MainGate MLP Fund

Class A (AMLPX)

Class C (MLCPX)

Class I (IMLPX)

6075 Poplar Avenue, Suite 720 | Memphis, TN 38119 | 855.MLP.FUND (855.657.3863) | www.maingatefunds.com

Annual Report

November 30, 2023

ANNUAL REPORT 2023 ● 3

Table of Contents

MainGate mlp fund

Dear Shareholder,

The MainGate MLP Fund (“Fund”) had the following average annual total returns for its fiscal year ended November 30, 2023 compared to the S&P 500 Index and the Alerian MLP Total Return Index.

| | | Inception | | 1 | | 5 | | 10 | | Since |

| | | Date | | Year | | Year | | Year | | Inception |

| MainGate MLP Fund – Class A without load | | 2/17/11 | | 17.62% | | 9.93% | | 2.77% | | 4.83% |

| MainGate MLP Fund – Class A with 5.75% maximum front-end load | | 2/17/11 | | 10.89% | | 8.63% | | 2.17% | | 4.35% |

| MainGate MLP Fund – Class I | | 2/17/11 | | 17.90% | | 10.19% | | 3.02% | | 5.09% |

| S&P 500 Index | | 2/17/11 | | 13.84% | | 12.51% | | 11.82% | | 12.23% |

| Alerian MLP Total Return Index | | 2/17/11 | | 23.29% | | 10.33% | | 2.29% | | 4.63% |

| MainGate MLP Fund – Class C without load | | 3/31/14 | | 16.83% | | 9.08% | | –– | | 1.21% |

| MainGate MLP Fund – Class C with 1.00% Contingent Deferred Sales Charge | | 3/31/14 | | 15.83% | | 9.08% | | –– | | 1.21% |

| S&P 500 Index | | 3/31/14 | | 13.84% | | 12.51% | | –– | | 11.75% |

| Alerian MLP Total Return Index | | 3/31/14 | | 23.29% | | 10.33% | | –– | | 2.01% |

Expense Ratios (Gross/Net): A Shares = 3.15%/3.14% | C Shares = 3.90%/3.89% | I Shares = 2.90%/2.89%. Gross and net expense ratios represent the percentages paid by investors and reflect a 1.41% deferred income tax expense which represents the performance impact of accrued deferred tax liabilities across the Fund, not individual share classes, for the fiscal year ended November 30, 2023 (the Fund had $0 in current tax expense and $10,861,413 in deferred tax expense). The Fund’s adviser has contractually agreed to cap the Fund’s total annual operating expenses (excluding brokerage fees and commissions; Class A 12b-1 fees; borrowing costs; taxes, such as Deferred Income Tax Expense; and extraordinary expenses) at 1.50% through March 31, 2025. The performance data shown For Class C with load reflects the Class C maximum deferred sales charge of 1.00%. Deferred income tax expense/(benefit) represents an estimate of the Fund’s potential tax expense/(benefit) if it were to recognize the unrealized gains/(losses) in the portfolio. An estimate of deferred income tax expense/(benefit) depends upon the Fund’s net investment income/(loss) and realized and unrealized gains/(losses) on its portfolio, which may vary greatly on a daily, monthly and annual basis depending on the nature of the Fund’s investments and their performance. An estimate of deferred income tax expenses/(benefit) cannot be reliably predicted from year to year.

The performance data quoted represents past performance. Past performance is no guarantee of future results. The investment return and the principal value of an investment will fluctuate and shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the information quoted. To obtain performance information current to the most recent month-end please call 855.MLP.FUND (855.657.3863). Performance data shown for Class A shares with load reflects the maximum sales charge of 5.75%. Performance data shown for Class C shares with load reflects the maximum deferred sales charge of 1.00%. Performance data shown for Class I shares does not reflect the deduction of a sales load or fee. Performance data shown “Without Load” does not reflect the deduction of the sales load or fee. If reflected, the load or fee would reduce the performance quoted.

ANNUAL REPORT 2023 ● 5

Happy New Year from MainGate!

Midstream Energy securities, measured by the Alerian MLP TR Index (AMZX)1, delivered an outstanding +26.6% total return for 2023*. This total return compares to the S&P 500 TR index (SPXT)2 which posted a +26.2% return driven primarily by concentrated outperformance of less than 10 names, and the S&P 500 Energy Sector3 which delivered a -0.7% total return in line with the market’s inability to extrapolate commodity prices into long-term value. The Midstream sector continues to stand out for its consistent performance and positive backdrop for fundamentals, attractive valuation4, and potential for increased cash returns to investors as we start 2024.

We continue to stand by our call that Midstream equities are de-coupling from WTI crude oil prices, which were down -10.7% in 2023. While this divergence with more recent history rhymes with the 2000-2011 period where the AMZX outperformed both the commodity and the SPXT, we believe there are a few other factors supporting our thoughts. First, the cash flow5 accruing to Midstream is more fee-based, contracted, and non-cyclical versus any other period in history. Second, with balance sheets in strong shape, the outlook for increased cash returns through dividend growth and equity repurchases is clear for investors, which gives the sector the ability to provide downside volatility protection when things go bump in the night. We highlighted the buyback potential for readers in our Q3:23 newsletter. Our updated analysis which accounts for index changes shows the AMZX constituents could potentially repurchase $67+ billion in equity through 2030, equating to nearly 92% of the total market capitalization – even higher if you float-adjust the shares outstanding6.

2024 outlook

Investing outlook

Our sector outlook is for another year of consistent cash flow performance, upside to cash returns, and increasing fundamental momentum going into what we see as a positive 2025.

Looking at the fund’s portfolio consensus expectations are for 7% adjusted DCF/u growth. Due to still high-versus-history coverage ratios of nearly 3.0x (DCF/u divided by paid distributions/dividends), we expect dividend/ distribution growth of ~10% using sellside consensus estimates. Combining yield7 plus growth factors yields a competitive range of total return. We believe there could be additional total return momentum generated through buybacks similar to the past 3 years8. Compared to the AMZX, consensus expects a 7.6% yield, 6% adjusted DCF/u growth, 2.1x coverage and 3.4% distribution growth.

If your information universe includes sellside research report(s), you have noticed their 2024 outlooks indicate a more cautious tone based on some combination of weak commodity forecasts for 1H:24, strong 2023 total returns, blips in new basin volumetric growth, or other idiosyncratic factors. Take heart, long-term investor; if these reasons for caution prove to be accurate, we believe this is an increased opportunity for you. First, we’re already staking the claim that commodity price performance is showing lower correlation to the AMZX, but admit it can bubble up for periods of time. Long term, we believe, capital returns from companies will outweigh short term periods of higher commodity price correlation9.

Second, we remind allocators of the trailing 3 year performance effect for asset classes, positively and negatively. Few institutional allocators, in our experience, buy at the bottom, instead they are more likely to wait until the “coast is clear”. When comparing to the AMZX trailing annualized 3 year total return of +32.4% to other asset classes, we struggle to find other asset classes comparing more favorably.

(unaudited)

*With the exception of the Fund returns on the previous page, all performance throughout this Shareholder Letter is based on the 2023 calendar year.

(1) Alerian MLP Index: A capitalization-weighted index of the most prominent energy Master Limited Partnerships. Visit http://www.alerian.com/indices/amz-index for more information, including performance. You cannot invest directly in an index. (2) S&P 500: A free-float capitalization-weighted index published since 1957 of the prices of 500 large-cap common stocks actively traded in the United States. (3) S&P 500 Energy Sector: The S&P 500® Energy comprises those companies included in the S&P 500 that are classified as members of the GICS® energy sector. (4) Valuation: The process of determining the current worth of an asset or a company. (5) Cash Flow: A measurement of the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income. (6) Actual share/unit repurchase may vary significantly. (7) Yield: Refers to the interest or dividends received from a security and is usually expressed annually as a percentage based on the investment’s cost, its current market value or its face value. (8) See footnote 6. (9) Correlation: The measure of the relationship between two data sets of variables.

6 | MainGate mlp fund

Annualized Returns as of 12/31/23

| Index | 5 Year | 3 Year | 1 Year |

| Alerian MLP Total Return Index | 12.03% | 32.43% | 26.56% |

| Alerian North American Midstream TR Index | 12.76% | 24.25% | 14.02% |

| S&P GSCI Total Return Index | 8.72% | 19.18% | -4.27% |

| Bloomberg WTI Cushing Crude Oil | 9.55% | 13.88% | -10.73% |

| S&P 500 Total Return Index | 15.69% | 10.00% | 26.29% |

| DJIA Total Return Index | 12.47% | 9.38% | 16.18% |

| MSCI World | 12.80% | 7.27% | 23.79% |

| NASDAQ | 18.81% | 6.07% | 44.70% |

| FTSE NAREIT Total Return Index | 7.59% | 5.70% | 11.36% |

| RUSSELL 2000 | 9.94% | 2.19% | 16.88% |

Still, giving credit to the market always seeking a forward-looking view, the sector’s attractive current valuation plus a strong outlook for cash returns through the end of the decade could push more institutions to “discover” the role Midstream can play in their portfolio (we try to assist on this topic in a latter section).

In short, we don’t see many reasons to be cautious regarding 2024 security performance beyond the normal respect for markets, geopolitics, interest rates and normal macro concerns.

Fundamental outlook

Midstream assets remain full, balance sheets remain strong, capital spending remains disciplined, and returns on invested capital (ROIC)10 continue to improve, at least for most companies. Energy commodity prices will behave, as always, depending on their markets, and our price outlook is not that different from consensus. We still expect commodity price performance to have little to do with Midstream security performance like 2023.

The consensus is for WTI crude oil to average $8011, which is moderately positive for producers, consistently positive for Midstreamers (full pipes, storage, docks, etc.), and good for consumers as well. This will likely keep natural gas liquids (NGLs) at similar levels to today, but because NGLs have to “price-to-clear”, opportunities should remain strong for Midstream companies to clip as many fees along their integrated value chains as possible.

Natural gas could have the most interesting performance in 2024 and deserves a bit more discussion. Winter thus far has turned out warmer than expectations pulling down current prices, and lowering the forward strip through the end of the year due to the associated build up in gas storage. However, current power demand growth of 5% Y/Y is tracking well above historical growth of less than 1%. In addition, to remind our readers, there is ~6 billion cubic feet per day (Bcf/d) of liquefied natural gas (LNG) export capacity coming online in 2025 with the potential for some facilities to arrive sooner in 2024. This could potentially add another ~6% of growth to current demand on the way towards sustaining an above average trend growth due to the addition of more LNG terminals through the end of the decade.

All this capacity growth creates, in industry verbiage, a “giant sucking sound” from global markets for secure, reliable, and clean natural gas. Midstream companies have been rapidly building cost efficient gas infrastructure such as intrastate pipelines, interconnects between pipelines, low-cost capacity expansions, gas storage capacity, etc. to serve this growth and should benefit from the increased utilization as well as potentially some marketing activities due to the higher logistical needs to get natural gas from anywhere to the U.S. Gulf Coast. In short, natural gas prices could have a bumpy year in 2024, but we believe they are setting up for a robust 2025, which the market may try to extrapolate sooner given the visibility to higher 2025 demand.

(unaudited)

(10) Return on Invested Capital: A return from an investment that is not considered income. (11) Reuters, “Slow demand set to keep oil price near $80/b in 2024”, 12/29/23.

ANNUAL REPORT 2023 ● 7

Energy sector investing thoughts

A recent analysis we did showed professional asset managers increased their allocation to Energy securities through 2023, but it was mostly passive to match the S&P 500 Energy sector, which potentially left them with losses, re-referencing the sector’s -0.7% total return. This was confirmed by analyzing the 30 largest open end mutual funds representing $2 trillion in assets under management (AUM) through September 30, 2023, showing the total capital was allocated 4.4% in total versus the S&P weight of 4.7%12. This is not really what we would call commitment.

Our point to all managers is you may have been investing in “Energy” but were you really aligning your investment process with your own analysis? Diving deeper into the index, was the generic investor consciously investing 76% into Exploration & Production (E&P)13, 9% to Midstream, 9% to Services and 6% to Refining? Focusing just on E&P and Midstream, if this same investor just split their allocation 50/50 between the E&P and Midstream constituents in the index (14 and 4, respectively) the return could have increased to a higher return. Applying active management with Midstream could potentially have boosted the return.

Obviously, Midstream’s return this year shows those investors using this as part of their energy allocation potentially outperformed those who were less active. But we believe investors are still thinking actively about Midstream and the role it can play in both their Energy and broader portfolio goals. Beyond retaining an attractive total return outlook, the sector presents a potentially lower risk, non-cyclical cash flow model, and is sufficiently large capitalization in nature for greater institutional adoption.

Referring back to our commodity price outlook, a virtually unchanged commodity price picture in 2024 is not terribly inspiring for production companies’ equity prices. Investors continue to demand producing companies return more capital than invest in growth, and expect excess commodity profits to be returned through dividend growth, special dividends, and buybacks. If there is not much growth in capital returns expected in 2024, other than corporate actions creating pockets of outperformance, we expect sentiment towards these companies to be fairly neutral. On the other hand, commodity prices are expected to remain consistent due to continued increases in production, which should keep Midstream companies’ assets well-utilized on primarily fee-based assets. This should allow them to return capital through dividend and distribution growth, and increased equity buybacks in addition to their strong yields. If history is an analog, equity prices should follow increased returns as investors continue to reward consistency of cash flow and capital return growth.

Midstream is a large capitalization space that should increasingly be appreciated by institutional investors. We looked at all U.S.-listed Energy companies (including Canadian companies with ADRs) with market capitalizations above $20 billion, and of the 33 companies, 12 are Midstream. That number drops to 8 when you exclude Master Limited Partnerships (MLPs) that are restricted in their eligibility for the S&P 500 or broader market-bench-marked funds, which are limited in their ability to own pass through entities. Therefore, these funds generally just exclude MLPs from their investment universe. However, investors who allocate capital instead through managers who can own Midstream companies regardless of tax status, primarily dedicated managers such as MainGate, remain an incremental source of funds – this is most of the people reading this newsletter, whether invested or not.

There continues to be encouraging signs of institutional receptivity, and the aforementioned 3 year numbers could be an important signal in 2024 to increase activity.

The capital return story is only beginning. Total returns could potentially follow these capital returns, and it is not inconceivable large allocators could increasingly embrace a low cash flow volatility, large capitalization sector through dedicated managers. That seems like a more realistic active approach to managing an Energy allocation beyond blind passivity.

(unaudited)

(12) Morningstar, 12/13/23. (13) Exploration & Production (E&P): The finding, augmenting, producing and merchandising of different types of oil and gas.

8 | MainGate mlp fund

Learnings from 2023

From our perspective, 2023 represented a year where balance began to return to the global energy discussion. The conversation amongst policy makers has absolutely switched to “it’s going to take everything (traditional and green/clean)”, while still preparing for green energy to take an increasing share of the growth of energy demand.

Topics we continue to monitor include:

| ● | Europe’s energy supply remains a year-to-year situation. |

| ● | Interest in Europe is shifting from green financing to embracing transition financing, which focuses on decarbonization and existing use for traditional fuels14. |

| ● | Higher interest rates have increased certain clean projects untenable return levels for many developers. |

| ● | State and local pushback to renewables development only pushes out clean energy objectives. This too has increased the cost of capital15 from a timeline perspective. |

| ● | Traditional energy companies can play an increasing role in energy transition goals. |

As students of market history, long term trends can be accurate, but mania around stock prices can indicate change is going to happen quicker than the general populace believes – until it doesn’t. Traditional energy equity investment has clearly been hampered by sentiment around electric vehicle (EV) companies and clean energy/energy transition companies since 2020. But the unwinding of stock prices for many of these companies in 2023 may also indicate investing in traditional energy equities has less sentimental pressure, particularly if you’re not facing the daily barrage of optimistic news stories of premature death.

Looking at EVs first, pundits have used their increased adoption rates to presume the imminent death of internal combustion engine (ICE) vehicles, and therefore imply not just peak but declining gasoline consumption. This narrative is increasingly being discredited. One example is the International Energy Agency (IEA)16 giving up on its assertion that peak consumption occurred in 2019, admitting 2024 won’t be the peak either, and they’re now not sure when the peak will be17. We can also look at the discreet example of Norway to see a real time example of EV sales penetration and the effect on oil demand. It’s estimated EVs were 83% of all new vehicle sales in 2023 (aided by strong government incentives), yet oil consumption has been essentially flat at 225 thousand barrels per day (MBpd) since 2020 as the decline in gasoline has been offset by increased consumption of diesel and other gas liquids18. Our research shows EVs’ effect on gasoline consumption will be mostly driven by the uptake in new EV vehicle sales in China and Western Europe, each driven by different objectives. China wants to decrease its reliance on oil, shifting more cars to the grid, which it can power with coal. Western European nations are driven by climate alarmism and are heavily subsidized or mandated. Even in aggressive growth scenarios for these two economies, we still see oil growth through the end of the decade.

The U.S. on the other hand is seeing the potential for slower growth in its EV adoption rate. Automakers are increasingly stuck with inventory, back-tracking from electric to hybrid19, or replacing expiring, government EV rebates by financing them on their own balance sheets (huh?!)20. In short, the U.S. will have little effect on gasoline growth estimates in the medium term, but weaker sentiment around EV adoption could provide at least a neutral backdrop for traditional energy companies.

The unwinding of energy transition stock prices is yet another example. This year they were exposed as construction stocks with unpredictable revenue and profitability masquerading as growth stocks with limitless total addressable markets (TAM). Investors may believe something in their minds (or hearts!), but they vote with their money. The S&P Global Clean Energy Index21 (SPGTCLNT) 2023 performance is indicative of “ask questions later”.

(unaudited)

(14) Bloomberg, LP “Transition Finance Takes Center Stage in 2024”, 1/3/24. (15) Cost of Capital: The cost of funds used for financing a business. (16) International Energy Agency (IEA): An autonomous organization which works to ensure reliable, affordable and clean energy for its 29 member countries and beyond. IEA’s four main areas of focus are: energy security, economic development, environmental awareness, and engagement worldwide. (17) Bloomberg, LP “The Peak in Gasoline Demand Turns Out to Be a Mirage”, 12/27/23. (18) Morgan Stanley, “The Cracking TImes”, 1/3/24. (19) Electrek, “Ford Will Follow Toyota As It Leans Into Hybrids, Scaling Back EV Targets”, 12/28/23. (20) Reuters, “GM Offers $7,500 Incentive for EVs Losing US Tax Credit”, 1/3/24. (21) The S&P Global Clean Energy Index provides liquid and tradable exposure to 30 companies from around the world that are involved in clean energy related businesses. The index is comprised of a diversified mix of Clean Energy Production and Clean Energy Equipment & Technology companies.The S&P Global Clean Energy Index is part of the S&P Global Thematic Indices. The series is designed to provide liquid exposure to emerging investment themes of water, clean energy and infrastructure that cut across traditional industry definitions and geographical boundaries. The series incorporates a unique selection and weighting scheme that provides diversified and tradable exposure for these themes.

ANNUAL REPORT 2023 ● 9

SPGTCLNT

But we’re not here to continue to throw dirt on a category of securities that may succeed at doing that on their own, with the spike the last 2 months of 2023 merely attributable to lower interest rate projections rather than an improvement in fundamentals. Many of these companies may re-emerge with different business models, which could make them more attractive to long term investors, no different than an online book seller in 1999 now accounting for 29% of web traffic for the two weeks before Christmas22. Our point is when investors recalibrate their macro viewpoints and express them through stocks, the case has to be made for a re-engagement of investor interest in traditional energy stocks.

Conclusion

Thank you to our investors. We have enjoyed the past year engaging with you and thank you for your continued trust in us as we embark on 2024. As always, we are happy to take a deeper dive on any of the topics mentioned in this quarter’s newsletter, or other thoughts you may have.

Sincerely,

|  |

| Geoffrey P. Mavar, Chairman | Matthew G. Mead, CEO |

(unaudited)

(22) Bloomberg, LP “Amazon Captured 29% of Online Orders Before Christmas”, 1/4/24.

10 | MainGate mlp fund

(unaudited)

Chickasaw Capital Management, LLC gives no guarantees with respect to the success of its investment management services and has not authorized any person to represent or guarantee any particular investment results. Any historical data provided herein are solely for the purpose of illustrating past performance and not as a representation or prediction that such performance could or will be achieved in the future. Securities are subject to numerous risks, including market, currency, economic, political and business risks. Investments in securities will not always be profitable, and investors may lose money, including principal. Past performance is no guarantee of future results. This is not an offer or solicitation with respect to the purchase or sale of any security.

Chickasaw Capital Management, LLC does not provide legal, tax or accounting advice. Any statement contained in this communication concerning U.S. tax matters is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties imposed on the relevant taxpayer. Clients of Chickasaw Capital Management, LLC should obtain their own independent tax advice based on their particular circumstances. Opinions expressed are current opinions as of the date appearing in this material only. No part of this material may be copied, photocopied or duplicated in any form, by any means, or redistributed without the prior written consent of Chickasaw Capital Management, LLC.

Mutual fund investing involves risk. Principal loss is possible. The Fund is nondiversified, meaning it may concentrate its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund.

The Fund will invest in Master Limited Partnerships (MLPs) which concentrate investments in the natural resource sector and are subject to the risks of energy prices and demand and the volatility of commodity investments. Damage to facilities and infrastructure of MLPs may significantly affect the value of an investment and may incur environmental costs and liabilities due to the nature of their business. MLPs are subject to significant regulation and may be adversely affected by changes in the regulatory environment.

MLPs are subject to certain risks inherent in the structure of MLPs, including complex tax structure risks, limited ability for election or removal of management, limited voting rights, potential dependence on parent companies or sponsors for revenues to satisfy obligations, and potential conflicts of interest between partners, members and affiliates. When the Fund invests in MLPs that operate energy-related businesses, its return on investment will be highly dependent on energy prices, which can be highly volatile.

Tax Risks

An investment in the Fund does not receive the same tax advantages as a direct investment in the MLP. The Fund is treated as a regular corporation or “C” corporation and is therefore subject to U.S. federal income tax on its taxable income at rates applicable to corporations (currently at a rate of 21%) as well as state and local income taxes. MLP Funds accrue deferred income taxes for future tax liabilities associated with the portion of MLP distributions considered to be a tax -deferred return of capital and for any net operating gains as well as capital appreciation of its investments. This deferred tax liability is reflected in the daily NAV and as a result the MLP Fund’s after- tax performance could differ significantly from the underlying assets even if the pre-tax performance is closely tracked. The potential tax benefits from investing in MLPs depend on them being treated as partnerships for federal income tax purposes. If the MLP is deemed to be a corporation then its income would be subject to federal taxation, reducing the amount of cash available for distribution to the Fund which could result in a reduction of the Fund’s value.

Investments in smaller companies involve additional risks, such as limited liquidity and greater volatility. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time (each, an “index”) are provided for your information only. Reference to this index does not imply that the portfolio will achieve returns, volatility or other results similar to the index. The composition of the index may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change over time. Indices are unmanaged. The figures for the indices do not reflect the deduction of any fees or expenses which would reduce returns. Investors cannot invest directly in indices.

The Alerian MLP Index is a composite of the most prominent energy Master Limited Partnerships that provides investors with an unbiased, comprehensive benchmark for this emerging asset class. The index, which is calculated using a float-adjusted, capitalization-weighted methodology, is disseminated real-time on a price-return basis (NYSE: AMZ), and the corresponding total-return index is disseminated daily (NYSE: AMZX). Relevant data points such as dividend yield are also published daily. For index values, constituents, and announcements regarding constituent changes, please visit www.alerian.com.

“Alerian MLP Index”, “AlerianMLP Total Return Index”, “AMZ” and “AMZX” are service marks of GKD Index Partners, LLC d/b/a Alerian (“Alerian”) and their use is granted under a license from Alerian.

Alerian does not guarantee the accuracy and/or completeness of the Alerian MLP Index or any data included therein and Alerian shall have no liability for any errors, omissions, interruptions or defects therein. Alerian makes no warranty, express or implied, representations or promises, as to results to be obtained by Licensee, or any other person or entity from the use of the Alerian MLP Index or any data included therein. Alerian makes no express or implied warranties, representations or promises, regarding the originality, merchantability, suitability, non-infringement, or fitness for a particular purpose or use with respect to the Alerian MLP Index or any data included therein. Without limiting any of the foregoing, in no event shall Alerian have any liability for any indirect, special, incidental, or consequential damages (including lost profits), arising out of the Alerian MLP Index or any data included therein, even if notified of the possibility of such damages.

Alerian North American Midstream TR Index: The Alerian Midstream Energy Index is a broad-based composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return (AMNA), total-return (AMNAX), net total-return (AMNAN), and adjusted net total-return (AMNTR) basis.

DJIA Total Return Index: Tracks the total return of The Dow Jones Industrial Average, a price-weighted average of 30 significant stocks traded on the New York Stock Exchange and the Nasdaq. Dividends are reinvested. The DJIA was invented by Charles Dow back in 1896.

The Energy MLP Classification Standard (“EMCS”) was developed by and is the exclusive property (and a service mark) of GKD Index Partners, LLC d/b/a Alerian (“Alerian”) and its use is granted under a license from Alerian. Alerian makes no warranties, express or implied, or representations with respect to such standard or classification (or the results to be obtained by the use thereof), and hereby expressly disclaims all warranties of originality, accuracy, completeness, merchantability, suitability, non-infringement, or fitness for a particular purpose with respect to any such standard or classification. No warranty is given that the standard or classification will conform to any description thereof or be free of omissions, errors, interruptions, or defects. Without limiting any of the foregoing, in no event shall Alerian have any liability for any indirect, special, incidental, or consequential damages (including lost profits), arising out of any such standard or classification, even if notified of the possibility of such damages.

FTSE NAREIT US Real Estate Total Return Index Series: Tracks the total return of the FTSE NAREIT US Real Estate Index Series which is designed to present investors with a comprehensive family of REIT performance indexes that spans the commercial real estate space across the US economy. Dividends are reinvested. The index series provides investors with exposure to all investment and property sectors. In addition, the more narrowly focused property sector and sub-sector indexes provide the facility to concentrate commercial real estate exposure in more selected markets.

MSCI World Total Return Index: Tracks the total return of the MSCI World Index, a market capitalization weighted index designed by Morgan Stanley Capital International to track the overall performance of commodity producers throughout the world. Dividends are reinvested. Stocks in the MSCI All Country World Commodity Producers Sector Capped Index are primarily focused on emerging market economies.

NASDAQ: A market-capitalization weighted index of the more than 3,000 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks. The index includes all Nasdaq listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debentures.

Russell 2000: An index measuring the performance approximately 2,000 small-cap companies in the Russell 3000 Index, which is made up of 3,000 of the biggest U.S. stocks. The Russell 2000 serves as a benchmark for small-cap stocks in the United States.

S&P 500 Energy comprises those companies included in the S&P 500 that are classified as members of the GICS® energy sector.

ANNUAL REPORT 2023 ● 11

S&P 500 Total Return Index tracks the total return of the S&P 500 Index, an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. Dividends are reinvested. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe.

S&P GSCI Total Return Index: Tracks the total return of the S&P GSCI, a composite index of commodity sector returns representing an unleveraged, long-only investment in commodity futures that is broadly diversified across the spectrum of commodities. Dividends are reinvested. The returns are calculated on a fully collateralized basis with full reinvestment.

Bloomberg WTI Cushing Crude Oil: West Texas Intermediate (WTI), also known as Texas light sweet, is a grade of crude oil used as a benchmark in oil pricing. This grade is described as light because of its relatively low density, and sweet because of its low sulfur content. It is the underlying commodity of Chicago Mercantile Exchange’s oil futures contracts.

Cash Flow is a revenue or expense stream that changes a cash account over a given period. Cash inflows usually arise from one of three activities - financing, operations or investing – although this also occurs as a result of donations or gifts in the case of personal finance. Cash outflows result from expenses or investments. This holds true for both business and personal finance. Cash flow can be attributed to a specific project, or to a business as a whole. Cash flow can be used as an indication of a company’s financial strength.

Correlation measures the extent of linear association of two variables.

Distributable Cash Flow (DCF) is calculated as net income plus depreciation and other noncash items, less maintenance capital expenditure requirements. Distributable cash flow (DCF) data is CCM calculated consensus of Wall Street estimates. The estimated consensus weighted average distributable cash flow (DCF) per unit growth rate for the AMZ and the fund’s portfolio incorporates market expectations by using the average annual growth rate using rolling-forward 24-month data. DCF growth rate is not a forecast of the portfolio’s future performance. DCF growth rate for the portfolio’s holdings does not guarantee a corresponding increase in the market value of the holding or the portfolio.

Distribution Coverage Ratio is calculated as cash available to limited partners divided by cash distributed to limited partners. It gives an indication of an MLP’s ability to make dividend payments to limited partner investors from operating cash flows. MLPs with a coverage ratio of in excess of 1.0 times are able to meet their dividend payments without external financing.

Distributions are quarterly payments, similar to dividends, made to Limited Partner (LP) and General Partner (GP) investors. These amounts are set by the GP and are supported by an MLP’s operating cash flows.

EBITDA is earnings before interest rates taxes depreciation and amortization.

Enterprise Value (EV) measures a company’s total value, often used as a more comprehensive alternative to market capitalization. EV includes in its calculation the market capitalization of a company but also short-term and long-term debt and any cash or cash equivalents on the company’s balance sheet.

EV/EBITDA is a ratio used to determine the value of a company. The enterprise multiple looks at a firm as a potential acquirer would, because it takes debt into account – an item which other multiples like the P/E ratio do not include. Enterprise multiple is calculated as: Enterprise multiple = EV/EBITDA.

Growth Capital Expenditures or Growth CapEx or GCX refers to the aggregate of all capital expenditures undertake to further growth prospects and/or expand operations and excludes any maintenance and regulatory capital expenditures.

iShares Global Clean Energy ETF: Tracks the investment results of an index composed of global equities in the clean energy sector.

Return on Invested Capital (ROIC) is the amount of money a company makes that is above the average cost it pays for its debt and equity capital. ROIC is used to assess a company’s efficiency at allocating the capital under its control to profitable investments. ROIC = EBIT (1 - Tax rate) / (Total Assets – Total Liabilities).

West Texas Intermediate (WTI), also known as Texas light sweet, is a grade of crude oil used as a benchmark in oil pricing. This grade is described as light because of its relatively low density, and sweet because of its low sulfur content. It is the underlying commodity of Chicago Mercantile Exchange’s oil futures contracts.

Yield refers to the cash dividend or distribution divided by the share or unit price at a particular point in time.

This material is provided for informational and educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell any security, product or service.

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

Investment Advisor: Chickasaw Capital Management, LLC | 6075 Poplar Avenue, Memphis, Tennessee 38119 | p 901.537.1866 or 800.743.5410, f 901.537.1890 | info@chickasawcap.com Portfolio Managers: Geoffrey P. Mavar, Principal | Matthew G. Mead, Principal

Earnings Growth is not a measure of the Fund’s future performance.

Distributed by Quasar Distributors, LLC.

12 | MainGate mlp fund

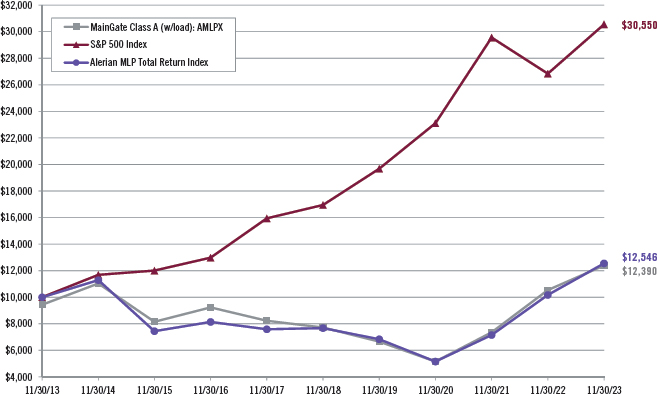

Hypothetical Growth of a $10,000 Investment | unaudited

This chart illustrates the performance of a hypothetical $10,000 investment made in Class A shares (w/load) during the time period shown.

Assumes reinvestment of dividends and capital gains. This chart does not imply any future performance.

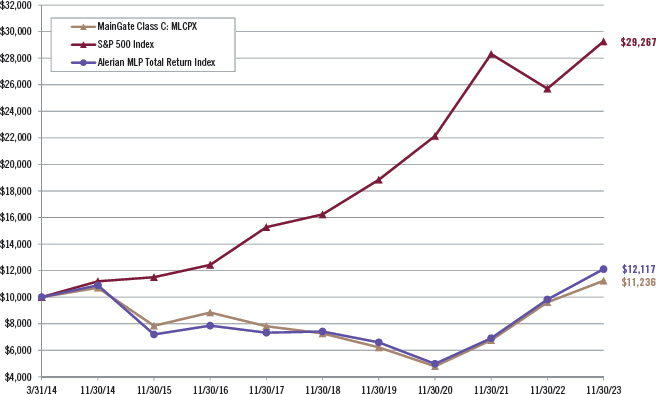

Hypothetical Growth of a $10,000 Investment | unaudited

This chart illustrates the performance of a hypothetical $10,000 investment made in Class C shares during the time period shown.

Assumes reinvestment of dividends and capital gains. This chart does not imply any future performance.

ANNUAL REPORT 2023 ● 13

Hypothetical Growth of a $1,000,000 Investment | unaudited

This chart illustrates the performance of a hypothetical $1,000,000 investment made in Class I shares during the time period shown.

Assumes reinvestment of dividends and capital gains. This chart does not imply any future performance.

Average Annual Returns | November 30, 2023 | unaudited

| | | 1 Year | | 5 Year | | 10 Year | | Since Inception | | Inception Date |

| Class A (without sales load) | | 17.62% | | 9.93% | | 2.77% | | 4.83% | | 2/17/11 |

| Class A (with sales load) | | 10.89% | | 8.63% | | 2.17% | | 4.35% | | 2/17/11 |

| Class C | | 16.83% | | 9.08% | | NA | | 1.21% | | 3/31/14 |

| Class C (with CDSC) | | 15.83% | | 9.08% | | NA | | 1.21% | | 3/31/14 |

| Class I | | 17.90% | | 10.19% | | 3.02% | | 5.09% | | 2/17/11 |

| S&P 500 Index | | 13.84% | | 12.51% | | 11.82% | | 12.23% | | 2/17/11 |

| S&P 500 Index | | 13.84% | | 12.51% | | NA | | 11.75% | | 3/31/14 |

| Alerian MLP Total Return Index | | 23.29% | | 10.33% | | 2.29% | | 4.63% | | 2/17/11 |

| Alerian MLP Total Return Index | | 23.29% | | 10.33% | | NA | | 2.01% | | 3/31/14 |

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855.MLP.FUND (855.657.3863) or by visiting www.maingatefunds.com.

Returns shown are calculated using the net asset values (“NAV’s”) that were used for shareholder transactions as of the respective period ends. These NAV’s, and the returns calculated from them, may differ from the NAV’s and returns shown elsewhere in this report.

Class A (with sales load) performance reflects the maximum sales charge of 5.75%. Class C (with CDSC) performance reflects the 1.00% contingent deferred sales charge. Class I is not subject to a sales charge or CDSC.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. The Alerian MLP Total Return Index is a capped, float-adjusted, capitaliziation-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities.

You cannot invest directly in an index.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of the Fund shares.

14 | MainGate mlp fund

Expense Example | unaudited

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested dividends, or other distributions; and exchange fees; and (2) ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the six-month period from June 1, 2023 to November 30, 2023.

Actual Expenses

For each class, the table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class, the second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expense you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or exchange fees. Therefore, the second line of the table for each class is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transaction costs were included, your costs would have been higher.

| | | | Actual Expenses | | Hypothetical Expenses | | | |

| | | | | | | | | | | | | |

| | Beginning

Account Value

(06/01/23) | | Ending

Account Value

(11/30/23) | | Expenses Paid

During Period (a)

(06/01/23–11/30/23) | | Ending

Account Value

(11/30/23) | | Expenses Paid

During Period (a)

(06/01/23–11/30/23) | | Net Annualized

Expense Ratio (b) | |

| | | | | | | | | | | | | |

| Class A | $1,000.00 | | $1,214.20 | | $9.71 | | $1,016.29 | | $8.85 | | 1.75% | |

| Class C | $1,000.00 | | $1,209.30 | | $13.85 | | $1,012.53 | | $12.61 | | 2.50% | |

| Class I | $1,000.00 | | $1,215.30 | | $8.33 | | $1,017.55 | | $7.59 | | 1.50% | |

| (a) | Expenses are calculated using each Fund’s annualized expense ratios for each class of shares, multiplied by the average account value for the period, then multiplying the actual number of days in the period (183), and then dividing that result by the actual number of days in the fiscal year (365). |

| (b) | Net annualized expense ratio excludes current and deferred federal income and state tax expenses, as applicable. |

ANNUAL REPORT 2023 ● 15

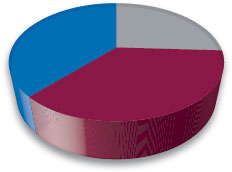

Allocation of Portfolio Assets

November 30, 2023 | unaudited

(expressed as a percentage of total investments)

Natural Gas Gathering/Processing* Natural Gas Gathering/Processing* | 38.0% |

Natural Gas/Natural Gas Liquid Pipelines and Storage* Natural Gas/Natural Gas Liquid Pipelines and Storage* | 35.9% |

Crude/Refined Products Pipelines and Storage* Crude/Refined Products Pipelines and Storage* | 26.1% |

*Master Limited Partnerships and Related Companies

Schedule of Investments | November 30, 2023

| Master Limited Partnerships and Related Companies - 100.0%(1) | | Shares | | | Fair Value | |

| Crude/Refined Products Pipelines and Storage - 26.0%(1) | | | | | | |

| Canada - 0.3%(1) | | | | | | |

| Enbridge, Inc. | | 70,000 | | | $2,440,900 | |

| United States - 25.7%(1) | | | | | | |

| Genesis Energy, L.P. | | 1,675,000 | | | 21,038,000 | |

| MPLX, L.P. | | 2,575,000 | | | 93,884,500 | |

| Phillips 66 | | 68,000 | | | 8,764,520 | |

| Plains All American Pipeline, L.P. | | 2,175,000 | | | 34,539,000 | |

| Plains GP Holdings, L.P. | | 2,895,000 | | | 46,783,200 | |

| | | | | | 205,009,220 | |

| Total Crude/Refined Products Pipelines and Storage | | | | | 207,450,120 | |

| | | | | | | |

| Natural Gas/Natural Gas Liquid Pipelines and Storage - 35.9%(1) | | | | | | |

| United States - 35.9%(1) | | | | | | |

| Cheniere Energy, Inc. | | 185,000 | | | 33,697,750 | |

| DT Midstream, Inc. | | 75,000 | | | 4,296,750 | |

| Energy Transfer, L.P. | | 6,891,250 | | | 95,719,463 | |

| Enterprise Products Partners, L.P. | | 2,413,000 | | | 64,620,140 | |

| Kinder Morgan, Inc. | | 419,000 | | | 7,361,830 | |

| ONEOK, Inc. | | 900,000 | | | 61,965,000 | |

| Williams Companies, Inc. | | 500,000 | | | 18,395,000 | |

| Total Natural Gas/Natural Gas Liquid Pipelines and Storage | | | | | 286,055,933 | |

| | | | | | | |

| Natural Gas Gathering/Processing - 38.0%(1) | | | | | | |

| United States - 38.0%(1) | | | | | | |

| Antero Midstream Corporation | | 605,000 | | | 8,058,600 | |

| Enlink Midstream, LLC | | 6,500,000 | | | 88,855,000 | |

| Kinetik Midstream, LLC | | 103,000 | | | 3,745,080 | |

| Targa Resources Corporation | | 1,100,000 | | | 99,495,000 | |

| Western Midstream Partners, L.P. | | 3,450,000 | | | 102,879,000 | |

| Total Natural Gas Gathering/Processing | | | | | 303,032,680 | |

| | | | | | | |

| Total Master Limited Partnerships and Related Companies (Cost $295,597,820) | | | | | 796,538,733 | |

| Total Investments - 99.9% (Cost $295,597,820)(1) | | | | | 796,538,733 | |

| Other Assets in Excess of Liabilities - 0.1%(1) | | | | | 1,046,664 | |

| Net Assets - 100.0%(1) | | | | | $797,585,397 | |

(1) Calculated as a percentage of net assets.

| 16 | MainGate mlp fund | The accompanying notes are an integral part of the financial statements. | |

Statement of Assets and Liabilities

November 30, 2023

| Assets | |

| Investments at fair value (cost $295,597,820) | $796,538,733 |

| Cash(1) | 12,789,970 |

| Receivable for Fund shares sold | 306,001 |

| Dividends receivable | 175,686 |

| Prepaid expenses | 80,583 |

| Total assets | 809,890,973 |

| Liabilities | |

| Deferred Tax Liability | 10,861,413 |

| Payable for Fund shares redeemed | 262,931 |

| Payable to Adviser(2) | 768,973 |

| Payable for 12b-1 distribution fee(2) | 48,412 |

| Payable to Trustees | 24,000 |

| Payable to Custodian(2) | 7,641 |

| Accrued expenses and other liabilities | 332,206 |

| Total liabilities | 12,305,576 |

| Net assets | $797,585,397 |

| Net Assets Consist of | |

| Paid-in capital | $910,132,853 |

| Total distributable earnings (loss), net of deferred taxes | (112,547,456) |

| Net assets | $797,585,397 |

(1) Credit Risk (See Note 4)

(2) Agreements and Related Party Transactions (See Note 5)

| Unlimited shares authorized, no par value | Class A | Class C | Class I |

| Net assets | $39,131,546 | $20,654,614 | $737,799,237 |

| Shares issued and outstanding | 5,087,830 | 2,937,032 | 90,923,783 |

| Net asset value, redemption price and minimum offering price per share | $7.69 | $7.03 | $8.11 |

| Maximum offering price per share (Net asset value/0.9425) | $8.16 | NA | NA |

Statement of Operations

Year Ended November 30, 2023

| Investment Income | |

| Distributions received from master limited partnerships | $44,647,228 |

| Less: return of capital on distributions from master limited partnerships | (44,647,228) |

| Distribution income received in excess of return of capital from master limited partnerships | — |

| Dividends from common stock(3,4) | 7,147,925 |

| Total Investment Income | 7,147,925 |

(3) The return of capital amount from C-Corporations was $1,552,039. (See Note 2)

(4) Net of foreign withholding tax of $36,401.

| Expenses | |

| Advisory fees(2) | 9,649,617 |

| Administrator fees(2) | 543,776 |

| Professional fees | 495,827 |

| Insurance expense | 228,270 |

| Transfer agent expense(2) | 199,595 |

| Reports to shareholders | 147,073 |

| Trustees’ fees | 96,000 |

| Compliance fees | 77,161 |

| Registration fees | 75,627 |

| Custodian fees and expenses(2) | 46,285 |

| Fund accounting fees(2) | 1,013 |

| 12b-1 distribution fee - Class A(2) | 88,368 |

| 12b-1 distribution fee - Class C(2) | 193,075 |

| Total Expenses | 11,841,687 |

| Less: expense reimbursement by Adviser(2) | (87,407) |

| Net Expenses | 11,754,280 |

| Net Investment Loss, before taxes | (4,606,355) |

| Deferred tax benefit | 208,811 |

| Net Investment Loss, net of taxes | (4,397,544) |

| Realized and Unrealized Gain/(Loss) on Investments | |

| Net realized gain on investments, before taxes | 123,426,505 |

| Deferred tax expense | (8,814,299) |

| Net realized gain on investments, net of taxes | 114,612,206 |

| Net change in unrealized appreciation/depreciation on investments, before taxes | 17,103,606 |

| Deferred tax expense | (2,255,925) |

| Net change in unrealized appreciation/depreciation on investments, net of taxes | 14,847,681 |

| Net Realized and Unrealized Gain/(Loss) on Investments | 129,459,887 |

| Increase in Net Assets Resulting from Operations | $125,062,343 |

| | The accompanying notes are an integral part of the financial statements. | ANNUAL REPORT 2023 ● 17 |

Statements of Changes in Net Assets

| Operations | Year Ended November 30, 2023 | Year Ended November 30, 2022 |

| Net investment income/(loss), net of tax | $(4,397,544) | $(3,635,802) |

| Net realized gain/(loss) on investments, net of tax | 114,612,206 | 62,162,401 |

| Net change in unrealized appreciation/depreciation on investments, net of taxes | 14,847,681 | 228,151,750 |

| Increase/(Decrease) in net assets resulting from operations | 125,062,343 | 286,678,349 |

| Dividends and Distributions to Class A Shareholders | | |

| Net investment income | (2,034,827) | (325,794) |

| Return of capital | – | (1,846,166) |

| Dividends and Distributions to Class C Shareholders | | |

| Net investment income | (1,199,306) | (195,319) |

| Return of capital | – | (1,106,806) |

| Dividends and Distributions to Class I Shareholders | | |

| Net investment income | (39,228,668) | (6,838,738) |

| Return of capital | – | (38,752,847) |

| Total dividends and distributions to Fund shareholders | (42,462,801) | (49,065,670) |

| Capital Share Transactions (Note 8) | | |

| Proceeds from shareholder subscriptions | 53,799,248 | 113,304,189 |

| Dividend reinvestments | 34,286,057 | 40,671,841 |

| Payments for redemptions | (211,373,631) | (286,531,714) |

| Decrease in net assets from capital share transactions | (123,288,326) | (132,555,684) |

| Total increase/(decrease) in net assets | (40,688,784) | 105,056,995 |

| Net Assets | | |

| Beginning of period | 838,274,181 | 733,217,186 |

| End of period | $797,585,397 | $838,274,181 |

| 18 | MainGate mlp fund | The accompanying notes are an integral part of the financial statements. | |

Financial Highlights: Class A Shares

| | Year Ended | Year Ended | Year Ended | Year Ended | Year Ended |

| Per Share Data(1) | November 30, | November 30, | November 30, | November 30, | November 30, |

| 2023 | 2022 | 2021 | 2020 | 2019 |

| Net Asset Value, beginning of period | $6.92 | $5.15 | $3.91 | $5.65 | $7.17 |

| Income from Investment Operations | | | | | |

| Net investment loss(2) | (0.05) | (0.04) | (0.07) | (0.06) | (0.05) |

| Net realized and unrealized gain (loss) on investments | 1.22 | 2.21 | 1.71 | (1.22) | (0.84) |

| Total increase (decrease) from investment operations | 1.17 | 2.17 | 1.64 | (1.28) | (0.89) |

| Less Distributions to Shareholders | | | | | |

| Net investment income | (0.40) | (0.06) | (0.06) | — | — |

| Return of capital | — | (0.34) | (0.34) | (0.46) | (0.63) |

| Total distributions to shareholders | (0.40) | (0.40) | (0.40) | (0.46) | (0.63) |

| Net Asset Value, end of year | $7.69 | $6.92 | $5.15 | $3.91 | $5.65 |

| Total Investment Return (excludes front-end sales load) | 17.62% | 43.28% | 42.66% | (22.61)% | (13.71)% |

| Supplemental Data and Ratios | | | | | |

| Net assets, end of year | $39,131,546 | $36,109,479 | $30,569,903 | $28,693,359 | $60,839,754 |

| Ratio of Expenses to Average Net Assets(3,4) | | | | | |

| Net deferred federal income and state tax (benefit) expense (“taxes”) | 1.41% | 0.00%‡ | 0.02% | 0.01% | 0.01% |

| Expenses (excluding taxes) before (waiver) recoupment | 1.75% | 1.69% | 1.68% | 1.72% | 1.69% |

| Expenses (excluding taxes) after (waiver) recoupment | 1.74% | 1.69% | 1.68% | 1.72% | 1.69% |

| Expenses (including taxes) before (waiver) recoupment | 3.15% | 1.69% | 1.70% | 1.73% | 1.70% |

| Net Fund Expenses | 3.14% | 1.69% | 1.70% | 1.73% | 1.70% |

| Ratio of Net Investment Income (Loss) to Average Net Assets(3,4) | | | | | |

| Net investment income (loss) (excluding taxes applied to net investment income (loss)) before waiver (recoupment) | (0.82)% | (0.67)% | (1.44)% | (1.32)% | (0.71)% |

| Net investment income (loss) (excluding taxes applied to net investment income (loss)) after waiver (recoupment) | (0.81)% | (0.67)% | (1.44)% | (1.32)% | (0.71)% |

| Net investment income (loss) (including taxes applied to net investment income (loss)) before waiver (recoupment) | (0.79)% | (0.67)% | (1.46)% | (1.33)% | (0.72)% |

| Net Investment Income (Loss) | (0.78)% | (0.67)% | (1.46)% | (1.33)% | (0.72)% |

| Portfolio turnover rate(5) | 8.27% | 3.26% | 20.80% | 36.65% | 66.39% |

‡ Less than 0.01%.

(1) Information presented relates to a share of Class A for the entire period.

(2) Calculated using average shares outstanding method.

(3) For the year ended November 30, 2023, the Fund did not accrue any state tax expense. For the year ended November 30, 2022, the Fund accrued $12,466 in state tax expense, of which $532 is attributable to Class A. For the year ended November 30, 2021, the Fund accrued $149,925 in state tax expense, of which $5,904 is attributable to Class A. For the year ended November 30, 2020, the Fund accrued $87,319 in state tax expense, of which $3,733 is attributable to Class A. For the year ended November 30, 2019, the Fund accrued $85,100 in state tax expense, of which $5,253 is attributable to Class A.

(4) For the year ended November 30, 2023, the Fund accrued $10,861,413 in net deferred tax expense, of which $497,327 is attributable to Class A.

(5) Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing between the classes of shares issued.

| | The accompanying notes are an integral part of the financial statements. | ANNUAL REPORT 2023 ● 19 |

Financial Highlights: Class C Shares

| | Year Ended | Year Ended | Year Ended | Year Ended | Year Ended |

| Per Share Data(1) | November 30, | November 30, | November 30, | November 30, | November 30, |

| 2023 | 2022 | 2021 | 2020 | 2019 |

| Net Asset Value, beginning of period | $6.40 | $4.82 | $3.72 | $5.43 | $6.97 |

| Income from Investment Operations | | | | | |

| Net investment loss(2) | (0.10) | (0.08) | (0.10) | (0.08) | (0.10) |

| Net realized and unrealized gain (loss) on investments | 1.13 | 2.06 | 1.60 | (1.17) | (0.81) |

| Total increase (decrease) from investment operations | 1.03 | 1.98 | 1.50 | (1.25) | (0.91) |

| Less Distributions to Shareholders | | | | | |

| Net investment income | (0.40) | (0.06) | (0.06) | — | — |

| Return of capital | — | (0.34) | (0.34) | (0.46) | (0.63) |

| Total distributions to shareholders | (0.40) | (0.40) | (0.40) | (0.46) | (0.63) |

| Net Asset Value, end of year | $7.03 | $6.40 | $4.82 | $3.72 | $5.43 |

| Total Investment Return (excludes contingent deferred sales charge) | 16.83% | 42.25% | 41.02% | (22.99)% | (14.42)% |

| Supplemental Data and Ratios | | | | | |

| Net assets, end of year | $20,654,614 | $19,980,563 | $17,119,406 | $16,108,024 | $33,310,916 |

| Ratio of Expenses to Average Net Assets(3,4) | | | | | |

| Net deferred federal income and state tax (benefit) expense (“taxes”) | 1.41% | 0.00%‡ | 0.02% | 0.01% | 0.01% |

| Expenses (excluding taxes) before (waiver) recoupment | 2.50% | 2.44% | 2.43% | 2.46% | 2.44% |

| Expenses (excluding taxes) after (waiver) recoupment | 2.49% | 2.44% | 2.43% | 2.46% | 2.44% |

| Expenses (including taxes) before (waiver) recoupment | 3.90% | 2.44% | 2.45% | 2.47% | 2.45% |

| Net Fund Expenses | 3.89% | 2.44% | 2.45% | 2.47% | 2.45% |

| Ratio of Net Investment Income (Loss) to Average Net Assets(3,4) | | | | | |

| Net investment income (loss) (excluding taxes applied to net investment income (loss)) before waiver (recoupment) | (1.57)% | (1.42)% | (2.19)% | (2.06)% | (1.46)% |

| Net investment income (loss) (excluding taxes applied to net investment income (loss)) after waiver (recoupment) | (1.56)% | (1.42)% | (2.19)% | (2.06)% | (1.46)% |

| Net investment income (loss) (including taxes applied to net investment income (loss)) before waiver (recoupment) | (1.54)% | (1.42)% | (2.21)% | (2.07)% | (1.47)% |

| Net Investment Income (Loss) | (1.53)% | (1.42)% | (2.21)% | (2.07)% | (1.47)% |

| Portfolio turnover rate(5) | 8.27% | 3.26% | 20.80% | 36.65% | 66.39% |

‡ Less than 0.01%.

(1) Information presented relates to a share of Class C for the entire period.

(2) Calculated using average shares outstanding method.

(3) For the year ended November 30, 2023, the Fund did not accrue any state tax expense. For the year ended November 30, 2022, the Fund accrued $12,466 in state tax expense, of which $297 is attributable to Class C. For the year ended November 30, 2021, the Fund accrued $149,925 in state tax expense, of which $3,367 is attributable to Class C. For the year ended November 30, 2020, the Fund accrued $87,319 in state tax expense, of which $2,149 is attributable to Class C. For the year ended November 30, 2019, the Fund accrued $85,100 in state tax expense, of which $2,996 is attributable to Class C.

(4) For the year ended November 30, 2023, the Fund accrued $10,861,413 in net deferred tax expense, of which $271,652 is attributable to Class C.

(5) Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing between the classes of shares issued.

| 20 | MainGate mlp fund | The accompanying notes are an integral part of the financial statements. | |

Financial Highlights: Class I Shares

| | Year Ended | Year Ended | Year Ended | Year Ended | Year Ended |

| Per Share Data(1) | November 30, | November 30, | November 30, | November 30, | November 30, |

| 2023 | 2022 | 2021 | 2020 | 2019 |

| Net Asset Value, beginning of period | $7.26 | $5.37 | $4.06 | $5.83 | $7.36 |

| Income from Investment Operations | | | | | |

| Net investment loss(2) | (0.04) | (0.03) | (0.06) | (0.05) | (0.03) |

| Net realized and unrealized gain (loss) on investments | 1.29 | 2.32 | 1.77 | (1.26) | (0.87) |

| Total increase (decrease) from investment operations | 1.25 | 2.29 | 1.71 | (1.31) | (0.90) |

| Less Distributions to Shareholders | | | | | |

| Net investment income | (0.40) | (0.06) | (0.06) | — | — |

| Return of capital | — | (0.34) | (0.34) | (0.46) | (0.63) |

| Total distributions to shareholders | (0.40) | (0.40) | (0.40) | (0.46) | (0.63) |

| Net Asset Value, end of year | $8.11 | $7.26 | $5.37 | $4.06 | $5.83 |

| Total Investment Return | 17.90% | 43.74% | 42.82% | (22.42)% | (13.48)% |

| Supplemental Data and Ratios | | | | | |

| Net assets, end of year | $737,799,237 | $782,184,139 | $685,527,877 | $747,728,099 | $967,800,549 |

| Ratio of Expenses to Average Net Assets(3,4) | | | | | |

| Net deferred federal income and state tax (benefit) expense (“taxes”) | 1.41% | 0.00%‡ | 0.02% | 0.01% | 0.01% |

| Expenses (excluding taxes) before (waiver) recoupment | 1.50% | 1.44% | 1.43% | 1.46% | 1.44% |

| Expenses (excluding taxes) after (waiver) recoupment | 1.49% | 1.44% | 1.43% | 1.46% | 1.44% |

| Expenses (including taxes) before (waiver) recoupment | 2.90% | 1.44% | 1.45% | 1.47% | 1.45% |

| Net Fund Expenses | 2.89% | 1.44% | 1.45% | 1.47% | 1.45% |

| Ratio of Net Investment Income (Loss) to Average Net Assets(3,4) | | | | | |

| Net investment income (loss) (excluding taxes applied to net investment income (loss)) before waiver (recoupment) | (0.57)% | (0.42)% | (1.19)% | (1.07)% | (0.46)% |

| Net investment income (loss) (excluding taxes applied to net investment income (loss)) after waiver (recoupment) | (0.56)% | (0.42)% | (1.19)% | (1.07)% | (0.46)% |

| Net investment income (loss) (including taxes applied to net investment income (loss)) before waiver (recoupment) | (0.54)% | (0.42)% | (1.21)% | (1.08)% | (0.47)% |

| Net Investment Income (Loss) | (0.53)% | (0.42)% | (1.21)% | (1.08)% | (0.47)% |

| Portfolio turnover rate(5) | 8.27% | 3.26% | 20.80% | 36.65% | 66.39% |

‡ Less than 0.01%.

(1) Information presented relates to a share of Class I for the entire period.

(2) Calculated using average shares outstanding method.

(3) For the year ended November 30, 2023, the Fund did not accrue any state tax expense. For the year ended November 30, 2022, the Fund accrued $12,466 in state tax expense, of which $11,637 is attributable to Class I. For the year ended November 30, 2021, the Fund accrued $149,925 in state tax expense, of which $140,654 is attributable to Class I. For the year ended November 30, 2020, the Fund accrued $87,319 in state tax expense, of which $81,437 is attributable to Class I. For the year ended November 30, 2019, the Fund accrued $85,100 in state tax expense, of which $76,851 is attributable to Class I.

(4) For the year ended November 30, 2023, the Fund accrued $10,861,413 in net deferred tax expense, of which $10,092,434 is attributable to Class I.

(5) Portfolio turnover is calculated on the basis of the Fund as a whole without distinguishing between the classes of shares issued.

| | The accompanying notes are an integral part of the financial statements. | ANNUAL REPORT 2023 ● 21 |

Notes to Financial Statements

November 30, 2023

1. Organization

MainGate MLP Fund (the “Fund”), a series of MainGate Trust (the “Trust”), is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end, non-diversified investment company. The Trust was established under the laws of Delaware by an Agreement and Declaration of Trust dated November 3, 2010. The Fund’s investment objective is total return. Class A and Class I commenced operations on February 17, 2011. Class C commenced operations on March 31, 2014.

The Fund offers three classes of shares: Class A, Class C and Class I. Depending on the size of the initial purchase, Class A shares are subject to a maximum 5.75% front-end sales charge or a 1.00% contingent deferred sales charge if shares are redeemed within 18 months. Class C shares have no front-end sales charge, but are subject to a 1.00% contingent deferred sales charge within 12 months of redemption. Class I shares have no sales charge. Class A shareholders pay Rule 12b-1 fees at the annual rate of 0.25% of average daily net assets. Class C shareholders pay Rule 12b-1 fees at the annual rate of 1.00% of average daily net assets. For the year ended November 30, 2023, contingent deferred sales charges of $0 and $808 were incurred by Class A and Class C shareholders, respectively.

2. Significant Accounting Policies

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Board Codification Topic 946 Financial Services—Investment Companies.

A. Use of Estimates. The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the recognition of distribution income and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

B. Investment Valuation. Fund investments are recognized at fair value, and subsequent changes in fair value are recognized in unrealized appreciation/(depreciation) on investments in the Statement of Operations. The Fund uses the following valuation methods to determine fair value as either current market value for investments for which market quotations are available, or if not available, a fair value, as determined in good faith pursuant to such policies and procedures as may be approved by the Trust’s Board of Trustees (“Board of Trustees”) from time to time. The valuation of the portfolio securities of the Fund currently includes the following processes:

| ● | Equity Securities: Securities listed on a securities exchange or an automated quotation system for which quotations are readily available, including securities traded over the counter, will be valued at the last quoted sale price on the principal exchange on which they are traded on the valuation date (or at approximately 4:00 p.m. Eastern Time if a security’s principal exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most recent quoted bid price. |

| ● | Fixed Income Securities: Debt and fixed income securities will be priced by independent, third-party pricing agents approved by the Board of Trustees. These third-party pricing agents will employ methodologies that they believe are appropriate, including actual market transactions, broker-dealer supplied valuations, matrix pricing, or other electronic data processing techniques. These techniques generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations. Debt obligations with remaining maturities of sixty days or less will be valued at their amortized cost, which approximates fair market value. |

| ● | Foreign Securities: Foreign securities are often principally traded on markets that close at different hours than U.S. markets. Such securities will be valued at their most recent closing prices on the relevant principal exchange even if the close of that exchange is earlier than the time of the Fund’s net asset value (“NAV”) calculation. However, securities traded in foreign markets which remain open as of the time of the NAV calculation will be valued at the most recent sales price as of the time of the NAV calculation. In addition, prices for certain foreign securities may be obtained from the Fund’s approved pricing sources. Chickasaw Capital Management, LLC (the “Adviser”) also monitors for the occurrence of significant events that may cast doubts on the reliability of previously obtained market prices for foreign securities held by the Fund. The prices for foreign securities will be reported in local currency and converted to U.S. dollars using currency exchange rates. Exchange rates will be provided daily by recognized independent pricing agents. The exchange rates used for the conversion will be captured as of the London close each day. |

C. Security Transactions, Investment Income and Expenses. Security transactions are accounted for on the date the securities are purchased or sold. Realized gains and losses are reported on a specific identified cost basis. Interest income is recognized on the accrual basis. Distributions are recorded on the ex-dividend date. Distributions received from the Fund’s investments in master limited partnerships (“MLPs”), including MLP general partnership interests, generally are comprised of ordinary income and return of capital. Withholding taxes on foreign dividends have

| 22 | MainGate mlp fund | The accompanying notes are an integral part of the financial statements. | |

been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and regulations.

For financial statement purposes, the Fund uses return of capital and income estimates to allocate the distribution income received. Such estimates are based on historical information available from each MLP and other industry sources. These estimates may subsequently be revised based on information received from MLPs after their tax reporting periods are concluded, as the actual character of these distributions is not known until after the fiscal year end of the Fund.

The Fund estimates the allocation of investment income and return of capital for the distributions received from MLPs within the Statement of Operations. For the year ended November 30, 2023, the Fund has estimated approximately 100% of the distributions from MLPs taxed as partnerships to be return of capital. Distributions from common stocks may also include income and return of capital. The Fund records the character of distributions received during the year based on estimates available. The characterization of distributions received by the Fund may be subsequently revised based on the information received from the MLPs and common stock after their tax reporting periods conclude.

Expenses are recorded on the accrual basis.

D. Dividends and Distributions to Shareholders. The Fund intends to make quarterly distributions from net income, which include the amount received as cash distributions from MLPs and common stock dividends. These activities are reported in the Statements of Changes in Net Assets.

Dividends and distributions to shareholders are recorded on the ex-dividend date. Dividends are reinvested in the Fund unless specifically instructed otherwise by a shareholder. The character of dividends and distributions to shareholders made during the period may differ from their ultimate characterization for federal income tax purposes. For the year ended November 30, 2023, the Fund’s dividends and distributions were expected to be comprised of 100% income and 0% return of capital. The tax character of distributions paid for the year ended November 30, 2023 will be determined in early 2024.

E. Federal Income Taxation. The Fund, taxed as a corporation, is obligated to pay federal and state income tax on its taxable income. Currently, the federal income tax rate for a corporation is 21%.

The Fund invests its assets primarily in MLPs, which generally are treated as partnerships for federal income tax purposes. As a limited partner in the MLPs, the Fund reports its allocable share of the MLP’s taxable income in computing its own taxable income. The Fund’s tax expense or benefit is included in the Statement of Operations based on the component of income or gains (losses) to which such expense or benefit relates. Deferred income taxes reflect the net tax effects of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for income tax purposes. A valuation allowance is recognized if, based on the weight of available evidence, it is more likely than not that some portion or all of the deferred income tax asset will not be realized.

The Fund’s policy is to classify interest and penalties associated with underpayment of federal and state income taxes as an income tax expense on the Statement of Operations. For the year ended November 30, 2023, the Fund did not have interest or penalties associated with underpayment of income taxes.

F. Indemnifications. Under the Fund’s organizational documents, its officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund may enter into contracts that provide general indemnification to other parties. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred, and may not occur. However, the Fund has not had prior claims or losses pursuant to these contracts.

G. Cash. Cash consists of deposits held with a bank.

3. Fair Value Measurements

Various inputs that are used in determining the fair value of the Fund’s investments are summarized in the three broad levels listed below:

| ● | Level 1: unadjusted quoted prices in active markets for identical securities that the Fund has the ability to access |

| ● | Level 2: other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.) |

| ● | Level 3: significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investments) |

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

These inputs are summarized in the three broad levels that follow.

| | | | | Fair Value Measurements at Reporting Date Using: | |

| | Description | | | Fair Value at

November 30, 2023 | | Quoted Prices in Active

Markets for Identical

Assets (Level 1) | | Significant Other

Observable

Inputs (Level 2) | | Significant

Unobservable

Inputs (Level 3) | |

| | Equity Securities | | | | | | | | | |

| | Master Limited Partnerships and and Related Companies(1) | | $796,538,733 | | $796,538,733 | | $ — | | $ — | |

| | Total | | $796,538,733 | | $796,538,733 | | $ — | | $ — | |

(1) All other industry classifications are identified in the Schedule of Investments.

4. Concentration Risk

The Fund seeks to achieve its investment objective by investing at least 80% of its net assets (plus any borrowings for investment purposes) in MLP interests under normal circumstances as determined in the prospectus. The investment objectives are included within the Schedule of Investments.

Credit Risk. The Fund maintains cash in bank accounts which, at times, may exceed United States federally insured limits.