UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-21653

DOMINI ADVISOR TRUST

(Exact Name of Registrant as Specified in Charter)

536 Broadway, 7th Floor, New York, New York 10012

(Address of Principal Executive Offices)

Amy L. Domini

Domini Social Investments LLC

536 Broadway, 7th Floor

New York, New York 10012

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code: 212-217-1100

Date of Fiscal Year End: July 31

Date of Reporting Period: July 31, 2006

Item 1. Reports to Stockholders.

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 follows.

Table of Contents

| 2 | Letter from the President | ||||

| Domini Social Equity Portfolio | |||||

| 4 | Performance Commentary | ||||

| 7 | Expense Example | ||||

| 9 | Social Profiles | ||||

| 13 | Portfolio of Investments | ||||

| Domini European Social Equity Portfolio | |||||

| 20 | Performance Commentary | ||||

| 23 | Expense Example | ||||

| 25 | Social Profiles | ||||

| 28 | Portfolio of Investments | ||||

| Financial Statements | |||||

| 32 | Domini Social Equity Trust | ||||

| 38 | Report of Independent Registered Public Accounting Firm | ||||

| 39 | Domini Social Equity Portfolio | ||||

| 47 | Report of Independent Registered Public Accounting Firm | ||||

| 48 | Domini European Social Equity Trust | ||||

| 55 | Report of Independent Registered Public Accounting Firm | ||||

| 56 | Domini European Social Equity Portfolio | ||||

| 64 | Report of Independent Registered Public Accounting Firm | ||||

| 65 | Board of Trustees' Consideration of Management and Submanagement Agreements | ||||

| 75 | Trustees and Officers | ||||

| 79 | Proxy Voting Information | ||||

| 79 | Quarterly Portfolio Schedule Information | ||||

| 79 | Proxy Results | ||||

| Back Cover | For More Information |

LETTER FROM THE PRESIDENT

Dear Fellow Shareholders:

The greatness of this nation has always rested upon its commitment to the ordinary women and men working in our factories, shops, farms, schools, mines, and other places of employment.

I grew up during the 1950s, an era in which a working person could support a family, buy a home, put the children through state university, and save for retirement — all on one salary. Thanks to the baby boomers from this era, this nation enjoyed the great expansion of the 1990s, when fields were developed that were unheard of in the past, such as computer technology, wireless phone communication, and drugs created through biotechnology. The giants of today's corporate leadership are the very products of America's commitment in the 1950s and '60s to maintaining fine public schools, paying workers enough so that their families could thrive, and providing the public with a degree of personal safety.

Since then, improvements in income have been enjoyed only by the richest among us. From 1972 to 2004, for instance, the real average income of the top 1% more than doubled — from about $300,000 to more than $700,000 — while the average income of the other 99% remained flat, at around $37,500. The income gap has widened, not narrowed.

There are many reasons for this. Increasing globalization has provided businesses access to a large pool of low-wage labor. CEO compensation has ballooned out of proportion to the wages earned by the average employee. Government policy, including tax cuts designed to benefit the rich, has arguably accelerated the concentration of wealth.

Although individual companies cannot reverse these broad trends, they can do a great deal to improve the well-being of their employees — not only by paying them fair wages and rewarding them for their contributions to the company, but by providing a range of benefits that may save them money, enrich their lives, and advance their careers.

At Domini Social Investments, we review our investments carefully. One of the primary indicators we use in evaluating a company is a supportive environment for employees. Creating such an environment is difficult, and no company does a perfect job of balancing the factors involved. In this report we profile some of the companies and agencies held in our portfolios that have made notable achievements in this area.

When someone makes the decision to work for a company, she or he makes what may be a life-changing commitment. Employees may invest their intellectual capital, develop specialized skills, sacrifice time that could otherwise be spent with their families, or even risk their own health and safety.

2

In fact, employers and employees can be viewed as participating in a partnership, and both parties have a responsibility to make it work. Employees must work diligently, and companies must in turn treat their employees fairly, assuring them, among other things, of a living wage and a comfortable retirement. But it should not stop there. The greatness of our nation over the next few decades will largely hinge on the workforce of today being able to give their children what baby boomers of the 1950s were given: an opportunity to excel. Companies that work to ensure a safe workplace, to encourage physical fitness, and to help employees deal with personal or family problems may benefit from increased employee productivity and loyalty. Where management and labor unions work respectfully with each other to balance their needs, both constituencies may find it easier to confront the challenges that businesses inevitably face.

By sharing their financial success through profit sharing, employee stock ownership, or other forms of involvement and empowerment, companies can help align their employees' sense of personal growth and satisfaction with the growth and success of the firm. Companies that take steps to assure equity in pay for men and women and the financial well-being of their retirees, and those that award bonuses for those who reach social and environmental goals — not just financial goals — help build their own credibility and align their reward systems with their goals for society.

The long-term success of a company depends on its relationship to a variety of stakeholders. Employees are among the most important of these stakeholders. As a social investor, you help encourage companies to adopt programs that promote the well-being of employees, which in turn strengthens our society.

Thank you for being a Domini shareholder. We appreciate your trust and your commitment to helping create a better future for everyone.

Very truly yours,

Amy Domini

amy@domini.com

3

Domini Social Equity Portfolio

PERFORMANCE COMMENTARY

For the year ended July 31, 2006, the Domini Social Equity Portfolio (Class A Shares) returned 0.51%, excluding sales charges, while the Standard & Poor's 500 Index (S&P 500) returned 5.38%.

Equity markets had modest gains for the 12-month period ended July 31, a year marked by concerns over oil prices and inflation.

Despite the impact of Hurricane Katrina and the spike in oil prices that followed, corporate earnings showed surprising strength in 2005, increasing approximately 15% over 2004. However, earnings grew at a decreasing rate over the last two quarters of 2005. A slowdown in earnings is consistent with the later stages of economic expansions.

The effect on oil prices of Hurricane Katrina and unrest in the Middle East heightened awareness that oil prices will remain vulnerable to production interruptions. Oil prices increased 26% during the 12 months ended July 31, ending at approximately $76 per barrel.

Comments by the Federal Reserve Board after its 17th consecutive interest rate increase this June suggested that the Fed believed that although economic growth was moderating, some inflation risks remained. Payroll data reported in early July showed a 3.9% annualized increase in wages.

Other economic statistics released during the six months ended July 31 pointed to a weakening economic environment. Nonfarm employment gains declined from an average of more than 176,000 jobs per month in the first quarter of 2006 to an estimated 112,000 jobs per month in April through July. Housing starts declined more than in any other period in the last eight years.

Although some Wall Street analysts predict that corporate profits will grow 12% in 2006, others estimate that one-third of recent profit increases have come from energy and materials companies. This source of profit growth is cyclical and could disappear as increased prices for energy and materials drag on the economy as a whole.

The performance of the Fund relative to the S&P 500 was hurt in part by its underweighting to the energy sector and its overweighting to the information technology sector. Negative return due to stock selection contributed to this effect. The Fund was hurt in particular by the Portfolio's overweighting in Dell and Intel.

The relative performance of the Fund was helped in part by its overweighting to the telecommunications services sector. The Fund was also helped by the Portfolio's overweighting to JPMorgan Chase and its avoidance of General Electric and Wal-Mart.

4

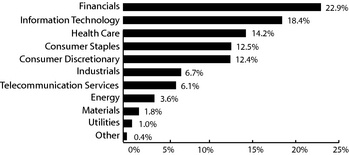

The Domini Social Equity Portfolio invests in the Domini Social Equity Trust. The table and the bar chart below provide information as of July 31, 2006, about the ten largest holdings of the Domini Social Equity Trust and its portfolio holdings by industry sector:

TEN LARGEST HOLDINGS

| COMPANY | % of NET ASSETS | COMPANY | % of NET ASSETS | ||||||||

| Microsoft | 3.66 | AT&T | 2.03 | ||||||||

| Johnson & Johnson | 3.21 | Cisco Systems | 1.89 | ||||||||

| Procter & Gamble | 3.20 | PepsiCo | 1.82 | ||||||||

| JPMorgan Chase | 2.75 | Intel | 1.82 | ||||||||

| Wells Fargo | 2.11 | Verizon Communications | 1.71 |

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS)

The holdings mentioned above are described in the Domini Social Equity Trust's (DSET) Portfolio of Investments at July 31, 2006, included herein. The composition of the DSET is subject to change.

Domini Social Equity Portfolio — Performance Commentary 5

AVERAGE ANNUAL TOTAL RETURNS

with maximum 4.75% sales charge

| Domini Social Equity Portfolio (DSEP) | S & P 500 | ||||||||||||||||||

| As of 6-30-06 | 1 Year(1) | 0.23 | % | 8.63 | % | ||||||||||||||

| 5 Year(1) | −0.01 | % | 2.49 | % | |||||||||||||||

| 10 Year(1) | 6.87 | % | 8.31 | % | |||||||||||||||

| Since Inception(1) | 9.01 | % | 10.32 | % | |||||||||||||||

| As of 7-31-06 | 1 Year(1) | −4.26 | % | 5.38 | % | ||||||||||||||

| 5 Year(1) | 0.02 | % | 2.82 | % | |||||||||||||||

| 10 Year(1) | 7.38 | % | 8.87 | % | |||||||||||||||

| Since Inception(1) | 8.96 | % | 10.31 | % | |||||||||||||||

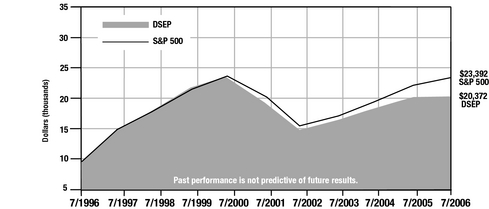

Comparison of $10,000 Investment in the

Domini Social Equity Portfolio and S&P 500

Past performance is no guarantee of future results. The Fund's returns quoted above represent past performance after all expenses. Economic and market conditions change, and both will cause investment return, principal value, and yield to fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, call 1-800-582-6757 or visit www.domini.com. A 2.00% redemption fee is charged on sales or exchanges of shares made less than 60 days after the settlement of purchase or acquisition through exchange, with certain exceptions. Performance data quoted above does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund's prospectus for further information.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Social Equity Portfolio is based on the Fund's net asset values and assumes all dividends and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money. Certain fees payable by the Fund were waived during the period, and the Fund's average annual total returns would have been lower had these not been waived.

The Standard & Poor's 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

(1)

The Domini Social Equity Portfolio, which commenced operations on May 1, 2005, invests all of its assets in the Domini Social Equity Trust (DSET), which has the same investment objectives as the Fund. The DSET commenced operations on June 3, 1991. Perfomance prior to the Fund's commencement of operations is the performance of the DSET adjusted for expenses of the Fund.

This material must be preceded or accompanied by the Fund's current prospectus. DSIL Investment Services LLC, Distributor. 09/06

6 Domini Social Equity Portfolio — Performance Commentary

DOMINI SOCIAL EQUITY PORTFOLIO

EXPENSE EXAMPLE

As a shareholder of the Domini Social Equity Portfolio, you incur two types of costs:

•

Transaction costs such as sales charges (loads) on purchases and redemption fees deducted from any redemption or exchange proceeds if you sell or exchange shares of the Fund after holding them less than 60 days

•

Ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses

This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on February 1, 2006, and held through July 31, 2006.

Actual Expenses

The line of the table captioned ‘‘Actual Expenses’’ below provides information about actual account value and actual expenses. You may use the information in this line, together with the amount invested, to estimate the expenses that you paid over the period as follows:

•

Divide your account value by $1,000.

•

Multiply your result in step 1 by the number in the first line under the heading ‘‘Expenses Paid During Period’’ in the table.

•

The result equals the estimated expenses you paid on your account during the period.

7

Hypothetical Expenses

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's return. The hypothetical account values and expenses may not be used to estimate actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical example that appears in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges and redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Domini Social Equity Portfolio | Beginning Account Value as of 2/1/2006 | Ending Account Value as of 7/31/06 | Expenses Paid During Period* 2/1/2006 − 7/31/2006 | ||||||||||||||||||||

| Actual Expenses | $ | 1,000.00 | $ | 978.50 | $ | 4.66 | |||||||||||||||||

| Hypothetical Expenses (5% return before expenses) | $ | 1,000.00 | $ | 1,020.08 | $ | 4.76 | |||||||||||||||||

*

Expenses are equal to the Fund's annualized expense ratio of 0.95% multiplied by average account value over the period, multiplied by 181, and divided by 365. The example reflects the aggregate expenses of the Fund and the Domini Social Equity Trust, the underlying portfolio in which the Fund invests.

8 Domini Social Equity Portfolio — Expense Example

Domini Social Equity Portfolio

Social Profiles

Employee Relations

Companies may invest in their employees in a variety of ways. Some companies offer exceptional compensation or family benefits, like Nordstrom and Bright Horizons Family Solutions, which are profiled below. Some empower their workers through decentralized decision-making (Granite Construction) or reenergize them through generous sabbaticals (Intel). Some excel in training (Men's Wearhouse) while others help give employees a sense of worth by encouraging them to contribute to society (CDW). Each of the companies profiled below appears in Fortune magazine's 2006 list of 100 Best Companies to Work For.

Other companies, including many in the portfolio of the Domini Social Equity Portfolio, are exceptional in their support for a diverse workforce that draws on the abilities of women, the handicapped, gays and lesbians, and people of various ethnic and religious backgrounds, or they have notably strong union relations.

In an economy increasingly dependent on service and information industries, the value of companies is increasingly tied to the skills and morale of their employees. By investing in their employees, American companies often find they reap important benefits in the form of a loyal, motivated, and productive workforce.

Bright Horizons Family Solutions (BFAM)

By investing in its employees, Bright Horizons Family Solutions, which operates 560 childcare and early education centers, has helped make childcare a more desirable profession.

Despite the importance of qualified daycare providers, daycare is often a poorly paid job. Bright Horizons, however, has opted to pay employees a rate more than 50% above the industry standard. Workers get a 50% discount on their own childcare, and 20 times a year they can use backup childcare for $10 a day.

According to the company, in addition to the 12 weeks of unpaid parental leave required by the Family and Medical Leave Act, both female and male Brights Horizons employees may use sick time and vacation time to extend their leave. Unused sick time and vacation time carry over from year to year, up to a total of 240 hours and 160 hours, respectively. Mothers may also use two to four weeks of paid disability leave (or more, depending on the situation) to replace income during the early months of the baby's life. The company also offers adoption aid, an eldercare resource and referral plan, and lactation rooms at various centers. Employees can take

9

advantage of alternative work schedules including flextime, compressed work weeks, part-time work, job sharing, and telecommuting.

The company and its foundation fund about 100 children's playrooms and educational centers, called Bright Spaces, in homeless shelters around the country. In November 2005, the company reported that it was supporting 100 Bright Spaces in 28 states and that roughly 4,000 children accessed these centers each month.

CDW (CDWC)

CDW, a direct marketer of computer products, encourages performance with incentives, including profit-sharing when the company does well. Employees who have worked at CDW at least three years are awarded all-expense-paid vacations anywhere in the U.S. if the company's sales goals are met. Employees enjoy a subsidized on-site cafeteria, an on-site fitness center, free meals for second-shift employees, free breakfasts on certain days of the week, a complimentary all-day beverage service, free turkeys or pies for Thanksgiving and Christmas, and a paid day off for community service.

CDW's generosity to its employees has helped spur generosity by its employees as well. Employees of CDW ordinarily enjoy an annual holiday party in Chicago that costs the company more than $1 million. In December 2005, employees chose to forego the company holiday party and donate the savings to relief for the victims of hurricanes in the Gulf Coast. The Louisiana Association of Business and Industry received $350,000 to launch its Small Business Reboot Program, and the company agreed to match up to $350,000 in donations made by employees. In August 2006, CDW reported that it had begun sending 300 employees on four-day ‘‘relief trips’’ to help rebuild homes destroyed by Hurricane Katrina.

Granite Construction (GVA)

Granite Construction — a major builder of highways and other construction projects — emphasizes integrity and uses stock ownership and decentralized decision-making to encourage its employees to feel involved in the company's success.

In 1984, when an offer was made to buy the company, Granite instead reserved majority ownership for an employee stock ownership plan. Each year shares were given to all employees. In 1990, in order to avoid using up capital buying back shares when employees retired, Granite went public to create a market for employee-owned shares. As of December 2005, Granite employees owned approximately 18% of the company. (Only non-union hourly and salaried employees participate in the plan.)

In 1990, the company introduced a week-long training program for young engineers, including a half day on ethical problems. The company drafted a new ethics policy based on a document by the company's founder, which

10 Domini Social Equity Portfolio — Social Profiles

asserted the company's people would ‘‘boldly contend for that which is right and firmly reject that which is wrong.’’

Each of Granite's divisions is run as an individual profit center. At each of the company's branches, branch managers are compensated according to the profitability of the branch. A system for employees to continually teach one another is described by the company as a ‘‘living learning process.’’ For the last ten years, the voluntary turnover rate among U.S. employees of Granite has reportedly been less than 9%.

Intel (INTC)

Intel, the well-known manufacturer of semiconductor chips, offers an impressive array of employee benefits, but one of the most unusual is its sabbatical program. Workers are eligible for an eight-week paid sabbatical every seven years. Employees report returning to work more committed and more energized.

In addition, Intel offers its employees a broad-based stock option plan and cash profit-sharing. Cash bonuses based on company profits are paid twice a year. An additional annual bonus is paid based on an employee's performance, the financial performance of the company, and the performance of the employee's business group.

In 2006, the magazine Careers & the disABLED ranked Intel number 19 among 50 companies with the best reputation for employing and accommodating the disabled. In 2005, for the fourth year, Working Mother magazine included Intel on its list of the 100 best workplaces for working mothers. Also in 2005, Intel was one of 101 companies to receive a perfect score of 100% on the Human Rights Campaign's Corporate Equality Index, which rates companies on their policies toward gay, lesbian, bisexual, and transgender people.

Men's Wearhouse (MW)

Men's Wearhouse, which sells men's clothing at discounted prices, encourages employee loyalty by investing substantially in their training.

Ninety-eight percent of regional and district managers have historically started in store positions. The company's Suits University offers a one-week training program for wardrobe consultants and managers, which covers consulting, customer service, corporate culture, merchandising, tailoring, and company benefits. The company also provides seasonal training seminars and in-store training and merchandising sessions. Long-time employees are eligible for a three-week paid sabbatical every five years — a notable policy for a retail store.

The company also uses its product to help men change their lives for the better. Men's Wearhouse sponsors organizations such as Working Wardrobes, Career Gear, and Law Suits, which offer free suits and alterations to help men faced with poverty and homelessness to dress for interviews and reenter the workforce.

Domini Social Equity Portfolio — Social Profiles 11

Nordstrom (JWN)

The Nordstrom department store chain is notable for its family-friendly policies. The company offers up to 84 days of family and medical leave per year, which may be used for maternity or paternity or a variety of family care situations. In addition to flextime and other alternative work options, the company offers a ‘‘Moms-to-Babies Maternity Management Program,’’ which helps provide access to covered prenatal care, education materials for expectant parents, obstetrical nurse case management, a pregnancy risk assessment, and breastfeeding information and support.

In addition to supporting its employees through its family benefits, Nordstrom has a policy of promoting from within. Most company managers and executives started on the selling floor and rose up through the company ranks, including members of the Nordstrom family. Former CEO and chair of the board John Whitacre began in the shoe department, former chair Bruce Nordstrom started in the stockroom, and president Blake Nordstrom began in the stockroom at age 14.

The company is widely cited as setting the benchmark for customer service in the department store industry, rewarding employees for good customer service as well as high sales.

The Fund invests in a portfolio designed to replicate the Domini 400 Social Index.SM All companies in the Fund's portfolio are measured against multiple standards of corporate accountability. We seek to avoid companies that manufacture alcohol, tobacco, or firearms, derive revenues from gambling operations, own or operate nuclear power plants, or earn significant revenues from weapons contracting. Before investing in any company, our social research providers at KLD Research & Analytics, Inc. (KLD) evaluate its social profile by weighing both strengths and weaknesses in the areas of community impact, diversity, employee relations, the environment, human rights, and product safety and usefulness. KLD is responsible for maintaining the Domini 400 Social Index and developing and applying its social and environmental standards. Special thanks to KLD for allowing us to reproduce portions of its research in these pages.

For extensive information about how we use social and environmental criteria to choose our investments, including brief social profiles of every company in the Fund's portfolio, visit www.domini.com.

Unlike other mutual funds, the Domini Social Equity Portfolio seeks to achieve its investment objective by investing all of its investable assets in a separate portfolio with an identical investment objective called the Domini Social Equity Trust (DSET). The companies discussed above can be found in the DSET's Portfolio of Investments at July 31, 2006, included herein. The composition of the DSET is subject to change.

The preceding profiles should not be deemed an offer to sell or a solicitation of an offer to buy the stock of any of the companies noted, or a recommendation concerning the merits of any of these companies as an investment.

Domini 400 Social IndexSM is a service mark of KLD Research & Analytics, Inc. (KLD), which is used under license. KLD is the owner of the Domini 400 Social Index. KLD determines the composition of the Index but is not the manager of the Domini Social Equity Trust, the Domini Social Equity Fund, the Domini Social Equity Portfolio, or the Domini Institutional Social Equity Fund.

Certain portions of these social profiles are copyright © 2006 by KLD Research & Analytics, Inc. and are reprinted here by permission. 09/06

12 Domini Social Equity Portfolio — Social Profiles

Item 1. Reports to Stockholders.

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 follows.

Domini Social Equity Trust

Portfolio of Investments

July 31, 2006

| Security | Shares | Value | ||||||||||||||

| Consumer Discretionary 12.4% | ||||||||||||||||

| American Greetings Corporation, Class A | 13,100 | $ | 295,143 | |||||||||||||

| AutoZone, Inc. (a) | 12,931 | 1,136,247 | ||||||||||||||

| Bandag, Inc. | 2,900 | 99,992 | ||||||||||||||

| Bed Bath & Beyond (a) | 69,900 | 2,340,252 | ||||||||||||||

| Best Buy Co., Inc. | 97,700 | 4,429,718 | ||||||||||||||

| Black & Decker Corp. | 18,361 | 1,294,634 | ||||||||||||||

| Bright Horizons Family Solutions, Inc. (a) | 6,400 | 246,080 | ||||||||||||||

| Centex Corporation | 29,100 | 1,376,721 | ||||||||||||||

| Champion Enterprises, Inc. (a) | 19,000 | 125,970 | ||||||||||||||

| Charming Shoppes, Inc. (a) | 26,300 | 271,153 | ||||||||||||||

| Circuit City Stores, Inc. | 38,100 | 933,450 | ||||||||||||||

| Claire's Stores, Inc. | 24,800 | 620,744 | ||||||||||||||

| Cooper Tire and Rubber Company | 15,300 | 152,847 | ||||||||||||||

| Darden Restaurants, Inc. | 31,200 | 1,054,560 | ||||||||||||||

| DeVry, Inc. (a) | 15,000 | 316,500 | ||||||||||||||

| Disney (Walt) Company (The) | 535,450 | 15,897,511 | ||||||||||||||

| Dollar General Corporation | 74,351 | 997,790 | ||||||||||||||

| Dow Jones & Company | 14,800 | 518,592 | ||||||||||||||

| Emmis Communications Corporation, Class A (a) | 8,860 | 131,305 | ||||||||||||||

| Family Dollar Stores Inc. | 38,800 | 881,536 | ||||||||||||||

| Foot Locker, Inc. | 39,000 | 1,059,630 | ||||||||||||||

| Gaiam, Inc. (a) | 5,300 | 71,497 | ||||||||||||||

| Gap Inc. | 127,797 | 2,217,278 | ||||||||||||||

| Genuine Parts Company | 41,500 | 1,728,060 | ||||||||||||||

| Harley-Davidson, Inc. | 66,000 | 3,762,000 | ||||||||||||||

| Harman International Industries, Inc. | 16,320 | 1,308,864 | ||||||||||||||

| Hartmarx Corporation (a) | 8,500 | 53,210 | ||||||||||||||

| Home Depot, Inc. (The) | 504,344 | 17,505,780 | ||||||||||||||

| Horton (D.R.), Inc. | 67,833 | 1,453,661 | ||||||||||||||

| Interface, Inc., Class A (a) | 11,400 | 139,878 | ||||||||||||||

| Johnson Controls, Inc. | 47,500 | 3,646,100 | ||||||||||||||

| KB Home | 17,800 | 756,856 | ||||||||||||||

| Lee Enterprises, Inc. | 10,900 | 270,647 | ||||||||||||||

| Leggett & Platt, Incorporated | 45,500 | 1,038,310 | ||||||||||||||

| Consumer Discretionary (Continued) | ||||||||||||||||

| Limited Brands | 83,830 | $ | 2,109,163 | |||||||||||||

| Liz Claiborne, Inc. | 26,200 | 926,170 | ||||||||||||||

| Lowe's Companies, Inc. | 378,573 | 10,732,545 | ||||||||||||||

| Mattel, Inc. | 96,785 | 1,746,001 | ||||||||||||||

| McClatchy Newspapers A, Class A | 6,700 | 284,013 | ||||||||||||||

| McDonald's Corporation | 303,700 | 10,747,943 | ||||||||||||||

| McGraw-Hill Companies | 87,800 | 4,943,140 | ||||||||||||||

| Media General, Inc., Class A | 5,600 | 204,008 | ||||||||||||||

| Men's Wearhouse, Inc. | 13,050 | 405,986 | ||||||||||||||

| Meredith Corporation | 10,200 | 481,746 | ||||||||||||||

| Modine Manufacturing Company | 8,700 | 205,059 | ||||||||||||||

| New York Times Company, Class A | 35,000 | 775,950 | ||||||||||||||

| Newell Rubbermaid, Inc. | 68,178 | 1,797,172 | ||||||||||||||

| NIKE, Inc., Class B | 46,300 | 3,657,700 | ||||||||||||||

| Nordstrom, Inc. | 52,600 | 1,804,180 | ||||||||||||||

| Office Depot (a) | 68,400 | 2,465,820 | ||||||||||||||

| Omnicom Group, Inc. | 41,800 | 3,699,718 | ||||||||||||||

| Penney (J.C.) Company, Inc. | 57,900 | 3,645,384 | ||||||||||||||

| Pep Boys – Manny, Moe & Jack | 14,000 | 150,920 | ||||||||||||||

| Phillips-Van Heusen Corporation | 11,700 | 415,701 | ||||||||||||||

| Pulte Homes, Inc. | 51,400 | 1,464,900 | ||||||||||||||

| Radio One, Inc. (a) | 2,300 | 16,445 | ||||||||||||||

| RadioShack Corporation | 33,700 | 544,929 | ||||||||||||||

| Ruby Tuesday, Inc. | 14,500 | 318,420 | ||||||||||||||

| Russell Corporation | 8,300 | 149,483 | ||||||||||||||

| Scholastic Corporation (a) | 9,000 | 258,750 | ||||||||||||||

| Scripps (E.W.) Company (The), Class A | 21,400 | 914,422 | ||||||||||||||

| Snap-On Incorporated | 14,550 | 611,246 | ||||||||||||||

| Spartan Motors, Inc. | 3,100 | 50,716 | ||||||||||||||

| Stanley Works | 16,700 | 757,679 | ||||||||||||||

| Staples, Inc. | 178,784 | 3,865,310 | ||||||||||||||

| Starbucks Corporation (a) | 187,114 | 6,410,526 | ||||||||||||||

| Stride Rite Corporation | 9,200 | 116,472 | ||||||||||||||

| Target Corporation | 210,200 | 9,652,384 | ||||||||||||||

| Tiffany & Co. | 35,500 | 1,121,445 | ||||||||||||||

13

Domini Social Equity Trust / Portfolio of Investments (Continued)

July 31, 2006

| Security | Shares | Value | |||||||||||||||||

| Consumer Discretionary (Continued) | |||||||||||||||||||

| Timberland Company (The) (a) | 13,400 | $ | 345,050 | ||||||||||||||||

| Time Warner, Inc. | 1,044,720 | 17,237,880 | |||||||||||||||||

| TJX Companies, Inc. | 111,700 | 2,722,129 | |||||||||||||||||

| Tribune Company | 43,800 | 1,301,298 | |||||||||||||||||

| Tupperware Corporation | 13,300 | 229,558 | |||||||||||||||||

| Univision Communications, Inc., Class A (a) | 53,800 | 1,796,920 | |||||||||||||||||

| Valassis Communications Inc. (a) | 12,300 | 252,519 | |||||||||||||||||

| Value Line, Inc. | 300 | 12,153 | |||||||||||||||||

| Washington Post Company, Class B | 1,400 | 1,079,400 | |||||||||||||||||

| Wendy's International, Inc. | 28,600 | 1,720,576 | |||||||||||||||||

| Whirlpool Corporation | 19,436 | 1,500,264 | |||||||||||||||||

| 173,781,709 | |||||||||||||||||||

| Consumer Staples 12.5% | |||||||||||||||||||

| Alberto-Culver Company, Class B | 18,850 | 918,749 | |||||||||||||||||

| Avon Products, Inc. | 109,943 | 3,187,248 | |||||||||||||||||

| Campbell Soup Company | 45,100 | 1,654,268 | |||||||||||||||||

| Chiquita Brands International, Inc. | 10,800 | 145,152 | |||||||||||||||||

| Church & Dwight Co., Inc. | 16,100 | 587,650 | |||||||||||||||||

| Clorox Company | 36,400 | 2,181,816 | |||||||||||||||||

| Coca-Cola Company | 500,600 | 22,276,700 | |||||||||||||||||

| Colgate-Palmolive Company | 125,200 | 7,426,864 | |||||||||||||||||

| Costco Wholesale Corporation | 114,630 | 6,047,879 | |||||||||||||||||

| CVS Corporation | 199,500 | 6,527,640 | |||||||||||||||||

| Dean Foods (a) | 33,500 | 1,257,255 | |||||||||||||||||

| Estée Lauder Companies, Inc. (The), Class A | 29,700 | 1,108,404 | |||||||||||||||||

| General Mills Incorporated | 87,500 | 4,541,250 | |||||||||||||||||

| Green Mountain Coffee, Inc. (a) | 1,300 | 51,727 | |||||||||||||||||

| Hain Celestial Group, Inc. (The) (a) | 9,500 | 205,200 | |||||||||||||||||

| Heinz (H.J.) Company | 81,793 | 3,432,852 | |||||||||||||||||

| Hershey Foods Corporation | 43,400 | 2,385,698 | |||||||||||||||||

| Consumer Staples (Continued) | |||||||||||||||||||

| Kellogg Company | 57,700 | $ | 2,779,409 | ||||||||||||||||

| Kimberly-Clark Corporation | 111,764 | 6,823,192 | |||||||||||||||||

| Kroger Company | 177,400 | 4,067,782 | |||||||||||||||||

| Longs Drug Stores Corporation | 6,600 | 271,392 | |||||||||||||||||

| McCormick & Company, Inc. | 33,100 | 1,160,486 | |||||||||||||||||

| PepsiAmericas, Inc. | 15,200 | 343,520 | |||||||||||||||||

| PepsiCo, Inc. | 404,070 | 25,609,957 | |||||||||||||||||

| Procter & Gamble Company | 801,387 | 45,037,948 | |||||||||||||||||

| Safeway Inc. | 109,100 | 3,063,528 | |||||||||||||||||

| Smucker (J.M.) Company | 14,505 | 647,358 | |||||||||||||||||

| SUPERVALU, Inc. | 50,680 | 1,373,935 | |||||||||||||||||

| Sysco Corporation | 152,200 | 4,200,720 | |||||||||||||||||

| Tootsie Roll Industries, Inc. | 6,837 | 185,625 | |||||||||||||||||

| United Natural Foods, Inc. (a) | 10,000 | 301,400 | |||||||||||||||||

| Walgreen Company | 246,659 | 11,538,708 | |||||||||||||||||

| Whole Foods Market, Inc. | 34,700 | 1,995,597 | |||||||||||||||||

| Wild Oats Markets, Inc. (a) | 6,550 | 117,180 | |||||||||||||||||

| Wrigley (Wm.) Jr. Company | 53,700 | 2,462,682 | |||||||||||||||||

| 175,916,771 | |||||||||||||||||||

| Energy 3.6% | |||||||||||||||||||

| Anadarko Petroleum Corporation | 111,470 | 5,098,638 | |||||||||||||||||

| Apache Corporation | 80,324 | 5,660,432 | |||||||||||||||||

| Cameron International Corp. (a) | 28,900 | 1,456,849 | |||||||||||||||||

| Chesapeake Energy Corp | 96,700 | 3,181,430 | |||||||||||||||||

| Devon Energy Corporation | 107,044 | 6,919,324 | |||||||||||||||||

| EOG Resources, Inc. | 59,400 | 4,404,510 | |||||||||||||||||

| Helmerich & Payne, Inc. | 26,000 | 719,680 | |||||||||||||||||

| Kinder Morgan, Inc. | 25,500 | 2,601,000 | |||||||||||||||||

| National Oilwell Varco, Inc. (a) | 42,400 | 2,842,496 | |||||||||||||||||

| Newfield Exploration (a) | 32,100 | 1,488,798 | |||||||||||||||||

| Noble Energy, Inc. | 44,000 | 2,226,840 | |||||||||||||||||

14

Domini Social Equity Trust / Portfolio of Investments (Continued)

July 31, 2006

| Security | Shares | Value | |||||||||||||||||

| Energy (Continued) | |||||||||||||||||||

| Pioneer Natural Resources Company | 32,200 | $ | 1,460,270 | ||||||||||||||||

| Rowan Companies, Inc. | 27,300 | 924,651 | |||||||||||||||||

| Smith International | 48,692 | 2,170,202 | |||||||||||||||||

| Sunoco, Inc. | 32,235 | 2,241,622 | |||||||||||||||||

| Williams Companies, Inc. | 145,277 | 3,522,967 | |||||||||||||||||

| XTO Energy Inc. | 88,993 | 4,181,781 | |||||||||||||||||

| 51,101,490 | |||||||||||||||||||

| Financials 22.9% | |||||||||||||||||||

| AFLAC, Inc. | 121,300 | 5,354,182 | |||||||||||||||||

| Allied Capital Corporation | 34,000 | 957,100 | |||||||||||||||||

| AMBAC Financial Group, Inc. | 25,500 | 2,119,305 | |||||||||||||||||

| American Express Company | 301,000 | 15,670,060 | |||||||||||||||||

| AmSouth Bancorporation | 83,700 | 2,398,842 | |||||||||||||||||

| BB&T Corporation | 133,900 | 5,622,461 | |||||||||||||||||

| Capital One Financial Corporation | 73,900 | 5,716,165 | |||||||||||||||||

| Cathay General Bancorp | 12,790 | 470,033 | |||||||||||||||||

| Chittenden Corporation | 11,920 | 336,382 | |||||||||||||||||

| Chubb Corporation | 100,800 | 5,082,336 | |||||||||||||||||

| Cincinnati Financial Corporation | 41,917 | 1,976,806 | |||||||||||||||||

| CIT Group | 48,500 | 2,226,635 | |||||||||||||||||

| Comerica Incorporated | 39,400 | 2,306,870 | |||||||||||||||||

| Edwards (A.G.), Inc. | 18,387 | 992,163 | |||||||||||||||||

| Equity Office Properties Trust | 89,900 | 3,408,109 | |||||||||||||||||

| Fannie Mae | 236,396 | 11,325,732 | |||||||||||||||||

| Fifth Third Bancorp | 136,711 | 5,214,158 | |||||||||||||||||

| First Horizon National Corporation | 29,500 | 1,236,050 | |||||||||||||||||

| FirstFed Financial Corp. (a) | 4,100 | 231,445 | |||||||||||||||||

| Franklin Resources, Inc. | 37,200 | 3,401,940 | |||||||||||||||||

| Freddie Mac | 168,300 | 9,737,838 | |||||||||||||||||

| Genl Growth Properties | 59,534 | 2,717,132 | |||||||||||||||||

| Golden West Financial | 62,900 | 4,633,214 | |||||||||||||||||

| Hartford Financial Services Group (The) | 73,900 | 6,269,676 | |||||||||||||||||

| Heartland Financial USA, Inc. | 3,000 | 80,520 | |||||||||||||||||

| Janus Capital Group Inc. | 50,126 | 811,540 | |||||||||||||||||

| KeyCorp | 99,100 | 3,656,790 | |||||||||||||||||

| Lincoln National Corporation | 69,759 | 3,953,940 | |||||||||||||||||

| Financials (Continued) | |||||||||||||||||||

| M&T Bank Corp. | 19,190 | $ | 2,339,645 | ||||||||||||||||

| Maguire Properties Inc. | 6,700 | 250,647 | |||||||||||||||||

| Marsh & McLennan Companies, Inc. | 133,800 | 3,616,614 | |||||||||||||||||

| MBIA, Inc. | 33,400 | 1,964,254 | |||||||||||||||||

| Medallion Financial Corp. | 4,300 | 52,632 | |||||||||||||||||

| Mellon Financial Corporation | 101,400 | 3,549,000 | |||||||||||||||||

| Merrill Lynch & Co., Inc. | 225,761 | 16,439,916 | |||||||||||||||||

| MGIC Investment Corporation | 21,700 | 1,234,947 | |||||||||||||||||

| Moody's Corporation | 59,300 | 3,254,384 | |||||||||||||||||

| Morgan (J.P.) Chase & Co. | 847,851 | 38,678,962 | |||||||||||||||||

| National City Corporation | 133,200 | 4,795,200 | |||||||||||||||||

| Northern Trust Corporation | 44,900 | 2,563,790 | |||||||||||||||||

| PNC Financial Services Group | 72,800 | 5,157,152 | |||||||||||||||||

| Popular Inc. | 69,496 | 1,250,233 | |||||||||||||||||

| Principal Financial Group, Inc. | 68,100 | 3,677,400 | |||||||||||||||||

| Progressive Corporation (The) | 191,512 | 4,632,675 | |||||||||||||||||

| ProLogis | 59,400 | 3,287,790 | |||||||||||||||||

| Regions Financial Corp. (New) | 111,600 | 4,049,964 | |||||||||||||||||

| SAFECO Corporation | 28,900 | 1,552,508 | |||||||||||||||||

| Schwab (Charles) Corporation | 253,100 | 4,019,228 | |||||||||||||||||

| SLM Corporation | 99,900 | 5,024,970 | |||||||||||||||||

| Sovereign Bancorp | 93,555 | 1,930,975 | |||||||||||||||||

| St. Paul Travelers Companies, Inc. (The) | 169,764 | 7,775,191 | |||||||||||||||||

| State Street Corporation | 80,700 | 4,846,842 | |||||||||||||||||

| SunTrust Banks, Inc. | 88,700 | 6,995,769 | |||||||||||||||||

| Synovus Financial Corporation | 77,950 | 2,202,867 | |||||||||||||||||

| T. Rowe Price Group, Inc. | 65,800 | 2,718,198 | |||||||||||||||||

| TradeStation Group, Inc. (a) | 5,100 | 74,562 | |||||||||||||||||

| U.S. Bancorp | 433,721 | 13,879,072 | |||||||||||||||||

| UnumProvident Corporation | 74,400 | 1,207,512 | |||||||||||||||||

| Wachovia Corporation. | 392,843 | 21,068,170 | |||||||||||||||||

15

Domini Social Equity Trust / Portfolio of Investments (Continued)

July 31, 2006

| Security | Shares | Value | |||||||||||||||||

| Financials (Continued) | |||||||||||||||||||

| Wainwright Bank & Trust Co. | 2,756 | $ | 30,344 | ||||||||||||||||

| Washington Mutual, Inc. | 234,142 | 10,466,147 | |||||||||||||||||

| Wells Fargo & Company | 409,848 | 29,648,404 | |||||||||||||||||

| Wesco Financial Corporation | 300 | 118,500 | |||||||||||||||||

| 322,261,888 | |||||||||||||||||||

| Health Care 14.2% | |||||||||||||||||||

| Affymetrix Inc (a) | 16,700 | 360,219 | |||||||||||||||||

| Allergan, Inc. | 37,105 | 4,001,774 | |||||||||||||||||

| Amgen, Inc. (a) | 287,953 | 20,081,842 | |||||||||||||||||

| Bard (C.R.), Inc. | 25,800 | 1,831,026 | |||||||||||||||||

| Bausch & Lomb Incorporated | 13,600 | 643,280 | |||||||||||||||||

| Baxter International, Inc. | 159,600 | 6,703,200 | |||||||||||||||||

| Becton Dickinson and Company | 60,500 | 3,988,160 | |||||||||||||||||

| Biogen Idec Inc. (a) | 84,350 | 3,552,822 | |||||||||||||||||

| Biomet, Inc. | 59,400 | 1,956,636 | |||||||||||||||||

| Boston Scientific Corporation (a) | 296,519 | 5,043,788 | |||||||||||||||||

| CIGNA Corporation | 29,400 | 2,682,750 | |||||||||||||||||

| Cross Country Healthcare, Inc. (a) | 5,200 | 92,924 | |||||||||||||||||

| Dionex Corporation (a) | 5,000 | 276,750 | |||||||||||||||||

| Fisher Scientific International (a) | 30,000 | 2,223,300 | |||||||||||||||||

| Forest Laboratories, Inc. (a) | 79,496 | 3,681,460 | |||||||||||||||||

| Gen-Probe Inc. (a) | 12,800 | 664,960 | |||||||||||||||||

| Genzyme Corporation (a) | 63,609 | 4,343,223 | |||||||||||||||||

| Gilead Sciences (a) | 110,900 | 6,818,132 | |||||||||||||||||

| Health Management Association, Class A | 60,100 | 1,223,636 | |||||||||||||||||

| Hillenbrand Industries, Inc. | 15,500 | 769,730 | |||||||||||||||||

| Humana, Inc. (a) | 40,800 | 2,281,944 | |||||||||||||||||

| IMS Health, Inc. | 48,013 | 1,317,477 | |||||||||||||||||

| Invacare Corporation | 7,700 | 161,931 | |||||||||||||||||

| Invitrogen Corporation (a) | 13,300 | 821,807 | |||||||||||||||||

| Johnson & Johnson | 723,137 | 45,232,218 | |||||||||||||||||

| King Pharmaceuticals Inc. (a) | 60,300 | 1,026,306 | |||||||||||||||||

| Manor Care, Inc. | 19,800 | 990,990 | |||||||||||||||||

| McKesson HBOC, Inc. | 74,720 | 3,765,141 | |||||||||||||||||

| Health Care (Continued) | |||||||||||||||||||

| MedImmune, Inc. (a) | 60,600 | $ | 1,538,028 | ||||||||||||||||

| Medtronic, Inc. | 294,934 | 14,900,066 | |||||||||||||||||

| Merck & Co., Inc. | 533,100 | 21,467,937 | |||||||||||||||||

| Millipore Corporation (a) | 12,800 | 801,920 | |||||||||||||||||

| Molina Healthcare Inc. (a) | 5,300 | 175,642 | |||||||||||||||||

| Mylan Laboratories, Inc. | 50,675 | 1,112,823 | |||||||||||||||||

| Patterson Companies, Inc. (a) | 34,200 | 1,137,492 | |||||||||||||||||

| Quest Diagnostics Incorporated | 39,400 | 2,368,728 | |||||||||||||||||

| St. Jude Medical, Inc. (a) | 88,600 | 3,269,340 | |||||||||||||||||

| Stryker Corporation | 71,335 | 3,246,456 | |||||||||||||||||

| Synovis Life Technologies, Inc. (a) | 2,600 | 23,036 | |||||||||||||||||

| Thermo Electron Corporation (a) | 40,500 | 1,498,905 | |||||||||||||||||

| UnitedHealth Group Incorporated | 329,182 | 15,744,775 | |||||||||||||||||

| Waters Corporation (a) | 25,800 | 1,049,544 | |||||||||||||||||

| Watson Pharmaceuticals (a) | 25,400 | 568,706 | |||||||||||||||||

| Zimmer Holdings, Inc. (a) | 60,591 | 3,831,775 | |||||||||||||||||

| 199,272,599 | |||||||||||||||||||

| Industrials 6.7% | |||||||||||||||||||

| 3M Company | 184,207 | 12,968,173 | |||||||||||||||||

| Alaska Air Group, Inc. (a) | 9,800 | 363,874 | |||||||||||||||||

| American Power Conversion | 43,400 | 732,592 | |||||||||||||||||

| AMR Corporation (a) | 44,800 | 985,600 | |||||||||||||||||

| Apogee Enterprises, Inc. | 7,400 | 106,338 | |||||||||||||||||

| Avery Dennison Corporation | 26,400 | 1,547,832 | |||||||||||||||||

| Baldor Electric Company | 7,000 | 207,200 | |||||||||||||||||

| Banta Corporation | 6,050 | 213,747 | |||||||||||||||||

| Brady Corporation, Class A | 12,000 | 405,120 | |||||||||||||||||

| CLARCOR, Inc. | 12,900 | 366,747 | |||||||||||||||||

| Cooper Industries, Inc., Class A | 22,900 | 1,973,064 | |||||||||||||||||

| Cummins, Inc. | 11,600 | 1,357,200 | |||||||||||||||||

| Deere & Company | 57,700 | 4,187,289 | |||||||||||||||||

| Deluxe Corporation | 11,200 | 190,400 | |||||||||||||||||

| Donaldson Company, Inc. | 16,900 | 555,841 | |||||||||||||||||

16

Domini Social Equity Trust / Portfolio of Investments (Continued)

July 31, 2006

| Security | Shares | Value | ||||||||||||||

| Industrials (Continued) | ||||||||||||||||

| Donnelley (R.R.) & Sons Company | 53,700 | $ | 1,567,503 | |||||||||||||

| Emerson Electric Company | 100,100 | 7,899,892 | ||||||||||||||

| Energy Conversion Devices (a) | 8,100 | 272,565 | ||||||||||||||

| Fastenal Company | 30,800 | 1,095,556 | ||||||||||||||

| FedEx Corporation | 74,600 | 7,811,366 | ||||||||||||||

| GATX Corporation | 12,600 | 493,794 | ||||||||||||||

| Graco, Inc. | 17,152 | 673,902 | ||||||||||||||

| Grainger (W.W.), Inc. | 18,900 | 1,173,501 | ||||||||||||||

| Granite Construction Incorporated | 8,225 | 357,705 | ||||||||||||||

| Herman Miller, Inc. | 17,300 | 491,493 | ||||||||||||||

| HNI Corporation | 12,600 | 511,686 | ||||||||||||||

| Hubbell Incorporated, Class B | 15,060 | 707,820 | ||||||||||||||

| Ikon Office Solutions | 32,800 | 452,968 | ||||||||||||||

| Illinois Tool Works, Inc. | 101,900 | 4,659,887 | ||||||||||||||

| JetBlue Airways Corporation (a) | 38,550 | 412,100 | ||||||||||||||

| Kadant Inc. (a) | 3,700 | 77,367 | ||||||||||||||

| Kansas City Southern Industries, Inc. (a) | 17,200 | 423,464 | ||||||||||||||

| Kelly Services, Inc. | 5,075 | 137,380 | ||||||||||||||

| Lawson Products, Inc. | 700 | 25,557 | ||||||||||||||

| Lincoln Electric Holdings, Inc. | 10,500 | 602,490 | ||||||||||||||

| Masco Corporation | 96,796 | 2,587,357 | ||||||||||||||

| Milacron, Inc. (a) | 12,633 | 10,991 | ||||||||||||||

| Monster Worldwide (a) | 31,500 | 1,260,000 | ||||||||||||||

| Nordson Corporation | 8,400 | 382,200 | ||||||||||||||

| Norfolk Southern Corporation | 101,500 | 4,407,130 | ||||||||||||||

| Pall Corp. | 31,100 | 811,088 | ||||||||||||||

| Pitney Bowes, Inc. | 54,300 | 2,243,676 | ||||||||||||||

| Robert Half International, Inc. | 42,600 | 1,378,536 | ||||||||||||||

| Ryder System, Inc. | 15,200 | 766,080 | ||||||||||||||

| Smith (A.O.) Corporation | 5,200 | 222,872 | ||||||||||||||

| Southwest Airlines Co. | 171,762 | 3,089,998 | ||||||||||||||

| SPX Corporation | 14,930 | 815,925 | ||||||||||||||

| Standard Register Company | 3,200 | 39,360 | ||||||||||||||

| Steelcase, Inc. | 13,300 | 195,377 | ||||||||||||||

| Tennant Company | 4,600 | 109,342 | ||||||||||||||

| Thomas & Betts Corporation (a) | 13,200 | 624,756 | ||||||||||||||

| Toro Company | 10,800 | 447,228 | ||||||||||||||

| Industrials (Continued) | ||||||||||||||||

| Trex Company, Inc. (a) | 2,600 | $ | 73,320 | |||||||||||||

| United Parcel Service, Inc., Class B | 265,159 | 18,272,106 | ||||||||||||||

| YRC Worldwide Inc. (a) | 14,780 | 587,948 | ||||||||||||||

| 94,334,303 | ||||||||||||||||

| Information Technology 18.4% | ||||||||||||||||

| 3Com Corporation (a) | 97,600 | 462,624 | ||||||||||||||

| Adaptec, Inc. (a) | 27,400 | 120,560 | ||||||||||||||

| ADC Telecommunications (a) | 29,228 | 357,458 | ||||||||||||||

| Adobe Systems Incorporated | 147,300 | 4,199,523 | ||||||||||||||

| Advanced Micro Devices, Inc. (a) | 120,000 | 2,326,800 | ||||||||||||||

| Advent Software, Inc. (a) | 4,200 | 131,124 | ||||||||||||||

| Analog Devices, Inc. | 88,600 | 2,864,438 | ||||||||||||||

| Andrew Corporation (a) | 39,300 | 332,085 | ||||||||||||||

| Apple Computer, Inc. (a) | 207,554 | 14,105,370 | ||||||||||||||

| Applied Materials, Inc. | 381,000 | 5,996,940 | ||||||||||||||

| Arrow Electronics, Inc. (a) | 30,200 | 853,452 | ||||||||||||||

| Autodesk, Inc. (a) | 57,600 | 1,964,736 | ||||||||||||||

| Automatic Data Processing, Inc. | 140,174 | 6,134,014 | ||||||||||||||

| BMC Software, Inc. (a) | 52,400 | 1,227,208 | ||||||||||||||

| CDW Corporation | 15,400 | 909,832 | ||||||||||||||

| Ceridian Corporation (a) | 35,700 | 857,157 | ||||||||||||||

| Cisco Systems, Inc. (a) | 1,489,158 | 26,581,470 | ||||||||||||||

| Coherent, Inc. (a) | 7,700 | 246,862 | ||||||||||||||

| Compuware Corporation (a) | 95,700 | 668,943 | ||||||||||||||

| Convergys Corp. (a) | 35,500 | 677,340 | ||||||||||||||

| Dell Inc. (a) | 554,794 | 12,027,934 | ||||||||||||||

| eBay Inc. (a) | 282,772 | 6,806,322 | ||||||||||||||

| Electronic Arts Inc. (a) | 74,300 | 3,500,273 | ||||||||||||||

| Electronic Data Systems Corporation | 125,600 | 3,001,840 | ||||||||||||||

| EMC Corporation (a) | 576,100 | 5,847,415 | ||||||||||||||

| Entegris, Inc. (a) | 20,000 | 189,000 | ||||||||||||||

| Gerber Scientific, Inc. (a) | 5,700 | 87,381 | ||||||||||||||

| Hewlett-Packard Company | 681,410 | 21,743,793 | ||||||||||||||

| Imation Corporation | 7,900 | 321,688 | ||||||||||||||

| Intel Corporation | 1,422,355 | 25,602,390 | ||||||||||||||

| Lexmark International Group, Inc. (a) | 25,600 | 1,383,680 | ||||||||||||||

17

Domini Social Equity Trust / Portfolio of Investments (Continued)

July 31, 2006

| Security | Shares | Value | ||||||||||||||||||||

| Information Technology (Continued) | ||||||||||||||||||||||

| LSI Logic Corporation (a) | 96,300 | $ | 789,660 | |||||||||||||||||||

| Lucent Technologies, Inc. (a) | 1,082,292 | 2,305,282 | ||||||||||||||||||||

| Merix Corporation (a) | 3,750 | 39,414 | ||||||||||||||||||||

| Micron Technology, Inc. (a) | 167,900 | 2,617,561 | ||||||||||||||||||||

| Microsoft Corporation | 2,142,810 | 51,491,724 | ||||||||||||||||||||

| Molex Incorporated | 35,646 | 1,130,691 | ||||||||||||||||||||

| National Semiconductor Corporation | 81,500 | 1,895,690 | ||||||||||||||||||||

| Novell, Inc. (a) | 62,500 | 405,625 | ||||||||||||||||||||

| Novellus Systems, Inc. (a) | 30,300 | 766,893 | ||||||||||||||||||||

| Palm Inc. (a) | 21,108 | 314,720 | ||||||||||||||||||||

| Paychex, Inc. | 81,500 | 2,785,670 | ||||||||||||||||||||

| Plantronics Inc. | 11,000 | 171,160 | ||||||||||||||||||||

| Polycom Inc. (a) | 21,700 | 481,740 | ||||||||||||||||||||

| Qualcomm, Inc. | 408,500 | 14,403,710 | ||||||||||||||||||||

| Red Hat, Inc. (a) | 39,200 | 928,256 | ||||||||||||||||||||

| Salesforce.com, Inc. (a) | 27,000 | 693,900 | ||||||||||||||||||||

| Sapient Corporation (a) | 19,800 | 95,040 | ||||||||||||||||||||

| Solectron Corporation (a) | 228,600 | 690,372 | ||||||||||||||||||||

| Sun Microsystems, Inc. (a) | 847,600 | 3,687,060 | ||||||||||||||||||||

| Symantec Corporation (a) | 254,600 | 4,422,402 | ||||||||||||||||||||

| Tektronix, Inc. | 20,400 | 556,308 | ||||||||||||||||||||

| Tellabs, Inc. (a) | 112,300 | 1,055,620 | ||||||||||||||||||||

| Texas Instruments, Inc. | 380,062 | 11,318,246 | ||||||||||||||||||||

| Xerox Corporation (a) | 225,400 | 3,175,886 | ||||||||||||||||||||

| Xilinx, Inc. | 82,800 | 1,680,012 | ||||||||||||||||||||

| 259,432,294 | ||||||||||||||||||||||

| Materials 1.8% | ||||||||||||||||||||||

| Air Products & Chemicals, Inc. | 54,400 | 3,477,792 | ||||||||||||||||||||

| Airgas, Inc. | 16,800 | 609,000 | ||||||||||||||||||||

| Aleris International, Inc. (a) | 7,900 | 323,426 | ||||||||||||||||||||

| Bemis Company, Inc. | 26,000 | 798,200 | ||||||||||||||||||||

| Cabot Corporation | 14,900 | 495,723 | ||||||||||||||||||||

| Calgon Carbon Corporation | 10,100 | 61,206 | ||||||||||||||||||||

| Caraustar Industries, Inc. (a) | 7,200 | 50,832 | ||||||||||||||||||||

| Crown Holdings, Inc. (a) | 41,700 | 694,722 | ||||||||||||||||||||

| Ecolab, Inc. | 43,900 | 1,890,773 | ||||||||||||||||||||

| Fuller (H.B.) Company | 7,300 | 291,854 | ||||||||||||||||||||

| Materials (Continued) | ||||||||||||||||||||||

| Lubrizol Corporation | 16,700 | $ | 714,259 | |||||||||||||||||||

| MeadWestvaco Corp. | 44,212 | 1,154,817 | ||||||||||||||||||||

| Minerals Technologies, Inc. | 5,000 | 253,100 | ||||||||||||||||||||

| Nucor Corporation | 76,193 | 4,051,182 | ||||||||||||||||||||

| Praxair, Inc. | 79,200 | 4,343,328 | ||||||||||||||||||||

| Rock-Tenn Company, Class A | 7,800 | 134,082 | ||||||||||||||||||||

| Rohm & Haas Company | 35,987 | 1,659,720 | ||||||||||||||||||||

| Schnitzer Steel Industries Inc., Class A | 5,300 | 179,670 | ||||||||||||||||||||

| Sealed Air Corporation | 20,300 | 958,972 | ||||||||||||||||||||

| Sigma-Aldrich Corporation | 16,700 | 1,160,650 | ||||||||||||||||||||

| Sonoco Products Company | 24,645 | 801,702 | ||||||||||||||||||||

| Valspar Corporation | 25,300 | 623,139 | ||||||||||||||||||||

| Wausau-Mosinee Paper Corporation | 12,800 | 156,672 | ||||||||||||||||||||

| Wellman, Inc. | 4,400 | 13,377 | ||||||||||||||||||||

| Worthington Industries, Inc. | 17,100 | 349,182 | ||||||||||||||||||||

| 25,247,380 | ||||||||||||||||||||||

| Telecommunication Services 6.1% | ||||||||||||||||||||||

| AT&T Inc. | 950,667 | 28,510,503 | ||||||||||||||||||||

| BellSouth Corporation | 441,979 | 17,312,317 | ||||||||||||||||||||

| Citizens Communications Company | 80,667 | 1,034,959 | ||||||||||||||||||||

| Sprint Corp. – FON Group | 727,799 | 14,410,420 | ||||||||||||||||||||

| Telephone and Data Systems, Inc. | 24,900 | 1,017,414 | ||||||||||||||||||||

| Verizon Communications | 712,622 | 24,100,876 | ||||||||||||||||||||

| 86,386,489 | ||||||||||||||||||||||

| Utilities 1.0% | ||||||||||||||||||||||

| AGL Resources, Inc. | 19,400 | 756,988 | ||||||||||||||||||||

| Cascade Natural Gas Corporation | 2,900 | 75,168 | ||||||||||||||||||||

| Cleco Corporation | 12,200 | 301,584 | ||||||||||||||||||||

| Energen Corporation | 18,300 | 779,946 | ||||||||||||||||||||

| Equitable Resources, Inc. | 30,000 | 1,080,300 | ||||||||||||||||||||

| IDACORP, Inc. | 10,600 | 395,168 | ||||||||||||||||||||

| KeySpan Corporation | 43,600 | 1,755,772 | ||||||||||||||||||||

| MGE Energy, Inc. | 5,100 | 165,648 | ||||||||||||||||||||

18

Domini Social Equity Trust / Portfolio of Investments (Continued)

July 31, 2006

| Security | Shares | Value | ||||||||||||||

| Utilities (Continued) | ||||||||||||||||

| National Fuel Gas Company | 21,100 | $ | 783,654 | |||||||||||||

| NICOR, Inc | 10,300 | 451,346 | ||||||||||||||

| NiSource, Inc. | 65,447 | 1,488,919 | ||||||||||||||

| Northwest Natural Gas Company | 6,500 | 246,805 | ||||||||||||||

| Ormat Technologies Inc. | 1,800 | 66,583 | ||||||||||||||

| OGE Energy Corporation | 22,600 | 855,410 | ||||||||||||||

| Peoples Energy Corporation | 9,400 | 396,774 | ||||||||||||||

| Utilities (Continued) | ||||||||||||||||

| Pepco Holdings, Inc. | 46,800 | $ | 1,146,600 | |||||||||||||

| Questar Corporation | 21,300 | 1,887,180 | ||||||||||||||

| Southern Union Company | 24,421 | 662,786 | ||||||||||||||

| WGL Holdings | 11,200 | 336,336 | ||||||||||||||

| 13,632,967 | ||||||||||||||||

| Total Investments — 99.6% | ||||||||||||||||

| (Cost $1,119,886,958)(b) | 1,401,367,890 | |||||||||||||||

| Other Assets, less liabilities — 0.4% | 6,252,996 | |||||||||||||||

| Net Assets — 100.0% | $ | 1,407,620,886 | ||||||||||||||

(a)

Non-income producing security.

(b)

The aggregate cost for federal income tax purposes is $1,232,086,974. The aggregate gross unrealized appreciation is $266,776,364 and the aggregate gross unrealized depreciation is $97,495,448, resulting in net unrealized appreciation of $169,280,916.

Copyright in the Domini 400 Social IndexSM is owned by KLD Research & Analytics, Inc., and the Index is reproduced here by permission. No portion of the Index may be reproduced or distributed by any means or in any medium without the express written consent of the copyright owner.

SEE NOTES TO FINANCIAL STATEMENTS

19

Domini European Social Equity Portfolio

Performance Commentary

From its inception on October 3, 2005, through July 31, 2006, the Domini European Social Equity Portfolio (Class A shares) returned 24.76%, excluding sales charges, while the Morgan Stanley Capital International Europe Index (MSCI Europe) returned 18.59%.

The Fund's share price is denominated in U.S. dollars and generally will be exposed to European currency movements. In addition to other risks, the Fund will benefit when European currencies strengthen against the dollar and will be hurt when European currencies weaken against the dollar.

European stocks turned in strong performance for the period from October 3, 2005, through July 31, 2006. The MSCI Europe index was up 11.05% in European currency terms and 18.59% in U.S. dollar terms. The broader international MSCI World index was up 8.29% in international currency terms and 10.75% in U.S. dollar terms.

The European economy grew at a gradually increasing rate in the second half of 2005. By the second quarter of 2006, economists expected the economy to grow at its fastest rate since 2000. Unemployment declined to 7.8% in the euro zone. The European Commission's index of economic sentiment increased to its highest level since March 2001. In the first quarter, GDP growth increased from 1.7% to 1.9% in the euro zone, and increased in the United Kingdom to 2.3%.

To curb inflationary pressure, the European Central Bank raised interest rates 0.25% in June, to 2.75%, while the Bank of England left interest rates at 4.50%. (In early August, the Bank of England increased interest rates by 0.25%, and the European Central Bank passed its third 0.25% increase of the calendar year.) With the U.S. and Japan raising rates as well, the world's three largest economies were in a ‘‘tightening’’ cycle. Higher interest rates were expected to increase borrowing costs, reducing corporate and consumer spending, and to increase the cost of financing, a major driver of acquisition- and merger-driven restructuring. Europe's mergers and acquisitions activity totaled more than $400 billion in the first quarter of 2006, more than twice as much as in the first quarter of the previous year. Although European companies increased their operating margins to 11% in 2005, equaling their peak levels in 2000, increased corporate costs may lower these margins.

The Fund's performance was helped in part by its underweighting to the energy sector and its overweighting to financials. The Fund was also helped by its overweighting to Arcelor (France: Materials), Schering (Germany: Pharmaceuticals and Biotechnology), and Fiat (Italy: Automobiles).

The Fund's performance was hurt in part by its overweighting to the consumer discretionary sector and its underweighting to materials. The

20

Fund's performance was hurt in particular by its overweighting to Dampskibssel Torm (Denmark: Energy), Arriva (United Kingdom: Transportation), and Seat Pagine (Italy: Media).

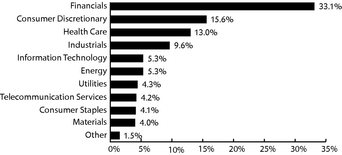

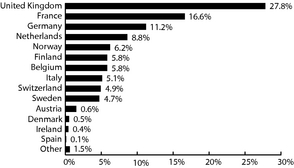

The Domini European Social Equity Portfolio invests in the Domini European Social Equity Trust. The table and the bar chart below provide information as of July 31, 2006, about the ten largest holdings of the Domini European Social Equity Trust and its portfolio holdings by industry sector and by country:

Ten Largest Holdings

| COMPANY | % OF NET ASSETS | COMPANY | % OF NET ASSETS | ||||||||

| GlaxoSmithKline | 3.89 | Norsk Hydro | 2.78 | ||||||||

| Sanofi-Aventis | 3.50 | National Grid | 2.73 | ||||||||

| ING Groep | 3.37 | Statoil | 2.55 | ||||||||

| BNP Paribas | 3.18 | KBC Groupe | 2.38 | ||||||||

| Société Générale | 2.93 | Muenchener Rueckver | 2.34 |

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS)

PORTFOLIO HOLDINGS BY COUNTRY (% OF NET ASSETS)

The holdings mentioned above are described in the Domini European Social Equity Trust's Portfolio of Investments at July 31, 2006, included herein. The composition of the Trust's portfolio is subject to change.

Domini European Social Equity Portfolio — Performance Commentary 21

| Total Return Since Inception (10/3/05) | |||||

| Domini European Social Equity Portfolio | 18.83%* | ||||

| MSCI Europe | 18.59% | ||||

Past performance is no guarantee of future results. The Fund's returns quoted above represent past performance after all expenses. Economic and market conditions change, and both will cause investment return, principal value, and yield to fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, call 1-800-582-6757 or visit www.domini.com. A 2.00% redemption fee is charged on sales or exchanges of shares made less than 60 days after the settlement of purchase or acquisition through exchange, with certain exceptions. Performance data quoted above does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund's prospectus for further information.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini European Social Equity Portfolio is based on the Fund's net asset values and assumes all dividends and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money. Certain fees payable by the Fund were waived during the period, and the Fund's average annual total returns would have been lower had these not been waived.

The Morgan Stanley Capital International Europe (MSCI Europe) is an unmanaged index of common stocks. Investors cannot invest directly in the MSCI Europe.

* Includes maximum sales charge of 4.75%

This material must be preceded or accompanied by the Fund's current prospectus. DSIL Investment Services LLC, Distributor. 09/06

22 Domini European Social Equity Portfolio — Performance Commentary

DOMINI EUROPEAN SOCIAL EQUITY PORTFOLIO

EXPENSE EXAMPLE

As a shareholder of the Domini European Social Equity Portfolio, you incur two types of costs:

•

Transaction costs such as sales charges (loads) on purchases and redemption fees deducted from any redemption or exchange proceeds if you sell or exchange shares of the Fund after holding them less than 60 days

•

Ongoing costs, including management fees, distribution (12b-1) fees, and other Fund expenses

This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The example is based on an investment of $1,000 invested on February 1, 2006, and held through July 31, 2006.

Actual Expenses

The line of the table captioned ‘‘Actual Expenses’’ below provides information about actual account value and actual expenses. You may use the information in this line, together with the amount invested, to estimate the expenses that you paid over the period as follows:

•

Divide your account value by $1,000.

•

Multiply your result in step 1 by the number in the first line under the heading ‘‘Expenses Paid During Period’’ in the table.

•

The result equals the estimated expenses you paid on your account during the period.

23

Hypothetical Expenses

The second line of the tables below provides information about hypothetical account values and hypothetical expenses based on the Fund's actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund's return. The hypothetical account values and expenses may not be used to estimate actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical example that appears in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges and redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Domini European Social Equity Portfolio | Beginning Account Value as of 2/1/2006 | Ending Account Value as of 7/31/2006 | Expenses Paid During Period* 2/1/2006 − 7/31/2006 | ||||||||||||||||||||

| Actual Expenses | $ | 1,000.00 | $ | 1,112.30 | $ | 8.38 | |||||||||||||||||

| Hypothetical Expenses (5% return before expenses) | $ | 1,000.00 | $ | 1,016.86 | $ | 8.00 | |||||||||||||||||

*

Expenses are equal to the Fund's annualized expense ratio of 1.60%, multiplied by average account value over the period, multiplied by 181, and divided by 365. The example reflects the aggregate expenses of the Fund and the Domini European Social Equity Trust, the underlying portfolio in which the Fund invests.

24 Domini European Social Equity Portfolio — Expense Example

Domini European Social Equity Portfolio

Social Profiles

Employee Relations

European workers often enjoy impressive employee benefits not only because of the generosity of their employers but because of government policy. While two weeks' vacation is a common standard in the United States, vacations in Europe are frequently six weeks and are often mandated by national law. The 35-hour work week adopted over the past several years in France and Germany has proven both popular with unions and controversial in management and political circles.

In France, companies are required to share profits with employees, and in Germany they are required to provide workers representation on corporate supervisory boards. Unionization of workers is often negotiated on a regional or national basis, rather than company by company. In countries where laws make it difficult for companies to lay off employees, training employees to handle new roles has become a higher priority than in the U.S.

Below, we profile three companies in the portfolio of the Domini European Social Equity Portfolio where the commitment to employees goes beyond the benefits required by law.

Lufthansa

Country: Germany

Industry: Transportation

Airlines such as Lufthansa were hard-hit after the terrorist attacks of September 11, 2001. Unlike airlines that responded by slashing their payroll, Lufthansa took steps to avoid laying off employees.

According to the company, cost-cutting measures began at the top, as Lufthansa's board of management decided to cut its own remuneration by 10%. Many managers and employees whose salaries were not covered by collective pay agreements took temporary cuts in their base salary. Those who were covered by such agreements negotiated other measures to cut costs, such as part-time work and reducing their unused vacation days, overtime, and extra work. The company reported that more than 400 employees agreed to take unpaid leave to help protect their fellow employees' jobs.

In addition to a commitment to ethnic and gender diversity, Lufthansa has sought out handicapped applicants for its call center in Berlin, and established a program called HR Development Over 40 to address the needs of older employees. A campaign called Flexibility for Fathers, launched in 2001, is aimed at motivating male employees to take a more active role in raising children.

25

Marks & Spencer

Country: United Kingdom

Industry: Retailing

In April 2006, as the British retailer Marks & Spencer was enjoying a resurgence in profits after several difficult years, the company decided to reward its employees. More than 50,000 shop-floor workers received bonuses of up to £500 with their July paychecks, and thousands of managers received more than £6,000. The payout totaled £70 million, and the company said it might award similar bonuses at the end of the year.

Through an innovative program called Marks & Start, the company reports that it helps disadvantaged people — single parents and people who are handicapped, homeless, or young and unemployed — to join the workforce, many of them as new Marks & Spencer employees. Launched in 2004, the program offers 2,500 work placements per year.

According to the company, participants are placed for two or four weeks in a Marks & Spencer store or office in the United Kingdom or Ireland. Each participant is assigned an employee mentor and is given travel expenses, free meals in store cafes, uniforms when necessary, and references when requested. More than 30% of the participants have been hired within 13 weeks of their placement, either with Marks & Spencer or another employer. Of 319 homeless people who have taken part in the program, 130 have found permanent employment, including 76 hired by Marks & Spencer.

Nokia

Country: Finland

Industry: Technology Hardware & Equipment

Jorma Ollila, who became CEO of Nokia in 1992, redirected the company from heavy machinery to the emerging field of cell phones. Ollila also built one of the world's biggest saunas, where Nokia employees reportedly hold regular business meetings to this day.

Although few of Nokia's other employee practices are as unusual, the company offers an impressive range of benefits and programs. Incentive programs for employees include rewards for individuals, teams, projects or programs, and a stock option plan. The company offers employees medical checkups, counseling, and insurance programs, as well as access to sporting, social, and cultural activities. Services aimed at improving work/life balance include telecommuting, flexible working hours, sabbaticals, and study leaves.

26 Domini European Social Equity Portfolio — Social Profiles

Each year an outside party conducts an employee survey called ‘‘Listening to You,’’ which covers topics such as employee motivation and involvement, leadership, and training and development. The ‘‘Ask HR’’ feature on Nokia's intranet allows employees to ask questions about employee practices, even anonymously, and receive a prompt and openly available response.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

Unlike other mutual funds, the Domini European Social Equity Portfolio seeks to achieve its investment objective by investing all of its investable assets in a separate portfolio with an identical investment objective called the Domini European Social Equity Trust (DESET).The companies discussed above can be found in the DESET's Portfolio of Investments at July 31, 2006, included herein. The composition of the DESET's portfolio is subject to change.

The preceding profiles should not be deemed an offer to sell or a solicitation of an offer to buy the stock of any of the companies noted, or a recommendation concerning the merits of any of these companies as an investment.

Domini European Social Equity Portfolio — Social Profiles 27

Domini European Social Equity Trust

Portfolio of Investments

July 31, 2006

| Country/ Security | Industry | Shares | Value | ||||||||||||||||||||||

| Austria – 0.6% | |||||||||||||||||||||||||

| voestalpine AG | Materials | 2,395 | $ | 353,501 | |||||||||||||||||||||

| 353,501 | |||||||||||||||||||||||||

| Belgium – 5.8% | |||||||||||||||||||||||||

| Bekaert SA | Capital Goods | 3,299 | 302,490 | ||||||||||||||||||||||

| Belgacom SA | Telecommunication Services | 12,993 | 438,236 | ||||||||||||||||||||||

| Fortis Group | Diversified Financials | 32,273 | 1,145,772 | ||||||||||||||||||||||

| Kbc Groep NV | Banks | 12,222 | 1,330,433 | ||||||||||||||||||||||

| 3,216,931 | |||||||||||||||||||||||||

| Denmark – 0.5% | |||||||||||||||||||||||||

| Danske Bank A/S | Banks | 7,856 | 300,958 | ||||||||||||||||||||||

| 300,958 | |||||||||||||||||||||||||

| Finland – 5.8% | |||||||||||||||||||||||||

| Kesko OYJ B shs | Food & Staples Retailing | 18,876 | 783,602 | ||||||||||||||||||||||

| Nokia Oyj | Technology Hardware & Equipment | 64,241 | 1,273,167 | ||||||||||||||||||||||

| Sampo Ins Co Ltd A shs | Insurance | 26,702 | 503,299 | ||||||||||||||||||||||

| Tietoenator OYJ | Software & Services | 10,560 | 251,466 | ||||||||||||||||||||||

| Uponor Oyj | Capital Goods | 16,001 | 435,960 | ||||||||||||||||||||||

| 3,247,494 | |||||||||||||||||||||||||

| France – 16.6% | |||||||||||||||||||||||||

| Assurances Generales de France | Insurance | 8,014 | 967,480 | ||||||||||||||||||||||

| BNP Paribas | Banks | 18,291 | 1,778,665 | ||||||||||||||||||||||

| Ciments Francais SA | Materials | 3,565 | 582,333 | ||||||||||||||||||||||

| CNP Assurances | Insurance | 7,090 | 674,521 | ||||||||||||||||||||||

| Natexis Banques Populaires | Banks | 2,486 | 608,804 | ||||||||||||||||||||||

| Neopost SA | Technology Hardware & Equipment | 5,680 | 617,937 | ||||||||||||||||||||||

| Sanofi-Aventis | Pharma, Biotech & Life Sciences | 20,627 | 1,959,758 | ||||||||||||||||||||||

| Schneider Electric SA | Capital Goods | 1,686 | 173,204 | ||||||||||||||||||||||

| Societe Generale Paris | Banks | 11,005 | 1,640,343 | ||||||||||||||||||||||

| Vivendi SA | Media | 8,612 | 291,350 | ||||||||||||||||||||||

| 9,294,395 | |||||||||||||||||||||||||

| Germany – 11.2% | |||||||||||||||||||||||||

| Adidas AG | Consumer Durables & Apparel | 2,992 | 139,442 | ||||||||||||||||||||||

| Beiersdorf | Household & Personal Products | 10,699 | 563,072 | ||||||||||||||||||||||

| Celesio AG | Pharma, Biotech & Life Sciences | 21,160 | 988,322 | ||||||||||||||||||||||

| Continental | Automobiles & Components | 4,368 | 445,938 | ||||||||||||||||||||||

| Deutsche Lufthansa Reg | Transportation | 46,323 | 864,854 | ||||||||||||||||||||||

| Fresenius AG | Health Care Equipment & Services | 4,693 | 741,435 | ||||||||||||||||||||||

| Hochtief AG | Capital Goods | 2,719 | 143,582 | ||||||||||||||||||||||