UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-23059

CLOUGH FUNDS TRUST

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

303.623.2577

(Registrant’s telephone number, including area code)

Sareena Khwaja-Dixon, Secretary

Clough Funds Trust

1290 Broadway, Suite 1100

Denver, CO 80203

(Name and address of agent for service)

Date of fiscal year end:October 31

Date of reporting period:November 1, 2018 - April 30, 2019

| Item 1. | Report to Stockholders. |

| Clough Global Long/Short Fund | Table of Contents |

| Shareholder Letter | 2 |

| Portfolio Performance | 5 |

| Disclosure of Fund Expenses | 8 |

| Statement of Investments | 9 |

| Statement of Assets and Liabilities | 12 |

| Statement of Operations | 13 |

| Statement of Changes in Net Assets | 14 |

| Financial Highlights | 15 |

| Notes to Financial Statements | 19 |

| Additional Information | 29 |

| Investment Advisory Agreement Approval | 30 |

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund’s annual and semi-annual shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Fund’s website at www.cloughglobal.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

Beginning on January 1, 2019, you may, notwithstanding the availability of shareholder reports online, elect to receive all future shareholder reports in paper free of charge. If you invest through a financial intermediary, you can contact your financial intermediary to request that you continue to receive paper copies of your shareholder reports. If you invest directly with the Fund, you can call 1-855-425-6844 to let the Fund know you wish to continue receiving paper copies of your shareholder reports.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by enrolling at http://www.cloughglobal.com/open-end-funds/overview/cloax.

| Clough Global Long/Short Fund | Shareholder Letter |

April 30, 2019 (Unaudited)

To Our Investors:

For the semi-annual period ending April 30th, 2019, the Clough Global Long/Short Fund (the “Fund”) had a total return of 4.77% for Class I, compared to 9.70% for the MSCI ACWI and 5.12% for the HFRI Equity Hedge Index. See total returns chart for the performance of all other share classes. The Fund had an average net exposure of 65.4% during this period.

During the period, the long-book contributed 7.71% to returns with an average exposure of 84.3%, while the short book detracted 2.44% from returns with an average exposure of -18.9%. By geography, companies domiciled in the U.S. contributed 3.87% to returns while companies in Italy detracted 0.46%. By sector, the largest contributor was Consumer Discretionary which added 2.56% to returns while Health Care was the largest detractor from returns, with a negative 0.65% impact.

Following is a summary of the key themes expressed in the Fund during the fiscal year-to-date:

The Semiconductor Cycle

The semiconductor cycle is acting in a traditional fashion. Mid-decade, strong smartphone sales hyped demand for semiconductors and manufacturers responded with aggressive capacity additions.

The Bitcoin boom, which took place at the same time as Apple and Samsung introduced new phones with heavy component needs, only intensified demand. Double-ordering, which always occurs at the top of cycles, made demand appear even stronger than it was, and smartphone producers were left heavy with excess semiconductor inventory when sales disappointed and Bitcoin collapsed. Dynamic random-access memory (“DRAM”) pricing started to weaken in mid-2018. Furthermore, large internet companies stopped buying DRAM as pricing started to decline. Since inventories had to be marked down in a falling market, what began as double-digit year-on-year declines in prices turned into the monthly year-on-year decline in rates which are expected to reach 30-40% by Q2 2019 in the case of DRAM.

But the industry should adjust to this quickly. For one, the number of memory suppliers has declined from twelve to three, as European and Taiwanese producers left the industry. We expect that the profit cycle for DRAM and flash memory next time around will be strong. Once 5G-enabled devices and signal infrastructure needs emerge, demand for memory should pick up strongly. The sources of demand have also changed. DRAM is now used by a much broader spectrum of customers. Demand used to be limited by the needs of smartphones, gamers and laptops, but now data centers and industrial uses dominate. Data center investment, artificial intelligence networks and related demand for chips will likely reaccelerate later in 2019 just as memory chip inventory depletes. DRAM pricing should be particularly strong under that scenario.

Asian Consumer Growth

India

As developed economies enter a slowdown, it is important to keep in mind that India offers 7% growth while Japan and Germany offer 1% growth or less. In India, an aspirational millennial population is beginning to migrate from India’s poor and inefficient northern and eastern provinces, to the south and west where the wealth is. That is a similar dynamic to one that powered China’s growth in the 2000s.

Also, over the past twenty-five years the NIFTY 50 Index, which is the benchmark broad-based stock market index for the Indian equity market, has returned 11.09% on an annualized basis, which places it among the top global markets. Indian firms have higher returns on equity (“ROE”) than their global peers (the top 500 companies in India generate ROE of 15% versus the emerging market average of 11%). And India’s talent pool is strong.

To keep up with demographics, India must generate one million jobs each month, and it is moving away from agriculture as a dominant employer. The number of agricultural employees has declined from 700 million to 400 million over the past decade, which indicates that India is very early in a productivity boom which could potentially span the next two decades. The demonetization strategy Prime Minister Modi put in place a few years ago drove 30% of the Indian population from the cash economy into the banks where they can now access credit. The new bankruptcy law has forced many of the state-owned banks to clear the books of shady loans and the highly public insolvency of the Non-Bank Financial Institutions puts the quality, publicly-traded banks in a margin sweet spot. They control most of the deposits, enjoy the lowest deposit costs, can lend profitably to the highest quality credit and control most of the loan pricing power in the economy.

While the government has announced a “Housing for All” program to fund millions of homes by the mid-2020s, private investment is picking up as well. Affordability is rising as incomes rise and housing costs remain stable. Mortgages outstanding equal 10% of gross domestic product (“GDP”) versus 60% in the U.S. Housing costs are tax deductible and mortgages are subsidized. In addition, interest rates in India are high and bank spreads are strong. With the state banking institution in a state of decline, depositors are moving to the private institutions.

| Clough Global Long/Short Fund | Shareholder Letter |

April 30, 2019 (Unaudited)

We believe demand for credit will come from both the household and corporate sectors. A badly needed construction boom is underway in India. Real estate borrowing in India is 4-5% of total credit, 80% of which is residential and therefore highly stable. Unsold inventory is falling and a cut in the Goods and Services tax is lifting profits and sentiment.

China

While debt issues still dominate negative investor perceptions of China, the real question is where can a 45% savings rate go? The consumption cycle in China still seems largely misunderstood by the market and it is underestimated.

A government policy of corporate deleveraging amid tariff concerns led China stocks to a 24% decline in 2018. At the same time, China’s securities markets suffered from a tight monetary policy and a concerted effort by the authorities to force deleveraging. But we think the 2019 recovery has legs. China’s equity market sells at a low price to book level, speculation is muted, earnings revisions are beginning to move up, and the central bank is increasing liquidity. These are all promising indicators.

China is always undergoing tremendous change and much of the slowing in that economy can be attributed to the decline in industrial and export activity, a segment forever plagued by excess, inefficient capacity and low returns on investment. However, household consumption and certain market segments, such as health services and others, are undercounted and growing rapidly. Wages are increasing in China and financial service companies will face growing demand.

The China negatives, on the other hand, are well known. China’s GDP reportedly slowed to 6.4% in 2018 and perhaps less. Either way, it was the slowest real rate of growth for that country in 30 years. Exports and industrial activity are slowing. China’s population is peaking, and the working age population will soon be declining. The number of births was the lowest since 1961 and even though China’s long standing “one child” policy was recently cancelled, they will continue to decline. The cliché-based fear is that China will grow old, with accompanying social costs, before it becomes rich. Political reform has seemingly stopped, and government is moving back to the type of autocracy which sooner or later becomes sclerotic. That is the negative outlook.

So why even consider investing in China? For one, we believe that much of this is already priced into the market. Historically, price to earnings ratios in China have ranged from 9x to 16x (excluding the rapid growth phase when they traded up to 37x), and they are at 11x today. Stocks are down so much in China that even a little good news should rally the market to some extent.

While China’s industrial sector is coming under pressure and producers of industrial goods from iPhones and appliances to precision machines and automobiles are experiencing declining sales, China’s current account balance is positive, its currency is strong and China’s consumer economy is still vibrant. Many consumer and technology companies are experiencing growing sales as consumer incomes rise.

Secondly, we believe consumer company profits are about to benefit from the “accelerator effect” – that is, the tendency of consumers to accelerate spending on higher end goods and services as incomes rise, promising growth in the consumer economy well above the national average. Per capita incomes in China average about $9,500 U.S. dollars and the number of high-income consumers is accelerating. As more consumers enter the middle class, and the number of middle- class Chinese rises from 300 million to an estimated 500 million by 2026, consumer spending should grow by an amount that may equal the total dollar value of U.S. consumer spending by 2026.

For the moment, the market’s attention is focused on the tariff issue and while that issue may yet take time to unfold, we note in the interim, that after visiting and investing in China for the better part of three decades, we have learned that China never does anything that is not in its own best interest. The absence of a trade deal means further deterioration in employment, which is something we think China will try to avoid at all costs.

Healthcare – Positioning for The Election Cycle

During the period we added to healthcare companies with classic “cash pay” businesses within healthcare (i.e. companies whose revenues stem from direct customer payments rather than government or private insurance reimbursements). These include positions in the dental and the animal health markets, bolstering our existing “science-heavy” portfolio.

As we move into the 2020 election cycle, we are looking for investments that boast strong fundamentals and sustainable mid-single digit growth over the next several years, but have little reimbursement, generic threat or drug pricing political rhetoric risk. Our holdings include three companies that we believe are uniquely positioned within the animal health industry, including a market leader in animal therapeutics, a market leader in animal diagnostics, and a recent spinoff in animal therapeutics.

| Semi-Annual Report | April 30, 2019 | 3 |

| Clough Global Long/Short Fund | Shareholder Letter |

April 30, 2019 (Unaudited)

We continue to be bullish on merger and acquisition (“M&A”) activity in the biotechnology and mid-cap pharmaceutical sub-sector. The industry has seen significant M&A activity in 2019, and we expect continued deal activity for the foreseeable future. We continue to add strategic assets to the portfolio. We believe that currently, roughly half of our healthcare holdings make reasonable acquisition targets, offering innovative competitive products, long patent protection, and management teams that are aligned with shareholders.

Short Book

Our long-standing short position in a basket of Europe’s weakest banks has been maintained. As Europe depends on its banks to fund growth, little wonder its economies are so weak. And there is no easy fix. Mergers make little sense since there is no evidence larger institutions would be any stronger. A European recession would complicate things. What long term refinancing operation (“LTRO”) and quantitative easing in Europe accomplished was to saddle the banks with huge holdings of peripheral country debt.

In a long period of excess liquidity and credit availability, the opportunity for capital destruction is rife. We have seen once iconic companies like Sears, General Electric and IBM buy back stock at prices far higher than today’s and reduce financial flexibility and ROIs in the process. We have seen capital destroyed on wasteful acquisitions and poor expansion strategies. Our sense is the securities markets will be less tolerant of such strategies going forward and we have identified short positions which we think are likely to benefit as a result.

In Conclusion

The Fund’s recent results are encouraging to us, particularly following the market chaos of the late 2018 equity sell-off. Amid that turmoil, we kept our high conviction long positions intact, because we believed that attempts to trade around the steep equity sell-offs risked the portfolio being whipsawed. During this period, the Fund’s modest short book helped to reduce volatility, which made holding our high conviction long positions more palatable.

We do not base our investment strategies on economic forecasts, but we do follow investment and credit cycles and we draw three conclusions from what we see today: (1) the dominant price trends are deflationary; (2) the Fed is more likely to ease than tighten; and (3) the economy will likely slow rather than fall into recession. No serious inventory imbalances are present (beyond what we outlined above within the semiconductor complex), and no serious overbuild in the nation’s capital stock which would undermine pricing and profitability is visible, such as the technology boom in 2000 or housing in 2008. We believe that although temporary technical factors can knock the market down, the likelihood of a serious liquidity squeeze seems remote at this point.

Sincerely,

|  |

| | |

| Charles I. Clough, Jr. | Vincent M. Lorusso, Jr. |

| Clough Global Long/Short Fund | Portfolio Performance |

April 30, 2019 (Unaudited)

Performance(as of April 30, 2019)

| | 1 Month | Quarter | 6 Month | 1 Year | 3 Year | Since Inception(a) |

| Class I - NAV(b)(c) | 1.17% | 3.70% | 4.77% | -2.86% | 6.39% | 2.47% |

| Investor Class - NAV(b)(g) | 1.09% | 3.64% | 4.62% | -3.14% | 6.04% | 2.16% |

| Class A - NAV(b)(h) | 1.09% | 3.64% | 4.62% | -3.14% | 6.04% | 3.04% |

| Class A - MOP(b)(h) | -4.48% | -2.03% | -1.16% | -8.50% | 4.07% | 1.43% |

| Class C - NAV(b) | 1.02% | 3.43% | 4.22% | -3.81% | 5.30% | 1.55% |

| Class C - CDSC(b) | 0.02% | 2.43% | 3.22% | -4.77% | 5.30% | 1.55% |

| MSCI All Country World Index(d) | 3.38% | 7.48% | 9.37% | 5.06% | 11.36% | 7.57% |

| HFRI Equity Hedge Index(e) | 1.63% | 4.09% | 5.05% | 0.98% | 6.92% | 4.35% |

| S&P 500 Index(f) | 4.05% | 9.48% | 9.76% | 13.49% | 14.87% | 10.88% |

The performance data quoted above represents past performance. Past performance is not a guarantee of future results. Investment return and value of the Fund shares will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Performance may be lower or higher than performance data quoted. Fund performance current to the most recent month-end is available by calling (855) 425-6844 or by visiting www.cloughglobal.com.

Maximum Offering Price (MOP) for Class A shares includes the Fund’s maximum sales charge of 5.50%. Performance shown at NAV does not include sales charges and would have been lower had it been taken into account. A Contingent Deferred Sales Charge (“CDSC”) of 1.00% may apply to Class C shares redeemed within the first 12 months after a purchase. The Fund imposes a 2.00% redemption fee on shares held for less than 30 days.

| (a) | Fund’s commencement date is September 30, 2015. The performance data quoted for the period prior to September 30, 2015 is that of an unregistered investment fund (the “Predecessor Fund”) that was managed by the Adviser since its inception and was reorganized into the Fund as of the date the Fund commenced investment operations. The Predecessor Fund was not a registered mutual fund and therefore was not subject to the same investment and tax restrictions as the Fund. Performance information reflects all fees and expenses incurred by the Predecessor Fund, and has not been adjusted to reflect Fund expenses. If it had been so adjusted, the Predecessor Fund’s performance would have been higher for that period. The Predecessor Fund commenced operations on January 2, 2015. |

| (b) | Returns shown prior to 9/30/2015 are based on the returns of the Predecessor Fund adjusted to reflect 12b-1 fees and shareholder services fees, as applicable. |

| (c) | Returns shown prior to 9/30/2015 are based on the returns of the Predecessor Fund. |

| (d) | The MSCI All Country World Index is a float-adjusted, capitalization weighted index that is designed to measure the equity market performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets. Both indices referenced herein reflect the reinvestment of dividends. The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages (www.msci.com). |

| (e) | An index designed by Hedge Fund Research, Inc. to represent the performance of investment managers who maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment processes can be employed by such managers to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation ranges of typical portfolios. The HFRI family of indices reserves the right to revise historical performance data for a period of up to four months following the as of date. The performance shown was calculated using current, available data at the time of publication, but is subject to change outside of the control of the Fund and its affiliates |

| (f) | The Standard & Poor’s composite index of 500 stocks, a widely recognized, unmanaged index of common stock prices. Index performance does not reflect fund performance. |

| (g) | On December 1, 2017, Class A was renamed Investor Class. |

| (h) | A new Class A commenced operations on June 29, 2018. |

Returns of less than 1 year are cumulative.

An investor cannot invest directly in an index.

| Semi-Annual Report | April 30, 2019 | 5 |

| Clough Global Long/Short Fund | Portfolio Performance & Allocation |

April 30, 2019 (Unaudited)

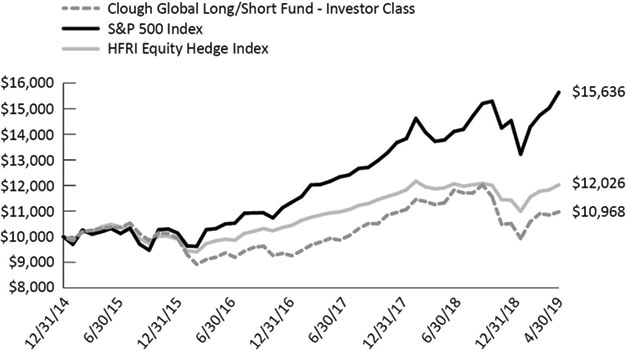

Performance of $10,000 Initial Investment(as of April 30, 2019)

The graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. The historical performance prior to September 30, 2015 is that of the Predecessor Fund. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Top Ten Long Holdings(as a % of Net Assets)* | |

| Carvana Co. | 2.02% |

| CRISPR Therapeutics AG | 1.98% |

| Microsoft Corp. | 1.71% |

| TransDigm Group, Inc. | 1.70% |

| JPMorgan Chase & Co. | 1.67% |

| Citigroup, Inc. | 1.65% |

| Morgan Stanley | 1.65% |

| Bank of America Corp. | 1.62% |

| Analog Devices, Inc. | 1.52% |

| Home Depot, Inc. | 1.47% |

| Top Ten Holdings | 16.99% |

| * | Holdings are subject to change |

| Sector Allocation** | Long Exposure % TNA | Short Exposure % TNA | Gross Exposure % TNA | Net Exposure % TNA |

| Health Care | 18.2% | -2.2% | 20.4% | 16.0% |

| Consumer Discretionary | 18.2% | -3.5% | 21.7% | 14.7% |

| Financials | 16.8% | -4.7% | 21.5% | 12.1% |

| Information Technology | 16.3% | -4.0% | 20.3% | 12.3% |

| Communication Services | 6.9% | -1.1% | 8.0% | 5.8% |

| Industrials | 2.9% | -1.0% | 3.9% | 1.9% |

| Materials | 0.9% | 0.0% | 0.9% | 0.9% |

| Real Estate | 1.2% | -2.1% | 3.3% | -0.9% |

| Consumer Staples | 4.0% | -4.2% | 8.2% | -0.2% |

| Total Investments | 85.4% | -22.8% | 108.2% | 62.6% |

| Clough Global Long/Short Fund | Portfolio Allocation |

April 30, 2019 (Unaudited)

| Country Allocation ** | Long Exposure % TNA | Short Exposure % TNA | Gross Exposure % TNA | Net Exposure % TNA |

| United States | 43.9% | -9.8% | 53.7% | 34.1% |

| U.S. Multinationals† | 16.6% | -3.5% | 20.1% | 13.1% |

| China | 12.4% | 0.0% | 12.4% | 12.4% |

| India | 6.7% | 0.0% | 6.7% | 6.7% |

| Other - Developed Markets | 0.6% | 0.0% | 0.6% | 0.6% |

| Japan | 0.5% | 0.0% | 0.5% | 0.5% |

| Other - Emerging Markets | 0.0% | -1.0% | 1.0% | -1.0% |

| Europe | 4.7% | -8.5% | 13.2% | -3.8% |

| Total Investments | 85.4% | -22.8% | 108.2% | 62.6% |

| ** | Allocation summaries and top ten long holdings calculated as percent of total net assets using market value of cash traded securities, notional value of derivative contracts and excluding short-term investments. |

| † | US Multinational Corporations – has more than 50% of revenues derived outside of the U.S. |

Semi-Annual Report | April 30, 2019 | 7 |

| Clough Global Long/Short Fund | Disclosure of Fund Expenses |

April 30, 2019 (Unaudited)

Examples. As a shareholder of the Clough Global Long/Short Fund (the “Fund”), you incur two types of costs: (1) transaction costs, including applicable redemption fees and sales charges (loads); and (2) ongoing costs, including management fees, distribution and service (12b-1) fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on November 1, 2018 and held through April 30, 2019.

Actual Expenses.The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period November 1, 2018 – April 30, 2019” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other mutual funds.

Please note that the expenses shown in the table are meant to highlight your ongoing Fund costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line of the table below is useful in comparing ongoing costs only and may not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| | Beginning

Account Value

11/01/18 | Ending

Account Value

4/30/19 | Expense Ratio(a)(b) | Expenses Paid During period 11/01/18 - 4/30/19(c) |

| Clough Global Long/Short Fund | | | | |

| Class I | | | | |

| Actual | $1,000.00 | $1,047.70 | 2.08% | $10.56 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,014.48 | 2.08% | $10.39 |

| Investor Class | | | | |

| Actual | $1,000.00 | $1,046.20 | 2.34% | $11.87 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,013.19 | 2.34% | $11.68 |

| Class A | | | | |

| Actual | $1,000.00 | $1,046.20 | 2.35% | $11.92 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,013.14 | 2.35% | $11.73 |

| Class C | | | | |

| Actual | $1,000.00 | $1,042.20 | 3.08% | $15.60 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,009.52 | 3.08% | $15.35 |

| (a) | Expense ratio excluding interest expense and dividends paid on borrowed securities for the Clough Global Long/Short Fund is 1.60%, 1.90%,1.85%, and 2.60% for Class I, Investor Class, Class A, and Class C respectively. |

| (b) | Annualized, based on the Fund's most recent fiscal half year expenses. |

| (c) | Expenses are equal to the Fund's annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half-year (181)/365 (to reflect the half-year period). |

| Clough Global Long/Short Fund | Statement of Investments |

April 30, 2019 (Unaudited)

| | | | Shares | | | | Value | |

| COMMON STOCKS 82.69% | | | | | | | | |

| Communication Services 6.85% | | | | | | | | |

| Alphabet, Inc. - Class C(a) | | | 320 | | | $ | 380,314 | |

| China Tower Corp., Ltd. - Class H | | | 1,888,000 | | | | 510,218 | |

| GCI Liberty, Inc. - Class A(a)(b) | | | 12,671 | | | | 755,445 | |

| IMAX Corp.(a) | | | 27,300 | | | | 665,574 | |

| Momo, Inc. - Sponsored ADR | | | 7,700 | | | | 270,039 | |

| Netflix, Inc.(a) | | | 1,181 | | | | 437,608 | |

| Softbank Group Corp. | | | 2,700 | | | | 280,071 | |

| T-Mobile US, Inc.(a)(b) | | | 3,600 | | | | 262,764 | |

| | | | | | | | 3,562,033 | |

| | | | | | | | | |

| Consumer Discretionary 18.24% | | | | | | | | |

| Alibaba Group Holding, Ltd. - Sponsored ADR(a) | | | 2,760 | | | | 512,173 | |

| Amazon.com, Inc.(a)(b) | | | 275 | | | | 529,793 | |

| ANTA Sports Products, Ltd. | | | 57,300 | | | | 403,922 | |

| At Home Group, Inc.(a) | | | 23,000 | | | | 540,270 | |

| Carvana Co.(a)(b) | | | 14,700 | | | | 1,051,932 | |

| Eicher Motors, Ltd. | | | 2,000 | | | | 585,685 | |

| Floor & Decor Holdings, Inc. - Class A(a) | | | 12,200 | | | | 585,844 | |

| Galaxy Entertainment Group, Ltd. | | | 68,500 | | | | 512,126 | |

| Home Depot, Inc.(b) | | | 3,750 | | | | 763,875 | |

| Lifestyle International Holdings, Ltd. | | | 145,000 | | | | 252,486 | |

| Mahindra & Mahindra, Ltd. | | | 64,982 | | | | 602,885 | |

| Pool Corp. | | | 2,900 | | | | 532,846 | |

| RH(a)(b) | | | 5,600 | | | | 597,576 | |

| Service Corp. International | | | 17,436 | | | | 725,512 | |

| TAL Education Group - ADR(a) | | | 8,100 | | | | 311,607 | |

| Vail Resorts, Inc. | | | 2,550 | | | | 583,567 | |

| Wayfair, Inc. - Class A(a) | | | 2,460 | | | | 398,889 | |

| | | | | | | | 9,490,988 | |

| | | | | | | | | |

| Consumer Staples 1.77% | | | | | | | | |

| Estee Lauder Cos., Inc. - Class A | | | 3,800 | | | | 652,878 | |

| L'Oreal SA | | | 977 | | | | 268,581 | |

| | | | | | | | 921,459 | |

| | | | | | | | | |

| Financials 16.82% | | | | | | | | |

| AIA Group, Ltd. | | | 40,600 | | | | 413,773 | |

| American International Group, Inc. | | | 6,000 | | | | 285,420 | |

| Bank of America Corp. | | | 27,550 | | | | 842,479 | |

| Bank of China, Ltd. - Class H | | | 323,000 | | | | 153,990 | |

| China Construction Bank Corp. - Class H | | | 174,000 | | | | 153,710 | |

China International Capital Corp., Ltd. - Class H | | | 111,600 | | | | 239,566 | |

CITIC Securities Co., Ltd. - Class H | | | 107,000 | | | | 231,328 | |

| Citigroup, Inc. | | | 12,149 | | | | 858,934 | |

| Golub Capital BDC, Inc. | | | 30,000 | | | | 552,900 | |

| Granite Point Mortgage Trust, Inc. | | | 38,600 | | | | 742,278 | |

| HDFC Bank, Ltd. | | | 20,801 | | | | 693,065 | |

| | | Shares | | Value |

| Financials (continued) | | | | | | | | |

| ICICI Bank, Ltd. | | | 117,807 | | | $ | 690,205 | |

Industrial & Commercial Bank of China - Class H | | | 206,000 | | | | 154,668 | |

| JPMorgan Chase & Co.(b) | | | 7,500 | | | | 870,375 | |

| Morgan Stanley(b) | | | 17,800 | | | | 858,850 | |

| Ping An Insurance Group Co. of China, Ltd. - Class H | | | 21,500 | | | | 258,856 | |

| Starwood Property Trust, Inc.(b) | | | 32,700 | | | | 753,735 | |

| | | | | | | | 8,754,132 | |

| Health Care 17.64% | | | | | | | | |

| Align Technology, Inc.(a)(b) | | | 1,520 | | | | 493,514 | |

| Amgen, Inc. | | | 1,750 | | | | 313,810 | |

| Apellis Pharmaceuticals, Inc.(a)(b) | | | 35,600 | | | | 705,236 | |

| Baxter International, Inc. | | | 3,400 | | | | 259,420 | |

| BeiGene, Ltd. - ADR(a) | | | 3,700 | | | | 459,651 | |

| BioMarin Pharmaceutical, Inc.(a) | | | 8,236 | | | | 704,425 | |

| Boston Scientific Corp.(a) | | | 6,800 | | | | 252,416 | |

| Correvio Pharma Corp.(a) | | | 137,570 | | | | 330,168 | |

| CRISPR Therapeutics AG(a) | | | 25,600 | | | | 1,028,864 | |

| Elanco Animal Health, Inc.(a)(b) | | | 12,700 | | | | 400,050 | |

| Equillium, Inc.(a) | | | 19,200 | | | | 119,808 | |

| Galapagos NV - Sponsored ADR(a) | | | 1,833 | | | | 210,795 | |

| Gossamer Bio, Inc.(a)(b) | | | 30,400 | | | | 515,584 | |

| GW Pharmaceuticals PLC - ADR(a) | | | 1,891 | | | | 320,165 | |

| IDEXX Laboratories, Inc.(a) | | | 870 | | | | 201,840 | |

| Idorsia, Ltd.(a)(c) | | | 30,821 | | | | 609,191 | |

| Illumina, Inc.(a) | | | 825 | | | | 257,400 | |

| Intra-Cellular Therapies, Inc.(a) | | | 18,300 | | | | 241,011 | |

| Masimo Corp.(a) | | | 1,900 | | | | 247,285 | |

| Teladoc Health, Inc.(a)(b) | | | 4,500 | | | | 255,960 | |

| Thermo Fisher Scientific, Inc. | | | 950 | | | | 263,578 | |

| Veracyte, Inc.(a) | | | 13,800 | | | | 315,606 | |

| Vertex Pharmaceuticals, Inc.(a) | | | 1,452 | | | | 245,359 | |

| WAVE Life Sciences, Ltd.(a) | | | 9,200 | | | | 244,076 | |

| Zoetis, Inc. | | | 1,810 | | | | 184,330 | |

| | | | | | | | 9,179,542 | |

| | | | | | | | | |

| Industrials 2.92% | | | | | | | | |

| Larsen & Toubro, Ltd. | | | 32,880 | | | | 637,497 | |

| TransDigm Group, Inc.(a)(b) | | | 1,830 | | | | 883,012 | |

| | | | | | | | 1,520,509 | |

| | | | | | | | | |

| Information Technology 16.34% | | | | | | | | |

| Adobe Systems, Inc.(a) | | | 2,180 | | | | 630,565 | |

| Analog Devices, Inc. | | | 6,800 | | | | 790,432 | |

| Broadcom, Ltd.(b) | | | 1,391 | | | | 442,895 | |

| Coupa Software, Inc.(a) | | | 2,050 | | | | 211,827 | |

| Guidewire Software, Inc.(a) | | | 2,600 | | | | 276,900 | |

| Inphi Corp(a) | | | 3,500 | | | | 159,810 | |

| KLA-Tencor Corp. | | | 5,610 | | | | 715,163 | |

| Micron Technology, Inc.(a)(b) | | | 17,400 | | | | 731,844 | |

| Microsoft Corp.(b) | | | 6,800 | | | | 888,080 | |

| Pluralsight, Inc. - Class A(a) | | | 8,800 | | | | 312,312 | |

| Semi-Annual Report | April 30, 2019 | 9 |

| Clough Global Long/Short Fund | Statement of Investments |

April 30, 2019 (Unaudited)

| | | Shares | | Value |

| Information Technology (continued) | | | | | | | | |

| Proofpoint, Inc.(a) | | | 3,620 | | | $ | 454,020 | |

| RingCentral, Inc. - Class A(a) | | | 2,900 | | | | 337,473 | |

| salesforce.com, Inc.(a)(b) | | | 3,355 | | | | 554,749 | |

| ServiceNow, Inc.(a) | | | 2,140 | | | | 581,031 | |

| Twilio, Inc. - Class A(a) | | | 1,700 | | | | 233,138 | |

| Visa, Inc. - Class A | | | 3,250 | | | | 534,398 | |

| WNS Holdings, Ltd. - ADR(a) | | | 4,900 | | | | 280,035 | |

| Xilinx, Inc. | | | 3,060 | | | | 367,628 | |

| | | | | | | | 8,502,300 | |

| | | | | | | | | |

| Materials 0.92% | | | | | | | | |

| Anhui Conch Cement Co., Ltd. - Class H | | | 78,500 | | | | 478,817 | |

| | | | | | | | | |

| Real Estate 1.19% | | | | | | | | |

| SBA Communications Corp.(a)(b) | | | 3,050 | | | | 621,376 | |

| | | | | | | | | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Cost $37,776,685) | | | | | | | 43,031,156 | |

| | | | | | | | | |

| EXCHANGE TRADED FUNDS 0.51% | | | | | | | | |

| Health Care 0.51% | | | | | | | | |

| iShares U.S. Medical Devices ETF | | | 1,180 | | | | 265,252 | |

| | | | | | | | | |

| TOTAL EXCHANGE TRADED FUNDS | | | | | | | | |

| (Cost $260,165) | | | | | | | 265,252 | |

| | | | | | | | | |

| SHORT-TERM INVESTMENTS 15.70% | | | | | | | | |

| Money Market Funds 15.70% | | | | | | | | |

| BlackRock Liquidity Funds, T-Fund Portfolio - Institutional Class (2.306% 7-day yield) | | | 8,171,313 | | | | 8,171,313 | |

| | | | | | | | | |

| TOTAL SHORT-TERM INVESTMENTS | | | | | | | | |

| (Cost $8,171,313) | | | | | | | 8,171,313 | |

| | | | | | | | | |

| Total Investments - 98.90% | | | | | | | | |

| (Cost $46,208,163) | | | | | | | 51,467,721 | |

| | | | | | | | | |

| Other Assets in Excess of Liabilities - 1.10%(d) | | | | | | | 573,646 | |

| | | | | | | | | |

| NET ASSETS - 100.00% | | | | | | $ | 52,041,367 | |

| SCHEDULE OF SECURITIES SOLDSHORT(a) | | Shares | | Value |

| COMMON STOCKS (22.17%) | | | | | | | | |

| Communication Services (1.06%) | | | | | | | | |

| AT&T, Inc. | | | (17,800 | ) | | $ | (551,088 | ) |

| | | | | | | | | |

| Consumer Discretionary (3.46%) | | | | | | | | |

| Dick's Sporting Goods, Inc. | | | (15,680 | ) | | | (580,160 | ) |

| Next PLC | | | (8,210 | ) | | | (617,300 | ) |

| Williams-Sonoma, Inc. | | | (10,560 | ) | | | (603,715 | ) |

| | | | | | | | (1,801,175 | ) |

| | | | | | | | | |

| Consumer Staples (4.19%) | | | | | | | | |

| Nestle SA | | | (5,941 | ) | | | (571,682 | ) |

| Tesco PLC | | | (184,741 | ) | | | (601,774 | ) |

| Walgreens Boots Alliance, Inc. | | | (9,500 | ) | | | (508,915 | ) |

| Wm Morrison Supermarkets PLC | | | (177,609 | ) | | | (500,030 | ) |

| | | | | | | | (2,182,401 | ) |

| | | | | | | | | |

| Financials (4.18%) | | | | | | | | |

| American Express Co. | | | (3,053 | ) | | | (357,903 | ) |

| Deutsche Bank AG | | | (53,100 | ) | | | (439,668 | ) |

| Mediobanca Banca di Credito Finanziario SpA | | | (46,357 | ) | | | (491,343 | ) |

| Societe Generale S.A. | | | (12,680 | ) | | | (401,342 | ) |

| UniCredit SpA | | | (35,211 | ) | | | (486,945 | ) |

| | | | | | | | (2,177,201 | ) |

| | | | | | | | | |

| Health Care (2.23%) | | | | | | | | |

| Alexion Pharmaceuticals, Inc. | | | (4,500 | ) | | | (612,585 | ) |

| McKesson Corp. | | | (4,581 | ) | | | (546,284 | ) |

| | | | | | | | (1,158,869 | ) |

| | | | | | | | | |

| Industrials (1.01%) | | | | | | | | |

| Stericycle, Inc. | | | (9,000 | ) | | | (525,510 | ) |

| | | | | | | | | |

| Information Technology (3.96%) | | | | | | | | |

| Amkor Technology, Inc. | | | (14,300 | ) | | | (129,558 | ) |

| AU Optronics Corp. - Sponsored ADR | | | (153,434 | ) | | | (535,485 | ) |

| International Business Machines Corp. | | | (3,760 | ) | | | (527,415 | ) |

| Manhattan Associates, Inc. | | | (4,900 | ) | | | (330,505 | ) |

| NetApp, Inc. | | | (7,400 | ) | | | (539,090 | ) |

| | | | | | | | (2,062,053 | ) |

| | | | | | | | | |

| Real Estate (2.08%) | | | | | | | | |

| AvalonBay Communities, Inc. | | | (2,680 | ) | | | (538,492 | ) |

| Clough Global Long/Short Fund | Statement of Investments |

April 30, 2019 (Unaudited)

SCHEDULE OF SECURITIES SOLD SHORT(a)(continued) | | Shares | | Value |

| Real Estate (continued) | | | | | | | | |

| Equity Residential | | | (7,100 | ) | | $ | (542,582 | ) |

| | | | | | | | (1,081,074 | ) |

| | | | | | | | | |

| TOTAL COMMON STOCKS | | | | | | | | |

| (Proceeds $11,575,690) | | | | | | | (11,539,371 | ) |

| | | | | | | | | |

| TOTAL SECURITIES SOLD SHORT | | | | | | | | |

| (Proceeds $11,575,690) | | | | | | $ | (11,539,371 | ) |

| (a) | Non-income producing security. |

| (b) | Pledged security; a portion or all of the security is pledged as collateral for securities sold short or total return swap contracts. As of April 30, 2019, the aggregate market value of those securities was $4,164,483, representing 8.00% of net assets. (See Note 1) |

| (c) | Security exempt from registration of the Securities Act of 1933. These securities may be resold in transactions exempt from registration under Rule 144A, normally to qualified institutional buyers. As of April 30, 2019, the aggregate value of those securities was $609,191 or 1.17% of net assets. |

| (d) | Includes cash which is being held as collateral for total return swap contracts and securities sold short. |

TOTAL RETURN SWAP CONTRACTS

| Counter Party | | Reference

Entity/Obligation | | Notional

Amount | | Floating Rate

Paid by the Fund | | Floating

Rate Index | | Termination

Date | | Market

Value | | Net Unrealized

Appreciation |

| Morgan Stanley | | Kweichow Moutai Co., Ltd. | | $ | 514,281 | | | 1D FEDEF + 250 bps | | 1 D FEDEF | | 1/8/2020 | | $ | 701,209 | | | $ | 186,928 | |

| | | | | $ | 514,281 | | | | | | | | | $ | 701,209 | | | $ | 186,928 | |

| Counter Party | | Reference

Entity/Obligation | | Notional

Amount | | Floating Rate

Paid by the Fund | | Floating

Rate Index | | Termination

Date | | Market

Value | | Net Unrealized

Depreciation |

| Morgan Stanley | | Banco Santander SA | | $ | (282,071 | ) | | 1D FEDEF -50 bps | | 1 D FEDEF | | 05/20/2020 | | $ | (298,951 | ) | | $ | (16,880 | ) |

| Morgan Stanley | | Jiangsu Yanghe Brewery | | | 438,934 | | | 1D FEDEF + 255 bps | | 1 D FEDEF | | 10/01/2020 | | $ | 434,885 | | | | (4,049 | ) |

| | | | | $ | 156,863 | | | | | | | | | $ | 135,934 | | | $ | (20,929 | ) |

Investment Abbreviations:

1D FEDEF - Federal Funds Effective Rate (Daily)

For Fund compliance purposes, the Fund’s sector classifications refer to any one of the sector sub-classifications used by one or more widely recognized market indexes, and/or as defined by the Fund's management. This definition may not apply for purposes of this report, which may combine sector sub-classifications for reporting ease. Sectors are shown as a percent of net assets. These sector classifications are unaudited.

See Notes to the Financial Statements.

| Semi-Annual Report | April 30, 2019 | 11 |

| Clough Global Long/Short Fund | Statement of Assets and Liabilities |

April 30, 2019 (Unaudited)

| ASSETS: | | | |

| | | | |

| Investments, at value (Cost - see below) | | $ | 51,467,721 | |

| Cash | | | 525,965 | |

| Deposit with broker for securities sold short | | | 11,618,316 | |

| Deposit with broker for total return swap contracts | | | 529,409 | |

| Unrealized appreciation on total return swap contracts | | | 186,928 | |

| Interest receivable - margin account | | | 17,041 | |

| Dividends receivable | | | 13,115 | |

| Interest receivable | | | 10,283 | |

| Receivable for investments sold | | | 1,206,842 | |

| Receivable for shares sold | | | 12,018 | |

| Prepaid expenses and other assets | | | 37,413 | |

| Total Assets | | | 65,625,051 | |

| | | | | |

| LIABILITIES: | | | | |

| | | | | |

| Securities sold short (Proceeds $11,575,690) | | | 11,539,371 | |

| Payable for investments purchased | | | 1,667,682 | |

| Payable for shares redeemed | | | 208,855 | |

| Unrealized depreciation on total return swap contracts | | | 20,929 | |

| Payable for total return swap contracts payments | | | 21,287 | |

| Dividends payable - short sales | | | 16,546 | |

| Accrued investment advisory fee | | | 23,844 | |

| Accrued distribution and service fees | | | 4,294 | |

| Accrued legal expense | | | 30,041 | |

| Accrued administration fee | | | 18,039 | |

| Other payables and accrued expenses | | | 32,796 | |

| Total Liabilities | | | 13,583,684 | |

| Net Assets | | $ | 52,041,367 | |

| Cost of Investments | | $ | 46,208,163 | |

| | | | | |

| COMPOSITION OF NET ASSETS: | | | | |

| | | | | |

| Paid-in capital | | $ | 51,714,871 | |

| Distributable Earnings | | | 326,496 | |

| Net Assets | | $ | 52,041,367 | |

| PRICING OF CLASS I SHARES: | | | | |

| Net Assets | | $ | 45,684,624 | |

| Shares outstanding of no par value, unlimited shares authorized | | | 4,075,550 | |

| Net Asset Value, offering and redemption price per share | | $ | 11.21 | |

| PRICING OF INVESTOR CLASS SHARES: | | | | |

| Net Assets | | $ | 2,648,818 | |

| Shares outstanding of no par value, unlimited shares authorized | | | 238,827 | |

| Net Asset Value, offering and redemption price per share | | $ | 11.09 | |

| PRICING OF CLASS A SHARES: | | | | |

| Net Assets | | $ | 174,328 | |

| Shares outstanding of no par value, unlimited shares authorized | | | 15,718 | |

| Net Asset Value, offering and redemption price per share | | $ | 11.09 | |

| Maximum offering price per share (NAV/0.945), based on maximum sales charge of 5.50% of the offering price | | $ | 11.74 | |

| PRICING OF CLASS C SHARES: | | | | |

| Net Assets | | $ | 3,533,597 | |

| Shares outstanding of no par value, unlimited shares authorized | | | 325,290 | |

| Net Asset Value, offering and redemption price per share | | $ | 10.86 | |

See Notes to the Financial Statements.

| Clough Global Long/Short Fund | Statement of Operations |

For the six months ended April 30, 2019 (Unaudited)

| INVESTMENT INCOME: | | | | |

| | | | | |

| Dividends (net of foreign withholding taxes of $5,087) | | $ | 343,819 | |

| Interest income - margin account | | | 81,553 | |

| Total Income | | | 425,372 | |

| | | | | |

| EXPENSES: | | | | |

| | | | | |

| Investment advisory fees | | | 355,352 | |

| Distribution and shareholder service fees: | | | | |

| Investor Class | | | 4,587 | |

| Class A | | | 313 | |

| Class C | | | 17,317 | |

| Administration fees | | | 47,405 | |

| Trustees fees | | | 39,873 | |

| Registration fees | | | 34,380 | |

| Dividend expense - short sales | | | 126,540 | |

| Custodian fees | | | 28,671 | |

| Audit & Tax Services fees | | | 22,179 | |

| Legal fees | | | 49,638 | |

| Printing fees | | | 11,422 | |

| Insurance fees | | | 11,229 | |

| Transfer agent fees | | | 24,950 | |

| Delegated transfer agent fees: | | | | |

| Class I | | | 3,221 | |

| Investor Class | | | 27 | |

| Class C | | | 42 | |

| Other expenses | | | 8,606 | |

| Total Expenses Before Waivers and/or Reimbursements | | | 785,752 | |

| Less fees waived and/or reimbursed by Adviser: | | | | |

| Class I | | | (191,864 | ) |

| Investor Class | | | (10,699 | ) |

| Class A | | | (728 | ) |

| Class C | | | (14,147 | ) |

| Net Expenses | | | 568,314 | |

| Net Investment Loss | | | (142,942 | ) |

| | | | | |

| NET REALIZED GAIN/(LOSS) ON: | | | | |

| Investment securities | | | (2,395,469 | ) |

| Securities sold short | | | 37,316 | |

| Total return swap contracts | | | 143,046 | |

| Foreign currency transactions | | | (42,543 | ) |

| Net realized loss | | | (2,257,650 | ) |

| NET CHANGE IN UNREALIZED APPRECIATION/DEPRECIATION ON: | | | | |

| Investment securities | | | 5,586,942 | |

| Securities sold short | | | (1,034,462 | ) |

| Total return swap contracts | | | 77,508 | |

| Translation of assets and liabilities denominated in foreign currencies | | | (796 | ) |

| Net change in unrealized appreciation | | | 4,629,192 | |

| Net realized and unrealized gain | | | 2,371,542 | |

| Net Increase in Net Assets from Operations | | $ | 2,228,600 | |

See Notes to the Financial Statements.

| Semi-Annual Report | April 30, 2019 | 13 |

| Clough Global Long/Short Fund | Statement of Changes in Net Assets |

| | | For the Six Months Ended April 30, 2019 (Unaudited) | | | For the Year Ended October 31, 2018 | |

| OPERATIONS: | | | | | | |

| | | | | | | |

| Net investment loss | | $ | (142,942 | ) | | $ | (369,740 | ) |

| Net realized loss | | | (2,257,650 | ) | | | (1,325,090 | ) |

| Net change in unrealized appreciation/(depreciation) | | | 4,629,192 | | | | (3,159,490 | ) |

| Net Increase/(Decrease) in Net Assets From Operations | | | 2,228,600 | | | | (4,854,320 | ) |

| | | | | | | | | |

| CAPITAL SHARE TRANSACTIONS: | | | | | | | | |

| Class I | | | | | | | | |

| Proceeds from shares sold | | | 3,364,971 | | | | 40,880,632 | |

| Payments for shares redeemed | | | (12,335,345 | ) | | | (13,523,671 | ) |

| Net Increase/(Decrease) in Net Assets From Class I Capital Share Transactions | | | (8,970,374 | ) | | | 27,356,961 | |

| | | | | | | | | |

| Investor Class(a) | | | | | | | | |

| Proceeds from shares sold | | | 84,431 | | | | 3,164,441 | |

| Payments for shares redeemed | | | (324,721 | ) | | | (424,647 | ) |

| Net Increase/(Decrease) in Net Assets From Investor Class Capital Share Transactions | | | (240,290 | ) | | | 2,739,794 | |

| | | | | | | | | |

| Class A(b) | | | | | | | | |

| Proceeds from shares sold | | | – | | | | 268,606 | |

| Payments for shares redeemed, net of redemption fees | | | (38,728 | ) | | | (39,847 | ) |

| Net Increase/(Decrease) in Net Assets From Class A Capital Share Transactions | | | (38,728 | ) | | | 228,759 | |

| | | | | | | | | |

| Class C | | | | | | | | |

| Proceeds from shares sold | | | 64,976 | | | | 3,909,708 | |

| Payments for shares redeemed | | | (234,183 | ) | | | (83,154 | ) |

| Net Increase/(Decrease) in Net Assets From Class C Capital Share Transactions | | | (169,207 | ) | | | 3,826,554 | |

| | | | | | | | | |

| Total Increase/(Decrease) in Net Assets | | $ | (7,189,999 | ) | | $ | 29,297,748 | |

| | | | | | | | | |

| NET ASSETS: | | | | | | | | |

| Beginning of period | | | 59,231,366 | | | | 29,933,618 | |

| End of period | | $ | 52,041,367 | | | $ | 59,231,366 | |

| (a) | On December 1, 2017, Class A was renamed Investor Class. |

| (b) | A new Class A commenced operations on June 29, 2018. |

See Notes to the Financial Statements.

| Clough Global Long/Short Fund – Class I | Financial Highlights |

For a share outstanding throughout the periods indicated

| | | For the Six Months Ended April 30, 2019 (Unaudited) | | | For the Year Ended October 31, 2018 | | | For the Year Ended October 31, 2017 | | | For the Year Ended October 31, 2016 | | | For the Period September 30, 2015 (commencement) to October 31, 2015 | |

| PER SHARE OPERATING PERFORMANCE: | | | | | | | | | | | | | | | |

| NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 10.70 | | | $ | 11.03 | | | $ | 9.40 | | | $ | 10.30 | | | $ | 10.00 | |

| INCOME/(LOSS) FROM OPERATIONS: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss(a) | | | (0.02 | ) | | | (0.07 | ) | | | (0.10 | ) | | | (0.12 | ) | | | (0.01 | ) |

| Net realized and unrealized gain/(loss) on investments | | | 0.53 | | | | (0.26 | ) | | | 1.73 | | | | (0.74 | ) | | | 0.31 | |

| Total from Investment Operations | | | 0.51 | | | | (0.33 | ) | | | 1.63 | | | | (0.86 | ) | | | 0.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO COMMON SHAREHOLDERS FROM: | | | | | | | | | | | | | | | | | | | | |

| Net realized gains | | | – | | | | – | | | | – | | | | (0.04 | ) | | | – | |

| Total Distributions to Common Shareholders | | | – | | | | – | | | | – | | | | (0.04 | ) | | | – | |

| Net asset value - end of period | | $ | 11.21 | | | $ | 10.70 | | | $ | 11.03 | | | $ | 9.40 | | | $ | 10.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Investment Return - Net Asset Value(b) | | | 4.77 | % | | | (2.99 | )% | | | 17.34 | % | | | (8.39 | )% | | | 3.00 | % |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | |

| Net assets attributable to common shares, end of period (in 000s) | | $ | 45,685 | | | $ | 52,684 | | | $ | 29,629 | | | $ | 44,003 | | | $ | 35,760 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS (including interest expense and dividend expense on securities sold short) | | | | | | | | | | | | | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 2.91 | %(c) | | | 2.85 | % | | | 3.21 | % | | | 3.76 | %(d) | | | 5.62 | %(c)(d) |

| Operating expenses including fee waivers/reimbursements | | | 2.08 | %(c) | | | 2.03 | % | | | 1.96 | % | | | 2.50 | %(d) | | | 2.32 | %(c)(d) |

| Net investment loss including fee waivers/reimbursements | | | (0.46 | )%(c) | | | (0.64 | )% | | | (0.96 | )% | | | (1.30 | )%(d) | | | (1.66 | )%(c)(d) |

| RATIOS TO AVERAGE NET ASSETS (excluding interest expense and dividend expense on securities sold short) | | | | | | | | | | | | | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 2.43 | %(c) | | | 2.42 | % | | | 2.85 | % | | | 2.86 | %(d) | | | 4.90 | %(c)(d) |

| Operating expenses including fee waivers/reimbursements | | | 1.60 | %(c) | | | 1.60 | % | | | 1.60 | % | | | 1.60 | %(d) | | | 1.60 | %(c)(d) |

| Net investment loss including fee waivers/reimbursements | | | (0.94 | )%(c) | | | (0.21 | )% | | | (0.60 | )% | | | (0.40 | )%(d) | | | (0.94 | )%(c)(d) |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE(e) | | | 127 | % | | | 156 | % | | | 237 | % | | | 261 | % | | | 22 | % |

| (a) | Per share amounts are based upon average shares outstanding. |

| (b) | Total investment return is for the period indicated and has not been annualized. The total investment return would have been lower had certain expenses not been waived / reimbursed during the period. The return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (d) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (e) | Portfolio turnover rate for periods less than one full year have not been annualized and is calculated at the Fund level. |

See Notes to the Financial Statements.

| Semi-Annual Report | April 30, 2019 | 15 |

| Clough Global Long/Short Fund – Investor Class | Financial Highlights |

For a share outstanding throughout the periods indicated

| | | For the Six Months Ended April 30, 2019 (Unaudited) | | | For the Year Ended October 31, 2018(a) | | | For the Year Ended October 31, 2017 | | | For the Year Ended October 31, 2016 | | | For the Period September 30, 2015 (commencement) to October 31, 2015 | |

| PER SHARE OPERATING PERFORMANCE: | | | | | | | | | | | | | | | |

| NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 10.60 | | | $ | 10.96 | | | $ | 9.37 | | | $ | 10.30 | | | $ | 10.00 | |

| INCOME/(LOSS) FROM OPERATIONS: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss(b) | | | (0.04 | ) | | | (0.11 | ) | | | (0.14 | ) | | | (0.15 | ) | | | (0.02 | ) |

| Net realized and unrealized gain/(loss) on investments | | | 0.53 | | | | (0.25 | ) | | | 1.73 | | | | (0.74 | ) | | | 0.32 | |

| Total from Investment Operations | | | 0.49 | | | | (0.36 | ) | | | 1.59 | | | | (0.89 | ) | | | 0.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO COMMON SHAREHOLDERS FROM: | | | | | | | | | | | | | | | | | | | | |

| Net realized gains | | | – | | | | – | | | | – | | | | (0.04 | ) | | | – | |

| Total Distributions to Common Shareholders | | | – | | | | – | | | | – | | | | (0.04 | ) | | | – | |

| Net asset value - end of period | | $ | 11.09 | | | $ | 10.60 | | | $ | 10.96 | | | $ | 9.37 | | | $ | 10.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Investment Return - Net Asset Value(c) | | | 4.62 | % | | | (3.28 | )% | | | 16.97 | %(d) | | | (8.68 | )%(d) | | | 3.00 | %(d) |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | |

| Net assets attributable to common shares, end of period (in 000s) | | $ | 2,649 | | | $ | 2,776 | | | $ | 210 | | | $ | 76 | | | $ | 27 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS (including interest expense and dividend expense on securities sold short) | | | | | | | | | | | | | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 3.16 | %(e) | | | 3.14 | % | | | 3.78 | % | | | 4.23 | %(f) | | | 6.44 | %(e)(f) |

| Operating expenses including fee waivers/reimbursements | | | 2.34 | %(e) | | | 2.33 | %(g) | | | 2.29 | %(g) | | | 2.85 | %(f) | | | 2.67 | %(e)(f) |

| Net investment loss including fee waivers/reimbursements | | | (0.72 | )%(e) | | | (0.93 | )% | | | (1.36 | )% | | | (1.57 | )%(f) | | | (2.00 | )%(e)(f) |

| RATIOS TO AVERAGE NET ASSETS (excluding interest expense and dividend expense on securities sold short) | | | | | | | | | | | | | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 2.68 | %(e) | | | 2.71 | % | | | 3.38 | % | | | 3.33 | %(f) | | | 5.72 | %(e)(f) |

| Operating expenses including fee waivers/reimbursements | | | 1.86 | %(e) | | | 1.90 | %(g) | | | 1.89 | %(g) | | | 1.95 | %(f) | | | 1.95 | %(e)(f) |

| Net investment loss including fee waivers/reimbursements | | | (1.20 | )%(e) | | | (0.50 | )% | | | (0.96 | )% | | | (0.67 | )%(f) | | | (1.28 | )%(e)(f) |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE(h) | | | 127 | % | | | 156 | % | | | 237 | % | | | 261 | % | | | 22 | % |

| (a) | On December 1, 2017, Class A was renamed Investor Class. |

| (b) | Per share amounts are based upon average shares outstanding. |

| (c) | Total investment return is for the period indicated and has not been annualized. The total investment return would have been lower had certain expenses not been waived / reimbursed during the period. The return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total investment return does not reflect the effect of sales charge. |

| (d) | Total investment return does not reflect the effect of sales charge. |

| (f) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (g) | According to the Fund's shareholder services plan, any amount of such payment not paid during the Fund's fiscal year for such services activities shall be reimbursed to the Fund as soon as practical after the end of the fiscal year. Fees were reimbursed to the Fund during the year ended October 31, 2018 and the year ended October 31, 2017, in the amounts of 0.05% and 0.06%, respectively of average net assets of the share class. |

| (h) | Portfolio turnover rate for periods less than one full year have not been annualized and is calculated at the Fund level. |

See Notes to the Financial Statements.

| Clough Global Long/Short Fund – Class A | Financial Highlights |

For a share outstanding throughout the periods indicated

| | | For the Six Months Ended April 30, 2019 (Unaudited) | | | For the Period June 29, 2018 (commencement) to October 31, 2018 | |

| PER SHARE OPERATING PERFORMANCE: | | | | | | |

| NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 10.60 | | | $ | 11.84 | |

| INCOME/(LOSS) FROM OPERATIONS: | | | | | | | | |

| Net investment loss(a) | | | (0.04 | ) | | | (0.02 | ) |

| Net realized and unrealized gain/(loss) on investments | | | 0.53 | | | | (1.22 | )(b) |

| Total from Investment Operations | | | 0.49 | | | | (1.24 | ) |

| Net asset value - end of period | | $ | 11.09 | | | $ | 10.60 | |

| | | | | | | | | |

| Total Investment Return - Net Asset Value(c) | | | 4.62 | % | | | (10.47 | )% |

| | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA: | | | | | | | | |

| Net assets attributable to common shares, end of period (in 000s) | | $ | 174 | | | $ | 209 | |

| | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS (including interest expense and dividend expense on securities sold short) | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 3.17 | %(d) | | | 2.91 | %(d)(e) |

| Operating expenses including fee waivers/reimbursements | | | 2.35 | %(d) | | | 2.32 | %(d)(e) |

| Net investment loss including fee waivers/reimbursements | | | (0.75 | )%(d) | | | (0.61 | )%(d)(e) |

| RATIOS TO AVERAGE NET ASSETS (excluding interest expense and dividend expense on securities sold short) | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 2.69 | %(d) | | | 2.44 | %(d)(e) |

| Operating expenses including fee waivers/reimbursements | | | 1.87 | %(d) | | | 1.85 | %(d)(e)(f) |

| Net investment loss including fee waivers/reimbursements | | | (1.23 | )%(d) | | | (0.14 | )%(d)(e) |

| | | | | | | | | |

| PORTFOLIO TURNOVER RATE(g) | | | 127 | % | | | 156 | % |

| (a) | Per share amounts are based upon average shares outstanding. |

| (b) | The per share amount varies from the net realized and unrealized gain/loss for the whole period because of the timing of sales of fund shares and per share amount of realized and unrealized gains and losses at such time. |

| (c) | Total investment return is for the period indicated and has not been annualized. The total investment return would have been lower had certain expenses not been waived / reimbursed during the period. The return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total investment return does not reflect the effect of sales charge. |

| (e) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (f) | According to the Fund's shareholder services plan, any amount of such payment not paid during the Fund's fiscal year for such services activities shall be reimbursed to the Fund as soon as practical after the end of the fiscal year. Fees were reimbursed to the Fund during the year ended October 31, 2018 in the amount of 0.10% of average net assets of the share class. |

| (g) | Portfolio turnover rate for periods less than one full year have not been annualized and is calculated at the Fund level. |

See Notes to the Financial Statements.

| Semi-Annual Report | April 30, 2019 | 17 |

| Clough Global Long/Short Fund – Class C | Financial Highlights |

For a share outstanding throughout the periods indicated

| | | For the Six Months Ended April 30, 2019 (Unaudited) | | | For the Year Ended October 31, 2018 | | | For the Year Ended October 31, 2017 | | | For the Year Ended October 31, 2016 | | | For the Period September 30, 2015 (commencement) to October 31, 2015 | |

| PER SHARE OPERATING PERFORMANCE: | | | | | | | | | | | | | | | |

| NET ASSET VALUE, BEGINNING OF PERIOD | | $ | 10.42 | | | $ | 10.84 | | | $ | 9.34 | | | $ | 10.30 | | | $ | 10.00 | |

| INCOME/(LOSS) FROM OPERATIONS: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss(a) | | | (0.08 | ) | | | (0.18 | ) | | | (0.20 | ) | | | (0.21 | ) | | | (0.02 | ) |

| Net realized and unrealized gain/(loss) on investments | | | 0.52 | | | | (0.24 | ) | | | 1.70 | | | | (0.71 | ) | | | 0.32 | |

| Total from Investment Operations | | | 0.44 | | | | (0.42 | ) | | | 1.50 | | | | (0.92 | ) | | | 0.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| DISTRIBUTIONS TO COMMON SHAREHOLDERS FROM: | | | | | | | | | | | | | | | | | | | | |

| Net realized gains | | | – | | | | – | | | | – | | | | (0.04 | ) | | | – | |

| Total Distributions to Common Shareholders | | | – | | | | – | | | | – | | | | (0.04 | ) | | | – | |

| Net asset value - end of period | | $ | 10.86 | | | $ | 10.42 | | | $ | 10.84 | | | $ | 9.34 | | | $ | 10.30 | |

| | | | | | | | | | | | | | | | | | | | | |

| Total Investment Return - Net Asset Value(b) | | | 4.22 | % | | | (3.87 | )% | | | 16.06 | % | | | (8.97 | )% | | | 3.00 | % |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS AND SUPPLEMENTAL DATA: | | | | | | | | | | | | | | | | | | | | |

| Net assets attributable to common shares, end of period (in 000s) | | $ | 3,534 | | | $ | 3,562 | | | $ | 95 | | | $ | 73 | | | $ | 26 | |

| | | | | | | | | | | | | | | | | | | | | |

| RATIOS TO AVERAGE NET ASSETS (including interest expense and dividend expense on securities sold short) | | | | | | | | | | | | | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 3.90 | %(c) | | | 3.79 | % | | | 4.33 | % | | | 4.78 | %(d) | | | 7.09 | %(c)(d) |

| Operating expenses including fee waivers/reimbursements | | | 3.08 | %(c) | | | 3.06 | % | | | 2.97 | % | | | 3.50 | %(d) | | | 3.32 | %(c)(d) |

| Net investment loss including fee waivers/reimbursements | | | (1.46 | )%(c) | | | (1.58 | )% | | | (2.03 | )% | | | (2.19 | )%(d) | | | (2.66 | )%(c)(d) |

| RATIOS TO AVERAGE NET ASSETS (excluding interest expense and dividend expense on securities sold short) | | | | | | | | | | | | | | | | | | | | |

| Operating expenses excluding fee waivers/reimbursements | | | 3.42 | %(c) | | | 3.32 | % | | | 3.96 | % | | | 3.88 | %(d) | | | 6.37 | %(c)(d) |

| Operating expenses including fee waivers/reimbursements | | | 2.60 | %(c) | | | 2.59 | % | | | 2.60 | % | | | 2.60 | %(d) | | | 2.60 | %(c)(d) |

| Net investment loss including fee waivers/reimbursements | | | (1.94 | )%(c) | | | (1.11 | )% | | | (1.66 | )% | | | (1.29 | )%(d) | | | (1.94 | )%(c)(d) |

| | | | | | | | | | | | | | | | | | | | | |

| PORTFOLIO TURNOVER RATE(e) | | | 127 | % | | | 156 | % | | | 237 | % | | | 261 | % | | | 22 | % |

| (a) | Per share amounts are based upon average shares outstanding. |

| (b) | Total investment return is for the period indicated and has not been annualized. The total investment return would have been lower had certain expenses not been waived / reimbursed during the period. The return shown does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total investment return does not reflect the effect of sales charge. |

| (d) | Expense ratios before reductions for startup periods may not be representative of longer term operating periods. |

| (e) | Portfolio turnover rate for periods less than one full year have not been annualized and is calculated at the Fund level. |

See Notes to the Financial Statements.

| Clough Global Long/Short Fund | Notes to Financial Statements |

April 30, 2019 (Unaudited)

1. ORGANIZATION AND SIGNIFICANT ACCOUNTING AND OPERATING POLICIES

Clough Funds Trust (the “Trust”) is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust was organized under the laws of the state of Delaware on March 17, 2015. The Trust currently offers shares of beneficial interest (“shares”) of the Clough Global Long/Short Fund (the “Fund”). The Fund’s commencement date is September 30, 2015. The Fund is a diversified investment company with an investment objective to seek to provide long-term capital appreciation. The Fund currently offers four Classes of shares: Class I, Investor Class, Class A and Class C. Prior to December 1, 2017, Investor Class shares were named Class A shares. On June 29, 2018, a new Class A commenced operations. Each share class of the Fund represents an investment in the same portfolio of securities, but each share class has its own expense structure. As of April 30, 2019, approximately 48% of the Fund is owned by affiliated parties. The Board of Trustees (the “Board”) may establish additional funds and classes of shares at any time in the future without shareholder approval.

The following is a summary of significant accounting policies followed by the Fund. These policies are in conformity with U.S. generally accepted accounting principles (“GAAP”). The preparation of financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements during the reporting period. Management believes the estimates and security valuations are appropriate; however, actual results may differ from those estimates, and the security valuations reflected in the financial statements may differ from the value the Fund ultimately realizes upon sale of the securities. The Fund is considered an investment company for financial reporting purposes under GAAP and follows the accounting and reporting guidance applicable to investment companies as codified in Accounting Standards Codification (“ASC”) Topic 946 – Investment Companies.

The net asset value (“NAV”) per share of the Fund is determined no less frequently than daily, on each day that the New York Stock Exchange (“NYSE” or the “Exchange”) is open for trading, as of the close of regular trading on the Exchange (normally 4:00 p.m. New York time). Trading may take place in foreign issues held by the Fund at times when the Fund is not open for business. As a result, the Fund’s NAV may change at times when it is not possible to purchase or sell shares of the Fund.

Investment Valuation: Securities held by the Fund for which exchange quotations are readily available are valued at the last sale price, or if no sale price or if traded on the over-the-counter market, at the mean of the bid and asked prices on such day. Most securities listed on a foreign exchange are valued at the last sale price at the close of the exchange on which the security is primarily traded. In certain countries market maker prices are used since they are the most representative of the daily trading activity. Market maker prices are usually the mean between the bid and ask prices. Certain markets are not closed at the time that the Fund prices its portfolio securities. In these situations, snapshot prices are provided by the individual pricing services or other alternate sources at the close of the NYSE as appropriate. Securities not traded on a particular day are valued at the mean between the last reported bid and the asked quotes, or the last sale price when appropriate; otherwise fair value will be determined by the board-appointed fair valuation committee. Debt securities for which the over-the-counter market is the primary market are normally valued on the basis of prices furnished by one or more pricing services or dealers at the mean between the latest available bid and asked prices. As authorized by the Board, debt securities (including short-term obligations that will mature in 60 days or less) may be valued on the basis of valuations furnished by a pricing service which determines valuations based upon market transactions for normal, institutional-size trading units of securities or a matrix method which considers yield or price of comparable bonds provided by a pricing service. Total return swaps are priced based on valuations provided by a Board approved independent third party pricing agent. If a total return swap price cannot be obtained from an independent third party pricing agent the Fund shall seek to obtain a bid price from at least one independent and/or executing broker.

If the price of a security is unavailable in accordance with the aforementioned pricing procedures, or the price of a security is unreliable, e.g., due to the occurrence of a significant event, the security may be valued at its fair value determined by management pursuant to procedures adopted by the Board. For this purpose, fair value is the price that the Fund reasonably expects to receive on a current sale of the security. Due to the number of variables affecting the price of a security, however; it is possible that the fair value of a security may not accurately reflect the price that the Fund could actually receive on a sale of the security.

A three-tier hierarchy has been established to classify fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

| Semi-Annual Report | April 30, 2019 | 19 |

| Clough Global Long/Short Fund | Notes to Financial Statements |

April 30, 2019 (Unaudited)

Various inputs are used in determining the value of the Fund’s investments as of the reporting period end. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

| Level 1 – | Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

| Level 2 – | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and |

| Level 3 – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. |

The following is a summary of the inputs used as of April 30, 2019, in valuing the Fund’s investments carried at value.

| Investments in Securities at Value* | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Common Stocks | | $ | 43,031,156 | | | $ | – | | | $ | – | | | $ | 43,031,156 | |

| Exchange Traded Funds | | | 265,252 | | | | – | | | | – | | | | 265,252 | |

| Short-Term Investments | | | 8,171,313 | | | | – | | | | – | | | | 8,171,313 | |

| TOTAL | | $ | 51,467,721 | | | $ | – | | | $ | – | | | $ | 51,467,721 | |

| | | | | | | | | | | | | | | | | |

| Other Financial Instruments | | | | | | | | | | | | | | | | |

| Assets | | | | | | | | | | | | | | | | |

| Total Return Swap Contracts** | | $ | – | | | $ | 186,928 | | | $ | – | | | $ | 186,928 | |

| Liabilities | | | | | | | | | | | | | | | | |

| Securities Sold Short | | | | | | | | | | | | | | | | |

| Common Stocks | | | (11,539,371 | ) | | | – | | | | – | | | | (11,539,371 | ) |

| Total Return Swap Contracts** | | | – | | | | (20,929 | ) | | | – | | | | (20,929 | ) |

| TOTAL | | $ | (11,539,371 | ) | | $ | 165,999 | | | $ | – | | | $ | (11,373,372 | ) |

| * | For detailed sector descriptions, see the accompanying Statement of Investments. |

| ** | Swap contracts are reported at their unrealized appreciation/(depreciation) at measurement date, which represents the change in the contract's value from trade date. |

Restricted Securities: Although the Fund will invest primarily in publicly traded securities, it may invest a portion of its assets (generally, 5% of its value) in restricted securities. Restricted securities are securities that may not be sold to the public without an effective registration statement under the Securities Act of 1933, as amended (the "Securities Act") or, if they are unregistered, may be sold only in a privately negotiated transaction or pursuant to an exemption from registration.

Restricted securities as of April 30, 2019 were as follows:

| Security | | % of Net Assets | | | Acquisition Dates | | Shares | | | Cost | | | Fair Value | |

| Idorsia, Ltd. | | 1.17% | | | 7/11/2018 - 2/7/2019 | | 30,821 | | | $ | 693,172 | | | $ | 609,191 | |

| | | 1.17% | | | | | | | | $ | 693,172 | | | $ | 609,191 | |

In the event a Board approved independent pricing service is unable to provide an evaluated price for a security or Clough Capital Partners L.P. (the “Adviser” or “Clough Capital”) believes the price provided is not reliable, securities of the Fund will be valued at fair value as described above. In these instances the Adviser may seek to find an alternative independent source, such as a broker/dealer to provide a price quote, or by using evaluated pricing models similar to the techniques and models used by the independent pricing service. These fair value measurement techniques may utilize unobservable inputs (Level 3).

On a monthly basis, the Fair Value Committee of the Fund meets and discusses securities that have been fair valued during the preceding month in accordance with the Fund’s Fair Value Procedures and reports quarterly to the Board on the results of those meetings.

For the six months ended April 30, 2019, the Fund did not have significant unobservable inputs (Level 3) used in determining fair value. Therefore, a reconciliation of assets in which significant unobservable inputs (Level 3) were used in determining fair value is not applicable.

| Clough Global Long/Short Fund | Notes to Financial Statements |

April 30, 2019 (Unaudited)

Class Expenses:Expenses that are specific to a class of shares are charged directly to that share class. Fees provided under the distribution (Rule 12b-1) and/or shareholder service plans for a particular class of the Fund are charged to the operations of such class.