Washington, D.C. 20549

Robert O. Judge

ITEM 1. REPORTS TO STOCKHOLDERS.

|

ANNUAL REPORTFOR THE YEAR ENDED

JUNE 30, 2017 |

| Schedule of Investments | 1 |

| Statement of Assets and Liabilities | 5 |

| Statement of Operations | 6 |

| Statements of Changes in Net Assets | 7 |

| Statement of Cash Flows | 8 |

| Financial Highlights | 9 |

| Notes to Financial Statements | 10 |

| Report of Independent Registered Public Accounting Firm | 18 |

| Other Information (Unaudited) | 19 |

| Trustees and Officers (Unaudited) | 21 |

|

SCHEDULE OF INVESTMENTS

JUNE 30, 2017

|

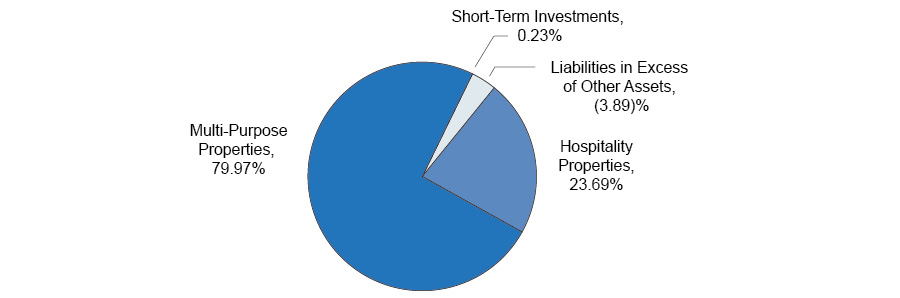

INVESTMENT TYPE AS A PERCENTAGE OF NET ASSETS AS FOLLOWS:

Description, State, Acquisition Date | Stated

Interest Rate | Effective Interest Rate | Maturity | | Cost | | | Principal | | | Fair Value | |

| 504 First Lien Loans — 103.66% | | | | | | | | | | | |

| Hospitality Properties — 23.69% | | | | | | | | | | | |

D S Hospitality, LLC, California, 3/10/2014(a) (b) | 1 Year Libor + 5.160% (5.430% Floor) | 6.570% | 3/15/2044 | | $ | 1,637,281 | | | $ | 1,606,414 | | | $ | 1,649,257 | |

McDonough Hospitality Plaza, LLC, Georgia, 12/14/2016(b) | 6.500%

(6.500% Fixed) | 5.250%* | 9/5/2024 | | | 4,502,847 | | | | 4,500,000 | | | | 4,498,245 | |

Moses Lake Investors, LLC, Washington, 9/18/2014(b) (c) | Prime + 2.250% (5.500% Floor) | 6.250% | 10/1/2039 | | | 982,016 | | | | 945,857 | | | | 983,218 | |

Vaibhav Laxmi, Inc., Illinois, 8/14/2015(b) | 5 Year Libor + 4.750% (6.500% Floor) | 6.000%* | 9/1/2026 | | | 1,635,423 | | | | 1,635,318 | | | | 1,615,662 | |

YC Anchorage Hotel Group, L.P., Alaska,

5/8/2014(a) (b) | 3 Year Libor + 5.180% (6.180% Floor) | 6.064%* | 5/15/2044 | | | 2,796,128 | | | | 2,797,580 | | | | 2,769,156 | |

| Total Hospitality Properties | | | | | | | | | | | | | | 11,515,538 | |

| | | | | | | | | | | | | | | | |

| Multi-Purpose Properties — 79.97% | | | | | | | | | | | | | | |

1250 Philadelphia, LLC, California, 10/3/2014(a) (b) | 5 Year Libor + 4.000% (5.930% Floor) | 5.930% | 10/15/2039 | | | 2,514,254 | | | | 2,422,958 | | | | 2,487,918 | |

413 East 53rd Street, LLC, New York, 2/4/2014(b) | 3 Year Libor + 4.170% (4.950% Floor) | 6.187% | 2/1/2044 | | | 1,667,304 | | | | 1,640,436 | | | | 1,690,535 | |

7410-7428 Bellaire, LLC, California, 8/22/2014(a) (b) | 5 Year Libor + 4.000% (5.780% Floor) | 5.780% | 9/15/2039 | | | 2,407,830 | | | | 2,320,922 | | | | 2,374,906 | |

77 West Mount Pleasant Avenue, LLC, New Jersey, 4/30/2015(b) | 3 Year Libor + 4.000% (5.125% Floor) | 5.125% | 5/1/2040 | | | 333,684 | | | | 319,100 | | | | 319,610 | |

AKT Elevon Partners, LLC, California, 9/17/2015(b) | 5 Year Libor + 3.880% (5.700% Floor) | 4.970%* | 10/1/2045 | | | 4,202,435 | | | | 4,204,924 | | | | 4,121,793 | |

See accompanying notes to financial statements.

1

|

SCHEDULE OF INVESTMENTS (continued)

JUNE 30, 2017

|

Description, State,

Acquisition Date — (continued) | Stated

Interest Rate | Effective Interest Rate | Maturity | | Cost | | | Principal | | | Fair Value | |

| Multi-Purpose Properties — (continued) | | | | | | | | | | | |

Anthony Ghostine, Kristina J. Ghostine, California, 12/1/2014(b) | 3 Year Libor + 5.150% (6.300% Floor) | 5.150%* | 12/1/2044 | | $ | 393,241 | | | $ | 393,241 | | | $ | 387,818 | |

BT Vineland, LLC, California, 1/5/2015(a) (b) | 3 Year Libor + 5.400% (6.740% Floor) | 5.340%* | 1/1/2045 | | | 925,425 | | | | 925,920 | | | | 916,781 | |

CBERT Rifle, LLC, Utah, 7/23/2015(b) | 5 Year Libor + 4.250% (5.147% Floor) | 5.147% | 9/1/2037 | | | 1,375,413 | | | | 1,335,099 | | | | 1,359,838 | |

CBERT Williston, LLC, Colorado, 9/18/2015(b) | 5 Year Libor + 4.250% (5.132% Floor) | 5.132% | 1/1/2038 | | | 1,262,375 | | | | 1,223,661 | | | | 1,231,175 | |

CV Investment Properties, LLC, Arizona,

5/29/2014(a) (b) | 5 Year Libor + 4.750% (6.000% Floor) | 6.270% | 10/30/2038 | | | 640,251 | | | | 608,904 | | | | 623,743 | |

Greenland Group US, LLC, New Jersey, 6/25/2014(b) | 6.375% (6.375% Floor) | 6.375% | 2/1/2037 | | | 251,180 | | | | 238,877 | | | | 247,702 | |

Grigorian Investments, LLC, California, 9/2/2014(b) | 5 Year Libor +4.500% (6.330% Floor) | 6.330% | 9/15/2039 | | | 534,299 | | | | 518,950 | | | | 527,575 | |

Marcus D. Chu, Tracey Chu, California, 3/13/2015(b) | 5 Year Libor + 4.750% (6.586% Floor) | 6.586% | 3/10/2040 | | | 1,788,418 | | | | 1,704,431 | | | | 1,752,360 | |

Mariano D. Cibran, Florida, 5/23/2016(b) | 3 Year Libor + 5.160% (6.160% Floor) | 6.240% | 6/1/2046 | | | 1,301,878 | | | | 1,259,531 | | | | 1,269,847 | |

None of Your Business, LLC, Illinois, 9/11/2014(b) | 3 Year Libor + 5.000% (6.250% Floor) | 6.250% | 9/15/2044 | | | 499,881 | | | | 483,261 | | | | 486,209 | |

Palomar Oaks Corp., California, 1/30/2014(b) | 5 Year Libor + 4.500% (6.280% Floor) | 6.280% | 2/1/2039 | | | 1,305,988 | | | | 1,283,256 | | | | 1,286,644 | |

PATC, LLC, California, 8/19/2014(a) (b) | 3 Year Libor + 3.250% (4.360% Floor) | 4.360% | 9/15/2044 | | | 3,976,281 | | | | 3,939,472 | | | | 3,920,208 | |

PennRose Studios, LLC, California,

12/17/2014(a) (b) | 3 Year Libor + 5.400% (6.630% Floor) | 5.230%* | 1/1/2045 | | | 890,314 | | | | 891,669 | | | | 884,348 | |

Rayr Holdings, LLC, California, 7/31/2015(b) | 3 Year Libor + 5.775% (7.025% Floor) | 7.025% | 7/1/2045 | | | 953,117 | | | | 907,814 | | | | 913,751 | |

Ruby View Investments, LLC, Oregon, 5/15/2014(b) | 5 Year Libor + 4.000% (6.500% Floor) | 6.500% | 6/26/2037 | | | 2,078,260 | | | | 1,986,437 | | | | 2,035,343 | |

Rug Palace, Inc. dba Rug Palace Expo, California, 2/27/2014(b) | Prime + 2.250% (5.500% Floor) | 5.120%* | 2/15/2044 | | | 667,508 | | | | 667,508 | | | | 676,239 | |

SGLP Enterprises, LLC, Smokin' Guns BBQ & Catering, Inc., Missouri, 3/18/2016(b) | 1 Month Libor + 4.500% | 5.580% | 9/12/2023 | | | 710,603 | | | | 701,149 | | | | 710,818 | |

Shiv Shakti Investments, LLC, Georgia, 6/20/2017(b) | 6.500% (6.500% Fixed) | 5.250%* | 12/15/2024 | | | 1,753,672 | | | | 1,750,000 | | | | 1,742,212 | |

South Washington Street Realty, LLC, Indiana, 7/21/2016(b) | 3 Year Libor + 5.160% (5.910% Floor) | 6.035% | 7/1/2046 | | | 306,983 | | | | 296,422 | | | | 292,738 | |

See accompanying notes to financial statements.

2

|

SCHEDULE OF INVESTMENTS (continued)

JUNE 30, 2017

|

Description, State,

Acquisition Date — (continued) | Stated

Interest Rate | Effective Interest Rate | Maturity | | Cost | | | Principal | | | Fair Value | |

| Multi-Purpose Properties — (continued) | | | | | | | | | | | |

Stanley Avenue Realty, LLC, New York, 9/17/2014(a) (b) | 4 Year Libor + 3.720% (5.370% Floor) | 4.770%* | 9/15/2044 | | $ | 1,867,959 | | | $ | 1,867,890 | | | $ | 1,873,269 | |

Storage Fit, LLC, California, 2/12/2015(b) | 5 Year Libor + 5.750% (7.390% Floor) | 5.140%* | 3/1/2045 | | | 411,785 | | | | 412,122 | | | | 406,261 | |

Summers Holdings, LLC, Missouri, 3/18/2016(b) | 1 Month Libor + 2.850% | 3.930% | 4/15/2021 | | | 495,932 | | | | 488,947 | | | | 496,115 | |

Watson Kellogg Property, LLC, Washington, 2/9/2015(a) (b) | 5 Year Libor + 4.250% (5.700% Floor) | 5.920% | 6/1/2040 | | | 656,433 | | | | 628,467 | | | | 643,934 | |

Watson Osburn Property, LLC, Washington, 2/9/2015(a) (b) | 5 Year Libor + 4.250% (5.700% Floor) | 5.880% | 6/1/2040 | | | 525,547 | | | | 502,333 | | | | 514,681 | |

Watson RathDrum Property, LLC, Washington, 2/9/2015(a) (b) | 5 Year Libor + 4.250% (5.700% Floor) | 5.920% | 6/1/2040 | | | 1,373,665 | | | | 1,319,298 | | | | 1,351,766 | |

ZC Park, LLC, Arizona, 10/17/2014(b) | 5 Year Libor + 4.000% (5.880% Floor) | 5.880% | 10/15/2044 | | | 1,363,342 | | | | 1,301,371 | | | | 1,325,980 | |

Total Multi-Purpose Properties | | | | | | | | | | | | | | 38,872,117 | |

| | | | | | | | | | | | | | | | |

| Total 504 First Lien Loans (identified cost of $50,988,952) | | | | | | | | | | $ | 50,387,655 | |

| | | Shares | | | Fair Value | |

| Short-Term Investments — 0.23% | | | | | | |

Federated Government Obligations Fund - Institutional Class, 0.82%(d) | | | 113,766 | | | $ | 113,766 | |

| Total Short-Term Investments (Cost $113,766) | | | | | | | 113,766 | |

| | | | | | | | | |

| Total Investments — 103.89% (Cost $51,102,718) | | | | | | | 50,501,421 | |

| Liabilities in Excess of Other Assets — (3.89)% | | | | | | | (1,890,453 | ) |

| Total Net Assets —100.00% | | | | | | $ | 48,610,968 | |

(a) | All or portion of these 504 First Lien Loans may serve as collateral for any debt extended on the line of credit (see Note 8). |

(b) | 504 First Lien Loans are restricted as to resale. The cost and fair value as of June 30, 2017 was $50,988,952 and $50,387,655, respectively. |

(c) | Represents an investment in the 504 First Lien Loan through a participation agreement with a financial institution. A participation agreement typically results in a contractual relationship only with a financial institution, not with the borrower. |

(d) | The rate shown is the annualized 7-day yield as of June 30, 2017. |

| * | The effective rate is net of a sub-servicing fee collected on the 504 First Lien Loan by the selling agent. As a result, the effective rate may be less than the 504 First Lien Loan floor rate. |

See accompanying notes to financial statements.

3

|

SCHEDULE OF INVESTMENTS (continued)

JUNE 30, 2017

|

INVESTMENT TYPE AS A PERCENTAGE OF NET ASSETS BY STATE:

| Hospitality Properties | |

| Alaska | 5.70% |

| California | 3.39% |

| Georgia | 9.26% |

| Illinois | 3.32% |

| Washington | 2.02% |

| Total Hospitality Properties | 23.69% |

| | |

| Multi-Purpose Properties | |

| Arizona | 4.01% |

| California | 42.50% |

| Colorado | 2.53% |

| Florida | 2.61% |

| Georgia | 3.58% |

| Illinois | 1.00% |

| Indiana | 0.60% |

| Missouri | 2.48% |

| New Jersey | 1.17% |

| New York | 7.34% |

| Oregon | 4.19% |

| Utah | 2.80% |

| Washington | 5.16% |

| Total Multi-Purpose Properties | 79.97% |

| | |

| Short-Term Investments | 0.23% |

| Total Investments | 103.89% |

| | |

| Liabilities in Excess of Other Assets | (3.89)% |

| | |

| Total Net Assets | 100.00% |

See accompanying notes to financial statements.

4

|

Statement of Assets and Liabilities

JUNE 30, 2017

|

| Assets: | | | |

| Investments in 504 First Lien Loans, at fair value (cost $50,988,952) | | $ | 50,387,655 | |

| Short-term investments, at fair value (cost $113,766) | | | 113,766 | |

| Receivables: | | | | |

| Interest | | | 199,345 | |

| Principal paydowns | | | 663 | |

| Prepaid expenses | | | 14,129 | |

| Total assets | | | 50,715,558 | |

| | | | | |

| Liabilities: | | | | |

| Payables: | | | | |

| Line of Credit | | | 2,000,000 | |

| Audit | | | 59,450 | |

| Legal | | | 10,926 | |

| Advisory fees | | | 10,157 | |

| Accounting and administration | | | 7,938 | |

| Chief Compliance Officer | | | 5,250 | |

| Transfer agent | | | 3,732 | |

| Custodian | | | 1,316 | |

| Accrued other expenses | | | 5,821 | |

| Total liabilities | | | 2,104,590 | |

| | | | | |

| Net Assets | | $ | 48,610,968 | |

| | | | | |

| Net Assets Consist of: | | | | |

| Capital (unlimited shares authorized, no par value) | | $ | 49,314,427 | |

| Accumulated undistributed net investment income | | | 2,887 | |

| Accumulated net realized loss on investments | | | (105,049 | ) |

| Accumulated net unrealized depreciation on investments | | | (601,297 | ) |

| Net Assets | | $ | 48,610,968 | |

| | | | | |

| Shares | | | | |

| Net assets applicable to outstanding shares | | $ | 48,610,968 | |

| Number of outstanding shares | | | 4,965,783 | |

| Net asset and redemption price value per share | | $ | 9.79 | |

Maximum offering price per share (Net asset value per share divided by 0.99)1 | | $ | 9.89 | |

1 | The offering price per share reflects a maximum sales charge of 1.00%. |

See accompanying notes to financial statements.

5

|

Statement of Operations

FOR THE Year ENDED

JUNE 30, 2017

|

| Investment Income: | | | |

| Interest | | $ | 2,617,586 | |

| Total investment income | | | 2,617,586 | |

| | | | | |

| Expenses: | | | | |

| Management fees | | | 883,122 | |

| Legal expense | | | 220,318 | |

| Accounting and administration expenses | | | 86,542 | |

| Audit expense | | | 78,400 | |

| Trustees' expenses | | | 65,270 | |

| Chief Compliance Officer expense | | | 61,761 | |

| Insurance expense | | | 35,755 | |

| Registration expense | | | 26,251 | |

| Transfer agent expense | | | 22,778 | |

| Interest expense | | | 20,195 | |

| Custodian expense | | | 12,801 | |

| Printing expense | | | 7,026 | |

| Miscellaneous | | | 47,403 | |

| Total expenses | | | 1,567,622 | |

| Less: Expenses waived | | | (664,305 | ) |

| Net expenses | | | 903,317 | |

| Net investment income | | | 1,714,269 | |

| | | | | |

| Net change in Unrealized Depreciation on Investments: | | | | |

| Net change in unrealized depreciation on investments | | | (1,960,235 | ) |

| Total net change in unrealized depreciation on investments | | | (1,960,235 | ) |

| | | | | |

| Net Decrease in Net Assets from Operations | | $ | (245,966 | ) |

See accompanying notes to financial statements.

6

|

StatementS of Changes in Net Assets

|

| | | Year Ended

June 30, 2017 | | | Year Ended

June 30, 2016 | |

Increase (Decrease) in Net Assets From: | | | | | | |

| Operations: | | | | | | |

| Net investment income | | $ | 1,714,269 | | | $ | 1,657,709 | |

| Net realized gain on investments | | | — | | | | 6,057 | |

| Net change in unrealized appreciation (depreciation) on investments | | | (1,960,235 | ) | | | 1,335,233 | |

| Net increase (decrease) in net assets from operations | | | (245,966 | ) | | | 2,998,999 | |

| | | | | | | | | |

| Distributions to Shareholders: | | | | | | | | |

| From net investment income | | | (1,748,325 | ) | | | (1,831,666 | ) |

| Total distributions to shareholders | | | (1,748,325 | ) | | | (1,831,666 | ) |

| | | | | | | | | |

| Capital Transactions: | | | | | | | | |

| Net proceeds from shares sold | | | — | | | | 8,000,000 | |

| Reinvestment of distributions | | | 453,786 | | | | 438,105 | |

| Cost of shares redeemed | | | (2,530,018 | ) | | | (2,737,731 | ) |

| Net increase (decrease) from capital transactions | | | (2,076,232 | ) | | | 5,700,374 | |

| | | | | | | | | |

| Total increase (decrease) in net assets | | | (4,070,523 | ) | | | 6,867,707 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Beginning of year | | | 52,681,491 | | | | 45,813,784 | |

| End of year | | $ | 48,610,968 | | | $ | 52,681,491 | |

| | | | | | | | | |

| Accumulated undistributed net investment income | | $ | 2,887 | | | $ | 259 | |

| | | | | | | | | |

| Capital Share Transactions: | | | | | | | | |

| Shares sold | | | — | | | | 795,228 | |

| Shares reinvested | | | 46,199 | | | | 43,634 | |

| Shares redeemed | | | (260,022 | ) | | | (271,600 | ) |

| Net increase (decrease) | | | (213,823 | ) | | | 567,262 | |

See accompanying notes to financial statements.

7

|

STATEMENT OF CASH FLOWS

FOR THE Year ENDED

JUNE 30, 2017

|

| Cash Flows from Operating Activities: | | | |

| Net decrease in net assets resulting from operations | | $ | (245,966 | ) |

| Adjustments to reconcile net decrease in net assets from operations to net cash provided by operating activities: | | | | |

| Purchase of investment securities | | | (6,567,535 | ) |

| Principal paydowns | | | 1,970,967 | |

| Net realized paydown losses | | | 38,106 | |

| Net sale of short-term investments | | | 4,668,275 | |

| Decrease in other assets | | | 3,586 | |

| Increase in interest receivable | | | (19,349 | ) |

| Decrease in receivables for principal paydowns | | | 108 | |

| Decrease in accrued expenses | | | (6,118 | ) |

| Amortization of premium on investments | | | 22,248 | |

| Net change in unrealized depreciation on investments | | | 1,960,235 | |

| Net cash provided by operating activities | | | 1,824,557 | |

| | | | | |

| Cash Flows from Financing Activities: | | | | |

| Shareholder redemptions paid | | | (2,530,018 | ) |

| Line of Credit borrowings | | | 3,000,000 | |

| Line of Credit repayments | | | (1,000,000 | ) |

| Cash distributions paid* | | | (1,294,539 | ) |

| Net cash used in financing activities | | | (1,824,557 | ) |

| | | | | |

| Net Decrease in Cash | | | — | |

| | | | | |

| Cash at beginning of year | | | — | |

| Cash at end of year | | $ | — | |

| | | | | |

| Supplemental Disclosure of Interest Expense Paid | | $ | 20,195 | |

| * | Noncash financing activities not included herein consist of reinvestment of dividends of $453,786. |

See accompanying notes to financial statements.

8

Per share income and capital changes for a share outstanding throughout the period.

| | | Year Ended

June 30, 2017 | | | Year Ended

June 30, 2016 | | | Year Ended

June 30, 2015 | | | Period Ended

June 30, 2014* | |

| Net asset value, beginning of year | | $ | 10.17 | | | $ | 9.93 | | | $ | 9.91 | | | $ | 10.00 | |

| | | | | | | | | | | | | | | | | |

| Income from Investment Operations: | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | | 0.34 | | | | 0.31 | | | | 0.20 | | | | (0.06 | ) |

| Net realized and unrealized gain (loss) on investments | | | (0.37 | ) | | | 0.28 | | | | 0.02 | | | | (0.03 | ) |

| Total from investment operations | | | (0.03 | ) | | | 0.59 | | | | 0.22 | | | | (0.09 | ) |

| | | | | | | | | | | | | | | | | |

| Less Distributions: | | | | | | | | | | | | | | | | |

| From net investment income | | | (0.35 | ) | | | (0.35 | ) | | | (0.20 | ) | | | — | |

| Total distributions | | | (0.35 | ) | | | (0.35 | ) | | | (0.20 | ) | | | — | |

| | | | | | | | | | | | | | | | | |

| Net asset value, end of year | | $ | 9.79 | | | $ | 10.17 | | | $ | 9.93 | | | $ | 9.91 | |

| | | | | | | | | | | | | | | | | |

| Total return | | | (0.30 | %) | | | 5.98 | % | | | 2.18 | % | | | (0.90 | %)1 |

| | | | | | | | | | | | | | | | | |

| Ratios/Supplemental Data: | | | | | | | | | | | | | | | | |

| Net assets, end of period (in thousands) | | $ | 48,611 | | | $ | 52,681 | | | $ | 45,814 | | | $ | 39,898 | |

| Ratio of expenses to average net assets | | | | | | | | | | | | | | | | |

| Before waiver inclusive of interest expense | | | 3.11 | % | | | 2.84 | % | | | 3.76 | % | | | 4.66 | %2 |

| After waiver inclusive of interest expense | | | 1.79 | % | | | 1.43 | % | | | 2.24 | % | | | 2.50 | %2 |

| Before waiver exclusive of interest expense | | | 3.07 | % | | | 2.83 | % | | | 3.76 | % | | | 4.66 | %2 |

| After waiver exclusive of interest expense | | | 1.75 | % | | | 1.42 | % | | | 2.24 | % | | | 2.50 | %2 |

| Ratio of net investment income (loss) to average net assets | | | 3.40 | % | | | 3.18 | % | | | 1.97 | % | | | (1.21 | %)2 |

| Portfolio turnover rate | | | 4 | % | | | 13 | % | | | 13 | % | | | 0.00 | %1 |

| * | Commenced operations on December 16, 2013 |

See accompanying notes to financial statements.

9

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

1. Organization

The 504 Fund (the “Fund”) was organized as a Delaware statutory trust on July 29, 2013 and is registered with the Securities and Exchange Commission (the “SEC”) as a closed-end, non-diversified management investment company under the Investment Company Act of 1940, as amended (the “1940 Act”), that operates as an “interval fund” pursuant to Rule 23c-3 under the 1940 Act. The Fund is managed by 504 Fund Advisors, LLC (the “Adviser”), an Illinois limited liability company registered under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). The Adviser is a subsidiary of Live Oak Bancshares, Inc. (“Live Oak”), a bank holding company. Government Loan Solutions, Inc. (“GLS”), also a subsidiary of Live Oak, provides the Adviser with data and research which is material to the Adviser’s valuation of the Fund’s investments. The Fund’s president is the chief executive officer of GLS and the chief investment officer of the Adviser, and the Fund’s secretary and treasurer is an employee of Live Oak and the chief executive officer of the Adviser. The offering of the Fund’s shares of beneficial interest in the Fund (the “Shares”) is registered under the Securities Act of 1933, as amended (the “Securities Act”). Shares are offered on a continuous basis monthly (generally as of the last business day of each month) at the net asset value (“NAV”) per Share plus a sales charge of up to 1.00%. There are an unlimited number of authorized Shares.

The Fund’s investment objectives are to provide current income, consistent with the preservation of capital, and to enable institutional Fund investors that are subject to regulatory examination for CRA compliance to claim favorable regulatory consideration of their investment under the Community Reinvestment Act of 1977, as amended (the “CRA”). The Fund seeks to achieve its objectives by investing primarily in a portfolio of 504 First Lien Loans secured by owner-occupied commercial real estate which represent the non-guaranteed portions of U.S. Small Business Administration (“SBA”) Section 504 transactions (“504 First Lien Loans”). 504 First Lien Loans are not guaranteed by the SBA, the U.S. government or by its agencies, instrumentalities or sponsored enterprises.

2. Accounting Policies

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Fund is an investment company and follows the investment company accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. In the normal course of business, the Fund has entered into contracts that contain a variety of representations which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. However, the Fund expects the risk of loss to be remote.

Investment Valuation – Investments for which market quotations are readily available are valued at current fair value, and all other investments are valued at fair value as determined in good faith by the Fund’s Board of Trustees (the “Board”), in accordance with the policies and procedures (the “Valuation Procedures”) adopted by the Board. The Board has a standing valuation committee (the “Valuation Committee”) that is composed of members appointed by the Board. The Valuation Committee operates under the Valuation Procedures approved by the Board. The Fund’s Valuation Committee makes quarterly reports to the Board concerning investments for which market quotations are not readily available. Investments in money market funds (short-term investments) are valued at the closing NAV per share.

10

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

2. Accounting Policies (continued)

504 First Lien Loans – The fair values of 504 First Lien Loans are analyzed using a pricing methodology designed to incorporate, among other things, the present value of the projected stream of cash flows on such investments (the “discounted cash flow” methodology). This pricing methodology takes into account a number of relevant factors, including changes in prevailing interest rates, yield spreads, the borrower’s creditworthiness, the debt service coverage ratio, lien position, delinquency status, frequency of previous late payments and the projected rate of prepayments. Newly purchased loans are initially fair valued at cost and subsequently analyzed using the discounted cash flow methodology. Loans with a pending short payoff will be fair valued at the anticipated recovery rate. Valuations of 504 First Lien Loans are determined no less frequently than weekly by the Board’s Valuation Committee.

Income – Interest income is recorded on the basis of interest accrued, adjusted for amortization of premium or accretion of discount using the effective yield. Fees associated with loan amendments are recognized immediately. Dividend income is recorded on the ex-dividend date for dividends received in cash and/or securities. 504 First Lien Loans will be placed in non-accrual status and related interest income reduced by ceasing current accruals and writing off interest receivables when the collection of all or a portion of interest has become doubtful as identified by the Adviser as part of the valuation process.

Distributions to Shareholders – The Fund expects to declare and pay dividends of net investment income quarterly and net realized capital gains annually. Unless shareholders specify otherwise, dividends will be reinvested in Shares of the Fund.

Use of Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Federal Income Taxes – The Fund intends to elect and to qualify each year to be treated as a regulated investment company under the provisions of Subchapter M of the Internal Revenue Code of 1986, as amended. In order to so qualify, the Fund must meet certain requirements with respect to the sources of its income, the diversification of its assets and the distribution of its income. If the Fund qualifies as a regulated investment company, it will not be subject to federal income or excise tax on income or net capital gains that it distributes in a timely manner to its shareholders in the form of investment company taxable income or net capital gain distributions.

Accounting for Uncertainty in Income Taxes – GAAP requires an evaluation of tax positions taken (or expected to be taken) in the course of preparing a Fund’s tax return to determine whether these positions meet a “more-likely-than-not” standard that, based on the technical merits, have a more than fifty percent likelihood of being sustained by a taxing authority upon examination. A tax position that meets the “more-likely-than-not” recognition threshold is measured to determine the amount of benefit to recognize in the financial statements. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations.

GAAP requires management of the Fund to analyze all open tax years for all major jurisdictions, which the Fund considers to be its federal and relevant state income tax filings. The open tax years for the Fund include all years since inception. As of and during the year ended June 30, 2017, the Fund did not record a liability for any unrecognized tax benefits. The Fund has no examination in progress and is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

Expenses – Fund expenses are charged to the Fund and recorded on an accrual basis.

11

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

2. Accounting Policies (continued)

Fair Value Measurements – Under GAAP for fair value measurements, a three-tier hierarchy to prioritize the assumptions, referred to as inputs, is used in valuation techniques to measure fair value. The three-tier hierarchy of inputs is summarized in the three broad levels listed below.

| | ● | Level 1 – Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date. |

| | ● | Level 2 – Other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.). |

| | ● | Level 3 – Significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of investment). |

The following table sets forth information about the levels within the fair value hierarchy at which the Fund’s investments are measured as of June 30, 2017:

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Hospitality Properties | | $ | — | | | $ | — | | | $ | 11,515,538 | | | $ | 11,515,538 | |

| Multi-Purpose Properties | | | — | | | | — | | | | 38,872,117 | | | | 38,872,117 | |

| Short-Term Investments | | | 113,766 | | | | — | | | | — | | | | 113,766 | |

| Total Investments | | $ | 113,766 | | | $ | — | | | $ | 50,387,655 | | | $ | 50,501,421 | |

For the year ended June 30, 2017, there were no transfers into or out of Level 1, Level 2 or Level 3.

Should a transfer between Levels occur, it is the Fund’s policy to recognize transfers in and out of all Levels at the end of the reporting period.

The following is a reconciliation of investments in which significant unobservable inputs (Level 3) were used in determining fair value:

| Investments | | Balance as of June 30, 2016 | | | Purchase and funding of investments | | | Proceeds from principal payments* | | | Net realized gain on investments | | | Net change in unrealized depreciation on investments | | | Amortization of discount and premium | | | Balance as of

June 30, 2017 | |

| Hospitality Properties | | $ | 7,329,428 | | | $ | 4,503,032 | | | $ | (101,558 | ) | | $ | — | | | $ | (214,198 | ) | | $ | (1,166 | ) | | $ | 11,515,538 | |

| Multi-Purpose Properties | | | 40,482,248 | | | | 2,064,503 | | | | (1,907,515 | ) | | | — | | | | (1,746,037 | ) | | | (21,082 | ) | | | 38,872,117 | |

| Total Investments | | $ | 47,811,676 | | | $ | 6,567,535 | | | $ | (2,009,073 | ) | | $ | — | | | $ | (1,960,235 | ) | | $ | (22,248 | ) | | $ | 50,387,655 | |

| * | Inclusive of net realized paydown losses. |

Change in unrealized depreciation included in the Statement of Operations attributable to Level 3 investments held as of the reporting date is $(1,926,489).

12

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

2. Accounting Policies (continued)

The following is a summary of quantitative information about significant unobservable valuation inputs for Level 3 fair value measurements for investments held as of June 30, 2017:

| Type of Level 3 Investments | Fair Value as of June 30, 2017 | Valuation Technique | Unobservable Inputs | Weighted Average | Range | Impact to Fair Value from an Increase in Input |

| Hospitality Properties | $ 11,515,538 | Discounted

Cash Flows | Purchase Price | $100.61 | $100-104 | Decrease** |

| | | | Debt Service Coverage Ratio | 1.73 | 1.25-2.74 | N/A* |

| | | | Effective Loan To Value Ratio | 46.70% | 42%-53% | Decrease |

| | | | Average Personal Credit Score | 721 | 687-761 | N/A* |

| Multi-Purpose Properties | $ 38,872,117 | Discounted

Cash Flows | Purchase Price | $102.34 | $100-105 | Decrease** |

| | | | Debt Service Coverage Ratio | 1.57 | 1.00-3.06 | N/A* |

| | | | Effective Loan To Value Ratio | 50.57% | 39%-64% | Decrease |

| | | | Average Personal Credit Score | 754 | 685-819 | N/A* |

| Total Investments | $ 50,387,655 | | | | | |

| * | A decrease in the input would result in a decrease in fair value. |

| ** | An increase in the spread from the Fund’s purchase price to the benchmark utilized within the fair value methodology would result in a decrease in fair value. |

3. Concentration of Risk

504 First Lien Loans Risk – The Fund predominantly invests in fixed or variable rate 504 First Lien Loans arranged through private negotiations between a small business borrower (the “Borrower”) and one or more 504 First Lien Loan lenders. 504 First Lien Loans are secured by real property and have a claim on the assets of the Borrower that is senior to the second lien held by a certified development company and any claims held by unsecured creditors. The 504 First Lien Loans the Fund will invest in are not rated. 504 First Lien Loans are subject to a number of risks, including credit risk, liquidity risk, valuation risk and interest rate risk. Although the 504 First Lien Loans in which the Fund will invest will be secured by real property, there can be no assurance that such real property can be readily liquidated or that the liquidation of such real property would satisfy the Borrower’s obligation in the event of non-payment of scheduled interest or principal, which could result in substantial loss to the Fund. In the event of the bankruptcy or insolvency of a Borrower, the Fund could experience delays or limitations with respect to its ability to realize the benefits of the real property securing a 504 First Lien Loan. In the event of a decline in the value of the already pledged real property, the Fund will be exposed to the risk that the value of the real property will not at all times equal or exceed the amount of the Borrower’s obligations under the 504 First Lien Loan. In general, the secondary trading market for 504 First Lien Loans is not fully-developed. No active trading market may exist for

13

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

3. Concentration of Risk (continued)

certain 504 First Lien Loans, which may make it difficult to value them. Illiquidity and adverse market conditions may mean that the Fund may not be able to sell certain 504 First Lien Loans quickly or at a fair price. To the extent that a secondary market does exist for certain 504 First Lien Loans, the market for them may be subject to irregular trading activity, wide bid/ask spreads and extended trade settlement periods.

Credit Risk – Credit risk is the risk that one or more debt instruments in the Fund’s portfolio will decline in price or fail to pay interest or principal when due because the borrower experiences a decline in its financial status. Losses may occur because the market value of a debt security is affected by the creditworthiness of the issuer and by general economic and specific industry conditions.

Qualification for CRA Credit Risk – Although the Adviser believes that the Fund’s 504 First Lien Loan investments will have the community development qualities that are eligible for favorable consideration as community development loans and qualified investments under the CRA, there is no guarantee that an investor will receive CRA credit for an investment in the Fund.

Geographic Concentration Risk – The Fund’s 504 First Lien Loan investments are concentrated in certain states as of June 30, 2017, which are listed in the last section of the Schedule of Investments. As a result, the Fund may be more susceptible to being adversely affected by any single occurrence in those states. Mortgaged properties in California, for example, may be particularly susceptible to economic risks of the state and certain types of hazards, such as earthquakes, floods, mudslides, wildfires and other natural disasters, for which there may or may not be insurance. As of June 30, 2017, 45.89% of the Fund’s investments were associated with properties located in California. Mortgaged properties in other states similarly may be adversely affected by natural disasters, for which there may not be insurance and which could result in substantial loss to the Fund.

Valuation Risk – Unlike publicly traded equity securities that trade on national exchanges, there is no central place or exchange for 504 First Lien Loans to trade. Due to the lack of centralized information and trading, the Adviser’s judgment plays a greater role in the valuation process and the valuation of 504 First Lien Loans. Uncertainties in the conditions of the financial market, unreliable reference data, lack of transparency and inconsistency of valuation models and processes may lead to inaccurate asset pricing. In addition, other market participants may value instruments differently than the Fund. As a result, the Fund may be subject to the risk that when a 504 First Lien Loan is sold in the market, the amount received by the Fund is less than the value that such 504 First Lien Loan is carried at on the Fund’s books.

For other risks associated with the Fund and its investments please refer to the “Risks” section in the Fund’s current prospectus.

4. Periodic Repurchase Offers

The Fund will make periodic offers to repurchase a portion of its outstanding Shares at NAV per Share. The Fund has adopted a fundamental policy to make repurchase offers once every twelve months. The Fund will offer to repurchase 5% of its outstanding Shares, unless the Board has approved a higher amount (but not more than 25% of its outstanding Shares). The Fund does not currently expect to charge a repurchase fee.

For the year ended June 30, 2017, the Fund had one repurchase offer as follows:

Repurchase Offer Notice | Repurchase Request Deadline | Repurchase Pricing Date | Repurchase Offer Amount | % of Shares

Repurchased | Number of

Shares Repurchased |

| December 15, 2016 | January 10, 2017 | January 20, 2017 | 5% | 5% | 260,022 |

14

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

5. Administration, Distribution, Transfer Agency and Custodian Agreements

The Fund and its administrator, UMB Fund Services, Inc. (“UMBFS”), are parties to an administration agreement under which UMBFS provides administrative and fund accounting services.

UMBFS also serves as the transfer agent and dividend disbursing agent for the Fund.

UMB Bank, N.A. serves as the custodian and escrow agent (the “Custodian”) for the Fund. The Custodian plays no role in determining the investment policies of the Fund or which securities are to be purchased and sold by the Fund.

The Fund and Foreside Fund Services, LLC (the “Distributor”) are parties to a distribution agreement under which the Distributor acts as the principal underwriter for the Fund.

6. Investment Advisory Agreement

The Fund has entered into an investment advisory agreement (the “Investment Advisory Agreement”) with the Adviser, effective April 1, 2015. Under the Investment Advisory Agreement, the Adviser makes investment decisions for the Fund and continuously reviews, supervises and administers the investment program of the Fund, subject to the supervision of, and policies established by, the Board. For providing these services, the Adviser will receive a fee from the Fund, accrued daily and paid monthly, at an annual rate equal to 1.75% of the Fund’s average daily net assets. In addition, the Adviser has contractually agreed to waive or reduce its adviser fees and/or reimburse expenses of the Fund to ensure that total annual Fund operating expenses after fee waiver and/or expense reimbursement (excluding any interest, leverage interest (i.e., any expenses incurred in connection with borrowings made by the Fund), taxes, brokerage commissions, acquired fund fees and expenses and extraordinary expenses and including organizational and offering costs) will not exceed 1.75% of the Fund’s average net assets pursuant to an operating expenses limitation agreement dated March 1, 2015 (the “Operating Expenses Limitation Agreement”). Under the terms of the Investment Advisory Agreement and the Operating Expenses Limitation Agreement, any such contractual reductions made by the Adviser in its fees or payment of expenses which are the Fund’s obligation are subject to reimbursement by the Fund to the Adviser for a period of three fiscal years following the end of the fiscal year in which such reduction or payment was accrued, except for initial organizational expenses which are subject to reimbursement by the Fund to the Adviser for a period of three years from the date on which such expenses were incurred. The Operating Expenses Limitation Agreement is in effect through at least January 1, 2018, and may be terminated only by, or with the consent of, the Board.

For the year ended June 30, 2017, the Adviser waived expenses totaling $664,305 that are subject to reimbursement.

As of June 30, 2017, the Adviser’s fees and expenses subject to reimbursement were as follows:

| June 30, 2018 | June 30, 2019 | June 30, 2020 |

| $ 371,559 | $ 562,480 | $ 664,305 |

7. Investment Transactions

For the year ended June 30, 2017, there were long term purchases of $6,567,535 and proceeds from principal payments of $1,970,967 in the Fund.

15

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

8. Revolving Credit Agreement

Effective July 1, 2016, the Fund entered into a secured, revolving line of credit facility with Park Sterling Bank with a maximum principal amount of $10 million for a period of one year, which expired on July 1, 2017. Effective July 1, 2017, the Fund renewed the agreement through October 1, 2018 with a maximum principal amount of $6 million. The line of credit is subject to a borrowing base of the lesser of either the aggregate principal amount of outstanding collateral 504 First Lien Loans or the aggregate market value of collateral 504 First Lien Loans (the “Borrowing Base”). The line of credit facility is secured by certain 504 First Lien Loans and all cash and cash equivalents held by the Fund that have been pledged as collateral. The Fund anticipates that this line of credit facility will be used for investment purposes, to satisfy repurchase requests from shareholders and to otherwise provide the Fund with liquidity. The Fund will incur additional interest and other expenses with respect to the use of this and other future line of credit facilities. A loan extension fee of $15,000 is payable on the line of credit. The interest rate on the line of credit facility is equal to 1-month LIBOR plus 2.50%. Collateral for the line of credit facility will be held by the Custodian. During the year ended June 30, 2017, the Fund paid $20,195 in interest on borrowings. The average interest rate and the average daily balance for borrowings under the line of credit facility for the year ended June 30, 2017, was 3.42% and $1,292,683, respectively. For the period July 1, 2016 to June 30, 2017, the maximum balance outstanding was $2,000,000. As of June 30, 2017, the interest rate on the line of credit facility was 3.72% and there are outstanding borrowings of $2,000,000.

9. Federal Tax Information

At June 30, 2017, gross unrealized appreciation (depreciation) of investments owned by the Fund, based on cost for federal income tax purposes, were as follows:

| Cost of investments | | $ | 51,102,718 | |

| Gross unrealized appreciation | | $ | 50,848 | |

| Gross unrealized depreciation | | | (652,145 | ) |

| Net unrealized depreciation on investments | | $ | (601,297 | ) |

GAAP requires that certain components of net assets be reclassified between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share. For the year ended June 30, 2017 permanent differences in book and tax accounting resulting primarily from differing treatments for paydowns and amortization of organizational costs have been reclassified to paid-in capital, accumulated net investment income and accumulated net realized loss on investments as follows:

Paid-In

Capital | Accumulated

Net Investment

Income (Loss) | Accumulated

Net Realized

Gain (Loss) |

| $1,422 | $36,684 | $(38,106) |

16

|

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2017

|

9. Federal Tax Information (continued)

As of June 30, 2017, the components of accumulated earnings (deficit) on a tax basis for the Fund were as follows:

| Undistributed ordinary income | | $ | 2,887 | |

| Undistributed long-term gains | | | — | |

| Tax accumulated earnings | | | 2,887 | |

| Accumulated capital and other losses | | $ | (105,049 | ) |

| Unrealized depreciation on investments | | | (601,297 | ) |

| Total accumulated earnings (deficit) | | $ | (703,459 | ) |

The tax character of distributions paid during the fiscal years ended June 30, 2017 and June 30, 2016 were as follows:

| | 2017 | | | 2016 | |

| Distribution paid from: | | | | | | |

| Ordinary income | | $ | 1,748,325 | | | $ | 1,831,666 | |

| Long-term capital gains | | | — | | | | — | |

| Total Distributions | | $ | 1,748,325 | | | $ | 1,831,666 | |

As of June 30, 2017, the Fund had a short-term capital loss carryover of $12,262 and long-term capital loss carryover of $92,787. To the extent that the Fund may realize future net capital gains, those gains will be offset by any of its unused capital loss carryforward. Future capital loss carryover utilization in any given year may be subject to Internal Revenue Code limitations.

10. Control Ownership

The beneficial ownership, either directly or indirectly, of more than 25% of the voting securities creates a presumption of control of the Fund, under Section 2(a)(9) of the 1940 Act. As of June 30, 2017, Northwest Federal Credit Union had ownership in the Fund in the amount of 51.00%.

11. Related Party Transaction

On November 22, 2016, the Trustees of the Fund who are not "interested persons" of the Fund as defined by the 1940 Act (the "Independent Trustees") approved the following compensation to be paid to Robert O. Judge in his capacity as President of the Fund: (a) an annual retainer of $10,000 (effective January 1, 2017) for service as President; and (b) $1,500 per Board meeting attended. For the year ended June 30, 2017, the Fund paid Mr. Judge $9,500 for his services as President.

12. Subsequent Events

The Fund has evaluated the events and transactions through the date the financial statements were issued and determined there were no subsequent events that required adjustments to our disclosure in the financial statements.

17

|

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

|

To the Shareholders and Board of Trustees of

The 504 Fund

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of The 504 Fund (the “Fund”) as of June 30, 2017, and the related statements of operations and cash flows for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of June 30, 2017, by correspondence with the custodian and counterparties. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of The 504 Fund as of June 30, 2017, the results of its operations and its cash flows for the year then ended, the changes in its net assets for each of the two years in the period then ended, and the financial highlights for each of the four periods in the period then ended, in conformity with accounting principles generally accepted in the United States of America.

As discussed in Note 2 to the financial statements, the financial statements include investments valued at $50,387,655 (103.66% of net assets) as of June 30, 2017, whose fair values have been estimated by management in accordance with policies approved by and under the general oversight of the Board of Trustees in the absence of readily determinable fair values.

COHEN & COMPANY, LTD.

Cleveland, Ohio

August 29, 2017

18

|

OTHER INFORMATION (UNAUDITED)

JUNE 30, 2017

|

Proxy Voting

For a description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, please call the Fund at 855-386-3504 and request a Statement of Additional Information. One will be mailed to you free of charge. The Statement of Additional Information is also available on the SEC’s website at http://www.sec.gov.

Information on how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge, upon request, by calling the Fund at 855-386-3504 or by accessing the SEC’s website http://www.sec.gov.

Disclosure of Portfolio Holdings

The Fund files a complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Fund’s Form N-Q is available on the SEC’s website at www.sec.gov, and may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

Basis for Approval of Advisory Agreement

At a meeting of the Board on February 7, 2017 (the “Meeting”), the Board, including a majority of the Independent Trustees, voting separately, approved the renewal of an investment advisory agreement (the “Advisory Agreement”) between the Fund and the Adviser.

At the Meeting, the Trustees reviewed materials (“Materials”) presented with regard to the Adviser, including relevant portions of responses by the Adviser to the request for information on behalf of the Independent Trustees, the Adviser’s organizational chart, a business continuity disaster recovery plan, a peer group comparative analysis prepared by UMBFS relating to the Fund’s investment advisory fee and net expense ratio, financial statements for the Adviser, biographical information for the Fund’s CCO, correspondence relating to the Fund’s and the Adviser’s recent SEC examinations, and a copy of the Adviser’s registration statement on Form ADV. The Board reviewed the terms of the Advisory Agreement and the Operating Expenses Limitation Agreement included in the Materials.

The Board then discussed with counsel to the Fund and counsel to the Independent Trustees the factors that may be relevant in determining whether to renew the Advisory Agreement between the Fund and the Adviser, including the following: (1) the nature, extent, and quality of the services provided by the Adviser; (2) the cost of the services provided and the profits realized by the Adviser from services rendered to the Fund; (3) comparative fee and expense data for the Fund; (4) the extent to which economies of scale would be realized as the Fund grows and whether the management fee for the Fund reflects these economies of scale for the benefit of the Fund; and (5) other financial benefits to the Adviser and its affiliates resulting from services rendered to the Fund. In their deliberations, the Trustees did not identify any particular information that was all-important or controlling.

Nature, Extent and Quality of Services Provided to the Fund. The Trustees considered the scope of services performed by the Adviser under the Advisory Agreement. In considering the nature, extent and quality of the services provided by the Adviser, the Board reviewed the resources and financial condition of the Adviser and certain of its affiliates, as well as the continued roles of Jordan M. Blanchard and Robert O. Judge, the Fund’s portfolio managers. The Adviser’s registration form on Form ADV was provided to the Board, as was the response of the Adviser to a detailed series of questions from counsel to the Independent Trustees which included, among other things, information about the background and experience of the portfolio managers who will continue to be primarily responsible for the day-to-day management of the Fund. The Board also considered other services to be provided to the Fund by the Adviser, such as monitoring adherence to the Fund’s investment

19

|

OTHER INFORMATION (UNAUDITED)

JUNE 30, 2017

|

restrictions and monitoring compliance with various Fund policies and procedures and with applicable securities regulations. Based on the factors above, as well as those discussed below, the Board concluded that it was satisfied with the nature, extent and quality of the services provided to the Fund by the Adviser.

Investment Performance of 504 Fund Advisors; Review of Fund Performance. The Board reviewed the Fund’s performance for the one-month, three-month, six-month, one-year, three-year and since inception periods ended December 31, 2016, on both an absolute basis and in comparison to benchmark indices, including the Bloomberg Barclays Aggregate Bond Index, the BofA Merrill Lynch 1-3 Year U.S. Corporate & Government Bond Index and the BofA Merrill Lynch 3-5 Year U.S. Corporate & Government Bond Index. The Board noted that the Fund is the Adviser’s only client. The Board also reviewed the Fund’s performance in comparison to a peer group compiled by the Fund’s administrator of closed-end loan participation funds, business development company funds, and an open-end mutual fund with an investment objective focusing on investments that will be deemed to be qualified under the CRA. Although past performance is not a guarantee or indication of future results, the Trustees determined that the performance obtained by the Adviser was satisfactory under current market conditions and the Fund and its shareholders were likely to benefit from the Adviser’s continued management of the Fund.

Cost of Services Provided and Profits Realized by 504 Fund Advisors. The Board considered the management fees and expense ratios of a peer group compiled by the Fund’s administrator of closed-end loan participation funds, business development company funds, and an open-end mutual fund with an investment objective focusing on investments that will be deemed to be qualified under the CRA, and concluded that the management fee was reasonable and the result of arm’s length negotiations. Additionally, the Board took into consideration that the Adviser has contractually agreed to limit the total annual operating expenses of the Fund to 1.75% through at least January 1, 2018, which has resulted in the Adviser waiving a significant portion of its management fees and the Adviser had not recouped those waivers from the Fund. The Board also evaluated the profitability of the Adviser from its relationship with the Fund, noting the Adviser’s representation that it was managing the Fund on an approximate break-even basis.

Economies of Scale. The Board noted that the Adviser is likely to realize economies of scale in managing the Fund as assets grow in size. The Board also noted that through fee waivers, the Adviser was in effect providing access to economies of scale to the Fund and its shareholders that may not have been achieved until the Fund reached significantly higher asset levels. With respect to the Adviser’s current fee structure and applicable expense waivers, the Board concluded that the current fee structure was reasonable and reflected a sharing of economies of scale between the Adviser and the Fund at the Fund’s current asset level.

Benefits Derived from the Relationship with the Fund. The Board considered the direct and indirect benefits that could be received by the Adviser from its association with the Fund. The Board also considered the compensation payable by the Fund to Mr. Judge in his capacity as President of the Fund. The Board determined that the benefits the Adviser may receive, including greater name recognition and the ability to attract additional investor assets, appear to be reasonable, and in many cases, may benefit the Fund.

20

|

TRUSTEES AND OFFICERS (UNAUDITED)

JUNE 30, 2017

|

Information pertaining to the Trustees and officers of the Fund is set forth below. Trustees who are not “interested persons” of the Fund as that term is defined in the 1940 Act are referred to as “Independent Trustees.” The business address of each Trustee or officer is c/o The 504 Fund, 1741 Tiburon Drive, Wilmington, North Carolina 28403. The Statement of Additional Information includes additional information about the Trustees and is available, without charge, upon request by calling the Fund at 855-386-3504.

Name and

Year of Birth | Position with

Fund and

Length of Term | Principal Occupations

in the Past 5 Years | Number of Portfolios in Fund Complex Overseen By Trustee | Other Directorships Held in the Past 5

Years |

| Independent Trustees | | | |

J. Clay Singleton,

Ph.D., CFA

Born: 1947 | Trustee

(Indefinite term; since 2013) | Retired; Professor Emeritus of Finance, Crummer Graduate School of Business, Rollins College (2002-2017); Consultant, Director of Indexes, PCE Investment Bankers (2005-2011) | 1 | Independent Trustee, USFS Funds Trust (an open-end investment company with two series) (2013-2014) |

Cornelius J. Lavelle

Born: 1944 | Trustee

(Indefinite term; since 2013) | Retired; Director-Institutional Equities, Citigroup Global Markets Inc. (multinational financial services firm) (1997-2009) | 1 | Independent Trustee, Broadview Funds Trust (an open-end investment company with one series) (since 2013); Independent Trustee, USFS Funds Trust (an open-end investment company with two series) (2013-2014) |

21

|

TRUSTEES AND OFFICERS (UNAUDITED)

JUNE 30, 2017

|

Name and

Year of Birth | Position with

Fund and

Length of Term | Principal Occupations

in the Past 5 Years | Number of Portfolios in Fund Complex Overseen By Trustee | Other Directorships Held in the Past 5

Years |

| Independent Trustees (continued) | | | |

George Stelljes, III

Born: 1961 | Chairman of the Board (Indefinite term; since August 2016) and Trustee

(Indefinite term; since 2013) | Managing Partner, St. John’s Capital, LLC (private investment fund) (since 2012); President, Chief Investment Officer and Director of the Gladstone Companies (family of public and private investment funds) (2001-2012) | 1 | Director, TICC Capital Corp. (business development company) (since 2016); Director, Intrepid Capital Corporation (asset management firm) (since 2003); Director, Gladstone Capital Corporation (business development company) (resigned 2012); Director, Gladstone Commercial Corporation (real estate investment trust) (resigned 2012); Director, Gladstone Investment Corporation (business development company) (resigned 2012); Director, Gladstone Land Corporation (real estate investment company) (resigned 2012) |

22

|

TRUSTEES AND OFFICERS (UNAUDITED)

JUNE 30, 2017

|

Name and

Year of Birth | Position with

Fund and

Length of Term | Principal Occupations

in the Past 5 Years | Number of Portfolios in Fund Complex Overseen By Trustee | Other Directorships Held in the Past 5

Years |

| Other Officers | | | | |

Robert O. Judge

Born: 1961 | President and Principal Executive Officer (Indefinite term; since August 2016) | Chief Investment Officer, 504 Fund Advisors, LLC (investment advisory firm) (since 2015); Portfolio Manager, The 504 Fund (since 2013); Chief Executive Officer of Government Loan Solutions, Inc. (a financial services company) (since 2006) | N/A | N/A |

Constantine Andrew (Dean) Pelos

Born: 1960 | Principal Financial Officer and Principal Accounting Officer (Indefinite term; since August 2016) and Chief Compliance Officer and AML Compliance Officer (Indefinite term; since 2015) | Director, Oyster Consulting, Inc. (compliance consulting to financial services firms) (since 2015); Senior Consultant, Oyster Consulting, Inc. (2013-2015); Investment Manager, LaSalle St. Securities, LLC (broker-dealer) (2009-2013); Partner, Head of Trading, Chief Compliance Officer, Sterling Investment Services, Inc. (broker-dealer) (1991-2009) | N/A | N/A |

Jordan M. Blanchard

Born: 1966 | Secretary and Treasurer (Indefinite term; since 2015) | Chief Executive Officer and Chief Operating Officer, 504 Fund Advisors, LLC (investment advisory firm) (since 2015); Portfolio Manager, The 504 Fund (since 2013); General Manager - Renewable Energy Lending, Live Oak Bank (since 2016); Managing Director of 504 Secondary Markets, Government Loan Solutions, Inc. (a financial services company) (2013-2015); President, Wholesale 504 Lending Consultants, LLC (financial services company) (2011-2012); Executive Vice President of Capital Markets, CDC Direct Capital (community development corporation subsidiary) (2009-2011) | N/A | N/A |

23

THIS PAGE INTENTIONALLY LEFT BLANK

THIS PAGE INTENTIONALLY LEFT BLANK

THE 504 FUND

1741 Tiburon Drive

Wilmington, NC 28403

INVESTMENT ADVISER

504 Fund Advisors, LLC

1741 Tiburon Drive

Wilmington, NC 28403

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

Cohen & Company, Ltd.

1350 Euclid Ave., Suite 800

Cleveland, OH 44115

LEGAL COUNSEL

Godfrey & Kahn, S.C.

833 East Michigan Street, Suite 1800

Milwaukee, WI 53202

CUSTODIAN

UMB Bank, N.A.

1010 Grand Boulevard

Kansas City, MO 64106

DISTRIBUTOR

Foreside Fund Services, LLC

Three Canal Plaza, Suite 100

Portland, Maine 04101

TRANSFER AGENT

UMB Fund Services, Inc.

235 West Galena Street

Milwaukee, WI 53212

There can be no assurance that the Fund will achieve its investment objectives. An investment in the Fund is an appropriate investment only for those investors who can tolerate a high degree of risk and do not require a liquid investment. Investors may lose some or all of their investment in the Fund. The Fund is not designed to be a complete investment program and may not be a suitable investment for all investors. The risk factors described are the principal risk factors associated with an investment in the Fund, as well as those factors associated with an investment in an investment company with similar investment objectives and investment policies.

This report is submitted for the general information of the shareholders of the Fund. It is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus, which includes information regarding the Fund’s risks, objectives, fees, expenses and experience of its management and other considerations.

ITEM 2. CODE OF ETHICS.

(a) The 504 Fund (the “registrant” or the “Fund”), as of the end of the period covered by this report, has adopted a code of ethics (the “code of ethics”) that applies to the registrant's principal executive officer, principal financial officer, principal accounting officer and controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party.

(c) There have been no amendments, during the period covered by this report, to the code of ethics.

(d) The registrant has not granted any waivers, during the period covered by this report, including an implicit waiver, from any provision of the code of ethics.

A copy of the registrant’s code of ethics is filed herewith.

ITEM 3. AUDIT COMMITTEE FINANCIAL EXPERT.

The registrant’s board of trustees has determined that there are two audit committee financial experts serving on its audit committee. Mr. George Stelljes, III and Dr. J. Clay Singleton are each qualified to serve as audit committee financial experts serving on its audit committee and each is "independent," as defined by Item 3 of Form N-CSR.

ITEM 4. PRINCIPAL ACCOUNTANT FEES AND SERVICES.

The registrant has engaged Cohen & Company, Ltd. to perform audit services, audit-related services, tax services and other services during the fiscal year ended June 30, 2017. “Audit services” refer to performing an audit of the registrant's annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years. “Audit-related services” refer to the assurance and related services by the principal accountant that are reasonably related to the performance of the audit. “Tax services” refer to professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning. The following table details the aggregate fees billed or expected to be billed for the fiscal years 2016 and 2017 for audit fees, audit-related fees, tax fees and other fees by Cohen & Company, Ltd.

The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre-approve all audit and non-audit services of the registrant, including services provided to any entity affiliated with the registrant.

The percentage of fees billed by Cohen & Company, Ltd. applicable to non-audit services pursuant to waiver of pre-approval requirement were as follows:

All of the principal accountant’s hours spent on auditing the registrant’s financial statements were attributed to work performed by full-time permanent employees of the principal accountant.

The following table indicates the non-audit fees billed or expected to be billed by the registrant’s accountant for services to the registrant and to the registrant’s investment adviser (and any other controlling entity, etc.) for the last two fiscal years.

The amount of fees billed by Cohen & Company, Ltd. applicable to non-audit fees were as follows:

ITEM 5. AUDIT COMMITTEE OF LISTED REGISTRANTS.

Not applicable.

ITEM 6. INVESTMENTS.

Schedule of Investments in securities of unaffiliated issuers as of the close of the reporting period is included as part of the report to shareholders filed under Item 1 of this Form.

ITEM 7. DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

Not applicable. During the period covered by this report, the Fund invested exclusively in non-voting securities. In the event that the Fund invests in voting securities, the Adviser will adopt proxy voting policies and procedures.

ITEM 8. PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES.

(a)(1) Identification of Portfolio Manager(s) and Description of Role of Portfolio Manager(s)

The following table provides biographical information about the Portfolio Managers, who are primarily responsible for the day-to-day portfolio management of the Fund as of the date hereof:

(a)(2) Other Accounts Managed by Portfolio Manager(s) or Management Team Member and Potential Conflicts of Interest

The following table provides information about portfolios and accounts, other than the Fund, for which the Portfolio Managers are primarily responsible for the day-to-day portfolio management as of June 30, 2017:

504 Fund Advisors, LLC (the "Adviser") serves as the Fund’s investment adviser. The Adviser and the portfolio managers will be subject to certain conflicts of interest in their management of the Fund. These conflicts will arise primarily from the involvement of the Adviser and the portfolio managers in other activities that may conflict with those of the Fund.

The Adviser believes that the portfolio managers have sufficient time and resources to discharge their responsibilities to the Fund. However, conflicts of interest may arise in allocating time, services or functions between the Fund and other entities or businesses to which a portfolio manager provides services. A portfolio manager will devote such time to the Fund as he believes is reasonably necessary to the conduct of the business of the Fund and its respective investments.

In the ordinary course of his business activities, a portfolio manager may engage in activities where the interests of the Fund and its shareholders conflict with the interest of other entities or businesses to which a portfolio manager provides services. Other present and future activities of the portfolio managers or such entities or businesses may give rise to additional conflicts of interest. In the event that a conflict of interest arises, a portfolio manager will attempt to resolve such conflicts in a fair and equitable manner and in accordance with the requirements and limitations of the Investment Company Act of 1940, as amended.

Mr. Blanchard is compensated by Live Oak Bank with a fixed salary plus a bonus based on the performance of Live Oak Bancshares, the holding company for Live Oak Bank. Mr. Judge is compensated by GLS with a fixed salary plus a bonus based upon the performance of GLS. Neither individual receives compensation from the Adviser or the Fund.

The following table sets forth the dollar range of equity securities beneficially owned by each Portfolio Manager in the Fund as of June 30, 2017:

ITEM 9. PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS.

There were no purchases made by or on behalf of the registrant or any “affiliated purchaser,” as defined in Rule 10b-18(a)(3) under the Exchange Act (17 CFR 240.10b-18(a)(3)), of shares or other units of any class of the registrant’s equity securities that is registered by the registrant pursuant to Section 12 of the Exchange Act (15 U.S.C. 781).

There were no purchases that do not satisfy the conditions of the safe harbor of Rule 10b-18 under the Exchange Act (17 CFR 240.10b-18), made in the period covered by this report.

ITEM 10. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

There have been no material changes to the procedures by which the shareholders may recommend nominees to the registrant's board of trustees, where those changes were implemented after the registrant last provided disclosure in response to the requirements of Item 407(c)(2)(iv) of Regulation S-K (17 CFR 229.407) (as required by Item 22(b)(15) of Schedule 14A (17 CFR 240.14a-101)), or this Item.

ITEM 11. CONTROLS AND PROCEDURES.

(a) The registrant's principal executive and principal financial officers, or persons performing similar functions, have concluded that the registrant's disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940, as amended (the "1940 Act") (17 CFR 270.30a-3(c))) are effective, as of a date within 90 days of the filing date of the report that includes the disclosure required by this paragraph, based on their evaluation of these controls and procedures required by Rule 30a-3(b) under the 1940 Act (17 CFR 270.30a-3(b)) and Rules 13a-15(b) or 15d-15(b) under the Securities Exchange Act of 1934, as amended (17 CFR 240.13a-15(b) or 240.15d-15(b)).

(b) There were no changes in the registrant's internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act (17 CFR 270.30a-3(d)) that occurred during the registrant's second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the registrant's internal control over financial reporting.

ITEM 12. EXHIBITS.

(a)(1) Registrant’s Code of Ethics is filed herewith.

(a)(2) Certifications pursuant to Rule 30a-2(a) under the 1940 Act and Section 302 of the Sarbanes-Oxley Act of 2002 are filed herewith.

(a)(3) Not applicable.

(b) Certifications pursuant to Rule 30a-2(b) under the 1940 Act and Section 906 of the Sarbanes-Oxley Act of 2002 are filed herewith.

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.