UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-09037

Nuveen Investment Trust III

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: September 30

Date of reporting period: March 31, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

Item 1. Reports to Stockholders.

Mutual Funds

Nuveen Taxable Bond Funds

For investors seeking attractive monthly income and portfolio diversification potential.

Semi-Annual Report

March 31, 2010

| | | | | | | | |

| Nuveen Short Duration Bond Fund | | | | Nuveen Multi-Strategy Core Bond Fund | | | | Nuveen High Yield Bond Fund |

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Chairman’s

Letter to Shareholders

Dear Shareholder,

The economic environment in which your Fund operates reflects continuing but uneven economic recovery. The U.S. and other major industrial countries are experiencing steady but comparatively low levels of economic growth, while emerging market countries are seeing a resumption of relatively strong economic expansion. The largest source of economic uncertainty is the potential impact of steps being considered by many governments to counteract the extraordinary governmental spending and credit expansion carried out to deal with the financial and economic crisis of 2008. Consequently, the implications for future tax rates, government spending, interest rates and the pace of economic recovery in the U.S. and other leading economies are extremely difficult to predict at the present time. The long term health of the global economy depends on restoring some measure of fiscal discipline around the world, but since all of the corrective steps require economic pain, it is not surprising that governments are reluctant to undertake them.

In the near term, governments remain committed to furthering economic recovery and realizing a meaningful reduction in their national unemployment rates. Such an environment should produce continued economic growth and, consequently, attractive investment opportunities. Over the longer term, the larger uncertainty mentioned earlier carries the risk of unexpected potholes in the road to sustained recovery. For this reason, Nuveen’s investment management teams are working hard to balance return and risk by building well-diversified portfolios, among other strategies. I encourage you to read the following commentary on the management of your Fund. As always, I also encourage you to contact your financial consultant if you have any questions about your Nuveen Fund investment.

On behalf of the other members of your Fund’s Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Board

May 21, 2010

Portfolio Manager’s Comments

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward looking statements and other views expressed herein are those of the portfolio manager as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Effective January 31, 2010, the Nuveen Multi-Strategy Income Fund changed its name to the Nuveen Multi-Strategy Core Bond Fund. There was no change in the Fund’s investment objectives, policies or portfolio management personnel.

The Nuveen Short Duration Bond Fund, Nuveen Multi-Strategy Core Bond Fund and Nuveen High Yield Bond Fund feature portfolio management by the Taxable Fixed Income group of Nuveen Asset Management. We recently spoke with Andrew Stenwall, Chief Investment Officer and Co-Director of Taxable Fixed Income at Nuveen Asset Management, and the Funds’ portfolio manager, about the performance and management of the Funds during the six-month reporting period ended March 31, 2010.

How did the Funds perform during the six-month period ended March 31, 2010?

The table on page five provides performance information for the Funds for the six-month, one-year, five-year and since inception periods ended March 31, 2010. The table also compares the Funds’ performance to appropriate benchmarks. Over this period, each Fund outperformed a comparative market index and underperformed the relevant Lipper group index. A more detailed account of each Fund’s relative performance is provided later in this report.

What are the Funds’ investment strategies and how were they applied during the six-month period ended March 31, 2010? How did these strategies influence performance?

Nuveen Short Duration Bond Fund

Over this period, the Nuveen Taxable Fixed Income team maintained its basic strategy of seeking to maximize total return through an active, risk managed approach that employed bottom-up analysis with deep specialization that looked at issuer fundamentals and relative value. By diversifying active investment strategies in the portfolio, we believe that we can manage portfolio returns across a wide array of economic and market environments. We employ fundamental credit analysis in an attempt to limit default risk and enhance returns throughout the credit cycle. We diversify across global interest rates in an effort to capture value in non U.S. bonds on a currency-hedged basis. We also use a quantitative approach to mortgage- and asset-backed securities analysis designed to evaluate both prepayment and credit risk and capture relative value. Lastly, we actively manage our non-U.S. dollar positions, which are designed to take advantage of opportunities in the changes in the value of the dollar versus other currencies.

For the reporting period, our position in asset-backed securities (ABS) performed well. In particular, ABS backed by credit cards and automobile loans positively contributed to performance. The Fund also benefited from our high yield positions, especially in the manufacturing, energy, service and utilities sectors. Generally speaking, lower quality, higher yielding sectors outperformed throughout the period. Our corporate bond positions in finance, manufacturing, energy, services and utilities all contributed positively to the Fund’s performance as well.

While our position in commercial mortgage-backed securities (CMBS) aided the Fund’s performance on a relative basis, our significant underweight versus the Lipper group accounted for the Fund’s underperformance against that index. We believe there are opportunities in CMBS, especially in the well-structured senior tranches. We remain wary of the mezzanine bonds and junior tranches. Also contributing to the Fund’s underperformance versus its Lipper group was its slightly shorter duration.

The Fund also used interest rate swaps to manage its exposure to U.S. interest rates. Looking at global fixed-income markets during the period, we generally had long exposure in securities issued in Australia, South Korea, Mexico, Norway, New Zealand, Turkey and Brazil. We generally had short exposure to securities issued in South Africa, the United Kingdom, Poland and Switzerland. Combined, these positions contributed neutrally to the Fund’s performance during the reporting period.

We also employed a currency overlay strategy, which involved taking both long (owning the actual security) and short (the Fund does not own the security, but has sold short through the delivery of a borrowed security) positions to manage the Fund’s currency exposure risk. The strategy detracted from performance, as several times throughout the period we were stopped out of our positions. When we re-entered, we were not able to fully re-coup all the losses. Throughout the period, we had long currency positions in Turkey, Brazil, Mexico, Poland, New Zealand, South Africa and Australia, which we exited by the end of the reporting period. Generally, we were short the Euro, British pound and Japanese yen.

Nuveen Multi-Strategy Core Bond Fund

During the reporting period, we continued to employ an investment strategy similar to the one used for the Nuveen Short Duration Bond Fund. We sought to maximize total return through an active, risk managed, relative value approach. By diversifying active investment strategies in the portfolio, we believed that we could better manage portfolio returns across a wide array of economic and market environments.

As with the Nuveen Short Duration Bond Fund, our position in asset-backed securities (ABS) performed well during the reporting period. In particular, ABS backed by credit cards and automobile loans positively contributed to performance. The Fund also benefited from our high yield positions, especially in the manufacturing, energy, service and utilities sectors. Generally speaking, lower quality, higher yielding sectors outperformed throughout the period. Our corporate bond positions in finance, manufacturing, energy, services and utilities all contributed positively to the Fund’s performance as well.

While our position in commercial mortgage-backed securities (CMBS) aided the Fund’s performance on a relative basis, our significant underweight versus the Lipper group accounted for the Fund’s underperformance compared with this index. We believe there are opportunities in CMBS, especially in the well-structured senior tranches. We remain wary of the mezzanine bonds and junior tranches. Also contributing to the Fund’s underperformance versus its Lipper group was its slightly shorter duration.

The Fund also used interest rate swaps to manage its exposure to U.S. interest rates. Looking at global fixed-income markets during the period, we generally had long exposure to securities issued in Australia, South Korea, Mexico, Norway, New Zealand, Turkey and Brazil. We generally held short exposure to securities issued in South Africa, the United Kingdom, Poland and Switzerland. Combined, these positions contributed neutrally to the Fund’s performance during the reporting period.

We also employed a currency overlay strategy, which involved taking both long (owning the actual security) and short (the Fund does not own the security, but has sold short through the delivery of a borrowed security) positions to manage the Fund’s currency exposure risk. The strategy detracted from performance, as several times throughout the period we were stopped out of our positions. When we re-entered we were not able to fully re-coup all the losses. Throughout the period we typically had long currency positions in Turkey, Brazil, Mexico, Poland, New Zealand, South Africa and Australia, which we exited by the end of the reporting period. Generally, we were short the Euro, British pound and Japanese yen.

Nuveen High Yield Bond Fund

Throughout the reporting period, we sought to maximize total return by investing in a diversified portfolio of high yield corporate debt securities. We continued to employ a disciplined, analytical, bottom-up approach with deep specialization that looked at issuer fundamentals and relative value. The Fund focused on BB/B rated credits, seeking securities with improving fundamentals and relatively strong cash flows that appeared under-priced compared to industry peers.

Sector selection continues to play an important role in navigating the high yield market, particularly during periods of high market volatility. The high yield market as a whole performed extremely well over the reporting period, as investors looked to invest in higher-yielding, lower quality sectors.

Our sector selection versus the Citigroup High Yield BB/B index impacted the Fund’s performance. In particular, our overweights in autos, media, metals & mining, secondary oil & gas, publishing and retail were positive contributors to performance. However, our underweights in the chemicals, banks/finance, gaming, homebuilders and transportation sectors negatively impacted relative performance, as these high-beta sectors performed very well.

It is also important to note that the Fund is limited in the amount of CCC-rated issues it can buy. Therefore, in many cases, it could not fully participate in the CCC-rated sectors that showed strong performance over the reporting period. As a result, the Fund underperformed its Lipper group. While our smaller CCC-rated allocation may detract

| * | Since inception returns for the Funds and the Lipper Indexes are as of 12/20/04. Since inception returns for the Citigroup Indexes are as of 12/31/04. |

| 1 | The Lipper Short Investment Grade Debt Funds Index represents the average total return for the 30 largest funds in the Lipper Short Investment Grade Debt Funds Category. The returns account for the effects of management fees and assume reinvestment of dividends, but do not reflect any applicable sales charges. You cannot invest directly in a Lipper index. |

| 2 | The Citigroup 1-3 Year Treasury Index is an index comprised of U.S. Treasury Notes and Bonds with maturities of one year or greater, but less than three years (minimum amount outstanding is $1 billion per issue). The index returns assume the reinvestment of dividends and do not reflect any sales charges. An index is not available for direct investment. |

| 3 | The Lipper Intermediate Investment Grade Debt Funds Index represents the average total return for the 30 largest funds in the Lipper Intermediate Investment Grade Debt Funds Category. The returns account for the effects of management fees and assume reinvestment of dividends, but do not reflect any applicable sales charges. You cannot invest directly in a Lipper index. |

| 4 | The Citigroup Broad Investment Grade Bond Index is an unmanaged index generally considered representative of the U.S. investment grade bond market. The index returns assume the reinvestment of dividends and do not reflect any sales charges. An index is not available for direct investment. |

| 5 | The Lipper High Current Yield Funds Index represents the average total return for the 30 largest funds in the Lipper High Current Yield Funds Category. The returns account for the effects of management fees and assume reinvestment of dividends, but do not reflect any applicable sales charges. You cannot invest directly in a Lipper index. |

| 6 | The Citigroup High Yield BB/B Index is a market capitalization-weighted index that comprises all high-yield issues rated BB or B by Standard & Poor’s for which Citigroup calculates a monthly return. The index returns assume the reinvestment of dividends and do not reflect any sales charges. An index is not available for direct investment. |

from performance during strong rallies in the high yield market, we beleve we benefit from our lower allocation when the market sells off.

Class A Shares – Average Annual Total Returns as of 3/31/10

| | | | | | | | | | |

| | | Cumulative | | Average Annual |

| | | 6-Month | | | | 1-Year | | 5-Year | | Since

Inception* |

Nuveen Short Duration Bond Fund | | | | | | | | | | |

A Shares at NAV | | 2.06% | | | | 8.20% | | 4.59% | | 4.25% |

A Shares at Offer | | 0.04% | | | | 6.02% | | 4.17% | | 3.85% |

Lipper Short Investment Grade Debt Funds Index1 | | 3.11% | | | | 10.70% | | 3.57% | | 3.36% |

Citigroup 1-3 Year Treasury Index2 | | 0.70% | | | | 1.34% | | 4.19% | | 3.94% |

Nuveen Multi-Strategy Core Bond Fund | | | | | | | | | | |

A Shares at NAV | | 2.93% | | | | 13.84% | | 5.97% | | 5.49% |

A Shares at Offer | | -0.95% | | | | 9.55% | | 5.16% | | 4.73% |

Lipper Intermediate Investment Grade Debt Funds Index3 | | 4.35% | | | | 16.91% | | 4.87% | | 4.53% |

Citigroup Broad investment Grade Bond Index4 | | 1.56% | | | | 6.44% | | 5.65% | | 5.28% |

Nuveen High Yield Bond Fund | | | | | | | | | | |

A Shares at NAV | | 9.63% | | | | 42.25% | | 5.63% | | 5.01% |

A Shares at Offer | | 4.39% | | | | 35.50% | | 4.60% | | 4.05% |

Lipper High Current Yield Funds Index5 | | 10.76% | | | | 51.20% | | 5.52% | | 5.01% |

Citigroup High Yield BB/B Index6 | | 8.30% | | | | 37.44% | | 5.14% | | 4.64% |

Six-month returns are cumulative; all other returns are annualized.

Returns quoted represent past performance which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. The Class A Share maximum sales charge is 2.00% for the Short Duration Fund, 3.75% for the Multi-Strategy Core Bond Fund and 4.75% for the High Yield Fund. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Footnote 7 — Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance, visit www.nuveen.com or call (800) 257-8787.

Please see each Fund’s Spotlight Page later in this report for more complete performance data and expense ratios.

Fund Spotlight as of 3/31/10 Nuveen Short Duration Bond Fund

| | | | | | | | |

| Quick Facts | | | | | | | | |

| | | A Shares | | C Shares | | R3 Shares | | I Shares |

Fund Symbol | | NSDAX | | NSCDX | | NSDTX | | NSDRX |

NAV | | $19.74 | | $19.77 | | $19.72 | | $19.70 |

Latest Monthly Dividend1 | | $0.0690 | | $0.0570 | | $0.0650 | | $0.0730 |

Inception Date | | 12/20/04 | | 12/20/04 | | 8/04/08 | | 12/20/04 |

Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Class A, C and I Share returns are actual. The returns for Class R3 Shares are actual for the period since class inception on 8/04/08; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains. Class A Shares have a 2.00% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a backend sales charge, if redeemed within twelve months of purchase. Class C Shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect an expense limitation by the Fund’s investment adviser.

| | | | |

| Average Annual Total Returns as of 3/31/10 |

| | |

| A Shares | | NAV | | Offer |

1-Year | | 8.20% | | 6.02% |

5-Year | | 4.59% | | 4.17% |

Since Inception | | 4.25% | | 3.85% |

| | |

| C Shares | | NAV | | |

1-Year | | 7.45% | | |

5-Year | | 3.82% | | |

Since Inception | | 3.49% | | |

| | |

| R3 Shares | | NAV | | |

1-Year | | 7.88% | | |

5-Year | | 4.31% | | |

Since Inception | | 3.98% | | |

| | |

| I Shares | | NAV | | |

1-Year | | 8.36% | | |

5-Year | | 4.81% | | |

Since Inception | | 4.48% | | |

| Yields | | | | |

| | |

| A Shares | | NAV | | Offer |

Dividend Yield4 | | 4.19% | | 4.11% |

30-Day Yield4 | | 2.09% | | — |

SEC 30-Day Yield5 | | — | | 2.04% |

| | |

| C Shares | | NAV | | |

Dividend Yield4 | | 3.46% | | |

SEC 30-Day Yield4 | | 1.34% | | |

| | |

| R3 Shares | | NAV | | |

Dividend Yield4 | | 3.96% | | |

SEC 30-Day Yield4 | | 1.83% | | |

| | |

| I Shares | | NAV | | |

Dividend Yield4 | | 4.45% | | |

SEC 30-Day Yield4 | | 2.33% | | |

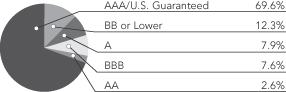

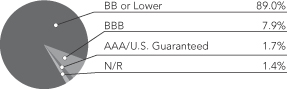

Portfolio Credit Quality2

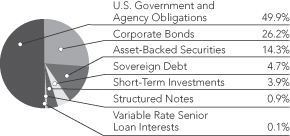

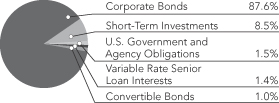

Portfolio Allocation3

| | |

| Net Assets ($000) | | $177,798 |

| | | | |

| Expense Ratios | | | | |

| Share Class | | Gross

Expense

Ratios | | Net

Expense

Ratios |

| Class A | | 1.14% | | 0.85% |

| Class C | | 1.88% | | 1.60% |

| Class R3 | | 1.38% | | 1.10% |

| Class I | | 0.86% | | 0.60% |

The expense ratios shown factor in Total Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a contractual commitment by the Fund’s investment adviser to waive fees and reimburse certain expenses through January 31, 2011. The expense ratios are those shown in the most recent Fund prospectus.

| 1 | Paid April 1, 2010. This is the latest monthly dividend declared during the period ended March 31, 2010. |

| 2 | As a percentage of total investments (excluding structured notes, short-term investments and investments in derivatives) as of March 31, 2010. The ratings disclosed are using the higher of Standard & Poor’s Group (“Standard & Poor’s”) or Moody’s Investor Service, Inc. (“Moody’s”) rating. Ratings below BBB by Standard & Poor’s or Baa by Moody’s are considered to be below investment grade. Holdings are subject to change. |

| 3 | As a percentage of total investments (excluding investments in derivatives) as of March 31, 2010. Holdings are subject to change. |

| 4 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 5 | The SEC 30-Day Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

Fund Spotlight as of 3/31/10 Nuveen Short Duration Bond Fund

| | |

| Corporate Debt: Industries1 | | |

Oil, Gas & Consumable Fuels | | 11.1% |

Commercial Banks | | 10.3% |

Diversified Telecommunication Services | | 9.5% |

Media | | 7.7% |

Metals & Mining | | 5.2% |

Diversified Financial Services | | 5.0% |

Capital Markets | | 4.1% |

Insurance | | 3.6% |

Wireless Telecommunication Services | | 3.2% |

Electric Utilities | | 3.1% |

Commercial Services & Supplies | | 2.9% |

Chemicals | | 2.7% |

Energy Equipment & Services | | 2.7% |

Machinery | | 2.3% |

Food & Staples Retailing | | 2.2% |

Household Products | | 2.2% |

Electronic Equipment & Instruments | | 2.1% |

Aerospace & Defense | | 1.7% |

Tobacco | | 1.6% |

Other | | 16.8% |

| 1 | As a percentage of total corporate debt holdings as of March 31, 2010. Corporate debt holdings include corporate bonds (high-yield investment grade rated), senior loans, convertible bonds, and any other debt instruments issued by a corporation (or that references a corporation) held by the Fund at the end of the reporting period. The percentage of “Other” corporate debt represents the total of all corporate debt industries that recalculated to less than 1.5% of total corporate debt holdings. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | Hypothetical Performance |

| | | Actual Performance | | | | (5% return before expenses) |

| | | A Shares | | C Shares | | R3 Shares | | I Shares | | | | A Shares | | C Shares | | R3 Shares | | I Shares |

| Beginning Account Value (10/01/09) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

| Ending Account Value (3/31/10) | | $ | 1,020.60 | | $ | 1,017.40 | | $ | 1,018.90 | | $ | 1,020.90 | | | | $ | 1,021.39 | | $ | 1,017.65 | | $ | 1,020.14 | | $ | 1,022.59 |

| Expenses Incurred During Period | | $ | 3.58 | | $ | 7.34 | | $ | 4.83 | | $ | 2.37 | | | | $ | 3.58 | | $ | 7.34 | | $ | 4.84 | | $ | 2.37 |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .71%, 1.46%, .96% and .47% for Classes A, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Fund Spotlight as of 3/31/10 Nuveen Multi-Strategy Core Bond Fund

| | | | | | | | | | |

| Quick Facts | | | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R3 Shares | | I Shares |

Fund Symbol | | NCBAX | | NBCBX | | NCBCX | | NMSTX | | NCBRX |

NAV | | $20.47 | | $20.58 | | $20.52 | | $20.48 | | $20.45 |

Latest Monthly Dividend1 | | $0.0900 | | $0.0780 | | $0.0775 | | $0.0860 | | $0.0945 |

Latest Capital Gain and Ordinary Income Distribution2 | | $0.0191 | | $0.0191 | | $0.0191 | | $0.0191 | | $0.0191 |

Inception Date | | 12/20/04 | | 12/20/04 | | 12/20/04 | | 8/04/08 | | 12/20/04 |

Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Class A, B, C and I Share returns are actual. The returns for Class R3 Shares are actual for the period since class inception on 8/04/08; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains. Class A Shares have a 3.75% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a backend sales charge, if redeemed within twelve months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect an expense limitation by the Fund’s investment adviser.

| | | | |

| Average Annual Total Returns as of 3/31/10 |

| A Shares | | NAV | | Offer |

1-Year | | 13.84% | | 9.55% |

5-Year | | 5.97% | | 5.16% |

Since Inception | | 5.49% | | 4.73% |

| B Shares | | w/o CDSC | | w/CDSC |

1-Year | | 12.22% | | 8.22% |

5-Year | | 5.27% | | 5.11% |

Since Inception | | 4.80% | | 4.64% |

| C Shares | | NAV | | |

1-Year | | 13.17% | | |

5-Year | | 5.21% | | |

Since Inception | | 4.74% | | |

| R3 Shares | | NAV | | |

1-Year | | 13.69% | | |

5-Year | | 5.72% | | |

Since Inception | | 5.25% | | |

| I Shares | | NAV | | |

1-Year | | 14.08% | | |

5-Year | | 6.22% | | |

Since Inception | | 5.74% | | |

| Yields | | | | |

| A Shares | | NAV | | Offer |

Dividend Yield5 | | 5.28% | | 5.08% |

30-Day Yield5 | | 3.49% | | — |

SEC 30-Day Yield6 | | — | | 3.36% |

| B Shares | | NAV | | |

Dividend Yield5 | | 4.55% | | |

SEC 30-Day Yield5 | | 2.74% | | |

| C Shares | | NAV | | |

Dividend Yield5 | | 4.53% | | |

SEC 30-Day Yield5 | | 2.74% | | |

| R3 Shares | | NAV | | |

Dividend Yield5 | | 5.04% | | |

SEC 30-Day Yield5 | | 3.24% | | |

| I Shares | | NAV | | |

Dividend Yield5 | | 5.55% | | |

SEC 30-Day Yield5 | | 3.70% | | |

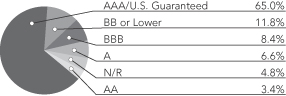

Portfolio Credit Quality3

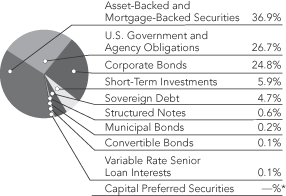

Portfolio Allocation4

| | |

| Net Assets ($000) | | $71,169 |

| | | | |

| Expense Ratios | | | | |

| Share Class | | Gross

Expense

Ratios | | Net

Expense

Ratios |

| Class A | | 1.38% | | 0.95% |

| Class B | | 2.12% | | 1.70% |

| Class C | | 2.16% | | 1.70% |

| Class R3 | | 1.61% | | 1.20% |

| Class I | | 1.06% | | 0.70% |

The expense ratios shown factor in Total Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a contractual commitment by the Fund’s investment adviser to waive fees and reimburse certain expenses through January 31, 2011. The expense ratios are those shown in the most recent Fund prospectus.

| * | Rounds to less than 0.1%. |

| 1 | Paid April 1, 2010. This is the latest monthly dividend declared during the period ended March 31, 2010. |

| 2 | Paid December 16, 2009. Capital gains are subject to federal taxation. |

| 3 | As a percentage of total investments (excluding structured notes, short-term investments and investments in derivatives) as of March 31, 2010. The ratings disclosed are using the higher of Standard & Poor’s Group (“Standard & Poor’s”) or Moody’s Investor Service, Inc. (“Moody’s”) rating. Ratings below BBB by Standard & Poor’s or Baa by Moody’s are considered to be below investment grade. Holdings are subject to change. |

| 4 | As a percentage of total investments (excluding investments in derivatives) as of March 31, 2010. Holdings are subject to change. |

| 5 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 6 | The SEC 30-Day Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

Fund Spotlight as of 3/31/10 Nuveen Multi-Strategy Core Bond Fund

| | |

| Corporate Debt: Industries1 | | |

Oil, Gas & Consumable Fuels | | 14.9% |

Diversified Telecommunication Services | | 9.8% |

Media | | 9.7% |

Capital Markets | | 5.8% |

Diversified Financial Services | | 5.4% |

Commercial Banks | | 5.2% |

Energy Equipment & Services | | 4.2% |

Electric Utilities | | 3.8% |

Chemicals | | 3.1% |

Industrial Conglomerates | | 3.0% |

Wireless Telecommunication Services | | 2.8% |

Metals & Mining | | 2.8% |

Food & Staples Retailing | | 2.4% |

Specialty Retail | | 2.4% |

Commercial Services & Supplies | | 2.0% |

Multi-Line Retail | | 1.8% |

Hotels, Restaurants & Leisure | | 1.7% |

Aerospace & Defense | | 1.6% |

Electronic Equipment & Instruments | | 1.5% |

Consumer Finance | | 1.5% |

Other | | 14.6% |

| 1 | As a percentage of total corporate debt holdings as of March 31, 2010. Corporate debt holdings include corporate bonds (high-yield investment grade rated), senior loans, convertible bonds, and any other debt instruments issued by a corporation (or that references a corporation) held by the Fund at the end of the reporting period. The percentage of “Other” corporate debt represents the total of all corporate debt industries that recalculated to less than 1.5% of total corporate debt holdings. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Actual Performance | | | | Hypothetical Performance

(5% return before expenses) |

| | | A Shares | | B Shares | | C Shares | | R3 Shares | | I Shares | | | | A Shares | | B Shares | | C Shares | | R3 Shares | | I Shares |

| Beginning Account Value (10/01/09) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

| Ending Account Value (3/31/10) | | $ | 1,029.30 | | $ | 1,026.10 | | $ | 1,027.00 | | $ | 1,029.10 | | $ | 1,030.10 | | | | $ | 1,020.84 | | $ | 1,017.20 | | $ | 1,017.15 | | $ | 1,019.70 | | $ | 1,022.14 |

| Expenses Incurred During Period | | $ | 4.15 | | $ | 7.83 | | $ | 7.88 | | $ | 5.31 | | $ | 2.83 | | | | $ | 4.13 | | $ | 7.80 | | $ | 7.85 | | $ | 5.29 | | $ | 2.82 |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .82%, 1.55%, 1.56%, 1.05% and .56% for Classes A, B, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Fund Spotlight as of 3/31/10 Nuveen High Yield Bond Fund

| | | | | | | | | | |

| Quick Facts | | | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R3 Shares | | I Shares |

Fund Symbol | | NHYAX | | NHBYX | | NHYCX | | NHYTX | | NHYRX |

NAV | | $16.98 | | $16.97 | | $16.94 | | $16.97 | | $16.97 |

Latest Monthly Dividend1 | | $0.1165 | | $0.1060 | | $0.1060 | | $0.1130 | | $0.1200 |

Inception Date | | 12/20/04 | | 12/20/04 | | 12/20/04 | | 8/04/08 | | 12/20/04 |

Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Class A, B, C and I Share returns are actual. The returns for Class R3 Shares are actual for the period since class inception on 8/04/08; returns prior to class inception are Class I Share returns adjusted for differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains. Class A Shares have a 4.75% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a backend sales charge, if redeemed within twelve months of purchase. Class B Shares have a CDSC that begins at 5% for redemptions during the first year and declines periodically until after six years when the charge becomes 0%. Class B Shares automatically convert to Class A Shares eight years after purchase. Class C Shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R3 Shares have no sales charge and are available to only certain retirement plan clients of financial intermediaries. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect an expense limitation by the Fund’s investment adviser.

| | | | |

| Average Annual Total Returns as of 3/31/10 |

| A Shares | | NAV | | Offer |

1-Year | | 42.25% | | 35.50% |

5-Year | | 5.63% | | 4.60% |

Since Inception | | 5.01% | | 4.05% |

| B Shares | | w/o CDSC | | w/CDSC |

1-Year | | 41.27% | | 37.27% |

5-Year | | 4.82% | | 4.68% |

Since Inception | | 4.21% | | 4.07% |

| C Shares | | NAV | | |

1-Year | | 41.26% | | |

5-Year | | 4.79% | | |

Since Inception | | 4.18% | | |

| R3 Shares | | NAV | | |

1-Year | | 41.94% | | |

5-Year | | 5.35% | | |

Since Inception | | 4.74% | | |

| I Shares | | NAV | | |

1-Year | | 42.61% | | |

5-Year | | 5.88% | | |

Since Inception | | 5.27% | | |

| Yields | | | | |

| A Shares | | NAV | | Offer |

Dividend Yield4 | | 8.23% | | 7.84% |

30-Day Yield4 | | 7.94% | | — |

SEC 30-Day Yield5 | | — | | 7.55% |

| B Shares | | NAV | | |

Dividend Yield4 | | 7.50% | | |

SEC 30-Day Yield4 | | 7.17% | | |

| C Shares | | NAV | | |

Dividend Yield4 | | 7.51% | | |

SEC 30-Day Yield4 | | 7.18% | | |

| R3 Shares | | NAV | | |

Dividend Yield4 | | 7.99% | | |

SEC 30-Day Yield4 | | 7.68% | | |

| I Shares | | NAV | | |

Dividend Yield4 | | 8.49% | | |

SEC 30-Day Yield4 | | 8.19% | | |

Portfolio Credit Quality2

Portfolio Allocation3

| | |

| Net Assets ($000) | | $136,977 |

| | | | |

| Expense Ratios | | | | |

| Share Class | | Gross

Expense

Ratios | | Net

Expense

Ratios |

| Class A | | 1.23% | | 1.20% |

| Class B | | 1.95% | | 1.95% |

| Class C | | 1.97% | | 1.95% |

| Class R3 | | 1.46% | | 1.45% |

| Class I | | 0.97% | | 0.95% |

The expense ratios shown factor in Total Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a contractual commitment by the Fund’s investment adviser to waive fees and reimburse certain expenses through January 31, 2011. The expense ratios are those shown in the most recent Fund prospectus.

| 1 | Paid April 1, 2010. This is the latest monthly dividend declared during the period ended March 31, 2010. |

| 2 | As a percentage of total investments (excluding short-term investments and investments in derivatives) as of March 31, 2010. The ratings disclosed are using the higher of Standard & Poor’s Group (“Standard & Poor’s”) or Moody’s Investor Service, Inc. (“Moody’s”) rating. Ratings below BBB by Standard & Poor’s or Baa by Moody’s are considered to be below investment grade. Holdings are subject to change. |

| 3 | As a percentage of total investments (excluding investments in derivatives) as of March 31, 2010. Holdings are subject to change. |

| 4 | Dividend Yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 5 | The SEC 30-Day Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

Fund Spotlight as of 3/31/10 Nuveen High Yield Bond Fund

| | |

| Corporate Debt: Industries1 | | |

Media | | 12.4% |

Oil, Gas & Consumable Fuels | | 12.2% |

Diversified Telecommunication Services | | 11.5% |

Metals & Mining | | 8.5% |

Wireless Telecommunication Services | | 5.6% |

Commercial Services & Supplies | | 5.2% |

Auto Components | | 5.0% |

Machinery | | 4.5% |

Energy Equipment & Services | | 3.9% |

Containers & Packaging | | 3.9% |

Hotels, Restaurants & Leisure | | 2.9% |

Electronic Equipment & Instruments | | 2.2% |

Chemicals | | 2.1% |

Aerospace & Defense | | 2.1% |

IT Services | | 1.9% |

Multi-Utilities | | 1.8% |

Specialty Retail | | 1.8% |

Household Products | | 1.7% |

Trading Companies & Distributors | | 1.7% |

Semiconductors & Equipment | | 1.6% |

Other | | 7.5% |

| 1 | As a percentage of total corporate debt holdings as of March 31, 2010. Corporate debt holdings include corporate bonds (high-yield investment grade rated), senior loans, convertible bonds and any other debt instruments issued by a corporation (or that references a corporation) held by the Fund at the end of the reporting period. The percentage of “Other” corporate debt represents the total of all corporate debt industries that recalculated to less than 1.5% of total corporate debt holdings. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Hypothetical Performance |

| | | Actual Performance | | | | (5% return before expenses) |

| | | A Shares | | B Shares | | C Shares | | R3 Shares | | I Shares | | | | A Shares | | B Shares | | C Shares | | R3 Shares | | I Shares |

| Beginning Account Value (10/01/09) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

| Ending Account Value (3/31/10) | | $ | 1,096.30 | | $ | 1,093.10 | | $ | 1,092.50 | | $ | 1,095.70 | | $ | 1,098.40 | | | | $ | 1,020.00 | | $ | 1,016.26 | | $ | 1,016.26 | | $ | 1,018.75 | | $ | 1,021.44 |

| Expenses Incurred During Period | | $ | 5.17 | | $ | 9.08 | | $ | 9.08 | | $ | 6.48 | | $ | 3.66 | | | | $ | 4.99 | | $ | 8.75 | | $ | 8.75 | | $ | 6.24 | | $ | 3.53 |

For each Class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of .99%, 1.74%, 1.74%, 1.24% and .70% for Classes A, B, C, R3 and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Portfolio of Investments (Unaudited)

Nuveen Short Duration Bond Fund

March 31, 2010

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | |

| | | CORPORATE BONDS – 26.7% | | | | | | | | | |

| | | | | |

| | | Aerospace & Defense – 0.5% | | | | | | | | | |

| | | | | |

| $ | 120 | | BAE Systems Holdings | | 6.400% | | 12/15/11 | | BBB+ | | $ | 128,442 |

| | | | | |

| | 100 | | Boeing Capital Corporation | | 6.500% | | 2/15/12 | | A | | | 109,293 |

| | | | | |

| | 235 | | Global Aviation Holdings, 144A | | 14.000% | | 8/15/13 | | BB– | | | 239,994 |

| | | | | |

| | 325 | | Northrop Grumman Corporation | | 3.700% | | 8/01/14 | | BBB | | | 332,886 |

| | 780 | | Total Aerospace & Defense | | | | | | | | | 810,615 |

| | | Auto Components – 0.3% | | | | | | | | | |

| | | | | |

| | 270 | | Affinia Group Inc. | | 9.000% | | 11/30/14 | | B3 | | | 270,000 |

| | | | | |

| | 210 | | ArvinMeritor Inc. | | 10.625% | | 3/15/18 | | Caa2 | | | 218,400 |

| | 480 | | Total Auto Components | | | | | | | | | 488,400 |

| | | Beverages – 0.4% | | | | | | | | | |

| | | | | |

| | 225 | | Anheuser Busch InBev, 144A | | 5.375% | | 11/15/14 | | BBB+ | | | 243,949 |

| | | | | |

| | 125 | | Diageo Finance BV | | 3.875% | | 4/01/11 | | A– | | | 128,500 |

| | | | | |

| | 240 | | Miller Brewing Company, 144A | | 5.500% | | 8/15/13 | | BBB+ | | | 257,154 |

| | 590 | | Total Beverages | | | | | | | | | 629,603 |

| | | Capital Markets – 1.1% | | | | | | | | | |

| | | | | |

| | 200 | | Bank of New York Mellon | | 4.300% | | 5/15/14 | | Aa2 | | | 210,737 |

| | | | | |

| | 325 | | Goldman Sachs Group, Inc. | | 6.600% | | 1/15/12 | | A1 | | | 352,790 |

| | | | | |

| | 585 | | Goldman Sachs Group, Inc. | | 5.500% | | 11/15/14 | | A1 | | | 628,218 |

| | | | | |

| | 150 | | Morgan Stanley | | 5.250% | | 11/02/12 | | A | | | 159,984 |

| | | | | |

| | 575 | | Morgan Stanley | | 6.000% | | 5/13/14 | | A | | | 621,645 |

| | 1,835 | | Total Capital Markets | | | | | | | | | 1,973,374 |

| | | Chemicals – 0.7% | | | | | | | | | |

| | | | | |

| | 365 | | Airgas, Inc. | | 4.500% | | 9/15/14 | | BBB | | | 377,078 |

| | | | | |

| | 250 | | E.I. Du Pont de Nemours and Company | | 4.750% | | 11/15/12 | | A | | | 268,825 |

| | | | | |

| | 110 | | E.I. Du Pont de Nemours and Company | | 3.250% | | 1/15/15 | | A | | | 110,791 |

| | | | | |

| | 160 | | IMC Global Inc. | | 7.300% | | 1/15/28 | | Baa2 | | | 171,770 |

| | | | | |

| | 375 | | Potash Corporation of Saskatchewan | | 3.750% | | 9/30/15 | | A– | | | 379,919 |

| | 1,260 | | Total Chemicals | | | | | | | | | 1,308,383 |

| | | Commercial Banks – 2.8% | | | | | | | | | |

| | | | | |

| | 350 | | BB&T Corporation | | 5.700% | | 4/30/14 | | A1 | | | 380,678 |

| | | | | |

| | 225 | | Citigroup Inc. | | 6.000% | | 2/21/12 | | A | | | 238,742 |

| | | | | |

| | 400 | | Citigroup Inc. | | 5.850% | | 7/02/13 | | A | | | 420,662 |

| | | | | |

| | 325 | | Citigroup Inc. | | 6.500% | | 8/19/13 | | A | | | 350,620 |

| | | | | |

| | 225 | | Credit Suisse First Boston, Note | | 6.125% | | 11/15/11 | | Aa1 | | | 241,811 |

| | | | | |

| | 260 | | Fifth Third Bancorp. | | 6.250% | | 5/01/13 | | Baa1 | | | 279,811 |

| | | | | |

| | 300 | | Household Finance Corporation | | 6.375% | | 11/27/12 | | A3 | | | 328,761 |

| | | | | |

| | 335 | | KeyCorp. | | 6.500% | | 5/14/13 | | BBB+ | | | 358,001 |

| | | | | |

| | 350 | | M&I Marshall & Ilsley Bank | | 4.850% | | 6/16/15 | | Baa1 | | | 311,592 |

| | | | | |

| | 200 | | PNC Funding Corporation | | 5.400% | | 6/10/14 | | A | | | 214,987 |

| | | | | |

| | 500 | | Regions Financial Corporation of the Bank of America | | 7.000% | | 3/01/11 | | BB+ | | | 503,874 |

| | | | | |

| | 230 | | US Bancorp | | 4.200% | | 5/15/14 | | Aa3 | | | 241,542 |

| | | | | |

| | 675 | | Wells Fargo & Company | | 5.250% | | 10/23/12 | | AA– | | | 727,653 |

| | | | | |

| | 275 | | Wells Fargo & Company | | 4.950% | | 10/16/13 | | A+ | | | 290,755 |

| | 4,650 | | Total Commercial Banks | | | | | | | | | 4,889,489 |

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | |

| | | Commercial Services & Supplies – 0.8% | | | | | | | | | |

| | | | | |

| $ | 60 | | Allied Waste North America | | 6.500% | | 11/15/10 | | BBB | | $ | 62,011 |

| | | | | |

| | 230 | | Browning Ferris-Allied Waste | | 9.250% | | 5/01/21 | | BBB | | | 282,272 |

| | | | | |

| | 310 | | GATX Corporation | | 4.750% | | 10/01/12 | | BBB+ | | | 323,769 |

| | | | | |

| | 310 | | Geokinetics Holdings Inc., 144A | | 9.750% | | 12/15/14 | | B | | | 292,175 |

| | | | | |

| | 300 | | Rental Service Corporation | | 9.500% | | 12/01/14 | | B– | | | 298,500 |

| | | | | |

| | 125 | | Waste Management Inc. | | 7.375% | | 8/01/10 | | BBB | | | 127,604 |

| | 1,335 | | Total Commercial Services & Supplies | | | | | | | | | 1,386,331 |

| | | Communications Equipment – 0.2% | | | | | | | | | |

| | | | | |

| | 125 | | Cisco Systems, Inc. | | 5.250% | | 2/22/11 | | A+ | | | 130,117 |

| | | | | |

| | 230 | | Paetec Holding Corporation, 144A | | 8.875% | | 6/30/17 | | B1 | | | 237,475 |

| | 355 | | Total Communications Equipment | | | | | | | | | 367,592 |

| | | Computers & Peripherals – 0.2% | | | | | | | | | |

| | | | | |

| | 170 | | Dell Inc. | | 3.375% | | 6/15/12 | | A2 | | | 176,759 |

| | | | | |

| | 100 | | Hewlett Packard Company | | 6.500% | | 7/01/12 | | A | | | 110,715 |

| | | | | |

| | 125 | | International Business Machines Corporation (IBM) | | 4.950% | | 3/22/11 | | A+ | | | 129,992 |

| | 395 | | Total Computers & Peripherals | | | | | | | | | 417,466 |

| | | Consumer Finance – 0.3% | | | | | | | | | |

| | | | | |

| | 275 | | American Express Credit Corporation | | 7.300% | | 8/20/13 | | A2 | | | 308,897 |

| | | | | |

| | 300 | | Provident Funding Associates, 144A, (WI/DD) | | 10.250% | | 4/15/17 | | Ba3 | | | 303,750 |

| | 575 | | Total Consumer Finance | | | | | | | | | 612,647 |

| | | Containers & Packaging – 0.1% | | | | | | | | | |

| | | | | |

| | 135 | | Rock-Tenn Company | | 5.625% | | 3/15/13 | | BBB– | | | 139,388 |

| | | | | |

| | 60 | | Tekni-Plex Inc. | | 10.875% | | 8/15/12 | | N/R | | | 56,400 |

| | 195 | | Total Containers & Packaging | | | | | | | | | 195,788 |

| | | Diversified Financial Services – 1.3% | | | | | | | | | |

| | | | | |

| | 153 | | Bank One Corporation | | 7.875% | | 8/01/10 | | A1 | | | 156,658 |

| | | | | |

| | 225 | | Capital One Financial Corporation | | 7.375% | | 5/23/14 | | Baa1 | | | 257,347 |

| | | | | |

| | 700 | | General Electric Capital Corporation | | 5.250% | | 10/19/12 | | AA+ | | | 751,927 |

| | | | | |

| | 850 | | JP Morgan Chase & Company | | 5.750% | | 1/02/13 | | A1 | | | 923,068 |

| | | | | |

| | 250 | | National Rural Utilities Cooperative Finance Corporation | | 7.250% | | 3/01/12 | | A | | | 275,125 |

| | 2,178 | | Total Diversified Financial Services | | | | | | | | | 2,364,125 |

| | | Diversified Telecommunication Services – 2.5% | | | | | | | | | |

| | | | | |

| | 210 | | Cequel Communication Holdings I, 144A | | 8.625% | | 11/15/17 | | B– | | | 216,825 |

| | | | | |

| | 195 | | Cincinnati Bell Inc. | | 8.375% | | 1/15/14 | | B2 | | | 201,581 |

| | | | | |

| | 455 | | Cincinnati Bell Inc. | | 8.750% | | 3/15/18 | | B2 | | | 461,256 |

| | | | | |

| | 575 | | Citizens Communications Company | | 9.000% | | 8/15/31 | | BB | | | 563,500 |

| | | | | |

| | 312 | | Cox Communications, Inc. | | 5.500% | | 10/01/15 | | Baa2 | | | 336,661 |

| | | | | |

| | 250 | | France Telecom | | 7.750% | | 3/01/11 | | A– | | | 265,480 |

| | | | | |

| | 250 | | Paetec Holding Corporation | | 8.875% | | 6/30/17 | | B1 | | | 258,125 |

| | | | | |

| | 790 | | Qwest Communications International Inc., 144A | | 7.125% | | 4/01/18 | | Ba3 | | | 819,625 |

| | | | | |

| | 310 | | Telecom Italia Capital | | 5.250% | | 10/01/15 | | BBB | | | 317,783 |

| | | | | |

| | 200 | | Telefonica Emisiones SAU | | 4.949% | | 1/15/15 | | A– | | | 211,414 |

| | | | | |

| | 150 | | Verizon Communications | | 5.875% | | 1/17/12 | | A | | | 159,843 |

| | | | | |

| | 400 | | Verizon Global Funding Company | | 4.900% | | 9/15/15 | | A | | | 429,879 |

Portfolio of Investments (Unaudited)

Nuveen Short Duration Bond Fund (continued)

March 31, 2010

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | |

| | | Diversified Telecommunication Services (continued) | | | | | | | | | |

| | | | | |

| $ | 270 | | Windstream Corporation, 144A | | 7.875% | | 11/01/17 | | Ba3 | | $ | 267,300 |

| | 4,367 | | Total Diversified Telecommunication Services | | | | | | | | | 4,509,272 |

| | | Electric Utilities – 0.8% | | | | | | | | | |

| | | | | |

| | 325 | | American Electric Power | | 5.250% | | 6/01/15 | | BBB | | | 347,869 |

| | | | | |

| | 198 | | Dominion Resources Inc. | | 5.700% | | 9/17/12 | | A– | | | 214,672 |

| | | | | |

| | 455 | | Edison Mission Energy | | 7.625% | | 5/15/27 | | B | | | 293,475 |

| | | | | |

| | 200 | | Exelon Generation Company LLC | | 5.350% | | 1/15/14 | | A3 | | | 213,441 |

| | | | | |

| | 4 | | FirstEnergy Corporation | | 6.450% | | 11/15/11 | | Baa3 | | | 4,244 |

| | | | | |

| | 400 | | Niagara Mohawk Power Company, 144A | | 3.553% | | 10/01/14 | | A– | | | 401,945 |

| | 1,582 | | Total Electric Utilities | | | | | | | | | 1,475,646 |

| | | Electrical Equipment – 0.1% | | | | | | | | | |

| | | | | |

| | 125 | | Emerson Electric Company | | 7.125% | | 8/15/10 | | A | | | 128,106 |

| | | Electronic Equipment & Instruments – 0.6% | | | | | | | | | |

| | | | | |

| | 365 | | Agilent Technologies Inc. | | 5.500% | | 9/14/15 | | BBB– | | | 391,726 |

| | | | | |

| | 225 | | Hewlett Packard Company | | 4.750% | | 6/02/14 | | A | | | 243,147 |

| | | | | |

| | 350 | | ViaSystems Inc., 144A | | 12.000% | | 1/15/15 | | B+ | | | 380,625 |

| | 940 | | Total Electronic Equipment & Instruments | | | | | | | | | 1,015,498 |

| | | Energy Equipment & Services – 0.7% | | | | | | | | | |

| | | | | |

| | 310 | | Crosstex Energy Finance, 144A | | 8.875% | | 2/15/18 | | B+ | | | 321,238 |

| | | | | |

| | 150 | | Halliburton Company | | 5.500% | | 10/15/10 | | A | | | 154,149 |

| | | | | |

| | 275 | | Kinder Morgan Energy Partners, L.P. | | 5.850% | | 9/15/12 | | BBB | | | 298,944 |

| | | | | |

| | 70 | | Parker Drilling Company, 144A | | 9.125% | | 4/01/18 | | B+ | | | 72,013 |

| | | | | |

| | 225 | | Rockies Express Pipeline Company, 144A | | 6.250% | | 7/15/13 | | BBB | | | 245,001 |

| | | | | |

| | 185 | | Trico Shipping AS, 144A | | 11.875% | | 11/01/14 | | B1 | | | 177,600 |

| | 1,215 | | Total Energy Equipment & Services | | | | | | | | | 1,268,945 |

| | | Food & Staples Retailing – 0.6% | | | | | | | | | |

| | | | | |

| | 250 | | CVS Caremark Corporation | | 5.750% | | 8/15/11 | | BBB+ | | | 264,375 |

| | | | | |

| | 325 | | Kroger Co | | 3.900% | | 10/01/15 | | BBB | | | 329,390 |

| | | | | |

| | 175 | | Safeway Inc. | | 4.950% | | 8/16/10 | | BBB | | | 177,801 |

| | | | | |

| | 250 | | Safeway Inc. | | 6.250% | | 3/15/14 | | BBB | | | 278,131 |

| | 1,000 | | Total Food & Staples Retailing | | | | | | | | | 1,049,697 |

| | | Food Products – 0.3% | | | | | | | | | |

| | | | | |

| | 250 | | General Mills, Inc. | | 6.000% | | 2/15/12 | | BBB+ | | | 272,130 |

| | | | | |

| | 175 | | Kraft Foods Inc. | | 5.625% | | 11/01/11 | | Baa2 | | | 185,938 |

| | 425 | | Total Food Products | | | | | | | | | 458,068 |

| | | Health Care Providers & Services – 0.1% | | | | | | | | | |

| | | | | |

| | 105 | | AMR-EmCare Holding Company Inc. | | 10.000% | | 2/15/15 | | Ba2 | | | 110,841 |

| | | | | |

| | 50 | | HCA Inc. | | 8.750% | | 9/01/10 | | B– | | | 51,250 |

| | 155 | | Total Health Care Providers & Services | | | | | | | | | 162,091 |

| | | Hotels, Restaurants & Leisure – 0.3% | | | | | | | | | |

| | | | | |

| | 180 | | Dave & Busters Inc. | | 11.250% | | 3/15/14 | | B– | | | 189,900 |

| | | | | |

| | 200 | | Harrah's Operating Company, Inc. | | 11.250% | | 6/01/17 | | B– | | | 216,500 |

| | | | | |

| | 175 | | Tricon Golbal Restaurants Incorporated | | 8.875% | | 4/15/11 | | BBB– | | | 187,732 |

| | 555 | | Total Hotels, Restaurants & Leisure | | | | | | | | | 594,132 |

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | |

| | | Household Products – 0.6% | | | | | | | | | |

| | | | | |

| $ | 350 | | Clorox Company | | 3.550% | | 11/01/15 | | BBB+ | | $ | 355,154 |

| | | | | |

| | 310 | | Norcraft Companies Finance, 144A | | 10.500% | | 12/15/15 | | B2 | | | 328,600 |

| | | | | |

| | 350 | | Procter and Gamble Company | | 3.150% | | 9/01/15 | | AA– | | | 355,871 |

| | 1,010 | | Total Household Products | | | | | | | | | 1,039,625 |

| | | Independent Power Producers & Energy Traders – 0.1% | | | | | | | | | |

| | | | | |

| | 285 | | Dynegy Holdings, Inc., Term Loan | | 7.750% | | 6/01/19 | | B | | | 216,600 |

| | | Industrial Conglomerates – 0.4% | | | | | | | | | |

| | | | | |

| | 125 | | Textron Financial Corporation | | 5.125% | | 2/03/11 | | Baa3 | | | 127,352 |

| | | | | |

| | 365 | | Timken Company | | 6.000% | | 9/15/14 | | BBB– | | | 388,545 |

| | | | | |

| | 155 | | Tyco International Group | | 6.000% | | 11/15/13 | | BBB+ | | | 171,434 |

| | 645 | | Total Industrial Conglomerates | | | | | | | | | 687,331 |

| | | Insurance – 1.0% | | | | | | | | | |

| | | | | |

| | 225 | | Allstate Life Global Funding | | 5.375% | | 4/30/13 | | AA– | | | 245,278 |

| | | | | |

| | 250 | | Berkshire Hathaway Inc. | | 5.000% | | 8/15/13 | | AA+ | | | 273,232 |

| | | | | |

| | 400 | | Genworth Life Institution Funding | | 5.875% | | 5/03/13 | | A | | | 408,488 |

| | | | | |

| | 275 | | Met Life Global Funding I | | 5.125% | | 4/10/13 | | AA– | | | 295,446 |

| | | | | |

| | 475 | | Prudential Financial Inc. | | 5.100% | | 9/20/14 | | A | | | 502,209 |

| | 1,625 | | Total Insurance | | | | | | | | | 1,724,653 |

| | | IT Services – 0.2% | | | | | | | | | |

| | | | | |

| | 215 | | First Data Corporation | | 9.875% | | 9/24/15 | | B– | | | 186,513 |

| | | | | |

| | 230 | | Fiserv Inc. | | 6.125% | | 11/20/12 | | Baa2 | | | 250,475 |

| | 445 | | Total IT Services | | | | | | | | | 436,988 |

| | | Machinery – 0.6% | | | | | | | | | |

| | | | | |

| | 250 | | Caterpillar Financial Services Corporation | | 6.200% | | 9/30/13 | | A | | | 282,567 |

| | | | | |

| | 250 | | Greenbrier Companies, Inc. | | 8.375% | | 5/15/15 | | CCC | | | 228,750 |

| | | | | |

| | 125 | | John Deere Capital Corporation | | 5.650% | | 7/25/11 | | A | | | 132,525 |

| | | | | |

| | 200 | | John Deere Capital Corporation | | 5.250% | | 10/01/12 | | A | | | 217,266 |

| | | | | |

| | 200 | | Toys R Us Property Company Inc., 144A | | 10.750% | | 7/15/17 | | B+ | | | 224,000 |

| | 1,025 | | Total Machinery | | | | | | | | | 1,085,108 |

| | | Media – 2.1% | | | | | | | | | |

| | | | | |

| | 300 | | AOL Time Warner | | 6.875% | | 5/01/12 | | BBB | | | 330,148 |

| | | | | |

| | 480 | | Clear Channel Communications, Inc. | | 10.750% | | 8/01/16 | | CCC– | | | 378,000 |

| | | | | |

| | 20 | | Clear Channel Worldwide Holdings Inc., 144A | | 9.250% | | 12/15/17 | | B | | | 20,875 |

| | | | | |

| | 110 | | Clear Channel Worldwide Holdings Inc., 144A | | 9.250% | | 12/15/17 | | B | | | 115,500 |

| | | | | |

| | 150 | | Comcast Corporation | | 5.450% | | 11/15/10 | | BBB+ | | | 153,842 |

| | | | | |

| | 350 | | Comcast Corporation | | 5.850% | | 11/15/15 | | BBB+ | | | 383,975 |

| | | | | |

| | 150 | | Cox Communications, Inc. | | 7.750% | | 11/01/10 | | Baa2 | | | 155,645 |

| | | | | |

| | 455 | | McClatchy Company, 144A | | 11.500% | | 2/15/17 | | B1 | | | 466,944 |

| | | | | |

| | 185 | | Nielsen Finance LLC Co | | 11.625% | | 2/01/14 | | B– | | | 209,975 |

| | | | | |

| | 40 | | Sinclair Broadcast Group | | 8.000% | | 3/15/12 | | CCC+ | | | 39,800 |

| | | | | |

| | 420 | | Sinclair Television Group, 144A | | 9.250% | | 11/01/17 | | B2 | | | 444,150 |

| | | | | |

| | 150 | | Time Warner Cable Inc. | | 5.400% | | 7/02/12 | | BBB | | | 161,111 |

| | | | | |

| | 105 | | Time Warner Cable Inc. | | 6.200% | | 7/01/13 | | BBB | | | 115,952 |

| | | | | |

| | 250 | | TL Acquisitions Inc., 144A | | 13.250% | | 7/15/15 | | CCC+ | | | 243,750 |

Portfolio of Investments (Unaudited)

Nuveen Short Duration Bond Fund (continued)

March 31, 2010

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | |

| | | Media (continued) | | | | | | | | | |

| | | | | |

| $ | 220 | | Valassis Communications Inc. | | 8.250% | | 3/01/15 | | B– | | $ | 227,150 |

| | | | | |

| | 125 | | Walt Disney Company | | 5.700% | | 7/15/11 | | A | | | 132,544 |

| | | | | |

| | 75 | | WMG Acquisition Group | | 9.500% | | 6/15/16 | | BB | | | 80,531 |

| | 3,585 | | Total Media | | | | | | | | | 3,659,892 |

| | | Metals & Mining – 1.4% | | | | | | | | | |

| | | | | |

| | 500 | | AK Steel Corporation | | 7.750% | | 6/15/12 | | BB– | | | 505,000 |

| | | | | |

| | 150 | | ArcelorMittal | | 5.375% | | 6/01/13 | | BBB | | | 159,778 |

| | | | | |

| | 200 | | BHP Billiton Finance Limited | | 5.500% | | 4/01/14 | | A+ | | | 220,270 |

| | | | | |

| | 230 | | Consol Energy Inc., 144A, (WI/DD) | | 8.000% | | 4/01/17 | | BB | | | 237,475 |

| | | | | |

| | 230 | | Consol Energy Inc., 144A, (WI/DD) | | 8.250% | | 4/01/20 | | BB | | | 237,475 |

| | | | | |

| | 240 | | Essar Steel Algoma Inc., 144A | | 9.375% | | 3/15/15 | | B+ | | | 243,600 |

| | | | | |

| | 550 | | Freeport McMoran Copper & Gold, Inc. | | 3.881% | | 4/01/15 | | BBB– | | | 556,188 |

| | | | | |

| | 140 | | Steel Dynamics, Inc., 144A | | 7.625% | | 3/15/20 | | BB+ | | | 144,200 |

| | | | | |

| | 160 | | Steel Dynamics, Inc. | | 7.375% | | 11/01/12 | | BB+ | | | 167,200 |

| | 2,400 | | Total Metals & Mining | | | | | | | | | 2,471,186 |

| | | Multi-Line Retail – 0.4% | | | | | | | | | |

| | | | | |

| | 150 | | Costco Wholesale Corporation | | 5.300% | | 3/15/12 | | A+ | | | 161,210 |

| | | | | |

| | 200 | | Home Depot, Inc. | | 5.400% | | 3/01/16 | | BBB+ | | | 216,394 |

| | | | | |

| | 250 | | Target Corporation | | 5.875% | | 3/01/12 | | A+ | | | 271,234 |

| | 600 | | Total Multi-Line Retail | | | | | | | | | 648,838 |

| | | Multi-Utilities – 0.2% | | | | | | | | | |

| | | | | |

| | 450 | | Bon-Ton Department Stores Inc. | | 10.250% | | 3/15/14 | | CCC | | | 441,000 |

| | | Oil, Gas & Consumable Fuels – 3.0% | | | | | | | | | |

| | | | | |

| | 125 | | Anadarko Petroleum Corporation | | 7.625% | | 3/15/14 | | BBB– | | | 143,831 |

| | | | | |

| | 100 | | Apache Corporation | | 6.250% | | 4/15/12 | | A– | | | 109,244 |

| | | | | |

| | 210 | | BP Capital Markets PLC | | 3.625% | | 5/08/14 | | Aa1 | | | 218,047 |

| | | | | |

| | 405 | | Cenovus Energy Inc., 144A | | 4.500% | | 9/15/14 | | BBB+ | | | 422,960 |

| | | | | |

| | 100 | | Chevron Corporation | | 3.950% | | 3/03/14 | | Aa1 | | | 104,529 |

| | | | | |

| | 200 | | Conoco Funding Co, Notes | | 6.350% | | 10/15/11 | | A1 | | | 215,822 |

| | | | | |

| | 153 | | Energy XXI Gulf Coast Inc., 144A | | 16.000% | | 6/15/14 | | B+ | | | 176,995 |

| | | | | |

| | 240 | | Enterprise Products Operating Group LLP | | 4.600% | | 8/01/12 | | BBB– | | | 253,300 |

| | | | | |

| | 265 | | Linn Energy LLC Finance Corporation, 144A, (WI/DD) | | 8.625% | | 4/15/20 | | Ba3 | | | 265,994 |

| | | | | |

| | 300 | | Massey Energy Company, Global Notes | | 6.875% | | 12/15/13 | | BB– | | | 305,625 |

| | | | | |

| | 340 | | McMoran Exploration Corporation | | 11.875% | | 11/15/14 | | B | | | 367,200 |

| | | | | |

| | 450 | | NFR Energy LLC/Finance Corporation, 144A | | 9.750% | | 2/15/17 | | B | | | 451,125 |

| | | | | |

| | 150 | | Ocean Energy Inc. | | 7.250% | | 10/01/11 | | BBB+ | | | 162,403 |

| | | | | |

| | 150 | | Phillips Petroleum Company | | 8.750% | | 5/25/10 | | A1 | | | 151,765 |

| | | | | |

| | 180 | | Sandridge Energy Inc. | | 8.625% | | 4/01/15 | | B+ | | | 175,950 |

| | | | | |

| | 260 | | Sandridge Energy Inc., 144A | | 8.750% | | 1/15/20 | | B+ | | | 254,800 |

| | | | | |

| | 300 | | StatOilHydro ASA | | 2.900% | | 10/15/14 | | Aa2 | | | 300,315 |

| | | | | |

| | 225 | | Stone Energy Corporation | | 6.750% | | 12/15/14 | | CCC+ | | | 199,125 |

| | | | | |

| | 365 | | Tesoro Petroleum Corporation | | 6.250% | | 11/01/12 | | BB+ | | | 367,738 |

| | | | | |

| | 150 | | Valero Energy Corporation | | 6.875% | | 4/15/12 | | BBB | | | 162,629 |

| | | | | |

| | 205 | | W&T Offshore, Inc., 144A | | 8.250% | | 6/15/14 | | B+ | | | 192,700 |

| | | | | |

| | 250 | | XTO Energy, Inc. | | 5.900% | | 8/01/12 | | BBB | | | 274,694 |

| | 5,123 | | Total Oil, Gas & Consumable Fuels | | | | | | | | | 5,276,791 |

| | | | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | |

| | | Paper & Forest Products – 0.1% | | | | | | | | | |

| | | | | |

| $ | 210 | | Buckeye Technologies Inc. | | 8.500% | | 10/01/13 | | BB | | $ | 215,775 |

| | | Pharmaceuticals – 0.1% | | | | | | | | | |

| | | | | |

| | 125 | | American Home Products Corporation, Wyeth | | 6.950% | | 3/15/11 | | AA | | | 132,611 |

| | | Real Estate – 0.1% | | | | | | | | | |

| | | | | |

| | 205 | | Potlatch Corporation, 144A | | 7.500% | | 11/01/19 | | Ba1 | | | 210,638 |

| | | Software – 0.1% | | | | | | | | | |

| | | | | |

| | 125 | | Oracle Corporation | | 5.000% | | 1/15/11 | | A | | | 129,298 |

| | | Specialty Retail – 0.3% | | | | | | | | | |

| | | | | |

| | 140 | | Michael's Stores | | 11.375% | | 11/01/16 | | CCC | | | 151,900 |

| | | | | |

| | 435 | | TJX Companies, Inc. | | 4.200% | | 8/15/15 | | A | | | 460,652 |

| | 575 | | Total Specialty Retail | | | | | | | | | 612,552 |

| | | Tobacco – 0.4% | | | | | | | | | |

| | | | | |

| | 225 | | Altria Group Inc. | | 8.500% | | 11/10/13 | | Baa1 | | | 263,207 |

| | | | | |

| | 75 | | Reynolds American Inc. | | 6.500% | | 7/15/10 | | BBB | | | 75,887 |

| | | | | |

| | 400 | | Reynolds American Inc. | | 7.250% | | 6/01/13 | | BBB | | | 445,098 |

| | 700 | | Total Tobacco | | | | | | | | | 784,192 |

| | | Trading Companies & Distributors – 0.0% | | | | | | | | | |

| | | | | |

| | 50 | | GATX Financial Corporation | | 5.125% | | 4/15/10 | | BBB+ | | | 50,041 |

| | | Wireless Telecommunication Services – 0.9% | | | | | | | | | |

| | | | | |

| | 250 | | AT&T/Cingular Wireless Services | | 8.125% | | 5/01/12 | | A | | | 282,254 |

| | | | | |

| | 160 | | Cricket Communications Inc. | | 10.000% | | 7/15/15 | | B– | | | 167,200 |

| | | | | |

| | 125 | | IntelSat Jackson Holding, 144A | | 8.500% | | 11/01/19 | | B+ | | | 131,875 |

| | | | | |

| | 215 | | MetroPCS Wireless Inc. | | 9.250% | | 11/01/14 | | B | | | 220,913 |

| | | | | |

| | 490 | | Sprint Capital Corporation | | 6.900% | | 5/01/19 | | BB– | | | 450,800 |

| | | | | |

| | 125 | | Vodafone Group PLC | | 5.500% | | 6/15/11 | | A– | | | 131,111 |

| | | | | |

| | 150 | | Vodafone Group PLC | | 5.000% | | 12/16/13 | | A– | | | 162,026 |

| | 1,515 | | Total Wireless Telecommunication Services | | | | | | | | | 1,546,179 |

| $ | 45,690 | | Total Corporate Bonds (cost $45,611,974) | | | | | | | | | 47,474,566 |

| | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | U.S. GOVERNMENT AND AGENCY OBLIGATIONS – 50.7% | | | | | | | | | |

| | | | | |

| | | U.S. Treasury Bonds/Notes – 50.7% | | | | | | | | | |

| | | | | |

| $ | 300 | | United States of America Treasury Bonds/Notes | | 8.000% | | 11/15/21 | | AAA | | $ | 408,844 |

| | | | | |

| | 650 | | United States of America Treasury Bonds/Notes | | 5.250% | | 2/15/29 | | AAA | | | 707,485 |

| | | | | |