UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-021979

Nuveen Investment Trust V

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: June 30, 2007

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

Item 1. Reports to Stockholders.

NUVEEN INVESTMENTS MUTUAL FUNDS

| | |

| | |

Semiannual Report dated June 30, 2007 | | For investors seeking a high level of current income and total return. |

Nuveen Investments Funds

Nuveen Preferred Securities Fund

NOW YOU CAN RECEIVE YOUR

NUVEEN INVESTMENTS FUND REPORTS FASTER.

NO MORE WAITING.

SIGN UP TODAY TO RECEIVE NUVEEN INVESTMENTS FUND INFORMATION BY E-MAIL.

It only takes a minute to sign up for E-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Investments Fund information is ready — no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report, and save it on your computer if your wish.

IT’S FAST, EASY & FREE:

www.investordelivery.com

if you get your Nuveen Investments Fund dividends and statements from your financial advisor or brokerage account.

(Be sure to have the address sheet that accompanied this report handy. You’ll need it to complete the enrollment process.)

OR

www.nuveen.com/accountaccess

if you get your Nuveen Investments Fund dividends and statements directly from Nuveen Investments.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Dear Shareholder,

Detailed information on your Nuveen Preferred Securities Fund’s performance can be found in the Portfolio Manager’s Comments and Fund Spotlight sections of this report. I urge you to take the time to read the Portfolio Manager’s Comments.

I also wanted to take this opportunity to report some important news about Nuveen Investments. The company has accepted a buyout offer from a private equity investment firm. While this may affect the corporate structure of Nuveen Investments, it will have no impact on the investment objectives of the Fund, its portfolio management strategies or its dividend policies. We will provide you with additional information about this transaction as more details become available.

Portfolio diversification is a recognized way to try to reduce some of the risk that comes with investing. Since one part of your portfolio may be going up when another is going down, portfolio diversification may help smooth your investment returns over time. In addition to providing a high level of current income and total return, an investment like your Fund may help you achieve and benefit from greater portfolio diversification. Your financial advisor can explain these potential advantages in more detail. I urge you to contact him or her soon for more information on this important investment strategy.

At Nuveen Investments, our mission continues to be to assist you and your financial advisor by offering investment services and products that can help you to secure your financial objectives. We are grateful that you have chosen us as a partner as you pursue your financial goals, and we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Timothy R. Schwertfeger

Chairman of the Board

August 15, 2007

“In addition to

providing a high level of

current income and total

return, an investment

like your Fund

may help you

achieve and benefit

from greater portfolio

diversification.”

Semiannual Report Page 1

Portfolio Manager’s Comments

Portfolio manager John Miller examines the investment philosophy for the Nuveen Preferred Securities Fund. John, who has 13 years of investment experience, has managed the Nuveen Preferred Securities Fund since its inception.

What were the general market conditions during this reporting period?

Economy: Although the U.S. economy grew at an anemic 0.7% annualized rate in 1Q07, market consensus is that 2Q07 Gross Domestic Product (GDP) has rebounded to over 3.0%. The U.S. housing market continues to languish as a result of oversupply, higher mortgage rates, stricter lending standards, and surging default rates. The labor market continues to create new jobs and unemployment hovers near six-year lows. Core inflation has trended lower during the first six months of 2007, but remains at the high end of the Fed’s 1% – 2% comfort zone.

Drilling down further, the economy generated an average of 145,000 non-farm jobs per month during the first half of 2007, surpassing economists’ expectations of roughly 120,000 per month. The unemployment rate is currently 4.5%. In the past six years, only March 2007 and October 2006 have posted a lower rate, each instance 4.4%. The service sector, which accounts for approximately 90% of the economy, added most of the new jobs.

Federal Reserves & Interest Rates: Since the beginning of the year, we have had four announcements out of the Federal Reserve. At each meeting the Fed has kept the overnight rate at 5.25%. Although core PCE, the Fed’s primary gauge for inflation, has been trending lower during the first half of 2007, it remains at the high end of the Fed’s comfort zone. Several factors such as low unemployment, high capacity utilization, falling productivity, a declining U.S. dollar, and solid global growth suggest that the downward trend in inflation could reverse at anytime. As a result, the Fed stated in its June 28 statement, “…the Committee’s predominant policy concern remains that inflation will fail to moderate as expected.”

In the U.S., longer rates have led the move higher. The spread between 2yr and 10yr U.S. Treasuries moved from -17bps at the beginning of 2007 to +10bps by the end of June 2007. No change in Fed policy or rhetoric and a general flight to quality from the sub-prime market have kept short-term treasury rates relatively steady. Further out the curve however, higher expectations for U.S. growth and inflation have forced yields higher.

Hybrids / Preferreds: While capital securities and $25 par securities performed quite well during the first couple of months of 2007, the asset class underperformed broader credit indices beginning in the latter portion of the first quarter. There were several large macro trends that caused a general re-pricing of risk across all asset classes, including the preferred sector. The U.S. 10yr treasury yield jumped over 3/4% between the end of February and early June. Over that same time period, the market experienced a spike in volatility and a material widening in credit spreads. All of these factors forced preferred market investors to reassess both credit and extension risk, material characteristics of the asset class.

There was roughly $60 billion of new issue supply in the capital security sector between January and June 2007, an unprecedented level. While the issuance was well received through the early part of spring, by late May demand began to wane as the market was both saturated with paper and subprime concerns had permeated surrounding asset classes. Another point of concern for the asset class was an announcement by S&P that it was reviewing several hybrid structures issued by insurers and reinsurers. There was speculation that S&P was reviewing covenants in the companies’ bank credit facilities that could affect dividend payments on the insurers’ and reinsurers’

Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The views expressed herein represent those of the portfolio manager as of the date of this report and are subject to change at any time, based on market conditions and other factors. The Fund disclaims any obligation to advise shareholders of such changes.

Semiannual Report Page 2

Class A Shares

Cumulative Total Returns as of 6/30/07

| | | | |

| | | 6-month | | Since

inception

(12/19/06) |

Nuveen Preferred Securities Fund | | | | |

A Shares at NAV | | -0.71% | | -0.66% |

A Shares at Offer | | -5.44% | | -5.39% |

Lipper Mixed-Asset Target Allocation Growth Funds Index1 | | 6.64% | | 6.64% |

Merrill Lynch Hybrid Securities Index2 | | 0.10% | | 0.10% |

Returns quoted represent past performance, which is no guarantee of future results. Returns at NAV would be lower if the sales charge were included. Returns less than one year are cumulative. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Class A shares have a 4.75% maximum sales charge. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Returns reflect a voluntary expense limitation by the Fund’s investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance, visit www.nuveen.com or call (800) 257-8787.

Please see the Fund’s Spotlight page later in this report for more complete performance data and expense ratios.

outstanding hybrid issues. Eventually nothing came to pass from S&P’s review, but it did revive investor concerns that rating agency activity might require additional risk premium.

How did the Fund perform during the six months ended June 30, 2007?

Class A shares at net asset value for the Nuveen Preferred Securities Fund underperformed its comparative indexes for the reporting period ended June 30, 2007. Although we believe that comparing the performance of the Fund with that of a asset allocation index may offer some insights into how the Fund performed relative to the general securities market, we also think that closely comparing the results of a preferred securities fund with an asset allocation index provides an incomplete picture, because most of the index’s results do not come from preferred securities.

What strategies were used to manage the Fund during the reporting period?

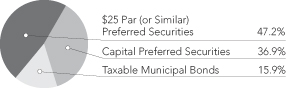

During the early part of the reporting period, the primary focus of the Fund was completing the invest-up. Throughout this period, we generally maintained a 65%/35% portfolio mix between the $25 par sector and the capital securities sector for the Fund. As the reporting period progressed, we began to strategically allocate away from both the $25 par sector and the capital securities sector in favor of taxable municipal bonds, which we felt offered both better relative value and a lower duration profile. At the close of the reporting period, the Fund held approximately 47% $25 par securities, 37% capital securities, and 16% taxable municipal bonds.

In the $25 par sector, we sold holdings from the brokerage and banking sectors which we judged to have limited upside potential and used the proceeds to help fund our allocation to taxable municipal bonds. In the capital securities sector, we sold some of our holdings and purchased others in the same sector that we believed provided better value.

| 1 | The Lipper Mixed-Asset Target Allocation Growth Funds Index is a managed index that represents the average annualized total returns of the 10 largest funds in the Lipper Mixed-Asset Target Allocation Growth Fund category. The since inception data for the index represents returns for the period 12/31/06–6/30/07, as returns for the index are calculated on a calendar month basis. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 2 | The Merrill Lynch Hybrid Securities Index is an unmanaged index consisting of a set of investment grade exchange-traded preferred stocks with outstanding market values of at least $50 million that are covered by Merrill Lynch Fixed Income Research. The index includes certain publicly issued, $25- and $1000-par securities with at least one year to maturity. The since inception data for the index represents returns for the period 12/31/06–6/30/07, as returns for the index are calculated on a calendar month basis. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

Semiannual Report Page 3

How did these strategies influence performance during the reporting period?

Although underperforming our internal benchmark index during the first quarter due primarily to the invest-up process, the Fund outperformed the same index during the second quarter. The outperformance was generated primarily through purchasing higher quality structures with extension protection, implementing a systematic duration hedging program while adhering to our stated investment process. We continuously monitored portfolio holdings on an option-adjusted-spread (OAS) basis, rotating out of positions which we felt offered limited upside into issues which we felt offered the possibility of outperforming over time. Additionally, we had success tactically adjusting our allocation between the $25 par and $1,000 par securities. Heavy retail participation in the $25 par sector caused the sector to lag broader market moves. During the second quarter, we tactically sold $25 par securities as the sector lagged in response to the push higher in interest rates and credit spreads. We subsequently redeployed these assets in the $1,000 capital securities sector.

Semiannual Report Page 4

Fund Spotlight as of 6/30/07 Nuveen Preferred Securities Fund

| | | | | | | | |

| Quick Facts | | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares |

NAV | | $19.41 | | $19.39 | | $19.39 | | $19.42 |

Inception Date | | 12/19/06 | | 12/19/06 | | 12/19/06 | | 12/19/06 |

Returns quoted represent past performance which is no guarantee of future results. Returns without sales charges would be lower if the sales charge were included. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Fund returns assume reinvestment of dividends and capital gains. Class A shares have a 4.75% maximum sales charge. Class B shares have a contingent deferred sales charge (CDSC), also known as a back-end sales charge, that for redemptions begins at 5% and declines periodically until after 6 years when the charge becomes 0%. Class B shares automatically convert to Class A shares eight years after purchase. Class C shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class R shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors.

| | | | |

| Cumulative Total Returns as of 6/30/07 |

| A Shares | | NAV | | Offer |

Since Inception | | -0.66% | | -5.39% |

| B Shares | | w/o CDSC | | w/CDSC |

Since Inception | | -1.07% | | -5.92% |

| C Shares | | NAV | | w/CDSC |

Since Inception | | -1.07% | | -2.04% |

| R Shares | | NAV | | |

Since Inception | | -0.51% | | |

| Yields |

| A Shares | | NAV | | Offer |

SEC 30-day yield2 | | 4.91% | | 4.68% |

Distibution Rate | | 5.94% | | 5.65% |

| B Shares | | NAV | | |

SEC 30-day yield | | 4.11% | | |

Distibution Rate | | 5.17% | | |

| C Shares | | NAV | | |

SEC 30-day yield | | 4.11% | | |

Distibution Rate | | 5.17% | | |

| R Shares | | NAV | | |

SEC 30-day yield | | 5.17% | | |

Distibution Rate | | 6.18% | | |

| | | | | | |

| Expense Ratios | | | | | | |

| | | |

| Share Class | | Gross

Expense

Ratio | | Net

Expense

Ratio | | As of

Date |

Class A | | 18.18% | | 1.23% | | 12/31/06 |

Class B | | 18.93% | | 1.99% | | 12/31/06 |

Class C | | 18.93% | | 1.99% | | 12/31/06 |

Class R | | 17.92% | | 0.98% | | 12/31/06 |

The expense ratios shown are estimated for the first fiscal year. The net expense ratio reflects a contractual commitment by the Fund’s investment adviser to waive fees and reimburse expenses through April 30, 2010. Absent the waiver and reimbursement, expenses would be higher and total returns would be less.

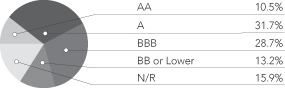

Credit Quality1

Portfolio Allocation1

| | |

| Portfolio Statistics |

Net Assets ($000) | | $5,044 |

Average Effective Maturity (Years) | | 38.38 |

Average Duration | | 5.53 |

Number of Stocks | | 27 |

| | | |

| Top Five Issuers1: |

Banco Santander | | 4.4% |

California Statewide Community Development Authority | | 4.0% |

Carter Plantation Land LLC | | 4.0% |

La Vernia Education Financing Corporation | | 4.0% |

Northern Palm Beach County Improvement District | | 3.9% |

| 1 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

| 2 | The SEC 30-Day Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Shares load in certain specified circumstances. |

Semiannual Report Page 5

Fund Spotlight as of 6/30/07 Nuveen Preferred Securities Fund

Industries1

| | |

Commercial Banks | | 26.3% |

Insurance | | 16.6% |

Municipals | | 15.9% |

Electric Utilities | | 7.4% |

Diversified Financial Services | | 7.1% |

Thrifts & Mortgage Finance | | 6.5% |

Capital Markets | | 6.3% |

Other | | 13.9% |

| 1 | As a percentage of total investments as of June 30, 2007. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | Hypothetical Performance |

| | | Actual Performance | | (5% annualized return before expenses) |

| | | | | | | | |

| | | A Shares | | B Shares | | C Shares | | R Shares | | A Shares | | B Shares | | C Shares | | R Shares |

Beginning Account Value (1/01/07) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

Ending Account Value (6/30/07) | | $ | 992.90 | | $ | 988.00 | | $ | 988.00 | | $ | 994.40 | | $ | 1,019.09 | | $ | 1,015.37 | | $ | 1,015.37 | | $ | 1,020.33 |

Expenses Incurred During Period | | $ | 5.68 | | $ | 9.37 | | $ | 9.37 | | $ | 4.45 | | $ | 5.76 | | $ | 9.49 | | $ | 9.49 | | $ | 4.51 |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 1.15%, 1.90%, 1.90% and 0.90% for Classes A, B, C and R, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Semiannual Report Page 6

Portfolio of Investments (Unaudited)

Nuveen Preferred Securities Fund

June 30, 2007

| | | | | | | | | | | | | | |

| Shares | | Description | | | | Coupon | | | | Ratings (1) | | Value |

| | | | | | | | | | | | | | |

| | | $25 PAR (OR SIMILAR) PREFERRED SECURITIES – 46.8% | | | | | | | | | | | |

| | | | | | |

| | | Airlines – 2.4% | | | | | | | | | | | |

| | | | | | |

| | 5,000 | | AMR Corporation | | | | 7.875% | | | | Caa1 | | $ | 123,000 |

| | | Capital Markets – 2.4% | | | | | | | | | | | |

| | | | | | |

| | 5,000 | | Morgan Stanley Capital Trust VII | | | | 6.600% | | | | A1 | | | 122,400 |

| | | Commercial Banks – 18.5% | | | | | | | | | | | |

| | | | | | |

| | 5,000 | | BAC Capital Trust V | | | | 6.000% | | | | Aa3 | | | 115,850 |

| | | | | | |

| | 4,000 | | Banco Santander, 144A | | | | 6.500% | | | | A | | | 98,125 |

| | | | | | |

| | 5,000 | | Citizens Funding Trust I | | | | 7.500% | | | | Baa1 | | | 127,032 |

| | | | | | |

| | 5,000 | | KeyCorp Capital Trust IX | | | | 6.750% | | | | A3 | | | 123,663 |

| | | | | | |

| | 5,000 | | National City Capital Trust II | | | | 6.625% | | | | A2 | | | 123,125 |

| | | | | | |

| | 5,000 | | Santander Finance, SA, 144A | | | | 5.880% | | | | A2 | | | 119,844 |

| | | | | | |

| | 4,000 | | USB Capital Trust XI | | | | 6.600% | | | | Aa3 | | | 98,880 |

| | | | | | |

| | 5,000 | | Zions Capital Trust B | | | | 8.000% | | | | A3 | | | 126,150 |

| | | Total Commercial Banks | | | | | | | | | | | 932,669 |

| | | |

| | | Diversified Financial Services – 7.1% | | | | | | | | | | | |

| | | | | | |

| | 4,800 | | Citigroup Capital XV | | | | 6.500% | | | | Aa2 | | | 118,200 |

| | | | | | |

| | 5,000 | | Deutsche Bank Capital Funding Trust VIII | | | | 6.375% | | | | A | | | 124,219 |

| | | | | | |

| | 5,000 | | GMAC LLC | | | | 7.375% | | | | BB+ | | | 114,000 |

| | | Total Diversified Financial Services | | | | | | | | | | | 356,419 |

| | | |

| | | Electric Utilities – 7.3% | | | | | | | | | | | |

| | | | | | |

| | 5,000 | | FPL Group Capital Inc. | | | | 6.600% | | | | A3 | | | 124,400 |

| | | | | | |

| | 4,500 | | Georgia Power Company | | | | 5.900% | | | | A | | | 105,255 |

| | | | | | |

| | 6,000 | | National Rural Utilities Cooperative Finance Corporation | | | | 5.950% | | | | A3 | | | 138,840 |

| | | Total Electric Utilities | | | | | | | | | | | 368,495 |

| | | |

| | | Household Durables – 2.1% | | | | | | | | | | | |

| | | | | | |

| | 4,000 | | M-I Homes | | | | 9.750% | | | | B | | | 104,850 |

| | | Insurance – 5.1% | | | | | | | | | | | |

| | | | | | |

| | 5,000 | | Aspen Insurance Holdings Limited | | | | 7.401% | | | | Ba1 | | | 124,500 |

| | | | | | |

| | 5,000 | | UnumProvident Financing Trust I (CORTS) | | | | 8.500% | | | | BBB | | | 130,300 |

| | | Total Insurance | | | | | | | | | | | 254,800 |

| | | |

| | | Real Estate Investment Trust – 1.9% | | | | | | | | | | | |

| | | | | | |

| | 4,000 | | Public Storage, Inc., Series M | | | | 6.625% | | | | BBB+ | | | 95,650 |

| | | Total $25 Par (or similar) Preferred Securities (cost $2,432,470) | | | | | | | | | | | 2,358,283 |

| | | |

| | | | | | |

Principal

Amount (000) | | Description | | | | Optional Call

Provisions (2) | | | | Ratings (1) | | Value |

| | | TAXABLE MUNICIPAL BONDS – 15.8% | | | | | | | | | | | |

| | | | | | |

| | | California – 4.0% | | | | | | | | | | | |

| | | | | | |

| $ | 200 | | California Statewide Community Development Authority, Lancer Educational Student Housing Revenue Bonds, California Baptist University,

Series 2007, 9.125%, 6/01/13 | | | | No Opt. Call | | | | N/R | | $ | 202,084 |

| | | Florida – 3.9% | | | | | | | | | | | |

| | | | | | |

| | 200 | | Northern Palm Beach County Improvement District, Florida, Water Control and Improvement Bonds, Development Unit 46,

Series 2007B, 8.250%, 8/01/21 | | | | 8/14 at 100.00 | | | | N/R | | | 195,880 |

| | | Louisiana – 4.0% | | | | | | | | | | | |

| | | | | | |

| | 200 | | Carter Plantation Land, Louisiana, Revenue Bonds,

Series 2007, 9.000%, 7/01/17 | | | | No Opt. Call | | | | N/R | | | 199,738 |

7

Portfolio of Investments (Unaudited)

Nuveen Preferred Securities Fund (continued)

June 30, 2007

| | | | | | | | | | | | | | |

Principal

Amount (000) | | Description | | | | Optional Call

Provisions (2) | | | | Ratings (1) | | Value |

| | | | | | | | | | | | | | |

| | | Texas – 3.9% | | | | | | | | | | | |

| | | | | | |

| $ | 200 | | La Vernia Education Financing Corporation, Texas, Charter School Revenue Bonds,

Riverwalk Education Foundation,

Series 2007B, 8.750%, 8/15/12 | | | | 8/11 at 100.00 | | | | N/R | | $ | 197,464 |

| $ | 800 | | Total Taxable Municipal Bonds (cost $798,865) | | | | | | | | | | | 795,166 |

| | | | | | |

Principal

Amount (000)/

Shares | | Description | | | | Coupon | | Maturity | | Ratings (1) | | Value |

| | | CAPITAL PREFERRED SECURITIES – 36.5% | | | | | | | | | | | |

| | | | | | |

| | | Capital Markets – 3.8% | | | | | | | | | | | |

| | | | | | |

| | 200 | | JP Morgan Chase Capital Trust XXII | | | | 6.450% | | 2/02/37 | | Aa3 | | $ | 190,690 |

| | | Commercial Banks – 7.5% | | | | | | | | | | | |

| | | | | | |

| | 200 | | BBVA International Perferred SA, Unipersonal | | | | 5.919% | | 10/18/49 | | A1 | | | 187,973 |

| | | | | | |

| | 200 | | HBOS PLC, Series 144A | | | | 6.657% | | 11/21/57 | | A1 | | | 192,468 |

| | 400 | | Total Commercial Banks | | | | | | | | | | | 380,441 |

| | | Insurance – 11.4% | | | | | | | | | | | |

| | | | | | |

| | 200 | | Liberty Mutual Group | | | | 7.800% | | 3/15/37 | | Baa3 | | | 188,827 |

| | | | | | |

| | 200 | | QBE Capital Funding Trust II, 144A | | | | 6.797% | | 6/01/49 | | BBB | | | 195,639 |

| | | | | | |

| | 200 | | XL Capital, Limited | | | | 6.500% | | 10/15/57 | | BBB | | | 188,168 |

| | 600 | | Total Insurance | | | | | | | | | | | 572,634 |

| | | Oil, Gas, & Consumable Fuels – 3.8% | | | | | | | | | | | |

| | | | | | |

| | 200 | | Enterprise Products Operating L.P. | | | | 7.034% | | 1/15/68 | | Ba1 | | | 193,150 |

| | | Road & Rail – 3.7% | | | | | | | | | | | |

| | | | | | |

| | 200 | | Burlington Northern Santa Fe Funding Trust I | | | | 6.613% | | 12/15/55 | | BBB | | | 183,167 |

| | | Thrifts & Mortgage Finance – 6.4% | | | | | | | | | | | |

| | | | | | |

| | 5 | | Sovereign Capital Trust V | | | | 7.750% | | 5/22/36 | | Baa1 | | | 129,950 |

| | | | | | |

| | 200 | | Washington Mutual Preferred Funding Delaware, Series A-1, 144A | | | | 6.534% | | 6/15/56 | | Baa1 | | | 193,699 |

| | 205 | | Total Thrifts & Mortgage Finance | | | | | | | | | | | 323,649 |

| | 1,805 | | Total Capital Preferred Securities (cost $1,916,160) | | | | | | | | | | | 1,843,731 |

| | | Total Investments (cost $5,147,495) – 99.1% | | | | | | | | | | | 4,997,180 |

| | | |

| | | Other Assets Less Liabilities – 0.9% | | | | | | | | | | | 47,166 |

| | | |

| | | Net Assets – 100% | | | | | | | | | | $ | 5,044,346 |

| | | |

8

Futures Contracts Outstanding at June 30, 2007:

| | | | | | | | | | | | | | |

| Type | | Contract

Position | | Number of

Contracts | | | Contract

Expiration | | Value at

6/30/07 | | | Unrealized

Appreciation

(Depreciation) |

| U.S Treasury Bond | | Short | | (4 | ) | | 9/07 | | $ | (431,000 | ) | | $ | 6,051 |

| | (1) | | Ratings: Using the higher of Standard & Poor’s or Moody’s rating. Ratings below BBB by Standard & Poor’s Group or Baa by Moody’s Investor Service, Inc. are considered to be below investment grade. |

| | (2) | | Optional Call Provisions: Dates (month and year) and prices of the earliest optional call or redemption. There may be other call provisions at varying prices at later dates. Certain mortgage-backed securities may be subject to periodic principal paydowns. |

| | 144A | | Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration which are normally those transactions with qualified institutional buyers. |

| | CORTS | | Corporate Backed Trust Securities. |

See accompanying notes to financial statements.

9

Statement of Assets and Liabilities (Unaudited)

Nuveen Preferred Securities Fund

June 30, 2007

| | | | |

Assets | | | | |

Investments, at market value (cost $5,147,495) | | $ | 4,997,180 | |

Cash | | | 43,701 | |

Receivables: | | | | |

Dividends | | | 8,097 | |

Fund Manager | | | 17,625 | |

Interest | | | 35,059 | |

Reclaims | | | 364 | |

Total assets | | | 5,102,026 | |

Liabilities | | | | |

Payable for variation margin on futures contracts | | | 3,875 | |

Accrued expenses: | | | | |

12b-1 distribution and service fees | | | 500 | |

Other | | | 27,840 | |

Dividends Payable | | | 25,465 | |

Total liabilities | | | 57,680 | |

Net assets | | $ | 5,044,346 | |

Class A Shares | | | | |

Net assets | | $ | 271,849 | |

Shares outstanding | | | 14,005 | |

Net asset value per share | | $ | 19.41 | |

Offering price per share (net asset value per share plus

maximum sales charge of 4.75% of offering price) | | $ | 20.38 | |

Class B Shares | | | | |

Net assets | | $ | 270,933 | |

Shares outstanding | | | 13,970 | |

Net asset value and offering price per share | | $ | 19.39 | |

Class C Shares | | | | |

Net assets | | $ | 270,933 | |

Shares outstanding | | | 13,970 | |

Net asset value and offering price per share | | $ | 19.39 | |

Class R Shares | | | | |

Net assets | | $ | 4,230,631 | |

Shares outstanding | | | 217,874 | |

Net asset value and offering price per share | | $ | 19.42 | |

| |

Net Assets Consist of: | | | | |

Capital paid-in | | $ | 5,192,470 | |

Undistributed (Over-distribution of) net investment income | | | 23,664 | |

Accumulated net realized gain (loss) from investments and derivative transactions | | | (27,524 | ) |

Net unrealized appreciation (depreciation) of investments and derivative transactions | | | (144,264 | ) |

Net assets | | $ | 5,044,346 | |

See accompanying notes to financial statements.

10

Statement of Operations (Unaudited)

Nuveen Preferred Securities Fund

Six Months Ended June 30, 2007

| | | | |

Investment Income | | | | |

Dividends (net of foreign tax withheld of $343) | | $ | 93,194 | |

Interest | | | 65,302 | |

Total investment income | | | 158,496 | |

Expenses | | | | |

Management fees | | | 18,262 | |

12b-1 service fees – Class A | | | 341 | |

12b-1 distribution and service fees – Class B | | | 1,363 | |

12b-1 distribution and service fees – Class C | | | 1,363 | |

Shareholders’ servicing agent fees and expenses | | | 128 | |

Custodian’s fees and expenses | | | 3,595 | |

Trustees’ fees and expenses | | | 56 | |

Professional fees | | | 26,516 | |

Shareholders’ reports – printing and mailing expenses | | | 21,187 | |

Federal and state registration fees | | | 384 | |

Other expenses | | | 1,089 | |

Total expenses before expense reimbursement | | | 74,284 | |

Custodian fee credit | | | (2,099 | ) |

Expense reimbursement | | | (46,721 | ) |

Net expenses | | | 25,464 | |

Net investment income | | | 133,032 | |

Realized and Unrealized Gain (Loss) | | | | |

Net realized gain (loss) from: | | | | |

Investments | | | (35,849 | ) |

Futures | | | 7,976 | |

Change in net unrealized appreciation (depreciation) of: | | | | |

Investments | | | (144,273 | ) |

Futures | | | 6,051 | |

Net realized and unrealized gain (loss) | | | (166,095 | ) |

Net increase (decrease) in net assets from operations | | $ | (33,063 | ) |

See accompanying notes to financial statements.

11

Statement of Changes in Net Assets (Unaudited)

Nuveen Preferred Securities Fund

| | | | | | | | |

| | | Six Months Ended

6/30/07 | | | For the Period

12/19/06

(commencement

of operations)

through 12/31/06 | |

Operations | | | | | | | | |

Net investment income | | $ | 133,032 | | | $ | 8,915 | |

Net realized gain (loss) from: | | | | | | | | |

Investments | | | (35,849 | ) | | | — | |

Futures | | | 7,976 | | | | — | |

Change in net unrealized appreciation (depreciation) of: | | | | | | | | |

Investments | | | (144,273 | ) | | | (6,042 | ) |

Futures | | | 6,051 | | | | — | |

Net increase (decrease) in net assets from operations | | | (33,063 | ) | | | 2,873 | |

Distributions to Shareholders | | | | | | | | |

From undistributed net investment income: | | | | | | | | |

Class A | | | (6,412 | ) | | | — | |

Class B | | | (5,537 | ) | | | — | |

Class C | | | (5,537 | ) | | | — | |

Class R | | | (102,103 | ) | | | — | |

Decrease in net assets from distributions to shareholders | | | (119,589 | ) | | | — | |

Fund Share Transactions | | | | | | | | |

Proceeds from sale of shares | | | 100,000 | | | | 4,900,000 | |

Proceeds from shares issued to shareholders due to reinvestment of distributions | | | 94,125 | | | | — | |

Net increase (decrease) in net assets from Fund share transactions | | | 194,125 | | | | 4,900,000 | |

Net increase (decrease) in net assets | | | 41,473 | | | | 4,902,873 | |

Net assets at the beginning of period | | | 5,002,873 | | | | 100,000 | |

Net assets at the end of period | | $ | 5,044,346 | | | $ | 5,002,873 | |

Undistributed (Over-distribution of) net investment income at the end of period | | $ | 23,664 | | | $ | 10,221 | |

See accompanying notes to financial statements.

12

Notes to Financial Statements (Unaudited)

1. General Information and Significant Accounting Policies

The Nuveen Investment Trust V (the “Trust”) is an open-end management investment company registered under the Investment Company Act of 1940, as amended. The Trust is comprised of the Nuveen Preferred Securities Fund (the “Fund”). The Trust was organized as a Massachusetts business trust on September 27, 2006.

Prior to the commencement of operations, the Fund had no operations other than those related to organizational matters, the initial capital contribution of $100,000 by Nuveen Asset Management (the “Adviser”), a wholly owned subsidiary of Nuveen Investments, Inc. (“Nuveen”), the recording of the organization expenses ($15,000) and offering costs ($85,000) and their reimbursement by Nuveen Investments, LLC, also a wholly owned subsidiary of Nuveen.

The Fund seeks to provide a high level of current income and total return. Under normal circumstances the Fund will invest at least 80% of its net assets in preferred securities and up to 20% of its assets in debt securities, U.S. government and agency debt and convertible preferred securities. The Fund may also invest in futures, forwards, options and swaps, or other financial instruments including credit default swaps.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements in accordance with U.S. generally accepted accounting principles.

Investment Valuation

Exchange-listed securities and instruments, other than futures, are generally valued at the last sales price on the exchange on which such securities are primarily traded. Securities or instruments traded on an exchange for which there are no transactions on a given day or securities or instruments not listed on an exchange are valued at the mean of the closing bid and asked prices. Securities traded on Nasdaq are valued at the Nasdaq Official Closing Price. The prices of fixed-income securities are generally provided by an independent pricing service approved by the Fund’s Board of Trustees and based on the mean between the bid and asked prices. Futures contracts are valued using closing settlement price or, in the absence of such a price, at the mean of the bid and asked prices. When price quotes are not readily available, the pricing service or, in the absence of a pricing service for a particular security or instrument, the Board of Trustees of the Fund, or its designee, may establish fair value using a wide variety of market data including yields or prices of securities of comparable quality, type of issue, coupon, maturity and rating, market quotes or indications of value from security dealers, evaluations of anticipated cash flows or collateral, general market conditions and other information and analysis, including the obligor’s credit characteristics considered relevant by the pricing service or the Board of Trustee’s designee. Short-term investments are valued at amortized cost, which approximates market value.

Investment Transactions

Investment transactions are recorded on a trade date basis. Realized gains and losses from investment transactions are determined on the specific identification method. Investments purchased on a when-issued/delayed delivery basis may have extended settlement periods. Any investments so purchased are subject to market fluctuation during this period. The Fund has instructed the custodian to segregate assets with a current value at least equal to the amount of the when-issued/delayed delivery purchase commitments. At June 30, 2007, the Fund had no such outstanding purchase commitments.

Investment Income

Dividend income is recorded on the ex-dividend date or, for foreign securities, when information is available. Interest income, which includes the amortization of premiums and accretion of discounts for financial reporting purposes, is recorded on an accrual basis.

Dividends and Distributions to Shareholders

Distributions to shareholders are recorded on the ex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from U.S. generally accepted accounting principles.

Dividends from net investment income are declared monthly. Net realized capital gains from investment transactions, if any, are declared and distributed to shareholders not less frequently than annually. Furthermore, capital gains are distributed only to the extent they exceed available capital loss carryforwards.

Federal Income Taxes

The Fund intends to distribute substantially all net investment income and net capital gains to shareholders and to otherwise comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies. Therefore, no federal income tax provision is required.

Flexible Sales Charge Program

The Fund offers Class A, B, C and R Shares, however, the Fund will issue Class B Shares only upon exchange of Class B Shares from another Nuveen fund or for purposes of dividend reinvestment. Class A Shares are generally sold with an up-front sales charge and incur a .25% annual 12b-1 service fee. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (“CDSC”) if redeemed within 18 months of purchase. Class B Shares incur a .75% annual 12b-1 distribution fee and a .25% annual 12b-1 service fee. An investor in Class B Shares agrees to pay a CDSC of up to 5% depending upon the length of time the shares are held by the investor (CDSC is reduced to 0% at the end of six years). Class B Shares convert to Class A Shares eight years after purchase. Class C Shares are sold without an up-front sales

13

Notes to Financial Statements (Unaudited) (continued)

charge but incur a .75% annual 12b-1 distribution fee and a .25% annual 12b-1 service fee. An investor purchasing Class C Shares agrees to pay a CDSC of 1% if Class C Shares are redeemed within one year of purchase. Class R Shares are not subject to any sales charge or 12b-1 distribution or service fees. Class R Shares are available only under limited circumstances.

Futures Contracts

The Fund is authorized to invest in futures contracts. Upon entering into a futures contract, a Fund is required to deposit with the broker an amount of cash or liquid securities equal to a specified percentage of the contract amount. This is known as the “initial margin.” Subsequent payments (“variation margin”) are made or received by a Fund each day, depending on the daily fluctuation of the value of the contract.

During the period the futures contract is open, changes in the value of the contract are recognized as an unrealized gain or loss by “marking-to-market” on a daily basis to reflect the changes in market value of the contract. When the contract is closed or expired, a Fund records a realized gain or loss equal to the difference between the value of the contract on the closing date and the value of the contract when originally entered into. Cash held by the broker to cover initial margin requirements on open futures contracts, if any, is noted in the Statement of Assets and Liabilities. Additionally, the Statement of Assets and Liabilities reflects a receivable and/or payable for the variation margin when applicable.

Risks of investments in futures contracts include the possible adverse movement of the securities or indices underlying the contracts, the possibility that there may not be a liquid secondary market for the contracts and/or that a change in the value of the contract may not correlate with a change in the value of the underlying securities or indices.

Repurchase Agreements

In connection with transactions in repurchase agreements, it is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. If the seller defaults, and the fair value of the collateral declines, realization of the collateral may be delayed or limited.

Expense Allocation

Expenses of the Fund that are not directly attributable to a specific class of shares are prorated among the classes based on the relative net assets of each class. Expenses directly attributable to a class of shares, which presently only include 12b-1 distribution and service fees, are recorded to the specific class.

Custodian Fee Credit

The Fund has an arrangement with the custodian bank whereby certain custodian fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. Such deposit arrangements are an alternative to overnight investments. Credits for cash balances may be offset by charges for any days on which the Fund overdraws its account at the custodian bank.

Indemnifications

Under the Trust’s organizational documents, its Officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business, the Trust enters into contracts that provide general indemnifications to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred. However, the Trust has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

Use of Estimates

The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results may differ from those estimates.

14

2. Fund Shares

Transactions in Fund shares were as follows:

| | | | | | | | | | |

| | | Six Months Ended

6/30/07 | | For the Period 12/19/06

(commencement of

operations) through 12/31/06 |

| | | Shares | | Amount | | Shares | | Amount |

Shares sold: | | | | | | | | | | |

Class A | | — | | $ | — | | 12,500 | | $ | 250,000 |

Class B | | — | | | — | | 12,500 | | | 250,000 |

Class C | | — | | | — | | 12,500 | | | 250,000 |

Class R | | 5,087 | | | 100,000 | | 207,500 | | | 4,150,000 |

| | | 5,087 | | | 100,000 | | 245,000 | | | 4,900,000.00 |

Shares issued to shareholders due to reinvestment

of distributions: | | | | | | | | | | |

Class A | | 255 | | | 5,068 | | — | | | — |

Class B | | 220 | | | 4,360 | | — | | | — |

Class C | | 220 | | | 4,360 | | — | | | — |

Class R | | 4,037 | | | 80,337 | | — | | | — |

| | | 4,732 | | | 94,125 | | — | | | — |

Net increase (decrease) | | 9,819 | | $ | 194,125 | | 245,000 | | $ | 4,900,000.00 |

3. Investment Transactions

Purchases and sales (including maturities but excluding short-term investments and derivative transactions) during the six months ended June 30, 2007, were as follows:

| | | |

Purchases: | | | |

Investment securities | | $ | 8,214,509 |

U.S. Government and agency obligations | | | — |

Sales and maturities: | | | |

Investment securities | | | 3,843,910 |

U.S. Government and agency obligations | | | 3,975,785 |

4. Income Tax Information

The following information is presented on an income tax basis based on information currently available to the Fund. Differences between amounts for financial statement and federal income tax purposes are primarily due to timing differences in the recognition of income and timing differences in recognizing certain gains and losses on investment transactions. To the extent that differences arise that are permanent in nature, such amounts are reclassified within the capital accounts on the Statement of Assets and Liabilities presented in the annual report, based on their federal tax basis treatment; temporary differences do not require reclassification. Temporary and permanent differences do not impact the net asset values of the Fund.

At June 30, 2007, the cost of investments was $5,146,171.

Gross unrealized appreciation and gross unrealized depreciation of investments at June 30, 2007, were as follows:

| | | | |

Gross unrealized: | | | | |

Appreciation | | $ | 9,190 | |

Depreciation | | | (158,181 | ) |

Net unrealized appreciation (depreciation) of investments | | $ | (148,991 | ) |

The tax components of undistributed net ordinary income and net long-term capital gains at December 31, 2006, the Fund’s last tax year end, were as follows:

| | | |

Undistributed net ordinary income* | | $ | 8,899 |

Undistributed net long-term capital gains | | | — |

* Net ordinary income consists of net taxable income derived from dividends, interest, and net short-term capital gains, if any.

5. Management Fees and Other Transactions with Affiliates

The Fund’s management fee is separated into two components – a complex-level component, based on the aggregate amount of all fund assets managed by the Adviser and a specific fund-level component, based only on the amount of assets within each individual

15

Notes to Financial Statements (Unaudited) (continued)

fund. This pricing structure enables Nuveen fund shareholders to benefit from growth in the assets within each individual fund as well as from growth in the amount of complex-wide assets managed by the Adviser.

The annual fund-level fee, payable monthly, for the Fund is based upon the average daily Managed Assets of the Fund as follows:

| | | |

| Average Daily Managed Assets | | Fund-Level Fee Rate | |

For the first $125 million | | .5500 | % |

For the next $125 million | | .5375 | |

For the next $250 million | | .5250 | |

For the next $500 million | | .5125 | |

For the next $1 billion | | .5000 | |

For Managed Assets over $2 billion | | .4750 | |

The annual complex-level fee, payable monthly, which is additive to the fund-level fee, for all Nuveen sponsored funds in the U.S., is based on the aggregate amount of total fund assets managed as stated in the tables below. As of June 30, 2007, the complex-level fee rate was .1828%.

Effective August 20, 2007, the complex-level fee schedule is as follows:

| | | |

| Complex-Level Asset Breakpoint Level(1) | | Effective Rate at Breakpoint Level | |

$55 billion | | .2000 | % |

$56 billion | | .1996 | |

$57 billion | | .1989 | |

$60 billion | | .1961 | |

$63 billion | | .1931 | |

$66 billion | | .1900 | |

$71 billion | | .1851 | |

$76 billion | | .1806 | |

$80 billion | | .1773 | |

$91 billion | | .1691 | |

$125 billion | | .1599 | |

$200 billion | | .1505 | |

$250 billion | | .1469 | |

$300 billion | | .1445 | |

Prior to August 20, 2007, the complex-level fee schedule was as follows:

| | | |

| Complex-Level Asset Breakpoint Level(1) | | Effective Rate at Breakpoint Level | |

$55 billion | | .2000 | % |

$56 billion | | .1996 | |

$57 billion | | .1989 | |

$60 billion | | .1961 | |

$63 billion | | .1931 | |

$66 billion | | .1900 | |

$71 billion | | .1851 | |

$76 billion | | .1806 | |

$80 billion | | .1773 | |

$91 billion | | .1698 | |

$125 billion | | .1617 | |

$200 billion | | .1536 | |

$250 billion | | .1509 | |

$300 billion | | .1490 | |

| (1) | The complex-level fee component of the management fee for the funds is calculated based upon the aggregate Managed Assets (“Managed Assets” means the average daily net assets of each fund including assets attributable to preferred stock issued by or borrowings by the Nuveen funds) of Nuveen-sponsored funds in the U.S. |

The management fee compensates the Adviser for overall investment advisory and administrative services and general office facilities. The Trust pays no compensation directly to those of its Trustees who are affiliated with the Adviser or to its Officers, all of whom receive remuneration for their services to the Trust from the Adviser or its affiliates. The Board of Trustees has adopted a deferred compensation plan for independent Trustees that enables Trustees to elect to defer receipt of all or a portion of the annual compensation they are entitled to receive from certain Nuveen advised funds. Under the plan, deferred amounts are treated as though equal dollar amounts had been invested in shares of select Nuveen advised funds.

The Adviser agreed to waive part of its management fees or reimburse certain expenses in order to limit operating expenses (excluding 12b-1 distribution and service fees, interest expense, taxes, fees incurred in acquiring and disposing of portfolio securities

16

and extraordinary expenses) from exceeding 1.00% of the average daily net assets through April 30, 2010 (1.25% after April 30, 2010). The Adviser may also voluntarily reimburse additional expenses from time to time. Voluntary reimbursements may be terminated at any time at the Adviser’s discretion.

All 12b-1 service fees collected on Class B Shares during the first year following a purchase, all 12b-1 distribution fees collected on Class B Shares, and all 12b-1 service and distribution fees collected on Class C Shares during the first year following a purchase are retained by the Distributor. During the six months ended June 30, 2007, the Distributor retained such 12b-1 fees as follows:

| | | |

12b-1 fees retained | | $ | 2,921 |

The remaining 12b-1 fees charged to the Fund were paid to compensate financial intermediaries for providing services to shareholders relating to their investments.

Agreement and Plan of Merger

On June 20, 2007, Nuveen Investments announced that it had entered into a definitive Agreement and Plan of Merger (“Merger Agreement”) with an investor group majority-led by Madison Dearborn Partners, LLC. Madison Dearborn Partners, LLC is a private equity investment firm based in Chicago, Illinois. The investor group includes affiliates of Merrill Lynch, Wachovia, Citigroup, Deutsche Bank and Morgan Stanley. It is anticipated that Merrill Lynch and its affiliates will be indirect “affiliated persons” (as that term is defined in the Investment Company Act of 1940) of the Fund. One important implication of this is that the Fund will not be able to buy or sell securities to or from Merrill Lynch, but the portfolio management team and Fund management do not expect that this will significantly impact the ability of the Fund to pursue its investment objectives and policies. Under the terms of the merger, each outstanding share of Nuveen Investments’ common stock (other than dissenting shares) will be converted into the right to receive a specified amount of cash, without interest. The merger is expected to be completed by the end of the year, subject to customary conditions, including obtaining the approval of Nuveen Investments shareholders, obtaining necessary fund and client consents sufficient to satisfy the terms of the Merger Agreement, and expiration of certain regulatory waiting periods. The obligations of Madison Dearborn Partners, LLC to consummate the merger are not conditioned on its obtaining financing.

The consummation of the merger will be deemed to be an “assignment” (as defined in the 1940 Act) of the investment management agreement between the Fund and the Adviser, and will result in the automatic termination of the Fund’s agreement. Prior to the consummation of the merger, it is anticipated that the Board of Trustees of the Fund will consider a new investment management agreement with the Adviser. If approved by the Board, the new agreement would be presented to the Fund’s shareholders for approval, and, if so approved by shareholders, would take effect upon consummation of the merger. There can be no assurance that the merger described above will be consummated as contemplated or that necessary shareholder approvals will be obtained.

6. New Accounting Pronouncements

Financial Accounting Standards Board Interpretation No. 48

Effective June 29, 2007, the Fund adopted Financial Accounting Standards Board Interpretation No. 48, “Accounting for Uncertainty in Income Taxes” (FIN 48). FIN 48 provides guidance regarding how uncertain tax positions should be recognized, measured, presented and disclosed in the financial statements. FIN 48 requires the evaluation of tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the applicable tax authority. Tax positions not deemed to meet the more-likely-than-not threshold would be recorded as a tax benefit or expense in the current year. Management of the Fund has concluded that there are no significant uncertain tax positions that require recognition in the Fund’s financial statements. Consequently, the adoption of FIN 48 had no impact on the net assets or results of operations of the Fund.

Financial Accounting Standards Board Statement of Financial Accounting Standards No. 157

In September 2006, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards (SFAS) No. 157, “Fair Value Measurements.” This standard establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements. SFAS No. 157 applies to fair value measurements already required or permitted by existing standards. SFAS No. 157 is effective for financial statements issued for fiscal years beginning after November 15, 2007, and interim periods within those fiscal years. The changes to current generally accepted accounting principles from the application of this standard relate to the definition of fair value, the methods used to measure fair value, and the expanded disclosures about fair value measurements. As of June 30, 2007, the Fund does not believe the adoption of SFAS No. 157 will impact the financial statement amounts; however, additional disclosures may be required about the inputs used to develop the measurements and the effect of certain of the measurements included within the Statement of Operations for the period.

17

Notes to Financial Statements (Unaudited) (continued)

7. Subsequent Events

Distributions from Shareholders

The Fund declared a dividend distribution from its net investment income which was paid on August 1, 2007, to shareholders of record on July 9, 2007, as follows:

| | | |

Dividend per share: | | | |

Class A | | $ | .0960 |

Class B | | | .0835 |

Class C | | | .0835 |

Class R | | | .1000 |

Expense Waiver and Reimbursement Policy Change

Effective September 1, 2007, the Adviser agreed to waive .05% of its management fees through April 30, 2010. The Adviser also agreed to reimburse other expenses through April 30, 2010 (excluding 12b-1 distribution and service fees, interest expense, taxes, fees incurred in acquiring and disposing of portfolio securities, and extraordinary expenses). Beginning May 1, 2010, the Adviser agreed to waive fees and reimburse expenses in order to limit total operating expenses (excluding 12b-1 distribution and services fees, interest expense, taxes, fees incurred in acquiring and disposing of portfolio securities, and extraordinary expenses) from exceeding 1.25% of the average daily net assets, subject to possible further reductions as a result of reductions in the complex-level fee component of the management fee.

18

Financial Highlights (Unaudited)

Selected data for a share outstanding throughout each period:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Class (Commencement Date) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Investment Operations | | | Less Distributions | | | | | | | | | Ratios/Supplemental Data | |

| PREFERRED SECURITIES | | | | | | | | | | | | | | | | | | | | | | | | | | | Ratios to Average

Net Assets

Before Credit/

Reimbursement | | | Ratios to Average

Net Assets After

Reimbursement(c) | | | Ratios to Average

Net Assets

After Credit/

Reimbursement(d) | | | | |

Period Ended

December 31, | | Beginning

Net

Asset

Value | | Net

Invest-

ment

Income(a) | | Net

Realized/

Unrealized

Gain

(Loss) | | | Total | | | Net

Invest-

ment

Income | | | Capital

Gains | | | Total | | | Ending

Net

Asset

Value | | | Total

Return(b) | | | Ending

Net

Assets

(000) | | Expenses | | | Net

Invest-

ment

Income | | | Expenses | | | Net

Invest-

ment

Income | | | Expenses | | | Net

Invest-

ment

Income | | | Portfolio

Turnover

Rate | |

| Class A (12/06) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2007(f) | | $ | 20.01 | | $ | .51 | | $ | (.65 | ) | | $ | (.14 | ) | | $ | (.46 | ) | | $ | — | | | $ | (.46 | ) | | $ | 19.41 | | | (.71 | )% | | $ | 272 | | 3.10 | %* | | 3.26 | %* | | 1.23 | %* | | 5.12 | %* | | 1.15 | %* | | 5.21 | %* | | 164 | % |

2006(e) | | | 20.00 | | | .03 | | | (.02 | ) | | | .01 | | | | — | | | | — | | | | — | | | | 20.01 | | | .05 | | | | 275 | | 18.18 | * | | (12.06 | )* | | 1.23 | * | | 4.88 | * | | 1.23 | * | | 4.88 | * | | — | |

| Class B (12/06) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2007(f) | | | 20.01 | | | .44 | | | (.66 | ) | | | (.22 | ) | | | (.40 | ) | | | — | | | | (.40 | ) | | | 19.39 | | | (1.12 | ) | | | 271 | | 3.85 | * | | 2.51 | * | | 1.98 | * | | 4.37 | * | | 1.90 | * | | 4.46 | * | | 164 | |

2006(e) | | | 20.00 | | | .03 | | | (.02 | ) | | | .01 | | | | — | | | | — | | | | — | | | | 20.01 | | | .05 | | | | 275 | | 18.93 | * | | (12.82 | )* | | 1.99 | * | | 4.12 | * | | 1.99 | * | | 4.12 | * | | — | |

| Class C (12/06) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2007(f) | | | 20.01 | | | .44 | | | (.66 | ) | | | (.22 | ) | | | (.40 | ) | | | — | | | | (.40 | ) | | | 19.39 | | | (1.12 | ) | | | 271 | | 3.85 | * | | 2.51 | * | | 1.98 | * | | 4.37 | * | | 1.90 | * | | 4.46 | * | | 164 | |

2006(e) | | | 20.00 | | | .03 | | | (.02 | ) | | | .01 | | | | — | | | | — | | | | — | | | | 20.01 | | | .05 | | | | 275 | | 18.93 | * | | (12.82 | )* | | 1.99 | * | | 4.12 | * | | 1.99 | * | | 4.12 | * | | — | |

| Class R (12/06) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2007(f) | | | 20.01 | | | .54 | | | (.65 | ) | | | (.11 | ) | | | (.48 | ) | | | — | | | | (.48 | ) | | | 19.42 | | | (.56 | ) | | | 4,231 | | 2.86 | * | | 3.50 | * | | .98 | * | | 5.38 | * | | .90 | * | | 5.47 | * | | 164 | |

2006(e) | | | 20.00 | | | .04 | | | (.03 | ) | | | .01 | | | | — | | | | — | | | | — | | | | 20.01 | | | .05 | | | | 4,178 | | 17.92 | * | | (11.81 | )* | | .98 | * | | 5.13 | * | | .98 | * | | 5.13 | * | | — | |

| (a) | Per share Net Investment Income is calculated using the average daily shares method. |

| (b) | Total return is the combination of changes in net asset value, reinvested dividend income at net asset value and reinvested capital gains distributions at net asset value, if any. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending net asset value. The actual reinvest price for the last dividend declared in the period may be different from the price used in the calculation. Total returns are not annualized. |

| (c) | After expense reimbursement from the Adviser, where applicable. |

| (d) | After custodian fee credit and expense reimbursement, where applicable. |

| (e) | For the period December 19, 2006 (commencement of operations) through December 31, 2006. |

| (f) | For the six months ended June 30, 2007. |

See accompanying notes to financial statements.

19

Annual Investment Management Agreement Approval Process

The Board Members are responsible for overseeing the performance of the investment adviser to the Fund and determining whether to approve the advisory arrangements. At a meeting held on November 14-16, 2006 (the “Initial Approval Meeting”), the Board Members of the Fund, including the Independent Board Members, unanimously approved the Investment Management Agreement between the Fund and Nuveen Asset Management (“NAM” or “Fund Adviser”). The Fund is sometimes referred to herein as a “New Fund.” The foregoing Investment Management Agreement with NAM is hereafter referred to as an “Original Investment Management Agreement”.

Subsequent to the Initial Approval Meeting, Nuveen Investments, Inc. (“Nuveen”), the parent company of NAM, entered into a merger agreement providing for the acquisition of Nuveen by Windy City Investments, Inc., a corporation formed by investors led by Madison Dearborn Partners, LLC (“MDP”), a private equity investment firm (the “Transaction”). The Original Investment Management Agreement, as required by Section 15 of the Investment Company Act of 1940 (the “1940 Act”) provides for its automatic termination in the event of its “assignment” (as defined in the 1940 Act). Any change in control of the adviser is deemed to be an assignment. The consummation of the Transaction will result in a change of control of NAM as well as its affiliated sub-advisers and therefore cause the automatic termination of the Original Investment Management Agreement, as required by the 1940 Act. Accordingly, in anticipation of the Transaction, at a meeting held on July 31, 2007 (the “July Meeting”), the Board Members, including the Independent Board Members, unanimously approved a new Investment Management Agreement (the “New Investment Management Agreement”) with NAM on behalf of the Fund to take effect immediately after the Transaction or shareholder approval of the new advisory contract, whichever is later. The 1940 Act also requires that the New Investment Management Agreement be approved by the Fund’s shareholders in order for it to become effective. Accordingly, to ensure continuity of advisory services, the Board Members, including the Independent Board Members, unanimously approved an Interim Investment Management Agreement to take effect upon the closing of the Transaction if shareholders have not yet approved the New Investment Management Agreement.

As NAM serves as adviser to other Nuveen funds, the Board Members already have a good understanding of the organization, operations and personnel of NAM. At a meeting held on May 21, 2007 (the “May Meeting”), many of the investment management contracts with other Nuveen funds advised by NAM (“Existing Funds”) were subject to their annual review. Although the Original Investment Management Agreement with the New Fund was recently initially approved and therefore not subject to the annual review at the May Meeting, the information provided and considerations made regarding NAM at the annual review as well as the initial approval continue to be relevant with respect to the evaluation of the New Investment Management Agreement. The Board therefore considered the foregoing as part of its deliberations of the New Investment Management Agreement. Accordingly, as indicated, the discussions immediately below outline the materials and information presented to the Board in connection with the Board’s prior annual review of NAM (to the extent applicable) and the analysis undertaken and the conclusions reached by the Board Members when determining to approve the Original Investment Management Agreement.

I. Approval of the Original Investment Management Agreement

During the course of the year, the Board received a wide variety of materials relating to the services provided by NAM and the performance of the Nuveen funds (as applicable). At each of its quarterly meetings, the Board reviewed investment performance (as applicable) and various matters relating to the operations of the Fund and other Nuveen funds, including the compliance program, shareholder services, valuation, custody, distribution and other information relating to the nature, extent and quality of services provided by NAM. Between the regularly scheduled quarterly meetings, the Board Members received information on particular matters as the need arose. In addition, as noted, because NAM already serves as adviser to other Nuveen funds, the information provided regarding NAM at the annual review at the May Meeting supplemented the information received at the initial approval.

In preparation for their consideration of NAM at the May Meeting, the Independent Board Members also received extensive materials, well in advance of the meeting, which outlined or are related to, among other things:

| • | | the nature, extent and quality of services provided by the Fund Adviser; |

| • | | the organization and business operations of the Fund Adviser, including the responsibilities of various departments and key personnel; |

| • | | each Existing Fund’s past performance as well as the Existing Fund’s performance compared to funds with similar investment objectives based on data and information provided by an independent third party and to recognized and/or customized benchmarks (as appropriate); |

| • | | the profitability of the Fund Adviser and certain industry profitability analyses for unaffiliated advisers; |

| • | | the expenses of the Fund Adviser in providing the various services; |

| • | | the advisory fees and total expense ratios of each Existing Fund, including comparisons of such fees and expenses with those of comparable, unaffiliated funds based on information and data provided by an independent third party (the “Peer Universe”) as well as compared to a subset of funds within the Peer Universe (the “Peer Group”) of the respective Existing Fund (as applicable); |

| • | | the advisory fees the Fund Adviser assesses to other types of investment products or clients; |

20

| • | | the soft dollar practices of the Fund Adviser, if any; and |

| • | | from independent legal counsel, a legal memorandum describing among other things, applicable laws, regulations and duties in reviewing and approving advisory contracts. |

At the Initial Approval Meeting, the Board Members received in advance of such meeting or at prior meetings similar materials, including the nature, extent and quality of services expected to be provided; the organization and operations of the Fund Adviser (including the responsibilities of various departments and key personnel); the expertise and background of the Fund Adviser; the profitability of Nuveen (which includes its wholly-owned advisory subsidiaries); the proposed management fees, including comparisons with peers; the expected expenses of the New Fund, including comparisons of the expense ratios with peers; and the soft dollar practices of the Fund Adviser. However, unlike Existing Funds, the New Fund did not have actual past performance at the time of approval.

At the May Meeting, NAM made a presentation to, and responded to questions from, the Board. At the May Meeting and applicable Initial Approval Meeting, the Independent Board Members met privately with their legal counsel to review the Board’s duties in reviewing advisory contracts and considering the approval or renewal of the advisory contracts (which include the sub-advisory contracts). The Independent Board Members, in consultation with independent counsel, reviewed the factors set out in judicial decisions and Securities and Exchange Commission (“SEC”) directives relating to the approval or renewal of advisory contracts. As outlined in more detail below, the Board Members considered all factors they believed relevant with respect to the New Fund, including, but not limited to, the following: (a) the nature, extent and quality of the services to be provided by the Fund Adviser; (b) the investment performance of the Fund and the Fund Adviser (as applicable); (c) the costs of the services to be provided and profits to be realized by the Fund Adviser and its affiliates; (d) the extent to which economies of scale would be realized; and (e) whether fee levels reflect those economies of scale for the benefit of the Fund’s investors. In addition, as noted, the Board Members met regularly throughout the year to oversee the Nuveen funds. In evaluating the advisory contracts, the Board Members also relied upon their knowledge of NAM, its services and the Nuveen funds resulting from their meetings and other interactions throughout the year. It is with this background that the Board Members considered each advisory contract.

A. Nature, Extent and Quality of Services

In considering the approval of the Original Investment Management Agreement, the Board Members considered the nature, extent and quality of the Fund Adviser’s services. The Board Members reviewed materials outlining, among other things, the Fund Adviser’s organization and business; the types of services that the Fund Adviser or its affiliates provide or are expected to provide to the Fund; and at the annual review, any initiatives Nuveen had taken for the applicable fund product line. As noted, the Board Members were already familiar with the organization, operations and personnel of NAM due to the Board Members’ experience in governing the other Nuveen funds and working with NAM on matters relating to the Nuveen funds.

At the May Meeting, the Board Members also recognized NAM’s investment in additional qualified personnel throughout the various groups in the organization and recommended to NAM that it continue to review staffing needs as necessary. The Board Members also recognized NAM’s investment of resources and efforts to continue to enhance and refine its investment processes.

In addition to advisory services, the Independent Board Members considered the quality of administrative and non-advisory services provided by NAM and noted that NAM and its affiliates provide the Fund with a wide variety of services and officers and other personnel as are necessary for the operations of the Fund, including:

| • | | oversight by shareholder services and other fund service providers; |

| • | | administration of Board relations; |

| • | | regulatory and portfolio compliance; and |

As the Fund operates in a highly regulated industry and given the importance of compliance, the Board Members considered, in particular, NAM’s compliance activities for the Fund and enhancements thereto. In this regard, the Board Members recognized the quality of NAM’s compliance team. The Board Members further noted NAM’s negotiations with other service providers and the corresponding reduction in certain service providers’ fees at the May Meeting.

Based on their review, the Board Members found that, overall, the nature, extent and quality of services provided (and expected to be provided) to the Fund under the Original Investment Management Agreement were satisfactory.

B. The Investment Performance of the New Fund and the Fund Adviser

The Fund did not have its own performance history at its Initial Approval Meeting. The Board Members, however, were familiar with NAM’s performance record on other Existing Funds.

21

Annual Investment Management Agreement Approval Process (continued)

C. Fees, Expenses and Profitability

1. Fees and Expenses

With respect to the New Fund, at the Initial Approval Meeting, the Board considered the New Fund’s proposed management fee structure, its sub-advisory fee arrangements and expected expense ratios in absolute terms as well as compared with the fees and expense ratios of comparable, unaffiliated funds and comparable, affiliated funds (if any). The Board Members also considered the applicable fund-level breakpoint schedule and complex-wide breakpoint schedule. Based on their review of the overall fee arrangements of the New Fund, the Board Members determined that the advisory fees and expected expenses of the New Fund were reasonable.

2. Comparisons with the Fees of Other Clients