Exhibit (c)(3)

CONFIDENTIAL

Discussion Materials – November 9, 2009

CONFIDENTIAL

Disclaimer

This presentation and the information contained herein is confidential and has been prepared exclusively for the benefit and internal use of the Special Committee of the Board of Directors of Rubio’s Restaurants, Inc. (the “Company”), in order to assist the Special Committee in evaluating, on a preliminary basis, the feasibility of a possible transaction or transactions and other strategic alternatives and does not convey any right of publication or disclosure, in whole or in part, to any other party without the prior written consent of Cowen. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by Cowen to the Special Committee.

The information in this presentation is based upon management forecasts supplied to Cowen and reflects prevailing conditions and Cowen’s views as of this date, all of which are accordingly subject to change. Cowen’s estimates constitute Cowen’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, Cowen has with your consent, assumed and relied, without independent investigation, upon the accuracy and completeness of all financial and other information provided to us by the management of the Company or which is publicly available or was otherwise reviewed by Cowen. Cowen’s analysis is not and does not purport to be appraisals of the assets, stock or business of the Company or any other entity. Cowen does not make representations as to the actual value which may be received in connection with a transaction or as to the price at which the Company’s securities may trade at any time. Cowen does not address any legal, tax or accounting effects of consummating a transaction or any other alternative. The information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other effects. This presentation does not represent a fairness opinion, recommendation, valuation or opinion of any kind. Cowen does not have any obligation to update, revise or reaffirm this presentation.

The information contained herein, as well as any other advice, services or other information provided to you by Cowen, is being provided pursuant to and subject to the terms of our engagement letter with the Board and may not be used or relied upon in any manner, nor are any duties or obligations created with respect thereto. This presentation does not constitute a commitment by Cowen or any of its affiliates to underwrite, subscribe for or place any securities to extend or arrange credit or to provide any other service.

Cowen policy mandates that no Cowen employee may directly or indirectly offer a company favorable research or threaten to change research as consideration or inducement for the receipt of business or compensation.

DISCUSSION MATERIALS

CONFIDENTIAL

Table of Contents

Page

I. Situation Overview 2

II. Restaurant Market Update 4

III. Rubio’s Overview 15

IV. Valuation Overview 32

V. Strategic Alternatives Overview 44

DISCUSSION MATERIALS

1

CONFIDENTIAL

I. Situation Overview

CONFIDENTIAL

Situation Overview

Cowen and Company, LLC is pleased to advise Rubio’s Special Committee of the Board of Directors in evaluating the Company’s alternatives

As part of this process, Cowen has considered the following Strategic Alternatives:

Status Quo

Share Repurchase

Acquisitions

Sale of the Company

I. SITUATION OVERVIEW

DISCUSSION MATERIALS

3

CONFIDENTIAL

II. Restaurant Market Update

CONFIDENTIAL

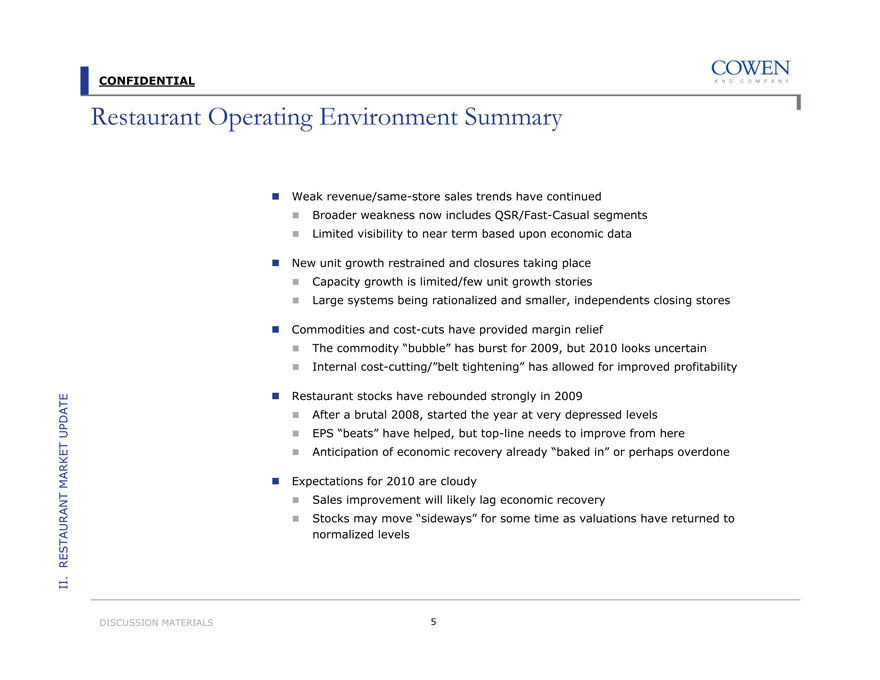

Restaurant Operating Environment Summary

Weak revenue/same-store sales trends have continued

Broader weakness now includes QSR/Fast-Casual segments

Limited visibility to near term based upon economic data

New unit growth restrained and closures taking place

Capacity growth is limited/few unit growth stories

Large systems being rationalized and smaller, independents closing stores

Commodities and cost-cuts have provided margin relief

The commodity “bubble” has burst for 2009, but 2010 looks uncertain

Internal cost-cutting/“belt tightening” has allowed for improved profitability

Restaurant stocks have rebounded strongly in 2009

After a brutal 2008, started the year at very depressed levels

EPS “beats” have helped, but top-line needs to improve from here

Anticipation of economic recovery already “baked in” or perhaps overdone

Expectations for 2010 are cloudy

Sales improvement will likely lag economic recovery

Stocks may move “sideways” for some time as valuations have returned to normalized levels

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

5

CONFIDENTIAL

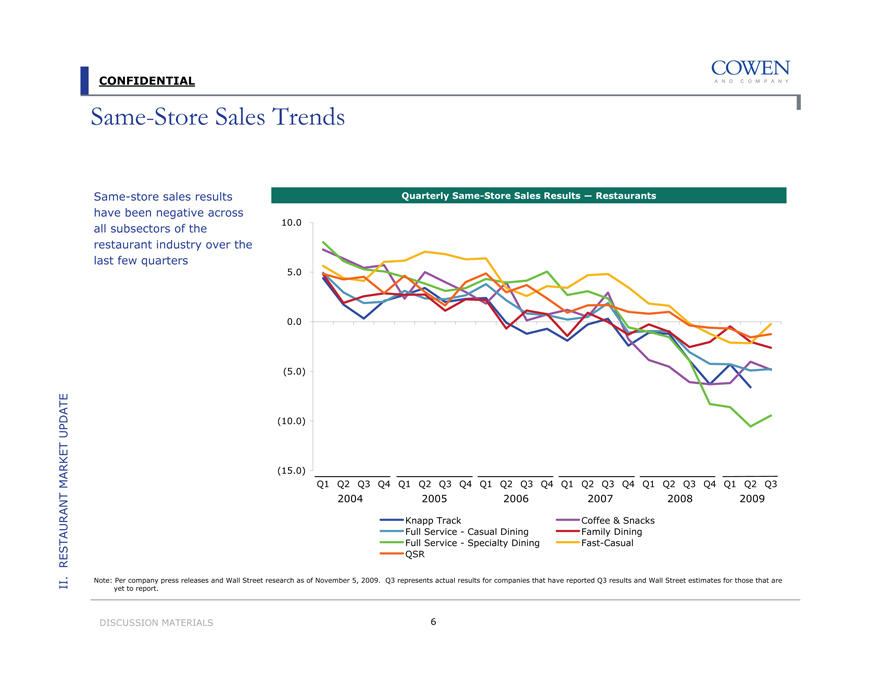

Same-Store Sales Trends

Same-store sales results have been negative across all subsectors of the restaurant industry over the last few quarters

Quarterly Same-Store Sales Results — Restaurants

10.0

5.0

0.0

(5.0)

(10.0)

(15.0)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 2004 2005 2006 2007 2008 2009

Knapp Track

Coffee & Snacks

Full Service - Casual Dining

Family Dining

Full Service - Specialty Dining

Fast-Casual

QSR

II. RESTAURANT MARKET UPDATE

Note: Per company press releases and Wall Street research as of November 5, 2009. Q3 represents actual results for companies that have reported Q3 results and Wall Street estimates for those that are yet to report.

DISCUSSION MATERIALS

6

CONFIDENTIAL

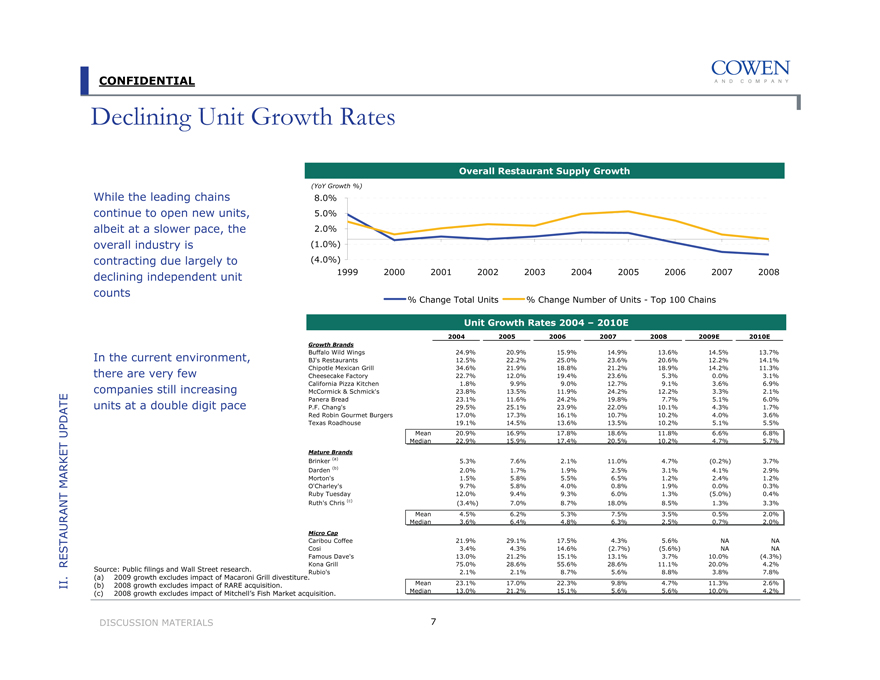

Declining Unit Growth Rates

While the leading chains continue to open new units, albeit at a slower pace, the overall industry is contracting due largely to declining independent unit counts

In the current environment, there are very few companies still increasing units at a double digit pace

Overall Restaurant Supply Growth

(YoY Growth %)

8.0%

5.0%

2.0%

(1.0%)

(4.0%)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

% Change Total Units % Change Number of Units - Top 100 Chains

Unit Growth Rates 2004 – 2010E

2004 2005 2006 2007 2008 2009E 2010E

Growth Brands

Buffalo Wild Wings 24.9% 20.9% 15.9% 14.9% 13.6% 14.5% 13.7%

BJ’s Restaurants 12.5% 22.2% 25.0% 23.6% 20.6% 12.2% 14.1%

Chipotle Mexican Grill 34.6% 21.9% 18.8% 21.2% 18.9% 14.2% 11.3%

Cheesecake Factory 22.7% 12.0% 19.4% 23.6% 5.3% 0.0% 3.1%

California Pizza Kitchen 1.8% 9.9% 9.0% 12.7% 9.1% 3.6% 6.9%

McCormick & Schmick’s 23.8% 13.5% 11.9% 24.2% 12.2% 3.3% 2.1%

Panera Bread 23.1% 11.6% 24.2% 19.8% 7.7% 5.1% 6.0%

P.F. Chang’s 29.5% 25.1% 23.9% 22.0% 10.1% 4.3% 1.7%

Red Robin Gourmet Burgers 17.0% 17.3% 16.1% 10.7% 10.2% 4.0% 3.6%

Texas Roadhouse 19.1% 14.5% 13.6% 13.5% 10.2% 5.1% 5.5%

Mean 20.9% 16.9% 17.8% 18.6% 11.8% 6.6% 6.8%

Median 22.9% 15.9% 17.4% 20.5% 10.2% 4.7% 5.7%

Mature Brands

Brinker (a) 5.3% 7.6% 2.1% 11.0% 4.7% (0.2%) 3.7%

Darden (b) 2.0% 1.7% 1.9% 2.5% 3.1% 4.1% 2.9%

Morton’s 1.5% 5.8% 5.5% 6.5% 1.2% 2.4% 1.2%

O’Charley’s 9.7% 5.8% 4.0% 0.8% 1.9% 0.0% 0.3%

Ruby Tuesday 12.0% 9.4% 9.3% 6.0% 1.3% (5.0%) 0.4%

Ruth’s Chris (c) (3.4%) 7.0% 8.7% 18.0% 8.5% 1.3% 3.3%

Mean 4.5% 6.2% 5.3% 7.5% 3.5% 0.5% 2.0%

Median 3.6% 6.4% 4.8% 6.3% 2.5% 0.7% 2.0%

Micro Cap

Caribou Coffee 21.9% 29.1% 17.5% 4.3% 5.6% NA NA

Cosi 3.4% 4.3% 14.6% (2.7%) (5.6%) NA NA

Famous Dave’s 13.0% 21.2% 15.1% 13.1% 3.7% 10.0% (4.3%)

Kona Grill 75.0% 28.6% 55.6% 28.6% 11.1% 20.0% 4.2%

Rubio’s 2.1% 2.1% 8.7% 5.6% 8.8% 3.8% 7.8%

Mean 23.1% 17.0% 22.3% 9.8% 4.7% 11.3% 2.6%

Median 13.0% 21.2% 15.1% 5.6% 5.6% 10.0% 4.2%

Source: Public filings and Wall Street research.

(a) 2009 growth excludes impact of Macaroni Grill divestiture.

(b) 2008 growth excludes impact of RARE acquisition.

(c) 2008 growth excludes impact of Mitchell’s Fish Market acquisition.

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

7

CONFIDENTIAL

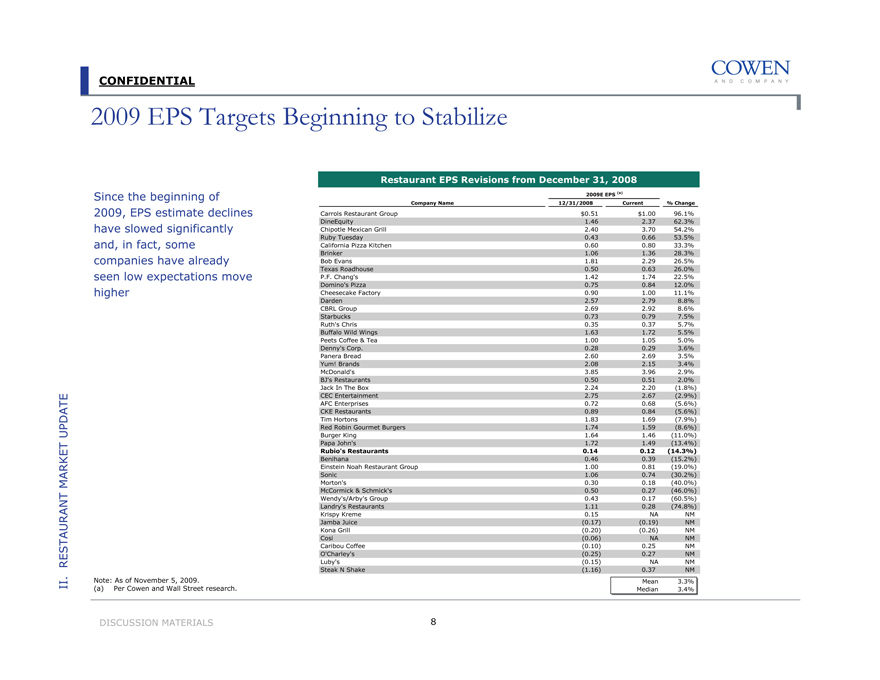

2009 EPS Targets Beginning to Stabilize

Since the beginning of 2009, EPS estimate declines have slowed significantly and, in fact, some companies have already seen low expectations move higher

Restaurant EPS Revisions from December 31, 2008

2009E EPS (a)

Company Name 12/31/2008 Current % Change

Carrols Restaurant Group $0.51 $1.00 96.1%

DineEquity 1.46 2.37 62.3%

Chipotle Mexican Grill 2.40 3.70 54.2%

Ruby Tuesday 0.43 0.66 53.5%

California Pizza Kitchen 0.60 0.80 33.3%

Brinker 1.06 1.36 28.3%

Bob Evans 1.81 2.29 26.5%

Texas Roadhouse 0.50 0.63 26.0%

P.F. Chang’s 1.42 1.74 22.5%

Domino’s Pizza 0.75 0.84 12.0%

Cheesecake Factory 0.90 1.00 11.1%

Darden 2.57 2.79 8.8%

CBRL Group 2.69 2.92 8.6%

Starbucks 0.73 0.79 7.5%

Ruth’s Chris 0.35 0.37 5.7%

Buffalo Wild Wings 1.63 1.72 5.5%

Peets Coffee & Tea 1.00 1.05 5.0%

Denny’s Corp. 0.28 0.29 3.6%

Panera Bread 2.60 2.69 3.5%

Yum! Brands 2.08 2.15 3.4%

McDonald’s 3.85 3.96 2.9%

BJ’s Restaurants 0.50 0.51 2.0%

Jack In The Box 2.24 2.20 (1.8%)

CEC Entertainment 2.75 2.67 (2.9%)

AFC Enterprises 0.72 0.68 (5.6%)

CKE Restaurants 0.89 0.84 (5.6%)

Tim Hortons 1.83 1.69 (7.9%)

Red Robin Gourmet Burgers 1.74 1.59 (8.6%)

Burger King 1.64 1.46 (11.0%)

Papa John’s 1.72 1.49 (13.4%)

Rubio’s Restaurants 0.14 0.12 (14.3%)

Benihana 0.46 0.39 (15.2%)

Einstein Noah Restaurant Group 1.00 0.81 (19.0%)

Sonic 1.06 0.74 (30.2%)

Morton’s 0.30 0.18 (40.0%)

McCormick & Schmick’s 0.50 0.27 (46.0%)

Wendy’s/Arby’s Group 0.43 0.17 (60.5%)

Landry’s Restaurants 1.11 0.28 (74.8%)

Krispy Kreme 0.15 NA NM

Jamba Juice (0.17) (0.19) NM

Kona Grill (0.20) (0.26) NM

Cosi (0.06) NA NM

Caribou Coffee (0.10) 0.25 NM

O’Charley’s (0.25) 0.27 NM

Luby’s (0.15) NA NM

Steak N Shake (1.16) 0.37 NM

Mean 3.3%

Median 3.4%

II. RESTAURANT MARKET UPDATE

Note: As of November 5, 2009.

(a) Per Cowen and Wall Street research.

DISCUSSION MATERIALS

8

CONFIDENTIAL

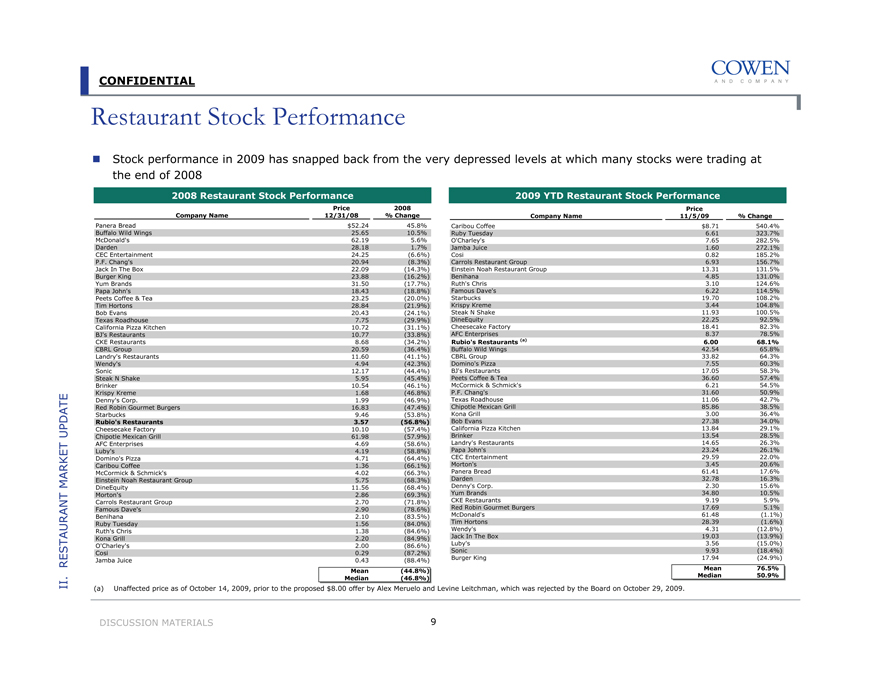

Restaurant Stock Performance

Stock performance in 2009 has snapped back from the very depressed levels at which many stocks were trading at the end of 2008

2008 Restaurant Stock Performance

Company Name Price 12/31/08 2008 % Change

Panera Bread $52.24 45.8%

Buffalo Wild Wings 25.65 10.5%

McDonald’s 62.19 5.6%

Darden 28.18 1.7%

CEC Entertainment 24.25 (6.6%)

P.F. Chang’s 20.94 (8.3%)

Jack In The Box 22.09 (14.3%)

Burger King 23.88 (16.2%)

Yum Brands 31.50 (17.7%)

Papa John’s 18.43 (18.8%)

Peets Coffee & Tea 23.25 (20.0%)

Tim Hortons 28.84 (21.9%)

Bob Evans 20.43 (24.1%)

Texas Roadhouse 7.75 (29.9%)

California Pizza Kitchen 10.72 (31.1%)

BJ’s Restaurants 10.77 (33.8%)

CKE Restaurants 8.68 (34.2%)

CBRL Group 20.59 (36.4%)

Landry’s Restaurants 11.60 (41.1%)

Wendy’s 4.94 (42.3%)

Sonic 12.17 (44.4%)

Steak N Shake 5.95 (45.4%)

Brinker 10.54 (46.1%)

Krispy Kreme 1.68 (46.8%)

Denny’s Corp. 1.99 (46.9%)

Red Robin Gourmet Burgers 16.83 (47.4%)

Starbucks 9.46 (53.8%)

Rubio’s Restaurants 3.57 (56.8%)

Cheesecake Factory 10.10 (57.4%)

Chipotle Mexican Grill 61.98 (57.9%)

AFC Enterprises 4.69 (58.6%)

Luby’s 4.19 (58.8%)

Domino’s Pizza 4.71 (64.4%)

Caribou Coffee 1.36 (66.1%)

McCormick & Schmick’s 4.02 (66.3%)

Einstein Noah Restaurant Group 5.75 (68.3%)

DineEquity 11.56 (68.4%)

Morton’s 2.86 (69.3%)

Carrols Restaurant Group 2.70 (71.8%)

Famous Dave’s 2.90 (78.6%)

Benihana 2.10 (83.5%)

Ruby Tuesday 1.56 (84.0%)

Ruth’s Chris 1.38 (84.6%)

Kona Grill 2.20 (84.9%)

O’Charley’s 2.00 (86.6%)

Cosi 0.29 (87.2%)

Jamba Juice 0.43 (88.4%)

Mean (44.8%)

Median (46.8%)

2009 YTD Restaurant Stock Performance

Company Name Price 11/5/09 % Change

Caribou Coffee $8.71 540.4%

Ruby Tuesday 6.61 323.7%

O’Charley’s 7.65 282.5%

Jamba Juice 1.60 272.1%

Cosi 0.82 185.2%

Carrols Restaurant Group 6.93 156.7%

Einstein Noah Restaurant Group 13.31 131.5%

Benihana 4.85 131.0%

Ruth’s Chris 3.10 124.6%

Famous Dave’s 6.22 114.5%

Starbucks 19.70 108.2%

Krispy Kreme 3.44 104.8%

Steak N Shake 11.93 100.5%

DineEquity 22.25 92.5%

Cheesecake Factory 18.41 82.3%

AFC Enterprises 8.37 78.5%

Rubio’s Restaurants (a) 6.00 68.1%

Buffalo Wild Wings 42.54 65.8%

CBRL Group 33.82 64.3%

Domino’s Pizza 7.55 60.3%

BJ’s Restaurants 17.05 58.3%

Peets Coffee & Tea 36.60 57.4%

McCormick & Schmick’s 6.21 54.5%

P.F. Chang’s 31.60 50.9%

Texas Roadhouse 11.06 42.7%

Chipotle Mexican Grill 85.86 38.5%

Kona Grill 3.00 36.4%

Bob Evans 27.38 34.0%

California Pizza Kitchen 13.84 29.1%

Brinker 13.54 28.5%

Landry’s Restaurants 14.65 26.3%

Papa John’s 23.24 26.1%

CEC Entertainment 29.59 22.0%

Morton’s 3.45 20.6%

Panera Bread 61.41 17.6%

Darden 32.78 16.3%

Denny’s Corp. 2.30 15.6%

Yum Brands 34.80 10.5%

CKE Restaurants 9.19 5.9%

Red Robin Gourmet Burgers 17.69 5.1%

McDonald’s 61.48 (1.1%)

Tim Hortons 28.39 (1.6%)

Wendy’s 4.31 (12.8%)

Jack In The Box 19.03 (13.9%)

Luby’s 3.56 (15.0%)

Sonic 9.93 (18.4%)

Burger King 17.94 (24.9%)

Mean 76.5%

Median 50.9%

(a) Unaffected price as of October 14, 2009, prior to the proposed $8.00 offer by Alex Meruelo and Levine Leitchman, which was rejected by the Board on October 29, 2009.

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

9

CONFIDENTIAL

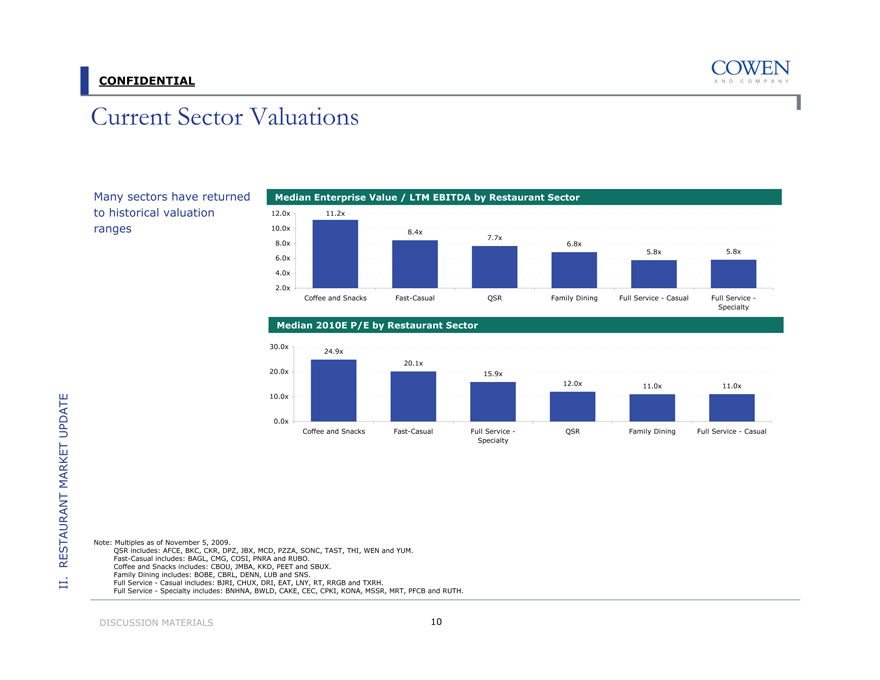

Current Sector Valuations

Many sectors have returned to historical valuation ranges

Median Enterprise Value / LTM EBITDA by Restaurant Sector

12.0x

10.0x

8.0x

6.0x

4.0x

2.0x

11.2x

8.4x

7.7x

6.8x

5.8x

5.8x

Coffee and Snacks

Fast-Casual

QSR

Family Dining

Full Service – Casual

Full Service – Specialty

Median 2010E P/E by Restaurant Sector

30.0x

20.0x

10.0x

0.0x

Coffee and Snacks

Fast-Casual

Full Service – Specialty

QSR

Family Dining

Full Service – Casual

24.9x

20.1x

15.9x

12.0x

11.0x

11.0x

Note:

Multiples as of November 5, 2009.

QSR includes: AFCE, BKC, CKR, DPZ, JBX, MCD, PZZA, SONC, TAST, THI, WEN and YUM. Fast-Casual includes: BAGL, CMG, COSI, PNRA and RUBO.

Coffee and Snacks includes: CBOU, JMBA, KKD, PEET and SBUX. Family Dining includes: BOBE, CBRL, DENN, LUB and SNS.

Full Service – Casual includes: BJRI, CHUX, DRI, EAT, LNY, RT, RRGB and TXRH.

Full Service – Specialty includes: BNHNA, BWLD, CAKE, CEC, CPKI, KONA, MSSR, MRT, PFCB and RUTH.

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

10

CONFIDENTIAL

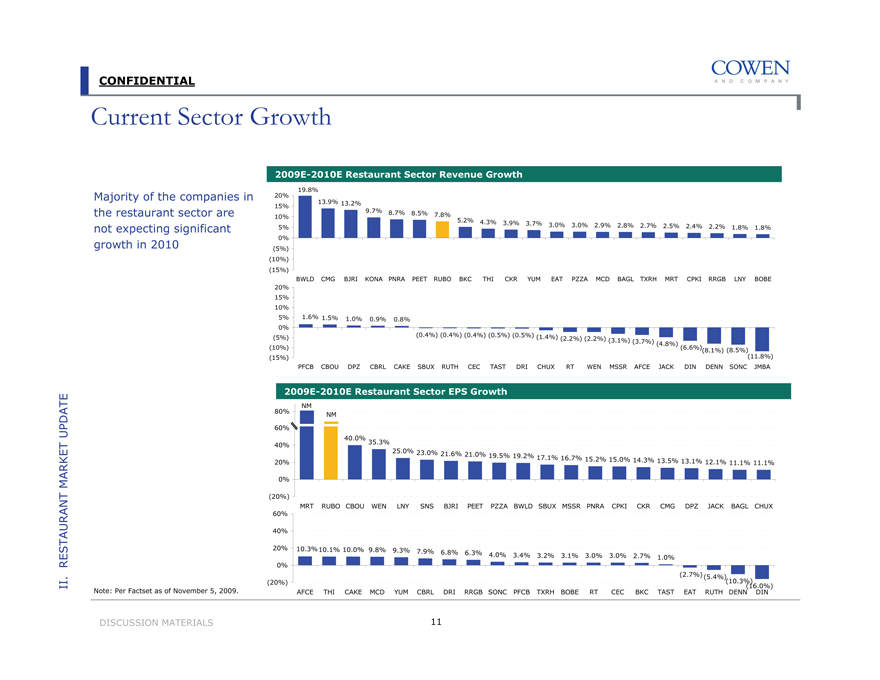

Current Sector Growth

Majority of the companies in the restaurant sector are not expecting significant growth in 2010

2009E-2010E Restaurant Sector Revenue Growth

20% 15% 10% 5% 0% (5%) (10%) (15%)

19.8% 13.9% 13.2% 9.7% 8.7% 8.5% 7.8% 5.2% 4.3% 3.9% 3.7% 3.0% 3.0% 2.9% 2.8% 2.7% 2.5% 2.4% 2.2% 1.8% 1.8%

BWLD CMG BJRI KONA PNRA PEET RUBO BKC THI CKR YUM EAT PZZA MCD BAGL TXRH MRT CPKI RRGB LNY BOBE

20% 15% 10% 5% 0% (5%) (10%) (15%)

1.6% 1.5% 1.0% 0.9% 0.8%

(0.4%) (0.4%) (0.4%) (0.5%) (0.5%) (1.4%)

(2.2%) (2.2%) (3.1%) (3.7%) (4.8%)

(6.6%) (8.1%) (8.5%) (11.8%)

PFCB CBOU DPZ CBRL CAKE SBUX RUTH CEC TAST DRI CHUX RT WEN MSSR AFCE JACK DIN DENN SONC JMBA

2009E-2010E Restaurant Sector EPS Growth

80% 60% 40% 20% 0% (20%)

NM NM

40.0%

35.3%

25.0% 23.0% 21.6%

21.0% 19.5% 19.2%

17.1% 16.7% 15.2% 15.0% 14.3% 13.5%

13.1% 12.1% 11.1% 11.1%

MRT RUBO CBOU WEN LNY SNS BJRI PEET PZZA BWLD SBUX MSSR PNRA CPKI CKR CMG DPZ JACK BAGL CHUX

60% 40% 20% 0% (20%)

10.3%10.1% 10.0% 9.8% 9.3% 7.9%

6.8% 6.3% 4.0% 3.4% 3.2%

3.1% 3.0% 3.0% 2.7% 1.0%

(2.7%) (5.4%) (10.3%) (16.0%)

AFCE THI CAKE MCD YUM CBRL DRI RRGB SONC PFCB TXRH BOBE RT CEC BKC TAST EAT RUTH DENN DIN

Note: Per Factset as of November 5, 2009.

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

11

CONFIDENTIAL

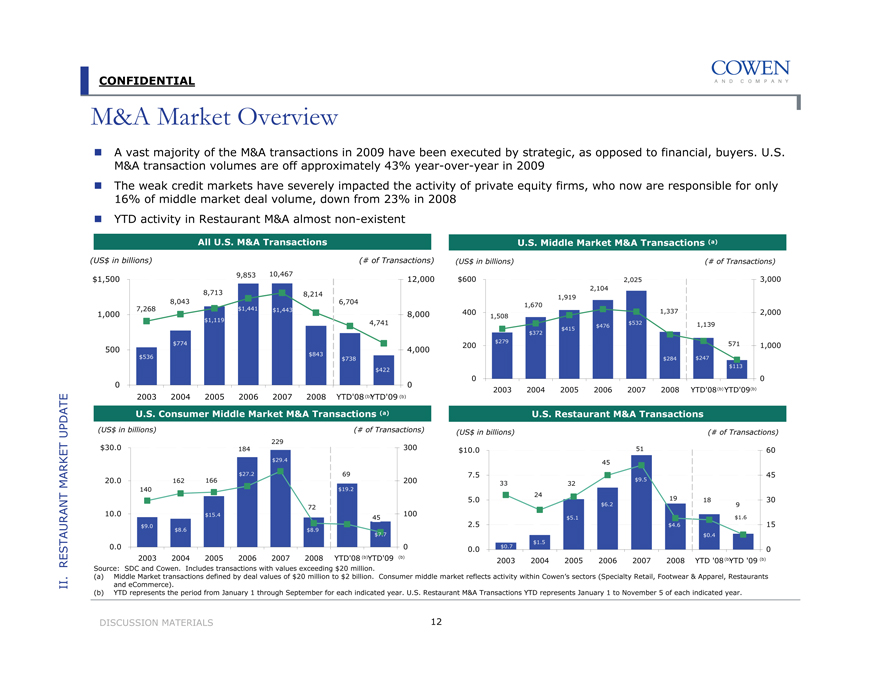

M&A Market Overview

A vast majority of the M&A transactions in 2009 have been executed by strategic, as opposed to financial, buyers. U.S. M&A transaction volumes are off approximately 43% year-over-year in 2009

The weak credit markets have severely impacted the activity of private equity firms, who now are responsible for only 16% of middle market deal volume, down from 23% in 2008

YTD activity in Restaurant M&A almost non-existent

All U.S. M&A Transactions

(US$ in billions) (# of Transactions)

9,853 10,467 $1,500 12,000 8,713 8,214 8,043 6,704 7,268 $1,441 $1,443 1,000 8,000 $1,119 4,741

$774

500 4,000 $536 $843 $738 $422

0 0 2003 2004 2005 2006 2007 2008 YTD’08 (b) YTD’09 (b)

U.S. Middle Market M&A Transactions (a)

(US$ in billions) (# of Transactions)

$600 2,025 3,000 2,104 1,919 400 1,670 1,337 2,000 1,508 $532 1,139 $476 $415 $372 $279 571 200 1,000 $284 $247 $113

0

0

2003 2004 2005 2006 2007 2008 YTD’08 (b) YTD’09(b)

U.S. Consumer Middle Market M&A Transactions (a)

(US$ in billions) (# of Transactions)

229 $30.0 184 300 $29.4

166 $27.2 69

20.0 162 200 140 $19.2

10.0 72 100 $15.4 45 $9.0 $8.6 $8.9 $7.7 0.0 0 2003 2004 2005 2006 2007 2008 YTD’08 (b)YTD’09 (b)

U.S. Restaurant M&A Transactions

(US$ in billions) (# of Transactions)

$10.0 51 60 45

7.5 45

$9.5

33 32 24

5.0 $6.2 19 18 9 30

$5.1 $1.6

2.5 $4.6 15

$0.4

$1.5

0.0 $0.7 0 2003 2004 2005 2006 2007 2008 YTD ‘08(b) YTD ‘09 (b)

Source: SDC and Cowen. Includes transactions with values exceeding $20 million.

(a) Middle Market transactions defined by deal values of $20 million to $2 billion. Consumer middle market reflects activity within Cowen’s sectors (Specialty Retail, Footwear & Apparel, Restaurants and eCommerce).

(b) YTD represents the period from January 1 through September for each indicated year. U.S. Restaurant M&A Transactions YTD represents January 1 to November 5 of each indicated year.

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

12

CONFIDENTIAL

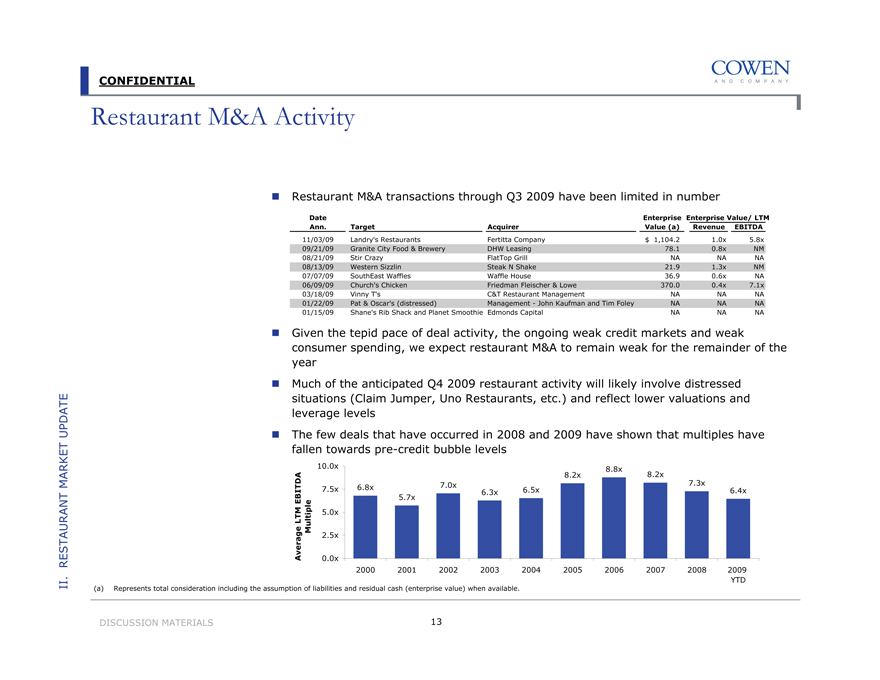

Restaurant M&A Activity

Restaurant M&A transactions through Q3 2009 have been limited in number

Enterprise Value/ LTM

Date Ann. Target Acquirer Enterprise Value (a) Revenue EBITDA

11/03/09 Landry’s Restaurants Fertitta Company $ 1,104.2 1.0x 5.8x

09/21/09 Granite City Food & Brewery DHW Leasing 78.1 0.8x NM

08/21/09 Stir Crazy FlatTop Grill NA NA NA

08/13/09 Western Sizzlin Steak N Shake 21.9 1.3x NM

07/07/09 SouthEast Waffles Waffle House 36.9 0.6x NA

06/09/09 Church’s Chicken Friedman Fleischer & Lowe 370.0 0.4x 7.1x

03/18/09 Vinny T’s C&T Restaurant Management NA NA NA

01/22/09 Pat & Oscar’s (distressed) Management - John Kaufman and Tim Foley NA NA NA

01/15/09 Shane’s Rib Shack and Planet Smoothie Edmonds Capital NA NA NA

Given the tepid pace of deal activity, the ongoing weak credit markets and weak consumer spending, we expect restaurant M&A to remain weak for the remainder of the year

Much of the anticipated Q4 2009 restaurant activity will likely involve distressed situations (Claim Jumper, Uno Restaurants, etc.) and reflect lower valuations and UPDATE leverage levels

The few deals that have occurred in 2008 and 2009 have shown that multiples have fallen towards pre-credit bubble levels

Average LTM EBITDA Multiple

10.0x 7.5x 5.0x 2.5x 0.0x

8.8x

8.2x

8.2x

7.0x

7.3x

6.8x

6.5x

6.4x

6.3x

5.7x

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 YTD

(a) Represents total consideration including the assumption of liabilities and residual cash (enterprise value) when available.

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

13

CONFIDENTIAL

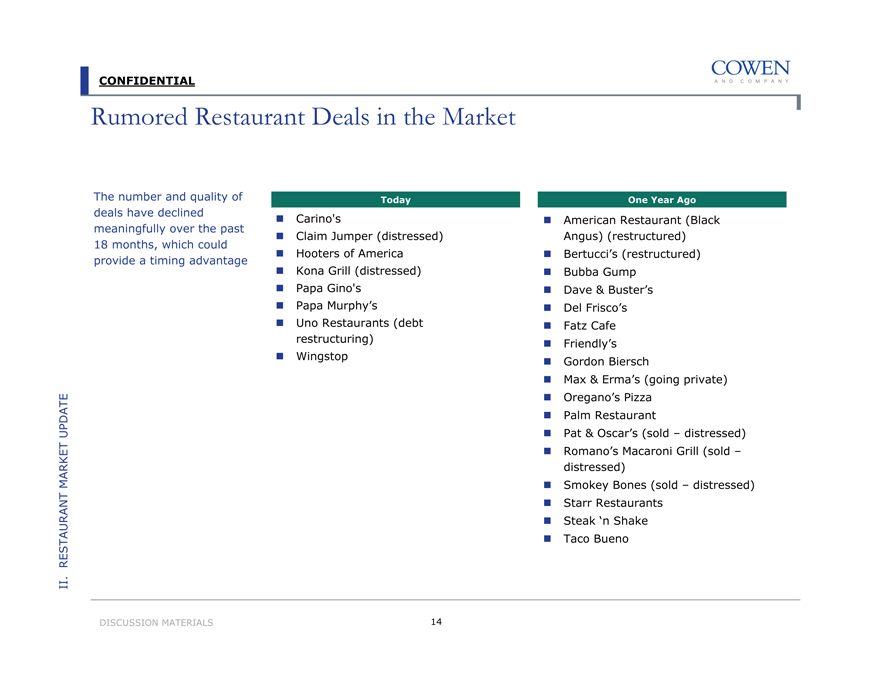

Rumored Restaurant Deals in the Market

The number and quality of deals have declined meaningfully over the past 18 months, which could provide a timing advantage

Today

Carino’s

Claim Jumper (distressed)

Hooters of America

Kona Grill (distressed)

Papa Gino’s

Papa Murphy’s

Uno Restaurants (debt restructuring)

Wingstop

One Year Ago

American Restaurant (Black Angus) (restructured)

Bertucci’s (restructured)

Bubba Gump

Dave & Buster’s

Del Frisco’s

Fatz Cafe

Friendly’s

Gordon Biersch

Max & Erma’s (going private)

Oregano’s Pizza

Palm Restaurant

Pat & Oscar’s (sold – distressed)

Romano’s Macaroni Grill (sold – distressed)

Smokey Bones (sold – distressed)

Starr Restaurants

Steak ‘n Shake

Taco Bueno

II. RESTAURANT MARKET UPDATE

DISCUSSION MATERIALS

14

CONFIDENTIAL

III. Rubio’s Overview

CONFIDENTIAL

YTD 2009 Operating Performance

While Rubio’s year-to-date 2009 results returned to profitability, the results don’t seem to portend a “break-out” to new, higher levels

Flat 2009 same-store sales results driven by significant increase in average check

Year-over-Year Comparable Performance

9 Months Ended September,

2008 2009 % Change

Total revenues $134.3 $143.4 6.8%

EBIT (a) 0.8 2.5 NM

EBITDA (a) 7.8 9.9 27.2%

Net Income (a) 0.5 1.6 NM

Same-store sales (3.1%) (0.1%) 3.0 pp

Average check 3.0% 6.1% 3.1 pp

Transactions (5.9%) (5.9%) 0.0 pp

III. RUBIO’S OVERVIEW

(a) Excludes asset impairment and loss on disposal (tax affected for net income).

DISCUSSION MATERIALS

16

CONFIDENTIAL

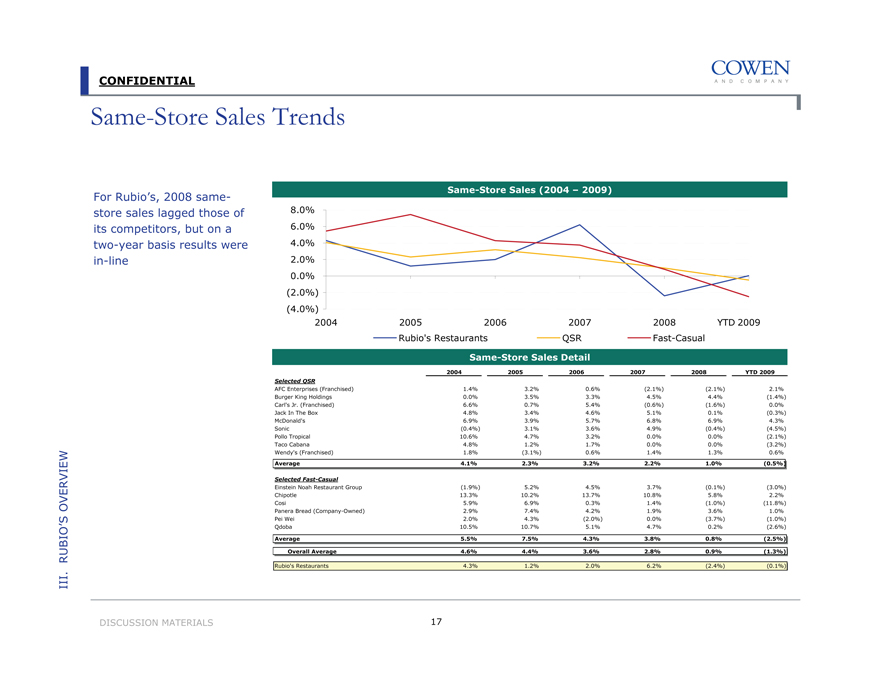

Same-Store Sales Trends

For Rubio’s, 2008 same-store sales lagged those of its competitors, but on a two-year basis results were in-line

Same-Store Sales (2004 – 2009)

8.0% 6.0% 4.0% 2.0% 0.0% (2.0%) (4.0%)

2004 2005 2006 2007 2008 YTD 2009 Rubio’s Restaurants QSR Fast-Casual

Same-Store Sales Detail

2004 2005 2006 2007 2008 YTD 2009

Selected QSR

AFC Enterprises (Franchised) 1.4% 3.2% 0.6% (2.1%) (2.1%) 2.1%

Burger King Holdings 0.0% 3.5% 3.3% 4.5% 4.4% (1.4%)

Carl’s Jr. (Franchised) 6.6% 0.7% 5.4% (0.6%) (1.6%) 0.0%

Jack In The Box 4.8% 3.4% 4.6% 5.1% 0.1% (0.3%)

McDonald’s 6.9% 3.9% 5.7% 6.8% 6.9% 4.3%

Sonic (0.4%) 3.1% 3.6% 4.9% (0.4%) (4.5%)

Pollo Tropical 10.6% 4.7% 3.2% 0.0% 0.0% (2.1%)

Taco Cabana 4.8% 1.2% 1.7% 0.0% 0.0% (3.2%)

Wendy’s (Franchised) 1.8% (3.1%) 0.6% 1.4% 1.3% 0.6%

Average 4.1% 2.3% 3.2% 2.2% 1.0% (0.5%)

Selected Fast-Casual

Einstein Noah Restaurant Group (1.9%) 5.2% 4.5% 3.7% (0.1%) (3.0%)

Chipotle 13.3% 10.2% 13.7% 10.8% 5.8% 2.2%

Cosi 5.9% 6.9% 0.3% 1.4% (1.0%) (11.8%)

Panera Bread (Company-Owned) 2.9% 7.4% 4.2% 1.9% 3.6% 1.0%

Pei Wei 2.0% 4.3% (2.0%) 0.0% (3.7%) (1.0%)

Qdoba 10.5% 10.7% 5.1% 4.7% 0.2% (2.6%)

Average 5.5% 7.5% 4.3% 3.8% 0.8% (2.5%)

Overall Average 4.6% 4.4% 3.6% 2.8% 0.9% (1.3%)

Rubio’s Restaurants 4.3% 1.2% 2.0% 6.2% (2.4%) (0.1%)

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

17

CONFIDENTIAL

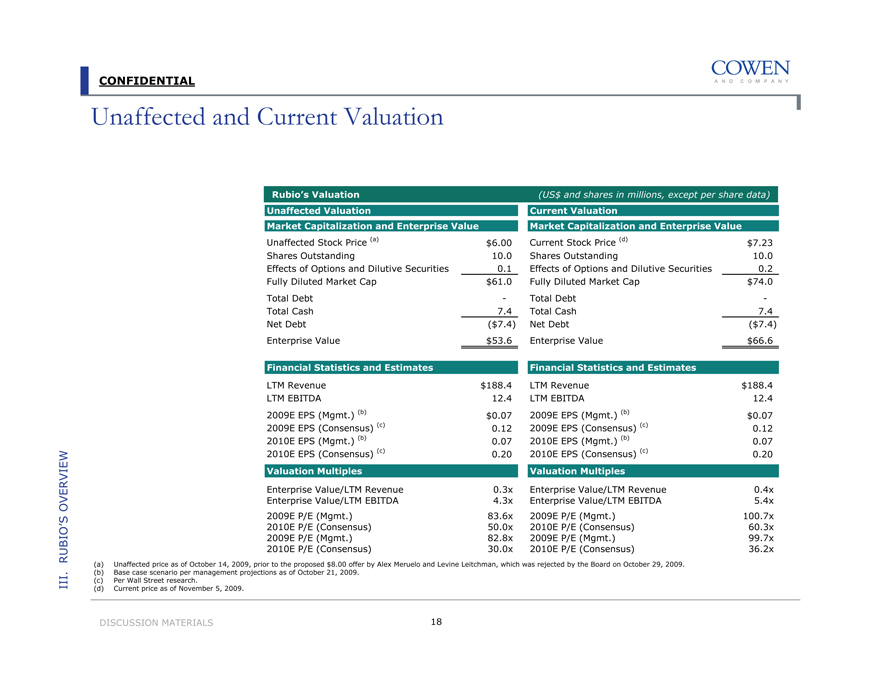

Unaffected and Current Valuation

Rubio’s Valuation

Unaffected Valuation

Market Capitalization and Enterprise Value

Unaffected Stock Price (a) $6.00

Shares Outstanding 10.0

Effects of Options and Dilutive Securities 0.1

Fully Diluted Market Cap $61.0

Total Debt -

Total Cash 7.4

Net Debt ($7.4)

Enterprise Value $53.6

Financial Statistics and Estimates

LTM Revenue $188.4

LTM EBITDA 12.4

2009E EPS (Mgmt.) (b) $0.07

2009E EPS (Consensus) (c) 0.12

2010E EPS (Mgmt.) (b) 0.07

2010E EPS (Consensus) (c) 0.20

Valuation Multiples

Enterprise Value/LTM Revenue 0.3x

Enterprise Value/LTM EBITDA 4.3x

2009E P/E (Mgmt.) 83.6x

2010E P/E (Consensus) 50.0x

2009E P/E (Mgmt.) 82.8x

2010E P/E (Consensus) 30.0x

(US$ and shares in millions, except per share data)

Current Valuation

Market Capitalization and Enterprise Value

Current Stock Price (d) $7.23

Shares Outstanding 10.0

Effects of Options and Dilutive Securities 0.2

Fully Diluted Market Cap $74.0

Total Debt -

Total Cash 7.4

Net Debt ($7.4)

Enterprise Value $66.6

Financial Statistics and Estimates

LTM Revenue $188.4

LTM EBITDA 12.4

2009E EPS (Mgmt.) (b) $0.07

2009E EPS (Consensus) (c) 0.12

2010E EPS (Mgmt.) (b) 0.07

2010E EPS (Consensus) (c) 0.20

Valuation Multiples

Enterprise Value/LTM Revenue 0.4x

Enterprise Value/LTM EBITDA 5.4x

2009E P/E (Mgmt.) 100.7x

2010E P/E (Consensus) 60.3x

2009E P/E (Mgmt.) 99.7x

2010E P/E (Consensus) 36.2x

(a) Unaffected price as of October 14, 2009, prior to the proposed $8.00 offer by Alex Meruelo and Levine Leitchman, which was rejected by the Board on October 29, 2009.

(b) Base case scenario per management projections as of October 21, 2009.

(c) Per Wall Street research.

(d) Current price as of November 5, 2009.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

18

CONFIDENTIAL

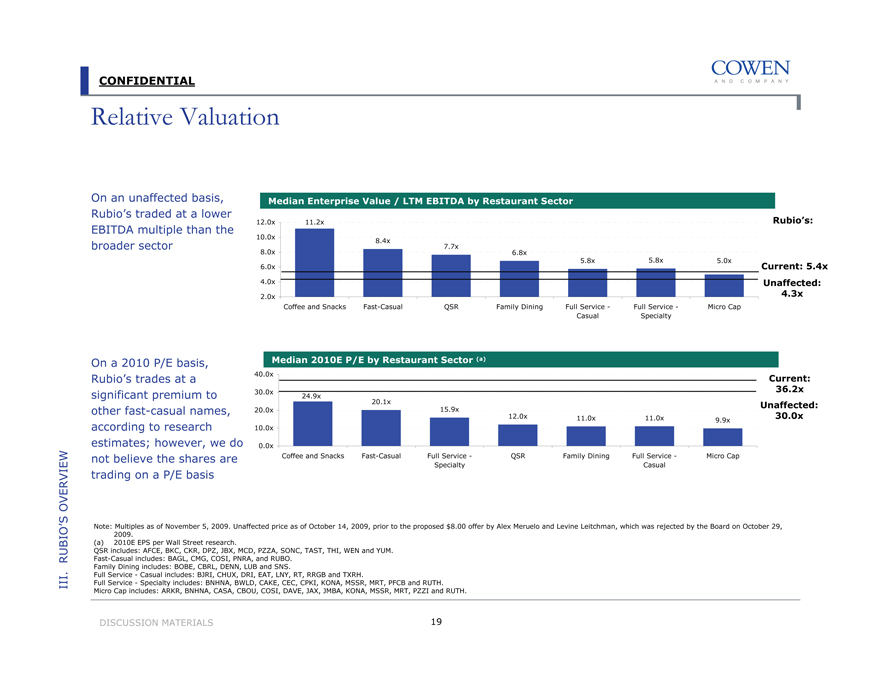

Relative Valuation

On an unaffected basis, Rubio’s traded at a lower EBITDA multiple than the broader sector

On a 2010 P/E basis, Rubio’s trades at a significant premium to other fast-casual names, according to research estimates; however, we do not believe the shares are trading on a P/E basis

Median Enterprise Value / LTM EBITDA by Restaurant Sector

12.0x 10.0x 8.0x 6.0x 4.0x 2.0x

11.2x

8.4x

7.7x

6.8x

5.8x

5.8x

5.0x

Coffee and Snacks Fast-Casual QSR Family Dining Full Service – Casual Full Service – Specialty Micro Cap

Rubio’s:

Current: 5.4x

Unaffected: 4.3x

Median 2010E P/E by Restaurant Sector (a)

40.0x 30.0x 20.0x 10.0x 0.0x

24.9x

20.1x

15.9x

12.0x

11.0x

11.0x

9.9x

Coffee and Snacks Fast-Casual Full Service – Specialty QSR Family Dining Full Service – Casual Micro Cap

Current: 36.2x

Unaffected: 30.0x

Note: Multiples as of November 5, 2009. Unaffected price as of October 14, 2009, prior to the proposed $8.00 offer by Alex Meruelo and Levine Leitchman, which was rejected by the Board on October 29, 2009.

(a) 2010E EPS per Wall Street research.

QSR includes: AFCE, BKC, CKR, DPZ, JBX, MCD, PZZA, SONC, TAST, THI, WEN and YUM. Fast-Casual includes: BAGL, CMG, COSI, PNRA, and RUBO.

Family Dining includes: BOBE, CBRL, DENN, LUB and SNS.

Full Service – Casual includes: BJRI, CHUX, DRI, EAT, LNY, RT, RRGB and TXRH.

Full Service – Specialty includes: BNHNA, BWLD, CAKE, CEC, CPKI, KONA, MSSR, MRT, PFCB and RUTH. Micro Cap includes: ARKR, BNHNA, CASA, CBOU, COSI, DAVE, JAX, JMBA, KONA, MSSR, MRT, PZZI and RUTH.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

19

CONFIDENTIAL

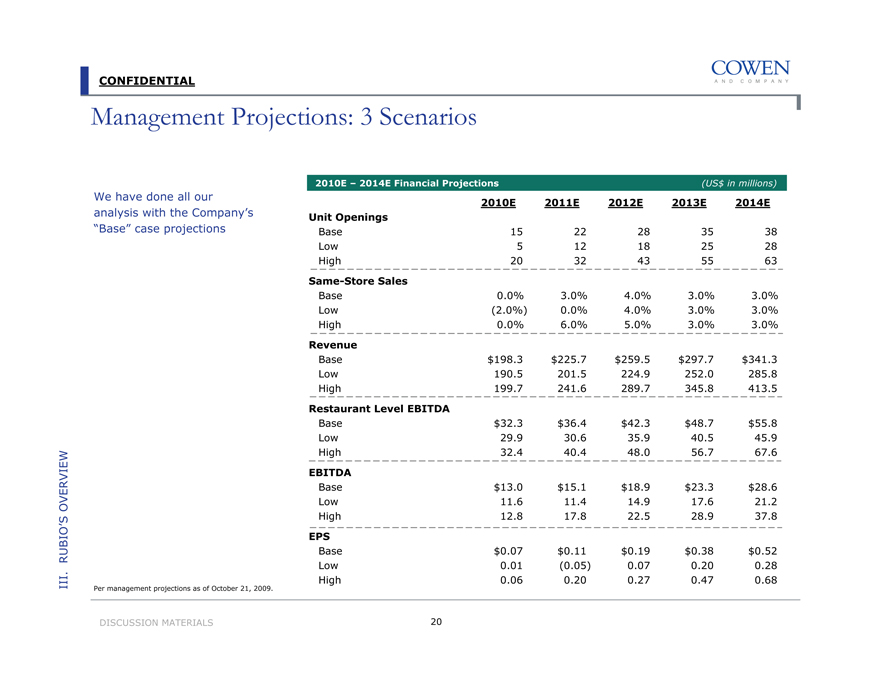

Management Projections: 3 Scenarios

We have done all our analysis with the Company’s “Base” case projections

2010E – 2014E Financial Projections (US$ in millions)

2010E 2011E 2012E 2013E 2014E

Unit Openings

Base 15 22 28 35 38

Low 5 12 18 25 28

High 20 32 43 55 63

Same-Store Sales

Base 0.0% 3.0% 4.0% 3.0% 3.0%

Low (2.0%) 0.0% 4.0% 3.0% 3.0%

High 0.0% 6.0% 5.0% 3.0% 3.0%

Revenue

Base $198.3 $225.7 $259.5 $297.7 $341.3

Low 190.5 201.5 224.9 252.0 285.8

High 199.7 241.6 289.7 345.8 413.5

Restaurant Level EBITDA

Base $32.3 $36.4 $42.3 $48.7 $55.8

Low 29.9 30.6 35.9 40.5 45.9

High 32.4 40.4 48.0 56.7 67.6

EBITDA

Base $13.0 $15.1 $18.9 $23.3 $28.6

Low 11.6 11.4 14.9 17.6 21.2

High 12.8 17.8 22.5 28.9 37.8

EPS

Base $0.07 $0.11 $0.19 $0.38 $0.52

Low 0.01 (0.05) 0.07 0.20 0.28

High 0.06 0.20 0.27 0.47 0.68

Per management projections as of October 21, 2009.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

20

CONFIDENTIAL

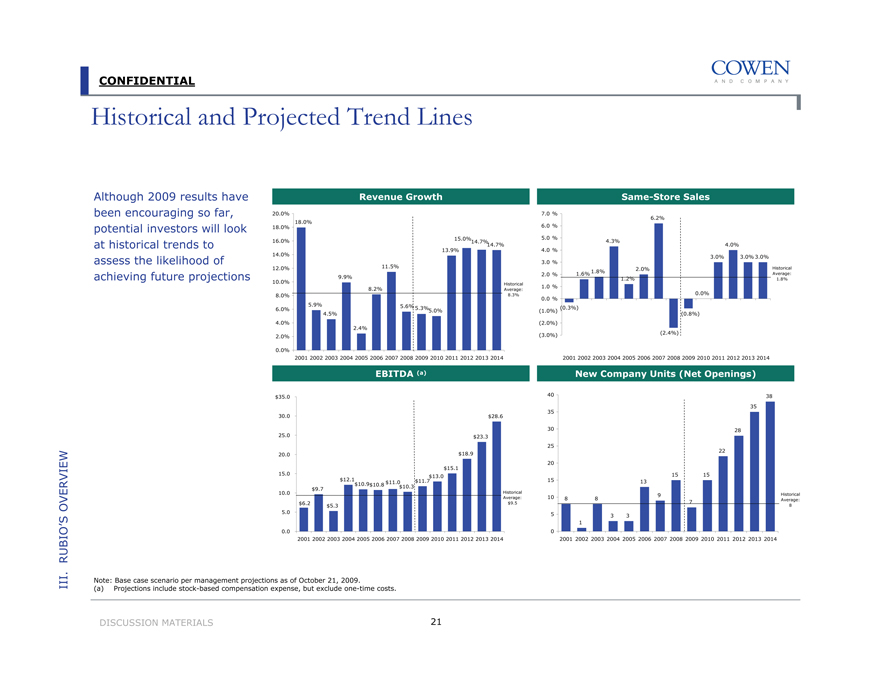

Historical and Projected Trend Lines

Although 2009 results have been encouraging so far, potential investors will look at historical trends to assess the likelihood of achieving future projections

20.0% 18.0% 16.0% 14.0% 12.0% 10.0% 8.0% 6.0% 4.0% 2.0% 0.0%

Revenue Growth

Historical Average: 8.3%

18.0%

11.5%

9.9%

8.2%

5.9%

5.6%

4.5%

5.3%

5.0%

2.4%

15.0%

14.7%

13.9%

14.7%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Same-Store Sales

7.0 % 6.0 % 5.0 % 4.0 % 3.0 % 2.0 % 1.0 % 0.0 % (1.0%) (2.0%) (3.0%)

6.2%

4.3%

4.0%

3.0%

3.0%

3.0%

1.6%

1.8%

2.0%

1.2%

0.0%

(0.3%)

(0.8%)

(2.4%)

Historical Average: 1.8%

EBITDA (a)

$35.0

30.0

25.0

20.0

15.0

10.0

5.0

0.0

$28.6

$23.3

$18.9

$15.1

$13.0

$12.1

$11.7

$10.9

$10.8

$11.0

$9.7

$10.3

$6.2

$5.3

Historical Average:

$9.5

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

New Company Units (Net Openings)

40 35 30 25 20 15 10 5 0

38

35

28

22

15

15

13

9

8

8

7

3

3

1

Historical Average: 8

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Note: Base case scenario per management projections as of October 21, 2009.

(a) Projections include stock-based compensation expense, but exclude one-time costs.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

21

CONFIDENTIAL

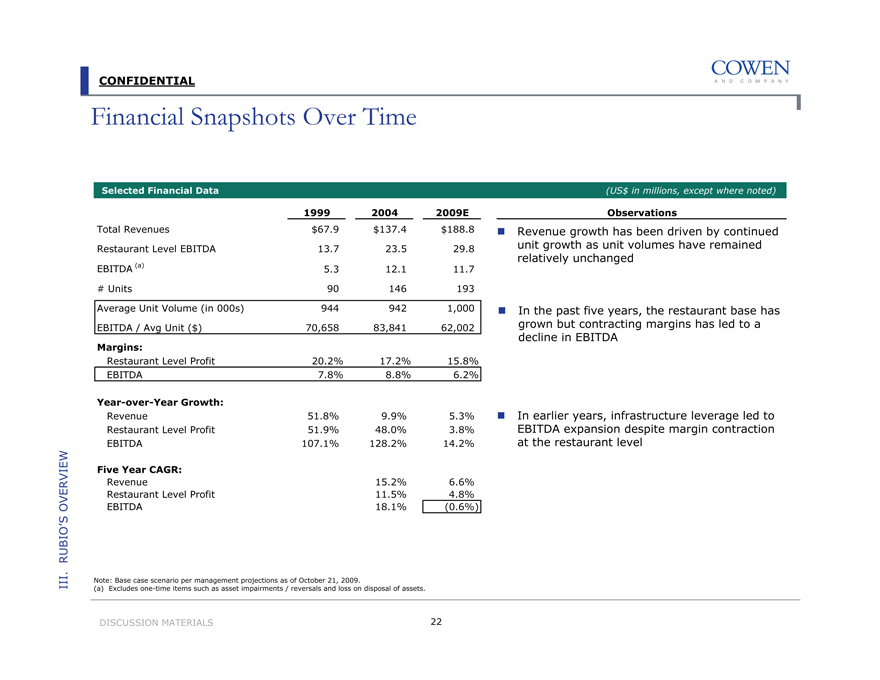

Financial Snapshots Over Time

Selected Financial Data

1999 2004 2009E

Total Revenues $67.9 $137.4 $188.8

Restaurant Level EBITDA 13.7 23.5 29.8

EBITDA (a) 5.3 12.1 11.7

# Units 90 146 193

Average Unit Volume (in 000s) 944 942 1,000

EBITDA / Avg Unit ($) 70,658 83,841 62,002

Margins:

Restaurant Level Profit 20.2% 17.2% 15.8%

EBITDA 7.8% 8.8% 6.2%

Year-over-Year Growth:

Revenue 51.8% 9.9% 5.3%

Restaurant Level Profit 51.9% 48.0% 3.8%

EBITDA 107.1% 128.2% 14.2%

Five Year CAGR:

Revenue 15.2% 6.6%

Restaurant Level Profit 11.5% 4.8%

EBITDA 18.1% (0.6%)

(US$ in millions, except where noted)

Observations

Revenue growth has been driven by continued unit growth as unit volumes have remained relatively unchanged

In the past five years, the restaurant base has grown but contracting margins has led to a decline in EBITDA

In earlier years, infrastructure leverage led to EBITDA expansion despite margin contraction at the restaurant level

Note: Base case scenario per management projections as of October 21, 2009.

(a) Excludes one-time items such as asset impairments / reversals and loss on disposal of assets.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

22

CONFIDENTIAL

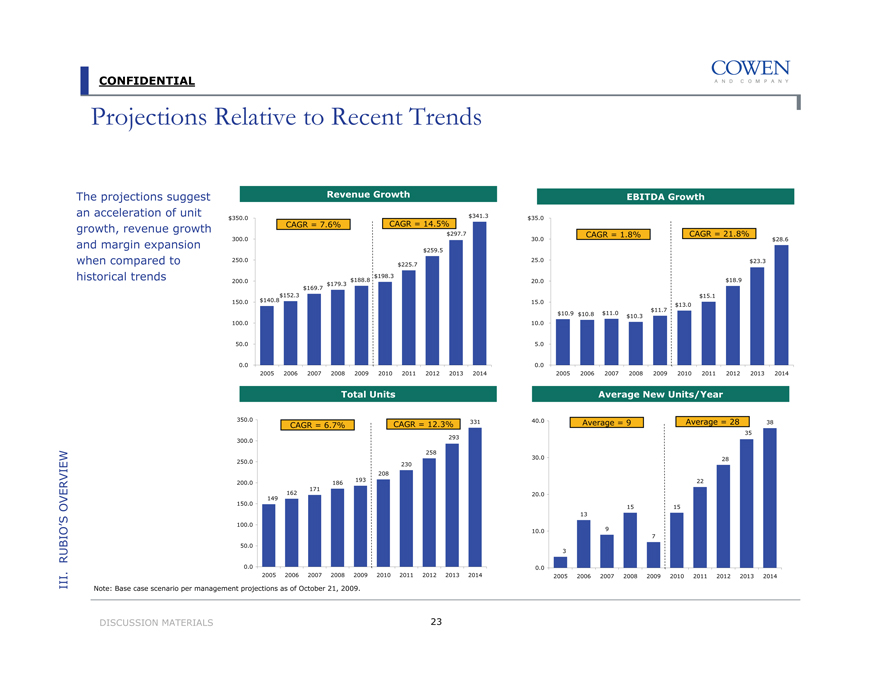

Projections Relative to Recent Trends

The projections suggest an acceleration of unit growth, revenue growth and margin expansion when compared to historical trends

Revenue Growth

$350.0 300.0 250.0 200.0 150.0 100.0 50.0 0.0

CAGR = 7.6%

CAGR = 14.5%

$297.7

$259.5

$225.7 $198.3 $188.8 $179.3 $169.7 $152.3 $140.8

$341.3

EBITDA Growth

$35.0

30.0

25.0

20.0

15.0

10.0

5.0

0.0

CAGR = 1.8%

CAGR = 21.8%

$28.6

$23.3

$18.9

$15.1

$11.7 $13.0

$10.9 $10.8 $11.0

$10.3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total Units

350.0

300.0

250.0

200.0

150.0

100.0

50.0

0.0

CAGR = 6.7%

CAGR = 12.3%

331

293

258 230 208 193 186 171 149 162

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Average New Units/Year

40.0

30.0

20.0

10.0

0.0

Average = 9

Average = 28

38

35

28

22

15

15

13

9

7

3

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Note: Base case scenario per management projections as of October 21, 2009.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

23

CONFIDENTIAL

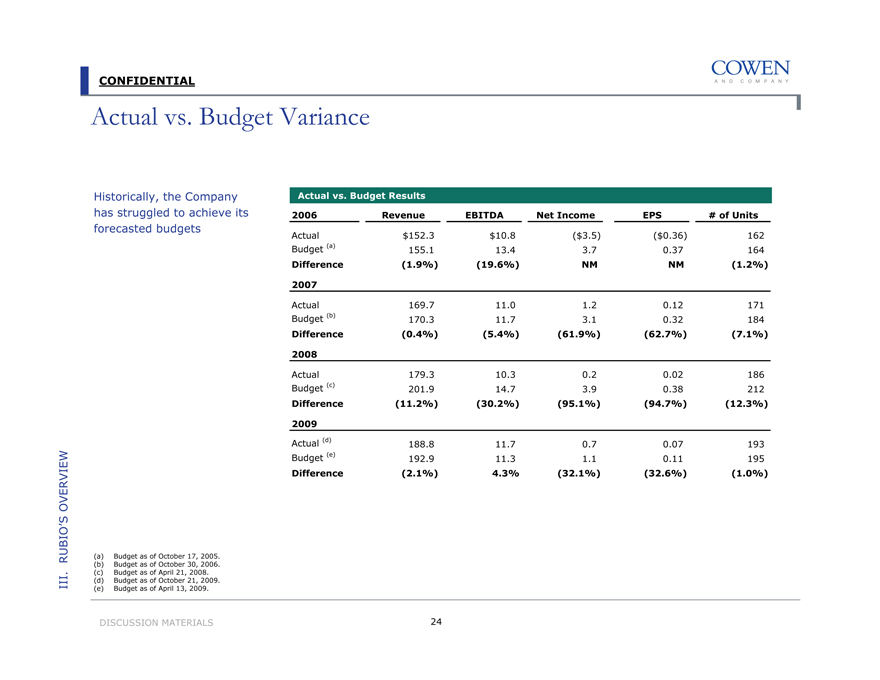

Actual vs. Budget Variance

Historically, the Company has struggled to achieve its forecasted budgets

Actual vs. Budget Results

2006 Revenue EBITDA Net Income EPS # of Units

Actual $152.3 $10.8 ($3.5) ($0.36) 162

Budget (a) 155.1 13.4 3.7 0.37 164

Difference (1.9%) (19.6%) NM NM (1.2%)

2007

Actual 169.7 11.0 1.2 0.12 171

Budget (b) 170.3 11.7 3.1 0.32 184

Difference (0.4%) (5.4%) (61.9%) (62.7%) (7.1%)

2008

Actual 179.3 10.3 0.2 0.02 186

Budget (c) 201.9 14.7 3.9 0.38 212

Difference (11.2%) (30.2%) (95.1%) (94.7%) (12.3%)

2009

Actual (d) 188.8 11.7 0.7 0.07 193

Budget (e) 192.9 11.3 1.1 0.11 195

Difference (2.1%) 4.3% (32.1%) (32.6%) (1.0%)

(a) Budget as of October 17, 2005.

(b) Budget as of October 30, 2006.

(c) Budget as of April 21, 2008.

(d) Budget as of October 21, 2009.

(e) Budget as of April 13, 2009.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

24

CONFIDENTIAL

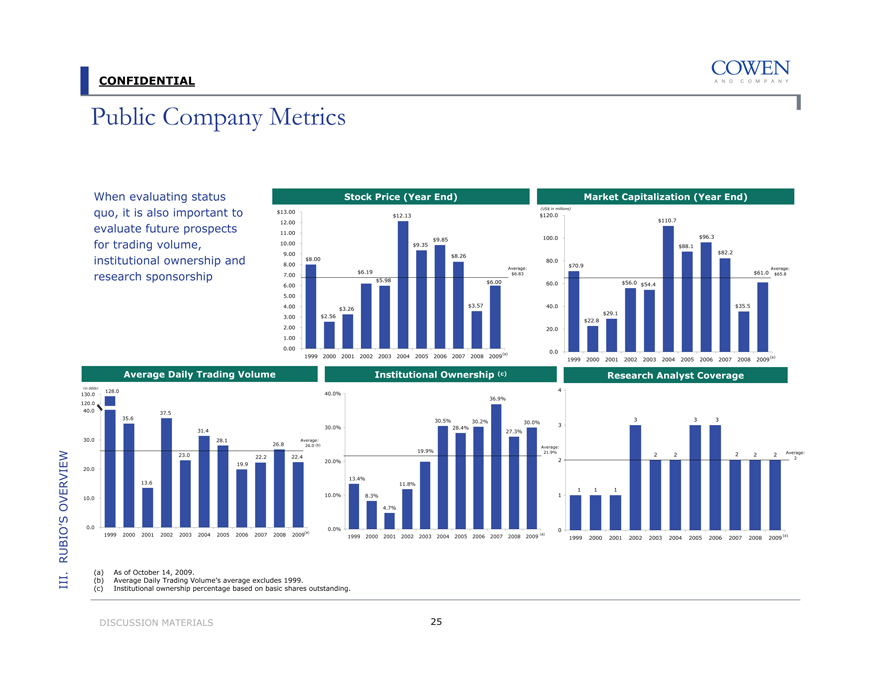

Public Company Metrics

When evaluating status quo, it is also important to evaluate future prospects for trading volume, institutional ownership and research sponsorship

Stock Price (Year End)

$13.00 12.00 11.00 10.00 9.00 8.00 7.00 6.00 5.00 4.00 3.00 2.00 1.00 0.00

$12.13

$9.35

$9.85

$8.26

$8.00

$6.19

$5.98

$6.00

$3.57

$3.26

$2.56

Average: $6.83

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009(a)

Market Capitalization (Year End)

(US$ in millions) $120.0

100.0

80.0

60.0

40.0

20.0

0.0

$110.7

$96.3

$88.1

$82.2

$70.9

$61.0

$56.0

$54.4

$35.5

$29.1

$22.8

Average: $65.8

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009(a)

Average Daily Trading Volume

(in 000s)

130.0 120.0

40.0

30.0

20.0

10.0

0.0

128.0

35.6

37.5

31.4

28.1

26.8

23.0

22.2

22.4

19.9

13.6

Average:

26.0 (b)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009(a)

Institutional Ownership (c)

40.0%

30.0%

20.0%

10.0%

0.0%

36.9%

30.5%

30.2%

30.0%

28.4%

27.3%

19.9%

13.4%

11.8%

8.3%

4.7%

Average: 21.9%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 (a)

Research Analyst Coverage

4

3

2

1

0

3

3

3

2

2

2

2

2

1

1

1

Average: 2

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 (a)

(a) As of October 14, 2009.

(b) Average Daily Trading Volume’s average excludes 1999.

(c) Institutional ownership percentage based on basic shares outstanding.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

25

CONFIDENTIAL

Challenges of a Micro-Cap Stock

Given the current economic and market environment, Rubio’s will likely continue to experience:

Lack of meaningful research coverage

Limited trading volume

A sub-$100 million market capitalization

Difficulty in expanding its institutional shareholder base

Volatility in stock price performance

Meaningful costs and risks associated with its public-company status

Without a material “break-out” in EBITDA growth to levels more in line with forward projections, the challenges of overcoming micro-cap status seem significant

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

26

CONFIDENTIAL

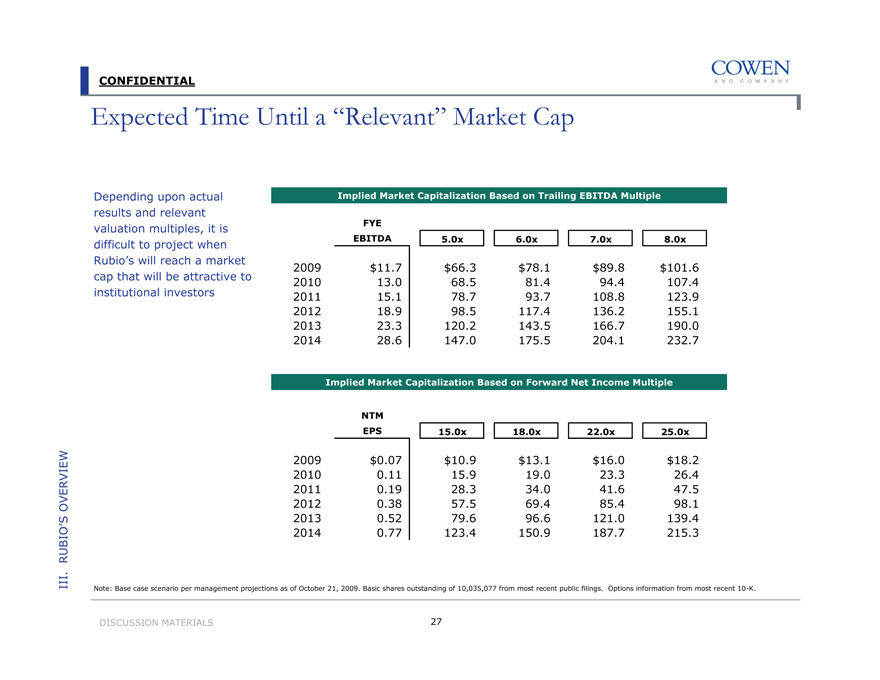

Expected Time Until a “Relevant” Market Cap

Depending upon actual results and relevant valuation multiples, it is difficult to project when Rubio’s will reach a market cap that will be attractive to institutional investors

Implied Market Capitalization Based on Trailing EBITDA Multiple

FYE EBITDA 5.0x 6.0x 7.0x 8.0x

2009 $11.7 $66.3 $78.1 $89.8 $101.6

2010 13.0 68.5 81.4 94.4 107.4

2011 15.1 78.7 93.7 108.8 123.9

2012 18.9 98.5 117.4 136.2 155.1

2013 23.3 120.2 143.5 166.7 190.0

2014 28.6 147.0 175.5 204.1 232.7

Implied Market Capitalization Based on Forward Net Income Multiple

NTM EPS 15.0x 18.0x 22.0x 25.0x

2009 $0.07 $10.9 $13.1 $16.0 $18.2

2010 0.11 15.9 19.0 23.3 26.4

2011 0.19 28.3 34.0 41.6 47.5

2012 0.38 57.5 69.4 85.4 98.1

2013 0.52 79.6 96.6 121.0 139.4

2014 0.77 123.4 150.9 187.7 215.3

Note: Base case scenario per management projections as of October 21, 2009. Basic shares outstanding of 10,035,077 from most recent public filings. Options information from most recent 10-K.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

27

CONFIDENTIAL

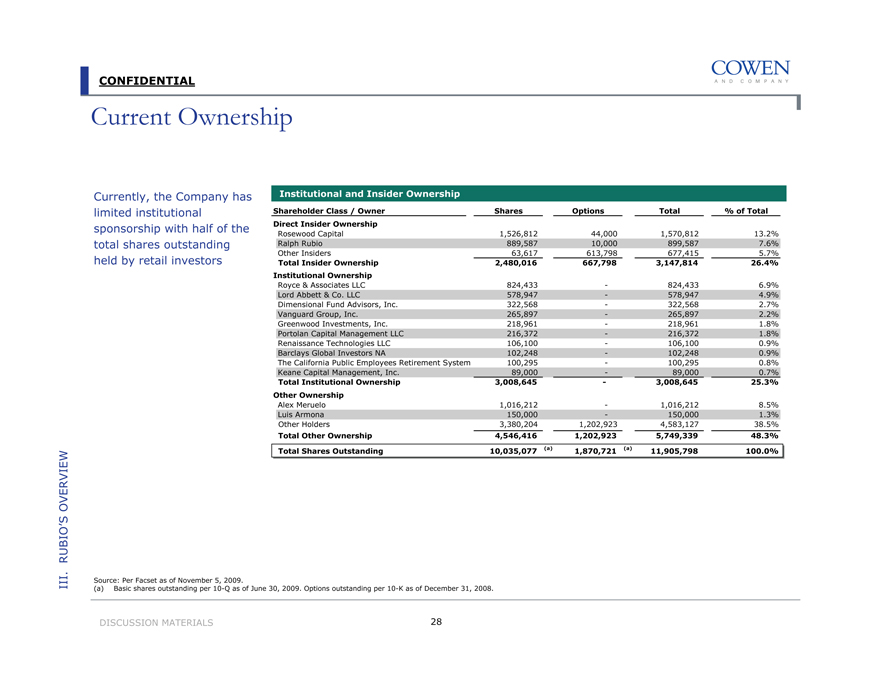

Current Ownership

Currently, the Company has limited institutional sponsorship with half of the total shares outstanding held by retail investors

Institutional and Insider Ownership

Shareholder Class / Owner Shares Options Total % of Total

Direct Insider Ownership

Rosewood Capital 1,526,812 44,000 1,570,812 13.2%

Ralph Rubio 889,587 10,000 899,587 7.6%

Other Insiders 63,617 613,798 677,415 5.7%

Total Insider Ownership 2,480,016 667,798 3,147,814 26.4%

Institutional Ownership

Royce & Associates LLC 824,433 - 824,433 6.9%

Lord Abbett & Co. LLC 578,947 - 578,947 4.9%

Dimensional Fund Advisors, Inc. 322,568 - 322,568 2.7%

Vanguard Group, Inc. 265,897 - 265,897 2.2%

Greenwood Investments, Inc. 218,961 - 218,961 1.8%

Portolan Capital Management LLC 216,372 - 216,372 1.8%

Renaissance Technologies LLC 106,100 - 106,100 0.9%

Barclays Global Investors NA 102,248 - 102,248 0.9%

The California Public Employees Retirement System 100,295 - 100,295 0.8%

Keane Capital Management, Inc. 89,000 - 89,000 0.7%

Total Institutional Ownership 3,008,645 - 3,008,645 25.3%

Other Ownership

Alex Meruelo 1,016,212 - 1,016,212 8.5%

Luis Armona 150,000 - 150,000 1.3%

Other Holders 3,380,204 1,202,923 4,583,127 38.5%

Total Other Ownership 4,546,416 1,202,923 5,749,339 48.3%

Total Shares Outstanding 10,035,077 (a) 1,870,721 (a) 11,905,798 100.0%

Source: Per Facset as of November 5, 2009.

(a) Basic shares outstanding per 10-Q as of June 30, 2009. Options outstanding per 10-K as of December 31, 2008.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

28

CONFIDENTIAL

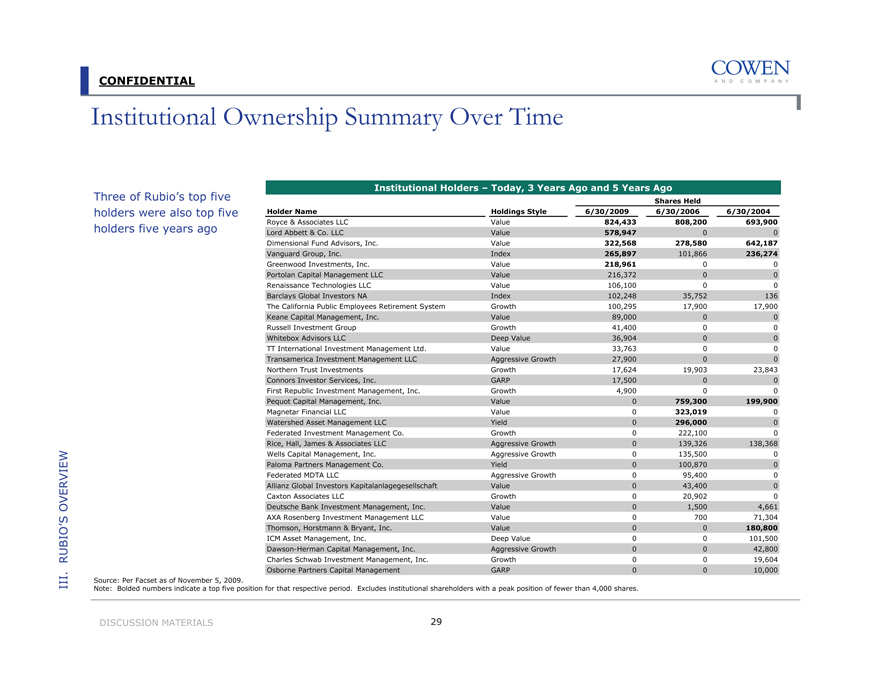

Institutional Ownership Summary Over Time

Three of Rubio’s top five holders were also top five holders five years ago

Institutional Holders – Today, 3 Years Ago and 5 Years Ago

Shares Held

Holder Name Holdings Style 6/30/2009 6/30/2006 6/30/2004

Royce & Associates LLC Value 824,433 808,200 693,900

Lord Abbett & Co. LLC Value 578,947 0 0

Dimensional Fund Advisors, Inc. Value 322,568 278,580 642,187

Vanguard Group, Inc. Index 265,897 101,866 236,274

Greenwood Investments, Inc. Value 218,961 0 0

Portolan Capital Management LLC Value 216,372 0 0

Renaissance Technologies LLC Value 106,100 0 0

Barclays Global Investors NA Index 102,248 35,752 136

The California Public Employees Retirement System Growth 100,295 17,900 17,900

Keane Capital Management, Inc. Value 89,000 0 0

Russell Investment Group Growth 41,400 0 0

Whitebox Advisors LLC Deep Value 36,904 0 0

TT International Investment Management Ltd. Value 33,763 0 0

Transamerica Investment Management LLC Aggressive Growth 27,900 0 0

Northern Trust Investments Growth 17,624 19,903 23,843

Connors Investor Services, Inc. GARP 17,500 0 0

First Republic Investment Management, Inc. Growth 4,900 0 0

Pequot Capital Management, Inc. Value 0 759,300 199,900

Magnetar Financial LLC Value 0 323,019 0

Watershed Asset Management LLC Yield 0 296,000 0

Federated Investment Management Co. Growth 0 222,100 0

Rice, Hall, James & Associates LLC Aggressive Growth 0 139,326 138,368

Wells Capital Management, Inc. Aggressive Growth 0 135,500 0

Paloma Partners Management Co. Yield 0 100,870 0

Federated MDTA LLC Aggressive Growth 0 95,400 0

Allianz Global Investors Kapitalanlagegesellschaft Value 0 43,400 0

Caxton Associates LLC Growth 0 20,902 0

Deutsche Bank Investment Management, Inc. Value 0 1,500 4,661

AXA Rosenberg Investment Management LLC Value 0 700 71,304

Thomson, Horstmann & Bryant, Inc. Value 0 0 180,800

ICM Asset Management, Inc. Deep Value 0 0 101,500

Dawson-Herman Capital Management, Inc. Aggressive Growth 0 0 42,800

Charles Schwab Investment Management, Inc. Growth 0 0 19,604

Osborne Partners Capital Management GARP 0 0 10,000

Source: Per Facset as of November 5, 2009.

Note: Bolded numbers indicate a top five position for that respective period. Excludes institutional shareholders with a peak position of fewer than 4,000 shares.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

29

CONFIDENTIAL

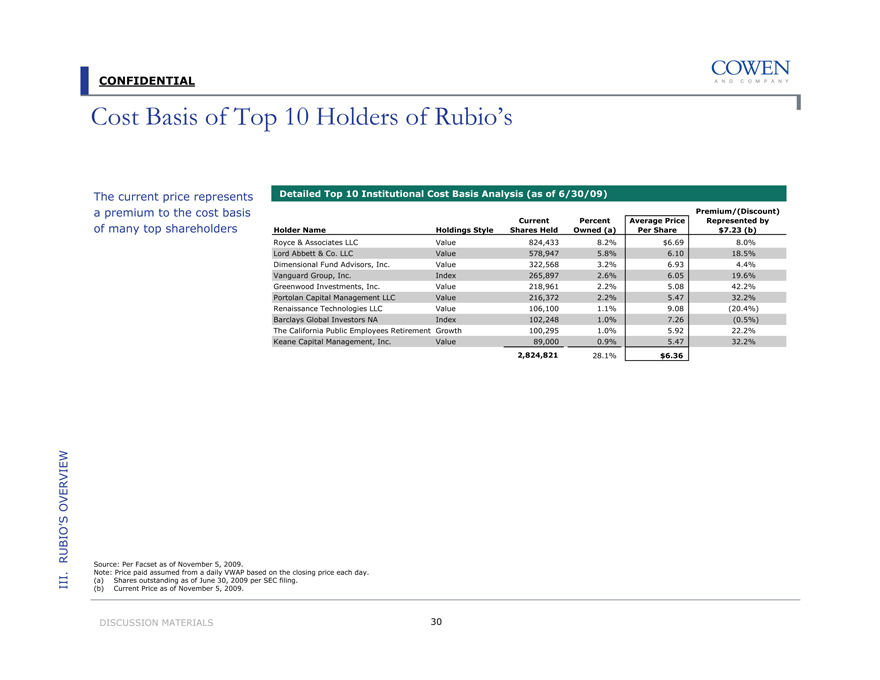

Cost Basis of Top 10 Holders of Rubio’s

The current price represents a premium to the cost basis of many top shareholders

Detailed Top 10 Institutional Cost Basis Analysis (as of 6/30/09)

Holder Name Holdings Style Current Shares Held Percent Owned (a) Average Price Per Share Premium/(Discount) Represented by $7.23 (b)

Royce & Associates LLC Value 824,433 8.2% $6.69 8.0%

Lord Abbett & Co. LLC Value 578,947 5.8% 6.10 18.5%

Dimensional Fund Advisors, Inc. Value 322,568 3.2% 6.93 4.4%

Vanguard Group, Inc. Index 265,897 2.6% 6.05 19.6%

Greenwood Investments, Inc. Value 218,961 2.2% 5.08 42.2%

Portolan Capital Management LLC Value 216,372 2.2% 5.47 32.2%

Renaissance Technologies LLC Value 106,100 1.1% 9.08 (20.4%)

Barclays Global Investors NA Index 102,248 1.0% 7.26 (0.5%)

The California Public Employees Retirement Growth 100,295 1.0% 5.92 22.2%

Keane Capital Management, Inc. Value 89,000 0.9% 5.47 32.2%

2,824,821 28.1% $6.36

Source: Per Facset as of November 5, 2009.

Note: Price paid assumed from a daily VWAP based on the closing price each day.

(a) Shares outstanding as of June 30, 2009 per SEC filing.

(b) Current Price as of November 5, 2009.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

30

CONFIDENTIAL

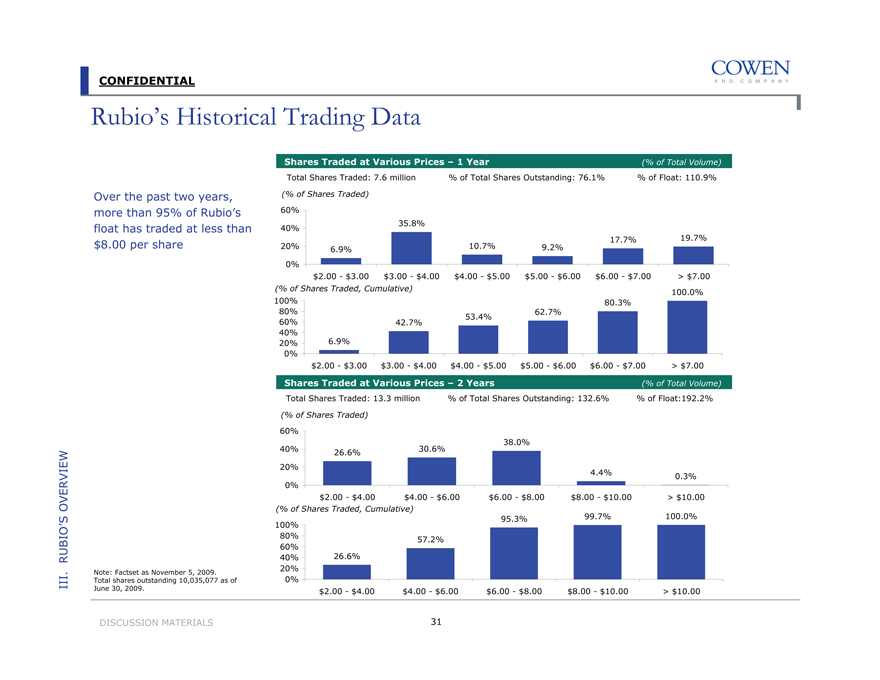

Rubio’s Historical Trading Data

Over the past two years, more than 95% of Rubio’s float has traded at less than

$8.00 per share

Shares Traded at Various Prices – 1 Year (% of Total Volume)

Total Shares Traded: 7.6 million % of Total Shares Outstanding: 76.1% % of Float: 110.9%

(% of Shares Traded)

60% 40% 20% 0%

35.8%

10.7% 17.7% 19.7%

6.9% 9.2%

$2.00 - $3.00 $3.00 - $4.00 $4.00 - $5.00 $5.00 - $6.00 $6.00 - $7.00 > $7.00

(% of Shares Traded, Cumulative)

100% 80% 60% 40% 20% 0%

100.0%

80.3%

62.7%

53.4%

42.7%

6.9%

$2.00 - $3.00 $3.00 - $4.00 $4.00 - $5.00 $5.00 - $6.00 $6.00 - $7.00 > $7.00

Shares Traded at Various Prices – 2 Years (% of Total Volume)

Total Shares Traded: 13.3 million % of Total Shares Outstanding: 132.6% % of Float:192.2%

(% of Shares Traded)

60% 40% 20% 0%

38.0%

26.6% 30.6%

4.4% 0.3%

$2.00 - $4.00 $4.00 - $6.00 $6.00 - $8.00 $8.00 - $10.00 > $10.00

(% of Shares Traded, Cumulative)

100% 80% 60% 40% 20% 0%

95.3% 99.7% 100.0%

57.2%

26.6%

$2.00 - $4.00 $4.00 - $6.00 $6.00 - $8.00 $8.00 - $10.00 > $10.00

Note: Factset as November 5, 2009. Total shares outstanding 10,035,077 as of June 30, 2009.

III. RUBIO’S OVERVIEW

DISCUSSION MATERIALS

31

CONFIDENTIAL

IV. Valuation Overview

CONFIDENTIAL

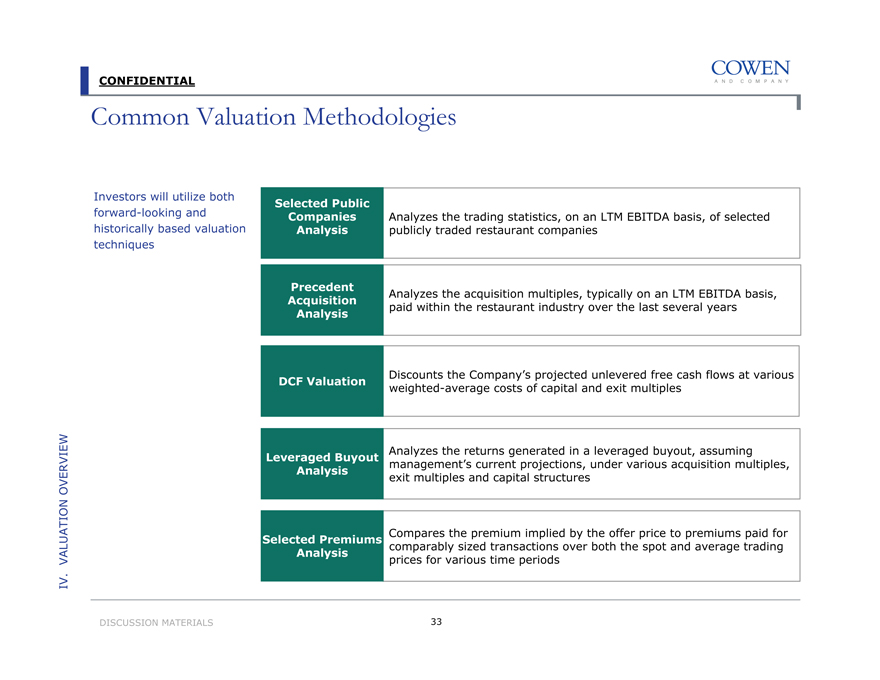

Common Valuation Methodologies

Investors will utilize both forward-looking and historically based valuation techniques

Selected Public Companies Analysis

Analyzes the trading statistics, on an LTM EBITDA basis, of selected publicly traded restaurant companies

Precedent Acquisition Analysis

Analyzes the acquisition multiples, typically on an LTM EBITDA basis, paid within the restaurant industry over the last several years

DCF Valuation

Discounts the Company’s projected unlevered free cash flows at various weighted-average costs of capital and exit multiples

Leveraged Buyout Analysis

Analyzes the returns generated in a leveraged buyout, assuming management’s current projections, under various acquisition multiples, exit multiples and capital structures

Selected Premiums Analysis

Compares the premium implied by the offer price to premiums paid for comparably sized transactions over both the spot and average trading prices for various time periods

IV. Valuation Overview

DISCUSSION MATERIALS

33

CONFIDENTIAL

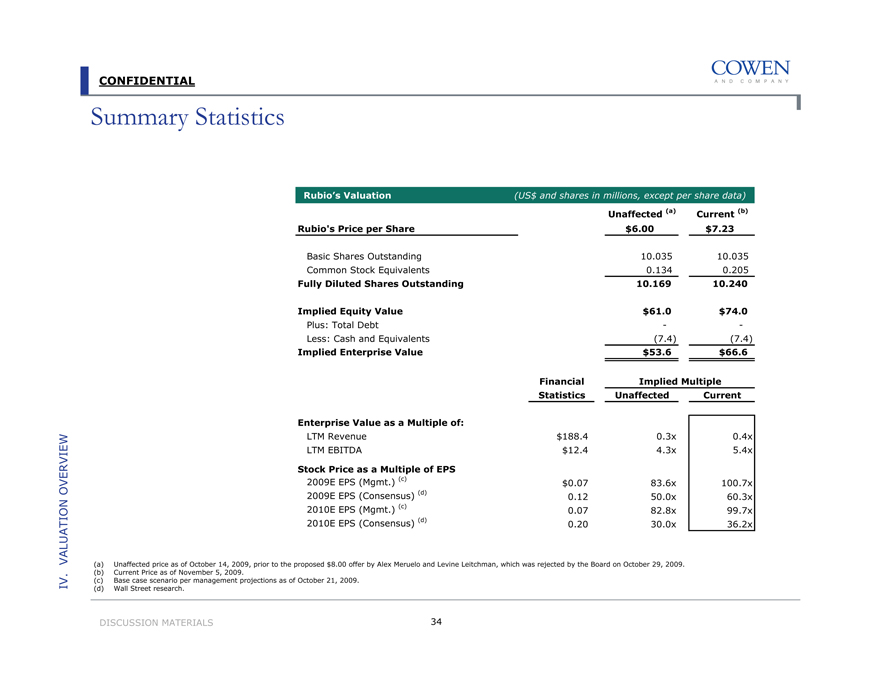

Summary Statistics

Rubio’s Valuation (US$ and shares in millions, except per share data)

Unaffected (a) Current (b)

Rubio’s Price per Share $6.00 $7.23

Basic Shares Outstanding 10.035 10.035

Common Stock Equivalents 0.134 0.205

Fully Diluted Shares Outstanding 10.169 10.240

Implied Equity Value $61.0 $74.0

Plus: Total Debt - -

Less: Cash and Equivalents (7.4) (7.4)

Implied Enterprise Value $53.6 $66.6

Financial Statistics Implied Multiple Unaffected Current

Enterprise Value as a Multiple of:

LTM Revenue $188.4 0.3x 0.4x

LTM EBITDA $12.4 4.3x 5.4x

Stock Price as a Multiple of EPS

2009E EPS (Mgmt.) (c) $0.07 83.6x 100.7x

2009E EPS (Consensus) (d) 0.12 50.0x 60.3x

2010E EPS (Mgmt.) (c) 0.07 82.8x 99.7x

2010E EPS (Consensus) (d) 0.20 30.0x 36.2x

(a) Unaffected price as of October 14, 2009, prior to the proposed $8.00 offer by Alex Meruelo and Levine Leitchman, which was rejected by the Board on October 29, 2009. (b) Current Price as of November 5, 2009.

(c) Base case scenario per management projections as of October 21, 2009. (d) Wall Street research.

IV. Valuation Overview

DISCUSSION MATERIALS

34

CONFIDENTIAL

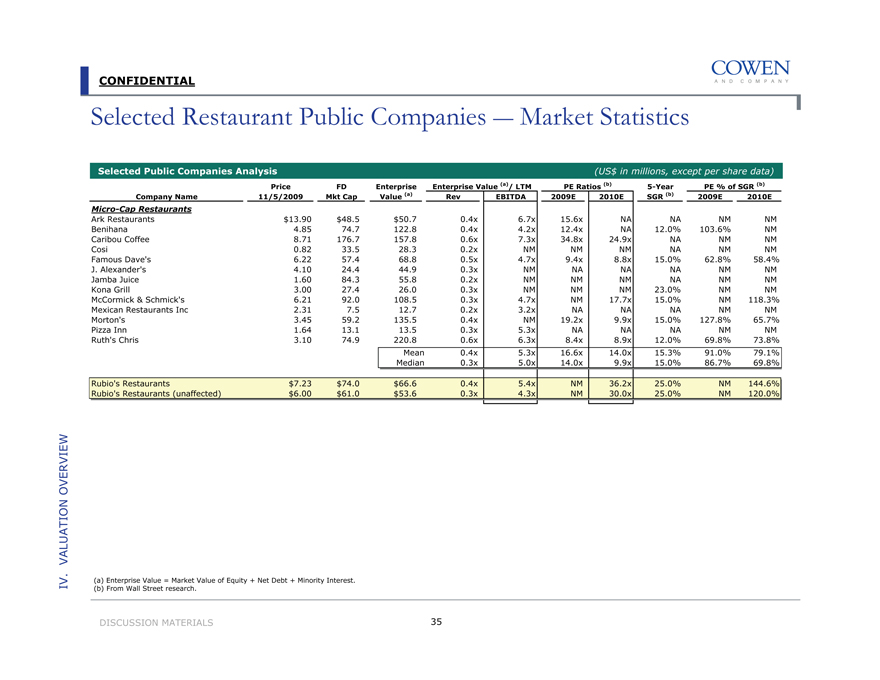

Selected Restaurant Public Companies — Market Statistics

Selected Public Companies Analysis

(US$ in millions, except per share data)

Enterprise Value (a)/ LTM PE Ratios (b) PE % of SGR (b)

Company Name Price 11/5/2009 FD Mkt Cap Enterprise Value (a) Rev EBITDA 2009E 2010E 5-Year SGR (b) 2009E 2010E

Micro-Cap Restaurants

Ark Restaurants $13.90 $48.5 $50.7 0.4x 6.7x 15.6x NA NA NM NM

Benihana 4.85 74.7 122.8 0.4x 4.2x 12.4x NA 12.0% 103.6% NM

Caribou Coffee 8.71 176.7 157.8 0.6x 7.3x 34.8x 24.9x NA NM NM

Cosi 0.82 33.5 28.3 0.2x NM NM NM NA NM NM

Famous Dave’s 6.22 57.4 68.8 0.5x 4.7x 9.4x 8.8x 15.0% 62.8% 58.4%

J. Alexander’s 4.10 24.4 44.9 0.3x NM NA NA NA NM NM

Jamba Juice 1.60 84.3 55.8 0.2x NM NM NM NA NM NM

Kona Grill 3.00 27.4 26.0 0.3x NM NM NM 23.0% NM NM

McCormick & Schmick’s 6.21 92.0 108.5 0.3x 4.7x NM 17.7x 15.0% NM 118.3%

Mexican Restaurants Inc 2.31 7.5 12.7 0.2x 3.2x NA NA NA NM NM

Morton’s 3.45 59.2 135.5 0.4x NM 19.2x 9.9x 15.0% 127.8% 65.7%

Pizza Inn 1.64 13.1 13.5 0.3x 5.3x NA NA NA NM NM

Ruth’s Chris 3.10 74.9 220.8 0.6x 6.3x 8.4x 8.9x 12.0% 69.8% 73.8%

Mean 0.4x 5.3x 16.6x 14.0x 15.3% 91.0% 79.1%

Median 0.3x 5.0x 14.0x 9.9x 15.0% 86.7% 69.8%

Rubio’s Restaurants $7.23 $74.0 $66.6 0.4x 5.4x NM 36.2x 25.0% NM 144.6%

Rubio’s Restaurants (unaffected) $6.00 $61.0 $53.6 0.3x 4.3x NM 30.0x 25.0% NM 120.0%

(a) Enterprise Value = Market Value of Equity + Net Debt + Minority Interest. (b) From Wall Street research.

IV. Valuation Overview

DISCUSSION MATERIALS

35

CONFIDENTIAL

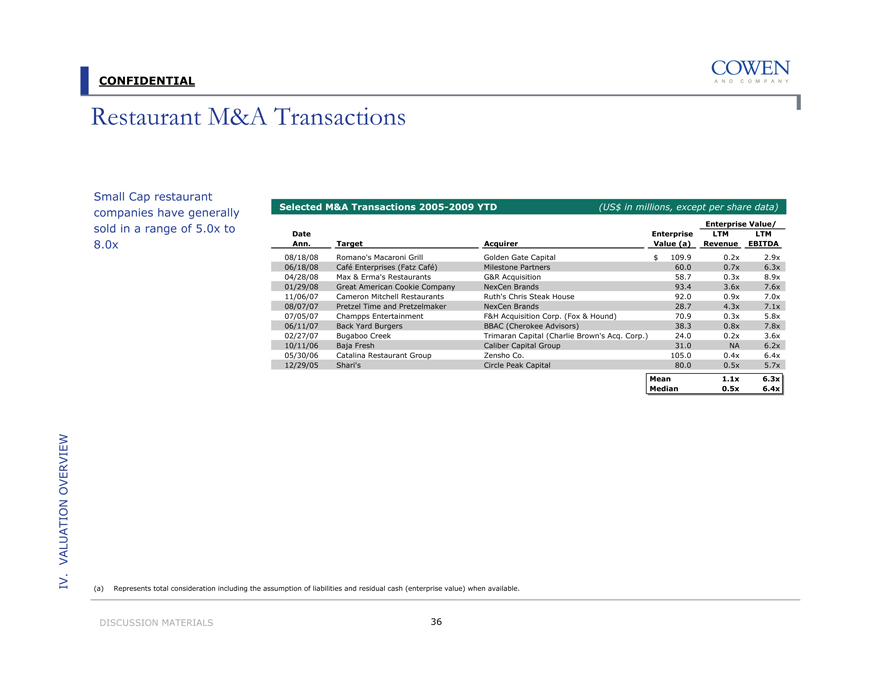

Restaurant M&A Transactions

Small Cap restaurant companies have generally sold in a range of 5.0x to 8.0x

Selected M&A Transactions 2005-2009 YTD (US$ in millions, except per share data)

Enterprise Value/

Date Ann. Target Acquirer Enterprise Value (a) LTM Revenue LTM EBITDA

08/18/08 Romano’s Macaroni Grill Golden Gate Capital $ 109.9 0.2x 2.9x

06/18/08 Café Enterprises (Fatz Café) Milestone Partners 60.0 0.7x 6.3x

04/28/08 Max & Erma’s Restaurants G&R Acquisition 58.7 0.3x 8.9x

01/29/08 Great American Cookie Company NexCen Brands 93.4 3.6x 7.6x

11/06/07 Cameron Mitchell Restaurants Ruth’s Chris Steak House 92.0 0.9x 7.0x

08/07/07 Pretzel Time and Pretzelmaker NexCen Brands 28.7 4.3x 7.1x

07/05/07 Champps Entertainment F&H Acquisition Corp. (Fox & Hound) 70.9 0.3x 5.8x

06/11/07 Back Yard Burgers BBAC (Cherokee Advisors) 38.3 0.8x 7.8x

02/27/07 Bugaboo Creek Trimaran Capital (Charlie Brown’s Acq. Corp.) 24.0 0.2x 3.6x

10/11/06 Baja Fresh Caliber Capital Group 31.0 NA 6.2x

05/30/06 Catalina Restaurant Group Zensho Co. 105.0 0.4x 6.4x

12/29/05 Shari’s Circle Peak Capital 80.0 0.5x 5.7x

Mean 1.1x 6.3x

Median 0.5x 6.4x

(a) Represents total consideration including the assumption of liabilities and residual cash (enterprise value) when available.

IV. Valuation Overview

DISCUSSION MATERIALS

36

CONFIDENTIAL

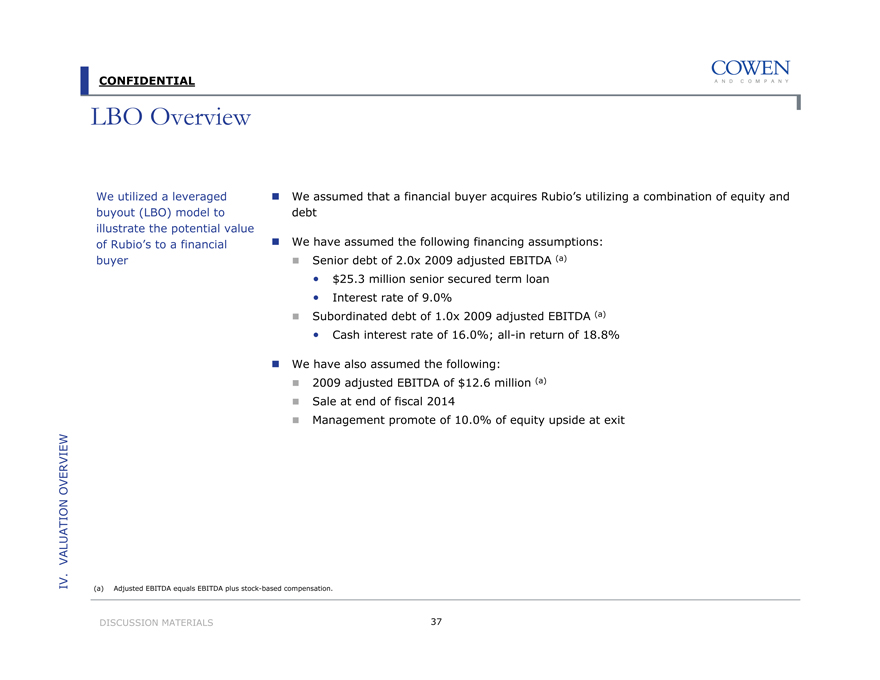

LBO Overview

We utilized a leveraged buyout (LBO) model to illustrate the potential value of Rubio’s to a financial buyer

We assumed that a financial buyer acquires Rubio’s utilizing a combination of equity and debt

We have assumed the following financing assumptions:

Senior debt of 2.0x 2009 adjusted EBITDA (a)

$25.3 million senior secured term loan

Interest rate of 9.0%

Subordinated debt of 1.0x 2009 adjusted EBITDA (a)

Cash interest rate of 16.0%; all-in return of 18.8%

We have also assumed the following:

2009 adjusted EBITDA of $12.6 million (a)

Sale at end of fiscal 2014

Management promote of 10.0% of equity upside at exit

(a) Adjusted EBITDA equals EBITDA plus stock-based compensation.

IV. Valuation Overview

DISCUSSION MATERIALS

37

CONFIDENTIAL

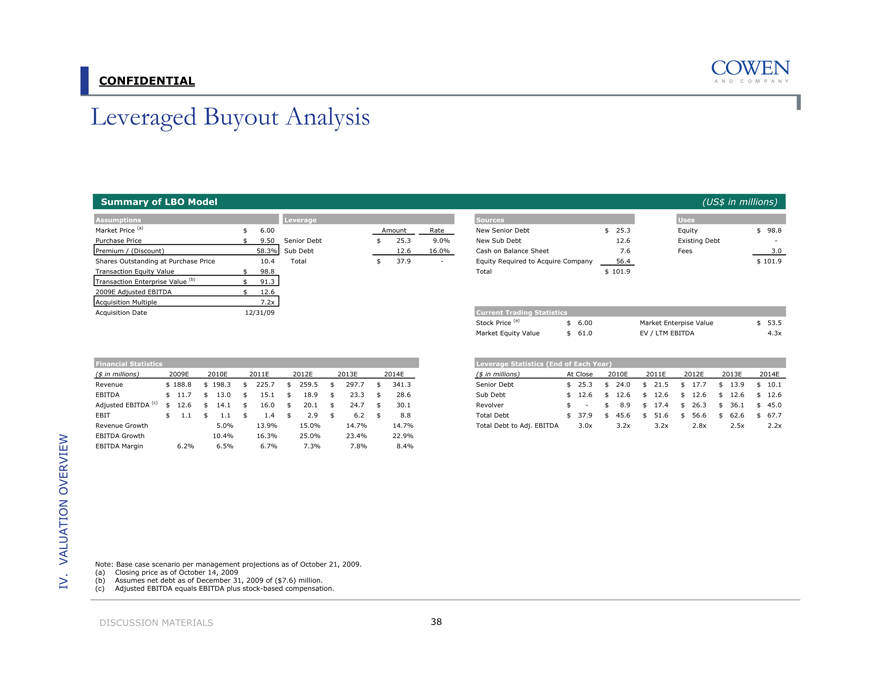

Leveraged Buyout Analysis

Summary of LBO Model

(US$ in millions)

Assumptions

Market Price (a) $ 6.00

Purchase Price $ 9.50

Premium / (Discount) 58.3%

Shares Outstanding at Purchase Price 10.4

Transaction Equity Value $ 98.8

Transaction Enterprise Value (b) $ 91.3

2009E Adjusted EBITDA $ 12.6

Acquisition Multiple 7.2x

Acquisition Date 12/31/09

Leverage

Amount Rate

Senior Debt $ 25.3 9.0%

Sub Debt 12.6 16.0%

Total $ 37.9 -

Sources

New Senior Debt $ 25.3

New Sub Debt 12.6

Cash on Balance Sheet 7.6

Equity Required to Acquire Company 56.4

Total $ 101.9

Uses

Equity $ 98.8

Existing Debt -

Fees 3.0

$ 101.9

Financial Statistics

($ in millions) 2009E 2010E 2011E 2012E 2013E 2014E

Revenue $ 188.8 $ 198.3 $ 225.7 $ 259.5 $ 297.7 $ 341.3

EBITDA $ 11.7 $ 13.0 $ 15.1 $ 18.9 $ 23.3 $ 28.6

Adjusted EBITDA (c) $ 12.6 $ 14.1 $ 16.0 $ 20.1 $ 24.7 $ 30.1

EBIT $ 1.1 $ 1.1 $ 1.4 $ 2.9 $ 6.2 $ 8.8

Revenue Growth 5.0% 13.9% 15.0% 14.7% 14.7%

EBITDA Growth 10.4% 16.3% 25.0% 23.4% 22.9%

EBITDA Margin 6.2% 6.5% 6.7% 7.3% 7.8% 8.4%

Current Trading Statistics

Stock Price (a) $ 6.00 Market Enterpise Value $ 53.5

Market Equity Value $ 61.0 EV / LTM EBITDA 4.3x

Leverage Statistics (End of Each Year)

($ in millions) At Close 2010E 2011E 2012E 2013E 2014E

Senior Debt $ 25.3 $ 24.0 $ 21.5 $ 17.7 $ 13.9 $ 10.1

Sub Debt $ 12.6 $ 12.6 $ 12.6 $ 12.6 $ 12.6 $ 12.6

Revolver $ - $ 8.9 $ 17.4 $ 26.3 $ 36.1 $ 45.0

Total Debt $ 37.9 $ 45.6 $ 51.6 $ 56.6 $ 62.6 $ 67.7

Total Debt to Adj. EBITDA 3.0x 3.2x 3.2x 2.8x 2.5x 2.2x

Note: Base case scenario per management projections as of October 21, 2009.

(a) Closing price as of October 14, 2009

(b) Assumes net debt as of December 31, 2009 of ($7.6) million.

(c) Adjusted EBITDA equals EBITDA plus stock-based compensation.

IV. Valuation Overview

DISCUSSION MATERIALS

38

CONFIDENTIAL

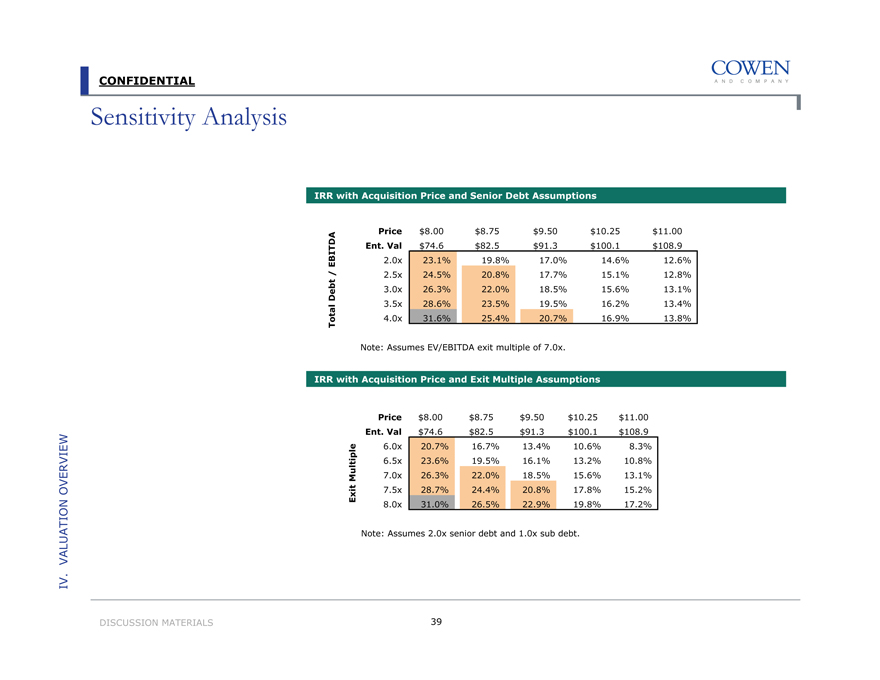

Sensitivity Analysis

IRR with Acquisition Price and Senior Debt Assumptions

Total Debt / EBITDA

Price $8.00 $8.75 $9.50 $10.25 $11.00

Ent. Val $74.6 $82.5 $91.3 $100.1 $108.9

2.0x 23.1% 19.8% 17.0% 14.6% 12.6%

2.5x 24.5% 20.8% 17.7% 15.1% 12.8%

3.0x 26.3% 22.0% 18.5% 15.6% 13.1%

3.5x 28.6% 23.5% 19.5% 16.2% 13.4%

4.0x 31.6% 25.4% 20.7% 16.9% 13.8%

Note: Assumes EV/EBITDA exit multiple of 7.0x.

IRR with Acquisition Price and Exit Multiple Assumptions

Exit Multiple

Price $8.00 $8.75 $9.50 $10.25 $11.00

Ent. Val $74.6 $82.5 $91.3 $100.1 $108.9

6.0x 20.7% 16.7% 13.4% 10.6% 8.3%

6.5x 23.6% 19.5% 16.1% 13.2% 10.8%

7.0x 26.3% 22.0% 18.5% 15.6% 13.1%

7.5x 28.7% 24.4% 20.8% 17.8% 15.2%

8.0x 31.0% 26.5% 22.9% 19.8% 17.2%

Note: Assumes 2.0x senior debt and 1.0x sub debt.

IV. Valuation Overview

DISCUSSION MATERIALS

39

CONFIDENTIAL

DCF Overview

We also utilized a discounted cash flow (DCF) model to calculate an implied value of Rubio’s

There are two key components to the DCF

The present value of the stream of unlevered cash flows in the projected period

The terminal value based on EBITDA in the outyear of the projected period

2009-2014 projections used for the DCF model were those provided by Rubio’s management

We presented the DCF with discount rates ranging from 18.0% to 22.0%

We assumed exit multiples in 2014 of 6.0x to 8.0x EBITDA

IV. VALUATION OVERVIEW

DISCUSSION MATERIALS

40

CONFIDENTIAL

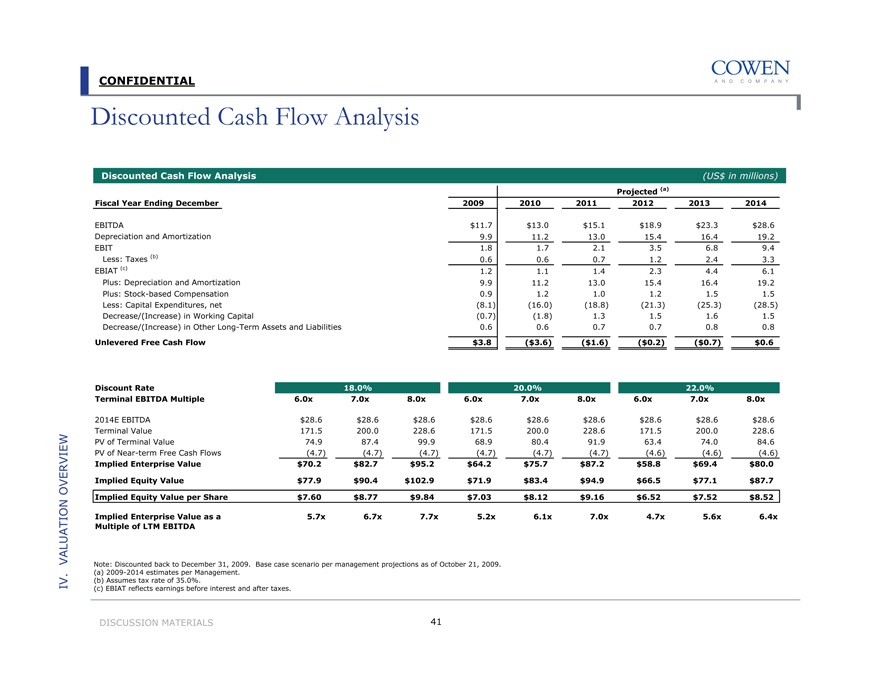

Discounted Cash Flow Analysis

Discounted Cash Flow Analysis

(US$ in millions)

Projected (a)

Fiscal Year Ending December

2009

2010

2011

2012

2013

2014

EBITDA

$11.7

$13.0

$15.1

$18.9

$23.3

$28.6

Depreciation and Amortization

9.9

11.2

13.0

15.4

16.4

19.2

EBIT

1.8

1.7

2.1

3.5

6.8

9.4

Less: Taxes (b)

0.6

0.6

0.7

1.2

2.4

3.3

EBIAT (c)

1.2

1.1

1.4

2.3

4.4

6.1

Plus: Depreciation and Amortization

9.9

11.2

13.0

15.4

16.4

19.2

Plus: Stock-based Compensation

0.9

1.2

1.0

1.2

1.5

1.5

Less: Capital Expenditures, net

(8.1)

(16.0)

(18.8)

(21.3)

(25.3)

(28.5)

Decrease/(Increase) in Working Capital

(0.7)

(1.8)

1.3

1.5

1.6

1.5

Decrease/(Increase) in Other Long-Term Assets and Liabilities

0.6

0.6

0.7

0.7

0.8

0.8

Unlevered Free Cash Flow

$3.8

($3.6)

($1.6)

($0.2)

($0.7)

$0.6

Discount Rate

18.0%

20.0%

22.0%

Terminal EBITDA Multiple

6.0x

7.0x

8.0x

6.0x

7.0x

8.0x

6.0x

7.0x

8.0x

2014E EBITDA

$28.6

$28.6

$28.6

$28.6

$28.6

$28.6

$28.6

$28.6

$28.6

Terminal Value

171.5

200.0

228.6

171.5

200.0

228.6

171.5

200.0

228.6

PV of Terminal Value

74.9

87.4

99.9

68.9

80.4

91.9

63.4

74.0

84.6

PV of Near-term Free Cash Flows

(4.7)

(4.7)

(4.7)

(4.7)

(4.7)

(4.7)

(4.6)

(4.6)

(4.6)

Implied Enterprise Value

$70.2

$82.7

$95.2

$64.2

$75.7

$87.2

$58.8

$69.4

$80.0

Implied Equity Value

$77.9

$90.4

$102.9

$71.9

$83.4

$94.9

$66.5

$77.1

$87.7

Implied Equity Value per Share

$7.60

$8.77

$9.84

$7.03

$8.12

$9.16

$6.52

$7.52

$8.52

Implied Enterprise Value as a

5.7x

6.7x

7.7x

5.2x

6.1x

7.0x

4.7x

5.6x

6.4x

Multiple of LTM EBITDA

Note: Discounted back to December 31, 2009. Base case scenario per management projections as of October 21, 2009. (a) 2009-2014 estimates per Management.

(b) |

| Assumes tax rate of 35.0%. |

(c) |

| EBIAT reflects earnings before interest and after taxes. |

IV. VALUATION OVERVIEW

DISCUSSION MATERIALS

41

CONFIDENTIAL

Valuation at Various Share Prices

Multiples at Various Share Prices

(US$ in millions)

Share Price

$6.00 (a)

$8.00

$8.50

$9.00

$9.50

$10.00

$10.50

$11.00

$11.50

$12.00

$12.50

$13.00

Premium/(Discount)

Current Price of $6.00

$0.00

33.3%

41.7%

50.0%

58.3%

66.7%

75.0%

83.3%

91.7%

100.0%

108.3%

116.7%

1-Week Average Price of $6.15

(2.5%)

30.0%

38.1%

46.3%

54.4%

62.5%

70.6%

78.8%

86.9%

95.0%

103.1%

111.3%

30-Day Average Price of $6.44

(6.8%)

24.2%

32.0%

39.8%

47.5%

55.3%

63.1%

70.8%

78.6%

86.4%

94.1%

101.9%

3-Month Average Price of $6.25

(4.0%)

28.0%

36.0%

44.0%

52.0%

60.1%

68.1%

76.1%

84.1%

92.1%

100.1%

108.1%

6-Month Average Price of $6.01

(0.1%)

33.2%

41.5%

49.9%

58.2%

66.5%

74.8%

83.2%

91.5%

99.8%

108.1%

116.5%

52-Week High of $7.85

(23.6%)

1.9%

8.3%

14.6%

21.0%

27.4%

33.8%

40.1%

46.5%

52.9%

59.2%

65.6%

52-Week Low of $2.16

177.8%

270.4%

293.5%

316.7%

339.8%

363.0%

386.1%

409.3%

432.4%

455.6%

478.7%

501.9%

Implied Equity Value

$61.0

$82.2

$87.5

$93.0

$98.8

$104.7

$110.6

$116.5

$122.4

$128.3

$134.3

$140.2

Implied Enterprise Value (b)

$53.6

$74.8

$80.1

$85.6

$91.4

$97.3

$103.2

$109.1

$115.0

$120.9

$126.8

$132.8

Fully Diluted Shares (Basic + CSEs)

10.169

10.273

10.292

10.330

10.405

10.472

10.534

10.593

10.646

10.695

10.741

10.786

Implied Enterprise Value/:

LTM EBITDA

4.3x

6.0x

6.5x

6.9x

7.4x

7.8x

8.3x

8.8x

9.3x

9.7x

10.2x

10.7x

Implied Equity Value/:

2009E EPS (Mgmt.) (c)

83.6x

111.5x

118.4x

125.4x

132.4x

139.3x

146.3x

153.3x

160.2x

167.2x

174.2x

181.1x

2009E EPS (Consensus) (d)

50.0x

66.7x

70.8x

75.0x

79.2x

83.3x

87.5x

91.7x

95.8x

100.0x

104.2x

108.3x

2010E EPS (Mgmt.) (c)

82.8x

110.4x

117.2x

124.1x

131.0x

137.9x

144.8x

151.7x

158.6x

165.5x

172.4x

179.3x

2010E EPS (Consensus) (d)

30.0x

40.0x

42.5x

45.0x

47.5x

50.0x

52.5x

55.0x

57.5x

60.0x

62.5x

65.0x

(a) Unaffected price as of October 14, 2009, prior to the proposed $8.00 offer by Alex Meruelo and Levine Leitchman, which was rejected by the Board on October 29, 2009. (b) Cash and debt figures from the period ending September 27, 2009.

(c) |

| Base case scenario per management projections as of October 21, 2009. (d) Per Wall Street Research. |

IV. VALUATION OVERVIEW

DISCUSSION MATERIALS 42

CONFIDENTIAL

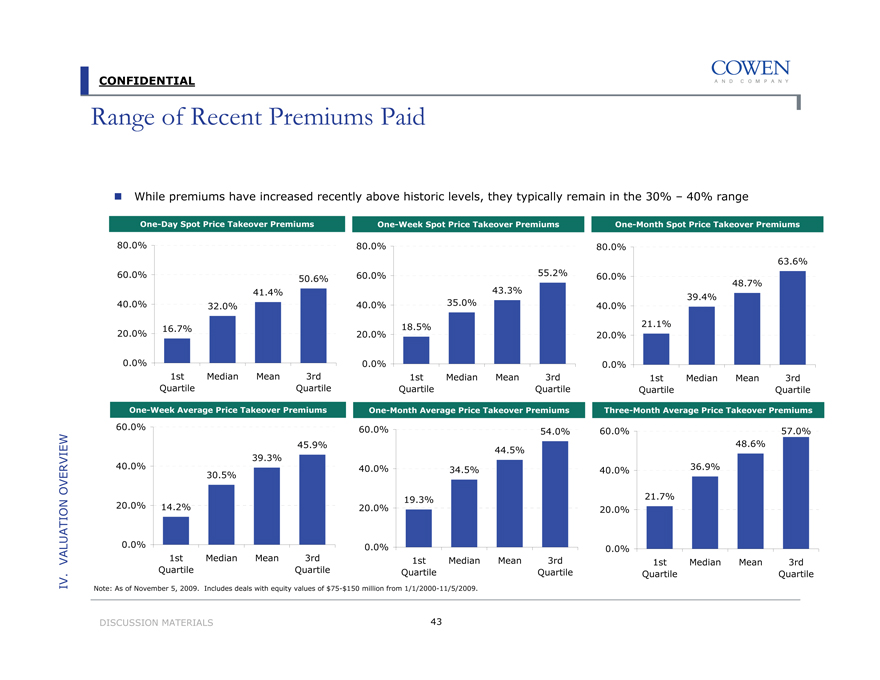

Range of Recent Premiums Paid

While premiums have increased recently above historic levels, they typically remain in the 30% – 40% range

One-Day Spot Price Takeover Premiums

80.0% 60.0% 40.0% 20.0% 0.0%

50.6%

41.4%

32.0%

16.7%

1st

Median

Mean

3rd

Quartile

Quartile

One-Week Spot Price Takeover Premiums

80.0% 60.0% 40.0% 20.0% 0.0%

55.2%

43.3%

35.0%

18.5%

1st

Median

Mean

3rd

Quartile

Quartile

One-Month Spot Price Takeover Premiums

80.0% 60.0% 40.0% 20.0% 0.0%

63.6%

48.7%

39.4%

21.1%

1st

Median

Mean

3rd

Quartile

Quartile

One-Week Average Price Takeover Premiums

60.0% 40.0% 20.0% 0.0%

45.9%

39.3%

30.5%

14.2%

5/81st

Median

Mean

3rd

Quartile

Quartile

One-Month Average Price Takeover Premiums

60.0% 40.0% 20.0% 0.0%

54.0%

44.5%

34.5%

19.3%

1st

Median

Mean

3rd

Quartile

Quartile

Three-Month Average Price Takeover Premiums

60.0% 40.0% 20.0% 0.0%

57.0%

48.6%

36.9%

21.7%

1st Median Mean 3rd Quartile Quartile

Note: As of November 5, 2009. Includes deals with equity values of $75-$150 million from 1/1/2000-11/5/2009.

IV. VALUATION OVERVIEW

DISCUSSION MATERIALS

43

CONFIDENTIAL

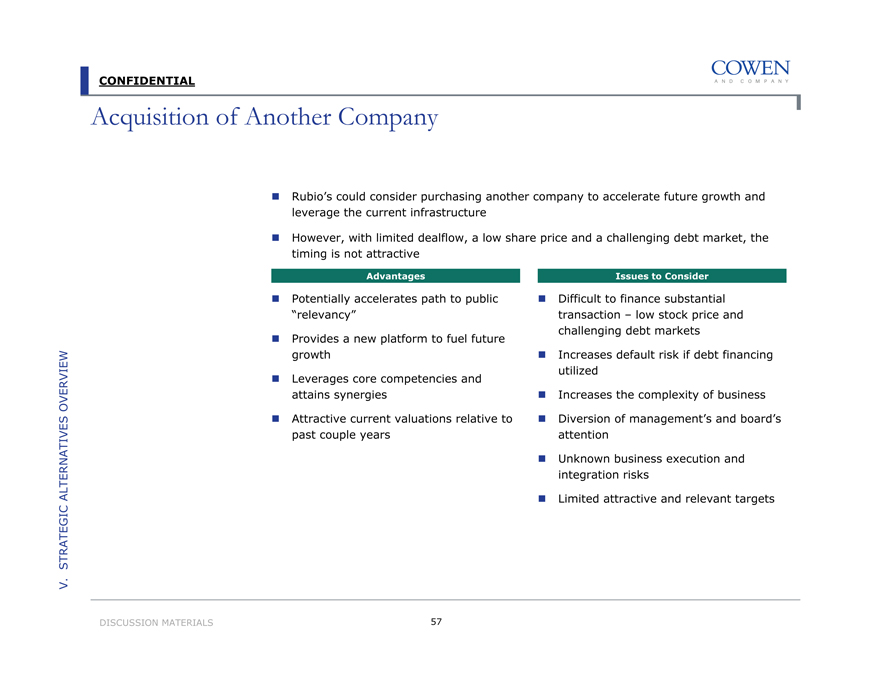

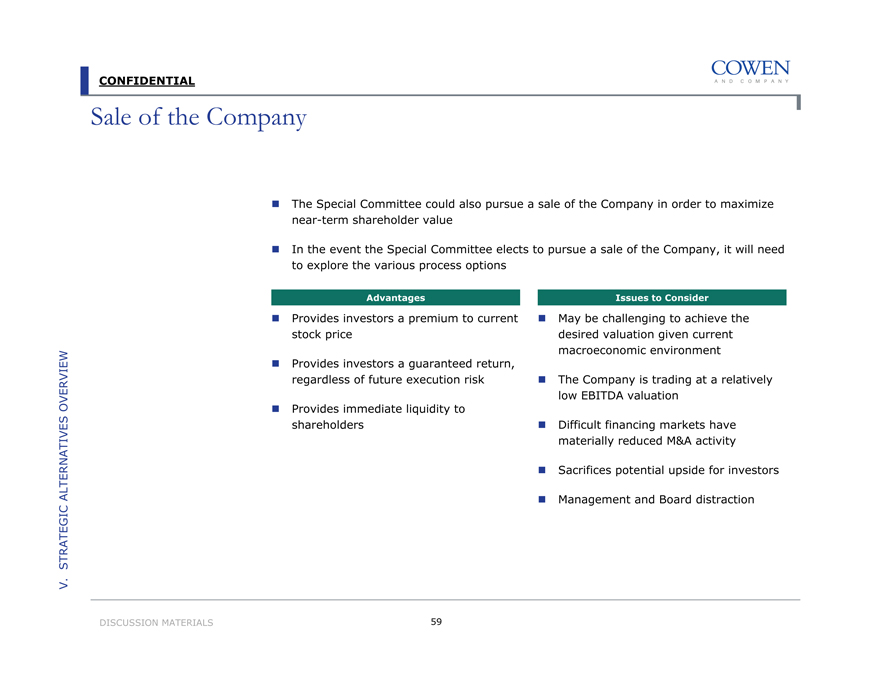

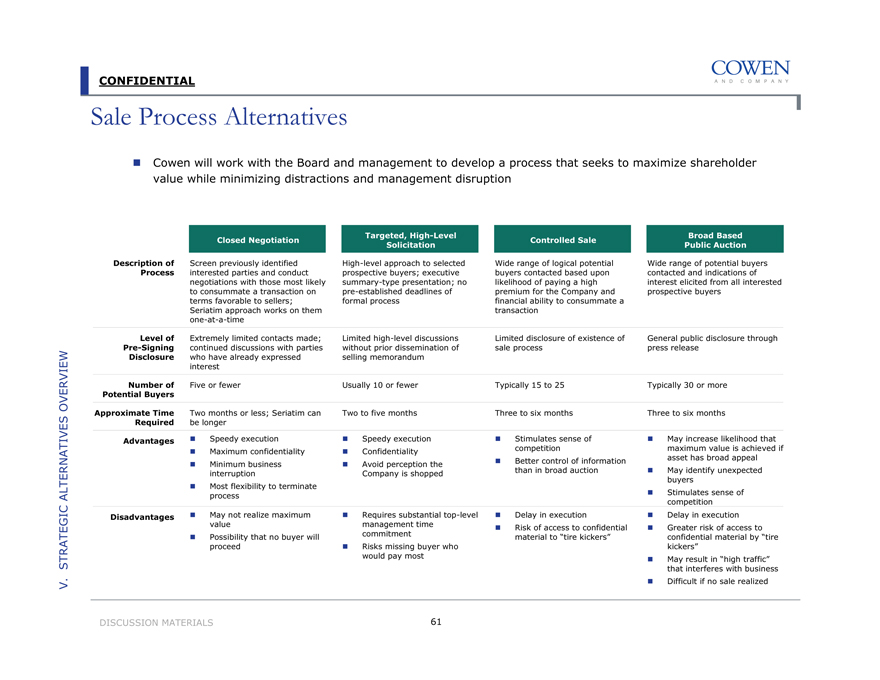

V. Strategic Alternatives Overview

CONFIDENTIAL

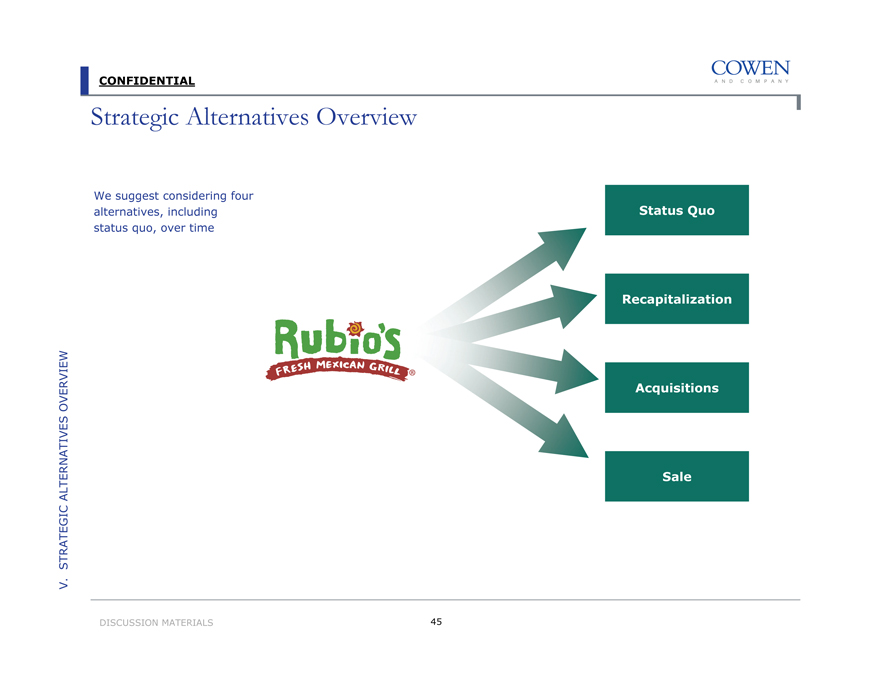

Strategic Alternatives Overview

We suggest considering four alternatives, including status quo, over time

V. STRATEGIC ALTERNATIVES OVERVIEW

DISCUSSION MATERIALS

Status Quo Recapitalization Acquisitions Sale

45

CONFIDENTIAL

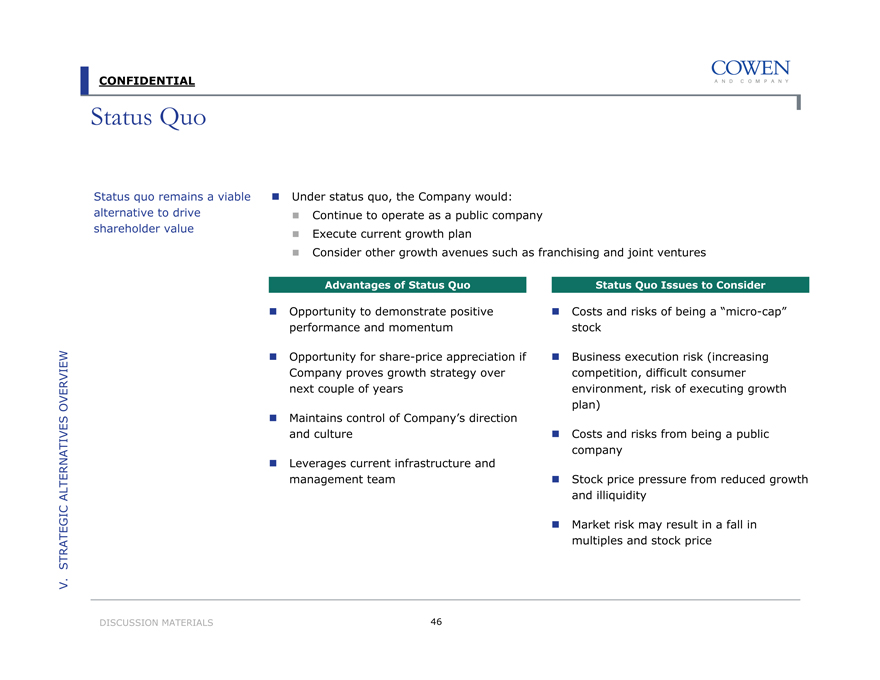

Status Quo

Status quo remains a viable alternative to drive shareholder value

Under status quo, the Company would:

Continue to operate as a public company

Execute current growth plan

Consider other growth avenues such as franchising and joint ventures

Advantages of Status Quo

Opportunity to demonstrate positive performance and momentum

Opportunity for share-price appreciation if Company proves growth strategy over next couple of years

Maintains control of Company’s direction and culture

Leverages current infrastructure and management team

Status Quo Issues to Consider

Costs and risks of being a “micro-cap” stock

Business execution risk (increasing competition, difficult consumer environment, risk of executing growth plan)

Costs and risks from being a public company

Stock price pressure from reduced growth and illiquidity

Market risk may result in a fall in multiples and stock price

V. STRATEGIC ALTERNATIVES OVERVIEW

DISCUSSION MATERIALS

46

CONFIDENTIAL

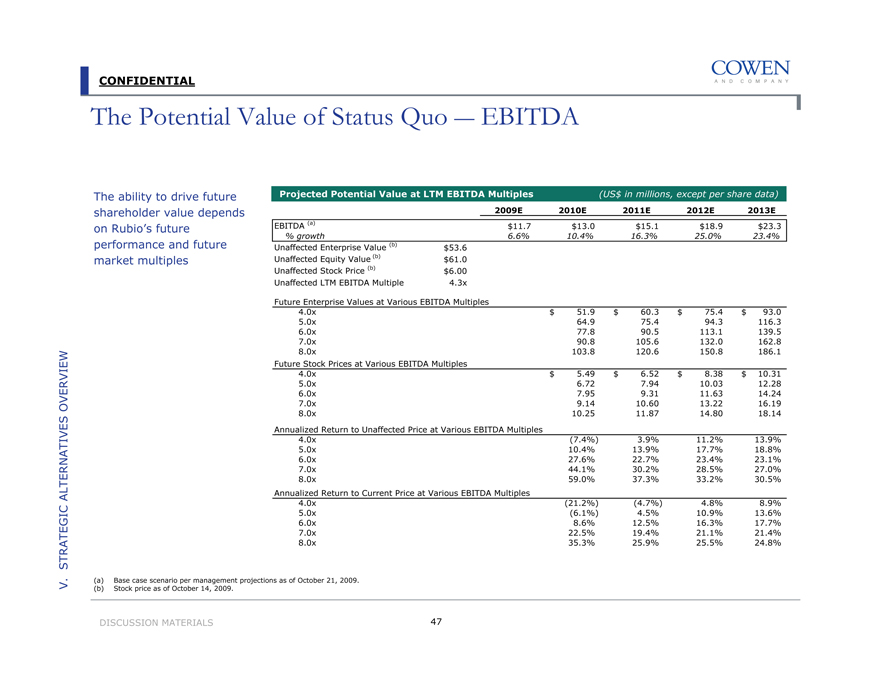

The Potential Value of Status Quo —EBITDA

The ability to drive future shareholder value depends on Rubio’s future performance and future market multiples

Projected Potential Value at LTM EBITDA Multiples

(US$ in millions, except per share data)

2009E

2010E

2011E

2012E

2013E

EBITDA (a)

$11.7

$13.0

$15.1

$18.9

$23.3

% growth

6.6%

10.4%

16.3%

25.0%

23.4%

Unaffected Enterprise Value (b)

$53.6

Unaffected Equity Value (b)

$61.0

Unaffected Stock Price (b)

$6.00

Unaffected LTM EBITDA Multiple

4.3x

Future Enterprise Values at Various EBITDA Multiples

4.0x

$ 51.9

$60.3

$75.4

$93.0

5.0x

64.9

75.4

94.3

116.3

6.0x

77.8

90.5

113.1

139.5

7.0x

90.8

105.6

132.0

162.8

8.0x

103.8

120.6

150.8

186.1

Future Stock Prices at Various EBITDA Multiples

4.0x

$ 5.49

$6.52

$8.38

$10.31

5.0x

6.72

7.94

10.03

12.28

6.0x

7.95

9.31

11.63

14.24

7.0x

9.14

10.60

13.22

16.19

8.0x

10.25

11.87

14.80

18.14

Annualized Return to Unaffected Price at Various EBITDA Multiples

4.0x

(7.4%)

3.9%

11.2%

13.9%

5.0x

10.4%

13.9%

17.7%

18.8%

6.0x

27.6%

22.7%

23.4%

23.1%

7.0x

44.1%

30.2%

28.5%

27.0%

8.0x

59.0%

37.3%

33.2%

30.5%

Annualized Return to Current Price at Various EBITDA Multiples

4.0x

(21.2%)

(4.7%)

4.8%

8.9%

5.0x

(6.1%)

4.5%

10.9%

13.6%

6.0x

8.6%

12.5%

16.3%

17.7%

7.0x

22.5%

19.4%

21.1%

21.4%

8.0x

35.3%

25.9%

25.5%

24.8%

(a) |

| Base case scenario per management projections as of October 21, 2009. (b) Stock price as of October 14, 2009. |

DISCUSSION MATERIALS 47

V. STRATEGIC ALTERNATIVES OVERVIEW

CONFIDENTIAL

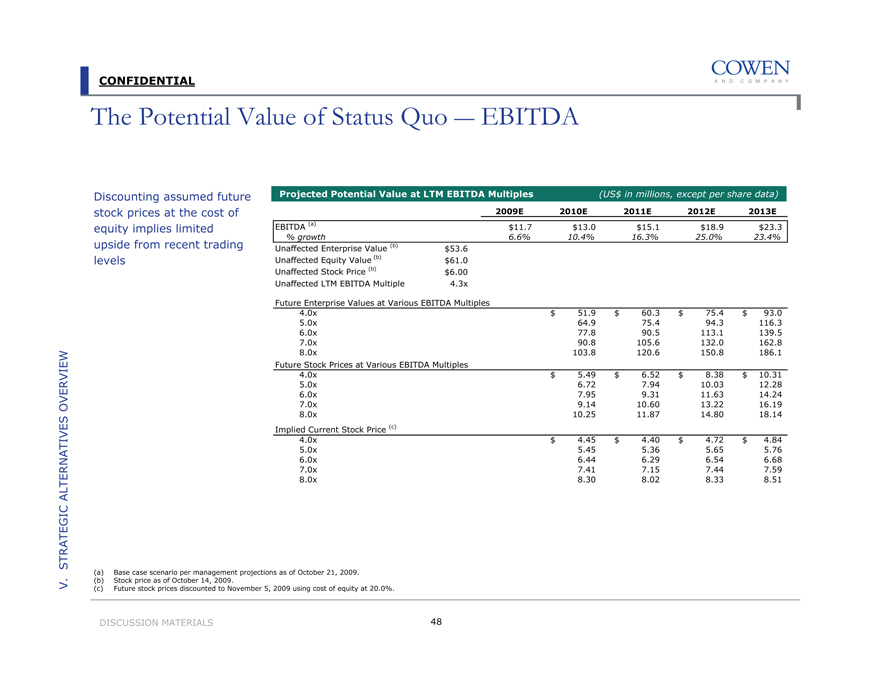

The Potential Value of Status Quo —EBITDA

Discounting assumed future stock prices at the cost of equity implies limited upside from recent trading levels

Projected Potential Value at LTM EBITDA Multiples

(US$ in millions, except per share data)

2009E

2010E

2011E

2012E

2013E

EBITDA (a)

$11.7

$13.0

$15.1

$18.9

$23.3

% growth

6.6%

10.4%

16.3%

25.0%

23.4%

Unaffected Enterprise Value (b)

$53.6

Unaffected Equity Value (b)

$61.0

Unaffected Stock Price (b)

$6.00

Unaffected LTM EBITDA Multiple

4.3x

Future Enterprise Values at Various EBITDA Multiples

4.0x

$51.9

$60.3

$75.4

$93.0

5.0x

64.9

75.4

94.3

116.3

6.0x

77.8

90.5

113.1

139.5

7.0x

90.8

105.6

132.0

162.8

8.0x

103.8

120.6

150.8

186.1

Future Stock Prices at Various EBITDA Multiples

4.0x

$5.49

$6.52

$8.38

$10.31

5.0x

6.72

7.94

10.03

12.28

6.0x

7.95

9.31

11.63

14.24

7.0x

9.14

10.60

13.22

16.19

8.0x

10.25

11.87

14.80

18.14

Implied Current Stock Price (c)

4.0x

$4.45

$4.40

$4.72

$4.84

5.0x

5.45

5.36

5.65

5.76

6.0x

6.44

6.29

6.54

6.68

7.0x

7.41

7.15

7.44

7.59

8.0x

8.30

8.02

8.33

8.51

(a) |

| Base case scenario per management projections as of October 21, 2009. (b) Stock price as of October 14, 2009. |

(c) |

| Future stock prices discounted to November 5, 2009 using cost of equity at 20.0%. |

DISCUSSION MATERIALS 48

V. STRATEGIC ALTERNATIVES OVERVIEW

CONFIDENTIAL

The Potential Value of Status Quo —Forward P/E

We believe it is unlikely the company will trade based on its current P/E multiple

A lack of significant ramp in absolute EPS until 2012 makes value creation difficult to assess

Projected Potential Value at Forward P/E Multiples

(US$ in millions, except per share data)

2009E

2010E

2011E

2012E

2013E

Forward Year EPS (a)

$0.07

$0.11

$0.19

$0.38

$0.52

% growth

(99.3%)

45.3%

78.6%

100.7%

37.0%

Unaffected Equity Value (b)

$61.0

Unaffected Stock Price (b)

$6.00

Unaffected 2010 P/E Multiple

30.0x

Future Stock Prices at Various P/E Multiples (b)

15.0x

$

1.58

$

2.82 $

5.66

$7.76

18.0x

1.90

3.39

6.80

9.31

20.0x

2.11

3.76

7.55

10.34

22.0x

2.32

4.14

8.31

11.38

25.0x

2.63

4.70

9.44

12.93

Annualized Return to Current Market Price at Various P/E Multiples

15.0x

(68.4%)

(29.5%)

(1.8%)

6.4%

18.0x

(63.0%)

(23.3%)

4.0%

11.1%

20.0x

(59.5%)

(19.4%)

7.6%

14.0%

22.0x

(56.0%)

(15.8%)

10.8%

16.6%

25.0x

(50.9%)

(10.7%)

15.4%

20.3%

Annualized Return to Current Price at Various P/E Multiples

15.0x

(73.1%)

(35.3%)

(7.4%)

1.7%

18.0x

(68.5%)

(29.6%)

(1.9%)

6.3%

20.0x

(65.5%)

(26.1%)

1.4%

9.0%

22.0x

(62.5%)

(22.8%)

4.5%

11.5%

25.0x

(58.2%)

(18.0%)

8.8%

15.0%

(a) |

| Base case scenario per management projections as of October 21, 2009. (b) Stock price as of October 14, 2009. |

DISCUSSION MATERIALS 49

V. STRATEGIC ALTERNATIVES OVERVIEW

CONFIDENTIAL

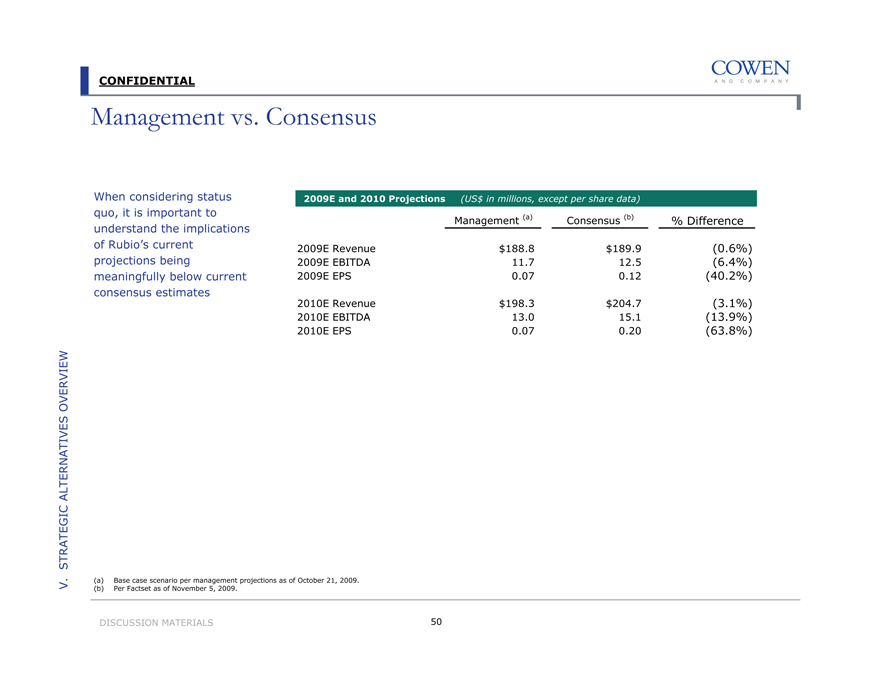

Management vs. Consensus

When considering status quo, it is important to understand the implications of Rubio’s current projections being meaningfully below current consensus estimates

2009E and 2010 Projections

(US$ in millions, except per share data)

Management (a)

Consensus (b)

% Difference

2009E

Revenue

$188.8

$189.9

(0.6%)

2009E

EBITDA

11.7

12.5

(6.4%)

2009E

EPS

0.07

0.12

(40.2%)

2010E

Revenue

$198.3

$204.7

(3.1%)

2010E

EBITDA

13.0

15.1

(13.9%)

2010E

EPS

0.07

0.20

(63.8%)

V. STRATEGIC ALTERNATIVES OVERVIEW

(a) |

| Base case scenario per management projections as of October 21, 2009. (b) Per Factset as of November 5, 2009. |

DISCUSSION MATERIALS 50

CONFIDENTIAL

Recapitalization

The Board may consider pursuing a levered recapitalization

A recapitalization plan can offer shareholders liquidity or a substantial cash distribution with the retention of an ongoing equity interest in the future growth of the restructured company

Delivers current value to shareholders on a basis that is otherwise available only in a takeover or LBO without forcing shareholders to relinquish control of ongoing equity interest

??While there are generally two main strategies related to a levered recapitalization (a one-time share repurchase and a one-time cash dividend), the share repurchase alternative is much more common

V. STRATEGIC ALTERNATIVES OVERVIEW

DISCUSSION MATERIALS

51

CONFIDENTIAL

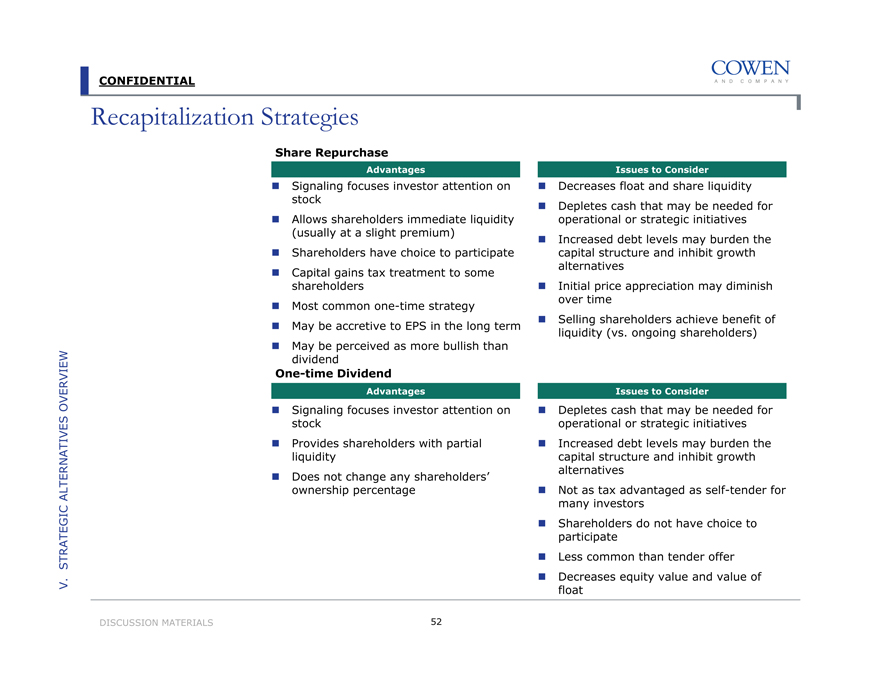

Recapitalization Strategies

Share Repurchase

Advantages

Signaling focuses investor attention on stock

Allows shareholders immediate liquidity (usually at a slight premium)

Shareholders have choice to participate

Capital gains tax treatment to some shareholders

Most common one-time strategy

May be accretive to EPS in the long term

May be perceived as more bullish than dividend

One-time Dividend

Advantages

Signaling focuses investor attention on stock

Provides shareholders with partial liquidity

Does not change any shareholders’ ownership percentage

Issues to Consider

Decreases float and share liquidity Depletes cash that may be needed for operational or strategic initiatives Increased debt levels may burden the capital structure and inhibit growth alternatives Initial price appreciation may diminish over time Selling shareholders achieve benefit of liquidity (vs. ongoing shareholders)

Issues to Consider

Depletes cash that may be needed for operational or strategic initiatives Increased debt levels may burden the capital structure and inhibit growth alternatives Not as tax advantaged as self-tender for many investors Shareholders do not have choice to participate Less common than tender offer Decreases equity value and value of float

V. STRATEGIC ALTERNATIVES OVERVIEW

DISCUSSION MATERIALS

52

CONFIDENTIAL

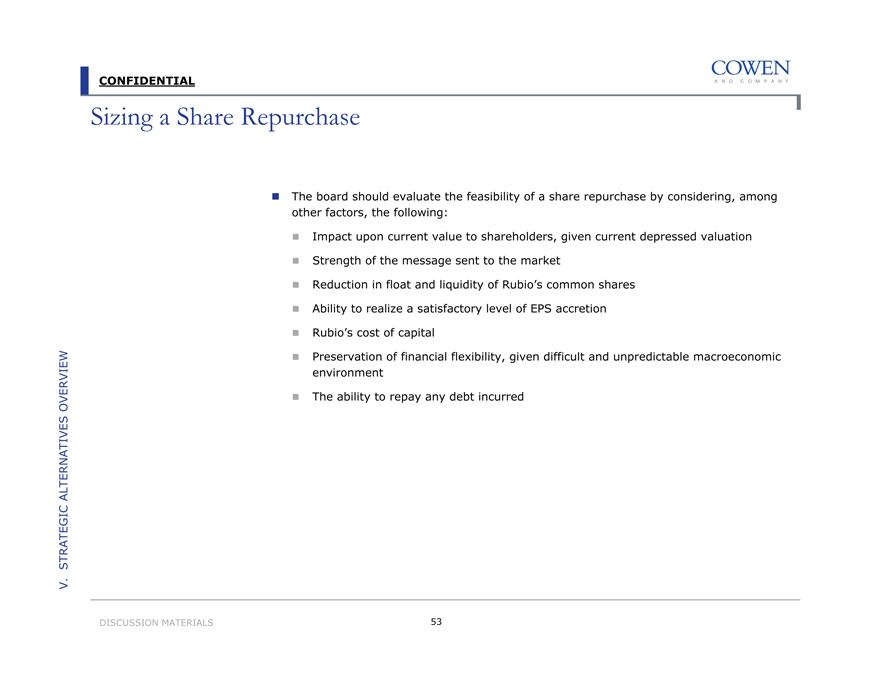

Sizing a Share Repurchase

The board should evaluate the feasibility of a share repurchase by considering, among other factors, the following:

Impact upon current value to shareholders, given current depressed valuation

Strength of the message sent to the market

Reduction in float and liquidity of Rubio’s common shares

Ability to realize a satisfactory level of EPS accretion

Rubio’s cost of capital

Preservation of financial flexibility, given difficult and unpredictable macroeconomic environment

The ability to repay any debt incurred

V. STRATEGIC ALTERNATIVES OVERVIEW

DISCUSSION MATERIALS

53

CONFIDENTIAL

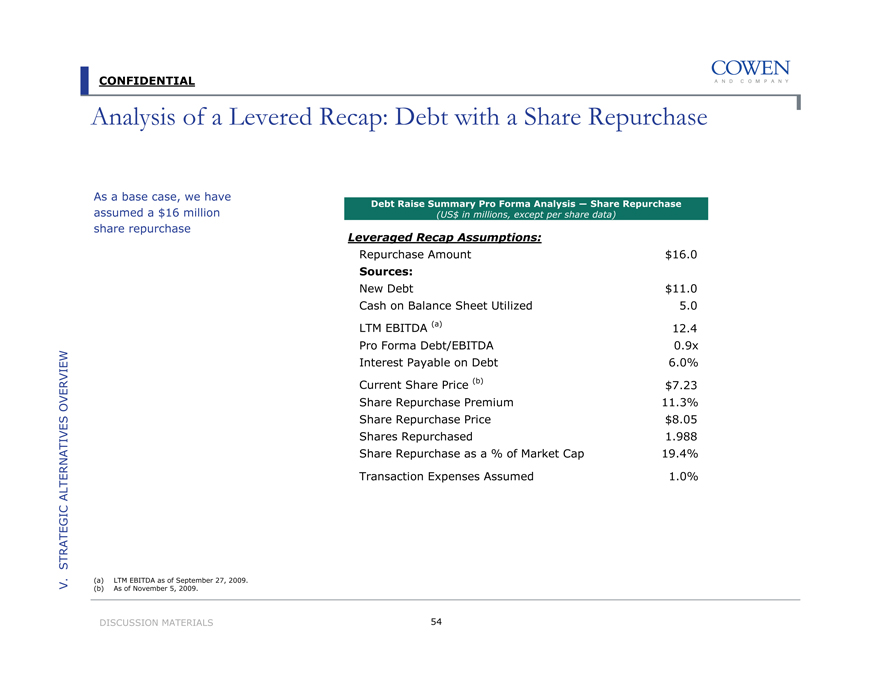

Analysis of a Levered Recap: Debt with a Share Repurchase

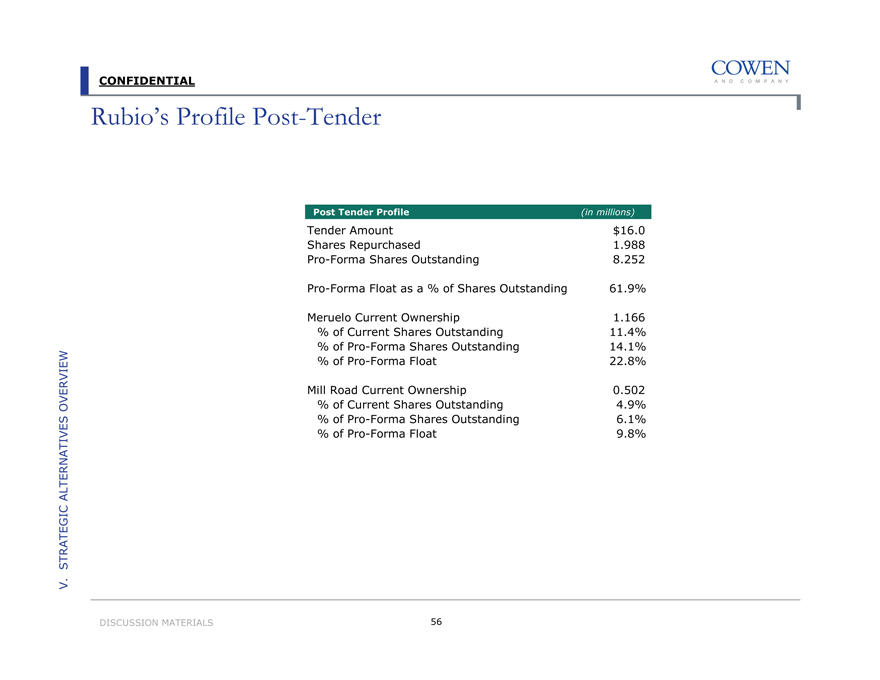

As a base case, we have assumed a $16 million share repurchase

Debt Raise Summary Pro Forma Analysis — Share Repurchase

(US$ in millions, except per share data)

Leveraged Recap Assumptions:

Repurchase Amount

$16.0

Sources:

New Debt

$11.0

Cash on Balance Sheet Utilized

5.0

LTM EBITDA (a)

12.4

Pro Forma Debt/EBITDA

0.9x

Interest Payable on Debt

6.0%

Current Share Price (b)

$7.23

Share Repurchase Premium

11.3%

Share Repurchase Price

$8.05

Shares Repurchased

1.988

Share Repurchase as a % of Market Cap

19.4%

Transaction Expenses Assumed

1.0%

V. STRATEGIC ALTERNATIVES OVERVIEW

(a) LTM EBITDA as of September 27, 2009. (b) As of November 5, 2009.

DISCUSSION MATERIALS 54

CONFIDENTIAL

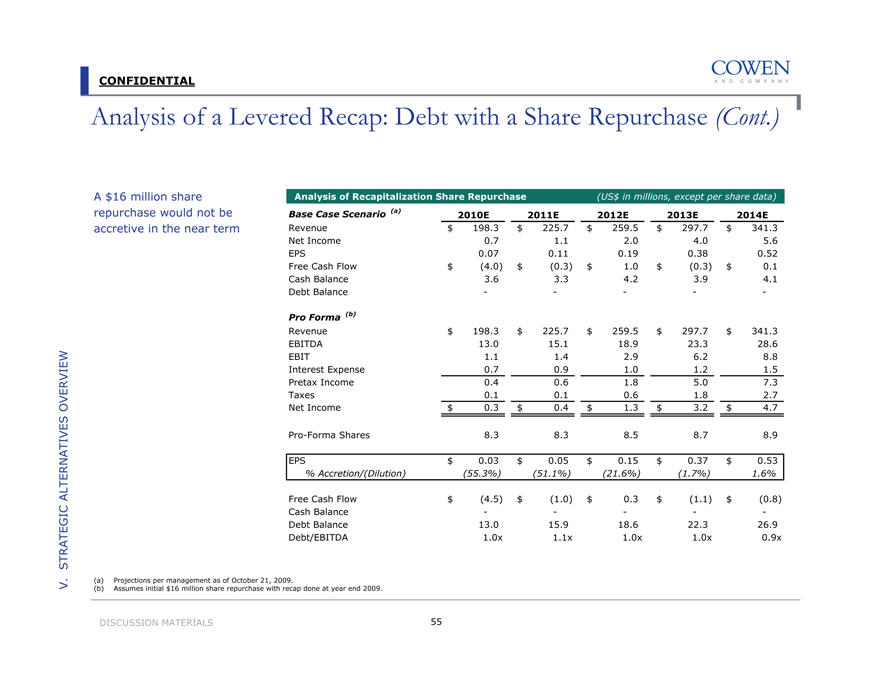

Analysis of a Levered Recap: Debt with a Share Repurchase (Cont.)

A $16 million share repurchase would not be accretive in the near term

Analysis of Recapitalization Share Repurchase

(US$ in millions, except per share data)

Base Case Scenario (a)

2010E

2011E

2012E

2013E

2014E

Revenue

$198.3

$225.7

$259.5

$297.7

$341.3

Net Income

0.7

1.1

2.0

4.0

5.6

EPS

0.07

0.11

0.19

0.38

0.52

Free Cash Flow

$(4.0)

$(0.3)

$1.0

$(0.3)

$0.1

Cash Balance

3.6

3.3

4.2

3.9

4.1

Debt Balance

—

—

—

—

—

Pro Forma (b)

Revenue

$198.3

$225.7

$259.5

$297.7

$341.3

EBITDA

13.0

15.1

18.9

23.3

28.6

EBIT

1.1

1.4

2.9

6.2

8.8

Interest Expense

0.7

0.9

1.0

1.2

1.5

Pretax Income

0.4

0.6

1.8

5.0

7.3

Taxes

0.1

0.1

0.6

1.8

2.7

Net Income

$0.3

$0.4

$1.3

$3.2

$4.7

Pro-Forma Shares

8.3

8.3

8.5

8.7

8.9

EPS

$0.03

$0.05

$0.15

$0.37

$0.53