UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22961

EA Series Trust

(Exact name of registrant as specified in charter)

19 E. Eagle Road

Havertown, PA 19083

(Address of principal executive offices) (Zip code)

19 E. Eagle Road

Havertown, PA 19083

(Name and address of agent for service)

(215) 330-4476

Registrant’s telephone number, including area code

Date of fiscal year end: September 30, 2024

Date of reporting period: September 30, 2024

Item 1. Report to Stockholders.

(a)

| | | | | | | | |

| Alpha Architect U.S. Quantitative Value ETF Ticker: QVAL Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/qval |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect U.S. Quantitative Value ETF (the “Fund”) for the period of October 1, 2023 to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/qval. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $36 | 0.32% |

| | | | | | | | | | | |

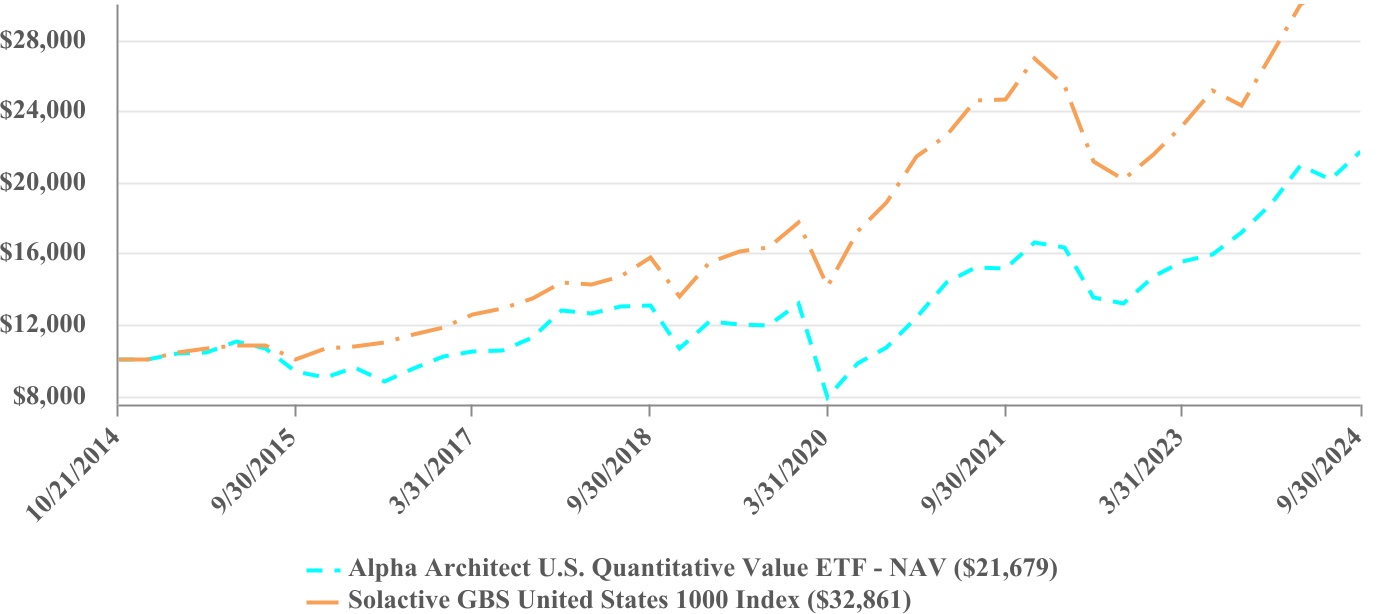

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | 5 Year | | Since Inception (10/21/2014) |

| Alpha Architect U.S. Quantitative Value ETF - NAV | | 26.33% | | 12.71% | | 8.09% |

| Solactive GBS United States 1000 Index | | 35.20% | | 15.06% | | 12.71% |

| | | | | | |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/qval for more recent performance information. |

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund returned 26.53% (NAV) for the Period vs. 35.20% for the Solactive GBS United States 1000 Index. During the Period, markets reacted positively to strong corporate earnings, resilient economic conditions, and Federal Reserve policy, with larger-cap stocks leading performance. The Fund’s tilt toward deeper value stocks as measured by EBIT/TEV contributed negatively to returns relative to the benchmark.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect U.S. Quantitative Value ETF Ticker: QVAL Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/qval |

|

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $376,221,478 | | Portfolio Turnover Rate* | | 223% |

| # of Portfolio Holdings | | 51 | | Advisory Fees Paid | | $1,023,524 |

| *Excludes impact of in-kind transactions. |

| | | | | | |

| | | | | |

SECTOR WEIGHTING

(as a % of Net Assets) |

| Consumer Discretionary | 26.9% |

| Industrials | 23.0% |

| Energy | 16.3% |

| Communication Services | 10.1% |

| Health Care | 9.6% |

| Materials | 6.1% |

| Information Technology | 4.0% |

| Consumer Staples | 3.7% |

| Cash & Cash Equivalents | 0.2% |

| | | | | |

TOP 10 HOLDINGS

(as a % of Net Assets) |

| Powell Industries, Inc. | 2.6% |

| Signet Jewelers Ltd. | 2.4% |

| Delta Air Lines, Inc. | 2.3% |

| Williams-Sonoma, Inc. | 2.3% |

| Freeport-McMoRan, Inc. | 2.2% |

| Tapestry, Inc. | 2.2% |

| Caterpillar, Inc. | 2.1% |

| Jabil, Inc. | 2.1% |

| Ulta Beauty, Inc. | 2.1% |

| CVS Health Corp. | 2.1% |

Material Fund Changes

This is a summary of certain changes to the Fund since October 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/qval or by calling (215) 330-4476.

Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as the Fund’s sub-adviser.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/qval. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect International Quantitative Value ETF Ticker: IVAL Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/ival |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect International Quantitative Value ETF (the “Fund”) for the period of October 1, 2023 to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/ival. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $45 | 0.42% |

| | | | | | | | | | | |

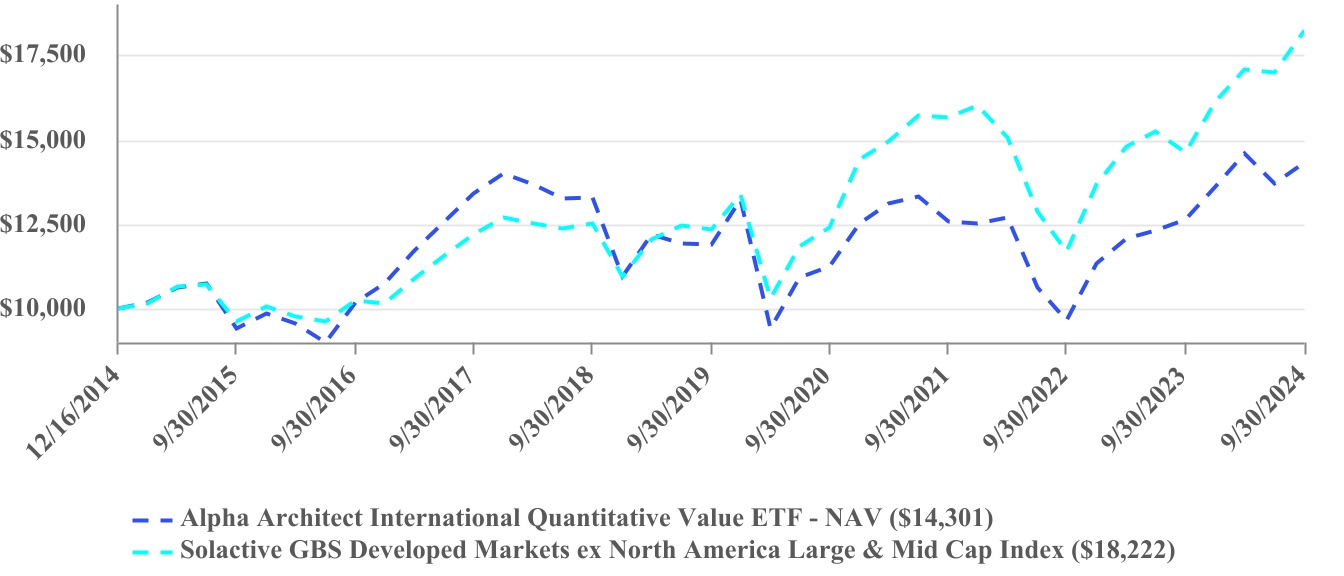

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | 5 Year | | Since Inception (12/16/2014) |

| Alpha Architect International Quantitative Value ETF - NAV | | 13.38% | | 3.79% | | 3.72% |

| Solactive GBS Developed Markets ex North America Large & Mid Cap Index | | 24.68% | | 8.12% | | 6.32% |

| | | | | | |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/ival for more recent performance information. |

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund returned 13.38% (NAV) for the Period vs. 24.68% for the Solactive GBS Developed Markets ex-North America Large Index. During the Period, markets reacted positively to strong corporate earnings, resilient economic conditions, and Federal Reserve policy, with larger-cap stocks leading performance. The Fund’s tilt toward deeper value stocks as measured by EBIT/TEV contributed negatively to returns relative to the benchmark.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect International Quantitative Value ETF Ticker: IVAL Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/ival |

|

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $150,759,000 | | Portfolio Turnover Rate* | | 155% |

| # of Portfolio Holdings | | 51 | | Advisory Fees Paid | | $632,933 |

| *Excludes impact of in-kind transactions. |

| | | | | | |

| | | | | |

SECTOR WEIGHTING

(as a % of Net Assets) |

| Industrials | 27.9% |

| Consumer Discretionary | 26.6% |

| Materials | 13.1% |

| Energy | 9.6% |

| Utilities | 8.0% |

| Consumer Staples | 8.0% |

| Information Technology | 3.9% |

| Real Estate | 1.9% |

| Investments Purchased with Proceeds from Securities Lending | 1.8% |

| Cash & Cash Equivalents | 0.1% |

| | | | | |

TOP 10 HOLDINGS

(as a % of Net Assets) |

| Rio Tinto Ltd. | 2.4% |

| Fortescue Ltd. | 2.4% |

| Rexel SA | 2.3% |

| SSAB AB - Class B | 2.2% |

| SKF AB - Class B | 2.2% |

| easyJet PLC | 2.1% |

| Aurizon Holdings Ltd. | 2.1% |

| Cie de Saint-Gobain SA | 2.1% |

| Yamazaki Baking Co. Ltd. | 2.1% |

| Fortum Oyj | 2.1% |

| | | | | |

COUNTRY WEIGHTING

(as a % of Net Assets) |

| Japan | 49.8% |

| France | 10.0% |

| Australia | 8.9% |

| United Kingdom | 7.9% |

| Sweden | 6.5% |

| Italy | 6.1% |

| Finland | 4.0% |

| Singapore | 2.0% |

| China | 1.9% |

| Portugal | 1.9% |

| United States | 1.9% |

Material Fund Changes

This is a summary of certain changes to the Fund since October 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/ival or by calling (215) 330-4476.

Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as the Fund’s sub-adviser.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/ival. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect U.S. Quantitative Momentum ETF Ticker: QMOM Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/qmom |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect U.S. Quantitative Momentum ETF (the “Fund”) for the period of October 1, 2023 to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/qmom. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $40 | 0.32% |

| | | | | | | | | | | |

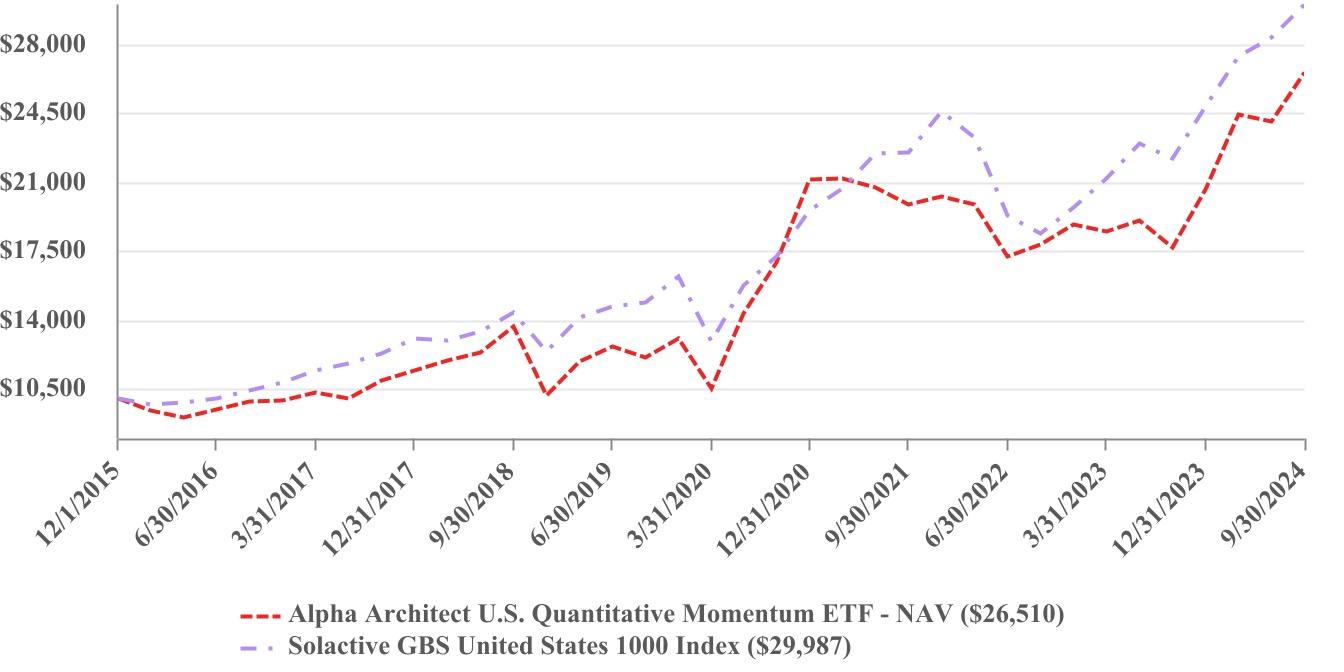

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | Since Inception (11/9/2022) |

| Alpha Architect U.S. Quantitative Momentum ETF - NAV | | 49.97% | 17.03% | 11.67% |

| | | | |

| Solactive GBS United States 1000 Index | | 35.20% | 15.06% | 13.24% |

| | | | |

| | | | |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/qmom for more recent performance information. |

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund returned 49.97% (NAV) for the Period vs. 35.20% for the Solactive GBS United States 1000 Index. During the Period, markets reacted positively to strong corporate earnings, resilient economic conditions, and Federal Reserve policy, with larger-cap stocks leading performance. The Fund’s tilt toward higher momentum stocks contributed positively to returns relative to the benchmark.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect U.S. Quantitative Momentum ETF Ticker: QMOM Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/qmom |

|

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $252,563,718 | | Portfolio Turnover Rate* | | 363% |

| # of Portfolio Holdings | | 51 | | Advisory Fees Paid | | $625,008 |

| *Excludes impact of in-kind transactions. |

| | | | | |

SECTOR WEIGHTING

(as a % of Net Assets) |

| Financials | 27.0% |

| Consumer Discretionary | 17.7% |

| Industrials | 16.1% |

| Information Technology | 13.9% |

| Utilities | 7.3% |

| Health Care | 5.9% |

| Communication Services | 4.2% |

| Consumer Staples | 3.9% |

| Materials | 2.1% |

| Energy | 1.6% |

| Cash & Cash Equivalents | 0.3% |

| | | | | |

TOP 10 HOLDINGS

(as a % of Net Assets) |

| Vistra Corp. | 2.7% |

| Constellation Energy Corp. | 2.5% |

| Zeta Global Holdings Corp. - Class A | 2.2% |

| Fair Isaac Corp. | 2.2% |

| Carpenter Technology Corp. | 2.1% |

| Blue Owl Capital, Inc. - Class A | 2.1% |

| EMCOR Group, Inc. | 2.1% |

| Meta Platforms, Inc. - Class A | 2.1% |

| Natera, Inc. | 2.1% |

| Trane Technologies PLC | 2.1% |

Material Fund Changes

This is a summary of certain changes to the Fund since October 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/qmom or by calling (215) 330-4476.

Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as the Fund’s sub-adviser.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/qmom. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect International Quantitative Momentum ETF Ticker: IMOM Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/imom |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect International Quantitative Momentum ETF (the “Fund”) for the period of October 1, 2023 to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/imom. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $46 | 0.42% |

| | | | | | | | | | | |

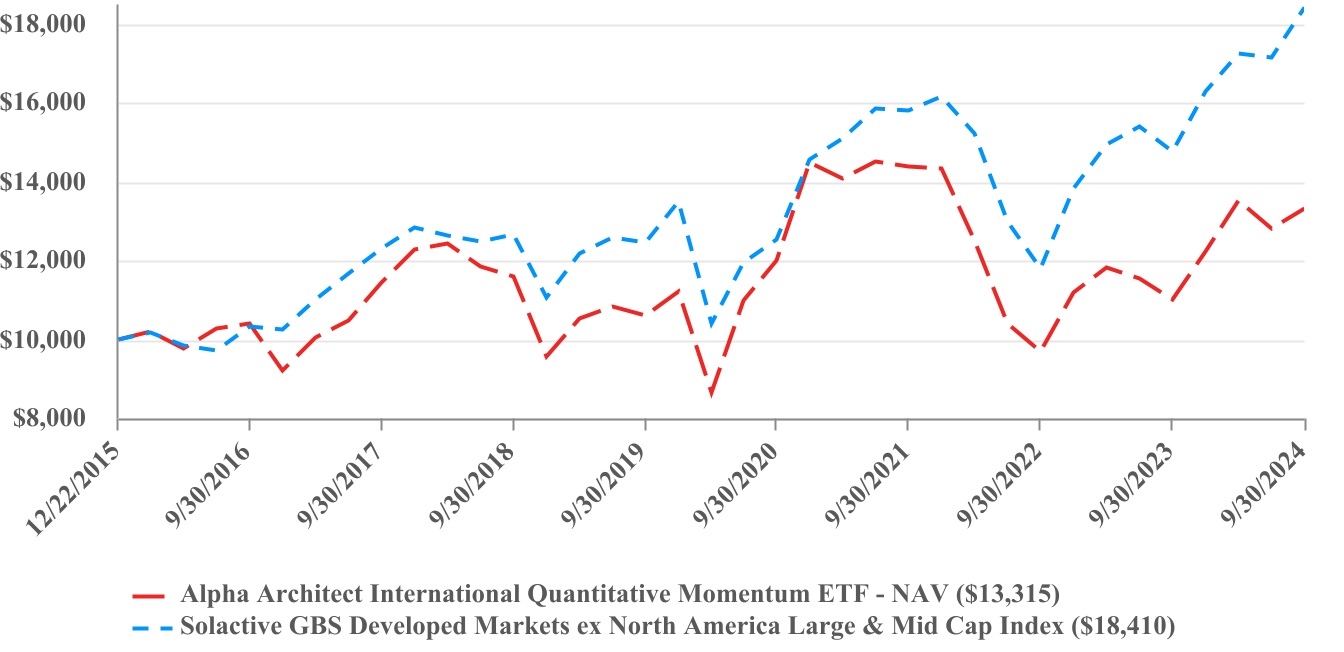

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | 5 Year | | Since Inception (12/22/2015) |

| Alpha Architect International Quantitative Momentum ETF - NAV | | 21.01% | | 4.65% | | 3.32% |

| | | | | | |

| Solactive GBS Developed Markets ex North America Large & Mid Cap Index | | 24.68% | | 8.12% | | 7.20% |

| | | | | | |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/ for more recent performance information. |

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund returned 21.01% (NAV) for the Period vs. 24.68% for the Solactive GBS Developed Markets ex-North America Large Index. During the Period, markets reacted positively to strong corporate earnings, resilient economic conditions, and Federal Reserve policy, with larger-cap stocks leading performance. The Fund’s tilt toward higher momentum stocks contributed negatively to returns relative to the benchmark.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect International Quantitative Momentum ETF Ticker: IMOM Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/imom |

|

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $82,652,321 | | Portfolio Turnover Rate* | | 219% |

| # of Portfolio Holdings | | 51 | | Advisory Fees Paid | | $332,566 |

| *Excludes impact of in-kind transactions. |

| | | | | |

SECTOR WEIGHTING

(as a % of Net Assets) |

| Financials | 31.8% |

| Industrials | 19.7% |

| Information Technology | 15.7% |

| Health Care | 8.4% |

| Communication Services | 6.2% |

| Materials | 6.2% |

| Consumer Discretionary | 5.9% |

| Consumer Staples | 2.1% |

| Energy | 1.9% |

| Real Estate | 1.3% |

| Cash & Cash Equivalents | 0.2% |

| | | | | |

TOP 10 HOLDINGS

(as a % of Net Assets) |

| Commerzbank AG | 2.5% |

| Telix Pharmaceuticals Ltd. | 2.4% |

| Pro Medicus Ltd. | 2.4% |

| Sea Ltd. - ADR | 2.3% |

| IHI Corp. | 2.2% |

| Rolls-Royce Holdings PLC | 2.2% |

| 3i Group PLC | 2.1% |

| Marks & Spencer Group PLC | 2.1% |

| Deutsche Bank AG | 2.1% |

| Asics Corp. | 2.1% |

| | | | | |

COUNTRY WEIGHTING

(as a % of Net Assets) |

| Japan | 27.0% |

| Italy | 9.9% |

| Australia | 8.7% |

| Germany | 8.4% |

| United Kingdom | 8.4% |

| Sweden | 7.8% |

| Denmark | 5.7% |

| Switzerland | 4.1% |

| Austria | 3.3% |

| Singapore | 2.3% |

| Israel | 2.0% |

| Spain | 2.0% |

| Ireland | 2.0% |

| Belgium | 1.9% |

| Norway | 1.9% |

| Portugal | 1.9% |

| Netherlands | 1.9% |

| United States | 0.2% |

Material Fund Changes

This is a summary of certain changes to the Fund since October 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/imom or by calling (215) 330-4476.

Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as the Fund’s sub-adviser.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/imom. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect Value Momentum Trend ETF Ticker: VMOT Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/vmot |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect Value Momentum Trend ETF (the “Fund”) for the period of October 1, 2023 to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/vmot. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $36 | 0.32% |

| | | | | | | | | | | |

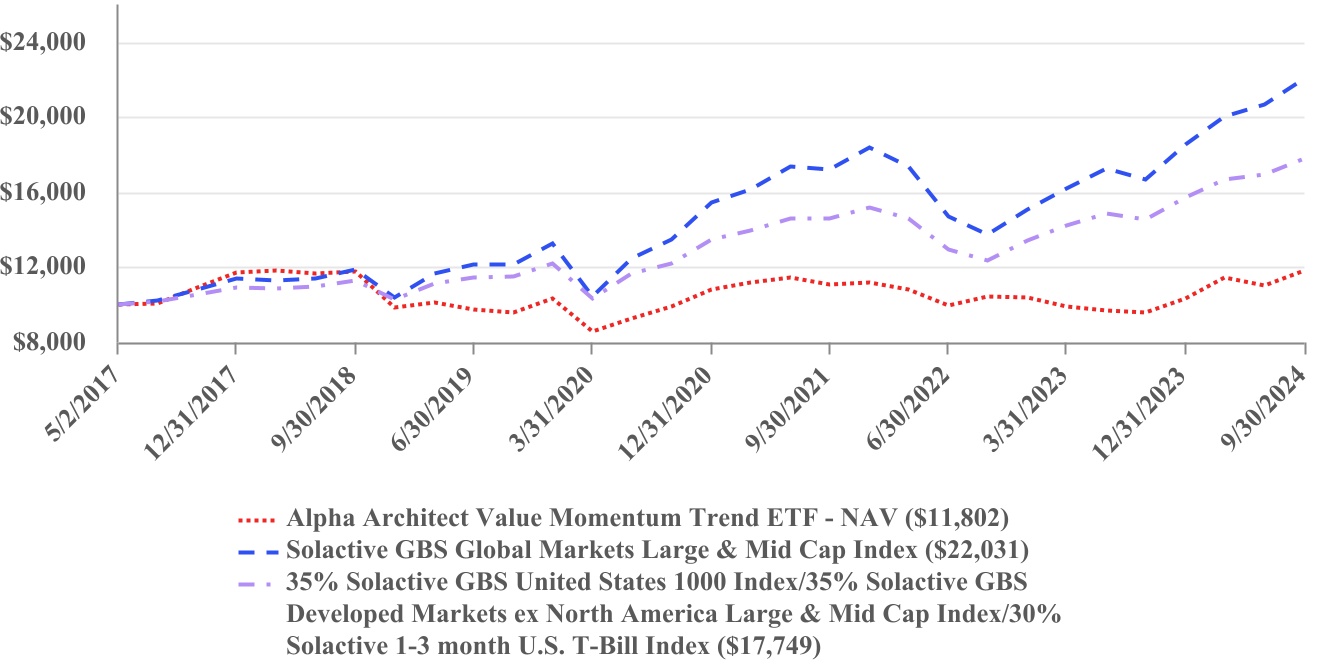

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | 5 Year | | Since Inception (5/2/2017) |

| Alpha Architect Value Momentum Trend ETF - NAV | | 23.05% | | 4.22% | | 2.26% |

| Solactive GBS Global Markets Large & Mid Cap Index | | 32.22% | | 12.66% | | 11.24% |

35% Solactive GBS United States 1000 Index/35% Solactive GBS Developed Markets ex North America Large & Mid Cap Index/30% Solactive 1-3 month U.S. T-Bill Index | | 22.25% | | 9.12% | | 8.05% |

| Solactive GBS United States 1000 Index | | 35.20% | | 15.06% | | 13.70% |

| Solactive GBS Developed Markets ex North America Large & Mid Cap Index | | 24.68% | | 8.12% | | 6.74% |

| Solactive 1-3 month U.S. T-Bill Index | | 5.51% | | 2.34% | | 2.15% |

| | | | | | |

| The Solactive GBS Global Markets Large & Mid Cap Index is provided as a broad measure of market performance. The 35% Solactive GBS United States 1000 Index/35% Solactive GBS Developed Markets ex North America Large & Mid Cap Index/30% Solactive 1-3 month U.S. T-Bill Index is provided as a measure of the Fund’s investment strategy and universe. |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/vmot for more recent performance information. |

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect Value Momentum Trend ETF Ticker: VMOT Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/vmot |

|

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund returned 23.05% (NAV) for the Period vs. 32.22% for the Solactive GBS Global Markets Large & Mid Cap Index. During the Period, markets reacted positively to strong corporate earnings, resilient economic conditions, and Federal Reserve policy, with larger-cap stocks leading performance. The Fund’s tilt toward (1) deeper value stocks as measured by EBIT/TEV, (2) higher momentum ex-U.S. stocks, (3) use of trend-following, and (4) relative value-momentum weighting detracted from returns relative to the benchmark, while exposure to higher momentum U.S. stocks contributed positively.

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $21,787,725 | | Advisory Fees | | $128,537 |

| # of Portfolio Holdings | | 5 | | Fees Waived and/or Expenses Reimbursed | | (37,970) |

| Portfolio Turnover Rate* | | 33% | | Net Advisory Fees Paid | | $90,567 |

| *Excludes impact of in-kind transactions. |

| | | | | |

SECTOR WEIGHTING

(as a % of Net Assets) |

| Exchange Traded Funds | 99.6% |

| Investments Purchased with Proceeds from Securities Lending | 10.8% |

| Cash & Cash Equivalents | 0.4% |

| | | | | |

TOP HOLDINGS

(as a % of Net Assets) |

| Alpha Architect US Quantitative Momentum ETF | 35.6% |

| Alpha Architect US Quantitative Value ETF | 29.9% |

| Alpha Architect International Quantitative Momentum ETF | 19.5% |

| Alpha Architect International Quantitative Value ETF | 14.6% |

Material Fund Changes

This is a summary of certain changes to the Fund since October 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/vmot or by calling (215) 330-4476.

Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as the Fund’s sub-adviser.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/vmot. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect High Inflation and Deflation ETF Ticker: HIDE Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/hide |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect High Inflation and Deflation ETF (the “Fund”) for the period of October 1, 2023, to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/hide. You can also request this information by contacting us at (215) 330-4476. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $24 | 0.24% |

| | | | | | | | | | | |

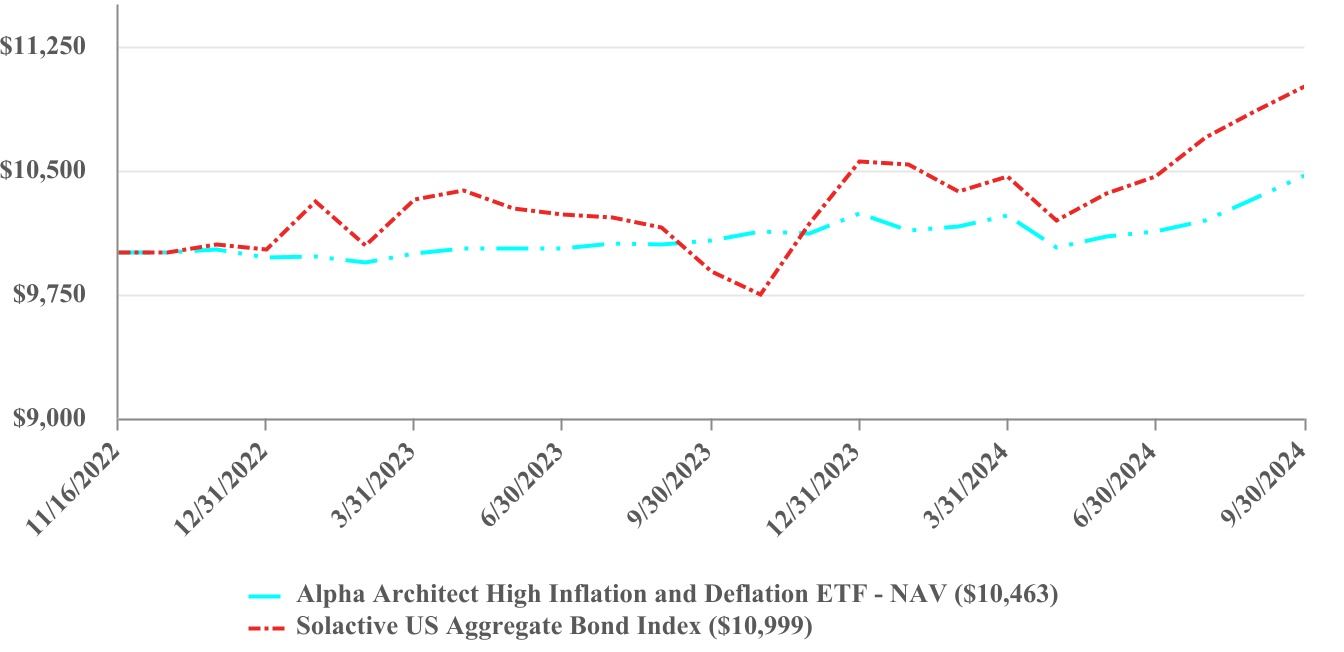

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | Since Inception (11/16/2022) |

| Alpha Architect High Inflation and Deflation ETF - NAV | | 3.91% | | 2.45% |

| | | | |

| Solactive US Aggregate Bond Index | | 11.25% | | 5.22% |

| | | | |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/hide for more recent performance information. |

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund returned 3.91% (NAV) for the Period vs. 11.25% for the Solactive US Aggregate Bond Index. During the Period, bond markets responded positively to strong corporate earnings, resilient economic conditions, and Federal Reserve policy. Bond markets also benefited from falling yields in the fiscal year. However, the Fund’s use of trend-following on REITs, bonds, and commodities contributed negatively to returns relative to the benchmark.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect High Inflation and Deflation ETF Ticker: HIDE Listed on: The Nasdaq Stock Market | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/hide |

|

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $30,270,823 | | Advisory Fees | | $62,674 |

| # of Portfolio Holdings | | 4 | | Fees Waived and/or Expenses Reimbursed | | (10,289) |

| Portfolio Turnover Rate* | | 267% | | Net Advisory Fees Paid | | $52,385 |

| *Excludes impact of in-kind transactions. |

| | | | | |

SECTOR WEIGHTING

(as a % of Net Assets) |

| Exchange Traded Funds | 75.8% |

| U.S. Treasury Bills | 23.7% |

| Cash & Cash Equivalents | 0.3% |

| | | | | |

TOP HOLDINGS

(as a % of Net Assets) |

| Schwab Intermediate-Term U.S. Treasury ETF | 51.2% |

| Vanguard Real Estate ETF | 24.6% |

| United States Treasury Bill 5.13%, 10/03/2024 | 23.6% |

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/hide. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect Tail Risk ETF Ticker: CAOS Listed on: Cboe BZX Exchange, Inc. | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/caos |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect Tail Risk ETF (the “Fund”) for the period of October 1, 2023 to September 30, 2024 (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/caos. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $55 | 0.53% |

| | | | | | | | | | | |

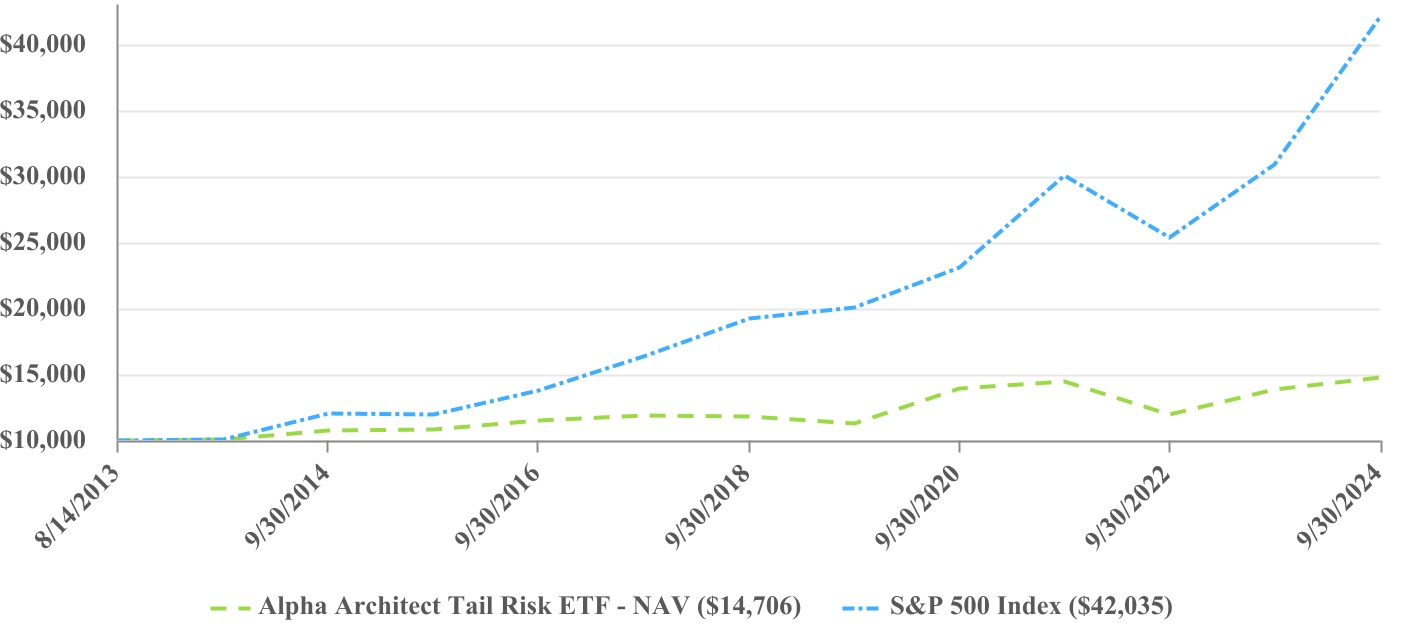

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | 5 Year | | 10 Year |

| Alpha Architect Tail Risk ETF - NAV | | 6.36% | | 5.48% | | 3.23% |

| S&P 500 Index | | 36.35% | | 15.98% | | 13.38% |

| | | | | | |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/caos for more recent performance information. |

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect Tail Risk ETF Ticker: CAOS Listed on: Cboe BZX Exchange, Inc. | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/caos |

|

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

As a tail risk fund, CAOS is designed to hedge against significant market downturns by using derivatives—primarily far-out-of-the-money put options on the S&P 500 Index—to protect portfolios during extreme market events. These far-out-of-the-money put options generally require periods of sharp market decline with an increase in implied volatility to gain value. If there is no such event, these options lose their value over time. To combat this erosion in value, the Fund employs two additional strategies in an effort to maintain its long volatility exposure while offering patient investors an opportunity for positive return during these sometimes long interim periods.

During the fiscal year, the equity market climbed higher, reducing the need for downside protection. The Fund trades short put spreads, which benefits the Fund should the market go higher. These put spreads involve selling a high strike put to gain market exposure, generally to the S&P 500 Index, and the purchase of a lower strike put on the same asset to limit any sizeable losses from the higher strike put. The maximum gain from this trade is the net premium collected at the outset of the trade, while the loss is equal to the difference in the strikes of the two put options less the initial net premium collected. This trade should benefit when the market climbs higher and was helpful to the Fund’s performance.

By the summer of 2024, growing concerns about a potential economic slowdown, coupled with speculation around possible rate cuts from the Federal Reserve, led to a modest increase in market volatility. The uptick in volatility towards the end of the fiscal year highlighted the potential of the Fund’s tail risk strategy. However, the degree to which the Federal Reserve sought to reduce short-term rates moderated. This delay permitted the Fund’s idle collateral to collect a stable return without equity market or volatility exposure. Similar to the put spread sales, the collateral yield positively contributed to the Fund return.

Overall, we believe the Fund provided valuable tail risk protection while managing hedging costs throughout the year, and it was well-positioned to deliver the intended downside protection as market conditions evolved.

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $248,524,832 | | Advisory Fees | | $1,192,650 |

| # of Portfolio Holdings | | 19 | | Fees Waived and/or Expenses Reimbursed | | (186,924) |

| Portfolio Turnover Rate* | | 14% | | Net Advisory Fees Paid | | $1,005,726 |

| *Excludes impact of in-kind transactions. |

| | | | | |

| ASSET CLASSES (as a % of Net Assets) |

| Purchased Options | 117.0% |

| Exchange Traded Funds | 11.7% |

| Written Options | (29.2)% |

| Cash & Cash Equivalents | 0.5% |

Material Fund Changes

This is a summary of certain changes to the Fund since October 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/caos or by calling (215) 330-4476.

Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as a sub-adviser to the Fund.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/caos. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect 1-3 Month Box ETF Ticker: BOXX Listed on: Cboe BZX Exchange, Inc. | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/boxx |

|

| | | | | | | | | | | |

| This annual shareholder report contains important information about the Alpha Architect 1-3 Month Box ETF (the “Fund”) for the period of November 1, 2023 to September 30, 2024, (the “Period”). You can find additional information about the Fund at https://funds.alphaarchitect.com/. You can also request this information by contacting us at (215) 330-4476. This report describes changes to the Fund that occurred during the Period. |

| | | | | | | | | | | |

WHAT WERE THE FUND COSTS FOR THE PERIOD?

(based on a hypothetical $10,000 investment) |

| COST OF $10,000 INVESTMENT | COST PAID AS A PERCENTAGE OF $10,000 INVESTMENT |

| $18 | 0.1949% |

| | | | | | | | | | | |

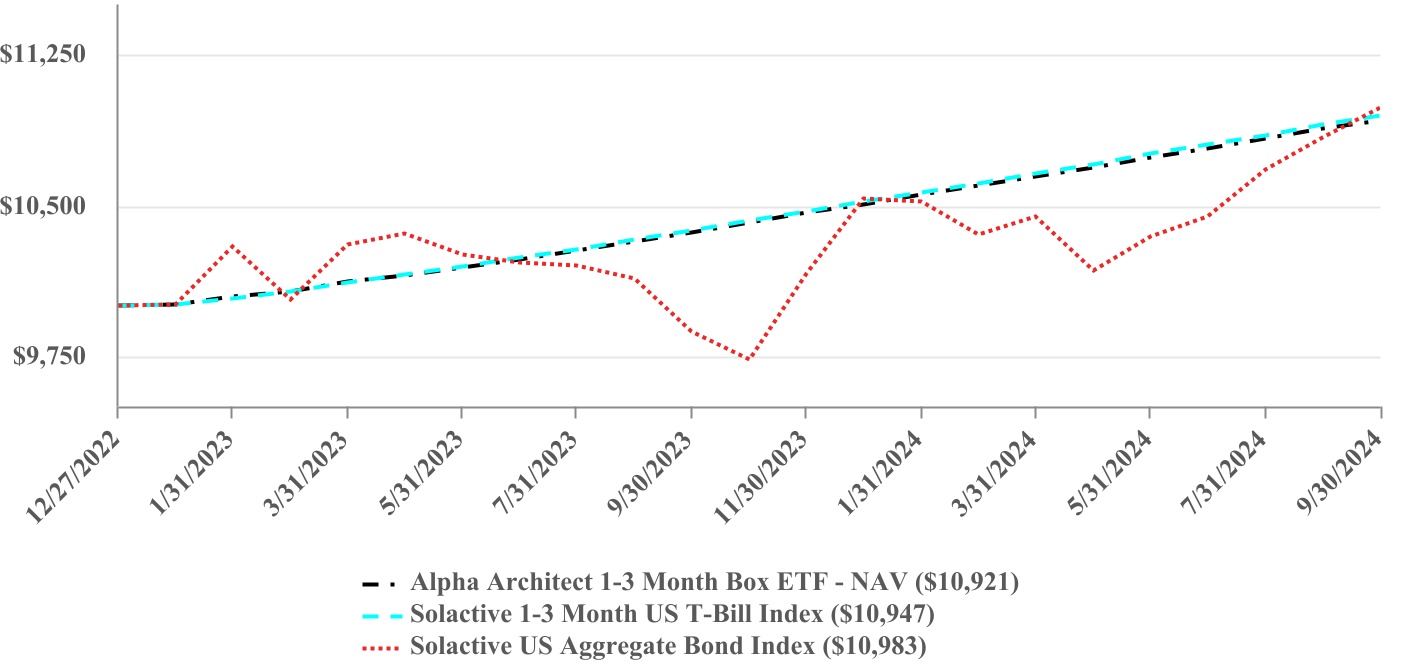

| PERFORMANCE OF A HYPOTHETICAL $10,000 INVESTMENT |

| | | | | | | | | | | | | | |

| AVERAGE ANNUAL TOTAL RETURNS |

| | 1 Year | | Since Inception (12/27/2022) |

| Alpha Architect 1-3 Month Box ETF - NAV | | 5.40% | | 5.14% |

| Solactive US Aggregate Bond Index | | 11.25% | | 5.48% |

| Solactive 1-3 Month US T-Bill Index | | 5.51% | | 5.28% |

| | | | |

| The Solactive US Aggregate Bond Index is provided as a broad measure of market performance. The Solactive 1-3 Month US T-Bill Index is provided as a measure of the Fund’s investment objective and strategy. |

The Fund’s past performance is not a good predictor of how the Fund will perform in the future. The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. Visit https://funds.alphaarchitect.com/boxx for more recent performance information. |

Annual Shareholder Report: September 30, 2024

| | | | | | | | |

| Alpha Architect 1-3 Month Box ETF Ticker: BOXX Listed on: Cboe BZX Exchange, Inc. | September 30, 2024 Annual Shareholder Report https://funds.alphaarchitect.com/boxx |

|

| | | | | | | | | | | |

| WHAT FACTORS INFLUENCED PERFORMANCE FOR THE PERIOD? |

The Fund benefited from the low-volatility environment and expectations for future rate cuts. The Fund primarily uses a strategy centered on derivatives, specifically box spreads utilizing options, such as those linked to the S&P 500.

•Stable Interest Rates: For much of the fiscal year, short-term interest rates remained stable, as the Federal Reserve maintained its interest rate policy after a period of aggressive tightening. This environment provided a consistent backdrop for the Fund’s box spread strategy, which aims to provide investment results that, before fees and expenses, equal or exceed the price and yield performance of an investment that tracks the 1-3 month sector of the United States Treasury Bill market.

•Increased Market Optimism in Mid-2024: By the summer of 2024, market sentiment shifted as expectations for rate cuts grew due to signs of economic slowing and inflation moderation. The Fund’s strategy benefited from the calm market environment as volatility remained low. This allowed the Fund to achieve modest positive returns without being impacted by the more pronounced shifts in longer-duration fixed-income securities.

•Derivatives Liquidity: Throughout the year, the liquidity of the options market, in which the Fund’s box spreads are executed, remained robust. This allowed the Fund to operate efficiently without major disruptions.

| | | | | | | | | | | | | | | | | | | | |

| KEY FUND STATISTICS (as of Period End) |

| Net Assets | | $3,968,953,465 | | Advisory Fees | | $8,116,529 |

| # of Portfolio Holdings | | 33 | | Fees Waived and/or Expenses Reimbursed | | (4,110,676) |

| Portfolio Turnover Rate* | | 0% | | Net Advisory Fees Paid | | $4,005,853 |

| *Portfolio turnover is not annualized and is calculated without regard to short-term securities having a maturity of less than one year. Excludes impact of in-kind transactions. |

| | | | | |

| ASSET CLASSES (as a % of net assets) |

| Purchased Options | 158.5% |

| Written Options | (58.5)% |

Material Fund Changes

This is a summary of certain changes to the Fund since November 1, 2023. For more complete information, you may review the Fund’s next prospectus, which we expect to be available by January 31, 2025, at funds.alphaarchitect.com/boxx or by calling (215) 330-4476.

•Effective June 21, 2024, the Fund’s Board of Trustees approved Alpha Architect, LLC to serve as a sub-adviser to the Fund.

•The Fund revised its principal investment strategies to reflect, among other things, its use of options on broad-based diversified assets such as the SPDR® S&P 500® ETF Trust for substantially all of the Fund’s holdings. The Fund also added “Tax Risk” as a principal investment risk.

•Effective November 12, 2024, the Adviser reduced the Fund’s management fee from 0.3949% to 0.2449%.

Availability of Additional Information

For additional information about the Fund, including its prospectus, financial information, holdings, and proxy information, visit https://funds.alphaarchitect.com/boxx. You can also request information by calling (215) 330-4476.

Householding

Householding is an option available to certain investors of the Fund. Householding is a method of delivery, based on the preference of the individual investor, in which a single copy of certain shareholder documents can be delivered to investors who share the same address, even if their accounts are registered under different names. Householding for the Fund is available through certain broker-dealers. If you are interested in enrolling in householding and receiving a single copy of prospectuses and other shareholder documents or you are currently enrolled in householding and wish to change your householding status, please contact your broker-dealer.

Annual Shareholder Report: September 30, 2024

(b) Not applicable

Item 2. Code of Ethics.

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer and principal financial officer. The registrant has not made any amendments to its code of ethics during the year covered by this report. The registrant has not granted any waivers from any provisions of the code of ethics during the year covered by this report.

A copy of the registrant’s Code of Ethics is incorporated by reference.

Item 3. Audit Committee Financial Expert.

The registrant’s Board of Trustees of the Trust has determined that there is at least one audit committee financial expert serving on its audit committee. Dr. Michael Pagano is an “audit committee financial expert” and is considered to be “independent” as each term is defined in Item 3 of Form N-CSR.

Item 4. Principal Accountant Fees and Services.

The registrant has engaged its principal accountant to perform audit services, audit-related services, tax services and other services during the past fiscal year. “Audit services” refer to performing an audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years. “Audit-related services” refer to the assurance and related services by the principal accountant that are reasonably related to the performance of the audit. “Tax services” refer to professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning, including review of the registrant’s tax returns and calculations of required income, capital gain and excise distributions. There were no “Other services” provided by the principal accountant. The following table details the aggregate fees billed or expected to be billed for the last fiscal year for audit fees, audit-related fees, tax fees and other fees by the principal accountant.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| QVAL | | IVAL | | QMOM | | IMOM |

| | FYE 9/30/2024 | FYE 9/30/2023 | | FYE 9/30/2024 | FYE 9/30/2023 | | FYE 9/30/2024 | FYE 9/30/2023 | | FYE 9/30/2024 | FYE 9/30/2023 |

| (a) Audit Fees | $8,750 | $8,750 | | $8,750 | $8,750 | | $8,750 | $8,750 | | $8,750 | $8,750 |

| (b) Audit-Related Fees | N/A | N/A | | N/A | N/A | | N/A | N/A | | N/A | N/A |

| (c) Tax Fees | $2,250 | $2,250 | | $2,250 | $2,250 | | $2,250 | $2,250 | | $2,250 | $2,250 |

| (d) All Other Fees | N/A | N/A | | N/A | N/A | | N/A | N/A | | N/A | N/A |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | VMOT | | HIDE | | CAOS | | BOXX |

FYE 9/30/2024 | FYE 9/30/2023 | | FYE 9/30/2024 | FYE 9/30/2023 | | FYE 9/30/2024 | FYE 9/30/2023 | | FYE 9/30/2024 | FYE 10/31/2023 |

| (a) Audit Fees | $8,750 | $8,750 | | $8,750 | $8,750 | | $11,000 | $8,750 | | $11,000 | $8,750 |

| (b) Audit-Related Fees | N/A | N/A | | N/A | N/A | | N/A | N/A | | N/A | N/A |

| (c) Tax Fees | $2,250 | $2,250 | | $2,250 | $2,250 | | $2,500 | $2,250 | | $2,500 | $2,250 |

| (d) All Other Fees | N/A | N/A | | N/A | N/A | | N/A | N/A | | N/A | N/A |

(e)(1) The audit committee has adopted pre-approval policies and procedures that require the audit committee to pre-approve all audit and non-audit services of the registrant, including services provided to any entity affiliated with the registrant.

(e)(2) None of the fees billed by any Fund's principal accountant were applicable to non-audit services pursuant to a waiver of the pre-approval requirement.

(f) All of the principal accountant’s hours spent on auditing the registrant’s financial statements were attributed to work performed by full-time permanent employees of the principal accountant.

(g) None of the fees billed by any Fund's principal accountant were applicable to non-audit services billed or expected to be billed to any Fund’s investment adviser.

(h) The audit committee of the board of trustees/directors has considered whether the provision of non-audit services that were rendered to the registrant's investment adviser is compatible with maintaining the principal accountant's independence and has concluded that the provision of such non-audit services by the accountant has not compromised the accountant’s independence.

(i) The registrant has not been identified by the U.S. Securities and Exchange Commission as having filed an annual report issued by a registered public accounting firm branch or office that is located in a foreign jurisdiction where the Public Company Accounting Oversight Board is unable to inspect or completely investigate because of a position taken by an authority in that jurisdiction..

(j) The registrant is not a foreign issuer.

Item 5. Audit Committee of Listed Registrants.

(a) The registrant is an issuer as defined in Rule 10A-3 under the Securities Exchange Act of 1934, (the “Act”) and has a separately-designated standing audit committee established in accordance with Section 3(a)(58)(A) of the Act. The independent members of the committee are as follows: Daniel Dorn, Chukwuemeka (Emeka) Oguh, and Michael Pagano.

(b) Not applicable.

Item 6. Investments

(a)

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.7% |

| Shares |

| Value |

| Advertising - 3.9% | | | |

|

| Interpublic Group of Cos., Inc. |

| 224,331 | |

| $ | 7,095,590 | |

| Omnicom Group, Inc. |

| 73,049 | |

| 7,552,536 | |

|

|

|

| 14,648,126 | |

|

|

|

|

|

| Apparel Retail - 2.1% | | | |

|

Urban Outfitters, Inc. (a) |

| 201,359 | |

| 7,714,063 | |

|

|

|

|

|

| Apparel, Accessories & Luxury Goods - 4.1% | | | |

|

| Carter's, Inc. |

| 110,644 | |

| 7,189,647 | |

| Tapestry, Inc. |

| 174,764 | |

| 8,210,413 | |

|

|

|

| 15,400,060 | |

|

|

|

|

|

| Brewers - 1.9% | | | |

|

| Molson Coors Beverage Co. - Class B |

| 126,708 | |

| 7,288,244 | |

|

|

|

|

|

| Broadcasting - 2.0% | | | |

|

| Fox Corp. - Class A |

| 176,808 | |

| 7,484,283 | |

|

|

|

|

|

| Building Products - 4.2% | | | |

|

| Owens Corning |

| 43,648 | |

| 7,704,745 | |

| UFP Industries, Inc. |

| 60,539 | |

| 7,943,322 | |

|

|

|

| 15,648,067 | |

|

|

|

|

|

| Cable & Satellite - 2.1% | | | |

|

| Comcast Corp. - Class A |

| 185,067 | |

| 7,730,249 | |

|

|

|

|

|

| Coal & Consumable Fuels - 2.0% | | | |

|

| CONSOL Energy, Inc. |

| 71,520 | |

| 7,484,568 | |

|

|

|

|

|

| Construction Machinery & Heavy Transportation Equipment - 8.0% | | | |

|

| Allison Transmission Holdings, Inc. |

| 79,687 | |

| 7,655,530 | |

| Caterpillar, Inc. |

| 20,657 | |

| 8,079,366 | |

| PACCAR, Inc. |

| 76,626 | |

| 7,561,453 | |

| Terex Corp. |

| 130,935 | |

| 6,927,771 | |

|

|

|

| 30,224,120 | |

|

|

|

|

|

| Copper - 2.2% | | | |

|

| Freeport-McMoRan, Inc. |

| 166,622 | |

| 8,317,770 | |

|

|

|

|

|

| Electrical Components & Equipment - 2.6% | | | |

|

| Powell Industries, Inc. |

| 44,557 | |

| 9,891,208 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

1

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.7% (CONTINUED) |

| Shares |

| Value |

| Electronic Manufacturing Services - 2.1% | | | |

|

| Jabil, Inc. |

| 67,180 | |

| $ | 8,050,179 | |

|

|

|

|

|

| Footwear - 3.9% | | | |

|

Crocs, Inc. (a) |

| 50,562 | |

| 7,321,883 | |

Skechers USA, Inc. - Class A (a) |

| 108,254 | |

| 7,244,358 | |

|

|

|

| 14,566,241 | |

|

|

|

|

|

| Health Care Facilities - 2.0% | | | |

|

Tenet Healthcare Corp. (a) |

| 44,488 | |

| 7,393,906 | |

|

|

|

|

|

Health Care Services - 2.1% | | | |

|

| CVS Health Corp. |

| 127,581 | |

| 8,022,293 | |

|

|

|

|

|

| Homebuilding - 4.0% | | | |

|

| KB Home |

| 88,372 | |

| 7,572,597 | |

| Lennar Corp. - Class A |

| 40,463 | |

| 7,586,003 | |

|

|

|

| 15,158,600 | |

|

|

|

|

|

| Homefurnishing Retail - 2.3% | | | |

|

| Williams-Sonoma, Inc. |

| 54,992 | |

| 8,519,361 | |

|

|

|

|

|

| Industrial Machinery & Supplies & Components - 3.9% | | | |

|

Gates Industrial Corp. PLC (a) |

| 406,127 | |

| 7,127,529 | |

| Snap-on, Inc. |

| 25,855 | |

| 7,490,452 | |

|

|

|

| 14,617,981 | |

|

|

|

|

|

| Integrated Telecommunication Services - 2.1% | | | |

|

| AT&T, Inc. |

| 352,825 | |

| 7,762,150 | |

|

|

|

|

|

| IT Consulting & Other Services - 1.9% | | | |

|

| Cognizant Technology Solutions Corp. - Class A |

| 93,996 | |

| 7,254,611 | |

|

|

|

|

|

| Leisure Products - 1.9% | | | |

|

Mattel, Inc. (a) |

| 383,120 | |

| 7,298,436 | |

|

|

|

|

|

| Managed Health Care - 5.5% | | | |

|

Centene Corp. (a) |

| 89,493 | |

| 6,737,033 | |

| Elevance Health, Inc. |

| 13,132 | |

| 6,828,640 | |

Molina Healthcare, Inc. (a) |

| 20,849 | |

| 7,183,732 | |

|

|

|

| 20,749,405 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

2

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.7% (CONTINUED) |

| Shares |

| Value |

| Oil & Gas Equipment & Services - 9.1% | | | |

|

| Baker Hughes Co. |

| 208,684 | |

| $ | 7,543,927 | |

| Halliburton Co. |

| 236,115 | |

| 6,859,141 | |

| Liberty Energy, Inc. |

| 358,817 | |

| 6,849,816 | |

| Schlumberger NV |

| 167,390 | |

| 7,022,010 | |

| Weatherford International PLC |

| 70,379 | |

| 5,976,585 | |

|

|

|

| 34,251,479 | |

|

|

|

|

|

| Oil & Gas Exploration & Production - 3.4% | | | |

|

| Devon Energy Corp. |

| 163,745 | |

| 6,405,704 | |

| SM Energy Co. |

| 161,818 | |

| 6,467,866 | |

|

|

|

| 12,873,570 | |

|

|

|

|

|

| Oil & Gas Refining & Marketing - 1.8% | | | |

|

| Marathon Petroleum Corp. |

| 41,185 | |

| 6,709,448 | |

|

|

|

|

|

| Other Specialty Retail - 6.6% | | | |

|

| Academy Sports & Outdoors, Inc. |

| 133,217 | |

| 7,774,544 | |

| Signet Jewelers Ltd. |

| 86,911 | |

| 8,964,001 | |

Ulta Beauty, Inc. (a) |

| 20,654 | |

| 8,036,884 | |

|

|

|

| 24,775,429 | |

|

|

|

|

|

| Paper & Plastic Packaging Products & Materials - 1.9% | | | |

|

| Graphic Packaging Holding Co. |

| 246,641 | |

| 7,298,107 | |

|

|

|

|

|

| Passenger Airlines - 2.3% | | | |

|

| Delta Air Lines, Inc. |

| 172,915 | |

| 8,782,353 | |

|

|

|

|

|

| Specialized Consumer Services - 2.0% | | | |

|

| H&R Block, Inc. |

| 115,263 | |

| 7,324,964 | |

|

|

|

|

|

| Steel - 2.0% | | | |

|

| Arch Resources, Inc. |

| 53,444 | |

| 7,383,823 | |

|

|

|

|

|

| Tobacco - 1.8% | | | |

|

| Altria Group, Inc. |

| 136,066 | |

| 6,944,809 | |

|

|

|

|

|

| Trading Companies & Distributors - 2.0% | | | |

|

| WESCO International, Inc. |

| 44,700 | |

| 7,508,706 | |

TOTAL COMMON STOCKS (Cost $346,457,717) | | |

| 375,076,609 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

3

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| SHORT-TERM INVESTMENTS - 0.2% | | Shares |

| Value |

| Money Market Funds - 0.2% |

| |

| |

First American Government Obligations Fund - Class X, 4.82% (b) |

| 907,975 | |

| $ | 907,975 | |

TOTAL SHORT-TERM INVESTMENTS (Cost $907,975) | | |

| 907,975 | |

|

|

|

|

|

TOTAL INVESTMENTS - 99.9% (Cost $347,365,692) | | |

| $ | 375,984,584 | |

| Other Assets in Excess of Liabilities - 0.1% | | |

| 236,894 | |

| TOTAL NET ASSETS - 100.0% |

| |

| $ | 376,221,478 | |

Percentages are stated as a percent of net assets.

| | |

| NV - Naamloze Vennootschap |

| | | | | | | | |

| (a) |

| Non-income producing security. |

| (b) |

| The rate shown represents the 7-day effective yield as of September 30, 2024. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by U.S. Bank Global Fund Services.

The accompanying notes are an integral part of these financial statements.

4

| | |

| ALPHA ARCHITECT INTERNATIONAL QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.0% |

| Shares |

| Value |

| Australia - 8.9% | | | |

|

| AGL Energy Ltd. |

| 376,277 | |

| $ | 3,077,436 | |

| Aurizon Holdings Ltd. |

| 1,294,828 | |

| 3,159,973 | |

| Fortescue Ltd. |

| 248,728 | |

| 3,556,082 | |

| Rio Tinto Ltd. |

| 40,718 | |

| 3,635,048 | |

|

|

|

| 13,428,539 | |

|

|

|

|

|

| China - 1.9% | | | |

|

| Yangzijiang Shipbuilding Holdings Ltd. |

| 1,495,130 | |

| 2,850,083 | |

|

|

|

|

|

| Finland - 4.0% | | | |

|

| Fortum Oyj |

| 188,683 | |

| 3,107,436 | |

| Nokia Oyj |

| 671,887 | |

| 2,934,808 | |

|

|

|

| 6,042,244 | |

|

|

|

|

|

| France - 10.0% | | | |

|

| Cie de Saint-Gobain SA |

| 34,406 | |

| 3,129,803 | |

| Cie Generale des Etablissements Michelin SCA |

| 75,847 | |

| 3,078,290 | |

| Eiffage SA |

| 27,562 | |

| 2,658,175 | |

| Engie SA |

| 166,146 | |

| 2,869,433 | |

| Rexel SA |

| 118,515 | |

| 3,426,097 | |

|

|

|

| 15,161,798 | |

|

|

|

|

|

| Italy - 6.1% | | | |

|

| Buzzi SpA |

| 77,865 | |

| 3,102,986 | |

| Enel SpA |

| 379,181 | |

| 3,028,467 | |

Saipem SpA (a) |

| 1,365,666 | |

| 3,007,703 | |

|

|

|

| 9,139,156 | |

|

|

|

|

|

Japan - 49.8%(b) | | | |

|

| Amada Co. Ltd. |

| 286,794 | |

| 2,908,347 | |

| Asahi Kasei Corp. |

| 411,579 | |

| 3,098,476 | |

| Bridgestone Corp. |

| 76,417 | |

| 2,924,289 | |

| Daito Trust Construction Co. Ltd. |

| 23,828 | |

| 2,886,384 | |

| Hitachi Construction Machinery Co. Ltd. |

| 119,438 | |

| 2,884,462 | |

| Honda Motor Co. Ltd. |

| 268,205 | |

| 2,813,143 | |

| Inpex Corp. |

| 197,660 | |

| 2,665,264 | |

Japan Airlines Co. Ltd. (c) |

| 176,584 | |

| 3,093,061 | |

| Komatsu Ltd. |

| 107,075 | |

| 2,954,666 | |

| Macnica Holdings, Inc. |

| 217,854 | |

| 3,010,319 | |

| Mazda Motor Corp. |

| 349,582 | |

| 2,602,559 | |

| Niterra Co. Ltd. |

| 99,064 | |

| 2,753,597 | |

The accompanying notes are an integral part of these financial statements.

5

| | |

| ALPHA ARCHITECT INTERNATIONAL QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.0% (CONTINUED) |

| Shares |

| Value |

Japan - 49.8%(b) (Continued) | | | | |

| Nitto Denko Corp. |

| 176,440 | |

| $ | 2,932,176 | |

| Persol Holdings Co. Ltd. |

| 1,499,448 | |

| 2,679,132 | |

| Sekisui Chemical Co. Ltd. |

| 193,975 | |

| 3,011,690 | |

| Shimamura Co. Ltd. |

| 54,974 | |

| 2,992,636 | |

| Subaru Corp. |

| 155,215 | |

| 2,680,422 | |

| Suntory Beverage & Food Ltd. |

| 80,131 | |

| 3,007,317 | |

| Suzuki Motor Corp. |

| 257,532 | |

| 2,853,503 | |

| Takashimaya Co. Ltd. |

| 379,627 | |

| 3,019,055 | |

| Toyo Tire Corp. |

| 200,003 | |

| 2,904,201 | |

| Toyota Motor Corp. |

| 155,232 | |

| 2,746,059 | |

| Toyota Tsusho Corp. |

| 154,325 | |

| 2,775,649 | |

| Yamaha Motor Co. Ltd. |

| 333,441 | |

| 2,969,591 | |

| Yamazaki Baking Co. Ltd. |

| 157,103 | |

| 3,110,361 | |

| Yokohama Rubber Co. Ltd. |

| 128,689 | |

| 2,875,972 | |

|

|

|

| 75,152,331 | |

|

|

|

|

|

| Portugal - 1.9% | | | |

|

| Galp Energia SGPS SA |

| 150,727 | |

| 2,818,738 | |

|

|

|

|

|

| Singapore - 2.0% | | | |

|

| Hafnia Ltd. |

| 416,653 | |

| 2,965,109 | |

|

|

|

|

|

| Sweden - 6.5% | | | |

|

| SKF AB - Class B |

| 165,923 | |

| 3,300,211 | |

| SSAB AB - Class B |

| 662,012 | |

| 3,389,635 | |

| Volvo AB - Class B |

| 117,102 | |

| 3,092,479 | |

|

|

|

| 9,782,325 | |

|

|

|

|

|

| United Kingdom - 7.9% | | | |

|

| easyJet PLC |

| 463,002 | |

| 3,218,860 | |

| Imperial Brands PLC |

| 101,482 | |

| 2,948,252 | |

| Shell PLC |

| 86,311 | |

| 2,798,296 | |

| Tesco PLC |

| 615,936 | |

| 2,953,811 | |

|

|

|

| 11,919,219 | |

TOTAL COMMON STOCKS (Cost $148,454,401) | | |

| 149,259,542 | |

|

|

|

|

|

| SHORT-TERM INVESTMENTS - 1.9% | |

|

|

|

| Investments Purchased with Proceeds from Securities Lending - 1.8% |

| |

| |

First American Government Obligations Fund - Class X, 4.82% (d) |

| 2,701,695 | |

| 2,701,695 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

6

| | |

| ALPHA ARCHITECT INTERNATIONAL QUANTITATIVE VALUE ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| SHORT-TERM INVESTMENTS - 1.9% | | Shares | | Value |

| Money Market Funds - 0.1% |

| |

| |

First American Government Obligations Fund - Class X, 4.82% (d) |

| 150,545 | |

| $ | 150,545 | |

TOTAL SHORT-TERM INVESTMENTS (Cost $2,852,240) | | |

| 2,852,240 | |

|

|

|

|

|

TOTAL INVESTMENTS - 100.9% (Cost $151,306,641) | | |

| $ | 152,111,782 | |

| Liabilities in Excess of Other Assets - (0.9)% | | |

| (1,352,782) | |

| TOTAL NET ASSETS - 100.0% |

| |

| $ | 150,759,000 | |

Percentages are stated as a percent of net assets.

| | |

| AB - Aktiebolag |

| PLC - Public Limited Company |

| SA - Sociedad Anónima |

| | | | | | | | |

| (a) |

| Non-income producing security. |

| (b) |

| To the extent that the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is more likely to be impacted by events or conditions affecting the country or region. See the Fund’s prospectus for additional risk disclosures. |

| (c) |

| All or a portion of this security is on loan as of September 30, 2024. The total market value of these securities was $2,549,585 which represented 1.7% of net assets. |

| (d) |

| The rate shown represents the 7-day effective yield as of September 30, 2024. |

The accompanying notes are an integral part of these financial statements.

7

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE MOMENTUM ETF |

| SCHEDULE OF INVESTMENTS |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.7% |

| Shares |

| Value |

| Aerospace & Defense - 4.1% | | | |

|

| General Electric Co. |

| 27,846 | |

| $ | 5,251,199 | |

| Howmet Aerospace, Inc. |

| 50,156 | |

| 5,028,139 | |

|

|

|

| 10,279,338 | |

|

|

|

|

|

| Apparel Retail - 1.8% | | | |

|

Abercrombie & Fitch Co. - Class A (a) |

| 33,252 | |

| 4,651,955 | |

|

|

|

|

|

| Application Software - 6.2% | | | |

|

Fair Isaac Corp. (a) |

| 2,825 | |

| 5,490,444 | |

Nutanix, Inc. - Class A (a) |

| 76,838 | |

| 4,552,651 | |

Zeta Global Holdings Corp. - Class A (a) |

| 184,961 | |

| 5,517,387 | |

|

|

|

| 15,560,482 | |

|

|

|

|

|

| Asset Management & Custody Banks - 8.2% | | | |

|

| Blue Owl Capital, Inc. - Class A |

| 276,487 | |

| 5,352,788 | |

| Carlyle Group, Inc. |

| 121,551 | |

| 5,233,986 | |

| KKR & Co., Inc. |

| 39,355 | |

| 5,138,976 | |

| StepStone Group, Inc. - Class A |

| 88,955 | |

| 5,055,313 | |

|

|

|

| 20,781,063 | |

|

|

|

|

|

| Automotive Retail - 1.8% | | | |

|

| Murphy USA, Inc. |

| 9,368 | |

| 4,617,206 | |

|

|

|

|

|

| Biotechnology - 2.1% | | | |

|

Natera, Inc. (a) |

| 41,684 | |

| 5,291,784 | |

|

|

|

|

|

| Building Products - 6.1% | | | |

|

| Carlisle Cos., Inc. |

| 11,530 | |

| 5,185,617 | |

| Lennox International, Inc. |

| 8,289 | |

| 5,008,960 | |

| Trane Technologies PLC |

| 13,540 | |

| 5,263,404 | |

|

|

|

| 15,457,981 | |

|

|

|

|

|

| Construction & Engineering - 2.1% | | | |

|

| EMCOR Group, Inc. |

| 12,425 | |

| 5,349,335 | |

|

|

|

|

|

| Consumer Electronics - 1.9% | | | |

|

| Garmin Ltd. |

| 26,601 | |

| 4,682,574 | |

|

|

|

|

|

| Consumer Finance - 3.5% | | | |

|

| Ally Financial, Inc. |

| 112,522 | |

| 4,004,658 | |

| Synchrony Financial |

| 96,805 | |

| 4,828,633 | |

|

|

|

| 8,833,291 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

8

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE MOMENTUM ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.7% (CONTINUED) |

| Shares |

| Value |

| Diversified Banks - 3.8% | | | |

|

| Fifth Third Bancorp |

| 114,178 | |

| $ | 4,891,385 | |

| PNC Financial Services Group, Inc. |

| 26,135 | |

| 4,831,055 | |

|

|

|

| 9,722,440 | |

|

|

|

|

|

| Electric Utilities - 4.6% | | | |

|

| Constellation Energy Corp. |

| 24,492 | |

| 6,368,410 | |

| NRG Energy, Inc. |

| 57,648 | |

| 5,251,733 | |

|

|

|

| 11,620,143 | |

|

|

|

|

|

| Food Retail - 2.0% | | | |

|

Sprouts Farmers Market, Inc. (a) |

| 46,611 | |

| 5,146,320 | |

|

|

|

|

|

| Footwear - 1.9% | | | |

|

Deckers Outdoor Corp. (a) |

| 30,722 | |

| 4,898,623 | |

|

|

|

|

|

| Health Care Facilities - 3.8% | | | |

|

Tenet Healthcare Corp. (a) |

| 29,493 | |

| 4,901,737 | |

| Universal Health Services, Inc. - Class B |

| 20,405 | |

| 4,672,949 | |

|

|

|

| 9,574,686 | |

|

|

|

|

|

| Homebuilding - 4.1% | | | |

|

| KB Home |

| 58,540 | |

| 5,016,292 | |

| Toll Brothers, Inc. |

| 33,920 | |

| 5,240,301 | |

|

|

|

| 10,256,593 | |

|

|

|

|

|

| Independent Power Producers & Energy Traders - 2.7% | | | |

|

| Vistra Corp. |

| 56,941 | |

| 6,749,786 | |

|

|

|

|

|

| Interactive Media & Services - 2.1% | | | |

|

| Meta Platforms, Inc. - Class A |

| 9,302 | |

| 5,324,837 | |

|

|

|

|

|

| Internet Services & Infrastructure - 1.8% | | | |

|

GoDaddy, Inc. - Class A (a) |

| 29,097 | |

| 4,561,828 | |

|

|

|

|

|

| Investment Banking & Brokerage - 3.9% | | | |

|

| Evercore, Inc. - Class A |

| 19,812 | |

| 5,019,172 | |

| Goldman Sachs Group, Inc. |

| 9,513 | |

| 4,709,981 | |

|

|

|

| 9,729,153 | |

|

|

|

|

|

| Movies & Entertainment - 2.1% | | | |

|

Spotify Technology SA (a) |

| 14,085 | |

| 5,190,745 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

9

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE MOMENTUM ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.7% (CONTINUED) |

| Shares |

| Value |

| Oil & Gas Equipment & Services - 1.6% | | | |

|

Tidewater, Inc. (a) |

| 54,902 | |

| $ | 3,941,415 | |

|

|

|

|

|

| Property & Casualty Insurance - 3.9% | | | |

|

| Allstate Corp. |

| 25,672 | |

| 4,868,695 | |

| Progressive Corp. |

| 19,276 | |

| 4,891,477 | |

|

|

|

| 9,760,172 | |

|

|

|

|

|

| Regional Banks - 1.8% | | | |

|

| Truist Financial Corp. |

| 109,139 | |

| 4,667,875 | |

|

|

|

|

|

| Reinsurance - 1.9% | | | |

|

| Reinsurance Group of America, Inc. |

| 22,064 | |

| 4,807,084 | |

|

|

|

|

|

| Restaurants - 6.2% | | | |

|

Brinker International, Inc. (a) |

| 68,497 | |

| 5,242,076 | |

| Texas Roadhouse, Inc. |

| 28,705 | |

| 5,069,303 | |

| Wingstop, Inc. |

| 12,627 | |

| 5,253,842 | |

|

|

|

| 15,565,221 | |

|

|

|

|

|

| Soft Drinks & Non-alcoholic Beverages - 1.9% | | | |

|

| Coca-Cola Consolidated, Inc. |

| 3,627 | |

| 4,774,583 | |

|

|

|

|

|

| Steel - 2.1% | | | |

|

| Carpenter Technology Corp. |

| 33,677 | |

| 5,374,176 | |

|

|

|

|

|

| Systems Software - 1.9% | | | |

|

Crowdstrike Holdings, Inc. - Class A (a) |

| 17,362 | |

| 4,869,520 | |

| | | | |

| Technology Hardware, Storage & Peripherals - 4.0% | | | |

|

| NetApp, Inc. |

| 40,364 | |

| 4,985,357 | |

Western Digital Corp. (a) |

| 74,430 | |

| 5,082,825 | |

|

|

|

| 10,068,182 | |

|

|

|

|

|

| Trading Companies & Distributors - 3.8% | | | |

|

Core & Main, Inc. - Class A (a) |

| 100,270 | |

| 4,451,988 | |

| FTAI Aviation Ltd. |

| 38,423 | |

| 5,106,417 | |

|

|

|

| 9,558,405 | |

TOTAL COMMON STOCKS (Cost $217,733,813) | | |

| 251,666,796 | |

|

|

|

|

|

The accompanying notes are an integral part of these financial statements.

10

| | |

| ALPHA ARCHITECT U.S. QUANTITATIVE MOMENTUM ETF |

| SCHEDULE OF INVESTMENTS (CONTINUED) |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| SHORT-TERM INVESTMENTS - 0.3% | | Shares |

| Value |

| Money Market Funds - 0.3% |

| |

| |

First American Government Obligations Fund - Class X, 4.82% (b) |

| 866,204 | |

| $ | 866,204 | |

TOTAL SHORT-TERM INVESTMENTS (Cost $866,204) | | |

| 866,204 | |

|

|

|

|

|

TOTAL INVESTMENTS - 100.0% (Cost $218,600,017) | | |

| $ | 252,533,000 | |

Other Assets in Excess of Liabilities - 0.0% (c) | | |

| 30,718 | |

| TOTAL NET ASSETS - 100.0% |

| |

| $ | 252,563,718 | |

| | |

| PLC - Public Limited Company |

| SA - Sociedad Anónima |

| | | | | | | | |

| (a) |

| Non-income producing security. |

| (b) |

| The rate shown represents the 7-day effective yield as of September 30, 2024. |

| (c) |

| Represents less than 0.05% of net assets. |

The Global Industry Classification Standard (GICS®) was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor’s Financial Services LLC (“S&P”). GICS is a service mark of MSCI, Inc. and S&P and has been licensed for use by U.S. Bank Global Fund Services.

The accompanying notes are an integral part of these financial statements.

11

| | |

| ALPHA ARCHITECT INTERNATIONAL QUANTITATIVE MOMENTUM ETF |

| SCHEDULE OF INVESTMENTS |

| September 30, 2024 |

| | | | | | | | | | | | | | |

| COMMON STOCKS - 99.2% |

| Shares |

| Value |

| Australia - 8.7% | | | |

|

| JB Hi-Fi Ltd. |

| 29,731 | |

| $ | 1,643,124 | |

| Pro Medicus Ltd. |

| 15,920 | |

| 1,961,865 | |

Telix Pharmaceuticals Ltd. (a) |

| 136,891 | |

| 1,961,872 | |

| Westpac Banking Corp. |

| 76,127 | |

| 1,669,431 | |

|

|

|

| 7,236,292 | |

|

|

|

|

|

| Austria - 3.3% | | | |

|

| Erste Group Bank AG |

| 30,354 | |

| 1,664,089 | |

Immofinanz AG (a) |

| 55,426 | |

| 1,108,088 | |

|

|

|

| 2,772,177 | |

|

|

|

|

|

| Belgium - 1.9% | | | |

|

| UCB SA |

| 8,749 | |

| 1,577,712 | |

|

|

|

|

|

| Denmark - 5.7% | | | |

|

| Novonesis (Novozymes) B |

| 23,728 | |

| 1,708,587 | |

| Pandora AS |

| 9,285 | |

| 1,528,655 | |

Zealand Pharma AS (a) |

| 12,473 | |

| 1,514,295 | |

|

|

|

| 4,751,537 | |

|

|

|

|

|

| Germany - 8.4% | | | |

|

| Commerzbank AG |

| 110,595 | |

| 2,034,377 | |

| Deutsche Bank AG |

| 100,818 | |

| 1,739,275 | |

| Rheinmetall AG |

| 2,710 | |

| 1,467,294 | |

| SAP SE |

| 7,504 | |

| 1,707,372 | |

|

|

|

| 6,948,318 | |

|

|

|

|

|

| Ireland - 2.0% | | | |

|