Brian R. Wiedmeyer, President

c/o U.S. Bancorp Fund Services, LLC

Port Street Quality Growth Fund

Institutional Class Shares — PSQGX

Annual Report

| www.portstreetinvest.com | March 31, 2022 |

(This Page Intentionally Left Blank.)

PORT STREET QUALITY GROWTH FUND

Dear Shareholders,

Thank you for the opportunity to report on the Fund’s strategy, performance, and outlook.

Quality Growth Fund Performance

For the six months ending March 31, 2022, the Port Street Quality Growth Fund (“Quality Growth”) returned 3.10%, while the S&P 500® returned 5.92%. For the twelve months ending March 31, 2022, Quality Growth returned 7.42%, while the S&P 500® returned 15.65%.

The Fund’s significant cash position (35%) led to performance lag relative to our benchmark during the last six months.

With the Federal Reserve finally ending Quantitative Easing, beginning to raise interest rates to stem inflation and beginning the process of shrinking their balance sheet, we believe that our strategy may outperform the benchmark as this market cycle comes to an end.

Quality Growth Fund Strategy

Quality Growth’s investment approach focuses on companies that can be purchased at market prices below their fair value with a record of consistent, above-average profit growth, strong balance sheets, sustainable competitive advantages, and capable management. The source of such growth is persistently above-average profitability, which, when combined with a sensible policy relating to the payout of such profits and intelligent re-investment, results in the compounding of retained earnings and long-term growth. Quality Growth’s investment strategy is designed to grow purchasing power in excess of inflation and outperform the general market over time while mitigating losses during periods of economic adversity.

Outlook

Inflation is the buzz word of the day, not just for investors, but for everyone in the world. The Federal Reserve was the beneficiary of 14 years of near scant inflation from 2008 to 2022 and was able to rise the tide for all public companies, through consequence-free increases in the money supply every time stocks wavered. They no longer have that same luxury.

The path forward for the Federal Reserve will lead to the return of real price discovery for stocks and a normalization of long term interest rates. We welcome both.

The Federal Reserve’s actions over the last 14 years has led to a boom for Zombie Companies. 656 companies in the Russell 3000® were classified as Zombie as of December 31, 2021. Rising interest rates and input costs will lead these companies to insolvency if nothing changes. Widespread bankruptcy will lead to further market contraction and will lead to buying opportunities for the Fund.

Contracting markets have led to outperformance over the benchmark in the past. We expect similar results this time around, as the Federal Reserve will not be able to bail out equity investors with additional quantitative easing, while they are simultaneously raising interest rates.

We also expect our disciplined investment process to hedge our investors from permanent capital impairment as this long-anticipated revaluation of assets occurs. Regardless of timing and direction, the capital preservation bias underlying our strategy will allow us the potential to protect capital in the current down period, and in turn, seek to allow better compounding capital over complete market cycles.

PORT STREET QUALITY GROWTH FUND

Thank you for your trust and confidence in our stewardship.

| Graham Pierce | Mac McCall |

| CEO | Senior Director |

Performance data quoted represents past performance; past performance does not guarantee future results.

Opinions expressed are those of the Investment Manager, and are subject to change, are not guaranteed and should not be considered investment advice.

Must be preceded or accompanied by a prospectus.

The S&P 500® Index is a stock market index based on the market capitalizations of 500 large companies having common stock listed on the NYSE or NASDAQ. It is not possible to directly invest in an index.

Zombie companies are defined as companies that earn just enough money to continue operating and service debt but are unable to pay off their debt.

The Russell 3000® Index is a market cap weighted equity index maintained by FTSE Russell which provides exposure to the entire U.S. stock market The index tracks the performance of the 3,000 largest U.S.-traded stocks, which represent about 97% of all U.S.-incorporated equity securities.

Fund holdings and sector allocations are subject to change and should not be considered a recommendation to buy or sell any security. For a complete list of Fund holdings, please refer to the Schedule of Investments in this report.

Mutual fund investing involves risk. Principal loss is possible. Investments in small-and mid-capitalization companies involve additional risks such as limited liquidity and greater volatility than large capitalization companies. Investments in foreign securities involve greater volatility; political, economic and currency risks; and differences in accounting methods. The Fund may have a relatively high concentration of assets in a single or smaller number of securities which can result in reduced diversification and greater volatility. A substantial cash/cash equivalent position can adversely impact Fund performance. In rising markets, holding cash or cash equivalents will negatively affect the Fund’s performance relative to its benchmark.

The Port Street Quality Growth Fund is distributed by Quasar Distributors, LLC.

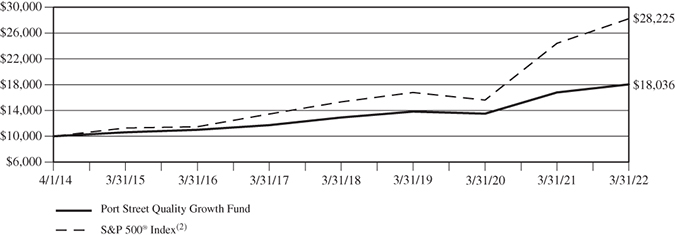

PORT STREET QUALITY GROWTH FUND

Value of $10,000 Investment (Unaudited)

The chart assumes an initial investment of $10,000. Performance reflects waivers of fee and operating expenses in effect. In the absence of such waivers, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate, so that your shares, when redeemed may be worth more or less than their original cost. Current performance of the fund may be lower or higher than the performance quoted. Performance data current to the most recent month-end may be obtained by calling 855-369-6220. Performance assumes the reinvestment of capital gains and income distributions. The performance does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annualized Rates of Return (%) – as of March 31, 2022

| | | | | Since |

| | 1 Year | 3 Year | 5 Year | Inception(1) |

| Port Street Quality Growth Fund | 7.42% | 9.28% | 9.01% | 7.65% |

S&P 500® Index(2) | 15.65% | 18.92% | 15.99% | 13.85% |

| (1) | The Fund commenced operations on April 1, 2014. |

| (2) | The S&P 500® Index is a stock market index based on the market capitalization of 500 large companies having common stock listed on the NYSE or NASDAQ. It is not possible to invest directly in an Index. |

The following is expense information for the Port Street Quality Growth Fund (the “Fund”) as disclosed in the Fund’s most recent prospectus dated July 29, 2021: Gross Expenses: 1.18%, Net Expenses: 0.97%.

Port Street Investments, LLC (the “Adviser”) has contractually agreed to reduce its management fees, and pay Fund expenses in order to ensure that Total Annual Fund Operating Expenses (excluding any acquired fund fees and expenses, leverage/borrowing interest, interest expense, dividends paid on short sales, taxes, brokerage commissions and other transactional expenses, and extraordinary expenses) do not exceed 0.97% of the Fund’s average daily net assets (the “Expense Cap”). After July 28, 2022, the Expense Cap for the Fund will be 1.15%, unless renewed by the Adviser for another year. Fees waived and expenses paid by the Adviser may be recouped by the Adviser for a period of 36 months following the month during which such fee waiver and expense payment was made if such recoupment can be achieved without exceeding the expense limit in effect at the time the fee waiver and expense payment occurred and the expense limit in place at the time of recoupment. The Operating Expenses Limitation Agreement is indefinite in term, but cannot be terminated through July 29, 2022. Thereafter, the agreement may be terminated at any time upon 60 days’ written noticed by the Trust’s Board of Trustees (the “Board”) or the Adviser, with the consent of the Board.

PORT STREET QUALITY GROWTH FUND

Expense Example (Unaudited)

March 31, 2022

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including brokerage commissions on purchases and sales of Fund shares, and (2) ongoing costs, including management fees, shareholder servicing fees, and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (October 1, 2021 – March 31, 2022).

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if transactional costs were included, your costs may have been higher.

| | Beginning | Ending | Expenses Paid |

| | Account Value | Account Value | During Period(1) |

| | (10/1/2021) | (3/31/2022) | (10/1/2021 to 3/31/2022) |

Institutional Class Actual(2) | $1,000.00 | $1,031.00 | $4.91 |

| Institutional Class Hypothetical | | | |

| (5% return before expenses) | $1,000.00 | $1,020.09 | $4.89 |

(1) | Expenses are equal to the Fund’s annualized expense ratio for the most recent six-month period of 0.97% multiplied by the average account value over the period, multiplied by 182/365 to reflect the one-half year period. |

(2) | Based on the actual return for the six-month period ended March 31, 2022 of 3.10%. |

PORT STREET QUALITY GROWTH FUND

Sector Allocation(1) (Unaudited)

as of March 31, 2022

(% of net assets)

Top Ten Equity Holdings(1) (Unaudited)

as of March 31, 2022

(% of net assets)

| | Raytheon Technologies Corp. | 4.0% | |

| | Oracle Corp. | 3.5% | |

| | Berkshire Hathaway, Inc., Class B | 3.4% | |

| | C.H. Robinson Worldwide, Inc. | 3.4% | |

| | Alphabet, Inc., Class A | 3.2% | |

| | Microsoft Corp. | 3.1% | |

| | Walt Disney Co. | 2.9% | |

| | Apple, Inc. | 2.7% | |

| | General Dynamics Corp. | 2.7% | |

| | Medtronic plc | 2.6% | |

(1) | Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security. |

PORT STREET QUALITY GROWTH FUND

Schedule of Investments

March 31, 2022

| | | Shares | | | Value | |

| COMMON STOCKS — 65.2% | | | | | | |

| | | | | | | |

| Communication Services — 6.1% | | | | | | |

| Alphabet, Inc., Class A* | | | 2,400 | | | $ | 6,675,240 | |

| Walt Disney Co.* | | | 44,600 | | | | 6,117,336 | |

| | | | | | | | 12,792,576 | |

| Consumer Discretionary — 6.0% | | | | | | | | |

| Home Depot, Inc. | | | 13,700 | | | | 4,100,821 | |

| NIKE, Inc., Class B | | | 31,300 | | | | 4,211,728 | |

| Starbucks Corp. | | | 46,200 | | | | 4,202,814 | |

| | | | | | | | 12,515,363 | |

| Consumer Staples — 7.4% | | | | | | | | |

| PepsiCo, Inc. | | | 14,500 | | | | 2,427,010 | |

| Procter & Gamble Co. | | | 15,700 | | | | 2,398,960 | |

| Reckitt Benckiser Group plc — ADR | | | 205,300 | | | | 3,169,832 | |

| Unilever plc — ADR | | | 114,600 | | | | 5,222,322 | |

| Walmart, Inc. | | | 15,600 | | | | 2,323,152 | |

| | | | | | | | 15,541,276 | |

| Financials — 3.4% | | | | | | | | |

| Berkshire Hathaway, Inc., Class B* | | | 20,000 | | | | 7,058,200 | |

| | | | | | | | | |

| Health Care — 10.7% | | | | | | | | |

| Becton, Dickinson & Co. | | | 11,900 | | | | 3,165,400 | |

| Biogen, Inc.* | | | 14,300 | | | | 3,011,580 | |

| Johnson & Johnson | | | 13,200 | | | | 2,339,436 | |

| Medtronic plc | | | 48,200 | | | | 5,347,790 | |

| Novo Nordisk — ADR | | | 47,500 | | | | 5,274,875 | |

| Roche Holding AG — ADR | | | 67,400 | | | | 3,330,234 | |

| | | | | | | | 22,469,315 | |

| Industrials — 11.3% | | | | | | | | |

| 3M Co. | | | 16,900 | | | | 2,516,072 | |

| C.H. Robinson Worldwide, Inc. | | | 65,400 | | | | 7,044,234 | |

| General Dynamics Corp. | | | 23,474 | | | | 5,661,459 | |

| Raytheon Technologies Corp. | | | 85,400 | | | | 8,460,578 | |

| | | | | | | | 23,682,343 | |

| Information Technology — 18.2% | | | | | | | | |

| Accenture plc, Class A | | | 9,571 | | | | 3,227,628 | |

| Adobe Systems, Inc.* | | | 9,726 | | | | 4,431,360 | |

| Apple, Inc. | | | 32,905 | | | | 5,745,542 | |

See Notes to the Financial Statements

PORT STREET QUALITY GROWTH FUND

Schedule of Investments – Continued

March 31, 2022

| | | Shares | | | Value | |

| Information Technology — 18.2% (Continued) | | | | | | |

| Cisco Systems, Inc. | | | 63,360 | | | $ | 3,532,954 | |

| Cognizant Technology Solutions Corp., Class A | | | 47,400 | | | | 4,250,358 | |

| Microsoft Corp. | | | 20,900 | | | | 6,443,679 | |

| Oracle Corp. | | | 87,700 | | | | 7,255,421 | |

| Visa, Inc., Class A | | | 14,807 | | | | 3,283,749 | |

| | | | | | | | 38,170,691 | |

| Materials — 2.1% | | | | | | | | |

| International Flavors & Fragrances, Inc. | | | 33,598 | | | | 4,412,425 | |

| Total Common Stocks | | | | | | | | |

| (Cost $88,879,867) | | | | | | | 136,642,189 | |

| | | | | | | | | |

| | | Par | | | | | |

| SHORT-TERM INVESTMENTS — 28.5% | | | | | | | | |

| U.S. Treasury Bills | | | | | | | | |

| 0.126%, 4/28/2022 (a)(b) | | $ | 10,000,000 | | | | 9,999,023 | |

| 0.265%, 5/26/2022 (a)(b) | | | 10,000,000 | | | | 9,995,875 | |

| 0.504%, 6/30/2022 (a)(b) | | | 10,000,000 | | | | 9,987,250 | |

| 0.746%, 7/28/2022 (a)(b) | | | 10,000,000 | | | | 9,975,335 | |

| 0.862%, 8/25/2022 (a)(b) | | | 10,000,000 | | | | 9,964,784 | |

| 0.998%, 9/29/2022 (a)(b) | | | 10,000,000 | | | | 9,949,559 | |

| Total Short-Term Investments | | | | | | | | |

| (Cost $59,897,454) | | | | | | | 59,871,826 | |

| Total Investments — 93.7% | | | | | | | | |

| (Cost $148,777,321) | | | | | | | 196,514,015 | |

| Other Assets and Liabilities, Net — 6.3% | | | | | | | 13,309,213 | |

| Total Net Assets — 100.0% | | | | | | $ | 209,823,228 | |

ADR — American Depositary Receipt

plc — Public Limited Company

| * | Non-income producing security |

| (a) | Rate shown is the effective yield as of March 31, 2022. |

| (b) | Level 2 security. |

See Notes to the Financial Statements

PORT STREET QUALITY GROWTH FUND

Statement of Assets and Liabilities

March 31, 2022

| ASSETS: | | | |

| Investments, at value | | | |

| (Cost: $148,777,321) | | $ | 196,514,015 | |

| Cash | | | 11,803,033 | |

| Dividends & interest receivable | | | 213,092 | |

| Receivable for capital shares sold | | | 1,724,091 | |

| Prepaid expenses | | | 21,675 | |

| Total assets | | | 210,275,906 | |

| | | | | |

| LIABILITIES: | | | | |

| Payable for investment securities purchased | | | 214,832 | |

| Payable to investment adviser | | | 114,576 | |

| Payable for fund administration & accounting fees | | | 31,082 | |

| Payable for capital shares redeemed | | | 24,326 | |

| Payable for audit fees | | | 19,055 | |

| Payable for transfer agent fees & expenses | | | 11,968 | |

| Accrued shareholder servicing fees | | | 10,165 | |

| Payable for trustee fees | | | 4,407 | |

| Payable for custody fees | | | 3,756 | |

| Payable for compliance fees | | | 3,503 | |

| Accrued expenses | | | 15,008 | |

| Total liabilities | | | 452,678 | |

| | | | | |

| NET ASSETS | | $ | 209,823,228 | |

| | | | | |

| NET ASSETS CONSIST OF: | | | | |

| Paid-in capital | | | 158,942,923 | |

| Total distributable earnings | | | 50,880,305 | |

| Net assets | | $ | 209,823,228 | |

| | | | | |

| Net assets | | $ | 209,823,228 | |

Shares issued and outstanding(1) | | | 12,633,147 | |

| Net asset value, redemption price and offering price per share | | $ | 16.61 | |

(1) | Unlimited shares authorized without par value. |

See Notes to the Financial Statements

PORT STREET QUALITY GROWTH FUND

Statement of Operations

For the Year Ended March 31, 2022

| INVESTMENT INCOME: | | | |

| Dividend income | | $ | 1,866,734 | |

| Less: Foreign taxes withheld | | | (24,567 | ) |

| Interest income | | | 36,522 | |

| Total investment income | | | 1,878,689 | |

| | | | | |

| EXPENSES: | | | | |

| Investment adviser fees (See Note 4) | | | 1,587,791 | |

| Fund administration & accounting fees (See Note 4) | | | 185,613 | |

| Shareholder servicing fees (See Note 5) | | | 115,334 | |

| Transfer agent fees & expenses (See Note 4) | | | 66,710 | |

| Federal & state registration fees | | | 35,820 | |

| Custody fees (See Note 4) | | | 21,345 | |

| Compliance fees (See Note 4) | | | 20,769 | |

| Audit fees | | | 19,050 | |

| Trustee fees (See Note 4) | | | 17,675 | |

| Other expenses | | | 11,988 | |

| Legal fees | | | 11,011 | |

| Postage & printing fees | | | 6,217 | |

| Insurance fees | | | 2,466 | |

| Total expenses before waiver | | | 2,101,789 | |

| Less: waiver from investment adviser (See Note 4) | | | (237,217 | ) |

| Net expenses | | | 1,864,572 | |

| | | | | |

| NET INVESTMENT INCOME | | | 14,117 | |

| | | | | |

| REALIZED AND UNREALIZED GAIN ON INVESTMENTS | | | | |

| Net realized gain on investments | | | 5,816,986 | |

| Net change in unrealized appreciation/depreciation on investments | | | 7,794,509 | |

| Net realized and unrealized gain on investments | | | 13,611,495 | |

| | | | | |

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | | $ | 13,625,612 | |

See Notes to the Financial Statements

PORT STREET QUALITY GROWTH FUND

Statements of Changes in Net Assets

| | | Year Ended | | | Year Ended | |

| | | March 31, 2022 | | | March 31, 2021 | |

| OPERATIONS: | | | | | | |

| Net investment income | | $ | 14,117 | | | $ | 4,618 | |

| Net realized gain on investments | | | 5,816,986 | | | | 2,999,045 | |

| Net change in unrealized | | | | | | | | |

| appreciation/depreciation on investments | | | 7,794,509 | | | | 29,446,689 | |

| Net increase in net assets resulting from operations | | | 13,625,612 | | | | 32,450,352 | |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS: | | | | | | | | |

| Proceeds from shares sold | | | 43,581,749 | | | | 73,004,016 | |

| Proceeds from reinvestment of distributions | | | 2,971,540 | | | | 2,465,216 | |

| Payments for shares redeemed | | | (28,174,544 | ) | | | (38,414,095 | ) |

| Net increase in net assets resulting | | | | | | | | |

| from capital share transactions | | | 18,378,745 | | | | 37,055,137 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

| Total distributions to shareholders | | | (3,753,442 | ) | | | (3,289,912 | ) |

| | | | | | | | | |

| TOTAL INCREASE IN NET ASSETS | | | 28,250,915 | | | | 66,215,577 | |

| | | | | | | | | |

| NET ASSETS: | | | | | | | | |

| Beginning of year | | | 181,572,313 | | | | 115,356,736 | |

| End of year | | $ | 209,823,228 | | | $ | 181,572,313 | |

See Notes to the Financial Statements

PORT STREET QUALITY GROWTH FUND

Financial Highlights

For a Fund share outstanding throughout the years.

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | March 31, | | | March 31, | | | March 31, | | | March 31, | | | March 31, | |

| | | 2022 | | | 2021 | | | 2020 | | | 2019 | | | 2018 | |

| PER SHARE DATA: | | | | | | | | | | | | | | | |

| Net asset value, beginning of year | | $ | 15.76 | | | $ | 12.91 | | | $ | 13.40 | | | $ | 12.73 | | | $ | 11.62 | |

| Investment operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.00 | (1)(2) | | | 0.00 | (1)(2) | | | 0.10 | | | | 0.09 | | | | 0.03 | |

| Net realized and unrealized | | | | | | | | | | | | | | | | | | | | |

| gain (loss) on investments | | | 1.18 | | | | 3.14 | | | | (0.39 | ) | | | 0.79 | | | | 1.15 | |

| Total from investment operations | | | 1.18 | | | | 3.14 | | | | (0.29 | ) | | | 0.88 | | | | 1.18 | |

| Less distributions from: | | | | | | | | | | | | | | | | | | | | |

| Net investment income | | | 0.00 | (1) | | | (0.02 | ) | | | (0.11 | ) | | | (0.07 | ) | | | (0.02 | ) |

| Net realized gains | | | (0.33 | ) | | | (0.27 | ) | | | (0.09 | ) | | | (0.14 | ) | | | (0.05 | ) |

| Total distributions | | | (0.33 | ) | | | (0.29 | ) | | | (0.20 | ) | | | (0.21 | ) | | | (0.07 | ) |

| Net asset value, end of year | | $ | 16.61 | | | $ | 15.76 | | | $ | 12.91 | | | $ | 13.40 | | | $ | 12.73 | |

| | | | | | | | | | | | | | | | | | | | | |

| TOTAL RETURN | | | 7.42 | % | | | 24.37 | % | | | -2.31 | % | | | 7.07 | % | | | 10.13 | % |

| | | | | | | | | | | | | | | | | | | | | |

| SUPPLEMENTAL DATA AND RATIOS: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (in millions) | | $ | 210.0 | | | $ | 181.6 | | | $ | 115.4 | | | $ | 110.2 | | | $ | 96.8 | |

| Ratio of expenses to average net assets: | | | | | | | | | | | | | | | | | | | | |

| Before expense waiver/recoupment | | | 1.09 | % | | | 1.13 | % | | | 1.18 | % | | | 1.16 | % | | | 1.19 | % |

| After expense waiver/recoupment | | | 0.97 | % | | | 0.97 | % | | | 0.97 | % | | | 1.13 | %(3) | | | 1.15 | % |

| Ratio of net investment income | | | | | | | | | | | | | | | | | | | | |

| to average net assets: | | | | | | | | | | | | | | | | | | | | |

| After expense waiver/recoupment | | | 0.01 | % | | | 0.00 | %(4) | | | 0.76 | % | | | 0.72 | % | | | 0.23 | % |

| | | | | | | | | | | | | | | | | | | | | |

| Portfolio turnover rate | | | 9 | % | | | 14 | % | | | 15 | % | | | 6 | % | | | 2 | % |

(1) | Amount per share is less than $0.005. |

(2) | Per share data calculated using the average shares method. |

(3) | Prior to February 13, 2019, the annual expense limitation was 1.15% of the average daily net assets of the Fund. Thereafter it was 0.97%. |

(4) | Amount is less than 0.005%. |

See Notes to the Financial Statements

PORT STREET QUALITY GROWTH FUND

Notes to the Financial Statements

March 31, 2022

1. ORGANIZATION

Managed Portfolio Series (the “Trust”) was organized as a Delaware statutory trust on January 27, 2011. The Trust is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Port Street Quality Growth Fund (the “Fund”) is a diversified series with its own investment objectives and policies within the Trust. The investment objective of the Fund is total return. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946, Financial Services – Investment Companies. The Fund commenced operations on April 1, 2014. The Fund currently offers an Institutional Class. Institutional Class shares are subject to a maximum 0.10% shareholder servicing fee. The Fund may issue an unlimited number of shares of beneficial interest, with no par value.

2. SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. These policies are in conformity with generally accepted accounting principles in the United States of America (“GAAP”).

Security Valuation – All investments in securities are recorded at their estimated fair value, as described in Note 3.

Federal Income Taxes – The Fund complies with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, necessary to qualify as a regulated investment company and distributes substantially all net taxable investment income and net realized gains to shareholders in a manner which results in no tax cost to the Fund. Therefore, no federal income or excise tax provision is required. As of and during the year ended March 31, 2022, the Fund did not have any tax positions that did not meet the “more-likely-than-not” threshold of being sustained by the applicable tax authority. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits on uncertain tax positions as income tax expense in the Statement of Operations. As of and during the year ended March 31, 2022, the Fund did not incur any interest or penalties. The Fund is not subject to examination by U.S. tax authorities for the tax years prior to the year ended March 31, 2019.

Security Transactions, Income and Distributions – The Fund follows industry practice and records security transactions on the trade date. Realized gains and losses on sales of securities are calculated on the basis of identified cost. Dividend income is recorded on the ex-dividend date and interest income is recorded on an accrual basis. Withholding taxes on foreign dividends have been provided for in accordance with the Fund’s understanding of the applicable country’s tax rules and regulations. Discounts and premiums on securities purchased are amortized over the expected life of the respective securities using the constant yield method.

The Fund distributes substantially all net investment income, if any, and net realized capital gains, if any, annually. Distributions to shareholders are recorded on the ex-dividend date. The treatment for financial reporting purposes of distributions made to shareholders during the year from net investment income or net realized capital gains may differ from their treatment for federal income tax purposes. These differences are caused primarily by differences in the timing of the recognition of certain components of income, expense or realized capital gain for federal income tax purposes. Where such differences are permanent in nature, GAAP requires that they be reclassified in the components of the net assets based on their ultimate characterization for federal income tax purposes. Any such reclassifications will have no effect on net assets, results of operations or net asset value (“NAV”) per share of the Fund. For the year ended March 31, 2022, the Fund increased paid-in capital by $365,541 and decreased distributable earnings by $365,541. The reclassification was due to the Fund’s utilization of earnings and profits distributed to shareholders as part of the dividends paid deduction.

PORT STREET QUALITY GROWTH FUND

Notes to the Financial Statements – Continued

March 31, 2022

Expenses – Expenses associated with a specific fund in the Trust are charged to that fund. Common Trust expenses are typically allocated evenly between funds of the Trust, or by other equitable means.

Use of Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

3. SECURITIES VALUATION

The Fund has adopted authoritative fair value accounting standards which establish an authoritative definition of fair value and set out a hierarchy for measuring fair value. These standards require additional disclosures about the various inputs and valuation techniques used to develop the measurements of fair value, a discussion in changes in valuation techniques and related inputs during the period and expanded disclosure of valuation Levels for major security types. These inputs are summarized in the three broad Levels listed below:

| Level 1 – | Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| | |

| Level 2 – | Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| | |

| Level 3 – | Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available. |

Following is a description of the valuation techniques applied to the Fund’s major categories of assets and liabilities measured at fair value on a recurring basis. The Fund’s investments are carried at fair value.

Short-Term Investments – Investments in other mutual funds, including money market funds, are valued at their NAV per share and are categorized in Level 1 of the fair value hierarchy. U.S. government securities are normally valued using a model that incorporates market observable data such as reported sales of similar securities, broker quotes, yields, bids, offers, and reference data. These securities are valued principally using dealer quotations. U.S. government securities are categorized in Level 2 of the fair value hierarchy depending on the inputs used and market activity levels for specific securities.

Equity Securities – Equity securities that are primarily traded on a national securities exchange are valued at the last sale price on the exchange on which they are primarily traded on the day of valuation or, if there has been no sale on such day, at the mean between the bid and ask prices. Securities traded primarily in the Nasdaq Global Market System for which market quotations are readily available are valued using the Nasdaq Official Closing Price (“NOCP”). If the NOCP is not available, such securities are valued at the last sale price on the day of valuation, or if there has been no sale on such day, at the mean between the bid and ask prices. To the extent these securities are actively traded and valuation adjustments are not applied, they are categorized in Level 1 of the fair value hierarchy.

Securities for which market quotations are not readily available, or if the closing price does not represent fair value, are valued following procedures approved by the Board of Trustees (the “Board”). These procedures consider many

PORT STREET QUALITY GROWTH FUND

Notes to the Financial Statements – Continued

March 31, 2022

factors, including the type of security, size of holding, trading volume and news events. There can be no assurance that the Fund could obtain the fair value assigned to a security if they were to sell the security at approximately the time at which the Fund determines their NAV per share. The Board has established a Valuation Committee to administer, implement, and oversee the fair valuation process, and to make fair value decisions when necessary. The Board regularly reviews reports that describe any fair value determinations and methods.

The inputs or methodology used for valuing securities are not an indication of the risk associated with investing in those securities. The following is a summary of the inputs used to value the Fund’s securities as of March 31, 2022:

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | $ | 136,642,189 | | | $ | — | | | $ | — | | | $ | 136,642,189 | |

| Short-Term Investments | | | — | | | | 59,871,826 | | | | — | | | | 59,871,826 | |

| Total Investments in Securities | | $ | 136,642,189 | | | $ | 59,871,826 | | | $ | — | | | $ | 196,514,015 | |

Refer to the Schedule of Investments for further information on the classification of investments.

4. INVESTMENT ADVISORY FEE AND OTHER TRANSACTIONS WITH AFFILIATES

The Trust has an agreement with Port Street Investments, LLC (the “Adviser”) to furnish investment advisory services to the Fund. Pursuant to an Investment Advisory Agreement between the Trust and the Adviser, the Adviser is entitled to receive, on a monthly basis, an annual advisory fee equal to 0.85% on the first $100 million of the Fund’s average daily net assets, 0.80% on the next $150 million of the Fund’s average daily net assets, 0.75% on the next $500 million of the Fund’s average daily net assets, and 0.70% on the Fund’s average daily net assets over $750 million.

The Adviser has engaged Saratoga Research & Investment Management (the “Sub-Adviser”) as the Sub-Adviser to the Fund. Subject to the supervision of the Adviser, the Sub-Adviser is primarily responsible for the day-to-day management of the Fund’s portfolio, including purchase, retention and sale of securities. Fees associated with these services are paid to the Sub-Adviser by the Adviser.

The Adviser has contractually agreed to waive its management fees, and pay Fund expenses, in order to ensure that total annual operating expenses (excluding acquired fund fees and expenses, leverage/borrowing interest, interest expense, taxes, dividends paid on short sales, brokerage commissions and extraordinary expenses) for the Fund do not exceed 0.97% of the Fund’s average daily net assets (the “Expense Cap”). After July 28, 2022, the Expense Cap for the Fund will be 1.15%, unless renewed by the Adviser for another year. Fees waived and expenses paid by the Adviser may be recouped by the Adviser for a period of thirty-six months following the date on which such fee waiver and expense payment was made, if such recoupment can be achieved without exceeding the expense limit in effect at the time the fee waiver and expense payment occurred and the expense limit in effect at the time of recoupment. The Operating Expenses Limitation Agreement is indefinite in term and cannot be terminated within a year of the effective date of the Fund’s prospectus. Thereafter, the agreement may be terminated at any time upon 60 days’ written notice by the Trust’s Board or the Adviser, with the consent of the board. Waived fees and reimbursed expenses subject to potential recovery by year of expiration are as follows:

Expiration | Amount | |

| April 2022 – March 2023 | $243,851 | |

| April 2023 – March 2024 | $250,254 | |

| April 2024 – March 2025 | $237,217 | |

PORT STREET QUALITY GROWTH FUND

Notes to the Financial Statements – Continued

March 31, 2022

U.S. Bancorp Fund Services, LLC (the “Administrator”), doing business as U.S. Bank Global Fund Services, acts as the Fund’s Administrator, Transfer Agent, and Fund Accountant. U.S. Bank N.A. (the “Custodian”) serves as the custodian to the Fund. The Custodian is an affiliate of the Administrator. The Administrator performs various administrative and accounting services for the Fund. The Administrator prepares various federal and state regulatory filings, reports and returns for the Fund; prepares reports and materials to be supplied to the Trustees; monitors the activities of the Custodian; coordinates the payment of the Fund’s expenses and reviews the Fund’s expense accruals. The officers of the Trust, including the Chief Compliance Officer, are employees of the Administrator. As compensation for its services, the Administrator is entitled to a monthly fee at an annual rate based upon the average daily net assets of the Fund, subject to annual minimums. Fees incurred by the Fund for administration and accounting, transfer agency, custody and chief compliance officer services for the year ended March 31, 2022, are disclosed in the Statement of Operations. A Trustee of the Trust is an interested person of the Adviser.

5. SHAREHOLDER SERVICING FEES

The Fund has entered into a shareholder servicing agreement (the “Agreement”) where the Adviser acts as the shareholder agent, under which the Fund may pay a servicing fee at a maximum annual rate of 0.10% of the average daily net assets of the Institutional Class. Payments to the Adviser under the Agreement may reimburse the Adviser for payments it makes to selected brokers, dealers and administrators which have entered into service agreements with the Adviser for services provided to shareholders of the Fund. Payments may also be made directly to the intermediaries providing shareholder services. The services provided by such intermediaries are primarily designed to assist shareholders of the Fund and include the furnishing of office space and equipment, telephone facilities, personnel and assistance to the Fund in servicing such shareholders. Services provided by such intermediaries also include the provision of support services to the Fund and includes establishing and maintaining shareholders’ accounts and record processing, purchase and redemption transactions, answering routine client inquiries regarding the Fund, and providing such other personal services to shareholders as the Fund may reasonably request. For the year ended March 31, 2022, the Fund incurred $115,334 in shareholder servicing fees under the Agreement.

6. CAPITAL SHARE TRANSACTIONS

Transactions in shares of the Fund were as follows:

| | | Year Ended | | | Year Ended | |

| | | March 31, 2022 | | | March 31, 2021 | |

| Shares sold | | | 2,632,858 | | | | 4,995,110 | |

| Shares issued to holders in reinvestment of dividends | | | 174,694 | | | | 161,125 | |

| Shares redeemed | | | (1,697,401 | ) | | | (2,569,203 | ) |

| Net increase in shares outstanding | | | 1,110,151 | | | | 2,587,032 | |

7. INVESTMENT TRANSACTIONS

The aggregate purchases and sales, excluding short-term investments, by the Fund for the year ended March 31, 2022, were as follows:

| | | Purchases | | | Sales | |

| U.S. Government Securities | | $ | — | | | $ | — | |

| Other Securities | | $ | 25,457,469 | | | $ | 11,485,381 | |

PORT STREET QUALITY GROWTH FUND

Notes to the Financial Statements – Continued

March 31, 2022

8. FEDERAL TAX INFORMATION

The aggregate gross unrealized appreciation and depreciation of securities held by the Fund and the total cost of securities for federal income tax purposes at March 31, 2022, were as follows:

| Aggregate Gross | Aggregate Gross | Net Unrealized | Federal Income |

Appreciation | Depreciation | Appreciation | Tax Cost |

| $50,166,051 | $(2,435,764) | $47,730,287 | $148,783,728 |

Any difference between book-basis and tax-basis unrealized appreciation is attributable primarily to the differences in tax treatment of wash sales.

At March 31, 2022, components of distributable earnings on a tax-basis were as follows:

| Undistributed | Undistributed | Net Unrealized | Total Distributable |

Ordinary Income | Long-Term Capital Gains | Appreciation | Earnings |

| $14,048 | $3,135,970 | $47,730,287 | $50,880,305 |

As of March 31, 2022, the Fund did not have any capital loss carryovers. A regulated investment company may elect for any taxable year to treat any portion of any qualified late year loss as arising on the first day of the next taxable year. Qualified late year losses are certain capital, and ordinary losses which occur during the portion of the Fund’s taxable year subsequent to October 31 and December 31, respectively. For the taxable year ended March 31, 2022, the Fund did not defer any qualified late year losses.

The tax character of distributions paid during the year ended March 31, 2022 were as follows:

| | Ordinary | Long-Term | | |

| | Income* | Capital Gains | Total | |

| | $461,915 | $3,291,527 | $3,753,442 | |

The tax character of distributions paid during the year ended March 31, 2021 were as follows:

| | Ordinary | Long-Term | | |

| | Income* | Capital Gains | Total | |

| | $461,315 | $2,828,597 | $3,289,912 | |

| * | For federal income tax purposes, distributions of short-term capital gains are treated as ordinary income. |

9. CONTROL OWNERSHIP

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities of a fund creates a presumption of control of the fund, under Section 2(a)(9) of the Investment Company Act of 1940. As of March 31, 2022, Charles Schwab & Co., Inc., for the benefit of its customers, owned 27.05% of the outstanding shares of the Fund.

10. COVID-19

The global outbreak of COVID-19 (commonly referred to as “coronavirus”) has disrupted economic markets and the prolonged economic impact is uncertain. The ultimate economic fallout from the pandemic, and the long-term impact on economies, markets, industries and individual issuers, are not known. The operational and financial performance of the issuers of securities in which the Fund invests depends on future developments, including the duration and

PORT STREET QUALITY GROWTH FUND

Notes to the Financial Statements – Continued

March 31, 2022

spread of the outbreak, and such uncertainty may in turn adversely affect the value and liquidity of the Fund’s investments, impair the Fund’s ability to satisfy redemption requests, and negatively impact the Fund’s performance.

11. REGULATORY UPDATE

In December 2020, the SEC adopted a new rule providing a framework for fund valuation practices (“Rule 2a-5”). Rule 2a-5 establishes requirements for determining fair value in good faith for purposes of the 1940 Act. Rule 2a-5 will permit fund boards to designate certain parties to perform fair value determinations, subject to board oversight and certain other conditions. Rule 2a-5 also defines when market quotations are “readily available” for purposes of the 1940 Act and the threshold for determining whether a fund must fair value a security. In connection with Rule 2a-5, the SEC also adopted related recordkeeping requirements and is rescinding previously issued guidance, including with respect to the role of a board in determining fair value and the accounting and auditing of fund investments. The Fund will be required to comply with the rules by September 8, 2022. Management is currently assessing the potential impact of the new rules on the Fund’s financial statements, if any.

PORT STREET QUALITY GROWTH FUND

Report of Independent Registered Public Accounting Firm

To the Shareholders of Port Street Quality Growth Fund and

Board of Trustees of Managed Portfolio Series

Opinion on the Financial Statements

We have audited the accompanying statements of assets and liabilities, including the schedule of investments, of Port Street Quality Growth Fund (the “Fund”), a series of Managed Portfolio Series, as of March 31, 2022, the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the related notes, and the financial highlights for each of the five years in the period then ended (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of March 31, 2022, the results of its operations for the year then ended, the changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the five years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of March 31, 2022, by correspondence with the custodian and brokers; when replies were not received from brokers, we performed other auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Funds’ auditor since 2014.

COHEN & COMPANY, LTD.

Milwaukee, Wisconsin

May 25, 2022

PORT STREET QUALITY GROWTH FUND

Approval of Investment Advisory Agreement (Unaudited)

Port Street Investments, LLC

Approval of Investment Sub-Advisory Agreement (Unaudited)

Saratoga Research & Investment Management

At the regular meeting of the Board of Trustees of Managed Portfolio Series (“Trust”) on February 22-23, 2022, the Trust’s Board of Trustees (“Board”), each of whom were present in person, including all of the Trustees who are not “interested persons” of the Trust, as that term is defined in Section 2(a)(19) of the Investment Company Act of 1940, as amended, (“Independent Trustees”) considered and approved the continuation of the Investment Advisory Agreement between the Trust and Port Street Investments, LLC (“Port Street” or the “Adviser”) regarding the Port Street Quality Growth Fund (the “Fund”) (the “Investment Advisory Agreement”) and the Investment Sub-Advisory Agreement between Port Street and Saratoga Research & Investment Management (“Saratoga” or “Sub-Adviser”) regarding the Fund (the “Investment Sub-Advisory Agreement”) for another annual term.

Prior to the meeting and at a meeting held on January 11, 2022, the Trustees received and considered information from Port Street, Saratoga and the Trust’s administrator designed to provide the Trustees with the information necessary to evaluate the continuance of the Investment Advisory Agreement and the Investment Sub-Advisory Agreement (“Support Materials”). Before voting to approve the continuance of the Investment Advisory Agreement and the Investment Sub-Advisory Agreement, the Trustees reviewed the Support Materials with Trust management and with counsel to the Independent Trustees, and received a memorandum from such counsel discussing the legal standards for their consideration of the renewal of the Investment Advisory Agreement and Investment Sub-Advisory Agreement. This information, together with the information provided to the Board throughout the course of the year, formed the primary (but not exclusive) basis for the Board’s determinations.

In determining whether to continue the Investment Advisory Agreement and the Investment Sub-Advisory Agreement, the Trustees considered all factors they believed relevant, including the following with respect to the Fund: (1) the nature, extent, and quality of the services provided by Port Street and Saratoga with respect to the Fund; (2) the Fund’s historical performance and the performance of other investment accounts managed by Port Street and Saratoga; (3) the costs of the services provided by Port Street and Saratoga and the profits realized by Port Street from services rendered to the Fund; (4) comparative fee and expense data for the Fund and other investment companies with similar investment objectives; (5) the extent to which economies of scale may be realized as the Fund grows, and whether the advisory fee for the Fund reflects such economies of scale for the Fund’s benefit; and (6) other benefits to Port Street and Saratoga resulting from its relationship with the Funds. In their deliberations, the Trustees weighed to varying degrees the importance of the information provided to them, did not identify any particular information that was all-important or controlling, and considered the information and made its determinations for each Fund separately and independently of the other Fund.

Based upon the information provided to the Board throughout the course of the year, including at an in-person presentation by representatives of Port Street, and the Support Materials, the Board concluded that the overall arrangements between the Trust and Port Street set forth in the Investment Advisory Agreement, and between Port Street and Saratoga as set forth in the Investment Sub-Advisory Agreement, as each agreement relates to the Fund, continue to be fair and reasonable in light of the services that Port Street and Saratoga perform, the investment advisory fees that each receives for such services, and such other matters as the Trustees considered relevant in the exercise of their reasonable business judgment. The material factors and conclusions that formed the basis of the Trustees’ determination to approve the continuation of the Investment Advisory Agreement and the Investment Sub-Advisory Agreement as it relates to each Fund are summarized below.

PORT STREET QUALITY GROWTH FUND

Approval of Investment Advisory Agreement (Unaudited) – Continued

Port Street Investments, LLC

Approval of Investment Sub-Advisory Agreement (Unaudited) – Continued

Saratoga Research & Investment Management

Nature, Extent and Quality of Services Provided. The Trustees considered the scope of services that Port Street provides under the Investment Advisory Agreement, noting that such services and responsibilities differ from those of the Sub-Adviser, and include, but are not limited to, the following with respect to the Fund: (1) providing for and supervising the general management and investment of the Fund’s securities portfolio through the use of a sub-adviser; (2) investing or overseeing the Sub-Adviser’s investment of the Fund’s assets consistent with the Fund’s investment objective and investment policies, and evaluating the Sub-Adviser’s performance results with respect to the Fund; (3) directly managing any portion of the Fund’s assets that the Adviser determines not to allocate to the Sub-Adviser and, with respect to such portion, determining the portfolio securities to be purchased, sold, or otherwise disposed of and the timing of such transactions; (4) voting or overseeing the Sub-adviser’s voting of all proxies with respect to the Fund’s portfolio securities; (5) maintaining and overseeing the Sub-Adviser’s maintenance of the required books and records for transactions that Port Street and/or Saratoga effected on behalf of the Fund; (6) selecting or overseeing the Sub-Adviser’s selection of broker-dealers to execute orders on behalf of the Fund; and (7) monitoring and maintaining the Fund’s compliance with policies and procedures of the Trust and with applicable securities laws, and overseeing the Sub-Adviser’s completion of the same. As part of that considerations the Trustees noted that the Adviser had currently allocated day-to-day portfolio management of all of the Fund’s assets to the Sub-Adviser. The Trustees reviewed Port Street’s assets under management, capitalization and financial statements and noted the fact that Port Street is under common control with Beacon Pointe Advisors, LLC (“Beacon Pointe”), a registered investment adviser with significant assets under management. In that regard, the Trustees concluded that Port Street has sufficient resources to support the management of the Fund. The Trustees also noted that the Trust and Adviser have obtained exemptive relief to allow the Adviser to operate the Fund in a “manager of managers” structure, which enables the Adviser to terminate and replace a sub-adviser without requesting shareholder approval. The Trustees considered the investment philosophy of Port Street’s portfolio managers and their investment industry experience. The Trustees concluded that they were satisfied with the nature, extent and quality of services that Port Street provides to the Fund under the Investment Advisory Agreement.

Similar to the review of Port Street, the Trustees considered the scope of distinct services that Saratoga provides under the Investment Sub-Advisory Agreement with respect to such portions of the Fund that the Adviser allocates to Saratoga’s management, and subject to the Adviser’s oversight, noting that such services include, but are not limited to, the following: (1) investing the Fund’s assets consistent with the Fund’s investment objective and investment policies; (2) determining the portfolio securities to be purchased, sold, or otherwise disposed of and the timing of such transactions; (3) voting proxies, if any, with respect to the Fund’s portfolio securities; (4) maintaining the required books and records for transactions Saratoga effected on behalf of the Fund; (5) selecting broker-dealers to execute orders on behalf of the Fund; and (6) monitoring and maintaining the Fund’s compliance with policies and procedures of the Trust and with applicable securities laws. The Trustees reviewed Saratoga’s assets under management, financial statements and its capitalization. The Trustees concluded that Saratoga had sufficient resources to support Saratoga’s management of the Fund. The Trustees noted the investment philosophy of Saratoga’s portfolio manager and his significant portfolio management experience. The Trustees concluded that they were satisfied with the nature, extent and quality of services that Saratoga provides to the Fund under the Investment Sub-Advisory Agreement.

PORT STREET QUALITY GROWTH FUND

Approval of Investment Advisory Agreement (Unaudited) – Continued

Port Street Investments, LLC

Approval of Investment Sub-Advisory Agreement (Unaudited) – Continued

Saratoga Research & Investment Management

Fund Historical Performance and the Overall Performance of Port Street and Saratoga. In assessing the quality of the portfolio management delivered by Port Street and Saratoga, the Trustees reviewed the short-term and long-term performance of the Fund on both an absolute basis and in comparison to appropriate benchmark indices, the Fund’s peer funds according to Morningstar classifications (the “Peer Group”), and as compiled by Barrington Partners (the, a “Morningstar BP Cohort”), and the composite of separate accounts that Saratoga manages utilizing a similar investment strategy as that of the Fund. The Trustees noted that the Fund had underperformed both the Peer Group and the Morningstar BP Cohort for the year-to-date, one-year, three-year and five-year periods ended September 30, 2021. The Trustees also considered that the Fund had underperformed its benchmark indexes for the year-to-date period ended September 30, 2021 and for the one-year, three-year, five-year and since inception periods ended December 31, 2020. The Trustees took into account that the Fund’s strategy contemplates the Fund holding a significant cash position, which impacted relative performance during periods reviewed by the Board. The Trustees also took into account that the Fund had achieved positive absolute returns across all reviewed periods since inception. The Trustees then observed that the investment performance of Saratoga’s similarly managed account composite generally tracked the Fund’s performance.

Cost of Advisory Services and Profitability. The Trustees considered the annual advisory fee that the Fund pays to Port Street under the Investment Advisory Agreement, as well as Port Street’s profitability analysis for services that Port Street rendered to the Fund during the 12 months ending September 30, 2021. The Trustees also considered the effect of an expense limitation agreement on Port Street’s compensation and that Port Street has contractually agreed to reduce its advisory fees and, if necessary, reimburse the Fund for operating expenses, as specified in the Fund’s prospectus. In that regard, the Trustees noted that Port Street had waived a portion of its advisory fees during the one-year period ended September 30, 2021. The Trustees observed that Port Street does not manage other accounts utilizing a similar investment strategy as that of the Fund for purposes of conducting a management fee comparison. The Trustees concluded that Port Street’s service relationship with the Fund had yielded a reasonable profit for Port Street.

The Trustees also considered the annual sub-advisory fee that Port Street pays to Saratoga under the Investment Sub-Advisory Agreement. While the Trustees noted the management fees Saratoga charges to separately managed accounts with similar investment strategies and similar asset levels to those of the Fund are generally higher than the sub-advisory fee for the Fund, the Trustees also noted the scope of services that Saratoga provides to the Fund pursuant to the Investment Sub-Advisory Agreement are more limited than the services Saratoga provides to these separately managed accounts. The Trustees noted that because the sub-advisory fees are paid by Port Street, the overall advisory fee paid by the Fund is not directly affected by the sub-advisory fees paid to Saratoga. Consequently, the Trustees did not consider the costs of services provided by Saratoga or the profitability of their relationship with the Fund to be material factors for consideration given that Saratoga is not affiliated with Port Street and, therefore, the sub-advisory fees were negotiated on an arm’s length basis.

Comparative Fee and Expense Data. The Trustees considered a comparative analysis of contractual expenses borne by the Fund and those of funds in the Morningstar BP Cohort. The Trustees noted the Fund’s management fee was higher than the Morningstar BP Cohort average. They also considered the total expenses of the Fund (after waivers and expense reimbursements) were higher than the Morningstar BP Cohort average. The Trustees took into

PORT STREET QUALITY GROWTH FUND

Approval of Investment Advisory Agreement (Unaudited) – Continued

Port Street Investments, LLC

Approval of Investment Sub-Advisory Agreement (Unaudited) – Continued

Saratoga Research & Investment Management

account that the advisory fees and total expenses (after waivers and expense reimbursements) borne by the Fund were well within the range of that borne by funds in the benchmark category. While recognizing that it is difficult to compare advisory fees because the scope of advisory services provided may vary from one investment adviser to another, the Trustees concluded that Port Street’s advisory fee and the portion of such fee that it allocates to Saratoga continues to be reasonable.

Economies of Scale. The Trustees considered whether the Fund would benefit from any economies of scale and noted the investment advisory fee for the Fund contains breakpoints and that the Fund’s assets had grown to the point where the initial breakpoint had been triggered. The Trustees noted that Port Street anticipates realizing additional economies of scale if Fund assets should increase materially from current levels. The Trustees concluded that the Fund was currently benefitting from economies of scale and would achieve additional benefits if the Fund’s assets were to grow materially from current levels.

Other Benefits. The Trustees considered the direct and indirect benefits that could be realized by the Adviser or the Sub-Adviser, and their affiliates, from their respective relationships with the Fund. The Trustees noted neither Port Street nor Saratoga utilizes soft dollar arrangements with respect to portfolio transactions and do not use affiliated brokers to execute the Fund’s portfolio transactions. The Trustees considered that the Adviser or the Sub-Adviser may receive some form of reputational benefit from services rendered to the Fund, but that such benefits are immaterial and cannot otherwise be quantified. The Trustees concluded that Port Street and Saratoga do not receive additional material benefits from their relationship with the Fund.

PORT STREET QUALITY GROWTH FUND

Additional Information (Unaudited)

March 31, 2022

TRUSTEES AND OFFICERS

| | | | Number of | | Other |

| | | | Portfolios | | Directorships |

| | Position(s) | Term of Office | in Trust | | Held by Trustee |

| Name, Address and | Held with | and Length of | Overseen | Principal Occupation(s) | During the |

Year of Birth | the Trust | Time Served | by Trustee | During the Past Five Years | Past Five Years |

| | | | | | |

| Independent Trustees | | | | | |

| | | | | | |

| Leonard M. Rush, CPA | Chairman, | Indefinite | 38 | Retired; Chief Financial Officer, | Independent Trustee, |

| 615 E. Michigan St. | Trustee | Term; Since | | Robert W. Baird & Co. | ETF Series Solutions |

| Milwaukee, WI 53202 | and Audit | April 2011 | | Incorporated, (2000-2011). | (60 Portfolios) |

| Year of Birth: 1946 | Committee | | | | (2012-Present) |

| | Chairman | | | | |

| | | | | | |

| David M. Swanson | Trustee and | Indefinite | 38 | Founder and Managing Principal, | Independent Trustee, |

| 615 E. Michigan St. | Nominating & | Term; Since | | SwanDog Strategic Marketing, LLC | ALPS Variable |

| Milwaukee, WI 53202 | Governance | April 2011 | | (2006-present); Executive Vice President, | Investment Trust |

| Year of Birth: 1957 | Committee | | | Calamos Investments (2004-2006). | (7 Portfolios) |

| | Chairman | | | | (2006-Present); |

| | | | | | Independent Trustee, |

| | | | | | RiverNorth Funds |

| | | | | | (3 Portfolios) |

| | | | | | (2018-Present); |

| | | | | | RiverNorth Managed |

| | | | | | Duration Municipal |

| | | | | | Income Fund Inc. |

| | | | | | (1 Portfolio) |

| | | | | | (2019-Present); |

| | | | | | RiverNorth Specialty |

| | | | | | Finance Corporation |

| | | | | | (1 Portfolio) |

| | | | | | (2018-Present); |

| | | | | | RiverNorth/ |

| | | | | | DoubleLine |

| | | | | | Strategic |

| | | | | | Opportunity Fund, |

| | | | | | Inc. (1 Portfolio) |

| | | | | | (2018-Present); |

| | | | | | RiverNorth |

| | | | | | Opportunities Fund, |

| | | | | | Inc. (1 Portfolio) |

| | | | | | (2015-Present); |

| | | | | | RiverNorth |

| | | | | | Opportunistic |

| | | | | | Municipal Income |

| | | | | | Fund, Inc. |

| | | | | | (1 Portfolio) |

| | | | | | (2018-Present); |

| | | | | | RiverNorth Flexible |

| | | | | | Municipal Income |

| | | | | | Fund (2020-Present). |

PORT STREET QUALITY GROWTH FUND

Additional Information (Unaudited) – Continued

March 31, 2022

| | | | Number of | | Other |

| | | | Portfolios | | Directorships |

| | Position(s) | Term of Office | in Trust | | Held by Trustee |

| Name, Address and | Held with | and Length of | Overseen | Principal Occupation(s) | During the |

Year of Birth | the Trust | Time Served | by Trustee | During the Past Five Years | Past Five Years |

| Robert J. Kern | Trustee | Indefinite | 38 | Retired (July 2018 – present); | None |

| 615 E. Michigan St. | | Term; Since | | Executive Vice President, | |

| Milwaukee, WI 53202 | | January 2011 | | U.S. Bancorp Fund Services, LLC | |

| Year of Birth: 1958 | | | | (1994-2018). | |

| | | | | | |

| Interested Trustee | | | | | |

| | | | | | |

| David A. Massart* | Trustee | Indefinite | 38 | Partner and Managing Director, | Independent Trustee, |

| 615 E. Michigan St. | | Term; Since | | Beacon Pointe Advisors, LLC | ETF Series Solutions |

| Milwaukee, WI 53202 | | April 2011 | | (since 2022); Co-Founder and Chief | (60 Portfolios) |

| Year of Birth: 1967 | | | | Investment Strategist, Next Generation | (2012-Present) |

| | | | | Wealth Management Inc. (2005-2021). | |

| | | | | | |

| Officers | | | | | |

| | | | | | |

| Brian R. Wiedmeyer | President and | Indefinite | N/A | Vice President, U.S. Bancorp Fund | N/A |

| 615 E. Michigan St. | Principal | Term; Since | | Services, LLC (2005-present). | |

| Milwaukee, WI 53202 | Executive | November 2018 | | | |

| Year of Birth: 1973 | Officer | | | | |

| | | | | | |

| Deborah Ward | Vice President, | Indefinite | N/A | Senior Vice President, U.S. Bancorp | N/A |

| 615 E. Michigan St. | Chief | Term; Since | | Fund Services, LLC (2004-present). | |

| Milwaukee, WI 53202 | Compliance | April 2013 | | | |

| Year of Birth: 1966 | Officer and | | | | |

| | Anti-Money | | | | |

| | Laundering | | | | |

| | Officer | | | | |

| | | | | | |

| Benjamin Eirich | Treasurer, | Indefinite | N/A | Assistant Vice President, U.S. Bancorp | N/A |

| 615 E. Michigan St. | Principal | Term; Since | | Fund Services, LLC (2008-present). | |

| Milwaukee, WI 53202 | Financial | August 2019 | | | |

| Year of Birth: 1981 | Officer and | (Treasurer); | | | |

| | Vice President | Indefinite | | | |

| | | Term; Since | | | |

| | | November 2018 | | | |

| | | (Vice President) | | | |

| | | | | | |

| John Hadermayer | Secretary | Indefinite | N/A | Vice President, U.S. Bank Global | N/A |

| 615 E. Michigan St. | | Term; Since | | Fund Services (2022-present); | |

| Milwaukee, WI 53202 | | May 2022 | | Executive Director, AQR Capital | |

| Year of Birth: 1977 | | | | Management, LLC (2013-2022). | |

| * | Mr. Massart is considered an “interested person” of this Fund, as defined by the 1940 Act, because he is a Partner and Managing Director of Beacon Point Advisors, LLC, which shares common control of Port Street Investments, LLC, the Fund’s Adviser. |

PORT STREET QUALITY GROWTH FUND

Additional Information (Unaudited) – Continued

March 31, 2022

| | | | Number of | | Other |

| | | | Portfolios | | Directorships |

| | Position(s) | Term of Office | in Trust | | Held by Trustee |

| Name, Address and | Held with | and Length of | Overseen | Principal Occupation(s) | During the |

Year of Birth | the Trust | Time Served | by Trustee | During the Past Five Years | Past Five Years |

| Douglas Schafer | Assistant | Indefinite | N/A | Assistant Vice President, U.S. Bancorp | N/A |

| 615 E. Michigan St. | Treasurer and | Term; Since | | Fund Services, LLC (2002-present). | |

| Milwaukee, WI 53202 | Vice President | May 2016 | | | |

| Year of Birth: 1970 | | (Assistant | | | |

| | | Treasurer); | | | |

| | | Indefinite | | | |

| | | Term; Since | | | |

| | | November 2018 | | | |

| | | (Vice President) | | | |

| | | | | | |

| Sara J. Bollech | Assistant | Indefinite | N/A | Officer, U.S. Bancorp Fund Services, | N/A |

| 615 E. Michigan St. | Treasurer and | Term: Since | | LLC (2007-present). | |

| Milwaukee, WI 53202 | Vice President | November 2021 | | | |

| Year of Birth: 1977 | | | | | |

| | | | | | |

| Peter A. Walker, CPA | Assistant | Indefinite | N/A | Officer, U.S. Bancorp Fund Services, | N/A |

| 615 E. Michigan St. | Treasurer and | Term: Since | | LLC (2016-present). | |

| Milwaukee, WI 53202 | Vice President | November 2021 | | | |

| Year of Birth: 1993 | | | | | |

PORT STREET QUALITY GROWTH FUND

Additional Information (Unaudited)

March 31, 2022

AVAILABILITY OF FUND PORTFOLIO INFORMATION

The Fund files complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Part F of Form N-PORT. The Fund’s Part F of Form N-PORT is available on the SEC’s website at www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. For information on the Public Reference Room call 1-800-SEC-0330. In addition, the Fund’s Part F of Form N-PORT is available without charge upon request by calling 1-855-282-2386.

AVAILABILITY OF PROXY VOTING INFORMATION

A description of the Fund’s Proxy Voting Policies and Procedures is available without charge, upon request, by calling 1-855-369-6220. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12 month period ended June 30, is available (1) without charge, upon request, by calling 1-855-369-6220, or (2) on the SEC’s website at www.sec.gov.

QUALIFIED DIVIDEND INCOME/DIVIDENDS RECEIVED DEDUCTION

For the fiscal year ended March 31, 2022, certain dividends paid by the Fund may be reported as qualified dividend income and may be eligible for taxation at capital gain rates. The percentage of dividends declared from ordinary income designated as qualified dividend income was 100.00% for the Fund. For corporate shareholders, the percent of ordinary income distributions qualifying for the corporate dividends received deduction for the fiscal year ended March 31, 2022, was 100.00% for the Fund. The percentage of taxable ordinary income distributions that are designated as short-term capital gain distributions under Internal Revenue Section 871(k)(2)(c) was 98.99%.

PORT STREET QUALITY GROWTH FUND

Privacy Notice (Unaudited)

The Fund collects only relevant information about you that the law allows or requires it to have in order to conduct its business and properly service you. The Fund collects financial and personal information about you (“Personal Information”) directly (e.g., information on account applications and other forms, such as your name, address, and social security number, and information provided to access account information or conduct account transactions online, such as password, account number, e-mail address, and alternate telephone number), and indirectly (e.g., information about your transactions with us, such as transaction amounts, account balance and account holdings).

The Fund does not disclose any non-public personal information about its shareholders or former shareholders other than for everyday business purposes such as to process a transaction, service an account, respond to court orders and legal investigations or as otherwise permitted by law. Third parties that may receive this information include companies that provide transfer agency, technology and administrative services to the Fund, as well as the Fund’s investment adviser who is an affiliate of the Fund. If you maintain a retirement/educational custodial account directly with the Fund, we may also disclose your Personal Information to the custodian for that account for shareholder servicing purposes. The Fund limits access to your Personal Information provided to unaffiliated third parties to information necessary to carry out their assigned responsibilities to the Fund. All shareholder records will be disposed of in accordance with applicable law. The Fund maintains physical, electronic and procedural safeguards to protect your Personal Information and requires its third party service providers with access to such information to treat your Personal Information with the same high degree of confidentiality.

In the event that you hold shares of the Fund through a financial intermediary, including, but not limited to, a broker-dealer, credit union, bank or trust company, the privacy policy of your financial intermediary governs how your non-public personal information is shared with unaffiliated third parties.

(This Page Intentionally Left Blank.)

INVESTMENT ADVISER

Port Street Investments, LLC

24 Corporate Plaza, Suite 150

Newport Beach, CA 92660

DISTRIBUTOR

Quasar Distributors, LLC

111 East Kilbourn Avenue, Suite 2200

Milwaukee, WI 53202

CUSTODIAN

U.S. Bank N.A.

1555 North Rivercenter Drive. Suite 302

Milwaukee, WI 53212

ADMINISTRATOR, FUND ACCOUNTANT

AND TRANSFER AGENT

U.S. Bancorp Fund Services, LLC

615 East Michigan Street

Milwaukee, WI 53202

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Cohen & Company, Ltd.

342 North Water Street, Suite 830

Milwaukee, WI 53202

LEGAL COUNSEL

Stradley Ronon Stevens & Young, LLP

2005 Market Street, Suite 2600

Philadelphia, PA 19103

This report should be accompanied or preceded by a prospectus.

The Fund’s Statement of Additional Information contains additional information about the

Fund’s trustees and is available without charge upon request by calling 1-855-369-6220.

Item 2. Code of Ethics.

The Registrant has adopted a code of ethics that applies to the Registrant’s principal executive officer and principal financial officer. The Registrant has not made any substantive amendments to its code of ethics during the period covered by this report.

The Registrant has not granted any waivers from any provisions of the code of ethics during the period covered by this report.

A copy of the Registrant’s code of ethics that applies to the Registrant’s principal executive officer and principal financial officer is filed herewith.

Item 3. Audit Committee Financial Expert.

The Registrant’s Board of Trustees has determined that there is at least one audit committee financial expert serving on its audit committee. Leonard M. Rush is the “audit committee financial expert” and is considered to be “independent” as each term is defined in Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

The Registrant has engaged its principal accountant to perform audit services, audit-related services, tax services and other services during the past two fiscal years. “Audit services” refer to performing an audit of the Registrant's annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years. “Audit-related services” refer to the assurance and related services by the principal accountant that are reasonably related to the performance of the audit. “Tax services” refer to professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning, including reviewing the Fund’s tax returns and distribution calculations. There were no “other services” provided by the principal accountant. For the fiscal years ended March 31, 2022, and March 31, 2021, the Fund’s principal accountant was Cohen & Company, Ltd. The following table details the aggregate fees billed or expected to be billed for the last two fiscal years for audit fees, audit-related fees, tax fees and other fees by the principal accountant.

| | FYE 3/31/2022 | FYE 3/31/2021 |

(a) Audit Fees | $14,000 | $14,000 |

(b) Audit-Related Fees | $0 | $0 |

(c) Tax Fees | $5,000 | $5,000 |

(d) All Other Fees | $0 | $0 |

(e)(1) The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre‑approve all audit and non‑audit services of the Registrant, including services provided to any entity affiliated with the Registrant.

(e)(2) The percentage of fees billed by Cohen & Company, Ltd. applicable to non-audit services pursuant to waiver of pre-approval requirement was as follows:

| | FYE 3/31/2022 | FYE 3/31/2021 |

Audit-Related Fees | 0% | 0% |

Tax Fees | 0% | 0% |

All Other Fees | 0% | 0% |

(f) All of the principal accountant’s hours spent on auditing the Registrant’s financial statements were attributed to work performed by full‑time permanent employees of the principal accountant.

(g) The following table indicates the non-audit fees billed or expected to be billed by the Registrant’s accountant for services to the Registrant and to the Registrant’s investment adviser (and any other controlling entity, etc.—not sub-adviser) for the last two years.

Non-Audit Related Fees | FYE 3/31/2022 | FYE 3/31/2021 |

Registrant | $0 | $0 |