As filed with the Securities and Exchange Commission on July 9, 2008

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21210

Alpine Income Trust

(Exact name of registrant as specified in charter)

615 East Michigan Street

3rd Floor

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Samuel A. Lieber

Alpine Woods Capital Investors, LLC

2500 Westchester Avenue, Suite 215

Purchase, NY 10577

(Name and address of agent for service)

1-888-785-5578

Registrant's telephone number, including area code

Date of fiscal year end: 10/31/2008

Date of reporting period: 04/30/2008

Item 1. Report to Stockholders.

Semi-Annual Report

April 30, 2008

April Dynamic Balance Fund

April Dynamic Dividend Fund

Alpine Dynamic Financial Services Fund

Alpine Dynamic Innovators Fund

Alpine Dynamic Transformations Fund

Alpine Municipal Money Market Fund

Alpine Ultra Short Tax Optimized Income Fund

TABLE OF CONTENTS |

EQUITY MANAGER REPORTS |

|

|

4 |

| |

7 |

| |

13 |

| |

16 |

| |

19 |

| |

FIXED INCOME MANAGER REPORTS |

|

|

24 |

| |

26 |

| |

30 |

| |

49 |

| |

51 |

| |

53 |

| |

60 |

| |

68 |

| |

78 |

| |

|

|

|

|

|

|

|

|

| Alpine’s Investment Outlook |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dear Investor:

The financial crisis which began unfolding last year has moderated somewhat over the six months ending April 30, 2008. The turning point was the Federal Reserve intervention in JPMorgan’s absorption of Bear Stearns on March 17. However, in its place broad economic concerns have spread, exacerbated by rapid rises of the cost of food and fuel. The American Presidential election cycle is now well underway, which in our opinion contributes not only uncertainty over the direction of future economic policies, but also a greater probability that additional government sponsored initiatives to stabilize the economy will not be forthcoming for the balance of the calendar year. Inflation, deflation and stagflation are features of a marketplace where the trends are myriad and weak.

The credit crisis which had engulfed the markets since last July was not a result of subprime loans, although they proved to be the stick which broke the proverbial camel’s back. We believe the culprit was the methods employed by Wall Street to package and sell a broad array of investible financial assets in a securitized format. We feel that the rating agencies’ models were deficient and permitted investment banks to ‘game the system’ creating excessively high proportions of AAA rated securities. The resultant lack of credibility which has descended upon once venerated investment rating companies, such as S&P, Moody’s and Fitch, appears to have virtually immobilized not only investment banking but also many bond trading functions which are critical to corporate and municipal activity. Over time, ‘the Street’ will hopefully create a new regime in which investment cash flows are more transparent, the structures simpler, and the cost of capital somewhat higher. We feel the credit delivery system is broken. The net result is that a significant portion of financial liquidity has been removed from the marketplace for the foreseeable future. This withdrawal of liquidity, combined with forced deleveraging of many financial service companies and banks, has made mortgage and corporate debt more expensive. It appears it is having the greatest effect in the U.S. where complex

securitizations were a dominant feature of the capital markets and to a lesser degree in the U.K. and Australia.

Even though consumer confidence in the U.S. is approaching historic low levels not seen since 1981(!), economic data remains mixed. The cost of living has been dramatically impacted by rising food and fuel costs which are continuing to ripple throughout the global economy. Unemployment has remained reasonably stable in most countries until the month of May; however, it is a lagging indicator, which could be affected by a weakening business climate. While incomes have remained reasonably stable and the level of consumer expenditures has also shown surprising sustainability, we suspect that falling employment levels and inflating prices could seriously squeeze households in both the U.S. and U.K. The impact of potentially declining consumption could further exacerbate the outlook for retail sales, which in turn may exacerbate the outlook for jobs and ultimately economic growth.

The traditional home sales season this spring in the U.S. is amongst the worst in recent memory and new home sales are currently running at levels not seen since 1991. Even though builders have managed to control the size of their inventories of homes for sale, it appears it is having no impact on the rising backlog of existing homes on the market. It should be noted that the owners of many of these homes for sale will not sell below a certain price unless they are forced to do so, either as a result of relocation or personal financial pressures. Thus, the actual downward pressure on home prices comes primarily from homes which have been foreclosed upon and are currently vacant, as opposed to new homes coming on to the market or existing homes where the owner/occupier seeks to relocate or buy another home.

Despite the negative economic backdrop, corporate earnings during the first quarter showed solid growth with the exception of the financial services sector. While the government’s economic stimulus program providing $100 billion worth of rebates will come through during

1

|

|

the second and third quarters, perhaps less than 40% of these funds will be reinserted into the economy, as many recipients either save or pay down previously established debt. Similarly, the continued benefit from low interest rates should start to benefit the economy now that risk premiums have improved and moderated somewhat. That said, credit conditions are somewhat tighter with loan to value ratios and debt coverage ratios returning to historic levels. On the other hand, government sponsored entities such as Fannie Mae and Freddie Mac have been permitted to raise the size of mortgages they can make, perhaps up to $625,000, so the trend of conforming fixed rate mortgages, once again the most established form of consumer debt, should continue.

While the Federal Reserve has done much to ameliorate the credit crisis, preventing a potential banking crisis and providing considerable liquidity for the credit markets, the Fed may not have many alternatives without effective government leadership. The global implications of a potential protracted downturn in the U.S. would have been far reaching 10 years ago. Today, however, the breadth of the global economy has created a more diverse array of users and producers of goods and services. While the U.S. represents roughly 4.6% of the world’s population, we still constitute 24% of Gross Domestic Product (GDP). Europe is virtually identical in both population and GDP contribution, thus, the balance of 53% of global GDP is produced by 91% of the population. As disproportionate as these comparative statistics are today, they are in fact less so than a decade ago. This reflects significant economic growth which has underpinned the so called “BRIC” countries (Brazil, Russia, India, China), in which 11% of global GDP is produced by 42% of the world’s population. As demographic drivers of demand such as population growth, expanding middle classes, increased mobility and leisure travel continue to expand, so does the rate of domestic consumption. These countries are no longer models of how cheap labor fuels an export

machine. Rather, they are continuing the transition from agrarian self-sufficiency to urban production which has entered a phase where enhanced productivity, sophistication, and internal focus are becoming more important. In a similar fashion, government monetary authorities as well as capital markets have become more sophisticated and more effective in regulating economic activity. The net result is that these economies are beginning to decouple from the U.S., Europe and Japan, and thus are somewhat less dependent upon them for growth. This trend should continue at a pace that reflects the growth disparity between countries over the next generation. If one assumes that the BRIC countries continue to grow at 6% per annum while Europe and the U.S. grow at 2%, then the respective GDP contribution will equal in nineteen years!

Despite this rather sober outlook, it has been Alpine’s experience that the greatest opportunities are derived from challenging investment environments. We believe there are pockets of growth as well as compelling valuations throughout the global capital markets. There also exists considerable risk. Our managers must approach the portfolio as a continuum of future potential outcomes and prepare multiple strategies to best protect and exploit the broad range of these outcomes. We hope this semi-annual report is helpful for you in understanding recent events and the manner in which we adapt to the investment challenges of today, and seek opportunities for tomorrow. This is Alpine’s approach to managing not only your investment dollars, but our personal investments in the funds we run.

Thank you for your interest.

Sincerely,

Samuel A. Lieber

Mutual fund investing involves risk. Principal loss is possible.

The letter and those that follow represent the opinions of Alpine Funds management and are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security.

Please refer to the schedules of portfolio investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security.

2

EQUITY MANAGER REPORTS

Alpine Dynamic Balance Fund | |

Alpine Dynamic Dividend Fund | |

Alpine Dynamic Financial Services Fund | |

Alpine Dynamic Innovators Fund | |

Alpine Dynamic Transformations Fund |

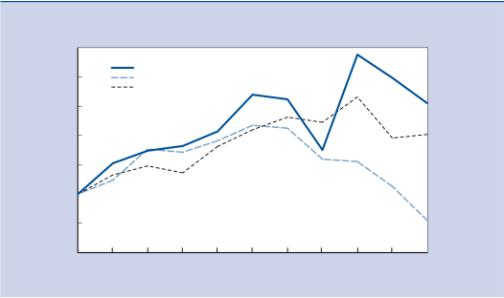

Value of a $10,000 Investment

$18,000

$17,000

$16,000

$15,000

$14,000

$13,000

$12,000

$11,000

$10,000

$9,000

$8,000

$7,000

Jun 7

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

01

01

02

02

03

03

04

04

05

05

06

06

07

07

08

$15,930

$12,256

Alpine Dynamic Balance Fund

S&P 500 Index

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Lipper Mixed-Asset Target Allocation Growth Funds Average is an average of Funds that, by portfolio practice, maintain a mix of between 60%–80% equity securities, with the remainder invested in bonds, cash, and cash equivalents. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500 Index and the Lipper Mixed-Asset Target Allocation Growth Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Balance Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Comparative Annualized Returns as of 4/30/08 | |||||||||||

|

| 6 Months (1) |

| 1 Year |

| 3 Years |

| 5 Years |

| Since Inception |

|

Alpine Dynamic Balance Fund |

| -5.44% |

| -7.04% |

| 4.56% |

| 9.27% |

| 6.98% |

|

S&P 500 Index |

| -9.64% |

| -4.68% |

| 8.23% |

| 10.62% |

| 2.99% |

|

Lipper Mixed-Asset Target Allocation Growth Funds Average |

| -6.80% |

| -1.63% |

| 7.68% |

| 9.18% |

| 4.06% |

|

Lipper Mixed-Asset Target Allocation Growth Fund Ranking |

| N/A |

| 629/669 |

| 513/555 |

| 185/425 |

| 22/324 |

|

(1) Not annualized. FINRA does not recognize rankings for less than one year.

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”), there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO allocations in the future.

4

Alpine Dynamic Balance Fund |

|

Portfolio Distributions* (Unaudited)

Financial/Banks 25.4% Information Technology 0.3% Cash & Cash Equivalents 0.8% Consumer Staples 2.5% Health Care 3.2% Energy 3.8% Utilities 4.7% Materials 10.3% Industrials 12.4% Consumer Discretionary 12.1% U.S. Gov't Obligations 24.4% Purchased Options 0.4% |

| Top 10 Holdings* (Unaudited) | |||||

| 1. |

| U.S. Treasury Bond, 5.250%, 11/15/2028 | 11.10% |

| ||

2. |

| U.S. Treasury Bond, 6.000%, 2/15/2026 | 7.47% |

| |||

3. |

| CONSOL Energy, Inc. | 5.53% |

| |||

4. |

| Allegheny Energy, Inc. | 3.47% |

| |||

5. |

| U.S. Treasury Bond, 6.250%, 8/15/2023 | 3.04% |

| |||

6. |

| Boston Properties, Inc. | 2.95% |

| |||

7. |

| Simon Property Group, Inc. | 2.74% |

| |||

8. |

| U.S. Treasury Note, 5.000%, 8/15/2011 | 2.73% |

| |||

9. |

| Eagle Materials, Inc. | 2.72% |

| |||

| 10. |

| Fannie Mae | 2.55% |

| ||

| ______________ * Portfolio holdings and sector distributions are as of 4/30/08 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. | ||||||

Commentary

Dear Investor:

The Alpine Dynamic Balance Fund had a -5.44% total return in the first half of fiscal year 2008, ending April 30th. This compares with -9.64% for the Standard & Poor’s 500 Index and -6.80% for the Lipper Mixed-Asset Target Allocation Growth Funds Average. The portfolio composition adhered to its basic balance, with 24% of assets in United States Treasury obligations and 1% in cash equivalent obligations. The equity portfolio reflected the extremely mixed trends of the stock market during this period of shifting valuations. We believe that the balanced approach of this Fund should enable us to provide both capital protection and growth opportunities.

The mixed market trends are strikingly clear when comparing the portfolio performance of the top five holdings in terms of gain during this period, with those of the bottom five. The following were the top five holdings performance: Mosaic Company +75.5%, Hess Corp. +48.6%, CONSOL Energy +43.7%, Southside Bancshares +15.9%, Diamond Offshore Drilling +13.3%.

Three of these holdings are energy related; Hess, a diversified oil producer and refiner, CONSOL Energy, a coal and natural gas producer and Diamond Offshore Drilling, an oil and gas well drilling company. Mosaic is a fertilizer company, benefiting by the rising demand for agricultural products. Southside Bancshares is a banking holding company located in eastern Texas.

The extraordinary negative volatility was shown by two homebuilders, Lennar Corp. and Standard Pacific Corp., and three companies in the financial or mortgage servicing business, Ambac Financial, MBIA Inc. and IndyMac Bancorp. Their average decline was over 70%.

The largest holding among the foregoing is CONSOL Energy, originally purchased in 2004 at a cost of $745,000 and valued at $4,371,840 on April 30 (at this writing, on June 16, 2008, the value is $5.76 million). The largest loss was in IndyMac Bancorp, purchased in 2006 and 2007 at a cost of $1,139,000 and valued at $78,975 on April 30th.

Large segments of the portfolio showed consistent earnings, dividends, and price improvement, as illustrated in our real estate investment trusts (10.1% of the portfolio), and commercial products and services (14.7%). Both are sectors based on comparatively long-term strategies, expected to yield significant growth and income from an undervalued base. There were sizeable appreciations since purchase of a number of these holdings; Boston Properties, up 76.6%, Simon Property Group, up 48%, Developers Diversified Realty, up 43.8%. In the commercial and industrial side, AMETEK Inc. has gained 63.8% since purchase, Honeywell International, 26.6%, and Autoliv Inc., 22.9%.

Financial services and banking holdings clearly produced mixed results. Notwithstanding the volatility in the financial industry, our two largest holdings in the field, JPMorgan Chase and Goldman Sachs, both produced modest positive returns in this period.

The portfolio was actively managed, yielding long-term gains of $2,321,000, and short-term gains of $757,000.

In equities we sought to take advantage of favorable short-term price swings both on the sell-side and on the buy-side. The largest single gains, in excess of $700,000 each, were recorded in the sale of shares of Simon Property Group and Union Pacific Corp. Pared back

5

Alpine Dynamic Balance Fund |

|

positions included Allegheny Energy, yielding gains of $485,000, and Goldman Sachs, yielding gains of $296,000, as well as in Chevron Corp. yielding $277,000. Larger shorter-term gains were from reduction of our position in Lennar Corp., resulting in a gain of $250,000 and elimination of Redecard S.A., with a gain of $172,000. Portfolio sector composition largely remained constant, although in November substantial profits were taken in long-term U.S. Treasury bonds due in 2028 and 2026, with monies subsequently reinvested.

We undoubtedly exhibited too much patience with financial institutions impacted by the mortgage crisis. In some situations, where we saw opportunities for what we perceived were long-term undervaluation, we experienced major falls. To this point there have been few signs of recovery in this segment of the financial markets. We have anticipated a quicker and greater response from Congressional and Administration legislation to alleviate challenges to both mortgage borrowers and lenders. These have not yet developed in any significant way. Based on historical parallels of the early 1990’s, and going back into the 1930’s, it should be possible to have Federal programs of meaningful assistance to both challenged borrowers and lenders. In our opinion, the forthcoming federal and congressional elections have surely been an excuse for inaction.

New portfolio commitments focused on companies we believed were undervalued due to inadequate recognition of their sustainable earning power even in a slowed economy. Examples include McGraw Hill Companies, whose shares we feel were sharply devalued as a result of market concerns over their ownership of Standard & Poor’s Corporation, a prominent bond rating agency. Another example of what we believe was temporary undervaluation was in the shares of PACCAR Inc., the largest manufacturer of heavy trucks. This company suffered a decline in its share price due to a change in regulation on diesel motors which accelerated purchases into late 2007 and presumably reduced demand for 2008.

The market apprehensions in our view did not adequately take account of the company’s strong international position, particularly manufacturing in Europe. Pediatrix Inc. was another acquisition where we believe the market had yet to recognize major new growth opportunities. The company, which had built a strong position in neonatal treatment facilities through a series of acquisitions, had entered the field of anesthesiology, a growth opportunity similar to its historical achievement. Darden Restaurants, Inc. experienced an adverse quarter of sales and we thought the market had reacted too negatively to the company just as it was about to enter a period of significant new growth.

Looking ahead, we recognize the challenges of a difficult phase of the overall economic environment. We are carefully taking advantage of cyclical trends, such as in the energy field where in fact our largest holding, CONSOL Energy, has been a long-term commitment with a 486% gain during the period of 2004 through April 30, 2008. We are also carefully taking advantage of a selection of temporary undervaluations caused by transient issues.

Our fixed income position remains the use of U.S. Treasury obligations because we think they provide the greatest clarity in participating in interest rate trends and flexibility for moving as they shift.

In closing we should note that we have enhanced income modestly through a selective use of option sales. This reflects our aim to maximize opportunity within the fundamentally conservative structure of this Fund.

We thank our investors for their sustained interest.

Sincerely,

Stephen A. Lieber

Samuel A. Lieber

Co-Portfolio Managers

This letter and those that follow represent the opinions of Alpine Funds management and are subject to change, are not guaranteed and should not be considered recommendations to buy or sell any security.

Please refer to the schedule of portfolio investments for fund holdings information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security.

Investing in this fund involves special risks, including but not limited to, options and futures transactions. Please refer to the prospectus for further details. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities.

Lipper Analytical Services, Inc. is an independent mutual fund research and rating service. Each Lipper average presents a universe of Funds with similar invest objectives. Rankings for the periods shown include dividends and distributions reinvested and do not reflect sales charges.

6

Value of a $10,000 Investment

$22,000

$21,000

Alpine Dynamic Dividend Fund

$20,000

S&P 500 Index

$19,000

$18,614

$14,747

Sep 22

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

Oct 31

Apr 30

03

03

04

04

05

05

06

06

07

07

08

$18,000

$17,000

$16,000

$15,000

$14,000

$13,000

$12,000

$11,000

$10,000

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Lipper Equity Income Funds Average is an average of funds that seek relatively high current income and income growth through investing 60% or more of their respective portfolios in equities. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500 Index and the Lipper Equity Income Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Comparative Annualized Returns as of 4/30/08 | |||||||||

| |||||||||

|

| 6 Months (1) |

| 1 Year |

| 3 Years |

| Since Inception |

|

Alpine Dynamic Dividend Fund |

| -13.67% |

| -10.26% |

| 9.75% |

| 14.44% |

|

S&P 500 Index |

| -9.64% |

| -4.68% |

| 8.23% |

| 8.80% |

|

Lipper Equity Income Funds Average |

| -8.82% |

| -5.54% |

| 8.20% |

| 10.29% |

|

Lipper Equity Income Fund Ranking |

| N/A |

| 237/275 |

| 50/217 |

| 8/172 |

|

(1) Not annualized. FINRA does not recognize rankings for less than one year.

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”), there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO allocations in the future.

7

Alpine Dynamic Dividend Fund |

|

|

|

| ||||

Portfolio Distributions* (Unaudited) |

| Top 10 Holdings* (Unaudited) | ||||

Industrials 21.0% Utilities 2.2% Telecommunication 10.1% Information Technology 1.3% Health Care 6.6% Consumer Staples 12.7% Materials 4.2% Energy 15.6% Financial - Banks 12.8% Consumer Discretionary 13.5% |

| 1. |

| Tele2 AB | 2.51% | |

2. |

| StatoilHydroASA | 2.48% | |||

3. |

| PepsiCo, Inc. | 2.14% | |||

4. |

| Genco Shipping & Trading Ltd | 2.04% | |||

5. |

| The Procter & Gamble Co. | 2.04% | |||

6. |

| Sampo Oyj | 2.01% | |||

7. |

| Diamond Offshore Drilling, Inc. | 2.01% | |||

8. |

| Regal Entertainment Group - Class A | 2.01% | |||

9. |

| Ship Finance International, Ltd. | 2.00% | |||

| 10. |

| Raytheon Co. | 1.99% | ||

| ______________ * Portfolio holdings and sector distributions areas of4/30/08 and are subject to change.Portfolio holdings are not recommendationsto buy or sell any securities. PortfolioDistributions and Top 10 Holdings do notinclude short-term investments. PortfolioDistributions percentages are based on totalinvestments and Top 10 Holdings percentagesare based on total net assets. | |||||

Commentary |

|

Dear Investor:

The Alpine Dynamic Dividend Fund (ADVDX) completed a difficult first half fiscal 2008 by achieving its objective of optimizing its tax-qualified dividend income distribution, but falling short of our objective of strong capital appreciation and total return. However, historically ADVDX has outperformed the major averages and equity income peer group and it is our goal to again provide this outperformance for our investors.

ADVDX declined by 13.67% including dividend reinvestments for the six months ended April 30, 2008 versus a 9.64% decline for the S&P 500 Stock Index and an 8.82% decline for the Lipper Equity Income Funds average for the same time period. Since inception on September 22, 2003, ADVDX has produced an annualized return of 14.44%, which compares favorably to a return of 8.80% for the S&P 500 Index and a 10.29% annualized return for the Lipper Equity Income Funds average. ADVDX ranks #8 based on total return out of 172 funds in the equity income category according to Lipper since inception on 9/22/03 through 4/30/08.

The global equity markets have been roiled over the past six months by a severe credit crisis that was spurred by the collapse of the U.S. residential housing market. While ADVDX did not have any direct exposure to the subprime mortgage industry that was the genesis of the credit problems, we did have investments in diversified global financial institutions and other non-financial businesses that relied on open credit markets to support growth and acquisitions. It is these businesses that have taken a substantial hit to their equity values, and we have been reducing our investments in these areas. This is illustrated in the decline in our financial sector exposure in ADVDX from 16.9% on 10/31/07 to 12.8% on 4/30/08.

Global equity markets have also been hit by a surge in commodity and energy costs which have negatively impacted corporate margins and have raised fears of global inflation, higher interest rates, and subsequently a slowdown in economic activity. We continue to be bullish on commodity and energy stocks based on supply constraints and increasing worldwide demand and have added to our positions in the equities in these sectors. However, ADVDX was hit by a sell off in the global industrial stocks on the fears of an impending economic slowdown. We have steadily repositioned the portfolio to where we believe are the best opportunities, and right now that is more toward hard assets versus financial assets. For example, we have taken our energy sector exposure up from 11.7% on 10/31/07 to 15.6% on 4/30/08. We have also added to our more defensive positions in consumer staples and telecom while decreasing our exp osure to consumer discretionary.

Also impacting the performance of ADVDX relative to the S&P 500 and our equity income peers has been our relatively large exposure to overseas markets, which have significantly underperformed the U.S. over the past six months. In addition to our multi-strategy and multi-cap approach, we also invest approximately 30-40% of our assets in international equities where we have found what we feel are attractive growth opportunities and larger dividend payouts than we see in the U.S. We do not actively manage our country weightings – we pick our holdings on a stock by stock basis based on dividend potential and total return. This bottoms up approach had taken a large portion of our international holdings to the Euro region which has been particularly hard hit as interest rates remain much higher there than in the US.

8

Alpine Dynamic Dividend Fund |

|

ADVDX is currently invested in equities based in 15 different countries, the majority of which would be considered mature countries. However we do have a small exposure to some emerging market economies and we continue to look for interesting dividend and capital appreciation opportunities in countries like Brazil, Mexico, and Russia. Following the United States, our current top countries are Sweden, Norway, Finland, Italy, and France. The average dividend yield for the major indices in these five countries is currently 4.63% which is more than double the yield on the S&P 500 Index of 2.27%.

The US has been one of the best performing major equity markets over the past six months largely due to the aggressive rate cuts by our Fed versus the European countries facing raising rates and the concern that a US slowdown will drag down Europe. For example, the Dow Jones STOXX Index, which is a broad representation of 600 companies in the European region, has declined by 27.61% from its high in mid-July 2007 through its low on March 17, 2008 versus a 20.25% decline for the S&P 500 Index from its high in mid-October 2007 through its low on 3/17/08.

We meet and talk with European management teams and analysts on a regular basis and the message continues to be that certain sectors of the economy like infrastructure and emerging consumer are strong, with many of our companies benefiting from growth in Asia and emerging markets. However, we are continuously doing our homework and we have lightened up on our European positions where we see increasing earnings risk from a potentially slowing global economy. In many cases, we believe that the market has oversold some great companies and we will ride out the near term turbulence and take a long term view for our investors.

ADVDX provides a strong dividend yield with a high level of qualified dividend income for investors

For the six months ended April 30, 2008, ADVDX paid $0.86 in dividend income, with nearly all of the distribution estimated to be qualified for the maximum taxable rate of 15%. For the twelve-months ended April 30, 2008 the Fund paid a total of $1.641 in dividend income. Based on a closing NAV price of $10.66 on 4/30/08, the $0.86 dividend payout represents a trailing six-month dividend yield of 8.08% for the Fund. This high level of dividend income is unique among equity oriented funds.

As of April 30, 2008 ADVDX paid a regular monthly minimum dividend of $0.07 per share. In addition, in the third month of each quarter the Fund has distributed excess dividend income that had been earned and accumulated during the quarter.

Our unique investment approach combines three sub-strategies: Dividend Capture, Value, and Growth

ADVDX combines three research-driven investment strategies – Dividend Capture, Value, and Growth – to maximize the amount of distributed dividend income that is qualified for reduced Federal income tax rates and to identify companies with the potential for dividend increases and capital appreciation. The Fund also offers some global diversification since a portion of the portfolio is invested in international dividend-paying equities. We scan the globe looking for what we feel are the best dividend opportunities for our investors, employing a multi-cap, multi-sector, and multi-style investment approach.

Our “Dividend Capture Strategy” enhances the qualified dividend income generated by the Fund

We run a portion of our portfolio with a dividend capture strategy, where we invest in typically high dividend yielding stocks or in special situations where large cash balances are being returned to shareholders as one-time special dividends. We seek to enhance the dividend return of this portfolio by electively rotating a portion of our high yielding holdings after the 61-day ownership period required to obtain the maximum 15% dividend tax rate.

Another facet of our dividend capture strategy is our search for core, long term holdings in companies that historically have generated consistent strong free cash flow and regular large dividend distributions, usually above 5%. Two of our largest holdings, Regal Entertainment with a 7.3% current yield and Ship Finance with a 7.8% dividend yield, are examples of this strategy.

Regal (RGC) is the largest theater owner in the U.S., generating 20% of total U.S. box office revenue. It is currently enjoying a rebound in theater attendance based on what has been perceived as higher quality movie selections. We expect the large-scale rollout of enhanced 3-D technology to theaters beginning in 2009 to act as a catalyst for an additional increase in movie attendance and an enhanced margin opportunity for Regal as 3-D movies command premium ticket prices.

Ship Finance (SFL) is one of the world’s largest ship owners with assets including crude oil tankers, dry bulk carriers, containerships, offshore supply vessels, and drilling rigs. The company’s fleet operates on long-term charters plus profit sharing agreements which has allowed SFL to benefit from strong growth in global shipping and commodity demand. In addition, the company returns most of its free cash flow to its investors with a current 7.8% dividend yield. SFL is continuing to expand its fleet of diversified assets which should support further earnings growth and dividend increases in the future.

9

Alpine Dynamic Dividend Fund |

|

Several of our top holdings as of April 30, 2008 were companies that announced special dividend payments associated with restructurings and/or excess cash, and we believe there is additional upside value to be realized following their dividend payments. Tele2 AB (TEL2B SS), based in Sweden, is an operator of mobile wireless networks throughout Europe with exposure to emerging market growth in Russia. The company has committed to returning excess cash to shareholders, with ADVDX receiving an annual and special dividend payment in May 2008 of 6.6%. And StatoilHydro ASA (STL NO), based in Norway, is well positioned as an integrated oil and gas company that operates drilling rigs in the North Sea, refineries in northern Europe, and retails gasoline in Scandinavia. We believe that Statoil offers attractive valuations relative to its future earnings outlook. In addition, the company provides an annual dividend yield of about 2.2% and also has returned excess cash to shareholders as special dividends in each of the past few years.

Our “Growth and Income Strategy” targets capital appreciation in addition to yield

Our second strategy identifies core growth and income stocks that may have slightly lower but still attractive current dividend yields and predictable earnings streams plus a catalyst for capital appreciation and dividend increases.

In our top 10 holdings, we would group Pepsi, Procter and Gamble, and Raytheon in this category. These companies are estimated to grow earnings annually by 10-15% over the next several years and each raised their dividends by 10-15% in 2008. We believe, in 2009, additional dividend increases may match earnings growth.

Two of our top growth and income holdings are considered more defensive consumer staple stocks with attractive earnings outlooks that are less tied to economic growth. PepsiCo (PEP) is a diversified beverage and snack company that is well positioned for double digit EPS growth through international expansion and the strength of its domestic portfolio of businesses. Pepsi has consistently increased its dividend and recently raised its annual payout by 13.3% to $1.70 per share, providing a current dividend yield of 2.6%. And Procter and Gamble (PG) is one of the world’s largest diversified consumer products company that is also benefiting from international expansion and strength in its core domestic brands. PG is also committed to dividend increases and recently raised its annual dividend by 14.3% to $1.60 per share.

Raytheon is an industry leader in aerospace, defense and government electronics. The company is benefiting from increasing worldwide demand for its systems such as missile defense, precision strike, radar, and intelligence gathering. Raytheon recently reported bookings up 23% year of year and a new record backlog. We believe the stock has been oversold based

on overblown concerns about cuts to future defense spending and we anticipate strong double digit earnings growth. Plus, the company recently increased its dividend payout by 10%.

Lastly, we would include Diamond Offshore Drilling (DO) as an attractive growth and income story in our top 10 holdings, growing earnings an estimated 20% in 2008 and 2009 and yielding a trailing twelve-month dividend yield of 3.15%. Diamond Offshore, based in Houston, Texas, is one of the largest operators of mid-deepwater rigs and it is seeing strong demand for its services as oil is getting harder to find and exploration is moving further out to sea. This is resulting in substantial increases on rates for its long term contracts and the expectation of possibly a doubling of earnings in the next two-three years. DO is generating significant free cash flows and has been returning it to shareholders as regular annual special dividends and has recently moved to quarterly special dividends of $1.25. We would expect the continuation of large cash returns in 2008 and 2009 as the company is committed to paying out about 80% of earnings as dividends.

Our “Value/Restructuring Strategy” looks for attractively valued or restructuring dividend payers

Our third major strategy is what we call “value with a catalyst or restructuring strategy”, where our internal research points to under-valued or mis-priced equity opportunities for companies with attractive dividend yields. We also look for turnaround situations or depressed earnings where we believe there is a catalyst for an earnings recovery or a restructuring or major corporate action that is expected to add value. The key characteristic for this strategy is low valuations relative to historical averages and above average dividend yields for a combined objective of capital appreciation and high qualified dividend income. We would categorize two of our top holdings in this strategy; Genco Shipping & Trading, and Sampo Oyj.

Genco Shipping & Trading (GNK) is one of the largest publicly traded dry bulk shipping companies that transports iron ore, coal, grain, steel products, and other minor dry bulk commodities along worldwide shipping routes. The company is benefiting from strong global demand for these commodities as well as increases in lengths of haul as the sourcing for many of the commodities are in countries that are far from the users. For example, China is now sourcing iron ore from Brazil which is double the length of haul from its traditional suppliers in Australia. In addition, Genco has been growing aggressively through acquisitions and is returning excess cash to shareholders with a current dividend yield of 6.3%, yet the company trades at very low multiples to future forward growth.

Sampo Oyj (SAMAS FH), based in Finland, is a comprehensive provider of insurance products in Scandinavia. Having exited its banking business at the

10

Alpine Dynamic Dividend Fund |

|

top of the market in 2007, they are looking to opportunistically deploy their excess capital and promote consolidation in the Scandinavian financial sector. The company is forecasted for solid 10% earnings growth and provides an attractive 7.2% annual dividend yield.

Outlook for 2008: We remain opportunistic and are focused on growth in NAV

The volatility over the past several months in global equity markets has provided challenges and opportunities. While our short term performance has been challenged, as fundamental investors we also see longer term opportunities. Particularly, within our value strategy, we are looking to take advantage of the recent declines in the equity markets to invest in still very strong companies with attractive dividend yields at more attractive valuations. While we do expect additional headline risks particularly in the financial sector for the remainder of 2008, we still believe that global economic growth will remain solid, albeit slower than in the previous several years, driven by demand from Asia and the emerging market economies. We continue to seek attractive global growth companies that are committed to returning cash to shareholders.

We continue to concentrate on global secular investment themes that we believe will outperform over the long term.

We remain bullish on global infrastructure and engineering companies as the rest of the world tries to catch up with the industrialized countries with regards to power plants, phones, roads, electricity, water treatment, sewage, and airports. In addition, the industrialized nations of the world have neglected their aging infrastructure and are now rebuilding and reinvesting. Some of the companies in our portfolio have been hit on concerns about rising capital costs and the need to finance these costly projects. However, while credit spreads have increased, the Fed’s actions to cut rates has offset some of this negative impact and our portfolio companies are confident in their ability to access capital markets. In addition, many of these projects are supported by governments that are long term in focus and less sensitive to short term economic swings. Some of our favorite stocks are the companies that may supply this growth for what we believe may be many years to come and at much higher prices than achieved in the past.

We also still like the long term secular story for the basic materials and energy sectors based also on constrained supply and growing global demand. For example, we like the long term secular outlook for deepwater drillers as oil is getting harder to find and exploration is moving further out to sea. We plan to continue to be nimble in these volatile yet potentially highly profitable sectors and we would look for attractive entry and exit points and we are aware of the impact of shorter term seasonal trading pattern. In addition, many of these

companies are producing record amounts of free cash flow and we expect continued increases in regular and special dividend payouts.

We also remain overweight in energy stocks as many of these companies have not reflected the recent spike in oil prices and we believe there will be upside earnings revisions. We also remain bullish on companies involved with corn, coal, and copper commodities.

We also participate in a variation on investing in commodity companies, and that is through increasing global trade. We look to participate in the increasing need for the movement of commodities globally through producers, financers, and operators in the shipping industry. Commodities such as oil, grain, iron ore, and coal are moving longer distances than ever and with higher volumes and frequencies. These companies tend to benefit from the overall growth in the world economies regardless of the price of the underlying commodity with many committed to returning cash as large dividends.

We also favor the industrial and machinery companies that are supplying global growth and are also benefiting from aerospace and defense spending. Our favorites are companies that have the majority of their revenue generated overseas and have booked strong backlogs with visibility on this revenue for several years out. However, we have recently lowered our overall exposure to the industrial sector as we look to take profits where we have had strong growth and where there may be a risk in earnings from a slowing global economy.

While the aging demographics of many of the industrialized countries may result in great long term growth opportunities in the healthcare sectors, we remain cautious on the large pharmaceutical companies where there are legislative and generic drug risks. We prefer to look for interesting opportunities in smaller cap niche healthcare which is being stimulated by demographic trends and advances in biotechnology and yet there is more limited generic risk.

While we remain positive on the outlook for sustainable global economic growth in 2008, we also believe that a slowing US economy and financial market turmoil makes it prudent to also have a meaningful exposure in the telecom, utilities and consumer staples sectors. These sectors tend to be large dividend payers and more defensive in nature. Within these groups, we continue to be selective and pick our holdings on a stock by stock basis where we see the best combination of earnings growth, valuation, and dividend opportunity.

At this time, we continue to remain cautious on the financial sector, as we believe there is still more write-downs on mortgage-related assets and downward earnings revisions. In addition, we believe the need to recapitalize balance sheets and the outlook for a reduction in high margin business opportunities will continue to dampen earnings outlooks beyond more

11

Alpine Dynamic Dividend Fund |

|

write-downs. Our strategy during the financial markets turmoil has been to add to the higher quality financial stocks on dips where we believe valuation have become very attractive. But overall we would not look to increase our weightings substantially until we believe that the downside risk is quantifiable and that the upside reward is meaningful.

Another sector that we remain cautious on at this time is consumer discretionary. General consumer spending is being impacted by the declining housing market and high energy prices, but this is balanced by overall employment levels which have remained resilient. And similar to the financial sector, we are consistently looking at opportunities within the global consumer sector where stocks may have been oversold and could offer long term value at current prices. If the housing and equity market volatility do spill over to the ever-resilient U.S. consumer or it start to impact employment levels, then we believe there is a higher risk of a general economic slowdown and we need to monitor this as investors could become more defensive.

In summary, in a slowing economic growth environment and financial market uncertainty, we believe investors will be drawn to high quality, internationally oriented,

and potentially more defensive stocks. That may bode well for dividend payers and our fundamental strategy of searching globally and in multi-caps and multi-sectors for investment opportunities. It is our plan to balance positive fundamentals in many of our secular growth themes with the risks of financial market turmoil, high oil prices, a potential economic slowdown in the U.S., and continued geopolitical uncertainties.

Our approach is to remain broadly diversified within the dividend-paying universe while actively looking for undervalued opportunities. It is our belief we will be able to continue to distribute our current dividend payouts to our shareholders by capitalizing on our research driven approach to identifying attractive situations as well as through our active management of the portfolio.

Thank you for your participation and we look forward to a prosperous year in 2008 and beyond.

Sincerely,

Jill K. Evans and Kevin Shacknofsky

Co-Portfolio Managers

______________

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security.

Investing in small and mid cap stocks involves additional risks such as limited liquidity and greater volatility as compared to large cap stocks.

Investing in foreign securities tends to involve greater volatility and political, economic and currency risks and differences in accounting methods.

Neither the Fund nor any of its representatives may give tax advice. Investors should consult their tax advisor for information concerning their particular situation.

Free cash flow: Cash not required for operations or for reinvestment. Often defined as earnings before interest (often obtained from the operating income line on the income statement) less capital expenditures less the change in working capital.

Earnings per share (EPS): Calculated by taking the total earnings divided by the number of shares outstanding.

Dividend Yield: The yield a company pays out to its shareholders in the form of dividends. It is calculated by taking the amount of dividends paid per share over a specific period of time and dividing by the stock’s price.

S&P 500 Electric Utility Index: Standard and Poor’s 500 Electric Utilities Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

DJ Select Dividend Index: The selection of stocks to the Dow Jones Select Dividend Index is based almost entirely on dividend yield and dividend history. Stocks are also required to have an annual average daily dollar trading volume of more than $1.5 million. These criteria help to ensure that the index represents the most widely traded of the market’s highest-yielding stocks.

12

Value of a $10,000 Investment

$15,000

Alpine Dynamic Financial Services Fund

$14,000

PHLX/KBW Bank Index

S&P 500 Index

$13,112

$13,000

$12,000

$12,044

$11,000

$10,000

$9,000

$9,102

$8,000

Nov 1

Jan 31

Apr 30

Jul 31

Oct 31

Jan 31

Apr 30

Jul 31

Oct 31

Jan 31

Apr 30

05

06

06

06

06

07

07

07

07

08

08

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The NASDAQ 100 Financial Index is a capitalization-weighted index of the 100 largest financial companies, as well as foreign issues, including American Depository Receipts (ADRs), traded on the NASDAQ National Market System (NASDAQ/NMS) and SmallCap Market. The PHLX/KBW Bank Index is a modified cap-weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Lipper Financial Services Funds Average is an average of funds whose primary objective is to invest primarily in equity securities of companies engaged in providing financial services. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The NASDAQ 100 Financial Index, the PHLX/KBW Bank Index, the S&P 500 Index and the Lipper Financial Services Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Financial Services Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Comparative Annualized Returns as of 4/30/08 | ||||||||||

|

|

|

|

|

| Since Inception | ||||

|

| 6 Months (1) |

| 1 Year |

| (11/1/2005) | ||||

Alpine Dynamic Financial Services Fund |

| -11.27% |

| -1.01% |

| 11.48% | ||||

NASDAQ 100 Financial Index |

| -11.84% |

| -12.29% |

| 0.04% | ||||

PHLX/KBW Bank Index |

| -18.10% |

| -25.74% |

| -3.51% | ||||

S&P 500 Index |

| -9.64% |

| -4.68% |

| 7.90% | ||||

Lipper Financial Services Funds Average |

| -17.20% |

| -21.14% |

| 2.42% | ||||

Lipper Financial Services Fund Ranking |

| N/A |

| 1/131 |

| 18/140 | ||||

(1) Not annualized. FINRA does not recognize rankings for less than one year.

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”), there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO allocations in the future.

13

Alpine Dynamic Financial Services Fund |

|

|

|

| ||||

Portfolio Distributions* (Unaudited) |

| Top 10 Holdings* (Unaudited) | ||||

|

| 1. |

| Intercontinental Exchange, Inc. |

| 5.54% |

Capital Markets 38.7% Consumer Finance 0.2% Transportation IT Services 3.1% Diversified Financial Services 4.6% Insurance 5.6% Thrifts & Mortgage Finance 14.2% Commerical Banks 31.8% |

| 2. |

| Ultra Short Financials ProShares Trust |

| 4.83% |

3. |

| Banco Estado Rio Grande Sul SA |

| 3.91% | ||

4. |

| Banco Panamericano SA |

| 3.76% | ||

5. |

| Alliance Bancorp, Inc. |

| 3.46% | ||

6. |

| Blackstone Group L P |

| 3.24% | ||

7. |

| Nymex Holdings Inc. |

| 3.21% | ||

8. |

| Sanders Morris Harris Group, Inc. |

| 3.11% | ||

9. |

| Fortress Investment Group LLC – Class A |

| 2.79% | ||

10. |

| Interactive Brokers Group, Inc. |

| 2.74% | ||

______________ | ||||||

* Portfolio holdings and sector distributions are as of 4/30/08 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Portfolio Distributions and Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. | ||||||

|

|

|

|

|

|

|

Commentary |

|

Dear Investor:

Alpine Dynamic Financial Services Fund reported a –11.27% total return during the six months ended April 30, 2008. This compares favorably to returns for the NASDAQ 100 Financial Index of -11.84% and the PHLX/KBW Bank Index of -18.10% during the same period.

The first half of fiscal 2008 was a difficult period for financial stocks with the nadir hit on the day the Bear Stearns bailout was announced. The actions taken by the Federal Reserve in the Bear Stearns transaction infused some investor confidence in the stability of the industry. It appears this renewed investor confidence has allowed many large institutions to raise billions of dollars in much needed capital. These recapitalization transactions should permit banks to more aggressively write-down the problems in their security and loan portfolios and de-lever their balance sheets. In our opinion this process of strengthening bank balance sheets is needed in order for financial stocks to mount an extended advance. We expect the early stages of a long term advance will be choppy with headline news driving both short-term rallies and declines. But with the sector still underweighted by institutional investors and heavily shorted by speculators, we believe future demand for financial stocks may be great. We also feel the recent decline in bank stocks provides a rare buying opportunity for long term oriented investors. The last

time bank valuations were this low was during the savings and loan crisis of the early 1990’s.

We anticipate the operating environment for the financial industry will remain challenging for the remainder of the year. From a macro-economic prospective, the weakening labor market combined with rising energy and food prices, declining home prices, and tighter credit is beginning to hamper consumer spending. This is causing economists to lower their growth projections for 2008. There is a concern that a prolonged decline in consumer spending could negatively affect the corporate sector which would cause further weakness in the labor market. Currently, banks are reporting that their commercial loan portfolios are performing well and that there is still demand for credit.

The area that is causing most of the problems for banks is the housing market. In speaking to bankers from around the country, the general opinion is for increases in delinquencies and charge-offs in construction, mortgage, and home equity loans for at least the next few quarters. Stabilization in the housing market is needed before trends improve. While an individual’s desire to own a home has not changed, their ability to afford a home has lessened. This should change if home prices readjust downward thus providing an opportunity for first-time homebuyers to enter the market. From the

14

Alpine Dynamic Financial Services Fund |

|

supply side, both builders and banks have been aggressive in selling excess inventory and home starts have declined meaningfully.

Most banks we have spoken to are being cautious and don’t expect balance sheet growth this year. Planned reductions in the residential construction loans may offset growth in other loan categories. Banks plan to grow their loan loss reserves this year and we expect more banks will announce capital raises and dividend cuts. On the positive side, we anticipate that the net interest margin will improve in the second half of the year. The rapid decline in the Fed funds rate hindered the margin as the rate charged on prime-based loans declines immediately while the rollover of CDs is spread over time. As the Federal Reserve holds rates steady, this should allow the repricing of CD rates to catch up with the decline in the prime rate. Competition for deposits is tough as troubled institutions are paying high rates to attach much needed funding. This is being offset on the loan side as risk is being priced into loan deals. Also helping the margin is a steeper yield curve.

We believe industry consolidation will slow during 2008 as acquirers wait until the real estate market stabilizes and they can better assess the risk of the balance sheets they are buying. When that time arrives, we anticipate a substantial increase in mergers. After a stressful period, we expect the boards of many banks are going to be willing sellers while the acquiring banks will want to take advantage of low deal valuations. We also expect to see small community banks doing merger of equal transactions with similar size banks in order to get scale, improve efficiency, and increase franchise value.

Although the immediate business climate is challenging for banks, longer term, we believe bank and thrift stocks offer the best potential return among the financial services sub-sectors coming out of this downturn. The stocks are starting at valuations not seen in over a decade. We expect the initial rally to begin when credit problems stabilize and banks start letting their loan loss reserves to flow back into earnings. Additional interest in the group should materialize

when the pace of industry consolidation increases. As fundamentals improve, we estimate that there will be a multi-year period of improving return on equity for the group which should help sustain investor interest in the sub-sector. Our holdings among banks and thrift stocks are primary in stocks we feel are attractively priced, in markets we believe will outperform in the next economic expansion, and are potential consolidation candidates.

In the short term, we believe companies with little or no credit exposure will outperform the overall financial sector. These include the owners of equity and derivative exchanges, brokers which only provide execution services, corporate financial advisors, and asset managers. Each of these groups has recently declined due to various investor concerns. While the concerns vary from group to group, they originate from the current weak capital market environment and lack of liquidity for leveraging and financing. As the capital markets improve and money flows increase, we anticipate that these companies, which have no over-hanging credit issues, will be the initial beneficiaries. Since our last report, we have increased our exposure to these groups.

In an effort to reduce the overall risk of the fund, we have diversified our holdings among the different sub-sectors of the financial industry. Some of these investments we believe will outperform in the short term while others we feel potentially offer the best long term return. We monitor industry trends for improvement or deterioration and direct our investments into or out of sub-sectors that are affected by these trends. We also actively search for attractively priced, oversold investment opportunities. While financial stocks have been under stress, we believe that once credit concerns subside the group offers attractive long term prospects. We wish to thank our investors for your continued support.

Sincerely,

Peter J. Kovalski

Portfolio Manager

The fund primarily invests in equity securities of financial services companies and will be affected by risk factors particular to this industry such as regulation, monetary and fiscal policies and interest rates, as well as general market risks. The fund invests in smaller companies, which involve additional risks such as liquidity and greater volatility. The fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods.

There is no assurance the fund will achieve its investment objective.

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security.

15

Value of a $10,000 Investment

$15,000

Alpine Dynamic Innovators Fund Russell

2000 Total Return Growth Index

$13,000

$12,972

$11,000

$10,739

$9,000

Jul 11

Aug 31

Oct 31

Dec 31

Feb 28

Apr 30

Jun 30

Aug 31

Oct 31

Dec 31

Feb 29

Apr 30

06

06

06

06

07

07

07

07

07

07

08

08

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The Russell 2000 Total Return Growth Index is constructed to provide a comprehensive and unbiased barometer of the small-cap growth market. Based on ongoing empirical research of investment manager behavior, the methodology used to determine growth probability approximates the aggregate small-cap growth manager’s opportunity set. The Lipper Small-Cap Growth Funds Average is an average of Funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The Russell 2000 Total Return Growth Index and the Lipper Small-Cap Growth Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Innovators Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

Comparative Annualized Returns as of 4/30/08 |

|

|

|

|

|

|

| |||

|

| 6 Months (1) |

| 1 Year |

| Since Inception |

| |||

Alpine Dynamic Innovators Fund |

| -9.79 | % |

| 13.21 | % |

| 15.53 | % |

|

Russell 2000 Total Return Growth Index |

| -14.14 | % |

| -6.71 | % |

| 4.03 | % |

|

Lipper Small-Cap Growth Funds Average |

| -16.55 | % |

| -7.94 | % |

| 5.00 | % |

|

Lipper Small-Cap Growth Fund Ranking |

| N/A |

|

| 1/598 |

|

| 12/543 |

|

|

(1) | Not annualized. FINRA does not recognize rankings for less than one year. |

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”), there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO allocations in the future.

16

Alpine Dynamic Innovators Fund |

|

|

|

| |||

Portfolio Distributions* (Unaudited) |

| Top 10 Holdings* (Unaudited) | |||

Financials 6.4% Energy 6.2% Consumer Discretionary 4.2% Materials 6.3% Cash & Cash Equivalents 12.2% Information Technology 19.4% Telecommunications 1.8% Industrials 14.1% Health Care 29.4% |

| 1. |

| Invitrogen Corp. | 3.31% |

2. |

| Itron, Inc. | 2.86% | ||

3. |

| Charles River Laboratories International, Inc. | 2.74% | ||

4. |

| Priceline.com, Inc. | 2.71% | ||

5. |

| Portfolio Recovery Associates, Inc. | 2.60% | ||

6. |

| MEMC Electronic Materials, Inc. | 2.53% | ||

7. |

| Logitech International S.A. | 2.35% | ||

8. |

| Air Products & Chemicals, Inc. | 2.32% | ||

9. |

| CME Group, Inc. | 2.16% | ||

| 10. |

| Inventiv Health, Inc. | 1.97% | |

| ______________ * Portfolio holdings and sector distributions are as of 4/30/08 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. | ||||

Commentary |

|

Dear Investor:

The performance of the Alpine Dynamic Innovators Fund for the first half of the fiscal year ended April 30, 2008 was -9.79%. This compares with -9.64% of the S&P 500 Index, and -14.14% for the Russell 2000 Total Return Growth Index. Since inception of the Fund on July 11, 2006, the cumulative performance is 29.72%, comparing with 12.68% for the S&P 500 Index and 7.39% for the Russell 2000 Total Return Growth Index.

After the 35% gain for the calendar year 2007, the Fund results were negatively impacted by the recessionary concerns building in 2007, notably in the technology sector. On occasion market volatility has obscured strong underlying trends in innovative companies. Illustratively, a dramatic change in valuation recently occurred for one of the Fund’s holdings, Sequenom, Inc. Originally purchased at $7.33 per share, its value at April 30th was $6.32, and by June 9th it closed at $12.83 per share. The reason for the sudden shift in valuation is that the company has announced its success in developing a genetic test to determine whether a child will be born with Downs Syndrome. The concept of innovation, as in this case, involves understanding the potentials for new developments and judging the timing for their impact. The largest single gain in the Fund to date had to do with an unexpected impact of a highly creative innovative data management source. We purchased shares of VMare, Inc. for its unique technology in high density data storage. Within a few months a bid was made for the company at a price which on April 30th, provided a 129.8% gain for the Fund.

Innovative opportunities can be accelerated by changing economic circumstances. One such example, in our opinion, is our holdings in Priceline.com, which has appreciated 44.7% since acquisition. This company offers travelers the opportunity to search out and negotiate extraordinary discounts, and it appears they have been favorably impacted by a slowing economy.

While anticipating innovative opportunities predominantly in the small to mid capitalization company environment, we believe the Fund is also benefiting identifying similar potential in larger capitalized companies. For example, Monsanto Company is already achieving, and anticipating even greater growth from its developments of high yield agricultural seeds. Large companies likely to be on the threshold of accelerating their growth through innovative products include such portfolio holdings as Air Products and Chemicals, Medtronic Inc., Merck & Company, CME Group, Inc., and Apple, Inc.

The search for innovative opportunity has led to medical technology and pharmaceutical products as the largest single grouping of holdings, with 26 companies. Next in number is electronic systems and instruments with 11 companies, followed by sectors as diverse as oil and gas exploration and development products, and energy efficiency systems. The size range of these companies is as extensive as from FMC Technologies $9.6 billion market value in oil and gas exploration, to Westport Innovations, a $446 million Canadian Dollar market value specialist in engine development for hydrogen vehicle power. With 30% of the portfolio invested in medical technology, healthcare and biotechnology, 19%

17

Alpine Dynamic Innovators Fund |

|

in electronic systems and communication, and 6% in energy systems, our present portfolio policy makes the statement as to where we think the greatest areas of innovation are likely to be in the period ahead.

Numerous portfolio changes during the fiscal half year reflected the volatile markets. A policy of risk avoidance involved short-term losses, as illustrated, in our opinion, by our largest losses in two stocks of electronic based companies, Formfactor Inc., and Garmin, Ltd., each with losses over 40%. We took significant profits on sharp run-ups as in the case of Google, Inc., paring back our position, and in the sale of Illumina, Inc., after an advance which more than doubled our investment and seemed, in our judgment, as discounting near term gains.

In its first 16 months of operation we feel that the Fund has established its strategy of focus on innovation, and demonstrated its leadership as a growth fund. In the

recent half year we have gone through a challenging period where many volatile stocks showed sharp moves over limited time cycles. We are adapting our strategies to evolving market environment and believe that the fundamental emphasis on innovative companies will allow the investment performance to move ahead, notwithstanding a slowing economy and uncertain equity markets.

We thank our initial and newly joining investors for their confidence in the potential of this Fund. We view it as an early stage growth vehicle and are dedicating resources to bring it to the next level.

Sincerely,

Stephen A. Lieber

Samuel A. Lieber

Co-Portfolio Managers

The Fund may invest in smaller and medium size companies, which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in micro-cap company stocks which are more volatile than those of larger companies and tend to perform poorly during times of economic stress.

The Fund may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods.

The Fund may invest in debt securities which typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities.

The Fund portfolio will involve short positions, which involves unlimited risk including the possibility that losses may exceed the original amount invested. The fund may also use options and future contracts, which have risks associated with unlimited losses in the underlying holdings due to unanticipated market movements and failure to correctly predict the direction of securities prices, interest rates and currency exchange rates. However, a mutual fund investor’s risk is limited to one’s amount of investment in a mutual fund.

The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security.

18

Value of a $10,000 Investment

$11,000

Alpine Dynamic Transformations Fund

S&P 500 Index

$10,090

$10,000

$9,497

$9,000

$8,000

Dec 31

Jan 31

Feb 29

Mar 31

Apr 30

07

08

08

08

0