UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Frank L. Newbauer, Esq.

Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246_ |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | May 31 | |

| Date of reporting period: | May 31, 2017 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

APEXcm SMALL/MID-CAP GROWTH FUND

(APSGX)

Annual Report

May 31, 2017

APEXcm SMALL/MID-CAP GROWTH FUND LETTER TO SHAREHOLDERS | May 31, 2017 |

Dear APEXcm Small/Mid-Cap Growth Fund Shareholder:

For the year ended May 31, 2017, the APEXcm Small/Mid-Cap Growth Fund (the “Fund”) returned +15.80% (net of fees). The Fund slightly underperformed its category benchmark, the Russell Midcap Growth Index, which returned +16.68%, and the Russell 2500 Growth Index (“Russell 2500 Growth”), which returned +17.85%, for the same one year period. We continue to invest for the long-term and believe a disciplined, prudent approach during this time of unpredictability will best serve our shareholders.

APEX PHILOSOPHY

We believe that the best way to provide value-added returns is to identify companies that exhibit certain favorable fundamental advantages and benefit from secular growth trends, allowing us to structure the portfolio in high-conviction areas of longer-term sustainable growth. Embedded in our portfolio construction is the recognition of companies at different stages of their growth cycle, which we designate as “stable” and “emerging” growth stocks. We believe that having a spectrum of growth companies ranging from those that are truly innovative and growing rapidly to those that are more established, can provide relative stability while allowing the opportunity to drive outperformance versus our benchmark and peers over time. In addition, we believe the SMID style provides the opportunity to invest in higher growth companies and capture a longer period of growth as these companies mature.

MARKET ENVIRONMENT

We began the reporting period in June 2016 with voters in the U.K. putting in motion a withdrawal from the European Union, prompting uncertainty and an intense move toward less risky assets. The Bank of England took aggressive action to steady the volatile response and mitigate near term economic concerns. The U.S. elections offered up another surprise in November with the Republicans winning the presidency and maintaining the majority in the House and Senate. Following what now appears to have been a commodity-driven industrial recession in the latter part of 2015 into 2016, the foundation for GDP growth was already stirring and would only be reinforced with the inclusion of proposed pro-growth strategies and significant fiscal stimulus from the new administration. As we moved into the second half of this reporting period, most markets rose in unison as stabilizing commodities and synchronized global growth provided a tailwind to the markets. Healthier industrial activity coupled with a weakening dollar, major emerging markets pulling out of a two year slump and the world’s most powerful economies finally showing signs of escaping the remnants of the financial crisis have, at least temporarily, offset the deferral of the Trump administration’s pro-growth strategies. We believe the prospects of lower taxes, less regulation and increased infrastructure spending still have the complacent equity markets buoying around all-time highs. It seems worrisome to reach new heights

1

concurrent with the Federal Reserve attempting to normalize monetary policy, key indicators of the health of housing, automotive and retail sectors reflecting fatigue and a buildup of emerging-market debt. With the U.S. economic expansion approaching eight years we would anticipate more market volatility as it wrestles with some weariness and the perception of a goldilocks environment of reasonable growth, benign inflation and continued accommodative central bank policy.

FUND PERFORMANCE FOR THE YEAR ENDED MAY 31, 2017

The Fund and the markets have recovered from the commodity-driven industrial recession in 2015/2016 and the ensuing anomalies of performance drivers appear to have normalized. Although the continuous shifting of market leadership can try investors’ patience, we believe the decisive driver of performance will be revenue and earnings growth supported by an improving global economic expansion.

Through all the twists and turns during the fiscal year, ultimately the Fund’s largest overweight – Information Technology – led the Russell 2500 Growth performance, up ~ 27.5% for this one year period. Our portfolio structure also added value during the reporting period as the overweights in Information Technology, Financials and Healthcare along with our underweights in Consumer Staples and Real Estate added approximately +2.2%. Towards the end of the reporting period Energy continued its decline and our overweight detracted ~-1.5%.

During the reporting period, the cash drag on the portfolio detracted approximately -0.7% from performance along with slightly negative stock selection detracting an additional ~- 0.8%. Stock selection was solid in Energy, Healthcare, Industrials, Materials and Real Estate, adding approximately +2.2%, but was offset by negative selection in Financials and Technology, which detracted ~-1.1%, as well as the consumer driven areas of Discretionary and Staples negatively impacting performance by approximately -2.0%. Although the Fund had some strong performers in the consumer sectors such as Burlington Stores, Wyndham Worldwide, China Lodging and Dave & Buster’s, several good businesses such as Michaels, Skechers (sold), Nordstrom and Carter’s lost value as brick and mortar retail continued to be under assault. Several other consumer businesses saw declines during this time period, such as Hain Celestial (sold), Boston Beer and IMAX. Although we see great value in these businesses, we continue to assess their growth opportunities in this ever changing consumer landscape.

Strong individual stock selection across multiple sectors was observed by top performers such as MercadoLibre, Align Technology, Arista Networks, IDEXX Laboratories and IAC/Interactive. These top five performers are good examples of our conviction in secular growth trends such as e-commerce and cloud computing (MercadoLibre, IAC, and Arista Networks) and the secular opportunities in Healthcare (Align Technology and IDEXX Labs). Although we noted significant winners in Healthcare, specialty pharma and biotech stocks have been in the crosshairs all year and three of the portfolio’s top five detractors were not immune to the downside volatility, absorbing significant declines in holdings Ophthotech (sold), Jazz Pharmaceuticals (sold) and Akorn (sold).

2

OUTLOOK

As we move into the second half of 2017, a lot of the anticipation of immediate change from the new administration has gradually dissipated. Infrastructure spending, deregulation, tax cuts and health care reform all remain possible but have gradually been discounted by the market for any meaningful impact in the near future. While the macro and political landscapes continue to swing and leadership in the market reallocates between risk/risk-off and secular/cyclical growth, fundamentals have improved during the most recent quarter with solid revenue growth and earnings growth (S&P Q1 earnings exhibited the strongest growth in almost six years) emerging as key drivers of performance. Although we remain concerned about the narrowing of winners in this market and investor complacency as we enter the second half of 2017, we believe the economy will remain resilient as synchronized global growth typically provides a sustained moderate but sturdy advance allowing for continued accommodative policies from central banks. There are still several risks such as tight labor markets fueling wage inflation, concern as to if or when higher sentiment and net worth translates into increased consumer spending and the impact of oil remaining below $50 per barrel highlight the challenging environment. We believe the length of this historic expansion still has some legs and we will be monitoring the rise in inflation expectations and compensation growth as keys to heightened central bank actions. Coincidently, growth must accelerate to support achievable earnings momentum and we will apply our cycle-tested investment process to balance these market undercurrents with our long-term secular views.

Sincerely,

Nitin N. Kumbhani

Vice Chairman and Chief of Growth Equity Strategies

Fiera Capital Inc.

Vice Chairman and Chief of Growth Equity Strategies

Fiera Capital Inc.

Index Definitions

Russell Midcap Growth Index measures the performance of the mid-capitalization growth sector of the U.S. equity market. It is a market capitalization weighted index representing the smallest 800 companies in the Russell 1000 Index.

Russell 2500 Growth Index is designed to measure the performance of those Russell 2500 companies with higher price-to-book ratios and higher forecasted growth values. The Russell 2500 Index covers the small and mid-capitalizations

3

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-888-575-4800.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit our website at www.apexcmfund.com or call 1-888-575-4800 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The APEXcm Small/Mid Cap Growth Fund is distributed by Ultimus Fund Distributors, LLC.

This Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. For a complete list of securities held by the Fund as of May 31, 2017, please see the Schedule of Investments section of the annual report. The opinions of the Adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates.

4

APEXcm SMALL/MID-CAP GROWTH FUND

PERFORMANCE INFORMATION

May 31, 2017 (Unaudited)

PERFORMANCE INFORMATION

May 31, 2017 (Unaudited)

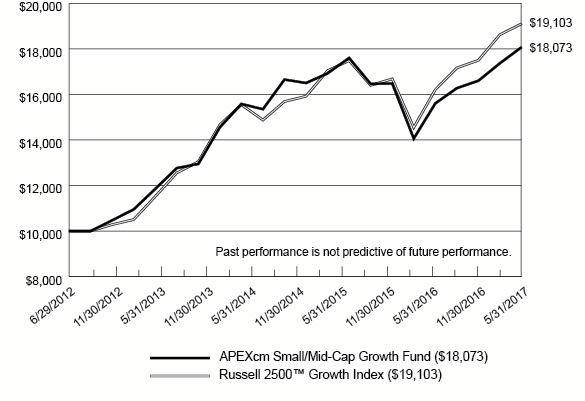

Comparison of the Change in Value of a $10,000 Investment in

APEXcm Small/Mid-Cap Growth Fund versus the Russell 2500TM Growth Index

Average Annual Total Returns For Periods Ended May 31, 2017 | ||||

| 1 Year | 3 Years | Since Inception(b) | ||

APEXcm Small/Mid-Cap Growth Fund(a) | 15.80% | 5.59% | 12.78% | |

Russell 2500TM Growth Index | 17.85% | 8.69% | 14.06% | |

(a) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(b) | The Fund commenced operations on June 29, 2012. |

5

APEXcm SMALL/MID-CAP GROWTH FUND

PORTFOLIO INFORMATION

May 31, 2017 (Unaudited)

PORTFOLIO INFORMATION

May 31, 2017 (Unaudited)

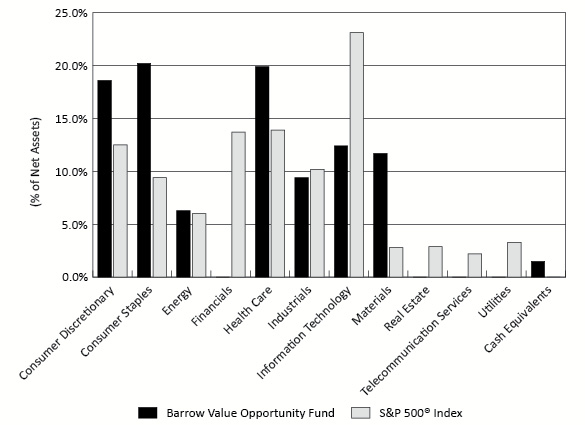

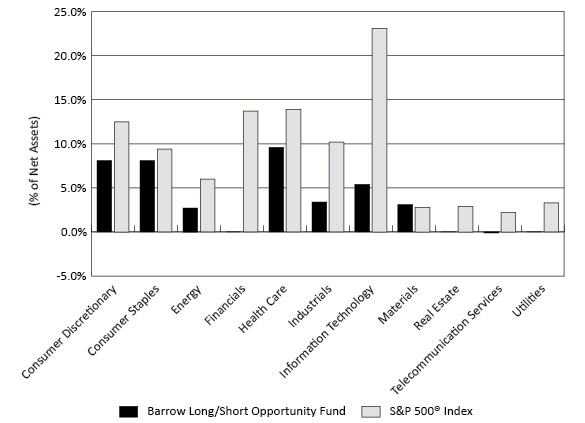

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

| Security Description | % of Net Assets |

| MercadoLibre, Inc. | 3.9% |

| Align Technology, Inc. | 3.0% |

| Arista Networks, Inc. | 2.9% |

| Trimble, Inc. | 2.0% |

| Reinsurance Group of America, Inc. | 2.0% |

| Foot Locker, Inc. | 1.9% |

| IAC/InterActiveCorp | 1.9% |

| CBRE Group, Inc. - Class A | 1.9% |

| United Rentals, Inc. | 1.8% |

| Berry Global Group, Inc. | 1.8% |

6

APEXcm SMALL/MID-CAP GROWTH FUND SCHEDULE OF INVESTMENTS May 31, 2017 | ||||||||

| COMMON STOCKS — 97.5% | Shares | Value | ||||||

| Consumer Discretionary — 20.0% | ||||||||

| Auto Components — 2.7% | ||||||||

| Autoliv, Inc. | 32,247 | $ | 3,576,837 | |||||

| BorgWarner, Inc. | 101,053 | 4,295,763 | ||||||

| 7,872,600 | ||||||||

| Hotels, Restaurants & Leisure — 5.7% | ||||||||

| China Lodging Group Ltd. - ADS * | 46,768 | 3,573,075 | ||||||

| Dave & Buster's Entertainment, Inc. * | 59,661 | 3,979,389 | ||||||

| Dunkin’ Brands Group, Inc. | 75,909 | 4,441,436 | ||||||

| Wyndham Worldwide Corporation | 47,727 | 4,819,950 | ||||||

| 16,813,850 | ||||||||

| Household Durables — 1.5% | ||||||||

| PulteGroup, Inc. | 191,788 | 4,347,834 | ||||||

| Media — 1.3% | ||||||||

| Cinemark Holdings, Inc. | 47,580 | 1,882,741 | ||||||

| IMAX Corporation * | 76,869 | 1,925,568 | ||||||

| 3,808,309 | ||||||||

| Multi-line Retail — 2.7% | ||||||||

| Burlington Stores, Inc. * | 48,807 | 4,775,765 | ||||||

| Nordstrom, Inc. | 74,396 | 3,109,753 | ||||||

| 7,885,518 | ||||||||

| Specialty Retail — 5.1% | ||||||||

| Foot Locker, Inc. | 94,085 | 5,589,590 | ||||||

| Lithia Motors, Inc. - Class A | 27,566 | 2,504,371 | ||||||

| Michaels Companies, Inc. (The) * | 164,749 | 3,184,598 | ||||||

| Williams-Sonoma, Inc. | 75,823 | 3,689,547 | ||||||

| 14,968,106 | ||||||||

| Textiles, Apparel & Luxury Goods — 1.0% | ||||||||

| Carter's, Inc. | 35,626 | 2,927,032 | ||||||

| Consumer Staples — 0.7% | ||||||||

| Beverages — 0.7% | ||||||||

| Boston Beer Company, Inc. (The) - Class A * | 14,020 | 2,001,355 | ||||||

| Energy — 3.4% | ||||||||

| Energy Equipment & Services — 0.4% | ||||||||

| Superior Energy Services, Inc. * | 112,870 | 1,170,462 | ||||||

7

APEXcm SMALL/MID-CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | ||||||||

| COMMON STOCKS — 97.5% (Continued) | Shares | Value | ||||||

| Energy — 3.4% (Continued) | ||||||||

| Oil, Gas & Consumable Fuels — 3.0% | ||||||||

| Cheniere Energy, Inc. * | 66,329 | $ | 3,231,549 | |||||

| Diamondback Energy, Inc. * | 36,213 | 3,359,118 | ||||||

| RSP Permian, Inc. * | 64,572 | 2,298,117 | ||||||

| 8,888,784 | ||||||||

| Financials — 5.8% | ||||||||

| Banks — 1.8% | ||||||||

| Bank of the Ozarks, Inc. | 57,771 | 2,553,478 | ||||||

| Western Alliance Bancorp * | 59,516 | 2,721,072 | ||||||

| 5,274,550 | ||||||||

| Capital Markets — 0.9% | ||||||||

| Evercore Partners, Inc. - Class A | 37,394 | 2,535,313 | ||||||

| Consumer Finance — 1.1% | ||||||||

| Navient Corporation | 227,887 | 3,288,409 | ||||||

| Insurance — 2.0% | ||||||||

| Reinsurance Group of America, Inc. | 46,317 | 5,766,930 | ||||||

| Health Care — 16.2% | ||||||||

| Biotechnology — 4.6% | ||||||||

| Alkermes plc * | 75,257 | 4,346,844 | ||||||

| Ionis Pharmaceuticals, Inc. * | 74,703 | 3,420,650 | ||||||

| Momenta Pharmaceuticals, Inc. * | 141,430 | 2,050,735 | ||||||

| Radius Health, Inc. * | 40,214 | 1,392,209 | ||||||

| TESARO, Inc. * | 15,318 | 2,287,131 | ||||||

| 13,497,569 | ||||||||

| Health Care Equipment & Supplies — 5.0% | ||||||||

| Align Technology, Inc. * | 60,073 | 8,722,600 | ||||||

| DexCom, Inc. * | 53,416 | 3,570,325 | ||||||

| ICU Medical, Inc. * | 13,701 | 2,209,971 | ||||||

| 14,502,896 | ||||||||

| Health Care Technology — 2.6% | ||||||||

| Medidata Solutions, Inc. * | 62,156 | 4,424,264 | ||||||

| Veeva Systems, Inc. - Class A * | 48,951 | 3,110,347 | ||||||

| 7,534,611 | ||||||||

| Life Sciences Tools & Services — 1.6% | ||||||||

| ICON plc * | 51,331 | 4,830,247 | ||||||

8

APEXcm SMALL/MID-CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | ||||||||

| COMMON STOCKS — 97.5% (Continued) | Shares | Value | ||||||

| Health Care — 16.2% (Continued) | ||||||||

| Pharmaceuticals — 2.4% | ||||||||

| Horizon Pharma plc * | 90,740 | $ | 907,400 | |||||

| Prestige Brands Holdings, Inc. * | 42,536 | 2,142,964 | ||||||

| Supernus Pharmaceuticals, Inc. * | 107,502 | 4,042,075 | ||||||

| 7,092,439 | ||||||||

| Industrials — 14.2% | ||||||||

| Airlines — 1.2% | ||||||||

| Hawaiian Holdings, Inc. * | 70,509 | 3,532,501 | ||||||

| Building Products — 0.8% | ||||||||

| Owens Corning | 37,082 | 2,313,917 | ||||||

| Construction & Engineering — 1.0% | ||||||||

| EMCOR Group, Inc. | 45,732 | 2,882,031 | ||||||

| Machinery — 5.6% | ||||||||

| Middleby Corporation (The) * | 35,416 | 4,545,998 | ||||||

| Nordson Corporation | 42,837 | 4,963,952 | ||||||

| Wabtec Corporation | 46,349 | 3,789,031 | ||||||

| Xylem, Inc. | 58,177 | 3,033,349 | ||||||

| 16,332,330 | ||||||||

| Professional Services — 0.7% | ||||||||

| WageWorks, Inc. * | 27,980 | 1,979,585 | ||||||

| Road & Rail — 1.6% | ||||||||

| Old Dominion Freight Line, Inc. * | 52,786 | 4,714,846 | ||||||

| Trading Companies & Distributors — 3.3% | ||||||||

| HD Supply Holdings, Inc. * | 109,824 | 4,431,398 | ||||||

| United Rentals, Inc. * | 49,663 | 5,399,858 | ||||||

| 9,831,256 | ||||||||

| Information Technology — 31.3% | ||||||||

| Communications Equipment — 2.9% | ||||||||

| Arista Networks, Inc. * | 56,648 | 8,348,782 | ||||||

| Electronic Equipment, Instruments & Components — 3.1% | ||||||||

| Dolby Laboratories, Inc. - Class A | 64,073 | 3,228,638 | ||||||

| Trimble, Inc. * | 164,679 | 5,935,031 | ||||||

| 9,163,669 | ||||||||

9

APEXcm SMALL/MID-CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | ||||||||

| COMMON STOCKS — 97.5% (Continued) | Shares | Value | ||||||

| Information Technology — 31.3% (Continued) | ||||||||

| Internet Software & Services — 5.8% | ||||||||

| IAC/InterActiveCorp * | 52,158 | $ | 5,546,482 | |||||

| MercadoLibre, Inc. | 41,240 | 11,345,536 | ||||||

| 16,892,018 | ||||||||

| IT Services — 9.3% | ||||||||

| Broadridge Financial Solutions, Inc. | 62,181 | 4,718,916 | ||||||

| CSRA, Inc. | 106,255 | 3,204,651 | ||||||

| Gartner, Inc. * | 32,621 | 3,901,472 | ||||||

| Global Payments, Inc. | 45,963 | 4,210,670 | ||||||

| Sabre Corporation | 167,676 | 3,760,973 | ||||||

| Teradata Corporation * | 84,098 | 2,292,511 | ||||||

| Total System Services, Inc. | 84,619 | 5,039,061 | ||||||

| 27,128,254 | ||||||||

| Semiconductors & Semiconductor Equipment — 4.1% | ||||||||

| Advanced Energy Industries, Inc. * | 53,779 | 4,137,218 | ||||||

| Entegris, Inc. * | 193,442 | 4,778,017 | ||||||

| Power Integrations, Inc. | 47,019 | 3,147,922 | ||||||

| 12,063,157 | ||||||||

| Software — 6.1% | ||||||||

| ACI Worldwide, Inc. * | 124,670 | 2,849,956 | ||||||

| BroadSoft, Inc. * | 76,188 | 3,047,520 | ||||||

| Fortinet, Inc. * | 115,281 | 4,535,155 | ||||||

| Guidewire Software, Inc. * | 49,310 | 3,275,170 | ||||||

| Splunk, Inc.* | 67,130 | 4,111,041 | ||||||

| 17,818,842 | ||||||||

| Materials — 4.0% | ||||||||

| Construction Materials — 1.3% | ||||||||

| Eagle Materials, Inc. | 41,146 | 3,880,068 | ||||||

| Containers & Packaging — 1.8% | ||||||||

| Berry Global Group, Inc. * | 90,915 | 5,272,161 | ||||||

| Paper & Forest Products — 0.9% | ||||||||

| KapStone Paper and Packaging Corporation | 120,619 | 2,548,679 | ||||||

| Real Estate — 1.9% | ||||||||

| Real Estate Management & Development — 1.9% | ||||||||

| CBRE Group, Inc. - Class A * | 158,537 | 5,529,771 | ||||||

Total Common Stocks (Cost $237,304,724) | $ | 285,238,681 | ||||||

10

APEXcm SMALL/MID-CAP GROWTH FUND SCHEDULE OF INVESTMENTS (Continued) | ||||||||

| MONEY MARKET FUNDS — 2.1% | Shares | Value | ||||||

Fidelity Institutional Money Market Portfolio - Class I, 0.67% (a) (Cost $6,281,250) | 6,281,250 | $ | 6,281,250 | |||||

Total Investments at Value — 99.6% (Cost $243,585,974) | $ | 291,519,931 | ||||||

| Other Assets in Excess of Liabilities — 0.4% | 1,177,339 | |||||||

| Net Assets — 100.0% | $ | 292,697,270 | ||||||

| ADS - American Depositary Shares | |

| * | Non-income producing security. |

(a) | The rate shown is the 7-day effective yield as of May 31, 2017 |

| See accompanying notes to financial statements. | |

11

APEXcm SMALL/MID-CAP GROWTH FUND STATEMENT OF ASSETS AND LIABILITIES May 31, 2017 | ||||

| ASSETS | ||||

| Investments in securities: | ||||

| At acquisition cost | $ | 243,585,974 | ||

| At value (Note 2) | $ | 291,519,931 | ||

| Receivable for capital shares sold | 1,262,062 | |||

| Dividends receivable | 183,625 | |||

| Other assets | 15,910 | |||

| Total assets | 292,981,528 | |||

| LIABILITIES | ||||

| Payable for capital shares redeemed | 24,899 | |||

| Payable to Adviser (Note 4) | 217,232 | |||

| Payable to administrator (Note 4) | 33,115 | |||

| Other accrued expenses and liabilities | 9,012 | |||

| Total liabilities | 284,258 | |||

| NET ASSETS | $ | 292,697,270 | ||

| NET ASSETS CONSIST OF: | ||||

| Paid-in capital | $ | 252,523,989 | ||

| Accumulated net investment loss | (493,639 | ) | ||

| Accumulated net realized losses from security transactions | (7,267,037 | ) | ||

| Net unrealized appreciation on investments | 47,933,957 | |||

| NET ASSETS | $ | 292,697,270 | ||

| Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 16,490,003 | |||

| Net asset value, offering price and redemption price per share (Note 2) | $ | 17.75 | ||

| See accompanying notes to financial statements. |

12

APEXcm SMALL/MID-CAP GROWTH FUND STATEMENT OF OPERATIONS For the Year Ended May 31, 2017 | ||||

| INVESTMENT INCOME | ||||

| Dividend income (net of foreign taxes of $4,024) | $ | 1,554,684 | ||

| EXPENSES | ||||

| Investment advisory fees (Note 4) | 2,727,551 | |||

| Administration fees (Note 4) | 267,480 | |||

| Fund accounting fees (Note 4) | 57,338 | |||

| Professional fees | 37,633 | |||

| Registration and filing fees | 31,281 | |||

| Custody and bank service fees | 30,488 | |||

| Compliance fees (Note 4) | 29,543 | |||

| Transfer agent fees (Note 4) | 18,887 | |||

| Printing of shareholder reports | 12,856 | |||

| Postage and supplies | 10,432 | |||

| Trustees’ fees and expenses (Note 4) | 9,611 | |||

| Insurance expense | 2,078 | |||

| Other expenses | 25,399 | |||

| Total expenses | 3,260,577 | |||

| Less fee reductions by the Adviser (Note 4) | (394,216 | ) | ||

| Net expenses | 2,866,361 | |||

| NET INVESTMENT LOSS | (1,311,677 | ) | ||

| REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | ||||

| Net realized losses from security transactions | (4,450,716 | ) | ||

| Net change in unrealized appreciation (depreciation) on investments | 46,120,751 | |||

| NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 41,670,035 | |||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 40,358,358 | ||

| See accompanying notes to financial statements. |

13

APEXcm SMALL/MID-CAP GROWTH FUND STATEMENTS OF CHANGES IN NET ASSETS | ||||||||

| Year Ended May 31, 2017 | Year Ended May 31, 2016 | |||||||

| FROM OPERATIONS | ||||||||

| Net investment loss | $ | (1,311,677 | ) | $ | (1,090,736 | ) | ||

| Net realized losses from security transactions | (4,450,716 | ) | (677,149 | ) | ||||

| Net change in unrealized appreciation (depreciation) on investments | 46,120,751 | (29,749,518 | ) | |||||

| Net increase (decrease) in net assets resulting from operations | 40,358,358 | (31,517,403 | ) | |||||

| DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

| From net realized gains | (743,317 | ) | (1,414,635 | ) | ||||

| CAPITAL SHARE TRANSACTIONS | ||||||||

| Proceeds from shares sold | 101,284,904 | 149,542,431 | ||||||

| Net asset value of shares issued in reinvestment of distributions to shareholders | 716,969 | 1,277,590 | ||||||

| Payments for shares redeemed | (107,870,747 | ) | (99,682,011 | ) | ||||

| Net increase (decrease) in net assets from capital share transactions | (5,868,874 | ) | 51,138,010 | |||||

| TOTAL INCREASE IN NET ASSETS | 33,746,167 | 18,205,972 | ||||||

| NET ASSETS | ||||||||

| Beginning of year | 258,951,103 | 240,745,131 | ||||||

| End of year | $ | 292,697,270 | $ | 258,951,103 | ||||

| ACCUMULATED NET INVESTMENT LOSS | $ | (493,639 | ) | $ | (529,959 | ) | ||

| CAPITAL SHARE ACTIVITY | ||||||||

| Shares sold | 6,277,194 | 9,569,552 | ||||||

| Shares reinvested | 44,671 | 81,740 | ||||||

| Shares redeemed | (6,682,018 | ) | (6,609,395 | ) | ||||

| Net increase (decrease) in shares outstanding | (360,153 | ) | 3,041,897 | |||||

| Shares outstanding at beginning of year | 16,850,156 | 13,808,259 | ||||||

| Shares outstanding at end of year | 16,490,003 | 16,850,156 | ||||||

| See accompanying notes to financial statements. |

14

APEXcm SMALL/MID-CAP GROWTH FUND FINANCIAL HIGHLIGHTS | ||||||||||||||||||||

| Per Share Data for a Share Outstanding Throughout Each Period | ||||||||||||||||||||

| Year Ended May 31, 2017 | Year Ended May 31, 2016 | Year Ended May 31, 2015 | Year Ended May 31, 2014 | Period Ended May 31, 2013(a) | ||||||||||||||||

| Net asset value at beginning of period | $ | 15.37 | $ | 17.43 | $ | 15.20 | $ | 12.69 | $ | 10.00 | ||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss) | (0.08 | ) | (0.06 | ) | (0.04 | ) | (0.03 | ) | 0.04 | (b) | ||||||||||

| Net realized and unrealized gains (losses) on investments | 2.50 | (1.92 | ) | 2.27 | 2.60 | 2.72 | ||||||||||||||

| Total from investment operations | 2.42 | (1.98 | ) | 2.23 | 2.57 | 2.76 | ||||||||||||||

| Less distributions: | ||||||||||||||||||||

| From net investment income | — | — | — | — | (0.07 | ) | ||||||||||||||

| From net realized gains | (0.04 | ) | (0.08 | ) | — | (0.06 | ) | — | ||||||||||||

| Total distributions | (0.04 | ) | (0.08 | ) | — | (0.06 | ) | (0.07 | ) | |||||||||||

| Net asset value at end of period | $ | 17.75 | $ | 15.37 | $ | 17.43 | $ | 15.20 | $ | 12.69 | ||||||||||

Total return (c) | 15.80 | % | (11.34 | %) | 14.67 | % | 20.26 | % | 27.65 | %(d) | ||||||||||

| Net assets at end of period (000's) | $ | 292,697 | $ | 258,951 | $ | 240,745 | $ | 88,477 | $ | 13,153 | ||||||||||

| Ratios/supplementary data: | ||||||||||||||||||||

| Ratio of total expenses to average net assets | 1.19 | % | 1.21 | % | 1.26 | % | 1.49 | % | 4.87 | %(e) | ||||||||||

Ratio of net expenses to average net assets (f) | 1.05 | % | 1.05 | % | 1.05 | % | 1.05 | % | 1.05 | %(e) | ||||||||||

Ratio of net investment income (loss) to average net assets (f) | (0.48 | %) | (0.42 | %) | (0.48 | %) | (0.38 | %) | 0.26 | %(e) | ||||||||||

| Portfolio turnover rate | 55 | % | 35 | % | 58 | % | 47 | % | 18 | %(d) | ||||||||||

(a) | Represents the period from the commencement of operations (June 29, 2012) through May 31, 2013. |

(b) | Calculated using weighted average shares outstanding during the period. |

(c) | Total return is a measure of the change in value of an investment in the Fund over the period covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses (Note 4). |

(d) | Not annualized. |

(e) | Annualized. |

(f) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

| See accompanying notes to financial statements. | |

15

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS

May 31, 2017

NOTES TO FINANCIAL STATEMENTS

May 31, 2017

1. Organization

APEXcm Small/Mid-Cap Growth Fund (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report. The Fund commenced operations on June 29, 2012.

The investment objective of the Fund is to seek to achieve long-term capital growth.

2. Significant Accounting Policies

In October 2016, the U.S. Securities and Exchange Commission (the “SEC”) adopted amendments to Regulation S-X which will impact financial statement presentation, particularly the presentation of derivative investments. Although still evaluating the impact, management believes that many of the Regulation S-X amendments are consistent with the Fund’s current financial statement presentation and expects that the Fund will be able to comply with the amendments by the August 1, 2017 compliance date.

The following is a summary of the Fund’s significant accounting policies. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Fund follows accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

Securities valuation – The Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. The Fund values its listed securities on the basis of the security’s last sale price on the security’s primary exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with procedures established by and under the general supervision of the Board of Trustees (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities

16

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTES TO FINANCIAL STATEMENTS (Continued)

or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s net asset value (“NAV”) may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

| ● | Level 1 – quoted prices in active markets for identical securities |

| ● | Level 2 – other significant observable inputs |

| ● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments as of May 31, 2017:

| Level 1 | Level 2 | Level 3 | Total | |||||||||||||

| Common Stocks | $ | 285,238,681 | $ | — | $ | — | $ | 285,238,681 | ||||||||

| Money Market Funds | 6,281,250 | — | — | 6,281,250 | ||||||||||||

| Total | $ | 291,519,931 | $ | — | $ | — | $ | 291,519,931 | ||||||||

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by industry type. As of May 31, 2017, the Fund did not have any transfers between Levels. In addition, the Fund did not hold derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of May 31, 2017. It is the Fund’s policy to recognize transfers between Levels at the end of the reporting period.

Share valuation – The NAV per share of the Fund is calculated daily by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of the Fund is equal to the NAV per share.

17

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTES TO FINANCIAL STATEMENTS (Continued)

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned. Withholding taxes on foreign dividends have been recorded in accordance with the Fund’s understanding of the appropriate country’s rules and tax rates.

Security transactions – Security transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on a specific identification basis.

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders – The Fund will distribute to shareholders any net investment income dividends and net realized capital gains distributions at least once each year. The amount of such dividends and distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions are recorded on the ex-dividend date. The tax character of the Fund’s distributions paid during the years ended May 31, 2017 and 2016 was as follows:

| Year Ended | Ordinary Income | Long-Term Capital Gains | Total Distributions | |||||||||

| May 31, 2017 | $ | — | $ | 743,317 | $ | 743,317 | ||||||

| May 31, 2016 | $ | 353,659 | $ | 1,060,976 | $ | 1,414,635 | ||||||

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986 (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

18

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTES TO FINANCIAL STATEMENTS (Continued)

The following information is computed on a tax basis for each item as of May 31, 2017:

| Tax cost of portfolio investments | $ | 245,069,986 | ||

| Gross unrealized appreciation | $ | 59,533,659 | ||

| Gross unrealized depreciation | (13,083,714 | ) | ||

| Net unrealized appreciation | 46,449,945 | |||

| Accumulated capital and other losses | (6,276,664 | ) | ||

| Accumulated earnings | $ | 40,173,281 |

The federal income tax cost of portfolio investments and the tax components of accumulated earnings may temporarily differ from the financial statement cost of portfolio investments and components of net assets (“book/tax difference”). These book/tax differences are due to the recognition of capital gains or losses under income tax regulations and GAAP, primarily due to the tax deferral of losses on wash sales.

Qualified late year losses incurred after December 31, 2016 and within the taxable year are deemed to arise on the first day of the Fund’s next taxable year. For the year ended May 31, 2017, the Fund deferred $493,639 of late year ordinary losses until June 1, 2017 for federal income tax purposes.

As of May 31, 2017, the Fund had the following capital loss carryforwards:

| Capital loss carryforward - short-term | $ | 5,562,683 | ||

| Capital loss carryforward - long-term | 220,342 | |||

| Total capital loss carryforwards | $ | 5,783,025 |

These capital loss carryforwards, which do no expire, may be utilized in future years to offset net realized capital gains, if any, prior to distributing such gains to shareholders.

For the year ended May 31, 2017, the Fund reclassified $1,347,997 of net investment loss and $743,317 of net realized loss against paid-in capital on its Statement of Assets and Liabilities. Such reclassifications, the result of permanent differences between financial statement and income tax reporting requirements, had no effect on the Fund’s total net assets or NAV per share.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for all open tax

19

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTES TO FINANCIAL STATEMENTS (Continued)

periods (periods ended May 31, 2014 through May 31, 2017) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. Federal.

3. Investment Transactions

During the year ended May 31, 2017, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $143,455,629 and $151,286,149, respectively.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by Fiera Capital, Inc. (the “Adviser”) pursuant to the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, the Fund pays the Adviser an advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.00% of its average daily net assets.

Pursuant to an Expense Limitation Agreement (“ELA”) between the Fund and the Adviser, the Adviser has contractually agreed, until October 1, 2017, to reduce investment advisory fees and reimburse other operating expenses to the extent necessary to limit total annual operating expenses of the Fund (exclusive of brokerage costs, taxes, interest, acquired fund fees and expenses, extraordinary expenses such as litigation and merger or reorganization costs, and other expenses not incurred in the ordinary course of the Fund’s business) to an amount not exceeding 1.05% of the Fund’s average daily net assets. Accordingly, during the year ended May 31, 2017, the Adviser reduced its advisory fees in the amount of $394,216.

Under the terms of the ELA, investment advisory fee reductions and expense reimbursements by the Adviser are subject to recoupment by the Adviser for a period of three years after such fees and expenses were incurred, provided the recoupments do not cause total annual operating expenses of the Fund to exceed the lesser of (i) the expense limitation then in effect, if any, or (ii) the expense limitation in effect at the time the expenses to be paid were incurred. As of May 31, 2017, the Adviser may seek recoupment of investment advisory fee reductions in the amount of $1,110,302 no later than the dates as stated below:

| May 31, 2018 | $ | 317,860 | ||

| May 31, 2019 | 398,226 | |||

| May 31, 2020 | 394,216 |

20

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTES TO FINANCIAL STATEMENTS (Continued)

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including, but not limited to, postage, supplies and costs of pricing the Fund’s portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain officers and a Trustee of the Trust are also officers of Ultimus and the Distributor.

TRUSTEE COMPENSATION

Effective October 1, 2016, each Trustee who is not an “interested person” of the Trust (“Independent Trustee”) receives a $1,000 annual retainer from the Fund, paid quarterly, except for the Board Chair who receives a $1,200 annual retainer from the Fund, paid quarterly. Each Independent Trustee also receives from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to October 1, 2016, the Fund paid each Independent Trustee a fee of $500 for each Board meeting attended, plus a $500 annual retainer.

PRINICIPAL HOLDERS OF FUND SHARES

As of May 31, 2017, the following shareholders owned of record 5% or more of the outstanding shares of the Fund:

| Name of Record Owner | % Ownership |

| UBS Financial Services, Inc. (for the benefit of its customers) | 30% |

| Charles Schwab & Company, Inc. (for the benefit of its customers) | 26% |

| National Financial Services LLC (for the benefit of its customers) | 15% |

| U.S. Bank, N.A. (for the benefit of its customers) | 6% |

A beneficial owner of 25% or more of a Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholder’s meeting.

5. Sector Risk

If a Fund has significant investments in the securities of issuers within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have

21

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

NOTES TO FINANCIAL STATEMENTS (Continued)

significant investments in that sector. In addition, this may increase the risk of loss in the Fund and increase the volatility of the Fund’s NAV per share. For instance, economic or market factors, regulatory changes or other developments may negatively impact all companies in a particular sector, and therefore the value of the Fund’s portfolio will be adversely affected. As of May 31, 2017, the Fund had 31.3% of the value of its net assets invested in stocks within the Information Technology sector.

6. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events, except as reflected in the following paragraph:

At an in-person meeting held on July 25, 2017, the Board approved the reorganization of the Fund into Fiera Capital Small/Mid-Cap Growth Fund, a series of Fiera Capital Series Trust (the “Acquiring Fund”). The Acquiring Fund will have the same investment objective, policies, and strategies of the Fund and be managed by the Adviser. The reorganization of the Fund is subject to shareholder approval. Shareholders of the Fund as of record date (to be determined) will be eligible to vote at the Special Meeting of Shareholders. All shareholders of record as of the record date will receive a combined proxy statement/prospectus describing the terms and conditions of the proposed reorganization along with proxy voting information.

22

APEXcm SMALL/MID-CAP GROWTH FUND

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Ultimus Managers Trust

and the Shareholders of APEXcm Small/Mid Cap Growth Fund

and the Shareholders of APEXcm Small/Mid Cap Growth Fund

We have audited the accompanying statement of assets and liabilities of APEXcm Small/Mid Cap Growth Fund, a series of shares of beneficial interest in Ultimus Managers Trust, (the “Fund”) including the schedule of investments, as of May 31, 2017, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the four-year period then ended and for the period from June 29, 2012 (commencement of operations) through May 31, 2013. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2017 by correspondence with the custodian. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of APEXcm Small/Mid Cap Growth Fund as of May 31, 2017, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the four-year period then ended and for the period June 29, 2012 through May 31, 2013, in conformity with accounting principles generally accepted in the United States of America.

| |

| BBD, LLP |

Philadelphia, Pennsylvania

July 27, 2017

July 27, 2017

23

APEXcm SMALL/MID-CAP GROWTH FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited)

ABOUT YOUR FUND’S EXPENSES (Unaudited)

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (December 1, 2016) and held until the end of the period (May 31, 2017).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the SEC requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

24

APEXcm SMALL/MID-CAP GROWTH FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued)

ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued)

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning Account Value December 1, 2016 | Ending Account Value May 31, 2017 | Expenses Paid During Period* | |

| Based on Actual Fund Return | $ 1,000.00 | $ 1,088.60 | $ 5.47 |

| Based on Hypothetical 5% Return (before expenses) | $ 1,000.00 | $ 1,019.70 | $ 5.29 |

| * | Expenses are equal to the Fund’s annualized net expense ratio of 1.05% for the period, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

OTHER INFORMATION (Unaudited)

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-888-575-4800, or on the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-888-575-4800, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-888-575-4800. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

25

APEXcm SMALL/MID-CAP GROWTH FUND

FEDERAL TAX INFORMATION (Unaudited)

FEDERAL TAX INFORMATION (Unaudited)

In accordance with federal tax requirements, the following provides shareholders with information concerning distributions made by the Fund during the year ended May 31, 2017. Certain dividends paid by the Fund may be subject to a maximum tax rate of 23.8%. The Fund intends to designate up to a maximum amount of $743,317 as a long-term capital gain distribution.

As required by federal regulations, complete information was computed and reported in conjunction with your 2016 Form 1099-DIV.

26

APEXcm SMALL/MID-CAP GROWTH FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

The Board of Trustees has overall responsibility for management of the Trust’s affairs. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement, or removal. The Trustees, in turn, elect the officers of the Fund to actively supervise its day-to-day operations. The officers have been elected for an annual term. Unless otherwise noted, each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. The following are the Trustees and executive officers of the Fund:

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years | Number of Funds in Trust Overseen by Trustee | Directorships of Public Companies Held by Trustee During Past 5 Years |

| Interested Trustees: | |||||

Robert G. Dorsey* Year of Birth: 1957 | Since February 2012 | Trustee (February 2012 to present) President (June 2012 to October 2013) | President and Managing Director of Ultimus Fund Solutions, LLC and Ultimus Fund Distributors, LLC (1999 to present) | 26 | None |

| Independent Trustees: | |||||

Janine L. Cohen Year of Birth: 1952 | Since January 2016 | Trustee | Retired since 2013; Chief Financial Officer from 2004 to 2013 and Chief Compliance Officer from 2008 to 2013 at AER Advisors, Inc. | 26 | None |

David M. Deptula Year of Birth: 1958 | Since June 2012 | Trustee | Vice President of Legal and Special Projects at Dayton Freight Lines, Inc. since 2016; Vice President of Tax Treasury at The Standard Register Inc. (formerly The Standard Register Company) from 2011 to 2016 | 26 | None |

27

APEXcm SMALL/MID-CAP GROWTH FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years | Number of Funds in Trust Overseen by Trustee | Directorships of Public Companies Held by Trustee During Past 5 Years |

| Independent Trustees (Continued): | |||||

John J. Discepoli Year of Birth: 1963 | Since June 2012 | Chairman (May 2016 to present) Trustee (June 2012 to present) | Owner of Discepoli Financial Planning, LLC (personal financial planning company) since 2004 | 26 | None |

| * | Mr. Dorsey is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the Investment Company Act of 1940 because of his relationship with the Trust’s administrator, transfer agent and distributor. |

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years |

| Executive Officers: | |||

David R. Carson Year of Birth: 1958 | Since April 2013 | Principal Executive Officer (April 2017 to present) President (October 2013 to present) Vice President (April 2013 to October 2013) | Vice President and Director of Client Strategies of Ultimus Fund Solutions, LLC (2013 to present); President, Unified Series Trust (2016 to present); Chief Compliance Officer, FSI LBAR Fund (2013 to 2016), The Huntington Funds (2005 to 2013), Huntington Strategy Shares (2012 to 2013), and Huntington Asset Advisors (2013); Vice President, Huntington National Bank (2001 to 2013) |

Jennifer L. Leamer Year of Birth: 1976 | Since April 2014 | Treasurer (October 2014 to present) Assistant Treasurer (April 2014 to October 2014) | Vice President, Mutual Fund Controller of Ultimus Fund Solutions, LLC (2014 to present); Business Analyst of Ultimus Fund Solutions, LLC (2007 to 2014) |

28

APEXcm SMALL/MID-CAP GROWTH FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

| Name and Year of Birth | Length of Time Served | Position(s) Held with Trust | Principal Occupation(s) During Past 5 Years |

| Executive Officers (Continued): | |||

Frank L. Newbauer Year of Birth: 1954 | Since February 2012 | Secretary (July 2017 to present) Assistant Secretary (April 2015 to July 2017) Secretary (February 2012 to April 2015) | Assistant Vice President of Ultimus Fund Solutions, LLC (2010 to present) |

Charles C. Black Year of Birth: 1979 | Since April 2015 | Chief Compliance Officer (January 2016 to present) Assistant Chief Compliance Officer (April 2015 to January 2016) | Senior Compliance Officer of Ultimus Fund Solutions, LLC (2015 to present); Chief Compliance Officer of The Caldwell & Orkin Funds, Inc. (2016 to present); Senior Compliance Manager at Touchstone Mutual Funds (2013 to 2015); Senior Compliance Manager at Fund Evaluation Group (2011 to 2013) |

Additional information about members of the Board and executive officers is available in the Fund’s Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call 1-888-575-4800.

29

|

BARROW VALUE OPPORTUNITY FUND

(BALIX)

BARROW LONG/SHORT OPPORTUNITY FUND

(BFSLX)

Annual Report

May 31, 2017

| BARROW VALUE OPPORTUNITY FUND LETTER TO SHAREHOLDERS | June 28, 2017 |

Dear Shareholder,

We are pleased to report on the status and performance of the Barrow Value Opportunity Fund (“the Fund”) for the twelve months ended May 31, 2017.

We believe that the Fund owns a well-positioned portfolio of equity interests in excellent businesses at attractive valuations. This portfolio is highly diversified by market capitalization segments (large, middle, small), industry sectors, and issuers. In selecting investments for the Fund, we search for businesses that we believe feature high returns on capital, wide operating margins, and low debt loads. Based on our estimates of intrinsic value, we believe our portfolio’s valuation is attractively low on an absolute basis and less expensive than the U.S. stock market as represented by the S&P 500® Index (the “S&P 500”).

The Fund’s long-term performance has been excellent, with an annual average total return of 14.62% since inception. The Fund has exceeded the total return of the S&P 500 in five of the past eight calendar years. During the most recent twelve months ended May 31, 2017, the Fund returned +12.14% net of all fees and expenses, which underperformed the S&P 500 by 5.33%.

Barrow Street Advisors, LLC (the “Advisor”) continues to use its proprietary private-equity approach to find companies that meet its Quality-meets-Value criteria. Using the Advisor’s extensive research, the Fund seeks to generate long-term capital appreciation by investing in companies with fundamental operating and financial attributes representative of both quality and value. To increase the Fund’s chances for success, the Fund invests in a variety of positions that are diversified across market capitalization and industry sectors.

Over the past twelve-months, we uncovered 120 new investment opportunities, composed of 50 small-caps, 27 mid-caps, and 43 large-caps, across seven different industry sectors. We believe all of these new additions to the Fund’s portfolio are excellent companies with strong balance sheets and robust earnings capabilities. These companies are generally using their ample free cash flow to: a) re-invest in growth opportunities at high rates of return on investment; b) pay dividends; c) repurchase stock at attractive valuations; and/or d) retire outstanding debt.

In keeping with our practice since the beginning of 2009, over the past twelve months the Fund’s investments were sourced by taking account of the opportunity set of all companies in our broad investment universe each time we committed capital to a new position. We believe this approach allows us to uncover excellent investment opportunities that arise from temporary market inefficiencies and to gather up the most compelling investments across a wide array of industries and market capitalizations, while avoiding the damaging behavioral biases inherent in concentrated-stock and sector-specialized investing.

��

1

Thirteen of the Fund’s holdings were announced as take-over targets over the past twelve months, which was approximately 2.6x the market average. The Fund has had investments in 93 take-overs since December 31, 20081, or roughly 3.5x the market average2. The control premiums we have captured by virtue of holding stocks that end up being merger targets has made repeated and meaningful contributions to the Fund’s total returns, and we expect continued benefits from this effect going forward. We typically sell companies from the Fund’s portfolio soon after they are announced as take-over targets and re-invest that capital.

Over the past twelve months, the Fund’s portfolio generated total returns, before fees and expenses, of +13.38%, including +12.40% for large-caps, +12.63% for mid-caps and +13.09% for small-caps. This compares to +17.47% for the S&P 500 (for large-caps), +17.16% for the S&P 400 Midcap (for mid-caps), and +20.36% for the Russell 2000 (for small-caps) over the same period. The Fund’s sectors with the best absolute performance were Industrials and Information Technology, which generated total returns of +28.01% and +22.68%, respectively. The Fund’s sectors with the worst absolute performance were Consumer Discretionary and Energy, which returned +2.84% and +6.75%, respectively.

Strategy Review

Given the Fund’s recent soft performance, we have carefully reviewed our “Quality-meets-Value” strategy. This process has reaffirmed our belief in the Fund’s investment process and approach. We remain committed to dispassionately purchasing diversified portfolios of quality businesses at prices below our estimate of their intrinsic value, and doing the inverse when selling short.

Over the past twelve months, “quality” stocks have significantly underperformed the overall market. The S&P 500 Quality Index has trailed the S&P 500 Index by 250 bps over this period (source: Bloomberg). While underperformance is frustrating, we remain optimistic as “quality” stocks have outperformed the market over most periods going back to 1994. The current “risk-on” stock market environment appears to be waning. In the long run, investment approaches that combine quality and value do very well.

Moving forward, we remain committed to: a) disciplined execution of our Quality-meets-Value strategy; b) resisting pressure to change our strategy due to periods of soft performance; and c) communicating what we do and why. We are willing to make adjustments with new information, but the bar is high.

You can find additional commentary and reports about the Advisor’s management of the Fund’s portfolio on the Barrow Funds’ website (www.barrowfunds.com).

Sincerely,

| Nicholas Chermayeff | Robert F. Greenhill, Jr. | David R. Bechtel |

| Co-Portfolio Manager, | Co-Portfolio Manager, | Principal, |

| Investment Committee | Investment Committee | Investment Committee |

2

1 | The investment related and performance information discussed above for periods prior to Barrow Value Opportunity Fund’s reorganization date (August 30, 2013) are based on the activities of the Fund’s predecessor, the Barrow Street Fund L.P., an unregistered limited partnership managed by the portfolio managers of Barrow Value Opportunity Fund (the “Predecessor Private Fund”). The Predecessor Private Fund was reorganized into the Institutional Class shares of the Barrow Value Opportunity Fund on August 30, 2013, the date that the Fund commenced operations (the “Reorganization”). Barrow Value Opportunity Fund has been managed in the same style and by the same portfolio managers since the Predecessor Private Fund’s inception on December 31, 2008. The performance information shows the Predecessor Private Fund’s returns calculated using the actual fees and expenses charged by the Predecessor Private Fund. This prior performance is net of management fees and other expenses, but does not include the effect of the Predecessor Private Fund’s performance fee, which was in place until October 7, 2012. Prior to the Reorganization, the Predecessor Private Fund was not subject to certain investment restrictions, diversification requirements, and other restrictions of the Investment Company Act of 1940, as amended, or Subchapter M of the Internal Revenue Code of 1986, as amended, which, if they had been applicable, might have adversely affected Barrow Value Opportunity Fund’s performance. |

2 | The frequency of merger and acquisition (“M&A”) activity in the Fund’s portfolio is calculated on a quarterly basis by dividing the cumulative number of portfolio holdings that have been announced as merger or acquisition targets by the cumulative number of unique holdings held in the Fund’s portfolio. The frequency of M&A activity in the market is calculated on a quarterly basis by dividing the cumulative number of publicly-traded U.S. common stocks that have been announced as acquisition targets per Bloomberg by the total universe of publicly-traded U.S. common stocks as identified by Bloomberg (approximately 10,000). |

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-877-767-6633.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit our website at www.barrowfunds.com or call 1-877-767-6633 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Advisor’s current opinions and views of the financial markets. Although the Advisor believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. For a complete list of securities held by the Fund as of May 31, 2017, please see the Schedule of Investments section of the Annual Report. The opinions of the Fund’s Advisor with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

BARROW VALUE OPPORTUNITY FUND

PERFORMANCE INFORMATION

May 31, 2017 (Unaudited)

PERFORMANCE INFORMATION

May 31, 2017 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment in

Barrow Value Opportunity Fund

versus the S&P 500® Index

Barrow Value Opportunity Fund

versus the S&P 500® Index

Average Annual Total Returns For the periods ended May 31, 2017 | ||||

| 1 Year | 5 Years | Since Inception(c) | ||

Barrow Value Opportunity Fund(a)(b) | 12.14% | 14.01% | 14.62% | |

S&P 500® Index | 17.47% | 15.42% | 14.83% | |

4

BARROW VALUE OPPORTUNITY FUND

PERFORMANCE INFORMATION

May 31, 2017 (Unaudited) (Continued)

PERFORMANCE INFORMATION

May 31, 2017 (Unaudited) (Continued)

Comparison of Yearly Returns with the S&P 500® Index | ||||

Barrow Value Opportunity Fund(a) | S&P 500® Index | Difference | ||

| Yearly Total Returns for Calendar Years: | ||||

| 2009 | 30.10% | 26.46% | 3.64% | |

| 2010 | 18.75% | 15.06% | 3.69% | |

| 2011 | 5.50% | 2.11% | 3.39% | |

| 2012 | 18.77% | 16.00% | 2.77% | |

| 2013 | 36.69% | 32.39% | 4.30% | |

| 2014 | 5.13% | 13.69% | (8.56%) | |

| 2015 | 0.81% | 1.38% | (0.57%) | |

| 2016 | 7.41% | 11.96% | (4.55%) | |

| Total Return Since Inception (not annualized, as of 12/31/16) | 201.26% | 194.48% | 6.78% | |

(a) | The Barrow Value Opportunity Fund (the “Fund”) performance includes the performance of the Barrow Street Fund L.P. (the “Predecessor Private Fund”), the Fund’s predecessor, for the periods before the Fund’s registration statement became effective. The Predecessor Private Fund was reorganized into the Fund at the close of business on August 30, 2013 (the “Reorganization”), the date the Fund commenced operations. The Fund has been managed in the same style and by the same portfolio managers since the Predecessor Private Fund’s inception on December 31, 2008. The Fund’s investment goals, policies, guidelines and restrictions are, in all material respects, equivalent to those of the Predecessor Private Fund. The performance of the Predecessor Private Fund is net of management fees of 1.50% of assets but does not include the effect of a 20% performance fee which was in place until October 7, 2012. Prior to the Reorganization, the Predecessor Private Fund was not subject to certain investment restrictions, diversification requirements and other restrictions of the Investment Company Act of 1940, as amended, or Subchapter M of the Internal Revenue Code of 1986, as amended. If such restrictions had been applicable, they might have adversely affected the Predecessor Private Fund’s performance. |

(b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. |

(c) | Represents the period from December 31, 2008(a) through May 31, 2017. |

5

| BARROW LONG/SHORT OPPORTUNITY FUND | |

| LETTER TO SHAREHOLDERS | |

Dear Shareholder,

We are pleased to report on the status and performance of the Barrow Long/Short Opportunity Fund (“the Fund”) for the twelve months ended May 31, 2017.

We believe the Fund owns a well-positioned long portfolio of equity positions in excellent businesses at attractive valuations that we believe feature high returns on capital, wide operating margins, and low debt load. The Fund also maintains short positions in the common stock of companies that we believe have poor business characteristics and are trading at high prices. The Fund’s long and short portfolios are highly diversified by market cap segments (large, mid, small), industry sectors, and issuers.

We believe the Fund is well positioned to do well in most future market conditions, especially a bear market. In our opinion, the Fund’s long and short portfolios are cheap and expensive, respectively, on an absolute basis and in relation to the U.S. stock market as represented by the S&P 500® Index (“S&P 500”). We believe the Fund’s short portfolio, the value of which is approximately 70% of the long portfolio, provides a meaningful hedge against the market’s potential downside volatility.

For the twelve months ended May 31, 2017, the Fund posted a total return of -3.38%, which compares to +17.47% for the S&P 500 and +10.89% for the HFRI Equity Hedge Index. The Fund underperformed the S&P 500 due mainly to the underperformance of its long positions.

The Fund maintains a target gross exposure of approximately 220% of its net assets, with long exposure of 130%, short exposure of 90%, and net exposure of 40%. For the twelve months ended May 31, 2017, the Fund’s long portfolio generated an unleveraged total return before fees and expenses of +13.25%, which underperformed the S&P 500 by 4.22%. The Fund’s short portfolio generated an unleveraged total return, before fees and expenses, of +19.93% or 2.46% more than the S&P 500. A positive return in the short portfolio results in negative return contributions to the Fund.

Barrow Street Advisors, LLC (the “Advisor”) continues to use its proprietary private equity approach to find companies that meet its Quality-meets-Value criteria. Using the Advisor’s extensive research, the Fund seeks to generate above-average returns through capital appreciation by investing long in companies with fundamental operating and financial attributes representative of both quality and value and selling short companies of both lower quality and high price. Using this approach the Fund continued to uncover potential opportunities to: 1) purchase quality companies trading at temporary discounts to their intrinsic values; and 2) sell short the stock of lower quality companies trading at prices well above their intrinsic values. To increase the Fund’s chances for success, the Fund invests in a variety of positions diversified across market capitalization and industry sectors.