UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22208

Valued Advisers Trust

(Exact name of registrant as specified in charter)

Ultimus Asset Services, LLC 225 Pictoria Drive, Suite 450 Cincinnati, OH 45246

(Address of principal executive offices) (Zip code)

Capitol Services, Inc.

615 S. Dupont Hwy.

Dover, DE 19901

(Name and address of agent for service)

With a copy to:

John H. Lively, Esq.

The Law Offices of John H. Lively & Associates, Inc.

A member firm of The 1940 Act Law GroupTM

11300 Tomahawk Creek Parkway,

Suite 310

Leawood, KS 66221

Registrant’s telephone number, including area code: 513-587-3400

Date of fiscal year end: 5/31

Date of reporting period: 5/31/17

Item 1. Reports to Stockholders.

ANNUAL

REPORT

May 31, 2017

BFS Equity Fund

185 Asylum Street • City Place II • Hartford, CT 06103 • (855) 575-2430

BFS Equity Fund

Letter to Shareholders

Dear Fellow Shareholders,

This annual report covers the period June 1, 2016 through May 31, 2017 – the BFS Equity Fund’s third full fiscal year.

The BFS Equity Fund (the “Fund”) was launched on November 8, 2013, with initial funds from investors of $1.1 million. On June 1, 2016, the Fund had net assets of $23.9 million. During the course of the fiscal year, the net assets of the Fund increased 13.8% to $27.2 million, as of May 31, 2017. This growth was driven by inflows from investors into the Fund, as well as by the positive investment return achieved by the Fund over the past fiscal year. As of May 31, 2017, there were approximately 550 investors in the Fund.

The Fund achieved a total return of 13.15% for the fiscal year commencing June 1, 2016 and ending May 31, 2017. This was less than the 17.47% total return of the S&P 500® Index and the 21.16% total return of the Dow Jones Industrial Average for the same period.

This report includes a commentary from the Lead Portfolio Manager, Tim Foster, and Co-Portfolio Managers, Tom Sargent and Keith LaRose. You will also find a listing of the portfolio holdings as of May 31, 2017, as well as financial statements and detailed information about the performance and positioning of the Fund.

The past fiscal year has been somewhat of a rollercoaster ride, dominated predominantly by the U.S. presidential election, the difficulty that the Trump administration has had getting a health care bill through Congress due to disunity of the Republicans in the House and Senate, the continuing media buzz about collusion with Russia by Trump operatives, the “resistance” by Democrats in Congress, and, finally, the sense that tax reform – one of the main planks of the Trump economic growth agenda – might not pass this year. Despite these factors, the market has ignored them and forged ahead. Corporate earnings growth has been positive the last three calendar quarters and appears to be accelerating, inflation has been muted, and stock market volatility is at very low levels. Even with the recent three hikes in the Fed Funds rate, it is unlikely that medium and longer term interest rates will rise significantly in the year ahead. With the earnings yield so much higher on U.S. stocks than bonds, it is likely that the stock market will continue to attract investors.

1

In closing, it is important to reiterate our belief that our investment strategy of investing in quality growth stocks purchased with a risk-mitigating approach and positioned to provide a margin of safety in the case of economic or market weakness is effective over the longer term. We believe the Fund’s ownership of shares in quality companies with sound business models, strong brands, good balance sheets, professional management, and robust cash flow should be able to withstand market corrections, even bear markets, and perform well over the longer term.

The Portfolio Managers of the Fund and I are shareholders together with you. We thank you for the trust that you have placed in us to manage your assets.

Sincerely

Stephen L. Willcox

President and CEO

Bradley, Foster & Sargent, Inc.

2

BFS Equity Fund

Portfolio Managers’ Letter

TO OUR SHAREHOLDERS

The BFS Equity Fund the (“Fund”) completed its third full fiscal year on May 31, 2017. The Fund returned a very healthy 13.15%, but lagged the performance of the S&P 500® Index (“S&P 500”), which returned 17.47% as well as the Dow Jones Industrial Average total return of 21.16%. The Fund is not managed to mimic either index. The S&P 500 is comprised of 500 different stocks, market cap weighted, so that the largest 10-20 names really drive the performance of the entire index. Apple’s 3.73% top weighting in the index with $776 billion in market capitalization makes Transocean’s 500th place at $3.4 billion market cap immaterial. The Dow Jones Industrial Average Index is comprised of 30 stocks, weighted by their relative absolute stock prices, where Goldman Sach’s $250 stock price trumps GE’s $29 stock price.

Generally, the Fund holds approximately 35 positions with individual weightings generally varying from 2-4%. We believe having about 35 names in the portfolio provides adequate diversification. At any time, we hold up to five individual securities within each of the S&P 500’s nine defined economic sectors. If we cannot find attractive values in a sector, such as Telecom or Utilities, which tend to perform poorly in a rising interest rate environment, we may opt not to own any (and, in fact, we do not own any, as of May 31, 2017). The S&P 500 Industrials sector includes sub categories such as Automotive, Aerospace, Agriculture, Mining Equipment, and Defense. Airlines may be attractive when Automobiles are not, so, unlike Utilities, a wider array of economic influences can drive individual stock performance. We may (and do) own more names in diverse sectors like Industrials, Technology, and Consumer Discretionary. Diversification is generally thought of as a good thing – it limits the impact of losses of any one holding. It is important to realize, as well, that diversification also limits the impact of gains. For the Fund, we want to identify what we believe to be the few best companies and/or best values across the most attractive sectors of the economy and focus our attention on those names. When an unforeseen event occurs that brings into question our assessment of what constitutes a best company or best value, then we will sell and move on. We strive to minimize stock selections that don’t work out, in order to limit the damage done.

MARKET COMMENTARY

As of March of this year, the bull market entered its ninth year. The S&P 500 has more than tripled since the March 2009 bottom, rising from a low of 676 to 2412 on May 31, 2017. The market appears extended to us, both in terms of time as well as magnitude.

3

Investor complacency as measured by the VIX index “anxiety gauge” is currently near its all-time low. Additionally, bond credit spreads have narrowed to near record lows. The market’s valuation is no longer below the long term mean, but is now somewhat above it on a P/E basis, but approaching the top decile of valuation by other metrics like market cap to GDP, the Shiller CAPE, or price to replacement value. The Federal Reserve is still in a very accommodative mode, but has recently taken three “baby steps” of raising the Federal Funds rate – each by 25 basis points. Inflation bottomed in the 1% range, but is now closer to 2%. Labor markets have been robust with the unemployment rate now down to 4.3%.

Bull markets do not die of old age, but there are plenty of potential catalysts that could shift current investor optimism into a dash for the hills – global conflicts from North Korea to Syria, not to mention internal U.S. political conflicts. A new president was elected last November on a platform of deregulation and lower taxes to stimulate the U.S. economy, but will that agenda ever see the light of day? And, will it work?

Our view of the near term investment outlook is modestly cautious. We sense the market has come too far, too soon, based on optimism of what could go right with the economy as opposed to consideration of how the market would react if something goes wrong. We do not foresee anything as dire as the 50% collapse during the bear markets of 2002 and 2008. The bubble in Technology stock valuations burst in the post Y2K and post 9/11 reality driving the 2002 bottom. The implosion of the Banking, Financial, and Housing sectors in 2008 led to the great recession of the next several years. Recession and a collapse of corporate profit growth is the real enemy to the market. The red flags of recession warning are simply not in place. No spike in inventories, inflation, or real interest rates. No inverted yield curve. No major shift in the Fed’s stance on a continued accommodative policy approach. As well, there are few signs of speculative excess. No IPO frenzy. No spike in M&A activity. No influx of capital to equity mutual funds and ETFs. In fact, the average investor who fled the equity markets after the second bear market (2009) of this new millennium parked his assets in bond funds and has never looked back.

Pending doom for the market? No, but a healthy pullback? We think there is a reasonable likelihood.

INVESTMENT STRATEGY

We have let our cash creep up a little to have some dry powder on hand. In a rising market, cash acts as an anchor to performance relative to an index, because the benchmark indices carry no cash. That is a risk we are willing to take when we see some signs of exuberance as in the large Technology stocks (including: Apple, Amazon, Alphabet, Microsoft, and Facebook). Despite continuing to like these names because of

4

their favorable growth prospects, we think there is a very reasonable prospect we will add back to these positions at lower prices in the not too distant future.

Patience is paramount in the portfolio management process. It requires patience to hold some cash reserves when reinvestment alternatives appear less than compelling. New event-driven opportunities will eventually present themselves – and it pays to be selective. An even more challenging patience is embracing the contrarian point of view. For example, our purchase of Nielsen Holdings has not, as yet, played out as we expected. This is the leading company in data gathering and analysis for the CPG (consumer packaged goods) industry, as well as measuring audience composition across all forms of media from traditional television to mobile streaming. Nielsen was the leader in these fields several decades ago when I first encountered the company through case studies and Nielsen remains the leader today. In fact, the value of competitive information only becomes more valuable. Retail sales were a little squishy during the past twelve months and discretionary spending by some of the CPG companies was curtailed. The market tends to treat any kind of earnings shortfall swiftly and severely, but similarly heaps rewards when expectations are exceeded. Temporary shortfall or systemic weakness? We will need to see how future earnings play out, but in the meantime we receive a very attractive 3.6% dividend yield to keep us patient.

We purchased Quintiles this past year under a similar investment thesis – the power of information. When Quintiles, a leading provider of clinical studies for the pharmaceutical and biopharmaceutical companies, acquired IMS, the leading purveyor of sales data for the global pharma industry, the merged companies were able to create a vertical data stream – from a medical compound’s birth to loss of patent protection. The value of this data continuum can be priceless. Quintiles has produced positive returns for the Fund. Nielsen has not. It takes a lot more patience to hold a stock that is not currently working than enjoying the ride on a stock that is. More often than not, it is those out-of-favor names that will provide the best returns going forward, while expectations for today’s winners become too challenging to exceed.

INVESTMENT COMMENTARY

The dark horse wins the biggest purse. It seemed virtually inconceivable that Donald Trump could win the U.S. presidential election last year. And even more inconceivable – that the stock market would surge better than 15% in the next several months. For stock investors? So far, so good under the new administration, but that advance has been largely in anticipation of policy promises that have yet to be implemented or achieved. Corporate earnings? We have had a little help from the U.S. dollar stabilizing versus other currencies. While hardly robust with oil prices back in the mid 40’s per barrel, prices are

5

somewhat higher than a year ago and much of the energy industry is shifting back to modest profits from heavy losses. Most other sectors enjoy near record profit margins that may come under pressure should labor costs rise under near full national employment, basic material inflation kick back in, and/or interest rates rise. Is there room for the market’s multiple to expand? The P/E of the S&P 500 was higher in the late nineties, but the current S&P 500 forward P/E at 18 is already above the thirty year mean of 16-17. Consumer confidence is at an all-time high, which has correlated very closely with the stock market. It is the second derivative that drives markets, however, and we see greater prospects for a moderation of good news items or acceleration of the bad news items. Thus we see a greater likelihood of a moderate pullback than further rally in the stock markets.

We believe the time is right for some caution and some patience. The road forward will surely hold some potholes and provide some new investment opportunities.

Some sector highlights of the past twelve months follow:

Technology

The Technology sector was both our heaviest weighted at 22.1% and highest earning sector at +28.6%, but weighted slightly lower than the S&P 500 Technology sector weighting of 23.2% and total return of +33.8%. We reduced our weighting to slightly below the S&P 500 during the first quarter of 2017, believing the powerful double digit gains were unsustainable. Our top performing stocks were Apple (+55.9%), Adobe (+42.6%), Microsoft (+35.0%), Alphabet (+31.8%) and Facebook (+27.5%). Two Tech names detracted modestly from performance: Cognizant (-17.8%) and Mastercard (-6.6%).

Industrials

The Fund’s Industrials holdings at 16.0% of the portfolio were the largest sector overweighting relative to the S&P 500 Industrials weighting of 10.2%. Given the wide ranging sub components, our Industrials exposure relates to several distinctive industries. John Deere in the agricultural sector was the standout performer (+57.9%), followed by heavy equipment manufacturer Caterpillar (+30.7%). Defense stocks did well with Raytheon (+29.2%) and United Technologies (+23.5%). Our biggest disappointment was the aforementioned Nielsen Holdings. Weakness in the retail space held back discretionary spending in Nielsen’s “Buy” space, but we have confidence in the faster growing “Media” space and feel the Buy space should pick up as well. The sector return for the Fund was +16.5% versus +21.8% for the S&P 500.

6

Healthcare

Despite the governmental scrutiny on rising healthcare costs, we still see healthcare as a growth industry. The Fund is overweighted in Healthcare at 15.5% versus the S&P 500 weighting of 13.9%. The Fund is more heavily weighted towards purveyors of all things “life science” – related versus traditional pharma. Zoetis, the leading animal science spin-out from Pfizer, was our top performer (+32.4%). Abbott Labs (+18.3%), J&J (+16.9%), Danaher (+14.7%) and Thermo Fisher (+14.3%) all contributed nicely, as well, driven by medical device and diagnostic equipment sales. Swiss drug maker, Novartis, was our weakest link (-9.6%). The strength of the Swiss Franc provided a currency headwind. The Fund showed excellent relative performance at +15.7% versus the S&P 500 Healthcare sector return of +8.6%.

Financials

The Fund’s holdings in the Financials sector totaled 12.4% of the portfolio, modestly under the S&P 500 Financials sector weighting of 13.7%. Our Financial sector return was +17.5% compared to the S&P 500 Financials return of +23.1%. Financials sharply underperformed the rest of the market pre-election and then sharply outperformed the market post-election. Results were strong across the board with the exception of Wells Fargo that disclosed fraudulent marketing activity later last year, spurring our sale of the position. J.P. Morgan was the hands down winner (+29.2%) with American Express and US Bancorp returning near +20.0% each, as well.

Consumer Discretionary

The Fund’s Consumer Discretionary sector weighting at 11.2% was close to the S&P 500’s sector weighting at 12.5%. For the sector as a whole, the Fund’s performance was +5.8% versus the S&P 500 Consumer Discretionary sector’s performance of +16.9%. The Fund’s performance was severely tarnished by a single issue – Under Armour. Under Armour hit, not a speed bump, but a wall, in its revenue trajectory and the stock declined (-43.0%). Amazon helped (+37.6%), but was overwhelmed by the decline in Under Armour. Retailers Home Depot (+18.8%) and Starbucks (+17.8%) also performed well.

Energy

After reaching a low in early 2016 of about $27 per barrel, oil rallied to near $60, but has since faded back to the high $40’s over the past year. Falling oil and natural gas prices led to negative returns for both the Fund of -0.9% and the S&P 500 of -0.8%. We own three stocks in this sector: one integrated major producer, Exxon (-6.3%), one oil service, Schlumberger (-6.4%), and one natural gas, Cabot (-3.0%). Global economies will continue to run on hydrocarbon fuels for many years to come. Given all of the global uncertainties and despite low current energy prices, we intend to maintain our exposure to energy.

7

Materials

Materials is a very broad sector and one driven by the vagaries of commodities pricing. Fertilizer prices are known for their volatility and are currently well below the levels of several years ago when corn prices were near double where they are today. We purchased Mosaic (+16.9%). We like the idea of being paid a healthy dividend yield while awaiting a commodities cycle to turn. We also own Ecolab (+6.1%), which is not driven by commodity prices, rather it is more of a service company providing essential cleaning/purification services and supplies. Our sector return of +23.0% was well ahead of the S&P 500 sector return of +15.4% with a weighting in the Fund of 4.5% versus the S&P 500 weighting of 2.8%.

Consumer Staples

We like the Consumer Staple sector for the defensive characteristics it offers, but we currently see little opportunity, given stretched stock prices. The sector offers only modest growth and currently sells at a high premium value to the market. The Fund is well underweighted at 3.1% versus the S&P 500 at 9.4%. Pepsi was our top performer (+19.7%), but we have been reducing the position due to the run up in valuation.

Utilities, Telecommunications and REITS

The Fund had only a single holding across these sectors, Spirit Realty. We were attracted by Spirit’s 6.0% dividend yield as a “safe” place to park some funds while awaiting either a pullback in the broad market or at least in one or more of our favored core positions. Unfortunately, it was Spirit that suffered the pullback, declining (-26.2%) with a first quarter earnings miss and a significant downgrade in earnings forecast by management.

CLOSING COMMENTS

The stock market has treated us well for the past eight plus years. Stock valuations have nearly doubled from 9-10 P/E multiples in 2009 to now 17-18. That is above the mean of 16x of the past several decades. The economy has grown at a below average rate for the past several years, 1-2% Real GDP growth. Now consensus forecasts call for growth accelerating to 2-3%. With the post-election 15% rally, the stock market has already priced in the improvement. Inflation has remained low and interest rates have been repressed through massive quantitative easing by the Federal Reserve. If economic growth does accelerate, it would be logical for interest rates and inflation to regress upward towards their long term mean values. Generally, rising rates and rising inflation present headwinds to the stock market.

Our expectation is that asset price inflation (i.e., record high market index prices) through central bank engineering is a tailwind that will soon be extinguished. Owning high quality

8

companies that can grow their earnings in more challenging economic conditions will be the winners going forward. Our research is focused on just those candidates. We will continue to refine the portfolio, seeking out new ideas for growth and weeding out names that show signs of weakness.

We, at Bradley, Foster & Sargent, Inc., look forward to serving you through our management of the Fund. Thank you for placing your capital under our care.

| Timothy Foster | Keith LaRose | Thomas Sargent | ||

| Lead Portfolio Manager | Co-Portfolio Manager | Co-Portfolio Manager |

9

BFS Equity Fund

ANNUAL PERFORMANCE REVIEW

(UNAUDITED)

The Fund lagged the performance of both the S&P 500 as well as the Dow Jones Industrial Average for the twelve month period commencing June 1, 2016 and ending May 31, 2017. The Fund returned 13.15% versus 17.47% for the S&P 500 and 21.16% for the Dow Jones Industrial Average.

Key Detractors from Relative Results

| • | The S&P 500, being market cap weighted, as well as the Dow Jones Industrial Average being market price weighted, create benchmarks quite different from the largely unit weighted BFS Equity Fund. |

| • | Two individual stocks were key detractors for the Fund for the twelve months ending May 31, 2017: Under Armour and Spirit Realty. The declines in both stocks related to the deep malaise affecting bricks and mortar retailing in the U.S. over this period. |

| • | Although not overweighted in the Energy sector, the sharp decline in oil prices led to negative returns for our Energy sector holdings, in particular, Exxon and Schlumberger. |

Key Contributors to Relative Results

| • | On the positive side, the Fund both over weighted and outperformed the S&P 500 Healthcare sector. Top performance came from both Abbott Labs and Thermo Fisher. |

| • | Exposure to top performing large cap growth stocks like Adobe, Apple, Alphabet, Amazon and Facebook was a significant positive contributor to the Fund’s absolute return. Reducing our exposure to these names during the period to less than market weights, as valuations became richer, limited returns relative to benchmarks. |

FUND INFORMATION

May 31, 2017

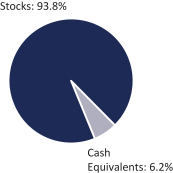

ASSET ALLOCATION

TEN LARGEST HOLDINGS (%) | FUND | |||

Chubb Ltd. | 4.0 | |||

U.S. Bancorp | 3.2 | |||

Thermo Fisher Scientific, Inc. | 3.2 | |||

Danaher Corp. | 3.1 | |||

JPMorgan Chase & Co. | 3.0 | |||

Raytheon Co. | 3.0 | |||

Automatic Data Processing, Inc. | 3.0 | |||

Exxon Mobil Corp. | 3.0 | |||

Amazon.com, Inc. | 2.9 | |||

Alphabet, Inc. — Class A | 2.9 | |||

SECTOR DIVERSIFICATION (%) | FUND | S&P 500 | ||||||

Information Technology | 22.1 | 23.2 | ||||||

Industrials | 16.0 | 10.2 | ||||||

Healthcare | 15.5 | 13.9 | ||||||

Financials | 12.4 | 13.7 | ||||||

Consumer Discretionary | 11.2 | 12.5 | ||||||

Energy | 7.3 | 6.0 | ||||||

Materials | 4.5 | 2.8 | ||||||

Consumer Staples | 3.1 | 9.4 | ||||||

Real Estate | 1.6 | 2.9 | ||||||

Telecommunication Services | 0.0 | 2.2 | ||||||

Utilities | 0.0 | 3.3 | ||||||

Cash Equivalents | 6.2 | 0.0 | ||||||

10

BFS Equity Fund

Investment Results (Unaudited)

Average Annual Total Returns(a) (For the periods ended May 31, 2017)

| One Year | Since Inception (November 8, 2013) | |||||||

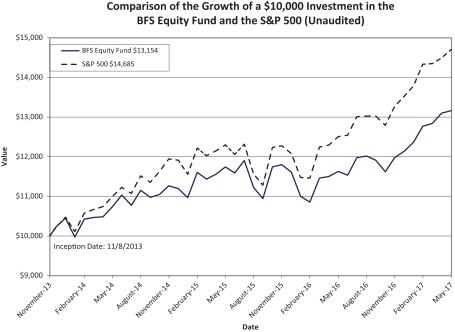

BFS Equity Fund | 13.15% | 8.01% | ||||||

S&P 500® Index(b) | 17.47% | 11.40% | ||||||

Dow Jones Industrial Average®(c) | 21.16% | 11.16% | ||||||

Total annual fund operating expenses, as disclosed in the BFS Equity Fund’s (the “Fund”) prospectus dated September 28, 2016, were 1.86% of average daily net assets (1.25% after fee waivers/expense reimbursements by Bradley, Foster & Sargent, Inc. (the “Adviser”)). The Adviser has contractually agreed to waive or limit its fees and assume other expenses of the Fund until September 30, 2017, so that total annual fund operating expenses does not exceed 1.00%. This contractual arrangement may only be terminated by mutual consent of the Adviser and the Board of Trustees of the Trust, and it will automatically terminate upon the termination of the investment advisory agreement between the Fund and the Adviser. This operating expense limitation does not apply to: (i) interest, (ii) taxes, (iii) brokerage commissions, (iv) other expenditures which are capitalized in accordance with generally accepted accounting principles, (v) other extraordinary expenses not incurred in the ordinary course of the Fund’s business, (vi) dividend expense on short sales, (vii) expenses incurred under a plan of distribution under Rule 12b-1, and (viii) expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, in any fiscal year. The operating expense limitation also excludes any “Fees and Expenses of Acquired Funds,” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including Exchange-Traded Funds (“ETF”), that have their own expenses. Each waiver or reimbursement of an expense by the Adviser is subject to repayment by the Fund within three years following the date in which the expense was incurred, provided that the Fund is able to make the repayment without exceeding the expense limitation in place at the time of the waiver or reimbursement.

The performance quoted represents past performance, which does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption Fund shares. The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. Current performance of a Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling (855) 575-2430.

| (a) | Average annual total returns reflect any change in price per share and assume the reinvestment of all distributions. The Fund’s returns reflect any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would have been lower. Total returns for periods less than one year are not annualized. |

| (b) | The S&P 500® Index (“S&P 500”) is a widely recognized unmanaged index of equity prices and is representative of a broader market and range of securities than is found in the Fund’s portfolio. The index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

| (c) | The Dow Jones Industrial Average® is a widely recognized unmanaged index of equity prices and is representative of a narrower market and range of securities than is found in the Fund’s portfolio. The index is an unmanaged benchmark that assumes reinvestment of all distributions and excludes the effect of taxes and fees. Individuals cannot invest directly in this index; however, an individual can invest in exchange traded funds or other investment vehicles that attempt to track the performance of a benchmark index. |

The Fund’s investment objectives, strategies, risks, charges and expenses must be considered carefully before investing. The prospectus contains this and other important information about the Fund and may be obtained by calling the same number as above. Please read it carefully before investing.

The Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

11

The chart above assumes an initial investment of $10,000 made on November 8, 2013 (commencement of operations) held through May 31, 2017. THE FUND’S RETURN REPRESENTS PAST PERFORMANCE AND DOES NOT GUARANTEE FUTURE RESULTS. The returns shown do not reflect deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investment returns and principal values will fluctuate so that your shares, when redeemed, may be worth more or less than their original purchase price.

Current performance may be lower or higher than the performance data quoted. For more information on the Fund, and to obtain performance data current to the most recent month end or to request a prospectus, please call (855) 575-2430. You should carefully consider the investment objectives, potential risks, management fees, and charges and expenses of the Fund before investing. The Fund’s prospectus contains this and other information about the Fund, and should be read carefully before investing.

The Fund is distributed by Unified Financial Securities, LLC, member FINRA/SIPC.

Availability of Portfolio Schedule (Unaudited)

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“SEC”) as of the end of the first and third quarters of each fiscal year on Form N-Q. The Fund’s Forms N-Q will be available at the SEC’s website at www.sec.gov. The Fund’s Form N-Q may be reviewed and copied at the Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling (800) SEC-0330.

12

BFS Equity Fund

Schedule of Investments

May 31, 2017

| Shares | Fair Value | |||||||

| COMMON STOCKS — 93.76% | ||||||||

| Aerospace & Defense — 5.69% | ||||||||

| 5,000 | Raytheon Co. | $ | 820,050 | |||||

| 6,000 | United Technologies Corp. | 727,680 | ||||||

|

| |||||||

| 1,547,730 | ||||||||

|

| |||||||

| Banks — 3.18% | ||||||||

| 17,000 | U.S. Bancorp | 865,130 | ||||||

|

| |||||||

| Beverages — 1.72% | ||||||||

| 4,000 | PepsiCo, Inc. | 467,480 | ||||||

|

| |||||||

| Chemicals — 4.52% | ||||||||

| 5,000 | Ecolab, Inc. | 664,200 | ||||||

| 25,000 | Mosaic Co./The | 565,750 | ||||||

|

| |||||||

| 1,229,950 | ||||||||

|

| |||||||

| Communications Equipment — 2.90% | ||||||||

| 25,000 | Cisco Systems, Inc. | 788,250 | ||||||

|

| |||||||

| Consumer Finance — 2.26% | ||||||||

| 8,000 | American Express Co. | 615,520 | ||||||

|

| |||||||

| Diversified Financial Services — 3.02% | ||||||||

| 10,000 | JPMorgan Chase & Co. | 821,500 | ||||||

|

| |||||||

| Electronic Equipment, Instruments & Components — 2.47% | ||||||||

| 9,000 | Amphenol Corp. — Class A | 671,400 | ||||||

|

| |||||||

| Energy Equipment & Services — 2.30% | ||||||||

| 9,000 | Schlumberger Ltd. | 626,310 | ||||||

|

| |||||||

| Equity Real Estate Investment Trusts — 1.60% | ||||||||

| 60,000 | Spirit Realty Capital, Inc. | 433,800 | ||||||

|

| |||||||

| Food Products — 1.37% | ||||||||

| 8,000 | Mondelez International, Inc. — Class A | 372,720 | ||||||

|

| |||||||

| Health Care Equipment & Supplies — 2.02% | ||||||||

| 12,000 | Abbott Laboratories | 547,920 | ||||||

|

| |||||||

| Hotels, Restaurants & Leisure — 2.11% | ||||||||

| 9,000 | Starbucks Corp. | 572,490 | ||||||

|

| |||||||

| Industrial Conglomerates — 5.64% | ||||||||

| 10,000 | Danaher Corp. | 849,400 | ||||||

| 25,000 | General Electric Co. | 684,500 | ||||||

|

| |||||||

| 1,533,900 | ||||||||

|

| |||||||

| Insurance — 3.95% | ||||||||

| 7,500 | Chubb Ltd. | 1,073,925 | ||||||

|

| |||||||

| Internet & Catalog Retail — 2.93% | ||||||||

| 800 | Amazon.com, Inc. * | 795,696 | ||||||

|

| |||||||

See accompanying notes which are an integral part of the financial statements.

13

BFS Equity Fund

Schedule of Investments (continued)

May 31, 2017

| Shares | Fair Value | |||||||

| COMMON STOCKS — (continued) | ||||||||

| Internet Software & Services — 5.69% | ||||||||

| 800 | Alphabet, Inc. — Class A * | $ | 789,672 | |||||

| 5,000 | Facebook, Inc. — Class A * | 757,300 | ||||||

|

| |||||||

| 1,546,972 | ||||||||

|

| |||||||

| IT Services — 3.01% | ||||||||

| 8,000 | Automatic Data Processing, Inc. | 818,960 | ||||||

|

| |||||||

| Life Sciences Tools & Services — 5.72% | ||||||||

| 8,000 | Quintiles IMS Holdings, Inc. * | 691,520 | ||||||

| 5,000 | Thermo Fisher Scientific, Inc. | 863,950 | ||||||

|

| |||||||

| 1,555,470 | ||||||||

|

| |||||||

| Machinery — 5.42% | ||||||||

| 4,000 | Caterpillar, Inc. | 421,720 | ||||||

| 3,500 | Deere & Co. | 428,610 | ||||||

| 10,000 | Fortive Corp. | 624,500 | ||||||

|

| |||||||

| 1,474,830 | ||||||||

|

| |||||||

| Media — 1.99% | ||||||||

| 5,000 | Walt Disney Co./The | 539,700 | ||||||

|

| |||||||

| Oil, Gas & Consumable Fuels — 5.00% | ||||||||

| 25,000 | Cabot Oil & Gas Corp. | 554,750 | ||||||

| 10,000 | Exxon Mobil Corp. | 805,000 | ||||||

|

| |||||||

| 1,359,750 | ||||||||

|

| |||||||

| Pharmaceuticals — 4.64% | ||||||||

| 4,000 | Johnson & Johnson | 513,000 | ||||||

| 12,000 | Zoetis, Inc. | 747,360 | ||||||

|

| |||||||

| 1,260,360 | ||||||||

|

| |||||||

| Professional Services — 2.41% | ||||||||

| 17,000 | Nielsen Holdings PLC | 654,160 | ||||||

|

| |||||||

| Software — 5.18% | ||||||||

| 5,000 | Adobe Systems, Inc. * | 709,300 | ||||||

| 10,000 | Microsoft Corp. | 698,400 | ||||||

|

| |||||||

| 1,407,700 | ||||||||

|

| |||||||

| Specialty Retail — 2.26% | ||||||||

| 4,000 | Home Depot, Inc./The | 614,040 | ||||||

|

| |||||||

| Technology Hardware, Storage & Peripherals — 2.81% | ||||||||

| 5,000 | Apple, Inc. | 763,800 | ||||||

|

| |||||||

| Textiles, Apparel & Luxury Goods — 1.95% | ||||||||

| 10,000 | NIKE, Inc. | 529,900 | ||||||

|

| |||||||

Total Common Stocks (Cost $20,290,164) | 25,489,363 | |||||||

|

| |||||||

See accompanying notes which are an integral part of the financial statements.

14

BFS Equity Fund

Schedule of Investments (continued)

May 31, 2017

| Shares | Fair Value | |||||||

| MONEY MARKET SECURITIES — 6.24% | ||||||||

| 1,696,196 | Fidelity Investments Money Market Government Portfolio — Institutional Class, 0.69% (a) | $ | 1,696,196 | |||||

|

| |||||||

Total Money Market Securities (Cost $1,696,196) | 1,696,196 | |||||||

|

| |||||||

Total Investments – 100.00% (Cost $21,986,360) | 27,185,559 | |||||||

|

| |||||||

Liabilities in Excess of Other Assets – (0.00)% | (409 | ) | ||||||

|

| |||||||

NET ASSETS – 100.00% | $ | 27,185,150 | ||||||

|

| |||||||

| (a) | Rate disclosed is the seven day effective yield as of May 31, 2017. |

| * | Non-income producing security. |

The industries shown on the schedule of investments are based on the Global Industry Classification Standard, or GICS® (“GICS”). The GICS was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by the Administrator.

See accompanying notes which are an integral part of the financial statements.

15

BFS Equity Fund

Statement of Assets and Liabilities

May 31, 2017

Assets | ||||

Investments in securities at fair value (cost $21,986,360) | $ | 27,185,559 | ||

Dividends receivable | 43,523 | |||

Prepaid expenses | 7,620 | |||

Total Assets | 27,236,702 | |||

Liabilities | ||||

Payable for fund shares redeemed | 5,451 | |||

Payable to Adviser | 7,287 | |||

Payable to Administrator | 6,783 | |||

Distribution fees accrued | 11,136 | |||

Other accrued expenses | 20,895 | |||

Total Liabilities | 51,552 | |||

Net Assets | $ | 27,185,150 | ||

Net Assets consist of: | ||||

Paid-in capital | $ | 22,226,668 | ||

Accumulated undistributed net investment income | 27,037 | |||

Accumulated net realized loss from investment transactions | (267,754 | ) | ||

Net unrealized appreciation on investments | 5,199,199 | |||

Net Assets | $ | 27,185,150 | ||

Shares outstanding (unlimited number of shares authorized, no par value) | 2,088,881 | |||

Net asset value, offering and redemption price per share | $ | 13.01 |

16

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Statement of Operations

For the year ended May 31, 2017

Investment Income |

| |||

Dividend income | $ | 401,688 | ||

Total investment income | 401,688 | |||

Expenses |

| |||

Investment Adviser | 188,205 | |||

Distribution (12b-1) | 62,735 | |||

Administrator | 38,000 | |||

Fund accounting | 25,000 | |||

Registration | 22,995 | |||

Transfer agent | 18,106 | |||

Audit | 17,100 | |||

Legal | 17,044 | |||

Printing | 11,722 | |||

Trustee | 6,912 | |||

Custodian | 4,247 | |||

Miscellaneous | 26,799 | |||

Total expenses | 438,865 | |||

Fees waived by Adviser | (124,587 | ) | ||

Net operating expenses | 314,278 | |||

Net investment income | 87,410 | |||

Net Realized and Change in Unrealized Gain on Investments |

| |||

Net realized gain on investment securities transactions | 545,073 | |||

Net change in unrealized appreciation of investment securities | 2,527,048 | |||

Net realized and change in unrealized gain on investments | 3,072,121 | |||

Net increase in net assets resulting from operations | $ | 3,159,531 | ||

17

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Statements of Changes in Net Assets

| Increase (Decrease) in Net Assets due to: | For the Year Ended May 31, 2017 | For the Year Ended May 31, 2016 | ||||||

Operations | ||||||||

Net investment income | $ | 87,410 | $ | 94,935 | ||||

Net realized gain/(loss) on investment securities transactions | 545,073 | (458,394 | ) | |||||

Net change in unrealized appreciation of investment securities | 2,527,048 | 217,958 | ||||||

Net increase (decrease) in net assets resulting from operations | 3,159,531 | (145,501 | ) | |||||

Distributions | ||||||||

From net investment income | (113,393 | ) | (69,881 | ) | ||||

Total distributions | (113,393 | ) | (69,881 | ) | ||||

Capital Transactions | ||||||||

Proceeds from shares sold | 1,862,217 | 5,178,205 | ||||||

Reinvestment of distributions | 101,818 | 62,385 | ||||||

Amount paid for shares redeemed | (1,709,170 | ) | (1,308,552 | ) | ||||

Net increase in net assets resulting from capital transactions | 254,865 | 3,932,038 | ||||||

Total Increase in Net Assets | 3,301,003 | 3,716,656 | ||||||

Net Assets |

| |||||||

Beginning of year | 23,884,147 | 20,167,491 | ||||||

End of year | $ | 27,185,150 | $ | 23,884,147 | ||||

Accumulated undistributed net investment income included in net assets at end of year | $ | 27,037 | $ | 53,020 | ||||

Share Transactions | ||||||||

Shares sold | 153,183 | 455,719 | ||||||

Shares issued in reinvestment of distributions | 8,443 | 5,364 | ||||||

Shares redeemed | (140,838 | ) | (118,087 | ) | ||||

Net increase in shares outstanding | 20,788 | 342,996 | ||||||

18

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Financial Highlights

(For a share outstanding during each period)

| For the Year Ended May 31, 2017 | For the Year Ended May 31, 2016 | For the Year Ended May 31, 2015 | For the Period Ended May 31, 2014(a) | |||||||||||||

Selected Per Share Data: | ||||||||||||||||

Net asset value, beginning of period | $11.55 | $11.69 | $10.73 | $10.00 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income from investment operations: | ||||||||||||||||

Net investment income | 0.04 | 0.04 | 0.02 | 0.04 | ||||||||||||

Net realized and unrealized gain/(loss) on investments | 1.47 | (0.15 | ) | 0.97 | 0.70 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total from investment operations | 1.51 | (0.11 | ) | 0.99 | 0.74 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Less distributions to shareholders from: | ||||||||||||||||

Net investment income | (0.05 | ) | (0.03 | ) | (0.03 | ) | (0.01 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total distributions | (0.05 | ) | (0.03 | ) | (0.03 | ) | (0.01 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net asset value, end of period | $13.01 | $11.55 | $11.69 | $10.73 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total Return(b) | 13.15 | % | (0.91 | )% | 9.27 | % | 7.36 | %(c) | ||||||||

Ratios and Supplemental Data: | ||||||||||||||||

Net assets, end of period (000) | $27,185 | $23,884 | $20,167 | $12,745 | ||||||||||||

Ratio of net expenses to average net assets | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | %(d) | ||||||||

Ratio of expenses to average net assets before waiver and reimbursement | 1.75 | % | 1.86 | % | 2.26 | % | 3.93 | %(d) | ||||||||

Ratio of net investment income to average net assets | 0.35 | % | 0.43 | % | 0.30 | % | 0.68 | %(d) | ||||||||

Portfolio turnover rate | 47.82 | % | 49.38 | % | 51.17 | % | 46.50 | %(c) | ||||||||

| (a) | For the period November 8, 2013 (commencement of operations) to May 31, 2014. |

| (b) | Total return in the above table represents the rate that the investor would have earned or lost on an investment in the Fund, assuming reinvestment of dividends, if any. |

| (c) | Not annualized |

| (d) | Annualized |

19

See accompanying notes which are an integral part of the financial statements.

BFS Equity Fund

Notes to the Financial Statements

May 31, 2017

NOTE 1. ORGANIZATION

The BFS Equity Fund (the “Fund”) was organized as an open-end diversified series of Valued Advisers Trust (the “Trust”) on July 23, 2013 and commenced operations on November 8, 2013. The Trust is a management investment company established under the laws of Delaware by an Agreement and Declaration of Trust dated June 13, 2008 (the “Trust Agreement”). The Trust Agreement permits the Trustees to issue an unlimited number of shares of beneficial interest of separate series without par value. The Fund is one of a series of funds authorized by the Board of Trustees (the “Board”). The Fund’s investment adviser is Bradley, Foster & Sargent, Inc. (the “Adviser”). The investment objective of the Fund is long-term appreciation through growth of principal and income.

NOTE 2. SIGNIFICANT ACCOUNTING POLICIES

The Fund is an investment company and follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Securities Valuation – All investments in securities are recorded at their estimated fair value as described in Note 3.

Federal Income Taxes – The Fund makes no provision for federal income or excise tax. The Fund has qualified and intends to qualify each year as a regulated investment company (“RIC”) under subchapter M of the Internal Revenue Code of 1986, as amended, by complying with the requirements applicable to RICs and by distributing substantially all of its taxable income. The Fund also intends to distribute sufficient net investment income and net capital gains, if any, so that it will not be subject to excise tax on undistributed income and gains. If the required amount of net investment income or gains is not distributed, the Fund could incur a tax expense.

As of, and during the fiscal year ended May 31, 2017, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the statement of operations. During the fiscal year ended May 31, 2017, the Fund did not incur any interest or penalties.

Expenses – Expenses incurred by the Trust that do not relate to a specific fund of the Trust are allocated to the individual funds based on each fund’s relative net assets or another appropriate basis.

Security Transactions and Related Income – The Fund follows industry practice and records security transactions on the trade date for financial reporting purposes. For financial statement and income tax purposes, the specific identification method is used for determining gains or losses.

20

BFS Equity Fund

Notes to the Financial Statements (continued)

May 31, 2017

Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Dividends and Distributions – The Fund intends to distribute its net investment income and net realized long-term and short-term capital gains, if any, at least annually. Dividends and distributions to shareholders, which are determined in accordance with income tax regulations, are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the period from net investment income or net realized capital gains may differ from their ultimate treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, they are reclassified among the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset values per share of the Fund.

NOTE 3. SECURITIES VALUATION AND FAIR VALUE MEASUREMENTS

Fair value is defined as the price that the Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. GAAP establishes a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and establish classification of fair value measurements for disclosure purposes.

Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below.

| • | Level 1 – unadjusted quoted prices in active markets for identical investments and/or registered investment companies where the value per share is determined and published and is the basis for current transactions for identical assets or liabilities at the valuation date. |

| • | Level 2 – other significant observable inputs (including, but not limited to, quoted prices for an identical security in an inactive market, quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| • | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments based on the best information available) |

21

BFS Equity Fund

Notes to the Financial Statements (continued)

May 31, 2017

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy which is reported is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

Equity securities that are traded on any stock exchange are generally valued at the last quoted sale price on the security’s primary exchange. Lacking a last sale price, an exchange traded security is generally valued at its last bid price. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. When using the market quotations and when the market is considered active, the security is classified as a Level 1 security. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with policies established by and under the general supervision of the Board. Under these policies, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used.

Investments in mutual funds, including money market mutual funds, are generally priced at the ending net asset value (“NAV”) provided by the pricing service of the funds. These securities will be categorized as Level 1 securities.

In accordance with the Trust’s valuation policies, the Adviser is required to consider all appropriate factors relevant to the value of securities for which it has determined other pricing sources are not available or reliable as described above. No single standard exists for determining fair value, because fair value depends upon the circumstances of each individual case. As a general principle, the current fair value of an issue of securities being valued by the Adviser would appear to be the amount that the Fund might reasonably expect to receive for them upon their current sale. Methods that are in accordance with this principle may, for example, be based on (i) a multiple of earnings; (ii) a discount from market prices of a similar freely traded security (including a derivative security or a basket of securities traded on other markets, exchanges or among dealers); or (iii) yield to maturity with respect to debt issues, or a combination of these and other methods. Fair-value pricing is permitted if, in the Adviser’s opinion, the validity of market quotations appears to be questionable based on factors such as evidence of a thin market in the security based on a small number of quotations, a significant event occurs after the close of a market but before the Fund’s NAV calculation that may affect a security’s value, or the Adviser is aware of any other data that calls into question the reliability of market quotations.

The following is a summary of the inputs used to value the Fund’s investments as of May 31, 2017:

| Valuation Inputs | ||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stocks(a) | $ | 25,489,363 | $ | – | $ | – | $ | 25,489,363 | ||||||||

Money Market Funds | 1,696,196 | – | – | 1,696,196 | ||||||||||||

Total | $ | 27,185,559 | $ | – | $ | – | $ | 27,185,559 | ||||||||

| (a) | Refer to Schedule of Investments for sector classifications. |

22

BFS Equity Fund

Notes to the Financial Statements (continued)

May 31, 2017

The Fund did not hold any investments during the reporting period for which other significant observable inputs (Level 2) were used in determining fair value. The Fund did not hold any investments during the reporting period for which significant unobservable inputs (Level 3) were used in determining fair value; therefore, no reconciliation of Level 3 securities is included for this reporting period. The Fund did not hold any derivative instruments during the reporting period.

The Trust recognizes transfers between fair value hierarchy levels at the end of the reporting period. There were no transfers between any levels as of May 31, 2017 based on input levels assigned at May 31, 2016.

NOTE 4. FEES AND OTHER TRANSACTIONS WITH AFFILIATES AND OTHER SERVICE PROVIDERS

Under the terms of the investment advisory agreement on behalf of the Fund (the “Agreement”), the Adviser manages the Fund’s investments subject to oversight of the Board. As compensation for its services, the Fund is obligated to pay the Adviser a fee computed and accrued daily and paid monthly at an annual rate of 0.75% of the average daily net assets of the Fund. For the fiscal year ended May 31, 2017, the Adviser earned a fee of $188,205 from the Fund before the waivers described below. At May 31, 2017, the Fund owed the Adviser $7,287.

The Adviser has contractually agreed to waive or limit its fee and reimburse other expenses of the Fund, until September 30, 2017, so that the ratio of total annual operating expenses does not exceed 1.00%. This operating expense limitation does not apply to interest, taxes, brokerage commissions, other expenditures which are capitalized in accordance with GAAP, other extraordinary expenses not incurred in the ordinary course of the Fund’s business, dividend expense on short sales, expenses incurred under a plan of distribution under Rule 12b-1, and expenses that the Fund has incurred but did not actually pay because of an expense offset arrangement, if applicable, incurred by the Fund in any fiscal year. The operating expense limitation also excludes any “Fees and Expenses of Acquired Funds,” which are the expenses indirectly incurred by the Fund as a result of investing in money market funds or other investment companies, including ETFs, that have their own expenses. Each fee waiver or expense reimbursement by the Adviser is subject to repayment by the Fund within the three years following the date in which the fee waiver or expense reimbursement occurred, provided that the Fund is able to make the repayment without exceeding the expense limitation that is in effect at the time of the repayment or at the time of the fee waiver or expense reimbursement, whichever is lower. For the fiscal year ended May 31, 2017, fees and expenses totaling $124,587 were waived or reimbursed by the Adviser. The maximum amounts subject to repayment by the Fund, pursuant to the aforementioned conditions are as follows:

| Recoverable through May 31, | Amount | |||||

| 2018 | $163,520 | |||||

| 2019 | 135,629 | |||||

| 2020 | 124,587 | |||||

23

BFS Equity Fund

Notes to the Financial Statements (continued)

May 31, 2017

The Trust retains Ultimus Asset Services, LLC (the “Administrator”) to provide the Fund with administration and compliance, fund accounting, and transfer agent services, including all regulatory reporting. For the fiscal year ended May 31, 2017, The Administrator earned fees of $38,000 for administration services, $25,000 for fund accounting services and $18,106 for transfer agent services. At May 31, 2017, the Fund owed the Administrator $6,783 for such services.

The officers and one trustee of the Trust are members of management and/or employees of the Administrator. Unified Financial Securities, LLC (the “Distributor”) acts as the principal distributor of the Fund’s shares. An officer of the Trust is an officer of the Distributor and such person may be deemed to be an affiliate of the Distributor.

The Fund has adopted a Distribution Plan (the “Plan”) pursuant to Rule 12b-1 under the Investment Company Act of 1940 (the “1940 Act”). The Plan provides that the Fund will pay the Distributor and/or any registered securities dealer, financial institution or any other person (the “Recipient”) a shareholder servicing fee of 0.25% of the average daily net assets of the Fund in connection with the promotion and distribution of the Fund’s shares or the provision of personal services to shareholders, including, but not necessarily limited to, advertising, compensation to underwriters, dealers and selling personnel, the printing and mailing of prospectuses to other than current Fund shareholders, the printing and mailing of sales literature and servicing shareholder accounts (“12b-1 Expenses”). The Fund or Distributor may pay all or a portion of these fees to any recipient who renders assistance in distributing or promoting the sale of shares, or who provides certain shareholder services, pursuant to a written agreement. For the fiscal year ended May 31, 2017, 12b-1 expense incurred by the Fund was $62,735. The Fund owed $11,136 for 12b-1 fees as of May 31, 2017.

NOTE 5. PURCHASES AND SALES OF SECURITIES

For the fiscal year ended May 31, 2017, purchases and sales of investment securities, other than short-term investments and short-term U.S. government obligations, were as follows:

Purchases | Sales | |||

| $11,698,818 | $ | 12,410,166 | ||

There were no purchases or sales of long-term U.S. government obligations during the fiscal year ended May 31, 2017.

NOTE 6. BENEFICIAL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a) (9) of the 1940 Act. At May 31, 2017, Charles Schwab & Co., Inc. (“Schwab”) owned, as record shareholder, 54% of the outstanding shares of the Fund. It is not known whether Schwab or any of the underlying beneficial owners owned or controlled more than 25% of the voting securities of the Fund.

24

BFS Equity Fund

Notes to the Financial Statements (continued)

May 31, 2017

NOTE 7. FEDERAL TAX INFORMATION

At May 31, 2017, the net unrealized appreciation (depreciation) of investments for tax purposes was as follows:

Gross Unrealized Appreciation | $ | 5,609,583 | ||

Gross Unrealized Depreciation | (428,924 | ) | ||

Net Unrealized Appreciation on Investments | $ | 5,180,659 |

At May 31, 2017, the aggregate cost of securities for federal income tax purposes was $22,004,900.

At May 31, 2017, the Fund’s most recent fiscal year end, the components of distributable earnings (accumulated losses) on a tax basis were as follows:

Undistributed ordinary income | $ | 27,037 | ||

Accumulated capital and other losses | (249,214 | ) | ||

Unrealized appreciation | 5,180,659 | |||

Total | $ | 4,958,482 |

The difference between book and tax basis appreciation was attributable primarily to the tax deferral of losses on wash sales.

The tax character of distributions paid for the fiscal years ended May 31, 2017 and May 31, 2016 were as follows:

| 2017 | 2016 | |||||||

Distributions paid from: | ||||||||

Ordinary Income | $ | 113,393 | $ | 69,881 | ||||

As of May 31, 2017, the Fund has available for federal tax purposes an unused capital loss carryforward of $249,214 short-term capital losses, respectively, with no expiration, which is available to offset against future taxable net capital gains. To the extent that these carryforwards are used to offset future gains, it is probable that the amount offset will not be distributed to shareholders.

During the fiscal year ended May 31, 2017, the Fund utilized $182,694 of its capital loss carryforward.

NOTE 8. COMMITMENTS AND CONTINGENCIES

The Fund indemnifies its officers and trustees for certain liabilities that may arise from performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred.

NOTE 9. SUBSEQUENT EVENTS

Management of the Fund has evaluated the need for disclosure and/or adjustments resulting from subsequent events through the date these financials were issued. Management has determined there were no items requiring adjustment of the financial statements or additional disclosure.

25

Report of Independent Registered Public Accounting Firm

To the Shareholders of BFS Equity Fund and

Board of Trustees of Valued Advisers Trust

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of BFS Equity Fund (the “Fund”), a series of Valued Advisers Trust, as of May 31, 2017, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2017, by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of BFS Equity Fund as of May 31, 2017, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

COHEN & COMPANY, LTD.

Cleveland, Ohio

July 24, 2017

26

BFS Equity Fund

Summary of Fund Expenses (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example in the table below is based on an investment of $1,000 invested at the beginning of the period, and held for the six month period from December 1, 2016 to May 31, 2017.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.60), then multiply the result by the number in the first line under the heading “Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratios and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), or redemption fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Beginning Account Value December 1, 2016 | Ending Account Value May 31, 2017 | Expenses Paid During the Period(a) | ||||||||||

Actual | $ | 1,000.00 | $ | 1,099.10 | $ | 6.54 | ||||||

Hypothetical(b) | $ | 1,000.00 | $ | 1,018.70 | $ | 6.29 | ||||||

| (a) | Expenses are equal to the Fund’s annualized net expense ratio of 1.25%, multiplied by the average account value over the period, multiplied by 182/365. |

| (b) | Assumes a 5% return before expenses. |

27

Additional Federal Income Tax Information (Unaudited):

The Form 1099-DIV you receive in January 2018 will show the tax status of all distributions paid to your account in calendar year 2017. Shareholders are advised to consult their own tax adviser with respect to the tax consequences of their investment in the Fund. As required by the Internal Revenue Code and/or regulations, shareholders must be notified regarding the status of qualified dividend income for individuals and the dividends received deduction for corporations.

Qualified Dividend Income: The Fund designates approximately 100%, or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for the reduced tax rate of 15%.

Dividends Received Deduction: Corporate shareholders are generally entitled to take the dividends received deduction on the portion of the Fund’s dividend distribution that qualifies under tax law. For the Fund’s fiscal year 2017 ordinary income dividends, 100% qualifies for the corporate dividends received deduction.

Trustees and Officers (Unaudited)

The Board of Trustees supervises the business activities of the Trust. Each Trustee serves as a trustee until termination of the Trust unless the Trustee dies, resigns, retires or is removed.

The following table provides information regarding each of the independent trustees.

| Name, Address*, Age, Position with Trust**, Term of Position with Trust | Principal Occupation During Past 5 Years and Other Directorships | Other Directorships | ||

Andrea N. Mullins, 50 Independent Trustee Since December 2013

Chairperson since March 2017 | Current: Private investor; Independent Contractor, SWM Advisors (since April 2014). | None. | ||

Ira Cohen, 58 Independent Trustee Since June 2010 | Current: Independent financial services consultant (since February 2005); Executive Vice President of Asset Management Services, Recognos Financial (since August 2015). | Trustee, Griffin Institutional Access Credit Fund (since January 2017); Trustee and Audit Committee Chairman, Griffin Institutional Real Estate Access Fund (since May 2014); Trustee, Angel Oak Funds Trust (since October 2014); Chairman (since April 2017). | ||

| * | The address for each trustee and officer is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. |

| ** | As of the date of this report, the Trust consists of 13 series. |

28

The following table provides information regarding the Trustee who is considered an “interested person” of the Trust, as that term is defined under the 1940 Act. Based on the experience of the Trustee, the Trust concluded that the individual described below should serve as a Trustee.

| Name, Address*, (Age), Position with Trust**, Term of Position with Trust | Principal Occupation During Past 5 Years | Other Directorships | ||

Mark J. Seger, 55 Trustee Since March 2017 | Current: President, Managing Director, and Co-Founder, Ultimus Fund Solutions, LLC (since 1999); Treasurer and Managing Director, Ultimus Fund Distributors, LLC (since 1999); President and Managing Director, Ultimus Asset Services, LLC (since 2016); Managing Director, Unified Financial Securities, LLC (since 2016). | None. | ||

| * | The address for each trustee and officer is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. |

| ** | As of the date of this report, the Trust consists of 13 series. |

The following table provides information regarding the officers of the Trust:

| Name, Address*, (Age), Position with Trust,** Term of Position with Trust | Principal Occupation During Past 5 Years | Other Directorships | ||

Bo J. Howell, 36 Principal Executive Officer and President Since March 2017 | Current: Vice President, Director of Fund Administration, Ultimus Fund Solutions, LLC (since 2014).

Previous: Counsel, Securities and Mutual Funds, Western & Southern Financial Group (2012 – 2014). | None. | ||

John C. Swhear, 56 Chief Compliance Officer and Vice President Since August 2008 | Current: Assistant Vice President and Associate Director of Fund Administration, Ultimus Fund Solutions, LLC (since April 2017); Chief Compliance Officer, Unified Financial Securities, LLC (since May 2007).

Previous: Associate Director of Compliance, Ultimus Fund Solutions, LLC (December 2015 to May 2017); Vice President of Legal Administration and Compliance, Huntington Asset Services, Inc. (n/k/a Ultimus Asset Services, LLC) (April 2007 to December 2015), Director (May 2014 to December 2015); Director, Unified Financial Securities, Inc. (n/k/a Unified Financial Securities, LLC) (May 2014 to December 2015). | None. | ||

Carol J. Highsmith, 52 Vice President Since August 2008

Secretary Since March 2014 | Current: Assistant Vice President, Ultimus Fund Solutions, LLC (since December 2015).

Previous: Employed in various positions with Huntington Asset Services, Inc. (n/k/a Ultimus Asset Services, LLC) (November 1994 to December 2015), most recently Vice President of Legal Administration (2005 to December 2015). | None. | ||

29

| Name, Address*, (Age), Position with Trust,** Term of Position with Trust | Principal Occupation During Past 5 Years | Other Directorships | ||

Matthew J. Miller, 41 Vice President Since December 2011 | Current: Assistant Vice President, Relationship Management, Ultimus Fund Solutions, LLC (since December 2015).

Previous: Employed in various positions with Huntington Asset Services, Inc. (n/k/a Ultimus Asset Services, LLC) ( July 1998 to December 2015), most recently Vice President of Relationship Management (2005 to December 2015). | None. | ||

Bryan W. Ashmus, 44 Principal Financial Officer and Treasurer Since December 2013 | Current: Vice President and Director of Financial Administration, Ultimus Fund Solutions, LLC (since December 2015).

Previous: Vice President and Manager of Financial Administration, Huntington Asset Services, Inc. (n/k/a Ultimus Asset Services, LLC) (September 2013 to December 2015); Vice President, Fund Administration, Citi Fund Services Ohio, Inc. (from May 2005 to September 2013). | None. | ||

| * | The address for each trustee and officer is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. |

| ** | As of the date of this report, the Trust consists of 13 series. |

Other Information (Unaudited)

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the trustees and is available without charge, upon request. You may call toll-free at (855) 575-2430 to request a copy of the SAI or to make shareholder inquiries.

30

March 9, 2017

FACTS | WHAT DOES VALUED ADVISERS TRUST DO WITH YOUR PERSONAL INFORMATION? | |

Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. | |

What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include: ◾ Social Security number ◾ account balances and account transactions ◾ account transactions, transaction or loss history and purchase history ◾ checking account information and wire transfer instructions When you are no longer our customer, we continue to share your information as described in this notice.

| |

How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons Valued Advisers Trust chooses to share; and whether you can limit this sharing.

|

Reasons we can share your personal information | Does Valued Advisers Trust share? | |

For our everyday business purposes — such as to process your transactions, maintain your account(s), respond to court orders and legal investigations, or report to credit bureaus | Yes | |

For our marketing purposes — to offer our products and services to you | Yes | |

For joint marketing with other financial companies | No | |

For our affiliates’ everyday business purposes — information about your transactions and experiences | No | |

For our affiliates’ everyday business purposes — information about your creditworthiness | No | |

For nonaffiliates to market to you | No |

Questions? | Call 1-855-575-2430. |

31

| Who we are | ||

Who is providing this notice?

| Valued Advisers Trust

| |

What we do

| ||

| How does Valued Advisers Trust protect my personal information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings.

| |

| How does Valued Advisers Trust collect my personal information? | We collect your personal information, for example, when you ◾ open an account or deposit money ◾ buy securities from us or sell securities to us ◾ make deposits or withdrawals from your account or provide account information ◾ give us your account information ◾ make a wire transfer ◾ tell us who receives the money ◾ tell us where to send the money ◾ show your government-issued ID ◾ show your driver’s license

| |

| Why can’t I limit all sharing? | Federal law gives you the right to limit only ◾ sharing for affiliates’ everyday business purposes — information about your creditworthiness ◾ affiliates from using your information to market to you ◾ sharing for nonaffiliates to market to you

State laws and individual companies may give you additional rights to limit sharing.

| |

Definitions

| ||

| Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies. | |

| Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies. ◾ Valued Advisers Trust does not share your personal information with nonaffiliates so they can market to you. | |

| Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you. ◾ Valued Advisers Trust doesn’t jointly market financial products or services to you. | |

32

Proxy Voting

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities and information regarding how the Fund voted those proxies during the most recent twelve month period ended June 30, is available without charge upon request by (1) calling the Fund at (855) 575-2430 and (2) from Fund documents filed with the Securities and Exchange Commission (“SEC”) on the SEC’s website at www.sec.gov.

TRUSTEES