UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-22558

BROOKFIELD INVESTMENT FUNDS

(Exact name of registrant as specified in charter)

BROOKFIELD PLACE

250 VESEY STREET, 15th Floor

NEW YORK, NEW YORK 10281-1023

(Address of principal executive offices) (Zip code)

BRIAN F. HURLEY, PRESIDENT

BROOKFIELD INVESTMENT FUNDS

BROOKFIELD PLACE

250 VESEY STREET 15th Floor

NEW YORK, NEW YORK 10281-1023

(Name and address of agent for service)

Registrant’s telephone number, including area code: (855)777-8001

Date of fiscal year end: December 31

Date of reporting period: December 31, 2018

Item 1. Reports to Shareholders.

Brookfield Public Securities Group LLC

* Please see inside front cover of the report for important information regarding future delivery of shareholder reports.

ANNUAL REPORT

December 31, 2018

Brookfield Global Listed Infrastructure Fund

Brookfield Global Listed Real Estate Fund

Brookfield U.S. Listed Real Estate Fund

Brookfield Real Assets Securities Fund

Brookfield Public Securities Group LLC (the “Firm”) is an SEC-registered investment adviser and represents the Public Securities platform of Brookfield Asset Management. The Firm provides global listed real assets strategies including real estate equities, infrastructure equities, energy nfrastructure equities, real asset debt and diversified real assets. With approximately $16.5 billion of assets under management as of December 31, 2018, the Firm manages separate accounts, registered funds and opportunistic strategies for institutional and individual clients, including financial institutions, public and private pension plans, insurance companies, endowments and foundations, sovereign wealth funds and high net worth investors. The Firm is a wholly owned subsidiary of Brookfield Asset Management, a leading global alternative asset manager with over $350 billion of assets under management as of December 31, 2018. For more information, go to www.brookfield.com.

Brookfield Investment Funds (the “Trust”) is managed by Brookfield Public Securities Group LLC. The Trust uses its website as a channel of distribution of material company information. Financial and other material information regarding the Trust is routinely posted on and accessible at www.brookfield.com.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Funds’ annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website (https://publicsecurities.brookfield.com/en), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a Fund electronically anytime by contacting your financial intermediary (such as a broker, investment adviser, bank or trust company) or, if you are a direct investor, by calling the Fund (toll-free) at 1-855-777-8001 or by sending an e-mail request to a Fund at publicsecurities.enquiries@brookfield.com.

Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with a Fund, you may call 1-855-777-8001 or send an email request to publicsecurities.enquiries@brookfield.com to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held within the fund complex if you invest directly with a Fund.

This report is for shareholder information. This is not a prospectus intended for the use in the purchase or sale of Fund shares.

| NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED |

[THIS PAGE IS INTENTIONALLY LEFT BLANK]

Dear Shareholders,

We are pleased to provide the Annual Report for Brookfield Global Listed Infrastructure Fund (the “Infrastructure Fund”), Brookfield Global Listed Real Estate Fund (the “Global Real Estate Fund”), Brookfield U.S. Listed Real Estate Fund (the “U.S. Real Estate Fund”) and Brookfield Real Assets Securities Fund (the “Real Assets Securities Fund”) (each, a “Fund”, and collectively, the “Funds”) for the year ended December 31, 2018.

Global markets whipsawed in 2018. In the first quarter the MSCI World Index1 snapped a seven-quarter streak of positive total returns. The decline was largely driven by fears that rising inflation, tighter job markets and fiscal stimulus would accelerate the pace of U.S. interest-rate hikes. Those fears appeared to subside as global equities drifted higher throughout the second and third quarters. However, global equities declined sharply in the fourth quarter amid concerns around slowing global economic growth related to ongoing trade disputes and geopolitical uncertainty; as well as tighter monetary policies by central banks.

The ongoing trade dispute between the U.S. and China continued to escalate throughout 2018, as the two imposed billions of dollars in tariffs on one another across hundreds of products. In December, the two nations announced a temporary truce to de-escalate the situation. However, the negative implications of these policies are beginning to appear in economies across the globe.

The U.S. Federal Reserve’s Federal Open Market Committee increased the target range for the federal funds rate on four occasions in 2018 (25 basis points each). At the press conference following the December announcement, Fed Chairman Jerome Powell appeared to spook markets when he indicated the unwinding of the Fed’s balance sheet holdings would remain on “autopilot.” Also during the quarter, the European Central Bank confirmed it would formally end its multi-trillion bond-buying program which began in March 2015.

With the exception of energy infrastructure, real asset equities outperformed broad market equities in 2018.2 Relative outperformance was particularly meaningful in the fourth quarter, when volatility increased. In our view, the relative outperformance of real assets over the recent market drawdown reflects on the historically defensive nature of companies that own and operate tangible real assets, such as real estate and infrastructure. For real estate, these defensive characteristics are driven by the contracted lease structures of commercial real estate properties. For infrastructure, the assets are usually long-lived with revenues that are contracted or regulated, often linked to inflation.

While we do see evidence of modest growth in the global economy, we also acknowledge an uptick of market and economic risks across the globe. We believe these conditions make listed real assets even more attractive for investors to own in their portfolios. These companies—which provide critical infrastructure and makeup the backbone of the global economy, have been shown to produce resilient cash flows throughout economic cycles.

In addition to performance information and additional discussion on factors impacting the Funds, this report provides the Funds’ audited financial statements and schedule of investments as of December 31, 2018.

We welcome your questions and comments, and encourage you to contact our Investor Relations team at (855) 777-8001 or visit us at www.brookfield.com for more information. Thank you for your support.

Brian F. Hurley

President

Brookfield Investment Funds

Craig Noble, CFA

CEO, Chief Investment Officer and Portfolio Manager

Brookfield Public Securities Group LLC

Letter to Shareholders(continued)

Past performance is no guarantee of future results.

Must be preceded or accompanied by a prospectus.

1 The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

2 Real Asset equities are represented by the Alerian MLP, FTSE EPRA Nareit Developed and Dow Jones Brookfield Global Infrastructure Composite Indexes. The Alerian MLP Index is a composite of the 50 most prominent energy MLPs calculated by Standard & Poor’s using a float-adjusted market-capitalization methodology. The index is disseminated by the New York Stock Exchange real-time on a price return basis (NYSE: AMZ) and on a total-return basis (NYSE:AMZX). The FTSE EPRA Nareit Developed Index is a free-float adjusted, liquidity, size and revenue screened index designed to track the performance of listed real estate companies and REITs worldwide. The Dow Jones Brookfield Global Infrastructure Composite Index is calculated and maintained by S&P Dow Jones Indices and comprises infrastructure companies with at least 70% of its annual cash flows derived from owning and operating infrastructure assets, including MLPs. Broad equities are represented by the MSCI World Index.

Indices are not managed and an investor cannot invest directly in an index.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2018 and subject to change based on subsequent developments.

The Funds’ portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Funds currently hold these securities. Please refer to the Schedules of Investments contained in this report for a full listing of Funds’ holdings.

Mutual fund investing involves risk. Principal loss is possible.

Quasar Distributors, LLC is the distributor of Brookfield Investment Funds.

A basis point (bps) is a unit that is equal to 1/100 of 1%, and is used to denote the change in a financial instrument.

2Brookfield Public Securities Group LLC

About Your Fund’s Expenses

As a shareholder of a Fund, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and contingent deferred sales charges and redemption fees on redemptions; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Fund Return

The table below provides information about actual account values and actual expenses. You may use the information on this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical account values and hypothetical expenses based on the Funds’ actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Funds’ actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Funds and other funds. To do so, compare this 5% hypothetical example with hypothetical examples that appear in shareholders’ reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) and redemption fees. Therefore, the hypothetical account values and expenses in the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs overall would have been higher.

| | Annualized Expense Ratio | Beginning Account Value

(07/01/18) | Ending Account Value

(12/31/18) | Expenses Paid During Period

(07/01/18–

12/31/18)(1) |

| INFRASTRUCTURE FUND | | | | |

| Actual | | | | |

Class A Shares

| 1.35% | $1,000.00 | $926.70 | $6.56 |

Class C Shares

| 2.10% | 1,000.00 | 923.20 | 10.18 |

Class Y Shares

| 1.10% | 1,000.00 | 928.10 | 5.35 |

Class I Shares

| 1.10% | 1,000.00 | 928.20 | 5.35 |

| Hypothetical (assuming a 5% return before expenses) | | | | |

Class A Shares

| 1.35% | 1,000.00 | 1,018.40 | 6.87 |

Class C Shares

| 2.10% | 1,000.00 | 1,014.62 | 10.66 |

Class Y Shares

| 1.10% | 1,000.00 | 1,019.66 | 5.60 |

Class I Shares

| 1.10% | 1,000.00 | 1,019.66 | 5.60 |

About Your Fund’s Expenses (continued)

| | Annualized Expense Ratio | Beginning Account Value

(07/01/18) | Ending Account Value

(12/31/18) | Expenses Paid During Period

(07/01/18–

12/31/18)(1) |

| GLOBAL REAL ESTATE FUND | | | | |

| Actual | | | | |

Class A Shares

| 1.20% | $1,000.00 | $917.00 | $5.80 |

Class C Shares

| 1.95% | 1,000.00 | 912.80 | 9.40 |

Class Y Shares

| 0.95% | 1,000.00 | 916.90 | 4.59 |

Class I Shares

| 0.95% | 1,000.00 | 917.60 | 4.59 |

| Hypothetical (assuming a 5% return before expenses) | | | | |

Class A Shares

| 1.20% | 1,000.00 | 1,019.16 | 6.11 |

Class C Shares

| 1.95% | 1,000.00 | 1,015.38 | 9.91 |

Class Y Shares

| 0.95% | 1,000.00 | 1,020.42 | 4.84 |

Class I Shares

| 0.95% | 1,000.00 | 1,020.42 | 4.84 |

| U.S. REAL ESTATE FUND | | | | |

| Actual | | | | |

Class A Shares

| 1.20% | $1,000.00 | $925.20 | $5.82 |

Class C Shares

| 1.95% | 1,000.00 | 921.10 | 9.44 |

Class Y Shares

| 0.95% | 1,000.00 | 926.20 | 4.61 |

Class I Shares

| 0.95% | 1,000.00 | 926.00 | 4.61 |

| Hypothetical (assuming a 5% return before expenses) | | | | |

Class A Shares

| 1.20% | 1,000.00 | 1,019.16 | 6.11 |

Class C Shares

| 1.95% | 1,000.00 | 1,015.38 | 9.91 |

Class Y Shares

| 0.95% | 1,000.00 | 1,020.42 | 4.84 |

Class I Shares

| 0.95% | 1,000.00 | 1,020.42 | 4.84 |

| REAL ASSETS SECURITIES FUND | | | | |

| Actual | | | | |

Class A Shares

| 1.35% | $1,000.00 | $923.40 | $6.54 |

Class C Shares

| 2.10% | 1,000.00 | 921.20 | 10.17 |

Class Y Shares

| 1.10% | 1,000.00 | 924.40 | 5.34 |

Class I Shares

| 1.10% | 1,000.00 | 924.30 | 5.34 |

| Hypothetical (assuming a 5% return before expenses) | | | | |

Class A Shares

| 1.35% | 1,000.00 | 1,018.40 | 6.87 |

Class C Shares

| 2.10% | 1,000.00 | 1,014.62 | 10.66 |

Class Y Shares

| 1.10% | 1,000.00 | 1,019.66 | 5.60 |

Class I Shares

| 1.10% | 1,000.00 | 1,019.66 | 5.60 |

| (1) | Expenses are equal to the Funds’ annualized expense ratio by class multiplied by the average account value over the period, multiplied by 184/365 (to reflect a six-month period). |

4Brookfield Public Securities Group LLC

Brookfield Global Listed Infrastructure Fund

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

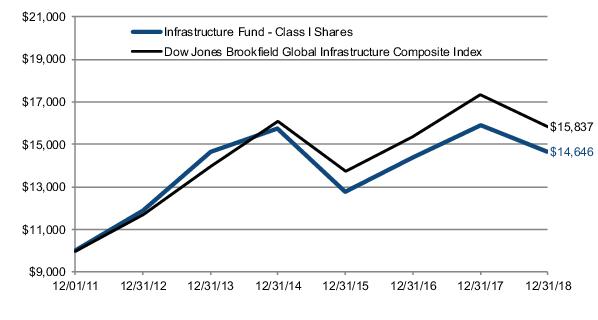

For the year ended December 31, 2018, the Infrastructure Fund, Class I had a total return of -7.95%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions, overperforming the Dow Jones Brookfield Global Infrastructure Composite Index1, which returned -8.54%.

By sector, the leading contributor to relative performance was the non-index Renewables/Electric Generation. Stock selection within the MLP and Toll Roads sector also contributed. Within the MLP sector, relative outperformance was due to a combination of overweight exposure to outperforming names, coupled with not owning a number of underperforming stocks. Relative outperformance within the Toll Roads sector was due to outperforming non-index holdings, as well as underweight exposure to several underperforming stocks.

Conversely, the Gas Utilities was the leading detractor from relative returns, driven by underweight exposure and stock selection. Underperformance was largely due to underweight exposure to Asia Pacific gas utilities, which performed well during the year. Stock selection within the Electricity Transmission & Distribution sector also detracted, driven by overweight exposure to PG&E Corporation (PCG, Electricity Transmission & Distribution, U.S.) and underweight allocations to a number of outperforming stocks in the group. An underweight allocation within Communications also detracted, largely driven by not owning select satellite companies. These companies outperformed amid speculation that the U.S. Federal Communications Commission is considering repurposing a portion of the C-band (3700-4200 MHz) spectrum from satellite services for next-generation 5G services.

By region, the U.S., Latin America and Canada were the leading contributors due to stock selection. Conversely, Asia Pacific was the leading detractor from relative performance due to stock selection and underweight exposure. Stock selection and overweight allocations in Continental Europe and the U.K. were also leading detractors.

By security, non-index holding Orsted A/S (ORSTED.DC, Renewables/Electric Generation, Continental Europe) was the leading contributor to relative returns. The timing of overweight exposure to Energy Transfer Operating, L.P. (ETP, MLP, U.S.) also contributed as the stock performed well amid the merger of Energy Transfer Equity, L.P. and Energy Transfer Partners, L.P., which simplified the overall structure of the company. The timing of underweight exposure to Edison International (EIX, Electricity Transmission & Distribution, U.S.) was also a leading contributor as the stock declined meaningfully following the Southern California wildfires.

Conversely, an overweight allocation to PG&E Corporation (PCG, Electricity Transmission & Distribution, U.S.) was the leading detractor from relative returns. The stock also declined meaningfully following the Northern California wildfires. Overweight exposure to Atlantia S.p.A (ATL.IM, Toll Roads, Continental Europe) also detracted as the stock fell following the Morandi bridge tragedy in Genoa, Italy. Underweight exposure to Hong Kong & China Gas Co. Ltd. (3.HK, Gas Utilities, Asia Pacific) also detracted as the stock rallied during the year.

INFRASTRUCTURE MARKET OVERVIEW

Listed infrastructure returns were negative in 2018, as measured by the Dow Jones Brookfield Global Infrastructure Composite Index, which declined 8.5% during the year. By region, the Americas was down 6.9%, while Asia Pacific and Europe rose 4.7% and 1.2%, respectively. By sector, Ports declined the most (−26.6%), followed by Water (−7.4%), Airports (−7.1%), Electricity Transmission & Distribution (−6.2%), Oil & Gas Storage & Transportation (−4.6%), Toll Roads (−2.3%) and Diversified (−0.7%). Only Communications (+6.5%) posted positive gains.

As measured by the Alerian MLP Index, Energy infrastructure continued on its recovery path during the first half of the year, driven by improved sentiment amid strong fundamentals and higher commodity prices. Within the MLP universe, however, returns varied as some companies were more adversely impacted by the surprise announcement in March from the Federal Energy Regulatory Commission (“FERC”) that disallowed an MLP to recover an income tax allowance in its cost of service rates.

The FERC made another surprise announcement on July 18, 2018 with a modified proposal that clarified the original March ruling. The modified proposal, in our view, substantially mitigates the potential rate reductions

Brookfield Global Listed Infrastructure Fund

through the removal of Accumulated Deferred Income Taxes (ADIT) from the rate base by allowing consolidated MLPs to include a federal income tax allowance in certain instances. At a minimum, the additional clarity provided by the modified proposal should ameliorate the uncertainty surrounding those names most impacted by the previous FERC actions.

After posting positive returns through the first three quarters, energy infrastructure stocks, as measured by the Alerian MLP Index2, declined in the fourth quarter as the price of West Texas Intermediate Crude Oil fell more than 35%.

Utilities generally outperformed global equities on a relative basis, especially during the fourth quarter in a flight to quality amid heightened volatility. Overall performance within the group, however, was hindered by California utilities, which underperformed following wildfires in the state. Select U.K. utilities also lagged amid regulatory uncertainty.3

Within the transports sector, ports were hit particularly hard amid global trade disputes. This small group of stocks declined roughly 27% during the year. Airports declined on a clouded outlook for global economic growth, as well as political uncertainty in certain regions. Toll roads fared the best among transports during the year.3

Despite uncertainty with regard to wireless carrier consolidation following the announcement of the T-Mobile and Sprint merger, several larger U.S. communication infrastructure companies posted positive returns during the Period. Certain satellite operators also performed well on speculation related to the C-band spectrum, where the U.S. Federal Communications Commission is considering repurposing a portion of that spectrum for next-generation 5G services.

1 The Dow Jones Brookfield Global Infrastructure Composite Index is calculated and maintained by S&P Dow Jones Indices and comprises infrastructure companies with at least 70% of its annual cash flows derived from owning and operating infrastructure assets, including MLPs.

2 The Alerian MLP Index is a composite of the 50 most prominent energy MLPs calculated by Standard & Poor’s using a float-adjusted market-capitalization methodology. The index is disseminated by the New York Stock Exchange real-time on a price return basis (NYSE: AMZ) and on a total-return basis (NYSE:AMZX).

3 Sector returns are represented by direct subsets of the Dow Jones Brookfield Global Infrastructure Index.

Indices are not managed and an investor cannot invest directly in an index.

OUTLOOK

Our outlook for the sector remains largely unchanged. We remain optimistic based on several factors: we believe volume growth is strong, valuations remain compelling and we think capital markets are recognizing the right projects. New projects continue to be announced to address takeaway constraints for crude oil and natural gas in key U.S. basins. As such, we believe these constraints should be short lived. Additionally, we are encouraged by the way corporate governance structures are improving and the shift toward models that are less reliant on equity markets to fund growth.

We maintain our preference for utilities exposed to low-cost renewables generation, as well as those located in favorable regulatory environments. We continue to monitor the regulatory impacts from the wildfires in California as new information comes to light. Regulatory risk also remains a concern for us among Chinese utilities, where regulatory changes can be swift and unexpected. We have seen select opportunities emerge, however, as these stocks have sold off in recent months. We have also begun to see some attractive relative valuations emerge among select European utilities.

Overall traffic trends in Europe remain favorable, where we prefer toll roads over airports. We recently took a more positive view on select toll roads in Brazil after meeting with management teams, in addition to the greater clarity in the market amid the election outcome. Conversely, we reduced our exposure to Mexico after the election of President Andrés Manuel López Obrador, who announced the cancellation of the partially completed $13 billion airport in Mexico City.

6Brookfield Public Securities Group LLC

Brookfield Global Listed Infrastructure Fund

We have shifted our holdings among U.S. communication tower companies toward those we view to be more defensive in nature. Among satellite operators, we are monitoring developments around the C-band spectrum. The U.S. Federal Communications Commission (FCC) is considering repurposing a portion of that spectrum for next-generation 5G services; and we continue to evaluate the value of these spectrum rights.

AVERAGE ANNUAL TOTAL RETURNS

| As of December 31, 2018 | 1 Year | 5 Years | Since Inception* |

| Class A Shares (excluding sales charge) | -8.23% | -0.26% | 5.13% |

| Class A Shares (including sales charge) | -12.56% | -1.22% | 4.40% |

| Class C Shares (excluding sales charge) | -8.92% | -1.02% | 3.29% |

| Class C Shares (including sales charge) | -9.80% | -1.02% | 3.29% |

| Class Y Shares | -8.03% | -0.01% | 5.52% |

| Class I Shares | -7.95% | 0.00% | 5.53% |

| Dow Jones Brookfield Global Infrastructure Composite Index | -8.54% | 2.61% | 6.70% |

* Class A was incepted on December 29, 2011, Class C was incepted on May 1, 2012 and Classes Y and I were incepted on December 1, 2011. The Dow Jones Brookfield Global Infrastructure Composite Total Return Index references Class I’s inception date. All returns shown in USD.

The table and graphs do not reflect the deductions of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855.244.4859. Performance shown including sales charge reflects the Class A maximum sales charge of 4.75% and the Class C Contingent Deferred Sales Charge (CDSC) of 1.00%. Performance data excluding sales charge does not reflect the deduction of the sales charge or CDSC and if reflected, the sales charge or fee would reduce the performance quoted.

The Fund’s gross and net expense ratios in the prospectus dated April 30, 2018, for Class A is 1.50% and 1.35%, Class C is 2.25% and 2.10%, Class Y is 1.25% and 1.10% and Class I is 1.25% and 1.10%, respectively for the year ended December 31, 2017.

The Adviser has contractually agreed to reimburse the Fund's expenses through May 1, 2019. There is no guarantee that such reimbursement will be continued after that date.

The graphs below illustrate a hypothetical investment of $10,000 in the Infrastructure Fund—Class I Shares from the commencement of investment operations on December 1, 2011 to December 31, 2018 compared to the Dow Jones Brookfield Global Infrastructure Composite Index.

Brookfield Global Listed Infrastructure Fund

Class I Shares

Disclosure

The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Brookfield Global Listed Infrastructure Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Infrastructure companies may be subject to a variety of factors that may adversely affect their business, including high interest costs, high leverage, regulation costs, economic slowdown, surplus capacity, increased competition, lack of fuel availability and energy conversation policies. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. The Fund invests in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. Investing in emerging markets may entail special risks relating to potential economic, political or social instability and the risks of nationalization, confiscation or the imposition of restrictions on foreign investment. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. Some securities held may be difficult to sell, particularly during times of market turmoil. If the Fund is forced to sell an illiquid asset to meet redemption, it may be forced to sell at a loss. Investing in MLPs involves certain risks related to investing in the underlying assets of the MLPs and risks associated with pooled investment vehicles. Using derivatives exposes the Fund to additional risks, may increase the volatility of the Fund’s net asset value and may not provide the result intended. Since the Fund will invest more than 25% of its total assets in securities in the Infrastructure industry, the Fund may be subject to greater volatility than a fund that is more broadly diversified.

Earnings growth is not a measure of the Fund’s future performance.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2018 and subject to change based on subsequent developments.

8Brookfield Public Securities Group LLC

Brookfield Global Listed Infrastructure Fund

Portfolio Characteristics (Unaudited)

December 31, 2018

| ASSET ALLOCATION BY GEOGRAPHY | Percent of Net Assets |

| United States | 46.4% |

| Canada | 12.9% |

| France | 8.1% |

| United Kingdom | 5.9% |

| Australia | 3.8% |

| Italy | 2.9% |

| China | 2.7% |

| Spain | 2.6% |

| Denmark | 2.0% |

| Japan | 1.4% |

| New Zealand | 1.3% |

| Brazil | 1.0% |

| Hong Kong | 0.8% |

| Mexico | 0.6% |

| Argentina | 0.1% |

| Other Assets in Excess of Liabilities | 7.5% |

| Total | 100.0% |

| ASSET ALLOCATION BY SECTOR | |

| Pipelines | 16.8% |

| Toll Roads | 14.9% |

| Master Limited Partnerships | 13.4% |

| Renewables/Electric Generation | 12.0% |

| Communications | 9.8% |

| Electricity Transmission & Distribution | 7.9% |

| Midstream | 6.8% |

| Gas Utilities | 5.6% |

| Airports | 3.0% |

| Water | 1.4% |

| Rail | 0.5% |

| Ports | 0.4% |

| Other Assets in Excess of Liabilities | 7.5% |

| Total | 100.0% |

| TOP TEN HOLDINGS | |

| Enbridge, Inc. | 7.3% |

| American Tower Corp. | 6.5% |

| Vinci SA | 5.2% |

| Enterprise Products Partners LP | 4.8% |

| Energy Transfer LP | 4.6% |

| National Grid PLC | 4.5% |

| The Williams Companies, Inc. | 4.3% |

| Kinder Morgan, Inc. | 3.3% |

| Atlantia SpA | 2.9% |

| Pembina Pipeline Corp. | 2.7% |

Brookfield Global Listed Infrastructure Fund

Schedule of Investments

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS – 92.5% | | | |

| ARGENTINA – 0.1% | | | |

| Airports – 0.1% | | | |

Corporacion America Airports SA1

| | | 37,555 | $248,990 |

| Total ARGENTINA | | | | 248,990 |

| AUSTRALIA – 3.8% | | | |

| Pipelines – 1.2% | | | |

APA Group

| | | 378,200 | 2,265,471 |

| Toll Roads – 2.6% | | | |

Transurban Group

| | | 620,170 | 5,090,063 |

| Total AUSTRALIA | | | | 7,355,534 |

| BRAZIL – 1.0% | | | |

| Toll Roads – 1.0% | | | |

CCR SA

| | | 299,841 | 864,793 |

EcoRodovias Infraestrutura e Logistica SA

| | | 429,900 | 1,038,596 |

| Total Toll Roads | | | | 1,903,389 |

| Total BRAZIL | | | | 1,903,389 |

| CANADA – 12.9% | | | |

| Pipelines – 11.9% | | | |

Enbridge, Inc.

| | | 452,800 | 14,066,253 |

Pembina Pipeline Corp.

| | | 175,100 | 5,195,796 |

TransCanada Corp.

| | | 102,935 | 3,675,711 |

| Total Pipelines | | | | 22,937,760 |

| Renewables/Electric Generation – 1.0% | | | |

Emera, Inc.

| | | 56,300 | 1,802,573 |

| Total CANADA | | | | 24,740,333 |

| CHINA – 2.7% | | | |

| Communications – 0.5% | | | |

China Tower Corporation Ltd.1,2

| | | 4,831,200 | 913,586 |

| Gas Utilities – 1.4% | | | |

ENN Energy Holdings Ltd.

| | | 298,600 | 2,653,888 |

| Pipelines – 0.4% | | | |

Kunlun Energy Company Ltd.

| | | 769,600 | 817,689 |

| Ports – 0.4% | | | |

China Merchants Port Holdings Company Ltd.

| | | 504,301 | 906,740 |

| Total CHINA | | | | 5,291,903 |

| DENMARK – 2.0% | | | |

| Renewables/Electric Generation – 2.0% | | | |

Orsted A/S2

| | | 57,500 | 3,847,773 |

| Total DENMARK | | | | 3,847,773 |

| FRANCE – 8.1% | | | |

| Airports – 0.7% | | | |

Aeroports de Paris

| | | 7,000 | 1,327,392 |

| Communications – 0.7% | | | |

Eutelsat Communications SA

| | | 69,700 | 1,373,172 |

See Notes to Financial Statements.

10Brookfield Public Securities Group LLC

Brookfield Global Listed Infrastructure Fund

Schedule of Investments (continued)

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS (continued) | | | |

| Renewables/Electric Generation – 1.5% | | | |

Engie SA

| | | 203,300 | $2,921,004 |

| Toll Roads – 5.2% | | | |

Vinci SA

| | | 120,700 | 9,925,414 |

| Total FRANCE | | | | 15,546,982 |

| HONG KONG – 0.8% | | | |

| Gas Utilities – 0.8% | | | |

Hong Kong & China Gas Company Ltd.

| | | 788,259 | 1,628,582 |

| Total HONG KONG | | | | 1,628,582 |

| ITALY – 2.9% | | | |

| Toll Roads – 2.9% | | | |

Atlantia SpA

| | | 265,200 | 5,488,357 |

| Total ITALY | | | | 5,488,357 |

| JAPAN – 1.4% | | | |

| Airports – 0.9% | | | |

Japan Airport Terminal Company Ltd.

| | | 51,000 | 1,763,044 |

| Rail – 0.5% | | | |

East Japan Railway Co.

| | | 10,800 | 953,750 |

| Total JAPAN | | | | 2,716,794 |

| MEXICO – 0.6% | | | |

| Toll Roads – 0.6% | | | |

Promotora y Operadora de Infraestructura SAB de CV

| | | 117,571 | 1,123,795 |

| Total MEXICO | | | | 1,123,795 |

| NEW ZEALAND – 1.3% | | | |

| Airports – 1.3% | | | |

Auckland International Airport Ltd.

| | | 516,900 | 2,494,788 |

| Total NEW ZEALAND | | | | 2,494,788 |

| SPAIN – 2.6% | | | |

| Toll Roads – 2.6% | | | |

Ferrovial SA

| | | 246,142 | 4,985,045 |

| Total SPAIN | | | | 4,985,045 |

| UNITED KINGDOM – 5.9% | | | |

| Electricity Transmission & Distribution – 4.5% | | | |

National Grid PLC

| | | 892,332 | 8,729,972 |

| Water – 1.4% | | | |

Severn Trent PLC

| | | 112,100 | 2,598,554 |

| Total UNITED KINGDOM | | | | 11,328,526 |

| UNITED STATES – 46.4% | | | |

| Communications – 8.6% | | | |

American Tower Corp.

| | | 79,103 | 12,513,304 |

Crown Castle International Corp.

| | | 36,400 | 3,954,132 |

| Total Communications | | | | 16,467,436 |

| Electricity Transmission & Distribution – 3.4% | | | |

Edison International

| | | 38,900 | 2,208,353 |

See Notes to Financial Statements.

Brookfield Global Listed Infrastructure Fund

Schedule of Investments (continued)

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS (continued) | | | |

PG&E Corp.1

| | | 74,634 | $1,772,558 |

Sempra Energy

| | | 24,600 | 2,661,474 |

| Total Electricity Transmission & Distribution | | | | 6,642,385 |

| Gas Utilities – 3.4% | | | |

Atmos Energy Corp.

| | | 32,200 | 2,985,584 |

NiSource, Inc.

| | | 143,900 | 3,647,865 |

| Total Gas Utilities | | | | 6,633,449 |

| Master Limited Partnerships – 13.4% | | | |

Energy Transfer LP

| | | 676,084 | 8,931,070 |

Enterprise Products Partners LP

| | | 376,169 | 9,249,996 |

Magellan Midstream Partners LP

| | | 63,200 | 3,606,192 |

MPLX LP

| | | 131,376 | 3,980,693 |

| Total Master Limited Partnerships | | | | 25,767,951 |

| Midstream – 6.8% | | | |

Cheniere Energy, Inc.1

| | | 59,700 | 3,533,643 |

Targa Resources Corp.

| | | 34,300 | 1,235,486 |

The Williams Companies, Inc.

| | | 374,300 | 8,253,315 |

| Total Midstream | | | | 13,022,444 |

| Pipelines – 3.3% | | | |

Kinder Morgan, Inc.

| | | 416,300 | 6,402,694 |

| Renewables/Electric Generation – 7.5% | | | |

American Electric Power Company, Inc.

| | | 30,400 | 2,272,096 |

CMS Energy Corp.

| | | 63,300 | 3,142,845 |

Entergy Corp.

| | | 50,400 | 4,337,928 |

FirstEnergy Corp.

| | | 99,200 | 3,724,960 |

NRG Energy, Inc.

| | | 23,900 | 946,440 |

| Total Renewables/Electric Generation | | | | 14,424,269 |

| Total UNITED STATES | | | | 89,360,628 |

Total COMMON STOCKS

(Cost $166,935,891)

| | | | 178,061,419 |

Total Investments – 92.5%

(Cost $166,935,891)

| | | | 178,061,419 |

Other Assets in Excess of Liabilities – 7.5%

| | | | 14,468,343 |

TOTAL NET ASSETS – 100.0%

| | | | $192,529,762 |

| 1 | — Non-income producing security. |

| 2 | — Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may only be resold in transactions exempt from registration, normally to qualified institutional buyers. As of December 31, 2018, the total value of all such securities was $4,761,359 or 2.5% of net assets. |

See Notes to Financial Statements.

12Brookfield Public Securities Group LLC

Brookfield Global Listed Real Estate Fund

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

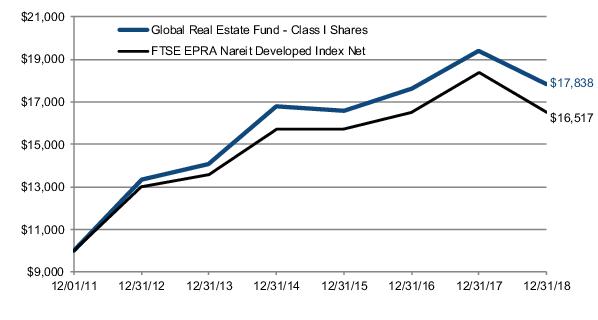

For the year ended December 31, 2018, the Global Real Estate Fund, Class I had a total return of -8.06%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions, underperforming the FTSE EPRA NAREIT Developed Index1, which returned -4.74%.

During the 12-month period ending December 31, 2018, the Retail sector was the leading contributor to relative performance due to stock selection and underweight exposure. We did not own a number of underperforming names in the sector during the year. The timing of our overweight exposure to Simon Property Group, Inc. (SPG, Retail, U.S.) contributed as well. The Healthcare sector was also a contributor, due to stock selection and overweight exposure. Conversely, Office was the leading sector detractor due to stock selection and overweight exposure. Office was the worst performing property type during the year and as a result, overweight and non-index holdings detracted from relative returns. Stock selection within the Residential and Data Centers sectors also detracted.

By region, Australia/New Zealand (stock selection) and Continental Europe (underweight exposure) were leading contributors. Conversely, Japan (stock selection) and the U.K. (overweight exposure) were the leading detractors from relative performance.

By security, underweight exposure to Unibail-Rodamco-Westfield (URW.NA, Retail, France) was the leading contributor to relative returns as the malaise that has plagued U.S. retail real estate now appears to be spreading to Europe. Overweight exposure to Simon Property Group, Inc. (SPG, Retail, U.S.) also contributed. Simon outperformed after reporting better-than-expected earnings, stable occupancy and positive re-leasing spreads. The company also began providing more detail on its redevelopment and development pipeline; and its pipeline of densification opportunities garnered positive attention. Overweight exposure to Dexus (DXS.AU, Diversified, Australia) contributed as well.

Conversely, overweight exposure to Land Securities Group PLC (LAND.LN, Diversified, U.K.) detracted as the stock declined on Brexit uncertainty. Non-index holding Leopalace21 Corporation (8848.JP, Residential, Japan) also detracted. The stock declined meaningfully in May 2018 after construction deficiencies were reported at some of the company’s apartments. Although we think the monetary costs related to repairing the deficiencies are not overly large, the long-term reputational effect on the company is much harder to estimate and could be much more damaging to the company’s long-term value. Lastly, overweight exposure to City Developments Limited (CIT.SP, Diversified, Singapore) detracted as well. Singapore real estate stocks took a leg down after the government enacting cooling measures. The government enacted stricter borrowing limits for first time buyers, meaning they have to put more cash up front. Stamp duties were also increased for foreign purchasers of residential property.

GLOBAL REAL ESTATE MARKET OVERVIEW

Global real estate securities, as measured by the FTSE EPRA Nareit Developed Index1 (the “Benchmark”) declined 4.7% during the year. By region, Europe, North America and Asia Pacific declined 12.1%, 3.9% and 1.5%, respectively.

By U.S. property type, Office posted the steepest declines during the year (−14.6%), followed by Hotels (−12.6%), Diversified (−7.9%), Retail (−7.2%), Industrial (−2.5%) and Mixed (0.0%). Conversely, Healthcare (+7.7%), Residential (+3.3%) and Self Storage (+2.9%) posted gains during the year.

Global real estate equities, as measured by the FTSE EPRA Nareit Developed Index, underperformed the broader equity market early in 2018 on fears that rising inflation, tighter job markets and fiscal stimulus would accelerate the pace of U.S. interest-rate hikes. Those fears appeared to subside throughout the year as global real estate equities drifted higher for six straight months through August.

In the final quarter of the year, nearly all asset classes sold off on concerns around slower economic growth as a result of global trade disputes, geopolitical uncertainty and tightening of monetary policies. Real estate equities

Brookfield Global Listed Real Estate Fund

were not immune to the downturn, but declined substantially less than broader equity markets, with the FTSE EPRA Nareit Developed Index1 down 5.5%, compared to the MSCI World Index2, which was off 13.3%.

Weakness for the year within the Office and Hotels sectors was largely a result of the clouded outlook on future growth. Performance within U.S. retail diverged, with higher quality operators outperforming those with lower quality portfolios. Outside the U.S., the malaise that has plagued U.S. retail real estate now appears to be spreading to Europe. Conversely, strong performance within the Healthcare sector was driven by improved fundamentals. Self Storage performed well despite supply concerns in a number of major metropolitan areas.3

1 The FTSE EPRA Nareit Developed Index is a free-float adjusted, liquidity, size and revenue screened index designed to track the performance of listed real estate companies and REITs worldwide.

2 The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

3 Sector returns represented by the U.S. portion of the FTSE EPRA Nareit Developed North America Index.

Indices are not managed and an investor cannot invest directly in an index.

OUTLOOK

Despite increased expectations that growth may slow in the coming years, the U.S. economy remains healthy and is expected to outperform developed market peers. We do not believe a recession is imminent, but we see elevated risks that growth is likely to slow. As such, we have positioned the portfolio toward what we believe to be more conservative holdings.

Within real estate, supply and demand appear relatively well balanced across most property types, and we are seeing inflationary rental growth. Leverage ratios have declined to the lowest levels ever recorded. In addition, many real estate companies have extended their average debt maturities to lock in lower-for-longer interest expenses moving forward. Our preference for companies with strong balance sheets is unchanged and we remain focused on companies with below average levels of leverage. We believe this is important from a portfolio construction standpoint in the current environment as companies with low leverage have the potential to perform better if we experience a downturn in the current business cycle.

Currently we see opportunities within U.S. multifamily residential real estate. New supply appears muted and jobs growth (which is a demand driver for apartments) remains strong. We are seeing attractive discounts to net asset value (NAV) in the Office sector. In particular, we see compelling opportunities in some West Coast and Sunbelt markets.

Conversely, we see fewer opportunities across the broader U.S. Retail sector. Our holdings are focused on what we believe to be the highest quality companies that operate in the most attractive markets. We are also less constructive within the Industrial sector amid lofty valuations and supply concerns.

Outside the U.S., we continue to see value in Japan, where we believe Japanese developers present attractive valuations on an absolute basis, as well as in relation to their J-REIT counterparts. We specifically like developers focused on the Tokyo office market, where demand is strong for new buildings. Elsewhere in Asia, we are cautious about Hong Kong, particularly the residential market given the tightening of China’s capital controls that have impacted property ownership, as well as uncertainty surrounding the ongoing U.S. trade conflict with China.

We continue to be positive on the U.K. market, despite the continued uncertainty on the Brexit resolution—although we have reduced retail exposure in favor of office properties where we still see good leasing demand. We have also begun to increase exposure in some Continental European markets as valuations have improved.

14Brookfield Public Securities Group LLC

Brookfield Global Listed Real Estate Fund

AVERAGE ANNUAL TOTAL RETURNS

| As of December 31, 2018 | 1 Year | 5 Years | Since Inception* |

| Class A Shares (excluding sales charge) | -8.23% | 4.64% | 6.41% |

| Class A Shares (including sales charge) | -12.61% | 3.63% | 5.63% |

| Class C Shares (excluding sales charge) | -8.98% | 3.84% | 5.61% |

| Class C Shares (including sales charge) | -9.86% | 3.84% | 5.61% |

| Class Y Shares | -8.12% | 4.88% | 8.52% |

| Class I Shares | -8.06% | 4.88% | 8.51% |

| FTSE EPRA Nareit Developed Index Net | -4.74% | 5.26% | 8.23% |

* Classes A and C were incepted on May 1, 2012 and Classes Y and I were incepted on December 1, 2011. The FTSE EPRA Nareit Developed Index references Class I's inception date (reflects no deduction for fees, expenses or taxes except the reinvestment of dividends net of non-U.S. withholding taxes). All returns shown in USD.

The table and graphs do not reflect the deductions of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855.244.4859. Performance shown including sales charge reflects the Class A maximum sales charge of 4.75% and the Class C Contingent Deferred Sales Charge (CDSC) of 1.00%. Performance data excluding sales charge does not reflect the deduction of the sales charge or CDSC and if reflected, the sales charge or fee would reduce the performance quoted.

The Fund’s gross and net expense ratios in the prospectus dated April 30, 2018, for Class A is 1.24% and 1.20%, Class C is 1.99% and 1.95%, Class Y is 0.99% and 0.95% and Class I is 0.99% and 0.95%, respectively for the year ended December 31, 2017.

The Adviser has contractually agreed to reimburse the Fund's expenses through May 1, 2019. There is no guarantee that such reimbursement will be continued after that date.

The graphs below illustrate a hypothetical investment of $10,000 in the Global Real Estate Fund—Class I Shares from the commencement of investment operations on December 1, 2011 to December 31, 2018 compared to the FTSE EPRA Nareit Developed Index.

Brookfield Global Listed Real Estate Fund

Class I Shares

Disclosure

The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Brookfield Global Listed Real Estate Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Investors should be aware of the risks involved with investing in a fund concentrating in REITs and real estate securities, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. Investing in emerging markets may entail special risks relating to potential economic, political or social instability and the risks of nationalization, confiscation or the imposition of restrictions on foreign investment. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. Some securities held may be difficult to sell, particularly during times of market turmoil. If the Fund is forced to sell an illiquid asset to meet redemption, the Fund may be forced to sell at a loss. Using derivatives exposes the Fund to additional risks, may increase the volatility of the Fund’s net asset value and may not provide the result intended. Since the Fund will invest more than 25% of its total assets in securities in the Real Estate industry, the Fund may be subject to greater volatility than a fund that is more broadly diversified.

Earnings growth is not a measure of the Fund’s future performance.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2018 and subject to change based on subsequent developments.

16Brookfield Public Securities Group LLC

Brookfield Global Listed Real Estate Fund

Portfolio Characteristics (Unaudited)

December 31, 2018

| ASSET ALLOCATION BY GEOGRAPHY | Percent of Net Assets |

| United States | 51.6% |

| Japan | 14.1% |

| United Kingdom | 9.3% |

| Germany | 6.2% |

| Australia | 5.4% |

| Hong Kong | 5.2% |

| France | 2.6% |

| Singapore | 1.6% |

| Canada | 1.5% |

| Spain | 1.5% |

| China | 0.9% |

| Other Assets in Excess of Liabilities | 0.1% |

| Total | 100.0% |

| ASSET ALLOCATION BY SECTOR | |

| Office | 29.2% |

| Diversified | 20.6% |

| Residential | 15.9% |

| Healthcare | 8.2% |

| Retail | 5.5% |

| Industrial | 5.2% |

| Self Storage | 5.1% |

| Net Lease | 4.5% |

| Hotel | 3.2% |

| Datacenters | 2.5% |

| Other Assets in Excess of Liabilities | 0.1% |

| Total | 100.0% |

| TOP TEN HOLDINGS | |

| Land Securities Group PLC | 4.8% |

| Simon Property Group, Inc. | 4.5% |

| Mid-America Apartment Communities, Inc. | 4.3% |

| Mitsubishi Estate Company Ltd. | 4.1% |

| Mitsui Fudosan Company Ltd. | 4.1% |

| Vonovia SE | 4.1% |

| Public Storage | 3.6% |

| AvalonBay Communities, Inc. | 3.3% |

| Prologis, Inc. | 3.1% |

| The GPT Group | 2.9% |

Brookfield Global Listed Real Estate Fund

Schedule of Investments

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS – 99.9% | | | |

| AUSTRALIA – 5.4% | | | |

| Diversified – 5.4% | | | |

Dexus

| | | 5,418,300 | $40,553,870 |

The GPT Group

| | | 12,524,868 | 47,131,597 |

| Total Diversified | | | | 87,685,467 |

| Total AUSTRALIA | | | | 87,685,467 |

| CANADA – 1.5% | | | |

| Industrial – 1.5% | | | |

Granite Real Estate Investment Trust

| | | 620,240 | 24,174,458 |

| Total CANADA | | | | 24,174,458 |

| CHINA – 0.9% | | | |

| Office – 0.9% | | | |

SOHO China Ltd.1

| | | 41,917,200 | 14,970,342 |

| Total CHINA | | | | 14,970,342 |

| FRANCE – 2.6% | | | |

| Office – 2.6% | | | |

Gecina SA

| | | 323,877 | 41,925,916 |

| Total FRANCE | | | | 41,925,916 |

| GERMANY – 6.2% | | | |

| Office – 2.1% | | | |

alstria office REIT-AG

| | | 2,481,652 | 34,744,959 |

| Residential – 4.1% | | | |

Vonovia SE

| | | 1,458,255 | 65,736,621 |

| Total GERMANY | | | | 100,481,580 |

| HONG KONG – 5.2% | | | |

| Diversified – 3.2% | | | |

CK Asset Holdings Ltd.

| | | 2,357,896 | 17,251,734 |

Wharf Real Estate Investment Company Ltd.

| | | 5,556,712 | 33,234,226 |

| Total Diversified | | | | 50,485,960 |

| Office – 2.0% | | | |

Hongkong Land Holdings Ltd.

| | | 5,166,900 | 32,572,840 |

| Total HONG KONG | | | | 83,058,800 |

| JAPAN – 14.1% | | | |

| Diversified – 2.0% | | | |

Activia Properties, Inc.

| | | 3,494 | 14,195,682 |

Invincible Investment Corp.

| | | 43,890 | 18,102,088 |

| Total Diversified | | | | 32,297,770 |

| Office – 9.9% | | | |

Daiwa Office Investment Corp.

| | | 1,482 | 9,348,338 |

Hulic Reit, Inc.

| | | 5,286 | 8,207,950 |

Kenedix Office Investment Corp.

| | | 1,439 | 9,184,879 |

Mitsubishi Estate Company Ltd.

| | | 4,257,103 | 66,979,170 |

Mitsui Fudosan Company Ltd.

| | | 2,960,152 | 65,750,623 |

| Total Office | | | | 159,470,960 |

See Notes to Financial Statements.

18Brookfield Public Securities Group LLC

Brookfield Global Listed Real Estate Fund

Schedule of Investments (continued)

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS (continued) | | | |

| Residential – 2.2% | | | |

Advance Residence Investment Corp.

| | | 6,278 | $17,332,404 |

Nippon Accommodations Fund, Inc.

| | | 3,842 | 18,556,650 |

| Total Residential | | | | 35,889,054 |

| Total JAPAN | | | | 227,657,784 |

| SINGAPORE – 1.6% | | | |

| Diversified – 1.6% | | | |

City Developments Ltd.

| | | 4,294,757 | 25,604,113 |

| Total SINGAPORE | | | | 25,604,113 |

| SPAIN – 1.5% | | | |

| Diversified – 1.5% | | | |

Merlin Properties Socimi SA

| | | 1,952,820 | 24,123,899 |

| Total SPAIN | | | | 24,123,899 |

| UNITED KINGDOM – 9.3% | | | |

| Diversified – 6.9% | | | |

Land Securities Group PLC

| | | 7,510,056 | 77,112,163 |

The British Land Company PLC

| | | 5,109,394 | 34,745,227 |

| Total Diversified | | | | 111,857,390 |

| Industrial – 0.6% | | | |

Tritax EuroBox PLC1,2

| | | 7,825,876 | 9,232,112 |

| Office – 1.8% | | | |

Derwent London PLC

| | | 345,200 | 12,551,943 |

Great Portland Estates PLC

| | | 1,928,082 | 16,207,512 |

| Total Office | | | | 28,759,455 |

| Total UNITED KINGDOM | | | | 149,848,957 |

| UNITED STATES – 51.6% | | | |

| Datacenters – 2.5% | | | |

Digital Realty Trust, Inc.

| | | 234,600 | 24,996,630 |

Equinix, Inc.

| | | 45,433 | 16,017,858 |

| Total Datacenters | | | | 41,014,488 |

| Healthcare – 8.2% | | | |

HCP, Inc.

| | | 1,282,762 | 35,827,542 |

Physicians Realty Trust

| | | 2,571,471 | 41,220,680 |

Ventas, Inc.

| | | 488,225 | 28,605,103 |

Welltower, Inc.

| | | 387,314 | 26,883,465 |

| Total Healthcare | | | | 132,536,790 |

| Hotel – 3.2% | | | |

Extended Stay America, Inc.

| | | 1,089,076 | 16,880,678 |

Park Hotels & Resorts, Inc.

| | | 587,722 | 15,269,018 |

RLJ Lodging Trust

| | | 1,234,923 | 20,252,736 |

| Total Hotel | | | | 52,402,432 |

| Industrial – 3.1% | | | |

Prologis, Inc.

| | | 846,900 | 49,729,968 |

See Notes to Financial Statements.

Brookfield Global Listed Real Estate Fund

Schedule of Investments (continued)

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS (continued) | | | |

| Net Lease – 4.5% | | | |

EPR Properties

| | | 249,800 | $15,994,694 |

MGM Growth Properties LLC

| | | 1,515,792 | 40,032,067 |

VEREIT, Inc.

| | | 2,212,237 | 15,817,495 |

| Total Net Lease | | | | 71,844,256 |

| Office – 9.9% | | | |

Boston Properties, Inc.

| | | 363,207 | 40,878,948 |

Cousins Properties, Inc.

| | | 2,585,400 | 20,424,660 |

Highwoods Properties, Inc.

| | | 605,121 | 23,412,131 |

Hudson Pacific Properties, Inc.

| | | 1,141,555 | 33,173,588 |

Kilroy Realty Corp.

| | | 663,584 | 41,726,162 |

| Total Office | | | | 159,615,489 |

| Residential – 9.6% | | | |

AvalonBay Communities, Inc.

| | | 303,900 | 52,893,795 |

Essex Property Trust, Inc.

| | | 134,549 | 32,992,760 |

Mid-America Apartment Communities, Inc.

| | | 721,828 | 69,078,940 |

| Total Residential | | | | 154,965,495 |

| Retail – 5.5% | | | |

Federal Realty Investment Trust

| | | 134,907 | 15,924,422 |

Simon Property Group, Inc.

| | | 433,133 | 72,762,013 |

| Total Retail | | | | 88,686,435 |

| Self Storage – 5.1% | | | |

CubeSmart

| | | 843,700 | 24,205,753 |

Public Storage

| | | 286,000 | 57,889,260 |

| Total Self Storage | | | | 82,095,013 |

| Total UNITED STATES | | | | 832,890,366 |

Total COMMON STOCKS

(Cost $1,681,341,653)

| | | | 1,612,421,682 |

Total Investments – 99.9%

(Cost $1,681,341,653)

| | | | 1,612,421,682 |

Other Assets in Excess of Liabilities – 0.1%

| | | | 1,980,571 |

TOTAL NET ASSETS – 100.0%

| | | | $1,614,402,253 |

| LLC— Limited Liability Company |

| 1 | — Non-income producing security. |

| 2 | — Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may only be resold in transactions exempt from registration, normally to qualified institutional buyers. As of December 31, 2018, the total value of all such securities was $9,232,112 or 0.6% of net assets. |

See Notes to Financial Statements.

20Brookfield Public Securities Group LLC

Brookfield U.S. Listed Real Estate Fund

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

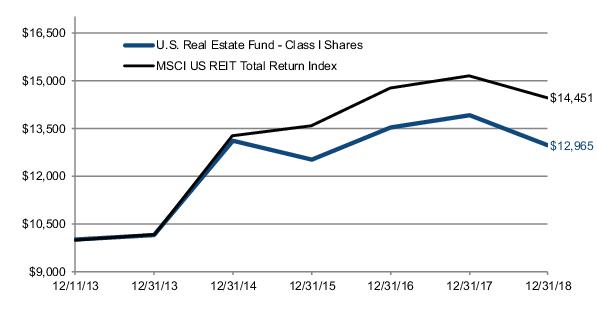

For the year ended December 31, 2018, the U.S. Real Estate Fund, Class I had a total return -6.90%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions, underperforming the MSCI U.S. REIT Index1, which returned -4.57%.

During the 12-month period ending December 31, 2018, the Retail sector was the leading contributor to relative performance due to stock selection. We did not own a number of underperforming names in the sector during the year. The timing of our overweight exposure to Simon Property Group, Inc. (SPG, Retail) contributed as well. Underweight exposure to the Diversified sector was also a leading contributor to relative returns, as was overweight exposure within the Healthcare sector.

Conversely, the Data Centers sector was the leading detractor from relative returns due to stock selection. The Office sector was also among the leading detractors due to stock selection and overweight exposure, as it was the worst performing property type during the year. Stock selection within Residential also detracted.

By security, the timing of our overweight exposure to Park Hotels & Resorts, Inc. (PK, Hotels) was the leading contributor to relative returns. An overweight allocation to Simon Property Group, Inc. (SPG, Retail) was also a leading contributor. Simon outperformed after reporting better-than-expected earnings, stable occupancy and positive re-leasing spreads. The company also began providing more detail on its redevelopment and development pipeline; and its pipeline of densification opportunities garnered positive attention. Overweight exposure to HCP, Inc. (HCP, Healthcare) was also a leading contributor during the year.

Conversely, overweight exposure to QTS Realty Trust, Inc. (QTS, Data Centers) was the leading detractor from relative returns. The stock declined meaningfully after the company unexpectedly announced a reorganization to exit the Cloud Managed Services business (often referred to as C3), along with a number of management changes. Overweight exposure to RLJ Lodging Trust (RLJ, Hotels) and non-index Extended Stay America, Inc. (STAY, Hotels) were also leading detractors, as the sector was one of the worst performers during the year.

U.S. REAL ESTATE MARKET OVERVIEW

U.S. real estate securities were down 4.6% for the year, as measured by the MSCI US REIT Index1 (the “Benchmark”). By U.S. property type, Office posted the steepest declines during the year (−14.6%), followed by Hotels (−12.6%), Diversified (−7.9%), Retail (−7.2%), Industrial (−2.5%) and Mixed (0.0%). Conversely, Healthcare (+7.7%), Residential (+3.3%) and Self Storage (+2.9%) posted gains during the year.2

U.S. real estate equities, as measured by the MSCI US REIT Index, underperformed the broader U.S. equity market early in 2018 on fears that rising inflation, tighter job markets and fiscal stimulus would accelerate the pace of U.S. interest-rate hikes. Those fears appeared to subside as U.S. real estate equities drifted higher for six straight months through August.

In the final quarter of the year, nearly all asset classes sold off on concerns around slower economic growth as a result of global trade disputes, geopolitical uncertainty and tightening of monetary policies. Real estate equities were not immune to the downturn, but declined substantially less than broader equity markets, with the MSCI US REIT Index down 6.7%, compared to the S&P 500 Index3, which was off 13.5%.

Weakness for the year within the Office and Hotels sectors was largely a result of the clouded outlook on future growth. Performance within U.S. retail diverged, with higher quality operators outperforming those with lower quality portfolios. Conversely, strong performance within the Healthcare sector was driven by improved fundamentals. Self Storage performed well despite supply concerns in a number of major metropolitan areas.4

1 The MSCI US REIT Index (RMS) is a total return market capitalization-weighted index which prices once per day after market close. It is calculated by MSCI and is composed of equity REITs that are included in the MSCI US Investable Market 2500 Index. You cannot invest directly in an index.

2 Sector returns represented by the U.S. portion of the FTSE EPRA NAREIT Developed North America Index. The FTSE EPRA NAREIT

Brookfield U.S. Listed Real Estate Fund

Developed Index is calculated by the FTSE Group. Performance is calculated by price, total return and net total return and the Index is calculated daily. Constituents must meet minimum market capitalization, liquidity requirements, and real estate activity requirements in order to be included within the Index. North American and Asian companies must be of a minimum of US$200 million in market capitalization with liquidity of US$100 million. European companies are bound by €50 million (approximately $60 million) market cap minimum and liquidity of €25 million (approximately $30 million).

3 The S&P 500® Index is an equity index of 500 widely held, large-capitalization U.S. companies. Special cash dividends trigger a price adjustment in the price return index. Indices are not managed and an investor cannot invest directly in an index.

4 Sector returns represented by the U.S. portion of the FTSE EPRA Nareit Developed North America Index.

Indices are not managed and an investor cannot invest directly in an index.

OUTLOOK

Despite increased expectations that growth may slow in the coming years, the U.S. economy remains healthy and is expected to outperform developed market peers. We do not believe a recession is imminent, but we see elevated risks that growth is likely to slow. As such, we have positioned the portfolio toward what we believe to be more conservative holdings.

Within real estate, supply and demand appear relatively well balanced across most property types, and we are seeing inflationary rental growth. Leverage ratios have declined to the lowest levels ever recorded. In addition, many real estate companies have extended their average debt maturities to lock in lower-for-longer interest expenses moving forward. Our preference for companies with strong balance sheets is unchanged and we remain focused on companies with below average levels of leverage. We believe this is important from a portfolio construction standpoint in the current environment as companies with low leverage have the potential to perform better if we experience a downturn in the current business cycle.

Currently we see opportunities within multifamily residential real estate. New supply appears muted and jobs growth (which is a demand driver for apartments) remains strong. We are seeing attractive discounts to net asset value (NAV) in the Office sector. In particular, we see compelling opportunities in some West Coast and Sunbelt markets.

Conversely, we see fewer opportunities across the broader Retail sector. Our holdings are focused on what we believe to be the highest quality companies that operate in the most attractive markets. We are also less constructive within the Industrial sector amid lofty valuations and supply concerns.

AVERAGE ANNUAL TOTAL RETURNS

| As of December 31, 2018 | 1 Year | 5 Years | Since Inception* |

| Class A Shares (excluding sales charge) | -7.14% | 4.72% | 5.00% |

| Class A Shares (including sales charge) | -11.53% | 3.71% | 3.99% |

| Class C Shares (excluding sales charge) | -7.86% | 3.98% | 4.26% |

| Class C Shares (including sales charge) | -8.75% | 3.98% | 4.26% |

| Class Y Shares | -6.98% | 5.04% | 5.33% |

| Class I Shares | -6.90% | 4.99% | 5.27% |

| MSCI US REIT Index | -4.57% | 7.79% | 7.55% |

* Classes A, C , Y and I were incepted on December 11, 2013. All returns shown in USD.

The table and graphs do not reflect the deductions of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Fund may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855.244.4859. Performance shown including sales charge reflects the Class A maximum sales charge of 4.75%

22Brookfield Public Securities Group LLC

Brookfield U.S. Listed Real Estate Fund

and the Class C Contingent Deferred Sales Charge (CDSC) of 1.00%. Performance data excluding sales charge does not reflect the deduction of the sales charge or CDSC and if reflected, the sales charge or fee would reduce the performance quoted.

The Fund’s gross and net expense ratios in the prospectus dated April 30, 2018, for Class A is 2.22% and 1.20%, Class C is 2.97% and 1.95%, Class Y is 1.97% and 0.95% and Class I is 1.97% and 0.95%, respectively for the year ended December 31, 2017.

The Adviser has contractually agreed to reimburse the Fund's expenses through May 1, 2019. There is no guarantee that such reimbursement will be continued after that date.

The graphs below illustrate a hypothetical investment of $10,000 in the U.S Real Estate Fund—Class I Shares from the commencement of investment operations on December 11, 2013 to December 31, 2018 compared to the MSCI US REIT Total Return Index.

Class I Shares

Disclosure

The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Brookfield U.S. Listed Real Estate Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Investors should be aware of the risks involved with investing in a fund concentrating in REITs and real estate securities, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments. Investments in foreign securities involve political, economic and currency risks, greater volatility and differences in accounting methods. Investing in emerging markets may entail special risks relating to potential economic, political or social instability and the risks of nationalization, confiscation or the imposition of restrictions on foreign investment. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. Some

Brookfield U.S. Listed Real Estate Fund

securities held may be difficult to sell, particularly during times of market turmoil. If the Fund is forced to sell an illiquid asset to meet redemption, the Fund may be forced to sell at a loss. Using derivatives exposes the Fund to additional risks, may increase the volatility of the Fund’s net asset value and may not provide the result intended. Since the Fund will invest more than 25% of its total assets in securities in the Real Estate industry, the Fund may be subject to greater volatility than a fund that is more broadly diversified. Using derivatives exposes the Fund to additional risks, may increase the volatility of the Fund’s net asset value and may not provide the result intended.

Earnings growth is not a measure of the Fund’s future performance.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on December 31, 2018 and subject to change based on subsequent developments.

24Brookfield Public Securities Group LLC

Brookfield U.S. Listed Real Estate Fund

Portfolio Characteristics (Unaudited)

December 31, 2018

| ASSET ALLOCATION BY SECTOR | Percent of Net Assets |

| Office | 17.1% |

| Residential | 16.1% |

| Healthcare | 15.0% |

| Retail | 11.2% |

| Self Storage | 10.0% |

| Net Lease | 8.9% |

| Datacenters | 8.2% |

| Hotel | 7.2% |

| Industrial | 5.3% |

| Other Assets in Excess of Liabilities | 1.0% |

| Total | 100.0% |

| TOP TEN HOLDINGS | |

| Simon Property Group, Inc. | 8.8% |

| Mid-America Apartment Communities, Inc. | 7.1% |

| Public Storage | 7.1% |

| AvalonBay Communities, Inc. | 6.0% |

| Prologis, Inc. | 5.3% |

| Equinix, Inc. | 5.2% |

| Physicians Realty Trust | 5.1% |

| MGM Growth Properties LLC | 5.0% |

| Kilroy Realty Corp. | 4.3% |

| Boston Properties, Inc. | 3.8% |

Brookfield U.S. Listed Real Estate Fund

Schedule of Investments

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS – 99.0% | | | |

| Datacenters – 8.2% | | | |

Digital Realty Trust, Inc.

| | | 3,800 | $404,890 |

Equinix, Inc.

| | | 2,000 | 705,120 |

| Total Datacenters | | | | 1,110,010 |

| Healthcare – 15.0% | | | |

HCP, Inc.

| | | 18,400 | 513,912 |

Physicians Realty Trust

| | | 42,329 | 678,534 |

Ventas, Inc.

| | | 7,500 | 439,425 |

Welltower, Inc.

| | | 5,500 | 381,755 |

| Total Healthcare | | | | 2,013,626 |

| Hotel – 7.2% | | | |

Extended Stay America, Inc.

| | | 19,000 | 294,500 |

Park Hotels & Resorts, Inc.

| | | 10,036 | 260,735 |

RLJ Lodging Trust

| | | 24,900 | 408,360 |

| Total Hotel | | | | 963,595 |

| Industrial – 5.3% | | | |

Prologis, Inc.

| | | 12,200 | 716,384 |

| Net Lease – 8.9% | | | |

EPR Properties

| | | 4,100 | 262,523 |

MGM Growth Properties LLC

| | | 25,384 | 670,391 |

VEREIT, Inc.

| | | 37,000 | 264,550 |

| Total Net Lease | | | | 1,197,464 |

| Office – 17.1% | | | |

Boston Properties, Inc.

| | | 4,600 | 517,730 |

Cousins Properties, Inc.

| | | 48,300 | 381,570 |

Highwoods Properties, Inc.

| | | 10,500 | 406,245 |

Hudson Pacific Properties, Inc.

| | | 14,200 | 412,652 |

Kilroy Realty Corp.

| | | 9,200 | 578,496 |

| Total Office | | | | 2,296,693 |

| Residential – 16.1% | | | |

AvalonBay Communities, Inc.

| | | 4,600 | 800,630 |

Essex Property Trust, Inc.

| | | 1,650 | 404,597 |

Mid-America Apartment Communities, Inc.

| | | 10,000 | 957,000 |

| Total Residential | | | | 2,162,227 |

| Retail – 11.2% | | | |

Federal Realty Investment Trust

| | | 2,700 | 318,708 |

Simon Property Group, Inc.

| | | 7,049 | 1,184,162 |

| Total Retail | | | | 1,502,870 |

| Self Storage – 10.0% | | | |

CubeSmart

| | | 13,800 | 395,922 |

See Notes to Financial Statements.

26Brookfield Public Securities Group LLC

Brookfield U.S. Listed Real Estate Fund

Schedule of Investments (continued)

December 31, 2018

| | | | Shares | Value |

| COMMON STOCKS (continued) | | | |

Public Storage

| | | 4,700 | $951,327 |

| Total Self Storage | | | | 1,347,249 |

Total COMMON STOCKS

(Cost $13,431,075)

| | | | 13,310,118 |

Total Investments – 99.0%

(Cost $13,431,075)

| | | | 13,310,118 |

Other Assets in Excess of Liabilities – 1.0%

| | | | 140,700 |

TOTAL NET ASSETS – 100.0%

| | | | $13,450,818 |

| LLC— Limited Liability Company |

See Notes to Financial Statements.

Brookfield Real Assets Securities Fund

MANAGEMENT DISCUSSION OF FUND PERFORMANCE

For the year ended December 31, 2018, the Real Assets Securities Fund, Class I had a total return -8.32%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions, underperforming the Fund’s Blended Index1, which returned -6.11%.

On an absolute performance basis, all asset class components of the strategy detracted during the period.

On a relative to the benchmark performance basis, REIT Preferreds contributed positively due to underweight exposure. Conversely, Global Real Estate was the leading detractor, driven primarily by security selection. Overweight exposure to Metals & Mining Equities was also a leading detractor from relative returns.

In the next section, we provide further detail on the performance of each asset class, along with our outlook for investing in real asset-related securities.

GLOBAL INFRASTRUCTURE SECURITIES

Listed infrastructure returns were negative in 2018, as measured by the Dow Jones Brookfield Global Infrastructure Composite Index2, which declined 8.5% during the year. By region, the Americas was down 6.9%, while Asia Pacific and Europe rose 4.7% and 1.2%, respectively. By sector, Ports declined the most (−26.6%), followed by Water (−7.4%), Airports (−7.1%), Electricity Transmission & Distribution (−6.2%), Oil & Gas Storage & Transportation (−4.6%), Toll Roads (−2.3%) and Diversified (−0.7%). Only Communications (+6.5%) posted positive gains.