united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-22483

Copeland Trust

(Exact name of Registrant as specified in charter)

Eight Tower Bridge, 161 Washington St., Suite #1325 Conshohocken, PA 19428

(Address of principal executive offices) (Zip code)

Ultimus Fund Solutions, LLC, 80 Arkay Drive Suite 10, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: (631) 470-2619

Date of fiscal year end: 11/30

Date of reporting period: 5/31/22

Item 1. Reports to Stockholders.

| Copeland | ||

| Dividend Growth Fund | ||

| Class A Shares: CDGRX | ||

| Class C Shares: CDCRX | ||

| Class I Shares: CDIVX | ||

| Copeland | ||

| Smid Cap Dividend Growth Fund | ||

| Class A Shares: CSDGX | ||

| Class I Shares: CSMDX | ||

| Copeland | ||

| International Small Cap Fund | ||

| Class A Shares: CISAX | ||

| Class I Shares: CSIIX | ||

| Semi-Annual Report | ||

| May 31, 2022 | ||

| Investor Information: 1-888-9-COPELAND | ||

| This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer of sale or solicitation of an offer to buy shares of the Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. | ||

| Distributed by Northern Lights Distributors, LLC | ||

| Member FINRA | ||

Copeland Dividend Growth Fund Semi-Annual Report

Semi-Annual Report

May 31, 2022

Dear Fellow Shareholders,

Copeland Capital Management is pleased to review the performance of the Copeland Dividend Growth Fund from the start of our fiscal year, December 1, 2021 for the six-month period ended May 31, 2022. Unless otherwise stated herein, all data and statistics that follow are as of May 31, 2022.

During the six-month period, Class I shares of the Fund fell 6.2%, besting the 8.9% decline registered by the S&P 500 Index. As fears surrounding inflation and Federal Reserve tightening took center stage, we are pleased to have outpaced the benchmark and partially shielded shareholders from the market downdraft. We have clearly entered a period of heightened market turbulence as the Federal Reserve seeks to strike a delicate balance amidst persistent inflation and slowing economic growth. Historically, during such periods, in our opinion, the downside protection afforded by a portfolio of high-quality dividend growth securities is of paramount importance.

Our stock selection in the Information Technology sector of the market bolstered Fund returns while those in the Real Estate sector were a drag. Oil and gas exploration company, Pioneer Natural Resources (PXD, 2.3% of holdings) was the top performing holding, advancing over 60% during the period. A sharp 75% increase in the price of WTI Crude Oil from $65 per barrel to $115 per barrel during the six-month period helped propel the shares higher. Pioneer used the lion’s share of its free cash flow to reward shareholders with a 95% increase in the quarterly variable dividend to $7.38 per share in the May quarter. Coupled with the quarterly base dividend payment, the distribution translated into an 11.5% dividend yield as the period drew to a close. The ongoing Russian invasion of Ukraine played a central role in driving crude oil prices higher and, at present, the conflict shows no sign of abating. Reflective of our strong relative performance in the Information Technology sector was CMC Materials (CCMP, 0.0% of holdings), which rose 43% during the period. In December, the supplier of materials to the semiconductor industry agreed to be acquired by competitor Entegris for a 35% premium. In early January, we elected to book the profit realized in the shares in favor of more compelling alternatives.

On the downside, Fund holding Cognex (CGNX, 1.1% of holdings) was a poor performer in the Fund, dipping over 37% during the period. While the provider of machine vision technology delivered better-than-expected March 2022 quarterly results, management guided June 2022 quarterly revenue and margins below Wall Street expectations, leading to a sell-off in the stock. Further, in June 2022, Cognex filed an 8-K disclosing that its primary third-party contract manufacturing facility in Indonesia experienced a large plant fire that resulted in loss or damage to a material portion of goods and inventory. We are awaiting additional information but expect the company can navigate through challenges and remain attracted to Cognex’s strong market position, favorable growth prospects, robust balance sheet, and healthy dividend growth. Cloud-based real estate broker eXp World Holdings (EXPI, 0.8% of holdings) was also a laggard, falling 46% during the period. Despite reporting strong Q4 2021 results, which included sales growth of 77% year-over-year and agent growth of 72% year-over-year, the stock sold off due to the broader market sentiment shift away from high growth stocks and fears around the impact of higher interest rates on residential real estate. We initiated our position in EXPI in January at a small initial weight and took advantage of the continued weakness in the share price to increase our position.

Concerns about inflation, the Russian invasion of Ukraine, and monetary policy tightening weighed on equity and fixed income markets during the period. The market continues to digest the reality of higher

1

rates, as the Federal Reserve raised the Federal Funds target rate by 75 basis points during the period. The monetary authority indicated that further increases would be necessary and that it would begin reducing its balance sheet holdings as of June 1, 2022. The Federal Reserve’s hawkish tone comes in response to persistently high inflation data. In May 2022, the Consumer Price Index increased 8.6% versus the prior year, the largest 12-month increase since December of 1981. Existing supply chain issues and price pressures were further exacerbated by the Russian invasion of Ukraine and renewed Covid related lockdowns in China.

It is our view that these challenges, which seem likely to persist for some time, highlight the importance of corporate fundamentals and valuations when considering any investment. Companies with positive free cash flow and profitability continue to outpace the market. Against this difficult macroeconomic and geopolitical backdrop, speculative investment approaches are retreating and, in our view, may encounter further downside risk. With strong business models and market positions, we continue to believe that shares of dividend growth companies remain poised for favorable risk-adjusted performance and are also well positioned should recent inflation and interest rate trends continue.

Thank you for the confidence you have placed in Copeland and for your investment in the Copeland Dividend Growth Fund.

The views and opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed. The Fund holdings discussed herein are for informational purposes only and should not be perceived as investment recommendations by Copeland Capital Management. Holdings are subject to change, may not represent current holdings and are subject to risk. Performance data quoted here represents past performance. Past performance is no guarantee of future results. The return quoted reflects fee waivers and expense reimbursements in effect and would have been lower in their absence. Current performance may be lower or higher than the performance quoted above. The risks of investing in the Copeland Funds vary from fund to fund; to see the risks of investing in an individual fund, please refer to that fund’s latest prospectus.

You cannot invest directly in any index. Index returns do not include a deduction for fees or expenses. The S&P 500® Index is a market-capitalization-weighted index of the stocks of 500 leading companies in major industries of the U.S. economy.

6684-NLD-07182022

2

Copeland SMID Cap Dividend Growth Fund

Semi-Annual Report

May 31, 2022

Dear Fellow Shareholders,

Copeland Capital Management is pleased to review the performance of the Copeland SMID Cap Dividend Growth Fund from December 1, 2021 through May 31, 2022. Unless otherwise stated herein, all data and statistics that follow are as of May 31, 2022.

During the six-month period, Class I shares of the Fund delivered a -4.5% return, besting the -10.7% decline posted by the Russell 2500 Index. As fears surrounding rising inflation and interest rates took center stage, we are pleased to have outpaced the benchmark and partially shielded shareholders from the market downdraft. We have clearly entered a period of heightened market turbulence as the Federal Reserve seeks to strike a delicate balance amidst persistent inflation and slowing economic growth. Historically, during such periods, in our opinion, the downside protection afforded by a portfolio of high-quality dividend growth securities is of paramount importance.

The Energy and Materials sectors delivered strong positive returns, reflecting the presence of many companies that benefit from rising commodity prices. Meanwhile the strong returns found broadly in the Utility sector reflected the increasingly cautious and defensive attitude of investors. On the other hand, stocks found in the Health Care and Technology sectors, most significantly among speculative growth companies that lack profits, suffered significant declines as investors eschewed risk. Discretionary stocks broadly retreated as consumers increasingly are struggling to spend in the face of high inflation, particularly as COVID-19 related government stimulus is exhausted.

Our stock selection in the Healthcare sector most significantly aided Fund returns. US Physical Therapy (USPH, 1.2% of holdings) rebounded 27%, driven by the reopening of its therapy centers as COVID-19 disruptions faded. The company effectively managed through a tight labor market and took patient volumes to record levels. The Fund’s Technology sector holdings also were materially more resilient than the benchmark. Mantech International (MANT, 1.2%) rallied 42% as defense stocks rebounded in response to Russia’s invasion of Ukraine. The company’s cyber intelligence capabilities, among many technology offerings, will be bolstered by increasing political support for higher defense budgets. Near the end of the period the company announced an agreement to be acquired by a private equity firm at a substantial premium. Finally, the top performing stocks in the portfolio were found in the Energy sector, led by Coterra Energy (CTRA, 1.7%) which appreciated 76%. Oil and natural gas prices were rising even before the Russian invasion of Ukraine, due to rebounding economic activity amidst a muted supply response. Coterra’s higher mix of natural gas was a particular tailwind, as Europe’s race to import natural gas from allies led to surging prices for the commodity in the U.S. The company committed to a capital allocation plan that will return at least 50% of free cash flow to shareholders. This led to a 20% increase in its base dividend as well as an additional variable dividend that increased the company’s total dividend yield to 7.1% based on the period end stock price.

Pressuring performance was our stock selection in the Financials sector. Hamilton Lane (HLNE, 1.3%) suffered a 33% decline as investors worried about weaker earnings at the alternative asset manager given the market decline. We are encouraged by strong new asset gathering and the company’s ability to invest this capital at attractive valuations for its clients, which will ultimately pay off when the equity market recovers. Cloud-based real estate broker eXp World Holdings (EXPI, 1.0% of holdings) was also a laggard, falling 47% during the period. Despite reporting strong Q4 2021 results, which included sales growth of

3

77% year-over-year and agent growth of 72% year-over-year, the stock sold off due to the broader market sentiment shift away from high growth stocks and fears around the impact of higher interest rates on residential real estate. We took advantage of the continued weakness in the share price to increase our position. Finally, Wingstop, Inc. (WING, 0.7%), a franchisor and operator of chicken wing restaurants, retreated 49% as investors soured on high growth stocks that enjoyed strong demand during the pandemic, as the company also dealt with inflation in chicken wing prices. The company delivered a $4 or 5% special dividend during the period, in addition to the 21% pace of growth in its base dividend. We remain confident in the company’s ability to maintain a premium growth rate as it expands from nearly 1700 to 4000 restaurants over time.

Concerns about inflation, the Russian invasion of Ukraine, and monetary policy tightening weighed on equity and fixed income markets during the period. The market continues to digest the reality of higher rates, as the Federal Reserve raised the Federal Funds target rate by 75 basis points during the period. The monetary authority indicated that further increases would be necessary and that it would begin reducing its balance sheet holdings as of June 1, 2022. The Fed’s hawkish tone comes in response to persistently high inflation data. In May, the Consumer Price Index increased 8.6% versus the prior year, the largest 12-month increase since December of 1981. Existing supply chain issues and price pressures were further exacerbated by the Russian invasion of Ukraine and renewed COVID-19 related lockdowns in China.

It is our view that these challenges, which seem likely to persist for some time, highlight the importance of corporate fundamentals and valuations when considering any investment. Companies with positive free cash flow and profitability continue to outpace the market. Against this difficult macroeconomic and geopolitical backdrop, speculative investment approaches are retreating and, in our view, may encounter further downside risk. With strong business models and market positions, we continue to believe that shares of dividend growth companies remain poised for favorable risk-adjusted performance and are also well positioned should recent inflation and interest rate trends continue.

Thank you for the confidence you have placed in Copeland and for your investment in the Copeland SMID Cap Dividend Growth Fund.

The views and opinions expressed in this letter are subject to change and may not be relied upon for investment advice. No forecasts can be guaranteed. The Fund holdings discussed herein are for informational purposes only and should not be perceived as investment recommendations by Copeland Capital Management. Holdings are subject to change, may not represent current holdings and are subject to risk. Performance data quoted here represents past performance. Past performance is no guarantee of future results. The return quoted reflects fee waivers and expense reimbursements in effect and would have been lower in their absence. Current performance may be lower or higher than the performance quoted above. The risks of investing in the Copeland Funds vary from fund to fund; to see the risks of investing in an individual fund, please refer to that fund’s latest prospectus.

You cannot invest directly in any index. Index returns do not include a deduction for fees or expenses. The Russell 2500 Index is comprised of the bottom 2500 companies in the Russell 3000 Index. The Russell 3000 Index measures the performance of the 3000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

6684-NLD-07182022

4

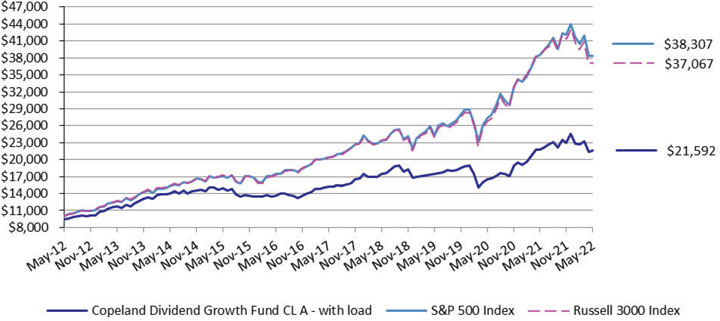

| Copeland Dividend Growth Fund |

| Portfolio Review (Unaudited) |

| May 31, 2012 through May 31, 2022 |

Performance of a $10,000 Investment (as of May 31, 2022)

| Average Annualized | Since | ||||

| Total Returns as of | Inception | ||||

| May 31, 2022 | Six Months | One Year | Five Year | Ten Year | Class I * |

| Copeland Dividend Growth Fund: | |||||

| Class A | |||||

| Without sales charge | (6.22)% | (1.07)% | 7.20% | 8.64% | — |

| With sales charge + | (11.61)% | (6.73)% | 5.93% | 8.00% | — |

| Class C | (6.50)% | (1.75)% | 6.40% | 7.84% | — |

| Class I | (6.16)% | (0.88)% | 7.37% | — | 7.81% |

| S&P 500 Index | (8.85)% | (0.30)% | 13.38% | 14.40% | 13.61% |

| Russell 3000 Index | (10.50)% | (3.68)% | 12.75% | 14.00% | 13.12% |

| * | Class A shares commenced operations on December 28, 2010. Class C commenced operations on January 5, 2012. Class I commenced operations March 1, 2013. |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The S&P 500 Index is an unmanaged market capitalization-weighted index which is comprised of 500 of the largest U.S. domiciled companies and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

The Russell 3000 Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. The performance and returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or redemption of Fund shares. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. For performance information current to the most recent month-end please call toll-free 1-888-9-COPELAND (1-888-926-7352). Additional information can be found by visiting our website, www.copelandfunds.com. The Fund’s gross annual operating expense ratio, as stated in the current prospectus, is 1.93%, 2.69%, and 1.75%, for Class A, Class C, and Class I shares, respectively, and its net annual operating expense ratio is 1.20%, 1.95%, and 1.05%, for Class A, Class C, and Class I shares, respectively. These ratios can fluctuate and may differ from the expense ratios disclosed in the Financial Highlights section of this report. The Fund’s investment adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, until at least March 31, 2023, to ensure that total annual fund operating expenses after fee deferral and/or reimbursement (exclusive of any taxes, leverage interest, borrowing interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expense on securities sold short, acquired fund fees and expenses or extraordinary expenses such as litigation) will not exceed 1.20%, 1.95% and 1.05% for Class A, Class C and Class I shares, respectively, subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after the fees have been deferred or reimbursed) if such recoupment can be achieved without exceeding the lesser of the expense limitation in effect at the time of the deferral and at the time of the repayment.

5

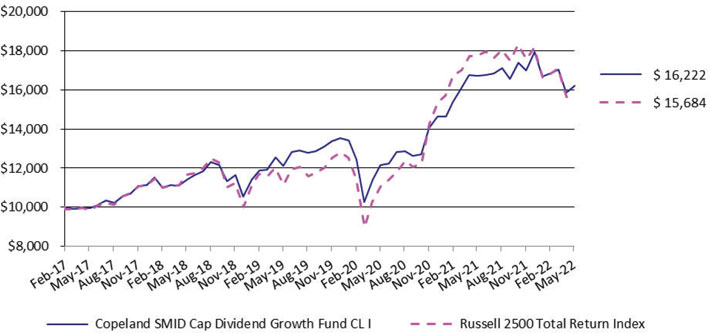

| Copeland SMID Cap Dividend Growth Fund |

| Portfolio Review (Unaudited) |

| February 27, 2017* through May 31, 2022 |

Performance of a $10,000 Investment (as of May 31, 2022)

| Since | Since | ||||

| Total Returns as of | Inception | Inception | |||

| May 31, 2022 | Six Months | One Year | Five Year | Class I * | Class A * |

| Copeland SMID Cap Dividend Growth Fund: | |||||

| Class I | (4.51)% | (3.09)% | 10.29% | 9.64% | — |

| Class A | |||||

| Without sales charge | (4.57)% | (3.34)% | — | — | 10.30% |

| With sales charge + | (10.03)% | (8.89)% | — | — | 8.33% |

| Russell 2500 Total Return Index | (10.72)% | (11.62)% | 9.76% | 8.94% | 10.36% |

| * | Class I shares commenced operations February 27, 2017. Class A commenced operations February 11, 2019 |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The Russell 2500 Total Return Index is comprised of the smallest 2500 companies in the Russell 3000 Index. The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market. Investors cannot invest directly in an index or benchmark.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. The performance and returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or redemption of Fund shares. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. For performance information current to the most recent month-end please call toll-free 1-888-9-COPELAND (1-888-926-7352). Additional information can be found by visiting our website, www.copelandfunds.com. The Fund’s gross annual operating expense ratio, as stated in the current prospectus is 2.10% and 1.87% for Class A and Class I shares, respectively, and its net annual operating expense ratio is 1.20% and 0.95% for Class A and Class I shares, respectively. This ratio can fluctuate and may differ from the expense ratio disclosed in the Financial Highlights section of this report. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, until at least March 31, 2023, to ensure that total annual fund operating expenses after fee deferral and/or reimbursement (exclusive of any taxes, leverage interest, borrowing interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expense on securities sold short, acquired fund fees and expenses or extraordinary expenses such as litigation) will not exceed 1.20% and 0.95% for Class A and Class I shares, respectively, subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after the fees have been deferred or reimbursed) if such recoupment can be achieved without exceeding the lesser of the expense limitation in effect at the time of the deferral and at the time of the repayment.

6

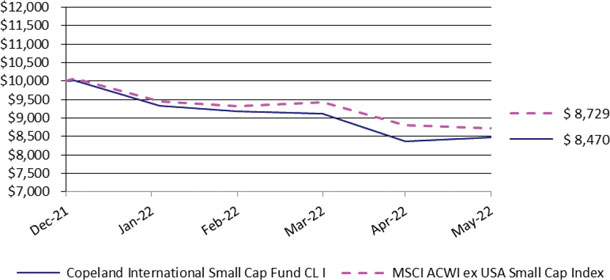

| Copeland International Small Cap Fund |

| Portfolio Review (Unaudited) |

| December 28, 2021* through May 31, 2022 |

Performance of a $10,000 Investment (as of May 31, 2022)

| Total Returns as of | Since |

| May 31, 2022 | Inception* |

| Copeland International Small Cap Fund: | |

| Class I | (15.30)% |

| Class A | |

| Without sales charge | (15.30)% |

| With sales charge + | (20.17)% |

| MSCI ACWI ex USA Small Cap Index | (12.71)% |

| * | The Fund commenced operations December 28, 2021. |

| + | Adjusted for initial maximum sales charge of 5.75%. |

The MSCI ACWI ex USA Small Cap Index captures small cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 24 Emerging Markets (EM) countries*. With 4,332 constituents, the index covers approximately 14% of the global equity opportunity set outside the US.

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. The performance and returns do not reflect the deduction of taxes that a shareholder may pay on Fund distributions or redemption of Fund shares. Total return is calculated assuming reinvestment of all dividends and distributions. Total returns would have been lower had the adviser not waived its fees and reimbursed a portion of the Fund’s expenses. For performance information current to the most recent month-end please call toll-free 1-888-9-COPELAND (1-888-926-7352). Additional information can be found by visiting our website, www.copelandfunds.com. The Fund’s gross annual operating expense ratio, as stated in the current prospectus is 2.27% and 2.12% for Class A and Class I shares, respectively, and its net annual operating expense ratio is 1.23% and 0.98% for Class A and Class I shares, respectively. This ratio can fluctuate and may differ from the expense ratio disclosed in the Financial Highlights section of this report. The Fund’s adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund, until at least March 31, 2023, to ensure that total annual fund operating expenses after fee deferral and/or reimbursement (exclusive of any taxes, leverage interest, borrowing interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expense on securities sold short, acquired fund fees and expenses or extraordinary expenses such as litigation) will not exceed 1.23% and 0.98% for Class A and Class I shares, respectively, subject to possible recoupment from the Fund in future years on a rolling three year basis (within the three years after the fees have been deferred or reimbursed) if such recoupment can be achieved without exceeding the lesser of the expense limitation in effect at the time of the deferral and at the time of the repayment.

7

| COPELAND DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 99.7% | ||||||||

| AEROSPACE & DEFENSE - 1.6% | ||||||||

| 4,058 | Huntington Ingalls Industries, Inc. | $ | 854,047 | |||||

| APPAREL & TEXTILE PRODUCTS - 1.1% | ||||||||

| 5,119 | NIKE, Inc., Class B | 608,393 | ||||||

| ASSET MANAGEMENT - 3.7% | ||||||||

| 2,785 | Ameriprise Financial, Inc. | 769,412 | ||||||

| 955 | BlackRock, Inc. | 638,971 | ||||||

| 8,045 | Hamilton Lane, Inc., Class A | 559,530 | ||||||

| 1,967,913 | ||||||||

| BANKING - 2.8% | ||||||||

| 6,952 | JPMorgan Chase & Company | 919,263 | ||||||

| 12,783 | Truist Financial Corporation | 635,826 | ||||||

| 1,555,089 | ||||||||

| BEVERAGES - 1.5% | ||||||||

| 3,289 | Constellation Brands, Inc., Class A | 807,351 | ||||||

| BIOTECH & PHARMA - 1.2% | ||||||||

| 3,739 | Zoetis, Inc. | 639,107 | ||||||

| CABLE & SATELLITE - 2.5% | ||||||||

| 477 | Cable One, Inc. | 621,579 | ||||||

| 16,284 | Comcast Corporation, Class A | 721,055 | ||||||

| 1,342,634 | ||||||||

| CHEMICALS - 2.4% | ||||||||

| 2,891 | Air Products and Chemicals, Inc. | 711,648 | ||||||

| 2,467 | Sherwin-Williams Company | 661,255 | ||||||

| 1,372,903 | ||||||||

| COMMERCIAL SUPPORT SERVICES - 2.6% | ||||||||

| 6,418 | Insperity, Inc. | 642,249 | ||||||

| 6,312 | Waste Connections, Inc. | 805,033 | ||||||

| 1,447,282 | ||||||||

The accompanying notes are an integral part of these financial statements.

8

| COPELAND DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 99.7% (Continued) | ||||||||

| CONSTRUCTION MATERIALS - 1.4% | ||||||||

| 2,949 | Carlisle Companies, Inc. | $ | 750,314 | |||||

| DATA CENTER REIT - 1.2% | ||||||||

| 982 | Equinix, Inc. | 674,722 | ||||||

| ELECTRIC UTILITIES - 3.0% | ||||||||

| 52,487 | Algonquin Power & Utilities Corporation | 764,211 | ||||||

| 11,458 | NextEra Energy, Inc. | 867,256 | ||||||

| 1,631,467 | ||||||||

| ELECTRICAL EQUIPMENT - 2.3% | ||||||||

| 12,068 | Cognex Corporation | 584,333 | ||||||

| 9,389 | Otis Worldwide Corporation | 698,541 | ||||||

| 1,282,874 | ||||||||

| ENGINEERING & CONSTRUCTION - 1.3% | ||||||||

| 5,285 | Tetra Tech, Inc. | 713,316 | ||||||

| HEALTH CARE FACILITIES & SERVICES - 8.0% | ||||||||

| 1,617 | Chemed Corporation | 783,275 | ||||||

| 12,253 | Encompass Health Corporation | 803,062 | ||||||

| 10,317 | Ensign Group, Inc. (The) | 837,431 | ||||||

| 2,281 | UnitedHealth Group, Inc. | 1,133,154 | ||||||

| 7,359 | US Physical Therapy, Inc. | 828,550 | ||||||

| 4,385,472 | ||||||||

| HOME CONSTRUCTION - 1.3% | ||||||||

| 9,177 | DR Horton, Inc. | 689,652 | ||||||

| HOUSEHOLD PRODUCTS - 0.9% | ||||||||

| 6,489 | Inter Parfums, Inc. | 478,888 | ||||||

| INDUSTRIAL REIT - 1.0% | ||||||||

| 4,084 | Innovative Industrial Properties, Inc. | 543,376 | ||||||

The accompanying notes are an integral part of these financial statements.

9

| COPELAND DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 99.7% (Continued) | ||||||||

| INFRASTRUCTURE REIT - 1.4% | ||||||||

| 3,129 | American Tower Corporation, Class A | $ | 801,431 | |||||

| INSURANCE - 1.6% | ||||||||

| 6,578 | Allstate Corporation (The) | 899,147 | ||||||

| LEISURE FACILITIES & SERVICES - 2.6% | ||||||||

| 4,058 | Churchill Downs, Inc. | 821,461 | ||||||

| 7,320 | Starbucks Corporation | 574,620 | ||||||

| 1,396,081 | ||||||||

| LEISURE PRODUCTS - 1.1% | ||||||||

| 7,957 | Brunswick Corporation | 598,605 | ||||||

| MEDICAL EQUIPMENT & DEVICES - 4.2% | ||||||||

| 3,819 | ResMed, Inc. | 777,014 | ||||||

| 3,527 | Steris plc | 804,861 | ||||||

| 3,077 | Stryker Corporation | 721,557 | ||||||

| 2,303,432 | ||||||||

| OIL & GAS PRODUCERS - 4.6% | ||||||||

| 8,010 | Diamondback Energy, Inc. | 1,217,680 | ||||||

| 4,615 | Pioneer Natural Resources Company | 1,282,693 | ||||||

| 2,500,373 | ||||||||

| PUBLISHING & BROADCASTING - 1.5% | ||||||||

| 4,721 | Nexstar Media Group, Inc., Class A | 827,214 | ||||||

| REAL ESTATE SERVICES - 0.8% | ||||||||

| 33,090 | eXp World Holdings, Inc. | 462,267 | ||||||

| RESIDENTIAL REIT - 1.2% | ||||||||

| 32,117 | UMH Properties, Inc. | 632,384 | ||||||

| RETAIL - CONSUMER STAPLES - 4.3% | ||||||||

| 4,004 | Casey’s General Stores, Inc. | 838,998 | ||||||

| 1,486 | Costco Wholesale Corporation | 692,803 | ||||||

The accompanying notes are an integral part of these financial statements.

10

| COPELAND DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 99.7% (Continued) | ||||||||

| RETAIL - CONSUMER STAPLES - 4.3% (Continued) | ||||||||

| 3,846 | Dollar General Corporation | $ | 847,428 | |||||

| 2,379,229 | ||||||||

| RETAIL - DISCRETIONARY - 4.9% | ||||||||

| 4,031 | Advance Auto Parts, Inc. | 765,325 | ||||||

| 2,016 | Home Depot, Inc. (The) | 610,344 | ||||||

| 13,606 | Monro, Inc. | 645,197 | ||||||

| 11,351 | TJX Companies, Inc. (The) | 721,583 | ||||||

| 2,742,449 | ||||||||

| SEMICONDUCTORS - 6.3% | ||||||||

| 1,777 | Broadcom, Inc. | 1,030,891 | ||||||

| 9,760 | Power Integrations, Inc. | 823,549 | ||||||

| 5,198 | Texas Instruments, Inc. | 918,798 | ||||||

| 5,171 | Universal Display Corporation | 653,149 | ||||||

| 3,426,387 | ||||||||

| SOFTWARE - 3.9% | ||||||||

| 1,459 | Intuit, Inc. | 604,697 | ||||||

| 3,182 | Microsoft Corporation | 865,091 | ||||||

| 10,397 | SS&C Technologies Holdings, Inc. | 665,304 | ||||||

| 2,135,092 | ||||||||

| SPECIALTY FINANCE - 2.8% | ||||||||

| 19,626 | Air Lease Corporation | 738,134 | ||||||

| 7,081 | Discover Financial Services | 803,623 | ||||||

| 1,541,757 | ||||||||

| STEEL - 1.5% | ||||||||

| 4,105 | Reliance Steel & Aluminum Company | 798,012 | ||||||

| TECHNOLOGY HARDWARE - 3.4% | ||||||||

| 6,790 | Apple, Inc. | 1,010,624 | ||||||

| 3,819 | Motorola Solutions, Inc. | 839,187 | ||||||

| 1,849,811 | ||||||||

| TECHNOLOGY SERVICES - 10.9% | ||||||||

| 2,650 | Accenture PLC, Class A | 790,919 | ||||||

| 9,469 | Booz Allen Hamilton Holding Corporation | 813,008 | ||||||

| 4,668 | Broadridge Financial Solutions, Inc. | 682,555 | ||||||

The accompanying notes are an integral part of these financial statements.

11

| COPELAND DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 99.7% (Continued) | ||||||||

| TECHNOLOGY SERVICES - 10.9% (Continued) | ||||||||

| 4,403 | CDW Corporation/DE | $ | 747,894 | |||||

| 7,010 | Fidelity National Information Services, Inc. | 732,545 | ||||||

| 1,989 | S&P Global, Inc. | 695,116 | ||||||

| 9,654 | TTEC Holdings, Inc. | 651,066 | ||||||

| 4,031 | Visa, Inc., Class A | 855,257 | ||||||

| 5,968,360 | ||||||||

| TELECOMMUNICATIONS - 1.3% | ||||||||

| 11,749 | Cogent Communications Holdings, Inc. | 709,522 | ||||||

| TRANSPORTATION & LOGISTICS - 1.6% | ||||||||

| 3,899 | Union Pacific Corporation | 856,922 | ||||||

| TOTAL COMMON STOCKS (Cost $48,839,358) | 54,573,275 | |||||||

| TOTAL INVESTMENTS - 99.7% (Cost $48,839,358) | $ | 54,573,275 | ||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES - 0.3% | 139,550 | |||||||

| NET ASSETS - 100.0% | $ | 54,712,825 | ||||||

| PLC | - Public Limited Company |

| REIT | - Real Estate Investment Trust |

| Portfolio Composition by Sector as of May 31, 2022 | ||||

| Sector | Percent of Net Assets | |||

| Technology | 24.4 | % | ||

| Health Care | 13.4 | % | ||

| Consumer Discretionary | 11.0 | % | ||

| Financials | 10.9 | % | ||

| Industrials | 9.4 | % | ||

| Consumer Staples | 6.7 | % | ||

| Real Estate | 5.7 | % | ||

| Materials | 5.3 | % | ||

| Communications | 5.3 | % | ||

| Energy | 4.6 | % | ||

| Utilities | 3.0 | % | ||

| Other Assets in Excess of Liabilities | 0.3 | % | ||

| Net Assets | 100.0 | % | ||

The accompanying notes are an integral part of these financial statements.

12

| COPELAND SMID CAP DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 98.5% | ||||||||

| AEROSPACE & DEFENSE - 1.2% | ||||||||

| 2,645 | Huntington Ingalls Industries, Inc. | $ | 556,667 | |||||

| ASSET MANAGEMENT - 4.1% | ||||||||

| 8,454 | Cohen & Steers, Inc. | 644,279 | ||||||

| 8,350 | Hamilton Lane, Inc., Class A | 580,743 | ||||||

| 27,955 | Kennedy-Wilson Holdings, Inc. | 588,732 | ||||||

| 1,813,754 | ||||||||

| BANKING - 5.9% | ||||||||

| 18,438 | Bank OZK | 764,624 | ||||||

| 31,663 | Home BancShares, Inc. | 715,267 | ||||||

| 5,809 | Popular, Inc. | 474,653 | ||||||

| 8,921 | Prosperity Bancshares, Inc. | 646,773 | ||||||

| 2,601,317 | ||||||||

| CABLE & SATELLITE - 1.6% | ||||||||

| 545 | Cable One, Inc. | 710,189 | ||||||

| CHEMICALS - 2.0% | ||||||||

| 21,316 | Element Solutions, Inc. | 453,818 | ||||||

| 2,671 | Quaker Chemical Corporation | 417,744 | ||||||

| 871,562 | ||||||||

| COMMERCIAL SUPPORT SERVICES - 5.6% | ||||||||

| 14,756 | ABM Industries, Inc. | 713,453 | ||||||

| 22,587 | GFL Environmental, Inc. | 690,485 | ||||||

| 6,794 | Insperity, Inc. | 679,876 | ||||||

| 2,689 | UniFirst Corporation | 439,490 | ||||||

| 2,523,304 | ||||||||

| CONSTRUCTION MATERIALS - 1.8% | ||||||||

| 3,086 | Carlisle Companies, Inc. | 785,171 | ||||||

| ELECTRIC UTILITIES - 1.7% | ||||||||

| 50,924 | Algonquin Power & Utilities Corporation | 741,453 | ||||||

| ELECTRICAL EQUIPMENT - 3.2% | ||||||||

| 9,569 | BWX Technologies, Inc. | 489,933 | ||||||

The accompanying notes are an integral part of these financial statements.

13

| COPELAND SMID CAP DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 98.5% (Continued) | ||||||||

| ELECTRICAL EQUIPMENT - 3.2% (Continued) | ||||||||

| 4,901 | Cognex Corporation | $ | 237,306 | |||||

| 2,541 | Littelfuse, Inc. | 686,578 | ||||||

| 1,413,817 | ||||||||

| ENGINEERING & CONSTRUCTION - 1.5% | ||||||||

| 4,815 | Tetra Tech, Inc. | 649,881 | ||||||

| FORESTRY, PAPER & WOOD PRODUCTS - 1.5% | ||||||||

| 8,921 | UFP Industries, Inc. | 688,701 | ||||||

| HEALTH CARE FACILITIES & SERVICES - 7.9% | ||||||||

| 1,608 | Chemed Corporation | 778,915 | ||||||

| 10,321 | Encompass Health Corporation | 676,438 | ||||||

| 10,710 | Ensign Group, Inc. (The) | 869,331 | ||||||

| 4,642 | Quest Diagnostics, Inc. | 654,615 | ||||||

| 4,616 | US Physical Therapy, Inc. | 519,715 | ||||||

| 3,499,014 | ||||||||

| HOME CONSTRUCTION - 0.8% | ||||||||

| 9,943 | KB Home | 342,934 | ||||||

| HOUSEHOLD PRODUCTS - 1.3% | ||||||||

| 7,780 | Inter Parfums, Inc. | 574,164 | ||||||

| INDUSTRIAL REIT - 1.0% | ||||||||

| 3,423 | Innovative Industrial Properties, Inc. | 455,430 | ||||||

| INSTITUTIONAL FINANCIAL SERVICES - 0.7% | ||||||||

| 2,853 | Evercore, Inc., Class A | 325,813 | ||||||

| INSURANCE - 1.1% | ||||||||

| 5,186 | Globe Life, Inc. | 505,998 | ||||||

| INTERNET MEDIA & SERVICES - 1.0% | ||||||||

| 7,650 | Shutterstock, Inc. | 460,530 | ||||||

The accompanying notes are an integral part of these financial statements.

14

| COPELAND SMID CAP DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 98.5% (Continued) | ||||||||

| LEISURE FACILITIES & SERVICES - 4.6% | ||||||||

| 3,734 | Churchill Downs, Inc. | $ | 755,873 | |||||

| 1,426 | Domino’s Pizza, Inc. | 517,880 | ||||||

| 8,958 | Travel + Leisure Company | 457,843 | ||||||

| 4,007 | Wingstop, Inc. | 319,198 | ||||||

| 2,050,794 | ||||||||

| LEISURE PRODUCTS - 1.5% | ||||||||

| 9,050 | Brunswick Corporation | 680,832 | ||||||

| MACHINERY - 3.8% | ||||||||

| 2,360 | Nordson Corporation | 514,197 | ||||||

| 2,749 | Snap-on, Inc. | 609,948 | ||||||

| 6,094 | Standex International Corporation | 567,351 | ||||||

| 1,691,496 | ||||||||

| MEDICAL EQUIPMENT & DEVICES - 3.4% | ||||||||

| 14,548 | LeMaitre Vascular, Inc. | 665,135 | ||||||

| 3,812 | Steris plc | 869,898 | ||||||

| 1,535,033 | ||||||||

| OIL & GAS PRODUCERS - 7.6% | ||||||||

| 21,420 | Coterra Energy, Inc. | 735,349 | ||||||

| 4,823 | Diamondback Energy, Inc. | 733,192 | ||||||

| 24,791 | Northern Oil and Gas, Inc. | 810,418 | ||||||

| 6,963 | Oasis Petroleum, Inc. | 1,105,237 | ||||||

| 3,384,196 | ||||||||

| PUBLISHING & BROADCASTING - 1.7% | ||||||||

| 4,361 | Nexstar Media Group, Inc., Class A | 764,134 | ||||||

| REAL ESTATE SERVICES - 1.0% | ||||||||

| 33,090 | eXp World Holdings, Inc. | 462,267 | ||||||

| RESIDENTIAL REIT - 1.4% | ||||||||

| 8,635 | NexPoint Residential Trust, Inc. | 634,500 | ||||||

The accompanying notes are an integral part of these financial statements.

15

| COPELAND SMID CAP DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 98.5% (Continued) | ||||||||

| RETAIL - CONSUMER STAPLES - 1.5% | ||||||||

| 3,112 | Casey’s General Stores, Inc. | $ | 652,088 | |||||

| RETAIL - DISCRETIONARY - 3.9% | ||||||||

| 27,579 | Aaron’s Company, Inc. (The) | 539,445 | ||||||

| 3,345 | Advance Auto Parts, Inc. | 635,082 | ||||||

| 11,799 | Monro, Inc. | 559,509 | ||||||

| 1,734,036 | ||||||||

| SEMICONDUCTORS - 4.7% | ||||||||

| 985 | CMC Materials, Inc. | 174,286 | ||||||

| 13,589 | Kulicke & Soffa Industries, Inc. | 736,116 | ||||||

| 8,532 | Power Integrations, Inc. | 719,930 | ||||||

| 3,700 | Universal Display Corporation | 467,347 | ||||||

| 2,097,679 | ||||||||

| SPECIALTY FINANCE - 1.3% | ||||||||

| 15,793 | Air Lease Corporation | 593,975 | ||||||

| STEEL - 1.8% | ||||||||

| 4,175 | Reliance Steel & Aluminum Company | 811,620 | ||||||

| TECHNOLOGY HARDWARE - 1.1% | ||||||||

| 20,876 | AudioCodes Ltd. | 479,313 | ||||||

| TECHNOLOGY SERVICES - 8.0% | ||||||||

| 2,547 | Booz Allen Hamilton Holding Corporation | 218,685 | ||||||

| 3,579 | Broadridge Financial Solutions, Inc. | 523,321 | ||||||

| 1,668 | FactSet Research Systems, Inc. | 636,810 | ||||||

| 3,475 | Jack Henry & Associates, Inc. | 653,718 | ||||||

| 5,666 | ManTech International Corporation, Class A | 541,953 | ||||||

| 2,079 | Morningstar, Inc. | 534,365 | ||||||

| 6,768 | TTEC Holdings, Inc. | 456,434 | ||||||

| 3,565,286 | ||||||||

| TELECOMMUNICATIONS - 3.0% | ||||||||

| 9,906 | Cogent Communications Holdings, Inc. | 598,223 | ||||||

The accompanying notes are an integral part of these financial statements.

16

| COPELAND SMID CAP DIVIDEND GROWTH FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 98.5% (Continued) | ||||||||

| TELECOMMUNICATIONS - 3.0% (Continued) | ||||||||

| 21,736 | Switch, Inc., Class A | $ | 733,590 | |||||

| 1,331,813 | ||||||||

| TRANSPORTATION & LOGISTICS - 1.4% | ||||||||

| 4,045 | Landstar System, Inc. | 612,534 | ||||||

| TRANSPORTATION EQUIPMENT - 1.6% | ||||||||

| 18,075 | Allison Transmission Holdings, Inc. | 723,181 | ||||||

| WHOLESALE - DISCRETIONARY - 1.3% | ||||||||

| 1,411 | Pool Corporation | 562,453 | ||||||

| TOTAL COMMON STOCKS (Cost $41,931,389) | 43,886,929 | |||||||

| TOTAL INVESTMENTS - 98.5% (Cost $41,931,389) | $ | 43,886,929 | ||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES - 1.5% | 685,535 | |||||||

| NET ASSETS - 100.0% | $ | 44,572,464 | ||||||

| LTD | - Limited Company |

| PLC | - Public Limited Company |

| REIT | - Real Estate Investment Trust |

| Portfolio Composition by Sector as of May 31, 2022 | ||||

| Sector | Percent of Net Assets | |||

| Industrials | 18.3 | % | ||

| Technology | 13.8 | % | ||

| Financials | 13.1 | % | ||

| Consumer Discretionary | 12.0 | % | ||

| Health Care | 11.3 | % | ||

| Energy | 7.6 | % | ||

| Communications | 7.3 | % | ||

| Materials | 7.1 | % | ||

| Real Estate | 3.5 | % | ||

| Consumer Staples | 2.8 | % | ||

| Utilities | 1.7 | % | ||

| Other Assets in Excess of Liabilities | 1.5 | % | ||

| Net Assets | 100.0 | % | ||

The accompanying notes are an integral part of these financial statements.

17

| COPELAND INTERNATIONAL SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 95.8% | ||||||||

| Australia - 1.7% | ||||||||

| 1,608 | Steadfast Group Ltd. | $ | 5,811 | |||||

| Austria - 1.9% | ||||||||

| 128 | BAWAG Group AG(a) | 6,548 | ||||||

| Canada - 13.4% | ||||||||

| 268 | Algonquin Power & Utilities Corporation | 3,898 | ||||||

| 139 | Canadian Apartment Properties Real Estate Investment Trust | 5,439 | ||||||

| 40 | Cargojet, Inc. | 4,706 | ||||||

| 308 | Freehold Royalties Ltd. | 3,823 | ||||||

| 395 | InterRent Real Estate Investment Trust | 4,272 | ||||||

| 86 | Toromont Industries Ltd. | 7,627 | ||||||

| 182 | Tourmaline Oil Corporation | 11,234 | ||||||

| 478 | Whitecap Resources, Inc. | 4,251 | ||||||

| 45,250 | ||||||||

| Cayman Islands - 1.6% | ||||||||

| 10,024 | Bosideng International Holdings, Ltd. | 5,334 | ||||||

| Denmark - 2.1% | ||||||||

| 81 | Royal Unibrew A/S | 7,107 | ||||||

| Finland - 1.3% | ||||||||

| 321 | Tokmanni Group Corporation Ord | 4,257 | ||||||

| France - 6.1% | ||||||||

| 56 | ARGAN S.A. | 6,736 | ||||||

| 89 | Ipsos(a) | 4,323 | ||||||

| 138 | Rubis S.C.A.(a) | 4,178 | ||||||

| 191 | Verallia S.A. | 5,293 | ||||||

| 20,530 | ||||||||

| Germany - 2.7% | ||||||||

| 220 | Hensoldt A.G. | 5,364 | ||||||

| 37 | LEG Immobilien A.G. | 3,813 | ||||||

| 9,177 | ||||||||

The accompanying notes are an integral part of these financial statements.

18

| COPELAND INTERNATIONAL SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 95.8% (Continued) | ||||||||

| Greece - 2.3% | ||||||||

| 511 | OPAP S.A. | $ | 7,627 | |||||

| Hong Kong - 2.7% | ||||||||

| 11,633 | CITIC Telecom International Ho | 3,943 | ||||||

| 1,381 | SITC International Holdings Company, Ltd. | 5,215 | ||||||

| 9,158 | ||||||||

| Italy - 4.8% | ||||||||

| 122 | Interpump Group SpA | 5,576 | ||||||

| 2,081 | Iren SpA(a) | 5,423 | ||||||

| 120 | Recordati SpA | 5,376 | ||||||

| 16,375 | ||||||||

| Japan - 22.6% | ||||||||

| 107 | Fujimi, Inc. | 4,839 | ||||||

| 245 | Fullcast Holdings Company Ltd. | 4,331 | ||||||

| 92 | Hamamatsu Photonics K.K. | 4,285 | ||||||

| 161 | Internet Initiative Japan, Inc. | 5,909 | ||||||

| 93 | JCU Corporation | 2,667 | ||||||

| 1 | Mitsui Fudosan Logistics Park, Inc. | 4,314 | ||||||

| 244 | Nichias Corporation(a) | 4,271 | ||||||

| 360 | NIPPON GAS CO. LTD. | 5,349 | ||||||

| 83 | Nissan Chemical Corporation | 4,666 | ||||||

| 142 | Okinawa Cellular Telephone Company | 5,658 | ||||||

| 65 | Open House Group Company, Ltd. | 2,706 | ||||||

| 227 | SBS Holdings, Inc. | 5,277 | ||||||

| 162 | Shoei Company, Ltd. | 6,037 | ||||||

| 104 | Taiyo Yuden Company Ltd.(a) | 4,240 | ||||||

| 313 | Takeuchi Manufacturing Company, Ltd. | 5,682 | ||||||

| 619 | Zeon Corporation | 6,553 | ||||||

| 76,784 | ||||||||

| Luxembourg - 3.0% | ||||||||

| 73 | Befesa S.A. | 4,861 | ||||||

| 95 | Stabilus S.A. | 5,286 | ||||||

| 10,147 | ||||||||

The accompanying notes are an integral part of these financial statements.

19

| COPELAND INTERNATIONAL SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 95.8% (Continued) | ||||||||

| Netherlands - 1.6% | ||||||||

| 63 | Euronext NV | $ | 5,457 | |||||

| Norway - 1.4% | ||||||||

| 130 | Kongsberg Gruppen ASA | 4,649 | ||||||

| Puerto Rico - 1.3% | ||||||||

| 54 | Popular, Inc. | 4,412 | ||||||

| Spain - 3.3% | ||||||||

| 81 | Laboratorios Farmaceuticos Rovi S.A.(a) | 5,434 | ||||||

| 71 | Vidrala S.A. | 5,669 | ||||||

| 11,103 | ||||||||

| Sweden - 2.7% | ||||||||

| 767 | Arjo AB, B Shares | 5,411 | ||||||

| 388 | Bravida Holding A.B. | 3,738 | ||||||

| 9,149 | ||||||||

| Switzerland - 2.5% | ||||||||

| 60 | Logitech International S.A.(a) | 3,669 | ||||||

| 220 | SIG Combibloc Group AG | 4,807 | ||||||

| 8,476 | ||||||||

| United Kingdom - 13.0% | ||||||||

| 889 | Advanced Medical Solutions Group plc | 3,375 | ||||||

| 398 | Avon Protection plc | 5,850 | ||||||

| 495 | Electrocomponents plc | 6,041 | ||||||

| 43 | Halma plc(a) | 1,208 | ||||||

| 476 | Hilton Food Group plc | 6,518 | ||||||

| 541 | OSB Group plc(a) | 3,539 | ||||||

| 1,075 | RWS Holdings plc | 5,363 | ||||||

| 483 | Unite Group plc | 7,040 | ||||||

| 302 | YouGov plc | 5,233 | ||||||

| 44,167 | ||||||||

| United States - 3.8% | ||||||||

| 105 | Inter Parfums, Inc. | 7,749 | ||||||

The accompanying notes are an integral part of these financial statements.

20

| COPELAND INTERNATIONAL SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Shares | Fair Value | |||||||

| COMMON STOCKS — 95.8% (Continued) | ||||||||

| United States - 3.8% (Continued) | ||||||||

| 94 | Kulicke & Soffa Industries, Inc. | $ | 5,092 | |||||

| 12,841 | ||||||||

| TOTAL COMMON STOCKS (Cost $364,376) | 324,359 | |||||||

| TOTAL INVESTMENTS - 95.8% (Cost $364,376) | $ | 324,359 | ||||||

| OTHER ASSETS IN EXCESS OF LIABILITIES - 4.2% | 14,293 | |||||||

| NET ASSETS - 100.0% | $ | 338,652 | ||||||

| A/S | - Anonim Sirketi |

| LTD | - Limited Company |

| NV | - Naamioze Vennootschap |

| PLC | - Public Limited Company |

| REIT | - Real Estate Investment Trust |

| S/A | - Société Anonyme |

| (a) | The fair value of this security has been determined in good faith under policies adopted by the Board of Trustees. |

| Portfolio Composition by Sector as of May 31, 2022 | ||||

| Sector | Percent of Net Assets | |||

| Industrials | 23.5 | % | ||

| Materials | 10.2 | % | ||

| Real Estate | 9.3 | % | ||

| Technology | 8.4 | % | ||

| Financials | 7.6 | % | ||

| Consumer Staples | 7.8 | % | ||

| Energy | 6.9 | % | ||

| Consumer Discretionary | 6.4 | % | ||

| Health Care | 5.8 | % | ||

| Communications | 5.6 | % | ||

| Utilities | 4.3 | % | ||

| Other Assets in Excess of Liabilities | 4.2 | % | ||

| Net Assets | 100.0 | % | ||

The accompanying notes are an integral part of these financial statements.

21

| COPELAND INTERNATIONAL SMALL CAP FUND |

| SCHEDULE OF INVESTMENTS (Unaudited) (Continued) |

| May 31, 2022 |

| Portfolio Composition by Country as of May 31, 2022 | ||||

| Sector | Percent of Net Assets | |||

| Japan | 22.7 | % | ||

| Canada | 13.4 | % | ||

| Great Britain | 11.0 | % | ||

| France | 7.7 | % | ||

| US | 7.2 | % | ||

| Germany | 5.7 | % | ||

| Italy | 4.8 | % | ||

| Hong Kong | 4.3 | % | ||

| Spain | 3.3 | % | ||

| Sw eden | 2.7 | % | ||

| Sw itzerland | 2.5 | % | ||

| Greece | 2.2 | % | ||

| Denmark | 2.1 | % | ||

| Austria | 1.9 | % | ||

| Australia | 1.7 | % | ||

| Norw ay | 1.4 | % | ||

| Finland | 1.2 | % | ||

| Other Assets in Excess of Liabilities | 4.2 | % | ||

| Net Assets | 100.0 | % | ||

The accompanying notes are an integral part of these financial statements.

22

| Copeland Trust |

| STATEMENTS OF ASSETS AND LIABILITIES (Unaudited) |

| May 31, 2022 |

| Copeland SMID | Copeland | |||||||||||

| Copeland Dividend | Cap Dividend | International | ||||||||||

| Growth Fund | Growth Fund | Small Cap Fund ** | ||||||||||

| Assets: | ||||||||||||

| Investments, at Cost | $ | 48,839,358 | $ | 41,931,389 | $ | 364,376 | ||||||

| Investments in Securities, at Market Value | $ | 54,573,275 | $ | 43,886,929 | $ | 324,359 | ||||||

| Cash | 104,110 | 648,201 | 8,517 | |||||||||

| Foreign Cash (Cost $0, $0, $124) | — | — | 125 | |||||||||

| Dividends and Interest Receivable | 106,360 | 70,068 | 1,041 | |||||||||

| Due from Investment Adviser | 20,975 | — | 25,108 | |||||||||

| Receivable for Fund Shares Sold | — | 7,154 | — | |||||||||

| Prepaid Expenses and Other Assets | 54,578 | 34,761 | — | |||||||||

| Total Assets | 54,859,298 | 44,647,113 | 359,150 | |||||||||

| Liabilities: | ||||||||||||

| Payable for Fund Shares Redeemed | 16,579 | 2,081 | — | |||||||||

| Payable to Investment Adviser | — | 2,336 | — | |||||||||

| Accrued Audit Fees | 29,485 | 22,686 | 5,064 | |||||||||

| Accrued Distribution Fees | 12,701 | 46 | — | |||||||||

| Payable to Related Parties | 39,481 | 33,434 | 6,020 | |||||||||

| Other Accrued Expenses | 48,227 | 14,066 | 9,414 | |||||||||

| Total Liabilities | 146,473 | 74,649 | 20,498 | |||||||||

| Net Assets | $ | 54,712,825 | $ | 44,572,464 | $ | 338,652 | ||||||

| Composition of Net Assets: | ||||||||||||

| At May 31, 2022, Net Assets consisted of: | ||||||||||||

| Paid-in-Capital | $ | 45,034,207 | $ | 41,587,858 | $ | 400,000 | ||||||

| Accumulated Earnings | 9,678,618 | 2,984,606 | (61,348 | ) | ||||||||

| Net Assets | $ | 54,712,825 | $ | 44,572,464 | $ | 338,652 | ||||||

| Class A Shares: | ||||||||||||

| Net Assets | $ | 16,085,103 | $ | 228,483 | $ | 8 | ||||||

| Shares Outstanding (no par value; unlimited number of shares authorized) | 1,319,061 | 16,162 | 1 | |||||||||

| Net Asset Value and Redemption Price Per Share* | $ | 12.19 | $ | 14.14 | $8.47 | + | ||||||

| Offering Price Per Share (NAV/$0.9425) Includes a Maximum Sales Charge of 5.75% | $ | 12.93 | $ | 15.00 | $ | 8.99 | ||||||

| Class C Shares: | ||||||||||||

| Net Assets | $ | 11,172,017 | ||||||||||

| Shares Outstanding (no par value; unlimited number of shares authorized) | 973,382 | |||||||||||

| Net Asset Value, Offering Price and Redemption Price Per Share* | $ | 11.48 | ||||||||||

| Class I Shares: | ||||||||||||

| Net Assets | $ | 27,455,705 | $ | 44,343,981 | $ | 338,644 | ||||||

| Shares Outstanding (no par value; unlimited number of shares authorized) | 2,280,145 | 3,122,757 | 39,999 | |||||||||

| Net Asset Value, Offering Price and Redemption Price Per Share* | $ | 12.04 | $ | 14.20 | $ | 8.47 | ||||||

| * | The Funds charge a 1.00% fee on shares redeemed less than 30 days after purchase or if shares held less than 30 days are redeemed for failure to maintain a balance that meets the minimum requirements listed in the Funds’ Prospectus. |

| ** | Fund commenced operations on December 28, 2021. |

| + | NAV may not recalculate due to rounding. |

The accompanying notes are an integral part of these financial statements.

23

| Copeland Trust |

| STATEMENTS OF OPERATIONS (Unaudited) |

| For the Six Months or Period Ended May 31, 2022 |

| Copeland SMID | Copeland | |||||||||||

| Copeland Dividend | Cap Dividend | International | ||||||||||

| Growth Fund | Growth Fund | Small Cap Fund * | ||||||||||

| Investment Income: | ||||||||||||

| Dividend Income | $ | 537,969 | $ | 421,193 | $ | 5,227 | ||||||

| Interest Income | — | — | 2 | |||||||||

| Less: Foreign Taxes Withholding | (4,567 | ) | (4,222 | ) | (514 | ) | ||||||

| Total Investment Income | 533,402 | 416,971 | 4,715 | |||||||||

| Expenses: | ||||||||||||

| Investment Advisory Fees | 227,536 | 152,360 | 1,174 | |||||||||

| Distribution Fees - Class C | 62,654 | — | — | |||||||||

| Distribution Fees - Class A | 21,599 | 269 | — | |||||||||

| Chief Compliance Officer Fees | 62,055 | 45,810 | 6,965 | |||||||||

| Trustees’ Fees | 42,400 | 24,938 | 4,902 | |||||||||

| Registration & Filing Fees | 39,893 | 23,361 | 770 | |||||||||

| Legal Fees | 36,195 | 21,585 | 3,927 | |||||||||

| Administration Fees | 33,485 | 23,411 | 9,380 | |||||||||

| Fund Accounting Fees | 23,884 | 17,761 | 12,764 | |||||||||

| Shareholder Service Fees - Class I | 12,346 | 3,041 | — | |||||||||

| Transfer Agent Fees | 12,104 | 15,956 | 2,184 | |||||||||

| Custody Fees | 11,074 | 3,649 | 2,110 | |||||||||

| Audit Fees | 9,802 | 7,686 | 5,064 | |||||||||

| Insurance Expense | 9,363 | 3,574 | — | |||||||||

| Printing Expense | 9,247 | 2,494 | 1,266 | |||||||||

| Non-Rule 12b-1 Shareholder Service Fees | 5,466 | 1,372 | 308 | |||||||||

| Miscellaneous Expenses | 2,897 | 2,202 | 1,716 | |||||||||

| Total Expenses | 622,000 | 349,469 | 52,530 | |||||||||

| Less: Fees Waived by Adviser | (227,536 | ) | (152,360 | ) | (1,174 | ) | ||||||

| Less: Other Expenses Reimbursed by Adviser | (6,914 | ) | (3,613 | ) | (49,885 | ) | ||||||

| Net Expenses | 387,550 | 193,496 | 1,471 | |||||||||

| Net Investment Income | 145,852 | 223,475 | 3,244 | |||||||||

| Net Realized and Unrealized Gain (Loss) on Investments and | ||||||||||||

| Foreign Currency Transactions: | ||||||||||||

| Net Realized Gain (Loss) on: | ||||||||||||

| Securities | 3,909,360 | 870,675 | (24,361 | ) | ||||||||

| Foreign Currency Transactions | — | — | (194 | ) | ||||||||

| 3,909,360 | 870,675 | (24,555 | ) | |||||||||

| Net Change in Unrealized Appreciation (Depreciation) on: | ||||||||||||

| Securities | (7,827,852 | ) | (2,972,125 | ) | (40,017 | ) | ||||||

| Foreign Currency Transactions | — | — | (20 | ) | ||||||||

| (7,827,852 | ) | (2,972,125 | ) | (40,037 | ) | |||||||

| Net Realized and Unrealized Loss on Investments and Foreign Currency Transactions: | (3,918,492 | ) | (2,101,450 | ) | (64,592 | ) | ||||||

| Net Decrease in Net Assets Resulting From Operations | $ | (3,772,640 | ) | $ | (1,877,975 | ) | $ | (61,348 | ) | |||

| * | Fund commenced operations on December 28, 2021. |

The accompanying notes are an integral part of these financial statements.

24

| Copeland Dividend Growth Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| For the | For the | |||||||

| Six Months Ended | Year Ended | |||||||

| May 31, 2022 | November 30, 2021 | |||||||

| (Unaudited) | ||||||||

| Operations: | ||||||||

| Net Investment Income | $ | 145,852 | $ | 141,972 | ||||

| Net Realized Gain on Investments | 3,909,360 | 9,117,466 | ||||||

| Net Change in Unrealized Appreciation (Depreciation) on investments | (7,827,852 | ) | 4,104,961 | |||||

| Net Increase (Decrease) in Net Assets Resulting From Operations | (3,772,640 | ) | 13,364,399 | |||||

| Distributions to Shareholders From: | ||||||||

| Total Distributions Paid | ||||||||

| Class A | (2,057,408 | ) | — | |||||

| Class C | (1,592,846 | ) | — | |||||

| Class I | (3,889,176 | ) | — | |||||

| Total Distributions to Shareholders | (7,539,430 | ) | — | |||||

| Beneficial Interest Transactions: | ||||||||

| Class A | ||||||||

| Proceeds from Shares Issued | 759,360 | 627,282 | ||||||

| Distributions Reinvested | 1,889,194 | — | ||||||

| Cost of Shares Redeemed | (1,640,843 | ) | (4,967,290 | ) | ||||

| Total Class A Shares | 1,007,711 | (4,340,008 | ) | |||||

| Class C | ||||||||

| Proceeds from Shares Issued | 7,604 | 83,941 | ||||||

| Distributions Reinvested | 1,568,803 | — | ||||||

| Cost of Shares Redeemed | (1,533,431 | ) | (4,690,002 | ) | ||||

| Redemption Fees | 4 | 25 | ||||||

| Total Class C Shares | 42,980 | (4,606,036 | ) | |||||

| Class I | ||||||||

| Proceeds from Shares Issued | 12,441 | 1,578,477 | ||||||

| Distributions Reinvested | 3,820,604 | — | ||||||

| Cost of Shares Redeemed | (4,059,397 | ) | (11,161,338 | ) | ||||

| Total Class I Shares | (226,352 | ) | (9,582,861 | ) | ||||

| Total Beneficial Interest Transactions | 824,339 | (18,528,905 | ) | |||||

| Decrease in Net Assets | (10,487,731 | ) | (5,164,506 | ) | ||||

| Net Assets: | ||||||||

| Beginning of Period | 65,200,556 | 70,365,062 | ||||||

| End of Period | $ | 54,712,825 | $ | 65,200,556 | ||||

| Share Activity: | ||||||||

| Class A | ||||||||

| Shares Issued | 58,981 | 49,937 | ||||||

| Distributions Reinvested | 139,424 | — | ||||||

| Shares Redeemed | (127,424 | ) | (370,466 | ) | ||||

| Total Activity Class A Shares | 70,981 | (320,529 | ) | |||||

| Class C | ||||||||

| Shares Issued | 632 | 6,508 | ||||||

| Distributions Reinvested | 122,563 | — | ||||||

| Shares Redeemed | (126,465 | ) | (373,185 | ) | ||||

| Total Activity Class C Shares | (3,270 | ) | (366,677 | ) | ||||

| Class I | ||||||||

| Shares Issued | 893 | 119,888 | ||||||

| Distributions Reinvested | 285,759 | — | ||||||

| Shares Redeemed | (322,576 | ) | (856,138 | ) | ||||

| Total Activity Class I Shares | (35,924 | ) | (736,250 | ) | ||||

The accompanying notes are an integral part of these financial statements.

25

| Copeland SMID Cap Dividend Growth Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| For the | For the | |||||||

| Six Months Ended | Year Ended | |||||||

| May 31, 2022 | November 30, 2021 | |||||||

| (Unaudited) | ||||||||

| Operations: | ||||||||

| Net Investment Income | $ | 223,475 | $ | 208,194 | ||||

| Net Realized Gain on Investments | 870,675 | 2,227,730 | ||||||

| Net Change in Unrealized Appreciation (Depreciation) on Investments | (2,972,125 | ) | 2,614,025 | |||||

| Net Increase (Decrease) in Net Assets Resulting From Operations | (1,877,975 | ) | 5,049,949 | |||||

| Distributions to Shareholders From: | ||||||||

| Total Distributions Paid | ||||||||

| Class A | (13,327 | ) | (283 | ) | ||||

| Class I | (2,360,113 | ) | (95,606 | ) | ||||

| Total Distributions to Shareholders | (2,373,440 | ) | (95,889 | ) | ||||

| Beneficial Interest Transactions: | ||||||||

| Class A | ||||||||

| Proceeds from Shares Issued | 32,013 | 74,799 | ||||||

| Distributions Reinvested | 13,327 | 282 | ||||||

| Cost of Shares Redeemed | — | — | ||||||

| Redemption Fees | 7 | 10 | ||||||

| Total Class A Shares | 45,347 | 75,091 | ||||||

| Class I | ||||||||

| Proceeds from Shares Issued | 13,218,472 | 17,596,082 | ||||||

| Distributions Reinvested | 2,131,974 | 88,162 | ||||||

| Cost of Shares Redeemed | (2,380,553 | ) | (9,072,094 | ) | ||||

| Redemption Fees | 1,265 | 2,222 | ||||||

| Total Class I Shares | 12,971,158 | 8,614,372 | ||||||

| Total Beneficial Interest Transactions | 13,016,505 | 8,689,463 | ||||||

| Increase in Net Assets | 8,765,090 | 13,643,523 | ||||||

| Net Assets: | ||||||||

| Beginning of Period | 35,807,374 | 22,163,851 | ||||||

| End of Period | $ | 44,572,464 | $ | 35,807,374 | ||||

| Share Activity: | ||||||||

| Class A | ||||||||

| Shares Issued | 2,243 | 4,790 | ||||||

| Distributions Reinvested | 869 | 21 | ||||||

| Total Activity Class A Shares | 3,112 | 4,811 | ||||||

| Class I | ||||||||

| Shares Issued | 905,400 | 1,162,033 | ||||||

| Distributions Reinvested | 138,530 | 6,492 | ||||||

| Shares Redeemed | (163,634 | ) | (598,801 | ) | ||||

| Total Activity Class I Shares | 880,296 | 569,724 | ||||||

The accompanying notes are an integral part of these financial statements.

26

| Copeland International Small Cap Fund |

| STATEMENT OF CHANGES IN NET ASSETS |

| For the | ||||

| Period Ended | ||||

| May 31, 2022 * | ||||

| (Unaudited) | ||||

| Operations: | ||||

| Net Investment Income | $ | 3,244 | ||

| Net Realized Loss on Investments and Foreign Currency Transactions | (24,555 | ) | ||

| Net Change in Unrealized Depreciation on Investments and Foreign Currency Transactions | (40,037 | ) | ||

| Net Decrease in Net Assets Resulting From Operations | (61,348 | ) | ||

| Beneficial Interest Transactions: | ||||

| Class A | ||||

| Proceeds from Shares Issued | 10 | |||

| Total Class A Shares | 10 | |||

| Class I | ||||

| Proceeds from Shares Issued | 399,990 | |||

| Total Class I Shares | 399,990 | |||

| Total Beneficial Interest Transactions | 400,000 | |||

| Increase in Net Assets | 338,652 | |||

| Net Assets: | ||||

| Beginning of Period | — | |||

| End of Period | $ | 338,652 | ||

| Share Activity: | ||||

| Class A | ||||

| Shares Issued | 1 | |||

| Total Activity Class A Shares | 1 | |||

| Class I | ||||

| Shares Issued | 39,999 | |||

| Total Activity Class I Shares | 39,999 | |||

| * | Fund commenced operations on December 28, 2021. |

The accompanying notes are an integral part of these financial statements.

27

| Copeland Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout each year/period presented.

| Class A | ||||||||||||||||||||||||

| Six Months | Year | Year | Year | Year | Year | |||||||||||||||||||

| Ended | Ended | Ended | Ended | Ended | Ended | |||||||||||||||||||

| May 31, 2022 | November 30, 2021 | November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017 | |||||||||||||||||||

| (Unaudited) | ||||||||||||||||||||||||

| Net Asset Value, Beginning of Year/Period | $ | 14.59 | $ | 11.99 | $ | 14.25 | $ | 15.18 | $ | 14.38 | $ | 12.27 | ||||||||||||

| Increase (Decrease) From Operations: | ||||||||||||||||||||||||

| Net investment income (a) | 0.04 | 0.04 | 0.01 | 0.10 | 0.04 | 0.06 | ||||||||||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.78 | ) | 2.56 | (0.48 | ) | 0.05 | 1.38 | 2.51 | ||||||||||||||||

| Other capital changes | — | — | 0.73 | (d) | — | — | — | |||||||||||||||||

| Total from operations | (0.74 | ) | 2.60 | 0.26 | 0.15 | 1.42 | 2.57 | |||||||||||||||||

| Distributions to shareholders from: | ||||||||||||||||||||||||

| Net investment income | (0.02 | ) | — | (0.09 | ) | (0.01 | ) | (0.03 | ) | (0.09 | ) | |||||||||||||

| Net realized gains | (1.64 | ) | — | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | |||||||||||||

| Total distributions | (1.66 | ) | — | (2.52 | ) | (1.08 | ) | (0.62 | ) | (0.46 | ) | |||||||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||

| Net Asset Value, End of Year/Period | $ | 12.19 | $ | 14.59 | $ | 11.99 | $ | 14.25 | $ | 15.18 | $ | 14.38 | ||||||||||||

| Total Return (c) | (6.22 | )% (f) | 21.68 | % | 2.24 | % | 1.32 | % | 10.33 | % | 21.63 | % | ||||||||||||

| Ratios/Supplemental Data | �� | |||||||||||||||||||||||

| Net assets, end of year/period (in 000’s) | $ | 16,085 | $ | 18,212 | $ | 18,800 | $ | 36,870 | $ | 52,779 | $ | 64,666 | ||||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||||||

| before reimbursement | 1.98 | % (e) | 1.93 | % | 2.13 | % | 1.74 | % | 1.71 | % | 1.82 | % | ||||||||||||

| net of reimbursement | 1.20 | % (e) | 1.20 | % | 1.44 | % | 1.45 | % | 1.45 | % | 1.45 | % | ||||||||||||

| Ratio of net investment income to average net assets | 0.57 | % (e) | 0.29 | % | 0.10 | % | 0.70 | % | 0.28 | % | 0.47 | % | ||||||||||||

| Portfolio turnover rate | 21 | % (f) | 34 | % | 170 | % | 244 | % | 30 | % | 27 | % | ||||||||||||

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. Sales loads are not reflected in total return. |

| (d) | As required by SEC standard per share data calculation methodology, this represents a balancing figure derived from the other amounts in the financial highlights tables that captures all other changes affecting net asset value per share. |

| (e) | Annualized. |

| (f) | Not Annualized. |

The accompanying notes are an integral part of these financial statements.

28

| Copeland Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout each year/period presented.

| Class C | ||||||||||||||||||||||||

| Six Months | Year | Year | Year | Year | Year | |||||||||||||||||||

| Ended | Ended | Ended | Ended | Ended | Ended | |||||||||||||||||||

| May 31, 2022 | November 30, 2021 | November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017 | |||||||||||||||||||

| (Unaudited) | ||||||||||||||||||||||||

| Net Asset Value, Beginning of Year/Period | $ | 13.85 | $ | 11.47 | $ | 13.73 | $ | 14.76 | $ | 14.06 | $ | 12.01 | ||||||||||||

| Increase (Decrease) From Operations: | ||||||||||||||||||||||||

| Net investment loss (a) | (0.01 | ) | (0.06 | ) | (0.07 | ) | (0.01 | ) | (0.07 | ) | (0.04 | ) | ||||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.72 | ) | 2.44 | (0.30 | ) | 0.05 | 1.36 | 2.46 | ||||||||||||||||

| Other capital changes | — | — | 0.54 | (d) | — | — | — | |||||||||||||||||

| Total from operations | (0.73 | ) | 2.38 | 0.17 | 0.04 | 1.29 | 2.42 | |||||||||||||||||

| Distributions to shareholders from: | ||||||||||||||||||||||||

| Net investment income | — | — | — | — | — | — | ||||||||||||||||||

| Net realized gains | (1.64 | ) | — | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | |||||||||||||

| Total distributions | (1.64 | ) | — | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | |||||||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||

| Net Asset Value, End of Year/Period | $ | 11.48 | $ | 13.85 | $ | 11.47 | $ | 13.73 | $ | 14.76 | $ | 14.06 | ||||||||||||

| Total Return (c) | (6.50 | )% (f) | 20.75 | % | 1.51 | % | 0.54 | % | 9.55 | % | 20.68 | % | ||||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||||||

| Net assets, end of year/period (in 000’s) | $ | 11,172 | $ | 13,530 | $ | 15,401 | $ | 25,271 | $ | 32,597 | $ | 35,487 | ||||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||||||

| before reimbursement | 2.73 | % (e) | 2.69 | % | 2.88 | % | 2.49 | % | 2.45 | % | 2.57 | % | ||||||||||||

| net of reimbursement | 1.95 | % (e) | 1.95 | % | 2.19 | % | 2.20 | % | 2.20 | % | 2.20 | % | ||||||||||||

| Ratio of net investment loss to average net assets | (0.19 | )% (e) | (0.46 | )% | (0.67 | )% | (0.05 | )% | (0.46 | )% | (0.28 | )% | ||||||||||||

| Portfolio turnover rate | 21 | % (f) | 34 | % | 170 | % | 244 | % | 30 | % | 27 | % | ||||||||||||

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (d) | As required by SEC standard per share data calculation methodology, this represents a balancing figure derived from the other amounts in the financial highlights tables that captures all other changes affecting net asset value per share. |

| (e) | Annualized. |

| (f) | Not Annualized. |

The accompanying notes are an integral part of these financial statements.

29

| Copeland Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout each year/period presented.

| Class I | ||||||||||||||||||||||||

| Six Months | Year | Year | Year | Year | Year | |||||||||||||||||||

| Ended | Ended | Ended | Ended | Ended | Ended | |||||||||||||||||||

| May 31, 2022 | November 30, 2021 | November 30, 2020 | November 30, 2019 | November 30, 2018 | November 30, 2017 | |||||||||||||||||||

| (Unaudited) | ||||||||||||||||||||||||

| Net Asset Value, Beginning of Year/Period | $ | 14.45 | $ | 11.85 | $ | 14.12 | $ | 15.08 | $ | 14.30 | $ | 12.24 | ||||||||||||

| Increase (Decrease) From Operations: | ||||||||||||||||||||||||

| Net investment income (a) | 0.04 | 0.06 | 0.03 | 0.11 | 0.07 | 0.08 | ||||||||||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.76 | ) | 2.54 | (0.38 | ) | 0.06 | 1.37 | 2.49 | ||||||||||||||||

| Other capital changes | — | — | 0.63 | (d) | — | — | — | |||||||||||||||||

| Total from operations | (0.72 | ) | 2.60 | 0.28 | 0.17 | 1.44 | 2.57 | |||||||||||||||||

| Distributions to shareholders from: | ||||||||||||||||||||||||

| Net investment income | (0.05 | ) | — | (0.12 | ) | (0.06 | ) | (0.07 | ) | (0.14 | ) | |||||||||||||

| Net realized gains | (1.64 | ) | — | (2.43 | ) | (1.07 | ) | (0.59 | ) | (0.37 | ) | |||||||||||||

| Total distributions | (1.69 | ) | — | (2.55 | ) | (1.13 | ) | (0.66 | ) | (0.51 | ) | |||||||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||||||||

| Net Asset Value, End of Year/Period | $ | 12.04 | $ | 14.45 | $ | 11.85 | $ | 14.12 | $ | 15.08 | $ | 14.30 | ||||||||||||

| Total Return (c) | (6.16 | )% (f) | 21.94 | % | 2.40 | % | 1.43 | % | 10.56 | % | 21.72 | % | ||||||||||||

| Ratios/Supplemental Data | ||||||||||||||||||||||||

| Net assets, end of year/period (in 000’s) | $ | 27,456 | $ | 33,459 | $ | 36,164 | $ | 66,649 | $ | 81,516 | $ | 75,097 | ||||||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||||||||||

| before reimbursement | 1.81 | % (e) | 1.75 | % | 1.98 | % | 1.58 | % | 1.53 | % | 1.57 | % | ||||||||||||

| net of reimbursement | 1.05 | % (e) | 1.05 | % | 1.29 | % | 1.30 | % | 1.30 | % | 1.30 | % | ||||||||||||

| Ratio of net investment income to average net assets | 0.70 | % (e) | 0.44 | % | 0.23 | % | 0.85 | % | 0.45 | % | 0.62 | % | ||||||||||||

| Portfolio turnover rate | 21 | % (f) | 34 | % | 170 | % | 244 | % | 30 | % | 27 | % | ||||||||||||

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the year/period. |

| (b) | Less than $0.01 per share. |

| (c) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. Had the Adviser not absorbed a portion of fund expenses, the total return would have been lower. |

| (d) | As required by SEC standard per share data calculation methodology, this represents a balancing figure derived from the other amounts in the financial highlights tables that captures all other changes affecting net asset value per share. |

| (e) | Annualized. |

| (f) | Not Annualized. |

The accompanying notes are an integral part of these financial statements.

30

| Copeland SMID Cap Dividend Growth Fund |

| FINANCIAL HIGHLIGHTS |

Certain information in the table below reflects financial results for one share of beneficial interest outstanding throughout the year/period presented.

| Class A | ||||||||||||||||

| Six Months | Year | Year | Period | |||||||||||||

| Ended | Ended | Ended | Ended | |||||||||||||

| May 31, 2022 | November 30, 2021 | November 30, 2020 | November 30, 2019 | * | ||||||||||||

| (Unaudited) | ||||||||||||||||

| Net Asset Value, Beginning of Year/Period | $ | 15.80 | $ | 13.14 | $ | 12.73 | $ | 11.10 | ||||||||

| Increase (Decrease) From Operations: | ||||||||||||||||

| Net investment income (a) | 0.06 | 0.06 | 0.10 | 0.10 | ||||||||||||

| Net gain (loss) from securities (both realized and unrealized) | (0.71 | ) | 2.63 | 0.50 | 1.53 | |||||||||||

| Total from operations | (0.65 | ) | 2.69 | 0.60 | 1.63 | |||||||||||

| Distributions to shareholders from: | ||||||||||||||||

| Net investment income | (0.04 | ) | (0.03 | ) | (0.05 | ) | — | |||||||||

| Net realized gains | (0.97 | ) | — | (0.14 | ) | — | ||||||||||

| Total distributions | (1.01 | ) | (0.03 | ) | (0.19 | ) | — | |||||||||

| Redemption fees (b) | 0.00 | 0.00 | 0.00 | 0.00 | ||||||||||||

| Net Asset Value, End of Year/Period | $ | 14.14 | $ | 15.80 | $ | 13.14 | $ | 12.73 | ||||||||

| Total Return (c) | (4.57 | )% (e) | 20.55 | % | 4.73 | % | 14.68 | % (e) | ||||||||

| Ratios/Supplemental Data | ||||||||||||||||

| Net assets, end of year/period (in 000’s) | $ | 228 | $ | 206 | $ | 108 | $ | 34 | ||||||||

| Ratio of expenses to average net assets: | ||||||||||||||||

| before reimbursement | 1.96 | % (d) | 2.10 | % | 2.72 | % | 3.04 | % (d) | ||||||||

| net of reimbursement | 1.20 | % (d) | 1.20 | % | 1.20 | % | 1.20 | % (d) | ||||||||

| Ratio of net investment income to average net assets | 0.83 | % (d) | 0.42 | % | 0.87 | % | 0.82 | % (d) | ||||||||

| Portfolio turnover rate | 14 | % (e) | 35 | % | 49 | % | 22 | % (e) | ||||||||

| * | Class A commenced operations on February 11, 2019. |

| (a) | Per share amounts are calculated using the average shares method, which more appropriately presents the per share data for the period/year. |

| (b) | Less than $0.01 per share. |