Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21682

BB&T Variable Insurance Funds

(Exact name of registrant as specified in charter)

434 Fayetteville Street Mall, 5th Floor

Raleigh, NC 27601-0575

(Address of principal executive offices) (Zip code)

E.G. Purcell, III, President

BB&T Variable Insurance Funds

434 Fayetteville Street Mall, 5th Floor

Raleigh, NC 27601-0575

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 228-1872

Date of fiscal year end: December 31

Date of reporting period: December 31, 2009

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

| Item 1. | Reports to Stockholders. |

The Report to Shareholders is attached herewith.

Table of Contents

Table of Contents

Fund Summary | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 6 | ||

| 7 | ||

| 8 | ||

Schedules of Portfolio Investments | ||

| 9 | ||

| 10 | ||

| 11 | ||

| 12 | ||

| 13 | ||

| 18 | ||

| 24 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 39 | ||

Table of Contents

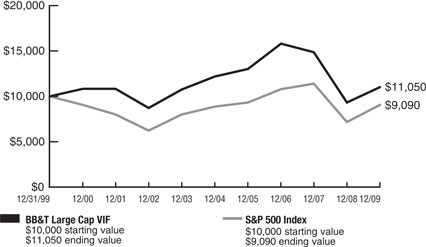

Performance Overview 12/31/1999 - 12/31/2009

Growth of a $10,000 investment

Portfolio Manager

Stephen L. Morgan, CFA

BB&T Asset Management, Inc.

Average Annual Returns

| 1 Year | 5 Year | 10 Years | ||||||

BB&T Large Cap VIF | 18.50 | % | -1.98 | % | 1.00% | |||

S&P 500 Index | 26.46 | % | 0.42 | % | -0.95% |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of distributions. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes. Value-based investments are subject to the risk that the broad market may not recognize their intrinsic value.

Q. How did the Fund perform during the 12-month period between January 1, 2009 and December 31, 2009?

A. The Fund returned 18.50%. That compared to a 26.46% return for its benchmark, the S&P 500 Index.1

Q. What factors affected the Fund’s performance?

A. The stock market performed well in 2009 due to expectations of an economic recovery and easing financial stress. The Federal Reserve’s accommodative monetary policy helped to support economic growth. Consumer spending rebounded from its 2008 lows, which also contributed to an economic recovery.2

Negative stock performance during the first two months of the year dragged on the Fund’s absolute returns. Investors fled risky assets amid the economic turmoil and persistent problems in the financial system.2

Sector selection made a positive contribution to relative performance during the period. Specifically, an overweight position in financials and an underweight stake in telecommunications services contributed to relative performance. In addition, individual positions in shares of an Internet services firm, a producer of gold, silver and copper, and a financial services firm contributed to the Fund’s returns relative to its benchmark index.2

Overall stock selection dragged on relative performance during the period, however. Selection within the financials and consumer discretionary sectors was responsible for the majority of the underperformance. Positions in a financial services firm, a consumer products company, and an international oil and gas firm were the largest individual detractors from relative performance.2

| 1 | The Fund is measured against the S&P 500 Index, a widely recognized, unmanaged index of common stocks. The index is unmanaged and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| 2 | Portfolio composition is as of December 31, 2009, and is subject to change. |

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the periods would have been lower.

2

Table of Contents

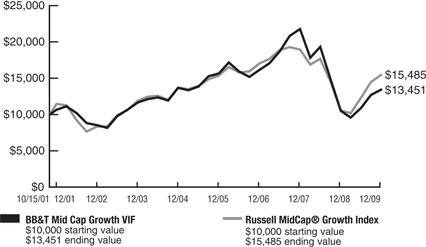

Performance Overview 10/15/2001 - 12/31/2009

Growth of a $10,000 investment

Portfolio Manager

Jeffrey J. Schappe

Chief Investment Officer

BB&T Asset Management, Inc.

Average Annual Returns (Inception 10/15/2001)

| 1 Year | 5 Year | Since Inception | ||||||

BB&T Mid Cap Growth VIF | 27.68 | % | -0.37 | % | 3.68% | |||

Russell MidCap® Growth Index | 46.29 | % | 2.40 | % | 5.50% |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of distributions. The inception date used for the Russell MidCap® Growth Index was 10/31/01. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Mid-capitalization funds typically carry additional risks since smaller companies generally have a higher risk of failure, and historically, their stocks have experienced a greater degree of market volatility than stocks on average.

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes.

Q. How did the Fund perform during the 12-month period between January 1, 2009 and December 31, 2009?

A. The Fund returned 27.68%. That compared to a 46.29% return for its benchmark, the Russell Midcap Growth® Index.1

Q. What factors affected the Fund’s performance?

A. The stock market performed well in 2009, due to expectations for an economic recovery and easing financial stress. The Federal Reserve’s accommodative monetary policy helped to support economic growth. Consumer spending rebounded from its 2008 lows, which also contributed to an economic recovery. Growth stocks performed especially well during the period. In particular, the information technology sector outperformed the overall market by a wide margin.2

Negative stock performance during the first two months of the year, when the economy had not yet shown any significant signs of recovery, dragged on the Fund’s absolute returns. Investors fled risky assets amid the economic turmoil and persistent problems in the financial system.2

Sector selection dragged on the Fund’s performance relative to its benchmark index. An overweight position in industrials and an underweight position in telecommunications services particularly detracted from relative returns. That said, underweight positions in utilities and consumer staples shares helped relative performance.2

Stock selection also reduced the Fund’s relative return. Specifically, positions in a regional financial services firm, a steel producer and a telecommunications firm detracted from relative performance. Conversely, positions in shares of a Chinese search engine, a mining and minerals development firm and a producer of gold, silver and copper boosted relative return.2

| 1 | The Fund is measured against the Russell MidCap® Growth Index, an unmanaged index which measures the performance of those securities in the Russell 1000 Index with higher price-to-book ratios and lower forecasted growth values. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| 2 | Portfolio composition is as of December 31, 2009, and is subject to change. |

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the periods would have been lower.

3

Table of Contents

BB&T Capital Manager Equity VIF

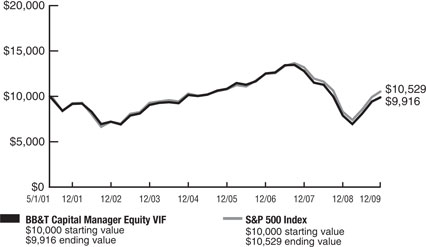

Performance Overview 5/01/2001 - 12/31/2009

Growth of a $10,000 investment

Portfolio Management Team

Managed by the BB&T Balanced Portfolio Management Team

Average Annual Returns (Inception 5/01/2001)

| 1 Year | 5 Year | Since Inception | ||||||

BB&T Capital Manager Equity VIF | 25.24 | % | -0.49 | % | -0.10% | |||

S&P 500 Index | 26.46 | % | 0.42 | % | 0.60% |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of distributions. The inception date used for the S&P 500 Index was 5/31/01. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes.

Q. How did the Fund perform during the 12-month period between January 1, 2009 and December 31, 2009?

A. The Fund returned 25.24%. That compared to a 26.46% return for the S&P 500 Index.1

Q. What factors affected the Fund���s performance?

A. The Fund normally invests in a combination of the BB&T Large Cap Fund, the BB&T Mid Cap Value Fund, the BB&T Mid Cap Growth Fund, the BB&T International Equity Fund, the BB&T Special Opportunities Fund, the BB&T Equity Income Fund, the BB&T Equity Index Fund, the BB&T U.S. Treasury Money Market Fund and various exchange-traded funds (collectively, “underlying Funds”).2

The stock market performed well in 2009. In the first two months of the year investors fled risky assets amid the economic turmoil and persistent problems in the financial system. Stocks generally performed poorly during that initial period, which dragged on the Fund’s absolute return. But aggressive global policy response to the economic crisis supported economic growth and helped increase investors’ appetite for risky assets, leading to a strong market rally. Consumer spending rebounded from its 2008 lows, which also contributed to the economic and market recovery.2

The Fund’s allocations to underlying Funds that invest in mid- and small-cap stocks contributed to relative returns, as mid- and small-cap shares outperformed the S&P 500. Mid-cap stocks comprise 32% of the Fund’s U.S. equity allocation, while small-cap stocks comprise 10%. An allocation to underlying Funds that invest in international stocks also made a positive contribution to relative performance, as foreign shares outperformed the benchmark index. International stocks comprise approximately 25% of the total equity allocation within the Fund.2

The Fund maintains a 60% allocation to underlying Funds that invest in value stocks, with a 40% allocation to underlying Funds that invest in growth stocks. The overweight allocation to value hurt relative returns during the period, as value shares’ performance lagged that of growth shares. The performance of the underlying equity Funds was also a net detractor from relative performance.2

| 1 | The Fund is measured against the S&P 500 Index, a widely recognized, unmanaged index of common stocks. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| 2 | Portfolio composition is as of December 31, 2009, and is subject to change. |

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the periods would have been lower.

4

Table of Contents

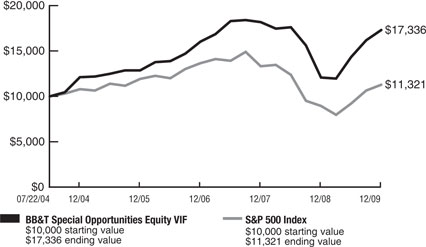

BB&T Special Opportunities Equity VIF

Performance Overview 7/22/2004 - 12/31/2009

Growth of a $10,000 investment

Portfolio Manager

George F. Shipp, CFA

Chief Investment Officer

Scott & Stringfellow LLC

Average Annual Returns (Inception 7/22/2004)

| 1 Year | 5 Year | Since Inception | ||||||

BB&T Special Opportunities Equity VIF | 43.53 | % | 7.42 | % | 10.63% | |||

S&P 500 Index | 26.46 | % | 0.42 | % | 2.32% |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of distributions. The inception date used for the S&P 500 Index was 07/31/04. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Equity securities (stocks) are more volatile and carry more risk than other forms of investments, including investments in high-grade fixed income securities. The net asset value per share of the Fund will fluctuate as the value of the securities in the portfolio changes. A concentrated portfolio may add a measure of volatility to performance, as major fluctuations in any one holding will likely affect the Fund more than a fund with greater diversification.

Q. How did the Fund perform during the 12-month period between January 1, 2009 and December 31, 2009?

A. The Fund returned 43.53%. That compared to a 26.46% return for its benchmark, the S&P 500 Index.1

Q. What factors affected the Fund’s performance?

A. Global stock markets rebounded sharply off their March 2009 lows, in response to the somewhat coordinated response of monetary authorities to flood the system with liquidity and keep credit flowing. With money markets and similar deposit products providing near zero yields, investors sought out higher returns in fixed income and equity markets. The Federal Reserve’s supply of essentially free money encouraged greater risk-taking. As a result, shares of smaller companies tended to provide the strongest returns. Shares of more-stable blue-chip companies benefited less from the 2009 rally.2

Favorable sector and security selection aided the Fund’s return relative to its benchmark. Throughout the year, the Fund held underweight positions in telecommunications companies, utilities and financials (the market’s worst, second-worst and fourth-worst performing sectors, respectively), while remaining overweight in technology stocks (the market’s strongest sector in 2009).2

Among the strongest gainers in the portfolio were stocks of a health care information technology company, a global oil producer, a specialty chemicals company, an optical glass manufacturer and a microchip design firm. Shares of two energy services providers, a broadband facilitator and an online marketplace company also provided strong double-digit returns for the year. Gains in those securities more than offset below-market performance from other stocks held by the Fund, including shares of a national cable operator and a global fast-food franchisor.2

| 1 | The Fund is measured against the S&P 500 Index, a widely recognized, unmanaged index of common stocks. The index does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| 2 | Portfolio composition is as of December 31, 2009, and is subject to change. |

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the periods would have been lower.

5

Table of Contents

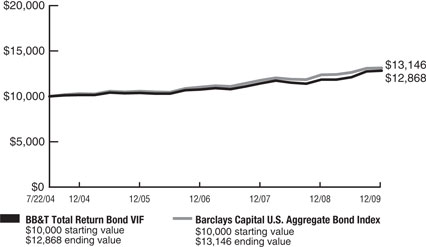

Performance Overview 7/22/2004 - 12/31/2009

Growth of a $10,000 investment

Portfolio Manager

Mark Montgomery, CFA

Managing Director and Fixed Income Portfolio Manager

Sterling Capital Management LLC

Average Annual Returns (Inception 7/22/2004)

| 1 Year | 5 Year | Since Inception | ||||||

BB&T Total Return Bond VIF | 8.57 | % | 4.81 | % | 4.74% | |||

Barclays Capital U.S. Aggregate Bond Index | 5.93 | % | 4.97 | % | 5.18% |

The chart represents a comparison of a hypothetical $10,000 investment in the indicated Fund versus a similar investment in the Fund’s benchmark, and includes the reinvestment of distributions. The inception date used for the Barclays Capital U.S. Aggregate Bond Index was 07/31/ 04. (The returns include the Fund level expenses, but exclude the insurance charges). Past performance does not guarantee future results. The value of the contract will fluctuate so that when redeemed, it may be worth more or less than the original investment.

Investment Concerns

Bonds offer a relatively stable level of income, although bond prices will fluctuate providing the potential for principal gain or loss. Intermediate-term, higher-quality bonds generally offer less risk than longer-term bonds and a lower rate of return.

The Fund is subject to the risk that principal value tends to react in opposition to the movement of interest rates and that a rising interest rate environment increases the risk of loss of principal.

Q. How did the Fund perform during the 12-month period between January 1, 2009 and December 31, 2009?

A. The Fund returned 8.57%. That compared to a 5.93% return for its benchmark, the Barclays Capital U.S. Aggregate Bond Index.1

Q. What factors affected the Fund’s performance?

A. High-quality corporate bonds, high-yield (“junk”) bonds and mortgage-backed and other structured securities all posted strong returns as confidence in the economy increased throughout the period. Government support programs such as the Public-Private Investment Fund and the Term Asset-Backed Securities Loan Facility helped bolster investors’ confidence and provide stability to the economy. In addition, Treasury and agency durations fell, boosting absolute returns.2

During the year, the Fund held overweight positions in several outperforming sectors, including corporate bonds, asset-backed securities, commercial mortgage-backed securities and private-label mortgages. Those larger-than-benchmark positions boosted returns relative to the index. The Fund’s underweight position in agency securities slightly reduced relative returns, on average.2

| 1 | The Fund is measured against Barclays Capital U.S. Aggregate Bond Index which is a market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed and mortgage-backed securities, with maturities of at least one year. The index is unmanaged and does not reflect the deduction of expenses associated with a mutual fund, such as investment management and fund accounting fees. The Fund’s performance reflects the deduction of fees for these services. Investors cannot invest directly in an index, although they can invest in its underlying securities. |

| 2 | Portfolio composition is as of December 31, 2009, and is subject to change. |

A portion of the Fund’s fees have been reduced. If fees had not been reduced, the Fund’s total return for the periods would have been lower.

6

Table of Contents

Summary of Portfolio Holdings (Unaudited)

December 31, 2009

Each BB&T Variable Insurance Fund’s portfolio composition was as follows at December 31, 2009:

| Percentage of net assets | ||

BB&T Large Cap VIF | ||

Consumer Discretionary | 6.9% | |

Consumer Staples | 11.4% | |

Energy | 13.9% | |

Financials | 12.7% | |

Health Care | 13.7% | |

Industrials | 10.9% | |

Information Technology | 17.9% | |

Materials | 5.9% | |

Telecommunication Services | 4.3% | |

Utilities | 2.0% | |

Cash Equivalents | 0.3% | |

| 99.9% | ||

BB&T Mid Cap Growth VIF | ||

Consumer Discretionary | 15.0% | |

Energy | 14.7% | |

Financials | 5.6% | |

Health Care | 7.3% | |

Industrials | 15.5% | |

Information Technology | 30.2% | |

Materials | 10.5% | |

Cash Equivalents | 5.4% | |

| 104.2% | ||

BB&T Capital Manager Equity VIF | ||

BB&T Equity Income Fund | 9.0% | |

BB&T Equity Index Fund | 0.8% | |

BB&T International Equity Fund | 21.1% | |

BB&T Large Cap Fund | 8.3% | |

BB&T Mid Cap Growth Fund | 8.9% | |

BB&T Mid Cap Value Fund | 13.1% | |

BB&T Special Opportunities Equity Fund | 4.8% | |

BB&T U.S. Treasury Money Market Fund | 2.0% | |

Exchange Traded Funds | 27.6% | |

Commodity Investment Company | 4.4% | |

| 100.0% | ||

BB&T Special Opportunities Equity VIF | ||

Consumer Discretionary | 6.0% | |

Consumer Staples | 2.7% | |

Energy | 5.7% | |

Financials | 1.6% | |

Health Care | 26.9% | |

Industrials | 5.2% | |

Information Technology | 31.4% | |

Materials | 2.2% | |

Cash Equivalents | 16.4% | |

| 98.1% | ||

BB&T Total Return Bond VIF | ||

Asset Backed Securities | 3.0% | |

Collateralized Mortgage Obligations | 10.8% | |

Commercial Mortgage-Backed Securities | 8.0% | |

Corporate Bonds | 37.5% | |

Fannie Mae | 19.3% | |

Foreign Government Bonds | 0.8% | |

Freddie Mac | 10.7% | |

Ginnie Mae | 5.8% | |

Municipal Bonds | 6.1% | |

U.S. Treasury Notes | 0.4% | |

Cash Equivalents | 0.1% | |

| 102.5% | ||

7

Table of Contents

Expense Example (Unaudited)

December 31, 2009

As a shareholder of the BB&T Variable Insurance Funds, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses.

These examples are intended to help you understand your ongoing costs (in dollars) of investing in the BB&T Variable Insurance Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

These examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from July 1, 2009 through December 31, 2009.

Actual Example

The table below provides information about actual account values and actual expenses. You may use the information below, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

| Beginning Account Value 7/1/09 | Ending Account Value 12/31/09 | Expenses Paid During Period 7/1/09 - 12/31/09* | Expense Ratio During Period 7/1/09 - 12/31/09 | |||||||

BB&T Large Cap VIF | $ | 1,000.00 | $ | 1,235.20 | $5.52 | 0.98% | ||||

BB&T Mid Cap Growth VIF | 1,000.00 | 1,230.50 | 6.02 | 1.07% | ||||||

BB&T Capital Manager Equity VIF | 1,000.00 | 1,219.10 | 2.13 | 0.38% | ||||||

BB&T Special Opportunities Equity VIF | 1,000.00 | 1,207.30 | 7.07 | 1.27% | ||||||

BB&T Total Return Bond VIF | 1,000.00 | 1,060.00 | 4.73 | 0.91% | ||||||

| * | Expenses are equal to the average account value times the Fund’s annualized expense ratio multiplied by the number of days in the most recent fiscal half-year divided by the number of days in the fiscal year. Expenses shown do not include annuity contract fees. |

Hypothetical Example for Comparison Purposes

The table below provides information about hypothetical account values and hypothetical expenses based on each BB&T Variable Insurance Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value 7/1/09 | Ending Account Value 12/31/09 | Expenses Paid During Period 7/1/09 - 12/31/09* | Expense Ratio During Period 7/1/09 - 12/31/09 | |||||||

BB&T Large Cap VIF | $ | 1,000.00 | $ | 1,020.27 | $4.99 | 0.98% | ||||

BB&T Mid Cap Growth VIF | 1,000.00 | 1,019.81 | 5.45 | 1.07% | ||||||

BB&T Capital Manager Equity VIF | 1,000.00 | 1,023.29 | 1.94 | 0.38% | ||||||

BB&T Special Opportunities Equity VIF | 1,000.00 | 1,018.80 | 6.46 | 1.27% | ||||||

BB&T Total Return Bond VIF | 1,000.00 | 1,020.62 | 4.63 | 0.91% | ||||||

| * | Expenses are equal to the average account value times the Fund’s annualized expense ratio multiplied by the number of days in the most recent fiscal half-year divided by the number of days in the fiscal year. Expenses shown do not include annuity contract fees. |

8

Table of Contents

Schedule of Portfolio Investments

December 31, 2009

| Shares | Fair Value | ||||

COMMON STOCKS (99.6%) | |||||

Consumer Discretionary (6.9%) | |||||

| 40,650 | Comcast Corp., Class A | $ | 685,359 | ||

| 13,700 | Genuine Parts Co. | 520,052 | |||

| 12,500 | Staples, Inc. | 307,375 | |||

| 22,200 | Walt Disney Co. (The) | 715,950 | |||

| 2,228,736 | |||||

Consumer Staples (11.4%) | |||||

| 18,200 | Campbell Soup Co. | 615,160 | |||

| 10,050 | CVS Caremark Corp. | 323,710 | |||

| 21,215 | Kraft Foods, Inc., Class A | 576,624 | |||

| 7,910 | PepsiCo, Inc. | 480,928 | |||

| 4,250 | Procter & Gamble Co. (The) | 257,678 | |||

| 13,610 | Sysco Corp. | 380,263 | |||

| 20,400 | Unilever PLC, ADR | 650,760 | |||

| 7,260 | Wal-Mart Stores, Inc. | 388,047 | |||

| 3,673,170 | |||||

Energy (13.9%) | |||||

| 7,200 | Anadarko Petroleum Corp. | 449,424 | |||

| 8,130 | Chevron Corp. | 625,929 | |||

| 15,290 | ConocoPhillips | 780,860 | |||

| 13,487 | Exxon Mobil Corp. | 919,679 | |||

| 11,175 | Schlumberger, Ltd. | 727,381 | |||

| 12,710 | Suncor Energy, Inc. | 448,790 | |||

| 6,110 | Transocean, Ltd.(a) | 505,908 | |||

| 4,457,971 | |||||

Financials (12.7%) | |||||

| 294 | Berkshire Hathaway, Inc. Class B(a) | 966,084 | |||

| 13,400 | JPMorgan Chase & Co. | 558,378 | |||

| 16,630 | MetLife, Inc. | 587,871 | |||

| 14,600 | State Street Corp. | 635,684 | |||

| 8,370 | Travelers Cos., Inc. (The) | 417,328 | |||

| 20,000 | U.S. Bancorp | 450,200 | |||

| 17,300 | Wells Fargo & Co. | 466,927 | |||

| 4,082,472 | |||||

Health Care (13.7%) | |||||

| 13,065 | Abbott Laboratories | 705,379 | |||

| 11,527 | Baxter International, Inc. | 676,404 | |||

| 9,450 | Johnson & Johnson | 608,675 | |||

| 17,000 | Medtronic, Inc. | 747,660 | |||

| 21,000 | Merck & Co., Inc. | 767,340 | |||

| 6,000 | Teva Pharmaceutical Industries, Ltd., ADR | 337,080 | |||

| 9,355 | WellPoint, Inc.(a) | 545,303 | |||

| 4,387,841 | |||||

Industrials (10.9%) | |||||

| 37,500 | ABB, Ltd., ADR(a) | 716,250 | |||

| 16,800 | Avery Dennison Corp. | 613,032 | |||

| 11,400 | Emerson Electric Co. | 485,640 | |||

| 38,750 | General Electric Co. | 586,288 | |||

| 6,390 | Lockheed Martin Corp. | 481,486 | |||

| 17,470 | Pall Corp. | 632,414 | |||

| 3,515,110 | |||||

Information Technology (17.9%) | |||||

| 34,800 | Applied Materials, Inc. | 485,112 | |||

| 26,000 | Cisco Systems, Inc.(a) | 622,440 | |||

| Shares | Fair Value | |||||

| COMMON STOCKS — (continued) | |||||

Information Technology — (continued) | ||||||

| 16,800 | Corning, Inc. | $ | 324,408 | |||

| 13,500 | eBay, Inc.(a) | 317,790 | ||||

| 546 | Google, Inc., Class A(a) | 338,509 | ||||

| 6,500 | Hewlett-Packard Co. | 334,815 | ||||

| 38,000 | Intel Corp. | 775,200 | ||||

| 3,150 | International Business Machines Corp. | 412,335 | ||||

| 37,500 | Microsoft Corp. | 1,143,375 | ||||

| 26,550 | Oracle Corp. | 651,537 | ||||

| 7,200 | QUALCOMM, Inc. | 333,072 | ||||

| 5,738,593 | ||||||

Materials (5.9%) | ||||||

| 22,500 | Barrick Gold Corp. | 886,050 | ||||

| 13,800 | E.I. du Pont de Nemours & Co. | 464,646 | ||||

| 6,600 | Monsanto Co. | 539,550 | ||||

| 1,890,246 | ||||||

Telecommunication Services (4.3%) | ||||||

| 21,300 | AT&T, Inc. | 597,039 | ||||

| 33,300 | Vodafone Group PLC, ADR | 768,897 | ||||

| 1,365,936 | ||||||

Utilities (2.0%) | ||||||

| 11,100 | Edison International | 386,058 | ||||

| 5,250 | Exelon Corp. | 256,568 | ||||

| 642,626 | ||||||

Total Common Stocks | 31,982,701 | |||||

| INVESTMENT COMPANY (0.3%) | |||||

| 98,368 | Federated Treasury Obligations Fund, Institutional Shares | 98,368 | ||||

Total Investment Company | 98,368 | |||||

| Principal Amount | ||||||

| SHORT TERM INVESTMENTS (0.0%) | ||||||

| $ | 29,800 | BNY Institutional Cash Reserve, Series B | 5,811 | |||

Total Short Term Investments | 5,811 | |||||

| Total Investments — 99.9% | 32,086,880 | ||||

| Net Other Assets (Liabilities) — 0.1% | 36,812 | ||||

| NET ASSETS — 100.0% | $ | 32,123,692 | |||

| (a) | Represents non-income producing security. |

ADR — American Depository Receipt

See accompanying notes to the financial statements.

9

Table of Contents

Schedule of Portfolio Investments

December 31, 2009

| Shares | Fair Value | ||||

COMMON STOCKS (98.8%) | |||||

Consumer Discretionary (15.0%) | |||||

| 1,200 | Amazon.com, Inc.(a) | $ | 161,424 | ||

| 6,450 | American Eagle Outfitters, Inc. | 109,521 | |||

| 8,035 | Cheesecake Factory (The)(a) | 173,476 | |||

| 5,860 | Darden Restaurants, Inc. | 205,510 | |||

| 4,900 | Dick’s Sporting Goods, Inc.(a) | 121,863 | |||

| 5,640 | JOS A Bank Clothiers, Inc.(a) | 237,952 | |||

| 4,500 | P.F. Chang’s China Bistro, Inc.(a) | 170,595 | |||

| 2,300 | Polo Ralph Lauren Corp. | 186,254 | |||

| 1,366,595 | |||||

Energy (14.7%) | |||||

| 5,790 | Alpha Natural Resources, Inc.(a) | 251,170 | |||

| 3,035 | Anadarko Petroleum Corp. | 189,445 | |||

| 14,900 | EXCO Resources, Inc. | 316,327 | |||

| 4,325 | National Oilwell Varco, Inc. | 190,689 | |||

| 4,390 | Petroleo Brasileiro SA, ADR | 209,315 | |||

| 3,850 | Southwestern Energy Co.(a) | 185,570 | |||

| 1,342,516 | |||||

Financials (5.6%) | |||||

| 625 | CME Group, Inc. | 209,969 | |||

| 5,900 | Piper Jaffray Cos.(a) | 298,599 | |||

| 508,568 | |||||

Health Care (7.3%) | |||||

| 6,510 | Alexion Pharmaceuticals, Inc.(a) | 317,818 | |||

| 2,300 | Celgene Corp.(a) | 128,064 | |||

| 12,250 | Mylan, Inc.(a)(b) | 225,768 | |||

| 671,650 | |||||

Industrials (15.5%) | |||||

| 6,985 | Aecom Technology Corp.(a) | 192,087 | |||

| 2,675 | C.H. Robinson Worldwide, Inc. | 157,103 | |||

| 4,525 | Duoyuan Global Water, Inc., ADR(a)(b) | 161,950 | |||

| 5,265 | Fluor Corp. | 237,136 | |||

| 10,650 | McDermott International, Inc.(a) | 255,706 | |||

| 11,470 | Orion Marine Group, Inc.(a) | 241,558 | |||

| 8,275 | Quanta Services, Inc.(a) | 172,451 | |||

| 1,417,991 | |||||

Information Technology (30.2%) | |||||

| 8,850 | Altera Corp. | 200,276 | |||

| 2,050 | Equinix, Inc.(a) | 217,608 | |||

| 6,150 | KLA-Tencor Corp. | 222,384 | |||

| 16,950 | Marvell Technology Group, Ltd.(a) | 351,713 | |||

| 13,125 | Nuance Communications, Inc.(a) | 203,962 | |||

| 8,830 | Red Hat, Inc.(a) | 272,847 | |||

| 8,550 | Rovi Corp.(a) | 272,488 | |||

| 3,600 | SINA Corp.(a)(b) | 162,648 | |||

| Shares | Fair Value | ||||||

| COMMON STOCKS — (continued) | ||||||

Information Technology — (continued) | |||||||

| 9,475 | VanceInfo Technologies, Inc., ADR(a) | $ | 182,015 | ||||

| 6,875 | Varian Semiconductor Equipment Associates, Inc.(a) | 246,675 | |||||

| 6,875 | Veeco Instruments, Inc.(a) | 227,150 | |||||

| 8,025 | Xilinx, Inc. | 201,106 | |||||

| 2,760,872 | |||||||

Materials (10.5%) | |||||||

| 2,415 | Air Products & Chemicals, Inc. | 195,760 | |||||

| 2,665 | Freeport-McMoRan Copper & Gold, Inc.(a) | 213,973 | |||||

| 4,490 | Nucor Corp. | 209,458 | |||||

| 9,700 | Teck Resources, Ltd., Class B(a) | 339,209 | |||||

| 958,400 | |||||||

Total Common Stocks | 9,026,592 | ||||||

| INVESTMENT COMPANY (1.8%) |

| |||||

| 163,214 | Federated Treasury Obligations Fund, Institutional Shares | 163,214 | |||||

Total Investment Company | 163,214 | ||||||

| Principal Amount | |||||||

| SECURITIES HELD AS COLLATERAL FOR | | |||||

| $ | 334,495 | Pool of Various Securities | 331,561 | ||||

Total Securities Held as Collateral for Securities on Loan (Cost $334,495) | 331,561 | ||||||

| Total Investments — 104.2% | 9,521,367 | |||||

| Net Other Assets (Liabilities) — (4.2)% | (385,900 | ) | ||||

| NET ASSETS — 100.0% | $ | 9,135,467 | ||||

| (a) | Represents non-income producing security. |

| (b) | Represents that all or a portion of the security was on loan as of December 31, 2009. |

ADR — American Depository Receipt

See accompanying notes to the financial statements.

10

Table of Contents

BB&T Capital Manager Equity VIF

Schedule of Portfolio Investments

December 31, 2009

| Shares | Fair Value | |||||

AFFILIATED INVESTMENT COMPANIES (68.0%) |

| |||||

| 58,718 | BB&T Equity Income Fund, Institutional Class | $ | 715,183 | |||

| 8,241 | BB&T Equity Index Fund, Institutional Class | 61,644 | ||||

| 326,146 | BB&T International Equity Fund, Institutional Class | 1,682,911 | ||||

| 62,020 | BB&T Large Cap Fund, Institutional Class | 658,028 | ||||

| 78,343 | BB&T Mid Cap Growth Fund, Institutional Class(a) | 705,869 | ||||

| 92,824 | BB&T Mid Cap Value Fund, Institutional Class | 1,044,267 | ||||

| 24,016 | BB&T Special Opportunities Equity Fund, Institutional Class(a) | 378,494 | ||||

| 159,013 | BB&T U.S. Treasury Money Market Fund, Institutional Class | 159,013 | ||||

Total Affiliated Investment Companies | 5,405,409 | |||||

EXCHANGE TRADED FUNDS (27.6%) |

| |||||

| 9,034 | iShares Russell 2000 Index Fund | 562,457 | ||||

| 14,587 | iShares S&P 500 Index Fund | 1,628,056 | ||||

Total Exchange Traded Funds | 2,190,513 | |||||

COMMODITY INVESTMENT COMPANY (4.4%) |

| |||||

| 41,184 | Credit Suisse Commodity Return Strategy Fund | 353,767 | ||||

Total Commodity Investment Company | 353,767 | |||||

Total Investments — 100.0% | 7,949,689 | |||||

Net Other Assets (Liabilities) — (0.0)% | (2,968 | ) | ||||

NET ASSETS — 100.0% | $ | 7,946,721 | ||||

| (a) | Represents non-income producing security. |

See accompanying notes to the financial statements.

11

Table of Contents

BB&T Special Opportunities Equity VIF

Schedule of Portfolio Investments

December 31, 2009

| Shares | Fair Value | ||||

COMMON STOCKS (81.7%) | |||||

Consumer Discretionary (6.0%) | |||||

| 87,000 | Comcast Corp., Class A | $ | 1,466,820 | ||

| 27,000 | Yum! Brands, Inc. | 944,190 | |||

| 2,411,010 | |||||

Consumer Staples (2.7%) | |||||

| 20,000 | Dole Food Co., Inc.(a) | 248,200 | |||

| 11,000 | Energizer Holdings, Inc.(a) | 674,080 | |||

| 2,569 | Ralcorp Holdings, Inc.(a) | 153,395 | |||

| 1,075,675 | |||||

Energy (5.7%) | |||||

| 12,000 | Apache Corp. | 1,238,040 | |||

| 10,000 | Halliburton Co. | 300,900 | |||

| 42,100 | Weatherford International, Ltd.(a) | 754,011 | |||

| 2,292,951 | |||||

Financials (1.6%) | |||||

| 1,900 | Markel Corp.(a) | 646,000 | |||

Health Care (26.9%) | |||||

| 29,000 | Allscripts-Misys Healthcare Solutions, Inc.(a)(b) | 586,670 | |||

| 21,000 | Baxter International, Inc. | 1,232,280 | |||

| 20,000 | Becton Dickinson & Co. | 1,577,200 | |||

| 60,000 | Bristol-Myers Squibb Co. | 1,515,000 | |||

| 30,000 | Gilead Sciences, Inc.(a) | 1,298,400 | |||

| 23,000 | McKesson Corp.(b) | 1,437,500 | |||

| 10,000 | MedCath Corp.(a) | 79,100 | |||

| 26,000 | Teva Pharmaceutical Industries, Ltd., ADR | 1,460,680 | |||

| 53,000 | UnitedHealth Group, Inc. | 1,615,440 | |||

| 10,802,270 | |||||

Industrials (5.2%) | |||||

| 14,000 | L-3 Communications Holdings, Inc. | 1,217,300 | |||

| 16,000 | SPX Corp. | 875,200 | |||

| 2,092,500 | |||||

Information Technology (31.4%) | |||||

| 80,000 | Activision Blizzard, Inc.(a) | 888,800 | |||

| 64,000 | Akamai Technologies, Inc.(a) | 1,621,120 | |||

| 215,000 | ARM Holdings PLC, ADR | 1,840,400 | |||

| 60,000 | Cisco Systems, Inc.(a)(b) | 1,436,400 | |||

| Shares | Fair Value | |||||

| COMMON STOCKS — (continued) | |||||

Information Technology — (continued) | ||||||

| 25,000 | Corning, Inc. | $ | 482,750 | |||

| 94,000 | Dell, Inc.(a)(b) | 1,349,840 | ||||

| 57,000 | eBay, Inc.(a) | 1,341,780 | ||||

| 30,000 | Harris Corp. | 1,426,500 | ||||

| 35,000 | Intuit, Inc.(a) | 1,074,850 | ||||

| 63,000 | Symantec Corp.(a) | 1,127,070 | ||||

| 12,589,510 | ||||||

Materials (2.2%) | ||||||

| 35,000 | Nalco Holding Co.(b) | 892,850 | ||||

Total Common Stocks | 32,802,766 | |||||

| INVESTMENT COMPANY (16.4%) | |||||

| 6,603,260 | Federated Treasury Obligations Fund, Institutional Shares | 6,603,260 | ||||

Total Investment Company | 6,603,260 | |||||

| Principal Amount | ||||||

| SHORT TERM INVESTMENTS (0.0%) | |||||

| $ | 37,343 | BNY Institutional Cash Reserve, Series B | 7,282 | |||

Total Short Term Investments | 7,282 | |||||

| Total Investments — 98.1% | 39,413,308 | ||||

| Net Other Assets (Liabilities) — 1.9% | 748,619 | ||||

| NET ASSETS — 100.0% | $ | 40,161,927 | |||

| (a) | Represents non-income producing security. |

| (b) | Security held as collateral for written call option. |

ADR — American Depository Receipt

See accompanying notes to the financial statements.

12

Table of Contents

Schedule of Portfolio Investments

December 31, 2009

| Principal Amount | Fair Value | |||||

| ASSET BACKED SECURITIES (3.0%) | |||||

| $ | 100,000 | American Express Credit Account Master Trust, Series 2007-8, Class B, 0.933%, 5/15/15* | $ | 95,800 | ||

| 250,000 | Bank of America Credit Card Trust, Series 2006-A6, Class A6, 0.263%, 11/15/13* | 246,902 | ||||

| 35,000 | Bank of America Credit Card Trust, Series 2008-A1, Class A1, 0.813%, 4/15/13* | 34,920 | ||||

| 98,000 | Chase Funding Mortgage Loan Asset-Backed Certificates, Series 2003-4, Class 1A5, STEP, 5.416%, 5/25/33(a) | 74,927 | ||||

| 79,000 | Honda Auto Receivables Owner Trust, Series 2009-2, Class A4, 4.430%, 7/15/15 | 83,191 | ||||

| 40,000 | MBNA Credit Card Master Note Trust, Series 2005-A4, Class A4, 0.273%, 11/15/12* | 39,869 | ||||

| 82,000 | World Omni Auto Receivables Trust, Series 2009-A, Class A4, 5.120%, 5/15/14 | 87,315 | ||||

Total Asset Backed Securities | 662,924 | |||||

| COLLATERALIZED MORTGAGE OBLIGATIONS | |||||

| 161,566 | Chase Mortgage Finance Corp., Series 2003-S7, Class A1, 0.631%, 8/25/18* | 149,124 | ||||

| 81,467 | Countrywide Home Loan Mortgage Pass Through Trust, Series 2004-7, Class 3A1, 4.050%, 5/25/34* | 75,309 | ||||

| 374,963 | Fannie Mae, Series 2009-70, Class PA, 5.000%, 8/25/35 | 395,979 | ||||

| 213,895 | Fannie Mae, Series 2009-86, Class CA, 4.500%, 9/25/24 | 223,378 | ||||

| 85,638 | Freddie Mac, Series 2906, Class VC, 5.000%, 12/15/15 | 90,828 | ||||

| 302,941 | Freddie Mac, Series 3578, Class AM, 4.500%, 9/15/16 | 315,326 | ||||

| 157,368 | MASTR Alternative Loans Trust, Series 2005-4, Class 4A1, 5.500%, 6/25/20 | 150,680 | ||||

| 57,783 | MASTR Asset Securitization Trust, Series 2004-1, Class 1A1, 5.000%, 2/25/34 | 57,644 | ||||

| 195,861 | RAAC, Series 2004-SP3, Class AI5, 4.890%, 12/25/32* | 187,262 | ||||

| 150,506 | RBSSP Resecuritization Trust, Series 2009-6, Class 2A1, 4.970%, 1/26/36*(b) | 141,385 | ||||

| 190,023 | Structured Adjustable Rate Mortgage Loan Trust, Series 2004-6, Class 4A1, 4.847%, 6/25/34* | 163,151 | ||||

| 123,229 | Structured Asset Securities Corp., Series 2005-6, Class 5A1, 5.000%, 5/25/35 | 117,818 | ||||

| 170,649 | Wells Fargo Mortgage Backed Securities Trust, Series 2004-BB, Class A2, 2.935%, 1/25/35* | 154,913 | ||||

| 182,730 | Wells Fargo Mortgage Backed Securities Trust, Series 2005-AR16, Class 6A3, 5.000%, 10/25/35* | 164,905 | ||||

Total Collateralized Mortgage Obligations (Cost $2,374,939) | 2,387,702 | |||||

| COMMERCIAL MORTGAGE-BACKED SECURITIES | |||||

| 150,000 | Bear Stearns Commercial Mortgage Securities, Series 2005-PWR8, Class A4, 4.674%, 6/11/41 | 143,491 | ||||

| 140,000 | Credit Suisse Mortgage Capital Certificates, Series 2009-RR1, Class A3A, 5.383%, 2/15/40(b) | 124,680 | ||||

| Principal Amount | Fair Value | |||||

| COMMERCIAL MORTGAGE-BACKED | |||||

| $ | 220,000 | CS First Boston Mortgage Securities Corp., Series 2005-C1, Class A3, 4.813%, 2/15/38 | $ | 219,647 | ||

| 76,740 | Greenwich Capital Commercial Funding Corp., Series 2005-GG3, Class A2, 4.305%, 8/10/42 | 76,598 | ||||

| 165,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Series 2003-CB7, Class A4, 4.879%, 1/12/38* | 165,699 | ||||

| 360,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Series 2005-CB11, Class A4, 5.335%, 8/12/37* | 355,254 | ||||

| 166,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Series 2005-LDP1, Class A3, 4.865%, 3/15/46 | 163,886 | ||||

| 210,000 | JP Morgan Chase Commercial Mortgage Securities Corp., Series 2006-CB15, Class A4, 5.814%, 6/12/43* | 202,092 | ||||

| 28,000 | Merrill Lynch/Countrywide Commercial Mortgage Trust, Series 2006-3, Class A3, 5.389%, 7/12/46* | 27,298 | ||||

| 220,000 | Morgan Stanley Capital I, Series 2005-HQ6, Class A4A, 4.989%, 8/13/42 | 212,954 | ||||

| 67,000 | Wachovia Bank Commercial Mortgage Trust, Series 2007-C33, Class A3, 5.902%, 2/15/51* | 65,894 | ||||

Total Commercial Mortgage-Backed Securities | 1,757,493 | |||||

| CORPORATE BONDS (37.5%) | |||||

Consumer Discretionary (3.4%) | ||||||

| 154,000 | Comcast Cable Communications Holdings, Inc., 9.455%, 11/15/22 | 198,066 | ||||

| 141,000 | Historic TW, Inc., 9.125%, 1/15/13 | 163,607 | ||||

| 203,000 | Time Warner Cable, Inc., 6.750%, 6/15/39 | 212,603 | ||||

| 175,000 | Viacom, Inc., 5.625%, 9/15/19 | 182,718 | ||||

| 756,994 | ||||||

Consumer Staples (2.5%) | ||||

| 96,000 | Altria Group, Inc., 9.950%, 11/10/38 | 125,137 | ||

| 255,000 | Anheuser-Busch InBev Worldwide, Inc., 4.125%, 1/15/15(b) | 258,914 | ||

| 55,000 | Brown University, 4.570%, 9/1/19 | 54,743 | ||

| 117,000 | CVS Caremark Corp., 6.125%, 9/15/39 | 115,959 | ||

| 554,753 | ||||

Energy (2.3%) | ||||

| 145,000 | Boardwalk Pipelines LP, 5.750%, 9/15/19 | 142,971 | ||

| 68,000 | Peabody Energy Corp., Series B, 6.875%, 3/15/13 | 68,765 | ||

| 105,000 | Plains All American Pipeline LP, 8.750%, 5/1/19 | 123,805 | ||

| 130,000 | Smith International, Inc., 9.750%, 3/15/19 | 164,675 | ||

| 500,216 | ||||

Financials (17.2%) | ||||

| 220,000 | Aflac, Inc., 8.500%, 5/15/19 | 253,438 | ||

| 221,000 | American Express Co., 8.125%, 5/20/19 | 261,899 | ||

| 266,000 | Bank of America Corp., 5.125%, 11/15/14(c) | 275,786 | ||

| 161,000 | Bank of America Corp., 5.750%, 12/1/17 | 164,867 | ||

| 65,000 | Bank of America Corp., 7.625%, 6/1/19 | 75,195 |

| Continued | ||||

13

Table of Contents

BB&T Total Return Bond VIF

Schedule of Portfolio Investments — (continued)

December 31, 2009

| Principal Amount | Fair Value | |||||

| CORPORATE BONDS — (continued) | |||||

Financials — (continued) | ||||||

| $ | 210,000 | Bear Stearns Cos., LLC (The), 7.250%, 2/1/18(c) | $ | 241,049 | ||

| 74,000 | Caterpillar Financial Services Corp., MTN, 7.150%, 2/15/19 | 85,573 | ||||

| 105,000 | Credit Suisse, New York, 5.300%, 8/13/19 | 107,832 | ||||

| 158,000 | ERP Operating LP REIT, 5.125%, 3/15/16 | 154,022 | ||||

| 30,000 | GATX Financial Corp., 5.125%, 4/15/10 | 30,218 | ||||

| 348,000 | General Electric Capital Corp., MTN, 6.875%, 1/10/39 | 359,374 | ||||

| 101,000 | Goldman Sachs Group, Inc. (The), 7.500%, 2/15/19 | 117,746 | ||||

| 148,000 | Goldman Sachs Group, Inc. (The), 6.125%, 2/15/33(c) | 148,626 | ||||

| 96,000 | Goldman Sachs Group, Inc. (The), 6.750%, 10/1/37 | 98,677 | ||||

| 190,000 | Hyundai Capital Services, Inc., 6.000%, 5/5/15(b) | 198,391 | ||||

| 162,000 | Merrill Lynch & Co., Inc., MTN, 6.875%, 4/25/18 | 174,545 | ||||

| 115,000 | MetLife, Inc., 6.750%, 6/1/16 | 128,782 | ||||

| 273,000 | Morgan Stanley, MTN, Series F, 6.625%, 4/1/18(c) | 295,159 | ||||

| 177,000 | Prudential Financial, Inc., MTN, Series B, 5.100%, 9/20/14 | 184,546 | ||||

| 113,000 | Simon Property Group LP REIT, 6.750%, 5/15/14 | 120,422 | ||||

| 114,000 | Wachovia Corp., 5.625%, 10/15/16 | 116,564 | ||||

| 194,000 | Wells Fargo & Co., 5.625%, 12/11/17(c) | 201,790 | ||||

| 3,794,501 | ||||||

Health Care (0.7%) | ||||||

| 90,000 | Laboratory Corp. of America | 94,099 | ||||

| 60,000 | Zimmer Holdings, Inc., 5.750%, 11/30/39 | 58,818 | ||||

| 152,917 | ||||||

Industrials (3.4%) | ||||||

| 186,000 | Allied Waste North America, Inc., 6.875%, 6/1/17(c) | 197,392 | ||||

| 240,000 | Corrections Corp. of America, 6.250%, 3/15/13(c) | 241,200 | ||||

| 60,000 | Goodrich (BF) Corp., 6.290%, 7/1/16 | 64,363 | ||||

| 110,000 | L-3 Communications Corp., 5.875%, 1/15/15 | 109,863 | ||||

| 142,000 | Roper Industries, Inc., 6.250%, 9/1/19 | 147,831 | ||||

| 760,649 | ||||||

Information Technology (2.4%) | ||||||

| 45,000 | Agilent Technologies, Inc., 5.500%, 9/14/15 | 47,169 | ||||

| 75,000 | CA, Inc., 5.375%, 12/1/19 | 75,421 | ||||

| 107,000 | Fiserv, Inc., 6.125%, 11/20/12 | 116,509 | ||||

| 269,000 | Xerox Corp., 6.350%, 5/15/18 | 280,602 | ||||

| 519,701 | ||||||

Materials (2.1%) | ||||||

| 225,000 | ArcelorMittal, 9.850%, 6/1/19 | 291,015 | ||||

| 118,000 | International Paper Co., 7.300%, 11/15/39 | 125,182 | ||||

| 35,000 | Valspar Corp., 7.250%, 6/15/19 | 38,408 | ||||

| 454,605 | ||||||

Telecommunication Services (2.8%) | ||||||

| 103,000 | America Movil SAB de CV, 6.375%, 3/1/35 | 106,325 | ||||

| 109,000 | AT&T, Inc., 6.400%, 5/15/38(c) | 112,016 | ||||

| Principal Amount | Fair Value | |||||

| CORPORATE BONDS — (continued) | |||||

Telecommunication Services — (continued) | ||||||

| $ | 58,000 | Telecom Italia Capital SA, 7.175%, 6/18/19 | $ | 64,662 | ||

| 100,000 | Telecom Italia Capital SA, 7.721%, 6/4/38 | 115,133 | ||||

| 51,000 | Verizon Communications, Inc., 6.350%, 4/1/19 | 56,265 | ||||

| 146,000 | Verizon Communications, Inc., 7.350%, 4/1/39 | 169,376 | ||||

| 623,777 | ||||||

Utilities (0.7%) | ||||||

| 144,000 | Ohio Power Co., Series K, 6.000%, 6/1/16 | 152,664 | ||||

Total Corporate Bonds | 8,270,777 | |||||

| MORTGAGE-BACKED SECURITIES (35.7%) | |||||

Fannie Mae(d) (19.2%) | ||||||

| 17,666 | 4.500%, 10/1/18, Pool #752030 | 18,414 | ||||

| 12,408 | 5.500%, 11/1/20, Pool #843972 | 13,212 | ||||

| 8,324 | 5.500%, 12/1/20, Pool #831138 | 8,863 | ||||

| 31,371 | 5.500%, 5/1/21, Pool #895628 | 33,404 | ||||

| 33,005 | 5.500%, 6/1/21, Pool #831526 | 35,021 | ||||

| 174,585 | 5.500%, 4/1/22, Pool #914937 | 185,000 | ||||

| 118,952 | 5.000%, 12/1/22, Pool #967350 | 124,506 | ||||

| 368,655 | 5.000%, 5/1/23, Pool #976197 | 385,672 | ||||

| 39,806 | 5.000%, 10/1/25, Pool #255894 | 41,273 | ||||

| 40,683 | 5.500%, 2/1/27, Pool #256600 | 42,956 | ||||

| 188,998 | 5.500%, 1/1/34, Pool #757571 | 198,644 | ||||

| 33,567 | 6.000%, 9/1/34, Pool #790912 | 35,801 | ||||

| 48,308 | 6.500%, 9/1/34, Pool #796569 | 52,007 | ||||

| 19,116 | 7.000%, 6/1/35, Pool #255820 | 20,976 | ||||

| 85,250 | 5.000%, 11/1/35, Pool #842402 | 87,652 | ||||

| 18,236 | 5.500%, 2/1/36, Pool #256101 | 19,156 | ||||

| 234,405 | 6.000%, 6/1/36, Pool #886959 | 248,982 | ||||

| 50,814 | 5.500%, 12/1/36, Pool #922224 | 53,289 | ||||

| 223,078 | 5.500%, 12/1/36, Pool #928043 | 233,942 | ||||

| 48,763 | 6.000%, 12/1/36, Pool #902054 | 51,796 | ||||

| 119,178 | 5.500%, 1/1/37, Pool #256552 | 124,982 | ||||

| 46,800 | 6.000%, 1/1/37, Pool #906095 | 49,710 | ||||

| 91,059 | 5.000%, 3/1/37, Pool #911395 | 93,553 | ||||

| 44,341 | 6.000%, 4/1/37, Pool #914725 | 47,036 | ||||

| 65,930 | 6.000%, 7/1/37, Pool #256800 | 69,937 | ||||

| 476,877 | 6.500%, 7/1/37, Pool #941315 | 511,227 | ||||

| 267,455 | 5.500%, 9/1/37, Pool #888638 | 280,271 | ||||

| 239,058 | 6.000%, 9/1/37, Pool #952420 | 253,588 | ||||

| 11,302 | 6.000%, 9/1/37, Pool #955005 | 11,989 | ||||

| 326,357 | 4.832%, 7/1/38, Pool #981430* | 341,448 | ||||

| 78,388 | 5.500%, 7/1/38, Pool #934323 | 82,144 | ||||

| 179,342 | 6.000%, 5/1/39, Pool #935238 | 190,102 | ||||

| 274,619 | 6.000%, 9/1/39, Pool #AD0132 | 291,310 | ||||

| 4,237,863 | ||||||

Freddie Mac(d) (10.7%) | ||||||

| 51,143 | 6.000%, 10/1/19, Pool #G11679 | 54,658 | ||||

| 25,257 | 5.500%, 10/1/21, Pool #G12425 | 26,807 | ||||

| 46,428 | 5.000%, 1/1/22, Pool #J04202 | 48,610 | ||||

| 72,926 | 5.000%, 5/1/22, Pool #J04788 | 76,353 | ||||

| 177,488 | 5.000%, 8/1/22, Pool #J05384 | 185,830 | ||||

| 172,037 | 5.500%, 12/1/22, Pool #G13665 | 182,596 | ||||

| 228,192 | 5.500%, 1/1/23, Pool #G12966 | 241,735 | ||||

| 236,183 | 6.000%, 11/1/23, Pool #G13325 | 252,143 | ||||

| 27,794 | 5.500%, 7/1/35, Pool #A36540 | 29,221 | ||||

| 14,307 | 6.000%, 7/1/35, Pool #A36304 | 15,233 | ||||

| 15,340 | 5.500%, 12/1/35, Pool #A40359 | 16,128 | ||||

| 44,027 | 5.500%, 2/1/36, Pool #G08111 | 46,205 | ||||

| Continued |

14

Table of Contents

BB&T Total Return Bond VIF

Schedule of Portfolio Investments — (continued)

December 31, 2009

| Principal Amount | Fair Value | |||||

| MORTGAGE-BACKED SECURITIES — (continued) | |||||

Freddie Mac(d) — (continued) | ||||||

| $ | 25,559 | 5.500%, 4/1/36, Pool #A44445 | $ | 26,823 | ||

| 105,264 | 6.000%, 9/1/36, Pool #A52325 | 111,909 | ||||

| 17,054 | 5.500%, 12/1/36, Pool #A80368 | 17,898 | ||||

| 94,405 | 5.878%, 12/1/36, Pool #1J1390* | 100,277 | ||||

| 68,509 | 5.500%, 4/1/37, Pool #G08192 | 71,845 | ||||

| 46,199 | 6.000%, 4/1/37, Pool #A58853 | 49,072 | ||||

| 39,460 | 5.000%, 6/1/37, Pool #G03094 | 40,511 | ||||

| 40,973 | 5.729%, 9/1/37, Pool #1Q0319* | 43,533 | ||||

| 147,421 | 6.500%, 12/1/37, Pool #A69955 | 157,939 | ||||

| 24,473 | 5.500%, 1/1/38, Pool #A71523 | 25,665 | ||||

| 73,558 | 5.242%, 4/1/38, Pool #783255* | 77,331 | ||||

| 189,750 | 5.500%, 6/1/38, Pool #A77678 | 198,980 | ||||

| 134,708 | 5.500%, 7/1/38, Pool #A78982 | 141,261 | ||||

| 60,484 | 5.500%, 7/1/38, Pool #G04388 | 63,426 | ||||

| 51,516 | 6.000%, 9/1/38, Pool #A81453 | 54,677 | ||||

| 2,356,666 | ||||||

Ginnie Mae (5.8%) | ||||||

| 245,268 | 5.500%, 9/15/38, Pool #782405 | 257,296 | ||||

| 187,000 | 5.000%, 1/15/39(e) | 192,289 | ||||

| 449,173 | 5.500%, 1/15/39, Pool #646685 | 471,161 | ||||

| 181,969 | 5.500%, 1/15/39, Pool #692307 | 190,876 | ||||

| 160,000 | 5.500%, 1/15/40(e) | 167,600 | ||||

| 1,279,222 | ||||||

Total Mortgage-Backed Securities | 7,873,751 | |||||

| MUNICIPAL BONDS (6.1%) | |||||

California (3.0%) | ||||||

| 230,000 | California State, Refunding G.O., Taxable, 6.200%, 10/1/19 | 223,914 | ||||

| 190,000 | California State, Water Utility Improvements G.O., Taxable, 5.450%, 4/1/15 | 191,110 | ||||

| 30,000 | Los Angeles Harbor Department, Crossover Refunding Revenue, Series A, Callable 8/1/12 | |||||

@ 100 (AMBAC), 5.500%, 8/1/14 | 31,670 | |||||

| 220,000 | Metropolitan Water District of Southern California, Water Utility Improvements Revenue, Callable 7/1/19 @ 100, 6.538%, 7/1/39 | 223,073 | ||||

| 669,767 | ||||||

District of Columbia (0.4%) | ||||||

| 70,000 | Metropolitan Washington Airports Authority, Refunding Revenue Bonds, Series D (NATL-RE), 5.000%, 10/1/11 | 74,169 | ||||

Florida (0.6%) | ||||||

| 135,000 | Greater Orlando Aviation Authority, FL, Port, Airport & Marina Improvements Revenue, Series A, Callable 2/1/10 @ 101 (NATL-RE FGIC), 5.250%, 10/1/12 | 136,658 | ||||

Iowa (0.8%) | ||||||

| 250,000 | Iowa Student Loan Liquidity Corporation, Student Loan Revenue Bonds, Series E, Taxable, Callable 1/11/10 @ 100 (AMBAC, GTD STD LNS), 0.000%, 12/1/31*(a)(f) | 182,500 | ||||

| Principal Amount | Fair Value | |||||

MUNICIPAL BONDS — (continued) | ||||||

New Jersey (1.0%) | ||||||

| $300,000 | Higher Education Student Assistance Authority, NJ, Student Loan Revenue, Series A, Callable 1/14/10 @ 100 (NATL-RE, GTD STD LNS), 0.718%, 6/1/36*(a)(f) | $ | 210,000 | |||

New York (0.3%) | ||||||

| 70,000 | New York & New Jersey Port Authority, Port, Airport & Marina Improvements Revenue, Series 122, Callable 2/1/10 @ 100.50 (General Obligation of Authority), 5.500%, 7/15/15 | 70,460 | ||||

Total Municipal Bonds | 1,343,554 | |||||

U.S. GOVERNMENT AGENCIES (0.1%) | ||||||

Fannie Mae (0.1%) | ||||||

| 26,000 | 4.125%, 4/15/14 | 27,652 | ||||

Total U.S. Government Agencies | 27,652 | |||||

U.S. TREASURY NOTES (0.4%) |

| |||||

| 42,000 | 3.750%, 11/15/18 | 41,997 | ||||

| 50,000 | 4.500%, 5/15/38(c) | 48,961 | ||||

Total U.S. Treasury Notes | 90,958 | |||||

FOREIGN GOVERNMENT BONDS (0.8%) |

| |||||

Qatar (0.8%) | ||||||

| 160,000 | Qatar Government International Bond, 4.000%, 1/20/15(b) | 160,400 | ||||

Total Foreign Government Bonds | 160,400 | |||||

| Shares | ||||||

INVESTMENT COMPANY (0.1%) |

| |||||

| 26,025 | Federated Treasury Obligations Fund, Institutional Shares | 26,025 | ||||

Total Investment Company | 26,025 | |||||

| Principal Amount | ||||||

SHORT TERM INVESTMENTS (0.0%) |

| |||||

| $17,758 | BNY Institutional Cash Reserve, Series B | 3,463 | ||||

Total Short Term Investments | 3,463 | |||||

Total Investments — 102.5% | 22,604,699 | |||||

Net Other Assets (Liabilities) — (2.5)% | (542,445 | ) | ||||

NET ASSETS — 100.0% | $ | 22,062,254 | ||||

| * | The interest rate for this variable rate note, which will change periodically, is |

| Continued |

15

Table of Contents

BB&T Total Return Bond VIF

Schedule of Portfolio Investments — (continued)

December 31, 2009

| based either on the prime rate or an index of market rates. The reflected rate is in effect as of December 31, 2009. The maturity date reflected is the final maturity date. |

| (a) | Illiquid. |

| (b) | Rule 144A, Section 4(2) or other security which is restricted as to resale to institutional investors. The Investment Advisor, using board approved procedures, has deemed these securities or a portion of these securities to be liquid. |

| (c) | Represents that all or a portion of the security was pledged as collateral for securities purchased on a when-issued basis. |

| (d) | On September 7, 2008, the Federal Housing Finance Agency (FHFA) placed Fannie Mae and Freddie Mac into conservatorship with FHFA as the conservator. The conservatorship is a statutory process designed to stabilize a troubled institution with the objective of returning the entities to normal business operations. |

| (e) | Represents securities purchase on a when-issued basis. At December 31, 2009, total cost of investment purchased on a when-issued basis was $365,399. |

| (f) | Security was fair valued under methods approved by the Board of Trustees. |

AMBAC — American Municipal Bond Insurance Corp.

FGIC — Financial Guaranty Insurance Corp.

G.O. — General Obligation

GTD STD LNS — Guaranteed Student Loans

MTN — Medium Term Note

NATL — National

RE — Reinsurance

REIT — Real Estate Investment Trust

STEP — Step Coupon Bond

| See accompanying notes to the financial statements. |

16

Table of Contents

(This page has been left blank intentionally.)

Table of Contents

Statements of Assets and Liabilities

December 31, 2009

| BB&T Large Cap VIF | BB&T Mid Cap Growth VIF | BB&T Capital Manager Equity VIF | BB&T Special Opportunities Equity VIF | BB&T Total Return Bond VIF | |||||||||||||||

Assets: | |||||||||||||||||||

Investments: | |||||||||||||||||||

Investments-unaffiliated, at cost | $ | 29,210,142 | $ | 7,289,949 | $ | 2,851,901 | $ | 33,856,442 | $ | 21,914,884 | |||||||||

Investments-affiliated, at cost | — | — | 6,062,644 | — | — | ||||||||||||||

Total investments, at cost* | 29,210,142 | 7,289,949 | 8,914,545 | 33,856,442 | 21,914,884 | ||||||||||||||

Unrealized appreciation (depreciation) | 2,876,738 | 2,231,418 | (964,856 | ) | 5,556,866 | 689,815 | |||||||||||||

Investments, at value | 32,086,880 | 9,521,367 | 7,949,689 | 39,413,308 | 22,604,699 | ||||||||||||||

Cash | — | — | — | — | 3,015 | ||||||||||||||

Interest and dividends receivable | 61,698 | 6,364 | 22,084 | 40,708 | 182,753 | ||||||||||||||

Receivable for investments sold | — | — | — | — | 41,714 | ||||||||||||||

Receivable for capital shares issued | 51,212 | 8,592 | — | 892,598 | — | ||||||||||||||

Receivable from Advisor | — | — | 8 | — | — | ||||||||||||||

Prepaid and other assets | 22,720 | 5,061 | 5,466 | 23,634 | 16,203 | ||||||||||||||

Total Assets | 32,222,510 | 9,541,384 | 7,977,247 | 40,370,248 | 22,848,384 | ||||||||||||||

Liabilities: | |||||||||||||||||||

Call options written (premiums received $ — , $ — , $ — , $81,688 and $ — , respectively) | — | — | — | 102,750 | — | ||||||||||||||

Payable for investments purchased | — | — | — | — | 366,407 | ||||||||||||||

Payable for capital shares redeemed | 2,154 | 49,785 | 19,521 | — | 364,076 | ||||||||||||||

Payable for collateral received on loaned securities | — | 334,495 | — | — | — | ||||||||||||||

Payable to securities lending agent | 29,800 | — | — | 37,343 | 17,758 | ||||||||||||||

Accrued expenses: | |||||||||||||||||||

Investment advisory fees | 13,765 | 4,262 | — | 23,125 | 3,484 | ||||||||||||||

Administration fees | 2,750 | 853 | — | 3,158 | 1,980 | ||||||||||||||

Audit fees | 32,082 | 11,779 | 7,713 | 32,535 | 22,592 | ||||||||||||||

Compliance service fees | 33 | 13 | 8 | 32 | 22 | ||||||||||||||

Trustee fees | 4 | — | — | 1 | 1 | ||||||||||||||

Printing fees | 7,129 | 1,165 | 1,097 | 4,477 | 3,643 | ||||||||||||||

Other fees | 11,101 | 3,565 | 2,187 | 4,900 | 6,167 | ||||||||||||||

Total Liabilities | 98,818 | 405,917 | 30,526 | 208,321 | 786,130 | ||||||||||||||

Net Assets: | $ | 32,123,692 | $ | 9,135,467 | $ | 7,946,721 | $ | 40,161,927 | $ | 22,062,254 | |||||||||

Net Assets Consist of: | |||||||||||||||||||

Capital | $ | 53,836,704 | $ | 12,860,528 | $ | 14,155,240 | $ | 37,703,591 | $ | 21,088,193 | |||||||||

Accumulated undistributed net investment income | 2,646 | — | 24,675 | 23,776 | 247,723 | ||||||||||||||

Accumulated realized gains (losses) from investments and written options | (24,592,396 | ) | (5,956,479 | ) | (5,268,338 | ) | (3,101,244 | ) | 36,523 | ||||||||||

Net unrealized appreciation/(depreciation) on investments and written options | 2,876,738 | 2,231,418 | (964,856 | ) | 5,535,804 | 689,815 | |||||||||||||

Net Assets | $ | 32,123,692 | $ | 9,135,467 | $ | 7,946,721 | $ | 40,161,927 | $ | 22,062,254 | |||||||||

Shares of Beneficial Interest Outstanding (unlimited number of shares authorized, no par value) | 4,219,843 | 1,036,416 | 1,347,814 | 2,810,504 | 2,126,547 | ||||||||||||||

Net Asset Value — offering and redemption price per share | $ | 7.61 | $ | 8.81 | $ | 5.90 | $ | 14.29 | $ | 10.37 | |||||||||

| * | The BB&T Mid Cap Growth VIF includes securities on loan of $324,671. |

See accompanying notes to the financial statements.

18

Table of Contents

BB&T Variable Insurance Funds

Statements of Operations

For the Year Ended December 31, 2009

| BB&T Large Cap VIF | BB&T Mid Cap Growth VIF | BB&T Capital Manager Equity VIF | BB&T Special Opportunities Equity VIF | BB&T Total Return Bond VIF | ||||||||||||||||

Investment Income: | ||||||||||||||||||||

Interest income | $ | — | $ | — | $ | — | $ | — | $ | 1,113,012 | ||||||||||

Dividend income - unaffiliated | 631,047 | 66,255 | 62,192 | 330,761 | 842 | |||||||||||||||

Dividend income - affiliated | — | — | 60,063 | — | — | |||||||||||||||

Foreign tax withholding | (2,469 | ) | (885 | ) | — | (16,846 | ) | — | ||||||||||||

Income from securities lending | 428 | 11,243 | — | 1,074 | 65 | |||||||||||||||

Total investment income | 629,006 | 76,613 | 122,255 | 314,989 | 1,113,919 | |||||||||||||||

Expenses: | ||||||||||||||||||||

Investment advisory fees (See Note 4) | 231,501 | 83,801 | 18,848 | 256,525 | 132,859 | |||||||||||||||

Administration fees (See Note 4) | 31,546 | 11,484 | — | 32,351 | 22,364 | |||||||||||||||

Audit fees | 29,904 | 8,926 | 7,277 | 36,104 | 34,463 | |||||||||||||||

Compliance service fees (See Note 4) | 354 | 131 | 86 | 359 | 252 | |||||||||||||||

Custodian fees | 1,186 | 3,293 | 134 | 2,500 | 1,484 | |||||||||||||||

Fund accounting fees (See Note 4) | 3,128 | 1,132 | 754 | 3,207 | 2,214 | |||||||||||||||

Insurance fees | 30,638 | 14,167 | 7,015 | 21,090 | 15,641 | |||||||||||||||

Legal fees | 27,357 | 9,661 | 5,977 | 26,819 | 20,573 | |||||||||||||||

Printing fees | 14,394 | 5,257 | 3,225 | 13,197 | 11,216 | |||||||||||||||

Transfer agent fees (See Note 4) | 10,435 | 3,804 | 2,502 | 10,537 | 7,465 | |||||||||||||||

Trustee fees | 2,156 | 777 | 511 | 2,061 | 1,504 | |||||||||||||||

Other fees | 5,675 | 18,995 | 3,429 | 7,416 | 24,220 | |||||||||||||||

Total expenses before waivers | 388,274 | 161,428 | 49,758 | 412,166 | 274,255 | |||||||||||||||

Less expenses waived or reimbursed by the Investment Advisor (See Note 4) | (75,081 | ) | (41,130 | ) | (18,848 | ) | (8,352 | ) | (65,995 | ) | ||||||||||

Net expenses | 313,193 | 120,298 | 30,910 | 403,814 | 208,260 | |||||||||||||||

Net investment income (loss) | 315,813 | (43,685 | ) | 91,345 | (88,825 | ) | 905,659 | |||||||||||||

Realized/Unrealized Gains (Losses) on Investments, Futures Contracts and Written Options: | ||||||||||||||||||||

Net realized gains (losses) from: | ||||||||||||||||||||

Investment transactions - unaffiliated | (2,881,881 | ) | (2,766,996 | ) | (362,788 | ) | (714,218 | ) | 607,175 | |||||||||||

Investment transactions - affiliated | — | — | (1,659,087 | ) | — | — | ||||||||||||||

Distributions from affiliated funds | — | — | (2,343 | ) | — | — | ||||||||||||||

Futures contracts | — | — | — | — | (91,552 | ) | ||||||||||||||

Written Options | — | — | — | 234,616 | — | |||||||||||||||

Change in unrealized appreciation/depreciation on: | ||||||||||||||||||||

Investments | 7,480,460 | 5,448,758 | 3,540,237 | 12,392,096 | 407,793 | |||||||||||||||

Futures contracts | — | — | — | — | (7,651 | ) | ||||||||||||||

Written Options | — | — | — | (25,495 | ) | — | ||||||||||||||

Net realized/unrealized gains on investments, futures contracts and written options | 4,598,579 | 2,681,762 | 1,516,019 | 11,886,999 | 915,765 | |||||||||||||||

Change in net assets from operations | $ | 4,914,392 | $ | 2,638,077 | $ | 1,607,364 | $ | 11,798,174 | $ | 1,821,424 | ||||||||||

See accompanying notes to the financial statements.

19

Table of Contents

BB&T Variable Insurance Funds

Statements of Changes in Net Assets

| BB&T Large Cap VIF | BB&T Mid Cap Growth VIF | |||||||||||||||

| For the Year Ended December 31, 2009 | For the Year Ended December 31, 2008 | For the Year Ended December 31, 2009 | For the Year Ended December 31, 2008 | |||||||||||||

From Investment Activities: | ||||||||||||||||

Operations: | ||||||||||||||||

Net investment income (loss) | $ | 315,813 | $ | 921,379 | $ | (43,685 | ) | $ | (53,697 | ) | ||||||

Net realized gains (losses) from investments and distributions from affiliated funds | (2,881,881 | ) | (21,659,986 | ) | (2,766,996 | ) | (3,193,231 | ) | ||||||||

Change in unrealized appreciation/depreciation of investments, futures contracts and written options | 7,480,460 | (6,116,076 | ) | 5,448,758 | (11,790,950 | ) | ||||||||||

Change in net assets from operations | 4,914,392 | (26,854,683 | ) | 2,638,077 | (15,037,878 | ) | ||||||||||

Distributions to Shareholders: | ||||||||||||||||

Net investment income | (313,190 | ) | (921,328 | ) | — | — | ||||||||||

Net realized gains from investment transactions | — | (12,646,677 | ) | — | (4,536,802 | ) | ||||||||||

Change in net assets from shareholders distributions | (313,190 | ) | (13,568,005 | ) | — | (4,536,802 | ) | |||||||||

Capital Transactions: | ||||||||||||||||

Proceeds from shares issued | 378,413 | 757,706 | 374,914 | 1,884,461 | ||||||||||||

Distributions reinvested | 313,190 | 13,568,005 | — | 4,536,802 | ||||||||||||

Value of shares redeemed | (9,147,412 | ) | (25,096,108 | ) | (6,047,269 | ) | (8,063,186 | ) | ||||||||

Change in net assets from capital transactions | (8,455,809 | ) | (10,770,397 | ) | (5,672,355 | ) | (1,641,923 | ) | ||||||||

Change in net assets | (3,854,607 | ) | (51,193,085 | ) | (3,034,278 | ) | (21,216,603 | ) | ||||||||

Net Assets: | ||||||||||||||||

Beginning of year | 35,978,299 | 87,171,384 | 12,169,745 | 33,386,348 | ||||||||||||

End of year | $ | 32,123,692 | $ | 35,978,299 | $ | 9,135,467 | $ | 12,169,745 | ||||||||

Accumulated undistributed net investment income | $ | 2,646 | $ | 23 | $ | — | $ | — | ||||||||

Share Transactions: | ||||||||||||||||

Issued | 60,519 | 74,734 | 50,915 | 158,834 | ||||||||||||

Reinvested | 50,035 | 1,571,115 | — | 425,991 | ||||||||||||

Redeemed | (1,433,681 | ) | (2,468,697 | ) | (777,503 | ) | (647,597 | ) | ||||||||

Change in Shares | (1,323,127 | ) | (822,848 | ) | (726,588 | ) | (62,772 | ) | ||||||||

See accompanying notes to the financial statements.

20

Table of Contents

BB&T Variable Insurance Funds

Statements of Changes in Net Assets

| BB&T Capital Manager Equity VIF | BB&T Special Opportunities Equity VIF | BB&T Total Return Bond VIF | |||||||||||||||||||

| For the Year Ended December 31, 2009 | For the Year Ended December 31, 2008 | For the Year Ended December 31, 2009 | For the Year Ended December 31, 2008 | For the Year Ended December 31, 2009 | For the Year Ended December 31, 2008 | ||||||||||||||||

| $ | 91,345 | $ | 158,507 | $ | (88,825 | ) | $ | 47,029 | $ | 905,659 | $ | 800,840 | |||||||||

| (2,024,218) | (3,000,889 | ) | (479,602 | ) | (1,430,745 | ) | 515,623 | (282,156 | ) | ||||||||||||

| 3,540,237 | (3,419,265 | ) | 12,366,601 | (12,504,758 | ) | 400,142 | 86,113 | ||||||||||||||

| 1,607,364 | (6,261,647 | ) | 11,798,174 | (13,888,474 | ) | 1,821,424 | 604,797 | ||||||||||||||

| (64,463) | (182,681 | ) | — | (47,020 | ) | (885,440 | ) | (803,726 | ) | ||||||||||||

| — | (3,211,624 | ) | (1,073,282 | ) | (1,229,604 | ) | — | — | |||||||||||||

| (64,463) | (3,394,305 | ) | (1,073,282 | ) | (1,276,624 | ) | (885,440 | ) | (803,726 | ) | |||||||||||

| 108,008 | 659,807 | 8,823,846 | 9,492,235 | 6,016,047 | 11,509,087 | ||||||||||||||||

| 64,463 | 3,394,305 | 1,073,282 | 1,276,625 | 885,440 | 803,726 | ||||||||||||||||

| (2,296,851) | (4,364,667 | ) | (7,143,652 | ) | (4,539,850 | ) | (6,771,543 | ) | (5,181,198 | ) | |||||||||||

| (2,124,380) | (310,555 | ) | 2,753,476 | 6,229,010 | 129,944 | 7,131,615 | |||||||||||||||

| (581,479) | (9,966,507 | ) | 13,478,368 | (8,936,088 | ) | 1,065,928 | 6,932,686 | ||||||||||||||

| 8,528,200 | 18,494,707 | 26,683,559 | 35,619,647 | 20,996,326 | 14,063,640 | ||||||||||||||||

| $ | 7,946,721 | $ | 8,528,200 | $ | 40,161,927 | $ | 26,683,559 | $ | 22,062,254 | $ | 20,996,326 | ||||||||||

| $24,675 | $ | 136 | $ | 23,776 | $ | 9 | $ | 247,723 | $ | 210,356 | |||||||||||

| 24,605 | 92,711 | 704,058 | 638,272 | 591,456 | 1,158,126 | ||||||||||||||||

| 11,466 | 526,651 | 80,516 | 88,168 | 87,393 | 81,352 | ||||||||||||||||

| (483,790) | (613,433 | ) | (573,467 | ) | (348,611 | ) | (665,610 | ) | (529,896 | ) | |||||||||||

| (447,719) | 5,929 | 211,107 | 377,829 | 13,239 | 709,582 | ||||||||||||||||

See accompanying notes to the financial statements.

21

Table of Contents

BB&T Variable Insurance Funds

Financial Highlights

Selected data for a share of beneficial interest outstanding throughout the years indicated.

| Investment Activities | Distributions | ||||||||||||||

| Net Asset Value, Beginning of Year | Net investment income (loss) | Net realized/ unrealized gains (losses) on investments | Total from Investment Activities | Net investment income | Net realized gains on investments | Total Distributions | |||||||||

BB&T Large Cap VIF | |||||||||||||||

Year Ended December 31, 2009 | $ | 6.49 | 0.07(c) | 1.12 | 1.19 | (0.07) | — | (0.07) | |||||||

Year Ended December 31, 2008 | $ | 13.69 | 0.16(c) | (4.63) | (4.47) | (0.16) | (2.57) | (2.73) | |||||||

Year Ended December 31, 2007 | $ | 16.75 | 0.23 | (1.08) | (0.85) | (0.31) | (1.90) | (2.21) | |||||||

Year Ended December 31, 2006 | $ | 14.00 | 0.27 | 2.68 | 2.95 | (0.20) | — | (0.20) | |||||||

Year Ended December 31, 2005 | $ | 13.35 | 0.26 | 0.65 | 0.91 | (0.26) | — | (0.26) | |||||||

BB&T Mid Cap Growth VIF | |||||||||||||||

Year Ended December 31, 2009 | $ | 6.90 | (0.03)(c) | 1.94 | 1.91 | — | — | — | |||||||

Year Ended December 31, 2008 | $ | 18.29 | (0.03)(c) | (8.40) | (8.43) | — | (2.96) | (2.96) | |||||||

Year Ended December 31, 2007 | $ | 15.16 | (0.03) | 5.09 | 5.06 | — (d) | (1.93) | (1.93) | |||||||

Year Ended December 31, 2006 | $ | 15.67 | 0.03 | 0.44 | 0.47 | (0.07) | (0.91) | (0.98) | |||||||

Year Ended December 31, 2005 | $ | 13.70 | (0.04) | 2.01 | 1.97 | — | — | — | |||||||

BB&T Capital Manager Equity VIF(e) | |||||||||||||||

Year Ended December 31, 2009 | $ | 4.75 | 0.06(c) | 1.14 | 1.20 | (0.05) | — | (0.05) | |||||||

Year Ended December 31, 2008 | $ | 10.33 | 0.09(c) | (3.50) | (3.41) | (0.10) | (2.07) | (2.17) | |||||||

Year Ended December 31, 2007 | $ | 11.65 | 0.25 | — (d) | 0.25 | (0.30) | (1.27) | (1.57) | |||||||

Year Ended December 31, 2006 | $ | 10.51 | 0.16 | 1.45 | 1.61 | (0.12) | (0.35) | (0.47) | |||||||

Year Ended December 31, 2005 | $ | 9.99 | 0.17 | 0.50 | 0.67 | (0.15) | — | (0.15) | |||||||

BB&T Special Opportunities Equity VIF | |||||||||||||||

Year Ended December 31, 2009 | $ | 10.27 | (0.03)(c) | 4.47 | 4.44 | — | (0.42) | (0.42) | |||||||

Year Ended December 31, 2008 | $ | 16.03 | 0.02(c) | (5.28) | (5.26) | (0.02) | (0.48) | (0.50) | |||||||

Year Ended December 31, 2007 | $ | 15.07 | (0.02) | 2.02 | 2.00 | — | (1.04) | (1.04) | |||||||

Year Ended December 31, 2006 | $ | 12.70 | (0.02) | 3.07 | 3.05 | (0.01) | (0.67) | (0.68) | |||||||

Year Ended December 31, 2005 | $ | 12.12 | (0.03) | 0.79 | 0.76 | — | (0.18) | (0.18) | |||||||

BB&T Total Return Bond VIF | |||||||||||||||

Year Ended December 31, 2009 | $ | 9.94 | 0.41(c) | 0.42 | 0.83 | (0.40) | — | (0.40) | |||||||

Year Ended December 31, 2008 | $ | 10.02 | 0.41(c) | (0.08) | 0.33 | (0.41) | — | (0.41) | |||||||

Year Ended December 31, 2007 | $ | 9.83 | 0.31 | 0.31 | 0.62 | (0.43) | — | (0.43) | |||||||

Year Ended December 31, 2006 | $ | 9.92 | 0.50 | (0.17) | 0.33 | (0.42) | — | (0.42) | |||||||

Year Ended December 31, 2005 | $ | 10.08 | 0.33 | (0.10) | 0.23 | (0.36) | (0.03) | (0.39) | |||||||

| (a) | Total return ratios assume reinvestment of distributions at net asset value. |

Total return ratios do not reflect charges pursuant to the terms of the insurance contracts funded by separate accounts that invest in the Fund’s shares.

| (b) | During the period certain fees were reduced. If such reductions had not occurred, the ratios would have been as indicated. |

| (c) | Per share net investment income (loss) has been calculated using the average daily shares method. |

| (d) | Amount is less than $0.005. |

| (e) | The expense ratios exclude the impact of fees/expenses paid by each underlying fund. |

See accompanying notes to the financial statements.

22

Table of Contents

| Ratios/Supplemental Data | |||||||||||||||

Net Asset Value, End of Year | Total Return(a) | Net Assets, End of Year (000) | Ratio of net expenses to average net assets | Ratio of net investment income (loss) to average net assets | Ratio of expenses to average net assets(b) | Portfolio turnover rate | |||||||||

| $ | 7.61 | 18.50 | % | $ | 32,124 | 1.00% | 1.01% | 1.24% | 137.52% | ||||||

| $ | 6.49 | (37.43 | )% | $ | 35,978 | 0.81% | 1.52% | 1.16% | 49.73% | ||||||

| $ | 13.69 | (5.87 | )% | $ | 87,171 | 0.77% | 1.50% | 1.08% | 52.81% | ||||||

| $ | 16.75 | 21.28 | % | $ | 93,143 | 0.77% | 1.72% | 1.01% | 45.76% | ||||||

| $ | 14.00 | 6.90 | % | $ | 113,648 | 0.79% | 1.95% | 1.05% | 21.76% | ||||||

| $ | 8.81 | 27.68 | % | $ | 9,135 | 1.06% | (0.39)% | 1.43% | 186.48% | ||||||

| $ | 6.90 | (51.78 | )% | $ | 12,170 | 0.84% | (0.23)% | 1.17% | 205.82% | ||||||

| $ | 18.29 | 35.02 | % | $ | 33,386 | 0.80% | (0.22)% | 1.05% | 127.76% | ||||||

| $ | 15.16 | 3.26 | % | $ | 25,460 | 0.78% | 0.25% | 1.02% | 160.04% | ||||||

| $ | 15.67 | 14.38 | % | $ | 39,090 | 0.78% | (0.28)% | 1.10% | 113.04% | ||||||

| $ | 5.90 | 25.24 | % | $ | 7,947 | 0.41% | 1.21% | 0.66% | 18.04% | ||||||

| $ | 4.75 | (38.22 | )% | $ | 8,528 | 0.31% | 1.15% | 0.59% | 61.04% | ||||||

| $ | 10.33 | 1.98 | % | $ | 18,495 | 0.18% | 2.27% | 0.51% | 40.70% | ||||||

| $ | 11.65 | 15.82 | % | $ | 18,222 | 0.17% | 1.15% | 0.54% | 20.55% | ||||||

| $ | 10.51 | 6.77 | % | $ | 28,722 | 0.26% | 1.68% | 0.55% | 3.24% | ||||||

| $ | 14.29 | 43.53 | % | $ | 40,162 | 1.26% | (0.28)% | 1.29% | 32.57% | ||||||