UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-22680 |

| Ultimus Managers Trust |

| (Exact name of registrant as specified in charter) |

| 225 Pictoria Drive, Suite 450 Cincinnati, Ohio | 45246 |

| (Address of principal executive offices) | (Zip code) |

Khimmara Greer

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 | Cincinnati, Ohio 45246 |

| (Name and address of agent for service) | |

| Registrant's telephone number, including area code: | (513) 587-3400 |

| Date of fiscal year end: | December 31 | |

| Date of reporting period: | December 31, 2022 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

| (a) |

Westwood Salient Global Real Estate Fund

Westwood Salient Select Income Fund

Westwood Broadmark Tactical Growth Fund

Westwood Salient MLP & Energy Infrastructure Fund

Westwood Broadmark Tactical Plus Fund

| Annual Report | December 31, 2022 |

| Investment Advisor: | |

| Westwood Management Corp. | |

WESTWOOD FUNDS

| TABLE OF CONTENTS |

| Shareholder Letter | 1 |

| Schedules of Investments | |

| Westwood Salient Global Real Estate Fund | 20 |

| Westwood Salient Select Income Fund | 22 |

| Westwood Broadmark Tactical Growth Fund | 24 |

| Westwood Salient MLP & Energy Infrastructure Fund | 25 |

| Westwood Broadmark Tactical Plus Fund | 27 |

| Statements of Assets and Liabilities | 28 |

| Statements of Operations | 30 |

| Statements of Changes in Net Assets | 32 |

| Financial Highlights | 36 |

| Notes to Financial Statements | 46 |

| Report of Independent Registered Public Accounting Firm | 67 |

| Change in Auditor | 69 |

| About Your Funds’ Expenses | 70 |

| Proxy Disclosure | 74 |

| Disclosure Regarding Approval of Investment Advisory Agreement | 76 |

| Trustees and Officers of Ultimus Managers Trust | 79 |

| Other Information | 81 |

| Other Federal Tax Information | 81 |

WESTWOOD FUNDS (Unaudited)

December 31, 2022

Dear Shareholders,

The previous 12 months can be summed up in three words: “massive economic change.” Over the last year, both the stock and bond markets as well as shareholders’ psyches have all executed an about-face. At the same time, the American economy went from ultra-low interest rates and a healthy economic backdrop to investors gauging just how deep a potential recession will be in 2023. The Federal Reserve (Fed) remains in the driver’s seat, but the car (economic growth) may be running low on fuel as roads are expected to remain bumpy over the next 12 months. The good news is that consumers have remained resilient, and this environment is where Westwood strategies typically seek to outperform, given our emphasis on bottom-up portfolio construction, focus on quality within our Value products, and tactical approach across our Multi-Asset suite.

As for Westwood Management Corp., we have also gone through change. On November 18, we completed the acquisition of the asset management business of Salient Partners, LP. As part of this transaction, we received shareholder approval to reorganize the funds below into the corresponding Westwood Funds.

| Salient MF Trust/Forward Funds Trust | Ultimus Managers Trust | |

| Pre-November 18, 2022 | Post November 18, 2022 | |

| Salient MLP & Energy Infrastructure Fund | à | Westwood Salient MLP & Energy Infrastructure Fund |

| Salient Global Real Estate Fund | à | Westwood Salient Global Real Estate Fund |

| Salient Select Income Fund | à | Westwood Salient Select Income Fund |

| Salient Tactical Growth Fund | à | Westwood Broadmark Tactical Growth Fund |

| Salient Tactical Plus Fund | à | Westwood Broadmark Tactical Plus Fund |

The newly acquired funds are now marketed under the Westwood Salient and Westwood Broadmark names and are managed by the same investment teams as before with no change to the stated investment objectives. We believe the strategies and teams, however, will benefit from increased scale, and broadened distribution, as well as additional risk oversight and performance analytics that Westwood provides to its current investment teams.

Westwood is excited for the future of the broader Westwood Funds family and thanks you for your trust in our abilities to provide world-class investment capabilities.

Where Are We Now?

This time last year, risk was on and the rising inflation risks were deemed almost necessary to keep the economy firing as most believed above-trend price pressures were transitory and would fade along with pandemic supply chain pressures. Unfortunately, that post-pandemic bullish momentum was stifled abruptly by a series of near-simultaneous events that flipped the risk switch quickly to “off.” As stocks began their wide-ranging selloff soon after the start of the year, Russia’s invasion of Ukraine not only introduced a grey swan into the mix but also added stress to an already fragile supply chain and quickly worsened global inflation as critical commodity prices, namely food and energy, soared. Growing inflation, abnormally strong consumer data and a resilient labor market have also forced the Fed to enact one of the most aggressive rate hike trajectories in history, driving the Fed funds rate from nearly 0% in January to 3.8% in November.

This series of events and quick-shifting investor sentiment battered the S&P 500 early in the year. High-valuation growth stocks, largely tech names, took the worst of the blow, but all major stock indexes had breached the widely accepted, deep correction level of 20% or more by mid-summer. Equities were able to recover more than half of that correction by mid-August, only to fall again by mid-October. Above-average market volatility persisted throughout the last 12 months.

1

WESTWOOD FUNDS (Unaudited)

In 2022, the stock market notched its 14th bear market since World War II and the fourth worst year since 1945, behind 2008 (-38.5%), 1974 (-29.7%) and 2002 (-23.4%)*. One of the major factors contributing to the stock market’s weakness was the Fed’s continued tight monetary policy and rising interest rates. The U.S. Treasury 10-year Note yield more than doubled during the year. The 10-year Note began the year with a 1.63% yield and ended at 3.88%. The U.S. Treasury 3-Month Bill yield soared from 0.08% at the beginning of the year to a 4.42% yield at the end of the year.

| * | Source: MacroTrends |

Stocks, Bonds and Commodities

Investors continued to exit riskier interest rate sensitive securities and moved into more safe-haven investments such as utilities, value stocks and short-term money market funds. The surging U.S. dollar is also contributing to earnings stress as a large portion of S&P 500 revenues are derived outside our borders. This means that foreign earnings reported domestically will be worth less, further reducing earnings growth potential.

Stocks have again recovered some of their ground since October, but it’s critical that investors acknowledge the headwinds that America faces and adjust their approach to the markets with a different set of tactics that may have been applied over the last decade or so.

There is no doubt the current environment is certainly atypical and, in many ways, unprecedented. The effects of the Fed’s hawkish actions are being felt across the economy, from a (quiet) housing correction to swaths of layoffs now beginning in what’s been a relatively resilient labor market. Corporate earnings in the most recent third quarter showed a continued deterioration of growth, with the earnings expansion rate just around 2%, the lowest reported by the S&P 500 since Q3 2020. The forward 12-month P/E ratio for the S&P 500 is 16.6, which is below the five-year average (18.5) but near the 10-year average (17.1).

In fixed income, government bond yields across all time periods trended higher (prices fell) for much of the year. From a global perspective, the losses in government bonds during the first half of 2022 were some of the deepest in history; corporate bond prices also logged losses not seen in decades while yields soared. Though the early portion of the third quarter offered some reprieve, corporate bond prices continued their march lower as the period ended. We believe there are opportunities in corporate bonds but keep a neutral allocation with a focus on higher-quality and investment grade selections in our multi-asset funds.

One inflationary respite could come from materials as traders continued to sell wide swaths of commodities such as gold, silver, lumber, metals and more as demand fears and a strengthening dollar added pressure. We see these trends continuing, except for oil and natural gas, which are likely to remain elevated and volatile due to complex logistical challenges related to the Russia-Ukraine war and demand for heat and electricity going into winter. As the world shifts its focus towards energy security we believe that hydrocarbons from politically friendly geographies like the U.S. will gain market share as governments work to reduce their reliance on Russia and other potentially riskier suppliers.

Global Markets: Risk Off

In Europe, many of the same headwinds as seen in the U.S. are mounting, such as supply chain disruptions and rising prices from energy to food and more, plus the region is facing an energy crisis related to the Russia-Ukraine conflict. The European Central Bank has also been raising its key borrowing rates but is slowing its pace as the bloc’s economies have weakened sharply. Asian markets are dealing with their own set of unique, varied challenges that add a level of murkiness to global growth estimates for the coming year.

Domestically, the Fed has some tough decisions to make as data still shows near-record-low unemployment and 40-year highs in inflation. The reality is that a greater level of uncertainty prevails, and investors continue to scour data,

2

WESTWOOD FUNDS (Unaudited)

seeking hard-to-find clues on where the economy and markets are headed from here. Increased chatter and the growing probability of a current or coming recession increased dramatically during the back half of the year as data continues to support above-trend inflation. The latest comments and forward guidance from the Fed and Chairman Powell specifically, also suggested that a recession will be necessary to get inflation back to the Fed’s target of 2%.

For investors, the main market stressor is not just inflation, but also the actions being taken to control it, which have already severely affected and will continue to impact consumers and corporate earnings. The Consumer Price Index has begun to slow, but still remains extremely high. Energy price declines in the back half of the year contributed heavily to the reductions, but food and other even more durable prices remain elevated.

The Russia-Ukraine war remains a wildcard that continues to complicate the task and effectiveness of central banks’ actions. The war’s effects add to logistical troubles, corporate earnings (as many western companies have withdrawn from doing business in Russia) and food supply and costs. We believe that the conflict is likely to be drawn out, driving headline risk and continued disturbances, both temporary and permanent, in global trade and logistics.

The Road Ahead

The current market environment continues to produce dislocations with respect to valuation and increased levels of fundamental skepticism that play to our strength. Now, more than ever, highly tactical and active investment approaches, with high conviction active selections and tactical balanced allocations, will be needed to help reduce volatility and produce alpha. As it has for over 30 years, our investment process continues to seek out mispriced opportunities where fundamental analysis can uncover value while maintaining a strong culture of risk management and a focus on limiting potential downside risks.

Investors will need to re-evaluate their strategy and tactics to best capture alpha in what’s likely to be more of a range-bound broad market in equities and bonds. Washington has few arrows in its quiver to address current market risks as any further stimulus is likely to stoke inflation, which is the one thing that must be quelled. We see a continued slowdown in earnings growth for the S&P 500 and expect continued volatility for both equities and fixed income in the coming months as effects of the Fed’s bellicose stance toward inflation and subsequent economy-slowing actions are realized, along with an increased number of market participants adjusting forecasts to account for those effects.

We believe that interest rates are in the process of peaking and bonds are beginning to find a bottom, providing attractive opportunities across our investment suite. Following the September meeting, the Fed supported our interest rate targets. The median Federal Open Market Committee (FOMC) member thinks the Fed’s target policy rate range will still be 4.50% to 4.75% (terminal rate) by the end of next year (2023), implying that the Fed doesn’t plan to deliver any rate cuts until 2024. With that, we see two- to five -year yields rising, while the longer duration 10-year is likely to remain range bound, effectively flattening the curve as tightening impacts growth outlooks.

As economic growth decelerates and the probability of a recession increases, high quality characteristics, which are a key feature across our mutual fund complex, are likely to be an important driver of excess returns. We also continue to like companies that maintain pricing power to manage through an inflationary environment and have the ability to reduce the impact of input costs or to pass those costs on to their customers. In summary, we continue to stick to our knitting, serving our investors during challenging market periods like we are in today.

Thank you for your trust.

Sincerely,

The Investment Team

The Westwood Funds

3

WESTWOOD FUNDS (Unaudited)

The information contained herein represents the views of the manager at a specific point in time and is based on information believed to be reliable. No representation or warranty is made concerning the accuracy or completeness of any data compiled herein. Any statements non-factual in nature constitute only current opinion, which is subject to change. Any statements concerning financial market trends are based on current market conditions, which will fluctuate. Past performance is not indicative of future results. All information provided herein is for informational purposes only and is not intended to be, and should not be interpreted as, an offer, solicitation, or recommendation to buy or sell or otherwise invest in any of the securities/sectors/countries that may be mentioned. Investing involves risk, including possible loss of principal. A discussion of each fund’s performance during the periods ended December 31, 2022, is presented below.

Westwood Salient Global Real Estate

The performance of the Westwood Salient Global Real Estate Fund for the periods ended December 31, 2022, was as follows:

| 2022 | ||

| 6 Months | Fiscal Year | |

| Westwood Salient Global Real Estate Fund – Institutional Shares (KIRYX) | -4.63% | -21.61% |

| Westwood Salient Global Real Estate Fund Fund – A Shares (KIRAX)* | -4.74% | -21.91% |

| Westwood Salient Global Real Estate Fund – C Shares (KIRCX) | -5.02% | -22.33% |

| FTSE EPRA Nareit Developed Index | -5.52% | -25.09% |

| MSCI World Index | 3.20% | -17.73% |

| * | Without sales charge |

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. The Adviser has contractually agreed to waive fees and reimburse expenses until April 30, 2024. In the absence of current fee waivers, total return and yield would have been reduced.

For the year ended December 31, 2022, Westwood Salient Global Real Estate Fund’s Institutional shares (the Fund) returned -21.61%, outperforming the Fund’s benchmark, the FTSE EPRA Nareit Developed Index, which returned -25.09%. The Fund, however, underperformed its secondary benchmark, the MSCI World Index, which returned -17.73%.

Despite ending on a somewhat positive note during the fourth quarter, 2022 will go down as one of the worst years for global investors in recent memory. In a dramatic reversal, investor sentiment shifted rapidly in the early part of 2022 as numerous economic signals presented a challenged economic climate. Chiefly among these was the elevated levels of inflation witnessed around the globe. In response, central banks, led by the Federal Reserve, ushered in a nearly unprecedented level of monetary tightening by rapidly increasing nominal interest rates throughout the year, which placed tremendous pressure on risk assets including on global REIT equities. On the geo -political front, Russia’s invasion of Ukraine in February and its related secondary effects impacting global trade and energy prices, added further uncertainty to the macro picture. As a result, most geographies and most property sectors experienced double-digit performance declines in 2022.

Investments in U.S. REITs suffered for the same reasons mentioned in the global macro section above. Additionally, slowing rent growth in multi-family, concerns around the return-to-office and tech downsizing in office, and tech weakness in data centers all contributed to negative performance. Our holdings in UK REITs were relatively diversified; however, all suffered for similar reasons as their U.S. peers. In domestic currency terms, Japanese REITs fared better

4

WESTWOOD FUNDS (Unaudited)

than those in most other territories; however, the material devaluing of the Japanese yen relative to the U.S. dollar heavily impacted the Fund’s performance, which is calculated in U.S. dollar terms.

Westwood Salient Select Income

The performance of the Westwood Salient Select Income Fund for the periods ended December 31, 2022, was as follows:

| 2022 | ||

| 6 Months | Fiscal Year | |

| Westwood Salient Select Income Fund – Institutional Shares (KIFYX) | -4.95% | -14.10% |

| Westwood Salient Select Income Fund – A Shares (KIFAX)* | -5.18% | -14.45% |

| Westwood Salient Select Income Fund – C Shares (KIFCX) | -5.38% | -14.92% |

| ICE BofA Fixed Rate Preferred Securities Index | -0.77% | -14.59% |

| * | Without sales charge |

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. The Adviser has contractually agreed to waive fees and reimburse expenses until April 30, 2024. In the absence of current fee waivers, total return and yield would have been reduced.

For the year ended December 31, 2022, Westwood Salient Select Income Fund’s Institutional shares (the Fund) returned -14.10%, outperforming the Fund’s benchmark, the ICE BofA Fixed Rate Preferred Securities Index, which returned -14.59%.

Despite ending on a somewhat positive note during the fourth quarter, 2022 will go down as one of the worst years for investors in recent memory. In a rather stunning reversal from the near euphoric investor sentiment the year prior, negative news emerged early in 2022 and essentially did not stop confounding investors. From Russia’s invasion of Ukraine in February and its resulting secondary effects impacting global trade and energy prices, to the hangover effect of the COVID-19 pandemic and the related elevated levels of inflation, investors struggled to position their portfolios for the deluge of difficult market signals. In nearly unprecedented fashion, the Fed hiked interest rates seven times in 2022, increasing the federal funds rate by 425 basis points (bps) over the course of the year, which placed significant pressure on REITs and REIT preferred securities. Due to uncertainty surrounding the economy and nominal interest rates, debt markets became materially constrained and the M&A market effectively halted, reducing the market’s ability to adequately value assets. Finally, there were effectively no new issuances of REIT preferred securities during the year, which normally provide price discovery and enhance liquidity in the REIT preferred markets.

Our Retail investments suffered primarily due to rising interest rates, which decreased the value of our preferred holdings. Additionally, a change of control event for the issuer of one of our securities resulted in a meaningful decline in the security’s credit quality. A class of preferred holders attempted to argue that the change of control event required a full calling of the security at par but were ultimately ruled against. Our Lodging investments were primarily impacted by rising interest rates as the underlying issuers reported strong performance throughout the year. Investments in the common equity of multi-family REITs were the largest detractor of performance in this sector. Slowing rent growth and leasing volumes led to downward adjustments in guidance by the REIT management teams, lowering valuations.

5

WESTWOOD FUNDS (Unaudited)

Westwood Broadmark Tactical Growth

The performance of the Westwood Broadmark Tactical Growth Fund for the periods ended December 31, 2022, was as follows:

| 2022 | ||

| 6 Months | Fiscal Year | |

| Westwood Broadmark Tactical Growth Fund – Institutional Shares (FTGWX) | -2.08% | -7.90% |

| Westwood Broadmark Tactical Growth Fund – A Shares (FTAGX)* | -2.30% | -8.27% |

| Westwood Broadmark Tactical Growth Fund – C Shares (FTGOX) | -2.53% | -8.75% |

| HFRX Equity Hedge Index | 1.61% | -3.18% |

| S&P 500 Index | 2.31% | -18.11% |

| * | Without sales charge |

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted.

For the year ended December 31, 2022, Westwood Broadmark Tactical Growth Fund’s Institutional Class shares returned -7.90%, underperforming the Fund’s primary benchmark, the HFRX Equity Hedge Index, which returned -3.18%. The Fund, however, outperformed its secondary benchmark, the S&P 500 Index, which declined -18.11%.

In 2022, the stock market notched its 14th bear market since World War II and the fourth worst year since 1945, behind 2008 (-38.5%), 1974 (-29.7%) and 2002 (-23.4%). One of the major factors contributing to the stock market’s weakness was the Fed’s continued tight monetary policy and rising interest rates. The U.S. Treasury 10-year Note yield more than doubled during the year. The 10-year Note began the year with a 1.63% yield and ended at 3.88%. The U.S. Treasury 3-Month Bill yield soared from 0.08% at the beginning of the year to a 4.42% yield at the end of the year.

Equity valuations have improved in the last year but are still high when adjusted for inflation. In addition, inflation fears have begun to shift to fears over earnings and the economy as we enter 2023. A tightening Fed into a slowing economy and continued high inflation is not a healthy environment for stocks. On the monetary front, while yields at the long end of the yield curve declined at the end of 2022, short-term interest rates rose while longer-term rates declined. The 3-month/10-year U.S. Treasury yield curve at the end of 2022 was the most negative since the 2008-2009 financial crisis. Historically, while timing is always uncertain, this inversion has often been a leading indicator of a future recession. In addition, since 1962, the market has shown a negative return during the periods when the 3-month/10-year yield curve was inverted. At the end of the year, the Fund’s investment team’s volume and breadth momentum models were negative across the board with short-term momentum also having turned negative.

The Fund employed derivative instruments during the year primarily to cushion the portfolio from declining stock prices. Futures contracts were used to help offset risk during these times. The use of futures detracted -0.91% from the Fund’s return for the year.

In accordance with the prospectus, you’ll note the sizeable cash position. The fund’s models are geared towards measuring market risk. Cash is utilized as a defensive measure when market risk is high.

6

WESTWOOD FUNDS (Unaudited)

As the Westwood Broadmark Tactical Growth Fund’s investment team looks ahead to 2023, there are several factors within its “Four Pillar Process” that the team will be watching:

| 1. | Valuation: Price earnings ratios adjusted for inflation (defined as the year-to-year change in the Consumer Price index) have declined from their lofty levels of a year ago, but they are still in overvalued territory. A decline in earnings and profits and potential recession in 2023 would be negative for equity valuations. Thus, it looks like this readjustment process has further to go before equities become more fairly valued. |

| 2. | Monetary factors and credit conditions: The yield curve comparing the 3-Month U.S. Treasury Bill yield with the 10-Year U.S. Treasury yield at the end of 2022 was at its greatest inversion since the 2008-2009 financial crisis. December was also the second consecutive month that short-term yields rose while longer-term yields declined. This inversion has occurred less than 12% of the time since 1962. Historical statistics show that during the time these inversions persisted, the S&P 500 has declined at an annual rate of -1.99%. Evidence that the yield curve is returning to normal would be a positive sign for the equity markets. |

| 3. | Sentiment: Investor sentiment became more pessimistic toward the end of 2022 as the stock market declined. This is positive from a contrary point of view. We note that investor sentiment is a condition and is not a trigger until it reaches an extreme. Nonetheless, the return of investor pessimism is a positive sign and the team will be watching for an extreme reading on this indicator in 2023 in order to provide the environment for a solid market low point. |

| 4. | Momentum: The team’s breadth momentum model, which measures the breadth of Standard & Poor’s industry groups, declined into negative territory at the end of 2022 and was negative a good part of the year. The team’s volume momentum model, which compares upside volume with downside volume, also remains in negative territory. The team would begin to raise market exposure if and when these momentum models return to positive territory. |

Westwood Salient MLP & Energy Infrastructure

The performance of the Westwood Salient MLP & Energy Infrastructure Fund for the periods ended December 31, 2022, was as follows:

| 2022 | ||

| 6 Months | Fiscal Year | |

| Westwood Salient MLP & Energy Infrastructure Fund – Institutional Shares (SMLPX) | 10.59% | 17.22% |

| Westwood Salient MLP & Energy Infrastructure Fund – A Shares (SMAPX)* | 10.52% | 17.00% |

| Westwood Salient MLP & Energy Infrastructure Fund – C Shares (SMFPX) | 10.08% | 15.98% |

| Westwood Salient MLP & Energy Infrastructure Fund – Ultra Shares (SMRPX) | 10.62% | 17.12% |

| Alerian Midstream Energy Select Index | 8.35% | 19.15% |

| * | Without sales charge |

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. The Adviser has contractually agreed to waive fees and reimburse expenses until April 30, 2024. In the absence of current fee waivers, total return and yield would have been reduced. Certain Funds may invest in MLPs taxed as partnerships. Due to a variety of factors, including significant non-cash deductions such as depreciation and depletion, MLPs have historically made cash distributions to limited partners that exceed the amount of taxable income allocable to such limited partners

7

WESTWOOD FUNDS (Unaudited)

or members. These excess cash distributions would not be treated as income to a Fund but rather would be treated as a return of capital to the extent of the Fund’s basis in the MLP. As a consequence, a Fund may make distributions that exceed its earnings and profits, which would be characterized as a return of capital to shareholders. A return of capital distribution will generally not be taxable, but will reduce each shareholder’s cost basis in Fund shares and result in a higher capital gain or lower capital loss when the Fund shares are sold. After a shareholder’s basis in Fund shares has been reduced to zero, distributions in excess of earnings and profits in respect of those Fund shares will be treated as gain from the sale of the Fund shares. As of 12/31/2022, the Westwood MLP and Energy Infrastructure Fund paid a minimum of $0.08/share in distributions per quarter.

For the year ended December 31, 2022, Westwood Salient MLP & Energy Infrastructure Fund’s Institutional shares (the Fund) returned 17.22%, underperforming the Fund’s benchmark, the Alerian Midstream Energy Select Total Return Index (AMEIX), which returned 19.15%.

2022 provided a positive market environment for master limited partnerships and midstream energy companies (businesses involved with the processing, storing, transporting and marketing of oil, natural gas and natural gas liquids). The year began with Russia’s march toward war with Ukraine and commodity prices responded strongly with oil moving up above $120 per barrel and natural gas reaching nearly $10/Mcf during the first half of the year. As the year progressed, worries of a slowdown in global growth brought volatility to the markets and uncertainty to energy demand. Increased uncertainty led to a choppier second half of the year for midstream equities. During the second half of the year, the U.S. government passed the Inflation Reduction Act (IRA) that accelerated investments in renewables and helped propel performance for the Fund’s renewable allocation. Ultimately, the favorable backdrop combined with continued capital discipline from the midstream industry led to healthy investment returns for the year.

The first quarter was marked by the Russian invasion of Ukraine. The invasion brought “energy security” back to the top of governments’ minds and caused oil prices to rise over 33% as measured by the West Texas Intermediate (WTI) benchmark and natural gas prices to increase over 50% during the quarter. Russia’s invasion of Ukraine is a massive geopolitical event that we believe will have long-term reverberations throughout the global energy landscape. Russia was the second largest producer globally of both crude oil and natural gas in 2020, with oil production of more than 10 million bpd (mmbpd) and natural gas production of almost 62 billion cubic feet per day (Bcf/d). It was also the fourth largest exporter of liquefied natural gas (LNG) at 3.9 Bcf/d. On the crude front, Russia exported north of 5 mmbpd with roughly half of those exports going to Europe. Natural gas exports are roughly 40% of Russia’s production, with Europe receiving 72% of those exports. Midstream providers, particularly natural gas and LNG focused businesses fared well during this period.

Another development during the first quarter was the de -correlation between the midstream industry and high yield spreads. Historically, there has been a close long-term relationship between high yield spreads (not rates) and midstream returns, but thankfully the two decoupled in early 2022. High yield spreads ended 2021 at 283 basis points (bps) and began to widen almost immediately in early January as inflation readings came in higher than expected and Federal Reserve governors espoused their intentions to aggressively raise rates. By late January, spreads reached 345 bps and continued to widen through mid-March — ultimately hitting 411 bps. The S&P 500 was down over 10% during this period, and in the not-too-distant past, the midstream space underperformed the broad market as spreads widened and that did not happen in 2022. Our thesis is that the breakdown in correlation to high yield spreads is an indication the midstream industry is now a net generator of capital through free cash flow. Without a need to raise capital today, companies should not be beholden to fluctuations in high yield spreads. We expect capital discipline to continue to favor the midstream space and for continued, substantial free cash flow generation to drive the long-term investment opportunity in the industry. For the quarter, the AMEIX index was up 21.5%.

As the year progressed, inflation became a much bigger concern and interest rate increases by the Fed Reserve began to drive markets. Higher than expected inflation caused a sharp correction in the broad market that resulted in a correction in the midstream industry as well. In early June, news started making the rounds that the Fed would

8

WESTWOOD FUNDS (Unaudited)

almost certainly raise rates by 75 basis points at their upcoming FOMC meeting to combat inflation, and markets fell sharply. The quarterly return for the AMEIX flipped from an 8.7% gain as of June 7 to a 9.5% loss by June 30 as investors began to fear that the Fed would overtighten and send the U.S. economy into recession, thus reducing energy demand.

By the start of the third quarter, investor focus shifted from the war in Ukraine to a potential recession in the United States. Concerns about a decline in energy demand due to recession caused oil prices to retreat throughout the quarter from their Ukraine war high above $120/bbl in early June to below $80/bbl by Sept. 30. Despite the sharp correction in oil prices, midstream companies held up well and the AMEIX index was down only 1% during the quarter. By October, the precipitous decline in oil prices was met with concern by OPEC and the cartel cut quotas by 2 million barrels per day to shore up the market and stabilize oil prices. OPEC’s cut coupled with inflation data beginning to trend softer resulted in a sharp rally during the fourth quarter with the AMEIX up 9.5% during the quarter.

While traditional energy companies had a healthy 2022, renewable energy infrastructure had a mixed year. January saw a strong shift away from growth stocks into value stocks, negatively impacting the Fund’s renewable allocation. The shift to value stocks led to a sharp decline in renewable companies’ stock prices through early May, with several of the Fund’s holdings down by over 25% at that point. Fortunately, earnings showed continued strength in the businesses, and the industry finally bottomed out in early June. During the summer, two developments helped to accelerate growth for the renewables industry which resulted in several companies returning to their 2021 highs. First, the Biden administration enacted a two-year moratorium on import tariffs for certain East Asian manufactured solar modules, which is expected to benefit utility scale solar installations, and second, the U.S. Government enacted the 2022 Inflation Reduction Act, which provides over $400 billion in subsidies for low carbon energy through 2032. We continue to believe that renewables play an integral part of the energy value chain and see significant long-term, secular opportunity owning companies that help bring that energy to market.

As previously stated, the Fund returned 17.2% in 2022 with several holdings driving performance throughout the year. The top contributors were predominantly within the gathering and processing, natural gas liquids (NGL) infrastructure and liquefied natural gas (LNG) sectors. The Fund’s top contributor to performance was Cheniere Energy, Inc. (Cheniere). Cheniere is the largest LNG exporter in the United States and is transitioning from a heavy capital investment cycle to a more sustained cash flow generation cycle. The company was instrumental in providing incremental natural gas cargoes to Europe as the continent disentangled itself from Russian natural gas this year. We continue to see favorable long-term growth opportunities for expanding Cheniere’s existing export facilities to handle more LNG, growing cash flows and earnings in coming years. The company’s growing cash flow stream gives management the ability to both reduce debt and repurchase stock, which could potentially generate more value to shareholders over time. Our investment in Cheniere is a testament to the total return approach the Fund employs to maximize long-term shareholder value rather than stretching for yield. Cheniere comprised an average portfolio weight of 8.7% and was up 48.2% for the year, contributing 456 basis points to the Fund’s overall performance.

The Fund’s second largest contributor to performance was Energy Transfer (ET). ET is a large integrated MLP that is transitioning from a debt reduction story to a growth, buyback and yield opportunity. Management guided to returning the distribution to its pre-pandemic crisis level of $1.22/unit implying over a 10% yield on the security as of the stock’s year end closing price. Additionally, ET is generating significant free cash flow above the current distribution giving management the flexibility to repurchase shares or raise the distribution further in the future. The company continues to grow through incremental investments in their existing footprint and offers, in our opinion, one of the cheapest and best ways to access the midstream industry at this juncture. ET was a 9.2% average weight in the portfolio, was up 56.0% for the year and contributed 438 bps to Fund performance.

Finally, our third largest portfolio contributor was Targa Resources Corp. (Targa). Targa is a fully integrated provider of natural gas and NGL services. The company gathers and processes natural gas and provides NGL transportation, storage, fractionation and export services. The company completed a large capital investment program and simplified

9

WESTWOOD FUNDS (Unaudited)

its corporate structure via several asset consolidations and dispositions during the year. Targa saw an acceleration of free cash flow generation in 2022 as production volumes grew throughout the year. With higher free cash flow, the company was able to reduce debt and buy back stock while still growing earnings meaningfully as compared to 2021. Targa comprised a 9.3% average weight in the portfolio during the year. The company was up 43.1% for 2022 and contributed 406 basis points to Fund performance.

While the Fund had good returns for the year, some holdings did detract from performance. The largest detractor for the year was Equitrans Midstream Corp. (ETRN). ETRN has had multiple legal setbacks for its Mountain Valley Pipeline (MVP) and continues to have difficulty securing all the permits for the pipeline. While we expect a resolution of the permitting process, the timeline continues to move further into the future. The company was an average weight of 3.4% in the portfolio and was down 30.3% for the year resulting in a negative contribution to the Fund of 159 basis points.

The second largest detractor for the year was the Fund’s investment in Heliogen. Heliogen is a concentrated solar company that is ramping up production over the coming three-year time frame. We believe the rotation from growth to value in the market negatively impacted the company’s stock performance along with delays on their project timeline. Heliogen had an average weight of 0.1% in the Fund and was down 75.9% during the year. The position detracted 128 basis points from Fund performance.

Finally, the third largest detractor for the year was the Fund’s investment in Keyera Corp. (Keyera). Keyera is an NGL infrastructure company in Canada with significant commodity sensitivity and a large project that has gone over budget and has experienced delays. We expect most of the delays to normalize in 2023 and 2024. The Fund owned an average of 2.4% of the position and detracted 71 basis points from Fund performance.

The Fund employed derivatives in 2022 in a limited way by writing calls on existing Fund positions. The call writing strategy generated $1.2 million in income for the Fund for the year, which amounts to 14 bps to overall performance.

2022 was a solid year for midstream equities despite the equity volatility toward the second half of the year. The year witnessed improvement in energy production in the United States, management teams staying capital disciplined and free cash flow growth above most analysts’ expectations. As we begin 2023, we see much of the same for the industry, with companies in the energy infrastructure space starting to provide preliminary 2023 guidance. So far the majority of companies are indicating healthier year-over-year cash flows in 2023. Furthermore, companies have already signaled their desire to continue returning capital to shareholders over increasing capital spending. The healthy growth in energy volumes, continued improvement in balance sheets and continued focus on capital discipline are anticipated to create a backdrop for continued success in 2023.

Westwood Broadmark Tactical Plus

The performance of the Westwood Broadmark Tactical Plus Fund for the periods ended December 31, 2022, was as follows:

| 2022 | ||

| 6 Months | Fiscal Year | |

| Westwood Broadmark Tactical Plus Fund – Institutional Shares (SBTIX) | 1.67% | -1.95% |

| Westwood Broadmark Tactical Plus Fund – A Shares (SBTAX)* | 1.48% | -2.18% |

| Westwood Broadmark Tactical Plus Fund – C Shares (SBTCX) | 1.22% | -2.82% |

| Westwood Broadmark Tactical Plus Fund – F Shares (BTPIX) | 1.81% | -1.65% |

| HFRX Equity Hedge Index | 1.61% | -3.18% |

| S&P 500 Index | 2.31% | -18.11% |

| * | Without sales charge |

10

WESTWOOD FUNDS (Unaudited)

The performance data quoted represents past performance. Past performance does not guarantee future results. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost and current performance may be lower or higher than the performance quoted. The Adviser has contractually agreed to waive fees and reimburse expenses until April 30, 2024. In the absence of current fee waivers, total return and yield would have been reduced.

For the year ended December 31, 2022, Westwood Broadmark Tactical Plus Fund’s Institutional Class shares returned -1.95%, outperforming the Fund’s primary benchmark, the HFRX Equity Hedge Index, which returned -3.18%. The Fund also outperformed its secondary benchmark, the S&P 500, which declined -18.11%.

In 2022, the stock market notched its 14th bear market since World War II and the fourth worst year since 1945, behind 2008 (-38.5%), 1974 (-29.7%) and 2002 (-23.4%). One of the major factors contributing to the stock market’s weakness was the Fed’s continued tight monetary policy and rising interest rates. The U.S. Treasury 10-year Note yield more than doubled during the year. The 10-year Note began the year with a 1.63% yield and ended at 3.88%. The U.S. Treasury 3-Month Bill yield soared from 0.08% at the beginning of the year to a 4.42% yield at the end of the year.

Equity valuations have improved in the last year but are still high when adjusted for inflation. In addition, inflation fears have begun to shift to fears over earnings and the economy as we enter 2023. A tightening Fed into a slowing economy and continued high inflation is not a healthy environment for stocks. On the monetary front, while yields at the long end of the yield curve declined at the end of 2022, short-term interest rates rose while longer-term rates declined. The 3-month/10-year U.S. Treasury yield curve at the end of 2022 was the most negative since the 2008-2009 financial crisis. Historically, while timing is always uncertain, this inversion has often been a leading indicator of a future recession. In addition, since 1962, the market has shown a negative return during the periods when the 3-month/10-year yield curve was inverted. At the end of the year, the team’s volume and breadth momentum models were negative across the board with short-term momentum also having turned negative.

The Fund regularly used options and futures during the year. A meaningful portion of the Fund’s return can be attributed to these derivative instruments.

In accordance with the prospectus, you’ll note the sizeable cash position. The fund’s models are geared towards measuring market risk. Cash is utilized as a defensive measure when market risk is high.

As the Westwood Broadmark Tactical Plus Fund’s investment team looks ahead to 2023, there are several factors within its “Four Pillar Process” that the team will be watching:

| 1. | Valuation: Price earnings ratios adjusted for inflation (defined as the year-to-year change in the Consumer Price Index) have declined from their lofty levels of a year ago, but they are still in overvalued territory. A decline in earnings and profits and potential recession in 2023 would be negative for equity valuations. Thus, it looks like this readjustment process has further to go before equities become more fairly valued. |

| 2. | Monetary factors and credit conditions: The yield curve comparing the 3-Month U.S. Treasury Bill yield with the 10-Year U.S. Treasury yield at the end of 2022 was at its greatest inversion since the 2008-2009 financial crisis. December 2022 was also the second consecutive month that short-term yields rose while longer-term yields declined. This inversion has occurred less than 12% of the time since 1962. Historical statistics show that during the time these inversions persisted, the S&P 500 has declined at an annual rate of -1.99%. Evidence that the yield curve is returning to normal would be a positive sign for the equity markets. |

| 3. | Sentiment: Investor sentiment became more pessimistic toward the end of 2022 as the stock market declined. This is positive from a contrary point of view. We note that investor sentiment is a condition and is not a trigger until it reaches an extreme. Nonetheless, the return of investor pessimism is a positive sign, |

11

WESTWOOD FUNDS (Unaudited)

and the team will be watching for an extreme reading on this indicator in 2023 in order to provide the environment for a solid market low point.

| 4. | Momentum: The team’s breadth momentum model, which measures the breadth of Standard & Poor’s industry groups, declined into negative territory at the end of 2022 and was negative a good part of the year. The team’s volume momentum model, which compares upside volume with downside volume, also remains in negative territory. The team would begin to raise market exposure if and when these momentum models return to positive territory. |

To determine if this Fund is an appropriate investment for you, carefully consider the Fund’s investment objectives, risk factors, charges and expenses before investing. This and other information can be found in the Fund’s prospectus, which may be obtained by calling 1.877.386.3944. Read the prospectus carefully before investing or sending money.

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month end are available by calling 1.877.386.3944.

An investor should consider the investment objectives, risks, charges and expenses of each Fund carefully before investing. The Funds’ prospectus contains this and other important information. To obtain a copy of the Funds’ prospectus, please visit the Funds’ website at www.westwoodfunds.com or call 1.877.386.3944 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Funds are distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Funds’ adviser’s current opinions and views of the financial markets. Although the Funds’ advisers believe it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Funds that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolios of the Funds, may be sold at any time, and may no longer be held by the Funds. For a complete list of securities held by the Funds as of December 31, 2022, see the Schedules of Investments section of this Report. The opinions of the Funds’ advisers with respect to those securities may change at any time.

Statements in the Letter to Shareholders that reflect projections or expectations for future financial or economic performance of the Funds and the market in general and statements of the Funds’ plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed, or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to factors noted with such forward-looking statements include, without limitation, general economic conditions, such as inflation, recession, and interest rates. Past performance is not a guarantee of future results.

12

WESTWOOD FUNDS (Unaudited)

Definition of the Comparative Indices & Key Terms

2022 Inflation Reduction Act covers new and reinstated tax laws that will affect individuals and businesses, including a number of credits and deductions. One provision changes the eligibility rules to claim a tax credit for clean vehicles. This took effect as soon as the law was signed.

Alerian Midstream Energy Select Index (AMEIX) is a composite of North American midstream energy infrastructure companies that are engaged in activities involving energy commodities. The capped, float-adjusted, capitalization-weighted index is disseminated in real time on a price-return basis.

Alpha is the measure of risk-adjusted performance.

FTSE EPRA Nareit Developed Index is designed to track the performance of listed real estate companies and REITs worldwide.

HFRX Equity Hedge Index comprises private funds with strategies that maintain both long and short positions primarily in equity securities and equity derivatives.

ICE BofA Fixed Rate Preferred Securities Index consists of investment-grade, fixed and fixed-to-floating rate U.S. dollar-denominated preferred securities.

MSCI World Index is a free float-adjusted market capitalization index designed to measure equity market performance in the global developed markets.

S&P 500 Index is an unmanaged capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic stock market through changes in the aggregate market value of 500 stocks representing all major industries.

13

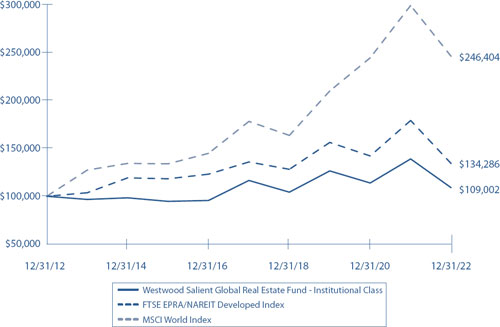

WESTWOOD SALIENT GLOBAL REAL ESTATE FUND (UNAUDITED)

Comparison of the Change in Value of a $100,000 Investment in Westwood Salient Global Real Estate

Fund - Institutional Class (a) versus the FTSE EPRA/NAREIT Developed Index and the MSCI World Index

Average Annual Total Returns (b) (for the periods ended December 31, 2022) | |||

| 1 Year | 5 Year | 10 Year | |

| Institutional Shares | -21.61% | -1.33% | 0.87% |

| A Class Shares with sales charge | -26.38% | -2.86% | -0.12% |

| A Class Shares without sales charge | -21.91% | -1.70% | 0.47% |

| C Class Shares with CDSC | -23.09% | -2.28% | -0.10% |

| C Class Shares without CDSC | -22.33% | -2.28% | -0.10% |

| FTSE EPRA/NAREIT Developed Index | -25.09% | -0.23% | 2.99% |

| MSCI World Index | -17.73% | 6.69% | 9.44% |

| (a) | The graph is based on Institutional Shares. Performance for A Class Shares would have been lower because it is subject to a maximum front-end sales charge of 3.00% and additional annual distribution expenses of 0.25%. Performance for C Class Shares would vary due to differences in fee structures. |

| (b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. If the Adviser had not limited certain expenses, the Fund’s total return would have been lower. |

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost. Past performance is no guarantee of future performance and should not be considered as a representation of the future results of the Fund. There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities. The Fund’s performance assumes the reinvestment of all dividends and all capital gains. Index returns assume reinvestment of dividends and, unlike the Fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

14

WESTWOOD SALIENT SELECT INCOME FUND (UNAUDITED)

Comparison of the Change in Value of a $100,000 Investment in Westwood Salient Select Income

Fund - Institutional Class (a) versus the ICE BofAML Fixed Rate Preferred Securities Index

Average Annual Total Returns (b) (for the periods ended December 31, 2022) | |||

| 1 Year | 5 Year | 10 Year | |

| Institutional Shares | -14.10% | 0.91% | 4.00% |

| A Class Shares with sales charge | -19.37% | -0.66% | 2.98% |

| A Class Shares without sales charge | -14.45% | 0.52% | 3.59% |

| C Class Shares with CDSC | -15.72% | -0.07% | 3.00% |

| C Class Shares without CDSC | -14.92% | -0.07% | 3.00% |

| ICE BofAML Fixed Rate Preferred Securities Index | -14.59% | 1.01% | 3.60% |

| (a) | The graph is based on Institutional Shares. Performance for A Class Shares would have been lower because it is subject to a maximum front-end sales charge of 3.00% and additional annual distribution expenses of 0.25%. Performance for C Class Shares would vary due to differences in fee structures. |

| (b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. If the Adviser had not limited certain expenses, the Fund’s total return would have been lower. |

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost. Past performance is no guarantee of future performance and should not be considered as a representation of the future results of the Fund. There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities. The Fund’s performance assumes the reinvestment of all dividends and all capital gains. Index returns assume reinvestment of dividends and, unlike the Fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

15

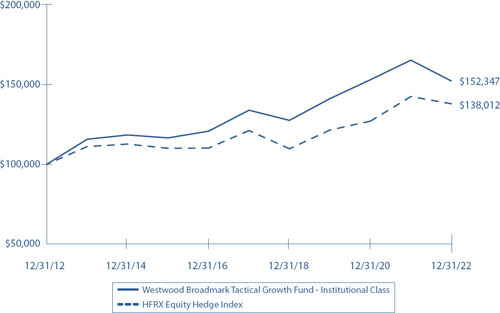

WESTWOOD BROADMARK TACTICAL GROWTH FUND (UNAUDITED)

Comparison of the Change in Value of a $100,000 Investment in Westwood Broadmark

Tactical Growth Fund - Institutional Class (a) versus the HFRX Equity Hedge Index

Average Annual Total Returns (b) (for the periods ended December 31, 2022) | |||

| 1 Year | 5 Year | 10 Year | |

| Institutional Shares | -7.90% | 2.60% | 4.30% |

| A Class Shares with sales charge | -13.55% | 0.97% | 3.21% |

| A Class Shares without sales charge | -8.27% | 2.18% | 3.82% |

| C Class Shares with CDSC | -9.63% | 1.59% | 3.30% |

| C Class Shares without CDSC | -8.75% | 1.59% | 3.30% |

| HFRX Equity Hedge Index | -3.18% | 2.63% | 3.27% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

| (a) | The graph is based on Institutional Shares. Performance for A Class Shares would have been lower because it is subject to a maximum front-end sales charge of 3.00% and additional annual distribution expenses of 0.25%. Performance for C Class Shares would vary due to differences in fee structures. |

| (b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. If the Adviser had not limited certain expenses, the Fund’s total return would have been lower. |

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost. Past performance is no guarantee of future performance and should not be considered as a representation of the future results of the Fund. There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities. The Fund’s performance assumes the reinvestment of all dividends and all capital gains. Index returns assume reinvestment of dividends and, unlike the Fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

16

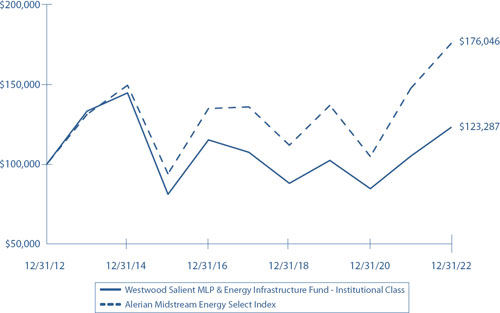

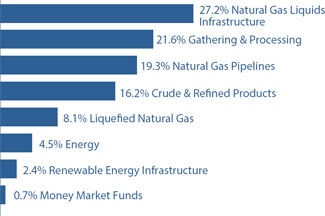

WESTWOOD SALIENT MLP & ENERGY INFRASTRUCTURE FUND (UNAUDITED)

Comparison of the Change in Value of a $100,000 Investment in Westwood Salient MLP & Energy

Infrastructure Fund - Institutional Class (a) versus the Alerian Midstream Energy Select Index

Average Annual Total Returns (b) (for the periods ended December 31, 2022) | |||||

| Since Inception | Since Inception | ||||

| 1 Year | 5 Year | 10 Year | (1/7/2013) | (1/4/2016) | |

| Institutional Shares | 17.22% | 2.76% | 2.12% | N/A | N/A |

| A Class Shares with sales charge | 10.57% | 1.36% | 1.32% | N/A | N/A |

| A Class Shares without sales charge | 17.00% | 2.53% | 1.90% | N/A | N/A |

| C Class Shares with CDSC | 14.98% | 1.73% | N/A | 0.71% | N/A |

| C Class Shares without CDSC | 15.98% | 1.73% | N/A | 0.71% | N/A |

| Ultra Shares | 17.12% | 2.84% | N/A | N/A | 6.12% |

| Alerian Midstream Energy Select Index | 19.15% | 5.28% | 5.82% | 5.45% | 9.27% |

| (a) | The graph is based on Institutional Shares. Performance for A Class Shares would have been lower because it is subject to a maximum front-end sales charge of 3.00% and additional annual distribution expenses of 0.25%. Performance for C Class Shares and Ultra Shares would vary due to differences in fee structures. |

| (b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. If the Adviser had not limited certain expenses, the Fund’s total return would have been lower. |

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost. Past performance is no guarantee of future performance and should not be considered as a representation of the future results of the Fund. There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities. The Fund’s performance assumes the reinvestment of all dividends and all capital gains. Index returns assume reinvestment of dividends and, unlike the Fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

17

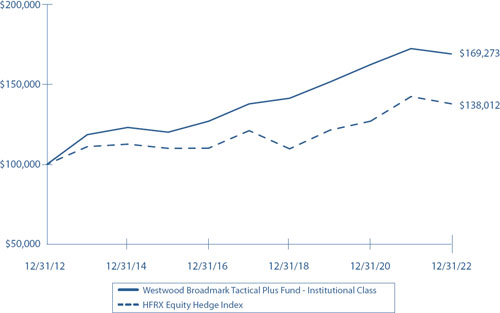

WESTWOOD BROADMARK TACTICAL PLUS FUND (UNAUDITED)

Comparison of the Change in Value of a $100,000 Investment in Westwood Broadmark

Tactical Plus Fund - Institutional Class (a) versus the HFRX Equity Hedge Index

Average Annual Total Returns (b) (for the periods ended December 31, 2022) | |||

| 1 Year | 5 Year | 10 Year | |

| Institutional Shares | -1.95% | 4.17% | 5.40% |

| A Class Shares with sales charge | -7.57% | 2.75% | 4.57% |

| A Class Shares without sales charge | -2.18% | 3.91% | 5.16% |

| C Class Shares with CDSC | -3.72% | 3.14% | 4.37% |

| C Class Shares without CDSC | -2.82% | 3.14% | 4.37% |

| F Class Shares | -1.65% | 4.49% | 5.73% |

| HFRX Equity Hedge Index | -3.18% | 2.63% | 3.27% |

| S&P 500 Index | -18.11% | 9.42% | 12.56% |

| (a) | The graph is based on Institutional Shares. Performance for A Class Shares would have been lower because it is subject to a maximum front-end sales charge of 3.00% and additional annual distribution expenses of 0.25%. Performance for C Class Shares and F Class Shares would vary due to differences in fee structures. |

| (b) | The Fund’s total returns do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. If the Adviser had not limited certain expenses, the Fund’s total return would have been lower. |

Institutional, A Class and C Class Shares of the Fund commenced operations on December 15, 2014. The returns prior to that date are those of an earlier iteration of the Fund, named Broadmark Tactical Plus Fund, which commenced operations on December 31, 2012. Performance for the period from December 31, 2012, to December 14, 2014, reflects the gross performance of the Investor Class shares of the predecessor fund adjusted to apply the fees and anticipated expenses of Institutional, A Class and C Class Shares of the Fund. All share classes of the Fund are invested in the same portfolio of

18

WESTWOOD BROADMARK TACTICAL PLUS FUND (UNAUDITED)

securities and returns only differ to the extent that fees and expenses of the classes are different. In the reorganization, Investor Class and Institutional Class Shares of the Broadmark Tactical Fund were exchanged for Class F Shares of the Salient Tactical Plus Fund.

The performance data quoted herein represents past performance and the return and value of an investment in the Fund will fluctuate so that, when redeemed, may be worth less than its original cost. Past performance is no guarantee of future performance and should not be considered as a representation of the future results of the Fund. There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities. The Fund’s performance assumes the reinvestment of all dividends and all capital gains. Index returns assume reinvestment of dividends and, unlike the Fund’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

19

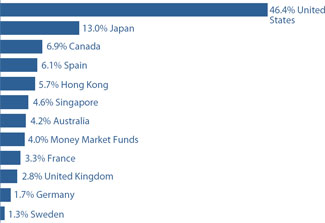

| WESTWOOD SALIENT GLOBAL REAL ESTATE FUND |

| DECEMBER 31, 2022 |

| Sector Weightings (Unaudited)† |

| † | Percentages are based on total investments. |

| SCHEDULE OF INVESTMENTS |

| COMMON STOCKS — 95.5% |

| Shares | Value | |||||||

| United States — 46.1% | ||||||||

| Alexandria Real Estate Equities, Inc. | 4,700 | $ | 684,649 | |||||

| American Tower Corp. | 2,000 | 423,720 | ||||||

| Americold Realty Trust, Inc. | 24,200 | 685,102 | ||||||

| Apple Hospitality REIT, Inc. | 45,000 | 710,100 | ||||||

| CubeSmart | 13,000 | 523,250 | ||||||

| DiamondRock Hospitality Co. | 20,000 | 163,800 | ||||||

| Digital Realty Trust, Inc. | 4,000 | 401,080 | ||||||

| Equinix, Inc. | 1,000 | 655,030 | ||||||

| Farmland Partners, Inc. | 30,000 | 373,800 | ||||||

| Federal Realty Investment Trust | 7,000 | 707,280 | ||||||

| Gaming and Leisure Properties, Inc. | 11,500 | 599,035 | ||||||

| Independence Realty Trust, Inc. | 25,000 | 421,500 | ||||||

| National Storage Affiliates Trust | 12,000 | 433,440 | ||||||

| PotlatchDeltic Corp. | 7,800 | 343,122 | ||||||

| Prologis, Inc. | 5,500 | 620,015 | ||||||

| Retail Opportunity Investments Corp. | 55,000 | 826,650 | ||||||

| Ventas, Inc. | 7,500 | 337,875 | ||||||

| VICI Properties, Inc. | 10,000 | 324,000 | ||||||

| 9,233,448 | ||||||||

| Singapore — 4.6% | ||||||||

| CapitaLand Integrated Commercial Trust | 60,786 | 92,712 | ||||||

| CapitaLand Investment, Ltd. | 300,000 | 829,108 | ||||||

| 921,820 | ||||||||

| France — 3.3% | ||||||||

| Gecina S.A. | 6,500 | 662,423 | ||||||

| COMMON STOCKS — continued |

| Shares | Value | |||||||

| Australia — 4.2% | ||||||||

| GPT Group (The) | 190,000 | $ | 541,828 | |||||

| Scentre Group | 154,000 | 299,740 | ||||||

| 841,568 | ||||||||

| Canada — 6.9% | ||||||||

| Granite Real Estate Investment Trust | 11,300 | 576,538 | ||||||

| Summit Industrial Income REIT | 47,500 | 796,023 | ||||||

| 1,372,561 | ||||||||

| United Kingdom — 2.8% | ||||||||

| Great Portland Estates Ltd. | 43,500 | 259,240 | ||||||

| Segro PLC | 32,700 | 301,142 | ||||||

| 560,382 | ||||||||

| Hong Kong — 5.7% | ||||||||

| Henderson Land Development Co., Ltd. | 63,000 | 219,312 | ||||||

| Link REIT | 43,000 | 314,641 | ||||||

| Sun Hung Kai Properties, Ltd. | 30,000 | 409,775 | ||||||

| Swire Properties, Ltd. | 76,000 | 192,497 | ||||||

| 1,136,225 | ||||||||

| Sweden — 1.3% | ||||||||

| Hufvudstaden AB - Class A | 18,300 | 260,538 | ||||||

| Spain — 6.1% | ||||||||

| Inmobiliaria Colonial S.A. | 95,000 | 611,250 | ||||||

| Merlin Properties Socimi S.A. | 65,000 | 609,816 | ||||||

| 1,221,066 | ||||||||

| Japan — 12.9% | ||||||||

| Mitsubishi Estate Co., Ltd. | 50,600 | 655,346 | ||||||

| Mitsui Fudosan Co., Ltd. | 38,000 | 694,414 | ||||||

| Sumitomo Realty & Development Co., Ltd. | 27,000 | 636,233 | ||||||

| Tokyo Tatemono Co., Ltd. | 49,500 | 599,168 | ||||||

| 2,585,161 | ||||||||

| Germany — 1.6% | ||||||||

| Vonovia SE | 14,000 | 329,891 | ||||||

| Total Common Stocks | ||||||||

| (Cost $20,401,432) | $ | 19,125,083 | ||||||

The accompanying notes are an integral part of the financial statements.

20

| WESTWOOD SALIENT GLOBAL REAL ESTATE FUND |

| DECEMBER 31, 2022 |

| MONEY MARKET FUNDS — 4.0% |

| Shares | Value | |||||||

| First American Government Obligations Fund - Class X, 4.09% (a) (Cost $800,067) | 800,067 | $ | 800,067 | |||||

| Investments at Value — 99.5% | ||||||||

| (Cost $21,201,499) | $ | 19,925,150 | ||||||

| Other Assets in Excess of Liabilities — 0.5% | 102,240 | |||||||

| Net Assets — 100.0% | $ | 20,027,390 | ||||||

| (a) | The rate shown is the 7-day effective yield as of December 31, 2022. |

AB - Aktiebolag

S.A. - Societe Anonyme

SE - Societe Europaea

The accompanying notes are an integral part of the financial statements.

21

| WESTWOOD SALIENT SELECT INCOME FUND |

| DECEMBER 31, 2022 |

| Sector Weightings (Unaudited)† |

| † | Percentages are based on total investments. |

| SCHEDULE OF INVESTMENTS |

| COMMON STOCKS — 21.9% |

| Shares | Value | |||||||

| Real Estate Investment Trusts (REITs) — 21.9% | ||||||||

| Farmland — 1.2% | ||||||||

| Farmland Partners, Inc. | 200,000 | $ | 2,492,000 | |||||

| �� | ||||||||

| Hotels — 4.7% | ||||||||

| Apple Hospitality REIT, Inc. | 320,000 | 5,049,600 | ||||||

| Gaming and Leisure Properties, Inc. | 100,100 | 5,214,209 | ||||||

| 10,263,809 | ||||||||

| Industrial — 4.2% | ||||||||

| Americold Realty Trust, Inc. | 145,000 | 4,104,950 | ||||||

| Prologis, Inc. | 45,000 | 5,072,850 | ||||||

| 9,177,800 | ||||||||

| Manufactured Homes — 2.1% | ||||||||

| Sun Communities, Inc. | 32,000 | 4,576,000 | ||||||

| Shopping Centers — 3.9% | ||||||||

| Phillips Edison & Co., Inc. | 80,000 | 2,547,200 | ||||||

| Retail Opportunity Investments Corp. | 397,000 | 5,966,910 | ||||||

| 8,514,110 | ||||||||

| Specialized — 1.0% | ||||||||

| Outfront Media, Inc. | 136,000 | 2,254,880 | ||||||

| Storage — 2.9% | ||||||||

| CubeSmart | 110,000 | 4,427,500 | ||||||

| National Storage Affiliates Trust | 50,000 | 1,806,000 | ||||||

| 6,233,500 | ||||||||

| COMMON STOCKS — continued |

| Shares | Value | |||||||

| Real Estate Investment Trusts (REITs) — continued | ||||||||

| Towers — 1.9% | ||||||||

| American Tower Corp. | 20,000 | $ | 4,237,200 | |||||

| Total Common Stocks | ||||||||

| (Cost $50,012,573) | $ | 47,749,299 | ||||||

| PREFERRED STOCKS — 72.7% | ||||||||

| Real Estate Investment Trusts (REITs) — 72.7% | ||||||||

| Apartments — 1.8% | ||||||||

| Centerspace - Series C, 6.63% | 158,980 | $ | 4,014,245 | |||||

| Data Centers — 3.4% | ||||||||

| DigitalBridge Group, Inc. - Series H, 7.13% | 240,000 | 4,535,976 | ||||||

| DigitalBridge Group, Inc. - Series I, 7.15% | 160,000 | 3,001,600 | ||||||

| 7,537,576 | ||||||||

| Diversified — 2.7% | ||||||||

| Armada Hoffler Properties, Inc. - Series A, 6.75% | 150,000 | 3,148,500 | ||||||

| CTO Realty Growth, Inc. - Series A, 6.38% | 133,683 | 2,733,817 | ||||||

| 5,882,317 | ||||||||

| Healthcare — 3.3% | ||||||||

| Global Medical REIT, Inc. - Series A, 7.50% | 290,000 | 7,284,800 | ||||||

| Hotels — 16.7% | ||||||||

| Chatham Lodging Trust - Series A, 6.63% | 190,000 | 3,807,600 | ||||||

| DiamondRock Hospitality Co. - Series A, 8.25% | 15,096 | 375,589 | ||||||

| Hersha Hospitality Trust - Series C, 6.88% | 260,000 | 5,190,900 | ||||||

| Hersha Hospitality Trust - Series D, 6.50% | 50,000 | 935,250 | ||||||

| Hersha Hospitality Trust - Series E, 6.50% | 275,000 | 5,087,500 | ||||||

| Pebblebrook Hotel Trust - Series G, 6.38% | 205,000 | 3,731,000 | ||||||

| Pebblebrook Hotel Trust - Series H, 5.70% | 90,148 | 1,487,442 | ||||||

| RLJ Lodging Trust - Series A, 1.95% | 390,000 | 9,278,100 | ||||||

| Summit Hotel Properties, Inc. - Series E, 6.250% | 222,386 | 4,065,216 | ||||||

| Summit Hotel Properties, Inc. - Series F, 5.875% | 151,000 | 2,586,630 | ||||||

| 36,545,227 | ||||||||

The accompanying notes are an integral part of the financial statements.

22

| WESTWOOD SALIENT SELECT INCOME FUND |

| DECEMBER 31, 2022 |

| PREFERRED STOCKS — continued |

| Shares | Value | |||||||

| Real Estate Investment Trusts (REITs) — continued | ||||||||

| Industrial — 5.6% | ||||||||

| LXP Industrial Trust - Series C, 6.50% | 205,514 | $ | 9,761,915 | |||||

| Plymouth Industrial REIT, Inc. - Series A, 7.50% | 100,000 | 2,498,000 | ||||||

| 12,259,915 | ||||||||

| Manufactured Homes — 0.5% | ||||||||

| UMH Properties, Inc. - Series D, 6.38% | 48,692 | 1,083,397 | ||||||

| Mortgage — 9.3% | ||||||||

| iStar, Inc. - Series D, 8.00% | 27,100 | 671,809 | ||||||

| iStar, Inc. - Series G, 7.65% | 400,000 | 9,812,000 | ||||||

| iStar, Inc. - Series I, 7.50% | 300,200 | 7,342,892 | ||||||

| KKR Real Estate Finance Trust, Inc. - Series A, 6.50% | 150,000 | 2,475,000 | ||||||

| 20,301,701 | ||||||||

| Office Property — 0.9% | ||||||||

| Hudson Pacific Properties - Series C, 4.80% | 42,625 | 534,091 | ||||||

| Vornado Realty Trust - Series M, 5.25% | 25,000 | 401,500 | ||||||

| Vornado Realty Trust - Series N, 5.25% | 60,500 | 982,520 | ||||||

| 1,918,111 | ||||||||

| Residential — 4.3% | ||||||||

| American Homes 4 Rent - Series G, 5.88% | 345,000 | 7,645,200 | ||||||

| American Homes 4 Rent - Series H, 6.25% | 71,000 | 1,649,039 | ||||||

| 9,294,239 | ||||||||

| Shopping Centers — 14.5% | ||||||||

| RPT Realty - Series D, 7.25% | 185,000 | 9,246,300 | ||||||

| Saul Centers, Inc. - Series D, 6.13% | 380,000 | 7,942,000 | ||||||

| Saul Centers, Inc. - Series E, 6.00% | 125,000 | 2,461,250 | ||||||

| Site Centers Corporation - Series A, 6.60% | 25,000 | 555,000 | ||||||

| Urstadt Biddle Properties, Inc. - Series H, 6.25% | 345,000 | 7,534,800 | ||||||

| Urstadt Biddle Properties, Inc. - Series K, 5.88% | 190,000 | 3,891,200 | ||||||

| 31,630,550 | ||||||||

| Single Tenant — 1.3% | ||||||||

| Spirit Realty Capital, Inc. - Series A, 6.00% | 130,000 | 2,892,500 | ||||||

| PREFERRED STOCKS — continued |

| Shares | Value | |||||||

| Real Estate Investment Trusts (REITs) — continued | ||||||||

| Specialized — 4.3% | ||||||||

| CorEnergy Infrastructure Trust, Inc. - Series A, 7.38% | 141,481 | $ | 1,612,884 | |||||

| EPR Properties - Series C, 5.75% | 31,000 | 557,070 | ||||||

| EPR Properties - Series E, 9.00% | 280,000 | 7,204,400 | ||||||

| 9,374,354 | ||||||||

| Storage — 4.1% | ||||||||

| National Storage Affiliates Trust - Series A, 6.00% | 400,000 | 8,942,000 | ||||||

| Total Preferred Stocks | ||||||||

| (Cost $155,660,808) | $ | 158,960,932 | ||||||

| MONEY MARKET FUNDS — 3.3% | ||||||||

| First American Government Obligations Fund - Class X, 4.09% (a) (Cost $7,218,880) | 7,218,880 | $ | 7,218,880 | |||||

| Investments at Value — 97.9% | ||||||||

| (Cost $212,892,261) | $ | 213,929,111 | ||||||

| Other Assets in Excess of Liabilities — 2.1% | 4,552,519 | |||||||

| Net Assets — 100.0% | $ | 218,481,630 | ||||||

| (a) | The rate shown is the 7-day effective yield as of December 31, 2022. |

REIT - Real Estate Investment Trust

The accompanying notes are an integral part of the financial statements.

23

| WESTWOOD BROADMARK TACTICAL GROWTH FUND |

| DECEMBER 31, 2022 |

| SCHEDULE OF INVESTMENTS |

| EXCHANGE-TRADED FUNDS — 20.1% |

| Shares | Value | |||||||

| Consumer Staples Select Sector SPDR® Fund (The) | 183,084 | $ | 13,648,912 | |||||

| Health Care Select Sector SPDR® Fund (The) | 101,697 | 13,815,538 | ||||||

| SPDR® Dow Jones Industrial Average ETF Trust | 39,992 | 13,250,549 | ||||||

| Utilities Select Sector SPDR® Fund (The) | 197,011 | 13,889,276 | ||||||

| Total Exchange-Traded Funds | ||||||||

| (Cost $53,420,648) | $ | 54,604,275 | ||||||

| MONEY MARKET FUNDS — 79.0% |

| Shares | Value | |||||||

| First American Government Obligations Fund - Class X, 4.09% (a) (Cost $214,244,298) | 214,244,298 | $ | 214,244,298 | |||||

| Investments at Value — 99.1% | ||||||||

| (Cost $267,664,946) | $ | 268,848,573 | ||||||

| Other Assets in Excess of Liabilities — 0.9% | 2,275,508 | |||||||

| Net Assets — 100.0% | $ | 271,124,081 | ||||||

| (a) | The rate shown is the 7-day effective yield as of December 31, 2022. |

ETF - Exchange-Traded Funds

S&P - Standard & Poor

SPDR - Standard and Poor’s Depository Receipts

| SCHEDULE OF FUTURES CONTRACTS SOLD SHORT |

| Value/ | ||||||||||||

| Expiration | Notional | Unrealized | ||||||||||

| FUTURES CONTRACTS SOLD SHORT ^ | Contracts | Date | Value | Depreciation* | ||||||||

| Index Futures | ||||||||||||

| E-Mini S&P® 500 Futures | 213 | 03/17/23 | $ | 41,119,650 | $ | (628,238 | ) | |||||

| * | Includes cumulative appreciation (depreciation) of futures contracts from the date that contracts were opened through December 31, 2022. Only current day variation margin is reported on the Statements of Assets and Liabilities. |