| OMB APPROVAL |

OMB Number: 3235-0570

Expires: August 31, 2020

Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANY

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Matthew J. Beck

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | August 31 | |

| Date of reporting period: | August 31, 2018 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Alambic Small Cap Value Plus Fund (ALAMX)

Alambic Small Cap Growth Plus Fund (ALGSX)

Alambic Mid Cap Value Plus Fund (ALMVX)

Alambic Mid Cap Growth Plus Fund (ALMGX)

Annual Report

August 31, 2018

ALAMBIC FUNDS | October 2018 |

Dear Alambic Funds Shareholder:

We are once again pleased to present you with the Alambic Funds’ Annual Report for our fiscal year ended August 31, 2018. This has been an interesting period in the US equity markets and, while portfolio management has been challenging, opportunities for small and mid-cap investors are plentiful for managers with the right strategy. We are honored to have had your support over the past year while we continued to refine our portfolios and validate our belief that a long-term view and disciplined systematic approach to fundamental investing will reward patient, value-focused investors.

The past fiscal year has been dominated first by the expectation, and then reality, of tax cuts, which drove multiples to near historical highs. During this period of “risk on” trading, growth and momentum stocks have consistently outperformed value stocks, and valuation has diminished as a return forecasting factor. Recent concerns over rising inflation, tighter Fed policy, and trade related conflicts have introduced higher volatility. However, volatility has dropped once again as investors appear to ignore the macro challenges for the time being.

Currently, US equities remain broadly expensive vs. history, with every size segment trading at double digit premiums to their historical median valuations. Earnings growth in many cases justifies current levels, but with shares being priced for near perfect results, many firms, particularly in the rapid growth sectors, are vulnerable to disappointing news. It appears that this is not a very popular bull market and, while the equity market keeps rising, investors seem to be focused on what will take the market lower instead of higher.

Performance Review

Alambic Small Cap Value Plus Fund (“ALAMX”)

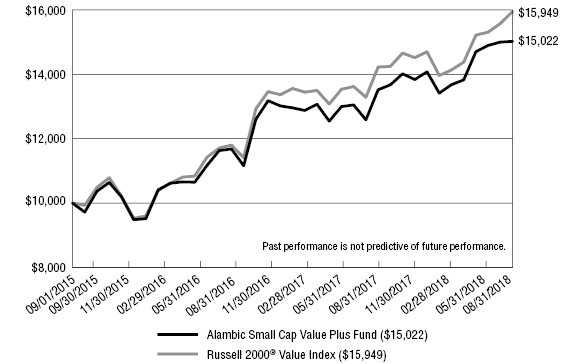

For the fiscal year ended 8/31/2018, ALAMX delivered a total return of 19.36%, compared to the 20.05% return for its benchmark, the Russel 2000 Value® Index. At the end of the fiscal year, this fund was placed in the 42nd percentile of its small cap value peers according to Morningstar. The Fund’s portfolio is managed with a focus on equities that are attractive from a fundamental value perspective and have a very low allocation to growth or momentum stocks. The Fund’s portfolio also tends to have a bias more towards smaller small cap stocks than most of our peer managers, and we tend to be underweight in the financial sector as well. The Funds’ portfolios continue to be built with a systematic, disciplined risk-controlled process, with the goal of delivering excess returns over time.

With the exception of periods where our underweight in financials hurt our performance, we have generally either tracked or beat our benchmark index, the Russell 2000 Value Index. Given that we use almost no growth or momentum factors for this portfolio during the selection process, we are happy with our returns.

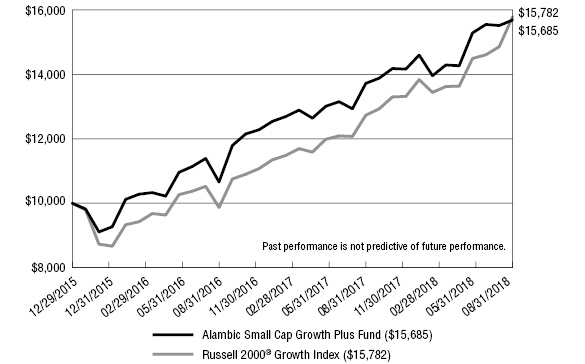

Alambic Small Cap Growth Plus Fund (“ALGSX”)

For the fiscal year ended 8/31/2018, ALGSX delivered a total return of 21.31%, compared to the 30.72% return for its benchmark, the Russell 2000 Growth® Index. The Fund’s portfolio Is managed with a focus on smaller market cap equities that score well on traditional growth factors, such as sales growth, cash flow growth and book value growth. Given our fundamental

1

value bias, we also include value-oriented stocks with certain growth characteristics, which results in our characteristic “value tilt.” Thus, we expect the Fund’s portfolio to outperform its benchmark during market cycles where value stocks outperform growth stocks. During periods where the value and growth stocks’ relative performance is roughly equivalent, we would expect our performance to exceed the benchmark over time, but by a lesser amount. Since inception, this fund has delivered an average annual total return of 18.33%.

Over the past 12 months, growth stocks have consistently outperformed value stocks. Our value bias in this fund relative to other small cap growth funds is reflected in its underperformance this year relative to its benchmark and its peer group. As growth stocks are now very expensive relative to value and earnings, we are broadening out across both sectors and expect this market trend to begin to reverse.

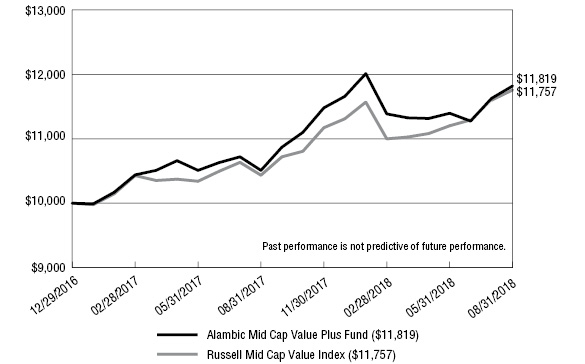

Alambic Mid Cap Value Plus Fund (“ALMVX”)

For the fiscal year ended 8/31/2018, ALMVX delivered a total return of 12.46%, compared to the 12.67% return for its benchmark, the Russell Mid Cap Value® Index. We manage the Fund’s portfolio without the traditional biases of our small cap funds relating to value factors and portfolio average market caps. Our focus on fundamental value stock selection, and the fact that we have avoided intentional portfolio biases, has resulted in returns during the past year that have often exceeded the benchmark.

As this fund was launched less than 2 years ago, its net assets are significantly lower than our small cap funds and, as a result, we carry fewer positions. This results in less diversification than the two small cap funds we manage, and sector weights and individual stocks can have a greater proportional impact on ALMVX’s performance than in those other funds. In the past year, occasional disappointing stock picks had a measurable impact on the fund’s performance, which would have been substantially reduced with a larger number of positions. Although we are pleased with the performance of this fund, we expect performance variability relative to its benchmark to decline as net assets increase.

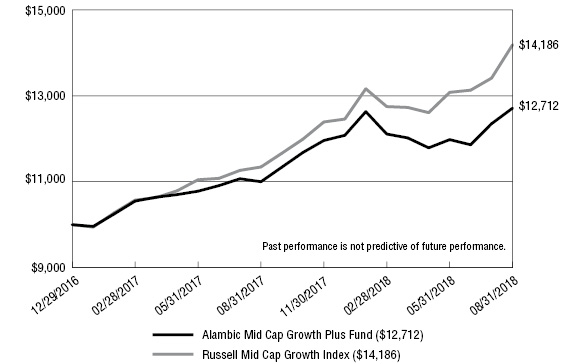

Alambic Mid Cap Growth Plus Fund (“ALMGX”)

For the fiscal year ended 8/31/2018, ALMGX delivered a total return of 15.56%, compared to the 25.06% return for its benchmark, the Russell Mid Cap Growth® Index. Consistent with our small cap growth fund, the Fund’s portfolio has a significant position in mid cap growth stocks, but also includes a significant number of value stocks that have certain growth characteristics. On a style basis, this fund is intentionally aligned more towards mid-cap core than mid cap growth. We expect this value bias to negatively impact the portfolio in strong growth/momentum driven markets, and this is what we experienced during the fiscal year. Conversely, we believe this fund should perform well relative to its benchmark in strong value driven markets.

As with the mid cap growth fund, this fund also has relatively low net assets and, thus, a considerably smaller number of positions than the small cap funds we manage. As it is difficult to maintain similar sector and market segment weights in this fund relative to its benchmark because of its small size, sector and segment imbalances are amplified.

We now have a three-year track record with the Alambic Small Cap Value Fund. We are developing a deeper understanding of how this fund, along with our more recent funds, performs in different market conditions. In some cases, we have tweaked our model to achieve a lower tracking error to our benchmarks, but in most cases, we will promote each fund with

2

the knowledge of its individual idiosyncrasies. We prefer to rely on our model’s long-term predictive characteristics and our systematic approach and will resist reacting to portfolio effects we see in the “rear view mirror.” We will continue to work on building optimal portfolios that will provide attractive returns over time, relative to each fund’s benchmark and its peers.

Thank you for your ongoing trust and commitment.

Sincerely

Albert Richards | Brian Thompson | Rob Slaymaker |

CEO | CRO | Partner |

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1-888-890-8988.

An investor should consider the investment objectives, risks, charges and expenses of the Funds carefully before investing. The Funds’ prospectus contains this and other important information. To obtain a copy of the Funds’ prospectus, please visit our website at http://alambicfunds.com or call 1-888-890-8988 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Alambic Funds are distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Funds that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Funds, may be sold at any time and may no longer be held by the Funds. For a complete list of securities held by the Funds as of August 31, 2018, please see the Schedule of Investments sections of the Annual Report. The opinions of the Funds’ Adviser with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Funds and the market in general and statements of the Funds’ plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

3

ALAMBIC SMALL CAP VALUE PLUS FUND

PERFORMANCE INFORMATION

August 31, 2018 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment

in Alambic Small Cap Value Plus Fund versus the

Russell 2000® Value Index.

Average Annual Total Returns | |||

1 Year | Since | ||

Alambic Small Cap Value Plus Fund(a) | 19.36% | 14.53% | |

Russell 2000® Value Index | 20.05% | 16.84% | |

(a) | The total returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund Shares. |

(b) | Commencement of operations for Alambic Small Cap Value Plus Fund was September 1, 2015. |

4

ALAMBIC SMALL CAP GROWTH PLUS FUND

PERFORMANCE INFORMATION

August 31, 2018 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment

in Alambic Small Cap Growth Plus Fund versus the

Russell 2000® Growth Index.

Average Annual Total Returns | |||

1 Year | Since | ||

Alambic Small Cap Growth Plus Fund(a) | 21.31% | 18.33% | |

Russell 2000® Growth Index | 30.72% | 18.61% | |

(a) | The total returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund Shares. |

(b) | Commencement of operations for Alambic Small Cap Growth Plus Fund was December 29, 2015. |

5

ALAMBIC MID CAP VALUE PLUS FUND

PERFORMANCE INFORMATION

August 31, 2018 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment

in Alambic Mid Cap Value Plus Fund versus the

Russell Mid Cap Value Index.

Average Annual Total Returns | |||

1 Year | Since | ||

Alambic Mid Cap Value Plus Fund(a) | 12.46% | 10.52% | |

Russell Mid Cap Value Index | 12.67% | 10.17% | |

(a) | The total returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund Shares. |

(b) | Commencement of operations for Alambic Mid Cap Value Plus Fund was December 29, 2016. |

6

ALAMBIC MID CAP GROWTH PLUS FUND

PERFORMANCE INFORMATION

August 31, 2018 (Unaudited)

Comparison of the Change in Value of a $10,000 Investment

in Alambic Mid Cap Growth Plus Fund versus the

Russell Mid Cap Growth Index.

Average Annual Total Returns | |||

1 Year | Since | ||

Alambic Mid Cap Growth Plus Fund(a) | 15.56% | 15.44% | |

Russell Mid Cap Growth Index | 25.06% | 23.27% | |

(a) | The total returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund Shares. |

(b) | Commencement of operations for Alambic Mid Cap Growth Plus Fund was December 29, 2016. |

7

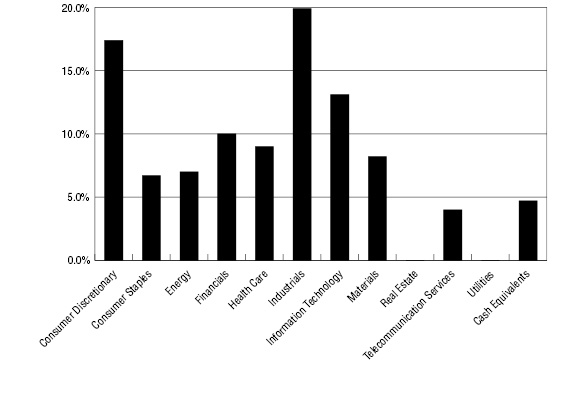

ALAMBIC SMALL CAP VALUE PLUS FUND

PORTFOLIO INFORMATION

August 31, 2018 (Unaudited)

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

Security Description | % of Net Assets |

ARC Document Solutions, Inc. | 2.6% |

Tredegar Corporation | 2.5% |

DSP Group, Inc. | 2.3% |

Xcerra Corporation | 2.2% |

Tower International, Inc. | 2.0% |

Bridgepoint Education, Inc. | 1.9% |

Speedway Motorsports, Inc. | 1.8% |

Ooma, Inc. | 1.8% |

Nautilus, Inc. | 1.6% |

Acacia Research Corporation | 1.6% |

8

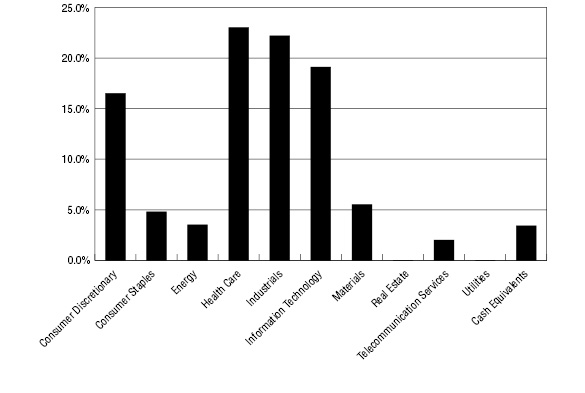

ALAMBIC SMALL CAP GROWTH PLUS FUND

PORTFOLIO INFORMATION

August 31, 2018 (Unaudited)

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

Security Description | % of Net Assets |

Xcerra Corporation | 3.0% |

Tredegar Corporation | 2.2% |

Commercial Vehicle Group, Inc. | 2.1% |

Tower International, Inc. | 1.9% |

DSP Group, Inc. | 1.9% |

Pfenex, Inc. | 1.7% |

Luminex Corporation | 1.7% |

EVERTEC, Inc. | 1.7% |

Natural Grocers by Vitamin Cottage, Inc. | 1.7% |

XO Group, Inc. | 1.6% |

9

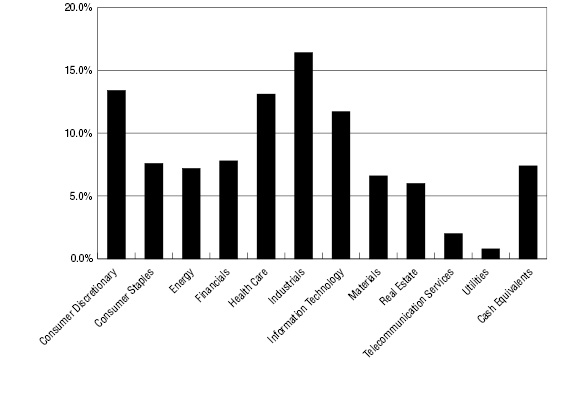

ALAMBIC MID CAP VALUE PLUS FUND

PORTFOLIO INFORMATION

August 31, 2018 (Unaudited)

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

Security Description | % of Net Assets |

Archer-Daniels-Midland Company | 2.7% |

AGCO Corporation | 2.6% |

Bio-Rad Laboratories, Inc. - Class A | 2.4% |

Xerox Corporation | 2.3% |

Allison Transmission Holdings, Inc. | 2.1% |

Hewlett Packard Enterprise Company | 2.0% |

United States Cellular Corporation | 2.0% |

Textron, Inc. | 1.8% |

Hunstman Corporation | 1.7% |

Viacom, Inc. - Class B | 1.6% |

10

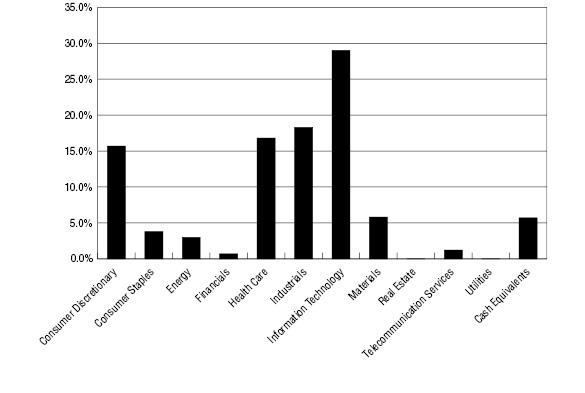

ALAMBIC MID CAP GROWTH PLUS FUND

PORTFOLIO INFORMATION

August 31, 2018 (Unaudited)

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

Security Description | % of Net Assets |

AGCO Corporation | 2.8% |

Xerox Corporation | 2.2% |

Bio-Rad Laboratories, Inc. - Class A | 2.2% |

Allison Transmission Holdings, Inc. | 2.2% |

Hewlett Packard Enterprise Company | 2.2% |

WestRock Company | 1.9% |

CA, Inc. | 1.8% |

Archer-Daniels-Midland Company | 1.7% |

Zebra Technologies Corporation - Class A | 1.7% |

Laureate Education, Inc. - Class A | 1.6% |

11

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% | Shares | Value | ||||||

Consumer Discretionary — 17.4% | ||||||||

Auto Components — 3.1% | ||||||||

Stoneridge, Inc. (a) | 781 | $ | 23,375 | |||||

Tenneco, Inc. | 250 | 10,698 | ||||||

Tower International, Inc. | 2,000 | 67,600 | ||||||

| 101,673 | ||||||||

Distributors — 0.2% | ||||||||

VOXX International Corporation (a) | 1,459 | 7,879 | ||||||

Diversified Consumer Services — 4.3% | ||||||||

American Public Education, Inc. (a) | 600 | 20,850 | ||||||

Bridgepoint Education, Inc. (a) | 5,455 | 64,151 | ||||||

K12, Inc. (a) | 2,450 | 40,572 | ||||||

Laureate Education, Inc. - Class A (a) | 1,100 | 17,567 | ||||||

| 143,140 | ||||||||

Hotels, Restaurants & Leisure — 2.5% | ||||||||

Carrols Restaurant Group, Inc. (a) | 200 | 3,160 | ||||||

Potbelly Corporation (a) | 1,487 | 20,149 | ||||||

Speedway Motorsports, Inc. | 3,400 | 60,826 | ||||||

| 84,135 | ||||||||

Household Durables — 1.2% | ||||||||

Bassett Furniture Industries, Inc. | 380 | 8,873 | ||||||

Flexsteel Industries, Inc. | 834 | 29,757 | ||||||

| 38,630 | ||||||||

Leisure Products — 1.6% | ||||||||

Nautilus, Inc. (a) | 3,587 | 52,550 | ||||||

Media — 3.5% | ||||||||

Gannett Company, Inc. | 1,700 | 17,476 | ||||||

Lee Enterprises, Inc. (a) | 17,729 | 50,528 | ||||||

MSG Networks, Inc. - Class A (a) | 1,165 | 28,309 | ||||||

Townsquare Media, Inc. - Class A (a) | 300 | 2,679 | ||||||

tronc, Inc. (a) | 1,012 | 16,698 | ||||||

| 115,690 | ||||||||

Specialty Retail — 0.5% | ||||||||

Ascena Retail Group, Inc. (a) | 2,100 | 9,618 | ||||||

Citi Trends, Inc. | 200 | 6,188 | ||||||

| 15,806 | ||||||||

Textiles, Apparel & Luxury Goods — 0.5% | ||||||||

Movado Group, Inc. | 200 | 8,520 | ||||||

Vera Bradley, Inc. (a) | 472 | 6,919 | ||||||

| 15,439 | ||||||||

12

See accompanying notes to financial statements.

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% (Continued) | Shares | Value | ||||||

Consumer Staples — 6.7% | ||||||||

Beverages — 0.5% | ||||||||

Boston Beer Company, Inc. (The) - Class A (a) | 20 | $ | 6,063 | |||||

Coca-Cola Bottling Company Consolidated | 40 | 6,782 | ||||||

Keurig Dr Pepper, Inc. | 100 | 2,280 | ||||||

| 15,125 | ||||||||

Food & Staples Retailing — 3.2% | ||||||||

Natural Grocers by Vitamin Cottage, Inc. (a) | 2,630 | 51,048 | ||||||

SpartanNash Company | 424 | 9,052 | ||||||

Village Super Market, Inc. - Class A | 1,609 | 46,951 | ||||||

| 107,051 | ||||||||

Food Products — 0.5% | ||||||||

Dean Foods Company | 2,196 | 16,734 | ||||||

Household Products — 2.3% | ||||||||

Central Garden & Pet Company - Class A (a) | 800 | 29,064 | ||||||

Oil-Dri Corporation of America | 1,150 | 46,748 | ||||||

| 75,812 | ||||||||

Personal Products — 0.2% | ||||||||

LifeVantage Corporation (a) | 500 | 6,280 | ||||||

Energy — 7.0% | ||||||||

Energy Equipment & Services — 1.5% | ||||||||

FTS International, Inc. (a) | 600 | 6,618 | ||||||

Helix Energy Solutions Group, Inc. (a) | 300 | 2,808 | ||||||

Mammoth Energy Services, Inc. | 800 | 21,984 | ||||||

Pioneer Energy Services Corporation (a) | 1,268 | 4,057 | ||||||

Superior Energy Services, Inc. (a) | 1,091 | 9,819 | ||||||

Unit Corporation (a) | 200 | 5,258 | ||||||

| 50,544 | ||||||||

Oil, Gas & Consumable Fuels — 5.5% | ||||||||

Adams Resources & Energy, Inc. | 1,018 | 46,727 | ||||||

Evolution Petroleum Corporation | 1,900 | 19,095 | ||||||

Overseas Shipholding Group, Inc. - Class A (a) | 10,712 | 36,742 | ||||||

PBF Energy, Inc. - Class A | 50 | 2,596 | ||||||

Renewable Energy Group, Inc. (a) | 600 | 16,170 | ||||||

VAALCO Energy, Inc. (a) | 14,379 | 34,797 | ||||||

W&T Offshore, Inc. (a) | 3,656 | 24,751 | ||||||

| 180,878 | ||||||||

Financials — 10.0% | ||||||||

Banks — 9.9% | ||||||||

Associated Banc-Corp | 300 | 8,175 | ||||||

Cadence Bancorporation | 600 | 16,950 | ||||||

Cathay General Bancorp | 200 | 8,460 | ||||||

13

See accompanying notes to financial statements.

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% (Continued) | Shares | Value | ||||||

Financials — 10.0% (Continued) | ||||||||

Banks — 9.9% (Continued) | ||||||||

Chemical Financial Corporation | 550 | $ | 31,416 | |||||

Columbia Banking System, Inc. | 350 | 14,788 | ||||||

Community Bank System, Inc. | 150 | 9,920 | ||||||

Customers Bancorp, Inc. (a) | 100 | 2,470 | ||||||

CVB Financial Corporation | 100 | 2,405 | ||||||

First Busey Corporation | 100 | 3,205 | ||||||

First Citizens BancShares, Inc. - Class A | 10 | 4,750 | ||||||

First Financial Bancorp | 300 | 9,420 | ||||||

First Financial Bankshares, Inc. | 100 | 6,040 | ||||||

First Midwest Bancorp, Inc. | 300 | 8,154 | ||||||

Fulton Financial Corporation | 300 | 5,460 | ||||||

Glacier Bancorp, Inc. | 100 | 4,568 | ||||||

Great Western Bancorp, Inc. | 500 | 21,770 | ||||||

Hancock Whitney Corporation | 300 | 15,465 | ||||||

Heartland Financial USA, Inc. | 150 | 9,120 | ||||||

Home BancShares, Inc. | 200 | 4,682 | ||||||

Hope Bancorp, Inc. | 600 | 10,506 | ||||||

IBERIABANK Corporation | 90 | 7,799 | ||||||

Independent Bank Corporation | 20 | 1,822 | ||||||

Independent Bank Group, Inc. | 50 | 3,463 | ||||||

International Bancshares Corporation | 50 | 2,342 | ||||||

MB Financial, Inc. | 200 | 9,692 | ||||||

Preferred Bank | 50 | 3,060 | ||||||

Renasant Corporation | 150 | 7,003 | ||||||

Republic First Bancorp, Inc. (a) | 500 | 3,900 | ||||||

ServisFirst Bancshares, Inc. | 150 | 6,465 | ||||||

Simmons First National Corporation - Class A | 200 | 6,320 | ||||||

South State Corporation | 260 | 21,437 | ||||||

TCF Financial Corporation | 200 | 5,070 | ||||||

UMB Financial Corporation | 180 | 13,543 | ||||||

United Bankshares, Inc. | 400 | 15,760 | ||||||

United Community Banks, Inc. | 600 | 18,204 | ||||||

Valley National Bancorp | 400 | 4,820 | ||||||

| 328,424 | ||||||||

Insurance — 0.1% | ||||||||

American Equity Investment Life Holding Company | 100 | 3,709 | ||||||

Health Care — 9.0% | ||||||||

Biotechnology — 2.5% | ||||||||

Acorda Therapeutics, Inc. (a) | 300 | 8,640 | ||||||

Calithera Biosciences, Inc. (a) | 1,499 | 8,170 | ||||||

14

See accompanying notes to financial statements.

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% (Continued) | Shares | Value | ||||||

Health Care — 9.0% (Continued) | ||||||||

Biotechnology — 2.5% (Continued) | ||||||||

Jounce Therapeutics, Inc. (a) | 1,894 | $ | 14,868 | |||||

Pfenex, Inc. (a) | 7,580 | 40,022 | ||||||

REGENXBIO, Inc. (a) | 50 | 3,522 | ||||||

Vanda Pharmaceuticals, Inc. (a) | 400 | 7,730 | ||||||

| 82,952 | ||||||||

Health Care Equipment & Supplies — 2.9% | ||||||||

Accuray, Inc. (a) | 2,567 | 10,268 | ||||||

AngioDynamics, Inc. (a) | 920 | 20,626 | ||||||

RTI Surgical, Inc. (a) | 5,465 | 24,456 | ||||||

Varex Imaging Corporation (a) | 1,300 | 40,820 | ||||||

| 96,170 | ||||||||

Health Care Providers & Services — 0.3% | ||||||||

American Renal Associates Holdings, Inc. (a) | 386 | 8,473 | ||||||

Health Care Technology — 1.9% | ||||||||

Allscripts Healthcare Solutions, Inc. (a) | 2,500 | 36,525 | ||||||

HealthStream, Inc. | 300 | 9,519 | ||||||

Quality Systems, Inc. (a) | 800 | 18,312 | ||||||

| 64,356 | ||||||||

Life Sciences Tools & Services — 1.0% | ||||||||

Luminex Corporation | 1,200 | 33,852 | ||||||

Pharmaceuticals — 0.4% | ||||||||

Assertio Therapeutics, Inc. (a) | 300 | 1,914 | ||||||

Lannett Company, Inc. (a) | 2,200 | 11,770 | ||||||

| 13,684 | ||||||||

Industrials — 19.9% | ||||||||

Aerospace & Defense — 2.0% | ||||||||

Engility Holdings, Inc. (a) | 200 | 6,942 | ||||||

Esterline Technologies Corporation (a) | 500 | 42,975 | ||||||

Moog, Inc. - Class A | 200 | 15,782 | ||||||

| 65,699 | ||||||||

Building Products — 1.9% | ||||||||

Armstrong Flooring, Inc. (a) | 1,964 | 34,390 | ||||||

NCI Building Systems, Inc. (a) | 1,800 | 30,420 | ||||||

| 64,810 | ||||||||

Commercial Services & Supplies — 3.6% | ||||||||

ARC Document Solutions, Inc. (a) | 26,200 | 84,364 | ||||||

Brady Corporation - Class A | 421 | 17,029 | ||||||

Kimball International, Inc. - Class B | 1,000 | 17,470 | ||||||

| 118,863 | ||||||||

15

See accompanying notes to financial statements.

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% (Continued) | Shares | Value | ||||||

Industrials — 19.9% (Continued) | ||||||||

Construction & Engineering — 1.3% | ||||||||

HC2 Holdings, Inc. (a) | 2,400 | $ | 15,048 | |||||

Orion Group Holdings, Inc. (a) | 3,100 | 26,722 | ||||||

| 41,770 | ||||||||

Electrical Equipment — 2.1% | ||||||||

Allied Motion Technologies, Inc. | 200 | 9,768 | ||||||

Atkore International Group, Inc. (a) | 600 | 16,428 | ||||||

Preformed Line Products Company | 540 | 44,118 | ||||||

| 70,314 | ||||||||

Machinery — 5.6% | ||||||||

AGCO Corporation | 550 | 32,813 | ||||||

Commercial Vehicle Group, Inc. (a) | 3,531 | 34,463 | ||||||

Global Brass & Copper Holdings, Inc. | 400 | 15,420 | ||||||

Hurco Companies, Inc. | 875 | 37,537 | ||||||

L.B. Foster Company - Class A (a) | 2,136 | 48,594 | ||||||

Meritor, Inc. (a) | 700 | 15,162 | ||||||

| 183,989 | ||||||||

Professional Services — 2.0% | ||||||||

Acacia Research Corporation (a) | 13,318 | 51,940 | ||||||

Heidrick & Struggles International, Inc. | 300 | 13,260 | ||||||

| 65,200 | ||||||||

Road & Rail — 0.7% | ||||||||

Covenant Transportation Group, Inc. - Class A (a) | 33 | 986 | ||||||

YRC Worldwide, Inc. (a) | 2,477 | 23,705 | ||||||

| 24,691 | ||||||||

Trading Companies & Distributors — 0.7% | ||||||||

BMC Stock Holdings, Inc. (a) | 500 | 11,250 | ||||||

Nexeo Solutions, Inc. (a) | 1,127 | 11,281 | ||||||

| 22,531 | ||||||||

Information Technology — 13.1% | ||||||||

Communications Equipment — 0.4% | ||||||||

Bel Fuse, Inc. - Class B | 200 | 5,730 | ||||||

Calix, Inc. (a) | 900 | 7,020 | ||||||

| 12,750 | ||||||||

Electronic Equipment, Instruments & Components — 0.4% | ||||||||

Insight Enterprises, Inc. (a) | 100 | 5,514 | ||||||

Vishay Precision Group, Inc. (a) | 200 | 8,660 | ||||||

| 14,174 | ||||||||

Internet Software & Services — 2.8% | ||||||||

Aerohive Networks, Inc. (a) | 8,300 | 35,026 | ||||||

eGain Corporation (a) | 700 | 10,010 | ||||||

Endurance International Group Holdings, Inc. (a) | 200 | 1,930 | ||||||

16

See accompanying notes to financial statements.

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% (Continued) | Shares | Value | ||||||

Information Technology — 13.1% (Continued) | ||||||||

Internet Software & Services — 2.8% (Continued) | ||||||||

QuinStreet, Inc. (a) | 800 | $ | 12,136 | |||||

XO Group, Inc. (a) | 1,140 | 34,268 | ||||||

| 93,370 | ||||||||

IT Services — 2.5% | ||||||||

EVERTEC, Inc. | 1,600 | 38,480 | ||||||

Sykes Enterprises, Inc. (a) | 1,469 | 44,423 | ||||||

| 82,903 | ||||||||

Semiconductors & Semiconductor Equipment — 6.2% | ||||||||

Amkor Technology, Inc. (a) | 2,100 | 18,333 | ||||||

DSP Group, Inc. (a) | 5,796 | 74,479 | ||||||

Nanometrics, Inc. (a) | 150 | 6,571 | ||||||

Photronics, Inc. (a) | 2,150 | 23,005 | ||||||

Veeco Instruments, Inc. (a) | 800 | 9,600 | ||||||

Xcerra Corporation (a) | 5,090 | 73,703 | ||||||

| 205,691 | ||||||||

Software — 0.3% | ||||||||

Agilysys, Inc. (a) | 333 | 5,351 | ||||||

American Software, Inc. - Class A | 267 | 4,801 | ||||||

| 10,152 | ||||||||

Technology Hardware, Storage & Peripherals — 0.5% | ||||||||

Avid Technology, Inc. (a) | 2,636 | 15,605 | ||||||

Materials — 8.2% | ||||||||

Chemicals — 4.0% | ||||||||

AdvanSix, Inc. (a) | 700 | 23,688 | ||||||

Kronos Worldwide, Inc. | 400 | 8,052 | ||||||

OMNOVA Solutions, Inc. (a) | 101 | 914 | ||||||

Tredegar Corporation | 3,825 | 83,959 | ||||||

Valhi, Inc. | 4,344 | 14,335 | ||||||

| 130,948 | ||||||||

Construction Materials — 1.5% | ||||||||

United States Lime & Minerals, Inc. | 674 | 51,150 | ||||||

Containers & Packaging — 1.6% | ||||||||

Owens-Illinois, Inc. (a) | 2,900 | 51,243 | ||||||

Metals & Mining — 1.1% | ||||||||

Cleveland-Cliffs, Inc. (a) | 200 | 2,010 | ||||||

Gold Resource Corporation | 4,738 | 24,448 | ||||||

Schnitzer Steel Industries, Inc. - Class A | 300 | 7,905 | ||||||

SunCoke Energy, Inc. (a) | 200 | 2,232 | ||||||

| 36,595 | ||||||||

17

See accompanying notes to financial statements.

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 95.3% (Continued) | Shares | Value | ||||||

Telecommunication Services — 4.0% | ||||||||

Diversified Telecommunication Services — 1.8% | ||||||||

Ooma, Inc. (a) | 3,600 | $ | 57,600 | |||||

Wireless Telecommunication Services — 2.2% | ||||||||

Spok Holdings, Inc. | 2,274 | 34,906 | ||||||

United States Cellular Corporation (a) | 900 | 38,484 | ||||||

| 73,390 | ||||||||

Total Common Stocks (Cost $2,753,798) | $ | 3,152,424 | ||||||

| ||||||||

RIGHTS — 0.0% (b) | Shares | Value | ||||||

Media General, Inc. - CVR (a)(c) (Cost $0) | 100 | $ | 5 | |||||

Total Investments at Value — 95.3% (Cost $2,753,798) | $ | 3,152,429 | ||||||

Other Assets in Excess of Liabilities — 4.7% | 154,296 | |||||||

Net Assets — 100.0% | $ | 3,306,725 | ||||||

CVR - Contingent Value Right.

| (a) | Non-income producing security. |

| (b) | Percentage rounds to less than 0.1%. |

| (c) | Illiquid security. Security value has been determined in good faith pursuant to procedures adopted by the Board of Trustees. The total value of such securities was $5 as of August 31, 2018, representing 0.0% (b) of net assets (Note 2). |

18

See accompanying notes to financial statements.

ALAMBIC SMALL CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 96.6% | Shares | Value | ||||||

Consumer Discretionary — 16.5% | ||||||||

Auto Components — 2.7% | ||||||||

Tenneco, Inc. | 550 | $ | 23,534 | |||||

Tower International, Inc. | 1,800 | 60,840 | ||||||

| 84,374 | ||||||||

Distributors — 0.0% (a) | ||||||||

VOXX International Corporation (b) | 150 | 810 | ||||||

Diversified Consumer Services — 4.6% | ||||||||

American Public Education, Inc. (b) | 600 | 20,850 | ||||||

Bridgepoint Education, Inc. (b) | 3,620 | 42,571 | ||||||

K12, Inc. (b) | 2,775 | 45,954 | ||||||

Laureate Education, Inc. - Class A (b) | 1,200 | 19,164 | ||||||

Weight Watchers International, Inc. (b) | 200 | 14,980 | ||||||

| 143,519 | ||||||||

Hotels, Restaurants & Leisure — 3.0% | ||||||||

BBX Capital Corporation | 680 | 5,052 | ||||||

Bojangles', Inc. (b) | 792 | 11,563 | ||||||

International Speedway Corporation - Class A | 300 | 13,245 | ||||||

Marcus Corporation (The) | 100 | 4,060 | ||||||

Potbelly Corporation (b) | 1,100 | 14,905 | ||||||

Speedway Motorsports, Inc. | 2,023 | 36,192 | ||||||

Town Sports International Holdings, Inc. (b) | 945 | 8,647 | ||||||

| 93,664 | ||||||||

Household Durables — 1.4% | ||||||||

Flexsteel Industries, Inc. | 1,055 | 37,643 | ||||||

LGI Homes, Inc. (b) | 142 | 8,179 | ||||||

| 45,822 | ||||||||

Leisure Products — 1.1% | ||||||||

Johnson Outdoors, Inc. - Class A | 60 | 6,077 | ||||||

Nautilus, Inc. (b) | 2,026 | 29,681 | ||||||

| 35,758 | ||||||||

Media — 2.0% | ||||||||

Gannett Company, Inc. | 400 | 4,112 | ||||||

Lee Enterprises, Inc. (b) | 8,810 | 25,108 | ||||||

MSG Networks, Inc. - Class A (b) | 500 | 12,150 | ||||||

Townsquare Media, Inc. - Class A (b) | 600 | 5,358 | ||||||

tronc, Inc. (b) | 900 | 14,850 | ||||||

| 61,578 | ||||||||

Specialty Retail — 0.5% | ||||||||

Citi Trends, Inc. | 400 | 12,376 | ||||||

Express, Inc. (b) | 300 | 3,366 | ||||||

| 15,742 | ||||||||

19

See accompanying notes to financial statements.

ALAMBIC SMALL CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 96.6% (Continued) | Shares | Value | ||||||

Consumer Discretionary — 16.5% (Continued) | ||||||||

Textiles, Apparel & Luxury Goods — 1.2% | ||||||||

Movado Group, Inc. | 300 | $ | 12,780 | |||||

Vera Bradley, Inc. (b) | 1,677 | 24,585 | ||||||

| 37,365 | ||||||||

Consumer Staples — 4.8% | ||||||||

Food & Staples Retailing — 2.4% | ||||||||

Natural Grocers by Vitamin Cottage, Inc. (b) | 2,700 | 52,407 | ||||||

SpartanNash Company | 3 | 64 | ||||||

Village Super Market, Inc. - Class A | 791 | 23,081 | ||||||

| 75,552 | ||||||||

Household Products — 2.0% | ||||||||

Central Garden & Pet Company - Class A (b) | 700 | 25,431 | ||||||

Energizer Holdings, Inc. | 250 | 15,898 | ||||||

Oil-Dri Corporation of America | 557 | 22,642 | ||||||

| 63,971 | ||||||||

Personal Products — 0.4% | ||||||||

LifeVantage Corporation (b) | 1,000 | 12,560 | ||||||

Energy — 3.5% | ||||||||

Energy Equipment & Services — 0.6% | ||||||||

Mammoth Energy Services, Inc. | 550 | 15,114 | ||||||

Superior Energy Services, Inc. (b) | 364 | 3,276 | ||||||

| 18,390 | ||||||||

Oil, Gas & Consumable Fuels — 2.9% | ||||||||

Adams Resources & Energy, Inc. | 511 | 23,455 | ||||||

Evolution Petroleum Corporation | 1,700 | 17,085 | ||||||

Overseas Shipholding Group, Inc. - Class A (b) | 2,048 | 7,024 | ||||||

VAALCO Energy, Inc. (b) | 10,221 | 24,735 | ||||||

W&T Offshore, Inc. (b) | 2,958 | 20,026 | ||||||

| 92,325 | ||||||||

Health Care — 23.0% | ||||||||

Biotechnology — 9.5% | ||||||||

Acorda Therapeutics, Inc. (b) | 800 | 23,040 | ||||||

AMAG Pharmaceuticals, Inc. (b) | 300 | 7,320 | ||||||

Amicus Therapeutics, Inc. (b) | 800 | 10,784 | ||||||

Calithera Biosciences, Inc. (b) | 1,000 | 5,450 | ||||||

ChemoCentryx, Inc. (b) | 200 | 2,636 | ||||||

Emergent BioSolutions, Inc. (b) | 250 | 15,500 | ||||||

Enanta Pharmaceuticals, Inc. (b) | 260 | 23,642 | ||||||

Genomic Health, Inc. (b) | 250 | 15,292 | ||||||

Halozyme Therapeutics, Inc. (b) | 1,200 | 22,092 | ||||||

Inovio Pharmaceuticals, Inc. (b) | 700 | 3,682 | ||||||

Jounce Therapeutics, Inc. (b) | 1,864 | 14,632 | ||||||

20

See accompanying notes to financial statements.

ALAMBIC SMALL CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 96.6% (Continued) | Shares | Value | ||||||

Health Care — 23.0% (Continued) | ||||||||

Biotechnology — 9.5% (Continued) | ||||||||

MacroGenics, Inc. (b) | 900 | $ | 19,683 | |||||

Pfenex, Inc. (b) | 10,359 | 54,696 | ||||||

PTC Therapeutics, Inc. (b) | 50 | 2,087 | ||||||

REGENXBIO, Inc. (b) | 350 | 24,657 | ||||||

Retrophin, Inc. (b) | 600 | 19,014 | ||||||

Vanda Pharmaceuticals, Inc. (b) | 1,700 | 32,853 | ||||||

| 297,060 | ||||||||

Health Care Equipment & Supplies — 5.1% | ||||||||

Accuray, Inc. (b) | 4,298 | 17,192 | ||||||

AngioDynamics, Inc. (b) | 1,220 | 27,352 | ||||||

Cardiovascular Systems, Inc. (b) | 100 | 3,853 | ||||||

Cerus Corporation (b) | 1,200 | 9,336 | ||||||

FONAR Corporation (b) | 100 | 2,620 | ||||||

Integer Holdings Corporation (b) | 250 | 19,975 | ||||||

Meridian Bioscience, Inc. | 100 | 1,570 | ||||||

Orthofix Medical, Inc. (b) | 350 | 18,746 | ||||||

RTI Surgical, Inc. (b) | 5,900 | 26,403 | ||||||

STAAR Surgical Company (b) | 700 | 33,390 | ||||||

| 160,437 | ||||||||

Health Care Providers & Services — 1.3% | ||||||||

American Renal Associates Holdings, Inc. (b) | 900 | 19,755 | ||||||

Cardinal Health, Inc. | 100 | 5,219 | ||||||

Express Scripts Holding Company (b) | 50 | 4,401 | ||||||

Select Medical Holdings Corporation (b) | 600 | 11,880 | ||||||

| 41,255 | ||||||||

Health Care Technology — 2.2% | ||||||||

Allscripts Healthcare Solutions, Inc. (b) | 2,300 | 33,603 | ||||||

HealthStream, Inc. | 908 | 28,811 | ||||||

Quality Systems, Inc. (b) | 300 | 6,867 | ||||||

| 69,281 | ||||||||

Life Sciences Tools & Services — 2.5% | ||||||||

Luminex Corporation | 1,900 | 53,599 | ||||||

Medpace Holdings, Inc. (b) | 400 | 23,916 | ||||||

| 77,515 | ||||||||

Pharmaceuticals — 2.4% | ||||||||

Innoviva, Inc. (b) | 1,000 | 14,520 | ||||||

Lannett Company, Inc. (b) | 300 | 1,605 | ||||||

Mylan N.V. (b) | 600 | 23,478 | ||||||

Nektar Therapeutics (b) | 250 | 16,622 | ||||||

Supernus Pharmaceuticals, Inc. (b) | 450 | 19,935 | ||||||

| 76,160 | ||||||||

21

See accompanying notes to financial statements.

ALAMBIC SMALL CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 96.6% (Continued) | Shares | Value | ||||||

Industrials — 22.2% | ||||||||

Aerospace & Defense — 2.0% | ||||||||

Engility Holdings, Inc. (b) | 800 | $ | 27,768 | |||||

Esterline Technologies Corporation (b) | 190 | 16,330 | ||||||

Moog, Inc. - Class A | 250 | 19,728 | ||||||

| 63,826 | ||||||||

Building Products — 1.5% | ||||||||

Armstrong Flooring, Inc. (b) | 938 | 16,424 | ||||||

Continental Building Products, Inc. (b) | 300 | 11,190 | ||||||

NCI Building Systems, Inc. (b) | 1,139 | 19,249 | ||||||

| 46,863 | ||||||||

Commercial Services & Supplies — 4.1% | ||||||||

ARC Document Solutions, Inc. (b) | 15,800 | 50,876 | ||||||

Brady Corporation - Class A | 537 | 21,722 | ||||||

Ennis, Inc. | 300 | 6,540 | ||||||

Herman Miller, Inc. | 600 | 22,980 | ||||||

Kimball International, Inc. - Class B | 1,451 | 25,349 | ||||||

| 127,467 | ||||||||

Construction & Engineering — 1.3% | ||||||||

Ameresco, Inc. - Class A (b) | 121 | 1,736 | ||||||

HC2 Holdings, Inc. (b) | 1,350 | 8,465 | ||||||

Orion Group Holdings, Inc. (b) | 3,700 | 31,894 | ||||||

| 42,095 | ||||||||

Electrical Equipment — 3.0% | ||||||||

Allied Motion Technologies, Inc. | 550 | 26,862 | ||||||

Atkore International Group, Inc. (b) | 1,000 | 27,380 | ||||||

Preformed Line Products Company | 325 | 26,553 | ||||||

Vicor Corporation (b) | 200 | 12,490 | ||||||

| 93,285 | ||||||||

Machinery — 6.9% | ||||||||

AGCO Corporation | 600 | 35,796 | ||||||

Allison Transmission Holdings, Inc. | 300 | 14,898 | ||||||

Commercial Vehicle Group, Inc. (b) | 6,707 | 65,460 | ||||||

Global Brass & Copper Holdings, Inc. | 800 | 30,840 | ||||||

Hurco Companies, Inc. | 734 | 31,489 | ||||||

L.B. Foster Company - Class A (b) | 774 | 17,608 | ||||||

Meritor, Inc. (b) | 900 | 19,494 | ||||||

| 215,585 | ||||||||

Professional Services — 2.6% | ||||||||

Acacia Research Corporation (b) | 9,475 | 36,952 | ||||||

Heidrick & Struggles International, Inc. | 427 | 18,873 | ||||||

Korn/Ferry International | 350 | 23,496 | ||||||

Resources Connection, Inc. | 200 | 3,310 | ||||||

| 82,631 | ||||||||

22

See accompanying notes to financial statements.

ALAMBIC SMALL CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 96.6% (Continued) | Shares | Value | ||||||

Industrials — 22.2% (Continued) | ||||||||

Road & Rail — 0.5% | ||||||||

YRC Worldwide, Inc. (b) | 1,512 | $ | 14,470 | |||||

Trading Companies & Distributors — 0.3% | ||||||||

BMC Stock Holdings, Inc. (b) | 400 | 9,000 | ||||||

Information Technology — 19.1% | ||||||||

Communications Equipment — 0.9% | ||||||||

Bel Fuse, Inc. - Class B | 700 | 20,055 | ||||||

Calix, Inc. (b) | 600 | 4,680 | ||||||

Digi International, Inc. (b) | 276 | 3,712 | ||||||

| 28,447 | ||||||||

Electronic Equipment, Instruments & Components —1.4% | ||||||||

Electro Scientific Industries, Inc. (b) | 300 | 6,585 | ||||||

Insight Enterprises, Inc. (b) | 350 | 19,299 | ||||||

Vishay Precision Group, Inc. (b) | 400 | 17,320 | ||||||

| 43,204 | ||||||||

Internet Software & Services — 4.5% | ||||||||

Aerohive Networks, Inc. (b) | 6,500 | 27,430 | ||||||

eGain Corporation (b) | 2,786 | 39,840 | ||||||

Endurance International Group Holdings, Inc. (b) | 600 | 5,790 | ||||||

QuinStreet, Inc. (b) | 1,000 | 15,170 | ||||||

XO Group, Inc. (b) | 1,720 | 51,703 | ||||||

| 139,933 | ||||||||

IT Services — 2.9% | ||||||||

EVERTEC, Inc. | 2,185 | 52,549 | ||||||

Sykes Enterprises, Inc. (b) | 1,300 | 39,312 | ||||||

| 91,861 | ||||||||

Semiconductors & Semiconductor Equipment — 6.1% | ||||||||

DSP Group, Inc. (b) | 4,586 | 58,930 | ||||||

Nanometrics, Inc. (b) | 550 | 24,096 | ||||||

Photronics, Inc. (b) | 301 | 3,221 | ||||||

Rudolph Technologies, Inc. (b) | 400 | 11,120 | ||||||

Xcerra Corporation (b) | 6,588 | 95,394 | ||||||

| 192,761 | ||||||||

Software — 2.7% | ||||||||

Agilysys, Inc. (b) | 1,567 | 25,182 | ||||||

American Software, Inc. - Class A | 1,226 | 22,043 | ||||||

OneSpan, Inc. (b) | 900 | 16,875 | ||||||

QAD, Inc. - Class A | 300 | 18,195 | ||||||

Rosetta Stone, Inc. (b) | 120 | 1,896 | ||||||

| 84,191 | ||||||||

23

See accompanying notes to financial statements.

ALAMBIC SMALL CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 96.6% (Continued) | Shares | Value | ||||||

Information Technology — 19.1% (Continued) | ||||||||

Technology Hardware, Storage & Peripherals — 0.6% | ||||||||

Avid Technology, Inc. (b) | 3,061 | $ | 18,121 | |||||

Materials — 5.5% | ||||||||

Chemicals — 3.6% | ||||||||

AdvanSix, Inc. (b) | 500 | 16,920 | ||||||

FutureFuel Corporation | 278 | 4,123 | ||||||

Kronos Worldwide, Inc. | 900 | 18,117 | ||||||

OMNOVA Solutions, Inc. (b) | 101 | 914 | ||||||

Tredegar Corporation | 3,200 | 70,240 | ||||||

Valhi, Inc. | 922 | 3,043 | ||||||

| 113,357 | ||||||||

Construction Materials — 0.8% | ||||||||

United States Lime & Minerals, Inc. | 300 | 22,767 | ||||||

Containers & Packaging — 0.2% | ||||||||

Owens-Illinois, Inc. (b) | 400 | 7,068 | ||||||

Metals & Mining — 0.9% | ||||||||

Cleveland-Cliffs, Inc. (b) | 1,100 | 11,055 | ||||||

Gold Resource Corporation | 2,389 | 12,327 | ||||||

Schnitzer Steel Industries, Inc. - Class A | 200 | 5,270 | ||||||

| 28,652 | ||||||||

Telecommunication Services — 2.0% | ||||||||

Diversified Telecommunication Services — 1.1% | ||||||||

Ooma, Inc. (b) | 2,185 | 34,960 | ||||||

Wireless Telecommunication Services — 0.9% | ||||||||

Spok Holdings, Inc. | 1,202 | 18,451 | ||||||

United States Cellular Corporation (b) | 200 | 8,552 | ||||||

| 27,003 | ||||||||

Total Investments at Value — 96.6% (Cost $2,561,443) | $ | 3,030,685 | ||||||

Other Assets in Excess of Liabilities — 3.4% | 106,738 | |||||||

Net Assets — 100.0% | $ | 3,137,423 | ||||||

(a) | Percentage rounds to less than 0.1%. |

(b) | Non-income producing security. |

24

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% | Shares | Value | ||||||

Consumer Discretionary — 13.4% | ||||||||

Auto Components — 1.7% | ||||||||

BorgWarner, Inc. | 180 | $ | 7,879 | |||||

Goodyear Tire & Rubber Company (The) | 250 | 5,672 | ||||||

Lear Corporation | 40 | 6,488 | ||||||

| 20,039 | ||||||||

Automobiles — 1.1% | ||||||||

General Motors Company | 370 | 13,339 | ||||||

Diversified Consumer Services — 1.5% | ||||||||

Laureate Education, Inc. - Class A (a) | 1,100 | 17,567 | ||||||

Hotels, Restaurants & Leisure — 0.9% | ||||||||

Wyndham Destinations, Inc. | 240 | 10,608 | ||||||

Household Durables — 1.0% | ||||||||

PulteGroup, Inc. | 400 | 11,180 | ||||||

Internet & Direct Marketing Retail — 0.2% | ||||||||

Qurate Retail, Inc. (a) | 100 | 2,079 | ||||||

Leisure Products — 0.6% | ||||||||

Brunswick Corporation | 100 | 6,642 | ||||||

Media — 2.1% | ||||||||

News Corporation - Class A | 450 | 5,881 | ||||||

Viacom, Inc. - Class B | 650 | 19,032 | ||||||

| 24,913 | ||||||||

Multi-Line Retail — 2.1% | ||||||||

Kohl's Corporation | 200 | 15,822 | ||||||

Macy's, Inc. | 150 | 5,483 | ||||||

Nordstrom, Inc. | 60 | 3,771 | ||||||

| 25,076 | ||||||||

Textiles, Apparel & Luxury Goods — 2.2% | ||||||||

Columbia Sportswear Company | 20 | 1,814 | ||||||

Ralph Lauren Corporation | 100 | 13,281 | ||||||

Skechers U.S.A., Inc. - Class A (a) | 350 | 10,318 | ||||||

| 25,413 | ||||||||

Consumer Staples — 7.6% | ||||||||

Beverages — 1.9% | ||||||||

Keurig Dr Pepper, Inc. | 400 | 9,120 | ||||||

Molson Coors Brewing Company - Class B | 60 | 4,004 | ||||||

25

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% (Continued) | Shares | Value | ||||||

Consumer Staples — 7.6% (Continued) | ||||||||

Beverages — 1.9% (Continued) | ||||||||

PepsiCo, Inc. | 80 | $ | 8,961 | |||||

| 22,085 | ||||||||

Food & Staples Retailing — 1.5% | ||||||||

Kroger Company (The) | 550 | 17,325 | ||||||

Food Products — 4.0% | ||||||||

Archer-Daniels-Midland Company | 620 | 31,248 | ||||||

Conagra Brands, Inc. | 250 | 9,187 | ||||||

Seaboard Corporation | 2 | 7,370 | ||||||

| 47,805 | ||||||||

Personal Products — 0.2% | ||||||||

Herbalife Nutrition Ltd. (a) | 40 | 2,264 | ||||||

Energy — 7.2% | ||||||||

Oil, Gas & Consumable Fuels — 7.2% | ||||||||

Apache Corporation | 40 | 1,753 | ||||||

Hess Corporation | 41 | 2,761 | ||||||

HollyFrontier Corporation | 200 | 14,904 | ||||||

Marathon Oil Corporation | 650 | 13,982 | ||||||

Marathon Petroleum Corporation | 120 | 9,875 | ||||||

Murphy Oil Corporation | 550 | 16,956 | ||||||

Newfield Exploration Company (a) | 250 | 6,820 | ||||||

Noble Energy, Inc. | 100 | 2,972 | ||||||

PBF Energy, Inc. - Class A | 200 | 10,384 | ||||||

Valero Energy Corporation | 30 | 3,536 | ||||||

| 83,943 | ||||||||

Financials — 7.8% | ||||||||

Banks — 4.4% | ||||||||

Bank OZK | 60 | 2,428 | ||||||

Citizens Financial Group, Inc. | 50 | 2,058 | ||||||

Comerica, Inc. | 60 | 5,849 | ||||||

East West Bancorp, Inc. | 140 | 8,875 | ||||||

Fifth Third Bancorp | 50 | 1,471 | ||||||

Huntington Bancshares, Inc. | 200 | 3,242 | ||||||

KeyCorp | 300 | 6,321 | ||||||

M&T Bank Corporation | 10 | 1,771 | ||||||

PacWest Bancorp | 40 | 2,020 | ||||||

Regions Financial Corporation | 100 | 1,946 | ||||||

SunTrust Banks, Inc. | 100 | 7,356 | ||||||

SVB Financial Group (a) | 10 | 3,227 | ||||||

26

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% (Continued) | Shares | Value | ||||||

Financials — 7.8% (Continued) | ||||||||

Banks — 4.4% (Continued) | ||||||||

Western Alliance Bancorporation (a) | 20 | $ | 1,153 | |||||

Wintrust Financial Corporation | 40 | 3,542 | ||||||

| 51,259 | ||||||||

Capital Markets — 1.4% | ||||||||

Ameriprise Financial, Inc. | 20 | 2,839 | ||||||

E*TRADE Financial Corporation (a) | 20 | 1,177 | ||||||

Eaton Vance Corporation | 80 | 4,218 | ||||||

MSCI, Inc. | 10 | 1,803 | ||||||

Northern Trust Corporation | 30 | 3,224 | ||||||

Raymond James Financial, Inc. | 20 | 1,861 | ||||||

T. Rowe Price Group, Inc. | 10 | 1,159 | ||||||

| 16,281 | ||||||||

Consumer Finance — 0.6% | ||||||||

Ally Financial, Inc. | 50 | 1,344 | ||||||

Discover Financial Services | 20 | 1,562 | ||||||

Synchrony Financial | 150 | 4,751 | ||||||

| 7,657 | ||||||||

Insurance — 1.4% | ||||||||

Aflac, Inc. | 40 | 1,850 | ||||||

Assurant, Inc. | 40 | 4,113 | ||||||

Berkley (W.R.) Corporation | 20 | 1,565 | ||||||

Lincoln National Corporation | 40 | 2,623 | ||||||

Markel Corporation (a) | 1 | 1,209 | ||||||

Principal Financial Group, Inc. | 20 | 1,104 | ||||||

Progressive Corporation (The) | 40 | 2,701 | ||||||

Torchmark Corporation | 20 | 1,758 | ||||||

| 16,923 | ||||||||

Health Care — 13.1% | ||||||||

Biotechnology — 1.0% | ||||||||

Regeneron Pharmaceuticals, Inc. (a) | 5 | 2,034 | ||||||

United Therapeutics Corporation (a) | 80 | 9,839 | ||||||

| 11,873 | ||||||||

Health Care Equipment & Supplies — 3.2% | ||||||||

DENTSPLY SIRONA, Inc. | 100 | 3,992 | ||||||

Hill-Rom Holdings, Inc. | 80 | 7,782 | ||||||

Hologic, Inc. (a) | 220 | 8,747 | ||||||

Zimmer Biomet Holdings, Inc. | 140 | 17,308 | ||||||

| 37,829 | ||||||||

Health Care Providers & Services — 2.1% | ||||||||

Cardinal Health, Inc. | 160 | 8,351 | ||||||

Express Scripts Holding Company (a) | 20 | 1,760 | ||||||

27

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% (Continued) | Shares | Value | ||||||

Health Care — 13.1% (Continued) | ||||||||

Health Care Providers & Services — 2.1% (Continued) | ||||||||

Molina Healthcare, Inc. (a) | 100 | $ | 13,800 | |||||

| 23,911 | ||||||||

Life Sciences Tools & Services — 4.4% | ||||||||

Agilent Technologies, Inc. | 220 | 14,859 | ||||||

Bio-Rad Laboratories, Inc. - Class A (a) | 85 | 27,650 | ||||||

Bruker Corporation | 260 | 9,251 | ||||||

| 51,760 | ||||||||

Pharmaceuticals — 2.4% | ||||||||

Merck & Company, Inc. | 80 | 5,487 | ||||||

Mylan N.V. (a) | 450 | 17,609 | ||||||

Nektar Therapeutics (a) | 80 | 5,319 | ||||||

| 28,415 | ||||||||

Industrials — 16.4% | ||||||||

Aerospace & Defense — 3.5% | ||||||||

Arconic, Inc. | 700 | 15,666 | ||||||

Curtiss-Wright Corporation | 20 | 2,679 | ||||||

Spirit AeroSystems Holdings, Inc. - Class A | 20 | 1,710 | ||||||

Textron, Inc. | 310 | 21,399 | ||||||

| 41,454 | ||||||||

Air Freight & Logistics — 0.7% | ||||||||

XPO Logistics, Inc. (a) | 80 | 8,520 | ||||||

Airlines — 0.9% | ||||||||

American Airlines Group, Inc. | 40 | 1,619 | ||||||

United Continental Holdings, Inc. (a) | 100 | 8,742 | ||||||

| 10,361 | ||||||||

Building Products — 1.3% | ||||||||

Owens Corning | 280 | 15,854 | ||||||

Construction & Engineering — 1.6% | ||||||||

EMCOR Group, Inc. | 100 | 8,010 | ||||||

Quanta Services, Inc. (a) | 300 | 10,377 | ||||||

| 18,387 | ||||||||

Industrial Conglomerates — 1.2% | ||||||||

Carlisle Companies, Inc. | 110 | 13,949 | ||||||

Machinery — 5.9% | ||||||||

AGCO Corporation | 520 | 31,023 | ||||||

Allison Transmission Holdings, Inc. | 500 | 24,830 | ||||||

Cummins, Inc. | 16 | 2,269 | ||||||

28

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% (Continued) | Shares | Value | ||||||

Industrials — 16.4% (Continued) | ||||||||

Machinery — 5.9% (Continued) | ||||||||

Oshkosh Corporation | 60 | $ | 4,216 | |||||

PACCAR, Inc. | 100 | 6,842 | ||||||

| 69,180 | ||||||||

Professional Services — 1.3% | ||||||||

ManpowerGroup, Inc. | 80 | 7,498 | ||||||

Robert Half International, Inc. | 100 | 7,818 | ||||||

| 15,316 | ||||||||

Information Technology — 11.7% | ||||||||

Communications Equipment — 0.7% | ||||||||

ARRIS International plc (a) | 300 | 7,773 | ||||||

Electronic Equipment, Instruments & Components — 2.1% | ||||||||

Dolby Laboratories, Inc. - Class A | 60 | 4,211 | ||||||

Jabil, Inc. | 400 | 11,824 | ||||||

Zebra Technologies Corporation - Class A (a) | 50 | 8,587 | ||||||

| 24,622 | ||||||||

IT Services — 1.7% | ||||||||

Alliance Data Systems Corporation | 30 | 7,157 | ||||||

International Business Machines Corporation | 10 | 1,465 | ||||||

MAXIMUS, Inc. | 120 | 7,980 | ||||||

Sabre Corporation | 150 | 3,917 | ||||||

| 20,519 | ||||||||

Semiconductors & Semiconductor Equipment — 1.0% | ||||||||

Mellanox Technologies Ltd. (a) | 140 | 11,648 | ||||||

Software — 1.6% | ||||||||

CA, Inc. | 230 | 10,074 | ||||||

Cadence Design Systems, Inc. (a) | 140 | 6,586 | ||||||

Citrix Systems, Inc. (a) | 20 | 2,280 | ||||||

| 18,940 | ||||||||

Technology Hardware, Storage & Peripherals — 4.6% | ||||||||

Hewlett Packard Enterprise Company | 1,400 | 23,142 | ||||||

Western Digital Corporation | 75 | 4,743 | ||||||

Xerox Corporation | 950 | 26,467 | ||||||

| 54,352 | ||||||||

Materials — 6.6% | ||||||||

Chemicals — 3.7% | ||||||||

Cabot Corporation | 100 | 6,492 | ||||||

Chemours Company (The) | 80 | 3,488 | ||||||

Eastman Chemical Company | 70 | 6,792 | ||||||

Huntsman Corporation | 640 | 19,514 | ||||||

29

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% (Continued) | Shares | Value | ||||||

Materials — 6.6% (Continued) | ||||||||

Chemicals — 3.7% (Continued) | ||||||||

Mosaic Company (The) | 100 | $ | 3,127 | |||||

Westlake Chemical Corporation | 40 | 3,783 | ||||||

| 43,196 | ||||||||

Containers & Packaging — 0.5% | ||||||||

Bemis Company, Inc. | 60 | 2,957 | ||||||

Owens-Illinois, Inc. (a) | 100 | 1,767 | ||||||

WestRock Company | 20 | 1,101 | ||||||

| 5,825 | ||||||||

Metals & Mining — 1.6% | ||||||||

Alcoa Corporation (a) | 80 | 3,574 | ||||||

Freeport-McMoRan, Inc. | 100 | 1,405 | ||||||

Nucor Corporation | 40 | 2,500 | ||||||

Reliance Steel & Aluminum Company | 20 | 1,758 | ||||||

Steel Dynamics, Inc. | 80 | 3,658 | ||||||

United States Steel Corporation | 200 | 5,936 | ||||||

| 18,831 | ||||||||

Paper & Forest Products — 0.8% | ||||||||

Louisiana-Pacific Corporation | 350 | 10,206 | ||||||

Real Estate — 6.0% | ||||||||

Equity Real Estate Investment Trusts (REITs) — 6.0% | ||||||||

Alexandria Real Estate Equities, Inc. | 10 | 1,284 | ||||||

Boston Properties, Inc. | 20 | 2,609 | ||||||

Brixmor Property Group, Inc. | 100 | 1,822 | ||||||

CyrusOne, Inc. | 40 | 2,678 | ||||||

Extra Space Storage, Inc. | 20 | 1,844 | ||||||

Gaming and Leisure Properties, Inc. | 300 | 10,737 | ||||||

Host Hotels & Resorts, Inc. | 150 | 3,230 | ||||||

Iron Mountain, Inc. | 50 | 1,805 | ||||||

Kimco Realty Corporation | 200 | 3,422 | ||||||

Macerich Company (The) | 100 | 5,874 | ||||||

Medical Properties Trust, Inc. | 300 | 4,515 | ||||||

Omega Healthcare Investors, Inc. | 50 | 1,653 | ||||||

Park Hotels & Resorts, Inc. | 150 | 5,017 | ||||||

Prologis, Inc. | 142 | 9,540 | ||||||

Realty Income Corporation | 60 | 3,514 | ||||||

Ventas, Inc. | 20 | 1,197 | ||||||

VICI Properties, Inc. | 100 | 2,091 | ||||||

Weyerhaeuser Company | 220 | 7,636 | ||||||

| 70,468 | ||||||||

30

See accompanying notes to financial statements.

ALAMBIC MID CAP VALUE PLUS FUND | ||||||||

COMMON STOCKS — 92.6% (Continued) | Shares | Value | ||||||

Telecommunication Services — 2.0% | ||||||||

Wireless Telecommunication Services — 2.0% | ||||||||

United States Cellular Corporation (a) | 540 | $ | 23,090 | |||||

Utilities — 0.8% | ||||||||

Electric Utilities — 0.4% | ||||||||

PG&E Corporation | 100 | 4,618 | ||||||

Multi-Utilities — 0.4% | ||||||||

CMS Energy Corporation | 60 | 2,954 | ||||||

Public Service Enterprise Group, Inc. | 40 | 2,094 | ||||||

| 5,048 | ||||||||

Total Common Stocks (Cost $963,956) | $ | 1,088,343 | ||||||

| ||||||||

RIGHTS — 0.0% (b) | Shares | Value | ||||||

Media General, Inc. - CVR (a)(c) (Cost $0) | 120 | $ | 6 | |||||

Total Investments at Value — 92.6% (Cost $963,956) | $ | 1,088,349 | ||||||

Other Assets in Excess of Liabilities — 7.4% | 86,640 | |||||||

Net Assets — 100.0% | $ | 1,174,989 | ||||||

CVR - Contingent Value Right

| (a) | Non-income producing security. |

| (b) | Percentage rounds to less than 0.1%. |

| (c) | Illiquid security. Security value has been determined in good faith pursuant to procedures adopted by the Board of Trustees. The total value of such securities was $6 as of August 31, 2018, representing 0.0% (b) of net assets (Note 2). |

31

See accompanying notes to financial statements.

ALAMBIC MID CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 94.3% | Shares | Value | ||||||

Consumer Discretionary — 15.7% | ||||||||

Auto Components — 2.6% | ||||||||

BorgWarner, Inc. | 260 | $ | 11,380 | |||||

Gentex Corporation | 350 | 8,183 | ||||||

Goodyear Tire & Rubber Company (The) | 350 | 7,942 | ||||||

Lear Corporation | 20 | 3,244 | ||||||

| 30,749 | ||||||||

Diversified Consumer Services — 1.6% | ||||||||

Laureate Education, Inc. - Class A (a) | 1,200 | 19,164 | ||||||

Hotels, Restaurants & Leisure — 1.2% | ||||||||

Darden Restaurants, Inc. | 20 | 2,321 | ||||||

Hyatt Hotels Corporation - Class A | 40 | 3,094 | ||||||

Texas Roadhouse, Inc. | 80 | 5,516 | ||||||

Wyndham Destinations, Inc. | 80 | 3,536 | ||||||

| 14,467 | ||||||||

Household Durables — 1.1% | ||||||||

PulteGroup, Inc. | 450 | 12,577 | ||||||

Internet & Direct Marketing Retail — 0.3% | ||||||||

Qurate Retail, Inc. (a) | 200 | 4,158 | ||||||

Leisure Products — 0.4% | ||||||||

Brunswick Corporation | 80 | 5,314 | ||||||

Media — 2.1% | ||||||||

Discovery, Inc. - Series A (a) | 300 | 8,349 | ||||||

News Corporation - Class A | 136 | 1,777 | ||||||

Viacom, Inc. - Class B | 500 | 14,640 | ||||||

| 24,766 | ||||||||

Multi-Line Retail — 2.5% | ||||||||

Kohl's Corporation | 180 | 14,240 | ||||||

Macy's, Inc. | 100 | 3,655 | ||||||

Nordstrom, Inc. | 180 | 11,313 | ||||||

| 29,208 | ||||||||

Specialty Retail — 1.3% | ||||||||

American Eagle Outfitters, Inc. | 250 | 6,490 | ||||||

Best Buy Company, Inc. | 40 | 3,182 | ||||||

Ross Stores, Inc. | 60 | 5,747 | ||||||

| 15,419 | ||||||||

32

See accompanying notes to financial statements.

ALAMBIC MID CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 94.3% (Continued) | Shares | Value | ||||||

Consumer Discretionary — 15.7% (Continued) | ||||||||

Textiles, Apparel & Luxury Goods — 2.6% | ||||||||

Columbia Sportswear Company | 120 | $ | 10,884 | |||||

Ralph Lauren Corporation | 60 | 7,969 | ||||||

Skechers U.S.A., Inc. - Class A (a) | 400 | 11,792 | ||||||

| 30,645 | ||||||||

Consumer Staples — 3.8% | ||||||||

Beverages — 0.8% | ||||||||

Keurig Dr Pepper, Inc. | 400 | 9,120 | ||||||

Food & Staples Retailing — 1.0% | ||||||||

Kroger Company (The) | 400 | 12,600 | ||||||

Food Products — 2.0% | ||||||||

Archer-Daniels-Midland Company | 400 | 20,160 | ||||||

Seaboard Corporation | 1 | 3,685 | ||||||

| 23,845 | ||||||||

Energy — 3.0% | ||||||||

Oil, Gas & Consumable Fuels — 3.0% | ||||||||

HollyFrontier Corporation | 130 | 9,688 | ||||||

Marathon Oil Corporation | 50 | 1,075 | ||||||

Murphy Oil Corporation | 400 | 12,332 | ||||||

Newfield Exploration Company (a) | 250 | 6,820 | ||||||

PBF Energy, Inc. - Class A | 100 | 5,192 | ||||||

Peabody Energy Corporation | 20 | 826 | ||||||

| 35,933 | ||||||||

Financials — 0.7% | ||||||||

Capital Markets — 0.7% | ||||||||

Ameriprise Financial, Inc. | 40 | 5,678 | ||||||

T. Rowe Price Group, Inc. | 20 | 2,318 | ||||||

| 7,996 | ||||||||

Health Care — 16.8% | ||||||||

Biotechnology — 3.4% | ||||||||

Alexion Pharmaceuticals, Inc. (a) | 20 | 2,445 | ||||||

BioMarin Pharmaceutical, Inc. (a) | 40 | 3,999 | ||||||

Incyte Corporation (a) | 140 | 10,347 | ||||||

Ionis Pharmaceuticals, Inc. (a) | 80 | 3,655 | ||||||

Neurocrine Biosciences, Inc. (a) | 40 | 4,918 | ||||||

United Therapeutics Corporation (a) | 130 | 15,989 | ||||||

| 41,353 | ||||||||

Health Care Equipment & Supplies — 4.0% | ||||||||

ABIOMED, Inc. (a) | 10 | 4,066 | ||||||

DexCom, Inc. (a) | 10 | 1,444 | ||||||

33

See accompanying notes to financial statements.

ALAMBIC MID CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 94.3% (Continued) | Shares | Value | ||||||

Health Care — 16.8% (Continued) | ||||||||

Health Care Equipment & Supplies — 4.0% (Continued) | ||||||||

Globus Medical, Inc. - Class A (a) | 60 | $ | 3,196 | |||||

Hill-Rom Holdings, Inc. | 100 | 9,727 | ||||||

Hologic, Inc. (a) | 300 | 11,928 | ||||||

Masimo Corporation (a) | 40 | 4,716 | ||||||

Zimmer Biomet Holdings, Inc. | 100 | 12,363 | ||||||

| 47,440 | ||||||||

Health Care Providers & Services — 2.9% | ||||||||

AmerisourceBergen Corporation | 100 | 8,997 | ||||||

Cardinal Health, Inc. | 140 | 7,307 | ||||||

McKesson Corporation | 10 | 1,287 | ||||||

Molina Healthcare, Inc. (a) | 100 | 13,800 | ||||||

WellCare Health Plans, Inc. (a) | 10 | 3,026 | ||||||

| 34,417 | ||||||||

Life Sciences Tools & Services — 3.9% | ||||||||

Agilent Technologies, Inc. | 100 | 6,754 | ||||||

Bio-Rad Laboratories, Inc. - Class A (a) | 80 | 26,024 | ||||||

Bruker Corporation | 190 | 6,760 | ||||||

Charles River Laboratories International, Inc. (a) | 55 | 6,793 | ||||||

| 46,331 | ||||||||

Pharmaceuticals — 2.6% | ||||||||

Mylan N.V. (a) | 450 | 17,609 | ||||||

Nektar Therapeutics (a) | 201 | 13,364 | ||||||

| 30,973 | ||||||||

Industrials — 18.3% | ||||||||

Aerospace & Defense — 3.3% | ||||||||

Arconic, Inc. | 600 | 13,428 | ||||||

Curtiss-Wright Corporation | 60 | 8,037 | ||||||

Textron, Inc. | 260 | 17,948 | ||||||

| 39,413 | ||||||||

Air Freight & Logistics — 0.4% | ||||||||

XPO Logistics, Inc. (a) | 40 | 4,260 | ||||||

Building Products — 0.1% | ||||||||

Owens Corning | 20 | 1,132 | ||||||

Construction & Engineering — 1.7% | ||||||||

EMCOR Group, Inc. | 100 | 8,010 | ||||||

Quanta Services, Inc. (a) | 350 | 12,106 | ||||||

| 20,116 | ||||||||

Industrial Conglomerates — 1.1% | ||||||||

Carlisle Companies, Inc. | 100 | 12,681 | ||||||

34

See accompanying notes to financial statements.

ALAMBIC MID CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 94.3% (Continued) | Shares | Value | ||||||

Industrials — 18.3% (Continued) | ||||||||

Machinery — 7.6% | ||||||||

AGCO Corporation | 560 | $ | 33,410 | |||||

Allison Transmission Holdings, Inc. | 520 | 25,823 | ||||||

Cummins, Inc. | 90 | 12,762 | ||||||

ITT, Inc. | 100 | 5,911 | ||||||

Oshkosh Corporation | 40 | 2,811 | ||||||

PACCAR, Inc. | 120 | 8,210 | ||||||

Parker-Hannifin Corporation | 10 | 1,756 | ||||||

| 90,683 | ||||||||

Professional Services — 3.1% | ||||||||

Korn/Ferry International | 60 | 4,028 | ||||||

ManpowerGroup, Inc. | 180 | 16,871 | ||||||

Robert Half International, Inc. | 200 | 15,636 | ||||||

| 36,535 | ||||||||

Road & Rail — 0.2% | ||||||||

Schneider National, Inc. - Class B | 100 | 2,705 | ||||||

Trading Companies & Distributors — 0.8% | ||||||||

United Rentals, Inc. (a) | 20 | 3,118 | ||||||

W.W. Grainger, Inc. | 20 | 7,081 | ||||||

| 10,199 | ||||||||

Information Technology — 29.0% | ||||||||

Communications Equipment — 2.1% | ||||||||

ARRIS International plc (a) | 350 | 9,068 | ||||||

F5 Networks, Inc. (a) | 80 | 15,130 | ||||||

| 24,198 | ||||||||

Electronic Equipment, Instruments & Components — 4.5% | ||||||||

Avnet, Inc. | 40 | 1,936 | ||||||

CDW Corporation | 20 | 1,751 | ||||||

Dolby Laboratories, Inc. - Class A | 220 | 15,442 | ||||||

Jabil, Inc. | 300 | 8,868 | ||||||

National Instruments Corporation | 120 | 5,730 | ||||||

Zebra Technologies Corporation - Class A (a) | 115 | 19,750 | ||||||

| 53,477 | ||||||||

IT Services — 5.6% | ||||||||

Alliance Data Systems Corporation | 60 | 14,315 | ||||||

Booz Allen Hamilton Holding Corporation | 200 | 10,232 | ||||||

Fiserv, Inc. (a) | 60 | 4,804 | ||||||

MAXIMUS, Inc. | 192 | 12,768 | ||||||

Sabre Corporation | 600 | 15,666 | ||||||

Teradata Corporation (a) | 220 | 9,123 | ||||||

| 66,908 | ||||||||

35

See accompanying notes to financial statements.

ALAMBIC MID CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 94.3% (Continued) | Shares | Value | ||||||

Information Technology — 29.0% (Continued) | ||||||||

Semiconductors & Semiconductor Equipment — 5.4% | ||||||||

Cypress Semiconductor Corporation | 500 | $ | 8,605 | |||||

KLA-Tencor Corporation | 30 | 3,486 | ||||||

Lam Research Corporation | 75 | 12,982 | ||||||

Maxim Integrated Products, Inc. | 40 | 2,419 | ||||||

Mellanox Technologies Ltd. (a) | 200 | 16,640 | ||||||

MKS Instruments, Inc. | 70 | 6,503 | ||||||

ON Semiconductor Corporation (a) | 650 | 13,871 | ||||||

| 64,506 | ||||||||

Software — 6.0% | ||||||||

CA, Inc. | 480 | 21,024 | ||||||

Cadence Design Systems, Inc. (a) | 220 | 10,349 | ||||||

Fair Isaac Corporation (a) | 50 | 11,549 | ||||||

Red Hat, Inc. (a) | 10 | 1,477 | ||||||

SS&C Technologies Holdings, Inc. | 160 | 9,495 | ||||||

Synopsys, Inc. (a) | 130 | 13,278 | ||||||

Zynga, Inc. - Class A (a) | 1,100 | 4,576 | ||||||

| 71,748 | ||||||||

Technology Hardware, Storage & Peripherals — 5.4% | ||||||||

Hewlett Packard Enterprise Company | 1,550 | 25,622 | ||||||

NetApp, Inc. | 140 | 12,153 | ||||||

Xerox Corporation | 950 | 26,467 | ||||||

| 64,242 | ||||||||

Materials — 5.8% | ||||||||

Chemicals — 2.3% | ||||||||

Cabot Corporation | 100 | 6,492 | ||||||

Chemours Company (The) | 20 | 872 | ||||||

Eastman Chemical Company | 30 | 2,911 | ||||||

Huntsman Corporation | 540 | 16,464 | ||||||

| 26,739 | ||||||||

Containers & Packaging — 1.9% | ||||||||

WestRock Company | 420 | 23,134 | ||||||

Metals & Mining — 1.0% | ||||||||

Alcoa Corporation (a) | 80 | 3,574 | ||||||

Nucor Corporation | 20 | 1,250 | ||||||

United States Steel Corporation | 250 | 7,420 | ||||||

| 12,244 | ||||||||

Paper & Forest Products — 0.6% | ||||||||

Louisiana-Pacific Corporation | 250 | 7,290 | ||||||

36

See accompanying notes to financial statements.

ALAMBIC MID CAP GROWTH PLUS FUND | ||||||||

COMMON STOCKS — 94.3% (Continued) | Shares | Value | ||||||

Telecommunication Services — 1.2% | ||||||||

Wireless Telecommunication Services — 1.2% | ||||||||

United States Cellular Corporation (a) | 340 | $ | 14,539 | |||||

Total Investments at Value — 94.3% (Cost $983,866) | $ | 1,123,224 | ||||||

Other Assets in Excess of Liabilities — 5.7% | 67,362 | |||||||

Net Assets — 100.0% | $ | 1,190,586 | ||||||

(a) | Non-income producing security. |

37

See accompanying notes to financial statements.

ALAMBIC FUNDS | ||||||||

| Alambic Small | Alambic Small | ||||||

ASSETS | ||||||||

Investments in securities: | ||||||||

At cost | $ | 2,753,798 | $ | 2,561,443 | ||||

At value (Note 2) | $ | 3,152,429 | $ | 3,030,685 | ||||

Cash (Note 2) | 169,773 | 111,463 | ||||||

Dividends receivable | 1,403 | 1,258 | ||||||

Receivable for investment securities sold | 88,356 | 68,664 | ||||||

Receivable from Adviser (Note 4) | 9,670 | 9,801 | ||||||

Other assets | 2,380 | 2,379 | ||||||

Total assets | 3,424,011 | 3,224,250 | ||||||

LIABILITIES | ||||||||

Payable for investment securities purchased | 104,005 | 73,548 | ||||||

Payable to administrator (Note 4) | 7,028 | 7,026 | ||||||

Other accrued expenses | 6,253 | 6,253 | ||||||

Total liabilities | 117,286 | 86,827 | ||||||

NET ASSETS | $ | 3,306,725 | $ | 3,137,423 | ||||

NET ASSETS CONSIST OF: | ||||||||

Paid-in capital | $ | 2,579,960 | $ | 2,310,096 | ||||

Accumulated net investment loss | (2,347 | ) | (6,623 | ) | ||||

Undistributed net realized gains from investment transactions | 330,481 | 364,708 | ||||||

Net unrealized appreciation on investments | 398,631 | 469,242 | ||||||

NET ASSETS | $ | 3,306,725 | $ | 3,137,423 | ||||

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 250,845 | 228,849 | ||||||

Net asset value, offering price and redemption price (Note 2) | $ | 13.18 | $ | 13.71 | ||||

See accompanying notes to financial statements. |

38

ALAMBIC FUNDS | ||||||||

| Alambic Mid | Alambic Mid | ||||||

ASSETS | ||||||||

Investments in securities: | ||||||||

At cost | $ | 963,956 | $ | 983,866 | ||||

At value (Note 2) | $ | 1,088,349 | $ | 1,123,224 | ||||

Cash (Note 2) | 81,505 | 67,229 | ||||||

Dividends receivable | 1,694 | 1,370 | ||||||

Receivable for investment securities sold | 31,325 | 37,517 | ||||||

Receivable from Adviser (Note 4) | 10,971 | 10,777 | ||||||

Other assets | 2,924 | 2,375 | ||||||

Total assets | 1,216,768 | 1,242,492 | ||||||

LIABILITIES | ||||||||

Payable for investment securities purchased | 29,166 | 39,293 | ||||||

Payable to administrator (Note 4) | 6,510 | 6,510 | ||||||

Other accrued expenses | 6,103 | 6,103 | ||||||

Total liabilities | 41,779 | 51,906 | ||||||

NET ASSETS | $ | 1,174,989 | $ | 1,190,586 | ||||

NET ASSETS CONSIST OF: | ||||||||

Paid-in capital | $ | 1,032,706 | $ | 962,454 | ||||

Undistributed net investment income | 6,697 | 3,057 | ||||||

Undistributed net realized gains from investment transactions | 11,193 | 85,717 | ||||||

Net unrealized appreciation on investments | 124,393 | 139,358 | ||||||

NET ASSETS | $ | 1,174,989 | $ | 1,190,586 | ||||

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 100,234 | 93,880 | ||||||

Net asset value, offering price and redemption price (Note 2) | $ | 11.72 | $ | 12.68 | ||||

See accompanying notes to financial statements. |

39

ALAMBIC FUNDS | ||||||||

| Alambic Small | Alambic Small | ||||||

INVESTMENT INCOME | ||||||||

Dividend income | $ | 35,322 | $ | 21,011 | ||||

Foreign withholding taxes on dividends | (2 | ) | (5 | ) | ||||

Total investment income | 35,320 | 21,006 | ||||||

EXPENSES | ||||||||

Professional fees | 37,152 | 37,152 | ||||||

Fund accounting fees (Note 4) | 30,314 | 29,291 | ||||||

Administration fees (Note 4) | 30,000 | 29,000 | ||||||

Investment advisory fees (Note 4) | 29,813 | 27,687 | ||||||

Compliance fees (Note 4) | 12,240 | 12,240 | ||||||

Transfer agent fees (Note 4) | 12,000 | 12,000 | ||||||

Trustees' fees and expenses (Note 4) | 10,009 | 10,009 | ||||||

Pricing costs | 4,496 | 4,372 | ||||||

Insurance expense | 2,680 | 2,680 | ||||||

Registration and filing fees | 2,108 | 2,107 | ||||||

Postage and supplies | 2,246 | 1,960 | ||||||

Printing of shareholder reports | 2,058 | 2,028 | ||||||

Other expenses | 7,010 | 7,095 | ||||||

Total expenses | 182,126 | 177,621 | ||||||

Less fee reductions and expense reimbursements by the Adviser (Note 4) | (152,313 | ) | (149,933 | ) | ||||

Net expenses | 29,813 | 27,688 | ||||||

NET INVESTMENT INCOME (LOSS) | 5,507 | (6,682 | ) | |||||

REALIZED AND UNREALIZED GAINS ON INVESTMENTS | ||||||||

Net realized gains from investment transactions | 375,360 | 479,597 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 162,454 | 81,190 | ||||||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 537,814 | 560,787 | ||||||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 543,321 | $ | 554,105 | ||||

See accompanying notes to financial statements. |

40

ALAMBIC FUNDS | ||||||||

| Alambic Mid | Alambic Mid | ||||||

INVESTMENT INCOME | ||||||||

Dividend income | $ | 18,886 | $ | 13,485 | ||||

Foreign withholding taxes on dividends | (10 | ) | (10 | ) | ||||

Total investment income | 18,876 | 13,475 | ||||||

EXPENSES | ||||||||

Professional fees | 37,152 | 37,152 | ||||||

Fund accounting fees (Note 4) | 26,112 | 26,112 | ||||||

Administration fees (Note 4) | 26,000 | 26,000 | ||||||

Compliance fees (Note 4) | 12,240 | 12,240 | ||||||

Transfer agent fees (Note 4) | 12,000 | 12,000 | ||||||

Trustees' fees and expenses (Note 4) | 10,009 | 10,009 | ||||||

Investment advisory fees (Note 4) | 7,779 | 7,867 | ||||||

Pricing costs | 3,516 | 2,971 | ||||||

Custody and bank service fees | 3,166 | 3,166 | ||||||

Insurance expense | 2,679 | 2,679 | ||||||

Registration and filing fees | 2,919 | 2,170 | ||||||

Printing of shareholder reports | 1,968 | 1,908 | ||||||

Postage and supplies | 1,838 | 1,834 | ||||||

Other expenses | 6,782 | 6,784 | ||||||

Total expenses | 154,160 | 152,892 | ||||||

Less fee reductions and expense reimbursements by the Adviser (Note 4) | (144,714 | ) | (143,339 | ) | ||||

Net expenses | 9,446 | 9,553 | ||||||

NET INVESTMENT INCOME | 9,430 | 3,922 | ||||||

REALIZED AND UNREALIZED GAINS ON INVESTMENTS | ||||||||

Net realized gains from investment transactions | 22,286 | 85,972 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 91,463 | 70,519 | ||||||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 113,749 | 156,491 | ||||||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 123,179 | $ | 160,413 | ||||

See accompanying notes to financial statements. |

41

ALAMBIC SMALL CAP VALUE PLUS FUND | ||||||||

| Year | Year | ||||||

FROM OPERATIONS | ||||||||

Net investment income | $ | 5,507 | $ | 1,201 | ||||

Net realized gains from investment transactions | 375,360 | 372,341 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 162,454 | (163,060 | ) | |||||

Net increase in net assets resulting from operations | 543,321 | 210,482 | ||||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | ||||||||

From net investment income | (4,978 | ) | (9,727 | ) | ||||

From net realized gains | (358,527 | ) | — | |||||

Total distributions to shareholders | (363,505 | ) | (9,727 | ) | ||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Proceeds from shares sold | 86,363 | 1,132,000 | ||||||