| OMB APPROVAL |

OMB Number: 3235-0570 Expires: January 31, 2017 Estimated average burden hours per response: 20.6 |

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246_ |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | November 30 | |

| Date of reporting period: | November 30, 2016 |

| Item 1. | Reports to Stockholders. |

LYRICAL U.S. VALUE EQUITY FUND

Institutional Class (LYRIX)

Investor Class (LYRBX)

LYRICAL U.S. HEDGED VALUE FUND

Institutional Class (LYRHX)

Investor Class (LYRDX)

Annual Report

November 30, 2016

LYRICAL FUNDS | December 16, 2016 |

Dear Fellow Shareholders,

Enclosed is the annual report to shareholders of the Lyrical U.S. Value Equity Fund (the “Value Fund”) and Lyrical U.S. Hedged Value Fund (the “Hedged Value Fund”) (collectively, the “Funds”). On behalf of the Funds and their investment adviser, Lyrical Asset Management LP, I would like to thank you for your investment.

Lyrical U.S. Value Equity Fund

Since its launch on February 4, 2013 through November 30, 2016, the Value Fund – Institutional Class has produced a cumulative total return of +78.72%, compared to the +59.53% cumulative total return for the S&P 500 Index (the “S&P 500”). For the twelve months ended November 30, 2016, the Value Fund – Institutional Class produced a total return of +10.73% compared to the total return for the S&P 500 of +8.06%. The biggest winners for the twelve month period ended November 30, 2016 were LNC (+52%), SYMC (+47%), and NCR (+43%). The biggest losers were HTZ (-55%), QVCA (-22%) and AFSI (-21%). We maintain our positions in each of these largest winners and detractors with the exception of AFSI.

In analyzing the Fund portfolio’s performance attribution, we find it helpful to examine both the investment success rate and any skew in the distribution of returns. Our success rate has been high over the life of the Value Fund, as 84% of the Fund’s investments posted gains, and 63% outperformed the S&P 500. Skew has also been a positive factor, as the Fund’s outperformers have outperformed by 50%, while our underperformers have underperformed by 35% over the life of the Fund. For the twelve month period ended November 30, 2016, 73% of the Fund’s investments posted gains, and 51% outperformed the S&P 500. For the twelve month period skew has been a positive factor as the Fund’s outperformers have outperformed by 16%, while our underperformers have underperformed by 13%.

During the life of the Value Fund we have sold sixteen positions, as four companies announced they were being acquired, nine approached our estimates of fair value, for one we lost conviction in our thesis, for one the company announced or completed acquisitions which increased the complexity and decreased analyzability and for one the risk/reward became less compelling than other opportunities. For each sale we added a new position from our pipeline of opportunities. We are still finding attractive stock opportunities to add to the portfolio, even as some of our existing positions begin to approach our estimates of fair value.

As of November 30, 2016, the valuation of our portfolio is 13.5x next twelve months consensus earnings. The S&P 500 has a valuation of 16.9x on this same basis, a premium of 25% over the Fund.

1

Lyrical U.S. Hedged Value Fund

In July 2014 we launched the Hedged Value Fund as a liquid alternatives product that employs the same long portfolio as the Value Fund (see discussion above). Sector exchange-traded fund (ETF) hedges are used on the short side to create a portfolio that aims to maintain net long exposures of 50%. This provides a hedged option for those wishing exposure to the long portfolio but unwilling to accept unhedged equity market exposure.

Since its launch on July 14, 2014 through November 30, 2016, the Hedged Value Fund – Institutional Class has produced a cumulative total return of +0.07%, compared to the +17.02% cumulative total return for the S&P 500. For the twelve months ended November 30, 2016, the Hedged Value Fund – Institutional Class produced a total return of +5.88% compared to the total return for the S&P 500 of +8.06%. In rising equity markets one should expect Hedged Value Fund’s performance to lag that of the S&P 500, as it did for both the above periods, as our hedges detract from total return.

Lyrical Asset Management’s Investment Philosophy and Portfolio Construction

As there have been a significant number of new investors since our previous letter to the Funds’ shareholders, we’d like to briefly outline our investment philosophy and portfolio construction approach.

We believe our strategy and approach to investing differentiate us from other investment managers, even those that share a value approach to investing. We are deep value investors and by this we mean that we look to invest in companies trading significantly below intrinsic value. We believe this separates us from other value managers who focus on relative value or core value approaches and whose portfolio characteristics have higher Price/Earnings, Price/Book and Price/Cash Flow multiples. We assess valuation based on current price relative to long-term normalized earnings, which contrasts us to those that rely on Price/Book or dividend yield. We only invest in what we consider to be quality businesses that we believe should earn good returns on invested capital, and avoid volatile businesses and companies with excessive leverage. Other value investors may consider owning any business regardless of quality if they believe the price is low enough. Lastly, we only invest in businesses we can understand, and avoid those that are excessively complex or require specialized technical knowledge, even though they may appear cheap from a high-level perspective.

We construct our portfolio purely bottom up and without regard to what is or is not contained in a benchmark. We are concerned with concentration risk, and have strict limits on how much capital can be invested in any one position or any one industry. Our long portfolio is constructed to be balanced and diversified across approximately 33 positions, giving us exposure to many different types of companies and situations without sacrificing our strict investment standards.

Thank you for your continued trust and interest in Lyrical Asset Management.

Sincerely,

Andrew Wellington

Portfolio Manager

2

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-888-884-8099.

An investor should consider the investment objectives, risks, charges and expenses of the Funds carefully before investing. The Funds’ prospectus contains this and other important information. To obtain a copy of the Funds’ prospectus please visit the Funds’ website at www.lyricalvaluefunds.com or call 1-888-884-8099 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Funds are distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Funds that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolios of the Funds, may be sold at any time, and may no longer be held by the Funds. For a complete list of securities held by the Funds as of November 30, 2016, please see the Schedules of Investments and Schedule of Securities Sold Short sections of the Annual Report. The opinions of the Funds’ adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Funds and the market in general and statements of the Funds’ plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

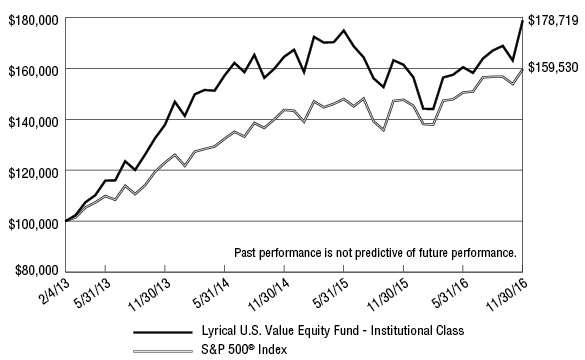

LYRICAL U.S. VALUE EQUITY FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $100,000 Investment in

Lyrical U.S. Value Equity Fund - Institutional Class(a) versus

the S&P 500® Index

Average Annual Total Returns (for the periods ended November 30, 2016) | ||

1 Year | Since | |

Lyrical U.S. Value Equity Fund - Institutional Class(b) | 10.73% | 16.42% |

Lyrical U.S. Value Equity Fund - Investor Class(b) | 10.36% | 6.70% |

S&P 500® Index(d) | 8.06% | 13.01%(e) |

(a) | The line graph above represents performance of the Institutional Class only, which will vary from the performance of the Investor Class based on the difference in fees paid by shareholders in the different classes. |

(b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(c) | Commencement of operations for Institutional Class shares was February 4, 2013. Commencement of operations for Investor Class shares was February 24, 2014. |

(d) | The S&P 500® Index is a market capitalization weighted index of 500 large companies that is widely used as a barometer of U.S. stock market performance. The index is unmanaged and shown for illustration purposes only. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

(e) | Represents the period from February 4, 2013 (date of commencement of operations of Institutional Class shares) through November 30, 2016. |

4

LYRICAL U.S. HEDGED VALUE FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $100,000 Investment in

Lyrical U.S. Hedged Value Fund - Institutional Class(a) versus

the S&P 500® Index

Average Annual Total Returns (for the periods ended November 30, 2016) | ||

1 Year | Since | |

Lyrical U.S. Hedged Value Fund - Institutional Class(b) | 5.88% | 0.03% |

Lyrical U.S. Hedged Value Fund - Investor Class(b) | 5.58% | (0.22%) |

S&P 500® Index(d) | 8.06% | 6.83% |

(a) | The line graph above represents performance of the Institutional Class only, which will vary from the performance of the Investor Class based on the difference in fees paid by shareholders in the different classes. |

(b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(c) | Commencement of operations for Institutional Class and Investor Class shares was July 14, 2014. |

(d) | The S&P 500® Index is a market capitalization weighted index of 500 large companies that is widely used as a barometer of U.S. stock market performance. The index is unmanaged and shown for illustration purposes only. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

5

LYRICAL U.S. VALUE EQUITY FUND

PORTFOLIO INFORMATION

November 30, 2016 (Unaudited)

Lyrical U.S. Value Equity Fund vs S&P 500® Index

Sector Diversification

Top Ten Equity Holdings

Security Description | % of |

Broadcom Ltd. | 6.1% |

Aetna, Inc. | 4.9% |

Comcast Corporation - Class A | 4.4% |

Corning, Inc. | 4.4% |

EOG Resources, Inc. | 4.4% |

Aflac, Inc. | 4.2% |

Lincoln National Corporation | 4.1% |

Symantec Corporation | 4.1% |

Suncor Energy, Inc. | 3.9% |

Johnson Controls International plc | 3.9% |

6

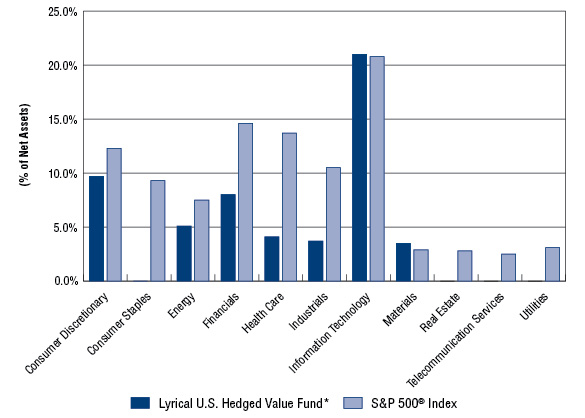

LYRICAL U.S. HEDGED VALUE FUND

PORTFOLIO INFORMATION

November 30, 2016 (Unaudited)

Lyrical U.S. Hedged Value Fund vs S&P 500® Index

Sector Diversification

* | The percentages above for Lyrical U.S. Hedged Value Fund represent the net percentages for the Fund and are computed by taking the net dollar exposure, including short positions, and dividing by the net assets of the Fund. |

Top Ten Long Positions

Security Description | % of |

Anthem, Inc. | 4.8% |

Aetna, Inc. | 4.8% |

Comcast Corporation - Class A | 4.8% |

Corning, Inc. | 4.8% |

TE Connectivity Ltd. | 4.7% |

Aflac, Inc. | 4.7% |

Lincoln National Corporation | 4.7% |

Broadcom Ltd. | 4.6% |

Symantec Corporation | 4.6% |

Celanese Corporation - Series A | 4.4% |

7

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

COMMON STOCKS — 99.9% | Shares | Value | ||||||

Consumer Discretionary — 13.7% | ||||||||

Auto Components — 3.4% | ||||||||

Goodyear Tire & Rubber Company (The) | 806,142 | $ | 24,740,498 | |||||

Tenneco, Inc. (a) | 180,828 | 10,659,810 | ||||||

35,400,308 | ||||||||

Household Durables — 3.2% | ||||||||

Whirlpool Corporation | 206,532 | 33,549,058 | ||||||

Internet & Direct Marketing Retail — 2.7% | ||||||||

Liberty Interactive Corporation QVC Group - Series A (a) | 1,387,442 | 28,733,924 | ||||||

Media — 4.4% | ||||||||

Comcast Corporation - Class A | 669,921 | 46,566,209 | ||||||

Energy — 11.2% | ||||||||

Energy Equipment & Services — 2.9% | ||||||||

National Oilwell Varco, Inc. | 822,966 | 30,746,010 | ||||||

Oil, Gas & Consumable Fuels — 8.3% | ||||||||

EOG Resources, Inc. | 446,593 | 45,784,714 | ||||||

Suncor Energy, Inc. | 1,300,599 | 41,437,084 | ||||||

87,221,798 | ||||||||

Financials — 16.8% | ||||||||

Capital Markets — 3.7% | ||||||||

Ameriprise Financial, Inc. | 343,724 | 39,256,718 | ||||||

Insurance — 13.1% | ||||||||

Aflac, Inc. | 619,964 | 44,253,030 | ||||||

Assurant, Inc. | 208,937 | 18,039,621 | ||||||

Lincoln National Corporation | 674,888 | 43,260,321 | ||||||

Willis Towers Watson plc | 254,209 | 31,615,973 | ||||||

137,168,945 | ||||||||

Health Care — 8.8% | ||||||||

Health Care Providers & Services — 8.8% | ||||||||

Aetna, Inc. | 392,069 | 51,298,308 | ||||||

Anthem, Inc. | 289,283 | 41,231,506 | ||||||

92,529,814 | ||||||||

Industrials — 13.7% | ||||||||

Commercial Services & Supplies — 3.9% | ||||||||

Johnson Controls International plc | 921,161 | 41,433,822 | ||||||

8

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

COMMON STOCKS — 99.9% (Continued) | Shares | Value | ||||||

Industrials — 13.7% (Continued) | ||||||||

Construction & Engineering — 1.4% | ||||||||

AECOM (a) | 406,654 | $ | 14,781,873 | |||||

Electrical Equipment — 3.9% | ||||||||

Eaton Corporation plc | 614,384 | 40,862,680 | ||||||

Road & Rail — 1.9% | ||||||||

Avis Budget Group, Inc. (a) | 314,468 | 12,040,980 | ||||||

Hertz Global Holdings, Inc. (a) | 325,383 | 8,193,144 | ||||||

20,234,124 | ||||||||

Trading Companies & Distributors — 2.6% | ||||||||

AerCap Holdings N.V. (a) | 628,023 | 26,910,785 | ||||||

Information Technology — 31.3% | ||||||||

Communications Equipment — 3.1% | ||||||||

ARRIS International plc (a) | 442,158 | 12,685,513 | ||||||

CommScope Holding Company, Inc. (a) | 555,859 | 19,999,807 | ||||||

32,685,320 | ||||||||

Electronic Equipment, Instruments & Components — 8.2% | ||||||||

Corning, Inc. | 1,906,302 | 45,808,437 | ||||||

TE Connectivity Ltd. | 604,454 | 40,885,269 | ||||||

86,693,706 | ||||||||

IT Services — 3.2% | ||||||||

Western Union Company (The) | 1,589,140 | 33,419,614 | ||||||

Semiconductors & Semiconductor Equipment — 7.6% | ||||||||

Broadcom Ltd. | 375,063 | 63,944,491 | ||||||

Microsemi Corporation (a) | 297,918 | 16,311,010 | ||||||

80,255,501 | ||||||||

Software — 4.1% | ||||||||

Symantec Corporation | 1,746,338 | 42,593,184 | ||||||

Technology Hardware, Storage & Peripherals — 5.1% | ||||||||

NCR Corporation (a) | 507,006 | 19,646,483 | ||||||

Western Digital Corporation | 537,223 | 34,199,616 | ||||||

53,846,099 | ||||||||

Materials — 4.4% | ||||||||

Chemicals — 3.5% | ||||||||

Celanese Corporation - Series A | 458,735 | 36,386,860 | ||||||

9

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

COMMON STOCKS — 99.9% (Continued) | Shares | Value | ||||||

Materials — 4.4% (Continued) | ||||||||

Containers & Packaging — 0.9% | ||||||||

Owens-Illinois, Inc. (a) | 499,286 | $ | 9,171,884 | |||||

Total Common Stocks (Cost $899,849,917) | $ | 1,050,448,236 | ||||||

MONEY MARKET FUNDS — 1.0% | Shares | Value | ||||||

Invesco Short-Term Investments Trust - Treasury Portfolio - Institutional Shares, 0.26% (b) (Cost $10,620,620) | 10,620,620 | $ | 10,620,620 | |||||

Total Investments at Value — 100.9% (Cost $910,470,537) | $ | 1,061,068,856 | ||||||

Liabilities in Excess of Other Assets — (0.9%) | (8,952,591 | ) | ||||||

Net Assets — 100.0% | $ | 1,052,116,265 | ||||||

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of November 30, 2016. |

N.V. — Naamloze Vennootschap |

plc — Public Limited Company |

See accompanying notes to financial statements. |

10

LYRICAL U.S. HEDGED VALUE FUND | ||||||||

COMMON STOCKS — 108.7% | Shares | Value | ||||||

Consumer Discretionary — 15.7% | ||||||||

Auto Components — 4.0% | ||||||||

Goodyear Tire & Rubber Company (The) (a) | 1,288 | $ | 39,528 | |||||

Tenneco, Inc. (b) | 283 | 16,683 | ||||||

56,211 | ||||||||

Household Durables — 3.7% | ||||||||

Whirlpool Corporation (a) | 315 | 51,168 | ||||||

Internet & Direct Marketing Retail — 3.2% | ||||||||

Liberty Interactive Corporation QVC Group - Series A (a) (b) | 2,156 | 44,651 | ||||||

Media — 4.8% | ||||||||

Comcast Corporation - Class A (a) | 964 | 67,008 | ||||||

Energy — 10.4% | ||||||||

Energy Equipment & Services — 2.3% | ||||||||

National Oilwell Varco, Inc. (a) | 871 | 32,541 | ||||||

Oil, Gas & Consumable Fuels — 8.1% | ||||||||

EOG Resources, Inc. (a) | 585 | 59,974 | ||||||

Suncor Energy, Inc. (a) | 1,657 | 52,792 | ||||||

112,766 | ||||||||

Financials — 18.8% | ||||||||

Capital Markets — 4.2% | ||||||||

Ameriprise Financial, Inc. (a) | 509 | 58,133 | ||||||

Insurance — 14.6% | ||||||||

Aflac, Inc. (a) | 921 | 65,741 | ||||||

Assurant, Inc. (a) | 352 | 30,392 | ||||||

Lincoln National Corporation | 1,021 | 65,446 | ||||||

Willis Towers Watson plc (a) | 346 | 43,032 | ||||||

204,611 | ||||||||

Health Care — 9.6% | ||||||||

Health Care Providers & Services — 9.6% | ||||||||

Aetna, Inc. (a) | 514 | 67,252 | ||||||

Anthem, Inc. (a) | 472 | 67,274 | ||||||

134,526 | ||||||||

Industrials — 15.4% | ||||||||

Commercial Services & Supplies — 4.3% | ||||||||

Johnson Controls International plc (a) | 1,319 | 59,329 | ||||||

11

LYRICAL U.S. HEDGED VALUE FUND | ||||||||

COMMON STOCKS — 108.7% (Continued) | Shares | Value | ||||||

Industrials — 15.4% (Continued) | ||||||||

Construction & Engineering — 1.5% | ||||||||

AECOM (a) (b) | 577 | $ | 20,974 | |||||

Electrical Equipment — 4.0% | ||||||||

Eaton Corporation plc (a) | 842 | 56,001 | ||||||

Road & Rail — 2.4% | ||||||||

Avis Budget Group, Inc. (a) (b) | 527 | 20,179 | ||||||

Hertz Global Holdings, Inc. (a) (b) | 522 | 13,144 | ||||||

33,323 | ||||||||

Trading Companies & Distributors — 3.2% | ||||||||

AerCap Holdings N.V. (a) (b) | 1,052 | 45,078 | ||||||

Information Technology — 33.3% | ||||||||

Communications Equipment — 3.5% | ||||||||

ARRIS International plc (b) | 703 | 20,169 | ||||||

CommScope Holding Company, Inc. (a) (b) | 800 | 28,784 | ||||||

48,953 | ||||||||

Electronic Equipment, Instruments & Components — 9.5% | ||||||||

Corning, Inc. (a) | 2,755 | 66,202 | ||||||

TE Connectivity Ltd. (a) | 975 | 65,949 | ||||||

132,151 | ||||||||

IT Services — 4.0% | ||||||||

Western Union Company (The) (a) | 2,662 | 55,982 | ||||||

Semiconductors & Semiconductor Equipment — 6.4% | ||||||||

Broadcom Ltd. (a) | 376 | 64,104 | ||||||

Microsemi Corporation (b) | 466 | 25,514 | ||||||

89,618 | ||||||||

Software — 4.6% | ||||||||

Symantec Corporation (a) | 2,628 | 64,097 | ||||||

Technology Hardware, Storage & Peripherals — 5.3% | ||||||||

NCR Corporation (b) | 836 | 32,395 | ||||||

Western Digital Corporation (a) | 656 | 41,761 | ||||||

74,156 | ||||||||

Materials — 5.5% | ||||||||

Chemicals — 4.4% | ||||||||

Celanese Corporation - Series A (a) | 774 | 61,393 | ||||||

12

LYRICAL U.S. HEDGED VALUE FUND | ||||||||

COMMON STOCKS — 108.7% (Continued) | Shares | Value | ||||||

Materials — 5.5% (Continued) | ||||||||

Containers & Packaging — 1.1% | ||||||||

Owens-Illinois, Inc. (a) (b) | 824 | $ | 15,137 | |||||

Total Common Stocks (Cost $1,482,677) | $ | 1,517,807 | ||||||

MONEY MARKET FUNDS — 1.2% | Shares | Value | ||||||

Invesco Short-Term Investments Trust - Treasury Portfolio - Institutional Shares, 0.26% (c) (Cost $16,436) | 16,436 | $ | 16,436 | |||||

Total Investments at Value — 109.9% (Cost $1,499,113) | $ | 1,534,243 | ||||||

Liabilities in Excess of Other Assets(d) — (9.9%) | (137,770 | ) | ||||||

Net Assets — 100.0% | $ | 1,396,473 | ||||||

(a) | All or a portion of the shares have been committed as collateral for open short positions (Note 2). |

(b) | Non-income producing security. |

(c) | The rate shown is the 7-day effective yield as of November 30, 2016. |

(d) | Includes cash held as margin deposits for short positions. |

N.V. — Naamloze Vennootschap |

plc — Public Limited Company |

See accompanying notes to financial statements. |

13

LYRICAL U.S. HEDGED VALUE FUND | ||||||||

EXCHANGE-TRADED FUNDS — 53.6% | Shares | Value | ||||||

Consumer Discretionary Select Sector SPDR® Fund (The) | 1,017 | $ | 83,242 | |||||

Energy Select Sector SPDR® Fund (The) | 997 | 74,207 | ||||||

Financial Select Sector SPDR® Fund (The) | 6,720 | 151,267 | ||||||

Health Care Select Sector SPDR® Fund (The) | 1,121 | 77,069 | ||||||

Industrial Select Sector SPDR® Fund (The) | 2,615 | 163,202 | ||||||

Materials Select Sector SPDR® Fund (The) | 561 | 28,016 | ||||||

Technology Select Sector SPDR® Fund (The) | 3,622 | 172,045 | ||||||

Total Securities Sold Short — 53.6% (Proceeds $679,510) | $ | 749,048 | ||||||

See accompanying notes to financial statements. |

14

LYRICAL FUNDS | ||||||||

| Lyrical U.S. | Lyrical U.S. | ||||||

ASSETS | ||||||||

Investments in securities: | ||||||||

At acquisition cost | $ | 910,470,537 | $ | 1,499,113 | ||||

At value (Note 2) | $ | 1,061,068,856 | $ | 1,534,243 | ||||

Deposits with brokers for securities sold short (Note 2) | — | 608,993 | ||||||

Dividends receivable | 1,558,493 | 2,324 | ||||||

Receivable for capital shares sold | 1,523,601 | 150 | ||||||

Receivable from Adviser (Note 4) | — | 15,067 | ||||||

Other assets | 17,597 | 5,661 | ||||||

Total assets | 1,064,168,547 | 2,166,438 | ||||||

LIABILITIES | ||||||||

Distributions payable | 2,627,445 | 595 | ||||||

Securities sold short, at value (Note 2) (proceeds $— and $679,510 respectively) | — | 749,048 | ||||||

Payable for capital shares redeemed | 8,230,645 | 4,777 | ||||||

Payable to Adviser (Note 4) | 1,058,522 | — | ||||||

Payable to administrator (Note 4) | 82,340 | 8,510 | ||||||

Accrued brokerage expense on securities sold short (Note 2) | — | 165 | ||||||

Other accrued expenses | 53,330 | 6,870 | ||||||

Total liabilities | 12,052,282 | 769,965 | ||||||

NET ASSETS | $ | 1,052,116,265 | $ | 1,396,473 | ||||

NET ASSETS CONSIST OF: | ||||||||

Paid-in capital | $ | 900,500,395 | $ | 1,430,321 | ||||

Accumulated net investment income (loss) | 15,200,942 | (133 | ) | |||||

Accumulated net realized gains (losses) from security transactions | (14,183,391 | ) | 693 | |||||

Net unrealized appreciation (depreciation) on: | ||||||||

Investments | 150,598,319 | 35,130 | ||||||

Securities sold short | — | (69,538 | ) | |||||

NET ASSETS | $ | 1,052,116,265 | $ | 1,396,473 | ||||

NET ASSET VALUE PER SHARE: | ||||||||

INSTITUTIONAL CLASS | ||||||||

Net assets applicable to Institutional Class | $ | 993,903,564 | $ | 821,429 | ||||

Institutional Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 59,884,896 | 84,959 | ||||||

Net asset value, offering price and redemption price per share (Note 2) | $ | 16.60 | $ | 9.67 | ||||

INVESTOR CLASS | ||||||||

Net assets applicable to Investor Class | $ | 58,212,701 | $ | 575,044 | ||||

Investor Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 3,522,978 | 59,838 | ||||||

Net asset value, offering price and redemption price per share (Note 2) | $ | 16.52 | $ | 9.61 | ||||

See accompanying notes to financial statements. |

15

LYRICAL FUNDS | ||||||||

| Lyrical U.S. | Lyrical U.S. | ||||||

INVESTMENT INCOME | ||||||||

Dividend income | $ | 29,084,905 | $ | 39,068 | ||||

Foreign withholding taxes on dividends | (297,672 | ) | (355 | ) | ||||

Total investment income | 28,787,233 | 38,713 | ||||||

EXPENSES | ||||||||

Investment advisory fees (Note 4) | 11,976,891 | (a) | 20,928 | |||||

Administration fees (Note 4) | 665,436 | 28,000 | ||||||

Distribution fees - Investor Class (Note 4) | 189,100 | 1,465 | ||||||

Fund accounting fees (Note 4) | 109,053 | 34,385 | ||||||

Transfer agent fees (Note 4) | 87,623 | 24,000 | ||||||

Compliance fees (Note 4) | 97,931 | 12,000 | ||||||

Custody and bank service fees | 92,402 | 6,552 | ||||||

Registration and filing fees | 85,848 | 10,086 | ||||||

Professional fees | 40,146 | 34,968 | ||||||

Postage and supplies | 38,132 | 3,230 | ||||||

Networking fees | 14,605 | 14,605 | ||||||

Trustees' fees and expenses (Note 4) | 10,165 | 10,165 | ||||||

Dividend expense on securities sold short (Note 2) | — | 14,191 | ||||||

Printing of shareholder reports | 10,813 | 3,220 | ||||||

Insurance expense | 2,546 | 2,546 | ||||||

Prime brokerage expense on securities sold short (Note 2) | — | 4,515 | ||||||

Other expenses | 33,582 | 5,611 | ||||||

Total expenses | 13,454,273 | 230,467 | ||||||

Fee reductions and expense reimbursements by Adviser (Note 4) | — | (186,666 | ) | |||||

Net expenses | 13,454,273 | 43,801 | ||||||

NET INVESTMENT INCOME (LOSS) | 15,332,960 | (5,088 | ) | |||||

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND SECURITIES SOLD SHORT | ||||||||

Net realized gains (losses) from: | ||||||||

Investments | 4,951,586 | 41,829 | ||||||

Securities sold short | — | (1,927 | ) | |||||

Net change in unrealized appreciation (depreciation) on: | ||||||||

Investments | 135,673,446 | 95,448 | ||||||

Securities sold short | — | (54,825 | ) | |||||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS AND SECURITIES SOLD SHORT | 140,625,032 | 80,525 | ||||||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 155,957,992 | $ | 75,437 | ||||

(a) | Includes $22,152 of prior years’ investment advisory fee reductions and expense reimbursements recouped by the Adviser (Note 4). |

See accompanying notes to financial statements. |

16

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

| Year | Year | ||||||

FROM OPERATIONS | ||||||||

Net investment income | $ | 15,332,960 | $ | 1,440,862 | ||||

Net realized gains from security transactions | 4,951,586 | 12,579,532 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 135,673,446 | (31,320,202 | ) | |||||

Net increase (decrease) in net assets resulting from operations | 155,957,992 | (17,299,808 | ) | |||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

From net investment income, Institutional Class | (1,403,762 | ) | (168,471 | ) | ||||

From net investment income, Investor Class | (6,340 | ) | — | |||||

From net realized gains, Institutional Class | (29,274,092 | ) | (11,690,275 | ) | ||||

From net realized gains, Investor Class | (2,366,361 | ) | (193,318 | ) | ||||

Decrease in net assets from distributions to shareholders | (33,050,555 | ) | (12,052,064 | ) | ||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | 653,121,923 | 339,352,309 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 24,129,237 | 9,377,973 | ||||||

Payments for shares redeemed | (395,236,728 | ) | (282,422,299 | ) | ||||

Net increase in Institutional Class net assets from capital share transactions | 282,014,432 | 66,307,983 | ||||||

Investor Class | ||||||||

Proceeds from shares sold | 59,719,286 | 118,329,002 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 2,323,727 | 181,114 | ||||||

Payments for shares redeemed | (66,805,457 | ) | (59,563,305 | ) | ||||

Net increase (decrease) in Investor Class net assets from capital share transactions | (4,762,444 | ) | 58,946,811 | |||||

TOTAL INCREASE IN NET ASSETS | 400,159,425 | 95,902,922 | ||||||

NET ASSETS | ||||||||

Beginning of year | 651,956,840 | 556,053,918 | ||||||

End of year | $ | 1,052,116,265 | $ | 651,956,840 | ||||

UNDISTRIBUTED NET INVESTMENT INCOME | $ | 15,200,942 | $ | 1,278,084 | ||||

See accompanying notes to financial statements. |

17

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

| Year | Year | ||||||

CAPITAL SHARE ACTIVITY | ||||||||

Institutional Class | ||||||||

Shares sold | 47,161,187 | 21,132,995 | ||||||

Shares issued in reinvestment of distributions to shareholders | 1,509,246 | 592,967 | ||||||

Shares redeemed | (26,574,555 | ) | (17,510,391 | ) | ||||

Net increase in shares outstanding | 22,095,878 | 4,215,571 | ||||||

Shares outstanding at beginning of year | 37,789,018 | 33,573,447 | ||||||

Shares outstanding at end of year | 59,884,896 | 37,789,018 | ||||||

Investor Class | ||||||||

Shares sold | 3,943,726 | 7,202,116 | ||||||

Shares issued in reinvestment of distributions to shareholders | 147,285 | 11,470 | ||||||

Shares redeemed | (4,510,214 | ) | (3,826,599 | ) | ||||

Net increase (decrease) in shares outstanding | (419,203 | ) | 3,386,987 | |||||

Shares outstanding at beginning of year | 3,942,181 | 555,194 | ||||||

Shares outstanding at end of year | 3,522,978 | 3,942,181 | ||||||

See accompanying notes to financial statements. |

18

LYRICAL U.S. HEDGED VALUE FUND | ||||||||

| Year | Year | ||||||

FROM OPERATIONS | ||||||||

Net investment loss | $ | (5,088 | ) | $ | (22,709 | ) | ||

Net realized gains (losses) from: | ||||||||

Investments | 41,829 | 21,575 | ||||||

Securities sold short | (1,927 | ) | (3,393 | ) | ||||

Net change in unrealized appreciation (depreciation) on: | ||||||||

Investments | 95,448 | (60,317 | ) | |||||

Securities sold short | (54,825 | ) | 2,207 | |||||

Net increase (decrease) in net assets resulting from operations | 75,437 | (62,637 | ) | |||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

From net realized gains, Institutional Class | (27,448 | ) | (54 | ) | ||||

From net realized gains, Investor Class | (20,037 | ) | (57 | ) | ||||

Decrease in net assets from distributions to shareholders | (47,485 | ) | (111 | ) | ||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | — | 220,000 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 26,757 | 54 | ||||||

Net increase in Institutional Class net assets from capital share transactions | 26,757 | 220,054 | ||||||

Investor Class | ||||||||

Proceeds from shares sold | 13,373 | 126,747 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 19,764 | 54 | ||||||

Payments for shares redeemed | (86,803 | ) | (94,359 | ) | ||||

Net increase (decrease) in Investor Class net assets from capital share transactions | (53,666 | ) | 32,442 | |||||

TOTAL INCREASE IN NET ASSETS | 1,043 | 189,748 | ||||||

NET ASSETS | ||||||||

Beginning of year | 1,395,430 | 1,205,682 | ||||||

End of year | $ | 1,396,473 | $ | 1,395,430 | ||||

ACCUMULATED NET INVESTMENT LOSS | $ | (133 | ) | $ | — | |||

See accompanying notes to financial statements. |

19

LYRICAL U.S. HEDGED VALUE FUND | ||||||||

| Year | Year | ||||||

CAPITAL SHARE ACTIVITY | ||||||||

Institutional Class | ||||||||

Shares sold | — | 21,883 | ||||||

Shares issued in reinvestment of distributions to shareholders | 2,782 | 6 | ||||||

Net increase in shares outstanding | 2,782 | 21,889 | ||||||

Shares outstanding at beginning of year | 82,177 | 60,288 | ||||||

Shares outstanding at end of year | 84,959 | 82,177 | ||||||

Investor Class | ||||||||

Shares sold | 1,471 | 12,770 | ||||||

Shares issued in reinvestment of distributions to shareholders | 2,067 | 6 | ||||||

Shares redeemed | (9,416 | ) | (9,763 | ) | ||||

Net increase (decrease) in shares outstanding | (5,878 | ) | 3,013 | |||||

Shares outstanding at beginning of year | 65,716 | 62,703 | ||||||

Shares outstanding at end of year | 59,838 | 65,716 | ||||||

See accompanying notes to financial statements. |

20

LYRICAL U.S. VALUE EQUITY FUND | ||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Period: | ||||||||||||||||

| Year 2016 | Year 2015 | Year 2014 | Period | ||||||||||||

Net asset value at beginning of period | $ | 15.63 | $ | 16.29 | $ | 13.78 | $ | 10.00 | ||||||||

Income (loss) from investment operations: | ||||||||||||||||

Net investment income (loss) | 0.24 | 0.04 | (0.00 | )(b) | 0.00 | (b) | ||||||||||

Net realized and unrealized gains (losses) on investments | 1.40 | (0.35 | ) | 2.66 | 3.78 | |||||||||||

Total from investment operations | 1.64 | (0.31 | ) | 2.66 | 3.78 | |||||||||||

Less distributions: | ||||||||||||||||

Dividends from net investment income | (0.04 | ) | (0.00 | )(b) | (0.00 | )(b) | — | |||||||||

Distributions from net realized gains | (0.63 | ) | (0.35 | ) | (0.15 | ) | — | |||||||||

Total distributions | (0.67 | ) | (0.35 | ) | (0.15 | ) | — | |||||||||

Net asset value at end of period | $ | 16.60 | $ | 15.63 | $ | 16.29 | $ | 13.78 | ||||||||

Total return (c) | 10.73 | % | (1.91 | %) | 19.41 | % | 37.80 | %(d) | ||||||||

Net assets at end of period (000's) | $ | 993,904 | $ | 590,582 | $ | 547,021 | $ | 97,948 | ||||||||

Ratios/supplementary data: | ||||||||||||||||

Ratio of total expenses to average net assets | 1.38 | % | 1.42 | % | 1.45 | % | 1.93 | %(e) | ||||||||

Ratio of net expenses to average net assets | 1.38 | % | 1.42 | % | 1.44 | %(f) | 1.45 | %(e)(f) | ||||||||

Ratio of net investment income (loss) to average net assets | 1.62 | % | 0.24 | % | (0.00 | %)(g)(f) | 0.01 | %(e)(f) | ||||||||

Portfolio turnover rate | 36 | % | 21 | % | 20 | % | 26 | %(d) | ||||||||

(a) | Represents the period from the commencement of operations (February 4, 2013) through November 30, 2013. |

(b) | Amount rounds to less than $0.01 per share. |

(c) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses for the periods ended November 30, 2014 and 2013 (Note 4). |

(d) | Not annualized. |

(e) | Annualized. |

(f) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

(g) | Amount rounds to less than 0.01%. |

See accompanying notes to financial statements. |

21

LYRICAL U.S. VALUE EQUITY FUND | ||||||||||||

Per Share Data for a Share Outstanding Throughout Each Period: | ||||||||||||

| Year 2016 | Year | Period | |||||||||

Net asset value at beginning of period | $ | 15.57 | $ | 16.27 | $ | 14.68 | ||||||

Income (loss) from investment operations: | ||||||||||||

Net investment income (loss) | 0.30 | 0.01 | (0.01 | ) | ||||||||

Net realized and unrealized gains (losses) on investments | 1.28 | (0.36 | ) | 1.60 | ||||||||

Total from investment operations | 1.58 | (0.35 | ) | 1.59 | ||||||||

Less distributions: | ||||||||||||

Distributions from net investment income | (0.00 | )(b) | — | — | ||||||||

Distributions from net realized gains | (0.63 | ) | (0.35 | ) | — | |||||||

Total distributions | (0.63 | ) | (0.35 | ) | — | |||||||

Net asset value at end of period | $ | 16.52 | $ | 15.57 | $ | 16.27 | ||||||

Total return (c) | 10.36 | % | (2.19 | %) | 10.83 | %(d) | ||||||

Net assets at end of period (000's) | $ | 58,213 | $ | 61,375 | $ | 9,033 | ||||||

Ratios/supplementary data: | ||||||||||||

Ratio of total expenses to average net assets | 1.70 | % | 1.72 | % | 2.39 | %(e) | ||||||

Ratio of net expenses to average net assets | 1.70 | % | 1.70 | %(f) | 1.70 | %(e)(f) | ||||||

Ratio of net investment income (loss) to average net assets | 1.39 | % | 0.03 | %(f) | (0.18 | %)(e)(f) | ||||||

Portfolio turnover rate | 36 | % | 21 | % | 20 | %(d)(g) | ||||||

(a) | Represents the period from the commencement of operations (February 24, 2014) through November 30, 2014. |

(b) | Amount rounds to less than $0.01 per share. |

(c) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses for the periods ended November 30, 2014 and 2013 (Note 4). |

(d) | Not annualized. |

(e) | Annualized. |

(f) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

(g) | Represents the year ended November 30, 2014. |

See accompanying notes to financial statements. |

22

LYRICAL U.S. HEDGED VALUE FUND | ||||||||||||

Per Share Data for a Share Outstanding Throughout Each Period: | ||||||||||||

| Year 2016 | Year | Period | |||||||||

Net asset value at beginning of period | $ | 9.45 | $ | 9.81 | $ | 10.00 | ||||||

Income (loss) from investment operations: | ||||||||||||

Net investment loss | (0.02 | ) | (0.13 | ) | (0.04 | ) | ||||||

Net realized and unrealized gains (losses) on investments and securities sold short | 0.57 | (0.23 | ) | (0.15 | ) | |||||||

Total from investment operations | 0.55 | (0.36 | ) | (0.19 | ) | |||||||

Less distributions: | ||||||||||||

Distributions from net realized gains | (0.33 | ) | (0.00 | )(b) | — | |||||||

Net asset value at end of period | $ | 9.67 | $ | 9.45 | $ | 9.81 | ||||||

Total return (c) | 5.88 | % | (3.66 | %) | (1.90% | )(d) | ||||||

Net assets at end of period (000's) | $ | 821 | $ | 777 | $ | 591 | ||||||

Ratios/supplementary data: | ||||||||||||

Ratio of total expenses to average net assets | 16.71 | % | 14.76 | % | 16.57 | %(e) | ||||||

Ratio of net expenses to average net assets (f) | 3.14 | % | 3.16 | % | 2.59 | %(e) | ||||||

Ratio of net expenses to average net assets excluding dividend expense (f) | 2.08 | % | 2.27 | % | 1.99 | %(e) | ||||||

Ratio of net expenses to average net assets excluding dividend expense and prime brokerage expense on securities sold short (f) | 1.75 | % | 1.75 | % | 1.75 | %(e) | ||||||

Ratio of net investment loss to average net assets (f) | (0.26 | %) | (1.49 | %) | (1.15 | %)(e) | ||||||

Portfolio turnover rate | 17 | % | 7 | % | 9 | %(d) | ||||||

(a) | Represents the period from the commencement of operations (July 14, 2014) through November 30, 2014. |

(b) | Amount rounds to less than $0.01 per share. |

(c) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and reimbursed expenses (Note 4). |

(d) | Not annualized. |

(e) | Annualized. |

(f) | Ratio was determined after advisory fee reductions and expense reimbursements (Note 4). |

See accompanying notes to financial statements. |

23

LYRICAL U.S. HEDGED VALUE FUND | ||||||||||||

Per Share Data for a Share Outstanding Throughout Each Period: | ||||||||||||

| Year 2016 | Year | Period | |||||||||

Net asset value at beginning of period | $ | 9.42 | $ | 9.80 | $ | 10.00 | ||||||

Income (loss) from investment operations: | ||||||||||||

Net investment loss | (0.06 | ) | (0.18 | ) | (0.05 | ) | ||||||

Net realized and unrealized gains (losses) on investments and securities sold short | 0.58 | (0.20 | ) | (0.15 | ) | |||||||

Total from investment operations | 0.52 | (0.38 | ) | (0.20 | ) | |||||||

Less distributions: | ||||||||||||

Distributions from net realized gains | (0.33 | ) | (0.00 | )(b) | — | |||||||

Net asset value at end of period | $ | 9.61 | $ | 9.42 | $ | 9.80 | ||||||

Total return (c) | 5.58 | % | (3.87 | %) | (2.00% | )(d) | ||||||

Net assets at end of period (000's) | $ | 575 | $ | 619 | $ | 614 | ||||||

Ratios/supplementary data: | ||||||||||||

Ratio of total expenses to average net assets | 17.54 | % | 15.49 | % | 16.95 | %(e) | ||||||

Ratio of net expenses to average net assets (f) | 3.39 | % | 3.41 | % | 2.84 | %(e) | ||||||

Ratio of net expenses to average net assets excluding dividend expense (f) | 2.34 | % | 2.52 | % | 2.24 | %(e) | ||||||

Ratio of net expenses to average net assets excluding dividend expense and prime brokerage expense on securities sold short (f) | 2.00 | % | 2.00 | % | 2.00 | %(e) | ||||||

Ratio of net investment loss to average net assets (f) | (0.53 | %) | (1.78 | %) | (1.38 | %)(e) | ||||||

Portfolio turnover rate | 17 | % | 7 | % | 9 | %(d) | ||||||

(a) | Represents the period from the commencement of operations (July 14, 2014) through November 30, 2014. |

(b) | Amount rounds to less than $0.01 per share. |

(c) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and reimbursed expenses (Note 4). |

(d) | Not annualized. |

(e) | Annualized. |

(f) | Ratio was determined after advisory fee reductions and expense reimbursements (Note 4). |

See accompanying notes to financial statements. |

24

LYRICAL FUNDS

NOTES TO FINANCIAL STATEMENTS

November 30, 2016

1. Organization

Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund (individually, a “Fund” and collectively, the “Funds”) are each a diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report. Lyrical U.S. Value Equity Fund commenced operations on February 4, 2013. Lyrical U.S. Hedged Value Fund commenced operations on July 14, 2014.

The investment objective of each Fund is to seek to achieve long-term capital growth.

Each Fund offers two classes of shares: Institutional Class shares (sold without any sales loads and distribution and/or shareholder service fees and requiring a $100,000 initial investment) and Investor Class shares (sold without any sales loads, but subject to a distribution and/or shareholder service fee of up to 0.25% of the average daily net assets attributable to Investor Class shares, and requiring a $2,500 initial investment). Each share class represents an ownership interest in the same investment portfolio.

2. Significant Accounting Policies

The following is a summary of the Funds’ significant accounting policies. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Funds follow accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

In October 2016, the Securities and Exchange Commission (the “SEC”) released its final rule on Investment Company Reporting Modernization (the “Rule”). The Rule, which introduces two new regulatory reporting forms for investment companies – Form N-PORT and Form N-CEN, also contains amendments to Regulation S-X which impact financial statement presentation, particularly the presentation of derivative investments. Although still evaluating the impact of the Rule, management believes that many of the Regulation S-X amendments are consistent with the Funds’ current financial statement presentation and expects that the Funds will be able to comply with the Rule’s Regulation S-X amendments by the August 1, 2017 compliance date.

Securities valuation – Each Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. The Funds value their listed securities on the basis of the security’s last sale price on the security’s primary exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. In the event that market quotations are not readily available or are considered unreliable due

25

LYRICAL FUNDS |

to market or other events, the Funds value their securities and other assets at fair value in accordance with procedures established by and under the general supervision of the Board of Trustees (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate each Fund’s net asset value (“NAV”) may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of each Fund’s investments. These inputs are summarized in the three broad levels listed below:

● | Level 1 – quoted prices in active markets for identical securities |

● | Level 2 – other significant observable inputs |

● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Funds’ investments and other financial instruments as of November 30, 2016:

Lyrical U.S. Value Equity Fund | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Investments in Securities | ||||||||||||||||

Common Stocks | $ | 1,050,448,236 | $ | — | $ | — | $ | 1,050,448,236 | ||||||||

Money Market Funds | 10,620,620 | — | — | 10,620,620 | ||||||||||||

Total | $ | 1,061,068,856 | $ | — | $ | — | $ | 1,061,068,856 | ||||||||

26

LYRICAL FUNDS |

Lyrical U.S. Hedged Value Fund | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Investments in Securities | ||||||||||||||||

Common Stocks | $ | 1,517,807 | $ | — | $ | — | $ | 1,517,807 | ||||||||

Money Market Funds | 16,436 | — | — | 16,436 | ||||||||||||

Total | $ | 1,534,243 | $ | — | $ | — | $ | 1,534,243 | ||||||||

Other Financial Instruments | ||||||||||||||||

Exchange-Traded Funds - Sold Short | $ | (749,048 | ) | $ | — | $ | — | $ | (749,048 | ) | ||||||

Refer to the Funds’ Schedules of Investments and Schedule of Securities Sold Short, as applicable, for a listing of securities by industry or sector type. As of November 30, 2016, the Funds did not have any transfers between Levels. In addition, the Funds did not hold any derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of November 30, 2016. It is the Funds’ policy to recognize transfers between Levels at the end of the reporting period.

Share valuation – The NAV per share of each class of each Fund is calculated daily by dividing the total value of the assets attributable to that class, less liabilities attributable to that class, by the number of shares outstanding of that class. The offering price and redemption price per share of each class of each Fund is equal to the NAV per share of such class.

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned. Withholding taxes on foreign dividends have been recorded in accordance with the Funds’ understanding of the appropriate country’s rules and tax rates.

Security transactions – Security transactions are accounted for on the trade date. Realized gains and losses on securities sold are determined on a specific identification basis.

Common expenses – Common expenses of the Trust are allocated among the Funds and the other series of the Trust based on the relative net assets of each series or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders – Each Fund distributes to shareholders any net investment income dividends and net realized capital gains distributions at least once each year. The amount of such dividends and distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to

27

LYRICAL FUNDS |

shareholders are recorded on the ex-dividend date. The tax character of distributions paid to shareholders by the Funds during the years ended November 30, 2016 and 2015 was as follows:

Year | Ordinary | Long-Term Capital Gains | Total | |

Lyrical U.S. Value Equity Fund - | 11/30/2016 | $ 3,276,517 | $ 27,401,337 | $ 30,677,854 |

Institutional Class | 11/30/2015 | $ 7,662,064 | $ 4,196,682 | $ 11,858,746 |

Lyrical U.S. Value Equity Fund - | 11/30/2016 | $ 116,943 | $ 2,255,758 | $ 2,372,701 |

Investor Class | 11/30/2015 | $ 123,919 | $ 69,399 | $ 193,318 |

Lyrical U.S. Hedged Value Fund - | 11/30/2016 | $ — | $ 27,448 | $ 27,448 |

Institutional Class | 11/30/2015 | $ 34 | $ 20 | $ 54 |

Lyrical U.S. Hedged Value Fund - | 11/30/2016 | $ — | $ 20,037 | $ 20,037 |

Investor Class | 11/30/2015 | $ 36 | $ 21 | $ 57 |

Lyrical U.S. Value Equity Fund made the following distributions subsequent to November 30, 2016 to shareholders of record on December 29, 2016:

Per Share | |||

Record | Ex-Date | Ordinary | |

Lyrical U.S. Value Equity Fund - Institutional Class | 12/29/2016 | 12/30/2016 | $ 0.2375 |

Lyrical U.S. Value Equity Fund - Investor Class | 12/29/2016 | 12/30/2016 | 0.1719 |

Short Positions – Lyrical U.S. Hedged Value Fund may sell securities short. For financial statement purposes, an amount equal to the settlement amount is included in the Statements of Assets and Liabilities as an asset and an equivalent liability is then subsequently marked-to-market daily to reflect the current value of the short position. Subsequent fluctuations in the market prices of securities sold, but not yet purchased, may require purchasing the securities at prices which may differ from the market value reflected on the Statements of Assets and Liabilities. The Fund is liable for any dividends payable on securities while those securities are in a short position and will also bear other costs, such as charges for the prime brokerage accounts, in connection with the short positions. These costs are reported as dividend expense and prime brokerage expense on securities sold short, respectively, in the Statements of Operations. As collateral for its short positions, the Fund is required under the Investment Company Act of 1940 (“1940 Act”) to maintain assets consisting of cash, cash equivalents or other liquid securities equal to the market value of the securities sold short. The deposits with brokers for securities sold short are reported on the Statements of Assets and Liabilities. The amount of collateral is required to be adjusted daily to reflect changes in the value of the securities

28

LYRICAL FUNDS |

sold short. To the extent Lyrical U.S. Hedged Value Fund invests the proceeds received from selling securities short, the Fund is engaging in a form of leverage. The use of leverage by the Fund may make any change in the Fund’s NAV greater than it would be without the use of leverage. Short sales are speculative transactions and involve special risks, including greater reliance on the ability of Lyrical Asset Management LP (the “Adviser”) to accurately anticipate the future value of a security.

The Fund typically takes short positions in shares of exchange-traded funds (“ETFs”), which are subject to additional risks including premium or discount risk (when the market value of an ETF’s shares trade at a premium or discount to the ETF’s NAV) and index-tracking risk.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – Each Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986 (the “Code”). Qualification generally will relieve each Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also each Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of November 30, 2016:

| Lyrical U.S. Value Equity Fund | Lyrical U.S. Hedged Value Fund | ||||||

Tax cost of portfolio investments | $ | 925,242,428 | $ | 1,499,113 | ||||

Gross unrealized appreciation | $ | 181,248,360 | $ | 188,052 | ||||

Gross unrealized depreciation | (45,421,932 | ) | (152,922 | ) | ||||

Net unrealized appreciation | 135,826,428 | 35,130 | ||||||

Net unrealized depreciation on securities sold short | — | (72,400 | ) | |||||

Undistributed ordinary income | 15,416,437 | — | ||||||

Undistributed long-term gains | 373,005 | 3,555 | ||||||

Accumulated capital and other losses | — | (133 | ) | |||||

Distributable earnings | $ | 151,615,870 | $ | (33,848 | ) | |||

29

LYRICAL FUNDS |

As of November 30, 2016, the proceeds of securities sold short on a tax basis is $676,648 for Lyrical U.S. Hedged Value Fund.

The difference between the federal income tax cost of portfolio investments and securities sold short and the financial statement cost of portfolio investments and securities sold short is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to the tax deferral of losses on wash sales.

Net qualified late year losses represent ordinary losses incurred after December 31, 2015 and specified capital losses incurred after October 31, 2016. These losses are deemed to arise on the first day of the Fund’s next taxable year. For the year ended November 30, 2016, Lyrical U.S. Hedged Value Fund intends to defer $133 of late year ordinary losses to December 1, 2016 for federal income tax purposes.

For the year ended November 30, 2016, the following reclassifications were made as a result of permanent differences between financial statement and income tax reporting requirements:

| Lyrical U.S. Value Equity Fund | Lyrical U.S. Hedged Value Fund | ||||||

Paid-in capital | $ | — | $ | (4,955 | ) | |||

Accumulated net investment income (loss) | — | 4,955 | ||||||

Accumulated net realized gains (losses) from security transactions | — | — | ||||||

The Funds recognize the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” of being sustained assuming examination by tax authorities. Management has reviewed the Funds’ tax positions for all open tax periods (periods ended November 30, 2013 through November 30, 2016 for Lyrical U.S. Value Equity Fund and November 30, 2014 through November 30, 2016 for Lyrical U.S. Hedged Value Fund) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Funds identify their major tax jurisdiction as U.S. Federal.

3. Investment Transactions

During the year ended November 30, 2016, cost of purchases and proceeds from sales of investment securities, other than short-term investments and short positions, amounted to $606,334,158 and $339,641,057, respectively, for Lyrical U.S. Value Equity Fund and $232,460 and $237,112, respectively, for Lyrical U.S. Hedged Value Fund.

30

LYRICAL FUNDS |

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

Each Fund’s investments are managed by the Adviser pursuant to the terms of an Investment Advisory Agreement. Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund pay the Adviser an investment advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.25% and 1.55%, respectively, of average daily net assets.

Pursuant to an Expense Limitation Agreement (“ELA”) between each Fund and the Adviser, the Adviser has contractually agreed, until March 31, 2018, to reduce investment advisory fees and reimburse other operating expenses to limit total annual operating expenses of the Funds (exclusive of brokerage costs, taxes, borrowing costs such as interest and dividend expenses on securities sold short, interest, acquired fund fees and expenses, extraordinary expenses such as litigation and merger or reorganization costs, and other expenses not incurred in the ordinary course of each Fund’s business) to an amount not exceeding the following percentages of average daily net assets attributable to each respective class:

| Institutional Class | Investor Class |

Lyrical U.S. Value Equity Fund | 1.45% | 1.70% |

Lyrical U.S. Hedged Value Fund | 1.75% | 2.00% |

Accordingly, during the year ended November 30, 2016, the Adviser did not collect any of its investment advisory fees from Lyrical U.S. Hedged Value Fund and, in addition, reimbursed other operating expenses of $165,738.

Under the terms of the ELA, investment advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause total annual fund operating expenses of the Funds to exceed the foregoing expense limitations. During the year ended November 30, 2016, the Adviser recouped from Lyrical U.S. Value Equity Fund $22,152 of prior years’ investment advisory fee reductions and expense reimbursements. As of November 30, 2016, the Adviser may seek recoupment of investment advisory fee reductions and expense reimbursements no later than the dates as stated below:

| November 30, 2017 | November 30, 2018 | November 30, 2019 | Total |

Lyrical U.S. Value Equity Fund | $ — | $ 2,918 | $ — | $ 2,918 |

Lyrical U.S. Hedged Value Fund | $ 59,418 | $ 164,816 | $ 186,666 | $ 410,900 |

The Principal Executive Officer of the Funds is also an officer of the Adviser.

31

LYRICAL FUNDS |

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance and transfer agency services to the Funds. Each Fund pays Ultimus fees in accordance with the agreements for such services. In addition, each Fund pays out-of-pocket expenses including but not limited to postage, supplies and costs of pricing its portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as the principal underwriter to each Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Funds).

A Trustee and certain officers of the Trust are also officers of Ultimus and/or the Distributor.

DISTRIBUTION PLAN

The Funds have adopted a plan of distribution (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act, which permits Investor Class shares of each Fund to directly incur or reimburse the Funds’ principal underwriter for certain expenses related to the distribution of its shares. The annual limitation for payment of expenses pursuant to the Plan is 0.25% of each Fund’s average daily net assets allocable to Investor Class shares. The Funds have not adopted a plan of distribution with respect to the Institutional Class shares. During the year ended November 30, 2016, the Investor Class shares of Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund incurred $189,100 and $1,465, respectively, of distribution fees under the Plan.

TRUSTEE COMPENSATION

Effective October 1, 2016, each Trustee who is not an “interested person” of the Trust (“Independent Trustee”) receives a $1,000 annual retainer from each Fund, paid quarterly, except for the Board Chair who receives a $1,200 annual retainer from each Fund, paid quarterly. Each Independent Trustee also receives from each Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to October 1, 2016, each Fund paid each Independent Trustee a fee of $500 for each Board meeting attended plus a $500 annual retainer.

32

LYRICAL FUNDS |

PRINCIPAL HOLDERS OF FUND SHARES

As of November 30, 2016, the following shareholders owned of record 5% or more of the outstanding shares of each class of each Fund:

NAME OF RECORD OWNER | % Ownership |

Lyrical U.S. Value Equity Fund - Institutional Class | |

Morgan Stanley Smith Barney LLC (for the benefit of its customers) | 37% |

Charles Schwab & Company, Inc. (for the benefit of its customers) | 17% |

Merrill Lynch, Pierce, Fenner & Smith (for the benefit of its customers) | 7% |

Lyrical U.S. Value Equity Fund - Investor Class | |

Charles Schwab & Company, Inc. (for the benefit of its customers) | 86% |

Lyrical U.S. Hedged Value Fund - Institutional Class | |

Lyrical Asset Management LP | 61% |

Ann S. Riesenberg | 24% |

George Wellington | 13% |

Lyrical U.S. Hedged Value Fund - Investor Class | |

Lyrical Asset Management LP | 86% |

A beneficial owner of 25% or more of a Fund’s outstanding shares may be considered a controlling person of that Fund. That shareholder’s vote could have a more significant effect on matters presented at a shareholder’s meeting.

5. Sector Risk

If a Fund has significant investments in the securities of issuers within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have significant investments in that sector. In addition, this may increase the risk of loss in the Fund and increase the volatility of the Fund’s NAV per share. Occasionally, market conditions, regulatory changes or other developments may negatively impact a particular sector. As of November 30, 2016, Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund had 31.3% and 33.3%, respectively, of the value of their net assets invested in stocks within the Information Technology sector.

6. Contingencies and Commitments

The Funds indemnify the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Funds. Additionally, in the normal course of business the Funds enter into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Funds’ maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Funds that have not yet occurred. However, based on experience, the Funds expect the risk of loss to be remote.

33

LYRICAL FUNDS |

7. Subsequent Events

The Funds are required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statements of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Funds are required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events except for the payment of ordinary income dividends subsequent to the end of the reporting period, as disclosed in Note 2.

34

LYRICAL FUNDS |

To the Board of Trustees of Ultimus Managers Trust

and the Shareholders of Lyrical U.S. Value Equity Fund

and Lyrical U.S. Hedged Value Fund

We have audited the accompanying statements of assets and liabilities of Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund, each a series of shares of beneficial interest in Ultimus Managers Trust (the “Funds”), including the schedules of investments, as of November 30, 2016, and the related statements of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years or periods presented. These financial statements and financial highlights are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of November 30, 2016 by correspondence with the custodian and brokers. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund as of November 30, 2016, and the results of their operations for the year then ended, the changes in their net assets for each of the years in the two-year period then ended and their financial highlights for each of the years or periods presented, in conformity with accounting principles generally accepted in the United States of America.

| |

BBD, LLP |

Philadelphia, Pennsylvania

January 26, 2017

35

LYRICAL FUNDS |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Funds, you incur ongoing costs, including management fees, class-specific expenses (such as distribution fees) and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (June 1, 2016) and held until the end of the period (November 30, 2016).

The table below illustrates each Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from each Fund’s actual return, and the fourth column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Funds. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare each Fund’s ongoing costs with those of other mutual funds. It assumes that each Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Funds’ actual return, the results do not apply to your investment. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (“SEC”) requires all mutual funds to calculate expenses based on a 5% return. You can assess each Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Funds do not charge transaction fees, such as purchase or redemption fees, nor do they carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

36

LYRICAL FUNDS

ABOUT YOUR FUNDS’ EXPENSES (Unaudited) (Continued)

More information about the Funds’ expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Funds’ prospectus.

| Beginning | Ending | Net Ratio(a) | Expenses Paid During Period(b) |

Lyrical U.S. Value Equity Fund | ||||

Institutional Class | ||||

Based on Actual Fund Returns | $ 1,000.00 | $ 1,114.00 | 1.38% | $ 7.29 |

Based on Hypothetical 5% Return (before expenses) | $ 1,000.00 | $ 1,018.10 | 1.38% | $ 6.96 |

Investor Class | ||||

Based on Actual Fund Returns | $ 1,000.00 | $ 1,111.70 | 1.70% | $ 8.97 |

Based on Hypothetical 5% Return (before expenses) | $ 1,000.00 | $ 1,016.50 | 1.70% | $ 8.57 |

Lyrical U.S. Hedged Value Fund | ||||

Institutional Class | ||||

Based on Actual Fund Returns | $ 1,000.00 | $ 1,066.20 | 3.00% | $ 15.50 |

Based on Hypothetical 5% Return (before expenses) | $ 1,000.00 | $ 1,010.00 | 3.00% | $ 15.08 |

Investor Class | ||||

Based on Actual Fund Returns | $ 1,000.00 | $ 1,065.40 | 3.25% | $ 16.78 |

Based on Hypothetical 5% Return (before expenses) | $ 1,000.00 | $ 1,008.75 | 3.25% | $ 16.32 |

(a) | Annualized, based on the Fund's most recent one-half year expenses. |

(b) | Expenses are equal to each Fund’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 183/366 (to reflect the one-half year period). |

37

LYRICAL FUNDS

OTHER INFORMATION (Unaudited)

A description of the policies and procedures that the Funds use to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-888-884-8099, or on the SEC’s website at http://www.sec.gov. Information regarding how the Funds voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-888-884-8099, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Funds with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-888-884-8099. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

FEDERAL TAX INFORMATION (Unaudited)

In accordance with federal tax requirements, the following provides shareholders with information concerning distributions from ordinary income and net realized gains made by each Fund during the fiscal year ended November 30, 2016. Certain dividends paid by the Funds may be subject to a maximum tax rate of 23.8%, as provided by the Jobs and Growth Tax Relief Reconciliation Act of 2003. Lyrical U.S. Value Equity Fund intends to designate up to a maximum amount of $3,393,460 as taxed at a maximum rate of 23.8%. Additionally, Lyrical U.S. Value Equity Fund and Lyrical U.S. Hedged Value Fund intend to designate up to a maximum amount of $29,657,095 and $47,485, respectively, as a long-term capital gain distribution. As required by federal regulations, complete information was computed and reported in conjunction with your 2016 Form 1099-DIV.

38

LYRICAL FUNDS

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

Overall responsibility for management of the Funds rests with the Board of Trustees. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement or removal. The Trustees, in turn, elect the officers of the Funds to actively supervise its day-to-day operations. The officers have been elected for an annual term. Unless otherwise noted, each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246.

Name and | Length of Time Served | Position Held | Principal Occupation(s) | Number of Funds in Trust Overseen by Trustee | Directorships of Public Companies Held by Trustee During Past 5 Years |

Interested Trustees: |

|

|

|

|

|