UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-09997

Baird Funds, Inc.

(Exact name of registrant as specified in charter)

777 East Wisconsin Avenue

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Andrew D. Ketter

Robert W. Baird & Co. Incorporated

777 East Wisconsin Avenue

Milwaukee, WI 53202

(Name and address of agent for service)

1-866-442-2473

Registrant's telephone number, including area code

Date of fiscal year end: December 31, 2013

Date of reporting period: December 31, 2013

Item 1. Reports to Stockholders.

Annual Report –

Baird Funds

December 31, 2013

Baird Short-Term Bond Fund

Baird Intermediate Bond Fund

Baird Intermediate Municipal Bond Fund

Baird Aggregate Bond Fund

Baird Core Plus Bond Fund

| Go Green. |  | Go Paperless. |

Sign up to receive your Baird Funds’ prospectuses and reports online.

Table of Contents

| Letter to Shareholders | 1 |

| 2013 Bond Market Overview | 2 |

| Baird Short-Term Bond Fund | 7 |

| Baird Intermediate Bond Fund | 17 |

| Baird Intermediate Municipal Bond Fund | 27 |

| Baird Aggregate Bond Fund | 40 |

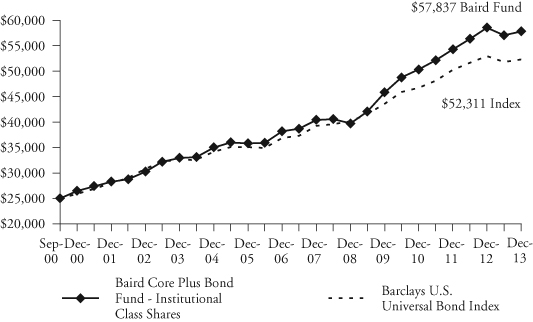

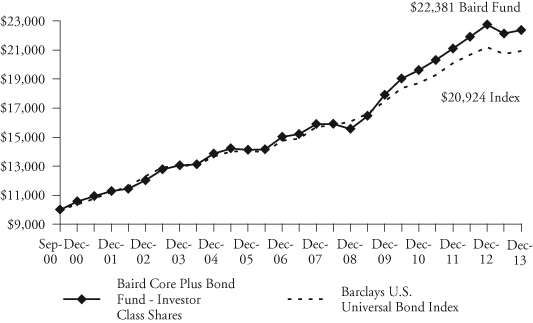

| Baird Core Plus Bond Fund | 50 |

| Additional Information on Fund Expenses | 60 |

| Statements of Assets and Liabilities | 62 |

| Statements of Operations | 64 |

| Statements of Changes in Net Assets | 65 |

| Financial Highlights | 70 |

| Notes to the Financial Statements | 80 |

| Report of Independent Registered Public Accounting Firm | 92 |

| Directors and Officers | 93 |

Disclosure Regarding the Board of Directors’ Approval of the Investment Advisory Agreement for Baird Bond Funds | 96 |

| Additional Information | 101 |

| Privacy Notice | A-1 |

This report has been prepared for shareholders and may be distributed to others only if preceded or accompanied by a current prospectus.

Cautionary Note on Analyses, Opinions and Outlooks: In this report we offer analyses and opinions on the performance of individual securities, companies, industries, sectors, markets, interest rates and governmental policies, including predictions, forecasts and outlooks regarding possible future events. These can generally be identified as such because the context of the statements may include such words as “believe,” “should,” “will,” “expects,” “anticipates,” “hopes” and words of similar effect. These statements reflect the portfolio managers’ good faith beliefs and judgments and involve risks and uncertainties, including the risk that the portfolio managers’ analyses, opinions and outlooks are or will prove to be inaccurate. It is inherently difficult to correctly assess and explain the performance of particular securities, sectors, markets, interest rate movements, governmental actions or general economic trends and conditions, and many unforeseen factors contribute to the performance of Baird Funds. Investors are, therefore, cautioned not to place undue reliance on subjective judgments contained in this report.

Baird Funds

1-866-442-2473

www.bairdfunds.com

February 27, 2014

Dear Shareholder,

Overall, 2013 proved to be a mixed year for bond investors as shorter duration investments generated modestly positive nominal returns and longer duration investments generated slightly negative nominal returns. Given this market dynamic, the disciplined, duration neutral strategy we employ against benchmarks coupled with our opportunistic ability to add value through yield curve positioning, sector allocation, and individual security selection were critical elements to our success in 2013 as all the Baird Bond Funds generated strong relative returns versus their respective benchmarks.

We strive to be good stewards of our shareholders’ assets. We employ a risk controlled, bottom-up process to investment decision making and portfolio management. This approach allows us to identify, research and invest based upon strong fundamentals that offer good relative value. We understand that our shareholders rely on us to maintain this consistent approach and focus on risk control to help them achieve their investment objectives through all market cycles.

Our long-term success rests on the trust you have placed in us and we want to thank you for your continued investment in the Baird Funds which experienced steady inflows during the year and increased total net assets to $9.3 billion at the end of 2013.

On the following pages, we review the bond market in 2013 and the performance and composition of each of the Baird Bond Funds.

We are privileged to provide you with fixed income investment management services and appreciate the confidence and trust you have placed in our experienced investment team.

Sincerely,

Mary Ellen Stanek, CFA

President

Baird Funds

Page 1

2013 Bond Market Overview

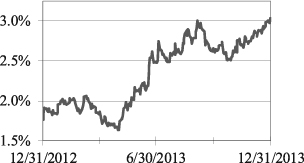

Treasury Yields Rise, Yield Curve Steepens on Introduction of Taper

The 10-year Treasury yield rose 127 bps in 2013, ending the year at its high (3.03%) as the Fed announced it will modestly reduce the pace of Quantitative Easing (QE) purchases from $85 to $75 billion per month and expects to further reduce and ultimately end purchases as the labor market and broader economy improve. The December announcement came after two months of nonfarm payroll reports showing job gains of over 200,000. The path to higher rates in 2013 was volatile (see chart below right) as sequestration (across the board federal spending cuts) pushed rates lower early in the year and then a partial government shutdown and eleventh hour vote to raise the debt ceiling to avoid technical default caused yields to drop in the fall. Despite these fiscal episodes, yields rose for the year primarily on the Fed’s move to taper QE bond purchases though modest improvement in the economy also contributed to the upward pressure on rates.

Treasury Yields

| 1 Year | |||

| Maturity | 12/31/12 | 12/31/13 | Change | |

| 1 | 0.14% | 0.11% | -0.03% | |

| 2 | 0.25% | 0.38% | 0.13% | |

| 3 | 0.35% | 0.76% | 0.41% | |

| 5 | 0.72% | 1.74% | 1.02% | |

| 7 | 1.18% | 2.45% | 1.27% | |

| 10 | 1.76% | 3.03% | 1.27% | |

| 30 | 2.95% | 3.97% | 1.02% | |

| 10 Year Treasury Yield | |

| |

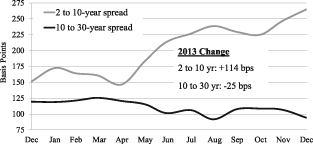

| Short End Steepens, Long End Flattens |

|

A Tale of Two Curves

As many anticipated, the Fed paired its decision to taper QE purchases with an announcement that it would likely keep the Fed Funds rate near zero “well past the time” the unemployment rate dips below its 6.5% threshold. Forward guidance anchored short term interest rates, creating a very steep yield curve from two to ten years. However, the ten to thirty year portion of the curve actually flattened by 25 bps for the year (see chart at right), in part due to demand from defined benefit pension plans reallocating into long term bonds as U.S. equity markets delivered a 30%+ performance in 2013.

Page 2

2013 Bond Market Overview

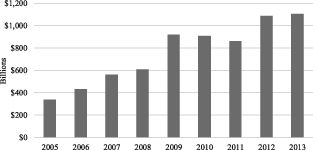

Record Issuance Year for Credit

U.S. investment grade credit issuance of $1.106 trillion set a new record, exceeding last year’s record of $1.086 trillion, according to Barclays data. Many corporations were looking to opportunistically fund their businesses while interest rates remained near historic lows. Apple set a record with the largest corporate issuance ever in the second quarter at $17 billion, only to be out-done by Verizon’s $49 billion debt issuance in the third quarter to help fund its $130 billion acquisition of Vodafone’s 45% stake in Verizon Wireless. Looking ahead, it is expected that gross issuance will decline 5% - 15% in 2014.

| Gross Issuance – Investment Grade Credit |

|

| Source: Barclays |

Corporate Yield Spreads Tighten Further

In spite of the record issuance, corporate spreads tightened significantly on strong investor demand and solid credit fundamentals (see chart below). Within investment grade credit, financial spreads tightened the most (-46 bps) as financial institutions continued fortifying balance sheets to comply with higher regulatory capital and liquidity requirements. The spread on financials (109 bps) is now less than industrials (114 bps), a relationship that was typical prior to 2008. Given the solid fundamentals, expanding regulation in the sector, and expected decline in supply, we believe financial spreads could continue to tighten vs. industrials. Very strong demand for yield in a low interest rate environment drove spreads on high yield corporates tighter (-129 bps). Away from corporates, agency pass-throughs tightened 16 bps as the Fed continued to purchase the majority of new issuance. Commercial mortgage-backed securities (CMBS) and asset-backed securities (ABS) spreads widened, reflecting some of the selling pressure on the market as bond mutual fund flows turned distinctly negative starting in June (see chart on next page).

Option-Adjusted Spreads (in bps)

| 1 Year | ||||

| 6/30/07 | 12/31/12 | 12/31/13 | Change | |

| U.S. Aggregate Index | 53 | 53 | 45 | -8 |

| U.S. Agency (non-mortgage) | 34 | 13 | 17 | 4 |

| Mortgage and ABS Sectors | ||||

| U.S. Agency Pass-throughs | 65 | 50 | 34 | -16 |

| Asset-Backed Securities | 57 | 43 | 55 | 12 |

| CMBS | 82 | 124 | 126 | 2 |

| Corporate Sectors | ||||

| U.S. Investment Grade | 97 | 141 | 114 | -27 |

| Industrial | 104 | 133 | 114 | -19 |

| Utility | 100 | 144 | 125 | -19 |

| Financial Institutions | 88 | 155 | 109 | -46 |

| U.S. High Yield | 292 | 511 | 382 | -129 |

| Source: Barclays |

Page 3

2013 Bond Market Overview

2013 Mutual Fund Net Flows

Source: ICI

Rising Yields Depress Returns

Most major bond indices and sectors posted negative returns for 2013 as rising yields detracted from returns. Only a handful of indices and sectors with shorter average durations (e.g. U.S. 1-3 Yr. Gov’t/Credit +0.64%, CMBS +0.23%), or with dramatic spread tightening (i.e. Corporate High Yield +7.44%) ended the year in positive territory. Treasuries (-2.75%) felt the full impact of the rise in rates in 2013 and municipals (-2.55%) followed close behind as mutual fund flows turned sharply negative mid-year (see chart above) and Detroit’s record bankruptcy filing and Puerto Rico’s challenges raised investors’ sensitivity to credit risk. Tightening spreads limited the fall of Investment Grade Corporates (-1.53%) while the return of the High Yield sector (+7.44%) mirrored the surge in equities. TIPS (-8.61%) were the weakest performing sector by far and moved back closer to fair value in 2013 (after an extended period of overvaluation) as inflation expectations eased and investors became painfully aware that while they do provide inflation protection, TIPS are not always an effective hedge against rising rates.

Total Returns of Selected Barclays Indices and Subsectors

| Barclays Index/Sector | December | 4th Quarter | 2013 |

| U.S. Aggregate Index | -0.57% | -0.14% | -2.02% |

| U.S. Gov’t/Credit Index | -0.62% | -0.03% | -2.35% |

| U.S. Intermediate Gov’t/Credit Index | -0.63% | -0.02% | -0.86% |

| U.S. 1-3 Yr. Gov’t/Credit Index | -0.13% | 0.18% | 0.64% |

| U.S. Treasury | -0.91% | -0.75% | -2.75% |

| U.S. Agency | -0.56% | -0.17% | -1.38% |

| MBS (Mortgage Backed Securities) | -0.47% | -0.42% | -1.41% |

| CMBS (Commercial Mortgage Backed Securities) | -0.29% | 0.53% | 0.23% |

| ABS (Asset-Backed Securities) | -0.22% | 0.32% | -0.27% |

| U.S. Corporate - Investment Grade | -0.16% | 1.11% | -1.53% |

| Corporate High Yield | 0.54% | 3.58% | 7.44% |

| Municipal Bond Index | -0.26% | 0.32% | -2.55% |

| TIPS (Treasury Inflation Protected Securities) | -1.47% | -2.00% | -8.61% |

Outlook

We expect economic growth to modestly improve in 2014 although many headwinds remain and inflation remains benign. The tapering of QE purchases will put some additional upward pressure on rates, although the magnitude of any rise will be limited by modest economic growth and tepid inflation. With the Fed keeping its policy rate near zero into 2015, the intermediate portion of the curve will remain very steep. As such, rolling down the yield curve will add significantly to returns of intermediate maturities. Due to the

Page 4

2013 Bond Market Overview

Taper, we see limited return potential for Treasuries and Agencies. Instead, we see good relative value in several non-government sectors along the steeper intermediate maturity segment of the curve. We expect Investment Grade Corporates to outperform, as strong fundamentals and reduced supply will allow spreads to tighten modestly. We also see attractive relative value in CMBS structures with superior credit enhancement. We hold a cautious view on Agency MBS as the Fed reduces extraordinarily accommodative purchases and the sector starts the year with historically tight spreads. With yields on Corporate High Yield at all-time lows, we are concerned that aggressive use of leverage could adversely impact the sector. In the municipal sector, higher yields and a steep curve brought in some demand from cross-over buyers. While state credit conditions are showing signs of improvement, high-profile challenges (e.g. Detroit, Puerto Rico) will keep investor sensitivity to credit risk high for municipals. Across tax-exempt markets we caution investors against going too far out the yield curve or too far down in quality given the high level of uncertainty and broad range of potential outcomes.

The Barclays Aggregate Bond Index is an index comprised of approximately 6,000 publicly traded bonds including U.S. Government, mortgage backed, corporate, and Yankee bonds with an average maturity of approximately 10 years.

The Barclays Government/Credit Index is a combination of the Government Index which measures government-bond general and Treasury funds, and the Credit Bond Index, which is a market value-weighted index which tracks the returns of all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC registered, investment grade Corporate Debt.

The Barclays Intermediate Government/Credit Index is a combination of the Government Index which measures government-bond general and Treasury funds, and the Credit Bond Index, which is a market value-weighted index which tracks the returns of all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC registered, investment grade Corporate Debt with maturities between one and ten years.

The Barclays Government/Credit Intermediate Index (1 – 3 yr) is a combination of the Government Index which measures government-bond general and Treasury funds, and the Credit Bond Index, which is a market value-weighted index which tracks the returns of all publicly issued, fixed-rate, nonconvertible, dollar-denominated, SEC registered, investment grade Corporate Debt with maturities between zero and three years.

The Barclays U.S. Treasury Index includes public obligations of the U.S. Treasury. Treasury bills are excluded by the maturity constraint of at least one year but are part of a separate Short Treasury Index. In addition, certain special issues, such as state and local government series bonds (SLGs), as well as U.S. Treasury TIPS, are excluded. STRIPS are excluded from the index because their inclusion would result in double-counting. Securities in the Index roll up to the U.S. Aggregate, U.S. Universal, and Global Aggregate Indices. The U.S. Treasury Index was launched on January 1, 1973.

The Barclays U.S. Agency Index: This index is the U.S. Agency component of the U.S. Government/Credit Index. It includes publicly issued debt of U.S. Government agencies, quasi-federal corporations, and corporate or foreign debt guaranteed by the U.S. Government (such as USAID securities). The largest issues are Fannie Mae, Freddie Mac, and the Federal Home Loan Bank System (FHLB). The index includes both callable and non-callable agency securities.

The Barclays U.S. Corporate – Investment Grade Index: This index is the Corporate component of the U.S. Credit Index. It includes publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered.

The Barclays CMBS (Commercial Mortgage Backed Securities) Index: This index is the CMBS component of the U.S. Aggregate Index. The Barclays CMBS ERISA-Eligible Index is the ERISA-eligible component of the Barclays CMBS Index. This index, which includes investment grade securities that are ERISA eligible under the underwriter’s exemption, is the only CMBS sector that is included in the U.S. Aggregate Index.

Page 5

2013 Bond Market Overview

The Barclays MBS (Mortgage Backed Securities) Index: This index is the U.S. MBS component of the U.S. Aggregate Index. The MBS Index covers the mortgage-backed pass-through securities of Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The MBS Index is formed by grouping the universe of over 600,000 individual fixed rate MBS pools into approximately 3,500 generic aggregates.

The Barclays ABS (Asset Backed Securities) Index: This index is the ABS component of the U.S. Aggregate Index. The ABS index has three subsectors: credit and charge cards, autos, and utility. The index includes pass-through, bullet, and controlled amortization structures. The ABS Index includes only the senior class of each ABS issue and the ERISA-eligible B and C tranche.

The Barclays Corporate High Yield Index: The Barclays U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. Original issue zeroes, step-up coupon structures, 144-As and pay-in-kind bonds (PIKs, as of October 1, 2009) are also included.

The Barclays Municipal Bond Index is a broad-based, total-return index. The bonds are all investment-grade, tax-exempt, and fixed-rate securities with long-term maturities (greater than 2 years). They are selected from issues larger than $50 million.

The Barclays TIPS Index consists of Treasury Inflation Protected Securities (TIPS). TIPS are securities whose principal is tied to the Consumer Price Index. TIPS pay interest semi-annually, based on the fixed rate applied to the adjusted principal.

A direct investment in an index is not possible.

Page 6

Baird Short-Term Bond Fund

December 31, 2013

The Baird Short-Term Bond Fund seeks an annual rate of total return, before Fund expenses, greater than the annual rate of total return of the Barclays 1-3 Year U.S. Government/Credit Bond Index. The Barclays 1-3 Year U.S. Government/Credit Bond Index is an unmanaged, market value weighted index of investment grade, fixed rate debt issues, including government and credit securities, with maturities between one and three years.

The Fund entered the year with a significant yield advantage over its benchmark and converted that advantage into strong absolute and relative returns versus its benchmark index in 2013. Our long-term commitment to duration neutrality was very important as well. A number of the themes that drove performance in 2012 continued to positively impact the portfolio relative to its benchmark in 2013. The primary factors contributing to the Fund’s outperformance over its benchmark are described below.

| • | The Fund’s overweight position to the corporate credit sector relative to the Fund’s benchmark positively impacted the Fund’s performance. Corporate bonds generally experienced favorable price returns relative to U.S. Treasuries of comparable maturity due to a significant narrowing of corporate bond spreads (the additional yield that investors demand above U.S. Treasury bonds for owning corporate debt) during the year. The narrowing was driven by generally solid corporate credit fundamentals and very strong investor demand. | |

| • | An overweight to the financial sub-sector in particular was an important contributor to the Fund’s relative outperformance as holdings in this sub-sector outperformed other investment grade corporate bonds. The financial sub-sector’s performance continued to be driven by both strong and improving credit fundamentals and strong investor demand. | |

| • | The Fund’s underweight to U.S. Treasuries and Agencies was a positive contributor to relative performance as nongovernment “spread sectors” such as corporate, mortgage-backed, and asset-backed securities outperformed equal-duration U.S. Government securities for the year. | |

| • | Exposure to commercial mortgage-backed securities (CMBS) had an overall positive impact on the Fund’s performance for the year. As part of the risk management for the Fund’s exposure to this sector, the Fund holds short maturity, select super-senior issues with significant credit enhancement. |

We are pleased with the Fund’s performance in 2013 and are confident in the individual issues and the overall structure of the Fund. The Fund continues to maintain a significant yield advantage over the benchmark and we are optimistic regarding the Fund’s relative performance as we head into 2014.

Page 7

Baird Short-Term Bond Fund

December 31, 2013

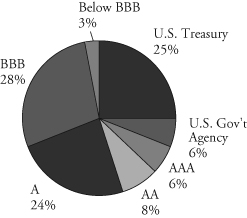

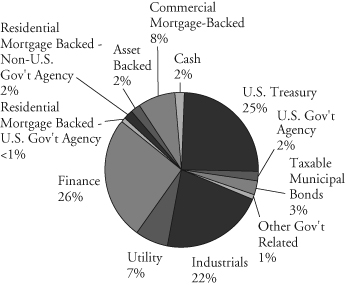

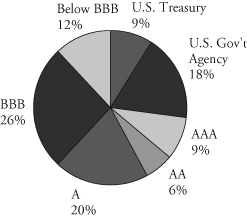

Portfolio Characteristics

Quality Distribution(1)

| Net Assets | $2,008,964,589 | |||

| SEC 30-Day | |||

Yield(2) | ||||

| Institutional Class | 1.38% | |||

| Investor Class | 1.10% | |||

| Average | ||||

| Effective | ||||

| Duration | 1.91 years | |||

| Average | ||||

| Effective | ||||

| Maturity | 2.35 years | |||

| Annualized | ||||

| Expense | ||||

| Ratio | ||||

| Institutional Class | 0.30% | |||

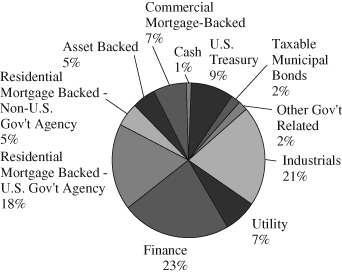

Sector Weightings(1) | Investor Class | 0.55%(3) | ||

| Portfolio | |||

| Turnover | ||||

| Rate | 45.1% | |||

| Number of | ||||

| Holdings | 473 | |||

| (1) | Percentages shown are based on the Fund’s total investments (less investments purchased with cash proceeds from securities lending). |

| (2) | SEC yields are based on SEC guidelines and are calculated for the 30 days ended December 31, 2013. |

| (3) | Includes 0.25% 12b-1 fee. |

Page 8

Baird Short-Term Bond Fund

December 31, 2013

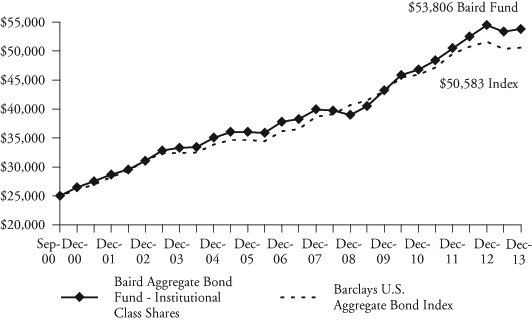

Institutional Class

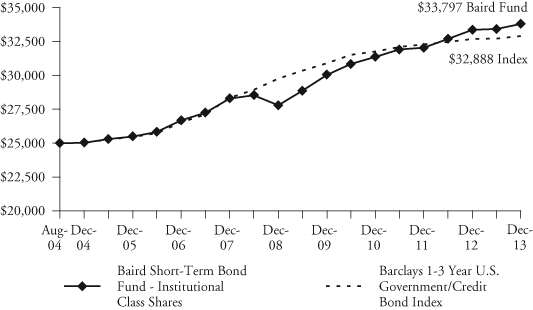

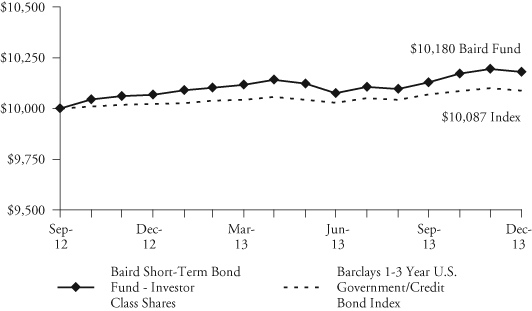

Value of a $25,000 Investment

Growth of a hypothetical investment of $25,000 made on the Fund’s inception date (8/31/04), assuming reinvestment of all distributions.

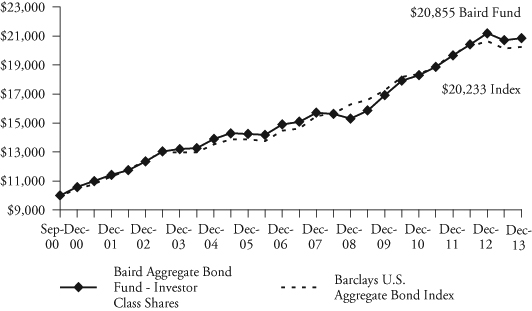

Investor Class

Value of a $10,000 Investment

Growth of a hypothetical investment of $10,000 made on the Fund’s inception date (9/19/12), assuming reinvestment of all distributions.

Page 9

Baird Short-Term Bond Fund

December 31, 2013

Total Returns

| Average Annual | ||||

| Since | Since | |||

| One | Five | Inception | Inception | |

| For the Periods Ended December 31, 2013 | Year | Years | (8/31/04) | (9/19/12) |

| Institutional Class Shares | 1.33% | 3.99% | 3.28% | N/A |

| Investor Class Shares | 1.11% | N/A | N/A | 1.40% |

Barclays 1-3 Year U.S. Government/Credit Bond Index(1) | 0.64% | 2.02% | 2.98% | 0.68% |

| (1) | The Barclays 1-3 Year U.S. Government/Credit Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt issues, including government and corporate securities, with maturities between one and three years. This index does not reflect any deduction for fees, expenses or taxes. A direct investment in an index is not possible. |

The line graph on the previous page and the returns shown in the table above reflect reinvestment of dividends and/or capital gains distributions in additional shares. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns reflect the actual performance for each period and do not include the impact of trades executed on the last business day of the period that were recorded on the first business day of the next period.

The Fund’s gross expense ratio for each Class, as reflected in the Fund’s current prospectus, is set forth under “Portfolio Characteristics”.

The Fund may invest in U.S. dollar denominated foreign securities which involve additional risks such as currency rate fluctuations, political and economic instability, and different and sometimes less strict financial reporting standards and regulation. The Fund may also invest in mortgage- and asset-backed securities, which include interest rate and prepayment risks more pronounced than those of other fixed income securities.

Past performance does not guarantee future results. Investment returns and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

For information about the performance of the Fund as of the most recent month-end, please call 1-866-44BAIRD or visit www.bairdfunds.com. Mutual fund performance changes over time and current performance may be lower or higher than that stated.

Page 10

Baird Short-Term Bond Fund

Summary Schedule of Investments, December 31, 2013

This schedule summarizes the Fund’s holdings by asset type. Details are reported for each of the Fund’s 50 largest individual holdings and for investments that, in total for any issuer, represent more than 1% of the Fund’s net assets. The total value of smaller holdings is reported as a single amount within each category.

The Fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter end. For the second and fourth fiscal quarters, the complete listing of the Fund’s holdings is available electronically in the Fund’s Form N-CSR at http://www.rwbaird.com/baird-funds/prospectus-applications/prospectus-applications.aspx and on the Securities and Exchange Commission’s website (www.sec.gov) or you can have it mailed to you without charge by calling 1-866-44BAIRD. For the first and third fiscal quarters, the Fund files the lists with the SEC on Form N-Q. Shareholders can look up the Fund’s Forms N-CSR and N-Q on the SEC’s website (www.sec.gov).

Long-Term Investments

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| U.S. Treasury Securities | ||||||||||||

| U.S. Treasury Bonds | ||||||||||||

| 2.375%, 07/31/2017@ | $ | 185,800,000 | $ | 194,146,508 | 9.7 | % | ||||||

| Total U.S. Treasury Securities | ||||||||||||

| (Cost $194,511,368) | 194,146,508 | 9.7 | % | |||||||||

| Taxable Municipal Bonds | ||||||||||||

| Rhode Island Housing & Mortgage Finance Corp/RI | ||||||||||||

| 3.000%, 10/01/2034 (Callable 10/01/2022) | 12,500,000 | 12,395,000 | 0.6 | % | ||||||||

| Other Taxable Municipal Bonds# | 44,037,927 | 2.2 | % | |||||||||

| Total Taxable Municipal Bonds | ||||||||||||

| (Cost $56,705,560) | 56,432,927 | 2.8 | % | |||||||||

| Other Government Related Securities | ||||||||||||

| Other Government Related Securities#~ | 22,958,440 | 1.1 | % | |||||||||

| Total Other Government Related Securities | ||||||||||||

| (Cost $22,822,243) | 22,958,440 | 1.1 | % | |||||||||

| Corporate Bonds | ||||||||||||

| Industrials | ||||||||||||

| America Movil, S.A.B. de C.V. | ||||||||||||

1.244%, 09/12/2016 f | 9,000,000 | 9,093,366 | 0.5 | % | ||||||||

| Computer Sciences Corporation | ||||||||||||

| 2.500%, 09/15/2015 | 9,550,000 | 9,747,847 | 0.5 | % | ||||||||

| Fidelity National Information Services, Inc. | ||||||||||||

| 7.875%, 07/15/2020 | 8,520,000 | 9,294,971 | 0.5 | % | ||||||||

| Ingredion Incorporated | ||||||||||||

| 1.800%, 09/25/2017 | 8,974,000 | 8,746,563 | 0.4 | % | ||||||||

| Marathon Oil Corporation | ||||||||||||

| 6.000%, 10/01/2017 | 7,805,000 | 8,845,258 | 0.4 | % | ||||||||

| Murphy Oil Corporation | ||||||||||||

| 2.500%, 12/01/2017 | 10,281,000 | 10,343,519 | 0.5 | % | ||||||||

| Pioneer Natural Resources Company | ||||||||||||

| 5.875%, 07/15/2016 | 10,000,000 | 11,092,870 | 0.6 | % | ||||||||

The accompanying notes are an integral part of these financial statements.

Page 11

Baird Short-Term Bond Fund

Summary Schedule of Investments, December 31, 2013

Long-Term Investments (cont.)

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| Plum Creek Timberlands, L.P. | ||||||||||||

| 5.875%, 11/15/2015 | $ | 9,550,000 | $ | 10,337,503 | 0.5 | % | ||||||

| Seagate HDD Cayman | ||||||||||||

6.875%, 05/01/2020 f | 8,400,000 | 9,082,500 | 0.4 | % | ||||||||

| Staples, Inc. | ||||||||||||

| 9.750%, 01/15/2014 | 9,555,000 | 9,584,773 | 0.5 | % | ||||||||

| Telecom Italia Capital, SA | ||||||||||||

5.250%, 10/01/2015 f | 10,960,000 | 11,521,700 | 0.6 | % | ||||||||

| The Valspar Corporation | ||||||||||||

| 5.100%, 08/01/2015 | 10,450,000 | 11,020,194 | 0.5 | % | ||||||||

| Time Warner Companies, Inc. | ||||||||||||

| 7.250%, 10/15/2017 | 7,831,000 | 9,335,382 | 0.5 | % | ||||||||

| Vale Canada Limited | ||||||||||||

5.700%, 10/15/2015 f | 8,000,000 | 8,561,896 | 0.4 | % | ||||||||

| Other Industrials#~ | 458,004,946 | 22.8 | % | |||||||||

| Total Industrials | ||||||||||||

| (Cost $591,982,346) | 594,613,288 | 29.6 | % | |||||||||

| Utility | ||||||||||||

| Entergy Corporation | ||||||||||||

| 4.700%, 01/15/2017 | 8,750,000 | 9,408,140 | 0.5 | % | ||||||||

| Gulfstream Natural Gas System, L.L.C. | ||||||||||||

| 6.950%, 06/01/2016 (Acquired 07/22/2013 | ||||||||||||

| through 08/27/2013, Cost $8,642,026)* | 7,646,000 | 8,573,865 | 0.4 | % | ||||||||

| National Grid PLC | ||||||||||||

6.300%, 08/01/2016 f | 9,611,000 | 10,808,377 | 0.5 | % | ||||||||

| Williams Partners L.P. | ||||||||||||

| 3.800%, 02/15/2015 | 9,000,000 | 9,298,089 | 0.5 | % | ||||||||

| Other Utility#~ | 125,734,701 | 6.2 | % | |||||||||

| Total Utility | ||||||||||||

| (Cost $162,448,865) | 163,823,172 | 8.1 | % | |||||||||

| Finance | ||||||||||||

| ABN AMRO Bank N.V. | ||||||||||||

| 1.036%, 10/28/2016 (Acquired 10/23/2013 | ||||||||||||

through 12/27/2013, Cost $9,953,753)* f | 9,950,000 | 9,964,925 | 0.5 | % | ||||||||

| Cie de Financement Foncier SA | ||||||||||||

| 2.500%, 09/16/2015 (Acquired 06/19/2012 | ||||||||||||

through 09/27/2013, Cost $8,807,060)* f | 8,600,000 | 8,846,037 | 0.4 | % | ||||||||

| Credit Agricole SA | ||||||||||||

| 1.096%, 10/03/2016 | ||||||||||||

(Acquired 09/26/2013, Cost $10,000,000)*@ f | 10,000,000 | 10,027,090 | 0.5 | % | ||||||||

| General Electric Capital Corporation: | ||||||||||||

| 0.894%, 07/12/2016 | 10,000,000 | 10,070,160 | 0.5 | % | ||||||||

| 5.625%, 09/15/2017 | 9,080,000 | 10,329,381 | 0.5 | % | ||||||||

| 1.000%-5.625%, 09/21/2015-05/01/2018@ | 8,925,000 | 9,347,803 | 0.5 | % | ||||||||

The accompanying notes are an integral part of these financial statements.

Page 12

Baird Short-Term Bond Fund

Summary Schedule of Investments, December 31, 2013

Long-Term Investments (cont.)

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| Hutchison Whampoa International Ltd. | ||||||||||||

| 4.625%, 09/11/2015 (Acquired 09/24/2012 | ||||||||||||

through 06/25/2013, Cost $9,547,825)* f | $ | 9,090,000 | $ | 9,619,238 | 0.5 | % | ||||||

| Kemper Corporation | ||||||||||||

| 6.000%, 11/30/2015 | 8,500,000 | 9,091,311 | 0.5 | % | ||||||||

| KeyBank National Association | ||||||||||||

| 7.413%, 05/06/2015 | 9,854,000 | 10,677,104 | 0.5 | % | ||||||||

| Macquarie Bank Limited | ||||||||||||

| 2.000%, 08/15/2016 (Acquired 08/07/2013 | ||||||||||||

through 09/27/2013, Cost $10,025,015)* f | 10,000,000 | 10,113,710 | 0.5 | % | ||||||||

| Manulife Financial Corp. | ||||||||||||

3.400%, 09/17/2015 f | 9,761,000 | 10,160,508 | 0.5 | % | ||||||||

| Nomura Holdings Inc. | ||||||||||||

2.000%, 09/13/2016 f | 9,155,000 | 9,230,684 | 0.5 | % | ||||||||

| The Bank of Tokyo-Mitsubishi UFJ, Ltd. | ||||||||||||

| 3.850%, 01/22/2015 | ||||||||||||

(Acquired 07/22/2013, Cost $10,307,280)* f | 10,000,000 | 10,315,700 | 0.5 | % | ||||||||

| The Bear Stearns Companies LLC | ||||||||||||

| 6.400%, 10/02/2017 | 7,700,000 | 8,936,320 | 0.4 | % | ||||||||

| Other Finance#~ | 478,094,625 | 23.8 | % | |||||||||

| Total Finance | ||||||||||||

| (Cost $609,070,808) | 614,824,596 | 30.6 | % | |||||||||

| Residential Mortgage-Backed Securities | ||||||||||||

| U.S. Government Agency Issues | ||||||||||||

| Other U.S. Government Agency Issues# | 1,152,444 | 0.1 | % | |||||||||

| Total U.S. Government Agency Issues | ||||||||||||

| (Cost $1,089,496) | 1,152,444 | 0.1 | % | |||||||||

| Non-U.S. Government Agency Issues | ||||||||||||

| Countrywide Alternative Loan Trust | ||||||||||||

| Series 2004-2CB, Class 1A8, 5.750%, 03/25/2034 | 8,960,070 | 9,129,845 | 0.5 | % | ||||||||

| MASTR Alternative Loan Trust: | ||||||||||||

| Series 2003-5, Class 7A1, 5.000%, 07/25/2018 | 12,607,177 | 13,140,347 | 0.6 | % | ||||||||

| Series 2003-9, Class 3A1, 4.750%, 11/25/2018 | 5,982,619 | 6,092,634 | 0.3 | % | ||||||||

| Series 2003-5, Class 4A1, 5.500%, 07/25/2033 | 9,273,386 | 9,727,420 | 0.5 | % | ||||||||

| Other Non-U.S. Government Agency Issues# | 16,461,276 | 0.8 | % | |||||||||

| Total Non-U.S. Government Agency Issues | ||||||||||||

| (Cost $54,873,028) | 54,551,522 | 2.7 | % | |||||||||

| Asset Backed Securities | ||||||||||||

| Accredited Mortgage Loan Trust | ||||||||||||

| Series 2006-2, Class A3, 0.315%, 09/25/2036 | 10,942,014 | 10,542,412 | 0.5 | % | ||||||||

| GSAA Trust | ||||||||||||

| Series 2005-8, Class A4, 0.435%, 06/25/2035 | 12,922,206 | 11,869,563 | 0.6 | % | ||||||||

The accompanying notes are an integral part of these financial statements.

Page 13

Baird Short-Term Bond Fund

Summary Schedule of Investments, December 31, 2013

Long-Term Investments (cont.)

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| Nationstar Home Equity Loan Trust | ||||||||||||

| Series 2006-B, Class AV3, 0.335%, 09/25/2036 | $ | 11,907,627 | $ | 11,594,349 | 0.6 | % | ||||||

| RASC Trust | ||||||||||||

| Series 2005-AHL2, Class A3, 0.515%, 10/25/2035 | 12,150,000 | 11,514,312 | 0.6 | % | ||||||||

| Other Asset Backed Securities#~ | 71,090,147 | 3.5 | % | |||||||||

| Total Asset Backed Securities | ||||||||||||

| (Cost $118,122,724) | 116,610,783 | 5.8 | % | |||||||||

| Commercial Mortgage-Backed Securities | ||||||||||||

| Bear Stearns Commercial Mortgage Securities | ||||||||||||

| Series 2005-PWR9, Class A4A, 4.871%, 09/11/2042 | 18,110,000 | 18,997,879 | 1.0 | % | ||||||||

| CD Commercial Mortgage Trust | ||||||||||||

| Series 2005-CD1, Class A4, 5.218%, 07/15/2044 | 17,551,848 | 18,609,610 | 0.9 | % | ||||||||

| COMM Mortgage Trust | ||||||||||||

| Series 2005-C6, Class A5A, 5.116%, 06/10/2044 | 13,407,000 | 14,099,418 | 0.7 | % | ||||||||

| Credit Suisse First Boston Mortgage Securities Corp. | ||||||||||||

| Series 2005-C5, Class A4, 5.100%, 08/15/2038 | 15,208,250 | 15,965,104 | 0.8 | % | ||||||||

| FHLMC Multifamily Structured | ||||||||||||

| Pass Through Certificates | ||||||||||||

| Series K-701, Class A2, 3.882%, 11/25/2017 | 10,000,000 | 10,762,920 | 0.5 | % | ||||||||

| J.P. Morgan Chase Commercial Mortgage Trust | ||||||||||||

| Series 2005-CB12, Class A4, 4.895%, 09/12/2037 | 10,549,000 | 11,047,577 | 0.6 | % | ||||||||

| Morgan Stanley Capital I Trust | ||||||||||||

| Series 2005-HQ7, Class A4, 5.207%, 11/14/2042 | 13,020,000 | 13,693,837 | 0.7 | % | ||||||||

| Wachovia Bank Commercial Mortgage Trust | ||||||||||||

| Series 2005-C22, Class A4, 5.289%, 12/15/2044 | 9,912,000 | 10,551,334 | 0.5 | % | ||||||||

| Other Commercial Mortgage Backed Securities#~ | 16,981,754 | 0.8 | % | |||||||||

| Total Commercial Mortgage Backed Securities | ||||||||||||

| (Cost $133,435,803) | 130,709,433 | 6.5 | % | |||||||||

| Total Long-Term Investments | ||||||||||||

| (Cost $1,945,062,241) | 1,949,823,113 | 97.0 | % | |||||||||

| Short-Term Investments | ||||||||||||

| Shares | ||||||||||||

| Money Market Mutual Funds | ||||||||||||

| Dreyfus Institutional Cash Advantage Fund, 0.06%« | 23,737,892 | 23,737,892 | 1.2 | % | ||||||||

| Short-Term Investments Trust – | ||||||||||||

| Liquid Assets Portfolio, 0.07%« | 39,000,000 | 39,000,000 | 1.9 | % | ||||||||

| Total Short-Term Investments | ||||||||||||

| (Cost $62,737,892) | 62,737,892 | 3.1 | % | |||||||||

The accompanying notes are an integral part of these financial statements.

Page 14

Baird Short-Term Bond Fund

Summary Schedule of Investments, December 31, 2013

Investments Purchased with Cash

Proceeds from Securities Lending

| % of | ||||||||||||

| Shares | Value | Net Assets | ||||||||||

| Investment Companies | ||||||||||||

| Mount Vernon Securities Lending | ||||||||||||

| Trust Prime Portfolio, 0.19%« | 204,124,977 | $ | 204,124,977 | 10.2 | % | |||||||

| Total Investment Companies | ||||||||||||

| (Cost $204,124,977) | 204,124,977 | 10.2 | % | |||||||||

| Total Investments Purchased With | ||||||||||||

| Cash Proceeds From Securities Lending | ||||||||||||

| (Cost $204,124,977) | 204,124,977 | 10.2 | % | |||||||||

| Total Investments | ||||||||||||

| (Cost $2,211,925,110) | 2,216,685,982 | 110.3 | % | |||||||||

| Liabilities in Excess of Other Assets | (207,721,393 | ) | (10.3 | )% | ||||||||

| TOTAL NET ASSETS | $ | 2,008,964,589 | 100.0 | % | ||||||||

Notes to Summary Schedule of Investments

| # | Represents the aggregate value, by category, of securities that are not among the 50 largest holdings and, in total for any issuer, represent 1% or less of net assets. | |

| * | Restricted Security Deemed Liquid | |

| @ | This security or portion of this security is out on loan at December 31, 2013. | |

| f | Foreign Security | |

| « | 7-Day Yield | |

| ~ | Groupings contain, in aggregate, restricted securities totaling $305,270,462 representing 15.20% of net assets. |

Summary of Fair Value Exposure at December 31, 2013

The Fund has adopted authoritative fair valuation accounting standards which establish a definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion on changes in valuation techniques and related inputs during the period. These standards define fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The fair value hierarchy is organized into three levels based upon the assumptions (referred to as “inputs”) used in pricing the asset or liability. These standards state that “observable inputs” reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from independent sources and “unobservable inputs” reflect an entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability. These inputs are summarized into three broad levels and described below:

Level 1 – | Unadjusted quoted prices in active markets for identical unrestricted securities. |

Level 2 – | Other significant observable inputs (including quoted prices for similar securities, quoted prices in inactive markets, dealer indications, interest rates, yield curves, prepayment speeds, credit risk, default rates, inputs corroborated by observable market data, etc.). |

Level 3 – | Significant unobservable inputs (including the Fund’s own assumptions about the factors that market participants would use in valuing the security) based on the best information available. |

The accompanying notes are an integral part of these financial statements.

Page 15

Baird Short-Term Bond Fund

Summary Schedule of Investments, December 31, 2013

Summary of Fair Value Exposure at December 31, 2013 (cont.)

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used to value the Fund’s investments as of December 31, 2013:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Fixed Income | ||||||||||||||||

| U.S. Treasury Securities | $ | — | $ | 194,146,508 | $ | — | $ | 194,146,508 | ||||||||

| Taxable Municipal Bonds | — | 56,432,927 | — | 56,432,927 | ||||||||||||

| Other Government Related Securities | — | 22,958,440 | — | 22,958,440 | ||||||||||||

| Corporate Bonds | — | 1,373,261,056 | — | 1,373,261,056 | ||||||||||||

| Residential Mortgage-Backed Securities – | ||||||||||||||||

| U.S. Government Agency Issues | — | 1,152,444 | — | 1,152,444 | ||||||||||||

| Residential Mortgage-Backed Securities – | ||||||||||||||||

| Non-U.S. Government Agency Issues | — | 54,551,522 | — | 54,551,522 | ||||||||||||

| Asset Backed Securities | — | 116,610,783 | — | 116,610,783 | ||||||||||||

| Commercial Mortgage-Backed Securities | — | 130,709,433 | — | 130,709,433 | ||||||||||||

| Total Fixed Income | — | 1,949,823,113 | — | 1,949,823,113 | ||||||||||||

| Short-Term Investments | ||||||||||||||||

| Money Market Mutual Funds | 62,737,892 | — | — | 62,737,892 | ||||||||||||

| Total Short-Term Investments | 62,737,892 | — | — | 62,737,892 | ||||||||||||

| Investments Purchased with Cash | ||||||||||||||||

| Proceeds from Securities Lending | ||||||||||||||||

| Investment Companies | 204,124,977 | — | — | 204,124,977 | ||||||||||||

| Total Investments Purchased with | ||||||||||||||||

| Cash Proceeds from Securities Lending | 204,124,977 | — | — | 204,124,977 | ||||||||||||

| Total Investments | $ | 266,862,869 | $ | 1,949,823,113 | $ | — | $ | 2,216,685,982 | ||||||||

Changes in valuation techniques may result in transfers into or out of assigned levels within the fair value hierarchy. There were no transfers between Level 1, Level 2 and Level 3 fair value measurements during the reporting period, as compared to their classification from the prior year’s annual report. See the Fund’s valuation policy in Note 2a to the financial statements.

The accompanying notes are an integral part of these financial statements.

Page 16

Baird Intermediate Bond Fund

December 31, 2013

The Baird Intermediate Bond Fund seeks an annual rate of total return, before Fund expenses, greater than the annual rate of total return of the Barclays Intermediate U.S. Government/Credit Bond Index. The Barclays Intermediate U.S. Government/Credit Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt issues, including government and credit securities, with maturities between one and ten years.

Although the Fund generated a negative absolute return for the year resulting from the rise in market yields, the Fund entered the year with a significant yield advantage over its benchmark and converted that advantage into strong relative returns versus its benchmark index in 2013. Our long-term commitment to duration neutrality was very important as well. A number of the themes that drove performance in 2012 continued to positively impact the portfolio relative to its benchmark in 2013. The primary factors contributing to the Fund’s outperformance over its benchmark in 2013 are described below.

| • | The Fund’s continued overweight position to the corporate credit sector relative to the Fund’s benchmark positively impacted the Fund’s performance. Corporate bonds generally experienced favorable price returns relative to U.S. Treasuries of comparable maturity due to a significant narrowing of corporate bond spreads (the additional yield that investors demand above U.S. Treasury bonds for owning corporate debt) during the year. The narrowing was driven by generally solid corporate credit fundamentals and very strong investor demand. | |

| • | An overweight to the financial sub-sector in particular was an important contributor to the Fund’s relative outperformance, as financials significantly outperformed other investment grade corporate bonds. The financial sub-sector’s performance was driven by both strong and improving credit fundamentals and strong investor demand. | |

| • | The Fund’s underweight to U.S. Treasuries and Agencies was a positive contributor to relative performance, as nongovernment “spread sectors” such as corporate, mortgage-backed, and asset-backed securities outperformed equal-duration U.S. Government securities for the year. | |

| • | Modest exposure to commercial mortgage-backed securities (CMBS) had an overall positive impact on the Fund’s performance for the year. As part of the risk management for the Fund’s exposure to this sector, the Fund holds short maturity, select super-senior issues with significant credit enhancement. | |

| • | The Fund’s modest exposure to non-U.S. Agency mortgage-backed securities was a positive contributor as prices for those securities generally rose during 2013. The Fund also benefited from relatively high coupon payments, an important consideration in the current low interest rate environment when income is reinvested as rates rise. |

We are pleased with the Fund’s relative performance to its benchmark in 2013 and are confident in the individual issues and the overall structure of the Fund. The Fund’s current significant yield advantage over the benchmark is meaningful and we are optimistic regarding the Fund’s relative performance as we head into 2014.

Page 17

Baird Intermediate Bond Fund

December 31, 2013

Portfolio Characteristics

Quality Distribution(1)

| Net Assets | $1,155,705,925 | |||

| SEC 30-Day | |||

Yield(2) | ||||

| Institutional Class | 2.08% | |||

| Investor Class | 1.84% | |||

| Average | ||||

| Effective | ||||

| Duration | 3.84 years | |||

| Average | ||||

| Effective | ||||

| Maturity | 4.39 years | |||

| Annualized | ||||

| Expense | ||||

| Ratio | ||||

Sector Weightings(1) | Institutional Class | 0.30% | ||

| Investor Class | 0.55%(3) | |||

| ||||

| Portfolio | ||||

| Turnover | ||||

| Rate | 45.1% | |||

| Number of | ||||

| Holdings | 422 | |||

| (1) | Percentages shown are based on the Fund’s total investments (less investments purchased with cash proceeds from securities lending). |

| (2) | SEC yields are based on SEC guidelines and are calculated for the 30 days ended December 31, 2013. |

| (3) | Includes 0.25% 12b-1 fee. |

Page 18

Baird Intermediate Bond Fund

December 31, 2013

Institutional Class

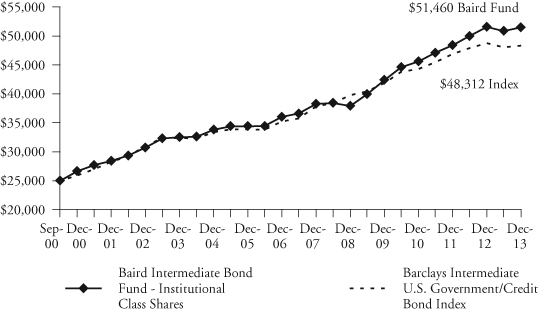

Value of a $25,000 Investment

Growth of a hypothetical investment of $25,000 made on the Fund’s inception date (9/29/00), assuming reinvestment of all distributions.

Investor Class

Value of a $10,000 Investment

Growth of a hypothetical investment of $10,000 made on the Fund’s inception date (9/29/00), assuming reinvestment of all distributions.

Page 19

Baird Intermediate Bond Fund

December 31, 2013

Total Returns

| Average Annual | ||||

| One | Five | Ten | Since | |

| For the Periods Ended December 31, 2013 | Year | Years | Years | Inception(1) |

| Institutional Class Shares | -0.17% | 6.29% | 4.69% | 5.60% |

| Investor Class Shares | -0.41% | 6.02% | 4.41% | 5.33% |

| Barclays Intermediate | ||||

U.S. Government/Credit Bond Index(2) | -0.86% | 3.96% | 4.09% | 5.10% |

| (1) | For the period from September 29, 2000 (commencement of operations) through December 31, 2013. |

| (2) | The Barclays Intermediate U.S. Government/Credit Bond Index is an unmanaged, market value weighted index of investment grade, fixed-rate debt issues, including government and corporate securities, with maturities between one and ten years. This index does not reflect any deduction for fees, expenses or taxes. A direct investment in an index is not possible. |

The line graph on the previous page and the returns shown in the table above reflect reinvestment of dividends and/or capital gains distributions in additional shares. The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns reflect the actual performance for each period and do not include the impact of trades executed on the last business day of the period that were recorded on the first business day of the next period.

The Fund’s gross expense ratio for each Class, as reflected in the Fund’s current prospectus, is set forth under “Portfolio Characteristics”.

The Fund may invest in U.S. dollar denominated foreign securities which involve additional risks such as currency rate fluctuations, political and economic instability, and different and sometimes less strict financial reporting standards and regulation. The Fund may also invest in mortgage- and asset-backed securities, which include interest rate and prepayment risks more pronounced than those of other fixed income securities.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

For information about the performance of the Fund as of the most recent month-end, please call 1-866-44BAIRD or visit www.bairdfunds.com. Mutual fund performance changes over time and current performance may be lower or higher than that stated.

Page 20

Baird Intermediate Bond Fund

Summary Schedule of Investments, December 31, 2013

This schedule summarizes the Fund’s holdings by asset type. Details are reported for each of the Fund’s 50 largest individual holdings and for investments that, in total for any issuer, represent more than 1% of the Fund’s net assets. The total value of smaller holdings is reported as a single amount within each category.

The Fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter end. For the second and fourth fiscal quarters, the complete listing of the Fund’s holdings is available electronically in the Fund’s Form N-CSR at http://www.rwbaird.com/baird-funds/prospectus-applications/prospectus-applications.aspx and on the Securities and Exchange Commission’s website (www.sec.gov) or you can have it mailed to you without charge by calling 1-866-44BAIRD. For the first and third fiscal quarters, the Fund files the lists with the SEC on Form N-Q. Shareholders can look up the Fund’s Forms N-CSR and N-Q on the SEC’s website (www.sec.gov).

Long-Term Investments

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| U.S. Treasury Securities | ||||||||||||

| U.S. Treasury Bonds: | ||||||||||||

| 3.875%, 05/15/2018@ | $ | 9,700,000 | $ | 10,691,224 | 0.9 | % | ||||||

| 9.125%, 05/15/2018@ | 13,950,000 | 18,505,540 | 1.6 | % | ||||||||

| 1.250%, 04/30/2019@ | 224,875,000 | 217,865,196 | 18.9 | % | ||||||||

| 7.875%, 02/15/2021@ | 31,000,000 | 42,179,375 | 3.6 | % | ||||||||

| Total U.S. Treasury Securities | ||||||||||||

| (Cost $290,915,764) | 289,241,335 | 25.0 | % | |||||||||

| U.S. Government Agency Issues | ||||||||||||

| Federal Home Loan Mortgage Corporation (FHLMC): | ||||||||||||

| 1.000%, 06/29/2017 | 9,200,000 | 9,144,818 | 0.8 | % | ||||||||

| 1.375%, 05/01/2020@ | 10,000,000 | 9,375,140 | 0.8 | % | ||||||||

| 2.375%, 01/13/2022@ | 300,000 | 286,790 | 0.0 | % | ||||||||

| Total U.S. Government Agency Issues | ||||||||||||

| (Cost $18,849,262) | 18,806,748 | 1.6 | % | |||||||||

| Taxable Municipal Bonds | ||||||||||||

| State of Illinois | ||||||||||||

| 3.636%, 02/01/2014 | 5,150,000 | 5,161,793 | 0.5 | % | ||||||||

| Other Taxable Municipal Bonds# | 28,805,070 | 2.5 | % | |||||||||

| Total Taxable Municipal Bonds | ||||||||||||

| (Cost $33,486,123) | 33,966,863 | 3.0 | % | |||||||||

| Other Government Related Securities | ||||||||||||

| Petrobras International Finance Company | ||||||||||||

3.875%, 01/27/2016 f | 4,175,000 | 4,298,004 | 0.4 | % | ||||||||

| Other Government Related Securities#~ | 10,607,760 | 0.9 | % | |||||||||

| Total Other Government Related Securities | ||||||||||||

| (Cost $13,984,332) | 14,905,764 | 1.3 | % | |||||||||

| Corporate Bonds | ||||||||||||

| Industrials | ||||||||||||

| Computer Sciences Corporation | ||||||||||||

| 2.500%, 09/15/2015@ | 4,500,000 | 4,593,227 | 0.4 | % | ||||||||

The accompanying notes are an integral part of these financial statements.

Page 21

Baird Intermediate Bond Fund

Summary Schedule of Investments, December 31, 2013

Long-Term Investments (cont.)

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| CVS Caremark Corporation | ||||||||||||

| 4.000%, 12/05/2023 | $ | 4,425,000 | $ | 4,415,637 | 0.4 | % | ||||||

| Fidelity National Information Services, Inc. | ||||||||||||

| 7.875%, 07/15/2020 | 4,800,000 | 5,236,603 | 0.4 | % | ||||||||

| Glencore Funding LLC | ||||||||||||

| 2.500%, 01/15/2019 (Acquired 05/22/2013 | ||||||||||||

| through 10/29/2013, Cost $4,292,532)* | 4,400,000 | 4,260,599 | 0.4 | % | ||||||||

| Hyundai Capital Services Inc. | ||||||||||||

| 6.000%, 05/05/2015 (Acquired 03/27/2013 | ||||||||||||

through 05/30/2013, Cost $5,883,634)* f | 5,549,000 | 5,901,317 | 0.5 | % | ||||||||

| Murphy Oil Corporation | ||||||||||||

| 3.700%, 12/01/2022 | 5,000,000 | 4,620,025 | 0.4 | % | ||||||||

| Mylan Inc. | ||||||||||||

| 6.000%, 11/15/2018 (Acquired 01/15/2013 | ||||||||||||

| through 02/12/2013, Cost $4,268,859)* | 4,000,000 | 4,262,380 | 0.4 | % | ||||||||

| Petrohawk Energy Corporation | ||||||||||||

| 7.250%, 08/15/2018 | 4,000,000 | 4,312,000 | 0.4 | % | ||||||||

| Telecom Italia Capital, SA | ||||||||||||

5.250%, 10/01/2015 f | 4,425,000 | 4,651,781 | 0.4 | % | ||||||||

| Warner Chilcott Co LLC / | ||||||||||||

| Warner Chilcott Finance LLC | ||||||||||||

7.750%, 09/15/2018 f | 5,000,000 | 5,412,500 | 0.5 | % | ||||||||

| Waste Management, Inc. | ||||||||||||

| 7.375%, 03/11/2019 | 5,000,000 | 6,047,305 | 0.5 | % | ||||||||

| Other Industrials#~ | 198,196,468 | 17.1 | % | |||||||||

| Total Industrials | ||||||||||||

| (Cost $248,407,897) | 251,909,842 | 21.8 | % | |||||||||

| Utility | ||||||||||||

| Ameren Corporation | ||||||||||||

| 8.875%, 05/15/2014 | 4,500,000 | 4,629,047 | 0.4 | % | ||||||||

| National Grid PLC | ||||||||||||

6.300%, 08/01/2016 f | 3,925,000 | 4,413,992 | 0.4 | % | ||||||||

| National Rural Utilities Corporation | ||||||||||||

| 10.375%, 11/01/2018 | 3,144,000 | 4,251,895 | 0.4 | % | ||||||||

| Other Utility#~ | 65,428,119 | 5.6 | % | |||||||||

| Total Utility | ||||||||||||

| (Cost $77,059,019) | 78,723,053 | 6.8 | % | |||||||||

| Finance | ||||||||||||

| ABN AMRO Bank N.V. | ||||||||||||

| 4.250%, 02/02/2017 | ||||||||||||

(Acquired 11/22/2013, Cost $4,853,428)* f | 4,500,000 | 4,824,369 | 0.4 | % | ||||||||

| BPCE | ||||||||||||

2.500%, 12/10/2018 f | 7,000,000 | 6,962,522 | 0.6 | % | ||||||||

The accompanying notes are an integral part of these financial statements.

Page 22

Baird Intermediate Bond Fund

Summary Schedule of Investments, December 31, 2013

Long-Term Investments (cont.)

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| Comerica Bank | ||||||||||||

| 5.200%, 08/22/2017 | $ | 4,095,000 | $ | 4,508,943 | 0.4 | % | ||||||

| Commonwealth Bank of Australia | ||||||||||||

| 5.000%, 10/15/2019 | ||||||||||||

(Acquired 03/02/2012, Cost $4,264,500)* f | 4,000,000 | 4,458,520 | 0.4 | % | ||||||||

| Deutsche Bank Aktiengesellschaft | ||||||||||||

3.250%, 01/11/2016 f | 4,250,000 | 4,444,926 | 0.4 | % | ||||||||

| First Tennessee Bank, National Association | ||||||||||||

| 5.650%, 04/01/2016 | 4,263,000 | 4,599,334 | 0.4 | % | ||||||||

| KeyBank National Association | ||||||||||||

| 7.413%, 05/06/2015 | 4,000,000 | 4,334,120 | 0.4 | % | ||||||||

| Macquarie Bank Limited | ||||||||||||

| 2.000%, 08/15/2016 | ||||||||||||

(Acquired 08/07/2013, Cost $4,998,250)* f | 5,000,000 | 5,056,855 | 0.4 | % | ||||||||

| The Goldman Sachs Group, Inc. | ||||||||||||

| 6.150%, 04/01/2018 | 3,900,000 | 4,472,041 | 0.4 | % | ||||||||

| The Huntington National Bank | ||||||||||||

| 1.300%, 11/20/2016 | 4,850,000 | 4,850,732 | 0.4 | % | ||||||||

| WEA Finance LLC / WT Finance Aust Pty Ltd | ||||||||||||

| 6.750%, 09/02/2019 | ||||||||||||

| (Acquired 11/21/2013, Cost $4,806,637)* | 4,000,000 | 4,756,020 | 0.4 | % | ||||||||

| Other Finance#~ | 247,426,557 | 21.4 | % | |||||||||

| Total Finance | ||||||||||||

| (Cost $293,148,726) | 300,694,939 | 26.0 | % | |||||||||

| Residential Mortgage-Backed Securities | ||||||||||||

| U.S. Government Agency Issues | ||||||||||||

| Other U.S. Government Agency Issues# | 1,329,800 | 0.1 | % | |||||||||

| Total U.S. Government Agency Issues | ||||||||||||

| (Cost $1,261,290) | 1,329,800 | 0.1 | % | |||||||||

| Non-U.S. Government Agency Issues | ||||||||||||

| Countrywide Alternative Loan Trust | ||||||||||||

| Series 2004-2CB, Class 1A8, 5.750%, 03/25/2034 | 5,145,064 | 5,242,553 | 0.5 | % | ||||||||

| Washington Mutual Mortgage Pass Through Certificates | ||||||||||||

| Series 2004-CB2, Class 3A, 6.000%, 08/25/2034 | 5,859,621 | 6,132,069 | 0.5 | % | ||||||||

| Other Non-U.S. Government Agency Issues#~ | 10,058,099 | 0.9 | % | |||||||||

| Total Non-U.S. Government Agency Issues | ||||||||||||

| (Cost $21,467,472) | 21,432,721 | 1.9 | % | |||||||||

| Asset Backed Securities | ||||||||||||

| Master Credit Card Trust | ||||||||||||

| Series 2012-2A, Class A, 0.780%, 04/21/2017 | ||||||||||||

(Acquired 10/24/2012, Cost $5,998,817)* f | 6,000,000 | 5,990,142 | 0.5 | % | ||||||||

| Soundview Home Loan Trust | ||||||||||||

| Series 2003-2, Class A2, 1.465%, 11/25/2033 | 4,851,513 | 4,792,504 | 0.4 | % | ||||||||

The accompanying notes are an integral part of these financial statements.

Page 23

Baird Intermediate Bond Fund

Summary Schedule of Investments, December 31, 2013

Long-Term Investments (cont.)

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| Specialty Underwriting & Residential Finance Trust | ||||||||||||

| Series 2004-BC4, Class A1A, 0.835%, 10/25/2035 | $ | 4,816,158 | $ | 4,683,184 | 0.4 | % | ||||||

| Other Asset Backed Securities#~ | 13,840,101 | 1.2 | % | |||||||||

| Total Asset Backed Securities | ||||||||||||

| (Cost $29,279,128) | 29,305,931 | 2.5 | % | |||||||||

| Commercial Mortgage-Backed Securities | ||||||||||||

| Bear Stearns Commercial Mortgage Securities | ||||||||||||

| Series 2005-PWR9, Class A4A, 4.871%, 09/11/2042 | 6,790,000 | 7,122,893 | 0.6 | % | ||||||||

| CD Commercial Mortgage Trust | ||||||||||||

| Series 2005-CD1, Class A4, 5.218%, 07/15/2044 | 7,000,000 | 7,421,855 | 0.6 | % | ||||||||

| Credit Suisse First Boston | ||||||||||||

| Mortgage Securities Corporation | ||||||||||||

| Series 2005-C5, Class A4, 5.100%, 08/15/2038 | 6,000,000 | 6,298,596 | 0.5 | % | ||||||||

| DBUBS Mortgage Trust | ||||||||||||

| Series 2011-LC3A, Class A2, 3.642%, 08/12/2044 | 5,000,000 | 5,252,645 | 0.4 | % | ||||||||

| FHLMC Multifamily Structured | ||||||||||||

| Pass Through Certificates: | ||||||||||||

| Series K-708, Class A2, 2.130%, 01/25/2019 | 8,300,000 | 8,266,053 | 0.7 | % | ||||||||

| Series K-003, Class A4, 5.053%, 01/25/2019 | 9,000,000 | 10,107,990 | 0.9 | % | ||||||||

| Series K-004, Class A2, 4.186%, 08/25/2019 | 5,875,000 | 6,381,125 | 0.5 | % | ||||||||

| Series K-005, Class A2, 4.317%, 11/25/2019 | 4,975,000 | 5,432,118 | 0.5 | % | ||||||||

| Series KF02, Class A3, 0.795%, 07/25/2020 | 9,992,432 | 9,996,569 | 0.9 | % | ||||||||

| 1.655%-4.251%, 11/25/2016-01/25/2020 | 7,783,000 | 8,019,563 | 0.7 | % | ||||||||

| J.P. Morgan Chase Commercial Mortgage Trust | ||||||||||||

| Series 2005-CB12, Class A4, 4.895%, 09/12/2037 | 5,000,000 | 5,236,315 | 0.5 | % | ||||||||

| Wachovia Bank Commercial Mortgage Trust | ||||||||||||

| Series 2005-C22, Class A4, 5.289%, 12/15/2044 | 5,000,000 | 5,322,505 | 0.5 | % | ||||||||

| Other Commercial Mortgage Backed Securities# | 6,518,765 | 0.6 | % | |||||||||

| Total Commercial Mortgage Backed Securities | ||||||||||||

| (Cost $91,727,345) | 91,376,992 | 7.9 | % | |||||||||

| Total Long-Term Investments | ||||||||||||

| (Cost $1,119,586,358) | 1,131,693,988 | 97.9 | % | |||||||||

| Short-Term Investments | ||||||||||||

| Shares | ||||||||||||

| Money Market Mutual Fund | ||||||||||||

| Short-Term Investments Trust – | ||||||||||||

| Liquid Assets Portfolio, 0.07%« | 21,500,000 | 21,500,000 | 1.9 | % | ||||||||

| Total Short-Term Investments | ||||||||||||

| (Cost $21,500,000) | 21,500,000 | 1.9 | % | |||||||||

The accompanying notes are an integral part of these financial statements.

Page 24

Baird Intermediate Bond Fund

Summary Schedule of Investments, December 31, 2013

Investments Purchased with Cash

Proceeds from Securities Lending

| % of | ||||||||||||

| Shares | Value | Net Assets | ||||||||||

| Investment Companies | ||||||||||||

| Mount Vernon Securities Lending | ||||||||||||

| Trust Prime Portfolio, 0.19%« | 227,595,639 | $ | 227,595,639 | 19.7 | % | |||||||

| Total Investment Companies | ||||||||||||

| (Cost $227,595,639) | 227,595,639 | 19.7 | % | |||||||||

| Total Investments Purchased With | ||||||||||||

| Cash Proceeds From Securities Lending | ||||||||||||

| (Cost $227,595,639) | 227,595,639 | 19.7 | % | |||||||||

| Total Investments | ||||||||||||

| (Cost $1,368,681,997) | 1,380,789,627 | 119.5 | % | |||||||||

| Liabilities in Excess of Other Assets | (225,083,702 | ) | (19.5 | )% | ||||||||

| TOTAL NET ASSETS | $ | 1,155,705,925 | 100.0 | % | ||||||||

Notes to Summary Schedule of Investments

| * | Restricted Security Deemed Liquid | |

| @ | This security or portion of this security is out on loan at December 31, 2013. | |

| f | Foreign Security | |

| « | 7-Day Yield | |

| # | Represents the aggregate value, by category, of securities that are not among the 50 largest holdings and, in total for any issuer, represent 1% or less of net assets. | |

| ~ | Groupings contain, in aggregate, restricted securities totaling $134,618,531 representing 11.65% of net assets. |

Summary of Fair Value Exposure at December 31, 2013

The Fund has adopted authoritative fair valuation accounting standards which establish a definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value and a discussion on changes in valuation techniques and related inputs during the period. These standards define fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The fair value hierarchy is organized into three levels based upon the assumptions (referred to as “inputs”) used in pricing the asset or liability. These standards state that “observable inputs” reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from independent sources and “unobservable inputs” reflect an entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability. These inputs are summarized into three broad levels and described below:

Level 1 – | Unadjusted quoted prices in active markets for identical unrestricted securities. |

Level 2 – | Other significant observable inputs (including quoted prices for similar securities, quoted prices in inactive markets, dealer indications, interest rates, yield curves, prepayment speeds, credit risk, default rates, inputs corroborated by observable market data, etc.). |

Level 3 – | Significant unobservable inputs (including the Fund’s own assumptions about the factors that market participants would use in valuing the security) based on the best information available. |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The accompanying notes are an integral part of these financial statements.

Page 25

Baird Intermediate Bond Fund

Summary Schedule of Investments, December 31, 2013

Summary of Fair Value Exposure at December 31, 2013 (cont.)

The following is a summary of the inputs used to value the Fund’s investments as of December 31, 2013:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Fixed Income | ||||||||||||||||

| U.S. Treasury Securities | $ | — | $ | 289,241,335 | $ | — | $ | 289,241,335 | ||||||||

| U.S. Government Agency Issues | — | 18,806,748 | — | 18,806,748 | ||||||||||||

| Taxable Municipal Bonds | — | 33,966,863 | — | 33,966,863 | ||||||||||||

| Other Government Related Securities | — | 14,905,764 | — | 14,905,764 | ||||||||||||

| Corporate Bonds | — | 631,327,834 | — | 631,327,834 | ||||||||||||

| Residential Mortgage-Backed Securities – | ||||||||||||||||

| U.S. Government Agency Issues | — | 1,329,800 | — | 1,329,800 | ||||||||||||

| Residential Mortgage-Backed Securities – | ||||||||||||||||

| Non-U.S. Government Agency Issues | — | 21,432,721 | — | 21,432,721 | ||||||||||||

| Asset Backed Securities | — | 29,305,539 | 392 | 29,305,931 | ||||||||||||

| Commercial Mortgage-Backed Securities | — | 91,376,992 | — | 91,376,992 | ||||||||||||

| Total Fixed Income | — | 1,131,693,596 | 392 | 1,131,693,988 | ||||||||||||

| Short-Term Investments | ||||||||||||||||

| Money Market Mutual Fund | 21,500,000 | — | — | 21,500,000 | ||||||||||||

| Total Short-Term Investments | 21,500,000 | — | — | 21,500,000 | ||||||||||||

| Investments Purchased with Cash | ||||||||||||||||

| Proceeds from Securities Lending | ||||||||||||||||

| Investment Companies | 227,595,639 | — | — | 227,595,639 | ||||||||||||

| Total Investments Purchased with | ||||||||||||||||

| Cash Proceeds from Securities Lending | 227,595,639 | — | — | 227,595,639 | ||||||||||||

| Total Investments | $ | 249,095,639 | $ | 1,131,693,596 | $ | 392 | $ | 1,380,789,627 | ||||||||

Changes in valuation techniques may result in transfers into or out of assigned levels within the fair value hierarchy. There were no transfers between Level 1, Level 2 and Level 3 fair value measurements during the reporting period, as compared to their classification from the prior year’s annual report. See the Fund’s valuation policy in Note 2a to the financial statements. One security priced at fair value by the Valuation Committee instead of the Fund’s pricing vendor is valued using Level 3 inputs.

Level 3 Reconciliation Disclosure

Following is a reconciliation of Level 3 assets for which significant unobservable inputs were used to determine fair value.

| Description | Investments in Securities | |||

| Balance as of December 31, 2012 | $ | 1,461 | ||

| Accrued discounts/premiums | — | |||

| Realized gain (loss) | (48,605 | ) | ||

| Change in unrealized appreciation (depreciation) | 47,635 | |||

| Purchases | — | |||

| Sales | (99 | ) | ||

| Transfers in and/or out of Level 3* | — | |||

| Balance as of December 31, 2013 | $ | 392 | ||

* Transfers between levels are recognized at the end of the reporting period.

The accompanying notes are an integral part of these financial statements.

Page 26

Baird Intermediate Municipal Bond Fund

December 31, 2013

The Baird Intermediate Municipal Bond Fund seeks current income that is substantially exempt from federal income tax. A secondary objective is to provide total return with relatively low volatility of principal. The Fund uses the Barclays 7-Year General Obligation Bond Index as its benchmark. The Barclays 7-Year General Obligation Bond Index is an unmanaged, market value weighted index consisting of investment grade state and local general obligation bonds that have been issued as part of an offering of at least $50 million; have a minimum amount outstanding of at least $5 million; have been issued within the last five years; and have a maturity of six to eight years.

Although the Fund had a negative absolute return in 2013 along with most of the municipal bond market, the Fund produced attractive relative results compared to its benchmark. Its focus on intermediate-maturity issues limited the impact of the increase in market yields, which produced sharply negative returns on longer issues in the market. Furthermore, the Fund’s emphasis on high-quality issues also contributed to relative performance as lower quality issues in the market underperformed due to investors’ heightened sensitivity to credit risk as a result of the City of Detroit’s bankruptcy filing.

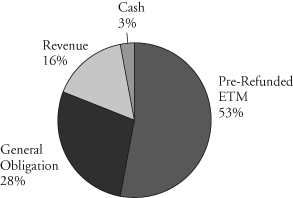

The Fund had a very broadly diversified portfolio at year end, with 53% of its investments in pre-refunded bonds. Pre-refunded municipal bonds are generally regarded as the safest municipal bonds available as their interest and principal payments are paid from an escrow account which holds U.S. Treasury and/or U.S. Agency securities. With its focus on high-quality holdings and intermediate duration, we believe the Fund is well-positioned for the uncertain environment for municipal bonds as we enter 2014.

Page 27

Baird Intermediate Municipal Bond Fund

December 31, 2013

Portfolio Characteristics

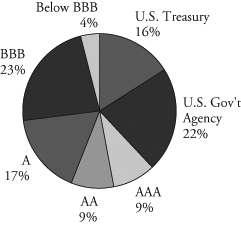

Quality Distribution(1)

| Net Assets | $1,006,994,598 | |||

| SEC 30-Day | |||

Yield(3) | ||||

| Institutional Class | 2.03% | |||

| Investor Class | 1.77% | |||

| Average | ||||

| Effective | ||||

| Duration | 4.88 years | |||

| Average | ||||

| Effective | ||||

| Maturity | 5.33 years | |||

| Annualized | ||||

| Expense | ||||

| Ratio | ||||

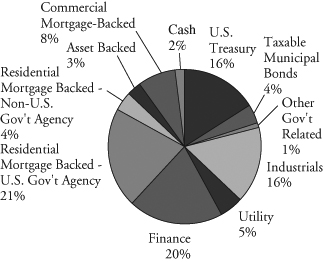

Sector Weightings(1) | Institutional Class | 0.30% | ||

| Investor Class | 0.55%(4) | |||

| ||||

| Portfolio | ||||

| Turnover | ||||

| Rate | 9.0% | |||

| Number of | ||||

| Holdings | 275 | |||

| (1) | Percentages shown are based on the Fund’s total investments. |

| (2) | Includes pre-refunded and escrowed-to-maturity (ETM) bonds. |

| (3) | SEC yields are based on SEC guidelines and are calculated for the 30 days ended December 31, 2013. |

| (4) | Includes 0.25% 12b-1 fee. |

Page 28

Baird Intermediate Municipal Bond Fund

December 31, 2013

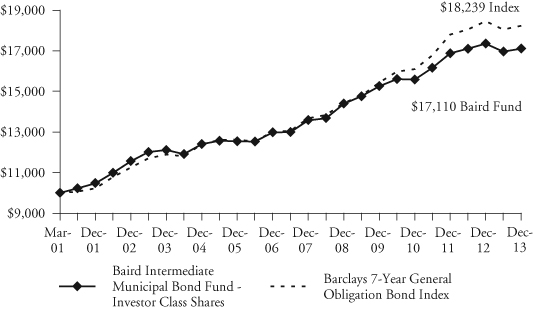

Value of a $25,000 Investment

Growth of a hypothetical investment of $25,000 made on the Fund’s inception date (3/30/01), assuming reinvestment of all distributions.

Investor Class

Value of a $10,000 Investment

Growth of a hypothetical investment of $10,000 made on the Fund’s inception date (3/30/01), assuming reinvestment of all distributions.

Page 29

Baird Intermediate Municipal Bond Fund

December 31, 2013

Total Returns

| Average Annual | ||||

| One | Five | Ten | Since | |

| For the Periods Ended December 31, 2013 | Year | Years | Years | Inception(1) |

| Institutional Class Shares | -1.19% | 3.77% | 3.78% | 4.57% |

| Investor Class Shares | -1.42% | 3.51% | 3.52% | 4.30% |

Barclays 7-Year General Obligation Bond Index(2) | -1.16% | 4.80% | 4.38% | 4.82% |

| (1) | For the period from March 30, 2001 (commencement of operations) through December 31, 2013. |

| (2) | The Barclays 7-Year General Obligation Bond Index is an unmanaged, market value weighted index comprised of investment grade state and local general obligation bonds that have been issued as part of an offering of at least $50 million, have a minimum amount outstanding of at least $5 million, have been issued within the last five years and have a maturity of six to eight years. This index does not reflect any deduction for fees, expenses or taxes. A direct investment in an index is not possible. |

The line graph on the previous page and the returns shown in the table above reflect reinvestment of dividends and/or capital gains distributions in additional shares. The returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns reflect the actual performance for each period and do not include the impact of trades executed on the last business day of the period that were recorded on the first business day of the next period.

The Fund’s gross expense ratio for each Class, as reflected in the Fund’s current prospectus, is set forth under “Portfolio Characteristics”.

The Fund may invest up to 25% of its total assets in municipal obligations issued by persons in the same state. As a result, changes in economic, business or political conditions of a particular state may have a disproportionate impact on the Fund’s share price. Municipal securities investments are not appropriate for all investors, especially those taxed at lower rates. The Fund may also invest in U.S. dollar denominated foreign securities which involve additional risks such as currency rate fluctuations, political and economic instability, and different and sometimes less strict financial reporting standards and regulation.

Past performance does not guarantee future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost.

For information about the performance of the Fund as of the most recent month-end, please call 1-866-44BAIRD or visit www.bairdfunds.com. Mutual fund performance changes over time and current performance may be lower or higher than that stated.

Page 30

Baird Intermediate Municipal Bond Fund

Summary Schedule of Investments, December 31, 2013

This schedule summarizes the Fund’s holdings by asset type. Details are reported for each of the Fund’s 50 largest individual holdings and for investments that, in total for any issuer, represent more than 1% of the Fund’s net assets. The total value of smaller holdings is reported as a single amount within each category.

The Fund reports a complete list of its holdings in regulatory filings four times in each fiscal year, at the quarter end. For the second and fourth fiscal quarters, the complete listing of the Fund’s holdings is available electronically in the Fund’s Form N-CSR at http://www.rwbaird.com/baird-funds/prospectus-applications/prospectus-applications.aspx and on the Securities and Exchange Commission’s website (www.sec.gov) or you can have it mailed to you without charge by calling 1-866-44BAIRD. For the first and third fiscal quarters, the Fund files the lists with the SEC on Form N-Q. Shareholders can look up the Fund’s Forms N-CSR and N-Q on the SEC’s website (www.sec.gov).

Long-Term Investments

| Principal | % of | |||||||||||

| Amount | Value | Net Assets | ||||||||||

| Municipal Bonds | ||||||||||||

| Alabama | ||||||||||||

| Other Alabama# | $ | 4,000,388 | 0.4 | % | ||||||||

| Total Alabama | ||||||||||||

| (Cost $3,793,792) | 4,000,388 | 0.4 | % | |||||||||

| Alaska | ||||||||||||

| Other Alaska# | 1,056,150 | 0.1 | % | |||||||||

| Total Alaska | ||||||||||||

| (Cost $1,013,067) | 1,056,150 | 0.1 | % | |||||||||

| Arizona | ||||||||||||

| Other Arizona# | 4,661,756 | 0.5 | % | |||||||||

| Total Arizona | ||||||||||||

| (Cost $4,514,269) | 4,661,756 | 0.5 | % | |||||||||

| Arkansas | ||||||||||||

| Other Arkansas# | 1,161,740 | 0.1 | % | |||||||||

| Total Arkansas | ||||||||||||

| (Cost $1,171,460) | 1,161,740 | 0.1 | % | |||||||||

| California | ||||||||||||

| San Joaquin Hills California Transportation | ||||||||||||

| Corridor Agency Toll Road Revenue: | ||||||||||||

| 0.000%, 01/01/2020 (ETM)^ | $ | 6,865,000 | 6,072,367 | 0.6 | % | |||||||

| 0.000%, 01/01/2023 (ETM)^ | 14,000,000 | 10,722,740 | 1.1 | % | ||||||||

| San Marcos California Public | ||||||||||||

| Facilities Authority Revenue | ||||||||||||