OMB APPROVAL | |

OMB Number: 3235-0570

Expires: August 31, 2020

Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 | Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) | |

Matthew J. Beck

| Ultimus Fund Solutions, LLC | 225 Pictoria Drive, Suite 450 | Cincinnati, Ohio 45246 |

| (Name and address of agent for service) | ||

| Registrant's telephone number, including area code: | (212) 888-8123 |

| Date of fiscal year end: | October 31 | |

| Date of reporting period: | October 31, 2018 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

STRALEM EQUITY FUND

LETTER TO SHAREHOLDERS

December 2018

Dear Shareholder,

Each year following the close of Stralem Equity Fund’s (the “Fund”) fiscal year on October 31, the Fund reports to you on its results and Stralem & Company Incorporated’s (Stralem) current investment outlook.

Performance

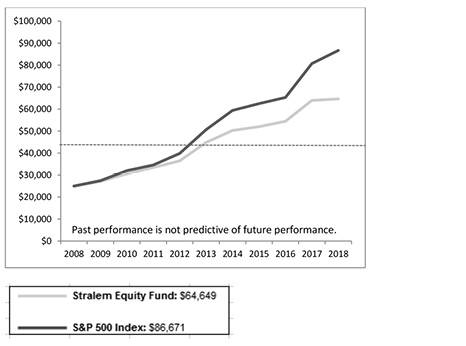

For the fiscal year ended October 31, 2018, the Fund (STEFX) provided a return of 1.13% before taxes and after fees and expenses but trailed the benchmark S&P 500 Index (the “Benchmark”) which returned 7.35% (which of course has no fees, taxes or expenses) as shown in the table below.

AVERAGE ANNUAL TOTAL RETURNS

BEFORE TAXES AND AFTER FEES AND EXPENSES

| Periods Ended 10/31/18 | |||

1 YR | 5 YRS | 10YRS | Since | |

Stralem Equity Fund | 1.13% | 7.60% | 9.97% | 5.60% |

S&P 500 Index | 7.35% | 11.34% | 13.24% | 5.39% |

* | Inception: January 18, 2000. |

Comparison of the Change in Value of a $25,000 Investment in

Stralem Equity Fund- vs. S&P 500 Index

1

PERFORMANCE NOTES: Stralem Equity Fund is advised by Stralem & Company Incorporated (“Stralem”), an independent, SEC registered investment adviser established in 1966. The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance data current to the most recent month end or to receive a prospectus, please call (866) 822-9555 toll free or visit the Fund’s website at www.stralemequityfund.com. Performance results for the Fund are stated after investment advisory fees and expenses (net) but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The Fund can suffer losses as well as gains. Performance results are calculated on a total return basis, which includes all income from dividends and interest and realized and unrealized gains or losses. Assuming dividends are reinvested, the growth in dollars of an investment in a period can be computed using these rates of return. The S&P 500 Index is widely used as a barometer of U.S. stock market performance. The S&P 500 Index is the Standard & Poor’s Composite Index of 500 Stocks, a widely recognized, unmanaged index of common stock prices. It is shown with dividends included and reflects no deduction for fees, expenses or taxes. |

From the market bottom in March of 2009 through the end of October 2018, the S&P 500 Index has returned an extraordinary 390% (17.9% annualized) fueled by a slow and steady economic recovery made possible by record-low interest rates, muted inflation and a very accommodative global monetary policy. Over this period, passive investment vehicles have outperformed their actively managed peers and attracted substantial amounts of assets.

As you can imagine, we at Stralem believe that blind faith in passive investing is a risky proposition that will ultimately be proven to be foolhardy. We believe fundamental stock research, risk-management and capital preservation matter, even if these investment tenets have appeared to be less than necessary in a market that only seems to grind higher. We believe that when historical volatility eventually returns, fundamentally advantaged stocks with stronger growth prospects, healthy cash generation, and superior balance sheets are likely to go down less and/or recover faster than weaker companies. Differentiation and dispersion in stock performance will re-emerge. While we can’t predict when this will happen, we believe it to be prudent to be prepared.

The end of calendar year 2017 was marked by anticipation of Congress passing the Tax Cuts and Jobs Act (TCJA), which lowered the statutory tax rates for individuals and corporations. While the impact to individuals can differ dramatically by state and tax bracket, the benefit to corporations is more straightforward, as the rate dropped to 21%. As analysts and investors began to incorporate this lower rate into their earnings estimates, the S&P 500, already near another record high with all-time high margins, was forecasted to grow earnings over 20% higher in 2018 than in 2017 -- a significant catalyst for a weary bull market nearly 10 years old. This fiscal stimulus also had the effect of boosting 2nd quarter GDP to 4.2% while driving unemployment down to 3.7%. And the S&P 500 responded by rallying over 15% from the start of the fiscal year (November 2017) through the end of September 2018.

However, as always, equity investors focus on more than just current year earnings, positive corporate commentary and earnings guidance are critical components in driving equity valuations and pushing up stock prices. Concurrent with Congress launching a new fiscal stimulus, the Federal Reserve (the “Fed”)

2

continued on its course of reversing the longstanding easy monetary policy program that had served as a stimulus since 2009. In addition to buying fewer bonds (Quantitative Tightening), the Fed raised interest rates three times in 2018 and has now raised a total of eight times since the end of 2015. These actions have led the 10-year Treasury yield to increase from a fiscal year low of 2.30% to a high of 3.25% -- well above the 2016 low of 1.31%. Higher rates historically serve as a brake on economic growth as the cost of debt increases, and input costs rise along with interest expense for corporations and consumers alike. The risk of higher rates is only amplified for highly levered companies that can easily choke on rapidly rising interest expenses.

In addition to higher interest rates, the Trump Administration’s hard-line trade policy in North America and China has caused indigestion for many large multi-national companies. These companies depend on China as a significant source of growth, while also relying on globally diverse and optimized supply chains that are easily disrupted by unnecessary tariffs and trade wars.

Through September of 2018, investors seemed more enamored with the accelerating GDP and increased earnings and drove the S&P 500 to new heights. But October brought more skepticism, as investors listened to CEOs discuss increasing wages, mounting inflation, higher interest rates and uncertainty around synchronized global growth clouding their visibility and confidence into 2019 and beyond. These collective worries seemed to trump the accelerated earnings growth and margin expansion, and the S&P 500 dropped 6.8% in the month of October – a potential turning point in the near decade long market rally.

Since the financial crisis Stralem has remained positioned with a slight conservative edge, allocating 35% of the portfolio to capital-preserving Down Market stocks and 65% of the portfolio emphasizing high-quality, larger-market-cap, globally exposed, stable and innovative growth-participating Up Market companies. Although this structure has predictably caused us to trail the S&P 500, we intentionally maintain it out of concern for the multitude of risks we see and are unwilling to ignore.

There have been only 5 market declines greater than 10% over the entire market rally since March 2009. The portfolio structure protected capital in each instance although each proved to merely be a speed bump on the way to a new record high.

While we may sound like a broken record, today just about every market pundit will agree that this market environment is not normal, nor is it likely to be sustainable indefinitely. One of the driving forces behind the rally, this loose monetary policy, has begun to reverse as the Federal Reserve continues on its path to raise rates and slowly unwind its QE policy. This is important because interest rates (and inflation) are inversely correlated with stock market valuations. And while we may still be in a “low rate” environment, and the tax cuts may have increased corporate profitability, the Fed has clearly pivoted and at some point, it will catch up to companies and the economy. Exactly when and to what magnitude is difficult to predict, but it is not hard to predict that more volatility is likely on the way.

3

In summary, despite our concerns about the overall market environment, we are confident in the portfolio’s positioning as well as in the companies we own. We continue to adhere to our time-tested process and discipline and believe “participation with protection” is the best way to build long-term wealth.

Portfolio Structure and Positioning

As of October 31, 2018, the overall allocation stood at 65% Up Market/ 35% Down Market.

Investment Outlook

While the Fund’s fiscal year began strongly based on hopes for faster GDP growth and higher corporate earnings as a result of Congress’ new tax plan, the year ended in a very different place.

Lower personal and corporate taxes drove GDP growth above 4%, unemployment below 4%, and corporate margins to all-time highs. The S&P 500 saw 2018 earnings growth above 20% -- an amazing result 10 years into a bull market. However, as we look forward to the end of calendar year 2018 and into 2019, from a market just off its all-time high, it is more challenging to be as optimistic about what comes next.

While companies are lapping the reduced tax rate, earnings growth peaked in 2018 and is expected to slow for the next 8 quarters. With wage growth creeping up, commodity prices elevated, interest rates higher and tariffs and trade decisions starting to bite, achieving new highs on corporate margins seems difficult.

In addition, while the new tax plan did drive some job growth and consumer spending while also goosing corporate margins and earnings, the outlook into 2019 is for lower GDP growth and lower S&P 500 earnings growth.

At present, with the tax cuts boosting earnings, S&P 500 valuations are only slightly above historical averages. However, with the pivot in monetary policy driving higher interest rates, there is increasing concern that we are approaching peak multiples. This does not necessarily portend the end of the bull market, but rather indicates that returns over the next several years will be more muted and there will be more dispersion among company performance based largely on growth, execution and reasonable valuations. As we said in some of our recent communiques to investors, to think higher interest rates will not have any impact on valuations is a potentially dangerous position and one for which we are actively preparing.

At Stralem, our mantra has long been “Participation with Protection”. At present, the protection element does not seem to be relevant; however, given views on both the macro economy and what we are seeing at the company level, we firmly believe it is more important than ever. However, we also recognize that market timing, and trying to speculate what could be the catalyst to derail the market’s nearly 10-year bull-run, are endeavors fraught with peril. So while maintaining a “Down-Market” protection component in the Large-Cap Equity Strategy, we also continuously try to identify and invest in the most exciting secular growth opportunities that will provide participation in strong markets.

4

Performance Attribution

The Fund’s relative underperformance for the fiscal year ended Oct 31, 2018 was driven proportionally by the Up Market sector (-2.46%) and by the Down Market sector (-2.59%).

The relative underperformance of the Up Market sector was driven by the New Industries category which led the market in FY18 and was up 15.0%. While the Fund had its share of New Industry winners, Adobe (+40.3%) and Microsoft (+30.7%), it did not own Apple (+31.4%) or Amazon (44.6%) which continued to make new highs. Another Fund holding, Broadcom, a high-cash flowing diversified semiconductor company that was up 48% in calendar year 2017, announced plans to buy Computer Associates (CA), a slower growing but high-cash flowing software company. While the deal makes financial sense and is earnings accretive, there was some investor angst about the strategic fit and the stock traded down 12.9%. We believe Broadcom’s CEO is a technology industry visionary with a long history of successful acquisitions, and we are content to wait and see how the company can integrate CA and cross-sell the hardware and software products and increase corporate margins.

In the New Products category, Thermo Fisher Scientific continues to execute incredibly well as it sells its diverse product lineup into the pharma and biotech laboratory testing market globally. While most companies find it difficult to navigate in China, Thermo Fisher continues to grow their sales as China prioritizes the biotechnology industry and Thermo sells their best-in-class solutions.

The Dominant Companies category was a mixed bag as strength in Visa (+26.2%), UnitedHealth Group (+26.0%), Intercontinental Exchange (+18.0%) and Lowe’s (+21.3%) was offset by D.R. Horton (-17.8%) and DowDupont (-23.8%). Visa continues to take advantage of the global secular trend to e-commerce, the shift to cashless, and the integration of Visa Europe which was neglected by its bank owners for many years. UnitedHealth Group continues to benefit from the increased population growth as the Affordable Care Act (ACA) was not repealed by Congress and near flawless execution on a growing client base. Intercontinental Exchange is consistently increasing it’s scale by bolting on smaller acquisition and selling more and more data to hungry investors – in both equities, derivatives and bonds. And lastly, Lowe’s, a perpetual underperformer relative to Home Depot, got a boost when some activist investors announced they were involved and would push for new management (we sold into this strength).

D.R. Horton struggled this fiscal year largely due to the increase in interest rates and the impact on mortgages. We strongly believe the secular trends are in place to drive more first-time homeownership among the Millenial cohort as well as Baby Boomers trading down and moving to locations with better weather. A spike in mortgage rates will always freeze the market temporarily and cause certain investors to sell, but we believe that D.R. Horton has the right product, in the right locations and should continue to execute well against a reasonable plan.

5

DowDupont performed very well in calendar year 2017 (+27.9%), when the merger was officially completed, and the company began to execute on its aggressive cost savings plan, while discussing the ultimate separation into 3 distinct, but focused companies. However, the stock traded sideways through most of the fiscal year until the energy complex sold off hard towards the end of September based on fears of trade wars with China and slowing global growth. Both inputs, as well as issues with U.S. farmers selling crops (namely soybeans) to China became yet another headwind for DowDupont. We still believe strongly in DowDupont’s products, it’s feedstock advantages, it’s innovation and its best-in-class product portfolio and we think that when separated out, each of its business units will obtain a higher multiple than they are afforded with a chemicals conglomerate.

The relative underperformance in the Down Market sector was driven by the High Yield category, where strength in Merck (+37.9%) and Pfizer (+27.4%) was offset by weakness in PPL (-14.5%), Philip Morris (-11.6%) and Abbvie (-10.4%). PPL’s and Philip Morris’ aforementioned difficulties led to both companies being sold from the Fund, and Abbvie’s weakness was likely related to the fact that the stock was up 60% in calendar year 2017.

Purchases and Sales

During the Fund’s fiscal year ended October 31, 2018, the Fund sold the following securities within the Up Market segment of the portfolio: biotechnology company Amgen (AMGN), home improvement retailer Lowe’s (LOW), packaged foods company Mondelez (MDLZ), and coffee retailer Starbucks (SBUX). The Fund also sold integrated oil and gas company Exxon Mobil (XOM), packaged foods company Kraft Heinz (KHI), international cigarette manufacturer Philip Morris (PM), and energy and utility company PPL (PPL) from the Down Market segment of the portfolio.

As replacements, the Fund purchased the following securities within the Up Market segment of the portfolio: orphan drug manufacturer Alexion Pharmaceuticals (ALXN), aerospace manufacturer Boeing (BA), cruise line company Carnival (CCL) and homebuilder D.R. Horton (DHI). We also purchased the following securities in our Down Market segment: large pharmaceutical manufacturer AbbVie (ABBV), regulated utility American Electric Power (AEP), global custody bank Bank of New York Mellon (BK), and oil and gas pipeline and storage company Kinder Morgan (KMI).

Amgen’s 1st-generation biotechnology drugs have been cash cows and performing very well, however, in recent quarters, the company has been experiencing attrition of its core franchise drugs due to biosimilar competition and the development of alternate cancer therapies. The company’s RGV (relative growth valuation) score has been weakening, and we expect will erode further as this trend continues.

6

While the overall home improvement category continues to be one of the best performers within Consumer Discretionary, Lowe’s management failed to execute consistently against their long-term goals and targets, and management changes are required. We have lost our patience and sold the stock based on better options.

Stralem’s 2013 thesis for buying Mondelez was centered around a 5-year margin-expansion program launched by CEO Irene Rosenfeld based on rationalizing a bloated cost structure. After successfully combining and modernizing production facilities, streamlining its supply chain and European distribution centers, and driving margins higher, future growth will be largely dependent on product innovations and additional market penetration and this has proven to be a challenge.

Starbucks was purchased based on strong sales in existing markets driven by more/better food and drink options, e-commerce initiatives built around the company’s Mobile Order and Pay, and rapid expansion in China. This thesis played out well for a couple years, but after some above average growth in North America, the company seems to be searching for additional innovation to drive traffic. Visionary CEO Howard Schulz is stepping down, and the company has settled into a period of slower sales growth.

In the Down Market, Exxon Mobil reached the end of a long run of decreasing capital expenditure intensity, which drove steadily improving free cash flow. This trend is likely to begin to reverse as the company increasingly feels the need to spend in order to replace reserves and take on more early-stage, but risky, large-scale projects.

Kraft Heinz has successfully applied the cost-cutting playbook of its activist investor (3G Capital) since Heinz acquired Kraft Foods in 2015. Unfortunately, the company has not been as successful in reinvigorating top-line through product innovation and organic growth. With the lack of organic growth, the company likely needs to make another major acquisition in order to provide the next boost through massive cost-cutting. However, since the failed $143 billion takeover bid for Unilever in early 2017, no such acquisition has been seriously on the radar, which has caused Kraft Heinz’s shares to languish.

Philip Morris International has benefitted from pricing power (due to inelastic demand) and aspirational consumption (trading up) in emerging countries. However, the company is investing heavily and transitioning its focus to ‘reduced-risk products’ (e-cigarettes), which initially saw some very strong conversion rates. However, in Q1 the adoption rate decelerated significantly and penetration in Japan seems to have plateaued far sooner than expected. We believe this is a true challenge to the business and decided to find a better option.

PPL has spent the last several years successfully transforming itself from a primarily non-regulated utility into an entirely regulated one. The issue with PPL is that its UK utility operations continue to play an outsize role not only in its overall profit generation but have also heaped uncertainty onto what should be steady, unexciting, regulated utility operations. Brexit and PPL’s UK sterling exposure were the main culprits for uncertainty starting in 2016, but that has now expanded to the suddenly tumultuous regulatory situation in the UK where electricity and gas bill inflation is under scrutiny.

7

Alexion Pharmaceuticals replaces Amgen in the New Products category within the Up Market. Alexion is an innovative orphan drug focused biotech company whose primary drug, Soliris, is a ‘C5 complement inhibitor’ that has proven extremely effective in treating the ‘ultra-rare’ genetic blood disorders paroxysmal nocturnal hemoglobinuria (PNH) and atypical hemolytic uremic syndrome (aHUS), both characterized by the death of red blood cells, which can cause blood clotting and organ damage. Soliris was also approved more recently for generalized myasthenia gravis (gMG), a rare but chronic and debilitating neuromuscular disorder. With a new management team, Alexion is leveraging its core competency of identifying and developing drugs for rare-disease populations and has several newer products in late stage clinical trials that are progressing very well.

Aerospace juggernaut Boeing was one of the Dominant Companies bought because it is in a cash flow sweet spot as it ramps up production of its improved fuel-efficient narrow-body 737 MAX and its wide-body 787 Dreamliner, and as unit costs come down as it reaches scale. The company is in the middle of a multi-decade increase in the global demand for air travel as emerging countries reach certain income thresholds and demand leisure travel. The company has a backlog of 5,800 aircraft valued at $486B, and while there is always a market risk, the company’s only real competitor, Airbus, has a 9+ year waiting list on planes as well – so the options for buyers remain limited. The company will generate a significant amount of free cash flow which will provide a bevy of options to the management team.

Carnival Corporation is another Dominant Company replacement and represents the largest player in the cruise industry, an oligopoly with significant barriers to entry (new ships cost over $1B), measured supply growth, strong demand based on affordability, and significant new market expansion opportunities as middle-class consumerism spreads through Asia. Carnival had a strong 2017 but the stock is not overly expensive; the company generates solid and stable cash flow with good visibility into passenger counts and revenues.

The final Dominant Company replacement is D.R. Horton, one of the largest homebuilders in America with a focus on more affordable first-time homebuyers, and retirees trading down in the fastest growing markets in the Southeast, South Central and Southwest. While mortgage rates are ticking higher, pent up demand among Millennials (the largest generation) that are finally beginning to marry and start families (homeownership rates are the lowest in 50 years) and the retiring and downsizing of the Baby Boomers remain as two strong secular drivers for home purchase—especially at D.R. Horton’s price points and in their very desirable geographies.

AbbVie replaces Kraft Heinz in the High Yield category within the Down Market sector. AbbVie is one of the largest pharmaceutical companies in the world, driven by sales of its autoimmune drug Humira, the largest-selling drug in the

8

world. While the “active ingredient” patent for Humira expired in 2016, AbbVie has successfully staved off biosimilar competition, and Humira sales continue to grow. The extension of market dominance for best-in-class Humira will provide abundant cash flow to keep increasing its dividend payout to investors, and to fill its future drug pipeline via acquisitions and internal development.

American Electric Power is a large regulated utility holding company whose service areas span much of the Midwest (11 states) and one that we ultimately found to be more attractive as an investment than PPL. The company operates the largest transmission network in the US (over 40,000 miles) and continues to invest heavily in its regulated transmission assets, propelling the growth of its regulated rate base. At the time of purchase, AEP sported a solid dividend yield of 3.8%, and over the last 5 years has increased its dividend at an annual rate of nearly 5%.

Bank of NY Mellon is an attractive Down Market investment because of its range of steady fee-generating businesses under its Investment Services arm (custody, execution & clearing, asset servicing, treasury services, issuer services) and its Investment Management arm. The company’s technology platforms represent a significant barrier to entry for competitors, it now has a firmly-entrenched cost-cutting and technology-oriented culture, and its new CEO, Charlie Scharf, will continue the technology transformation, just as he successfully engineered at Visa.

Kinder Morgan replaces Exxon in the Low Price to Cash Flow category within the Down Market. Kinder is the largest energy infrastructure company in North America, operating 84,000 miles of pipelines that transport natural gas and other refined petroleum products, along with more than 150 terminals that transload and store petroleum and chemical products. The U.S. shale revolution, Mexican natural gas demand and increasing LNG exports are boosting demand for energy infrastructure, and Kinder generates stable, fee-based cash flow primarily under take-or-pay contracts. Kinder lives within its cash flow (which fully funds expansion capex and dividends), has a transparent corporate structure (unlike opaque MLP structures) and works hard to align management’s and shareholders’ incentives.

Conclusion

Stralem’s long-held investment discipline is based on the principle of “participation with protection” which is based on the understanding that when it comes to building sustainable wealth, the impact of preserving capital in falling markets far outstrips the importance of outperforming in rising ones. So despite the challenges of outperforming the S&P 500 Index from the market low in 2009, Stralem chose not to chase performance for performance sake and remained disciplined awaiting a return to a more “normalized” historical environment. This normalized environment has taken longer to occur than we, or most Wall Street pundits, have expected, however it may finally be upon us.

While the U.S. and global economies have undergone a fair amount of upheaval since the election of Donald Trump and his “America First” doctrine, the critical change to the market is the pivot from easy to tighter monetary policy by the Federal Reserve. While the Fed began raising rates and unwinding the balance sheet in 2015, it is only recently that markets and companies have begun to feel the bite. The recent tax cuts created a sugar high that resulted in record earnings growth and margins, but only served to delay the inevitable. Nearly 10 years into a one-way bull market that has achieved record after record, despite record low volatility, the economy and stock market will likely need to revert to more normalized conditions which, means greater volatility and more muted returns. Stralem continues to be convinced that fundamental analysis, investment prudence and discipline will once again prove to be critical.

9

Market corrections – both large and small – happen, and they typically occur when least expected. At Stralem, even at the cost of sometimes trailing the Benchmark, we will remain steadfast in our discipline and patient in our approach – continuing to maintain an allocation to downside protection while seeking fundamentally advantaged, high quality companies that meet our criteria for growth and valuation. A return to fundamental investing unencumbered by very loose monetary policy should, in our view, amply reward such discipline.

Please do not hesitate to contact us with any questions.

Sincerely,

Andrea Baumann Lustig

President, Stralem & Company Incorporated

10

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-866-822-9555.

An investor should consider the investment objectives, risks, charges, and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please visit the Fund’s website at www.stralemequityfund.com or call 1-866-822-9555 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of Stralem’s current opinions and views of the financial markets. Although Stralem believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time, and may no longer be held by the Fund. For a complete list of securities held by the Fund as of October 31, 2018, please see the Schedule of Investments section of the annual report. The opinions of Stralem with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Fund and the market in general and statements of the Fund’s plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements, include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

11

STRALEM EQUITY FUND

PORTFOLIO INFORMATION

October 31, 2018 (Unaudited)

As of October 31, 2017 | As of October 31, 2018 | ||||||||||||||||

|

| Value | % of Total | Value | % of Total | ||||||||||||

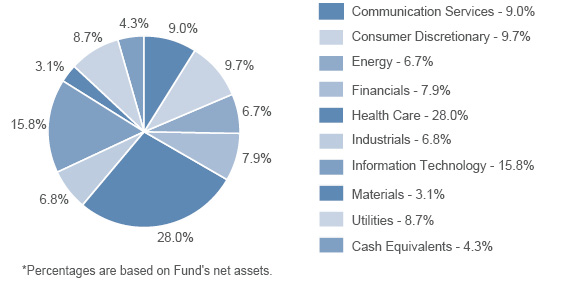

UP MARKET | NEW PRODUCTS | $ | 13,516,674 | 9.9 | % | $ | 12,103,796 | 12.5 | % | ||||||||

NEW INDUSTRIES | 26,535,346 | 19.4 | % | 17,883,847 | 18.5 | % | |||||||||||

DOMINANT COMPANIES | 50,299,002 | 36.7 | % | 32,447,888 | 33.5 | % | |||||||||||

DOWN MARKET | LOW PRICE TO CASH FLOW | 11,756,714 | 8.6 | % | 10,810,753 | 11.2 | % | ||||||||||

HIGH YIELD | 30,411,986 | 22.2 | % | 20,108,204 | 20.8 | % | |||||||||||

MONEY MARKET | 4,351,561 | 3.2 | % | 3,345,210 | 3.5 | % | |||||||||||

| $ | 136,871,283 | 100.0 | % | $ | 96,699,698 | 100.0 | % | ||||||||||

12

STRALEM EQUITY FUND

SCHEDULE OF INVESTMENTS

October 31, 2018

COMMON STOCKS — 95.7% | Shares | Value | ||||||

Communication Services — 9.0% | ||||||||

Diversified Telecommunication Services — 3.0% | ||||||||

AT&T, Inc. | 96,700 | $ | 2,966,756 | |||||

Interactive Media & Services — 6.0% | ||||||||

Alphabet, Inc. - Class A (a) | 2,800 | 3,053,624 | ||||||

Facebook, Inc. - Class A (a) | 18,400 | 2,792,936 | ||||||

| 5,846,560 | ||||||||

Consumer Discretionary — 9.7% | ||||||||

Auto Components — 3.0% | ||||||||

Aptiv plc | 38,300 | 2,941,440 | ||||||

Hotels, Restaurants & Leisure — 3.4% | ||||||||

Carnival Corporation | 58,750 | 3,292,350 | ||||||

Household Durables — 3.3% | ||||||||

D.R. Horton, Inc. | 88,900 | 3,196,844 | ||||||

Energy — 6.7% | ||||||||

Oil, Gas & Consumable Fuels — 6.7% | ||||||||

Chevron Corporation | 19,400 | 2,166,010 | ||||||

EOG Resources, Inc. | 20,000 | 2,106,800 | ||||||

Kinder Morgan, Inc. | 129,500 | 2,204,090 | ||||||

| 6,476,900 | ||||||||

Financials — 7.9% | ||||||||

Capital Markets — 5.7% | ||||||||

Bank of New York Mellon Corporation (The) | 45,250 | 2,141,683 | ||||||

Intercontinental Exchange, Inc. | 44,250 | 3,409,020 | ||||||

| 5,550,703 | ||||||||

Insurance — 2.2% | ||||||||

Chubb Ltd. | 17,550 | 2,192,170 | ||||||

Health Care — 28.0% | ||||||||

Biotechnology — 7.7% | ||||||||

AbbVie, Inc. | 36,250 | 2,822,062 | ||||||

Alexion Pharmaceuticals, Inc. (a) | 21,450 | 2,403,902 | ||||||

Celgene Corporation (a) | 31,950 | 2,287,620 | ||||||

| 7,513,584 | ||||||||

See notes to financial statements. |

13

STRALEM EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 95.7% (Continued) | Shares | Value | ||||||

Health Care — 28.0% (Continued) | ||||||||

Health Care Equipment & Supplies — 5.9% | ||||||||

Abbott Laboratories | 35,650 | $ | 2,457,711 | |||||

Danaher Corporation | 33,000 | 3,280,200 | ||||||

| 5,737,911 | ||||||||

Health Care Providers & Services — 3.4% | ||||||||

UnitedHealth Group, Inc. | 12,600 | 3,293,010 | ||||||

Life Sciences Tools & Services — 2.6% | ||||||||

Thermo Fisher Scientific, Inc. | 10,750 | 2,511,738 | ||||||

Pharmaceuticals — 8.4% | ||||||||

Johnson & Johnson | 17,450 | 2,442,825 | ||||||

Merck & Company, Inc. | 40,100 | 2,951,761 | ||||||

Pfizer, Inc. | 66,300 | 2,854,878 | ||||||

| 8,249,464 | ||||||||

Industrials — 6.8% | ||||||||

Aerospace & Defense — 3.5% | ||||||||

Boeing Company (The) | 9,500 | 3,371,170 | ||||||

Air Freight & Logistics — 3.3% | ||||||||

FedEx Corporation | 14,800 | 3,261,032 | ||||||

Information Technology — 15.8% | ||||||||

IT Services — 3.4% | ||||||||

Visa, Inc. - Class A | 24,250 | 3,342,862 | ||||||

Semiconductors & Semiconductor Equipment — 3.1% | ||||||||

Broadcom, Inc. | 13,400 | 2,994,766 | ||||||

Software — 9.3% | ||||||||

Adobe Systems, Inc. (a) | 12,300 | 3,022,848 | ||||||

Microsoft Corporation | 28,100 | 3,001,361 | ||||||

Oracle Corporation | 61,800 | 3,018,312 | ||||||

| 9,042,521 | ||||||||

Materials — 3.1% | ||||||||

Chemicals — 3.1% | ||||||||

DowDuPont, Inc. | 56,750 | 3,059,960 | ||||||

See notes to financial statements. |

14

STRALEM EQUITY FUND

SCHEDULE OF INVESTMENTS (Continued)

COMMON STOCKS — 95.7% (Continued) | Shares | Value | ||||||

Utilities — 8.7% | ||||||||

Electric Utilities — 5.8% | ||||||||

American Electric Power Company, Inc. | 38,700 | $ | 2,839,032 | |||||

Duke Energy Corporation | 34,350 | 2,838,341 | ||||||

| 5,677,373 | ||||||||

Multi-Utilities — 2.9% | ||||||||

Dominion Energy, Inc. | 39,700 | 2,835,374 | ||||||

Total Common Stocks (Cost $66,963,586) | $ | 93,354,488 | ||||||

MONEY MARKET FUNDS — 3.4% | Shares | Value | ||||||

Dreyfus Treasury Securities Cash Management Fund - Investor Shares, 1.77% (b) (Cost $3,345,210) | 3,345,210 | $ | 3,345,210 | |||||

Total Investments at Value — 99.1% (Cost $70,308,796) | $ | 96,699,698 | ||||||

Other Assets in Excess of Liabilities — 0.9% | 848,369 | |||||||

Net Assets — 100.0% | $ | 97,548,067 | ||||||

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of October 31, 2018. |

See notes to financial statements. | |

15

STRALEM EQUITY FUND

STATEMENT OF ASSETS AND LIABILITIES

October 31, 2018

ASSETS | ||||

Investments, at value (Note 2) (Cost $70,308,796) | $ | 96,699,698 | ||

Cash | 114,745 | |||

Receivable for investment securities sold | 693,782 | |||

Dividends receivable | 141,763 | |||

Other assets | 7,182 | |||

Total Assets | 97,657,170 | |||

LIABILITIES | ||||

Payable to Investment Adviser (Note 4) | 61,477 | |||

Payable to administrator (Note 4) | 15,090 | |||

Accrued expenses | 32,536 | |||

Total Liabilities | 109,103 | |||

NET ASSETS | $ | 97,548,067 | ||

NET ASSETS CONSIST OF: | ||||

Paid-in capital | $ | 48,957,850 | ||

Accumulated earnings | 48,590,217 | |||

Net Assets | $ | 97,548,067 | ||

Shares of beneficial interest outstanding | 9,769,566 | |||

Net asset value, offering price and redemption price per share (a) | $ | 9.98 |

(a) | Redemption price varies based on length of time held (Note 2). |

See notes to financial statements. | |

16

STRALEM EQUITY FUND

STATEMENT OF OPERATIONS

For the Year Ended October 31, 2018

INVESTMENT INCOME | ||||

Dividends (net of foreign withholding taxes of $11) | $ | 2,613,779 | ||

EXPENSES | ||||

Investment advisory fees (Note 4) | 1,330,260 | |||

Administration fees (Note 4) | 120,492 | |||

Professional fees | 61,798 | |||

Fund accounting fees (Note 4) | 42,732 | |||

Registration and filing fees | 16,700 | |||

Compliance fees (Note 4) | 15,432 | |||

Transfer agent fees (Note 4) | 15,000 | |||

Trustees’ fees and expenses (Note 4) | 12,932 | |||

Bank service fees | 6,916 | |||

Printing | 4,960 | |||

Postage and supplies | 4,805 | |||

Insurance expense | 2,953 | |||

Other | 20,812 | |||

Total Expenses | 1,655,792 | |||

Investment advisory fee reductions (Note 4) | (445,789 | ) | ||

Net Expenses | 1,210,003 | |||

NET INVESTMENT INCOME | 1,403,776 | |||

REALIZED AND UNREALIZED GAINS (LOSSES) ON INVESTMENTS | ||||

Net realized gains from investment transactions | 21,339,408 | |||

Net change in unrealized appreciation (depreciation) on investments | (20,505,741 | ) | ||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 833,667 | |||

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 2,237,443 |

See notes to financial statements. |

17

STRALEM EQUITY FUND

STATEMENTS OF CHANGES IN NET ASSETS

| Year | Year | ||||||

OPERATIONS | ||||||||

Net investment income | $ | 1,403,776 | $ | 1,372,588 | ||||

Net realized gains from investment transactions | 21,339,408 | 7,346,411 | ||||||

Net change in unrealized appreciation (depreciation) on investments | (20,505,741 | ) | 12,604,924 | |||||

Net increase in net assets resulting from operations | 2,237,443 | 21,323,923 | ||||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | (8,723,481 | ) | (19,648,609 | ) | ||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Proceeds from shares sold | 5,181,862 | 5,811,367 | ||||||

Net asset value of shares issued in reinvestment of distributions | 6,957,351 | 16,004,485 | ||||||

Proceeds from redemption fees (Note 2) | 64 | 5 | ||||||

Payments for shares redeemed | (44,946,201 | ) | (29,615,038 | ) | ||||

Net decrease in net assets from capital share transactions | (32,806,924 | ) | (7,799,181 | ) | ||||

TOTAL DECREASE IN NET ASSETS | (39,292,962 | ) | (6,123,867 | ) | ||||

NET ASSETS | ||||||||

Beginning of year | 136,841,029 | 142,964,896 | ||||||

End of year | $ | 97,548,067 | $ | 136,841,029 | ||||

CAPITAL SHARE ACTIVITY | ||||||||

Shares sold | 505,521 | 597,266 | ||||||

Shares reinvested | 690,899 | 1,720,912 | ||||||

Shares redeemed | (4,426,909 | ) | (2,909,110 | ) | ||||

Net decrease in shares outstanding | (3,230,489 | ) | (590,932 | ) | ||||

Shares outstanding, beginning of year | 13,000,055 | 13,590,987 | ||||||

Shares outstanding, end of year | 9,769,566 | 13,000,055 | ||||||

(a) | The presentation of Distributions to Shareholders has been updated to reflect the changes prescribed in amendments to Regulation S-X, effective November 5, 2018 (Note 2). For the year ended October 31, 2017, distributions to shareholders consisted of $2,109,539 from net investment income and $17,539,070 from net realized gains from investment transactions. As of October 31, 2017, undistributed net investment income was $975,373. |

See notes to financial statements. | |

18

STRALEM EQUITY FUND

FINANCIAL HIGHLIGHTS

(For a share outstanding throughout each year) | ||||||||||||||||||||

Year Ended October 31, | ||||||||||||||||||||

| 2018 | 2017 | 2016 | 2015 | 2014 | |||||||||||||||

Net asset value, beginning of year | $ | 10.53 | $ | 10.52 | $ | 15.53 | $ | 17.45 | $ | 16.77 | ||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||

Net investment income | 0.13 | 0.12 | 0.22 | 0.23 | 0.24 | |||||||||||||||

Net realized and unrealized gains on investments | 0.00 | (a) | 1.49 | 0.24 | 0.34 | 1.70 | ||||||||||||||

Total from investment operations | 0.13 | 1.61 | 0.46 | 0.57 | 1.94 | |||||||||||||||

Less distributions: | ||||||||||||||||||||

Dividends from net investment income | (0.11 | ) | (0.17 | ) | (0.25 | ) | (0.25 | ) | (0.26 | ) | ||||||||||

Distributions from net realized gains | (0.57 | ) | (1.43 | ) | (5.22 | ) | (2.24 | ) | (1.00 | ) | ||||||||||

Total distributions | (0.68 | ) | (1.60 | ) | (5.47 | ) | (2.49 | ) | (1.26 | ) | ||||||||||

Proceeds from redemption fees collected (Note 2) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | 0.00 | (a) | ||||||||||

Net asset value, end of year | $ | 9.98 | $ | 10.53 | $ | 10.52 | $ | 15.53 | $ | 17.45 | ||||||||||

Total return (b) | 1.13 | % | 17.36 | % | 4.72 | % | 3.43 | % | 12.18 | % | ||||||||||

Ratios/supplemental data: | ||||||||||||||||||||

Net assets, end of year (000’s) | $ | 97,548 | $ | 136,841 | $ | 142,965 | $ | 190,800 | $ | 318,237 | ||||||||||

Ratio of total expenses to average net assets | 1.30 | % | 1.28 | % | 1.42 | % | 1.21 | % | 1.12 | % | ||||||||||

Ratio of net expenses to average net assets (c) | 0.95 | % | 0.95 | % | 0.98 | % | 0.98 | % | 0.98 | % | ||||||||||

Ratio of net investment income to average net assets (c) | 1.10 | % | 1.03 | % | 1.52 | % | 1.17 | % | 1.27 | % | ||||||||||

Portfolio turnover rate | 32 | % | 7 | % | 8 | % | 33 | % | 19 | % | ||||||||||

(a) | Amount rounds to less than $0.01 per share. |

(b) | Total return is the measure of the change in value of an investment in the Fund over the periods covered, which assumes any dividends or capital gains distributions are reinvested in shares of the Fund. Returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. The total returns would be lower if the Adviser had not reduced advisory fees and/or reimbursed expenses (Note 4). |

(c) | Ratio was determined after advisory fee reductions and/or expense reimbursements by the Adviser (Note 4). |

See notes to financial statements. | |

19

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS

October 31, 2018

1. | ORGANIZATION |

Stralem Equity Fund (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”). The Trust is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund was reorganized into the Trust on October 17, 2016. It was formerly a series of Stralem Fund.

The Fund’s investment objective is to seek long-term capital appreciation.

2. | SIGNIFICANT ACCOUNTING POLICIES |

In August 2018, the U.S. Securities and Exchange Commission (the “SEC”) adopted regulations that eliminated or amended disclosure requirements that were redundant or outdated in light of changes in SEC requirements, accounting principles generally accepted in the United States of America (“GAAP”), International Financial Reporting Standards or changes in technology or the business environment. These regulations were effective November 5, 2018, and the Fund is complying with them effective with these financial statements.

The Fund follows accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services – Investment Companies.” The following is a summary of the Fund’s significant accounting policies used in the preparation of its financial statements. These policies are in conformity with GAAP.

New Accounting Pronouncement — In August 2018, FASB issued Accounting Standards Update No. 2018-13 (“ASU 2018-13”), “Disclosure Framework – Changes to the Disclosure Requirements for Fair Value Measurement,” which amends the fair value measurement disclosure requirements of ASC Topic 820, “Fair Value Measurement” (“ASC 820”). ASU 2018-13 includes new, eliminated, and modified disclosure requirements for ASC 820. In addition, ASU 2018-13 clarifies that materiality is an appropriate consideration of entities when evaluating disclosure requirements. ASU 2018-13 is effective for fiscal years beginning after December 15, 2019, including interim periods therein. Early adoption is permitted and the Fund has adopted ASU 2018-13 with these financial statements.

Investment valuation:

The Fund’s portfolio securities are valued as of the close of business of the regular session of trading on the New York Stock Exchange (“NYSE”) (normally 4:00 p.m., Eastern time) on each day the NYSE is open. Securities which are traded on stock exchanges are valued at the closing price on the day the securities are being valued, or, if not traded on a particular day, at the closing mean price. Securities quoted by NASDAQ are valued at the NASDAQ Official Closing Price.

20

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Securities traded in the over-the-counter market are valued at the last sale price, if available, otherwise, at the last quoted mean price. Investments in money market funds are valued at net asset value (“NAV”). When using a quoted price and when the market for the security is considered active, the security will be classified as Level 1 within the fair value hierarchy (see below). In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value pursuant to procedures established by and under the direction of the Board of Trustees (the “Board”) of the Trust. Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s NAV may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

Level 1 – quoted prices in active markets for identical securities

Level 2 – other significant observable inputs

Level 3 – significant unobservable inputs

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the above fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments by security type as of October 31, 2018:

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stocks | $ | 93,354,488 | $ | — | $ | — | $ | 93,354,488 | ||||||||

Money Market Funds | 3,345,210 | — | — | 3,345,210 | ||||||||||||

Total | $ | 96,699,698 | $ | — | $ | — | $ | 96,699,698 | ||||||||

21

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by sector and industry type. There were no Level 2 or Level 3 securities or derivative instruments held by the Fund as of October 31, 2018.

Share valuation and redemption fees:

The NAV per share of the Fund is calculated daily by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share is equal to the NAV per share, except that shares are subject to a redemption fee of 1% if shares are redeemed within 60 days of purchase. During the years ended October 31, 2018 and 2017, proceeds from redemption fees totaled $64 and $5, respectively.

Investment transactions and income:

Investment transactions are accounted for on the trade date. Realized gains and losses on sales of investments are calculated on a specific identification basis. Dividend income is recorded on the ex-dividend date, and interest income is recognized on the accrual basis. Withholding taxes on foreign dividends have been recorded in accordance with the Fund’s understanding of the applicable country’s rules and tax rates.

Common Expenses:

Common expenses of the Trust are allocated among the Fund and other series of the Trust based on the relative net assets of each series or the nature of the services performed and the relative applicability to each series.

Distributions to shareholders:

Distributions arising from net investment income and net realized capital gains are declared and paid to shareholders annually. The amount of distributions from net investment income and net realized capital gains are determined in accordance with federal income tax regulations, which may differ from GAAP. The tax character of distributions paid to shareholders during the years ended October 31, 2018 and 2017 was as follows:

Years Ended | Ordinary | Long-Term | Total | |||||||||

October 31, 2018 | $ | 1,508,018 | $ | 7,215,463 | $ | 8,723,481 | ||||||

October 31, 2017 | $ | 2,489,305 | $ | 17,159,304 | $ | 19,648,609 | ||||||

Use of estimates:

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

22

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Federal Income Tax:

The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986, as amended (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent its net investment income and net realized capital gains are distributed in accordance with the Code.

In order to avoid imposition of a federal excise tax applicable to regulated investment companies, the Fund must declare and pay as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of October 31, 2018:

Cost of portfolio investments | $ | 70,484,723 | ||

Gross unrealized appreciation | $ | 29,823,260 | ||

Gross unrealized depreciation | (3,608,285 | ) | ||

Net unrealized appreciation | 26,214,975 | |||

Undistributed ordinary income | 1,302,359 | |||

Undistributed long-term capital gains | 21,072,883 | |||

Distributable earnings | $ | 48,590,217 |

The difference between the federal income tax cost of portfolio investments and the financial statement cost of portfolio investments is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are due to the tax deferral of losses on wash sales.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for all open tax years (generally three years) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements.

3. | INVESTMENT TRANSACTIONS |

During the year ended October 31, 2018, cost of purchases and proceeds from sales of investment securities, other than short-term investments, amounted to $38,757,354 and $78,756,256, respectively.

23

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

4. | TRANSACTIONS WITH RELATED PARTIES |

INVESTMENT ADVISORY AGREEMENT

Pursuant to an Investment Advisory Agreement with Stralem & Company Incorporated (the “Adviser”), the Fund pays the Adviser an advisory fee, payable quarterly, based on the average weekly net assets of the Fund, equal to 1.25% per annum of the first $50 million of such net assets; 1.00% per annum of the next $50 million of such net assets; and 0.75% per annum of such net assets in excess of $100 million.

The Adviser has agreed contractually, until at least March 1, 2020, to reduce its advisory fees and reimburse other expenses to the extent necessary to limit total annual operating expenses (excluding brokerage costs; taxes; interest; costs to organize the Fund; acquired fund fees and expenses; and extraordinary expenses, such as litigation and merger or reorganization costs and other expenses not incurred in the ordinary course of the Fund’s business) to an amount not exceeding 0.95% of the Fund’s average daily net assets. During the year ended October 31, 2018, the Adviser reduced its advisory fees in the amount of $445,789.

Advisory fee reductions and expense reimbursements by the Adviser are subject to repayment by the Fund for a period of three years after such fees and expenses were incurred, provided that the repayments do not cause total annual operating expenses to exceed the lesser of (i) the expense limitation then in effect, if any, and (ii) the expense limitation in effect at the time the expenses to be repaid were incurred. Prior to March 1, 2020, this agreement may not be modified or terminated without the approval of the Board. This agreement will terminate automatically if the Investment Advisory Agreement is terminated. As of October 31, 2018, the amount of fee reductions and expense reimbursements available for recovery by the Adviser is $877,641, which must be recovered no later than the dates stated below:

October 31, 2020 | $ | 431,852 | ||

October 31, 2021 | 445,789 | |||

| $ | 877,641 |

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides administration, fund accounting, compliance, and transfer agent services for the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including, but not limited to, postage, supplies and costs of pricing the Fund’s portfolio securities.

24

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Pursuant to a Distribution Agreement with Ultimus Fund Distributors, LLC (the “Distributor”), the Distributor provides distribution services and serves as principal underwriter for the Fund. The Distributor is a wholly owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain officers and a Trustee of the Trust are also officers of Ultimus and the Distributor.

TRUSTEE COMPENSATION

Effective August 1, 2018, each Trustee who is not an “interested person” of the Trust (“Independent Trustee”) receives a $1,300 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who receives a $1,500 annual retainer from the Fund, paid quarterly. Each Independent Trustee also receives from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses. Prior to August 1, 2018, each Independent Trustee received a $1,000 annual retainer from the Fund, paid quarterly, except for the Board Chairperson who received a $1,200 annual retainer from the Fund, paid quarterly. Each Independent Trustee also received from the Fund a fee of $500 for each Board meeting attended plus reimbursement for travel and other meeting-related expenses.

PRINCIPAL HOLDER OF FUND SHARES

As of October 31, 2018, the following shareholder owned of record 25% or more of the outstanding shares of the Fund:

Name of Record Owner | % Ownership |

Pershing LLC (for the benefit of its customers) | 77% |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholders’ meeting.

5. | SECTOR RISK |

If the Fund has significant investments in the securities of issuers within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have significant investments in that sector. In addition, this may increase the risk of loss in the Fund and increase the volatility of the Fund’s NAV per share. Occasionally, market conditions, regulatory changes or other developments may negatively impact this sector, and therefore the value of the Fund’s portfolio will be adversely affected. As of October 31, 2018, the Fund had 28.0% of the value of its net assets invested in securities within the Health Care sector.

25

STRALEM EQUITY FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

6. | CONTINGENCIES AND COMMITMENTS |

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, the Fund has not had any prior claims or losses pursuant to these arrangements.

7. | SUBSEQUENT EVENTS |

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

26

STRALEM EQUITY FUND

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders of Stralem Equity Fund and

Board of Trustees of Ultimus Managers Trust

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Stralem Equity Fund (the “Fund”), a series of Ultimus Managers Trust, as of October 31, 2018, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, including the related notes, and the financial highlights for each of the three years in the period then ended (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of October 31, 2018, the results of its operations for the year then ended, the changes in Its net assets for each of the two years in the period then ended, and the financial highlights for each of the three years in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

The Fund’s financial statements and financial highlights for the years ended prior to October 31, 2016, were audited by other auditors, whose report dated December 10, 2015, expressed an unqualified opinion on those financial statements and financial highlights.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of October 31, 2018, by correspondence with the custodian and brokers. Our audits also included evaluating the accounting principles used and

27

STRALEM EQUITY FUND

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM (Continued)

significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2016.

COHEN & COMPANY, LTD.

Cleveland, Ohio

December 20, 2018

28

STRALEM EQUITY FUND

DISCLOSURE OF FUND EXPENSES (Unaudited)

As a shareholder of the Fund, you incur ongoing costs, including management fees and other Fund expenses, which are deducted from the Fund’s gross income. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period (May 1, 2018) and held until the end of the period (October 31, 2018).

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

| Beginning | Ending | Expenses Paid |

Based on Actual Fund Return | $ 1,000.00 | $ 1,011.10 | $ 4.82 |

Based on Hypothetical 5% Return | $ 1,000.00 | $ 1,020.42 | $ 4.84 |

* | Expenses are equal to the Fund’s annualized net expense ratio of 0.95% for the period, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). |

29

STRALEM EQUITY FUND

ADDITIONAL INFORMATION (Unaudited)

PROXY VOTING POLICIES AND PROCEDURES

A description of the Fund’s proxy voting policies and procedures is available, without charge, upon request by calling toll free (866) 822-9555, or on the SEC website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is also available, without charge, upon request by calling toll free (866) 822-9555, or on the SEC website at http://www.sec.gov.

QUARTERLY PORTFOLIO HOLDINGS

The Fund’s Forms N-Q containing a complete schedule of portfolio holdings as of the end of the first and third quarters of each fiscal year are available on the SEC’s website at http://www.sec.gov or are available upon request, without charge, by calling toll free at (866) 822-9555.

HOUSEHOLDING

The Fund will generally send only one copy of the summary prospectus, proxy material, annual report and semi-annual report to shareholders residing at the same “household.” This reduces Fund expenses which benefits all shareholders, minimizes the volume of mail you receive and eliminates duplicates of the same information. If you need additional copies of these documents, a copy of the prospectus or do not want your mailings to be “householded,” please send us a written request or call us toll free at (866) 822-9555.

OTHER FEDERAL TAX INFORMATION (Unaudited)

For the fiscal year ended October 31, 2018, the Fund designated $7,215,463 as long-term capital gain distributions subject to a maximum tax rate of 20%.

Qualified Dividend Income — The Fund designates 100% of its ordinary income dividends, or up to the maximum amount of such dividends allowable pursuant to the Internal Revenue Code, as qualified dividend income eligible for the reduced tax rate of 15%.

Dividends Received Deduction — Corporate shareholders are generally entitled to take the dividends received deduction on the portion of the Fund’s dividend distributions that qualifies under tax law. For the fiscal year ended October 31, 2018, 100% of ordinary income dividends qualified for the corporate dividends received deduction.

30

STRALEM EQUITY FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

The Board has overall responsibility for management of the Trust’s affairs. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement, or removal. The Trustees, in turn, elect the officers of the Fund to actively supervise its day-to-day operations. The officers have been elected for an annual term. Each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. The following are the Trustees and executive officers of the Fund:

Name and | Length | Position(s) | Principal | Number | Directorships |

Interested Trustees: | |||||

Robert G. Dorsey* Year of Birth: 1957 | Since February | Trustee (February 2012 to present)

President (June 2012 to October 2013) | Managing Director (1999 to present), Co-CEO (April 2018 to present), and President (1999 to April 2018) of Ultimus Fund Solutions, LLC and its subsidiaries (except as otherwise noted for FINRA-regulated broker dealer entities) | 19 | Interested Trustee of Capitol Series Trust (10 Funds) |

Independent Trustees: | |||||

Janine L. Cohen Year of Birth: 1952 | Since | Trustee | Retired since 2013; Chief Financial Officer from 2004 to 2013 and Chief Compliance Officer from 2008 to 2013 at AER Advisors, Inc. | 19 | None |

31

STRALEM EQUITY FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

Name and | Length of Time Served | Position(s) Held with Trust | Principal | Number of Funds in Trust Overseen by | Directorships of Public Companies Held by Trustee During Past 5 Years |

David M. Deptula Year of Birth: 1958 | Since | Trustee | Vice President of Legal and Special Projects at Dayton Freight Lines, Inc. since 2016; Vice President of Tax Treasury at The Standard Register Inc. (formerly The Standard Register Company) from 2011 to 2016 | 19 | None |

John J. Discepoli Year of Birth: 1963 | Since | Chairperson (May 2016

Trustee (June 2012 to present) | Owner of Discepoli Financial Planning, LLC (personal financial planning company) since 2004 | 19 | None |

* | Mr. Dorsey is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the 1940 Act, as amended, because of his relationship with the Trust’s administrator, transfer agent and distributor. |

Name and | Length of Time Served | Position(s) | Principal Occupation(s) During Past 5 Years |

Executive Officers: | |||

David R. Carson Year of Birth: 1958 | Since | Principal

President (October 2013 to present)

Vice President (April 2013 to October 2013) | Vice President and Director of Client Strategies of Ultimus Fund Solutions, LLC (2013 to present); President, Unified Series Trust (2016 to present); Chief Compliance Officer, FSI Low Beta Absolute Return Fund (2013 to 2016); Chief Compliance Officer, The Huntington Funds (2005 to 2013), Huntington Strategy Shares (2012 to 2013), and Huntington Asset Advisors (2013); Vice President, Huntington National Bank (2001 to 2013) |

32

STRALEM EQUITY FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

Name and | Length of Time Served | Position(s) | Principal Occupation(s) During Past 5 Years |

Todd E. Heim Year of Birth: 1967 | Since 2014 | Vice President (2014 to present) | Vice President, Relationship Management Director of Ultimus Fund Solutions, LLC (2018 to present); Client Implementation Manager of Ultimus Fund Solutions, LLC (2014 to 2018); Naval Flight Officer of United States Navy (1989 to 2017); Business Project Manager of Vantiv, Inc. (2013 to 2014) |

Jennifer L. Leamer Year of Birth: 1976 | Since | Treasurer (October 2014 to present)

Assistant Treasurer (April 2014 to October 2014) | Vice President, Mutual Fund Controller of Ultimus Fund Solutions, LLC (2014 to present); Business Analyst of Ultimus Fund Solutions, LLC (2007 to 2014) |

Daniel D. Bauer Year of Birth: 1977 | Since | Assistant Treasurer (April 2016 to present) | Assistant Mutual Fund Controller (September 2015 to present) and Fund Accounting Manager (March 2012 to August 2015) of Ultimus Fund Solutions, LLC |

Matthew J. Beck Year of Birth: 1988 | Since | Secretary | Senior Attorney of Ultimus Fund Solutions, LLC (2018 to present); General Counsel of The Nottingham Company (2014 to 2018) |

Natalie S. Anderson Year of Birth: 1975 | Since | Assistant Secretary (April 2016 to present) | Legal Administration Manager (July 2016 to present) and Paralegal (January 2015 to June 2016) of Ultimus Fund Solutions, LLC; Senior Paralegal of Unirush, LLC (October 2011 to January 2015) |

Charles C. Black Year of Birth: 1979 | Since | Chief Compliance Officer

Assistant Chief Compliance Officer (April 2015 to January 2016) | Senior Compliance Officer of Ultimus Fund Solutions, LLC (2015 to present); Chief Compliance Officer of The Caldwell & Orkin Funds, Inc. (2016 to present); Senior Compliance Manager for Touchstone Mutual Funds (2013 to 2015); Senior Compliance Manager for Fund Evaluation Group (2011 to 2013) |

Additional information about members of the Board and executive officers is available in the Fund’s Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call 1-866-822-9555.

33

STRALEM EQUITY FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited)

The Board of Trustees (the “Board”), including the Independent Trustees voting separately, has reviewed and approved the Fund’s Investment Advisory Agreement with the Stralem & Company, Incorporated (the “Adviser”) for an additional one-year term (the “Agreement”). The Board approved the Agreement at an in-person meeting held on July 23-24, 2018, at which all of the Trustees were present.

Legal counsel advised the Board during its deliberations. Additionally, the Board received and reviewed a substantial amount of information provided by the Adviser in response to requests of the Board and counsel. In deciding whether to approve the renewal of the Investment Advisory Agreement, the Board recalled its review of the materials related to the Fund and the Adviser throughout the preceding 12 months and its numerous discussions with Trust management and the Adviser about the operations and performance of the Fund during that period. The Board further considered those materials and discussions and other numerous factors, including

The nature, extent, and quality of the services provided by the Adviser. In this regard, the Board reviewed the services being provided by the Adviser to the Fund including, without limitation, its investment advisory services since the Fund’s inception, the Adviser’s compliance policies and procedures, its efforts to promote the Fund and assist in its distribution, and its compliance program. After reviewing the foregoing information and further information in a memorandum from the Adviser (e.g., descriptions of its business and Form ADV), the Board concluded that the quality, extent, and nature of the services provided by Adviser were satisfactory and adequate for the Fund.

The investment performance of the Fund. In this regard, the Board compared the performance of the Fund with the performance of its benchmark index, custom peer group and related Morningstar category. The Board noted that while the Fund had underperformed its custom peer group’s average and median performance for the one year period and underperformed its custom peer group’s average and median performance since the Fund’s inception and underperformed its Morningstar category’s (Large Cap Blend Category Under $250 million, True No-Load) median and average performance for the one year period, and underperformed the median and underperformed the average performance since the Fund’s inception, the Adviser had satisfactorily explained its performance results for the Fund. The Board also considered the consistency of the Adviser’s management with the Fund’s investment objective and policies. Following discussion of the investment performance of the Fund and its performance relative to its Morningstar category, the Adviser’s experience in managing a mutual fund and separate accounts, its historical investment performance, and other factors, the Board concluded that the investment performance of the Fund has been satisfactory.

34

STRALEM EQUITY FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)