UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-021979

Nuveen Investment Trust V

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Kevin J. McCarthy

Nuveen Investments

333 West Wacker Drive Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: December 31

Date of reporting period: June 30, 2009

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policy making roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss.3507.

Item 1. Reports to Stockholders.

Mutual Funds

Nuveen Taxable Fixed Income Funds

For investors seeking a high level of current income and total return.

Semi-Annual Report

June 30, 2009

|

| Nuveen Preferred Securities Fund |

LIFE IS COMPLEX.

Nuveen makes things e-simple.

It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Investments Fund information is ready. No more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish.

Free e-Reports right to your e-mail!

www.investordelivery.com

If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account.

OR

www.nuveen.com/accountaccess

If you receive your Nuveen Fund dividends and statements directly from Nuveen.

| | | | | | |

| Must be preceded by or accompanied by a prospectus. | | NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

Chairman’s

Letter to Shareholders

Dear Shareholder,

The problems in the U.S. financial system and the slowdown in global economic activity continue to create a very difficult environment for the U.S. economy. The administration, the Federal Reserve System and Congress have initiated a variety of programs directed at restoring liquidity to the financial markets, providing financial support for critical financial institutions and stimulating economic activity. There are encouraging signs that these initiatives are beginning to have a constructive impact. It is not possible to predict whether the actions taken to date will be sufficient to restore more normal conditions in the financial markets or enable the economy to stabilize and set a course toward recovery. However, the speed and scope of the government’s actions are very encouraging and more importantly, reflect a commitment to act decisively to meet the economic challenges we face.

The performance information in the attached report reflects the impact of many forces at work in the equity and fixed-income markets. The comments by the portfolio manager describe the strategies being used to pursue your Fund’s long-term investment goals. Parts of the financial markets continue to experience serious dislocations and thorough research and strong investment disciplines have never been more important in identifying risks and opportunities. I hope you will read this information carefully.

Your Board is particularly sensitive to our shareholders’ concerns in these uncertain times. We believe that frequent and thorough communication is essential in this regard and encourage you to visit the Nuveen website: www.nuveen.com, for recent developments in all Nuveen funds. We also encourage you to communicate with your financial consultant for answers to your questions and to seek advice on your long-term investment strategy in the current market environment.

On behalf of myself and the other members of your Fund’s Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

Robert P. Bremner

Chairman of the Nuveen Fund Board

August 24, 2009

Portfolio Manager’s Comments

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio manager as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Fund disclaims any obligation to update publicly or revise any forward-looking statements or views expressed herein.

The Nuveen Preferred Securities Fund features management by Nuveen Asset Management (NAM), an affiliate of Nuveen Investments. Douglas Baker, CFA, has served as the Fund’s portfolio manager since its inception in 2006, and has more than ten years of investment industry experience. Here Doug discusses the Fund’s performance and investment strategy for the six-month period ended June 30, 2009.

How did the Fund perform during the six months ended June 30, 2009?

The table on page four provides performance information for the Fund for the six-month period ended June 30, 2009. The table also compares the Fund’s performance to special and general market indexes. A more detailed discussion of the Fund’s relative performance is provided later in this report.

What strategies were used to manage the Fund during the reporting period?

The Fund continued to witness meaningful net investor inflows during the first six months of 2009. The second quarter was especially busy, with assets under management growing by approximately 132%. We continued to deploy these cash inflows into credits favored by our research team, as well as toward efforts to modify or adjust allocations across trust preferred, enhanced trust preferred, and perpetual preferred security structures. For example, starting in the first quarter of 2009 and continuing through the second quarter, the Fund increasingly allocated assets to perpetual preferred security structures, which tend to be lower in a company’s capital structure, for those names in which we held the strongest conviction. It was our opinion, these perpetual structures offered an attractive risk/return profile for appropriate credits.

As of June 30, 2009, about 30% of the Fund’s assets were invested in perpetual maturity, non-cumulative distribution structures. This allocation was not broad-based across all issuers represented in the Fund; rather, with the input from our research team, we initiated relative overweights to non-cumulative structures for those credits that we deemed to have a negligible likelihood of deferring distributions. In doing so, the Fund was able to capture the larger yields associated with non-cumulative structures. In most instances, these non-cumulative structures also paid qualified dividend income (QDI) distributions currently taxed at a maximum rate of 15%.

During the period, individual investor buying and selling generated price volatility for exchange-listed $25 par preferred securities – especially when compared to the $1000 par preferred structures generally traded over-the-counter by institutions. We sought to take advantage of the resulting price dislocations by toggling between $25 par and $1000 par securities as opportunities presented themselves. As of period end, the Fund

was allocated roughly 50% / 50% between $25 par and $1000 par structures, while the allocation was closer to 70% / 30% at the end of the first quarter. We also continued to build a relative overweight in financial services holdings, while decreasing our relative exposure to utilities. We did not add to our taxable municipal sleeve, as we believed that preferred / hybrid securities offered better risk/ return profiles.

We believe supply and demand technical factors still benefit the preferred / hybrid asset class. Although there were a handful of new issue deals during the second quarter of 2009, we continue to believe that meaningful new issue flow will be negligible for several more quarters. While preferred and hybrid securities rallied during the second quarter, the spread levels existing at period end meant that the cost of issuing new securities was still somewhat prohibitive. In addition, the exchanges and tenders of preferred and hybrid securities discussed earlier materially reduced the amount of securities outstanding, likely contributing to scarcity value for the asset class.

During the six-month period ended June 30, 2009, the Fund (Class A Shares at NAV) returned 15.46%, outpacing the comparative indexes and benchmarks shown in this report. Driving this outperformance was the Fund’s increasing tactical allocation to non-cumulative security structures. As discussed previously, these securities had underperformed materially in previous periods due to headline risk surrounding the financial services sector, and subsequent fears concerning potential preferred / hybrid distribution deferrals. During the second quarter, investors received meaningful clarity regarding several of the most prominent issues vexing the asset class. As a result, spreads compressed disproportionately more for the perpetual maturity, non-cumulative structures. Also contributing to the Fund’s relative outperformance was the toggling between the $25 par and $1000 par structures. The six months ended June 30, 2009, contained some fairly volatile periods. As individual and institutional investors responded differently to rapidly changing market conditions, the Fund was able to capture significant relative value opportunities between the two segments.

| * | Six-month returns are cumulative; one-year and since inception returns are annualized. |

| 1 | The Merrill Lynch Hybrid Securities Index is an unmanaged index consisting of a set of investment grade exchange-traded preferred stocks with outstanding market values of at least $50 million that are covered by Merrill Lynch Fixed Income Research. The index includes certain publicly issued, $25- and $1000-par securities with at least one year to maturity. The since inception data for the index represents returns for the period 12/31/06 – 12/31/08, as returns for the index are calculated on a calendar month basis. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 2 | The Market Benchmark Index is comprised of a 60% weighting in the Merrill Lynch Hybrid Securities Index, a 35% weighting in the Barclays Capital USD Capital Securities Index and a 5% weighting in the Merrill Lynch REIT Preferred Stock Index. The Merrill Lynch Hybrid Securities Index is an unmanaged index consisting of a set of investment grade exchange-traded preferred stocks with outstanding market values of at least $50 million that are covered by Merrill Lynch Fixed Income Research. The Barclays Capital USD Capital Securities Index contains securities generally viewed as hybrid fixed income securities that either receive regulatory capital treatment or a degree of “equity credit” from the rating agencies. This generally includes Tier 2/Lower Tier 2 bonds, perpetual step-up debt, step-up preferred securities, and term preferred securities. The Merrill Lynch REIT Preferred Stock Index is an unmanaged index of investment grade REIT preferred shares with a deal size in excess of $100 million, weighted by capitalization and considered representative of investment grade preferred real estate stock performance. The since inception data for the index represents returns for the period 12/31/06 – 12/31/08, as returns for the index are calculated on a calendar month basis. The returns assume reinvestment of dividends and do not reflect any applicable sales charges. You cannot invest directly in an index. |

| 3 | The S&P 500 Index is an unmanaged index generally considered representative of the U.S. stock market. The index returns assume reinvestment of dividends, but do not reflect any applicable sales charges. You cannot invest directly in an index. |

Class A Shares – Average Annual Total Returns*

For periods ended 6/30/09

| | | | | | |

| | | 6-Month | | 1-Year | | Since

inception

(12/19/06) |

Nuveen Preferred Securities Fund | | | | | | |

A Shares at NAV | | 15.46% | | -12.08% | | -9.25% |

A Shares at Offer | | 9.94% | | -16.27% | | -10.99% |

Merrill Lynch Hybrid Securities Index1 | | -0.06% | | -8.09% | | -8.83% |

Market Benchmark Index2 | | 4.05% | | -6.73% | | -6.65% |

S&P 500 Index3 | | 3.16% | | -26.21% | | -13.91% |

Returns quoted represent past performance which is no guarantee of future results. Returns less than one year are cumulative. Current performance may be higher or lower than the performance shown. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Class A Shares have a 4.75% maximum sales charge. Returns at NAV would be lower if sales charges were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. Returns reflect a voluntary expense limitation by the Fund’s investment adviser that may be modified or discontinued at any time without notice. For the most recent month-end performance, visit www.nuveen.com or call (800) 257-8787.

Please see the Fund’s Spotlight Page later in this report for more complete performance data and expense ratios.

Fund Spotlight as of 6/30/09 Nuveen Preferred Securities Fund

| | | | | | |

| Quick Facts | | | | | | |

| | | A Shares | | C Shares | | I Shares1 |

Fund Symbols | | NPSAX | | NPSCX | | NPSRX |

NAV | | $12.83 | | $12.84 | | $12.83 |

Latest Monthly Dividend2 | | $0.0970 | | $0.0900 | | $0.0995 |

Inception Date | | 12/19/06 | | 12/19/06 | | 12/19/06 |

Returns quoted represent past performance which is no guarantee of future results. Investment returns and principal value will fluctuate so that when shares are redeemed, they may be worth more or less than their original cost. Current performance may be higher or lower than the performance shown. Returns without sales charges would be lower if the sales charge were included. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of shares. For the most recent month-end performance visit www.nuveen.com or call (800) 257-8787.

Returns reflect differences in sales charges and expenses, which are primarily differences in distribution and service fees. Fund returns assume reinvestment of dividends and capital gains. Class A Shares have a 4.75% maximum sales charge. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (CDSC), also known as a back-end sales charge, if redeemed within twelve months of purchase. Class C Shares have a 1% CDSC for redemptions within less than one year, which is not reflected in the one-year total return. Class I Shares have no sales charge and may be purchased under limited circumstances or by specified classes of investors. Returns may reflect an expense limitation by the Fund’s investment adviser.

| | | | |

| Average Annual Total Returns as of 6/30/09 |

| | |

| A Shares | | NAV | | Offer |

1-Year | | -12.08% | | -16.27% |

Since Inception | | -9.25% | | -10.99% |

| | |

| C Shares | | NAV | | |

1-Year | | -12.65% | | |

Since Inception | | -9.91% | | |

| | |

| I Shares | | NAV | | |

1-Year | | -11.82% | | |

Since Inception | | -9.01% | | |

| Yields |

| | |

| A Shares | | NAV | | Offer |

Dividend yield5 | | 9.07% | | 8.64% |

30-day yield5 | | 9.12% | | — |

SEC 30-day yield5,6 | | — | | 8.68% |

| | |

| C Shares | | NAV | | |

Dividend yield5 | | 8.41% | | |

30-day yield5 | | 8.35% | | |

| | |

| I Shares | | NAV | | |

Dividend yield5 | | 9.31% | | |

SEC 30-day yield5 | | 9.37% | | |

| | |

| Top Five Issuers3: |

Wells Fargo & Company | | 10.5% |

JP Morgan Chase & Company | | 9.9% |

| Bank of America Corporation | | 7.0% |

| MetLife Inc. | | 5.4% |

| Morgan Stanley | | 4.4% |

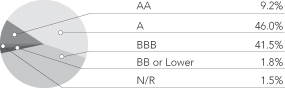

Portfolio Credit Quality3

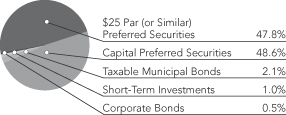

Portfolio Allocation4

| | |

| Portfolio Statistics |

| Net Assets ($000) | | $165,203 |

| Average Effective Maturity (Years) | | 43.01 |

| Average Duration | | 8.07 |

| Number of Positions/Holdings | | 173 |

| | | |

| | | | | | |

| Expense Ratios | | | | | | |

| Share Class | | Gross

Expense

Ratios | | Net

Expense

Ratios | | As of

Date |

| Class A | | 1.64% | | 0.94% | | 12/31/08 |

| Class C | | 2.32% | | 1.69% | | 12/31/08 |

| Class I | | 1.26% | | 0.69% | | 12/31/08 |

The expense ratios shown factor in Total Annual Fund Operating Expenses including management fees and other fees and expenses. The Net Expense Ratios reflect a contractual commitment by the Fund’s investment adviser to waive fees and reimburse expenses through April 30, 2010. The Net Expense Ratios also reflect a custodian fee credit whereby certain fees and expenses are reduced by credits earned on the Fund’s cash on deposit with the bank. There is no guarantee that the Fund will earn such credits in the future. Absent the waiver, reimbursement and custodian fee credit, the Net Expense Ratios would be higher and total returns would be less.

| 1 | Effective May 1, 2008, Class R Shares were renamed Class I Shares. See the Fund’s prospectus for more information. |

| 3 | As a percentage of total investments (excluding short-term investments and investments in derivatives) as of June 30, 2009. Holdings are subject to change. |

| 4 | As a percentage of total investments (excluding investments in derivatives) as of June 30, 2009. Holdings are subject to change. |

| 5 | Dividend yield is the most recent dividend per share (annualized) divided by the appropriate price per share. The SEC 30-Day Yield is computed under an SEC standardized formula and is based on the maximum offer price per share. The 30-Day Yield is computed under the same formula but is based on the Net Asset Value (NAV) per share. The Dividend yield may differ from the SEC 30-Day yield because the Fund may be paying out more or less than it is earning and it may not include the effect of amortization of bond premium. |

| 6 | The SEC 30-Day Yield on A Shares at NAV applies only to A Shares purchased at no-load pursuant to the Fund’s policy permitting waiver of the A Share load in certain specified circumstances. |

Fund Spotlight as of 6/30/09 Nuveen Preferred Securities Fund

| | |

| Industries1 | | |

Commercial Banks | | 40.3% |

Diversified Financial Services | | 23.5% |

Insurance | | 14.8% |

Capital Markets | | 14.1% |

Short-Term Investments | | 1.0% |

Other | | 6.3% |

| 1 | As a percentage of total investments (excluding investments in derivatives) as of June 30, 2009. Holdings are subject to change. |

Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including front and back end sales charges (loads) or redemption fees, where applicable; and (2) ongoing costs, including management fees; distribution and service (12b-1) fees, where applicable; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example below is based on an investment of $1,000 invested at the beginning of the period and held for the period.

The information under “Actual Performance,” together with the amount you invested, allows you to estimate actual expenses incurred over the reporting period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60) and multiply the result by the cost shown for your share class, in the row entitled “Expenses Incurred During Period” to estimate the expenses incurred on your account during this period.

The information under “Hypothetical Performance,” provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you incurred for the period. You may use this information to compare the ongoing costs of investing in the Fund and other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as front and back end sales charges (loads) or redemption fees, where applicable. Therefore, the hypothetical information is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds or share classes. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | Hypothetical Performance |

| | | Actual Performance | | | | (5% annualized return before expenses) |

| | | A Shares | | C Shares | | I Shares | | | | A Shares | | C Shares | | I Shares |

| Beginning Account Value (1/01/09) | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 | | | | $ | 1,000.00 | | $ | 1,000.00 | | $ | 1,000.00 |

| Ending Account Value (6/30/09) | | $ | 1,154.60 | | $ | 1,149.70 | | $ | 1,156.20 | | | | $ | 1,020.08 | | $ | 1,016.36 | | $ | 1,021.32 |

| Expenses Incurred During Period | | $ | 5.08 | | $ | 9.06 | | $ | 3.74 | | | | $ | 4.76 | | $ | 8.50 | | $ | 3.51 |

For each class of the Fund, expenses are equal to the Fund’s annualized net expense ratio of 0.95%, 1.70% and 0.70% for Classes A, C and I, respectively, multiplied by the average account value over the period, multiplied by 181/365 (to reflect the one-half year period).

Portfolio of Investments (Unaudited)

Nuveen Preferred Securities Fund

June 30, 2009

| | | | | | | | | |

| Shares | | Description (1) | | Coupon | | Ratings (2) | | Value |

| | | | | | | | | |

| | $25 PAR (OR SIMILAR) PREFERRED SECURITIES – 48.0% | | | | | | | |

| | | | |

| | Capital Markets – 9.3% | | | | | | | |

| | | | |

| 40,000 | | Ameriprise Financial, Inc. | | 7.750% | | A | | $ | 864,000 |

| | | | |

| 11,862 | | BNY Capital Trust IV, Series E | | 6.875% | | Aa3 | | | 296,550 |

| | | | |

| 27,520 | | BNY Capital Trust V, Series F | | 5.950% | | Aa3 | | | 618,099 |

| | | | |

| 15,128 | | Credit Suisse | | 7.900% | | Aa3 | | | 339,472 |

| | | | |

| 14,600 | | Deutsche Bank Capital Funding Trust I | | 7.350% | | Aa3 | | | 280,904 |

| | | | |

| 47,664 | | Deutsche Bank Capital Funding Trust II | | 6.550% | | Aa3 | | | 856,999 |

| | | | |

| 108,040 | | Deutsche Bank Capital Funding Trust V | | 8.050% | | Aa3 | | | 2,240,848 |

| | | | |

| 4,100 | | Deutsche Bank Capital Funding Trust VIII | | 6.375% | | Aa3 | | | 75,358 |

| | | | |

| 85,300 | | Deutsche Bank Contingent Capital Trust III | | 7.600% | | Aa3 | | | 1,683,822 |

| | | | |

| 5,000 | | Goldman Sachs Group Inc., Series D | | 4.000% | | A3 | | | 80,250 |

| | | | |

| 42,179 | | Goldman Sachs Group Inc. | | 6.200% | | A3 | | | 959,572 |

| | | | |

| 46,801 | | Morgan Stanley Capital Trust III | | 6.250% | | A3 | | | 898,579 |

| | | | |

| 1,900 | | Morgan Stanley Capital Trust V | | 5.750% | | A3 | | | 34,295 |

| | | | |

| 97,458 | | Morgan Stanley Capital Trust VI | | 6.600% | | A3 | | | 1,985,219 |

| | | | |

| 182,406 | | Morgan Stanley Capital Trust VII | | 6.600% | | A3 | | | 3,582,454 |

| | | | |

| 33,515 | | Morgan Stanley Capital Trust VIII | | 6.450% | | A3 | | | 649,856 |

| | Total Capital Markets | | | | | | | 15,446,277 |

| | Commercial Banks – 19.1% | | | | | | | |

| | | | |

| 46,000 | | ABN AMRO Capital Fund Trust V | | 5.900% | | A2 | | | 535,900 |

| | | | |

| 185,632 | | ABN AMRO Capital Fund Trust VII | | 6.080% | | A2 | | | 2,125,486 |

| | | | |

| 52,600 | | Banco Santander Finance | | 6.800% | | A2 | | | 1,017,810 |

| | | | |

| 66,600 | | Banco Santander Finance | | 6.500% | | A2 | | | 1,198,800 |

| | | | |

| 21,500 | | Banco Santander Finance | | 4.000% | | A2 | | | 241,875 |

| | | | |

| 125,700 | | Barclays Bank PLC | | 8.125% | | BBB+ | | | 2,595,705 |

| | | | |

| 20,000 | | Barclays Bank PLC | | 7.750% | | BBB+ | | | 392,800 |

| | | | |

| 40,141 | | BB&T Capital Trust V | | 8.950% | | A2 | | | 1,021,588 |

| | | | |

| 21,650 | | Fifth Third Capital Trust VI | | 7.250% | | Baa2 | | | 347,916 |

| | | | |

| 113,478 | | Fifth Third Capital Trust VII | | 8.875% | | Baa2 | | | 2,224,169 |

| | | | |

| 31,512 | | HSBC Finance Corporation | | 6.875% | | A | | | 674,042 |

| | | | |

| 500 | | HSBC Finance Corporation | | 6.000% | | A | | | 9,555 |

| | | | |

| 48,948 | | HSBC Holdings PLC | | 8.125% | | A– | | | 1,164,473 |

| | | | |

| 6,899 | | KeyCorp Capital Trust V | | 5.875% | | Baa2 | | | 117,214 |

| | | | |

| 146,936 | | KeyCorp Capital Trust X | | 8.000% | | Baa2 | | | 2,737,418 |

| | | | |

| 3,187 | | KeyCorp Capital VIII | | 7.000% | | Baa2 | | | 54,816 |

| | | | |

| 19,462 | | M&T Capital Trust IV | | 8.500% | | Baa1 | | | 481,685 |

| | | | |

| 15,600 | | Merrill Lynch Capital Trust II | | 6.450% | | Baa3 | | | 249,912 |

| | | | |

| 10,000 | | Merrill Lynch Capital Trust III | | 7.375% | | Baa3 | | | 182,000 |

| | | | |

| 26,985 | | Merrill Lynch Capital Trust III | | 7.000% | | Baa3 | | | 451,189 |

| | | | |

| 4,400 | | National City Capital Trust II | | 6.625% | | Baa1 | | | 82,632 |

| | | | |

| 23,100 | | National City Capital Trust IV | | 8.000% | | Baa1 | | | 512,820 |

| | | | |

| 71,832 | | PNC Financial Services, Series F | | 9.875% | | Baa2 | | | 1,810,166 |

| | | | |

| 16,350 | | Regions Financing Trust III | | 8.875% | | BB+ | | | 325,038 |

| | | | |

| 25,784 | | SunTrust Capital Trust IX | | 7.875% | | Baa2 | | | 547,910 |

| | | | |

| 75,867 | | U.S. Bancorp. | | 7.875% | | A2 | | | 1,885,295 |

Portfolio of Investments (Unaudited)

Nuveen Preferred Securities Fund (continued)

June 30, 2009

| | | | | | | | | |

| Shares | | Description (1) | | Coupon | | Ratings (2) | | Value |

| | | | | | | | | |

| | Commercial Banks (continued) | | | | | | | |

| | | | |

| 22,481 | | USB Capital Trust XI | | 6.600% | | A1 | | $ | 501,326 |

| | | | |

| 23,883 | | USB Capital XII | | 6.300% | | A1 | | | 502,498 |

| | | | |

| 6,100 | | Wachovia Capital Trust IX | | 6.375% | | A3 | | | 115,412 |

| | | | |

| 37,475 | | Wachovia Capital Trust X | | 7.850% | | A3 | | | 837,566 |

| | | | |

| 205,194 | | Wells Fargo & Company | | 8.000% | | A– | | | 4,575,826 |

| | | | |

| 15,000 | | Wells Fargo Capital Trust XII | | 7.875% | | A3 | | | 358,800 |

| | | | |

| 70,180 | | Wells Fargo Capital Trust XIV | | 8.625% | | A3 | | | 1,775,554 |

| | Total Commercial Banks | | | | | | | 31,655,196 |

| | Consumer Finance – 0.0% | | | | | | | |

| | | | |

| 5,000 | | HSBC Finance Corporation | | 6.360% | | Baa2 | | | 79,500 |

| | Diversified Financial Services – 15.1% | | | | | | | |

| | | | |

| 7,000 | | BAC Capital Trust I | | 7.000% | | Baa3 | | | 132,440 |

| | | | |

| 10,000 | | BAC Capital Trust II | | 7.000% | | Baa3 | | | 191,000 |

| | | | |

| 19,850 | | BAC Capital Trust VIII | | 6.000% | | Baa3 | | | 330,503 |

| | | | |

| 2,829 | | BAC Capital Trust X | | 6.250% | | Baa3 | | | 49,819 |

| | | | |

| 27,172 | | BAC Capital Trust XII | | 6.875% | | Baa3 | | | 496,976 |

| | | | |

| 20,645 | | Bank One Capital Trust VI | | 7.200% | | A1 | | | 474,835 |

| | | | |

| 31,388 | | Bear Stearns Capital Trust III | | 7.800% | | A1 | | | 742,326 |

| | | | |

| 22,400 | | Citigroup Capital Trust IX | | 6.000% | | A1 | | | 303,744 |

| | | | |

| 18,500 | | Citigroup Capital Trust VII | | 7.125% | | Baa3 | | | 295,075 |

| | | | |

| 48,300 | | Citigroup Capital Trust VIII | | 6.950% | | Baa3 | | | 748,167 |

| | | | |

| 26,595 | | Citigroup Capital Trust XI | | 6.000% | | Baa3 | | | 362,224 |

| | | | |

| 23,400 | | Citigroup Capital X | | 6.100% | | Baa3 | | | 328,068 |

| | | | |

| 56,600 | | Citigroup Capital XV | | 6.500% | | Baa3 | | | 1,019,366 |

| | | | |

| 100,200 | | Citigroup Capital XVI | | 6.450% | | Baa3 | | | 1,699,392 |

| | | | |

| 51,400 | | Citigroup Capital XVII | | 6.350% | | Baa3 | | | 822,400 |

| | | | |

| 11,600 | | Citigroup Capital XX | | 7.875% | | Baa3 | | | 217,616 |

| | | | |

| 185,767 | | Countrywide Capital IV Trust | | 6.750% | | Baa3 | | | 3,055,867 |

| | | | |

| 376,300 | | Countrywide Capital Trust III | | 7.000% | | Baa3 | | | 6,419,678 |

| | | | |

| 28,401 | | Fleet Capital Trust VIII | | 7.200% | | Baa3 | | | 518,318 |

| | | | |

| 2,300 | | General Electric Capital Corporation | | 6.625% | | AA+ | | | 54,694 |

| | | | |

| 500 | | General Electric Capital Corporation | | 6.000% | | AA+ | | | 10,865 |

| | | | |

| 106,551 | | ING Groep N.V. | | 8.500% | | BBB | | | 2,072,417 |

| | | | |

| 111,725 | | JP Morgan Chase & Company | | 8.625% | | A2 | | | 2,842,284 |

| | | | |

| 38,100 | | JP Morgan Chase Capital Trust XXVI | | 8.000% | | A1 | | | 955,929 |

| | | | |

| 5,060 | | JP Morgan Capital XXIV | | 6.875% | | A1 | | | 115,368 |

| | | | |

| 14,905 | | JP Morgan Chase Capital Trust X | | 7.000% | | A1 | | | 359,211 |

| | | | |

| 3,573 | | JP Morgan Chase Capital Trust XI | | 5.875% | | A1 | | | 73,389 |

| | | | |

| 1,000 | | MBNA Capital E | | 8.100% | | Baa3 | | | 19,750 |

| | | | |

| 12,300 | | MBNA Corporation, Capital Trust D | | 8.125% | | Baa3 | | | 240,096 |

| | Total Diversified Financial Services | | | | | | | 24,951,817 |

| | Electric Utilities – 1.0% | | | | | | | |

| | | | |

| 11,500 | | American Electric Power | | 8.750% | | Baa3 | | | 307,165 |

| | | | |

| 7,400 | | DTE Energy Trust I | | 7.800% | | Baa3 | | | 184,408 |

| | | | |

| 1,000 | | DTE Energy Trust II | | 7.500% | | Baa3 | | | 24,800 |

| | | | | | | | | | |

| Shares | | Description (1) | | Coupon | | Ratings (2) | | Value |

| | | | | | | | | | |

| | | Electric Utilities (continued) | | | | | | | |

| | | | |

| | 21,200 | | FPL Group Capital Inc. | | 7.450% | | A3 | | $ | 550,776 |

| | | | |

| | 9,700 | | FPL Group Capital Inc. | | 6.600% | | A3 | | | 241,530 |

| | | | |

| | 11,534 | | National Rural Utilities Cooperative Finance Corporation | | 6.750% | | A3 | | | 273,471 |

| | | Total Electric Utilities | | | | | | | 1,582,150 |

| | | Insurance – 1.1% | | | | | | | |

| | | | |

| | 2,400 | | Aegon N.V. | | 6.500% | | Baa1 | | | 35,760 |

| | | | |

| | 11,600 | | Aegon N.V. | | 7.250% | | Baa1 | | | 197,200 |

| | | | |

| | 10,000 | | Allianz SE | | 8.375% | | A+ | | | 224,500 |

| | | | |

| | 20,300 | | Financial Security Assurance Holdings | | 6.250% | | A+ | | | 294,350 |

| | | | |

| | 20,393 | | Lincoln National Capital VI, Series F | | 6.750% | | Baa3 | | | 362,995 |

| | | | |

| | 2,100 | | MetLife Inc., Series B | | 6.500% | | Baa1 | | | 43,155 |

| | | | |

| | 1,200 | | PLC Capital Trust III | | 7.500% | | BBB | | | 22,008 |

| | | | |

| | 2,000 | | PLC Capital Trust IV | | 7.250% | | BBB | | | 39,340 |

| | | | |

| | 13,200 | | Protective Life Corporation | | 7.250% | | BBB | | | 249,348 |

| | | | |

| | 11,949 | | Prudential Financial Inc. | | 9.000% | | BBB+ | | | 281,757 |

| | | Total Insurance | | | | | | | 1,750,413 |

| | | Multi-Utilities – 0.2% | | | | | | | |

| | | | |

| | 13,300 | | Xcel Energy Inc. | | 7.600% | | Baa2 | | | 336,889 |

| | | Real Estate Investment Trust – 1.9% | | | | | | | |

| | | | |

| | 17,996 | | Duke Realty Corpoation, Series O | | 8.375% | | Baa3 | | | 316,010 |

| | | | |

| | 15,390 | | Harris Preferred Capital Corporation, Series A | | 7.375% | | A1 | | | 329,808 |

| | | | |

| | 10,300 | | Kimco Realty Corporation, Series G | | 7.750% | | Baa2 | | | 212,695 |

| | | | |

| | 5,900 | | Prologis Trust, Series G | | 6.750% | | Baa3 | | | 96,760 |

| | | | |

| | 5,000 | | PS Business Parks, Inc. | | 7.000% | | Baa3 | | | 92,250 |

| | | | |

| | 48,080 | | Public Storage, Inc., Series K | | 7.250% | | Baa1 | | | 1,062,568 |

| | | | |

| | 41,864 | | Public Storage, Inc., Series M | | 6.625% | | Baa1 | | | 836,024 |

| | | | |

| | 8,930 | | Vornado Realty Trust, Series H | | 6.750% | | Baa3 | | | 164,580 |

| | | Total Real Estate Investment Trust | | | | | | | 3,110,695 |

| | | Thrifts & Mortgage Finance – 0.2% | | | | | | | |

| | | | |

| | 12,900 | | Sovereign Capital Trust V | | 7.750% | | BBB+ | | | 274,126 |

| | | U.S. Agency – 0.1% | | | | | | | |

| | | | |

| | 7,000 | | Federal Home Loan Mortgage Corporation (3) | | 6.420% | | Ca | | | 11,200 |

| | | | |

| | 45,000 | | Federal Home Loan Mortgage Corporation (3) | | 8.375% | | Ca | | | 54,900 |

| | | | |

| | 45,000 | | Federal National Mortgage Association (3) | | 8.250% | | Ca | | | 57,600 |

| | | | |

| | 60,000 | | Federal National Mortgage Association (3) | | 8.250% | | Ca | | | 80,400 |

| | | Total U.S. Agency | | | | | | | 204,100 |

| | | Total $25 Par (or similar) Preferred Securities (cost $70,089,350) | | | | | | | 79,391,163 |

| | | | |

Principal

Amount (000) | | Description (1) | | Optional Call

Provisions (4) | | Ratings (2) | | Value |

| | | | | | | | | | |

| | | TAXABLE MUNICIPAL BONDS – 2.2% | | | | | | | |

| | | | |

| | | California – 0.4% | | | | | | | |

| | | | |

| $ | 485 | | California Municipal Finance Authority, Educational Facilities Revenue Bonds, OCEAA Project, Series 2008B, 11.000%, 10/01/14 | | No Opt. Call | | N/R | | $ | 472,351 |

| | | | |

| | 200 | | California Statewide Community Development Authority, Lancer Educational Student Housing Revenue Bonds, California Baptist University, Series 2007, 9.125%, 6/01/13, 144A | | No Opt. Call | | N/R | | | 195,972 |

| | 685 | | Total California | | | | | | | 668,323 |

Portfolio of Investments (Unaudited)

Nuveen Preferred Securities Fund (continued)

June 30, 2009

| | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Optional Call

Provisions (4) | | Ratings (2) | | Value |

| | | | | | | | | | |

| | | Florida – 0.4% | | | | | | | |

| | | | |

| $ | 200 | | Northern Palm Beach County Improvement District, Florida, Water Control and Improvement Bonds, Development Unit 46, Series 2007B, 8.250%, 8/01/21 | | 8/14 at 100.00 | | N/R | | $ | 181,564 |

| | | | |

| | 500 | | Seminole Tribe of Florida, Special Obligation Bonds, Series 2007B,

7.804%, 10/01/20, 144A | | No Opt. Call | | BBB | | | 421,880 |

| | 700 | | Total Florida | | | | | | | 603,444 |

| | | Idaho – 0.1% | | | | | | | |

| | | | |

| | 125 | | Idaho Housing and Finance Association NonProfit Facilities Revenue Bonds, Liberty Charter School, Inc, Series 2008B, 7.500%, 6/01/12 | | No Opt. Call | | BBB | | | 122,573 |

| | | Louisiana – 0.3% | | | | | | | |

| | | | |

| | 195 | | Carter Plantation Land Louisiana, Revenue Bonds, 9.000%, 7/01/17, 144A (5) | | 10/09 at 100.00 | | N/R | | | 109,627 |

| | | | |

| | 440 | | Louisiana Local Government Environmental Facilities and Community Development Authority, Federal Taxable Solid Waste Revenue Bonds, CWI White Oaks Landfill, Series 2007B, 9.750%, 3/01/22 | | 3/10 at 102.00 | | N/R | | | 344,247 |

| | 635 | | Total Louisiana | | | | | | | 453,874 |

| | | New York – 0.2% | | | | | | | |

| | | | |

| | 260 | | New York City Industrial Development Agency, New York, Civic Facility Revenue Bonds, Special Needs Facilities Pooled Program, Series 2008A-2, 7.500%, 7/01/09 | | No Opt. Call | | N/R | | | 260,000 |

| | | Texas – 0.4% | | | | | | | |

| | | | |

| | 600 | | Danbury Higher Education Authority Inc., Texas, Golden Rule Charter School Revenue Bonds, Series 2008B, 10.000%, 8/15/18 | | No Opt. Call | | BB+ | | | 554,064 |

| | | | |

| | 175 | | La Vernia Education Financing Corporation, Texas, Charter School Revenue Bonds, Riverwalk Education Foundation, Series 2007B, 8.750%, 8/15/12 | | 8/11 at 100.00 | | N/R | | | 173,334 |

| | 775 | | Total Texas | | | | | | | 727,398 |

| | | Washington – 0.4% | | | | | | | |

| | | | |

| | 745 | | Washington State Economic Development Finance Authority, Revenue Bonds, Coeur D’Alene Fiber Fuels Inc., Series 2007H, 10.000%, 12/01/11 | | No Opt. Call | | N/R | | | 649,402 |

| $ | 3,925 | | Total Taxable Municipal Bonds (cost $3,922,271) | | | | | | | 3,485,014 |

| | | | | | | | | | | | | | |

| | | | | | |

Principal

Amount (000) | | Description (1) | | | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | | | |

| | | CORPORATE BONDS – 0.5% | | | | | | | | | | | |

| | | | | | |

| | | Insurance – 0.5% | | | | | | | | | | | |

| | | | | | |

| $ | 700 | | QBE Insurance Group Limited, 144A | | | | 9.750% | | 3/14/14 | | A | | $ | 760,213 |

| $ | 700 | | Total Corporate Bonds (cost $579,518) | | | | | | | | | | | 760,213 |

| | | | | | |

Principal

Amount (000)/

Shares | | Description (1) | | | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | | | | |

| | | CAPITAL PREFERRED SECURITIES – 48.7% | | | | | | | | | | | |

| | | | | | |

| | | Capital Markets – 4.8% | | | | | | | | | | | |

| | | | | | |

| | 500 | | Credit Suisse | | | | 5.860% | | 11/15/57 | | Aa3 | | $ | 325,457 |

| | | | | | |

| | 1,000 | | Goldman Sachs Capital II | | | | 5.793% | | 12/01/57 | | A3 | | | 609,810 |

| | | | | | |

| | 500 | | Goldman Sachs Group, Inc. | | | | 6.345% | | 2/15/34 | | A2 | | | 404,494 |

| | | | | | |

| | 3,520 | | Mellon Capital Trust IV | | | | 6.244% | | 6/20/49 | | A1 | | | 2,359,836 |

| | | | | | |

| | 500 | | MUFG Capital Finance | | | | 6.346% | | 7/25/16 | | A2 | | | 438,302 |

| | | | | | |

| | 1,000 | | State Street Capital Trust | | | | 8.250% | | 9/15/58 | | A3 | | | 845,340 |

| | | | | | |

| | 400 | | UBS Capital IX | | | | 6.189% | | 4/15/42 | | A2 | | | 270,100 |

| | | | | | |

| | 3,850 | | UBS Perferred Funding Trust I | | | | 8.622% | | 10/01/51 | | A1 | | | 2,742,286 |

| | | Total Capital Markets | | | | | | | | | | | 7,995,625 |

| | | | | | | | | | | |

Principal

Amount (000)/

Shares | | Description (1) | | Coupon | | Maturity | | Ratings (2) | | Value |

| | | | | | | | | | | |

| | Commercial Banks – 21.3% | | | | | | | | | |

| | | | | |

| 3,350 | | Barclays Bank PLC, 144A | | 8.550% | | 6/15/15 | | BBB+ | | $ | 2,278,000 |

| | | | | |

| 650 | | Barclays Bank PLC, Reg S | | 8.550% | | 12/15/49 | | BBB+ | | | 455,000 |

| | | | | |

| 420 | | BBVA International Unipersonal | | 5.919% | | 4/18/58 | | A2 | | | 248,136 |

| | | | | |

| 1,000 | | BNP Paribas, 144A | | 7.195% | | 12/25/57 | | Aa3 | | | 731,774 |

| | | | | |

| 500 | | BOI Capital Funding 2, 144A | | 5.571% | | 8/01/56 | | B | | | 187,700 |

| | | | | |

| 2,000 | | Comerica Capital Trust II | | 6.576% | | 2/20/37 | | A3 | | | 1,182,542 |

| | | | | |

| 2,370 | | Credit Agricole, S.A, 144A | | 6.637% | | 5/30/49 | | Aa3 | | | 1,394,209 |

| | | | | |

| 2,475 | | HSBC Financial Capital Trust IX | | 5.911% | | 11/30/35 | | Baa1 | | | 1,309,829 |

| | | | | |

| 200 | | Lloyd’s Banking Group PLC, 144A | | 6.657% | | 5/21/49 | | B3 | | | 72,100 |

| | | | | |

| 400 | | Lloyd’s Banking Group PLC, 144A | | 6.267% | | 11/14/49 | | B3 | | | 136,143 |

| | | | | |

| 300 | | Mizuho Capital Investment I Limited, 144A | | 6.686% | | 3/30/49 | | Baa1 | | | 227,345 |

| | | | | |

| 6,200 | | PNC Preferred Funding Trust III, 144A | | 8.700% | | 3/15/58 | | Baa2 | | | 5,096,446 |

| | | | | |

| 5,000 | | Rabobank Nederland, 144A | | 11.000% | | 12/31/49 | | Aa2 | | | 5,576,595 |

| | | | | |

| 500 | | Societe Generale, 144A | | 5.922% | | 4/05/57 | | A1 | | | 310,425 |

| | | | | |

| 480 | | Sovereign Capital Trust VI | | 7.908% | | 6/13/56 | | BBB+ | | | 360,672 |

| | | | | |

| 2,000 | | Standard Chartered PLC, 144A | | 7.014% | | 7/30/37 | | Baa2 | | | 1,423,454 |

| | | | | |

| 4,900 | | USB Realty Corporation, 144A | | 6.091% | | 4/15/49 | | A2 | | | 2,843,651 |

| | | | | |

| 1,550 | | Wachovia Capital Trust III | | 5.800% | | 3/15/42 | | A– | | | 930,316 |

| | | | | |

| 11,080 | | Wells Fargo Capital Trust XIII | | 7.700% | | 9/26/58 | | A– | | | 9,203,436 |

| | | | | |

| 1,365 | | Wells Fargo Capital Trust XV | | 9.750% | | 9/26/49 | | A– | | | 1,321,753 |

| | Total Commercial Banks | | | | | | | | | 35,289,526 |

| | Diversified Financial Services – 8.5% | | | | | | | | | |

| | | | | |

| 5,300 | | ING Capital Funding Trust III | | 8.439% | | 12/30/49 | | BBB | | | 3,339,970 |

| | | | | |

| 12,221 | | JP Morgan Chase & Company | | 7.900% | | 4/30/49 | | A2 | | | 10,724,295 |

| | Total Diversified Financial Services | | | | | | | | | 14,064,265 |

| | Industrial Conglomerates – 0.4% | | | | | | | | | |

| | | | | |

| 1,000 | | General Electric Capital Corporation | | 6.375% | | 11/15/67 | | Aa3 | | | 668,184 |

| | Insurance – 13.4% | | | | | | | | | |

| | | | | |

| 3,100 | | Assured Guaranty US Holdings, Series A | | 6.400% | | 12/15/66 | | A3 | | | 1,582,789 |

| | | | | |

| 2,010 | | AXA SA, 144A | | 6.379% | | 6/14/57 | | Baa1 | | | 1,289,524 |

| | | | | |

| 2,000 | | Financial Security Assurance Holdings, 144A | | 6.400% | | 12/15/36 | | A– | | | 1,040,000 |

| | | | | |

| 750 | | Genworth Financial Inc. | | 6.150% | | 11/15/66 | | Ba1 | | | 337,955 |

| | | | | |

| 1,000 | | Hartford Financial Services Group Inc. | | 8.125% | | 6/15/18 | | Ba1 | | | 700,980 |

| | | | | |

| 1,000 | | Liberty Mutual Group Inc., 144A | | 10.750% | | 6/15/58 | | Baa3 | | | 721,205 |

| | | | | |

| 400 | | Liberty Mutual Group, 144A | | 7.800% | | 3/15/37 | | Baa3 | | | 224,406 |

| | | | | |

| 1,000 | | Lincoln National Corporation | | 7.000% | | 5/17/66 | | BBB | | | 640,000 |

| | | | | |

| 2,500 | | MetLife Capital Trust IV, 144A | | 7.875% | | 12/15/67 | | Baa1 | | | 2,029,950 |

| | | | | |

| 2,000 | | MetLife Capital Trust X, 144A | | 9.250% | | 4/08/68 | | BBB+ | | | 1,784,094 |

| | | | | |

| 5,000 | | MetLife Inc., WI/DD | | 10.750% | | 8/01/69 | | Baa1 | | | 4,999,050 |

| | | | | |

| 4,950 | | Prudential Financial Inc. | | 8.875% | | 6/15/18 | | BBB+ | | | 4,114,395 |

| | | | | |

| 1,000 | | Swiss Re Capital I, 144A | | 6.854% | | 5/25/49 | | A– | | | 551,037 |

| | | | | |

| 500 | | Symetra Financial Corporation, 144A | | 8.300% | | 10/15/37 | | Ba1 | | | 216,486 |

| | | | | |

| 485 | | ZFS Finance USA Trust II, 144A | | 6.450% | | 12/15/65 | | A | | | 373,450 |

| | | | | |

| 2,050 | | ZFS Finance USA Trust V, 144A | | 6.500% | | 5/09/67 | | A | | | 1,517,000 |

| | Total Insurance | | | | | | | | | 22,122,321 |

| | Oil, Gas & Consumable Fuels – 0.1% | | | | | | | | | |

| | | | | |

| 200 | | Enterprise Products Operating LP | | 7.034% | | 1/15/68 | | Ba1 | | | 147,714 |

| | Road & Rail – 0.2% | | | | | | | | | |

| | | | | |

| 400 | | Burlington Northern Santa Fe Funding Trust I | | 6.613% | | 12/15/55 | | Baa3 | | | 317,237 |

| | Total Capital Preferred Securities (cost $71,959,117) | | | | | | | | | 80,604,872 |

Portfolio of Investments (Unaudited)

Nuveen Preferred Securities Fund (continued)

June 30, 2009

| | | | | | | | | | |

Principal

Amount (000) | | Description (1) | | Coupon | | Maturity | | Value |

| | | | | | | | | | |

| | | SHORT-TERM INVESTMENTS – 1.1% | | | | | | | |

| | | | |

| | | U.S. Government and Agency Obligations – 0.3% | | | | | | | |

| | | | |

| $ | 500 | | U.S. Treasury Bills | | 0.000% | | 8/27/09 | | $ | 499,896 |

| | | | |

| | | Repurchase Agreements – 0.8% | | | | | | | |

| | | | |

| | 1,241 | | Repurchase Agreement with State Street Bank, dated 6/30/09, repurchase price $1,241,237, collateralized by $1,270,000 U.S. Treasury Bills, 0.000%, due 12/10/09, value $1,268,222 | | 0.000% | | 7/01/09 | | | 1,241,237 |

| $ | 1,741 | | Total Short-Term Investments (cost $1,741,118) | | | | | | | 1,741,133 |

| | | Total Investments (cost $148,291,374) – 100.5% | | | | | | | 165,982,395 |

| | | Other Assets Less Liabilities – (0.5)% | | | | | | | (779,499) |

| | | Net Assets – 100% | | | | | | $ | 165,202,896 |

Investments in Derivatives

Futures Contracts outstanding at June 30, 2009:

| | | | | | | | | | | | | |

| Type | | Contract

Position | | Number of

Contracts | | Contract

Expiration | | Value at

June 30, 2009 | | Unrealized

Appreciation

(Depreciation) | |

U.S. 30-Year Treasury Bonds | | Long | | 25 | | 9/09 | | $ | 2,958,984 | | $ | (51,345 | ) |

| | (1) | | All percentages shown in the Portfolio of Investments are based on net assets. |

| | (2) | | Ratings: Using the higher of Standard & Poor’s Group (“Standard & Poor’s”) or Moody’s Investor Service, Inc. (“Moody’s”) rating. Ratings below BBB by Standard & Poor’s or Baa by Moody’s are considered to be below investment grade. |

| | (3) | | Non-income producing security; denotes that the issuer has defaulted on the payment of dividends. |

| | (4) | | Optional Call Provisions: Dates (month and year) and prices of the earliest optional call or redemption. There may be other call provisions at varying prices at later dates. Certain mortgage-backed securities may be subject to periodic principal paydowns. |

| | (5) | | The Fund’s Adviser has concluded this issue is not likely to meet its future interest payment obligations and has directed the Fund’s custodian to cease accruing additional income on the Fund’s records. |

| | WI/DD | | Purchased on a when-issued or delayed delivery basis. |

| | 144A | | Investment is exempt from registration under Rule 144A of the Securities Act of 1933, as amended. These investments may only be resold in transactions exempt from registration which are normally those transactions with qualified institutional buyers. |

| | Reg S | | Regulation S allows United States companies to sell securities to persons or entities located outside of the United States without registering those securities with the Securities and Exchange Commission. Specifically, Regulation S provides a safe harbor from the registration requirements of the Securities Act for the offers and sales of securities by both foreign and domestic issuers that are made outside the United States. |

See accompanying notes to financial statements.

Statement of Assets and Liabilities (Unaudited)

June 30, 2009

| | | | |

Assets | | | | |

Investments, at value (cost $148,291,374) | | $ | 165,982,395 | |

Deposits with brokers for open futures contracts | | | 2,000 | |

Receivables: | | | | |

Dividends | | | 255,739 | |

From Adviser | | | 62,169 | |

Interest | | | 1,225,278 | |

Shares sold | | | 6,931,458 | |

Other assets | | | 35 | |

Total assets | | | 174,459,074 | |

Liabilities | | | | |

Payables: | | | | |

Dividends | | | 582,857 | |

Investments purchased | | | 8,252,197 | |

Shares redeemed | | | 248,419 | |

Variation margin on futures contracts | | | 5,078 | |

Accrued expenses: | | | | |

12b-1 distribution and service fees | | | 33,455 | |

Other | | | 134,172 | |

Total liabilities | | | 9,256,178 | |

Net assets | | $ | 165,202,896 | |

Class A Shares | | | | |

Net assets | | $ | 70,118,225 | |

Shares outstanding | | | 5,463,885 | |

Net asset value per share | | $ | 12.83 | |

Offering price per share (net asset value per share plus

maximum sales charge of 4.75% of offering price) | | $ | 13.47 | |

Class C Shares | | | | |

Net assets | | $ | 26,091,971 | |

Shares outstanding | | | 2,031,350 | |

Net asset value and offering price per share | | $ | 12.84 | |

Class I Shares | | | | |

Net assets | | $ | 68,992,700 | |

Shares outstanding | | | 5,376,396 | |

Net asset value and offering price per share | | $ | 12.83 | |

Net Assets Consist of: | | | | |

Capital paid-in | | $ | 160,648,450 | |

Undistributed (Over-distribution of) net investment income | | | (312,460 | ) |

Accumulated net realized gain (loss) from investments and derivative transactions | | | (12,772,770 | ) |

Net unrealized appreciation (depreciation) of investments and derivative transactions | | | 17,639,676 | |

Net assets | | $ | 165,202,896 | |

See accompanying notes to financial statements.

Statement of Operations (Unaudited)

Six Months Ended June 30, 2009

| | | | |

Investment Income | | | | |

Dividends | | $ | 3,314,549 | |

Interest | | | 2,074,469 | |

Total Investment Income | | | 5,389,018 | |

Expenses | | | | |

Management fees | | | 343,710 | |

12b-1 service fees – Class A | | | 45,420 | |

12b-1 distribution and service fees – Class C | | | 63,483 | |

Shareholders’ servicing agent fees and expenses | | | 87,611 | |

Custodian’s fees and expenses | | | 17,905 | |

Trustees’ fees and expenses | | | 2,034 | |

Professional fees | | | 19,745 | |

Shareholders’ reports – printing and mailing expenses | | | 48,851 | |

Federal and state registration fees | | | 83,832 | |

Other expenses | | | 6,283 | |

Total expenses before custodian fee credit and expense reimbursement | | | 718,874 | |

Custodian fee credit | | | (2 | ) |

Expense reimbursement | | | (289,227 | ) |

Net expenses | | | 429,645 | |

Net investment income | | | 4,959,373 | |

Realized and Unrealized Gain (Loss) | | | | |

Net realized gain (loss) from: | | | | |

Investments | | | (6,394,257 | ) |

Futures contracts | | | (113,825 | ) |

Change in net unrealized appreciation (depreciation) of: | | | | |

Investments | | | 28,078,356 | |

Futures contracts | | | (117,590 | ) |

Net realized and unrealized gain (loss) | | | 21,452,684 | |

Net increase (decrease) in net assets from operations | | $ | 26,412,057 | |

See accompanying notes to financial statements.

Statement of Changes in Net Assets (Unaudited)

| | | | | | | | |

| | | Six Months Ended

6/30/09 | | | Year Ended

12/31/08 | |

Operations | | | | | | | | |

Net investment income | | $ | 4,959,373 | | | $ | 3,535,044 | |

Net realized gain (loss) from: | | | | | | | | |

Investments | | | (6,394,257 | ) | | | (6,250,471 | ) |

Futures contracts | | | (113,825 | ) | | | 110,401 | |

Change in net unrealized appreciation (depreciation) of: | | | | | | | | |

Investments | | | 28,078,356 | | | | (8,580,750 | ) |

Futures contracts | | | (117,590 | ) | | | 66,245 | |

Net increase (decrease) in net assets from operations | | | 26,412,057 | | | | (11,119,531 | ) |

Distributions to Shareholders | | | | | | | | |

From net investment income: | | | | | | | | |

Class A | | | (2,080,863 | ) | | | (355,033 | ) |

Class B | | | — | | | | — | |

Class C | | | (695,883 | ) | | | (92,502 | ) |

Class I (1) | | | (2,510,432 | ) | | | (3,062,416 | ) |

Tax return of capital | | | | | | | | |

Class A | | | — | | | | (39,419 | ) |

Class B | | | — | | | | — | |

Class C | | | — | | | | (10,312 | ) |

Class I (1) | | | — | | | | (340,963 | ) |

Decrease in net assets from distributions to shareholders | | | (5,287,178 | ) | | | (3,900,645 | ) |

Fund Share Transactions | | | | | | | | |

Proceeds from sale of shares | | | 104,352,168 | | | | 71,899,868 | |

Proceeds from shares issued to shareholders due to reinvestment of distributions | | | 2,382,936 | | | | 1,040,675 | |

| | | 106,735,104 | | | | 72,940,543 | |

Cost of shares redeemed | | | (30,202,501 | ) | | | (10,955,497 | ) |

Net increase (decrease) in net assets from Fund share transactions | | | 76,532,603 | | | | 61,985,046 | |

Net increase (decrease) in net assets | | | 97,657,482 | | | | 46,964,870 | |

Net assets at the beginning of period | | | 67,545,414 | | | | 20,580,544 | |

Net assets at the end of period | | $ | 165,202,896 | | | $ | 67,545,414 | |

Undistributed (Over-distribution of) net investment income at the end of period | | $ | (312,460 | ) | | $ | 15,345 | |

(1) Effective May 1, 2008, Class R Shares were renamed Class I Shares.

See accompanying notes to financial statements.

Notes to Financial Statements (Unaudited)

1. General Information and Significant Accounting Policies

The Nuveen Investment Trust V (the “Trust”) is an open-end management investment company registered under the Investment Company Act of 1940, as amended. The Trust is comprised of the Nuveen Preferred Securities Fund (the “Fund”). The Trust was organized as a Massachusetts business trust on September 27, 2006.

The Fund seeks to provide a high level of current income and total return. Under normal circumstances, the Fund will invest at least 80% of its net assets in preferred securities. At least 60% of the preferred securities in which the Fund invests will be rated BBB/Baa or higher at the time of purchase by at least one independent rating agency, or if unrated, judged to be of comparable quality by Nuveen Asset Management (the “Adviser”), a wholly-owned subsidiary of Nuveen Investments Inc. (“Nuveen). The Fund may invest up to 40% of its net assets in securities rated below investment grade (BB/Ba or lower) at the time of purchase, which are commonly referred to as “high yield,” “high risk” or “junk” securities. The Fund may invest up to 35% of its net assets in U.S. dollar-denominated securities of non-U.S. issuers and up to 10% of its total assets in other open or closed-end funds that invest in similar types of securities. The Fund may invest up to 20% of its net assets in debt securities, U.S. government and agency debt, taxable municipal securities and convertible preferred securities. Under normal circumstances, the Fund may invest up to 15% of its net assets in securities and other instruments that, at the time of investment, are illiquid (i.e., securities that are not readily marketable). The Fund may also invest in forwards, futures, options and swap contracts, or other derivative financial instruments including credit default swaps.

Effective March 31, 2008, Class B shares are no longer available for the Fund. As of March 31, 2008, all outstanding Class B Shares for the Fund were owned by Nuveen and transferred to Class I Shares on May 2, 2008.

During the current reporting period, the Fund’s Board of Trustees approved a change in the Fund’s fiscal year end from December 31 to September 30.

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements in accordance with US generally accepted accounting principles.

Investment Valuation

Exchange-listed securities are generally valued at the last sales price on the securities exchange on which such securities are primarily traded. Securities traded on a securities exchange for which there are no transactions on a given day or securities not listed on a securities exchange are valued at the mean of the closing bid and asked prices. Securities traded on NASDAQ are valued at the NASDAQ Official Closing Price. The prices of fixed-income securities are generally provided by an independent pricing service approved by the Fund’s Board of Trustees. Futures contracts are valued using the closing settlement price or, in the absence of such a price, at the mean of the bid and asked prices. When market price quotes are not readily available, the pricing service or, in the absence of a pricing service for a particular investment or derivative instrument, the Board of Trustees of the Fund, or its designee may establish fair value using a wide variety of market data including yields or prices of investments of comparable quality, type of issue, coupon, maturity and rating, market quotes or indications of value from security dealers, evaluations of anticipated cash flows or collateral, general market conditions and other information and analysis, including the obligor’s credit characteristics considered relevant. Short-term investments are valued at amortized cost, which approximates value.

Investment Transactions

Investment transactions are recorded on a trade date basis. Realized gains and losses from investment transactions are determined on the specific identification method. Investments purchased on a when-issued/delayed delivery basis may have extended settlement periods. Any investments so purchased are subject to market fluctuation during this period. The Fund has instructed the custodian to segregate assets with a current value at least equal to the amount of the when-issued/delayed delivery purchase commitments. At June 30, 2009, the Fund outstanding when-issued/delayed purchase commitments of $4,999,050.

Investment Income

Dividend income is recorded on the ex-dividend date or, for foreign securities, when information is available. Interest income, which includes the amortization of premiums and accretion of discounts for financial reporting purposes, is recorded on an accrual basis. Interest income also includes paydown gains and losses, if any.

Income Taxes

The Fund intends to distribute substantially all of its net investment income and net capital gains to shareholders and to otherwise comply with the requirements of Subchapter M of the Internal Revenue Code applicable to regulated investment companies. Therefore, no federal income tax provision is required.

For all open tax years and all major taxing jurisdictions, management of the Fund has concluded that there are no significant uncertain tax positions that would require recognition in the financial statements. Open tax years are those that are open for examination by taxing authorities (i.e., generally the last four tax year ends and the interim tax period since then). Furthermore, management of the Fund is also not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Dividends and Distributions to Shareholders

Dividends from net investment income are declared monthly. Net realized capital gains from investment transactions, if any, are declared and distributed to shareholders at least annually. Furthermore, capital gains are distributed only to the extent they exceed available capital loss carryforwards.

Distributions to shareholders are recorded on the ex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from US generally accepted accounting principles.

Flexible Sales Charge Program

Class A Shares are generally sold with an up-front sales charge and incur a .25% annual 12b-1 service fee. Class A Share purchases of $1 million or more are sold at net asset value without an up-front sales charge but may be subject to a contingent deferred sales charge (“CDSC”) if redeemed within twelve months of purchase. Class C Shares are sold without an up-front sales charge but incur a .75% annual 12b-1 distribution fee and a .25% annual 12b-1 service fee. Class C Shares are subject to a CDSC of 1% if redeemed within one year of purchase. Class I Shares are not subject to any sales charge or 12b-1 distribution or service fees.

Futures Contracts

The Fund is subject to interest rate risk in the normal course of pursuing its investment objectives and is authorized to invest in futures contracts in an attempt to gain exposure to, or hedge against changes in interest rates. Upon entering into a futures contract, the Fund is required to deposit with the broker an amount of cash or liquid securities equal to a specified percentage of the contract amount. This is known as the “initial margin.” Cash held by the broker to cover initial margin requirements on open futures contracts, if any, is recognized as “Deposits with brokers for open futures contracts” on the Statement of Assets and Liabilities. Subsequent payments (“variation margin”) are made or received by the Fund each day, depending on the daily fluctuation of the value of the contract. Variation margin is recognized as a receivable or payable for “Variation margin on futures contracts” on the Statement of Assets and Liabilities, when applicable.

During the period the futures contract is open, changes in the value of the contract are recorded as an unrealized gain or loss by “marking-to-market” on a daily basis to reflect the changes in market value of the contract and is recognized as “Change in net unrealized appreciation (depreciation) of futures contracts” on the Statement of Operations. When the contract is closed or expired, the Fund records a realized gain or loss equal to the difference between the value of the contract on the closing date and value of the contract when originally entered into and is recognized as “Net realized gain (loss) from futures contracts” on the Statement of Operations.

Risks of investments in futures contracts include the possible adverse movement of the securities or indices underlying the contracts, the possibility that there may not be a liquid secondary market for the contracts and/or that a change in the value of the contract may not correlate with a change in the value of the underlying securities or indices.

The average number of futures contracts outstanding during the six months ended June 30, 2009, was 12. Refer to Footnote 3 – Derivative Instruments and Hedging Activities for further details on futures contract activity.

Market and Counterparty Credit Risk

In the normal course of business the Fund may invest in financial instruments and enter into financial transactions where risk of potential loss exists due to changes in the market (market risk) or failure of the other party to the transaction to perform (counterparty credit risk). The potential loss could exceed the value of the financial assets recorded on the financial statements. Financial assets, which potentially expose the Fund to counterparty credit risk, consist principally of cash due from counterparties on forward, option and swap transactions. The extent of the Fund’s exposure to counterparty credit risk in respect to these financial assets approximates their carrying value as recorded on the Statement of Assets and Liabilities. Futures contracts expose the Fund to minimal counterparty credit risk as they are exchange traded and the exchange’s clearinghouse, which is counterparty to all exchange traded futures, guarantees the futures contracts against default.

The Fund helps manage counterparty credit risk by entering into agreements only with counterparties the Adviser believes have the financial resources to honor their obligations and by having the Adviser monitor the financial stability of the counterparties. Additionally, counterparties may be required to pledge collateral daily (based on the daily valuation of the financial asset) on behalf of the Fund with a value approximately equal to the amount of any unrealized gain above a pre-determined threshold. Reciprocally, when the Fund has an unrealized loss, the Fund has instructed the custodian to pledge assets of the Fund as collateral with a value approximately equal to the amount of the unrealized loss above a pre-determined threshold. Collateral pledges are monitored and subsequently adjusted if and when the valuations fluctuate, either up or down, by at least the predetermined threshold amount.

Repurchase Agreements

In connection with transactions in repurchase agreements, it is the Fund’s policy that its custodian take possession of the underlying collateral securities, the fair value of which exceeds the principal amount of the repurchase transaction, including accrued interest, at all times. If the seller defaults, and the fair value of the collateral declines, realization of the collateral may be delayed or limited.

Expense Allocation

Expenses of the Fund that are not directly attributable to a specific class of shares are prorated among the classes based on the relative net assets of each class. Expenses directly attributable to a class of shares, which presently only include 12b-1 distribution and service fees, are recorded to the specific class.

Notes to Financial Statements (Unaudited) (continued)

Custodian Fee Credit

The Fund has an arrangement with the custodian bank whereby certain custodian fees and expenses are reduced by net credits earned on the Fund’s cash on deposit with the bank. Such deposit arrangements are an alternative to overnight investments. Credits for cash balances may be offset by charges for any days on which the Fund overdraws its account at the custodian bank.

Indemnifications

Under the Trust’s organizational documents, its Officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust. In addition, in the normal course of business, the Trust enters into contracts that provide general indemnifications to other parties. The Trust’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Trust that have not yet occurred. However, the Trust has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

Use of Estimates

The preparation of financial statements in conformity with US generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results may differ from those estimates.

2. Fair Value Measurements

In determining the value of the Fund’s investments various inputs are used. These inputs are summarized in the three broad levels listed below:

| | |

| Level 1 – | | Quoted prices in active markets for identical securities. |

| Level 2 – | | Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). |

| Level 3 – | | Significant unobservable inputs (including management’s assumptions in determining the fair value of investments). |

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities.

The following is a summary of the Fund’s fair value measurements as of June 30, 2009:

| | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | Level 3 | | Total | |

Investments: | | | | | | | | | | | | | | |

Preferred Securities* | | $ | 79,391,163 | | | $ | 80,604,872 | | $ | — | | $ | 159,996,035 | |

Taxable Municipal Bonds | | | — | | | | 3,485,014 | | | — | | | 3,485,014 | |

Corporate Bonds | | | — | | | | 760,213 | | | — | | | 760,213 | |

Short-Term Investments | | | 1,741,133 | | | | — | | | — | | | 1,741,133 | |

Derivatives: | | | | | | | | | | | | | | |

Futures Contracts** | | | (51,345 | ) | | | — | | | — | | | (51,345 | ) |

Total | | $ | 81,080,951 | | | $ | 84,850,099 | | $ | — | | $ | 165,931,050 | |

| * | Preferred Securities may include Convertible Preferred Securities, $25 Par (or similar) Preferred Securities and Capital Preferred Securities. |

| ** | Represents net unrealized appreciation (depreciation). |

The following is a reconciliation of the Fund’s Level 3 investments held at the beginning and end of the measurement period:

| | | | |

| | | Level 3

Investments | |

Balance at beginning of period | | $ | 700,000 | |

Gains (losses): | | | | |

Net realized gains (losses) | | | — | |

Net change in unrealized appreciation (depreciation) | | | 51,512 | |

Net purchases at cost (sales at proceeds) | | | — | |

Net discounts (premiums) | | | 8,701 | |

Net transfers in to (out of) at end of period fair value | | | (760,213 | ) |

Balance at end of period | | $ | — | |

3. Derivative Instruments and Hedging Activities

During the current fiscal period, the Fund adopted the provisions of Statement of Financial Accounting Standards No. 161 (SFAS No. 161) “Disclosures about Derivative Instruments and Hedging Activities.” This standard is intended to enhance financial statement disclosures for derivative instruments and hedging activities and enable investors to better understand: a) how and why a fund uses derivative instruments; b) how derivative instruments are accounted for; and c) how derivative instruments affect a fund’s financial position, results of operations and cash flows, if any. The Fund records derivative instruments at fair value with changes in fair value recognized on the Statement of Operations. Even though the Fund’s investments in derivatives may represent economic hedges, they are considered to be non-hedge transactions for SFAS No. 161 disclosure purposes. For additional information on the derivative instruments in which the Fund was invested during and at the end of the reporting period, refer to the Portfolio of Investments, Financial Statements and Footnote 1 – General Information and Significant Accounting Policies.

The following table presents the fair value of all derivative instruments held by the Fund as of June 30, 2009, the location of these instruments on the Statement of Assets and Liabilities, and the primary underlying risk exposure.

| | | | | | | | | | | | |

| | | | | Location on the Statement of Assets and Liabilities |

Underlying Risk

Exposure | | Derivative

Instrument | | Asset Derivatives | | Liability Derivatives |

| | | Location | | Value | | Location | | Value |

Interest Rate | | Futures | | — | | $

| —

| | Deposits with brokers for open futures contracts and Payable for variation margin on futures contracts* | | $ | 51,345 |

| * | Value represents cumulative unrealized appreciation (depreciation) of futures contracts as reported in the Portfolio of Investments and not the deposits with brokers, if any, or the receivable or payable for variation margin on futures contracts presented on the Statement of Assets and Liabilities. |

The following tables present the amount of net realized gain (loss) and change in net unrealized appreciation (depreciation) recognized for the six months ended June 30, 2009, on derivative instruments, as well as the primary risk exposure associated with each.

| | | | |

| Net Realized Gain (Loss) from Futures | | | |

Risk Exposure | | | | |

Interest Rate | | $ | (113,825 | ) |

| | | | |

| Change in Net Unrealized Appreciation (Depreciation) of Futures | | | |

Risk Exposure | | | | |

Interest Rate | | $ | (117,590 | ) |

4. Fund Shares

Transactions in Fund shares were as follows:

| | | | | | | | | | | | | | |

| | | Six Months Ended

6/30/09 | | | Year Ended

12/31/08 | |

| | | Shares | | | Amount | | | Shares | | | Amount | |

Shares sold: | | | | | | | | | | | | | | |

Class A | | 4,872,136 | | | $ | 50,922,086 | | | 2,293,754 | | | $ | 26,123,279 | |

Class B* | | — | | | | — | | | — | | | | — | |

Class C | | 1,636,235 | | | | 18,003,655 | | | 538,244 | | | | 6,214,381 | |

Class I | | 3,243,473 | | | | 35,426,427 | | | 2,530,870 | | | | 39,562,208 | |

Shares issued to shareholders due to reinvestment of distributions: | | | | | | | | | | | | | | |

Class A | | 85,969 | | | | 943,971 | | | 16,592 | | | | 194,768 | |

Class B* | | — | | | | — | | | 318 | | | | 5,496 | |

Class C | | 27,316 | | | | 292,352 | | | 4,494 | | | | 54,997 | |

Class I | | 109,377 | | | | 1,146,613 | | | 57,175 | | | | 785,414 | |

| | | 9,974,506 | | | | 106,735,104 | | | 5,441,447 | | | | 72,940,543 | |

Shares redeemed: | | | | | | | | | | | | | | |

Class A | | (1,400,336 | ) | | | (14,524,513 | ) | | (423,124 | ) | | | (4,520,859 | ) |

Class B* | | — | | | | — | | | (14,780 | ) | | | (253,326 | ) |

Class C | | (178,445 | ) | | | (1,880,059 | ) | | (10,956 | ) | | | (123,500 | ) |

Class I | | (1,265,659 | ) | | | (13,797,929 | ) | | (463,163 | ) | | | (6,057,812 | ) |

| | | (2,844,440 | ) | | | (30,202,501 | ) | | (912,023 | ) | | | (10,955,497 | ) |

Net increase (decrease) | | 7,130,066 | | | $ | 76,532,603 | | | 4,529,424 | | | $ | 61,985,046 | |

| * | Effective March 31, 2008, Class B Shares were no longer available to the Funds and transferred to Class I Shares on May 2, 2008. |

5. Investment Transactions

Purchases and sales (including maturities but excluding short-term investments and derivative transactions) during the six months ended June 30, 2009, aggregated $100,480,599 and $23,552,145, respectively.

Notes to Financial Statements (Unaudited) (continued)

6. Income Tax Information

The following information is presented on an income tax basis. Differences between amounts for financial statement and federal income tax purposes are primarily due to timing differences in recognizing taxable market discount, amortization of premium on taxable debt securities and timing differences in recognizing certain gains and losses on investment transactions. To the extent that differences arise that are permanent in nature, such amounts are reclassified within the capital accounts on the Statement of Assets and Liabilities presented in the annual report, based on their federal tax basis treatment; temporary differences do not require reclassification. Temporary and permanent differences do not impact the net asset value of the Fund.

At June 30, 2009, the cost of investments was $148,794,933.

Gross unrealized appreciation and gross unrealized depreciation of investments at June 30, 2009, were as follows:

| | | | |

Gross unrealized: | | | | |

Appreciation | | $ | 24,538,950 | |

Depreciation | | | (7,351,488 | ) |

Net unrealized appreciation (depreciation) of investments | | $ | 17,187,462 | |

The tax components of undistributed net ordinary income and net long-term capital gains at December 31, 2008, the Fund’s last tax year end, were as follows:

| | | |

Undistributed net ordinary income* | | $ | — |

Undistributed net long-term capital gains | | | — |

| * | Net ordinary income consists of net taxable income derived from dividends, interest, and net short-term capital gains, if any. |

The tax character of distributions paid during the Fund’s last tax year ended December 31, 2008, was designated for purposes of the dividends paid deduction as follows:

| | | |

Distributions from ordinary income* | | $ | 3,509,653 |

Distributions from net long-term capital gains | | | — |

Tax return of capital | | | 390,694 |

| * | Net ordinary income consists of net taxable income derived from dividends, interest, and net short-term capital gains, if any. |