UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K/A

(Amendment No. 1)

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended January 3, 2015 | |

| OR | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| Commission file number: 1-32383 | ||

| BlueLinx Holdings Inc. | ||

| (Exact name of registrant as specified in its charter) | ||

| Delaware | 77-0627356 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 4300 Wildwood Parkway, Atlanta, Georgia | 30339 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: 770-953-7000

Securities registered pursuant to Section 12(b) of the Act

| Title of Each Class | Name of Each Exchange on Which Registered | |

Common stock, par value $0.01 per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o | Accelerated filer o | Non-accelerated filer o | Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant as of July 5, 2014 was $34,205,977, based on the closing price on the New York Stock Exchange of $1.26 per share on July 3, 2014.

As of February 19, 2015, the registrant had 89,416,236 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Part III of this Annual Report on Form 10-K incorporates by reference to the registrant’s definitive Proxy Statement, to be filed with the Securities and Exchange Commission within 120 days of the close of the fiscal year ended January 3, 2015.

Explanatory Note

This Amendment No. 1 to BlueLinx Holdings Inc. Annual Report on Form 10-K hereby amends the Annual Report on Form 10-K originally filed solely to include Exhibits 21.1 and 23.1 that were inadvertently excluded from the Form 10-K filed with the Securities and Exchange Commission on February 20, 2015, and address non-material typographical errors in the Form 10-K as originally filed.

Except as expressly set forth above, this Amendment does not, and does not purport to, amend, update, or restate the information in any other item of the Form 10-K or reflect any events that have occurred after the filing of the original Form 10-K.

BLUELINX HOLDINGS INC.

ANNUAL REPORT ON FORM 10-K

For the fiscal year ended January 3, 2015

TABLE OF CONTENTS

As used herein, unless the context otherwise requires, “BlueLinx,” the “Company,” “we,” “us,” and “our” refer to BlueLinx Holdings Inc. and its subsidiaries. BlueLinx Corporation is the wholly-owned operating subsidiary of BlueLinx Holdings Inc. and is referred to herein as the “operating company” when necessary. Reference to “fiscal 2014” refers to the 52-week period ended January 3, 2015. Reference to “fiscal 2013” refers to the 53-week period ended January 4, 2014. Reference to “fiscal 2012” refers to the 52-week period ended December 29, 2012.

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains information that may constitute “forward-looking statements.” Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. However, the absence of these words or similar expressions does not mean that a statement is not forward-looking. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future — including statements relating to volume growth, share of sales and earnings per share growth, and statements expressing general views about future operating results — are forward-looking statements. Management believes that these forward-looking statements are reasonable as and when made. However, caution should be taken not to place undue reliance on any such forward-looking statements because such statements speak only as of the date when made. Our Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. In addition, forward-looking statements are subject to certain risks and uncertainties that could cause actual results to differ materially from our Company’s historical experience and our present expectations or projections. These risks and uncertainties include, but are not limited to, those described in Item 1A Risk Factors and elsewhere in this report and those described from time to time in our future reports filed with the Securities and Exchange Commission.

4

PART I

ITEM 1. BUSINESS

Company Overview

We are a leading distributor of building products in North America. The Company is headquartered in Atlanta, Georgia, with executive offices located at 4300 Wildwood Parkway, Atlanta, Georgia, and we operate our distribution business through a network of 49 distribution centers. We serve all major metropolitan areas in the United States (“U.S.”) and, as of January 3, 2015, we distributed approximately 10,000 products from over 750 suppliers to service approximately 11,500 customers nationwide, including dealers, industrial manufacturers, manufactured housing producers, and home improvement retailers.

The Company was incorporated on March 8, 2004 as ABP Distribution Holdings, Inc (“ABP”). On May 7, 2004, Georgia-Pacific Corporation (“Georgia-Pacific”) sold the assets of its distribution division to ABP. ABP subsequently merged into BlueLinx Holdings Inc. On December 17, 2004, we consummated an initial public offering of our common stock.

Fiscal Year

Fiscal 2014 contained 52 weeks, fiscal 2013 contained 53 weeks, and fiscal 2012 contained 52 weeks.

Products and Services

We distribute products in two principal categories: structural products and specialty products. Structural products, which represented approximately 41%, 44%, and 42% of our fiscal 2014, fiscal 2013, and fiscal 2012 gross sales, respectively, include plywood, oriented strand board (“OSB”), rebar and remesh, lumber and other wood products primarily used for structural support, walls and flooring in construction projects. Additional end uses of our structural products include outdoor decks, sheathing, crates, and boxes. Specialty products, which represented approximately 59%, 56%, and 58% of our fiscal 2014, fiscal 2013, and fiscal 2012 gross sales, respectively, include roofing, insulation, specialty panels, moulding, engineered wood products, vinyl products (used primarily in siding), outdoor living, particle board, and metal products (excluding rebar and remesh). In some cases, these products are branded by us.

We also provide a wide range of value-added services and solutions to our customers and suppliers including:

•providing “less-than-truckload” delivery services;

•pre-negotiated program pricing plans;

•inventory stocking;

•automated order processing through an electronic data interchange, or “EDI”, that provides a direct link between us

and our customers;

•intermodal distribution services, including railcar unloading and cargo reloading onto customers’ trucks; and

•backhaul services, when otherwise empty trucks are returning from customer deliveries.

Distribution Channels

We sell products through three main distribution channels: warehouse sales, reload sales, and direct sales.

Warehouse sales are delivered from our warehouses to dealers, home improvement centers, and industrial users. Warehouse sales accounted for approximately 71% of our fiscal 2014, fiscal 2013, and fiscal 2012 gross sales.

Reload sales are similar to warehouse sales but are shipped from third-party warehouses where we store owned product in order to enhance operating efficiencies. This channel is employed primarily to service strategic customers that would be less economical to service from our warehouses, and to distribute large volumes of imported products from port facilities. Reload sales accounted for approximately10% of our fiscal 2014 and fiscal 2013 gross sales, and 9% of our fiscal 2012 gross sales.

Direct sales are shipped from the manufacturer to the customer without our taking physical inventory possession. This channel requires the lowest amount of committed capital and fixed costs. Direct sales accounted for approximately 19% of our fiscal 2014 and fiscal 2013 gross sales, and 20% of our 2012 gross sales.

5

Competition

The U.S. building products distribution market is a highly fragmented market, served by a small number of multi-regional distributors, several regionally focused distributors and a large number of independent local distributors. Local and regional distributors tend to be closely held and often specialize in a limited number of segments, in which they offer a broader selection of products. Some of our multi-regional competitors are part of larger companies and therefore have access to greater financial and other resources than those to which we have access. We compete on the basis of breadth of product offering, consistent availability of product, product price and quality, reputation, service, and distribution facility location.

Two of our largest competitors are Boise Cascade Company and Weyerhaeuser Company. Most major markets in which we operate are served by the distribution arm of at least one of these companies.

Seasonality

We are exposed to fluctuations in quarterly sales volumes and expenses due to seasonal factors common in the building products distribution industry. The first and fourth quarters are typically our slowest quarters due to the impact of poor weather on the construction market. Our second and third quarters are typically our strongest quarters, reflecting a substantial increase in construction due to more favorable weather conditions. Our working capital, accounts receivable, and accounts payable generally peak in the third quarter, while inventory generally peaks in the second quarter in anticipation of the summer building season.

Employees

As of January 3, 2015, we employed approximately 1,700 employees. We consider our relationship with our employees generally to be good.

Executive Officers

The following are the current executive officers of our Company as of February 19, 2015:

Mitchell B. Lewis, age 52, has served as our President and Chief Executive Officer, and as a Director of BlueLinx Holdings Inc. since January 2014. Mr. Lewis has held numerous leadership positions in the building products industry since 1992, including President and Chief Executive Officer of Euramax Holdings, Inc. from February 2008, through November 2013. Mr. Lewis also served as Chief Operating Officer in 2005, Executive Vice President in 2002, and group Vice President in 1997, of Euramax Holdings, Inc. and its predecessor companies. Prior to being appointed group Vice President, Mr. Lewis served as President of Amerimax Building Products, Inc. Prior to 1992, Mr. Lewis served as Corporate Counsel with Alumax Inc. and practiced law with Alston & Bird LLP, specializing in mergers and acquisitions.

Susan C. O’Farrell, age 51, has served as our Senior Vice President, Chief Financial Officer, Treasurer, and Principal Accounting Officer since May 2014. Prior to joining us, Ms. O’Farrell was a senior financial executive holding several roles with The Home Depot since 1999. As the Vice President of Finance, she led teams supporting the retail organization. Ms. O’Farrell was also responsible for the finance function for The Home Depot’s At Home Services Group. Ms. O’Farrell led the financial operations of The Home Depot, as well as served as the VP Finance for the $26 billion Northern Division of the company. Ms. O’Farrell began her career with Andersen Consulting, LLP, leaving as an Associate Partner in 1996 for a strategic information systems role with AGL Resources. Ms. O’Farrell earned a Bachelor of Science degree in Business Administration from Auburn University and attended Emory University’s Executive Leadership program.

Robert P. McKagen, age 55, has served as our Senior Vice President of Sales and Operations since 2012. Prior to 2012, Mr. McKagan served as the Company’s Vice President Supply Chain since 2009, and Regional Vice President of the Southern Region from the Company’s inception in 2004. Mr. McKagen has approximately 30 years of industry experience. He received a Bachelor in Business Administration from Florida Atlantic University.

Sara E. Epstein, age 37, has served as our Vice President, General Counsel and Corporate Secretary since February 2013, and our Senior Counsel and Corporate Secretary since March 2010. Prior to joining us, Ms. Epstein was an attorney with Jones Day. Ms. Epstein received a Juris Doctor degree from Tulane University and a Bachelor of Arts degree from Tufts University.

Environmental and Other Governmental Regulations

The Company is subject to various federal, state, provincial and local laws, rules, and regulations. We are subject to environmental laws, rules and regulations that limit discharges into the environment, establish standards for the handling, generation, emission, release, discharge, treatment, storage and disposal of hazardous materials, substances and wastes, and require cleanup of contaminated soil and groundwater. These laws, ordinances, and regulations are complex, change frequently

6

and have tended to become more stringent over time. Many of them provide for substantial fines and penalties, orders (including orders to cease operations), and criminal sanctions for violations. They may also impose liability for property damage and personal injury stemming from the presence of, or exposure to, hazardous substances. In addition, certain of our operations require us to obtain, maintain compliance with, and periodically renew permits.

Certain of these laws, including the Comprehensive Environmental Response, Compensation, and Liability Act, may require the investigation and cleanup of an entity’s or its predecessor’s current or former properties, even if the associated contamination was caused by the operations of a third party. These laws also may require the investigation and cleanup of third-party sites at which an entity or its predecessor sent hazardous wastes for disposal, notwithstanding that the original disposal activity accorded with all applicable requirements. Liability under such laws may be imposed jointly and severally, and regardless of fault.

We are also subject to the requirements of the U.S. Department of Labor Occupational Safety and Health Administration (“OSHA”). In order to maintain compliance with applicable OSHA requirements, we have established uniform safety and compliance procedures for our operations, and implemented measures to prevent workplace injuries.

The U.S. Department of Transportation (“DOT”) regulates our operations in domestic interstate commerce. We are subject to safety requirements governing interstate operations prescribed by the DOT. Vehicle dimensions and driver hours of service also remain subject to both federal and state regulation.

We incur and will continue to incur costs to comply with the requirements of environmental, health and safety, and transportation laws, ordinances, and regulations. We anticipate that these requirements could become more stringent in the future, and we cannot assure you that compliance costs will not be material.

Securities Exchange Act Reports

The Company maintains a website at www.BlueLinxCo.com. The information on the Company’s website is not incorporated by reference in this Annual Report on Form 10-K. We make available on or through our website certain reports, and amendments to those reports, that we file with or furnish to the U.S. Securities and Exchange Commission (the “SEC”) in accordance with the Securities Exchange Act of 1934. These include our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and proxy statements. Additionally, our code of ethics, board committee charters, and corporate governance guidelines are available on our website. If we make substantial amendments to our code of ethics, or grant any waiver, including any implicit waiver, we will disclose the nature of such amendment or waiver on our website or in a report on Form 8-K.

We make information available on our website free of charge as soon as reasonably practicable after we electronically file the information with, or furnish it to, the SEC. In addition, copies of this information will be made available, free of charge, on written request, by writing to BlueLinx Holdings Inc., Attn: Corporate Secretary, 4300 Wildwood Parkway, Atlanta, Georgia, 30339.

ITEM 1A. RISK FACTORS

In addition to the other information contained in this Form 10-K, the following risk factors should be considered carefully in evaluating our business. Our business, financial condition, or results of operations could be materially adversely affected by any of these risks. Additional risks not presently known to us or that we currently deem immaterial may also impair our business and operations.

Our industry is highly cyclical, and prolonged periods of weak demand or excess supply may reduce our net sales and/or margins, which may reduce our net income or cause us to incur losses.

The building products distribution industry is subject to cyclical market pressures. Prices of building products are determined by overall supply and demand in the market. Market prices of building products historically have been volatile and cyclical, and we have limited ability to control the timing and amount of pricing changes. Demand for building products is driven mainly by factors outside of our control, such as general economic and political conditions, interest rates, availability of mortgage financing, the construction, repair and remodeling markets, industrial markets, weather, and population growth. The supply of building products fluctuates based on available manufacturing capacity, and excess capacity in the industry can result in significant declines in market prices for those products. To the extent that prices and volumes experience a sustained or sharp decline, our net sales and margins likely would decline as well. Because we have substantial fixed costs, a decrease in sales and margin generally may have a significant adverse impact on our financial condition, operating results, and cash flows.

Additionally, many of the building products which we distribute, including OSB, plywood, lumber, and particleboard, are commodities that are widely available from other distributors or manufacturers, with prices and volumes determined frequently

7

in an auction market based on participants’ perceptions of short-term supply and demand factors. At times, the purchase price for any one or more of the products we produce or distribute may fall below our purchase costs, requiring us to incur short-term losses on product sales.

All of these factors make it difficult to forecast our operating results.

Our industry is dependent on the homebuilding industry, and any future downturns would materially affect our business, liquidity, and operating results.

Our sales depend heavily on the strength of national and local new residential construction, home improvement, and remodeling markets. The strength of these markets depends on new housing starts and residential renovation projects, which are a function of many factors beyond our control. Some of these factors include general economic conditions, employment levels, job and household formation, interest rates, housing prices, tax policy, availability of mortgage financing, prices of commodity wood and steel products, immigration patterns, regional demographics, and consumer confidence. Our results of operations were adversely affected by the severe downturn in new housing activity in the U.S., and, while conditions are improving, any future downturns in the markets that we serve or in the economy generally may have a material adverse effect on our operating results, liquidity, and financial condition. Reduced levels of construction activity may result in continued intense price competition among building materials suppliers, which may adversely affect our gross margins. We cannot provide assurance that our responses to future downturns in the economy in general, and in the residential housing market in particular, will be successful.

A significant portion of our sales are on credit to our customers. Material changes in their creditworthiness or our inability to forecast deterioration in their credit position could have a material adverse effect on our operating results, cash flow, and liquidity.

The majority of our sales are on account where we provide credit to our customers. Market disruptions could cause economic downturns, which may lead to lower demand for our products and increased incidence of customers’ inability to pay their accounts. Bankruptcies by our customers may cause us to incur bad debt expense at levels higher than historically experienced. In fiscal 2014, less than 0.1% in bad debt expense to total net sales was incurred related to credit sales. Our customers generally are susceptible to the same economic business risks as those to which we are exposed. Furthermore, we may not necessarily be aware of any deterioration in our customers’ financial position. If our customers’ financial position were to become significantly impaired, it could have a material impact on our bad debt exposure, which may result in a material adverse effect on our operating results, cash flow and liquidity. In addition, certain of our suppliers may be impacted as well, causing disruption or delay of product availability. These events could have a material adverse impact on our results of operations, cash flow, and financial position.

Our cash flows and capital resources may be insufficient to make required payments on our substantial indebtedness, future indebtedness, or to maintain our required level of excess liquidity.

We have a substantial amount of debt which could have important consequences to you. For example, it could:

| • | make it difficult for us to satisfy our debt obligations; |

| • | make us more vulnerable to general adverse economic and industry conditions; |

| • | limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions, and other general corporate requirements; |

| • | expose us to interest rate fluctuations because the interest rate on the debt under our U.S. revolving credit facility is variable; |

| • | require us to dedicate a substantial portion of our cash flows to payments on our debt, thereby reducing the availability of our cash flows for operations and other purposes; |

| • | limit our flexibility in planning for, or reacting to, changes in our business, and the industry in which we operate; and |

| • | place us at a competitive disadvantage compared to competitors that may have proportionately less debt, and therefore may be in a better position to obtain favorable credit terms. |

8

In addition, our ability to make scheduled payments or refinance our obligations depends on our successful financial and operating performance, cash flows, and capital resources, which in turn depend upon prevailing economic conditions and certain financial, business, and other factors, many of which are beyond our control. These factors include, among others:

| • | economic and demand factors affecting the building products distribution industry; |

| • | external factors affecting availability of credit; |

| • | pricing pressures; |

| • | increased operating costs; |

| • | competitive conditions; and |

| • | other operating difficulties. |

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell material assets or operations, obtain additional capital, or restructure our debt. Obtaining additional capital or restructuring our debt could be accomplished in part through new or additional borrowings or placements of debt or securities. There is no assurance that we could obtain additional capital or refinance our debt on terms acceptable to us, or at all. In the event that we are required to dispose of material assets or operations to meet our debt service and other obligations, the value realized on the disposition of such assets or operations will depend on market conditions and the availability of buyers. Accordingly, any such sale may not, among other things, be for a sufficient dollar amount. Our obligations under the revolving credit facilities are secured by a first priority security interest in all of our operating subsidiaries and BlueLinx Building Products Canada Ltd.’s (“BlueLinx Canada”) (for the Canadian revolving credit facility) inventories, accounts receivable, and proceeds from those items. In addition, our mortgage loan is secured by the majority of our real property. The foregoing encumbrances may limit our ability to dispose of material assets or operations. We may incur substantial additional indebtedness in the future, including under the revolving credit facilities. Our incurring additional indebtedness would intensify the risks described above.

The instruments governing our indebtedness contain various covenants limiting the discretion of our management in operating our business, including requiring us to maintain a minimum level of excess liquidity.

Our revolving credit facilities and mortgage loan contain various restrictive covenants and restrictions, including financial covenants customary for asset-based loans that limit management’s discretion in operating our business. In particular, these instruments limit our ability to, among other things:

| • | incur additional debt; |

| • | grant liens on assets; |

| • | make investments, including capital expenditures; |

| • | sell or acquire assets outside the ordinary course of business; |

| • | engage in transactions with affiliates; and |

| • | make fundamental business changes. |

As of January 3, 2015, the U.S. revolving credit facility requires us to maintain a fixed charge coverage ratio of 1.1 to 1.0 in the event our excess availability under the U.S. revolving credit facility falls below the greater of $33.2 million during the time the Tranche A Loan is outstanding, and $31.8 million at all times thereafter; or the amount equal to 12.5% of the lesser of the borrowing base or $467.5 million during the time the Tranche A Loan is outstanding, and $447.5 million at all times thereafter (the “Excess Availability Threshold”). If we fail to maintain this minimum excess availability, the U.S. revolving credit facility requires us to (i) maintain certain financial ratios, which we would not meet with current operating results, and (ii) limit our capital expenditures, which would have a negative impact on our ability to finance working capital needs and capital expenditures.

If we fail to comply with the restrictions in the U.S. revolving credit facility, the Canadian revolving credit facility, the mortgage loan documents, or any other current or future financing agreements, a default may allow the creditors under the relevant instruments to accelerate the related debts and to exercise their remedies under these agreements, which typically will include the right to declare the principal amount of that debt, together with accrued and unpaid interest, and other related amounts, immediately due and payable, to exercise any remedies the creditors may have to foreclose on assets that are subject to liens securing that debt, and to terminate any commitments they had made to supply further funds.

We source many products internationally, and are exposed to risks associated with doing business globally.

We import a variety of products from countries located in Asia, South America, and the Middle East. The business, regulatory, and political environments in these countries differ from those in the U.S. Our global sourcing strategy is subject to risks and uncertainties, including changes in foreign country regulatory requirements; differing business practices associated with foreign operations; imposition of foreign tariffs and other trade barriers; political, legal, and economic instability; foreign

9

currency exchange rate fluctuations; foreign country tax rules, regulations and other requirements, such as changes in tax rates and statutory and judicial interpretations in tax laws; inflation; differing labor laws and changes in those laws; government price controls; and work stoppages and disruptions in the shipping of imported and exported products.

Our transportation operations are subject to significant governmental regulation.

We use our own fleet of tractors and trailers to service customers throughout the U.S. Our transportation operations are subject to the regulatory jurisdiction and broad administrative powers of the DOT. If we fail to comply adequately with DOT regulations or regulations become more stringent, we could experience increased inspections, regulatory authorities could take remedial action including imposing fines or shutting down our operations or we could be subject to increased audit and compliance costs. If any of these events were to occur, our results of operations, business, cash flow, and financial condition would be adversely affected.

Environmental laws impose risks and costs on us.

Our operations are subject to federal, state, provincial, and local laws, rules, and regulations governing the protection of the environment, including, but not limited to, those regulating discharges into the air and water, the use, handling and disposal of hazardous or toxic substances, the management of wastes, the cleanup of contamination, and the control of noise and odors. We have made, and will continue to make, expenditures to comply with these requirements. While we believe, based upon current information, that we are in substantial compliance with all applicable environmental laws, rules, and regulations, we could be subject to potentially significant fines or penalties for any failure to comply. Moreover, under certain environmental laws, a current or previous owner or operator of real property, and parties that generate or transport hazardous substances that are disposed of at that real property, may be held liable for the cost to investigate or clean up such real property, and for related damages to natural resources. We may be subject to liability, including liability for investigation and cleanup costs, if contamination is discovered at one of our current or former warehouse facilities, or at a landfill or other location where we have disposed of, or arranged for the disposal of, wastes. We have an indemnification agreement with Georgia-Pacific, which has agreed to indemnify us against any claim arising from environmental conditions in connection with the properties we acquired when we purchased the assets of its distribution division on May 7, 2004. However, any remediation costs either not related to conditions existing prior to May 7, 2004 or on properties acquired after May 7, 2004 may not be covered by indemnification. We also carry environmental insurance, but certain remediation costs may not be covered by insurance. In addition, we could be subject to claims brought pursuant to applicable laws, rules, or regulations for property damage or personal injury resulting from the environmental impact of our operations. Increasingly stringent environmental requirements, more aggressive enforcement actions, the discovery of unknown conditions, or the bringing of future claims may cause our expenditures for environmental matters to increase, and we may incur material costs associated with these matters.

Product shortages, loss of key suppliers, and our dependence on third-party suppliers and manufacturers could affect our financial health.

Our ability to offer a wide variety of products to our customers is dependent upon our ability to obtain adequate product supply from manufacturers and other suppliers. Generally, our products are obtainable from various sources and in sufficient quantities. However, the loss of, or a substantial decrease in the availability of, products from our suppliers or the loss of key supplier arrangements could adversely impact our financial condition, operating results, and cash flows.

Although in many instances we have agreements with our suppliers, these agreements are generally terminable by either party on limited notice. Failure by our suppliers to continue to supply us with products on commercially reasonable terms, or at all, could have a material adverse effect on our financial condition, operating results, and cash flows.

Our industry is highly fragmented and competitive. If we are unable to compete effectively, our net sales and operating results will be reduced.

The building products distribution industry is highly fragmented and competitive, and the barriers to entry for local competitors are relatively low. Competitive factors in our industry include pricing and availability of product, service, and delivery capabilities, customer relationships, geographic coverage, and breadth of product offerings. Also, financial stability is important to suppliers and customers in choosing distributors for their products, and affects the favorability of the terms on which we are able to obtain our products from our suppliers and sell our products to our customers.

Some of our competitors are part of larger companies, and therefore have access to greater financial and other resources than those to which we have access. In addition, certain product manufacturers sell and distribute their products directly to customers. Additional manufacturers of products distributed by us may elect to sell and distribute directly to end-users in the future or enter into exclusive supply arrangements with other distributors. Finally, we may not be able to maintain our costs at a level sufficiently low for us to compete effectively. If we are unable to compete effectively, our net sales and net income will be reduced.

10

A significant percentage of our employees are unionized. Wage increases or work stoppages by our unionized employees may reduce our results of operations.

As of January 3, 2015, we employed approximately 1,700 persons. Approximately 34% of our employees were represented by various labor union collective bargaining agreements, of which approximately 30% are up for renewal in fiscal 2015. Although we have generally had good relations with our unionized employees, and expect to renew collective bargaining agreements as they expire, no assurances can be provided that we will be able to reach a timely agreement as to the renewal of the agreements, and their expiration or continued work under an expired agreement, as applicable, could result in a work stoppage. In addition, we may become subject to material cost increases, or additional work rules imposed by agreements with labor unions. The foregoing could increase our selling, general, and administrative expenses in absolute terms and/or as a percentage of net sales. In addition, work stoppages or other labor disturbances may occur in the future, which could adversely impact our net sales and/or selling, general, and administrative expenses. All of these factors could negatively impact our operating results and cash flows.

Increases in the cost of employee benefits, such as pension benefits, could impact our financial results and cash flow.

Unfavorable changes in the cost of our pension retirement benefits and current employees’ medical benefits could materially adversely impact our financial results and cash flow. We sponsor a defined benefit pension plan covering many of our hourly unionized employees. Our estimates of the amount and timing of our future funding obligations for our defined benefit pension plans are based upon various assumptions. These assumptions include, but are not limited to, the discount rate, projected return on plan assets, compensation increase rates, mortality rates, retirement patterns, and turnover rates. In addition, the amount and timing of our pension funding obligations are influenced by funding requirements that are established by the Employee Retirement Income and Security Act of 1974 (“ERISA”), the Pension Protection Act, Congressional Acts, or other governing bodies.

We participate in various multi-employer pension plans in the U.S. The majority of these plans are underfunded. If, in the future, we choose to withdraw from these plans, we likely would need to record a withdrawal liability, which may be material to our financial results.

Failure to comply with governmental laws and regulations could harm our business.

Our business is subject to regulation by various federal, state, local, and foreign governmental agencies, including agencies responsible for monitoring and enforcing employment and labor laws, workplace safety, product safety, environmental laws, consumer protection laws, anti-bribery laws, import/export controls, federal securities laws, and tax laws and regulations. Noncompliance with applicable regulations or requirements could subject us to investigations, sanctions, mandatory product recalls, enforcement actions, disgorgement of profits, fines, damages, civil and criminal penalties, or injunctions. If any governmental sanctions are imposed, or if we do not prevail in any possible civil or criminal litigation, our business, operating results, and financial condition could be materially adversely affected. In addition, responding to any actions would likely result in a significant diversion of management’s attention and resources, and an increase in professional fees. Enforcement actions and sanctions could harm our business, operating results, and financial condition.

Affiliates of Cerberus control us and may have conflicts of interest with other stockholders.

Cerberus Capital Management, L.P. (“Cerberus”), a private investment firm, beneficially owned approximately 53% of our common stock as of January 3, 2015. As a result, Cerberus is able to control the election of our directors, determine our corporate and management policies and determine, without the consent of our other stockholders, the outcome of most corporate transactions or other matters submitted to our stockholders for approval, including potential mergers or acquisitions, asset sales, and other significant corporate transactions. This concentrated ownership position limits other stockholders’ ability to influence corporate matters and, as a result, we may take actions that some of our stockholders may not view as beneficial.

Two of our nine directors are employees of or current advisors to Cerberus. Cerberus also has sufficient voting power to amend our organizational documents. The interests of Cerberus may not coincide with the interests of other holders of our common stock. Additionally, Cerberus is in the business of making investments in companies, and may, from time to time, acquire and hold interests in businesses that compete directly or indirectly with us. Cerberus may also pursue, for its own account, acquisition opportunities that may be complementary to our business, and as a result, those acquisition opportunities may not be available to us. So long as Cerberus continues to own a significant amount of the outstanding shares of our common stock, it will continue to be able to strongly influence or effectively control our decisions, including potential mergers or acquisitions, asset sales, and other significant corporate transactions. In addition, because we are a controlled company within the meaning of the New York Stock Exchange rules, we are exempt from the NYSE requirements that our board be composed of a majority of independent directors, that our compensation committee be composed entirely of independent directors, and that we maintain a nominating/corporate governance committee composed entirely of independent directors.

11

Even if Cerberus no longer controls us in the future, certain provisions of our charter documents and agreements and Delaware law could discourage, delay, or prevent a merger or acquisition at a premium price.

Our Second Amended and Restated Certificate of Incorporation and Amended and Restated Bylaws contain provisions that:

| • | permit us to issue, without any further vote or action by the stockholders, up to 30 million shares of preferred stock in one or more series and, with respect to each series, to fix the number of shares constituting the series and the designation of the series, the voting powers (if any) of the shares of such series, and the preferences and other special rights, if any, and any qualifications, limitations or restrictions, of the shares of the series; and |

| • | limit the stockholders’ ability to call special meetings. |

These provisions may discourage, delay or prevent a merger or acquisition at a premium price.

In addition, we are subject to Section 203 of the General Corporation Law of the State of Delaware, or the “DGCL”, which also imposes certain restrictions on mergers and other business combinations between us and any holder of 15% or more of our common stock. Further, certain of our incentive plans provide for vesting of stock options and/or payments to be made to our employees in connection with a change of control, which could discourage, delay or prevent a merger or acquisition at a premium price.

We are subject to information technology security risks and business interruption risks, and may incur increasing costs in an effort to minimize those risks.

Our business employs information technology systems and a website that allow for the secure storage and transmission of customers’ proprietary information. We also employ information technology systems to secure other confidential information, such as employee data. Security breaches could expose us to a risk of loss or misuse of this information, litigation, and potential liability. We may not have the resources or technical sophistication to anticipate or prevent rapidly evolving types of cyber attacks. Any compromise of our security could result in a violation of applicable privacy and other laws, significant legal and financial exposure, damage to our reputation, and a loss of confidence in our security measures, which could harm our business. As cyber attacks become more sophisticated generally, we may be required to incur significant costs to strengthen our systems from outside intrusions, and/or obtain insurance coverage related to the threat of such attacks.

Additionally, our business is reliant upon information technology systems to place orders with our vendors and process orders from our customers. Disruption in these systems could materially impact our ability to buy and sell our products.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

ITEM 2. PROPERTIES

We operate our business out of 49 warehouse facilities. Additionally, two owned properties are held for sale, in Newtown, Connecticut, and Shreveport, Louisiana; and our leased Stockton, California property, is being marketed for sublease. The total square footage under roof at our owned warehouses is approximately 9.3 million square feet. Certain of our owned warehouse facilities secure our mortgage loan. The following table summarizes our real estate facilities including their inside square footage:

| Property Type | Number | Owned Facilities (sq. ft.) | Leased Facilities (sq. ft.) | |||||

| Office Space (1) | 3 | — | 167,308 | |||||

| Warehouses and other real property | 52 | 9,257,366 | 340,600 | |||||

| TOTAL | 55 | 9,257,366 | 507,908 | |||||

| (1) | Includes corporate headquarters in Atlanta, and sales centers in Denver and Vancouver. |

We also store materials, such as lumber and rebar, outdoors at all of our warehouse locations, which increases warehouse distribution and storage capacity. We believe that substantially all of our property and equipment is in good condition, subject to normal wear and tear. We believe that our facilities have sufficient capacity to meet current and projected distribution needs.

12

ITEM 3. LEGAL PROCEEDINGS

We are, and from time to time may be, a party to routine legal proceedings incidental to the operation of our business. The outcome of any pending or threatened proceedings is not expected to have a material adverse effect on our financial condition, operating results, or cash flows, based on our current understanding of the relevant facts. Legal expenses incurred related to these contingencies generally are expensed as incurred. We establish reserves for pending or threatened proceedings when the costs associated with such proceedings become probable and reasonably can be estimated.

ITEM 4. MINE SAFETY DISCLOSURES

Not applicable.

13

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our equity securities consist of one class of common stock, which is traded on the New York Stock Exchange under the symbol “BXC”. The following table sets forth, for the periods indicated, the range of the high and low sales prices for the common stock as quoted on the New York Stock Exchange:

| High | Low | ||||||

| Fiscal Year Ended January 3, 2015 | |||||||

| First Quarter | $ | 1.96 | $ | 1.25 | |||

| Second Quarter | $ | 1.47 | $ | 1.07 | |||

| Third Quarter | $ | 1.39 | $ | 1.11 | |||

| Fourth Quarter | $ | 1.35 | $ | 1.11 | |||

| Fiscal Year Ended January 4, 2014 | |||||||

| First Quarter | $ | 3.48 | $ | 2.42 | |||

| Second Quarter | $ | 3.10 | $ | 1.90 | |||

| Third Quarter | $ | 2.29 | $ | 1.56 | |||

| Fourth Quarter | $ | 2.14 | $ | 1.57 | |||

As of February 19, 2015, there were 44 shareowner accounts of record, and, as of that date we estimate there were approximately 2,200 beneficial owners holding our common stock in nominee or “street” name.

We do not pay dividends on our common stock. Future dividend payments, if dividends are declared at a future date, are subject to contractual restrictions under our U.S. revolving credit facility.

14

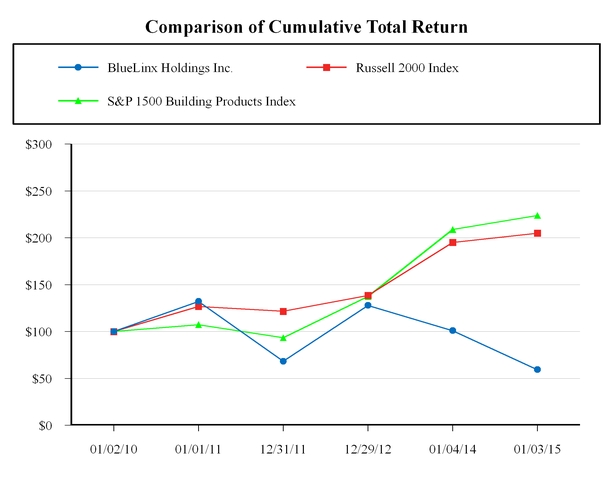

Performance Graph

The chart below compares the quarterly percentage change in the cumulative total stockholder return on our common stock with the cumulative total return on the Russell 2000 Index and S&P 1500 Building Products Index for the period commencing January 2, 2010, and ending January 3, 2015, assuming an investment of $100 and the reinvestment of dividends (if any).

Cumulative Total Return

Years Ending

| Base Period | |||||||||||||||||||||||

| Company Name/Index | 1/2/2010 | 1/1/2011 | 12/31/2011 | 12/29/2012 | 1/4/2014 | 1/3/2015 | |||||||||||||||||

| BlueLinx Holdings Inc. | $ | 100 | $ | 132.13 | $ | 68.25 | $ | 127.86 | $ | 100.97 | $ | 59.34 | |||||||||||

| Russell 2000 Index | $ | 100 | $ | 126.85 | $ | 121.56 | $ | 138.56 | $ | 195.07 | $ | 204.94 | |||||||||||

| S&P 1500 Building Products Index | $ | 100 | $ | 107.38 | $ | 93.42 | $ | 137.26 | $ | 208.72 | $ | 223.76 | |||||||||||

15

ITEM 6. SELECTED FINANCIAL DATA

The following tables sets forth certain historical financial data of our Company. The selected financial data for the fiscal years ended January 3, 2015, January 4, 2014, December 29, 2012, December 31, 2011, and January 1, 2011, have been derived from our audited financial statements included elsewhere in this Annual Report on Form 10-K, or from prior financial statements. The following information should be read in conjunction with our financial statements and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Year Ended January 3, 2015 | Year Ended January 4, 2014 | Year Ended December 29, 2012 | Year Ended December 31, 2011 | Year Ended January 1, 2011 | |||||||||||||||

| (In thousands, except per share data) | |||||||||||||||||||

| Statements of Operations Data: | |||||||||||||||||||

| Net sales | $ | 1,979,393 | $ | 2,151,972 | $ | 1,907,842 | $ | 1,755,431 | $ | 1,804,418 | |||||||||

| Net income (loss) | $ | (13,872 | ) | $ | (40,618 | ) | $ | (23,027 | ) | $ | (38,567 | ) | $ | (53,243 | ) | ||||

| Per Share Data: | |||||||||||||||||||

| Basic net income (loss) per share applicable to common stock | $ | (0.16 | ) | $ | (0.51 | ) | $ | (0.35 | ) | $ | (0.82 | ) | $ | (1.59 | ) | ||||

| Diluted net income (loss) per share applicable to common stock | $ | (0.16 | ) | $ | (0.51 | ) | $ | (0.35 | ) | $ | (0.82 | ) | $ | (1.59 | ) | ||||

| Other Financial Data: | |||||||||||||||||||

| EBITDA (1) | 22,684 | (12,490 | ) | 14,081 | 1,791 | (11,099 | ) | ||||||||||||

| Adjusted EBITDA (1) | 24,583 | 1,324 | 6,028 | (8,181 | ) | (10,138 | ) | ||||||||||||

| Balance Sheet Data (at end of period): | |||||||||||||||||||

| Cash and cash equivalents | $ | 4,522 | $ | 5,034 | $ | 5,188 | $ | 4,898 | $ | 14,297 | |||||||||

| Working capital | 297,652 | 294,899 | 272,403 | 233,414 | 236,168 | ||||||||||||||

| Total assets | 538,982 | 528,489 | 542,451 | 501,282 | 525,019 | ||||||||||||||

Total debt (2) | 413,976 | 405,077 | 381,498 | 338,384 | 384,256 | ||||||||||||||

| Stockholders’ equity (deficit) | (36,026 | ) | (5,898 | ) | (20,592 | ) | 8,374 | $ | 991 | ||||||||||

| (1) | EBITDA is an amount equal to net income (loss) plus interest expense and all interest expense related items (e.g. write-off of debt issuance costs, charges associated with mortgage refinancing), income taxes, and depreciation and amortization. Adjusted EBITDA is an amount equal to net income (loss) plus interest expense and all interest expense related items (e.g. write-off of debt issuance costs, charges associated with mortgage refinancing), income taxes, depreciation and amortization, and further adjusted to exclude non-cash items and certain other adjustments to Consolidated Net Income (Loss). We present EBITDA and Adjusted EBITDA because they are important measures used by management to evaluate operating performance and helps to enhance investors’ overall understanding of the financial performance of our business. However, EBITDA and Adjusted EBITDA are not presentations made in accordance with accounting principles generally accepted in the United States (“GAAP”), and are not intended to present a superior measure of the financial condition from those determined under GAAP. EBITDA and Adjusted EBITDA, as used herein, are not necessarily comparable to other similarly titled captions of other companies due to differences in methods of calculation. |

We believe EBITDA and Adjusted EBITDA are helpful in highlighting operating trends. We further believe that EBITDA and Adjusted EBITDA are frequently used by securities analysts, investors, and other interested parties in their evaluation of companies, many of which present an EBITDA or Adjusted EBITDA measure when reporting their results. We compensate for the limitations of using non-GAAP financial measures by using them to supplement GAAP results to provide a more complete understanding of the factors and trends affecting the business than using GAAP results alone.

| (2) | Total debt represents long-term debt related to our mortgage and revolving credit facilities, including current maturities and capital lease obligations. |

16

A reconciliation of net income (loss) to EBITDA and Adjusted EBITDA for each of the respective periods indicated is as follows:

Year Ended January 3, 2015 | Year Ended January 4, 2014 | Year Ended December 29, 2012 | Year Ended December 31, 2011 | Year Ended January 1, 2011 | |||||||||||||||

| (In thousands) | |||||||||||||||||||

| Net income (loss) | $ | (13,872 | ) | $ | (40,618 | ) | $ | (23,027 | ) | $ | (38,567 | ) | $ | (53,243 | ) | ||||

| Interest expense | 26,771 | 28,024 | 28,157 | 28,834 | 29,368 | ||||||||||||||

| Provision for (benefit from) income taxes | 312 | (9,013 | ) | 386 | 962 | (589 | ) | ||||||||||||

| Depreciation and amortization | 9,473 | 9,117 | 8,565 | 10,562 | 13,365 | ||||||||||||||

| EBITDA (1) | 22,684 | (12,490 | ) | 14,081 | 1,791 | (11,099 | ) | ||||||||||||

| Gain on sale of properties | (5,251 | ) | (5,220 | ) | (9,885 | ) | (10,604 | ) | — | ||||||||||

| Share-based compensation expense, excluding restructuring | 2,351 | 3,222 | 2,797 | 1,974 | 3,978 | ||||||||||||||

| Restructuring, severance, debt fees, and other | 4,799 | 12,123 | — | 1,382 | 1,092 | ||||||||||||||

| Loss (gain) from closed distribution centers | — | 3,689 | (489 | ) | 477 | (1,933 | ) | ||||||||||||

| Gain from insurance settlement | — | — | (476 | ) | (1,230 | ) | — | ||||||||||||

| Gain from modification of lease agreement | — | — | — | (1,971 | ) | — | |||||||||||||

| OSB lawsuit settlement gain | — | — | — | — | (5,206 | ) | |||||||||||||

| Tender offer expenses | — | — | — | — | 3,030 | ||||||||||||||

| Adjusted EBITDA (1) | $ | 24,583 | $ | 1,324 | $ | 6,028 | $ | (8,181 | ) | $ | (10,138 | ) | |||||||

| (1) | See above regarding calculation and presentation of EBITDA and Adjusted EBITDA. |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion should be read in conjunction with our consolidated financial statements and related notes and other financial information appearing elsewhere in this Form 10-K. In addition to historical information, the following discussion and other parts of this Form 10-K contain forward-looking information that involves risks and uncertainties. Our actual results could differ materially from those anticipated by this forward-looking information due to the factors discussed under “Risk Factors,” “Cautionary Statement Concerning Forward-Looking Statements”, and elsewhere in this Form 10-K.

Executive Level Overview

Company Background

BlueLinx is a leading distributor of building products in North America. With a combination of market position and coverage, the strength of a local and national sales force, the buying power of centralized procurement, and the efficiencies of centralized accounting and systems technologies, BlueLinx is able to provide a wide range of value-added services and solutions to our customers and suppliers.

Industry Conditions

Many of the factors that cause our operations to fluctuate are seasonal or cyclical in nature. Conditions in the U.S. housing market continue to be at historically low levels. Nevertheless, we believe that the housing recovery is progressing, and that U.S. housing demand will improve in the long term.

17

Factors That Affect Our Operating Results

Our results of operations and financial performance are influenced by a variety of factors, including the following:

•changes in the prices, supply and/or demand for products which we distribute;

•inventory management and commodities pricing;

| • | new housing starts and inventory levels of existing homes for sale; |

| • | general economic and business conditions in the U.S.; |

| • | acceptance by our customers of our privately branded products; |

| • | financial condition and credit worthiness of our customers; |

| • | continuation of supply from our key vendors; |

| • | reliability of the technologies we utilize; |

| • | activities of competitors; |

| • | changes in significant operating expenses; |

| • | fuel costs; |

| • | risk of losses associated with accidents; |

| • | exposure to product liability claims; |

| • | changes in the availability of capital and interest rates; |

| • | adverse weather patterns or conditions; |

| • | acts of cyber intrusion; |

| • | variations in the performance of the financial markets, including the credit markets; and |

•risk factors discussed under Item 1A Risk Factors and elsewhere in this Annual Report on Form 10-K.

Key Business Metrics

Net Sales

Net sales result primarily from the distribution of products to dealers, industrial manufacturers, manufactured housing producers, and home improvement retailers. All revenues recognized are net of trade allowances, cash discounts, and sales returns. In addition, we provide inventory to certain customers through pre-arranged agreements on a consignment basis. When the consigned inventory is sold by the customer, we recognize revenue on a gross basis. Net sales may not be comparable year-over-year due to closed facilities, fiscal calendar weeks in the year, and market-driven fluctuations in the prices of the inventories we sell.

Gross Profit

Gross profit primarily represents revenues less the product cost from our suppliers (net of earned rebates and discounts), including the cost of inbound freight. The cost of outbound freight, purchasing, receiving, and warehousing are included in selling, general, and administrative expenses within operating expenses. Our gross profit may not be comparable to that of other companies, as other companies may include all or some of the costs related to their distribution network in cost of sales. Market price fluctuations, particularly on structural products vulnerable to commodity price variability, may impact our gross profit.

Adjusted EBITDA

Adjusted EBITDA is an amount equal to net income (loss) plus interest expense and all interest expense related items (e.g., write-off of debt issuance costs, charges associated with mortgage refinancing), income taxes, depreciation and amortization, and further adjusted to exclude non-cash items and certain other adjustments to Consolidated Net Income (Loss). We present Adjusted EBITDA because it is a primary measure used by management to evaluate operating performance and helps to enhance investors’ overall understanding of the financial performance of our business. However, Adjusted EBITDA is not a presentation made in accordance with GAAP, and is not intended to present a superior measure of the financial condition from those determined under GAAP. Adjusted EBITDA, as used herein, is not necessarily comparable to other similarly titled captions of other companies due to differences in methods of calculation.

We believe Adjusted EBITDA is helpful in highlighting operating trends. We further believe that Adjusted EBITDA is frequently used by securities analysts, investors and other interested parties in their evaluation of companies, many of which present an Adjusted EBITDA measure when reporting their results. We compensate for the limitations of using non-GAAP financial measures by using them to supplement GAAP results to provide a more complete understanding of the factors and trends affecting the business than using GAAP results alone.

18

Results of Operations

Fiscal 2014 Compared to Fiscal 2013

The following table sets forth our results of operations for fiscal 2014 and fiscal 2013. Fiscal 2014 contained 52 weeks, and fiscal 2013 contained 53 weeks.

Fiscal 2014 | % of Net Sales | Fiscal 2013 | % of Net Sales | ||||||||||

| (Dollars in thousands) | |||||||||||||

| Net sales | $ | 1,979,393 | 100.0 | % | $ | 2,151,972 | 100.0 | % | |||||

| Gross profit | 229,104 | 11.6 | % | 228,483 | 10.6 | % | |||||||

| Selling, general, and administrative | 206,095 | 10.4 | % | 240,667 | 11.2 | % | |||||||

| Depreciation and amortization | 9,473 | 0.5 | % | 9,117 | 0.4 | % | |||||||

| Operating (loss) income | 13,536 | 0.7 | % | (21,301 | ) | (1.0 | )% | ||||||

| Interest expense, net | 26,771 | 1.4 | % | 28,024 | 1.3 | % | |||||||

| Other expense (income), net | 325 | — | % | 306 | — | % | |||||||

| Loss before (benefit from) provision for income taxes | (13,560 | ) | (0.7 | )% | (49,631 | ) | (2.3 | )% | |||||

| (Benefit from) provision for income taxes | 312 | — | % | (9,013 | ) | (0.4 | )% | ||||||

| Net income (loss) | $ | (13,872 | ) | (0.7 | )% | $ | (40,618 | ) | (1.9 | )% | |||

The following table sets forth changes in net sales by product category, sales variances due to changes in unit volume, and dollar and percentage changes in unit volume and price versus comparable prior periods. Certain prior year amounts have been reclassified to conform to the current year product mix of structural and specialty products.

| Fiscal 2014 | Fiscal 2013 | ||||||

| (Dollars in millions) | |||||||

| Sales by category | |||||||

| Structural products | $ | 831 | $ | 966 | |||

| Specialty products | 1,169 | 1,202 | |||||

| Other (1) | (21 | ) | (16 | ) | |||

| Total sales | $ | 1,979 | $ | 2,152 | |||

| Sales variances $ | |||||||

| Unit volume $ change | $ | (90 | ) | $ | 182 | ||

| Price/other (2) | (83 | ) | 62 | ||||

| Total $ change | $ | (173 | ) | $ | 244 | ||

| Sales variances % | |||||||

| Unit volume % change | (4.3 | )% | 10.0 | % | |||

| Price/other % change (1) | (3.7 | )% | 2.8 | % | |||

| Total % change | (8.0 | )% | 12.8 | % | |||

(1)“Other” includes unallocated allowances and discounts.

(2)“Other” includes unallocated allowances, discounts, and the impact of unit volume changes related to the five distribution centers closed as part of the restructuring activities in fiscal 2013 (the “2013 restructuring”).

19

The following table sets forth changes in gross margin dollars and percentages by product category, and percentage changes in unit volume growth by product, versus comparable prior periods. Certain prior year amounts have been reclassified to conform to the current year product mix of structural and specialty products.

| Fiscal 2014 | Fiscal 2013 | ||||||

| (Dollars in millions) | |||||||

| Gross Profit $ by category | |||||||

| Structural products | $ | 69 | $ | 69 | |||

| Specialty products | 156 | 155 | |||||

| Other (1) | 4 | 4 | |||||

| Total gross profit | $ | 229 | $ | 228 | |||

| Gross margin % by category | |||||||

| Structural products | 8.3 | % | 7.2 | % | |||

| Specialty products | 13.4 | % | 12.9 | % | |||

| Total gross margin % | 11.6 | % | 10.6 | % | |||

| Unit volume % change by product (2) | |||||||

| Structural products | (9.9 | )% | 12.2 | % | |||

| Specialty products | 0.1 | % | 8.4 | % | |||

| Total unit volume % change | (4.3 | )% | 10.0 | % | |||

(1)“Other” includes unallocated allowances and discounts.

(2)Excludes the impact of unit volume changes related to the five distribution centers closed as part of the 2013 restructuring.

Net sales. Net sales decreased by 8.0%, or $172.6 million, from $2.2 billion in fiscal 2013 to $2.0 billion in fiscal 2014. This decrease was primarily related to the $85.6 million impact of the five distribution centers closed as part of the 2013 restructuring and the $19.2 million impact from fiscal 2013 containing 53 weeks versus 52 weeks in fiscal 2014. In addition, the Company focused on the profitability of every sale, and pursued low profit structural business less aggressively. As a result, structural unit volumes were down approximately $83.0 million for the year, partially offset by unit volume increases in specialty products.

Gross profit. Total gross profit for fiscal 2014 was $229.1 million, or 11.6% of sales, compared to $228.5 million and 10.6% in fiscal 2013. The increase in gross profit primarily was due to an improvement in the gross margin of structural products. Structural products were 42.0% of sales in fiscal 2014, and 45.0% of sales in fiscal 2013. Structural gross margin percentage increased 110 basis points year over year to 8.3% in fiscal 2014 from 7.2% in fiscal 2013. Specialty gross margin percentage improved 50 basis points year over year to 13.4% in fiscal 2014 from 12.9% in fiscal 2013.

Selling, general, and administrative. Selling, general, and administrative expenses for fiscal 2014 were $206.1 million, or 10.4% of net sales, compared to $240.7 million, or 11.2% of net sales, during fiscal 2013. The decrease in selling, general, and administrative expenses primarily was due to cost control measures implemented in fiscal 2014, including cost savings realized from fiscal 2013 restructuring efforts of $3.3 million in fiscal 2014. Payroll, commissions, and incentives decreased year over year by $16.3 million. Third party freight improved by $3.4 million, of which $2.3 million is specifically related to discontinued operations, and the remaining $1.1 million improvement is driven by lower sales volume and cost control efforts. Additionally, bad debt expense improved by $1.6 million due to continued favorable accounts receivable performance.

Interest expense, net. Interest expense for fiscal 2014 was $26.8 million compared to $28.0 million for fiscal 2013. The decrease of $1.2 million relates to a decrease in interest expense related to our mortgage, due to principal payments on the mortgage. Although borrowings on the U.S. revolving credit facility increased by a net $18.4 million during fiscal 2014, a decline in interest rates resulted in interest expense on the U.S. revolving credit facility remaining flat from fiscal 2013 to fiscal 2014, at approximately $11.4 million for both years.

Provision for (benefit from) income taxes. Our effective tax rate was (2.3)% and 18.2% for fiscal 2014 and fiscal 2013, respectively. The effective tax rate for fiscal 2014 largely is due to a full valuation allowance recorded against our tax benefit related to our fiscal 2014 loss. The effective tax rate for fiscal 2013 largely is due to a full valuation allowance recorded against our tax benefit and an allocation of income tax expense to other comprehensive income (loss) for an actuarial gain associated with our pension plan which resulted in a benefit to continuing operations. The effect of the valuation allowance for fiscal 2014 and fiscal 2013 was offset by state income taxes, gross receipts taxes, and foreign income taxes recorded on a separate company basis partially offset by various refundable tax credits.

20

Fiscal 2013 Compared to Fiscal 2012

The following table sets forth our results of operations for fiscal 2013 and fiscal 2012. Fiscal 2013 contained 53 weeks, and fiscal 2012 contained 52 weeks.

Fiscal 2013 | % of Net Sales | Fiscal 2012 | % of Net Sales | ||||||||||

| (Dollars in thousands) | |||||||||||||

| Net sales | $ | 2,151,972 | 100.0 | % | $ | 1,907,842 | 100.0 | % | |||||

| Gross profit | 228,483 | 10.6 | % | 230,070 | 12.1 | % | |||||||

| Selling, general, and administrative | 240,667 | 11.2 | % | 215,996 | 11.3 | % | |||||||

| Depreciation and amortization | 9,117 | 0.4 | % | 8,565 | 0.4 | % | |||||||

| Operating (loss) income | (21,301 | ) | (1.0 | )% | 5,509 | 0.3 | % | ||||||

| Interest expense, net | 28,024 | 1.3 | % | 28,157 | 1.5 | % | |||||||

| Other expense (income), net | 306 | — | % | (7 | ) | — | % | ||||||

| Loss before (benefit from) provision for income taxes | (49,631 | ) | (2.3 | )% | (22,641 | ) | (1.2 | )% | |||||

| (Benefit from) provision for income taxes | (9,013 | ) | (0.4 | )% | 386 | — | % | ||||||

| Net income (loss) | $ | (40,618 | ) | (1.9 | )% | $ | (23,027 | ) | (1.2 | )% | |||

The following table sets forth changes in net sales by product category, sales variances due to changes in unit volume and dollar and percentage changes in unit volume and price versus comparable prior periods. Certain prior year amounts have been reclassified to conform to the current year product mix of structural and specialty products.

| Fiscal 2013 | Fiscal 2012 | ||||||

| (Dollars in millions) | |||||||

| Sales by category | |||||||

| Structural products | $ | 966 | $ | 804 | |||

| Specialty products | 1,202 | 1,112 | |||||

| Other (1) | (16 | ) | (8 | ) | |||

| Total sales | $ | 2,152 | $ | 1,908 | |||

| Sales variances $ | |||||||

| Unit volume $ change | $ | 182 | $ | 42 | |||

| Price/other (2) | 62 | 111 | |||||

| Total $ change | $ | 244 | $ | 153 | |||

| Sales variances % | |||||||

| Unit volume % change | 10.0 | % | 2.5 | % | |||

| Price/other % change (1) | 2.8 | % | 6.2 | % | |||

| Total % change | 12.8 | % | 8.7 | % | |||

(1)“Other” includes unallocated allowances and discounts.

(2)“Other” includes unallocated allowances, discounts, and the impact of unit volume changes related to the five distribution centers closed as part of the 2013 restructuring.

21

The following table sets forth changes in gross profit dollars and gross margin percentages by product category, and percentage changes in unit volume growth by product, versus comparable prior periods. Certain prior year amounts have been reclassified to conform to the current year product mix of structural and specialty products.

| Fiscal 2013 | Fiscal 2012 | ||||||

| (Dollars in millions) | |||||||

| Gross Profit $ by category | |||||||

| Structural products | $ | 69 | $ | 77 | |||

| Specialty products | 155 | 146 | |||||

| Other (1) | 4 | 7 | |||||

| Total gross profit | $ | 228 | $ | 230 | |||

| Gross margin % by category | |||||||

| Structural products | 7.2 | % | 9.5 | % | |||

| Specialty products | 12.9 | % | 13.2 | % | |||

| Total gross margin % | 10.6 | % | 12.1 | % | |||

| Unit volume % change by product (2) | |||||||

| Structural products | 12.2 | % | 0.8 | % | |||

| Specialty products | 8.4 | % | 3.6 | % | |||

| Total unit volume % change | 10.0 | % | 2.5 | % | |||

(1)“Other” includes unallocated allowances and discounts.

(2)Excludes the impact of unit volume changes related to the five distribution centers closed as part of the 2013 restructuring.

Net sales. For fiscal year 2013, net sales increased by 12.8%, or $244.1 million, to $2.2 billion. Sales during the fiscal year were positively impacted by a 15.5% increase in single family housing starts. Structural sales increased by $162.1 million, or 20.2% from 2012, as a result of a 10.1% increase in structural product prices and a 12.2% increase in unit volume. In addition, specialty sales increased $86.0 million, or 7.7% from 2012, as a result of a 8.4% increase in unit volume and a 0.6% increase in specialty product prices.

Gross profit. Gross profit for fiscal 2013 was $228.5 million, or 10.6% of sales, compared to $230.1 million and 12.1% 2012. Declines in gross margin were driven by volatility in wood-based structural product pricing, primarily during the second quarter of fiscal 2013. The declines in gross margin further were impacted by a greater percentage of our sales being comprised of lower gross margin structural products. In addition, we experienced lower margin sales as we sold through inventory at the five distribution centers we closed during the third quarter of fiscal 2013.

Selling, general, and administrative. Selling, general, and administrative expenses for fiscal 2013 were $240.7 million, or 11.2% of net sales, compared to $216.0 million, or 11.3% of net sales, during fiscal 2012. The increase in selling, general, and administrative expenses primarily was due to $11.2 million of restructuring and other charges associated with the fiscal 2013 restructuring and a change in executive leadership. During fiscal 2013 there were also increases in third party freight, professional fees, and general maintenance and supplies of $2.3 million, $1.9 million, and $1.3 million, respectively. These changes were partially offset by a decrease in payroll of $1.2 million related to a reduced headcount from the 2013 restructuring and change in executive leadership.

The gain recorded in selling, general and administrative expenses during fiscal 2013 was a $5.2 million gain on sales of properties. During fiscal 2012, other gains recorded in selling, general, and administrative expenses were comprised primarily of $9.9 million in gain on sales of properties. The increases to third party freight and general maintenance and supplies largely are due to the increase in revenue during fiscal 2013. The increase in professional fees relates to certain non-recurring activities requiring the services of various professionals. These activities included capital raising initiatives, freeze of the non-union participants in the pension plan, contribution of certain real properties to the pension plan, and the waiver process for the 2012 minimum required contribution of the pension plan.

Provision for (benefit from) income taxes. Our effective tax rates were 18.2% and (1.7)% for fiscal 2013 and fiscal 2012, respectively. The effective tax rate for fiscal 2013 largely is due to a full valuation allowance recorded against our tax benefit and an allocation of income tax expense to other comprehensive income (loss) for an actuarial gain associated with our pension plan resulting in a benefit to continuing operations. The main driver of the actuarial pension gain is an increase in the market value of the underlying assets and a decrease in the pension liability resulting largely from the change in the underlying

22

discount rate assumption, which increased from 4.24% in fiscal 2012 to 5.00% in fiscal 2013. The effective tax rate for fiscal 2012 largely is due to a full valuation allowance recorded against our tax benefit related to our fiscal 2012 loss.

Liquidity and Capital Resources

We expect our primary sources of liquidity to be cash flows from sales in the normal course of our operations, and borrowings under our revolving credit facilities, and we expect that these sources will fund our ongoing cash requirements for the foreseeable future. As the Company’s revenue performance improves as expected, increases in inventory to meet demand and resulting increases in accounts receivable from sales may cause the excess availability to decrease. While the Company believes that the amounts currently available from its revolving credit facilities and other sources would be sufficient to fund its routine operations and working capital requirements for at least the next 12 months, the Company believes that additional working capital will provide it with a stronger liquidity position and allow it to more fully participate in the improving housing market.

Sources and Uses of Cash

Operating Activities

During fiscal 2014, cash flows used in operating activities totaled $12.3 million. The primary driver of cash flows used in operations was a net loss of $13.9 million, which included non-cash charges of $7.3 million, a decrease in receivables of $5.8 million, and an increase in inventories of $19.0 million. These changes were partially offset by an increase in accounts payable of $7.0 million. Our cash flows used in operations continue to improve year over year, as 2014 cash flows from operating activities improved by $27.6 million compared to the fiscal 2013 cash used in operations of $39.9 million, which largely were driven by a net loss of $40.6 million. Cash used in operations in fiscal 2012 was $74.3 million, which was primarily a result of large increases in accounts receivable and inventories during that year, of $18.6 million and $44.5 million, respectively.

Investing Activities

During fiscal 2014, our net cash provided by investing activities was $4.4 million, which included expenditures for property and equipment of approximately $3.0 million, and proceeds from the disposition of property and equipment of $7.4 million, which included $6.9 million related to the sale of the Portland, Oregon distribution center. The fiscal 2014 expenditures were primarily to purchase information technology, leasehold improvements, and certain machinery and equipment. The majority of our capital expenditures for fiscal 2014 and 2013 have been and likely will continue to be paid from our U.S. revolving credit facility. In fiscal 2015, we intend to make additional investments in information technology for our sales force. Additionally, we intend to lease additional vehicles under capital leases with a third party leasing company as part of our efforts to continually replenish our fleet.

During fiscal 2013 and 2012, net cash provided by investment activities of $5.5 million and $16.4 million, respectively, substantially were driven by the sale of real properties.

Financing Activities