Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22167

Allianz Funds Multi-Strategy Trust

(Exact name of registrant as specified in charter)

1633 Broadway, New York, NY 10019

(Address of principal executive offices) (Zip code)

Scott Whisten

1633 Broadway, New York, NY 10019

(Name and address of agent for service)

Registrant’s telephone number, including area code: 212-739-3367

Date of fiscal year end: September 30

Date of reporting period: March 31, 2018

Table of Contents

Item 1. Report to Shareholders

Allianz Multi-Strategy Funds

SHARE CLASSES A, C, R, P, INSTITUTIONAL, R6, ADMINISTRATIVE

Semiannual Report

March 31, 2018

AllianzGI Retirement 2020 Fund

AllianzGI Retirement 2025 Fund

AllianzGI Retirement 2030 Fund

AllianzGI Retirement 2035 Fund

AllianzGI Retirement 2040 Fund

AllianzGI Retirement 2045 Fund

AllianzGI Retirement 2050 Fund

AllianzGI Retirement 2055 Fund

AllianzGI Multi Asset Income Fund (formerly AllianzGI Retirement Income Fund)

AllianzGI Global Allocation Fund

AllianzGI Best Styles Emerging Markets Equity Fund

AllianzGI Best Styles Global Equity Fund

AllianzGI Best Styles International Equity Fund

AllianzGI Best Styles U.S. Equity Fund

AllianzGI Convertible Fund

AllianzGI Emerging Markets Consumer Fund

AllianzGI Emerging Markets Debt Fund

AllianzGI Emerging Markets Small-Cap Fund

AllianzGI Europe Equity Dividend Fund

AllianzGI Global Dynamic Allocation Fund

AllianzGI Global Fundamental Strategy Fund

AllianzGI Global High Yield Fund

AllianzGI Global Sustainability Fund

AllianzGI Global Water Fund

AllianzGI High Yield Bond Fund

AllianzGI International Growth Fund

AllianzGI International Small-Cap Fund

AllianzGI Micro Cap Fund

AllianzGI NFJ Emerging Markets Value Fund

AllianzGI NFJ International Small-Cap Value Fund

AllianzGI PerformanceFee Managed Futures Strategy Fund

AllianzGI PerformanceFee Structured US Equity Fund

AllianzGI PerformanceFee Structured US Fixed Income Fund

AllianzGI Real Estate Debt Fund

AllianzGI Short Duration High Income Fund

AllianzGI Structured Return Fund

AllianzGI U.S. Equity Hedged Fund

AllianzGI Ultra Micro Cap Fund

This material is authorized for use only when preceded or accompanied by the current Allianz Multi-Strategy Funds, prospectus. Investors should consider the investment objectives, risks, charges and expenses of each Fund carefully before investing. This and other information is contained in the Funds’ prospectuses and summary prospectuses. Please read the prospectus carefully before you invest.

Receive this report electronically and eliminate paper mailings.

To enroll, go to us.allianzgi.com/edelivery.

Table of Contents

| 2–3 | Letter from the President | |||

| 4–105 | Fund Summaries | |||

| 106–107 | Important Information | |||

| 108–111 | Benchmark Descriptions | |||

| 112–197 | Schedules of Investments | |||

| 198–211 | Statements of Assets and Liabilities | |||

| 212–224 | Statements of Operations | |||

| 226–241 | Statements of Changes in Net Assets | |||

| 242–301 | Financial Highlights | |||

| 302–379 | Notes to Financial Statements | |||

| 380 | Changes to the Board of Trustees and Fund Officers | |||

| 381–385 | Matters Relating to the Trustees’ Consideration of the Investment Management Agreements | |||

| 386–387 | Privacy Policy |

A Word About Risk: A fund may be subject to various risks as described in its prospectus. Some of those risks may include, but are not limited to, the following: derivatives risk, smaller company risk, non-US investment risk, focused investment risk and specific sector investment risks. Use of derivative instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, counterparty risk, management risk and the risk that a fund is unable to close out a position when it is most advantageous to do so. Portfolios investing in derivatives could lose more than the principal amount invested in those instruments. Investing in foreign securities may entail risk due to foreign economic and political developments; this risk may be enhanced when investing in emerging markets. Smaller companies may be more volatile than larger companies and may entail more risk. Concentrating investments in individual sectors may add additional risk and additional volatility compared to a diversified equity portfolio. AllianzGI target-date funds seek to manage risk and return by blending two separately-managed portfolios: a return-generating portfolio for growth potential, and a defensive portfolio for principal protection. The balance grows increasingly defensive over time until the target date is reached, after which the Fund’s assets roll into a retirement income strategy. The principal values of the Funds are not guaranteed at any time, including the target date. Please refer to each Fund’s applicable current prospectus for complete details.

Table of Contents

Thomas J. Fuccillo

President & CEO

Dear Shareholder,

The US economy continued to expand during the six-month period ended March 31, 2018. This trend also occurred outside the US, and global inflation remained well-contained. Against this backdrop, US and international equities generated positive results. Elsewhere, the US bond market posted a modest decline during the reporting period.

Six Months in Review

For the six-month period ended March 31, 2018, US stocks, as measured by the Standard & Poor’s 500 Index, gained 5.84%. Two measures of stock performance in developed international and global markets, the MSCI EAFE (Europe, Australasia and Far East) Index (net) and the MSCI World Index (net), returned 2.63% and 4.15%, respectively, in dollar-denominated terms. Elsewhere, the MSCI Emerging Markets Index (net) rose 8.96%. With respect to bonds, the Bloomberg Barclays US Credit Index returned -1.10%, whereas the Bloomberg Barclays Global High Yield Index rose 0.50%. The Bloomberg Barclays US Government Bond Index returned 0.51%, while the broader bond market index, as measured by the Bloomberg Barclays US Aggregate Bond Index, returned -1.08%.

Turning to the US economy, gross domestic product (“GDP”), the value of goods and services produced in the country, the broadest measure of economic activity and the principal indicator of economic performance, expanded at an annual pace of 3.2% and 2.9% during the third and fourth quarters of 2017, respectively. The Commerce Department’s initial estimate for the first quarter of 2018 — released after the reporting period had ended — showed that GDP grew at an annual pace of 2.3%.

The US Federal Reserve (the “Fed”) raised interest rates twice during the reporting period, in December 2017 and March 2018. With the rate hike in March, the federal funds rate moved to a range between 1.50% and 1.75%. This marked the Fed’s sixth rate hike since December 2015 and the first under new Chairman Jerome Powell. Meanwhile, in October 2017, the Fed started to gradually reduce its balance sheet — a process that will likely take several years. The Fed’s actions during the reporting period were well telegraphed and there were minimal market disruptions.

| 2 | March 31, 2018 | | Semiannual Report |

Table of Contents

Outlook

Since the depths of the global financial crisis, central banks have supported financial markets and the economies they serve through expansionary monetary policies, increasing their balance sheets to previously unheard-of sizes. In our opinion, the strong growth in corporate profits and diminishing fears of deflation show that this approach has worked, and central banks will be careful not to stifle current gains.

So, while we anticipate the scale of central bank support will diminish in 2018 — led by the Fed — we expect the overall shift to be slow and the precise actions to vary from one central bank to the next. In our view, interest rates will stay low overall in 2018. Consequently, we believe investors should continue to keep a careful eye on inflation, particularly because official data appear to understate rises in real-world costs. In addition to macroeconomic considerations, we believe several dominant investment themes, including geopolitical risk and business disruption, will persist in 2018.

Against this backdrop, we will continue to use our fundamental research and insights — and our strong global network — to help our clients balance risk and reward. Where appropriate, we will also seek to capitalize on volatility spikes and prepare to trim exposure to risky assets if cyclical data start to lose momentum.

On behalf of Allianz Global Investors U.S. LLC, the Funds’ investment manager, thank you for investing with us. We encourage you to consult with your financial advisor and to visit our website, us.allianzgi.com, for additional information. We remain dedicated to serving your investment needs.

Sincerely,

Thomas J. Fuccillo

President & Chief Executive Officer

Past performance is no guarantee of future results. Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

Receive this report electronically and eliminate paper mailings.

To enroll, go to us.allianzgi.com/edelivery.

| Semiannual Report | | March 31, 2018 | 3 |

Table of Contents

Unaudited

For the period of October 1, 2017 through March 31, 2018, as provided by the Multi-Asset US Group.

Fund Insights

For the six-month period ended March 31, 2018, Class A shares at net asset value (“NAV”) of the AllianzGI Target-Date Funds (the “Funds”) returned between 0.74% and 3.38% with longer dated Funds posting more favorable results. In terms of relative performance, all strategies underperformed their respective benchmarks (Morningstar Lifetime Moderate series) for the six-month period.

Market Overview

The six-month period ending on March 31, 2018 is best characterized as one which began with markets being supported by optimism about global growth and mostly positive political developments. About midway through the period, however, market expectations began to reset.

Global equities appreciated through January buoyed by optimism about the trajectory of global growth. Late in the fourth quarter, the passage of the Tax Cuts and Jobs Act provided an additional boost to sentiment around US equities in light of positive implications for corporate earnings. In terms of economic expansion, we received confirmation that the US economy expanded at a greater than 3.0% rate for two consecutive quarters (on a quarter-over-quarter annualized rate) and that in the US and almost all major economies, the labor market continued to tighten. And yet inflation failed to materialize in spite of such improvements, while official forecasts (from the US Federal Reserve (the “Fed”)) and unofficial ones (from consumer sentiment surveys) suggested that the absence of inflation would continue in the US and in most major economies. Emerging market assets continued to benefit from the “spillover” effects of strong global growth, with its attendant boost to international trade and support for some industrial commodity prices (such as copper) that benefit key commodity exporters. In addition, emerging markets benefited from a weaker US dollar and persistent inflows of foreign capital.

However, signs of rising inflationary pressures and higher bond yields led to a sharp correction in early February. For the remainder of the period macroeconomic and policy uncertainty forced a recalibration of expectations among market participants across asset classes. As of January, markets expected the Fed to increase its benchmark interest rate two times during 2018 and markets seemed to have grown complacent with the low volatility environment of the previous two years. Several new themes arose during the reporting period including (i) a re-emergence of volatility, (ii) renewed vigilance about the possibility of creeping inflation, and (iii) revised forecasts for the pace and magnitude of increases in the Fed’s benchmark interest rate. In this new context, we observed a spike in the Chicago Board Options Exchange Volatility Index (“VIX”) of around 300% during the first week of February, a correction in US equities of more than 6% intraday during the day following a report showing that US wages in January increased more than expected, and an increase in yields on 10-Year Treasuries of roughly 40 basis points by the end of the period.

In March, these factors, combined with the looming threat of a global trade war linked to the White House’s announcement of steep tariffs on steel and aluminum, weighed on markets. Later in March, the technology sector suffered in the wake of several company-specific events, including the launch of a federal investigation into Facebook’s alleged privacy breach.

Overall, the best performing assets for the six-month period were emerging market equities and emerging market bonds followed by global and US equities. Among the worst performing assets were corporate and US government bonds.

Portfolio Review

An overweight to global equities, especially in emerging markets and US equities, provided a tailwind to performance during the reporting period across the board. In addition, selection in equities detracted from performance as the Funds underperformed their respective benchmarks. In addition, selection in bonds also had a negative impact as the AllianzGI Advanced Core Bond Portfolio also underperformed the Bloomberg Barclays US Aggregate Bond Index. Lastly, opportunistic positions in energy and industrial metals commodities also detracted from the Funds’ performance.

At the end of the reporting period, the Funds maintained an underweight position in US government bonds (duration weighted) and an overweight position in global equities including emerging markets, although less so than at the start of the period. The Funds also have an opportunistic position in US bank loans, which are floating rate instruments and which we believe should outperform traditional corporate credit in a rising interest rate environment.

Outlook

Overall, despite the recent volatility in markets, there is still evidence to support a prolonged period of synchronized global growth. As of the end of the quarter, around the world more than two-thirds of countries (developed and emerging) were producing above-average economic data changes. In addition, monetary policy remains accommodative in historical terms as the removal of excess liquidity has been gradual and we believe monetary policy will likely remain accommodative. Although the Fed raised its benchmark interest rate in March and provided more hawkish guidance for the next two years, comments from new Fed Chair Jerome Powell suggest that policy will move at a measured pace. For its part, the European Central Bank signaled that it will not increase the policy rate in 2018. Inflation remains low albeit higher than at the end of last year. Inflation expectations, especially survey-based measures, however, are more elevated.

As of the end of the quarter, our market cycle signals and fundamental analysis recommend a neutral position for global equities favoring emerging markets and US equities and with a small underweight to Europe and the United Kingdom. On the fixed income side, we are neutral to modestly underweight US bonds and long periphery European bonds and emerging market local bonds.

* The “Target-Date Funds” are the AllianzGI Retirement 2020 Fund, the AllianzGI Retirement 2025 Fund, the AllianzGI Retirement 2030 Fund, the AllianzGI Retirement 2035 Fund, the AllianzGI Retirement 2040 Fund, the AllianzGI Retirement 2045 Fund, the AllianzGI Retirement 2050 Fund, and the AllianzGI Retirement 2055 Fund.

| 4 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

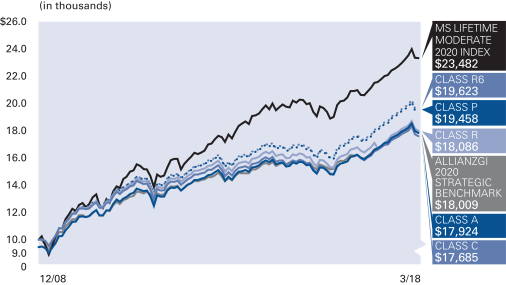

AllianzGI Retirement 2020 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2020 Fund Class A | 0.74% | 6.87% | 3.64% | 7.17% | ||||||||||||||

| AllianzGI Retirement 2020 Fund Class A (adjusted) | –4.80% | 0.99% | 2.47% | 6.51% | |||||||||||||

| AllianzGI Retirement 2020 Fund Class C | 0.33% | 6.09% | 2.86% | 6.35% | ||||||||||||||

| AllianzGI Retirement 2020 Fund Class C (adjusted) | –0.65% | 5.09% | 2.86% | 6.35% | |||||||||||||

| AllianzGI Retirement 2020 Fund Class R | 0.58% | 7.71% | 2.89% | 6.61% | |||||||||||||

| AllianzGI Retirement 2020 Fund Class P | 0.87% | 7.15% | 3.94% | 7.46% | |||||||||||||

| AllianzGI Retirement 2020 Fund Class R6 | 0.90% | 7.29% | 4.04% | 7.56% | |||||||||||||

| AllianzGI Retirement 2020 Fund Administrative Class | 0.80% | 6.94% | 3.68% | 7.21% | ||||||||||||||

| Morningstar Lifetime Moderate 2020 Index | 2.67% | 8.19% | 6.12% | 9.67% | |||||||||||||

| AllianzGI 2020 Strategic Benchmark | 1.78% | 7.31% | 4.06% | 6.57% | |||||||||||||

| Lipper Mixed-Asset Target 2020 Funds Average | 1.95% | 7.14% | 5.32% | 8.63% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 29, 2008. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2008.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.19% for Class A shares, 1.94% for Class C shares, 1.44% for Class R shares, 0.79% for Class P shares, 0.69% for Class R6 shares, and 1.04% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.70% for Class C shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| AllianzGI Global Dynamic Allocation | 63.3% | |||

| AllianzGI Advanced Core Bond | 17.2% | |||

| AllianzGI Best Styles U.S. Equity | 6.0% | |||

| Vanguard Mortgage-Backed Securities | 2.3% | |||

| AllianzGI Short Duration High Income | 1.2% | |||

| iShares TIPS Bond | 1.1% | |||

| Vanguard Intermediate-Term Corporate Bond | 0.9% | |||

| AllianzGI Emerging Markets Small-Cap | 0.7% | |||

| Other | 0.7% | |||

| Cash & Equivalents — Net | 6.6% |

| Semiannual Report | | March 31, 2018 | 5 |

Table of Contents

Unaudited

AllianzGI Retirement 2020 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,007.40 | $1,003.30 | $1,005.80 | $1,008.70 | $1,009.00 | $1,008.00 | ||||||

| Expenses Paid During Period | $1.75 | $5.49 | $3.50 | $0.25 | $0.02 | $1.50 | ||||||

| Hypothetical Performance | ||||||||||||

| (5% return before expenses) | ||||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,023.19 | $1,019.45 | $1,021.44 | $1,024.68 | $1,024.92 | $1,023.44 | ||||||

| Expenses Paid During Period | $1.77 | $5.54 | $3.53 | $0.25 | $0.02 | $1.51 | ||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.35% for Class A, 1.10% for Class C, 0.70% for Class R, 0.05% for Class P, less than 0.005% for Class R6 and 0.30% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 6 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

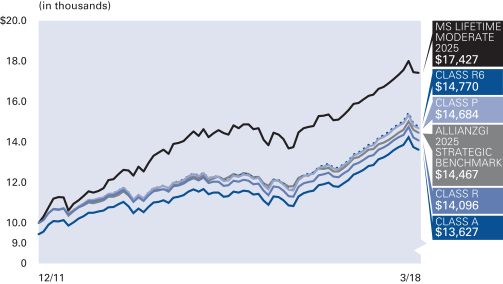

AllianzGI Retirement 2025 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2025 Fund Class A | 1.76% | 8.99% | 4.50% | 6.00% | ||||||||||||||

| AllianzGI Retirement 2025 Fund Class A (adjusted) | –3.84% | 3.00% | 3.32% | 5.05% | |||||||||||||

| AllianzGI Retirement 2025 Fund Class R | 1.57% | 8.61% | 4.12% | 5.61% | |||||||||||||

| AllianzGI Retirement 2025 Fund Class P | 1.88% | 9.31% | 4.81% | 6.31% | |||||||||||||

| AllianzGI Retirement 2025 Fund Class R6 | 1.91% | 9.38% | 4.91% | 6.41% | |||||||||||||

| AllianzGI Retirement 2025 Fund Administrative Class | 1.76% | 9.05% | 4.55% | 6.04% | ||||||||||||||

| Morningstar Lifetime Moderate 2025 Index | 3.08% | 9.31% | 7.00% | 9.25% | |||||||||||||

| AllianzGI 2025 Strategic Benchmark | 2.56% | 8.99% | 4.89% | 6.06% | |||||||||||||

| Lipper Mixed-Asset Target 2025 Funds Average | 2.48% | 8.65% | 6.45% | 8.30% | ||||||||||||||

* Cumulative returns

† The Fund began operations on December 19, 2011. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2011.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.23% for Class A shares, 1.48% for Class R shares, 0.83% for Class P shares, 0.73% for Class R6 shares and 1.08% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| AllianzGI Global Dynamic Allocation | 72.0% | |||

| AllianzGI Advanced Core Bond | 13.6% | |||

| AllianzGI Best Styles U.S. Equity | 9.4% | |||

| AllianzGI Emerging Markets Small-Cap | 0.6% | |||

| AllianzGI Short Duration High Income | 0.5% | |||

| iShares TIPS Bond | 0.5% | |||

| AllianzGI Emerging Markets Debt | 0.3% | |||

| Cash & Equivalents — Net | 3.1% |

| Semiannual Report | | March 31, 2018 | 7 |

Table of Contents

Unaudited

AllianzGI Retirement 2025 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,017.60 | $1,015.70 | $1,018.80 | $1,019.10 | $1,017.60 | |||||

| Expenses Paid During Period | $1.56 | $3.32 | $0.05 | $0.02 | $1.31 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,023.39 | $1,021.64 | $1,024.88 | $1,024.92 | $1,023.64 | |||||

| Expenses Paid During Period | $1.56 | $3.33 | $0.05 | $0.02 | $1.31 | |||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.31% for Class A, 0.66% for Class R, 0.01% for Class P, less than 0.005% for Class R6 and 0.26% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 8 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

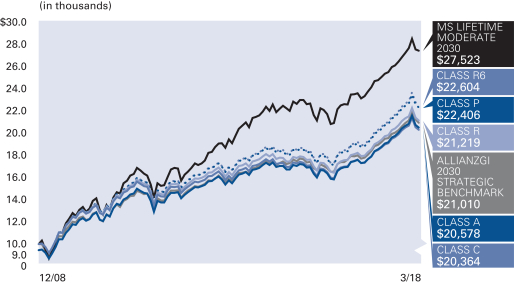

AllianzGI Retirement 2030 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2030 Fund Class A | 2.31% | 10.62% | 5.22% | 8.77% | ||||||||||||||

| AllianzGI Retirement 2030 Fund Class A (adjusted) | –3.32% | 4.54% | 4.04% | 8.11% | |||||||||||||

| AllianzGI Retirement 2030 Fund Class C | 1.95% | 9.77% | 4.43% | 8.00% | ||||||||||||||

| AllianzGI Retirement 2030 Fund Class C (adjusted) | 0.98% | 8.77% | 4.43% | 8.00% | |||||||||||||

| AllianzGI Retirement 2030 Fund Class R | 2.17% | 10.26% | 4.85% | 8.47% | |||||||||||||

| AllianzGI Retirement 2030 Fund Class P | 2.46% | 10.91% | 5.53% | 9.11% | |||||||||||||

| AllianzGI Retirement 2030 Fund Class R6 | 2.54% | 11.02% | 5.64% | 9.21% | |||||||||||||

| AllianzGI Retirement 2030 Fund Administrative Class | 2.38% | 10.68% | 5.27% | 8.87% | ||||||||||||||

| Morningstar Lifetime Moderate 2030 Index | 3.61% | 10.66% | 7.92% | 11.57% | |||||||||||||

| AllianzGI 2030 Strategic Benchmark | 3.24% | 10.47% | 5.70% | 8.36% | |||||||||||||

| Lipper Mixed-Asset Target 2030 Funds Average | 3.15% | 10.12% | 7.17% | 10.23% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 29, 2008. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2008.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.22% for Class A shares, 1.97% for Class C shares, 1.47% for Class R shares, 0.82% for Class P shares, 0.72% for Class R6 shares and 1.07% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.70% for Class C shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| AllianzGI Global Dynamic Allocation | 70.4% | |||

| AllianzGI Best Styles U.S. Equity | 13.0% | |||

| AllianzGI Best Styles Global Equity | 9.0% | |||

| AllianzGI Advanced Core Bond | 3.0% | |||

| AllianzGI Emerging Markets Small-Cap | 1.1% | |||

| Vanguard FTSE All World ex-U.S. Small-Cap | 0.5% | |||

| Cash & Equivalents — Net | 3.0% |

| Semiannual Report | | March 31, 2018 | 9 |

Table of Contents

Unaudited

AllianzGI Retirement 2030 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,023.10 | $1,019.50 | $1,021.70 | $1,024.60 | $1,025.40 | $1,023.80 | ||||||

| Expenses Paid During Period | $1.61 | $5.39 | $3.38 | $0.10 | $0.02 | $1.36 | ||||||

| Hypothetical Performance | ||||||||||||

| (5% return before expenses) | ||||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,023.34 | $1,019.60 | $1,021.59 | $1,024.83 | $1,024.92 | $1,023.59 | ||||||

| Expenses Paid During Period | $1.61 | $5.39 | $3.38 | $0.10 | $0.02 | $1.36 | ||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.32% for Class A, 1.07% for Class C, 0.67% for Class R, 0.02% for Class P, less than 0.005% for Class R6 and 0.27% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 10 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

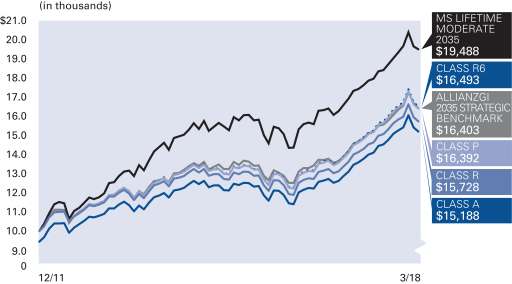

AllianzGI Retirement 2035 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2035 Fund Class A | 2.78% | 11.75% | 5.93% | 7.85% | ||||||||||||||

| AllianzGI Retirement 2035 Fund Class A (adjusted) | –2.88% | 5.60% | 4.74% | 6.88% | |||||||||||||

| AllianzGI Retirement 2035 Fund Class R | 2.63% | 11.41% | 5.57% | 7.48% | |||||||||||||

| AllianzGI Retirement 2035 Fund Class P | 2.96% | 12.07% | 6.26% | 8.19% | |||||||||||||

| AllianzGI Retirement 2035 Fund Class R6 | 3.00% | 12.22% | 6.37% | 8.29% | |||||||||||||

| AllianzGI Retirement 2035 Fund Administrative Class | 2.77% | 11.77% | 5.98% | 7.90% | ||||||||||||||

| Morningstar Lifetime Moderate 2035 Index | 4.14% | 11.95% | 8.65% | 11.21% | |||||||||||||

| AllianzGI 2035 Strategic Benchmark | 3.84% | 11.82% | 6.43% | 8.20% | |||||||||||||

| Lipper Mixed-Asset Target 2035 Funds Average | 3.76% | 11.74% | 8.13% | 9.91% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 19, 2011. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2011.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.15% for Class A shares, 1.40% for Class R shares, 0.75% for Class P shares, 0.65% for Class R6 shares and 1.00% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| AllianzGI Global Dynamic Allocation | 46.7% | |||

| AllianzGI Best Styles Global Equity | 30.6% | |||

| AllianzGI Best Styles U.S. Equity | 15.5% | |||

| AllianzGI Advanced Core Bond | 2.5% | |||

| AllianzGI Emerging Markets Small-Cap | 1.1% | |||

| Vanguard FTSE All World ex-U.S. Small-Cap | 0.9% | |||

| Cash & Equivalents — Net | 2.7% |

| Semiannual Report | | March 31, 2018 | 11 |

Table of Contents

Unaudited

AllianzGI Retirement 2035 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,027.80 | $1,026.30 | $1,029.60 | $1,030.00 | $1,027.70 | |||||

| Expenses Paid During Period | $1.97 | $3.74 | $0.46 | $0.02 | $1.72 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,022.99 | $1,021.24 | $1,024.48 | $1,024.92 | $1,023.24 | |||||

| Expenses Paid During Period | $1.97 | $3.73 | $0.45 | $0.02 | $1.72 | |||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.39% for Class A, 0.74% for Class R, 0.09% for Class P, 0.005% for Class R6 and 0.34% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 12 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2040 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2040 Fund Class A | 3.08% | 12.52% | 6.42% | 10.12% | ||||||||||||||

| AllianzGI Retirement 2040 Fund Class A (adjusted) | –2.59% | 6.33% | 5.22% | 9.45% | |||||||||||||

| AllianzGI Retirement 2040 Fund Class C | 2.69% | 11.63% | 5.63% | 9.28% | ||||||||||||||

| AllianzGI Retirement 2040 Fund Class C (adjusted) | 1.72% | 10.63% | 5.63% | 9.28% | |||||||||||||

| AllianzGI Retirement 2040 Fund Class R | 2.93% | 12.11% | 6.06% | 9.77% | |||||||||||||

| AllianzGI Retirement 2040 Fund Class P | 3.24% | 12.85% | 6.76% | 10.43% | |||||||||||||

| AllianzGI Retirement 2040 Fund Class R6 | 3.28% | 12.98% | 6.86% | 10.53% | |||||||||||||

| AllianzGI Retirement 2040 Fund Administrative Class | 3.07% | 12.56% | 6.48% | 10.16% | ||||||||||||||

| Morningstar Lifetime Moderate 2040 Index | 4.51% | 12.86% | 9.03% | 12.47% | |||||||||||||

| AllianzGI 2040 Strategic Benchmark | 4.31% | 12.85% | 6.97% | 9.72% | |||||||||||||

| Lipper Mixed-Asset Target 2040 Funds Average | 4.03% | 12.25% | 8.25% | 11.12% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 29, 2008. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2008.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.09% for Class A shares, 1.84% for Class C shares, 1.34% for Class R shares, 0.69% for Class P shares, 0.59% for Class R6 shares and 0.94% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.70% for Class C shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

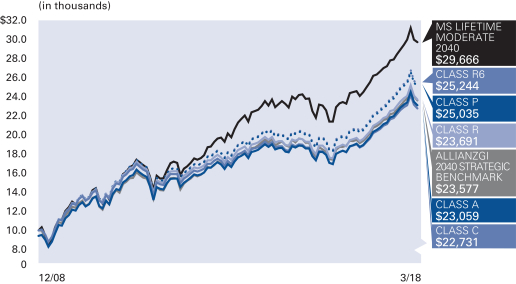

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| AllianzGI Best Styles Global Equity | 44.7% | |||

| AllianzGI Global Dynamic Allocation | 32.8% | |||

| AllianzGI Best Styles U.S. Equity | 18.1% | |||

| Vanguard FTSE All World ex-U.S. Small-Cap | 1.1% | |||

| AllianzGI Emerging Markets Small-Cap | 1.1% | |||

| Cash & Equivalents — Net | 2.2% |

| Semiannual Report | | March 31, 2018 | 13 |

Table of Contents

Unaudited

AllianzGI Retirement 2040 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,030.80 | $1,026.90 | $1,029.30 | $1,032.40 | $1,032.80 | $1,030.70 | ||||||

| Expenses Paid During Period | $2.23 | $6.01 | $4.00 | $0.71 | $0.20 | $1.97 | ||||||

| Hypothetical Performance | ||||||||||||

| (5% return before expenses) | ||||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,022.74 | $1,019.00 | $1,020.99 | $1,024.23 | $1,024.73 | $1,022.99 | ||||||

| Expenses Paid During Period | $2.22 | $5.99 | $3.98 | $0.71 | $0.20 | $1.97 | ||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.44% for Class A, 1.19% for Class C, 0.79% for Class R, 0.14% for Class P, 0.04% for Class R6 and 0.39% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 14 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2045 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2045 Fund Class A | 3.20% | 13.03% | 6.84% | 8.93% | ||||||||||||||

| AllianzGI Retirement 2045 Fund Class A (adjusted) | –2.48% | 6.81% | 5.64% | 7.95% | |||||||||||||

| AllianzGI Retirement 2045 Fund Class R | 2.98% | 12.60% | 6.47% | 8.55% | |||||||||||||

| AllianzGI Retirement 2045 Fund Class P | 3.32% | 13.31% | 7.18% | 9.27% | |||||||||||||

| AllianzGI Retirement 2045 Fund Class R6 | 3.41% | 13.44% | 7.30% | 9.37% | |||||||||||||

| AllianzGI Retirement 2045 Fund Administrative Class | 3.24% | 13.11% | 6.90% | 8.97% | ||||||||||||||

| Morningstar Lifetime Moderate 2045 Index | 4.68% | 13.31% | 9.11% | 11.70% | |||||||||||||

| AllianzGI 2045 Strategic Benchmark | 4.56% | 13.40% | 7.22% | 9.29% | |||||||||||||

| Lipper Mixed-Asset Target 2045 Funds Average | 4.31% | 13.10% | 8.84% | 10.76% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 19, 2011. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2011.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.06% for Class A shares, 1.31% for Class R shares, 0.66% for Class P shares, 0.56% for Class R6 shares and 0.91% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

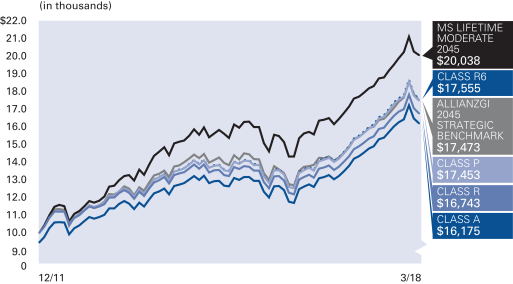

Fund Allocation (as of March 31, 2018)

| AllianzGI Best Styles Global Equity | 53.9% | |||

| AllianzGI Global Dynamic Allocation | 22.0% | |||

| AllianzGI Best Styles U.S. Equity | 18.9% | |||

| Vanguard FTSE All World ex-U.S. Small-Cap | 1.3% | |||

| AllianzGI Emerging Markets Small-Cap | 1.0% | |||

| Cash & Equivalents — Net | 2.9% |

| Semiannual Report | | March 31, 2018 | 15 |

Table of Contents

Unaudited

AllianzGI Retirement 2045 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,032.00 | $1,029.80 | $1,033.20 | $1,034.10 | $1,032.40 | |||||

| Expenses Paid During Period | $2.43 | $4.20 | $0.91 | $0.41 | $2.18 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,022.54 | $1,020.79 | $1,024.03 | $1,024.53 | $1,022.79 | |||||

| Expenses Paid During Period | $2.42 | $4.18 | $0.91 | $0.40 | $2.17 | |||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.48% for Class A, 0.83% for Class R, 0.18% for Class P, 0.08% for Class R6 and 0.43% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 16 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2050 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2050 Fund Class A | 3.31% | 13.14% | 6.89% | 10.55% | ||||||||||||||

| AllianzGI Retirement 2050 Fund Class A (adjusted) | –2.37% | 6.92% | 5.68% | 9.88% | |||||||||||||

| AllianzGI Retirement 2050 Fund Class C | 2.91% | 12.30% | 6.08% | 9.74% | ||||||||||||||

| AllianzGI Retirement 2050 Fund Class C (adjusted) | 1.94% | 11.30% | 6.08% | 9.74% | |||||||||||||

| AllianzGI Retirement 2050 Fund Class R | 3.13% | 12.77% | 6.50% | 10.22% | |||||||||||||

| AllianzGI Retirement 2050 Fund Class P | 3.47% | 13.50% | 7.22% | 10.88% | |||||||||||||

| AllianzGI Retirement 2050 Fund Class R6 | 3.47% | 13.56% | 7.32% | 10.98% | |||||||||||||

| AllianzGI Retirement 2050 Fund Administrative Class | 3.31% | 13.16% | 6.94% | 10.62% | ||||||||||||||

| Morningstar Lifetime Moderate 2050 Index | 4.72% | 13.47% | 9.05% | 12.51% | |||||||||||||

| AllianzGI 2050 Strategic Benchmark | 4.66% | 13.61% | 7.28% | 9.90% | |||||||||||||

| Lipper Mixed-Asset Target 2050+ Funds Average | 4.23% | 12.76% | 8.69% | 11.37% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 29, 2008. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2008.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.05% for Class A shares, 1.80% for Class C shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.70% for Class C shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

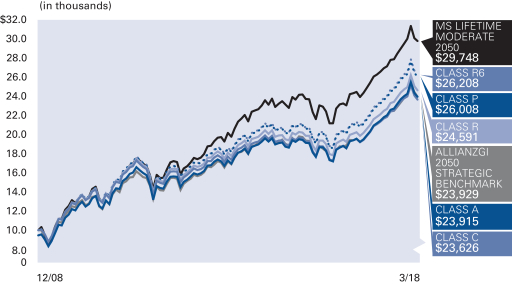

Fund Allocation (as of March 31, 2018)

| AllianzGI Best Styles Global Equity | 58.9% | |||

| AllianzGI Best Styles U.S. Equity | 18.4% | |||

| AllianzGI Global Dynamic Allocation | 17.5% | |||

| Vanguard FTSE All World ex-U.S. Small-Cap | 1.4% | |||

| AllianzGI Emerging Markets Small-Cap | 1.0% | |||

| Cash & Equivalents — Net | 2.8% |

| Semiannual Report | | March 31, 2018 | 17 |

Table of Contents

Unaudited

AllianzGI Retirement 2050 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,033.10 | $1,029.10 | $1,031.30 | $1,034.70 | $1,034.70 | $1,033.10 | ||||||

| Expenses Paid During Period | $2.48 | $6.27 | $4.25 | $0.96 | $0.46 | $2.23 | ||||||

| Hypothetical Performance | ||||||||||||

| (5% return before expenses) | ||||||||||||

| Class A | Class C | Class R | Class P | Class R6 | Administrative Class | |||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | ||||||

| Ending Account Value (3/31/18) | $1,022.49 | $1,018.75 | $1,020.74 | $1,023.98 | $1,024.48 | $1,022.74 | ||||||

| Expenses Paid During Period | $2.47 | $6.24 | $4.23 | $0.96 | $0.45 | $2.22 | ||||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.49% for Class A, 1.24% for Class C, 0.84% for Class R, 0.19% for Class P, 0.09% for Class R6 and 0.44% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 18 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Retirement 2055 Fund

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

| AllianzGI Retirement 2055 Fund Class A | 3.38% | 13.18% | 6.90% | 9.08% | ||||||||||||||

| AllianzGI Retirement 2055 Fund Class A (adjusted) | –2.31% | 6.95% | 5.69% | 8.11% | |||||||||||||

| AllianzGI Retirement 2055 Fund Class R | 3.20% | 12.81% | 6.52% | 8.71% | |||||||||||||

| AllianzGI Retirement 2055 Fund Class P | 3.51% | 13.48% | 7.21% | 9.42% | |||||||||||||

| AllianzGI Retirement 2055 Fund Class R6 | 3.58% | 13.64% | 7.33% | 9.53% | |||||||||||||

| AllianzGI Retirement 2055 Fund Administrative Class | 3.39% | 13.24% | 6.94% | 9.13% | ||||||||||||||

| Morningstar Lifetime Moderate 2055 Index | 4.73% | 13.57% | 8.96% | 11.57% | |||||||||||||

| AllianzGI 2055 Strategic Benchmark | 4.66% | 13.61% | 7.28% | 9.34% | |||||||||||||

| Lipper Mixed-Asset Target 2055+ Funds Average | 4.51% | 13.57% | 9.19% | 11.11% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 19, 2011. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2011.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.05% for Class A shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

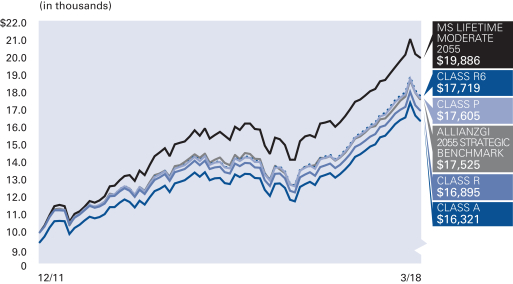

Fund Allocation (as of March 31, 2018)

| AllianzGI Best Styles Global Equity | 58.8% | |||

| AllianzGI Best Styles U.S. Equity | 18.3% | |||

| AllianzGI Global Dynamic Allocation | 17.5% | |||

| Vanguard FTSE All World ex-U.S. Small-Cap | 1.4% | |||

| AllianzGI Emerging Markets Small-Cap | 1.0% | |||

| Cash & Equivalents — Net | 3.0% |

| Semiannual Report | | March 31, 2018 | 19 |

Table of Contents

Unaudited

AllianzGI Retirement 2055 Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,033.80 | $1,032.00 | $1,035.10 | $1,035.80 | $1,033.90 | |||||

| Expenses Paid During Period | $2.48 | $4.26 | $0.96 | $0.46 | $2.23 | |||||

| Hypothetical Performance | ||||||||||

| (5% return before expenses) | ||||||||||

| Class A | Class R | Class P | Class R6 | Administrative Class | ||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||

| Ending Account Value (3/31/18) | $1,022.49 | $1,020.74 | $1,023.98 | $1,024.48 | $1,022.74 | |||||

| Expenses Paid During Period | $2.47 | $4.23 | $0.96 | $0.45 | $2.22 | |||||

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.49% for Class A, 0.84% for Class R, 0.19% for Class P, 0.09% for Class R6 and 0.44% for Administrative Class), multiplied by the average account value over the period, multiplied by 182/365. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| 20 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Multi Asset Income Fund (formerly AllianzGI Retirement Income Fund)

For the period of October 1, 2017 through March 31, 2018, as provided by the Multi-Asset US Group.

Fund Insights

For the six-month period ended March 31, 2018, Class A shares at net asset value (“NAV”) of the AllianzGI Multi Asset Income Fund (the “Fund”) returned -1.59%, underperforming the Bloomberg Barclays US Universal Bond Index (the “benchmark”), which returned -1.00%.

Market Overview

The six-month period ending on March 31, 2018 is best characterized as one which began with markets being supported by optimism about global growth and mostly positive political developments. About midway through the period, however, market expectations began to reset.

Global equities appreciated through January buoyed by optimism about the trajectory of global growth. Late in the fourth quarter, the passage of the Tax Cuts and Jobs Act provided an additional boost to sentiment around US equities in light of positive implications for corporate earnings. In terms of economic expansion, we received confirmation that the US economy expanded at a greater than 3.0% rate for two consecutive quarters (on a quarter-over-quarter annualized rate) and that in the US and almost all major economies, the labor market continued to tighten. And yet inflation failed to materialize in spite of such improvements, while official forecasts (from the US Federal Reserve (the “Fed”)) and unofficial ones (from consumer sentiment surveys) suggested that the absence of inflation would continue in the US and in most major economies. Emerging market assets continued to benefit from the “spillover” effects of strong global growth, with its attendant boost to international trade and support for some industrial commodity prices (such as copper) that benefit key commodity exporters. In addition, emerging markets benefited from a weaker US dollar and persistent inflows of foreign capital.

However, signs of rising inflationary pressures and higher bond yields led to a sharp correction in early February. For the remainder of the period macroeconomic and policy uncertainty forced a recalibration of expectations among market participants across asset classes. As of January, markets expected the Fed to increase its benchmark interest rate two times during 2018 and markets seemed to have grown complacent with the low volatility environment of the previous two years. Several new themes arose including (i) a re-emergence of volatility, (ii) renewed vigilance about the possibility of creeping inflation, and (iii) revised forecasts for the pace and magnitude of increases in the Fed’s benchmark interest rate. In this new context, we observed a spike in the Chicago Board Options Exchange Volatility Index (“VIX”) of around 300% during the first week of February, a correction in US equities of more than 6% intraday during the day following a report showing that US wages in January increased more than expected, and an increase in yields on 10-Year Treasuries of roughly 40 basis points by the end of the period.

In March, these factors, combined with the looming threat of a global trade war linked to the White House’s announcement of steep tariffs on steel and aluminum, weighed on markets. Later in March, the technology sector suffered in the wake of several company-specific events including the launch of a federal investigation into Facebook’s alleged privacy breach.

Overall, the best performing assets for the six-month period were emerging market equities and emerging market bonds followed by global and US equities. Among the worst performing assets were corporate and US government bonds.

Portfolio Review

Given the Fund’s focus on generating a relatively high level of income via dividends and interest, the Fund was overweight with respect to REITs and held an opportunistic position in MLPs during the reporting period; these two positions were responsible for most of the Fund’s underperformance. The Fund benefited from the use of high dividend paying equities and from a positive allocation effect in developed Asian and emerging market equities. The use of flexible income-oriented core strategies and the AllianzGI Short Duration High Income Fund offset the negative contribution from the Fund’s treasury positions.

The Fund is currently overweight with respect to equities, including preferred stocks and convertible securities, bank loans and emerging market debt, and underweight with respect to traditional high yield bonds, investment grade bonds and overall duration.

Overall, the Fund seeks to maintain a highly diversified mix of income sources throughout all market environments to mitigate portfolio risks.

Outlook

Overall, despite the recent volatility in markets, there is still evidence to support a prolonged period of synchronized global growth. As of the end of the quarter, around the world more than two-thirds of countries (developed and emerging) were producing above-average economic data changes. In addition, monetary policy remains accommodative in historical terms as the removal of excess liquidity has been gradual and we believe monetary policy will likely remain accommodative. Although the Fed raised its benchmark interest rate in March and provided more hawkish guidance for the next two years, comments from new Fed Chair Jerome Powell suggest that policy will move at a measured pace. For its part, the European Central Bank signaled that it will not increase the policy rate in 2018. Inflation remains low albeit higher than at the end of last year. Inflation expectations, especially survey-based measures, however, are more elevated.

As of the end of the quarter, our market cycle signals and fundamental analysis recommend a neutral position for global equities favoring emerging markets and US equities and with a small underweight to Europe and the United Kingdom. On the fixed income side, we are neutral to modestly underweight US bonds and long periphery European bonds and emerging market local bonds.

| Semiannual Report | | March 31, 2018 | 21 |

Table of Contents

Unaudited

AllianzGI Multi Asset Income Fund (formerly AllianzGI Retirement Income Fund) (cont’d)

Average Annual Total Return for the period ended March 31, 2018

| 6 Month* | 1 Year | 5 Year | Since Inception† | |||||||||||||||

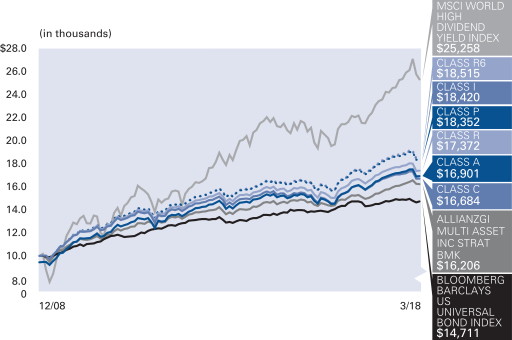

| AllianzGI Multi Asset Income Fund Class A | –1.59% | 2.28% | 2.95% | 6.48% | ||||||||||||||

| AllianzGI Multi Asset Income Fund Class A (adjusted) | –7.00% | –3.34% | 1.79% | 5.83% | |||||||||||||

| AllianzGI Multi Asset Income Fund Class C | –2.01% | 1.47% | 2.16% | 5.69% | ||||||||||||||

| AllianzGI Multi Asset Income Fund Class C (adjusted) | –2.95% | 0.51% | 2.16% | 5.69% | |||||||||||||

| AllianzGI Multi Asset Income Fund Class R | –1.76% | 1.87% | 2.59% | 6.14% | |||||||||||||

| AllianzGI Multi Asset Income Fund Class P | –1.43% | 2.56% | 3.26% | 6.78% | |||||||||||||

| AllianzGI Multi Asset Income Fund Class R6 | –1.37% | 2.68% | 3.37% | 6.88% | |||||||||||||

| AllianzGI Multi Asset Income Fund Administrative Class | –1.57% | 2.32% | 2.79% | 6.42% | ||||||||||||||

| AllianzGI Multi Asset Income Fund Institutional Class | –1.45% | 2.57% | 3.30% | 6.82% | |||||||||||||

| Bloomberg Barclays US Universal Bond Index | –1.00% | 1.52% | 2.19% | 4.26% | |||||||||||||

| AllianzGI Multi Asset Income Strategic Benchmark | 0.81% | 5.15% | 2.93% | 5.36% | |||||||||||||

| MSCI World High Dividend Yield Index | 0.24% | 8.04% | 6.87% | 10.53% | |||||||||||||

| Lipper Mixed-Asset Target Today Funds Average | 1.11% | 5.04% | 3.62% | 6.37% | ||||||||||||||

* Cumulative return

† The Fund began operations on December 29, 2008. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on December 31, 2008.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum initial sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.20% for Class A shares, 1.95% for Class C shares, 1.45% for Class R shares, 0.80% for Class P shares, 0.75% for Institutional Class, 0.70% for Class R6 shares and 1.05% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2020. The Fund’s expense ratios net of this reduction are 0.95% for Class A shares, 1.70% for Class C shares, 1.30% for Class R shares, 0.65% for Class P shares, 0.60% for Institutional Class, 0.55% for Class R6 shares and 0.90% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

| 22 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Multi Asset Income Fund (formerly AllianzGI Retirement Income Fund) (cont’d)

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| PIMCO Income | 12.8% | |||

| AllianzGI Short Duration High Income | 10.2% | |||

| PIMCO Investment Grade Corporate Bond | 7.6% | |||

| AllianzGI Emerging Markets Debt | 7.4% | |||

| AllianzGI Europe Equity Dividend | 6.8% | |||

| PIMCO Preferred and Capital Securites | 6.0% | |||

| PIMCO Mortgage Opportunities | 5.0% | |||

| AllianzGI High Yield Bond | 5.0% | |||

| Other | 26.8% | |||

| Cash & Equivalents — Net | 12.4% |

| Shareholder Expense Example | Actual Performance | |||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class* | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (3/31/18) | $984.10 | $979.90 | $982.40 | $985.70 | $969.60 | $986.30 | $984.30 | |||||||

| Expenses Paid During Period | $1.93 | $5.63 | $3.66 | $0.45 | $0.06 | $0.01 | $1.68 | |||||||

| Hypothetical Performance | ||||||||||||||

| (5% return before expenses) | ||||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class* | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (3/31/18) | $1,022.99 | $1,019.25 | $1,021.24 | $1,024.48 | $1,024.73 | $1,024.92 | $1,023.24 | |||||||

| Expenses Paid During Period | $1.97 | $5.74 | $3.73 | $0.45 | $0.20 | $0.02 | $1.72 | |||||||

* Institutional Class commenced operations on February 1, 2018. The Actual expense example for Institutional Class is based on the period since inception; the Actual expense example for Class A, Class C, Class R, Class P, Class R6, and Administrative Class and the Hypothetical expense example for all classes are based on the period beginning October 1, 2017. If the Hypothetical expense example for Institutional Class had been based on the period since inception, the Ending Account Value and Expenses Paid During Period would have been: $1,007.88 and $0.06, respectively.

For each class of the Fund, expenses (net of fee waiver and reimbursement, if any) are equal to the annualized expense ratio for the class (0.39% for Class A, 1.14% for Class C, 0.74% for Class R, 0.09% for Class P, 0.04% for Institutional Class, less than 0.005% for Class R6 and 0.34% for Administrative Class), multiplied by the average account value over the period, multiplied by 182 (58 for Institutional Class)/365 for the Actual expense example and 182/365 for the Hypothetical expense example. These expenses do not include the expenses of the investment companies in which the Fund invests, which are indirectly borne by Fund shareholders.

| Semiannual Report | | March 31, 2018 | 23 |

Table of Contents

Unaudited

AllianzGI Global Allocation Fund

For the period of October 1, 2017 through March 31, 2018, as provided by the Multi-Asset US Group.

Fund Insights

For the six-month period ended March 31, 2018, Class A shares at net asset value (“NAV”) of the AllianzGI Global Allocation Fund (the “Fund”) returned 1.80%, underperforming the 60% MSCI ACWI, 40% Bloomberg Barclays US Aggregate Bond Index (the “benchmark”), which returned 2.45%.

Market Overview

The six-month period ending on March 31, 2018 is best characterized as one which began with markets being supported by optimism about global growth and mostly positive political developments. About midway through the period, however, market expectations began to reset.

Global equities appreciated through January buoyed by optimism about the trajectory of global growth. Late in the fourth quarter, the passage of the Tax Cuts and Jobs Act provided an additional boost to sentiment around US equities in light of positive implications for corporate earnings. In terms of economic expansion, we received confirmation that the US economy expanded at a greater than 3.0% rate for two consecutive quarters (on a quarter-over-quarter annualized rate) and that in the US and almost all major economies, the labor market continued to tighten. And yet inflation failed to materialize in spite of such improvements, while official forecasts (from the US Federal Reserve (the “Fed”)) and unofficial ones (from consumer sentiment surveys) suggested that the absence of inflation would continue in the US and in most major economies. Emerging market assets continued to benefit from the “spillover” effects of strong global growth, with its attendant boost to international trade and support for some industrial commodity prices (such as copper) that benefit key commodity exporters. In addition, emerging markets benefited from a weaker US dollar and persistent inflows of foreign capital.

However, signs of rising inflationary pressures and higher bond yields led to a sharp correction in early February. For the remainder of the reporting period macroeconomic and policy uncertainty forced a recalibration of expectations among market participants across asset classes. As of January, markets expected the Fed to increase its benchmark interest rate two times during 2018 and seemed to have grown complacent with the low volatility environment of the previous two years. Several new themes arose during the reporting period including (i) a re-emergence of volatility, (ii) renewed vigilance about the possibility of creeping inflation, and (iii) revised forecasts for the pace and magnitude of increases in the Fed’s benchmark interest rate. In this new context, we observed a spike in the Chicago Board Options Exchange Volatility Index (“VIX”) of around 300% during the first week of February, a correction in US equities of more than 6% intraday during the day following a report showing that US wages in January increased more than expected, and an increase in yields on 10-Year Treasuries of roughly 40 basis points by the end of the period.

In March, these factors, combined with the looming threat of a global trade war linked to the White House’s announcement of steep tariffs on steel and aluminum, weighed on markets. Later in March, the technology sector suffered in the wake of several company-specific events, including the launch of a federal investigation into Facebook’s alleged privacy breach.

Overall, the best performing assets for the six-month period were emerging market equities and emerging market bonds followed by global and US equities. Among the worst performing assets were corporate and US government bonds.

Portfolio Review

An overweight to global equities, especially in emerging markets and US equities, provided a tailwind to performance during the reporting period across the board. In addition, selection in equities detracted from performance as the Fund underperformed its benchmark. In the opportunistic portion of the portfolio, performance benefitted from exposure to small-cap stocks in both emerging markets and the US. Other opportunistic holdings such as high yield bonds and UK government bonds detracted from the Fund’s performance. In addition, exposure to commodities and selected currencies through a managed futures strategy detracted from the Fund’s performance. The Fund’s exposure to US Treasuries ultimately detracted, although positioning helped intermittently, including as exposure was decreased when yields went up in February.

At the end of the reporting period, the Fund maintained an underweight position in US government bonds (duration weighted) and an overweight position with respect to global equities including emerging markets, although less so than at the start of the reporting period.

Outlook

Overall, despite the recent volatility in markets, there is still evidence to support a prolonged period of synchronized global growth. As of the end of the quarter, around the world more than two-thirds of countries (developed and emerging) were producing above-average economic data changes. In addition, monetary policy remains accommodative in historical terms as the removal of excess liquidity has been gradual and we believe monetary policy will likely remain accommodative. Although the Fed raised its benchmark interest rate in March and provided more hawkish guidance for the next two years, comments from new Fed Chair Jerome Powell suggest that policy will move at a measured pace. For its part, the European Central Bank signaled that it will not increase the policy rate in 2018. Inflation remains low albeit higher than at the end of last year. Inflation expectations, especially survey-based measures, however, are more elevated.

As of the end of the quarter, our market cycle signals and fundamental analysis recommend a neutral position for global equities favoring emerging markets and US equities and with a small underweight to Europe and the United Kingdom. On the fixed income side, we are neutral to modestly underweight US bonds and long periphery European bonds and Emerging Market local bonds.

| 24 | March 31, 2018 | | Semiannual Report |

Table of Contents

Unaudited

AllianzGI Global Allocation Fund (cont’d)

Average Annual Total Return for the period ended March 31, 2018

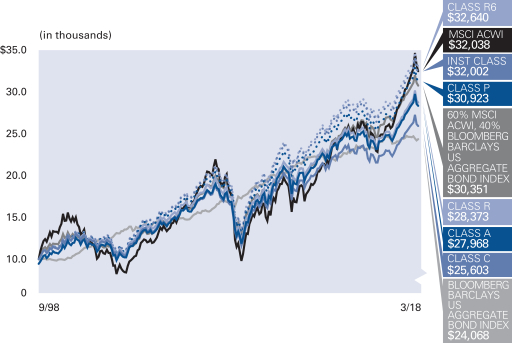

| 6 Month* | 1 Year | 5 Year | 10 Year | Since Inception† | ||||||||||||||||||

| AllianzGI Global Allocation Fund Class A | 1.80% | 9.64% | 4.84% | 5.09% | 5.72% | |||||||||||||||||

| AllianzGI Global Allocation Fund Class A (adjusted) | –3.80% | 3.61% | 3.66% | 4.50% | 5.42% | ||||||||||||||||

| AllianzGI Global Allocation Fund Class C | 1.47% | 8.85% | 4.06% | 4.32% | 4.94% | |||||||||||||||||

| AllianzGI Global Allocation Fund Class C (adjusted) | 0.54% | 7.85% | 4.06% | 4.32% | 4.94% | ||||||||||||||||

| AllianzGI Global Allocation Fund Class R | 1.77% | 9.52% | 4.68% | 4.89% | 5.49% | ||||||||||||||||

| AllianzGI Global Allocation Fund Class P | 1.96% | 9.97% | 5.12% | 5.34% | 5.96% | ||||||||||||||||

| AllianzGI Global Allocation Fund Institutional Class | 1.97% | 9.79% | 5.07% | 5.40% | 6.14% | ||||||||||||||||

| AllianzGI Global Allocation Fund Administrative Class | 1.85% | 9.80% | 4.86% | 5.13% | 5.78% | ||||||||||||||||

| AllianzGI Global Allocation Fund R6 | 1.95% | 10.08% | 5.18% | 5.51% | 6.25% | ||||||||||||||||

| MSCI ACWI | 4.71% | 14.85% | 9.20% | 5.57% | 6.15% | ||||||||||||||||

| 60% MSCI ACWI, 40% Bloomberg Barclays US Aggregate Bond Index | 2.45% | 9.29% | 6.33% | 5.15% | 5.86% | ||||||||||||||||

| Bloomberg Barclays US Aggregate Bond Index | –1.08% | 1.20% | 1.82% | 3.63% | 4.61% | ||||||||||||||||

| Lipper Alternative Global Macro Funds Average | 0.64% | 4.89% | 2.17% | 3.17% | 5.12% | |||||||||||||||||

* Cumulative return

† The Fund began operations on September 30,1998. Benchmark return comparisons began on the fund inception date. Lipper performance comparisons began on September 30, 1998.

Performance quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than performance shown. For performance current to the most recent month-end, visit our website at us.allianzgi.com. Investment return and the principal value will fluctuate. Shares may be worth more or less than original cost when redeemed. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and the contingent deferred sales charge (CDSC) of 1% on Class C shares, which may apply to shares redeemed during the first year of ownership. Returns do not reflect deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. See pages 106 and 107 for more information. The Fund’s gross expense ratios are 1.53% for Class A shares, 2.28% for Class C shares, 1.72% for Class R shares, 1.26% for Class P shares, 1.36% for Institutional Class shares, 1.21% for Class R6 shares and 1.47% for Administrative Class shares. These ratios do not include an expense reduction, contractually guaranteed through at least January 31, 2019. The Fund’s expense ratios net of this reduction are 1.01% for Class A shares, 1.78% for Class C shares, 1.21% for Class R shares, 0.81% for Class P shares, 0.81% for Institutional Class shares, 0.71% for Class R6 shares and 0.96% for Administrative Class shares. Expense ratio information is as of the Fund’s current prospectus dated February 1, 2018.

Cumulative Returns Through March 31, 2018

Fund Allocation (as of March 31, 2018)

| AllianzGI Best Styles Global Equity | 39.7% | |||

| AllianzGI Advanced Core Bond | 25.6% | |||

| AllianzGI Best Styles Global Managed Volatility | 10.4% | |||

| AllianzGI International Growth | 5.3% | |||

| AllianzGI Emerging Markets Debt | 4.3% | |||

| AllianzGI PerformanceFee Managed Futures Strategy | 4.1% | |||

| iShares iBoxx $ Investment Grade Corporate Bond | 2.9% | |||

| iShares MBS | 1.9% | |||

| Other | 2.8% | |||

| Cash & Equivalents — Net | 3.0% |

| Semiannual Report | | March 31, 2018 | 25 |

Table of Contents

Unaudited

AllianzGI Global Allocation Fund (cont’d)

| Shareholder Expense Example | Actual Performance | |||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (3/31/18) | $1,018.00 | $1,014.70 | $1,017.70 | $1,019.60 | $1,019.70 | $1,019.50 | $1,018.50 | |||||||

| Expenses Paid During Period | $3.02 | $6.83 | $4.02 | $1.86 | $2.01 | $1.52 | $2.77 | |||||||

| Hypothetical Performance | ||||||||||||||

| (5% return before expenses) | ||||||||||||||

| Class A | Class C | Class R | Class P | Institutional Class | Class R6 | Administrative Class | ||||||||

| Beginning Account Value (10/1/17) | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | $1,000.00 | |||||||

| Ending Account Value (3/31/18) | $1,021.94 | $1,018.15 | $1,020.94 | $1,023.09 | $1,022.94 | $1,023.44 | $1,022.19 | |||||||

| Expenses Paid During Period | $3.02 | $6.84 | $4.03 | $1.87 | $2.02 | $1.51 | $2.77 | |||||||