UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number811-22558

BROOKFIELD INVESTMENT FUNDS

(Exact name of registrant as specified in charter)

BROOKFIELD PLACE

250 VESEY STREET, 15th Floor

NEW YORK, NEW YORK 10281-1023

(Address of principal executive offices) (Zip code)

BRIAN F. HURLEY, PRESIDENT

BROOKFIELD INVESTMENT FUNDS

BROOKFIELD PLACE

250 VESEY STREET 15th Floor

NEW YORK, NEW YORK 10281-1023

(Name and address of agent for service)

Registrant’s telephone number, including area code: (855)777-8001

Date of fiscal year end: September 30

Date of reporting period: September 30, 2019

Item 1. Reports to Shareholders.

Brookfield

20

19

ANNUAL REPORT

SEPTEMBER 30, 2019

Center Coast Brookfield

Energy Infrastructure Fund

* Please see inside front cover of the report for important information regarding future delivery of shareholder reports.

Brookfield Public Securities Group LLC (the “Firm”) is an SEC-registered investment adviser and represents the Public Securities platform of Brookfield Asset Management. The Firm provides global listed real assets strategies including real estate equities, infrastructure and energy infrastructure equities, multi-real-asset-class strategies and real asset debt. With over $19 billion of assets under management as of September 30, 2019, the Firm manages separate accounts, registered funds and opportunistic strategies for institutional and individual clients, including financial institutions, public and private pension plans, insurance companies, endowments and foundations, sovereign wealth funds and high net worth investors. The Firm is a wholly owned subsidiary of Brookfield Asset Management, a leading global alternative asset manager with over $500 billion of assets under management as of September 30, 2019. For more information, go to www.brookfield.com.

Center Coast Brookfield Energy Infrastructure Fund (the “Fund”) is managed by Brookfield Public Securities Group LLC. The Fund uses its website as a channel of distribution of material company information. Financial and other material information regarding the Fund is routinely posted on and accessible at https://publicsecurities.brookfield.com/en.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website (https://publicsecurities.brookfield.com/en), and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker, investment adviser, bank or trust company) or, if you are a direct investor, by calling the Fund (toll-free) at 1-855-777-8001 or by sending an e-mail request to the Fund atpublicsecurities.enquiries@brookfield.com.

Beginning on January 1, 2019, you may elect to receive all future reports in paper free of charge. If you invest through a financial intermediary, you may contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you may call 1-855-777-8001 or send an email request topublicsecurities.enquiries@brookfield.com to let the Fund know you wish to continue receiving paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held in your account if you invest through your financial intermediary or all funds held within the fund complex if you invest directly with the Fund.

This report is for shareholder information. This is not a prospectus intended for use in the purchase or sale of Fund shares.

| NOT FDIC INSURED | MAY LOSE VALUE | NOT BANK GUARANTEED |

[THIS PAGE IS INTENTIONALLY LEFT BLANK]

Dear Shareholders,

We are pleased to provide the Annual Report for Center Coast Brookfield Energy Infrastructure Fund (the “Fund”) for the fiscal year ended September 30, 2019.

Broader equity and fixed-income markets posted gains during the period with the MSCI World1, S&P 5002 and Bloomberg Barclays Global Aggregate Bond3 Indexes returning +2.42%, +4.25% and +7.60%, respectively. Energy infrastructure lagged broader markets returning -8.13%, as measured by the Alerian MLP Index4, as commodity price volatility and technical selling in late 2018 heavily contributed to the sector’s underperformance during the fiscal year.

From a macroeconomic perspective, the period was marked by slowing economic growth and falling interest rates amid dovish monetary policy. Domestically, the U.S. continued to lead the developed world in terms of economic growth, although the pace of that growth moderated somewhat throughout the period. The ongoing U.S.-China trade dispute continued to gain steam, with additional tariffs levied throughout the period and no clear resolution expected in the near future.

In response to slowing economic growth and the perceived increased risks to economic growth, the U.S. Federal Reserve’s Federal Open Market Committee (“the FOMC”) reversed course during the period. After raising the target for the federal funds rate at its meeting in December 2018, the FOMC then cut its benchmark rate twice by 25 basis points at both of the August and September 2019 meetings.

Globally, the Eurozone continued to lag the U.S. in terms of economic growth and in response, the European Central Bank resumed stimulus measures in an attempt to combat the region’s economic malaise. The People’s Bank of China also increased its stimulus measures to combat a slowing Chinese economy, some of which can be attributed to the U.S-China trade dispute.

Looking ahead we expect modest, albeit slowing, global economic growth. We do, however, acknowledge heightened market and economic risks related to ongoing geopolitical uncertainty, including trade disputes, Brexit and the upcoming U.S. presidential election, among others. Given the wholesale measures (discussed in greater detail in the Management Discussion of Fund Performance) the asset class has undertaken over the last several years coupled with the sector’s historical relative cash flow stability versus the broader energy industry, we believe energy infrastructure has the ability to show defensiveness in an uncertain environment.

In addition to performance information, this report provides an overview of market conditions and a discussion of factors affecting the Fund’s investment performance, together with the Fund’s audited financial statements as of September 30, 2019.

We welcome your questions and comments, and encourage you to contact our Investor Relations team at (855) 777-8001 or visit us at www.brookfield.com for more information. Thank you for your support.

Sincerely,

Brian F. Hurley

President

Center Coast Brookfield Energy Infrastructure Fund

David W. Levi, CFA

Chief Executive Officer

Brookfield Public Securities Group LLC

Past performance is no guarantee of future results.

1 The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets.

Letter to Shareholders(continued)

2 The S&P 500 Index is an unmanaged weighted index of 500 large company stocks that is widely-recognized as representative of the performance of the U.S. stock market. Indexes are not managed and an investor cannot invest directly in an index.

3 The Bloomberg Barclays Global Aggregate Bond Index tracks the performance of investment grade public debt issued in the major domestic and eurobond markets, including global bonds.

4 The Alerian MLP Index is the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX).

Indices are not managed and an investor cannot invest directly in an index.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are primarily as of the close of business on September 30, 2019 and subject to change based on subsequent developments.

The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of Fund’s holdings.

Mutual fund investing involves risk. Principal loss is possible.

Quasar Distributors, LLC is the distributor of Brookfield Investment Funds.

Diversification does not assure a profit, nor does it protect against a loss in a declining market.

Must be preceded or accompanied by a prospectus.

2Brookfield Public Securities Group LLC

About Your Fund’s Expenses

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments and contingent deferred sales charges and redemption fees on redemptions; and (2) ongoing costs, including management fees, distribution (12b-1) fees and other fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Fund Return

The table below provides information about actual account values and actual expenses. You may use the information on this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The table below also provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with hypothetical examples that appear in shareholders’ reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) and redemption fees. Therefore, the hypothetical account values and expenses in the table are useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs overall would have been higher.

| | Annualized Expense Ratio | Beginning Account Value

(04/01/19) | Ending Account Value

(09/30/19) | Expenses Paid During Period

(04/01/19–

09/30/19)(1) |

| Actual | | | | |

Class Y Shares

| 1.25% | $1,000.00 | $937.60 | $6.07 |

| Hypothetical (assuming a 5% return before expenses) | | | | |

Class Y Shares

| 1.25% | $1,000.00 | 1,018.80 | 6.33 |

| (1) | Expenses are equal to the Fund’s annualized expense ratio by class multiplied by the average account value over the period, multiplied by 183/365 (to reflect a six-month period). |

Center Coast Brookfield Energy Infrastructure Fund

Management Discussion of Fund Performance

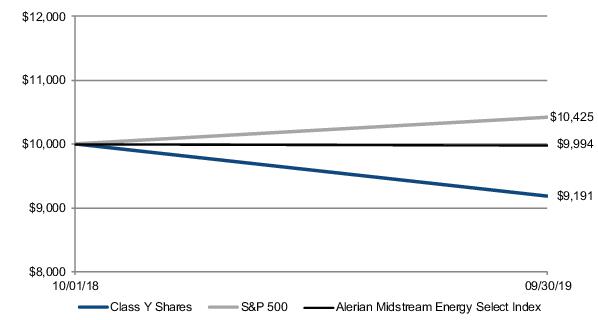

For the fiscal year ended September 30, 2019, the Fund's Class Y had a total return of -8.09%, which assumes the reinvestment of dividends and is exclusive of brokerage commissions, underperforming the S&P 5001 and Alerian Midstream Energy Select Index2, which returned 4.25% and -0.06%, respectively.

MARKET OVERVIEW

Introduction

Fiscal First Quarter (October – December 2018) (-18.83% NAV total return by the Fund's Y share class)

The Fund’s fiscal first quarter came to a disappointing end due to a combination of broader market volatility, crude oil price weakness and year-end tax loss selling. Over the same time period, the Fund’s benchmark, the Alerian MLP Index3 (“AMZ”) posted a -17.30% return for the third worst quarterly performance for the index on record.

The asset class was defined by uncertainty over much of the calendar year. Numerous midstream companies engaged in “simplification” transactions during the first half of the fiscal year, which contributed to the volatility. Simplifications are transactions in which incentive distribution rights are retired in exchange for various financial considerations, and/or two or more affiliated public entities merge in a corporate transaction or series of corporate transactions. However, each transaction and transition itself is difficult to predict (i.e., uncertain) and sometimes results in a distribution cut and/or unexpected tax bill. Even the most seasoned industry vets were caught off guard and surprised by many of the announced simplification transactions and distribution cuts.

In addition to simplification, most midstream companies took steps to eliminate the ongoing need for equity capital markets to fund growth (the transition to “self-funding”). This too can involve a corporate action or corporate finance decision that is difficult to predict and often impacts growth projections and/or distributions, making it difficult to value and invest in the equity of a company.

Despite the disappointing ending, we headed into 2019 optimistic given fundamentals remained constructive while the often-painful process of simplification was largely over. The industry exited the calendar year with both record levels of supply and demand while midstream companies positioned themselves with little need for external equity, distribution coverage levels higher than they were at the peak of the market and leverage levels lower than they had been in years.

Fiscal Second Quarter (January – March 2019) (20.32% NAV total return by the Fund's Y share class)

The Fund outperformed the AMZ for the three months ended March 31, 2019 and beat the Index’s strongest-ever quarterly return in its 23 year history (+19.74% in Q1 of 2013). Other than the quarterly return, it was a fairly boring quarter. There were some project announcements, modest earnings surprises, some Mergers & Acquisitions here and there, ongoing regulatory battles, and a few small equity offerings, but nothing extraordinary or shocking. The level of activity felt normal, like what you would expect in any given quarter—no major surprises, no Federal Energy Regulatory Commission policy change, no unexpected distribution cuts, no Exploration & Production bankruptcy fears, no unwanted tax bills, no game-changers. And this is exactly what we want! Boring, in our opinion, is better.

Conversely, underperformance during the period, and beyond, tracked names that: announced project delays, revised guidance, have complicated balance sheets, and generally just over-promised the market and under-delivered results. It helps to have scale, integration, balance sheet flexibility, and management experience, which is where our portfolios remained biased.

As previously discussed, the corporate and financing maturation process was largely behind us – at the end of the Fund’s fiscal second quarter, just 7% of the midstream market cap remained in an IDR-paying structure. In addition, public equity issuance virtually evaporated, from $50+ billion over a three year-span from 2014-2016 to ~$5bn expected from 2019-2021 by some sell-side estimates. The transition allowed companies to actually be “boring” and execute the plan with a cleaner, more mature structure built for stability in a lower-for-longer,

4Brookfield Public Securities Group LLC

Center Coast Brookfield Energy Infrastructure Fund

post-shale world. With all of that said, and as odd as it may sound, our hope was for the trend of “boring is better” to continue for the rest of the year.

Fiscal Third Quarter (April – June 2019) (-2.35% NAV total return by the Fund's Y share class)

The fund’s fiscal third quarter was largely a continuation of the “boring is better” trend, outside of the broader market and commodities volatility. Industry bellwethers outperformed as energy investors continued showing very little patience for the old investment paradigm: for midstream, using equity capital markets to fund growth (“Midstream 1.0”), while for oil & gas producers, growing production for growth’s sake (instead of focusing on free cash flow).

During the Fund’s fiscal third quarter, midstream outperformed broader energy indices and energy commodities, potentially showing that the measures the sector had taken to adjust its corporate finance model could be starting to pay off for investors. From April to June, the AMZ outperformed:

| • | Broader energy by 3% |

| • | Oil & gas producers by 11% |

| • | Oilfield services by 14% |

| • | U.S. crude oil by 3% |

| • | U.S. natural gas by 11% |

| • | U.S. natural gas liquids (NGLs) by 21%4 |

Energy commodities went on a wild ride yet again in the second calendar quarter, driven by changing supply/demand fundamentals, up-and-down trade war news, and other geopolitical tensions. U.S. crude rallied 10% from the end of the first quarter to late April but had trekked down 15% by mid-June before finally finishing the quarter down only 3%. U.S. gas prices were under pressure virtually the entire quarter, and U.S. NGL prices had their lowest quarterly average since the third quarter of 2016 despite wide pricing spreads to Europe and Asia, signaling the need for more export capacity to get high-demand liquids to market. Amidst this choppiness, midstream equities continued to be “boring.”

Fiscal Fourth Quarter (July – September 2019) (-3.98% NAV total return by the Fund's Y share class)

While the prior quarters saw a continuation of “boring is better”, the end of the fund’s fiscal year delivered a handful of surprises, a bit of drama, and a noticeable increase in volatility. Some of this volatility showed up in response to continued weakness in natural gas and natural gas liquids (“NGL”) prices. Importantly, the primary cause of this commodity price weakness is record supply, which is what moves through midstream assets to create cash flow (record cash flow, we might add).

The challenge, however, is that the extreme success of some basins is starting to impact other basins halfway across the country, and even halfway across the world. The Permian Basin—largely viewed as the “best” basin in North America—is taking absolutely no prisoners as it continues to produce record levels of crude oil that comes out of the ground along with “associated” natural gas and NGLs. Producers view these associated hydrocarbons as a byproduct and, in our opinion, it’s hard to compete with byproduct economics. As long as crude prices incentivize drilling in the Permian (and the Bakken and Rockies, to a lesser extent), associated gas and NGLs will most likely make it incrementally more difficult for basins relying on dry or wet gas economics to compete.

Further, with the ongoing completion of export facilities, North America’s excess natural gas and NGLs started to pressure prices abroad. Despite the interim volatility this has created, cheap natural gas prices have tended to stimulate demand which could result in long-term tailwinds for the industry as a whole. Cheap natural gas import

Center Coast Brookfield Energy Infrastructure Fund

prices abroad should accelerate the transition away from “dirtier” fuels such as coal and heating oil, helping reduce global carbon emissions.

Perhaps the most dramatic event of the quarter, however, was the brazen attack on Saudi Arabia’s Abqaiq and Khurais oil facilities on September 14th. Although Saudi Arabia has been able to return production back to pre-attack levels as of the writing of this letter, crude oil prices jumped more than 10% the following Monday morning (September 16, 2019), and many believed that a geopolitical risk premium would be embedded in crude oil prices—and energy equities—for the foreseeable future. Yet, shockingly, global crude oil prices erased all their gains in two weeks, and the near-term portion of the Brent futures curve is actually lower as of this writing than it was before the attack.5

The end of the Fund’s fiscal year felt like a common refrain: any major news had little or no impact due to overwhelming negative energy sentiment and broader market jitters. So, what continues to make us excited about this asset class? The cash flow. It’s sustainable, in our view, and we believe with simplification mostly behind us, balance sheets healthier, and financing less equity dependent, it should finally start accruing to the benefit of equity investors in a sustainable way. In the current sub 2% interest rate world, we think this can matter. At a minimum we think it will provide attractive income—an important component of total return—and could mitigate risk to the extent volatility picks up meaningfully. In the meantime, we’ll continue to celebrate the fundamentals, point out the myriad valuation disconnects, and hope that someone eventually listens even if, for now, it feels like we’re shouting into the void.

1The S&P 500 Index is an unmanaged weighted index of 500 large company stocks that is widely-recognized as representative of the performance of the U.S. stock market. Indexes are not managed and an investor cannot invest directly in an index.

2The Alerian Midstream Energy Select Index is a composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents are engaged in midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMEI) and on a total-return basis (AMEIX).

3The Alerian MLP Index is the leading gauge of energy infrastructure Master Limited Partnerships (MLPs). The capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities, is disseminated real-time on a price-return basis (AMZ) and on a total-return basis (AMZX).

4Broader energy is represented by the IXE Index, Oil & gas producers by the SPSIOP Index, Oilfield services by the OSX Index, U.S. crude oil by West Texas Intermediate (WTI), U.S. natural gas by Henry Hub, and U.S. NGLs by Mont Belvieu is the U.S. benchmark for NGL prices. The Energy Select Sector (“IXE”) Index is one of the eleven Select Sector Indices that seeks to track their respective Global Industry Classification Standard (GICS®) sectors. The IXE tracks companies within the Energy GICS® sector, which is comprised of companies that are engaged in exploration & production, refining & marketing and storage & transportation of oil & gas and coal & consumable fuels. The sector also includes companies that offer oil & gas equipment and services. The S&P Oil & Gas Exploration & Production Select Industry (“SPSIOP”) Index is a sub-index of the Energy Select Sector Index. The index comprises stocks in the S&P Total Market Index that are classified in the GICS oil & gas exploration & production sub-industry. The PHLX Oil Service Sector (“OSX”) Index is designed to track the performance of a set of companies involved in the oil services sector. Henry Hub is the U.S. benchmark for natural gas spot and futures pricing. West Texas Intermediate (“WTI”) is the U.S. benchmark for crude oil prices.

5Bloomberg Brent Spot Prices and 10/4/2019 Brent Futures Curve vs. 9/13/2019 Brent Futures Curve.

Indices are not managed and an investor cannot invest directly in an index.

6Brookfield Public Securities Group LLC

Center Coast Brookfield Energy Infrastructure Fund

AVERAGE ANNUAL TOTAL RETURNS

| Average Annual Total Returns for fiscal year ended September 30, 2019 | One Year† | Since Inception1 |

| Class Y Shares | -8.09% | -8.09% |

| S&P 500 Index2 | 4.25% | 4.25% |

| Alerian Midstream Energy Select Index3 | -0.06% | -0.06% |

† Returns for less than one year are not annualized.

1 Class Y Shares commenced operations on October 1, 2018.

2 The S&P 500 Index references Class Y's inception date.

3 The Alerian Midstream Energy Select Index references Class Y's inception date.

Performance data quoted represents past performance; past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance of the Funds may be lower or higher than the performance quoted. Performance data current to the most recent month end may be obtained by calling 855.244.4859.

Investment performance reflects fee waivers, expenses and reimbursements in effect. In the absence of such waivers, total return and NAV would be reduced.

The gross expense ratio in the prospectus dated January 28, 2019 is 4.00% for Class Y Shares, as applicable to investors.

The Fund’s gross and net expense ratios in the financial highlights of this report are as follows: Class Y is 6.17% and 1.25% for the fiscal year ended September 30, 2019.

The Adviser has contractually agreed to reimburse the Fund's expenses through October 1, 2020. There is no guarantee that such reimbursement will be continued after that date.

The graph below illustrates a hypothetical investment of $10,000 in the Fund—Class Y Shares from the commencement of investment operations on October 1, 2018 to September 30, 2019 compared to the Alerian Midstream Energy Select Index.

Center Coast Brookfield Energy Infrastructure Fund

Disclosure

The Fund’s portfolio holdings are subject to change without notice. The mention of specific securities is not a recommendation or solicitation for any person to buy, sell or hold any particular security. There is no assurance that the Fund currently holds these securities. Please refer to the Schedule of Investments contained in this report for a full listing of fund holdings.

Earnings growth is not a measure of the Fund’s future performance.

A Basis Point is one hundredth of one percent (0.01%). Cash flow refers to the amount of cash generated and used by a company over a given period.

Mutual fund investing involves risk. Principal loss is possible. Investing in Master Limited Partnerships (“MLPs”) involves additional risks as compared to the risks of investing in common stock, including risks related to cash flow, dilution and voting rights. The Fund’s investments are concentrated in the energy infrastructure industry with an emphasis on securities issued by MLPs, which may increase volatility. Energy infrastructure companies are subject to risks specific to the industry such as fluctuations in commodity prices, reduced volumes of natural gas or other energy commodities, environmental hazards, changes in the macroeconomic or the regulatory environment or extreme weather. MLPs may trade less frequently than larger companies due to their smaller capitalizations which may result in erratic price movement or difficulty in buying or selling. The Fund invests in small and mid-cap companies, which involve additional risks such as limited liquidity and greater volatility. Additional management fees and other expenses are associated with investing in MLPs. Additionally, investing in MLPs involves material income tax risks and certain other risks. Actual results, performance or events may be affected by, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) changes in laws and regulations and (5) changes in the policies of governments and/or regulatory authorities. An investment in the Fund may not receive the same tax advantages as a direct investment in the MLP. This material is provided for general and educational purposes only, and is not intended to provide legal, tax or investment advice or to avoid legal penalties that may be imposed under U.S. federal tax laws. Investors should contact their own legal or tax advisors to learn more about the rules that may affect individual situations.

These views represent the opinions of Brookfield Public Securities Group LLC and are not intended to predict or depict the performance of any investment. These views are as of the close of business on September 30, 2019 and subject to change based on subsequent developments.

8Brookfield Public Securities Group LLC

Center Coast Brookfield Energy Infrastructure Fund

Portfolio Characteristics (Unaudited)

September 30, 2019

| Asset Allocation by Sector | Percent of

Total Investments |

| Master Limited Partnerships | |

| Pipeline Transportation | Natural Gas | 10.3% |

| Pipeline Transportation | Petroleum | 8.5% |

| Gathering + Processing | 6.1% |

| Total Master Limited Partnerships | 24.9% |

| Common Stocks | |

| Gathering + Processing | 36.6% |

| Pipeline Transportation | Petroleum | 17.3% |

| Pipeline Transportation | Natural Gas | 13.1% |

| Other | Liquefaction | 8.1% |

| Total Common Stocks | 75.1% |

| Total | 100.0% |

| TOP TEN HOLDINGS | Percent of

Net Assets |

| Williams Companies, Inc. | 9.0% |

| Targa Resources Corp. | 8.9% |

| Cheniere Energy, Inc. | 8.0% |

| Pembina Pipeline Corp. | 6.3% |

| ONEOK, Inc. | 6.1% |

| Enterprise Products Partners LP | 5.1% |

| Energy Transfer LP | 5.1% |

| Plains GP Holdings LP | 4.7% |

| MPLX LP | 4.6% |

| Equitrans Midstream Corp. | 4.5% |

Center Coast Brookfield Energy Infrastructure Fund

Schedule of Investments

September 30, 2019

| | | | Shares | Value |

| MASTER LIMITED PARTNERSHIPS – 24.8% | | | |

| Gathering + Processing – 6.1% | | | |

MPLX LP

| | | 7,482 | $209,571 |

Western Midstream Partners LP

| | | 2,772 | 68,995 |

| Total Gathering + Processing | | | | 278,566 |

| Pipeline Transportation | Natural Gas – 10.2% | | | |

Energy Transfer LP

| | | 18,000 | 235,440 |

Enterprise Products Partners LP

| | | 8,247 | 235,699 |

| Total Pipeline Transportation | Natural Gas | | | | 471,139 |

| Pipeline Transportation | Petroleum – 8.5% | | | |

Magellan Midstream Partners LP

| | | 2,176 | 144,204 |

Phillips 66 Partners LP

| | | 1,282 | 72,587 |

Plains All American Pipeline LP

| | | 8,319 | 172,619 |

| Total Pipeline Transportation | Petroleum | | | | 389,410 |

Total MASTER LIMITED PARTNERSHIPS

(Cost $1,188,630)

| | | | 1,139,115 |

| COMMON STOCKS – 74.4% | | | |

| Gathering + Processing – 36.3% | | | |

Altus Midstream Co. (n)

| | | 46,395 | 131,298 |

Antero Midstream Corp.

| | | 18,699 | 138,373 |

EnLink Midstream LLC

| | | 18,435 | 156,698 |

ONEOK, Inc.

| | | 3,818 | 281,348 |

Rattler Midstream LP (n)

| | | 7,637 | 136,091 |

Targa Resources Corp.

| | | 10,234 | 411,100 |

Williams Companies, Inc.

| | | 17,139 | 412,364 |

| Total Gathering + Processing | | | | 1,667,272 |

| Other | Liquefaction – 8.0% | | | |

Cheniere Energy, Inc. (n)

| | | 5,837 | 368,081 |

| Pipeline Transportation | Natural Gas – 13.0% | | | |

Equitrans Midstream Corp.

| | | 14,252 | 207,367 |

Kinder Morgan, Inc.

| | | 9,379 | 193,301 |

TC Energy Corp. (u)

| | | 3,793 | 196,439 |

| Total Pipeline Transportation | Natural Gas | | | | 597,107 |

| Pipeline Transportation | Petroleum – 17.1% | | | |

Enbridge, Inc. (u)

| | | 3,993 | 140,074 |

Pembina Pipeline Corp. (u)

| | | 7,784 | 288,553 |

Plains GP Holdings LP

| | | 10,181 | 216,143 |

Tallgrass Energy LP

| | | 7,041 | 141,806 |

| Total Pipeline Transportation | Petroleum | | | | 786,576 |

Total COMMON STOCKS

(Cost $3,643,749)

| | | | 3,419,036 |

Total Investments – 99.2%

(Cost $4,832,379)

| | | | 4,558,151 |

Other Assets in Excess of Liabilities – 0.8%

| | | | 38,716 |

TOTAL NET ASSETS – 100.0%

| | | | $4,596,867 |

See Notes to Financial Statements.

10Brookfield Public Securities Group LLC

Center Coast Brookfield Energy Infrastructure Fund

Schedule of Investments (continued)

September 30, 2019

| The following notes should be read in conjunction with the accompanying Schedule of Investments. |

| LP— Limited Partnership |

| LLC— Limited Liability Company |

| (n) | — Non-income producing security. |

| (u) | — Foreign security or a U.S. security of a foreign company. |

See Notes to Financial Statements.

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Statement of Assets and Liabilities

September 30, 2019

| Assets: | |

Investments in securities, at value (cost $4,832,379)

| $4,558,151 |

Cash

| 49,250 |

Dividends receivable

| 5,824 |

Net receivable from Adviser

| 21,491 |

Receivable for investments sold

| 3,983 |

Prepaid expenses

| 74 |

Total assets

| 4,638,773 |

| Liabilities: | |

Trustees' fee payable

| 1,368 |

Accrued expenses

| 40,538 |

Total liabilities

| 41,906 |

Commitments and contingencies (Note 8)

| |

Net Assets

| $4,596,867 |

| Composition of Net Assets: | |

Paid-in capital

| $5,013,542 |

Accumulated losses

| (416,675) |

Net assets applicable to capital shares outstanding

| $4,596,867 |

| Net Assets | |

| Class Y Shares — Net Assets | $4,596,867 |

Shares outstanding

| 501,693 |

Net asset value and redemption price per share

| $9.16 |

See Notes to Financial Statements.

12Brookfield Public Securities Group LLC

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Statement of Operations

For the Fiscal Year Ended September 30, 2019

| Investment Income: | |

Dividends and distributions from common stocks (net of foreign withholding tax of $6,143)

| $163,637 |

Distributions from master limited partnerships

| 121,691 |

Total dividends and distributions

| 285,328 |

Less return of capital distributions

| (194,228) |

Total investment income

| 91,100 |

| Expenses: | |

Investment advisory fees (Note 3)

| 46,494 |

Administration fees (Note 3)

| 6,974 |

Organizational fees

| 138,112 |

Audit and tax services

| 33,216 |

Trustees' fees

| 17,932 |

Reports to shareholders

| 15,483 |

Legal fees

| 11,200 |

Custodian fees

| 6,581 |

Miscellaneous

| 4,389 |

Transfer agent fees

| 3,594 |

Fund accounting fees

| 2,276 |

Registration fees

| 650 |

Insurance

| 187 |

Interest expense

| 7 |

Total operating expenses

| 287,095 |

Less expenses reimbursed by the investment adviser (Note 3)

| (228,978) |

Net expenses

| 58,117 |

Net investment income

| 32,983 |

| Realized and Unrealized Gain (Loss): | |

Net realized gain (loss) on:

| |

Investments

| (161,941) |

Foreign currency transactions

| 37 |

Net realized loss

| (161,904) |

Net change in unrealized (appreciation) depreciation on:

| |

Investments

| (274,228) |

Foreign currency translations

| 16 |

Net change in unrealized depreciation

| (274,212) |

Net realized and unrealized loss

| (436,116) |

Net decrease in net assets resulting from operations

| $(403,133) |

See Notes to Financial Statements.

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Statements of Changes in Net Assets

| | For the

Fiscal Year

Ended

September 30,

2019 |

| Increase (Decrease) in Net Assets Resulting from Operations: | |

Net investment income

| $32,983 |

Net realized loss

| (161,904) |

Net unrealized depreciation

| (274,212) |

Net decrease in net assets resulting from operations

| (403,133) |

| Distributions to Shareholders: | |

| From distributable earnings: | |

Class Y shares

| (13,542) |

Total distributions paid

| (13,542) |

| Capital Share Transactions (Note 6): | |

Subscriptions

| 5,000,000 |

Reinvestment of distributions

| 13,542 |

Net increase in capital share transactions

| 5,013,542 |

Total increase in net assets

| 4,596,867 |

| Net Assets: | |

Beginning of year

| — |

End of year

| $4,596,867 |

See Notes to Financial Statements.

14Brookfield Public Securities Group LLC

Center Coast Brookfield Energy Infrastructure Fund

Financial Highlights

| Class Y | For the

Fiscal Year

Ended

September 30,

2019 |

| Per Share Operating Performance: | |

Net asset value, beginning of period

| $10.00 |

Net investment income1

| 0.07 |

Net realized and unrealized gain (loss)1

| (0.88) |

Net increase (decrease) in net asset value resulting from operations

| (0.81) |

Distributions from distributable earnings

| (0.03) |

Net asset value, end of period

| $9.16 |

| Total Investment Return† | -8.09% |

| Ratios to Average Net Assets/Supplementary Data: | |

Net assets, end of period (000s)

| $4,597 |

Gross operating expenses

| 6.17% |

| Net expenses, including fee waivers and reimbursement and exlcuding organizational fees | 3.20% |

Net expenses, including fee waivers and reimbursement

| 1.25% |

Net investment income

| (4.21)% |

Net investment income, excluding the effect of fee waivers and reimbursement

| 0.71% |

Portfolio turnover rate

| 96% |

| † | Total investment return is computed based upon the net asset value of the Fund’s shares and excludes the effects of sales charges or contingent deferred sales charges, if applicable. Distributions are assumed to be reinvested at the net asset value of the Class on the ex-date of the distribution. |

| 1 | Per share amounts presented are based on average shares outstanding throughout the period indicated. |

See Notes to Financial Statements.

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements

September 30, 2019

1.Organization

Brookfield Investment Funds, a Delaware statutory trust (the “Trust”), is registered as an open-end management investment company under the under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust consists of seven different series of underlying portfolios as of September 30, 2019. Center Coast Brookfield Energy Infrastructure Fund (the “Fund”), a series of the Trust, is non-diversified as the term is defined in the 1940 Act. The Fund's Class Y Shares commenced operations on October 1, 2018. Shares of the Fund are not offered for sale as of the date of this report. As of September 30, 2019, Brookfield Public Securities Group LLC (the “Adviser”) owns Class Y shares in the Fund.

The Fund currently has four classes of shares: Class A, Class C, Class Y and Class I shares. Each class represents an interest in the same portfolio of assets and has identical voting, dividend, liquidation and other rights except that: (i) Class A shares have a maximum front end sales charge of 4.75% and Class C shares have a maximum deferred sales charge of 1.00%; (ii) Class A shares have a 12b-1 fee of 0.25% and Class C shares have a 12b-1 fee of 1.00%; and (iii) each class has exclusive voting rights with respect to matters relating to its own distribution arrangements. Currently, the Fund is not publicly offering any share class to investors.

The Adviser, a wholly-owned subsidiary of Brookfield Asset Management Inc., is registered as an investment adviser under the Investment Advisers Act of 1940, as amended, and serves as investment adviser to the Fund.

The Fund’s primary investment objective is to seek total return through growth of capital and current income. The Fund's investment objective is not fundamental and may be changed by the Trust's Board of Trustees (the “Board”) without shareholder approval, upon not less than 60 days prior written notice to shareholders. There can be no assurance that the Fund will achieve its investment objective.

2.Significant Accounting Policies

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The Fund is an investment company within the scope of Financial Accounting Standards Board (“FASB”) Accounting Standards Update (“ASU”) 2013-08 and follows accounting and reporting guidance under FASB Accounting Standards Codification (“ASC”) Topic 946,Financial Services-Investment Companies.

Valuation of Investments:The Fund’s Board has adopted procedures for the valuation of the Fund’s securities. The Adviser oversees the day to day responsibilities for valuation determinations under these procedures. The Board regularly reviews the application of these procedures to the securities in the Fund’s portfolio. The Adviser’s Valuation Committee is comprised of senior members of the Adviser’s management team. There can be no assurance that the Fund could purchase or sell a portfolio security at the price used to calculate the Fund’s net asset value (“NAV”).

Investments in equity securities listed or traded on any securities exchange or traded in the over-the-counter market are valued at the last trade price as of the close of business on the valuation date. Prices of foreign equities that are principally traded on certain foreign markets will generally be adjusted daily pursuant to a fair value pricing service approved by the Board in order to reflect an adjustment for the factors occurring after the close of certain foreign markets but before the NYSE Close. When fair value pricing is employed, the value of the portfolio securities used to calculate the Fund’s NAV may differ from quoted or official closing prices. Investments in open-end registered investment companies, if any, are valued at the NAV as reported by those investment companies.

16Brookfield Public Securities Group LLC

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

Debt securities, including U.S. government securities, listed corporate bonds, other fixed income and asset-backed securities, and unlisted securities and private placement securities, are generally valued at the bid prices furnished by an independent pricing service or, if not valued by an independent pricing service, using bid prices obtained from active and reliable market makers in any such security or a broker-dealer. The broker-dealers or pricing services use multiple valuation techniques to determine fair value. In instances where sufficient market activity exists, the broker-dealers or pricing services may utilize a market-based approach through which quotes from market makers are used to determine fair value. In instances where sufficient market activity may not exist or is limited, the broker-dealers or pricing services may also utilize proprietary valuation models which may consider market transactions in comparable securities and the various relationships between securities in determining fair value and/or market characteristics such as benchmark yield curves, option-adjusted spreads, credit spreads, estimated default rates, coupon-rates, anticipated timing of principal repayments, underlying collateral, and other unique security features in order to estimate the relevant cash flows, which are then discounted to calculate the fair values. Short-term debt securities with remaining maturities of sixty days or less are valued at amortized cost of discount or premium to maturity, unless such valuation, in the judgment of the Adviser's Valuation Committee, does not represent fair value.

Securities for which market prices are not readily available or which cannot be valued using the sources described above will be valued using an internal proprietary fair value methodology. For any security warranting such fair value measurement, a memorandum, including the specific methodology and supporting information, will be provided to the Valuation Committee by a portfolio manager or analyst looking to fair value a particular security utilizing the internal proprietary fair value methodology. A portfolio manager or analyst shall use their best efforts to maximize the use of relevant observable inputs and minimize the use of unobservable inputs within their valuation technique. The Valuation Committee shall review the memorandum and supporting information provided by a portfolio manager or analyst and consider all relevant factors as it deems appropriate before approving the fair value recommendation.

The Fund may use the internally determined fair value of a security to calculate its NAV when, for example, (1) a portfolio security is not traded in a public market or the principal market in which the security trades is closed, (2) trading in a portfolio security is suspended and not resumed prior to the normal market close, (3) a portfolio security is not traded in significant volume for a substantial period, or (4) the Adviser determines that the quotation or price for a portfolio security provided by a broker-dealer or an independent pricing service is inaccurate.

The internally determined fair value of securities may be difficult to determine and thus judgment plays a greater role in the valuation process. The fair valuation methodology may include or consider the following guidelines, as appropriate: (1) evaluation of all relevant factors, including, but not limited to, pricing history, current market level, supply and demand of the respective security; (2) comparison to the values and current pricing of securities that have comparable characteristics; (3) knowledge of historical market information with respect to the security; (4) other factors relevant to the security which would include, but not be limited to, duration, yield, fundamental analytical data, the Treasury yield curve, and credit quality.

The values assigned to internally fair valued investments are based on available information and do not necessarily represent amounts that might ultimately be realized, since such amounts depend on future developments inherent in investments. Changes in the fair valuation of portfolio securities may be less frequent and of greater magnitude than changes in the price of portfolio securities valued at their last sale price, by an independent pricing service, or based on market quotations. Imprecision in estimating fair value can also impact the amount of unrealized appreciation or depreciation recorded for a particular portfolio security and differences in the assumptions used could result in a different determination of fair value, and those differences could be material.

The Fund has established methods of fair value measurements in accordance with GAAP. Fair value denotes the price that the Fund would receive upon selling an investment in a timely transaction to an independent buyer in the principal or most advantageous market of the investment. A three-tier hierarchy has been established to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk, for example, the risk inherent in a particular valuation technique used to measure fair value including such a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances. The three-tier hierarchy of inputs is summarized in the three broad levels listed below.

| Level 1 - | quoted prices in active markets for identical assets or liabilities |

| Level 2 - | quoted prices in markets that are not active or other significant observable inputs (including, but not limited to: quoted prices for similar assets or liabilities, quoted prices based on recently executed transactions, interest rates, credit risk, etc.)

|

| Level 3 - | significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of assets or liabilities) |

The Adviser’s valuation policy, as previously stated, establishes parameters for the sources and types of valuation analysis, as well as, the methodologies and inputs the Valuation Committee uses in determining fair value. If the Valuation Committee determines that additional techniques, sources or inputs are appropriate or necessary in a given situation, such additional work will be undertaken.

To assess the continuing appropriateness of security valuations, the Adviser (or its third party service provider, who is subject to oversight by the Adviser), regularly compares its prior day prices, prices on comparable securities and sale prices to the current day prices and challenges those prices that exceed certain tolerance levels with the third party pricing service or broker source. For those securities valued by fair valuations, the Adviser’s Valuation Committee reviews and affirms the reasonableness of the valuations based on such methodologies and fair valuation determinations on a regular basis after considering all relevant information that is reasonably available.

The inputs or methodology used for valuing investments are not necessarily an indication of the risk associated with investing in those securities.

The following table summarizes the Fund’s investments valuation inputs categorized in the disclosure hierarchy as of September 30, 2019:

| Valuation Inputs | Level 1 | | Level 2 | | Level 3 | | Total |

Common Stocks

| $3,419,036 | | $— | | $— | | $3,419,036 |

Master Limited Partnerships

| 1,139,115 | | — | | — | | 1,139,115 |

Total Investments

| $4,558,151 | | $— | | $— | | $4,558,151 |

For further information regarding security characteristics, see the Schedule of Investments.

Investment Transactions and Investment Income: Securities transactions are recorded on the trade date. Realized gains and losses from securities transactions are calculated on the identified cost basis. Interest income is recorded on the accrual basis. Discounts and premiums on securities are accreted and amortized, respectively, on a daily basis, using the effective yield to maturity method adjusted based on management’s assessment of the collectability of such interest. Dividend income is recorded on the ex-dividend date.

Master Limited Partnerships: A master limited partnership (“MLP”) is an entity receiving partnership taxation treatment under the U.S. Internal Revenue Code of 1986 (the “Code”), the partnership interests or “units” of which

18Brookfield Public Securities Group LLC

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

are traded on securities exchanges like shares of corporate stock. Holders of MLP units generally have limited control and voting rights on matters affecting the partnership.

The Fund invests in MLPs, which generally are treated as partnerships for federal income tax purposes. If an MLP does not meet current legal requirements to maintain partnership status, or if it is unable to do so because of tax law changes, it would be taxed as a corporation or other form of taxable entity and there could be a material decrease in the value of its securities. Additionally, if tax law changes to eliminate or reduce tax deductions such as depletion, depreciation and amortization expense deductions that MLPs have been able to use to offset a significant portion of their taxable income, it could significantly reduce the value of the MLPs held by the Fund and could cause a greater portion of the income and gain allocated to the Fund to be subject to U.S. federal, state and local corporate income taxes, which would reduce the amount the Fund can distribute to shareholders and could increase the percentage of Fund distributions treated as dividends instead of tax-deferred return of capital.

Depreciation or other cost recovery deductions passed through to the Fund from investments in MLPs in a given year generally will reduce the Fund’s taxable income (and earnings and profits), but those deductions may be recaptured in the Fund’s taxable income (and earnings and profits) in subsequent years when the MLPs dispose of their assets or when the Fund disposes of its interests in the MLPs. When deductions are recaptured, distributions to the Fund’s shareholders may be taxable.

Return of Capital Estimates:A distribution received from the Fund’s investments in MLPs generally is comprised of income and return of capital. The Fund records investment income and return of capital based on estimates made at the time such distributions are received. Such estimates are based on historical information available from each MLP and other industry sources. These estimates may subsequently be revised based on information received from MLPs after their tax reporting periods are concluded. For the fiscal year ended September 30, 2019, the Fund estimated that 100% of the MLP distributions received would be treated as return of capital.

Expenses: Expenses directly attributable to the Fund are charged directly to the Fund, while expenses which are attributable to the Fund and other investment companies advised by the Adviser are allocated among the respective investment companies, including the Fund, based upon relative average net assets, evenly or a combination of average net assets and evenly.

Distributions to Shareholders: The Fund’s dividend distribution policy is intended to provide monthly distributions to its common shareholders at a rate that over time is similar to the distribution rate the Fund receives from the MLPs in which it invests, without offset for the expenses of the Fund. The Fund is not required to make such distributions and therefore the amount, if any, and/or the frequency of payment is subject to change. The amount of the Fund’s distributions is based on, among other considerations, distributions the Fund actually receives from portfolio investments, including returns of capital, and estimated future cash flows. Because the Fund’s distribution policy takes into consideration estimated future cash flows from its underlying holdings, and to permit the Fund to maintain a stable distribution rate, the Fund’s distributions may exceed, or be below the amount the Fund actually receives from its portfolio investments. Additionally, since the Fund’s distribution rate is not derived from the Fund’s investment income or loss, the Fund’s distributions may not represent yield or investment return on the Fund’s portfolio. To the extent that the distributions paid exceed the distributions the Fund has received, the distributions will reduce the Fund’s net assets. Consequently, the Fund may maintain cash reserves, borrow or may be required to sell certain investments at times when it would not otherwise be desirable to do so in order to pay the expenses of the Fund. The Fund is not required to make such distributions and, as a result, the Fund could in the future decide not to make such distributions or not to make distributions at a rate that over time is similar to the distribution rate that it receives from the MLPs in which it invests. Furthermore, unlike the MLPs in which it invests, the Fund is not a pass through entity. Consequently, the tax characterization of the distributions paid by the Fund, as dividend income or return of capital, may differ greatly from those of the underlying MLPs.

Distributions, if any, are declared and distributed monthly. The estimated characterization of the distributions paid will be either a dividend (ordinary or qualified income) or distribution (return of capital). This estimate is based on the Fund’s operating results during the period. It is anticipated that a portion of its distributions will be comprised of

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

return of capital as a result of the tax character of cash distributions made by the Fund’s investments. The actual characterization of the distributions made during the period will not be determined until after the end of the fiscal year. For the fiscal year ended September 30, 2019, the Fund estimates that its distributions will be largely characterized as return of capital. The Fund will inform shareholders of the final tax character of the distributions on IRS Form DIV in February 2020.

The portion of the Fund’s distributions that may be classified as return of capital is uncertain and can be materially impacted by events that are not subject to the control of the Fund’s Adviser (e.g., mergers, acquisitions, reorganizations and other capital transactions occurring at the individual MLP level, changes in the tax characterization of distributions received from the MLP investments held by the Fund, changes in tax laws, etc.). The return of capital portion may also be impacted by the Fund’s strategy, which may recognize gains on its holdings. Because of these factors, the portion of the Fund’s distributions that are classified as return of capital may vary materially from year to year. Accordingly, there is no guarantee that future distributions will maintain the same classification for tax purposes as past distributions.

The distributions are determined in accordance with federal income tax regulations and are recorded on the ex-dividend date. The character may differ from GAAP. These differences between book-basis and tax-basis are either considered temporary or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require reclassification.

Energy Industry Concentration Risk: A substantial portion of the MLPs in which the Fund invests are engaged primarily in the energy industry. As a result, the Fund will be concentrated in the energy industry, and will therefore be susceptible to adverse economic, environmental or regulatory occurrences effecting the energy industry.

New Accounting Pronouncements: In August 2018, FASB issued ASU 2018-13, Fair Value Measurement (Topic 820): Disclosure Framework — Changes to the Disclosure Requirements for Fair Value Measurement. The primary focus of ASU 2018-13 is to improve the effectiveness of the disclosure requirements for fair value measurements. In general, the amendments in ASU 2018-13 are effective for all entities for fiscal years and interim periods within those fiscal years, beginning after December 15, 2019. An entity is permitted to early adopt upon the issuance of ASU 2018-13. Management has implemented the amendments and there was no material impact on the Fund’s financial statements.

3.Investment Advisory Agreement and Related Party Transactions

The Fund has entered into an investment advisory agreement (the “Advisory Agreement”) with the Adviser under which the Adviser is responsible for the management of the Fund’s portfolio and provides the necessary personnel, facilities, equipment and certain other services necessary to the operations of the Fund. The Advisory Agreement provides that the Fund shall pay the Adviser a fee, computed daily and payable monthly, at an annual rate of 1.00% of the Fund’s average daily net assets.

Pursuant to operating expense limitation agreement (the “Expense Limitation Agreement”), the Adviser has contractually agreed to waive all or a portion of its investment advisory or administration fees, as presented above, and/or to reimburse certain expenses of the Fund to the extent necessary to maintain the Fund’s total annual operating expenses after fee waiver and/or expense reimbursement (excluding any front-end or contingent deferred charges, brokerage commissions and other transactional expenses, acquired fund fees and expenses, interest, taxes, and extraordinary expenses, such as litigation; and other expenses not incurred in the ordinary course of a Fund’s business) at no more than 1.50% for Class A Shares, 2.25% for Class C Shares, 1.25% for Class I Shares and 1.25% for Class Y Shares. The Expense Limitation Agreement will continue until at least October 1, 2020 and may not be terminated by the Fund or the Adviser before such time. Thereafter, the Expense Limitation Agreement may only be terminated or amended to increase the expense cap as of October 1st of each calendar year, provided that in the case of a termination by the Adviser, the Adviser will provide the Board with written notice of its intention to terminate the arrangement prior to the expiration of its then current term. Pursuant

20Brookfield Public Securities Group LLC

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

to the Expense Limitation Agreement, any waivers and/or reimbursements made by the Adviser are subject to recoupment from the Fund for a period not to exceed three years after the occurrence of the waiver and/or reimbursement, provided that the Fund is able to effect such payment to the Adviser and remain in compliance with the expense cap in effect at the time the waivers and/or reimbursements occurred.

The amount of investment advisory fees waived and/or expenses reimbursed available to be recouped before expiration is $228,978 for fiscal year ended September 30, 2019. For the fiscal year ended September 30, 2019, the Adviser did not recoup any expenses.

The Fund has entered into an Administration Agreement with the Adviser and the Adviser has entered into a sub-administration agreement with U.S. Bancorp Fund Services, LLC (“Sub-Administrator”). The Adviser and Sub-Administrator perform administrative services necessary for the operation of the Fund, including maintaining certain books and records of the Fund and preparing reports and other documents required by federal, state, and other applicable laws and regulations, and providing the Fund with administrative office facilities. For these services, the Fund pays to the Adviser a monthly fee at an annual rate of 0.15% of the Fund’s average daily net Assets. The Adviser is responsible for any fees due to the Sub-Administrator.

Certain officers and/or trustees of the Trust are officers and/or employees of the Adviser.

4.Purchases and Sales of Investments

For the fiscal year ended September 30, 2019, purchases and sales of investments, excluding short-term investments were $9,505,951 and $4,317,071, respectively.

5.Shares of Beneficial Interest

The Trust’s Declaration of Trust authorizes the issuance of an unlimited number of full and fractional shares of beneficial interest. With respect to each series, the Trust may offer more than one class of shares. The Trust reserves the right to create and issue additional series or classes. Each share of a series or class represents an equal proportionate interest in that series or class with each other share of that series or class.

The shares of each series or class participate equally in the earnings, dividends and assets of the particular series or class.

| | 20191 |

| Class Y | Shares | | Amount |

Subscriptions

| 500,000 | | $5,000,000 |

Reinvestment of distributions

| 1,693 | | 13,542 |

Redemptions

| — | | — |

Net Increase

| 501,693 | | $5,013,542 |

1 For the Fiscal Year Ended September 30, 2019.

6.Credit Facility

U.S. Bank, N.A. (the “Bank”) has made available to the Trust, a credit facility, pursuant to a separate Loan and Security Agreement, for temporary or extraordinary purposes. The maximum line of credit as of September 30, 2019 for the Trust is $75,000,000. Advances are not collateralized by a first lien against the Fund’s assets. For fiscal year ended September 30, 2019, the average interest rate on the outstanding principal amount for the Fund was 5.00%.

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

During the fiscal year ended September 30, 2019, the Fund utilized the credit facility for 1 day and had an outstanding average daily loan balance of $16,000. The maximum amount outstanding during the period was $16,000 and the interest expense amounted to $7. At of September 30, 2019, the Fund did not have an amount outstanding on the credit facility.

7.Federal Income Tax Information

The Fund intends to continue to meet the requirements of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Therefore, no federal income or excise tax provision is required. The Fund may incur an excise tax to the extent it has not distributed all of its taxable income on a calendar year basis.

GAAP provides guidance for how uncertain tax positions should be recognized, measured, presented and disclosed in the financial statements. An evaluation of tax positions taken in the course of preparing the Funds’ tax returns to determine whether the tax positions are “more-likely-than-not” of being sustained by the taxing authority is required. Tax benefits of positions not deemed to meet the more-likely-than-not threshold would be booked as a tax expense in the current year and recognized as: a liability for unrecognized tax benefits; a reduction of an income tax refund receivable; a reduction of a deferred tax asset; an increase in a deferred tax liability; or a combination thereof. As of September 30, 2019, The Fund has determined that there are no uncertain tax positions or tax liabilities required to be accrued.

The Fund has reviewed the taxable year open for examination (i.e. not barred by the applicable statute of limitations) by taxing authorities of all major jurisdictions, including the Internal Revenue Service. As of September 30, 2019, open taxable year consisted of the taxable period from October 1, 2018 (commencement of operations) to September 30, 2019. No examination of the Funds’ tax returns is currently in progress.

Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from GAAP.

The tax character of distribution paid of $13,542 for the year ended September 30, 2019 was from ordinary income (including short-term capital gains).

At September 30, 2019, the Fund’s most recently completed tax year-end, the components of net assets (excluding paid-in capital) on a tax basis were as follows:

Capital loss carryforward(1)

| $(11,947) |

Undistributed ordinary income

| 51,024 |

Other accumulated losses

| (61,055) |

Tax basis unrealized depreciation on investments and foreign currency

| (394,697) |

Total Tax basis net accumulated losses

| $(416,675) |

(1) To the extent that future capital gains are offset by capital loss carryforwards, such gains will not be distributed.

As of September 30, 2019, the Fund’s capital loss carryforwards was $11,947 from short-term capital gains which will not expire.

Federal Income Tax Basis: The federal income tax basis of the Fund’s investments, not including foreign currency translation, at September 30, 2019 was as follows:

| Cost of Investments | Gross Unrealized Appreciation | Gross Unrealized Depreciation | Net Unrealized Appreciation |

$4,952,848

| $206,978 | $(601,675) | $(394,697) |

22Brookfield Public Securities Group LLC

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Notes to Financial Statements (continued)

September 30, 2019

Capital Account Reclassifications: Because federal income tax regulations differ in certain respects from GAAP, income and capital gain distributions, if any, determined in accordance with tax regulations may differ from net investment income and realized gains recognized for financial reporting purposes. These differences are primarily due to differing treatments for wash sales, partnership income/expense and return of capital. Permanent book and tax differences, if any, relating to shareholder distributions will result in reclassifications to paid-in-capital or to undistributed capital gains. These reclassifications have no effect on net assets or NAV per share.

At September 30, 2019, the Fund’s most recently completed tax year-end, the Fund’s components of net assets were increased or (decreased) by (29,472) and 29,472 for distributions in excess of net investment income and accumulated net realized loss, respectively.

8.Indemnification

Under the Fund’s organizational documents, its officers and directors are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Fund enters into contracts with its vendors and others that provide for indemnification. The Fund’s maximum exposure under these arrangements is unknown, since this would involve the resolution of certain claims, as well as future claims that may be made, against the Fund. Thus, an estimate of the financial impact, if any, of these arrangements cannot be made at this time. However, based on experience, the Fund expects the risk of loss due to these warranties and indemnities to be unlikely.

9.Subsequent Events

GAAP requires recognition in the financial statements of the effects of all subsequent events that provide additional evidence about conditions that existed at the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made.

Management has evaluated subsequent events in the preparation of the Fund’s financial statements and has determined that herein, there are no additional events that require recognition or disclosure in the financial statements.

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Report of Independent Registered Public Accounting Firm

September 30, 2019

To the shareholders of Center Coast Brookfield Energy Infrastructure Fund and the Board of Trustees of Brookfield Investment Funds

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statement of assets and liabilities of Center Coast Brookfield Energy Infrastructure Fund (the “Fund”), a series of the Brookfield Investment Trust, including the schedule of investments, as of September 30, 2019, the related statements of operations and changes in net assets and the financial highlights for the year then ended, and the related notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of September 30, 2019, and the results of its operations, changes in its net assets, and the financial highlights for the year ended September 30, 2019, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements and financial highlights based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. Our procedures included confirmation of securities owned as of September 30, 2019, by correspondence with the custodian and brokers. We believe that our audit provides a reasonable basis for our opinion.

DELOITTE & TOUCHE LLP

Chicago, Illinois

November 27, 2019

We have served as the auditor of one or more of Brookfield Public Securities Group LLC's investment companies since 2011.

24Brookfield Public Securities Group LLC

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Tax Information

September 30, 2019

QUALIFIED DIVIDEND INCOME/DIVIDENDS RECEIVED DEDUCTION

For the fiscal year ended September 30, 2019, certain dividends paid by the Funds may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. The percentage of dividends declared from ordinary income designated as qualified dividend income was 100.00%.

For corporate shareholders, the percentage of ordinary distributions qualifying for the corporate dividends received deductions for the year ended September 30, 2019 was 100.00%.

The percentage of taxable ordinary income distributions that are designated as short-term capital gain distributions under the Internal Revenue Section 871(k)(2)(C) for each Fund was 0.00%.

CENTER COAST BROOKFIELD ENERGY INFRASTRUCTURE FUND

Information Concerning Trustees and Officers (Unaudited)

September 30, 2019

The following tables provide information concerning the trustees and officers of the Fund.

Trustees of the Fund

| Name, Address and Year of Birth | Position(s) Held with Funds | Principal Occupation(s) During Past 5 Years and Other Directorships Held by Director | Number of Portfolios in Fund Complex |

| Independent Trustees | | | |

Edward A. Kuczmarski

c/o Brookfield Place,

250 Vesey Street,

New York, New York

10281-1023

Born: 1949 | Trustee and Independent Chairman of the Board, Member of the Audit Committee, Chairman of the Nominating and Compensation Committee

Served Since 2018 | Director/Trustee of several investment companies advised by the Adviser (2011-Present); Certified Public Accountant and Retired Partner of Crowe Horwath LLP (1980-2013); Trustee of the Empire Builder Tax Free Bond Fund (1984-2013); Director of ISI Funds (2007-2015); Trustee of the Daily Income Fund (2006-2015), Director of the California Daily Tax Free Income Fund, Inc. (2006-2015); Trustee of the Stralem Funds (2014-2016). | 10 |

Stuart A. McFarland

c/o Brookfield Place,

250 Vesey Street,