| OMB APPROVAL | |

OMB Number: 3235-0570

Expires: August 31, 2020

Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Matthew J. Beck

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246 | |

| (Name and address of agent for service) | |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | November 30 | |

| Date of reporting period: | November 30, 2018 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

LYRICAL U.S. VALUE EQUITY FUND

Institutional Class (LYRIX)

Investor Class (LYRBX)

Annual Report

November 30, 2018

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of the Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by contacting the Fund at 1-888-884-8099 or, if you own these shares through a financial intermediary, by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting the Fund at 1-888-884-8099. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all funds held with the fund complex or at your financial intermediary.

LYRICAL U.S. VALUE EQUITY FUND | November 30, 2018 |

Dear Fellow Shareholders,

Enclosed is the Annual Report to shareholders of the Lyrical U.S. Value Equity Fund (the “Fund”). On behalf of the Fund and its investment adviser, Lyrical Asset Management LP, I would like to thank you for your investment.

The Fund’s differentiated value investing approach ran into some stiff cross-currents this past fiscal year. Intermittent market environments in which value investing falls out of favor are not unusual even as this period marked the first significant such stretch since we launched the Fund. We are excited for the prospects of the Fund going forward.

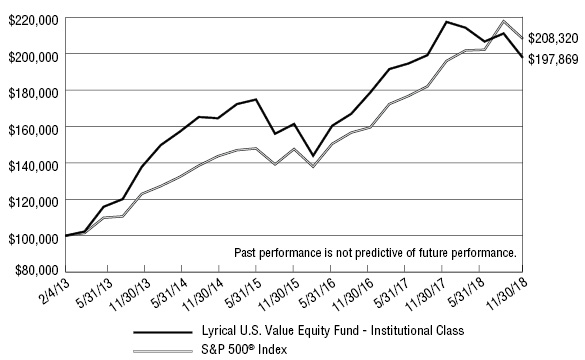

Since its launch on February 4, 2013 through November 30, 2018, the Fund’s Institutional Class has produced a cumulative total return of +97.87%, compared to the +108.32% cumulative total return for the S&P 500® Index (the “S&P 500”). For the twelve months ended November 30, 2018, the Fund’s Institutional Class produced a total return of -9.02% compared to the total return for the S&P 500 of +6.27%. For the twelve months ended November 30, 2018, the three positions that most positively impacted performance were HCA Healthcare, Inc. (HCA), Anthem, Inc. (ANTM), and Microsemi Corporation (MSCC) with contributions of 288 basis points (“bps”) (up 71%), 123 bps (up 25%) and 27 bps (up 27%), respectively; conversely, the three positions that most negatively impacted performance were Western Digital Corporation (WDC), Flex Ltd. (FLEX), and Affiliated Managers Group, Inc. (AMG) which detracted 178 bps (down 40%), 146 bps (down 52%) and 131 bps (down 43%), respectively.

In analyzing the Fund portfolio’s performance attribution, we find it helpful to examine both the investment success rate and any skew in the distribution of returns. Over the life of the Fund, 77% of the Fund’s investments posted gains, and 50% outperformed the S&P 500. Skew has been a positive factor, as the Fund’s outperformers have outperformed by 71%, while our underperformers have underperformed by 64% over the life of the Fund. For the twelve month period ended November 30, 2018, 32% of the Fund’s investments posted gains, and 16% outperformed the S&P 500. For the twelve month period, skew has been a negative factor as the Fund’s outperformers have outperformed by 19%, while our underperformers have underperformed by 23%.

During the life of the Fund we have sold twenty-four positions, as seven companies announced they were being acquired, fourteen approached our estimates of fair value, for one we lost conviction in our thesis, for one the company announced or completed acquisitions which increased the complexity and decreased analyzability and for one the risk/reward became less compelling than other opportunities. For each sale we added a new position from our pipeline of opportunities.

As of November 30, 2018, the valuation of our portfolio is 10.1 times the next twelve months consensus earnings. The S&P 500 has a valuation of 16.5 times earnings on this same basis, a premium of 63% over the Fund.

1

Lyrical Asset Management’s Investment Philosophy and Portfolio Construction

For the new investors since our previous letter to the Fund’s shareholders, we’d like to briefly outline our investment philosophy and portfolio construction approach.

We believe our strategy and approach to investing differentiate us from other investment managers, even those that share a value approach to investing. We are deep value investors and by this we mean that we look to invest in companies trading significantly below intrinsic value. This separates us from other value managers who focus on relative value or core value approaches and whose portfolio characteristics have higher Price/Earnings, Price/Book and Price/Cash Flow multiples. We assess valuation based on current price relative to long-term normalized earnings, which contrasts us to those that rely on Price/Book or dividend yield. We only invest in what we consider to be quality businesses that we believe should earn good returns on invested capital, and avoid volatile businesses and companies with excessive leverage. Other value investors may consider owning any business regardless of quality if they believe the price is low enough. Lastly, we only invest in businesses we can understand and avoid those that are excessively complex or require specialized technical knowledge, even though they may appear cheap from a high-level perspective.

We construct our portfolio purely bottom up and without regard to what is or is not contained in a benchmark. We are concerned with concentration risk and have strict limits on how much capital can be invested in any one position or any one industry. Our long portfolio is constructed to be balanced and diversified across approximately 33 positions, giving us exposure to many different types of companies and situations without sacrificing our strict investment standards.

Thank you for your continued trust and interest in Lyrical Asset Management.

Sincerely,

Andrew Wellington

Portfolio Manager

2

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling1-888-884-8099.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit the Fund’s website atwww.lyricalvaluefunds.com or call1-888-884-8099and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolios of the Fund, may be sold at any time, and may no longer be held by the Fund. For a complete list of securities held by the Funds as of November 30, 2018, please see the Schedules of Investments section of this Report. The opinions of the Fund’s adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

LYRICAL U.S. VALUE EQUITY FUND

PERFORMANCE INFORMATION (Unaudited)

Comparison of the Change in Value of a $100,000 Investment in

Lyrical U.S. Value Equity Fund - Institutional Class(a) versus

the S&P 500® Index

Average Annual Total Returns (for the periods ended November 30, 2018) | ||||

1 Year | 5 Years | Since | ||

Lyrical U.S. Value Equity Fund - Institutional Class(b) | (9.02%) | 7.50% | 12.44% | |

Lyrical U.S. Value Equity Fund - Investor Class(b) | (9.30%) | N/A | 5.94% | |

S&P 500® Index(d) | 6.27% | 11.12% | 13.44%(e) | |

(a) | The line graph above represents performance of the Institutional Class only, which will vary from the performance of the Investor Class based on the difference in fees paid by shareholders in the different classes. |

(b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

(c) | Commencement of operations for Institutional Class shares was February 4, 2013. Commencement of operations for Investor Class shares was February 24, 2014. |

(d) | The S&P 500® Index is a market capitalization weighted index of 500 large companies that is widely used as a barometer of U.S. stock market performance. The index is unmanaged and shown for illustration purposes only. An investor cannot invest in an index and its returns are not indicative of the performance of any specific investment. |

(e) | Represents the period from February 4, 2013 (date of commencement of operations of Institutional Class shares) through November 30, 2018. |

4

LYRICAL U.S. VALUE EQUITY FUND

PORTFOLIO INFORMATION

November 30, 2018 (Unaudited)

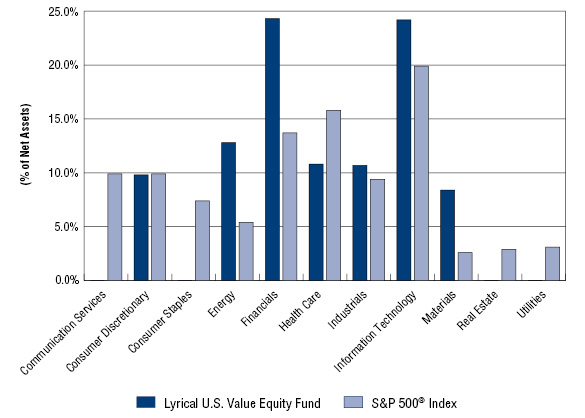

Lyrical U.S. Value Equity Fund vs S&P 500® Index

Sector Diversification

Top Ten Equity Holdings

Security Description | % of |

HCA Healthcare, Inc. | 5.5% |

Aflac, Inc. | 5.3% |

Anthem, Inc. | 5.3% |

Broadcom, Inc. | 5.2% |

Microchip Technology, Inc. | 5.2% |

Celanese Corporation - Series A | 5.0% |

Willis Towers Watson plc | 5.0% |

Ameriprise Financial, Inc. | 5.0% |

EOG Resources, Inc. | 4.9% |

Lincoln National Corporation | 4.7% |

5

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

COMMON STOCKS — 101.0% | Shares | Value | ||||||

Consumer Discretionary — 9.8% | ||||||||

Auto Components — 3.3% | ||||||||

Adient plc | 243,158 | $ | 5,757,981 | |||||

Goodyear Tire & Rubber Company (The) | 813,762 | 18,846,728 | ||||||

Tenneco, Inc. - Class A | 181,153 | 6,113,914 | ||||||

| 30,718,623 | ||||||||

Household Durables — 2.9% | ||||||||

Whirlpool Corporation | 216,277 | 27,279,018 | ||||||

Internet & Direct Marketing Retail — 3.6% | ||||||||

Qurate Retail, Inc.(a) | 1,481,885 | 32,927,485 | ||||||

Energy — 12.8% | ||||||||

Energy Equipment & Services — 3.3% | ||||||||

National Oilwell Varco, Inc. | 962,796 | 30,915,380 | ||||||

Oil, Gas & Consumable Fuels — 9.5% | ||||||||

EOG Resources, Inc. | 443,099 | 45,776,557 | ||||||

Suncor Energy, Inc. | 1,311,713 | 42,355,213 | ||||||

| 88,131,770 | ||||||||

Financials — 24.3% | ||||||||

Capital Markets — 7.1% | ||||||||

Affiliated Managers Group, Inc. | 176,413 | 19,603,013 | ||||||

Ameriprise Financial, Inc. | 355,619 | 46,141,565 | ||||||

| 65,744,578 | ||||||||

Insurance — 17.2% | ||||||||

Aflac, Inc. | 1,079,893 | 49,394,306 | ||||||

Assurant, Inc. | 204,663 | 19,901,430 | ||||||

Lincoln National Corporation | 697,307 | 43,909,422 | ||||||

Willis Towers Watson plc | 290,146 | 46,263,779 | ||||||

| 159,468,937 | ||||||||

Health Care — 10.8% | ||||||||

Health Care Providers & Services — 10.8% | ||||||||

Anthem, Inc. | 169,265 | 49,098,699 | ||||||

HCA Healthcare, Inc. | 354,159 | 50,995,354 | ||||||

| 100,094,053 | ||||||||

Industrials — 10.7% | ||||||||

Building Products — 4.1% | ||||||||

Johnson Controls International plc | 1,089,715 | 37,900,288 | ||||||

6

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

COMMON STOCKS — 101.0% (Continued) | Shares | Value | ||||||

Industrials — 10.7% (Continued) | ||||||||

Construction & Engineering — 1.6% | ||||||||

AECOM(a) | 446,514 | $ | 14,359,890 | |||||

Road & Rail — 1.6% | ||||||||

Avis Budget Group, Inc.(a) | 304,358 | 8,914,646 | ||||||

Hertz Global Holdings, Inc.(a) | 315,446 | 5,901,994 | ||||||

| 14,816,640 | ||||||||

Trading Companies & Distributors — 3.4% | ||||||||

AerCap Holdings N.V.(a) | 602,888 | 31,874,689 | ||||||

Information Technology — 24.2% | ||||||||

Communications Equipment — 1.1% | ||||||||

CommScope Holding Company, Inc.(a) | 589,692 | 10,673,425 | ||||||

Electronic Equipment, Instruments & Components — 5.1% | ||||||||

Arrow Electronics, Inc.(a) | 277,396 | 21,351,170 | ||||||

Flex Ltd.(a) | 1,728,101 | 15,120,884 | ||||||

Tech Data Corporation(a) | 121,811 | 10,956,899 | ||||||

| 47,428,953 | ||||||||

IT Services — 3.2% | ||||||||

Western Union Company (The) | 1,574,642 | 29,493,045 | ||||||

Semiconductors & Semiconductor Equipment — 10.4% | ||||||||

Broadcom, Inc. | 204,218 | 48,483,396 | ||||||

Microchip Technology, Inc. | 635,432 | 47,657,400 | ||||||

| 96,140,796 | ||||||||

Technology Hardware, Storage & Peripherals — 4.4% | ||||||||

NCR Corporation(a) | 478,512 | 13,259,567 | ||||||

Western Digital Corporation | 598,353 | 27,159,243 | ||||||

| 40,418,810 | ||||||||

Materials — 8.4% | ||||||||

Chemicals — 5.0% | ||||||||

Celanese Corporation - Series A | 462,160 | 46,645,809 | ||||||

Containers & Packaging — 3.4% | ||||||||

Crown Holdings, Inc.(a) | 427,047 | 21,898,970 | ||||||

Owens-Illinois, Inc.(a) | 518,759 | 9,539,978 | ||||||

| 31,438,948 | ||||||||

Total Common Stocks (Cost $803,651,505) | $ | 936,471,137 | ||||||

7

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

MONEY MARKET FUNDS — 0.4% | Shares | Value | ||||||

Invesco Short-Term Investments Trust - Treasury Portfolio - Institutional Shares, 2.13%(b) (Cost $4,055,774) | 4,055,774 | $ | 4,055,774 | |||||

Investments at Value — 101.4% (Cost $807,707,279) | $ | 940,526,911 | ||||||

Liabilities in Excess of Other Assets — (1.4%) | (13,349,851 | ) | ||||||

Net Assets — 100.0% | $ | 927,177,060 | ||||||

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of November 30, 2018. |

See accompanying notes to financial statements. | |

8

LYRICAL U.S. VALUE EQUITY FUND | ||||

ASSETS | ||||

Investments in securities: | ||||

At cost | $ | 807,707,279 | ||

At value (Note 2) | $ | 940,526,911 | ||

Receivable for capital shares sold | 8,864,184 | |||

Receivable for investment securities sold | 14,890,650 | |||

Dividends receivable | 1,715,895 | |||

Other assets | 31,834 | |||

Total assets | 966,029,474 | |||

LIABILITIES | ||||

Distributions payable | 15,590,959 | |||

Payable for capital shares redeemed | 21,960,306 | |||

Payable to Adviser (Note 4) | 1,177,005 | |||

Payable to administrator (Note 4) | 90,045 | |||

Accrued distribution fees (Note 4) | 419 | |||

Other accrued expenses | 33,680 | |||

Total liabilities | 38,852,414 | |||

NET ASSETS | $ | 927,177,060 | ||

NET ASSETS CONSIST OF: | ||||

Paid-in capital | $ | 843,271,568 | ||

Accumulated earnings | 83,905,492 | |||

NET ASSETS | $ | 927,177,060 | ||

NET ASSET VALUE PER SHARE: | ||||

INSTITUTIONAL CLASS | ||||

Net assets applicable to Institutional Class | $ | 907,365,757 | ||

Institutional Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 58,340,526 | |||

Net asset value, offering price and redemption price per share (Note 2) | $ | 15.55 | ||

INVESTOR CLASS | ||||

Net assets applicable to Investor Class | $ | 19,811,303 | ||

Investor Class shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 1,284,312 | |||

Net asset value, offering price and redemption price per share (Note 2) | $ | 15.43 | ||

See accompanying notes to financial statements. |

9

LYRICAL U.S. VALUE EQUITY FUND | ||||

INVESTMENT INCOME | ||||

Dividend income | $ | 18,604,116 | ||

Foreign withholding taxes on dividends | (232,829 | ) | ||

Total investment income | 18,371,287 | |||

EXPENSES | ||||

Investment advisory fees (Note 4) | 14,926,281 | |||

Administration fees (Note 4) | 755,782 | |||

Compliance fees (Note 4) | 121,511 | |||

Fund accounting fees (Note 4) | 120,755 | |||

Transfer agent fees (Note 4) | 118,401 | |||

Custody and bank service fees | 91,372 | |||

Distribution fees - Investor Class (Note 4) | 84,486 | |||

Registration and filing fees | 66,498 | |||

Postage and supplies | 49,344 | |||

Professional fees | 44,383 | |||

Networking fees | 39,784 | |||

Borrowing costs (Note 5) | 12,625 | |||

Printing of shareholder reports | 10,595 | |||

Trustees' fees and expenses (Note 4) | 10,151 | |||

Insurance expense | 6,552 | |||

Other expenses | 36,099 | |||

Total expenses | 16,494,619 | |||

Expense reimbursements by Adviser (Note 4) | (6,222 | ) | ||

Net expenses | 16,488,397 | |||

NET INVESTMENT INCOME | 1,882,890 | |||

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS AND FOREIGN CURRENCIES | ||||

Net realized gains from investments | 50,802,676 | |||

Net realized losses from foreign currency transactions (Note 2) | (4,989 | ) | ||

Net change in unrealized appreciation (depreciation) on investments | (163,561,509 | ) | ||

NET REALIZED AND UNREALIZED LOSSES ON INVESTMENTSAND FOREIGN CURRENCIES | (112,763,822 | ) | ||

NET DECREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | (110,880,932 | ) | |

See accompanying notes to financial statements. |

10

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

| Year | Year | ||||||

FROM OPERATIONS | ||||||||

Net investment income | $ | 1,882,890 | $ | 245,607 | ||||

Net realized gains from investment transactions | 50,802,676 | 75,451,576 | ||||||

Net realized losses from foreign currency transactions | (4,989 | ) | — | |||||

Net change in unrealized appreciation (depreciation) on investments | (163,561,509 | ) | 145,782,822 | |||||

Net increase (decrease) in net assets resulting from operations | (110,880,932 | ) | 221,480,005 | |||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

Institutional Class | (77,051,597 | ) | (88,896,292 | ) | ||||

Investors Class | (1,717,444 | ) | (3,128,810 | ) | ||||

Decrease in net assets from distributions to shareholders | (78,769,041 | ) | (92,025,102 | ) | ||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Institutional Class | ||||||||

Proceeds from shares sold | 456,135,603 | 340,448,217 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 61,458,585 | 67,241,541 | ||||||

Payments for shares redeemed | (542,065,326 | ) | (408,713,799 | ) | ||||

Net decrease in Institutional Class net assets from capital share transactions | (24,471,138 | ) | (1,024,041 | ) | ||||

Investor Class | ||||||||

Proceeds from shares sold | 4,889,814 | 7,832,427 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 1,617,814 | 2,940,288 | ||||||

Payments for shares redeemed | (18,570,922 | ) | (37,958,377 | ) | ||||

Net decrease in Investor Class net assets from capital share transactions | (12,063,294 | ) | (27,185,662 | ) | ||||

TOTAL INCREASE (DECREASE) IN NET ASSETS | (226,184,405 | ) | 101,245,200 | |||||

NET ASSETS | ||||||||

Beginning of year | 1,153,361,465 | 1,052,116,265 | ||||||

End of year | $ | 927,177,060 | $ | 1,153,361,465 | ||||

(a) | The presentation of Distributions to Shareholders has been updated to reflect the changes prescribed in amendments to Regulations S-X, effective November 5, 2018 (Note 2). For the year ended November 30, 2017, distributions to shareholders for the Institutional Class consisted of $14,603,810 and $74,292,482 from net investment income and net realized gains, respectively, and for the Investor Class consisted of $605,949 and $2,522,861 from net investment income and net realized gains, respectively. As of November 30, 2017, undistributed net investment income was $236,790. |

See accompanying notes to financial statements. | |

11

LYRICAL U.S. VALUE EQUITY FUND | ||||||||

| Year | Year | ||||||

CAPITAL SHARE ACTIVITY | ||||||||

Institutional Class | ||||||||

Shares sold | 25,680,359 | 19,205,975 | ||||||

Shares issued in reinvestment of distributions to shareholders | 3,949,556 | 3,695,697 | ||||||

Shares redeemed | (31,270,758 | ) | (22,805,199 | ) | ||||

Net increase (decrease) in shares outstanding | (1,640,843 | ) | 96,473 | |||||

Shares outstanding at beginning of year | 59,981,369 | 59,884,896 | ||||||

Shares outstanding at end of year | 58,340,526 | 59,981,369 | ||||||

Investor Class | ||||||||

Shares sold | 268,775 | 441,214 | ||||||

Shares issued in reinvestment of distributions to shareholders | 104,804 | 162,690 | ||||||

Shares redeemed | (1,073,442 | ) | (2,142,707 | ) | ||||

Net decrease in shares outstanding | (699,863 | ) | (1,538,803 | ) | ||||

Shares outstanding at beginning of year | 1,984,175 | 3,522,978 | ||||||

Shares outstanding at end of year | 1,284,312 | 1,984,175 | ||||||

See accompanying notes to financial statements. |

12

LYRICAL U.S. VALUE EQUITY FUND | ||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Year: | ||||||||||||||||||||

| Year | Year | Year | Year | Year | |||||||||||||||

Net asset value at beginning of year | $ | 18.62 | $ | 16.60 | $ | 15.63 | $ | 16.29 | $ | 13.78 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment income (loss) | 0.03 | (a) | 0.01 | (a) | 0.24 | 0.04 | (0.00 | )(b) | ||||||||||||

Net realized and unrealized gains (losses) on investments and foreign currencies | (1.70 | ) | 3.54 | 1.40 | (0.35 | ) | 2.66 | |||||||||||||

Total from investment operations | (1.67 | ) | 3.55 | 1.64 | (0.31 | ) | 2.66 | |||||||||||||

Less distributions: | ||||||||||||||||||||

Dividends from net investment income | (0.01 | ) | (0.24 | ) | (0.04 | ) | (0.00 | )(b) | (0.00 | )(b) | ||||||||||

Distributions from net realized gains | (1.39 | ) | (1.29 | ) | (0.63 | ) | (0.35 | ) | (0.15 | ) | ||||||||||

Total distributions | (1.40 | ) | (1.53 | ) | (0.67 | ) | (0.35 | ) | (0.15 | ) | ||||||||||

Net asset value at end of year | $ | 15.55 | $ | 18.62 | $ | 16.60 | $ | 15.63 | $ | 16.29 | ||||||||||

Total return(c) | (9.02 | %) | 21.70 | % | 10.73 | % | (1.91 | %) | 19.41 | % | ||||||||||

Net assets at end of year (000's) | $ | 907,366 | $ | 1,116,584 | $ | 993,904 | $ | 590,582 | $ | 547,021 | ||||||||||

Ratios/supplementary data: | ||||||||||||||||||||

Ratio of total expenses to average net assets | 1.37 | % | 1.37 | % | 1.38 | % | 1.42 | % | 1.45 | % | ||||||||||

Ratio of net expenses to average net assets | 1.37 | % | 1.37 | % | 1.38 | % | 1.42 | % | 1.44 | %(d) | ||||||||||

Ratio of net investment income (loss) to average net assets | 0.17 | % | 0.03 | % | 1.62 | % | 0.24 | % | (0.00 | %)(d)(e) | ||||||||||

Portfolio turnover rate | 39 | % | 22 | % | 36 | % | 21 | % | 20 | % | ||||||||||

(a) | Per share net investment income has been determined on the basis of average number of shares outstanding during the period. |

(b) | Amount rounds to less than $0.01 per share. |

(c) | Total return is a measure of the change in value of an investment in the Fund over the years covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses for the year ended November 30, 2014 (Note 4). |

(d) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

(e) | Amount rounds to less than 0.01%. |

See accompanying notes to financial statements. | |

13

LYRICAL U.S. VALUE EQUITY FUND | ||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Period: | ||||||||||||||||||||

| Year | Year | Year | Year | Period | |||||||||||||||

Net asset value at beginning of period | $ | 18.54 | $ | 16.52 | $ | 15.57 | $ | 16.27 | $ | 14.68 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment income (loss) | (0.03 | )(b) | (0.05 | )(b) | 0.30 | 0.01 | (0.01 | ) | ||||||||||||

Net realized and unrealized gains (losses) on investments and foreign currencies | (1.69 | ) | 3.53 | 1.28 | (0.36 | ) | 1.60 | |||||||||||||

Total from investment operations | (1.72 | ) | 3.48 | 1.58 | (0.35 | ) | 1.59 | |||||||||||||

Less distributions: | ||||||||||||||||||||

Distributions from net investment income | — | (0.17 | ) | (0.00 | )(c) | — | — | |||||||||||||

Distributions from net realized gains | (1.39 | ) | (1.29 | ) | (0.63 | ) | (0.35 | ) | — | |||||||||||

Total distributions | (1.39 | ) | (1.46 | ) | (0.63 | ) | (0.35 | ) | — | |||||||||||

Net asset value at end of period | $ | 15.43 | $ | 18.54 | $ | 16.52 | $ | 15.57 | $ | 16.27 | ||||||||||

Total return(d) | (9.30 | %) | 21.32 | % | 10.36 | % | (2.19 | %) | 10.83 | %(e) | ||||||||||

Net assets at end of period (000's) | $ | 19,811 | $ | 36,777 | $ | 58,213 | $ | 61,375 | $ | 9,033 | ||||||||||

Ratios/supplementary data: | ||||||||||||||||||||

Ratio of total expenses to average net assets | 1.72 | % | 1.70 | % | 1.70 | % | 1.72 | % | 2.39 | %(f) | ||||||||||

Ratio of net expenses to average net assets | 1.70 | %(g) | 1.70 | % | 1.70 | % | 1.70 | %(g) | 1.70 | %(f)(g) | ||||||||||

Ratio of net investment income (loss) to average net assets | (0.18 | %)(g) | (0.32 | %) | 1.39 | % | 0.03 | %(g) | (0.18 | %)(f)(g) | ||||||||||

Portfolio turnover rate | 39 | % | 22 | % | 36 | % | 21 | % | 20 | %(e)(h) | ||||||||||

(a) | Represents the period from the commencement of operations (February 24, 2014) through November 30, 2014. |

(b) | Per share net investment loss has been determined on the basis of average number of shares outstanding during the period. |

(c) | Amount rounds to less than $0.01 per share. |

(d) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses for the periods ended November 30, 2018, 2015 and 2014 (Note 4). |

(e) | Not annualized. |

(f) | Annualized. |

(g) | Ratio was determined after advisory fee reductions and/or expense reimbursements (Note 4). |

(h) | Represents the year ended November 30, 2014 |

See accompanying notes to financial statements. | |

14

LYRICAL U.S. VALUE EQUITY FUND

NOTES TO FINANCIAL STATEMENTS

November 30, 2018

1. Organization

Lyrical U.S. Value Equity Fund (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report.

The investment objective of the Fund is to seek to achieve long-term capital growth.

The Fund offers two classes of shares: Institutional Class shares (sold without any sales loads and distribution and/or shareholder service fees and requiring a $100,000 initial investment) and Investor Class shares (sold without any sales loads, but subject to a distribution and/or shareholder service fee of up to 0.25% of the average daily net assets attributable to Investor Class shares, and requiring a $2,500 initial investment). Each share class represents an ownership interest in the same investment portfolio.

2. Significant Accounting Policies

In August 2018, the U.S. Securities and Exchange Commission (the “SEC”) adopted regulations that eliminated or amended disclosure requirements that were redundant or outdated in light of changes in SEC requirements, accounting principles generally accepted in the United States of America (“GAAP”), International Financial Reporting Standards or changes in technology or the business environment. These regulations were effective November 5, 2018, and the Fund is complying with them effective with these financial statements.

The following is a summary of the Fund’s significant accounting policies. The policies are in conformity with GAAP. The Fund follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services – Investment Companies.”

New accounting pronouncement – In August 2018, FASB issued Accounting Standards Update No. 2018-13 (“ASU 2018-13”), “Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement,” which amends the fair value measurement disclosure requirements of ASC Topic 820 (“ASC 820”), “Fair Value Measurement.” ASU 2018-13 includes new, eliminated, and modified disclosure requirements for ASC 820. In addition, ASU 2018-13 clarifies that materiality is an appropriate consideration of entities when evaluating disclosure requirements. ASU 2018-13 is effective for fiscal years beginning after December 15, 2019, including interim periods therein. Early adoption is permitted and the Fund has adopted ASU 2018-13 with these financial statements.

Securities valuation – The Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. The Fund values its listed securities on the basis of the security’s last sale price on the security’s primary

15

LYRICAL U.S. VALUE EQUITY FUND |

exchange, if available, otherwise at the exchange’s most recently quoted mean price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. When using a quoted price and when the market is considered active, the security will be classified as Level 1 within the fair value hierarchy (see below). In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with procedures established by and under the general supervision of the Board of Trustees (the “Board”). Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s net asset value (“NAV”) may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

● | Level 1 – quoted prices in active markets for identical securities |

● | Level 2 – other significant observable inputs |

● | Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments as of November 30, 2018:

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stocks | $ | 936,471,137 | $ | — | $ | — | $ | 936,471,137 | ||||||||

Money Market Funds | 4,055,774 | — | — | 4,055,774 | ||||||||||||

Total | $ | 940,526,911 | $ | — | $ | — | $ | 940,526,911 | ||||||||

16

LYRICAL U.S. VALUE EQUITY FUND |

Refer to the Fund’s Schedule of Investments for a listing of securities by industry type. As of November 30, 2018, the Fund did not hold any derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3).

Share valuation – The NAV per share of each class of the Fund is calculated daily by dividing the total value of the assets attributable to that class, less liabilities attributable to that class, by the number of shares outstanding of that class. The offering price and redemption price per share of each class of the Fund is equal to the NAV per share of such class.

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned. Withholding taxes on foreign dividends have been recorded in accordance with the Fund’s understanding of the applicable country’s rules and tax rates.

Investment transactions – Investment transactions are accounted for on the trade date. Realized gains and losses on investments sold are determined on a specific identification basis.

Foreign currency translation – Investment securities and other assets and liabilities denominated in or expected to settle in foreign currencies, if any, are translated into U.S. dollars based on exchange rates on the following basis:

A. | The fair values of investment securities and other assets and liabilities are translated as of the close of the NYSE each day. |

B. | Purchases and sales of investment securities and income and expenses are translated at the rate of exchange prevailing as of 4:00 p.m. Eastern time on the respective date of such transactions. |

C. | The Fund does not isolate that portion of the results of operations caused by changes in foreign exchange rates on investments from those caused by changes in market prices of securities held. Such fluctuations are included with the net realized and unrealized gains or losses on investments. |

Reported net realized foreign exchange gains or losses arise from 1) purchases and sales of foreign currencies and 2) the difference between the amounts of dividends and foreign withholding taxes recorded on the Fund’s books and the U.S. dollar equivalent of the amounts actually received or paid. Reported net unrealized foreign exchange gains and losses, if any, arise from changes in the value of assets and liabilities that result from changes in exchange rates.

Allocation between Classes – Investment income earned, realized capital gains and losses, and unrealized appreciation and depreciation are allocated daily to each Class of the Fund based upon its proportionate share of total net assets of the Fund. Class-specific

17

LYRICAL U.S. VALUE EQUITY FUND |

expenses are charged directly to the Class incurring the expense. Common expenses which are not attributable to a specific Class are allocated daily to each Class of shares of the Fund based upon its proportionate share of total net assets of the Fund

Distributions to shareholders – The Fund distributes to shareholders any net investment income dividends and net realized capital gains distributions at least once each year. The amount of such dividends and distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date. The tax character of distributions paid to shareholders by the Fund during the years ended November 30, 2018 and 2017 was as follows:

Year Ended | Ordinary | Long-Term | Total | |||||||||

11/30/2018 | $ | 377,148 | $ | 78,391,893 | $ | 78,769,041 | ||||||

11/30/2017 | $ | 21,153,113 | $ | 70,871,989 | $ | 92,025,102 | ||||||

The Fund made the following ordinary income distribution to the Institutional Class of shares subsequent to November 30, 2018 to shareholders of record on December 27, 2018:

| Record Date | Ex-Date | Per Share | |||||||||

Institutional Class | 12/27/2018 | 12/28/2018 | $ | 0.0507 | ||||||||

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986, as amended (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

18

LYRICAL U.S. VALUE EQUITY FUND |

The following information is computed on a tax basis for each item as of November 30, 2018:

Tax cost of portfolio investments | $ | 865,329,247 | ||

Gross unrealized appreciation | $ | 181,108,617 | ||

Gross unrealized depreciation | (105,910,953 | ) | ||

Net unrealized appreciation | 75,197,664 | |||

Undistributed ordinary income | 1,871,300 | |||

Undistributed long-term capital gains | 6,836,528 | |||

Distributable earnings | $ | 83,905,492 |

The difference between the federal income tax cost of portfolio investments and the financial statement cost of portfolio investments is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to the tax deferral of losses on wash sales.

For the year ended November 30, 2018, the following reclassification was made as a result of permanent differences between the financial statement and income tax reporting requirements:

Paid-in capital | $ | 7,515,308 | ||

Distributable earnings | $ | (7,515,308 | ) |

This reclassification has no effect on the Fund’s total net asset or its net asset value per share and is due to the utilization of earnings and profits on shareholder redemptions.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” of being sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for all open tax years (generally three years) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. Federal.

3. Investment Transactions

During the year ended November 30, 2018, cost of purchases and proceeds from sales of investment securities, other than short-term investments, amounted to $448,085,553 and $560,230,265, respectively.

19

LYRICAL U.S. VALUE EQUITY FUND |

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by Lyrical Asset Management L.P. (the “Adviser”) pursuant to the terms of an Investment Advisory Agreement. The Fund pays the Adviser an investment advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.25% of average daily net assets.

Pursuant to an Expense Limitation Agreement (“ELA”) between the Fund and the Adviser, the Adviser has contractually agreed, until March 31, 2020, to reduce investment advisory fees and reimburse other operating expenses to limit total annual operating expenses of the Fund (exclusive of brokerage costs; taxes; interest; borrowing costs such as interest and dividend expenses on securities sold short; costs to organize the Fund; acquired fund fees and expenses; extraordinary expenses such as litigation and merger or reorganization costs; and other expenses not incurred in the ordinary course of the Fund’s business) to an amount not exceeding the following percentages of average daily net assets attributable to each respective class:

Institutional Class | Investor Class |

1.45% | 1.70% |

Accordingly, during the year ended November 30, 2018, the Adviser reimbursed other operating expenses of $6,222 for Investor Class shares.

Under the terms of the ELA, investment advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause total annual fund operating expenses to exceed the lesser of (i) the expense limitation then in effect, if any, and (ii) the expense limitation in effect at the time the expenses to be repaid were incurred. As of November 30, 2018, the Adviser may seek repayment of expense reimbursements of $6,222 no later than November 30, 2021.

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including, but not limited to, postage, supplies and costs of pricing its portfolio securities.

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as the principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated partially by the Adviser and partially by the Investor Class shares of the Fund for acting as principal underwriter.

20

LYRICAL U.S. VALUE EQUITY FUND |

A Trustee and certain officers of the Trust are also officers of Ultimus and/or the Distributor.

DISTRIBUTION PLAN

The Fund has adopted a plan of distribution (the “Plan”), pursuant to Rule 12b-1 under the Investment Company Act of 1940, as amended (the “1940 Act”), which permits Investor Class shares of the Fund to directly incur or reimburse the Fund’s principal underwriter for certain expenses related to the distribution of its shares. The annual limitation for payment of expenses pursuant to the Plan is 0.25% of the Fund’s average daily net assets allocable to Investor Class shares. The Fund has not adopted a plan of distribution with respect to the Institutional Class shares. During the year ended November 30, 2018, the Investor Class shares incurred $84,486 of distribution fees under the Plan.

TRUSTEE COMPENSATION

Effective August 1, 2018, each Trustee who is not an “interested person” of the Trust (“Independent Trustee”) receives a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who receives a $1,500 annual retainer from the Fund, paid in quarterly installments. Each Independent Trustee also receives from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to August 1, 2018, each Independent Trustee received a $1,000 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who received a $1,200 annual retainer from the Fund, paid quarterly. Each Independent Trustee also received from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses.

PRINCIPAL HOLDER OF FUND SHARES

As of November 30, 2018, the following shareholder owned of record 25% or more of the outstanding shares of the Investor Class of the Fund:

NAME OF RECORD OWNER | % Ownership |

Lyrical U.S. Value Equity Fund - Investor Class | |

Charles Schwab & Company, Inc. (for the benefit of its customers) | 64% |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person of the Fund. That shareholder’s vote could have a more significant effect on matters presented at a shareholders’ meeting.

5. Borrowing Costs

From time to time, the Fund may have an overdrawn cash balance at the custodian due to redemptions or market movements. When this occurs, the Fund will incur borrowing costs charged by the custodian. Accordingly, during the year ended November 30, 2018, the Fund incurred $12,625 of borrowing costs charged by the custodian.

21

LYRICAL U.S. VALUE EQUITY FUND |

6. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statements of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events other than the payment of net investment income dividends on December 28, 2018, as discussed in Note 2.

22

LYRICAL U.S. VALUE EQUITY FUND |

To the Board of Trustees of Ultimus Managers Trust

and the Shareholders of Lyrical U.S. Value Equity Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Lyrical U.S. Value Equity Fund, a series of shares of beneficial interest in Ultimus Managers Trust (the“Fund”), including the schedule of investments, as of November 30, 2018, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended and the financial highlights for each of the years in the five-year period then ended for Institutional Class Shares and each of the years in the four-year period then ended and the period from February 24, 2014 (commencement of operations) to November 30, 2014 for Investor Class Shares, and the related notes (collectively referred to as the“financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of November 30, 2018, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years or periods in the five-year period then ended as described in the previous sentence, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

23

LYRICAL U.S. VALUE EQUITY FUND |

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of November 30, 2018 by correspondence with the custodian and brokers, or by other appropriate auditing procedures where replies from brokers were not received. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

| |

BBD, LLP |

We have served as the auditor of one or more of the Funds in the Ultimus Managers Trust since 2013.

Philadelphia, Pennsylvania

January 24, 2019

24

LYRICAL U.S. VALUE EQUITY FUND |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees, class-specific expenses (such as distribution fees) and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (June 1, 2018) and held until the end of the period (November 30, 2018).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the fourth column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the SEC requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

25

LYRICAL U.S. VALUE EQUITY FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued)

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning | Ending | Net | Expenses |

Lyrical U.S. Value Equity Fund | ||||

Institutional Class | ||||

Actual | $1,000.00 | $957.30 | 1.37% | $6.72 |

Hypothetical 5% Return (before expenses) | $1,000.00 | $1,018.20 | 1.37% | $6.93 |

Investor Class | ||||

Actual | $1,000.00 | $955.90 | 1.70% | $8.34 |

Hypothetical 5% Return (before expenses) | $1,000.00 | $1,016.55 | 1.70% | $8.59 |

(a) | Annualized, based on the Fund’s most recent one-half year expenses. |

(b) | Expenses are equal to the Fund’s annualized net expense ratio multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

26

LYRICAL U.S. VALUE EQUITY FUND

OTHER INFORMATION (Unaudited)

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-888-884-8099, or on the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-888-884-8099, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-888-884-8099. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov.

FEDERAL TAX INFORMATION (Unaudited)

Qualified Dividend Income – The Fund designates 100% of its ordinary income dividends, or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for the reduced tax rate of 15%.

Dividends Received Deduction– Corporate shareholders are generally entitled to take the dividends received deduction on the portion of the Fund’s dividend distribution that qualifies under tax law. For the fiscal year ended November 30, 2018, 100% of ordinary income dividends qualifies for the corporate dividends received deduction.

Long-Term Capital Gains– For the year ended November 30, 2018, the Fund designates $85,907,200 as long-term capital gains distributions.

27

LYRICAL U.S. VALUE EQUITY FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

The Board of Trustees has overall responsibility for management of the Trust’s affairs. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement, or removal. The Trustees, in turn, elect the officers of the Trust to actively supervise its day-to-day operations. The officers have been elected for an annual term. Each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. The following are the Trustees and executive officers of the Trust:

Name and | Length of | Position(s) | Principal | Number | Directorships |

Interested Trustees: |

|

|

|

|

|

Robert G. Dorsey* | Since February 2012 | Trustee | Managing Director (1999 to present), Co-CEO (April 2018 to present), and President (1999 to April 2018) of Ultimus Fund Solutions, LLC and its subsidiaries (except as otherwise noted for FINRA-regulated broker dealer entities) | 19 | Interested Trustee of Capitol Series Trust (10 Funds) |

Independent Trustees: |

|

|

|

|

|

Janine L. Cohen | Since January 2016 | Trustee | Retired since 2013; Chief Financial Officer from 2004 to 2013 and Chief Compliance Officer from 2008 to 2013 at AER Advisors, Inc. | 19 | None |

David M. Deptula | Since June 2012 | Trustee | Vice President of Legal and Special Projects at Dayton Freight Lines, Inc. since 2016; Vice President of Tax Treasury at Standard Register Inc. (formerly The Standard Register Company) from 2011 to 2016 | 19 | None |

28

LYRICAL U.S. VALUE EQUITY FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

Name and | Length of | Position(s) | Principal | Number | Directorships |

Independent Trustees: (continued) |

|

|

|

| |

John J. Discepoli | Since June 2012 | Chairman (May 2016 to present) | Owner of Discepoli Financial Planning, LLC (personal financial planning company) since 2004 | 19 | None |

* | Mr. Dorsey is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the 1940 Act because of his relationship with the Trust’s administrator, transfer agent and distributor. |

Name and | Length of | Position(s) | Principal Occupation(s) |

Executive Officers: | |||

David R. Carson | Since 2013 | Principal Executive Officer | Vice President and Director of Client Strategies of Ultimus Fund Solutions, LLC (2013 to present); President, Unified Series Trust (2016 to present); Chief Compliance Officer, FSI Low Beta Absolute Return Fund (2013 to 2016) |

Todd E. Heim | Since 2014 | Vice | Vice President, Relationship Management Director of Ultimus Fund Solutions, LLC (2018 to present); Client Implementation Manager of Ultimus Fund Solutions, LLC (2014 to 2018); Naval Flight Officer of United States Navy (1989 to 2017); Business Project Manager of Vantiv, Inc. (2013 to 2014) |

Jennifer L. Leamer | Since 2014 | Treasurer | Vice President, Mutual Fund Controller of Ultimus Fund Solutions, LLC (2014 to present); Business Analyst of Ultimus Fund Solutions, LLC (2007 to 2014) |

29

LYRICAL U.S. VALUE EQUITY FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

Name and | Length of | Position(s) | Principal Occupation(s) |

Executive Officers: (continued) | |||

Daniel D. Bauer Year of Birth: 1977 | Since 2016 | Assistant Treasurer | Assistant Mutual Fund Controller (2015 to present) and Fund Accounting Manager (2012 to 2015) of Ultimus Fund Solutions, LLC |

Matthew J. Beck | Since 2018 | Secretary | Senior Attorney of Ultimus Fund Solutions, LLC (2018 to present); General Counsel of the Nottingham Company (2014 to 2018) |

Natalie S. Anderson Year of Birth: 1975 | Since 2016 | Assistant Secretary | Legal Administration Manager (2016 to present) and Paralegal (2015 to 2016) of Ultimus Fund Solutions, LLC; Senior Paralegal of Unirush, LLC (2011 to 2015) |

Charles C. Black | Since 2015 | Chief Compliance Officer | Senior Compliance Officer of Ultimus Fund Solutions, LLC (2015 to present); Chief Compliance Officer of The Caldwell & Orkin Funds, Inc. (2016 to present); Senior Compliance Manager for Touchstone Mutual Funds (2013 to 2015) |

Additional information about members of the Board and executive officers is available in the Fund’s Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call 1-866-884-8099.

30

LYRICAL U.S. VALUE EQUITY FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited)

The Board of Trustees (the “Board”), including the Independent Trustees voting separately, has reviewed and approved the Fund’s Investment Advisory Agreement with Lyrical Asset Management LP (the “Adviser”) for an additional one-year term (the “Agreement”). The Board approved the Agreement at an in-person meeting held on October 22-23, 2018, at which all of the Trustees were present.

Legal counsel advised the Board during its deliberations. Additionally, the Board received and reviewed a substantial amount of information provided by the Adviser in response to requests of the Board and counsel. In deciding whether to approve the renewal of the Investment Advisory Agreement, the Board recalled its review of the materials related to the Fund and the Adviser throughout the preceding 12 months and its numerous discussions with Trust management and the Adviser about the operations and performance of the Fund during that period. The Board further considered those materials and discussions and other numerous factors, including.

The nature, extent, and quality of the services provided by the Adviser.In this regard, the Board reviewed the services being provided by the Adviser to the Fund including, without limitation, its investment advisory services since the Fund’s inception; its compliance procedures and practices; its efforts to promote the Fund and assist in its distribution; and its compliance program. After reviewing the foregoing information and further information in the Adviser’s memorandum to the Board (e.g., description of its business and Form ADV), the Board concluded that the quality, extent, and nature of the services provided by the Adviser to the Fund were satisfactory and adequate.

The investment performance of the Fund. In this regard, the Board compared the performance of the Fund with the performance of its benchmark index, custom peer group, and Morningstar category. The Board also considered the consistency of the Adviser’s management with the Fund’s investment objective and policies. The Board noted that the Fund had underperformed relative to the average and median of its custom peer group for the one-year period, outperformed the average and underperformed the median for the three-year period, and outperformed the average and median for the five-year and since inception periods. The Board also noted that the Fund had underperformed relative to the average and median of its Morningstar category (Large Cap Value Funds $1 Billion - $5 Billion, True No-Loan) for the one- and three-year periods, but outperformed for the five-year and since inception periods. The Board indicated that the Adviser had satisfactorily explained its performance results for the Fund. Following additional discussion of the investment performance of the Fund; the Adviser’s experience in managing mutual funds, private funds, and separate accounts; the Adviser’s historical investment performance; and other factors, the Board concluded that the investment performance of the Fund has been satisfactory.

31

LYRICAL U.S. VALUE EQUITY FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

The costs of the services provided and profits realized by the Adviser and its affiliates from their relationship with the Fund.In this regard, the Board considered the Adviser’s staffing; methods of operating; the education and experience of its personnel; its compliance program, policies and procedures; its financial condition and the level of commitment to the Fund and, generally, the Adviser’s advisory business; the asset level of the Fund; the overall expenses of the Fund, including the advisory fee; and the differences in fees and services to the Adviser’s other similar clients. The Board considered its discussion with the Adviser regarding the Adviser’s expense limitation agreement with the Fund (the “ELA”), and considered the Adviser’s past fee reductions and expense reimbursements for the Fund. The Board further took into account the Adviser’s willingness to continue the ELA for the Fund until at least April 1, 2020.

The Board also considered potential benefits for the Adviser in managing the Fund, including promotion of the Adviser’s name. The Board compared the Fund’s advisory fee and overall expense ratio to the average and median advisory fees and expense ratios for its custom peer group and Morningstar categories and fees charged to the Adviser’s other client accounts. In considering the comparison in fees and expense ratios between the Fund and other comparable funds, the Board looked at the differences in types of funds being compared, the style of investment management, the size of the Fund, and the nature of the investment strategies. The Board also considered the Adviser’s commitment to limit the Fund’s expenses under the ELA. The Board noted that the 1.25% advisory fee for the Fund was above the average and median for the Fund’s custom peer group, and above the average and median for the other funds in the Fund’s Morningstar category (Large Cap Value Funds $1 Billion - $5 Billion, True No-Loan). The Board further noted that the overall expense ratio for the Fund of 1.37% was higher than the average and median expense ratio for the other funds in each the Fund’s custom peer group and Morningstar category (Large Cap Value Funds $1 Billion - $5 Billion, True No-Loan). The Board also compared the fees paid by the Fund to the fees paid by other clients of the Adviser, and considered the similarities and differences of services received by such other clients as compared to the services received by the Fund. The Board noted that the fee structures applicable to the Adviser’s other clients were not indicative of any unreasonableness with respect to the advisory fees payable by the Fund. The Board further considered the investment strategy and style used by the Adviser in managing the portfolio of the Fund. Following these comparisons and considerations and upon further consideration and discussion of the foregoing, the Board concluded that the advisory fee to be paid to the Adviser by the Fund is fair and reasonable.

The extent to which economics of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefit of the Fund’s investors.In this regard, the Board considered that the Fund’s fee arrangements with the Adviser involve both the advisory fee and the ELA. The Board determined that while the advisory fee remained the same as asset levels increased, the shareholders of the Fund have experienced in the past, and may again experience in the future, benefits from the ELA.

32

LYRICAL U.S. VALUE EQUITY FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

Following further discussion of the Fund’s asset level, expectations for asset growth, and level of fees, the Board determined that the fee arrangements with the Adviser were fair and reasonable in relation to the nature and quality of services being provided by the Adviser.

Brokerage and portfolio transactions. In this regard, the Board considered the Adviser’s policies and procedures and performance in seeking best execution for its clients, including the Fund. The Board also considered the historical portfolio turnover rate for the Fund; the process by which evaluations are made of the overall reasonableness of commissions paid; the process by which the Adviser evaluates best execution; the method and basis for selecting and evaluating the broker-dealers used; and any anticipated allocation of portfolio business to persons affiliated with the Adviser. After further review and discussion, the Board determined that the Adviser’s practices regarding brokerage and portfolio transactions are satisfactory.

Possible conflicts of interest. In evaluating the possibility for conflicts of interest, the Board considered such matters as the experience and abilities of the advisory personnel assigned to the Fund; the Adviser’s process for allocating trades among the Fund and its other clients; and the substance and administration of the Adviser’s Code of Ethics. Following further consideration and discussion, the Board found for the Fund that the Adviser’s standards and practices relating to the identification and mitigation of potential conflicts of interests were satisfactory.

After full consideration of the above factors as well as other factors, the Board unanimously concluded that approval of the Agreement was in the best interests of the Fund and its shareholders. It was noted that in the Trustees’ deliberations regarding the approval of the continuance of the Agreement, the Trustees did not identify any particular information or factor that was all-important or controlling, and that each individual Trustee may have attributed different weights to various factors listed above.

33

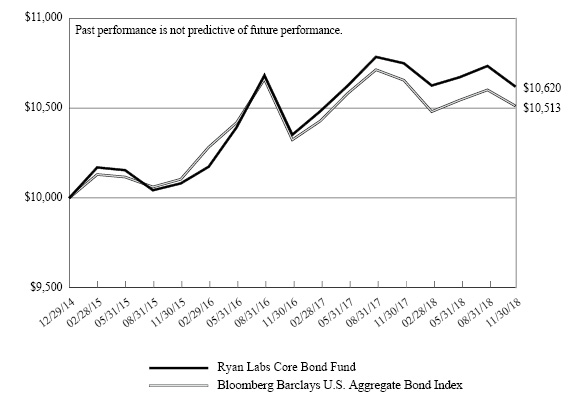

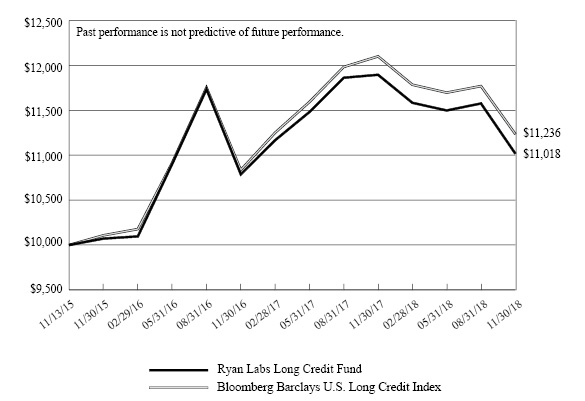

RYAN LABS CORE BOND FUND

(RLCBX)

RYAN LABS LONG CREDIT FUND

(RLLCX)

Annual Report

November 30, 2018

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Funds’ shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Funds or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Funds electronically by contacting the Funds at 1-866-561-3087 or, if you own these shares through a financial intermediary, by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Funds that you wish to continue receiving paper copies of your shareholder reports by contacting the Funds at 1-866-561-3087. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held with the Fund complex or at your financial intermediary.

RYAN LABS FUNDS | November 30, 2018 |

Dear Shareholders,

Following is the Annual Report to shareholders of Ryan Labs Core Bond Fund and Ryan Labs Long Credit Fund (collectively, the “Funds”) for the H2 2018. On behalf of the investment manager, Ryan Labs Asset Management, Inc., we would like to thank you for your continued investment.

MARKET RECAP

Continuing uncertainty on the effects of a trade war with China weighed heavily on markets, as well as liquidity being pulled back by multiple central banks - from the US Fed’s balance sheet reduction or “quantitative tightening” to the end of QE by the ECB. Investment grade spreads widened in August, giving back nearly half of the July tightening, on concerns of heavy issuance in September. Though September saw the much-anticipated supply, issuance was well received. Spreads widened in October and November on the backdrop of Brexit related uncertainty, the anticipated Dec Fed rate hike and Fed’s 2019 policy, plunge in oil prices, and volatility returning to the equity market. Year to date through November, investment grade corporate supply was down 12%. Tax reform and resulting repatriation of offshore cash was the primary driver for the decline in IG corporate supply. WTI Crude traded as high as $76.41 per barrel during the quarter, its highest level since November 2014 and traded as low as $50.93 towards the end of November 2018 on international trade concerns and supply glut. During the quarter, the Federal Reserve raised the federal funds rate by 25 basis points for the third time this year, to a range of 2.0% to 2.25%. As we write this commentary, the Fed raised rates for the fourth time in December. The U.S. 2s/10s yield curve spread has been flattening at a rapid pace. It has narrowed from its 2018 high at 78 bps to 20 bps at the end of November. The yield on 30-year Treasury was 3.29% as of November 30, 2018. In the investment grade structured markets, Agency MBS continued to underperform as the 10-year treasury had remained elevated above 3%. The 30-year fixed rate mortgage rate has touched 5%, causing prepayments speeds to come in at some their slowest levels since the financial crisis. ABS and CMBS mezzanine credit weakened in concert with macro volatility but held in well compared with higher beta corporate credit. The securitized sector overall has been the beneficiary of perceived insulation from global macro concerns such as a trade war with China.

RYAN LABS CORE BOND FUND (RLCBX)

INVESTMENT PHILOSOPHY

The investment objective of Ryan Labs Core Bond Fund (the “Core Bond Fund”) is to seek total return (consisting of current income and capital appreciation) versus the Bloomberg Barclays U.S. Aggregate Bond Index (the “Core Bond Benchmark”). The Core Bond Fund seeks this investment objective while providing protection against interest rate risk. We attempt to accomplish this investment objective by investing at least 80% of Core Bond Fund assets in U.S. dollar-denominated, investment-grade debt securities. The portfolio’s sensitivity to interest rate changes is intended to track the market for domestic, investment-grade fixed-income securities.

1

The modified duration of the Core Bond Fund’s investment portfolio at the end of each calendar month will typically be within half a year of the Core Bond Benchmark. The primary strategies utilized for value-add are sector rotation, issue selection, and yield curve positioning.

PERFORMANCE SUMMARY