UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-10575

ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND, INC.

(Exact name of registrant as specified in charter)

1345 Avenue of the Americas, New York, New York 10105

(Address of principal executive offices) (Zip code)

Joseph J. Mantineo

AllianceBernstein L.P.

1345 Avenue of the Americas

New York, New York 10105

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 221-5672

Date of fiscal year end: October 31, 2016

Date of reporting period: April 30, 2016

ITEM 1. REPORTS TO STOCKHOLDERS.

APR 04.30.16

SEMI-ANNUAL REPORT

ALLIANCE CALIFORNIA

MUNICIPAL INCOME FUND

(NYSE: AKP)

Investment Products Offered

|

• Are Not FDIC Insured • May Lose Value • Are Not Bank Guaranteed |

You may obtain a description of the Fund’s proxy voting policies and procedures, and information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, without charge. Simply visit AB’s website at www.abglobal.com, or go to the Securities and Exchange Commission’s (the “Commission”) website at www.sec.gov, or call AB at (800) 227-4618.

The Fund files its complete schedule of portfolio holdings with the Commission for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q are available on the Commission’s website at www.sec.gov. The Fund’s Forms N-Q may also be reviewed and copied at the Commission’s Public Reference Room in Washington, DC; information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

AllianceBernstein Investments, Inc. (ABI) is the distributor of the AB family of mutual funds. ABI is a member of FINRA and is an affiliate of AllianceBernstein L.P., the Adviser of the funds.

The [A/B] logo is a registered service mark of AllianceBernstein and AllianceBernstein® is a registered service mark used by permission of the owner, AllianceBernstein L.P.

June 24, 2016

Semi-Annual Report

This report provides management’s discussion of fund performance for Alliance California Municipal Income Fund (the “Fund”) for the semi-annual reporting period ended April 30, 2016. The Fund is a closed-end fund and its shares are listed and traded on the New York Stock Exchange.

Investment Objectives and Policies

This Fund seeks to provide high current income exempt from regular federal and California state income tax by investing substantially all of its net assets in municipal securities that are exempt from state taxes. The Fund will normally invest at least 80%, and normally substantially all, of its net assets in municipal securities paying interest that is exempt from regular federal and California state income tax. In addition, the Fund normally invests at least 75% of its net assets in investment-grade municipal securities or unrated municipal securities considered to be of comparable quality as determined by the Fund’s investment adviser, AllianceBernstein L.P. (the “Adviser”). The Fund may invest up to 25% of its net assets in municipal securities rated below investment-grade and unrated municipal securities considered to be of comparable quality. The Fund intends to invest primarily in municipal securities that pay interest that is not subject to the federal alternative minimum Tax (“AMT”), but may invest without limit in municipal securities paying interest that is subject to the federal AMT. For more information regarding the Fund’s risks, please see “Disclosures and Risks” on pages 4-5 and “Note G—Risks Involved in Investing in the Fund” of the Notes to Financial Statements on pages 31-34.

Investment Results

The table on page 6 provides performance data for the Fund and its benchmark, the Barclays Municipal Bond Index, for the six- and 12-month periods ended April 30, 2016.

The Fund outperformed its benchmark for the six- and 12-month periods. An underweight in both the state and local general obligation (“GO”) sectors contributed to performance for both periods, relative to the benchmark, as did security selection in the water and special tax sectors. Security selection in the education sector also contributed to performance for the six-month period. For the 12-month period, security selection in the local GO sector contributed to performance, while security selection in the industrial and transportation sectors detracted from performance.

Leverage, achieved through the usage of auction rate preferred shares, tender option bonds (“TOBs”) and variable rate municipal term preferred shares, benefited the Fund’s absolute total return and income over both periods. The Fund used interest rate swaps for hedging purposes over both periods, which had an immaterial impact on performance.

Market Review and Investment Strategy

Intermediate- and long-maturity bonds had strong returns over both periods as falling global commodity prices and slowing economic growth drove yields lower. Shorter-maturity bonds underperformed as the US Federal Reserve increased the Federal Funds rate above its zero target to 0.25% for the first time

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 1 | |

since 2008. Across fixed-income sectors, municipals had strong performance due primarily to a combination of continued investor demand and limited supply. The total volume of outstanding municipal bonds has declined since 2010, unlike the corporate and Treasury markets which have seen an increase in issuance. In the opinion of the Fund’s Senior Investment Management Team (the “Team”), municipal credit continues to do well, as economic growth and tax receipts are correlated, which has caused tax revenues for state and local governments to hit all-time highs. State and local governments have kept payrolls and expenditures in check as government employment is approximately 500,000 below the peak during the financial crisis. The Team continues to overweight credit (municipal bonds rated A and below) and underweight the longest maturity bonds in the Fund.

California’s fiscal improvement has continued as the state’s economy and tax revenue growth has been sustained, and policymakers have continued to manage state finances prudently. California’s economy, particularly in the Bay Area, is growing more rapidly than the rest of the nation. The state, which faced a $26 billion deficit in January 2010, has since restrained spending and passed a series of tax increases, which together have balanced the state’s budget. The state has also focused on paying down debt and controlling growth of liabilities like pensions. As a result, California’s bond ratings have been rising and the Team believes this will continue during 2016. Over the next 12 months, steady revenue collections, which are historically volatile in California due in part to its highly

progressive income tax, should be a key factor to continued credit improvement. Ongoing fiscal discipline in the budgetary process will also be important, and the Team anticipates that the state may continue to use its robust revenues to pay down debts incurred during previous recessions and to build reserves for the inevitable next recession. While the Team is mindful of California’s history of strained finances, weak governance, and headline risk, the Team also recognizes that the state’s general obligation bonds are constitutionally protected and that debt service is paid second only after education.

The Fund may purchase municipal securities that are insured under policies issued by certain insurance companies. Historically, insured municipal securities typically received a higher credit rating, which meant that the issuer of the securities paid a lower interest rate. As a result of declines in the credit quality and associated downgrades of most fund insurers, insurance has less value than it did in the past. The market now values insured municipal securities primarily based on the credit quality of the issuer of the security with little value given to the insurance feature. In purchasing such insured securities, the Adviser evaluates the risk and return of municipal securities through its own research. If an insurance company’s rating is downgraded or the company becomes insolvent, the prices of municipal securities insured by the insurance company may decline. As of April 30, 2016, the Fund’s percentages of investments in municipal bonds that are insured and in insured municipal bonds that have been pre-refunded or

| | |

| 2 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

escrowed to maturity were 7.56% and 0.00%, respectively.

Since February 2008, auctions of the auction rate preferred shares have had fewer buyers than sellers and, as a result, the auctions have “failed”. The failed auctions did not lower the credit quality of the auction rate preferred shares, but rather meant that a holder was unable to sell the auction rate preferred securities in the auctions, so that there was a loss of liquidity for the holders of the auction rate preferred shares. When an auction fails, the auction rate preferred shares pay interest on a formula-based maximum rate based on AA-commercial paper and short-term municipal bond rates. In the extremely low short-term interest rate environment of recent years, the interest rates resulting from such a formula have been much lower than the returns on the Fund’s investments and the cost of alternative forms of leverage available to the Fund. However, to the extent that the cost of this leverage increases in the future and earnings from the Fund’s investments do not increase, the Fund’s net investment returns may decline.

In July 2015, the Fund announced a tender offer of up to 100% of its outstanding auction rate preferred shares at a price equal to 94% of the

liquidation preference of $25,000 per share. The result of accepting tendered shares in September 2015, and replacing the leverage associated with these shares with an alternative form of leverage, was to increase the Fund’s net asset value, but at least in the near term to increase the cost of leverage. Over time, the Team believes diversifying its sources of leverage will lead to lower borrowing costs.

The Team continues to explore, and discuss with the Board of Directors, other liquidity and leverage options, including TOBs, which it has used in the past; this may result in additional auction rate preferred shares being redeemed in the future. The Fund is not required to redeem any auction rate preferred shares, and the Team expects to continue to rely on the auction rate preferred shares for a portion of the Fund’s leverage exposure.

On June 23, 2016, the UK voted to leave the European Union (“EU”) in a popular referendum. At this moment in time, the UK remains a member of the EU and the rules and regulations remain unchanged, as do all the protections in place. Exactly how the UK’s role in the EU will change will become clear over time. The Adviser continues to monitor the heightened market volatility.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 3 | |

DISCLOSURES AND RISKS

Alliance California Municipal Income Fund Shareholder Information

Weekly comparative net asset value (“NAV”) and market price information about the Fund is published each Saturday in Barron’s and in other newspapers in a table called “Closed End Funds”. Daily NAVs and market price information, and additional information regarding the Fund, is available at www.abglobal.com and www.nyse.com. For additional shareholder information regarding this Fund, please see page 47.

Benchmark Disclosure

The Barclays Municipal Bond Index is unmanaged and does not reflect fees and expenses associated with the active management of a fund portfolio. The Barclays Municipal Bond Index represents the performance of the long-term tax-exempt bond market consisting of investment-grade bonds. An investor cannot invest directly in an index, and its results are not indicative of the performance for any specific investment, including the Fund. In addition, the Index does not reflect the use of leverage, whereas the Fund utilizes leverage.

A Word About Risk

Among the risks of investing in the Fund are changes in the general level of interest rates or changes in bond credit quality ratings. Changes in interest rates have a greater effect on bonds with longer maturities than on those with shorter maturities. Please note, as interest rates rise, existing bond prices fall and can cause the value of your investment in the Fund to decline. While the Fund invests principally in bonds and other fixed-income securities, in order to achieve its investment objectives, the Fund may at times use certain types of investment derivatives, such as options, futures, forwards and swaps. These instruments involve risks different from, and in certain cases, greater than, the risks presented by more traditional investments. At the discretion of the Fund’s Adviser, the Fund may invest up to 25% of its net assets in municipal bonds that are rated below investment grade (i.e., “junk bonds”). These securities involve greater volatility and risk than higher-quality fixed-income securities. The Fund will invest substantially all of its net assets in California municipal bonds and is therefore susceptible to political, economic or regulatory factors specifically affecting California municipal bond issuers.

Leverage Risk: The Fund uses financial leverage for investment purposes, which involves leverage risk. The Fund’s outstanding auction preferred shares and variable rate munifund term preferred shares (together “preferred shares”) result in leverage. The Fund may also use other types of financial leverage, including TOBs, either in combination with, or in lieu of, the preferred shares. The Fund utilizes leverage to seek to enhance the yield and NAV attributable to its Common Stock. These objectives may not be achieved in all interest rate environments. Leverage creates certain risks for holders of Common Stock, including the likelihood of greater volatility of the NAV and market price of the Common Stock. If income from the securities purchased from the funds made available by leverage is not sufficient to cover the cost of leverage, the Fund’s return will be less than if leverage had not been used. As a result, the amounts available for distribution to Common Stockholders as dividends and other distributions will be reduced. During periods of rising short-term interest rates, the interest paid on the auction rate preferred stock or the floaters issued in connection with the Fund’s TOB transactions would increase. In addition, the interest paid on inverse floaters held by the Fund, whether issued in connection with the Fund’s TOB transactions or purchased in a secondary market transaction, would decrease. Under such circumstances, the Fund’s income and distributions to Common Stockholders may decline, which would adversely affect the Fund’s yield and possibly the market value of its shares. If rising short-term rates coincide with a period of rising long-term rates, the value of the long-term municipal bonds purchased with the proceeds of leverage would decline, adversely affecting the net asset value attributable to the Fund’s Common Stock and possibly the market value of the shares.

Tax Risk: There is no guarantee that all of the Fund’s income will remain exempt from federal or state income taxes. From time to time, the US government and the US

(Disclosures, Risks and Note about Historical Performance continued on next page)

| | |

| 4 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Disclosures and Risks

DISCLOSURES AND RISKS

(continued from previous page)

Congress consider changes in federal tax law that could limit or eliminate the federal tax exemption for municipal bond income, which would in effect reduce the net income received by shareholders from the Fund by increasing taxes on that income. In such event, the Fund’s NAV could also decline as yields on municipal bonds, which are typically lower than those on taxable bonds, would be expected to increase to approximately the yield of comparable bonds.

Market Risk: The value of the Fund’s assets will fluctuate as the bond market fluctuates. The value of the Fund’s investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events that affect large portions of the market.

Credit Risk: An issuer or guarantor of a fixed-income security, or the counterparty to a derivatives or other contract, may be unable or unwilling to make timely payments of interest or principal, or to otherwise honor its obligations. The issuer or guarantor may default, causing a loss of the full principal amount of a security. The degree of risk for a particular security may be reflected in its credit rating. There is the possibility that the credit rating of a fixed-income security may be downgraded after purchase, which may adversely affect the value of the security. Investments in fixed-income securities with lower ratings tend to have a higher probability that an issuer will default or fail to meet its payment obligations.

Interest Rate Risk: Changes in interest rates will affect the value of investments in fixed-income securities. When interest rates rise, the value of investments in fixed-income securities tends to fall and this decrease in value may not be offset by higher income from new investments. Interest rate risk is generally greater for fixed-income securities with longer maturities or durations.

Inflation Risk: This is the risk that the value of assets or income from investments will be less in the future as inflation decreases the value of money. As inflation increases, the value of the Fund’s assets can decline as can the value of the Fund’s distributions. This risk is significantly greater for fixed-income securities with longer maturities.

Derivatives Risk: Investments in derivatives may be illiquid, difficult to price, and leveraged so that small changes may produce disproportionate losses for the Fund, and may be subject to counterparty risk to a greater degree than more traditional investments.

Duration Risk: Duration is a measure that relates the expected price volatility of a fixed-income security to changes in interest rates. The duration of a fixed-income security may be shorter than or equal to full maturity of a fixed-income security. Fixed-income securities with longer durations have more risk and will decrease in price as interest rates rise. For example, a fixed-income security with a duration of three years will decrease in value by approximately 3% if interest rates increase by 1%.

Liquidity Risk: Liquidity risk occurs when certain investments become difficult to purchase or sell. Difficulty in selling less liquid securities may result in sales at disadvantageous prices affecting the value of your investment in the Fund. Causes of liquidity risk may include low trading volumes and large positions. Municipal securities may have more liquidity risk than other fixed-income securities because they trade less frequently and the market for municipal securities is generally smaller than many other markets.

Management Risk: The Fund is subject to management risk because it is an actively managed investment fund. The Adviser will apply its investment techniques and risk analyses in making investment decisions, but there is no guarantee that its techniques will produce the intended results.

These risks are fully discussed in the Fund’s prospectus. As with all investments you may lose money by investing in the Fund.

An Important Note About Historical Performance

The performance on the following page represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance information shown. All fees and expenses related to the operation of the Fund have been deducted. Performance assumes reinvestment of distributions and does not account for taxes.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 5 | |

Disclosures and Risks

HISTORICAL PERFORMANCE

| | | | | | | | | | |

| | | | | | | | | | |

THE FUND VS. ITS BENCHMARK

PERIODS ENDED APRIL 30, 2016 (unaudited) | | Returns | | | |

| | 6 Months | | | 12 Months | | | |

| Alliance California Municipal Income Fund (NAV) | | | 7.28% | | | | 12.28% | | | |

|

| Barclays Municipal Bond Index | | | 3.55% | | | | 5.29% | | | |

|

| The Fund’s market price per share on April 30, 2016 was $15.11. The Fund’s NAV price per share on April 30, 2016 was $15.86. For additional Financial Highlights, please see pages 36-38. |

| | | | | | | | | | |

See Disclosures, Risks and Note about Historical Performance on pages 4-5.

| | |

| 6 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Historical Performance

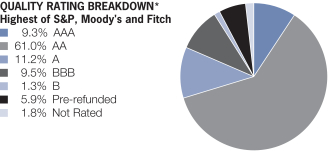

PORTFOLIO SUMMARY

April 30, 2016 (unaudited)

PORTFOLIO STATISTICS

Net Assets ($mil): $135.7

| * | | All data are as of April 30, 2016. The Fund’s quality rating breakdown is expressed as a percentage of the Fund’s total investments in municipal securities and may vary over time. The Fund also enters into derivative transactions, which may be used for hedging or investment purposes (see “Portfolio of Investments” section of the report for additional details). The quality ratings are determined by using the Standard & Poor’s Ratings Services (“S&P”), Moody’s Investors Services, Inc. (“Moody’s”) and Fitch Ratings, Ltd. (“Fitch”). The Fund considers the credit ratings issued by S&P, Moody’s and Fitch and uses the highest rating issued by the agencies. These ratings are a measure of the quality and safety of a bond or portfolio, based on the issuer’s financial condition. AAA is the highest (best) and D is the lowest (worst). If applicable, the pre-refunded category includes bonds which are secured by US government securities and therefore are deemed high-quality investment-grade by the Adviser. If applicable, Not Applicable (N/A) includes non-creditworthy investments; such as, equities, currency contracts, futures and options. If applicable, the Not Rated category includes bonds that are not rated by a nationally recognized statistical rating organization. The Adviser evaluates the creditworthiness of non-rated securities based on a number of factors including, but not limited to, cash flows, enterprise value and economic environment. |

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 7 | |

Portfolio Summary

PORTFOLIO OF INVESTMENTS

April 30, 2016 (unaudited)

| | | | | | | | |

| | | Principal Amount (000) | | | U.S. $ Value | |

| |

| | | | | | | | |

MUNICIPAL OBLIGATIONS – 156.2% | | | | | | | | |

Long-Term Municipal Bonds – 156.2% | | | | | | | | |

California – 142.3% | | | | | | | | |

Abag Finance Authority for Nonprofit Corps.

(Bijou Woods Associates LP)

Series 2001A

5.30%, 12/01/31 | | $ | 2,735 | | | $ | 2,742,986 | |

Anaheim Public Financing Authority

(City of Anaheim CA Lease)

Series 2014A

5.00%, 5/01/33-5/01/39 | | | 4,750 | | | | 5,654,150 | |

Bay Area Toll Authority

Series 2013S

5.00%, 4/01/33 | | | 5,000 | | | | 5,910,200 | |

Beaumont Financing Authority

AMBAC Series 2007C

5.00%, 9/01/26 | | | 755 | | | | 778,503 | |

Bellflower Redevelopment Agency

(9920 Flora Vista LP)

Series 2002A

5.50%, 6/01/35 | | | 2,775 | | | | 2,744,225 | |

California Econ Recovery

Series 2009A

5.25%, 7/01/21 (Pre-refunded/ETM) | | | 535 | | | | 609,456 | |

California Health Facilities Financing Authority

(California-Nevada Methodist Homes)

Series 2015

5.00%, 7/01/45 | | | 3,000 | �� | | | 3,521,880 | |

California Municipal Finance Authority

(Azusa Pacific University)

Series 2015B

5.00%, 4/01/35-4/01/41 | | | 2,040 | | | | 2,274,445 | |

California Pollution Control Financing Authority

(Poseidon Resources Channelside LP)

Series 2012

5.00%, 7/01/37(a) | | | 3,450 | | | | 3,575,511 | |

California School Finance Authority

(Alliance College-Ready Public Schools Facilities Corp.)

Series 2015A

5.00%, 7/01/30(a) | | | 1,700 | | | | 1,859,205 | |

California School Finance Authority

(Green DOT Public Schools Obligated Group)

Series 2015A

5.00%, 8/01/45(a) | | | 1,500 | | | | 1,614,855 | |

California State Public Works Board

Series 2011G

5.25%, 12/01/26 (Pre-refunded/ETM) | | | 6,000 | | | | 7,357,380 | |

| | |

| 8 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Portfolio of Investments

| | | | | | | | |

| | |

| | | Principal Amount (000) | | | U.S. $ Value | |

| |

| | | | | | | | |

California Statewide Communities Development Authority

(Bentley School)

Series 2010A

7.00%, 7/01/40 | | $ | 2,625 | | | $ | 3,108,893 | |

California Statewide Communities Development Authority

(Buck Institute for Research on Aging)

AGM Series 2014

5.00%, 11/15/44 | | | 4,000 | | | | 4,552,960 | |

California Statewide Communities Development Authority

(Collis P. and Howard Huntington Memorial Hospital Trust)

Series 2014B

5.00%, 7/01/44 | | | 1,000 | | | | 1,142,190 | |

City of Los Angeles Department of Airports

(Los Angeles Intl Airport)

Series 2009A

5.25%, 5/15/29 | | | 1,700 | | | | 1,922,224 | |

Series 2010A

5.00%, 5/15/27 | | | 1,440 | | | | 1,667,606 | |

City of San Francisco CA Public Utilities Commission Wastewater Revenue

Series 2013B

5.00%, 10/01/32 | | | 4,735 | | | | 5,695,779 | |

Fullerton Redevelopment Agency Successor Agency

(Marshall B Ketchum University)

AGC Series 2004

5.00%, 4/01/21 | | | 2,050 | | | | 2,127,367 | |

Garden Grove Unified School District

Series 2013C

5.00%, 8/01/34 | | | 3,650 | | | | 4,333,280 | |

Jurupa Public Financing Authority

Series 2014A

5.00%, 9/01/30-9/01/32 | | | 2,475 | | | | 2,934,165 | |

Long Beach Bond Finance Authority

(Aquarium of the Pacific)

Series 2012

5.00%, 11/01/27 | | | 3,500 | | | | 4,117,190 | |

Los Angeles Community College District/CA

Series 2008F-1

5.00%, 8/01/28 (Pre-refunded/ETM) | | | 4,200 | | | | 4,598,958 | |

Los Angeles Community Redevelopment Agency

(Los Angeles Community Redevelopment Agency Sales Tax)

AMBAC Series 2002A

5.375%, 12/01/26 | | | 6,635 | | | | 6,655,568 | |

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 9 | |

Portfolio of Investments

| | | | | | | | |

| | |

| | | Principal Amount (000) | | | U.S. $ Value | |

| |

| | | | | | | | |

Los Angeles County Metropolitan Transportation Authority

(Los Angeles County Metropolitan Transportation Authority Sales Tax)

Series 2009

5.00%, 7/01/25 | | $ | 6,700 | | | $ | 7,560,146 | |

Series 2013B

5.00%, 7/01/33 | | | 1,675 | | | | 2,022,194 | |

Los Angeles County Sanitation Districts Financing Authority

Series 2015A

5.00%, 10/01/33 | | | 1,400 | | | | 1,682,674 | |

Los Angeles Department of Water & Power WTR

Series 2013B

5.00%, 7/01/32 | | | 6,185 | | | | 7,467,027 | |

Napa Valley Unified School District

Series 2016C

4.00%, 8/01/46 | | | 2,500 | | | | 2,728,175 | |

Norco Community Redevelopment Agency Successor Agency

(Norco Redevelopment Agency Project No 1)

Series 2010

5.875%, 3/01/32 | | | 420 | | | | 492,324 | |

6.00%, 3/01/36 | | | 325 | | | | 381,147 | |

Peralta Community College District

Series 2014A

4.00%, 8/01/31 | | | 4,100 | | | | 4,504,055 | |

Port of Los Angeles

Series 2009C

5.00%, 8/01/26 | | | 5,550 | | | | 6,250,576 | |

Richmond Community Redevelopment Agency

Series 2010A

5.75%, 9/01/24-9/01/25 | | | 530 | | | | 614,181 | |

6.00%, 9/01/30 | | | 370 | | | | 430,850 | |

Riverside County Infrastructure Financing Authority

(Riverside County Infrastructure Financing Authority Lease)

Series 2015A

4.00%, 11/01/37 | | | 1,225 | | | | 1,308,815 | |

Riverside County Transportation Commission

(Riverside County Transportation Commission Sales Tax)

Series 2013A

5.25%, 6/01/32 | | | 2,000 | | | | 2,432,700 | |

Sacramento City Unified School District/CA

Series 2011

5.50%, 7/01/29 | | | 4,000 | | | | 4,780,280 | |

| | |

| 10 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Portfolio of Investments

| | | | | | | | |

| | |

| | | Principal Amount (000) | | | U.S. $ Value | |

| |

| | | | | | | | |

San Bernardino County Transportation Authority

5.00% SBDTRN, 3/01/32-3/01/34(b) | | $ | 6,040 | | | $ | 7,205,011 | |

San Diego County Water Authority Financing Corp.

Series 2013

5.00%, 5/01/31 | | | 4,300 | | | | 5,200,979 | |

San Diego Public Facilities Financing Authority

5.00%, 5/15/36(b) | | | 5,000 | | | | 6,122,750 | |

San Diego Public Facilities Financing Authority

(San Diego Public Facilities Financing Authority Lease)

Series 2010A

5.10%, 9/01/29 | | | 2,360 | | | | 2,706,967 | |

San Diego Unified School District/CA

Series 2013C

5.00%, 7/01/32 | | | 5,125 | | | | 6,130,474 | |

San Francisco Bay Area Rapid Transit District

(San Francisco Bay Area Rapid Transit District Sales Tax)

Series 2012A

5.00%, 7/01/36 | | | 3,730 | | | | 4,403,675 | |

San Francisco Municipal Transportation Agency

Series 2013

5.00%, 3/01/28-3/01/31 | | | 6,070 | | | | 7,327,441 | |

San Joaquin Hills Transportation Corridor Agency

Series 2014A

5.00%, 1/15/44 | | | 3,900 | | | | 4,283,019 | |

San Mateo Joint Powers Financing Authority

(San Mateo Joint Powers Financing Authority Lease)

Series 2014

5.00%, 6/15/31 | | | 1,250 | | | | 1,521,188 | |

San Mateo Union High School District

Series 2013A

5.00%, 9/01/33 | | | 4,180 | | | | 4,881,446 | |

Southern California Public Power Authority

(Los Angeles Department of Water & Power PWR)

Series 2010

5.00%, 7/01/27 | | | 2,525 | | | | 2,867,390 | |

State of California

Series 2013

5.00%, 11/01/31 | | | 2,000 | | | | 2,449,800 | |

Turlock Irrigation District

Series 2011

5.50%, 1/01/41 | | | 1,200 | | | | 1,386,468 | |

University of California

Series 2012G

5.00%, 5/15/31 | | | 8,000 | | | | 9,522,240 | |

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 11 | |

Portfolio of Investments

| | | | | | | | |

| | |

| | | Principal Amount (000) | | | U.S. $ Value | |

| |

| | | | | | | | |

Walnut Energy Center Authority

Series 2014

5.00%, 1/01/33 | | $ | 2,500 | | | $ | 2,960,625 | |

| | | | | | | | |

| | | | | | | 193,123,593 | |

| | | | | | | | |

Florida – 3.2% | | | | | | | | |

Florida Higher Educational Facilities Financial Authority

(Nova Southeastern University, Inc.)

Series 2016

5.00%, 4/01/33(c) | | | 1,000 | | | | 1,186,910 | |

Miami Beach Health Facilities Authority

(Mount Sinai Medical Center of Florida, Inc.)

Series 2014

5.00%, 11/15/39 | | | 2,750 | | | | 3,101,643 | |

| | | | | | | | |

| | | | | | | 4,288,553 | |

| | | | | | | | |

Guam – 1.7% | | | | | | | | |

Guam Power Authority

Series 2012A

5.00%, 10/01/34 | | | 2,000 | | | | 2,244,560 | |

| | | | | | | | |

| | |

Indiana – 0.8% | | | | | | | | |

Richmond Hospital Authority

(Reid Hospital & Health Care Services, Inc.)

Series 2015

5.00%, 1/01/39 | | | 1,000 | | | | 1,139,200 | |

| | | | | | | | |

| | |

Minnesota – 1.0% | | | | | | | | |

City of Minneapolis MN

(Fairview Health Services Obligated Group)

Series 2015A

5.00%, 11/15/33 | | | 1,100 | | | | 1,286,153 | |

| | | | | | | | |

| | |

Missouri – 0.8% | | | | | | | | |

Joplin Industrial Development Authority

(Freeman Health System)

Series 2015

5.00%, 2/15/35 | | | 1,000 | | | | 1,131,150 | |

| | | | | | | | |

| | |

Nevada – 1.4% | | | | | | | | |

Henderson Local Improvement Districts

AGM Series 2007A

5.00%, 3/01/18 | | | 1,810 | | | | 1,906,021 | |

| | | | | | | | |

| | |

New York – 4.2% | | | | | | | | |

Metropolitan Transportation Authority

Series 2014C

5.00%, 11/15/32 | | | 4,745 | | | | 5,707,760 | |

| | | | | | | | |

| | |

| 12 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Portfolio of Investments

| | | | | | | | |

| | |

| | | Principal Amount (000) | | | U.S. $ Value | |

| |

| | | | | | | | |

Ohio – 0.0% | | | | | | | | |

Columbiana County Port Authority

(Apex Environmental LLC)

Series 2004

7.125%, 8/01/25(d) | | $ | 500 | | | $ | 10,000 | |

Series 2014

10.635%, 8/01/25(d) | | | 67 | | | | 1,346 | |

| | | | | | | | |

| | | | | | | 11,346 | |

| | | | | | | | |

Pennsylvania – 0.8% | | | | | | | | |

Pennsylvania Economic Development Financing

Authority

(PA Bridges Finco LP)

Series 2015

5.00%, 12/31/38 | | | 1,000 | | | | 1,122,680 | |

| | | | | | | | |

| | |

Total Investments – 156.2%

(cost $193,205,959) | | | | | | | 211,961,016 | |

Other assets less liabilities – (34.2)% | | | | | | | (46,410,563 | ) |

Auction Preferred Shares at liquidation value – (22.0)% | | | | | | | (29,875,000 | ) |

| | | | | | | | |

| | |

Net Assets Applicable to Common Shareholders – 100.0%(e) | | | | | | $ | 135,675,453 | |

| | | | | | | | |

INTEREST RATE SWAPS (see Note C)

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Rate Type | | | | |

Swap Counterparty | | Notional

Amount

(000) | | | Termination

Date | | | Payments

made

by the Fund | | | Payments

received

by the

Fund | | | Unrealized

Appreciation/

(Depreciation) | |

Merrill Lynch Capital Services, Inc. | | $ | 2,300 | | | | 10/21/16 | | | | SIFMA | * | | | 4.129 | % | | $ | 43,737 | |

| | | | | | | | | | | | | | | | | | | | |

| * | | Variable interest rate based on the Securities Industry & Financial Markets Association (SIFMA) Municipal Swap Index. |

| (a) | | Security is exempt from registration under Rule 144A of the Securities Act of 1933. These securities are considered liquid and may be resold in transactions exempt from registration, normally to qualified institutional buyers. At April 30, 2016, the aggregate market value of these securities amounted to $7,049,571 or 5.2% of net assets. |

| (b) | | Security represents the underlying municipal obligation of an inverse floating rate obligation held by the Fund (see Note I). |

| (c) | | When-Issued or delayed delivery security. |

| (e) | | Portfolio percentages are calculated based on net assets applicable to common shareholders. |

As of April 30, 2016, the Fund’s percentages of investments in municipal bonds that are insured and in insured municipal bonds that have been pre-refunded or escrowed to maturity are 7.6% and 0.0%, respectively.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 13 | |

Portfolio of Investments

Glossary:

AGC – Assured Guaranty Corporation

AGM – Assured Guaranty Municipal

AMBAC – Ambac Assurance Corporation

ETM – Escrowed to Maturity

See notes to financial statements.

| | |

| 14 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Portfolio of Investments

STATEMENT OF ASSETS & LIABILITIES

April 30, 2016 (unaudited)

| | | | |

| Assets | | | | |

Investments in securities, at value | | | | |

Unaffiliated issuers (cost $193,205,959) | | $ | 211,961,016 | |

Interest and dividends receivable | | | 2,857,150 | |

Deferred offering costs | | | 225,981 | |

Unrealized appreciation on interest rate swaps | | | 43,737 | |

| | | | |

Total assets | | | 215,087,884 | |

| | | | |

| Liabilities | | | | |

Due to custodian | | | 2,932 | |

Variable Rate MuniFund Term Preferred Shares, at liquidation value | | | 40,125,000 | |

Payable for floating rate notes issued* | | | 7,950,000 | |

Payable for investment securities purchased | | | 1,183,120 | |

Advisory fee payable | | | 113,034 | |

Interest expense payable | | | 57,523 | |

Dividends payable—preferred shares | | | 3,103 | |

Other liabilities | | | 13,980 | |

Accrued expenses | | | 88,739 | |

| | | | |

Total liabilities | | | 49,537,431 | |

| | | | |

| Auction Preferred Shares, at Liquidation Value | | | | |

Auction Preferred shares, $.001 par value per share; 3,240 shares authorized, 1,195 shares issued and outstanding at $25,000 per share liquidation preference | | $ | 29,875,000 | |

| | | | |

Net Assets Applicable to Common Shareholders | | $ | 135,675,453 | |

| | | | |

| Composition of Net Assets Applicable to Common Shareholders | | | | |

Common stock, $.001 par value per share; 1,999,996,760 shares authorized, 8,554,668 shares issued and outstanding | | $ | 8,555 | |

Additional paid-in capital | | | 122,415,038 | |

Distributions in excess of net investment income | | | (122,718 | ) |

Accumulated net realized loss on investment transactions | | | (5,424,216 | ) |

Net unrealized appreciation on investments | | | 18,798,794 | |

| | | | |

Net Assets Applicable to Common Shareholders | | $ | 135,675,453 | |

| | | | |

Net Asset Value Applicable to Common Shareholders

(based on 8,554,668 common shares outstanding) | | $ | 15.86 | |

| | | | |

| * | | Represents short-term floating rate certificates issued by tender option bond trusts (see Note H). |

See notes to financial statements.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 15 | |

Statement of Assets & Liabilities

STATEMENT OF OPERATIONS

Six Months Ended April 30, 2016 (unaudited)

| | | | | | | | |

| Investment Income | | | | | | | | |

Interest | | $ | 4,057,742 | | | | | |

Dividends—Affiliated issuers | | | 1,573 | | | $ | 4,059,315 | |

| | | | | | | | |

| Expenses | | | | | | | | |

Advisory fee (see Note B) | | | 659,395 | | | | | |

Auction Preferred Shares-auction agent’s fees | | | 9,239 | | | | | |

Custodian | | | 44,137 | | | | | |

Audit and tax | | | 31,806 | | | | | |

Legal | | | 26,797 | | | | | |

Printing | | | 17,684 | | | | | |

Registration fees | | | 11,908 | | | | | |

Directors’ fees | | | 9,719 | | | | | |

Transfer agency | | | 9,133 | | | | | |

Miscellaneous | | | 29,484 | | | | | |

| | | | | | | | |

Total expenses before interest expense, fees and amortization of offering costs | | | 849,302 | | | | | |

Interest expense, fees and amortization of offering costs | | | 343,642 | | | | | |

| | | | | | | | |

Total expenses | | | | | | | 1,192,944 | |

| | | | | | | | |

Net investment income | | | | | | | 2,866,371 | |

| | | | | | | | |

| Realized and Unrealized Gain (Loss) on Investment Transactions | | | | | | | | |

Net realized gain on: | | | | | | | | |

Investment transactions | | | | | | | 335,470 | |

Swaps | | | | | | | 46,649 | |

Net change in unrealized appreciation/depreciation of: | | | | | | | | |

Investments | | | | | | | 5,952,145 | |

Swaps | | | | | | | (48,608 | ) |

| | | | | | | | |

Net gain on investment transactions | | | | | | | 6,285,656 | |

| | | | | | | | |

| Dividends to Auction Preferred Shareholders from | | | | | | | | |

Net investment income | | | | | | | (59,668 | ) |

| | | | | | | | |

Net Increase in Net Assets Applicable to Common Shareholders Resulting from Operations | | | | | | $ | 9,092,359 | |

| | | | | | | | |

See notes to financial statements.

| | |

| 16 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Statement of Operations

STATEMENT OF CHANGES IN NET ASSETS

APPLICABLE TO COMMON SHAREHOLDERS

| | | | | | | | |

| | | Six Months Ended

April 30, 2016

(unaudited) | | | Year Ended

October 31,

2015 | |

| Increase (Decrease) in Net Assets Applicable to Common Shareholders Resulting from Operations | | | | | | | | |

Net investment income | | $ | 2,866,371 | | | $ | 6,394,156 | |

Net realized gain on investment transactions | | | 382,119 | | | | 1,566,266 | |

Net change in unrealized appreciation/depreciation of investments | | | 5,903,537 | | | | (2,652,119 | ) |

| Dividends to Auction Preferred Shareholders from | | | | | | | | |

Net investment income | | | (59,668 | ) | | | (80,388 | ) |

| | | | | | | | |

Net increase in net assets applicable to common shareholders resulting from operations | | | 9,092,359 | | | | 5,227,915 | |

| Dividends and Distributions to Common Shareholders from | | | | | | | | |

Net investment income | | | (3,033,913 | ) | | | (6,436,532 | ) |

| Common Stock Transactions | | | | | | | | |

Net increase | | | – 0 | – | | | 2,488,667 | |

| | | | | | | | |

Total increase | | | 6,058,446 | | | | 1,280,050 | |

| Net Assets Applicable to Common Shareholders | | | | | | | | |

Beginning of period | | | 129,617,007 | | | | 128,336,957 | |

| | | | | | | | |

End of period (including distributions in excess of net investment income and undistributed net investment income of ($122,718) and $104,492, respectively) | | $ | 135,675,453 | | | $ | 129,617,007 | |

| | | | | | | | |

See notes to financial statements.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 17 | |

Statement of Changes in Net Assets Applicable to Common Shareholders

STATEMENT OF CASH FLOWS

For the Six Months Ended April 30, 2016 (unaudited)

| | | | | | | | |

| Cash flows from operating activities | | | | | | | | |

Net increase in net assets from operations | | | | | | $ | 9,152,027 | |

| Reconciliation of net increase in net assets from operations to net increase in cash from operating activities: | | | | | | | | |

Decrease in interest and dividends receivable | | $ | 10,062 | | | | | |

Net accretion of bond discount and amortization of bond premium | | | 570,816 | | | | | |

Decrease in payable for investments purchased | | | (33,011 | ) | | | | |

Decrease in other assets | | | 17,879 | | | | | |

Decrease in accrued expenses | | | (69,251 | ) | | | | |

Purchases of long-term investments | | | (14,341,145 | ) | | | | |

Purchases of short-term investments | | | (5,264,153 | ) | | | | |

Proceeds from disposition of long-term investments | | | 14,785,249 | | | | | |

Proceeds from disposition of short-term investments | | | 5,264,153 | | | | | |

Proceeds on swaps, net | | | 46,649 | | | | | |

Net realized gain on investment transactions | | | (382,119 | ) | | | | |

Net change in unrealized appreciation/depreciation on investment transactions | | | (5,903,537 | ) | | | | |

| | | | | | | | |

Total adjustments | | | | | | | (5,298,408 | ) |

| | | | | | | | |

Net increase in cash from operating activities | | | | | | $ | 3,853,619 | |

| | | | | | | | |

| Cash flows from financing activities | | | | | | | | |

Decrease in due to custodian | | | (262,641 | ) | | | | |

Cash dividends paid | | | (3,090,978 | ) | | | | |

Decrease in payable for floating rate notes issued | | | (500,000 | ) | | | | |

| | | | | | | | |

Net decrease in cash from financing activities | | | | | | | (3,853,619 | ) |

| | | | | | | | |

Net increase in cash | | | | | | | — | |

Net change in cash | | | | | | | | |

Cash at beginning of period | | | | | | | — | |

| | | | | | | | |

Cash at end of period | | | | | | $ | — | |

| | | | | | | | |

Supplemental disclosure of cash flow information: | | | | | | | | |

Interest expense paid during the period | | $ | 331,108 | | | | | |

In accordance with U.S. GAAP, the Fund has included a Statement of Cash Flows as a result of its substantial investments in floating rate notes and Variable Rate MuniFund Term Preferred Shares throughout the period.

See notes to financial statements.

| | |

| 18 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Statement of Cash Flows

NOTES TO FINANCIAL STATEMENTS

April 30, 2016 (unaudited)

NOTE A

Significant Accounting Policies

Alliance California Municipal Income Fund, Inc. (the “Fund”) was incorporated in the State of Maryland on November 9, 2001 and is registered under the Investment Company Act of 1940 as a diversified, closed-end management investment company. The financial statements have been prepared in conformity with U.S. generally accepted accounting principles (“U.S. GAAP”) which require management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements and amounts of income and expenses during the reporting period. Actual results could differ from those estimates. The Fund is an investment company under U.S. GAAP and follows the accounting and reporting guidance applicable to investment companies. The following is a summary of significant accounting policies followed by the Fund.

1. Security Valuation

Portfolio securities are valued at their current market value determined on the basis of market quotations or, if market quotations are not readily available or are deemed unreliable, at “fair value” as determined in accordance with procedures established by and under the general supervision of the Fund’s Board of Directors (the “Board”).

In general, the market values of securities which are readily available and deemed reliable are determined as follows: securities listed on a national securities exchange (other than securities listed on the NASDAQ Stock Market, Inc. (“NASDAQ”)) or on a foreign securities exchange are valued at the last sale price at the close of the exchange or foreign securities exchange. If there has been no sale on such day, the securities are valued at the last traded price from the previous day. Securities listed on more than one exchange are valued by reference to the principal exchange on which the securities are traded; securities listed only on NASDAQ are valued in accordance with the NASDAQ Official Closing Price; listed or over the counter (“OTC”) market put or call options are valued at the mid level between the current bid and ask prices. If either a current bid or current ask price is unavailable, AllianceBernstein L.P. (the “Adviser”) will have discretion to determine the best valuation (e.g. last trade price in the case of listed options); open futures are valued using the closing settlement price or, in the absence of such a price, the most recent quoted bid price. If there are no quotations available for the day of valuation, the last available closing settlement price is used; U.S. Government securities and any other debt instruments having 60 days or less remaining until maturity are generally valued at market by an independent pricing vendor, if a market price is available. If a market price is not available, the securities are valued at amortized cost. This methodology is commonly used for short term securities that have an original maturity of 60 days or less, as well as short term securities that had an original term to maturity that exceeded 60 days. In instances when amortized cost is utilized, the Valuation Committee (the

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 19 | |

Notes to Financial Statements

“Committee”) must reasonably conclude that the utilization of amortized cost is approximately the same as the fair value of the security. Such factors the Committee will consider include, but are not limited to, an impairment of the creditworthiness of the issuer or material changes in interest rates. Fixed-income securities, including mortgage-backed and asset-backed securities, may be valued on the basis of prices provided by a pricing service or at a price obtained from one or more of the major broker-dealers. In cases where broker-dealer quotes are obtained, the Adviser may establish procedures whereby changes in market yields or spreads are used to adjust, on a daily basis, a recently obtained quoted price on a security. Swaps and other derivatives are valued daily, primarily using independent pricing services, independent pricing models using market inputs, as well as third party broker-dealers or counterparties. Investment companies are valued at their net asset value each day.

Securities for which market quotations are not readily available (including restricted securities) or are deemed unreliable are valued at fair value. Factors considered in making this determination may include, but are not limited to, information obtained by contacting the issuer, analysts, analysis of the issuer’s financial statements or other available documents. In addition, the Fund may use fair value pricing for securities primarily traded in non-U.S. markets because most foreign markets close well before the Fund values its securities at 4:00 p.m., Eastern Time. The earlier close of these foreign markets gives rise to the possibility that significant events, including broad market moves, may have occurred in the interim and may materially affect the value of those securities. To account for this, the Fund may frequently value many of its foreign equity securities using fair value prices based on third party vendor modeling tools to the extent available.

2. Fair Value Measurements

In accordance with U.S. GAAP regarding fair value measurements, fair value is defined as the price that the Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants at the measurement date. U.S. GAAP establishes a framework for measuring fair value, and a three-level hierarchy for fair value measurements based upon the transparency of inputs to the valuation of an asset or liability (including those valued based on their market values as described in Note A.1 above). Inputs may be observable or unobservable and refer broadly to the assumptions that market participants would use in pricing the asset or liability. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions that market participants would use in pricing the asset or liability based on the best information available in the circumstances. Each investment is assigned a level

| | |

| 20 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Notes to Financial Statements

based upon the observability of the inputs which are significant to the overall valuation. The three-tier hierarchy of inputs is summarized below.

| | • | | Level 1—quoted prices in active markets for identical investments |

| | • | | Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.) |

| | • | | Level 3—significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The fair value of debt instruments, such as bonds, and over-the-counter derivatives is generally based on market price quotations, recently executed market transactions (where observable) or industry recognized modeling techniques and are generally classified as Level 2. Pricing vendor inputs to Level 2 valuations may include quoted prices for similar investments in active markets, interest rate curves, coupon rates, currency rates, yield curves, option adjusted spreads, default rates, credit spreads and other unique security features in order to estimate the relevant cash flows which are then discounted to calculate fair values. If these inputs are unobservable and significant to the fair value, these investments will be classified as Level 3. In addition, non-agency rated investments are classified as Level 3.

Other fixed income investments, including non-U.S. government and corporate debt, are generally valued using quoted market prices, if available, which are typically impacted by current interest rates, maturity dates and any perceived credit risk of the issuer. Additionally, in the absence of quoted market prices, these inputs are used by pricing vendors to derive a valuation based upon industry or proprietary models which incorporate issuer specific data with relevant yield/spread comparisons with more widely quoted bonds with similar key characteristics. Those investments for which there are observable inputs are classified as Level 2. Where the inputs are not observable, the investments are classified as Level 3.

The following table summarizes the valuation of the Fund’s investments by the above fair value hierarchy levels as of April 30, 2016:

| | | | | | | | | | | | | | | | |

Investments in Securities: | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Assets: | | | | | | | | | | | | | | | | |

Long-Term Municipal Bonds | | $ | – 0 | – | | $ | 208,062,274 | | | $ | 3,898,742 | | | $ | 211,961,016 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | | – 0 | – | | | 208,062,274 | | | | 3,898,742 | | | | 211,961,016 | |

Other Financial Instruments(a): | | | | | | | | | | | | | | | | |

Assets: | | | | | | | | | | | | | | | | |

Interest Rate Swaps | | | – 0 | – | | | 43,737 | | | | – 0 | – | | | 43,737 | |

Liabilities: | | | – 0 | – | | | – 0 | – | | | – 0 | – | | | – 0 | – |

| | | | | | | | | | | | | | | | |

Total(b) | | $ | – 0 | – | | $ | 208,106,011 | | | $ | 3,898,742 | | | $ | 212,004,753 | |

| | | | | | | | | | | | | | | | |

| (a) | | Other financial instruments are derivative instruments, such as futures, forwards and swaps, which are valued at the unrealized appreciation/depreciation on the instrument. |

| (b) | | There were no transfers between any levels during the reporting period. |

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 21 | |

Notes to Financial Statements

The Fund recognizes all transfers between levels of the fair value hierarchy assuming the financial instruments were transferred at the beginning of the reporting period.

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value.

| | | | | | | | |

| | | Long-Term

Municipal

Bonds | | | Total | |

Balance as of 10/31/15 | | $ | 3,876,970 | | | $ | 3,876,970 | |

Accrued discounts/(premiums) | | | (3,202 | ) | | | (3,202 | ) |

Realized gain (loss) | | | (397,407 | ) | | | (397,407 | ) |

Change in unrealized appreciation/depreciation | | | 592,285 | | | | 592,285 | |

Purchases | | | – 0 | – | | | – 0 | – |

Sales | | | (169,904 | ) | | | (169,904 | ) |

Transfers in to Level 3 | | | – 0 | – | | | – 0 | – |

Transfers out of Level 3 | | | – 0 | – | | | – 0 | – |

| | | | | | | | |

Balance as of 4/30/16 | | $ | 3,898,742 | | | $ | 3,898,742 | |

| | | | | | | | |

Net change in unrealized appreciation/depreciation from investments held as of 4/30/16(a) | | $ | 246,225 | | | $ | 246,225 | |

| | | | | | | | |

| (a) | | The unrealized appreciation/depreciation is included in net change in unrealized appreciation/depreciation on investments and other financial instruments in the accompanying statement of operations. |

As of April 30, 2016, all Level 3 securities were priced by third party vendors.

The Adviser established the Committee to oversee the pricing and valuation of all securities held in the Fund. The Committee operates under pricing and valuation policies and procedures established by the Adviser and approved by the Board, including pricing policies which set forth the mechanisms and processes to be employed on a daily basis to implement these policies and procedures. In particular, the pricing policies describe how to determine market quotations for securities and other instruments. The Committee’s responsibilities include: 1) fair value and liquidity determinations (and oversight of any third parties to whom any responsibility for fair value and liquidity determinations is delegated), and 2) regular monitoring of the Adviser’s pricing and valuation policies and procedures and modification or enhancement of these policies and procedures (or recommendation of the modification of these policies and procedures) as the Committee believes appropriate.

The Committee is also responsible for monitoring the implementation of the pricing policies by the Adviser’s Pricing Group (the “Pricing Group”) and a third party which performs certain pricing functions in accordance with the pricing policies. The Pricing Group is responsible for the oversight of the third party on a day-to-day basis. The Committee and the Pricing Group perform a series of activities to provide reasonable assurance of the accuracy of prices including: 1) periodic vendor due diligence meetings, review of methodologies, new

| | |

| 22 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Notes to Financial Statements

developments and processes at vendors, 2) daily comparison of security valuation versus prior day for all securities that exceeded established thresholds, and 3) daily review of unpriced, stale, and variance reports with exceptions reviewed by senior management and the Committee.

In addition, several processes outside of the pricing process are used to monitor valuation issues including: 1) performance and performance attribution reports are monitored for anomalous impacts based upon benchmark performance, and 2) portfolio managers review all portfolios for performance and analytics (which are generated using the Adviser’s prices).

3. Taxes

It is the Fund’s policy to meet the requirements of the Internal Revenue Code applicable to regulated investment companies and to distribute all of its investment company taxable income and net realized gains, if any, to shareholders. Therefore, no provisions for federal income or excise taxes are required.

In accordance with U.S. GAAP requirements regarding accounting for uncertainties in income taxes, management has analyzed the Fund’s tax positions taken or expected to be taken on federal and state income tax returns for all open tax years (the current and the prior three tax years) and has concluded that no provision for income tax is required in the Fund’s financial statements.

4. Investment Income and Investment Transactions

Dividend income is recorded on the ex-dividend date or as soon as the Fund is informed of the dividend. Interest income is accrued daily. Investment transactions are accounted for on the date the securities are purchased or sold. Investment gains or losses are determined on the identified cost basis. The Fund amortizes premiums and accretes original issue discounts and market discounts as adjustments to interest income.

5. Dividends and Distributions

Dividends and distributions to shareholders, if any, are recorded on the ex-dividend date. Income dividends and capital gains distributions are determined in accordance with federal tax regulations and may differ from those determined in accordance with U.S. GAAP. To the extent these differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax basis treatment; temporary differences do not require such reclassification.

NOTE B

Advisory Fee and Other Transactions with Affiliates

Under the terms of an investment advisory agreement, the Fund pays the Adviser an advisory fee at the annual rate of 0.65% of the Fund’s average daily net assets. Such advisory fee, which is calculated on the basis of the assets attributable to the Fund’s common and preferred shareholders, is accrued daily and paid monthly. In computing daily net assets for purposes of determining the

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 23 | |

Notes to Financial Statements

advisory fee payable, the Fund calculates daily the value of the total assets of the Fund, minus the value of the total liabilities of the Fund, except that the aggregate liquidation preference of the VMTP shares, which is a liability for financial reporting purposes, is not deducted.

Under the terms of the Shareholder Inquiry Agency Agreement with AllianceBernstein Investor Services, Inc. (“ABIS”), a wholly-owned subsidiary of the Adviser, the Fund reimburses ABIS for costs relating to servicing phone inquiries on behalf of the Fund. During the six months ended April 30, 2016, there was no reimbursement paid to ABIS.

The Fund may invest in the AB Fixed-Income Shares, Inc.—Government STIF Portfolio (“Government STIF Portfolio”), an open-end management investment company managed by the Adviser. The Government STIF Portfolio is offered as a cash management option to mutual funds and other institutional accounts of the Adviser, and is not currently available for direct purchase by members of the public. The Government STIF Portfolio currently pays no investment management fees but does bear its own expenses. A summary of the Fund’s transactions in shares of the Government STIF Portfolio for the six months ended April 30, 2016 is as follows:

| | | | | | | | | | | | | | | | | | |

Market Value October 31, 2015 (000) | | | Purchases

at Cost

(000) | | | Sales

Proceeds

(000) | | | Market Value April 30, 2016 (000) | | | Dividend

Income

(000) | |

| $ | – 0 – | | | $ | 5,264 | | | $ | 5,264 | | | $ | – 0 – | | | $ | 2 | |

NOTE C

Investment Transactions

Purchases and sales of investment securities (excluding short-term investments) for the six months ended April 30, 2016 were as follows:

| | | | | | | | |

| | | Purchases | | | Sales | |

Investment securities (excluding U.S. government securities) | | $ | 14,341,145 | | | $ | 14,714,085 | |

U.S. government securities | | | – 0 | – | | | – 0 | – |

The cost of investments for federal income tax purposes was substantially the same as the cost for financial reporting purposes. Accordingly, gross unrealized appreciation and unrealized depreciation (excluding swap transactions) are as follows:

| | | | |

Gross unrealized appreciation | | $ | 18,785,832 | |

Gross unrealized depreciation | | | (30,775 | ) |

| | | | |

Net unrealized appreciation | | $ | 18,755,057 | |

| | | | |

| | |

| 24 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Notes to Financial Statements

1. Derivative Financial Instruments

The Fund may use derivatives in an effort to earn income and enhance returns, to replace more traditional direct investments, to obtain exposure to otherwise inaccessible markets (collectively, “investment purposes”), or to hedge or adjust the risk profile of its portfolio.

The principal types of derivatives utilized by the Fund, as well as the methods in which they may be used are:

The Fund may enter into swaps to hedge its exposure to interest rates or credit risk. A swap is an agreement that obligates two parties to exchange a series of cash flows at specified intervals based upon or calculated by reference to changes in specified prices or rates for a specified amount of an underlying asset. The payment flows are usually netted against each other, with the difference being paid by one party to the other. In addition, collateral may be pledged or received by the Fund in accordance with the terms of the respective swaps to provide value and recourse to the Fund or its counterparties in the event of default, bankruptcy or insolvency by one of the parties to the swap.

Risks may arise as a result of the failure of the counterparty to the swap to comply with the terms of the swap. The loss incurred by the failure of a counterparty is generally limited to the net interim payment to be received by the Fund, and/or the termination value at the end of the contract. Therefore, the Fund considers the creditworthiness of each counterparty to a swap in evaluating potential counterparty risk. This risk is mitigated by having a netting arrangement between the Fund and the counterparty and by the posting of collateral by the counterparty to the Fund to cover the Fund’s exposure to the counterparty. Additionally, risks may arise from unanticipated movements in interest rates or in the value of the underlying securities. The Fund accrues for the interim payments on swaps on a daily basis, with the net amount recorded within unrealized appreciation/depreciation of swaps on the statement of assets and liabilities, where applicable. Once the interim payments are settled in cash, the net amount is recorded as realized gain/(loss) on swaps on the statement of operations, in addition to any realized gain/(loss) recorded upon the termination of swaps. Upfront premiums paid or received are recognized as cost or proceeds on the statement of assets and liabilities and are amortized on a straight line basis over the life of the contract. Amortized upfront premiums are included in net realized gain/(loss) from swaps on the statement of operations. Fluctuations in the value of swaps are recorded as a component of net change in unrealized appreciation/depreciation of swaps on the statement of operations.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 25 | |

Notes to Financial Statements

Interest Rate Swaps:

The Fund is subject to interest rate risk exposure in the normal course of pursuing its investment objectives. Because the Fund holds fixed rate bonds, the value of these bonds may decrease if interest rates rise. To help hedge against this risk and to maintain its ability to generate income at prevailing market rates, the Fund may enter into interest rate swaps. Interest rate swaps are agreements between two parties to exchange cash flows based on a notional amount. The Fund may elect to pay a fixed rate and receive a floating rate, or, receive a fixed rate and pay a floating rate on a notional amount.

In addition, a Fund may also enter into interest rate swap transactions to preserve a return or spread on a particular investment or portion of its portfolio, or protect against an increase in the price of securities the Fund anticipates purchasing at a later date. Interest rate swaps involve the exchange by a Fund with another party of their respective commitments to pay or receive interest (e.g., an exchange of floating rate payments for fixed rate payments) computed based on a contractually-based principal (or “notional”) amount. Interest rate swaps are entered into on a net basis (i.e., the two payment streams are netted out, with the Fund receiving or paying, as the case may be, only the net amount of the two payments).

During the six months ended April 30, 2016, the Fund held interest rate swaps for hedging purposes.

The Fund typically enters into International Swaps and Derivatives Association, Inc. Master Agreements (“ISDA Master Agreement”) or similar master agreements (collectively, “Master Agreements”) with its derivative contract counterparties in order to, among other things, reduce its credit risk to counterparties. ISDA Master Agreements include provisions for general obligations, representations, collateral and events of default or termination. Under an ISDA Master Agreement, the Fund typically may offset with the counterparty certain derivative financial instrument’s payables and/or receivables with collateral held and/or posted and create one single net payment (close-out netting) in the event of default or termination.

Various Master Agreements govern the terms of certain transactions with counterparties, including transactions such as derivative transactions, repurchase and reverse repurchase agreements. These Master Agreements typically attempt to reduce the counterparty risk associated with such transactions by specifying credit protection mechanisms and providing standardization that improves legal certainty. Cross-termination provisions under Master Agreements typically provide that a default in connection with one transaction between the Fund and a counterparty gives the non-defaulting party the right to terminate any other transactions in place with the defaulting party to create one single net payment due to/due from the defaulting party. In the event of a default by a

| | |

| 26 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Notes to Financial Statements

Master Agreements counterparty, the return of collateral with market value in excess of the Fund’s net liability, held by the defaulting party, may be delayed or denied.

The Fund’s Master Agreements may contain provisions for early termination of OTC derivative transactions in the event the net assets of the Fund decline below specific levels (“net asset contingent features”). If these levels are triggered, the Fund’s counterparty has the right to terminate such transaction and require the Fund to pay or receive a settlement amount in connection with the terminated transaction. For additional details, please refer to netting arrangements by counterparty tables below.

At April 30, 2016, the Fund had entered into the following derivatives:

| | | | | | | | | | |

| | | Asset Derivatives | | | Liability Derivatives |

Derivative Type | | Statement of

Assets and

Liabilities

Location | | Fair Value | | | Statement of

Assets and

Liabilities

Location | | Fair Value |

Interest rate contracts | | Unrealized appreciation on interest rate swaps | | $ | 43,737 | | | | | |

| | | | | | | | | | |

Total | | | | $ | 43,737 | | | | | |

| | | | | | | | | | |

| | | | | | | | | | |

Derivative Type | | Location of Gain or (Loss) on

Derivatives Within

Statement of

Operations | | Realized Gain

or (Loss) on

Derivatives | | | Change in

Unrealized

Appreciation or

(Depreciation) | |

Interest rate contracts | | Net realized gain (loss) on swaps; Net change in unrealized appreciation/depreciation of swaps | | $ | 46,649 | | | $ | (48,608 | ) |

| | | | | | | | | | |

Total | | | | $ | 46,649 | | | $ | (48,608 | ) |

| | | | | | | | | | |

The following table represents the average monthly volume of the Fund’s derivative transactions during the six months ended April 30, 2016:

| | | | |

Interest Rate Swaps: | | | | |

Average notional amount | | $ | 2,300,000 | |

For financial reporting purposes, the Fund does not offset derivative assets and derivative liabilities that are subject to netting arrangements in the statement of assets and liabilities.

All derivatives held at period end were subject to netting arrangements. The following table presents the Fund’s derivative assets and liabilities by counterparty

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 27 | |

Notes to Financial Statements

net of amounts available for offset under Master Agreements (“MA”) and net of the related collateral received/ pledged by the Fund as of April 30, 2016:

| | | | | | | | | | | | | | | | | | | | |

Counterparty | | Derivative

Assets

Subject to a

MA | | | Derivative

Available for

Offset | | | Cash

Collateral

Received | | | Security

Collateral

Received | | | Net Amount

of Derivatives

Assets | |

OTC Derivatives: | | | | | | | | | | | | | | | | | | | | |

Merrill Lynch Capital Services, Inc. | | $ | 43,737 | | | $ | – 0 | – | | $ | – 0 | – | | $ | – 0 | – | | $ | 43,737 | |

| | | | | | | | | | | | | | | | | | | | |

Total | | $ | 43,737 | | | $ | – 0 | – | | $ | – 0 | – | | $ | – 0 | – | | $ | 43,737 | ^ |

| | | | | | | | | | | | | | | | | | | | |

| ^ | | Net amount represents the net receivable/(payable) that would be due from/to the counterparty in the event of default or termination. The net amount from OTC financial derivative instruments can only be netted across transactions governed under the same master agreement with the same counterparty. |

NOTE D

Common Stock

There are 8,554,668 shares of common stock outstanding at April 30, 2016. During the six months ended April 30, 2016 and year ended October 31, 2015, the Fund did not issue any shares in connection with the Fund’s dividend reinvestment plan.

NOTE E

Auction Preferred Shares

The Fund has 3,240 shares authorized, and 1,195 shares issued and outstanding of auction preferred shares (“APS”), consisting of 771 shares of Series M and 424 shares of series T. The APS have a liquidation value of $25,000 per share plus accumulated, unpaid dividends. The dividend rate on the APS may change every 7 days as set by the auction agent for Series M and T. Due to the recent failed auctions, the dividend rate is the “maximum rate” set by the terms of the APS, which is based on AA commercial paper rates and short-term municipal bond rates. The dividend rate on Series M is 0.67% effective through May 2, 2016. The dividend rate on Series T is 0.67% effective through May 3, 2016.

At certain times, the Fund may voluntarily redeem the APS in certain circumstances. The Fund is not required to redeem any of its APS and expects to continue to rely on the APS for a portion of its leverage exposure. The Fund may also pursue other liquidity solutions for the APS. During the year ended October 31, 2015, the Fund conducted a tender offer (the “Offer”) for its APS at a price reflecting a discount to its liquidation preference. The Fund offered to purchase up to 100% of its APS, at a price equal to 94% of the liquidation preference of $25,000 per share (or $23,500 per share), plus any unpaid dividends accrued through the termination date of the Offer. The Offer expired on Monday, August 24, 2015, and all shares that were validly tendered and not withdrawn during the offering period were accepted for payment. In aggregate,

| | |

| 28 | | • ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND |

Notes to Financial Statements

the Fund accepted for payment 1,707 APS, which represented approximately $42,675,000 or 59% of its outstanding APS (at $25,000 per share). Payment for such shares was made by the Fund on September 1, 2015. APS that were not tendered remain outstanding. The shares accepted represent, approximately 47% and 71% of outstanding Series M and Series T, respectively. The difference of $2,560,500 between the liquidation preference of the APS and the actual purchase price of the tendered APS, net of legal, printing, mailing, information agent and registration fees of $71,833, was recorded by the Fund as “Net increase on tendered and repurchased Auction Preferred Shares” on the statement of changes in net assets. The Fund financed the tender offer payment by issuing Variable Rate MuniFund Term Preferred Shares.

Variable Rate MuniFund Term Preferred Shares

During the year ended October 31, 2015, the Fund also completed a private offering of Variable Rate MuniFund Term Preferred Shares (“VMTPS”), having a liquidation preference of $25,000 per share. The Fund issued and sold 1,605 VMTPS in its offering. The net proceeds from the offering were used to repurchase the APS that were accepted for payment pursuant to the Offer. The VMTPS rank pari passu with the remaining outstanding APS but are subject to a mandatory redemption by the Fund in September 2022. The cost of leverage to the Fund resulting from the issuance of VMTPS is expected to vary over time and to differ from, and in some cases may exceed, the cost of leverage associated with the APS, as is the case at April 30, 2016, although the Adviser anticipates that, in general, an increase in interest rates beyond a certain level may result in the VMTPS being more economical to the Fund.

VMTPS generally do not trade, and market quotations are generally not available. VMTPS are short-term or short/intermediate-term instruments that pay a variable dividend rate tied to a short-term index, plus an additional fixed “spread” amount established at the time of issuance. As of April 30, 2016, the dividend rate for the VMTPS was 1.71%. In the Fund’s statement of assets and liabilities, the aggregate liquidation preference of the VMTPS is shown as a liability in accordance with U.S. GAAP because the VMTPS have a stated mandatory redemption date.

Dividends on the VMTPS (which are treated as interest payments for financial reporting purposes) are set weekly. Unpaid dividends on VMTPS are recorded as “Interest expense payable” on the statement of assets and liabilities. Dividends accrued on VMTPS are recorded as a component of “Interest expense, fees and amortization of offering costs” on the statement of operations.

Costs incurred by the Fund in connection with its offering of VMTPS were recorded as a deferred charge, which are amortized over the life of the shares and are recorded as “Deferred offering costs” on the statement of assets and liabilities and included within “Interest expense, fees and amortization of offering costs” on the statement of operations. The VMTPS are treated as equity for tax purposes.

| | | | |

| ALLIANCE CALIFORNIA MUNICIPAL INCOME FUND • | | | 29 | |

Notes to Financial Statements