united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-21872

Mutual Fund Series Trust

(Exact name of registrant as specified in charter)

4221 North 203rd Street, Suite 100 Elkhorn, Nebraska 68022-3474

(Address of principal executive offices) (Zip code)

Ultimus Fund Solutions ___

80 Arkay Drive, Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 402-895-1600

Date of fiscal year end: 3/31

Date of reporting period: 3/31/24

Explanatory Note: The registrant is filing this amendment to its filing on Form N-CSR for the year ended March 31, 2024, which was originally filed with the Securities and Exchange Commission on June 11, 2024 (Accession Number 0001580642-24-003144), solely to correct the title of Michael Schoonover and Erik Naviloff to reflect as Principal Executive Officer and Principal Financial Officer and update Items 11a and 11b to reflect the internal control impact of the material weakness on Form N-CSR.

ITEM 1. REPORTS TO SHAREHOLDERS.

Annual Report

AlphaCentric Income Opportunities Fund

Class A: IOFAX Class C: IOFCX Class I: IOFIX

AlphaCentric Premium Opportunity Fund

Class A: HMXAX Class C: HMXCX Class I: HMXIX

AlphaCentric Robotics and Automation Fund

Class A: GNXAX Class C: GNXCX Class I: GNXIX

AlphaCentric Symmetry Strategy Fund

Class A: SYMAX Class C: SYMCX Class I: SYMIX

AlphaCentric LifeSci Healthcare Fund

Class A: LYFAX Class C: LYFCX Class I: LYFIX

AlphaCentric Strategic Income Fund

Class A: SIIAX Class C: SIICX Class I: SIIIX

March 31, 2024

AlphaCentric Advisors LLC

53 Palmeras Street, Suite 601

San Juan, PR 00901

1-844-223-8637

March 31, 2024

AlphaCentric Income Opportunities Fund (IOFIX | IOFAX | IOFCX) (unaudited)

Dear Shareholders:

We hope this letter finds you navigating the most recent bout of “surprise” well – a lot has changed in the last year. We believe markets are finally starting to feel better, a welcome change.

The Federal Reserve’s efforts painted a better picture and began stages of a recovery, although the Fund returned -3.61% (Class I) versus 1.70% for the Bloomberg US Aggregate for the period 3/31/2023 – 3/31/2024.

Fed Chair Powell’s pause in July of 2023 allowed the markets to breathe half a sigh of relief, and yet inflation remained an overhanging issue. His comments at the end of 2023 led to a more positive market tone heading into 2024, but the market perhaps got ahead of itself in forecasting as many as six Fed Funds cuts. Those hopes were successively dashed with Q1 reports revealing sticky prices and continued strength in wages, and some even suggesting that a hike might be on the table. This of course kept investors “on the sidelines” and willing to stay in higher-interest money market funds, trying to avoid duration calls until clearer signals arrive.

Revisions in jobs data imply emerging softness in labor, which could be a component of the Fed’s dual mandate despite inflation/pricing data having received most of the headline emphasis. We feel that conditions are supportive of no further hikes at the very least and believe that cuts will be the next step although “data dependent,” as Chair Powell likes to say. And along those lines we continue to be firmly convinced of the Fund’s portfolio and positioning, as the Fund’s sector remains cheap relative to other asset classes and offers potentially higher upside with solid collateral characteristics. As mentioned in the past, housing fundamentals and mortgage borrower profiles, in particular for the seasoned, legacy securities emphasized in the Fund, have kept improving.

As always, thank you for your support and best wishes for the year!

Sincerely,

Garrison Point Fund Management Team

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

The Fund’s returns for the fiscal year ended 3/31/24 and for the period since inception through 3/31/24, as compared to the Benchmark Index, were as follows:

| | | Since Inception |

| | Fiscal Year Ended 3/31/2024 | 5/28/2015 |

| Class I | -3.61 | 2.32 |

| | | |

| Class A | -3.86 | 2.06 |

| | | |

| Class A w/ Sales Charge | -8.39 | 1.50 |

| | | |

| Class C | -4.62 | 1.30 |

| | | |

| Bloomberg US Agg Bond Index (1) | 1.70 | 1.20 |

| (1) | Bloomberg US Aggregate Bond Index: A market capitalization-weighted index that is designed to measure the performance of the U.S. investment grade bond market with maturities of more than one year. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 4.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 5412-NLD-5/14/2024.

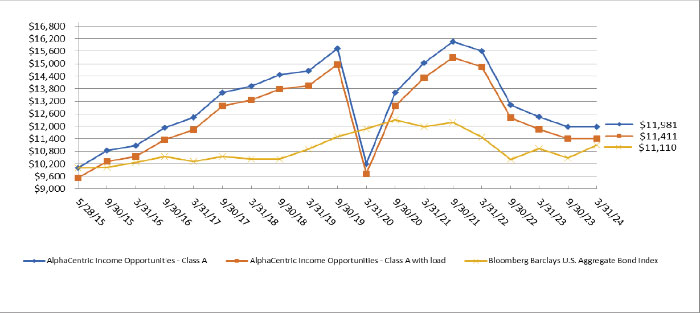

AlphaCentric Income Opportunities Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2024

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmark:

| | | Annualized | Annualized | Annualized |

| | One Year | Three Years | Five Years | Since Inception+ |

| Class A (IOFAX) | (3.86)% | (7.32)% | (3.95)% | 2.06% |

| Class A (IOFAX) with 4.75% load | (8.39)% | (8.80)% | (4.88)% | 1.50% |

| Class C (IOFCX) | (4.62)% | (8.02)% | (4.69)% | 1.30% |

| Class I (IOFIX) | (3.61)% | (7.07)% | (3.72)% | 2.32% |

| Bloomberg U.S. Aggregate Bond Index ** | 1.70% | (2.46)% | 0.36% | 1.20% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 4.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 28, 2024. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2024, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.74%, 2.49% and 1.49% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the adviser from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus were 2.18%, 2.93% and 1.93% for the Fund’s Class A, Class C, and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus were 1.90%, 2.65% and 1.65% for the Fund’s Class A, Class C, and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The Bloomberg U.S. Aggregate Bond Index is commonly used as a benchmark by both passive and active investors to measure portfolio performance relative to the U.S. dollar-denominated investment grade fixed-rate taxable bond market. It is also an informational measure of broad market returns commonly applied to fixed income instruments. Investors cannot invest directly in an index. |

| + | The AlphaCentric Income Opportunities Fund commenced operations on May 28, 2015. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | | % of Net Assets | |

| Non-Agency Residential Mortgage Backed Securities | | | 105.1 | % |

| Short Term Investment | | | 0.0 | % * |

| Liabilities In Excess Of Other Assets | | | (5.1 | )% |

| | | | 100.0 | % |

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

March 31, 2024

AlphaCentric Premium Opportunity Fund (HMXIX | HMXAX | HMXCX) (unaudited)

Dear Shareholders:

We are pleased to provide our Annual Letter to Shareholders. Thank you for your support and for being an investor in the Fund.

Investment Strategy

The portfolio strategy utilized by the Fund seeks to achieve capital appreciation with lower overall volatility than the equity market. The strategy attempts to achieve its objective by investing in a systematically managed portfolio of long and short call and put options and futures on the Standard & Poor’s 500 Index (the “Index”) and/or other securities that represent the return of the Index (such as exchange traded funds), as well as investments tied to measures of market volatility such as volatility exchange traded funds and futures on the VIX Index, which reflect the market’s expected fluctuation (volatility).

In addition to option strategies such as call ratios, strangles and straddles, the strategy uses futures, options on futures, and a variety of derivative instruments in an attempt to achieve capital efficiency. Relying on the embedded leverage of these markets, the Fund aims to hold between 70% and 85% of assets in U.S. Treasury bills or similar investments. Treasury bills act as a source of defense as well as potential upside, aligning with the overall dual mandate of balancing offense and defense. The income they generate, especially in a higher rate environment, helps enhance risk-adjusted returns for investors.

Fund Performance

For the fiscal year ended March 31, 2024, the Fund returned +14.17% (Class I shares). This return represented 48% of the S&P 500 total return.

Several quarters during the fiscal year acted as great examples of the Fund’s multiple return streams and ability to shift and react dynamically to different market environments. The second quarter of 2023 highlighted the Fund’s ability to capture returns from option strategies not related to the market’s upside or downside; earning 0.68% in May 2023.

The third quarter of 2023 highlighted the Fund’s ability to truncate the downside, with a loss of 0.57%. And the fourth quarter of 2023 highlighted the Fund’s ability to participate in the market’s upside, with a gain for the Fund of 5.77%.

On the flip side, October 2023 and Q1 of 2024 were more difficult periods. In October 2023, with our models shifting into defense mode as the S&P teetered on the edge of a -10% correction, only to see the market rally strongly into the end of the year. While we can look back now and lament that our downside defense cost the Fund from capturing more of the market’s upside, it sure felt good to have that defense on as the market stared a full-blown correction in the face.

Q1 2024 was different. Without volatility falling to new all-time lows as the S&P hit new all-time highs, the Fund’s option strategies capped the upside capture of the Fund somewhat, providing a slight headwind even as we participated meaningfully in the upside.

With the Fund participating in market upside both through direct exposure in S&P futures markets, and through the capture of volatility erosion as markets rise in price, the removal of one of those legs can lessen the Fund’s participation some.

Market Outlook

Looking out into the year ahead, it really feels like a reset and start of a new market regime that could last multiple years. Sort of like a new football season after living through the drama, wins and losses of the year before, but this ’season’ having been the entire post-COVID period, and the new ’season’ perhaps lasting several years.

Markets are essentially in a neutral stance, at or close to all-time highs as of the end of March 2024, but with valuations (Shiller CAPE Ratio) about midway between 2020 lows and 2021 highs. Bond and interest rate markets look set to normalize, with potential delays in easing, but the likelihood of further hikes much diminished.

Meanwhile, volatility has erased the echo of the COVID spike and become much more of a two-way market with volatility sellers and volatility downside reintroduced to the market. Meanwhile, volatility does remain low, and markedly lower than the bulk of the past three years. This allows the Fund to more cheaply invest in structures which potentially increase in value as the market decreases.

Sincerely,

Russell Kellites

Portfolio Manager

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

The Fund’s returns for the fiscal year ended 3/31/24 and for the period since inception through 3/31/24, as compared to the Benchmark Index, were as follows:

| | Fiscal Year Ended 3/31/2024 | Since Inception* |

| Class A | 13.83 | 7.12 |

| | | |

| Class A with Sales Charge | 7.31 | 6.28 |

| | | |

| Class C | 12.98 | 6.42 |

| | | |

| S&P 500 TR Index1 | 29.88 | 14.56 |

| | | |

| Class I | 14.17 | 9.41 |

| | | |

| S&P 500 TR Index1 | 29.88 | 14.50 |

| * | Fund Inception: 9/1/2011 (Class I) & 9/30/2016 (Class A & C). The Performance shown before September 30, 2016, is for the Fund’s Predecessor Fund (Theta Funds, L.P.) The Fund’s management practices, investment goals, policies, objectives, guidelines and restrictions are, in all material respects, equivalent to the predecessor limited partnership. From its inception date, the predecessor limited partnership was not subject to certain investment restrictions, diversification requirements and other restrictions of the Investment Company Act of 1940, as amended, if they had been applicable, it might have adversely affected its performance. In addition, the predecessor limited partnership was not subject to sales loads that would have adversely affected performance. Performance of the predecessor fund is not an indicator of future results. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Dividends are not assured. Investments in mutual funds involve risks. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com.

3374-NLD-05/14/2024

| 1 | The S&P 500 Total Return Index by Standard & Poor’s Corp. is a capitalization-weighted index comprising 500 widely held common stocks listed on various exchanges, representing the performance of the stock market generally. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index, although individuals may invest in exchange traded funds or other investment vehicles that attempt to track the performance of an index. The Fund may or may not purchase the types of securities represented by the S&P 500 Total Return Index. Investors cannot invest directly in an index. |

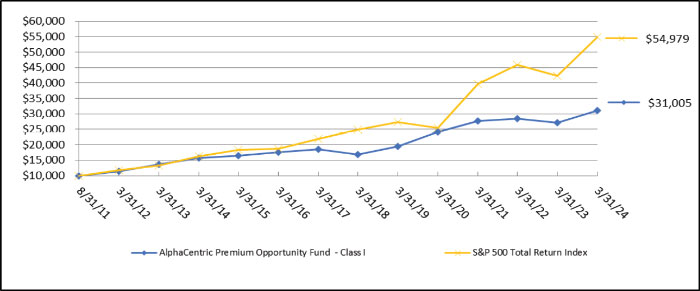

AlphaCentric Premium Opportunity Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2024

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmark:

| | | Annualized | Annualized | Annualized | Annualized | Annualized |

| | One Year | Three Years | Five Years | Ten Years | Since Inception+ | Since Inception++ |

| Class A (HMXAX) without load | 13.83% | 3.57% | 9.42% | — | 7.12% | — |

| Class A (HMXAX) with 5.75% load | 7.31% | 1.55% | 8.13% | — | 6.28% | — |

| Class C (HMXCX) | 12.98% | 2.79% | 8.71% | — | 6.42% | — |

| Class I (HMXIX) +++ | 14.17% | 3.84% | 9.69% | 7.04% | — | 9.41% |

| S&P 500 Total Return Index ** | 29.88% | 11.49% | 15.05% | 12.96% | 14.56% | 14.50% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 28, 2024. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2024, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 2.24%, 2.99% and 1.99% for the Fund’s Class A, Class C and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the adviser from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus were 2.45%, 3.20% and 2.20% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus were 2.32%, 3.07%, and 2.07% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

| + | The AlphaCentric Premium Opportunity Fund Class A and Class C commenced operations on September 30, 2016. |

| ++ | The AlphaCentric Premium Opportunity Fund Class I, formerly a private fund, commenced operations on August 31, 2011. |

| +++ | The Fund acquired all of the assets and liabilities of Theta Funds, L.P. (the “Predecessor Fund”) in a tax-free reorganization on September 30, 2016. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund, so the Predecessor Fund became the Class I shares of the Fund. The Fund’s investment objective, policies and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies and guidelines. The Predecessor Fund commenced operations on August 31, 2011. Updated performance information will be available at no cost by calling 1-844-ACFUNDS (844-223-8637) or visiting the Fund’s website at www.AlphaCentricFunds.com. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type ** | | % of Net Assets | |

| U.S. Government & Agencies | | | 33.1 | % |

| Short-Term Investments | | | 24.1 | % |

| Future Options Purchased | | | 1.1 | % |

| Index Options Purchased | | | 0.1 | % |

| Written Future Options | | | (0.9 | )% |

| Other Assets in Excess of Liabilities | | | 42.5 | % |

| | | | 100.0 | % |

| ** | - Does not include derivative investments. |

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

March 31, 2024

Dear AlphaCentric Robotics and Automation Fund (the “Fund”) Investor:

The narrative of the past year has been dominated by two major themes, but just seven major stocks. The first major theme was underscored by the view that artificial intelligence (AI) would usher in a new era – similar to the advent of the internet, or electricity – according to some vocal pundits. Seven stocks, including Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta, and Tesla became widely regarded as the leaders in the race to AI supremacy. As we write, the dominance of the so-called “Magnificent Seven” has become so extreme that they collectively account for nearly 30% of the market-cap of the S&P 500. The second major theme was the indication by the Federal Reserve Board that they were done raising rates, and that they would likely begin “normalizing” rates with at least three cuts before year-end 2024. Of course, the street initially took that to mean seven rate cuts over the next year. The street has subsequently trimmed that expectation to just one cut in September as inflation continues to run too hot.

March 31, 2024 marked the end of the fiscal year for the Fund. Since the end of the last fiscal year, the Fund posted a 5.85% total return (Class I share). The S&P 500 TR Index recorded a gain of 29.88% during the same period. A bifurcation of returns between the Magnificent Seven described above and the average S&P 500 stock significantly distorted and exaggerated the performance of the major cap-weighted indexes. Since the Fund did not own any of these seven overvalued and overhyped stocks, the Fund experienced a relative performance deficit over the past 12-month period versus the benchmark index.

Geopolitical developments in the Middle East between Israel and its adversaries – Hamas, Hezbollah, Houthis, and Iran – specifically with respect to the shipping routes that pass through the Red Sea and the Suez Canal, have put pressure on energy prices and have negatively impacted supply chains since October 7th. The evidence continues to suggest that capital expenditures spending priorities have resumed their focus on robotics and automation solutions, but there has been a notable impact on the timing of new projects and initiatives. Nevertheless, it remains our view that the mandate to improve operational efficiencies will remain foremost as companies large and small adapt to the new realities of the post-COVID world.

While mergers and acquisitions (M&A) have helped the Fund’s performance in previous years, the termination of the iRobot acquisition by Amazon has many small-cap companies in the space rethinking their timelines for profitability. Our strategy of focusing on leading-edge technologies and the core end-market beneficiaries of the automation theme has benefitted from M&A activity in the past, but it has never been dependent upon M&A for success. Indeed, we engaged in a culling of certain profitless growth stories from the Fund’s holdings in 1Q24. This portfolio management action has allowed us to further consolidate the Fund around the strongest fundamental growth stories in the robotics and automation universe – those which are generating high free cash flow growth – and with which we currently maintain the highest conviction.

During the past year, the Fund’s top performing position was Doosan Robotics, up 115% during the period. The company is a leading provider of advanced industrial robots for production process automation based in South Korea. Their products are used primarily for precision assembly tasks in the automotive, consumer electronics, healthcare and food & beverage industries. A new addition in 2023, automated voice pioneer, SoundHound AI, was the second largest contributor to the Fund’s results last year. The stock gained 83% year-over-year. The company’s proprietary independent voice AI platform allows its customers across the automotive, hospitality, entertainment, and electronics industries to voice-enable their products and services. Procept BioRobotics, the Fund’s fourth largest holding, logged the number three performance rank last year, posting an annual total return of 79%. The maker of the AQUABEAM advanced, image-guided, surgical robotic system is setting new standards in safety and efficacy for the treatment of BHP.

While these examples were important to the Fund’s fiscal year results, they simply represent the broad array of companies and technologies that populate the Fund’s holdings. The Fund remains laser-focused on identifying and capitalizing upon advances and innovative technologies that are changing the world by investing in the companies that are driving this change.

Thank you for your support and participation in the Fund.

Sincerely,

Brian Gahsman, Portfolio Manager

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

The Fund’s returns for the fiscal year ended 3/31/24 and for the period since inception through 3/31/24, as compared to the Benchmark Index, were as follows:

| | Fiscal Year Ended | Since Inception |

| | 3/31/2024 | 5/31/17 |

| Class I | 5.85 | 5.49 |

| | | |

| Class A | 5.60 | 5.23 |

| | | |

| Class A w/Sales Charge | -0.49 | 4.32 |

| | | |

| Class C | 4.79 | 4.44 |

| | | |

| S&P 500 Total Return Index1 | 29.88 | 14.05 |

| | | |

| MSCI AC World Index TR Gross2 | 23.81 | 10.44 |

| + | The AlphaCentric Robotics and Automation Fund Class A, Class C and Class I commenced operations on May 31, 2017. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com.

3353-NLD-05022024

| 1 | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. |

| 2 | The MSCI AC World Index TR Gross represents the Modern Index Strategy and captures all sources of equity returns in 23 developed and 24 emerging markets. |

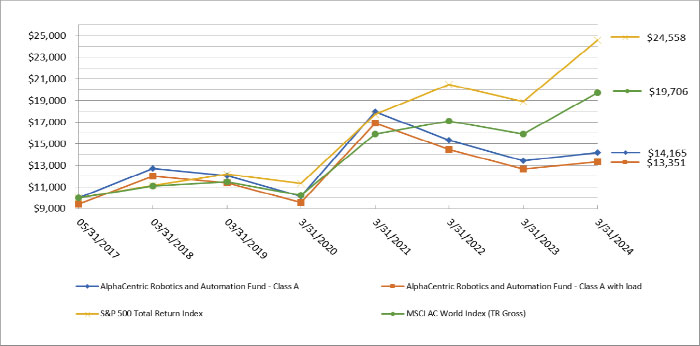

AlphaCentric Robotics and Automation Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2024

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmarks:

| | | | Annualized | Annualized | Annualized |

| | | One Year | Three Years | Five Years | Since Inception+ |

| | Class A (GNXAX) without load | 5.60% | (7.58)% | 3.27% | 5.23% |

| | Class A (GNXAX) with 5.75% load | (0.49)% | (9.38)% | 2.05% | 4.32% |

| | Class C (GNXCX) | 4.79% | (8.28)% | 2.50% | 4.44% |

| | Class I (GNXIX) | 5.85% | (7.37)% | 3.52% | 5.49% |

| | S&P 500 Total Return Index ** | 29.88% | 11.49% | 15.05% | 14.05% |

| | MSCI AC World Index (TR Gross) *** | 23.81% | 7.46% | 11.45% | 10.44% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 28, 2024. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2024, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.65%, 2.40% and 1.40% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the adviser from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus for the Fund’s period of operation are 2.31%, 3.06% and 2.06% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses shown in the August 1, 2023 prospectus for the Fund’s period of operation are 1.65%, 2.40% and 1.40% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

| *** | The MSCI AC World Index (TR Gross) represents the Modern Index Strategy and captures all sources of equity returns in 23 developed and 24 emerging markets. Investors cannot invest directly in an index. |

| + | The AlphaCentric Robotics and Automation Fund Class A, Class C and Class I commenced operations on May 31, 2017. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | | % of Net Assets | |

| Common Stocks | | | 98.7 | % |

| Investment Purchased as Securities Lending Collateral | | | 26.6 | % |

| Money Market Fund | | | 2.3 | % |

| Liabilities In Excess Of Other Assets | | | (27.6 | )% |

| | | | 100.0 | % |

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

March 31, 2024

AlphaCentric Symmetry Strategy Fund (SYMIX | SYMAX | SYMCX) (unaudited)

Dear Shareholders:

The Fund returned 9.57% (Class I shares) for fiscal year 2024, while the blended MSCI World/U.S. Aggregate Bond Blended Index (“Benchmark”) returned 14.23%. The traditional portfolio, which invests in stocks and credit, contributed the bulk of the gains as equity markets broadly increased and credit spreads tightened. The alternative portfolio, which invests in commodities, fixed income and currencies, detracted a little with commodity positions generating positive returns that were offset by losses in fixed income and currency markets. This is largely the mirror image of last year, and that diversification is at the heart of the strategy, resulting in a return of 6.03% annually over the last three years compared to 3.28% annually for the Benchmark.

The past year was characterized by the continued bumpy drop in inflation which, using the headline Consumer Price Index (CPI) number, peaked at 9% in the summer of 2022. A year later it hit 3% and since then has bounced around somewhat stubbornly just north of that level. Core CPI has had a similar trajectory. Inflation falling and the end point for rate rises coming into clearer view was supportive for equity valuations and credit spreads, particularly as the feared recession that rate rises would cause failed to materialize. Indeed, the unemployment rate in the US has been 4% or less since January 2022. Remarkable resilience. Equity and credit exposures remained at the upper end of the target ranges after being rebuilt in the early part of 2023 and stayed high through the year. The strategy holds positions in several industrials that continue to perform well, beneficiaries of the infrastructure and fiscal packages passed through Congress during this administration. It takes time for the legislation to filter its way through to the real economy and be spent, we are seeing it now and it will continue for the next few years. United Rentals and Paccar Inc. are good examples of this type of business, both reported strong fundamentals in the most recent quarter and are leaders in the spaces in which they operate. Although at the index level the equity markets look expensive, under the surface there are many companies at much cheaper valuations executing on their business consistently.

As the inflationary panic subsided somewhat, the alternative side that tends to thrive on panics and volatility did its job, contributing through the first part of the year before seeing some losses as many of the trends that have done so well over the past few years began to subside. The nature of trend following is that one is always positioned at the end of trends. As rate hike fears subsided and markets moved to price rate cuts (too many too quickly as it turned out) the alternative side reduced short, fixed income positions. This is why we rebalance religiously between the elements of the strategy, maintaining the symmetry.

As we look ahead over the next 12 months, we believe the outlook for the US economy remains fairly upbeat. As we noted briefly above, the fiscal packages will likely support growth over the rest of the year. Alongside that, assuming the inflation story doesn’t lead central banks to restart hikes, a gradual easing of policy as inflation continues to normalize should help support the interest rate sensitive sectors of the economy, some of which have been struggling. The US economy has under produced housing for years leading to construction continuing apace on the residential side, and a newly reinvigorated industrial policy around key industries of the future has led to a boom in manufacturing construction. Throw in some AI based activity as companies compete to not get left behind in the brave new world and some higher commodity prices helping the oil space and the economy looks in fine shape for now.

One thing to note, we think monetary policy at this juncture has the potential to be powerful if the economy were to slow and inflation comes down. Generally speaking, it has been the interest rate sensitive sectors that have slowed. If the Federal Reserve reduces rates in response to a slowing economy, we could see a wave of refinancing and pent-up activity coming back quite quickly. For all the talk of homeowners being locked into their 3% rates, life has been continuing apace. People have families and get new jobs. Home sales are down some 25% from pre pandemic levels – there is still a lot of activity in the 75% that are moving. They will refinance mortgages quickly, and at some point, other borrowers may tap the increased equity in their homes for consumption as well. Housing equity is at record levels. The Fed looks less stuck than it has for a while – again assuming inflation cooperates.

As it relates to the strategy, the key areas where we see risks of derailment are in the areas where the alternative side can potentially shine brightest. Oil and copper price spikes setting off inflation again could be a real worry for the stock market, the strategy can take direct exposures there. A generally stickier inflation path may challenge equity valuations, the ability to participate in rising bond yields through shorts in bond markets and longs in the USD also allows flexibility

to adapt to what may be ahead. Being able to adapt to changing times and take long and short positions in a broader range of markets is at the core of the strategy approach.

Thank you for your support, and we hope that you stay healthy and safe in 2024.

Sincerely,

Mount Lucas Management LP Team

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

The Fund’s returns for the fiscal year ended 3/31/24 and for the period since inception through 3/31/24, as compared to the Benchmark Index, were as follows:

| | Fiscal Year | |

| | Ended | |

| | 3/31/2024 | Since Inception* |

| Class A | 9.28 | 4.86 |

| | | |

| Class A w/ Sales Charge | 3.00 | 3.53 |

| | | |

| Class C | 8.46 | 4.06 |

| | | |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (1) | 5.27 | 1.99 |

| | | |

| MSCI World/Bloomberg U.S. Aggregate Bond Blended Index (2) | 14.23 | 6.33 |

| | | |

| Class I | 9.57 | 3.74 |

| | | |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (1) | 5.27 | 1.44 |

| | | |

MSCI World/Bloomberg U.S. Aggregate Bond Blended Index (2) | 14.23 | 5.13 |

| * | Inception (annualized): 9/1/14 (I Share) | 8/9/19 (A & C Shares) |

The Fund acquired all of the assets and liabilities of MLM Symmetry Fund, LP (the “Predecessor Fund”) in a tax-free reorganization on August 9, 2019. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund. The Fund’s investment objectives, policies, restrictions, and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies, restrictions, and guidelines. The Fund’s sub-advisor was the adviser to the Predecessor Fund.

| (1) | BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income. Investors cannot invest directly in an index. |

| (2) | MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across all 23 developed markets countries. It covers approximately 85% of the free float-adjusted market capitalization in each country. The Bloomberg U.S. Aggregate Bond index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Dividends are not assured. Investments in mutual funds involve risks. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 5411-NLD-5/14/2024

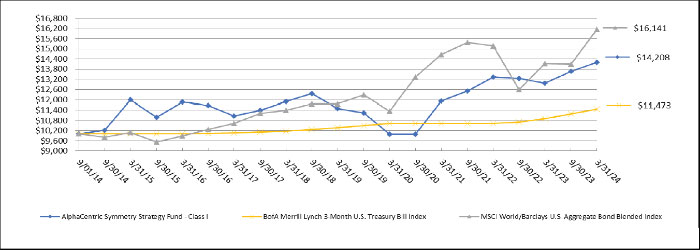

AlphaCentric Symmetry Strategy Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2024

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmarks:

| | | Annualized | Annualized | Annualized | Annualized |

| | One Year | Three Years | Five Years | Since Inception+ | Since Inception++ |

| Class A (SYMAX) without load | 9.28% | 5.80% | — | 4.86% | — |

| Class A (SYMAX) with 5.75% load | 3.00% | 3.73% | — | 3.53% | — |

| Class C (SYMCX) | 8.46% | 4.98% | — | 4.06% | — |

| Class I (SYMIX) +++ | 9.57% | 6.03% | 4.34% | — | 3.74% |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index ** | 5.27% | 2.60% | 2.03% | 1.99% | 1.44% |

| MSCI World/Bloomberg U.S. Aggregate Bond Blended Index *** | 14.23% | 3.28% | 6.53% | 6.33% | 5.13% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 28, 2024. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2024, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.85%, 2.60% and 1.60% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the adviser from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus are 2.03%, 2.78% and 1.78% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses shown in the August 1, 2023 prospectus are 1.93%, 2.68% and 1.68% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | BofA Merrill Lynch 3-Month U.S. Treasury Bill Index tracks the performance of the U.S. dollar denominated U.S. Treasury Bills publicly issued in the U.S. domestic market with a remaining term to final maturity of less than 3 months. Investors cannot invest directly in an index. |

| *** | MSCI World/Bloomberg U.S. Aggregate Bond Blended Index reflects an unmanaged portfolio of 60% of the MSCI World Index and 40% of the Bloomberg U.S. Aggregate Bond Index. Investors cannot invest directly in an index. |

| + | The AlphaCentric Symmetry Strategy Fund Class A, Class C commenced operations on August 8, 2019. |

| ++ | The AlphaCentric Symmetry Strategy Fund Class I, formerly a private fund, commenced operations on September 1, 2014. |

| +++ | The Fund acquired all of the assets and liabilities of MLM Symmetry Fund, LP (the “Predecessor Fund”) in a tax-free reorganization on August 9, 2019. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund. The Fund’s investment objectives, policies, restrictions, and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies, restrictions, and guidelines. The Fund’s sub-advisor was the adviser to the Predecessor Fund. The financial statements for the Predecessor Fund can be found in the Fund’s SAI. The performance information set forth below reflects the historical performance of the Predecessor Fund shares. Updated performance information will be available at no cost by calling 1-844-ACFUNDS (844-223-8637) or visiting the Fund’s website at www.AlphaCentricFunds.com |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type * | | % of Net Assets | |

| Exchange-Traded Funds | | | 34.9 | % |

| Common Stocks | | | 30.4 | % |

| U.S. Government & Agencies | | | 19.6 | % |

| Short-term Investment | | | 13.1 | % |

| Other Assets in Excess of Liabilities | | | 2.0 | % |

| | | | 100.0 | % |

| * | Does not include derivative investments. |

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

March 31, 2024

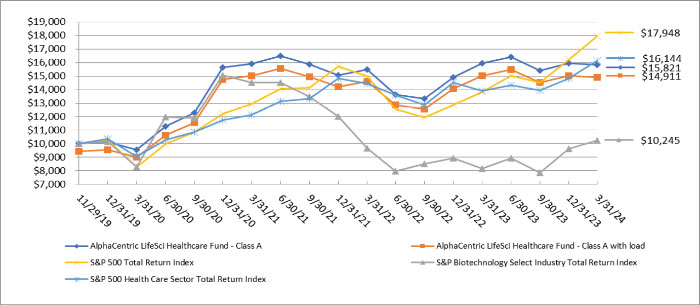

AlphaCentric LifeSci Healthcare Fund (LYFIX | LYFAX | LYFCX) (unaudited)

Dear Shareholders:

Performance

The Fund experienced fits and starts for the fiscal year ended March 31, 2024 as fundamental, thesis-driven stock picking took a back seat to macro considerations. Waxing and waning expectations for rate cuts from the Federal Reserve drove volatility in the S&P Biotechnology Select Index (“Index”) which was inversely correlated to the 10-year treasury yield. The Fund created alpha from holdings benefiting from Mergers & Acquisitions (M&A) transactions, favorable earnings announcements, positive fundamental company-specific news and avoidance of negative clinical or regulatory developments through October before the fed “pivot party” strongly increased select risk asset prices through the end of March. October was a tough month for the Index with >80% of the components in the red, with more than half of these down over 10%. Remarkably, before the rally, a record >30% of the entire biotech universe was trading below cash value, and more than 70% had an enterprise value below $100 million. The momentum factor had been the primary driver of returns in the last few months of the fiscal year, with many depressed biotech companies not participating in the rally – particularly small-cap commercial companies. The Fund did not attempt to chase momentum names that were bid up and held a number of value-oriented commercial companies that appeared to be mispriced. The Fund remains nimble and continues to seek asymmetric risk/reward opportunities for the portfolio that are poised to create potential value regardless of the trajectory of the broader economic environment.

Market Overview

The fiscal year ended with the Financial Times reporting US small-cap stocks had the worst performance run versus large cap peers in more than 20 years. Expectations are growing among strategists that the Fed intends to enact a soft removal of the 2% inflation target with Powell's comments that the goal will be reached "over time." The Index remains in the midst of the longest and deepest bear market in its history. We believe this should eventually be a tailwind for the many biotech stocks that remain left for dead, especially small-cap commercial companies. The Fed may be further motivated to start cutting rates despite some hotter economic data, due to the $1.1 trillion in interest payments on US government debt made in the past 12 months. Additionally, government spending is now growing at ~10% year-over-year, adding ~$1.0 trillion to the debt every 100 days. Although uncertainty remains regarding the timing and magnitude of potential interest rate cuts, US 2-Year/10-Year Spreads have been inverted for a record >625 days (prior record was 624 in August ’78) and it appears we are closer to the end of the interest rate cycle than the beginning.

Following half a decade of consecutive outperformance from 2011-2015, biotech has underperformed the Nasdaq from 2016-2023 for 8 years and the S&P 500 for 5 of those 8 years. Expectations for lower interest rates, sustained biotech M&A activity, continued new approvals of cutting-edge new therapies, and resurgent capital markets activity appear to be converging to potentially reverse biotech’s record relative underperformance. To be sure, the Federal Trade Commission’s defeat at blocking Amgen's (AMGN) ~$28 billion acquisition of Horizon Therapeutics (HZNP) bolstered expectations for sustained deal activity. Pharma drug sales were +3% in 2023 and are forecasted to grow 7% compounded through 2028 setting the backdrop sustained demand for new innovations.

The Food and Drug Administration (FDA) remained constructive in the fiscal year, given that 2023 was a banner year for new pharmaceutical products with 55 approvals, more than all prior years but two since 1985 (59 new drug approvals in 2018 and 1996). Included was the landmark approval of the first medicine incorporating gene editing technology. Crisper Therapeutics' (CRSP) Casgevy was approved for Sickle Cell Disease (SCD) and will be priced at $2.2 million per treatment. BioMarin (BMRN) continued the streak of high-profile regulatory approvals with FDA clearance of the first gene therapy for hemophilia A. BMRN plans to price Roctavian at $2.9 million per patient. FDA approved another gene therapy by giving the nod to Krystal Biotech's (KRYS) Vyjuvek for patients with dystrophic epidermolysis bullosa (DEB) with mutation(s) in the collagen type VII alpha 1 chain (COL7A1) gene. List price equates to >$1 million per patient per year for induction and ~$600k for maintenance use, leading KRYS to estimate a >$750 million global market opportunity despite there being only ~3000 DEB patients in the US. Finally, Seres Therapeutics (MCRB) announced the watershed regulatory approval oral microbiome therapy Vowst for the prevention of recurrence of C. difficile infection. The therapy will be priced at $17.5K per course and is the first microbiome therapy approval by the agency. Investor sentiment for

an accommodative FDA has become sanguine to the point where new approvals are even expected for certain drugs that fail to meet prespecified clinical criteria.

Fund Overview

The Fund benefited from M&A activity during the fiscal year with exposure to Cymabay Therapeutics (CBAY), NuVation Bio (NUVB), Immunogen (IMGN), Karuna Therapeutics (KRTX), Mirati Therapeutics (MRTX) and Point Biopharma (PNT). Gilead (GILD) announced the acquisition of CBAY for $4.3 billion representing a ~25% premium to prior close. The deal was generally well-received and values the company at 4-8x peak sales of lead drug seladelpar for primary biliary cirrhosis (PBC). The deal emphasizes pharma's seemingly insatiable appetite for differentiated assets. The Fund also benefited from the all-stock merger of NuVation Bio (NUVB) with AnHeart Therapeutics (private). The acquisition adds taletrectinib, a next-generation, potentially best-in-class ROS1 inhibitor with Breakthrough Therapy Designations currently enrolling two pivotal studies for the treatment of patients with ROS1-positive NSCLC. NUVB had been trading at a negative enterprise value and rallied on the news of the deal. Abbvie (ABBV) announced the acquisition of IMGN for a total equity value of approximately $10.1 billion, representing a 95% premium to the prior closing price. Valuation was ~5.5x consensus 2030 revenue estimates, in line with other recent oncology deals such as Pfizer's (PFE) purchase of Seagen (SGEN).

Bristol Myers (BMY) announced plans to acquire Karuna Therapeutics (KRTX) for $330 per share in an all-cash deal representing a 53% premium and $14 billion in value. The deal emphasized the value for novel mechanisms in established CNS indications such as schizophrenia. Bristol Myers (BMY) also announced the acquisition of Mirati Therapeutics (MRTX) for $4.9 billion cash upfront plus a contingent value right (CVR) for an additional $1 billion. Eli Lilly (LLY) stepped in front of pivotal data with the $1.4 billion purchase on PNT. The deal was an 87% premium to the prior close. Curiously, the announcement came ahead of PNT2002's Phase III SPLASH dataset in Q4 for pre-chemo prostate cancer. It turned out the SPLASH data came in below expectations and PNT would likely have faced a significant drawdown if it were not for the pending acquisition. The Fund was fortunate to benefit from LLY’s apparent strategic interest in acquiring a radiopharmaceutical platform and manufacturing assets regardless of the outcome of the SPLASH trial. The Fund continues to strive to increase exposure to holdings that might benefit from M&A transactions.

The Fund participated in a number of primary share transactions providing capital to directly fund R&D initiatives during the year. Specifically, the Fund participated in the $87 million private placement in Perspective therapeutics (CATX). The deal helped enable the company to advance its radiopharmaceutical pipeline focused on the alpha emitting isotope PB-212. The transaction was priced at $0.37 and shares closed the fiscal year at $1.19. Likewise, the Fund participated in an $88 million private placement for Vyne Therapeutics (VYNE). Prior to the deal, VYNE was trading at a depressed valuation of only ~$7 million market cap and the financing provides the company with ample runway to reach the next set of clinical milestones. The Fund also joined the syndicate for Abivax’s (ABVX) $236 million US NASDAQ IPO. The deal was intended to fund the company through phase 3 clinical data for lead inflammatory drug obefazimod in Ulcerative colitis. The Fund continues to look for primary share purchase opportunities that provide capital to allow companies to get through key development goals and potentially unlock value in the process.

The Fund’s companies with robust revenue and cash flow growth profiles continued to execute, but operational progress has not consistently translated into favorable share price performance as many SMID cap commercial companies remain under macro pressure. The Fund also benefited from shareholder capital return initiatives. For example, United Therapeutics (UTHR) announced a $1 billion accelerated share repurchase program (~9% of shares outstanding).

Outlook

The biotech bear market has been around quite a while, after completing its twelfth quarter to end the fiscal year. Signs of life are abounding as the Relative Strength Index for the Index went from 25 to 75 in less than four months to end the fiscal year, taking less than half the time as the last such move from the pandemic lockdowns. Many companies remain at depressed valuations, having yet to participate in the broader risk asset rally setting up for a long-anticipated reversal of the record relative underperformance. We continue to expect sustained biotech M&A activity, new approvals of cutting edge novel therapies and resurgent capital markets activity to create value in the sector. Of course, the ultimate realization of lower interest rates has the potential to position the risk for biotech to the upside once again.

Sincerely,

Mark Charest, Ph.D.

Founding Partner and Portfolio Manager

LifeSci Fund Management

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

The Fund’s returns for the fiscal year ended 3/31/24 and for the period since inception through 3/31/24, as compared to the Benchmark Index, were as follows:

| | Fiscal Year Ended 3/31/2024 | Since Inception 11/29/2019 |

| Class I | -0.56 | 11.39 |

| Class A | -0.79 | 11.16 |

| Class A w/ Sales Charge | -6.47 | 9.65 |

| Class C | -1.50 | 10.53 |

| S&P Biotechnology Select Industry Index1 | 25.67 | 0.56 |

| S&P 500 Total Return Index2 | 29.88 | 14.44 |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com.

5410-NLD-5/14/2024

1 The S&P Biotechnology Select Industry Index represents the biotechnology sub-industry portion of the S&P Total Markets Index (S&P TMI). The S&P TMI tracks all the U.S. common stocks listed on the NYSE, NYSE American, NASDAQ National Market and NASDAQ Small Cap exchanges. The S&P Biotechnology Select Industry Index is a modified equal weight index and typically consists of approximately 70 companies. Investors cannot invest directly in an index.

2 The S&P 500 Total Return Index is a widely recognized, unmanaged index of the approximately 500 largest companies in the United States as measured by market capitalization.

AlphaCentric LifeSci Healthcare Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2024

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmarks:

| | | Annualized | Annualized |

| | One Year | Three Years | Since Inception+ |

| Class A (LYFAX) without load | (0.79)% | (0.21)% | 11.16% |

| Class A (LYFAX) with 5.75% load | (6.47)% | (2.16)% | 9.65% |

| Class C (LYFCX) | (1.50)% | (0.96)% | 10.53% |

| Class I (LYFIX) | (0.56)% | 0.04% | 11.39% |

| S&P 500 Total Return Index ** | 29.88% | 11.49% | 14.44% |

| S&P Biotechnology Select Industry Total Return Index *** | 25.67% | (11.00)% | 0.56% |

| S&P 500 Health Care Sector Total Return Index **** | 16.09% | 10.01% | 11.68% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 28, 2024. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2024, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.65%, 2.40% and 1.40% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the adviser from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus are 2.00%, 2.75% and 1.75% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses as shown in the August 1, 2023 prospectus are 1.65%, 2.40% and 1.40% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

| *** | S&P Biotechnology Select Industry Total Return Index is designed to measure the performance of narrow GICS® sub-industries. The Index comprises stocks in the S&P Total Market Index that are classified in the GICS biotechnology sub-industry. Investors cannot invest directly in an index. |

| **** | S&P 500 Health Care Sector Total Return Index is designed to measure the performance of narrow GICS® health care sub-industries. The Index comprises stocks in the S&P Total Market Index that are classified in the GICS health care sub-industry. Investors cannot invest directly in an index. |

| + | The AlphaCentric LifeSci Healthcare Fund Class A, Class C and Class I commenced operations on November 29, 2019. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | | % of Net Assets | |

| Common Stocks | | | 93.8 | % |

| Short-term Investments | | | 6.2 | % |

| Liabilities in Excess of Other Assets | | | (0.0 | )% * |

| | | | 100.0 | % |

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

March 31, 2024

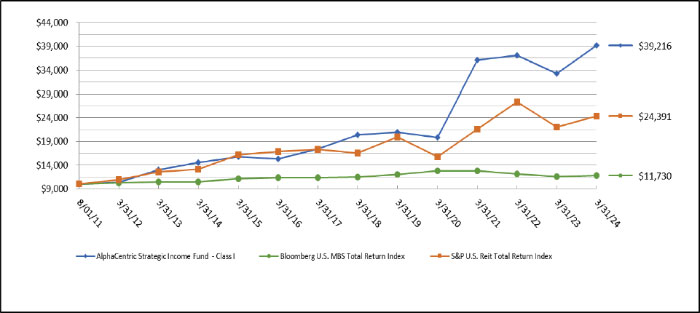

Dear AlphaCentric Strategic Income Fund (“the Fund”) Investor:

The Fund’s performance for the year ended March 31, 2024, was 18.00% (for the Class I Shares) versus 10.36% for the S&P U.S. REIT Index and 1.39% for the Bloomberg Barclays U.S. Mortgage-Backed Securities Index. The Fund also outperformed most other funds in Morningstar’s Real Estate Fund category for the same period.

Typical real estate funds continue to take predominantly equity type risk in commercial real estate by virtue of their extensive holdings of common shares in equity REITs. On the contrary, typical mortgage bond funds are hamstrung by their inability to take advantage of tangential opportunities in the equity market. We believe the Fund’s flexibility to invest “across the capital structure” differentiates it from most funds in the space and enables it to construct a portfolio capable of producing attractive risk-adjusted returns.

As financial pundits look back at 2023 and summarize economic and market developments, there is one common theme – surprise. While the twists and turns of markets throughout the year were somewhat unpredictable, by the end of the year, investors were generally rewarded for taking risk and resisting the allure of 5% money market rates. While depleted asset values at poorly hedged banks were unsurprising to us given our involvement in the mortgage bond market, the prospect of financial market contagion and a potential credit crunch became a significant risk in 2023. As we discussed at the time, tightening financial conditions stemming from the bank turmoil also ironically had the potential to be the knockout punch in the fight against inflation. While inflation wasn’t knocked out in 2023, as the year progressed upward, consumer price pressure increasingly appeared to be “on the ropes.” However, the market rebound in the middle of the year proved to be short-lived as rates sold off sharply in the August-October period. Inflation and jobs numbers moderated again in November and market sentiment sharply shifted in the context of a more highly probable “soft landing.” Although the “Magnificent 7” were responsible for almost half of the U.S. equity market gains by the end of the year, the rally in 4Q2023 put most parts of the market into positive territory for 2023.

The main theme of the Fund continued to play off the strength in the U.S. residential housing market. The Fund continued to be overweight in subsectors tied to residential mortgage credit – ranging from residential mortgage REITs to RMBS bonds. We believe when there is discernable fundamental strength in one part of the market, investors are apt to invest lower down in the capital structure to find the best risk/reward. Despite a historic rise in interest rates in 2022, as we anticipated, housing data remained relatively resilient throughout 2023. Low housing supply and ample mortgage borrower equity continued to be the drivers of strength in the housing market and correspondingly low residential mortgage defaults.

The rally across risk assets at the end of 2023 spilled over into 1Q2024 as many equities continued to march higher. Once a pipe dream, the “soft landing” scenario became the base case for many market participants. However, “animal spirits” were less present in real estate-related equities in 1Q2024 as REIT indices underperformed the broader market. This underperformance was mainly a result of the markets’ recognition that stubbornly high interest rates will likely continue to be a headwind for commercial property valuations. Most regional bank stocks, unsurprisingly to us, and an area of the market where the Fund has no exposure, also posted losses for 1Q2024 as commercial real estate woes, depleted asset prices, and deposit flight risk remain unresolved issues.

Yields across our target markets remain elevated and support the Fund’s managed monthly distribution of nine cents per share. This is the equivalent of an annualized yield of 6.58% based on the March 31, 2024 NAV.

In our opinion, the recent underperformance of residential mortgage equities and some parts of the structured credit market has presented an attractive opportunity. Looking ahead to the remainder of 2024, we believe many mortgage-related equities which are trading at unusually large discounts to book value are poised to generate attractive total returns. We also see deep value opportunities in certain parts of the structured (RMBS and CMBS) and corporate credit markets.

We believe the Fund is we are well-positioned for 2024 as it is focused on deep value opportunities in fundamentally sound parts of the real estate market. As fundamentals and market pricing evolve, we will aim to make use of the Fund’s flexibility and take advantage of dislocations in different parts of the real estate/mortgage markets.

We thank you for your investment and remind you that we are also investors in the Fund. Have a happy and healthy 2024!

Sincerely,

David Gregory

Portfolio Manager

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

The Fund’s returns for the fiscal year ended 3/31/24 and for the period since inception through 3/31/24, as compared to the Benchmark Index, were as follows:

| | Fiscal Year Ended | |

| | 3/31/2024 | Since Inception* |

| Class I | 18.00 | 11.39 |

| | | |

| S&P US REIT Index1 | 10.36 | 7.29 |

| | | |

| Bloomberg U.S. Mortgage Backed Securities Index USD2 | 1.39 | 1.27 |

| | | |

| Class A | 17.77 | 1.84 |

| | | |

| Class A w/ Sales Charge | 12.18 | 0.12 |

| | | |

| Class C | 16.88 | 1.08 |

| | | |

| S&P US REIT Index1 | 10.36 | 1.21 |

| | | |

| Bloomberg U.S. Mortgage Backed Securities Index USD2 | 1.39 | -3.12 |

| | | |

| Class I 30-Day SEC Yield – Subsidized | 6.22% | |

| | | |

| Class I 30-Day SEC Yield – Un-Subsidized | 5.44% | |

| * | Inception (annualized): 8/1/2011 (I Share) | 5/28/2021 (A & C Shares) |

Performance before May 28, 2021 is for the Fund’s Predecessor Fund (Strategos Deep Value Fund LP). The prior performance is net of management fees and other expenses including the effect of the performance fee. The Predecessor Fund had an investment objective and strategies that were, in all material respects, the same as those of the Fund, and was managed in a manner that, in all material respects, complied with the investment guidelines and restrictions of the Fund. From its inception to May 28, 2021, the Predecessor Fund was not subject to certain investment restrictions, diversification requirements and other restrictions of the Investment Company Act of 1940 or the Internal Revenue Code, which if they had been applicable, might have adversely affected its performance. In addition, the Predecessor Fund was not subject to sales loads that would have adversely affected performance. Performance of the Predecessor Fund is not an indicator of future results.

The 30-Day SEC Yield represents net investment income earned by the Fund over the 30-day period ending 3/31/2024, expressed as an annual percentage rate based on the Fund’s share price at the end of the 30-day period. Subsidized SEC 30-Day Yield reflects fee waivers and/or expense reimbursements during the period.

| 1 | The Bloomberg U.S. Mortgage Backed Securities Index tracks fixed-rate agency mortgage backed pass-through securities guaranteed by Ginnie Mae, Fannie Mae, and Freddie Mac. Investors cannot invest directly in an index. |

| 2 | The S&P U.S. States REIT Index defines and measures the investable universe of publicly traded real estate investment trusts domiciled in the United States. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 4.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 3354-NLD-05/06/2024

AlphaCentric Strategic Income Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2024

The Fund’s performance figures* for the periods ended March 31, 2024, compared to its benchmarks:

| | | Annualized | Annualized | Annualized | Annualized | Annualized |

| | One Year | Three Years | Five Years | Ten Years | Since Inception+ | Since Inception++ |

| Class A (SIIAX) | 17.77% | — | — | — | 1.84% | — |

| Class A (SIIAX) with 4.75% load | 12.18% | — | — | — | 0.12% | — |

| Class C (SIICX) | 16.88% | — | — | — | 1.08% | — |

| Class I (SIIIX) +++ | 18.00% | 2.76% | 13.41% | 10.46% | — | 11.39% |

| Bloomberg U.S. MBS Total Return Index ** | 1.39% | (2.84)% | (0.39)% | 1.12% | (3.12)% | 1.27% |

| S&P U.S. REIT Index Total Return *** | 10.36% | 4.10% | 4.04% | 6.45% | 1.21% | 7.29% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 4.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 28, 2024. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2024, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.74%, 2.49% and 1.49% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the adviser from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s estimated total annual operating expenses as shown in the August 1, 2023 prospectus for the Fund’s initial fiscal period are 2.38%, 3.13% and 2.13% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses shown in the August 1, 2023 prospectus for the Fund’s initial fiscal period are 1.75%, 2.50% and 1.50% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The Bloomberg U.S. MBS Total Return Index tracks fixed-rate agency mortgage backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). Investors cannot invest directly in an index. |

| *** | The S&P U.S. REIT Index Total Return defines and measures the investable universe of publicly traded real estate investment trusts domiciled in the United States.. Investors cannot invest directly in an index or benchmark. |

| + | The AlphaCentric Strategic Income Fund Class A and Class C commenced operations on May 28, 2021. |

| ++ | The AlphaCentric Strategic Income Fund Class I commenced operations on April 1, 2011. |

| +++ | The Fund acquired all of the assets and liabilities of Strategos Deep Value Fund LP (the “Predecessor Fund”) in a tax-free reorganization on May 28, 2021. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund. The Fund’s investment objectives, policies, restrictions, and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies, restrictions, and guidelines. The Fund’s sub-advisor is Goshen Rock Capital, LLC (“GRC”). GRC is an SEC registered investment advisor founded in 2021. The financial statements for the Predecessor Fund can be found in the Fund’s SAI. The performance information set forth below reflects the historical performance of the Predecessor Fund shares. Updated performance information will be available at no cost by calling 1-844-ACFUNDS (844-223-8637) or visiting the Fund’s website at www.AlphaCentricFunds.com |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | | % of Net Assets | |

| Common Stocks | | | 41.4 | % |

| Preferred Stocks | | | 14.5 | % |

| Asset Backed Securities | | | 12.4 | % |

| Convertible Bonds | | | 12.2 | % |

| Short-Term Investment | | | 9.2 | % |

| Corporate Bonds | | | 4.2 | % |

| U.S. Government & Agencies | | | 2.5 | % |

| Collateralized Mortgage Obligations | | | 2.1 | % |

| Exchange-Traded Fund | | | 0.8 | % |

| Other Assets in Excess of Liabilities | | | 0.7 | % |

| | | | 100.0 | % |