united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22153

Dunham Funds

(Exact name of registrant as specified in charter)

6256 Greenwich Dr. Ste 550, San Diego, CA 92122

(Address of principal executive offices) (Zip code)

Timothy Burdick

Ultimus Fund Solutions LLC., 4221 N 203rd St., Suite 100, Elkhorn, NE 68022

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2649

Date of fiscal year end: 10/31

Date of reporting period: 10/31/22

Item 1. Reports to Stockholders.

Dear Fellow Shareholders:

One of the persistent themes throughout this fiscal year has been “uncertainty”. This was and still is applicable to the outlook for containing substantially-elevated inflation, the War in Ukraine, and the severity of a U.S. recession (and a global recession). These significant unknowns have translated into volatile declines in both equity and bond markets around the globe. Although there have been some parallels identified between the current economic environment and the Global Financial Crisis, one of the notable contrasts relates to how bond markets have suffered. In the Global Financial Crisis, adequate refuge could be found in investment-grade bonds. However, in the current environment global bonds1 on average were punished even more than global stocks2. The same was true when solely considering the past 12 months for the United States – U.S. investment-grade bonds3 fell more than U.S. stocks4, in general. Without bonds as a potential safe haven, on the surface it appeared that many investors were relegated to a nearly 20 percent decline irrespective of their allocation to bonds versus equities. However, as we have exposure to numerous asset classes below the broad categorizations of “equities” and “bonds”, this environment provided opportunities for some asset classes and strategies to shine – or to at least provide significant downside protection where broad bonds failed to do so.

As the Federal Open Market Committee pursued aggressive monetary policy in its attempt to cool rampantly rising inflation, securities with the highest sensitivities to changes in interest rates experienced substantial principal declines. However, some asset classes within the bond market, such as bank loans5, have coupons that adjust along with the rising rates. This resulted in those securities on average experiencing a much more muted decline during this fiscal year. Similarly, fixed income-oriented strategies that do not primarily rely on collecting meaningful yields, such as long/short credit strategies, also found opportunities to prevail on a relative basis. A commonality with the Global Financial Crisis was the high correlations between most equity asset classes. This does not mean that all equity styles or capitalizations performed the same, but they broadly traveled in the same direction during the fiscal year, despite having disparate fundamental drivers. As we look toward an eventual recovery in the equity and bond markets, we believe it is important to maintain diversification across asset classes and to remain disciplined and methodical, especially when many other investors are not.

I continue to personally invest alongside you, and I remain confident that we at Dunham have the tools and the discipline to succeed as our economy recovers. You can continue to rely on us to apply a rational and unemotional approach. We thank you for your continued trust and the confidence you have placed in us. We take that trust very seriously. We look forward to servicing the investment needs for you and your family for generations to come.

Sincerely,

Jeffrey A. Dunham

President

Dunham & Associates

October 31, 2022

| 1 | As measured by the Bloomberg Global Aggregate Bond Index |

| 2 | As measured by the MSCI All Country World Index NR |

| 3 | As measured by the Bloomberg U.S. Aggregate Bond Index |

| 4 | As measured by the S&P 500 Index |

| 5 | As measured by the Morningstar LSTA US Leveraged Loan Index |

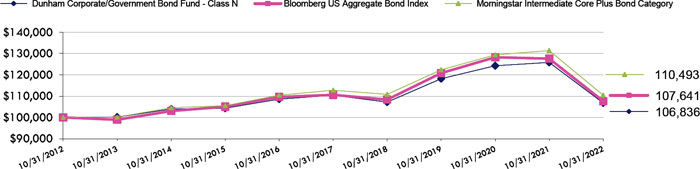

| Dunham Corporate/Government Bond Fund (Unaudited) |

| Message from the Sub-Adviser (Virtus Fixed Income Advisers, LLC) |

Asset Class Recap

Investment-grade bonds have historically exhibited negative correlation to equities during times of heightened volatility. However, in the most recent fiscal quarter and fiscal year, investment-grade bonds have sold off in tandem with equity markets as the asset classes’ duration adversely impacted performance. During the year, the Federal Open Market Committee became increasingly hawkish as persistent inflation, coupled with data illustrating a strong consumer and resilient job market, helped provide justification for a series of hikes in the Fed Funds rate. The Federal Reserve hiked 50 basis points in May, 75 basis points in June, and another 75 basis points in July. This represented the largest 3 -month percentage change in the Fed Funds rate since the early 1980s. Although some economic data showed signs of a slowing economy, inflation remained persistent prompting the Federal Reserve to raise rates another 75 basis points in September and retain their hawkish stance on their outlook. Meanwhile, the U.S. Treasury yield curve inverted as the 2-year U.S. Treasury yield rose 398 basis points to 4.48 percent, and the 10-year U.S. Treasury yield increased 243 basis points to 4.05 percent. A yield curve inversion has historically preceded a recession, exacerbating concerns of an upcoming economic slowdown. During the fiscal year, intermediate- term BBB-rated corporate bond spreads increased 279 basis points, intermediate-term single-B rated bonds experienced 162 basis points of widening, and intermediate-term CCC-rated corporate bonds jumped 179 basis points. Intermediate-term BBB-rated corporate bond yields reached 6.31% in October, the highest point since coming out of the Great Financial Crisis in 2009. For the fiscal year, investment-grade bonds as measured by the Bloomberg U.S. Aggregate Bond Index, declined 15.7 percent, underperforming equity markets, as measured by the S&P 500 index, which declined 14.6 percent.

Allocation Review

Nearly two-thirds of broad U.S. investment-grade bonds in the benchmark index are represented by Treasury and government agency bonds. Therefore, most of the performance of the benchmark index is dictated by how those U.S. government-related bonds perform, and far less is dependent on the performance of corporate bonds and non-agency mortgage-backed securities. During the fiscal year, U.S. Treasury bonds, as measured by the BofA U.S. Treasury & Agency Index, fell 14.4 percent. As the Fund had approximately 17 percent allocated to Treasury and government agency bonds, this is far less than what is represented by the benchmark index, and this significant underweight generally contributed to relative performance during the year. The Fund’s largest exposure was to investment-grade corporate bonds, comprising more than 27 percent of the Fund. Investment-grade corporate bonds, as measured by the BofA U.S. Corporate Index, declined 19.3 percent during the fiscal year. The Fund’s off-benchmark exposure to bank loans was one of the strongest positive contributions to Fund performance. The Fund had an approximate 8.0 percent allocation and increased approximately 1.2 percent over the fiscal year. Throughout the fiscal year, the Sub-Adviser decreased the allocations to government bonds, high-yield bonds, and bank loans and increased the allocation to municipal bonds and securitized products. The Fund did not have any exposure to derivatives during the fiscal quarter that meaningfully affected performance.

Holdings Insights

The bank loan exposure within the Fund provided one of the strongest contributors to relative and absolute performance over the fiscal year. This includes the Caesars Resort Collection, LLC Floating Rate, Due 10/02/2024 (BL252667) (holding weight*: 0.25 percent), an American hotel and casino entertainment company. This loan performed well over the fiscal year as a result of the market’s expectations for a refinancing, solid operating performance, and declining digital losses. The gaming consumer remained resilient over the fiscal year with encouraging trends in Las Vegas while regional markets have leveled back down to more consistent pre-covid levels. Another bank loan that contributed to Fund performance over the fiscal year was the INEOS US Finance, LLC Floating Rate, Due 03/31/2024 (BL2552414) (holding weight*: 0.40 percent), a chemical manufacturer. As a result of this company’s credit strength and strong fundamentals, it was able to refinance its short-maturity loans amid a difficult commodity chemical environment. Despite the allocation to investment-grade corporates detracting from Fund performance, the General Electric Company Floating Rate, Due 06/15/2169 (369604BQ5) (holding weight*: 0.30 percent), an American multinational conglomerate, was one of the strongest contributors to Fund performance over the fiscal year. This credit pays a floating rate, so the coupon has risen from 3.5 percent to begin the year to 6.6 percent by the end of the fiscal year. This credit benefited from the rise in interest rates and received a tailwind as the company made progress toward the spinoff of its Healthcare unit. Over the fiscal year, this credit increased by 4.7 percent.

Investment-grade corporate bonds that detracted from Fund performance include the Bank of America Corporation 2.687%, Until 04/22/2031, Due 04/22/2032 (06051GJT7) (holding weight*: 0.96 percent) and the JPMorgan Chase & Company 1.953%, Due 02/4/2032 (46647PBX3) (holding weight*: 0.96 percent). These bonds underperformed due to their relatively longer duration plus robust issuance from the major banks during the most recent fiscal quarter and year. This heavy issuance came while demand drivers were weak, exacerbating the spread widening for banks. These credits declined by 21.4 percent and 21.8 percent, respectively. The exposure to municipal bonds also detracted from Fund performance as the asset class fell in-line with the taxable fixed income market as the appetite for long-duration securities ceased. A municipal bond within the Fund that detracted from Fund performance was the State of Texas 3.211%, Due 04/01/2044 (882724QP5) (holding weight*: 0.78 percent). Over the fiscal quarter, the price of this credit declined from $105.25 to $74.82.

Sub-Adviser Outlook

The Sub-Adviser is cautiously optimistic for the remainder of the year; however, Federal Reserve hawkishness and Russia remain a key area of focus for investors. The Sub-Adviser believes that markets now face a mild version of stagflation as they absorb the impact of the end of 13 years of monetary and fiscal policy stimulus. Policy rate hikes, central bank balance sheet run-offs, and fiscal contraction all hitting at the same time have darkened the outlook for global growth and inflation. While nowhere as bad as the late 1970s and 80s, the Sub-Adviser expects weaker growth that falls short of a deep recession combined with lower (but still elevated) inflation will stop financial markets from a robust rally. At the same time, equity, Treasury, and credit markets have corrected meaningfully. As a result, the Sub-Adviser sees long-term value in certain areas of the bond market. The Sub- Adviser will look to use selloffs to add small amounts of select bonds in sectors where it has de-risked and now have lower relative exposure.

| * | Holdings percentage(s) of total investments, cash and unsettled trades excluding collateral for securities loaned as of 10/31/2022. |

Growth of $100,000 Investment

Total Returns (a) as of October 31, 2022

| | | Annualized | Annualized |

| | One Year | Five Years | Ten Years |

| Class N | (15.12)% | (0.66)% | 0.66% |

| Class A with load of 4.50% | (19.11)% | (1.80)% | (0.04)% |

| Class A without load | (15.29)% | (0.89)% | 0.42% |

| Class C | (15.68)% | (1.39)% | (0.08)% |

| Bloomberg US Aggregate Bond Index | (15.68)% | (0.54)% | 0.74% |

| Morningstar Intermediate Core Plus Bond Category | (15.92)% | (0.41)% | 1.00% |

| (a) | Total Returns are calculated based on traded NAVs. |

The Bloomberg US Aggregate Bond Index is an unmanaged index which represents the U.S. investment-grade fixed-rate bond market (including government and corporate securities, mortgage pass-through securities and asset-backed securities). Investors cannot invest directly in an index or benchmark.

The Morningstar Intermediate Core Plus Bond Category is generally representative of intermediate-term bond mutual funds that primarily invest in corporate and other investment-grade U.S. fixed-income securities and typically have durations of 3.5 to 6.0 years. Funds in this category also invest in high-yield and foreign bonds.

As disclosed in the Trust’s latest registration statement, the Fund’s total annual operating expenses, including underlying funds, are 1.25% for Class N, 2.00% for Class C and 1.50% for Class A. Class A shares are subject to a sales load of 4.50% and a deferred sales charge of up to 0.75%. The performance data quoted here represents past performance, which is not indicative of future results. Current performance may be lower or higher than the performance data quoted. The investment return and NAV will fluctuate, so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated assuming reinvestment of all dividends and capital gains distributions, if any. The returns do not reflect the deductions of taxes a shareholder would pay on the redemption of Fund shares or Fund distributions. For performance information current to the most recent month-end, please call 1-800-442-4358 or visit our website www.dunham.com.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | ASSET BACKED SECURITIES — 32.4% | | | | | | | | | | |

| | | | | AUTO LOAN — 6.6% | | | | | | | | | | |

| | 280,000 | | | American Credit Acceptance Receivables Trust Series 2021-2 C(a) | | | | 0.9700 | | 07/13/27 | | $ | 272,425 | |

| | 220,000 | | | American Credit Acceptance Receivables Trust Series 2022-1 D(a) | | | | 2.4600 | | 03/13/28 | | | 195,236 | |

| | 112,638 | | | Americredit Automobile Receivables Trust Series 2018-1 D | | | | 3.8200 | | 03/18/24 | | | 112,531 | |

| | 230,000 | | | AmeriCredit Automobile Receivables Trust Series 2020-3 C | | | | 1.0600 | | 08/18/26 | | | 215,255 | |

| | 155,000 | | | Avis Budget Rental Car Funding AESOP, LLC Series 2019-3A A(a) | | | | 2.3600 | | 03/20/26 | | | 143,905 | |

| | 140,000 | | | Carmax Auto Owner Trust Series 2019-1 C | | | | 3.7400 | | 01/15/25 | | | 139,568 | |

| | 175,000 | | | Carvana Auto Receivables Trust Series 2019-3A D(a) | | | | 3.0400 | | 04/15/25 | | | 173,341 | |

| | 225,000 | | | Carvana Auto Receivables Trust Series 2021-P3 B | | | | 1.4200 | | 08/10/27 | | | 195,183 | |

| | 107,556 | | | Carvana Auto Receivables Trust Series 2021-N1 C | | | | 1.3000 | | 01/10/28 | | | 101,363 | |

| | 178,222 | | | Carvana Auto Receivables Trust Series 2021-N2 C | | | | 1.0700 | | 03/10/28 | | | 168,520 | |

| | 225,000 | | | CPS Auto Receivables Trust Series 2019-D E(a) | | | | 3.8600 | | 10/15/25 | | | 218,054 | |

| | 89,579 | | | Credito Real USA Auto Receivables Trust Series 2021-1A A(a) | | | | 1.3500 | | 02/16/27 | | | 87,146 | |

| | 7,291 | | | First Investors Auto Owner Trust Series 2019-1A C(a) | | | | 3.2600 | | 03/17/25 | | | 7,285 | |

| | 180,000 | | | Flagship Credit Auto Trust Series 2020-4 C(a) | | | | 1.2800 | | 02/16/27 | | | 171,466 | |

| | 180,000 | | | Foursight Capital Automobile Receivables Trust Series 2022-1 B(a) | | | | 2.1500 | | 05/17/27 | | | 166,239 | |

| | 86,581 | | | LAD Auto Receivables Trust Series 2022-1A A(a) | | | | 5.2100 | | 06/15/27 | | | 85,035 | |

| | 140,000 | | | OneMain Direct Auto Receivables Trust Series 2021-1A B(a) | | | | 1.2600 | | 07/14/28 | | | 120,731 | |

| | 275,000 | | | Santander Drive Auto Receivables Trust Series 2021-3 C | | | | 0.9500 | | 09/15/27 | | | 263,066 | |

| | 195,000 | | | Santander Drive Auto Receivables Trust Series 2022-5 C | | | | 4.7400 | | 10/15/28 | | | 187,442 | |

| | 263,748 | | | United Auto Credit Securitization Trust Series 2021-1 C(a) | | | | 0.8400 | | 06/10/26 | | | 260,686 | |

| | 17,814 | | | Veros Automobile Receivables Trust Series 2020-1 B(a) | | | | 2.1900 | | 06/16/25 | | | 17,777 | |

| | 170,000 | | | Westlake Automobile Receivables Trust Series 2020-3A C(a) | | | | 1.2400 | | 11/17/25 | | | 164,796 | |

| | 345,000 | | | Westlake Automobile Receivables Trust Series 2022-1A B(a) | | | | 2.7500 | | 03/15/27 | | | 331,565 | |

| | | | | | | | | | | | | | 3,798,615 | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 8.7% | | | | | | | | | | |

| | 134,532 | | | AJAX Mortgage Loan Trust Series 2021-A A1(a),(b) | | | | 1.0650 | | 09/25/65 | | | 115,509 | |

| | 120,825 | | | Angel Oak Mortgage Trust Series 2020-R1 A2(a),(b) | | | | 1.2470 | | 12/26/24 | | | 106,577 | |

| | 71,724 | | | Angel Oak Mortgage Trust Series 2021-8 A1(a),(b) | | | | 1.8200 | | 11/25/66 | | | 57,578 | |

| | 103,837 | | | Arroyo Mortgage Trust Series 2019-1 A1(a),(b) | | | | 3.8050 | | 01/25/49 | | | 96,911 | |

| | 44,000 | | | Arroyo Mortgage Trust Series 2019-2 A1(a),(b) | | | | 3.3470 | | 04/25/49 | | | 40,971 | |

| | 88,229 | | | Bunker Hill Loan Depositary Trust Series 2019-2 A1(a),(c) | | | | 2.8790 | | 07/25/49 | | | 81,445 | |

| | 38,334 | | | Chase Mortgage Finance Corporation Series 2016-SH2 M2(a),(b) | | | | 3.7500 | | 02/25/44 | | | 33,303 | |

| | 51,322 | | | Chase Mortgage Finance Corporation Series 2016-SH1 M2(a),(b) | | | | 3.7500 | | 04/25/45 | | | 42,903 | |

| | 132,234 | | | CIM Trust Series 2021-NR4 A1(a),(c) | | | | 2.8160 | | 10/25/61 | | | 121,585 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | ASSET BACKED SECURITIES — 32.4% (Continued) | | | | | | | | | | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 8.7% (Continued) | | | | | | | | | | |

| | 137,502 | | | COLT A1Trust Series 2020-RPL1 A1(a),(b) | | | | 1.3900 | | 01/25/65 | | $ | 118,056 | |

| | 74,776 | | | COLT Funding, LLC Series 2021-3R A1(a),(b) | | | | 1.0510 | | 12/25/64 | | | 60,270 | |

| | 69,045 | | | CSMC Series 2021-NQM1 A1(a),(b) | | | | 0.8090 | | 05/25/65 | | | 63,050 | |

| | 154,271 | | | CSMC Trust Series 2020-RPL4 A1(a),(b) | | | | 2.0000 | | 01/25/60 | | | 136,031 | |

| | 25,315 | | | CSMC Trust Series 2020-NQM1 A1(a),(c) | | | | 1.2080 | | 05/25/65 | | | 22,763 | |

| | 21,640 | | | Ellington Financial Mortgage Trust Series 2019-2 A3(a),(b) | | | | 3.0460 | | 11/25/59 | | | 20,417 | |

| | 23,406 | | | Flagstar Mortgage Trust Series 2017-1 1A3(a),(b) | | | | 3.5000 | | 03/25/47 | | | 20,684 | |

| | 11,549 | | | Galton Funding Mortgage Trust Series 2018-1 A23(a),(b) | | | | 3.5000 | | 11/25/57 | | | 10,379 | |

| | 34,804 | | | JP Morgan Mortgage Series 2017-5 A1(a),(b) | | | | 3.1780 | | 12/15/47 | | | 33,364 | |

| | 220,000 | | | LHOME Mortgage Trust Series 2021-RTL1 A1(a),(b) | | | | 2.0900 | | 09/25/26 | | | 211,203 | |

| | 100,000 | | | METLIFE S.E.CURITIZATION TRUST Series 2017-1A M1(a),(b) | | | | 3.4240 | | 04/25/55 | | | 88,826 | |

| | 40,612 | | | METLIFE S.E.CURITIZATION TRUST Series 2019-1A A1A(a),(b) | | | | 3.7500 | | 04/25/58 | | | 39,576 | |

| | 199,632 | | | Mill City Mortgage Loan Trust Series 2019-1 M2(a),(b) | | | | 3.5000 | | 10/25/69 | | | 166,461 | |

| | 170,000 | | | New Residential Mortgage Loan Trust Series 2022-RTL1 A1F(a) | | | | 4.3360 | | 12/25/26 | | | 161,426 | |

| | 169,939 | | | New Residential Mortgage Loan Trust Series 2014-3A AFX3(a),(b) | | | | 3.7500 | | 11/25/54 | | | 156,522 | |

| | 163,994 | | | New Residential Mortgage Loan Trust Series 2016-3A B1(a),(b) | | | | 4.0000 | | 09/25/56 | | | 149,239 | |

| | 42,476 | | | New Residential Mortgage Loan Trust Series 2016-4A A1(a),(b) | | | | 3.7500 | | 11/25/56 | | | 38,865 | |

| | 333,017 | | | New Residential Mortgage Loan Trust Series 2017-2A A3(a),(b) | | | | 4.0000 | | 03/25/57 | | | 312,509 | |

| | 89,318 | | | New Residential Mortgage Loan Trust Series 2018-1A A1A(a),(b) | | | | 4.0000 | | 12/25/57 | | | 84,064 | |

| | 54,517 | | | New Residential Mortgage Loan Trust Series 2021-NQ2R A1(a),(b) | | | | 0.9410 | | 09/25/58 | | | 50,953 | |

| | 215,000 | | | New Residential Mortgage Loan Trust Series 2019-RPL2 M2(a),(b) | | | | 3.7500 | | 02/25/59 | | | 177,605 | |

| | 419,890 | | | New Residential Mortgage Loan Trust Series 2020-1A A1B(a),(b) | | | | 3.5000 | | 10/25/59 | | | 385,722 | |

| | 15,370 | | | OBX Trust Series 2019-INV1 A3(a),(b) | | | | 4.5000 | | 11/25/48 | | | 14,626 | |

| | 97,239 | | | Onslow Bay Mortgage Loan Trust Series 2021-NQM4 A1(a) | | | | 1.9570 | | 08/25/61 | | | 75,877 | |

| | 135,000 | | | Palisades Mortgage Loan Trust Series 2021-RTL1 A1(a),(c) | | | �� | 2.8570 | | 06/25/26 | | | 127,311 | |

| | 191,360 | | | PRET, LLC Series 2021-RN3 A1(a),(c) | | | | 1.8430 | | 09/25/51 | | | 173,107 | |

| | 32,368 | | | Provident Funding Mortgage Loan Trust Series 2019-1 A2(a),(b) | | | | 3.0000 | | 12/25/49 | | | 26,797 | |

| | 182,175 | | | PRPM, LLC Series 2021-2 A1(a),(b) | | | | 2.1150 | | 03/25/26 | | | 168,702 | |

| | 62,255 | | | RCKT Mortgage Trust Series 2020-1 A1(a),(b) | | | | 3.0000 | | 02/25/50 | | | 50,948 | |

| | 104,277 | | | RCO VI Mortgage, LLC Series 2022-1 A1(a),(c) | | | | 3.0000 | | 01/25/27 | | | 97,780 | |

| | 79,207 | | | Residential Mortgage Loan Trust Series 2020-1 A1(a),(b) | | | | 2.3760 | | 02/25/24 | | | 74,955 | |

| | 13,543 | | | Residential Mortgage Loan Trust Series 2019-2 A1(a),(b) | | | | 2.9130 | | 05/25/59 | | | 13,283 | |

| | 225,000 | | | ROC Securities Trust Series 2021-RTL1 A1(a),(b) | | | | 2.4870 | | 08/25/26 | | | 212,526 | |

| | 165,627 | | | SG Residential Mortgage Trust Series 2021-1 A3(a),(b) | | | | 1.5600 | | 07/25/61 | | | 131,256 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | ASSET BACKED SECURITIES — 32.4% (Continued) | | | | | | | | | | |

| | | | | COLLATERALIZED MORTGAGE OBLIGATIONS — 8.7% (Continued) | | | | | | | | | | |

| | 78,459 | | | Starwood Mortgage Residential Trust Series 2020-1 A1(a),(b) | | | | 2.2750 | | 02/25/50 | | $ | 77,807 | |

| | 25,646 | | | Starwood Mortgage Residential Trust Series 2020-3 A1(a),(b) | | | | 1.4860 | | 04/25/65 | | | 24,625 | |

| | 365,000 | | | Towd Point Mortgage Trust Series 2021-1 A2(a),(b) | | | | 2.7500 | | 11/25/61 | | | 279,981 | |

| | 50,441 | | | Verus Securitization Trust Series 2019-INV2 A1(a),(b) | | | | 2.9130 | | 07/25/59 | | | 49,343 | |

| | 100,000 | | | Verus Securitization Trust Series 2019-4 M1(a),(b) | | | | 3.2070 | | 11/25/59 | | | 86,757 | |

| | 26,047 | | | Verus Securitization Trust Series 2020-1 A1(a),(c) | | | | 2.4170 | | 01/25/60 | | | 24,614 | |

| | 49,161 | | | Verus Securitization Trust Series 2021-2 A1(a),(b) | | | | 1.0310 | | 02/25/66 | | | 39,614 | |

| | 30,202 | | | Wells Fargo Mortgage Backed Securities Series 2020-4 A1(a),(b) | | | | 3.0000 | | 07/25/50 | | | 24,669 | |

| | | | | | | | | | | | | | 4,979,345 | |

| | | | | CREDIT CARD — 0.7% | | | | | | | | | | |

| | 410,000 | | | Genesis Sales Finance Master Trust Series 2020-AA A(a) | | | | 1.6500 | | 09/22/25 | | | 399,983 | |

| | | | | | | | | | | | | | | |

| | | | | NON AGENCY CMBS — 2.5% | | | | | | | | | | |

| | 144,979 | | | Angel Oak SB Commercial Mortgage Trust Series 2020-SBC1 A1(a),(b) | | | | 2.0680 | | 05/25/50 | | | 137,689 | |

| | 90,000 | | | BPR Trust Series 2021-KEN A(a),(d) | | US0001M + 1.250% | | 4.6620 | | 02/15/29 | | | 87,447 | |

| | 160,000 | | | BX Trust Series 2019-OC11 B(a) | | | | 3.6050 | | 12/09/41 | | | 127,407 | |

| | 130,000 | | | BX Trust Series 2019-OC11 D(a),(b) | | | | 4.0750 | | 12/09/41 | | | 101,899 | |

| | 233,239 | | | CHC Commercial Mortgage Trust Series 2019-CHC A(a),(d) | | US0001M + 1.120% | | 4.5320 | | 06/15/34 | | | 228,850 | |

| | 100,475 | | | Citigroup Commercial Mortgage Trust Series 2015-GC27 A4 | | | | 2.8780 | | 02/10/48 | | | 95,266 | |

| | 305,000 | | | GCT Commercial Mortgage Trust Series 2021-GCT A(a),(d) | | US0001M + 0.800% | | 4.2120 | | 02/15/23 | | | 287,191 | |

| | 185,000 | | | Hilton USA Trust Series 2016-SFP B(a) | | | | 3.3230 | | 11/05/35 | | | 170,175 | |

| | 157,297 | | | Onslow Bay Mortgage Loan Trust Series 2021-NQM2 A1(a),(b) | | | | 1.1010 | | 05/25/61 | | | 121,861 | |

| | 62,000 | | | WFRBS Commercial Mortgage Trust Series 2014-C24 AS | | | | 3.9310 | | 11/15/47 | | | 58,809 | |

| | | | | | | | | | | | | | 1,416,594 | |

| | | | | OTHER ABS — 9.6% | | | | | | | | | | |

| | 230,000 | | | American Homes 4 Rent Trust Series 2014-SFR2 C(a) | | | | 4.7050 | | 10/17/36 | | | 222,829 | |

| | 220,000 | | | American Homes 4 Rent Trust Series 2015-SFR2 C(a) | | | | 4.6910 | | 10/17/45 | | | 210,646 | |

| | 175,000 | | | AMSR Trust Series 2020-SFR1 B(a) | | | | 2.1200 | | 04/17/37 | | | 158,355 | |

| | 250,000 | | | AMSR Trust Series 2020-SFR2 C(a) | | | | 2.5330 | | 07/17/37 | | | 227,459 | |

| | 100,000 | | | AMSR Trust Series 2020-SFR2 D(a) | | | | 3.2820 | | 07/17/37 | | | 91,752 | |

| | 83,664 | | | Aqua Finance Trust Series 2019-A A(a) | | | | 3.1400 | | 07/16/40 | | | 78,513 | |

| | 275,000 | | | Aqua Finance Trust Series 2019-A C(a) | | | | 4.0100 | | 07/16/40 | | | 251,507 | |

| | 270,000 | | | Aqua Finance Trust Series 2020-AA B(a) | | | | 2.7900 | | 07/17/46 | | | 235,087 | |

| | 100,000 | | | CCG Receivables Trust Series 2019-2 B(a) | | | | 2.5500 | | 03/15/27 | | | 98,715 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | ASSET BACKED SECURITIES — 32.4% (Continued) | | | | | | | | | | |

| | | | | OTHER ABS — 9.6% (Continued) | | | | | | | | | | |

| | 220,000 | | | CCG Receivables Trust Series 2021-1 C(a) | | | | 0.8400 | | 06/14/27 | | $ | 203,668 | |

| | 105,152 | | | CF Hippolyta, LLC Series 2020-1 A1(a) | | | | 1.6900 | | 07/15/60 | | | 92,540 | |

| | 64,269 | | | Corevest American Finance Trust Series 2020-1 A1(a) | | | | 1.8320 | | 03/15/50 | | | 59,692 | |

| | 100,000 | | | Corevest American Finance Trust Series 2019-3 C(a) | | | | 3.2650 | | 10/15/52 | | | 81,326 | |

| | 198,556 | | | Corevest American Finance Trust Series 2020-4 A(a) | | | | 1.1740 | | 12/15/52 | | | 173,612 | |

| | 240,000 | | | Dext A.B.S, LLC Series 2020-1 B(a) | | | | 1.9200 | | 11/15/27 | | | 228,816 | |

| | 285,000 | | | FirstKey Homes Trust Series 2021-SFR1 D(a) | | | | 2.1890 | | 08/17/28 | | | 234,620 | |

| | 375,000 | | | FirstKey Homes Trust Series 2020-SFR2 B(a) | | | | 1.5670 | | 10/19/37 | | | 325,447 | |

| | 26,554 | | | Foundation Finance Trust Series 2019-1A A(a) | | | | 3.8600 | | 11/15/34 | | | 25,953 | |

| | 97,752 | | | HIN Timeshare Trust Series 2020-A C(a) | | | | 3.4200 | | 10/09/39 | | | 89,239 | |

| | 129,025 | | | Jersey Mike’s Funding Series 2019-1A A2(a) | | | | 4.4330 | | 02/15/50 | | | 115,350 | |

| | 69,670 | | | MVW, LLC Series 2020-1A A(a) | | | | 1.7400 | | 10/20/37 | | | 60,868 | |

| | 33,268 | | | Octane Receivables Trust Series 2020-1A A(a) | | | | 1.7100 | | 02/20/25 | | | 32,846 | |

| | 152,572 | | | Oportun Funding, LLC Series 2022-1 A(a) | | | | 3.2500 | | 06/15/29 | | | 148,920 | |

| | 46,319 | | | Orange Lake Timeshare Trust Series 2019-A B(a) | | | | 3.3600 | | 04/09/38 | | | 43,422 | |

| | 265,000 | | | Progress Residential Series 2021-SFR3 D(a) | | | | 2.2880 | | 05/17/26 | | | 223,079 | |

| | 201,000 | | | Progress Residential Series 2021-SFR1 C(a) | | | | 1.5550 | | 04/17/38 | | | 168,526 | |

| | 550,000 | | | Progress Residential Trust Series 2020-SFR2 E(a) | | | | 5.1150 | | 06/17/37 | | | 517,120 | |

| | 275,000 | | | Purchasing Power Funding, LLC Series 2021-A A(a) | | | | 1.5700 | | 10/15/25 | | | 263,925 | |

| | 265,000 | | | Regional Management Issuance Trust Series 2021-1 A(a) | | | | 1.6800 | | 03/17/31 | | | 240,358 | |

| | 60,614 | | | Sierra Timeshare Receivables Funding, LLC Series 2020-2A B(a) | | | | 2.3200 | | 07/20/37 | | | 55,652 | |

| | 85,275 | | | Taco Bell Funding, LLC Series 2016-1A A23(a) | | | | 4.9700 | | 05/25/46 | | | 81,118 | |

| | 200,000 | | | Tricon American Homes Trust Series 2020-SFR2 D(a) | | | | 2.2810 | | 11/17/27 | | | 161,962 | |

| | 165,000 | | | Tricon American Homes Trust Series 2019-SFR1 C(a) | | | | 3.1490 | | 03/17/38 | | | 147,907 | |

| | 160,000 | | | Tricon Residential Trust Series 2021-SFR1 B(a) | | | | 2.2440 | | 07/17/38 | | | 138,257 | |

| | | | | | | | | | | | | | 5,489,086 | |

| | | | | RESIDENTIAL MORTGAGE — 4.2% | | | | | | | | | | |

| | 89,087 | | | Ajax Mortgage Loan Trust Series 2019-D A1(a),(c) | | | | 2.9560 | | 09/25/65 | | | 82,572 | |

| | 155,874 | | | Pretium Mortgage Credit Partners, LLC Series 2021-NPL1 A1(a),(c) | | | | 2.2390 | | 09/27/60 | | | 147,665 | |

| | 135,000 | | | Towd Point Mortgage Trust Series 2016-4 B1(a),(b) | | | | 3.8300 | | 07/25/56 | | | 122,286 | |

| | 115,000 | | | Towd Point Mortgage Trust Series 2017-1 M1(a),(b) | | | | 3.7500 | | 10/25/56 | | | 106,183 | |

| | 460,000 | | | Towd Point Mortgage Trust Series 2017-4 A2(a),(b) | | | | 3.0000 | | 06/25/57 | | | 408,011 | |

| | 160,000 | | | Towd Point Mortgage Trust Series 2017-6 A2(a),(b) | | | | 3.0000 | | 10/25/57 | | | 144,506 | |

| | 140,000 | | | Towd Point Mortgage Trust Series 2018-6 A1B(a),(b) | | | | 3.7500 | | 03/25/58 | | | 129,257 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | ASSET BACKED SECURITIES — 32.4% (Continued) | | | | | | | | | | |

| | | | | RESIDENTIAL MORTGAGE — 4.2% (Continued) | | | | | | | | | | |

| | 300,000 | | | Towd Point Mortgage Trust Series 2018-6 A2(a),(b) | | | | 3.7500 | | 03/25/58 | | $ | 264,303 | |

| | 100,886 | | | Towd Point Mortgage Trust Series 2018-4 A1(a),(b) | | | | 3.0000 | | 06/25/58 | | | 91,314 | |

| | 255,000 | | | Towd Point Mortgage Trust Series 2019-2 A2(a),(b) | | | | 3.7500 | | 12/25/58 | | | 211,865 | |

| | 235,000 | | | Towd Point Mortgage Trust Series 2019-4 A2(a),(b) | | | | 3.2500 | | 10/25/59 | | | 191,818 | |

| | 100,000 | | | Towd Point Mortgage Trust Series 2020-1 M1(a),(b) | | | | 3.5000 | | 01/25/60 | | | 76,151 | |

| | 97,249 | | | VCAT Asset Securitization, LLC Series 2021-NPL3 A1(a),(c) | | | | 1.7430 | | 05/25/51 | | | 86,500 | |

| | 58,201 | | | VCAT, LLC Series 2021-NPL2 A1(a),(c) | | | | 2.1150 | | 03/27/51 | | | 53,097 | |

| | 69,896 | | | VOLT C, LLC Series 2021-NPL9 A1(a),(c) | | | | 1.9920 | | 05/25/51 | | | 63,071 | |

| | 79,054 | | | VOLT CVI, LLC Series 2021-NP12 A1(a),(c) | | | | 2.7340 | | 12/26/51 | | | 72,713 | |

| | 175,639 | | | VOLT XCII, LLC Series 2021-NPL1 A1(a),(c) | | | | 1.8920 | | 02/27/51 | | | 159,224 | |

| | | | | | | | | | | | | | 2,410,536 | |

| | | | | STUDENT LOANS — 0.1% | | | | | | | | | | |

| | 72,354 | | | Commonbond Student Loan Trust Series 2020-1 A(a) | | | | 1.6900 | | 10/25/51 | | | 62,916 | |

| | | | | | | | | | | | | | | |

| | | | | TOTAL ASSET BACKED SECURITIES (Cost $20,679,892) | | | | | | | | | 18,557,075 | |

| | | | | | | | | | | | | | | |

| | | | | CORPORATE BONDS — 34.3% | | | | | | | | | | |

| | | | | AEROSPACE & DEFENSE — 0.7% | | | | | | | | | | |

| | 108,000 | | | Boeing Company (The) | | | | 5.9300 | | 05/01/60 | | | 91,198 | |

| | 236,000 | | | Huntington Ingalls Industries, Inc. | | | | 2.0430 | | 08/16/28 | | | 189,660 | |

| | 80,000 | | | Spirit AeroSystems, Inc.(a) | | | | 5.5000 | | 01/15/25 | | | 77,310 | |

| | 85,000 | | | TransDigm, Inc. | | | | 5.5000 | | 11/15/27 | | | 77,211 | |

| | | | | | | | | | | | | | 435,379 | |

| | | | | ASSET MANAGEMENT — 1.4% | | | | | | | | | | |

| | 92,000 | | | Blackstone Private Credit Fund | | | | 2.6250 | | 12/15/26 | | | 75,570 | |

| | 125,000 | | | Blue Owl Finance, LLC(a) | | | | 3.1250 | | 06/10/31 | | | 90,759 | |

| | 245,000 | | | Charles Schwab Corporation (The)(d) | | H15T10Y + 3.079% | | 4.0000 | | 03/01/69 | | | 182,280 | |

| | 155,000 | | | Citadel, L.P.(a) | | | | 4.8750 | | 01/15/27 | | | 143,456 | |

| | 250,000 | | | Drawbridge Special Opportunities Fund, L.P. /(a) | | | | 3.8750 | | 02/15/26 | | | 226,878 | |

| | 128,000 | | | OWL Rock Core Income Corporation | | | | 4.7000 | | 02/08/27 | | | 112,644 | |

| | | | | | | | | | | | | | 831,587 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | AUTOMOTIVE — 0.5% | | | | | | | | | | |

| | 106,000 | | | Ford Motor Company | | | | 3.2500 | | 02/12/32 | | $ | 79,562 | |

| | 70,000 | | | Ford Motor Company(g) | | | | 4.7500 | | 01/15/43 | | | 48,961 | |

| | 140,000 | | | Tenneco, Inc.(a) | | | | 5.1250 | | 04/15/29 | | | 139,049 | |

| | | | | | | | | | | | | | 267,572 | |

| | | | | BANKING — 4.8% | | | | | | | | | | |

| | 200,000 | | | Banco Mercantil del Norte S.A.(a),(d) | | H15T10Y + 5.034% | | 6.6250 | | 01/24/70 | | | 150,300 | |

| | 715,000 | | | Bank of America Corporation(d) | | SOFRRATE + 1.320% | | 2.6870 | | 04/22/32 | | | 552,967 | |

| | 230,000 | | | Bank of America Corporation(d) | | H15T5Y + 1.200% | | 2.4820 | | 09/21/36 | | | 164,501 | |

| | 200,000 | | | Barclays plc(d) | | H15T1Y + 3.500% | | 7.4370 | | 11/02/33 | | | 199,621 | |

| | 200,000 | | | BBVA Bancomer S.A.(a),(d) | | H15T5Y + 2.650% | | 5.1250 | | 01/18/33 | | | 162,246 | |

| | 113,000 | | | Citigroup, Inc.(d) | | SOFRRATE + 1.280% | | 4.0020 | | 02/24/28 | | | 108,061 | |

| | 175,000 | | | JPMorgan Chase & Company(d) | | SOFRRATE + 1.180% | | 3.8800 | | 02/24/28 | | | 169,576 | |

| | 425,000 | | | JPMorgan Chase & Company(d) | | SOFRRATE + 1.065% | | 1.9530 | | 02/04/32 | | | 311,481 | |

| | 140,000 | | | JPMorgan Chase & Company(d) | | SOFRRATE + 2.580% | | 5.7170 | | 09/14/33 | | | 130,662 | |

| | 47,000 | | | JPMorgan Chase & Company Series HH(d) | | SOFRRATE + 3.125% | | 4.6000 | | 08/01/68 | | | 42,060 | |

| | 205,000 | | | Santander Holdings USA, Inc. | | | | 4.4000 | | 07/13/27 | | | 185,369 | |

| | 200,000 | | | Texas Capital Bancshares, Inc.(d) | | H15T5Y + 3.150% | | 4.0000 | | 05/06/31 | | | 173,309 | |

| | 185,000 | | | Truist Financial Corporation(d) | | H15T10Y + 4.349% | | 5.1000 | | 03/01/69 | | | 162,836 | |

| | 330,000 | | | Wells Fargo & Company(d) (g) | | H15T5Y + 3.453% | | 3.9000 | | 03/15/69 | | | 280,376 | |

| | | | | | | | | | | | | | 2,793,365 | |

| | | | | BEVERAGES — 0.4% | | | | | | | | | | |

| | 200,000 | | | Bacardi Ltd.(a) | | | | 4.7000 | | 05/15/28 | | | 185,943 | |

| | 75,000 | | | Central American Bottling Corp / CBC Bottling(a) | | | | 5.2500 | | 04/27/29 | | | 65,865 | |

| | | | | | | | | | | | | | 251,808 | |

| | | | | BIOTECH & PHARMA — 0.7% | | | | | | | | | | |

| | 40,000 | | | Bausch Health Companies, Inc.(a) | | | | 5.7500 | | 08/15/27 | | | 25,335 | |

| | 160,000 | | | Mylan N.V. | | | | 3.9500 | | 06/15/26 | | | 145,817 | |

| | 45,000 | | | Par Pharmaceutical, Inc.(a) | | | | 7.5000 | | 04/01/27 | | | 34,506 | |

| | 120,000 | | | Teva Pharmaceutical Finance Netherlands III BV(g) | | | | 3.1500 | | 10/01/26 | | | 101,609 | |

| | 681 | | | Viatris, Inc.(a) | | | | 2.3000 | | 06/22/27 | | | 560 | |

| | 150,000 | | | Viatris, Inc. | | | | 2.3000 | | 06/22/27 | | | 123,416 | |

| | | | | | | | | | | | | | 431,243 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | CABLE & SATELLITE — 0.1% | | | | | | | | | | |

| | 14,000 | | | CCO Holdings, LLC / CCO Holdings Capital(a) | | | | 6.3750 | | 09/01/29 | | $ | 12,936 | |

| | 40,000 | | | CCO Holdings, LLC / CCO Holdings Capital(a) | | | | 4.7500 | | 03/01/30 | | | 33,687 | |

| | 45,000 | | | CCO Holdings, LLC / CCO Holdings Capital(a) (g) | | | | 4.5000 | | 08/15/30 | | | 36,904 | |

| | | | | | | | | | | | | | 83,527 | |

| | | | | CHEMICALS — 1.1% | | | | | | | | | | |

| | 185,000 | | | Albemarle Corporation | | | | 5.0500 | | 06/01/32 | | | 168,885 | |

| | 80,000 | | | Avient Corporation(a) | | | | 7.1250 | | 08/01/30 | | | 76,608 | |

| | 235,000 | | | Bayport Polymers, LLC(a) | | | | 5.1400 | | 04/14/32 | | | 203,551 | |

| | 245,000 | | | Nutrition & Biosciences, Inc.(a) | | | | 2.3000 | | 11/01/30 | | | 184,254 | |

| | | | | | | | | | | | | | 633,298 | |

| | | | | COMMERCIAL SUPPORT SERVICES — 0.1% | | | | | | | | | | |

| | 50,000 | | | Aramark Services, Inc.(a) | | | | 6.3750 | | 05/01/25 | | | 49,595 | |

| | | | | | | | | | | | | | | |

| | | | | CONSUMER SERVICES — 0.1% | | | | | | | | | | |

| | 60,000 | | | Carriage Services, Inc.(a) | | | | 4.2500 | | 05/15/29 | | | 46,262 | |

| | | | | | | | | | | | | | | |

| | | | | DIVERSIFIED INDUSTRIALS — 0.3% | | | | | | | | | | |

| | 181,000 | | | General Electric Company Series D(d) | | US0003M + 3.330% | | 6.6230 | | 06/15/69 | | | 175,118 | |

| | | | | | | | | | | | | | | |

| | | | | ELECTRIC UTILITIES — 0.8% | | | | | | | | | | |

| | 238,000 | | | Puget Energy, Inc. | | | | 2.3790 | | 06/15/28 | | | 196,806 | |

| | 244,000 | | | Southern Company (The)(d) | | H15T5Y + 2.915% | | 3.7500 | | 09/15/51 | | | 193,233 | |

| | 80,000 | | | Vistra Corporation(a),(d) | | H15T5Y + 6.930% | | 8.0000 | | 04/15/70 | | | 76,194 | |

| | | | | | | | | | | | | | 466,233 | |

| | | | | ENGINEERING & CONSTRUCTION — 0.5% | | | | | | | | | | |

| | 140,000 | | | Global Infrastructure Solutions, Inc.(a) | | | | 7.5000 | | 04/15/32 | | | 103,816 | |

| | 238,000 | | | Sempra Infrastructure Partners, L.P.(a) | | | | 3.2500 | | 01/15/32 | | | 186,390 | |

| | | | | | | | | | | | | | 290,206 | |

| | | | | FORESTRY, PAPER & WOOD PRODUCTS — 0.1% | | | | | | | | | | |

| | 90,000 | | | Suzano Austria GmbH | | | | 2.5000 | | 09/15/28 | | | 71,784 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | GAS & WATER UTILITIES — 0.3% | | | | | | | | | | |

| | 220,000 | | | Brooklyn Union Gas Company (The)(a) | | | | 4.8660 | | 08/05/32 | | $ | 197,418 | |

| | | | | | | | | | | | | | | |

| | | | | HEALTH CARE FACILITIES & SERVICES — 0.4% | | | | | | | | | | |

| | 125,000 | | | HCA, Inc.(g) | | | | 5.2500 | | 06/15/49 | | | 101,135 | |

| | 205,000 | | | Universal Health Services, Inc.(a) | | | | 2.6500 | | 01/15/32 | | | 146,021 | |

| | | | | | | | | | | | | | 247,156 | |

| | | | | HOME CONSTRUCTION — 0.8% | | | | | | | | | | |

| | 100,000 | | | M/I Homes, Inc. | | | | 4.9500 | | 02/01/28 | | | 85,949 | |

| | 105,000 | | | Masco Corporation | | | | 2.0000 | | 02/15/31 | | | 77,555 | |

| | 105,000 | | | Masco Corporation | | | | 3.1250 | | 02/15/51 | | | 60,504 | |

| | 235,000 | | | PulteGroup, Inc. | | | | 6.3750 | | 05/15/33 | | | 218,520 | |

| | | | | | | | | | | | | | 442,528 | |

| | | | | HOUSEHOLD PRODUCTS — 0.3% | | | | | | | | | | |

| | 170,000 | | | Church & Dwight Company, Inc. | | | | 5.0000 | | 06/15/52 | | | 148,449 | |

| | | | | | | | | | | | | | | |

| | | | | INDUSTRIAL SUPPORT SERVICES — 0.3% | | | | | | | | | | |

| | 200,000 | | | Ashtead Capital, Inc.(a) | | | | 5.5000 | | 08/11/32 | | | 180,893 | |

| | | | | | | | | | | | | | | |

| | | | | INSTITUTIONAL FINANCIAL SERVICES — 2.9% | | | | | | | | | | |

| | 125,000 | | | Bank of New York Mellon Corporation (The)(d) | | SOFRINDX + 2.074% | | 5.8340 | | 10/25/33 | | | 125,165 | |

| | 160,000 | | | Bank of New York Mellon Corporation (The)(d) | | H15T5Y + 4.358% | | 4.7000 | | 09/20/68 | | | 153,600 | |

| | 370,000 | | | Brookfield Finance, Inc. | | | | 2.7240 | | 04/15/31 | | | 286,678 | |

| | 175,000 | | | Goldman Sachs Group, Inc. (The)(d) | | SOFRRATE + 1.090% | | 1.9920 | | 01/27/32 | | | 127,770 | |

| | 290,000 | | | Jefferies Group, LLC / Jefferies Group Capital | | | | 2.6250 | | 10/15/31 | | | 206,373 | |

| | 285,000 | | | Morgan Stanley(g) | | | | 3.1250 | | 07/27/26 | | | 260,242 | |

| | 175,000 | | | Morgan Stanley(g) | | | | 6.3750 | | 07/24/42 | | | 177,215 | |

| | 175,000 | | | Northern Trust Corporation | | | | 6.1250 | | 11/02/32 | | | 175,199 | |

| | 160,000 | | | State Street Corporation(d) (g) | | SOFRRATE + 1.726% | | 4.1640 | | 08/04/33 | | | 141,829 | |

| | | | | | | | | | | | | | 1,654,071 | |

| | | | | INSURANCE — 2.5% | | | | | | | | | | |

| | 150,000 | | | Allstate Corporation (The)(d) | | US0003M + 2.938% | | 5.7500 | | 08/15/53 | | | 137,858 | |

| | 185,000 | | | Ascot Group Ltd.(a) | | | | 4.2500 | | 12/15/30 | | | 153,561 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | INSURANCE — 2.5% (Continued) | | | | | | | | | | |

| | 170,000 | | | Brighthouse Financial, Inc. | | | | 5.6250 | | 05/15/30 | | $ | 158,219 | |

| | 156,000 | | | Corebridge Financial, Inc.(a),(d) | | H15T5Y + 3.846% | | 6.8750 | | 12/15/52 | | | 139,965 | |

| | 175,000 | | | Liberty Mutual Group, Inc.(a),(d) | | H15T5Y + 3.315% | | 4.1250 | | 12/15/51 | | | 132,765 | |

| | 275,000 | | | Lincoln National Corporation(d) | | US0003M + 2.040% | | 6.2830 | | 04/20/67 | | | 208,159 | |

| | 160,000 | | | MetLife, Inc.(d) | | H15T5Y + 3.576% | | 3.8500 | | 03/15/69 | | | 140,998 | |

| | 76,000 | | | MetLife, Inc.(d) | | US0003M + 2.959% | | 5.8750 | | 09/15/66 | | | 68,220 | |

| | 230,000 | | | Prudential Financial, Inc.(d) | | US0003M + 3.920% | | 5.6250 | | 06/15/43 | | | 227,753 | |

| | 59,000 | | | Prudential Financial, Inc.(d) | | H15T5Y + 3.162% | | 5.1250 | | 03/01/52 | | | 50,438 | |

| | 33,000 | | | Prudential Financial, Inc.(d) (g) | | H15T5Y + 3.234% | | 6.0000 | | 09/01/52 | | | 30,123 | |

| | | | | | | | | | | | | | 1,448,059 | |

| | | | | LEISURE PRODUCTS — 0.2% | | | | | | | | | | |

| | 166,000 | | | Brunswick Corporation | | | | 2.4000 | | 08/18/31 | | | 115,618 | |

| | | | | | | | | | | | | | | |

| | | | | MACHINERY — 0.3% | | | | | | | | | | |

| | 155,000 | | | Pentair Finance Sarl | | | | 5.9000 | | 07/15/32 | | | 145,974 | |

| | | | | | | | | | | | | | | |

| | | | | MEDICAL EQUIPMENT & DEVICES — 0.8% | | | | | | | | | | |

| | 124,000 | | | Bio-Rad Laboratories, Inc. | | | | 3.3000 | | 03/15/27 | | | 111,931 | |

| | 39,000 | | | Bio-Rad Laboratories, Inc. | | | | 3.7000 | | 03/15/32 | | | 32,463 | |

| | 175,000 | | | DENTSPLY SIRONA, Inc. | | | | 3.2500 | | 06/01/30 | | | 136,647 | |

| | 243,000 | | | Illumina, Inc. | | | | 2.5500 | | 03/23/31 | | | 185,551 | |

| | | | | | | | | | | | | | 466,592 | |

| | | | | METALS & MINING — 1.5% | | | | | | | | | | |

| | 135,000 | | | Alliance Resource Operating Partners, L.P. /(a)(g) | | | | 7.5000 | | 05/01/25 | | | 132,625 | |

| | 70,000 | | | Cleveland-Cliffs, Inc.(a) | | | | 6.7500 | | 03/15/26 | | | 69,609 | |

| | 140,000 | | | FMG Resources August 2006 Pty Ltd.(a) | | | | 5.8750 | | 04/15/30 | | | 124,559 | |

| | 205,000 | | | Freeport-McMoRan, Inc. (g) | | | | 5.4500 | | 03/15/43 | | | 169,040 | |

| | 185,000 | | | Glencore Funding, LLC(a) | | | | 2.8500 | | 04/27/31 | | | 143,296 | |

| | 205,000 | | | Teck Resources Ltd. | | | | 6.1250 | | 10/01/35 | | | 192,252 | |

| | | | | | | | | | | | | | 831,381 | |

| | | | | OIL & GAS PRODUCERS — 3.8% | | | | | | | | | | |

| | 70,000 | | | Chesapeake Escrow Issuer, LLC B(a) | | | | 5.5000 | | 02/01/26 | | | 67,956 | |

| | 125,000 | | | DT Midstream, Inc.(a) | | | | 4.1250 | | 06/15/29 | | | 108,373 | |

| | 170,000 | | | Enbridge, Inc.(d) | | H15T5Y + 4.418% | | 7.6250 | | 01/15/83 | | | 162,790 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | OIL & GAS PRODUCERS — 3.8% (Continued) | | | | | | | | | | |

| | 175,000 | | | Energy Transfer, L.P.(d) | | H15T5Y + 5.694% | | 6.5000 | | 11/15/69 | | $ | 150,938 | |

| | 125,000 | | | EQM Midstream Partners, L.P.(a) | | | | 7.5000 | | 06/01/30 | | | 121,731 | |

| | 245,000 | | | Flex Intermediate Holdco, LLC(a) | | | | 3.3630 | | 06/30/31 | | | 189,070 | |

| | 165,000 | | | HF Sinclair Corporation(a) | | | | 5.8750 | | 04/01/26 | | | 160,575 | |

| | 45,000 | | | Kinder Morgan, Inc. | | | | 7.7500 | | 01/15/32 | | | 48,937 | |

| | 200,000 | | | Lundin Energy Finance BV(a) | | | | 2.0000 | | 07/15/26 | | | 172,438 | |

| | 105,000 | | | Occidental Petroleum Corporation(g) | | | | 6.1250 | | 01/01/31 | | | 105,657 | |

| | 70,000 | | | Parsley Energy, LLC / Parsley Finance Corporation(a) | | | | 4.1250 | | 02/15/28 | | | 63,735 | |

| | 200,000 | | | Pertamina Persero PT(a) | | | | 6.4500 | | 05/30/44 | | | 180,988 | |

| | 185,000 | | | Petroleos Mexicanos | | | | 7.6900 | | 01/23/50 | | | 120,845 | |

| | 250,000 | | | Reliance Industries Ltd.(a) | | | | 2.8750 | | 01/12/32 | | | 188,180 | |

| | 65,000 | | | Sabine Pass Liquefaction, LLC | | | | 4.2000 | | 03/15/28 | | | 59,304 | |

| | 225,000 | | | Transcanada Trust(d) | | H15T5Y + 3.986% | | 5.6000 | | 03/07/82 | | | 192,766 | |

| | 95,000 | | | Venture Global Calcasieu Pass, LLC(a) | | | | 3.8750 | | 08/15/29 | | | 82,194 | |

| | | | | | | | | | | | | | 2,176,477 | |

| | | | | OIL & GAS SERVICES & EQUIPMENT — 0.0%(e) | | | | | | | | | | |

| | 21,712 | | | Transocean Guardian Ltd.(a) | | | | 5.8750 | | 01/15/24 | | | 21,133 | |

| | | | | | | | | | | | | | | |

| | | | | REAL ESTATE INVESTMENT TRUSTS — 2.0% | | | | | | | | | | |

| | 220,000 | | | EPR Properties | | | | 4.7500 | | 12/15/26 | | | 189,578 | |

| | 155,000 | | | GLP Capital, L.P. / GLP Financing II, Inc. | | | | 5.7500 | | 06/01/28 | | | 144,021 | |

| | 23,000 | | | GLP Capital, L.P. / GLP Financing II, Inc. | | | | 3.2500 | | 01/15/32 | | | 17,196 | |

| | 25,000 | | | MPT Operating Partnership, L.P. / MPT Finance(g) | | | | 4.6250 | | 08/01/29 | | | 19,603 | |

| | 125,000 | | | MPT Operating Partnership, L.P. / MPT Finance(g) | | | | 3.5000 | | 03/15/31 | | | 86,292 | |

| | 170,000 | | | Office Properties Income Trust | | | | 4.5000 | | 02/01/25 | | | 141,388 | |

| | 240,000 | | | Phillips Edison Grocery Center Operating | | | | 2.6250 | | 11/15/31 | | | 171,786 | |

| | 105,000 | | | Retail Opportunity Investments Partnership, L.P. | | | | 4.0000 | | 12/15/24 | | | 100,128 | |

| | 225,000 | | | Retail Properties of America, Inc. | | | | 4.7500 | | 09/15/30 | | | 192,277 | |

| | 75,000 | | | Service Properties Trust | | | | 4.9500 | | 02/15/27 | | | 60,827 | |

| | | | | | | | | | | | | | 1,123,096 | |

| | | | | REAL ESTATE OWNERS & DEVELOPERS — 0.4% | | | | | | | | | | |

| | 275,000 | | | Ontario Teachers’ Cadillac Fairview Properties(a) | | | | 2.5000 | | 10/15/31 | | | 207,824 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | RETAIL - DISCRETIONARY — 0.5% | | | | | | | | | | |

| | 175,000 | | | BlueLinx Holdings, Inc.(a) | | | | 6.0000 | | 11/15/29 | | $ | 142,891 | |

| | 159,000 | | | Dick’s Sporting Goods, Inc. | | | | 3.1500 | | 01/15/32 | | | 120,643 | |

| | | | | | | | | | | | | | 263,534 | |

| | | | | SEMICONDUCTORS — 0.6% | | | | | | | | | | |

| | 171,000 | | | Broadcom, Inc. | | | | 4.1500 | | 11/15/30 | | | 147,160 | |

| | 222,000 | | | Entegris Escrow Corporation(a) | | | | 4.7500 | | 04/15/29 | | | 196,547 | |

| | | | | | | | | | | | | | 343,707 | |

| | | | | SOFTWARE — 0.2% | | | | | | | | | | |

| | 90,000 | | | Consensus Cloud Solutions, Inc.(a) | | | | 6.5000 | | 10/15/28 | | | 79,570 | |

| | 45,000 | | | Oracle Corporation | | | | 3.8500 | | 04/01/60 | | | 27,142 | |

| | | | | | | | | | | | | | 106,712 | |

| | | | | SPECIALTY FINANCE — 1.2% | | | | | | | | | | |

| | 214,000 | | | Ally Financial, Inc. Series B(d) | | H15T5Y + 3.868% | | 4.7000 | | 08/15/69 | | | 155,820 | |

| | 145,000 | | | Aviation Capital Group, LLC(a) | | | | 3.5000 | | 11/01/27 | | | 117,840 | |

| | 125,000 | | | Avolon Holdings Funding Ltd.(a) | | | | 4.3750 | | 05/01/26 | | | 109,952 | |

| | 182,000 | | | Capital One Financial Corporation(d) | | SOFRRATE + 1.337% | | 2.3590 | | 07/29/32 | | | 125,373 | |

| | 120,000 | | | Ladder Capital Finance Holdings LLLP / Ladder(a) | | | | 4.2500 | | 02/01/27 | | | 101,117 | |

| | 65,000 | | | OneMain Finance Corporation | | | | 6.8750 | | 03/15/25 | | | 63,252 | |

| | | | | | | | | | | | | | 673,354 | |

| | | | | TECHNOLOGY HARDWARE — 1.4% | | | | | | | | | | |

| | 289,000 | | | CDW, LLC / CDW Finance Corporation | | | | 3.5690 | | 12/01/31 | | | 227,979 | |

| | 154,000 | | | Dell International, LLC / EMC Corporation | | | | 8.1000 | | 07/15/36 | | | 163,233 | |

| | 200,000 | | | HP, Inc. | | | | 5.5000 | | 01/15/33 | | | 177,957 | |

| | 50,000 | | | Motorola Solutions, Inc. | | | | 4.6000 | | 05/23/29 | | | 45,988 | |

| | 210,000 | | | TD SYNNEX Corporation | | | | 2.3750 | | 08/09/28 | | | 167,169 | |

| | | | | | | | | | | | | | 782,326 | |

| | | | | TECHNOLOGY SERVICES — 0.6% | | | | | | | | | | |

| | 137,000 | | | Kyndryl Holdings, Inc. | | | | 2.7000 | | 10/15/28 | | | 99,232 | |

| | 245,000 | | | Leidos, Inc. | | | | 2.3000 | | 02/15/31 | | | 181,270 | |

| | 75,000 | | | Science Applications International Corporation(a) | | | | 4.8750 | | 04/01/28 | | | 68,403 | |

| | | | | | | | | | | | | | 348,905 | |

| | | | | TELECOMMUNICATIONS — 0.9% | | | | | | | | | | |

| | 160,000 | | | Level 3 Financing, Inc.(a) | | | | 4.2500 | | 07/01/28 | | | 132,437 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | CORPORATE BONDS — 34.3% (Continued) | | | | | | | | | | |

| | | | | TELECOMMUNICATIONS — 0.9% (Continued) | | | | | | | | | | |

| | 125,000 | | | Sprint Spectrum Company, LLC / Sprint Spectrum(a) | | | | 4.7380 | | 03/20/25 | | $ | 123,121 | |

| | 265,000 | | | T-Mobile USA, Inc. | | | | 3.8750 | | 04/15/30 | | | 234,117 | |

| | | | | | | | | | | | | | 489,675 | |

| | | | | TOBACCO & CANNABIS — 0.4% | | | | | | | | | | |

| | 215,000 | | | BAT Capital Corporation | | | | 7.7500 | | 10/19/32 | | | 219,915 | |

| | | | | | | | | | | | | | | |

| | | | | TRANSPORTATION & LOGISTICS — 0.4% | | | | | | | | | | |

| | 219,238 | | | Alaska Airlines 2020-1 Class A Pass Through Trust(a) | | | | 4.8000 | | 08/15/27 | | | 205,323 | |

| | | | | | | | | | | | | | | |

| | | | | TOTAL CORPORATE BONDS (Cost $23,433,241) | | | | | | | | | 19,667,097 | |

| | | | | | | | | | | | | | | |

| | | | | MUNICIPAL BONDS — 6.2% | | | | | | | | | | |

| | | | | CITY — 0.7% | | | | | | | | | | |

| | 340,000 | | | City of Bristol VA | | | | 4.2100 | | 01/01/42 | | | 277,849 | |

| | 145,000 | | | City of San Antonio TX | | | | 1.9630 | | 02/01/33 | | | 107,491 | |

| | | | | | | | | | | | | | 385,340 | |

| | | | | GOVERNMENT LEASE — 0.2% | | | | | | | | | | |

| | 145,000 | | | Texas Public Finance Authority | | | | 2.1400 | | 02/01/35 | | | 102,651 | |

| | | | | | | | | | | | | | | |

| | | | | HOSPITALS — 0.2% | | | | | | | | | | |

| | 135,000 | | | Idaho Health Facilities Authority | | | | 5.0200 | | 03/01/48 | | | 117,364 | |

| | | | | | | | | | | | | | | |

| | | | | LOCAL AUTHORITY — 1.4% | | | | | | | | | | |

| | 320,000 | | | San Diego County Regional Airport Authority | | | | 5.5940 | | 07/01/43 | | | 304,985 | |

| | 600,000 | | | State of Texas | | | | 3.2110 | | 04/01/44 | | | 448,940 | |

| | 35,000 | | | Texas Transportation Commission State Highway Fund | | | | 4.0000 | | 10/01/33 | | | 30,395 | |

| | | | | | | | | | | | | | 784,320 | |

| | | | | MISCELLANEOUS TAX — 1.4% | | | | | | | | | | |

| | 765,000 | | | Metropolitan Transportation Authority | | | | 5.0000 | | 11/15/45 | | | 778,804 | |

| | | | | | | | | | | | | | | |

| | | | | SALES TAX — 0.0%(e) | | | | | | | | | | |

| | 20,000 | | | Sales Tax Securitization Corporation | | | | 3.4110 | | 01/01/43 | | | 14,345 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | | | (%) | | Maturity | | Fair Value | |

| | | | | MUNICIPAL BONDS — 6.2% (Continued) | | | | | | | | | | |

| | | | | WATER AND SEWER — 2.3% | | | | | | | | | | |

| | 705,000 | | | Broward County FL Water & Sewer Utility Revenue | | | | 4.0000 | | 10/01/47 | | $ | 626,495 | |

| | 625,000 | | | New York State Environmental Facilities | | | | 5.0000 | | 06/15/51 | | | 650,902 | |

| | 160,000 | | | Santa Clara Valley Water District | | | | 2.9670 | | 06/01/50 | | | 101,099 | |

| | | | | | | | | | | | | | 1,378,496 | |

| | | | | TOTAL MUNICIPAL BONDS (Cost $4,284,017) | | | | | | | | | 3,561,320 | |

| | | | | | | | | | | | | | | |

| | | | | NON U.S. GOVERNMENT & AGENCIES — 1.0% | | | | | | | | | | |

| | | | | SOVEREIGN — 1.0% | | | | | | | | | | |

| | 300,000 | | | Dominican Republic International Bond(a) (g) | | | | 4.8750 | | 09/23/32 | | | 232,290 | |

| | 200,000 | | | Emirate of Dubai Government International Bonds | | | | 5.2500 | | 01/30/43 | | | 168,312 | |

| | 200,000 | | | Mexico Government International Bond | | | | 2.6590 | | 05/24/31 | | | 155,799 | |

| | | | | TOTAL NON U.S. GOVERNMENT & AGENCIES (Cost $677,101) | | | | | | | | | 556,401 | |

| | | | | | | | | | | | | | | |

| | | | | | | Spread | | | | | | | | |

| | | | | TERM LOANS — 4.9% | | | | | | | | | | |

| | | | | AEROSPACE & DEFENSE — 0.1% | | | | | | | | | | |

| | 70,876 | | | TransDigm, Inc.(d) | | US0001M + 2.250% | | 5.9240 | | 05/30/25 | | | 69,373 | |

| | | | | | | | | | | | | | | |

| | | | | AUTOMOTIVE — 0.1% | | | | | | | | | | |

| | 71,356 | | | Cooper-Standard Automotive, Inc.(d) | | US0002M + 2.000% | | 5.1150 | | 11/02/23 | | | 65,211 | |

| | | | | | | | | | | | | | | |

| | | | | BIOTECH & PHARMA — 0.1% | | | | | | | | | | |

| | 64,838 | | | Perrigo Investments, LLC(d) | | TSFR1M + 2.500% | | 5.6340 | | 04/07/29 | | | 64,108 | |

| | | | | | | | | | | | | | | |

| | | | | CABLE & SATELLITE — 0.1% | | | | | | | | | | |

| | 79,130 | | | Directv Financing, LLC(d) | | US0001M + 5.000% | | 8.1150 | | 07/22/27 | | | 75,609 | |

| | | | | | | | | | | | | | | |

| | | | | CHEMICALS — 0.4% | | | | | | | | | | |

| | 230,487 | | | INEOS US Finance, LLC(d) | | US0002M + 2.000% | | 5.1150 | | 03/31/24 | | | 229,006 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | TERM LOANS — 4.9% (Continued) | | | | | | | | | | |

| | | | | CONTAINERS & PACKAGING — 0.1% | | | | | | | | | | |

| | 70,837 | | | Berry Global, Inc.(d) | | US0001M + 1.750% | | 5.0500 | | 07/01/26 | | $ | 69,926 | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | | | | ELECTRICAL EQUIPMENT — 0.1% | | | | | | | | | | |

| | 70,242 | | | Brookfield WEC Holdings, Inc.(d) | | US0001M + 2.750% | | 5.8650 | | 08/01/25 | | | 69,163 | |

| | | | | | | | | | | | | | | |

| | | | | FOOD — 0.1% | | | | | | | | | | |

| | 87,272 | | | Hostess Brands, LLC(d) | | US0001M + 2.250% | | 5.3650 | | 08/03/25 | | | 86,093 | |

| | | | | | | | | | | | | | | |

| | | | | HEALTH CARE FACILITIES & SERVICES — 0.2% | | | | | | | | | | |

| | 54,436 | | | Agiliti Health, Inc.(d) | | US0001M + 2.750% | | 5.9380 | | 10/18/25 | | | 53,619 | |

| | 71,596 | | | Legacy LifePoint Health, LLC(d) | | US0001M + 3.750% | | 6.8710 | | 11/16/25 | | | 63,542 | |

| | | | | | | | | | | | | | 117,161 | |

| | | | | INDUSTRIAL SUPPORT SERVICES — 0.1% | | | | | | | | | | |

| | 68,613 | | | Resideo Funding, Inc.(d) | | US0001M + 2.250% | | 5.5700 | | 02/09/28 | | | 67,713 | |

| | | | | | | | | | | | | | | |

| | | | | INSTITUTIONAL FINANCIAL SERVICES — 0.1% | | | | | | | | | | |

| | 39,000 | | | Citadel Securities, L.P.(d) | | TSFR1M + 3.000% | | 6.1490 | | 02/02/28 | | | 38,870 | |

| | | | | | | | | | | | | | | |

| | | | | LEISURE FACILITIES & SERVICES — 0.7% | | | | | | | | | | |

| | 143,645 | | | Caesars Resort Collection, LLC(d) | | US0001M + 2.750% | | 5.8650 | | 10/02/24 | | | 142,287 | |

| | 70,000 | | | Hilton Worldwide Finance, LLC(d) | | US0001M + 1.750% | | 5.3360 | | 06/21/26 | | | 68,871 | |

| | 39,900 | | | Scientific Games Corporation(d) | | SOFRRATE + 3.000% | | 6.4020 | | 04/07/29 | | | 39,460 | |

| | 68,581 | | | Station Casinos, LLC(d) | | US0001M + 2.250% | | 5.3700 | | 01/31/27 | | | 67,299 | |

| | 68,968 | | | UFC Holdings, LLC(d) | | US0006M + 2.750% | | 7.1100 | | 04/29/26 | | | 67,572 | |

| | | | | | | | | | | | | | 385,489 | |

| | | | | MACHINERY — 0.2% | | | | | | | | | | |

| | 71,268 | | | Alliance Laundry Systems, LLC(d) | | US0003M + 3.500% | | 7.4090 | | 09/30/27 | | | 68,951 | |

| | 71,551 | | | Standard Industries, Inc.(d) | | US0006M + 2.500% | | 6.6750 | | 08/06/28 | | | 70,219 | |

| | | | | | | | | | | | | | 139,170 | |

| | | | | OIL & GAS PRODUCERS — 0.3% | | | | | | | | | | |

| | 57,181 | | | CITGO Petroleum Corporation(d) | | US0001M + 6.250% | | 9.3650 | | 03/27/24 | | | 57,353 | |

| | 69,283 | | | Freeport LNG Investments LLLP(d) | | US0003M + 3.500% | | 7.7430 | | 11/17/28 | | | 64,996 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | Spread | | (%) | | Maturity | | Fair Value | |

| | | | | TERM LOANS — 4.9% (Continued) | | | | | | | | | | |

| | | | | OIL & GAS PRODUCERS — 0.3% (Continued) | | | | | | | | | | |

| | 69,200 | | | Oryx Midstream Services Permian Basin, LLC(d) | | US0001M + 3.250% | | 6.2110 | | 09/30/28 | | $ | 68,320 | |

| | | | | | | | | | | | | | 190,669 | |

| | | | | PUBLISHING & BROADCASTING — 0.1% | | | | | | | | | | |

| | 41,179 | | | Nexstar Broadcasting, Inc.(d) | | US0001M + 2.500% | | 5.6150 | | 06/20/26 | | | 40,852 | |

| | | | | | | | | | | | | | | |

| | | | | SOFTWARE — 0.5% | | | | | | | | | | |

| | 111,830 | | | Applied Systems, Inc.(d) | | US0001M + 2.000% | | 5.2500 | | 09/19/24 | | | 110,602 | |

| | 69,313 | | | CCC Intelligent Solutions, Inc.(d) | | US0003M + 2.500% | | 5.3650 | | 09/17/28 | | | 68,043 | |

| | 68,098 | | | Sophia, L.P.(d) | | US0003M + 3.250% | | 7.1740 | | 10/07/27 | | | 65,658 | |

| | 66,908 | | | UKG, Inc.(d) | | US0001M + 3.250% | | 6.9980 | | 05/03/26 | | | 64,715 | |

| | | | | | | | | | | | | | 309,018 | |

| | | | | TECHNOLOGY HARDWARE — 0.1% | | | | | | | | | | |

| | 69,412 | | | NCR Corporation(d) | | US0001M + 2.500% | | 5.3100 | | 08/08/26 | | | 66,809 | |

| | | | | | | | | | | | | | | |

| | | | | TECHNOLOGY SERVICES — 0.6% | | | | | | | | | | |

| | 58,685 | | | Blackhawk Network Holdings, Inc.(d) | | US0001M + 3.000% | | 7.0770 | | 05/22/25 | | | 56,558 | |

| | 64,932 | | | Dun & Bradstreet Corporation (The)(d) | | US0001M + 3.250% | | 6.8460 | | 02/08/26 | | | 64,040 | |

| | 69,226 | | | NAB Holdings, LLC(d) | | SOFRRATE + 3.000% | | 6.7030 | | 11/18/28 | | | 66,630 | |

| | 57,040 | | | Peraton Corporation(d) | | US0001M + 3.750% | | 6.8650 | | 02/24/28 | | | 55,044 | |

| | 69,164 | | | Tenable, Inc.(d) | | US0006M + 2.750% | | 5.5560 | | 06/17/28 | | | 67,146 | |

| | | | | | | | | | | | | | 309,418 | |

| | | | | TELECOMMUNICATIONS — 0.2% | | | | | | | | | | |

| | 23,965 | | | CenturyLink, Inc.(d) | | US0001M + 2.250% | | 5.3650 | | 03/15/27 | | | 22,370 | |

| | 96,533 | | | SBA Senior Finance II, LLC(d) | | US0001M + 1.750% | | 4.8700 | | 04/11/25 | | | 95,871 | |

| | | | | | | | | | | | | | 118,241 | |

| | | | | TRANSPORTATION & LOGISTICS — 0.7% | | | | | | | | | | |

| | 24,644 | | | Air Canada(d) | | US0006M + 3.500% | | 6.4210 | | 07/27/28 | | | 24,108 | |

| | 101,387 | | | Brown Group Holding, LLC(d) | | US0003M + 2.500% | | 5.6150 | | 04/22/28 | | | 98,768 | |

| | 66,500 | | | Mileage Plus Holdings, LLC(d) | | US0003M + 5.250% | | 8.7770 | | 06/25/27 | | | 68,024 | |

| | 73,506 | | | PODS, LLC(d) | | US0001M + 3.000% | | 6.1150 | | 03/19/28 | | | 70,934 | |

| | 70,000 | | | SkyMiles IP Ltd.(d) | | US0003M + 3.750% | | 7.9930 | | 09/16/27 | | | 70,744 | |

| | | | | | | | | | | | | | 332,578 | |

| | | | | TOTAL TERM LOANS (Cost $2,898,912) | | | | | | | | | 2,844,477 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Principal | | | | | Coupon Rate | | | | | |

| Amount ($) | | | | | (%) | | Maturity | | Fair Value | |

| | | | | U.S. GOVERNMENT & AGENCIES — 18.1% | | | | | | | | |

| | | | | AGENCY FIXED RATE — 0.8% | | | | | | | | |

| | 8,409 | | | Fannie Mae Pool 735061 | | 6.0000 | | 11/01/34 | | $ | 8,631 | |

| | 10,793 | | | Fannie Mae Pool 866009 | | 6.0000 | | 03/01/36 | | | 11,183 | |

| | 76,025 | | | Fannie Mae Pool 938574 | | 5.5000 | | 09/01/36 | | | 77,757 | |

| | 26,884 | | | Fannie Mae Pool 310041 | | 6.5000 | | 05/01/37 | | | 28,653 | |

| | 12,166 | | | Fannie Mae Pool 962752 | | 5.0000 | | 04/01/38 | | | 12,178 | |

| | 15,200 | | | Fannie Mae Pool 909175 | | 5.5000 | | 04/01/38 | | | 15,586 | |

| | 56,806 | | | Fannie Mae Pool 909220 | | 6.0000 | | 08/01/38 | | | 58,198 | |

| | 49,085 | | | Fannie Mae Pool AS7026 | | 4.0000 | | 04/01/46 | | | 46,039 | |

| | 86,197 | | | Fannie Mae Pool BJ9260 | | 4.0000 | | 04/01/48 | | | 79,785 | |

| | 84,807 | | | Freddie Mac Gold Pool G01980 | | 5.0000 | | 12/01/35 | | | 85,000 | |

| | 11,525 | | | Freddie Mac Gold Pool G05888 | | 5.5000 | | 10/01/39 | | | 11,832 | |

| | | | | | | | | | | | 434,842 | |

| | | | | U.S. TREASURY BONDS — 5.3% | | | | | | | | |

| | 1,040,000 | | | United States Treasury Bond | | 2.8750 | | 05/15/49 | | | 806,914 | |

| | 1,440,000 | | | United States Treasury Bond | | 2.0000 | | 02/15/50 | | | 912,206 | |

| | 2,500,000 | | | United States Treasury Bond | | 1.3750 | | 08/15/50 | | | 1,326,270 | |

| | | | | | | | | | | | 3,045,390 | |

| | | | | U.S. TREASURY NOTES — 12.0% | | | | | | | | |

| | 625,000 | | | United States Treasury Note | | 2.5000 | | 04/30/24 | | | 605,688 | |

| | 2,505,000 | | | United States Treasury Note | | 2.6250 | | 02/15/29 | | | 2,281,311 | |

| | 485,000 | | | United States Treasury Note | | 0.8750 | | 11/15/30 | | | 381,180 | |

| | 715,000 | | | United States Treasury Note | | 1.6250 | | 05/15/31 | | | 590,350 | |

| | 540,000 | | | United States Treasury Note | | 2.8750 | | 05/15/32 | | | 488,869 | |

| | 2,045,000 | | | United States Treasury Note | | 1.8750 | | 02/15/51 | | | 1,246,092 | |

| | 1,135,000 | | | United States Treasury Note | | 1.8750 | | 11/15/51 | | | 688,005 | |

| | 175,000 | | | United States Treasury Note | | 2.2500 | | 02/15/52 | | | 116,785 | |

| | 655,000 | | | United States Treasury Note | | 2.8750 | | 05/15/52 | | | 505,885 | |

| | | | | | | | | | | | 6,904,165 | |

| | | | | TOTAL U.S. GOVERNMENT & AGENCIES (Cost $14,577,068) | | | | | | | 10,384,397 | |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| Shares | | | | | Fair Value | |

| | | | | SHORT-TERM INVESTMENTS — 6.5% | | | | |

| | | | | MONEY MARKET FUNDS - 3.5% | | | | |

| | 1,988,883 | | | Fidelity Government Portfolio, Class I, 2.86% (Cost $1,988,883)(f) | | $ | 1,988,883 | |

| | | | | | | | | |

| | | | | COLLATERAL FOR SECURITIES LOANED – 3.0% | | | | |

| | 1,727,778 | | | Mount Vernon Liquid Assets Portfolio, LLC, 3.24% (Cost $1,727,778) (f),(h) | | | 1,727,778 | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS – 103.4% (Cost $70,266,892) | | $ | 59,287,428 | |

| | | | | LIABILITIES IN EXCESS OF OTHER ASSETS- (3.4%) | | | (1,749,810 | ) |

| | | | | NET ASSETS - 100.0% | | $ | 57,537,618 | |

| LLC | - Limited Liability Company |

| NV | - Naamioze Vennootschap |

| PLC | - Public Limited Company |

| REIT | - Real Estate Investment Trust |

| H15T1Y | US Treasury Yield Curve Rate T Note Constant Maturity 1 Year |

| H15T5Y | US Treasury Yield Curve Rate T Note Constant Maturity 5 Year |

| H15T10Y | US Treasury Yield Curve Rate T Note Constant Maturity 10 Year |

| SOFRINDX | Secured Overnight Financing Rate Compounded |

| SOFRRATE | Secured Overnight Financing Rate |

| TSFR1M | Secured Overnight Financing Rate 1 month |

| US0001M | ICE LIBOR USD 1 Month |

| US0002M | ICE LIBOR USD 2 Month |

| US0003M | ICE LIBOR USD 3 Month |

| US0006M | ICE LIBOR USD 6 Month |

See accompanying notes which are an integral part of these financial statements.

| DUNHAM CORPORATE/GOVERNMENT BOND FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| October 31, 2022 |

| (a) | Security exempt from registration under Rule 144A or Section 4(2) of the Securities Act of 1933. The security may be resold in transactions exempt from registration, normally to qualified institutional buyers. As of October 31, 2022 the total market value of 144A securities is 23,826,876 or 41.1% of net assets. |

| (b) | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| (c) | Step bond. Coupon rate is fixed rate that changes on a specified date. The rate shown is the current rate at October 31, 2022. |

| (d) | Variable rate security; the rate shown represents the rate on October 31, 2022. |

| (e) | Percentage rounds to less than 0.1%. |

| (f) | Rate disclosed is the seven day effective yield as of October 31, 2022. |

| (g) | All or a portion of these securities are on loan. Total loaned securities had a value of $1,687,743 at October 31, 2022. |

| (h) | The Trust’s securities lending policies and procedures require that the borrower: deliver cash or U.S. Government securities as collateral with respect to each new loan of U.S. securities, equal to at least 102% of the value of the portfolio securities loaned, and (ii) at all times thereafter mark-to-market the collateral on a daily basis so that the market value of such collateral is at least 100% of the value of securities loaned. From time to time the collateral may not be 102% due to end of day market movement. The next business day additional collateral is obtained/received from the borrower to replenish/reestablish 102%. |

| Portfolio Composition * - (Unaudited) |

| Corporate Bonds | | | 33.2 | % | | Term Loans | | | 4.8 | % |

| Asset Backed Securities | | | 31.3 | % | | Short-Term Investments | | | 3.4 | % |

| U.S. Government & Agencies | | | 17.5 | % | | Collateral for Securities Loaned | | | 2.9 | % |

| Municipal Bonds | | | 6.0 | % | | Non U.S. Government & Agencies | | | 0.9 | % |

| | | | | | | Total | | | 100.0 | % |

| * | Based on total value of investments as of October 31, 2022. Does not include derivative holdings. Percentage may differ from Schedule of Investments which are based on Fund net assets. |

See accompanying notes which are an integral part of these financial statements.

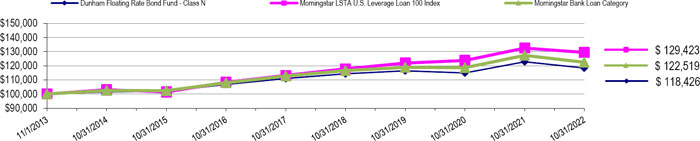

| Dunham Floating Rate Bond Fund (Unaudited) |

| Message from the Sub-Adviser (PineBridge Investments, LLC) |

Asset Class Recap

The most recent market environment has seen nearly all risk assets experience significant declines. This included investment-grade corporate bonds, as measured by the Bloomberg US Credit Index, which declined 8.7 percent in the fourth fiscal quarter and plummeted 18.9 percent since the start of the fiscal year. High-yield bonds, as measured by the ICE BofA U.S. Cash Pay High-Yield Index, decreased 3.6 percent during the final fiscal quarter and 11.3 percent during the 12-month period ended October 31, 2022. This dispersion in returns was primarily due to the lower interest rate sensitivity generally exhibited by high-yield bonds versus their investment-grade counterparts. As the 5-year and 10-year U.S. Treasury Bond yields increased 3.0 percent and 2.5 percent, respectively during the fiscal year, the bonds with higher interest rate sensitivity broadly experienced significant declines. However, bonds with low interest rate sensitivity, such as floating rate securities, generally sustained smaller losses. For example, the Morningstar LSTA US Leveraged Loan 100 Index, which is comprised of bank loans with coupons tied to a market reference rate such as LIBOR or SOFR, only declined 2.3 percent over the fiscal year and was only down 0.1 percent during the fourth fiscal quarter. Securitized asset pools, known as collateralized loan obligations (CLO), comprised of these floating rate securities, as measured by the Palmer Square CLO Debt Index, declined 1.2 percent over the fourth fiscal quarter and fell 6.9 percent during the fiscal year. During the fiscal year, 3-month LIBOR increased 4.3 percent, which exceeded the yield increases on intermediate-term and long-term U.S. Treasuries. As the Federal Reserve has indicated that its pace of interest rate increases will remain aggressive until inflation has been tempered, interest rate sensitive bonds may remain under pressure, while floating rate securities may see the focus shift toward concerns regarding credit quality and increases in default rates. In mid-October, Fitch Ratings projected that the U.S. high yield default rate may finish 2023 between 2.5 percent and 3.5 percent, reflecting growing macroeconomic headwinds and its expectation of a U.S. recession. However, the forecast remains below both the 3.8 percent 21-year historic average and the 5.2 percent default rate reached in 2020.

Allocation Review

The Fund continued to primarily hold floating rate securities, which was predominately comprised of bank loans and CLOs. In aggregate, the Fund held 91 percent in these two categories, with close to 10 percent allocated to CLOs and 81 percent allocated to bank loans. The Fund’s allocation to CLOs generally detracted from overall performance, as the demand for CLOs declined, particularly demand for the higher rated tranches. The Fund also had approximately 7 percent allocated to fixed coupon high-yield corporate bonds, which provided mixed results, but as a whole fell more than the average bank loan in the Fund during the fiscal year. The Fund also had a higher allocation to single- B and CCC rated securities versus the Morningstar LSTA US Leveraged Loan 100 Index. The Fund’s lower exposure to BBB-rated bank loans was the largest underweight versus the benchmark index, as the Fund had less than one percent in BBB-rated loans and the benchmark index had nearly 8 percent. The Fund’s largest credit quality overweight was in the single-B space, as the Fund had close to 77 percent exposure versus 59 percent in the benchmark index. The largest sector overweights were to the consumer services and diversified financial services sectors, while the largest underweights were to the software & services and telecommunication services sectors. The Fund did not have any exposure to derivatives during the twelve-month period that meaningfully affected performance.

Holdings Insights

While the second half of the fiscal year began with a negative reversal for some of the stronger performers from the first half of the fiscal year, the final three months of the fiscal year saw some of those holdings rebound. For example, within the bank loan holdings, the Fund continued to hold Playa Resorts Holding BV Floating Rate due 4/27/2024 (BL2699181) (holding weight*: 0.64 percent). Playa Resorts is an owner, operator, and developer of all - inclusive resorts in Mexico and the Caribbean. The bank loan’s price had declined 2.3 percent in the third fiscal quarter, but rebounded 1.3 percent in the fourth fiscal quarter. This strong finish to the fiscal year brought the price decline for the Playa Resorts bank loan to a negative 0.1 percent for the 12-month period ended October 31, 2022, which made it a positive total return when including the floating coupon of 3-month LIBOR plus 275 basis points. One of the strongest contributors during the final fiscal quarter was Hornblower Sub, LLC due 4/27/2025 (BL3489657) (holding weight*: 1.06 percent), a charter yacht, dining cruise, and ferry service company. The Hornblower bank loan was one of the largest detractors from the Fund for the fiscal year, with its price declining 22.0 percent, but surged 6.0 percent in the final fiscal quarter. When considering its floating coupon of 1-month LIBOR plus 475 basis points, the impact for the fiscal year was marginally offset.