UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-10371

LORD ABBETT TRUST I

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, NJ 07302

(Address of principal executive offices) (Zip code)

Lawrence B. Stoller, Vice President, Secretary, and Chief Legal Officer

90 Hudson Street, Jersey City, NJ 07302

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 7/31

Date of reporting period: 7/31/2022

| Item 1: | Report(s) to Shareholders. |

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Climate Focused Bond Fund

Emerging Markets Equity Fund

International Growth Fund

Mid Cap Innovation Growth Fund

Short Duration High Yield Fund

For the period ended July 31, 2022

Lord Abbett Trust I

Lord Abbett Climate Focused Bond Fund, Lord Abbett Emerging Markets Equity Fund, Lord Abbett International Growth Fund, Lord Abbett Mid Cap Innovation Growth Fund, and Lord Abbett Short Duration High Yield Fund

Annual Report

For the period year ended July 31, 2022

From left to right: James L.L. Tullis, Independent Chairman of the Lord Abbett Funds and Douglas B. Sieg, Trustee, President, and Chief Executive Officer of the Lord Abbett Funds. | | Dear Shareholders: We are pleased to provide you with this overview of the performance of the Funds for the period year ended July 31, 2022. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For detailed and timely information about the Funds, please visit our website at www.lordabbett.com, where you can also access the quarterly commentaries that provide updates on each Fund’s performance and other portfolio related updates. Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come. Best regards,

Douglas B. Sieg

Trustee, President and Chief Executive Officer |

| | | |

Lord Abbett Climate Focused Bond Fund

For the fiscal year ended July 31, 2022, the Fund returned -8.72%, reflecting performance at the net asset value of Class A shares with all distributions reinvested, compared to its benchmark, the ICE BofA Green Bond Index (USD Hedged)1, which returned -11.44% over the same period. The Bloomberg Global Aggregate Bond

Index (USD Hedged)2 returned -7.77% over the same period.

Risk assets finished lower for the twelve-month period as negative sentiment overwhelmed markets. Looking closer, the period was defined by two distinct periods of economic activity. In the second half of 2021, U.S. markets exhibited more stability as a result of continued central bank liquidity and corporate earnings surprises. Additionally, markets

1

continued to benefit from vaccine progress against the COVID-19 virus and momentum surrounding economic reopening in the U.S. Specifically, the U.S. economy generated meaningful growth, notching gains of 2.3% and 6.9% in the third and fourth quarters of 2021, respectively.

U.S. markets, however, met increasing headwinds towards the latter half of 2021, including the increased spread of new COVID-19 variants. These new variants, namely Delta and Omicron, decreased vaccine efficacy in reducing transmission of COVID-19, leading to new waves of positive infections. Higher infection rates placed increased weight on supply chain and input price pressures, and many companies faced labor shortages as workers were sidelined with the virus. This was particularly evident during the spike in Omicron at the end of December 2021, with a record-high in daily average positive cases. Yet, the negative sentiment around Omicron quickly reversed as it was determined that cases were generally less severe than prior strains, and updated guidelines from the Centers for Disease Control and Prevention shortened quarantine times to help alleviate the COVID-19 induced labor constraints.

Moving into 2022, markets were facing higher and more persistent inflation. Inflationary pressures had built up in the fourth quarter of 2021 by an imbalance between supply and demand dynamics across multiple industries, exacerbated by COVID-19 labor issues. This became evident with headline U.S. consumer price index (CPI) rising 6.8% year-over-year in

November 2021, the fastest pace since 1982. Prices continued increasing throughout the first half of 2022, led by energy, food, and used cars. This surge in prices resulted in headline inflation rising 9.1% year-over-year in July 2022, the fastest annual increase in over 40 years.

The steady rise in prices forced the U.S. Federal Reserve (Fed) into a more aggressive approach to combating inflation. Throughout the first half of the twelve-month period, the Fed had remained mostly consistent in its messaging around expectations that price pressures would be transitory. However, more persistent CPI prints caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Three additional rate hikes of 50 bps, 75 bps and 75 bps followed in the succeeding months as inflation readings continued to come in hotter-than-expected, resulting in a federal funds rate of 2.25% by the end of July.

Bond yields shot up from near record lows in reaction to this shift in policy, with the 10-year breaching 3% for the first time since 2018. However, short-term rates increased at a much faster clip, leading to a bearish curve flattening trend that caused periods of brief yield curve inversion. This was reflected in the 5-year and 30-year U.S. Treasury spread inverting for the first time since 2006, and the 2- year and 10-year Treasury spread inverting, albeit briefly, for the first time

2

since 2019. These inversions led to increasing concerns of a potential recession in the United States. Key macroeconomic indicators also pointed to a potential recession in the United States, culminating in the U.S. economy contracting for two consecutive quarters.

Despite rising recessionary signs, select bright spots in the U.S. economy supported the idea that a potential recession would be shallow. For example, the U.S. labor market stood strong with the national unemployment rate remaining low, at around 3.6%, its lowest level in decades.

Bond markets rebounded at the end of the period as credit markets exhibited strong returns for the month of July. U.S. high yield bonds gained approximately 6% in July alone, driven by better-than-expected earnings and expectations for a shallower Fed tightening cycle. The 10-year Treasury yield fell sharply at the end of the period as markets started to price in peak inflation rates and a slowing in the pace of Fed rate hikes.

From an environmental, social and governance (ESG) perspective, global ESG bond supply from corporate issuers slowed throughout the period. Approximately $211 billion of ESG bonds were issued during the first half of 2022, approximately 13% below the $242 billion issued in the same period in 2021. We believe this slowdown was likely due to the broader decline in corporate bond issuance as the global financing environment has become stricter, rather than a lack of desire from companies to issue ESG bonds. For example, from a composition standpoint, the percentage of total corporate supply

with an ESG label has increased compared to 2021. Green, sustainability and sustainability-linked bonds (SLBs) all saw strong market growth, whereas growth in social bonds lagged considerably.

The Fund invests in the securities of issuers we believe have, or will have, a positive impact on the climate through an issuer’s operations, products, or services. Our investment process focuses on five key climate-related themes including: clean energy, energy efficiency, low carbon transportation, clean water and resource management, and other environmental areas such as recycling and waste management. Within this universe, the Fund’s underweight allocation to sovereign debt was the most significant contributor to relative performance for the quarter. Specifically, the Fund primarily benefited from underweight exposure to sovereign debt within the Eurozone relative to its benchmark, mainly France, Italy, and the United Kingdom. Issuers from these regions faced challenges during the period from high inflation, surging energy prices and ongoing geopolitical instability caused by the Russian-Ukrainian War, dampening gross domestic product outlooks for each of these countries. Separately, the European Central Bank surprised markets with a much more hawkish stance on inflation than expected, leading to speculation of increased interest rate hikes in the near term.

An underweight allocation relative to the Fund’s benchmark and security selection within investment grade corporate debt contributed positively to relative returns. The underweight allocation, specifically to

3

European credit, helped performance as these credits came under pressure from a bleaker economic outlook within the Eurozone. The Fund’s shorter duration profile within U.S. corporate debt was also a positive contributor to relative returns during the period as U.S. Treasury yields continued to rise.

The Fund’s overweight allocation to high yield corporate debt dragged on returns. Both U.S. and European high yield sectors were impacted as global inflation surged and recessionary scenarios became increasingly probable, leading to significant spread widening in lower-rated credit.

An off-benchmark allocation to convertible bonds also detracted from performance. These securities, which were issued primarily by renewable energy companies, significantly underperformed as equity-like securities, particularly growth-oriented investments, sold off near the end of the period.

Lord Abbett International Growth Fund

For the fiscal year ended July 31, 2022, the Fund returned -23.41%, reflecting performance at the net asset value of Class A shares (USD), compared to its benchmark, the MSCI All Country World Index ex USA Growth (Net)3, which returned -20.51% over the same period.

Global equities finished lower for the twelve-month period as bearish sentiment overwhelmed markets. Looking closer, the period was defined by two distinct periods of economic activity. In the second half of 2021, U.S. markets exhibited more stability, supported by continued central bank liquidity and corporate earnings surprises.

Additionally, continued vaccine progress against the COVID-19 virus and momentum surrounding economic reopening in developed markets provided tailwinds. Specifically, the U.S. economy showed signs of meaningful growth, notching gains of 2.3% and 6.9% in the third and fourth quarters of 2021, respectively. Meanwhile, Eurozone gross domestic product (GDP) grew 2.3% and 0.4% and China’s economy grew 0.7% and 1.5% over the same time periods.

U.S. markets, however, were met with increasing headwinds towards the latter half of 2021, including the increased spread of new COVID-19 variants. These new variants, namely Delta and Omicron, decreased vaccine efficacy in reducing transmission of COVID-19, leading to new waves of positive infections. Higher infection rates placed increased weight on supply chain and input price pressures, and many companies faced labor shortages as workers were sidelined with the virus. This was particularly evident during the spike in Omicron at the end of December 2021, with a peak average of over 800,000 daily positive cases. Yet, the negative sentiment around Omicron quickly reversed as it was determined that cases were generally less severe than prior strains, and updated CDC guidelines shortened quarantine times to help alleviate the COVID-19 induced labor constraints.

Moving into 2022, investor risk appetite shifted lower due primarily to a combination of higher and more persistent inflation. Inflationary pressures had built up in the fourth quarter of 2021 by an imbalance between supply and demand dynamics across multiple industries,

4

exacerbated by COVID-19 labor issues. This became evident with headline U.S. consumer price index (CPI) rising 6.8% year-on-year in November 2021, the fastest pace since 1982. Prices continued increasing throughout the first half of 2022, led by energy, food, and used cars. This surge in prices culminated in July 2022 as headline inflation came in at 9.1% year-on-year, the fastest annual increase in over 40 years. Meanwhile, inflation data outside the U.S. was also high, with June inflation readings for Canada, the U.K, and Eurozone coming in at 8.1%, 9.4%, and 8.9%, respectively.

There were a number of developments indicating an increasing possibility of an approaching recession for global economies. Namely, the U.S. economy contracted for a second straight quarter in Q2, falling -0.9% quarter-over-quarter. The July flash services Purchasing Managers Index (PMI) fell into contraction territory, and flash manufacturing PMI slumped to the lowest level in two years. The weakness in the U.S. GDP report was widespread, with falls in construction, investment, and government spending. In addition, initial jobless claims came in at an eight-month high in July. There was a flurry of high-profile hiring freezes and layoff announcements. Second quarter earnings also provided some cautious takeaways, including lower retail guidance on general merchandise softness from inflation, tech companies pointing to continued deterioration in digital advertising and consumer electronics, and home builders commenting on a slowdown in housing demand. Commodity prices also softened towards the end of the period, yet it was widely believed to be a function of

growth and demand concerns rather than improvements on the supply chains that continued to be affected by COVID-19 and geopolitical issues. The U.S. labor market remained strong, however, putting into question whether the economy is in fact in a technical recession. National unemployment remained low at around 3.5%, its lowest level in decades, and employers continued to add labor at a healthy yet more moderate rate. Meanwhile, many forecast a recession in the Eurozone later this year, as energy-driven inflation is not expected to ease much due to the Russia-Ukraine conflict, even with central banks starting to raise rates.

The steady rise in prices forced the U.S. Federal Reserve (Fed) into a more aggressive approach to combating inflation. Throughout the first half of the twelve- month period, the Fed had remained mostly consistent in its messaging around expectations that price pressures would be transitory. However, more persistent CPI prints caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Three additional rate hikes of 50 bps, 75 bps and 75 bps, followed in the succeeding months as inflation readings continued to come in hotter-than-expected, resulting in a federal funds rate of 2.25% by the end of July.

Meanwhile, in an attempt to reduce inflationary pressures, the European Central Bank (ECB) raised its three key interest rates by 50bp during its July 2022

5

meeting, ending eight years of negative rates with its first increase since 2011. Inflation in the Euro Area continued to march higher and break record rates, showing no signs of peaking, and approaching double-digits. The central bank also said that further normalization of interest rates will be appropriate in the upcoming meetings.

Although most central banks around the world withdrew crisis-mode stimulus, the Bank of Japan (BoJ) appeared undeterred. The BoJ maintained its key short-term interest rate at -0.1% and that for 10-year bond yields around 0% during its July meeting; but cut its 2022 GDP growth forecast to 2.4% from its April forecast of 2.9%, citing a slowdown in overseas economies and persistent supply chain issues due to the prolonged war in Ukraine. The BoJ reiterated that it would not hesitate to take extra easing measures if needed, a sign that it will remain an outlier among a global wave of central banks tightening policies. The central bank also mentioned that it would continue to buy unlimited amounts of the bonds to defend an implicit 0.25% cap every market day, as it had been doing since April.

Similar to equity market performance in the U.S., non-U.S. equity markets experienced a strong decline during the last twelve months, before rallying in July. Against a weaker global growth backdrop, markets increasingly priced in interest rate cuts from the Fed in 2023. This anticipation of a policy pivot supported risk assets over the month. Global growth stocks benefited most, delivering 11.5% total return in July, recouping some of their heavy year-to-

date losses. Emerging Markets equities meaningfully underperformed their developed markets peers, as a strong U.S. dollar and rising oil prices proved to be major headwinds. Weighing particularly hard on the index was underperformance in Chinese equities, as the country continued to grapple with the Omicron outbreak and a series of rolling lockdown measures enacted in various cities.

During the period, the Fund’s underperformance relative to its benchmark was driven by stock selection, particularly within the Industrials, Information Technology and Consumer Discretionary sectors. Within Industrials, companies that are dependent on intricate supply chains or that are in the logistics space suffered most. In the latter segment, Autostore Holdings, a robotic and software technology company that provides cubic storage automation, detracted most from Fund performance. Although the proliferation of e-commerce and labor wage inflation pressures provide a strong investment case for warehouse automation, sentiment deteriorated around high-growth stocks such as this one. Another detractor in this space was DSV A/S, a global logistics company based in Denmark. We believe this will be another beneficiary of supply chain bottlenecks, but the stock was punished due to its high growth profile. This was a common theme in the Information Technology sector as well. Some of the largest detractors from Fund performance during this twelve-month period were high growth stocks that performed very well last year. Examples are Keyence Corp., a Japanese company that is the global leader in machine vision and

6

plays into the portfolio’s industrial automation theme. Another is Adyen NV, a Netherlands-based company that is in the payments business – a space that is rife with competition.

Within the Consumer Discretionary sector, holdings in Alibaba, a Chinese e-commerce company, detracted most from Fund performance, as regulatory pressures from China’s government proved to be a strong headwind. To add to Alibaba’s woes, the failed IPO spinoff of Ant Financial sent shares trading lower. The Fund’s investment in shares of Anta Sports Products, Ltd. also detracted from relative performance, as continued COVID lockdowns in China put a damper on production, and as inflationary pressures worried investors.

Conversely, stock selection within the Energy sector contributed positively to relative performance over the period. Equinor ASA was one of the largest contributors to relative performance as oil prices rallied. WTI Crude futures breached $100 per barrel in March for the first time since September 2014, and prices faced additional upward pressure from lower supply given increased sanctions on Russia. Equinor engages in the exploration and production of petroleum in Norway. Pembina Pipeline Corp., a midstream services company based in Canada also benefited.

Stock selection in Health Care was another bright spot. The largest contributor to relative performance was Novo Nordisk, a Danish health care company with the world’s leading diabetes franchise. The company’s most exciting

recent development has been in its Diabetes & Obesity Care segment, where its revolutionary drug Wegovy has had tremendous results for weight loss in people. On the drug’s injectible pen regiment, the average patient was able to reduce their weight by 17%. This is a prescription drug that has proven to have limited effects. Furthermore, Novo can cross-sell this drug into the same population that relies on its diabetes drugs. Another winner in this sector was AstraZeneca PLC, a U.K.-based pharmaceutical company. AstraZeneca has a big oncology business which has had a few huge wins recently. The company acquired the rights to a class of drugs from a Japanese company, Daiichi Sankyo, one of which is likely to be the second line drug of choice for breast cancer, which is notably a very large market.

Lord Abbett Mid Cap Innovation Growth Fund

For the fiscal year ended July 31, 2022, the Fund returned -29.93%, reflecting performance at the net asset value of Class A shares with all distributions reinvested, compared to its benchmark, the Russell MidCap® Growth Index,4 which returned -21.76% over the same period.

U.S. markets faced many challenges throughout the twelve-month period ending July 31, 2022, including increased volatility stemming from the emergence of the Delta and Omicron variants of COVID-19, supply chain dislocations, labor shortages, inflationary pressures, less accommodative fiscal and monetary policy, and geopolitical tensions related to Russia’s invasion of Ukraine. The Dow Jones Industrial

7

Average and S&P 500® Index5 fell -4.14% and -4.64%, respectively, while the tech-heavy Nasdaq Composite lost -14.95%. Value stocks6 significantly outperformed growth stocks7 (-1.65% vs -12.65%), while large cap stocks8 outperformed small cap stocks9 (-6.87% vs -14.29%).

Despite the aforementioned challenges, the period began with a positive tone driven by accommodative monetary policy, continued vaccine progress, upside in corporate earnings surprises, and momentum surrounding the gradual reopening of global economies. However, sentiment began to shift in the latter half of the third quarter of 2021, as markets had to endure the increased spread of the Delta variant of COVID-19. Global markets were also affected by negative headlines overseas, namely China’s regulatory crackdown of the private education and technology sectors, as well as worries about the impacts of a default by Chinese real estate developer Evergrande. These headwinds culminated in a volatile September with all major U.S. indices finishing in negative territory. Specifically, the S&P 500® Index snapped a streak of seven consecutive months of positive returns in September, with the worst month of performance since March 2020.

In December, global markets had to grapple with the emergence of the newly discovered Omicron variant. The World Health Organization designated the newly discovered mutation as a “variant of concern”, particularly due to its increased transmissibility and then-unknown severity. This led to one of the largest selloffs and worst one-day performance of

U.S. risk assets since the start of the pandemic, as fears that the world would succumb to a new wave of infections emerged. Yet, the negative sentiment regarding Omicron quickly reversed as cases proved to be generally less severe than prior strains.

Inflationary concerns began to take focus towards the end of 2021. Headline core consumer price index readings had hovered a little above 5% year-over-year for most of 2021, which led investors to question whether this period of rising prices would be more persistent than originally thought. However, this debate was intensified by November’s headline consumer price index which rose 6.8% year-over-year. This was the fastest pace since 1982, and enhanced inflation fears among investors. The sharp increase in prices was generally due to an imbalance between supply and demand dynamics across multiple industries, led initially by energy, food, and used cars. Although positive COVID-19 cases plummeted throughout the quarter from Omicron’s surge in late 2021, many companies faced labor shortages, with workers sidelined with the virus, exacerbating supply chain issues, and adding to inflationary pressures.

Energy costs were the primary driver of inflation for the period, rising more than 30% year-over-year by the end of June. The energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s military invasion of Ukraine. Investors were concerned about the secondary effects of the war, particularly

8

from a commodity and supply chain standpoint. Russia has been a large global exporter of oil and certain minerals, and the various sanctions set on Russia from Western nations led to a surge in commodity prices, with crude oil reaching over $100 per barrel for the first time since 2014.

The surge in prices forced the U.S. Federal Reserve (Fed) into a more aggressive approach to combating inflation. Throughout the first half of the twelve-month period, the Fed remained mostly consistent in its messaging around expectations that price pressures would be transitory, and the peak inflation theme gained traction even as economists suggested that ‘transitory’ might be longer than expected. However, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Three additional rate hikes of 50 bps, 75 bps and 75 bps, respectively, followed in the succeeding months as inflation prints continued to come in hotter than expected, resulting in a federal funds rate of 2.25% by the end of July. Bond yields shot up in reaction to this shift in policy, exhibiting a bearish curve flattening trend and ultimately leading to periods of brief yield curve inversion, as shorter-term yields moved higher than longer- term yields. This trend was reflected in the 5-year and 30-year U.S. Treasury spread inverting for the first time since 2006, and the 2-year and 10-year Treasury spread

inverting, albeit briefly, for the first time since 2019. However, towards the end of the period, 10-year Treasury yields fell sharply.

Key macroeconomic indicators continued to trend lower throughout the period, with the U.S. reporting negative gross domestic product of -1.6% in the first quarter of 2022 and -0.9% in the second quarter. Worries among investors that a recession was pending continued to grow, and consumer sentiment dropped in the second quarter, reaching levels worse than during the COVID-19 pandemic and nearly as bad as the worst periods during the global financial crisis of 2008.

Despite rising recessionary signs, select bright spots in the U.S. economy throughout the first half of 2022 supported the idea that a potential recession would be shallow. For example, the U.S. labor market remained strong, with the national unemployment rate remaining low, at around 3.6% as of the end of June. This was its lowest level in decades. Employers also continued to add labor at a healthy rate, adding approximately 457,000 jobs per month for the period. Separately, consumer balance sheets remained robust, with cash at record high levels, providing a level of flexibility for individuals to absorb price increases.

Over the course of the period, high innovation small and midcap companies, particularly those aggressively reinvesting in research & development to drive future revenues and earnings, underperformed lower growth, lower valuation names within the Russell MidCap® Growth Index. Given the environment of increased

9

volatility and uncertainty, investors largely sought safety over innovation, which had a negative impact on the Fund’s relative returns.

The Fund’s position in DocuSign, Inc., a provider of cloud-based electronic signature solutions, was the largest individual detractor from relative performance over the period. After greatly benefitting from the accelerated adoption of work-from-home solutions throughout the initial onset of COVID-19, DocuSign’s stock price started to turn negatively in July 2021. However, the stock price took a major tumble in December after the company reported fourth quarter guidance that fell short of analyst estimates. Soon after the earnings report, several analysts downgraded the stock.

The Fund’s position in EPAM Systems, Inc., a developer of software products and digital platform engineering services, was also a notable detractor from relative performance over the period. After sustained stock price appreciation since the beginning of the pandemic, EPAM stock was in a period of consolidation throughout the beginning of 2022 as high-growth and richly valued technology stocks were adversely impacted by the rotation away from growth to value. Additionally, EPAM was also negatively impacted by the Russian invasion of Ukraine, as a large percentage of its workforce is based in Ukraine, Russia, and Belarus.

Conversely, the Fund’s position in Lantheus Holdings, Inc., a developer of innovative diagnostic and therapeutic agents, was a primary contributor to

relative performance. Shares of the stock soared following the company’s strong first quarter of 2022 earnings report. Management also raised its 2022 guidance, which was primarily driven by the accelerated adoption of PYLARIFY®, a diagnostic imaging agent for prostate cancer. As of the end of the period, Lantheus Holdings was among the Fund’s largest active overweights relative to the Fund’s benchmark.

Within the semiconductor and semi equipment industry, the Fund’s position in Enphase Energy, Inc., a developer of solar micro-inverters, energy generation monitoring software, and battery energy storage products, was also a prominent contributor to relative performance. Shares of the stock soared after the company reported quarterly earnings results that were above consensus estimates. Management also significantly raised guidance for the remainder of the year, as the company expected strong demand for its solar, storage, EV, and energy management solutions. As of the end of the period, Enphase was the Fund’s largest active overweight relative to the Fund’s benchmark.

Lord Abbett Short Duration High Yield Fund

For the fiscal year ended July 31, 2022, the Fund returned -4.04%, reflecting performance at the net asset value of Class A shares with all distributions reinvested, compared to its benchmark, the ICE BofA High Yield U.S. Corporate Cash Pay BB-B (1-5yrs) USD Index10, which returned -3.57% over the same period.

10

Credit risk assets finished lower for the 12-month period as bearish sentiment overwhelmed markets. Looking closer, the period was defined by two distinct periods of economic activity. In the second half of 2021, U.S. markets exhibited more stability, propped up by continued central bank liquidity and corporate earnings surprises. Additionally, markets continued to benefit from vaccine progress against the COVID-19 virus and momentum surrounding economic reopening in the U.S. Specifically, the U.S. economy showed signs of meaningful growth, notching gains of 2.3% and 6.9% in the third and fourth quarters of 2021, respectively.

U.S. markets, however, were met with increasing headwinds towards the latter half of 2021, including the increased spread of new COVID-19 variants. These new variants, namely Delta and Omicron, decreased vaccine efficacy in reducing transmission of COVID-19, leading to new waves of positive infections. Higher infection rates placed increased weight on supply chain and input price pressures, and many companies faced labor shortages as workers were sidelined with the virus. This was particularly evident during the spike in Omicron at the end of December 2021 with a record-high in daily average positive cases. Yet, the negative sentiment around Omicron quickly reversed as it was determined that cases were generally less severe than prior strains, and updated guidelines from the Centers for Disease Control and Prevention shortened quarantine times to help alleviate the COVID-19 induced labor constraints.

Moving into 2022, investor sentiment turned negative due primarily to a combination of higher and more persistent inflation. Inflationary pressures had built up in the fourth quarter of 2021 by an imbalance between supply and demand dynamics across multiple industries, exacerbated by COVID-19 labor issues. This became evident with headline U.S. consumer price index (CPI) rising 6.8% year-over-year in November 2021, the fastest pace since 1982. Prices continued increasing throughout the first half of 2022, led by energy, food, and used cars. This surge in prices culminated in July 2022 as headline inflation came in at 9.1% year- over-year, the fastest annual increase in over 40 years.

The steady rise in prices forced the U.S. Federal Reserve (Fed) into a more aggressive approach to combating inflation. Throughout the first half of the twelve- month period, the Fed had remained mostly consistent in its messaging around expectations that price pressures would be transitory. However, more persistent CPI prints caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Three additional rate hikes of 50 bps, 75 bps, and 75 bps followed in the succeeding months as inflation readings continued to come in hotter-than-expected, resulting in a federal funds rate of 2.25% by the end of July.

Bond yields shot up from near record lows in reaction to this shift in policy, with

11

the 10-year breaching 3% for the first time since 2018. However, short-term rates increased at a much faster clip, leading to a bearish curve flattening trend that caused periods of brief yield curve inversion. This was reflected in the 5-year and 30-year U.S. Treasury spread inverting for the first time since 2006, and the 2- year and 10-year Treasury spread inverting, albeit briefly, for the first time since 2019. These inversions caused heightened concerns regarding a potential recession in the United States.

Key macroeconomic indicators continued to point to a potential recession in the United States throughout the period, resulting in the U.S. economy contracting for two consecutive quarters. Consumer sentiment also dropped in the second quarter of 2022, reaching levels worse than during the COVID-19 pandemic and nearly as bad as the worst periods during the great financial crisis of 2007-2008.

Despite rising recessionary signs, select bright spots in the U.S. economy throughout the first half of 2022 supported the idea that a potential recession would be shallow. For example, the U.S. labor market stood strong with the national unemployment rate remaining low, at around 3.6%, which was its lowest level in decades. Performance rebounded at the end of the period as credit markets exhibited strong returns for the month of July. U.S. high yield bonds gained approximately 6% in July alone, as better-than-expected earnings and expectations for a shallower Fed tightening cycle were tailwinds. Interest rates showed signs of rallying, as the 10-year Treasury yield fell

sharply as markets started to price in peak inflation rates and a slowing in the pace of Fed rate hikes.

With respect to performance, the increased concerns surrounding growth in the U.S. economy led to the underperformance from some of the Fund’s cyclical exposures. Namely, security selection within the Services and Leisure sectors detracted from relative performance. Relative to its benchmark, the Fund was overweight certain issuers in these sectors, which faced increased headwinds due to inflationary pressures, mainly from higher labor costs causing downward pressure on profit margins. High inflation also dampened expectations on U.S. consumer spending, leading many consumer-driven businesses to revise future revenue outlooks lower.

From a credit standpoint, security selection within BB-rated credits detracted from the Fund’s relative performance. Despite holding an underweight allocation to the sector, relative to the benchmark, the Fund was overweight select BB credits that faced increased selling pressure as their more liquid profiles led them to be attractive sources of cash for investors moving out of the high yield asset class. These issuers were primarily within the Automotive, Consumer Goods, and Financial Services sectors.

The Fund’s overweight allocation (relative to its benchmark) and security selection within the Energy sector were positive contributors to performance during the period. The Fund benefited from select holdings in the Exploration & Production (E&P) subsector, which received support

12

from the continued rally in oil prices. Specifically, WTI Crude futures breached $100 per barrel for the first time since 2014, and prices faced favorable technical support from lower supply given the increased sanctions on Russian oil exports.

Security selection within the Basic Industry sector also contributed positively to relative returns. The Fund was underweight companies within the Chemicals subsector that faced idiosyncratic credit issues. The Fund also

1 The ICE BofA Green Bond Index (USD Hedged) tracks securities issued for qualified green purposes that promote climate change mitigation or adaption. Qualifying bonds must have a clearly designated use of proceeds that is solely applied toward projects or activities that promote climate change mitigation or adaptation or other environmental sustainability purposes as outlined by the ICMA Green Bond Principles.

2 The Bloomberg Global Aggregate Bond Index (USD Hedged) provides a broad-based measure of the global investment-grade fixed-income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate indexes. The index also includes eurodollar and euro-yen corporate bonds, Canadian government securities, and U.S. dollar investment-grade 144A securities. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and an investor cannot invest directly in an index.

3 The MSCI All Country World Index ex USA Growth (Net) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

4 The Russell MidCap® Growth Index measures the performance of those Russell MidCap® Index companies with higher price-to-book ratios and higher forecasted growth values.

5 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance.

benefitted from its opportunistic allocation to bank loans, which have outperformed high yield corporate bonds since the start of 2022, as the asset class has been generally more insulated from interest rate volatility due to its floating rate nature.

The Funds’ portfolios are actively managed and, therefore, holdings and the weightings of a particular issuer or particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

6 As represented by the Russell 3000® Value Index as of 7/31/2022.

7 As represented by the Russell 3000® Growth Index as of 7/31/2022.

8 As represented by the Russell 1000® Index as of 7/31/2022.

9 As represented by the Russell 2000® Index as of 7/31/2022.

10 The ICE BofA High Yield U.S. Corporate Cash Pay BB-B (1-5yrs) USD Index consists of BB-B rated U.S. dollar-denominated corporate bonds publicly issued in the U.S. domestic market with maturities of 1 to 5 years. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and an investor cannot invest directly in an index.

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information

Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Funds will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

13

Except where noted, comparative Fund performance does not account for the deduction of sales charges and would be different if sales charges were included. Each Fund offers classes of shares with distinct pricing options. For a full description of the differences in pricing alternatives, please see each Fund’s prospectus.

During certain periods shown, expense waivers and reimbursements were in place. Without such expense waivers and reimbursements, each Fund’s returns would have been lower.

The annual commentary above discusses the views of the Funds’ management and various portfolio holdings of the Funds as of July 31, 2022. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not

a recommendation to buy or sell securities. Because the Funds’ portfolios are actively managed and may change significantly, the Funds may no longer own the securities described above or may have otherwise changed their positions in the securities. For more recent information about the Funds’ portfolio holdings, please visit www.lordabbett.com.

A Note about Risk: See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with each Fund, please see each Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

14

Climate Focused Bond Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the ICE BofA Green Bond Index (USD Hedged) and Bloomberg Global Aggregate Bond Index (USD Hedged), assuming reinvestment of all dividends and distributions. The Fund has adopted the ICE BofA Green Bond Index (USD Hedged), a more broad-based index, as its primary benchmark index. The performance of other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursements of expense, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended July 31, 2022

| | | 1 Year | | Life of Class | |

| Class A3 | | -10.79% | | -2.46% | |

| Class C4 | | -10.18% | | -2.15% | |

| Class F5 | | -8.53% | | -1.23% | |

| Class F35 | | -8.47% | | -1.16% | |

| Class I5 | | -8.53% | | -1.23% | |

| Class R35 | | -8.98% | | -1.73% | |

| Class R45 | | -8.76% | | -1.48% | |

| Class R55 | | -8.53% | | -1.23% | |

| Class R65 | | -8.47% | | -1.16% | |

1 Reflects the deduction of the maximum initial sales charge of 2.25%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance. Performance of the index began on May 28, 2020.

3 Class A shares commenced operations on May 20, 2020 and performance for the Class began on May 28, 2020. Total return, which is the percent change in net asset value, after deduction of the maximum initial sales charge of 2.25% applicable to Class A shares, with all dividends and

distributions reinvested for the period shown ended July 31, 2022, is calculated using the SEC required uniform method to compute such return.

4 Class C shares commenced operations on May 20, 2020 and performance for the Class began on May 28, 2020. The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Commenced operations on May 20, 2020 and performance for the Classes began on May 28, 2020. Performance is at net asset value.

15

International Growth Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the MSCI All Country World Index ex USA Growth (Net), assuming reinvestment of all dividends and distributions. The performance of other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursements of expense, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended July 31, 2022

| | | 1 Year | | Life of Class | |

| Class A3 | | -27.81% | | -25.65% | |

| Class C4 | | -24.72% | | -22.11% | |

| Class F5 | | -23.27% | | -21.37% | |

| Class F35 | | -23.13% | | -21.25% | |

| Class I5 | | -23.27% | | -21.37% | |

| Class R35 | | -23.61% | | -21.74% | |

| Class R45 | | -23.41% | | -21.56% | |

| Class R55 | | -23.27% | | -21.37% | |

| Class R65 | | -23.13% | | -21.25% | |

1 Reflects the deduction of the maximum initial sales charge of 5.75%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance. Performance of the index began on June 24, 2021.

3 Class A shares commenced operations on June 18, 2021 and performance for the Class began on June 24, 2021. Total return, which is the percent change in net asset value, after deduction of the maximum initial sales charge of 5.75% applicable to Class A shares, with all dividends and distributions reinvested for the period shown ended July 31,

2022, is calculated using the SEC required uniform method to compute such return.

4 Class C shares commenced operations on June 18, 2021 and performance for the Class began on June 24, 2021. The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date.

5 Commenced operations on June 18, 2021 and performance for the Classes began on June 24, 2021. Performance is at net asset value.

16

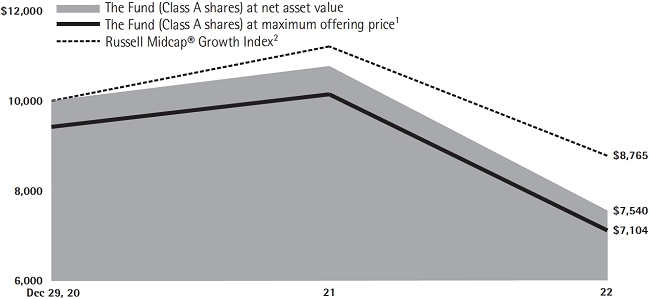

Mid Cap Innovation Growth Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the Russell Midcap® Growth Index, assuming reinvestment of all dividends and distributions. The performance of other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursements of expense, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended July 31, 2022

| | | 1 Year | | Life of Class | |

| Class A3 | | -33.94% | | -19.39% | |

| Class C4 | | -31.13% | | -16.91% | |

| Class F5 | | -29.75% | | -16.07% | |

| Class F35 | | -29.68% | | -16.03% | |

| Class I5 | | -29.75% | | -16.07% | |

| Class R35 | | -30.09% | | -16.49% | |

| Class R45 | | -29.93% | | -16.31% | |

| Class R55 | | -29.75% | | -16.07% | |

| Class R65 | | -29.68% | | -16.03% | |

1 Reflects the deduction of the maximum initial sales charge of 5.75%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance. Performance of the index began on December 29, 2020.

3 Class A shares commenced operations on December 28, 2020 and performance for the Class began on December 29, 2020. Total return, which is the percent change in net asset value, after deduction of the maximum initial sales charge of 5.75% applicable to Class A shares, with all dividends and distributions reinvested for the period shown ended July 31,

2022, is calculated using the SEC required uniform method to compute such return.

4 Class C shares commenced operations on December 28, 2020 and performance for the Class began on December 29, 2020. The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date.

5 Commenced operations on December 28, 2020 and performance for the Classes began on December 29, 2020. Performance is at net asset value.

17

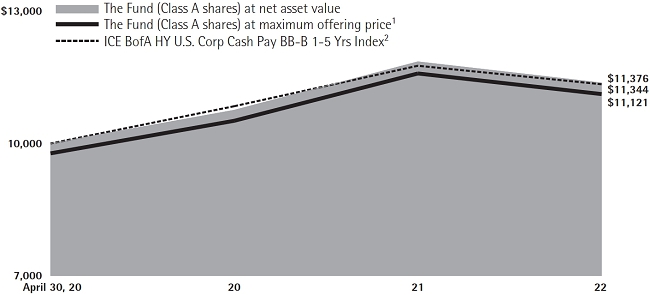

Short Duration High Yield Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the ICE BofA HY U.S. Corp Cash Pay BB-B 1-5 Yrs Index, assuming reinvestment of all dividends and distributions. The performance of other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursements of expense, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum Applicable

Sales Charge for the Periods Ended July 31, 2022

| | | 1 Year | | Life of Class | |

| Class A3 | | -6.17% | | 4.83% | |

| Class C4 | | -5.60% | | 5.10% | |

| Class F5 | | -3.85% | | 6.10% | |

| Class F35 | | -3.79% | | 6.17% | |

| Class I5 | | -3.94% | | 6.06% | |

| Class R35 | | -4.31% | | 5.58% | |

| Class R45 | | -4.08% | | 5.84% | |

| Class R55 | | -3.83% | | 6.11% | |

| Class R65 | | -3.80% | | 6.16% | |

1 Reflects the deduction of the maximum initial sales charge of 2.25%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of the index is not necessarily representative of the Fund’s performance. Performance of the index began on April 30, 2020.

3 Class A shares commenced operations on April 22, 2020 and performance for the Class began on April 30, 2020. Total return, which is the percent change in net asset value, after deduction of the maximum initial sales charge of 2.25% applicable to Class A shares, with all dividends and

distributions reinvested for the period shown ended July 31, 2022, is calculated using the SEC required uniform method to compute such return.

4 Class C shares commenced operations on April 22, 2020 and performance for the Class began on April 30, 2020. The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Commenced operations on April 22, 2020 and performance for the Classes began on April 30, 2020. Performance is at net asset value.

18

Expense Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments (these charges vary among the share classes); and (2) ongoing costs, including management fees; distribution and service (12b-1) fees (these charges vary among the share classes); and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (February 1, 2022 through July 31, 2022 for Climate Focused Bond Fund, International Growth Fund, Mid Cap Innovation Growth Fund and Short Duration High Yield Fund. March 2, 2022, commencement of operations for Emerging Markets Equity Fund through July 31, 2022).

Actual Expenses

For each class of each Fund, the first line of the applicable table on the following pages provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 2/1/22 – 7/31/22 for Climate Focused Bond Fund, International Growth Fund, Mid Cap Innovation Growth Fund and Short Duration High Yield Fund. 3/2/22, commencement of operations for Emerging Markets Equity Fund – 7/31/22” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of each Fund, the second line of the applicable table on the following pages provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

19

Climate Focused Bond Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | | 2/1/22 | | 7/31/22 | | 2/1/22 -

7/31/22 | |

| Class A | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 939.20 | | | $3.13 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.57 | | | $3.26 | |

| Class C | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 936.40 | | | $6.19 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,018.40 | | | $6.46 | |

| Class F | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 940.10 | | | $2.16 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.56 | | | $2.26 | |

| Class F3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 940.40 | | | $1.88 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.86 | | | $1.96 | |

| Class I | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 940.10 | | | $2.16 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.56 | | | $2.26 | |

| Class R3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 937.80 | | | $4.56 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.08 | | | $4.76 | |

| Class R4 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 939.00 | | | $3.37 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.32 | | | $3.51 | |

| Class R5 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 940.10 | | | $2.16 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.56 | | | $2.26 | |

| Class R6 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 940.40 | | | $1.88 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.86 | | | $1.96 | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (0.65% for Class A, 1.29% for Class C, 0.45% for Class F, 0.39% for Class F3, 0.45% for Class I, 0.95% for Class R3, 0.70% for Class R4, 0.45% for Class R5 and 0.39% for Class R6) multiplied by the average account value over the period, multiplied by 181/365 (to reflect one-half year period). |

20

Portfolio Holdings Presented by Sector

July 31, 2022

| Sector* | | %** |

| Asset Backed Securities | | | 2.10 | % |

| Basic Materials | | | 1.56 | % |

| Communication Services | | | 1.78 | % |

| Consumer, Cyclical | | | 3.46 | % |

| Consumer, Non-cyclical | | | 3.90 | % |

| Energy | | | 6.62 | % |

| Financials | | | 18.88 | % |

| Foreign Government | | | 24.63 | % |

| Industrials | | | 10.00 | % |

| Mortgage-Backed Securities | | | 1.67 | % |

| Municipal | | | 2.91 | % |

| Technology | | | 1.31 | % |

| U.S. Government | | | 2.36 | % |

| Utilities | | | 15.12 | % |

| Repurchase Agreements | | | 3.70 | % |

| Total | | | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

21

Emerging Markets Equity Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | | 3/2/22 | | 7/31/22 | | 3/2/22 –

7/31/22 | |

| Class A | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 904.70 | | | $4.92 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,015.66 | | | $5.20 | |

| Class C | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 902.00 | | | $7.88 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,012.53 | | | $8.34 | |

| Class F | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 905.30 | | | $3.93 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,016.70 | | | $4.16 | |

| Class F3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 906.00 | | | $3.61 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,017.03 | | | $3.82 | |

| Class I | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 905.30 | | | $3.93 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,016.70 | | | $4.16 | |

| Class R6 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 906.00 | | | $3.61 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,017.03 | | | $3.82 | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.24% for Class A, 1.99% for Class C, 0.99% for Class F, 0.91% for Class F3, 0.99% for Class I and 0.91% for Class R6) multiplied by the average account value over the period, multiplied by 152/365 (to reflect the period March 2, 2022, commencement of operations, to July 31, 2022). |

22

Portfolio Holdings Presented by Sector

July 31, 2022

| Sector* | | %** |

| Communication Services | | | 9.15 | % |

| Consumer Discretionary | | | 16.34 | % |

| Consumer Staples | | | 8.33 | % |

| Energy | | | 5.84 | % |

| Financials | | | 22.62 | % |

| Health Care | | | 3.76 | % |

| Industrials | | | 5.62 | % |

| Information Technology | | | 18.31 | % |

| Materials | | | 5.59 | % |

| Real Estate | | | 2.03 | % |

| Utilities | | | 2.41 | % |

| Total | | | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

23

International Growth Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | | 2/1/22 | | 7/31/22 | | 2/1/22 -

7/31/22 | |

| Class A | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 847.70 | | | $4.86 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,019.54 | | | $5.31 | |

| Class C | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 845.50 | | | $8.28 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,015.82 | | | $9.05 | |

| Class F | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 848.70 | | | $3.71 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.78 | | | $4.06 | |

| Class F3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 849.50 | | | $3.35 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.17 | | | $3.66 | |

| Class I | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 848.70 | | | $3.71 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.78 | | | $4.06 | |

| Class R3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 846.80 | | | $6.00 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,018.30 | | | $6.56 | |

| Class R4 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 847.70 | | | $4.86 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,019.54 | | | $5.31 | |

| Class R5 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 848.70 | | | $3.71 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.78 | | | $4.06 | |

| Class R6 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 849.50 | | | $3.35 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.17 | | | $3.66 | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.06% for Class A, 1.81% for Class C, 0.81% for Class F, 0.73% for Class F3, 0.81% for Class I, 1.31% for Class R3, 1.06% for Class R4, 0.81% for Class R5 and 0.73% for Class R6) multiplied by the average account value over the period, multiplied by 181/365 (to reflect one-half year period). |

24

Portfolio Holdings Presented by Sector

July 31, 2022

| Sector* | | %** |

| Communication Services | | | 3.85 | % |

| Consumer Discretionary | | | 16.36 | % |

| Consumer Staples | | | 13.01 | % |

| Energy | | | 3.10 | % |

| Financials | | | 8.85 | % |

| Health Care | | | 14.84 | % |

| Industrials | | | 13.78 | % |

| Information Technology | | | 19.03 | % |

| Materials | | | 5.88 | % |

| Utilities | | | 1.30 | % |

| Total | | | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

25

Mid Cap Innovation Growth Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | | 2/1/22 | | 7/31/22 | | 2/1/22 -

7/31/22 | |

| Class A | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 849.70 | | | $4.86 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,019.54 | | | $5.31 | |

| Class C | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 846.30 | | | $8.29 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,015.82 | | | $9.05 | |

| Class F | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 850.90 | | | $3.72 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.78 | | | $4.06 | |

| Class F3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 851.00 | | | $3.35 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.17 | | | $3.66 | |

| Class I | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 850.90 | | | $3.72 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.78 | | | $4.06 | |

| Class R3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 848.60 | | | $6.00 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,018.30 | | | $6.56 | |

| Class R4 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 849.70 | | | $4.86 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,019.54 | | | $5.31 | |

| Class R5 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 850.90 | | | $3.72 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,020.78 | | | $4.06 | |

| Class R6 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 851.00 | | | $3.35 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.17 | | | $3.66 | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.06% for Class A, 1.81% for Class C, 0.81% for Class F, 0.73% for Class F3, 0.81% for Class I, 1.31% for Class R3, 1.06% for Class R4, 0.81% for Class R5 and 0.73% for Class R6) multiplied by the average account value over the period, multiplied by 181/365 (to reflect one-half year period). |

26

Portfolio Holdings Presented by Sector

July 31, 2022

| Sector* | | %** |

| Communication Services | | | 3.34 | % |

| Consumer Discretionary | | | 12.21 | % |

| Consumer Staples | | | 3.86 | % |

| Energy | | | 2.28 | % |

| Financials | | | 2.56 | % |

| Health Care | | | 22.47 | % |

| Industrials | | | 6.25 | % |

| Information Technology | | | 42.96 | % |

| Materials | | | 1.21 | % |

| Real Estate | | | 1.41 | % |

| Repurchase Agreements | | | 1.45 | % |

| Total | | | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

27

Short Duration High Yield Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | Beginning

Account

Value | | Ending

Account

Value | | Expenses

Paid During

Period† | |

| | | | 2/1/22 | | 7/31/22 | | 2/1/22 -

7/31/22 | |

| Class A | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 958.80 | | | $3.45 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.27 | | | $3.56 | |

| Class C | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 955.60 | | | $6.89 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,017.75 | | | $7.10 | |

| Class F | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 959.80 | | | $2.48 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.27 | | | $2.56 | |

| Class F3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 959.90 | | | $2.28 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.46 | | | $2.36 | |

| Class I | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 958.80 | | | $2.48 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.27 | | | $2.56 | |

| Class R3 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 957.50 | | | $4.90 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,019.79 | | | $5.06 | |

| Class R4 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 958.60 | | | $3.69 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,021.03 | | | $3.81 | |

| Class R5 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 959.80 | | | $2.48 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.27 | | | $2.56 | |

| Class R6 | | | | | | | | | | |

| Actual | | | $1,000.00 | | $ | 959.00 | | | $2.28 | |

| Hypothetical (5% Return Before Expenses) | | | $1,000.00 | | $ | 1,022.46 | | | $2.36 | |

| † | For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (0.71% for Class A, 1.42% for Class C, 0.51% for Class F, 0.47% for Class F3, 0.51% for Class I, 1.01% for Class R3, 0.76% for Class R4, 0.51% for Class R5 and 0.47% for Class R6) multiplied by the average account value over the period, multiplied by 181/365 (to reflect one-half year period). |

28

Portfolio Holdings Presented by Sector

July 31, 2022

| Sector* | | %** |

| Asset Backed Securities | | | 3.31 | % |

| Basic Materials | | | 3.56 | % |

| Communication Services | | | 10.02 | % |

| Consumer, Cyclical | | | 21.52 | % |

| Consumer, Non-cyclical | | | 14.78 | % |

| Diversified | | | 0.31 | % |

| Energy | | | 22.16 | % |

| Financials | | | 9.49 | % |

| Industrials | | | 8.87 | % |

| Mortgage-Backed Securities | | | 0.68 | % |

| Technology | | | 1.55 | % |

| Utilities | | | 3.05 | % |

| Repurchase Agreements | | | 0.70 | % |

| Total | | | 100.00 | % |

| * | | A sector may comprise several industries. |

| ** | | Represents percent of total investments. |

29

Schedule of Investments

CLIMATE FOCUSED BOND FUND July 31, 2022

| | | Interest | | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | | Date | | Amount | | | Value | |

| LONG-TERM INVESTMENTS 94.62% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| ASSET-BACKED SECURITIES 2.06% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Automobiles 1.05% | | | | | | | | | | | | | | |

| Tesla Auto Lease Trust 2019-A C† | | | 2.68% | | | 1/20/2023 | | $ | 125,000 | | | $ | 124,757 | |

| Tesla Auto Lease Trust 2021-A B† | | | 1.02% | | | 3/20/2025 | | | 100,000 | | | | 95,394 | |

| Total | | | | | | | | | | | | | 220,151 | |

| | | | | | | | | | | | | | | |

| Other 1.01% | | | | | | | | | | | | | | |

| GoodLeap Sustainable Home Solutions Trust 2022-1GS A† | | | 2.70% | | | 1/20/2049 | | | 141,706 | | | | 127,453 | |

| Sunrun Demeter Issuer 2021-2A A† | | | 2.27% | | | 1/30/2057 | | | 98,039 | | | | 84,706 | |

| Total | | | | | | | | | | | | | 212,159 | |

| Total Asset-Backed Securities (cost $465,860) | | | | | | | | | | | | | 432,310 | |

| | | | | | | | | | | | | | | |

| CONVERTIBLE BONDS 1.01% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Auto Manufacturers 0.20% | | | | | | | | | | | | | | |

| Lucid Group, Inc.† | | | 1.25% | | | 12/15/2026 | | | 12,000 | | | | 7,653 | |

| NIO, Inc. (China)(a) | | | 0.50% | | | 2/1/2027 | | | 8,000 | | | | 6,152 | |

| Tesla, Inc. | | | 2.00% | | | 5/15/2024 | | | 2,000 | | | | 28,692 | |

| Total | | | | | | | | | | | | | 42,497 | |

| | | | | | | | | | | | | | | |

| Energy-Alternate Sources 0.74% | | | | | | | | | | | | | | |

| Enphase Energy, Inc. | | | Zero Coupon | | | 3/1/2026 | | | 37,000 | | | | 44,511 | |

| NextEra Energy Partners LP† | | | Zero Coupon | | | 6/15/2024 | | | 14,000 | | | | 14,175 | |

| Plug Power, Inc. | | | 3.75% | | | 6/1/2025 | | | 3,000 | | | | 12,844 | |

| SolarEdge Technologies, Inc. (Israel)(a) | | | Zero Coupon | | | 9/15/2025 | | | 30,000 | | | | 44,145 | |

| SunPower Corp. | | | 4.00% | | | 1/15/2023 | | | 16,000 | | | | 17,256 | |

| Sunrun, Inc. | | | Zero Coupon | | | 2/1/2026 | | | 30,000 | | | | 22,650 | |

| Total | | | | | | | | | | | | | 155,581 | |

| | | | | | | | | | | | | | | |

| REITS 0.07% | | | | | | | | | | | | | | |

| HAT Holdings I LLC/HAT Holdings II LLC† | | | Zero Coupon | | | 5/1/2025 | | | 15,000 | | | | 13,995 | |

| Total Convertible Bonds (cost $222,596) | | | | | | | | | | | | | 212,073 | |

| | | | | | | | | | | | | | | |

| CORPORATE BONDS 65.29% | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Agriculture 0.50% | | | | | | | | | | | | | | |

| Darling Ingredients, Inc.† | | | 5.25% | | | 4/15/2027 | | | 67,000 | | | | 67,196 | |

| Darling Ingredients, Inc.† | | | 6.00% | | | 6/15/2030 | | | 36,000 | | | | 37,280 | |

| Total | | | | | | | | | | | | | 104,476 | |

| | |

| 30 | See Notes to Financial Statements. |

Schedule of Investments (continued)

CLIMATE FOCUSED BOND FUND July 31, 2022

| | | Interest | | | Maturity | | Principal | | | Fair | |

| Investments | | Rate | | | Date | | Amount | | | Value | |

| Apparel 0.46% | | | | | | | | | | | | | | |

| Chanel Ceres plc(b) | | | 0.50% | | | 7/31/2026 | | EUR | 100,000 | | | $ | 96,015 | |

| | | | | | | | | | | | | | | |

| Auto Manufacturers 1.00% | | | | | | | | | | | | | | |

| Ford Motor Co. | | | 3.25% | | | 2/12/2032 | | $ | 35,000 | | | | 29,277 | |

| Hyundai Capital Services, Inc. (South Korea)(a) | | | 1.25% | | | 2/8/2026 | | | 200,000 | | | | 180,859 | |

| Total | | | | | | | | | | | | | 210,136 | |

| | | | | | | | | | | | | | | |

| Auto Parts & Equipment 0.74% | | | | | | | | | | | | | | |

| Aptiv plc (Ireland)(a) | | | 4.35% | | | 3/15/2029 | | | 35,000 | | | | 33,817 | |

| BorgWarner, Inc. | | | 3.375% | | | 3/15/2025 | | | 65,000 | | | | 63,943 | |

| Dana, Inc. | | | 4.25% | | | 9/1/2030 | | | 68,000 | | | | 56,707 | |

| Total | | | | | | | | | | | | | 154,467 | |

| | | | | | | | | | | | | | | |

| Banks 9.01% | | | | | | | | | | | | | | |

| ABN AMRO Bank NV (Netherlands)†(a) | | | 2.47%

(1 Yr. Treasury

CMT + 1.10% | )# | | 12/13/2029 | | | 200,000 | | | | 174,312 | |

| AIB Group plc(b) | | | 2.875%

(5 Yr. EUSA + 3.30% | )# | | 5/30/2031 | | EUR | 100,000 | | | | 96,763 | |

| Bank of America Corp. | | | 2.456%

(3 Mo. LIBOR + .87% | )# | | 10/22/2025 | | $ | 100,000 | | | | 96,146 | |

| Bank of Ireland Group plc(b) | | | 0.375%

(1 Yr. EUSA + .77% | )# | | 5/10/2027 | | EUR | 100,000 | | | | 92,598 | |

| Bank of Nova Scotia (The) (Canada)(a) | | | 0.65% | | | 7/31/2024 | | $ | 125,000 | | | | 117,914 | |

| Bank of Nova Scotia (The) (Canada)(a) | | | 2.375% | | | 1/18/2023 | | | 80,000 | | | | 79,806 | |

| BNP Paribas SA (France)†(a) | | | 1.675%

(SOFR + .91% | )# | | 6/30/2027 | | | 200,000 | | | | 178,822 | |

| CaixaBank SA(b) | | | 1.25%

(5 Yr. EUSA + 1.63% | )# | | 6/18/2031 | | EUR | 100,000 | | | | 91,587 | |

| Citigroup, Inc. | | | 1.678%

(SOFR + 1.67% | )# | | 5/15/2024 | | $ | 125,000 | | | | 123,048 | |

| Danske Bank A/S(b) | | | 0.75%

(1 Yr. EUAMDB + .88% | )# | | 6/9/2029 | | EUR | 100,000 | | | | 89,566 | |

| Industrial & Commercial Bank of China Ltd. (Luxembourg)(a) | | | 2.875% | | | 10/12/2022 | | $ | 200,000 | | | | 199,906 | |

| JPMorgan Chase & Co. | | | 0.768%

(SOFR + .49% | )# | | 8/9/2025 | | | 111,000 | | | | 103,692 | |

| Kreditanstalt fuer Wiederaufbau (Germany)(a) | | | 0.75% | | | 9/30/2030 | | | 150,000 | | | | 127,738 | |

| Kreditanstalt fuer Wiederaufbau (Germany)(a) | | | 2.00% | �� | | 10/4/2022 | | | 112,000 | | | | 111,894 | |

| Landesbank Baden-Wuerttemberg(b) | | | 1.50% | | | 2/3/2025 | | GBP | 100,000 | | | | 115,802 | |