OMB APPROVAL

OMB Number: 3235-0570

Expires: October 31, 2006

Estimated average burden hours per response: 19.3

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-08895

ING Funds Trust

(Exact name of registrant as specified in charter)

7337 E. Doubletree Ranch Rd., Scottsdale, AZ | | 85258 |

(Address of principal executive offices) | | (Zip code) |

The Corporation Trust Company, 1209 Orange Street, Wilmington, DE 19801

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-800-992-0180

Date of fiscal year end: | March 31 |

| |

Date of reporting period: | September 30, 2006 |

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1):

Funds

Semi-Annual Report

September 30, 2006

Classes A, B, C, I, M, O, Q and R

Fixed Income Funds

n ING GNMA Income Fund

n ING High Yield Bond Fund

n ING Intermediate Bond Fund

n ING National Tax-Exempt Bond Fund

Money Market Funds

n ING Classic Money Market Fund

n ING Institutional Prime Money Market Fund

E-Delivery Sign-up – details inside

E-Delivery Sign-up – details inside

This report is submitted for general information to shareholders of the ING Funds. It is not authorized for distribution to prospective shareholders unless accompanied or preceded by a prospectus which includes details regarding the funds' investment objectives, risks, charges, expenses and other information. This information should be read carefully.

TABLE OF CONTENTS

| President's Letter | | | 1 | | |

|

| Market Perspective | | | 2 | | |

|

| Portfolio Managers' Reports | | | 4 | | |

|

| Shareholder Expense Examples | | | 14 | | |

|

| Statements of Assets and Liabilities | | | 17 | | |

|

| Statements of Operations | | | 21 | | |

|

| Statements of Changes in Net Assets | | | 23 | | |

|

| Financial Highlights | | | 26 | | |

|

| Notes to Financial Statements | | | 39 | | |

|

| Portfolios of Investments | | | 54 | | |

|

Go Paperless with E-Delivery!

Go Paperless with E-Delivery!

Sign up now for on-line prospectuses, fund reports, and proxy statements. In less than five minutes, you can help reduce paper mail and lower fund costs.

Just go to www.ingfunds.com, click on the E-Delivery icon from the home page, follow the directions and complete the quick 5 Steps to Enroll.

You will be notified by e-mail when these communications become available on the internet. Documents that are not available on the internet will continue to be sent by mail.

(THIS PAGE INTENTIONALLY LEFT BLANK)

PRESIDENT'S LETTER

JAMES M. HENNESSY

Dear Shareholder,

In its recent meetings, the Federal Reserve Board (the "Fed") has stopped a two-year trend of raising interest rates. That string of 17 consecutive rate hikes was interpreted by many analysts as a sign that the Fed was concerned about containing inflation.

The Fed's latest actions put us in a climate that economist refer to as a "plateau." Historically, there have been six similar plateaus since 1982 and during four of those periods the Standard & Poor's 500® Composite Stock Price ("S&P 500®") Index experienced significant growth in the three months following the decrease of Fed interest rates.1

Although past market performance cannot guarantee future market success, I believe the arrival of a "plateau" offers one more reason to be optimistic about the future. So far in 2006, we have seen robust corporate earnings, significant levels of dividend payouts on the part of companies and impressive merger and acquisition announcements.

Whatever the future holds and whatever the economic climate, we at ING Funds continue to work hard to provide you, the investor, with an array of investment choices that enable you to build a smart and diversified portfolio. We also continue to expand and improve our customer service department to ensure that your needs are met promptly and that we indeed continue to make attaining your future goals easier.

On behalf of everyone here at ING Funds, I thank you for your continued support.

Sincerely,

James M. Hennessey

President

ING Funds

October 27, 2006

1 Research provided by ING Investment Management Co. based on S&P 500® Index performance 1987-2006.

The views expressed in the President's Letter reflect those of the President as of the date of the letter. Any such views are subject to change at any time based upon market or other conditions and ING Funds disclaims any responsibility to update such views. These views may not be relied on as investment advice and because investment decisions for an ING Fund are based on numerous factors, may not be relied on as an indication of investment intent on behalf of any ING Fund. Reference to specific company securities should not be construed as recommendations or investment advice.

For more complete information, or to obtain a prospectus on any ING fund, please call your Investment Professional or ING Fund Distributor, LLC at (800) 992-0180 or log on to www.ingfunds.com. The prospectus should be read carefully before investing. Consider the fund's investment objectives, risks, and charges and expenses carefully before investing. The prospectus contains this and other information about the fund. Check with your Investment Professional to determine which funds are available for sale within their firm. Not all funds are available for sale at all firms.

1

MARKET PERSPECTIVE: SIX MONTHS ENDED SEPTEMBER 30, 2006

It did not take long for U.S. fixed income investors to start scratching their heads. At the start of our new fiscal year, the feet of the new Federal Reserve Board (the "Fed") Chairman Dr. Ben Bernanke had seemed already to be firmly under the desk, as in March, the Federal Open Market Committee ("FOMC") had raised rates for the fifteenth time since June 2004. However, the minutes from the March meeting said that the end of the tightening cycle was near, and by the end of April, Dr. Bernanke himself seemed to hint at a pause after May. The statement issued with the sixteenth rate increase on May 10 also suggested somewhat ambivalently, that this was possible. Meanwhile the price of oil and other commodities (and stock markets) had been making new records. The combination of inflationary press ures and a Fed about to go on hold lifted the yield on the ten-year Treasury note/bond through 5% for the first time in nearly four years, to 5.19% on May 12. Importantly, the spread over the three-month Treasury Bill yield was now at its high for the year, as many began to wonder if Dr. Bernanke was just a little bit soft on inflation. Dr. Bernanke's reputation was taking a knock. The respected academic who espoused plain-speaking openness to make policy clear had succeeded in achieving the opposite. He needed to re-establish his inflation fighting credentials by going on the offensive.

About a week later, after another high core Consumer Price Index figure, a Federal Reserve official cast doubt on an FOMC pause. Over the next few weeks he would be joined by every one of his colleagues, each of whom pointedly stressed that inflation was the prime concern. By June 13, the ten-year Treasury yield was back below 5% and the curve inverted over much of its range. Investors feared that with all this tough talk the FOMC would now have to keep raising rates, even as the economy was obviously cooling, evidenced by a shockingly weak employment report on June 2 and a slumping housing market that had driven so much of the consumer spending in recent years. So the seventeenth interest rate increase to 5.25% on June 29 surprised no one, and the month ended with every yield on the Treasury curve lower than the federal funds rate: the market's vote that the FOMC had already gone too far.

The announcement accompanying the increase however, had been couched in relatively mild language. Could the FOMC now, at last, be done?

Not everyone believed it and the doubts intensified when renewed conflict in the Middle East sent the price of a barrel of oil to another all-time peak on July 14. The next FOMC meeting was August 8 and with only a week to go, futures contracts were still signaling a rate increase in the balance. But the flow of data, especially on housing, had pointed almost without exception to cooling demand and gross domestic product ("GDP") growth in the second quarter was in fact reported to have slipped to 2.5%. Finally, a tame employment report on August 4 showed the unemployment rate up and wage growth benign. Most commentators felt that this had now eliminated the chance of another rate increase, even as British Petroleum's closure of the Prudhoe Bay oilfield on August 7 caused the oil price to take another run at a record, failing by just 5 cents per barrel. At the August 8 meeting, the FOMC did indeed leave rates unchanged, citing the 17 prior in creases and "other factors restraining aggregate demand". Those factors became increasingly evident and it was soon the consensus view that the FOMC got it right. Housing data continued to deteriorate, with the first drop in home prices in 11 years, falling sales and record inventories of unsold homes. The FOMC even referred at its September 19 meeting, to the role a vibrant housing market had played in spurring GDP growth, and again took no action. The perception of a weakening economy sent (especially longer) rates onto a downward trajectory and as September drew to a close, the three-month Treasury Bill yield exceeded that of the ten-year Treasury Note by the most since January 2001. For the six months ended September 30, 2006, the ten-year yield fell by 22 basis points ("bps") to 4.63% while the three-month rose by 25 bps to 4.76%. The broader Lehman Brothers Aggregate Bond Index (1) returned 3.73%, the Lehman Brothers High Yield Bond Index (2) 4.40%.

After the best first calendar quarter since 1998 for global equities, reality had set in by mid-May as investors were gripped by fears described above that inflation fighting central bankers would raise interest rates by more than enough to choke off global growth. But from a low point a month later, stock markets found reasons to form a base and recover. In the U.S., it was high and rising corporate profits. The same could be said for Continental Europe, despite a hawkish European Central Bank, p lus improving economic fundamentals. Markets were also supported by broadly based merger and acquisition initiatives. This helped UK stocks as did a recovery in housing prices. All markets cheered the FOMC's pause, while after the failed attempt at a new record on August 7,

2

MARKET PERSPECTIVE: SIX MONTHS ENDED SEPTEMBER 30, 2006

oil prices slid more than 18% by September 30 as seasonal and political pressures eased. Only Japan, burdened by the first increase in interest rates in six years, could not eke out a gain. For the six-month period ended September 30, 2006 the Morgan Stanley Capital International ("MSCI") World® Index (3) in local currencies, including net reinvested dividends, returned 1.8%).

(1) The Lehman Brothers Aggregate Bond Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. Government, mortgage-backed, asset-backed and corporate debt securities.

(2) The Lehman Brothers High Yield Bond Index is an unmanaged index that measures the performance of fixed-income securities generally representative of corporate bonds rated below investment-grade.

(3) The MSCI World® Index is an unmanaged index that measures the performance of over 1,400 securities listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East.

All indices are unmanaged and investors cannot invest directly in an index.

Past performance does not guarantee future results. The performance quoted represents past performance. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. The Funds' performance is subject to change since the period's end and may be lower or higher than the performance data shown. Please call (800) 992-0180 or log on to www.ingfunds.com to obtain performance data current to the most recent month end.

Market Perspective reflects the views of the ING Chief Investment Risk Officer only through the end of the period, and is subject to change based on market and other conditions.

3

ING GNMA INCOME FUND

PORTFOLIO MANAGERS' REPORT

The ING GNMA Income Fund (the "Fund") seeks a high level of current income, consistent with liquidity and safety of principal, through investment primarily in Government National Mortgage Association ("GNMA") mortgage-backed securities (also known as GNMA Certificates) that are guaranteed as to the timely payment of principal and interest by the U.S. government. The Fund is managed by Denis P. Jamison, CFA, Senior Vice President and Senior Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Securities issued by the U.S. Treasury are backed by the full faith and credit of the U.S. government. Securities issued by individual agencies and organizations may be backed by the full faith and credit of the U.S. government as to principal or interest but are not direct obligations of the U.S. Treasury. Securities of some agencies and organizations are backed solely by the entity's own resources or by the ability of the entity to borrow from the U.S. Treasury. Government securities also include certain mortgage-related securities that are sponsored by a U.S. government agency or organization and are not direct obligations of the U.S. government.

Performance: For the six months ended September 30, 2006, the Fund's Class A shares, excluding sales charges, provided a total return of 3.09% compared to the Lehman Brothers Mortgage-Backed Securities Index, which returned 3.64% for the same period.

Portfolio Specifics: The bond market went on a rollercoaster ride during the six-month period ended September 30. Worries about higher inflation and the extent to which the U.S. Federal Reserve Board (the "Fed") would tighten monetary supply colored prices during the period. Bond yields rose steadily until mid-June, at which point they moved back to levels seen in the spring as investors perceived an imminent change in Fed monetary policy.

The Fund performed well during this period, although it was unable to keep up with its broad mortgage benchmark because the return on GNMA securities lagged those of Federal National Mortgage Association ("FNMA") and Federal Home Loan Mortgage Corporation ("FHLMC") mortgages. It's worth noting that this same disparity occurred in 2005, but the gap in the relative returns among the mortgage groups closed in the final quarter. Hopefully, this scenario will play out again this year. Despite underperforming its benchmark, the Fund maintained a strong competitive position relative to its peer group.

There was an exceptionally strong bid for call protected multi-family GNMA mortgages during much of the second and third quarters. Dealers were anxious to buy these securities in order to place them into collaterized mortgage obligations. We steadily sold during this period, realizing a gain of about $1.2 million for these securities. In addition, our U.S. Treasury bond trading activity was quite profitable, generating $1 million in capital gains. Our multi-family loan portfolio is now down to about $30 million, versus more than $100 million as of March 31, 2006.

GNMA mortgages were hammered in the second quarter, posting a return of -0.4% compared with slight gains for FNMA and FHLMC securities. GNMAs didn't make up any of this lost ground during the summer. The Fund must hold 80% of its assets in GNMA securities while the Lehman Brothers Mortgage-Backed Securities Index has only a 10% exposure to the sector.

Institutional investors, especially foreign based ones new to the U.S. mortgage market, increasingly are viewing the full, faith and credit guaranteed GNMA mortgages as interchangeable with the agency guaranteed FHLMC and FNMA securities. This has been clearly reflected in a narrowing of the price spread between these securities. For example, on January 20, 2006 GNMA 5.5% mortgages were 15/8% richer than their FNMA cousins. By the end of the third quarter, this spread had narrowed to 26/32%. Unfortunately, for GNMA investors, the spread could get even narrower. The securities have traded as tight as a quarter of a point apart during the last four years.

Current Strategy and Outlook: While rollercoaster rides are very exciting, especially when you're falling, you ultimately end the ride where you began. This sums up our feelings about the current bond market. Over the next few quarters, we believe will likely see plenty of small rallies and reversals but little market direction. We expect investors will get frustrated by the lack of change in Fed monetary policy and become bullish on one-off signs of economic weakness. Directionless markets usually offer lots of opportunities to take short-term trading profits. We intend to maintain a 10%-plus liquidity position in order to have readily available funds to purchase longer-dated U.S. Treasury bonds as oversold conditions develop. With the yield curve inverted, this strategy entails little cost in terms of current income and believe there are profits to be mad e. We also feel that newly minted project loans offer little value compared with single family mortgages. Accordingly, we are not going to rebuild our position as we expect sales of multi-family loans will not be positive going forward.

Investment Types

as of September 30, 2006

(as a percent of net assets)

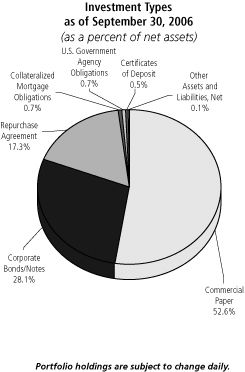

| U.S. Government Agency Obligations | | | 83.0 | % | |

| U.S. Treasury Bills | | | 14.5 | % | |

| U.S. Treasury Obligations | | | 3.2 | % | |

| Other Assets and Liabilities, Net | | | (0.7 | )% | |

| Total | | | 100.0 | % | |

Portfolio holdings are subject to change daily.

4

ING GNMA INCOME FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended September 30, 2006 | |

| | |

1 Year | |

5 Year | |

10 Year | | Since

Inception

of Class B

October 6,

2000 | | Since

Inception

of Class C

October 13,

2000 | | Since

Inception

of Class I

January 7,

2002 | | Since

Inception

of Class M

February 23,

2001 | | Since

Inception

of Class Q

February 26,

2001 | |

| Including Sales Charge: | |

| Class A(1) | | | (1.00 | )% | | | 2.95 | % | | | 5.52 | % | | | — | | | | — | | | | — | | | | — | | | | — | | |

| Class B(2) | | | (1.76 | )% | | | 2.83 | % | | | — | | | | 4.56 | % | | | — | | | | — | | | | — | | | | — | | |

| Class C(3) | | | 2.19 | % | | | 3.18 | % | | | — | | | | — | | | | 4.64 | % | | | — | | | | — | | | | — | | |

| Class I | | | 4.25 | % | | | — | | | | — | | | | — | | | | — | | | | 4.71 | % | | | — | | | | — | | |

| Class M(4) | | | (0.04 | )% | | | 2.74 | % | | | — | | | | — | | | | — | | | | — | | | | 3.65 | % | | | — | | |

| Class Q | | | 3.86 | % | | | 4.00 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | 4.81 | % | |

| Excluding Sales Charge: | |

| Class A | | | 3.92 | % | | | 3.95 | % | | | 6.04 | % | | | — | | | | — | | | | — | | | | — | | | | — | | |

| Class B | | | 3.18 | % | | | 3.16 | % | | | — | | | | 4.70 | % | | | — | | | | — | | | | — | | | | — | | |

| Class C | | | 3.18 | % | | | 3.18 | % | | | — | | | | — | | | | 4.64 | % | | | — | | | | — | | | | — | | |

| Class I | | | 4.25 | % | | | — | | | | — | | | | — | | | | — | | | | 4.71 | % | | | — | | | | — | | |

| Class M | | | 3.27 | % | | | 3.43 | % | | | — | | | | — | | | | — | | | | — | | | | 4.25 | % | | | — | | |

| Class Q | | | 3.86 | % | | | 4.00 | % | | | — | | | | — | | | | — | | | | — | | | | — | | | | 4.81 | % | |

Lehman Brothers Mortgage-Backed

Securities Index(5) | | | 4.19 | % | | | 4.53 | % | | | 6.29 | % | | | 5.79 | %(6) | | | 5.79 | %(6) | | | 4.76 | %(7) | | | 5.12 | %(8) | | | 5.12 | %(8) | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING GNMA Income Fund against the Index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 4.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5%, 2% and 1% for the 1 year, 5 year and since inception returns, respectively.

(3) Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) Reflects deduction of the maximum Class M sales charge of 3.25%.

(5) The Lehman Brothers Mortgage-Backed Securities Index is an unmanaged index composed of fixed income security mortgage pools sponsored by GNMA, FNMA and FHLMC, including GNMA Graduated Payment Mortgages.

(6) Since inception performance for index is shown from October 1, 2000.

(7) Since inception performance for index is shown from January 1, 2002.

(8) Since inception performance for index is shown from March 1, 2001.

5

ING HIGH YIELD BOND FUND

PORTFOLIO MANAGERS' REPORT

The ING High Yield Bond Fund (the "Fund") seeks to provide investors with a high level of current income and total return. The Fund is managed by Greg Jacobs, CFA and Kurt Kringelis, CFA, CPA, ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended September 30, 2006, the Fund's Class A shares, excluding sales charges, provided a total return of 3.19% compared to the Lehman Brothers High Yield Bond Index and the Lehman Brothers High Yield Bond Index — 2% Issuer Constrained, which returned 4.33% and 3.69%, respectively, for the same period.

Portfolio Specifics: Over the last six months, activity in the U.S. Treasury market has highlighted the uncertainty in the direction of the U.S. economy. In April, the bond market was attuned to contrasting signs of economic vigor and comments by the Federal Reserve Board (the "Fed") perceived as dovish. Fed Chairman Ben Bernanke's statement that "at some point in the future the Committee may decide to take no action at one or more meetings in the interest of allowing more time to receive information relevant to the outlook" was widely interpreted as a likely pause in interest rates in June. First quarter GDP indicated that the economy grew at a 4.8% real annualized pace — although this strong number must be coupled with the very weak 1.7% 4th quarter result in 2005 for a clearer picture. Data from the domestic manufacturing sector continues to surpris e on the upside, and consumer confidence was unfazed by spiraling energy costs. This combined with increasing inflation metrics, caused concern in the bond market, driving rates up 30-40 basis points across the curve.

By June, the market focus shifted to concerns of a weakening economy. Less than inspiring reports on payrolls, consumer spending, Institute of Supply Management surveys of business activity, and construction outlays pointed to some softness. Despite these anemic reports, wage gains are clearly evident and inflation remains above tolerances. The Federal Open Market Committee (the "FOMC") did, however, raise the overnight rate to 5.25% at their June 29th meeting, but the FOMC introduced some "dovish" language that might be interpreted as more cautious on the economic picture. Weakening economic indicators, combined with the Fed statements, set the table for a Treasury rally in third quarter. During the quarter, the Treasury market erased the second quarter losses, with the 10 year Treasury rallying 50 basis points.

Like the U.S. Treasury market, the high-yield market found a catalyst in the Fed's decision to hold rates where they were and was able to provide investors with positive total returns, as the market took the dovish signals from the Fed as a cue to regain an appetite for risk. For the last six months, the Lehman High Yield 2% Issuer-Constrained Index had a total return of 3.69%. Treasury-relative returns remained positive at 0.22%. Year-to-date, the high-yield market generated a very respectable total return of 6.39% with an excess return of 3.76%. During the period, lower quality issuance outperformed higher quality, as distressed securities outperformed the benchmark by 1.57% and CCC-rated securities on average outperformed the benchmark by 2.45%. During the six months, B-rated and BB-rated issues on average underperformed by 0.20% and 0.75%, respectively.

The Fund continues to be overweight the middle tier B-rated part of the universe and underweight BBs and distressed. This weighting had a neutral impact on the Fund during the period as the benefit of being underweight high-quality issuance was offset by the impact of being underweight the lowest quality part of the universe. The Fund continued to benefit from a strategic overweight in cable, as the sector outperformed the benchmark by 6.40% for the period. The sector showed signs of fundamental improvement during the period. In addition, the Fund shifted from an underweight to an overweight position in automotives. For the period, the industry outperformed the benchmark by 7.23%. The negative impact of being underweight during the first part of the six month period was offset by the benefit of being overweight during the latter half.

Current Outlook and Strategy: The Fed's decision to stop raising rates in August and September fostered a new market consensus for the timing of future rate hikes, with many observers forecasting this pause could last for sometime due to the softness in the residential real estate market and related industries. Indeed, some observers contend that the Fed's next move will be to ease rates sometime in the first quarter of 2007. At present, we disagree with that view. We believe the swift downturn in most residential housing measures clearly has the FOMC concerned, and may well be the primary reason for the Fed's continuing pause. Energy and base metal prices have come off their highs, although this may have more to do with the end of the summer driving season and a decrease in commodity speculation than a barometer of economic activity.

Just like Pluto's reclassification from a planet to asteroid due to its stature, inflation is being perceived as insufficient in size to be of a major concern. Yet, inflation may re-emerge as an issue for policy makers in the future. However, the Fed seems willing to wait for irrefutable evidence, and is more concerned about a slowdown in growth than a rise in core CPI. Nevertheless, the economic climate presents a dilemma to the FOMC, whose next move will be highly dependent on incoming data and its ongoing assessment of the real estate slowdown.

Despite some concerns of a large expected new issue calendar, we believe that accounts have ample cash to put to work for the rest of the year. Fundamentally, we believe the outlook remains relatively favorable for the high yield market as we approach what is likely the mid-point of this credit cycle. As a result, we believe that the market is likely to remain stable through the fourth quarter, despite entering a historically volatile season. We continue to believe that the biggest threat to spreads would come from unwelcome increases in future inflationary data which could present the FED with difficult choices in the event of a continued slowing of the economy with rising inflationary pressures.

Top Ten Industries

as of September 30, 2006

(as a percent of net assets)

| Media | | | 15.5 | % | |

| Telecommunications | | | 11.2 | % | |

| Diversified Financial Services | | | 10.9 | % | |

| Chemicals | | | 7.5 | % | |

| Commercial Services | | | 4.9 | % | |

| Entertainment | | | 4.7 | % | |

| Retail | | | 4.3 | % | |

| Forest Products & Paper | | | 4.2 | % | |

| Electric | | | 3.2 | % | |

| Healthcare - Services | | | 2.7 | % | |

Portfolio holdings are subject to change daily.

6

ING HIGH YIELD BOND FUND

PORTFOLIO MANAGERS' REPORT

| Average Annual Total Returns for the Periods Ended September 30, 2006 | |

| | |

1 Year | |

5 Year | | Since Inception

December 15, 1998 | |

| Including Sales Charge: | |

| Class A(1) | | | 1.41 | % | | | 6.87 | % | | | 5.27 | % | |

| Class B(2) | | | 0.63 | % | | | 6.87 | % | | | 5.15 | % | |

| Class C(3) | | | 4.62 | % | | | 7.19 | % | | | 5.16 | % | |

| Excluding Sales Charge: | |

| Class A | | | 6.41 | % | | | 7.93 | % | | | 5.93 | % | |

| Class B | | | 5.61 | % | | | 7.17 | % | | | 5.15 | % | |

| Class C | | | 5.61 | % | | | 7.19 | % | | | 5.16 | % | |

| Lehman Brothers High Yield Bond Index(4) | | | 8.07 | % | | | 10.51 | % | | | 6.04 | %(6) | |

| Lehman Brothers High Yield Bond Index — 2% Issuer Constrained(5) | | | 7.23 | % | | | 10.54 | % | | | 14.10 | %(6) | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING High Yield Bond Fund against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 4.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively.

(3) Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The Lehman Brothers High Yield Bond Index is an unmanaged index that measures the performance of fixed-income securities that are similar, but not identical, to those in the Fund's portfolio.

(5) This index is the 2% Issuer Cap component of the Lehman Brothers High Yield Bond Index.

(6) Since inception performance for index is shown from December 1, 1998.

7

ING INTERMEDIATE BOND FUND

PORTFOLIO MANAGERS' REPORT

The ING Intermediate Bond Fund (the "Fund") seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity. The Fund is managed by James B. Kauffmann, ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended September 30, 2006, the Fund's Class A shares, excluding sales charges, provided a total return of 3.12% compared to 3.73% for the Lehman Brothers Aggregate Bond ("LBAB") Index.

Portfolio Specifics: The LBAB Index posted a total return of 3.73% during the six-month period which was characterized by a marked shift in market sentiment. In the second quarter, the bond market was acutely attuned to contrasting signs of economic vigor and a perceived dovish posture by the U.S. Federal Reserve Board ("Fed"). By the third quarter, the great guessing game focused on the decline in the U.S. residential real estate market and the perceived end of the Fed's tightening cycle. After 17 consecutive rate hikes, the Federal Open Market Committee ("FOMC") decided not to raise the federal funds rate at its August and September meetings, keeping it at 5.25%. Markets quickly forecast the Fed cutting rates as soon as December, despite core inflation remaining above the Fed's comfort zone. During the period, the collapse of Amaranth, an energy trading h edge fund, was also a notable event. Energy prices moved lower during the period, pleasing consumers but not investors with energy exposure. A record level of corporate debt was issued. The yield curve inverted leaving short-term interest rates higher than long-term. The yield on the two-year Treasury declined 0.13% to close at 4.68%; the yield on the five-year Treasury declined 0.23% to close at 4.58%; and the yield on the ten-year Treasury declined 0.22% to close at 4.63%.

Two major themes dominated the Fund's performance during the period. Tactical overweight positions in securitized assets such as mortgage-backed securities — especially adjustable rate mortgages and commercial mortgage-backed securities — helped the Fund, while the Fund's short duration acted as a drag. Duration positioning was the main reason for the Fund's underperformance especially in the latter part of the period.

The portfolio was underweight longer-dated corporate bonds in the face of miniscule yield spreads, or risk compensation; however, tactical allocations to longer maturity credits helped performance. We fared relatively well during the late May and early June market hiccup. A brief sell-off in riskier assets worldwide soon abated, yet the Fund's position in some foreign banks and trusts was not beneficial. During July, by contrast, a small exposure to a large re-insurer had a slight negative impact on the portfolio as Hurricane Ernesto, the only major notable storm in a benign hurricane season compared to 2005, developed and then faded. A minor position in a pipeline company whose previously announced leveraged buyout was re-priced also acted as a slight drag. A long-dated utility and several minerals extractors in South America performed well on a relative basis.

The Fund had a small high yield position, but the high yield bond market outperformed the broader market, indicating that a more sizable commitment was warranted. The same can be said for emerging market debt which performed well during the period.

Current Outlook and Strategy: The Fed's decision to stop raising rates in August and September fostered a new market consensus for the timing of future rate hikes, with many observers forecasting this pause could last for some time due to the softness in the residential real estate market and related industries. Indeed, some observers contend that the Fed's next move will be to ease rates sometime in the first quarter of 2007. At present, we disagree with that view. The swift downturn in most residential housing measures clearly has the FOMC concerned and may well be the primary reason for the Fed's continuing pause. Energy and base metal prices have come off their highs, although this may have more to do with the end of the summer driving season and a decrease in commodity speculation than a barometer of economic activity.

Just like Pluto's reclassification from a planet to an asteroid due to its stature, inflation is being perceived as insufficient in size to be of a major concern. Yet inflation may re-emerge as an issue for policy makers in the future. The Fed seems willing to wait for irrefutable evidence, and is more concerned about a slowdown in growth than a rise in the core consumer price index (CPI). Nevertheless, the economic climate presents a dilemma to the FOMC, whose next move will be highly dependent on incoming data and its ongoing assessment of the real estate slowdown. We believe that the yield curve will become steeper, and anticipate that long-term rates will rise more than short-term rates. While this stance may be a bit early, the position is not hindered by elapsed time or forgone yield. The portfolio is shorter in duration than the index.

We believe that corporate bond investors are not being adequately compensated for risk in the present market. Mergers and acquisition announcements as well as news of firms taking themselves private continue unabated. Such actions by companies are rarely good news for corporate bondholders. Yet credit spreads remain generally tight in the face of some $200 billion of new leveraged buyouts. The credit portfolio remains defensively positioned with a slight underweight. Our mortgage team has constructed a portfolio designed to offset an increase in volatility with a particular focus on ARMs and structured product such as collateralized mortgage obligations. The portfolio's mortgage sector position is now neutral relative to the index.

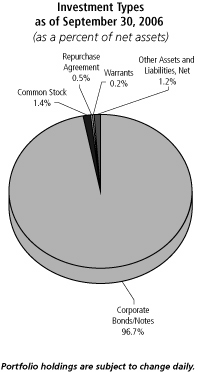

Investment Types

as of September 30, 2006

(as a percent of net assets)

| U.S. Government Agency Obligations | | | 31.4 | % | |

| Collateralized Mortgage Obligations | | | 28.1 | % | |

| Corporate Bonds/Notes | | | 25.3 | % | |

| U.S. Treasury Obligations | | | 11.9 | % | |

| Asset-Backed Securities | | | 6.7 | % | |

| Repurchase Agreement | | | 4.8 | % | |

| Preferred Stock | | | 2.0 | % | |

| Municipal Bonds | | | 0.7 | % | |

| Other Assets and Liabilities, Net* | | | (10.9 | )% | |

| Total | | | 100.0 | % | |

* Includes short-term investment related to securities lending collateral.

Portfolio holdings are subject to change daily.

8

ING INTERMEDIATE BOND FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended September 30, 2006 | |

| | | 1 Year | | 5 Year | | Since

Inception

of Class A, B and C

December 15,

1998 | | Since

Inception

of Class I

January 8,

2002 | | Since

Inception

of Class O

August 13,

2004 | | Since

Inception

of Class R

March 16,

2004 | |

| Including Sales Charge: | |

| Class A(1) | | | (1.65 | )% | | | 4.27 | % | | | 5.77 | % | | | — | | | | — | | | | — | | |

| Class B(2) | | | (2.42 | )% | | | 4.16 | % | | | 5.62 | % | | | — | | | | — | | | | — | | |

| Class C(3) | | | 1.52 | % | | | 4.52 | % | | | 5.64 | % | | | — | | | | — | | | | — | | |

| Class I | | | 3.59 | % | | | — | | | | — | | | | 5.61 | % | | | — | | | | — | | |

| Class O | | | 3.17 | % | | | — | | | | — | | | | — | | | | 3.39 | % | | | — | | |

| Class R | | | 3.02 | % | | | — | | | | — | | | | — | | | | — | | | | 2.60 | % | |

| Excluding Sales Charge: | |

| Class A | | | 3.28 | % | | | 5.29 | % | | | 6.43 | % | | | — | | | | — | | | | — | | |

| Class B | | | 2.49 | % | | | 4.48 | % | | | 5.62 | % | | | — | | | | — | | | | — | | |

| Class C | | | 2.51 | % | | | 4.52 | % | | | 5.64 | % | | | — | | | | — | | | | — | | |

| Class I | | | 3.59 | % | | | — | | | | — | | | | 5.61 | % | | | — | | | | — | | |

| Class O | | | 3.17 | % | | | — | | | | — | | | | — | | | | 3.39 | % | | | — | | |

| Class R | | | 3.02 | % | | | — | | | | — | | | | — | | | | — | | | | 2.60 | % | |

| Lehman Brothers Aggregate Bond Index(4) | | | 3.67 | % | | | 4.81 | % | | | 5.51 | %(5) | | | 5.06 | %(6) | | | 4.01 | %(7) | | | 2.85 | %(8) | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING Intermediate Bond Fund against the Index indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charges and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will ßuctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reßect those of the portfolio manager, only through the end of the period as stated on the cover. The portfolio manager's views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 4.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively.

(3) Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The Lehman Brothers Aggregate Bond Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. government, mortgage-backed, asset-backed and corporate debt securities.

(5) Since inception performance for index is shown from December 1, 1998.

(6) Since inception performance for index is shown from January 1, 2002.

(7) Since inception performance for index is shown from August 1, 2004.

(8) Since inception performance for index is shown from April 1, 2004.

9

ING NATIONAL TAX-EXEMPT BOND FUND

PORTFOLIO MANAGERS' REPORT

The ING National Tax-Exempt Bond Fund (the "Fund") seeks to provide investors with a high level of current income that is exempt from federal income taxes, consistent with the preservation of capital. The Fund is managed by Robert Schonbrunn, Portfolio Manager, Karen Cronk, Managing Director and Portfolio Manager, and Rink Kilbride, ING Investment Management Co. — the Sub-Adviser.

Performance: For the six months ended September 30, 2006, the Fund's Class A shares, excluding sales charges, provided a total return of 3.10% compared to the Lehman Brothers Municipal Bond Index and the Lehman Brothers Aggregate Bond Index, which returned 3.44% and 3.73%, respectively, for the same period.

Portfolio Specifics: The most significant factor that impacted the municipal bond market over the past six months was the change in the direction of interest rates. In the second quarter interest rates moved higher as the Federal Reserve Board ("Fed") continued to raise the federal funds rate. However, after seventeen consecutive rate increases, the Fed paused in August, and interest rates declined in the third quarter. In March, the Fund was positioned defensively and had a relatively low level of sensitivity to interest rate changes. Toward the end of the second quarter, we gradually shifted the portfolio into longer-term issues to increase the Fund's sensitivity to interest rate changes in anticipation of a shift in rates. This strategy had a positive impact on the portfolio by offsetting the negative effect of rising interest rates earlier in the period and also positioned the portfolio to benefit from the rate decline in the third quarter. The relationship of short to long rates, known as the yield curve, flattened as short rates rose faster than longer rates. The portfolio held overweight positions in both short-term and long-term bonds with relatively little in the intermediate maturity sector. This barbell structure performed well as the yield curve flattened. Lower-quality bonds outperformed higher-quality bonds earlier in the year, but became over-valued as interest rates declined. The Fund participated in the lower-quality sector with BBB-rated hospital and tobacco issues during the second quarter. However, we recently shifted the portfolio into higher-quality issues such as municipal housing issues that generate relatively high yields and serve as a replacement for lower-quality bonds. The Fund's yield to maturity of 4.17% was competitively high and positively contributed to the Fund's total return over the period.

Current Strategy and Outlook: We believe there is a high probability that the Fed has completed its two-year program to control the risk of rising inflation. This policy shift has positive longer-term implications for the bond market as interest rates are likely to decline. Weakness in the housing market and the broader impact of lower housing asset values on consumer sentiment and consumer spending will dampen economic activity and should hold inflation at acceptable levels. In the near term, while some analysts are concerned that rising labor costs may extend the period before interest rates decline, we believe the longer-term trend may favor generally lower interest rates. In this environment, we are maintaining a higher sensitivity to interest rate movements using longer-maturity bonds which will enable us to participate in the potential drop in rates a nd also to earn the higher yields available on longer-term bonds. We are gradually shifting assets from the longer and shorter ends of the yield curve and building up the intermediate maturity sector to improve yields. We expect to maintain our focus on higher-quality bonds until yields on the lower-quality sectors widen to more attractive levels.

10

ING NATIONAL TAX-EXEMPT BOND FUND

PORTFOLIO MANAGERS' REPORT

| | | Average Annual Total Returns for the Periods Ended September 30, 2006 | |

| | | 1 Year | | 5 Year | | Since Inception

November 8, 1999 | |

| Including Sales Charge: | |

| Class A(1) | | | (1.50 | )% | | | 3.26 | % | | | 4.42 | % | |

| Class B(2) | | | (2.24 | )% | | | 3.17 | % | | | 4.37 | % | |

| Class C(3) | | | 1.69 | % | | | 3.52 | % | | | 4.39 | % | |

| Excluding Sales Charge: | |

| Class A | | | 3.45 | % | | | 4.28 | % | | | 5.17 | % | |

| Class B | | | 2.68 | % | | | 3.51 | % | | | 4.37 | % | |

| Class C | | | 2.67 | % | | | 3.52 | % | | | 4.39 | % | |

| Lehman Brothers Municipal Bond Index(4) | | | 4.45 | % | | | 5.17 | % | | | 6.29 | %(6) | |

| Lehman Brothers Aggregate Bond Index(5) | | | 3.67 | % | | | 4.81 | % | | | 6.27 | %(6) | |

Based on a $10,000 initial investment, the table above illustrates the total return of ING National Tax-Exempt Bond Fund against the indices indicated. An index is unmanaged and has no cash in its portfolio, imposes no sales charge and incurs no operating expenses. An investor cannot invest directly in an index. The Fund's performance is shown both with and without the imposition of sales charges.

The performance table does not reflect the deduction of taxes that a shareholder will pay (if any) on Fund distributions or the redemption of Fund shares.

The performance shown may include the effect of fee waivers and/or expense reimbursements by the Investment Adviser and/or other service providers, which have the effect of increasing total return. Had all fees and expenses been considered, the total returns would have been lower.

Performance data represents past performance and is no assurance of future results. Investment return and principal value of an investment in the Fund will fluctuate. Shares, when sold, may be worth more or less than their original cost. The Fund's performance may be lower or higher than the performance data shown. Please log on to www.ingfunds.com or call (800) 992-0180 to get performance through the most recent month end.

This report contains statements that may be "forward-looking" statements. Actual results may differ materially from those projected in the "forward-looking" statements.

The views expressed in this report reflect those of the portfolio managers, only through the end of the period as stated on the cover. The portfolio managers' views are subject to change at any time based on market and other conditions.

Fund holdings are subject to change daily.

(1) Reflects deduction of the maximum Class A sales charge of 4.75%.

(2) Reflects deduction of the Class B deferred sales charge of 5% and 2% for the 1 year and 5 year returns, respectively.

(3) Reflects deduction of the Class C deferred sales charge of 1% for the 1 year return.

(4) The Lehman Brothers Municipal Bond Index is an unmanaged index of approximately 1,100 investment grade tax-exempt bonds classified into four sectors: general obligation, revenue, insured and pre-refunded.

(5) The Lehman Brothers Aggregate Bond Index is a widely recognized, unmanaged index of publicly issued investment grade U.S. government, mortgage-backed, asset-backed and corporate debt securities.

(6) Since inception performance for index is shown from November 1, 1999.

11

ING CLASSIC MONEY MARKET FUND

PORTFOLIO MANAGERS' REPORT

ING Classic Money Market Fund (the "Fund") seeks to provide investors with a high level of current return, consistent with the preservation of capital and liquidity, and the maintenance of a stable $1.00 net asset value per share. The Fund is managed by David S. Yealy, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: After seventeen consecutive quarter-point increases in the federal funds rate, the Federal Open Market Committee ("FOMC") voted to keep the rate at 5.25% at its August 8th and September 20th meetings. The FOMC indicated that economic growth could be expected to slow due to a decline in the housing market and higher energy prices. Inflation continues to increase, albeit at a slower pace, and is above the perceived Federal Reserve Board ("Fed") comfort zone remaining a concern to both the Fed and the markets. But, while inflation is a concern, the market has shifted from pricing in a potential Fed increase to pricing in a potential Fed rate cut in late 2006 or early 2007. Short-term money market security yields have declined accordingly.

Our primary investment strategy, which we have had in place since the second half of 2004, did not change significantly during the period. The Fund benefited from interest-rate sensitive floating-rate securities owned throughout the six-month period. In addition to our emphasis on floating-rate securities, we continued to focus on very short maturity securities that typically performed well in a rising rate environment. We made selective purchases in the two-to-three month maturity range only when the market fully priced in future Fed rate increases. For a brief period in June, the market priced in a more aggressive Fed funds rate with the 1-Year London Interbank Offered Rate nearing 5.80%. We took the opportunity to extend the Fund's weighted average maturity ("WAM") from approximately 20 days to 40 days by investing approximately 5% of the Fund in fixed-rate securities with maturities greater than six months. This maturity extension positi oned the Fund to take advantage of the shift in the FOMC's rate posture during the third quarter, and the markets' reaction to such a shift. The fixed-rate securities with maturities longer than six months added a yield premium over shorter securities. We elected to sell a portion of the longer-term fixed-rate securities at a gain during the third quarter as the market priced in future Fed rate cuts. We ended the quarter with a WAM of 31 days.

Current Strategy and Outlook: Statements released by the Fed after each FOMC meeting indicated that the central bank was still concerned with the risks associated with rising inflation. Fed committee members, including Chairman Ben Bernanke, have also continued to express concerns about inflation during recent speeches and public appearances. The market seemed to ignore these concerns, and instead focused on the housing decline and its potential impact on future economic growth. We believe that the market has over reacted. There is still the potential that inflation will become more of a concern and the Fed could be forced to either hold rates where they are for an extended period of time or even raise them. We expect more opportunities in the near-term to extend our weighted average maturity at higher yields than what is currently priced into the market fo r short-term money market securities.

12

ING INSTITUTIONAL PRIME MONEY MARKET FUND

PORTFOLIO MANAGERS' REPORT

The ING Institutional Money Market Fund (the "Fund") seeks to provide investors with a high level of current income, consistent with the preservation of capital and liquidity and the maintenance of a stable $1.00 net asset value per share. The Fund is managed by David S. Yealy, Portfolio Manager, ING Investment Management Co. — the Sub-Adviser.

Portfolio Specifics: After seventeen consecutive quarter-point increases in the federal funds rate, the Federal Open Market Committee ("FOMC") voted to keep the rate at 5.25% at its August 8th and September 20th meetings. The FOMC indicated that economic growth could be expected to slow due to a decline in the housing market and higher energy prices. Inflation continues to increase, albeit at a slower pace, and is above the perceived Federal Reserve Board's ("FED") comfort zone remaining a concern to both the Fed and the markets. But, while inflation is a concern, the market has shifted from pricing in a potential Fed increase to pricing in a potential Fed rate cut in late 2006 or early 2007. Short-term money market security yields have declined accordingly.

Our primary investment strategy, which we have had in place since the second half of 2004, did not change significantly during the period. The Fund benefited from interest-rate sensitive floating-rate securities owned throughout the six-month period. In addition to our emphasis on floating-rate securities, we continued to focus on very short maturity securities that typically performed well in a rising rate environment. We made selective purchases in the two-to-three month maturity range only when the market fully priced in future Fed rate increases. For a brief period in June the market priced in a more aggressive fed funds rate with the 1-Year London Interbank Offered Rate nearing 5.80%. We took the opportunity to extend the Fund's weighted average maturity (WAM) from approximately 20 days to 40 days by investing approximately 10% of the Fund in fixed-rate securities with maturities greater than six months. This maturity extension position ed the Fund to take advantage of the shift in the FOMC's rate posture during the third quarter, and the markets' reaction to such a shift. The fixed-rate securities with maturities longer than six months added a yield premium over shorter securities. We elected to sell a portion of the longer-term fixed-rate securities at a gain during the third quarter as the market priced in future Fed rate cuts. We ended the quarter with a WAM of 31 days.

Current Strategy and Outlook: Statements released by the Fed after each FOMC meeting indicated that the central bank was still concerned with the risks associated with rising inflation. Fed committee members, including Chairman Ben Bernanke, have also continued to express concerns about inflation during recent speeches and public appearances. The market seemed to ignore these concerns, and instead focused on the housing decline and its potential impact on future economic growth. We believe that the market has over reacted. There is still the potential that inflation will become more of a concern and the Fed could be forced to either hold rates where they are for an extended period of time or even raise them. We expect more opportunities in the near-term to extend our weighted average maturity at higher yields than what is currently priced into the market fo r short-term money market securities.

13

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED)

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution [and/or service] (12b–1) fees; and other Fund expenses. These Examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2006 to September 30, 2006.

Actual Expenses

The first section of the table shown, "Actual Fund Return," provides information about actual account values and actual expenses. You may use the information in this section, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first section under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second section of the table shown, "Hypothetical 5% Return," provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the hypothetical lines of the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| ING GNMA Income Fund | | Beginning

Account

Value

April 1, 2006 | | Ending

Account

Value

September 30, 2006 | | Annualized

Expense

Ratio | | Expenses Paid

During the

Six Months Ended

September 30, 2006* | |

| Actual Fund Return | |

| Class A | | $ | 1,000.00 | | | $ | 1,030.90 | | | | 0.95 | % | | $ | 4.84 | | |

| Class B | | | 1,000.00 | | | | 1,027.30 | | | | 1.70 | | | | 8.64 | | |

| Class C | | | 1,000.00 | | | | 1,027.30 | | | | 1.70 | | | | 8.64 | | |

| Class I | | | 1,000.00 | | | | 1,032.60 | | | | 0.65 | | | | 3.31 | | |

| Class M | | | 1,000.00 | | | | 1,028.10 | | | | 1.46 | | | | 7.42 | | |

| Class Q | | | 1,000.00 | | | | 1,030.00 | | | | 0.91 | | | | 4.63 | | |

| Hypothetical (5% return before expenses) | |

| Class A | | $ | 1,000.00 | | | $ | 1,020.31 | | | | 0.95 | % | | $ | 4.81 | | |

| Class B | | | 1,000.00 | | | | 1,016.55 | | | | 1.70 | | | | 8.59 | | |

| Class C | | | 1,000.00 | | | | 1,016.55 | | �� | | 1.70 | | | | 8.59 | | |

| Class I | | | 1,000.00 | | | | 1,021.81 | | | | 0.65 | | | | 3.29 | | |

| Class M | | | 1,000.00 | | | | 1,017.75 | | | | 1.46 | | | | 7.38 | | |

| Class Q | | | 1,000.00 | | | | 1,020.51 | | | | 0.91 | | | | 4.61 | | |

* Expenses are equal to each Fund's respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/365 to reflect the most recent fiscal half-year.

14

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) (CONTINUED)

| ING High Yield Bond Fund | | Beginning

Account

Value

April 1, 2006 | | Ending

Account

Value

September 30, 2006 | | Annualized

Expense

Ratio | | Expenses Paid

During the

Six Months Ended

September 30, 2006* | |

| Actual Fund Return | |

| Class A | | $ | 1,000.00 | | | $ | 1,031.90 | | | | 1.10 | % | | $ | 5.60 | | |

| Class B | | | 1,000.00 | | | | 1,029.20 | | | | 1.85 | | | | 9.41 | | |

| Class C | | | 1,000.00 | | | | 1,021.20 | | | | 1.85 | | | | 9.41 | | |

| Hypothetical (5% return before expenses) | |

| Class A | | $ | 1,000.00 | | | $ | 1,019.55 | | | | 1.10 | % | | $ | 5.57 | | |

| Class B | | | 1,000.00 | | | | 1,015.79 | | | | 1.85 | | | | 9.35 | | |

| Class C | | | 1,000.00 | | | | 1,015.79 | | | | 1.85 | | | | 9.35 | | |

| ING Intermediate Bond Fund | |

| Actual Fund Return | |

| Class A | | $ | 1,000.00 | | | $ | 1,031.20 | | | | 0.69 | % | | $ | 3.51 | | |

| Class B | | | 1,000.00 | | | | 1,027.20 | | | | 1.44 | | | | 7.32 | | |

| Class C | | | 1,000.00 | | | | 1,027.30 | | | | 1.44 | | | | 7.32 | | |

| Class I | | | 1,000.00 | | | | 1,031.70 | | | | 0.38 | | | | 1.94 | | |

| Class O | | | 1,000.00 | | | | 1,030.10 | | | | 0.69 | | | | 3.51 | | |

| Class R | | | 1,000.00 | | | | 1,029.80 | | | | 0.94 | | | | 4.78 | | |

| Hypothetical (5% return before expenses) | |

| Class A | | $ | 1,000.00 | | | $ | 1,021.61 | | | | 0.69 | % | | $ | 3.50 | | |

| Class B | | | 1,000.00 | | | | 1,017.85 | | | | 1.44 | | | | 7.28 | | |

| Class C | | | 1,000.00 | | | | 1,017.85 | | | | 1.44 | | | | 7.28 | | |

| Class I | | | 1,000.00 | | | | 1,023.16 | | | | 0.38 | | | | 1.93 | | |

| Class O | | | 1,000.00 | | | | 1,021.61 | | | | 0.69 | | | | 3.50 | | |

| Class R | | | 1,000.00 | | | | 1,020.36 | | | | 0.94 | | | | 4.76 | | |

| ING National Tax-Exempt Bond Fund | |

| Actual Fund Return | |

| Class A | | $ | 1,000.00 | | | $ | 1,031.00 | | | | 0.87 | % | | $ | 4.43 | | |

| Class B | | | 1,000.00 | | | | 1,027.20 | | | | 1.62 | | | | 8.23 | | |

| Class C | | | 1,000.00 | | | | 1,027.10 | | | | 1.62 | | | | 8.23 | | |

| Hypothetical (5% return before expenses) | |

| Class A | | $ | 1,000.00 | | | $ | 1,020.71 | | | | 0.87 | % | | $ | 4.41 | | |

| Class B | | | 1,000.00 | | | | 1,016.95 | | | | 1.62 | | | | 8.19 | | |

| Class C | | | 1,000.00 | | | | 1,016.95 | | | | 1.62 | | | | 8.19 | | |

* Expenses are equal to each Fund's respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/365 to reflect the most recent fiscal half-year.

15

SHAREHOLDER EXPENSE EXAMPLES (UNAUDITED) (CONTINUED)

| ING Classic Money Market Fund | | Beginning

Account

Value

April 1, 2006 | | Ending

Account

Value

September 30, 2006 | | Annualized

Expense

Ratio | | Expenses Paid

During the

Six Months Ended

September 30, 2006* | |

| Actual Fund Return | |

| Class A | | $ | 1,000.00 | | | $ | 1,022.50 | | | | 0.77 | % | | $ | 3.90 | | |

| Class B | | | 1,000.00 | | | | 1,019.40 | | | | 1.36 | | | | 6.88 | | |

| Class C | | | 1,000.00 | | | | 1,019.40 | | | | 1.36 | | | | 6.88 | | |

| Hypothetical (5% return before expenses) | |

| Class A | | $ | 1,000.00 | | | $ | 1,021.21 | | | | 0.77 | % | | $ | 3.90 | | |

| Class B | | | 1,000.00 | | | | 1,018.25 | | | | 1.36 | | | | 6.88 | | |

| Class C | | | 1,000.00 | | | | 1,018.25 | | | | 1.36 | | | | 6.88 | | |

| ING Institutional Prime Money Market Fund | |

| Actual Fund Return | | $ | 1,000.00 | | | $ | 1,025.50 | | | | 0.17 | % | | $ | 0.86 | | |

Hypothetical (5% return before

| |

| expenses) | | $ | 1,000.00 | | | $ | 1,024.22 | | | | 0.17 | % | | $ | 0.86 | | |

* Expenses are equal to each Fund's respective annualized expense ratios multiplied by the average account value over the period, multiplied by 183/365 to reflect the most recent fiscal half-year.

16

STATEMENTS OF ASSETS AND LIABILITIES AS OF SEPTEMBER 30, 2006 (UNAUDITED)

| | | ING

GNMA Income

Fund | | ING

High Yield

Bond

Fund | | ING

Intermediate

Bond

Fund | |

| ASSETS: | |

| Investments in securities at value+* | | $ | 537,990,113 | | | $ | 169,026,890 | | | $ | 1,071,159,567 | | |

| Short-term investments** | | | 90,365,126 | | | | — | | | | — | | |

| Short-term investments at amortized cost | | | — | | | | — | | | | 169,060,933 | | |

| Repurchase agreement | | | — | | | | 796,000 | | | | 48,524,000 | | |

| Cash | | | 550,069 | | | | 198,237 | | | | 1,325,454 | | |

| Cash collateral for futures | | | — | | | | 70,781 | | | | 625,673 | | |

| Foreign currencies at value*** | | | — | | | | — | | | | 9,092,721 | | |

| Receivables: | |

| Investment securities sold | | | 111 | | | | 1,894,900 | | | | 63,257,141 | | |

| Fund shares sold | | | 640,510 | | | | 91,413 | | | | 2,557,392 | | |

| Dividends and interest | | | 2,810,442 | | | | 3,357,974 | | | | 7,425,370 | | |

| Unrealized appreciation on swap agreements | | | — | | | | — | | | | 419,141 | | |

| Prepaid expenses | | | 50,898 | | | | 23,831 | | | | 147,991 | | |

| Reimbursement due from manager | | | — | | | | 1,447 | | | | — | | |

| Total assets | | | 632,407,269 | | | | 175,461,473 | | | | 1,373,595,383 | | |

| LIABILITIES: | |

| Payable for investment securities purchased | | | 7,258,053 | | | | 2,129,911 | | | | 191,003,326 | | |

| Payable for fund shares redeemed | | | 701,324 | | | | 413,673 | | | | 1,482,292 | | |

| Payable for futures variation margin | | | — | | | | 7,969 | | | | 112,832 | | |

| Payable upon receipt of securities loaned | | | — | | | | — | | | | 169,060,933 | | |

| Unrealized depreciation on swap agreements | | | — | | | | — | | | | 255,888 | | |

| Income distribution payable | | | — | | | | 485,280 | | | | 733,316 | | |

| Payable to affiliates | | | 472,179 | | | | 167,442 | | | | 473,223 | | |

| Payable for borrowings against line of credit | | | — | | | | 200,000 | | | | — | | |

| Payable for trustees fees | | | 4,682 | | | | 8,782 | | | | 3,638 | | |

| Other accrued expenses and liabilities | | | 280,981 | | | | 168,117 | | | | 135,633 | | |

| Total liabilities | | | 8,717,219 | | | | 3,581,174 | | | | 363,261,081 | | |

| NET ASSETS | | $ | 623,690,050 | | | $ | 171,880,299 | | | $ | 1,010,334,302 | | |

| NET ASSETS WERE COMPRISED OF: | |

| Paid-in capital | | $ | 642,275,759 | | | $ | 565,803,610 | | | $ | 1,027,706,825 | | |

Undistributed net investment income

(accumulated net investment loss) | | | 835,257 | | | | (193,562 | ) | | | (33,911 | ) | |

Accumulated net realized loss on investments,

foreign currency related transactions, futures, and swaps | | | (15,914,180 | ) | | | (394,668,274 | ) | | | (16,447,885 | ) | |

Net unrealized appreciation or depreciation on investments,

foreign currency related transactions, futures, and swaps | | | (3,506,786 | ) | | | 938,525 | | | | (890,727 | ) | |

| NET ASSETS | | $ | 623,690,050 | | | $ | 171,880,299 | | | $ | 1,010,334,302 | | |

| + Including securities loaned at value | | $ | — | | | $ | — | | | $ | 165,718,213 | | |

| * Cost of investments in securities | | $ | 541,547,691 | | | $ | 168,167,627 | | | $ | 1,071,556,819 | | |

| ** Cost of short-term investments | | $ | 90,314,334 | | | $ | — | | | $ | — | | |

| *** Cost of foreign currencies | | $ | — | | | $ | — | | | $ | 9,417,983 | | |

See Accompanying Notes to Financial Statements

17

STATEMENTS OF ASSETS AND LIABILITIES AS OF SEPTEMBER 30, 2006 (UNAUDITED) (CONTINUED)

| | | ING

GNMA Income

Fund | | ING

High Yield

Bond

Fund | | ING

Intermediate

Bond

Fund | |

| Class A: | |

| Net assets | | $ | 503,588,287 | | | $ | 98,722,649 | | | $ | 636,697,359 | | |

| Shares authorized | | | unlimited | | | | unlimited | | | | unlimited | | |

| Par value | | $ | 0.001 | | | $ | 0.001 | | | $ | 0.001 | | |

| Shares outstanding | | | 60,382,897 | | | | 11,356,859 | | | | 62,474,306 | | |

| Net asset value and redemption price per share | | $ | 8.34 | | | $ | 8.69 | | | $ | 10.19 | | |

| Maximum offering price per share (2.50%)(1) | | $ | 8.55 | | | $ | 8.91 | | | $ | 10.45 | | |

| Class B: | |

| Net assets | | $ | 66,621,459 | | | $ | 56,941,528 | | | $ | 54,484,198 | | |

| Shares authorized | | | unlimited | | | | unlimited | | | | unlimited | | |

| Par value | | $ | 0.001 | | | $ | 0.001 | | | $ | 0.001 | | |

| Shares outstanding | | | 8,029,817 | | | | 6,554,067 | | | | 5,356,607 | | |

| Net asset value and redemption price per share(2) | | $ | 8.30 | | | $ | 8.69 | | | $ | 10.17 | | |

| Maximum offering price per share | | $ | 8.30 | | | $ | 8.69 | | | $ | 10.17 | | |

| Class C: | |

| Net assets | | $ | 35,352,752 | | | $ | 16,216,122 | | | $ | 74,423,132 | | |

| Shares authorized | | | unlimited | | | | unlimited | | | | unlimited | | |

| Par value | | $ | 0.001 | | | $ | 0.001 | | | $ | 0.001 | | |

| Shares outstanding | | | 4,255,031 | | | | 1,865,476 | | | | 7,311,548 | | |

| Net asset value and redemption price per share(2) | | $ | 8.31 | | | $ | 8.69 | | | $ | 10.18 | | |

| Maximum offering price per share | | $ | 8.31 | | | $ | 8.69 | | | $ | 10.18 | | |

| Class I: | |

| Net assets | | $ | 17,909,092 | | | | n/a | | | $ | 194,187,050 | | |

| Shares authorized | | | unlimited | | | | n/a | | | | unlimited | | |

| Par value | | $ | 0.001 | | | | n/a | | | $ | 0.001 | | |

| Shares outstanding | | | 2,145,606 | | | | n/a | | | | 19,048,698 | | |

| Net asset value and redemption price per share | | $ | 8.35 | | | | n/a | | | $ | 10.19 | | |

| Maximum offering price per share | | $ | 8.35 | | | | n/a | | | $ | 10.19 | | |

| Class M: | |

| Net assets | | $ | 134,502 | | | | n/a | | | | n/a | | |

| Shares authorized | | | unlimited | | | | n/a | | | | n/a | | |

| Par value | | $ | 0.001 | | | | n/a | | | | n/a | | |

| Shares outstanding | | | 16,101 | | | | n/a | | | | n/a | | |

| Net asset value and redemption price per share | | $ | 8.35 | | | | n/a | | | | n/a | | |

| Maximum offering price per share (3.25%)(3) | | $ | 8.63 | | | | n/a | | | | n/a | | |

| Class O: | |

| Net assets | | | n/a | | | | n/a | | | $ | 49,651,404 | | |

| Shares authorized | | | n/a | | | | n/a | | | | unlimited | | |

| Par value | | | n/a | | | | n/a | | | $ | 0.001 | | |

| Shares outstanding | | | n/a | | | | n/a | | | | 4,870,233 | | |

| Net asset value and redemption price per share | | | n/a | | | | n/a | | | $ | 10.19 | | |

| Maximum offering price per share | | | n/a | | | | n/a | | | $ | 10.19 | | |

| Class Q: | |

| Net assets | | $ | 83,958 | | | | n/a | | | | n/a | | |

| Shares authorized | | | unlimited | | | | n/a | | | | n/a | | |

| Par value | | $ | 0.001 | | | | n/a | | | | n/a | | |

| Shares outstanding | | | 10,049 | | | | n/a | | | | n/a | | |

| Net asset value and redemption price per share | | $ | 8.35 | | | | n/a | | | | n/a | | |

| Maximum offering price per share | | $ | 8.35 | | | | n/a | | | | n/a | | |

| Class R: | |

| Net assets | | | n/a | | | | n/a | | | $ | 891,159 | | |

| Shares authorized | | | n/a | | | | n/a | | | | unlimited | | |

| Par value | | | n/a | | | | n/a | | | $ | 0.001 | | |

| Shares outstanding | | | n/a | | | | n/a | | | | 87,305 | | |

| Net asset value and redemption price per share | | | n/a | | | | n/a | | | $ | 10.21 | | |

| Maximum offering price per share | | | n/a | | | | n/a | | | $ | 10.21 | | |

(1) Maximum offering price is computed at 100/97.50 of net asset value. On purchases of $100,000 or more, the offering price is reduced.

(2) Redemption price per share may be reduced for any applicable contingent deffered sales charges.

(3) Maximum offering price is computed at 100/96.75 of net asset value. On purchases of $50,000 or more, the offering price is reduced.

See Accompanying Notes to Financial Statements

18

STATEMENTS OF ASSETS AND LIABILITIES AS OF SEPTEMBER 30, 2006 (UNAUDITED) (CONTINUED)

| | | ING

National Tax-

Exempt Bond

Fund | | ING

Classic

Money Market

Fund | | ING

Institutional Prime

Money Market

Fund | |

| ASSETS: | |

| Investments in securities at value* | | $ | 25,380,453 | | | $ | — | | | $ | — | | |

| Short-term investments at amortized cost | | | — | | | | 748,963,164 | | | | 116,563,464 | | |

| Repurchase agreement | | | — | | | | 28,139,000 | | | | 24,393,000 | | |

| Cash | | | 1,223,560 | | | | 139,095 | | | | 6,087 | | |

| Receivables: | |

| Fund shares sold | | | 15,559 | | | | 586,506 | | | | — | | |

| Dividends and interest | | | 343,068 | | | | 2,112,305 | | | | 319,699 | | |

| Prepaid expenses | | | 33,097 | | | | 197,719 | | | | 65,973 | | |

| Reimbursement due from manager | | | 993 | | | | — | | | | — | | |

| Total assets | | | 26,996,730 | | | | 780,137,789 | | | | 141,348,223 | | |

| LIABILITIES: | |

| Payable for fund shares redeemed | | | 178 | | | | 423,450 | | | | — | | |

| Income distribution payable | | | 72,869 | | | | 24,607 | | | | 214,035 | | |

| Payable to affiliates | | | 16,984 | | | | 430,788 | | | | 20,503 | | |

| Payable for trustees fees | | | 1,249 | | | | 5,758 | | | | 787 | | |

| Other accrued expenses and liabilities | | | 17,860 | | | | 101,751 | | | | 44,620 | | |

| Total liabilities | | | 109,140 | | | | 986,354 | | | | 262,412 | | |

| NET ASSETS | | $ | 26,887,590 | | | $ | 779,151,435 | | | $ | 141,085,811 | | |

| NET ASSETS WERE COMPRISED OF: | |

| Paid-in capital | | $ | 26,096,321 | | | $ | 779,308,654 | | | $ | 141,053,137 | | |

Undistributed net investment income

(distributions in excess of net investment income) | | | (1,275 | ) | | | (1,534 | ) | | | 29,357 | | |

| Accumulated net realized gain (loss) on investments | | | 191,232 | | | | (155,685 | ) | | | 3,317 | | |

| Net unrealized appreciation on investments | | | 601,312 | | | | — | | | | — | | |

| NET ASSETS | | $ | 26,887,590 | | | $ | 779,151,435 | | | $ | 141,085,811 | | |

| * Cost of investments in securities | | $ | 24,779,141 | | | $ | — | | | $ | — | | |

See Accompanying Notes to Financial Statements

19

STATEMENTS OF ASSETS AND LIABILITIES AS OF SEPTEMBER 30, 2006 (UNAUDITED) (CONTINUED)

| | | ING

National Tax-

Exempt Bond

Fund | | ING

Classic

Money Market

Fund | | ING

Institutional Prime

Money Market

Fund | |

| Class A: | |

| Net assets | | $ | 22,415,654 | | | $ | 747,942,115 | | | $ | 141,085,811 | | |

| Shares authorized | | | unlimited | | | | unlimited | | | | unlimited | | |

| Par value | | $ | 0.001 | | | $ | 0.001 | | | $ | 0.001 | | |

| Shares outstanding | | | 2,157,251 | | | | 748,070,380 | | | | 141,082,173 | | |

| Net asset value and redemption price per share | | $ | 10.39 | | | $ | 1.00 | | | $ | 1.00 | | |

| Maximum offering price per share (2.50%)(1) | | $ | 10.66 | | | $ | 1.00 | | | $ | 1.00 | | |

| Class B: | |

| Net assets | | $ | 2,843,819 | | | $ | 24,678,978 | | | | n/a | | |

| Shares authorized | | | unlimited | | | | unlimited | | | | n/a | | |

| Par value | | $ | 0.001 | | | $ | 0.001 | | | | n/a | | |

| Shares outstanding | | | 273,881 | | | | 24,701,330 | | | | n/a | | |

| Net asset value and redemption price per share(2) | | $ | 10.38 | | | $ | 1.00 | | | | n/a | | |

| Maximum offering price per share | | $ | 10.38 | | | $ | 1.00 | | | | n/a | | |

| Class C: | |