We expect the U.S. economy may experience solid but potentially tepid growth in 2010 as two key engines of growth remain sluggish. One is that overall consumption in the U.S. is expected to remain weak as a result of the continued deleveraging of the average U.S. household from the credit binge of the mid 2000’s. Secondly, small businesses are being hindered by rising taxes and healthcare costs and tight credit conditions from the still fragile U.S. banking system. Consequently, it looks like employment growth will remain subdued and the unemployment rate may remain stubbornly high relative to traditional economic recoveries and in comparison to the 4.7% rate that the U.S. experienced in January 2008. The U.S. government has made tremendous efforts to avert a financial meltdown, but in the end, the key to revitalizing household cash flows and driving sustainable economic growth must be centered on solutions for housing and unemployment.

Within the context of this potentially tepid growth outlook in the U.S., it is likely that inflation will remain subdued through 2010, which is positive for equity valuations. There is still a significant output gap in the U.S. with excess capacity in the labor market, industrial utilization, and rental properties which make up the majority of the inflation rate. We do anticipate upward pressure on commodity and energy prices in 2010 based on tighter supply-demand fundamentals driven by stronger global growth and we continue to look for opportunities to invest in these areas. So even if the Fed begins to raise rates in 2010 from its historically low level of 0.25 basis points, we expect the overall interest rate environment should remain accommodative throughout 2010 and this should be positive for the U.S. equity markets. Early in an economic recovery it is traditional for long rates to rise as money comes out of treasuries and into higher risk alternatives.

We are more optimistic about the outlook for economic growth outside of the U.S. and we continue to look for a combination of growth and income opportunities for our investors that have the potential to capitalize on this growth. We believe the two biggest drivers for our positive outlook are coming from the strong economic outlooks in China and Brazil. China is expected to maintain its substantial stimulus spending program and Brazil has benefitted from strong consumer growth and the infrastructure buildouts heading into the Soccer World Cup games in 2014 and the summer Olympics in 2016. Therefore, we expect that global companies that are exposed to the emerging market consumers, commodities, and energy could be outperformers in 2010. In addition, U.S. companies that have exposure to these strong global markets should also outperform as the dollar is expected to remain relatively weak and these companies have also benefitted from cost cutting efforts and strong margin leverage on rising revenues.

We are aware that there are still many identifiable risks to a solid global growth outlook in 2010 that need to be balanced and monitored. We believe one of the key risks for low inflation and sustainable economic growth is a policy mistake by Central Banks that withdraws the current accommodative monetary actions too soon. For example, we will be closely watching the impact on the credit markets when the U.S. Fed begins to withdrawal its quantitative easing programs, such as the expected wind down of the buying of mortgages in early 2010. This could result in an unwarranted rise in mortgage rates amidst an expected wave of continued foreclosures in 2010 and could further damage our still fragile financial system. Another risk is that that European Central Bank’s deep-rooted fears of inflation may result in actions to raise rates too quickly which would put pressure on banks in the weaker areas of Europe, such as Poland, Spain, Ireland or Greece. Lastly, if China moves to restrict bank lending and thereby slowing its growth, that could be a risk for equities.

We Will Maintain Our Balanced Approach In 2010

The volatility over the past 18 months in global equity markets has provided challenges and opportunities. Our goal is to keep our portfolio balanced and maintain our “barbell” approach to our stock selections. What we mean is that a portion of the portfolio will continue to be invested in more defensive companies with a history of strong and sustainable earnings and cash flow growth with the potential for increasing dividends. These are companies in sectors like healthcare, consumer staples, telecom, and utilities where earnings and dividend growth should be more resilient in economic downturns. On the other end of the barbell, we are searching for attractive value opportunities in some strong companies in the more cyclical sectors like energy, materials, consumer discretionary and industrials where prices had been punished during the economic downturn and where we believe long term growth prospects are still attractive.

We are on watch for continued headline risks particularly in the financial sector in first half 2010 as the recent problems in Dubai, Greece and Spain remind of us lingering debt issues and still inflated global asset valuations. However, we remain optimistic that these risks can be contained and that global economic growth will continue to improve in 2010. In addition, we are hopeful that 2010 will be an attractive environment for ADVDX’s investment strategy as fundamental investors focus on high quality and attractive dividend payers. With real global interest rates still close to zero, we would expect capital to search for sustainable yield opportunities in equities which was the case coming out of the bear market in the mid-70’s.

In summary, we see both catalysts and risks in 2010. Our approach during these uncertain times is to remain broadly diversified within the dividend-paying universe

| |

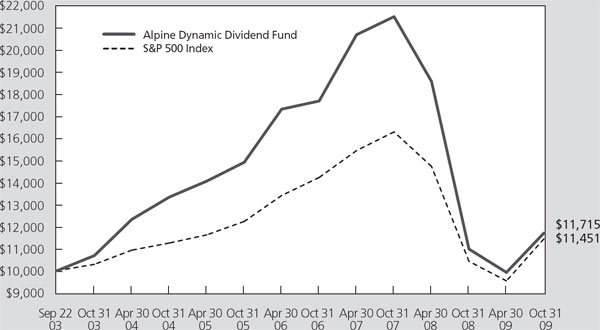

Alpine Dynamic Dividend Fund |

|

| | |

while actively scanning the globe for undervalued opportunities and high quality cash flow generators. We are confident that we should be able to continue to distribute attractive dividend payouts by capitalizing on our research driven approach to identifying value opportunities as well as through our active management of the portfolio. We are hopeful that equities will continue to be an attractive asset class relative to bonds and cash in 2010 and that ADVDX will continue to offer strong capital appreciation and total return potential for our investors.

Thank you for your support of ADVDX and we look forward to a prosperous and peaceful year in 2010 and beyond.

Sincerely,

Jill K. Evans and Kevin Shacknofsky

Co-Portfolio Managers

Diversification does not assure a profit or protect against loss in a declining market.

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. Current and future portfolio holdings are subject to risk.

Investing in small and mid cap stocks involves additional risks such as limited liquidity and greater volatility as compared to large cap stocks. Investing in foreign securities tends to involve greater volatility and political, economic and currency risks and differences in accounting methods.

Neither the Fund nor any of its representatives may give tax advice. Investors should consult their tax advisor for information concerning their particular situation.

Free cash flow: Cash not required for operations or for reinvestment. Often defined as earnings before interest (often obtained from the operating income line on the income statement) less capital expenditures less the change in working capital.

Earnings per share (EPS): Calculated by taking the total earnings divided by the number of shares outstanding.

Earnings Growth is a measure of a company’s net income over a specific period, generally one year, is a key indicator for measuring a company’s success, and the driving force behind stock price appreciation.

Dividend Yield: The yield a company pays out to its shareholders in the form of dividends. It is calculated by taking the amount of dividends paid per share over a specific period of time and dividing by the stock’s price.

A basis point is one hundredth of a percentage point (0.01%).

Beta measures the volatility of the fund, as compared to that of the overall market. The Market’s beta is set at 1.00; a beta higher than 1.00 is considered to be more volatile than the market, while a beta lower than 1.00 is considered to be less volatile.

Book value: net asset value of a company, calculated by subtracting total liabilities from total assets.

Euro Stoxx 50 Index is The Dow Jones EURO STOXX 50 Index, Europe’s leading Blue-chip index for the Eurozone, provides a Blue-chip representation of supersector leaders in the Eurozone. The index covers 50 stocks from 12 Eurozone countries: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain.

The Dow Jones EURO STOXX 50 Index is licensed to financial institutions to serve as underlying for a wide range of investment products such as Exchange Traded Funds (ETF), Futures and Options, and structured products worldwide.

S&P 500 Financial Select Sector Index: Standard and Poor’s 500 Financials Index is a capitalization-weighted index. The parent index is S&P 500. This is a GICS Level 1 Sector group. One cannot invest directly in an index.

14

| |

Alpine Accelerating Dividend Fund |

|

|

| | | | | | | | | | |

Comparative Annualized Returns as of 10/31/09 (Unaudited) |

| | | | | | | | | | |

| | 3 Months (1) | | 6 Months (1) | | Since Inception

(11/05/2008) (1) | |

|

|

|

|

|

|

|

|

Alpine Accelerating Dividend Fund | | 6.00 | % | | 16.43 | % | | 14.80 | % | |

|

|

|

|

|

|

|

|

|

|

|

S&P 500 Index | | 5.48 | % | | 20.04 | % | | 11.58 | % | |

|

|

|

|

|

|

|

|

|

|

|

Dow Jones Industrial Average | | 6.65 | % | | 20.73 | % | | 9.81 | % | |

|

|

|

|

|

|

|

|

|

|

|

Lipper Equity Income Funds Average(2) | | 5.41 | % | | 20.26 | % | | 16.48 | % | |

|

|

|

|

|

|

|

|

|

|

|

Gross Expense Ratio: 3.41%(3) | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.41%(3) | | | | | | | | | | |

| | | | | | | | | | | |

|

(1) Not annualized. |

(2) The since inception return and represents the annualized return for the period beginning 11/6/2008. |

(3) As disclosed in the prospectus dated February 27, 2009. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Dow Jones Industrial Average is a price weighted average of 30 actively traded shares of large cap U.S. industrial corporations. The Lipper Equity Income Funds Average is an average of Funds that seek relatively high current income and income growth through investing 60% or more of their respective portfolios in equities. The S&P 500 Index, the Dow Jones Industrial Average, and the Lipper Equity Income Funds Average are unmanaged and do not reflect fees associated with a mutual fund, such as investment adviser fees. The performance for the Accelerating Dividend Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

The adviser contractually agreed to waive a portion of its fees and to absorb certain fund expenses. This arrangement will remain in effect unless the Board of Trustees approves its modification or termination.

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”) and/or secondary offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary offerings in the future.

|

|

Portfolio Distributions* (Unaudited) |

| | | | | |

|

Top 10 Holdings* (Unaudited) |

1. | | Alcon, Inc. | | 4.11% | |

2. | | Sigma-Aldrich Corp. | | 3.42% | |

3. | | Chubb Corp. | | 3.20% | |

4. | | Chevron Corp. | | 3.15% | |

5. | | Kimberly-Clark Corp. | | 2.77% | |

6. | | Sonoco Products Co. | | 2.75% | |

7. | | Sysco Corp. | | 2.72% | |

8. | | El Paso Pipeline Partners LP | | 2.54% | |

9. | | United Technologies Corp. | | 2.53% | |

10. | | Burlington Northern

Santa Fe Corporation | | 2.48% | |

| | |

| |

* | Portfolio holdings and sector distributions are as of 10/31/09 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. |

|

15

| |

Alpine Accelerating Dividend Fund |

|

| | |

|

|

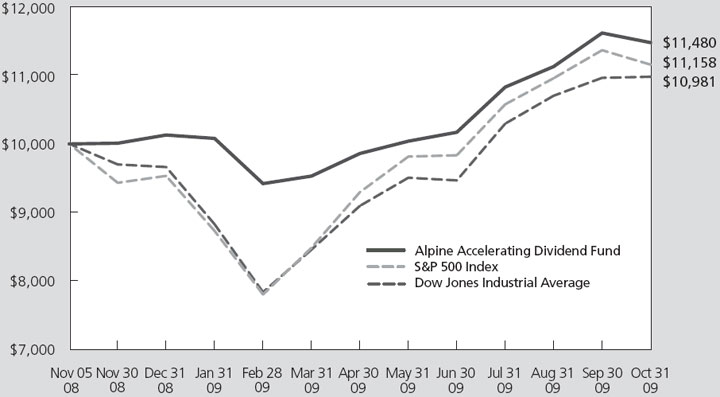

Value of a $10,000 Investment (Unaudited) |

|

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Dear Investor:

We completed our first year of operation with the Alpine Accelerating Dividend Fund, initially launched on November 5, 2008. Since inception through the period ending October 31, 2009, the Fund produced a total return of 14.80%. This compares favorably with a total return of 11.58% for the Standard & Poor’s 500 Average and 9.81% for the Dow Jones Industrial Average for the same period.

The objective of the Accelerating Dividend Fund is to invest in dividend-paying companies which we feel have the potential to accelerate their dividends in the future, based on our analysis of their growth prospects and cash flow generating capabilities. The Fund aims to achieve a sustainable and rising stream of dividend income as well as long-term capital appreciation. We believe dividend acceleration is best sustained by companies with consistent sales or service growth, defensible margins and a strong balance sheet and liquidity profile.

While a limited universe of companies have provided increasing dividends for a sustained period of time, even fewer have demonstrated sustained dividend

acceleration. We use a selective screening process to identify companies with this potential. We feel that in the long-run, these companies provide better risk-adjusted returns for investors while simultaneously providing a buffer against dramatic declines in the stock market and excessive volatility. It is important to recognize that these companies may not outperform the broader market in all environments. For example, when markets rebound off their troughs, more speculative, higher-beta stocks tend to outperform as companies with riskier financial profiles that possessed a higher probability of financial distress recover off their dramatically low valuations. However, when viewed over a longer investment horizon and through a full economic cycle, we feel that companies with more conservative balance sheets and credit profiles should ultimately outperform, especially on a risk-adjusted basis. This point is clearly demonstrated in a recent Wall Street Journal article – “Dividend Payers Return to the Fore” (November 21, 2009 page B1). The article references an analysis from Standard & Poor’s which shows that in the past 10 years, dividend-paying stocks have outperformed non-dividend-paying stocks in every year except for 2003 and 2009. Both of these represented rebound years following bear

16

| |

Alpine Accelerating Dividend Fund |

|

| | |

markets where higher-beta, more speculative stocks outperformed.

Growing, or even sustaining, dividends in the recent environment was extremely difficult, as evidenced by a record number of dividend cuts experienced from companies across various sectors. Even dividend stalwarts such as General Electric, Pfizer and US Bancorp, who have a long and proud history of dividend increases were forced to cut their dividends significantly earlier this year. Strikingly, based on the S&P Dividend Aristocrats, 8 companies that have consistently increased their dividends each year for at least 25 years were forced to slash their dividends this year.

Illustrative of companies we deem capable of meeting these standards are the top performing holdings in the brief history of this Fund. The following are the top performers from inception through October 31, 2009: Suntrust Banks +69%, Alcon +63%, Occidental Petroleum Corp +38%, Sigma Aldrich +37%, J&J Snack Foods +34% and JM Smucker Co +33%. In addition, Burlington Northern Corp, in which we had a 10% gain as of October 31, subsequently announced its sale to Berkshire Hathaway, Inc. on November 3 for a 23% premium to its previous closing price. Burlington, which was a top 10 holding of the fund, has a history of dividend acceleration as well as the ability to generate strong operating cash flow even during a deep recessionary environment. These companies are not concentrated in any one particular area, but conversely represent a broad cross-section of numerous industries including financials, oil and gas, chemicals and consumer products. On the other hand, several companies in our portfolio posted disappointing results: Regions Financial -12%, Accenture -10%, WGL Holdings - -9%, CPFL Energia -8% and Exelon Corp -7%.

Regions Financial is a large regional bank headquartered in Alabama with a Southeast concentration in its loan portfolio. The bank was included in the group of 19 large banks that were stress tested by the Fed earlier this year and raised the requisite amount of capital dictated by the stress tests. From a long term value perspective, we continue to feel that Regions offers compelling return potential while the downside risks have likely been mitigated through the regulatory assessment and resultant capital increases. However, we recognize that similar to other US regional banks, the recovery timeline is not short and expect earnings to be below normal operating levels for several years. While Regions was forced to virtually eliminate their dividend earlier this year in order to preserve capital, we expect future dividend increases to be concurrent with a reduction in loan loss provisioning and recovery in earnings.

Accenture, a historical dividend accelerator with a strong balance sheet, is a provider of management and

technology consulting services to corporations. We believe that the Company may continue to benefit from global corporate demand for outsourcing solutions and more efficient use of IT technology to enhance productivity and reduce cost. As a result, we feel that Accenture’s business model and financial results will prove to be more resilient in a slow economy. WGL and Exelon are US utility companies and CPFL Energia is a Brazilian utility. Although utilities underperformed the broader market (S&P 500) through October 31, we believe that the sector was positioned for a rebound as investors reduce risk appetite and rotate into more defensive names. Utilities have historically provided attractive dividend yields and cash flow characteristics, and, as discussed below, represent a meaningful part of our portfolio.

Three of our largest industry groups and corresponding percent of portfolio are Oil and Gas – 8.4%, Electric Utilities – 7.9% and Healthcare Equipment and Supplies – 7.7%. We feel that our investments in the energy sector should benefit from the significant infrastructure spending domestically as well as in the emerging markets (i.e, China, Brazil). The utility sector may provide very attractive dividend yields and a conservative corporate profile. Despite a challenged dividend environment, utilities’ steady revenue streams should support the continuation of high dividend payouts. The healthcare equipment companies in our portfolio have solid balance sheets and a history of strong cash flow generation. We feel that they have the capability to increase their dividend even through a continued weak economy, and are also more insulated than pharmaceuticals to the risks associated with the impending healthcare legislation. It is our intention to continue to look for investments that meet our criteria without assuming excessive risk by overly concentrating in one particular sector or geographic region.

We aim to be selective in identifying companies that we feel are best positioned to maintain their historical dividend trajectories by deploying a three-pronged approach. First, we look for companies that internally generate enough free cash flow from their core operations to support their dividends and even fund share repurchases. Second, we monitor the ratio of cash flow to adjusted net income to indentify companies whose core earnings (adjusted for depreciation and amortization) are running in-line with the amount of cash flow from operations. Third, we favor companies with stronger liquidity profiles and an ability to service their debt even under adverse profitability scenarios. We seek companies with more unencumbered balance sheets which retain flexibility in recessions enabling them to avoid franchise-destroying actions, such as forced divestitures of strategic assets. Companies with fortress balance sheets should be better positioned to take advantage of market opportunities and enhance

17

| |

Alpine Accelerating Dividend Fund |

|

| | |

their franchise at the expense of competitors by acquiring assets at the bottom, rather than the top, of the cycle.

Despite the strong rebound in equity markets this year and evidence of the resumption of economic growth in the US, we remain cautious on the economy and feel that the recovery will be tepid with speed-bumps along the way. The consumer and corporate deleveraging process will likely continue for several years as the aggregate leverage in our system remains very elevated relative to historical standards. While the pace of labor cuts appears to be decreasing as evidenced by the recent decline in initial unemployment claims, unemployment has continued to climb due to a lack of private sector hiring. It will likely take years for us to recover these lost jobs – by the Fed’s own estimates it will take until 2012 to bring the unemployment rate back down to 8%, a level we have not seen since 1984! Massive government support of the real estate sector through Fannie, Freddie, the FHA and tax credits has increased transaction flow and put a floor on prices, but the market has not demonstrated an ability to stand on its own without stimulus. Finally, emerging markets such as China, which have contributed enormously to the recovery of commodity prices and global trade this year, must ensure that capital flows and local stimulus do not create speculative bubbles that can derail their recoveries. These forces, coupled with an increasing consumer savings rate, will remain a headwind to a potential recovery in the near-term.

There are reasons to be optimistic. Our financial institutions have been repairing their balance sheets and should emerge from this crisis as better-capitalized and more prudent risk managers. Emerging markets such as China, Brazil and India have demonstrated their ability to decouple from OECD (The Organization for Economic Co-operation and Development) economies and will likely be the leading contributors to global economic growth. In addition, the rapid pace of innovation should continue to create growth, jobs and attractive opportunities for returns. Given the logic of a cautious macro-economic stance, we remain optimistic that companies which meet the high standards of dividend growth and strong liquidity, basic to this strategy, should better withstand a protracted difficult recovery phase while providing attractive capital growth opportunities for investors.

We firmly believe that our strategy should provide investors with attractive risk-adjusted returns through the cycle, and thank our shareholders for their confidence in our management during these unprecedented and volatile market conditions.

Sincerely,

Stephen A. Lieber

David Burg

Co-Portfolio Managers

|

|

Past performance is not a guarantee of future results. |

|

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Current and future holdings are subject to risk. |

|

Investing in small and mid cap stocks involves additional risks such as limited liquidity and greater volatility as compared to large cap stocks. Investing in foreign securities tends to involve greater volatility and political, economic and currency risks and differences in accounting methods. |

|

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income. |

|

Beta measures the volatility of the fund, as compared to that of the overall market. The Market’s beta is set at 1.00; a beta higher than 1.00 is considered to be more volatile than the market, while a beta lower than 1.00 is considered to be less volatile. |

18

| |

Alpine Dynamic Financial Services Fund |

|

|

| | | | | | | | | | | | | |

|

Comparative Annualized Returns as of 10/31/09 (Unaudited) |

| | 6 Months (1) | | 1 Year | | 3 Years | | Since Inception

(11/1/2005) | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Alpine Dynamic Financial Services Fund | | 31.48 | % | | 21.83 | % | | -4.46 | % | | 1.45 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NASDAQ 100 Financial Index | | 9.37 | % | | -13.85 | % | | -13.28 | % | | -7.58 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PHLX/KBW Bank Index | | 29.50 | % | | -25.96 | % | | -25.48 | % | | -16.37 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

S&P 500 Index | | 20.04 | % | | 9.80 | % | | -7.02 | % | | -1.58 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lipper Financial Services Funds Average(2) | | 25.21 | % | | -2.14 | % | | -18.48 | % | | -11.12 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lipper Financial Services Funds Ranking(2) | | N/A | | | 7/84 | | | 3/69 | | | 3/59 | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Expense Ratio: 2.19%(3) | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.97%(3) | | | | | | | | | | | | | |

|

| |

(1) | Not annualized. FINRA does not recognize rankings for less than one year. |

(2) | The since inception return and ranking represents the annualized return for the period beginning 11/3/2005. |

(3) | As disclosed in the prospectus dated February 27, 2009. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The NASDAQ 100 Financial Index is a capitalization-weighted index of the 100 largest financial companies, as well as foreign issues, including American Depository Receipts (ADRs), traded on the NASDAQ National Market System (NASDAQ/NMS) and SmallCap Market. The PHLX/KBW Bank Index is a modified cap-weighted index consisting of 24 exchange-listed and National Market System stocks, representing national money center banks and leading regional institutions. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Lipper Financial Services Funds Average is an average of funds whose primary objective is to invest primarily in equity securities of companies engaged in providing financial services. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The NASDAQ 100 Financial Index, the PHLX/KBW Bank Index, the S&P 500 Index and the Lipper Financial Services Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Financial Services Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

The adviser contractually agreed to waive a portion of its fees and to absorb certain fund expenses. This arrangement will remain in effect unless the Board of Trustees approves its modification or termination.

The Fund’s past performance benefitted significantly from initial public offerings (“IPOs”) of certain issuers, and there is no assurance that the Fund can replicate this performance in the future. To the extent that the Fund’s historical performance resulted from gains derived from participation in Secondary offerings, there is no guarantee that these results can be replicated or that the Fund will be able to participate to the same degree in IPO and Secondary offerings in the future.

| |

|

| |

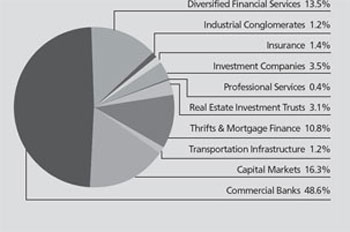

Portfolio Distributions* (Unaudited) | Top 10 Holdings* (Unaudited) |

| | | |

1. | United Western Bancorp, Inc. | | 6.04% |

2. | The Bancorp, Inc. | | 5.81% |

3. | IntercontinentalExchange, Inc. | | 5.48% |

4. | Banco do Estado do Rio Grande | | |

| do Sul SA | | 4.55% |

5. | Metro Bancorp, Inc. | | 4.50% |

6. | Synovus Financial Corp. | | 3.98% |

7. | Blackstone Group LP | | 3.40% |

8. | Alliance Bancorp, Inc. | | |

| of Pennsylvania | | 3.31% |

9. | American Capital Agency Corp. | | 3.29% |

10. | 1st United Bancorp, Inc. | | 3.23% |

| | |

| |

* | Portfolio holdings and sector distributions are as of 10/31/09 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets.

|

19

| |

Alpine Dynamic Financial Services Fund |

|

| | |

|

| |

|

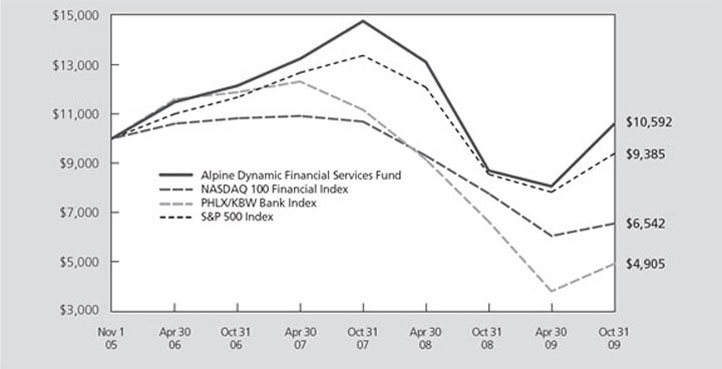

Value of a $10,000 Investment (Unaudited) |

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Dear Investor:

Alpine Dynamic Financial Services Fund generated a 21.83% total return for the fiscal year ended October 31, 2009. This compares favorably to the Fund’s benchmarks which showed total returns of -13.85% for the NASDAQ 100 Financial Index and the PHLX/KBW Bank Index of -25.96% during the same period.

While the Fund’s performance in fiscal 2009 was materially better than the prior year, the market proved equally challenging. At the beginning of fiscal 2008, the outlook for the financial industry was slowly deteriorating due to the problems in residential real estate. The pace at which the industry’s fundamentals were deteriorating dramatically accelerated after the demise of Bear Stearns Co. and through the end of the fiscal year 2008. The speed, depth, and breadth of the decline made it difficult to find investments which would not be significantly affected by market conditions. Equity market volatility continued into fiscal 2009. The year started in the depths of the global financial crisis. With the capital funding markets seized up, governments around the world were forced to infuse capital and liquidity into their bank system in

order to restore order and confidence back to the capital markets. Although governments and their central banks around the world did what they could through fiscal and monetary policies to stabilize the situation, the outlook for the financial industry continued to deteriorate. In the first quarter of calendar 2009, there was talk by politicians both in the US and abroad about potentially nationalizing their large banks. At this point investor sentiment toward the banking industry was at its lowest. The ability for banks to raise much needed capital from the private sector was impossible. Then, in early March, two banks that were considered potential nationalization candidates, Bank of America and Citicorp, both disclosed improving operating trends in the March quarter. This marked the nadir for the bank indexes as hedge funds scrambled to cover their short positions and portfolio managers, who as a group were significantly underweight financials at the beginning of the year, were quickly increasing their sector allocation on the news. Investor confidence has continued to improve through the remainder of the fiscal year as earnings for some of the large financial companies beat consensus estimates and recent economic data point to less contraction than originally

20

| |

Alpine Dynamic Financial Services Fund |

|

| | |

anticipated. This improved outlook is attributable to a high level of Government intervention which includes fiscal spending and targeted stimulus programs. In addition, the housing market data has also begun to improve thanks in part to the Federal Reserve’s program of purchasing mortgages and Agency securities and the Government’s first time home ownership program.

The challenge of fiscal 2009 was the rapid change in investor sentiment toward the capital markets and the financial sector. This year was truly a tale of two markets. The first period was represented by risk aversion, a strong dollar, weak commodity prices, and extreme consumer and investor pessimism. During this period financial stocks were among the worst performing sectors. The second period was in complete contrast with risk taking, weak dollar, strong commodity prices, and improving consumer and investor sentiment. During this period financial stocks were among the best performing sectors. The quickness in the change of investor sentiment and the strength of the rally in financial stocks has caused an adjustment in our investment tactics. With the fundamentals of the industry weak, the outlook uncertain, and no established long term trend, we became more short term focused. Profits were taken if a market rally caused an investment to advance meaningfully in a short period of time in order to protect against a possible quick reversal.

A common characteristic of sector funds is the concentration risk of the industry the fund invests in. We try to reduce this risk by diversifying our investments into different subsectors within the financial industry, and different business models within those subsectors, as well as different geographical markets. This is done with the belief that as some subsectors underperform the group there will be other subsectors outperforming. This was the case in fiscal 2009. The Fund’s best performing holdings were the foreign financial companies. The Brazilian companies were by far the strongest. Banco Panamericano had a total return of 204%, Banco Estado Rio Grande Sul’s total return was 183%, and BM&F Bovespa’s total return was 146%. Another area of outperformance this fiscal year was asset management companies. Within this subsector, the stocks of the alternative investment managers had the best returns. Our holding of Och-Ziff Capital Management generated a total return of 166%, Fortress Investment Group a 103% total return, and Blackstone Group a 62% total return. The next best performing subsector was the security brokerage firms. Among this group our holdings of the niche firms like MF Global, GFI Group, and JMP Group generated the best returns.

On the downside, the worst performing subsector was the domestic banks. A number of the underperforming holdings were banks in the Southeast with exposure to Florida. The sharp decline in the State’s real estate market negatively affected the performance of banks

such as, Bank of Florida Corporation (-76%), Superior Bancorp (-61%), and The South Financial Group (-86%).

The improved investor sentiment toward financials has allowed one important condition needed to resolve the banking crisis to appear. That condition is the opening of the capital markets to equity issuance by banks. In order for the industry to address their problem assets and repay Government TARP money much capital is needed from the private sector. Starting in the summer there has been a wave of banks recapitalizing their balance sheets. These equity raises have been of two types. A defensive offering in which a bank uses the proceeds to rebuild their low capital base and increase their loan loss reserve and an offensive offering in which a bank uses the proceeds to repay TARP money and build excess capital to make acquisitions. We expect both of these types of equity issuances to continue into 2010. The Fund has participated in many of these offerings. We believe the defensive offerings help diminish the overriding concern of capital adequacy while the offensive offerings prove a potential catalyst if the issuing banks are successful in acquiring failed institutions. As a result of our participating in these offerings, the commercial banks category has increased as a percentage of the portfolio distribution over last year end. Two of our largest holdings, The Bancorp Inc. and United Western Bancorp, were purchased in these offerings.

As the industry cleanses itself of weaker institutions, rational pricing of loans and deposits has been returning. Loan underwriting standards are once again prudent. Risk is now being priced into loans while debt coverage and collateral requirements are stricter. We would expect the vintage of loans being underwritten today should perform very well over their life. On the funding side of the balance sheet, the exit of many troubled banks with liquidity problems has dramatically reduced the outlying special Certificate of Deposit (CD) rate promotions. In addition, the bank regulators are beginning to rein in troubled banks from offering CD rates that are way above the prevailing local market rates. Also helping the funding side of the balance sheet is the liquidity that is coming back to the wholesale money market which is reducing the cost of short term borrowing. These factors have allowed the net interest margin for many banks to increase in the third quarter. We believe margins could improve further in the coming quarters as maturing CDs continue to reprice lower and new loans are being underwritten with interest rate floors above their indexed rate. The balance sheets of some banks are also positioned to see widening margins in a rising interest rate environment. Thus, any movement up in rates after the Federal Reserve completes their mortgage purchase program could benefit these banks.

We believe that banks may continue to strengthen their capital ratios. This is being done through the issuance of additional capital and reducing the size of their balance

21

| |

Alpine Dynamic Financial Services Fund |

|

| | |

sheet. Banks have been reducing the thin margin, wholesale side of their balance sheet. These tend to be liquid securities funded with short term borrowings. The banks are also weeding out their loan portfolios accounts with weakening financials and clients which have no other bank products than their loan. Bankers are marketing for relationship customers who want to do all their banking business with them. These accounts are more profitable and tend to stay with a bank longer than rate shoppers.

Our concern with the banking industry is the continuing deterioration of credit quality. We expect loan charge-offs will continue to remain elevated for another year. While residential real estate appears to be stabilizing, the lingering effect of the recession is exerting stress on commercial real estate. This is the main worry and focus of bank examiners. The regulators are requiring banks with commercial real estate concentration to reduce their exposure. Another unknown is the potential for new banking regulation which may hinder the industry’s profitability. We understand that the regulators are

already requiring many banks to maintain capital ratios well in excess of the well-capitalized guidelines.

Longer term, we see the banking industry emerging out of the current recession a stronger and more disciplined industry. As the economy recovers and the credit cycle turns upward, we expect that banks will find themselves with excess capital and loan loss reserves as they did in the early 1990s. This could lead to acceleration in healthy bank mergers and stock buybacks. We look for signs of increasing consumption and private investment as early indicators to a sustained economic recovery.

While we believe 2010 holds some challenges for banks, the industry is in much better shape than it was a year ago. We wish to thank you for your continued support as we pass through these unusual times.

Sincerely,

Peter J. Kovalski

Portfolio Manager

The fund primarily invests in equity securities of financial services companies and will be affected by risk factors particular to this industry such as regulation, monetary and fiscal policies and interest rates, as well as general market risks. The fund invests in smaller companies, which involve additional risks such as liquidity and greater volatility. The fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods.

There is no assurance the fund will achieve its investment objective.

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Current and future portfolio holdings are subject to risk.

Diversification does not assure a profit or protect against loss in a declining market.

22

| |

Alpine Dynamic Innovators Fund |

|

|

| | | | | | | | | | |

| |

Comparative Annualized Returns as of 10/31/09 (Unaudited) | | | | | |

| | | | | | | | | | |

| | 6 Months (1) | | 1 Year | | 3 Years | | Since Inception

(07/11/2006) | |

|

|

|

|

|

|

|

|

|

|

|

Alpine Dynamic Innovators Fund | | 42.38 | % | | 19.03% | | -5.99% | | -4.57% | |

|

|

|

|

|

|

|

|

|

|

|

Russell 2000 Total Return Growth Index | | 15.70 | % | | 11.34% | | -6.88% | | -4.28% | |

|

|

|

|

|

|

|

|

|

|

|

S&P 500 Index | | 20.04 | % | | 9.80% | | -7.02% | | -3.96% | |

|

|

|

|

|

|

|

|

|

|

|

Lipper Small-Cap Growth Funds Average(2) | | 16.74 | % | | 13.12% | | -7.54% | | -4.47% | |

|

|

|

|

|

|

|

|

|

|

|

Lipper Small-Cap Growth Funds Ranking(2) | | N/A | | | 140/557 | | 144/475 | | 258/465 | |

|

|

|

|

|

|

|

|

|

|

|

Gross Expense Ratio: 1.38%(3) | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.42%(3) | | | | | | | | | | |

| |

(1) Not annualized. FINRA does not recognize rankings for less than one year.

(2) The since inception return and ranking represents the annualized return for the period beginning 7/13/2006.

(3) As disclosed in the prospectus dated February 27, 2009.

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The Russell 2000 Total Return Growth Index is constructed to provide a comprehensive and unbiased barometer of the small-cap growth market. Based on ongoing empirical research of investment manager behavior, the methodology used to determine growth probability approximates the aggregate small-cap growth manager’s opportunity set. The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The S&P 500 Index is unmanaged and does not reflect the deduction of fees associated with a mutual fund, such as investment advisory fees. The Lipper Small-Cap Growth Funds Average is an average of Funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three year weighted basis) less than 250% of the dollar-weighted median of the smallest 500 of the middle 1,000 securities of the S&P SuperComposite 1500 Index. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The Russell 2000 Total Return Growth Index, S&P 500 Index and the Lipper Small-Cap Growth Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Innovators Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

The adviser contractually agreed to waive a portion of its fees and to absorb certain fund expenses. This arrangement will remain in effect unless the Board of Trustees approves its modification or termination.

|

The Fund’s past performance benefitted significantly from initial public offerings (“IPOs”) of certain issuers, and there is no assurance that the Fund can replicate this performance in the future. To the extent that the Fund’s historical performance resulted from gains derived from participation in Secondary offerings, there is no guarantee that these results can be replicated or that the Fund will be able to participate to the same degree in IPO and Secondary offerings in the future. |

|

| |

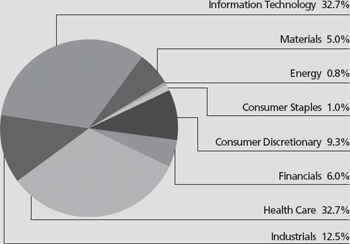

Portfolio Distributions* (Unaudited)

Top 10 Holdings* (Unaudited)

| | | | | |

1. | | Itron, Inc. | | 7.03% | |

2. | | ANSYS, Inc. | | 5.99% | |

3. | | Priceline.com, Inc. | | 5.68% | |

4. | | FLIR Systems, Inc. | | 5.26% | |

5. | | Alcon, Inc. | | 5.14% | |

6. | | Logitech International SA | | 5.05% | |

7. | | Air Products & Chemicals, Inc. | | 4.86% | |

8. | | Life Technologies Corp. | | 4.67% | |

9. | | inVentiv Health, Inc. | | 4.28% | |

10. | | PowerSecure International, Inc. | | 4.27% | |

| | |

| |

* | Portfolio holdings and sector distributions are as of 10/31/09 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. |

23

| |

Alpine Dynamic Innovators Fund |

|

| | |

|

| |

|

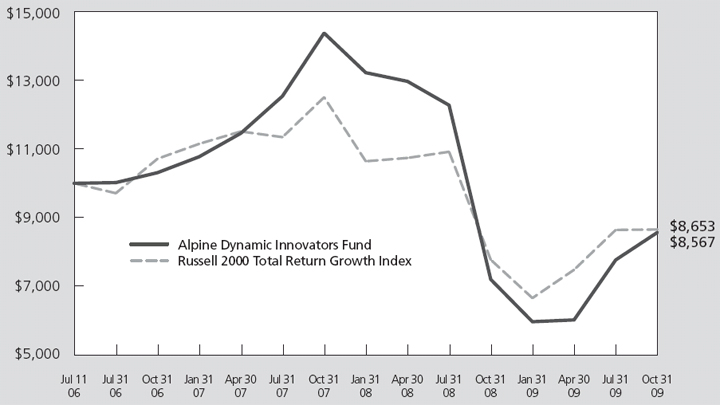

Value of a $10,000 Investment (Unaudited) |

|

|

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Dear Investor:

The Alpine Dynamic Innovators Fund provided a 19.03% return for the fiscal year ended October 31, 2009. This compares with the 9.80% return of the Standard & Poor’s 500 Average and 11.34% for the Russell 2000 Total Return Growth Index for the same period.

Since inception of the Fund on July 11, 2006, cumulative performance is -4.57% compared with the -3.96% for the Standard & Poor’s 500 Index and -4.28% for the Russell 2000 Total Return Growth Index.

The Fund has returned to the positive results experienced in its first calendar year, 2007, which produced a 35% gain in net asset value per share. While past performance is not a guarantee of future results, we believe that the initial results suggest that the concept of concentrating on innovation has now been proven. We seek demonstrated technological leadership, new disruptive technologies, introduction of new and better products and innovative business models. The negative results of the following year, 2008, certainly challenged this Fund’s portfolio as so many others. It is very reassuring that sizeable gains in shares of many

companies with innovative opportunities provided significant outperformance in fiscal 2009.

The leadership of the Fund’s investment performance in this fiscal year were shares in a group of companies with successful innovative business activities or strategies. The top ten among the Fund’s forty-three holdings produced gains ranging from 65% to 209% during this fiscal year.

First in percentage return was Priceline.com Inc.’s 208.9% return. The company’s profits grew with its innovations in an internet based hotel reservation system which allows interactive bidding by customers.

Second in percentage return was Imdex Limited, up 153.4%, an Australian oil and gas drilling system developer and manufacturer of energy production equipment.

Third in return was Westport Innovations, Inc., up 135.9%, a Canadian developer of natural gas fuel systems for automotive engines with key alliances in the U.S. markets with Ford Motor and Cummins Engine.

Power Secure International, Inc. was fourth in gain, up 110.6%. It provides energy management and

24

| |

Alpine Dynamic Innovators Fund |

|

| | |

conservation solutions to utilities and their customers to selectively regulate and reduce consumption.

Scientific Learning Corp., up 102%, was fifth. It has led in the development of internet based computer learning systems for cognitive enhancement.

The group of holdings which gained under 100%, but over 65%, were led by Allscript-Misys Healthcare Solutions, with a 97.3% return. It develops and supplies computer patient data systems for healthcare professionals. In another phase of the healthcare business, Inventiv Health, with a 78.2% return, provides marketing strategies and services for the pharmaceutical industry. Flowserve Corp., which gained 73.7%, is the leader in flow control systems for the oil and natural gas industries. Alcon, Inc., up 67.6%, is the dominant producer of specialty medications for vision and eyecare. Among the top ten is Life Technologies Corp., which gained 65.3%, a major specialty provider of biotechnology tools for medical research and healthcare institutions.

The companies we mention are predominantly small to mid-size enterprises. But, the portfolio strategy will not be limited to the smaller companies. We seek out any significant opportunity for innovation. For example, the largest company among the Fund’s holdings is Hewlett Packard Company, now being enhanced by proposed new acquisitions.

While we are pleased to report strong results in our top ten holdings, there have been others with disappointment and some where losses have been taken. Most disappointing was Sequenom, Inc., with a

loss of - -82.7% recorded after the company disclosed errors in genetic sequencing data which they had published. Promising specialized medical technology companies did prove negative with losses reported in CardioNet, Inc. (-71.3%), Synovis Life Technologies (-31.4%) and Abiomed (-39.3%). We recognize that intensive analysis is necessary in such fields as biotechnology and medical product innovation which may have risks offsetting often remarkable benefits. Other investments in the medical field which could benefit from enlarged government programs, notably stimulus money, include Alscrips-Mysis Healthcare, Mednax Inc. and Quality Systems, Inc.

The early stages of economic recovery have usually provided companies with increasing cash flow to devote to capital investment and marketing for innovative products. We anticipate that this trend may develop even with a limited pace of recovery. Concentration on innovation when successful should drive growth and provide a stream of potential opportunities for investment in this Fund’s strategic areas.

Our organization has added to its research staff and capabilities. We anticipate bringing their wider knowledge to our search for innovative businesses. We thank our shareholders for their continuing support.

Sincerely,

Stephen A. Lieber

Samuel A. Lieber

Co-Portfolio Managers

| |

| |

Past performance is not a guarantee of future results. |

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. Current and future portfolio holdings are subject to risk.

The Fund may invest in smaller and medium size companies, which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in micro-cap company stocks which are more volatile than those of larger companies and tend to perform poorly during times of economic stress. The Fund may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. The Fund may invest in debt securities which typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. The Fund’s portfolio will involve short positions, which involves unlimited risk including the possibility that losses may exceed the original amount invested. The Fund may also use options and future contracts, which have risks associated with unlimited losses of the underlying holdings due to unanticipated market movements and failure to correctly predict the direction of securities prices, interest rates and currency exchange rates. However, a mutual fund investor’s risk is limited to one’s amount of investment in a mutual fund.

Cash flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

25

| |

Alpine Dynamic Transformations Fund |

|

|

| | | | | | | | | | |

|

Comparative Annualized Returns as of 10/31/09 (Unaudited) |

| | 6 Months (1) | | 1 Year | | Since Inception

(12/31/2007) | |

|

|

|

|

|

|

|

|

Alpine Dynamic Transformations Fund | | 31.51 | % | | 33.61 | % | | -13.05 | % | |

|

|

|

|

|

|

|

|

|

|

|

S&P 500 Index | | 20.04 | % | | 9.80 | % | | -15.29 | % | |

|

|

|

|

|

|

|

|

|

|

|

NASDAQ Composite Index | | 19.62 | % | | 20.09 | % | | -12.40 | % | |

|

|

|

|

|

|

|

|

|

|

|

Lipper Mid-Cap Core Funds Average | | 19.40 | % | | 17.52 | % | | -14.43 | % | |

|

|

|

|

|

|

|

|

|

|

|

Lipper Mid-Cap Core Funds Ranking | | N/A | | | 19/370 | | 128/352 | |

|

|

|

|

|

|

|

|

|

|

|

Gross Expense Ratio: 3.00%(2) | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.40%(2) | | | | | | | | | | |

| | | | | | | | |

| |

(1) | Not annualized. FINRA does not recognize rankings for less than one year. |

(2) | As disclosed in the prospectus dated February 27, 2009. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The NASDAQ Composite Index is a stock market index of all of the common stocks and similar securities listed on the NASDAQ stock market, meaning that it has over 3,000 components. It is highly followed in the U.S. as an indicator of the performance of stocks of technology companies and growth companies. The Lipper Mid-Cap Core Funds Average is an average of funds that invest at least 75% of their equity assets in companies with market capitalizations below Lipper’s USDE large cap floor. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500 Index, NASDAQ Composite Index and the Lipper Mid-Cap Core Funds Average are unmanaged and do not reflect fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Transformations Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

The adviser contractually agreed to waive a portion of its fees and to absorb certain fund expenses. This arrangement will remain in effect unless the Board of Trustees approves its modification or termination.

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”) and/or secondary offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary offerings in the future.

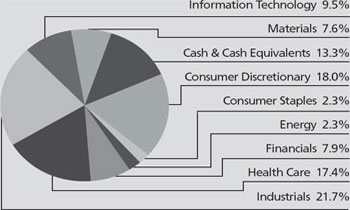

Portfolio Distributions* (Unaudited)

| | | | |

Top 10 Holdings*(Unaudited) | | | |

1. | Pall Corp. | | 9.03 | % |

2. | Intuitive Surgical, Inc. | | 7.01 | % |

3. | Priceline.com, Inc. | | 6.74 | % |

4. | Autoliv, Inc. | | 5.73 | % |

5. | CME Group, Inc. | | 5.17 | % |

6. | Walter Energy, Inc. | | 4.99 | % |

7. | Teleflex, Inc. | | 4.95 | % |

8. | Clean Harbors, Inc. | | 4.34 | % |

9. | Emergency Medical Services Corp. | | 4.10 | % |

10. | Hewlett-Packard Co. | | 4.05 | % |

| | |

| |

* | Portfolio holdings and sector distributions are as of 10/31/09 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. |

26

| |

Alpine Dynamic Transformations Fund |

|

| | |

|

| |

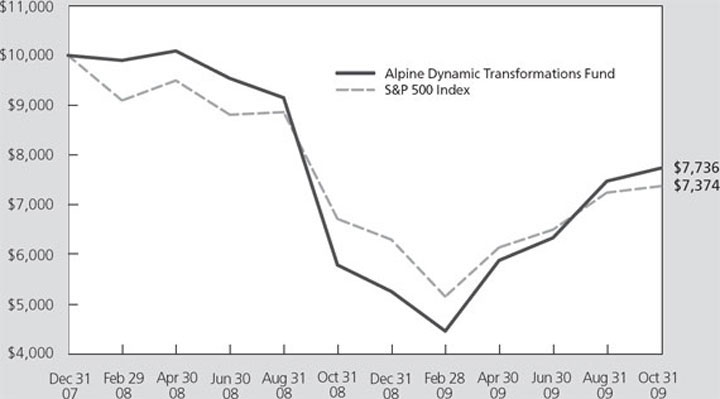

Value of a $10,000 Investment (Unaudited) |

|

|

|

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Dear Investor:

The Alpine Dynamic Transformations Fund return for its first fiscal year to October 31, 2009 was 33.61%. This compared with the 9.80% for the Standard & Poor’s 500 Average and 20.09% for the NASDAQ.

The Dynamic Transformations Fund started January 1, 2008 in, what is often referred to in the investment field, as an incubation stage. In essence, the beginning of a new mutual fund strategy is a “proof of concept”. We believe that the central concept of the Fund – that there should be exceptional growth opportunities through investment in companies which are in the process of enhancing their business through transforming strategies, often literally a business culture change – has now been proven.

The strategy is well illustrated through the performance over the last year in the top ten performing holdings of the Fund.

The number one performer, up 199.8%, was Priceline.com, Inc. Priceline is leading the transformation of its industry, a specialty business of providing customer negotiated hotel, travel and cruise reservations. It has achieved sustained and large

profitability gains in an environment where travel became much more competitive as demand declined.

The second largest gainer was PNC Financial Services Group, with a 112.4% total return. This major regional bank headquartered in Western Pennsylvania, positioned itself to potentially benefit by the 2008 crisis in the banking industry through acquisition of a major Cleveland, Ohio banking system, National City, Inc. Its recent financial results compare outstandingly with a typical bank. The third largest return was in State Street Corp., at 101.3%. State Street, a major trust bank, had lost some of its investment standing during the banking crisis through its ownership of unconsolidated lending vehicles. Investor confidence began to be restored when the management announced write-downs on these vehicles to eliminate the risk of further losses.

The next largest gain was 69.9% in the shares of CME Group, Inc. CME is the parent of Chicago Mercantile Exchange and other exchanges. It is the largest exchange in the field of derivatives. Much of the investment crisis of 2008 was impacted by derivative obligations being traded outside of the exchange structures in an unregulated fashion. There now is growing expectation that regulations will require that

27

| |

Alpine Dynamic Transformations Fund |

|

| | |

exchanges such as CME take on this additional transaction volume, which should enhance growth opportunity in a transformational manner.

Walter Investment Management Corp. and Walter Energy Inc. rose 68.4% and 67.8%, respectively. These gains reflected a true transformation in the shares of Walter when the company separated its two businesses, mortgage investment management and energy resources. This particularly enabled concentration on the high growth potential metallurgical coal mining subsidiary. Autoliv Corp. provided a 61.9% return. This international manufacturer of auto safety equipment, seatbelts and airbags, has begun a new product program with the introduction of infrared safety equipment to be installed on cars in order to identify nighttime risks, particularly highlighting pedestrians.

A transformation program was initiated by Starbucks Corp., up 44.5%, recognizing that the company had lost its historical growth luster. Combining reduction in the number of stores with changes in product and even introduction of instant coffees, Starbucks appears to have regained a growth trend.

Intuitive Surgical Inc., up 42.6% continued its growth in a transformational fashion by achieving increased sales of disposable operating room products. Historically, an outstanding growth company based on its robotic surgery equipment, the company’s sales of supplies this year sustained growth when recessionary conditions reduced hospital investment in major systems.

Of the underperforming holdings in the Fund during this period, many had transformational trends that we feel are still not fully realized in the profits column. For example, General Electric Company (-9.9%) was bought in November at a price substantially identical to that which it held the end of the fiscal year. We expected then, and expect now, that General Electric should succeed in the transformation of the capital position of its extensive financial operations, and thus, bring back acceptable investment returns.

There are many other holdings with interesting potential for their transformations, such as Snap-On Tools, Inc. – the automotive tools specialist – which has developed a new line of tools which include diagnostic capabilities.

The severely competitive conditions of the recessionary environment, the managerial preoccupation with the most efficient use of capital and the necessity of seeking out new approaches to, and sources of, profits all lead to potential transformational business opportunities. But, not all results are satisfactory or even profitable. This is well illustrated by the Fund’s largest realized loss in this fiscal period, the 96% decline in the value of shares in Federal National Mortgage Association, Fannie Mae. During the early phase of the financial crisis of 2008 we believed that Fannie Mae was on the threshold of obtaining new support from proposed legislation discussed at that time by Sen. Dodd and Congressman Frank. No such support emerged and, instead, the government threw the company into a conservatorship. While still not fully resolved, this wiped out virtually all the market value. This is not an economic event which we would anticipate being repeated. Other negative performers in the fiscal year period included Ambac Financial Group (-51.1%), Helix Energy Solutions (-51.3%) and Flotek Industries

(-67.4%).

The essence of the transformation concept of investing is to recognize and select important and promising changes in corporate culture. Many have provided outstanding investment gains and we believe that the Fund’s brief experience suggests that it is well positioned to potentially benefit by strong continuing trends in a recovering economy. We appreciate the interest of our investors in our strategy.

Sincerely,

Stephen A. Lieber, Portfolio Manager

Sarah Hunt, Associate Portfolio Manager

The Fund may invest in smaller and medium size companies, which involve additional risks such as limited liquidity and greater volatility. The Fund may also invest in micro-cap company stocks which are more volatile than those of larger companies and tend to perform poorly during times of economic stress. The Fund may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. The Fund may invest in debt securities which typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. The fund may also use options and future contracts, which have risks associated with unlimited losses of the underlying holdings due to unanticipated market movements and failure to correctly predict the direction of securities prices, interest rates and currency exchange rates.

Please refer to the schedule of portfolio investments for fund holding information. Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. Current and future portfolio holdings are subject to risk.

The NASDAQ Composite Index is a market capitalization-weighted index that is designed to represent the performance of the National Market System which includes over 5,000 stocks traded only over-the-counter and not on an exchange. You cannot invest directly in an index.

28

| |

Alpine Dynamic Balance Fund |

|

|

| | | | | | | | | | | | | |

|

Comparative Annualized Returns as of 10/31/09 (Unaudited) |

| | | | | | | | | | | | | |

| | 6 Months (1) | | 1 Year | | 3 Years | | 5 Years | | Since Inception

(6/7/2001) | |

|

|

|

|

|

|

|

|

|

|

|

|

Alpine Dynamic Balance Fund | | 11.28 | % | | 11.03 | % | -8.48 | % | -1.45 | % | 2.61 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

S&P 500 Index | | 20.04 | % | | 9.80 | % | -7.02 | % | 0.33 | % | -0.59 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lipper Mixed-Asset Target Allocation Growth Funds Average | | 18.00 | % | | 15.96 | % | -3.22 | % | 2.05 | % | 1.65 | % | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Lipper Mixed-Asset Target Allocation Growth Funds Ranking | | N/A | | | 553/651 | 535/540 | 438/442 | 67/278 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gross Expense Ratio: 1.25%(2) | | | | | | | | | | | | | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net Expense Ratio: 1.25%(2) | | | | | | | | | | | | | |

| |

| |

(1) | Not annualized. FINRA does not recognize rankings for less than one year. |

(2) | As disclosed in the prospectus dated February 27, 2009. |

Performance data quoted represents past performance and is not predictive of future results. Investment return and principal value of the Fund fluctuate, so that the shares, when redeemed, may be worth more or less than their original cost. Performance current to the most recent month end may be lower or higher than performance quoted and may be obtained by calling 1-888-785-5578. Performance data shown does not reflect the 1.00% redemption fee imposed on shares held for fewer than 2 months. If it did, total returns would be reduced.

The S&P 500 Index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries. The Lipper Mixed-Asset Target Allocation Growth Funds Average is an average of Funds that, by portfolio practice, maintain a mix of between 60%–80% equity securities, with the remainder invested in bonds, cash, and cash equivalents. Lipper Rankings for the periods shown are based on Fund total returns with dividends and distributions reinvested and do not reflect sales charges. The S&P 500 Index and the Lipper Mixed-Asset Target Allocation Growth Funds Average are unmanaged and do not reflect the deduction of fees associated with a mutual fund, such as investment adviser fees. The performance for the Dynamic Balance Fund reflects the deduction of fees for these value-added services. Investors cannot directly invest in an index.

|

To the extent that the Fund’s historical performance resulted from gains derived from participation in initial public offerings (“IPOs”) and/or secondary offerings, there is no guarantee that these results can be replicated in future periods or that the Fund will be able to participate to the same degree in IPO/Secondary offerings in the future. |

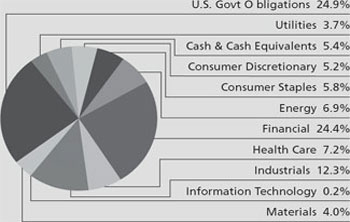

Portfolio Distributions* (Unaudited)

| | | | |

Top 10 Holdings* (Unaudited) | | | |

1. | U.S. Treasury Bond,

5.250%, 11/15/2028 | | 14.42 | % |

2. | U.S. Treasury Bond,

6.000%, 02/15/2026 | | 6.65 | % |

3. | CONSOL Energy, Inc. | | 4.57 | % |

4. | U.S. Treasury Note,

5.000%, 08/15/2011 | | 3.90 | % |

5. | JPMorgan Chase & Co. | | 3.45 | % |

6. | Simon Property Group, Inc. | | 2.91 | % |

7. | Johnson & Johnson | | 2.89 | % |

8. | Eagle Materials, Inc. | | 2.20 | % |

9. | Allegheny Energy, Inc. | | 2.11 | % |

10. | State Street Corp. | | 1.97 | % |

| | |

| |

* | Portfolio holdings and sector distributions are as of 10/31/09 and are subject to change. Portfolio holdings are not recommendations to buy or sell any securities. Top 10 Holdings do not include short-term investments. Portfolio Distributions percentages are based on total investments and Top 10 Holdings percentages are based on total net assets. |

| |

29

| |

Alpine Dynamic Balance Fund |

|

| | |

|

|

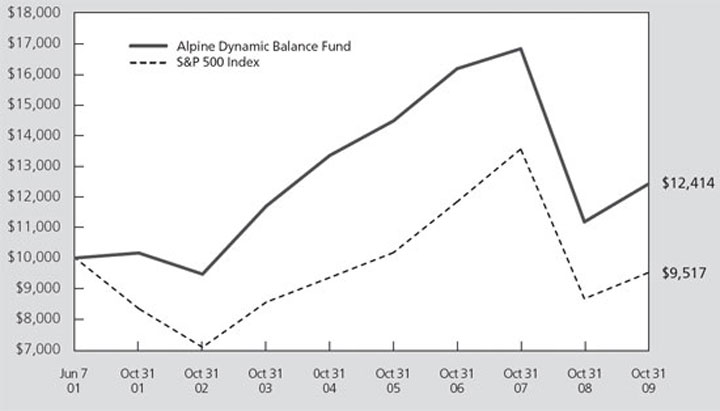

Value of a $10,000 Investment (Unaudited) |

|

|

This chart represents a comparison of a hypothetical $10,000 investment in the Fund versus a similar investment in the Fund’s benchmark. The graph and the table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment performance reflects the waiver and recovery of certain fees. Without the waiver and recovery of fees, the Fund’s total return would have differed.

Dear Investor:

The Alpine Dynamic Balance Fund provided an 11.03% return for its fiscal year ending October 31, 2009. This return compared with 9.80% from the Standard & Poor’s 500 Index and the 15.96% from the Lipper Mixed-Asset Target Allocation Growth Fund Index. Since inception on June 7, 2001, the Fund has provided a 2.61% average annual rate of return as compared with -0.59% for the Standard & Poor’s 500 Index and 1.65% for the Lipper Mixed-Asset Target Allocation Growth Fund Index.

The Dynamic Balance Fund investments include diverse strategies and types of investment vehicle. Central to the program is the continuing utilization of a substantial portion of the Fund holdings in United States Treasury obligations; 25% of assets at fiscal year end. This is an actively managed segment of the portfolio aimed to add to total return by taking advantage of cyclical trends in the markets for U.S. Treasury obligations while providing income.

A major component of the Fund strategy is investing in stocks of comparatively large capitalization companies

which have demonstrated long term records of substantial dividend payment and increases. These holdings accounted for 40% of the portfolio at fiscal year end. Another segment is aimed at participating in cyclical opportunities for corporate profits growth. These stock holdings accounted for 30% of the portfolio at fiscal year end.

Within the different equity investment segments, sector commitments included real estate investment trusts and operating companies (10.6%), diversified financial services (4.8%), and commercial banks (4.5%). Portfolio results varied significantly across these different categories of investment, reflecting the high level of volatility in the fiscal year. Among equities, the top performer during our fiscal year was Temple Inland Inc., a packaging company whose shares provided a 111.3% total return. Ventas Inc., a real estate operating company, produced a 96.2% return, while ProLogis, a distribution center real estate operator, brought a 78.4% return. Among financials, the outstanding return was 75.7% in the shares of Goldman Sachs, followed by title insurer Fidelity National Financial Inc. with a 69.3% return. A variety of issues produced significant returns; with 24

30

| |

Alpine Dynamic Balance Fund |

|

| | |

different holdings providing returns ranging from 30% to 111%. Historically low volatility issues had important recoveries after the fall of prices in 2008. Illustratively, our holdings in the Walgreen Company total return was 56.3%, Darden Restaurants, 43.2%, American Electric Power, 22.4%, Honeywell International, 20.6%, J.C. Penney, 19.7%, 3M Company, 18.9%, Colgate Palmolive, 17.7%.

The major challenged area of the portfolio was in financials. Bank of America (-36.6%), Wells Fargo (-4.5%) and regional institutions, such as Southside Bankshares, Inc. (-4.3%), New York Community Bank (-20.1%), and Webster Financial (-40.9%), encountered severe challenges to their financial status and adverse volatility for their shares.