PRELIMINARY AND CONFIDENTIAL SUBJECT TO MATERIAL REVISION FOR DISCUSSION PURPOSES ONLY July 1, 2024 Exhibit (c)(4) Project Augusta Discussion Materials for the Conflicts Committee Strictly Confidential. Not for Distribution.

EXECUTIVE SUMMARY 3 01 9 PRELIMINARY FINANCIAL ANALYSES 02 20 PRELIMINARY PREMIUMS PAID DATA 03 23 APPENDIX 04 24 Additional Response Considerations 35 Public Market Observations 42 Weighted Average Cost of Capital 49 Preliminary Selected Benchmarking Data 58 DISCLAIMER 05

EXECUTIVE SUMMARY 01 01 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

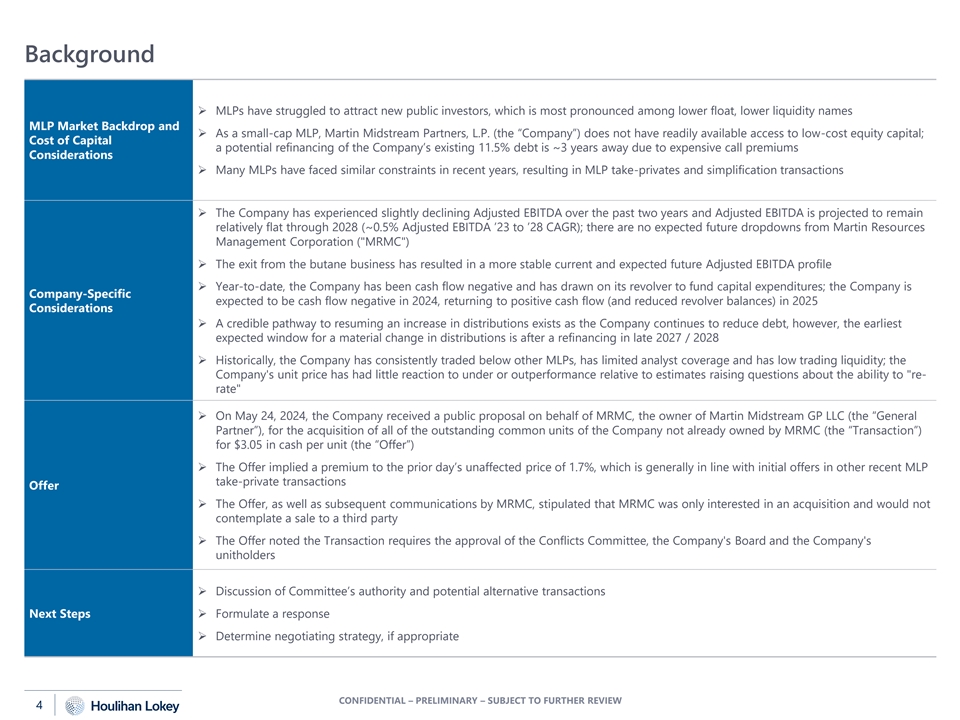

Background ➢ MLPs have struggled to attract new public investors, which is most pronounced among lower float, lower liquidity names MLP Market Backdrop and ➢ As a small-cap MLP, Martin Midstream Partners, L.P. (the “Company”) does not have readily available access to low-cost equity capital; Cost of Capital a potential refinancing of the Company’s existing 11.5% debt is ~3 years away due to expensive call premiums Considerations ➢ Many MLPs have faced similar constraints in recent years, resulting in MLP take-privates and simplification transactions ➢ The Company has experienced slightly declining Adjusted EBITDA over the past two years and Adjusted EBITDA is projected to remain relatively flat through 2028 (~0.5% Adjusted EBITDA ’23 to ’28 CAGR); there are no expected future dropdowns from Martin Resources Management Corporation ( MRMC ) ➢ The exit from the butane business has resulted in a more stable current and expected future Adjusted EBITDA profile ➢ Year-to-date, the Company has been cash flow negative and has drawn on its revolver to fund capital expenditures; the Company is Company-Specific expected to be cash flow negative in 2024, returning to positive cash flow (and reduced revolver balances) in 2025 Considerations ➢ A credible pathway to resuming an increase in distributions exists as the Company continues to reduce debt, however, the earliest expected window for a material change in distributions is after a refinancing in late 2027 / 2028 ➢ Historically, the Company has consistently traded below other MLPs, has limited analyst coverage and has low trading liquidity; the Company's unit price has had little reaction to under or outperformance relative to estimates raising questions about the ability to re- rate ➢ On May 24, 2024, the Company received a public proposal on behalf of MRMC, the owner of Martin Midstream GP LLC (the “General Partner”), for the acquisition of all of the outstanding common units of the Company not already owned by MRMC (the “Transaction”) for $3.05 in cash per unit (the “Offer”) ➢ The Offer implied a premium to the prior day’s unaffected price of 1.7%, which is generally in line with initial offers in other recent MLP take-private transactions Offer ➢ The Offer, as well as subsequent communications by MRMC, stipulated that MRMC was only interested in an acquisition and would not contemplate a sale to a third party ➢ The Offer noted the Transaction requires the approval of the Conflicts Committee, the Company's Board and the Company's unitholders ➢ Discussion of Committee’s authority and potential alternative transactions Next Steps➢ Formulate a response ➢ Determine negotiating strategy, if appropriate CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 4

Overview of the Proposed Transaction ➢ MRMC Parties ➢ Martin Midstream Partners, L.P. ➢ MRMC proposes to acquire 100% of the common units owned by unitholders Summary➢ $3.05 in cash per unit (the “Consideration”) ➢ The Company will merge with a wholly owned subsidiary of MRMC, and the Company will no longer remain public ➢ Approval of the Board of Directors of MRMC ➢ Approval of the Conflicts Committee Timing and Approvals ➢ Approval of the Board of Directors of Martin Midstream GP LLC ➢ Approval of the Company's unitholders [majority of all common units] ➢ MRMC has no interest at this time in selling any of its or its subsidiaries' interests in the Company or the General Partner or pursuing other strategic alternatives involving the Company or the General Partner ➢ MRMC anticipates financing the merger consideration with cash on hand and borrowings under its existing and additional Other credit facilities ➢ No financing condition expected, as is customary ➢ 13E-3 Transaction Source: Offer. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 5

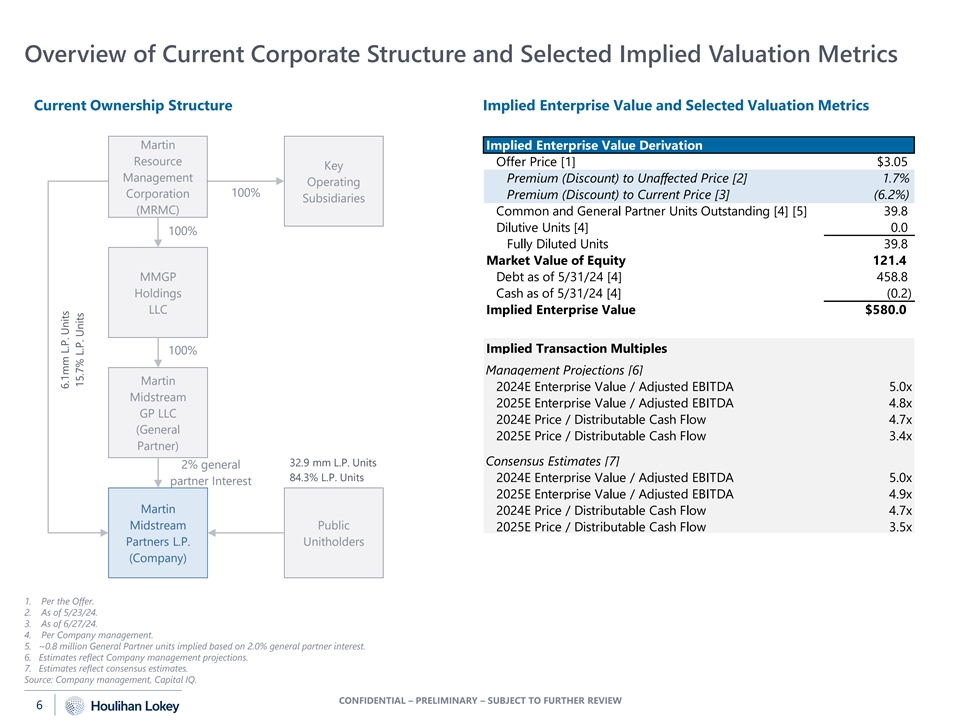

Overview of Current Corporate Structure and Selected Implied Valuation Metrics Current Ownership Structure Implied Enterprise Value and Selected Valuation Metrics Martin Implied Enterprise Value Derivation Resource Offer Price [1] $3.05 Key Management Premium (Discount) to Unaffected Price [2] 1.7% Operating 100% Corporation Premium (Discount) to Current Price [3] (6.2%) Subsidiaries (MRMC) Common and General Partner Units Outstanding [4] [5] 39.8 Dilutive Units [4] 0.0 100% Fully Diluted Units 39.8 Market Value of Equity 121.4 MMGP Debt as of 5/31/24 [4] 458.8 Holdings Cash as of 5/31/24 [4] (0.2) LLC Implied Enterprise Value $580.0 Implied Transaction Multiples 100% Management Projections [6] Martin 2024E Enterprise Value / Adjusted EBITDA 5.0x Midstream 2025E Enterprise Value / Adjusted EBITDA 4.8x GP LLC 2024E Price / Distributable Cash Flow 4.7x (General 2025E Price / Distributable Cash Flow 3.4x Partner) Consensus Estimates [7] 32.9 mm L.P. Units 2% general 84.3% L.P. Units 2024E Enterprise Value / Adjusted EBITDA 5.0x partner Interest 2025E Enterprise Value / Adjusted EBITDA 4.9x Martin 2024E Price / Distributable Cash Flow 4.7x Midstream Public 2025E Price / Distributable Cash Flow 3.5x Partners L.P. Unitholders (Company) 1. Per the Offer. 2. As of 5/23/24. 3. As of 6/27/24. 4. Per Company management. 5. ~0.8 million General Partner units implied based on 2.0% general partner interest. 6. Estimates reflect Company management projections. 7. Estimates reflect consensus estimates. Source: Company management, Capital IQ. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 6 6.1mm L.P. Units 15.7% L.P. Units

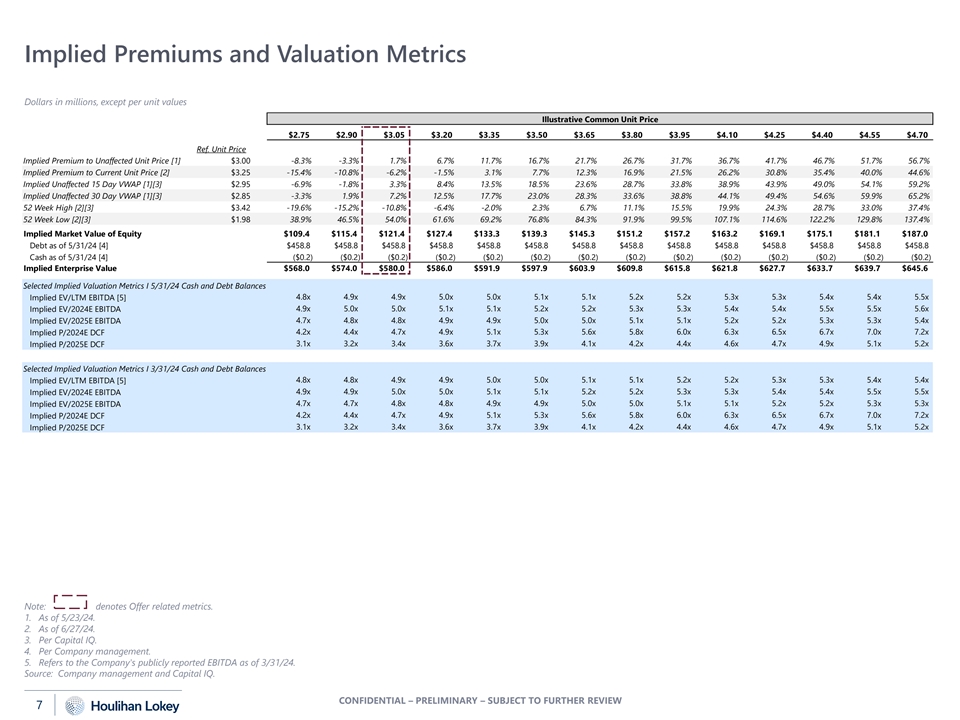

Implied Premiums and Valuation Metrics Dollars in millions, except per unit values Illustrative Common Unit Price $2.75 $2.90 $3.05 $3.20 $3.35 $3.50 $3.65 $3.80 $3.95 $4.10 $4.25 $4.40 $4.55 $4.70 Ref. Unit Price Implied Premium to Unaffected Unit Price [1] $3.00 -8.3% -3.3% 1.7% 6.7% 11.7% 16.7% 21.7% 26.7% 31.7% 36.7% 41.7% 46.7% 51.7% 56.7% Implied Premium to Current Unit Price [2] $3.25 -15.4% -10.8% -6.2% -1.5% 3.1% 7.7% 12.3% 16.9% 21.5% 26.2% 30.8% 35.4% 40.0% 44.6% Implied Unaffected 15 Day VWAP [1][3] $2.95 -6.9% -1.8% 3.3% 8.4% 13.5% 18.5% 23.6% 28.7% 33.8% 38.9% 43.9% 49.0% 54.1% 59.2% Implied Unaffected 30 Day VWAP [1][3] $2.85 -3.3% 1.9% 7.2% 12.5% 17.7% 23.0% 28.3% 33.6% 38.8% 44.1% 49.4% 54.6% 59.9% 65.2% 52 Week High [2][3] $3.42 -19.6% -15.2% -10.8% -6.4% -2.0% 2.3% 6.7% 11.1% 15.5% 19.9% 24.3% 28.7% 33.0% 37.4% 52 Week Low [2][3] $1.98 38.9% 46.5% 54.0% 61.6% 69.2% 76.8% 84.3% 91.9% 99.5% 107.1% 114.6% 122.2% 129.8% 137.4% Implied Market Value of Equity $109.4 $115.4 $121.4 $127.4 $133.3 $139.3 $145.3 $151.2 $157.2 $163.2 $169.1 $175.1 $181.1 $187.0 Debt as of 5/31/24 [4] $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 $458.8 Cash as of 5/31/24 [4] ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) ($0.2) Implied Enterprise Value $568.0 $574.0 $580.0 $586.0 $591.9 $597.9 $603.9 $609.8 $615.8 $621.8 $627.7 $633.7 $639.7 $645.6 Selected Implied Valuation Metrics I 5/31/24 Cash and Debt Balances Implied EV/LTM EBITDA [5] 4.8x 4.9x 4.9x 5.0x 5.0x 5.1x 5.1x 5.2x 5.2x 5.3x 5.3x 5.4x 5.4x 5.5x Implied EV/2024E EBITDA 4.9x 5.0x 5.0x 5.1x 5.1x 5.2x 5.2x 5.3x 5.3x 5.4x 5.4x 5.5x 5.5x 5.6x 4.7x 4.8x 4.8x 4.9x 4.9x 5.0x 5.0x 5.1x 5.1x 5.2x 5.2x 5.3x 5.3x 5.4x Implied EV/2025E EBITDA 4.2x 4.4x 4.7x 4.9x 5.1x 5.3x 5.6x 5.8x 6.0x 6.3x 6.5x 6.7x 7.0x 7.2x Implied P/2024E DCF 3.1x 3.2x 3.4x 3.6x 3.7x 3.9x 4.1x 4.2x 4.4x 4.6x 4.7x 4.9x 5.1x 5.2x Implied P/2025E DCF Selected Implied Valuation Metrics I 3/31/24 Cash and Debt Balances 4.8x 4.8x 4.9x 4.9x 5.0x 5.0x 5.1x 5.1x 5.2x 5.2x 5.3x 5.3x 5.4x 5.4x Implied EV/LTM EBITDA [5] 4.9x 4.9x 5.0x 5.0x 5.1x 5.1x 5.2x 5.2x 5.3x 5.3x 5.4x 5.4x 5.5x 5.5x Implied EV/2024E EBITDA Implied EV/2025E EBITDA 4.7x 4.7x 4.8x 4.8x 4.9x 4.9x 5.0x 5.0x 5.1x 5.1x 5.2x 5.2x 5.3x 5.3x Implied P/2024E DCF 4.2x 4.4x 4.7x 4.9x 5.1x 5.3x 5.6x 5.8x 6.0x 6.3x 6.5x 6.7x 7.0x 7.2x 3.1x 3.2x 3.4x 3.6x 3.7x 3.9x 4.1x 4.2x 4.4x 4.6x 4.7x 4.9x 5.1x 5.2x Implied P/2025E DCF Note: denotes Offer related metrics. 1. As of 5/23/24. 2. As of 6/27/24. 3. Per Capital IQ. 4. Per Company management. 5. Refers to the Company's publicly reported EBITDA as of 3/31/24. Source: Company management and Capital IQ. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 7

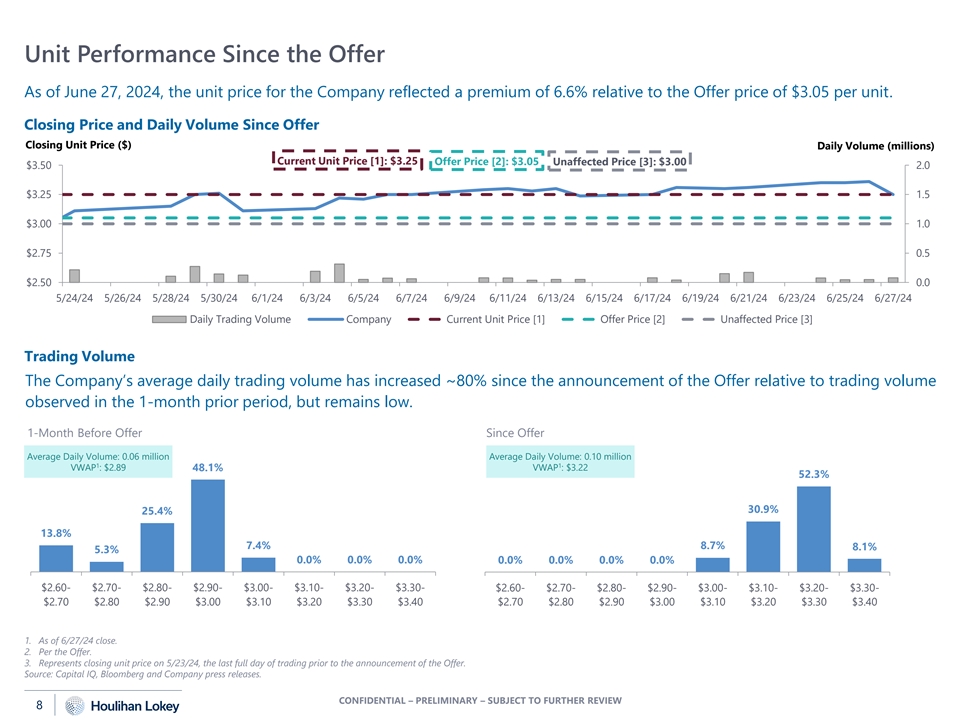

Unit Performance Since the Offer As of June 27, 2024, the unit price for the Company reflected a premium of 6.6% relative to the Offer price of $3.05 per unit. Closing Price and Daily Volume Since Offer Closing Unit Price ($) Daily Volume (millions) Current Unit Price [1]: $3.25 Offer Price [2]: $3.05 Unaffected Price [3]: $3.00 $3.50 2.0 $3.25 1.5 $3.00 1.0 $2.75 0.5 $2.50 0.0 5/24/24 5/26/24 5/28/24 5/30/24 6/1/24 6/3/24 6/5/24 6/7/24 6/9/24 6/11/24 6/13/24 6/15/24 6/17/24 6/19/24 6/21/24 6/23/24 6/25/24 6/27/24 Daily Trading Volume Company Current Unit Price [1] Offer Price [2] Unaffected Price [3] Trading Volume The Company’s average daily trading volume has increased ~80% since the announcement of the Offer relative to trading volume observed in the 1-month prior period, but remains low. 1-Month Before Offer Since Offer Average Daily Volume: 0.06 million Average Daily Volume: 0.10 million 1 1 VWAP : $2.89 VWAP : $3.22 48.1% 52.3% 30.9% 25.4% 13.8% 7.4% 8.7% 8.1% 5.3% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% $2.60- $2.70- $2.80- $2.90- $3.00- $3.10- $3.20- $3.30- $2.60- $2.70- $2.80- $2.90- $3.00- $3.10- $3.20- $3.30- $2.70 $2.80 $2.90 $3.00 $3.10 $3.20 $3.30 $3.40 $2.70 $2.80 $2.90 $3.00 $3.10 $3.20 $3.30 $3.40 1. As of 6/27/24 close. 2. Per the Offer. 3. Represents closing unit price on 5/23/24, the last full day of trading prior to the announcement of the Offer. Source: Capital IQ, Bloomberg and Company press releases. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 8

PRELIMINARY FINANCIAL ANALYSES 02 02 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

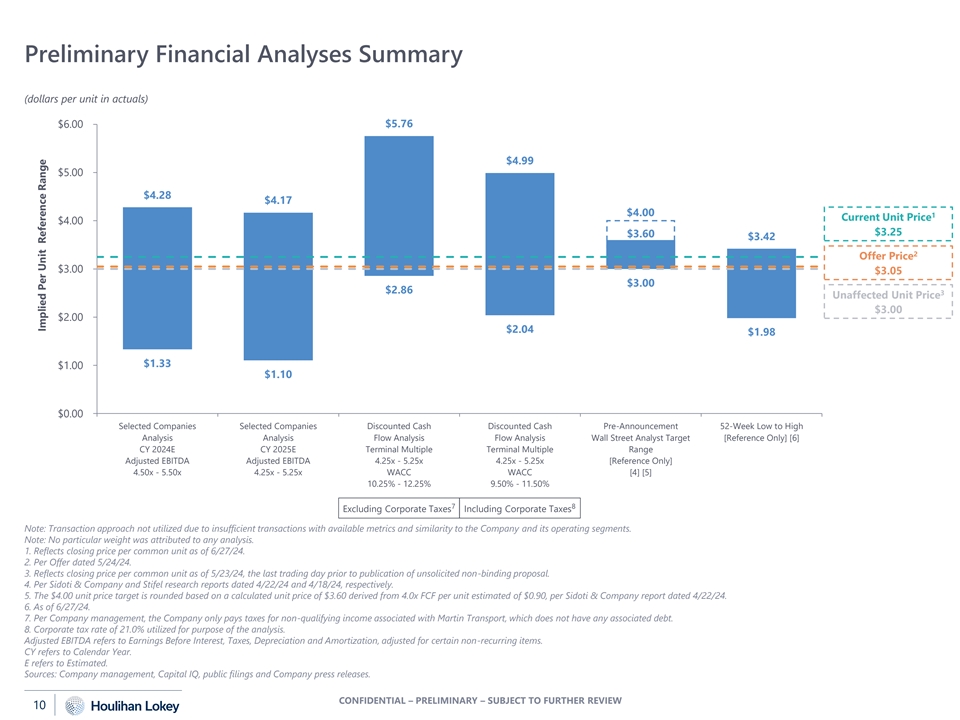

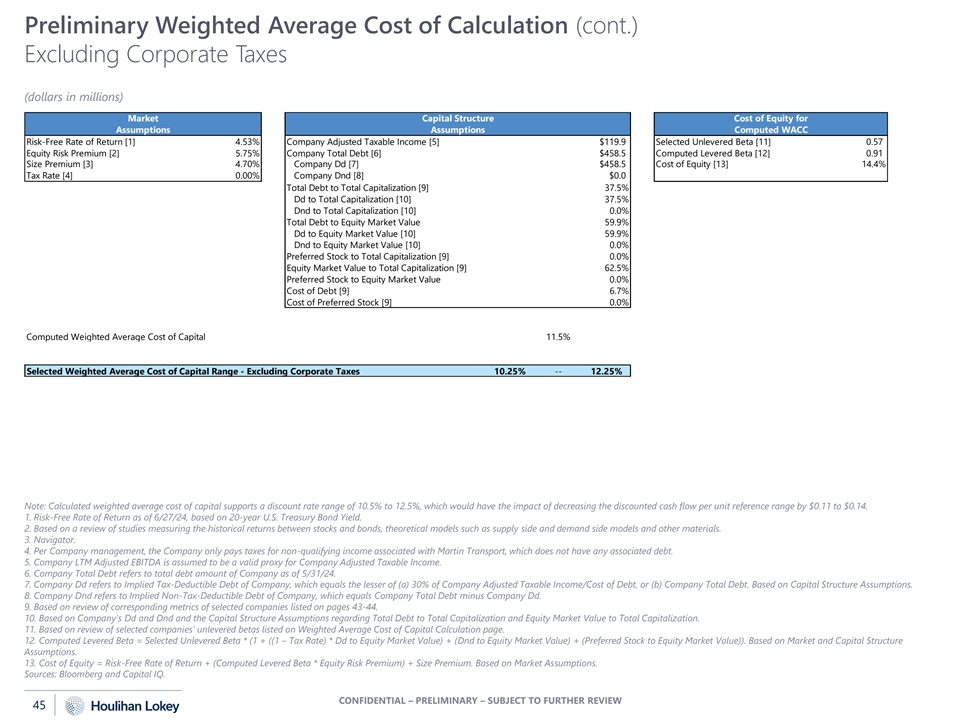

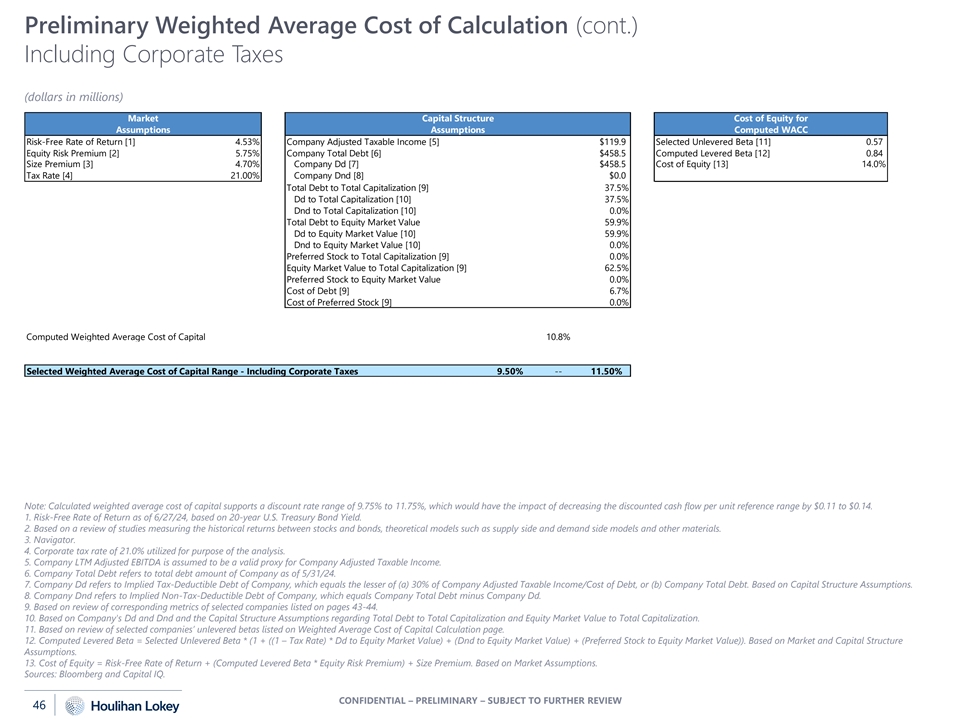

Preliminary Financial Analyses Summary (dollars per unit in actuals) $6.00 $5.76 $4.99 $5.00 $4.28 $4.17 $4.00 1 Current Unit Price $4.00 $3.25 $3.60 $3.42 2 Offer Price $3.00 $3.05 $3.00 $2.86 3 Unaffected Unit Price $3.00 $2.00 $2.04 $1.98 $1.33 $1.00 $1.10 $0.00 Selected Companies Selected Companies Discounted Cash Discounted Cash Pre-Announcement 52-Week Low to High Analysis Analysis Flow Analysis Flow Analysis Wall Street Analyst Target [Reference Only] [6] CY 2024E CY 2025E Terminal Multiple Terminal Multiple Range Adjusted EBITDA Adjusted EBITDA 4.25x - 5.25x 4.25x - 5.25x [Reference Only] 4.50x - 5.50x 4.25x - 5.25x WACC WACC [4] [5] 10.25% - 12.25% 9.50% - 11.50% 7 8 Excluding Corporate Taxes Including Corporate Taxes Note: Transaction approach not utilized due to insufficient transactions with available metrics and similarity to the Company and its operating segments. Note: No particular weight was attributed to any analysis. 1. Reflects closing price per common unit as of 6/27/24. 2. Per Offer dated 5/24/24. 3. Reflects closing price per common unit as of 5/23/24, the last trading day prior to publication of unsolicited non-binding proposal. 4. Per Sidoti & Company and Stifel research reports dated 4/22/24 and 4/18/24, respectively. 5. The $4.00 unit price target is rounded based on a calculated unit price of $3.60 derived from 4.0x FCF per unit estimated of $0.90, per Sidoti & Company report dated 4/22/24. 6. As of 6/27/24. 7. Per Company management, the Company only pays taxes for non-qualifying income associated with Martin Transport, which does not have any associated debt. 8. Corporate tax rate of 21.0% utilized for purpose of the analysis. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. CY refers to Calendar Year. E refers to Estimated. Sources: Company management, Capital IQ, public filings and Company press releases. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 10 Implied Per Unit Reference Range

Preliminary Financial Analyses Summary (cont.) (dollars and units in millions, except per unit values) Excluding Corporate Taxes [1] Including Corporate Taxes [2] Selected Companies Selected Companies Discounted Cash Discounted Cash Analysis Analysis Flow Analysis Flow Analysis CY 2024E CY 2025E Terminal Multiple Terminal Multiple Adjusted EBITDA Adjusted EBITDA 4.25x -- 5.25x 4.25x -- 5.25x Discount Rate Discount Rate Corresponding Base Amount $115.3 $119.9 10.25% -- 12.25% 9.50% -- 11.50% Selected Multiples Range 4.50x -- 5.50x 4.25x -- 5.25x Implied Enterprise Value Reference Range $518.8 -- $634.1 $509.7 -- $629.7 $579.5 -- $692.9 $547.0 -- $662.4 Cash and Cash Equivalents as of 5/31/24 [3] 0.2 -- 0.2 0.2 -- 0.2 0.2 -- 0.2 0.2 -- 0.2 Implied Total Enterprise Value Reference Range $519.0 -- $634.3 $509.9 -- $629.9 $579.7 -- $693.1 $547.2 -- $662.6 Total Debt as of 5/31/24 [3] (458.5) -- (458.5) (458.5) -- (458.5) (458.5) -- (458.5) (458.5) -- (458.5) Implied Total Equity Value Reference Range Pre-Contingent Liability $60.5 -- $175.8 $51.4 -- $171.4 $121.2 -- $234.6 $88.7 -- $204.1 Contingent Liability [4] (7.5) -- (5.5) (7.5) -- (5.5) (7.5) -- (5.5) (7.5) -- (5.5) Implied Total Equity Value Reference Range $53.0 -- $170.3 $43.9 -- $165.9 $113.7 -- $229.1 $81.2 -- $198.6 Units Outstanding [5] 39.8 -- 39.8 39.8 -- 39.8 39.8 -- 39.8 39.8 -- 39.8 Implied Per Unit Reference Range $1.33 -- $4.28 $1.10 -- $4.17 $2.86 -- $5.76 $2.04 -- $4.99 1. Per Company management, the Company only pays taxes for non-qualifying income associated with Martin Transport, which does not have any associated debt. 2. Corporate tax rate of 21.0% utilized for purpose of the analysis. 3. Per Company management. 4. Refers to the Company's potential financial exposure associated with certain litigation related matters and potential insurance claims related to the oil spill that occurred on 6/15/24 and Marine bridge incident that occurred on 5/15/24, per Company management. 5. Represents ~39.0 million common units and ~0.8 million units to account for the General Partner's 2% economic interest, per Company management. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. CY refers to Calendar Year. E refers to Estimated. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 11

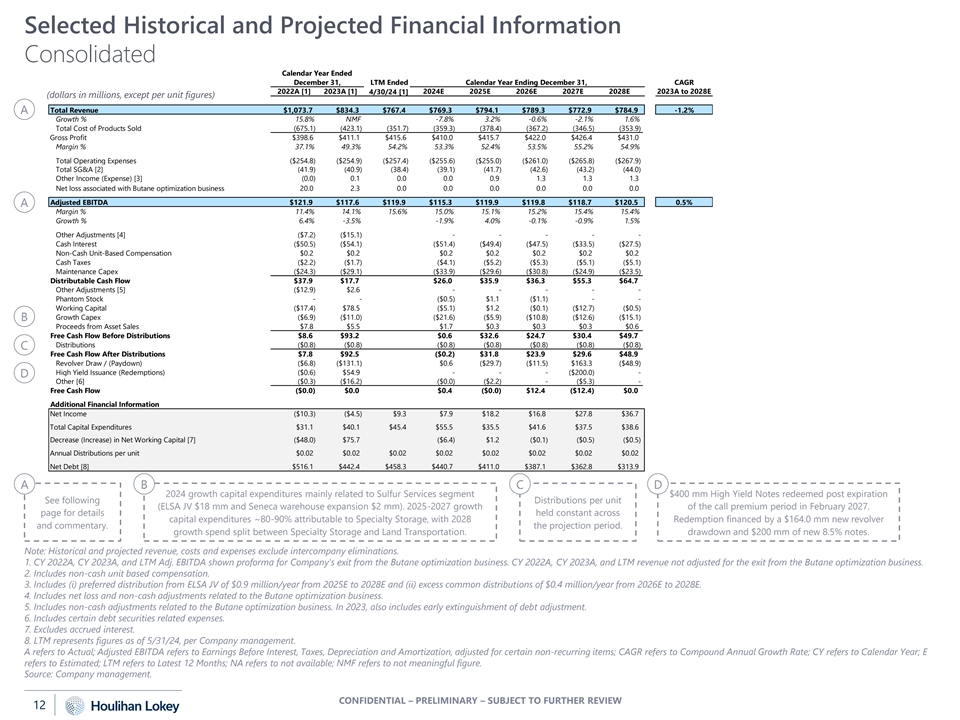

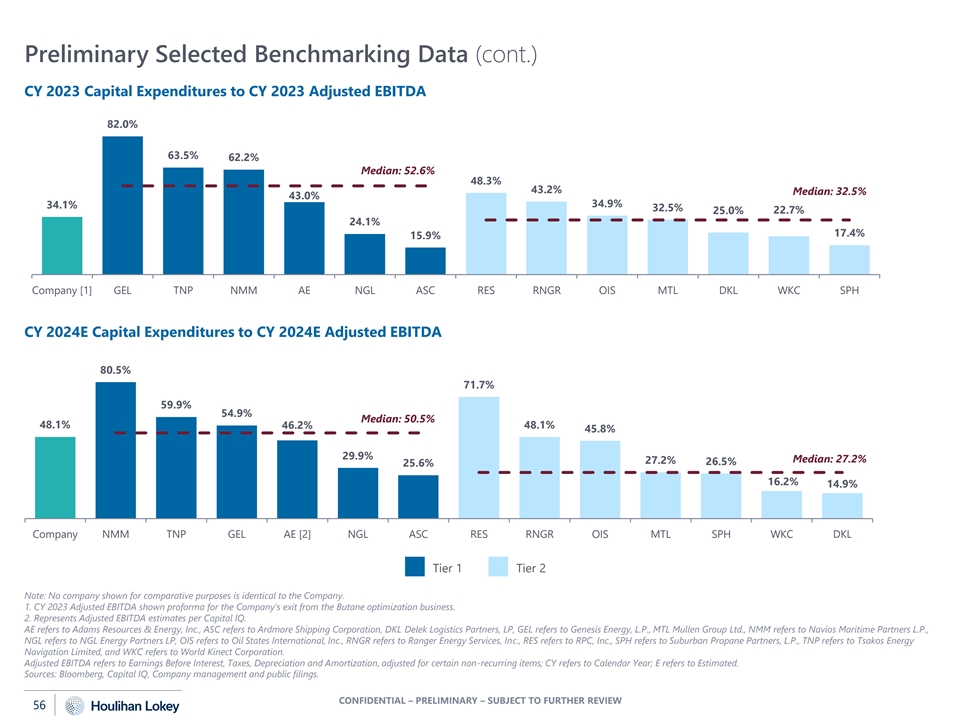

Selected Historical and Projected Financial Information Consolidated Calendar Year Ended December 31, LTM Ended Calendar Year Ending December 31, CAGR 2022A [1] 2023A [1] 4/30/24 [1] 2024E 2025E 2026E 2027E 2028E 2023A to 2028E (dollars in millions, except per unit figures) Total Revenue $1,073.7 $834.3 $767.4 $769.3 $794.1 $789.3 $772.9 $784.9 -1.2% A Growth % 15.8% NMF -7.8% 3.2% -0.6% -2.1% 1.6% Total Cost of Products Sold (675.1) (423.1) (351.7) (359.3) (378.4) (367.2) (346.5) (353.9) Gross Profit $398.6 $411.1 $415.6 $410.0 $415.7 $422.0 $426.4 $431.0 Margin % 37.1% 49.3% 54.2% 53.3% 52.4% 53.5% 55.2% 54.9% Total Operating Expenses ($254.8) ($254.9) ($257.4) ($255.6) ($255.0) ($261.0) ($265.8) ($267.9) Total SG&A [2] (41.9) (40.9) (38.4) (39.1) (41.7) (42.6) (43.2) (44.0) Other Income (Expense) [3] (0.0) 0.1 0.0 0.0 0.9 1.3 1.3 1.3 Net loss associated with Butane optimization business 20.0 2.3 0.0 0.0 0.0 0.0 0.0 0.0 Adjusted EBITDA $121.9 $117.6 $119.9 $115.3 $119.9 $119.8 $118.7 $120.5 0.5% A Margin % 11.4% 14.1% 15.6% 15.0% 15.1% 15.2% 15.4% 15.4% Growth % 6.4% -3.5% -1.9% 4.0% -0.1% -0.9% 1.5% Other Adjustments [4] ($7.2) ($15.1) - - - - - Cash Interest ($50.5) ($54.1) ($51.4) ($49.4) ($47.5) ($33.5) ($27.5) Non-Cash Unit-Based Compensation $0.2 $0.2 $0.2 $0.2 $0.2 $0.2 $0.2 Cash Taxes ($2.2) ($1.7) ($4.1) ($5.2) ($5.3) ($5.1) ($5.1) Maintenance Capex ($24.3) ($29.1) ($33.9) ($29.6) ($30.8) ($24.9) ($23.5) Distributable Cash Flow $37.9 $17.7 $26.0 $35.9 $36.3 $55.3 $64.7 Other Adjustments [5] ($12.9) $2.6 - - - - - Phantom Stock - - ($0.5) $1.1 ($1.1) - - Working Capital ($17.4) $78.5 ($5.1) $1.2 ($0.1) ($12.7) ($0.5) Growth Capex ($6.9) ($11.0) ($21.6) ($5.9) ($10.8) ($12.6) ($15.1) B Proceeds from Asset Sales $7.8 $5.5 $1.7 $0.3 $0.3 $0.3 $0.6 Free Cash Flow Before Distributions $8.6 $93.2 $0.6 $32.6 $24.7 $30.4 $49.7 Distributions ($0.8) ($0.8) ($0.8) ($0.8) ($0.8) ($0.8) ($0.8) C Free Cash Flow After Distributions $7.8 $92.5 ($0.2) $31.8 $23.9 $29.6 $48.9 Revolver Draw / (Paydown) ($6.8) ($131.1) $0.6 ($29.7) ($11.5) $163.3 ($48.9) High Yield Issuance (Redemptions) ($0.6) $54.9 - - - ($200.0) - D Other [6] ($0.3) ($16.2) ($0.0) ($2.2) - ($5.3) - Free Cash Flow ($0.0) $0.0 $0.4 ($0.0) $12.4 ($12.4) $0.0 Additional Financial Information Net Income ($10.3) ($4.5) $9.3 $7.9 $18.2 $16.8 $27.8 $36.7 Total Capital Expenditures $31.1 $40.1 $45.4 $55.5 $35.5 $41.6 $37.5 $38.6 Decrease (Increase) in Net Working Capital [7] ($48.0) $75.7 ($6.4) $1.2 ($0.1) ($0.5) ($0.5) Annual Distributions per unit $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 $0.02 Net Debt [8] $516.1 $442.4 $458.3 $440.7 $411.0 $387.1 $362.8 $313.9 A B C D 2024 growth capital expenditures mainly related to Sulfur Services segment $400 mm High Yield Notes redeemed post expiration See following Distributions per unit (ELSA JV $18 mm and Seneca warehouse expansion $2 mm). 2025-2027 growth of the call premium period in February 2027. page for details held constant across capital expenditures ~80-90% attributable to Specialty Storage, with 2028 Redemption financed by a $164.0 mm new revolver and commentary. the projection period. growth spend split between Specialty Storage and Land Transportation. drawdown and $200 mm of new 8.5% notes. Note: Historical and projected revenue, costs and expenses exclude intercompany eliminations. 1. CY 2022A, CY 2023A, and LTM Adj. EBITDA shown proforma for Company's exit from the Butane optimization business. CY 2022A, CY 2023A, and LTM revenue not adjusted for the exit from the Butane optimization business. 2. Includes non-cash unit based compensation. 3. Includes (i) preferred distribution from ELSA JV of $0.9 million/year from 2025E to 2028E and (ii) excess common distributions of $0.4 million/year from 2026E to 2028E. 4. Includes net loss and non-cash adjustments related to the Butane optimization business. 5. Includes non-cash adjustments related to the Butane optimization business. In 2023, also includes early extinguishment of debt adjustment. 6. Includes certain debt securities related expenses. 7. Excludes accrued interest. 8. LTM represents figures as of 5/31/24, per Company management. A refers to Actual; Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items; CAGR refers to Compound Annual Growth Rate; CY refers to Calendar Year; E refers to Estimated; LTM refers to Latest 12 Months; NA refers to not available; NMF refers to not meaningful figure. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 12

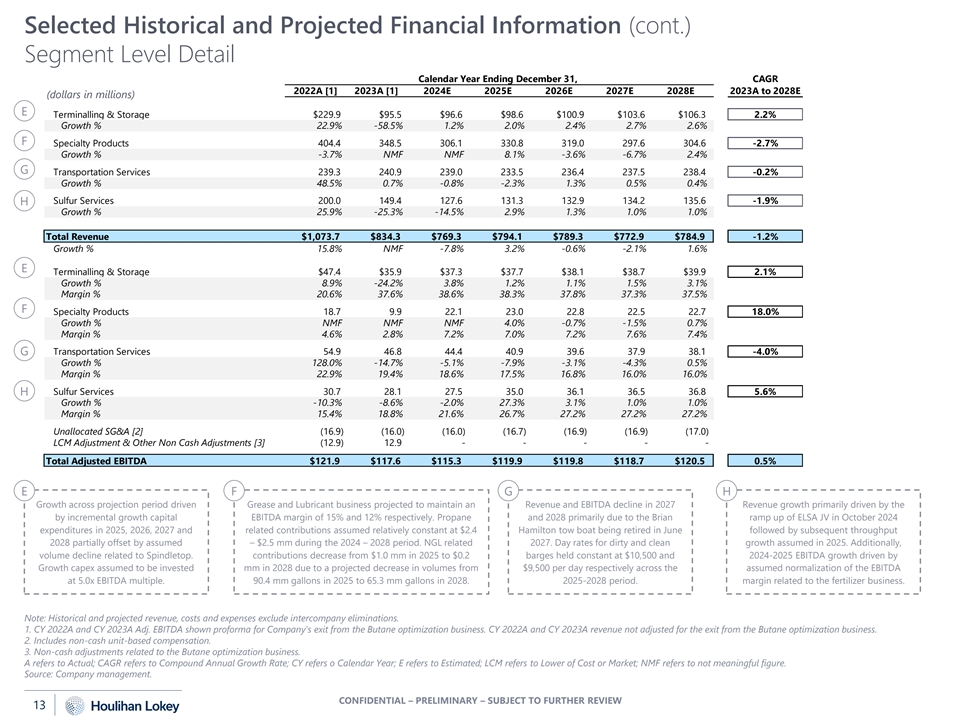

Selected Historical and Projected Financial Information (cont.) Segment Level Detail Calendar Year Ending December 31, CAGR 2022A [1] 2023A [1] 2024E 2025E 2026E 2027E 2028E 2023A to 2028E (dollars in millions) E Terminalling & Storage $229.9 $95.5 $96.6 $98.6 $100.9 $103.6 $106.3 2.2% Growth % 22.9% -58.5% 1.2% 2.0% 2.4% 2.7% 2.6% F Specialty Products 404.4 348.5 306.1 330.8 319.0 297.6 304.6 -2.7% Growth % -3.7% NMF NMF 8.1% -3.6% -6.7% 2.4% G Transportation Services 239.3 240.9 239.0 233.5 236.4 237.5 238.4 -0.2% Growth % 48.5% 0.7% -0.8% -2.3% 1.3% 0.5% 0.4% Sulfur Services 200.0 149.4 127.6 131.3 132.9 134.2 135.6 -1.9% H Growth % 25.9% -25.3% -14.5% 2.9% 1.3% 1.0% 1.0% Total Revenue $1,073.7 $834.3 $769.3 $794.1 $789.3 $772.9 $784.9 -1.2% Growth % 15.8% NMF -7.8% 3.2% -0.6% -2.1% 1.6% E Terminalling & Storage $47.4 $35.9 $37.3 $37.7 $38.1 $38.7 $39.9 2.1% Growth % 8.9% -24.2% 3.8% 1.2% 1.1% 1.5% 3.1% Margin % 20.6% 37.6% 38.6% 38.3% 37.8% 37.3% 37.5% F Specialty Products 18.7 9.9 22.1 23.0 22.8 22.5 22.7 18.0% Growth % NMF NMF NMF 4.0% -0.7% -1.5% 0.7% Margin % 4.6% 2.8% 7.2% 7.0% 7.2% 7.6% 7.4% Transportation Services 54.9 46.8 44.4 40.9 39.6 37.9 38.1 -4.0% G Growth % 128.0% -14.7% -5.1% -7.9% -3.1% -4.3% 0.5% Margin % 22.9% 19.4% 18.6% 17.5% 16.8% 16.0% 16.0% Sulfur Services 30.7 28.1 27.5 35.0 36.1 36.5 36.8 5.6% H Growth % -10.3% -8.6% -2.0% 27.3% 3.1% 1.0% 1.0% Margin % 15.4% 18.8% 21.6% 26.7% 27.2% 27.2% 27.2% Unallocated SG&A [2] (16.9) (16.0) (16.0) (16.7) (16.9) (16.9) (17.0) LCM Adjustment & Other Non Cash Adjustments [3] (12.9) 12.9 - - - - - Total Adjusted EBITDA $121.9 $117.6 $115.3 $119.9 $119.8 $118.7 $120.5 0.5% E F G H Growth across projection period driven Grease and Lubricant business projected to maintain an Revenue and EBITDA decline in 2027 Revenue growth primarily driven by the by incremental growth capital EBITDA margin of 15% and 12% respectively. Propane and 2028 primarily due to the Brian ramp up of ELSA JV in October 2024 expenditures in 2025, 2026, 2027 and related contributions assumed relatively constant at $2.4 Hamilton tow boat being retired in June followed by subsequent throughput 2028 partially offset by assumed – $2.5 mm during the 2024 – 2028 period. NGL related 2027. Day rates for dirty and clean growth assumed in 2025. Additionally, volume decline related to Spindletop. contributions decrease from $1.0 mm in 2025 to $0.2 barges held constant at $10,500 and 2024-2025 EBITDA growth driven by Growth capex assumed to be invested mm in 2028 due to a projected decrease in volumes from $9,500 per day respectively across the assumed normalization of the EBITDA at 5.0x EBITDA multiple. 90.4 mm gallons in 2025 to 65.3 mm gallons in 2028. 2025-2028 period. margin related to the fertilizer business. Note: Historical and projected revenue, costs and expenses exclude intercompany eliminations. 1. CY 2022A and CY 2023A Adj. EBITDA shown proforma for Company's exit from the Butane optimization business. CY 2022A and CY 2023A revenue not adjusted for the exit from the Butane optimization business. 2. Includes non-cash unit-based compensation. 3. Non-cash adjustments related to the Butane optimization business. A refers to Actual; CAGR refers to Compound Annual Growth Rate; CY refers o Calendar Year; E refers to Estimated; LCM refers to Lower of Cost or Market; NMF refers to not meaningful figure. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 13

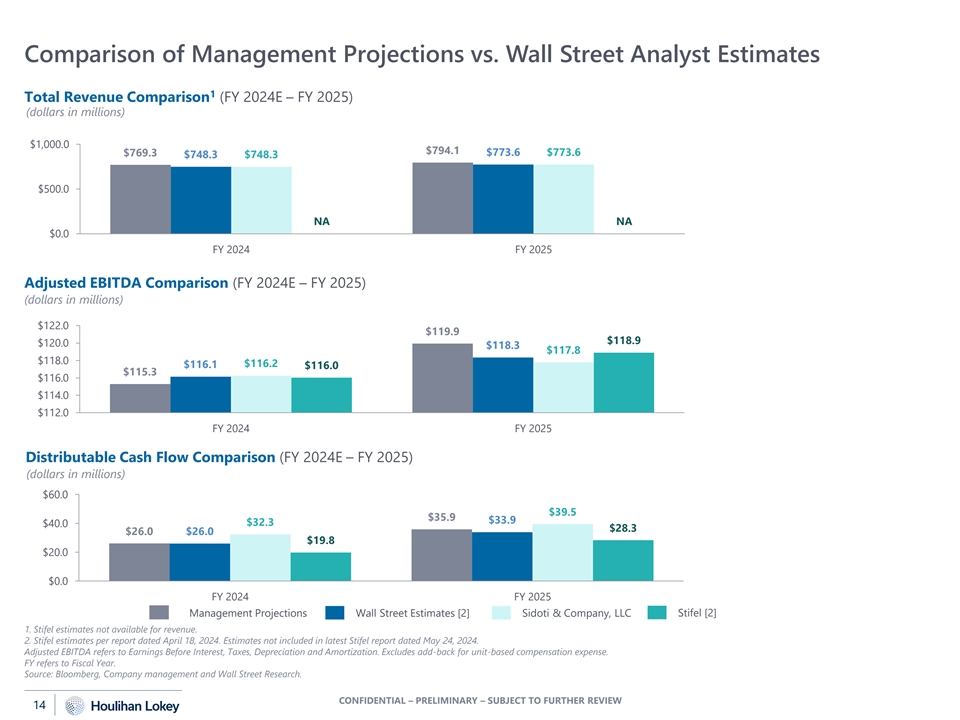

Comparison of Management Projections vs. Wall Street Analyst Estimates 1 Total Revenue Comparison (FY 2024E – FY 2025) (dollars in millions) $1,000.0 $794.1 $769.3 $773.6 $773.6 $748.3 $748.3 $500.0 NA NA $0.0 FY 2024 FY 2025 Adjusted EBITDA Comparison (FY 2024E – FY 2025) (dollars in millions) $122.0 $119.9 $118.9 $120.0 $118.3 $117.8 $118.0 $116.1 $116.2 $116.0 $115.3 $116.0 $114.0 $112.0 FY 2024 FY 2025 Distributable Cash Flow Comparison (FY 2024E – FY 2025) (dollars in millions) $60.0 $39.5 $35.9 $33.9 $40.0 $32.3 $28.3 $26.0 $26.0 $19.8 $20.0 $0.0 FY 2024 FY 2025 Management Projections Wall Street Estimates [2] Sidoti & Company, LLC Stifel [2] 1. Stifel estimates not available for revenue. 2. Stifel estimates per report dated April 18, 2024. Estimates not included in latest Stifel report dated May 24, 2024. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization. Excludes add-back for unit-based compensation expense. FY refers to Fiscal Year. Source: Bloomberg, Company management and Wall Street Research. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 14

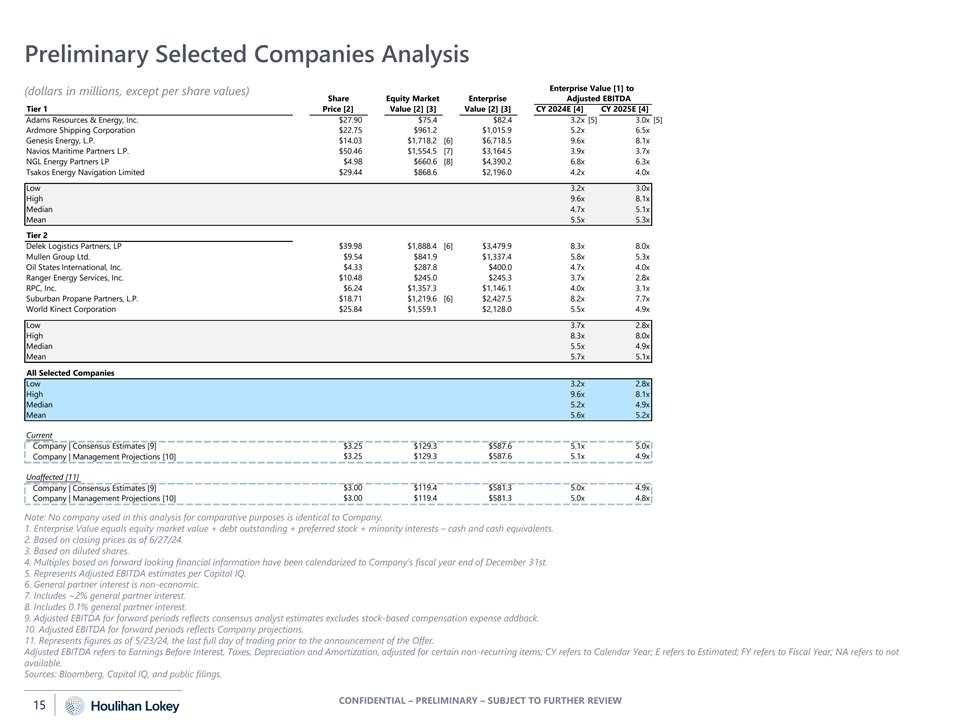

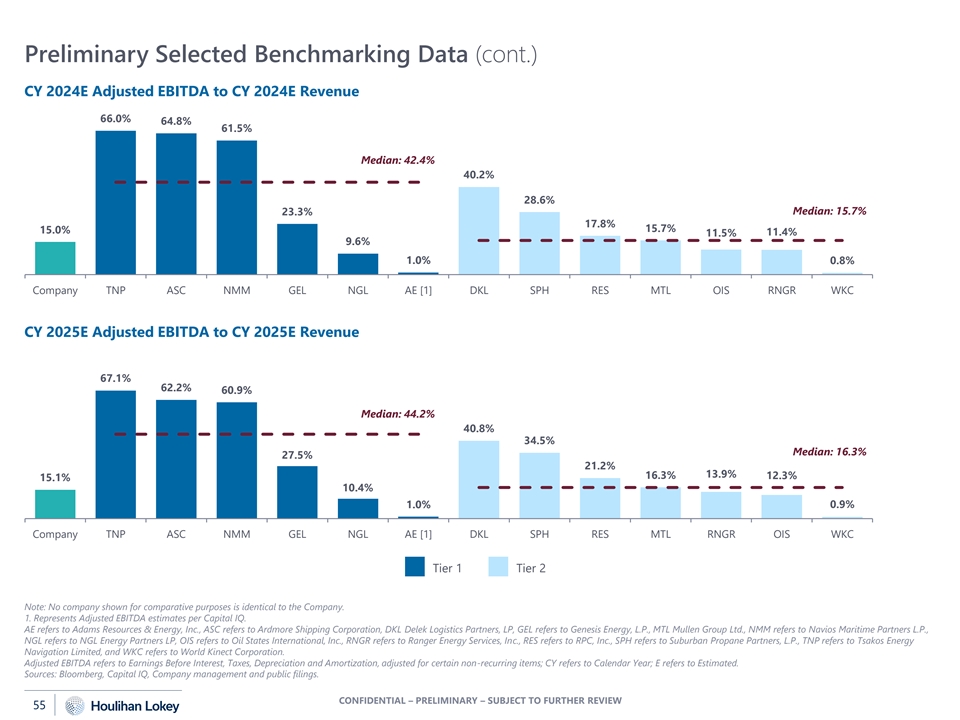

Preliminary Selected Companies Analysis Enterprise Value [1] to (dollars in millions, except per share values) Share Equity Market Enterprise Adjusted EBITDA Tier 1 Price [2] Value [2] [3] Value [2] [3] CY 2024E [4] CY 2025E [4] Adams Resources & Energy, Inc. $27.90 $75.4 $82.4 3.2x [5] 3.0x [5] Ardmore Shipping Corporation $22.75 $961.2 $1,015.9 5.2x 6.5x Genesis Energy, L.P. $14.03 $1,718.2 [6] $6,718.5 9.6x 8.1x Navios Maritime Partners L.P. $50.46 $1,554.5 [7] $3,164.5 3.9x 3.7x NGL Energy Partners LP $4.98 $660.6 [8] $4,390.2 6.8x 6.3x Tsakos Energy Navigation Limited $29.44 $868.6 $2,196.0 4.2x 4.0x Low 3.2x 3.0x High 9.6x 8.1x Median 4.7x 5.1x Mean 5.5x 5.3x Tier 2 Delek Logistics Partners, LP $39.98 $1,888.4 [6] $3,479.9 8.3x 8.0x Mullen Group Ltd. $9.54 $841.9 $1,337.4 5.8x 5.3x Oil States International, Inc. $4.33 $287.8 $400.0 4.7x 4.0x Ranger Energy Services, Inc. $10.48 $245.0 $245.3 3.7x 2.8x RPC, Inc. $6.24 $1,357.3 $1,146.1 4.0x 3.1x Suburban Propane Partners, L.P. $18.71 $1,219.6 [6] $2,427.5 8.2x 7.7x World Kinect Corporation $25.84 $1,559.1 $2,128.0 5.5x 4.9x Low 3.7x 2.8x High 8.3x 8.0x Median 5.5x 4.9x Mean 5.7x 5.1x All Selected Companies Low 3.2x 2.8x High 9.6x 8.1x Median 5.2x 4.9x Mean 5.6x 5.2x Current Company | Consensus Estimates [9] $3.25 $129.3 $587.6 5.1x 5.0x $3.25 $129.3 $587.6 5.1x 4.9x Company | Management Projections [10] Unaffected [11] Company | Consensus Estimates [9] $3.00 $119.4 $581.3 5.0x 4.9x Company | Management Projections [10] $3.00 $119.4 $581.3 5.0x 4.8x Note: No company used in this analysis for comparative purposes is identical to Company. 1. Enterprise Value equals equity market value + debt outstanding + preferred stock + minority interests – cash and cash equivalents. 2. Based on closing prices as of 6/27/24. 3. Based on diluted shares. 4. Multiples based on forward looking financial information have been calendarized to Company’s fiscal year end of December 31st. 5. Represents Adjusted EBITDA estimates per Capital IQ. 6. General partner interest is non-economic. 7. Includes ~2% general partner interest. 8. Includes 0.1% general partner interest. 9. Adjusted EBITDA for forward periods reflects consensus analyst estimates excludes stock-based compensation expense addback. 10. Adjusted EBITDA for forward periods reflects Company projections. 11. Represents figures as of 5/23/24, the last full day of trading prior to the announcement of the Offer. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items; CY refers to Calendar Year; E refers to Estimated; FY refers to Fiscal Year; NA refers to not available. Sources: Bloomberg, Capital IQ, and public filings. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 15

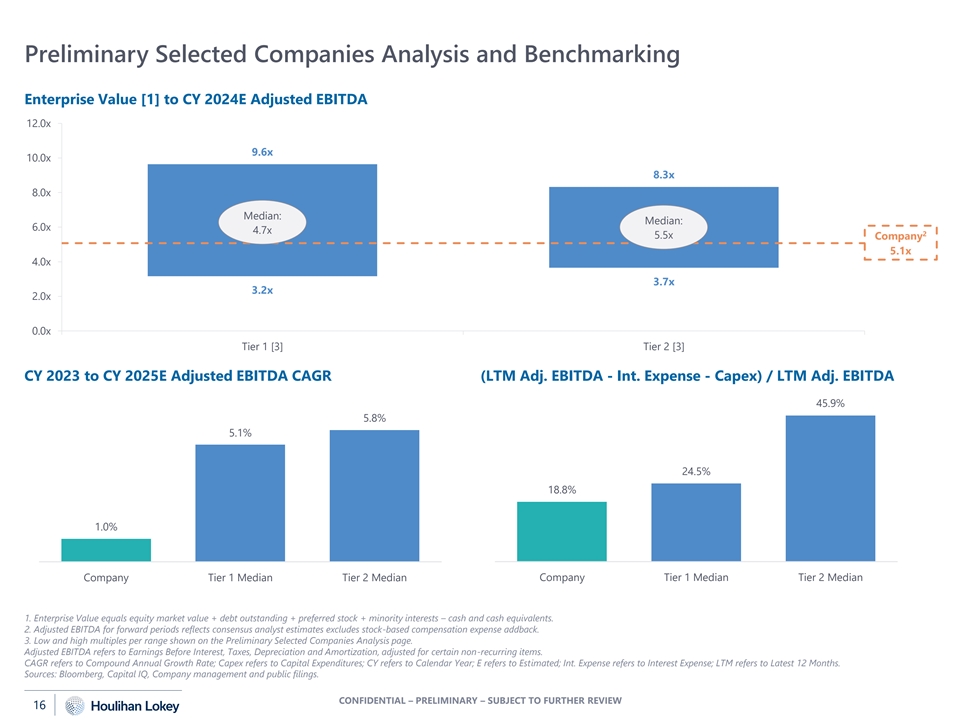

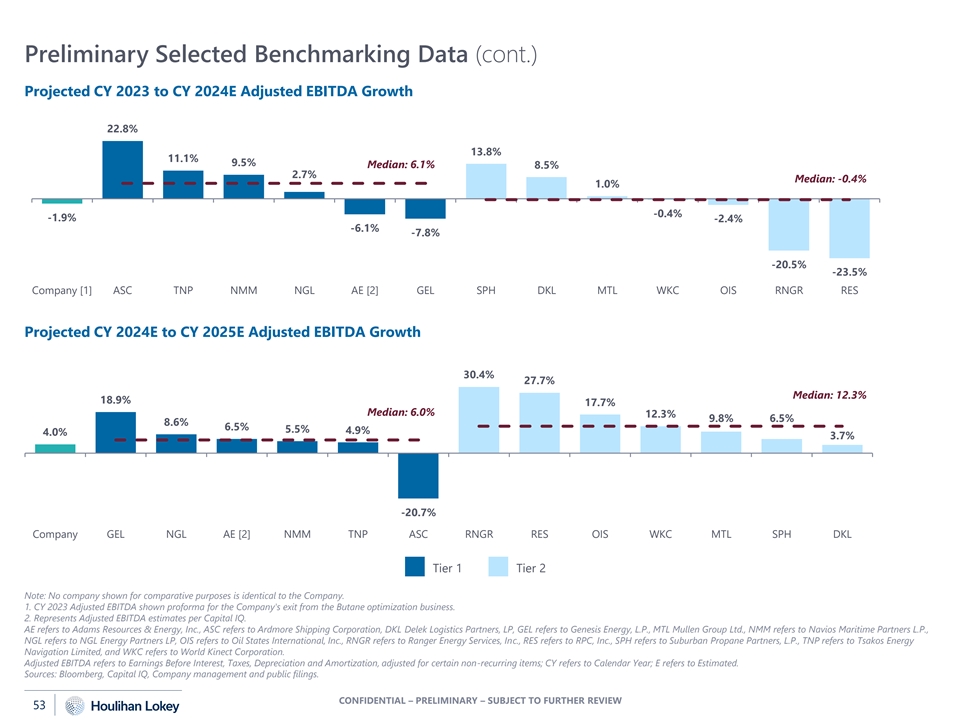

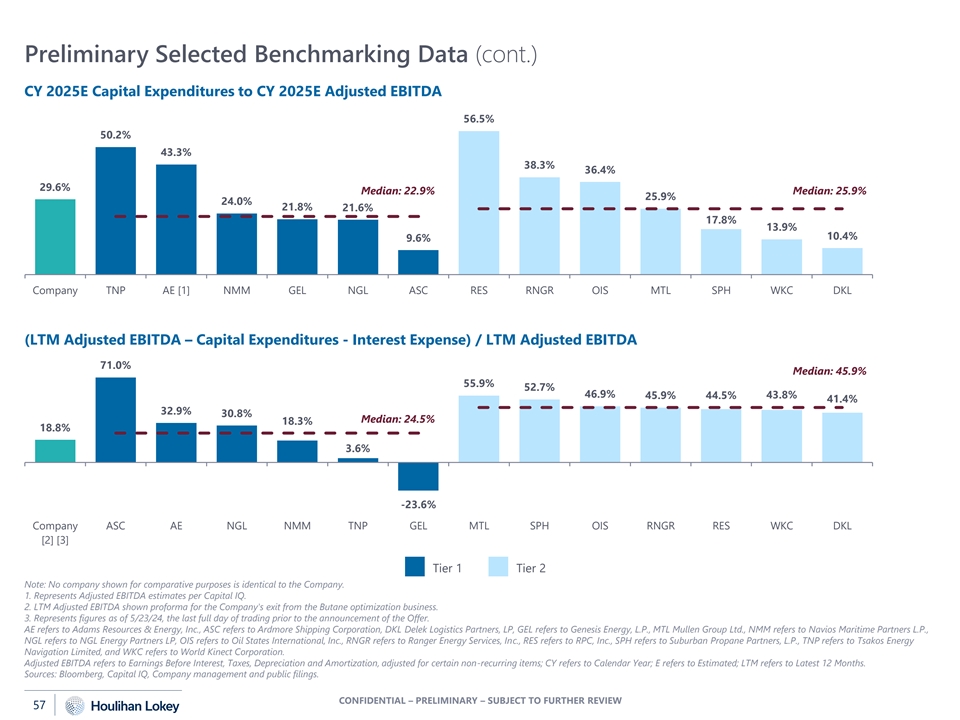

Preliminary Selected Companies Analysis and Benchmarking Enterprise Value [1] to CY 2024E Adjusted EBITDA 12.0x 9.6x 10.0x 8.3x 8.0x Median: Median: 6.0x 4.7x 2 5.5x Company 5.1x 4.0x 3.7x 3.2x 2.0x 0.0x Tier 1 [3] Tier 2 [3] CY 2023 to CY 2025E Adjusted EBITDA CAGR (LTM Adj. EBITDA - Int. Expense - Capex) / LTM Adj. EBITDA 45.9% 5.8% 5.1% 24.5% 18.8% 1.0% Company Tier 1 Median Tier 2 Median Company Tier 1 Median Tier 2 Median 1. Enterprise Value equals equity market value + debt outstanding + preferred stock + minority interests – cash and cash equivalents. 2. Adjusted EBITDA for forward periods reflects consensus analyst estimates excludes stock-based compensation expense addback. 3. Low and high multiples per range shown on the Preliminary Selected Companies Analysis page. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. CAGR refers to Compound Annual Growth Rate; Capex refers to Capital Expenditures; CY refers to Calendar Year; E refers to Estimated; Int. Expense refers to Interest Expense; LTM refers to Latest 12 Months. Sources: Bloomberg, Capital IQ, Company management and public filings. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 16

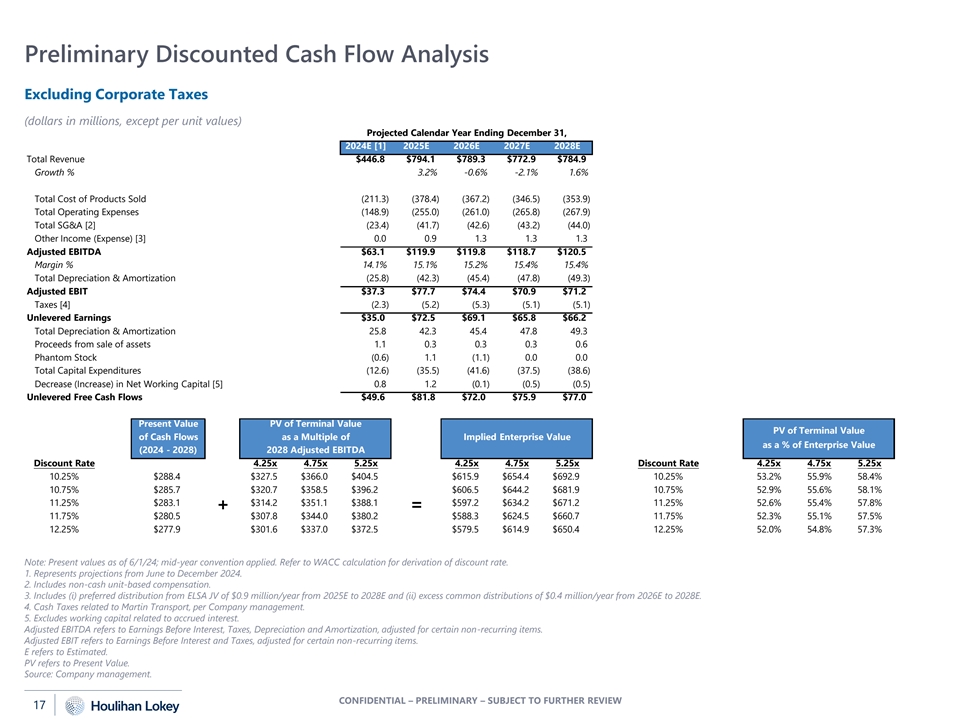

Preliminary Discounted Cash Flow Analysis Excluding Corporate Taxes (dollars in millions, except per unit values) Projected Calendar Year Ending December 31, 2024E [1] 2025E 2026E 2027E 2028E Total Revenue $446.8 $794.1 $789.3 $772.9 $784.9 Growth % 3.2% -0.6% -2.1% 1.6% Total Cost of Products Sold (211.3) (378.4) (367.2) (346.5) (353.9) Total Operating Expenses (148.9) (255.0) (261.0) (265.8) (267.9) Total SG&A [2] (23.4) (41.7) (42.6) (43.2) (44.0) Other Income (Expense) [3] 0.0 0.9 1.3 1.3 1.3 Adjusted EBITDA $63.1 $119.9 $119.8 $118.7 $120.5 Margin % 14.1% 15.1% 15.2% 15.4% 15.4% Total Depreciation & Amortization (25.8) (42.3) (45.4) (47.8) (49.3) Adjusted EBIT $37.3 $77.7 $74.4 $70.9 $71.2 Taxes [4] (2.3) (5.2) (5.3) (5.1) (5.1) Unlevered Earnings $35.0 $72.5 $69.1 $65.8 $66.2 Total Depreciation & Amortization 25.8 42.3 45.4 47.8 49.3 Proceeds from sale of assets 1.1 0.3 0.3 0.3 0.6 Phantom Stock (0.6) 1.1 (1.1) 0.0 0.0 Total Capital Expenditures (12.6) (35.5) (41.6) (37.5) (38.6) Decrease (Increase) in Net Working Capital [5] 0.8 1.2 (0.1) (0.5) (0.5) Unlevered Free Cash Flows $49.6 $81.8 $72.0 $75.9 $77.0 Present Value PV of Terminal Value PV of Terminal Value of Cash Flows as a Multiple of Implied Enterprise Value as a % of Enterprise Value (2024 - 2028) 2028 Adjusted EBITDA Discount Rate 4.25x 4.75x 5.25x 4.25x 4.75x 5.25x Discount Rate 4.25x 4.75x 5.25x 10.25% $288.4 $327.5 $366.0 $404.5 $615.9 $654.4 $692.9 10.25% 53.2% 55.9% 58.4% 10.75% $285.7 $320.7 $358.5 $396.2 $606.5 $644.2 $681.9 10.75% 52.9% 55.6% 58.1% 11.25% $283.1 $314.2 $351.1 $388.1 $597.2 $634.2 $671.2 11.25% 52.6% 55.4% 57.8% + = 11.75% $280.5 $307.8 $344.0 $380.2 $588.3 $624.5 $660.7 11.75% 52.3% 55.1% 57.5% 12.25% $277.9 $301.6 $337.0 $372.5 $579.5 $614.9 $650.4 12.25% 52.0% 54.8% 57.3% Note: Present values as of 6/1/24; mid-year convention applied. Refer to WACC calculation for derivation of discount rate. 1. Represents projections from June to December 2024. 2. Includes non-cash unit-based compensation. 3. Includes (i) preferred distribution from ELSA JV of $0.9 million/year from 2025E to 2028E and (ii) excess common distributions of $0.4 million/year from 2026E to 2028E. 4. Cash Taxes related to Martin Transport, per Company management. 5. Excludes working capital related to accrued interest. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. Adjusted EBIT refers to Earnings Before Interest and Taxes, adjusted for certain non-recurring items. E refers to Estimated. PV refers to Present Value. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 17

Preliminary Discounted Cash Flow Analysis (cont.) Including Corporate Taxes (dollars in millions, except per unit values) Projected Calendar Year Ending December 31, 2024E [1] 2025E 2026E 2027E 2028E Total Revenue $446.8 $794.1 $789.3 $772.9 $784.9 Growth % 3.2% -0.6% -2.1% 1.6% Total Cost of Products Sold (211.3) (378.4) (367.2) (346.5) (353.9) Total Operating Expenses (148.9) (255.0) (261.0) (265.8) (267.9) Total SG&A [2] (23.4) (41.7) (42.6) (43.2) (44.0) Other Income (Expense) [3] 0.0 0.9 1.3 1.3 1.3 Adjusted EBITDA $63.1 $119.9 $119.8 $118.7 $120.5 Margin % 14.1% 15.1% 15.2% 15.4% 15.4% Total Depreciation & Amortization (25.8) (42.3) (45.4) (47.8) (49.3) Adjusted EBIT $37.3 $77.7 $74.4 $70.9 $71.2 Taxes [4] (9.0) (18.8) (18.3) (17.6) (17.5) Unlevered Earnings $28.3 $58.9 $56.1 $53.3 $53.7 Total Depreciation & Amortization 25.8 42.3 45.4 47.8 49.3 Proceeds from sale of assets 1.1 0.3 0.3 0.3 0.6 Phantom Stock (0.6) 1.1 (1.1) 0.0 0.0 Total Capital Expenditures (12.6) (35.5) (41.6) (37.5) (38.6) Decrease (Increase) in Net Working Capital [5] 0.8 1.2 (0.1) (0.5) (0.5) Unlevered Free Cash Flows $43.0 $68.2 $59.0 $63.4 $64.5 Present Value PV of Terminal Value PV of Terminal Value of Cash Flows as a Multiple of Implied Enterprise Value as a % of Enterprise Value (2024 - 2028) 2028 Adjusted EBITDA Discount Rate 4.25x 4.75x 5.25x 4.25x 4.75x 5.25x Discount Rate 4.25x 4.75x 5.25x 9.50% $245.0 $337.9 $377.6 $417.4 $582.9 $622.6 $662.4 9.50% 58.0% 60.6% 63.0% 10.00% $242.7 $330.9 $369.8 $408.7 $573.6 $612.5 $651.5 10.00% 57.7% 60.4% 62.7% 10.50% $240.4 $324.1 $362.2 $400.3 $564.5 $602.7 $640.8 10.50% 57.4% 60.1% 62.5% + = 11.00% $238.2 $317.4 $354.8 $392.1 $555.7 $593.0 $630.3 11.00% 57.1% 59.8% 62.2% 11.50% $236.0 $311.0 $347.6 $384.1 $547.0 $583.6 $620.2 11.50% 56.9% 59.6% 61.9% Note: Present values as of 6/1/24; mid-year convention applied. Refer to WACC calculation for derivation of discount rate. 1. Represents projections from June to December 2024. 2. Includes non-cash unit-based compensation. 3. Includes (i) preferred distribution from ELSA JV of $0.9 million/year from 2025E to 2028E and (ii) excess common distributions of $0.4 million/year from 2026E to 2028E. 4. Cash Taxes related to Martin Transport, per Company management, plus 21% Corporate Tax on pretax income not attributed to Martin Transport. Terminal period taxes based on 2028E effective rate. 5. Excludes working capital related to accrued interest. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. Adjusted EBIT refers to Earnings Before Interest and Taxes, adjusted for certain non-recurring items. E refers to Estimated. PV refers to Present Value. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 18

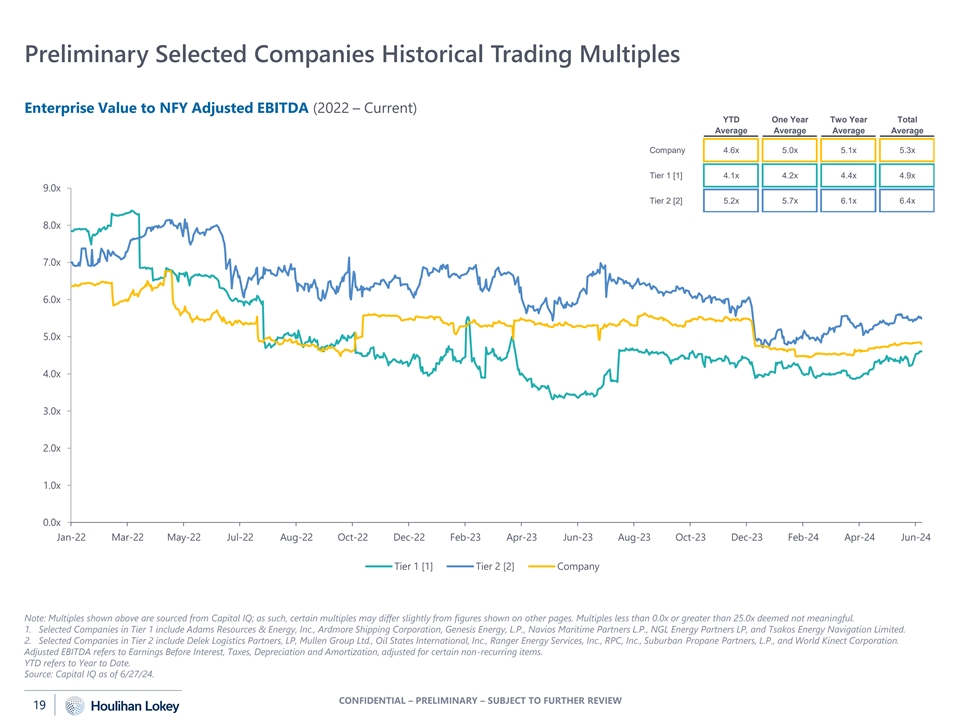

Preliminary Selected Companies Historical Trading Multiples Enterprise Value to NFY Adjusted EBITDA (2022 – Current) YTD One Year Two Year Total Average Average Average Average Company 4.6x 5.0x 5.1x 5.3x Tier 1 [1] 4.1x 4.2x 4.4x 4.9x 9.0x Tier 2 [2] 5.2x 5.7x 6.1x 6.4x 8.0x 7.0x 6.0x 5.0x 4.0x 3.0x 2.0x 1.0x 0.0x Jan-22 Mar-22 May-22 Jul-22 Aug-22 Oct-22 Dec-22 Feb-23 Apr-23 Jun-23 Aug-23 Oct-23 Dec-23 Feb-24 Apr-24 Jun-24 Tier 1 [1] Tier 2 [2] Company Note: Multiples shown above are sourced from Capital IQ; as such, certain multiples may differ slightly from figures shown on other pages. Multiples less than 0.0x or greater than 25.0x deemed not meaningful. 1. Selected Companies in Tier 1 include Adams Resources & Energy, Inc., Ardmore Shipping Corporation, Genesis Energy, L.P., Navios Maritime Partners L.P., NGL Energy Partners LP, and Tsakos Energy Navigation Limited. 2. Selected Companies in Tier 2 include Delek Logistics Partners, LP, Mullen Group Ltd., Oil States International, Inc., Ranger Energy Services, Inc., RPC, Inc., Suburban Propane Partners, L.P., and World Kinect Corporation. Adjusted EBITDA refers to Earnings Before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. YTD refers to Year to Date. Source: Capital IQ as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 19

PRELIMINARY PREMIUMS PAID DATA 04 03 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

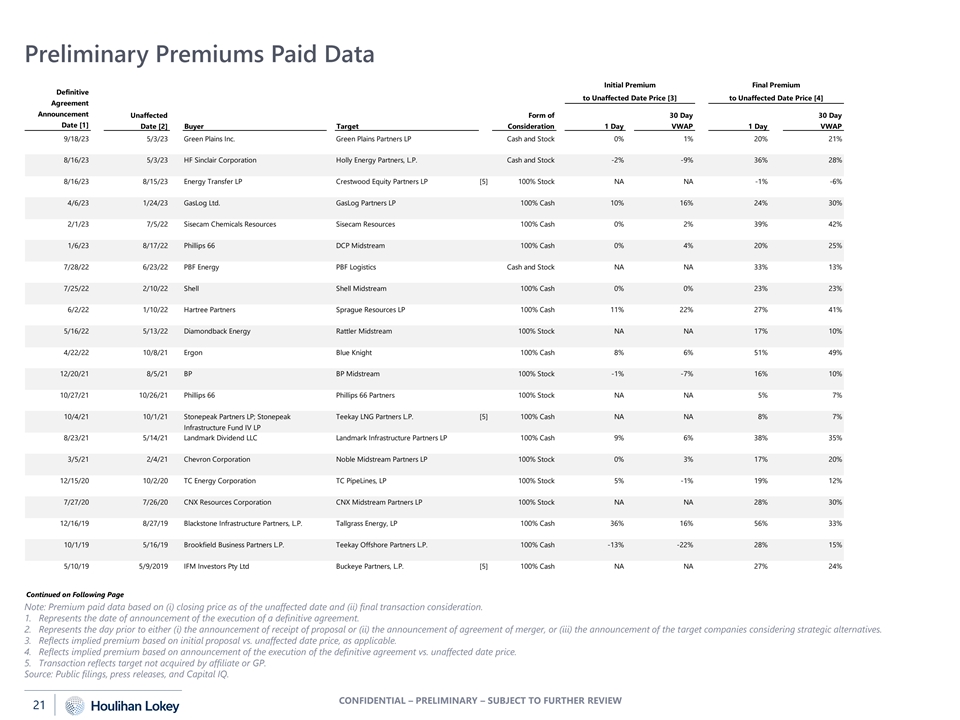

Preliminary Premiums Paid Data Initial Premium Final Premium Definitive to Unaffected Date Price [3] to Unaffected Date Price [4] Agreement Announcement Unaffected Form of 30 Day 30 Day Date [1] Date [2] Buyer Target Consideration 1 Day VWAP 1 Day VWAP 9/18/23 5/3/23 Green Plains Inc. Green Plains Partners LP Cash and Stock 0% 1% 20% 21% 8/16/23 5/3/23 HF Sinclair Corporation Holly Energy Partners, L.P. Cash and Stock -2% -9% 36% 28% 8/16/23 8/15/23 Energy Transfer LP Crestwood Equity Partners LP [5] 100% Stock NA NA -1% -6% 4/6/23 1/24/23 GasLog Ltd. GasLog Partners LP 100% Cash 10% 16% 24% 30% 2/1/23 7/5/22 Sisecam Chemicals Resources Sisecam Resources 100% Cash 0% 2% 39% 42% 1/6/23 8/17/22 Phillips 66 DCP Midstream 100% Cash 0% 4% 20% 25% 7/28/22 6/23/22 PBF Energy PBF Logistics Cash and Stock NA NA 33% 13% 7/25/22 2/10/22 Shell Shell Midstream 100% Cash 0% 0% 23% 23% 6/2/22 1/10/22 Hartree Partners Sprague Resources LP 100% Cash 11% 22% 27% 41% 5/16/22 5/13/22 Diamondback Energy Rattler Midstream 100% Stock NA NA 17% 10% 4/22/22 10/8/21 Ergon Blue Knight 100% Cash 8% 6% 51% 49% 12/20/21 8/5/21 BP BP Midstream 100% Stock -1% -7% 16% 10% 10/27/21 10/26/21 Phillips 66 Phillips 66 Partners 100% Stock NA NA 5% 7% 10/4/21 10/1/21 Stonepeak Partners LP; Stonepeak Teekay LNG Partners L.P. [5] 100% Cash NA NA 8% 7% Infrastructure Fund IV LP 8/23/21 5/14/21 Landmark Dividend LLC Landmark Infrastructure Partners LP 100% Cash 9% 6% 38% 35% 3/5/21 2/4/21 Chevron Corporation Noble Midstream Partners LP 100% Stock 0% 3% 17% 20% 12/15/20 10/2/20 TC Energy Corporation TC PipeLines, LP 100% Stock 5% -1% 19% 12% 7/27/20 7/26/20 CNX Resources Corporation CNX Midstream Partners LP 100% Stock NA NA 28% 30% 12/16/19 8/27/19 Blackstone Infrastructure Partners, L.P. Tallgrass Energy, LP 100% Cash 36% 16% 56% 33% 10/1/19 5/16/19 Brookfield Business Partners L.P. Teekay Offshore Partners L.P. 100% Cash -13% -22% 28% 15% 5/10/19 5/9/2019 IFM Investors Pty Ltd Buckeye Partners, L.P. [5] 100% Cash NA NA 27% 24% Continued on Following Page Note: Premium paid data based on (i) closing price as of the unaffected date and (ii) final transaction consideration. 1. Represents the date of announcement of the execution of a definitive agreement. 2. Represents the day prior to either (i) the announcement of receipt of proposal or (ii) the announcement of agreement of merger, or (iii) the announcement of the target companies considering strategic alternatives. 3. Reflects implied premium based on initial proposal vs. unaffected date price, as applicable. 4. Reflects implied premium based on announcement of the execution of the definitive agreement vs. unaffected date price. 5. Transaction reflects target not acquired by affiliate or GP. Source: Public filings, press releases, and Capital IQ. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 21

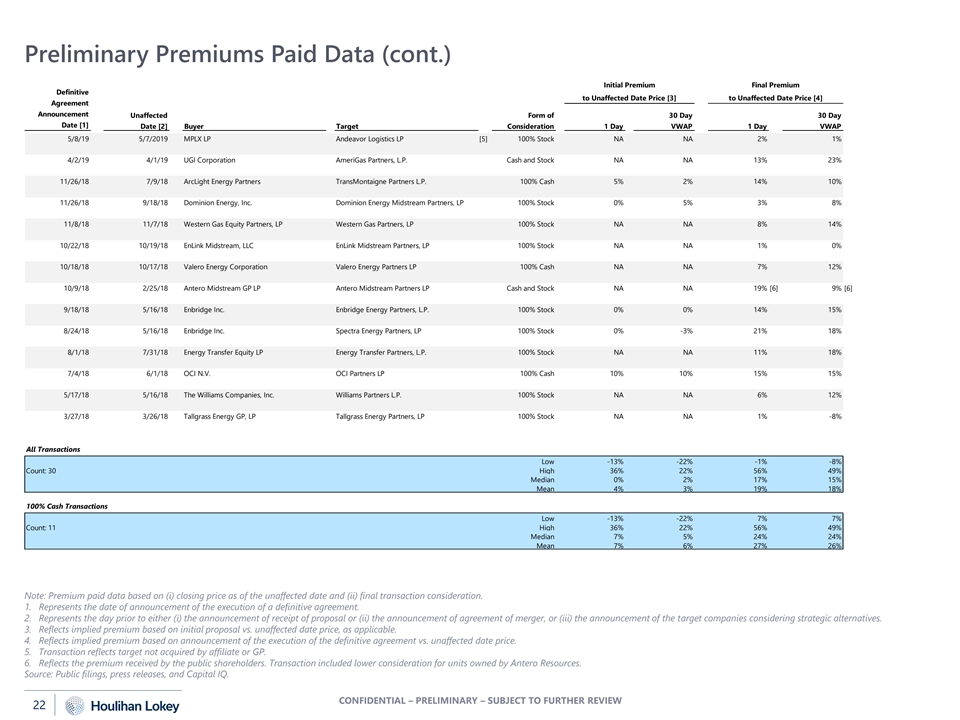

Preliminary Premiums Paid Data (cont.) Initial Premium Final Premium Definitive to Unaffected Date Price [3] to Unaffected Date Price [4] Agreement Announcement Unaffected Form of 30 Day 30 Day Date [1] Date [2] Buyer Target Consideration 1 Day VWAP 1 Day VWAP 5/8/19 5/7/2019 MPLX LP Andeavor Logistics LP [5] 100% Stock NA NA 2% 1% 4/2/19 4/1/19 UGI Corporation AmeriGas Partners, L.P. Cash and Stock NA NA 13% 23% 11/26/18 7/9/18 ArcLight Energy Partners TransMontaigne Partners L.P. 100% Cash 5% 2% 14% 10% 11/26/18 9/18/18 Dominion Energy, Inc. Dominion Energy Midstream Partners, LP 100% Stock 0% 5% 3% 8% 11/8/18 11/7/18 Western Gas Equity Partners, LP Western Gas Partners, LP 100% Stock NA NA 8% 14% 10/22/18 10/19/18 EnLink Midstream, LLC EnLink Midstream Partners, LP 100% Stock NA NA 1% 0% 10/18/18 10/17/18 Valero Energy Corporation Valero Energy Partners LP 100% Cash NA NA 7% 12% 10/9/18 2/25/18 Antero Midstream GP LP Antero Midstream Partners LP Cash and Stock NA NA 19% [6] 9% [6] 9/18/18 5/16/18 Enbridge Inc. Enbridge Energy Partners, L.P. 100% Stock 0% 0% 14% 15% 8/24/18 5/16/18 Enbridge Inc. Spectra Energy Partners, LP 100% Stock 0% -3% 21% 18% 8/1/18 7/31/18 Energy Transfer Equity LP Energy Transfer Partners, L.P. 100% Stock NA NA 11% 18% 7/4/18 6/1/18 OCI N.V. OCI Partners LP 100% Cash 10% 10% 15% 15% 5/17/18 5/16/18 The Williams Companies, Inc. Williams Partners L.P. 100% Stock NA NA 6% 12% 3/27/18 3/26/18 Tallgrass Energy GP, LP Tallgrass Energy Partners, LP 100% Stock NA NA 1% -8% All Transactions Low -13% -22% -1% -8% Count: 30 High 36% 22% 56% 49% Median 0% 2% 17% 15% Mean 4% 3% 19% 18% 100% Cash Transactions Low -13% -22% 7% 7% Count: 11 High 36% 22% 56% 49% Median 7% 5% 24% 24% Mean 7% 6% 27% 26% Note: Premium paid data based on (i) closing price as of the unaffected date and (ii) final transaction consideration. 1. Represents the date of announcement of the execution of a definitive agreement. 2. Represents the day prior to either (i) the announcement of receipt of proposal or (ii) the announcement of agreement of merger, or (iii) the announcement of the target companies considering strategic alternatives. 3. Reflects implied premium based on initial proposal vs. unaffected date price, as applicable. 4. Reflects implied premium based on announcement of the execution of the definitive agreement vs. unaffected date price. 5. Transaction reflects target not acquired by affiliate or GP. 6. Reflects the premium received by the public shareholders. Transaction included lower consideration for units owned by Antero Resources. Source: Public filings, press releases, and Capital IQ. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 22

APPENDIX 06 04 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

APPENDIX Additional Response Considerations 07 04 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

Unit Trading Activity Prior to the Offer Closing Unit Price (dollars in actuals) Closing Unit Price 1-Month VWAP: $2.89 3-Month VWAP: $2.69 6-Month VWAP: $2.55 1-Year VWAP: $2.57 3-Year VWAP: $3.17 5-Year VWAP: $2.81 $7.00 $6.00 5/24/24: Offer Announced $5.00 $4.00 $3.00 $2.00 $1.00 $0.00 May-19 May-20 May-21 May-22 May-23 May-24 Note: VWAPs shown are as of 5/23/24. VWAP refers to Volume Weighted Average Price. Source: Bloomberg as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 25

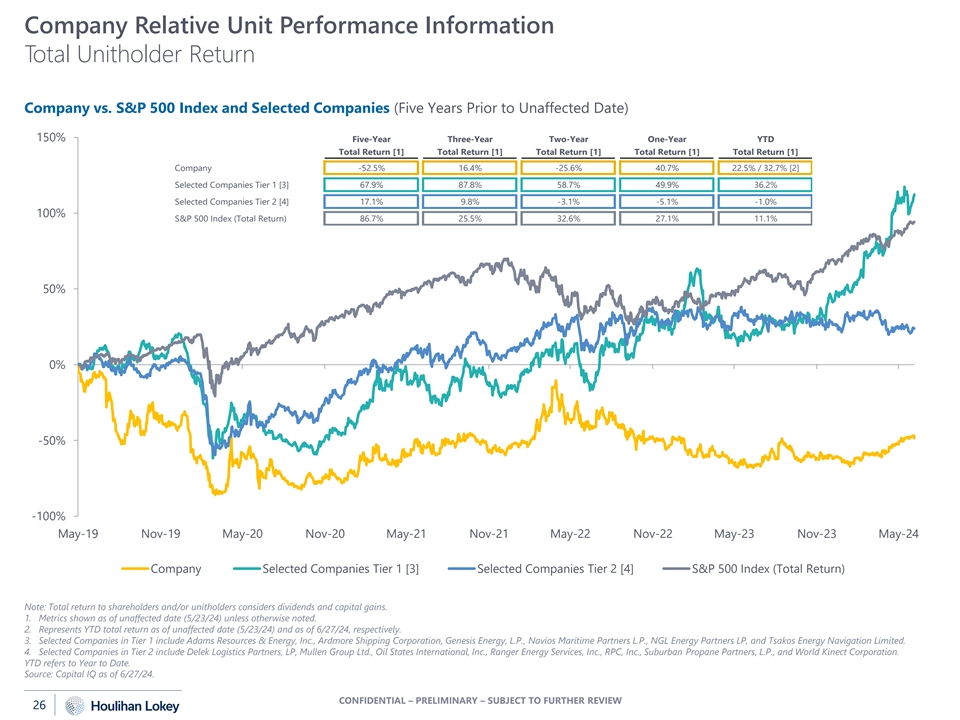

Company Relative Unit Performance Information Total Unitholder Return Company vs. S&P 500 Index and Selected Companies (Five Years Prior to Unaffected Date) 150% Five-Year Three-Year Two-Year One-Year YTD Total Return [1] Total Return [1] Total Return [1] Total Return [1] Total Return [1] Company -52.5% 16.4% -25.6% 40.7% 22.5% / 32.7% [2] Selected Companies Tier 1 [3] 67.9% 87.8% 58.7% 49.9% 36.2% Selected Companies Tier 2 [4] 17.1% 9.8% -3.1% -5.1% -1.0% 100% S&P 500 Index (Total Return) 86.7% 25.5% 32.6% 27.1% 11.1% 50% 0% -50% -100% May-19 Nov-19 May-20 Nov-20 May-21 Nov-21 May-22 Nov-22 May-23 Nov-23 May-24 Company Selected Companies Tier 1 [3] Selected Companies Tier 2 [4] S&P 500 Index (Total Return) Note: Total return to shareholders and/or unitholders considers dividends and capital gains. 1. Metrics shown as of unaffected date (5/23/24) unless otherwise noted. 2. Represents YTD total return as of unaffected date (5/23/24) and as of 6/27/24, respectively. 3. Selected Companies in Tier 1 include Adams Resources & Energy, Inc., Ardmore Shipping Corporation, Genesis Energy, L.P., Navios Maritime Partners L.P., NGL Energy Partners LP, and Tsakos Energy Navigation Limited. 4. Selected Companies in Tier 2 include Delek Logistics Partners, LP, Mullen Group Ltd., Oil States International, Inc., Ranger Energy Services, Inc., RPC, Inc., Suburban Propane Partners, L.P., and World Kinect Corporation. YTD refers to Year to Date. Source: Capital IQ as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 26

Recent Unit Price Performance Daily Volume (millions) Closing Unit Price ($) $4.00 1.6 Current Unit Price [1]: $3.25 $3.50 1.4 $3.00 1.2 $2.50 1.0 Q4 $2.00 Q1 0.8 Q2 Q1 FY 22 FY 23 Q3 FY 23 FY 24 Q4 FY 23 $1.50 0.6 FY 23 2 ▲ 0.9% 2 2 ▼ 2.0% 2 ▲ 0.0% ▲ 3.4% 2 $1.00 0.4 ▲ 0.4% 2 ▼ 0.5% $0.50 0.2 $0.00 0.0 1/1/23 3/1/23 5/1/23 7/1/23 9/1/23 11/1/23 1/1/24 3/1/24 5/1/24 Daily Trading Volume Company Current Unit Price [1] 90-Day Average Daily Trading Volume (in millions) [3] 0.1 % of Total Units Outstanding 0.3% 90-Day Average Daily Trading Value (in millions) [3] $0.3 % of Market Value of Equity 0.3% Number of Analysts Covering the Company [4] 2 Total Public Float [5] [6] 28.2 Comparison of Reported Financials and Wall Street Estimates % of Total Units Outstanding 70.9% (dollars in millions) Fiscal Year Ended December 31, 2022 2023 2024 Q4 Q1 Q2 Q3 Q4 Q1 Total Adjusted Total Adjusted Total Adjusted Total Adjusted Total Adjusted Total Adjusted Revenue EBITDA Revenue EBITDA Revenue EBITDA Revenue EBITDA Revenue EBITDA Revenue EBITDA Consensus Wall Street Estimate [7] NA $23.2 NA $32.5 NA $33.0 NA $26.2 $178.0 $25.6 $199.0 $31.3 Reported Financials $243.4 $17.8 $244.5 $30.6 [8] $195.6 $31.8 [8] $176.7 $26.2 $181.1 $29.2 $180.8 $30.4 % Difference NA -23.4% NA -6.0% NA -3.6% NA -0.1% 1.7% 14.1% -9.1% -2.7% 1. As of 6/27/24 close. 2. Refers to percentage change between closing unit price directly prior to reported earnings and closing unit price on subsequent trading day, per Capital IQ. 3. Per Capital IQ. 4. Per Bloomberg. 5. Per public filings. 6. Represents common units outstanding. Does not reflect unit acquisitions or disposals not publicly disclosed as of 6/27/24. 7. Refers to consensus Bloomberg and Wall Street analyst estimates for relevant financial metric directly prior to reported earnings. 8. The reported Adjusted EBITDA figures for Q1 2023 and Q2 2023 are shown pro forma for the Company’s exit from the Butane optimization business. Source: Capital IQ, Bloomberg and Company press releases. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 27

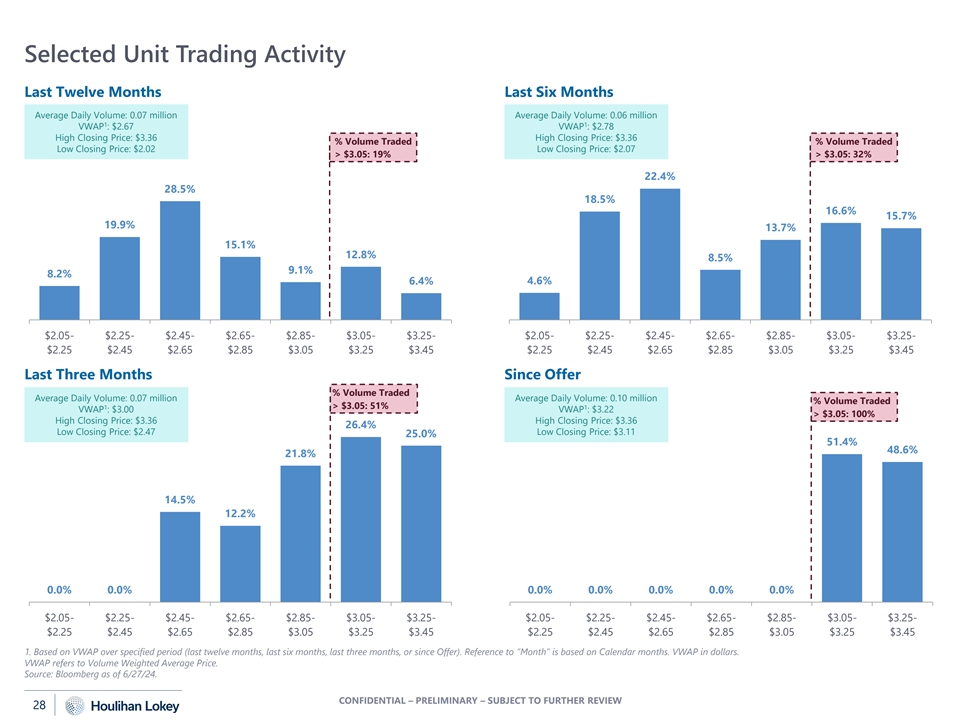

Selected Unit Trading Activity Last Twelve Months Last Six Months Average Daily Volume: 0.07 million Average Daily Volume: 0.06 million 1 1 VWAP : $2.67 VWAP : $2.78 High Closing Price: $3.36 High Closing Price: $3.36 % Volume Traded % Volume Traded Low Closing Price: $2.02 Low Closing Price: $2.07 > $3.05: 19% > $3.05: 32% 22.4% 28.5% 18.5% 16.6% 15.7% 19.9% 13.7% 15.1% 12.8% 8.5% 9.1% 8.2% 4.6% 6.4% $2.05- $2.25- $2.45- $2.65- $2.85- $3.05- $3.25- $2.05- $2.25- $2.45- $2.65- $2.85- $3.05- $3.25- $2.25 $2.45 $2.65 $2.85 $3.05 $3.25 $3.45 $2.25 $2.45 $2.65 $2.85 $3.05 $3.25 $3.45 Last Three Months Since Offer % Volume Traded Average Daily Volume: 0.07 million Average Daily Volume: 0.10 million % Volume Traded 1 > $3.05: 51% 1 VWAP : $3.00 VWAP : $3.22 > $3.05: 100% High Closing Price: $3.36 High Closing Price: $3.36 26.4% Low Closing Price: $2.47 Low Closing Price: $3.11 25.0% 51.4% 48.6% 21.8% 14.5% 12.2% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% $2.05- $2.25- $2.45- $2.65- $2.85- $3.05- $3.25- $2.05- $2.25- $2.45- $2.65- $2.85- $3.05- $3.25- $2.25 $2.45 $2.65 $2.85 $3.05 $3.25 $3.45 $2.25 $2.45 $2.65 $2.85 $3.05 $3.25 $3.45 1. Based on VWAP over specified period (last twelve months, last six months, last three months, or since Offer). Reference to “Month” is based on Calendar months. VWAP in dollars. VWAP refers to Volume Weighted Average Price. Source: Bloomberg as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 28

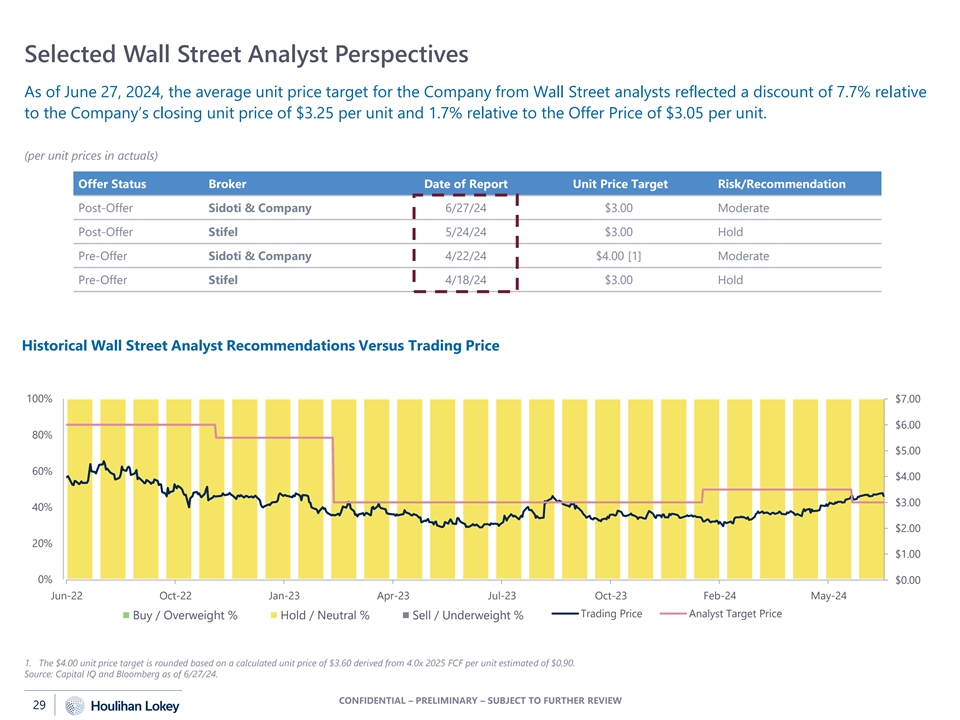

Selected Wall Street Analyst Perspectives As of June 27, 2024, the average unit price target for the Company from Wall Street analysts reflected a discount of 7.7% relative to the Company’s closing unit price of $3.25 per unit and 1.7% relative to the Offer Price of $3.05 per unit. (per unit prices in actuals) Offer Status Broker Date of Report Unit Price Target Risk/Recommendation Post-Offer Sidoti & Company 6/27/24 $3.00 Moderate Post-Offer Stifel 5/24/24 $3.00 Hold Pre-Offer Sidoti & Company 4/22/24 $4.00 [1] Moderate Pre-Offer Stifel 4/18/24 $3.00 Hold Historical Wall Street Analyst Recommendations Versus Trading Price 100% $7.00 $6.00 80% $5.00 60% $4.00 $3.00 40% $2.00 20% $1.00 0% $0.00 Jun-22 Oct-22 Jan-23 Apr-23 Jul-23 Oct-23 Feb-24 May-24 Trading Price Analyst Target Price Buy / Overweight % Hold / Neutral % Sell / Underweight % 1. The $4.00 unit price target is rounded based on a calculated unit price of $3.60 derived from 4.0x 2025 FCF per unit estimated of $0.90. Source: Capital IQ and Bloomberg as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 29

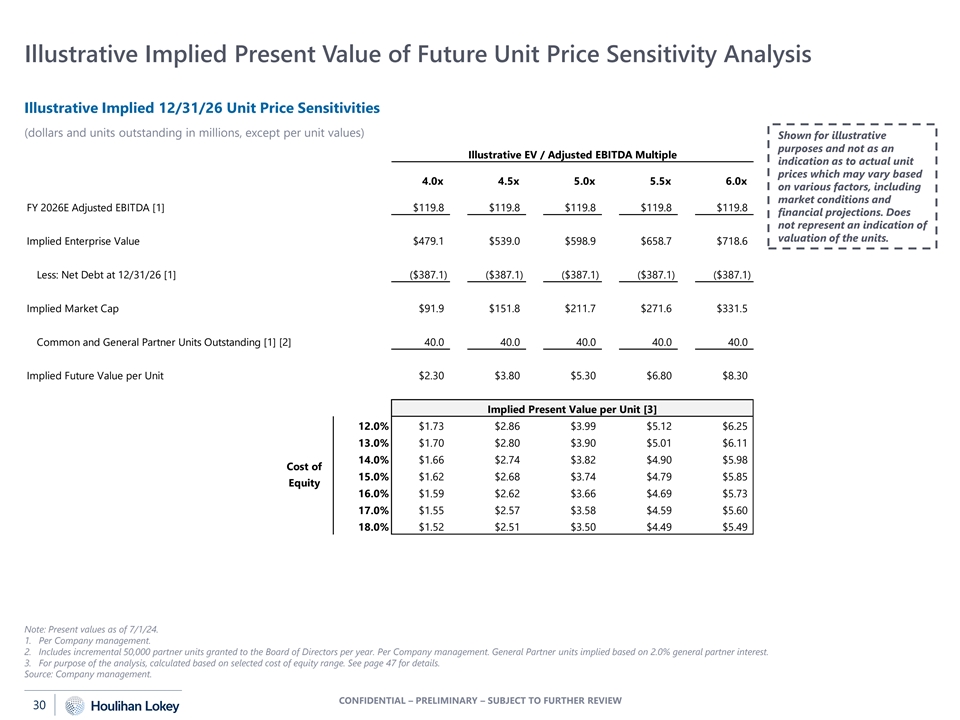

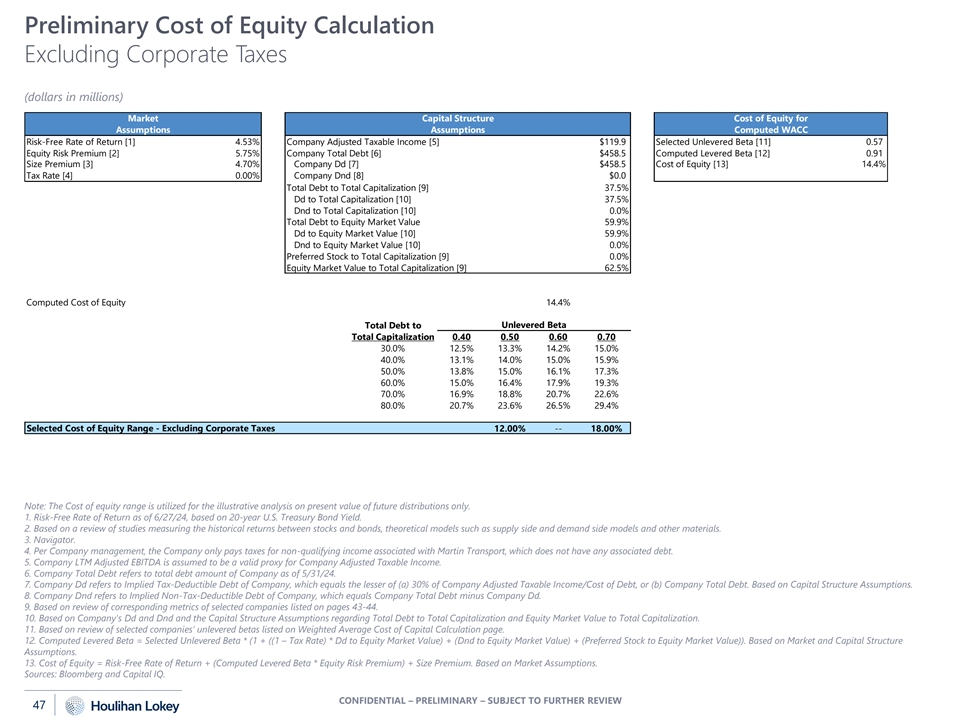

Illustrative Implied Present Value of Future Unit Price Sensitivity Analysis Illustrative Implied 12/31/26 Unit Price Sensitivities (dollars and units outstanding in millions, except per unit values) Shown for illustrative purposes and not as an Illustrative EV / Adjusted EBITDA Multiple indication as to actual unit prices which may vary based 4.0x 4.5x 5.0x 5.5x 6.0x on various factors, including market conditions and FY 2026E Adjusted EBITDA [1] $119.8 $119.8 $119.8 $119.8 $119.8 financial projections. Does not represent an indication of valuation of the units. Implied Enterprise Value $479.1 $539.0 $598.9 $658.7 $718.6 Less: Net Debt at 12/31/26 [1] ($387.1) ($387.1) ($387.1) ($387.1) ($387.1) Implied Market Cap $91.9 $151.8 $211.7 $271.6 $331.5 Common and General Partner Units Outstanding [1] [2] 40.0 40.0 40.0 40.0 40.0 Implied Future Value per Unit $2.30 $3.80 $5.30 $6.80 $8.30 Implied Present Value per Unit [3] 12.0% $1.73 $2.86 $3.99 $5.12 $6.25 13.0% $1.70 $2.80 $3.90 $5.01 $6.11 14.0% $1.66 $2.74 $3.82 $4.90 $5.98 Cost of 15.0% $1.62 $2.68 $3.74 $4.79 $5.85 Equity 16.0% $1.59 $2.62 $3.66 $4.69 $5.73 17.0% $1.55 $2.57 $3.58 $4.59 $5.60 18.0% $1.52 $2.51 $3.50 $4.49 $5.49 Note: Present values as of 7/1/24. 1. Per Company management. 2. Includes incremental 50,000 partner units granted to the Board of Directors per year. Per Company management. General Partner units implied based on 2.0% general partner interest. 3. For purpose of the analysis, calculated based on selected cost of equity range. See page 47 for details. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 30

Illustrative Present Value of Future Distributions The below assumes (for illustrative purposes only) that following de-levering to below 3x Net Debt / LTM EBITDA, the Company initiates distributions in FY 2028, ramping up to a level consistent with a 1.6x distribution coverage ratio in 2031, based on discussions with Company management. Implied present values are based on a terminal distribution coverage ratio range of ~1.3x to ~2.0x and selected cost of equity range of 12-18%. 2024E [1] 2025E 2026E 2027E 2028E 2029E 2030E 2031E (dollars and units outstanding in millions, except per unit values) Distributable Cash [2] [a] $13.0 $35.9 $36.3 $55.3 $64.7 $64.7 $64.7 $64.7 Free Cash Flow Before Distributions [2] $0.3 $32.6 $24.7 $30.4 $49.7 $49.7 $49.7 $49.7 Illustrative Distibutions [3] [b] ($0.4) ($0.8) ($0.8) ($0.8) ($10.0) ($20.0) ($30.0) ($40.0) Implied Distribution per Unit ($0.01) ($0.02) ($0.02) ($0.02) ($0.25) ($0.50) ($0.75) ($0.99) Implied Distribution Coverage Ratio [4] [a]/[b] 32.7x 45.0x 45.7x 69.5x 6.5x 3.2x 2.2x 1.6x Implied Distribution Ratio [5] [b]/[a] 0.0x 0.0x 0.0x 0.0x 0.2x 0.3x 0.5x 0.6x Total Units (millions) [6] 39.8 39.9 40.0 40.0 40.1 40.1 40.2 40.2 Credit-Related Metrics Beginning Cash $0.1 $0.5 $0.5 $12.9 $0.5 $0.5 $30.2 $49.8 Change in Cash 0.2 (0.0) 12.4 (12.4) 0.0 29.7 19.7 9.7 Ending Cash $0.5 $0.5 $12.9 $0.5 $0.5 $30.2 $49.8 $59.5 Total Debt [7] $441.2 $411.5 $400.0 $363.3 $323.7 $323.7 $323.7 $323.7 Net Debt / Adjusted EBITDA [8] 3.8x 3.4x 3.2x 3.1x 2.7x 2.4x 2.3x 2.2x Free Cash Flow Before Distributions Coverage Ratio [9] 0.8x 41.0x 31.0x 38.2x 5.0x 2.5x 1.7x 1.2x Liquidity [10] $109.3 $139.0 $162.9 $37.2 $76.8 $106.5 $126.2 $135.9 • Additional liquidity may be necessary to potentially Implied Present Value of Distributions Per Unit [11] refinance the Company’s debt 2031 Terminal Distribution Coverage Ratio in the future 2.05x 1.90x 1.75x 1.60x 1.45x 1.30x 1.00x represents the upper bound Implied Terminal Free Cash Flow Before Distributions Coverage Ratio [9] 1.57x 1.46x 1.34x 1.23x 1.11x 1.00x to theoretical distributions • Distribution coverage ratios Implied Terminal Distribution $31.5 $34.0 $37.0 $40.4 $44.6 $49.8 of MLPs have trended higher in recent years, generally Implied Distribution per Unit $0.78 $0.85 $0.92 $1.01 $1.11 $1.24 Shown for illustrative purposes between ~1.5x and ~2.0x 12.0% $4.29 $4.52 $4.79 $5.12 $5.51 $5.99 and not as an indication as to 13.0% $3.83 $4.03 $4.27 $4.55 $4.89 $5.31 • MLPs frequently have actual unit prices which may significant latitude on the 14.0% $3.44 $3.62 $3.82 $4.07 $4.37 $4.73 vary based on various factors, Cost of definitions of capital 15.0% $3.11 $3.26 $3.45 $3.66 $3.92 $4.24 including market conditions Equity expenditures and other items 16.0% $2.82 $2.96 $3.12 $3.31 $3.54 $3.82 and financial projections. Does used to calculate distributable 17.0% $2.58 $2.70 $2.84 $3.01 $3.21 $3.46 not reflect an indication of cash 18.0% $2.36 $2.47 $2.59 $2.74 $2.92 $3.15 valuation of the units. See the following page for footnotes. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 31

Illustrative Present Value of Future Distributions (cont.) Note: Present values as of 7/1/24; mid-year convention applied. 1. Reflects stub period as of 7/1/24. 2. Held constant after 2028E. 3. For purpose of the illustrative analysis, assumes total distribution amounts of $10 mm, $20 mm, $30 mm and $40 mm for each of 2028E, 2029E, 2030E and 2031E respectively. 4. Defined as Distributable Cash Flow divided by total Distributions in a given year. 5. Defined as total Distributions divided by Distributable Cash Flow in a given year. 6. Includes incremental 50,000 partner units granted to the Board of Directors per year. Per Company management. 0.8 million General Partner units implied based on 2.0% general partner interest. 7. For purpose of the illustrative analysis, (i) 2028 Free Cash Flow After Distributions is assumed to be utilized to pay down the revolver and (ii) the revolver balance is held constant after 2028. 8. For purpose of the illustrative analysis, the Company's adjusted EBITDA is assumed to be held constant after 2028. 9. Defined as Free Cash Flow Before Distributions divided by total Distributions in a given year. 10. Assumes $150 mm of total credit facility availability from 2024 till January 2027 and $200 mm thereafter. Per Company management. 11. For purpose of the illustrative analysis, utilizes terminal perpetual growth rate of 0%. Source: Company management. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 32

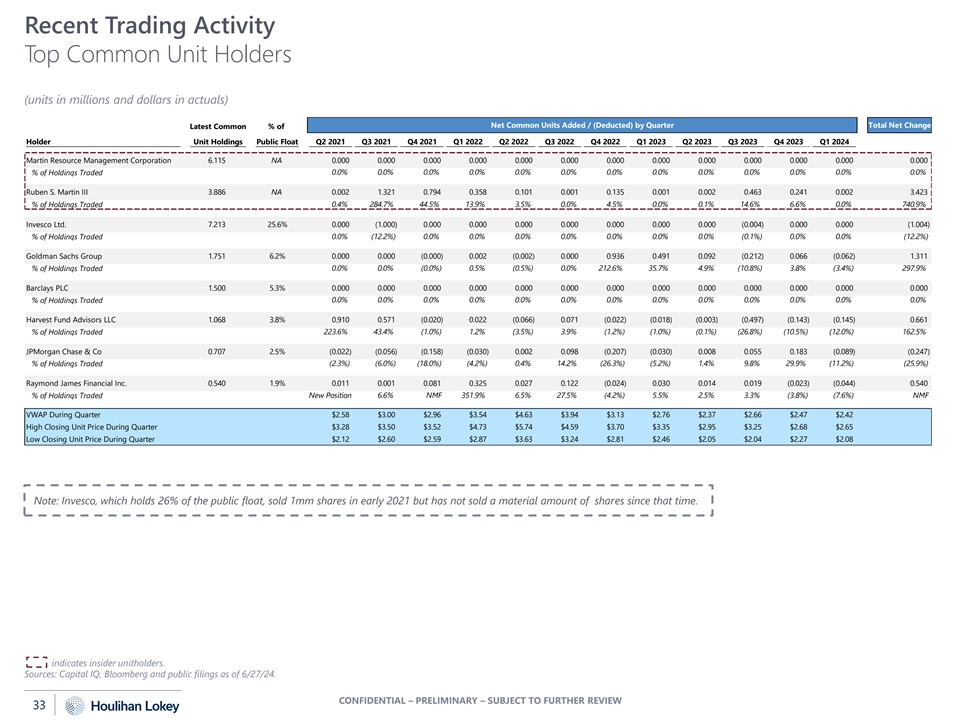

Recent Trading Activity Top Common Unit Holders (units in millions and dollars in actuals) Net Common Units Added / (Deducted) by Quarter Total Net Change Latest Common % of Holder Unit Holdings Public Float Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q2 2022 Q3 2022 Q4 2022 Q1 2023 Q2 2023 Q3 2023 Q4 2023 Q1 2024 Martin Resource Management Corporation 6.115 NA 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% % of Holdings Traded Ruben S. Martin III 3.886 NA 0.002 1.321 0.794 0.358 0.101 0.001 0.135 0.001 0.002 0.463 0.241 0.002 3.423 0.4% 284.7% 44.5% 13.9% 3.5% 0.0% 4.5% 0.0% 0.1% 14.6% 6.6% 0.0% 740.9% % of Holdings Traded Invesco Ltd. 7.213 25.6% 0.000 (1.000) 0.000 0.000 0.000 0.000 0.000 0.000 0.000 (0.004) 0.000 0.000 (1.004) 0.0% (12.2%) 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% (0.1%) 0.0% 0.0% (12.2%) % of Holdings Traded Goldman Sachs Group 1.751 6.2% 0.000 0.000 (0.000) 0.002 (0.002) 0.000 0.936 0.491 0.092 (0.212) 0.066 (0.062) 1.311 0.0% 0.0% (0.0%) 0.5% (0.5%) 0.0% 212.6% 35.7% 4.9% (10.8%) 3.8% (3.4%) 297.9% % of Holdings Traded Barclays PLC 1.500 5.3% 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 0.000 % of Holdings Traded 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% Harvest Fund Advisors LLC 1.068 3.8% 0.910 0.571 (0.020) 0.022 (0.066) 0.071 (0.022) (0.018) (0.003) (0.497) (0.143) (0.145) 0.661 % of Holdings Traded 223.6% 43.4% (1.0%) 1.2% (3.5%) 3.9% (1.2%) (1.0%) (0.1%) (26.8%) (10.5%) (12.0%) 162.5% JPMorgan Chase & Co 0.707 2.5% (0.022) (0.056) (0.158) (0.030) 0.002 0.098 (0.207) (0.030) 0.008 0.055 0.183 (0.089) (0.247) % of Holdings Traded (2.3%) (6.0%) (18.0%) (4.2%) 0.4% 14.2% (26.3%) (5.2%) 1.4% 9.8% 29.9% (11.2%) (25.9%) Raymond James Financial Inc. 0.540 1.9% 0.011 0.001 0.081 0.325 0.027 0.122 (0.024) 0.030 0.014 0.019 (0.023) (0.044) 0.540 % of Holdings Traded New Position 6.6% NMF 351.9% 6.5% 27.5% (4.2%) 5.5% 2.5% 3.3% (3.8%) (7.6%) NMF VWAP During Quarter $2.58 $3.00 $2.96 $3.54 $4.63 $3.94 $3.13 $2.76 $2.37 $2.66 $2.47 $2.42 High Closing Unit Price During Quarter $3.28 $3.50 $3.52 $4.73 $5.74 $4.59 $3.70 $3.35 $2.95 $3.25 $2.68 $2.65 Low Closing Unit Price During Quarter $2.12 $2.60 $2.59 $2.87 $3.63 $3.24 $2.81 $2.46 $2.05 $2.04 $2.27 $2.08 Note: Invesco, which holds 26% of the public float, sold 1mm shares in early 2021 but has not sold a material amount of shares since that time. indicates insider unitholders. Sources: Capital IQ, Bloomberg and public filings as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 33

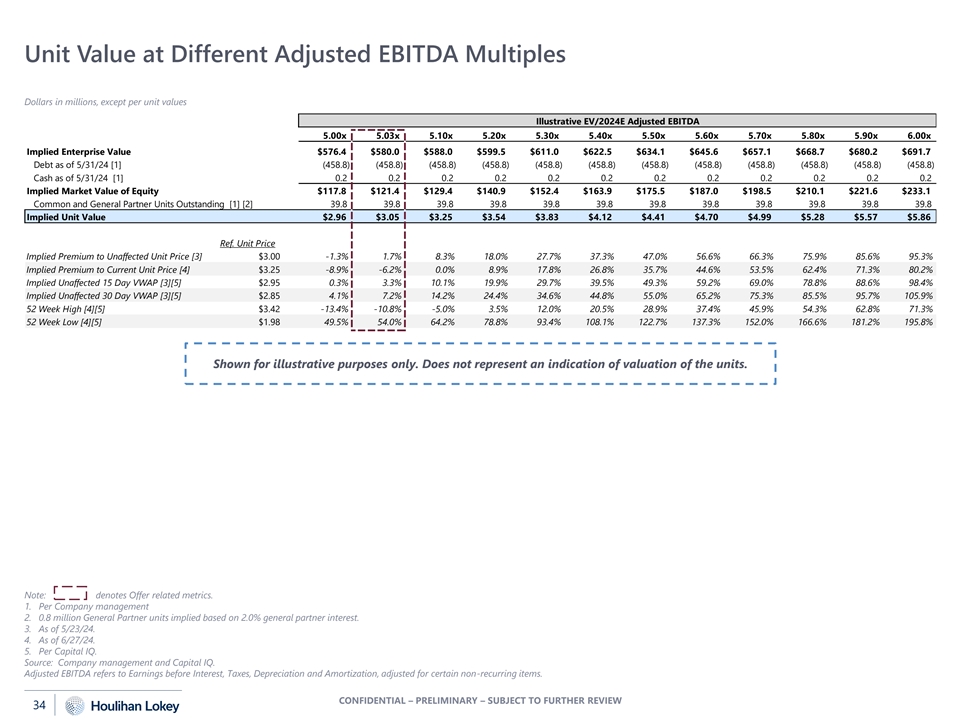

Unit Value at Different Adjusted EBITDA Multiples Dollars in millions, except per unit values Illustrative EV/2024E Adjusted EBITDA 5.00x 5.03x 5.10x 5.20x 5.30x 5.40x 5.50x 5.60x 5.70x 5.80x 5.90x 6.00x Implied Enterprise Value $576.4 $580.0 $588.0 $599.5 $611.0 $622.5 $634.1 $645.6 $657.1 $668.7 $680.2 $691.7 Debt as of 5/31/24 [1] (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) (458.8) Cash as of 5/31/24 [1] 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.2 Implied Market Value of Equity $117.8 $121.4 $129.4 $140.9 $152.4 $163.9 $175.5 $187.0 $198.5 $210.1 $221.6 $233.1 Common and General Partner Units Outstanding [1] [2] 39.8 39.8 39.8 39.8 39.8 39.8 39.8 39.8 39.8 39.8 39.8 39.8 Implied Unit Value $2.96 $3.05 $3.25 $3.54 $3.83 $4.12 $4.41 $4.70 $4.99 $5.28 $5.57 $5.86 Ref. Unit Price Implied Premium to Unaffected Unit Price [3] $3.00 -1.3% 1.7% 8.3% 18.0% 27.7% 37.3% 47.0% 56.6% 66.3% 75.9% 85.6% 95.3% Implied Premium to Current Unit Price [4] $3.25 -8.9% -6.2% 0.0% 8.9% 17.8% 26.8% 35.7% 44.6% 53.5% 62.4% 71.3% 80.2% Implied Unaffected 15 Day VWAP [3][5] $2.95 0.3% 3.3% 10.1% 19.9% 29.7% 39.5% 49.3% 59.2% 69.0% 78.8% 88.6% 98.4% Implied Unaffected 30 Day VWAP [3][5] $2.85 4.1% 7.2% 14.2% 24.4% 34.6% 44.8% 55.0% 65.2% 75.3% 85.5% 95.7% 105.9% 52 Week High [4][5] $3.42 -13.4% -10.8% -5.0% 3.5% 12.0% 20.5% 28.9% 37.4% 45.9% 54.3% 62.8% 71.3% 52 Week Low [4][5] $1.98 49.5% 54.0% 64.2% 78.8% 93.4% 108.1% 122.7% 137.3% 152.0% 166.6% 181.2% 195.8% Shown for illustrative purposes only. Does not represent an indication of valuation of the units. Note: denotes Offer related metrics. 1. Per Company management 2. 0.8 million General Partner units implied based on 2.0% general partner interest. 3. As of 5/23/24. 4. As of 6/27/24. 5. Per Capital IQ. Source: Company management and Capital IQ. Adjusted EBITDA refers to Earnings before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 34

APPENDIX Public Market Observations 05 04 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

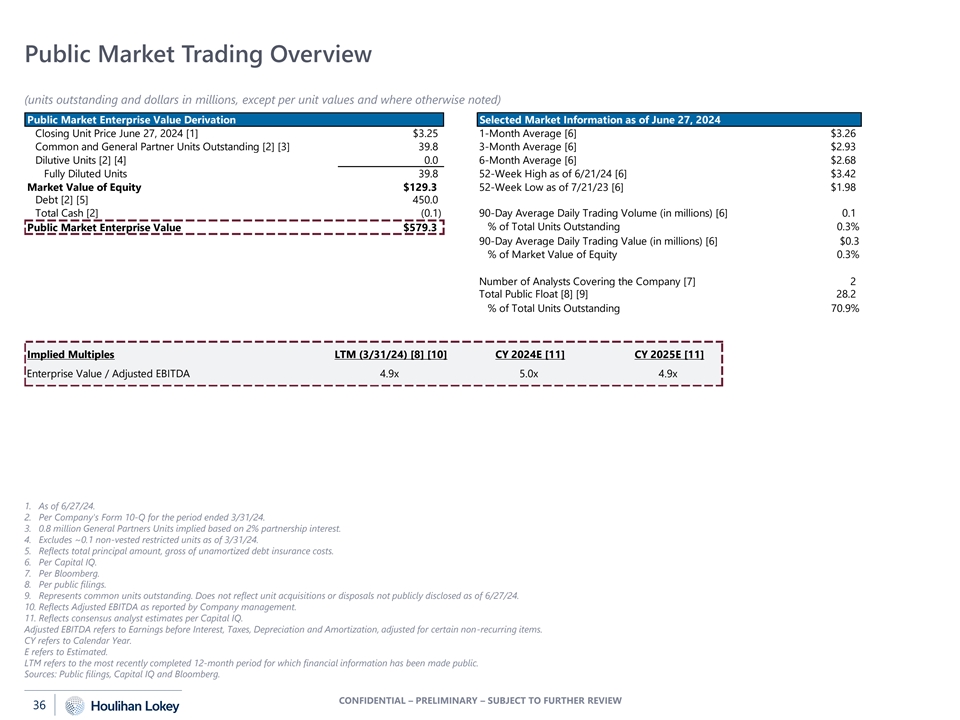

Public Market Trading Overview (units outstanding and dollars in millions, except per unit values and where otherwise noted) Public Market Enterprise Value Derivation Selected Market Information as of June 27, 2024 Closing Unit Price June 27, 2024 [1] $3.25 1-Month Average [6] $3.26 Common and General Partner Units Outstanding [2] [3] 39.8 3-Month Average [6] $2.93 Dilutive Units [2] [4] 0.0 6-Month Average [6] $2.68 Fully Diluted Units 39.8 52-Week High as of 6/21/24 [6] $3.42 Market Value of Equity $129.3 52-Week Low as of 7/21/23 [6] $1.98 Debt [2] [5] 450.0 Total Cash [2] (0.1) 90-Day Average Daily Trading Volume (in millions) [6] 0.1 % of Total Units Outstanding 0.3% Public Market Enterprise Value $579.3 90-Day Average Daily Trading Value (in millions) [6] $0.3 % of Market Value of Equity 0.3% Number of Analysts Covering the Company [7] 2 Total Public Float [8] [9] 28.2 % of Total Units Outstanding 70.9% Implied Multiples LTM (3/31/24) [8] [10] CY 2024E [11] CY 2025E [11] CY 2025E [11] Enterprise Value / Adjusted EBITDA 4.9x 5.0x 4.9x #VALUE! 1. As of 6/27/24. 2. Per Company's Form 10-Q for the period ended 3/31/24. 3. 0.8 million General Partners Units implied based on 2% partnership interest. 4. Excludes ~0.1 non-vested restricted units as of 3/31/24. 5. Reflects total principal amount, gross of unamortized debt insurance costs. 6. Per Capital IQ. 7. Per Bloomberg. 8. Per public filings. 9. Represents common units outstanding. Does not reflect unit acquisitions or disposals not publicly disclosed as of 6/27/24. 10. Reflects Adjusted EBITDA as reported by Company management. 11. Reflects consensus analyst estimates per Capital IQ. Adjusted EBITDA refers to Earnings before Interest, Taxes, Depreciation and Amortization, adjusted for certain non-recurring items. CY refers to Calendar Year. E refers to Estimated. LTM refers to the most recently completed 12-month period for which financial information has been made public. Sources: Public filings, Capital IQ and Bloomberg. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 36

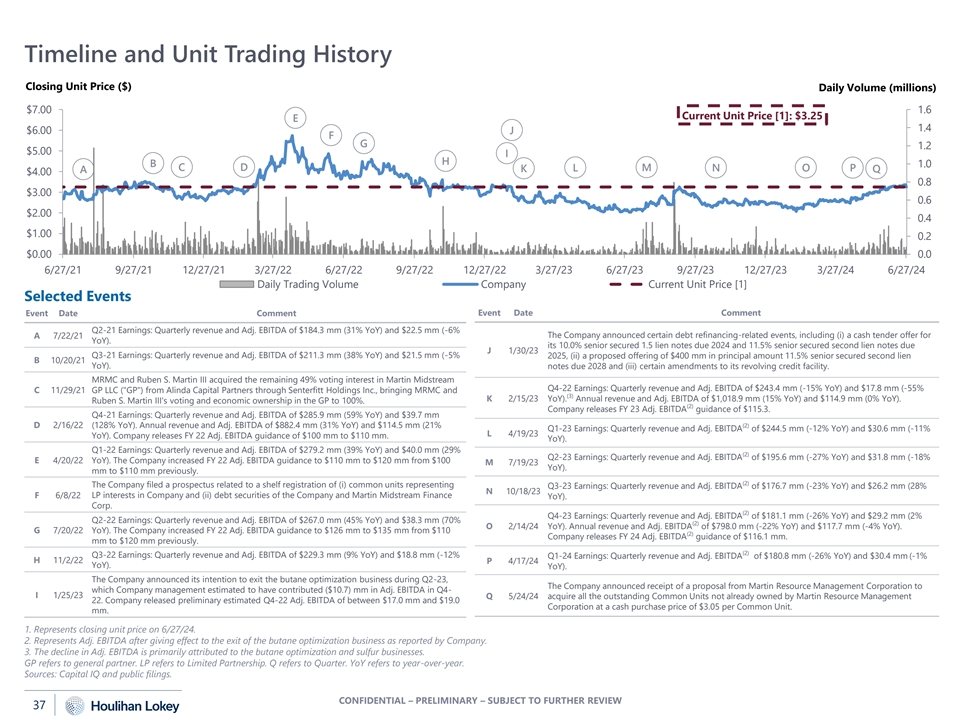

Timeline and Unit Trading History Closing Unit Price ($) Daily Volume (millions) $7.00 1.6 Current Unit Price [1]: $3.25 E 1.4 $6.00 J F G 1.2 $5.00 I H B 1.0 C D K L M N O P Q A $4.00 0.8 $3.00 0.6 $2.00 0.4 $1.00 0.2 $0.00 0.0 6/27/21 9/27/21 12/27/21 3/27/22 6/27/22 9/27/22 12/27/22 3/27/23 6/27/23 9/27/23 12/27/23 3/27/24 6/27/24 Daily Trading Volume Company Current Unit Price [1] Selected Events Event Date Comment Event Date Comment Q2-21 Earnings: Quarterly revenue and Adj. EBITDA of $184.3 mm (31% YoY) and $22.5 mm (-6% A 7/22/21 The Company announced certain debt refinancing-related events, including (i) a cash tender offer for YoY). its 10.0% senior secured 1.5 lien notes due 2024 and 11.5% senior secured second lien notes due J 1/30/23 Q3-21 Earnings: Quarterly revenue and Adj. EBITDA of $211.3 mm (38% YoY) and $21.5 mm (-5% 2025, (ii) a proposed offering of $400 mm in principal amount 11.5% senior secured second lien B 10/20/21 YoY). notes due 2028 and (iii) certain amendments to its revolving credit facility. MRMC and Ruben S. Martin III acquired the remaining 49% voting interest in Martin Midstream Q4-22 Earnings: Quarterly revenue and Adj. EBITDA of $243.4 mm (-15% YoY) and $17.8 mm (-55% C 11/29/21 GP LLC ( GP ) from Alinda Capital Partners through Senterfitt Holdings Inc., bringing MRMC and (3) K 2/15/23 YoY). Annual revenue and Adj. EBITDA of $1,018.9 mm (15% YoY) and $114.9 mm (0% YoY). Ruben S. Martin III's voting and economic ownership in the GP to 100%. (2) Company releases FY 23 Adj. EBITDA guidance of $115.3. Q4-21 Earnings: Quarterly revenue and Adj. EBITDA of $285.9 mm (59% YoY) and $39.7 mm D 2/16/22 (128% YoY). Annual revenue and Adj. EBITDA of $882.4 mm (31% YoY) and $114.5 mm (21% (2) Q1-23 Earnings: Quarterly revenue and Adj. EBITDA of $244.5 mm (-12% YoY) and $30.6 mm (-11% L 4/19/23 YoY). Company releases FY 22 Adj. EBITDA guidance of $100 mm to $110 mm. YoY). Q1-22 Earnings: Quarterly revenue and Adj. EBITDA of $279.2 mm (39% YoY) and $40.0 mm (29% (2) Q2-23 Earnings: Quarterly revenue and Adj. EBITDA of $195.6 mm (-27% YoY) and $31.8 mm (-18% E 4/20/22 YoY). The Company increased FY 22 Adj. EBITDA guidance to $110 mm to $120 mm from $100 M 7/19/23 YoY). mm to $110 mm previously. (2) The Company filed a prospectus related to a shelf registration of (i) common units representing Q3-23 Earnings: Quarterly revenue and Adj. EBITDA of $176.7 mm (-23% YoY) and $26.2 mm (28% N 10/18/23 F 6/8/22 LP interests in Company and (ii) debt securities of the Company and Martin Midstream Finance YoY). Corp. (2) Q4-23 Earnings: Quarterly revenue and Adj. EBITDA of $181.1 mm (-26% YoY) and $29.2 mm (2% Q2-22 Earnings: Quarterly revenue and Adj. EBITDA of $267.0 mm (45% YoY) and $38.3 mm (70% (2) O 2/14/24 YoY). Annual revenue and Adj. EBITDA of $798.0 mm (-22% YoY) and $117.7 mm (-4% YoY). G 7/20/22 YoY). The Company increased FY 22 Adj. EBITDA guidance to $126 mm to $135 mm from $110 (2) Company releases FY 24 Adj. EBITDA guidance of $116.1 mm. mm to $120 mm previously. (2) Q3-22 Earnings: Quarterly revenue and Adj. EBITDA of $229.3 mm (9% YoY) and $18.8 mm (-12% Q1-24 Earnings: Quarterly revenue and Adj. EBITDA of $180.8 mm (-26% YoY) and $30.4 mm (-1% H 11/2/22 P 4/17/24 YoY). YoY). The Company announced its intention to exit the butane optimization business during Q2-23, The Company announced receipt of a proposal from Martin Resource Management Corporation to which Company management estimated to have contributed ($10.7) mm in Adj. EBITDA in Q4- I 1/25/23 Q 5/24/24 acquire all the outstanding Common Units not already owned by Martin Resource Management 22. Company released preliminary estimated Q4-22 Adj. EBITDA of between $17.0 mm and $19.0 Corporation at a cash purchase price of $3.05 per Common Unit. mm. 1. Represents closing unit price on 6/27/24. 2. Represents Adj. EBITDA after giving effect to the exit of the butane optimization business as reported by Company. 3. The decline in Adj. EBITDA is primarily attributed to the butane optimization and sulfur businesses. GP refers to general partner. LP refers to Limited Partnership. Q refers to Quarter. YoY refers to year-over-year. Sources: Capital IQ and public filings. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 37

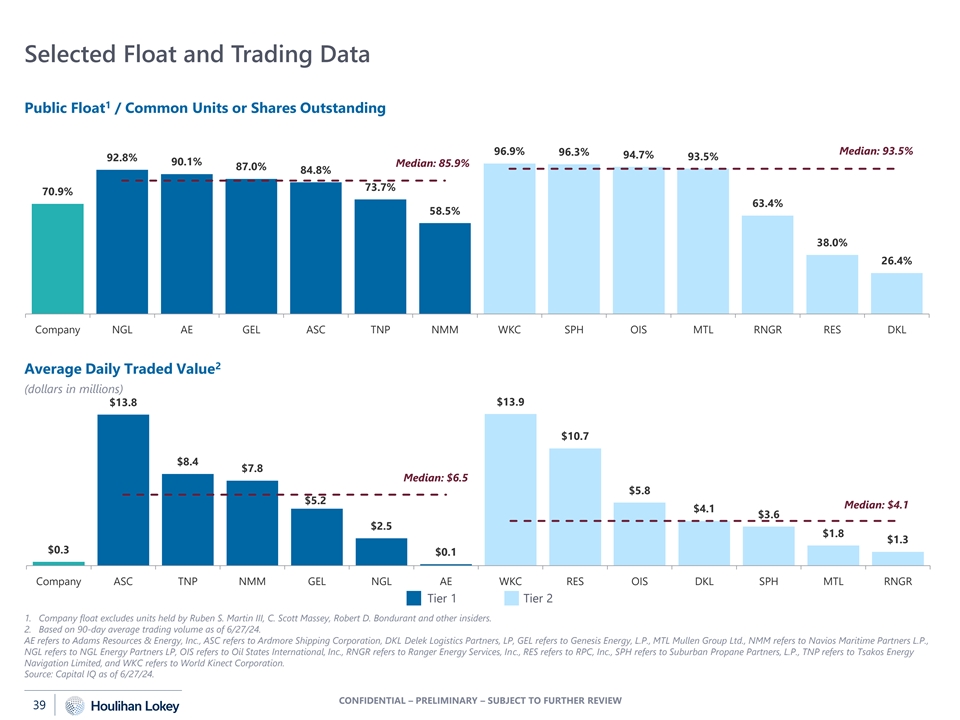

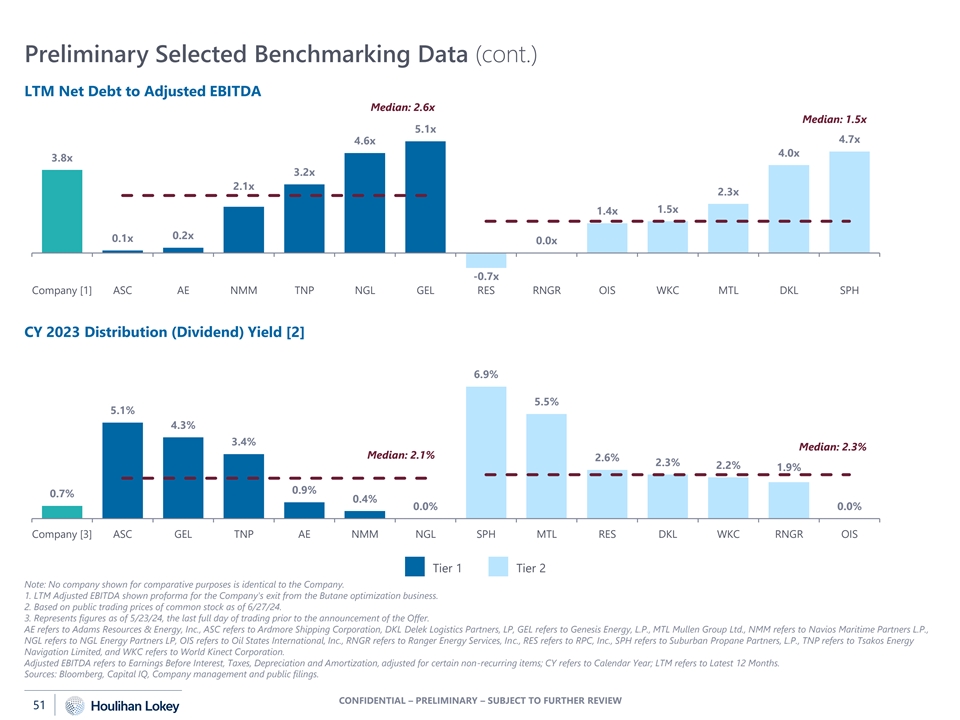

Selected Float and Trading Data 1 Average Daily Volume / Common Units or Shares Outstanding 2.5% 1.6% 1.0% 0.9% Median: 0.7% 0.7% 0.7% 0.6% Median: 0.5% 0.3% 0.3% 0.3% 0.2% 0.2% 0.2% 0.2% Company ASC TNP NMM GEL NGL AE OIS WKC RES RNGR SPH DKL MTL 1 2 Average Daily Volume / Public Float 2.7% 1.9% 1.8% 1.3% Median: 1.0% 1.0% 1.0% 1.0% 0.9% Median: 0.7% 0.4% 0.4% 0.3% 0.3% 0.2% 0.2% Company ASC TNP NMM GEL NGL AE OIS RES RNGR WKC DKL SPH MTL Tier 1 Tier 2 1. Based on 90-day average trading volume as of 6/27/24. 2. Company float excludes units held by Ruben S. Martin III, C. Scott Massey, Robert D. Bondurant and other insiders. AE refers to Adams Resources & Energy, Inc., ASC refers to Ardmore Shipping Corporation, DKL Delek Logistics Partners, LP, GEL refers to Genesis Energy, L.P., MTL Mullen Group Ltd., NMM refers to Navios Maritime Partners L.P., NGL refers to NGL Energy Partners LP, OIS refers to Oil States International, Inc., RNGR refers to Ranger Energy Services, Inc., RES refers to RPC, Inc., SPH refers to Suburban Propane Partners, L.P., TNP refers to Tsakos Energy Navigation Limited, and WKC refers to World Kinect Corporation. Source: Capital IQ as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 38

Selected Float and Trading Data 1 Public Float / Common Units or Shares Outstanding 96.9% Median: 93.5% 96.3% 94.7% 93.5% 92.8% 90.1% Median: 85.9% 87.0% 84.8% 73.7% 70.9% 63.4% 58.5% 38.0% 26.4% Company NGL AE GEL ASC TNP NMM WKC SPH OIS MTL RNGR RES DKL 2 Average Daily Traded Value (dollars in millions) $13.9 $13.8 $10.7 $8.4 $7.8 Median: $6.5 $5.8 $5.2 Median: $4.1 $4.1 $3.6 $2.5 $1.8 $1.3 $0.3 $0.1 Company ASC TNP NMM GEL NGL AE WKC RES OIS DKL SPH MTL RNGR Tier 1 Tier 2 1. Company float excludes units held by Ruben S. Martin III, C. Scott Massey, Robert D. Bondurant and other insiders. 2. Based on 90-day average trading volume as of 6/27/24. AE refers to Adams Resources & Energy, Inc., ASC refers to Ardmore Shipping Corporation, DKL Delek Logistics Partners, LP, GEL refers to Genesis Energy, L.P., MTL Mullen Group Ltd., NMM refers to Navios Maritime Partners L.P., NGL refers to NGL Energy Partners LP, OIS refers to Oil States International, Inc., RNGR refers to Ranger Energy Services, Inc., RES refers to RPC, Inc., SPH refers to Suburban Propane Partners, L.P., TNP refers to Tsakos Energy Navigation Limited, and WKC refers to World Kinect Corporation. Source: Capital IQ as of 6/27/24. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 39

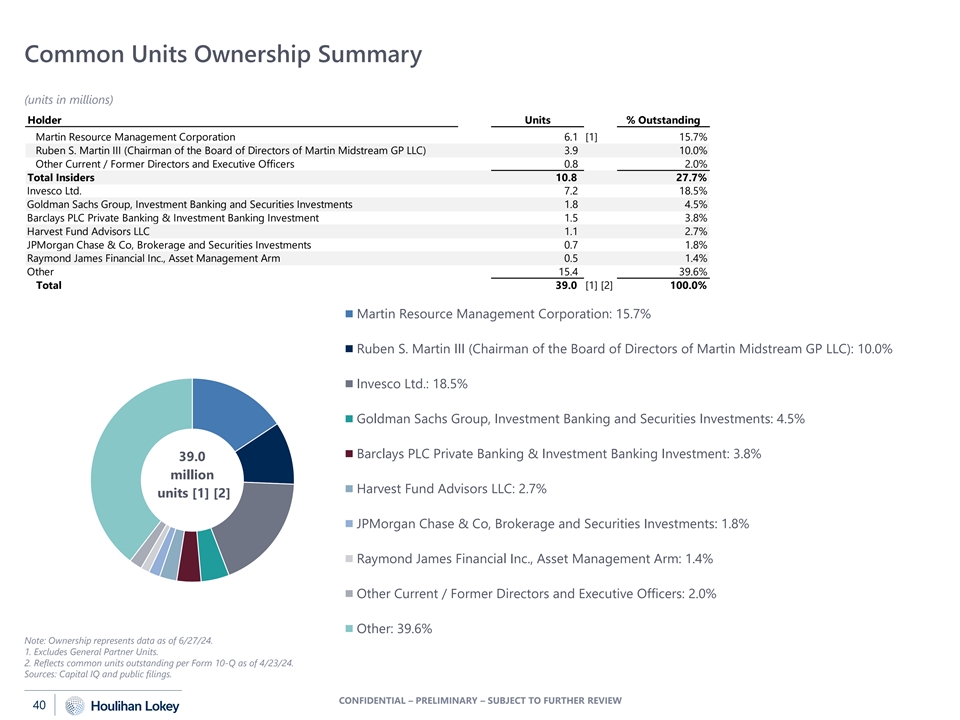

Common Units Ownership Summary (units in millions) Holder Units % Outstanding Martin Resource Management Corporation 6.1 [1] 15.7% Ruben S. Martin III (Chairman of the Board of Directors of Martin Midstream GP LLC) 3.9 10.0% Other Current / Former Directors and Executive Officers 0.8 2.0% Total Insiders 10.8 27.7% Invesco Ltd. 7.2 18.5% Goldman Sachs Group, Investment Banking and Securities Investments 1.8 4.5% Barclays PLC Private Banking & Investment Banking Investment 1.5 3.8% Harvest Fund Advisors LLC 1.1 2.7% JPMorgan Chase & Co, Brokerage and Securities Investments 0.7 1.8% Raymond James Financial Inc., Asset Management Arm 0.5 1.4% Other 15.4 39.6% Total 39.0 [1] [2] 100.0% Martin Resource Management Corporation: 15.7% Ruben S. Martin III (Chairman of the Board of Directors of Martin Midstream GP LLC): 10.0% Invesco Ltd.: 18.5% Goldman Sachs Group, Investment Banking and Securities Investments: 4.5% Barclays PLC Private Banking & Investment Banking Investment: 3.8% 39.0 million Harvest Fund Advisors LLC: 2.7% units [1] [2] JPMorgan Chase & Co, Brokerage and Securities Investments: 1.8% Raymond James Financial Inc., Asset Management Arm: 1.4% Other Current / Former Directors and Executive Officers: 2.0% Other: 39.6% Note: Ownership represents data as of 6/27/24. 1. Excludes General Partner Units. 2. Reflects common units outstanding per Form 10-Q as of 4/23/24. Sources: Capital IQ and public filings. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 40

Selected Wall Street Analyst Commentary (unit prices in actuals) Date of Report & Analyst Comments Recommendation “We suspect investors are jockeying for a boost to the initial offer of $3.05 per unit before the deal closes given the stock has closed above this price since the announcement.” 6/27/24 Sidoti & “Recently, MMLP incurred what we consider to be two minor environmental incidents. On May 15, multiple media sources reported that a barge owned by MMLP collided with the Pelican Island Bridge near Galveston, Company (Risk: Moderate/ $3.00) TX. Earlier this week, MMLP reported a crude oil pipeline spill of approximately 2,000 barrels near the Smackover refinery in Arkansas. While these issues are unfortunate, we do not see either, or both collectively, having a meaningful effect on MMLP.” “MMLP has historically traded at a discount to peers, given its capital structure, elevated leverage, and minimal growth; we believe the offer reflects that discount. In our view, the parent company is the natural acquirer and we do not foresee a competing offer from another company, considering the nature of 5/28/24 Sidoti & MMLP’s business and assets.” Company (Risk: Moderate/ $3.00) “MMLP units are up 14% in the last month and 30% year-to-date. In our view, the strong performance likely reflects balance sheet improvement and potential for additional shareholder returns, as did our prior price target.” “Given MRMC is the logical buyer, we would not anticipate any other bidders to come into play and would not expect a material change to the buyout offer. That said, given MMLP's investment in the DSM Semichem JV 5/24/24 Stifel and longer-term prospects associated with the JV, we believe this could drive incremental value for MMLP (Hold / $3.00) unitholders. Overall, given MMLP's core assets were not mainstream midstream assets, and it was a micro-cap company, we believe the assets fit best in private hands.” “Our $4 price target is based on 4x our revised 2025 FCF per share estimate of $0.90 (from $0.92). MMLP 4/22/24 Sidoti & shares trade at a discount to other small-cap energy companies. We contend the valuation gap fails to Company (Risk: Moderate/ $4.00) reflect the repositioning of the company.” “MMLP… not[ed] upside potential for additional customers to utilize the ELSA produced by the JV. [While] potential upside does exist due to the reshoring trend and chip production expansion in the US, we view it as a longer-term opportunity. At this time, we are maintaining our Hold rating and our $3.00 target 4/18/24 Stifel price.” (Hold / $3.00) “MMLP is trading at 4.8x EV/LP EBITDA. Our 5.0x target multiple applied against our LP EBITDA estimate results in a $3.00 target price.” Source: Wall Street Research. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 41 Prior to Offer Subsequent to Offer

APPENDIX Weighted Average Cost of Capital 06 04 CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW

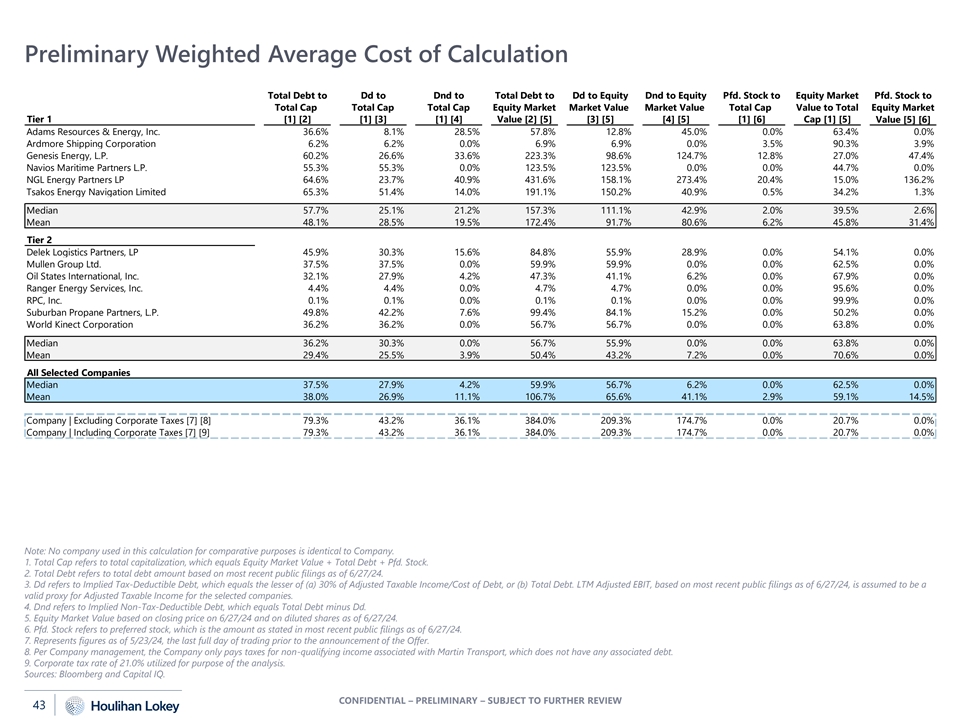

Preliminary Weighted Average Cost of Calculation Total Debt to Dd to Dnd to Total Debt to Dd to Equity Dnd to Equity Pfd. Stock to Equity Market Pfd. Stock to Total Cap Total Cap Total Cap Equity Market Market Value Market Value Total Cap Value to Total Equity Market Tier 1 [1] [2] [1] [3] [1] [4] Value [2] [5] [3] [5] [4] [5] [1] [6] Cap [1] [5] Value [5] [6] Adams Resources & Energy, Inc. 36.6% 8.1% 28.5% 57.8% 12.8% 45.0% 0.0% 63.4% 0.0% Ardmore Shipping Corporation 6.2% 6.2% 0.0% 6.9% 6.9% 0.0% 3.5% 90.3% 3.9% Genesis Energy, L.P. 60.2% 26.6% 33.6% 223.3% 98.6% 124.7% 12.8% 27.0% 47.4% Navios Maritime Partners L.P. 55.3% 55.3% 0.0% 123.5% 123.5% 0.0% 0.0% 44.7% 0.0% NGL Energy Partners LP 64.6% 23.7% 40.9% 431.6% 158.1% 273.4% 20.4% 15.0% 136.2% Tsakos Energy Navigation Limited 65.3% 51.4% 14.0% 191.1% 150.2% 40.9% 0.5% 34.2% 1.3% Median 57.7% 25.1% 21.2% 157.3% 111.1% 42.9% 2.0% 39.5% 2.6% Mean 48.1% 28.5% 19.5% 172.4% 91.7% 80.6% 6.2% 45.8% 31.4% Tier 2 Delek Logistics Partners, LP 45.9% 30.3% 15.6% 84.8% 55.9% 28.9% 0.0% 54.1% 0.0% Mullen Group Ltd. 37.5% 37.5% 0.0% 59.9% 59.9% 0.0% 0.0% 62.5% 0.0% Oil States International, Inc. 32.1% 27.9% 4.2% 47.3% 41.1% 6.2% 0.0% 67.9% 0.0% Ranger Energy Services, Inc. 4.4% 4.4% 0.0% 4.7% 4.7% 0.0% 0.0% 95.6% 0.0% RPC, Inc. 0.1% 0.1% 0.0% 0.1% 0.1% 0.0% 0.0% 99.9% 0.0% Suburban Propane Partners, L.P. 49.8% 42.2% 7.6% 99.4% 84.1% 15.2% 0.0% 50.2% 0.0% World Kinect Corporation 36.2% 36.2% 0.0% 56.7% 56.7% 0.0% 0.0% 63.8% 0.0% Median 36.2% 30.3% 0.0% 56.7% 55.9% 0.0% 0.0% 63.8% 0.0% Mean 29.4% 25.5% 3.9% 50.4% 43.2% 7.2% 0.0% 70.6% 0.0% All Selected Companies Median 37.5% 27.9% 4.2% 59.9% 56.7% 6.2% 0.0% 62.5% 0.0% Mean 38.0% 26.9% 11.1% 106.7% 65.6% 41.1% 2.9% 59.1% 14.5% Company | Excluding Corporate Taxes [7] [8] 79.3% 43.2% 36.1% 384.0% 209.3% 174.7% 0.0% 20.7% 0.0% Company | Including Corporate Taxes [7] [9] 79.3% 43.2% 36.1% 384.0% 209.3% 174.7% 0.0% 20.7% 0.0% Note: No company used in this calculation for comparative purposes is identical to Company. 1. Total Cap refers to total capitalization, which equals Equity Market Value + Total Debt + Pfd. Stock. 2. Total Debt refers to total debt amount based on most recent public filings as of 6/27/24. 3. Dd refers to Implied Tax-Deductible Debt, which equals the lesser of (a) 30% of Adjusted Taxable Income/Cost of Debt, or (b) Total Debt. LTM Adjusted EBIT, based on most recent public filings as of 6/27/24, is assumed to be a valid proxy for Adjusted Taxable Income for the selected companies. 4. Dnd refers to Implied Non-Tax-Deductible Debt, which equals Total Debt minus Dd. 5. Equity Market Value based on closing price on 6/27/24 and on diluted shares as of 6/27/24. 6. Pfd. Stock refers to preferred stock, which is the amount as stated in most recent public filings as of 6/27/24. 7. Represents figures as of 5/23/24, the last full day of trading prior to the announcement of the Offer. 8. Per Company management, the Company only pays taxes for non-qualifying income associated with Martin Transport, which does not have any associated debt. 9. Corporate tax rate of 21.0% utilized for purpose of the analysis. Sources: Bloomberg and Capital IQ. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 43

Preliminary Weighted Average Cost of Calculation (cont.) Levered Unlevered Equity Risk Size Cost of Cost of Cost of Pfd. Tier 1 Beta [1] Beta [2] Premium [3] Premium [4] Equity [5] Debt [6] Stock [7] WACC Adams Resources & Energy, Inc. 0.88 0.57 5.75% 4.70% 14.3% 6.5% NA 11.4% Ardmore Shipping Corporation 0.84 0.76 5.75% 1.14% 10.5% 8.4% 8.5% 10.3% Genesis Energy, L.P. 1.38 0.37 5.75% 1.39% 13.8% 7.4% [8] 11.2% 9.6% Navios Maritime Partners L.P. 1.34 0.60 5.75% 1.39% 13.6% 7.1% NA 10.0% NGL Energy Partners LP 1.02 0.15 5.75% 1.14% 11.6% 8.6% 10.2% 9.4% Tsakos Energy Navigation Limited 1.09 0.37 5.75% 1.14% 12.0% 6.7% 9.4% 8.5% Median 1.06 0.47 12.8% 7.2% 9.8% 9.8% Mean 1.09 0.47 12.6% 7.4% 9.8% 9.9% Tier 2 8.2% [8] Delek Logistics Partners, LP 0.97 0.53 5.75% 1.21% 11.3% NA 9.9% Mullen Group Ltd. 1.01 0.70 5.75% 1.14% 11.5% 3.9% NA 8.6% Oil States International, Inc. 1.64 1.11 5.75% 1.99% 15.9% 5.6% NA 12.6% Ranger Energy Services, Inc. 0.50 0.49 5.75% 1.99% 9.4% 6.1% NA 9.3% RPC, Inc. 0.74 0.74 5.75% 1.39% 10.2% 8.4% NA 10.2% Suburban Propane Partners, L.P. 0.79 0.40 5.75% 1.39% 10.5% 5.6% NA 8.1% World Kinect Corporation 0.87 0.60 5.75% 1.39% 10.9% 5.6% NA 9.0% Median 0.87 0.60 10.9% 5.6% NA 9.3% Mean 0.93 0.65 11.4% 6.2% NA 9.7% All Selected Companies Median 0.97 0.57 11.5% 6.7% 9.8% 9.6% Mean 1.01 0.57 12.0% 6.8% 9.8% 9.8% Company | Excluding Corporate Taxes [9] [10] 0.73 0.15 5.75% 4.70% 13.6% 8.4% [8] NA 9.5% Company | Including Corporate Taxes [9] [11] 0.73 0.17 5.75% 4.70% 13.6% 8.4% [8] NA 8.7% Note: No company used in this calculation for comparative purposes is identical to Company. 1. Based on actual levered beta per Bloomberg 5-year weekly as of 6/27/24. 2. Unlevered Beta = Levered Beta/(1 + ((1 – tax rate) * Dd to Equity Market Value) + (Dnd to Equity Market Value) + (Pfd. Stock to Equity Market Value)). 3. Based on review of studies measuring the historical returns between stocks and bonds, theoretical models such as supply-side and demand-side models and other materials. 4. Kroll Cost of Capital Navigator ( Navigator ). 5. Cost of Equity = Risk-Free Rate of Return + (Levered Beta * Equity Risk Premium) + Size Premium. Risk-Free Rate of Return as of 6/27/24, based on 20-year U.S. Treasury Bond Yield. 6. Based on selected company weighted average interest rate per most recent public filings as of 6/27/24. 7. Based on selected company weighted average preferred dividend per most recent public filings 6/27/24. 8. Cost of debt incorporated market based yield for certain securities. 9. Represents figures as of 5/23/24, the last full day of trading prior to the announcement of the Offer. 10. Per Company management, the Company only pays taxes for non-qualifying income associated with Martin Transport, which does not have any associated debt. 11. Corporate tax rate of 21.0% utilized for purpose of the analysis. NA refers to not available. Sources: Bloomberg and Capital IQ. CONFIDENTIAL – PRELIMINARY – SUBJECT TO FURTHER REVIEW 44