UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-09561

(Investment Company Act File Number)

Century Capital Management Trust

(Exact Name of Registrant as Specified in Charter)

c/o Century Capital Management, LLC

100 Federal Street, Boston, MA 02110

(Address of Principal Executive Offices)

Jennifer Mortimer

Century Capital Management, LLC

100 Federal Street, Boston, MA 02110

(Name and Address of Agent for Service)

(617) 482-3060

(Registrant’s Telephone Number)

Date of Fiscal Year End: October 31

Date of Reporting Period: October 31, 2014

| Item 1. | Reports to Shareholders. |

Table of Contents

| Page | |

| Letter to Shareholders | 1 |

| Fund Summaries | |

| Century Shares Trust | 5 |

| Century Small Cap Select Fund | 8 |

| Century Growth Opportunities Fund | 11 |

| Portfolio of Investments | |

| Century Shares Trust | 14 |

| Century Small Cap Select Fund | 16 |

| Century Growth Opportunities Fund | 18 |

| Statements of Assets and Liabilities | 20 |

| Statements of Operations | 21 |

| Statements of Changes in Net Assets | 22 |

| Financial Highlights | |

| Century Shares Trust | 24 |

| Century Small Cap Select Fund | 25 |

| Century Growth Opportunities Fund | 27 |

| Notes to Financial Statements | 28 |

| Report of Independent Registered Public Accounting Firm | 37 |

| Disclosure of Fund Expenses | 38 |

| Tax Information | 39 |

| Approval of Investment Management Agreements | 40 |

| Trustees and Officers | 44 |

This report is submitted for the general information of the shareholders of Century Shares Trust, Century Small Cap Select Fund, and Century Growth Opportunities Fund (each a “Fund” and collectively, the “Funds”). It is not authorized for distribution to prospective investors in a Fund unless it is preceded by or accompanied by the Fund’s current prospectus. The prospectus includes important information about the Fund’s objective, risks, charges and expenses, experience of its management, and other information. Please read the prospectus carefully before you invest.

The views expressed in this report are those of the Funds’ Portfolio Managers as of October 31, 2014, the end of the reporting period. Any such views are subject to change at any time and may not reflect the Portfolio Managers’ views on the date that this report is first published or anytime thereafter. These views are intended to assist shareholders in understanding their investments and do not constitute investment advice. There is no assurance that the Funds will continue to invest in the securities mentioned in this report.

| Letter to Shareholders |

| October 31, 2014 (Unaudited) |

Dear Fellow Shareholders,

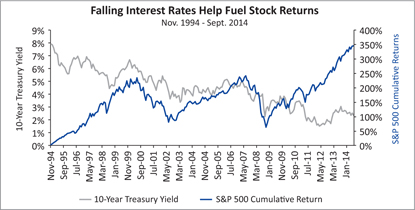

As the recent November election tide recedes, we reflect on several recurring themes driving the equity markets. First, US economic growth continues to grind higher. Second, the Federal Reserve halted its quantitative easing program to keep interest rates low. Third, the resurgence in American energy production is contributing to sustainably lower costs for consumers and corporations alike. Fourth, global growth is sputtering, and geopolitical risks (Ebola, Russia, Ukraine, ISIL uprising, slowdowns in Asia and Latin America) reinforce the perception that our domestic economy remains the safest port among a storm of concerns affecting other continents.

The resulting influx of foreign investment onto US shores helps 1) lower our interest rates and 2) raise the value of our dollar currency. These favorable conditions may not last, but we expect our economy will benefit from the surprisingly low inflation and cheaper imported goods that provide tailwinds to spending and investment opportunities over the coming months. On the other hand, our exported goods (representing 15% of GDP) will become more expensive.

Source: Bank of America (Data as of 10/31/2014;

Date Range 11/30/1994 through 9/30/2014)

Slow and Steady Wins the Race

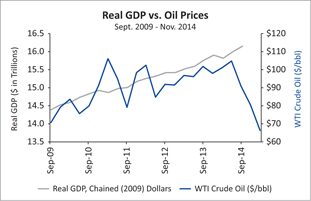

The current outlook seems favorable for investors. US gross domestic product (GDP) grew at an annual rate of 3.9% in the third quarter of 2014, capping the fastest 6-months of growth in a decade. The unemployment rate fell to 5.8% in October, the lowest level since July of 2008. With unemployment and oil prices at multi-year lows, the average consumer or corporation has more discretionary dollars to help sustain GDP growth over the next year. Each one cent drop in gasoline prices equals a $1 billion increase in discretionary income. Additionally, interest rates remain at historic lows, with the 10 year Treasury bond yield hovering around 2.4%. Given this backdrop, the Conference Board’s index of leading economic indicators (LEI) continues its steady march upward, suggesting our “slow and steady” domestic recovery will stay on track into 2015.

Source: Bureau of Economic Analysis (Data as of 12/02/2014;

Date Range Real GDP: 09/30/2009 through 9/30/2014;

Date Range WTI Crude Oil: 09/30/2009 through 11/28/2014)

Past performance is not indicative of future results.

S&P 500® Index is a broad-based, unmanaged measurement of changes in stock market conditions based on the average of 500 widely held common stocks. One cannot invest directly in an index.

1

| Letter to Shareholders |

| October 31, 2014 (Unaudited) |

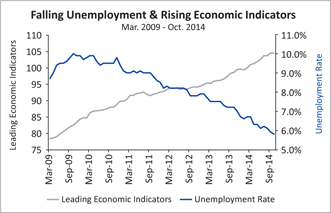

We are all familiar with the Aesop’s Fable about the race between the Tortoise and the Hare, and its lesson in the virtues of patience and persistence. The prolonged and underwhelming pace of this recovery from the 2008-2009 economic crisis resembles the tortoise’s slow but relentless progress to victory, while most previous recoveries mimic the Hare’s speed, with rapid growth but shorter duration. We believe this slower pace creates a more resilient economic foundation to sustain this expansion beyond next year.

Source: Bank of America (Data as of 10/31/2014;

Date Range 3/31/2009 through 10/31/2014)

This 6-year protracted recovery somehow bypassed the average retail investor, who was scared by the 2008-09 downturn and remained on the sidelines, missing out on the favorable investment returns since then. At Century, our long term investment style is more similar to the tortoise than the hare. We invest in quality growth businesses that the market under appreciates, in our opinion. We try to gain an in-depth understanding of each company’s risks and rewards, as well as the industry dynamics that may shift over time. We expect our discipline and research-intensive approach will help investors achieve their investment goals over a full market cycle.

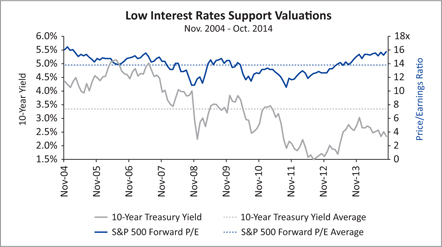

In our view, US companies remain financially strong and equity valuations are reasonable. Profit margins are high, balance sheets have low debt and strong cash positions, and corporate earnings continue to beat expectations. Given the strong returns for equities over the past several years, we believe the equity markets are fairly valued, with price-to-earnings valuations hovering at or above historical averages. While valuations are important investment factors, they need to be viewed in the context of low interest rates, which tend to support higher valuations for stocks.

Source: Bank of America (Data as of 10/31/2014;

Date Range 11/30/2004 through 10/31/2014)

Past performance is not indicative of future results.

Price to earnings (P/E) ratio is the value of a company’s stock price to company earnings.

2

| Letter to Shareholders |

| October 31, 2014 (Unaudited) |

Federal Reserve Exiting Markets

Improving economic growth, falling unemployment rates and strong equity returns provided sufficient reason for the Federal Reserve to exit its stimulus program. Throughout the past year, the Federal Reserve began tapering its monetary easing program by cutting bond purchases from a peak of $85 billion per month to zero, when the program was halted in October. As the economy continues to recover, many expect the Federal Reserve to start raising rates in the second half of 2015. As a result of the Federal Reserve backing away from market intervention, correlations between stocks have fallen suggesting that companies are again being valued on their own growth and profitability “fundamentals,” as opposed to trading on news headlines. Lower correlations are generally positive for active managers, such as Century, who employ a fundamental research-intensive investment process.

Global Growth and Geopolitical Risks

While the US recovery appears to be intact, the global economic landscape faces challenges. The Eurozone has anemic growth, double-digit unemployment and could be heading towards its third recession in six years. Germany, the Eurozone’s largest and most resilient economy is forecasting growth of only 1.2% and 1.3% in 2014 and 2015, respectively. Other European Union nations’ expected growth rates are much lower, while economic sanctions and low oil prices may force Russia into a recession.

Further east, there are concerns that Japan’s and China’s economies are slowing. China’s consumer price index decelerated to 1.6% in October, the lowest level since January 2010. While low inflation is generally welcome, it is the latest indication of sluggish demand.

We are seeing a myriad of geopolitical risks that have shaken investor confidence, ranging from the Ukraine-Russian conflict and various Middle East concerns (Syria, ISIL uprising into neighboring countries) to the Ebola crisis and naval skirmishes in the South China Sea. This year has witnessed negative surprises for President Obama’s foreign policy initiatives that raise investor concerns but also reinforce the current strength of our own domestic economic engine.

Looking Forward

As we start 2015 with a Republican-led Congress, the expectations for cooperation between the President and Congress could not be lower. We hope this consensus is wrong, and meaningful progress is made on such topics as immigration and tax reform. Bipartisan leadership may be improbable, but it would help to ensure the current economic tailwinds continue and encourage corporations to make long-term investments.

We keep the following thoughts in mind: The US economy remains in a strong competitive position. We expect periods of volatility will provide opportunities to improve our portfolio holdings in quality growth enterprises. Historically, stocks have proven to be an excellent asset class for growing capital appreciation over the long term.

Correlation is a statistical measure of how an index moves in relation to another index or model portfolio. A correlation ranges from -1 to 1. A correlation of 1 means the two indexes have moved in lockstep with each other. A correlation of -1 means the two indexes have moved in exactly the opposite direction.

3

| Letter to Shareholders |

| October 31, 2014 (Unaudited) |

In general, markets move upward in jagged lines, and thoughtful long term investors win by acting more like tortoises than hares. Patience and persistence allow investors to take advantage of volatility when others run for the exits. Periodic market pullbacks are healthy adjustments to changes in fundamentals and sentiment. Currently, we continue to see favorable economic growth, improving employment and low inflation setting the stage for this domestic recovery to continue. We are not seeing the normal signs of a bear market developing, unless the geopolitical issues arrive on our shores.

We hope to earn your trust over the coming year, and we wish you all a happy holiday season.

Respectfully submitted,

Alexander L. Thorndike

Chairman of the Century Funds

4

| Fund Commentary |

| CENTURY SHARES TRUST | October 31, 2014 (Unaudited) |

HOW DID THE PORTFOLIO PERFORM?

For the one-year period ended October 31, 2014, Century Shares Trust’s shares returned +17.29%, outperforming the Russell 1000 Growth Index (R1000G), the Fund’s benchmark, which returned +17.11%. The S&P 500 Index gained +17.27%.

WHAT FACTORS INFLUENCED PERFORMANCE?

The Fund’s performance was primarily driven by stock selection. The Healthcare, Consumer Discretionary and Materials sectors were the largest contributors to performance. Exposures to the Information Technology, Industrials and Utilities sectors detracted most from performance.

Century Shares Trust’s performance was positively impacted by several stocks. Specifically, Actavis Plc. (pharmaceuticals), LyondellBasell Industries N.V. (chemicals), Apple, Inc. (media devices), Alexion Pharmaceuticals, Inc. (biotechnology) and Celgene Corp. (biotechnology). Actavis lifted as investors applauded the accretive acquisitions of Warner Chilcott and Forest Labs. LyondellBasell benefited from inexpensive raw materials (i.e. natural gas-linked ethane feedstock) and operational improvements. Alexion traded up on strong financial results. Apple appreciated on strong iPhone sales and by actively returning capital to shareholders. Celgene outperformed due to FDA approval of its oral inhibitor drug, Otezla (apremilast), that treats patients with moderate to severe plaque psoriasis.

Conversely, Urban Outfitters, Inc. (specialty retail), Masco Corp. (building products), eBay, Inc. (ecommerce), Marvell Technology Group Ltd. (semiconductors) and HCP, Inc. (healthcare real estate) detracted from performance. Urban Outfitters traded down on weaker gross margins. Masco posted lower than expected results that were affected by harsh weather earlier in the year. eBay encountered several issues including a security breach, a decline in traffic and the departure of the head of its PayPal unit. Marvell Technology depreciated on signs of an increasingly competitive mobile market. HCP, Inc. traded down on concerns that low deal volume might lead to unattractive real estate transactions.

HOW WAS THE PORTFOLIO POSITIONED AT PERIOD END?

We continue to be encouraged by the strength of the domestic economy and the stock market. While companies continue to have strong earnings and solid balance sheets, it is harder to find stocks trading at reasonable valuations than it was a few years ago. The domestic economy continued to perform well; however, Europe, Latin America and Asia have been areas of concern. Additionally, geopolitical risks ranging from the Russia – Ukraine conflict to the rise of ISIL have the ability to disturb stock market appreciation domestically and abroad.

The portfolio is diversified across almost every sector while maintaining overweight positions in the Consumer Discretionary, Healthcare and Financials sectors. Conversely, the portfolio is underweight in the Consumer Staples, Energy and Materials sectors.

Past performance is not indicative of future results. Current performance may be lower or higher than the performance data quoted.

5

| Fund Commentary |

| CENTURY SHARES TRUST | October 31, 2014 (Unaudited) |

Risks: The Fund may invest a significant portion of assets in a limited number of companies or in companies within the same market sector. As a result, the Fund may be more susceptible to financial, market and economic events affecting particular companies or sectors and therefore may experience greater price volatility than funds with more diversified portfolios. Please read the Fund’s prospectus for details regarding the Fund’s risk profile.

| Ten Largest Holdings* | |

ACTAVIS PLC Pharmaceuticals | 4.57% |

GOOGLE, INC. Internet Software & Services | 4.53% |

APPLE, INC. Technology Hardware, Storage & Peripherals | 4.42% |

AMERICAN TOWER CORP. Real Estate Investment Trust (REITs) | 3.95% |

WESTERN UNION CO. IT Services | 3.76% |

CELGENE CORP. Biotechnology | 3.72% |

DOLLAR TREE, INC. Multiline Retail | 3.53% |

PEPSICO, INC. Beverages | 3.52% |

DIRECTV Media | 3.40% |

CERNER CORP. Health Care Technology | 3.20% |

| Sector Allocation* | |

| Information Technology | 27.6% |

| Consumer Discretionary | 22.7% |

| Health Care | 16.4% |

| Industrials | 12.6% |

| Financials | 7.4% |

| Consumer Staples | 6.6% |

| Energy | 2.0% |

| Materials | 0.9% |

| Cash, Cash Equivalents, & Other Net Assets | 3.8% |

| * | Based on the Fund’s net assets at October 31, 2014 and subject to change. |

6

| Performance Summary |

| CENTURY SHARES TRUST | October 31, 2014 (Unaudited) |

Institutional Shares

The returns shown below represent past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be higher or lower than the Fund’s past performance. For the most recent month‐end performance, please call 800‐303‐1928.

As stated in the Fund’s current prospectus, the total (gross) operating expenses are 1.11% for the Institutional Shares. The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted to reflect the deduction of taxes that a shareholder would pay on these distributions or the redemption of Fund shares. Shares held less than 90 days may be subject to a 1% redemption fee.

| Average Annual Total Returns October 31, 2014 | ||||

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Century Shares Trust - Institutional Shares | 17.29% | 17.60% | 15.82% | 7.70% |

Russell 1000® Growth Index | 17.11% | 19.30% | 17.43% | 9.05% |

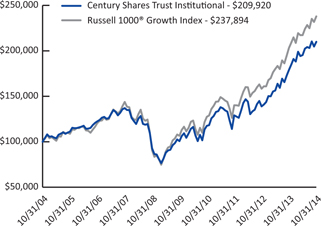

Growth of $100,000 for the period ended October 31, 2014

The graph and table reflect the change in value of a hypothetical investment in the Fund, including reinvest of dividends and distributions, compared with the listed indices. Index returns assume reinvestment of dividends and, unlike Fund returns, do not reflect any fees or expenses. It is not possible to invest directly in an index. Minimum initial investment for Institutional Shares is $100,000.

The Russell 1000® Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000® companies with higher price-to-book ratios and higher forecasted growth values.

7

| Fund Commentary |

| CENTURY SMALL CAP SELECT FUND | October 31, 2014 (Unaudited) |

HOW DID THE PORTFOLIO PERFORM?

For the one-year period ended October 31, 2014, Century Small Cap Select Fund Institutional Shares returned +6.79% and the Investor Shares returned +6.47%, underperforming the Russell 2000 Growth Index (R2000G), the Fund’s benchmark, which returned +8.26%.

WHAT FACTORS INFLUENCED PERFORMANCE?

Stock selection was the primary driver of the Fund’s performance. The Financials, Healthcare and Energy sectors were the largest contributors to portfolio performance as Jazz Pharmaceuticals Plc. (biotechnology), Akorn, Inc. (pharmaceuticals), Palo Alto Networks, Inc. (cybersecurity software), Acadia Healthcare Company, Inc. (healthcare), and Gentherm, Inc. (auto parts) fared well. Jazz Pharmaceuticals announced a drug licensing partnership. Akorn appreciated on news of two acquisitions and stronger pricing for one of its products. Palo Alto Networks traded up on continued market share gains and the increasing need for cybersecurity solutions. Acadia Healthcare’s outperformance was primarily driven by the acquisition of a UK based provider of mental health services. Gentherm appreciated on favorable auto sales trends and market share gains.

Conversely, the Information Technology, Materials and Industrials sectors were the largest detractors from portfolio performance as Web.com Group, Inc. (internet), Cumulus Media, Inc. (media), DSW, Inc. (apparel), Movado Group, Inc. (apparel) and Key Energy Services, Inc. (oil and gas services) traded down. Web.com declined on weaker than expected earnings results. Cumulus Media traded down on slowing advertising growth trends. DSW sold off on pricing pressures from aggressive retailers and weakening trends in women’s shoes. Movado was weaker due to slower watch demand. Key Energy fell on disappointing results.

HOW WAS THE PORTFOLIO POSITIONED AT PERIOD END?

We continue to be encouraged by the strength of the domestic economy, low inflation and energy prices and believe the Fund to be well positioned to generate attractive returns into 2015. We believe that current valuation levels are fair and earnings growth will be the primary driver of stock returns for the foreseeable future, as opposed to multiple expansion. We are also keeping an eye on slowing global growth and the potential for geopolitical risks to derail stock price appreciation.

The portfolio is currently overweight in the Information Technology, Financials and Industrials sectors and is underweight in the Consumer Staples, Materials and Healthcare sectors. As always, we remain focused on finding quality growth companies trading at valuations that we believe are attractive.

Past performance is not indicative of future results. Current performance may be lower or higher than the performance data quoted.

8

| Fund Commentary |

| CENTURY SMALL CAP SELECT FUND | October 31, 2014 (Unaudited) |

Risks: The Fund concentrates its investments in the financial services and health care group of industries (at least 25% of the Fund’s assets in the aggregate). Concentration in a particular industry subjects the Fund to the risks associated with that industry, and as a result, the Fund may be subject to greater price volatility than funds with less concentrated portfolios. In addition, the Fund invests in smaller companies which pose greater risks than those associated with larger, more established companies. Please read the Fund’s prospectus for details regarding the Fund’s risk profile.

| Ten Largest Holdings* | |

J2 GLOBAL, INC. Internet Software & Services | 3.71% |

DEALERTRACK TECHNOLOGIES, INC. Internet Software & Services | 3.39% |

COHEN & STEERS, INC. Capital Markets | 3.29% |

HERMAN MILLER, INC. Commercial Services & Supplies | 3.19% |

ACADIA HEALTHCARE CO., INC. Health Care Providers & Services | 3.15% |

AKORN, INC. Pharmaceuticals | 2.92% |

CAI INTERNATIONAL, INC. Trading Companies & Distributors | 2.67% |

EAGLE BANCORP, INC. Banks | 2.62% |

BROOKDALE SENIOR LIVING, INC. Health Care Providers & Services | 2.62% |

PROOFPOINT, INC. Software | 2.58% |

| Sector Allocation* | |

| Information Technology | 28.8% |

| Health Care | 21.2% |

| Consumer Discretionary | 16.2% |

| Industrials | 16.0% |

| Financials | 9.1% |

| Materials | 3.5% |

| Energy | 2.4% |

| Cash, Cash Equivalents, & Other Net Assets | 2.8% |

| * | Based on the Fund’s net assets at October 31, 2014 and subject to change. |

9

| Performance Summary |

| CENTURY SMALL CAP SELECT FUND | October 31, 2014 (Unaudited) |

Institutional Shares and Investor Shares

The returns shown below represent past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be higher or lower than the Fund’s past performance. For the most recent month‐end performance, please call 800‐303‐1928.

As stated in the Fund’s current prospectus, the total (gross) operating expenses are 1.12% for the Institutional Shares and 1.41% for the Investor Shares. Returns would have been lower during the 10 year period if certain fees had not been waived or expenses reimbursed. The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted to reflect the deduction of taxes that a shareholder would pay on these distributions or the redemption of Fund shares. Shares held less than 90 days may be subject to a 1% redemption fee.

| Average Annual Total Returns October 31, 2014 | ||||

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Century Small Cap Select Fund - Institutional Shares | 6.79% | 14.88% | 17.27% | 7.37% |

| Century Small Cap Select Fund - Investor Shares | 6.47% | 14.50% | 16.88% | 7.01% |

Russell 2000® Growth Index | 8.26% | 18.42% | 18.61% | 9.42% |

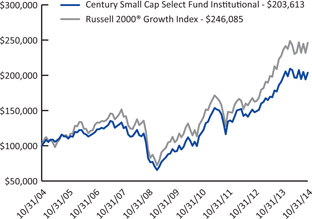

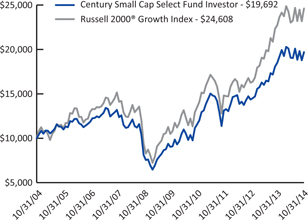

Growth of $100,000 for the period ended October 31, 2014 Institutional Shares | Growth of $10,000 for the period ended October 31, 2014 Investor Shares |

|  |

The graphs and table reflect the change in value of a hypothetical investment in the Fund, including reinvest of dividends and distributions, compared with the index. Index returns assume reinvestment of dividends and, unlike Fund returns, do not reflect any fees or expenses. It is not possible to invest directly in an index. Minimum initial investment for Institutional Shares is $100,000.

The Russell 2000® Growth Index measures the performance of the small-cap growth segment of the U.S. equity universe. It includes those Russell 2000® companies with higher price-to-value ratios and higher forecasted growth values. Index returns assume reinvestment of dividends but, unlike Fund returns, do not reflect fees or expenses. One cannot invest directly in an index.

10

| Fund Commentary |

| CENTURY GROWTH OPPORTUNITIES FUND | October 31, 2014 (Unaudited) |

HOW DID THE PORTFOLIO PERFORM?

For the one-year period ended October 31, 2014, Century Growth Opportunities Fund Institutional Shares returned +13.04%, outperforming the Russell 2500 Growth Index (R2500G), which returned +10.24%.

WHAT FACTORS INFLUENCED PERFORMANCE?

The Fund’s outperformance was primarily a result of stock selection. The Healthcare, Industrials and Consumer Discretionary sectors were the largest contributors to portfolio attribution as Jazz Pharmaceuticals Plc., (biotechnology), Salix Pharmaceuticals, Ltd. (medical devices), United Rentals, Inc. (equipment rental), Palo Alto Networks, Inc. (cyber security software) and White Wave Food Company (food and beverage) fared well. Jazz Pharmaceuticals’ partnership with Aerial BioPharma, LLC improved Jazz’s product offering and sales growth profile. Salix lifted from an accretive acquisition of Santarus, Inc. United Rentals benefited from the trend of renting, rather than owning industrial machinery. Palo Alto Networks lifted on continued market share gains from incumbent vendors. White Wave Food Company benefited from increased adoption of non-dairy milk beverages.

Conversely, Materials, Energy and Telecommunication Services detracted most from performance as ULTA Salon, Cosmetics & Fragrance, Inc. (retail store), Mercadolibre, Inc. (ecommerce platform), Web.com Group, Inc. (internet services) BroadSoft, Inc. (software) and Key Energy Services, Inc. (energy services) traded down. ULTA Salon missed earnings as their new CEO decided to reinvest in the business and reset earnings expectations. Mercadolibre traded down on Venezuela devaluation concerns and a slowing South American economy. Web.com declined on fears of competitive pressures from Google. Broadsoft suffered from deteriorating operations and missed earnings. Key Energy Services reported operating leverage that was below expectations.

HOW WAS THE PORTFOLIO POSITIONED AT PERIOD END?

Given the strong equity returns of the past few years, the portfolio is focused on companies where we believe future earnings growth, as opposed to multiple expansion, will drive stock price appreciation. While we are encouraged by the growth of the domestic economy, healthy corporate earnings and company balance sheets, we recognize that global growth is slowing and geopolitical risks remain.

The portfolio is currently overweight in the Information Technology, Consumer Discretionary and Healthcare sectors and underweight the Materials, Financials and Industrial sectors. As always, we remain focused on finding quality growth companies trading at valuations that we believe are attractive.

Past performance is not indicative of future results. Current performance may be lower or higher than the performance data quoted.

11

| Fund Commentary |

| CENTURY GROWTH OPPORTUNITIES FUND | October 31, 2014 (Unaudited) |

Risks: The Fund invests mainly in small‐cap and mid‐cap companies, which, historically, have been more volatile in price than the stocks of large‐cap companies. The Fund may invest in foreign companies, which involves risks not associated with investing solely in U.S. companies, such as currency fluctuations, unfavorable political developments, or economic instability. These risks are magnified in emerging markets. Please read the Fund’s prospectus for details regarding the Fund’s risk profile.

| Ten Largest Holdings* | |

MAXIMUS, INC. IT Services | 2.47% |

AKORN, INC. Pharmaceuticals | 2.43% |

GRAND CANYON EDUCATION, INC. Diversified Consumer Services | 2.33% |

G&K SERVICES, INC., CLASS A Commercial Services & Supplies | 2.31% |

UNITED RENTALS, INC. Trading Companies & Distributors | 2.28% |

KANSAS CITY SOUTHERN Road & Rail | 2.26% |

ALKERMES PLC Biotechnology | 2.25% |

SNAP-ON, INC. Machinery | 2.24% |

LANDS' END, INC. Internet & Catalog Retail | 2.24% |

CARDTRONICS, INC. IT Services | 2.24% |

| Sector Allocation* | |

| Information Technology | 25.6% |

| Consumer Discretionary | 22.6% |

| Health Care | 19.8% |

| Industrials | 15.5% |

| Financials | 6.2% |

| Consumer Staples | 4.1% |

| Energy | 2.7% |

| Telecommunication Services | 2.1% |

| Cash, Cash Equivalents, & Other Net Assets | 1.4% |

| * | Based on the Fund’s net assets at October 31, 2014 and subject to change. |

12

| Performance Summary |

| CENTURY GROWTH OPPORTUNITIES FUND | October 31, 2014 (Unaudited) |

Institutional Shares

The returns shown below represent past performance. Past performance does not guarantee future results. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than the original cost. Current performance may be higher or lower than the Fund’s past performance. For the most recent month‐end performance, please call 800‐303‐1928.

As stated in the Fund’s current prospectus, the total (gross) operating expenses are 1.12%. The Adviser has agreed contractually to limit the operating expenses for the Fund’s Institutional Shares to 1.10% through February 28, 2015. Returns would have been lower during all periods if certain fees had not been waived or expenses reimbursed. The Fund’s total returns include the reinvestment of dividend and capital gain distributions, but have not been adjusted to reflect the deduction of taxes that a shareholder would pay on these distributions or the redemption of Fund shares. Shares held less than 90 days may be subject to a 1% redemption fee.

| Average Annual Total Returns October 31, 2014 | |||

| 1 Year | 3 Years | Since Inception* | |

| Century Growth Opportunities Fund - Institutional Shares | 13.04% | 13.76% | 12.10% |

| Russell 2500® Growth Index | 10.24% | 18.64% | 16.81% |

| * | Fund inception date of November 17, 2010. |

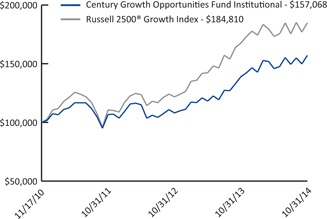

Growth of $100,000 for the period ended October 31, 2014

The graph and table reflect the change in value of a hypothetical investment in the Fund, including reinvest of dividends and distributions, compared with the listed indices. Index returns assume reinvestment of dividends and, unlike Fund returns, do not reflect any fees or expenses. It is not possible to invest directly in an index. Minimum initial investment for Institutional Shares is $100,000.

The Russell 2500® Growth Index measures the performance of the small- to mid-cap growth segment of the U.S. equity universe. It includes those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values. Index returns assume reinvestment of dividends but, unlike Fund returns, do not reflect fees or expenses. One cannot invest directly in an index.

13

| Portfolio of Investments |

| CENTURY SHARES TRUST | October 31, 2014 |

| Shares | Value | |||||||

| COMMON STOCKS - 96.2% | ||||||||

| Consumer Discretionary - 22.7% | ||||||||

| Hotels, Restaurants & Leisure - 3.9% | ||||||||

| 32,639 | Panera Bread Co., Class A(a) | $ | 5,275,768 | |||||

| 44,087 | Starbucks Corp. | 3,331,214 | ||||||

| 8,606,982 | ||||||||

| Household Durables - 2.6% | ||||||||

| 33,146 | Whirlpool Corp. | 5,702,769 | ||||||

| Internet & Catalog Retail - 2.8% | ||||||||

| 20,180 | Amazon.com, Inc.(a) | 6,164,183 | ||||||

| Media - 3.4% | ||||||||

| 87,308 | DIRECTV(a) | 7,577,461 | ||||||

| Multiline Retail - 3.5% | ||||||||

| 129,521 | Dollar Tree, Inc.(a) | 7,845,087 | ||||||

| Specialty Retail - 4.6% | ||||||||

| 133,528 | Dick’s Sporting Goods, Inc. | 6,058,165 | ||||||

| 41,995 | Home Depot, Inc. | 4,095,353 | ||||||

| 10,153,518 | ||||||||

| Textiles, Apparel & Luxury Goods - 1.9% | ||||||||

| 42,615 | Fossil Group, Inc.(a) | 4,332,241 | ||||||

| Total Consumer Discretionary | 50,382,241 | |||||||

| Consumer Staples - 6.6% | ||||||||

| Beverages - 3.5% | ||||||||

| 81,428 | PepsiCo, Inc. | 7,830,931 | ||||||

| Food & Staples Retailing - 1.1% | ||||||||

| 27,240 | CVS Health Corp. | 2,337,464 | ||||||

| Household Products - 2.0% | ||||||||

| 67,899 | Colgate-Palmolive Co. | 4,541,085 | ||||||

| Total Consumer Staples | 14,709,480 | |||||||

| Energy - 2.0% | ||||||||

| Energy Equipment & Services - 2.0% | ||||||||

| 79,751 | FMC Technologies, Inc.(a) | 4,469,246 | ||||||

| Financials - 7.4% | ||||||||

| Diversified Financial Services - 3.5% | ||||||||

| 4 | Berkshire Hathaway, Inc., Class A(a) | 840,000 | ||||||

| 69,329 | Moody’s Corp. | 6,879,517 | ||||||

| 7,719,517 | ||||||||

| Shares | Value | |||||||

| Financials - 7.4% (continued) | ||||||||

| Real Estate Investment Trust (REITs) - 3.9% | ||||||||

| 90,115 | American Tower Corp. | $ | 8,786,212 | |||||

| Total Financials | 16,505,729 | |||||||

| Health Care - 16.4% | ||||||||

| Biotechnology - 6.4% | ||||||||

| 31,473 | Alexion Pharmaceuticals, Inc.(a) | 6,022,673 | ||||||

| 77,228 | Celgene Corp.(a) | 8,270,347 | ||||||

| 14,293,020 | ||||||||

| Health Care Equipment & Supplies - 1.1% | ||||||||

| 21,466 | Zimmer Holdings, Inc. | 2,387,878 | ||||||

| Health Care Providers & Services - 1.1% | ||||||||

| 33,666 | Express Scripts Holding Co.(a) | 2,586,222 | ||||||

| Health Care Technology - 3.2% | ||||||||

| 112,397 | Cerner Corp.(a) | 7,119,226 | ||||||

| Pharmaceuticals - 4.6% | ||||||||

| 41,937 | Actavis PLC(a) | 10,179,787 | ||||||

| Total Health Care | 36,566,133 | |||||||

| Industrials - 12.6% | ||||||||

| Aerospace & Defense - 2.9% | ||||||||

| 52,149 | Boeing Co. | 6,513,932 | ||||||

| Air Freight & Logistics - 1.6% | ||||||||

| 33,335 | United Parcel Service, Inc., Class B | 3,497,175 | ||||||

| Electrical Equipment - 2.0% | ||||||||

| 68,289 | Emerson Electric Co. | 4,374,593 | ||||||

| Professional Services - 3.0% | ||||||||

| 107,988 | Verisk Analytics, Inc., Class A(a) | 6,733,052 | ||||||

| Road & Rail - 3.1% | ||||||||

| 59,425 | Union Pacific Corp. | 6,920,041 | ||||||

| Total Industrials | 28,038,793 | |||||||

| Information Technology - 27.6% | ||||||||

| Internet Software & Services - 7.4% | ||||||||

| 30,797 | Equinix, Inc. | 6,433,494 | ||||||

| 8,952 | Google, Inc., Class A(a) | 5,083,572 | ||||||

| 8,952 | Google, Inc., Class C(a) | 5,004,884 | ||||||

| 16,521,950 | ||||||||

See Notes to Financial Statements.

14

| Portfolio of Investments |

| CENTURY SHARES TRUST | October 31, 2014 |

| Shares | Value | |||||||

| Information Technology - 27.6% (continued) | ||||||||

| IT Services - 9.4% | ||||||||

| 131,134 | Cognizant Technology Solutions Corp., Class A(a) | $ | 6,405,896 | |||||

| 25,363 | Visa, Inc., Class A | 6,123,389 | ||||||

| 493,649 | Western Union Co. | 8,372,287 | ||||||

| 20,901,572 | ||||||||

| Software - 6.4% | ||||||||

| 49,952 | Adobe Systems, Inc.(a) | 3,502,634 | ||||||

| 76,737 | Citrix Systems, Inc.(a) | 4,928,817 | ||||||

| 123,947 | Microsoft Corp. | 5,819,312 | ||||||

| 14,250,763 | ||||||||

| Technology Hardware, Storage & Peripherals - 4.4% | ||||||||

| 91,015 | Apple, Inc. | 9,829,620 | ||||||

| Total Information Technology | 61,503,905 | |||||||

| Materials - 0.9% | ||||||||

| Chemicals - 0.9% | ||||||||

| 21,406 | LyondellBasell Industries NV, Class A | 1,961,432 | ||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $168,574,774) | 214,136,959 | |||||||

| SHORT-TERM INVESTMENTS - 3.9% | ||||||||

| Money Market Mutual Funds - 3.9% | ||||||||

| 8,551,595 | State Street Institutional U.S. Government Money Market Fund - Investment Class (0.00%(b) 7 Day Yield) | 8,551,595 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $8,551,595) | 8,551,595 | |||||||

| TOTAL INVESTMENTS - 100.1% | ||||||||

| (Cost, $177,126,369) | 222,688,554 | |||||||

| Liabilities in Excess of Other Assets - (0.1%) | (137,422 | ) | ||||||

| NET ASSETS - 100.0% | $ | 222,551,132 | ||||||

| (a) | Non-income producing security. |

| (b) | Less than 0.005%. |

| Abbreviations: | |

| NV - | Naamloze Vennootschap (Dutch: Limited Liability Company) |

| PLC - | Public Limited Company |

See Notes to Financial Statements.

15

| Portfolio of Investments |

| CENTURY SMALL CAP SELECT FUND | October 31, 2014 |

| Shares | Value | |||||||

| COMMON STOCKS - 97.2% | ||||||||

| Consumer Discretionary - 16.2% | ||||||||

| Auto Components - 2.5% | ||||||||

| 229,917 | Gentherm, Inc.(a) | $ | 9,587,539 | |||||

| Diversified Consumer Services - 1.6% | ||||||||

| 153,152 | Sotheby’s | 6,074,008 | ||||||

| Hotels, Restaurants & Leisure - 2.8% | ||||||||

| 139,776 | Papa John’s International, Inc. | 6,535,926 | ||||||

| 332,298 | Ruth’s Hospitality Group, Inc. | 4,044,066 | ||||||

| 10,579,992 | ||||||||

| Household Durables - 2.7% | ||||||||

| 195,790 | Ryland Group, Inc. | 7,011,240 | ||||||

| 57,749 | Universal Electronics, Inc.(a) | 3,285,341 | ||||||

| 10,296,581 | ||||||||

| Internet & Catalog Retail - 2.5% | ||||||||

| 275,224 | HomeAway, Inc.(a) | 9,605,318 | ||||||

| Multiline Retail - 0.7% | ||||||||

| 68,769 | Burlington Stores, Inc.(a) | 2,884,172 | ||||||

| Textiles, Apparel & Luxury Goods - 3.4% | ||||||||

| 59,845 | Hanesbrands, Inc. | 6,320,231 | ||||||

| 188,911 | Movado Group, Inc. | 6,668,558 | ||||||

| 12,988,789 | ||||||||

| Total Consumer Discretionary | 62,016,399 | |||||||

| Energy - 2.4% | ||||||||

| Energy Equipment & Services - 1.1% | ||||||||

| 336,521 | Basic Energy Services, Inc.(a) | 4,341,121 | ||||||

| Oil, Gas & Consumable Fuels - 1.3% | ||||||||

| 575,136 | Penn Virginia Corp.(a) | 4,928,915 | ||||||

| Total Energy | 9,270,036 | |||||||

| Financials - 9.1% | ||||||||

| Banks - 2.6% | ||||||||

| 280,528 | Eagle Bancorp, Inc.(a) | 10,079,371 | ||||||

| Capital Markets - 3.3% | ||||||||

| 294,847 | Cohen & Steers, Inc. | 12,637,143 | ||||||

| Diversified Financial Services - 1.9% | ||||||||

| 348,956 | Marlin Business Services Corp. | 7,376,930 | ||||||

| Insurance - 1.3% | ||||||||

| 188,783 | American Equity Investment Life Holding Co. | 4,872,489 | ||||||

| Total Financials | 34,965,933 | |||||||

| Shares | Value | |||||||

| Health Care - 21.2% | ||||||||

| Biotechnology - 1.9% | ||||||||

| 127,221 | Anacor Pharmaceuticals, Inc.(a) | $ | 3,741,569 | |||||

| 134,260 | NPS Pharmaceuticals, Inc.(a) | 3,678,724 | ||||||

| 7,420,293 | ||||||||

| Health Care Equipment & Supplies - 0.9% | ||||||||

| 292,765 | Endologix, Inc.(a) | 3,337,521 | ||||||

| Health Care Providers & Services - 11.0% | ||||||||

| 195,351 | Acadia Healthcare Co., Inc.(a) | 12,121,530 | ||||||

| 161,491 | Air Methods Corp.(a) | 7,627,220 | ||||||

| 353,552 | AMN Healthcare Services, Inc.(a) | 6,063,417 | ||||||

| 298,582 | Brookdale Senior Living, Inc.(a) | 10,065,199 | ||||||

| 219,050 | PharMerica Corp.(a) | 6,284,544 | ||||||

| 42,161,910 | ||||||||

| Life Sciences Tools & Services - 3.8% | ||||||||

| 248,615 | Cambrex Corp.(a) | 5,240,804 | ||||||

| 122,320 | ICON PLC(a) | 6,435,255 | ||||||

| 84,125 | WuXi PharmaTech (Cayman), Inc., Sponsored ADR(a) | 3,171,513 | ||||||

| 14,847,572 | ||||||||

| Pharmaceuticals - 3.6% | ||||||||

| 251,650 | Akorn, Inc.(a) | 11,211,008 | ||||||

| 15,067 | Jazz Pharmaceuticals PLC(a) | 2,543,912 | ||||||

| 13,754,920 | ||||||||

| Total Health Care | 81,522,216 | |||||||

| Industrials - 16.0% | ||||||||

| Building Products - 1.2% | ||||||||

| 237,217 | NCI Building Systems, Inc.(a) | 4,713,502 | ||||||

| Commercial Services & Supplies - 3.2% | ||||||||

| 382,563 | Herman Miller, Inc. | 12,242,016 | ||||||

| Electrical Equipment - 1.9% | ||||||||

| 162,184 | Generac Holdings, Inc.(a) | 7,353,422 | ||||||

| Machinery - 2.9% | ||||||||

| 102,778 | Greenbrier Companies, Inc. | 6,427,736 | ||||||

| 62,396 | Nordson Corp. | 4,776,414 | ||||||

| 11,204,150 | ||||||||

See Notes to Financial Statements.

16

| Portfolio of Investments |

| CENTURY SMALL CAP SELECT FUND | October 31, 2014 |

| Shares | Value | |||||||

| Industrials - 16.0% (continued) | ||||||||

| Professional Services - 2.5% | ||||||||

| 370,755 | Kforce, Inc. | $ | 8,582,978 | |||||

| 32,404 | On Assignment, Inc.(a) | 942,956 | ||||||

| 9,525,934 | ||||||||

| Road & Rail - 1.6% | ||||||||

| 122,883 | Saia, Inc.(a) | 6,023,725 | ||||||

| Trading Companies & Distributors - 2.7% | ||||||||

| 487,975 | CAI International, Inc.(a) | 10,271,874 | ||||||

| Total Industrials | 61,334,623 | |||||||

| Information Technology - 28.8% | ||||||||

| Communications Equipment - 3.7% | ||||||||

| 66,853 | Palo Alto Networks, Inc.(a) | 7,066,362 | ||||||

| 1,074,414 | Sonus Networks, Inc.(a) | 3,728,216 | ||||||

| 94,375 | Ubiquiti Networks, Inc. | 3,375,794 | ||||||

| 14,170,372 | ||||||||

| Internet Software & Services - 11.3% | ||||||||

| 173,995 | comScore, Inc.(a) | 7,332,149 | ||||||

| 78,113 | Constant Contact, Inc.(a) | 2,762,076 | ||||||

| 276,440 | Dealertrack Technologies, Inc.(a) | 13,006,502 | ||||||

| 99,432 | Demandware, Inc.(a) | 5,960,949 | ||||||

| 263,724 | j2 Global, Inc. | 14,264,831 | ||||||

| 43,326,507 | ||||||||

| IT Services - 1.3% | ||||||||

| 72,558 | Virtusa Corp.(a) | 2,973,427 | ||||||

| 107,672 | WNS Holdings Ltd., Sponsored ADR(a) | 2,176,051 | ||||||

| 5,149,478 | ||||||||

| Semiconductors & Semiconductor Equipment - 8.8% | ||||||||

| 163,956 | Cavium, Inc.(a) | 8,412,582 | ||||||

| 196,073 | Inphi Corp.(a) | 3,035,210 | ||||||

| 368,513 | Integrated Device Technology, Inc.(a) | 6,047,298 | ||||||

| 201,674 | Mellanox Technologies Ltd.(a) | 9,032,979 | ||||||

| 161,848 | Monolithic Power Systems, Inc. | 7,152,063 | ||||||

| 33,680,132 | ||||||||

| Shares | Value | |||||||

| Information Technology - 28.8% (continued) | ||||||||

| Software - 3.7% | ||||||||

| 225,460 | Proofpoint, Inc.(a) | $ | 9,929,259 | |||||

| 176,932 | VASCO Data Security International, Inc.(a) | 4,479,918 | ||||||

| 14,409,177 | ||||||||

| Total Information Technology | 110,735,666 | |||||||

| Materials - 3.5% | ||||||||

| Construction Materials - 1.7% | ||||||||

| 75,439 | Eagle Materials, Inc. | 6,595,632 | ||||||

| Metals & Mining - 1.8% | ||||||||

| 152,058 | U.S. Silica Holdings, Inc. | 6,827,404 | ||||||

| Total Materials | 13,423,036 | |||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $297,541,581) | 373,267,909 | |||||||

| SHORT-TERM INVESTMENTS - 3.7% | ||||||||

| Money Market Mutual Funds - 3.7% | ||||||||

| 14,277,761 | State Street Institutional U.S. Government Money Market Fund - Investment Class (0.00%(b) 7 Day Yield) | 14,277,761 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $14,277,761) | 14,277,761 | |||||||

| TOTAL INVESTMENTS - 100.9% | ||||||||

| (Cost, $311,819,342) | 387,545,670 | |||||||

| Liabilities in Excess of Other Assets - (0.9%) | (3,320,336 | ) | ||||||

| NET ASSETS - 100.0% | $ | 384,225,334 | ||||||

| (a) | Non-income producing security. |

| (b) | Less than 0.005%. |

| Abbreviations: | |

| ADR - | American Depositary Receipt |

| Ltd. - | Limited |

| PLC - | Public Limited Company |

See Notes to Financial Statements.

17

| Portfolio of Investments |

| CENTURY GROWTH OPPORTUNITIES FUND | October 31, 2014 |

| Shares | Value | |||||||

| COMMON STOCKS - 98.6% | ||||||||

| Consumer Discretionary - 22.6% | ||||||||

| Auto Components - 1.4% | ||||||||

| 29,286 | Gentherm, Inc.(a) | $ | 1,221,226 | |||||

| Diversified Consumer Services - 4.3% | ||||||||

| 42,438 | Grand Canyon Education, Inc.(a) | 2,032,780 | ||||||

| 70,909 | ServiceMaster Global Holdings, Inc.(a) | 1,700,398 | ||||||

| 3,733,178 | ||||||||

| Hotels, Restaurants & Leisure - 3.3% | ||||||||

| 33,943 | Choice Hotels International, Inc. | 1,815,951 | ||||||

| 19,740 | Fiesta Restaurant Group, Inc.(a) | 1,088,661 | ||||||

| 2,904,612 | ||||||||

| Household Durables - 2.2% | ||||||||

| 29,384 | Jarden Corp.(a) | 1,912,605 | ||||||

| Internet & Catalog Retail - 3.3% | ||||||||

| 27,903 | HomeAway, Inc.(a) | 973,815 | ||||||

| 41,175 | Lands’ End, Inc.(a) | 1,954,577 | ||||||

| 2,928,392 | ||||||||

| Multiline Retail - 3.9% | ||||||||

| 38,050 | Big Lots, Inc. | 1,736,982 | ||||||

| 41,217 | Burlington Stores, Inc.(a) | 1,728,641 | ||||||

| 3,465,623 | ||||||||

| Textiles, Apparel & Luxury Goods - 4.2% | ||||||||

| 20,436 | Deckers Outdoor Corp.(a) | 1,787,333 | ||||||

| 17,579 | Hanesbrands, Inc. | 1,856,518 | ||||||

| 3,643,851 | ||||||||

| Total Consumer Discretionary | 19,809,487 | |||||||

| Consumer Staples - 4.1% | ||||||||

| Food & Staples Retailing - 2.1% | ||||||||

| 27,075 | United Natural Foods, Inc.(a) | 1,841,641 | ||||||

| Food Products - 2.0% | ||||||||

| 46,804 | WhiteWave Foods Co.(a) | 1,742,513 | ||||||

| Total Consumer Staples | 3,584,154 | |||||||

| Energy - 2.7% | ||||||||

| Energy Equipment & Services - 1.6% | ||||||||

| 36,261 | FMSA Holdings, Inc.(a) | 445,648 | ||||||

| Shares | Value | |||||||

| Energy - 2.7% (continued) | ||||||||

| Energy Equipment & Services - 1.6% (continued) | ||||||||

| 38,753 | Superior Energy Services, Inc. | $ | 974,638 | |||||

| 1,420,286 | ||||||||

| Oil, Gas & Consumable Fuels - 1.1% | ||||||||

| 18,579 | Gulfport Energy Corp.(a) | 932,294 | ||||||

| Total Energy | 2,352,580 | |||||||

| Financials - 6.2% | ||||||||

| Banks - 2.2% | ||||||||

| 59,982 | PrivateBancorp, Inc. | 1,938,619 | ||||||

| Real Estate Investment Trusts (REITs) - 4.0% | ||||||||

| 21,781 | Camden Property Trust | 1,669,949 | ||||||

| 158,042 | Education Realty Trust, Inc. | 1,779,553 | ||||||

| 3,449,502 | ||||||||

| Total Financials | 5,388,121 | |||||||

| Health Care - 19.8% | ||||||||

| Biotechnology - 2.8% | ||||||||

| 38,843 | Alkermes PLC(a) | 1,963,514 | ||||||

| 38,865 | Dyax Corp.(a) | 480,760 | ||||||

| 2,444,274 | ||||||||

| Health Care Equipment & Supplies - 4.5% | ||||||||

| 23,040 | CareFusion Corp.(a) | 1,321,805 | ||||||

| 10,422 | Cooper Companies, Inc. | 1,708,166 | ||||||

| 16,421 | Cyberonics, Inc.(a) | 862,102 | ||||||

| 3,892,073 | ||||||||

| Health Care Providers & Services - 6.0% | ||||||||

| 28,141 | Team Health Holdings, Inc.(a) | 1,759,938 | ||||||

| 15,970 | Universal Health Services, Inc., Class B | 1,656,249 | ||||||

| 41,130 | VCA, Inc.(a) | 1,874,294 | ||||||

| 5,290,481 | ||||||||

| Life Sciences Tools & Services - 2.1% | ||||||||

| 45,009 | Cambrex Corp.(a) | 948,790 | ||||||

| 16,175 | PAREXEL International Corp.(a) | 878,464 | ||||||

| 1,827,254 | ||||||||

| Pharmaceuticals - 4.4% | ||||||||

| 47,649 | Akorn, Inc.(a) | 2,122,763 | ||||||

| 26,054 | Endo International PLC(a) | 1,743,533 | ||||||

| 3,866,296 | ||||||||

| Total Health Care | 17,320,378 | |||||||

See Notes to Financial Statements.

18

| Portfolio of Investments |

| CENTURY GROWTH OPPORTUNITIES FUND | October 31, 2014 |

| Shares | Value | |||||||

| Industrials - 15.5% | ||||||||

| Commercial Services & Supplies - 3.6% | ||||||||

| 32,036 | G&K Services, Inc., Class A | $ | 2,020,511 | |||||

| 21,737 | U.S. Ecology, Inc. | 1,092,936 | ||||||

| 3,113,447 | ||||||||

| Machinery - 5.2% | ||||||||

| 28,221 | Greenbrier Companies, Inc. | 1,764,941 | ||||||

| 11,289 | Nordson Corp. | 864,173 | ||||||

| 14,839 | Snap-on, Inc. | 1,960,826 | ||||||

| 4,589,940 | ||||||||

| Professional Services - 2.2% | ||||||||

| 47,489 | FTI Consulting, Inc.(a) | 1,917,606 | ||||||

| Road & Rail - 2.2% | ||||||||

| 16,092 | Kansas City Southern | 1,975,936 | ||||||

| Trading Companies & Distributors - 2.3% | ||||||||

| 18,086 | United Rentals, Inc.(a) | 1,990,545 | ||||||

| Total Industrials | 13,587,474 | |||||||

| Information Technology - 25.6% | ||||||||

| Communications Equipment - 4.9% | ||||||||

| 13,984 | F5 Networks, Inc.(a) | 1,719,752 | ||||||

| 16,554 | Palo Alto Networks, Inc.(a) | 1,749,758 | ||||||

| 22,226 | Ubiquiti Networks, Inc. | 795,024 | ||||||

| 4,264,534 | ||||||||

| Electronic Equipment, Instruments & Components - 1.3% | ||||||||

| 15,046 | Zebra Technologies Corp., Class A(a) | 1,109,642 | ||||||

| Internet Software & Services - 1.2% | ||||||||

| 17,048 | Demandware, Inc.(a) | 1,022,028 | ||||||

| IT Services - 8.8% | ||||||||

| 50,913 | Cardtronics, Inc.(a) | 1,954,550 | ||||||

| 5,993 | FleetCor Technologies, Inc.(a) | 902,306 | ||||||

| 44,483 | MAXIMUS, Inc. | 2,155,646 | ||||||

| 47,581 | VeriFone Systems, Inc.(a) | 1,772,868 | ||||||

| 22,703 | Virtusa Corp.(a) | 930,369 | ||||||

| 7,715,739 | ||||||||

| Semiconductors & Semiconductor Equipment - 6.6% | ||||||||

| 19,061 | Cavium, Inc.(a) | 978,020 | ||||||

| 86,883 | Integrated Device Technology, Inc.(a) | 1,425,750 | ||||||

| 36,718 | Mellanox Technologies Ltd.(a) | 1,644,599 | ||||||

| Shares | Value | |||||||

| Information Technology - 25.6% (continued) | ||||||||

| Semiconductors & Semiconductor Equipment - 6.6% (continued) | ||||||||

| 25,615 | NXP Semiconductor NV(a) | $ | 1,758,726 | |||||

| 5,807,095 | ||||||||

| Software - 2.8% | ||||||||

| 28,962 | Proofpoint, Inc.(a) | 1,275,487 | ||||||

| 46,694 | VASCO Data Security International, Inc.(a) | 1,182,292 | ||||||

| 2,457,779 | ||||||||

| Total Information Technology | 22,376,817 | |||||||

| Telecommunication Services - 2.1% | ||||||||

| Diversified Telecommunication Services - 2.1% | ||||||||

| 53,402 | Cogent Communications Holdings, Inc. | 1,812,464 | ||||||

| TOTAL COMMON STOCKS | ||||||||

| (Cost $71,398,044) | 86,231,475 | |||||||

| SHORT-TERM INVESTMENTS - 1.2% | ||||||||

| Money Market Mutual Funds - 1.2% | ||||||||

| 1,001,515 | State Street Institutional U.S. Government Money Market Fund - Investment Class (0.00%(b) 7 Day Yield) | 1,001,515 | ||||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $1,001,515) | 1,001,515 | |||||||

| TOTAL INVESTMENTS - 99.8% | ||||||||

| (Cost, $72,399,559) | 87,232,990 | |||||||

| Other Assets in Excess of Liabilities - 0.2% | 187,115 | |||||||

| NET ASSETS - 100.0% | $ | 87,420,105 | ||||||

| (a) | Non-income producing security. |

| (b) | Less than 0.005%. |

| Abbreviations: | |

| Ltd. - | Limited |

| NV - | Naamloze Vennootschap (Dutch: Limited Liability Company) |

| PLC - | Public Limited Company |

See Notes to Financial Statements.

19

| Statements of Assets and Liabilities |

| October 31, 2014 |

Century Shares Trust | Century Small Cap Select Fund | Century Growth Opportunities Fund | ||||||||||

| ASSETS: | ||||||||||||

| Investments, at value (Note 1) (cost - see below) | $ | 222,688,554 | $ | 387,545,670 | $ | 87,232,990 | ||||||

| Receivable for investments sold | – | 5,907,628 | 891,997 | |||||||||

| Receivable for fund shares subscribed | 1,274 | 344,958 | 95,917 | |||||||||

| Dividends receivable | 265,068 | 7,544 | 22,065 | |||||||||

| Prepaid expenses | 4,146 | 8,471 | 1,813 | |||||||||

| Total Assets | 222,959,042 | 393,814,271 | 88,244,782 | |||||||||

| LIABILITIES: | ||||||||||||

| Payable to Affiliates: | ||||||||||||

| Investment adviser fees (Note 4) | 145,181 | 296,165 | 69,586 | |||||||||

| Administration fees (Note 5) | 18,148 | – | 6,992 | |||||||||

| Distribution and service fees (Note 6) | – | 32,899 | – | |||||||||

| Payable for investments purchased | – | 8,803,572 | 662,305 | |||||||||

| Payable for shares redeemed | 129,503 | 293,525 | 8,510 | |||||||||

| Payable to trustees | 16,934 | 35,403 | 7,619 | |||||||||

| Accrued expenses and other liabilities | 98,144 | 127,373 | 69,665 | |||||||||

| Total Liabilities | 407,910 | 9,588,937 | 824,677 | |||||||||

| NET ASSETS | $ | 222,551,132 | $ | 384,225,334 | $ | 87,420,105 | ||||||

| NET ASSETS CONSIST OF: | ||||||||||||

| Paid-in capital | $ | 123,666,342 | $ | 257,721,200 | $ | 56,466,776 | ||||||

| Accumulated net investment loss | – | – | (596,361 | ) | ||||||||

| Accumulated net realized gain on investments | 53,322,605 | 50,777,806 | 16,716,259 | |||||||||

| Unrealized appreciation in value of investments | 45,562,185 | 75,726,328 | 14,833,431 | |||||||||

| NET ASSETS | $ | 222,551,132 | $ | 384,225,334 | $ | 87,420,105 | ||||||

| Net Assets: | ||||||||||||

| Institutional Shares | $ | 222,551,132 | $ | 266,044,661 | $ | 87,420,105 | ||||||

| Investor Shares | N/A | $ | 118,180,673 | N/A | ||||||||

| Shares Outstanding (Note 2): | ||||||||||||

| Institutional Shares | 8,982,358 | 7,720,964 | 5,637,637 | |||||||||

| Investor Shares | N/A | 3,568,158 | N/A | |||||||||

| Net Asset Value Per Share | ||||||||||||

(Represents both the offering and redemption price)(a) | ||||||||||||

| Institutional Shares | $ | 24.78 | $ | 34.46 | $ | 15.51 | ||||||

| Investor Shares | N/A | $ | 33.12 | N/A | ||||||||

| Cost of investments | $ | 177,126,369 | $ | 311,819,342 | $ | 72,399,559 | ||||||

| (a) | A redemption fee may be assessed for shares redeemed within 90 days after purchase. (Note 1) |

See Notes to Financial Statements.

20

| Statements of Operations |

| For the Year Ended October 31, 2014 |

Century Shares Trust | Century Small Cap Select Fund | Century Growth Opportunities Fund | ||||||||||

| INVESTMENT INCOME: | ||||||||||||

| Dividends | $ | 2,210,246 | $ | 1,663,490 | $ | 290,865 | ||||||

| Foreign taxes withheld | (9,633 | ) | – | (571 | ) | |||||||

| Total Investment Income | 2,200,613 | 1,663,490 | 290,294 | |||||||||

| EXPENSES: | ||||||||||||

| Investment adviser fees (Notes 4 and 7) | 1,712,967 | 3,931,983 | 714,361 | |||||||||

| Distribution and service fees (Note 6): | ||||||||||||

| Investor Shares | – | 262,519 | – | |||||||||

| Administrative fees | 214,121 | – | 89,295 | |||||||||

| Transfer agency fees | 140,075 | 306,007 | 18,303 | |||||||||

| Fund accounting fees | 25,782 | 48,456 | 13,276 | |||||||||

| Custodian fees | 18,386 | 35,343 | 32,017 | |||||||||

| Insurance fees | 15,015 | 31,713 | 6,979 | |||||||||

| Professional fees | 60,943 | 75,768 | 52,571 | |||||||||

| Registration fees | 23,199 | 40,045 | 17,120 | |||||||||

| Trustee fees | 74,375 | 144,270 | 30,432 | |||||||||

| Printing fees | 44,328 | 48,833 | 3,536 | |||||||||

| Other expenses | 10,558 | 25,264 | 7,460 | |||||||||

Total Expenses | 2,339,749 | 4,950,201 | 985,350 | |||||||||

| Adviser waivers/reimbursements (Note 7) | – | – | (3,288 | ) | ||||||||

| Net Expenses | 2,339,749 | 4,950,201 | 982,062 | |||||||||

| NET INVESTMENT LOSS | (139,136 | ) | (3,286,711 | ) | (691,768 | ) | ||||||

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | ||||||||||||

| Net realized gain on investments | 53,680,617 | 57,842,711 | 18,260,490 | |||||||||

| Long-term capital gains from other investment companies | 36,899 | – | – | |||||||||

| Net change in unrealized depreciation of investments | (19,688,444 | ) | (27,150,382 | ) | (6,570,681 | ) | ||||||

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | 34,029,072 | 30,692,329 | 11,689,809 | |||||||||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 33,889,936 | $ | 27,405,618 | $ | 10,998,041 | ||||||

See Notes to Financial Statements.

21

| |

| Century Shares Trust | ||||||||

| For the Year Ended October 31, | ||||||||

| 2014 | 2013 | |||||||

| OPERATIONS: | ||||||||

| Net investment income/(loss) | $ | (139,136 | ) | $ | 290,829 | |||

| Net realized gain on investments | 53,680,617 | 11,876,647 | ||||||

| Long-term capital gains from other investment companies | 36,899 | – | ||||||

| Change in net unrealized appreciation/(depreciation) | (19,688,444 | ) | 34,752,330 | |||||

| Net increase in net assets resulting from operations | 33,889,936 | 46,919,806 | ||||||

| DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||

| Institutional Shares | ||||||||

| From net investment income | – | (399,960 | ) | |||||

| From net realized gains on investments | (11,893,456 | ) | (21,366,224 | ) | ||||

| Investor Shares | ||||||||

| From net investment income | – | – | ||||||

| From net realized gains on investments | – | – | ||||||

| Total distributions | (11,893,456 | ) | (21,766,184 | ) | ||||

| CAPITAL SHARE TRANSACTIONS: | ||||||||

| Increase/(decrease) in net assets from capital share transactions (Note 2) | (716,312 | ) | 1,582,539 | |||||

| Redemption fees | 33 | 441 | ||||||

| Net increase/(decrease) from share transactions | (716,279 | ) | 1,582,980 | |||||

| Total increase | 21,280,201 | 26,736,602 | ||||||

| NET ASSETS: | ||||||||

| Beginning of year | 201,270,931 | 174,534,329 | ||||||

| End of year* | $ | 222,551,132 | $ | 201,270,931 | ||||

| *Including accumulated net investment loss | $ | – | $ | (166,506 | ) | |||

See Notes to Financial Statements.

22

Statements of Changes in Net Assets | |

| Century Small Cap Select Fund | Century Growth Opportunities Fund | ||||||||||||||

| For the Year Ended October 31, | For the Year Ended October 31, | ||||||||||||||

| 2014 | 2013 | 2014 | 2013 | ||||||||||||

| $ | (3,286,711 | ) | $ | (962,493 | ) | $ | (691,768 | ) | $ | (273,374 | ) | ||||

| 57,842,711 | 64,324,461 | 18,260,490 | 8,886,734 | ||||||||||||

| – | – | – | – | ||||||||||||

| (27,150,382 | ) | 45,785,839 | (6,570,681 | ) | 16,179,917 | ||||||||||

| 27,405,618 | 109,147,807 | 10,998,041 | 24,793,277 | ||||||||||||

| – | – | – | (173,998 | ) | |||||||||||

| (14,887,988 | ) | – | (987,358 | ) | – | ||||||||||

| – | – | – | – | ||||||||||||

| (6,555,307 | ) | – | – | – | |||||||||||

| (21,443,295 | ) | – | (987,358 | ) | (173,998 | ) | |||||||||

| (50,603,727 | ) | (73,741,581 | ) | (16,003,874 | ) | (25,491,806 | ) | ||||||||

| 4,834 | 11,434 | 372 | – | ||||||||||||

| (50,598,893 | ) | (73,730,147 | ) | (16,003,502 | ) | (25,491,806 | ) | ||||||||

| (44,636,570 | ) | 35,417,660 | (5,992,819 | ) | (872,527 | ) | |||||||||

| 428,861,904 | 393,444,244 | 93,412,924 | 94,285,451 | ||||||||||||

| $ | 384,225,334 | $ | 428,861,904 | $ | 87,420,105 | $ | 93,412,924 | ||||||||

| $ | – | $ | (2,663,042 | ) | $ | (596,361 | ) | $ | (560,030 | ) | |||||

23

| Financial Highlights |

CENTURY SHARES TRUST INSTITUTIONAL SHARES | For a share outstanding throughout the periods presented |

| For the Year Ended October 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 22.41 | $ | 19.81 | $ | 20.66 | $ | 19.65 | $ | 16.84 | ||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||

Net investment income/(loss)(a) | (0.02 | ) | 0.03 | 0.05 | (0.02 | ) | (0.01 | ) | ||||||||||||

| Net realized and unrealized gain on investments | 3.72 | 5.09 | 1.28 | 1.93 | 2.82 | |||||||||||||||

| Total income from investment operations | 3.70 | 5.12 | 1.33 | 1.91 | 2.81 | |||||||||||||||

| LESS DISTRIBUTIONS FROM: | ||||||||||||||||||||

| Net investment income | – | (0.05 | ) | (0.06 | ) | (0.01 | ) | (0.00 | )(b) | |||||||||||

| Net realized gain on investment transactions | (1.33 | ) | (2.47 | ) | (2.12 | ) | (0.89 | ) | – | |||||||||||

| Total distributions | (1.33 | ) | (2.52 | ) | (2.18 | ) | (0.90 | ) | (0.00 | )(b) | ||||||||||

| REDEMPTION FEES | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | ||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 24.78 | $ | 22.41 | $ | 19.81 | $ | 20.66 | $ | 19.65 | ||||||||||

| TOTAL RETURN | 17.29 | % | 28.85 | % | 7.63 | % | 9.79 | % | 16.72 | % | ||||||||||

| RATIOS AND SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (000's) | $ | 222,551 | $ | 201,271 | $ | 174,534 | $ | 178,201 | $ | 177,042 | ||||||||||

| Ratio of expenses to average net assets | 1.09 | % | 1.11 | % | 1.12 | % | 1.13 | % | 1.15 | % | ||||||||||

| Ratio of net investment income/(loss) to average net assets | (0.06 | %) | 0.16 | % | 0.24 | % | (0.10 | %) | (0.05 | %) | ||||||||||

| PORTFOLIO TURNOVER RATE | 126 | % | 39 | % | 79 | % | 72 | % | 67 | % | ||||||||||

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Less than $0.005 per share. |

See Notes to Financial Statements.

24

| Financial Highlights |

CENTURY SMALL CAP SELECT FUND INSTITUTIONAL SHARES | For a share outstanding throughout the periods presented |

| For the Year Ended October 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 33.94 | $ | 26.27 | $ | 23.91 | $ | 20.99 | $ | 16.34 | ||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||

Net investment loss(a) | (0.24 | ) | (0.04 | ) | (0.12 | ) | (0.09 | ) | (0.05 | ) | ||||||||||

| Net realized and unrealized gain on investments | 2.48 | 7.71 | 2.48 | 3.01 | 4.70 | |||||||||||||||

| Total income from investment operations | 2.24 | 7.67 | 2.36 | 2.92 | 4.65 | |||||||||||||||

| LESS DISTRIBUTIONS FROM: | ||||||||||||||||||||

| Net realized gain on investment transactions | (1.72 | ) | – | – | – | – | ||||||||||||||

| Total distributions | (1.72 | ) | – | – | – | – | ||||||||||||||

| REDEMPTION FEES | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | ||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 34.46 | $ | 33.94 | $ | 26.27 | $ | 23.91 | $ | 20.99 | ||||||||||

| TOTAL RETURN | 6.79 | % | 29.20 | % | 9.87 | % | 13.86 | % | 28.52 | % | ||||||||||

| RATIOS AND SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (000's) | $ | 266,045 | $ | 300,833 | $ | 281,480 | $ | 254,724 | $ | 249,429 | ||||||||||

| Ratio of expenses to average net assets | 1.11 | % | 1.12 | % | 1.10 | % | 1.11 | % | 1.13 | % | ||||||||||

| Ratio of net investment loss to average net assets | (0.71 | %) | (0.14 | %) | (0.48 | %) | (0.37 | %) | (0.25 | %) | ||||||||||

| PORTFOLIO TURNOVER RATE | 97 | % | 91 | % | 53 | % | 75 | % | 85 | % | ||||||||||

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Less than $0.005 per share. |

See Notes to Financial Statements.

25

| Financial Highlights |

CENTURY SMALL CAP SELECT FUND INVESTOR SHARES | For a share outstanding throughout the periods presented |

| For the Year Ended October 31, | ||||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | 2010 | ||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 32.78 | $ | 25.45 | $ | 23.25 | $ | 20.49 | $ | 16.00 | ||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||

Net investment loss(a) | (0.33 | ) | (0.13 | ) | (0.21 | ) | (0.17 | ) | (0.11 | ) | ||||||||||

| Net realized and unrealized gain on investments | 2.39 | 7.46 | 2.41 | 2.92 | 4.60 | |||||||||||||||

| Total income from investment operations | 2.06 | 7.33 | 2.20 | 2.75 | 4.49 | |||||||||||||||

| LESS DISTRIBUTIONS FROM: | ||||||||||||||||||||

| Net realized gain on investment transactions | (1.72 | ) | – | – | – | – | ||||||||||||||

| Total distributions | (1.72 | ) | – | – | – | – | ||||||||||||||

| REDEMPTION FEES | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.01 | 0.00 | (b) | |||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 33.12 | $ | 32.78 | $ | 25.45 | $ | 23.25 | $ | 20.49 | ||||||||||

| TOTAL RETURN | 6.47 | % | 28.80 | % | 9.46 | % | 13.47 | % | 28.06 | % | ||||||||||

| RATIOS AND SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (000's) | $ | 118,181 | $ | 128,029 | $ | 111,965 | $ | 116,678 | $ | 92,618 | ||||||||||

| Ratio of expenses to average net assets | 1.40 | % | 1.41 | % | 1.47 | % | 1.48 | % | 1.50 | % | ||||||||||

| Ratio of net investment loss to average net assets | (1.00 | %) | (0.44 | %) | (0.84 | %) | (0.71 | %) | (0.61 | %) | ||||||||||

| PORTFOLIO TURNOVER RATE | 97 | % | 91 | % | 53 | % | 75 | % | 85 | % | ||||||||||

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Less than $0.005 per share. |

See Notes to Financial Statements.

26

| Financial Highlights |

CENTURY GROWTH OPPPORTUNITIES FUND INSTITUTIONAL SHARES | For a share outstanding throughout the periods presented |

| For the Year Ended October 31, | For the Period November 17, 2010 (Inception) to October 31, | |||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 13.87 | $ | 10.81 | $ | 10.67 | $ | 10.00 | ||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||

Net investment loss(a) | (0.11 | ) | (0.03 | ) | (0.02 | ) | (0.07 | ) | ||||||||

| Net realized and unrealized gain on investments | 1.90 | 3.11 | 0.16 | 0.74 | ||||||||||||

| Total income from investment operations | 1.79 | 3.08 | 0.14 | 0.67 | ||||||||||||

| LESS DISTRIBUTIONS FROM: | ||||||||||||||||

| Net investment income | – | (0.02 | ) | – | – | |||||||||||

| Net realized gain on investment transactions | (0.15 | ) | – | – | – | |||||||||||

| Total distributions | (0.15 | ) | (0.02 | ) | – | – | ||||||||||

| REDEMPTION FEES | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | 0.00 | (b) | ||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 15.51 | $ | 13.87 | $ | 10.81 | $ | 10.67 | ||||||||

| TOTAL RETURN | 13.04 | % | 28.54 | % | 1.31 | % | 6.70 | %(c) | ||||||||

| RATIOS AND SUPPLEMENTAL DATA | ||||||||||||||||

| Net assets, end of period (000's) | $ | 87,420 | $ | 93,413 | $ | 94,285 | $ | 7,323 | ||||||||

| Ratio of expenses to average net assets without giving effect to contractual expense agreement | 1.10 | % | 1.12 | % | 1.20 | % | 3.62 | %(d) | ||||||||

| Ratio of expenses to average net assets | 1.10 | % | 1.10 | % | 1.10 | % | 1.10 | %(d) | ||||||||

| Ratio of net investment loss to average net assets | (0.77 | %) | (0.27 | %) | (0.18 | %) | (0.64 | %)(d) | ||||||||

| PORTFOLIO TURNOVER RATE | 165 | % | 155 | % | 148 | % | 119 | %(c) | ||||||||

| (a) | Per share numbers have been calculated using the average shares method. |

| (b) | Less than $0.005 per share. |

| (c) | Not annualized. |

| (d) | Annualized. |

See Notes to Financial Statements.

27

| Notes to Financial Statements |

| October 31, 2014 |

1. SIGNIFICANT ACCOUNTING POLICIES

Century Capital Management Trust (the “Trust”) is registered under the Investment Company Act of 1940, as amended (“1940 Act”) as an open-end management investment company organized as a Massachusetts business trust. Century Shares Trust, Century Small Cap Select Fund, and Century Growth Opportunities Fund (each a “Fund” and, collectively, the “Funds”) are diversified series of the Trust. The following are significant accounting policies consistently followed by the Funds and are in conformity with accounting principles generally accepted in the United States (GAAP). Each Fund is considered an investment company for financial reporting purposes under GAAP.

The investment objective of Century Shares Trust is to seek long-term growth of principal and income. The investment objective of each of Century Small Cap Select Fund and Century Growth Opportunities Fund is to seek long-term capital growth.

A. Security Valuations — Equity securities are valued at the last reported sale price or official closing price on the primary exchange or market on which they are traded, as reported by an independent pricing service. If no sale price or official closing price is reported, market value is generally determined based on quotes or closing prices obtained from a quotation reporting system, established market maker, or reputable pricing service. For unlisted securities and for exchange-listed securities for which there are no reported sales or official closing prices, fair value is generally determined using closing bid prices. In the absence of readily available market quotes, securities and other assets will be valued at fair value, as determined in good faith under procedures established by and under the general supervision of the Funds’ Board of Trustees. Short-term obligations, maturing in 60 days or less, are valued at amortized cost, which approximates fair value. Investments in open-end mutual funds are valued at their closing net asset value each business day.

A three-tier hierarchy has been established to classify fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of each Fund’s investments as of the reporting period end. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

Level 1 — | Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Funds have the ability to access at the measurement date; |

| Level 2 — | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; |

Level 3 — | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

28

| Notes to Financial Statements |

| October 31, 2014 |

The following is a summary of the inputs used as of October 31, 2014 in valuing the Funds’ investments carried at fair value:

| Century Shares Trust | ||||||||||||||||

| Investments in Securities at Value* | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Common Stocks | $ | 214,136,959 | $ | ��� | $ | – | $ | 214,136,959 | ||||||||

| Short-Term Investments | 8,551,595 | – | – | 8,551,595 | ||||||||||||

| TOTAL | $ | 222,688,554 | $ | – | $ | – | $ | 222,688,554 | ||||||||

| Century Small Cap Select Fund | ||||||||||||||||

| Investments in Securities at Value* | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Common Stocks | $ | 373,267,909 | $ | – | $ | – | $ | 373,267,909 | ||||||||

| Short-Term Investments | 14,277,761 | – | – | 14,277,761 | ||||||||||||

| TOTAL | $ | 387,545,670 | $ | – | $ | – | $ | 387,545,670 | ||||||||

| Century Growth Opportunities Fund | ||||||||||||||||

| Investments in Securities at Value* | Level 1 - Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Common Stocks | $ | 86,231,475 | $ | – | $ | – | $ | 86,231,475 | ||||||||

| Short-Term Investments | 1,001,515 | – | – | 1,001,515 | ||||||||||||

| TOTAL | $ | 87,232,990 | $ | – | $ | – | $ | 87,232,990 | ||||||||

| * | At October 31, 2014 the Funds held investments in common stocks classified as Level 1, with corresponding major categories as shown on each Fund’s Portfolio of Investments. |

The Funds recognize transfers into and out of all levels at the end of the reporting period. There were no transfers into or out of Levels 1 and 2 during the period.

There were no securities classified as Level 3 securities during the period, thus, a reconciliation of assets in which significant unobservable inputs (Level 3) were used is not applicable for these Funds.

29

| Notes to Financial Statements |

| October 31, 2014 |

B. Security Transactions — Security transactions are recorded on a trade date basis. Gain or loss on sales is determined by the use of the highest cost-method, for both financial reporting and federal income tax purposes. Dividend income is recorded on the ex-dividend date. Payments received from certain investments held by the Funds may be comprised of dividends, capital gains and return of capital. The Funds originally estimate the expected classification of such payments. The amounts may subsequently be reclassified upon receipt of information from the issuer. The Funds may invest in equity securities issued or guaranteed by companies organized and based in countries outside of the United States. These securities may be traded on foreign securities exchanges or in foreign over-the-counter markets. Foreign dividend income is recorded on ex-dividend date or as soon as practicable after the Fund determines the existence of a dividend declaration after exercising reasonable due diligence. Foreign income and capital gain on some foreign securities may be subject to foreign withholding taxes, which are accrued as applicable. Interest income is recorded daily on an accrual basis.

C. Use of Estimates — The preparation of these financial statements in accordance with GAAP incorporates estimates made by management in determining the reported amounts of assets, liabilities, income and expenses of the Funds. Actual results could differ from those estimates.

D. Risks and Uncertainty — Century Shares Trust may invest a significant portion of assets in a limited number of companies. As a result, the Fund may be more susceptible to financial, market and economic events affecting particular companies and therefore may experience greater price volatility than funds with more diversified portfolios.