UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22781

Goldman Sachs Trust II

(Exact name of registrant as specified in charter)

200 West Street

15th Floor

New York, New York 10282

(Address of principal executive offices) (Zip code)

| | |

Copies to: |

Robert Griffith, Esq. | | Stephen H. Bier, Esq. |

Goldman Sachs & Co. LLC | | Dechert LLP |

200 West Street | | 1095 Avenue of the Americas |

New York, New York 10282 | | New York, NY 10036 |

(Name and address of agents for service)

Registrant’s telephone number, including area code: (212) 902-1000

Date of fiscal year end: October 31

Date of reporting period: October 31, 2023

| ITEM 1. | REPORTS TO STOCKHOLDERS. |

| | The Annual Report to Shareholders is filed herewith. |

Active Equity Multi-Manager Funds

| | |

| ∎ | | MULTI-MANAGER INTERNATIONAL EQUITY |

| | |

| ∎ | | MULTI-MANAGER U.S. SMALL CAP EQUITY |

TABLE OF CONTENTS

| | | | | | |

| | | | |

| NOT FDIC-INSURED | | May Lose Value | | No Bank Guarantee | | |

MARKET REVIEW

Active Equity Multi-Manager Funds

Market Review

The global equity markets recorded strong gains during the 12-month period ended October 31, 2023 (the “Reporting Period”). Performance was driven by macro factors, chief among them rising interest rates, inflation data, volatile energy prices and speculation about whether central banks would achieve soft or hard economic landings. (A soft landing, in economics, is a cyclical downturn that avoids recession. It typically describes attempts by central banks to raise interest rates just enough to stop an economy from overheating and experiencing high inflation, without causing a significant increase in unemployment, or a hard landing.)

During the Reporting Period, global equities, as represented by the MSCI All Country World Index (Net Total Return, Unhedged, USD) (“MSCI ACWI Index”), generated a return of 10.5%. The majority of the gains occurred during the first nine months of the Reporting Period. The final three months saw corrections across most regions and sectors within the MSCI ACWI Index. (A correction is a condition in which securities prices fall 10% or more from recent highs.)

Non-U.S. developed markets stocks, as represented by the MSCI® EAFE® Index (Net, Unhedged, USD), performed best, posting a return of 14.4% during the Reporting Period overall, with value stocks outpacing growth stocks. From a regional standpoint, Japanese and European equities were the strongest performers. Despite significant depreciation in the Japanese yen relative to the U.S. dollar, Japan’s stock market was one of the best performing developed markets regions, as it benefited from continuation of the central bank’s accommodative monetary policy, rising share buybacks and growing corporate investment. Market technicals (i.e., supply/demand conditions) also supported the performance of Japanese equities, as investment inflows increased, perhaps driven by optimism that long-promised corporate governance reforms were finally starting to bear fruit. As for European equities, they appreciated significantly early in the Reporting Period, recovering from previously depressed levels. Investors had been bearish on European stocks due both to inflation worries, especially concerns about energy price inflation caused by Russia’s invasion of Ukraine, and to rising interest rates and overall economic weakness. However, reduced energy demand because of a warmer than expected winter, success in securing alternative energy imports and generous government support for the consumer improved investor sentiment, led to a significant rally in European equity performance. Challenges then followed, with March 2023 especially difficult, as a U.S. regional banking crisis spilled over to European banks, leading to the high-profile bankruptcy of Credit Suisse but not much further fallout due to prompt government intervention. European equities were volatile for the rest of the Reporting Period, with the outlook for economies and interest rates weighing on market sentiment. Overall, macroeconomic fundamentals in European countries were lethargic during the Reporting Period, with Germany, for example, entering a technical recession and its inflation remaining above target, although employment in the country stayed robust. (A technical recession is commonly defined as two consecutive quarters of negative growth in a country’s gross domestic product.)

In the U.S., where growth stocks beat value stocks by a wide margin, the broad equity market generated a return of 9.5%, as measured by the Russell 1000® Index. The rally in growth stocks was led by the so-called “Magnificent Seven” (specifically, Apple, Microsoft, Alphabet, Amazon.com, Nvidia, Meta Platforms and Tesla), which were responsible for almost all of the U.S equity market’s gains in the first half of 2023. The rally was driven by a combination of factors, including a reversal of previous multiples compression and the strong fundamental performance of some of these companies. (Multiple compression, or valuation derating, is when a company’s valuation multiples, such as the price/earnings ratio, is reduced either because of increased earnings without a corresponding increase in stock price or because of a decreased stock price without a corresponding decrease in earnings.) Many of the Magnificent Seven were beneficiaries of investor optimism about artificial intelligence (“AI”) following the release of ChatGPT as well as excitement about generative AI. Within the U.S. equity market, small-cap stocks, as measured by the Russell 2000® Index, recorded a decline of 8.6% during the Reporting Period. Geopolitical strife, inflation concerns and uncertainty over U.S. Federal Reserve monetary policy created a difficult backdrop for small-cap equities, which are generally considered more volatile and cyclical than their large-cap counterparts.

Emerging markets equities returned 10.8%, as measured by the MSCI Emerging Markets Index (Net, USD, Unhedged), during the Reporting Period. Chinese equities posted the strongest gains, with the MSCI China All Shares Index (Net Total Return, USD, Unhedged) notching a 21.1% return during the Reporting Period, though performance was highly volatile. At first, Chinese equities benefited from the reopening of the country’s economy following COVID-19-related lockdowns, but they subsequently weakened, as an expected surge in consumer spending did not materialize due in part to worries about China’s property crisis and level of unemployment. These investor concerns were exacerbated by geopolitical and regulatory issues.

1

Looking Ahead

At the end of the Reporting Period, many investors continued to debate whether central banks could engineer soft landings or if protracted economic declines were more probable. Although inflation had come down substantially, central banks remained cautious at the end of the Reporting Period about declaring victory due to the potentially sticky components of core inflation, such as wages, that could keep inflation above policymakers’ desired 2% target in major developed markets economies. In most developed markets countries, consumer spending was solid and employment robust, and we thought investors would continue assessing whether this strength could be sustained. In the emerging markets, some countries, such as Mexico, India and Indonesia, were benefiting from “near-shoring” trends wherein Western firms were trying to reduce supply-chain dependency on China, leading to increased investment in other emerging markets countries. Meanwhile, China’s future path was a point of debate, with many investors bearish for both the short term and long term and no signs apparent of a clear catalyst that might fuel a rally without significant government stimulus. Geopolitical risks also remained top of mind for many investors at the end of the Reporting Period, as the Russia/Ukraine war entered another winter, Israel/Hamas war risks escalated and impacted the broader Middle East region, and trade tensions persisted between the U.S. and China.

2

FUND RESULTS

Multi-Manager International Equity Fund

|

| |

Investment Objective The Fund seeks to provide long-term capital growth. |

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs External Investing Group (“XIG”) (formerly, the Goldman Sachs Alternative Investments & Manager Selection (“AIMS”) Group) discusses the Multi-Manager International Equity Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2023 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class P Shares generated an average annual total return of 15.32%. This return compares to the 14.40% average annual total return of the Fund’s benchmark, the MSCI Europe, Australasia and Far East (“EAFE”) Index (Net, USD, Unhedged) (the “MSCI® EAFE® Index”), during the same time period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund uses a multi-manager approach and generally seeks to achieve its investment objective by dynamically allocating its assets among unaffiliated investment managers (“Underlying Managers”) that employ an international equity investment strategy. XIG is responsible for making recommendations with respect to hiring, terminating or replacing the Fund’s Underlying Managers as well as for determining the Fund’s asset allocations. XIG applies a multifaceted process with respect to manager due diligence, portfolio construction and risk management. |

| | During the Reporting Period, the Fund generated a positive absolute return and outperformed the Index on a relative basis. These relative results can be attributed to the performance of the Fund’s Underlying Managers overall. During the Reporting Period, the Fund allocated capital to four Underlying Managers as part of its top-level strategy allocation—Causeway Capital Management LLC (“Causeway”), Lazard Asset Management LLC (“Lazard”), Massachusetts Financial Services Company doing business as MFS Investment Management (“MFS”) and WCM Investment Management (“WCM”). |

| | Of the four Underlying Managers, two produced positive absolute returns and two produced negative absolute returns during the Reporting Period. On a relative basis, value-oriented Underlying Manager Causeway and core-oriented Underlying Manager MFS outperformed their respective benchmark indices during the Reporting Period. Core-oriented Underlying Manager Lazard and growth-oriented Underlying Manager WCM underperformed their respective benchmark indices. |

| Q | Which international equity strategies most significantly affected Fund performance? |

| A | During the Reporting Period, value-oriented Underlying Manager Causeway significantly outperformed its benchmark index, the MSCI® EAFE® Index. The gains were due in part to style tailwinds, as value stocks generally outpaced growth stocks within the MSCI® EAFE® Index during the Reporting Period. The strategy also benefited from strong stock selection within the industrials and financials sectors. |

| | Core-oriented Underlying Manager MFS outperformed the MSCI® EAFE® Index, its benchmark index, driven by broad-based positive stock selection across the communication services, industrials and materials sectors. Effective stock selection within communication services was highlighted by out-of-benchmark exposure to Asian gaming companies, while exposure to European chemical and industrial gas providers added to relative performance in the materials sector. The strategy’s lack of exposure to real estate also contributed positively given that rising interest rates pressured that sector during the Reporting Period. Conversely, stock selection across the health care and financials sectors, as well as an overweight position versus the MSCI® EAFE® Index in the consumer staples sector, detracted somewhat from relative performance. Within health care, exposure to medical equipment makers and to Japanese pharmaceutical companies hampered returns. Within financials, the strategy was hurt by its lack of exposure to Japanese banks, which appreciated amid higher Japanese interest rates and an improved economic growth outlook. From a regional perspective, stock selection in the U.K. and an underweight in Asia ex Japan, especially the strategy’s lack of exposure to Australia, added to relative returns. However, stock selection in Japan—namely, a preference for health care, retailers and manufacturers over banks—and out-of-benchmark exposure to North America, predominantly to Canadian transportation and financials, detracted from relative performance. |

| | Lazard, another core-oriented Underlying Manager, underperformed its benchmark index, the MSCI® EAFE® Index, primarily because of poor stock selection in the financials, health care and consumer discretionary sectors. |

3

| | However, stock selection in information technology, consumer staples and communication services contributed positively, partially offsetting these negative results. On a regional basis, stock selection in continental Europe was the largest detractor from relative performance, while stock selection in the U.K. added most to returns. |

| | Growth-oriented Underlying Manager WCM underperformed its benchmark index, the MSCI ACWI ex-USA Index, during the Reporting Period, due primarily to weak stock selection within the information technology and financials sectors. These losses were partially offset by an overweight in the health care sector as well as lack of exposure to the real estate sector, which added value. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Fund used forward foreign currency exchange contracts to take positions in select non-U.S. markets. The use of forward foreign currency exchange contracts had a negative impact on the Fund’s performance. Rights were employed to give the Fund the opportunity, but not the obligation, to buy additional shares in specific stocks at a discount. Warrants were utilized to give the Fund the right, but not the obligation, to buy or sell specific stocks at a certain price before expiration. The use of rights and warrants each had a neutral impact on the Fund’s performance during the Reporting Period. |

| Q | Were there any notable changes in the Fund’s allocations during the Reporting Period? |

| A | There were no notable changes to the Fund’s allocations during the Reporting Period. At the beginning and end of the Reporting Period, the Fund’s assets were allocated approximately 30% to MFS, 29% to Causeway, 20% to WCM and 20% to Lazard, with the remainder invested in cash and cash equivalents. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | We intend to continue to position the Fund in alignment with our longer-term strategic views within the international equity complex. We further intend to continue to monitor allocations and Underlying Manager performance as we seek to generate long-term capital growth. |

4

FUND BASICS

Multi-Manager International Equity Fund

as of October 31, 2023

|

|

| TOP TEN HOLDINGS AS OF 10/31/23 ± |

| | | | | | | |

| | |

Holding | | % of Net Assets | | Line of Business |

| | |

Novo Nordisk AS Class B | | | | 3.1 | % | | Pharmaceuticals |

Compass Group PLC | | | | 1.9 | | | Hotels, Restaurants & Leisure |

RELX PLC | | | | 1.9 | | | Professional Services |

Canadian Pacific Kansas City Ltd. | | | | 1.7 | | | Ground Transportation |

Rolls-Royce Holdings PLC | | | | 1.7 | | | Aerospace & Defense |

Nestle SA | | | | 1.6 | | | Food Products |

ICON PLC ADR | | | | 1.5 | | | Life Sciences Tools & Services |

Samsung Electronics Co. Ltd. | | | | 1.5 | | | Technology Hardware, Storage & Peripherals |

Roche Holding AG | | | | 1.5 | | | Pharmaceuticals |

Aon PLC Class A | | | | 1.5 | | | Insurance |

| ± | The top 10 holdings may not be representative of the Fund’s future investments. The top 10 holdings exclude investments in money market funds. |

|

|

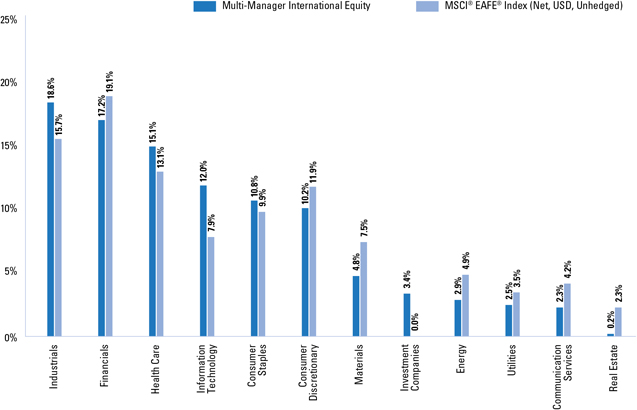

| FUND VS. BENCHMARK SECTOR ALLOCATION† |

As of October 31, 2023

| † | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of the total value of the Fund’s equity investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. Figures in the above graph may not sum to 100% due to the exclusion of other assets and liabilities. |

| | For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance. |

5

|

| MULTI-MANAGER INTERNATIONAL EQUITY FUND |

Performance Summary

October 31, 2023

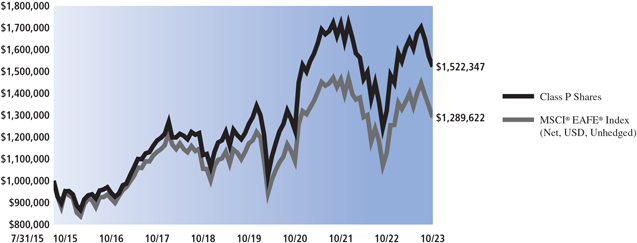

The following graph shows the value, as of October 31, 2023, of a $1,000,000 investment made on July 31, 2015 (commencement of operations) in Class P Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the MSCI® EAFE® Index (Net, USD, Unhedged) is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

|

|

Multi-Manager International Equity Fund’s Lifetime Performance |

| | Performance of a $1,000,000 investment, with distributions reinvested, from July 31, 2015 through October 31, 2023. |

| | | | | | | | | | | | | | | | | |

| | | | |

| | | Average Annual Total Return through October 31, 2023* | | One Year | | Five Years | | Since Inception |

| | | | |

| | Class P Shares (Commenced July 31, 2015) | | 15.32% | | 6.37% | | 5.22% |

| | * | Because Class P Shares does not involve a sales charge, such a charge is not applied to its Average Annual Total Return. |

6

FUND RESULTS

Multi-Manager U.S. Small Cap Equity Fund

|

| |

Investment Objective The Fund seeks to provide long-term capital growth. |

Portfolio Management Discussion and Analysis

Below, the Goldman Sachs External Investing Group (“XIG”) (formerly, the Goldman Sachs Alternative Investments & Manager Selection (“AIMS”) Group) discusses the Multi-Manager U.S. Small Cap Equity Fund’s (the “Fund”) performance and positioning for the 12-month period ended October 31, 2023 (the “Reporting Period”).

| Q | How did the Fund perform during the Reporting Period? |

| A | During the Reporting Period, the Fund’s Class P Shares generated an average annual total return of -5.00%. This return compares to the -8.56% average annual total return of the Fund’s benchmark, the Russell 2000® Total Return Index (the “Index”), during the same time period. |

| Q | What key factors were responsible for the Fund’s performance during the Reporting Period? |

| A | The Fund uses a multi-manager approach and generally seeks to achieve its investment objective by dynamically allocating its assets among unaffiliated investment managers (“Underlying Managers”) that employ a small-cap equity investment strategy. XIG is responsible for making recommendations with respect to hiring, terminating or replacing the Fund’s Underlying Managers as well as for determining the Fund’s asset allocations. XIG applies a multifaceted process with respect to manager due diligence, portfolio construction and risk management. |

| | The Fund generated a negative absolute return during the Reporting Period but outperformed the Index. The relative outperformance can be attributed to the performance of the Fund’s Underlying Managers overall. At various points during the Reporting Period, the Fund allocated capital to four Underlying Managers, one of which managed two strategies, as part of its top-level strategy allocation—Boston Partners Global Investors (“Boston Partners”), Brown Advisory, LLC (“Brown Advisory”), Victory Capital Management, Inc. (“Victory RS” and “Victory Sycamore”) and Westfield Capital Management Company, L.P. (“Westfield”). |

| | The three Underlying Managers with allocated capital during the entire Reporting Period generated negative absolute returns. Victory RS generated a negative absolute return between the beginning of the Reporting Period and |

| | March 13, 2023, when its assets were redeemed. Westfield generated a negative absolute return between March 6, 2023, when it was allocated capital, and the end of the Reporting Period. |

| | On a relative basis, value-oriented Underlying Manager Boston Partners, value-oriented Underlying Manager Victory Sycamore and growth-oriented Underlying Manager Brown Advisory outperformed their respective benchmark indices during the Reporting Period. Growth-oriented Underlying Manager Victory RS underperformed its benchmark index between the start of the Reporting Period and March 13, 2023. Westfield, a growth-oriented Underlying Manager, outperformed its benchmark index between March 6, 2023 and the end of the Reporting Period. |

| Q | Which small-cap equity strategies most significantly affected Fund performance? |

| A | Value-oriented Underlying Manager Boston Partners outperformed its benchmark index, the Russell 2000® Value Index, the most during the Reporting Period. Strong stock selection and a relative underweight in the health care sector, as well as effective selection and an overweight in information technology, added to performance. These positive results were partially offset by stock selection within the energy and materials sectors, which detracted. |

| | Victory Sycamore, the other value-oriented Underlying Manager, also outperformed its benchmark index, the Russell 2000® Value Index, during the Reporting Period. The relative outperformance was driven by effective stock selection and an underweight in the health care sector as well as by an overweight in the industrials sector. An underweight in the energy sector, as well as weak stock selection in consumer discretionary, detracted, partly offsetting these positive results. |

7

| | Growth-oriented Underlying Manager Brown Advisory outperformed its benchmark index, the Russell 2000® Growth Index, during the Reporting Period, due to strong selection within health care, communication services and real estate. Partly offsetting these results was stock selection within consumer discretionary and financials, which detracted from relative performance. |

| | Victory RS, a growth-oriented Underlying Manager, underperformed its benchmark index, the Russell 2000® Growth Index, between the beginning of the Reporting Period and March 13, 2023 when its assets were redeemed. The negative results were driven by weak stock selection in the health care sector, notably among biotechnology companies. Selection in consumer discretionary also detracted from relative returns as did selection in information technology, specifically software stocks. On the positive side, stock selection in the industrials and energy sectors added to relative performance. |

| | Westfield, a growth-oriented Underlying Manager, outperformed its benchmark index, the Russell 2000® Growth Index, between March 6, 2023, when it was allocated assets, and the end of the Reporting Period. Its outperformance was primarily attributable to effective stock selection in the health care sector, particularly among biotechnology companies. A relative overweight in financials and stock selection in real estate further added to returns. Conversely, stock selection in the industrials and consumer discretionary sectors detracted from relative performance during the Reporting Period. |

| Q | How did the Fund use derivatives and similar instruments during the Reporting Period? |

| A | During the Reporting Period, the Fund did not use derivatives or similar instruments. |

| Q | Were there any notable changes in the Fund’s allocations during the Reporting Period? |

| A | At the beginning of the Reporting Period, the Fund’s assets were allocated approximately 36% to Brown Advisory, 29% to Boston Partners, 25% to Victory Sycamore and 9% to Victory RS, with the remainder invested in cash and cash equivalents. |

| | In December 2022, XIG reduced the Fund’s allocation to value-oriented Underlying Manager Boston Partners and redeployed the capital to Victory Sycamore, the Fund’s other value-oriented Underlying Manager. |

| | Effective January 24, 2023, Westfield became a growth-oriented Underlying Manager for the Fund but was not allocated capital at that time. |

| | In March 2023, the Fund’s allocation to growth-oriented Underlying Manager Victory RS was eliminated and the capital reallocated to Westfield. This redeployment allowed XIG to allocate assets to a strategy in which it had greater conviction while keeping the Fund in balance from both a risk budget and style perspective. Subsequently, XIG increased the Fund’s allocation to Westfield by reducing its allocation to growth-oriented Brown Advisory. Lastly, after substantial outperformance by value-oriented Victory Sycamore, XIG trimmed the Fund’s allocation to that Underlying Manager and further increased its allocation to Westfield. These adjustments allowed the Fund to reach an equal weighting between its growth-oriented and value-oriented Underlying Managers. |

| | At the end of the Reporting Period, the Fund’s assets were allocated approximately 29.50% to Brown Advisory, 24.75% to Boston Partners, 24.75% to Victory Sycamore and 20.00% to Westfield, with the remainder in cash and cash equivalents. |

| Q | What is the Fund’s tactical view and strategy for the months ahead? |

| A | We intend to continue to position the Fund in alignment with our longer-term strategic views within the U.S. small-cap equity complex. We further intend to continue to monitor allocations and Underlying Manager performance as we seek to generate long-term capital growth. |

8

FUND BASICS

Multi-Manager U.S. Small Cap Equity Fund

as of October 31, 2023

|

|

| TOP TEN HOLDINGS AS OF 10/31/23 ± |

| | | | | | | |

| | |

Holding | | % of Net Assets | | Line of Business |

ChampionX Corp. | | | | 1.3 | % | | Energy Equipment & Services |

Curtiss-Wright Corp. | | | | 0.9 | | | Aerospace & Defense |

Casella Waste Systems, Inc. Class A | | | | 0.9 | | | Commercial Services & Supplies |

Bright Horizons Family Solutions, Inc. | | | | 0.9 | | | Diversified Consumer Services |

Haemonetics Corp. | | | | 0.9 | | | Health Care Equipment & Supplies |

Casey’s General Stores, Inc. | | | | 0.9 | | | Consumer Staples Distribution & Retail |

Wintrust Financial Corp. | | | | 0.9 | | | Banks |

Ascendis Pharma AS ADR | | | | 0.9 | | | Biotechnology |

FTI Consulting, Inc. | | | | 0.8 | | | Professional Services |

Dynatrace, Inc. | | | | 0.8 | | | Software |

| ± | The top 10 holdings may not be representative of the Fund’s future investments. The top 10 holdings exclude investments in money market funds. |

|

|

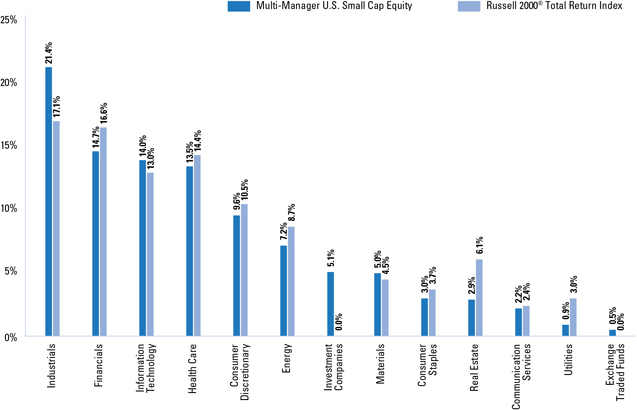

| FUND VS. BENCHMARK SECTOR ALLOCATION † |

As of October 31, 2023

| † | The Fund is actively managed and, as such, its composition may differ over time. Consequently, the Fund’s overall sector allocations may differ from the percentages contained in the graph above. The graph categorizes investments using the Global Industry Classification Standard (“GICS”), however, the sector classifications used by the portfolio management team may differ from GICS. The percentage shown for each investment category reflects the value of investments in that category as a percentage of the total value of the Fund’s equity investments. The graph depicts the Fund’s investments but may not represent the Fund’s market exposure due to the exclusion of certain derivatives, if any, as listed in the Additional Investment Information section of the Schedule of Investments. Figures in the above graph may not sum to 100% due to the exclusion of other assets and liabilities. |

| | For more information about your Fund, please refer to www.GSAMFUNDS.com. There, you can learn more about your Fund’s investment strategies, holdings, and performance. |

9

|

| MULTI-MANAGER U. S. SMALL CAP EQUITY FUND |

Performance Summary

October 31, 2023

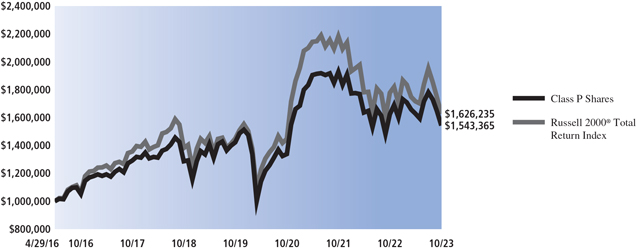

The following graph shows the value, as of October 31, 2023, of a $1,000,000 investment made on April 29, 2016 (commencement of operations) in Class P Shares at NAV. For comparative purposes, the performance of the Fund’s benchmark, the Russell 2000® Total Return is shown. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. Returns do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The returns set forth below represent past performance. Past performance does not guarantee future results. The Fund’s investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance quoted below. Please visit our web site at www.GSAMFUNDS.com to obtain the most recent month-end returns.

|

|

| Multi-Manager U.S. Small Cap Equity Fund’s Lifetime Performance |

| | Performance of a $1,000,000 investment, with distributions reinvested, from April 29, 2016 through October 31, 2023 |

| | | | | | | | | | | | | | | | | |

| | | | |

| | | Average Annual Total Return through October 31, 2023* | | One Year | | Five Years | | Since Inception |

| | | | |

| | Class P Shares (Commenced April 29, 2016) | | -5.00% | | 3.70% | | 5.95% |

| | * | Because Class P Shares does not involve a sales charge, such a charge is not applied to its Average Annual Total Return. |

10

FUND BASICS

Index Definitions

Market Review

MSCI All Country World Index Investable Market Index is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets.

MSCI China All Shares Index captures large and mid-cap representation across China A shares, B shares, H shares, Red chips, P chips and foreign listings (e.g., American Depositary Receipts). The index aims to reflect the opportunity set of China share classes listed in Hong Kong, Shanghai, Shenzhen and outside of China.

Russell 1000® Index measures the performance of the large-cap segment of the U.S. equity universe. The Russell 1000® Index is a subset of the Russell 3000® Index and includes approximately 1000 of the largest securities based on a combination of their market cap and current index membership. The Russell 1000® Index represents approximately 92% of the U.S. market. The Russell 1000® Index is constructed to provide a comprehensive and unbiased barometer for the large-cap segment and is completely reconstituted annually to ensure new and growing equities are reflected.

Russell 2000® Total Return Index is an unmanaged index of common stock prices that measures the performance of the 2000 smallest companies in the Russell 3000® Index. The Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

Multi-Manager International Equity Fund

MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 developed markets countries.

MSCI® EAFE® Index is a stock market index that is designed to measure the equity market performance of developed markets in Europe, Australasia and the Far East, excluding the U.S. and Canada.

Multi-Manager U.S. Small Cap Equity Fund

Russell 2000® Growth Index measures the performance of the small-cap growth stocks of the U.S. equity universe.

Russell 2000® Total Return Index is an unmanaged index of common stock prices that measures the performance of the 2000 smallest companies in the Russell 3000® Index. The Index is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

Russell 2000® Value Index measures the performance of the small-cap value stocks of the U.S. equity universe.

It is not possible to invest directly in an unmanaged index.

11

|

| MULTI-MANAGER INTERNATIONAL EQUITY FUND |

Schedule of Investments

October 31, 2023

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks – 95.8% | |

| |

| | | | | Belgium – 0.9% | |

| | | | | 117,981 | | | Anheuser-Busch InBev SA (Beverages) | | $ | 6,712,889 | |

| | | | | 82,195 | | | KBC Group NV (Banks) | | | 4,523,589 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 11,236,478 | |

| | | | | | |

| | | | | Bermuda* – 0.7% | |

| | | | | 99,310 | | | Arch Capital Group Ltd. (Insurance) | | | 8,608,191 | |

| | | | | | |

| | | | | Brazil – 0.2% | |

| | | | | 816,219 | | | Banco Bradesco SA ADR (Banks) | | | 2,277,251 | |

| | | | | | |

| | | | | Canada – 4.8% | |

| | | | | 87,493 | | | Alimentation Couche-Tard, Inc.

(Consumer Staples Distribution & Retail) | | | 4,762,824 | |

| | | | | 151,828 | | | CAE, Inc.* (Aerospace & Defense) | | | 3,170,679 | |

| | | | | 46,879 | | | Canadian National Railway Co.

(Ground Transportation) | | | 4,958,861 | |

| | | | | 299,501 | | | Canadian Pacific Kansas City Ltd.

(Ground Transportation) | | | 21,258,824 | |

| | | | | 18,862 | | | Intact Financial Corp. (Insurance) | | | 2,650,133 | |

| | | | | 54,624 | | | National Bank of Canada (Banks) | | | 3,396,201 | |

| | | | | 273,523 | | | Suncor Energy, Inc. (Oil, Gas & Consumable Fuels) | | | 8,858,062 | |

| | | | | 44,290 | | | Thomson Reuters Corp.

(Professional Services) | | | 5,305,219 | |

| | | | | 70,013 | | | Toronto-Dominion Bank (Banks) | | | 3,910,731 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 58,271,534 | |

| | | | | | |

| | | | | China – 1.2% | |

| | | | | 28,935 | | | Alibaba Group Holding Ltd. ADR* (Broadline Retail) | | | 2,388,295 | |

| | | | | 2,024,000 | | | Beijing Capital International Airport Co. Ltd. Class H* (Transportation Infrastructure) | | | 745,515 | |

| | | | | 157,800 | | | NetEase, Inc. (Entertainment) | | | 3,377,165 | |

| | | | | 169,900 | | | Tencent Holdings Ltd. (Interactive Media & Services) | | | 6,287,783 | |

| | | | | 44,736 | | | Yum China Holdings, Inc. (Hotels, Restaurants & Leisure) | | | 2,351,324 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 15,150,082 | |

| | | | | | |

| | | | | Denmark – 4.7% | |

| | | | | 73,406 | | | Carlsberg AS Class B (Beverages) | | | 8,748,022 | |

| | | | | 36,677 | | | DSV AS (Air Freight & Logistics) | | | 5,481,044 | |

| | | | | 9,072 | | | Genmab AS* (Biotechnology) | | | 2,564,499 | |

| | | | | 396,488 | | | Novo Nordisk AS Class B (Pharmaceuticals) | | | 38,251,658 | |

| | | | | 98,371 | | | Vestas Wind Systems AS*

(Electrical Equipment) | | | 2,132,168 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 57,177,391 | |

| | | | | | |

| | | | | Finland – 0.4% | |

| | | | | 115,594 | | | Sampo OYJ Class A (Insurance) | | | 4,546,174 | |

| | | | | | |

| | | | | France – 12.1% | |

| | | | | 88,711 | | | Air Liquide SA (Chemicals) | | | 15,200,822 | |

| | | | | | |

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | �� | | Common Stocks (continued) | |

| | | | | France (continued) | |

| | | | | 417,040 | | | Alstom SA (Machinery) | | $ | 5,647,748 | |

| | | | | 184,151 | | | AXA SA (Insurance) | | | 5,456,472 | |

| | | | | 37,147 | | | BNP Paribas SA (Banks) | | | 2,136,101 | |

| | | | | 140,995 | | | Bureau Veritas SA (Professional Services) | | | 3,211,553 | |

| | | | | 47,136 | | | Capgemini SE (IT Services) | | | 8,330,290 | |

| | | | | 222,727 | | | Carrefour SA (Consumer Staples Distribution & Retail) | | | 3,904,730 | |

| | | | | 75,874 | | | Cie de Saint-Gobain SA (Building Products) | | | 4,130,137 | |

| | | | | 89,079 | | | Cie Generale des Etablissements Michelin SCA (Automobile Components) | | | 2,646,399 | |

| | | | | 142,449 | | | Danone SA (Food Products) | | | 8,474,356 | |

| | | | | 54,133 | | | Dassault Systemes SE (Software) | | | 2,229,921 | |

| | | | | 554,174 | | | Engie SA (Multi-Utilities) | | | 8,814,073 | |

| | | | | 33,802 | | | EssilorLuxottica SA (Health Care Equipment & Supplies) | | | 6,120,982 | |

| | | | | 12,954 | | | Kering SA (Textiles, Apparel & Luxury Goods) | | | 5,268,411 | |

| | | | | 38,353 | | | Legrand SA (Electrical Equipment) | | | 3,317,779 | |

| | | | | 14,098 | | | L’Oreal SA (Personal Products) | | | 5,925,819 | |

| | | | | 21,603 | | | LVMH Moet Hennessy Louis Vuitton SE (Textiles, Apparel & Luxury Goods) | | | 15,466,243 | |

| | | | | 60,723 | | | Pernod Ricard SA (Beverages) | | | 10,782,968 | |

| | | | | 67,536 | | | Sanofi SA (Pharmaceuticals) | | | 6,132,690 | |

| | | | | 93,700 | | | Schneider Electric SE (Electrical Equipment) | | | 14,416,429 | |

| | | | | 31,299 | | | Thales SA (Aerospace & Defense) | | | 4,619,030 | |

| | | | | 174,214 | | | Valeo SE (Automobile Components) | | | 2,301,905 | |

| | | | | 33,924 | | | Vinci SA (Construction & Engineering) | | | 3,751,127 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 148,285,985 | |

| | | | | | |

| | | | | Germany–7.0% | |

| | | | | 25,337 | | | Allianz SE (Insurance) | | | 5,935,002 | |

| | | | | 167,608 | | | Bayer AG (Pharmaceuticals) | | | 7,242,100 | |

| | | | | 57,185 | | | Beiersdorf AG (Personal Products) | | | 7,520,971 | |

| | | | | 62,130 | | | Continental AG (Automobile Components) | | | 4,056,403 | |

| | | | | 39,178 | | | Deutsche Boerse AG (Capital Markets) | | | 6,448,562 | |

| | | | | 377,743 | | | Deutsche Telekom AG (Diversified Telecommunication Services) | | | 8,198,407 | |

| | | | | 22,994 | | | Gerresheimer AG (Life Sciences Tools & Services) | | | 2,144,724 | |

| | | | | 72,508 | | | Infineon Technologies AG

(Semiconductors & Semiconductor Equipment) | | | 2,117,974 | |

| | | | | 115,708 | | | LANXESS AG (Chemicals) | | | 2,651,399 | |

| | | | | 62,515 | | | Merck KGaA (Pharmaceuticals) | | | 9,442,165 | |

| | | | | 10,719 | | | MTU Aero Engines AG (Aerospace & Defense) | | | 2,014,708 | |

| | | | | | |

12 The accompanying notes are an integral part of these financial statements.

MULTI-MANAGER INTERNATIONAL EQUITY FUND

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks (continued) | |

| | | | | Germany (continued) | |

| | | | | 121,049 | | | RWE AG (Independent Power and Renewable Electricity Producers) | | $ | 4,631,989 | |

| | | | | 125,568 | | | SAP SE (Software) | | | 16,842,728 | |

| | | | | 68,137 | | | Schott Pharma AG & Co. KGaA* (Life Sciences Tools & Services) | | | 1,975,424 | |

| | | | | 30,944 | | | Siemens AG (Industrial Conglomerates) | | | 4,106,233 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 85,328,789 | |

| | | | | | |

| | | | | Hong Kong – 1.0% | |

| | | | | 1,298,400 | | | AIA Group Ltd. (Insurance) | | | 11,275,050 | |

| | | | | 1,171,000 | | | ESR Group Ltd.(a) (Real Estate Management & Development) | | | 1,504,612 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 12,779,662 | |

| | | | | | |

| | | | | India – 1.4% | |

| | | | | 425,874 | | | HDFC Bank Ltd. (Banks) | | | 7,556,934 | |

| | | | | 316,710 | | | ICICI Bank Ltd. ADR (Banks) | | | 7,027,795 | |

| | | | | 46,273 | | | Tata Consultancy Services Ltd.

(IT Services) | | | 1,873,297 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 16,458,026 | |

| | | | | | |

| | | | | Ireland – 6.7% | |

| | | | | 38,611 | | | Accenture PLC Class A (IT Services) | | | 11,470,942 | |

| | | | | 58,074 | | | Aon PLC Class A (Insurance) | | | 17,968,096 | |

| | | | | 340,220 | | | Experian PLC (Professional Services) | | | 10,321,862 | |

| | | | | 75,346 | | | ICON PLC ADR* (Life Sciences Tools & Services) | | | 18,381,410 | |

| | | | | 30,573 | | | Linde PLC (Chemicals) | | | 11,683,778 | |

| | | | | 142,761 | | | Ryanair Holdings PLC ADR* (Passenger Airlines) | | | 12,520,140 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 82,346,228 | |

| | | | | | |

| | | | | Israel – 0.7% | |

| | | | | 712,965 | | | Bank Leumi Le-Israel BM (Banks) | | | 4,592,148 | |

| | | | | 25,511 | | | Check Point Software Technologies Ltd.* (Software) | | | 3,424,852 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 8,017,000 | |

| | | | | | |

| | | | | Italy – 3.8% | |

| | | | | 1,528,944 | | | Enel SpA (Electric Utilities) | | | 9,705,095 | |

| | | | | 321,925 | | | Eni SpA (Oil, Gas & Consumable Fuels) | | | 5,262,722 | |

| | | | | 37,934 | | | Ferrari NV (Automobiles) | | | 11,482,769 | |

| | | | | 2,106,773 | | | Intesa Sanpaolo SpA (Banks) | | | 5,489,810 | |

| | | | | 550,827 | | | UniCredit SpA (Banks) | | | 13,809,020 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 45,749,416 | |

| | | | | | |

| | | | | Japan – 9.1% | |

| | | | | 295,200 | | | Advantest Corp. (Semiconductors & Semiconductor Equipment) | | | 7,603,944 | |

| | | | | 126,200 | | | BayCurrent Consulting, Inc. (Professional Services) | | | 3,168,471 | |

| | | | | | |

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks (continued) | |

| | | | | Japan (continued) | |

| | | | | 60,500 | | | Daikin Industries Ltd.

(Building Products) | | $ | 8,722,822 | |

| | | | | 313,400 | | | Denso Corp. (Automobile Components) | | | 4,627,768 | |

| | | | | 266,800 | | | FANUC Corp. (Machinery) | | | 6,621,014 | |

| | | | | 132,100 | | | Hitachi Ltd. (Industrial Conglomerates) | | | 8,373,367 | |

| | | | | 48,900 | | | Hoya Corp. (Health Care Equipment & Supplies) | | | 4,707,534 | |

| | | | | 16,500 | | | Keyence Corp. (Electronic Equipment, Instruments & Components) | | | 6,387,454 | |

| | | | | 107,000 | | | Kobe Bussan Co. Ltd. (Consumer Staples Distribution & Retail) | | | 2,648,042 | |

| | | | | 211,600 | | | Koito Manufacturing Co. Ltd. (Automobile Components) | | | 3,170,346 | |

| | | | | 127,500 | | | Kokusai Electric Corp.*

(Semiconductors & Semiconductor Equipment) | | | 2,077,684 | |

| | | | | 26,200 | | | Kose Corp. (Personal Products) | | | 1,735,776 | |

| | | | | 112,200 | | | Kubota Corp. (Machinery) | | | 1,509,005 | |

| | | | | 82,500 | | | Kyocera Corp. (Electronic Equipment, Instruments & Components) | | | 4,066,541 | |

| | | | | 245,200 | | | Mitsubishi Electric Corp.

(Electrical Equipment) | | | 2,811,588 | |

| | | | | 445,200 | | | Murata Manufacturing Co. Ltd.

(Electronic Equipment, Instruments & Components) | | | 7,625,999 | |

| | | | | 239,900 | | | Olympus Corp. (Health Care Equipment & Supplies) | | | 3,203,949 | |

| | | | | 276,600 | | | Renesas Electronics Corp.*

(Semiconductors & Semiconductor Equipment) | | | 3,633,312 | |

| | | | | 77,700 | | | Seven & i Holdings Co. Ltd.

(Consumer Staples Distribution & Retail) | | | 2,846,827 | |

| | | | | 75,300 | | | Shin-Etsu Chemical Co. Ltd. (Chemicals) | | | 2,251,724 | |

| | | | | 8,100 | | | SMC Corp. (Machinery) | | | 3,740,280 | |

| | | | | 64,100 | | | Sony Group Corp. (Household Durables) | | | 5,329,200 | |

| | | | | 48,200 | | | Sumitomo Mitsui Financial Group, Inc. (Banks) | | | 2,323,624 | |

| | | | | 72,200 | | | Suzuki Motor Corp. (Automobiles) | | | 2,802,227 | |

| | | | | 185,000 | | | Takeda Pharmaceutical Co. Ltd. (Pharmaceuticals) | | | 5,021,774 | |

| | | | | 118,900 | | | Terumo Corp. (Health Care Equipment & Supplies) | | | 3,252,888 | |

| | | | | 70,300 | | | ZOZO, Inc. (Specialty Retail) | | | 1,336,737 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 111,599,897 | |

| | | | | | |

| | | | | Mexico – 0.4% | |

| | | | | 560,700 | | | Arca Continental SAB de CV (Beverages) | | | 5,027,920 | |

| | | | | | |

The accompanying notes are an integral part of these financial statements. 13

|

| MULTI-MANAGER INTERNATIONAL EQUITY FUND |

Schedule of Investments (continued)

October 31, 2023

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks (continued) | |

| | | | | Netherlands – 5.9% | |

| | | | | 8,839 | | | Adyen NV*(a) (Financial Services) | | $ | 5,961,780 | |

| | | | | 47,667 | | | Airbus SE (Aerospace & Defense) | | | 6,391,008 | |

| | | | | 185,400 | | | Akzo Nobel NV (Chemicals) | | | 12,437,501 | |

| | | | | 17,714 | | | ASM International NV (Semiconductors & Semiconductor Equipment) | | | 7,310,215 | |

| | | | | 22,700 | | | ASML Holding NV (Semiconductors & Semiconductor Equipment) | | | 13,619,167 | |

| | | | | 837,464 | | | ING Groep NV (Banks) | | | 10,736,728 | |

| | | | | 342,784 | | | Koninklijke Philips NV* (Health Care Equipment & Supplies) | | | 6,520,600 | |

| | | | | 79,325 | | | QIAGEN NV* (Life Sciences Tools & Services) | | | 2,956,292 | |

| | | | | 36,357 | | | Randstad NV (Professional Services) | | | 1,882,738 | |

| | | | | 159,073 | | | Universal Music Group NV (Entertainment) | | | 3,895,511 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 71,711,540 | |

| | | | | | |

| | | | | Portugal – 0.6% | |

| | | | | 883,450 | | | EDP - Energias de Portugal SA

(Electric Utilities) | | | 3,712,696 | |

| | | | | 201,722 | | | Galp Energia SGPS SA (Oil, Gas & Consumable Fuels) | | | 3,036,876 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,749,572 | |

| | | | | | |

| | | | | Singapore – 1.0% | |

| | | | | 364,400 | | | DBS Group Holdings Ltd. (Banks) | | | 8,754,096 | |

| | | | | 148,600 | | | United Overseas Bank Ltd. (Banks) | | | 2,931,089 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 11,685,185 | |

| | | | | | |

| | | | | South Korea – 1.9% | |

| | | | | 68,621 | | | Samsung Electronics Co. Ltd. (Technology Hardware, Storage & Peripherals) | | | 3,415,602 | |

| | | | | 11,838 | | | Samsung Electronics Co. Ltd. GDR (Technology Hardware, Storage & Peripherals) | | | 14,803,130 | |

| | | | | 56,234 | | | SK Hynix, Inc. (Semiconductors & Semiconductor Equipment) | | | 4,883,479 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 23,102,211 | |

| | | | | | |

| | | | | Spain – 1.3% | |

| | | | | 37,214 | | | Aena SME SA(a) (Transportation Infrastructure) | | | 5,399,776 | |

| | | | | 120,070 | | | Amadeus IT Group SA

(Hotels, Restaurants & Leisure) | | | 6,852,732 | |

| | | | | 329,581 | | | Iberdrola SA (Electric Utilities) | | | 3,665,606 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 15,918,114 | |

| | | | | | |

| | | | | Sweden – 1.2% | |

| | | | | 50,003 | | | Assa Abloy AB Class B (Building Products) | | | 1,065,817 | |

| | | | | | |

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks (continued) | |

| | | | | Sweden (continued) | |

| | | | | 323,706 | | | Atlas Copco AB Class A (Machinery) | | $ | 4,191,675 | |

| | | | | 68,930 | | | Evolution AB(a)

(Hotels, Restaurants & Leisure) | | | 6,142,036 | |

| | | | | 363,770 | | | Hexagon AB Class B

(Electronic Equipment, Instruments & Components) | | | 2,964,591 | |

| | | | | 6,460 | | | Sandvik AB (Machinery) | | | 110,033 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 14,474,152 | |

| | | | | | |

| | | | | Switzerland – 7.7% | |

| | | | | 84,801 | | | ABB Ltd. (Electrical Equipment) | | | 2,849,119 | |

| | | | | 74,490 | | | Cie Financiere Richemont SA Class A (Textiles, Apparel & Luxury Goods) | | | 8,787,992 | |

| | | | | 46,934 | | | Julius Baer Group Ltd.

(Capital Markets) | | | 2,781,388 | |

| | | | | 401 | | | Lonza Group AG (Life Sciences Tools & Services) | | | 140,432 | |

| | | | | 175,817 | | | Nestle SA (Food Products) | | | 18,959,881 | |

| | | | | 120,082 | | | Novartis AG (Pharmaceuticals) | | | 11,242,024 | |

| | | | | 1,397 | | | Partners Group Holding AG

(Capital Markets) | | | 1,479,232 | |

| | | | | 70,063 | | | Roche Holding AG (Pharmaceuticals) | | | 18,055,905 | |

| | | | | 30,100 | | | Sika AG (Chemicals) | | | 7,203,212 | |

| | | | | 16,452 | | | Sonova Holding AG (Health Care Equipment & Supplies) | | | 3,899,342 | |

| | | | | 364,059 | | | UBS Group AG (Capital Markets) | | | 8,554,086 | |

| | | | | 20,151 | | | Zurich Insurance Group AG (Insurance) | | | 9,571,575 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 93,524,188 | |

| | | | | | |

| | | | | Taiwan – 0.6% | |

| | | | | 235,000 | | | Taiwan Semiconductor Manufacturing Co. Ltd. (Semiconductors & Semiconductor Equipment) | | | 3,838,139 | |

| | | | | 44,612 | | | Taiwan Semiconductor Manufacturing Co. Ltd. ADR (Semiconductors & Semiconductor Equipment) | | | 3,850,462 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 7,688,601 | |

| | | | | | |

| | | | | United Kingdom – 17.5% | |

| | | | | 361,387 | | | Allfunds Group PLC (Capital Markets) | | | 1,849,624 | |

| | | | | 113,082 | | | AstraZeneca PLC (Pharmaceuticals) | | | 14,158,274 | |

| | | | | 5,167,525 | | | Barclays PLC (Banks) | | | 8,294,114 | |

| | | | | 45,350 | | | Berkeley Group Holdings PLC (Household Durables) | | | 2,229,251 | |

| | | | | 1,594,663 | | | BP PLC (Oil, Gas & Consumable Fuels) | | | 9,737,033 | |

| | | | | 177,924 | | | British American Tobacco PLC (Tobacco) | | | 5,315,018 | |

| | | | | | |

14 The accompanying notes are an integral part of these financial statements.

MULTI-MANAGER INTERNATIONAL EQUITY FUND

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks (continued) | |

| | | | | United Kingdom (continued) | |

| | | | | 141,711 | | | Coca-Cola Europacific Partners PLC (Beverages) | | $ | 8,266,723 | |

| | | | | 917,348 | | | Compass Group PLC (Hotels, Restaurants & Leisure) | | | 23,127,588 | |

| | | | | 320,705 | | | Diageo PLC (Beverages) | | | 12,127,772 | |

| | | | | 47,433 | | | Ferguson PLC (Trading Companies & Distributors) | | | 7,124,614 | |

| | | | | 375,571 | | | GSK PLC (Pharmaceuticals) | | | 6,695,214 | |

| | | | | 785,062 | | | HSBC Holdings PLC (Banks) | | | 5,668,474 | |

| | | | | 409,325 | | | Informa PLC (Media) | | | 3,546,585 | |

| | | | | 555,474 | | | Kingfisher PLC (Specialty Retail) | | | 1,418,412 | |

| | | | | 1,025,667 | | | Legal & General Group PLC (Insurance) | | | 2,642,633 | |

| | | | | 47,755 | | | London Stock Exchange Group PLC (Capital Markets) | | | 4,818,242 | |

| | | | | 976,998 | | | NatWest Group PLC (Banks) | | | 2,125,768 | |

| | | | | 1,094,045 | | | Prudential PLC (Insurance) | | | 11,439,751 | |

| | | | | 150,101 | | | Reckitt Benckiser Group PLC (Household Products) | | | 10,042,796 | |

| | | | | 657,740 | | | RELX PLC (Professional Services) | | | 22,969,094 | |

| | | | | 108,342 | | | Rio Tinto PLC (Metals & Mining) | | | 6,912,269 | |

| | | | | 7,891,928 | | | Rolls-Royce Holdings PLC* (Aerospace & Defense) | | | 20,773,316 | |

| | | | | 168,057 | | | Segro PLC (Industrial REITs) | | | 1,460,775 | |

| | | | | 259,752 | | | Shell PLC (Oil, Gas & Consumable Fuels) | | | 8,485,483 | |

| | | | | 943,625 | | | Tesco PLC (Consumer Staples Distribution & Retail) | | | 3,096,560 | |

| | | | | 74,387 | | | Unilever PLC (Personal Products) | | | 3,523,014 | |

| | | | | 245,599 | | | WH Smith PLC (Specialty Retail) | | | 3,462,752 | |

| | | | | 333,567 | | | WPP PLC (Media) | | | 2,872,418 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 214,183,567 | |

| | | | | | |

| | | | | United States – 2.4% | |

| | | | | 53,027 | | | Atlassian Corp. Class A* (Software) | | | 9,578,797 | |

| | | | | 16,313 | | | EPAM Systems, Inc.* (IT Services) | | | 3,549,219 | |

| | | | | 3,943 | | | Mettler-Toledo International, Inc.* (Life Sciences Tools & Services) | | | 3,884,644 | |

| | | | | 33,224 | | | STERIS PLC (Health Care Equipment & Supplies) | | | 6,976,376 | |

| | | | | 44,799 | | | Waste Connections, Inc. (Commercial Services & Supplies) | | | 5,801,470 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 29,790,506 | |

| | | | | | |

| | | | | Uruguay* – 0.6% | |

| | | | | 6,320 | | | MercadoLibre, Inc. (Broadline Retail) | | | 7,841,477 | |

| | | | | | |

| | | |

| TOTA L C OMMON S TOCKS

(Cost $1,022,822,030) | | $ | 1,169,529,137 | |

| | | | | | |

| | | | | | | | | | | | |

| | | | Shares | | | Dividend

Rate | | Value | |

| |

| | | | | Investment Company(b) – 3.3% | |

| | | |

| Goldman Sachs Financial Square Government Fund —

Institutional Shares |

|

| | | | | 40,942,755 | | | 5.258% | | $ | 40,942,755 | |

| | | | | (Cost $ 40,942,755) | |

| | | | | | |

| | | |

| TOTAL INVESTMENTS – 99.1%

(Cost $ 1,063,764,785) | | $ | 1,210,471,892 | |

| | | | | | |

| | | |

| OTHER ASSETS IN EXCESS OF

LIABILITIES – 0.9% | | | 10,579,442 | |

| | | | | | |

| | | | | NET ASSETS – 100.0% | | $ | 1,221,051,334 | |

| | | | | | |

The percentage shown for each investment category reflects the value of investments in that category as a percentage of net assets.

| | * | Non-income producing security. |

| | (a) | Exempt from registration under Rule 144A of the Securities Act of 1933. |

| | (b) | Represents an Affiliated Issuer. |

| | | | |

|

| SECTOR ALLOCATION AS OF OCTOBER 31, 2023 | |

| |

| Sector | | % of Total

Market Value | |

Industrials | | | 18.6% | |

Financials | | | 17.2 | |

Health Care | | | 15.1 | |

Information Technology | | | 12.0 | |

Consumer Staples | | | 10.8 | |

Consumer Discretionary | | | 10.2 | |

Materials | | | 4.8 | |

Investment Company | | | 3.4 | |

Energy | | | 2.9 | |

Utilities | | | 2.5 | |

Communication Services | | | 2.3 | |

Real Estate | | | 0.2 | |

| |

| | | 100.0% | |

| |

| | |

Investment Abbreviations: |

ADR | | —American Depositary Receipt |

GDR | | —Global Depository Receipt |

PLC | | —Public Limited Company |

|

The accompanying notes are an integral part of these financial statements. 15

|

| MULTI-MANAGER U.S. SMALL CAP EQUITY FUND |

Schedule of Investments

October 31, 2023

| | | | | | | | |

| | |

Shares | | Description | | Value | |

| |

| | Common Stocks – 94.0% | |

| |

| | Aerospace & Defense – 2.5% | |

| | 33,040 | | Curtiss-Wright Corp. | | $ | 6,568,683 | |

| | 67,360 | | Hexcel Corp. | | | 4,170,931 | |

| | 106,431 | | Leonardo DRS, Inc.* | | | 2,029,639 | |

| | 39,300 | | Mercury Systems, Inc.* | | | 1,414,014 | |

| | 32,492 | | Woodward, Inc. | | | 4,051,752 | |

| | | | | | | | |

| | | | | | | 18,235,019 | |

| | | |

| |

| | Air Freight & Logistics* – 0.5% | |

| | 50,280 | | Hub Group, Inc. Class A | | | 3,456,750 | |

| | | |

| |

| | Automobile Components – 1.1% | |

| | 31,894 | | LCI Industries | | | 3,460,180 | |

| | 32,540 | | Visteon Corp.* | | | 3,746,330 | |

| | 13,728 | | XPEL, Inc.* | | | 635,607 | |

| | | | | | | | |

| | | | | | | 7,842,117 | |

| | | |

| |

| | Automobiles – 0.1% | |

| | 8,456 | | Thor Industries, Inc. | | | 743,536 | |

| | | |

| |

| | Banks – 5.0% | |

| | 20,016 | | Ameris Bancorp | | | 746,597 | |

| | 25,700 | | Bank of Hawaii Corp. | | | 1,269,323 | |

| | 29,582 | | Berkshire Hills Bancorp, Inc. | | | 580,103 | |

| | 28,621 | | Dime Community Bancshares, Inc. | | | 526,340 | |

| | 41,860 | | First Merchants Corp. | | | 1,143,197 | |

| | 28,214 | | Hancock Whitney Corp. | | | 971,408 | |

| | 54,602 | | Heritage Commerce Corp. | | | 446,644 | |

| | 72,955 | | Hope Bancorp, Inc. | | | 639,086 | |

| | 34,800 | | Independent Bank Corp. | | | 1,698,240 | |

| | 33,300 | | Lakeland Financial Corp. | | | 1,640,025 | |

| | 88,962 | | OceanFirst Financial Corp. | | | 1,126,259 | |

| | 89,535 | | Old National Bancorp | | | 1,226,629 | |

| | 35,526 | | Peapack-Gladstone Financial Corp. | | | 830,243 | |

| | 19,405 | | Preferred Bank | | | 1,155,956 | |

| | 98,188 | | Prosperity Bancshares, Inc. | | | 5,355,173 | |

| | 67,750 | | Renasant Corp. | | | 1,652,422 | |

| | 26,164 | | S&T Bancorp, Inc. | | | 673,985 | |

| | 58,650 | | SouthState Corp. | | | 3,876,765 | |

| | 39,500 | | UMB Financial Corp. | | | 2,477,440 | |

| | 26,386 | | Univest Financial Corp. | | | 439,591 | |

| | 29,891 | | Western Alliance Bancorp | | | 1,228,520 | |

| | 82,845 | | Wintrust Financial Corp. | | | 6,187,693 | |

| | | | | | | | |

| | | | | | | 35,891,639 | |

| | | |

| |

| | Biotechnology* – 4.1% | |

| | 98,670 | | 89bio, Inc. | | | 730,158 | |

| | 166,709 | | Abcam PLC ADR | | | 3,820,970 | |

| | 85,052 | | Alkermes PLC | | | 2,057,408 | |

| | 68,953 | | Ascendis Pharma AS ADR | | | 6,158,192 | |

| | 23,101 | | Blueprint Medicines Corp. | | | 1,359,725 | |

| | 57,506 | | Catalyst Pharmaceuticals, Inc. | | | 713,649 | |

| | 82,360 | | Cerevel Therapeutics Holdings, Inc. | | | 1,947,814 | |

| | 23,820 | | CRISPR Therapeutics AG | | | 927,313 | |

| | 10,706 | | Karuna Therapeutics, Inc. | | | 1,783,727 | |

| | 23,818 | | MoonLake Immunotherapeutics | | | 1,234,011 | |

| | 40,753 | | Neurocrine Biosciences, Inc. | | | 4,521,138 | |

| | | |

| | | | | | | | |

| | |

Shares | | Description | | Value | |

| |

| | Common Stocks – (continued) | |

| |

| | Biotechnology* – (continued) | |

| | 135,130 | | Rocket Pharmaceuticals, Inc. | | $ | 2,445,853 | |

| | 44,834 | | Vaxcyte, Inc. | | | 2,156,515 | |

| | | | | | | | |

| | | | | | | 29,856,473 | |

| | | |

| |

| | Building Products – 2.4% | |

| | 32,999 | | AAON, Inc. | | | 1,797,786 | |

| | 23,650 | | Apogee Enterprises, Inc. | | | 1,015,058 | |

| | 153,871 | | AZEK Co., Inc.* | | | 4,031,420 | |

| | 24,100 | | Gibraltar Industries, Inc.* | | | 1,466,726 | |

| | 79,000 | | Hayward Holdings, Inc.* | | | 829,500 | |

| | 147,476 | | Janus International Group, Inc.* | | | 1,380,375 | |

| | 11,485 | | Masonite International Corp.* | | | 908,923 | |

| | 28,767 | | PGT Innovations, Inc.* | | | 861,284 | |

| | 20,000 | | UFP Industries, Inc. | | | 1,903,400 | |

| | 103,981 | | Zurn Elkay Water Solutions Corp. | | | 2,751,337 | |

| | | | | | | | |

| | | | | | | 16,945,809 | |

| | | |

| |

| | Capital Markets – 1.6% | |

| | 28,270 | | Avantax, Inc.* | | | 729,649 | |

| | 333,009 | | BGC Group, Inc. Class A | | | 1,954,763 | |

| | 36,650 | | Cohen & Steers, Inc. | | | 1,914,596 | |

| | 20,459 | | Evercore, Inc. Class A | | | 2,663,352 | |

| | 13,000 | | Houlihan Lokey, Inc. | | | 1,306,760 | |

| | 57,070 | | StepStone Group, Inc. Class A | | | 1,615,081 | |

| | 11,909 | | StoneX Group, Inc.* | | | 1,135,166 | |

| | | | | | | | |

| | | | | | | 11,319,367 | |

| | | |

| |

| | Chemicals – 3.4% | |

| | 47,275 | | AdvanSix, Inc. | | | 1,302,426 | |

| | 13,923 | | Ashland, Inc. | | | 1,066,919 | |

| | 71,500 | | Avient Corp. | | | 2,260,830 | |

| | 94,800 | | Axalta Coating Systems Ltd.* | | | 2,486,604 | |

| | 148,696 | | Ecovyst, Inc.* | | | 1,368,003 | |

| | 82,214 | | HB Fuller Co. | | | 5,438,456 | |

| | 50,004 | | Ingevity Corp.* | | | 2,014,161 | |

| | 24,600 | | Innospec, Inc. | | | 2,410,800 | |

| | 16,858 | | Methanex Corp. | | | 695,393 | |

| | 35,775 | | Minerals Technologies, Inc. | | | 1,933,997 | |

| | 26,700 | | Orion SA | | | 542,010 | |

| | 23,023 | | Quaker Chemical Corp. | | | 3,308,866 | |

| | | | | | | | |

| | | | | | | 24,828,465 | |

| | | |

| |

| | Commercial Services & Supplies – 3.9% | |

| | 31,401 | | ABM Industries, Inc. | | | 1,235,315 | |

| | 51,608 | | Brink’s Co. | | | 3,450,511 | |

| | 86,786 | | Casella Waste Systems, Inc. Class A* | | | 6,548,004 | |

| | 127,867 | | CoreCivic, Inc.* | | | 1,623,911 | |

| | 25,764 | | MSA Safety, Inc. | | | 4,067,620 | |

| | 113,538 | | Rentokil Initial PLC ADR | | | 2,905,437 | |

| | 9,250 | | UniFirst Corp. | | | 1,520,978 | |

| | 70,283 | | Viad Corp.* | | | 1,702,957 | |

| | 41,380 | | Waste Connections, Inc. | | | 5,358,710 | |

| | | | | | | | |

| | | | | | | 28,413,443 | |

| | | |

16 The accompanying notes are an integral part of these financial statements.

MULTI-MANAGER U.S. SMALL CAP EQUITY FUND

| | | | | | | | |

| | | Shares | | Description | | Value | |

| |

| | Common Stocks – (continued) | |

| |

| | Communications Equipment* – 1.3% | |

| | 50,610 | | Calix, Inc. | | $ | 1,676,203 | |

| | 48,500 | | Ciena Corp. | | | 2,046,700 | |

| | 25,757 | | Clearfield, Inc. | | | 618,683 | |

| | 76,574 | | Extreme Networks, Inc. | | | 1,578,956 | |

| | 12,910 | | F5, Inc. | | | 1,957,027 | |

| | 477,772 | | Infinera Corp. | | | 1,399,872 | |

| | | | | | | | |

| | | | | | | 9,277,441 | |

| | | |

| |

| | Construction & Engineering – 1.2% | |

| | 1,280 | | Comfort Systems USA, Inc. | | | 232,768 | |

| | 3,300 | | EMCOR Group, Inc. | | | 681,945 | |

| | 28,731 | | Granite Construction, Inc. | | | 1,163,031 | |

| | 4,700 | | MYR Group, Inc.* | | | 544,401 | |

| | 33,254 | | Primoris Services Corp. | | | 999,615 | |

| | 14,839 | | Valmont Industries, Inc. | | | 2,921,948 | |

| | 61,520 | | WillScot Mobile Mini Holdings Corp.* | | | 2,424,503 | |

| | | | | | | | |

| | | | | | | 8,968,211 | |

| | | |

| |

| | Construction Materials – 0.4% | |

| | 8,500 | | Eagle Materials, Inc. | | | 1,308,235 | |

| | 54,000 | | Summit Materials, Inc. Class A* | | | 1,776,600 | |

| | | | | | | | |

| | | | | | | 3,084,835 | |

| | | |

| |

| | Consumer Finance – 1.0% | |

| | 22,161 | | FirstCash Holdings, Inc. | | | 2,413,776 | |

| | 11,172 | | Nelnet, Inc. Class A | | | 947,497 | |

| | 292,717 | | SLM Corp. | | | 3,805,321 | |

| | | | | | | | |

| | | | | | | 7,166,594 | |

| | | |

| |

| | Consumer Staples Distribution & Retail – 1.1% | |

| | 22,803 | | Casey’s General Stores, Inc. | | | 6,200,364 | |

| | 33,900 | | Performance Food Group Co.* | | | 1,958,064 | |

| | | | | | | | |

| | | | | | | 8,158,428 | |

| | | |

| |

| | Containers & Packaging – 0.8% | |

| | 46,000 | | Silgan Holdings, Inc. | | | 1,842,760 | |

| | 46,000 | | Sonoco Products Co. | | | 2,383,260 | |

| | 53,475 | | TriMas Corp. | | | 1,294,630 | |

| | | | | | | | |

| | | | | | | 5,520,650 | |

| | | |

| |

| | Diversified Consumer Services – 2.1% | |

| | 86,596 | | Bright Horizons Family Solutions, Inc.* | | | 6,413,300 | |

| | 36,981 | | Frontdoor, Inc.* | | | 1,069,860 | |

| | 224,437 | | Laureate Education, Inc. | | | 3,173,539 | |

| | 430,651 | | Mister Car Wash, Inc.* | | | 2,239,385 | |

| | 38,905 | | Stride, Inc.* | | | 2,138,997 | |

| | | | | | | | |

| | | | | | | 15,035,081 | |

| | | |

| |

| | Diversified Telecommunication Services – 0.4% | |

| | 42,405 | | Cogent Communications Holdings, Inc. | | | 2,755,477 | |

| | | |

| |

| | Electric Utilities – 0.5% | |

| | 21,500 | | IDACORP, Inc. | | | 2,036,265 | |

| | | |

| | | | | | | | |

| | | Shares | | Description | | Value | |

| |

| | Common Stocks – (continued) | |

| |

| | Electric Utilities – (continued) | |

| | 18,000 | | MGE Energy, Inc. | | $ | 1,289,340 | |

| | 10,857 | | Portland General Electric Co. | | | 434,497 | |

| | | | | | | | |

| | | | | | | 3,760,102 | |

| | | |

| |

| | Electrical Equipment – 1.0% | |

| | 9,509 | | Acuity Brands, Inc. | | | 1,540,173 | |

| | 12,415 | | Atkore, Inc.* | | | 1,542,936 | |

| | 14,219 | | EnerSys | | | 1,216,862 | |

| | 31,225 | | NEXTracker, Inc. Class A* | | | 1,085,381 | |

| | 67,030 | | Sensata Technologies Holding PLC | | | 2,136,916 | |

| | | | | | | | |

| | | | | | | 7,522,268 | |

| | | |

| |

| | Electronic Equipment, Instruments & Components – 3.5% | |

| | 19,400 | | Advanced Energy Industries, Inc. | | | 1,692,844 | |

| | 50,538 | | Avnet, Inc. | | | 2,341,426 | |

| | 30,986 | | Belden, Inc. | | | 2,196,907 | |

| | 23,600 | | Crane NXT Co. | | | 1,227,200 | |

| | 20,890 | | Fabrinet* | | | 3,237,950 | |

| | 38,618 | | Insight Enterprises, Inc.* | | | 5,533,960 | |

| | 18,866 | | Littelfuse, Inc. | | | 4,087,696 | |

| | 12,740 | | OSI Systems, Inc.* | | | 1,328,400 | |

| | 8,100 | | Plexus Corp.* | | | 796,392 | |

| | 14,725 | | Rogers Corp.* | | | 1,809,555 | |

| | 44,000 | | ScanSource, Inc.* | | | 1,337,600 | |

| | | | | | | | |

| | | | | | | 25,589,930 | |

| | | |

| |

| | Energy Equipment & Services – 3.7% | |

| | 72,927 | | Cactus, Inc. Class A | | | 3,423,193 | |

| | 298,203 | | ChampionX Corp. | | | 9,184,652 | |

| | 61,857 | | Expro Group Holdings NV* | | | 974,248 | |

| | 53,000 | | Helmerich & Payne, Inc. | | | 2,097,210 | |

| | 95,411 | | National Energy Services Reunited Corp.* | | | 539,072 | |

| | 27,050 | | Noble Corp. PLC | | | 1,262,965 | |

| | 293,149 | | Patterson-UTI Energy, Inc. | | | 3,722,992 | |

| | 90,366 | | ProPetro Holding Corp.* | | | 947,036 | |

| | 99,432 | | Select Water Solutions, Inc. | | | 739,774 | |

| | 11,443 | | Tidewater, Inc.* | | | 782,129 | |

| | 52,125 | | U.S. Silica Holdings, Inc.* | | | 629,149 | |

| | 22,266 | | Weatherford International PLC* | | | 2,072,742 | |

| | | | | | | | |

| | | | | | | 26,375,162 | |

| | | |

| |

| | Entertainment* – 0.3% | |

| | 9,721 | | Take-Two Interactive Software, Inc. | | | 1,300,184 | |

| | 84,606 | | Vivid Seats, Inc. Class A | | | 497,483 | |

| | | | | | | | |

| | | | | | | 1,797,667 | |

| | | |

| |

| | Financial Services – 3.0% | |

| | 42,986 | | Essent Group Ltd. | | | 2,030,659 | |

| | 21,253 | | Federal Agricultural Mortgage Corp. Class C | | | 3,157,346 | |

| | 114,660 | | Flywire Corp.* | | | 3,083,207 | |

| | 170,220 | | Marqeta, Inc. Class A* | | | 880,037 | |

| | 67,516 | | NCR Atleos Corp.* | | | 1,489,403 | |

| | 49,810 | | Shift4 Payments, Inc. Class A* | | | 2,217,541 | |

| | | |

The accompanying notes are an integral part of these financial statements. 17

|

| MULTI-MANAGER U.S. SMALL CAP EQUITY FUND |

Schedule of Investments (continued)

October 31, 2023

| | | | | | | | |

| | |

Shares | | Description | | Value | |

| |

| | Common Stocks – (continued) | |

| |

| | Financial Services – (continued) | |

| | 22,156 | | Voya Financial, Inc. | | $ | 1,479,356 | |

| | 24,796 | | Walker & Dunlop, Inc. | | | 1,606,781 | |

| | 35,888 | | WEX, Inc.* | | | 5,974,634 | |

| | | | | | | | |

| | | | | | | 21,918,964 | |

| | | |

| |

| | Food Products – 1.2% | |

| | 56,355 | | Fresh Del Monte Produce, Inc. | | | 1,408,875 | |

| | 44,094 | | Hostess Brands, Inc. * | | | 1,472,739 | |

| | 16,900 | | Ingredion, Inc. | | | 1,581,502 | |

| | 7,200 | | Lancaster Colony Corp. | | | 1,218,024 | |

| | 73,589 | | Simply Good Foods Co.* | | | 2,744,134 | |

| | | | | | | | |

| | | | | | | 8,425,274 | |

| | | |

| |

| | Gas Utilities – 0.1% | |

| | 17,700 | | ONE Gas, Inc. | | | 1,069,080 | |

| | | |

| |

| | Ground Transportation – 1.1% | |

| | 18,613 | | Knight-Swift Transportation Holdings, Inc. | | | 909,989 | |

| | 93,300 | | Marten Transport Ltd. | | | 1,640,214 | |

| | 8,710 | | Saia, Inc.* | | | 3,122,448 | |

| | 67,000 | | Werner Enterprises, Inc. | | | 2,433,440 | |

| | | | | | | | |

| | | | | | | 8,106,091 | |

| | | |

| |

| | Health Care Equipment & Supplies* – 3.6% | |

| | 60,458 | | Establishment Labs Holdings, Inc. | | | 1,770,210 | |

| | 73,066 | | Haemonetics Corp. | | | 6,227,415 | |

| | 7,400 | | ICU Medical, Inc. | | | 725,644 | |

| | 45,381 | | Inari Medical, Inc. | | | 2,755,081 | |

| | 30,652 | | Inmode Ltd. | | | 585,453 | |

| | 15,170 | | Inspire Medical Systems, Inc. | | | 2,232,417 | |

| | 30,900 | | Integer Holdings Corp. | | | 2,508,153 | |

| | 20,250 | | Integra LifeSciences Holdings Corp. | | | 728,190 | |

| | 57,706 | | Lantheus Holdings, Inc. | | | 3,727,808 | |

| | 57,742 | | OrthoPediatrics Corp. | | | 1,412,369 | |

| | 5,353 | | QuidelOrtho Corp. | | | 326,961 | |

| | 155,950 | | SI-BONE, Inc. | | | 2,652,710 | |

| | | | | | | | |

| | | | | | | 25,652,411 | |

| | | |

| |

| | Health Care Providers & Services – 3.8% | |

| | 207,450 | | Accolade, Inc.* | | | 1,348,425 | |

| | 139,050 | | agilon health, Inc.* | | | 2,502,900 | |

| | 175,967 | | Alignment Healthcare, Inc.* | | | 1,210,653 | |

| | 9,418 | | Amedisys, Inc.* | | | 861,653 | |

| | 12,851 | | AMN Healthcare Services, Inc.* | | | 974,877 | |

| | 3,550 | | Chemed Corp. | | | 1,997,407 | |

| | 66,215 | | Encompass Health Corp. | | | 4,142,410 | |

| | 60,166 | | HealthEquity, Inc.* | | | 4,312,699 | |

| | 158,587 | | LifeStance Health Group, Inc.* | | | 924,562 | |

| | 338,389 | | NeoGenomics, Inc.* | | | 4,744,214 | |

| | 113,590 | | Option Care Health, Inc.* | | | 3,149,851 | |

| | 64,385 | | PetIQ, Inc. * | | | 1,208,506 | |

| | | | | | | | |

| | | | | | | 27,378,157 | |

| | | |

| |

| | Health Care Technology* – 0.6% | |

| | 140,703 | | Definitive Healthcare Corp. | | | 810,449 | |

| | | |

| | | | | | | | |

| | |

Shares | | Description | | Value | |

| |

| | Common Stocks – (continued) | |

| |

| | Health Care Technology* – (continued) | |

| | 121,434 | | Phreesia, Inc. | | $ | 1,658,789 | |

| | 166,800 | | Veradigm, Inc. | | | 2,200,092 | |

| | | | | | | | |

| | | | | | | 4,669,330 | |

| | | |

| |

| | Hotel & Resort REITs – 0.3% | |

| | 115,000 | | Apple Hospitality REIT, Inc. | | | 1,803,200 | |

| | | |

| |

| | Hotels, Restaurants & Leisure – 2.3% | |

| | 31,510 | | Bloomin’ Brands, Inc. | | | 735,443 | |

| | 123,584 | | Bowlero Corp. Class A* | | | 1,246,963 | |

| | 9,582 | | Choice Hotels International, Inc. | | | 1,058,811 | |

| | 40,711 | | Churchill Downs, Inc. | | | 4,471,696 | |

| | 23,912 | | Dave & Buster’s Entertainment, Inc.* | | | 835,485 | |

| | 41,532 | | First Watch Restaurant Group, Inc.* | | | 694,000 | |

| | 45,608 | | International Game Technology PLC | | | 1,159,355 | |

| | 37,530 | | Texas Roadhouse, Inc. | | | 3,810,796 | |

| | 14,050 | | Wingstop, Inc. | | | 2,567,919 | |

| | | | | | | | |

| | | | | | | 16,580,468 | |

| | | |

| |

| | Household Durables – 1.3% | |

| | 5,300 | | Helen of Troy Ltd.* | | | 521,096 | |

| | 28,246 | | M/I Homes, Inc.* | | | 2,318,149 | |

| | 25,700 | | Meritage Homes Corp. | | | 2,930,314 | |

| | 23,765 | | Tempur Sealy International, Inc. | | | 948,937 | |

| | 9,047 | | TopBuild Corp.* | | | 2,069,592 | |

| | 144,192 | | Vizio Holding Corp. Class A* | | | 733,937 | |

| | | | | | | | |

| | | | | | | 9,522,025 | |

| | | |

| |

| | Household Products* – 0.4% | |

| | 66,100 | | Central Garden & Pet Co. Class A | | | 2,623,509 | |

| | | |

| |

| | Industrial REITs – 0.9% | |

| | 24,830 | | EastGroup Properties, Inc. | | | 4,053,498 | |

| | 28,400 | | First Industrial Realty Trust, Inc. | | | 1,201,320 | |

| | 47,670 | | STAG Industrial, Inc. | | | 1,583,597 | |

| | | | | | | | |

| | | | | | | 6,838,415 | |

| | | |

| |

| | Insurance – 3.9% | |

| | 30,700 | | AMERISAFE, Inc. | | | 1,564,779 | |

| | 33,218 | | Assured Guaranty Ltd. | | | 2,072,803 | |

| | 52,421 | | Axis Capital Holdings Ltd. | | | 2,993,239 | |

| | 20,108 | | Employers Holdings, Inc. | | | 764,104 | |

| | 38,500 | | First American Financial Corp. | | | 1,980,440 | |

| | 19,600 | | Hanover Insurance Group, Inc. | | | 2,297,316 | |

| | 7,540 | | Kinsale Capital Group, Inc. | | | 2,517,682 | |

| | 31,766 | | Palomar Holdings, Inc.* | | | 1,590,841 | |

| | 14,200 | | Primerica, Inc. | | | 2,714,472 | |

| | 38,100 | | Ryan Specialty Holdings, Inc. * | | | 1,645,920 | |

| | 25,300 | | Safety Insurance Group, Inc. | | | 1,901,801 | |

| | 21,600 | | Selective Insurance Group, Inc. | | | 2,248,776 | |

| | 15,000 | | Stewart Information Services Corp. | | | 655,050 | |

| | 2,381 | | White Mountains Insurance Group Ltd. | | | 3,406,616 | |

| | | | | | | | |

| | | | | | | 28,353,839 | |

| | | |

18 The accompanying notes are an integral part of these financial statements.

MULTI-MANAGER U.S. SMALL CAP EQUITY FUND

| | | | | | | | | | | | |

| | | |

Shares | | | Description | | Value | |

| |

| | | | | Common Stocks – (continued) | |

| |

| | | | | Interactive Media & Services* – 0.9% | |

| | | | | 300,830 | | | Angi, Inc. | | $ | 484,336 | |

| | | | | 46,690 | | | Bumble, Inc. Class A | | | 627,514 | |

| | | | | 28,585 | | | Cars.com, Inc. | | | 435,350 | |

| | | | | 154,223 | | | Pinterest, Inc. Class A | | | 4,608,183 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 6,155,383 | |

| | | | | | |

| |

| | | | | IT Services – 0.3% | |

| | | | | 30,634 | | | Hackett Group, Inc. | | | 682,832 | |

| | | | | 24,000 | | | Perficient, Inc.* | | | 1,396,560 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 2,079,392 | |

| | | | | | |

| |

| | | | | Leisure Products – 1.0% | |

| | | | | 30,540 | | | BRP, Inc. | | | 2,065,115 | |

| | | | | 16,900 | | | Brunswick Corp. | | | 1,174,043 | |

| | | | | 193,467 | | | Clarus Corp. | | | 1,120,174 | |

| | | | | 112,875 | | | Mattel, Inc.* | | | 2,153,655 | |

| | | | | 82,389 | | | Topgolf Callaway Brands Corp.* | | | 1,006,793 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 7,519,780 | |

| | | | | | |

| |

| | | | | Life Sciences Tools & Services – 1.1% | |

| | | | | 6,480 | | | Bio-Rad Laboratories, Inc. Class A* | | | 1,783,815 | |