UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-21732

Mercer Funds

(Exact Name of Registrant as Specified in Charter)

99 High Street

Boston, MA 02110

(Address of Principal Executive Offices)(Zip Code)

Caroline Hulme, Esq.

Mercer Investments LLC

99 High Street

Boston, MA 02110

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code: (617) 747-9500

Date of Fiscal Year End: March 31, 2023

Date of Reporting Period: March 31, 2023

| Item 1. | Reports to Stockholders. |

(a) The Report to Shareholders is attached herewith.

Mercer FundsTM

Annual Report

March 31, 2023

Mercer US Large Cap Equity Fund |

Mercer US Small/Mid Cap Equity Fund |

Mercer Non-US Core Equity Fund |

Mercer Core Fixed Income Fund |

Mercer Opportunistic Fixed Income Fund |

Mercer Emerging Markets Equity Fund |

Mercer Global Low Volatility Equity Fund |

This report has been prepared for Mercer Funds shareholders. It is not authorized for distribution to prospective investors unless accompanied or preceded by a current Mercer Funds prospectus. The prospectus contains more complete information about the Funds’ investment objectives, risks, and expenses. Investors are reminded to read the prospectus carefully before investing.

MERCER FUNDS

TABLE OF CONTENTS

Management's Discussion of Fund Performance (Unaudited)

Mercer US Large Cap Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the Russell 1000® Index1.

Investment Strategy

The Fund invests principally in equity securities (such as common stock) issued by large capitalization U.S. companies. The Fund employs a “core equity” investment strategy by investing in both growth and value oriented equity securities. The Fund may invest in derivative instruments to gain market exposure on cash balances or to reduce market exposure in anticipation of liquidity needs.

Performance

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -10.94% compared to its benchmark, the Russell 1000® Index, return of -8.39%. Performance for the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged and cannot be invested in directly.

The Sub-Advisers

As of March 31, 2023, the Fund employed six sub-advisers: Brandywine Global Investment Management LLC (Brandywine), O’Shaughnessy Asset Management LLC (OSAM), Polen Capital Management LLC (Polen), Jennison Associates LLC (Jennison), Delaware Investments Fund Advisers, a series of Macquarie Investment Management Business Trust (Macquarie), and Parametric Portfolio Associates LLC (Parametric).

Brandywine, a deep value manager, focuses on cheap stocks that trade at a significant discount to intrinsic value, with strong free cash flows and quality balance sheets.

OSAM is a yield focused quantitative value manager that seeks stocks that rank high based on valuation, quality and shareholder yield.

Polen is a concentrated quality growth manager, focused on finding high quality companies, with sustainable, above-average earnings growth.

Jennison is a growth manager who selects stocks with long-term competitive advantages that are growing earnings faster or longer than the broad market.

Macquarie is a quality value manager who invests in strong, high quality businesses with sound balance sheets and free cash flow generation.

Parametric utilizes exchange-traded futures to generate market exposure corresponding to the Fund’s benchmark.

Market Commentary and Fund Performance

Amidst a backdrop of rising inflation, liquidity tightening from the Federal Reserve and the war in Ukraine and its implications on the energy supply and prices, the U.S. market saw a sharp sell-off that started in the first quarter of 2022 and continued throughout much of the fiscal year. Volatility was persistent throughout the U.S. markets as a result of multi-decade high inflation prints and the Federal Reserve’s determination to fight it via tighter financial conditions. In the summer months, there was the perception that the Federal Reserve would pivot from its hawkish stance after inflation reached its peak sending the U.S. market on a strong rally. With the Fed reaffirming its hawkish stance in Jackson Hole in August, the rally ended and was followed by a sharp sell-off through the end of the summer and into the fall. In early October after the market reached oversold levels, another strong rally ensued through the end of November culminating with another sell-off in December through the end of 2022.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Large Cap Equity Fund

After 2022 ended with widespread pessimism and investors had renewed optimism for 2023, the U.S. markets experienced a sharp rally in which companies that experienced severe volatility in 2022 saw a sharp reversal in momentum as their share prices soared in January. This beta2 rally quickly waned as inflation crept higher, the jobs report came in stronger than expected and hopes for a dovish Fed policy waned. In addition, Silicon Valley Bank, the bank of choice for many tech companies and entrepreneurs collapsed, which initiated a contagion effect on others such as Signature Bank. The banking failures and the sharp reversals in interest rate expectations became the main storyline of the first quarter in 2023.

Within the Russell 1000® Index, the Fund’s benchmark, the best performing sectors for the fiscal year were Energy 12.5%, Consumer Staples 1.0% and Industrials -0.2%. The worst performing sectors were Real Estate -19.5%, Consumer Discretionary -18.8% and Communication Services -18.1%. Information Technology, the largest sector in Russell 1000® Index returned -6.7%. Health Care, Utilities, Materials and Financials returned -3.9%, -6.0%, -8.1% and -14.1%, respectively.

The Mercer US Large Cap Equity Fund lagged the Russell 1000® Index for the period, with value oriented managers, Brandywine and OSAM, outperforming, and growth and higher quality managers, Jennison and Polen, underperforming their respective benchmarks. Macquarie, a quality value manager, moderately lagged its benchmark.

Jennison lagged the Russell 1000® Growth Index3 by 5.3%. Significant underperformance of higher growth, higher valuation stocks was a major headwind. The majority of underperformance came from security selection in Communication Services and Information Technology as well from being overweight in the Consumer Discretionary and Communication Services sectors. Overweight positions to Snap, Tesla, Atlassian and Crowdstrike were among the largest detractors from performance. On the positive side, the portfolio’s healthcare, semiconductor and luxury consumer exposure added to relative performance.

Polen lagged the Russell 1000® Growth Index by 6.0%. Significant underperformance resulted from weaker security selection and sector allocation. Specifically, stock selection within Information Technology, Consumer Discretionary and Health Care detracted as did an overweight position in Communication Services. The portfolio’s lack of exposure to Consumer Staples and Industrials detracted from relative results. The largest detractors included Meta, DocuSign, and PayPal.

Macquarie underperformed the Russell 1000® Value Index4 by 0.4%. Macquarie’s underperformance was driven by security selection in a number of sectors such as Financials, Communication Services, Health Care, and Real Estate. Stronger security selection in Information Technology and Utilities were the largest positive contributors.

OSAM outperformed the Russell 1000® Value Index by 0.8%. Security selection in Information Technology, Health Care, Consumer Discretionary, and Energy led to outperformance. Security selection in Communication Services and Financials detracted. OSAM’s higher than index exposure to equities lower value multiples, such as price to earnings and price to cash flow, was a tailwind as companies with value characteristics tended to outperform during the period.

Brandywine outperformed the Russell 1000® Value Index by 1.4%. Security selection in Communication Services, Financials and Consumer Discretionary as well as being underweight to Real Estate were the largest positive contributors. Security selection in Materials and being underweight to Industrials detracted. Brandywine’s higher than index exposure to inexpensively priced equities was a tailwind as companies with value characteristics tended to outperform during the period.

Parametric utilizes exchange-traded futures to replicate the Fund’s benchmark, aiming to provide broad, passive, equity market exposure to the Fund’s liquidity sleeve, and seeking to create positive returns on assets that would have otherwise been earning cash or cash equivalent returns. Performance differences versus the benchmark are largely a result of cash flow effects related to daily subscription/redemption activity and through financing costs of futures relative to interest earned on cash.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Large Cap Equity Fund

Risk Considerations

The Fund invests in both growth stocks and value stocks. Growth stocks may be particularly sensitive to market conditions. Investing in value stocks involves the risk that an investment made in undervalued securities may not appreciate in value as anticipated or remain undervalued for long periods of time. The Fund may invest in derivative instruments such as exchange-listed equity futures contracts, which may cause the Fund to experience greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify the risk of loss for the Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Large Cap Equity Fund

March 31, 2023

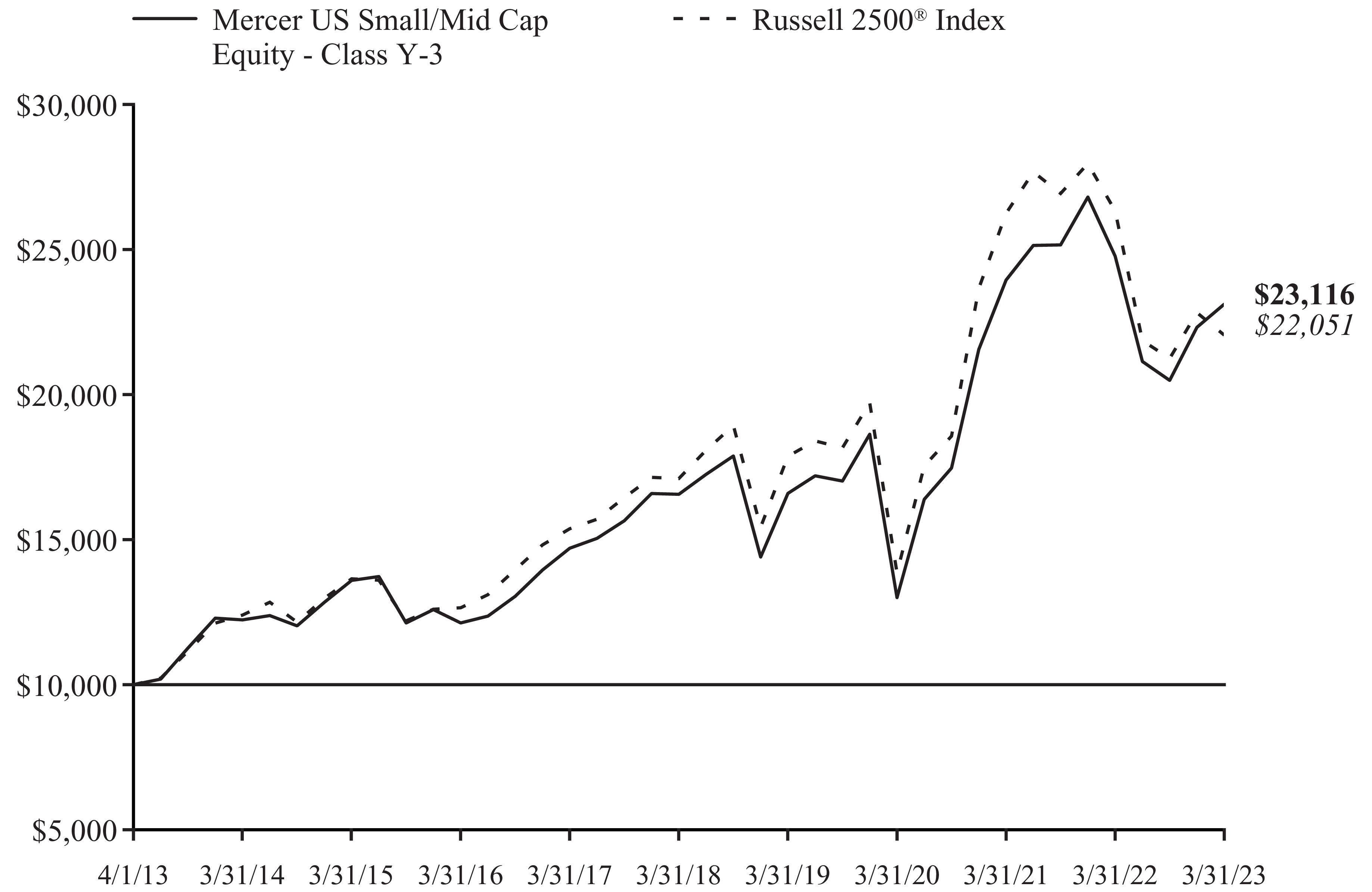

Comparison of Change in Value of a hypothetical $10,000 Investment in Mercer US Large Cap Equity Class Y-3 Shares vs. the Russell 1000® Index for the period 4/1/13 through 3/31/23

AVERAGE ANNUAL TOTAL RETURNS | | | | |

| | | | |

Mercer US Large Cap Equity Fund – Class Y-3 – 8/15/2005 | | | | |

| | | | |

1 Russell 1000® Index measures the performance of the large cap segment of the U.S. equity universe.

2 Beta is a measure of how an individual asset moves (on average) when the overall stock market increases or decreases.

3 Russell 1000® Growth Index measures the performance of the large-cap growth segment of the US equity universe.

4 Russell 1000® Value Index measures the performance of the large-cap value segment of the US equity universe.

The Fund's total annual gross operating expense for Class Y-3 is 0.58%. Please see the Fund's most recent Prospectus.

The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Large Cap Equity Fund

March 31, 2023

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-888-887-0619 or visit the Trust’ s website at https://www.mercer.us/what-we-do/wealth-and-investments/delegated-solutions-us.html for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Please see the Schedule of Investments for a complete list of Fund holdings.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Small/Mid Cap Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, comprised primarily of capital appreciation. The benchmark for the Fund is the Russell 2500® Index1.

Investment Strategy

The Fund invests principally in equity securities issued by small-to-medium capitalization U.S. companies. The Fund employs a “core equity” investment strategy by investing in both growth and value oriented equity securities. The Fund may invest in derivative instruments to gain market exposure on cash balances or to reduce market exposure in anticipation of liquidity needs.

Performance

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -6.69% compared to its benchmark, the Russell 2500® Index, return of -10.39%. Performance for the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisers

As of March 31, 2023, the Fund employed six sub-advisers: Westfield Capital Management Company, L.P. (Westfield), GW&K Investment Management LLC (GW&K), Loomis, Sayles & Company, L.P. (Loomis), LSV Asset Management (LSV), River Road Asset Management, LLC (River Road) and Parametric Portfolio Associates LLC (Parametric).

Westfield, a traditional growth manager, employs a fundamental, bottom-up approach, which seeks to identify reasonably priced stocks with high earnings growth potential. A bottom-up approach focuses on the analysis of individual stocks and de-emphasizes the significance of macroeconomic and market cycles with the assumption individual companies can do well even in an industry that is not performing, at least on a relative basis.

GW&K uses a bottom-up fundamental research process in order to identify high quality companies with sustainable long-term earnings growth rates.

Loomis looks to provide a lower volatility approach to high growth investing by seeking companies with high quality business models that have differentiated and sustainable growth opportunities.

LSV, a quantitative value manager, using mathematical and statistical methods, seeks deep value, out-of-favor companies with recent momentum. LSV avoids introducing any judgmental biases or behavioral weaknesses into their investment process.

River Road, a fundamental absolute value manager, seeks to buy stocks at a discount to their fair value and sell them at or in excess of that value, and focuses on purchasing companies that are priced at a modest discount to their absolute value and possess superior fundamental business characteristics.

Parametric utilizes exchange-traded futures to generate market exposure corresponding to the Fund’s benchmark.

Market Commentary and Fund Performance

Amidst a backdrop of rising inflation, liquidity tightening from the Federal Reserve and the war in Ukraine and its implications on the energy supply and prices, the U.S. market saw a sharp sell-off that started in the first quarter of 2022 and continued throughout much of the fiscal year. Volatility was persistent throughout the U.S. markets as a result of multi-decade high inflation prints and the Federal Reserve’s determination to fight it via tighter financial conditions. In the summer months, there was the perception that the Federal Reserve would pivot from its hawkish stance after inflation reached its peak sending the U.S. market on a strong rally. With the Fed reaffirming its hawkish stance in Jackson Hole in August, the rally ended and was followed by a sharp sell-off through the end of the summer and into the fall. In early October after the market reached oversold levels, another strong rally ensued through the end of November culminating with another sell-off in December through the end of 2022.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Small/Mid Cap Equity Fund

After 2022 ended with widespread pessimism and investors had renewed optimism for 2023, the U.S. markets experienced a sharp rally in which companies that experienced severe volatility in 2022 saw a sharp reversal in momentum as their share prices soared in January. This beta2 rally quickly waned as inflation crept higher, the jobs report came in stronger than expected and hopes for a dovish Fed policy waned. In addition, Silicon Valley Bank, the bank of choice for many tech companies and entrepreneurs collapsed, which initiated a contagion effect on others such as Signature Bank. The banking failures and the sharp reversals in interest rate expectations became the main storyline of the first quarter in 2023.

Within the Russell 2500® Index, the Fund’s benchmark, the best performing sectors for the fiscal year were consumer staples and industrials with returns of 1.5% and -1.4%, respectively. Underperforming sectors for the fiscal year were communication services and real estate, with returns of -24.1% and -21.5%, respectively. The top performing industries for the fiscal year were construction & engineering and beverages with returns of 18.6% and 15.05%, respectively. The underperforming industries for the fiscal year were office REITs and interactive media & services with returns of -52.0% and -41.2%, respectively.

The Mercer US Small/Mid Cap Equity Fund outperformed the Russell 2500® Index by 3.7% for the period. The Fund’s exposure to value, quality and lower beta profile were tailwinds towards performance for the year. Security selection, particularly in the industrials, consumer discretionary and consumer staples sectors contributed towards performance while selection in the information technology and real estate sectors detracted from performance for the fiscal year. From an allocation standpoint, the Fund’s underweight positions in the real estate and communication services sectors contributed towards performance while the Fund’s underweight positions in the energy and utilities sectors detracted from performance.

Westfield outperformed the Russell 2500® Growth Index3 by 4.7% for the fiscal year. In addition, their strong security selection in the industrials and information technology sectors contributed towards performance for the fiscal year. From an allocation standpoint, their underweight positioning in the consumer discretionary and communication services sectors coupled with their overweight positioning in the financials and industrials sectors also contributed towards performance. Westfield’s lack of exposure to the consumer staples sector detracted from performance for the fiscal year.

GW&K’s outperformed the Russell 2500® Index by 4.2% and it can be attributed to its exposure to higher quality and lower beta stocks. In addition, their strong security selection in the industrials, consumer staples and consumer discretionary sectors contributed towards their performance despite their selection in the information technology sector. From an allocation standpoint, their lack of exposure to the communication services sector combined with an underweight to financials contributed towards performance while their underweight positioning in the energy sector weighed on performance for the fiscal year.

LSV’s outperformance versus the Russell 2500® Value Index4 by 5.2% for the period was driven by their deeper value style being in favor, which is evident with their security selection across multiple sectors contributing towards performance. From an allocation standpoint, their underweight to the real estate sector combined with an overweight to the consumer staples and consumer discretionary sectors contributed towards performance despite their underweight to the industrials and energy sectors.

River Road’s outperformance versus the Russell 2500® Value Index by 7.9% for the period was attributed to their lack of exposure to REITs and banks within the financials sector. In addition, their overweight in the industrials sector combined with their strong security selection in the financials sector contributed towards performance for the fiscal year.

Loomis’ exposure to quality growth coupled with their lower beta approach to high growth investing were tailwinds towards performance for the fiscal year despite their underperformance versus the Russell 2500® Growth Index by -0.57%. Despite their strong security selection in the industrials and consumer discretionary sectors, their security selection in the information technology and health care sectors detracted from performance versus the Russell 2500® Growth Index. From an allocation standpoint, their lack of exposure to the real estate sector coupled with an overweight to the consumer staples and industrials sectors contributed towards performance, while their underweight to the energy sector weighed on performance for the full fiscal year.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Small/Mid Cap Equity Fund

Parametric utilizes exchange-traded futures replicating the Fund’s benchmark to provide broad, passive, equity market exposure to the Fund’s liquidity sleeve, creating positive returns on assets that would have otherwise been earning cash or cash equivalent returns. Performance differences versus the benchmark are largely a result of cash flow effects related to daily subscription/redemption activity and through financing costs of futures relative to interest earned on cash.

Risk Considerations

The Fund invests in both growth stocks and value stocks. Growth stocks may be particularly sensitive to market conditions. Investing in value stocks involves the risk that an investment made in undervalued securities may not appreciate in value as anticipated or remain undervalued for long periods of time. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may invest in derivative instruments such as exchange-listed equity futures contracts, which may cause the Fund to experience greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify the risk of loss for the Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Small/Mid Cap Equity Fund

March 31, 2023

Comparison of Change in Value of a hypothetical $10,000 Investment in Mercer US Small/Mid Cap Equity Class Y-3 Shares vs. the Russell 2500® Index for the period 4/1/13 through 3/31/23

AVERAGE ANNUAL TOTAL RETURNS | | | | |

| | | | |

Mercer US Small/Mid Cap Equity Fund – Class Y-3 – 8/15/2005 | | | | |

| | | | |

1 Russell 2500® Index measures the performance of the small-to mid-cap segment of the U.S. equity universe. The Russell 2500® Index is a subset of the Russell 3000® Index. It includes approximately 2,500 of the smallest securities based on a combination of their market cap and current index membership.

2 Beta is a measure of how an individual asset moves (on average) when the overall stock market increases or decreases.

3 Russell 2500® Growth Index measures the performance of the small to mid-cap growth segment of the US equity universe.

4 Russell 2500® Value Index measures the performance of the small to mid-cap value segment of the US equity universe.

The Fund's total annual gross operating expense for Class Y-3 is 0.94%. Please see the Fund's most recent Prospectus.

The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer US Small/Mid Cap Equity Fund

March 31, 2023

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-888-887-0619 or visit the Trust’ s website at https://www.mercer.us/what-we-do/wealth-and-investments/delegated-solutions-us.html for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Please see the Schedule of Investments for a complete list of Fund holdings.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Non-US Core Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the MSCI EAFE® Index1.

Investment Strategy

The Fund invests principally in equity securities issued by non-U.S. companies of any capitalization, located in the world’s developed and emerging capital markets. The Fund employs a “core equity” investment strategy that seeks to meet the Fund’s investment objective by investing in both growth- and value-oriented equity securities.

Performance

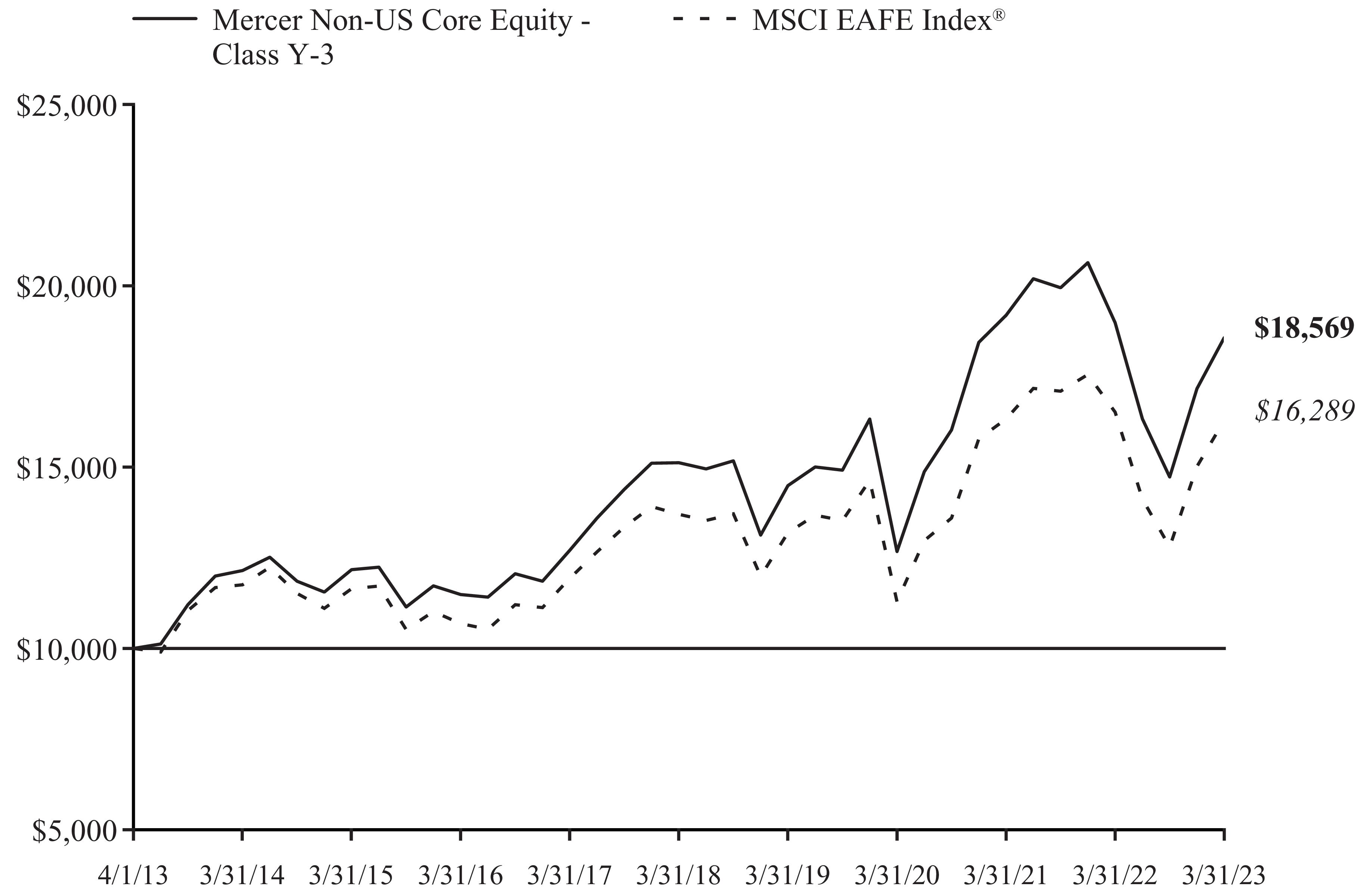

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -2.17% and the I share class performance was -2.47% compared to its benchmark return of -1.38%. Performance for the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisers

As of March 31, 2023, the Fund employed five sub-advisers: Arrowstreet Capital, Limited Partnership (Arrowstreet), American Century Investment Management, Inc. (American Century), Massachusetts Financial Services Company (MFS), LSV Asset Management (LSV) and Parametric Portfolio Associates LLC (Parametric).

Arrowstreet’s strategy seeks to outperform international equity benchmarks through a risk-controlled core approach. Arrowstreet combines sound investment intuition and research with rigorous quantitative tools to identify mispriced stocks around the world. Arrowstreet believes that the key to generating returns in excess of the benchmark involves evaluating the prospects of a security considering the characteristics of the stock itself (direct effects), characteristics of other related stocks (indirect effects) as well as attractiveness of the country and sector basket to which the stock belongs to.

American Century manages its portfolio based on an investment philosophy that companies exhibiting improving or accelerating growth will outperform the market over time. American Century constructs its portfolio through a bottom-up stock selection, which focuses on individual stock selection rather than macroeconomic and market cycles, within a risk aware framework. American Century’s thorough research process seeks to identify companies that are exhibiting an improvement or acceleration in growth where it believes that growth is sustainable but that the earnings power of the company is generally underestimated. American Century can opportunistically invest in emerging market stocks.

MFS’s investment process is based on a fundamental, bottom-up stock selection of high quality companies whose long-term value MFS believes is not adequately reflected in the stock price.

LSV utilizes a quantitative approach, which uses mathematical and statistical methods and seeks deep value stocks that have fallen out of favor with the market, but have recent momentum, either in terms of price or earnings. LSV believes that long-term results are achieved through systematic exploitation of judgmental biases and behavioral weaknesses that influence investor decisions. LSV aims to exploit these biases through the disciplined application of quantitative techniques to drive bottom-up security selection.

Parametric utilizes exchange-traded futures to generate market exposure corresponding to the Fund’s benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Non-US Core Equity Fund

Market Commentary and Fund Performance

2023 fiscal year was a turbulent period for capital markets. Multi-decade high inflation rates, fueled by very accommodative fiscal and monetary policy of the prior two years, supply chain disruptions and commodity price spikes, further escalated by Russia’s invasion of Ukraine, were front and center for policy makers and investors. In response to the stubbornly high inflation prints, global central banks initiated one of the most aggressive hiking cycles in decades. With rates rising sharply, the precipitous decline in equity markets which began in January of 2022 continued until October when the global markets bottomed and investor sentiment reached its trough. In contrast to the first half of the fiscal year, the second half experienced strong rallies as investors began to bet on moderating inflation, slowing interest rate hikes by central banks and a possibility of soft landing.

For the year ended March 31, 2023, U.S. equities, measured using the Russell 1000® Index2, declined by 8.39%. Compared to the U.S., international developed markets performed better, with the MSCI EAFE® Index (the Fund’s benchmark) decreasing by 1.38% over the period. The MSCI Emerging Markets® Index3 declined by 10.70% for the 12-month period ended March 31, 2023. In local currency terms MSCI EAFE® Index and MSCI Emerging Markets® Index posted higher returns, as the US dollar appreciated compared to other major currencies.

Fears of looming recession and weak Chinese demand from the prolonged zero COVID policy put pressure on the commodity prices in the second half of the year, resulting in poor returns from commodity producing countries such as Saudi Arabia, South Africa, Canada, Australia and Brazil. These countries were among the best performers in the prior fiscal year. India and Taiwan which performed well during prior fiscal year also had weak returns. On the other hand, European equities with attractive valuations from prior year’s sharp underperformance showed best returns. Chinese equities, which were the worst performing major market in the 2022 fiscal year, rallied sharply in May-June and again between October and January, as the country officially emerged from COVID lockdown. However, on both occasions, these rallies were followed by sharp reversals, leaving Chinese equities with a 6.3% decline for the year.

Triggered by rising interest rates and expensive valuations, the sharp underperformance of companies with high earnings growth and higher profitability characteristics continued in the first three quarters of the fiscal year. In the fourth quarter, this trend reversed, making the underperformance of the growth versus value equities less pronounced. The persistent outperformance of energy stocks also reversed in the fourth quarter of the fiscal year. Smaller market capitalization companies were under significantly more pressure compared to mega and larger market capitalization companies. Momentum was the worst performing equity style across all major markets. For the year, value was the best performing investment style followed by lower volatility.

For the fiscal year, in Europe, Australasia and Far East (EAFE) markets, energy 10.4%, consumer discretionary 5.6% and consumer staples 1.7% were the best performing sectors while real estate -20.0%, materials -6.2% and communication services -6.1% were the worst performers.

Arrowstreet outperformed the Fund’s benchmark by 1.6%. Arrowstreet’s tilt towards value stocks was a tailwind. Among largest positive contributors were being underweight to real estate and overweight to energy. Germany was the most significant country-level positive contributor in large part due to positive security selection in German consumer discretionary and financials sectors. Weaker security selection in health care, primarily due to negative selection in United Kingdom and Swiss health care names was a detractor. Additionally, being underweight to French consumer discretionary names also contributed negatively. Russia was the most significant country-level detractor due to strategy’s exposure to Russian energy stocks.

American Century lagged the Fund’s benchmark by 5.1%. Companies with high and accelerating earnings growth characteristics continued to experience sharp-selloff during the 2023 fiscal year; this environment was a major headwind for American Century. The majority of underperformance came from security selection in information technology, consumer discretionary, materials, industrials, and financials.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Non-US Core Equity Fund

MFS underperformed the Fund’s benchmark by 2%. Weak security selection within both materials and industrials detracted from relative results. Being underweight to the energy sector further weakened relative performance. Conversely, an overweight exposure to consumer staples and strong security selection within the information technology sector strengthened relative results. The strategy’s relative currency exposure, resulting primarily from differences between the strategy’s and its benchmark’s exposures to holdings of securities denominated in foreign currencies also contributed to relative performance.

LSV outperformed the Fund’s benchmark by 1.2%. LSV’s tilt towards lower market capitalization stocks was a headwind; higher than benchmark exposure to value stocks was a tailwind. Stronger security selection in industrials and financials were largest positive contributors. Security selection in health care and consumer discretionary were main detractors.

Parametric utilizes exchange-traded futures replicating the Fund’s benchmark, aiming to provide broad, passive, equity market exposure to the Fund’s liquidity sleeve, and seeking to create positive returns on assets that would have otherwise been earning cash or cash equivalent returns. Performance differences versus the benchmark are largely a result of cash flow effects related to daily subscription/redemption activity and through financing costs of futures relative to interest earned on cash.

Risk Considerations

The Fund invests in foreign and emerging market securities which involves certain risks such as currency volatility, political and social instability and reduced market liquidity. Emerging markets may be more volatile and less liquid than more developed markets and therefore may involve greater risks. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may invest in derivative instruments such as exchange-listed equity futures contracts, which may cause the Fund to experience greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify the risk of loss for the Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Non-US Core Equity Fund

March 31, 2023

Comparison of Change in Value of a hypothetical $10,000 Investment in Mercer Non-US Core Equity Class Y-3 Shares vs. the MSCI EAFE Index® for the period 4/1/13 through 3/31/23

AVERAGE ANNUAL TOTAL RETURNS | | | | |

| | | | |

Mercer Non-US Core Equity Fund – Class Y-3 – 8/18/2006 | | | | |

Mercer Non-US Core Equity Fund – Class I – 7/22/2021 | | | | |

| | | | |

1 MSCI EAFE® Index measures the performance of equity securities in developed markets outside of North America, including Europe, Australasia, and the Far East.

2 Russell 1000® Index measures the performance of the large cap segment of the U.S. equity universe.

3 MSCI Emerging Markets® Index measures the performance of equity securities in global emerging markets.

The Fund's total annual gross operating expense for Class Y-3 is 0.76% and for Class I is 1.01% Please see the Fund's most recent Prospectus.

The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Non-US Core Equity Fund

March 31, 2023

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-888-887-0619 or visit the Trust’ s website at https://www.mercer.us/what-we-do/wealth-and-investments/delegated-solutions-us.html for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Please see the Schedule of Investments for a complete list of Fund holdings.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Core Fixed Income Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide total return, consisting of both current income and capital appreciation. The benchmark for the Fund is the Bloomberg U.S. Aggregate Bond™ Index1.

Investment Strategy

The Fund invests principally in investment grade fixed income securities, including government securities, corporate bonds and securitized bonds, such as mortgage and asset-backed securities. The Fund may also invest in non-investment grade bonds (sometimes called high yield or junk bonds), non-U.S. dollar denominated bonds, and bonds issued by issuers located in emerging capital markets. The Fund may also invest in certain derivative instruments, such as options, futures, and swap agreements. The Fund may engage in transactions in derivatives for a variety of purposes, including changing the investment characteristics of its portfolio, enhancing total returns or as a substitute for taking a position in an underlying asset.

Performance

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -5.20% compared to its benchmark return of -4.78%. For the fiscal year ended March 31, 2023, the Fund’s I share class performance was -5.42% compared to its benchmark return of -4.78%. Performance for the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisers

As of March 31, 2023, the Fund employed three sub-advisers: Manulife Investment Management (US) LLC (Manulife), Income Research & Management (IR&M) and PGIM Fixed Income, a business unit of PGIM, Inc. (Prudential).

Manulife manages its allocated portion of the Fund by seeking to produce superior results through bottom-up active management of sector allocation and issue selection, combined with yield curve positioning. Duration is also managed in line with the benchmark. The investment team capitalizes on their disciplined investment process and adds value by following a relative value approach to sector allocation and issue selection while engaging in intensive fundamental credit research and identifying points on the yield curve with the greatest return potential.

IR&M manages its allocated portion of the Fund based on the belief that careful security selection and higher portfolio income provide superior returns over the long term. Portfolios are constructed using a disciplined, bottom-up investment approach to select attractive securities from the U.S. fixed income universe. A bottom-up approach focuses on the analysis of individual issuers and de-emphasizes the significance of macroeconomic and market cycles with the assumption individual companies can do well even in an industry that is not performing, at least on a relative basis.

Prudential manages its allocated portion of the Fund by seeking to maximize excess return opportunities from sustainable alpha2 sources, such as sector allocation and bottom-up security selection. This process is coupled with a diligent daily portfolio risk evaluation and monitoring process. Research-based security selection is a major source of added value and incorporates both fundamental analysis, by measuring a security’s intrinsic value to determine if undervalued or overvalued, as well as proprietary models, by using software and other means of analysis to gain a competitive edge, which identify relative value and detailed technical review of issuers across both benchmark and non-benchmark sectors, with an emphasis on credit-oriented sectors.

Market Commentary and Fund Performance

For the 12-month period ended March 31, 2023, U.S. fixed income market returns, as measured by the Bloomberg U.S. Aggregate Bond™ Index, were -4.78%, mainly driven by a move structurally higher in U.S. interest rates.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Core Fixed Income Fund

Rising consumer prices as measured by the Consumer Price Index (CPI)3 fed in to U.S. monetary policy action, creating the need for one of the most aggressive hiking cycles on record. U.S. inflation as measured by CPI hit a four-decade high of 9.1% in June 2022, with large increases in the cost of gasoline, shelter and food. During the fiscal year, the Fed hiked +50 basis points (bps)4 in May 2022, +75bps in June, July, September, and November 2022, +50bps in December 2022, +25bps in February 2023, and +25bps in March 2023 with the federal funds rate ending the period at 4.75-5%. As indication that Fed action is gaining traction, U.S. inflation eased in March 2023 with CPI rising 5.0% from a year earlier, marking the ninth straight monthly deceleration since the peak in June 2022.

Investment grade credit spreads ended the period at 138bps (1.38%), widening from their March 2022 level of 116bps (1.16%). Front end rates steadily climbed higher for the period, while the 10 and 30-year Treasuries peaked around November 2022 and have since come down. The 3-month T-Bill ended the period at a rate of 4.85%, 433bps higher than its March 2022 level of 0.52%. The 10-year Treasury ended the period at a rate of 3.48%, 116bps higher than its March 2022 level of 2.32%. Perhaps the biggest market signal thus far of tighter conditions and worrying growth outlook is the shape of the curve. The spread between 10-year yields and 3-month yields was +180bps in March 2022, and now sits at an extreme inversion...-137bps.

The Fund’s return was negative in relative terms as it underperformed the Bloomberg U.S. Aggregate Bond™ Index for the fiscal year ended March 31, 2023. The majority of underperformance was due to the Fund’s strategic overweight to spread sectors during a period when credit-sensitive sectors generally lagged, with the majority of underperformance occurring during the early stages of the period.

The respective performance results of each Sub-adviser was in line with expectations based on risk posture. Manulife has the largest share of the risk-allocation within the Fund. Manulife’s bias towards corporate credit and allocation to “higher quality” high yield bonds led the manager to underperform for the fiscal year.

Prudential had a marginally less aggressive allocation to spread sectors relative to Manulife, but was still overweight relative to the Fund’s benchmark. The majority of underperformance relative to the benchmark was due to the portfolio’s long spread risk position in the first quarter of the fiscal year as volatility in risk markets increased and spreads widened in response to the Russia-Ukraine conflict and growing concerns over stickier inflation.

IR&M outperformed the Fund’s benchmark over the trailing 12-month period. The bias towards higher quality corporate bonds as well as their tactical rotation of spread exposure led them to outperform.

Risk Considerations

The Fund is subject to the risks that the underlying bonds in its portfolio are subject to, including credit, prepayment, call and interest rate risk. As interest rates rise, the value of bond prices will decline. The Fund may invest in foreign securities, which may expose the Fund to currency and exchange rate fluctuations, derivatives (such as futures, options, or swaps) and high yield bonds (also known as “junk” bonds). These investments may cause the Fund to experience greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify the risk of loss for the Fund. The Fund may also experience high portfolio turnover, which may result in higher transaction costs and capital gains.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Core Fixed Income Fund

March 31, 2023

Comparison of Change in Value of a hypothetical $10,000 Investment in Mercer Core Fixed Income Class Y-3 Shares vs. the Bloomberg U.S. Aggregate Bond™ Index for the period 4/1/13 through 3/31/23

AVERAGE ANNUAL TOTAL RETURNS | | | | |

| | | | |

Mercer Core Fixed Income Fund – Class Y-3 – 8/15/2005 | | | | |

Mercer Core Fixed Income Fund – Class I – 12/27/2021 | | | | |

Bloomberg U.S. Aggregate Bond™ Index | | | | |

1 Bloomberg U.S. Aggregate Bond(TM) Index is an index that measures the performance of securities from the Bloomberg U.S. Government/ Corporate Bond Index, Mortgage-Backed Securities Index, Asset-Backed Securities Index, and Commercial Mortgage-Backed Securities Index. The Bloomberg U.S. Aggregate BondTM Index is a broad representation of the investment-grade fixed-income market in the United States and includes U.S. government and corporate debt securities, mortgage- and asset-backed securities, and international U.S. dollar-denominated bonds. All securities contained in the Bloomberg U.S. Aggregate BondTM Index have a minimum term to maturity of one year.

2 Alpha measures the amount that the investment has returned in comparison to the market index or other broad benchmark that it is compared against.

3 Consumer price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Indexes are available for the U.S. and various geographic areas. Average price data for select utility, automotive fuel, and food items are also available.

4 Basis Points: A common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Core Fixed Income Fund

March 31, 2023

The Fund's total annual gross operating expense for Class Y-3 is 0.39% and for Class I is 0.64% Please see the Fund's most recent Prospectus.

The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-888-887-0619 or visit the Trust’ s website at https://www.mercer.us/what-we-do/wealth-and-investments/delegated-solutions-us.html for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Please see the Schedule of Investments for a complete list of Fund holdings.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Opportunistic Fixed Income Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The Fund’s primary benchmark is the ICE Bank of America Merrill Lynch Global High Yield 2% Constrained Index Unhedged1. The Fund’s secondary benchmark2 is a blended benchmark consisting of 35% Bloomberg Global Aggregate Corporate Total Return Index Hedged3, 17.5% Bloomberg Global High Yield Index4, 10.5% JP Morgan CEMBI Diversified Index5, 7% S&P/LSTA Leveraged Loan Index6, and 30% JP Morgan GBI-EM Diversified Index7.

Investment Strategy

The Fund invests principally in fixed income securities of U.S. and non-U.S. issuers, including those in emerging and frontier markets. The Fund invests in various strategic and tactical global bond market opportunities without limitations in geography, issuer type, quality and currency denomination. The Fund may invest in derivatives such as futures (including among others, interest rate futures), swaps (currency, interest rate, credit default and total return), forwards, options, and credit-linked notes. The Fund may engage in transactions in derivatives for a variety of purposes, including hedging, risk management, efficient portfolio management, enhance total returns, or as a substitute for taking position in the underlying asset.

Performance

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -2.96% compared to its primary benchmark return of -2.47% and secondary benchmark return of -2.54%, Performance of the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisers

As of March 31, 2023, the Fund employed four sub-advisers, Western Asset Management Company, LLC and Western Asset Management Company Limited (as sub-subadviser) (together referred to as WAMCO), Loomis, Sayles & Company, L.P. (Loomis), BlackRock International Limited (BlackRock), and Colchester Global Investors Limited (Colchester).

In managing its allocated portion of the Fund’s portfolio, Loomis invests in debt of issuers globally. Loomis produces country specific credit cycle views and forward looking financial market regimes as inputs to portfolio construction. Security selection is then carried out by the investment team with input from a team of credit analysts who maintain a comprehensive database of internal ratings. The investment team will also engage in active duration positioning although security and sector selections are identified as main drivers of performance.

In managing its allocated portion of the Fund’s portfolio, WAMCO employs an active, team-managed investment approach around a long-term, value-oriented investment philosophy. The portfolio seeks to harvest income opportunities by constructing a diversified portfolio that includes investment-grade and high yield corporate credit, non-dollar debt, bank loans, Credit Loan Obligations (CLO), emerging markets sovereign and corporate debt, and a variety of structured credit (Residential Mortgage Backed Security (RMBS), Commercial Mortgage Backed Securities (CMBS), Asset Backed Securities (ABS)). Western seeks to add value through sector rotation, issue selection, duration management, yield curve positioning, and tail risk hedging.

In managing its allocated portion of the Fund’s portfolio, Colchester invests in sovereign debt issued by emerging market borrowers denominated in each issuer’s local currency. Colchester’s portfolio construction process is based on a quantitative model, using mathematical and statistical methods, that promotes allocation to countries and currencies identified based on attractive real yields for bonds and attractive valuations for currencies, complemented by sound financial characteristics and Environmental, Social and Governance (ESG) considerations.

In managing its allocated portion of the Fund’s portfolio, BlackRock invests in emerging market debt securities denominated in local currency. BlackRock’s portfolio construction process implements a top down philosophy focused on identifying economic or market themes that impact asset prices. The themes inform the team’s market views and portfolios are positioned to benefit from directional moves in the market.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Opportunistic Fixed Income Fund

Market Commentary and Fund Performance

For the 12-month period ended March 31, 2023, U.S. fixed income market returns, as measured by the Bloomberg U.S. Aggregate Bond™ Index8, were -4.78%, driven mainly by a structural move higher in US interest rates. Rising consumer prices as measured by the Consumer Price Index (CPI) fed in to US monetary policy action, creating the need for one of the most aggressive hiking cycles on record. U.S. inflation as measured by CPI hit a four-decade high of 9.1% in June 2022, with large increases in the cost of gasoline, shelter and food. During the fiscal year, the Fed hiked +50 basis points (bps) in May 2022, +75bps in June, July, September, and November 2022, +50bps in December 2022, +25bps in February 2023, and +25bps in March 2023 with the federal funds rate ending the period at 4.75-5%. As indication that Fed action is gaining traction, U.S. inflation eased to 5.0% as of March 2023, marking the ninth straight monthly deceleration since the peak in June 2022.

Investment grade credit spreads ended the period at 138bps (1.38%), widening from their March 2022 level of 116bps (1.16%). Front end rates steadily climbed higher for the period, while the 10 and 30-year Treasuries peaked around November 2022 and have since come down. The 3-month T-Bill ended the period at a rate of 4.85%, 433bps higher than its March 2022 level of 0.52%. The 10-year Treasury ended the period at a rate of 3.48%, 116bps higher than its March 2022 level of 2.32%. Perhaps the biggest market signal thus far of tighter conditions and worrying growth outlook is the shape of the curve. The spread between 10 year yields and 2 year yields was +180bps in March 2022, and now sits at an extreme inversion…-137bps.

JPM GBI-EM Global Diversified Index of local currency Emerging Market government returned -0.72% in U.S. dollar terms over the 12-month period ending March 31, 2023. The asset class was challenged by heightened inflation and recession concerns, global central banks’ policy tightening and geopolitical uncertainty over the ongoing Russia-Ukraine war.

During the period, WAMCO and Loomis underperformed their component of the Fund’s secondary benchmark with both managers struggling to meaningfully capitalize on opportunistic sector exposures. WAMCO had mixed performance with duration and yield curve positioning detracting while sector allocation in investment grade corporates, high yield corporates, and emerging market debt offset some of the underperformance. Loomis’ underperformance was driven by sector allocation in investment grade corporates and emerging market debt.

During the period, Blackrock and Colchester outperformed their component of the Fund’s secondary benchmark, the JPM GBI-EM Diversified Index government bond benchmark. BlackRock’s macro regime shifting investment approach helped to take advantage of broad market correlation shifts and idiosyncratic opportunities. Colchester benefited from continuing their fundamental real-yield valuation approach. The repricing higher of out-of-benchmark positions in Russian government bonds in the first half of the fiscal year added to performance while both managers sought too tactically trim exposure.

Risk Considerations

The Fund invests in non-investment grade and emerging market fixed income securities that involve certain risks such as higher volatility, currency fluctuation, political and social instability and reduced market liquidity. The Fund is subject to the risks that the underlying bonds in its portfolio are subject to, including credit, prepayment, call and interest rate risk. As interest rates rise, the value of bond prices will decline. The Fund may invest in foreign securities, which may expose the Fund to currency and exchange rate fluctuations, derivatives (such as futures, options and swaps) and high yield bonds (also known as “junk” bonds). These investments may cause the Fund to experience greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify the risk of loss for the Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Opportunistic Fixed Income Fund

March 31, 2023

Comparison of Change in Value of a hypothetical $10,000 Investment in Mercer Opportunistic Fixed Income Class Y-3 Shares vs. the ICE Bank of America Merrill Lynch Global High Yield 2% Constrained Index Unhedged, the Fund’s Secondary Index for the period 8/21/13 through 3/31/23

AVERAGE ANNUAL TOTAL RETURNS | | | | |

| | | | |

Mercer Opportunistic Fixed Income Fund – Class Y-3 – 8/21/2013 | | | | |

ICE Bank of America Merrill Lynch Global High Yield 2% Constrained Index Unhedged | | | | |

| | | | |

1 ICE Bank of America Merrill Lynch Global High Yield 2.0% Constrained Index Unhedged contains all securities in The Bank of America Merrill Lynch Global High Yield Index but caps issuer exposure at 2%. Index constituents are capitalization-weighted, based on their current amount outstanding, provided the total allocation to an individual issuer does not exceed 2%. Issuers that exceed the limit are reduced to 2% and the face value of each of their bonds is adjusted on a pro-rata basis.

2 The Fund’s secondary benchmark is a blended benchmark consisting of 35% Bloomberg Global Aggregate Corporate Total Return Index Hedged, 17.5% Bloomberg Global High Yield Index, 10.5% JP Morgan CEMBI Diversified Index, 7% S&P/LSTA Leveraged Loan Index, and 30% JP Morgan GBI-EM Diversified Index.

3 Bloomberg Global Aggregate Corporate Total Return Index Hedged is a measure of global investment grade, fixed-rate corporate debt. This multi-currency benchmark includes bonds from developed and emerging markets issuers within the industrial, utility and financial sectors.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Opportunistic Fixed Income Fund

March 31, 2023

4 Bloomberg Global High Yield Index is a multi-currency flagship measure of the global high yield debt market. The index represents the union of the US High Yield, the Pan-European High Yield, and Emerging Markets (EM) Hard Currency High Yield Indices.

5 J.P. Morgan CEMBI Broad Diversified Core Index (CEMBI CORE) tracks the performance of US dollar denominated bonds issued by emerging market corporate entities. The CEMBI CORE follows the methodology of the flagship J.P. Morgan CEMBI Broad Diversified (CEMBIB Dividend) closely, while offering a more liquid and higher credit quality subset.

6 S&P (Standard and Poor’s/LSTA (Loan Syndications and Trading Association) Leveraged Loan 100 Index is designed to measure the performance of the U.S. leveraged loan market based upon market weightings, spreads, and interest payments.

7 J.P. Morgan Government Bond Index-Emerging Markets (GBI-EM) Indices are comprehensive Emerging Markets debt benchmarks that track local currency bonds issued by Emerging Market governments. The GBI-EM Indices are comprised of only those countries from the GBI universe that meet our criteria for an Emerging Market, resulting in 18 countries from four regions. For the Diversified version of the Index, the methodology uses only a limited portion of a country’s current face amount outstanding for calculating weights. The adjusted face amount used in calculating a country’s weight is based on the respective country’s relative size in the index and the average size of all countries.

8 Bloomberg U.S. Aggregate Bond(TM) Index is an index that measures the performance of securities from the Bloomberg U.S. Government/Corporate Bond Index, Mortgage-Backed Securities Index, Asset-Backed Securities Index, and Commercial Mortgage-Backed Securities Index. The Bloomberg U.S. Aggregate Bond Index is a broad representation of the investment-grade fixed-income market in the United States and includes U.S. government and corporate debt securities, mortgage- and asset-backed securities, and international U.S. dollar-denominated bonds. All securities contained in the Bloomberg U.S. Aggregate Bond Index have a minimum term to maturity of one year.

The Fund's total annual gross operating expense for Class Y-3 is 0.90%. Please see the Fund's most recent Prospectus.

The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-888-887-0619 or visit the Trust’ s website at https://www.mercer.us/what-we-do/wealth-and-investments/delegated-solutions-us.html for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Please see the Schedule of Investments for a complete list of Fund holdings.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Emerging Markets Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the MSCI Emerging Markets® Index1.

Investment Strategy

The Fund invests principally in equity securities of large, medium and small capitalization companies, located in emerging markets, other investments that are tied economically to emerging markets, as well as in American, European and Global Depositary receipts. Stock index futures and various types of swaps may be used to implement the country selection component of the Fund’s investment strategy. Currency forwards may be used to make stock-selection and country allocation decisions independently of the underlying currency.

Performance

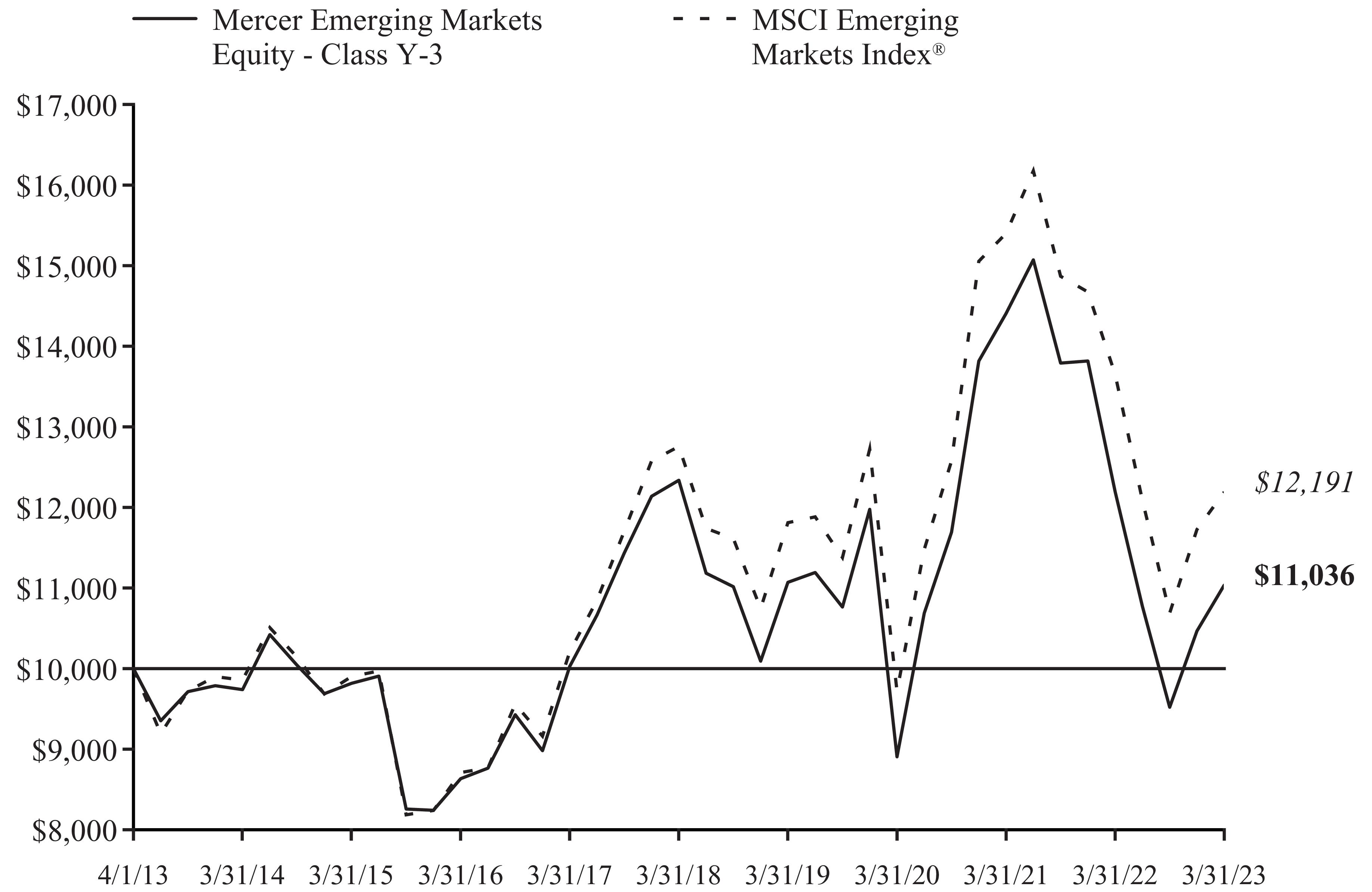

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -9.51% compared to its benchmark return of -10.70%. Performance for the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisers

As of March 31, 2023, the Fund employed six sub-advisers and one sub-subadviser: Barrow, Hanley, Mewhinney &Strauss, LLC (Barrow Hanley), William Blair Investment Management LLC (William Blair), Origin Asset Management LLP (Origin), Bennbridge U.S. LLC which utilizes certain personnel of Skerryvore Asset Management LLP (together referred to as Bennbridge/Skerryvore), Schroder Investment Management North America Inc. and Schroder Investment Management North America Limited (as sub-subadviser) (together, referred to as Schroders) and Parametric Portfolio Associates LLC (Parametric). Barrow Hanley replaced Grantham, Mayo, Van Otterloo & Co. LLC as sub-adviser to the Fund on December 22, 2022.

Barrow Hanley manages a fundamentally driven, value oriented strategy. Their process focuses on identifying companies trading in the bottom 1/3rd of the Emerging Markets universe from a valuation standpoint, and conducts in-depth fundamental analysis to identify strong companies positioned well for a business turnaround.

William Blair has a quality growth philosophy and process focused on finding those companies that can achieve a higher growth rate for a longer period of time than the market expects. William Blair looks for companies with experienced and motivated management teams, unique business models and attractive financial characteristics.

Origin’s portfolio is managed using a quantitative process focused on companies with high and improving cash flow return on investment, selling at discounted valuations of expected future growth versus historical growth and that also display fundamental and price momentum. The portfolio is managed to have a higher tracking error and high active share.

Bennbridge/Skerryvore manages a high quality, concentrated equity strategy with an emphasis on preservation of capital, and sustainability of the businesses in which they invest. The strategy is low turnover, and concentrated, roughly 30-60 names.

Schroders manages a dedicated China allocation for the Fund to exploit alpha opportunities within the country. The strategy is a bottom up, fundamental strategy, relying on a team of experienced analysts and PMs to source and evaluate potential investments. The strategy is based on the belief that investing in quality businesses, with sustainable competitive advantages, and focus on shareholder value, trading at reasonable valuations will outperform over time.

Parametric utilizes exchange-traded futures to generate market exposure corresponding to the Fund’s benchmark.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Emerging Markets Equity Fund

Market Commentary and Fund Performance

2023 fiscal year was a turbulent period for capital markets. Multi-decade high inflation rates, fueled by very accommodative fiscal and monetary policy of the prior two years, supply chain disruptions and commodity price spikes, further escalated by Russia’s invasion of Ukraine, were front and center for policy makers and investors. In response to the stubbornly high inflation prints, global central banks initiated one of the most aggressive hiking cycles in decades. With rates rising sharply, the precipitous decline in equity markets which began in January of 2022 continued until October when the global markets bottomed and investor sentiment reached its trough. In contrast to the first half of the fiscal year, the second half experienced strong rallies as investors began to bet on moderating inflation, slowing interest rate hikes by central banks and a possibility of soft landing.

For the year ended March 31, 2023, U.S. equities, measured using the Russell 1000® Index2, declined by 8.39%. Compared to the U.S., international developed markets performed better, with the MSCI EAFE® Index3 decreasing by 1.39% over the period. The MSCI Emerging Markets® Index (the Fund’s benchmark) declined by 10.70% for the 12-month period ended March 31, 2023. In local currency terms MSCI EAFE® Index and MSCI Emerging Markets® Index posted higher returns, as the US dollar appreciated compared to other major currencies.

Fears of looming recession and weak Chinese demand from the prolonged zero COVID policy put pressure on the commodity prices in the second half of the year, resulting in poor returns from commodity producing countries such as Saudi Arabia, South Africa, Canada, Australia and Brazil. These countries were among the best performers in the prior fiscal year. India and Taiwan which performed well during prior fiscal year also had weak returns. On the other hand, European equities with attractive valuations from prior year’s sharp underperformance showed best returns. Chinese equities, which were the worst performing major market in the 2022 fiscal year, rallied sharply in May-June and again between October and January, as the country officially emerged from COVID lockdown. However, on both occasions, these rallies were followed by sharp reversals, leaving Chinese equities with 6.3% decline for the year.

Triggered by rising interest rates and expensive valuations, the sharp underperformance of companies with high earnings growth and higher profitability characteristics continued in the first three quarters of the fiscal year. In the fourth quarter, this trend reversed, making the underperformance of the growth versus value equities less pronounced. The persistent outperformance of energy stocks also reversed in the fourth quarter of the fiscal year. Smaller market capitalization companies were under significantly more pressure compared to mega and larger market capitalization companies. Momentum was the worst performing equity style across all major markets. For the year value was the best performing investment style followed by lower volatility.

For the 12-month period ending March 31, 2023, the Mercer Emerging Markets Equity Fund outperformed the MSCI Emerging Markets® Index by approximately 1.2%. The Fund’s outperformance was driven in large part by strong performance from two sub-advisers, Schroders and Bennbridge/Skerryvore

Barrow Hanley, the newly appointed manager in the fund outperformed by 0.4% since their inception in December of 2022. Contributing to performance was a general underweight to India, which pulled back during the period on concerns around Adani Enterprises, a large influential Indian industrial conglomerate. Strong stock selection in Brazil and Taiwan along with a general underweight to commodity producers in the Middle East were also additive to performance.

The William Blair Emerging Markets strategy underperformed the MSCI Emerging Markets® Index by 4.0% over the trailing 12-month period ending March 31st. Blair’s focus on high growth, high quality and long-duration assets was significantly out of style as markets favored low-valuation stocks. Nearly all of the trailing 12-month relative underperformance can be traced to the fourth quarter where markets saw a sharp country and industry rotation in the wake of China’s decisive U-turn on its zero-COVID policy and rapid relaxation of travel restrictions. Against this backdrop, stock selection was generally challenged in China, India, and South Korea, particularly within technology, consumer, and financial names. On the positive side Mexico and Indonesia were bright spots on a relative basis.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Emerging Markets Equity Fund

Bennbridge/Skerryvore outperformed by 10.2% for the year ending 3/31/23. The portfolio’s focus on higher quality businesses with strong alignment with minority shareholders was beneficial during a choppy period for emerging markets. The team added value across sectors and countries, with notable winners in Brazil (WEG SA), India (Cipla) and consumer names (China Resource Beer, Heineken, Unilever, and Fomento Economico).

Origin underperformed by 3.8% during the period as momentum shifted throughout the year, creating headwinds to a core tenant of their investment philosophy. Chinese and Taiwanese holdings in particular were a large detractor, especially within financials and industrials. On the positive side, holdings in Brazil and a general underweight to the Middle East contributed.

The portion of the Fund allocated to Schroders, which pursues investment opportunities in China, outperformed for the year. Strong security selection across a number of industries added value, with holdings in industrials and in companies tied to the electric vehicle (EV) supply chain and renewable energy (solar) space being notable outperformers. Strong relative performance in real estate (selection and underweight), along with an allocation to gold miners, also added value.

Parametric utilizes exchange-traded futures to replicate the Fund’s benchmark, aiming to provide broad, passive, equity market exposure to the Fund’s liquidity sleeve and seeking to create positive returns on assets that would have otherwise been earning cash or cash equivalent returns. Performance differences versus the benchmark are largely a result of cash flow effects related to daily subscription/redemption activity and through financing costs

of futures relative to interest earned on cash.

Risk Considerations

The Fund invests in emerging market securities which involves certain risks such as currency volatility, political and social instability and reduced market liquidity. Emerging markets may be more volatile and less liquid than more developed markets and therefore may involve greater risks. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. The Fund may invest in derivatives (such as futures, forwards, options, or swaps), which may cause the Fund to experience greater volatility and less liquidity. Derivatives may be more sensitive to changes in market conditions and may amplify the risk of loss for the Fund.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Emerging Markets Equity Fund

March 31, 2023

Comparison of Change in Value of a hypothetical $10,000 Investment in Mercer Emerging Markets Equity Class Y-3 Shares vs. the MSCI Emerging Markets Index® for the period 4/1/13 through 3/31/23

AVERAGE ANNUAL TOTAL RETURNS | | | | |

| | | | |

Mercer Emerging Markets Equity Fund – Class Y-3 – 5/1/2012 | | | | |

MSCI Emerging Markets Index® | | | | |

1 MSCI Emerging Markets® Index measures the performance of equity securities in global emerging markets.

2 Russell 1000® Index measures the performance of the large cap segment of the U.S. equity universe.

3 MSCI EAFE® Index measures the performance of equity securities in developed markets outside of North America, including Europe, Australasia, and the Far East.

The Fund's total annual gross operating expense for Class Y-3 is 0.87%. Please see the Fund's most recent Prospectus.

The performance of other classes, when launched, will vary from the performance of the class shown based on the difference in fees and expenses paid by shareholders investing in different share classes. The Fund may charge a 2% redemption fee on shares owned less than 30 days.

The table and graph assume reinvestment of dividends and capital gains, but do not reflect a deduction of taxes an investor might pay on fund distributions or upon redemption of fund shares. Performance shown reflects a fee waiver and/or expense reimbursement. Without this waiver/reimbursement, returns would have been lower.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Emerging Markets Equity Fund

March 31, 2023

The data quoted represents past performance and does not guarantee future results. Current performance of the Fund may be lower or higher than the performance quoted. Please call 1-888-887-0619 or visit the Trust’ s website at https://www.mercer.us/what-we-do/wealth-and-investments/delegated-solutions-us.html for the Fund’s most recent month-end performance. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than when purchased.

Fund holdings and sector allocations are subject to change and are not a recommendation to buy or sell any security. Please see the Schedule of Investments for a complete list of Fund holdings.

Management's Discussion of Fund Performance (Unaudited) (Continued)

Mercer Global Low Volatility Equity Fund

Investment Objective and Benchmark

The investment objective of the Fund is to provide long-term total return, which includes capital appreciation and income. The benchmark for the Fund is the MSCI World® Index1.

Investment Strategy

The Fund invests principally in equity securities of U.S. and foreign issuers, of large, medium and small capitalization companies. Stock index futures and various types of swaps may be used to implement the equity security selection component of the Fund’s investment strategy. Currency forwards may be used to make stock- selection and country allocation decisions independently of the underlying currency.

Performance

For the fiscal year ended March 31, 2023, the Fund’s Y-3 share class performance was -4.53% compared to its benchmark return of -7.02%. Performance for the Fund is reported net of fees and operating expenses while the benchmark returns do not include expenses of any kind as indexes are unmanaged.

The Sub-Advisers