Item 1. Report to Stockholders.

2 Q1 2020 Annual Report

THE WEITZ PHILOSOPHY

Finding quality at a discount

There are no shortcuts in value investing. At Weitz, we dig for opportunities using a robust quality scoring process. We analyze hundreds of ideas to find strong, well-managed but undervalued companies that offer reasonable risk-adjusted returns. It’s simple – but it’s not easy. We do the due diligence, analyze, ask tough questions and push for answers. We wait for the right opportunities. Then, and only then, do we invest your money.

Fundamental Research-Driven Process

Our research-driven investment approach means deeply understanding our investable universe so we can capitalize on opportunities that arise out of market inefficiencies. Each of our analysts focuses on finding opportunities in specific industries, ensuring deep, ongoing research within their own areas of expertise. We also encourage a generalist mentality where all investment team members vet new ideas. All investment decisions are backed by thorough analysis, logical strategies, extensive debate and our team’s commitment to long-term growth.

Bottom-Up Focus

Our focus is on finding well-run companies with strong fundamentals and outstanding long-term prospects. Valuation is our North Star. When a security is selling at a significant discount to its intrinsic value, that’s when we buy. And when it’s not selling at a discount, we have the discipline and patience to wait for the price to come our way.

High-Conviction Investing

We believe there are a limited number of great investment ideas and that intrinsic value doesn’t change with the daily ebbs and flows of the market. Our high-conviction approach means we know what we own inside and out, allowing our funds to be highly concentrated.

Today we are responsible for approximately $3 billion in investments for our shareholders – individuals, corporations, pension plans, foundations and endowments. And our commitment remains the same: to put your goals first. Always. We do so through our expertise, our flexibility, and our drive to uncover investments that can help you preserve and grow wealth.

We’re right beside you

Weitz employees have a strong commitment of investing their own assets in our mutual funds. By aligning our goals with yours, you can have confidence that we’re treating your money as if it were our own.

Q1 2020 Annual Report 3

Beginning on January 1, 2021, paper copies of the Fund’s shareholder reports will no longer be sent by mail unless specifically requested from the Fund or from your financial intermediary (such as a financial adviser). Instead, the reports will be made available at weitzinvestments.com and you will be notified by mail each time a report is posted. You will continue to receive other Fund regulatory documents (such as prospectuses or supplements) in paper unless you have elected to receive all Fund documents electronically.

If you would like to continue to receive the Fund’s future shareholder reports in paper free of charge after January 1, 2021, you may make that request (1) by contacting your financial intermediary; or (2) if you invest directly with the Fund, by calling 800-304-9745.

If you already receive shareholder reports and other Fund documents electronically, you will not be affected by this change, and you need not take any action. If you do not receive shareholder reports and other Fund documents electronically but would like to do so, contact your financial intermediary or, if you invest directly with the Fund, call 800-304-9745. An election to receive shareholder reports electronically will apply to all Funds held with the Weitz Funds and may apply to all funds held with your financial intermediary.

The management of Weitz Funds has chosen paper for the 84 page report from a paper manufacturer certified under the Sustainable Forestry Initiative ® standard.

Portfolio composition is subject to change at any time and references to specific securities, industries, and sectors referenced in this report are not recommendations to purchase or sell any particular security. Current and future portfolio holdings are subject to risk. See the Schedules of Investments included in this report for the percent of assets in each of the Funds invested in particular industries or sectors.

4 Q1 2020 Annual Report

VALUE MATTERSApril 7, 2020 Dear Fellow Shareholder,

The first quarter of 2020 felt like stepping through the looking glass into another world. COVID-19 is the story of the moment. Attempts to slow its spread have put the country and much of the world in a kind of “time out” that has paralyzed economies and raised anxiety levels everywhere. Our first priorities are to make sure that our colleagues, friends, families and clients are physically safe and that we are as prepared as possible for a siege that could last weeks or months.

The daily reports on new cases as well as the shortages of tests and medical supplies are keeping the country on edge. Healthcare systems in a growing number of hot spots are struggling to build capacity ahead of the mounting cases. The good news is that the country has taken notice, and addressing the shortages is now a priority. New and more widely available tests should allow for more effective policy responses. Increased production of personal protective equipment (PPE) for medical professionals, ventilators and thousands of temporary hospital beds will help us manage through the crisis. Potential drug treatments are being tested, and while the ultimate defense, an effective vaccine, may be a year or more away, it seems highly likely that one will be developed. When that happens, it will be clear that we can coexist with this virus, if not eradicate it.

It will likely take a while to get the upper hand on the virus, but we do not doubt that the country will get through it. In the meantime, our business continuity strategy has enabled our team to work remotely without disruption. As always, we continue our fundamental research and business model analysis. And, we stay in contact with company management teams, with a focus on understanding the impact this new reality will have on their businesses. The future will be different for most companies, and we aspire to own the ones that can thrive in a post-COVID world.

1st Quarter Results

The volatility in stock and bond markets in the first quarter was extreme. A number of companies’ stock prices fell over 50%, rallied significantly and then sagged again as rumors, margin calls and other non-fundamental factors played havoc with trading. The quarterly performance reflected in the table following this letter could have been very different if the quarter had ended on a different day, and they will no doubt be out of date by the time you read this letter. Quarterly results are rarely predictive of longer-term results, and all we can tell for sure is that investors are extremely confused and afraid.

Our stock funds were all down for the quarter, though some fared better than others, which was at least partly due to the portfolio weightings of some very large, mature companies that generally held up better than smaller companies. One bright spot in terms of relative performance was the Partners III Opportunity Fund, which is structurally different from our other equity portfolios, being partly hedged and generally less exposed to the stock market. But it was not immune from the carnage. [See Partners III’s portfolio holdings later in this report for securities sold short, which includes hedges against, and therefore less overall exposure to, the S&P 500.]

Our fixed income funds, in spite of severe bond market chaos, did their jobs of providing ballast for investors’ portfolios. Returns ranged from small gains for the Ultra Short Government Fund and the Nebraska Tax-Free Income Fund to small declines for the Short Duration Income Fund and the Core Plus Income Fund. The leaders of our fixed income team, Tom Carney and Nolan Anderson, made some very opportunistic purchases during the quarter, and though corporate and asset-backed bond prices are currently depressed, we believe shareholders will benefit from these portfolio maneuvers. Tom and Nolan will elaborate further in their Fixed Income Insights.

We do not relish using red ink in our reports, but we feel good about the stocks and bonds that we own and the moves that our portfolio managers made during the quarter. This update is short on specific investments details, but our portfolio managers provide a lot of information about this busy quarter in their individual fund perspectives.

"The future will be different for most companies, and we aspire to own the ones that can thrive in a post-COVID world."

Changing Changelessness

So, we have a recession (“a rose by any other name…”). It is a big one that came on suddenly. But with a combined 80+ years of industry experience between the two of us, we’ve managed through many recessions and bear markets. Whatever the cause, the stock and bond market reactions are ultimately driven by people, and people react in predictable ways. Hence the excuse to dust off “changing changelessness,” the favorite catchphrase of my (Wally’s) high school Latin teacher, Dr. Romeo (yes, that was his real name).

There are some unique aspects of the current economic situation, including the threat of catching a potentially deadly disease. And while the odds of becoming infected and developing dangerous symptoms is low, the disease is new and not well understood. So, understandably, anxiety is high. On top of that, there’s an oil price war raging between Russia and Saudi Arabia while, simultaneously, demand for oil has collapsed. This has a very specific and devastating impact on the domestic “oil patch” (and those who live in it, serve it and lend to it).

Q1 2020 Annual Report 5

What makes the current situation so jarring is that the economy more or less shut down overnight. Generally, recessions begin in a weak sector or two, spread to others and gradually affect the whole economy. This time, as communities across the country began to stay at home, it was as if the power switch for the economy was suddenly flipped off.

It is small comfort that St. Louis Fed president James Bullard prefers to call this recession a “National Pandemic Adjustment Period.” The disruption to lives and economic activity feels like the real thing. But the country has, in effect, been put into an “induced coma” to allow it to heal, making it plausible that the patient’s recovery may be quicker and more robust once the coma is lifted. That is the hope of policymakers. Extraordinary monetary and fiscal measures are now in place to sustain the economy during this period. Stimulative measures (e.g. infrastructure spending) are likely to follow to make sure the recovery is powerful.

The Liquidity Crisis

In response to the Great Financial Crisis of 2008-09, the Federal Reserve (Fed) lowered interest rates and flooded the markets with newly created money. That was a reasonable policy response, and the economy recovered. By keeping credit cheap and readily available long after the crisis was over, they arguably encouraged imprudent lending and excessive borrowing.

A great deal of borrowing is done on a short-term basis because short rates are generally lower than longer-term rates. The expectation is that collateral will maintain its value and loans will be renewed or extended. Periodically, lenders become concerned about the creditworthiness of borrowers and “tighten” or withdraw credit. This results in forced sales of collateral, including stocks and bonds. In extreme cases, distress selling of assets turns into a figurative run on the bank. The sudden shutdown of economic activity in response to the virus has raised the prospect of loan defaults by individuals and companies and has triggered a classic liquidity crisis.

Fortunately, the Fed and Treasury learned important lessons during the last crisis, and being independent entities, they have been able to swing into action very quickly. Their focus has been on the bond markets, which are much larger than the stock market and more crucial to day-to-day economic activity. They started with treasuries and AAA bonds. Stabilizing the market for the most risk-averse investors was key to restoring faith in the rest of the credit markets. Multiple trillions of dollars have been injected to assure credit is available to desperate, but creditworthy, borrowers. Most of this money is not at risk and will not be lost by the government, but its presence restores confidence.

This process is not complete as of the end of March, but there are signs that the credit markets are settling down and reopening for normal lending and borrowing. This is a critical first step to addressing the bigger issue of the recession. Credit must be available for normal business activities and for companies that must make workout arrangements with their creditors. When buyers and sellers can transact because they want to and not because they have to, business can return to normal. With an end to the liquidity crisis, hopefully within a few weeks, the country will be able to address a more familiar and manageable challenge – the recession.

Lower Earnings, Changing Business Models, Opportunities for Patient Investors

Investing in any environment, but particularly during a recession, requires patience, discipline and realistic expectations. But as history has shown time and time again, it can be done. Based on the assumption that the economy will remain subdued for months, we are building a prolonged recession into the earnings models we use to estimate business values. Each business is different, and we are just beginning to understand how companies are impacted by people staying home as well as the potential benefits to come from the smorgasbord of fiscal and monetary programs. If Bullard and other economists are correct and we have a V-shaped recovery, that will be a bonus.

One of the complicating factors is that the public health prescription of shutting down the economy and having everyone stay at home is the flip side of the economic health prescription of getting everybody back to work. Hopefully, with widespread testing and effective treatment, our policymakers will find the right balance between isolating the sick, protecting the most vulnerable and carefully reopening the country. The polarized

“Investing in any environment, but particularly during a recession, requires patience, discipline and realistic expectations.”

political climate may complicate the policy discussion, but whether done well or poorly, the U.S. (and the rest of the world) will eventually reopen for business and life.

Investing in the Thick of the Crisis

We are remaining invested. Given the extreme uncertainty as to the length and depth of the health crisis and economic recession, we are being conservative in our assessments of business values. On the other hand, in periods of market distress, stock prices usually overshoot to the downside and subsequent recoveries can be just as explosive to the upside. Bear markets scare some investors and wear out others. At some point, the markets turn, usually for no apparent reason. We do not know when this bear will end, nobody does. But we firmly

6 Q1 2020 Annual Report

believe that if we try to sidestep it and to “get back in when the coast is clear,” we will miss the initial snapback and an important part of potential future returns.

We are emphasizing quality over absolute cheapness. All stocks have been affected by the recent decline, and some of those most obviously impacted by the pandemic look extraordinarily cheap. Investors have a way of extrapolating the negatives of the recent past far into the future and pricing stocks accordingly. We are looking for mispriced assets, but we are not interested in any stock for which the investment thesis begins, “If this company survives the recession….” On the contrary, the recent extreme volatility has created an opportunity for us to buy more of some of our favorite stocks and to establish positions in some great businesses which we have aspired to own for some time. These very high-quality stocks may not bounce as rapidly initially, but we believe they will provide very strong returns for our portfolios over the next 5-10 years.

We are trying to anticipate behavioral changes by consumers and workers. One of the most interesting questions our investment team has been discussing is “How will consumer behavior change as a result of the pandemic?” Human nature does not seem to change over time, but an extended period of working remotely and social distancing may have lasting impacts. Attitudes toward the role of government may also change. The relative values of Netflix vs. movie theaters may seem clear, but all industries will be affected. We are trying to be imaginative about potential changes and to be humble about our ability to predict.

Management is key. Quality of management and corporate culture are always important criteria for evaluating a business. We need to be able to trust management to keep the balance sheet strong and adjust the business model to fit changing conditions. With the “downside” protected (first things first!), some of our companies will be able to “play offense.” Berkshire Hathaway is famous for being there to “help” other companies in a crisis. Warren Buffett has made legendary investments in times of financial stress as has John Malone at Liberty Media. Other CEOs have also been adept at acquiring assets and businesses opportunistically.

Recognizing a market bottom. The stock market always turns back up before it is clear that the danger has passed. All investors will be watching the shape of the infection curve and trying to predict the end of the COVID crisis. There will probably be several false starts and the market’s bottoming process may take many months. We will not be able to “call the bottom” accurately, but that is not our objective.

Our goals are to (a) preserve capital, (b) understand evolving risks and opportunities, and (c) position our portfolios for strong returns over the coming years.

Outlook

As a country, we are experiencing something new and surreal, and the psychological trauma may be more significant than the physical or economic. As investors, we are less certain than usual about how near-term events will unfold. The good news is that the country’s capacity to respond to the healthcare emergency is ramping up rapidly. The human ingenuity being displayed in dealing with shortages and developing treatments has been very encouraging. The government has made unprecedented financial and policy responses. Stories of extraordinary work by healthcare workers and ordinary people are amazing. China and other Asian countries that were affected early are beginning to reopen. There are logical reasons for hope and optimism even if our fears and uncertainty persist.

“There are logical reasons for hope and optimism even if our fears and uncertainty persist.”

We are especially thankful to our colleagues who are capably working under new and unusual circumstances and for our clients who have been very supportive through this entire situation. We are in this together, and we believe that we will get through it and return to a changed, but recognizable, version of normal.

As always, we’re here to support you and want to ensure you’re as informed as possible. Please don’t hesitate to reach out to your Weitz representative if we can be of assistance.

Best regards,

|  |

| | |

| Wally Weitz | Brad Hinton |

wally@weitzinvestments.com | brad@weitzinvestments.com |

As of 3/31/2020, the following portfolio company constituted a portion of the net assets of Balanced Fund, Hickory Fund, Partners III Opportunity Fund, Partners Value Fund, and Value Fund as follows: Berkshire Hathaway Inc.-Class B: 2.5%, 0%, 11.1%, 7.1%, and 7.4%.

Over time, the Liberty Media family of companies has included a large number of entities, including these current portfolio companies, which as of 3/31/2020, constituted a portion of the net assets of Balanced Fund, Hickory Fund, Partners III Opportunity Fund, Partners Value Fund, and Value Fund as follows:

• Charter Communications, Inc.-Class A: 1.8%, 0%, 0%, 0%, and 0%.

• GCI Liberty, Inc.-Class A: 0%, 4.0%, 0.5%, 0%, and 0%.

• Liberty Braves Group-Series A & C: 0%, 1.3%, 0%, 0%, and 0%.

• Liberty Broadband Corp.-Series A & C: 0%, 9.0%, 5.5%, 6.9%, and 0%.

• Liberty Broadband Corp.-Series C: 0%, 0%, 0%, 0%, and 7.1%.

• Liberty Formula One Group-Series A & C: 0%, 1.2%, 0%, 0%, and 0%.

• Liberty Global plc-Class C: 0%, 3.0%, 4.6%, 3.0%, and 2.0%.

• Liberty Latin America Ltd.-Class C: 0%, 2.8%, 0.7%, 2.4%, and 0%.

• Liberty SiriusXM Group-Series A & C: 0%, 4.3%, 3.6%, 4.4%, and 0%.

• Liberty SiriusXM Group-Series C: 0%, 0%, 0%, 0%, and 2.7%.

Qurate Retail, Inc.-Series A: 0%, 2.4%, 1.0%, 0%, and 0%.

Portfolio composition is subject to change at any time. Current and future portfolio holdings are subject to risk.

Q1 2020 Annual Report 7

This page intentionally left blank

8 Q1 2020 Annual Report

DISCLOSURES

Data quoted is past performance and current performance may be lower or higher. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. All investments involve risks, including possible loss of principal. Please visit weitzinvestments. com for the most recent month-end performance.

Investment results reflect applicable fees and expenses and assume all distributions are reinvested but do not reflect the deduction of taxes an investor would pay on distributions or share redemptions. Net and Gross Expense Ratios are as of the Fund’s most recent prospectus. Certain Funds have entered into fee waiver and/or expense reimbursement arrangements with the Investment Advisor. In these cases, the Advisor has contractually agreed to waive a portion of the Advisor’s fee and reimburse certain expenses (excluding taxes, interest, brokerage costs, acquired fund fees and expenses and extraordinary expenses) to limit the total annual fund operating expenses of the Class’s average daily net assets through Contractual Expiration Date of 07/31/2020. The Net Expense Ratio reflects the total annual fund operating expenses of the Fund after taking into account any such fee waiver and/or expense reimbursement, if any; total returns would have been lower had there been no waivers or reimbursements.

Performance quoted for the Balanced, Partners Value and Value Funds’ Institutional Class shares before their inception is derived from the historical performance of the Investor Class shares, which have not been adjusted for the expenses of the Institutional Class shares, had they, returns would have been different.

Performance quoted for the Partners III Opportunity and Short Duration Income Funds’ Investor Class shares before their inception is derived from the historical performance of the Institutional Class shares, which have not been adjusted for the expenses of the Institutional Class shares, had they, returns would have been different.

Index performance is hypothetical and is shown for illustrative purposes only. You cannot invest directly in an index. See page 81 for a description of all indices. The Since Inception return for the Russell 1000 Value and CPI +1% is from 5/31/1986 and 12/31/1988, respectively. All other indices Since Inception return are since the Fund’s inception. The inception date of the Bloomberg Barclays 1-3 Year U.S. Aggregate and 5-Year Municipal Bond was 12/31/1992 and 1/29/1988, respectively.

On 12/29/2006, the Nebraska Tax-Free Income Fund succeeded to substantially all of the assets of Weitz Income Partners Limited Partnership. On 12/31/1993, Partners Value Fund succeeded to substantially all of the assets of Weitz Partners II Limited Partnership. On 12/30/2005, Partners III Opportunity Fund succeeded to substantially all of the assets of Weitz Partners III Limited Partnership. The investment objectives, policies and restrictions of the Funds are materially equivalent to those of the Partnerships, and the Partnerships were managed at all times with full investment authority by the Investment Adviser. The performance information includes performance for the Partnerships. The Partnerships were not registered under the Investment Company Act of 1940 and, therefore, were not subject to certain investment or other restrictions or requirements imposed by the 1940 Act or the Internal Revenue Code. If the Partnerships had been registered under the 1940 Act, the Partnerships’ performance might have been adversely affected.

Effective 12/16/2016, the Ultra Short Government Fund revised its principal investment strategies. Prior to that date, the Fund operated as a “government money market fund” and maintained a stable net asset value of $1.00 per share. Performance prior to 12/16/2016 reflects the Fund’s prior principal investment strategies and may not be indicative of future performance results.

Effective 12/16/2016, the Short Duration Income Fund revised its principal investment strategies. Since that time the Fund has generally maintained an average effective duration between one to three and a half years. Prior to that date, the Fund maintained a dollar–weighted average maturity of between two to five years. Performance prior to 12/16/2016 reflects the Fund’s prior principal investment strategies and may not be indicative of future performance results.

Effective 03/29/2019, the Hickory Fund invests the majority of its assets in the common stock of medium–sized companies, which the Fund considers to be companies with a market capitalization, at the time of initial purchase, of greater than $1 billion and less than or equal to the market capitalization of the largest company in the Russell Midcap Index. Prior to that date, the Fund invested the majority of its assets in the common stock of smaller– and medium–sized companies, which the Fund considered to be companies with a market capitalization, at the time of initial purchase, of less than $10 billion.

Q1 2020 Annual Report 9

| | | | | | | | | | |

| | | | ANNUALIZED | | | |

| | | | | | Since Fund

| Inception | Net | Gross |

| EQUITY | QTD | YTD | 1 YR | 5 YR | 10 YR

| Inception* | Date | Expense | Expense

|

| Hickory Fund (WEHIX) | (27.69)% | (27.69)% | (15.67)% | (2.20)% | 5.85% | 8.20% | 4/1/1993* | 1.09% | 1.27% |

Russell Midcap® | (27.07) | (27.07) | (18.31) | 1.85 | 8.77 | 9.52 | | | |

| Partners III Opportunity Fund - Investor (WPOIX) | (16.30) | (16.30) | (6.40) | 0.70 | 7.33 | 11.55 | 8/1/2011 | 2.13 | 2.13 |

| Partners III Opportunity Fund - Institutional (WPOPX) | (16.17) | (16.17) | (5.83) | 1.22 | 7.72 | 11.66 | 6/1/1983* | 1.56 | 1.56 |

S&P 500® | (19.60) | (19.60) | (6.98) | 6.73 | 10.53 | 10.42 | | | |

Russell 3000® | (20.90) | (20.90) | (9.13) | 5.77 | 10.15 | 10.14 | | | |

| Partners Value Fund - Investor (WPVLX) | (26.32) | (26.32) | (14.82) | (2.00) | 6.01 | 10.64 | 6/1/1983* | 1.09 | 1.27 |

| Partners Value Fund - Institutional (WPVIX) | (26.26) | (26.26) | (14.59) | (1.75) | 6.16 | 10.68 | 7/31/2014 | 0.89 | 1.07 |

S&P 500® | (19.60) | (19.60) | (6.98) | 6.73 | 10.53 | 10.42 | | | |

Russell 3000® | (20.90) | (20.90) | (9.13) | 5.77 | 10.15 | 10.14 | | | |

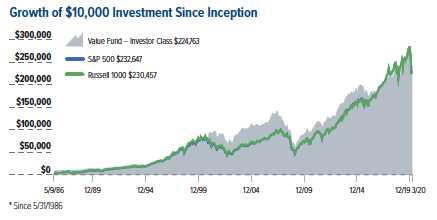

| Value Fund - Investor (WVALX) | (18.98) | (18.98) | (5.77) | 2.53 | 8.27 | 9.61 | 5/9/1986* | 1.09 | 1.23 |

| Value Fund - Institutional (WVAIX) | (18.94) | (18.94) | (5.55) | 2.76 | 8.41 | 9.65 | 7/31/2014 | 0.89 | 1.08 |

S&P 500® | (19.60) | (19.60) | (6.98) | 6.73 | 10.53 | 9.72 | | | |

Russell 1000® | (20.22) | (20.22) | (8.03) | 6.22 | 10.39 | 9.69 | | | |

| | | | | | | | | | |

| | | | ANNUALIZED | | | |

| | | | | | Since Fund | Inception | Net | Gross |

| ALLOCATION | QTD | YTD | 1 YR | 5 YR | 10 YR | Inception* | Date | Expense | Expense |

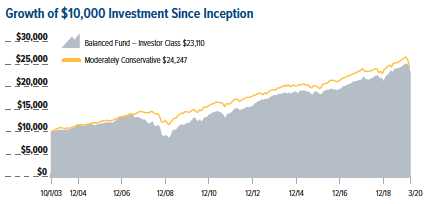

| Balanced Fund - Investor (WBALX) | (7.95)% | (7.95)% | 0.35% | 3.77% | 6.01% | 5.20% | 10/1/2003* | 0.85% | 1.30% |

| Balanced Fund - Institutional (WBAIX) | (7.89) | (7.89) | 0.45 | 3.79 | 6.02 | 5.21 | 3/29/2019 | 0.70 | 0.97 |

Morningstar Moderately Conservative Target Risk | (8.16) | (8.16) | (0.81) | 3.56 | 5.11 | 5.51 | | | |

| | | | | | | | | | |

| | | | ANNUALIZED | | | |

| | | | | | Since Fund

| Inception | Net | Gross |

| FIXED INCOME | QTD | YTD | 1 YR | 5 YR | 10 YR

| Inception* | Date | Expense | Expense

|

| Core Plus Income Fund - Investor (WCPNX) | (3.12)% | (3.12)% | 1.38% | 2.70% | N/A% | 2.89% | 7/31/2014* | 0.50% | 1.42% |

| Core Plus Income Fund - Institutional (WCPBX) | (2.99) | (2.99) | 1.56 | 2.93 | N/A | 3.11 | 7/31/2014* | 0.40 | 0.96 |

Bloomberg Barclays U.S. Aggregate Bond | 3.15 | 3.15 | 8.93 | 3.35 | N/A | 3.65 | | | |

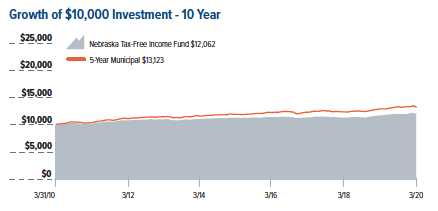

| Nebraska Tax-Free Income Fund (WNTFX) | 0.38 | 0.38 | 2.55 | 1.31 | 1.89 | 4.45 | 10/1/1985* | 0.45 | 0.89 |

Bloomberg Barclays 5-Year Municipal Bond | (1.04) | (1.04) | 2.19 | 2.07 | 2.75 | N/A | | | |

| Short Duration Income Fund - Investor (WSHNX) | (2.19) | (2.19) | 0.26 | 1.27 | 1.81 | 4.82 | 8/1/2011 | 0.55 | 0.92 |

| Short Duration Income Fund - Institutional (WEFIX) | (2.15) | (2.15) | 0.44 | 1.49 | 2.00 | 4.89 | 12/23/1988* | 0.48 | 0.63 |

Bloomberg Barclays 1-3 Year U.S. Aggregate | 1.79 | 1.79 | 4.63 | 1.93 | 1.64 | N/A | | | |

U.S. Consumer Price Index (CPI) Plus 1.00% | 0.69 | 0.69 | 2.56 | 2.82 | 2.74 | 3.49 | | | |

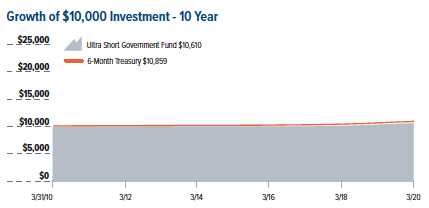

| Ultra Short Government Fund (SAFEX) | 0.75 | 0.75 | 2.44 | 1.16 | 0.59 | 2.36 | 8/1/1991* | 0.20 | 0.61 |

ICE BofAML U.S. 6-Month Treasury Bill | 0.94 | 0.94 | 2.85 | 1.44 | 0.83 | 2.93 | | | |

* Denotes the Funds inception date and the date from which Since Inception Performance is calculated.

10 Q1 2020 Annual Report

April 16, 2020

Dear Fellow Shareholder,

The analogies to describe the year’s first quarter, particularly the month of March, could seemingly fill a book. The unfortunate human and economic drama that continues to unfold across the globe will certainly be forever etched on the world’s collective memory. And while it’s important to provide this update on the markets (as out of date as it may soon become in this rapidly changing environment), our hearts, minds and prayers remain with all of those who have suffered and are suffering the direct human effects of the coronavirus outbreak. It’s also important to remember those who have suffered direct economic consequences resulting from the fight against the disease, including a historic number of job losses. Since the whole world is in this predicament together, hopefully the words from World Health Organization chief Tedros Adhanom Ghebreyesus will bring solace: that the “amazing spirit of human solidarity must become more infectious than the virus itself” and that “we can only succeed together.”

Market Update

The placid beginning to the year, with gently rising stock and bond prices, increasingly became unnerved as evidence grew that COVID-19 would not abide by any national or continental border. The overall market unease that had been rising due to the spread of this invisible enemy escalated on March 8 as Saudi Arabia and Russia initiated an oil price war that led to the biggest oil price decline in decades. In market parlance, a single black swan is a rare sight (just as they’re rare outside of their native Australian habitat), but in March, a viral outbreak and an oil spat among OPEC+ members was akin to two black swan sightings in the same month. If the COVID-19 outbreak in China was like the butterfly effect where a local event had international repercussions, the OPEC+ price war was the Titanic hitting the iceberg. Collapsing aggregate demand due to efforts to slow the spread of the coronavirus was met by an upward supply shock as Saudi Arabia and Russia tried to outmatch each other in flooding the world with oil.

The result was dislocations in both the stock and bond markets which hadn’t occurred since the Great Recession of 2008, and that was quickly morphing into a discussion that “D”, as in Depression, was a more likely descriptor for today. Markets froze and arguably seized up, particularly fixed-income markets, with price discovery becoming challenging. Many mutual funds/index funds and ETFs faced liquidity issues during this period. In order to meet redemption requests, massive bid-lists in the hundreds of millions (looking to sell) were distributed on a Sunday (something that this management has never seen before). Buyers became scarce, if existent at all, and clearing prices for those who had to sell certain types of investments were frequently at significant discounts to not only the price at which they had been valued only a day before but arguably at a meaningful discount to true intrinsic value.

At Weitz, we are pleased to report that we did not have to sell any investments at what we considered to be an unwanted and unwarranted discount. While we may have experienced meaningful (unrealized) markdowns on fixed-income securities we own due to others having to sell them at markdowns, we also benefited from liquidity in the form of U.S. Treasuries and other highly rated securities. We’ve never forgotten the sage advice a long-time shareholder in Indianapolis imparted many years ago about the importance of having real liquidity at the times you need it most.

To help mitigate the market’s liquidity issues, the Federal Reserve (Fed) intervened to support the flow of credit to households and businesses by reducing the Federal Funds rate to a range of 0-0.25% (down 1.5% since year end) and flooding the market with liquidity. These liquidity mechanisms were aimed to support a variety of markets experiencing stress – including Treasuries, agency commercial and residential mortgage-backed securities, corporate bonds, asset-backed securities, municipal bonds, commercial paper, a program to support small businesses and more. “Essentially unlimited” and “we’re not going to run out of ammunition” were comments used by Fed Chair Jerome Powell to reinforce the Fed’s resolve to take drastic action to help support the economy. One area, however, that did not benefit from the recent monetary or fiscal largesse was non-agency mortgage-backed securities, which had a direct impact on long-time portfolio holding Redwood Trust (RWT). Please see our fixed-income funds quarterly commentaries for a more detailed discussion of this and other portfolio-specific topics.

Coupled with the massive fiscal stimulus from Washington, a semblance of calm (albeit with uneasy undertones) settled on the markets by quarter end. One could possibly compare this calm to the eye of a hurricane.

Q1 2020 Annual Report 11

We collectively seem to have survived its first impact, which took the form of a significant liquidity event. The next phase of the storm, while difficult to predict with any certainty, may involve solvency issues related to the economic downshift so many businesses are experiencing. We are preparing for that possibility.

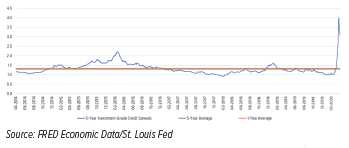

The graph below shows the changes of select Treasury rates over the past quarter and year. Across the yield curve (a line that plots yields / interest rates of bonds with differing maturity dates), interest rates have precipitously declined by a full percent (100 basis points) or more.

Spreads on corporate bonds went sharply upward in the first quarter resulting in meaningful underperformance compared to U.S. Treasury bonds. A broad measure of investment-grade corporate bond spreads, compiled by ICE BofAML, rose as high as 400 basis points, nearly three times its level at year end, before receding to 305 basis points as of March 31. The chart below depicts the path of investment-grade credit spreads for the past five years (blue line) against the one- (orange) and five-year (gray) averages. Overall, corporate bond credit spreads are meaningfully above where they have been over the last five years – and we feel offer compelling value across many industries.

First Quarter Results

Our fixed income funds, despite severe bond market dislocations, did their jobs of providing ballast for investors’ portfolios. Returns ranged from small gains for the Ultra Short Government Fund and the Nebraska Tax-Free Income Fund to small declines for the Short Duration Income Fund and the Core Plus Income Fund.

Like our equity teammates, we do not relish using red ink in our reports. Negative returns are frustrating, but they often come with a proverbial silver lining. When securities prices are being set as much (or more) by fear than reality, it can present opportunities for those able and willing to take advantage of dislocations between price and value. We believe that the net effect of any unrealized depreciation (which we generally expect to recover at or before maturity) on the investments we already own and the new investments that have been added to the portfolios have meaningfully improved our forward return profile.

For additional insights, please see this quarter’s Value Matters from Co-Chief Investment Officers Wally Weitz and Brad Hinton. We are arguably biased, but we think the message is particularly insightful this quarter. Also, please review the equity and balanced funds’ Quarterly Commentaries for detailed analysis around specific moves our equity portfolio managers made during the quarter.

Unintended Consequences

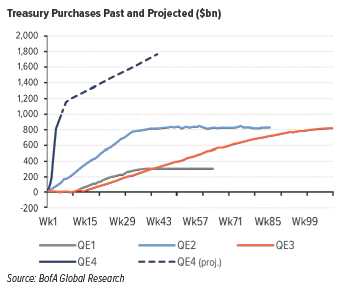

The following two charts present topics to analyze in depth another day – but they are ones we will be monitoring in the months and quarters ahead. In an effort to support the flow of credit in the U.S. financial system, the Fed has embarked on its largest quantitative easing program ever, projected to be orders of magnitude larger than previous iterations. Its balance sheet could reach a previously unfathomable $9 trillion, more than double where it stood at the end of 2019 and $8 trillion higher than its level prior to the Great Recessison.

The Fed is presently fighting the specter of deflation, but its ugly twin, inflation, may reappear sometime in the not-too-distant future with damaging purchasing power implications for fixed-income investors. Even if the health pandemic recedes sooner than some predict, governments around the globe are likely to continue their elevated spending whether or not it remains necessary to do so. Worries of a deflationary bust might quickly turn into an almighty inflationary boom.

12 Q1 2020 Annual Report

Outlook – what a difference a month can make

In several of our previous quarterly correspondence pieces, we had bemoaned the lack of favorable risk/ reward opportunities to deploy capital on behalf of our shareholders (see the “price is what you pay – value is what you receive” section in our Q4 2019 Fixed Income Insights on our website). And as the second month of the new year was ending, we had considered penning a commentary letter about how poor forward returns appeared at the time. Well, March came crashing upon all of us as rising fear about the coronavirus invasion turned markets into what seemed like a version of Rod Serling’s Twilight Zone (specifically 1960’s classic The Monsters are Due on Maple Street, in which mysterious, frightening events suddenly turn a neighborhood upside down). The financial markets became unnerved and increasingly fearful. The U.S. credit default swap index on North American investment grade debt (often dubbed the ‘fear gauge’) that was referenced in our previous Fixed Income Insights went from an all-time low to a multi-year high.

The result has been a rapid repricing of credit risk that has meaningfully and favorably shifted the risk/ reward relationship. At quarter end, the forward returns (as measured by yield-to-worst) for our fixed-income portfolios are at levels they have not been at in many years. We believe this is a solid starting place.

In our fixed income investments, we strive to (a) preserve capital, (b) maintain a strong liquidity position, (c) understand evolving risks and opportunities, (d) selectively take advantage of favorable risk/reward opportunities, and (e) conduct consistent, thorough research and credit surveillance.

Q1 2020 Annual Report 13

While these are difficult times, rest assured that we remain ready to take advantage of any further valuation disparities that may develop, and we strive to remain your trusted partner.

|  |

| | |

| Tom Carney | Nolan Anderson |

tom@weitzinvestments.com | nolan@weitzinvestments.com |

As of 3/31/2020, the following portfolio company constituted a portion of the net assets of Balanced Fund, Core Plus Income Fund, Hickory Fund, Nebraska Tax-Free Income Fund, Partners III Opportunity Fund, Partners Value Fund, Short Duration Income Fund, Ultra Short Government Fund and Value Fund as follows: Redwood Trust, Inc.: 0.5%, 1.3%, 1.7%, 0%, 1.1%, 1.5%, 2.1%, 0%, and 0%.

Portfolio composition is subject to change at any time. Current and future portfolio holdings are subject to risk.

Definitions: Investment Grade Bonds are those securities rated at least BBB- by one or more credit ratings agencies. Non-Investment Grade Bonds are those securities (commonly referred to as “high yield” or “junk” bonds) rated below BBB- by two or more credit ratings agencies. Yield to Worst (YTW) is the lowest potential yield that can be received on a bond portfolio without the issuers actually defaulting.

14 Q1 2020 Annual Report

CoStar Group: Dominant Services with a World of White Space

By Jon Baker, CFA

CoStar Group is a leading provider of commercial real estate information services. With an army of researchers, a massive proprietary database, and a track record of consistent investment, its services have become essential tools for real estate professionals. The group has built a wide moat that we believe is unlikely to be crossed by any competitor. CoStar Group scores high in our quality assessment and has a clean balance sheet. We have been able to buy the company at what we believe is a significant discount to intrinsic value, making it a prime example of our Quality-at-a-Discount (QuaD) investing approach.

Founded in 1987, the group has grown into the largest provider of data, analytics, and online marketplaces to the commercial real estate industries in the United States and the United Kingdom. CoStar Group currently has three businesses that attract our interest. They are:

| • | CoStar Suite: The group’s original real estate data service. |

| • | LoopNet: A listing venue for for-sale and for-lease commercial properties. |

| • | Apartments.com: Along with related subsequent acquisitions, a collection of online consumer marketplaces serving the U.S. apartment rental market. |

Prior to its 2012 acquisition, LoopNet (at least tangentially) competed with the group’s original service, CoStar Suite. Now under the same roof, a delineation of purpose exists, and the two can invest and grow without collisions of effort.

Weathering the Storm

Before we delve any deeper into the businesses themselves, let’s give reality its due. COVID-19 will likely exact payment in some form from nearly every business we could own. This period of upheaval will undoubtedly impact CoStar’s customers, and their renewal rates –normally above 90% – are unlikely to be spared in the coming year. But as we look at what the business could become over the next decade, we and other owners have several things working in our favor. CoStar has over a billion dollars in cash on the balance sheet and no debt. While management has a history of creating value through acquisitions, they have never mortgaged the company’s future to do so. Each of the group’s three primary businesses dominates its field. They are all plumbing massive, growing markets. They enjoy high incremental margins and earn very attractive returns on capital. Each business has exhibited great operating momentum coming into this period, and none lies directly in the crosshairs of the virus itself.

CoStar Suite

The group’s original data service, CoStar Suite, began as an outsourced research department serving commercial real estate brokerages in the Washington, D.C., area. Over the decades, it expanded along two axes: deepening coverage within existing markets and expanding to new ones. As coverage grew, so too did CoStar’s universe of users, starting with brokers and expanding to lenders, owners, and service providers. New market expansion requires an upfront investment in data gathering, which is expensed through the income statement. Thus, any period of CoStar’s accelerating coverage has taken a chunk out of reported earnings in a way that misrepresents underlying value creation. This may well happen again with an acceleration in Europe, and we would welcome it.

The beating heart of CoStar’s subscription business is a research department some 1,600 strong, tracking 110 billion square feet of real estate across 400 markets and 1,400 submarkets. The annual research budget alone dwarfs the relevant revenue of any competitor. Additionally, CoStar’s own investment in data collection is effectively doubled by input from its subscribers themselves. That user effort is unlikely to be duplicated on a second network, especially one offering only a fraction of CoStar’s audience. This inexorably growing layer cake of data uniquely offers comparability across both geography and time – something no upstart could approach without immense losses over a period of many years. CoStar Suite’s cost to serve each new subscriber is effectively zero, and the cost to research its next geographic market can be leveraged over the largest user base in the industry. With a management team intent on continually growing both subscribers and coverage, we believe CoStar Suite has a global glide path and will never be caught from behind.

LoopNet

Whereas CoStar Suite is a ‘free to submit, pay to view’ subscription-based information service, sister company LoopNet is a ‘pay to submit, free to view’ marketing venue. LoopNet has aggregated the largest audience of commercial real estate professionals in the U.S. To put the tremendous size of its audience in perspective, LoopNet’s web traffic is 22x that of its 50 largest

Q1 2020 Annual Report 15

competitors combined. Anyone wishing to put for-sale or for-lease opportunities in front of that audience must pay the ferryman.

While only about a quarter of CoStar Suite’s size, LoopNet boasts higher margins, has been growing more quickly and is about to benefit from a widened marketing aperture. As international expansion continues, we believe management will want to own information services as well as marketing venues in each geographical region it serves.

Apartments.com

Lastly, and perhaps most importantly, we have 2014 addition Apartments.com and related subsequent acquisitions. These are websites that allow apartment owners to advertise vacancies to apartment hunters. The business reminds us of online travel agent Booking. com’s early years in Europe. Both of these online marketplaces serve as an intermediary, helping two ultra-fragmented groups make sense of one another in a highly efficient manner.

While Apartments.com has large fixed costs, its marginal costs to serve each next renter or landlord approach zero. Thus, topline growth falls disproportionally to the pre-marketing income line, creating additional capacity for marketing investment, which spurs further growth and so on. As the largest player in the U.S., Apartments. com is the only apartment listing platform that can efficiently buy national television advertising. Along with a scaled investment in user experience, the business’s greater branding increases conversion rates on search engine marketing (SEM) investment. Higher conversion means higher returns on SEM and – for an aggressive management team that is not remotely solving for near-term margin maximization – perhaps the ability to tip nearly all other players off the board.

Search-engine marketing (SEM) is the practice of marketing a business using paid advertisements that appear on search engine results pages.

In 2019, Apartments.com and CoStar Group’s other apartment rental websites already had two-thirds click share in the U.S. In second place was the highly leveraged, and now bankrupt, RentPath with 17% share. While RentPath had been aggressively shopped for 18 months, a stalking-horse bid from CoStar Group was the only interest surfaced. It’s likely that CoStar’s acquisition of RentPath will either be approved by the Department of Justice, or RentPath will evaporate (and its volumes potentially move to Apartments.com regardless). If this set of circumstances doesn’t already trouble competitors, they should consider the additional $100 million in marketing expenditure, on top of an already industry-dwarfing $150 million in 2019, that CoStar Group intends to spend this year.

Click share is the number of clicks received compared to the estimated total number of achievable clicks in a search or marketing campaign.

About two-thirds of large apartment communities already advertise on CoStar Group’s rental websites. But as the company continues to invest in both consumer awareness and utility, their share of assisted transactions can continue to deepen. There is also a massive, yet largely untapped, population of smaller communities and independent owners to which CoStar is turning its gaze.

Biggest Threats

As is the case with the online travel agents, Google will be an ever-present threat to the apartment rentals business. However, like Booking.com, Apartments.com’s approach to customer acquisition is SEM-heavy and more closely aligned with Google’s goals than free-riding marketing models. In addition, Apartments.com has access to real-time market data from both CoStar Suite and the apartment rental sites that can be shared with paying landlords. And unlike Booking.com, Apartments.com is already looking to get its hooks deeper into both renters and landlords via other convenient services, offered at no additional cost.

Regarding other players in real estate services, including household names such as Zillow and Redfin, we believe CoStar Group’s industry-leading research investment and marketing budget will allow the company’s data services and marketplaces to remain unrivaled.

Despite CoStar’s dominant position, we don’t currently see any cause for anti-trust concern. The ongoing RentPath acquisition aside, we believe the company’s future acquisition activity will focus upon complementary – rather than competing – markets and services. Because of this, we believe CoStar is unlikely to raise alarm bells with regulators.

16 Q1 2020 Annual Report

Competent Hands at the Wheel

None of the futures discussed here are given. Each of these businesses may need to pivot somewhat from the approaches that have earned each so much success to date. But CoStar Group is governed by a rarity – a founder and team that have managed adaptably for decades, with a balance of both prudence and aggressiveness. With respect to discretionary investment – both organic and acquired – CoStar’s management team has hit for both power and a high batting average. They also have the means and mindset to continue to invest through this period of uncertainty. If all is right in the world by next year, there will certainly be stocks of less advantaged companies that will outperform CoStar’s. But for the coming decade, we believe the qualities of CoStar Group’s businesses can make it a meaningful creator of wealth for the Funds’ shareholders.

As of 03/31/2020, each of the following portfolio companies constituted a portion of the net assets of Balanced Fund, Hickory Fund, Partners III Opportunity Fund, Partners Value Fund, and Value Fund as follows: Alphabet, Inc.-Class C (GOOG) 1.9%, 0%, 5.2%, 6.4%, and 7.1%. CoStar Group, Inc. (CSGP) 0%, 2.8%, 0.7%, 2.8%, and 2.7%.

As of 03/31/2020 Booking Holdings, Inc. (BKNG), Redfin Corp. (RDFN) and Zillow Group, Inc. (ZG) were not held in any Weitz Funds.

Holdings are subject to change and may not be representative of current or future investments.

Jon Baker, CFA, joined Weitz Investments in 1997. Prior to joining the firm, he audited equity funds (including the Weitz Funds) as a certified public accountant at McGladrey & Pullen. Jon has a bachelor’s in accounting and computer applications from the University of Notre Dame.

Q1 2020 Annual Report 17

This page intentionally left blank

18 Q1 2020 Annual Report

Portfolio Managers: Wally Weitz, CFA & Drew Weitz

Investment Style: Mid-Cap Value

The Hickory Fund returned -27.69% in the first quarter of 2020, compared to -27.07% for the Russell Midcap index (the Fund’s primary benchmark). For the year ending March 31, 2020, the Fund returned -15.67% compared to -18.31% for the benchmark.

The COVID-19 crisis has unfurled at an alarming pace, disrupting our daily lives and the global economy seemingly overnight. The situation remains incredibly dynamic as investors grapple with the consequences of the virus itself, the potential consequences of shutting down economies (both here and abroad) and the power of monetary policy and fiscal stimulus to combat the recession. The magnitude of this uncertainty has manifested itself in violent swings in stock prices, volatility we’ve not experienced since the Great Financial Crisis of 2008-2009. Against this highly fluid backdrop, our commentary reflects performance and activity through March 31, a period that incorporates the beginning of the pandemic but obviously not its eventual resolution.

Stocks and other risk assets were pummeled as the economy ground to a near halt in March, and only three stocks contributed positively to performance. EverArc Holdings and Equity Commonwealth both derive nearly all their value from the large sums of cash sitting on their balance sheets. Acquisition vehicle EverArc Holdings raised capital in late 2019 and continues to evaluate opportunities to purchase one or more operating businesses. Market-wide asset price declines suggest improving potential returns when EverArc ultimately deploys its war chest of cash. In recent years, Equity Commonwealth opted to capitalize on frothy commercial real estate prices by liquidating nearly all its portfolio for cash. Today, this war chest gives chairman Sam Zell and company lots of optionality for value creation. Lastly, as the market swooned, we initiated a new position in IDEX Corp. (maker of highly engineered pumps, dispensing solutions, and other components enabling the movement of fluids and gasses) which has delivered strong early returns.

The rest of our holdings participated in the sell-off to varying degrees, but long-time holding Redwood Trust deserves individual attention. The non-agency mortgage market is under tremendous duress, and we believe the initial shock was more about liquidity than solvency. Extreme volatility in loan portfolio pricing stemming from the COVID-19 pandemic has pressured the sector’s funding model, with no relief from government intervention in sight. Redwood’s management has equal measures of integrity, resolve and experience; if anyone can safely navigate these waters, we like their chances. The team has taken several difficult, decisive steps to shore up liquidity, and we think they have invested (and marked) with appropriate conservatism. The potential upside case is clear, yet we cannot be sure that this unprecedented disruption will not further impair their business. More to follow next quarter.

Other top detractors include several companies that participate in elements of the auto industry (CarMax, Axalta and Liberty SiriusXM) as investors first feared supply chain shocks for auto manufacturers and then demand shocks from fewer vehicle sales and miles driven. There is no doubt that business (and earnings) will be challenged for these (and nearly all) companies in the coming quarters, but we remain confident that their long-term prospects are sound. Colfax’s recent purchase of medical devices and services company DJO (and sale of its Air & Gas Handling business) improved its business mix, but its overall cyclicality and balance sheet leverage had investors heading to the exits. We believe management’s strategy is sound, but we ultimately sold our shares to pursue potentially more attractive opportunities.

On balance, the Fund was a seller of equities in the quarter, including actions that we took towards portfolio reshaping. In addition to Colfax, we closed our positions in Perspecta and Fortune Brands to take advantage of the new opportunity set. We also trimmed relative outperformers LICT Corp and Black Knight to manage their weights as their position sizes rose relative to the rest of our portfolio holdings. In addition, we reduced our position in Expedia Group by nearly two-thirds in late February and early March as the potential travel slowdown started coming into focus. On the buy side, we continue to build up newer positions at lower price points (e.g. First Hawaiian, Markel and Vulcan Materials), as well as older holdings where investors’ fear appeared overdone (e.g. Liberty Global and Liberty Latin America). We initiated three new positions in the portfolio, including IDEX Corp. (mentioned above), CoStar Group and HEICO Corporation (detailed below). These three companies are characterized by the highest Weitz Quality Scores (Q1’s or Q2’s on a Q1-Q7 ranking) and strong balance sheets with low-to-no net debt.

CoStar Group is the leading provider of data, analytics and marketing services to commercial real estate brokers and tenants as well as the operator of the rental marketplace, Apartments.com. Research Analyst Jon Baker, CFA, details the business and our investment thesis in this quarter’s Analyst Corner feature. HEICO Corporation’s largest segment designs, manufactures and sells FAA-approved jet engine and other aircraft replacement parts, typically at price points below those offered by original equipment manufacturers (OEMs). With airlines all but grounded, aftermarket demand for HEICO parts and overhaul services has surely suffered. However, we think it is unlikely that air travel is permanently impaired. As planes return to service, HEICO’s value proposition will help them gain market share. HEICO’s conservative balance should allow them to not only survive this temporary halt but to continue their strategy of bolt-on acquisitions at attractive prices to accelerate business value growth.

As we move into the second quarter, much is still uncertain. Although there are some encouraging headlines and governments around the globe are acting aggressively to head off the worst, we are proceeding with caution. Using our quality-at-a-discount or “QuaD investing” framework, we continue to seek (and act upon) investment opportunities which we believe can deliver superior returns over a multi-year time horizon, even while the near-term outlook remains clouded. We appreciate our shareholders’ trust and the opportunity to invest alongside you.

Q1 2020 Annual Report 19

| | | | | | | | | | | |

| Returns | | | | Annualized

| | |

| | | | | | | | Since Fund | | |

| | | | | | | | Inception | Net | Gross |

| QTD | YTD | 1 YR | 3 YR | 5 YR | 10 YR | 20 YR | (4/1/1993) | Expense | Expense |

| WEHIX | (27.69)% | (27.69)% | (15.67)% | (4.13)% | (2.20)% | 5.85% | 3.61% | 8.20% | 1.09% | 1.27% |

| Russell Midcap | (27.07) | (27.07) | (18.31) | (0.81) | 1.85 | 8.77 | 6.79 | 9.52 | | |

| | |

| Top 10 Stock Holdings | |

| % of Net Assets |

Liberty Broadband Corp. - Series A & C | 9.0 |

LICT Corp. | 6.3 |

Laboratory Corp. of America Holdings | 4.7 |

Equity Commonwealth | 4.6 |

EverArc Holdings Ltd. | 4.4 |

Liberty SiriusXM Group - Series A & C | 4.3 |

GCI Liberty, Inc. - Class A | 4.0 |

ACI Worldwide, Inc. | 3.8 |

Black Knight, Inc. | 3.4 |

Markel Corp. | 3.4 |

| 47.9 |

| | | | |

| Top Performers | | | |

| | Average | |

| | Return | Weight | Contribution |

| EverArc Holdings Ltd. | 11.1% | 3.2% | 0.26% |

| IDEX Corp. | (19.5) | 0.2 | 0.24 |

| Equity Commonwealth | (3.4) | 3.6 | 0.04 |

| | |

| Industry Breakdown | |

| % of Net Assets |

Communication Services | 31.9 |

Information Technology | 15.1 |

Industrials | 9.3 |

Consumer Discretionary | 9.2 |

Materials | 8.9 |

Financials | 7.6 |

Health Care | 4.7 |

Real Estate | 4.6 |

Other Common Stock & Warrants | 4.4 |

Cash Equivalents/Other | 4.3 |

| 100.0 |

| | | | |

| Bottom Performers | | | |

| | Average | |

| Return | Weight | Contribution |

Redwood Trust, Inc. | (68.6)% | 3.7% | (3.89)% |

Colfax Corp. | (45.6) | 3.1 | (2.09) |

Liberty SiriusXM Group - Series A & C | (34.4) | 4.4 | (1.66) |

Axalta Coating Systems Ltd. | (43.2) | 3.5 | (1.62) |

CarMax, Inc. | (38.6) | 3.7 | (1.54) |

Data quoted is past performance and current performance may be lower or higher. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. All investments involve risks, including possible loss of principal. Please visit weitzinvestments.com for the most recent month-end performance.

Investment results reflect applicable fees and expenses and assume all distributions are reinvested but do not reflect the deduction of taxes an investor would pay on distributions or share redemptions. Net and Gross Expense Ratios are as of the Fund’s most recent prospectus. The Fund has entered into fee waiver and/or expense reimbursement arrangements with the Investment Advisor. The Advisor has contractually agreed to waive a portion of the Advisor’s fee and reimburse certain expenses (excluding taxes, interest, brokerage costs, acquired fund fees and expenses and extraordinary expenses) to limit the total annual fund operating expenses of the Class’s average daily net assets through 07/31/2020. The Net Expense Ratio reflects the total annual fund operating expenses of the Fund after taking into account any such fee waiver and/or expense reimbursement, if any; total returns would have been lower had there been no waivers or reimbursements.

See page 8 for additional performance disclosures. See page 81 for a description of all indices.

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter. Return shown is the actual quarterly return of the security or combination of share classes.

Source (Top Performers, Bottom Performers): FactSet Analytics

20 Q1 2020 Annual Report

PARTNERS III OPPORTUNITY FUND

Portfolio Manager: Wally Weitz, CFA

Investment Style: Multi-Cap Alternative

The Partners III Opportunity Fund’s Institutional Class returned -16.17% in the first quarter of 2020 compared to -19.60% for the S&P 500 (the Fund’s primary benchmark) and -20.90% for the Russell 3000. For the year ending March 31, 2020, the Fund returned -5.83% compared to -6.98% for the S&P 500 and -9.13% for the Russell 3000.

There was extreme volatility in the stock and bond markets during the first quarter of 2020. The COVID-19 crisis has unfolded at an alarming pace, putting the country and much of the world in a kind of economic “time out.” Investors are encouraged to read our latest Value Matters for a deeper analysis of the current investing climate. As detailed below, Fund performance was helped by some very large, mature companies that generally outperformed smaller companies, while the Fund’s index short positions provided some additional ballast. Nevertheless, we were not immune from the swoon. We always prefer to report relative outperformance but acknowledge that does not fully dull the sting of negative absolute results.

Despite the overall gloom, there were a few bright spots in the quarterly numbers. Acquisition vehicle EverArc Holdings raised capital in late 2019 and continues to evaluate opportunities to purchase one or more operating businesses. Market-wide asset price declines suggest improving potential returns when EverArc ultimately deploys its war chest of cash. Amazon managed a small positive return likely due to a shift in retail market share as consumers adjusted to shelter-in-place orders. We also generated positive returns from our sales of Expedia Group and Colfax, which were valuation-driven and completed before the market impact of the outbreak was truly underway. Not surprisingly, our index short positions collectively delivered the greatest positive contributions, providing a partial hedge for the portfolio’s decline.

Our remaining holdings participated to varying degrees in the overall sell-off. Berkshire Hathaway’s position size magnified its market-like return, while others like Liberty Global and Liberty SiriusXM suffered more meaningful markdowns as investors struggled to project the duration and depth of the coming recession, and investors grew even more negative on DXC Technology, despite progress on their divestiture plan (and planned debt reduction). We empathize with investors’ near-term uncertainty, but we remain focused on the businesses’ long-term opportunities which we believe are sound.

Long-time holding Redwood Trust faces a less clear path. The non-agency mortgage market is under tremendous duress, and we believe the initial shock was more about liquidity than solvency. Extreme volatility in loan portfolio pricing stemming from the COVID-19 pandemic has pressured the sector’s funding model, with no relief from government intervention in sight. Redwood’s management has equal measures of integrity, resolve and experience; if anyone can safely navigate these waters, we like their chances. The team has taken several difficult, decisive steps to shore up liquidity, and we think they have invested (and marked) with appropriate conservatism. The upside case is clear, yet we also cannot be sure that this unprecedented disruption will not further impair their business. More to follow next quarter.

We were active on both the buy and sell sides of the ledger during the first quarter. In addition to Colfax and Expedia, we also completed a sale of Perspecta, while we began two new company investments and one new long ETF position. Among our new investments is CoStar Group, the leading provider of data, analytics and marketing services to commercial real estate brokers and tenants as well as the operator of the rental marketplace, Apartments.com. Research Analyst Jon Baker, CFA, provides a more detailed description and summary of our investment thesis in this quarter’s Analyst Corner feature. We also began buying Vulcan Materials (a high-quality provider of aggregates and other building materials to both private and public-sector customers) late in the quarter after its shares were swept up in the overall market decline. We also added a significant new holding of the Financial Select Sector SPDR ETF. Financial stocks (banks, in particular) have disproportionately slumped as rock-bottom interest rates pressure banks’ ability to earn an attractive margin on their loans while an economic slowdown creates concern around consumer and commercial credit. It’s true that banks played a central role in the Great Financial Crisis of 2008-2009, but today banks are much better capitalized and not the epicenter of our current troubles. We believe the magnitude of these declines has been overdone. In the past, we have constructed “baskets” of individual securities to express an “industry thesis.” Today, we can simply and efficiently do the same by purchasing the sector ETF instead.

Within the short book, we closed our SiriusXM short (a hedge that had protected prior gains in Liberty SiriusXM) at a gain and covered the remaining shares of our Dollar General short at a loss. On balance, we reduced our index short position during the quarter, covering layers of our S&P 500 Index ETF short at various levels during the market decline. Though our Index shorts were positive to the portfolio during the market’s quarter decline, the shares covered resulted in a loss. These moves resulted in a gross short exposure equal to 11% of net assets at quarter end (down from 19% on December 31). Our gross long exposure also declined to 90% (from 97%) during the quarter, resulting in an effective net long position of 79% of net assets.

Despite an uncertain near term, we are confident that the world will recover from the current health crisis. As we continue to navigate through this difficult period, our goal remains unchanged: to identify attractive investment opportunities that can deliver strong returns for years to come.

Q1 2020 Annual Report 21

| | | | | | | | | | | |

| Returns | | | | Annualized | | |

| | | | | | | | Since Fund | | |

| | | | | | | | Inception | Net | Gross |

| QTD | YTD | 1 YR | 3 YR | 5 YR | 10 YR | 20 YR | (6/1/1983) | Expense | Expense |

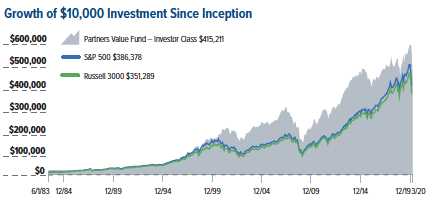

| WPOIX - Investor Class | (16.30)% | (16.30)% | (6.40)% | 1.67% | 0.70% | 7.33% | 8.58% | 11.55% | 2.13% | 2.13% |

| WPOPX - Institutional Class | (16.17) | (16.17) | (5.83) | 2.24 | 1.22 | 7.72 | 8.78 | 11.66 | 1.56 | 1.56 |

| S&P 500 | (19.60) | (19.60) | (6.98) | 5.10 | 6.73 | 10.53 | 4.79 | 10.42 | | |

| Russell 3000 | (20.90) | (20.90) | (9.13) | 4.00 | 5.77 | 10.15 | 4.91 | 10.14 | | |

| | |

| Top 10 Holdings | |

| % of Net Assets |

Berkshire Hathaway Inc. - Class B | 11.1 |

Intelligent Systems Corp. | 9.3 |

Liberty Broadband Corp. - Series A & C | 5.5 |

Visa Inc. - Class A | 5.3 |

Markel Corp. | 5.3 |

Alphabet, Inc. - Class C | 5.2 |

Mastercard Inc. - Class A | 5.2 |

Liberty Global plc - Class C | 4.6 |

The Financial Select Sector SPDR Fund | 4.5 |

Facebook, Inc. - Class A | 4.2 |

| 60.2 |

| | | | |

| Top Performers | | | |

| | Average | |

| Return | Weight | Contribution |

SPDR S&P 500 ETF Trust (short) | (19.4)% | (14.6)% | 3.33% |

EverArc Holdings Ltd. | 11.1 | 3.3 | 0.32 |

Invesco QQQ Trust, Series 1 (short) | (10.3) | (1.5) | 0.25 |

Sirius XM Holdings, Inc. (short) | (30.8) | (0.9) | 0.23 |

Amazon.com, Inc. | 5.5 | 2.4 | 0.18 |

| | |

| Industry Breakdown | |

| % of Net Assets |

Information Technology | 27.5 |

Communication Services | 24.3 |

Financials | 19.0 |

Consumer Discretionary | 5.1 |

Health Care | 2.7 |

Materials | 2.4 |

Industrials | 0.7 |

Other Common Stock & Warrants | 4.0 |

Exchange Traded Funds | 4.5 |

Securities Sold Short | (11.2) |

Short Proceeds/Other | 21.0 |

| 100.0 |

| | | | |

| Bottom Performers | | | |

| | Average | |

| Return | Weight | Contribution |

Berkshire Hathaway Inc. - Class B | (19.3)% | 10.9% | (2.23)% |

Redwood Trust, Inc. | (68.6) | 2.2 | (2.00) |

Liberty SiriusXM Group - Series A & C | (34.4) | 4.2 | (1.75) |

DXC Technology Co. | (64.8) | 2.1 | (1.69) |

Liberty Global plc - Class C | (27.9) | 5.2 | (1.48) |

Data quoted is past performance and current performance may be lower or higher. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, and shares, when redeemed, may be worth more or less than their original cost. All investments involve risks, including possible loss of principal. Please visit weitzinvestments.com for the most recent month-end performance.

Investment results reflect applicable fees and expenses and assume all distributions are reinvested but do not reflect the deduction of taxes an investor would pay on distributions or share redemptions. Net and Gross Expense Ratios are as of the Fund’s most recent prospectus.

See page 8 for additional performance disclosures. See page 81 for a description of all indices.

Contributions to Fund performance are based on actual daily holdings. Securities may have been bought or sold during the quarter. Return shown is the actual quarterly return of the security or combination of share classes.

Source (Top Performers, Bottom Performers): FactSet Analytics

22 Q1 2020 Annual Report

Portfolio Managers: Wally Weitz, CFA & Brad Hinton, CFA

Investment Style: Multi-Cap Value

The Partners Value Fund’s Institutional Class returned -26.26% during the first quarter compared to -20.90% for the Russell 3000 and -19.60% for the S&P 500, the Fund’s primary benchmark. For the year ending March 31, 2020, the Fund’s Institutional Class returned -14.59% compared to -9.13% for the Russell 3000 and -6.98% for the S&P 500. The markets quickly took back most of the Fund’s 2019 outsized gains. The March swoon was particularly harsh for small-cap stocks, mid-cap stocks and all but the highest-quality companies.

The COVID-19 outbreak has taken center stage and upended life around the globe. The U.S. economy has temporarily ground to a near halt. The short-term effects, reactions and implications are unprecedented, and the Fund declined more than its benchmark during this turmoil. Before we get into stock specifics, it is helpful to highlight a few broad themes:

Large-cap stocks declined far less than small- and mid-cap stocks

We wrote last quarter about the concept of splitting the portfolio into a large-cap basket and a mid-cap basket. More than 70 percent of the quarter’s negative contribution came from our mid-cap basket. In fact, our large-cap basket would have outperformed the broader market indices by several hundred basis points on a stand-alone basis.

Higher-quality stocks declined far less than lower-quality stocks

Our proprietary quality scoring (QS) system rates stocks on a QS1-QS7 scale, with QS1 being the highest quality. Our portfolio consists of companies rated QS1-QS4 only; we generally exclude low-quality (QS5-QS7) businesses. QS1 and QS2 stocks held up well, performing slightly better than the broad market. Our QS3 stocks were impacted more, and our QS4 stocks gapped even lower still. QS3 and QS4 stocks accounted for roughly two-thirds of the quarter’s negative contribution.

These trends are not surprising in a cascading market correction. We strongly believe that through a market cycle, mid-cap companies should have a prominent place in a multi-cap, best-ideas strategy. We also believe that carefully curated, well-researched QS3 and QS4 companies can add excess return to a portfolio over the long haul. To paraphrase Warren Buffett, we are willing to endure a lumpier path to a higher place. This view, too, has been out of favor as recent mid-quality volatility has been mostly one-sided. Mid-sized, mid-quality stocks have often meant double trouble in this market environment.

Expedia Group and IDEX were the only positive contributors to results during the quarter. We sold Expedia Group at a large gain after the company reported encouraging earnings and before the COVID-19 outbreak took hold. The fortuitous sale was triggered by our valuation discipline. In contrast, we bought multi-platform industrial IDEX into the teeth of the drawdown, and the stock enjoyed a nice bounce by quarter end. Detractors included Colfax, Liberty SiriusXM and CarMax, which all fit the mid-sized, mid-quality mold. We sold Colfax to upgrade the portfolio, while we think the other two stocks have tremendous return potential from their quarter end, depressed price levels.

Long-time holding Redwood Trust faces a less clear path. The non-agency mortgage market is under tremendous duress, and we believe the initial shock was more about liquidity than solvency. Extreme volatility in loan portfolio pricing stemming from the COVID-19 pandemic has pressured the sector’s funding model, with no relief from government intervention in sight. Redwood’s management has equal measures of integrity, resolve and experience; if anyone can safely navigate these waters, we like their chances. The team has taken several difficult, decisive steps to shore up liquidity, and we think they have invested (and marked) with appropriate conservatism. The upside case is clear, yet we also cannot be sure that this unprecedented disruption will not further impair their business. More to follow next quarter.

For the year ending March 31, 2020, Liberty Broadband, Marvell Technology and Expedia (sold) were the largest contributors. Marvell is a good example of a mid-sized, mid-quality company that bucked the trend and helped fund performance. Beyond Redwood Trust, material detractors included Qurate Retail, Colfax and DXC Technology. We sold these three stocks to focus on more durable companies as the opportunity set widened, with little sacrifice to the Fund’s return potential in our view.

As volatility increased throughout the quarter, we took several steps to reshape and improve the portfolio. Drawing on excellent work from the equity research team, we bought CoStar Group (real estate information, analytics and marketplaces), HEICO (aerospace products) and IDEX (multi-platform industrials). In addition to timely sales of travel companies Expedia and Booking Holdings, we eliminated Colfax, Qurate Retail and TransDigm Group. We also materially increased our positions in Markel, Vulcan Materials and ACI Worldwide. We think the resulting portfolio is sturdier, with an even more attractive risk-reward profile.

Valuation remains our North Star, and we think our stocks are attractively priced despite the negative headlines and hazy 2020 outlook. Our appraisals are more fluid than usual given the extreme nature of the COVID-19 disruption. Wider ranges are more useful than point estimates, and our current view is that the portfolio currently trades at a price-to-value in the low to mid 70s. Even with some margin for error, these discounted valuation levels suggest above-average long run return potential.

Q1 2020 Annual Report 23

| | | | | | | | | | | |

| Returns | | | | Annualized | | |

| | | | | | | | Since Fund | | |

| | | | | | | | Inception | Net | Gross |

| QTD | YTD | 1 YR | 3 YR | 5 YR | 10 YR | 20 YR | (6/1/1983) | Expense | Expense |