| NOTES TO THE FINANCIAL STATEMENTS | |

| CONQUER RISK FUNDS | |

| June 30, 2024 | |

| | | | | | | | | | |

| 1.) ORGANIZATION | | | | | | | | | |

The Conquer Risk Funds (the “Funds”) are each a series of PFS Funds (the “Trust”). The Trust is an open-end management investment company that was organized in Massachusetts by an Agreement and Declaration of Trust dated January 13, 2000, as amended on January 20, 2011. The Trust is registered as an open-end investment company under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust may offer an unlimited number of shares of beneficial interest in a number of separate series, each series representing a distinct fund with its own investment objectives and policies. Conquer Risk Defensive Bull Fund (“Defensive Bull Fund”), Conquer Risk Managed Volatility Fund (“Managed Volatility Fund”), Conquer Risk Tactical Opportunities Fund (“Tactical Opportunities Fund”) and Conquer Risk Tactical Rotation Fund (“Tactical Rotation Fund”) (each a “Fund” and collectively the “Funds”) were each organized as a non-diversified series of the Trust, on June 9, 2020 and commenced operations on July 1, 2020. As of June 30, 2024, there were twelve series authorized by the Trust. The investment advisor to the Funds is Potomac Fund Management, Inc. (the “Advisor”). Significant accounting policies of the Funds are presented below.

|

| | | | | | | | | | |

| 2.) SIGNIFICANT ACCOUNTING POLICIES | | | | | | | |

| The Funds are investment companies and accordingly follow the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946 Financial Services - Investment Companies. The financial statements are prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Funds follow the significant accounting policies described in this section. |

| | | | | | | | | | |

| SECURITY VALUATION | | | | | | | | | |

All investments in securities are valued as described in Note 3. The Trust’s Board of Trustees (“Board”) has designated the Advisor as “Valuation Designee” pursuant to Rule 2a-5 under the 1940 Act.

|

| | | | | | | | | | |

| SHARE VALUATION | | | | | | | | | |

Each Fund’s net asset value (the “NAV”) is generally calculated as of the close of trading on the New York Stock Exchange (the “Exchange”) (normally 4:00 p.m. Eastern time) every day the Exchange is open. The NAV for each Fund is calculated by taking the total value of the Fund’s assets, subtracting its liabilities, and then dividing by the total number of shares outstanding, rounded to the nearest cent. The offering price and redemption price per share is equal to the net asset value per share.

|

| | | | | | | | | | |

| FEDERAL INCOME TAXES | | | | | | | | | |

The Funds’ policy is to continue to comply with the requirements of the Internal Revenue Code that are applicable to regulated investment companies and to distribute all of their taxable income to shareholders. Therefore, no federal income tax provision is required. It is the Funds’ policy to distribute annually, prior to the end of the calendar year, dividends sufficient to satisfy excise tax requirements of the Internal Revenue Code. This Internal Revenue Code requirement may cause an excess of distributions over the book year-end accumulated income. In addition, it is the Funds’ policy to distribute annually, after the end of the fiscal year, any remaining net investment income and net realized capital gains.

|

| | | | | | | | | | |

The Funds recognize the tax benefits of certain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Funds’ tax positions, and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years. The Funds identify their major tax jurisdictions as U.S. Federal and State tax authorities; the Funds are not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months. The Funds recognize interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statements of Operations. During the fiscal year ended June 30, 2024, the Funds did not incur any interest or penalties.

|

| | | | | | | | | | |

| FUND OF FUND STRUCTURE | | | | | | | | | |

Each Fund invests in portfolios of exchange traded funds (ETFs) and open-end mutual funds (the "Underlying Funds"). The shares of many ETFs frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurances that the market discount or market premium on shares of any ETFs purchased by the Funds will not change. For further information on how each Fund values the Underlying Funds, see Note 3.

|

| | | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS | | | | | | | |

| Distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The Funds may utilize earnings and profits distributed to shareholders on redemptions of shares as part of the dividends paid deduction. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassification will have no effect on net assets, results of operations or net asset values per share of any Fund. |

| | | | | | | | | | |

| USE OF ESTIMATES | | | | | | | | | |

The financial statements are prepared in accordance with GAAP, which requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

|

| | | | | | | | | | |

| OTHER | | | | | | | | | |

The Funds record security transactions based on a trade date. Dividend income is recognized on the ex-dividend date, and interest income, if any, is recognized on an accrual basis. The Funds use the specific identification method in computing gain or loss on the sale of investment securities. Long-term capital gain distributions are recorded as capital gain distributions from investment companies, and short-term capital gain distributions are recorded as dividend income. Additionally, the Funds may hold investments which are structured as master limited partnerships (“MLPs”) for tax purposes. It is common for distributions from MLPs to exceed taxable earnings and profits resulting in the excess portion of such dividends to be designated as return of capital. Annually, income or loss from MLPs is reclassified upon receipt of the MLPs K-1. For financial reporting purposes, management does not estimate the tax character of MLP distributions for which actual information has not been reported.

|

| | | | | | | | | | |

| EXPENSES | | | | | | | | | |

Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual Fund based on each Fund’s relative net assets or by another appropriate method.

|

| | | | | | | | | | |

| 3.) SECURITIES VALUATIONS | | | | | | | | | |

The Funds utilize various methods to measure the fair value of their investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

|

| | | | | | | | | | |

Level 1 - Unadjusted quoted prices in active markets for identical assets or liabilities that the Funds have the ability to access.

|

| | | | | | | | | | |

Level 2 - Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

|

| | | | | | | | | | |

Level 3 - Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

|

| | | | | | | | | | |

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in level 3.

|

| | | | | | | | | | |

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

|

| | | | | | | | | | |

| VALUATION OF FUND ASSETS | | | | | | | | | |

A description of the valuation techniques applied to each Fund's major categories of assets measured at fair value on a recurring basis follows.

|

| | | | | | | | | | |

Equity securities (exchange traded funds). Equity securities generally are valued by using market quotations, but may be valued on the basis of prices furnished by a pricing service when the Valuation Designee believes such prices accurately reflect the fair value of such securities. Securities that are traded on any stock exchange or on the NASDAQ over-the-counter market are generally valued by the pricing service at the last quoted sale price. Lacking a last sale price, an equity security is generally valued by the pricing service at its last bid price. Generally, if the security is traded in an active market and is valued at the last sale price, the security is categorized as a level 1 security, and if an equity security is valued by the pricing service at its last bid, it is generally categorized as a level 2 security. When market quotations are not readily available, when the Valuation Designee determines that the market quotation or the price provided by the pricing service does not accurately reflect the current fair value, or when restricted securities are being valued, such securities are valued as determined in good faith by the Valuation Designee, subject to review of the Board of Trustees, and are categorized in level 2 or level 3, when appropriate.

|

| | | | | | | | | | |

Money market funds. Money market funds are valued at NAV provided by the funds and are classified in level 1 of the fair value hierarchy.

|

| | | | | | | | | | |

Mutual funds. Mutual funds are valued at the NAV as reported by the underlying fund and are classified in level 1 of the fair value hierarchy. The underlying mutual funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value by the methods established by the boards of the underlying funds. In the event a mutual fund does not report its net asset value, the Fund will value such an asset using its fair value procedures which incorporate, among other information, price changes from reference indexes or reference funds to assist in the valuation of a non-reporting mutual fund.

|

| | | | | | | | | | |

In accordance with the Trust’s fair value pricing guidelines, the Valuation Designee is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. There is no standard procedure for determining fair value, since fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Valuation Designee would appear to be the amount which the owner might reasonably expect to receive for them upon their current sale. Methods which are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. The Board maintains responsibilities for the fair value determinations under Rule 2a-5 under the 1940 Act and oversees the Valuation Designee.

|

| | | | | | | | | | |

The following tables summarize the inputs used to value each Fund’s assets measured at fair value as of June 30, 2024:

|

| | | | | | | | | | |

| Defensive Bull Fund: | | | | | | | | | |

| Valuation Inputs of Assets | | Level 1 | | Level 2 | | Level 3 | | Total |

| Exchange Traded Funds | | $1,178,201,718 | | $ - | | $ - | | $1,178,201,718 |

| Money Market Funds | | 9,666,331 | | - | | - | | 9,666,331 |

| Total | | $1,187,868,049 | | $ - | | $ - | | $1,187,868,049 |

| | | | | | | | | | |

| Managed Volatility Fund: | | | | | | | | | |

| Valuation Inputs of Assets | | Level 1 | | Level 2 | | Level 3 | | Total |

| Exchange Traded Funds | | $ 121,320,598 | | $ - | | $ - | | $ 121,320,598 |

| Money Market Funds | | 1,094,892 | | - | | - | | 1,094,892 |

| Total | | $ 122,415,490 | | $ - | | $ - | | $ 122,415,490 |

| | | | | | | | | | |

| Tactical Opportunities Fund: | | | | | | | | | |

| Valuation Inputs of Assets | | Level 1 | | Level 2 | | Level 3 | | Total |

| Exchange Traded Funds | | $ 112,707,359 | | $ - | | $ - | | $ 112,707,359 |

| Money Market Funds | | 2,111,440 | | - | | - | | 2,111,440 |

| Total | | $ 114,818,799 | | $ - | | $ - | | $ 114,818,799 |

| | | | | | | | | | |

| Tactical Rotation Fund: | | | | | | | | | |

| Valuation Inputs of Assets | | Level 1 | | Level 2 | | Level 3 | | Total |

| Exchange Traded Funds | | $ 146,772,261 | | $ - | | $ - | | $ 146,772,261 |

| Money Market Funds | | 3,028,159 | | - | | - | | 3,028,159 |

| Total | | $ 149,800,420 | | $ - | | $ - | | $ 149,800,420 |

| | | | | | | | | | |

| The Funds did not hold any level 3 assets during the fiscal year ended June 30, 2024. |

| | | | | | | | | | |

| The Funds did not invest in derivative instruments during the fiscal year ended June 30, 2024. |

| | | | | | | | | | |

| 4.) INVESTMENT ADVISORY AGREEMENT AND SERVICES AGREEMENT | | | |

The Funds have entered into an investment advisory agreement (“Management Agreement”) with the Advisor. The Advisor manages the investment portfolio of each Fund, subject to the policies adopted by the Trust’s Board of Trustees. Under the Management Agreement, the Advisor, at its own expense and without reimbursement from the Trust, furnishes office space and all necessary office facilities, equipment and executive personnel necessary for managing the assets of each Fund. The Advisor receives an investment management fee equal to 1.25% of each Fund’s average daily net assets up to $100 million, 1.00% of each Fund’s average daily net assets between $100 million and $200 million and 0.90% of each Fund’s average daily net assets in excess of $200 million.

|

| | | | | | | | | | |

For the fiscal year ended June 30, 2024, the Advisor earned management fees in the amounts of $8,600,353, $1,349,873, $1,286,386 and $1,459,321 for the Defensive Bull Fund, Managed Volatility Fund, Tactical Opportunities Fund and Tactical Rotation Fund, respectively. At June 30, 2024, $899,093, $119,095, $112,703 and $140,050 was due to the Advisor from Defensive Bull Fund, Managed Volatility Fund, Tactical Opportunities Fund and Tactical Rotation Fund, respectively.

|

| | | | | | | | | | |

| Additionally, the Funds have a Services Agreement with the Advisor (the “Services Agreement”). Effective October 3, 2023, under the Services Agreement the Advisor receives an additional fee of 0.50% of a Fund’s average daily net assets up to $25 million, and 0.20% of such assets in excess of $25 million for services provided under the agreement and is also obligated to pay the operating expenses of a Fund excluding management fees, brokerage fees and commissions, 12b-1 fees (if any), taxes, borrowing costs (such as (a) interest and (b) dividend expenses on securities sold short), ADR fees, the cost of acquired funds and extraordinary expenses. From November 1, 2021 through October 2, 2023, under the Services Agreement the Advisor received a service fee of 0.50% of each Fund's average daily net assets up to $25 million, 0.20% of each Fund's average daily net assets from $25 million to $100 million, and 0.10% of such assets in excess of $100 million and was obligated to pay the operating expenses of each Fund excluding management fees, brokerage fees and commissions, 12b-1 fees (if any), taxes, borrowing costs (such as (a) interest and (b) dividend expenses on securities sold short), ADR fees, the cost of acquired funds and extraordinary expenses. Prior to November 1, 2021, under the Services Agreement the Advisor received a service fee of 0.65% of each Fund's average daily net assets up to $25 million, 0.35% of each Fund's average daily net assets from $25 million to $100 million, and 0.25% of such assets in excess of $100 million and was obligated to pay the operating expenses of each Fund excluding management fees, brokerage fees and commissions, 12b-1 fees (if any), taxes, borrowing costs (such as (a) interest and (b) dividend expenses on securities sold short), ADR fees, the cost of acquired funds and extraordinary expenses. Additionally, under the Services Agreement the Advisor supervises each Fund's business affairs. The Advisor coordinates for the provision of the services of a Chief Compliance Officer for the Trust with respect to each Fund, executive and administrative services including, but are not limited to, the coordination of all third parties furnishing services to each Fund, review of the books and records of each Fund maintained by such third parties, and such other actions with respect to each Fund as may be necessary in the opinion of the Advisor to perform its duties under the Services Agreement. |

| | | | | | | | | | |

For the fiscal year ended June 30, 2024, the Advisor earned services fees of $1,723,892, $297,386, $280,289 and $317,107 from Defensive Bull Fund, Managed Volatility Fund, Tactical Opportunities Fund and Tactical Rotation Fund, respectively. At June 30, 2024, $197,749, $25,868, $24,590 and $30,059 was due to the Advisor from Defensive Bull Fund, Managed Volatility Fund, Tactical Opportunities Fund and Tactical Rotation Fund, respectively.

|

| | | | | | | | | | |

| 5.) RELATED PARTY TRANSACTIONS | | | | | | | |

Certain officers and a Trustee of the Trust are also officers of Premier Fund Solutions, Inc. (the “Administrator”). These individuals receive benefits from the Administrator resulting from administration fees paid to the Administrator of the Fund by the Adviser.

|

| | | | | | | | | | |

The Trustees who are not interested persons of the Funds were each paid $6,000, for a total of $24,000, in Trustees fees for the fiscal year ended June 30, 2024. Under the Services Agreements, the Advisor pays these fees.

|

| | | | | | | | | | |

| 6.) INVESTMENTS | | | | | | | | | |

For the fiscal year ended June 30, 2024, purchases and sales of investment securities other than U.S. Government obligations and short-term investments were as follows:

|

| | | | | | | | | | |

| | Defensive | Managed | | Tactical | | Tactical |

| | Bull Fund | Volatility Fund | | Opportunities Fund | | Rotation Fund |

| Purchases | $ 14,939,491,361 | $ 611,339,595 | $ 1,631,407,608 | $1,502,222,751 |

| Sales | $ 14,495,819,678 | $ 560,689,837 | $ 1,616,325,756 | $1,447,385,294 |

| | | | | | | | | | |

There were no purchases or sales of U.S. Government obligations.

|

| | | | | | | | | | |

| 7.) CONTROL OWNERSHIP | | | | | | | | | |

The beneficial ownership, either directly or indirectly, of more than 25% of the voting shares of a fund creates a presumption of control of the fund, under section 2(a)(9) of the 1940 Act, as amended. As of June 30, 2024, National Financial Services, LLC (“NFS”), located in New York, New York, and Charles Schwab & Co., Inc. located in San Francisco, California, each held for the benefit of its customers, accounts in excess of 25% of the voting shares of each fund noted below. The Funds do not know whether any underlying accounts of NFS or TD Ameritrade, owned or controlled 25% or more of the voting securities of each Fund.

|

| | | | | | | | | | |

| | | Charles Schwab | | NFS | | | | | |

| Defensive Bull Fund | | 47.32% | | – ** | | | | | |

| Managed Volatility Fund | | 39.94% | | – ** | | | | | |

| Tactical Opportunities Fund | | 39.69% | | 27.52% | | | | | |

| Tactical Rotation Fund | | 45.61% | | 26.34% | | | | | |

| | | | | | | | | | |

| ** Balance under 25% as of June 30, 2024. |

| | | | | | | | | | |

| 8.) TAX MATTERS | | | | | | | | | |

For federal income tax purposes, at June 30, 2024 the cost of securities on a tax basis and the composition of gross unrealized appreciation (the excess of value over tax cost) and depreciation (the excess of tax cost over value) were as follows:

|

| | | | | | | | | | |

| | | Defensive | | Managed | | Tactical | | Tactical |

| | | Bull Fund | | Volatility Fund | | Opportunities Fund | | Rotation Fund |

| Cost of Investments | | $1,193,288,248 | $ 123,241,559 | | $ 117,316,876 | $ 150,491,117 |

| | | | | | | | | | |

| Gross Unrealized Appreciation | | $ - | $ 45,202 | | $ 139,041 | $ 833,626 |

| Gross Unrealized Depreciation | | (5,420,199) | (871,271) | | (2,637,118) | (1,524,323) |

| Net Unrealized Appreciation | | | | | | |

| (Depreciation) on Investments | | $ (5,420,199) | $ (826,069) | | $ (2,498,077) | $ (690,697) |

| | | | | | | | | | |

The tax character of distributions paid during the fiscal years ended June 30, 2024 and June 30, 2023 were as follows:

|

| | | | | | | | | | |

| | | Fiscal Year Ended | | | | Fiscal Year Ended | | | |

| | | June 30, 2024 | | | June 30, 2023 | | |

| Defensive Bull Fund | | | | | | | | | |

| Ordinary Income | | $ 72,611,422 | | | $ 549,021 | | |

| Long-term Capital Gain | | - | | | - | | |

| | | $ 72,611,422 | | | $ 549,021 | | |

| | | | | | | | | | |

| Managed Volatility Fund | | | | | | | | | |

| Ordinary Income | | $ 2,611,519 | | | $ 328,375 | | |

| Tax-Exempt Income | | 568,874 | | | 71,321 | | |

| Long-term Capital Gain | | - | | | - | | |

| | | $ 3,180,393 | | | $ 399,696 | | |

| | | | | | | | | | |

| Tactical Opportunities Fund | | | | | | | | | |

| Ordinary Income | | $ 615,611 | | | $ - | | |

| Long-term Capital Gain | | - | | | - | | |

| | | $ 615,611 | | | $ - | | |

| | | | | | | | | | |

| Tactical Rotation Fund | | | | | | | | | |

| Ordinary Income | | $ 1,154,589 | | | $ 81,288 | | |

| Long-term Capital Gain | | - | | | - | | |

| | | $ 1,154,589 | | | $ 81,288 | | |

| | | | | | | | | | |

As of June 30, 2024, the components of distributable earnings on a tax basis were as follows:

|

| | | | | | | | | | |

| | | | | Defensive Bull Fund | | | | Managed Volatility Fund | |

| Undistributed Ordinary Income | | | $ 138,149,716 | | | $ 1,299,975 | |

| Undistributed Tax-Exempt Income | | - | | | 248,590 | |

| Accumulated Capital and Other Losses | - | | | (477,138) | |

| Unrealized Depreciation - Net | | | (5,420,199) | | | (826,069) | |

| | | | $ 132,729,517 | | | $ 245,358 | |

| | | | | | | | | | |

| | | | | Tactical Opportunities Fund | | | | Tactical Rotation Fund | |

| Undistributed Ordinary Income | | | | $ 4,868,877 | | | | $ 6,946,817 | |

| Unrealized Depreciation - Net | | | | (2,498,077) | | | | (690,697) | |

| | | | | $ 2,370,800 | | | | $ 6,256,120 | |

| | | | | | | | | | |

As of June 30, 2024, the primary differences between book and tax basis unrealized appreciation (depreciation) were attributable to the tax deferral of wash sales.

|

| | | | | | | | | | |

As of June 30, 2024, accumulated capital and other losses include the following:

|

| | | | | | | | | | |

| Managed Volatility Fund | | | | | | | | | |

| Short Term Capital Loss Carryforward | $477,138 | | | | | | | |

| | | | | | | | | | |

Under current tax law, post-October capital losses incurred after October 31 of a fund’s fiscal year end may be deferred and treated as occurring on the first business day of the following fiscal year for tax purposes. Capital loss carryforwards have no expiration. During the fiscal year ended June 30, 2024, Managed Volatility, Tactical Opportunities, and Tactical Rotation utilized available capital loss carryforwards of $1,385,467, $3,881,178, and $1,464,261, respectively.

|

| | | | | | | | | | |

| 9.) LEVERAGED ETF RISKS | | | | | | | | | |

The Funds may invest in leveraged Exchange Traded Funds (“ETFs”). The net asset value and market price of leveraged ETFs are usually more volatile than the value of the tracked index or of other ETFs that do not use leverage. Inverse and leveraged ETFs use investment techniques and financial instruments that may be considered aggressive, including the use of derivative transactions. Most leveraged ETFs are designed to achieve their stated objectives on a daily basis. Their performance over long periods of time can differ significantly from the performance of the underlying index during the same period of time. This effect can be magnified in volatile markets.

|

| | | | | | | | | | |

| 10.) AFFILIATED ISSUER TRANSCTIONS | | | | | | | |

When a Fund holds more than 5% of the outstanding shares of an investment, that investment is consider to be an affiliated investment of the Fund. During the fiscal year ended June 30, 2024, Defensive Bull Fund had the following transactions with affiliated companies:

|

| | | | | | | | | | |

| | | | | Direxion Daily S&P | | | | | |

| | | | | 500 3X Bull Shares | | | | | |

| Security Name | | | | ETF | | | | | |

| Value as of June 30, 2023 | | | | $ 215,078,294 | | | | |

| Purchases | | | | 4,054,311,062 | | | | |

| Sales | | | | (3,945,027,688) | | | | |

| Change in Unrealized Gain | | | | (12,850,251) | | | | |

| Realized Gain | | | | 66,528,406 | | | | |

| Value as of June 30, 2024 | | | | $ 378,039,823 | | | | |

| Shares Balance as of June 30, 2024 | | | 2,588,073 | | | | |

| Dividends | | | | $ 1,320,378 | | | | |

| Capital Gain Distributions | | | | $ - | | | | |

| | | | | | | | | | |

Also, during the fiscal year ended June 30, 2024, Tactical Rotation Fund had the following transactions with affiliated companies:

|

| | | | | | | | | | |

| | | | | Direxion Daily Mid | | | | | |

| | | | | Cap Bull 3X | | | | | |

| Security Name | | | | Shares ETF | | | | | |

| Value as of June 30, 2023 | | | | $ - | | | | |

| Purchases | | | | 69,635,899 | | | | |

| Sales | | | | (53,329,539) | | | | |

| Change in Unrealized Gain | | | | 256,701 | | | | |

| Realized Gain | | | | 1,523,060 | | | | |

| Value as of June 30, 2024 | | | | $ 18,086,121 | | | | |

| Shares Balance as of June 30, 2024 | | | 377,502 | | | | |

| Dividends | | | | $ - | | | | |

| Capital Gain Distributions | | | | $ - | | | | |

| | | | | | | | | | |

There were no affiliated investment transactions in Managed Volatility Fund and Tactical Opportunities Fund during the fiscal year ended June 30, 2024.

|

| | | | | | | | | | |

| 11.) CONTINGENCIES AND COMMITMENTS | | | | | | | |

The Trust indemnifies its officers and the Board for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, each Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. Each Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against a Fund that have not yet occurred. However, based on experience, the risk of loss due to these warranties and indemnities appears to be remote.

|

| | | | | | | | | | |

| 12.) SUBSEQUENT EVENTS | | | | | | | | | |

Subsequent events after the date of the Statements of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has concluded that there is no impact requiring adjustment to or disclosure in the financial statements.

|

| Item 11. Statement Regarding Basis for Approval of Investment Advisory Contract. | |

| | | | | | | | | | |

| On June 21, 2024, the Board of Trustees (the “Board” or the “Trustees”) considered the renewal of the Management Agreement (the “Management Agreement”) between Potomac Fund Management, Inc. (“Potomac”) and the Trust with respect to the Conquer Risk Funds. In approving the continuation of the Management Agreement, the Board considered and evaluated the following factors: (i) the nature, extent and quality of the services provided by Potomac to the Conquer Risk Funds; (ii) the investment performance of the Conquer Risk Funds; (iii) the cost of the services to be provided and the profits to be realized by Potomac from the relationship with the Conquer Risk Funds; (iv) the extent to which economies of scale will be realized as the Conquer Risk Funds grow and whether the fee levels reflect these economies of scale to the benefit of shareholders; and (v) Potomac’s practices regarding possible conflicts of interest. |

| | | | | | | | | | |

| In assessing these factors and reaching its decisions, the Board took into consideration information furnished for the Board’s review and consideration throughout the year at its regular Board meetings, as well as information specifically prepared and/or presented in connection with the annual renewal process. The Board also considered the presentation made by a representative of Potomac at the Meeting. The Board requested and was provided with information and reports relevant to the annual renewal of the Management Agreement, as well as information relevant to their consideration of the Management Agreement including: (i) information regarding the services and support provided to the Conquer Risk Funds and their shareholders by Potomac; (ii) assessments of the investment performance of the Conquer Risk Funds by the portfolio manager from Potomac; (iii) commentary on the reasons for the performance; (iv) presentations addressing Potomac’s investment philosophy, investment strategy, personnel and operations; (v) compliance and audit related information concerning the Conquer Risk Funds and Potomac; (vi) disclosure information contained in the registration statement of the Trust and the Form ADV of Potomac; and (vii) a memorandum from legal counsel that summarized the fiduciary duties and responsibilities of the Board in reviewing and approving the Management Agreement, including the material factors set forth above and the types of information included in each factor that should be considered by the Board in order to make an informed decision. The Board also requested and received various informational materials including, without limitation: (i) documents containing information about Potomac, including financial information, a description of personnel and the services provided to the Conquer Risk Funds, information on investment advice, performance, summaries of the Conquer Risk Funds’ expenses, compliance program, current legal matters, and other general information; (ii) comparative expense and performance information for other mutual funds with strategies similar to the Conquer Risk Funds; (iii) the anticipated effect of size on the Conquer Risk Funds’ performance and expenses; and (iv) benefits to be realized by Potomac from its relationship with the Conquer Risk Funds. The Board did not identify any particular information that was most relevant to its consideration to approve the Management Agreement and each Trustee may have afforded a different weight to the various factors. |

| |

| 1. The nature, extent, and quality of the services provided by Potomac. |

| | | | | | | | | | |

| In this regard, the Board considered the responsibilities of Potomac under the Management Agreement. The Board reviewed the services provided by Potomac to the Conquer Risk Funds including, without limitation, the procedures for formulating investment recommendations and assuring compliance with the Conquer Risk Funds’ investment objectives and limitations; Potomac’s coordination of services for the Conquer Risk Funds among the service providers; and the efforts of Potomac to promote the Conquer Risk Funds and grow assets. The Board considered: Potomac’s staffing, personnel, and methods of operating; the education and experience of its personnel; and its compliance programs, policies, and procedures. After reviewing the foregoing and further information from Potomac, the Board concluded that the quality, extent, and nature of the services provided by Potomac was satisfactory and adequate for the Conquer Risk Funds. |

| | | | | | | | | | |

| 2. The investment performance of the Conquer Risk Funds and Potomac. |

| | | | | | | | | | |

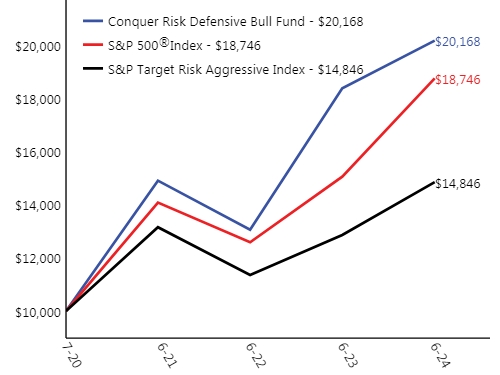

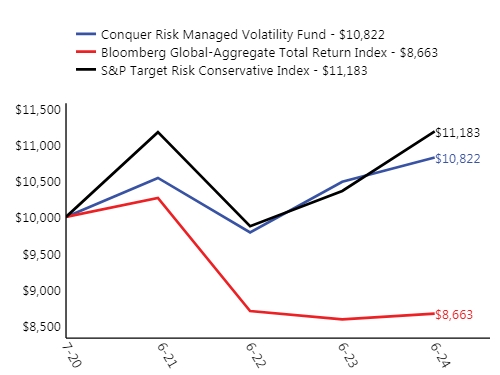

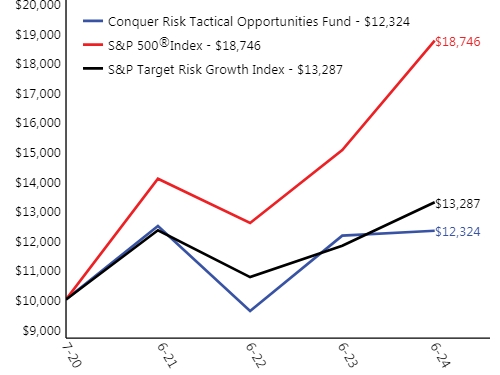

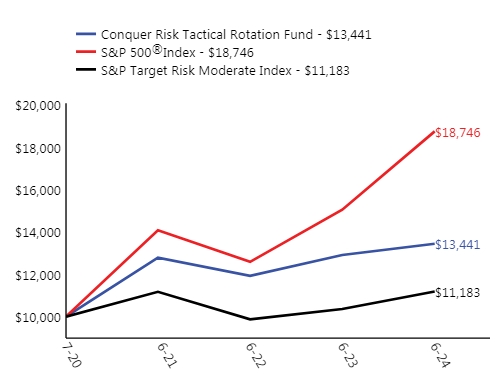

| In considering the investment performance of the Conquer Risk Funds and Potomac, the Trustees compared the performance of the Conquer Risk Funds with the performance of funds with similar objectives managed by other investment advisers, as well as with aggregated peer group data. As to the performance of the Conquer Risk Funds, the Trustees compared each Conquer Risk Fund’s performance to its Morningstar category, (each, a “Category”) and to a group of funds of similar size, style and objective, derived from the Category (the “Peer Group”). The performance data from the Category and the Peer Group covered periods ended March 31, 2024. The Trustees noted that with respect to the Conquer Risk Defensive Bull Fund, for the 1-year period ended March 31, 2024, the Fund had underperformed the average of its Category (US Fund Tactical Allocation Funds), Peer Group, S&P Target Risk Aggressive Index and the S&P 500 Index. For the 3-year period ended March 31, 2024, the Fund had outperformed the average of its Category, Peer Group, S&P Target Risk Aggressive Index, and had underperformed compared to the S&P 500 Index. The Trustees noted that with respect to the Conquer Risk Managed Volatility Fund, for the 1-year period ended March 31, 2024, the Fund had underperformed the average of its Category (US Fund Multisector Bond Funds), Peer Group, S&P Target Risk Conservative Index and had outperformed compared to the Bloomberg Global-Aggregate Total Return Index. For the 3-year period ended March 31, 2024, the Fund had outperformed the average of its Category, Peer Group, S&P Target Risk Conservative Index and Bloomberg Global-Aggregate Total Return Index. The Trustees noted that with respect to the Conquer Risk Tactical Opportunities Fund, for the 1-year and 3-year periods ended March 31, 2024, the Fund had underperformed the average of its Category (US Fund Tactical Allocation Funds), Peer Group, S&P Target Risk Growth Index and S&P 500 Index. The Trustees noted that with respect to the Conquer Risk Tactical Rotation Fund, for the 1-year and 3-year periods ended March 31, 2024, the Fund had underperformed the average of its Category (US Fund Tactical Allocation Funds), Peer Group, S&P Target Risk Moderate Index and S&P 500 Index. The Trustees reflected on the management style utilized for each of the Conquer Risk Funds and noted the positive performance of each of the Conquer Risk Funds in a difficult market environment. After reviewing and discussing the investment performance of each of the Conquer Risk Funds further, Potomac’s experience managing the Conquer Risk Funds, and other relevant factors, the Board concluded, in light of all the facts and circumstances, that the investment performance of each of the Conquer Risk Funds and Potomac was satisfactory. |

| | | | | | | | | | |

| 3. The costs of the services to be provided and the profits to be realized by Potomac from the relationship with the Conquer Risk Funds. |

| | | | | | | | | | |

| In considering the costs of the services to be provided and profits to be realized by Potomac from the relationship with the Conquer Risk Funds, the Trustees considered: (1) Potomac’s financial condition and the level of commitment to the Conquer Risk Funds and Potomac by the principals of Potomac; (2) the asset level of the Conquer Risk Funds; (3) the overall expenses of the Conquer Risk Funds; and (4) the nature and frequency of advisory fee payments. The Trustees reviewed information provided by Potomac regarding its profits associated with managing the Conquer Risk Funds. The Trustees also considered potential benefits for Potomac in managing the Conquer Risk Funds, noting it was created to provide an efficient structure for clients of Potomac to access the investment strategy. The Trustees then compared the fees and expenses of the Conquer Risk Funds (including the management fee) to other comparable mutual funds. The Trustees reviewed the fees under the Management Agreement and compared them to the average management fee of the Category and Peer Group, noting that each of the Conquer Risk Funds’ management fee was higher than the average management fee for its Category and Peer Group, respectively. The Trustees also reviewed the net expense ratios of each Conquer Risk Fund and compared them to the average net expense ratio of the Category and Peer Group, noting that each of the Conquer Risk Funds’ net expense ratio was higher than the average net expense ratio of its Category and Peer Group, with the exception of the Conquer Risk Defensive Bull Fund’s net expense ratio, which was lower than the average net expense ratio of its Category and Peer Group. The Board also noted that each of the Conquer Risk Funds’ management fees and expense ratios were within the range of funds in its Category and Peer Group. The Board noted that Potomac doesn’t offer similar strategies as employed by the Conquer Risk Funds to non-mutual fund clients. The Trustees also considered that under the contractual arrangements with Potomac, it was required to pay most of the Conquer Risk Funds’ operating expenses out of its assets. The Trustees also considered a profitability analysis of Potomac’s relationship with the Fund. Based on the foregoing, the Board concluded that the fee arrangements to Potomac and the profitability of Potomac, considering all the facts and circumstances, were fair and reasonable in relation to the nature and quality of the services provided by Potomac. |

| | | | | | | | | | |

| 4. The extent to which economies of scale would be realized as the Conquer Risk Funds grow and whether advisory fee levels reflect these economies of scale for the benefit of the Conquer Risk Funds’ investors. |

| | | | | | | | | | |

| In this regard, the Board considered the Conquer Risk Funds’ fee arrangements with Potomac. The Board discussed the breakpoints included in the Management Agreement and the Services Agreement and the impact on shareholders. It was further noted that under the Services Agreement, Potomac is obligated to pay certain of the Conquer Risk Funds’ operating expenses which had the effect of limiting the overall fees paid by each Fund. Following further discussion of the Conquer Risk Funds’ projected asset levels, expectations for growth, and levels of fees, the Board determined that each of the Conquer Risk Fund’s fee arrangement with Potomac was fair and reasonable and reasonable in relation to the nature and quality of the services to be provided by Potomac. |

| | | | | | | | | | |

| 5. Possible conflicts of interest and benefits to Potomac. | | | | |

| | | | | | | | | | |

| In evaluating the possibility for conflicts of interest, the Board considered such matters as: the experience and ability of the advisory personnel assigned to the Conquer Risk Funds; the basis of decisions to buy or sell securities for the Conquer Risk Funds; the method for bunching of portfolio securities transactions; and the substance and administration of Potomac’s Code of Ethics and other relevant policies described in Potomac’s Form ADV and compliance manual. Following further consideration and discussion, the Board indicated that Potomac’s standards and practices relating to the identification and mitigation of potential conflicts of interest were satisfactory. The Trustees noted Potomac’s utilization of soft dollars and the benefits that could be derived by the Funds. |

| | | | | | | | | | |

| After further discussion and careful review by the Board, the Board determined that the compensation payable under the Management Agreement was fair, reasonable and within a range of what could have been negotiated at arms-length in light of all the surrounding circumstances, and they approved the Management Agreement for another one-year term. |