UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-10303

Buffalo Funds

(Exact name of registrant as specified in charter)

5420 W. 61st Place

Shawnee Mission, KS 66205

(Address of principal executive offices) (Zip code)

Clay E. Brethour

5420 W. 61st Place

Shawnee Mission, KS 66205

(Name and address of agent for service)

(913) 677-7778

Registrant’s telephone number, including area code

Date of fiscal year end: March 31, 2015

Date of reporting period: March 31, 2015

Item 1. Reports to Stockholders.

Message to Our Shareholders

Message to Our Shareholders

O

ur most recent fiscal year, ended March 31, 2015, anniversaries the stock market’s sixth year of the current bull market. In general there are a number of issues facing the market which we believe will increase its “choppiness” going forward. We believe this volatility will transition the market place from a general momentum market, into a “stock-pickers” market, which may provide opportunities for our shareholders to outperform.

While the U.S. market is in its sixth year of recovery from the “great” recession, the health of the economy continues to be mixed. According to the U.S. Bureau of Labor Statistics, the U.S. unemployment rate stood at 5.5% in March 2015, its lowest level since 2008. Wage inflation remains muted, and the general economy has felt more “Wall Street” driven than ‘Main Street”. Given the strengthening of U.S. companies’ balance sheets over the past several years, the economy is in a favorable position going forward.

Our shareholders living in the Northeast certainly understand the slowing of the economy, given the significant impact of that region’s record snowfall. However, there are a number of other factors affecting the entire country, notably the port strikes impacting the movement of goods throughout the U.S. The recently released 2015 first quarter gross domestic product initial report showed the economy grew only 0.2%.

The mixed economic news has put a hold on the Federal Reserve’s imminent rise in short-term interest rates. The initial consensus view of a mid-year increase has been revised to this fall, and is expected to be in smaller increments than previously anticipated. We would not be surprised to see the Fed wait until 2016 to raise rates, given the unprecedented Quantitative Easing programs initiated throughout the world. In addition to India and China, the European Central Bank and the Bank of Japan have lowered interest rates in support of their respective countries’ monetary stimulus policies.

The current environment places the Fed in a precarious position. Low interest rates prevail throughout the world. The current yield on the 10-year U.S. Treasury note of 2.1% is high compared to its German counterpart’s yield of 0.36%. Capital throughout the world has gravitated towards the highest return. This gravitation has led to the strengthening of the U.S. Dollar Index and having an adverse impact on multinational companies. The Fed will be sensitive to a strengthening dollar, particularly since 71.2% of the U.S. Dollar Index is weighted towards the euro and the yen, which represent 57.6% and 13.6%, respectively.

Regardless of the timing, interest rates are unsustainably low throughout the world and even negative in some countries within Europe. In a rising interest-rate environment, stock-pickers (actively managed funds) have historically outperformed passive funds. We believe our investment strategy of constructing our Funds with detailed bottom-up analysis of companies should benefit from our internally identified broad secular growth trends providing shareholders with a group of companies which has the potential to grow long-term, regardless of overall economic conditions.

As always, we appreciate your trust in our management teams and our organization. We will continue to work diligently to meet your expectations.

Sincerely,

Clay E. Brethour

President

Active investing has higher management fees because of the manager’s increased level of involvement while passive investing has lower management and operating fees. Investing in both actively and passively managed mutual funds involves risk and principal loss is possible. Both actively and passively managed mutual funds generally have daily liquidity. There are no guarantees regarding the performance of actively and passively managed mutual funds. Actively managed mutual funds may have higher portfolio turnover than passively managed funds. Excessive turnover can limit returns and can incur capital gains.

The Funds’ investment objectives, risks, charges and expenses must be considered carefully before investing. The Prospectus contains this and other important information about the investment company, and it may be obtained by calling 1-800-49-BUFFALO or visiting www.buffalofunds. com. Read it carefully before investing.

Past performance does not guarantee future results. Mutual fund investing involves risk. Principal loss is possible.

The opinions expressed above are those of the author, are subject to change and are not guaranteed and should not be considered investment advice.

The Buffalo Funds are distributed by Quasar Distributors, LLC.

2

Portfolio Management Review

Buffalo Discovery Fund

While growth slowed in the first quarter of 2015, over the past year the United States economy outperformed other developed markets delivering relatively consistent and modest expansion. Growth in U.S. gross domestic product (GDP) reached 2.2% in 2014, consistent with 2013. The first quarter 2015 initial measurement of GDP growth came in at 0.2% for a myriad of reasons. A harsh winter in the northeast and the west coast port closures arising from the dock workers’ strike both contributed to the deceleration. The strength of the U.S. dollar relative to other developed and developing market currencies, as these economies provide stimulus to drive economic expansion, has negatively impacted U.S. exports. In addition, the drop in oil prices had an impact on GDP, reducing corporate profits from the energy sector. The offset is reduced manufacturing input costs resulting in increased corporate profit from the industrial sector and increased consumer discretionary income driving retail sales growth, yet these positive effects typically lag. So the economy faced some headwinds in the first quarter of 2015, and consequently expectations for first quarter earnings have come down.

However, despite a relatively slow start to 2015 in terms of domestic economic growth, the equity market has continued its ascent with the Russell 3000 Growth Index returning 4.05% in the most recent quarter and 15.76% for the twelve months ending March 31, 2015. The strength of the dollar has led some foreign investors to the U.S. capital markets as a perceived safe haven. Fixed income yields remained depressed and equities offered an attractive alternative. The moderating pace of U.S. economic growth is likely to delay the inevitable interest rate hikes expected from the Federal Reserve to late-2015 from mid-2015. Expectations remain high for U.S. economic growth to accelerate for the remainder of the calendar year. These factors present a favorable backdrop for equities.

The Buffalo Discovery Fund invests in companies which create value through the commercial application of innovative products, services, or intellectual property. The Fund invests in companies across all market capitalizations and sectors. While we are cognizant of the macroeconomic environment, our top down process is driven by the Buffalo secular trends rather than predictions related to global economic factors. The majority of our research efforts focus on bottom up stock and company analysis. Whether we buy, trim or exit a holding is primarily driven by the investment thesis and valuation.

The Buffalo Discovery Fund returned 15.56% in fiscal 2015, roughly in-line with the Russell 3000 Growth Index, which appreciated 15.76% in the same period. The Fund outperformed its peers, as measured by the Lipper Multi

Cap Growth Funds Index, which gained 14.25% for the year. Sector allocation relative to the benchmark was strong driven by the Fund’s almost 1400 basis point overweight healthcare, the top performing sector in the benchmark. Stock selection was a modest detractor in the period. Strong stock selection in Consumer Discretionary, Financial and Healthcare holdings was more than offset by weak selection within the energy and industrial sectors. The precipitous fall in the price of crude oil, due to what we believe is a near-term oversupply issue, had a profound impact on the operating performance of our companies with exposure to the oil and gas end markets.

The top three contributors to the Fund in fiscal year 2015 were Hospira, Apple and Allergan. Hospira, a maker of lower cost injectable drugs, was the Fund’s largest holding entering fiscal 2015 given the company’s focus on containing health care costs and the attractive valuation of the equity. In February 2015, Pfizer announced plans to acquire Hospira for cash consideration of $90 per share, a significant premium to where the equity was trading. Apple’s stock appreciated in response to the iPhone 6 launch which exceeded expectations and drove upward earnings revisions. Allergan has a strong global healthcare franchise in two highly profitable businesses, aesthetic medicine and ophthalmology. Particularly in aesthetic medicine Allergan has several products with unmatched brand equity. Given these strong and sustainable fundamentals, the company became an acquisition target in fiscal 2015 with several suitors. Actavis ultimately had the winning bid and has completed the acquisition.

The three top detractors in the period were CARBO Ceramics, Chart Industries and Forum Energy Technologies, all companies with exposure to energy end markets. Oil had a big move over the past year, peaking in June 2014 at nearly $107 a barrel, then reaching a low in the $40s in March of 2015. The decrease in the price accelerated after Organization of the Petroleum Exporting Countries (OPEC) November 2014 decision to not cut its output quota in spite of lower worldwide demand for oil. OPEC decided to instead focus its efforts on maintaining market share, and in some instances, increasing market share in particular markets by driving the price of oil to a level that would make it uneconomical for non-OPEC members to compete. The majority of the incremental worldwide crude oil production for the past several years has been the result of non-OPEC producers, which have taken market share away from OPEC. In North America, the number of rigs drilling for oil has dropped significantly with the drop in oil prices, negatively impacting two of the Fund’s holdings; CARBO Ceramics and Forum Energy Technologies. We believe that the valuation of these two stocks is attractive and that they will recover as the oil supply contracts, driving the price of oil higher.

3

Portfolio Management Review

(Continued)

The lower crude prices also pressured the incentives to incorporate the use of natural gas as a substitute for diesel, negatively impacting Chart Industries, a leading manufacturer of equipment used in the liquefied natural gas (LNG) supply chain. Additionally, China took a hiatus in the build out of its LNG infrastructure as its economy slowed. More recently interest in the LNG build out in China has resurfaced. North America is also exploring increased investment in LNG facilities to export natural gas. These factors reinforce our belief that Chart Industries’ long term outlook is bright.

The Buffalo Discovery Fund ended fiscal 2015 holding 73 stocks, up from 69 at the end of fiscal 2014. During the year eighteen new positions were added to the Fund and fourteen holdings were eliminated, a few of which were acquired by other companies. Cash at the end of the fiscal year was 7.1%, up from 5.6% at the end of fiscal 2014. This cash level is outside the normal range as we reduced the Fund’s exposure to Healthcare in the last week of the quarter. We see ample opportunities to reinvest the excess cash and plan to do so in the near term opportunistically.

We are optimistic U.S. economic growth will accelerate for the remainder of 2015. The harsh winter is behind us, the west coast ports are working through backlogs, employment and wage growth are improving and residential housing continues its recovery. We believe that the U.S. economy can deliver modest growth consistent with the last several years for the full year 2015. The upside case would be that global GDP growth accelerates driven by economic stimulus emanating from the Euro Zone, Japan and China. Many cash-generating, pro-cyclical companies within the technology and industrial sectors have been reluctant to invest their excess liquidity due to wavering business confidence, and instead have returned it to shareholders and paid down debt. An acceleration of global economic growth would favor growers over payers, and discretionary over stable businesses. Increased business confidence should ultimately lead to increased business growth investment, as opposed to return of capital. If global GDP accelerates, we believe investors will rotate into pro-cyclical multinational companies. Furthermore the valuations of the pro-cyclical multinational companies appear attractive compared to more defensive areas such as healthcare. Healthcare stocks have led the market the past three years. And while growth remains robust, the stock prices frequently incorporate that growth. Our valuation discipline led us to exit two of our biotech holdings in that last quarter of fiscal 2015. We plan to reinvest that capital into stocks that could offer a more compelling risk reward, which at this juncture appears to be more pro-cyclical industrial and technology companies, as well as within the energy sector.

Buffalo Dividend Focus Fund

For the twelve month period ending March 31, 2015, the Buffalo Dividend Focus Fund returned 18.86%, significantly outperforming the benchmark S&P 500 Index which had a return of 12.73%.

While the Fund’s allocation across various sectors had a negative impact for the year, we more than offset that impact through stock selection. In terms of relative sector contributions, Energy was the largest contributor to the Fund’s outperformance in the year ending 3/31/2015, followed by Industrials. The largest detractors from relative performance were Health Care and our cash position. Our cash position averaged approximately 10.7% for the year and caused a 1.0% drag to our performance.

In the Energy sector we have found a number of master limited partnerships (MLP’s) that we are attracted to due to their stable cash flow generating asset base, generous yields, and strong distribution growth. Many of these companies are engaged in the midstream segment of the energy markets, which is the link between the exploration and production of crude oil and natural gas from the wellhead and the delivery of these commodities to refineries or other end use markets. Assets included in the midstream segment include transportation pipelines, storage, natural gas processing, and natural gas fractionation just to name a few. Many (but not all) of these types of midstream assets have stable fee structures that have very little direct commodity price risk, thus allowing the assets to produce a steady and growing source of cash flow that allows the asset owners to pay stable and growing distributions.

Dominion Midstream Partners and Shell Midstream Partners are just a couple examples of MLP’s that performed well in the past year for the Fund. Although these two MLP’s own different assets in different geographies throughout the midstream value chain in the U.S., the thesis for owning them is relatively straightforward. They both have, in our view, great assets and strong parent companies that will likely sell assets down to the partnership over time and should allow them to grow significantly in the future. We believe both partnerships could be able to grow their distribution at 15% or greater per year for at least the next three years.

In the Industrials segment, the Fund benefited from positive stock selection relative to the benchmark. Notable winners included Robert Half and Southwest Airlines. Robert Half was up approximately 46% for the Fund during the period while Southwest Airlines was up approximately 72%. Robert Half benefited from the improving labor market as unemployment continued to decline. Southwest Airlines benefited from a more rational airline industry as well as the tailwind of declining energy prices as fuel is a large component of their cost structure.

4

Our worst performing sector relative to the benchmark was Health Care. Notable relative detractors during the year included both stocks that were owned (Novo Nordisk, GlaxoSmithKline, and Sanofi) as well as stock that were not owned, namely companies that do not have a dividend but contributed nicely to the benchmark return such as Celgene and Actavis. GlaxoSmithKline performed poorly due to worries by the market that the company’s dividend might be at risk of being cut. Sanofi and Novo Nordisk both suffered from concerns over pricing power in the insulin market, while Sanofi also suffered from the board’s decision to abruptly remove CEO Chris Viehbacher based on the board’s concerns over a lack of communication by Viehbacher with the board.

Going forward, we continue to have a consistent message in that we look for companies that we believe 1) exhibit long-term sustainable competitive advantages, 2) have a history of growing their revenues, earnings, and dividends, 3) generate significant amounts of free cash flow, 4) have rock solid balance sheets, 5) have management teams who exhibit stellar capital allocation skills and whose interests are aligned with shareholders, and 6) are trading at an adequate discount to our estimate of fair value. As the market has moved up and multiples have expanded over the last year, it has become more difficult to continue to find undervalued companies. We continue to search for companies that meet our criteria for purchase and sell those that no longer exhibit the qualities we desire.

Buffalo Emerging Opportunities Fund

The Buffalo Emerging Opportunities Fund focuses on early stage growth companies that have the potential to deliver significant capital appreciation over the long term. The Fund invests primarily in companies with a market capitalization below $1 billion.

This past fiscal year began with concerns over stretched valuations in the technology sector. As the year progressed, geopolitical issues including the Ukraine crisis and downward volatility in foreign currencies and commodities developed. Despite these events, the broader markets continued their march higher as the U.S. economy continued to advance and successfully navigate the weakness in a number of other geographies.

For the 12-month period ending March 31, 2015, the Buffalo Emerging Opportunities Fund posted a return of -0.71%, trailing the Russell 2000 Growth Index return of 12.06%. The underperformance was due primarily to stock selection as we construct our portfolio by investing in premier, early stage growth companies with less attention paid to the weightings and allocations of our benchmark. While that can lead to periods of outperformance such as the

trailing three and five years, it can also lead to periods of underperformance as seen in the past 12 months ended March 31, 2015.

During the year, the Information Technology sector was the largest drag on performance, resulting in a -4.75% variance versus the Russell 2000 Growth Index. Poor stock selection was the culprit as a number of our technology holdings posted large negative returns. One of the contributors to the underperformance in the sector was voxeljet, an early stage 3D printing company with significant exposure to automotive and industrial applications. While the company continues to grow rapidly and expand its footprint, investors’ appetite and willingness to pay higher multiples for these small cap growth stocks dipped during the past year as evidenced by the decline in this particular name. Despite the underperformance during the past year, we remain overweight the Technology sector given the focus on innovation lining up well with the Fund’s objectives of long-term growth of capital.

Other noteworthy contributors to the underperformance were the Consumer Discretionary and Consumer Staples sectors which caused -3.26% and -2.11% of relative shortfall, respectively, during the year. In the Consumer Discretionary sector, Black Diamond, a leading global equipment provider for climbing, skiing and mountaineering, posted disappointing results in their efforts to expand their brand into outdoor apparel. In the Consumer Staples category, Boulder Brands, a leading provider of gluten-free food brands, struggled with key input cost inflation along with slowing category growth of gluten free foods.

While the drag from the Healthcare sector was more modest at -0.97%, we were underweight the sector as it rose 28% during the fiscal year, leading all benchmark sectors. Healthcare now represents close to 25% of the Russell 2000 Growth Index with 15% of the index being the biotech and pharmaceuticals industries. Record volumes of mergers and acquisitions combined with a wave of innovative new drugs as well as a more streamlined Food and Drug Administration (FDA) approval process has caused a “melt up” in the majority of these type of healthcare companies. The broad-based, multi-year outperformance of this area of the market has drawn comparisons to the late 90’s tech boom given that many are high-risk, single product companies that have business models that are cash flow and earnings negative. Not every drug can generate $500 million-$1 billion in sales and given that so many of these companies are valued as such, then it stands to reason that market forces will correct these imbalances over time. As a reminder, our investment process typically avoids these types of companies due to the binary nature of the outcomes. For example, if company A does not get approval of a particular drug then the value of the company can quite literally be less than half of

5

Portfolio Management Review

(Continued)

what it was the previous day, which is not a risk we think is worth taking when running a more concentrated portfolio of 45-65 small-cap companies.

The collapse in oil prices, a surging United States dollar, the West Coast port strike and harsh winter weather have taken a toll on U.S. economic results to begin calendar 2015. However, during the current bull market that dates back to March 2009, economic metrics have disappointed in some fashion during the first quarter over the past five years only to yield to stronger results in the summer and fall months. Time will tell if this occurs again in 2015, but early indicators point to stronger data in the second quarter.

By many metrics, valuations for small caps are above historical averages; however, we believe this data point is somewhat mitigated by the fact that investors remain decidedly unenthusiastic towards the asset class based on mutual fund flows, which have been negative for four straight quarters. Small cap equity fund outflows in the December 2014 quarter even exceeded the worst quarter of outflows from the 2008 financial crisis!

After a strong five-year run for the Fund, the past year clearly fell short of our expectations. We continue to work diligently to attempt to best position the Fund going forward. As the economic outlook and investor sentiment ebbs and flows, our job remains the same in terms of identifying attractively valued, early-stage growth companies that have robust structural growth potential and defensible business models. We will use upward and downward market volatility to attempt to best position the Fund for long-term capital appreciation.

As a reminder, the Fund initiated a soft-close in November 2013 that remains in effect today. The Fund remains open to additional investments from existing investors, all clients of existing Advisors, Consultants, and Employer Sponsored Retirement Plans (401k, etc.). Please visit www.buffalofunds.com for more information.

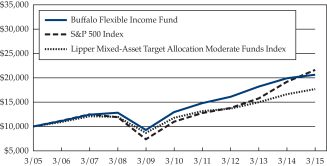

Buffalo Flexible Income Fund

For the twelve months ended March 31, 2015, the Buffalo Flexible Income Fund returned 3.33%. During the same time period, the S&P 500 returned 12.73% and the Bank of America Merrill Lynch High Yield Master II Index returned 2.05%.

Equity

| • | For the fiscal year ended March 31, 2015, the equity portion of the portfolio returned 6.19% compared to 12.73% for the S&P 500 Index. The Flexible Income Fund’s equity component is primarily focused on large cap dividend payers which we believe possess significant competitive advantages. The primary sectors that led to the underperformance were Healthcare, Energy and |

Information Technology. The underperformance in Healthcare was due to both security selection and sector allocation. The Fund was roughly 350bps underweight the best performing sector in the S&P. Security selection also contributed to the underperformance in the sector as the fund is focused on dividend paying stocks and consequently did not have exposure to some non-dividend paying healthcare stocks that generated strong returns such as Actavis, Celgene and Gilead. Additionally, some of the dividend paying stocks the Fund owned did not perform as well as the sector including GlaxoSmithKline (GSK) and Baxter. GSK underperformed due to anemic sales growth and margin pressure which reflect increased competition and underwhelming new product launches and pipeline development. The deteriorating financials ultimately led the company to suspend its share repurchases and the market also became nervous about the sustainability of the dividend. However, we continue to believe in the Company’s prospects and expect new products to drive improved financial performance over the coming years. Baxter underperformed due to poor strategic execution in plasma, competition to key products and uncertainty over the upcoming company spin-off. The negative performance within Energy was due entirely to its overweight position as Energy was the worst performing sector over the past 12 months. The underperformance in IT was due to an underweight position and security selection. The Fund was roughly 700bps underweight the sector and the sector was one of the better performing sectors over the past 12 months. As it relates to security selection, the Fund was underweight Apple and did not have exposure to some non-dividend paying stocks such as Facebook that performed well over the past 12 months. |

Fixed income

| • | The fixed income portion of the Buffalo Flexible Income Fund generated a return of 3.56% over the past 12 months which compares favorably to the 2.05% return for the Bank of America Merrill Lynch Master II Index. The outperformance was primarily due to security selection within the Consumer Discretionary sector while the Energy and Health Care sectors also positively contributed to returns over the past twelve months. Within the Consumer Discretionary segment, the Lions Gate Entertainment (LGF) convertible notes were the top performer. LGF continues to execute on its growth strategy and there has also been speculation that LGF could potentially be acquired due its growing TV and film content. The outperformance in the Energy sector was driven by a modest underweight in one of |

6

the worst performing sectors while Healthcare outperformance was driven by an overweight in one of the better performing sectors. |

As we look ahead, we remain focused on finding attractive yield opportunities that we believe have favorable risk reward outlooks. Within the equity space we remain focused on large cap dividend payers as well as select MLPs. Within fixed income, we are primarily focused on three asset classes, high yield bonds, convertible bonds and floating rate bank debt.

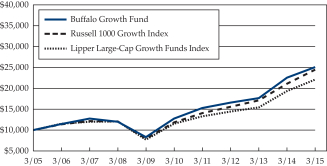

Buffalo Growth Fund

The Buffalo Growth Fund invests in high quality growth companies with an emphasis on large capitalization stocks. We seek to invest in companies that have benefited from long-term secular growth trends that comprise our premier universe. Then we perform bottoms-up fundamental analysis that culminates in a valuation that incorporates both an upside target and downside risk exposure. The Growth Fund owns a portfolio of companies where we believe the upside potential exceeds downside risk exposure. Our belief is the market frequently overreacts to short term news providing what we view as attractive opportunities to purchase companies with long term growth opportunities. We use these opportunities to build a portfolio of high quality growth companies with the potential for competitive returns.

For the fiscal year ending March 31, 2015, the Buffalo Growth Fund returned 11.32% compared to 16.09% for the benchmark Russell 1000 Growth Index. The underperformance relative to the index was most significant in the Consumer Discretionary and Industrials sectors, which was offset by outperformance within the Information Technology sector.

The performance of our holdings within the Industrial sector was most impacted by the decline in oil prices. The most notable detractor was Chart Industries, where lower oil prices contributed to slower than anticipated adoption of liquefied natural gas (LNG) for use in industrial transportation within the U.S. and China. The decline in oil prices has compressed the economic advantage of using LNG as an alternative to diesel. However, we believe more stringent emissions standards and low natural gas prices will catalyze LNG adoption over the long-term. As a result, we used weakness in shares as an opportunity to increase our ownership.

Within the Consumer Discretionary sector, performance was most impacted by Coach and Discovery Communications. With Coach we believed that a good management team combined with a strong brand would enable it to execute a product refresh that would rejuvenate sales growth. However, sales growth proved elusive and

management determined it needed to embark on a more significant turnaround. Discovery Communications we believed had an advantaged content cost structure with the potential for increased distribution globally that would yield competitive returns. The thesis was challenged by the secular shift towards video on demand offerings, like Netflix, that has surpassed expectations and created more competition for audiences than anticipated. This will be a long-term headwind that could dilute returns on capital by impacting both distribution and advertising revenues. We exited our positions in Coach and Discovery as our long term outlook for each company was impaired during the year.

Turning to the top contributors in the Fund, Allergan benefitted from consolidation in the Health Care sector. The company owns a strong global franchise in aesthetic medicine and ophthalmology, where it has several products with unmatched brand equity. Given these strong and sustainable fundamentals, the company became an acquisition target with Actavis ultimately winning a competitive bidding process.

Within the Information Technology sector, Apple and Facebook, were also top contributors. Apple, which has built a strong competitive position in the mobile device market, produced a strong product cycle with the introduction of the iPhone 6 that resulted in market share gains. In addition, Apple introduced a watch that marked its first new product category since the iPad. Facebook shares climbed as it continued to rapidly grow sales and market share in digital advertising, particularly on mobile devices. It has built a suite of applications including the flagship Facebook app, Messenger, Instagram, and WhatsApp that have each successfully signed up between 300 million to over a billion users. The suite of apps provides it with a strong competitive advantage in audience reach that has proved attractive to advertisers.

While we are disappointed to have trailed the benchmark index for the fiscal year period, we recognize that periods of underperformance are an inevitable risk associated with seeking differentiated returns. However, we believe over the long-term our approach of seeking out high quality growth companies with the patience to buy at prices attractive for long-term capital returns have the potential to win out.

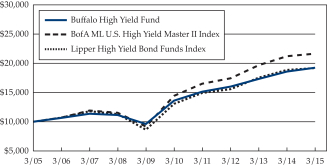

Buffalo High Yield Fund

The Buffalo High Yield Fund returned 3.58% for the fiscal year ended March 31, 2015. During the period, the Fund outperformed by 153 basis points (bps) our primary benchmark, the BofA Merrill Lynch High Yield Master II Index (the “Index”) which had a return of 2.05% during the comparable period. Our outperformance relative to the Index can largely be attributed the Fund’s strategy of owning higher credit quality issues with shorter durations,

7

Portfolio Management Review

(Continued)

significant underweight in the Energy sector compared to the Index, and strong returns from the Fund’s common stock holdings. In fiscal 2015, higher returns in the high yield universe were directly correlated with higher credit quality as the “BB” rated sector returned 4.6% versus the “CCC”* sector losing -3.4%. According to JP Morgan, the Energy sector was the worst performing industry losing -8.0% in fiscal 2015 which benefited the Fund relative to the Index as the Fund’s Energy allocation was 5.2% compared to the Index’s 13.0% weighting. From an asset class perspective, contributions from our holdings of straight corporate bonds, bank loans, convertible preferred and common stocks all outperformed the Index. Our convertible bonds and cash holdings underperformed the Index.

A more detailed look at the portfolio demonstrates how the performance was generated during the fiscal year 2015:

| APPROXIMATE WEIGHTING RANGE | APPROXIMATE ASSET CLASS RETURN | |||||||||||

| LOW | HIGH | |||||||||||

Straight Corporates Bonds | 61 | % | 69 | % | 5 | % | ||||||

Convertibles Bonds | 16 | 17 | 1 | |||||||||

Bank Loans | 1 | 2 | 2 | |||||||||

Convertible Preferred Stocks | 2 | 2 | 10 | |||||||||

Common Stocks | 5 | 6 | 19 | |||||||||

Cash | 5 | 15 | 0 | |||||||||

|

| |||||||||||

Total | 4 | |||||||||||

Primary contributors to the straight corporate bond portfolio included Lions Gate 5.25% ‘18, Philips VanHeusen 7.75% ‘23, AAR Corp 7.25% ‘22 and FTI Consulting 6% ‘22. These bonds were relatively large weights within the portfolio, offered high credit quality with short duration, and performed well as lower quality and longer duration bonds declined. Securities that underperformed in this asset class included Kratos Defense & Security 7% ‘19, Hornbeck Offshore Services 5.875% ‘20 and Rent-a-Center 4.75% ‘21.

Two of the Fund’s largest convertible bond holdings, Lions Gate 1.25% ‘18 and Lions Gate 4% ‘17 generated strong returns. Fully offsetting these gains though, were losses sustained in General Cable 4.5% ‘29, Dealertrack 1.5% ‘17 and Servicesource 1.5% ‘18. As an asset class, convertible bonds contributed the least to the Fund’s total returns in fiscal 2015.

The Fund only owned two convertible preferred stock positions during the fiscal year 2015. HealthSouth 6.5% was a strong contributor as the underlying stock gained more than 25% during the year. The other convertible preferred, AMG Capital 5.15%, had virtually no impact on the Fund’s returns.

Within the common stock segment of the portfolio, names that contributed most positively to performance include FirstService Corproration, AbbVie, and Abbott Laboratories.

All of the common stock positions contributed positive returns to the Fund performance during the fiscal year.

The same factors that affected the high yield market during the 2014 fiscal year persisted throughout fiscal year 2015. Fixed income products, including high yield, continued to trade at relatively elevated levels driven by factors such as: (i) continued accommodative monetary policies from the Fed and uncertainty about the timing of interest rate increases; (ii) strong demand for yield securities outweighing supply; (iii) generally strong corporate earnings and a muted default environment; and (iv) investor complacency about the potential impact of geopolitical risks (such as turmoil in the Middle East and default risk in Greece). However, the precipitous drop in the price of crude oil during the second half of calendar year 2014 was a new significant factor that negatively influenced high yield returns as the Energy sector has the largest weighting in the Index. This weakness in high yield energy names caused spreads and yields to end the fiscal year higher than the near all-time lows when the year started, but still well below historical average levels. The spread to worst and yield to worst for the Index on March 31, 2015 were 494 bps and 6.2%, respectively, compared to 394 bps and 5.3% on March 31, 2014 and the 582 bps and 9.4% historical twenty year averages.

Within this environment, we have been managing the Fund cautiously. We believe that many bonds are not trading at levels that offer appealing risk/reward tradeoffs, and that the potential for a rising rate environment would lead to increased market volatility and more appealing investment opportunities. Our allocation of a portion of the Fund into common stocks and convertible securities reflects our belief that these securities offer better return opportunity relative to highly-speculative and richly valued CCC-rated bonds. We believe many CCC-rated and long duration bonds could underperform materially in a deteriorating market environment while offering minimal upside at current levels. We will continue to deploy cash to the opportunities that we believe offer the most appealing risk/reward tradeoffs with a bias toward high credit quality, relatively short duration, and attractive relative values.

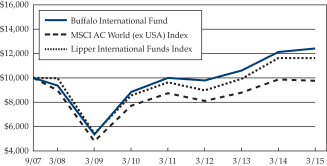

Buffalo International Fund

Markets tend to lead economies but the latest economic data suggests global economies are slowly responding as the conductors increase their tempo, with Japanese inflation coming in at 2.2% for the most recent month, Europe posting positive and accelerating GDP growth (off of a very low base) helped in part by Euro depreciation, and China’s official Purchasing Managers’ Index (PMI) landing in expansionary territory after suggesting contraction in manufacturing earlier in the year. With Europe, Japan and

8

China looking somewhat better, the mood in emerging markets has also seemingly turned the corner.

European, Japan and Hong Kong markets have responded very favorably, especially in the past few months, most posting solid returns on a local currency basis. On a U.S. dollar adjusted basis, the MSCI AC World (ex USA) Index posted a negative 1.01% return for the trailing twelve months ending March 31, 2015. Comparatively, the Buffalo International Fund posted a positive 2.32% return for the last twelve months, beating our benchmark.

Our emphasis on long-term growth through our weightings in Healthcare and Information Technology and our underweighting in Energy provided a positive boost to performance for the trailing twelve months, offset somewhat by our weighting and selection in Consumer Staples.

Notable significant positive performers for the year included Avago Technologies, Kuka AG, and Actavis PLC. Avago, a maker of RF signal filters has benefited from increasing penetration of 4G smartphones with increasing RF band connectivity. Kuka is a robotics manufacturer which has benefited from a switch of capital for labor as total labor costs continue to rise sharply in developing markets, and Actavis benefited from the resiliency of healthcare spending along with increased visibility on the synergies captured from recent acquisition activity.

All was not completely rosy, however, and we did have our fair share of laggards. Technip and Vallourec were the bigger detractors from performance – both being impacted by the significant slowdown in energy development spending. While each has secular growth aspects within the industry, they weren’t able to overcome the dramatic drop in all things energy in the fourth quarter of 2014. The Fund’s performance was also held back by holding cash due to our inclination to buy when stocks are down, not up. We ended the year with our cash balance at approximately 10%, above our longer-term goal of less than 5%.

With the European Central Bank baton pass, we’re happy to see international markets coming back in vogue with market participants. We’re also mindful that recent performance can change as markets rotate in and out of industries, as they sell winners and bid up under-performers. Our investment process favors a long-term secular growth perspective coupled within the context of our country specific macro analyses. We don’t fancy ourselves as global macro traders. While we don’t subscribe to the “buy anything and everything” approach in this environment, we continue to believe there are ample opportunities across the globe for investors. Our process remains unchanged. We look for companies that are exposed to secular growth trends, have improving balance sheets and sustainable

business models and whose valuation has the potential to provide appropriate prospective returns relative to their risks.

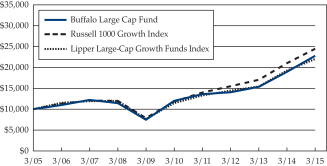

Buffalo Large Cap Fund

While growth slowed in the first quarter of 2015, over the past year the United States economy outperformed other developed markets delivering relatively consistent and modest expansion. Growth in U.S. gross domestic product (GDP) reached 2.2% in 2014, consistent with 2013. The first quarter 2015 initial measurement of GDP growth came in at 0.2% for a myriad of reasons. A harsh winter in the northeast and the west coast port closures arising from the dock workers’ strike contributed to the deceleration. The strength of the U.S. dollar relative to other developed and developing market currencies has negatively impacted U.S. exports, as these economies provide stimulus to drive economic expansion. In addition, the drop in oil prices had an impact on GDP, reducing corporate profits from the Energy sector. The offset is reduced manufacturing input costs resulting in increased corporate profit from the Industrial sector and increased Consumer Discretionary income driving retail sales growth, yet these positive effects typically lag. So the economy faced some headwinds in the first quarter of 2015, and consequently expectations for first quarter earnings have come down.

However, despite a relatively slow start to 2015 in terms of domestic economic growth, the equity market has continued its ascent with the Russell 1000 Growth Index returning 3.8% in the most recent quarter, and 16.1% for the twelve months ending March 31, 2015. The strength of the dollar has led some foreign investors to the U.S. capital markets as a perceived safe haven. Fixed income yields remain depressed and equities offer an attractive alternative. The moderating pace of U.S. economic growth is likely to delay the inevitable interest rate hikes expected from the Federal Reserve to late-2015 from mid-2015. Expectations remain high for U.S. economic growth to accelerate for the remainder of the calendar year. These factors present a favorable backdrop for U.S. equities.

While we are cognizant of the macroeconomic environment, our top down process is driven by the Buffalo secular trends rather than predictions related to global economic factors. By focusing on bottom up stock and company analysis, we believe that we can add more value to the investment process and Fund returns. The decision to buy, trim or exit a holding is driven by the investment thesis and valuation. The Buffalo Large Cap Fund holds the equity of secular growth companies which are beneficiaries of one of the Buffalo long term growth trends, and possess the following four characteristics:

| • | The company has a leadership position (a market share taker) in an attractive market with limited competition |

9

Portfolio Management Review

(Continued)

| • | The company’s products or services are value added |

| • | The company has a growth opportunity in North America |

| • | The company has a history of delivering a compelling return on invested capital and that pattern is expected to continue into the future. |

Our investment horizon is long term and we strive for low turnover. The focus on high quality companies, and the valuation discipline, is designed to position the Buffalo Large Cap Fund to potentially outperform its peers, particularly in a down market.

In the fiscal year 2015, the Buffalo Large Cap Fund returned 20.29% outperforming its benchmark, the Russell 1000 Growth Index, by 420 basis points, which returned 16.09%. The relative outperformance was driven by stock selection within the Consumer and Healthcare sectors. In fact, the top two contributors to the Fund for the year were healthcare holdings.

More specifically, the top three contributors to the Fund in fiscal year 2015 were Hospira, Biomarin and Apple. Hospira, a maker of lower cost injectable drugs, was the Fund’s largest holding entering fiscal 2015 given the company’s focus on containing health care costs and the attractive valuation of the equity. In February 2015, Pfizer announced plans to acquire Hospira for cash consideration of $90 per share, a significant premium to where the equity was trading. BioMarin, develops, manufactures and commercializes biologic drugs to treat rare diseases. The stock appreciated in anticipation of the FDA approval of a pipeline asset, drisapersen for Duchenne’s muscular dystrophy, which is currently under review at the agency. Duchenne’s muscular dystrophy is a debilitating disorder that affects male children starting at around age three and reduces life expectancy to about 30 years of age. Currently no drugs are available to treat this disease. Apple’s stock appreciated in response to the iPhone 6 launch which exceeded expectations and drove upward earnings revisions.

The three top detractors in the period were Precision Castparts, Discovery Communications and Qualcomm. Precision Castparts (PCP) is primarily a commercial aerospace supplier, but also has some modest exposure to oil and gas end markets. Precision Castparts had multiple earnings misses over the past year. The misses are attributable to the oversupply fundamentals in the oil/gas industry, as well as weak commercial aerospace product demand, which is not consistent with that end market’s strong growth dynamics. Since the commercial aerospace end market is strong, we believe that growth should return in the near-term in PCP’s commercial aerospace product offerings which should be a positive catalyst for the stock. Discovery Communications,

which owns and operates a number of cable networks in the U.S. and internationally, disappointed as U.S. advertising revenue growth was slower than investors expected while costs were higher than expected. Advertising growth has slowed in the U.S. as companies divert ad dollars from traditional venues to online and mobile internet properties. We believe this shift creates a significant headwind for Discovery Communications threatening its secular growth. As a result we exited the position during the year. Qualcomm was a detractor for several reasons. Chinese semiconductor manufacturers have failed to pay the licenses fees Qualcomm is owed based on the company’s intellectual property. These disputes are near a resolution and the license fees should be recovered over the next one to two years. In addition, a key customer did not use a Qualcomm processor in its latest generation handset. This issue will impact Qualcomm’s growth this year, but we are optimistic that Qualcomm can regain the business in future product cycles.

The Buffalo Large Cap Fund ended fiscal 2015 holding the equity of 46 companies up from 42 at the end of fiscal 2014. During the year ten new positions were added to the Fund (excluding the Google share split), and seven eliminated. The majority of the turnover was in the Healthcare and Consumer holdings. In Healthcare, several stocks reached extreme valuations and we reallocated those funds to equities that offered a more compelling risk reward. In the Consumer sector, we made a conscious effort to increase the Fund’s exposure to take advantage of growth in the automobile and healthy living end markets. Cash at the end of the fiscal year was 5.3% of net assets, modestly above the normal range for the Fund of 2-5%.

We are optimistic U.S. economic growth will accelerate in fiscal 2016. The harsh winter is behind us, the west coast ports are working through backlogs, employment and wage growth are improving and residential housing continues its recovery. We believe that the U.S. economy can deliver modest growth this year consistent with the last several years. The upside case would be that global GDP growth accelerates driven by economic stimulus emanating from the Europe and Asia. In the most recent quarter equity markets outside the U.S., specifically in Europe, China and Japan, outperformed the U.S. equity markets. Given this, the Buffalo Large Cap Fund remains committed to holding high quality companies with a growth opportunity in North America. We look for companies that are beneficiaries of the Buffalo secular growth trends. Frequently, growth opportunities in the U.S. translate into opportunities in the international markets. Therefore, the Fund has modest exposure to accelerating global economic growth, if that scenario materializes. Yet the Buffalo Large Cap Fund has greater leverage to growth companies in North America because we believe these companies are among the most

10

innovative, and have the potential to deliver strong, predictable and profitable growth over the intermediate and long term.

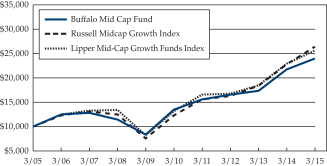

Buffalo Mid Cap Fund

The Buffalo Mid Cap Fund advanced 10.43% for the fiscal year ending March 31, 2015. This result, while fairly strong on an absolute basis, underperformed the Russell Midcap Growth Index return of 15.56% over the same timeframe. Strong stock selection from the portfolio’s consumer stocks helped contribute to the 10%+ portfolio return during the period and included gains from WhiteWave Foods, LifeTime Fitness, and Under Armour which advanced by 55.06%, 47.42%, and 40.40% respectively. WhiteWave Foods which manufactures, markets, distributes, and sells branded plant-based foods and beverages, coffee creamers, premium dairy products and organic produce across North America and Europe advanced throughout the year as the company generated a strong organic net sales increases within North America and Europe. LifeTime Fitness, which develops and operates resort-like fitness and recreational centers, was acquired by a private equity firm for a nice premium. While Under Armour, the high-tech sporting equipment and apparel company, generated strong sales growth and gross margin expansion over the year in all product areas including international, footwear, women’s, youth and direct-to-consumer. The company continued to benefit from its strong brand awareness translating into significant market share gains.

The top contributor to the Fund’s performance during the period was the health care-related company Hospira, Inc. Hospira, a maker of lower cost injectable drugs, was the Fund’s largest holding given the company’s focus on containing health care costs and the attractive valuation of the equity. In February 2015, Pfizer announced plans to acquire Hospira for cash consideration of $90 per share, a significant premium to where the equity was trading and helped contribute to the stock’s 103.03% return during the period. Unfortunately, despite Hospira’s strong contribution to the portfolio the Healthcare sector overall was an area of relative weakness for the portfolio due to an underweight position in biotechnology, an area which produced very strong performance for the index. Most of the companies operating in the biotech industry do not meet our quality parameters due to their ongoing reliance on external capital raises to fund their business rather than from internal cash flow and so it has been difficult to participate in this sector. While it is frustrating to not fully participate in the party that has been going on within biotech, we feel the prudent decision long term is to stick to our process.

Other areas of weakness for the portfolio which led to the performance shortfall compared to the index occurred within our energy-related positions due to plunging oil

prices during the past 12 months. For example, CARBO Ceramics, a supplier of ceramic and resin-coated proppant for fracturing oil and gas wells, declined significantly after management reported disappointing results throughout the year and offered weak future guidance. The company has continued to lower guidance due to a decline in demand as operators experiment with utilizing more sand versus ceramic proppant. The company is also experiencing an increase in competition from imports and domestic players. We believe that the movement by operators into different completion methods will eventually result in a reversion back to ceramic or a mixture of sand/ceramic proppant to optimize well productivity and economic return over the life of the well. With that said, this reversion may take some time to materialize, therefore we’ve made the decision to exit the position for better potential risk/reward opportunities in the near term.

The Industrial area also experienced poor selection effect relative to the index with Chart Industries contributing to almost half of the underperformance. The company is a leading manufacturer of equipment used in the liquefied natural gas (LNG) supply chain and declined over 55% during the past year as sentiment surrounding slow adoption of LNG within the transportation sector and decelerating growth in China contributed to the stock’s sell off. We continue to believe LNG will be integrated into transportation vehicles in both China and the U.S., driven by stringent emissions regulations and the prospect of long-term low natural gas prices in North America. Chart Industries remains favorably positioned to attempt to benefit from this adoption through the supply chain of LNG to the end markets.

Idea generation has been strong and we feel good about the portfolio’s current positioning. Relative performance versus the benchmark and peers so far this year (2015) has been solid, which is encouraging. Regarding portfolio changes, we added five new securities during the period, eliminated two, and one was acquired. We are currently overweight Consumer Discretionary and Financials and are monitoring these exposures closely. The portfolio ended the period with 54 positions, a number that may continue to expand as we use market volatility as an opportunity to establish new ideas.

Looking ahead we believe the U.S. economy is on a self-sustaining path. Rising real wages, more plentiful job opportunities, better access to credit, low inflation and dramatically lower oil prices should lead to higher consumer confidence. The decline of oil prices and sizable movements in the currency markets can create volatility in the capital markets as the impact works its way through the financial system. A stronger U.S. dollar creates a headwind for U.S. multinational company earnings and margins, while mid

11

Portfolio Management Review

(Continued)

cap companies have more limited exposure to currency headwinds and typically sell more of their products and services into the domestic market, which currently has a more favorable macroeconomic backdrop. As always, we are diligently searching for those premier mid cap growth companies that have benefited from secular growth tailwinds, trading at reasonable valuations, with the potential to deliver significant capital appreciation over the long term.

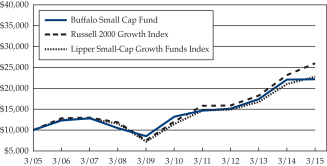

Buffalo Small Cap Fund

The Buffalo Small Cap Fund produced a return 0.56% for the fiscal year ending March 31, 2015. This result was obviously disappointing on an absolute and benchmark relative basis as the Russell 2000 Growth Index produced a return of 12.06% over the same timeframe.

Healthcare drove over half of the index’s return during the period as biotechnology and pharmaceutical shares rocketed on continued merger and acquisition activity in the sector. Record volumes of mergers and acquisitions combined with a wave of innovative new drugs as well as a more streamlined FDA approval process has caused a tremendous amount of investor speculation toward future earnings potential of many of these companies, in our opinion. The multi-year advance of stock prices in this area is reminiscent of the late 90’s tech boom given that many are high-risk, single product companies that have negative cash flow and no earnings. We don’t believe every new drug can generate a $1 billion in sales, so while many of these companies are valued as such, it stands to reason that market forces will find price multiple equilibrium over time. Most of the companies operating in the biotech industry do not meet our quality parameters due to their ongoing reliance on external capital raises to fund their business rather than from internal cash flow and so it has been difficult to participate in this sector. While our more established pharmaceutical and contract research holdings such as Akorn and ICON enjoyed substantial returns during the period, our underweight position to healthcare, and biotech in particular, hampered our relative return. While it is frustrating to not fully participate in the party that has been going on within biotech, we feel the prudent decision long term is to stick to our process.

Outside of Health Care the relative shortfall of the Fund during the past year was the result of poor stock performance among the portfolio’s Consumer and Technology stocks. Consumer stocks cost the portfolio over 350 basis points in relative performance. While we had a couple of solid performers in that area like LifeTime Fitness, which was acquired by a private equity firm for a nice premium, they were more than offset by the weakness from Pandora and Lumber Liquidators, which accounted for most of the underperformance in the sector. Lumber Liquidators, the specialty

retailer of hardwood flooring, declined by over 67% the past year exacerbated by a 60 Minutes story on the company claiming their laminate flooring sourced in China emits dangerous levels of formaldehyde. Although we believe the 60 Minutes analysis was flawed due to an improper testing technique that is not used by anyone in the industry or regulatory boards that ultimately decide appropriate levels of emissions, the report undoubtedly did some damage to the company’s brand. It will likely take some time for Lumber Liquidators to repair this damage and therefore we have trimmed the position as we believe the stock will tread water until the company sorts out the situation and reestablishes confidence in their products with consumers.

The Information Technology sector was also a major detractor during the past year and amounted to over 500 basis points of the relative performance shortfall when compared to the benchmark. Stratasys Ltd., a leader in 3D printing technology, was responsible for a large part of the underperformance, declining by over 50% during the period due to a reduction in earnings from most estimates from increased investments and weaker revenue growth due to a product issue with their desktop 3D printer line, Makerbot. While most investors expected increased investments, the product issue was a disappointing surprise and we have trimmed the position accordingly. Among the portfolio’s software as a service holdings, there was weakness in Cornerstone Ondemand which declined by about 40%. Cornerstone, a leading provider of talent management tools for recruiting, employee training and development, and other services declined due to lower than expected new business booking trends. This position has been trimmed due to execution issues and slowing growth. Overall we have been evaluating several new technology ideas for the portfolio and are monitoring ideal entry points based on what we view as attractive valuations.

Other areas of weakness for the portfolio which led to the performance shortfall compared to the index occurred within our energy-related positions due to plunging oil prices during the past 12 months. For example, CARBO Ceramics, a supplier of ceramic and resin-coated proppant for fracturing oil and gas wells, declined significantly after management reported disappointing results throughout the year and offered weak future guidance. The company has continued to lower guidance due to a decline in demand as operators experiment with utilizing more sand versus ceramic proppant. The company is also experiencing an increase in competition from imports and domestic players. We believe that the movement by operators into different completion methods will eventually result in a reversion back to ceramic or a mixture of sand/ceramic proppant to optimize well productivity and economic return over the life of the well. With that said, this reversion may take some

12

time to materialize, therefore we’ve made the decision to exit the position for better potential risk/reward opportunities in the near term.

The Industrial area also experienced poor selection effect relative to the index with Chart Industries contributing to the underperformance. The company is a leading manufacturer of equipment used in the liquefied natural gas (LNG) supply chain and declined over 55% during the past year as sentiment surrounding slow adoption of LNG within the transportation sector and decelerating growth in China contributed to the stock’s sell off. We continue to believe LNG will be integrated into transportation vehicles in both China and the U.S., driven by stringent emissions regulations and the prospect of long-term low natural gas prices in North America. Chart Industries remains favorably positioned to potentially benefit from this adoption through the supply chain of LNG to the end markets.

On a positive note, the Financial Services sector continues to provide solid relative performance. The portfolio’s investment in Wisdomtree, an innovator in exchange traded funds (ETFs), led our positive stock selection results within financials overall. Wisdomtree’s stock advanced over 63% during the year as strength in the U.S. dollar and a positive backdrop for global equities has led to continued growth in asset flows into the company’s currency hedged equity products. Overall our exposure to financials is now nearly 15% of portfolio assets, an overweight position of 700 basis points. As always, stocks come into the portfolio from the bottom up on their own merits and we are not trying to make any sector call here. However, as with any significant bet we make in the portfolio, we will continue to monitor this risk exposure closely.

We ended the period with 59 stocks in the portfolio up from 52 at year end, and while new idea generation remains strong, we remain steadfast in our quality and valuation parameters. The number of holdings in the portfolio will

likely tick up over the coming quarters but remain within our target range of 50 – 70 stocks. More new ideas have the added benefit of squeezing out old portfolio positions that have limited or no upside to our fair value estimates, and also stocks where our investment thesis has not played out or the company has failed to execute.

Outlook

Looking ahead we believe the U.S. economy is on a self-sustaining path. Rising real wages, more plentiful job opportunities, better access to credit, low inflation and dramatically lower oil prices should lead to higher consumer confidence. The decline in oil prices and sizable movements in the currency markets can create volatility in the capital markets as the impact works its way through the financial system. A stronger U.S. dollar creates a headwind for U.S. multinational company earnings and margins, while small-cap companies have more limited exposure to currency headwinds and typically sell more of their products and services into the domestic market, which currently has a more favorable macroeconomic backdrop. As always, we are diligently searching for those premier small cap growth companies that have benefited from secular growth tailwinds, trading at reasonable valuations, with the potential to deliver significant capital appreciation over the long term. We appreciate the continued confidence in our process and are laser focused on seeking to achieve outstanding performance relative to our benchmark and peers.

Sincerely,

| ||

John C. Kornitzer President, KCM |

A basis point is one hundredth of a percentage point (0.01%)

Free Cash Flow is revenue less operating expenses including interest expense and maintenance capital spending. It is the discretionary cash that a company has after all expenses and is available for purposes such as dividend payments, investing back into the business, or share repurchases.

Return of Capital is a return from an investment that is not considered income. The return of capital is when some or all of the money an investor has in an investment is paid back to him or her, thus decreasing the value of the investment.

Return on Invested Capital is used to assess a company’s efficiency at allocating the capital under its control to profitable investments. The return on invested capital measure gives a sense of how well a company is using its money to generate returns.

Spread to worst is the difference in overall returns between two different classes of securities, or returns from the same class, but different representative securities. It measures the difference from the worst performing security to the best, and can be seen as a measure of dispersion of returns within a given market or between markets.

Yield to worst is the lowest potential yield that can be received on a bond without the issuer actually defaulting.

| * | According to S&P, an obligation rated ‘CCC’ is currently vulnerable and dependent on favorable business, financial and economic conditions to meet financial commitments. |

13

Investment Results

Total Returns as of March 31, 2015

| AVERAGE ANNUAL | ||||||||||||||||||||||||

| GROSS EXPENSE RATIO* | THREE MONTHS | ONE YEAR | FIVE YEARS | TEN YEARS | SINCE INCEPTION | |||||||||||||||||||

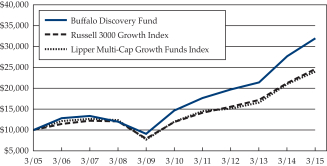

Buffalo Discovery Fund (inception date 4/16/01) | 1.01% | 7.50% | 15.56% | 16.94% | 12.33% | 9.24% | ||||||||||||||||||

Russell 3000 Growth Index | N/A | 4.05% | 15.76% | 15.71% | 9.41% | 4.83% | ||||||||||||||||||

Lipper Multi-Cap Growth Funds Index | N/A | 4.61% | 14.25% | 14.93% | 9.13% | 6.01% | ||||||||||||||||||

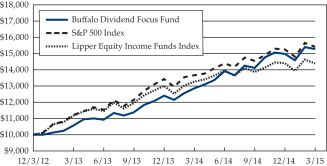

Buffalo Dividend Focus Fund (inception date 12/03/12) | 0.94% | 1.93% | 18.86% | N/A | N/A | 20.01% | ||||||||||||||||||

S&P 500 Index | N/A | 0.95% | 12.73% | N/A | N/A | 20.44% | ||||||||||||||||||

Lipper Equity Income Funds Index | N/A | -0.01% | 8.46% | N/A | N/A | 17.22% | ||||||||||||||||||

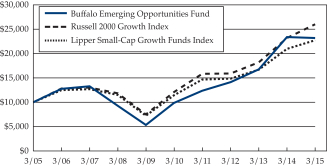

Buffalo Emerging Opportunities Fund (inception date 5/21/04) | 1.49% | 3.66% | -0.71% | 18.63% | 8.78% | 8.66% | ||||||||||||||||||

Russell 2000 Growth Index | N/A | 6.63% | 12.06% | 16.58% | 10.02% | 10.01% | ||||||||||||||||||

Lipper Small-Cap Growth Funds Index | N/A | 5.74% | 8.34% | 14.74% | 8.56% | 8.73% | ||||||||||||||||||

Buffalo Flexible Income Fund (inception date 8/12/94) | 1.03% | 0.86% | 3.33% | 9.79% | 7.49% | 7.48% | ||||||||||||||||||

S&P 500 Index | N/A | 0.95% | 12.73% | 14.47% | 8.01% | 9.61% | ||||||||||||||||||

Lipper Mixed-Asset Target Allocation Moderate Funds Index | N/A | 1.83% | 6.06% | 8.44% | 5.85% | 7.22% | ||||||||||||||||||

Buffalo Growth Fund (inception date 5/19/95) | 0.91% | 4.00% | 11.32% | 14.56% | 9.63% | 10.16% | ||||||||||||||||||

Russell 1000 Growth Index | N/A | 3.84% | 16.09% | 15.63% | 9.36% | 8.63% | ||||||||||||||||||

Lipper Large-Cap Growth Funds Index | N/A | 3.44% | 14.26% | 13.94% | 8.24% | 7.62% | ||||||||||||||||||

Buffalo High Yield Fund (inception date 5/19/95) | 1.02% | 2.74% | 3.58% | 7.19% | 6.79% | 7.61% | ||||||||||||||||||

Bank of America Merrill Lynch U.S. High Yield Master II Index | N/A | 2.54% | 2.05% | 8.40% | 8.04% | 7.55% | ||||||||||||||||||

Lipper High Yield Bond Funds Index | N/A | 2.47% | 1.80% | 8.01% | 6.76% | 6.20% | ||||||||||||||||||

Buffalo International Fund (inception date 9/28/07) | 1.08% | 4.37% | 2.32% | 7.01% | N/A | 2.92% | ||||||||||||||||||

MSCI AC World (ex USA) Index | N/A | 3.49% | -1.01% | 4.82% | N/A | -0.22% | ||||||||||||||||||

Lipper International Funds Index | N/A | 5.07% | 0.19% | 6.35% | N/A | 0.61% | ||||||||||||||||||

Buffalo Large Cap Fund (inception date 5/19/95) | 0.97% | 6.27% | 20.29% | 13.67% | 8.60% | 9.41% | ||||||||||||||||||

Russell 1000 Growth Index | N/A | 3.84% | 16.09% | 15.63% | 9.36% | 8.63% | ||||||||||||||||||

Lipper Large-Cap Growth Funds Index | N/A | 3.44% | 14.26% | 13.94% | 8.24% | 7.62% | ||||||||||||||||||

Buffalo Mid Cap Fund (inception date 12/17/01) | 1.01% | 7.05% | 10.43% | 12.28% | 9.15% | 8.75% | ||||||||||||||||||

Russell Midcap Growth Index | N/A | 5.38% | 15.56% | 16.43% | 10.19% | 9.01% | ||||||||||||||||||

Lipper Mid-Cap Growth Funds Index | N/A | 5.07% | 11.85% | 14.27% | 9.87% | 7.98% | ||||||||||||||||||

Buffalo Small Cap Fund (inception date 4/14/98) | 1.00% | 3.86% | 0.56% | 10.98% | 8.29% | 12.13% | ||||||||||||||||||

Russell 2000 Growth Index | N/A | 6.63% | 12.06% | 16.58% | 10.02% | 5.79% | ||||||||||||||||||

Lipper Small-Cap Growth Funds Index | N/A | 5.74% | 8.34% | 14.74% | 8.56% | 6.46% | ||||||||||||||||||

| * | As reported in the Funds’ Prospectus dated July 29, 2014. |

| Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current as of the most recent month-end may be obtained by calling 1-800-49-BUFFALO or by visiting the website at www.buffalofunds.com. |

| The Buffalo Discovery, Dividend Focus, Flexible Income, International, Large Cap, Mid Cap, and Growth Funds impose a 2.00% redemption fee on shares held for less than 60 days and the Buffalo High Yield, Emerging Opportunities and Small Cap Funds impose a 2.00% redemption fee on shares held less than 180 days. |

14

The Funds’ returns shown do not reflect the deduction of taxes that a shareholder would pay on distributions or the redemption of shares. The benchmark returns shown, excluding the Lipper Indices, reflect the reinvestment of dividends and capital gains but do not reflect the deduction of any investment management fees, other expenses or taxes. The performance of the Lipper Indices is presented net of the Funds’ fees and expenses; however, applicable sales charges are not taken into consideration. One cannot invest directly in an index.

The Russell 3000 Growth Index measures the performance of the broad growth segment of the U.S. equity universe. It includes those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Lipper Multi-Cap Growth Funds Index is an unmanaged index that reflects the net asset value weighted return of 30 of the largest multi-cap growth funds tracked by Lipper. Its returns include net reinvested dividends. The S&P 500 Index is a capitalization weighted index of 500 large capitalization stocks which is designed to measure broad domestic securities markets. The Lipper Mixed-Asset Target Allocation Moderate Funds Index is an average of funds that, by portfolio practice, maintain a mix of between 40%-60% equity securities, with the remainder invested in bonds, cash, and cash equivalents. The total return of the Lipper Average does not include the effect of sales charges. You cannot invest directly in a Lipper Average. The Russell 1000 Growth Index measures the performance of those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Lipper Large-Cap Growth Funds Index is an unmanaged, equally weighted performance index of the 30 largest qualifying mutual funds (based on net assets) in the Lipper Large-Cap classification. The Bank of America Merrill Lynch U.S. High Yield Master II Index tracks the performance of below investment grade U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market. The Lipper High Yield Bond Funds Index is a widely recognized index of the 30 largest mutual funds that invest primarily in high yield bonds. The MSCI AC World (ex USA) Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, excluding the U.S. The Lipper International Funds Index is an unmanaged, equally weighted performance index of the 30 largest qualifying mutual funds (based on net assets) in the Lipper International classifications. The Russell Midcap Growth Index measures the performance of those Russell Midcap companies with higher price-to-book ratios and higher forecasted growth values. The Lipper Mid-Cap Growth Funds Index is an unmanaged, equally weighted performance index of the 30 largest qualifying mutual funds (based on net assets) in the Lipper Mid-Cap classification. The Russell 2000 Growth Index measures the performance of those Russell 2000 Index companies with higher price-to-book ratios and higher forecasted growth values. The Lipper Small-Cap Growth Funds Index is an unmanaged, equally weighted performance index of the 30 largest qualifying mutual funds (based on net assets) in the Lipper Small-Cap classification. Lipper Equity Income Funds Index tracks funds that seek relatively high current income and growth of income by investing at least 65% of their portfolio in dividend-paying equity securities. These funds’ gross or net yield must be at least 125% of the average gross or net yield of the U.S. diversified equity fund universe. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index.

Please refer to the prospectus for special risks associated with investing in the Buffalo Funds, including, but not limited to, risks involved with investments in science and technology, foreign, debt, lower- or non-rated securities and smaller companies.

Fund holdings and sector allocations are subject to change at any time and should not be considered a recommendation to buy or sell any security. Please refer to the Schedule of Investments for a complete list of Fund holdings.

15

Buffalo Discovery Fund

Growth of a $10,000 Investment

Buffalo Dividend Focus Fund

Growth of a $10,000 Investment

Buffalo Emerging Opportunities Fund

Growth of a $10,000 Investment

Buffalo Flexible Income Fund

Growth of a $10,000 Investment

Buffalo Growth Fund

Growth of a $10,000 Investment

Buffalo High Yield Fund

Growth of a $10,000 Investment

Buffalo International Fund

Growth of a $10,000 Investment

Buffalo Large Cap Fund

Growth of a $10,000 Investment

16

Buffalo Mid Cap Fund

Growth of a $10,000 Investment

Buffalo Small Cap Fund

Growth of a $10,000 Investment

17

Expense Example

As a shareholder of the Funds, you incur two types of costs: (1) transaction costs (including redemption fees) and (2) ongoing costs, including management fees and other Fund specific expenses. The examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2014 – March 31, 2015).

ACTUAL EXPENSES

The first line of the tables below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during the period. Although the Funds charge no sales load or transaction fees, you will be assessed fees for outgoing wire transfers, returned checks and stop payment orders at prevailing rates charged by U.S. Bancorp Fund Services, LLC, the Funds’ transfer agent. If you request that a redemption be made by wire transfer, currently a $15.00 fee is charged by the Funds’ transfer agent. You will be charged a redemption fee equal to 2.00% of the net amount of the redemption if you redeem your shares of the Buffalo Flexible Income, Dividend Focus, International, Large Cap, Mid Cap, Discovery and Growth Funds within 60 days of purchase. The Buffalo High Yield, Emerging Opportunities and Small Cap Funds will charge a redemption fee equal to 2.00% of the net amount of the redemption if you redeem your shares

within 180 days of purchase. To the extent a Fund invests in shares of other investment companies as part of its investment strategy, you will indirectly bear your proportionate share of any fees and expenses charged by the underlying funds in which the Fund invests in addition to the expenses of the Fund. Actual expenses of the underlying funds are expected to vary among the various underlying funds. These expenses are not included in the examples below. The examples below include management fees, registration fees and other expenses. However, the examples below do not include portfolio trading commissions and related expenses and other extraordinary expenses as determined under U.S. generally accepted accounting principles.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES