UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-10041 |

|

JNL Investors Series Trust |

(Exact name of registrant as specified in charter) |

|

1 Corporate Way, Lansing, Michigan | | 48951 |

(Address of principal executive offices) | | (Zip code) |

|

225 West Wacker Drive, Suite 1200, Chicago, Illinois 60606 |

(Mailing address) |

|

Steven J. Fredricks Jackson National Asset Management, LLC 225 West Wacker Drive, Suite 1200 Chicago, Illinois 60606 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (312) 338-5800 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2014 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. §3507.

Item 1. Report to Shareholders.

ANNUAL REPORT

December 31, 2014

· JNL® Investors Series Trust

This report is for the general information of qualified and non-qualified plan participants, as well as contract/policyowners of the PerspectiveSM, Perspective II®, Perspective AdvisorsSM, Perspective Advisors IISM, PerspectiveSM L Series, CuriangardSM, Perspective AdvantageSM, Perspective Focus®, Perspective Investor VUL®, Ultimate Investor® VUL, Jackson AdvisorSM VUL, Defined Strategies®, Fifth Third Perspective, Retirement Latitudes®, Perspective (New York), Perspective II (New York), Perspective Advisors II (New York), Perspective L Series (New York), Curiangard (New York), Perspective Advisors (New York), Perspective Focus (New York) and Perspective Investor VUL (New York). Not all the portfolios are available in all of the products. Jackson® is the marketing name for Jackson National Life Insurance Company® (Home Office: Lansing, Michigan) and Jackson National Life Insurance Company of New York® (Home Office: Purchase, New York).

JNL/PPM America Funds

PPM America, Inc. (Unaudited)

Market Summary: U.S. fixed income performed resiliently during the year, and in stark contrast with 2013, higher quality credits generally outperformed lower quality segments. For instance, the Barclays U.S. Aggregate Bond Index advanced 5.97%, and the Barclays U.S. Corporate Investment Grade Index gained 7.46%, while the Bank of America ("BofA") Merrill Lynch U.S. High Yield Master II Index returned 2.51%, and the S&P/LSTA Leveraged Loan Index delivered 1.60%. For most of the year, interest rates drifted lower, aiding higher quality fixed income's performance. Compared to 2013 year end, five and 10-year U.S. Treasury yields ended -10 basis points ("bps") and -87 bps lower, respectively.

Slowing global growth, heightened geopolitical tensions, fears of deflation and plummeting oil prices were among the factors that contributed to investors' demand for the relative safety of U.S. Treasuries. These issues pressured Treasury yields downward despite the conclusion of quantitative easing, improving U.S. economic health and the anticipation of an increase in the federal funds rate in the coming year. However, in December third quarter gross domestic

product was revised upward to 5%, the biggest quarterly gain since 2006, reinforcing previous indications of domestic economic improvement and encouraging short term rates upward.

Though low interest rates provided a favorable tailwind for U.S. fixed income assets, corporate bond yields failed to follow Treasury yields lower, resulting in wider credit spreads. Investment grade and high yield corporate credit spreads increased 14 bps and 104 bps, respectively, during the year as measured by Barclays U.S. Credit Index and BofA Merrill Lynch U.S. High Yield Master II Index. High yield spread widening was exacerbated by a structural reduction in market liquidity, which diminished broker dealers' ability to behave as market makers. While wider spreads reflected investors' more cautious sentiment toward risk, many credit supportive themes remained prevalent during the year. These included reasonable corporate credit metrics, low borrowing costs and the absence of a material increase in defaults.

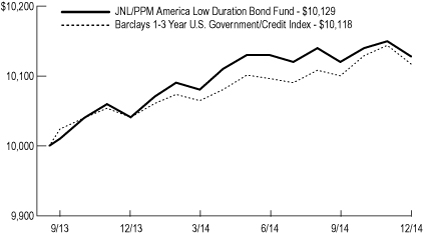

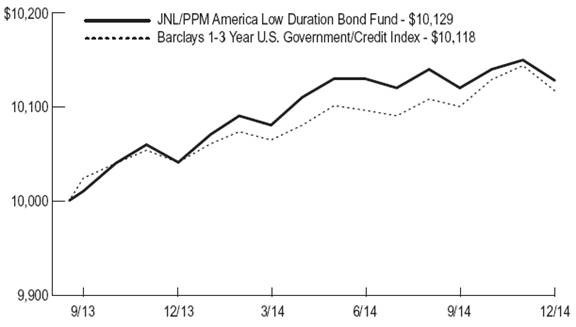

JNL/PPM America Low Duration Bond Fund

Portfolio Composition†:

Financials | | | 30.4 | % | |

Non-U.S. Government Agency ABS | | | 28.5 | | |

Government Securities | | | 13.4 | | |

U.S. Government Agency MBS | | | 3.4 | | |

Consumer Discretionary | | | 3.4 | | |

Health Care | | | 3.2 | | |

Consumer Staples | | | 3.2 | | |

Industrials | | | 2.8 | | |

Materials | | | 2.1 | | |

Utilities | | | 1.7 | | |

Telecommunication Services | | | 1.3 | | |

Information Technology | | | 0.7 | | |

Energy | | | 0.2 | | |

Short Term Investments | | | 5.7 | | |

Total Investments | | | 100.0 | % | |

†Total Investments as of December 31, 2014

Portfolio Manager Commentary: For the year ended December 31, 2014, JNL/PPM America Low Duration Bond Fund outperformed its benchmark by posting a return of 0.88% for

Class A shares, compared to 0.77% for the Barclays 1-3 Year U.S. Government/Credit Index.

The investment results were positively impacted primarily by an overweight to corporate bonds and, to a lesser degree, exposure to asset, commercial mortgage and mortgage backed securities. Though broad investment grade and high yield corporate credit spreads ended the year wider, the Fund's allocation to these asset classes positively contributed to performance results. The Fund's underexposure to shorter dated U.S. Treasuries also supported relative outperformance, as front end Treasury yields rose during the year in response to better economic data readings. Furthermore, in light of heightened global uncertainties, demand for short term fixed income strategies was robust, and despite U.S. economic progress, the U.S. Federal Reserve ("Fed") refrained from raising the Fed funds rate.

We expect moderate U.S. growth, in the 2-3% range, to persist over the next twelve months and that inflation is likely to remain muted, particularly

given the sharp decline in oil prices. Our view is that shorter dated interest rates are biased upward in the coming year; however, we do not anticipate a material acceleration. Although U.S. economic data continues to improve, we think that the Fed will take stagnant global growth and ongoing geopolitical risks into consideration and exercise caution when it begins its tightening cycle. Furthermore, we think that the aforementioned issues can help support demand for the asset class, as ensuing volatility can be reasonably expected to materialize. We anticipate remaining overweight in credit securities, rather than Treasuries. Specifically, we have trimmed down our asset backed securities and Treasury positions in favor of corporates, as valuations (i.e., credit spreads) are slightly more attractive, and credit fundamentals remain healthy. We are also closely monitoring the dislocations in the high yield market and may selectively add credits with compelling risk/return potential at attractive entry points.

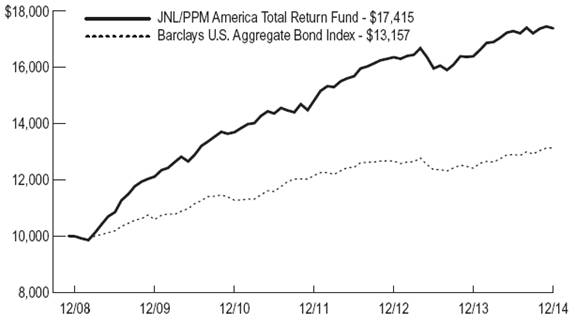

JNL/PPM America Total Return Fund

Portfolio Composition†:

Financials | | | 26.4 | % | |

U.S. Government Agency MBS | | | 17.3 | | |

Government Securities | | | 11.2 | | |

Energy | | | 7.2 | | |

Consumer Discretionary | | | 5.7 | | |

Non-U.S. Government Agency ABS | | | 5.6 | | |

Health Care | | | 4.4 | | |

Materials | | | 3.9 | | |

Utilities | | | 3.4 | | |

Industrials | | | 3.0 | | |

Telecommunication Services | | | 2.8 | | |

Consumer Staples | | | 1.5 | | |

Information Technology | | | 1.3 | | |

Short Term Investments | | | 6.3 | | |

Total Investments | | | 100.0 | % | |

†Total Investments as of December 31, 2014

Portfolio Manager Commentary: For the year ended December 31, 2014, JNL/PPM America Total Return Fund outperformed its benchmark by posting a return of 6.06% for Class A shares,

compared to 5.97% for the Barclays U.S. Aggregate Bond Index. The Fund also outperformed its Morningstar peer group average return of 5.85%, placing it in the 20th percentile of the U.S. Open Ended Intermediate Term Bond category.

Though broad credit spreads widened during the year, the Fund outperformed relative to the index. This was primarily due to the Fund's individual security selection within its overweight to corporate bonds. Within corporates, the Fund's allocation to high yield bonds detracted from results, whereas banking and health care were strong contributors. Performance was also positively influenced by the Fund's underexposure to shorter dated U.S. Treasuries, as front end yields rose during 2014 in response to improving U.S. economic data. Underweight positioning to mortgage-backed securities, sovereigns, and agency debt negatively impacted performance.

We are optimistic toward the U.S. economic growth outlook over the next twelve to twenty-four months; however, we are also cognizant of potential

reverberations from various international factors, including slowing global growth and diverging central bank policies. While we think that firmer U.S. economic data could pave the way for the U.S. Federal Reserve to begin its tightening cycle, we believe that, in order to avoid derailing economic progress, it will likely exercise caution in doing so. Although total return potential is likely to be relatively subdued over the coming year, we believe there is modest room for spread tightening. As a result, we are maintaining our overweight to corporates and underweight to Treasuries, as we think the fundamental credit environment is still supportive. Within the corporate space, we have increased our positioning in the pharmaceutical sector, as merger and acquisition activity and shareholder activism have resulted in compelling valuations for certain credits. Furthermore, we are closely monitoring the dislocations and opportunities within high yield corporates and could selectively add those credits we find compelling.

JNL/PPM America Funds (continued)

PPM America, Inc. (Unaudited)

JNL/PPM America Low Duration Bond Fund

Average Annual Total Returns | |

| 1 Year | | | 0.88 | % | |

Since Inception | | | 1.00 | % | |

(Inception date September 16, 2013) | |

JNL/PPM America Total Return Fund

Average Annual Total Returns | |

| 1 Year | | | 6.06 | % | |

| 5 Year | | | 7.52 | % | |

Since Inception | | | 9.68 | % | |

(Inception date December 29, 2008) | |

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but not do not reflect the deduction of insurance charges.

| JNL/PPM America Funds |

PPM America, Inc. (Unaudited) |

Market Summary: U.S. fixed income performed resiliently during the year, and in stark contrast with 2013, higher quality credits generally outperformed lower quality segments. For instance, the Barclays U.S. Aggregate Bond Index advanced 5.97%, and the Barclays U.S. Corporate Investment Grade Index gained 7.46%, while the Bank of America (“BofA”) Merrill Lynch U.S. High Yield Master II Index returned 2.51%, and the S&P/LSTA Leveraged Loan Index delivered 1.60%. For most of the year, interest rates drifted lower, aiding higher quality fixed income’s performance. Compared to 2013 year end, five and 10-year U.S. Treasury yields ended -10 basis points (“bps”) and -87 bps lower, respectively.

Slowing global growth, heightened geopolitical tensions, fears of deflation and plummeting oil prices were among the factors that contributed to investors’ demand for the relative safety of U.S. Treasuries. These issues pressured Treasury yields downward despite the conclusion of quantitative easing, improving U.S. economic health and the anticipation of an increase in the federal funds rate in the coming year. However, in December third quarter gross domestic product was revised upward to 5%, the biggest quarterly gain since 2006, reinforcing previous indications of domestic economic improvement and encouraging short term rates upward.

Though low interest rates provided a favorable tailwind for U.S. fixed income assets, corporate bond yields failed to follow Treasury yields lower, resulting in wider credit spreads. Investment grade and high yield corporate credit spreads increased 14 bps and 104 bps, respectively, during the year as measured by Barclays U.S. Credit Index and BofA Merrill Lynch U.S. High Yield Master II Index. High yield spread widening was exacerbated by a structural reduction in market liquidity, which diminished broker dealers’ ability to behave as market makers. While wider spreads reflected investors’ more cautious sentiment toward risk, many credit supportive themes remained prevalent during the year. These included reasonable corporate credit metrics, low borrowing costs and the absence of a material increase in defaults.

JNL/PPM America Low Duration Bond Fund

Portfolio Composition†: | | | |

Financials | | 30.4 | % |

Non-U.S. Government Agency ABS | | 28.5 | |

Government Securities | | 13.4 | |

U.S. Government Agency MBS | | 3.4 | |

Consumer Discretionary | | 3.4 | |

Health Care | | 3.2 | |

Consumer Staples | | 3.2 | |

Industrials | | 2.8 | |

Materials | | 2.1 | |

Utilities | | 1.7 | |

Telecommunication Services | | 1.3 | |

Information Technology | | 0.7 | |

Energy | | 0.2 | |

Short Term Investments | | 5.7 | |

Total Investments | | 100.0 | % |

† Total Investments as of December 31, 2014

Portfolio Manager Commentary: For the year ended December 31, 2014, JNL/PPM America Low Duration Bond Fund outperformed its benchmark by posting a return of 0.88% for Class A shares, compared to 0.77% for the Barclays 1-3 Year U.S. Government/Credit Index.

The investment results were positively impacted primarily by an overweight to corporate bonds and, to a lesser degree, exposure to asset, commercial mortgage and mortgage backed securities. Though broad investment grade and high yield corporate credit spreads ended the year wider, the Fund’s allocation to these asset classes positively contributed to performance results. The Fund’s underexposure to shorter dated U.S. Treasuries also supported relative outperformance, as front end Treasury yields rose during the year in response to better economic data readings. Furthermore, in light of heightened global uncertainties, demand for short term fixed income strategies was robust, and despite U.S. economic progress, the U.S. Federal Reserve (“Fed”) refrained from raising the Fed funds rate.

We expect moderate U.S. growth, in the 2-3% range, to persist over the next twelve months and that inflation is likely to remain muted, particularly given the sharp decline in oil prices. Our view is that shorter dated interest rates are biased upward in the coming year; however, we do not anticipate a material acceleration. Although U.S. economic data continues to improve, we think that the Fed will take stagnant global growth and ongoing geopolitical risks into consideration and exercise caution when it begins its tightening cycle. Furthermore, we think that the aforementioned issues can help support demand for the asset class, as ensuing volatility can be reasonably expected to materialize. We anticipate remaining overweight in credit securities, rather than Treasuries. Specifically, we have trimmed down our asset backed securities and Treasury positions in favor of corporates, as valuations (i.e., credit spreads) are slightly more attractive, and credit fundamentals remain healthy. We are also closely monitoring the dislocations in the high yield market and may selectively add credits with compelling risk/return potential at attractive entry points.

JNL/PPM America Total Return Fund

Portfolio Composition†: | | | |

Financials | | 26.4 | % |

U.S. Government Agency MBS | | 17.3 | |

Government Securities | | 11.2 | |

Energy | | 7.2 | |

Consumer Discretionary | | 5.7 | |

Non-U.S. Government Agency ABS | | 5.6 | |

Health Care | | 4.4 | |

Materials | | 3.9 | |

Utilities | | 3.4 | |

Industrials | | 3.0 | |

Telecommunication Services | | 2.8 | |

Consumer Staples | | 1.5 | |

Information Technology | | 1.3 | |

Short Term Investments | | 6.3 | |

Total Investments | | 100.0 | % |

† Total Investments as of December 31, 2014

Portfolio Manager Commentary: For the year ended December 31, 2014, JNL/PPM America Total Return Fund outperformed its benchmark by posting a return of 6.06% for Class A shares, compared to 5.97% for the Barclays U.S. Aggregate Bond Index. The Fund also outperformed its Morningstar peer group average return of 5.85%, placing it in the 20th percentile of the U.S. Open Ended Intermediate Term Bond category.

Though broad credit spreads widened during the year, the Fund outperformed relative to the index. This was primarily due to the Fund’s individual security selection within its overweight to corporate bonds. Within corporates, the Fund’s allocation to high yield bonds detracted from results, whereas banking and health care were strong contributors. Performance was also positively influenced by the Fund’s underexposure to shorter dated U.S. Treasuries, as front end yields rose during 2014 in response to improving U.S. economic data. Underweight positioning to mortgage-backed securities, sovereigns, and agency debt negatively impacted performance.

We are optimistic toward the U.S. economic growth outlook over the next twelve to twenty-four months; however, we are also cognizant of potential reverberations from various international factors, including slowing global growth and diverging central bank policies. While we think that firmer U.S. economic data could pave the way for the U.S. Federal Reserve to begin its tightening cycle, we believe that, in order to avoid derailing economic progress, it will likely exercise caution in doing so. Although total return potential is likely to be relatively subdued over the coming year, we believe there is modest room for spread tightening. As a result, we are maintaining our overweight to corporates and underweight to Treasuries, as we think the fundamental credit environment is still supportive. Within the corporate space, we have increased our positioning in the pharmaceutical sector, as merger and acquisition activity and shareholder activism have resulted in compelling valuations for certain credits. Furthermore, we are closely monitoring the dislocations and opportunities within high yield corporates and could selectively add those credits we find compelling.

JNL/PPM America Low Duration Bond Fund

Average Annual Total Returns | | | |

1 Year | | 0.88 | % |

Since Inception

(Inception date September 16, 2013) | | 1.00 | % |

JNL/PPM America Total Return Fund

Average Annual Total Returns | | | |

1 Year | | 6.06 | % |

5 Year | | 7.52 | % |

Since Inception

(Inception date December 29, 2008) | | 9.68 | % |

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Performance numbers are net of all Fund operating expenses, but not do not reflect the deduction of insurance charges.

JNL Investors Series Trust

Schedules of Investments

December 31, 2014

| | Shares/ Par† | | Value | |

JNL/PPM America Low Duration Bond Fund | | | | | |

NON-U.S. GOVERNMENT AGENCY ASSET-BACKED SECURITIES - 29.9% | | | | | |

AEP Texas Central Transition Funding III LLC | | | | | |

0.88%, 12/01/17 | | $ | 645,070 | | $ | 644,621 | |

1.98%, 06/01/20 | | 1,250,000 | | 1,248,079 | |

American Express Credit Account Master Trust | | | | | |

0.99%, 08/17/15 | | 3,300,000 | | 3,306,795 | |

0.77%, 10/15/15 | | 5,100,000 | | 5,101,504 | |

1.26%, 06/15/17 | | 1,340,000 | | 1,337,106 | |

American Express Issuance Trust II, 0.61%, 03/15/18 (a) | | 1,105,000 | | 1,099,682 | |

AmeriCredit Automobile Receivables Trust | | | | | |

1.78%, 05/08/15 | | 525,000 | | 526,622 | |

2.67%, 12/08/15 | | 330,000 | | 334,033 | |

1.12%, 01/08/16 | | 1,210,000 | | 1,213,779 | |

2.85%, 08/08/16 | | 555,590 | | 557,137 | |

4.20%, 11/08/16 | | 183,000 | | 184,126 | |

2.86%, 01/09/17 | | 775,466 | | 779,580 | |

1.31%, 11/08/17 | | 1,423,000 | | 1,427,424 | |

0.96%, 04/09/18 | | 400,000 | | 400,477 | |

1.79%, 03/08/19 | | 1,825,000 | | 1,822,536 | |

2.38%, 06/10/19 | | 219,000 | | 220,872 | |

Bank of America Credit Card Trust, 5.17%, 06/15/19 | | 1,500,000 | | 1,620,637 | |

Bank of The West Auto Trust, 1.65%, 10/15/18 (b) | | 1,022,000 | | 1,020,098 | |

Bear Stearns Commercial Mortgage Securities REMIC | | | | | |

5.74%, 09/11/17 (a) | | 489,000 | | 534,911 | |

5.69%, 06/11/50 (a) | | 2,737,000 | | 2,969,440 | |

Bear Stearns Commercial Mortgage Securities Trust REMIC, 5.47%, 01/12/45 (a) | | 1,079,831 | | 1,156,939 | |

California Republic Auto Receivables Trust | | | | | |

1.09%, 04/17/17 | | 2,500,000 | | 2,496,252 | |

1.23%, 10/16/17 | | 2,179,572 | | 2,187,464 | |

1.57%, 08/15/18 | | 3,000,000 | | 2,991,825 | |

1.79%, 10/15/18 | | 1,458,000 | | 1,458,464 | |

Capital One Multi-Asset Execution Trust | | | | | |

0.96%, 11/15/16 | | 5,000,000 | | 4,980,940 | |

1.48%, 09/15/17 | | 3,000,000 | | 3,001,191 | |

CarMax Auto Owner Trust | | | | | |

2.08%, 03/15/18 | | 585,000 | | 593,267 | |

0.97%, 04/16/18 | | 3,000,000 | | 3,006,273 | |

1.91%, 03/15/19 | | 200,000 | | 201,017 | |

1.16%, 06/17/19 | | 1,826,000 | | 1,819,673 | |

Centerpoint Energy Transition Bond Co. III LLC, 4.19%, 02/01/17 | | 544,624 | | 560,027 | |

CenterPoint Energy Transition Bond Co. IV LLC, 0.90%, 04/15/17 | | 6,523,135 | | 6,532,535 | |

Chase Issuance Trust | | | | | |

0.41%, 02/15/17 (a) | | 5,000,000 | | 4,968,310 | |

0.62%, 02/15/17 (a) | | 3,000,000 | | 2,982,438 | |

1.58%, 08/15/19 | | 500,000 | | 489,347 | |

REMIC, 1.36%, 05/15/15 (a) | | 500,000 | | 501,760 | |

Chrysler Capital Auto Receivables Trust, 0.83%, 09/17/18 (b) | | 3,296,000 | | 3,292,229 | |

Citibank Credit Card Issuance Trust | | | | | |

1.02%, 02/22/17 | | 8,000,000 | | 7,971,584 | |

5.50%, 03/24/17 | | 1,375,000 | | 1,390,108 | |

Citigroup Commercial Mortgage Trust REMIC, 5.43%, 10/15/49 | | 4,000,000 | | 4,235,320 | |

Citigroup/Deutsche Bank Commercial Mortgage Trust REMIC, 5.23%, 10/15/15 (a) | | 2,102,000 | | 2,157,283 | |

CNH Equipment Trust | | | | | |

2.04%, 10/17/16 | | 547,876 | | 548,193 | |

1.01%, 02/15/17 | | 6,625,000 | | 6,599,149 | |

0.99%, 11/15/18 | | 1,960,000 | | 1,944,540 | |

1.50%, 05/15/20 | | 325,000 | | 323,515 | |

COMM Mortgage Trust REMIC, 0.72%, 09/10/17 | | 875,607 | | 872,971 | |

Credit Suisse First Boston Mortgage Securities Corp. REMIC, 5.58%, 05/15/36 (a) | | 240,671 | | 242,352 | |

Dell Equipment Finance Trust | | | | | |

0.94%, 06/22/20 (b) | | 290,000 | | 289,700 | |

1.36%, 06/22/20 (b) | | 100,000 | | 99,891 | |

Discover Card Execution Note Trust | | | | | |

0.61%, 11/16/15 (a) | | 1,200,000 | | 1,198,757 | |

1.04%, 10/17/16 | | 5,000,000 | | 4,994,460 | |

1.39%, 10/16/17 | | 2,000,000 | | 1,996,118 | |

Ford Credit Auto Owner Trust | | | | | |

3.21%, 04/15/15 | | 119,000 | | 120,012 | |

2.27%, 10/15/15 | | 2,000,000 | | 2,022,334 | |

1.95%, 04/15/18 | | 1,549,000 | | 1,546,010 | |

1.54%, 03/15/19 | | 2,500,000 | | 2,487,077 | |

1.71%, 05/15/19 | | 415,000 | | 415,875 | |

1.90%, 09/15/19 | | 185,000 | | 185,549 | |

1.97%, 04/15/20 | | 553,000 | | 551,424 | |

Ford Credit Floorplan Master Owner Trust | | | | | |

1.50%, 09/15/16 | | 1,000,000 | | 1,008,261 | |

1.20%, 02/15/17 | | 3,111,000 | | 3,102,753 | |

GE Equipment Midticket LLC | | | | | |

0.95%, 04/22/16 | | 2,000,000 | | 2,005,554 | |

1.14%, 05/22/18 | | 3,000,000 | | 2,998,149 | |

GE Equipment Small Ticket LLC, 1.39%, 11/25/16 (b) | | 3,520,000 | | 3,545,238 | |

GE Equipment Transportation LLC | | | | | |

0.92%, 09/24/16 | | 850,000 | | 851,839 | |

0.97%, 04/23/17 | | 1,112,000 | | 1,111,039 | |

1.23%, 04/24/17 | | 515,000 | | 513,139 | |

1.30%, 08/24/17 | | 5,000,000 | | 5,005,565 | |

1.48%, 01/23/18 | | 801,000 | | 800,415 | |

GreatAmerica Leasing Receivables Funding LLC | | | | | |

0.61%, 11/15/15 (b) | | 1,676,435 | | 1,676,539 | |

0.78%, 12/15/15 (b) | | 1,105,732 | | 1,106,616 | |

1.16%, 12/15/16 (b) | | 1,458,000 | | 1,461,469 | |

0.89%, 01/15/17 (b) | | 3,846,000 | | 3,843,981 | |

1.47%, 01/15/18 (b) | | 545,000 | | 542,484 | |

Harley-Davidson Motorcycle Trust, 1.31%, 03/15/15 | | 4,680,705 | | 4,688,957 | |

Huntington Auto Trust | | | | | |

1.71%, 12/15/15 | | 200,000 | | 201,556 | |

1.07%, 06/15/16 | | 275,000 | | 275,381 | |

Hyundai Auto Receivables Trust | | | | | |

1.35%, 04/15/17 | | 300,000 | | 299,773 | |

2.10%, 06/15/17 | | 2,148,000 | | 2,174,390 | |

1.39%, 03/15/18 | | 395,000 | | 395,880 | |

0.79%, 07/16/18 | | 1,935,000 | | 1,932,428 | |

0.90%, 12/17/18 | | 2,988,000 | | 2,979,616 | |

John Deere Owner Trust, 1.07%, 11/15/17 | | 3,500,000 | | 3,487,354 | |

JPMorgan Mortgage Trust REMIC, 3.00%, 10/25/26 (a) (b) | | 2,422,211 | | 2,486,550 | |

LB-UBS Commercial Mortgage Trust REMIC, 5.06%, 09/15/40 (a) | | 575,000 | | 585,445 | |

MMCA Auto Owner Trust | | | | | |

1.57%, 08/15/17 (b) | | 258,851 | | 260,069 | |

1.21%, 12/16/19 (b) | | 3,405,000 | | 3,404,762 | |

Morgan Stanley Capital I Trust REMIC | | | | | |

5.91%, 07/11/17 (a) | | 2,422,047 | | 2,634,175 | |

5.33%, 11/12/41 | | 2,493,596 | | 2,637,040 | |

| | | | | | | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

5.65%, 06/11/42 (a) | | 4,000,000 | | 4,355,156 | |

4.99%, 06/12/47 (a) | | 535,000 | | 542,683 | |

Sierra Receivables Funding Co. LLC, 2.38%, 03/20/29 (b) | | 1,350,838 | | 1,363,045 | |

Sierra Timeshare Receivables Funding LLC | | | | | |

3.37%, 02/20/21 (b) | | 729,175 | | 743,615 | |

3.51%, 11/20/25 (b) | | 531,333 | | 538,117 | |

Springleaf Mortgage Loan Trust REMIC, 1.87%, 09/25/57 (a) (b) | | 2,044,145 | | 2,038,812 | |

Volvo Financial Equipment LLC, 0.82%, 04/16/18 (b) | | 2,332,000 | | 2,327,679 | |

Wachovia Bank Commercial Mortgage Trust REMIC, 5.42%, 07/15/41 (a) | | 1,761,418 | | 1,762,929 | |

Wells Fargo Mortgage Backed Securities Trust REMIC, 2.62%, 12/25/34 (a) | | 596,066 | | 603,284 | |

Westlake Automobile Receivables Trust, 1.12%, 07/15/15 (b) | | 1,808,242 | | 1,810,144 | |

World Omni Auto Receivables Trust, 1.49%, 04/15/16 | | 565,000 | | 568,051 | |

Total Non-U.S. Government Agency Asset-Backed Securities (cost $187,050,097) | | | | 186,431,564 | |

CORPORATE BONDS AND NOTES - 51.4% | | | | | |

CONSUMER DISCRETIONARY - 3.5% | | | | | |

Dollar General Corp., 1.88%, 04/15/18 (c) | | 2,000,000 | | 1,932,582 | |

GLP Capital LP, 4.38%, 11/01/18 (c) | | 1,037,000 | | 1,060,333 | |

Home Depot Inc., 2.00%, 06/15/19 | | 3,500,000 | | 3,508,578 | |

MGM Resorts International, 6.63%, 07/15/15 | | 2,000,000 | | 2,035,000 | |

Time Warner Cable Inc., 6.75%, 07/01/18 | | 4,500,000 | | 5,160,946 | |

Toll Brothers Finance Corp., 4.00%, 12/31/18 | | 2,077,000 | | 2,082,193 | |

Toyota Motor Credit Corp. | | | | | |

1.13%, 05/16/17 | | 2,000,000 | | 1,993,176 | |

2.13%, 07/18/19 | | 2,000,000 | | 2,005,930 | |

Unitymedia Hessen GmbH & Co. KG, 7.50%, 03/15/19 (b) | | 2,000,000 | | 2,100,000 | |

| | | | 21,878,738 | |

CONSUMER STAPLES - 3.4% | | | | | |

Altria Group Inc., 2.63%, 01/14/20 | | 2,500,000 | | 2,507,257 | |

Bunge Ltd. Finance Corp., 5.10%, 07/15/15 | | 3,232,000 | | 3,302,458 | |

Church & Dwight Co. Inc., 2.45%, 12/15/19 | | 2,000,000 | | 1,998,946 | |

ConAgra Foods Inc., 1.30%, 01/25/16 | | 3,000,000 | | 2,999,976 | |

Kimberly-Clark Corp., 1.90%, 05/22/19 | | 2,500,000 | | 2,483,185 | |

Kroger Co. | | | | | |

0.76%, 10/17/16 (a) | | 1,000,000 | | 998,377 | |

1.20%, 10/17/16 | | 2,844,000 | | 2,838,585 | |

Mondelez International Inc., 2.25%, 02/01/19 | | 2,500,000 | | 2,489,733 | |

WM Wrigley Jr. Co. | | | | | |

1.40%, 10/21/16 (b) | | 909,000 | | 909,990 | |

2.00%, 10/20/17 (b) | | 468,000 | | 471,410 | |

| | | | 20,999,917 | |

ENERGY - 0.2% | | | | | |

Transocean Inc., 5.05%, 12/15/16 (d) | | 1,500,000 | | 1,507,619 | |

FINANCIALS - 31.9% | | | | | |

Abbey National Treasury Services Plc, 2.35%, 09/10/19 | | 2,308,000 | | 2,300,229 | |

ABN AMRO Bank NV, 4.25%, 02/02/17 (b) | | 5,000,000 | | 5,268,300 | |

AerCap Ireland Capital Ltd., 2.75%, 05/15/17 (b) | | 1,698,000 | | 1,664,040 | |

Ally Financial Inc. | | | | | |

4.63%, 06/26/15 | | 1,250,000 | | 1,259,375 | |

2.75%, 01/30/17 | | 1,500,000 | | 1,495,320 | |

American Express Credit Corp. | | | | | |

0.74%, 07/29/16 (a) | | 500,000 | | 501,873 | |

1.13%, 06/05/17 | | 3,000,000 | | 2,991,678 | |

Ameriprise Financial Inc., 5.65%, 11/15/15 | | 1,391,000 | | 1,447,305 | |

Bank of America Corp. | | | | | |

3.63%, 03/17/16 | | 655,000 | | 673,528 | |

6.00%, 09/01/17 | | 3,000,000 | | 3,308,181 | |

2.00%, 01/11/18 | | 963,000 | | 962,268 | |

2.60%, 01/15/19 | | 537,000 | | 541,176 | |

Bank of America NA, 5.30%, 03/15/17 | | 750,000 | | 805,670 | |

Bank of Montreal, 2.38%, 01/25/19 | | 1,600,000 | | 1,615,378 | |

Bank of Nova Scotia, 0.66%, 12/13/16 (a) | | 700,000 | | 701,734 | |

BB&T Corp., 2.45%, 01/15/20 | | 3,000,000 | | 2,992,017 | |

Caisse Centrale Desjardins, 1.55%, 09/12/17 (b) | | 3,000,000 | | 2,987,769 | |

Capital One Bank USA NA | | | | | |

1.20%, 02/13/17 | | 3,000,000 | | 2,974,155 | |

2.25%, 02/13/19 | | 3,000,000 | | 2,978,274 | |

2.40%, 09/05/19 (e) | | 2,627,000 | | 2,614,175 | |

Capital One Financial Corp., 1.00%, 11/06/15 | | 630,000 | | 629,482 | |

Caterpillar Financial Services Corp. | | | | | |

1.00%, 03/03/17 | | 2,000,000 | | 1,995,282 | |

2.25%, 12/01/19 | | 3,000,000 | | 3,003,285 | |

CIT Group Inc. | | | | | |

4.75%, 02/15/15 (b) | | 2,500,000 | | 2,507,069 | |

4.25%, 08/15/17 | | 1,000,000 | | 1,020,000 | |

Citigroup Inc., 1.35%, 03/10/17 | | 2,000,000 | | 1,990,682 | |

CNH Capital LLC, 3.88%, 11/01/15 | | 4,250,000 | | 4,271,250 | |

Commonwealth Bank of Australia | | | | | |

1.40%, 09/08/17 | | 2,500,000 | | 2,486,600 | |

2.25%, 03/13/19 | | 3,000,000 | | 3,013,980 | |

Compass Bank, 1.85%, 09/29/17 | | 2,000,000 | | 1,991,612 | |

Corp. Andina de Fomento, 1.50%, 08/08/17 | | 2,250,000 | | 2,236,221 | |

Daimler Finance North America LLC, 1.38%, 08/01/17 (b) | | 3,500,000 | | 3,483,903 | |

Discover Bank, 2.00%, 02/21/18 | | 4,250,000 | | 4,238,924 | |

Equity One Inc. | | | | | |

6.00%, 09/15/16 | | 200,000 | | 214,788 | |

6.25%, 01/15/17 | | 2,053,000 | | 2,222,490 | |

ERP Operating LP, 2.38%, 07/01/19 | | 2,000,000 | | 1,991,452 | |

Fifth Third Bancorp, 3.63%, 01/25/16 | | 1,000,000 | | 1,024,826 | |

Fifth Third Bank, 2.38%, 04/25/19 | | 3,000,000 | | 3,013,659 | |

First Horizon National Corp., 5.38%, 12/15/15 | | 5,096,000 | | 5,276,663 | |

First Tennessee Bank NA, 5.05%, 01/15/15 | | 2,000,000 | | 2,003,327 | |

Ford Motor Credit Co. LLC | | | | | |

1.50%, 01/17/17 | | 6,000,000 | | 5,968,032 | |

1.68%, 09/08/17 | | 3,000,000 | | 2,976,336 | |

General Electric Capital Corp. | | | | | |

5.40%, 02/15/17 (c) | | 2,500,000 | | 2,714,190 | |

5.63%, 05/01/18 | | 1,420,000 | | 1,597,829 | |

General Motors Financial Co. Inc., 2.75%, 05/15/16 | | 4,000,000 | | 4,065,000 | |

Goldman Sachs Group Inc. | | | | | |

1.04%, 12/15/17 (a) | | 2,000,000 | | 1,997,046 | |

2.38%, 01/22/18 | | 5,000,000 | | 5,050,495 | |

2.55%, 10/23/19 | | 2,000,000 | | 1,990,462 | |

HCP Inc., 6.30%, 09/15/16 | | 1,500,000 | | 1,623,982 | |

Hospitality Properties Trust, 5.63%, 03/15/17 | | 2,752,000 | | 2,947,717 | |

HSBC Bank Plc, 1.50%, 05/15/18 (b) | | 3,000,000 | | 2,967,549 | |

HSBC USA Inc., 2.63%, 09/24/18 | | 3,000,000 | | 3,077,034 | |

Huntington National Bank, 1.30%, 11/20/16 | | 3,875,000 | | 3,860,132 | |

Intesa Sanpaolo SpA, 3.13%, 01/15/16 | | 1,400,000 | | 1,422,354 | |

JPMorgan Chase & Co. | | | | | |

1.37%, 09/22/15 (a) | | 2,015,000 | | 2,026,457 | |

1.35%, 02/15/17 | | 2,224,000 | | 2,224,076 | |

0.78%, 04/25/18 (a) | | 3,000,000 | | 2,993,121 | |

Kreditanstalt fuer Wiederaufbau, 0.50%, 07/15/16 | | 2,193,000 | | 2,190,544 | |

Lloyds Bank Plc, 4.20%, 03/28/17 | | 2,000,000 | | 2,115,280 | |

Mid-America Apartments LP, 5.50%, 10/01/15 | | 2,245,000 | | 2,319,604 | |

Mizuho Bank Ltd., 1.70%, 09/25/17 (b) (c) | | 3,000,000 | | 2,985,864 | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

Morgan Stanley | | | | | |

5.55%, 04/27/17 | | 4,000,000 | | 4,341,992 | |

1.88%, 01/05/18 | | 2,069,000 | | 2,063,983 | |

2.38%, 07/23/19 (c) | | 2,000,000 | | 1,992,624 | |

National Australia Bank Ltd. | | | | | |

2.25%, 07/01/19 (b) | | 2,250,000 | | 2,249,021 | |

2.40%, 12/09/19 (b) | | 2,000,000 | | 1,996,646 | |

Prologis International Funding II, 4.88%, 02/15/20 (b) | | 900,000 | | 957,114 | |

Regions Financial Corp., 5.75%, 06/15/15 | | 3,500,000 | | 3,572,660 | |

Royal Bank of Scotland Group Plc, 2.55%, 09/18/15 | | 1,000,000 | | 1,009,998 | |

Royal Bank of Scotland Plc | | | | | |

4.38%, 03/16/16 | | 260,000 | | 268,854 | |

1.88%, 03/31/17 | | 5,300,000 | | 5,296,115 | |

Santander Holdings USA Inc. | | | | | |

3.00%, 09/24/15 | | 2,000,000 | | 2,023,942 | |

4.63%, 04/19/16 | | 2,000,000 | | 2,083,816 | |

SLM Corp., 3.88%, 09/10/15 | | 3,612,000 | | 3,639,090 | |

SunTrust Bank | | | | | |

0.52%, 08/24/15 (a) | | 2,000,000 | | 1,995,996 | |

1.35%, 02/15/17 | | 4,000,000 | | 4,000,600 | |

Toronto-Dominion Bank, 1.13%, 05/02/17 | | 1,100,000 | | 1,093,652 | |

Union Bank NA, 2.63%, 09/26/18 | | 3,000,000 | | 3,044,238 | |

USAA Capital Corp., 2.13%, 06/03/19 (b) | | 2,800,000 | | 2,792,815 | |

Wells Fargo & Co. | | | | | |

0.76%, 07/20/16 (a) | | 875,000 | | 877,692 | |

1.15%, 06/02/17 | | 2,000,000 | | 1,989,822 | |

2.13%, 04/22/19 (c) | | 3,500,000 | | 3,499,083 | |

| | | | 198,600,797 | |

HEALTH CARE - 3.4% | | | | | |

Actavis Funding SCS | | | | | |

1.30%, 06/15/17 | | 3,500,000 | | 3,437,542 | |

2.45%, 06/15/19 | | 1,000,000 | | 982,947 | |

Becton Dickinson and Co., 1.80%, 12/15/17 | | 1,565,000 | | 1,570,892 | |

Medco Health Solutions Inc., 2.75%, 09/15/15 | | 1,500,000 | | 1,519,854 | |

Medtronic Inc., 2.50%, 03/15/20 (b) | | 3,889,000 | | 3,899,201 | |

Mylan Inc., 1.35%, 11/29/16 | | 4,000,000 | | 3,981,484 | |

Perrigo Co. Plc, 1.30%, 11/08/16 | | 2,523,000 | | 2,512,671 | |

Thermo Fisher Scientific Inc., 2.40%, 02/01/19 | | 1,307,000 | | 1,308,949 | |

Ventas Realty LP, 1.55%, 09/26/16 | | 1,895,000 | | 1,903,105 | |

| | | | 21,116,645 | |

INDUSTRIALS - 2.9% | | | | | |

Bombardier Inc., 4.25%, 01/15/16 (b) | | 1,500,000 | | 1,515,000 | |

Cobham Plc, 2.68%, 10/28/17 (e) (f) | | 2,500,000 | | 2,473,346 | |

Eaton Corp., 1.50%, 11/02/17 | | 3,000,000 | | 2,982,843 | |

John Deere Capital Corp., 1.55%, 12/15/17 (c) | | 2,500,000 | | 2,501,490 | |

Penske Truck Leasing Co. LP | | | | | |

3.75%, 05/11/17 (b) | | 2,000,000 | | 2,090,344 | |

3.05%, 01/09/20 (b) | | 4,000,000 | | 3,996,888 | |

Ryder System Inc., 2.45%, 09/03/19 | | 2,500,000 | | 2,482,387 | |

| | | | 18,042,298 | |

INFORMATION TECHNOLOGY - 0.8% | | | | | |

Hewlett-Packard Co., 2.75%, 01/14/19 | | 2,500,000 | | 2,503,195 | |

Oracle Corp., 2.25%, 10/08/19 | | 2,250,000 | | 2,266,074 | |

| | | | 4,769,269 | |

MATERIALS - 2.1% | | | | | |

Anglo American Capital Plc, 1.18%, 04/15/16 (a) (b) | | 1,216,000 | | 1,217,223 | |

FMG Resources August 2006 Pty Ltd., 6.00%, 04/01/17 (b) (c) | | 1,500,000 | | 1,434,375 | |

Freeport-McMoRan Inc., 2.30%, 11/14/17 | | 2,000,000 | | 2,002,550 | |

LyondellBasell Industries NV, 5.00%, 04/15/19 | | 2,500,000 | | 2,726,910 | |

Martin Marietta Materials Inc., 1.36%, 06/30/17 (a) | | 1,051,000 | | 1,062,523 | |

Monsanto Co., 2.13%, 07/15/19 | | 5,000,000 | | 4,981,520 | |

| | | | 13,425,101 | |

TELECOMMUNICATION SERVICES - 1.4% | | | | | |

America Movil SAB de CV, 5.75%, 01/15/15 | | 4,000,000 | | 4,007,613 | |

Verizon Communications Inc. | | | | | |

2.50%, 09/15/16 | | 1,500,000 | | 1,533,665 | |

1.35%, 06/09/17 | | 3,000,000 | | 2,987,241 | |

| | | | 8,528,519 | |

UTILITIES - 1.8% | | | | | |

AES Corp., 3.23%, 06/01/19 (a) | | 1,049,000 | | 1,022,775 | |

Berkshire Hathaway Energy Co., 2.40%, 02/01/20 (b) (c) | | 3,000,000 | | 2,986,938 | |

Dominion Gas Holdings LLC, 2.50%, 12/15/19 | | 2,000,000 | | 2,004,962 | |

Pepco Holdings Inc., 2.70%, 10/01/15 | | 2,670,000 | | 2,702,451 | |

Southern California Edison Co., 1.13%, 05/01/17 | | 1,517,000 | | 1,513,707 | |

Southern Co., 2.38%, 09/15/15 | | 900,000 | | 909,898 | |

| | | | 11,140,731 | |

Total Corporate Bonds and Notes (cost $320,739,057) | | | | 320,009,634 | |

GOVERNMENT AND AGENCY OBLIGATIONS - 17.6% | | | | | |

GOVERNMENT SECURITIES - 14.0% | | | | | |

Federal Home Loan Bank - 1.0% (g) | | | | | |

Federal Home Loan Bank | | | | | |

2.00%, 09/09/16 | | 4,835,000 | | 4,943,391 | |

1.13%, 12/08/17 | | 1,000,000 | | 997,956 | |

| | | | 5,941,347 | |

Federal Home Loan Mortgage Corp. - 0.6% (g) | | | | | |

Federal Home Loan Mortgage Corp., 1.25%, 08/01/19 (c) | | 4,000,000 | | 3,926,144 | |

Federal National Mortgage Association - 0.2% (g) | | | | | |

Federal National Mortgage Association, 1.13%, 04/27/17 | | 1,200,000 | | 1,207,129 | |

Sovereign - 0.3% | | | | | |

Korea Land & Housing Corp., 1.88%, 08/02/17 (b) | | 1,905,000 | | 1,899,213 | |

U.S. Treasury Securities - 11.9% | | | | | |

U.S. Treasury Note | | | | | |

0.63%, 12/31/16 | | 5,500,000 | | 5,494,412 | |

0.88%, 04/15/17 - 11/15/17 | | 50,674,000 | | 50,544,603 | |

1.00%, 09/15/17 (c) | | 1,525,000 | | 1,525,357 | |

1.00%, 12/15/17 | | 4,000,000 | | 3,990,936 | |

1.25%, 10/31/18 | | 13,000,000 | | 12,914,694 | |

| | | | 74,470,002 | |

U.S. GOVERNMENT AGENCY MORTGAGE-BACKED SECURITIES - 3.6% | | | | | |

Federal Home Loan Mortgage Corp. - 0.9% | | | | | |

Federal Home Loan Mortgage Corp. | | | | | |

4.00%, 02/01/26 | | 281,838 | | 301,092 | |

2.50%, 03/15/30, TBA (h) | | 4,000,000 | | 4,049,352 | |

REMIC, 3.00%, 02/15/39 | | 1,548,980 | | 1,588,112 | |

| | | | 5,938,556 | |

Federal National Mortgage Association - 2.0% | | | | | |

Federal National Mortgage Association | | | | | |

4.00%, 04/01/26 - 01/01/31 | | 4,217,030 | | 4,524,264 | |

4.50%, 05/01/26 | | 230,116 | | 248,731 | |

3.50%, 03/01/27 | | 2,828,788 | | 3,002,010 | |

2.75%, 02/01/44 (a) | | 2,143,775 | | 2,213,641 | |

REMIC, 4.00%, 09/25/29 | | 105,000 | | 110,207 | |

REMIC, 3.50%, 12/25/30 | | 2,069,211 | | 2,159,911 | |

| | | | 12,258,764 | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

Government National Mortgage Association - 0.7% | | | | | |

Government National Mortgage Association | | | | | |

2.50%, 11/20/42 (a) | | 696,035 | | 715,432 | |

3.00%, 03/20/44 (a) | | 2,118,883 | | 2,198,838 | |

REMIC, 4.50%, 11/20/39 | | 1,322,538 | | 1,404,476 | |

| | | | 4,318,746 | |

Total Government and Agency Obligations

(cost $109,973,647) | | | | 109,959,901 | |

SHORT TERM INVESTMENTS - 6.0% | | | | | |

Investment Companies - 3.8% | | | | | |

JNL Money Market Fund, 0.01% (i) (j) | | 23,606,728 | | 23,606,728 | |

Securities Lending Collateral - 2.2% | | | | | |

Securities Lending Cash Collateral Fund LLC, 0.22% (i) (j) | | 13,573,160 | | 13,573,160 | |

Total Short Term Investments (cost $37,179,888) | | | | 37,179,888 | |

Total Investments - 104.9% (cost $654,942,689) | | | | 653,580,987 | |

Other Assets and Liabilities, Net - (4.9%) | | | | (30,540,249 | ) |

Total Net Assets - 100.0% | | | | $ | 623,040,738 | |

| | | | | | |

(a) Variable rate security. Rate stated was in effect as of December 31, 2014.

(b) The Sub-Adviser has deemed this security which is exempt from registration under the Securities Act of 1933 (“1933 Act”), as amended, to be liquid based on procedures approved by the Trust’s Board of Trustees. As of December 31, 2014, the aggregate value of these liquid securities was $84,231,710 which represented 13.5% of net assets.

(c) All or a portion of the security was on loan.

(d) The interest rate for this security is inversely affected by upgrades or downgrades to the credit rating of the issuer.

(e) The Sub-Adviser has deemed this security to be illiquid based on procedures approved by the Trust’s Board of Trustees.

(f) Security fair valued in good faith in accordance with the procedures approved by the Trust’s Board of Trustees. Good faith fair valued securities may be classified as Level 2 or Level 3 for Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 820 “Fair Value Measurement,” based on applicable valuation inputs. See FASB Topic 820 in the Notes to Financial Statements.

(g) Securities in this category are direct debt of the agency and not collateralized by mortgages.

(h) All or a portion of the investment was purchased on a delayed delivery basis. As of December 31, 2014, the total payable of investments purchased on a delayed delivery basis was $4,051,250.

(i) Investment in affiliate.

(j) Yield changes daily to reflect current market conditions. Rate was the quoted yield as of December 31, 2014.

| | Shares/ Par† | | Value | |

JNL/PPM America Total Return Fund | | | | | |

NON-U.S. GOVERNMENT AGENCY ASSET-BACKED SECURITIES - 5.8% | | | | | |

American Airlines Pass-Through Trust | | | | | |

5.60%, 07/15/20 (a) (b) | | $ | 3,094,470 | | $ | 3,160,227 | |

4.95%, 01/15/23 | | 1,584,923 | | 1,697,848 | |

American Express Credit Account Master Trust, 0.99%, 08/17/15 | | 477,000 | | 477,982 | |

American Tower Trust I, 3.07%, 03/15/23 (c) | | 6,596,000 | | 6,557,281 | |

AmeriCredit Automobile Receivables Trust | | | | | |

1.59%, 08/08/15 | | 473,000 | | 475,222 | |

1.73%, 02/08/17 | | 679,815 | | 680,908 | |

4.26%, 02/08/17 | | 158,000 | | 160,057 | |

1.31%, 11/08/17 | | 606,000 | | 607,884 | |

1.07%, 03/08/18 | | 905,000 | | 906,099 | |

Aventura Mall Trust REMIC, 3.74%, 12/05/20 (c) (d) | | 1,575,000 | | 1,671,593 | |

Banc of America Commercial Mortgage Trust REMIC, 5.75%, 07/10/17 (d) | | 622,049 | | 678,249 | |

Bear Stearns Commercial Mortgage Securities REMIC | | | | | |

5.74%, 09/11/17 (d) | | 500,000 | | 546,944 | |

5.69%, 06/11/50 (d) | | 1,463,000 | | 1,587,245 | |

Capital One Multi-Asset Execution Trust, 4.90%, 02/17/15 | | 2,595,000 | | 2,608,260 | |

Citigroup Mortgage Loan Trust REMIC, 3.50%, 08/25/23 (a) (b) (d) | | 2,821,593 | | 2,887,683 | |

Commercial Mortgage Pass-Through Certificates REMIC, 3.92%, 09/10/24 | | 3,902,000 | | 4,164,858 | |

Continental Airlines Inc. Pass-Through Trust | | | | | |

6.25%, 04/11/20 | | 642,762 | | 675,299 | |

4.15%, 04/11/24 (e) | | 1,912,545 | | 1,963,954 | |

4.00%, 10/29/24 | | 2,155,745 | | 2,190,884 | |

DBUBS Mortgage Trust REMIC, 3.74%, 06/01/17 (c) | | 3,033,838 | | 3,108,040 | |

Dell Equipment Finance Trust | | | | | |

0.94%, 06/22/20 (c) | | 565,000 | | 564,415 | |

1.36%, 06/22/20 (c) | | 166,000 | | 165,820 | |

Delta Air Lines Inc. Pass-Through Trust | | | | | |

6.20%, 07/02/18 | | 786 | | 867 | |

4.95%, 05/23/19 | | 169,568 | | 181,437 | |

Ford Credit Auto Owner Trust, 1.97%, 04/15/20 | | 1,256,000 | | 1,252,422 | |

Greenwich Capital Commercial Funding Corp. REMIC, 5.44%, 01/10/17 | | 139,000 | | 148,249 | |

GS Mortgage Securities Trust REMIC | | | | | |

3.55%, 04/10/22 (c) | | 2,500,000 | | 2,604,895 | |

4.95%, 01/10/45 (c) | | 847,000 | | 948,747 | |

JPMorgan Chase Commercial Mortgage Securities Trust REMIC, 5.70%, 04/12/17 (d) | | 1,860,000 | | 1,995,998 | |

JPMorgan Mortgage Trust REMIC, 3.00%, 10/25/26 (c) (d) | | 2,906,653 | | 2,983,860 | |

Morgan Stanley Bank of America Merrill Lynch Trust REMIC, 2.86%, 09/15/22 | | 3,000,000 | | 3,004,386 | |

Morgan Stanley Capital I Trust REMIC, 5.91%, 07/11/17 (d) | | 4,593,355 | | 4,995,650 | |

Morgan Stanley Re-REMIC Trust REMIC, 5.80%, 04/12/17 (c) (d) | | 1,295,945 | | 1,389,413 | |

MVW Owner Trust, 2.15%, 04/22/30 (c) | | 1,034,676 | | 1,034,998 | |

SBA Tower Trust, 2.90%, 10/15/44 (c) | | 5,000,000 | | 5,013,175 | |

Sierra Receivables Funding Co. LLC | | | | | |

2.84%, 05/20/19 (c) | | 450,424 | | 456,770 | |

2.38%, 03/20/29 (c) | | 245,582 | | 247,802 | |

United Air Lines Pass-Through Trust, 9.75%, 01/15/17 | | 53,963 | | 59,326 | |

Total Non-U.S. Government Agency Asset-Backed Securities (cost $62,766,289) | | | | 63,854,747 | |

CORPORATE BONDS AND NOTES - 62.0% | | | | | |

CONSUMER DISCRETIONARY - 6.0% | | | | | |

A&E Television Networks LLC | | | | | |

3.11%, 08/22/19 (b) (f) | | 1,000,000 | | 996,044 | |

3.63%, 08/22/22 (b) (f) | | 1,000,000 | | 994,288 | |

3.78%, 08/22/24 (b) (f) | | 1,000,000 | | 993,967 | |

British Sky Broadcasting Group Plc | | | | | |

2.63%, 09/16/19 (c) | | 1,435,000 | | 1,435,532 | |

3.75%, 09/16/24 (c) | | 1,970,000 | | 1,982,064 | |

Charter Communications Term Loan, 4.25%, 08/12/21 (d) | | 550,000 | | 553,097 | |

Delphi Corp. | | | | | |

6.13%, 05/15/21 | | 185,000 | | 201,650 | |

5.00%, 02/15/23 | | 1,867,000 | | 1,992,985 | |

Dollar General Corp., 3.25%, 04/15/23 (e) | | 1,883,000 | | 1,713,991 | |

| | | | | | | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

DreamWorks Animation SKG Inc., 6.88%, 08/15/20 (c) | | 824,000 | | 844,600 | |

Four Seasons Hotels Ltd. New Term Loan, 3.50%, 06/27/20 (d) | | 1,148,463 | | 1,122,622 | |

General Motors Co. | | | | | |

5.00%, 04/01/35 | | 3,500,000 | | 3,647,315 | |

6.25%, 10/02/43 | | 1,285,000 | | 1,535,061 | |

GLP Capital LP | | | | | |

4.38%, 11/01/18 (e) | | 277,000 | | 283,233 | |

4.88%, 11/01/20 | | 311,000 | | 314,888 | |

5.38%, 11/01/23 | | 242,000 | | 250,470 | |

Grupo Televisa SAB, 5.00%, 05/13/45 | | 2,099,000 | | 2,118,791 | |

JC Penney Corp. Inc. Term Loan, 6.00%, 05/22/18 (d) | | 878,875 | | 860,568 | |

KB Home | | | | | |

4.75%, 05/15/19 | | 2,316,000 | | 2,281,260 | |

7.50%, 09/15/22 | | 409,000 | | 433,540 | |

Media General Financing Sub Inc., 5.88%, 11/15/22 (c) | | 1,084,000 | | 1,073,160 | |

Men’s Wearhouse Inc., 7.00%, 07/01/22 (c) (e) | | 368,000 | | 378,120 | |

NAI Entertainment Holdings, 5.00%, 08/01/18 (c) | | 228,000 | | 233,700 | |

NBCUniversal Enterprise Inc., 5.25%, (callable at 100 beginning 03/19/21) (c) (g) | | 1,589,000 | | 1,648,588 | |

Netflix Inc., 5.75%, 03/01/24 (c) | | 1,720,000 | | 1,788,800 | |

Numericable Group SA | | | | | |

4.88%, 05/15/19 (c) | | 3,381,000 | | 3,351,416 | |

5.38%, 05/15/22 (c), EUR | | 1,000,000 | | 1,248,775 | |

NVR Inc., 3.95%, 09/15/22 | | 4,573,000 | | 4,690,517 | |

Schaeffler Finance BV | | | | | |

3.25%, 05/15/19 (c), EUR | | 1,296,000 | | 1,583,911 | |

3.50%, 05/15/22 (c), EUR | | 570,000 | | 701,870 | |

Schaeffler Holding Finance BV, 5.75%, 11/15/21 (c), EUR | | 1,407,000 | | 1,813,210 | |

Scientific Games International Inc., 7.00%, 01/01/22 (a) (b) | | 2,447,000 | | 2,477,587 | |

Seminole Indian Tribe of Florida, 6.54%, 10/01/20 (c) | | 840,000 | | 894,600 | |

SES SA | | | | | |

3.60%, 04/04/23 (c) | | 652,000 | | 658,564 | |

5.30%, 04/04/43 (c) | | 464,000 | | 515,381 | |

Shea Homes LP, 8.63%, 05/15/19 (e) | | 627,000 | | 658,350 | |

Sirius XM Radio Inc., 6.00%, 07/15/24 (c) | | 4,426,000 | | 4,536,650 | |

Taylor Morrison Communities Inc. | | | | | |

7.75%, 04/15/20 (c) | | 1,100,000 | | 1,166,000 | |

7.75%, 04/15/20 (c) | | 673,000 | | 713,380 | |

Tenneco Inc. | | | | | |

6.88%, 12/15/20 | | 1,750,000 | | 1,850,625 | |

5.38%, 12/15/24 (e) | | 1,065,000 | | 1,091,625 | |

Time Warner Cable Inc. | | | | | |

6.75%, 06/15/39 | | 371,000 | | 485,001 | |

5.88%, 11/15/40 | | 252,000 | | 300,473 | |

5.50%, 09/01/41 | | 1,291,000 | | 1,500,043 | |

TRW Automotive Inc. | | | | | |

7.25%, 03/15/17 (c) | | 100,000 | | 110,500 | |

4.50%, 03/01/21 (c) | | 867,000 | | 871,335 | |

4.45%, 12/01/23 (c) | | 825,000 | | 829,125 | |

Univision Communications Inc. Incremental Term Loan, 4.00%, 03/01/20 (d) | | 1,051,175 | | 1,025,947 | |

Wynn Las Vegas LLC, 7.75%, 08/15/20 (e) | | 2,900,000 | | 3,089,167 | |

| | | | 65,842,386 | |

CONSUMER STAPLES - 1.5% | | | | | |

Bunge Ltd. Finance Co., 8.50%, 06/15/19 (h) | | 100,000 | | 122,554 | |

ConAgra Foods Inc., 4.65%, 01/25/43 | | 1,183,000 | | 1,234,659 | |

Constellation Brands Inc., 4.25%, 05/01/23 | | 208,000 | | 206,440 | |

JBS Investments GmbH, 7.25%, 04/03/24 (c) | | 1,445,000 | | 1,419,712 | |

Lorillard Tobacco Co., 7.00%, 08/04/41 | | 812,000 | | 1,025,276 | |

Mars Inc. | | | | | |

2.19%, 10/11/17 (b) (f) | | 2,850,000 | | 2,843,493 | |

3.74%, 10/11/27 (b) (f) | | 1,200,000 | | 1,206,390 | |

SABMiller Holdings Inc., 3.75%, 01/15/22 (c) | | 1,602,000 | | 1,672,023 | |

Sysco Corp., 4.35%, 10/02/34 | | 3,955,000 | | 4,257,898 | |

Tyson Foods Inc. | | | | | |

3.95%, 08/15/24 | | 929,000 | | 960,327 | |

4.88%, 08/15/34 | | 1,010,000 | | 1,107,941 | |

5.15%, 08/15/44 (e) | | 549,000 | | 616,623 | |

| | | | 16,673,336 | |

ENERGY - 7.4% | | | | | |

Access Midstream Partners LP | | | | | |

4.88%, 05/15/23 | | 1,377,000 | | 1,397,655 | |

4.88%, 03/15/24 | | 1,041,000 | | 1,056,615 | |

Alpha Natural Resources Inc. | | | | | |

9.75%, 04/15/18 (e) | | 1,700,000 | | 765,000 | |

6.25%, 06/01/21 (e) | | 1,397,000 | | 391,160 | |

Arch Coal Inc. | | | | | |

8.00%, 01/15/19 (c) (e) | | 887,000 | | 492,285 | |

9.88%, 06/15/19 (e) | | 2,064,000 | | 701,760 | |

BP Capital Markets Plc, 2.75%, 05/10/23 | | 2,796,000 | | 2,614,610 | |

California Resources Corp. | | | | | |

5.00%, 01/15/20 (c) (e) | | 2,500,000 | | 2,168,750 | |

5.50%, 09/15/21 (c) | | 1,804,000 | | 1,542,420 | |

6.00%, 11/15/24 (c) (e) | | 1,818,000 | | 1,536,210 | |

Calumet Specialty Products Partners LP, 6.50%, 04/15/21 (c) | | 2,325,000 | | 2,069,250 | |

Chesapeake Energy Corp., 3.48%, 04/15/19 (d) | | 4,617,000 | | 4,524,660 | |

Chesapeake Midstream Partners LP, 5.88%, 04/15/21 | | 957,000 | | 997,673 | |

Concho Resources Inc., 5.50%, 04/01/23 | | 2,164,000 | | 2,174,171 | |

Continental Resources Inc., 4.50%, 04/15/23 | | 876,000 | | 833,208 | |

DCP Midstream LLC, 5.85%, 05/21/43 (c) (d) | | 2,184,000 | | 2,118,480 | |

Diamond Offshore Drilling Inc., 4.88%, 11/01/43 (e) | | 700,000 | | 596,342 | |

Energy XXI Gulf Coast Inc., 6.88%, 03/15/24 (c) (e) | | 959,000 | | 517,860 | |

Enterprise Products Operating LLC | | | | | |

3.75%, 02/15/25 | | 2,087,000 | | 2,094,947 | |

4.95%, 10/15/54 | | 1,337,000 | | 1,368,470 | |

EP Energy LLC, 6.88%, 05/01/19 | | 1,000,000 | | 1,015,000 | |

Fieldwood Energy LLC 1st Lien Term Loan, 3.88%, 09/28/18 (d) | | 1,584,999 | | 1,497,824 | |

Jupiter Resources Inc., 8.50%, 10/01/22 (c) | | 3,000,000 | | 2,257,500 | |

Kinder Morgan Inc. | | | | | |

3.05%, 12/01/19 | | 3,500,000 | | 3,472,175 | |

5.30%, 12/01/34 | | 2,500,000 | | 2,537,640 | |

Linden Term Loan B, 3.75%, 12/01/20 (d) | | 505,349 | | 497,456 | |

Linn Energy LLC, 6.50%, 09/15/21 (e) | | 2,759,000 | | 2,234,790 | |

Memorial Production Partners LP, 6.88%, 08/01/22 (c) | | 2,317,000 | | 1,760,920 | |

Penn Virginia Corp., 8.50%, 05/01/20 (e) | | 850,000 | | 680,000 | |

Petrobras Global Finance BV | | | | | |

2.00%, 05/20/16 | | 4,150,000 | | 3,963,872 | |

4.38%, 05/20/23 (e) | | 2,381,000 | | 2,047,850 | |

Petroleos Mexicanos, 2.29%, 02/15/24 | | 3,097,950 | | 3,078,250 | |

Phillips 66 | | | | | |

4.65%, 11/15/34 | | 1,750,000 | | 1,793,747 | |

4.88%, 11/15/44 | | 1,750,000 | | 1,791,206 | |

Plains Exploration & Production Co., 6.75%, 02/01/22 | | 2,099,000 | | 2,308,900 | |

Regency Energy Partners LP | | | | | |

5.88%, 03/01/22 | | 2,278,000 | | 2,272,305 | |

5.00%, 10/01/22 | | 1,080,000 | | 1,020,600 | |

Seadrill Ltd., 6.13%, 09/15/17 (c) (e) (i) | | 3,726,000 | | 3,297,510 | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

SM Energy Co., 6.13%, 11/15/22 (c) | | 2,685,000 | | 2,523,900 | |

Targa Resources Partners LP, 4.13%, 11/15/19 (c) | | 3,856,000 | | 3,711,400 | |

Tesoro Logistics LP | | | | | |

5.50%, 10/15/19 (c) | | 454,000 | | 450,595 | |

6.25%, 10/15/22 (c) | | 656,000 | | 654,360 | |

Transocean Inc. | | | | | |

2.50%, 10/15/17 (h) | | 1,000,000 | | 884,106 | |

6.38%, 12/15/21 (h) | | 1,824,000 | | 1,682,547 | |

3.80%, 10/15/22 (e) (h) | | 2,015,000 | | 1,632,805 | |

Ultra Petroleum Corp., 6.13%, 10/01/24 (c) (e) | | 2,451,000 | | 2,107,860 | |

| | | | 81,136,644 | |

FINANCIALS - 27.3% | | | | | |

Abbey National Treasury Services Plc, 4.00%, 03/13/24 | | 3,354,000 | | 3,491,641 | |

AerCap Ireland Capital Ltd. | | | | | |

2.75%, 05/15/17 (c) | | 152,000 | | 148,960 | |

4.50%, 05/15/21 (c) | | 288,000 | | 291,600 | |

AIG SunAmerica Global Financing X, 6.90%, 03/15/32 (c) | | 1,696,000 | | 2,335,268 | |

Bank of America Corp. | | | | | |

6.25% (callable at 100 beginning 09/05/24) (g) | | 2,683,000 | | 2,651,976 | |

6.50% (callable at 100 beginning 10/23/24) (g) | | 2,197,000 | | 2,236,326 | |

3.30%, 01/11/23 | | 7,078,000 | | 7,078,545 | |

4.20%, 08/26/24 | | 3,000,000 | | 3,056,175 | |

4.25%, 10/22/26 | | 2,559,000 | | 2,553,255 | |

Barclays Bank Plc | | | | | |

7.63%, 11/21/22 | | 1,279,000 | | 1,398,491 | |

7.75%, 04/10/23 (d) | | 1,009,000 | | 1,099,810 | |

3.75%, 05/15/24 | | 7,200,000 | | 7,421,407 | |

Barclays Plc, 8.25%, (callable at 100 beginning 12/15/18) (e) (g) | | 5,300,000 | | 5,432,071 | |

BlackRock Inc., 3.38%, 06/01/22 | | 1,062,000 | | 1,095,095 | |

Capital One Bank USA NA, 2.40%, 09/05/19 (b) | | 7,568,000 | | 7,531,053 | |

Capital One NA, 2.95%, 07/23/21 (b) | | 2,005,000 | | 1,992,455 | |

CDP Financial Inc., 3.15%, 07/24/24 (c) | | 3,000,000 | | 3,058,659 | |

Chubb Corp., 6.38%, 03/29/67 (d) | | 100,000 | | 107,205 | |

Citigroup Inc. | | | | | |

5.90% (callable at 100 beginning 02/15/23) (g) | | 1,375,000 | | 1,340,625 | |

4.05%, 07/30/22 | | 2,025,000 | | 2,095,187 | |

5.30%, 05/06/44 | | 3,000,000 | | 3,287,007 | |

Credit Agricole SA, 6.63%, (callable at 100 beginning 09/23/19) (c) (g) | | 2,400,000 | | 2,326,200 | |

Credit Suisse | | | | | |

3.00%, 10/29/21 | | 2,390,000 | | 2,378,843 | |

3.63%, 09/09/24 | | 4,728,000 | | 4,809,506 | |

Credit Suisse AG | | | | | |

7.50% (callable at 100 beginning 12/11/23) (c) (e) (g) | | 4,748,000 | | 4,937,920 | |

6.50%, 08/08/23 (c) | | 8,211,000 | | 9,013,387 | |

Discover Financial Services, 3.95%, 11/06/24 | | 3,500,000 | | 3,518,350 | |

Duke Realty LP, 8.25%, 08/15/19 | | 100,000 | | 123,370 | |

Fifth Third Bank, 2.38%, 04/25/19 | | 6,000,000 | | 6,027,318 | |

Five Corners Funding Trust, 4.42%, 11/15/23 (c) | | 6,695,000 | | 7,079,434 | |

Ford Motor Credit Co. LLC | | | | | |

5.00%, 05/15/18 | | 6,898,000 | | 7,495,008 | |

2.38%, 03/12/19 | | 2,250,000 | | 2,234,336 | |

General Electric Capital Corp. | | | | | |

6.25% (callable at 100 beginning 12/15/22) (g) | | 7,744,000 | | 8,431,280 | |

7.13% (callable at 100 beginning 06/15/22) (g) | | 4,425,000 | | 5,149,594 | |

3.10%, 01/09/23 | | 3,900,000 | | 3,948,730 | |

General Motors Financial Co. Inc., 4.38%, 09/25/21 | | 2,819,000 | | 2,942,331 | |

GFI Group Inc, 10.38%, 07/19/18 (h) | | 2,250,000 | | 2,598,750 | |

Goldman Sachs Group Inc. | | | | | |

5.70% (callable at 100 beginning 05/10/19) (e) (g) | | 6,892,000 | | 6,971,258 | |

2.38%, 01/22/18 | | 8,108,000 | | 8,189,883 | |

2.55%, 10/23/19 | | 3,500,000 | | 3,483,309 | |

4.00%, 03/03/24 | | 4,564,000 | | 4,738,112 | |

3.85%, 07/08/24 | | 1,895,000 | | 1,943,508 | |

6.75%, 10/01/37 | | 1,500,000 | | 1,886,063 | |

Guggenheim Partners Investment Management Holdings LLC Initial Term Loan, 4.25%, 07/17/20 (d) | | 495,000 | | 489,555 | |

Hospitality Properties Trust, 4.50%, 03/15/25 (e) | | 3,338,000 | | 3,360,274 | |

HSBC Holdings Plc | | | | | |

5.63% (callable at 100 beginning 01/17/20) (e) (g) | | 3,037,000 | | 3,047,630 | |

6.38% (callable at 100 beginning 09/17/24) (g) | | 3,431,000 | | 3,465,310 | |

4.25%, 03/14/24 | | 3,450,000 | | 3,590,008 | |

5.25%, 03/14/44 | | 525,000 | | 588,081 | |

Icahn Enterprises LP | | | | | |

3.50%, 03/15/17 | | 1,500,000 | | 1,500,000 | |

4.88%, 03/15/19 | | 2,518,000 | | 2,511,705 | |

6.00%, 08/01/20 | | 1,363,000 | | 1,404,163 | |

International Lease Finance Corp. | | | | | |

4.88%, 04/01/15 | | 1,000,000 | | 1,007,250 | |

8.63%, 01/15/22 | | 750,000 | | 930,000 | |

Intesa Sanpaolo SpA, 5.02%, 06/26/24 (c) | | 7,200,000 | | 6,987,708 | |

Invesco Finance Plc, 3.13%, 11/30/22 | | 1,778,000 | | 1,762,119 | |

JPMorgan Chase & Co. | | | | | |

5.00% (callable at 100 beginning 07/01/19) (g) | | 2,500,000 | | 2,446,093 | |

7.90% (callable at 100 beginning 04/30/18) (g) | | 1,774,000 | | 1,909,356 | |

3.20%, 01/25/23 | | 4,109,000 | | 4,110,734 | |

3.63%, 05/13/24 | | 3,000,000 | | 3,070,809 | |

4.13%, 12/15/26 | | 3,750,000 | | 3,739,770 | |

Legg Mason Inc., 2.70%, 07/15/19 | | 1,883,000 | | 1,892,095 | |

Liberty Mutual Group Inc., 4.85%, 08/01/44 (c) | | 2,800,000 | | 2,846,127 | |

Lloyds Bank PLC, 2.35%, 09/05/19 | | 5,000,000 | | 4,996,395 | |

Mizuho Bank Ltd. | | | | | |

1.70%, 09/25/17 (c) | | 3,000,000 | | 2,985,864 | |

2.45%, 04/16/19 (c) | | 3,286,000 | | 3,264,621 | |

Mizuho Financial Group Cayman 3 Ltd., 4.60%, 03/27/24 (c) | | 4,000,000 | | 4,144,688 | |

Morgan Stanley | | | | | |

2.38%, 07/23/19 | | 8,596,000 | | 8,564,298 | |

4.88%, 11/01/22 | | 4,381,000 | | 4,652,964 | |

4.10%, 05/22/23 | | 5,008,000 | | 5,070,289 | |

3.88%, 04/29/24 | | 3,446,000 | | 3,535,720 | |

3.70%, 10/23/24 | | 3,125,000 | | 3,167,563 | |

4.35%, 09/08/26 | | 2,138,000 | | 2,150,775 | |

Murray Street Investment Trust I, 4.65%, 03/09/17 (i) | | 4,250,000 | | 4,485,688 | |

National Rural Utilities Cooperative Finance Corp., 4.75%, 04/30/43 (d) | | 3,146,000 | | 3,117,686 | |

PNC Financial Services Group Inc., 4.85%, (callable at 100 beginning 06/01/23) (e) (g) | | 581,000 | | 548,367 | |

Prologis International Funding II, 4.88%, 02/15/20 (c) | | 2,222,000 | | 2,363,008 | |

Prudential Financial Inc., 5.88%, 09/15/42 (d) | | 1,502,000 | | 1,584,610 | |

Royal Bank of Scotland Group Plc | | | | | |

6.13%, 12/15/22 | | 1,317,000 | | 1,433,431 | |

6.10%, 06/10/23 | | 3,370,000 | | 3,655,085 | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

6.00%, 12/19/23 | | 1,740,000 | | 1,883,373 | |

5.13%, 05/28/24 | | 3,384,000 | | 3,442,174 | |

Santander UK Plc, 5.00%, 11/07/23 (c) | | 1,152,000 | | 1,216,738 | |

Societe Generale SA, 6.00%, (callable at 100 beginning 01/27/20) (c) (e) (g) | | 1,121,000 | | 1,020,110 | |

Stena AB, 7.00%, 02/01/24 (c) (e) | | 1,332,000 | | 1,218,780 | |

Tanger Properties LP, 3.75%, 12/01/24 | | 3,500,000 | | 3,527,128 | |

Union Bank NA, 2.25%, 05/06/19 | | 4,300,000 | | 4,285,625 | |

USAA Capital Corp., 2.13%, 06/03/19 (c) | | 4,100,000 | | 4,089,479 | |

Wells Fargo & Co. | | | | | |

4.48%, 01/16/24 | | 1,455,000 | | 1,551,328 | |

4.10%, 06/03/26 | | 6,093,000 | | 6,227,393 | |

| | | | 298,771,268 | |

HEALTH CARE - 4.6% | | | | | |

Actavis Funding SCS | | | | | |

3.85%, 06/15/24 | | 794,000 | | 798,056 | |

4.85%, 06/15/44 | | 1,630,000 | | 1,654,020 | |

Bayer US Finance LLC, 2.38%, 10/08/19 (c) | | 2,000,000 | | 2,007,936 | |

Becton Dickinson and Co. | | | | | |

2.68%, 12/15/19 | | 2,086,000 | | 2,113,433 | |

3.73%, 12/15/24 | | 883,000 | | 908,746 | |

4.69%, 12/15/44 | | 1,109,000 | | 1,194,350 | |

Forest Laboratories Inc., 5.00%, 12/15/21 (c) | | 1,268,000 | | 1,373,023 | |

Gilead Sciences Inc. | | | | | |

3.50%, 02/01/25 | | 1,705,000 | | 1,750,012 | |

4.80%, 04/01/44 | | 1,302,000 | | 1,444,249 | |

4.50%, 02/01/45 | | 1,493,000 | | 1,595,717 | |

HCA Inc. | | | | | |

3.75%, 03/15/19 | | 3,119,000 | | 3,122,899 | |

4.25%, 10/15/19 | | 2,464,000 | | 2,500,960 | |

Howard Hughes Medical Institute, 3.50%, 09/01/23 | | 2,046,000 | | 2,139,478 | |

Mayo Clinic Rochester, 3.77%, 11/15/43 | | 600,000 | | 592,782 | |

Medtronic Inc. | | | | | |

3.50%, 03/15/25 (c) | | 4,879,000 | | 4,991,070 | |

4.38%, 03/15/35 (c) | | 3,016,000 | | 3,199,542 | |

4.63%, 03/15/45 (c) | | 4,062,000 | | 4,403,167 | |

Memorial Sloan-Kettering Cancer Center | | | | | |

5.00%, 07/01/42 | | 997,000 | | 1,170,545 | |

4.13%, 07/01/52 | | 587,000 | | 583,605 | |

Merck & Co. Inc., 4.15%, 05/18/43 | | 1,520,000 | | 1,617,145 | |

Novartis Capital Corp., 2.40%, 09/21/22 | | 1,027,000 | | 1,017,411 | |

Omnicare Inc. | | | | | |

4.75%, 12/01/22 | | 266,000 | | 269,325 | |

5.00%, 12/01/24 | | 174,000 | | 178,350 | |

Perrigo Finance Plc | | | | | |

3.50%, 12/15/21 | | 2,850,000 | | 2,883,242 | |

4.90%, 12/15/44 | | 943,000 | | 999,276 | |

Pfizer Inc., 4.30%, 06/15/43 | | 1,700,000 | | 1,820,603 | |

Walgreens Boots Alliance Inc., 3.80%, 11/18/24 | | 2,884,000 | | 2,941,391 | |

Zoetis Inc., 4.70%, 02/01/43 | | 684,000 | | 696,159 | |

| | | | 49,966,492 | |

INDUSTRIALS - 3.1% | | | | | |

AECOM Technology Corp., 5.88%, 10/15/24 (c) | | 1,203,000 | | 1,230,068 | |

Aircastle Ltd., 4.63%, 12/15/18 | | 1,270,000 | | 1,276,350 | |

Algeco Scotsman Global Finance Plc, 10.75%, 10/15/19 (c) | | 1,700,000 | | 1,462,000 | |

Bombardier Inc. | | | | | |

4.75%, 04/15/19 (c) (e) | | 5,607,000 | | 5,628,026 | |

6.13%, 01/15/23 (c) (e) | | 1,056,000 | | 1,077,120 | |

Florida East Coast Holdings Corp., 6.75%, 05/01/19 (c) | | 1,583,000 | | 1,567,170 | |

General Electric Co. | | | | | |

3.50%, 10/02/18 | | 5,100,000 | | 5,202,000 | |

2.70%, 10/09/22 | | 2,825,000 | | 2,826,147 | |

Huntington Ingalls Industries Inc., 5.00%, 12/15/21 (c) | | 1,283,000 | | 1,305,453 | |

IHS Inc., 5.00%, 11/01/22 (c) | | 1,072,000 | | 1,061,280 | |

International Lease Finance Corp. | | | | | |

2.19%, 06/15/16 (d) | | 1,750,000 | | 1,747,812 | |

6.75%, 09/01/16 (c) | | 1,100,000 | | 1,171,500 | |

7.13%, 09/01/18 (c) | | 1,000,000 | | 1,120,000 | |

4.63%, 04/15/21 (e) | | 2,237,000 | | 2,276,147 | |

Meritor Inc. | | | | | |

6.75%, 06/15/21 | | 2,057,000 | | 2,149,565 | |

6.25%, 02/15/24 | | 952,000 | | 966,280 | |

Schaeffler AG New Term Loan B, 4.25%, 05/15/20 | | 1,200,000 | | 1,198,200 | |

United Continental Holdings Inc., 6.00%, 07/15/28 (e) | | 1,100,000 | | 1,047,750 | |

| | | | 34,312,868 | |

INFORMATION TECHNOLOGY - 1.4% | | | | | |

CDK Global Inc., 3.30%, 10/15/19 (c) | | 1,382,000 | | 1,376,360 | |

Oracle Corp., 4.30%, 07/08/34 | | 5,000,000 | | 5,353,360 | |

SAP Ireland US-Financial Services Ltd. | | | | | |

2.82%, 11/15/20 (b) (f) | | 2,485,000 | | 2,477,853 | |

3.18%, 11/15/22 (b) (f) | | 2,485,000 | | 2,476,184 | |

ViaSat Inc., 6.88%, 06/15/20 | | 3,092,000 | | 3,215,680 | |

| | | | 14,899,437 | |

MATERIALS - 4.1% | | | | | |

Alcoa Inc., 5.13%, 10/01/24 | | 1,684,000 | | 1,784,653 | |

Arch Western Finance LLC Term Loan, 6.25%, 05/14/18 (d) | | 977,476 | | 806,828 | |

Ardagh Packaging Finance Plc, 3.24%, 12/15/19 (c) (d) | | 3,350,000 | | 3,232,750 | |

Barrick Gold Corp. | | | | | |

3.85%, 04/01/22 | | 399,000 | | 383,975 | |

4.10%, 05/01/23 (e) | | 1,800,000 | | 1,751,756 | |

Cemex Finance LLC | | | | | |

9.38%, 10/12/22 (c) | | 855,000 | | 953,325 | |

6.00%, 04/01/24 (c) | | 1,171,000 | | 1,141,725 | |

Cemex SAB de CV, 6.50%, 12/10/19 (c) | | 3,290,000 | | 3,370,605 | |

FMG Resources August 2006 Pty Ltd., 8.25%, 11/01/19 (c) (e) | | 1,450,000 | | 1,319,500 | |

FMG Resources Pty Ltd. New Term Loan B, 3.75%, 06/30/19 (d) | | 1,862,190 | | 1,687,144 | |

Freeport-McMoRan Copper & Gold Inc. | | | | | |

3.10%, 03/15/20 (e) | | 3,450,000 | | 3,355,929 | |

5.45%, 03/15/43 | | 1,263,000 | | 1,194,260 | |

Freeport-McMoRan Inc. | | | | | |

4.55%, 11/14/24 (e) | | 1,803,000 | | 1,750,763 | |

5.40%, 11/14/34 | | 5,878,000 | | 5,730,492 | |

LYB International Finance BV, 4.00%, 07/15/23 | | 1,020,000 | | 1,043,401 | |

Methanex Corp., 5.65%, 12/01/44 | | 1,569,000 | | 1,604,218 | |

Monsanto Co. | | | | | |

3.38%, 07/15/24 | | 493,000 | | 500,922 | |

4.70%, 07/15/64 | | 3,253,000 | | 3,410,852 | |

Rain CII Carbon LLC, 8.25%, 01/15/21 (c) (e) | | 3,508,000 | | 3,586,930 | |

Samarco Mineracao SA | | | | | |

4.13%, 11/01/22 (c) | | 685,000 | | 602,800 | |

5.38%, 09/26/24 (c) | | 4,273,000 | | 3,961,071 | |

Sealed Air Corp., 4.88%, 12/01/22 (c) | | 1,077,000 | | 1,068,922 | |

Teck Resources Ltd., 3.75%, 02/01/23 | | 879,000 | | 787,840 | |

| | | | 45,030,661 | |

TELECOMMUNICATION SERVICES - 3.0% | | | | | |

Altice Financing SA, 7.88%, 12/15/19 (c) | | 324,000 | | 331,742 | |

Crown Castle Towers LLC, 4.88%, 08/15/20 (c) | | 1,450,000 | | 1,593,878 | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

Frontier Communications Corp. | | | | | |

6.25%, 09/15/21 (e) | | 400,000 | | 402,000 | |

6.88%, 01/15/25 | | 511,000 | | 511,000 | |

Inmarsat Finance Plc, 4.88%, 05/15/22 (c) | | 3,417,000 | | 3,382,830 | |

SES Global Americas Holdings GP, 5.30%, 03/25/44 (c) | | 1,524,000 | | 1,706,150 | |

Telefonica Moviles Chile SA, 2.88%, 11/09/15 (c) | | 100,000 | | 101,121 | |

Verizon Communications Inc. | | | | | |

5.15%, 09/15/23 | | 4,925,000 | | 5,438,347 | |

6.40%, 09/15/33 | | 3,106,000 | | 3,825,918 | |

4.40%, 11/01/34 | | 2,000,000 | | 1,987,962 | |

6.55%, 09/15/43 | | 6,008,000 | | 7,697,143 | |

5.01%, 08/21/54 (a) (b) | | 4,473,000 | | 4,627,538 | |

Windstream Corp. Term Loan B-4, 3.50%, 01/15/20 (d) | | 980,000 | | 966,937 | |

| | | | 32,572,566 | |

UTILITIES - 3.6% | | | | | |

Abengoa Yield Plc, 7.00%, 11/15/19 (c) (e) | | 2,315,000 | | 2,280,275 | |

AES Corp., 3.23%, 06/01/19 (d) | | 2,660,000 | | 2,593,500 | |

Atlantic City Electric Co., 3.38%, 09/01/24 | | 3,386,000 | | 3,428,460 | |

Dynegy Finance I Inc., 6.75%, 11/01/19 (c) | | 1,010,000 | | 1,027,675 | |

Electricite de France SA, 5.25%, (callable at 100 beginning 01/29/23) (c) (e) (g) | | 7,570,000 | | 7,759,250 | |

Enel SpA, 8.75%, 09/24/73 (c) (d) | | 1,872,000 | | 2,173,860 | |

FirstEnergy Corp. | | | | | |

4.25%, 03/15/23 (h) | | 883,000 | | 911,092 | |

7.38%, 11/15/31 | | 1,575,000 | | 1,906,326 | |

FirstEnergy Transmission LLC, 5.45%, 07/15/44 (c) | | 1,680,000 | | 1,810,815 | |

Oglethorpe Power Corp., 4.55%, 06/01/44 | | 2,344,000 | | 2,471,260 | |

Oncor Electric Delivery Co. LLC | | | | | |

6.80%, 09/01/18 | | 2,250,000 | | 2,622,650 | |

4.10%, 06/01/22 | | 1,679,000 | | 1,803,192 | |

Pacific Gas & Electric Co., 4.30%, 03/15/45 | | 2,007,000 | | 2,060,101 | |

PPL WEM Holdings Plc, 3.90%, 05/01/16 (c) | | 200,000 | | 205,943 | |

Puget Energy Inc., 6.00%, 09/01/21 | | 1,650,000 | | 1,930,248 | |

RJS Power Holdings LLC, 5.13%, 07/15/19 (c) | | 3,350,000 | | 3,308,125 | |

Texas Competitive Electric Holdings Co. LLC Term Loan, 3.75%, 05/05/16 (d) | | 1,269,802 | | 1,272,977 | |

| | | | 39,565,749 | |

Total Corporate Bonds and Notes (cost $675,863,486) | | | | 678,771,407 | |

GOVERNMENT AND AGENCY OBLIGATIONS - 29.8% | | | | | |

GOVERNMENT SECURITIES - 11.7% | | | | | |

Municipals - 0.1% | | | | | |

Port Authority of New York & New Jersey, GO, 4.46%, 10/01/62 | | 1,490,000 | | 1,581,531 | |

U.S. Treasury Securities - 11.6% | | | | | |

U.S. Treasury Bond | | | | | |

3.75%, 08/15/41 | | 5,348,000 | | 6,451,025 | |

3.13%, 11/15/41 | | 10,120,000 | | 10,932,757 | |

U.S. Treasury Note | | | | | |

1.63%, 03/31/19 - 06/30/19 | | 44,844,000 | | 45,002,042 | |

1.50%, 05/31/19 | | 12,868,000 | | 12,836,834 | |

2.00%, 11/15/21 - 02/15/22 | | 13,292,000 | | 13,319,248 | |

1.75%, 05/15/22 | | 1,835,000 | | 1,803,460 | |

2.75%, 02/15/24 | | 29,579,000 | | 31,106,489 | |

2.50%, 05/15/24 | | 4,850,000 | | 4,992,469 | |

| | | | 126,444,324 | |

U.S. GOVERNMENT AGENCY MORTGAGE-BACKED SECURITIES - 18.1% | | | | | |

Federal Home Loan Mortgage Corp. - 2.8% | | | | | |

Federal Home Loan Mortgage Corp. | | | | | |

3.00%, 06/01/29 - 03/01/43 | | 7,085,742 | | 7,245,479 | |

6.00%, 07/01/37 - 09/01/37 | | 242,342 | | 274,280 | |

5.00%, 02/01/38 - 08/01/40 | | 2,331,161 | | 2,576,478 | |

5.50%, 03/01/39 - 07/01/39 | | 678,111 | | 759,047 | |

4.50%, 03/01/42 | | 5,705,837 | | 6,190,962 | |

3.50%, 04/01/42 - 06/01/42 | | 5,721,273 | | 5,957,378 | |

4.00%, 03/01/43 - 11/01/44 | | 3,609,102 | | 3,864,287 | |

4.50%, 09/01/44, TBA (j) | | 3,628,041 | | 3,944,261 | |

| | | | 30,812,172 | |

Federal National Mortgage Association - 10.7% | | | | | |

Federal National Mortgage Association | | | | | |

4.00%, 04/01/26 - 09/01/40 | | 19,903,327 | | 21,268,117 | |

3.00%, 06/01/27 - 12/01/44 | | 34,956,012 | | 35,619,969 | |

2.50%, 01/01/28 - 12/01/29 | | 11,026,782 | | 11,237,311 | |

3.50%, 12/01/28 - 08/01/44 | | 15,757,802 | | 16,484,880 | |

5.50%, 12/01/33 - 08/01/38 | | 3,549,647 | | 3,993,028 | |

5.00%, 06/01/35 | | 3,233,062 | | 3,579,422 | |

6.00%, 08/01/37 - 01/01/38 | | 426,048 | | 483,621 | |

4.50%, 08/01/40 - 02/01/41 | | 14,686,202 | | 15,975,524 | |

4.50%, 01/15/45, TBA (j) | | 543,000 | | 589,292 | |

3.50%, 02/15/45, TBA (j) | | 317,000 | | 329,423 | |

4.00%, 02/15/45, TBA (j) | | 7,491,000 | | 7,971,731 | |

| | | | 117,532,318 | |

Government National Mortgage Association - 4.6% | | | | | |

Government National Mortgage Association | | | | | |

4.50%, 03/15/40 | | 737,233 | | 807,454 | |

5.00%, 08/20/41 | | 1,687,864 | | 1,881,482 | |

3.50%, 08/20/42 - 06/20/43 | | 13,441,024 | | 14,125,426 | |

2.50%, 05/20/43 (d) | | 2,356,942 | | 2,414,067 | |

3.00%, 05/20/43 | | 1,706,239 | | 1,745,992 | |

4.00%, 05/20/44 | | 11,875,009 | | 12,740,192 | |

3.50%, 01/15/45, TBA (j) | | 3,955,000 | | 4,149,847 | |

4.50%, 01/15/45, TBA (j) | | 1,677,000 | | 1,832,052 | |

Government National Mortgage Association | | | | | |

4.50%, 08/20/43 | | 4,357,137 | | 4,766,311 | |

4.00%, 05/20/44 | | 4,905,697 | | 5,305,007 | |

| | | | 49,767,830 | |

Total Government and Agency Obligations (cost $320,047,504) | | | | 326,138,175 | |

PREFERRED STOCKS - 0.5% | | | | | |

ENERGY - 0.1% | | | | | |

NuStar Logistics LP, 7.63%, 01/15/43 (e) | | 48,000 | | 1,238,400 | |

FINANCIALS - 0.4% | | | | | |

Allstate Corp., 5.10%, 01/15/53 | | 49,000 | | 1,241,170 | |

Goldman Sachs Group Inc., 5.50%, (callable at 25 beginning 05/10/23) (g) | | 76,000 | | 1,854,400 | |

U.S. Bancorp - Series G, 6.00%, (callable at 25 beginning 04/15/17) (e) (g) | | 44,500 | | 1,206,840 | |

| | | | 4,302,410 | |

Total Preferred Stocks (cost $5,519,040) | | | | 5,540,810 | |

SHORT TERM INVESTMENTS - 6.7% | | | | | |

Investment Company - 2.6% | | | | | |

JNL Money Market Fund, 0.01% (k) (l) | | 27,883,831 | | 27,883,831 | |

See accompanying Notes to Financial Statements.

| | Shares/ Par† | | Value | |

Securities Lending Collateral - 4.1% | | | | | |

Securities Lending Cash Collateral Fund LLC, 0.22% (k) (l) | | 44,951,314 | | 44,951,314 | |

Total Short Term Investments (cost $72,835,145) | | | | 72,835,145 | |

Total Investments - 104.8% (cost $1,137,031,648) | | | | 1,147,140,284 | |

Other Assets and Liabilities, Net - (4.8%) | | | | (52,418,959 | ) |

Total Net Assets - 100.0% | | | | $ | 1,094,721,325 | |

| | | | | | |

(a) Security is restricted to resale to institutional investors. See Restricted Securities in the Notes to Schedules of Investments.

(b) The Sub-Adviser has deemed this security to be illiquid based on procedures approved by the Trust’s Board of Trustees.

(c) The Sub-Adviser has deemed this security which is exempt from registration under the 1933 Act to be liquid based on procedures approved by the Trust’s Board of Trustees. As of December 31, 2014, the aggregate value of these liquid securities was $222,648,684 which represented 20.3% of net assets.

(d) Variable rate security. Rate stated was in effect as of December 31, 2014.

(e) All or a portion of the security was on loan.

(f) Security fair valued in good faith in accordance with the procedures approved by the Trust’s Board of Trustees. Good faith fair valued securities may be classified as Level 2 or Level 3 for Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 820 “Fair Value Measurement,” based on applicable valuation inputs. See FASB Topic 820 in the Notes to Financial Statements.

(g) Perpetual security.

(h) The interest rate for this security is inversely affected by upgrades or downgrades to the credit rating of the issuer.

(i) Security is a “step-up” bond where the coupon may increase or step up at a future date. Rate stated was the coupon as of December 31, 2014.

(j) All or a portion of the investment was purchased on a delayed delivery basis. As of December 31, 2014, the total payable of investments purchased on a delayed delivery basis was $18,764,860.

(k) Investment in affiliate.

(l) Yield changes daily to reflect current market conditions. Rate was the quoted yield as of December 31, 2014.

| | Shares/ Par† | | Value | |

JNL Money Market Fund | | | | | |

CORPORATE BONDS AND NOTES - 14.2% | | | | | |

CONSUMER DISCRETIONARY - 0.3% | | | | | |

Toyota Motor Credit Corp., 0.23%, 10/29/15 (a) | | $ | 6,000,000 | | $ | 6,000,000 | |

FINANCIALS - 12.6% | | | | | |

American Honda Finance Corp. | | | | | |

0.23%, 06/04/15 (a) | | 33,000,000 | | 33,000,000 | |

0.23%, 10/07/15 (a) | | 20,000,000 | | 20,000,000 | |

BPCE SA, 0.48%, 05/27/15 (a) | | 30,000,000 | | 30,000,000 | |