UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-09037

Nuveen Investment Trust III

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive, Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: September 30

Date of reporting period: March 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

Item 1. Reports to Stockholders.

Mutual Funds

Nuveen Taxable Bond Funds

For investors seeking a high level of current income and capital appreciation.

Semi-Annual Report

March 31, 2013

| | | | | | |

| | | Share Class / Ticker Symbol |

| | | |

| Fund Name | | Class A | | Class C | | Class I |

Nuveen Symphony Credit Opportunities Fund | | NCOAX | | NCFCX | | NCOIX |

Nuveen Symphony Floating Rate Income Fund | | NFRAX | | NFFCX | | NFRIX |

Nuveen Symphony High Yield Bond Fund | | NSYAX | | NSYCX | | NSYIX |

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund distributions and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund distributions and statements directly from Nuveen.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Table of Contents

Chairman’s

Letter to Shareholders

Dear Shareholders,

The global economy continues to struggle with low growth rates. The European Central Bank’s commitment to “do what it takes” to support sovereign debt markets has stabilized the broader euro area financial markets. The larger member states of the European Union (EU) are working diligently on a tighter financial and banking union and meaningful progress is being made. However, economic conditions in the southern tier members are not improving and their political leaders are becoming more forceful in their demands for loosening the current EU fiscal targets and timetables. Economic growth in emerging market countries continues to be buffeted by lower overseas demand for their manufactured products and raw materials.

In the U.S., the Fed’s commitment to low interest rates through Quantitative Easing is the subject of increasing debate in its policy making deliberations and many independent economists are expressing concern about the economic distortions resulting from negative real interest rates. There are encouraging signs in Congress that both political parties are working toward compromises on previously irreconcilable issues such as reforming immigration laws and the tax code. It is too early to tell whether those efforts will produce meaningful results or pave the way for cooperation on the major fiscal issues that loom ahead. Over the longer term, there are some positive trends for the U.S. economy: house prices are clearly recovering, banks and corporations continue to strengthen their financial positions and incentives for capital investment in the U.S. by domestic and foreign corporations are increasing due to more competitive energy and labor costs.

During the last eighteen months, U.S. investors have benefited from strong returns in the domestic equity markets and steady total returns in many fixed income markets. However, many macroeconomic risks remain unresolved, including negotiating through the many U.S. fiscal issues, achieving a better balance between fiscal discipline and encouraging economic growth in the euro area and reducing the potential economic impact of geopolitical issues, particularly in the Middle East and East Asia. In the face of these uncertainties, the experienced investment professionals at Nuveen Investments seek out investments that are enjoying positive and sustainable returns. At the same time they are always on the alert for risks in markets that are subject to the excessive optimism that can accompany an extended period of abnormally low interest rates. Monitoring this process is a critical function for the Fund Board as it oversees your Nuveen Fund on your behalf.

As always, I encourage you to communicate with your financial consultant if you have any questions about your investment in a Nuveen Fund. On behalf of the other members of your Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Board

May 24, 2013

Portfolio Managers’ Comments

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

These Funds are managed by Symphony Asset Management LLC, (Symphony), an affiliate of Nuveen Investments. Gunther Stein, director of investment strategies at Symphony, and Jenny Rhee manage the Nuveen Symphony Credit Opportunities Fund and the Nuveen Symphony High Yield Bond Fund, while Gunther and Scott Caraher oversee the investments of the Nuveen Symphony Floating Rate Income Fund.

Here the managers discuss their key strategies and the performance of the Funds for the six-month reporting period ended March 31, 2013. The Nuveen Symphony High Yield Bond Fund has an abbreviated reporting period from the Fund’s commencement of operations on December 10, 2012 through March 31, 2013.

How did the Funds perform during the six-month reporting period ended March 31, 2013?

The tables in the Fund Performance and Expense Ratios section of this report provide total return performance information for the Funds’ Class A Shares at net asset value (NAV) for the six-month, one-year and since inception periods ended March 31, 2013. The tables also compare the Funds’ returns to comparative market indexes and Lipper classification averages. A more detailed account of each Fund’s performance is provided later in this report.

What was the primary investment strategy for each Fund and how did this strategy affect the Fund’s performance for the six-month period ended March 31, 2013?

Nuveen Symphony Credit Opportunities Fund

The Fund’s Class A Shares at NAV outperformed the BofA Merrill Lynch U.S. High Yield Master II Index, the Custom Benchmark Index and the Lipper High Yield Funds Classification Average during the reporting period. In previous reports the Market Benchmark Index was used as the primary comparative index. During the reporting period, the Market Benchmark Index was renamed the Custom Benchmark Index and given secondary benchmark status. The former secondary benchmark for the Fund, the BofA Merrill Lynch U.S. High Yield Master II Index, became the primary index. Both indexes will be used for performance comparison going forward.

The Fund seeks current income and capital appreciation by investing primarily in debt instruments such as bonds, loans and convertible securities, a substantial portion of which may be rated below investment grade or, if unrated, we deem to be of comparable quality. The Fund may utilize derivatives, including options; futures contracts; options on futures contracts; swap agreements, including interest rate swaps, total return swaps, and credit default swaps; and options on swap agreements.

We base our investment process on fundamental, bottom-up credit analysis. Analysts assess sector dynamics, company business models and asset quality. Specific recommendations are based on an analysis of the relative value of the various types of debt within a company’s capital structure. Inherent in our credit analysis process is the evaluation of potential upside and downside to any credit. As such, we concentrate our efforts on sectors where there is sufficient transparency to assess the downside risk and where firms have assets to support meaningful recovery in case of default. In its focus on downside protection, we favor opportunities where valuations can be quantified and risks assessed.

During the reporting period, high yield bonds and leveraged loans posted strong results. For the fourth quarter 2012 (the most recent data available at the time this report was prepared), Credit Suisse reported bond issuance was $97.4 billion. Senior loan issuance was also robust, with a volume of $96.3 billion. Although investor demand for high yield credit remained strong throughout the earlier part of 2012, investor appetites shifted in the fourth quarter. High yield bond mutual funds saw outflows while loan mutual funds saw inflows. Despite the outflows in the fourth quarter 2012, heavy demand throughout the year led to an increase in the average high yield bond price and a corresponding decrease in yields to near record lows.

During the first quarter of 2013, investors continued to allocate money to risk assets. Although high yield bonds and senior loans lagged equities, they outperformed investment grade bonds and the 10-year Treasury.

During the reporting period, default rates remained well below the historical average long term default rate of 4.2%, according to Credit Suisse. Meanwhile, for fourth quarter the default rate was recorded by Credit Suisse as .59% (or 2.35% annualized).

The Fund benefited from exposure to HD Supply Inc. We owned several of the high yield bond facilities. HD Supply is the commercial arm of Home Depot. The company has performed well recently amid speculation of an IPO. Also enhancing the Fund’s performance were the bonds of Claire’s Stores, Inc., which announced strong earnings during the reporting period. The term loans of Clear Channel also benefited performance. The company is one of the leading global media and entertainment companies specializing in radio, digital, outdoor, mobile, live events, and on-demand entertainment and information services for local communities. The company was expected to address near-term maturities with refinancing transactions. Given Clear Channel’s leverage, this is seen as an overall positive for the company.

Several holdings that detracted from performance included Cengage Learning Acquisitions, Inc., Term Loan. The textbook and software maker announced disappointing earnings during the period. The company also continues to seek merger and acquisition related solutions. Additionally lagging the market was Fairpoint Communications 8.75% bonds. The holding was involved in an amendment and refinancing during the period. Lastly, the B-2 term loan of Toys R Us detracted from performance. The company announced weak holiday sales during the first quarter of 2013.

Nuveen Symphony Floating Rate Income Fund

The Fund’s Class A Shares at NAV outperformed both the Credit Suisse Leveraged Loan Index and the Lipper Loan Participation Funds Classification Average during the reporting period.

The Fund seeks current income and capital appreciation by investing primarily in floating rate loans and other floating rate securities, a substantial portion of which will be rated below investment-grade. The Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in floating rate securities. Floating rate securities are defined to include floating rate loans, other floating rate debt securities, money market securities and shares of money market and short-term bond funds. The Fund may invest up to 20% of its net assets in other securities, which would primarily be fixed rate debt securities, convertible securities and equity securities received as a result of the restructuring of an issuer’s debt. A substantial portion of the Fund’s assets generally will be invested in securities rated below investment grade or, if unrated, we deemed to be of comparable quality. The Fund may utilize derivatives, including options; futures contracts; options on futures contracts; swap agreements, including interest rate swaps, total return swaps, and credit default swaps; and options on swap agreements.

We base our investment process on fundamental, bottom-up credit analysis. Analysts assess sector dynamics, company business models and asset quality. Inherent in our credit analysis process is the evaluation of potential upside and downside to any credit. As such, we concentrate our efforts on sectors where there is sufficient transparency to assess the downside risk and where firms have assets to support meaningful recovery in case of default. In our focus on downside protection, we favor opportunities where valuations can be quantified and risks assessed.

During the period, the Fund’s capital was deployed into assets that we believe offer attractive current income and yield for the associated risk profile. Fundamentally, we feel that many of these companies have stable businesses, good asset coverage for senior debt holders, and can perform well in a stable to slow-growth environment.

Helping performance were the term loans of Clear Channel, as the media concern was expected to address near-term maturities with refinancing transactions. Also helping performance was exposure to IASIS Healthcare bonds and loans.

Detracting from performance was Cengage Learning Acquisitions, Inc. The textbook and software maker announced disappointing earnings during the period. The company continues to seek merger and acquisition-related solutions. Spectrum Brands, which is a global and diversified consumer products company, also detracted from performance. The company announced an acquisition during the period along with $1 billion of new issue bonds to finance the transaction.

Nuveen Symphony High Yield Bond Fund

The Fund’s Class A Shares at NAV outperformed both the BofA Merrill Lynch U.S. High Yield Master II Index and the Lipper High Yield Funds Classification Average during the abbreviated reporting period from December 10, 2012 through March 31, 2013.

The Fund seeks current income and capital appreciation by investing primarily in below investment grade bonds using a bottom up, research driven process. The Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in bonds rated below investment-grade or, if unrated, we deemed to be of comparable quality. The Fund may invest up to 20% of its net assets, collectively, in the bank loans, convertible securities and equity securities.

We base our investment process on fundamental, bottom-up credit analysis. Analysts assess sector dynamics, company business models and asset quality. Specific recommendations are based on an analysis of the relative value of the various types of debt within a company’s capital structure. Inherent in our credit analysis process is the evaluation of potential upside and downside to any credit. As such, we concentrate our efforts on sectors where there is sufficient transparency to assess the downside risk and where firms have assets to support meaningful recovery in case of default. In its focus on downside protection, we favor opportunities where valuations can be quantified and risks assessed.

During the first quarter of 2013, investors continued to allocate money to risk assets. Although high yield bonds and senior loans lagged equities, they outperformed investment grade bonds and the 10-year Treasury for the first quarter 2013. During the abbreviated reporting period, default rates remained well below the historical average long term default rate of 4.2%, according to Credit Suisse. In the first quarter of 2013, the default rate totaled .12%.

The Fund benefited from its exposure to IASIS Healthcare bonds and loans. This is despite being in a sector that is generally somewhat exposed to medicare reimbursement cuts. Holdings that contributed to performance included the term loans of Clear Channel. The company is one of the leading global media and entertainment companies specializing in radio, digital, outdoor, mobile, live events, and on-demand entertainment and information services for local communities. The company was expected to address near-term maturities with refinancing transactions. Given Clear Channel’s leverage, this is seen as an overall positive for the company. Additionally, Tempur Pedic bonds contributed to performance. The company announced better than expected Q4 2012 earnings.

Risk Considerations

Mutual fund investing involves risk; principal loss is possible. Debt or fixed income securities such as those held by the Funds are subject to market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices fall. Below investment grade or high yield debt securities are subject to liquidity risk and heightened credit risk. Foreign investments involve additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. The value of a Fund’s convertible securities may decline in response to such factors as rising interest rates and fluctuations in the market price of the underlying securities. These Funds are subject to loan settlement risk due to the lack of established settlement standards or remedies for failure to settle. Because each Fund currently has less assets than a larger fund, large inflows and outflows may impact the Fund’s market exposure and subsequently its performance. Redemption of a large number of shares may subject each Fund and its shareholders to leverage risk and disrupt the overall composition of the Fund’s portfolio and thereby impede the ability to pursue the investment strategy.

Fund Performance and Expense Ratios

The Fund Performance and Expense Ratios for each Fund are shown on the following three pages.

Returns quoted represent past performance, which is no guarantee of future results. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Returns may reflect a contractual agreement between certain Funds and the investment adviser to waive certain fees and expenses; see Notes to Financial Statements, Footnote 7 — Management Fees and Other Transactions with Affiliates for more information. In addition, returns may reflect a voluntary expense limitation by the Funds’ investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains.

Comparative index and Lipper return information is provided for the Funds’ Class A Shares at net asset value (NAV) only.

The expense ratios shown reflect the Funds’ total operating expenses (before fee waivers and/or expense reimbursements, if any) as shown in the Funds’ most recent prospectus. The expense ratios include management fees and other fees and expenses.

Fund Performance and Expense Ratios (continued)

Nuveen Symphony Credit Opportunities Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of March 31, 2013

| | | | | | | | | | | | |

| | |

| | | Cumulative | | | Average Annual | |

| | | |

| | | 6-Month | | | 1-Year | | | Since

Inception* | |

Class A Shares at NAV | | | 6.90% | �� | | | 13.07% | | | | 11.09% | |

Class A Shares at maximum Offering Price | | | 1.83% | | | | 7.70% | | | | 9.26% | |

BofA Merrill Lynch U.S. High Yield Master II Index** | | | 6.17% | | | | 13.06% | | | | 10.38% | |

Custom Benchmark Index** | | | 5.27% | | | | 11.12% | | | | 8.84% | |

Lipper High Yield Funds Classification Average** | | | 5.95% | | | | 11.80% | | | | 9.51% | |

| | | | | | | | | | | | |

Class C Shares | | | 6.48% | | | | 12.22% | | | | 10.24% | |

Class I Shares | | | 6.98% | | | | 13.35% | | | | 11.36% | |

Class A Shares have a maximum 4.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 1.12% | | | | 1.07% | |

Class C Shares | | | 1.87% | | | | 1.82% | |

Class I Shares | | | 0.87% | | | | 0.82% | |

The Fund’s investment adviser has agreed to waive fees and/or reimburse expenses through January 31, 2014, so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fee and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.85% (1.35% after January 31, 2014) of the average daily net assets of any class of Fund shares. The expense limitation expiring January 31, 2014, may be terminated or modified prior to that date only with the approval of the Board of Trustees of the Fund. The expense limitation in effect thereafter may be terminated or modified only with the approval of shareholders of the Fund.

| * | Since inception returns are from 4/28/10. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Fund Performance and Expense Ratios (continued)

Nuveen Symphony Floating Rate Income Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Average Annual Total Returns as of March 31, 2013

| | | | | | | | | | | | |

| | |

| | | Cumulative | | | Average Annual | |

| | | |

| | | 6-Month | | | 1-Year | | | Since

Inception** | |

Class A Shares at NAV | | | 5.12% | | | | 9.34% | | | | 7.11% | |

Class A Shares at maximum Offering Price* | | | 1.97% | | | | 6.06% | | | | 5.42% | |

Credit Suisse Leveraged Loan Index*** | | | 3.93% | | | | 8.27% | | | | 5.33% | |

Lipper Loan Participation Funds Classification Average*** | | | 3.74% | | | | 7.51% | | | | 5.12% | |

| | | |

Class C Shares | | | 4.74% | | | | 8.48% | | | | 6.29% | |

Class I Shares | | | 5.30% | | | | 9.60% | | | | 7.36% | |

Class A Shares have a maximum 4.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 1.90% | | | | 1.07% | |

Class C Shares | | | 2.69% | | | | 1.82% | |

Class I Shares | | | 1.62% | | | | 0.82% | |

The Fund’s investment adviser has agreed to waive fees and/or reimburse expenses through January 31, 2014, so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.85% (1.10% after January 31, 2014) of the average daily net assets of any class of Fund shares. This expense limitation expiring January 31, 2014, may be terminated or modified prior to that date only with the approval of the Board of Trustees of the Fund. The expense limitation in effect thereafter may be terminated or modified only with the approval of shareholders of the Fund.

| * | Effective April 1, 2013 (subsequent to the close of this reporting period) Class A Shares have a maximum 3.00% sales charge (Offering Price). |

| ** Since | inception returns are from 5/2/11. |

| *** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Fund Performance and Expense Ratios (continued)

Nuveen Symphony High Yield Bond Fund

Refer to the first page of this Fund Performance and Expense Ratios section for further explanation of the information included within this page.

Fund Performance

Cumulative Total Returns as of March 31, 2013

| | | | |

| | | | |

| |

| | | Since

Inception* | |

Class A Shares at NAV | | | 6.30% | |

Class A Shares at maximum Offering Price | | | 1.25% | |

BofA Merrill Lynch U.S. High Yield Master II Index** | | | 3.43% | |

Lipper High Yield Funds Classification Average** | | | 3.39% | |

| |

Class C Shares | | | 6.10% | |

Class I Shares | | | 6.40% | |

Class A Shares have a maximum 4.75% sales charge (Offering Price). Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within eighteen months of purchase. Class C Shares have a 1% CDSC for redemptions within less than twelve months, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

Expense Ratios as of Most Recent Prospectus

| | | | | | | | |

| | |

| | | Gross

Expense

Ratios | | | Net

Expense

Ratios | |

Class A Shares | | | 1.29% | | | | 1.10% | |

Class C Shares | | | 2.04% | | | | 1.85% | |

Class I Shares | | | 1.04% | | | | 0.85% | |

The Fund’s investment adviser has agreed to waive fees and/or reimburse expenses through January 31, 2015, so that total annual Fund operating expenses (excluding 12b-1 distribution and/or service fees, interest expenses, taxes, acquired fund fees and expenses, fees incurred in acquiring and disposing of portfolio securities and extraordinary expenses) do not exceed 0.85% of the average daily net assets of any class of Fund shares. This expense limitation expiring January 31, 2015, may be terminated or modified prior to that date only with the approval of the Board of Trustees of the Fund. The expense limitation in effect thereafter may be terminated or modified only with the approval of shareholders of the Fund.

| * | Since inception returns are from 12/10/12. |

| ** | Refer to the Glossary of Terms Used in this Report for definitions. Indexes and Lipper averages are not available for direct investment. |

Yields as of March 31, 2013

Dividend Yield is the most recent dividend per share (annualized) divided by the offering price per share.

The SEC 30-Day Yield is a standardized measure of a Fund’s yield that accounts for the future amortization of premiums or discounts of bonds held in the Fund’s portfolio. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. Dividend Yield may differ from the SEC 30-Day Yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium.

Nuveen Symphony Credit Opportunities Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares1 | | | 5.73% | | | | 4.49% | |

Class C Shares | | | 5.28% | | | | 3.95% | |

Class I Shares | | | 6.26% | | | | 5.02% | |

Nuveen Symphony Floating Rate Income Fund

| | | | | | | | |

| | |

| | | Dividend

Yield | | | SEC 30-Day

Yield | |

Class A Shares1 | | | 4.61% | | | | 2.71% | |

Class C Shares | | | 4.09% | | | | 2.11% | |

Class I Shares | | | 5.08% | | | | 3.02% | |

Nuveen Symphony High Yield Bond Fund

| | | | |

| |

| | | SEC 30-Day

Yield | |

Class A Shares1 | | | 5.71% | |

Class C Shares | | | 5.25% | |

Class I Shares | | | 6.26% | |

| 1 | The SEC Yield for Class A shares quoted in the table reflects the maximum sales load. Investors paying a reduced load because of volume discounts, investors paying no load because they qualify for one of the several exclusions from the load, and existing shareholders who previously paid a load but would like to know the SEC Yield applicable to their shares on a going-forward basis, should understand that the SEC Yield effectively applicable to them would be higher than the figure quoted in the table. |

Holding Summaries as of March 31, 2013

This data relates to the securities held in each Fund’s portfolio of investments. It should not be construed as a measure of performance for the Fund itself.

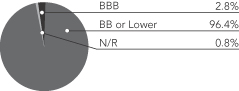

Ratings shown are the highest rating given by one of the following national rating agencies: Standard & Poor’s Group, Moody’s Investors Service, Inc. or Fitch, Inc. Credit ratings are subject to change. AAA, AA, A, and BBB are investment grade ratings; BB, B, CCC, CC, C and D are below-investment grade ratings. Certain bonds backed by U.S. Government or agency securities are regarded as having an implied rating equal to the rating of such securities. Holdings designated N/R are not rated by these national rating agencies.

Nuveen Symphony Credit

Opportunities Fund

Portfolio Credit Quality1

Nuveen Symphony Floating Rate Income Fund

Portfolio Credit Quality2

| | | | |

| Portfolio Allocation3 | | | |

| Corporate Bonds | | | 66.6% | |

| Variable Rate Senior Loan Interests | | | 26.1% | |

| Short-Term Investments | | | 8.5% | |

| Convertible Bonds | | | 1.1% | |

$1,000 Par (or similar) Institutional Structures | | | 0.3% | |

| Common Stocks | | | 0.2% | |

| Other4 | | | (2.8)% | |

| | | | |

| Portfolio Allocation3 | | | |

| Variable Rate Senior Loan Interests | | | 75.5% | |

| Short-Term Investments | | | 28.4% | |

| Corporate Bonds | | | 17.1% | |

| Other4 | | | (21.0)% | |

| | | | |

| Portfolio Composition3 | | | |

| Health Care Providers & Services | | | 8.6% | |

| Media | | | 6.9% | |

| Oil, Gas & Consumable Fuels | | | 6.8% | |

| Commercial Services & Supplies | | | 4.8% | |

| Wireless Telecommunication Services | | | 4.2% | |

| Hotels, Restaurants & Leisure | | | 4.2% | |

| Diversified Telecommunication Services | | | 3.3% | |

| Food & Staples Retailing | | | 3.1% | |

| Food Products | | | 3.1% | |

| Specialty Retail | | | 2.9% | |

| Chemicals | | | 2.9% | |

| Household Products | | | 2.7% | |

| Software | | | 2.6% | |

| Health Care Equipment & Supplies | | | 2.5% | |

| Distributors | | | 2.5% | |

| Communications Equipment | | | 2.4% | |

| Pharmaceuticals | | | 2.1% | |

| Machinery | | | 2.1% | |

| Household Durables | | | 2.0% | |

| IT Services | | | 2.0% | |

| Diversified Financial Services | | | 1.9% | |

| Containers & Packaging | | | 1.8% | |

| Short-Term Investments | | | 8.5% | |

| Other5 | | | 16.1% | |

| | | | |

| Portfolio Composition3 | | | |

| Media | | | 9.3% | |

| Pharmaceuticals | | | 7.0% | |

| Health Care Providers & Services | | | 6.4% | |

| Food Products | | | 5.6% | |

| Wireless Telecommunication Services | | | 4.7% | |

| Oil, Gas & Consumable Fuels | | | 4.7% | |

| Hotels, Restaurants & Leisure | | | 4.5% | |

| Health Care Equipment & Supplies | | | 4.0% | |

| Software | | | 4.0% | |

| Commercial Services & Supplies | | | 3.9% | |

| Short-Term Investments | | | 28.4% | |

| Other6 | | | 17.5% | |

| 1 | As a percentage of total long-term investments (excluding common stocks). Holdings are subject to change. |

| 2 | As a percentage of total long-term investments. Holdings are subject to change. |

| 3 | As a percentage of net assets. Holdings are subject to change. |

| 4 | Other assets less liabilities. |

| 5 | Includes other assets less liabilities and all industries less than 1.8% of net assets. |

| 6 | Includes other assets less liabilities and all industries less than 3.9% of net assets. |

Holding Summaries as of March 31, 2013 (continued)

Nuveen Symphony High Yield Bond Fund

Portfolio Credit Quality1

| | | | |

| Portfolio Allocation2 | | | |

| Corporate Bonds | | | 89.5% | |

| Variable Rate Senior Loan Interests | | | 8.6% | |

| Other3 | | | 1.9% | |

| | | | |

| Portfolio Composition3 | | | |

| Media | | | 10.7% | |

| Commercial Services & Supplies | | | 9.9% | |

| Hotels, Restaurants & Leisure | | | 9.5% | |

| Oil, Gas & Consumable Fuels | | | 8.8% | |

| Machinery | | | 7.6% | |

| Specialty Retail | | | 7.2% | |

| Distributors | | | 5.6% | |

| Household Durables | | | 5.0% | |

| Building Products | | | 5.0% | |

| Health Care Providers & Services | | | 4.9% | |

| Containers & Packaging | | | 4.8% | |

| Health Care Equipment & Supplies | | | 4.1% | |

| Other4 | | | 16.9% | |

| 1 | As a percentage of total investments. Holdings are subject to change. |

| 2 | As a percentage of net assets. Holdings are subject to change. |

| 3 | Other assets less liabilities. |

| 4 | Includes other assets less liabilities and all industries less than 4.1% of net assets. |

Expense Examples

As a shareholder of one or more of the Funds, you incur two types of costs: (1) transaction costs, including up-front and back-end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. The Examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. Since the expense examples for Nuveen Symphony High Yield Bond Fund reflect only 112 days of the Fund’s operations, they may not provide a meaningful understanding of the Fund’s ongoing expenses.

The Examples below are based on an investment of $1,000 invested at the beginning of the period and held through the end of the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the respective Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transaction costs were included, your costs would have been higher.

Nuveen Symphony Credit Opportunities Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | | | | (5% annualized return before expenses) | |

| | | A Shares | | | C Shares | | | I Shares | | | | | A Shares | | | C Shares | | | I Shares | |

| Beginning Account Value (10/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (3/31/13) | | $ | 1,069.00 | | | $ | 1,064.80 | | | $ | 1,069.80 | | | | | $ | 1,019.75 | | | $ | 1,016.01 | | | $ | 1,020.94 | |

| Expenses Incurred During Period | | $ | 5.36 | | | $ | 9.21 | | | $ | 4.13 | | | | | $ | 5.24 | | | $ | 9.00 | | | $ | 4.03 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.04%, 1.79% and .80% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Nuveen Symphony Floating Rate Income Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | | | | (5% annualized return before expenses) | |

| | | A Shares | | | C Shares | | | I Shares | | | | | A Shares | | | C Shares | | | I Shares | |

| Beginning Account Value (10/01/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (3/31/13) | | $ | 1,051.20 | | | $ | 1,047.40 | | | $ | 1,053.00 | | | | | $ | 1,019.60 | | | $ | 1,015.86 | | | $ | 1,020.84 | |

| Expenses Incurred During Period | | $ | 5.47 | | | $ | 9.29 | | | $ | 4.20 | | | | | $ | 5.39 | | | $ | 9.15 | | | $ | 4.13 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.07%, 1.82% and .82% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period).

Nuveen Symphony High Yield Bond Fund

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | Hypothetical Performance | |

| | | Actual Performance | | | | | (5% annualized return before expenses) | |

| | | A Shares | | | C Shares | | | I Shares | | | | | A Shares | | | C Shares | | | I Shares | |

| Beginning Account Value (12/10/12) | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | | | | | $ | 1,000.00 | | | $ | 1,000.00 | | | $ | 1,000.00 | |

| Ending Account Value (3/31/13) | | $ | 1,063.00 | | | $ | 1,061.00 | | | $ | 1,064.00 | | | | | $ | 1,012.06 | | | $ | 1,009.76 | | | $ | 1,012.83 | |

| Expenses Incurred During Period | | $ | 3.39 | | | $ | 5.75 | | | $ | 2.60 | | | | | $ | 3.30 | | | $ | 5.61 | | | $ | 2.53 | |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.07%, 1.82% and .82% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 112/365 (to reflect the 112 days in the period since the Fund’s commencement of operations).

Portfolio of Investments (Unaudited)

Nuveen Symphony Credit Opportunities Fund

March 31, 2013

| | | | | | | | | | | | | | | | | | | | |

| Shares | | | Description (1) | | | | | | | | | | | Value | |

| | | | COMMON STOCKS – 0.2% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Media – 0.2% | | | | | | | | | | | | | | | | |

| | | | | |

| | 11,546 | | | Tribune Company | | | | | | | | | | | | | | $ | 656,390 | |

| | | | | |

| | 9,292 | | | Tribune Company, (3) | | | | | | | | | | | | | | | — | |

| | | | Total Media | | | | | | | | | | | | | | | 656,390 | |

| | | | Paper & Forest Products – 0.0% | | | | | | | | | | | | | | | | |

| | | | | |

| | 30,709 | | | Catalyst Paper Corporation, (2), (4) | | | | | | | | | | | | | | | 69,529 | |

| | | | Total Common Stocks (cost $478,435) | | | | | | | | | | | | | | | 725,919 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | | | | Ratings (5) | | | Value | |

| | | | $1,000 PAR (OR SIMILAR) INSTITUTIONAL STRUCTURES – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | IT Services – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,000 | | | Zayo Escrow Corporation | | | 8.125% | | | | | | | | B1 | | | $ | 1,120,000 | |

| | | | Total $1,000 Par (or similar) Institutional Structures (cost $1,000,000) | | | | | | | | | | | | | | | 1,120,000 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | CONVERTIBLE BONDS – 1.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Health Care Equipment & Supplies – 0.4% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,537 | | | Hologic Inc. | | | 2.000% | | | | 12/15/43 | | | | N/R | | | $ | 1,610,967 | |

| | | | Health Care Providers & Services – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 500 | | | LifePoint Hospitals, Inc. | | | 3.500% | | | | 5/15/14 | | | | BB– | | | | 545,313 | |

| | | | | |

| | 500 | | | Omnicare, Inc. | | | 3.250% | | | | 12/15/35 | | | | B+ | | | | 499,375 | |

| | 1,000 | | | Total Health Care Providers & Services | | | | | | | | | | | | | | | 1,044,688 | |

| | | | Life Sciences Tools & Services – 0.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 500 | | | Charles River Laboratories International, Inc. | | | 2.250% | | | | 6/15/13 | | | | BB+ | | | | 504,063 | |

| | | | Multiline Retail – 0.0% | | | | | | | | | | | | | | | | |

| | | | | |

| | 200 | | | Saks, Inc. | | | 2.000% | | | | 3/15/24 | | | | BB | | | | 200,875 | |

| | | | Semiconductors & Equipment – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | ON Semiconductor Corporation | | | 2.625% | | | | 12/15/26 | | | | BB+ | | | | 1,040,000 | |

| $ | 4,237 | | | Total Convertible Bonds (cost $4,171,513) | | | | | | | | | | | | | | | 4,400,593 | |

| | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | CORPORATE BONDS – 66.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Aerospace & Defense – 0.8% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,150 | | | Bombardier Inc., 144A | | | 6.125% | | | | 1/15/23 | | | | BB | | | $ | 1,193,125 | |

| | | | | |

| | 750 | | | Sequa Corporation, 144A | | | 7.000% | | | | 12/15/17 | | | | CCC+ | | | | 759,375 | |

| | | | | |

| | 1,000 | | | TransDigm Inc. | | | 7.750% | | | | 12/15/18 | | | | B– | | | | 1,097,500 | |

| | 2,900 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | 3,050,000 | |

| | | | Airlines – 0.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 3,000 | | | Continental Airlines, Inc., 144A | | | 6.750% | | | | 9/15/15 | | | | Ba2 | | | | 3,142,500 | |

| | | | Auto Components – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 500 | | | Sonic Automotive Inc. | | | 7.000% | | | | 7/15/22 | | | | BB– | | | | 551,875 | |

| | | | | |

| | 500 | | | Tenneco Inc. | | | 7.750% | | | | 8/15/18 | | | | BB | | | | 550,000 | |

| | 1,000 | | | Total Auto Components | | | | | | | | | | | | | | | 1,101,875 | |

Portfolio of Investments (Unaudited)

Nuveen Symphony Credit Opportunities Fund (continued)

March 31, 2013

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | Chemicals – 2.5% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 500 | | | Ferro Corporation | | | 7.875% | | | | 8/15/18 | | | | B1 | | | $ | 518,750 | |

| | | | | |

| | 7,000 | | | Hexion US Finance, 144A | | | 6.625% | | | | 4/15/20 | | | | B1 | | | | 7,017,500 | |

| | | | | |

| | 1,600 | | | Ineos Finance PLC, 144A | | | 8.375% | | | | 2/15/19 | | | | BB– | | | | 1,770,000 | |

| | | | | |

| | 500 | | | PolyOne Corporation | | | 7.375% | | | | 9/15/20 | | | | BB– | | | | 552,500 | |

| | 9,600 | | | Total Chemicals | | | | | | | | | | | | | | | 9,858,750 | |

| | | | Commercial Services & Supplies – 3.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,500 | | | 313 Group Incorporated, 144A | | | 6.375% | | | | 12/01/19 | | | | B1 | | | | 2,481,250 | |

| | | | | |

| | 1,500 | | | Aramark Corporation, 144A | | | 5.750% | | | | 3/15/20 | | | | B– | | | | 1,533,750 | |

| | | | | |

| | 3,000 | | | Ceridian Corporation, 144A | | | 8.875% | | | | 7/15/19 | | | | B1 | | | | 3,491,250 | |

| | | | | |

| | 810 | | | Ceridian Corporation, 144A | | | 11.000% | | | | 3/15/21 | | | | CCC | | | | 868,725 | |

| | | | | |

| | 54 | | | Ceridian Corporation | | | 12.250% | | | | 11/15/15 | | | | CCC | | | | 55,823 | |

| | | | | |

| | 6,000 | | | Harland Clarke Holdings | | | 9.500% | | | | 5/15/15 | | | | B– | | | | 5,917,500 | |

| | | | | |

| | 500 | | | Mead Products LLC/ACCO Brands, 144A | | | 6.750% | | | | 4/30/20 | | | | BB | | | | 533,750 | |

| | | | | |

| | 225 | | | Tervita Corporation, 144A | | | 8.000% | | | | 11/15/18 | | | | B2 | | | | 232,594 | |

| | 14,589 | | | Total Commercial Services & Supplies | | | | | | | | | | | | | | | 15,114,642 | |

| | | | Communications Equipment – 1.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Avaya Inc., 144A | | | 9.000% | | | | 4/01/19 | | | | B1 | | | | 2,080,000 | |

| | | | | |

| | 1,000 | | | IntelSat Jackson Holdings | | | 7.250% | | | | 4/01/19 | | | | B | | | | 1,092,500 | |

| | | | | |

| | 1,000 | | | IntelSat Jackson Holdings | | | 7.500% | | | | 4/01/21 | | | | B | | | | 1,112,500 | |

| | | | | |

| | 2,000 | | | Nortel Networks Limited, (8) | | | 0.000% | | | | 7/15/11 | | | | BB– | | | | 2,095,000 | |

| | 6,000 | | | Total Communications Equipment | | | | | | | | | | | | | | | 6,380,000 | |

| | | | Computers & Peripherals – 0.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | 800 | | | Seagate HDD Cayman | | | 7.750% | | | | 12/15/18 | | | | BB+ | | | | 877,000 | |

| | | | | |

| | 1,500 | | | Sungard Data Systems Inc., 144A | | | 6.625% | | | | 11/01/19 | | | | B– | | | | 1,548,750 | |

| | 2,300 | | | Total Computers & Peripherals | | | | | | | | | | | | | | | 2,425,750 | |

| | | | Containers & Packaging – 1.5% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,750 | | | Ardagh Packaging Finance / MP HD USA, 144A | | | 7.000% | | | | 11/15/20 | | | | B3 | | | | 1,798,125 | |

| | | | | |

| | 1,000 | | | Ardagh Packaging Finance PLC, 144A | | | 7.375% | | | | 10/15/17 | | | | Ba3 | | | | 1,095,000 | |

| | | | | |

| | 1,000 | | | Ardagh Packaging Finance PLC, 144A | | | 7.375% | | | | 10/15/17 | | | | Ba3 | | | | 1,093,750 | |

| | | | | |

| | 1,250 | | | Reynolds Group | | | 7.875% | | | | 8/15/19 | | | | B+ | | | | 1,378,125 | |

| | | | | |

| | 500 | | | Reynolds Group | | | 6.875% | | | | 2/15/21 | | | | B+ | | | | 532,500 | |

| | 5,500 | | | Total Containers & Packaging | | | | | | | | | | | | | | | 5,897,500 | |

| | | | Distributors – 2.2% | | | | | | | | | | | | | | | | |

| | | | | |

| | 7,590 | | | HD Supply Inc., 144A | | | 11.500% | | | | 7/15/20 | | | | CCC+ | | | | 8,994,150 | |

| | | | Diversified Consumer Services – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Servicemaster Company | | | 8.000% | | | | 2/15/20 | | | | BB– | | | | 1,072,500 | |

| | | | Diversified Financial Services – 1.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Charter Communications, CCO Holdings LLC | | | 7.375% | | | | 6/01/20 | | | | BB– | | | | 1,108,750 | |

| | | | | |

| | 2,000 | | | Harland Clarke Holdings | | | 5.040% | | | | 5/15/15 | | | | B– | | | | 1,920,000 | |

| | | | | |

| | 2,000 | | | Jefferies Finance LLC, 144A | | | 7.375% | | | | 4/01/20 | | | | CCC+ | | | | 2,035,000 | |

| | 5,000 | | | Total Diversified Financial Services | | | | | | | | | | | | | | | 5,063,750 | |

| | | | Diversified Telecommunication Services – 3.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,213 | | | Cincinnati Bell Inc. | | | 8.375% | | | | 10/15/20 | | | | B1 | | | | 1,261,520 | |

| | | | | |

| | 1,500 | | | CyrusOne LP Finance, 144A | | | 6.375% | | | | 11/15/22 | | | | B+ | | | | 1,571,250 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | Diversified Telecommunication Services (continued) | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 2,000 | | | IntelSat Limited, 144A, (WI/DD) | | | 7.750% | | | | 6/01/21 | | | | CCC+ | | | $ | 2,035,000 | |

| | | | | |

| | 3,000 | | | IntelSat Limited, 144A, (WI/DD) | | | 8.125% | | | | 6/01/23 | | | | CCC+ | | | | 3,048,750 | |

| | | | | |

| | 2,000 | | | Level 3 Financing Inc., 144A | | | 7.000% | | | | 6/01/20 | | | | BB– | | | | 2,095,000 | |

| | | | | |

| | 2,000 | | | Level 3 Financing Inc. | | | 8.625% | | | | 7/15/20 | | | | BB– | | | | 2,230,000 | |

| | | | | |

| | 1,000 | | | Windstream Corporation | | | 7.500% | | | | 4/01/23 | | | | BB+ | | | | 1,060,000 | |

| | 12,713 | | | Total Diversified Telecommunication Services | | | | | | | | | | | | | | | 13,301,520 | |

| | | | Energy Equipment & Services – 1.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Hornbeck Offshore Services Inc. | | | 5.875% | | | | 4/01/20 | | | | BB– | | | | 2,070,000 | |

| | | | | |

| | 3,000 | | | Offshore Group Investment Limited | | | 7.125% | | | | 4/01/23 | | | | B– | | | | 3,067,500 | |

| | 5,000 | | | Total Energy Equipment & Services | | | | | | | | | | | | | | | 5,137,500 | |

| | | | Food & Staples Retailing – 1.9% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,600 | | | Rite Aid Corporation | | | 9.250% | | | | 3/15/20 | | | | CCC+ | | | | 1,806,000 | |

| | | | | |

| | 500 | | | Rite Aid Corporation | | | 8.000% | | | | 8/15/20 | | | | BB– | | | | 565,000 | |

| | | | | |

| | 5,000 | | | U.S. Foodservice, 144A | | | 8.500% | | | | 6/30/19 | | | | CCC+ | | | | 5,306,250 | |

| | 7,100 | | | Total Food & Staples Retailing | | | | | | | | | | | | | | | 7,677,250 | |

| | | | Food Products – 0.7% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Chiquita Brands International Inc., Corporate Bond, 144A | | | 7.875% | | | | 2/01/21 | | | | B1 | | | | 1,048,750 | |

| | | | | |

| | 1,500 | | | JBS USA LLC, 144A | | | 8.250% | | | | 2/01/20 | | | | BB | | | | 1,638,750 | |

| | 2,500 | | | Total Food Products | | | | | | | | | | | | | | | 2,687,500 | |

| | | | Gas Utilities – 0.5% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | AmeriGas Finance LLC | | | 7.000% | | | | 5/20/22 | | | | Ba2 | | | | 2,175,000 | |

| | | | Health Care Equipment & Supplies – 1.9% | | | | | | | | | | | | | | | | |

| | | | | |

| | 500 | | | Apria Healthcare Group Inc. | | | 12.375% | | | | 11/01/14 | | | | B– | | | | 510,000 | |

| | | | | |

| | 1,500 | | | Biomet Inc., 144A | | | 6.500% | | | | 8/01/20 | | | | B– | | | | 1,591,874 | |

| | | | | |

| | 500 | | | DJO Finance LLC/DJO Finance Corporation, 144A | | | 8.750% | | | | 3/15/18 | | | | B– | | | | 557,500 | |

| | | | | |

| | 2,400 | | | Kinetic Concepts | | | 10.500% | | | | 11/01/18 | | | | B | | | | 2,598,000 | |

| | | | | |

| | 2,400 | | | Kinetic Concepts | | | 12.500% | | | | 11/01/19 | | | | CCC+ | | | | 2,364,000 | |

| | | | | |

| | 165 | | | Rotech Healthcare Inc. | | | 10.750% | | | | 10/15/15 | | | | Caa1 | | | | 165,000 | |

| | 7,465 | | | Total Health Care Equipment & Supplies | | | | | | | | | | | | | | | 7,786,374 | |

| | | | Health Care Providers & Services – 6.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Aviv Healthcare Properties LP | | | 7.750% | | | | 2/15/19 | | | | BB | | | | 1,075,000 | |

| | | | | |

| | 500 | | | Capella Healthcare Inc. | | | 9.250% | | | | 7/01/17 | | | | B | | | | 541,250 | |

| | | | | |

| | 1,000 | | | HCA Holdings Inc. | | | 6.250% | | | | 2/15/21 | | | | B– | | | | 1,066,250 | |

| | | | | |

| | 4,000 | | | IASIS Healthcare Capital Corporation | | | 8.375% | | | | 5/15/19 | | | | CCC+ | | | | 4,205,000 | |

| | | | | |

| | 3,000 | | | Prospect Medical Holdings Inc., 144A | | | 8.375% | | | | 5/01/19 | | | | B2 | | | | 3,195,000 | |

| | | | | |

| | 1,385 | | | Symbion Inc. | | | 8.000% | | | | 6/15/16 | | | | B | | | | 1,464,638 | |

| | | | | |

| | 500 | | | Universal Health Services Inc. | | | 7.000% | | | | 10/01/18 | | | | BB– | | | | 543,750 | |

| | | | | |

| | 2,000 | | | Universal Hospital Services Inc., 144A | | | 7.625% | | | | 8/15/20 | | | | B+ | | | | 2,152,500 | |

| | | | | |

| | 2,000 | | | Vanguard Health Holding LLC/Inc., 144A | | | 7.750% | | | | 2/01/19 | | | | B– | | | | 2,140,000 | |

| | | | | |

| | 1,200 | | | Vanguard Health Holding LLC/Inc. | | | 8.000% | | | | 2/01/18 | | | | B– | | | | 1,276,500 | |

| | | | | |

| | 7,000 | | | Wolverine Healthcare Analytics, 144A | | | 10.625% | | | | 6/01/20 | | | | CCC+ | | | | 7,980,000 | |

| | 23,585 | | | Total Health Care Providers & Services | | | | | | | | | | | | | | | 25,639,888 | |

| | | | Health Care Technology – 0.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 500 | | | MedAssets Inc., 144A | | | 8.000% | | | | 11/15/18 | | | | B– | | | | 546,250 | |

Portfolio of Investments (Unaudited)

Nuveen Symphony Credit Opportunities Fund (continued)

March 31, 2013

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | Hotels, Restaurants & Leisure – 3.2% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,000 | | | Caesars Operating Escrow, 144A | | | 9.000% | | | | 2/15/20 | | | | B– | | | $ | 1,006,250 | |

| | | | | |

| | 350 | | | Carrols Restaurant Group, 144A | | | 11.250% | | | | 5/15/18 | | | | B– | | | | 394,188 | |

| | | | | |

| | 3,000 | | | Landry’s Holdings, 144A | | | 10.250% | | | | 1/01/18 | | | | CCC+ | | | | 3,142,500 | |

| | | | | |

| | 1,000 | | | Landry’s Restaurants Inc., 144A | | | 9.375% | | | | 5/01/20 | | | | BB– | | | | 1,077,500 | |

| | | | | |

| | 1,200 | | | MGM Resorts International Inc. | | | 7.750% | | | | 3/15/22 | | | | B+ | | | | 1,332,000 | |

| | | | | |

| | 2,000 | | | Pinnacle Entertainment Inc. | | | 7.750% | | | | 4/01/22 | | | | B | | | | 2,147,500 | |

| | | | | |

| | 2,000 | | | RHP Hotel Properties LP Finance, 144A | | | 5.000% | | | | 4/15/21 | | | | BB | | | | 2,015,000 | |

| | | | | |

| | 1,500 | | | Station Casinos LLC, 144A | | | 7.500% | | | | 3/01/21 | | | | CCC+ | | | | 1,541,250 | |

| | 12,050 | | | Total Hotels, Restaurants & Leisure | | | | | | | | | | | | | | | 12,656,188 | |

| | | | Household Durables – 1.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,440 | | | Libbey Glass Inc. | | | 6.875% | | | | 5/15/20 | | | | B+ | | | | 1,553,400 | |

| | | | | |

| | 1,000 | | | RSI Home Products Incorporated, 144A | | | 6.875% | | | | 3/01/18 | | | | B+ | | | | 1,015,000 | |

| | | | | |

| | 1,000 | | | Spectrum Brands Inc., 144A | | | 6.375% | | | | 11/15/20 | | | | BB– | | | | 1,073,750 | |

| | | | | |

| | 750 | | | Tempur Pedic International Inc., 144A | | | 6.875% | | | | 12/15/20 | | | | B+ | | | | 800,625 | |

| | 4,190 | | | Total Household Durables | | | | | | | | | | | | | | | 4,442,775 | |

| | | | Household Products – 2.7% | | | | | | | | | | | | | | | | |

| | | | | |

| | 5,000 | | | 313 Group Incorporated, 144A | | | 8.750% | | | | 12/01/20 | | | | CCC+ | | | | 5,056,250 | |

| | | | | |

| | 3,000 | | | Serta Simmons Holdings LLC, 144A | | | 8.125% | | | | 10/01/20 | | | | CCC+ | | | | 3,116,250 | |

| | | | | |

| | 1,500 | | | Spectrum Brands Inc., 144A | | | 6.625% | | | | 11/15/22 | | | | BB– | | | | 1,627,500 | |

| | | | | |

| | 1,000 | | | Spectrum Brands Inc. | | | 9.500% | | | | 6/15/18 | | | | Ba3 | | | | 1,132,500 | |

| | 10,500 | | | Total Household Products | | | | | | | | | | | | | | | 10,932,500 | |

| | | | Independent Power Producers & Energy Traders – 0.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,500 | | | NRG Energy Inc., 144A | | | 6.625% | | | | 3/15/23 | | | | BB | | | | 1,590,000 | |

| | | | Insurance – 0.5% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Fidelity & Guaranty Life Holdings Inc., 144A | | | 6.375% | | | | 4/01/21 | | | | BB– | | | | 2,040,000 | |

| | | | IT Services – 0.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 3,000 | | | First Data Corporation, 144A | | | 7.375% | | | | 6/15/19 | | | | BB– | | | | 3,191,250 | |

| | | | Leisure Equipment & Products – 0.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | PC Merger Sub Inc., 144A | | | 8.875% | | | | 8/01/20 | | | | CCC+ | | | | 2,195,000 | |

| | | | Machinery – 2.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,750 | | | Cleaver-Brooks Inc., 144A | | | 8.750% | | | | 12/15/19 | | | | B | | | | 1,887,813 | |

| | | | | |

| | 1,500 | | | NES Rental Holdings Inc., 144A | | | 12.250% | | | | 4/15/15 | | | | CCC+ | | | | 1,586,250 | |

| | | | | |

| | 2,000 | | | Terex Corporation | | | 6.000% | | | | 5/15/21 | | | | B+ | | | | 2,105,000 | |

| | | | | |

| | 3,000 | | | Xerium Technologies | | | 8.875% | | | | 6/15/18 | | | | B | | | | 2,872,500 | |

| | 8,250 | | | Total Machinery | | | | | | | | | | | | | | | 8,451,563 | |

| | | | Media – 4.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,750 | | | Cequel Communications Holding I LLC Capital | | | 6.375% | | | | 9/15/20 | | | | B– | | | | 1,815,625 | |

| | | | | |

| | 1,000 | | | Charter Communications, CCO Holdings LLC | | | 7.000% | | | | 1/15/19 | | | | BB– | | | | 1,077,500 | |

| | | | | |

| | 1,000 | | | Charter Communications, CCO Holdings LLC | | | 6.625% | | | | 1/31/22 | | | | BB– | | | | 1,072,500 | |

| | | | | |

| | 109 | | | Clear Channel Communications, Inc., 144A | | | 9.000% | | | | 12/15/19 | | | | CCC+ | | | | 104,776 | |

| | | | | |

| | 1,000 | | | Clear Channel Communications, Inc., 144A | | | 11.250% | | | | 3/01/21 | | | | CCC+ | | | | 1,025,000 | |

| | | | | |

| | 2,000 | | | Clear Channel Communications, Inc. | | | 4.900% | | | | 5/15/15 | | | | CCC– | | | | 1,855,000 | |

| | | | | |

| | 2,500 | | | Clear Channel Communications, Inc. | | | 11.000% | | | | 8/01/16 | | | | CCC– | | | | 1,975,000 | |

| | | | | |

| | 500 | | | Clear Channel Worldwide Holdings Inc. | | | 7.625% | | | | 3/15/20 | | | | B | | | | 516,875 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | Media (continued) | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 1,100 | | | Clear Channel Worldwide Holdings Inc. | | | 7.625% | | | | 3/15/20 | | | | B | | | $ | 1,148,125 | |

| | | | | |

| | 337 | | | Entravision Communications Corporation | | | 8.750% | | | | 8/01/17 | | | | B+ | | | | 365,645 | |

| | | | | |

| | 4,000 | | | McGraw-Hill Global Education Holdings, 144A | | | 9.750% | | | | 4/01/21 | | | | BB | | | | 3,960,000 | |

| | | | | |

| | 1,000 | | | Mediacom LLC | | | 7.250% | | | | 2/15/22 | | | | B | | | | 1,100,000 | |

| | | | | |

| | 500 | | | UnityMedia Hessen GmBH, 144A | | | 7.500% | | | | 3/15/19 | | | | BB– | | | | 546,875 | |

| | | | | |

| | 1,000 | | | UPCB Finance Limited, 144A | | | 7.250% | | | | 11/15/21 | | | | BB– | | | | 1,105,000 | |

| | | | | |

| | 500 | | | UPCB Finance VI Limited, 144A | | | 6.875% | | | | 1/15/22 | | | | BB– | | | | 543,750 | |

| | | | | |

| | 1,000 | | | WideOpenWest Finance Capital Corporation, 144A | | | 10.250% | | | | 7/15/19 | | | | CCC+ | | | | 1,112,500 | |

| | 19,296 | | | Total Media | | | | | | | | | | | | | | | 19,324,171 | |

| | | | Metals & Mining – 0.7% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Global Brass and Copper, 144A | | | 9.500% | | | | 6/01/19 | | | | B | | | | 1,107,500 | |

| | | | | |

| | 500 | | | Novellis Inc. | | | 8.750% | | | | 12/15/20 | | | | B | | | | 563,750 | |

| | | | | |

| | 1,100 | | | Walter Energy Inc., 144A | | | 8.500% | | | | 4/15/21 | | | | B | | | | 1,127,500 | |

| | 2,600 | | | Total Metals & Mining | | | | | | | | | | | | | | | 2,798,750 | |

| | | | Multiline Retail – 0.7% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,390 | | | Bon-Ton Department Stores Inc. | | | 10.250% | | | | 3/15/14 | | | | CCC | | | | 1,396,950 | |

| | | | | |

| | 1,300 | | | Revlon Consumer Products, 144A | | | 5.750% | | | | 2/15/21 | | | | B1 | | | | 1,304,875 | |

| | 2,690 | | | Total Multiline Retail | | | | | | | | | | | | | | | 2,701,825 | |

| | | | Oil, Gas & Consumable Fuels – 6.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Calumet Specialty Products | | | 9.375% | | | | 5/01/19 | | | | B | | | | 1,120,000 | |

| | | | | |

| | 250 | | | Chaparral Energy Inc., 144A | | | 7.625% | | | | 11/15/22 | | | | B– | | | | 273,124 | |

| | | | | |

| | 1,400 | | | Cheniere Energy Inc., 144A | | | 5.625% | | | | 2/01/21 | | | | BB+ | | | | 1,452,500 | |

| | | | | |

| | 2,000 | | | Drill Rigs Holdings Inc., 144A | | | 6.500% | | | | 10/01/17 | | | | B | | | | 2,020,000 | |

| | | | | |

| | 500 | | | EPL Oil & Gas Inc., 144A | | | 8.250% | | | | 2/15/18 | | | | B– | | | | 530,000 | |

| | | | | |

| | 1,250 | | | Everest Acquisition LLC Finance, 144A | | | 7.750% | | | | 9/01/22 | | | | B | | | | 1,381,250 | |

| | | | | |

| | 1,000 | | | Genesis Energy LP | | | 7.875% | | | | 12/15/18 | | | | B1 | | | | 1,097,500 | |

| | | | | |

| | 500 | | | Halcon Resources Limited Liability Corporation, 144A | | | 8.875% | | | | 5/15/21 | | | | CCC+ | | | | 538,750 | |

| | | | | |

| | 2,000 | | | Laredo Petroleum Inc. | | | 7.375% | | | | 5/01/22 | | | | B– | | | | 2,190,000 | |

| | | | | |

| | 2,000 | | | Linn Energy LLC Finance Corporation, 144A | | | 6.250% | | | | 11/01/19 | | | | B | | | | 2,045,000 | |

| | | | | |

| | 2,850 | | | Magnum Hunter Resources Corporation | | | 9.750% | | | | 5/15/20 | | | | CCC+ | | | | 2,992,500 | |

| | | | | |

| | 2,000 | | | Oasis Petroleum Inc. | | | 6.500% | | | | 11/01/21 | | | | B | | | | 2,180,000 | |

| | | | | |

| | 2,000 | | | PetroBakken Energy Limited, 144A | | | 8.625% | | | | 2/01/20 | | | | CCC+ | | | | 2,040,000 | |

| | | | | |

| | 3,000 | | | Plains Exploration & Production Company | | | 6.500% | | | | 11/15/20 | | | | B1 | | | | 3,315,000 | |

| | | | | |

| | 1,300 | | | Range Resources Corporation | | | 5.000% | | | | 3/15/23 | | | | BB | | | | 1,329,250 | |

| | | | | |

| | 1,600 | | | Shelf Drill Holdings Limited, 144A | | | 8.625% | | | | 11/01/18 | | | | B1 | | | | 1,696,000 | |

| | 24,650 | | | Total Oil, Gas & Consumable Fuels | | | | | | | | | | | | | | | 26,200,874 | |

| | | | Paper & Forest Products – 0.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,332 | | | Catalyst Paper Corporation | | | 11.000% | | | | 10/30/17 | | | | N/R | | | | 1,854,079 | |

| | | | | |

| | 500 | | | Unifrax I LLC / Unifrax Holdings, 144A | | | 7.500% | | | | 2/15/19 | | | | B– | | | | 515,000 | |

| | 2,832 | | | Total Paper & Forest Products | | | | | | | | | | | | | | | 2,369,079 | |

| | | | Personal Products – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,000 | | | Prestige Brands Inc. | | | 8.125% | | | | 2/01/20 | | | | B– | | | | 1,128,750 | |

| | | | Pharmaceuticals – 0.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | 53 | | | Angiotech Pharmaceuticals Inc. | | | 5.000% | | | | 12/01/13 | | | | N/R | | | | 53,199 | |

Portfolio of Investments (Unaudited)

Nuveen Symphony Credit Opportunities Fund (continued)

March 31, 2013

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Ratings (5) | | | Value | |

| | | | Pharmaceuticals (continued) | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 897 | | | Angiotech Pharmaceuticals Inc. | | | 9.000% | | | | 12/01/16 | | | | N/R | | | $ | 900,363 | |

| | | | | |

| | 750 | | | Warner Chilcott Company LLC | | | 7.750% | | | | 9/15/18 | | | | BB | | | | 801,563 | |

| | 1,700 | | | Total Pharmaceuticals | | | | | | | | | | | | | | | 1,755,125 | |

| | | | Real Estate Investment Trust – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,200 | | | Istar Financial Inc. | | | 9.000% | | | | 6/01/17 | | | | B+ | | | | 1,341,000 | |

| | | | Road & Rail – 0.7% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,250 | | | Avis Budget Car Rental, 144A, (WI/DD) | | | 5.500% | | | | 4/01/23 | | | | BB– | | | | 1,246,875 | |

| | | | | |

| | 1,000 | | | Avis Budget Car Rental | | | 8.250% | | | | 1/15/19 | | | | B+ | | | | 1,108,750 | |

| | | | | |

| | 500 | | | Swift Services Holdings Inc. | | | 10.000% | | | | 11/15/18 | | | | B+ | | | | 572,500 | |

| | 2,750 | | | Total Road & Rail | | | | | | | | | | | | | | | 2,928,125 | |

| | | | Software – 1.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 400 | | | Emdeon Incorporated | | | 11.000% | | | | 12/31/19 | | | | CCC+ | | | | 461,000 | |

| | | | | |

| | 2,000 | | | First Data Corporation, (WI/DD) | | | 10.625% | | | | 6/15/21 | | | | B– | | | | 2,022,500 | |

| | | | | |

| | 850 | | | Infor Us Inc. | | | 11.500% | | | | 7/15/18 | | | | B– | | | | 998,750 | |

| | | | | |

| | 750 | | | Infor Us Inc. | | | 9.375% | | | | 4/01/19 | | | | B– | | | | 850,312 | |

| | 4,000 | | | Total Software | | | | | | | | | | | | | | | 4,332,562 | |

| | | | Specialty Retail – 2.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 3,000 | | | Claire’s Stores, Inc., 144A | | | 9.000% | | | | 3/15/19 | | | | B2 | | | | 3,390,000 | |

| | | | | |

| | 1,000 | | | Claire’s Stores, Inc. | | | 10.500% | | | | 6/01/17 | | | | CCC | | | | 1,012,500 | |

| | | | | |

| | 1,000 | | | Claire’s Stores, Inc. | | | 8.875% | | | | 3/15/19 | | | | CCC | | | | 1,055,000 | |

| | | | | |

| | 2,850 | | | Jo-Ann Stores Holdings Inc., 144A | | | 9.750% | | | | 10/15/19 | | | | CCC+ | | | | 2,992,500 | |

| | 7,850 | | | Total Specialty Retail | | | | | | | | | | | | | | | 8,450,000 | |

| | | | Textiles, Apparel & Luxury Goods – 0.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Levi Strauss & Company | | | 6.875% | | | | 5/01/22 | | | | BB– | | | | 2,190,000 | |

| | | | | |

| | 1,000 | | | Perry Ellis International | | | 7.875% | | | | 4/01/19 | | | | B+ | | | | 1,050,000 | |

| | 3,000 | | | Total Textiles, Apparel & Luxury Goods | | | | | | | | | | | | | | | 3,240,000 | |

| | | | Thrifts & Mortgage Finance – 0.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,500 | | | Nationstar Mortgage LLC Capital Corporation | | | 6.500% | | | | 7/01/21 | | | | B+ | | | | 1,563,750 | |

| | | | Trading Companies & Distributors – 0.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Rexel SA, 144A, (WI/DD) | | | 5.250% | | | | 6/15/20 | | | | BB | | | | 2,025,000 | |

| | | | | |

| | 1,200 | | | United Rentals Financing Escrow Corporation, 144A | | | 7.375% | | | | 5/15/20 | | | | B+ | | | | 1,332,000 | |

| | 3,200 | | | Total Trading Companies & Distributors | | | | | | | | | | | | | | | 3,357,000 | |

| | | | Wireless Telecommunication Services – 3.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | CenturyLink Inc. | | | 5.625% | | | | 4/01/20 | | | | BB+ | | | | 2,045,000 | |

| | | | | |

| | 2,000 | | | Digicel Limited, 144A | | | 6.000% | | | | 4/15/21 | | | | B1 | | | | 1,990,000 | |

| | | | | |

| | 2,000 | | | FairPoint Communications Inc., 144A | | | 8.750% | | | | 8/15/19 | | | | B | | | | 1,940,000 | |

| | | | | |

| | 1,700 | | | MetroPCS Wireless Inc., 144A | | | 6.250% | | | | 4/01/21 | | | | BB | | | | 1,729,750 | |

| | | | | |

| | 2,500 | | | MetroPCS Wireless Inc., 144A | | | 6.625% | | | | 4/01/23 | | | | BB | | | | 2,550,000 | |

| | | | | |

| | 1,000 | | | Nortel Networks Limited, (8) | | | 10.125% | | | | 7/15/13 | | | | N/R | | | | 1,140,000 | |

| | | | | |

| | 1,000 | | | Syniverse Holdings Inc. | | | 9.125% | | | | 1/15/19 | | | | B– | | | | 1,097,500 | |

| | 12,200 | | | Total Wireless Telecommunication Services | | | | | | | | | | | | | | | 12,492,250 | |

| $ | 253,300 | | | Total Corporate Bonds (cost $253,406,494) | | | | | | | | | | | | | | | 266,535,236 | |

| | | | | | | | | | | | | | | | | | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity (6) | | | Ratings (5) | | | Value | |

| | | | VARIABLE RATE SENIOR LOAN INTERESTS – 26.1% (7) | | | | | | | | | | | | | | | | |

| | | | | |

| | | | Aerospace & Defense – 0.7% | | | | | | | | | | | | | | | | |

| | | | | |

| $ | 2,000 | | | Beechcraft Holdings LLC, Exit Term Loan B | | | 5.750% | | | | 2/15/20 | | | | BB– | | | $ | 2,012,500 | |

| | | | | |

| | 878 | | | Hamilton Sundstrand, Term Loan, First Lien | | | 4.000% | | | | 12/13/19 | | | | B1 | | | | 884,804 | |

| | 2,878 | | | Total Aerospace & Defense | | | | | | | | | | | | | | | 2,897,304 | |

| | | | Airlines – 0.6% | | | | | | | | | | | | | | | | |

| | | | | |

| | 2,000 | | | Delta Air Lines, Inc., Term Loan B1 | | | 5.250% | | | | 10/18/18 | | | | Ba2 | | | | 2,034,376 | |

| | | | | |

| | 500 | | | United Air Lines, Inc., Term Loan B, (WI/DD) | | | TBD | | | | TBD | | | | Ba2 | | | | 506,094 | |

| | 2,500 | | | Total Airlines | | | | | | | | | | | | | | | 2,540,470 | |

| | | | Auto Components – 0.5% | | | | | | | | | | | | | | | | |

| | | | | |

| | 998 | | | FleetPride Corporation, Term Loan, First Lien | | | 5.250% | | | | 11/16/19 | | | | B1 | | | | 1,011,839 | |

| | | | | |

| | 955 | | | Schaeffler AG, Term Loan C | | | 4.250% | | | | 1/07/17 | | | | Ba3 | | | | 966,938 | |

| | 1,953 | | | Total Auto Components | | | | | | | | | | | | | | | 1,978,777 | |

| | | | Biotechnology – 0.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 294 | | | Grifols, Inc., Term Loan | | | 4.250% | | | | 6/01/17 | | | | BB | | | | 297,106 | |

| | | | Capital Markets – 0.7% | | | | | | | | | | | | | | | | |

| | | | | |

| | 850 | | | American Capital, LTD., Senior Secured Term Loan | | | 5.500% | | | | 8/15/16 | | | | B+ | | | | 864,875 | |

| | | | | |

| | 1,962 | | | Walter Investment Management First Lien Term Loan | | | 5.750% | | | | 11/28/17 | | | | B+ | | | | 2,000,117 | |

| | 2,812 | | | Total Capital Markets | | | | | | | | | | | | | | | 2,864,992 | |

| | | | Chemicals – 0.4% | | | | | | | | | | | | | | | | |

| | | | | |

| | 891 | | | Ineos US Finance LLC, Term Loan B | | | 6.500% | | | | 5/04/18 | | | | B+ | | | | 906,315 | |

| | | | | |

| | 489 | | | Univar, Inc., Term Loan | | | 5.000% | | | | 6/30/17 | | | | B+ | | | | 494,207 | |

| | 1,380 | | | Total Chemicals | | | | | | | | | | | | | | | 1,400,522 | |

| | | | Commercial Services & Supplies – 1.0% | | | | | | | | | | | | | | | | |

| | | | | |

| | 833 | | | Aramark Corporation, Term Loan, Tranche D | | | 4.000% | | | | 2/20/20 | | | | BB– | | | | 843,375 | |

| | | | | |

| | 435 | | | CCS Income Trust, Term Loan, First Lien | | | 6.250% | | | | 5/12/18 | | | | B2 | | | | 440,270 | |

| | | | | |

| | 2,491 | | | Ceridian Corporation, Extended Term Loan | | | 5.953% | | | | 5/09/17 | | | | B1 | | | | 2,541,232 | |

| | 3,759 | | | Total Commercial Services & Supplies | | | | | | | | | | | | | | | 3,824,877 | |

| | | | Communications Equipment – 0.8% | | | | | | | | | | | | | | | | |

| | | | | |

| | 998 | | | Alcatel-Lucent, Term Loan C | | | 7.250% | | | | 1/29/19 | | | | BB– | | | | 1,014,853 | |

| | | | | |

| | 998 | | | CompuCom Systems, Inc., Term Loan, First Lien | | | 6.500% | | | | 10/04/18 | | | | B+ | | | | 1,010,800 | |

| | | | | |

| | 995 | | | Zayo Group LLC, Term Loan B, (WI/DD) | | | TBD | | | | TBD | | | | B1 | | | | 1,007,064 | |

| | 2,991 | | | Total Communications Equipment | | | | | | | | | | | | | | | 3,032,717 | |

| | | | Consumer Finance – 0.1% | | | | | | | | | | | | | | | | |

| | | | | |

| | 375 | | | Springleaf Financial Funding Company, Term Loan | | | 5.500% | | | | 5/10/17 | | | | B3 | | | | 378,105 | |

| | | | Containers & Packaging – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 712 | | | Reynolds Group Holdings, Inc., Term Loan | | | 4.750% | | | | 9/28/18 | | | | B+ | | | | 722,967 | |

| | | | | |

| | 351 | | | Sealed Air Corporation, Term Loan B1 | | | 4.000% | | | | 10/03/18 | | | | Ba1 | | | | 357,302 | |

| | 1,063 | | | Total Containers & Packaging | | | | | | | | | | | | | | | 1,080,269 | |

| | | | Distributors – 0.3% | | | | | | | | | | | | | | | | |

| | | | | |

| | 1,244 | | | HD Supply, Inc., Term Loan B | | | 4.500% | | | | 10/12/17 | | | | B+ | | | | 1,275,621 | |