UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21897

Manager Directed Portfolios

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Scott M. Ostrowski, President

Manager Directed Portfolios

c/o U.S. Bank Global Fund Services

811 East Wisconsin Avenue, 8th Floor

Milwaukee, WI 53202

(Name and address of agent for service)

(414) 765-4339

Registrant's telephone number, including area code

Date of fiscal year end: December 31, 2022

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

Spyglass Growth Fund

Annual Report

December 31, 2022

Spyglass Growth Fund

Table of Contents

| Letter to Shareholders | | | 3 |

| Investment Highlights | | | 8 |

| Sector Allocation of Portfolio Assets | | | 9 |

| Schedule of Investments | | | 10 |

| Statement of Assets and Liabilities | | | 12 |

| Statement of Operations | | | 13 |

| Statements of Changes in Net Assets | | | 14 |

| Financial Highlights | | | 15 |

| Notes to Financial Statements | | | 16 |

| Report of Independent Registered Public Accounting Firm | | | 25 |

| Expense Example | | | 26 |

| Statement Regarding Liquidity Risk Management Program | | | 28 |

| Notice to Shareholders | | | 29 |

| Trustees and Officers | | | 30 |

| Approval of the Spyglass Growth Fund Investment Advisory Agreement | | | 33 |

| Notice of Privacy Policy and Practices | | | 36 |

Spyglass Growth Fund

Letter to Shareholders

(Unaudited)

Dear Shareholders,

For the fiscal year ended December 31, 2022, the Spyglass Growth Fund – Institutional Shares (the “Fund”) generated a negative return of 47.23%(1). This performance was unfavorable compared to the negative return of 26.72% for its benchmark, the Russell Midcap Growth Index (which includes the reinvestment of dividends, interest income, and capital gains), and to the negative return of 18.11% for the S&P 500 Index (which includes the reinvestment of dividends, interest income, and capital gains), as a comparison for the broader equity market performance.

The Fund invests in dynamic companies, operating in rapidly growing industries that are being led by results-oriented, entrepreneurial management teams. The Fund’s strategy remains consistent as it attempts to identify companies that are benefiting from secular growth and are well positioned to compete in the industries in which they operate.

The Fund’s top five performers during 2022 were Twitter, Inc., Ascendis Pharma A/S, TransDigm Group, Inc., Five Below, Inc., and Ulta Beauty, Inc. Two of these five holdings were not in the portfolio at the end of 2022 – Twitter, Inc., which was sold in the second quarter of 2022, and Ulta Beauty, Inc., which was sold in the third quarter of 2022. Twitter, Inc., a leading social media company, was a top performer for the Fund in 2022. Spyglass exited the position in the second quarter of 2022 after a definitive agreement was reached for the Company to be acquired by Elon Musk. Ascendis Pharma A/S, a leading global biopharmaceutical company, was a top performer for the Fund in 2022. The Company’s lead asset, SKYTROFA, exceeded expectations throughout the year. Additionally, the Company reported positive clinical data for its TransCon PTH and TransCon CNP clinical programs. TransDigm Group, Inc., a leading global aerospace company, was a top performer for the Fund in 2022. The Company reported solid results throughout its fiscal year and benefitted from growing air traffic volumes around the globe. Five Below, Inc., a value-oriented specialty retailer, was a top performer for the Fund in 2022. Despite a challenging macro environment leading the Company to reduce its initial full year guidance, Five Below reported strong results and accelerating momentum in the second half of the year while continuing to open up more new stores and roll out new growth initiatives. Ulta Beauty, Inc., the largest beauty retailer in the US, was a top performer for the Fund in 2022. Spyglass exited the position in the third quarter of 2022. Spyglass assessed the Company as fairly valued and viewed the risk-reward as relatively balanced, therefore it was deemed prudent to reallocate the capital to more attractive opportunities elsewhere in the portfolio.

| | | | | Since |

| | One-Year | Three-Year | Five-Years | Inception(2) |

Spyglass Growth Fund – Institutional Shares(1) | (47.23%) | (7.17%) | 3.73% | 6.35% |

As of December 31, 2022.

(1) Performance verified by US Bank Global Fund Services. Past performance does not guarantee future results.

(2) Inception date October 1, 2015.

Three-year, five-year, and since inception performance is annualized.

Spyglass Growth Fund

In 2022, the Fund’s five biggest detractors were AppLovin Corporation, Affirm Holdings, Inc., Lyft, Inc., Momentive Global Inc., and Peloton Interactive, Inc. AppLovin Corporation, a leading software solutions provider for app developers, was a bottom contributor for the Fund in 2022. Industry-wide headwinds weighed on the growth of the mobile app ecosystem as the year progressed, thereby reducing the willingness of app developers to spend on user acquisition and limiting the AppLovin’s revenue potential. Affirm Holdings, Inc., a leading financial technology company, was a bottom contributor for the Fund in 2022. Despite an overall healthy demand environment, ongoing interest rate hikes impacted the Company’s go-forward growth rate, ultimately leading it to lower its fiscal year 2023 growth expectations. Lyft, Inc., a leading ride-sharing company, was a bottom contributor for the Fund in 2022. Investors were disappointed with Lyft’s investments in driver supply which weighed on profitability during the year. However, Spyglass believes these investments have set up Lyft to generate more consistent earnings growth in 2023 and beyond. Momentive Global Inc., a developer of survey software, was a bottom contributor for the Fund in 2022. Broad-based macroeconomic uncertainty led to slower new deal activity and existing customers consuming a lower amount of existing survey credits. Peloton Interactive, Inc., a leading exercise equipment and media company, was a bottom contributor for the Fund in 2022. The Company brought on a new CEO who is pursuing a turnaround that is focused on reducing the expense base and reaccelerating revenue growth.

In 2022, rising inflation and rising interest rates were the primary focus of investors with the Federal Reserve delivering seven rate hikes totaling an increase of 4.25%. The Fed has not tightened rates this aggressively since the early 1980s. Across asset classes, this was a tough year to be an investor. Commodities were the only major asset class to achieve gains in 2022. Both bonds and equities lost value. However, this was the best year for Value’s relative performance compared to Growth since the year 2000. The S&P 500 Value Index outperformed the Growth Index by more than 2400 basis points while the Russell 2000 Value Index outperformed the Growth Index by more than 1400 basis points. From a sector perspective, cyclical and defensive sectors led the way in 2022. In the S&P 500 Index and the Russell Midcap Growth Index, Energy stocks rose 64.6% and 59.1%, respectively, while Utilities rose 1.6% and 2.9%, respectively. No other sectors were positive for the year, but sectors such as Industrials and Materials only declined modestly relative to more growth-oriented sectors such as Technology, Communications, and Consumer Discretionary. Given this backdrop, which included fear of a recession, a ground war in Europe, and lingering effects of the COVID-19 pandemic, investor sentiment continued to be particularly bearish.

As long-term investors in rapidly growing companies, Spyglass typically utilizes time – often measured in years – for the fundamentals of our portfolio companies to evolve. Given the market environment in 2022, investors appeared defensive and seemed to gravitate quickly to companies with strong current earnings and lower P/E multiples. Low P/E multiples are often associated with safety and value; however, they also tend to be

Spyglass Growth Fund

associated with businesses that offer low levels of growth. While cyclical low-growth industries such as Energy, Industrials, and Materials outperformed in 2022 as investor dollars prioritized short-term safety, Spyglass historically does not invest in these sectors because the Spyglass research engine is built to capitalize on the opportunity to unlock potential alpha embedded in what we see as tomorrow’s leading growth companies. We believe these companies will not only grow rapidly but also generate high levels of earnings and free cash flow. Spyglass seeks companies that grow their revenues, and ultimately their earnings, at approximately 20% per year on average. We invest in these companies until the stock price intercepts our calculated present value. The intention of the Spyglass Growth Fund is not to lose less money by owning stocks that might go down less, rather our objective is to drive capital appreciation by owning world class growth businesses where share price gains outrun the market averages over time.

As growth stocks came under pressure in 2022, the market seemed increasingly focused on interest rates, inflation, and the impact of a potential recession. Notably, the conversation around innovation in the economy faded into the background. At Spyglass, we are perpetually trying to find those companies that will benefit from an ever-evolving economy. The spring of 2023 will hopefully mark the end of a three-year economic episode that was dramatically impacted by the COVID-19 pandemic. The pandemic and the resulting turbulence—economic and social—have been enormous distractions from the progress in fields such as artificial intelligence and genomics when we look out. While we are not satisfied with the results of the last quarter or the last year, we remain as optimistic as ever that investing with a value orientation in rapidly growing companies, operating in dynamic sectors of the economy, and being led by entrepreneurs, will allow us to generate returns that exceed the long-term average returns of the market. Every day we are reminded that innovation changes the world. While the pessimists can sound smart, the future belongs to the optimists.

We want to thank you for your confidence in the Spyglass Growth Fund. We will continue to invest your money alongside ours, and we look forward to updating you at the end of 2023.

Sincerely,

Spyglass Capital Management, LLC

SPY000121

Spyglass Growth Fund

Disclosures:

The opinions expressed are subject to change, are not guaranteed and should not be considered investment advice. Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Please see Schedule of Investments for a complete list of holdings. Top ten holdings as of December 31, 2022: Ascendis Pharma A/S (6.94%); Affiliated Managers Group, Inc. (5.29%); GoDaddy, Inc. (5.27%); TransDigm Group, Inc. (5.26%); Nutanix, Inc. (5.15%); ZoomInfo Technologies Inc. (5.15%); Exact Sciences Corp. (4.99%); Five Below, Inc. (4.56%); Vail Resorts, Inc. (4.39%); and Leslie’s, Inc. (4.38%).

The Fund’s investment objectives, risks, charges and expenses must be read and considered carefully before investing. The Prospectus contains this and other important information about the investment company. It may be obtained through this website, or a free hard-copy version is available by calling (toll free) 888-878-5680. Read the prospectus carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. The Fund is non-diversified, meaning it may focus its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. Medium- and small-capitalization companies tend to have limited liquidity and greater price volatility than large-capitalization companies.

The Russell Midcap® Growth Index measures the performance of those Russell Midcap® companies with higher price/book ratios and higher forecasted growth values. The S&P 500® is widely regarded as the best single gauge of large-cap U.S. equities. The index measures the performance of the large-cap segment of the market. Considered to be a proxy of the U.S. equity market, the index is composed of 500 constituent companies. The price/earnings ratio is the ratio of a company’s stock price to the company’s earnings per share. The price-to-book ratio (P/B Ratio) is a ratio used to compare a stock’s market value to its book value. An investment cannot be made directly in an index.

Performance of the Russell Midcap® Growth Index is included for informational purposes to show the general trend in the midcap equity market for the periods indicated and is not intended to imply that the portfolio was similar to the index either in composition or element of risk. The volatility of indices may be materially different from the performance of Spyglass’ strategy. The Russell Midcap® Growth Index is an unmanaged stock market index that measures the performance of those Russell Midcap® companies. Investors cannot invest directly in an index; Index performance does not reflect trading commissions and costs. Due to these differences, comparison to an index should not be relied upon as an accurate measure of comparison.

On December 29, 2017, Spyglass Partners Fund LP, a limited partnership managed by the Advisor (the “Predecessor Partnership”), converted into the Institutional Shares class of the Fund by contributing all of its assets to the Fund in exchange for Institutional Shares of the Fund. The Predecessor Partnership was formed on October 1, 2015, to serve as a pooled investment vehicle for accredited investors, and since inception the Predecessor Partnership maintained investment policies, objectives, guidelines, and restrictions that were, in all material respects, equivalent to those of the Fund. From the date of inception through the time of the conversion, the Predecessor Partnership was managed by the Advisor and the same portfolio manager as the Fund. The conversion date was December 29, 2017 (inception) and the Fund commenced operations on January 2, 2018. The Fund’s performance prior to 2018 is that of the Predecessor Partnership and the returns reflect the deduction of the 1% management fee and expenses, paid by the Predecessor

Spyglass Growth Fund

Partnership, without provision for state or local taxes. The performance includes gains or losses plus income and the reinvestment of all dividends and interest. Other than the Predecessor Partnership, the Advisor did not manage any accounts materially equivalent to the Fund during the period of the Predecessor Partnership’s performance shown above. The Predecessor Partnership was not registered under the 1940 Act, and was not subject to certain investment limitations, diversification requirements, and other restrictions imposed by the 1940 Act and the Internal Revenue Code of 1986, as amended (the “Code”), which, if applicable, may have adversely affected its performance. For periods beginning January 1, 2018, the Fund’s net performance is calculated on a daily basis and also includes a deduction of 1% management fee and is subject to a 1% expense cap, which differs in certain respects from the methods used to compute total returns for the Predecessor Partnership.

The Spyglass Growth Fund is distributed by: ALPS Distributors, Inc., member FINRA, an unaffiliated entity.

Performance Disclosure:

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost, and current performance may be higher or lower than the performance quoted. For performance data current to the most recent month end, please call 1.888.878.5680.

Fee waiver language(can be shortened just keep the word “contractual” in shortened version):

Pursuant to a contractual operating expense limitation between Spyglass Capital Management LLC (the “Advisor”), the Fund’s investment adviser, and the Fund, the Advisor has agreed to waive its management fees and/or reimburse Fund expenses to ensure that Total Annual Fund Operating Expenses (excluding any frontend or contingent deferred loads, Rule 12b-1 plan fees, shareholder servicing plan fees, taxes, leverage (i.e., any expenses incurred in connection with borrowings made by the Fund), interest (including interest incurred in connection with bank and custody overdrafts), brokerage commissions and other transactional expenses, expenses incurred in connection with any merger or reorganization, dividends or interest on short positions, acquired fund fees and expenses or extraordinary expenses such as litigation (collectively, “Excludable Expenses”)) do not exceed 1.00% of the Fund’s average daily net assets, through at least April 30, 2023, unless terminated sooner by, or with the consent of, the Trust's Board of Trustees (the “Board of Trustees” or the “Board”). To the extent the Fund incurs Excludable Expenses, Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement will exceed 1.00%. The Advisor may request recoupment of previously waived fees and paid expenses from the Fund for up to three years from the date such fees and expenses were waived or paid, if such reimbursement will not cause the Fund's total expense ratio to exceed the lesser of: (1) the expense limitation in place at the time of the waiver and/or expense payment; or (2) the expense limitation in place at the time of the recoupment.

Spyglass Growth Fund

| INVESTMENT HIGHLIGHTS |

| (Unaudited) |

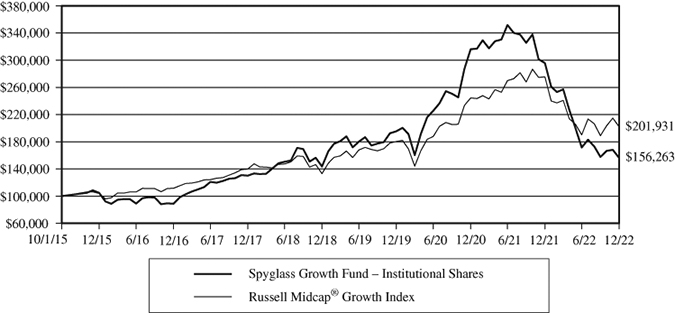

Comparison of the Change in Value of a Hypothetical $100,000 Investment

in the Spyglass Growth Fund – Institutional Shares and

Russell Midcap Growth Index

| Annualized Total Return Periods Ended | One | Three | Five | Since Inception |

| December 31, 2022: | Year | Year | Year | (10/1/2015) |

| Spyglass Growth Fund – | | | | |

Institutional Shares(1)(2) | -47.23% | -7.17% | 3.73% | 6.35% |

| Russell Midcap Growth Index | -26.72% | 3.85% | 7.64% | 10.18% |

Expense ratios*: Gross 1.05%, Net 1.00% (Institutional Shares)

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 1-888-878-5680.

This chart illustrates the performance of a hypothetical $100,000 investment made in the Fund on October 1, 2015, the Fund’s inception date. Returns reflect the reinvestment of dividends and capital gain distributions. The performance data and expense ratios shown reflect a contractual fee waiver made by the Adviser, currently, through April 30, 2024. In the absence of fee waivers, returns would be reduced. The performance data and graph do not reflect the deduction of taxes that a shareholder may pay on dividends, capital gain distributions, or redemption of Fund shares. This chart does not imply any future performance.

| * | The expense ratios presented are from the most recent prospectus. The expense ratio for the fiscal year ended December 31, 2022 was 1.09% (Gross); 1.00% (Net) for the Institutional Shares. |

| (1) | Fund commenced operations on January 2, 2018. |

| (2) | The performance data quoted for periods prior to January 2, 2018 is that of the Spyglass Partners Fund Limited Partnership (the “Partnership”). The Partnership commenced operations on October 1, 2015. The Partnership was not a registered mutual fund and was not subject to the same investments and tax restrictions as the Fund. If it had been, the Partnership’s performance might have been lower. |

Spyglass Growth Fund

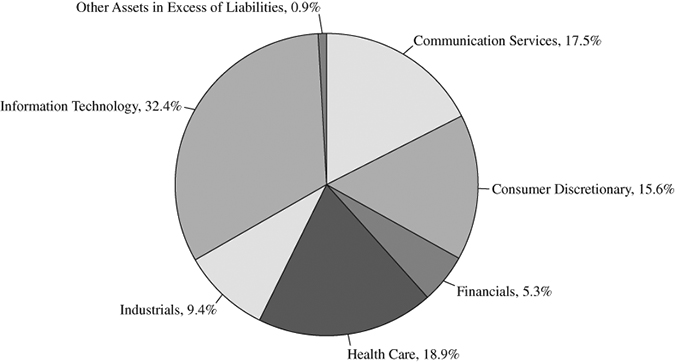

| SECTOR ALLOCATION OF PORTFOLIO ASSETS |

| at December 31, 2022 |

Percentages represent market value as a percentage of net assets.

Note: For Presentation purposes, the Fund has grouped some of the industry categories for purposes of categorizing securities for compliance with Section 8(b)(1) of the Investment Company Act of 1940, as amended, the Fund uses more specific industry classifications.

Spyglass Growth Fund

| SCHEDULE OF INVESTMENTS |

| at December 31, 2022 |

| | | Number of | | | | |

| COMMON STOCKS – 99.1% | | Shares | | | Value | |

| | | | | | | |

| COMMUNICATION SERVICES – 17.5% | | | | | | |

| Cable One, Inc. | | | 24,836 | | | $ | 17,679,755 | |

| Match Group, Inc. (a) | | | 574,058 | | | | 23,817,666 | |

| Roku, Inc. (a) | | | 299,343 | | | | 12,183,260 | |

| Spotify Technology SA – ADR (a) | | | 278,105 | | | | 21,956,390 | |

| ZoomInfo Technologies, Inc. (a) | | | 1,051,956 | | | | 31,674,395 | |

| TOTAL COMMUNICATION SERVICES | | | | | | | 107,311,466 | |

| | | | | | | | | |

| | | | | | | | | |

| CONSUMER DISCRETIONARY – 15.6% | | | | | | | | |

| Five Below, Inc. (a) | | | 158,354 | | | | 28,008,072 | |

| Leslie’s, Inc. (a) | | | 2,205,054 | | | | 26,923,709 | |

| Peloton Interactive, Inc. (a) | | | 1,778,350 | | | | 14,120,099 | |

| Vail Resorts, Inc. | | | 113,179 | | | | 26,976,215 | |

| TOTAL CONSUMER DISCRETIONARY | | | | | | | 96,028,095 | |

| | | | | | | | | |

| FINANCIALS – 5.3% | | | | | | | | |

| Affiliated Managers Group, Inc. | | | 205,189 | | | | 32,508,093 | |

| TOTAL FINANCIALS | | | | | | | 32,508,093 | |

| | | | | | | | | |

| HEALTH CARE – 18.9% | | | | | | | | |

| Ascendis Pharma A/S – ADR (a) | | | 349,291 | | | | 42,658,910 | |

| Exact Sciences Corp. (a) | | | 620,686 | | | | 30,730,164 | |

| Pacira BioSciences, Inc. (a) | | | 425,459 | | | | 16,426,972 | |

| Oak Street Health, Inc. (a) | | | 1,222,071 | | | | 26,286,747 | |

| TOTAL HEALTH CARE | | | | | | | 116,102,793 | |

| | | | | | | | | |

| INDUSTRIALS – 9.4% | | | | | | | | |

| Lyft, Inc. (a) | | | 2,309,239 | | | | 25,447,814 | |

| TransDigm Group, Inc. | | | 51,332 | | | | 32,321,194 | |

| TOTAL INDUSTRIALS | | | | | | | 57,769,008 | |

The accompanying notes are an integral part of these financial statements.

Spyglass Growth Fund

| SCHEDULE OF INVESTMENTS (Continued) |

| at December 31, 2022 |

| | | Number of | | | | |

| COMMON STOCKS – 99.1% (Continued) | | Shares | | | Value | |

| | | | | | | |

| INFORMATION TECHNOLOGY – 32.4% | | | | | | |

| Affirm Holdings, Inc. (a) | | | 1,639,228 | | | $ | 15,851,335 | |

| AppLovin Corp. (a) | | | 1,356,972 | | | | 14,288,915 | |

| Datadog, Inc. (a) | | | 319,613 | | | | 23,491,556 | |

| GoDaddy, Inc. (a) | | | 432,792 | | | | 32,381,497 | |

| Momentive Global, Inc. (a) | | | 2,449,675 | | | | 17,147,725 | |

| Nutanix, Inc. (a) | | | 1,219,234 | | | | 31,761,046 | |

| Palo Alto Networks, Inc. (a) | | | 176,963 | | | | 24,693,417 | |

| Pure Storage, Inc. (a) | | | 670,288 | | | | 17,936,907 | |

| Splunk, Inc. (a) | | | 249,533 | | | | 21,482,296 | |

| TOTAL INFORMATION TECHNOLOGY | | | | | | | 199,034,694 | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Cost $789,044,132) – 99.1% | | | | | | | 608,754,149 | |

| Other Assets in Excess of Liabilities – 0.9% | | | | | | | 5,783,704 | |

| TOTAL NET ASSETS – 100.0% | | | | | | $ | 614,537,853 | |

Percentages are stated as a percent of net assets.

ADR – American Depositary Receipt

| (a) | Non-income producing security. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI and S&P and has been licensed for use by U.S. Bank Global Fund Services.

The accompanying notes are an integral part of these financial statements.

Spyglass Growth Fund

| STATEMENT OF ASSETS AND LIABILITIES |

| at December 31, 2022 |

| Assets: | | | |

| Investments, at value (cost of $789,044,132) | | $ | 608,754,149 | |

| Cash | | | 399,759 | |

| Receivables: | | | | |

| Securities sold | | | 12,138,722 | |

| Fund shares sold | | | 1,913,724 | |

| Dividends Receivable | | | 221,016 | |

| Prepaid expenses | | | 30,349 | |

| Total assets | | | 623,457,719 | |

| | | | | |

| Liabilities: | | | | |

| Payables: | | | | |

| Securities purchased | | | 6,190,835 | |

| Fund shares redeemed | | | 2,101,696 | |

| Investment advisory fees | | | 482,261 | |

| Administration and fund accounting fees | | | 68,701 | |

| Custody fees | | | 14,179 | |

| Transfer agent fees and expenses | | | 28,524 | |

| Other accrued expenses | | | 33,670 | |

| Total liabilities | | | 8,919,866 | |

| | | | | |

| Net assets | | $ | 614,537,853 | |

| | | | | |

| Net assets consist of: | | | | |

| Paid in capital | | $ | 1,404,766,153 | |

| Total accumulated losses | | | (790,228,300 | ) |

| Net assets | | $ | 614,537,853 | |

| | | | | |

| Institutional Shares: | | | | |

| Net assets applicable to outstanding Institutional Shares | | $ | 614,537,853 | |

| Shares issued (Unlimited number of beneficial | | | | |

| interest authorized, $0.01 par value) | | | 65,138,803 | |

| Net asset value, offering price and redemption price per share | | $ | 9.43 | |

The accompanying notes are an integral part of these financial statements.

Spyglass Growth Fund

| STATEMENT OF OPERATIONS |

| For the Year Ended December 31, 2022 |

| Investment income: | | | |

| Dividends | | $ | 2,855,711 | |

| Total investment income | | | 2,855,711 | |

| | | | | |

| Expenses: | | | | |

| Investment advisory fees (Note 4) | | | 11,958,727 | |

| Administration and fund accounting fees (Note 4) | | | 443,291 | |

| Transfer agent fees and expenses | | | 203,895 | |

| Federal and state registration fees | | | 148,492 | |

| Custody fees | | | 128,002 | |

| Reports to shareholders | | | 31,094 | |

| Legal fees | | | 24,677 | |

| Trustees’ fees and expenses | | | 16,213 | |

| Audit fees | | | 14,992 | |

| Compliance expense | | | 12,441 | |

| Other | | | 34,683 | |

| Total expenses before reimbursement from advisor | | | 13,016,507 | |

| Expense reimbursement from advisor (Note 4) | | | (1,050,279 | ) |

| Net expenses | | | 11,966,228 | |

| Net investment loss | | | (9,110,517 | ) |

| | | | | |

| Realized and unrealized loss: | | | | |

| Net realized loss on investments | | | (543,588,532 | ) |

| Net change in unrealized depreciation on investments | | | (326,034,688 | ) |

| Net realized and unrealized loss | | | (869,623,220 | ) |

| Net decrease in net assets resulting from operations | | $ | (878,733,737 | ) |

The accompanying notes are an integral part of these financial statements.

Spyglass Growth Fund

| STATEMENTS OF CHANGES IN NET ASSETS |

| |

| | | Year ended | | | Year Ended | |

| | | December 31, 2022 | | | December 31, 2021 | |

| Operations: | | | | | | |

| Net investment loss | | $ | (9,110,517 | ) | | $ | (21,991,524 | ) |

| Net realized gain (loss) on investments | | | (543,588,532 | ) | | | 209,523,057 | |

| Net change in unrealized | | | | | | | | |

| appreciation (depreciation) on investments | | | (326,034,688 | ) | | | (385,280,190 | ) |

| Net decrease in net assets | | | | | | | | |

| resulting from operations | | | (878,733,737 | ) | | | (197,748,657 | ) |

| | | | | | | | | |

| Distributions: | | | | | | | | |

| Distributed earnings | | | (385,085 | ) | | | (292,699,584 | ) |

| Total distributions | | | (385,085 | ) | | | (292,699,584 | ) |

| | | | | | | | | |

| Capital Share Transactions: | | | | | | | | |

| Proceeds from shares sold | | | 502,904,743 | | | | 1,098,995,294 | |

| Proceeds from shares issued to | | | | | | | | |

| holders in reinvestment of dividends | | | 301,758 | | | | 236,144,946 | |

| Cost of shares redeemed | | | (1,074,273,282 | ) | | | (522,730,441 | ) |

| Net increase (decrease) in net assets | | | | | | | | |

| from capital share transactions | | | (571,066,781 | ) | | | 812,409,799 | |

| Total increase (decrease) in net assets | | | (1,450,185,603 | ) | | | 321,961,558 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of year | | | 2,064,723,456 | | | | 1,742,761,898 | |

| End of year | | $ | 614,537,853 | | | $ | 2,064,723,456 | |

| | | | | | | | | |

| Changes in Shares Outstanding: | | | | | | | | |

| Shares sold | | | 38,335,470 | | | | 48,483,426 | |

| Shares issued to holders in | | | | | | | | |

| reinvestment of dividends | | | 31,142 | | | | 13,579,353 | |

| Shares redeemed | | | (88,718,265 | ) | | | (25,097,954 | ) |

| Net increase (decrease) in shares outstanding | | | (50,351,653 | ) | | | 36,964,825 | |

The accompanying notes are an integral part of these financial statements.

Spyglass Growth Fund

For a capital share outstanding throughout each period

Institutional Shares

| | | | | | | | | | | | | | | January 2, 2018* | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | through | |

| | | December 31, | | | December 31, | | | December 31, | | | December 31, | | | December 31, | |

| | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018 | |

| Net Asset Value – | | | | | | | | | | | | | | | |

| Beginning of Period | | $ | 17.88 | | | $ | 22.19 | | | $ | 14.09 | | | $ | 10.52 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | |

| Income from | | | | | | | | | | | | | | | | | | | | |

| Investment Operations: | | | | | | | | | | | | | | | | | | | | |

Net investment loss1 | | | (0.10 | ) | | | (0.22 | ) | | | (0.17 | ) | | | (0.10 | ) | | | (0.10 | ) |

| Net realized and unrealized | | | | | | | | | | | | | | | | | | | | |

| gain (loss) on investments | | | (8.34 | ) | | | (1.28 | ) | | | 8.87 | | | | 3.89 | | | | 1.14 | |

| Total from | | | | | | | | | | | | | | | | | | | | |

| investment operations | | | (8.44 | ) | | | (1.50 | ) | | | 8.70 | | | | 3.79 | | | | 1.04 | |

| | | | | | | | | | | | | | | | | | | | | |

| Less Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from | | | | | | | | | | | | | | | | | | | | |

| net realized gains | | | (0.01 | ) | | | (2.81 | ) | | | (0.60 | ) | | | (0.22 | ) | | | (0.52 | ) |

| Total distributions | | | (0.00 | ) | | | (2.81 | ) | | | (0.60 | ) | | | (0.22 | ) | | | (0.52 | ) |

| | | | | | | | | | | | | | | | | | | | | |

| Net Asset Value – | | | | | | | | | | | | | | | | | | | | |

| End of Period | | $ | 9.43 | | | $ | 17.88 | | | $ | 22.19 | | | $ | 14.09 | | | $ | 10.52 | |

| | | | | | | | | | | | | | | | | | | | | |

Total Return

| | | (47.23 | )%

| | | (6.42

| )%

| | | 61.82

| % | | | 36.03 | %

| | | 10.36 | %^ |

| | | | | | | | | | | | | | | | | | | | | |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of | | | | | | | | | | | | | | | | | | | | |

| period (thousands) | | $ | 614,538 | | | $ | 2,064,723 | | | $ | 1,742,762 | | | $ | 253,018 | | | $ | 41,530 | |

| Ratio of operating expenses | | | | | | | | | | | | | | | | | | | | |

| to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Before reimbursements | | | 1.09 | % | | | 1.05 | % | | | 1.09 | % | | | 1.21 | % | | | 1.78 | %+ |

| After reimbursements | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % | | | 1.00 | % | | | 1.00 | %+ |

| Ratio of net investment loss | | | | | | | | | | | | | | | | | | | | |

| to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Before reimbursements | | | (0.85 | )% | | | (1.00 | )% | | | (1.04 | )% | | | (0.97 | )% | | | (1.61 | )%+ |

| After reimbursements | | | (0.76 | )% | | | (0.95 | )% | | | (0.95 | )% | | | (0.76 | )% | | | (0.83 | )%+ |

Portfolio turnover rate

| | | 54 | %

| | | 51

| %

| | | 38 | % | | | 39

| %

| | | 66 | %^

|

| * | Commencement of operations for Institutional Shares was January 2, 2018. |

+ | Annualized |

| ^ | Not Annualized |

1 | The net investment loss per share was calculated using the average shares outstanding method. |

The accompanying notes are an integral part of these financial statements.

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS |

| at December 31, 2022 |

NOTE 1 – ORGANIZATION

The Spyglass Growth Fund (the “Fund”) is a series of Manager Directed Portfolios (the “Trust”). The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), and was organized as a Delaware statutory trust on April 4, 2006. The Fund is an open-end investment management company and is a non-diversified series of the Trust. The Fund acquired the assets of Spyglass Partners Fund, LP, a Delaware investment limited partnership (the “Predecessor Private Fund”), in a tax-free conversion completed at the close of business on December 29, 2017. The Fund did not have any operations prior to December 29, 2017 other than those relating to organizational matters and registration of its shares under applicable securities law. The Fund commenced operations on January 2, 2018, and currently only offers Institutional Shares. The Predecessor Private Fund had an investment objective and investment policies that were, in all material respects, equivalent to those of the Fund. However, the Predecessor Private Fund was not registered as an investment company under the 1940 Act, and was not subject to certain investment limitations, diversification requirements, liquidity requirements and other restrictions imposed by the 1940 Act and Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). Upon completion of the conversion, the net assets of the Fund were $16,225,831. The number of shares of the Fund issued in connection with the conversion was 1,622,583, and the amount of net unrealized gains on the portfolio securities transferred to the Fund was $2,060,757. Spyglass Capital Management LLC (the “Advisor”) serves as the investment advisor to the Fund. As an investment company, the Fund follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 Financial Services – Investment Companies. The investment objective of the Fund is to seek long term capital appreciation.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund. These policies are in conformity with U.S. generally accepted accounting principles (“GAAP”).

| | A. | Security Valuation: All investments in securities are recorded at their estimated fair value, as described in Note 3. |

| | | |

| | B. | Federal Income Taxes: It is the Fund’s policy to comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Therefore, no federal income or excise tax provisions are required. |

| | | |

| | | The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions to be taken or expected to be taken on a tax return. The tax |

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

| | | returns for the Fund for the prior three fiscal years are open for examination. The Fund identifies its major tax jurisdictions as U.S. Federal and the state of Delaware. |

| | | |

| | C. | Securities Transactions, Income and Distributions: Securities transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on the basis of identified cost. Interest income is recorded on an accrual basis. Dividend income and distributions to shareholders are recorded on the ex-dividend date. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates. |

| | | |

| | | The Fund distributes substantially all of its net investment income, if any, and net realized capital gains, if any, annually. Distributions from net realized gains for book purposes may include short-term capital gains. All short-term capital gains are included in ordinary income for tax purposes. The amount of dividends and distributions to shareholders from net investment income and net realized capital gains is determined in accordance with federal income tax regulations, which may differ from GAAP. To the extent these book/tax differences are permanent, such amounts are reclassified within the capital accounts based on their federal tax treatment. |

| | | |

| | | The Fund is charged for those expenses that are directly attributable to it, such as investment advisory, custody and transfer agent fees. Expenses that are not attributable to a Fund are typically allocated among the funds in the Trust proportionately based on allocation methods approved by the Board of Trustees (the “Board”). Common expenses of the Trust are typically allocated among the funds in the Trust based on a fund’s respective net assets, or by other equitable means. |

| | | |

| | D. | Use of Estimates: The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets during the reporting period. Actual results could differ from those estimates. |

| | | |

| | E. | Reclassification of Capital Accounts: GAAP requires that certain components of net assets relating to permanent differences be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. |

| | | |

| | F. | Events Subsequent to the Fiscal Period End: In preparing the financial statements as of December 31, 2022 and through the date the financial statements were available to be issued, management considered the impact of subsequent events for potential recognition or disclosure in the financial statements and had concluded that no additional disclosures are necessary. |

| | | |

| | G. | Recent Accounting Pronouncements and Rule Issuances: In October 2020, the SEC adopted new regulations governing the use of derivatives by registered |

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

| | | investment companies (“Rule 18f-4”). Rule 18f-4 will impose limits on the amount of derivatives a Fund can enter into, eliminate the asset segregation framework currently used by funds to comply with Section 18 of the 1940 Act, and require funds whose use of derivatives is greater than a limited specified amount to establish and maintain a comprehensive derivatives risk management program and appoint a derivatives risk manager. Funds will be required to comply with Rule 18f-4 by August 19, 2022. It is not currently clear what impact, if any, Rule 18f-4 will have on the availability, liquidity or performance of derivatives. Management is currently evaluating the potential impact of Rule 18f-4 on the Fund. When fully implemented, Rule 18f-4 may require changes in how a Fund uses derivatives, adversely affect the Fund’s performance and increase costs related to the Fund’s use of derivatives. As of December 31, 2022, the Fund did not invest in any derivatives. |

| | | |

| | | In December 2020, the SEC adopted a new rule providing a framework for fund valuation practices (“Rule 2a-5”). Rule 2a-5 establishes requirements for determining fair value in good faith for purposes of the 1940 Act. Rule 2a-5 will permit fund boards to designate certain parties to perform fair value determinations, subject to board oversight and certain other conditions. Rule 2a-5 also defines when market quotations are “readily available” for purposes of the 1940 Act and the threshold for determining whether a fund must fair value a security. In connection with Rule 2a-5, the SEC also adopted related recordkeeping requirements and is rescinding previously issued guidance, including with respect to the role of a board in determining fair value and the accounting and auditing of fund investments. The Funds will be required to comply with the rules by September 8, 2022. Management is currently assessing the potential impact of the new rules on the Funds’ financial statements. |

NOTE 3 – SECURITIES VALUATION

The Fund has adopted authoritative fair value accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value, a discussion of changes in valuation techniques and related inputs during the period and expanded disclosure of valuation levels for major security types. These inputs are summarized in the three broad levels listed below:

| | Level 1 – | Unadjusted, quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access at the date of measurement. |

| | | |

| | Level 2 – | Other significant observable inputs (including, but not limited to, quoted prices in active markets for similar instruments, quoted prices in markets that are not active for identical or similar instruments, and model-derived valuations in which all significant inputs and significant value drivers are |

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

| | | observable in active markets, such as interest rates, prepayment speeds, credit risk curves, default rates, and similar data). |

| | | |

| | Level 3 – | Significant unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

Following is a description of the valuation techniques applied to the Fund’s major categories of assets and liabilities measured at fair value on a recurring basis.

Equity Securities: Equity securities, including common stocks, preferred stocks, foreign-issued common stocks, exchange-traded funds, closed-end mutual funds and real estate investment trusts (REITs), that are primarily traded on a national securities exchange shall be valued at the last sale price on the exchange on which they are primarily traded on the day of valuation or, if there has been no sale on such day, at the mean between the bid and asked prices. Securities primarily traded in the NASDAQ Global Market System for which market quotations are readily available shall be valued using the NASDAQ Official Closing Price (“NOCP”). If the NOCP is not available, such securities shall be valued at the last sale price on the day of valuation, or if there has been no sale on such day, at the mean between the bid and asked prices. Over-the-counter securities that are not traded on a listed exchange are valued at the last sale price in the over-the-counter market. Over-the-counter securities which are not traded in the NASDAQ Global Market System shall be valued at the mean between the bid and asked prices. To the extent these securities are actively traded and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy.

Registered Investment Companies: Investments in registered investment companies (e.g., mutual funds) are generally priced at the ending NAV provided by the applicable registered investment company’s service agent and will be classified in Level 1 of the fair value hierarchy.

Short-Term Debt Securities: Debt securities, including short-term debt instruments having a maturity of less than 60 days, are valued at the evaluated mean price supplied by an approved pricing service. Pricing services may use various valuation methodologies including matrix pricing and other analytical pricing models as well as market transactions and dealer quotations. In the absence of prices from a pricing service, the securities will be priced in accordance with the procedures adopted by the Board. Short-term securities are generally classified in Level 1 or Level 2 of the fair market hierarchy depending on the inputs used and market activity levels for specific securities.

The Board has delegated day-to-day valuation issues to a Valuation Committee of the Trust which, as of June 30, 2022, was comprised of officers of the Trust. The function of the Valuation Committee is to value securities where current and reliable market quotations are not readily available, or the closing price does not represent fair value, by following procedures approved by the Board. These procedures consider many factors, including the

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

type of security, size of holding, trading volume and news events. All actions taken by the Valuation Committee are subsequently reviewed and ratified by the Board.

Depending on the relative significance of the valuation inputs, fair valued securities may be classified in either level 2 or level 3 of the fair value hierarchy.

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities. The following is a summary of the fair valuation hierarchy of the Fund’s securities as of December 31, 2022:

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | | | | | | | | | | | |

| Communication Services | | $ | 107,311,466 | | | $ | — | | | $ | — | | | $ | 107,311,466 | |

| Consumer Discretionary | | | 96,028,095 | | | | — | | | | — | | | | 96,028,095 | |

| Financials | | | 32,508,093 | | | | — | | | | — | | | | 32,508,093 | |

| Health Care | | | 116,102,793 | | | | — | | | | — | | | | 116,102,793 | |

| Industrials | | | 57,769,008 | | | | — | | | | — | | | | 57,769,008 | |

| Information Technology | | | 199,034,694 | | | | — | | | | — | | | | 199,034,694 | |

| Total Common Stocks | | | 608,754,149 | | | | — | | | | — | | | | 608,754,149 | |

| Total Investments in Securities | | $ | 608,754,149 | | | $ | — | | | $ | — | | | $ | 608,754,149 | |

NOTE 4 – INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

For the fiscal year ended December 31, 2022, the Advisor provided the Fund with investment management services under an Investment Advisory Agreement. The Advisor furnishes all investment advice, office space, and facilities, and provides most of the personnel needed by the Fund. As compensation for its services, the Advisor is entitled to a monthly fee at an annual rate of 1.00% for the Spyglass Growth Fund based upon the average daily net assets of the Fund. For the fiscal year ended December 31, 2022, the Fund incurred $11,958,727 in advisory fees.

The Fund is responsible for its own operating expenses. The Advisor has contractually agreed to waive its management fees and/or absorb expenses of the Fund to ensure that the total annual operating expenses [excluding front-end or contingent deferred loads, Rule 12b-1 plan fees, shareholder servicing plan fees, taxes, leverage, interest, brokerage commissions and other transactional expenses, expenses in connection with a merger or reorganization, dividends or interest on short positions, acquired fund fees and expenses or extraordinary expenses (collectively, “Excludable Expenses”)] do not exceed the following amounts of the average daily net assets for the Institutional Shares:

Spyglass Growth Fund

| | Institutional Shares | 1.00% | |

For the fiscal year ended December 31, 2022, the Advisor reduced its fees and absorbed Fund expenses in the amount of $1,050,279 for the Fund. The waivers and

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

reimbursements will remain in effect through April 30, 2024 unless terminated sooner by, or with the consent of, the Board.

The Advisor may request recoupment of previously waived fees and paid expenses in any subsequent month in the three-year period from the date of the management fee reduction and expense payment if the aggregate amount actually paid by the Fund toward the operating expenses for such fiscal year (taking into account the reimbursement) will not cause the Fund’s expenses to exceed the lesser of: (1) the expense limitation in place at the time of the management fee reduction and expense payment; or (2) the expense limitation in place at the time of the reimbursement. Any such reimbursement is also contingent upon Board of Trustees review and approval at the time the reimbursement is made. Such reimbursement may not be paid prior to the Fund’s payment of current ordinary operating expenses. Cumulative expenses subject to recapture pursuant to the aforementioned conditions expire as follows:

| | Amount | | Expiration | |

| | | 732,905 | | 12/31/2023 | |

| | | 1,213,828 | | 12/31/2024 | |

| | | 1,050,279 | | 12/31/2025 | |

U.S. Bancorp Fund Services, LLC, doing business as U.S. Bank Global Fund Services, LLC (“Fund Services” or the “Administrator”) acts as the Fund’s Administrator under an Administration Agreement. The Administrator prepares various federal and state regulatory filings, reports and returns for the Fund; prepares reports and materials to be supplied to the Trustees; monitors the activities of the Fund’s custodian, transfer agent and accountants; coordinates the preparation and payment of the Fund’s expenses and reviews the Fund’s expense accruals. Fund Services also serves as the fund accountant and transfer agent to the Fund. Vigilant Compliance, LLC serves as the Chief Compliance Officer to the Fund. U.S. Bank N.A., an affiliate of Fund Services, serves as the Fund’s custodian. For the fiscal year ended December 31, 2022, the Fund incurred the following expenses for administration, fund accounting, transfer agency and custody fees:

| | Administration & fund accounting | | $ | 443,291 | |

| | Custody | | $ | 128,002 | |

| | Transfer agency | | $ | 203,895 | |

At December 31, 2022, the Fund had payables due to Fund Services for administration, fund accounting and transfer agency fees and to U.S. Bank N.A. for custody fees in the following amounts:

| | Administration & fund accounting | | $ | 68,701 | |

| | Custody | | $ | 14,179 | |

| | Transfer agency | | $ | 28,524 | |

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

ALPS Distributor, Inc. (the “Distributor”) acts as the Fund’s principal underwriter in a continuous public offering of the Fund’s shares.

Certain officers of the Fund are employees of the Administrator and are not paid any fees by the Fund for serving in such capacities.

NOTE 5 – SECURITIES TRANSACTIONS

For the fiscal year ended December 31, 2022, the cost of purchases and the proceeds from sales of securities, excluding short-term securities, were as follows:

| | | | Purchases | | | Sales | |

| | Spyglass Growth Fund | | $ | 651,665,252 | | | $ | 1,219,410,820 | |

There were no purchases or sales of long-term U.S. Government securities.

NOTE 6 – INCOME TAXES AND DISTRIBUTIONS TO SHAREHOLDERS

As of December 31, 2022, the components of accumulated earnings/(losses) on a tax basis were as follows:

| | Cost of investments(a) | | | 932,744,181 | |

| | Gross unrealized appreciation | | | 101,131,704 | |

| | Gross unrealized depreciation | | | (425,121,736 | ) |

| | Net unrealized depreciation | | | (323,990,032 | ) |

| | Undistributed ordinary income | | | — | |

| | Undistributed long-term capital gain | | | — | |

| | Total distributable earnings | | | — | |

| | Other accumulated losses | | | (466,238,268 | ) |

| | Total accumulated earnings | | | (790,228,300 | ) |

| | (a) | The difference between the book basis and tax basis net unrealized depreciation and cost is attributable primarily to wash sales. | |

For tax purposes, the Fund had no post October capital loss deferrals at December 31, 2022.

As of December 31, 2022, the Fund had long-term capital losses in the amount of $75,362,962 and short-term tax basis capital losses in the amount of $387,539,553 to offset future capital gains.

The tax character of distributions paid during the year ended December 31, 2022 and the year ended December 31, 2021 was as follows:

| | | | Fiscal Year Ended | | | Fiscal Year Ended | |

| | | | December 31, 2022 | | | December 31, 2021 | |

| | Ordinary income | | $ | 385,085 | | | $ | 120,508,378 | |

| | Long-Term Capital Gains | | | — | | | | 172,191,206 | |

| | Total | | $ | 385,085 | | | $ | 292,699,584 | |

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

For the fiscal year ended December 31, 2022, the effect of permanent “book/tax” reclassifications resulted in increases and decreases to components of the Funds’ net assets as follows:

| | | | Total Accumulated | | | Paid-In | |

| | | | Earnings/Loss | | | Capital | |

| | Spyglass Growth Fund | | $ | 9,495,602 | | | $ | (9,495,602 | ) |

NOTE 7 – PRINCIPAL RISKS

Below are summaries of some, but not all, of the principal risks of investing in the Fund, each of which could adversely affect the Fund’s NAV, market price, yield, and total return. Further information about investment risks is available in the Fund’s prospectus and Statement of Additional Information.

General Market Risk; Recent Market Events: The value of the Fund’s shares will fluctuate based on the performance of the Fund’s investments and other factors affecting the securities markets generally. Certain investments selected for the Fund’s portfolio may be worth less than the price originally paid for them, or less than they were worth at an earlier time. The value of the Fund’s investments may go up or down, sometimes dramatically and unpredictably, based on current market conditions, such as real or perceived adverse political or economic conditions, inflation, changes in interest rates, lack of liquidity in the fixed income markets or adverse investor sentiment.

U.S. and international markets have experienced volatility in recent months and years due to a number of economic, political and global macro factors, including the impact of the coronavirus (COVID-19) global pandemic, which has resulted in a public health crisis, business interruptions, growth concerns in the U.S. and overseas, layoffs, rising unemployment claims, changed travel and social behaviors and reduced consumer spending. The effects of COVID-19 may lead to a substantial economic downturn or recession in the U.S. and global economies, the recovery from which is uncertain and may last for an extended period of time.

Equity Market Risk: Equity securities are susceptible to general stock market fluctuations due to economic, market, political and issuer-specific considerations and to potential volatile increases and decreases in value as market confidence in and perceptions of their issuers change.

Small-Cap and Mid-Cap Company Risk: Small-Cap and Mid-Cap companies often have less predictable earnings, more limited product lines, markets, distribution channels or financial resources, and the management of such companies may be dependent upon one or few key people. The market movements of equity securities of these companies may be more abrupt and volatile than the market movements of equity securities of larger, more established companies, or the stock market in general. Because of these movements, and because small-cap and mid-cap companies tend to be bought and sold less often and in smaller amounts, they are generally less liquid than the equity securities of larger companies.

Spyglass Growth Fund

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| at December 31, 2022 |

Management Risk: The ability of the Fund to meet its investment objective is directly related to the Advisor’s management of the Fund. The value of your investment in the Fund may vary with the effectiveness of the Advisor’s research, analysis and asset allocation among portfolio securities. If the investment strategies do not produce the expected results, the value of your investment could be diminished or even lost entirely.

Non-Diversified Fund Risk: Because the Fund is “non-diversified,” it may invest a greater percentage of its assets in the securities of a single issuer. As a result, a decline in the value of an investment in a single issuer could cause the Fund’s overall value to decline to a greater degree than if the Fund held a more diversified portfolio.

Sector Emphasis Risk: Although the Advisor selects stocks based on their individual merits, some economic sectors will represent a larger portion of the Fund’s overall investment portfolio than other sectors. Potential negative market or economic developments affecting one of the larger sectors could have a greater impact on the Fund than on a fund with fewer holdings in that sector.

Information Technology Sector Risk: Technology companies face intense competition, which may have an adverse effect on profit margins. Technology companies may have limited product lines, markets, financial resources or personnel. The products of technology companies may face obsolescence due to rapid technological developments and frequent new product introduction, unpredictable changes in growth rates, and competition for the services of qualified personnel. Information technology companies may be smaller and less experienced companies, with limited product lines, markets or financial resources and fewer experienced management or marketing personnel. Information technology companies may be subject to additional risks, including loss of patent, copyright, and trademark protections, as well as evolving industry standards.

REIT Risk: A REIT’s share price may decline because of adverse developments affecting the real estate industry, including changes in interest rates. The returns from REITs may trail returns from the overall market. The Fund’s investments in REITs may be subject to special tax rules, or a particular REIT may fail to qualify for the favorable federal income tax treatment applicable to REITs, the effect of which may have adverse tax consequences for the Fund and shareholders.

Cash and Cash Equivalent Risk: At various times, the Fund may have cash balances that exceed federally insured limits. It is the opinion of management that the solvency of the financial institutions are not of a particular concern at this time.

NOTE 8 – GUARANTEES AND INDEMNIFICATIONS

In the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

Spyglass Growth Fund

| REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

| |

To the Board of Trustees of Manager Directed Portfolios

and the Shareholders of Spyglass Growth Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Spyglass Growth Fund, a series of shares of beneficial interest in Manager Directed Portfolios (the “Fund”), including the schedule of investments, as of December 31, 2022, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the four-year period then ended and for the period from January 2, 2018 (commencement of operations) through December 31, 2018, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of December 31, 2022, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended, and its financial highlights for each of the years in the four-year period then ended and for the period from January 2, 2018 through December 31, 2018, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2022 by correspondence with the custodian, brokers, or by other appropriate auditing procedures where replies from brokers were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in the Manager Directed Portfolios since 2007.

Philadelphia, Pennsylvania

March 1, 2023

Spyglass Growth Fund

| EXPENSE EXAMPLE |

| December 31, 2022 (Unaudited) |

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period indicated and held for the entire period from July 1, 2022 to December 31, 2022 for the Institutional Shares.

Actual Expenses

The information in the table under the heading “Actual” provides information about actual account values and actual expenses. You may use the information in these columns together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the row entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period. There are some account fees that are charged to certain types of accounts, such as Individual Retirement Accounts (generally, a $15 fee is charged to the account annually) that would increase the amount of expenses paid on your account. The example below does not include portfolio trading commissions and related expenses and other extraordinary expenses as determined under generally accepted accounting principles.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical (5% return before expenses)” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. As noted above, there are some account fees that are charged to certain types of accounts that would increase the amount of expense paid on your account.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the information under the heading “Hypothetical (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Spyglass Growth Fund

| EXPENSE EXAMPLE (Continued) |

| December 31, 2022 (Unaudited) |

| | Beginning | Ending | Expenses Paid |

| | Account Value | Account Value | During Period |

| | 7/1/2022 | 12/31/2022 | 7/1/2022 – 12/31/2022(1) |

| Actual | | | |

| Institutional Shares | $1,000.00 | $ 910.80 | $4.82 |

| | | | |

| Hypothetical (5% return | | | |

| before expenses) | | | |

| Institutional Shares | $1,000.00 | $1,020.16 | $5.09 |

| (1) | Expenses are equal to the Institutional Shares’ annualized expense ratio of 1.00% multiplied by the average account value over the period, multiplied by 184/365 (to reflect the period). |

Spyglass Growth Fund

| STATEMENT REGARDING LIQUIDITY RISK MANAGEMENT PROGRAM |

| (Unaudited) |

In accordance with Rule 22e-4 under the Investment Company Act of 1940, as amended, the Fund, a series of Manager Directed Portfolios (the “Trust”), has adopted and implemented a liquidity risk management program tailored specifically to the Fund (the “Program”). The Program seeks to promote effective liquidity risk management for the Fund and to protect Fund shareholders from dilution of their interests. The Board has designated the Fund’s investment adviser to serve as the administrator of the Program (the “Program Administrator”). Personnel of the Fund’s investment adviser conduct the day-to-day operation of the Program pursuant to policies and procedures administered by the Program Administrator. The Program Administrator is required to provide a written annual report to the Board and the chief compliance officer of the Trust regarding the adequacy and effectiveness of the Program, including the operation of the Fund’s highly liquid investment minimum, and any material changes to the Program.

Under the Program, the Program Administrator manages the Fund’s liquidity risk, which is the risk that the Fund could not meet shareholder redemption requests without significant dilution of remaining shareholders’ interests in the Fund. The Program assesses liquidity risk under both normal and reasonably foreseeable stressed market conditions. This risk is managed by monitoring the degree of liquidity of the Fund’s investments, limiting the amount of the Fund’s illiquid investments, and utilizing various risk management tools and facilities available to the Fund for meeting shareholder redemptions, among other means. The Program Administrator’s process of determining the degree of liquidity of the Fund’s investments is supported by one or more third-party liquidity assessment vendors.

On November 18, 2022, the Board reviewed the Program Administrator’s assessment of the operation and effectiveness of the Program for the period December 15, 2021 through September 30, 2022 (the “Report”) and a memorandum regarding the Report prepared by the Trust’s chief compliance officer. The Report noted that the Fund’s portfolio is expected to continue to primarily hold highly liquid investments and the determination that the Fund be designated as a “primarily highly liquid fund” (as defined in Rule 22e-4) remains appropriate. The Fund can therefore continue to rely on the exclusion in Rule 22e-4 from the requirements to determine and review a highly liquid investment minimum for the Fund and to adopt policies and procedures for responding to a highly liquid investment minimum shortfall. The Report noted that there were no breaches of the Fund’s restriction on holding illiquid investments exceeding 15% of its net assets during the review period. The Report confirmed that the Fund’s investment strategy was appropriate for an open-end management investment company. The Report also indicated that no material changes had been made to the Program during the review period.

The Program Administrator determined that the Fund is reasonably likely to be able to meet redemption requests without adversely affecting non-redeeming Fund shareholders through significant dilution. The Program Administrator concluded that the during the review period, the Program was adequately designed and effectively operating to monitor the liquidity risk to the Fund, taking into account the size of the Fund, the type of business conducted, and other relevant factors.

Spyglass Growth Fund

| NOTICE TO SHAREHOLDERS |

| at December 31, 2022 (Unaudited) |

How to Obtain a Copy of the Fund’s Proxy Voting Policies

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-888-878-5680 or on the U.S. Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov.

How to Obtain a Copy of the Fund’s Proxy Voting Records for the most recent 12-Month Period Ended June 30

Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available no later than August 31 without charge, upon request, by 1-888-878-5680. Furthermore, you can obtain the Fund’s proxy voting records on the SEC’s website at http://www.sec.gov.

Quarterly Filings on Form N-PORT

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Part F of Form N-PORT. The Fund’s Part F of Form N-PORT is available on the SEC’s website at http://www.sec.gov. Information included in the Fund’s Part F of Form N-PORT is also available, upon request, by calling 1-888-878-5680.

Qualified Dividend Income/Dividends Received Deduction

For the fiscal year ended December 31, 2022 certain dividends paid by the Funds may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. The percentage of dividends declared from ordinary income designated as qualified dividend income was as follows:

| | Spyglass Growth Fund | | | 0.48 | % |

For corporate shareholders, the percent of ordinary income distributions qualifying for the corporate dividends received deduction for the fiscal year ended December 31, 2022 was as follows:

| | Spyglass Growth Fund | | | 0.48 | % |

The percentage of taxable ordinary income distributions that are designated as short-term capital gain distributions under Internal Revenue Section 871(k)(2)(C) for each Fund were as follows:

| | Spyglass Growth Fund | | | 100.00 | % |

Spyglass Growth Fund

| TRUSTEES AND OFFICERS |

| (Unaudited) |

The business and affairs of the Trust are managed under the oversight of the Board, subject to the laws of the State of Delaware and the Trust’s Agreement and Declaration of Trust. The Board, as of January 1, 2021, is currently comprised of four trustees who are not interested persons of the Trust within the meaning of the 1940 Act (the “Independent Trustees”). The Trustees are responsible for deciding matters of overall policy and overseeing the actions of the Trust’s service providers. The officers of the Trust conduct and supervise the Trust’s daily business operations.

| | | | Number of | |

| | | | Funds | Other |

| | Position(s) Held | | in Fund | Directorships |

| Name, | with the Trust | | Complex | Held by Trustee |

| Year of Birth | and Length of | Principal Occupation(s) | Overseen by | During the Past |

and Address(1) | Time Served(2) | During the Past Five Years | Trustee(3) | Five Years |

| INDEPENDENT TRUSTEES | | | | |

| | | | | |

| Gaylord B. Lyman | Trustee and | Senior Portfolio Manager, | 10 | None |

| (Born 1962) | Audit Committee | Affinity Investment Advisors, | | |

| | Chairman, since | LLC, since 2017; Managing | | |

| | April 2015 | Director of Kohala Capital | | |

| | | Partners, LLC (2011 – 2016). | | |

| | | | | |

| Scott Craven Jones | Trustee since | Managing Director, Carne Global | 10 | Trustee, Madison |

| (Born 1962) | July 2016 and | Financial Services (US) LLC | | Funds, since 2019 |

| | Lead Independent | (a provider of independent | | (18 portfolios); |

| | Trustee since | governance and distribution | | Trustee, XAI |

| | May 2017 | support for the asset management | | Octagon Floating |

| | | industry), since 2013; interim | | Rate & |

| | | Managing Director, Park Agency, | | Alternative |

| | | Inc., since 2020. | | Income Term |

| | | | | Trust, since 2017 |

| | | | | (2 portfolios); |

| | | | | Director, |

| | | | | Guestlogix Inc. |

| | | | | (a provider of |

| | | | | ancillary-focused |

| | | | | technology to the |

| | | | | travel industry) |

| | | | | (2015 – 2016). |

Spyglass Growth Fund

| TRUSTEES AND OFFICERS (Continued) |

| (Unaudited) |

| | | | Number of | |

| | | | Funds | Other |

| | Position(s) Held | | in Fund | Directorships |

| Name, | with the Trust | | Complex | Held by Trustee |

| Year of Birth | and Length of | Principal Occupation(s) | Overseen by | During the Past |

and Address(1) | Time Served(2) | During the Past Five Years | Trustee(3) | Five Years |

| Lawrence T. | Trustee since | Senior Vice President and Chief | 10 | None |

| Greenberg | July 2016 | Legal Officer, The Motley Fool | | |

| (Born 1963) | | Holdings, Inc., since 1996; | | |

| | | Venture Partner and General | | |

| | | Counsel, Motley Fool Ventures | | |

| | | LP, since 2018; Manager, Motley | | |

| | | Fool Wealth Management, LLC, | | |

| | | since 2013; Adjunct Professor, | | |

| | | Washington College of Law, | | |

| | | American University, since 2006; | | |

| | | General Counsel Motley Fool | | |

| | | Asset Management, LLC | | |

| | | (2008 – 2019). | | |

| | | | | |

| James R. Schoenike | Trustee since | Distribution consultant since | 10 | None |

| (Born 1959) | July 2016(4) | 2018, President and CEO, Board | | |

| | | of Managers, Quasar Distributors, | | |

| | | LLC (2013 – 2018). | | |

(1) | The address of each Trustee as it relates to the Trust’s business is c/o U.S. Bank Global Fund Services, 615 East Michigan Street, Milwaukee, WI 53202. |

(2) | Each Trustee serves during the continued lifetime of the Trust until he dies, resigns, is declared bankrupt or incompetent by a court of competent jurisdiction, or is removed. |

(3) | The Trust currently has nine active portfolios. |

(4) | Prior to January 1, 2021, Mr. Schoenike was considered to be an “interested person” of the Fund by virtue of his previous position as President of Quasar Distributors, LLC. |