UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-21653

DOMINI ADVISOR TRUST

(Exact Name of Registrant as Specified in Charter)

536 Broadway, 7th Floor, New York, New York 10012

(Address of Principal Executive Offices)

Amy Domini Thornton

Domini Social Investments LLC

536 Broadway, 7th Floor

New York, New York 10012

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code: 212-217-1100

Date of Fiscal Year End: July 31

Date of Reporting Period: July 31, 2007

Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 follows.

TABLE OF CONTENTS

| 2 |

| Letter from the President |

| 4 |

| Domini News |

| 5 |

| The Way You Invest Matters: Climate Change |

| 10 |

| The Way You Invest Matters: Activism |

|

| Fund Performance and Holdings | |

| 11 |

| Economic and Market Background |

| 14 |

| Domini Social Equity Portfolio |

| 20 |

| Domini European Social Equity Portfolio |

| 27 |

| Domini PacAsia Social Equity Portfolio |

| 35 |

| Domini EuroPacific Social Equity Portfolio |

| 44 |

| Expense Example |

| 47 |

| Financial Statements |

|

| Domini Social Equity Trust | |

|

| Domini European Social Equity Trust | |

|

| Domini PacAsia Social Equity Trust | |

|

| Domini EuroPacific Social Equity Trust | |

|

| Report of Independent Registered Public Accounting Firm | |

| 62 |

| Financial Statements |

|

| Domini Social Equity Portfolio | |

|

| Domini European Social Equity Portfolio | |

|

| Domini PacAsia Social Equity Portfolio | |

|

| Domini EuroPacific Social Equity Portfolio | |

|

| Report of Independent Registered Public Accounting Firm | |

| 79 |

| Board of Trustees’ Consideration of Management and Submanagement Agreements |

| 85 |

| Trustees and Officers |

| 90 |

| Proxy Voting Information |

| 90 |

| Quarterly Portfolio Schedule Information |

THE WAY YOU INVEST MATTERS |

LETTER FROM THE PRESIDENT

Dear Fellow Shareholders:

These have been twelve difficult months for many Americans, offering reasons for worry but also opportunities to make a difference. The Iraq war drags on, and even its supporters have become discouraged. Extreme weather conditions — including a tornado that touched down a mere six miles from our New York offices — highlight a climate crisis driven by our dependence on oil. The cost of filling our gas tanks has gone so high that people go into debt just to pay their bills. More and more families face foreclosure, in many cases because a deceptive financing company has sold them a mortgage they can’t afford.

Our highways are collapsing, just as the levees failed in Louisiana. Billions of dollars once invested in America’s infrastructure continue to pour into war, and into corporate welfare for pharmaceutical, agricultural, and weapons companies. Government functions have been transferred into corporate hands, often via no-bid contracts that prioritize private profit over public good.

So where do we see opportunities? Two recent trends show promise, and both connect directly to the work that you and I do as social investors.

First, some leading corporations are coming to realize their responsibility to people and the planet. Global warming presents an interesting example. Here in the U.S., some companies are far ahead of government, which has so far utterly failed to play its part. Several years back, when Domini began to talk to companies about climate change, it seemed unlikely that corporations — including many that don’t meet Domini’s investment standards — would lobby for regulation of carbon. But today many of them do. Social investors played a crucial role here, and in this report we highlight ways in which your investments matter in seeking solutions to climate change.

Second, strong global markets have in recent years been driven largely by developments beyond our borders. What baby boomers did for the 20th century American economy, the emerging economies are now doing for global growth and prosperity.

The widely touted “three billion new consumers” in emerging economies have created a huge new market for products and services that we in the West now take for granted: cell phones, potable water, transportation and energy systems. New technologies offer these countries a chance to develop faster, more efficiently, and with less environmental damage than we experienced in the West. Yet we find ourselves at a fork in the road, as these emerging populations grow so quickly that the future cannot come fast enough. They demand oil and coal, paper, timber, and weapons; they foul their waters with mercury and cover their exports with lead paint.

Our challenge, as social investors, is to emphasize the future while managing the present. Our role, internationally, is the same as it has been

2 |

|

THE WAY YOU INVEST MATTERS |

in the U.S.: telling companies, through our investments, that they must behave responsibly toward the environment and communities that are the foundation of their prosperity.

We at Domini are proud of our decision to invest globally. Our funds now enable us to communicate your values of fairness and sustainability to companies around the world, and to make an impact on a global scale. Corporations need to know that there are investors who believe that responsibility to people and the planet matter just as much as rewards for executives and Wall Street. Together, we are perfectly positioned to deliver that crucial message.

Thank you, as always, for your decision to invest with us.

Very truly yours,

Amy Domini

amy@domini.com

KEEP IN TOUCH WITH DOMINI |

If you’re a Domini shareholder, you receive a report like this twice each year. But your dollars are working for change all year long, and now there’s a great way to stay in touch. When you sign up for Domini Updates, here’s what you’ll get:

• | Our email newsletter Investing Matters, with convenient links to quarterly Social Impact Updates and fund commentaries. |

• | Domini Action Alerts, giving you an opportunity to speak out on issues from child labor to global warming. (More than 400 people responded to our recent Action Alert asking the SEC to preserve ordinary investors’ right to file shareholder resolutions. We know our voices were heard, as the SEC cited Domini’s email in its resulting proposal.) |

To get Domini Updates, visit www.domini.com and sign up on our home page.

We will not “spam” you or overwhelm you with emails, and we will never sell or rent your email address to anyone, for any reason. (Please visit our website for more information about our Privacy Policy.) And you can, of course, unsubscribe from Domini Updates at any time.

If you invest directly with Domini, you can also sign up for paperless E-Delivery of your statements and reports — just log into your account and select E-Delivery from the “Account Maintenance” drop-down menu. If you invest through a financial advisor, brokerage firm, or employer-sponsored retirement plan, why not ask your advisor or plan sponsor how to receive your documents electronically? It can reduce your carbon footprint, save trees, and unclutter your life, all with just a few strokes of your keyboard!

| 3 |

THE WAY YOU INVEST MATTERS |

DOMINI NEWS

Protecting Shareholders’ Voices: On behalf of our investors, Domini has filed or co-filed about 150 shareholder resolutions since 1994, and voted in favor of hundreds more — helping us convince companies to report greenhouse gas emissions, publish sustainability reports, disclose political contributions, prohibit discrimination against gay and lesbian employees, and more.

In late July, a sharply divided Securities and Exchange Commission proposed two rules governing the nomination of corporate directors. The SEC also raised questions that could eliminate or severely impair shareholders’ ability to file resolutions if they become the basis of a formal rule. In the run-up to the SEC’s July meeting, more than 400 people had responded to a Domini Action Alert in defense of shareholder rights. Their comments gained the attention of the SEC, which referred to them in a footnote to its proposal.

This important issue remains unresolved, and we continue to work with our colleagues around the world to protect these critical tools for corporate accountability. We encourage you to visit www.domini.com to sign up for email updates, including future Action Alerts on matters impacting corporate accountability and social investing.

Domini Votes for Change: A recent study published at www.fundvotes.com highlighted the wide gap in the use of proxy votes between “mainstream” and socially responsible mutual funds. Mainstream fund companies examined in the study voted for only 13% of the social and environmental proxy resolutions presented to them, including resolutions on global warming. Socially responsible fund families, as a group, voted for 83% of the resolutions on average, and Domini voted for 94% of them. Domini was one of four mutual fund managers rated “most activist” in the most recent assessment by The Corporate Library, a respected information source on corporate governance.

New International Funds Gain Assets: Just seven months after their launch, the Domini PacAsia Social Equity Trust and Domini EuroPacific Social Equity Trust have over $40 million in combined assets under management. These new funds empower shareholders to bring about social and environmental change on a global scale, drawing companies around the world into dialogue on such issues as global warming, sweatshop labor, and product safety.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

4 |

|

THE WAY YOU INVEST MATTERS |

THE WAY YOU INVEST MATTERS: CLIMATE CHANGE

Climate change has become one of the pressing issues — perhaps the pressing issue — of our time.

With a clear scientific consensus about global warming and its human causes, research and discussion are focusing not on proving that climate change is occurring, but on understanding its consequences and developing ways to reverse it. These consequences are in the news virtually every day: from receding glaciers and melting polar ice to accelerating desertification, from changing crop patterns to the increasing severity of storms. Clearly, urgent action is needed.

The scale of the threat will require change at many levels of our society and economy. Certainly, government will have to take a leading role, through regulation, tax policy, and technology investment. Individual action, too, will be crucial. Changing light bulbs, riding bikes, using mass transit or fuel-efficient cars, eating locally grown foods, turning down the heat in the winter or the air conditioning in the summer — all of these, when done by enough of us, can have an impact.

Corporations must address this crisis too. Big companies decide, in large part, what kinds of products will be made available to us — and how they are manufactured, how the raw materials are mined or harvested, how they are transported to market, and how they reenter the waste stream.

Through their investments, millions of ordinary working people are the ultimate owners of the world’s corporations. On climate change, as on other important issues of sustainability and fairness, we use our investment decisions and our voice as owners to encourage companies to clean up after themselves, to innovate, to reduce emissions, and to create solutions. In this report, we look at some of the ways in which your investments are making a difference on climate change.

Domini’s Response

In addressing the climate crisis, Domini brings to bear all of the tools of the social investor — applying thoughtful investment standards, conducting in-depth company research, engaging in direct dialogue with the companies we own, speaking out for investors on public policy — in an effort to maximize our shareholders’ impact.

Our investment process begins with an in-house research team, which uses our Global Investment Standards to compile a list of eligible investments. Our subadvisors then use that list as the basis for selecting securities and constructing portfolios. (Details on Domini’s standards are available at www.domini.com.) Using a top-down/bottom-up approach, we evaluate how industries, specific business lines or “subindustries,” and finally individual companies contribute to climate change.

5

THE WAY YOU INVEST MATTERS |

Within the energy sector, for instance, we tend to favor natural gas (a relatively cleaner “transitional” fuel) over oil (a major contributor to climate change) or nuclear power (which we exclude from our portfolios due to concerns about waste disposal and nuclear weapons proliferation). Of course, alternative energy sources like wind or solar are vastly preferable to any of those, and our investment standards lead us to seek out companies like the Japanese technology firm Kyocera, which has shown a commitment to solar energy.

Key factors for a climate change evaluation can include evaluation of greenhouse gas emission reduction strategies, energy efficiency, use of renewable energy, forestry or recycling practices, and development of products that empower consumers to reduce their carbon footprint. In the energy sector, for example, the Norwegian company Statoil has addressed climate change through carbon sequestration and the use of emissions trading, while the U.S. energy companies Unit and XTO Energy derive most of their revenue fr om natural gas production and distribution. Each of these companies meets our standards for investment. Meanwhile, many of the energy companies that are common in “mainstream” mutual funds — notably, much of “Big Oil” — are excluded from Domini portfolios.

When Domini analysts evaluate a company’s sustainability record, they need information. Because social investors like ourselves are asking questions, thousands of companies now produce reports on the long-term sustainability of their business activities. It’s a business truism that what gets reported gets measured, and what gets measured gets managed. Often, a company that agrees to report its carbon emissions begins trying to reduce the emission that they now have to report.

This impact continues when we engage companies directly. In 2006, working with the Carbon Disclosure Project, we wrote to more than 200 U.S. and European companies asking them to disclose their greenhouse gas emissions and climate change policies. Domini’s efforts over the years have been credited with significant improvements in the responsiveness of U.S. companies to this global survey. After we filed shareholder resolutions and engaged them in dialogue, three oil and gas producers held by the Domini Social Equity Portfolio — Apache, Anadarko, and Devon Energy — agreed to begin public reporting about their response to climate change. Working together with other social investors, public and private pension funds, and environmental organizations, we have seen concrete change in corporate behavior taking place.

Domini has taken a lead role in pressing companies to adopt more sustainable forestry policies, as part of our overall approach to climate change. Kimberly-Clark — the manufacturer of Kleenex — recently agreed to publicly state a preference for wood fiber certified by the Forest Stewardship Council (FSC) after two years of dialogue with Domini. This signal to the marketplace, from the world’s largest tissue manufacturer, should reduce demand for wood from endangered forests, and increase demand for responsibly harvested wood. The implications for climate change are enormous.

6 | The Way You Invest Matters: Climate Change |

THE WAY YOU INVEST MATTERS |

The climate crisis has no quick and easy solutions. Facing this challenge will require that thousands of corporations worldwide begin placing sustainability at the forefront of their business decisions. On your behalf, Domini is sending companies this message.

Focus on: Transportation

While climate change is an issue that we look at across all industries, for some it plays more of a key role than for others. Transportation, for instance, is one of the three largest contributors to global warming, accounting for more than 13% of the total impact. But within this industry, some subindustries have greater impact than others, and each has its particular set of challenges.

Because fuel is an important component of transportation costs, we believe that more energy-efficient companies are well positioned to both reduce carbon emissions and maximize their profitability.

Certain modes of transportation are preferable to others in terms of their impact on the climate. Shipping by sea and rail tends to be the most fuel-efficient means of transporting goods, while air freight and long-haul trucking are much more carbon-intensive. For long-haul people-moving, there are few practical alternatives to air travel, despite its substantial negative impact on global warming, but we look closely at the business models of airline companies to see which ones are trying to minimize their impact. In local and regional transportation, public transportation by rail or bus is generally preferable. Travel by car, meanwhile, is often the least fuel-efficient method of moving people.

Within this sector, the overall shape of Fund portfolios often reflects these preferences. In addition, within each sub-industry, we seek to identify companies that are developing innovative, efficient solutions to the industry’s pressing challenges. Here are some examples:

Public Transportation

Based in the U.K., Arriva provides bus and train service in nine European countries. The company reports that it reduces its environmental impact by using a range of fuels, including ultra-low-sulfur diesel and compressed natural gas, and is conducting trials of vegetable-oil fuel in its German rail operations. In March 2007, the company introduced what the company says is the world’s first hybrid double-decker bus in London. Arriva says that all its new buses comply with the latest environmental requirements, and that older buses have been retrofitted with cleaner engines.

Central Japan Railway owns and operates a high-speed train that links the cities of the “Tokaido” region — Tokyo, Nagoya, and Osaka — and provides conventional rail service. Japan’s Minister of Environment has reportedly praised the company’s aggressive introduction of energy- efficient railroad cars. According to the company, a cogeneration system at the company’s JR Central Towers facility uses exhaust heat from power

The Way You Invest Matters: Climate Change | 7 |

THE WAY YOU INVEST MATTERS |

generation to improve energy efficiency and reduce CO2 emissions. Solar panels generate electricity at its Kyoto station and its research facility in Komaki.

Airlines

Although it is hard to envision real progress in reducing the greenhouse gas effects of the airline industry, Air France stands out for its fuel efficiency initiatives. The company says it increases fuel efficiency by reducing the weight of onboard equipment, operating with optimally clean engines, and replacing some training flights with flight simulators. The Air France fleet is also younger than the industry average. By replacing Boeing 747s with newer 777-300s, the company reports that low-altitude hydrocarbon emissions are cut by 35%, carbon monoxide by 12%, and nitrogen oxides by 8%. Air France has spoken out for a worldwide system of emissions trading, and believes that mobile sources like aircraft should be added to the European Union’s emis sions trading system.

Automobiles

Although automobiles are a significant contributor to global warming, FIAT’s fleet is reportedly one of the most fuel-efficient in Europe. Fiat’s research effort, which by 2005, according to the company, included nearly 900 employees focusing exclusively on issues of energy, environment, and sustainability, has developed prototype hybrid and fuel-cell engines, and is developing a prototype hydrogen-fueled car. Fiat manufactures cars that run on bioethanol for use in Brazil, and its Panda Natural Power car runs on compressed natural gas.

By introducing high-efficiency hybrid versions of its most popular cars, like the Civic, the Japanese automaker Honda Motor has reportedly gained 31% of the world market share for hybrid vehicles. The company has announced that it will sell advanced diesel cars to meet California’s new emissions standards, and (like Fiat) bioethanol vehicles for the Brazilian market. Honda developed and has started to sell a next- generation fuel-cell car, which emits only water.

Delivery Services

United Parcel Service reported as of December 2006 that it operated a fleet of more than 10,000 low-emission and alternative-fuel vehicles worldwide. It measures its U.S. fuel consumption in terms of gallons used per package delivered, and operates one of the largest private fleets in the country to run on compressed natural gas. The company says that its flight planning system saved nearly $1 million in fuel each month in 2005.

Through its Driving Clean program, the Dutch delivery service TNT seeks to reduce the environmental impact of its fleet of vehicles. In addition to working with the Dutch government to retrofit vehicles with diesel particulate filters, the company is investing in technology that complies with Euro 5, an environmental standard that becomes compulsory in

8 | The Way You Invest Matters: Climate Change |

THE WAY YOU INVEST MATTERS |

November 2009. The company says it has built six filling stations that supply an additive called AdBlue, which reduces nitrogen oxides from exhaust, and in 2006 it bought 165 trucks that meet the Euro 5 standard. TNT reports that it is investigating the use of hybrid vehicles in Australia and Turkey, uses compressed natural gas in Berlin, and runs about 53 vehicles in Amsterdam on canola oil. In December 2006, it reportedly introduced a high-performance 7.5-metric-ton zero emission electric vehicle for use in London.

Unlike other mutual funds, the Domini Social Equity Portfolio, Domini European Social Equity Portfolio, Domini PacAsia Social Equity Portfolio, and Domini EuroPacific Social Equity Portfolio seek to achieve their investment objectives by investing all of their investable assets, respectively, in separate portfolios with identical investment objectives called the Domini Social Equity Trust (DSET), Domini European Social Equity Trust (DESET), Domini PacAsia Social Equity Trust (DASET), and Domini EuroPacific Social Equity Trust (DUSET). References to each Domini Fund include the applicable Domini Trust, unless the context otherwise requires.

The holdings discussed above can be found in the portfolios of the Domini Funds, included herein. The composition of the Funds’ portfolios is subject to change.

As of July 31, 2007, the companies discussed above were held in the portfolios of the following Domini Funds: Anadarko, Apache, Devon Energy, Kimberly-Clark, Unit, UPS, and XTO Energy were held by the Domini Social Equity Portfolio. Air France, Arriva, Fiat, Statoil, and TNT were held by the Domini European Social Equity Portfolio. Central Japan Railway, Honda Motor, and Kyocera were held by the Domini PacAsia Social Equity Portfolio. Air France, Central Japan Railway, Fiat, Honda Motor, Kyocera, Statoil, and TNT were held by the Domini EuroPacific Social Equity Portfolio.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The preceding profiles should not be deemed an offer to sell or a solicitation of an offer to buy the stock of any of the companies noted, or a recommendation concerning the merits of any of these companies as an investment.

The Way You Invest Matters: Climate Change | 9 |

THE WAY YOU INVEST MATTERS |

THE WAY YOU INVEST MATTERS: ACTIVISM

As a Domini shareholder, you make a difference in the world. By applying social and environmental standards to our holdings, Domini and its shareholders create accountability, encourage transparency, spur demand for more information, and reshape the way the world thinks about corporations and their role in our lives. By engaging in dialogue with the companies we invest in, filing shareholder resolutions, and actively voting our proxies, we make our voices heard on a wide range of issues. By investing in underserved communities, we enable people to buy homes, start businesses, and revitalize their neighborhoods, an important part of building a more fair and sustainable economy.

Here are a few recent highlights of Domini’s shareholder activism, which each year includes meetings with dozens of companies on a wide range of important issues. (For more information, visit our website, www.domini.com.)

Rights for Coffee Farmers: Over the past year, we expressed our strong concerns to Starbucks officials about their dispute with the government of Ethiopia over ownership of the names of its prime coffee-growing regions, culminating in a detailed letter to the CEO. We also helped enable representatives of Oxfam and Ethiopian coffee farmers to ask questions at the company’s annual meeting. In June, the company reversed its position, and signed a historic agreement acknowledging Ethiopian rights to these names, which should help Ethiopian farmers more effectively market their coffees, and ultimately capture their fair share of the profits. By participating in this engagement, we contribut ed to an important achievement for Ethiopian farmers by creating a more sustainable business model for this highly sought-after commodity.

Gender Diversity in Japan: Domini’s proxy voting guidelines require that when a company has an all-male board, we vote against the entire slate of directors. Among the 46 Japanese companies that we held, we voted against the board slate of all but one: Sony, which has one woman on its board.

A First in Europe: Domini filed its first shareholder resolution in Europe, with the British transportation company FirstGroup, on behalf of the Domini European Social Equity Portfolio and the Domini EuroPacific Social Equity Portfolio. The proposal, which addresses allegations of anti-union activity at a U.S. school bus subsidiary, was co-filed with labor unions and more than 140 FirstGroup employees. Domini’s participation was critical in allowing the unions to meet onerous British filing requirements. Our engagement with the company included a meeting with senior executives, including the CEO and chairman, in London.

10 |

|

FUND PERFORMANCE AND HOLDINGS

ECONOMIC AND MARKET BACKGROUND

United States Markets Financial markets in the U.S. were generally strong for the year ended July 31, 2007. The S&P 500 Index returned 16.13% and the bond market (as measured by the Lehman Brothers Intermediate Aggregate Index, or LBIA) returned 5.50%.

Stock market performance for the period was driven by corporate earnings and resilient consumer spending, sustained by reasonably strong employment. The Dow Jones Industrial Average passed 14,000 for the first time in mid-July — but the end of the month saw a sharp downturn caused by the crisis in the subprime mortgage market, a slowdown in housing, and a global tightening of credit.

American workers have now experienced five years of economic growth without a sustained increase in wages. American consumers are also being squeezed by increases in their fixed costs — including higher interest rates on their credit card and mortgage debt, and increased food, fuel, and healthcare costs.

The residential real estate market has cooled markedly over the past year. One result is the recent meltdown of the subprime mortgage market. Though subprime lending — home loans to borrowers who don’t qualify for standard mortgages — can make it possible for lower-income people to purchase their own homes, it is vulnerable to abusive “predatory lending” practices. The recent softening of the housing market, coinciding with the expiration of low “promotional” interest rates, has made it much more difficult for borderline borrowers to make ends meet, and foreclosure rates have risen sharply. Because many of these mortgages are “packaged” by Wall Street into mortgage-backed bonds, this development presents significant challenges for the bond market, and triggered the stock market’s late-July downturn, which continued beyond the end of the period.

The Federal Reserve, seeking to balance its goals of inflation control and economic growth, held the Fed funds rate steady at 5.25% through July 2007 (although market turmoil caused the Fed to lower its overnight discount rate in August). High oil and food prices continued to present a risk of inflation.

European Markets The European stock market had strong returns for the year ended July 31, 2007. In local currency terms, the MSCI Europe Index returned 19.56% for the year. Viewed in U.S. dollar terms, the MSCI Europe Index produced a total return of 28.27%, as the dollar continued to weaken against the euro and other currencies.

Underlying Europe’s strong markets for the year was accelerating economic growth. The German economy, the largest in Europe, grew

| 11 |

almost 3% in 2006, the fastest rate since 2000, and grew at a rate of more than 3% in early 2007, despite the impact of an increase to the value added tax. Consumer confidence has rebounded and unemployment has fallen, although many of the new jobs created in the past year have been temporary and lower paid.

The election in May of Nicolas Sarkozy to the French presidency reflects a view that change is needed in order to improve France’s economic performance, which has lagged that of Germany and the U.K. In June, Prime Minister Tony Blair was succeeded by Gordon Brown, the former Chancellor of the Exchequer. As chief economic policy maker in Blair’s cabinet, Brown held office during a period of low inflation, low interest rates, and low unemployment.

Economic indicators in the euro zone continue to be generally positive. Business confidence has remained high, while consumer confidence has weakened only slightly. Although June’s inflation rate was 1.9%, within the European Central Bank’s definition of price stability, the bank increased short-term interest rates for the second time in 2007, from 3.75% to 4.00%.

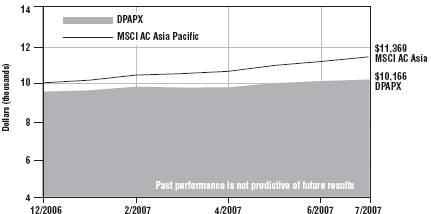

Asian Markets Asia-Pacific stock markets had strong returns for the period since the inception of the Domini PacAsia Social Equity Portfolio and Domini EuroPacific Social Equity Portfolio. For the period from December 27, 2006, through July 31, 2007, the MSCI All Country Asia Pacific Index returned 11.12% in local currency terms. Viewed in U.S. dollar terms, the index produced a total return of 13.69%.

Although Asian banks and major investors in Asia have little direct exposure to the U.S. market in subprime mortgages, analysts expressed concern that Asian markets could be hurt by the indirect effects of the crisis, such as a falling U.S. dollar or decreased U.S. demand for Asian products.

Japan, the region’s largest market, continues to enjoy its longest economic recovery since World War II, with the economy reportedly growing at a strong annual rate of 3.3% as of the first quarter of 2007. Surveys of manufacturers show that business confidence remains high as exporters benefit from the weak yen, which makes Japanese exports more competitive, and from strong demand in Asian markets.

One of the best-performing markets in the region in 2007 was China, fueled by a rapidly expanding economy that many believe may be overheating. Meanwhile, social and environmental concerns in China were widely reported, including severe air pollution, slave labor at Chinese mines and brick factories, and issues of product and food safety among Chinese exports.

Domini believes that concerned investors should — without loosening their social and environmental standards — seek out forward-looking

12 | Economic and Market Backgroud |

companies in China, stimulate dialogue about fair and sustainable business practices, and press companies whenever possible to improve their social and environmental performance. For our part, Domini will continue to encourage U.S. companies with business ties to China to use their influence to improve conditions.

Economic and Market Backgroud | 13 |

DOMINI SOCIAL EQUITY PORTFOLIO

PERFORMANCE COMMENTARY

For the year ended July 31, 2007, the Domini Social Equity Portfolio (the “Fund”) returned 14.69%, excluding sales charges, underperforming the Standard and Poor’s 500 Index (S&P 500) return by 1.44%.

During the four months ended November 29, 2006, the Fund was managed as an index fund. In this period, the Fund’s performance was helped by its underweighting to the energy sector, which underperformed as oil and gas prices declined, and its overweighting to the information technology sector. Stocks that helped performance included Microsoft and Cisco Systems. In the same four-month period, the Fund’s performance was hurt by an overweighting in the consumer staples sector and by stock selection within the financials sector.

On November 30, 2006, the Fund transitioned to an active investment strategy, and Wellington Management Company became the Fund’s submanager.

During the eight months following this transition, the Fund was hurt by its underweighting to the energy sector and its overweighting to the financials sector. The big three oil companies, which do not meet Domini’s sustainability standards for Fund investment, performed well, in part due to high oil prices during the period. However, these negative effects of sector allocation were largely offset by positive effects in other sectors.

The Fund’s active investment process is designed to highlight stock selection as a primary factor driving the Fund’s performance relative to its benchmark. During this eight-month period, the Fund was helped by its investments in two industrial companies that manufacture diesel engines: Navistar (which also makes trucks and school buses) and Cummins. Cummins’ share price nearly doubled during this period, as its earnings exceeded analysts’ expectations.

The Fund was hurt by its positions in several technology stocks. Lexmark International stock declined more than 40% during the eight months since the Fund’s transition, due to weakness in its inkjet printing business. The stock of semiconductor manufacturer Micron Technology, which like Lexmark is no longer held by the fund, declined about 20%, in part due to declining prices caused by an oversupply of memory chips. Apple Computer’s stock rose more than 40%, driven by strong sales of Macintosh computers and iPod music players, and by market expectations for the new iPhone. However, the percentage of Apple stock in the Fund’s portfolio was less than its percentage in the S&P 500.

14 |

|

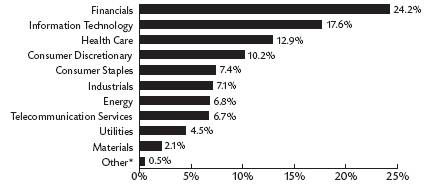

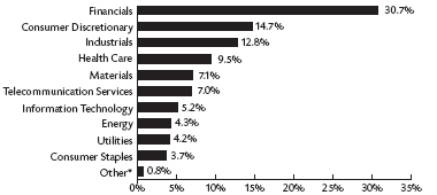

The Domini Social Equity Portfolio invests in the Domini Social Equity Trust. The table and bar chart below provide information as of July 31, 2007, about the ten largest holdings of the Domini Social Equity Trust and its portfolio holdings by industry sector:

TEN LARGEST HOLDINGS

| % NET | |

COMPANY |

| ASSETS |

Intl Business Machines Corp. |

| 3.79% |

Verizon Communications Inc. |

| 3.46% |

JP Morgan Chase & Co. |

| 3.40% |

Citigroup Inc. |

| 3.25% |

Hewlett-Packard Company |

| 3.23% |

Merck & Co. Inc. |

| 3.16% |

Bank of America Corporation |

| 2.94% |

Johnson & Johnson |

| 2.63% |

Goldman Sachs Group Inc. |

| 2.62% |

Microsoft Corp. |

| 2.41% |

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS)

* | Other reflects Repurchase Agreements and Other Assets, less liabilities. |

The holdings mentioned above are described in the Domini Social Equity Trust’s Portfolio of Investments at July 31, 2007, included herein. The composition of the Trust’s portfolio is subject to change.

Domini Social Equity Portfolio — Performance Commentary | 15 |

AVERAGE ANNUAL TOTAL RETURNS

|

|

|

| Domini Social Equity |

| Domini Social Equity |

| S&P 500 | |||

|

| 1 year |

| 14.62 | % |

| 20.34 | % |

| 20.59 | % |

As of |

| 5 Year |

| 7.82 | % |

| 8.88 | % |

| 10.70 | % |

6-30-07 |

| 10 Year |

| 5.69 | % |

| 6.20 | % |

| 7.13 | % |

|

| Since Inception(1) |

| 9.71 | % |

| 10.05 | % |

| 10.93 | % |

|

| 1 Year |

| 9.24 | % |

| 14.69 | % |

| 16.13 | % |

As of |

| 5 Year |

| 8.51 | % |

| 9.57 | % |

| 11.81 | % |

7-31-07 |

| 10 Year |

| 4.31 | % |

| 4.82 | % |

| 5.98 | % |

|

| Since Inception(1) |

| 9.34 | % |

| 9.67 | % |

| 10.66 | % |

COMPARISON OF $10,000 INVESTMENT IN THE

DOMINI SOCIAL EQUITY PORTFOLIO (WITH 4.75% MAXIMUM SALES CHARGE) AND S&P 500

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Economic and market conditions change, and both will cause investment return, principal value, and yield to fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, call 1-800-582-6757 or visit www.domini.com. A 2.00% redemption fee is charged on sales or exchanges of shares made less than 60 days after the settlement of purchase or acquisition through exchange, with certain exceptions. Performance data quoted ab ove does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Social Equity Portfolio is based on the Fund’s net asset values and assumes all dividends and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured.

You may lose money. Certain fees payable by the Fund were waived during the period, and the Fund’s average annual total returns would have been lower had these not been waived.

For the period reported in its current prospectus, the Fund’s gross annual operating expenses were estimated to total 37.76% of net assets. Until November 30, 2007, Domini has contractually agreed to waive fees and reimburse expenses to limit the Fund’s expenses, on a per annum basis, to 1.13% of net assets.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

______________(1) | The Domini Social Equity Portfolio, which commenced operations on May 1, 2005, invests all of its assets in the Domini Social Equity Trust (DSET), which has the same investment objectives as the Fund. The DSET commenced operations on June 3, 1991. Performance prior to the Fund’s commencement of operations is the performance of the DSET adjusted for expenses of the Fund. |

This material must be preceded or accompanied by the Fund’s current prospectus. DSIL Investment Services LLC, Distributor. 09/07

16 | Domini Social Equity Portfolio — Performance Commentary |

DOMINI SOCIAL EQUITY TRUST

PORTFOLIO OF INVESTMENTS

JULY 31, 2007

SECURITY |

| SHARES |

| VALUE |

| |

Common Stocks – 99.5% |

|

|

|

|

|

|

Consumer Discretionary – 10.2% |

|

|

|

|

|

|

Amazon.com, Inc. |

| 41,000 |

| $ | 3,220,140 |

|

AutoZone Inc. (a) |

| 54,047 |

|

| 6,853,700 |

|

Best Buy Co., Inc. |

| 858 |

|

| 38,258 |

|

Big Lots, Inc. (a) |

| 231,100 |

|

| 5,976,246 |

|

Bright Horizons Family Solutions, Inc. (a) |

| 443 |

|

| 17,188 |

|

CBS Corporation, Class B |

| 699,300 |

|

| 22,181,796 |

|

Coach Inc. (a) |

| 176,500 |

|

| 8,023,690 |

|

Comcast Corporation, Class A (a) |

| 6,750 |

|

| 177,323 |

|

Cooper Tire & Rubber |

| 172,000 |

|

| 3,954,280 |

|

Disney (Walt) Company (The) |

| 285,937 |

|

| 9,435,921 |

|

Family Dollar Stores Inc. |

| 986 |

|

| 29,205 |

|

Gap Inc. |

| 2,187 |

|

| 37,616 |

|

Home Depot, Inc. (The) |

| 3,344 |

|

| 124,296 |

|

Horton, (D.R.), Inc. |

| 1,975 |

|

| 32,232 |

|

Interface Inc., Class A |

| 1,268 |

|

| 23,369 |

|

J.C. Penney Company Inc. |

| 111,417 |

|

| 7,580,813 |

|

Johnson Controls Inc. |

| 818 |

|

| 92,557 |

|

Limited Brands |

| 868 |

|

| 20,962 |

|

Lowe’s Companies, Inc. |

| 2,686 |

|

| 75,235 |

|

Mattel Inc. |

| 642,100 |

|

| 14,710,511 |

|

McDonald’s Corporation |

| 413,974 |

|

| 19,816,935 |

|

McGraw-Hill Companies |

| 1,512 |

|

| 91,476 |

|

Meredith Corporation |

| 623 |

|

| 35,193 |

|

NIKE Inc., Class B |

| 2,388 |

|

| 134,803 |

|

Nordstrom, Inc. |

| 595 |

|

| 28,310 |

|

Pulte Homes, Inc. |

| 1,594 |

|

| 30,828 |

|

Radio One, Inc. (a) |

| 2,279 |

|

| 13,948 |

|

RadioShack Corporation |

| 130,200 |

|

| 3,271,926 |

|

Scholastic Corporation (a) |

| 722 |

|

| 23,234 |

|

Staples, Inc. |

| 1,858 |

|

| 42,771 |

|

Starbucks Corporation (a) |

| 2,378 |

|

| 63,445 |

|

Target Corporation |

| 1,736 |

|

| 105,150 |

|

Time Warner, Inc. |

| 171,076 |

|

| 3,294,924 |

|

Washington Post Company, Class B |

| 95 |

|

| 75,121 |

|

Wendy’s International, Inc. |

| 1,823 |

|

| 63,860 |

|

Whirlpool Corporation |

| 222,063 |

|

| 22,674,853 |

|

|

|

|

|

| 132,372,115 |

|

Consumer Staples – 7.4% |

|

|

|

|

|

|

Avon Products, Inc. |

| 1,706 |

| $ | 61,433 |

|

Church & Dwight Co., Inc. |

| 70,785 |

|

| 3,472,712 |

|

Coca Cola Company |

| 349,484 |

|

| 18,211,611 |

|

Colgate-Palmolive Company |

| 1,796 |

|

| 118,536 |

|

CVS Caremark Corporation |

| 1,905 |

|

| 67,037 |

|

Estee Lauder Companies, Inc., Class A |

| 457,149 |

|

| 20,580,848 |

|

General Mills Inc. |

| 137,400 |

|

| 7,642,188 |

|

Green Mountain Coffee, Inc. (a) |

| 966 |

|

| 28,642 |

|

Hershey Company (The) |

| 1,736 |

|

| 80,030 |

|

J.M. Smucker Company (The), New Common |

| 181,941 |

|

| 10,154,127 |

|

Kimberly-Clark Corporation |

| 1,456 |

|

| 97,945 |

|

Kroger Company |

| 697,377 |

|

| 18,103,907 |

|

PepsiCo, Inc. |

| 4,153 |

|

| 272,520 |

|

Procter & Gamble Company |

| 62,301 |

|

| 3,853,940 |

|

SunOpta Inc. (a) |

| 2,500 |

|

| 28,175 |

|

Supervalu Inc. |

| 326,300 |

|

| 13,596,921 |

|

United Natural Foods, Inc. (a) |

| 732 |

|

| 19,932 |

|

Walgreen Company |

| 1,964 |

|

| 86,770 |

|

Wild Oats Markets, Inc. (a) |

| 1,259 |

|

| 20,270 |

|

|

|

|

|

| 96,497,544 |

|

Energy – 6.8% |

|

|

|

|

|

|

Anadarko Petroleum Corporation |

| 4,618 |

|

| 232,424 |

|

Apache Corporation |

| 66,462 |

|

| 5,366,807 |

|

Devon Energy Corporation |

| 3,970 |

|

| 296,202 |

|

ENSCO International, Inc. |

| 131,300 |

|

| 8,018,491 |

|

EOG Resources, Inc. |

| 3,008 |

|

| 210,861 |

|

Metretek Technologies, Inc. (a) |

| 1,700 |

|

| 23,885 |

|

National Oilwell Varco Inc. |

| 33,800 |

|

| 4,059,718 |

|

Noble Corporation |

| 47,100 |

|

| 4,825,866 |

|

Noble Energy, Inc. |

| 90,200 |

|

| 5,514,828 |

|

Tidewater Inc. |

| 316,600 |

|

| 21,661,772 |

|

Unit Corporation (a) |

| 424,800 |

|

| 23,389,487 |

|

XTO Energy Inc. |

| 266,916 |

|

| 14,554,929 |

|

|

|

|

|

| 88,155,270 |

|

17

DOMINI SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JULY 31, 2007

SECURITY |

| SHARES |

| VALUE |

| |

Financials – 24.2% |

|

|

|

|

|

|

Allstate Corporation |

| 240,200 |

| $ | 12,766,630 |

|

American Express Company |

| 3,876 |

|

| 226,901 |

|

Assurant, Inc. |

| 112,700 |

|

| 5,716,144 |

|

Bank of America Corporation |

| 804,000 |

|

| 38,125,680 |

|

Chubb Corporation |

| 191,666 |

|

| 9,661,883 |

|

CIT Group, Inc. |

| 258,400 |

|

| 10,640,912 |

|

Citigroup, Inc. |

| 903,200 |

|

| 42,062,024 |

|

Fannie Mae |

| 242,416 |

|

| 14,506,173 |

|

FirstFed Financial Corp. (a) |

| 142,600 |

|

| 6,445,520 |

|

Freddie Mac |

| 2,222 |

|

| 127,254 |

|

Goldman Sachs Group, Inc. (The) |

| 180,300 |

|

| 33,957,702 |

|

Hartford Financial Services Group (The) |

| 226,038 |

|

| 20,766,111 |

|

Heartland Financial USA, Inc. |

| 498 |

|

| 8,487 |

|

Lehman Brothers Holdings Inc. |

| 46,200 |

|

| 2,864,400 |

|

Medallion Financial Corporation |

| 1,275 |

|

| 14,650 |

|

Morgan (J.P.) Chase & Co. |

| 1,001,530 |

|

| 44,077,335 |

|

Nationwide Financial Services, Inc., Class A |

| 224,600 |

|

| 12,781,986 |

|

Popular Inc. |

| 4,111 |

|

| 54,224 |

|

Prudential Financial, Inc. |

| 204,100 |

|

| 18,089,383 |

|

SunTrust Banks, Inc. |

| 156,426 |

|

| 12,248,156 |

|

Travelers Companies, Inc. (The) |

| 482,652 |

|

| 24,509,069 |

|

U.S. Bancorp |

| 5,163 |

|

| 154,632 |

|

Wachovia Corporation |

| 68,783 |

|

| 3,247,245 |

|

Washington Mutual, Inc. |

| 4,331 |

|

| 162,542 |

|

Wells Fargo & Company |

| 6,826 |

|

| 230,514 |

|

|

|

|

|

| 313,445,557 |

|

Health Care – 12.9% |

|

|

|

|

|

|

Amgen, Inc. (a) |

| 150,766 |

|

| 8,102,165 |

|

Baxter International, Inc. |

| 301,422 |

|

| 15,854,797 |

|

Becton Dickinson & Company |

| 2,202 |

|

| 168,145 |

|

Conceptus, Inc. (a) |

| 1,100 |

|

| 17,820 |

|

Express Scripts, Inc. (a) |

| 125,200 |

|

| 6,276,276 |

|

Forest Laboratories, Inc. (a) |

| 233,000 |

|

| 9,366,600 |

|

Genentech, Inc. (a) |

| 1,600 |

|

| 119,008 |

|

Gilead Sciences, Inc. (a) |

| 155,210 |

|

| 5,778,468 |

|

Invacare Corporation |

| 1,260 |

|

| 25,893 |

|

Johnson & Johnson |

| 563,424 |

| $ | 34,087,152 |

|

Kinetic Concepts, Inc. (a) |

| 144,500 |

|

| 8,883,860 |

|

Medtronic, Inc. |

| 3,455 |

|

| 175,065 |

|

Merck & Co., Inc. |

| 823,602 |

|

| 40,891,839 |

|

Watson Pharmaceuticals, Inc. (a) |

| 384,300 |

|

| 11,690,406 |

|

Zimmer Holdings, Inc. (a) |

| 335,843 |

|

| 26,115,152 |

|

|

|

|

| 167,552,646 |

| |

Industrials – 7.1% |

|

|

|

|

|

|

3M Company |

| 2,664 |

|

| 236,883 |

|

Baldor Electric Company |

| 1,190 |

|

| 54,312 |

|

Brady Corporation, Class A |

| 654 |

|

| 22,883 |

|

Cooper Industries, Ltd., Class A |

| 2,386 |

|

| 126,267 |

|

Cummins Inc. |

| 182,232 |

|

| 21,630,937 |

|

Deere & Company |

| 70,100 |

|

| 8,441,442 |

|

Deluxe Corporation |

| 265,200 |

|

| 10,013,952 |

|

Donnelley (R.R.) & Sons Company |

| 2,118 |

|

| 89,507 |

|

Emerson Electric Company |

| 4,408 |

|

| 207,485 |

|

Evergreen Solar, Inc. (a) |

| 1,700 |

|

| 14,161 |

|

Fuel Tech, Inc. (a) |

| 700 |

|

| 19,579 |

|

FuelCell Energy, Inc. (a) |

| 2,600 |

|

| 19,136 |

|

Granite Construction Incorporated |

| 737 |

|

| 47,898 |

|

Herman Miller, Inc. |

| 896 |

|

| 27,355 |

|

Illinois Tool Works, Inc. |

| 2,800 |

|

| 154,140 |

|

JetBlue Airways Corporation (a) |

| 2,293 |

|

| 22,586 |

|

Kadant Inc. (a) |

| 627 |

|

| 16,898 |

|

Monster Worldwide, Inc. (a) |

| 835 |

|

| 32,473 |

|

Navistar International Corporation (a) |

| 134,900 |

|

| 8,498,700 |

|

PACCAR Inc. |

| 206,900 |

|

| 16,928,558 |

|

Pitney Bowes, Inc. |

| 1,457 |

|

| 67,168 |

|

Ryder System, Inc. |

| 154,684 |

|

| 8,410,169 |

|

Southwest Airlines Co. |

| 3,478 |

|

| 54,465 |

|

Tennant Company |

| 1,296 |

|

| 49,961 |

|

Trex Company, Inc. (a) |

| 888 |

|

| 14,830 |

|

United Parcel Service, Inc., Class B |

| 1,873 |

|

| 141,824 |

|

YRC Worldwide Inc. (a) |

| 506,579 |

|

| 16,271,317 |

|

|

|

|

|

| 91,614,886 |

|

Information Technology – 17.6% |

|

|

|

|

|

|

Apple Inc. (a) |

| 1,312 |

|

| 172,869 |

|

Applied Materials, Inc. |

| 301,000 |

|

| 6,634,040 |

|

Arrow Electronics, Inc. |

| 146,900 |

|

| 5,614,518 |

|

18

DOMINI SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JULY 31, 2007

SECURITY |

| SHARES |

| VALUE |

| |

Information Technology (Continued) |

|

|

|

|

|

|

Cisco Systems, Inc. (a) |

| 8,816 |

| $ | 254,871 |

|

Convergys Corporation (a) |

| 218,300 |

|

| 4,158,615 |

|

Dell Inc. (a) |

| 301,684 |

|

| 8,438,101 |

|

eBay Inc. (a) |

| 2,176 |

|

| 70,502 |

|

Electronic Data Systems Corporation |

| 980,900 |

|

| 26,474,491 |

|

Google Inc., Class A (a) |

| 300 |

|

| 153,000 |

|

Hewlett-Packard Company |

| 908,347 |

|

| 41,811,212 |

|

Intel Corporation |

| 10,039 |

|

| 237,121 |

|

International Business Machines Corporation |

| 444,500 |

|

| 49,183,925 |

|

Itron, Inc. (a) |

| 445 |

|

| 35,346 |

|

Jabil Circuit, Inc. |

| 1,500 |

|

| 33,796 |

|

Juniper Networks, Inc. (a) |

| 1,900 |

|

| 56,924 |

|

LAM Research Corporation (a) |

| 338,900 |

|

| 19,601,976 |

|

MEMC Electronic Materials, Inc. (a) |

| 129,700 |

|

| 7,953,204 |

|

Microsoft Corporation |

| 1,076,952 |

|

| 31,220,838 |

|

Motorola, Inc. |

| 5,000 |

|

| 84,950 |

|

Power Integrations, Inc. (a) |

| 600 |

|

| 15,901 |

|

QUALCOMM, Inc. |

| 3,434 |

|

| 143,026 |

|

SunPower Corporation, Class A (a) |

| 400 |

|

| 28,213 |

|

Symantec Corporation (a) |

| 425,846 |

|

| 8,176,243 |

|

Texas Instruments, Inc. |

| 3,628 |

|

| 127,669 |

|

Western Digital Corporation (a) |

| 526,800 |

|

| 11,247,180 |

|

Xerox Corporation (a) |

| 375,198 |

|

| 6,550,957 |

|

|

|

|

| 228,479,488 |

| |

Materials – 2.1% |

|

|

|

|

|

|

Airgas, Inc. |

| 1,159 |

|

| 54,125 |

|

Ecolab, Inc. |

| 1,757 |

|

| 73,987 |

|

International Paper Company |

| 3,000 |

|

| 111,210 |

|

Lubrizol Corporation |

| 88,200 |

|

| 5,526,612 |

|

MeadWestvaco Corporation |

| 2,666 |

|

| 86,752 |

|

Nucor Corporation |

| 189,116 |

|

| 9,493,623 |

|

Rock-Tenn Company, Class A |

| 592 |

|

| 18,187 |

|

Rohm and Haas Company |

| 1,510 |

|

| 85,345 |

|

Schnitzer Steel Industries Inc., Class A |

| 1,269 |

| $ | 68,767 |

|

Sonoco Products Company |

| 1,260 |

|

| 46,204 |

|

United States Steel Corporation |

| 115,300 |

|

| 11,332,837 |

|

|

|

|

|

| 26,897,649 |

|

Telecommunication Services – 6.7% |

|

|

|

|

|

|

AT&T Inc. |

| 747,904 |

|

| 29,287,921 |

|

CenturyTel, Inc. |

| 271,200 |

|

| 12,439,944 |

|

Sprint Nextel Corp. |

| 5,159 |

|

| 105,914 |

|

Verizon Communications Inc. |

| 1,053,538 |

|

| 44,901,789 |

|

|

|

|

|

| 86,735,568 |

|

Utilities – 4.5% |

|

|

|

|

|

|

Atmos Energy Corporation |

| 130,000 |

|

| 3,649,100 |

|

CenterPoint Energy, Inc. |

| 936,700 |

|

| 15,436,816 |

|

Energen Corporation |

| 435,247 |

|

| 23,028,919 |

|

ONEOK, Inc. |

| 187,100 |

|

| 9,495,325 |

|

Pepco Holdings, Inc. |

| 250,200 |

|

| 6,772,914 |

|

WGL Holdings |

| 8,577 |

|

| 256,795 |

|

|

|

|

|

| 58,639,869 |

|

Total Common Stocks |

|

|

|

|

|

|

(Cost $1,180,493,385) |

|

|

|

| 1,290,390,592 |

|

Repurchase Agreements – 0.4% |

|

|

|

|

|

|

State Street Bank & Trust, dated 7/31/07, 3.52% due 8/1/07, maturity amount $4,790,465 (collateralized by U.S. Government Agency Mortgage Securities, Fannie Mae, 31359MZ22, 5.45%, 10/18/2021, market value $4,886,869) |

| 4,789,996 |

|

| 4,789,996 |

|

Total Repurchase Agreements |

|

|

|

|

|

|

(Cost $4,789,996) |

|

|

|

| 4,789,996 |

|

Total Investments – 99.9% |

|

|

|

|

|

|

(Cost $1,185,283,381) (b) |

|

|

|

| 1,295,180,588 |

|

Other Assets, less liabilities – 0.1% |

|

|

|

| 889,974 |

|

Net Assets – 100.0% |

|

|

| $ | 1,296,070,562 |

|

(a) | Non-income producing security. |

(b) | The aggregate cost for federal income tax purposes is $1,229,563,689. The aggregrate gross unrealized appreciation is $103,861,105 and the aggregate gross unrealized depreciation is $38,244,206, resulting in net unrealized appreciation of $65,616,899. |

SEE NOTES TO FINANCIAL STATEMENTS

19

DOMINI EUROPEAN SOCIAL EQUITY PORTFOLIO

PERFORMANCE COMMENTARY

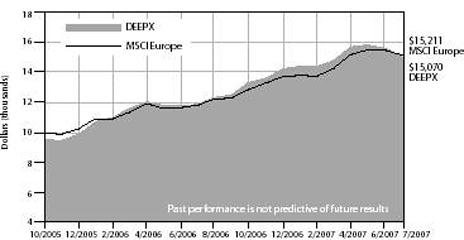

For the year ended July 31, 2007, the Domini European Social Equity Portfolio (the “Fund”) returned 26.82%, excluding sales charges, underperforming the Morgan Stanley Capital International Europe Index (MSCI Europe) by 1.45%.

The Fund’s performance relative to its benchmark was hurt by its position in the Irish fruit and produce distributor Fyffes. The company’s share price declined in the second quarter after it failed to meet analysts’ earnings expectations, which it attributed in part to an increase in fuel prices. The Fund was also hurt by its position in the French pharmaceutical company Sanofi-Aventis.

The Fund’s position in the Italian automaker Fiat was a positive contributor to returns, as its stock price doubled during the year. (See our discussion of Fiat in “The Way You Invest Matters: Global Warming.”) The exclusion of the integrated oil company BP also contributed to the Fund’s relative performance, as BP’s stock performance was essentially flat in a year when the market was rising sharply. The company, which does not meet Domini’s investment standards, has suffered setbacks including the departure of its CEO and maintenance problems at its facility in Prudhoe Bay, Alaska.

The Fund was helped by its positions in the British company Aggreko, which rents power generators, and the Swedish bus and truck manufacturer Scania, which claims to be the world’s only supplier of ethanol-powered commercial vehicles. The Fund was also helped by its avoidance of the British pharmaceutical company AstraZeneca, which does not meet our investment standards.

20 |

|

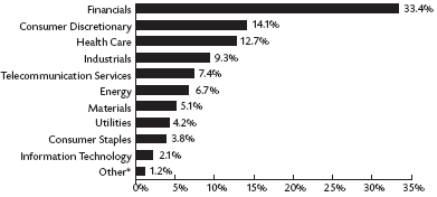

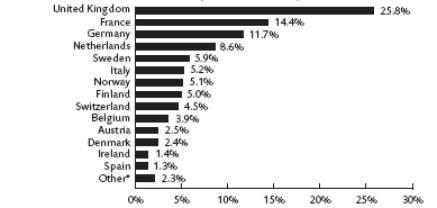

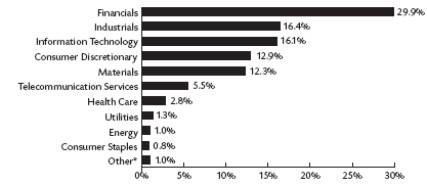

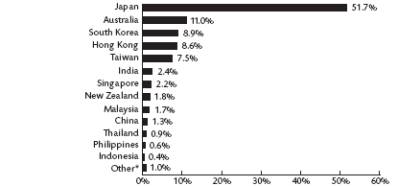

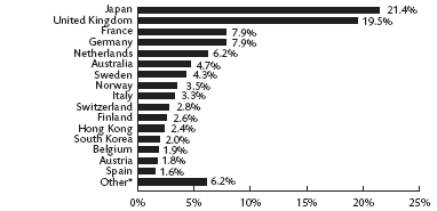

The Domini European Social Equity Portfolio invests in the Domini European Social Equity Trust. The table and bar chart below provide information as of July 31, 2007, about the ten largest holdings of the Domini European Social Equity Trust and its portfolio holdings by industry sector and by country:

TEN LARGEST HOLDINGS

COMPANY |

| % NET |

|

Vivendi SA |

| 3.02% |

|

Swiss Re-Reg |

| 2.92% |

|

Sanofi-Aventis |

| 2.78% |

|

Fiat SPA |

| 2.65% |

|

Royal Bank of Scotland Group |

| 2.64% |

|

Statoil ASA |

| 2.64% |

|

UniCredito Italiano SPA |

| 2.23% |

|

Muenchener Rueckver AG-Reg |

| 2.21% |

|

Allianz SE-Reg |

| 2.12% |

|

National Grid PLC |

| 2.04% |

|

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS)

* Other reflects Repurchase Agreements and Other Assets, less liabilities.

PORTFOLIO HOLDINGS BY COUNTRY (% OF NET ASSETS)

* Other reflects Turkey, Poland, Portugal, Repurchase Agreements, and Other Assets, less liabilities.

______________The holdings mentioned above are described in the Domini European Social Equity Trust’s Portfolio of Investments at July 31, 2007, included herein. The composition of the Trust’s portfolio is subject to change.

Domini European Social Equity Portfolio — Performance Commentary | 21 |

AVERAGE ANNUAL TOTAL RETURNS

|

|

|

| Domini European Social |

| Domini European Social |

| MSCI |

|

As of |

| 1 Year |

| 26.88% |

| 33.20% |

| 33.07% |

|

6-30-07 |

| Since Inception(1) |

| 29.35% |

| 33.02% |

| 28.84% |

|

As of |

| 1 Year |

| 20.79% |

| 26.82% |

| 28.27% |

|

7-31-07 |

| Since Inception(1) |

| 25.20% |

| 28.59% |

| 25.85% |

|

COMPARISON OF $10,000 INVESTMENT IN THE

DOMINI EUROPEAN SOCIAL EQUITY PORTFOLIO (WITH 4.75% MAXIMUM SALES CHARGE) AND THE MSCI EUROPE

Past performance is no guarantee of future results. The fund’s returns quoted above represent past performance after all expenses. Economic and market conditions change, and both will cause investment return, principal value, and yield to fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, call 1-800-582-6757 or visit www.domini.com. A 2.00% redemption fee is charged on sales or exchanges of shares made less than 60 days after the settlement of purchase or acquisition through exchange, with certain exceptions. Performance data quo ted above does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini European Social Equity Portfolio is based on the Fund’s net asset values and assumes all dividends and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money. Certain fees payable by the Fund were waived during the period, and the Fund’s average annual total returns would have been lower had these not been waived.

For the period reported in its current prospectus, the Fund’s gross annual operating expenses were estimated to total 30.44% of net assets. Until November 30, 2007, Domini has contractually agreed to waive fees and reimburse expenses to limit the Fund’s expenses, on a per annum basis, to 1.57% of net assets.

The Morgan Stanley Capital International Europe Index (MSCI Europe) is an unmanaged index of common stocks. Investors cannot invest directly in the MSCI Europe.

______________(1) | Since October 3, 2005 |

This material must be preceded or accompanied by the Fund’s current prospectus. DSIL Investment Services LLC, Distributor. 09/07

22 | Domini European Social Equity Portfolio — Performance Commentary |

DOMINI EUROPEAN SOCIAL EQUITY TRUST

PORTFOLIO OF INVESTMENTS

JULY 31, 2007

COUNTRY/ SECURITY |

| INDUSTRY |

| SHARES |

|

| VALUE |

|

Common Stocks – 98.8% |

|

|

|

|

|

|

|

|

Austria – 2.5% |

|

|

|

|

|

|

|

|

Immoeast AG (a) |

| Real Estate |

| 62,915 |

| $ | 817,378 |

|

Immofinanz AG (a) |

| Real Estate |

| 107,410 |

|

| 1,350,676 |

|

OMV AG |

| Energy |

| 2,399 |

|

| 149,123 |

|

Voestalpine AG |

| Materials |

| 11,768 |

|

| 979,526 |

|

|

|

|

|

|

|

| 3,296,703 |

|

Belgium – 3.9% |

|

|

|

|

|

|

|

|

Belgacom SA |

| Telecommunication Services |

| 48,604 |

|

| 1,968,715 |

|

Fortis |

| Diversified Financials |

| 41,009 |

|

| 1,617,109 |

|

Omega Pharma SA |

| Health Care Equipment & Services |

| 19,098 |

|

| 1,638,734 |

|

|

|

|

|

|

|

| 5,224,558 |

|

Denmark – 2.4% |

|

|

|

|

|

|

|

|

Dampskibsselskabet Torm |

| Energy |

| 45,252 |

|

| 1,803,004 |

|

Danske Bank A/S |

| Banks |

| 7,856 |

|

| 331,022 |

|

H. Lundbeck A/S |

| Pharma, Biotech & Life Sciences |

| 5,300 |

|

| 136,396 |

|

Sydbank A/S |

| Banks |

| 18,800 |

|

| 954,824 |

|

|

|

|

|

|

|

| 3,225,246 |

|

Finland – 5.0% |

|

|

|

|

|

|

|

|

Elisa OYJ – A Shares |

| Telecommunication Services |

| 14,545 |

|

| 411,374 |

|

Kesko OYJ – B Shares |

| Food & Staples Retailing |

| 27,708 |

|

| 1,468,107 |

|

Metso OYJ |

| Capital Goods |

| 7,144 |

|

| 452,425 |

|

Orion OYJ |

| Pharma, Biotech & Life Sciences |

| 73,462 |

|

| 1,925,050 |

|

Outokumpu OYJ |

| Materials |

| 21,597 |

|

| 669,260 |

|

Rautaruukki OYJ |

| Materials |

| 26,846 |

|

| 1,759,840 |

|

|

|

|

|

|

|

| 6,686,056 |

|

France – 14.4% |

|

|

|

|

|

|

|

|

Air France – KLM |

| Transportation |

| 33,873 |

|

| 1,525,426 |

|

BNP Paribas |

| Banks |

| 23,573 |

|

| 2,592,584 |

|

Credit Agricole SA |

| Banks |

| 18,360 |

|

| 701,883 |

|

France Telecom SA |

| Telecommunication Services |

| 94,621 |

|

| 2,545,099 |

|

Lafarge SA |

| Materials |

| 1,395 |

|

| 236,411 |

|

Michelin (CDGE) – B |

| Automobiles & Components |

| 5,884 |

|

| 777,256 |

|

Sanofi – Aventis |

| Pharma, Biotech & Life Sciences |

| 44,329 |

|

| 3,714,994 |

|

Societe Generale |

| Banks |

| 8,920 |

|

| 1,533,942 |

|

Ste Des Ciments Francais – A |

| Materials |

| 3,576 |

|

| 813,204 |

|

Valeo |

| Automobiles & Components |

| 13,920 |

|

| 714,038 |

|

Vivendi SA |

| Media |

| 94,767 |

|

| 4,027,413 |

|

|

|

|

|

|

|

| 19,182,250 |

|

Germany – 11.7% |

|

|

|

|

|

|

|

|

Allianz SE – Reg |

| Insurance |

| 13,278 |

|

| 2,824,930 |

|

Altana AG |

| Pharma, Biotech & Life Sciences |

| 36,224 |

|

| 851,066 |

|

Celesio AG |

| Health Care Equipment & Services |

| 40,107 |

|

| 2,410,227 |

|

Deutsche Lufthansa – Reg |

| Transportation |

| 63,951 |

|

| 1,795,338 |

|

Deutsche Telekom AG – Reg |

| Telecommunication Services |

| 34,069 |

|

| 588,077 |

|

Epcos AG |

| Technology Hardware & Equipment |

| 37,186 |

|

| 749,176 |

|

Fresenius SE |

| Health Care Equipment & Services |

| 28,437 |

|

| 2,065,576 |

|

Merck KGAA |

| Pharma, Biotech & Life Sciences |

| 5,829 |

|

| 727,650 |

|

Muenchener Rueckver AG – Reg |

| Insurance |

| 17,158 |

|

| 2,956,565 |

|

ProSieben Sat.1 Media AG |

| Media |

| 17,237 |

|

| 622,053 |

|

|

|

|

|

|

|

| 15,590,658 |

|

23

DOMINI EUROPEAN SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JULY 31, 2007

COUNTRY/ SECURITY |

| INDUSTRY |

| SHARES |

|

| VALUE |

|

Ireland – 1.4% |

|

|

|

|

|

|

|

|

Fyffes PLC |

| Food & Staples Retailing |

| 1,375,229 |

| $ | 1,505,491 |

|

Kerry Group PLC – A |

| Food & Beverage |

| 14,438 |

|

| 383,032 |

|

|

|

|

|

|

|

| 1,888,523 |

|

Italy – 5.2% |

|

|

|

|

|

|

|

|

Banca Popolare Emilia Romagna |

| Banks |

| 20,412 |

|

| 495,969 |

|

Fiat SPA |

| Automobiles & Components |

| 120,134 |

|

| 3,534,901 |

|

UniCredito Italiano SPA |

| Banks |

| 350,135 |

|

| 2,971,701 |

|

|

|

|

|

|

|

| 7,002,571 |

|

Netherlands – 8.6% |

|

|

|

|

|

|

|

|

Arcelor Mittal |

| Materials |

| 33,829 |

|

| 2,075,604 |

|

Fugro NV – CVA |

| Energy |

| 16,388 |

|

| 1,091,097 |

|

ING Groep NV – CVA |

| Diversified Financials |

| 50,956 |

|

| 2,152,174 |

|

Koninkijke KPN NV |

| Telecommunication Services |

| 87,899 |

|

| 1,360,673 |

|

OCE NV |

| Technology Hardware & Equipment |

| 65,016 |

|

| 1,505,327 |

|

SNS Reaal |

| Insurance |

| 49,704 |

|

| 1,106,471 |

|

TNT NV |

| Transportation |

| 44,686 |

|

| 1,918,695 |

|

Unilever NV – CVA |

| Food & Beverage |

| 8,276 |

|

| 250,255 |

|

|

|

|

|

|

|

| 11,460,296 |

|

Norway – 5.1% |

|

|

|

|

|

|

|

|

Norsk Hydro ASA |

| Energy |

| 26,828 |

|

| 1,033,879 |

|

Orkla ASA |

| Capital Goods |

| 46,500 |

|

| 875,107 |

|

Petroleum Geo – Services |

| Energy |

| 16,167 |

|

| 384,520 |

|

Statoil ASA |

| Energy |

| 118,967 |

|

| 3,520,287 |

|

Tandberg ASA |

| Technology Hardware & Equipment |

| 25,104 |

|

| 569,314 |

|

Telenor ASA |

| Telecommunication Services |

| 23,978 |

|

| 439,016 |

|

|

|

|

|

|

|

| 6,822,123 |

|

Poland – 0.3% |

|

|

|

|

|

|

|

|

Globe Trade Centre SA (a) |

| Real Estate |

| 10,681 |

|

| 147,548 |

|

Polish Oil & Gas |

| Energy |

| 166,817 |

|

| 292,894 |

|

|

|

|

|

|

| 440,442 |

| |

Portugal – 0.2% |

|

|

|

|

|

|

|

|

Banco Espirito Santo – Reg |

| Banks |

| 10,373 |

|

| 243,529 |

|

|

|

|

|

|

|

| 243,529 |

|

Spain – 1.3% |

|

|

|

|

|

|

|

|

Gas Natural SDG SA |

| Utilities |

| 25,993 |

|

| 1,492,474 |

|

Telefonica SA |

| Telecommunication Services |

| 10,472 |

|

| 245,205 |

|

|

|

|

|

|

|

| 1,737,679 |

|

Sweden – 5.9% |

|

|

|

|

|

|

|

|

Electrolux AB – Ser B |

| Consumer Durables & Apparel |

| 27,600 |

|

| 690,186 |

|

Eniro AB |

| Media |

| 61,200 |

|

| 753,990 |

|

Industrivarden AB – C Shares |

| Diversified Financials |

| 34,800 |

|

| 716,688 |

|

Investor AB – B Shares |

| Diversified Financials |

| 20,200 |

|

| 522,493 |

|

Nordea AB |

| Banks |

| 61,223 |

|

| 986,447 |

|

Scania AB – B Shares |

| Capital Goods |

| 76,600 |

|

| 1,825,375 |

|

SSAB Svenskt Stal AB – Ser A |

| Materials |

| 7,050 |

|

| 252,983 |

|

SSAB Svenskt Stal AB – Ser A Rights (c) |

| Materials |

| 7,050 |

|

| 24,458 |

|

Swedbank AB |

| Banks |

| 49,700 |

|

| 1,804,818 |

|

Teliasonera AB |

| Telecommunication Services |

| 44,500 |

|

| 336,442 |

|

|

|

|

|

|

|

| 7,913,880 |

|

24

DOMINI EUROPEAN SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JULY 31, 2007

COUNTRY/ SECURITY |

| INDUSTRY |

| SHARES |

|

| VALUE |

|

Switzerland – 4.5% |

|

|

|

|

|

|

|

|

Novartis AG – Reg Shares |

| Pharma, Biotech & Life Sciences |

| 19,482 |

| $ | 1,049,457 |

|

Rieter Holding AG |

| Automobiles & Components |

| 993 |

|

| 522,848 |

|

Swiss Re – Reg |

| Insurance |

| 45,478 |

|

| 3,896,937 |

|

The Swatch Group AG – Reg |

| Consumer Durables & Apparel |

| 9,901 |

|

| 576,802 |

|

|

|

|

|

|

|

| 6,046,044 |

|

Turkey – 0.6% |

|

|

|

|

|

|

|

|

Ihlas Holding (a) |

| Capital Goods |

| 262,048 |

|

| 143,533 |

|

Trakya Cam Sanayii A.S. |

| Capital Goods |

| 92,053 |

|

| 344,453 |

|

Turk Sise ve Cam Fabrikalari AS |

| Consumer Durables & Apparel |

| 64,938 |

|

| 289,864 |

|

|

|

|

|

|

|

| 777,850 |

|

United Kingdom – 25.8% |

|

|

|

|

|

|

|

|

3i Group PLC |

| Diversified Financials |

| 101,733 |

|

| 2,204,144 |

|

Aggreko PLC |

| Commercial Services & Supplies |

| 47,281 |

|

| 519,670 |

|

Arriva PLC |

| Transportation |

| 47,675 |

|

| 756,839 |

|

Aviva PLC |

| Insurance |

| 63,993 |

|

| 889,716 |

|

Barclays PLC |

| Banks |

| 177,780 |

|

| 2,498,261 |

|

Barratt Developments PLC |

| Consumer Durables & Apparel |

| 24,983 |

|

| 468,191 |

|

Bellway PLC |

| Consumer Durables & Apparel |

| 11,578 |

|

| 289,142 |

|

BG Group PLC |

| Energy |

| 38,952 |

|

| 633,906 |

|

Bovis Homes Group PLC |

| Consumer Durables & Apparel |

| 21,038 |

|

| 327,619 |

|

BT Group PLC |

| Telecommunication Services |

| 263,647 |

|

| 1,671,703 |

|

Drax Group PLC |

| Utilities |

| 97,495 |

|

| 1,351,755 |

|

Firstgroup PLC |

| Transportation |

| 49,226 |

|