UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22321

MAINSTAY FUNDS TRUST

(Exact name of Registrant as specified in charter)

51 Madison Avenue, New York, NY 10010

(Address of principal executive offices) (Zip code)

J. Kevin Gao, Esq.

169 Lackawanna Avenue

Parsippany, New Jersey 07054

(Name and address of agent for service)

Registrant’s telephone number, including area code: (212)576-7000

Date of fiscal year end: October 31

Date of reporting period: April 30, 2013

| Item 1. | Reports to Stockholders. |

MainStay Epoch U.S. Equity Yield Fund

Message from the President and Semiannual Report

Unaudited | April 30, 2013

This page intentionally left blank

Message from the President

The U.S. stock market advanced during the six months ended April 30, 2013, generally providing double-digit returns at all capitalization levels. Value stocks tended to outpace growth stocks among large- and mid-capitalization companies, while growth stocks tended to outpace value stocks among smaller companies.

The market’s advance, however, was far from uniform. Stocks declined in early November, both before and immediately after the U.S. presidential election. Following a sharp recovery, stocks climbed until mid-December, when a Congressional stalemate on the fiscal cliff led to a brief decline. Another dip occurred in late February as investors speculated that the Federal Open Market Committee (FOMC) might stop purchasing mortgage-backed securities sooner than expected. Stocks also dipped in mid-April, as consumer sentiment dropped after the Boston marathon bombing. Despite these setbacks, U.S. stocks continued to trend upward during the six-month reporting period.

International stock markets also advanced, with several regional differences. Accommodative action by the Bank of Japan helped lower the yen and lift Japanese stocks to their highest levels since 2008. In Europe, stocks did well until early February, bolstered by the promise of support for the euro. As the year progressed, however, economic contraction, rising unemployment and systematic banking concerns took a toll on investor enthusiasm. In China, manufacturing slowed as the nation sought to balance growth and inflation risks. On the Korean peninsula, tensions rose as North Korea continued to threaten its neighbors, which added an undercurrent of caution to the market.

During the six months ended April 30, 2013, the FOMC kept the federal funds rate in a range close to zero. The FOMC also continued its direct purchases of mortgage-backed securities and longer-term U.S. government securities. With short-term interest rates likely to remain at low levels, many bond investors pursued higher yields by lengthening maturities and assuming greater risk. As a result, bonds with higher risk profiles tended

to outperform higher-quality investment-grade bonds and U.S. Treasury securities. Cash and cash equivalents essentially returned zero.

With wide variations in the performance of various asset classes, some investors might be tempted to chase higher returns by shifting back and forth between stocks and bonds. Since no one can predict where the market will move next, however, we encourage investors to select an appropriate mix of investments for their risk tolerance and time horizon and to stick with that mix, making only minor adjustments over time.

At MainStay Funds, our portfolio managers use a similar approach. Careful security selection and thoughtful sell disciplines help them pursue the investment objectives of their respective Funds. Using the principal investment strategies outlined in the Prospectus, they focus primarily on providing long-term investment potential for our shareholders.

Has this approach proved successful? In its most recent rankings, Barron’s listed MainStay Funds as the #1 fund family over the past 10 years. We were also the only mutual fund family that has appeared in Barron’s top six for the past five consecutive years.

The pages that follow provide additional insight into the specific market events, investment decisions and securities that shaped your MainStay Fund(s) during the six months ended April 30, 2013. We encourage you to read the semiannual report(s) carefully and to evaluate your results with your long-term financial goals in mind.

Sincerely,

Stephen P. Fisher

President

The opinions expressed are as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

To qualify for the Lipper/Barron’s Fund Survey, a fund family must have at least three funds in Lipper’s general U.S.-stock category, one in world equity (which combines global and international funds), one mixed-equity fund (which holds stocks and bonds), two taxable-bond funds, and one tax-exempt fund. Fund loads and 12b-1 fees aren’t included in the calculation of returns because the aim is to measure the manager’s skill. Each fund’s return is measured against all funds in its Lipper category, resulting in a percentile ranking which is then weighted by asset size relative to the fund family’s other assets in its general classifications. Finally, the score is multiplied by the general classification weightings as determined by the entire Lipper universe of funds.

Source: Barron’s, 2/9/13. Overall, MainStay Funds ranked number 56 for the one-year period, 20 for the five-year period and one for the 10-year period ended December 31, 2012, out of 62, 53 and 46 fund families, respectively. MainStay ranked number three for the 10-year period in 2009, 2010 and 2011 from among 48, 46 and 45 fund families, respectively. MainStay ranked number six from among 48 fund families for the 10-year period in 2008. Past performance is no guarantee of future results, which will vary. For the most recent MainStay Funds performance, please visit our website at mainstayinvestments.com. All mutual funds are subject to market risk and will fluctuate in value.

Not part of the Semiannual Report

Table of Contents

Investors should refer to the Fund’s Summary Prospectus and/or Prospectus and consider the Fund’s investment objectives, strategies, risks, charges and expenses carefully before investing. The Summary Prospectus and/or Prospectus contain this and other information about the Fund. You may obtain copies of the Fund’s Summary Prospectus, Prospectus and Statement of Additional Information free of charge, upon request, by calling toll-free 800-MAINSTAY (624-6782), by writing to NYLIFE Distributors LLC, Attn: MainStay Marketing Department, 169 Lackawanna Avenue, Parsippany, New Jersey 07054 or by sending an e-mail to MainStayShareholderServices@nylim.com. These documents are also available via the MainStay Funds’ website at mainstayinvestments.com/documents. Please read the Summary Prospectus and/or Prospectus carefully before investing.

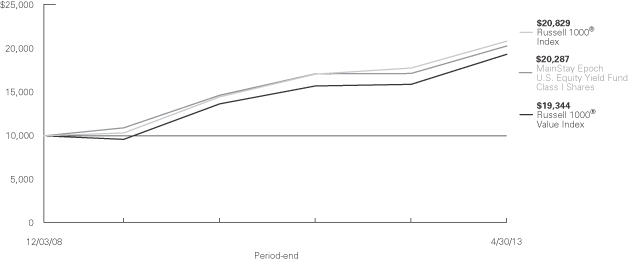

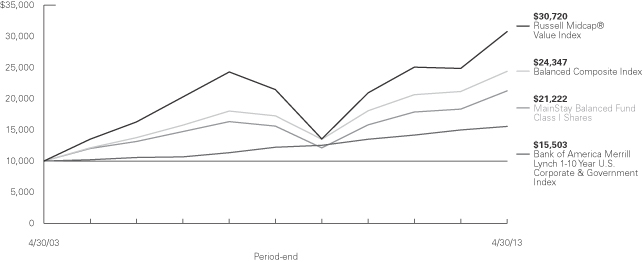

Investment and Performance Comparison1 (Unaudited)

Performance data quoted represents past performance. Past performance is no guarantee of future results. Because of market volatility, current performance may be lower or higher than the figures shown. Investment return and principal value will fluctuate, and as a result, when shares are redeemed, they may be worth more or less than their original cost. The graph below depicts the historical performance of Class I shares of the Fund. Performance will vary from class to class based on differences in class-specific expenses and sales charges. For performance information current to the most recent month-end, please call 800-MAINSTAY (624-6782) or visit mainstayinvestments.com.

Average Annual Total Returns for the Period Ended April 30, 2013

| | | | | | | | | | | | | | | | | | | | |

| Class | | Sales Charge | | | | Six Months | | | One Year | | | Since

Inception

(12/3/08) | | | Gross

Expense

Ratio2 | |

| Investor Class Shares3 | | Maximum 5.5% Initial Sales Charge | | With sales charges Excluding sales charges | |

| 10.04

16.44 | %

| |

| 11.61

18.10 | %

| |

| 15.56

17.05 | %

| |

| 2.14

2.14 | %

|

| Class | | Sales Charge | | | | Six Months | | | One Year | | | Since

Inception

(2/3/09) | | | Gross

Expense

Ratio2 | |

| Class A Shares4 | | Maximum 5.5% Initial Sales Charge | | With sales charges Excluding sales charges | |

| 10.02

16.42 | %

| |

| 11.58

18.08 | %

| |

| 15.61

17.16 | %

| |

| 2.19

2.19 | %

|

| Class | | Sales Charge | | | | Six Months | | | One Year | | | Since

Inception

(12/3/08) | | | Gross

Expense

Ratio2 | |

| Class C Shares3 | | Maximum 1% CDSC if Redeemed Within One Year of Purchase | | With sales charges Excluding sales charges | |

| 15.02

15.94 | %

| |

| 16.33

17.26 | %

| |

| 16.25

16.25 | %

| |

| 2.89

2.89 | %

|

| Class | | Sales Charge | | | | Six Months | | | One Year | | | Since

Inception

(12/3/08) | | | Gross

Expense

Ratio2 | |

| Class I Shares4 | | No Sales Charge | | | | | 16.57 | % | | | 18.31 | % | | | 17.41 | % | | | 1.94 | % |

| 1. | The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on distributions or Fund share redemptions. Total returns reflect maximum applicable sales charges as indicated in the table above, changes in share price, and reinvestment of dividend and capital gain distributions. The graph assumes the initial investment amount shown above and reflects the deduction of all sales charges that would have applied for the period of investment. Performance figures reflect certain fee waivers and/or expense limitations, without which total returns may have been lower. For more information on share classes and current fee waivers and/or expense limitations, please refer to the notes to the financial statements. |

| 2. | The gross expense ratios presented reflect the Fund’s “Total Annual Fund Operating Expenses” from the most recent Prospectus and may differ from other expense ratios disclosed in this report. |

| 3. | Performance figures for Investor Class and Class C shares, first offered on November 16, 2009, include the historical performance of Class I shares from December 3, 2008 through November 15, 2009 adjusted for differences in certain expenses and fees. Unadjusted, the performance shown for Investor Class and Class C shares would likely have been different. |

| 4. | Performance figures for Class I shares and Class A shares include the historical performance of the Institutional shares from December 3, 2008 |

The footnotes on the next page are an integral part of the table and graph and should be carefully read in conjunction with them.

| | | | |

| mainstayinvestments.com | | | 5 | |

| | | | | | | | | | | | |

| Benchmark Performance | | Six Months | | | One Year | | | Since

Inception

of the Fund | |

Russell 1000® Value Index5 | | | 16.31 | % | | | 21.80 | % | | | 16.14 | % |

Russell 1000® Index6 | | | 15.05 | | | | 17.17 | | | | 18.11 | |

Average Lipper Large-Cap Core Fund7 | | | 14.17 | | | | 15.80 | | | | 17.15 | |

and the Class P shares from February 3, 2009, respectively, of the Epoch U.S. Large Cap Equity Fund (the predecessor to the Fund), through November 15, 2009. The Epoch U.S. Large Cap Equity Fund was subject to a different fee structure and was advised by Epoch Investment Partners, Inc.

| 5. | The Russell 1000® Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000® Index companies with lower price-to-book ratios and lower expected growth values. The Fund selected the Russell 1000® Value Index as its primary benchmark because it believes that this index is more reflective of its current investment style. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 6. | The Russell 1000® Index measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1,000 of the largest securities based on a combination of their market cap and current index membership. The Russell |

| | 1000® Index represents approximately 92% of the U.S. market. The Fund has selected the Russell 1000® Index as its secondary benchmark. Results assume reinvestment of all dividends and capital gains. An investment cannot be made directly in an index. |

| 7. | The average Lipper large-cap core fund is representative of funds that, by portfolio practice, invest at least 75% of their equity assets in companies with market capitalizations (on a three-year weighted basis) above Lipper’s U.S. Diversified Equity large-cap floor. Large-cap core funds have more latitude in the companies in which they invest. These funds typically have an average price-to-earnings ratio, price-to-book ratio, and three-year sales-per-share growth value, compared to the S&P 500® Index. This benchmark is a product of Lipper Inc. Lipper Inc. is an independent monitor of fund performance. Results are based on average total returns of similar funds with all dividend and capital gain distributions reinvested. |

The footnotes on the preceding page are an integral part of the table and graph and should be carefully read in conjunction with them.

| | |

| 6 | | MainStay Epoch U.S. Equity Yield Fund |

Cost in Dollars of a $1,000 Investment in MainStay Epoch U.S. Equity Yield Fund (Unaudited)

The example below is intended to describe the fees and expenses borne by shareholders during the six-month period from November 1, 2012, to April 30, 2013, and the impact of those costs on your investment.

Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including exchange fees and sales charges (loads) on purchases (as applicable), and (2) ongoing costs, including management fees, distribution and/or service (12b-1) fees, and other Fund expenses (as applicable). This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from November 1, 2012, to April 30, 2013.

This example illustrates your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six months ended April 30, 2013. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then

multiply the result by the number under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in the Fund with the ongoing costs of investing in other Funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other Funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as exchange fees or sales charges (loads). Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | |

| Share Class | | Beginning

Account

Value

11/1/12 | | | Ending Account

Value (Based

on Actual

Returns and

Expenses)

4/30/13 | | | Expenses

Paid

During

Period1 | | | Ending Account

Value (Based

on Hypothetical

5% Annualized

Return and

Actual Expenses)

4/30/13 | | | Expenses

Paid

During

Period1 | |

| | | | | |

| Investor Class Shares | | $ | 1,000.00 | | | $ | 1,164.40 | | | $ | 7.35 | | | $ | 1,018.00 | | | $ | 6.85 | |

| | | | | |

| Class A Shares | | $ | 1,000.00 | | | $ | 1,164.20 | | | $ | 7.08 | | | $ | 1,018.20 | | | $ | 6.61 | |

| | | | | |

| Class C Shares | | $ | 1,000.00 | | | $ | 1,159.40 | | | $ | 11.35 | | | $ | 1,014.30 | | | $ | 10.59 | |

| | | | | |

| Class I Shares | | $ | 1,000.00 | | | $ | 1,165.70 | | | $ | 5.80 | | | $ | 1,019.40 | | | $ | 5.41 | |

| 1. | Expenses are equal to the Fund’s annualized expense ratio of each class (1.37% for Investor Class, 1.32% for Class A, 2.12% for Class C and 1.08% for Class I) multiplied by the average account value over the period, divided by 365 and multiplied by 181 (to reflect the six-month period). The table above represents the actual expenses incurred during the six-month period. |

| | | | |

| mainstayinvestments.com | | | 7 | |

Industry Composition as of April 30, 2013 (Unaudited)

| | | | |

| Multi-Utilities | | | 8.2 | % |

| Aerospace & Defense | | | 6.6 | |

| Oil, Gas & Consumable Fuels | | | 6.5 | |

| Pharmaceuticals | | | 6.1 | |

| Electric Utilities | | | 5.9 | |

| Tobacco | | | 5.7 | |

| Commercial Services & Supplies | | | 4.1 | |

| Diversified Telecommunication Services | | | 3.9 | |

| Food Products | | | 3.6 | |

| Beverages | | | 3.3 | |

| Household Products | | | 3.2 | |

| Media | | | 3.2 | |

| Semiconductors & Semiconductor Equipment | | | 3.1 | |

| Insurance | | | 2.8 | |

| Electrical Equipment | | | 2.6 | |

| IT Services | | | 2.4 | |

| Computers & Peripherals | | | 2.2 | |

| Software | | | 1.8 | |

| Chemicals | | | 1.7 | |

| | | | |

| Gas Utilities | | | 1.7 | % |

| Leisure Equipment & Products | | | 1.7 | |

| Food & Staples Retailing | | | 1.5 | |

| Capital Markets | | | 1.4 | |

| Commercial Banks | | | 1.3 | |

| Energy Equipment & Services | | | 1.3 | |

| Real Estate Investment Trusts | | | 1.3 | |

| Industrial Conglomerates | | | 1.2 | |

| Distributors | | | 1.0 | |

| Health Care Equipment & Supplies | | | 1.0 | |

| Hotels, Restaurants & Leisure | | | 1.0 | |

| Specialty Retail | | | 1.0 | |

| Diversified Financial Services | | | 0.9 | |

| Air Freight & Logistics | | | 0.5 | |

| Containers & Packaging | | | 0.5 | |

| Machinery | | | 0.5 | |

| Short-Term Investment | | | 1.3 | |

| Other Assets, Less Liabilities | | | 4.0 | |

| | | | |

| | | 100.0 | % |

| | | | |

See Portfolio of Investments beginning on page 11 for specific holdings within these categories.

Top Ten Holdings as of April 30, 2013 (excluding short-term investment)

| | |

| 8 | | MainStay Epoch U.S. Equity Yield Fund |

Portfolio Management Discussion and Analysis (Unaudited)

Questions answered by portfolio managers Eric Sappenfield, Michael Welhoelter, CFA, William Priest, CFA, John Tobin, PhD, CFA, and Kera Van Valen, CFA, of Epoch Investment Partners, Inc., the Fund’s Subadvisor.

How did MainStay Epoch U.S. Equity Yield Fund perform relative to its peers and its benchmark for the six months ended April 30, 2013?

Excluding all sales charges, MainStay Epoch U.S. Equity Yield Fund returned 16.44% for Investor Class shares, 16.42% for Class A shares and 15.94% for Class C shares for the six months ended April 30, 2013. Over the same period, Class I shares returned 16.57%. All share classes outperformed the 14.17% return of the average Lipper1 large-cap core fund for the same period. Investor Class, Class A and Class I shares outperformed—and Class C shares underperformed—the 16.31% return of the Russell 1000® Value Index2 for the six months ended April 30, 2013. The Russell 1000® Value Index is the Fund’s broad-based securities-market index. See page 5 for Fund returns with applicable sales charges.

Were there any changes to the Fund during the reporting period?

Effective February 28, 2013, John Tobin and Kera Van Valen were added as portfolio managers.

What factors affected the Fund’s relative performance during the reporting period?

The Fund provided strong absolute returns that reflected growth in cash flows and shareholder yield—including dividends, share buybacks and debt reduction—from its holdings. The Fund’s absolute performance was also supported by the global rally in equities during the reporting period.

Relative to the Russell 1000® Value Index, the Fund’s emphasis on sustainable shareholder yield was a positive factor in an environment where market gains were led by defensive companies with strong shareholder-yield characteristics. The Fund’s relative returns were hurt by not owning the large banks and some information technology companies that saw a jump in share prices during the reporting period.

During the reporting period, which sectors were the strongest positive contributors to the Fund’s relative performance and which sectors were particularly weak?

The strongest positive contributors to the Fund’s performance relative to the Russell 1000® Value Index were the materials, energy and industrials sectors. (Contributions take weightings and total returns into account.) The Fund had less exposure than the Index to materials and energy companies. This positioning enhanced results, as these sectors had the weakest returns during the reporting period. The Fund’s holdings in the materials and industrials sectors appreciated more than securities in the comparable sectors of the Russell 1000® Value Index.

Results lagged the Russell 1000® Value Index in the information technology and financials sectors. While the Fund’s overweight position relative to the Index in information technology was a positive factor, stock selection in the sector detracted. Fund returns were hindered in the financials sector by the Fund’s avoidance of the large banks, many of which did not meet our shareholder-yield criteria. The Fund’s residual cash position also detracted from relative performance in a rising equity market.

During the reporting period, which individual stocks made the strongest positive contributions to the Fund’s absolute performance and which stocks detracted the most?

The individual stocks that made the strongest positive contributors to the Fund’s absolute performance were hard disk manufacturer Seagate Technology, drug company AbbVie and health and hygiene company Kimberly-Clark. Seagate Technology reported strong results on improved pricing and stock repurchases. In January 2013, Abbott Laboratories split into two companies: Abbott Laboratories (a global health care company) and AbbVie (the biotechnology and pharmaceutical part of the business). The Fund’s position in Abbott Laboratories was also split into two parts, but AbbVie has a higher dividend commitment to its shareholders. We sold the Fund’s position in Abbott Laboratories, which has a lower dividend payment but a higher growth component. Kimberly-Clark reported strong international sales and improved profit margins. The company increased its dividend during the reporting period and has a buyback program that we believe is attractive.

During the reporting period, the most substantial detractors from the Fund’s absolute performance were Pitney Bowes, Darden Restaurants and ONEOK Partners. We sold the Fund’s position in Pitney Bowes, a company that provides hardware, software and services for physical and digital communications. The company continued to see pressure on its core businesses, and its priorities for capital allocation became unclear to us. We also sold the Fund’s position in casual dining restaurant operator Darden Restaurants after weak sales and an acquisition announcement reduced our confidence that the Fund would accumulate returns through dividends and share repurchases. Natural gas company ONEOK Partners reported a drop in earnings due to lower prices for natural gas liquids. With volumes up and new projects near completion, we continued to have confidence in the company’s ability to deliver shareholder yield, and thus held the position at the end of the reporting period.

Did the Fund make any significant purchases or sales during the reporting period?

We added a Fund position in retail pharmacy CVS Caremark after management confirmed its intention to return $5 billion to

| 1. | See footnote on page 6 for more information on Lipper Inc. |

| 2. | See footnote on page 6 for more information on the Russell 1000® Value Index. |

| | | | |

| mainstayinvestments.com | | | 9 | |

shareholders in 2013 through a combination of dividends and share repurchases. We believe that modest revenue growth, coupled with margin expansion, should allow CVS Caremark to continue generating strong free cash flow. We also established a Fund position in Health Care REIT, which operates a growing portfolio of medical office buildings. The company has a large dividend yield and plans on reducing its debt.

In addition to the sales already mentioned, we exited the Fund’s position in Diebold, a maker of ATMs. We sold the stock on the view that the company’s earnings and cash flows were being hurt by an intensifying slowdown among U.S. regional banks.

How did the Fund’s sector weightings change during the reporting period?

The Fund’s sector weightings are the result of buying and selling individual stocks and changed little during the reporting period. The most significant shifts were modest increases in energy and utilities and modest decreases in industrials and telecommunication services.

How was the Fund positioned at the end of April 2013?

As of April 30, 2013, the Fund had more exposure than the Russell 1000® Value Index to the consumer staples and utilities sectors, where an abundance of companies not only generate strong cash flows but also—as part of their capital-allocation decisions—emphasize returning capital to shareholders. As of the same date, the Fund remained significantly underweight in the financials sector, which makes up more than one-quarter of the Russell 1000® Value Index. Many of the larger financials, especially banks, were forced to cut dividends and issue new stock during the financial crisis. During the reporting period, many of these same banks continued to have their dividends restricted by regulators. These companies are still using cash to fortify their capital bases rather than provide shareholder yield. As a result, they are not appropriate candidates for the Fund at this time.

The opinions expressed are those of the portfolio managers as of the date of this report and are subject to change. There is no guarantee that any forecast made will come to pass. This material does not constitute investment advice and is not intended as an endorsement of any specific investment.

| | |

| 10 | | MainStay Epoch U.S. Equity Yield Fund |

Portfolio of Investments April 30, 2013 (Unaudited)

| | | | | | | | |

| | |

| | | Shares | | | Value | |

| | | | | | | | |

| Common Stocks 94.7%† | | | | | | | | |

Aerospace & Defense 6.6% | |

Boeing Co. (The) | | | 1,165 | | | $ | 106,493 | |

General Dynamics Corp. | | | 1,670 | | | | 123,513 | |

Honeywell International, Inc. | | | 2,455 | | | | 180,541 | |

Lockheed Martin Corp. | | | 2,035 | | | | 201,648 | |

¨Raytheon Co. | | | 3,575 | | | | 219,434 | |

United Technologies Corp. | | | 1,415 | | | | 129,175 | |

| | | | | | | | |

| | | | | | | 960,804 | |

| | | | | | | | |

Air Freight & Logistics 0.5% | |

United Parcel Service, Inc. Class B | | | 785 | | | | 67,384 | |

| | | | | | | | |

| | |

Beverages 3.3% | | | | | | | | |

Coca-Cola Co. (The) | | | 3,420 | | | | 144,769 | |

Coca-Cola Enterprises, Inc. | | | 3,320 | | | | 121,612 | |

Molson Coors Brewing Co. Class B | | | 2,665 | | | | 137,514 | |

PepsiCo., Inc. | | | 920 | | | | 75,872 | |

| | | | | | | | |

| | | | | | | 479,767 | |

| | | | | | | | |

Capital Markets 1.4% | |

BlackRock, Inc. | | | 475 | | | | 126,587 | |

Waddell & Reed Financial, Inc. Class A | | | 1,940 | | | | 83,168 | |

| | | | | | | | |

| | | | | | | 209,755 | |

| | | | | | | | |

Chemicals 1.7% | |

Dow Chemical Co. (The) | | | 1,625 | | | | 55,104 | |

E.I. du Pont de Nemours & Co. | | | 2,035 | | | | 110,928 | |

RPM International, Inc. | | | 2,300 | | | | 74,520 | |

| | | | | | | | |

| | | | | | | 240,552 | |

| | | | | | | | |

Commercial Banks 1.3% | |

Bank of Hawaii Corp. | | | 1,505 | | | | 71,773 | |

M&T Bank Corp. | | | 1,095 | | | | 109,719 | |

| | | | | | | | |

| | | | | | | 181,492 | |

| | | | | | | | |

Commercial Services & Supplies 4.1% | |

Deluxe Corp. | | | 3,575 | | | | 136,351 | |

R.R. Donnelley & Sons Co. | | | 6,995 | | | | 86,108 | |

Republic Services, Inc. | | | 3,930 | | | | 133,934 | |

¨Waste Management, Inc. | | | 5,865 | | | | 240,348 | |

| | | | | | | | |

| | | | | | | 596,741 | |

| | | | | | | | |

Computers & Peripherals 2.2% | |

Apple, Inc. | | | 240 | | | | 106,260 | |

Seagate Technology PLC | | | 5,600 | | | | 205,520 | |

| | | | | | | | |

| | | | | | | 311,780 | |

| | | | | | | | |

Containers & Packaging 0.5% | |

Bemis Co., Inc. | | | 1,805 | | | | 71,027 | |

| | | | | | | | |

|

Distributors 1.0% | |

Genuine Parts Co. | | | 1,840 | | | | 140,447 | |

| | | | | | | | |

| | | | | | | | |

| | |

| | | Shares | | | Value | |

| | | | | | | | |

Diversified Financial Services 0.9% | |

CME Group, Inc. | | | 2,203 | | | $ | 134,075 | |

| | | | | | | | |

| | | | | | | | |

|

Diversified Telecommunication Services 3.9% | |

AT&T, Inc. | | | 4,395 | | | | 164,637 | |

¨CenturyLink, Inc. | | | 5,855 | | | | 219,972 | |

Verizon Communications, Inc. | | | 3,390 | | | | 182,755 | |

| | | | | | | | |

| | | | | | | 567,364 | |

| | | | | | | | |

Electric Utilities 5.9% | |

Duke Energy Corp. | | | 2,810 | | | | 211,312 | |

Entergy Corp. | | | 1,030 | | | | 73,367 | |

Northeast Utilities | | | 3,323 | | | | 150,631 | |

PPL Corp. | | | 5,380 | | | | 179,584 | |

Southern Co. | | | 2,655 | | | | 128,051 | |

Westar Energy, Inc. | | | 3,155 | | | | 110,299 | |

| | | | | | | | |

| | | | | | | 853,244 | |

| | | | | | | | |

Electrical Equipment 2.6% | |

Eaton Corp. PLC | | | 2,890 | | | | 177,475 | |

Emerson Electric Co. | | | 3,455 | | | | 191,787 | |

| | | | | | | | |

| | | | | | | 369,262 | |

| | | | | | | | |

Energy Equipment & Services 1.3% | |

Diamond Offshore Drilling, Inc. | | | 2,709 | | | | 187,192 | |

| | | | | | | | |

|

Food & Staples Retailing 1.5% | |

CVS Caremark Corp. | | | 1,260 | | | | 73,307 | |

Wal-Mart Stores, Inc. | | | 1,915 | | | | 148,834 | |

| | | | | | | | |

| | | | | | | 222,141 | |

| | | | | | | | |

Food Products 3.6% | |

Campbell Soup Co. | | | 3,695 | | | | 171,485 | |

Hershey Co. (The) | | | 1,940 | | | | 172,970 | |

Kraft Foods Group, Inc. | | | 3,455 | | | | 177,898 | |

| | | | | | | | |

| | | | | | | 522,353 | |

| | | | | | | | |

Gas Utilities 1.7% | |

ONEOK, Inc. | | | 2,910 | | | | 149,457 | |

WGL Holdings, Inc. | | | 2,135 | | | | 98,680 | |

| | | | | | | | |

| | | | | | | 248,137 | |

| | | | | | | | |

Health Care Equipment & Supplies 1.0% | |

Medtronic, Inc. | | | 2,990 | | | | 139,573 | |

| | | | | | | | |

|

Hotels, Restaurants & Leisure 1.0% | |

McDonald’s Corp. | | | 1,350 | | | | 137,889 | |

| | | | | | | | |

|

Household Products 3.2% | |

Colgate-Palmolive Co. | | | 640 | | | | 76,423 | |

¨Kimberly-Clark Corp. | | | 2,470 | | | | 254,879 | |

Procter & Gamble Co. (The) | | | 1,705 | | | | 130,893 | |

| | | | | | | | |

| | | | | | | 462,195 | |

| | | | | | | | |

| † | Percentages indicated are based on Fund net assets. |

| ¨ | | Among the Fund’s 10 largest holdings, as of April 30, 2013, excluding short-term investment. May be subject to change daily. |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | 11 | |

Portfolio of Investments April 30, 2013 (Unaudited) (continued)

| | | | | | | | |

| | |

| | | Shares | | | Value | |

| Common Stocks (continued) | | | | | | | | |

| | | | | | | | |

Industrial Conglomerates 1.2% | |

3M Co. | | | 1,695 | | | $ | 177,483 | |

| | | | | | | | |

|

Insurance 2.8% | |

Arthur J. Gallagher & Co. | | | 5,070 | | | | 215,221 | |

Marsh & McLennan Cos., Inc. | | | 2,820 | | | | 107,188 | |

Travelers Companies, Inc. (The) | | | 975 | | | | 83,275 | |

| | | | | | | | |

| | | | | | | 405,684 | |

| | | | | | | | |

IT Services 2.4% | |

Automatic Data Processing, Inc. | | | 2,615 | | | | 176,094 | |

Paychex, Inc. | | | 4,540 | | | | 165,302 | |

| | | | | | | | |

| | | | | | | 341,396 | |

| | | | | | | | |

Leisure Equipment & Products 1.7% | |

¨Mattel, Inc. | | | 5,425 | | | | 247,706 | |

| | | | | | | | |

|

Machinery 0.5% | |

Deere & Co. | | | 763 | | | | 68,136 | |

| | | | | | | | |

|

Media 3.2% | |

Comcast Corp. Class A | | | 4,260 | | | | 167,375 | |

Regal Entertainment Group Class A | | | 5,975 | | | | 107,192 | |

Time Warner, Inc. | | | 3,124 | | | | 186,753 | |

| | | | | | | | |

| | | | | | | 461,320 | |

| | | | | | | | |

Multi-Utilities 8.2% | |

CMS Energy Corp. | | | 5,435 | | | | 162,724 | |

Dominion Resources, Inc. | | | 2,335 | | | | 144,023 | |

Integrys Energy Group, Inc. | | | 2,180 | | | | 134,201 | |

NiSource, Inc. | | | 6,430 | | | | 197,594 | |

SCANA Corp. | | | 1,980 | | | | 107,316 | |

TECO Energy, Inc. | | | 4,960 | | | | 94,885 | |

Vectren Corp. | | | 3,065 | | | | 115,121 | |

¨Wisconsin Energy Corp. | | | 5,125 | | | | 230,317 | |

| | | | | | | | |

| | | | | | | 1,186,181 | |

| | | | | | | | |

Oil, Gas & Consumable Fuels 6.5% | |

Chevron Corp. | | | 565 | | | | 68,936 | |

ConocoPhillips | | | 2,390 | | | | 144,475 | |

Enterprise Products Partners, L.P. | | | 1,715 | | | | 104,015 | |

Exxon Mobil Corp. | | | 695 | | | | 61,848 | |

Kinder Morgan Energy Partners, L.P. | | | 1,195 | | | | 105,698 | |

MarkWest Energy Partners, L.P. | | | 1,505 | | | | 95,116 | |

ONEOK Partners, L.P. | | | 1,715 | | | | 92,781 | |

Royal Dutch Shell PLC, ADR | | | 2,150 | | | | 146,135 | |

Spectra Energy Corp. | | | 3,820 | | | | 120,445 | |

| | | | | | | | |

| | | | | | | 939,449 | |

| | | | | | | | |

Pharmaceuticals 6.1% | |

¨AbbVie, Inc. | | | 5,290 | | | | 243,605 | |

Bristol-Myers Squibb Co. | | | 4,595 | | | | 182,513 | |

¨Johnson & Johnson | | | 2,735 | | | | 233,104 | |

¨Merck & Co., Inc. | | | 4,635 | | | | 217,845 | |

| | | | | | | | |

| | | | | | | 877,067 | |

| | | | | | | | |

| | | | | | | | |

| | |

| | | Shares | | | Value | |

| | | | | | | | |

Real Estate Investment Trusts 1.3% | |

Health Care REIT, Inc. | | | 1,505 | | | $ | 112,830 | |

Ventas, Inc. | | | 1,010 | | | | 80,426 | |

| | | | | | | | |

| | | | | | | 193,256 | |

| | | | | | | | |

Semiconductors & Semiconductor Equipment 3.1% | |

Intel Corp. | | | 3,230 | | | | 77,358 | |

KLA-Tencor Corp. | | | 2,555 | | | | 138,609 | |

Linear Technology Corp. | | | 1,750 | | | | 63,875 | |

Microchip Technology, Inc. | | | 4,595 | | | | 167,350 | |

| | | | | | | | |

| | | | | | | 447,192 | |

| | | | | | | | |

Software 1.8% | |

Microsoft Corp. | | | 3,905 | | | | 129,256 | |

Oracle Corp. | | | 4,195 | | | | 137,512 | |

| | | | | | | | |

| | | | | | | 266,768 | |

| | | | | | | | |

Specialty Retail 1.0% | |

Home Depot, Inc. (The) | | | 1,935 | | | | 141,932 | |

| | | | | | | | |

|

Tobacco 5.7% | |

¨Altria Group, Inc. | | | 7,020 | | | | 256,300 | |

Lorillard, Inc. | | | 3,575 | | | | 153,332 | |

Philip Morris International, Inc. | | | 2,160 | | | | 206,474 | |

Reynolds American, Inc. | | | 4,350 | | | | 206,277 | |

| | | | | | | | |

| | | | | | | 822,383 | |

| | | | | | | | |

Total Common Stocks

(Cost $11,870,570) | | | | | | | 13,679,127 | |

| | | | | | | | |

| | |

| | | | | | | | |

| | | Principal

Amount | | | | |

| Short-Term Investment 1.3% | |

Repurchase Agreement 1.3% | | | | | | | | |

State Street Bank and Trust Co.

0.01%, dated 4/30/13

due 5/1/13

Proceeds at Maturity $182,418 (Collateralized by a Federal National Mortgage Assocation security with a rate of 2.00% and a maturity date of 11/2/22, with a Principal Amount of $190,000 and a Market Value of $189,931) | | $ | 182,418 | | | | 182,418 | |

| | | | | | | | |

Total Short-Term Investment

(Cost $182,418) | | | | | | | 182,418 | |

| | | | | | | | |

Total Investments

(Cost $12,052,988) (a) | | | 96.0 | % | | | 13,861,545 | |

Other Assets, Less Liabilities | | | 4.0 | | | | 580,188 | |

Net Assets | | | 100.0 | % | | $ | 14,441,733 | |

| | | | |

| 12 | | MainStay Epoch U.S. Equity Yield Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

| (a) | As of April 30, 2013, cost is $12,046,132 for federal income tax purposes and net unrealized appreciation is as follows: |

| | | | |

Gross unrealized appreciation | | $ | 1,815,541 | |

Gross unrealized depreciation | | | (128 | ) |

| | | | |

Net unrealized appreciation | | $ | 1,815,413 | |

| | | | |

The following abbreviation is used in the above portfolio:

ADR—American Depositary Receipt.

The following is a summary of the fair valuations according to the inputs used as of April 30, 2013, for valuing the Fund’s assets.

Asset Valuation Inputs

| | | | | | | | | | | | | | | | |

Description | | Quoted

Prices in

Active

Markets for

Identical

Assets (Level 1) | | | Significant

Other

Observable

Inputs (Level 2) | | | Significant

Unobservable

Inputs

(Level 3) | | | Total | |

| Investments in Securities (a) | | | | | | | | | | | | | | | | |

| Common Stocks | | $ | 13,679,127 | | | $ | — | | | $ | — | | | $ | 13,679,127 | |

| Short-Term Investment | | | | | | | | | | | | | | | | |

Repurchase Agreement | | | — | | | | 182,418 | | | | — | | | | 182,418 | |

| | | | | | | | | | | | | | | | |

| Total Investments in Securities | | $ | 13,679,127 | | | $ | 182,418 | | | $ | — | | | $ | 13,861,545 | |

| | | | | | | | | | | | | | | | |

| (a) | For a complete listing of investments and their industries, see the Portfolio of Investments. |

The Fund recognizes transfers between the levels as of the beginning of the period.

For the period ended April 30, 2013, the Fund did not have any transfers between Level 1 and Level 2 fair value measurements. (See Note 2)

As of April 30, 2013, the Fund did not hold any investments with significant unobservable inputs (Level 3). (See Note 2)

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | 13 | |

Statement of Assets and Liabilities as of April 30, 2013 (Unaudited)

| | | | |

| Assets | |

Investment in securities, at value

(identified cost $12,052,988) | | $ | 13,861,545 | |

Receivables: | | | | |

Fund shares sold | | | 511,105 | |

Investment securities sold | | | 302,767 | |

Dividends and interest | | | 23,134 | |

Manager (See Note 3) | | | 2,224 | |

Other assets | | | 34,293 | |

| | | | |

Total assets | | | 14,735,068 | |

| | | | |

| |

| Liabilities | | | | |

Payables: | | | | |

Investment securities purchased | | | 159,055 | |

Transfer agent (See Note 3) | | | 51,392 | |

Fund shares redeemed | | | 46,647 | |

Professional fees | | | 22,347 | |

Shareholder communication | | | 9,039 | |

NYLIFE Distributors (See Note 3) | | | 1,231 | |

Trustees | | | 187 | |

Accrued expenses | | | 3,437 | |

| | | | |

Total liabilities | | | 293,335 | |

| | | | |

Net assets | | $ | 14,441,733 | |

| | | | |

| |

| Composition of Net Assets | | | | |

Shares of beneficial interest outstanding (par value of $.001 per share) unlimited number of shares authorized | | $ | 1,148 | |

Additional paid-in capital | | | 12,374,805 | |

| | | | |

| | | 12,375,953 | |

Undistributed net investment income | | | 94,715 | |

Accumulated net realized gain (loss) on investments | | | 162,508 | |

Net unrealized appreciation (depreciation) on investments | | | 1,808,557 | |

| | | | |

Net assets | | $ | 14,441,733 | |

| | | | |

| | | | |

Investor Class | | | | |

Net assets applicable to outstanding shares | | $ | 768,925 | |

| | | | |

Shares of beneficial interest outstanding | | | 61,485 | |

| | | | |

Net asset value per share outstanding | | $ | 12.51 | |

Maximum sales charge (5.50% of offering price) | | | 0.73 | |

| | | | |

Maximum offering price per share outstanding | | $ | 13.24 | |

| | | | |

Class A | | | | |

Net assets applicable to outstanding shares | | $ | 3,671,083 | |

| | | | |

Shares of beneficial interest outstanding | | | 292,636 | |

| | | | |

Net asset value per share outstanding | | $ | 12.54 | |

Maximum sales charge (5.50% of offering price) | | | 0.73 | |

| | | | |

Maximum offering price per share outstanding | | $ | 13.27 | |

| | | | |

Class C | | | | |

Net assets applicable to outstanding shares | | $ | 670,605 | |

| | | | |

Shares of beneficial interest outstanding | | | 54,771 | |

| | | | |

Net asset value and offering price per share outstanding | | $ | 12.24 | |

| | | | |

Class I | | | | |

Net assets applicable to outstanding shares | | $ | 9,331,120 | |

| | | | |

Shares of beneficial interest outstanding | | | 739,065 | |

| | | | |

Net asset value and offering price per share outstanding | | $ | 12.63 | |

| | | | |

| | | | |

| 14 | | MainStay Epoch U.S. Equity Yield Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Statement of Operations for the six months ended April 30, 2013 (Unaudited)

| | | | |

| Investment Income (Loss) | |

Income | | | | |

Dividends | | $ | 454,264 | |

Interest | | | 16 | |

| | | | |

Total income | | | 454,280 | |

| | | | |

Expenses | | | | |

Manager (See Note 3) | | | 81,197 | |

Registration | | | 29,174 | |

Professional fees | | | 21,167 | |

Custodian | | | 14,175 | |

Transfer agent (See Note 3) | | | 13,769 | |

Shareholder communication | | | 11,137 | |

Distribution/Service—Investor Class (See Note 3) | | | 710 | |

Distribution/Service—Class A (See Note 3) | | | 2,429 | |

Distribution/Service—Class C (See Note 3) | | | 2,277 | |

Trustees | | | 286 | |

Miscellaneous | | | 5,612 | |

| | | | |

Total expenses before waiver/reimbursement | | | 181,933 | |

Expense waiver/reimbursement from Manager (See Note 3) | | | (67,351 | ) |

| | | | |

Net expenses | | | 114,582 | |

| | | | |

Net investment income (loss) | | | 339,698 | |

| | | | |

|

| Realized and Unrealized Gain (Loss) on Investments | |

Net realized gain (loss) on investments | | | 400,658 | |

Net change in unrealized appreciation (depreciation) on investments | | | 1,551,761 | |

| | | | |

Net realized and unrealized gain (loss) on investments | | | 1,952,419 | |

| | | | |

Net increase (decrease) in net assets resulting from operations | | $ | 2,292,117 | |

| | | | |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | 15 | |

Statements of Changes in Net Assets

for the six months ended April 30, 2013 (Unaudited) and the year ended October 31, 2012

| | | | | | | | |

| | | 2013 | | | 2012 | |

| Increase (Decrease) in Net Assets | |

Operations: | | | | | | | | |

Net investment income (loss) | | $ | 339,698 | | | $ | 2,027,911 | |

Net realized gain (loss) on investments | | | 400,658 | | | | 52,371,551 | |

Net change in unrealized appreciation (depreciation) on investments | | | 1,551,761 | | | | (26,396,938 | ) |

| | | | |

Net increase (decrease) in net assets resulting from operations | | | 2,292,117 | | | | 28,002,524 | |

| | | | |

Dividends and distributions to shareholders: | | | | | | | | |

From net investment income: | | | | | | | | |

Investor Class | | | (4,245 | ) | | | (807 | ) |

Class A | | | (8,995 | ) | | | (1,962 | ) |

Class C | | | (2,900 | ) | | | — | |

Class I | | | (228,843 | ) | | | (1,686,234 | ) |

| | | | |

| | | (244,983 | ) | | | (1,689,003 | ) |

| | | | |

From net realized gain on investments: | | | | | | | | |

Investor Class | | | (99,362 | ) | | | (13,870 | ) |

Class A | | | (247,854 | ) | | | (30,125 | ) |

Class C | | | (78,416 | ) | | | (13,749 | ) |

Class I | | | (5,915,562 | ) | | | (13,880,465 | ) |

| | | | |

| | | (6,341,194 | ) | | | (13,938,209 | ) |

| | | | |

Total dividends and distributions to shareholders | | | (6,586,177 | ) | | | (15,627,212 | ) |

| | | | |

Capital share transactions: | | | | | | | | |

Net proceeds from sale of shares | | | 3,299,544 | | | | 57,657,095 | |

Net asset value of shares issued to shareholders in reinvestment of dividends and distributions | | | 4,002,164 | | | | 4,407,737 | |

Cost of shares redeemed | | | (27,922,850 | ) | | | (304,719,709 | ) |

| | | | |

Increase (decrease) in net assets derived from capital share transactions | | | (20,621,142 | ) | | | (242,654,877 | ) |

| | | | |

Net increase (decrease) in net assets | | | (24,915,202 | ) | | | (230,279,565 | ) |

|

| Net Assets | |

Beginning of period | | | 39,356,935 | | | | 269,636,500 | |

| | | | |

End of period | | $ | 14,441,733 | | | $ | 39,356,935 | |

| | | | |

Undistributed net investment income at end of period | | $ | 94,715 | | | $ | — | |

| | | | |

| | | | |

| 16 | | MainStay Epoch U.S. Equity Yield Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Financial Highlights selected per share data and ratios

| | | | | | | | | | | | | | | | | | | | |

| | | Investor Class | |

| | | Six months

ended

April 30, | | | Year ended October 31, | | | January 1,

2010

through

October 31, | | | November 16,

2009**

through

December 31, | |

| | | 2013* | | | 2012 | | | 2011 | | | 2010*** | | | 2009 | |

Net asset value at beginning of period | | $ | 13.54 | | | $ | 12.66 | | | $ | 13.51 | | | $ | 12.67 | | | $ | 12.38 | |

| | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (a) | | | 0.15 | | | | 0.13 | | | | 0.04 | | | | 0.03 | | | | 0.02 | |

Net realized and unrealized gain (loss) on investments | | | 1.62 | | | | 1.46 | | | | 0.51 | | | | 0.81 | | | | 0.30 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 1.77 | | | | 1.59 | | | | 0.55 | | | | 0.84 | | | | 0.32 | |

| | | | | | | | | | | | | | | | | | | | |

Less dividends and distributions: | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.12 | ) | | | (0.04 | ) | | | (0.05 | ) | | | — | | | | (0.03 | ) |

From net realized gain on investments | | | (2.68 | ) | | | (0.67 | ) | | | (1.35 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (2.80 | ) | | | (0.71 | ) | | | (1.40 | ) | | | — | | | | (0.03 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value at end of period | | $ | 12.51 | | | $ | 13.54 | | | $ | 12.66 | | | $ | 13.51 | | | $ | 12.67 | |

| | | | | | | | | | | | | | | | | | | | |

Total investment return (b) | | | 16.44 | %(c) | | | 13.22 | % | | | 4.06 | % | | | 6.63 | %(c) | | | 2.60 | %(c) |

Ratios (to average net assets)/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 2.49 | %†† | | | 1.02 | % | | | 0.27 | % | | | 0.25 | %†† | | | 1.11 | %†† |

Net expenses | | | 1.37 | %†† | | | 1.21 | %(d) | | | 1.36 | % | | | 1.40 | %†† | | | 1.19 | %†† |

Expenses (before waiver/reimbursement) | | | 2.03 | %†† | | | 1.50 | %(d) | | | 1.36 | % | | | 1.43 | %†† | | | 1.19 | %†† |

Portfolio turnover rate | | | 17 | % | | | 50 | % | | | 54 | % | | | 54 | % | | | 54 | % |

Net assets at end of period (in 000’s) | | $ | 769 | | | $ | 444 | | | $ | 273 | | | $ | 74 | | | $ | 28 | |

| ** | Commencement of operations. |

| *** | The Fund changed its fiscal year end from December 31 to October 31. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (c) | Total investment return is not annualized. |

| (d) | Net of interest expense which is less than one-tenth of a percent. (See Note 6) |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | 17 | |

Financial Highlights selected per share data and ratios

| | | | | | | | | | | | | | | | | | | | |

| | | Class A | |

| | | Six months

ended

April 30, | | | Year ended October 31, | | | January 1,

2010

through

October 31, | | | February 3,

2009**

through

December 31, | |

| | | 2013* | | | 2012 | | | 2011 | | | 2010*** | | | 2009 | |

Net asset value at beginning of period | | $ | 13.56 | | | $ | 12.68 | | | $ | 13.52 | | | $ | 12.67 | | | $ | 10.24 | |

| | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (a) | | | 0.14 | | | | 0.12 | | | | 0.05 | | | | 0.02 | | | | 0.08 | |

Net realized and unrealized gain (loss) on investments | | | 1.62 | | | | 1.47 | | | | 0.51 | | | | 0.83 | | | | 3.33 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 1.76 | | | | 1.59 | | | | 0.56 | | | | 0.85 | | | | 3.41 | |

| | | | | | | | | | | | | | | | | | | | |

Less dividends and distributions: | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.10 | ) | | | (0.04 | ) | | | (0.05 | ) | | | — | | | | (0.10 | ) |

From net realized gain on investments | | | (2.68 | ) | | | (0.67 | ) | | | (1.35 | ) | | | — | | | | (0.88 | ) |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (2.78 | ) | | | (0.71 | ) | | | (1.40 | ) | | | — | | | | (0.98 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value at end of period | | $ | 12.54 | | | $ | 13.56 | | | $ | 12.68 | | | $ | 13.52 | | | $ | 12.67 | |

| | | | | | | | | | | | | | | | | | | | |

Total investment return (b) | | | 16.42 | %(c) | | | 13.24 | % | | | 4.18 | % | | | 6.71 | %(c) | | | 33.59 | %(c) |

Ratios (to average net assets)/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 2.35 | %†† | | | 0.89 | % | | | 0.41 | % | | | 0.19 | %†† | | | 0.76 | %†† |

Net expenses | | | 1.32 | %†† | | | 1.31 | %(d) | | | 1.25 | % | | | 1.34 | %†† | | | 1.35 | %†† |

Expenses (before waiver/reimbursement) | | | 1.98 | %†† | | | 1.62 | %(d) | | | 1.25 | % | | | 1.37 | %†† | | | 1.44 | %†† |

Portfolio turnover rate | | | 17 | % | | | 50 | % | | | 54 | % | | | 54 | % | | | 54 | % |

Net assets at end of period (in 000’s) | | $ | 3,671 | | | $ | 1,090 | | | $ | 534 | | | $ | 850 | | | $ | 127 | |

| ** | Commencement of operations. |

| *** | The Fund changed its fiscal year end from December 31 to October 31. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (c) | Total investment return is not annualized. |

| (d) | Net of interest expense which is less than one-tenth of a percent. (See Note 6) |

| | | | |

| 18 | | MainStay Epoch U.S. Equity Yield Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Financial Highlights selected per share data and ratios

| | | | | | | | | | | | | | | | | | | | |

| | | Class C | |

| | | Six months

ended

April 30, | | | Year ended October 31, | | | January 1,

2010

through

October 31, | | | November 16,

2009**

through

December 31, | |

| | | 2013* | | | 2012 | | | 2011 | | | 2010*** | | | 2009 | |

Net asset value at beginning of period | | $ | 13.34 | | | $ | 12.53 | | | $ | 13.42 | | | $ | 12.67 | | | $ | 12.38 | |

| | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) (a) | | | 0.10 | | | | 0.03 | | | | (0.05 | ) | | | (0.07 | ) | | | 0.01 | |

Net realized and unrealized gain (loss) on investments | | | 1.58 | | | | 1.45 | | | | 0.51 | | | | 0.82 | | | | 0.30 | |

| | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 1.68 | | | | 1.48 | | | | 0.46 | | | | 0.75 | | | | 0.31 | |

| | | | | | | | | | | | | | | | | | | | |

Less dividends and distributions: | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.10 | ) | | | — | | | | — | | | | — | | | | (0.02 | ) |

From net realized gain on investments | | | (2.68 | ) | | | (0.67 | ) | | | (1.35 | ) | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (2.78 | ) | | | (0.67 | ) | | | (1.35 | ) | | | — | | | | (0.02 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net asset value at end of period | | $ | 12.24 | | | $ | 13.34 | | | $ | 12.53 | | | $ | 13.42 | | | $ | 12.67 | |

| | | | | | | | | | | | | | | | | | | | |

Total investment return (b) | | | 15.94 | %(c) | | | 12.49 | % | | | 3.30 | % | | | 5.92 | % (c)(d) | | | 2.51 | %(c) |

Ratios (to average net assets)/Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 1.70 | %†† | | | 0.23 | % | | | (0.42 | %) | | | (0.63 | %)†† | | | 0.37 | %†† |

Net expenses | | | 2.12 | %†† | | | 1.98 | %(e) | | | 2.10 | % | | | 2.15 | % †† | | | 1.94 | %†† |

Expenses (before waiver/reimbursement) | | | 2.78 | %†† | | | 2.23 | %(e) | | | 2.10 | % | | | 2.18 | % †† | | | 1.94 | %†† |

Portfolio turnover rate | | | 17 | % | | | 50 | % | | | 54 | % | | | 54 | % | | | 54 | % |

Net assets at end of period (in 000’s) | | $ | 671 | | | $ | 393 | | | $ | 208 | | | $ | 33 | | | $ | 26 | |

| ** | Commencement of operations. |

| *** | The Fund changed its fiscal year end from December 31 to October 31. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. |

| (c) | Total investment return is not annualized. |

| (d) | Total investment return may reflect adjustments to conform to generally accepted accounting principles. |

| (e) | Net of interest expense which is less than one-tenth of a percent. (See Note 6) |

| | | | | | |

The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. | | mainstayinvestments.com | | | 19 | |

Financial Highlights selected per share data and ratios

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | Class I | |

| | | Six months

ended

April 30, | | | Year ended October 31, | | | January 1,

2010

through

October 31, | | | Year ended

December 31, | | | December 3,

2008**

through

December 31, | |

| | | 2013* | | | 2012 | | | 2011 | | | 2010*** | | | 2009 | | | 2008 | |

Net asset value at beginning of period | | $ | 13.62 | | | $ | 12.75 | | | $ | 13.58 | | | $ | 12.70 | | | $ | 10.85 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 0.21 | (a) | | | 0.14 | (a) | | | 0.09 | (a) | | | 0.04 | (a) | | | 0.11 | (a) | | | 0.01 | |

Net realized and unrealized gain (loss) on investments | | | 1.58 | | | | 1.48 | | | | 0.51 | | | | 0.84 | | | | 2.74 | | | | 0.85 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total from investment operations | | | 1.79 | | | | 1.62 | | | | 0.60 | | | | 0.88 | | | | 2.85 | | | | 0.86 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Less dividends and distributions: | | | | | | | | | | | | | | | | | | | | | | | | |

From net investment income | | | (0.10 | ) | | | (0.08 | ) | | | (0.08 | ) | | | — | | | | (0.12 | ) | | | (0.01 | ) |

From net realized gain on investments | | | (2.68 | ) | | | (0.67 | ) | | | (1.35 | ) | | | — | | | | (0.88 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions | | | (2.78 | ) | | | (0.75 | ) | | | (1.43 | ) | | | — | | | | (1.00 | ) | | | (0.01 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value at end of period | | $ | 12.63 | | | $ | 13.62 | | | $ | 12.75 | | | $ | 13.58 | | | $ | 12.70 | | | $ | 10.85 | |

| | | | | | | | | | | | | | | | | | | | | | | | |

Total investment return (b) | | | 16.57 | %(c) | | | 13.43 | % | | | 4.43 | % | | | 6.93 | %(c) | | | 26.53 | % | | | 8.59 | %(c) |

Ratios (to average net assets)/Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income (loss) | | | 3.53 | %†† | | | 1.06 | % | | | 0.67 | % | | | 0.40 | %†† | | | 0.98 | % | | | 1.28 | %†† |

Net expenses | | | 1.08 | %†† | | | 1.05 | %(d) | | | 1.00 | % | | | 1.09 | %†† | | | 1.09 | % | | | 1.09 | %†† |

Expenses (before waiver/reimbursement) | | | 1.74 | %†† | | | 1.10 | %(d) | | | 1.00 | % | | | 1.12 | %†† | | | 1.19 | % | | | 1.16 | %†† |

Portfolio turnover rate | | | 17 | % | | | 50 | % | | | 54 | % | | | 54 | % | | | 54 | % | | | 1 | % |

Net assets at end of period (in 000’s) | | $ | 9,331 | | | $ | 37,430 | | | $ | 268,622 | | | $ | 229,830 | | | $ | 155,231 | | | $ | 98,778 | |

| ** | Commencement of operations. |

| *** | The Fund changed its fiscal year end from December 31 to October 31. |

| (a) | Per share data based on average shares outstanding during the period. |

| (b) | Total investment return is calculated exclusive of sales charges and assumes the reinvestment of dividends and distributions. Class I shares are not subject to sales charges. |

| (c) | Total investment return is not annualized. |

| (d) | Net of interest expense which is less than one-tenth of a percent. (See Note 6) |

| | | | |

| 20 | | MainStay Epoch U.S. Equity Yield Fund | | The notes to the financial statements are an integral part of,

and should be read in conjunction with, the financial statements. |

Notes to Financial Statements (Unaudited)

Note 1–Organization and Business

MainStay Funds Trust (the “Trust”) was organized as a Delaware statutory trust on April 28, 2009, and is governed by a Declaration of Trust. The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end investment management company, and is comprised of thirty-three funds (collectively referred to as the “Funds”). These financial statements and notes relate only to the MainStay Epoch U.S. Equity Yield Fund (the “Fund”), a diversified fund. Prior to September 17, 2012, the Fund’s name was MainStay Epoch U.S. Equity Fund, with a different investment objective, investment strategies, and investment process. The Fund is the successor to the Epoch U.S. Large Cap Equity Fund (the “Predecessor Fund”), which was a series of a different registered investment company for which Epoch Investment Partners, Inc. served as investment advisor. The financial statements of the Fund reflect the historical results of the Institutional Class and Class P shares of the Predecessor Fund prior to its reorganization. Upon the completion of the reorganization, the Class I and Class A shares of the Fund assumed the performance, financial and other information of the Institutional Class and Class P shares of the Predecessor Fund, respectively. All information and references to periods prior to November 16, 2009 refer to the Predecessor Fund.

The Fund currently offers four classes of shares. Investor Class and Class C shares commenced operations on November 16, 2009. Class A and Class I shares commenced operations (under former designations) on February 3, 2009 and December 3, 2008, respectively. Investor Class and Class A shares are offered at net asset value (“NAV”) per share plus an initial sales charge. No sales charge applies to investments of $1 million or more (and certain other qualified purchases) in Investor Class and Class A shares, but a contingent deferred sales charge (“CDSC”) is imposed on certain redemptions made within one year of the date of purchase. Class C shares are offered at NAV without an initial sales charge, although a 1.00% CDSC may be imposed on redemptions made within one year of the date of purchase of Class C shares. Class I shares are offered at NAV and are not subject to a sales charge. Depending upon eligibility, Investor Class shares may convert to Class A shares and Class A shares may convert to Investor Class shares. The four classes of shares have the same voting (except for issues that relate solely to one class), dividend, liquidation and other rights, and the same terms and conditions, except that Class C shares are subject to higher distribution and/or service fee rates than Investor Class and Class A shares under a distribution plan pursuant to Rule 12b-1 under the 1940 Act. Class I shares are not subject to a distribution and/or service fee.

The Fund’s investment objective is to seek current income and capital appreciation.

Note 2–Significant Accounting Policies

The Fund prepares its financial statements in accordance with generally accepted accounting principles (“GAAP”) in the United States of America and follows the significant accounting policies described below.

(A) Securities Valuation. Investments are valued as of the close of regular trading on the New York Stock Exchange (“Exchange”) (generally 4:00 p.m. Eastern time) on each day the Fund is open for business (“valuation date”).

The Board of Trustees (the “Board”) has adopted procedures for the valuation of the Fund’s securities and has delegated the responsibility for valuation determination under those procedures to the Valuation Committee of the Fund (the “Valuation Committee”). The Board has authorized the Valuation Committee to appoint a Valuation Sub-Committee (the “Sub-Committee”) to deal in the first instance with questions that arise or cannot be resolved under these procedures. The Sub-Committee meets (in person, via electronic mail or via teleconference) on an as-needed basis. The Valuation Committee meets at a later time, as necessary, to ensure that actions taken by the Sub-Committee were appropriate. The procedures recognize that, subject to the oversight of the Board and unless otherwise noted, the responsibility for day-to-day valuation of portfolio assets (including securities for which market prices are not readily available) rests with New York Life Investment Management LLC ( “New York Life Investments” or the “Manager”), aided to whatever extent necessary by the Subadvisor (as defined in Note 3(A)) of the Fund.

To assess the appropriateness of security valuations, the Manager or the Fund’s third party service provider who is subject to oversight by the Manager, regularly compares prior day prices, prices on comparable securities and the sale prices to the prior and current day prices and challenges prices exceeding certain tolerance levels with third party pricing services or broker sources. For those securities valued by recommendation, whether through a standardized fair valuation methodology or a fair valuation determination, the Valuation Committee reviews and affirms the reasonableness of the valuation based on such methodologies and determinations on a regular basis after considering all relevant information that is reasonably available.

“Fair value” is defined as the price that the Fund would receive upon selling an investment in an orderly transaction to an independent buyer in the principal or most advantageous market of the investment. Fair value measurements are determined within a framework that has established a three-tier hierarchy which maximizes the use of observable market data and minimizes the use of unobservable inputs to establish classification of fair value measurements for disclosure purposes. “Inputs” refers broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, such as the risk inherent in a particular valuation technique used to measure fair value using a pricing model and/or the risk inherent in the inputs for the valuation technique. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability based on market data obtained from sources independent of the Fund. Unobservable inputs reflect the Fund’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the information available in the circumstances. The inputs or methodology used for valuing securities may not be an indication of the risks associated with investing in those securities. The three-tier hierarchy of inputs is summarized in the three broad Levels listed below.

| • | | Level 1—quoted prices in active markets for identical investments |

| • | | Level 2—other significant observable inputs (including quoted prices for similar investments in active markets, interest rates and yield curves, prepayment speeds, credit risks, etc.) |

| | | | |

| mainstayinvestments.com | | | 21 | |

Notes to Financial Statements (Unaudited) (continued)

| • | | Level 3—significant unobservable inputs (including the Fund’s own assumptions about the assumptions that market participants would use in determining the fair value of investments) |

The aggregate value by input level, as of April 30, 2013, for the Fund’s investments is included at the end of the Fund’s Portfolio of Investments.

The valuation techniques used by the Fund to measure fair value maximize the use of observable inputs and minimize the use of unobservable inputs. The Fund may utilize third party vendor evaluations, whose prices may be derived from one or more of the following standard inputs:

| | |

• Benchmark Yields | | • Reported Trades |

• Broker Dealer Quotes | | • Issuer Spreads |

• Two-sided markets | | • Benchmark securities |

• Bids/Offers | | • Reference Data (corporate actions or material event notices) |

• Industry and economic events | | • Comparable bonds |

• Equity and credit default swap curves | | • Monthly payment information |

Securities for which market values cannot be determined using the methodologies described above are valued by methods deemed in good faith by the Fund’s Valuation Committee, following the procedures established by the Board, to represent fair value. Under these procedures, the Fund primarily employs a market-based approach which may use related or comparable assets or liabilities, recent transactions, market multiples, book values, and other relevant information. The Fund may also use an income-based valuation approach in which the anticipated future cash flows of the investment are discounted to calculate fair value. Discounts may also be applied due to the nature or duration of any restrictions on the disposition of the investments. Due to the inherent uncertainty of valuations of such investments, the fair values may differ significantly from the values that would have been used had an active market existed. For the six-month period ended April 30, 2013, there have been no changes to the fair value methodologies.

Equity and non-equity securities which may be valued in this manner include, but are not limited to: (i) a security for which the trading has been halted or suspended; (ii) a debt security that has recently gone into default and for which there is not a current market quotation; (iii) a security of an issuer that has entered into a restructuring; (iv) a security that has been de-listed from a national exchange; (v) a security for which the market price is not available from a third party pricing source or, if so provided, does not, in the opinion of the Fund’s Manager or Subadvisor reflect the security’s market value; and (vi) a security whose principal market has been temporarily closed at a time when, under normal conditions, it would be open. Securities for which market quotations or observable inputs are not readily available are generally categorized as Level 3 in the hierarchy. As of April 30, 2013, the Fund did not hold any securities that were fair valued in such a manner.

Certain events may occur between the time that foreign markets close, on which securities held by the Fund principally trade, and the time at which the Fund’s NAV is calculated. These events may include, but are not limited to, situations relating to a single issuer in a market sector, significant fluctuations in U.S. or foreign markets, natural disasters,

armed conflicts, governmental actions or other developments not tied directly to the securities markets. Should the Manager or Subadvisor conclude that such events may have affected the accuracy of the last price of such securities reported on the local foreign market, the Manager or Subadvisor may, pursuant to procedures adopted by the Board, adjust the value of the local price to reflect the estimated impact on the price of such securities as a result of such events. In this instance, securities are generally categorized as Level 3 in the hierarchy. Additionally, foreign equity securities are also fair valued whenever the movement of a particular index exceeds certain thresholds. In such cases, the securities are fair valued by applying factors provided by a third party vendor in accordance with the Fund’s policies and procedures and are generally categorized as Level 2 in the hierarchy. As of April 30, 2013, certain foreign equity securities held by the Fund were not fair valued in such a manner.

Equity securities and Exchange Traded Funds are valued at the latest quoted sales prices as of the close of regular trading on the Exchange on each valuation date. Securities that are not traded on the valuation date are valued at the mean of the latest quoted bid and ask prices. Prices normally are taken from the principal market in which each security trades. Futures contracts are valued at the last posted settlement price on the market where such futures are primarily traded. Options contracts are valued at the last posted settlement price on the market where such options are principally traded. Investments in other mutual funds are valued at their respective NAVs as of the close of the Exchange on the valuation date. These securities are generally categorized as Level 1 in the hierarchy.

Temporary cash investments acquired over 60 days to maturity are valued using the latest bid prices or using valuations based on a matrix system (which considers such factors as security prices, yields, maturities, and ratings), both as furnished by independent pricing services. Other temporary cash investments which mature in 60 days or less (“Short-Term Investments”) are valued at amortized cost. The amortized cost method involves valuing a security at its cost on the date of purchase and thereafter assuming a constant amortization to maturity of the difference between such cost and the value on maturity date. Amortized cost approximates the current fair value of a security. Securities valued at amortized cost are not valued using a quoted price in an active market. These securities are generally categorized as Level 2 in the hierarchy.

(B) Income Taxes. The Fund’s policy is to comply with the requirements of the Internal Revenue Code of 1986, as amended (the “Internal Revenue Code”), applicable to regulated investment companies and to distribute all of the taxable income to the shareholders of the Fund within the allowable time limits. Therefore, no federal, state and local income tax provision is required.

Management evaluates its tax positions to determine if the tax positions taken meet the minimum recognition threshold in connection with accounting for uncertainties in income tax positions taken or expected to be taken for the purposes of measuring and recognizing tax liabilities in the financial statements. Recognition of tax benefits of an uncertain tax position is required only when the position is “more likely than not” to be sustained assuming examination by taxing authorities. Management has analyzed the Fund’s tax positions taken on federal, state and local income tax returns for all open tax years (for up to three tax years), and

| | |

| 22 | | MainStay Epoch U.S. Equity Yield Fund |

has concluded that no provision for federal, state and local income tax is required in the Fund’s financial statements. The Fund’s federal, state and local income and federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state and local departments of revenue.

(C) Dividends and Distributions to Shareholders. Dividends and distributions are recorded on the ex-dividend date. The Fund intends to declare and pay dividends of net investment income and distributions of net realized capital and currency gains, if any, at least annually. Unless the shareholder elects otherwise, all dividends and distributions are reinvested in the same class of shares of the Fund, at NAV. Dividends and distributions to shareholders are determined in accordance with federal income tax regulations and may differ from GAAP.

(D) Security Transactions and Investment Income. The Fund records security transactions on the trade date. Realized gains and losses on security transactions are determined using the identified cost method. Dividend income is recognized on the ex-dividend date and interest income is accrued as earned using the effective interest rate method. Discounts and premiums on Short-Term Investments are accreted and amortized, respectively, on the straight-line method.

Investment income and realized and unrealized gains and losses on investments of the Fund are allocated to separate classes of shares pro rata based upon their relative net assets on the date the income is earned or realized and unrealized gains and losses are incurred.