|

Exhibit (c)(6)

Strictly Confidential

Presentation to the Conflicts Committee of the Board of Directors of CPP

GP LLC

November 1, 2016 / Confidential

Jefferies LLC

Member SIPC

Disclaimer

Strictly Confidential

The following pages contain materials provided to the Conflicts Committee of the Board of Directors (the “Committee”) of

CPP GP LLC, the general partner of Columbia Pipeline Partners, LP (“CPPL”), by Jefferies LLC (“Jefferies”) in

connection with a transaction involving CPPL and Columbia Pipeline Group (“CPGX”).

These materials were prepared on a confidential basis in connection with an oral presentation to the Committee and not with a view toward complying with the disclosure standards under state or federal securities laws. These materials are for use of the Committee and may not be used for any other purpose or disclosed to any party without Jefferies’ prior written consent.

The information contained in this presentation is based solely on publicly available information or information furnished to Jefferies by CPGX management. Jefferies has relied, without independent investigation or verification, on the accuracy, completeness and fair presentation of all such information and the conclusions contained herein are conditioned upon such information (whether written or oral) being accurate, complete and fairly presented in all respects. These materials are necessarily based on economic, market and other conditions as they exist on, and information made available as of, the date hereof. None of Jefferies, its affiliates or its or their respective employees, directors, officers, contractors, advisors, members, successors or agents makes any representation or warranty in respect of the accuracy, completeness or fair presentation of any information or any conclusion contained herein.

Neither Jefferies nor any of its affiliates is an advisor as to legal, tax, accounting or regulatory matters in any jurisdiction. These materials are not and should not be construed as a fairness opinion.

Jefferies consents to the use of this presentation by CPPL for purposes of public disclosure in the Schedule13E-3.

Jefferies LLC / November 2016

i

Jefferies

|

Table of Contents

Strictly Confidential

Transaction Overview 1

Market Update 5

Valuation Analysis 11

Appendix

Weighted Average Cost of Capital Analyses 25

Jefferies LLC / November 2016 ii

|

Strictly Confidential

Transaction Overview

Jefferies LLC / November 2016 1

|

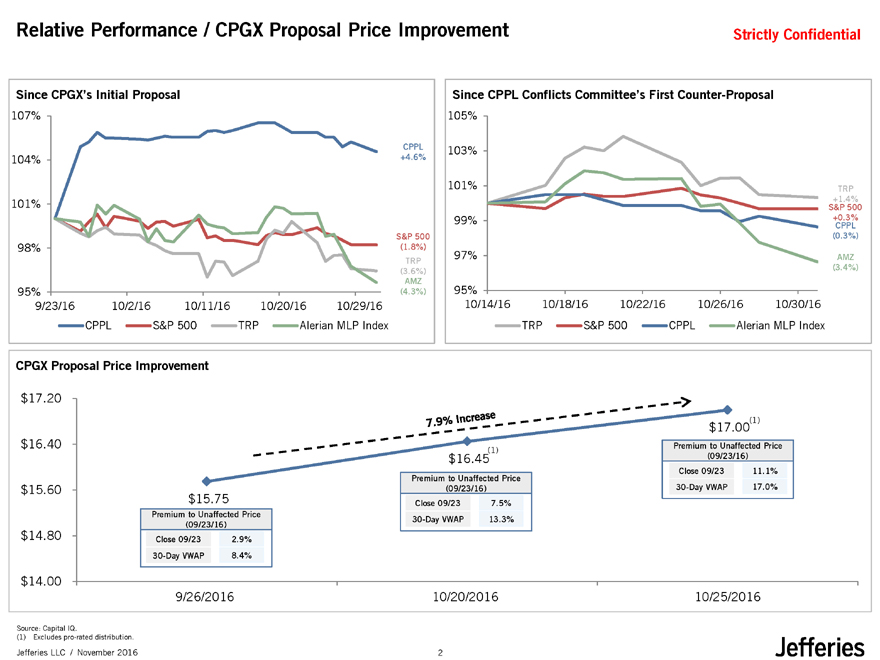

Relative Performance / CPGX Proposal Price Improvement

Strictly Confidential

Since CPGX’s Initial Proposal

107%

CPPL

104% +4.6%

101%

S&P 500

98% (1.8%)

TRP

(3.6%)

AMZ

95% (4.3%)

9/23/16 10/2/16 10/11/1610/20/1610/29/16

CPPL S&P 500TRPAlerian MLP Index

Since CPPL Conflicts Committee’s First Counter-Proposal

105%

103%

101% TRP

+1.4%

S&P 500

99% +0.3% CPPL

(0.3%)

97% AMZ

(3.4%)

95%

10/14/16 10/18/16 10/22/1610/26/1610/30/16

TRP S&P 500CPPLAlerian MLP Index

Source: Capital IQ.

(1) Excludes pro-rated distribution.

Jefferies LLC / November 2016 2

|

CPGX Purchase Price Analysis

($Millions, except per unit values)

Strictly Confidential

Transaction Overview

CPGX’s Purchase Price

Purchase Price Per CPPL Unit $17.00

CPPL Common Units Outstanding 53.8

Implied Common Unit Equity Purchase Price $915.3

Purchase Price

Purchase Price Analysis Metric Price$17.00

Premium / (Discount) to CPPL: Unaffected Price (as of 09/23/16) $15.3011.1%

10-Day VWAP (as of 09/23/16) 14.9213.9%

20-Day VWAP (as of 09/23/16) 14.6715.9%

30-Day VWAP (as of 09/23/16) 14.5217.0%

52-Week High 19.49(12.8%)

52-Week Low 11.7744.4%

Current Price (as of 10/31/16) 16.006.3%

Median Wall Street Consensus Price Target(1) 17.000.0%

IPO Price (as of 02/06/15) 23.00(26.1%)

Purchase Price $17.00

CPPL Fully Diluted Units Outstanding (MM) 100.7

Implied CPPL Transaction Equity Value $1,711.1

Plus: Implied GP Value(2) $8.9

Plus: CPPL Revolver(3) 53.8

Plus: OpCo Debt Attributable to CPPL(4) 179.1

Plus: Preferred(3) -

Plus: Non-Controlling Interest(3) -

Less: Cash & Cash Equivalents(4) 1.6

Implied CPPL Enterprise Value $1,951.4

Implied

Transaction

CPPL Statistics Statistic(3)Multiple

Implied Transaction Total Enterprise Value / 2017E EBITDA Attributable to CPPL $120.216.2x

Implied Transaction Total Enterprise Value / 2018E EBITDA Attributable to CPPL 166.811.7x

Source: Public filings, Capital IQ and Wall Street research. (1) See page 10.

(2) Implied value of GP interest based on 2016E GP distributions capitalized at current LP yield. (3) Per Q3 2016E Financial Summary provided by CPGX Management.

(4) CPPL’s pro rata share of OpCo’s consolidated net debt, per Q3 2016E Financial Summary provided by CPGX Management.

Jefferies LLC / November 2016 3

|

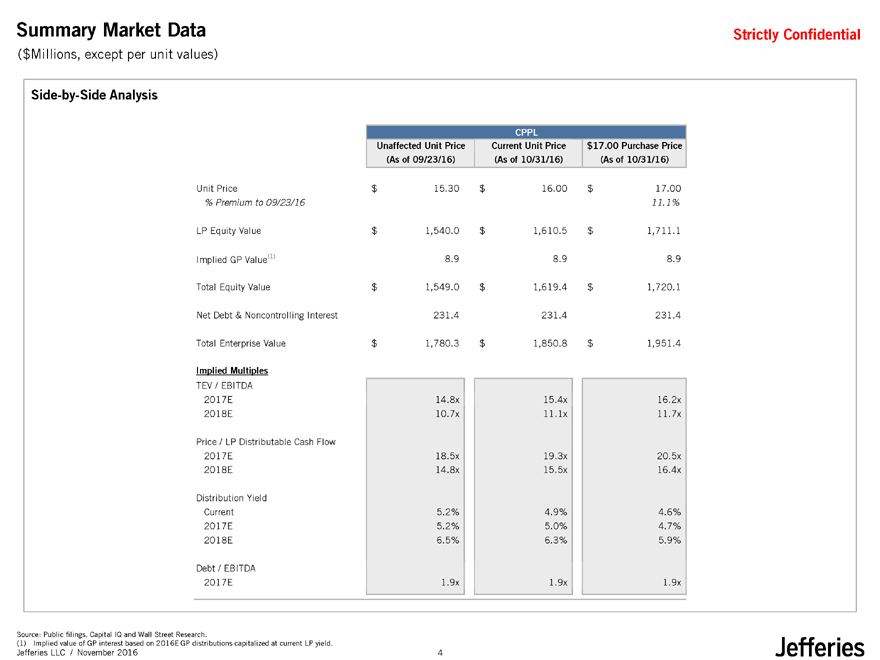

Summary Market Data

($Millions, except per unit values)

Strictly Confidential

Side-by-Side Analysis

CPPL

Unaffected Unit Price Current Unit Price$17.00 Purchase Price

(As of 09/23/16)(As of 10/31/16)(As of 10/31/16)

Unit Price $15.30$16.00$17.00

% Premium to 09/23/16 11.1%

LP Equity Value $1,540.0$1,610.5$1,711.1

Implied GP Value(1) 8.98.98.9

Total Equity Value $1,549.0$1,619.4$1,720.1

Net Debt & Noncontrolling Interest 231.4231.4231.4

Total Enterprise Value $1,780.3$1,850.8$1,951.4

Implied Multiples

TEV / EBITDA

2017E 14.8x15.4x16.2x

2018E 10.7x11.1x11.7x

Price / LP Distributable Cash Flow

2017E 18.5x19.3x20.5x

2018E 14.8x15.5x16.4x

Distribution Yield

Current 5.2%4.9%4.6%

2017E 5.2%5.0%4.7%

2018E 6.5%6.3%5.9%

Debt / EBITDA

2017E 1.9x1.9x1.9x

Source: Public filings, Capital IQ and Wall Street Research.

(1) Implied value of GP interest based on 2016E GP distributions capitalized at current LP yield.

Jefferies LLC / November 2016 4

|

Strictly Confidential

Market Update

Jefferies LLC / November 2016 5

|

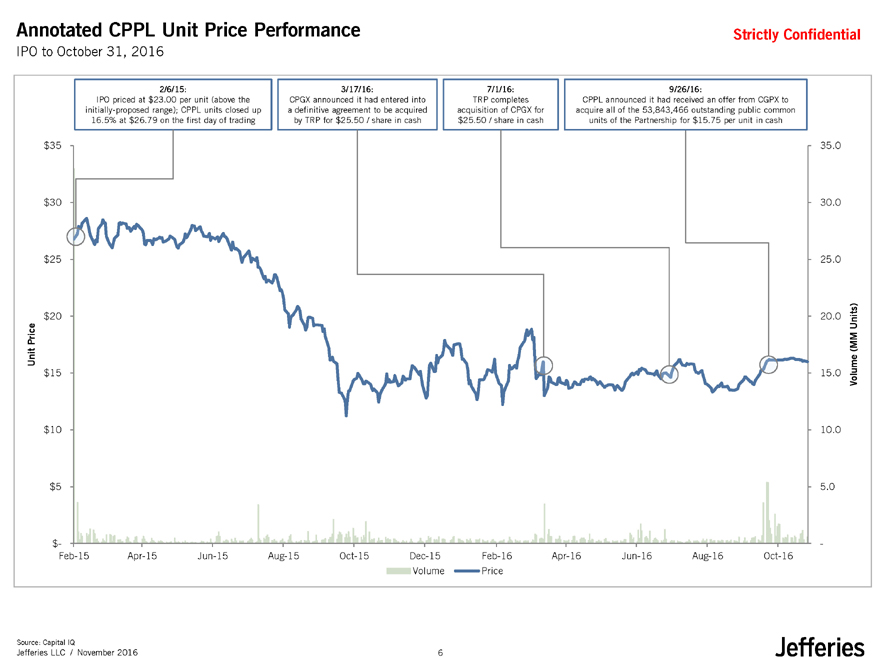

Annotated CPPL Unit Price Performance

IPO to October 31, 2016

Strictly Confidential

2/6/15:3/17/16:7/1/16:9/26/16:

IPO priced at $23.00 per unit (above theCPGX announced it had entered intoTRP completesCPPL announced it had received an offer from CGPX to

initially-proposed range); CPPL units closed up a definitive agreement to be acquiredacquisition of CPGX foracquire all of the 53,843,466 outstanding public common

16.5% at $26.79 on the first day of tradingby TRP for $25.50 / share in cash$25.50 / share in cashunits of the Partnership for $15.75 per unit in cash

$35 35.0

$30 30.0

$25 25.0

$20 20.0Units)

Price (MM

Unit

$15 15.0Volume

$10 10.0

$5 5.0

$- -

Feb-15 Apr-15Jun-15Aug-15Oct-15Dec-15Feb-16Apr-16Jun-16Aug-16Oct-16

VolumePrice

Source: Capital IQ

Jefferies LLC / November 2016 6

|

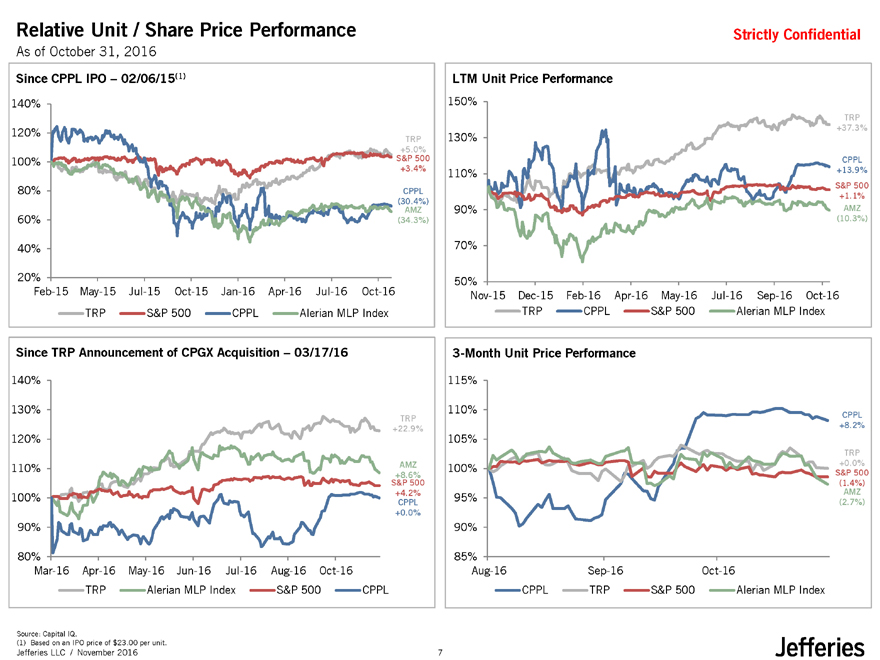

Relative Unit / Share Price Performance

As of October 31, 2016

Strictly Confidential

Since CPPL IPO – 02/06/15(1)

140%

120% TRP

+5.0%

100% S&P 500

+3.4%

80% CPPL

(30.4%)

AMZ

60% (34.3%)

40%

20%

Feb-15 May-15 Jul-15 Oct-15 Jan-16Apr-16 Jul-16 Oct-16

TRP S&P 500 CPPLAlerian MLP Index

LTM Unit Price Performance

150%

TRP

+37.3%

130%

CPPL

110% +13.9%

S&P 500

+1.1%

90% AMZ

(10.3%)

70%

50%

Nov-15 Dec-15 Feb-16 Apr-16 May-16Jul-16 Sep-16 Oct-16

TRP CPPL S&P 500Alerian MLP Index

Since TRP Announcement of CPGX Acquisition – 03/17/16

140%

130%

TRP

+22.9%

120%

110% AMZ

+8.6%

S&P 500

100% +4.2%

CPPL

+0.0%

90%

80%

Mar-16 Apr-16 May-16 Jun-16 Jul-16 Aug-16 Oct-16

TRP Alerian MLP Index S&P 500CPPL

3-Month Unit Price Performance

115%

110% CPPL

+8.2%

105%

TRP

+0.0%

100% S&P 500

(1.4%)

AMZ

95% (2.7%)

90%

85%

Aug-16 Sep-16 Oct-16

CPPL TRP S&P 500Alerian MLP Index

Source: Capital IQ.

(1) Based on an IPO price of $23.00 per unit.

Jefferies LLC / November 2016 7

|

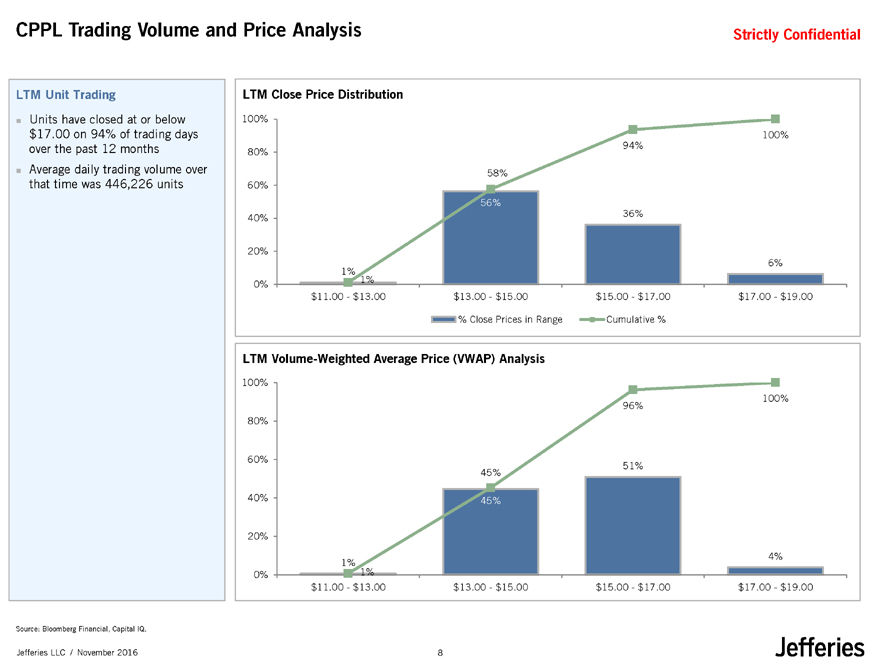

CPPL Trading Volume and Price Analysis

Strictly Confidential

LTM Unit Trading

Units have closed at or below $17.00 on 94% of trading days over the past 12 months Average daily trading volume over that time was 446,226 units

LTM Close Price Distribution

100%

100%

80% 94%

58%

60%

56%

40% 36%

20%

6%

1% 1%

0%

$11.00—$13.00 $13.00—$15.00 $15.00—$17.00$17.00—$19.00

% Close Prices in Range Cumulative %

LTM Volume-Weighted Average Price (VWAP) Analysis

100%

100%

96%

80%

60%

45%51%

40% 45%

20%

1% 4%

0% 1%

$11.00—$13.00 $13.00—$15.00$15.00—$17.00$17.00—$19.00

Source: Bloomberg Financial, Capital IQ.

Jefferies LLC / November 2016 8

|

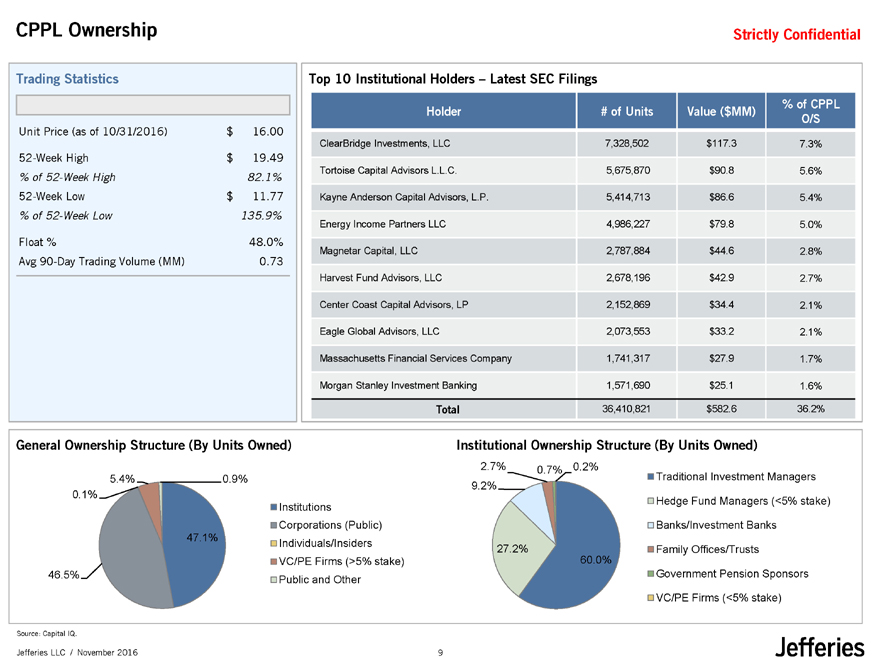

CPPL Ownership

Strictly Confidential

Trading Statistics

Unit Price (as of 10/31/2016) $16.00

52-Week High $19.49

% of 52-Week High 82.1%

52-Week Low $11.77

% of 52-Week Low 135.9%

Float % 48.0%

Avg 90-Day Trading Volume (MM) 0.73

Top 10 Institutional Holders – Latest SEC Filings

Holder # of Units Value ($MM)% of CPPL

O/S

ClearBridge Investments, LLC 7,328,502 $117.37.3%

Tortoise Capital Advisors L.L.C. 5,675,870 $90.85.6%

Kayne Anderson Capital Advisors, L.P. 5,414,713 $86.65.4%

Energy Income Partners LLC 4,986,227 $79.85.0%

Magnetar Capital, LLC 2,787,884 $44.62.8%

Harvest Fund Advisors, LLC 2,678,196 $42.92.7%

Center Coast Capital Advisors, LP 2,152,869 $34.42.1%

Eagle Global Advisors, LLC 2,073,553 $33.22.1%

Massachusetts Financial Services Company 1,741,317 $27.91.7%

Morgan Stanley Investment Banking 1,571,690 $25.11.6%

Total 36,410,821 $582.636.2%

General Ownership Structure (By Units Owned)

5.4% 0.9%

0.1%

Institutions

Corporations (Public)

47.1% Individuals/Insiders

VC/PE Firms (>5% stake)

46.5% Public and Other

Institutional Ownership Structure (By Units Owned)

2.7% 0.7% 0.2%

Traditional Investment Managers

9.2%

Hedge Fund Managers (<5% stake)

Banks/Investment Banks

27.2% Family Offices/Trusts

60.0%

Government Pension Sponsors

VC/PE Firms (<5% stake)

Source: Capital IQ.

Jefferies LLC / November 2016 9

|

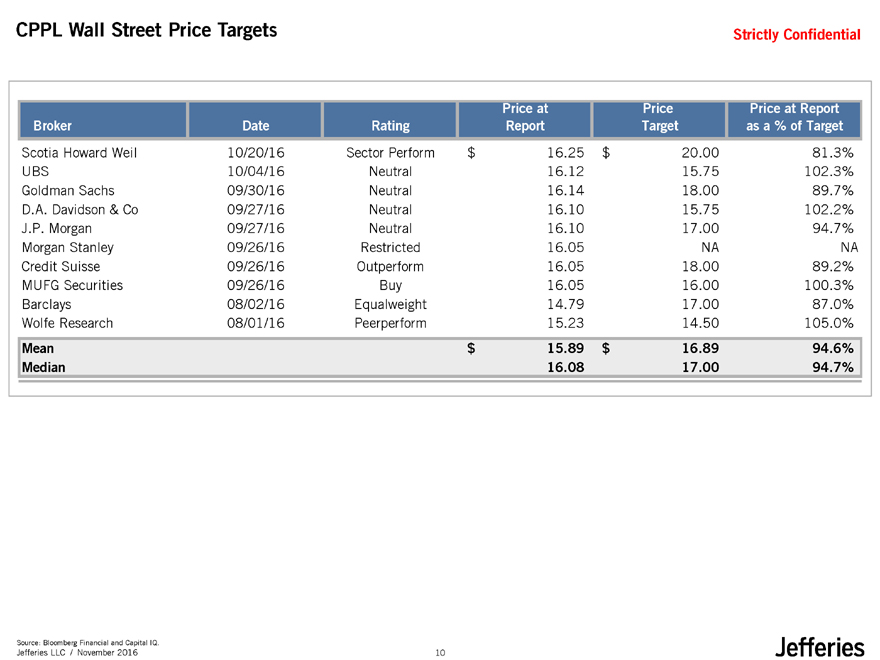

CPPL Wall Street Price Targets

Strictly Confidential

Price atPricePrice at Report

Broker Date RatingReportTargetas a % of Target

Scotia Howard Weil 10/20/16 Sector Perform$16.25$20.0081.3%

UBS 10/04/16 Neutral16.1215.75102.3%

Goldman Sachs 09/30/16 Neutral16.1418.0089.7%

D.A. Davidson & Co 09/27/16 Neutral16.1015.75102.2%

J.P. Morgan 09/27/16 Neutral16.1017.0094.7%

Morgan Stanley 09/26/16 Restricted16.05NANA

Credit Suisse 09/26/16 Outperform16.0518.0089.2%

MUFG Securities 09/26/16 Buy16.0516.00100.3%

Barclays 08/02/16 Equalweight14.7917.0087.0%

Wolfe Research 08/01/16 Peerperform15.2314.50105.0%

Mean $15.89$16.8994.6%

Median 16.0817.0094.7%

Source: Bloomberg Financial and Capital IQ.

Jefferies LLC / November 2016 10

|

Strictly Confidential

Valuation Analysis

Jefferies LLC / November 2016 11

|

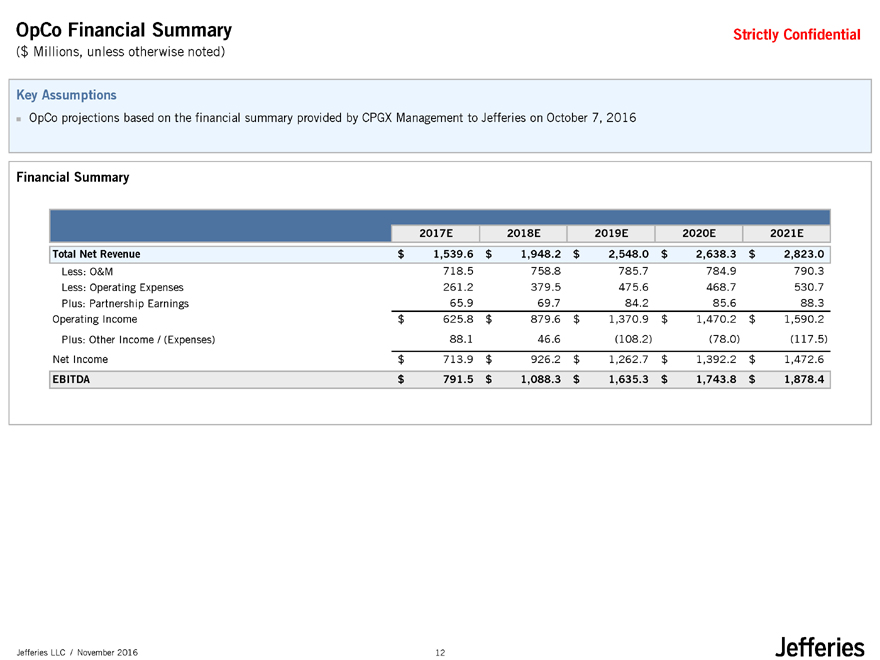

OpCo Financial Summary

($ Millions, unless otherwise noted)

Strictly Confidential

Key Assumptions

OpCo projections based on the financial summary provided by CPGX Management to Jefferies on October 7, 2016

Financial Summary

2017E 2018E2019E2020E2021E

Total Net Revenue $ 1,539.6 $1,948.2$2,548.0$2,638.3$2,823.0

Less: O&M 718.5 758.8785.7784.9790.3

Less: Operating Expenses 261.2 379.5475.6468.7530.7

Plus: Partnership Earnings 65.9 69.784.285.688.3

Operating Income $ 625.8 $879.6$1,370.9$1,470.2$1,590.2

Plus: Other Income / (Expenses) 88.1 46.6(108.2)(78.0)(117.5)

Net Income $ 713.9 $926.2$1,262.7$1,392.2$1,472.6

EBITDA $ 791.5 $1,088.3$1,635.3$1,743.8$1,878.4

Jefferies LLC / November 2016 12

|

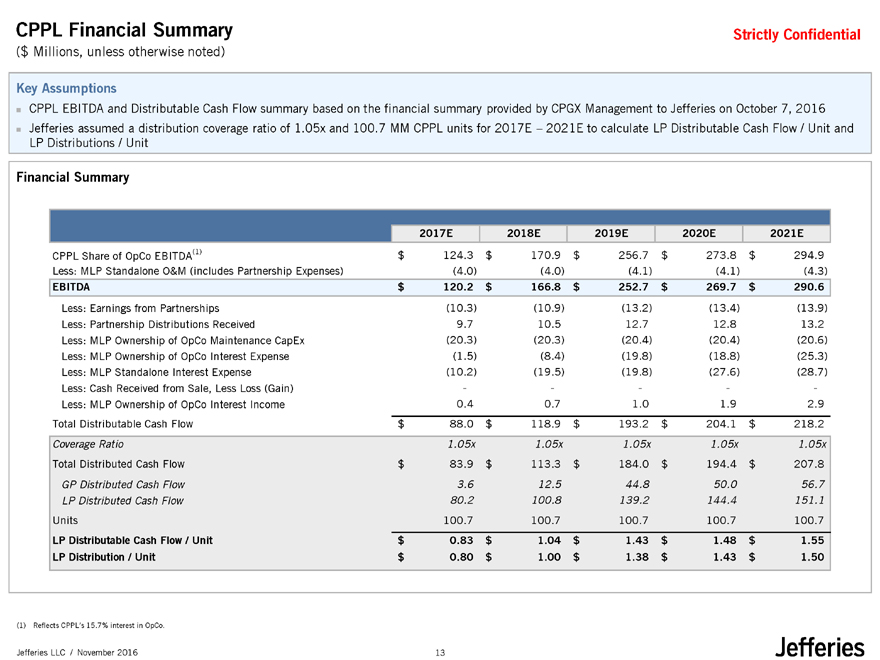

CPPL Financial Summary

($ Millions, unless otherwise noted)

Strictly Confidential

Key Assumptions

CPPL EBITDA and Distributable Cash Flow summary based on the financial summary provided by CPGX Management to Jefferies on October 7, 2016 Jefferies assumed a distribution coverage ratio of 1.05x and 100.7 MM CPPL units for 2017E – 2021E to calculate LP Distributable Cash Flow / Unit and LP Distributions / Unit

Financial Summary

2017E 2018E2019E2020E2021E

CPPL Share of OpCo EBITDA(1) $ 124.3 $170.9$256.7$273.8$294.9

Less: MLP Standalone O&M (includes Partnership Expenses) (4.0) (4.0)(4.1)(4.1)(4.3)

EBITDA $ 120.2 $166.8$252.7$269.7$290.6

Less: Earnings from Partnerships (10.3) (10.9)(13.2)(13.4)(13.9)

Less: Partnership Distributions Received 9.7 10.512.712.813.2

Less: MLP Ownership of OpCo Maintenance CapEx (20.3) (20.3)(20.4)(20.4)(20.6)

Less: MLP Ownership of OpCo Interest Expense (1.5) (8.4)(19.8)(18.8)(25.3)

Less: MLP Standalone Interest Expense (10.2) (19.5)(19.8)(27.6)(28.7)

Less: Cash Received from Sale, Less Loss (Gain) - ----

Less: MLP Ownership of OpCo Interest Income 0.4 0.71.01.92.9

Total Distributable Cash Flow $ 88.0 $118.9$193.2$204.1$218.2

Coverage Ratio 1.05x 1.05x1.05x1.05x1.05x

Total Distributed Cash Flow $ 83.9 $113.3$184.0$194.4$207.8

GP Distributed Cash Flow 3.6 12.544.850.056.7

LP Distributed Cash Flow 80.2 100.8139.2144.4151.1

Units 100.7 100.7100.7100.7100.7

LP Distributable Cash Flow / Unit $ 0.83 $1.04$1.43$1.48$1.55

LP Distribution / Unit $ 0.80 $1.00$1.38$1.43$1.50

(1) Reflects CPPL’s 15.7% interest in OpCo.

Jefferies LLC / November 2016 13

|

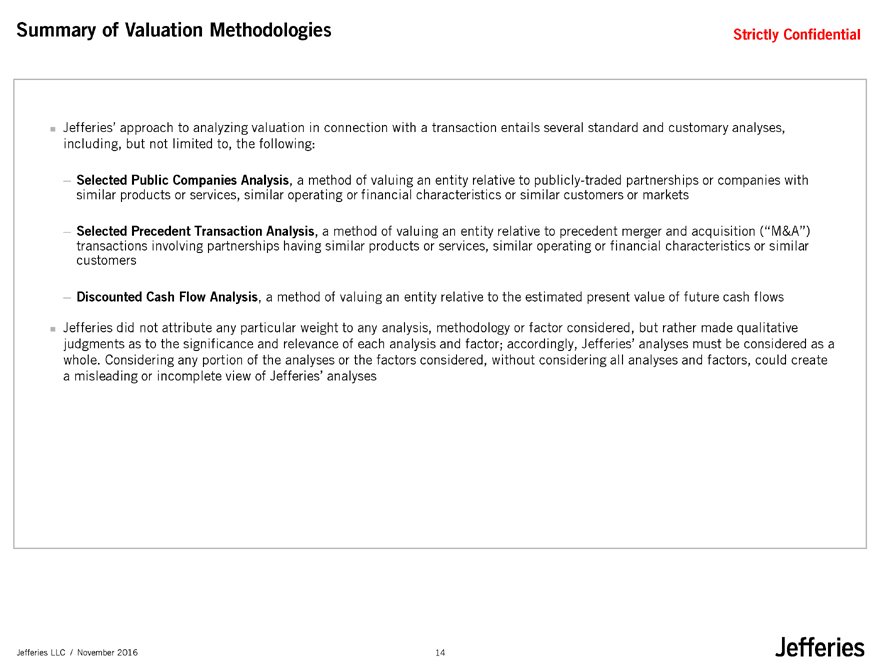

Summary of Valuation Methodologies

Strictly Confidential

Jefferies’ approach to analyzing valuation in connection with a transaction entails several standard and customary analyses,

including, but not limited to, the following:

— Selected Public Companies Analysis, a method of valuing an entity relative to publicly-traded partnerships or companies with

similar products or services, similar operating or financial characteristics or similar customers or markets

— Selected Precedent Transaction Analysis, a method of valuing an entity relative to precedent merger and acquisition (“M&A”)

transactions involving partnerships having similar products or services, similar operating or financial characteristics or similar

customers

— Discounted Cash Flow Analysis, a method of valuing an entity relative to the estimated present value of future cash flows

Jefferies did not attribute any particular weight to any analysis, methodology or factor considered, but rather made qualitative

judgments as to the significance and relevance of each analysis and factor; accordingly, Jefferies’ analyses must be considered as a

whole. Considering any portion of the analyses or the factors considered, without considering all analyses and factors, could create

a misleading or incomplete view of Jefferies’ analyses

Jefferies LLC / November 2016 14

|

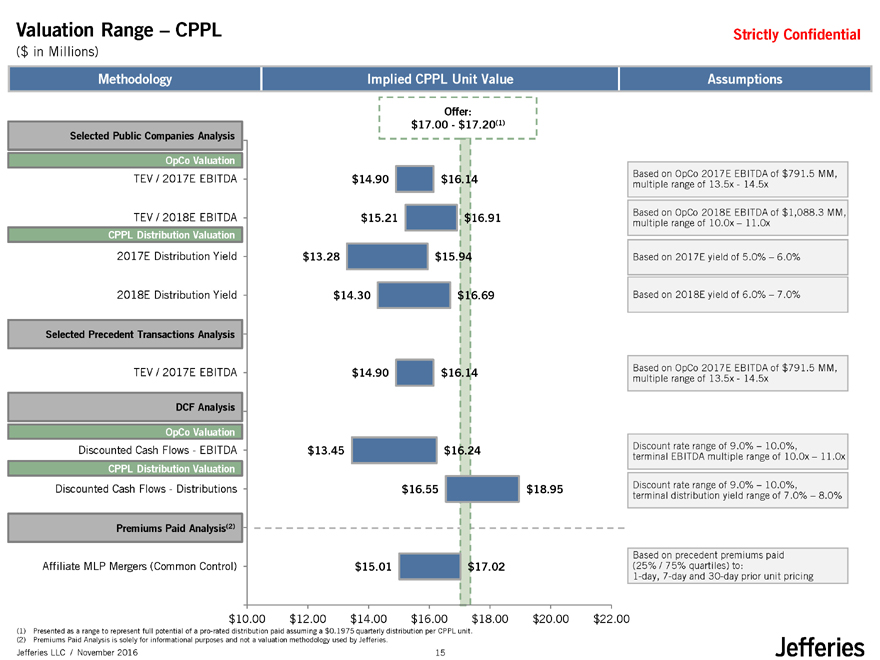

Valuation Range – CPPL

($ in Millions)

Strictly Confidential

Methodology

Selected Public Companies Analysis

OpCo Valuation

TEV / 2017E EBITDA

TEV / 2018E EBITDA

CPPL Distribution Valuation

2017E Distribution Yield

2018E Distribution Yield

Selected Precedent Transactions Analysis

TEV / 2017E EBITDA

DCF Analysis

OpCo Valuation

Discounted Cash Flows—EBITDA

CPPL Distribution Valuation

Discounted Cash Flows—Distributions

Premiums Paid Analysis(2)

Affiliate MLP Mergers (Common Control)

Implied CPPL Unit Value

Offer:

$17.00—$17.20(1)

$14.90 $16.14

$15.21 $16.91

$13.28 $15.94

$14.30 $16.69

$14.90 $16.14

$13.45 $16.24

$16.55 $18.95

$15.01 $17.02

Assumptions

Based on OpCo 2017E EBITDA of $791.5 MM, multiple range of 13.5x—14.5x

Based on OpCo 2018E EBITDA of $1,088.3 MM, multiple range of 10.0x – 11.0x

Based on 2017E yield of 5.0% – 6.0%

Based on 2018E yield of 6.0% – 7.0%

Based on OpCo 2017E EBITDA of $791.5 MM, multiple range of 13.5x—14.5x

Discount rate range of 9.0% – 10.0%, terminal EBITDA multiple range of 10.0x – 11.0x

Discount rate range of 9.0% – 10.0%, terminal distribution yield range of 7.0% – 8.0%

Based on precedent premiums paid (25% / 75% quartiles) to: 1-day, 7-day and 30-day prior unit pricing

$10.00 $12.00 $14.00 $16.00 $18.00 $20.00 $22.00

(1) Presented as a range to represent full potential of a pro-rated distribution paid assuming a $0.1975 quarterly distribution per CPPL unit. (2) Premiums Paid Analysis is solely for informational purposes and not a valuation methodology used by Jefferies.

Jefferies LLC / November 2016 15

|

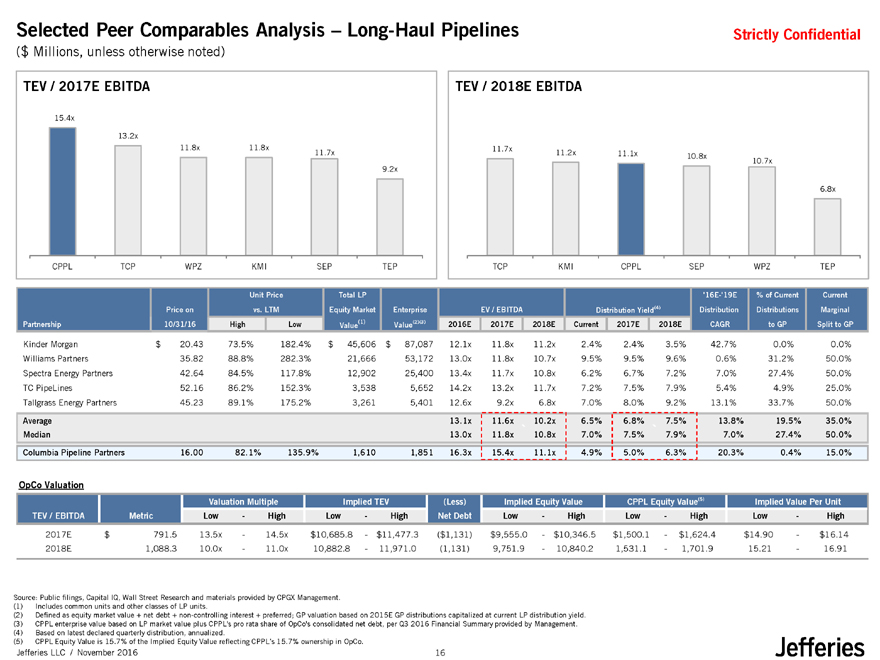

Selected Peer Comparables Analysis – Long-Haul Pipelines

($ Millions, unless otherwise noted)

Strictly Confidential

TEV / 2017E EBITDA

15.4x

13.2x

11.8x11.8x11.7x

9.2x

CPPL TCP WPZKMISEPTEP

TEV / 2018E EBITDA

11.7x 11.2x 11.1x10.8x

10.7x

6.8x

TCP KMI CPPLSEPWPZTEP

Unit PriceTotal LP’16E-‘19E% of CurrentCurrent

Price on vs. LTMEquity MarketEnterpriseEV / EBITDADistribution Yield(4)DistributionDistributionsMarginal

Partnership 10/31/16 HighLowValue(1)Value(2)(3)2016E2017E2018ECurrent2017E2018ECAGRto GPSplit to GP

Kinder Morgan $ 20.43 73.5%182.4%$ 45,606$87,08712.1x11.8x11.2x2.4%2.4%3.5%42.7%0.0%0.0%

Williams Partners 35.82 88.8%282.3%21,66653,17213.0x11.8x10.7x9.5%9.5%9.6%0.6%31.2%50.0%

Spectra Energy Partners 42.64 84.5%117.8%12,90225,40013.4x11.7x10.8x6.2%6.7%7.2%7.0%27.4%50.0%

TC PipeLines 52.16 86.2%152.3%3,5385,65214.2x13.2x11.7x7.2%7.5%7.9%5.4%4.9%25.0%

Tallgrass Energy Partners 45.23 89.1%175.2%3,2615,40112.6x9.2x6.8x7.0%8.0%9.2%13.1%33.7%50.0%

Average 13.1x11.6x10.2x6.5%6.8%7.5%13.8%19.5%35.0%

Median 13.0x11.8x`10.8x7.0%7.5%`7.9%7.0%27.4%50.0%

Columbia Pipeline Partners 16.00 82.1%135.9%1,6101,85116.3x15.4x11.1x4.9%5.0%6.3%20.3%0.4%15.0%

OpCo Valuation

Valuation MultipleImplied TEV(Less)Implied Equity ValueCPPL Equity Value(5)Implied Value Per Unit

TEV / EBITDA MetricLow- HighLow- HighNet DebtLow- HighLow-HighLow-High

2017E $791.513.5x- 14.5x$10,685.8- $11,477.3($1,131)$9,555.0- $10,346.5$1,500.1-$1,624.4$14.90-$16.14

2018E 1,088.310.0x- 11.0x10,882.8- 11,971.0(1,131)9,751.9- 10,840.21,531.1-1,701.915.21-16.91

Source: Public filings, Capital IQ, Wall Street Research and materials provided by CPGX Management. (1) Includes common units and other classes of LP units.

(2) Defined as equity market value + net debt + non-controlling interest + preferred; GP valuation based on 2015E GP distributions capitalized at current LP distribution yield. (3) CPPL enterprise value based on LP market value plus CPPL’s pro rata share of OpCo’s consolidated net debt, per Q3 2016 Financial Summary provided by Management. (4) Based on latest declared quarterly distribution, annualized.

(5) CPPL Equity Value is 15.7% of the Implied Equity Value reflecting CPPL’s 15.7% ownership in OpCo.

Jefferies LLC / November 2016 16

|

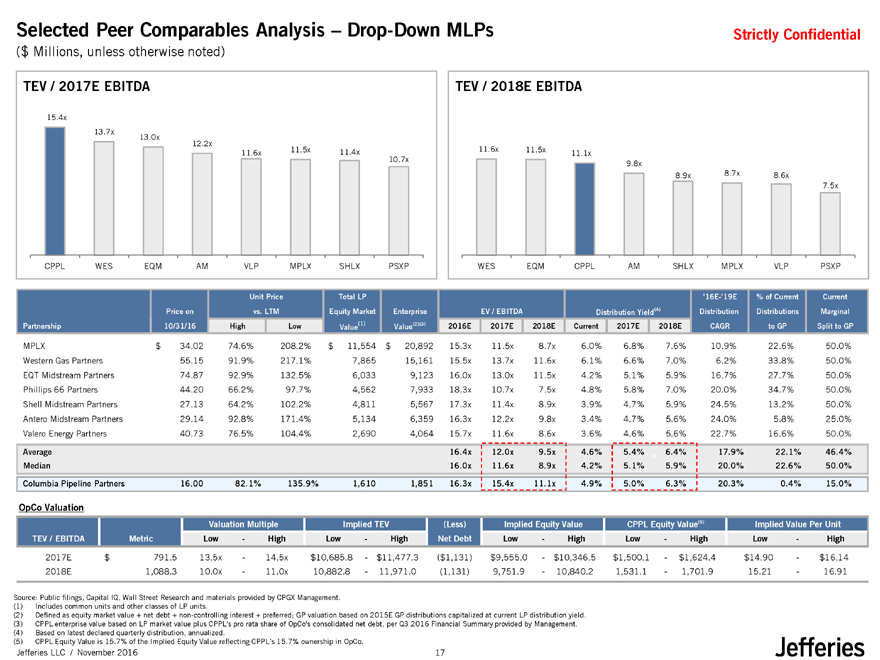

Selected Peer Comparables Analysis – Drop-Down MLPs

($ Millions, unless otherwise noted)

Strictly Confidential

TEV / 2017E EBITDA

15.4x

13.7x 13.0x

12.2x

11.6x11.5x11.4x

10.7x

CPPL WES EQMAMVLPMPLXSHLXPSXP

TEV / 2018E EBITDA

11.6x 11.5x 11.1x

9.8x

8.9x8.7x8.6x

7.5x

WES EQM CPPLAMSHLXMPLXVLPPSXP

Unit PriceTotal LP’16E-‘19E% of CurrentCurrent

Price on vs. LTMEquity MarketEnterpriseEV / EBITDADistribution Yield(4)DistributionDistributionsMarginal

Partnership 10/31/16 HighLowValue(1)Value(2)(3)2016E2017E2018ECurrent2017E2018ECAGRto GPSplit to GP

MPLX $ 34.02 74.6%208.2%$ 11,554$20,89215.3x11.5x8.7x6.0%6.8%7.6%10.9%22.6%50.0%

Western Gas Partners 55.15 91.9%217.1%7,86515,16115.5x13.7x11.6x6.1%6.6%7.0%6.2%33.8%50.0%

EQT Midstream Partners 74.87 92.9%132.5%6,0339,12316.0x13.0x11.5x4.2%5.1%5.9%16.7%27.7%50.0%

Phillips 66 Partners 44.20 66.2%97.7%4,5627,93318.3x10.7x7.5x4.8%5.8%7.0%20.0%34.7%50.0%

Shell Midstream Partners 27.13 64.2%102.2%4,8115,56717.3x11.4x8.9x3.9%4.7%5.9%24.5%13.2%50.0%

Antero Midstream Partners 29.14 92.8%171.4%5,1346,35916.3x12.2x9.8x3.4%4.7%5.6%24.0%5.8%25.0%

Valero Energy Partners 40.73 76.5%104.4%2,6904,06415.7x11.6x8.6x3.6%4.6%5.6%22.7%16.6%50.0%

Average 16.4x12.0x9.5x4.6%5.4%6.4%17.9%22.1%46.4%

Median 16.0x11.6x8.9x4.2%5.1%`5.9%20.0%22.6%50.0%

Columbia Pipeline Partners 16.00 82.1%135.9%1,6101,85116.3x15.4x11.1x4.9%5.0%6.3%20.3%0.4%15.0%

OpCo Valuation

Valuation MultipleImplied TEV(Less)Implied Equity ValueCPPL Equity Value(5)Implied Value Per Unit

TEV / EBITDA MetricLow- HighLow- HighNet DebtLow- HighLow-HighLow-High

2017E $791.513.5x- 14.5x$10,685.8- $11,477.3($1,131)$9,555.0- $10,346.5$1,500.1-$1,624.4$14.90-$16.14

2018E 1,088.310.0x- 11.0x10,882.8- 11,971.0(1,131)9,751.9- 10,840.21,531.1-1,701.915.21-16.91

Source: Public filings, Capital IQ, Wall Street Research and materials provided by CPGX Management.

(1) Includes common units and other classes of LP units.

(2) Defined as equity market value + net debt + non-controlling interest + preferred; GP valuation based on 2015E GP distributions capitalized at current LP distribution yield.

(3) CPPL enterprise value based on LP market value plus CPPL’s pro rata share of OpCo’s consolidated net debt, per Q3 2016 Financial Summary provided by Management.

(4) Based on latest declared quarterly distribution, annualized.

(5) CPPL Equity Value is 15.7% of the Implied Equity Value reflecting CPPL’s 15.7% ownership in OpCo.

Jefferies LLC / November 2016 17

|

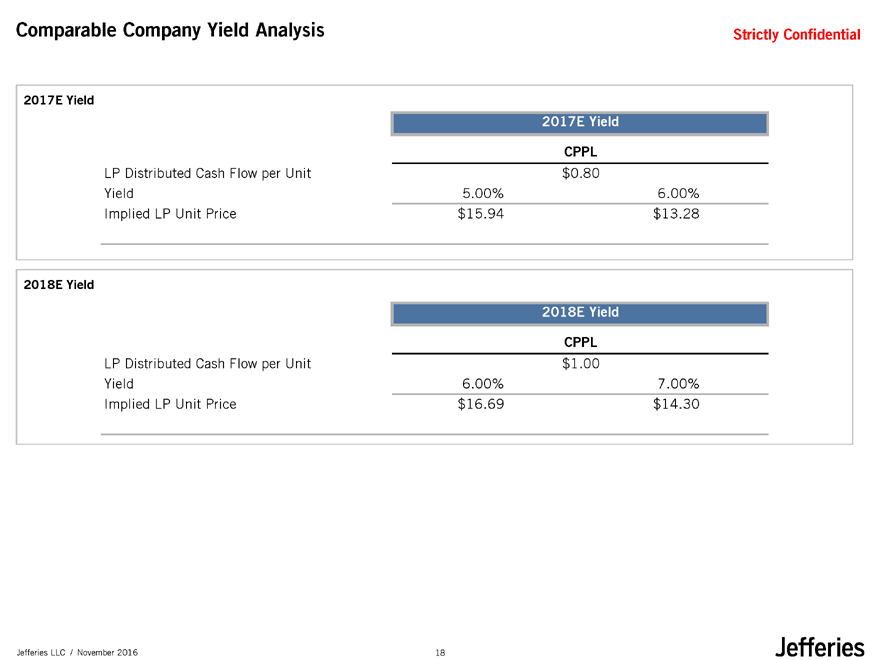

Comparable Company Yield Analysis

Strictly Confidential

2017E Yield

2017E Yield

CPPL

LP Distributed Cash Flow per Unit $0.80

Yield 5.00%6.00%

Implied LP Unit Price $15.94$13.28

2018E Yield

2018E Yield

CPPL

LP Distributed Cash Flow per Unit $1.00

Yield 6.00%7.00%

Implied LP Unit Price $16.69$14.30

Jefferies LLC / November 2016 18

|

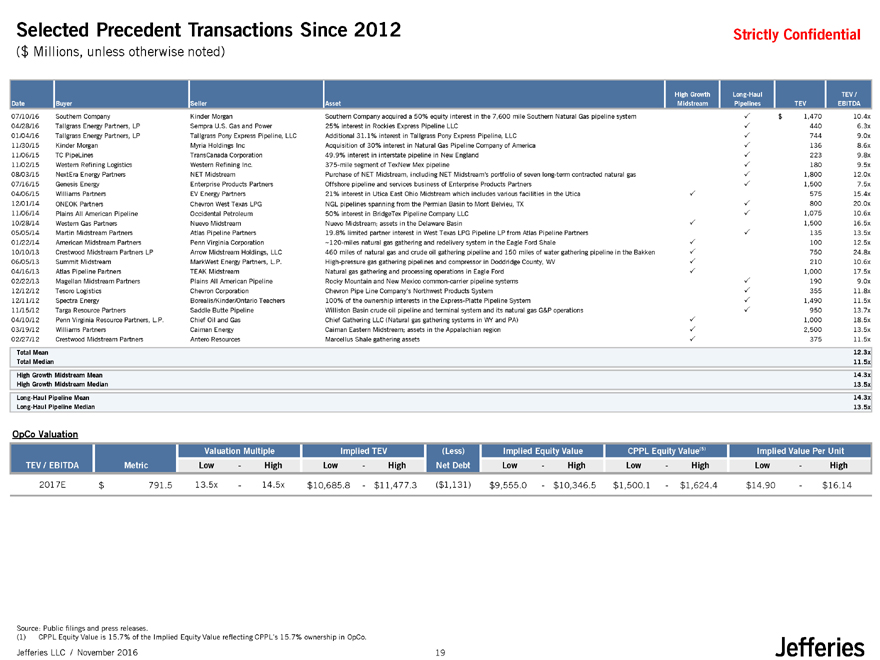

Selected Precedent Transactions Since 2012

($ Millions, unless otherwise noted)

Strictly Confidential

High GrowthLong-HaulTEV /

Date Buyer SellerAssetMidstreamPipelinesTEVEBITDA

07/10/16 Southern Company Kinder MorganSouthern Company acquired a 50% equity interest in the 7,600 mile Southern Natural Gas pipeline systemP$1,47010.4x

04/28/16 Tallgrass Energy Partners, LP Sempra U.S. Gas and Power25% interest in Rockies Express Pipeline LLCP4406.3x

01/04/16 Tallgrass Energy Partners, LP Tallgrass Pony Express Pipeline, LLCAdditional 31.1% interest in Tallgrass Pony Express Pipeline, LLCP7449.0x

11/30/15 Kinder Morgan Myria Holdings IncAcquisition of 30% interest in Natural Gas Pipeline Company of AmericaP1368.6x

11/06/15 TC PipeLines TransCanada Corporation49.9% interest in interstate pipeline in New EnglandP2239.8x

11/02/15 Western Refining Logistics Western Refining Inc.375-mile segment of TexNew Mex pipelineP1809.5x

08/03/15 NextEra Energy Partners NET MidstreamPurchase of NET Midstream, including NET Midstream’s portfolio of seven long-term contracted natural gasP1,80012.0x

07/16/15 Genesis Energy Enterprise Products PartnersOffshore pipeline and services business of Enterprise Products PartnersP1,5007.5x

04/06/15 Williams Partners EV Energy Partners21% interest in Utica East Ohio Midstream which includes various facilities in the UticaP57515.4x

12/01/14 ONEOK Partners Chevron West Texas LPGNGL pipelines spanning from the Permian Basin to Mont Belvieu, TXP80020.0x

11/06/14 Plains All American Pipeline Occidental Petroleum50% interest in BridgeTex Pipeline Company LLCP1,07510.6x

10/28/14 Western Gas Partners Nuevo MidstreamNuevo Midstream; assets in the Delaware BasinP1,50016.5x

05/05/14 Martin Midstream Partners Atlas Pipeline Partners19.8% limited partner interest in West Texas LPG Pipeline LP from Atlas Pipeline PartnersP13513.5x

01/22/14 American Midstream Partners Penn Virginia Corporation~120-miles natural gas gathering and redelivery system in the Eagle Ford ShaleP10012.5x

10/10/13 Crestwood Midstream Partners LP Arrow Midstream Holdings, LLC460 miles of natural gas and crude oil gathering pipeline and 150 miles of water gathering pipeline in the BakkenP75024.8x

06/05/13 Summit Midstream MarkWest Energy Partners, L.P.High-pressure gas gathering pipelines and compressor in Doddridge County, WVP21010.6x

04/16/13 Atlas Pipeline Partners TEAK MidstreamNatural gas gathering and processing operations in Eagle FordP1,00017.5x

02/22/13 Magellan Midstream Partners Plains All American PipelineRocky Mountain and New Mexico common-carrier pipeline systemsP1909.0x

12/12/12 Tesoro Logistics Chevron CorporationChevron Pipe Line Company’s Northwest Products SystemP35511.8x

12/11/12 Spectra Energy Borealis/Kinder/Ontario Teachers100% of the ownership interests in the Express-Platte Pipeline SystemP1,49011.5x

11/15/12 Targa Resource Partners Saddle Butte PipelineWilliston Basin crude oil pipeline and terminal system and its natural gas G&P operationsP95013.7x

04/10/12 Penn Virginia Resource Partners, L.P. Chief Oil and GasChief Gathering LLC (Natural gas gathering systems in WY and PA)P1,00018.5x

03/19/12 Williams Partners Caiman EnergyCaiman Eastern Midstream; assets in the Appalachian regionP2,50013.5x

02/27/12 Crestwood Midstream Partners Antero ResourcesMarcellus Shale gathering assetsP37511.5x

Total Mean 12.3x

Total Median 11.5x

High Growth Midstream Mean 14.3x

High Growth Midstream Median 13.5x

Long-Haul Pipeline Mean 14.3x

Long-Haul Pipeline Median 13.5x

OpCo Valuation

Valuation MultipleImplied TEV(Less)Implied Equity ValueCPPL Equity Value(5)Implied Value Per Unit

TEV / EBITDA MetricLow-HighLow- HighNet DebtLow- HighLow-HighLow-High

2017E $791.513.5x-14.5x$10,685.8- $11,477.3($1,131)$9,555.0- $10,346.5$1,500.1-$1,624.4$14.90-$16.14

Source: Public filings and press releases.

(1) CPPL Equity Value is 15.7% of the Implied Equity Value reflecting CPPL’s 15.7% ownership in OpCo.

Jefferies LLC / November 2016 19

|

Strictly Confidential

Jefferies LLC / November 2016

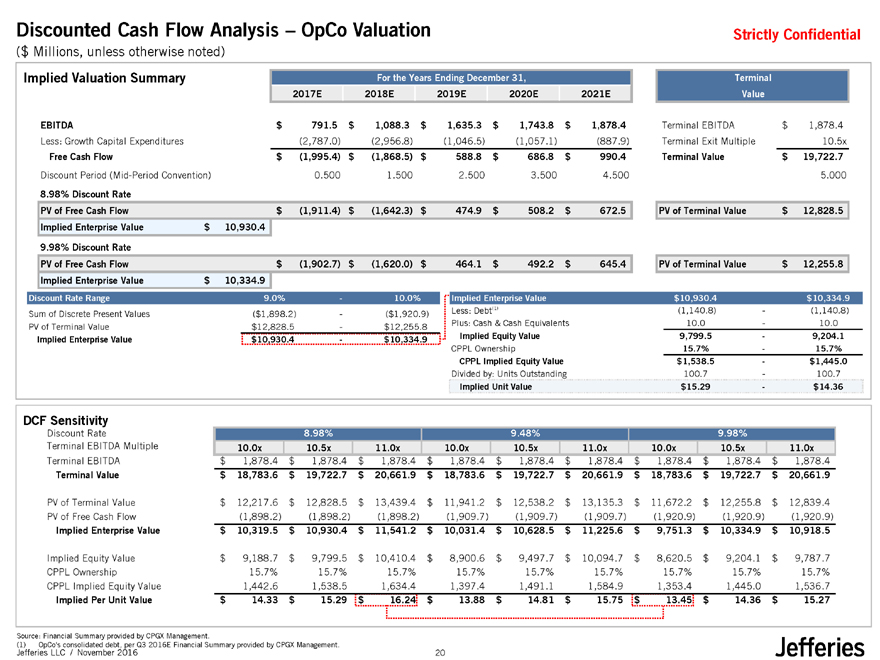

Implied Valuation Summary

DCF Sensitivity

Discounted Cash Flow Analysis – OpCo Valuation

($ Millions, unless otherwise noted)

Source: Financial Summary provided by CPGX Management.

(1) OpCo’s consolidated debt, per Q3 2016E Financial Summary provided by CPGX Management.

For the Years Ending December 31, Terminal

2017E 2018E 2019E 2020E 2021E Value

EBITDA $ 791.5 $ 1,088.3 $ 1,635.3 $ 1,743.8 $ 1,878.4 Terminal EBITDA $ 1,878.4

Less: Growth Capital Expenditures (2,787.0) (2,956.8) (1,046.5) (1,057.1) (887.9) Terminal Exit Multiple 10.5x

Free Cash Flow $ (1,995.4) $ (1,868.5) $ 588.8 $ 686.8 $ 990.4 Terminal Value $ 19,722.7

Discount Period (Mid-Period Convention) 0.500 1.500 2.500 3.500 4.500 5.000

8.98% Discount Rate

PV of Free Cash Flow $ (1,911.4) $ (1,642.3) $ 474.9 $ 508.2 $ 672.5 PV of Terminal Value $ 12,828.5

Implied Enterprise Value $ 10,930.4

9.98% Discount Rate

PV of Free Cash Flow $ (1,902.7) $ (1,620.0) $ 464.1 $ 492.2 $ 645.4 PV of Terminal Value $ 12,255.8

Implied Enterprise Value $ 10,334.9

Discount Rate Range 9.0%—10.0%

Sum of Discrete Present Values ($1,898.2)—($1,920.9)

PV of Terminal Value $12,828.5—$12,255.8

Implied Enterprise Value $10,930.4—$10,334.9

Implied Enterprise Value $10,930.4 $10,334.9

Less: Debt(1) (1,140.8)—(1,140.8)

Plus: Cash & Cash Equivalents 10.0—10.0

Implied Equity Value 9,799.5—9,204.1

CPPL Ownership 15.7%—15.7%

CPPL Implied Equity Value $1,538.5—$1,445.0

Divided by: Units Outstanding 100.7—100.7

Implied Unit Value $15.29—$14.36

Discount Rate 8.98% 9.48% 9.98%

Terminal EBITDA Multiple 10.0x 10.5x 11.0x 10.0x 10.5x 11.0x 10.0x 10.5x 11.0x

Terminal EBITDA $ 1,878.4 $ 1,878.4 $ 1,878.4 $ 1,878.4 $ 1,878.4 $ 1,878.4 $ 1,878.4 $ 1,878.4 $ 1,878.4

Terminal Value $ 18,783.6 $ 19,722.7 $ 20,661.9 $ 18,783.6 $ 19,722.7 $ 20,661.9 $ 18,783.6 $ 19,722.7 $ 20,661.9

PV of Terminal Value $ 12,217.6 $ 12,828.5 $ 13,439.4 $ 11,941.2 $ 12,538.2 $ 13,135.3 $ 11,672.2 $ 12,255.8 $ 12,839.4

PV of Free Cash Flow (1,898.2) (1,898.2) (1,898.2) (1,909.7) (1,909.7) (1,909.7) (1,920.9) (1,920.9) (1,920.9)

Implied Enterprise Value $ 10,319.5 $ 10,930.4 $ 11,541.2 $ 10,031.4 $ 10,628.5 $ 11,225.6 $ 9,751.3 $ 10,334.9 $ 10,918.5

Implied Equity Value $ 9,188.7 $ 9,799.5 $ 10,410.4 $ 8,900.6 $ 9,497.7 $ 10,094.7 $ 8,620.5 $ 9,204.1 $ 9,787.7

CPPL Ownership 15.7% 15.7% 15.7% 15.7% 15.7% 15.7% 15.7% 15.7% 15.7%

CPPL Implied Equity Value 1 ,442.6 1 ,538.5 1 ,634.4 1 ,397.4 1 ,491.1 1 ,584.9 1 ,353.4 1 ,445.0 1 ,536.7

Implied Per Unit Value $ 1 4.33 $ 1 5.29 $ 1 6.24 $ 1 3.88 $ 1 4.81 $ 1 5.75 $ 1 3.45 $ 1 4.36 $ 1 5.27

20

|

Strictly Confidential

Jefferies LLC / November 2016

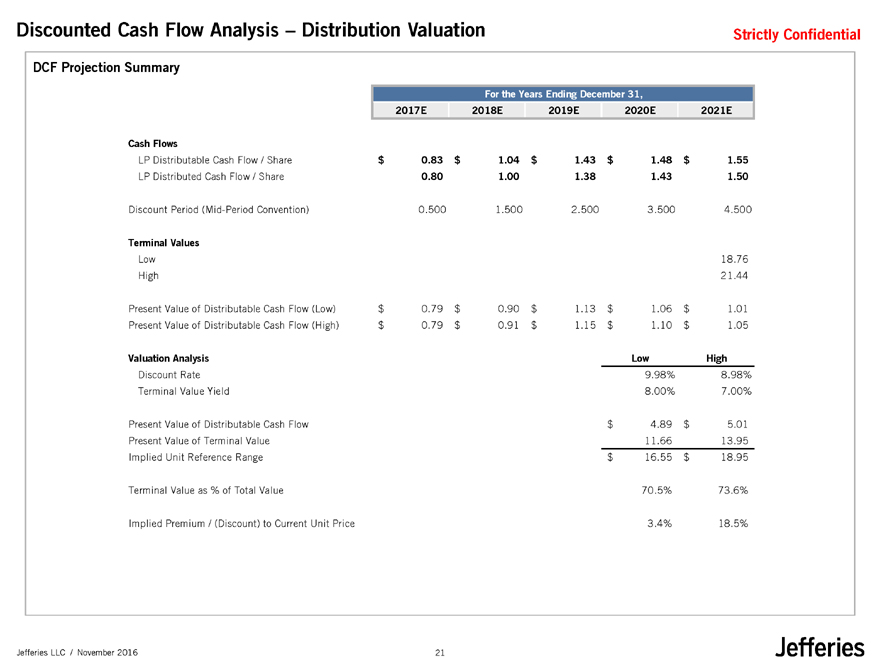

DCF Projection Summary

Discounted Cash Flow Analysis – Distribution Valuation

For the Years Ending December 31,

2017E 2018E 2019E 2020E 2021E

Cash Flows

LP Distributable Cash Flow / Share $ 0.83 $ 1.04 $ 1.43 $ 1.48 $ 1.55

LP Distributed Cash Flow / Share 0.80 1.00 1.38 1.43 1.50

Discount Period (Mid-Period Convention) 0.500 1.500 2.500 3.500 4.500

Terminal Values

Low 18.76

High 21.44

Present Value of Distributable Cash Flow (Low) $ 0.79 $ 0.90 $ 1.13 $ 1.06 $ 1.01

Present Value of Distributable Cash Flow (High) $ 0.79 $ 0.91 $ 1.15 $ 1.10 $ 1.05

Valuation Analysis Low High

Discount Rate 9.98% 8.98%

Terminal Value Yield 8.00% 7.00%

Present Value of Distributable Cash Flow $ 4.89 $ 5.01

Present Value of Terminal Value 11.66 13.95

Implied Unit Reference Range $ 16.55 $ 18.95

Terminal Value as % of Total Value 70.5% 73.6%

Implied Premium / (Discount) to Current Unit Price 3.4% 18.5%

21

|

Strictly Confidential

Jefferies LLC / November 2016

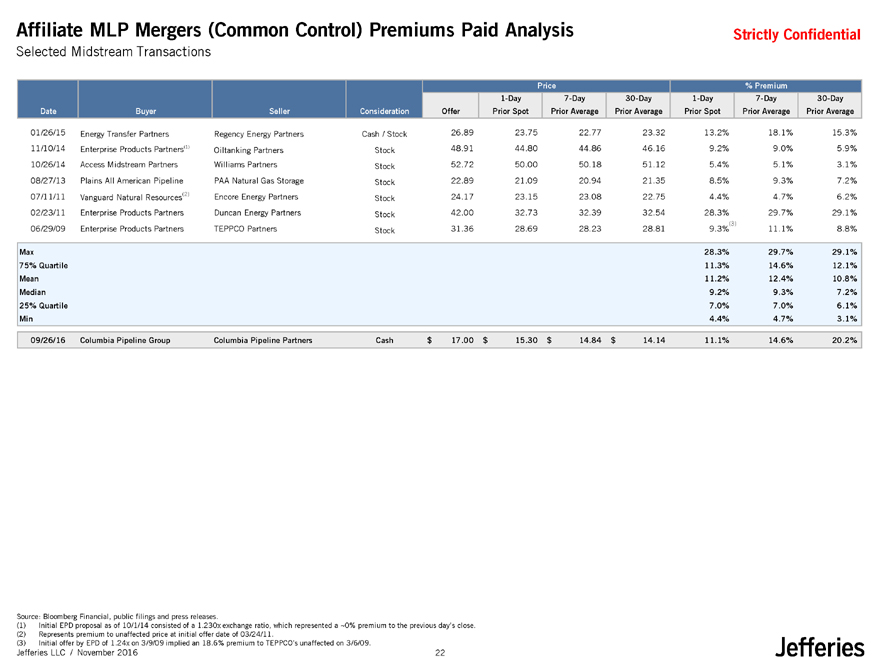

Affiliate MLP Mergers (Common Control) Premiums Paid Analysis

Selected Midstream Transactions

Source: Bloomberg Financial, public filings and press releases.

(1) Initial EPD proposal as of 10/1/14 consisted of a 1.230x exchange ratio, which represented a ~0% premium to the previous day’s close.

(2) Represents premium to unaffected price at initial offer date of 03/24/11.

(3) Initial offer by EPD of 1.24x on 3/9/09 implied an 18.6% premium to TEPPCO’s unaffected on 3/6/09.

(3)

Price % Premium

1-Day 7-Day 30-Day 1-Day 7-Day 30-Day

Date Buyer Seller Consideration Offer Prior Spot Prior Average Prior Average Prior Spot Prior Average Prior Average

01/26/15 Energy Transfer Partners Regency Energy Partners Cash / Stock 26.89 23.75 22.77 23.32 13.2% 18.1% 15.3%

11/10/14 Enterprise Products Partners(1) Oiltanking Partners Stock 48.91 44.80 44.86 46.16 9.2% 9.0% 5.9%

10/26/14 Access Midstream Partners Williams Partners Stock 52.72 50.00 50.18 51.12 5.4% 5.1% 3.1%

08/27/13 Plains All American Pipeline PAA Natural Gas Storage Stock 22.89 21.09 20.94 21.35 8.5% 9.3% 7.2%

07/11/11 Vanguard Natural Resources(2) Encore Energy Partners Stock 24.17 23.15 23.08 22.75 4.4% 4.7% 6.2%

02/23/11 Enterprise Products Partners Duncan Energy Partners Stock 42.00 32.73 32.39 32.54 28.3% 29.7% 29.1%

06/29/09 Enterprise Products Partners TEPPCO Partners Stock 31.36 28.69 28.23 28.81 9.3% 11.1% 8.8%

Max 28.3% 29.7% 29.1%

75% Quartile 11.3% 14.6% 12.1%

Mean 11.2% 12.4% 10.8%

Median 9.2% 9.3% 7.2%

25% Quartile 7.0% 7.0% 6.1%

Min 4.4% 4.7% 3.1%

09/26/16 Columbia Pipeline Group Columbia Pipeline Partners Cash $ 17.00 $ 15.30 $ 14.84 $ 14.14 11.1% 14.6% 20.2%

22

|

Strictly Confidential

Jefferies LLC / November 2016

Affiliate MLP Mergers (Common Control) Premiums Paid Analysis (Cont’d)

Source: Bloomberg Financial, public filings and press releases.

Based on Unaffected Price (As of 09/23/16)

% Premium

1-Day 7-Day 30-Day

Implied Price per Unit Valuation Prior Spot Prior Average Prior Average

Unit Price Before Offer $ 15.30 $ 14.84 $ 14.14

High 28.3% 29.7% 29.1%

75% Quartile 11.3% 14.6% 12.1%

Mean 11.2% 12.4% 10.8%

Median 9.2% 9.3% 7.2%

25% Quartile 7.0% 7.0% 6.1%

Low 4.4% 4.7% 3.1%

Implied Value per Unit

High $ 19.63 $ 19.24 $ 18.26

75% Quartile 17.02 17.00 15.85

Mean 17.01 16.68 15.68

Median 16.70 16.22 15.17

25% Quartile 16.37 15.88 15.01

Low 15.97 15.53 14.59

23

|

Strictly Confidential

Jefferies LLC / November 2016

Appendix

24

|

Strictly Confidential

Jefferies LLC / November 2016

Weighted Average Cost of Capital Analyses

25

|

Strictly Confidential

Jefferies LLC / November 2016

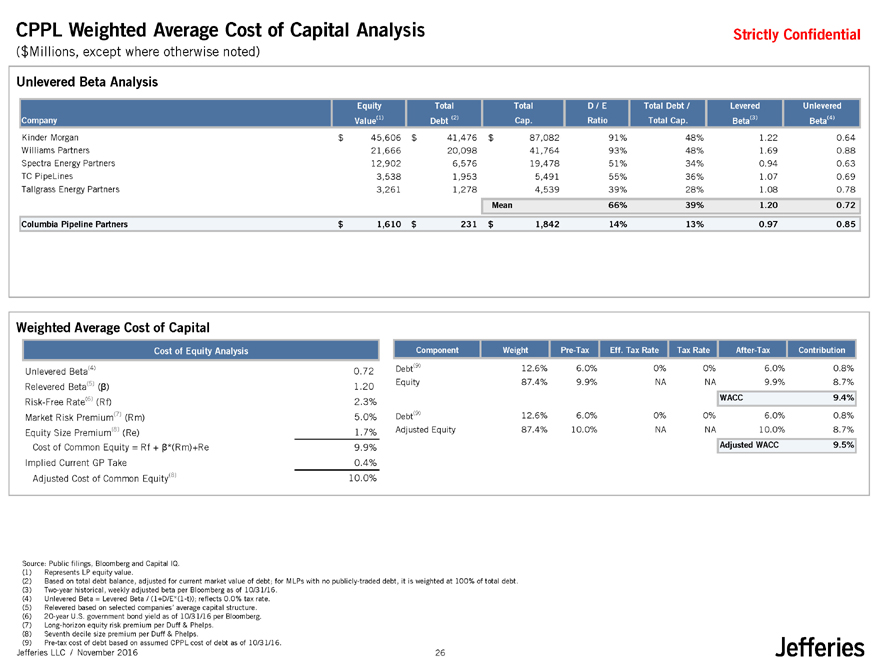

CPPL Weighted Average Cost of Capital Analysis

Source: Public filings, Bloomberg and Capital IQ.

(1) Represents LP equity value.

(2) Based on total debt balance, adjusted for current market value of debt; for MLPs with no publicly-traded debt, it is weighted at 100% of total debt.

(3) Two-year historical, weekly adjusted beta per Bloomberg as of 10/31/16.

(4) Unlevered Beta = Levered Beta / (1+D/E*(1-t)); reflects 0.0% tax rate.

(5) Relevered based on selected companies’ average capital structure.

(6) 20-year U.S. government bond yield as of 10/31/16 per Bloomberg.

(7) Long-horizon equity risk premium per Duff & Phelps.

(8) Seventh decile size premium per Duff & Phelps.

(9) Pre-tax cost of debt based on assumed CPPL cost of debt as of 10/31/16.

Unlevered Beta Analysis

Weighted Average Cost of Capital

($Millions, except where otherwise noted)

Equity Total Total D / E Total Debt / Levered Unlevered

Company Value(1) Debt (2) Cap. Ratio Total Cap. Beta(3) Beta(4)

Kinder Morgan $ 45,606 $ 41,476 $ 87,082 91% 48% 1.22 0.64

Williams Partners 21,666 20,098 41,764 93% 48% 1.69 0.88

Spectra Energy Partners 12,902 6,576 19,478 51% 34% 0.94 0.63

TC PipeLines 3,538 1,953 5,491 55% 36% 1.07 0.69

Tallgrass Energy Partners 3,261 1,278 4,539 39% 28% 1.08 0.78

Mean 66% 39% 1.20 0.72

Columbia Pipeline Partners $ 1,610 $ 231 $ 1,842 14% 13% 0.97 0.85

Cost of Equity Analysis

Unlevered Beta(4) 0.72

Relevered Beta(5) (?) 1.20

Risk-Free Rate(6) (Rf) 2.3%

Market Risk Premium(7) (Rm) 5.0%

Equity Size Premium(8) (Re) 1.7%

Cost of Common Equity = Rf + ?*(Rm)+Re 9.9%

Implied Current GP Take 0.4%

Adjusted Cost of Common Equity(8) 10.0%

Component Weight Pre-Tax Eff. Tax Rate Tax Rate After-Tax Contribution

Debt(9) 12.6% 6.0% 0% 0% 6.0% 0.8%

Equity 87.4% 9.9% NA NA 9.9% 8.7%

WACC 9.4%

Debt(9) 12.6% 6.0% 0% 0% 6.0% 0.8%

Adjusted Equity 87.4% 10.0% NA NA 10.0% 8.7%

Adjusted WACC 9.5%

26