UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-22037 | ||||||

| |||||||

Stone Harbor Investment Funds | |||||||

(Exact name of registrant as specified in charter) | |||||||

| |||||||

1290 Broadway, Suite 1100 Denver, CO |

| 80203 | |||||

(Address of principal executive offices) |

| (Zip code) | |||||

| |||||||

Adam J. Shapiro, Esq. c/o Stone Harbor Investment Partners LP 31 West 52nd Street, 16th Floor New York, NY 10019 | |||||||

(Name and address of agent for service) | |||||||

| |||||||

With copies To:

John M. Loder, Esq. Ropes & Gray LLP One International Place Boston, MA 02110-2624 | |||||||

| |||||||

Registrant’s telephone number, including area code: | (303) 623-2577 |

| |||||

| |||||||

Date of fiscal year end: | May 31 |

| |||||

| |||||||

Date of reporting period: | August 16, 2007 - May 31, 2008 |

| |||||

Item 1. Reports to Stockholders.

Table of Contents

Letter to Shareholders |

| 2 |

|

|

|

Disclosure of Fund Expenses |

| 5 |

|

|

|

Summary of Portfolio Holdings |

| 6 |

|

|

|

Growth of a $10,000 Investment |

| 7 |

|

|

|

Report of Independent Registered Public Accounting Firm |

| 8 |

|

|

|

Statement of Investments |

|

|

Emerging Markets Debt Fund |

| 9 |

High Yield Bond Fund |

| 16 |

|

|

|

Statement of Assets & Liabilities |

| 33 |

|

|

|

Statement of Operations |

| 34 |

|

|

|

Statement of Changes in Net Assets |

|

|

Emerging Markets Debt Fund |

| 35 |

High Yield Bond Fund |

| 36 |

|

|

|

Financial Highlights |

|

|

Emerging Markets Debt Fund |

| 37 |

High Yield Bond Fund |

| 38 |

|

|

|

Notes to Financial Statements |

| 39 |

|

|

|

Additional Information |

| 45 |

|

|

|

Trustees and Officers |

| 48 |

Letter to Shareholders

Dear Shareholder,

We once again thank you for your investment in the Stone Harbor Investment Funds. Our goal is to produce long-term returns that exceed market benchmarks at risk levels comparable to, or less than, the general level of market risk. We will also strive to keep you well informed about information pertaining to your investment in our funds. If you have questions, please feel free to a call us at 212-548-1200.

PERFORMANCE

The two Stone Harbor institutional mutual funds underperformed their benchmarks on a net return basis for the six month period ended May 31, 2008. The High Yield Bond Fund returned 1.64% net of expenses, versus the Citigroup High Yield Market Capped Index return of 2.34%. In the same period the Stone Harbor Emerging Markets Debt Fund returned 1.90% net of expenses, as compared to the JP Morgan EMBI Global Diversified Index return of 2.29%. Both funds, however, remain ahead of benchmark on a net basis since their inception date of August 16, 2007; 5.09% net for the High Yield Bond Fund versus 4.69% for the benchmark, and 10.46% net for the Emerging Markets Debt Fund versus its benchmark of 9.27%.

THE MARKETS

The credit shocks of 2007 have carried over into 2008. Last year’s concerns over lax lending practices, particularly in the housing sector, led to tighter credit conditions and a dramatic economic slowdown. This year housing prices, as reported by the Case Schiller / S & P index, have declined over 15 % on a year-on-year basis and delinquencies on home mortgages have reached levels not seen since the 1930s.As a result, financial institutions have taken massive write-offs in their credit portfolios, and the Federal Reserve Bank has been left with no choice but to step in dramatically to calm the storm. Since the beginning of 2008, the Fed has lowered their overnight funds target by 225 basis points, forced a bailout of Bear Stearns, and given investment banks unprecedented access to the discount window.

Against this backdrop, it would be fair to say that navigating the waters of the credit markets for the past six months has been difficult. Investors have continued to favor the safety of U.S. government debt and credit risk has been approached with great caution. Spreads versus governments in all fixed income asset classes have been quite volatile as investors remained concerned about U.S. economic prospects. Credit spreads in the high yield market, as measured by our Citigroup High Yield benchmark, have widened by 75 basis points since December 1, 2007, while emerging debt spreads remained unchanged. Ironically, credit spreads in both markets were significantly wider just two months earlier in March.

In the Emerging Debt Fund country investments making positive contributions to performance were Colombia, Brazil and Ecuador. Investments in Argentina detracted from Fund performance. In the High Yield Fund, credits of homebuilders made a sudden recovery, and we have continued to under- weight this sector. Our over-weight of publishers also hurt our relative returns to benchmark.

Looking forward, the uncertainty of economic conditions forces us to remain cautious. The market has become extremely conscious of the threat of global inflation. Central banks face the difficult balancing act of trying to create enough economic stimulus to prevent recession, while at the same time maintaining the perception that they are vigilant against the threat of accelerating inflation. This will be a difficult task to accomplish. As a result, we believe that in the months ahead, spread volatility is likely to remain

2

at higher levels. We are comfortable that investors will achieve attractive long-term returns even from current spread levels, but opportunities for better returns seem likely later in the year.

BOND PERFORMANCE COMPARISONS

The charts below depict the performance of various debt market indices over our reporting period. As can be seen, The Stone Harbor Funds fared well in comparison.

|

| Dec. 1, 2007 to |

|

|

| May 31, 2008 (%) |

|

Citigroup Treasury 1-10 Year (1) |

| 2.01 |

|

Lehman U.S. Corporate Investment Grade (2) |

| -0.05 |

|

Citigroup High Yield Market Capped Index (3) |

| 2.34 |

|

JP Morgan EMBI Global Diversified Index (4) |

| 2.29 |

|

|

|

|

|

Stone Harbor High Yield Bond Fund (Gross) |

| 1.92 |

|

Stone Harbor High Yield Bond Fund (Net) |

| 1.64 |

|

Stone Harbor Emerging Markets Debt Fund (Gross) |

| 2.28 |

|

Stone Harbor Emerging Markets Debt Fund (Net) |

| 1.90 |

|

3

Sincerely,

![]()

Thomas W. Brock

Chairman of the Board of Trustees

June 30, 2008

(1) |

| The Citigroup US Treasury 1-10 Year Benchmark (On-The-Run) Index measures total returns for the current ten year on-the-run Treasuries that have been in existence for the entire month. |

(2) |

| The Lehman Brothers U.S. Corporate Investment Grade Index is comprised of publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered. |

(3) |

| The Citigroup High Yield Market Capped Index represents a modified version of the High Yield Market Index by delaying the entry of fallen angel issues and capping the par value of individual issuers at US$5 billion par amount outstanding. |

(4) |

| The JPMorgan EMBI Global Diversified is a uniquely-weighted version of the EMBI Global (Which tracks total returns for U.S.-dollar-denominated debt instruments issued by emerging markets sovereign and qua-si-sovereign entities: Brady bonds, loans, Eurobonds. Currently, the EMBI Global covers 196 instruments across 28 countries). It limits the weights of those index countries with larger debt stocks by only including specified portions of these countries’ eligible current face amounts of debt outstanding. The countries covered in the EMBI Global Diversified are identical to those covered by the EMBI Global. |

This report must be preceded or accompanied by a prospectus. For more complete information including charges and expenses, please call 1-866-699-8158 to receive a prospectus. Read the prospectus carefully before investing or sending money.

Past performance is no guarantee of future results. The performance data quoted represents past performance and current returns may be lower or higher. Total return figures include change in share price, reinvestment of dividends and capital gains and do not reflect taxes that a shareholder would pay on fund distributions or on the redemption of fund shares. The investment return and net asset value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. [To obtain performance information for the most recent month end, please call 1-866-699-8158.]

For more complete information on the Funds, you may request additional prospectuses by calling 1-866-699-8158. You should consider each Fund’s investment objectives, risk, charges and expenses carefully before you invest. Information about these and other important information is in the Funds’ prospectus which you should read carefully before investing.

Not FDIC insured. May lose value. No bank guarantee.

4

Disclosure of Fund Expenses

For the period August 16, 2007 (Inception) to May 31, 2008

Example. As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and/or redemption fees (if applicable) and (2) ongoing costs, including management fees and other Fund expenses. The below examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on December 1, 2007 and held until May 31, 2008.

Actual Expenses. The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending ac- count balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect transaction fees, such as redemption fees, sales charges (loads) or exchange fees.Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transaction fees were included, your costs would have been higher.

|

| Beginning |

| Ending |

|

|

| Expenses |

| |||

|

| Account Value |

| Account Value |

| Expense |

| Paid During |

| |||

|

| 12/01/2007 |

| 05/31/2008 |

| Ratio (a) |

| Period (b) |

| |||

STONE HARBOR EMERGING MARKETS DEBT FUND |

|

|

|

|

|

|

|

|

| |||

Institutional Class |

|

|

|

|

|

|

|

|

| |||

Actual |

| $ | 1,000.00 |

| $ | 1,019.00 |

| 0.75 | % | $ | 3.78 |

|

Hypothetical |

| $ | 1,000.00 |

| $ | 1,021.26 |

| 0.75 | % | $ | 3.78 |

|

|

|

|

|

|

|

|

|

|

| |||

STONE HARBOR HIGH YIELD BOND FUND |

|

|

|

|

|

|

|

|

| |||

Institutional Class |

|

|

|

|

|

|

|

|

| |||

Actual |

| $ | 1,000.00 |

| $ | 1,016.40 |

| 0.55 | % | $ | 2.76 |

|

Hypothetical |

| $ | 1,000.00 |

| $ | 1,022.26 |

| 0.55 | % | $ | 2.77 |

|

(a) |

| Annualized, based on the Portfolio’s most recent fiscal half-year expenses. |

(b) |

| Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183), divided by 366. Note this expense example is typically based on a six-month period. |

5

Summary of Portfolio Holdings

May 31, 2008 (Unaudited)

Under SEC Rules, all funds are required to include in their annual and semi-annual shareholder reports a presentation of portfolio holdings in a table, chart or graph by reasonably identifiable categories. The following tables which present holdings as a percent of total net assets (“TNA”) are provided in compliance with such requirements.

EMERGING MARKETS DEBT FUND

Country Breakout |

| % of TNA |

|

Argentina |

| 6.95 | % |

Brazil |

| 13.41 | % |

Chile |

| 0.32 | % |

Colombia |

| 6.78 | % |

Ecuador |

| 2.67 | % |

El Savador |

| 3.68 | % |

Gabon |

| 1.29 | % |

Indonesia |

| 6.45 | % |

Iraq |

| 2.37 | % |

Ireland |

| 1.56 | % |

Lebanon |

| 1.11 | % |

Luxembourg |

| 2.07 | % |

Malaysia |

| 3.58 | % |

Mexico |

| 5.94 | % |

Panama |

| 4.56 | % |

Peru |

| 4.12 | % |

Philippines |

| 7.03 | % |

Russia |

| 4.42 | % |

Singapore |

| 0.05 | % |

South Africa |

| 1.85 | % |

Tunisia |

| 0.51 | % |

Turkey |

| 4.61 | % |

Ukraine |

| 2.67 | % |

Uruguay |

| 2.87 | % |

Venezuela |

| 5.44 | % |

Total |

| 96.31 | % |

Other Assets in Excess of Liabilities |

| 3.69 | % |

Total Net Assets |

| 100.00 | % |

HIGH YIELD BOND FUND

Industry Breakout |

| % of TNA |

|

Advertising |

| 2.15 | % |

Aerospace - Defense |

| 3.99 | % |

Agriculture |

| 0.72 | % |

Apparel |

| 0.77 | % |

Auto Manufacturers |

| 1.73 | % |

Beverages |

| 1.26 | % |

Building Products |

| 0.97 | % |

Chemicals |

| 3.37 | % |

Coal |

| 1.04 | % |

Commercial Services |

| 4.17 | % |

Distribution - Wholesale |

| 0.34 | % |

Diversified Financial Services |

| 6.17 | % |

Electric |

| 5.51 | % |

Electrical Components & Equipment |

| 0.27 | % |

Entertainment |

| 3.54 | % |

Environmental Control |

| 0.92 | % |

Food |

| 1.58 | % |

Forest Products & Paper |

| 1.13 | % |

Healthcare-Products |

| 1.53 | % |

Healthcare-Services |

| 3.71 | % |

Holding Companies-Diversified |

| 0.12 | % |

Home Furnishings |

| 0.14 | % |

Hotels & Motels |

| 0.47 | % |

Internet |

| 0.27 | % |

Investment Companies |

| 0.43 | % |

Iron/Steel |

| 1.03 | % |

Lodging |

| 0.96 | % |

Machinery - Construction & Mining |

| 0.53 | % |

Media |

| 7.40 | % |

Miscellaneous Manufacturers |

| 1.11 | % |

Office Furnishings |

| 0.22 | % |

Office-Business Equipment |

| 1.46 | % |

Oil & Gas |

| 5.49 | % |

Oil & Gas Services |

| 1.16 | % |

Packaging & Containers |

| 2.00 | % |

Pharmaceuticals |

| 0.57 | % |

Pipelines |

| 4.59 | % |

Real Estate Investment Trusts |

| 1.70 | % |

Research Services |

| 0.37 | % |

Retail |

| 2.93 | % |

Semiconductors |

| 0.64 | % |

Telecommunications |

| 7.48 | % |

Transportation |

| 0.61 | % |

Total |

| 86.55 | % |

Other Assets in Excess of Liabilities |

| 13.45 | % |

Total Net Assets |

| 100.00 | % |

6

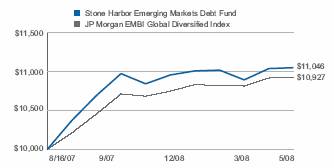

Growth of a $10,000 Investment

May 31, 2008 (Unaudited)

STONE HARBOR EMERGING MARKETS DEBT FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor Emerging Markets Debt Fund and the JP Morgan Emerging Bond Index Global Diversified

The JP Morgan Emerging Bond Index Global Diversified is a uniquely-weighted version of the EMBI Global (Which tracks total returns for U.S.-dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds. Currently, the EMBI Global covers 196 instruments across 28 countries). It limits the weights of those index countries with larger debt stocks by only including specified portions of these countries eligible current face amounts of debt outstanding. The countries covered in the EMBI Global Diversified are identical to those covered by the EMBI Global.

STONE HARBOR HIGH YIELD BOND FUND

Comparison of Change in Value of $10,000 Investment in Stone Harbor High Yield Bond Fund and the Citigroup High Yield Market Capped Index

The Citigroup High Yield Market Capped Index represents a modified version of the High Yield Market Index by delaying the entry of fallen angel issues and capping the par value of individual issuers at US $5 billion par amount outstanding.

7

Report of Independent Registered Public Accounting Firm

May 31, 2008

To the Shareholders of Stone Harbor Investment Funds:

We have audited the accompanying statements of assets and liabilities of Stone Harbor Investment Funds, including the Stone Harbor High Yield Bond Fund and Stone Harbor Emerging Markets Debt Fund (collectively, the “Funds”), including the statements of investments, as of May 31, 2008, and the related statements of operations and net assets, and the financial highlights for the period from August 16, 2008 (inception) to May 31, 2008. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based

on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States).Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. The Funds are not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. Our audits included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Funds’ internal control over financial reporting. Accordingly, we express no such opinion. An audit also-includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of May 31, 2008, by correspondence with the custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of each of the funds constituting the Stone Harbor Investment Funds as of May 31, 2008, and the results of its operations, and the net assets, and its financial highlights for the period from August 16, 2008 (inception) to May 31, 2008, in conformity with accounting principles generally accepted in the United States of America.

DELOITTE & TOUCHE LLP

Denver, Colorado

July 30, 2008

8

Statement of Investments

May 31, 2008 |

| Emerging Markets Debt Fund |

|

|

|

| Principal |

| Market Value |

| |

Interest Rate/Maturity Date |

| Currency |

| Amount * |

| (Expressed in U.S. $) |

| |

|

|

|

|

|

|

|

| |

SOVEREIGN DEBT OBLIGATIONS - 86.88% |

|

|

|

|

|

|

| |

Argentina - 6.95% |

|

|

|

|

|

|

| |

Republic of Argentina |

|

|

|

|

|

|

| |

8.750%, 02/04/2003(1) |

| EUR |

| 57,000 |

| $ | 27,460 |

|

7.000%, 03/18/2004(1) |

| EUR |

| 30,000 |

| 14,103 |

| |

7.000%, 03/18/2004(1) |

| EUR |

| 58,000 |

| 13,918 |

| |

9.000%, 05/24/2005(1) |

| EUR |

| 25,000 |

| 11,733 |

| |

9.000%, 04/26/2006(1) |

| EUR |

| 58,000 |

| 27,040 |

| |

10.000%, 01/03/2007(1) |

| ITL |

| 140,000,000 |

| 35,395 |

| |

10.250%, 01/26/2007(1) |

| EUR |

| 661,000 |

| 323,576 |

| |

8.000%, 02/26/2008(1) |

| EUR |

| 93,000 |

| 44,514 |

| |

7.000%, 09/12/2013 |

|

|

| 165,000 |

| 131,019 |

| |

7.000%, 04/17/2017 |

|

|

| 145,000 |

| 102,205 |

| |

8.280%, 12/31/2033(2) |

|

|

| 727,003 |

| 594,325 |

| |

1.330%, 12/31/2038(3) |

|

|

| 100,000 |

| 36,850 |

| |

|

|

|

|

|

| 1,362,138 |

| |

Brazil - 11.18% |

|

|

|

|

|

|

| |

Nota Do Tesouro Nacional |

|

|

|

|

|

|

| |

Series F, 10.000%, 01/01/2014 |

| BRL |

| 625,000 |

| 332,687 |

| |

Series F, 10.000%, 01/01/2017 |

| BRL |

| 1,775,000 |

| 906,412 |

| |

Republic of Brazil |

|

|

|

|

|

|

| |

8.500%, 09/24/2012 |

| EUR |

| 290,000 |

| 504,327 |

| |

8.000%, 01/15/2018 |

|

|

| 390,000 |

| 445,868 |

| |

|

|

|

|

|

| 2,189,294 |

| |

Chile - 0.32% |

|

| �� |

|

|

|

| |

Republic of Chile |

|

|

|

|

|

|

| |

5.500%, 01/15/2013 |

|

|

| 60,000 |

| 62,124 |

| |

|

|

|

|

|

|

|

| |

Colombia - 6.78% |

|

|

|

|

|

|

| |

Republic of Colombia |

|

|

|

|

|

|

| |

10.750%, 01/15/2013 |

|

|

| 30,000 |

| 37,313 |

| |

4.870%, 11/16/2015(4) |

|

|

| 100,000 |

| 106,125 |

| |

7.375%, 01/27/2017 |

|

|

| 100,000 |

| 113,875 |

| |

11.750%, 02/25/2020 |

|

|

| 385,000 |

| 584,718 |

| |

9.850%, 06/28/2027 |

| COP |

| 824,000,000 |

| 431,824 |

| |

10.375%, 01/28/2033 |

|

|

| 35,000 |

| 53,200 |

| |

|

|

|

|

|

| 1,327,055 |

| |

9

|

|

|

| Principal |

| Market Value |

| |

Interest Rate/Maturity Date |

| Currency |

| Amount * |

| (Expressed in U.S. $) |

| |

|

|

|

|

|

|

|

| |

Ecuador - 2.67% |

|

|

|

|

|

|

| |

Republic of Ecuador |

|

|

|

|

|

|

| |

9.375%, 12/15/2015 |

|

|

| 85,000 |

| $ | 91,163 |

|

10.000%, 08/15/2030 |

|

|

| 425,000 |

| 431,375 |

| |

|

|

|

|

|

| 522,538 |

| |

El Salvador - 3.68% |

|

|

|

|

|

|

| |

Republic of El Salvador |

|

|

|

|

|

|

| |

7.750%, 01/24/2023 |

|

|

| 153,000 |

| 171,743 |

| |

7.650%, 06/15/2035 |

|

|

| 513,000 |

| 548,910 |

| |

|

|

|

|

|

| 720,653 |

| |

Gabon - 1.29% |

|

|

|

|

|

|

| |

Republic of Gabonese |

|

|

|

|

|

|

| |

8.200%, 12/12/2017(5) |

|

|

| 235,000 |

| 252,331 |

| |

|

|

|

|

|

|

|

| |

Indonesia - 6.45% |

|

|

|

|

|

|

| |

Indonesia Government Credit Linked Note |

|

|

|

|

|

|

| |

8.705%, 02/20/2010(6)(7) |

| IDR |

| 1,000,000,000 |

| 87,493 |

| |

8.410%, 02/20/2010(6)(7) |

| IDR |

| 1,943,000,000 |

| 169,999 |

| |

8.443%, 02/20/2010(6)(7) |

| IDR |

| 1,954,000,000 |

| 170,962 |

| |

12.500%, 03/15/2013(6) |

| IDR |

| 1,000,000,000 |

| 106,924 |

| |

Republic of Indonesia |

|

|

|

|

|

|

| |

8.500%, 10/12/2035 |

|

|

| 100,000 |

| 107,750 |

| |

7.750%, 01/17/2038 |

|

|

| 635,000 |

| 620,713 |

| |

|

|

|

|

|

| 1,263,841 |

| |

Iraq - 2.37% |

|

|

|

|

|

|

| |

Republic of Iraq |

|

|

|

|

|

|

| |

5.800%, 01/15/2028 |

|

|

| 625,000 |

| 464,063 |

| |

|

|

|

|

|

|

|

| |

Lebanon - 1.11% |

|

|

|

|

|

|

| |

Lebanese Republic |

|

|

|

|

|

|

| |

4.000%, 12/31/2017 |

|

|

| 275,000 |

| 218,213 |

| |

|

|

|

|

|

|

|

| |

Malaysia - 2.62% |

|

|

|

|

|

|

| |

Malaysia |

|

|

|

|

|

|

| |

3.833%, 09/28/2011 |

| MYR |

| 1,455,000 |

| 452,330 |

| |

3.461%, 07/31/2013 |

| MYR |

| 200,000 |

| 60,694 |

| |

|

|

|

|

|

| 513,024 |

| |

10

|

|

|

| Principal |

| Market Value |

| |

Interest Rate/Maturity Date |

| Currency |

| Amount * |

| (Expressed in U.S. $) |

| |

|

|

|

|

|

|

|

| |

Mexico - 3.89% |

|

|

|

|

|

|

| |

United Mexican States |

|

|

|

|

|

|

| |

7.250%, 12/15/2016 |

| MXN |

| 2,090,000 |

| $ | 190,982 |

|

5.625%, 01/15/2017 |

|

|

| 194,000 |

| 199,918 |

| |

8.300%, 08/15/2031 |

|

|

| 140,000 |

| 179,795 |

| |

6.750%, 09/27/2034 |

|

|

| 175,000 |

| 191,406 |

| |

|

|

|

|

|

| 762,101 |

| |

Panama - 4.56% |

|

|

|

|

|

|

| |

Republic of Panama |

|

|

|

|

|

|

| |

7.250%, 03/15/2015 |

|

|

| 457,000 |

| 504,642 |

| |

9.375%, 01/16/2023 |

|

|

| 25,000 |

| 32,750 |

| |

8.875%, 09/30/2027 |

|

|

| 46,000 |

| 59,570 |

| |

9.375%, 04/01/2029 |

|

|

| 16,000 |

| 21,668 |

| |

6.700%, 01/26/2036 |

|

|

| 260,000 |

| 273,650 |

| |

|

|

|

|

|

| 892,280 |

| |

Peru - 4.12% |

|

|

|

|

|

|

| |

Republic of Peru |

|

|

|

|

|

|

| |

9.875%, 02/06/2015 |

|

|

| 115,000 |

| 146,050 |

| |

8.375%, 05/03/2016 |

|

|

| 360,000 |

| 433,800 |

| |

8.750%, 11/21/2033 |

|

|

| 120,000 |

| 159,000 |

| |

6.550%, 03/14/2037 |

|

|

| 65,000 |

| 68,413 |

| |

|

|

|

|

|

| 807,263 |

| |

Philippines - 7.03% |

|

|

|

|

|

|

| |

Republic of Philippines |

|

|

|

|

|

|

| |

8.250%, 01/15/2014 |

|

|

| 207,000 |

| 233,909 |

| |

8.875%, 03/17/2015 |

|

|

| 58,000 |

| 68,150 |

| |

9.375%, 01/18/2017 |

|

|

| 635,000 |

| 782,637 |

| |

7.500%, 09/25/2024 |

|

|

| 145,000 |

| 157,869 |

| |

9.500%, 02/02/2030 |

|

|

| 30,000 |

| 38,962 |

| |

6.375%, 01/15/2032 |

|

|

| 100,000 |

| 96,000 |

| |

|

|

|

|

|

| 1,377,527 |

| |

Russia - 4.42% |

|

|

|

|

|

|

| |

Russian Federation |

|

|

|

|

|

|

| |

7.500%, 03/31/2030 |

|

|

| 762,390 |

| 866,377 |

| |

|

|

|

|

|

|

|

| |

South Africa - 1.85% |

|

|

|

|

|

|

| |

Republic of South Africa |

|

|

|

|

|

|

| |

6.500%, 06/02/2014 |

|

|

| 323,000 |

| 338,141 |

| |

8.500%, 06/23/2017 |

|

|

| 20,000 |

| 23,600 |

| |

|

|

|

|

|

| 361,741 |

| |

11

|

|

|

| Principal |

| Market Value |

| |

Interest Rate/Maturity Date |

| Currency |

| Amount * |

| (Expressed in U.S. $) |

| |

|

|

|

|

|

|

|

| |

Turkey - 4.61% |

|

|

|

|

|

|

| |

Republic of Turkey |

|

|

|

|

|

|

| |

6.750%, 04/03/2018 |

|

|

| 75,000 |

| $ | 74,438 |

|

7.375%, 02/05/2025 |

|

|

| 100,000 |

| 100,563 |

| |

8.000%, 02/14/2034 |

|

|

| 35,000 |

| 36,654 |

| |

6.875%, 03/17/2036 |

|

|

| 485,000 |

| 441,955 |

| |

7.250%, 03/05/2038 |

|

|

| 265,000 |

| 250,343 |

| |

|

|

|

|

|

| 903,953 |

| |

Ukraine - 2.67% |

|

|

|

|

|

|

| |

Ukraine Government |

|

|

|

|

|

|

| |

6.875%, 03/04/2011(5) |

|

|

| 110,000 |

| 112,063 |

| |

6.385%, 06/26/2012 |

|

|

| 100,000 |

| 99,750 |

| |

7.650%, 06/11/2013 |

|

|

| 300,000 |

| 311,625 |

| |

|

|

|

|

|

| 523,438 |

| |

Uruguay - 2.87% |

|

|

|

|

|

|

| |

Republic of Uruguay |

|

|

|

|

|

|

| |

8.000%, 11/18/2022 |

|

|

| 510,000 |

| 561,000 |

| |

7.875%, 01/15/2033(2) |

|

|

| 800 |

| 868 |

| |

|

|

|

|

|

| 561,868 |

| |

Venezuela - 5.44% |

|

|

|

|

|

|

| |

Republic of Venezuela |

|

|

|

|

|

|

| |

5.375%, 08/07/2010 |

|

|

| 130,000 |

| 123,175 |

| |

10.750%, 09/19/2013 |

|

|

| 245,000 |

| 256,025 |

| |

8.500%, 10/08/2014 |

|

|

| 40,000 |

| 37,800 |

| |

7.000%, 12/01/2018 |

|

|

| 75,000 |

| 60,825 |

| |

7.650%, 04/21/2025 |

|

|

| 480,000 |

| 379,200 |

| |

9.375%, 01/13/2034 |

|

|

| 235,000 |

| 207,975 |

| |

|

|

|

|

|

| 1,065,000 |

| |

TOTAL SOVEREIGN DEBT OBLIGATIONS |

|

|

|

|

| 17,016,822 |

| |

|

|

|

|

|

|

|

| |

CORPORATE BONDS - 9.43% |

|

|

|

|

|

|

| |

Brazil - 2.23% |

|

|

|

|

|

|

| |

GTL Trade Finance, Inc. |

|

|

|

|

|

|

| |

7.250%, 10/20/2017(5) |

|

|

| 100,000 |

| 102,375 |

| |

National Development Co. |

|

|

|

|

|

|

| |

6.369%, 06/16/2018(5) |

|

|

| 160,000 |

| 162,000 |

| |

12

|

|

|

| Principal |

| Market Value |

| |

Interest Rate/Maturity Date |

| Currency |

| Amount * |

| (Expressed in U.S. $) |

| |

|

|

|

|

|

|

|

| |

Petrobras International Finance Co. |

|

|

|

|

|

|

| |

5.875%, 03/01/2018 |

|

|

| 175,000 |

| $ | 171,832 |

|

|

|

|

|

|

| 436,207 |

| |

Ireland - 1.56% |

|

|

|

|

|

|

| |

VIP Finance Ireland Ltd. for OJSC Vimpel Communications |

|

|

|

|

|

|

| |

8.375%, 04/30/2013(5)(8) |

|

|

| 300,000 |

| 306,390 |

| |

|

|

|

|

|

|

|

| |

Luxembourg - 2.07% |

|

|

|

|

|

|

| |

RSHB Capital SA for OJSC Russian Agricultural Bank |

|

|

|

|

|

|

| |

7.750%, 05/29/2018(5)(8) |

|

|

| 200,000 |

| 201,800 |

| |

VTB Capital SA |

|

|

|

|

|

|

| |

6.875%, 05/29/2018(5) |

|

|

| 205,000 |

| 204,487 |

| |

|

|

|

|

|

| 406,287 |

| |

Malaysia - 0.96% |

|

|

|

|

|

|

| |

Petronas Capital Ltd. |

|

|

|

|

|

|

| |

7.875%, 05/22/2022 |

|

|

| 155,000 |

| 187,181 |

| |

|

|

|

|

|

|

|

| |

Mexico - 2.05% |

|

|

|

|

|

|

| |

Pemex Project Funding Master Trust |

|

|

|

|

|

|

| |

5.750%, 03/01/2018 |

|

|

| 400,000 |

| 401,520 |

| |

|

|

|

|

|

|

|

| |

Singapore - 0.05% |

|

|

|

|

|

|

| |

DBS Bank Ltd. |

|

|

|

|

|

|

| |

5.000%, 11/15/2019(4)(5) |

|

|

| 10,000 |

| 9,401 |

| |

|

|

|

|

|

|

|

| |

Tunisia - 0.51% |

|

|

|

|

|

|

| |

Banque Centrale de Tunisie |

|

|

|

|

|

|

| |

7.375%, 04/25/2012 |

|

|

| 60,000 |

| 64,950 |

| |

8.250%, 09/19/2027 |

|

|

| 30,000 |

| 34,849 |

| |

|

|

|

|

|

| 99,799 |

| |

TOTAL CORPORATE BONDS |

|

|

|

|

| 1,846,785 |

| |

|

|

|

|

|

|

|

| |

MONEY MARKET MUTUAL FUNDS - 7.05% |

|

|

|

|

|

|

| |

Dreyfus Cash Advantage Plus Fund(2.83% 7-day yield) |

|

|

| 1,381,709 |

| 1,381,709 |

| |

|

|

|

|

|

|

|

| |

TOTAL MONEY MARKET MUTUAL FUNDS |

|

|

|

|

| 1,381,709 |

| |

13

|

|

|

| Principal |

| Market Value |

| |

Interest Rate/Maturity Date |

| Currency |

| Amount * |

| (Expressed in U.S. $) |

| |

|

|

|

|

|

|

|

|

|

Total Investments - 103.36% |

|

|

|

|

| $ | 20,245,316 |

|

Liabilities in Excess of Other Assets - (3.36)% |

|

|

|

|

| $ | (657,910 | ) |

|

|

|

|

|

|

|

| |

Net Assets - 100% |

|

|

|

|

| $ | 19,587,406 |

|

* |

| The principal/contract amount of each security is stated in the currency in which the bond is denominated (U.S. Dollar unless otherwise notated). See below. |

BRL | Brazilian Real |

COP | Colombian Peso |

EUR | Euro Currency |

IDR | Indonesian Rupiah |

ITL | Italian Lira |

MXN | Mexican Peso |

MYR | Malaysian Ringgit |

(1) | Security is currently in default/non-income producing. |

(2) | Pay-in-kind securities. |

(3) | Step Bond. Coupon increases periodically based upon a predetermined schedule. Interest rate disclosed is the stated rate at a set date in the future. |

(4) | Floating or variable rate security. Interest rate disclosed is that which is in effect at May 31, 2008. |

(5) | Security exempt from registration under Rule 144A of the Securities Act of 1933. Under procedures approved by the Board of Trustees, such securities have been determined to be liquid by the Investment Advisor and may be resold, normally to qualified buyers in transactions exempt from registration. Total market value of Rule 144Asecurities amounts to $1,350,847, which represents approximately 6.90% of net assets as of May 31, 2008. |

(6) | The security is issued by JP Morgan Securities, Inc. |

(7) | Zero coupon bond reflects effective yield on the date of purchase. |

(8) | “OJSC” Open Joint Stock Company - A business whose capital is held in transferable shares of stock by its joint owners. |

See Notes to Financial Statements

14

OUTSTANDING FORWARD FOREIGN CURRENCY CONTRACTS

Contract |

| Contracted |

| Purchase/Sale |

| Expiration |

| Value on |

| Current |

| Unrealized |

| |||

Description |

| Amount |

| Contract |

| Date |

| Settlement Date |

| Value |

| Depreciation |

| |||

BRL |

| 1,460,817 | (BRL) | Purchase |

| 06/03/2008 |

| $ | 896,536 |

| $ | 894,928 |

| $ | (1,608 | ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

BRL |

| 1,460,817 | (BRL) | Sale |

| 06/03/2008 |

| $ | 870,000 |

| $ | 894,928 |

| $ | (24,928 | ) |

COP |

| 414,460,000 | (COP) | Sale |

| 06/19/2008 |

| 230,000 |

| 236,373 |

| (6,373 | ) | |||

EUR |

| 661,850 | (EUR) | Sale |

| 07/16/2008 |

| 970,385 |

| 1,026,137 |

| (55,752 | ) | |||

|

|

|

|

|

|

|

|

|

| $ | 2,157,438 |

| $ | (87,053 | ) | |

15

Statement of Investments

May 31, 2008 |

| High Yield Bond Fund |

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

CORPORATE BONDS - 81.39% |

|

|

|

|

| |

Advertising - 2.15% |

|

|

|

|

| |

Interep National Radio Sales, Inc. |

|

|

|

|

| |

Series B, 10.000%, 07/01/2008 |

| 4,000 |

| $ | 2,700 |

|

Lamar Media Corp. |

|

|

|

|

| |

6.625%, 08/15/2015 |

| 710,000 |

| 672,725 |

| |

Series B, 6.625%, 08/15/2015 |

| 330,000 |

| 312,675 |

| |

Series C, 6.625%, 08/15/2015 |

| 200,000 |

| 189,500 |

| |

RH Donnelley Corp. |

|

|

|

|

| |

Series A-1, 6.875%, 01/15/2013 |

| 250,000 |

| 168,750 |

| |

Series A-2, 6.875%, 01/15/2013 |

| 25,000 |

| 16,875 |

| |

Series A-3, 8.875%, 01/15/2016 |

| 380,000 |

| 262,200 |

| |

8.875%, 10/15/2017(1) |

| 1,000,000 |

| 675,000 |

| |

|

|

|

| 2,300,425 |

| |

Aerospace - Defense - 3.58% |

|

|

|

|

| |

Alliant Techsystems, Inc. |

|

|

|

|

| |

6.750%, 04/01/2016 |

| 390,000 |

| 387,075 |

| |

DRS Technologies, Inc. |

|

|

|

|

| |

6.875%, 11/01/2013 |

| 50,000 |

| 51,375 |

| |

6.625%, 02/01/2016 |

| 20,000 |

| 20,950 |

| |

7.625%, 02/01/2018 |

| 335,000 |

| 362,638 |

| |

Esterline Technologies Corp. |

|

|

|

|

| |

7.750%, 06/15/2013 |

| 325,000 |

| 332,313 |

| |

6.625%, 03/01/2017 |

| 150,000 |

| 152,250 |

| |

L-3 Communications Corp. |

|

|

|

|

| |

7.625%, 06/15/2012 |

| 1,531,000 |

| 1,563,533 |

| |

Series B, 6.375%, 10/15/2015 |

| 100,000 |

| 96,875 |

| |

Moog, Inc. |

|

|

|

|

| |

6.250%, 01/15/2015 |

| 410,000 |

| 397,700 |

| |

TransDigm, Inc. |

|

|

|

|

| |

7.750%, 07/15/2014 |

| 450,000 |

| 462,375 |

| |

|

|

|

| 3,827,084 |

| |

Agriculture - 0.72% |

|

|

|

|

| |

Reynolds American, Inc. |

|

|

|

|

| |

7.625%, 06/01/2016 |

| 730,000 |

| 765,878 |

| |

|

|

|

|

|

| |

Airlines - 0.00%(2) |

|

|

|

|

| |

Continental Airlines, Inc. |

|

|

|

|

| |

Series 981C, 6.541%, 09/15/2009 |

| 743 |

| 743 |

| |

16

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Apparel - 0.77% |

|

|

|

|

| |

Levi Strauss & Co. |

|

|

|

|

| |

9.750%, 01/15/2015 |

| 785,000 |

| $ | 826,213 |

|

|

|

|

|

|

| |

Auto Manufacturers - 1.29% |

|

|

|

|

| |

Ford Motor Co. |

|

|

|

|

| |

7.450%, 07/16/2031 |

| 410,000 |

| 285,975 |

| |

8.900%, 01/15/2032 |

| 25,000 |

| 18,875 |

| |

General Motors Corp. |

|

|

|

|

| |

8.375%, 07/15/2033 |

| 1,560,000 |

| 1,076,400 |

| |

|

|

|

| 1,381,250 |

| |

Beverages - 1.13% |

|

|

|

|

| |

Constellation Brands, Inc. |

|

|

|

|

| |

8.375%, 12/15/2014 |

| 675,000 |

| 708,750 |

| |

7.250%, 09/01/2016 |

| 445,000 |

| 445,000 |

| |

7.250%, 05/15/2017 |

| 50,000 |

| 49,625 |

| |

|

|

|

| 1,203,375 |

| |

Building Materials - 0.38% |

|

|

|

|

| |

Associated Materials, Inc. |

|

|

|

|

| |

11.250%, 03/01/2014(3) |

| 130,000 |

| 89,375 |

| |

Interline Brands, Inc. |

|

|

|

|

| |

8.125%, 06/15/2014 |

| 175,000 |

| 171,500 |

| |

Nortek, Inc. |

|

|

|

|

| |

8.500%, 09/01/2014 |

| 150,000 |

| 105,750 |

| |

NTK Holdings, Inc. |

|

|

|

|

| |

10.750%, 03/01/2014(3) |

| 75,000 |

| 37,594 |

| |

|

|

|

| 404,219 |

| |

Chemicals - 3.03% |

|

|

|

|

| |

Airgas, Inc. |

|

|

|

|

| |

6.250%, 07/15/2014 |

| 425,000 |

| 426,063 |

| |

Hercules, Inc. |

|

|

|

|

| |

6.750%, 10/15/2029 |

| 475,000 |

| 456,000 |

| |

Lyondell Chemical Co. |

|

|

|

|

| |

8.375%, 08/15/2015(1) |

| 525,000 |

| 378,000 |

| |

MacDermid, Inc. |

|

|

|

|

| |

9.500%, 04/15/2017(1) |

| 225,000 |

| 219,375 |

| |

Nalco Co. |

|

|

|

|

| |

7.750%, 11/15/2011 |

| 375,000 |

| 384,375 |

| |

8.875%, 11/15/2013 |

| 355,000 |

| 375,413 |

| |

17

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

NewMarket Corp. |

|

|

|

|

| |

7.125%, 12/15/2016 |

| 405,000 |

| $ | 400,950 |

|

Nova Chemicals Corp. |

|

|

|

|

| |

6.500%, 01/15/2012 |

| 645,000 |

| 603,074 |

| |

|

|

|

| 3,243,250 |

| |

Coal - 1.04% |

|

|

|

|

| |

Arch Western Finance LLC |

|

|

|

|

| |

6.750%, 07/01/2013(4) |

| 450,000 |

| 446,625 |

| |

Peabody Energy Corp. |

|

|

|

|

| |

Series B, 6.875%, 03/15/2013 |

| 490,000 |

| 497,350 |

| |

7.375%, 11/01/2016 |

| 35,000 |

| 35,963 |

| |

7.875%, 11/01/2026 |

| 125,000 |

| 127,500 |

| |

|

|

|

| 1,107,438 |

| |

Commercial Services - 4.08% |

|

|

|

|

| |

ARAMARK Corp. |

|

|

|

|

| |

6.373%, 02/01/2015(4) |

| 65,000 |

| 62,725 |

| |

8.500%, 02/01/2015 |

| 780,000 |

| 802,425 |

| |

Cadmus Communications Corp. |

|

|

|

|

| |

8.375%, 06/15/2014 |

| 200,000 |

| 170,000 |

| |

Cenveo Corp. |

|

|

|

|

| |

7.875%, 12/01/2013 |

| 100,000 |

| 87,250 |

| |

Corrections Corp. of America |

|

|

|

|

| |

7.500%, 05/01/2011 |

| 10,000 |

| 10,125 |

| |

6.250%, 03/15/2013 |

| 999,000 |

| 989,009 |

| |

6.750%, 01/31/2014 |

| 75,000 |

| 75,188 |

| |

Deluxe Corp. |

|

|

|

|

| |

7.375%, 06/01/2015 |

| 345,000 |

| 316,106 |

| |

Education Management, LLC |

|

|

|

|

| |

8.750%, 06/01/2014 |

| 475,000 |

| 459,563 |

| |

10.250%, 06/01/2016 |

| 195,000 |

| 186,713 |

| |

The Geo Group, Inc. |

|

|

|

|

| |

8.250%, 07/15/2013 |

| 275,000 |

| 283,250 |

| |

Iron Mountain, Inc. |

|

|

|

|

| |

8.625%, 04/01/2013 |

| 25,000 |

| 25,500 |

| |

7.750%, 01/15/2015 |

| 575,000 |

| 589,375 |

| |

8.750%, 07/15/2018 |

| 285,000 |

| 304,950 |

| |

|

|

|

| 4,362,179 |

| |

Distribution - Wholesale - 0.34% |

|

|

|

|

| |

Baker & Taylor, Inc. |

|

|

|

|

| |

11.500%, 07/01/2013(1) |

| 395,000 |

| 361,425 |

| |

18

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Diversified Financial Services - 5.91% |

|

|

|

|

| |

AmeriCredit Corp. |

|

|

|

|

| |

8.500%, 07/01/2015 |

| 110,000 |

| $ | 89,238 |

|

Ford Motor Credit Co. LLC |

|

|

|

|

| |

7.375%, 10/28/2009 |

| 275,000 |

| 267,923 |

| |

9.875%, 08/10/2011 |

| 1,075,000 |

| 1,017,861 |

| |

8.000%, 12/15/2016 |

| 460,000 |

| 386,741 |

| |

Global Cash Access LLC |

|

|

|

|

| |

8.750%, 03/15/2012 |

| 448,000 |

| 448,000 |

| |

GMAC LLC |

|

|

|

|

| |

5.850%, 01/14/2009 |

| 450,000 |

| 442,121 |

| |

5.625%, 05/15/2009 |

| 224,000 |

| 216,278 |

| |

7.250%, 03/02/2011 |

| 125,000 |

| 107,130 |

| |

6.875%, 09/15/2011 |

| 375,000 |

| 316,379 |

| |

6.000%, 12/15/2011 |

| 150,000 |

| 120,802 |

| |

7.000%, 02/01/2012 |

| 375,000 |

| 306,370 |

| |

6.625%, 05/15/2012 |

| 105,000 |

| 84,716 |

| |

8.000%, 11/01/2031 |

| 20,000 |

| 15,356 |

| |

Hughes Network Systems LLC |

|

|

|

|

| |

9.500%, 04/15/2014 |

| 160,000 |

| 162,400 |

| |

Petroplus Finance Ltd. |

|

|

|

|

| |

6.750%, 05/01/2014(1) |

| 110,000 |

| 101,475 |

| |

7.000%, 05/01/2017(1) |

| 550,000 |

| 499,125 |

| |

Pinnacle Foods Finance LLC |

|

|

|

|

| |

9.250%, 04/01/2015 |

| 475,000 |

| 439,375 |

| |

Rainbow National Services LLC |

|

|

|

|

| |

8.750%, 09/01/2012(1) |

| 200,000 |

| 206,000 |

| |

Sensus Metering Systems, Inc. |

|

|

|

|

| |

8.625%, 12/15/2013 |

| 125,000 |

| 121,563 |

| |

Southern Star Central Corp. |

|

|

|

|

| |

6.750%, 03/01/2016 |

| 25,000 |

| 24,219 |

| |

6.750%, 03/01/2016(1) |

| 475,000 |

| 460,156 |

| |

Vanguard Health Holding Co. II LLC |

|

|

|

|

| |

9.000%, 10/01/2014 |

| 465,000 |

| 480,113 |

| |

|

|

|

| 6,313,341 |

| |

Electric - 5.51% |

|

|

|

|

| |

TheAES Corp. |

|

|

|

|

| |

9.375%, 09/15/2010 |

| 118,000 |

| 125,670 |

| |

8.875%, 02/15/2011 |

| 131,000 |

| 137,878 |

| |

7.750%, 03/01/2014 |

| 275,000 |

| 276,375 |

| |

8.000%, 10/15/2017 |

| 850,000 |

| 857,438 |

| |

19

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Edison Mission Energy |

|

|

|

|

| |

7.500%, 06/15/2013 |

| 55,000 |

| $ | 56,375 |

|

7.200%, 05/15/2019 |

| 290,000 |

| 284,200 |

| |

7.625%, 05/15/2027 |

| 960,000 |

| 909,599 |

| |

Mirant Americas Generation LLC |

|

|

|

|

| |

8.500%, 10/01/2021 |

| 175,000 |

| 169,750 |

| |

Mirant North America LLC |

|

|

|

|

| |

7.375%, 12/31/2013 |

| 765,000 |

| 774,563 |

| |

NRG Energy, Inc. |

|

|

|

|

| |

7.250%, 02/01/2014 |

| 425,000 |

| 417,563 |

| |

7.375%, 02/01/2016 |

| 640,000 |

| 625,600 |

| |

Texas Competitive Electric Holdings Co. LLC |

|

|

|

|

| |

10.250%, 11/01/2015(1) |

| 1,225,000 |

| 1,257,155 |

| |

|

|

|

| 5,892,166 |

| |

Electrical Components & Equipment - 0.27% |

|

|

|

|

| |

Belden, Inc. |

|

|

|

|

| |

7.000%, 03/15/2017 |

| 300,000 |

| 294,000 |

| |

|

|

|

|

|

| |

Entertainment - 3.35% |

|

|

|

|

| |

AMC Entertainment, Inc. |

|

|

|

|

| |

8.000%, 03/01/2014 |

| 50,000 |

| 45,500 |

| |

11.000%, 02/01/2016 |

| 240,000 |

| 244,800 |

| |

Cinemark, Inc. |

|

|

|

|

| |

9.750%, 03/15/2014(3) |

| 735,000 |

| 701,925 |

| |

Great Canadian Gaming Corp. |

|

|

|

|

| |

7.250%, 02/15/2015(1) |

| 430,000 |

| 419,250 |

| |

Isle of Capri Casinos, Inc. |

|

|

|

|

| |

7.000%, 03/01/2014 |

| 170,000 |

| 130,475 |

| |

Marquee Holdings, Inc. |

|

|

|

|

| |

12.000%, 08/15/2014(3) |

| 540,000 |

| 437,400 |

| |

Penn National Gaming, Inc. |

|

|

|

|

| |

6.875%, 12/01/2011 |

| 25,000 |

| 24,625 |

| |

Pinnacle Entertainment, Inc. |

|

|

|

|

| |

8.250%, 03/15/2012 |

| 425,000 |

| 430,313 |

| |

8.750%, 10/01/2013 |

| 175,000 |

| 180,250 |

| |

7.500%, 06/15/2015(1) |

| 230,000 |

| 190,900 |

| |

Seneca Gaming Corp. |

|

|

|

|

| |

7.250%, 05/01/2012 |

| 695,000 |

| 674,150 |

| |

Series B, 7.250%, 05/01/2012 |

| 105,000 |

| 101,850 |

| |

|

|

|

| 3,581,438 |

| |

20

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Environmental Control - 0.92% |

|

|

|

|

| |

Allied Waste North America, Inc. |

|

|

|

|

| |

7.250%, 03/15/2015 |

| 900,000 |

| $ | 897,750 |

|

Series B, 7.125%, 05/15/2016 |

| 50,000 |

| 49,375 |

| |

Browning-Ferris Industries, Inc. |

|

|

|

|

| |

9.250%, 05/01/2021 |

| 35,000 |

| 36,356 |

| |

Safety-Kleen Services, Inc. |

|

|

|

|

| |

9.250%, 06/01/2008(5) |

| 50,000 |

| 10 |

| |

|

|

|

| 983,491 |

| |

Food - 1.58% |

|

|

|

|

| |

Del Monte Corp. |

|

|

|

|

| |

8.625%, 12/15/2012 |

| 625,000 |

| 643,749 |

| |

Dole Food Co., Inc. |

|

|

|

|

| |

8.625%, 05/01/2009 |

| 300,000 |

| 295,500 |

| |

7.250%, 06/15/2010 |

| 325,000 |

| 303,063 |

| |

8.750%, 07/15/2013 |

| 65,000 |

| 58,013 |

| |

Pilgrim’s Pride Corp. |

|

|

|

|

| |

9.250%, 11/15/2013 |

| 100,000 |

| 105,750 |

| |

8.375%, 05/01/2017 |

| 325,000 |

| 285,188 |

| |

|

|

|

| 1,691,263 |

| |

Forest Products & Paper - 0.75% |

|

|

|

|

| |

Appleton Papers, Inc. |

|

|

|

|

| |

8.125%, 06/15/2011 |

| 120,000 |

| 116,400 |

| |

Series B, 9.750%, 06/15/2014 |

| 200,000 |

| 192,000 |

| |

Buckeye Technologies, Inc. |

|

|

|

|

| |

8.000%, 10/15/2010 |

| 111,000 |

| 111,555 |

| |

8.500%, 10/01/2013 |

| 350,000 |

| 353,500 |

| |

NewPage Corp. |

|

|

|

|

| |

10.000%, 05/01/2012 |

| 30,000 |

| 32,100 |

| |

|

|

|

| 805,555 |

| |

Healthcare-Products - 1.53% |

|

|

|

|

| |

Accellent, Inc. |

|

|

|

|

| |

10.500%, 12/01/2013 |

| 430,000 |

| 394,525 |

| |

Advanced Medical Optics, Inc. |

|

|

|

|

| |

7.500%, 05/01/2017 |

| 475,000 |

| 446,500 |

| |

Boston Scientific Corp. |

|

|

|

|

| |

6.000%, 06/15/2011 |

| 675,000 |

| 664,875 |

| |

6.400%, 06/15/2016 |

| 50,000 |

| 47,875 |

| |

7.000%, 11/15/2035 |

| 100,000 |

| 86,500 |

| |

|

|

|

| 1,640,275 |

| |

21

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Healthcare-Services - 3.48% |

|

|

|

|

| |

Community Health Systems, Inc. |

|

|

|

|

| |

8.875%, 07/15/2015 |

| 625,000 |

| $ | 647,656 |

|

DaVita, Inc. |

|

|

|

|

| |

7.250%, 03/15/2015 |

| 920,000 |

| 903,900 |

| |

HCA, Inc. |

|

|

|

|

| |

9.250%, 11/15/2016 |

| 500,000 |

| 529,375 |

| |

9.625%, 11/15/2016(6) |

| 25,000 |

| 26,438 |

| |

National Mentor Holdings, Inc. |

|

|

|

|

| |

11.250%, 07/01/2014 |

| 175,000 |

| 182,875 |

| |

Psychiatric Solutions, Inc. |

|

|

|

|

| |

7.750%, 07/15/2015 |

| 680,000 |

| 700,400 |

| |

United Surgical Partners International, Inc. |

|

|

|

|

| |

8.875%, 05/01/2017 |

| 125,000 |

| 123,125 |

| |

9.250%, 05/01/2017(6) |

| 620,000 |

| 610,700 |

| |

|

|

|

| 3,724,469 |

| |

Holding Companies-Diversified - 0.12% |

|

|

|

|

| |

Atlantic Broadband Finance LLC |

|

|

|

|

| |

9.375%, 01/15/2014 |

| 135,000 |

| 126,394 |

| |

|

|

|

|

|

| |

Home Furnishings - 0.14% |

|

|

|

|

| |

Norcraft Cos LP |

|

|

|

|

| |

9.000%, 11/01/2011 |

| 35,000 |

| 35,700 |

| |

Norcraft Holdings LP |

|

|

|

|

| |

9.750%, 09/01/2012(3) |

| 125,000 |

| 116,875 |

| |

|

|

|

| 152,575 |

| |

Internet - 0.05% |

|

|

|

|

| |

FTD, Inc. |

|

|

|

|

| |

7.750%, 02/15/2014 |

| 50,000 |

| 50,500 |

| |

|

|

|

|

|

| |

Investment Companies - 0.43% |

|

|

|

|

| |

Intelsat Jackson Holdings Ltd. |

|

|

|

|

| |

11.250%, 06/15/2016 |

| 450,000 |

| 461,250 |

| |

|

|

|

|

|

| |

Iron/Steel - 1.03% |

|

|

|

|

| |

RathGibson, Inc. |

|

|

|

|

| |

11.250%, 02/15/2014 |

| 400,000 |

| 396,000 |

| |

22

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Steel Dynamics, Inc. |

|

|

|

|

| |

7.375%, 11/01/2012(1) |

| 450,000 |

| $ | 455,625 |

|

6.750%, 04/01/2015 |

| 250,000 |

| 245,625 |

| |

|

|

|

| 1,097,250 |

| |

Lodging - 0.96% |

|

|

|

|

| |

Caesars Entertainment, Inc. |

|

|

|

|

| |

7.875%, 03/15/2010 |

| 200,000 |

| 190,500 |

| |

MGM Mirage |

|

|

|

|

| |

6.000%, 10/01/2009 |

| 35,000 |

| 34,956 |

| |

8.500%, 09/15/2010 |

| 225,000 |

| 230,906 |

| |

8.375%, 02/01/2011 |

| 75,000 |

| 74,719 |

| |

Station Casinos, Inc. |

|

|

|

|

| |

6.000%, 04/01/2012 |

| 60,000 |

| 50,700 |

| |

7.750%, 08/15/2016 |

| 525,000 |

| 439,688 |

| |

|

|

|

| 1,021,469 |

| |

Machinery - Construction & Mining - 0.53% |

|

|

|

|

| |

Terex Corp. |

|

|

|

|

| |

8.000%, 11/15/2017 |

| 550,000 |

| 565,125 |

| |

|

|

|

|

|

| |

Media - 6.82% |

|

|

|

|

| |

CanWest MediaWorks, Inc. |

|

|

|

|

| |

8.000%, 09/15/2012 |

| 450,000 |

| 415,125 |

| |

CCH I Holdings LLC |

|

|

|

|

| |

10.000%, 05/15/2014 |

| 25,000 |

| 15,875 |

| |

CCH I Holdings LLC |

|

|

|

|

| |

11.750%, 05/15/2014(3) |

| 230,000 |

| 152,950 |

| |

12.125%, 01/15/2015(3) |

| 25,000 |

| 16,375 |

| |

CCH I Holdings, LLC |

|

|

|

|

| |

11.000%, 10/01/2015 |

| 945,000 |

| 807,974 |

| |

CCO Holdings LLC |

|

|

|

|

| |

8.750%, 11/15/2013 |

| 75,000 |

| 71,625 |

| |

Charter Communications Operating, LLC |

|

|

|

|

| |

8.375%, 04/30/2014(1) |

| 50,000 |

| 49,375 |

| |

CSC Holdings, Inc. |

|

|

|

|

| |

Series B, 7.625%, 04/01/2011 |

| 575,000 |

| 577,875 |

| |

6.750%, 04/15/2012 |

| 175,000 |

| 170,625 |

| |

Dex Media, Inc. |

|

|

|

|

| |

8.000%, 11/15/2013 |

| 20,000 |

| 16,000 |

| |

9.000%, 11/15/2013(3) |

| 100,000 |

| 78,000 |

| |

9.000%, 11/15/2013(3) |

| 150,000 |

| 117,000 |

| |

23

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Dex Media West LLC |

|

|

|

|

| |

Series B, 8.500%, 08/15/2010 |

| 20,000 |

| $ | 20,150 |

|

Series B, 9.875%, 08/15/2013 |

| 44,000 |

| 42,515 |

| |

Echostar DBS Corp. |

|

|

|

|

| |

5.750%, 10/01/2008 |

| 55,000 |

| 55,138 |

| |

7.000%, 10/01/2013 |

| 25,000 |

| 24,313 |

| |

6.625%, 10/01/2014 |

| 350,000 |

| 330,750 |

| |

7.125%, 02/01/2016 |

| 610,000 |

| 585,600 |

| |

Idearc, Inc. |

|

|

|

|

| |

8.000%, 11/15/2016 |

| 940,000 |

| 676,799 |

| |

Radio One, Inc. |

|

|

|

|

| |

Series B, 8.875%, 07/01/2011 |

| 430,000 |

| 362,813 |

| |

The Reader’s Digest Association, Inc. |

|

|

|

|

| |

9.000%, 02/15/2017(1) |

| 470,000 |

| 363,075 |

| |

Rogers Cable, Inc. |

|

|

|

|

| |

8.750%, 05/01/2032 |

| 175,000 |

| 197,599 |

| |

Salem Communications Holding Corp. |

|

|

|

|

| |

7.750%, 12/15/2010 |

| 445,000 |

| 418,856 |

| |

Sinclair Television Group, Inc. |

|

|

|

|

| |

8.000%, 03/15/2012 |

| 358,000 |

| 366,055 |

| |

Univision Communications, Inc. |

|

|

|

|

| |

9.750%, 03/15/2015(1)(6) |

| 675,000 |

| 513,000 |

| |

Videotron Ltee |

|

|

|

|

| |

6.875%, 01/15/2014 |

| 670,000 |

| 664,974 |

| |

6.375%, 12/15/2015 |

| 185,000 |

| 177,600 |

| |

|

|

|

| 7,288,036 |

| |

Miscellaneous Manufacturers - 1.11% |

|

|

|

|

| |

Blount, Inc. |

|

|

|

|

| |

8.875%, 08/01/2012 |

| 50,000 |

| 51,000 |

| |

Koppers, Inc. |

|

|

|

|

| |

9.875%, 10/15/2013 |

| 50,000 |

| 53,250 |

| |

Koppers Holdings, Inc. |

|

|

|

|

| |

9.875%, 11/15/2014(3) |

| 250,000 |

| 231,250 |

| |

RBS Global, Inc. |

|

|

|

|

| |

9.500%, 08/01/2014 |

| 460,000 |

| 463,450 |

| |

SPX Corp. |

|

|

|

|

| |

7.625%, 12/15/2014(1) |

| 375,000 |

| 390,469 |

| |

|

|

|

| 1,189,419 |

| |

Office-Business Equipment - 1.46% |

|

|

|

|

| |

Xerox Capital Trust I |

|

|

|

|

| |

8.000%, 02/01/2027 |

| 1,595,000 |

| 1,556,785 |

| |

24

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Office Furnishings - 0.06% |

|

|

|

|

| |

Interface, Inc. |

|

|

|

|

| |

9.500%, 02/01/2014 |

| 65,000 |

| $ | 68,250 |

|

|

|

|

|

|

| |

Oil & Gas - 5.49% |

|

|

|

|

| |

Chaparral Energy, Inc. |

|

|

|

|

| |

8.500%, 12/01/2015 |

| 625,000 |

| 556,249 |

| |

9.375%, 02/01/2017(4) |

| 145,000 |

| 129,413 |

| |

Chesapeake Energy Corp. |

|

|

|

|

| |

7.625%, 07/15/2013 |

| 275,000 |

| 281,188 |

| |

7.000%, 08/15/2014 |

| 50,000 |

| 50,063 |

| |

7.750%, 01/15/2015 |

| 550,000 |

| 572,687 |

| |

6.375%, 06/15/2015 |

| 150,000 |

| 144,375 |

| |

6.250%, 01/15/2018 |

| 285,000 |

| 268,613 |

| |

7.250%, 12/15/2018 |

| 550,000 |

| 548,624 |

| |

EXCO Resources, Inc. |

|

|

|

|

| |

7.250%, 01/15/2011 |

| 900,000 |

| 887,624 |

| |

Hilcorp Energy I LP |

|

|

|

|

| |

7.750%, 11/01/2015(1) |

| 270,000 |

| 265,275 |

| |

9.000%, 06/01/2016(1) |

| 205,000 |

| 213,713 |

| |

Newfield Exploration Co. |

|

|

|

|

| |

7.125%, 05/15/2018 |

| 450,000 |

| 446,063 |

| |

Pioneer Natural Resources Co. |

|

|

|

|

| |

6.650%, 03/15/2017 |

| 425,000 |

| 410,259 |

| |

Range Resources Corp. |

|

|

|

|

| |

7.250%, 05/01/2018 |

| 225,000 |

| 229,500 |

| |

SandRidge Energy, Inc. |

|

|

|

|

| |

8.000%, 06/01/2018(1) |

| 425,000 |

| 432,438 |

| |

Stone Energy Corp. |

|

|

|

|

| |

8.250%, 12/15/2011 |

| 425,000 |

| 429,250 |

| |

|

|

|

| 5,865,334 |

| |

Oil & Gas Services - 1.16% |

|

|

|

|

| |

Complete Production Services, Inc. |

|

|

|

|

| |

8.000%, 12/15/2016 |

| 425,000 |

| 432,438 |

| |

Dresser-Rand Group, Inc. |

|

|

|

|

| |

7.375%, 11/01/2014 |

| 805,000 |

| 805,000 |

| |

|

|

|

| 1,237,438 |

| |

Packaging & Containers - 2.00% |

|

|

|

|

| |

CrownAmericas LLC |

|

|

|

|

| |

7.750%, 11/15/2015 |

| 430,000 |

| 453,650 |

| |

25

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Graphic Packaging International, Inc. |

|

|

|

|

| |

8.500%, 08/15/2011 |

| 410,000 |

| $ | 416,150 |

|

9.500%, 08/15/2013 |

| 260,000 |

| 263,250 |

| |

Owens Brockway Glass Container, Inc. |

|

|

|

|

| |

8.250%, 05/15/2013 |

| 500,000 |

| 519,999 |

| |

Series $, 6.750%, 12/01/2014 |

| 275,000 |

| 279,813 |

| |

Owens-Illinois, Inc. |

|

|

|

|

| |

7.500%, 05/15/2010 |

| 50,000 |

| 51,250 |

| |

Packaging Dynamics Finance Corp. |

|

|

|

|

| |

10.000%, 05/01/2016(1) |

| 225,000 |

| 149,625 |

| |

Radnor Holdings Corp. |

|

|

|

|

| |

11.000%, 03/15/2010(5) |

| 25,000 |

| 313 |

| |

|

|

|

| 2,134,050 |

| |

Pharmaceuticals - 0.57% |

|

|

|

|

| |

Valeant Pharmaceuticals International |

|

|

|

|

| |

7.000%, 12/15/2011 |

| 630,000 |

| 611,100 |

| |

|

|

|

|

|

| |

Pipelines - 4.59% |

|

|

|

|

| |

ANR Pipeline Co. |

|

|

|

|

| |

7.375%, 02/15/2024 |

| 60,000 |

| 63,755 |

| |

7.000%, 06/01/2025 |

| 10,000 |

| 10,279 |

| |

Atlas Pipeline Partners LP |

|

|

|

|

| |

8.125%, 12/15/2015 |

| 400,000 |

| 415,000 |

| |

Copano Energy LLC |

|

|

|

|

| |

7.750%, 06/01/2018(1) |

| 450,000 |

| 449,438 |

| |

Dynegy Holdings, Inc. |

|

|

|

|

| |

8.375%, 05/01/2016 |

| 920,000 |

| 929,200 |

| |

7.125%, 05/15/2018 |

| 75,000 |

| 69,563 |

| |

7.750%, 06/01/2019 |

| 160,000 |

| 152,400 |

| |

7.625%, 10/15/2026 |

| 25,000 |

| 22,375 |

| |

El Paso Corp. |

|

|

|

|

| |

7.250%, 06/01/2018 |

| 175,000 |

| 176,531 |

| |

7.800%, 08/01/2031 |

| 800,000 |

| 809,262 |

| |

Targa Resources, Inc. |

|

|

|

|

| |

8.500%, 11/01/2013 |

| 630,000 |

| 609,525 |

| |

Tennessee Gas Pipeline Co. |

|

|

|

|

| |

8.375%, 06/15/2032 |

| 150,000 |

| 167,114 |

| |

Transcontinental Gas Pipe Line Corp. |

|

|

|

|

| |

6.400%, 04/15/2016 |

| 50,000 |

| 50,625 |

| |

26

|

| Principal |

|

|

| |

Interest Rate/Maturity Date |

| Amount |

| Market Value |

| |

|

|

|

|

|

| |

Williams Cos, Inc. |

|

|

|

|

| |

7.875%, 09/01/2021 |

| 625,000 |

| $ | 684,375 |

|

8.750%, 03/15/2032 |

| 250,000 |

| 292,500 |

| |

|

|

|

| 4,901,942 |

| |

Real Estate Investment Trusts - 1.66% |

|

|

|

|

| |

Felcor Lodging LP |

|

|

|

|

| |

8.500%, 06/01/2011 |

| 525,000 |

| 536,813 |

| |