united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-23066

Northern Lights Fund Trust IV

(Exact name of registrant as specified in charter)

17605 Wright Street, Omaha, Nebraska 68130

(Address of principal executive offices) (Zip code)

Wendy Wang, Gemini Fund Services, LLC.

80 Arkay Drive, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 631-470-2612

Date of fiscal year end: 8/31

Date of reporting period: 8/31/18

Item 1. Reports to Stockholders.

| ||

| Anchor Tactical Credit Strategies Fund | ||

| Institutional Class (ATCSX) | ||

| Anchor Tactical Equity Strategies Fund | ||

| Institutional Class (ATESX) | ||

| Anchor Tactical Municipal Strategies Fund | ||

| Institutional Class (ATMSX) | ||

| Anchor Tactical Real Estate Fund | ||

| Institutional Class (ARESX) | ||

| Annual Report | ||

| August 31, 2018 | ||

| 1-844-594-1226 | ||

| www.anchorcapitalfunds.com | ||

| This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer of sale or solicitation of an offer to buy shares of the Anchor Funds. Such offering is made only by prospectus, which includes details as to offering price and other material information. | ||

| Distributed by Northern Lights Distributors, LLC. | ||

| Member FINRA | ||

Anchor Tactical Credit Strategies Fund

Annual Shareholder Report (Unaudited)

August 31, 2018

It is my pleasure to present the annual report for the Anchor Tactical Credit Strategies Fund for the year ended August 31, 2018. On behalf of the entire team at Anchor Capital, I would like to thank you for your investment in the Anchor Tactical Credit Strategies Fund.

Performance

The Anchor Tactical Credit Strategies Fund returned -1.65% for the fiscal year ending August 31, 2018. The Fund’s benchmark, the HFRX Absolute Return Index, and the Fund’s Morningstar Category, the Long-Short Credit category, returned 2.21% and 1.40% respectively.

Market and Fund Performance Commentary

The Fund’s process for risk management utilizing cash and short1 positions to hedge volatility performed as expected over the past year. The Fund’s underperformance was due to the hedging of exposure during market volatility in early 2018. After the trend was reestablished, the Fund went long and produced last-three-month returns in excess of the benchmark (1.25% for the Fund versus 0.52% for the HFRX Absolute Return Index).

The credit market saw rising volatility in the second quarter of 2018 as trade tensions escalated between US and key trading partners. The expectation of rising interest rates also suppressed valuations, as did concerns about widening spreads and the sustainability of strong economic growth in the US.

Market Outlook

With a tightening monetary policy outlook, global liquidity is declining and volatility in credit markets is likely to rise. We also anticipate rising volatility in higher-yield segments as assets are reallocated to lower-risk segments. At this point in the credit cycle, navigating these changes will require disciplined risk management. The current environment should be well suited for the Anchor Tactical Credit Strategies Fund.

Eric Leake

President, CIO

Anchor Capital Management Group, Inc.

| 1 | Short: The sale of a borrowed security, commodity or currency with the expectation that the asset will fall in value. |

| 7574-NLD-10/12/2018 | www.anchor-capital.com | 15 Enterprise, Suite 450 |

| Aliso Viejo, CA 92656 USA | ||

| (800) 290-8633 main | ||

| (949) 382-1497 fax |

1

Anchor Tactical Equity Strategies Fund

Annual Shareholder Report (Unaudited)

August 31, 2018

It is my pleasure to present the annual report for the Anchor Tactical Equity Strategies Fund for the period ended August 31, 2018. On behalf of the entire team at Anchor Capital, I would like to thank you for your investment in the Anchor Tactical Equity Strategies Fund.

Performance

The Anchor Tactical Equity Strategies Fund returned 16.33% for the fiscal year ending August 31, 2018. The Fund’s benchmark, the S&P 500 Total Return Index, and the Fund’s Morningstar Category, the Long-Short Equity category, returned 19.66% and 7.15% respectively.

Market and Fund Performance Commentary

The Fund has continued to benefit from the rising US stock market, while successfully navigating much of the market volatility and drawdown.

Market Outlook

Despite continued strong performance in US equities, market risks are beginning to become apparent. The current bull market is the longest in post-WWII history, but there is growing evidence of slowing momentum in developed international and emerging markets. As the result of rising interest rates, the US Dollar has continued to gain. The strong dollar in conjunction with looming tariffs, has caused international and emerging markets to come under pressure. With continued rate hikes expected through the end of the year and the slowing of international growth, we would expect the US markets to become more volatile and pose greater challenges for continued growth.

For these reasons, we believe that now more than ever investors will need to pay attention to risks, a climate well suited for the Anchor Tactical Equity Strategies Fund.

Eric Leake

President, CIO

Anchor Capital Management Group, Inc.

| 7575-NLD-10/12/2018 | www.anchor-capital.com | 15 Enterprise, Suite 450 |

| Aliso Viejo, CA 92656 USA | ||

| (800) 290-8633 main | ||

| (949) 382-1497 fax |

2

Anchor Tactical Municipal Strategies Fund

Annual Shareholder Report (Unaudited)

August 31, 2018

It is my pleasure to present the annual report for the Anchor Tactical Municipal Strategies Fund for the period ended August 31, 2018. On behalf of the entire team at Anchor Capital, I would like to thank you for your investment in the Anchor Tactical Municipal Strategies Fund.

Performance

The Anchor Tactical Municipal Strategies Fund returned 0.25% for the 1-year period ending August 31, 2018. The Fund’s benchmark, the SPDR Bloomberg Barclays U.S. Municipal Bond Index, and the Fund’s Morningstar Category, the Intermediate-Term Bond category, returned 0.49% and -0.98% respectively.

Market and Fund Performance Commentary

This was an active year in the municipal bond space. Debate over tax reform in late 2017 generated a surge in supply in December 2017, with three times the issuance in December 2017 relative to December 2016. Demand was also supported by tax reform, with the expectation that residents of high-tax states will continue to seek out municipal bonds to improve tax-efficiency.

Early in the year, however, municipal bonds plunged on concerns of accelerated rate rises. The Fund took a defensive posture for the early part of 2018, missing most of the benchmark’s intra-month declines but losing ground on upswings in market pricing.

Market Outlook

Tax reform and rising interest rates are likely to support market demand for municipal bonds while dampening supply. However, decisions regarding the pace of interest rate acceleration may foster volatility. We anticipate ample opportunity for the Fund’s risk models to generate positive returns in the quarters ahead.

Eric Leake

President, CIO

Anchor Capital Management Group, Inc.

| 7576-NLD- 10/12/2018 | www.anchor-capital.com | 15 Enterprise, Suite 450 |

| Aliso Viejo, CA 92656 USA | ||

| (800) 290-8633 main | ||

| (949) 382-1497 fax |

3

Anchor Tactical Real Estate Fund

Annual Shareholder Report (Unaudited)

August 31, 2018

It is my pleasure to present the annual report for the Anchor Tactical Real Estate Fund for the period ended August 31, 2018. On behalf of the entire team at Anchor Capital, I would like to thank you for your investment in the Anchor Tactical Real Estate Fund.

Performance

The Anchor Tactical Real Estate Fund returned -1.36% for the fiscal year ending August 31, 2018. The Fund’s benchmark, the Dow Jones U.S. Select Real Estate Securities Total Return Index, and the Fund’s Morningstar Category, the Long-Short Equity category, returned 7.80% and 5.69% respectively. While the Fund dramatically outperformed in the beginning of the year, it’s continued defensive position has caused the recent underperformance.

Market and Fund Performance Commentary

REIT performance in 2017 and early 2018 was driven by concerns over rising interest rates. As rates trended higher this year volatility also trended relatively higher in the sector. The Fund’s underperformance resulted from it continued defensive positioning.

Market Outlook

The REIT market suffered large losses in the first quarter but has been able to recover into August. We remain cautious on the sector as interest rates continue to rise and the home builders continue to breakdown. Ongoing Federal Reserve tightening and rising interest rates continues to pose a major threat to the real estate market going forward.

For these reasons, we believe that markets may continue a pattern of higher than normal volatility and risk, a climate well suited for the Anchor Tactical Real Estate Fund.

Eric Leake

President, CIO

Anchor Capital Management Group, Inc.

| 7573-NLD-10/12/2018 | www.anchor-capital.com | 15 Enterprise, Suite 450 |

| Aliso Viejo, CA 92656 USA | ||

| (800) 290-8633 main | ||

| (949) 382-1497 fax |

4

| Anchor Tactical Credit Strategies Fund* |

| Portfolio Review (Unaudited) |

| August 31, 2018 |

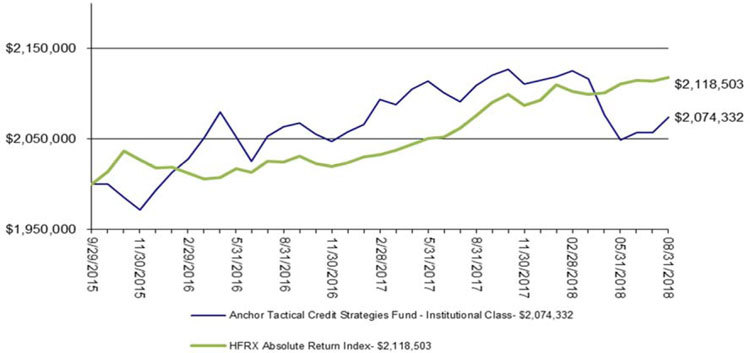

The Fund’s Institutional Class performance figures for the periods ended August 31, 2018, compared to its benchmark (assumes an initial investment of $2,000,000):

| One Year | Since Inception* | |

| Anchor Tactical Credit Strategies Fund - Institutional Class | (1.65)% | 1.26% |

| HFRX Absolute Return Index** | 2.21% | 1.99% |

| * | The Fund commenced operations on September 29, 2015. |

| ** | The HFRX Absolute Return Index is designed to be representative of the overall composition of the Hedge Fund Universe. It is comprised of all eligible hedge fund strategies including, but not limited to, convertible arbitrage, distressed securities, equity hedge, equity market neutral, event driven, macro, merger arbitrage, and relative value arbitrage. As a component of the optimization process, the index selects constituents which characteristically exhibit lower volatilities and lower correlations to standard directional benchmarks of equity market and hedge fund industry performance. Hedge Fund Research, Inc. (HFR) utilizes a UCITSIII compliant methodology to construct the HFRX Hedge Fund Indices. The methodology is based on defined and predetermined rules and objective criteria to select and rebalance components to maximize representation of the Hedge Fund Universe. HFRX Indices utilize state-of-the-art quantitative techniques and analysis, multi-level screening, cluster analysis, Monte-Carlo simulations and optimization techniques to ensure that each Index is a pure representation of its corresponding investment focus. Investors cannot invest directly in an index, and unlike the Fund, returns do not reflect any fees, expenses or sales charges. |

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. The returns shown do not reflect the deduction of taxes that a shareholder would have to pay on Fund distributions or the redemption of the Fund shares. The Fund’s total expenses, as shown in the December 29, 2017 prospectus, is 2.97%. Updated information regarding the Fund’s expense ratio is available in the Financial Highlights. The Adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund through August 31, 2018, (exclusive of any front-end or contingent deferred loads, brokerage fees and commissions, fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example, options and swap fees and expenses), acquired fund fees and expenses, borrowing costs (such as interest and dividend expense on securities sold short), taxes and extraordinary expenses, such as litigation) to 2.25% of the Fund’s average daily net assets. For performance information current to the most recent month-end, please call 1-844-594-1226.

| PORTFOLIO COMPOSITION* (Unaudited) | ||||

| % of Net Assets | ||||

| Closed-End Fund | 4.6 | % | ||

| Exchange Traded Funds | 94.2 | % | ||

| Other Assets Less Liabilities | 1.2 | % | ||

| Total | 100.0 | % | ||

| Please refer to the Portfolio of Investments in this report for a detailed analysis of the Fund’s holdings. |

5

| Anchor Tactical Equity Strategies Fund* |

| Portfolio Review (Unaudited) |

| August 31, 2018 |

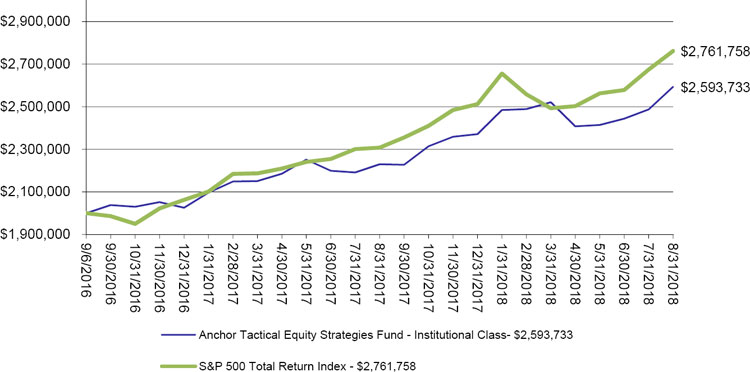

The Fund’s Institutional Class performance figures for the period ended August 31, 2018, compared to its benchmark (assumes an initial l investment of $2,000,000):

| One Year | Since Inception* | |

| Anchor Tactical Equity Strategies Fund - Institutional Class | 16.33% | 14.00% |

| S&P 500 Total Return Index** | 19.66% | 17.67% |

| * | The Fund commenced operations on September 6, 2016. |

| ** | The S&P 500 Total Return Index is an unmanaged market capitalization-weighted index which is comprised of 500 of the largest U.S. domiciled companies and includes the reinvestment of all dividends. Investors cannot invest directly in an index or benchmark. |

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. The returns shown do not reflect the deduction of taxes that a shareholder would have to pay on Fund distributions or the redemption of the Fund shares. The Adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund through August 31, 2018, (exclusive of any front-end or contingent deferred loads, brokerage fees and commissions, fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example, options and swap fees and expenses), acquired fund fees and expenses, borrowing costs (such as interest and dividend expense on securities sold short), taxes and extraordinary expenses, such as litigation) to 2.25% of the Fund’s average daily net assets. For performance information current to the most recent month-end, please call 1-844-594-1226.

Per the fee table in the Fund’s December 29, 2017 prospectus, the Fund’s Total Annual Operating Expense Ratio is 2.51%. Updated information regarding the Fund’s expense ratio is available in the Financial Highlights.

| Portfolio Composition (Unaudited) | ||||

| % of Net Assets | ||||

| Exchange Traded Funds | 98.8 | % | ||

| Other Assets Less Liabilities | 1.2 | % | ||

| Total | 100.0 | % | ||

| Please refer to the Portfolio of Investments in this report for a detailed analysis of the Fund’s holdings. |

6

| Anchor Tactical Municipal Strategies Fund* |

| Portfolio Review (Unaudited) |

| August 31, 2018 |

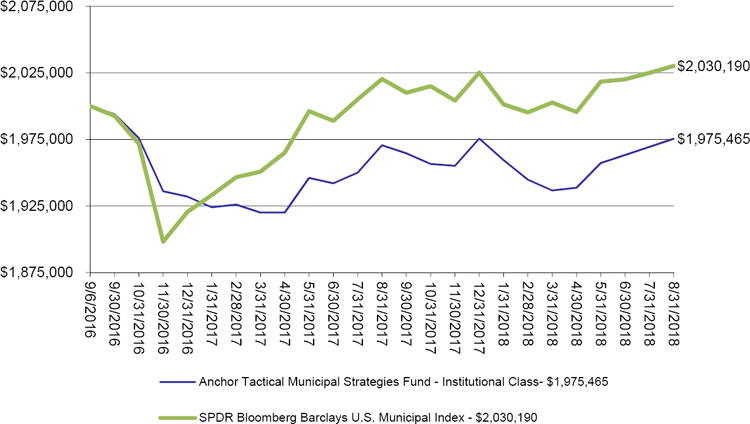

The Fund’s Institutional Class performance figures for the period ended August 31, 2018, compared to its benchmark (assumes an initial investment of $2,000,000):

| One Year | Since Inception* | |

| Anchor Tactical Municipal Strategies Fund - Institutional Class | 0.25% | (0.62)% |

| SPDR Bloomberg Barclays U.S. Municipal Index** | 0.49% | 0.76% |

| * | The Fund commenced operations on September 6, 2016. |

| ** | The SPDR Bloomberg Barclays U.S. Municipal Index covers the USD-denominated long-term tax exempt bond market. Investors cannot invest directly in an index or benchmark. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. |

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. The returns shown do not reflect the deduction of taxes that a shareholder would have to pay on Fund distributions or the redemption of the Fund shares. The Adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund through August 31, 2018, (exclusive of any front-end or contingent deferred loads, brokerage fees and commissions, fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example, options and swap fees and expenses), acquired fund fees and expenses, borrowing costs (such as interest and dividend expense on securities sold short), taxes and extraordinary expenses, such as litigation) to 2.25% of the Fund’s average daily net assets. For performance information current to the most recent month-end, please call 1-844-594-1226.

Per the fee table in the Fund’s December 29, 2017 prospectus, the Fund’s Total Annual Operating Expense Ratio is 2.43%. Updated information regarding the Fund’s expense ratio is available in the Financial Highlights.

| Portfolio Composition (Unaudited) | ||||

| % of Net Assets | ||||

| Closed-End Funds | 50.0 | % | ||

| Mutual Funds | 49.8 | % | ||

| Other Assets Less Liabilities | 0.2 | % | ||

| Total | 100.0 | % | ||

| Please refer to the Portfolio of Investments in this report for a detailed analysis of the Fund’s holdings. |

7

| Anchor Tactical Real Estate Fund* |

| Portfolio Review (Unaudited) |

| August 31, 2018 |

The Fund’s Institutional Class performance figures for the period ended August 31, 2018, compared to its benchmark (assumes an initial investment of $2,000,000):

| One Year | Since Inception* | |

| Anchor Tactical Real Estate Fund - Institutional Class | (1.36)% | (1.90)% |

| Dow Jones U.S. Select Real Estate Securities Total Return Index** | 7.80% | 1.60% |

| * | The Fund commenced operations on September 6, 2016. |

| ** | The Dow Jones U.S. Select Real Estate Securities Total Return Index is designed to measure the performance of publicly traded real estate securities. Investors cannot invest directly in an index or benchmark. The index is designed to serve as a proxy for direct real estate investment, in part by excluding companies whose performance may be driven by factors other than the value of real estate. |

Past performance is not predictive of future results. The investment return and principal value of an investment will fluctuate. An investor’s shares, when redeemed, may be worth more or less than the original cost. Total return is calculated assuming reinvestment of all dividends and distributions. The returns shown do not reflect the deduction of taxes that a shareholder would have to pay on Fund distributions or the redemption of the Fund shares. The Adviser has contractually agreed to reduce its fees and/or absorb expenses of the Fund through August 31, 2018, (exclusive of any front-end or contingent deferred loads, brokerage fees and commissions, fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example, options and swap fees and expenses), acquired fund fees and expenses, borrowing costs (such as interest and dividend expense on securities sold short), taxes and extraordinary expenses, such as litigation) to 2.25% of the Fund’s average daily net assets. For performance information current to the most recent month-end, please call 1-844-594-1226.

Per the fee table in the Fund’s December 29, 2017 prospectus, the Fund’s Total Annual Operating Expense Ratio is 2.33%. Updated information regarding the Fund’s expense ratio is available in the Financial Highlights.

| Portfolio Composition (Unaudited) | ||||

| % of Net Assets | ||||

| Exchange Traded Funds (Long) | 93.8 | % | ||

| Exchange Traded Funds (Short) | (18.2 | )% | ||

| Other Assets Less Liabilities | 24.4 | % | ||

| Total | 100.0 | % | ||

| Please refer to the Portfolio of Investments in this report for a detailed analysis of the Fund’s holdings. |

8

| Anchor Tactical Credit Strategies Fund |

| PORTFOLIO OF INVESTMENTS |

| August 31, 2018 |

| Shares | Value | |||||||

| CLOSED-END FUND - 4.6% | ||||||||

| DEBT FUND - 4.6% | ||||||||

| 207,049 | PIMCO High Income Fund | $ | 1,846,877 | |||||

| TOTAL CLOSED-END FUND (Cost- $1,838,435) | ||||||||

| EXCHANGE TRADED FUNDS - 94.2% | ||||||||

| DEBT FUNDS - 94.2% | ||||||||

| 88,055 | iShares 1 -3 Year Treasury Bond ETF | 7,338,504 | ||||||

| 175,000 | iShares iBoxx $ High Yield Corporate Bond ETF | 15,113,000 | ||||||

| 50,000 | SPDR Bloomberg Barclays Convertible Securities ETF | 2,717,500 | ||||||

| 350,000 | SPDR Bloomberg Barclays High Yield Bond ETF | 12,600,000 | ||||||

| TOTAL EXCHANGE TRADED FUNDS (Cost - $37,525,397) | 37,769,004 | |||||||

| TOTAL INVESTMENTS (Cost - $39,363,832) - 98.8% | $ | 39,615,881 | ||||||

| CASH & OTHER ASSETS LESS LIABILITIES - 1.2% | 469,815 | |||||||

| NET ASSETS - 100.0% | $ | 40,085,696 | ||||||

ETF - Exchange Traded Fund

See accompanying notes to financial statements.

9

| Anchor Tactical Equity Strategies Fund |

| PORTFOLIO OF INVESTMENTS |

| August 31, 2018 |

| Shares | Value | |||||||

| EXCHANGE TRADED FUNDS - 98.8% | ||||||||

| EQUITY FUNDS - 98.8% | ||||||||

| 449,925 | Powershares QQQ Trust Series 1 | $ | 83,978,501 | |||||

| 1,000,000 | ProShares UltraShort S&P500 | 33,550,000 | ||||||

| 50,000 | SPDR S&P 500 ETF Trust | 14,515,500 | ||||||

| 600,000 | WisdomTree U.S. Quality Dividend Growth Fund | 26,352,000 | ||||||

| TOTAL EXCHANGE TRADED FUNDS (Cost - $153,637,036) | 158,396,001 | |||||||

| TOTAL INVESTMENTS(Cost - $153,637,036) - 98.8% | $ | 158,396,001 | ||||||

| CASH & OTHER ASSETS LESS LIABILITIES - 1.2% | 1,864,356 | |||||||

| NET ASSETS - 100.0% | $ | 160,260,357 | ||||||

ETF - Exchange Traded Fund

See accompanying notes to financial statements.

10

| Anchor Tactical Municipal Strategies Fund |

| PORTFOLIO OF INVESTMENTS |

| August 31, 2018 |

| Shares | Value | |||||||

| CLOSED-END FUNDS - 50.0% | ||||||||

| DEBT FUNDS - 50.0% | ||||||||

| 78,422 | BlackRock California Municipal Income Trust | $ | 1,001,449 | |||||

| 75,640 | BlackRock MuniHoldings California Quality Fund, Inc. | 985,589 | ||||||

| 74,846 | BlackRock MuniYield California Fund, Inc. | 1,009,672 | ||||||

| 74,209 | BlackRock MuniYield California Quality Fund, Inc. | 987,722 | ||||||

| 77,088 | Invesco California Value Municipal Income Trust | 926,598 | ||||||

| 147,492 | Nuveen California AMT-Free Quality Municipal Income Fund | 1,979,343 | ||||||

| 195,678 | Nuveen California Quality Municipal Income Fund | 2,641,653 | ||||||

| 26,451 | PIMCO California Municipal Income Fund | 447,022 | ||||||

| 53,958 | PIMCO California Municipal Income Fund II | 477,528 | ||||||

| 35,994 | PIMCO California Municipal Income Fund III | 391,975 | ||||||

| TOTAL CLOSED-END FUNDS (Cost - $10,838,739) | 10,848,551 | |||||||

| MUTUAL FUNDS - 49.8% | ||||||||

| DEBT FUNDS - 49.8% | ||||||||

| 289,055 | American Century California High - Yield Municipal Fund - Investor Class | 3,043,744 | ||||||

| 805,785 | Nuveen California High Yield Municipal Bond Fund - Class R | 7,759,711 | ||||||

| TOTAL MUTUAL FUNDS (Cost - $10,849,525) | 10,803,455 | |||||||

| TOTAL INVESTMENTS (Cost - $21,688,264) - 99.8% | $ | 21,652,006 | ||||||

| CASH & OTHER ASSETS LESS LIABILITIES - 0.2% | 36,946 | |||||||

| NET ASSETS - 100.0% | $ | 21,688,952 | ||||||

See accompanying notes to financial statements.

11

| Anchor Tactical Real Estate Fund |

| PORTFOLIO OF INVESTMENTS |

| August 31, 2018 |

| Shares | Value | |||||||

| EXCHANGE TRADED FUNDS - 93.8% | ||||||||

| EQUITY FUNDS - 93.8% | ||||||||

| 125,000 | iShares U.S. Real Estate ETF | $ | 10,397,500 | |||||

| 286,700 | Real Estate Select Sector SPDR Fund | 9,704,795 | ||||||

| 118,092 | Vanguard Real Estate ETF | 9,925,633 | ||||||

| TOTAL EXCHANGE TRADED FUNDS (Cost - $29,451,485) | 30,027,928 | |||||||

| TOTAL INVESTMENTS(Cost - $29,451,485) - 93.8% | $ | 30,027,928 | ||||||

| SECURITIES SOLD SHORT (Premiums Received - $5,773,822) - (18.2)% | (5,828,250 | ) | ||||||

| CASH AND OTHER ASSETS LESS LIABILITIES - 24.4% | 7,792,518 | |||||||

| NET ASSETS - 100.0% | $ | 31,992,196 | ||||||

ETF - Exchange Traded Fund

| SECURITIES SOLD SHORT - (18.2)% | ||||||||

| EXCHANGE TRADED FUNDS - (18.2)% | ||||||||

| EQUITY FUNDS - (18.2)% | ||||||||

| (75,000 | ) | iShares U.S. Home Construction ETF | $ | (2,826,750 | ) | |||

| (75,000 | ) | SPDR S&P Homebuilders ETF | (3,001,500 | ) | ||||

| TOTAL EXCHANGE TRADED FUNDS (Premiums Received - $5,773,822) | $ | (5,828,250 | ) |

See accompanying notes to financial statements.

12

| Anchor Funds |

| STATEMENTS OF ASSETS AND LIABILITIES |

| August 31, 2018 |

| Anchor Tactical | Anchor Tactical | |||||||||||||||

| Anchor Tactical Credit | Equity Strategies | Municipal | Anchor Tactical | |||||||||||||

| Strategies Fund | Fund | Strategies Fund | Real Estate Fund | |||||||||||||

| ASSETS | ||||||||||||||||

| Investment securities: | ||||||||||||||||

| At cost | $ | 39,363,832 | $ | 153,637,036 | $ | 21,688,264 | $ | 29,451,485 | ||||||||

| At value | $ | 39,615,881 | $ | 158,396,001 | $ | 21,652,006 | $ | 30,027,928 | ||||||||

| Cash | 495,450 | 2,098,168 | 71,866 | 2,036,911 | ||||||||||||

| Deposits with Broker | 1,099 | — | 11,909 | 5,884,429 | ||||||||||||

| Receivable for Fund shares sold | 202,437 | 168,306 | 2,231 | 8,017 | ||||||||||||

| Dividends and interest receivable | 3,088 | 13,875 | 60,394 | 4,094 | ||||||||||||

| Prepaid expenses | 23,612 | 27,543 | 24,356 | 22,293 | ||||||||||||

| TOTAL ASSETS | 40,341,567 | 160,703,893 | 21,822,762 | 37,983,672 | ||||||||||||

| LIABILITIES | ||||||||||||||||

| Securities sold short (Premiums received of $ - , $ - , $ -, and $5,773,822, respectively) | — | — | — | 5,828,250 | ||||||||||||

| Due to Broker | — | 74 | — | — | ||||||||||||

| Payable for Fund shares redeemed | 108,925 | 140,723 | 53,592 | 59,459 | ||||||||||||

| Investment advisory fees payable | 54,844 | 211,153 | 23,167 | 42,725 | ||||||||||||

| Distribution (12b-1) fees payable | 7,632 | 32,993 | 4,648 | 6,676 | ||||||||||||

| Payable to related parties | 8,713 | 10,986 | 5,522 | 7,002 | ||||||||||||

| Accrued expenses and other liabilities | 75,757 | 47,607 | 46,881 | 47,364 | ||||||||||||

| TOTAL LIABILITIES | 255,871 | 443,536 | 133,810 | 5,991,476 | ||||||||||||

| NET ASSETS | $ | 40,085,696 | $ | 160,260,357 | $ | 21,688,952 | $ | 31,992,196 | ||||||||

| Net Assets Consist Of: | ||||||||||||||||

| Paid in capital | 42,551,628 | 144,219,011 | 24,899,776 | 36,426,922 | ||||||||||||

| Undistributed net investment loss | (401,971 | ) | — | — | (291,430 | ) | ||||||||||

| Accumulated net realized gain (loss) from investments and securities sold short | (2,316,010 | ) | 11,282,381 | (3,174,566 | ) | (4,665,311 | ) | |||||||||

| Net unrealized appreciation (depreciation) on investments and securities sold short | 252,049 | 4,758,965 | (36,258 | ) | 522,015 | |||||||||||

| NET ASSETS | $ | 40,085,696 | $ | 160,260,357 | $ | 21,688,952 | $ | 31,992,196 | ||||||||

| Institutional Class | ||||||||||||||||

| Net Assets | $ | 40,085,696 | $ | 160,260,357 | $ | 21,688,952 | $ | 31,992,196 | ||||||||

| Shares of beneficial interest outstanding ($0 par value, unlimited shares authorized) | 4,118,942 | 13,210,010 | 2,239,862 | 3,358,405 | ||||||||||||

| Net asset value, offering and redemption price per share (Net assets/Shares of Beneficial Interest) | $ | 9.73 | $ | 12.13 | $ | 9.68 | $ | 9.53 | ||||||||

See accompanying notes to financial statements.

13

| Anchor Funds |

| STATEMENTS OF OPERATIONS |

| For the Year Ended August 31, 2018 |

| Anchor Tactical | ||||||||||||||||

| Anchor Tactical Credit | Anchor Tactical Equity | Municipal Strategies | Anchor Tactical Real | |||||||||||||

| Strategies Fund | Strategies Fund | Fund | Estate Fund | |||||||||||||

| INVESTMENT INCOME | ||||||||||||||||

| Dividends | $ | 2,296,487 | $ | 689,190 | $ | 1,964,066 | $ | 2,642,638 | ||||||||

| Interest | 84,740 | 179,166 | 11,171 | 200,522 | ||||||||||||

| TOTAL INVESTMENT INCOME | 2,381,227 | 868,356 | 1,975,237 | 2,843,160 | ||||||||||||

| EXPENSES | ||||||||||||||||

| Investment advisory fees | 1,107,294 | 1,470,406 | 814,852 | 1,494,231 | ||||||||||||

| Dividend expense on securities sold short | 887,904 | 83,453 | — | 218,861 | ||||||||||||

| Interest expense on securities sold short | 297,943 | — | — | 14,501 | ||||||||||||

| Distribution (12b-1) fees | 173,015 | 229,751 | 127,321 | 233,474 | ||||||||||||

| Administrative services fees | 55,308 | 74,933 | 41,332 | 76,716 | ||||||||||||

| Custodian fees | 41,737 | 12,043 | 15,985 | 15,546 | ||||||||||||

| Registration fees | 35,000 | 32,889 | 32,987 | 32,787 | ||||||||||||

| Accounting services fees | 32,951 | 35,572 | 29,246 | 37,593 | ||||||||||||

| Printing and postage expenses | 15,798 | 13,598 | 13,894 | 19,388 | ||||||||||||

| Audit fees | 13,400 | 13,400 | 13,400 | 13,400 | ||||||||||||

| Legal fees | 13,320 | 14,624 | 17,000 | 16,794 | ||||||||||||

| Trustees' fees and expenses | 9,566 | 13,785 | 13,566 | 12,485 | ||||||||||||

| Compliance officer fees | 9,377 | 6,803 | 8,470 | 11,729 | ||||||||||||

| Transfer agent fees | 9,242 | 8,975 | 8,837 | 9,542 | ||||||||||||

| Miscellaneous expense | 8,720 | 5,437 | 6,839 | 8,990 | ||||||||||||

| Insurance expense | 7,767 | 4,531 | 5,709 | 6,488 | ||||||||||||

| TOTAL EXPENSES | 2,718,342 | 2,020,200 | 1,149,438 | 2,222,525 | ||||||||||||

| Less: Fees waived by the Adviser | — | — | (6,605 | ) | — | |||||||||||

| NET EXPENSES | 2,718,342 | 2,020,200 | 1,142,833 | 2,222,525 | ||||||||||||

| NET INVESTMENT INCOME (LOSS) | (337,115 | ) | (1,151,844 | ) | 832,404 | 620,635 | ||||||||||

| REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | ||||||||||||||||

| Net realized gain (loss) from: | ||||||||||||||||

| Investments | (291,707 | ) | 14,967,935 | 446,115 | 406,667 | |||||||||||

| Securities sold short | (248,643 | ) | (2,528,191 | ) | 4,788 | (3,204,491 | ) | |||||||||

| Net change in unrealized appreciation (depreciation) on: | ||||||||||||||||

| Investments | (359,487 | ) | 3,498,045 | (1,448,228 | ) | (1,824,751 | ) | |||||||||

| Securities sold short | — | — | — | (54,428 | ) | |||||||||||

| NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS | (899,837 | ) | 15,937,789 | (997,325 | ) | (4,677,003 | ) | |||||||||

| NET INCREASE (DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | $ | (1,236,952 | ) | $ | 14,785,945 | $ | (164,921 | ) | $ | (4,056,368 | ) | |||||

See accompanying notes to financial statements.

14

| Anchor Funds |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Anchor Tactical | Anchor Tactical | |||||||||||||||

| Credit Strategies Fund | Equity Strategies Fund | |||||||||||||||

| For the | For the | For the | For the | |||||||||||||

| Year Ended | Year Ended | Year Ended | Period Ended | |||||||||||||

| August 31, 2018 | August 31, 2017* | August 31, 2018 | August 31, 2017** | |||||||||||||

| FROM OPERATIONS: | ||||||||||||||||

| Net investment income (loss) | $ | (337,115 | ) | $ | 2,677,541 | $ | (1,151,844 | ) | $ | (680,438 | ) | |||||

| Net realized gain (loss) from investments and securities sold short | (540,350 | ) | 481,665 | 12,439,744 | 5,314,814 | |||||||||||

| Net change in unrealized appreciation (depreciation) on investments | (359,487 | ) | (621,079 | ) | 3,498,045 | 1,260,920 | ||||||||||

| Net increase (decrease) in net assets resulting from operations | (1,236,952 | ) | 2,538,127 | 14,785,945 | 5,895,296 | |||||||||||

| DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||

| From net investment income ($0.13, $0.28, $ -, and $ - per share, respectively) | (1,041,231 | ) | (3,246,985 | ) | — | — | ||||||||||

| From net realized gains ($0.04, $ 0.14, $0.67, and $0.09 per share, respectively) | (292,634 | ) | (1,889,257 | ) | (4,171,001 | ) | (494,486 | ) | ||||||||

| Net decrease in net assets from distributions to shareholders | (1,333,865 | ) | (5,136,242 | ) | (4,171,001 | ) | (494,486 | ) | ||||||||

| FROM SHARES OF BENEFICIAL INTEREST: | ||||||||||||||||

| Proceeds from shares sold | 31,371,929 | 76,542,727 | 169,814,613 | 101,395,585 | ||||||||||||

| Reinvestment of dividends | 1,333,201 | 5,136,214 | 4,171,001 | 494,486 | ||||||||||||

| Payments for shares redeemed | (80,835,660 | ) | (132,097,375 | ) | (84,707,633 | ) | (46,988,836 | ) | ||||||||

| Redemption fees | 2,892 | 33,631 | 1,638 | 63,749 | ||||||||||||

| Net increase (decrease) in net assets from shares of beneficial interest | (48,127,638 | ) | (50,384,803 | ) | 89,279,619 | 54,964,984 | ||||||||||

| TOTAL INCREASE (DECREASE) IN NET ASSETS | (50,698,455 | ) | (52,982,918 | ) | 99,894,563 | 60,365,794 | ||||||||||

| NET ASSETS | ||||||||||||||||

| Beginning of Period | 90,784,151 | 143,767,069 | 60,365,794 | — | ||||||||||||

| End of Period ǂ | $ | 40,085,696 | $ | 90,784,151 | $ | 160,260,357 | $ | 60,365,794 | ||||||||

| ǂ Includes undistributed net investment income (loss) of: | $ | (401,971 | ) | $ | 18,202 | $ | — | $ | — | |||||||

| SHARE ACTIVITY | ||||||||||||||||

| Institutional Class: | ||||||||||||||||

| Shares sold | 3,174,701 | 7,556,618 | 14,723,999 | 9,848,475 | ||||||||||||

| Shares reinvested | 133,715 | 510,508 | 373,077 | 48,622 | ||||||||||||

| Shares redeemed | (8,211,264 | ) | (13,056,325 | ) | (7,351,021 | ) | (4,433,142 | ) | ||||||||

| Net increase (decrease) in shares of beneficial interest outstanding | (4,902,848 | ) | (4,989,199 | ) | 7,746,055 | 5,463,955 | ||||||||||

| * | Formerly the Investor Class of the Anchor Tactical Credit Strategies Fund. |

| ** | The Fund commenced operations on September 6, 2016. |

See accompanying notes to financial statements.

15

| Anchor Funds |

| STATEMENTS OF CHANGES IN NET ASSETS (Continued) |

| Anchor Tactical | Anchor Tactical | |||||||||||||||

| Municipal Strategies Fund | Real Estate Fund | |||||||||||||||

| For the | For the | For the | For the | |||||||||||||

| Year Ended | Period Ended | Year Ended | Period Ended | |||||||||||||

| August 31, 2018 | August 31, 2017* | August 31, 2018 | August 31, 2017* | |||||||||||||

| FROM OPERATIONS: | ||||||||||||||||

| Net investment income (loss) | $ | 832,404 | $ | 19,929 | $ | 620,635 | $ | (165,245 | ) | |||||||

| Net realized gain (loss) from investments and securities sold short | 450,903 | (3,625,469 | ) | (2,797,824 | ) | (1,870,724 | ) | |||||||||

| Distributions of capital gains from underlying investment companies | — | — | — | 3,387 | ||||||||||||

| Net change in unrealized appreciation (depreciation) on investments and securities sold short | (1,448,228 | ) | 1,411,970 | (1,879,179 | ) | 2,401,194 | ||||||||||

| Net increase (decrease) in net assets resulting from operations | (164,921 | ) | (2,193,570 | ) | (4,056,368 | ) | 368,612 | |||||||||

| DISTRIBUTIONS TO SHAREHOLDERS: | ||||||||||||||||

| From net investment income ($0.19, $0.00** and $0.10, and $ - per share, respectively) | (906,693 | ) | (20,276 | ) | (1,068,727 | ) | — | |||||||||

| Net decrease in net assets from distributions to shareholders | (906,693 | ) | (20,276 | ) | (1,068,727 | ) | — | |||||||||

| FROM SHARES OF BENEFICIAL INTEREST: | ||||||||||||||||

| Proceeds from shares sold | 11,367,230 | 152,128,877 | 62,695,431 | 141,010,033 | ||||||||||||

| Reinvestment of dividends | 906,660 | 20,276 | 1,063,431 | — | ||||||||||||

| Payments for shares redeemed | (60,579,173 | ) | (78,968,814 | ) | (125,887,334 | ) | (42,171,831 | ) | ||||||||

| Redemption fees | 2,849 | 96,507 | 33 | 38,916 | ||||||||||||

| Net increase (decrease) in net assets from shares of beneficial interest | (48,302,434 | ) | 73,276,846 | (62,128,439 | ) | 98,877,118 | ||||||||||

| TOTAL INCREASE (DECREASE) IN NET ASSETS | (49,374,048 | ) | 71,063,000 | (67,253,534 | ) | 99,245,730 | ||||||||||

| NET ASSETS | ||||||||||||||||

| Beginning of Period | 71,063,000 | — | 99,245,730 | — | ||||||||||||

| End of Period ǂ | $ | 21,688,952 | $ | 71,063,000 | $ | 31,992,196 | $ | 99,245,730 | ||||||||

| ǂ Includes undistributed net investment income (loss) of: | $ | — | $ | 69,638 | $ | (291,430 | ) | $ | — | |||||||

| SHARE ACTIVITY | ||||||||||||||||

| Institutional Class: | ||||||||||||||||

| Shares sold | 1,167,235 | 15,365,338 | 6,474,525 | 14,576,799 | ||||||||||||

| Shares reinvested | 93,631 | 2,061 | 106,893 | — | ||||||||||||

| Shares redeemed | (6,237,356 | ) | (8,151,047 | ) | (13,395,911 | ) | (4,403,901 | ) | ||||||||

| Net increase (decrease) in shares of beneficial interest outstanding | $ | (4,976,490 | ) | 7,216,352 | $ | (6,814,493 | ) | 10,172,898 | ||||||||

| * | The Fund commenced operations on September 6, 2016. |

| ** | Amount is less than $0.005. |

See accompanying notes to financial statements.

16

| Anchor Tactical Credit Strategies Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period Presented.

| Institutional Class ** | ||||||||||||

| For the | For the | Period | ||||||||||

| Year Ended | Year Ended | Ended | ||||||||||

| August 31, 2018 | August 31, 2017 | August 31, 2016* | ||||||||||

| Net asset value, beginning of period | $ | 10.06 | $ | 10.26 | $ | 10.00 | ||||||

| Activity from investment operations: | ||||||||||||

| Net investment income (loss) (1) | (0.05 | ) | 0.23 | 0.07 | ||||||||

| Net realized and unrealized gain (loss) on investments | (0.11 | ) | (0.01 | ) | 0.25 | |||||||

| Total from investment operations | (0.16 | ) | 0.22 | 0.32 | ||||||||

| Less distributions: | ||||||||||||

| From net investment income | (0.13 | ) | (0.28 | ) | (0.06 | ) | ||||||

| From net realized gains | (0.04 | ) | (0.14 | ) | — | |||||||

| Total distributions | (0.17 | ) | (0.42 | ) | (0.06 | ) | ||||||

| Paid-in capital from redemption fees (1) | 0.00 | (7) | 0.00 | (7) | — | |||||||

| Net asset value, end of period | $ | 9.73 | $ | 10.06 | $ | 10.26 | ||||||

| Total return (2) | (1.65 | )% | 2.22 | % | 3.17 | % (3) | ||||||

| Net assets, end of period (000s) | $ | 40,086 | $ | 90,784 | $ | 143,767 | ||||||

| Ratio of expenses to average net assets (5) | 3.94 | % | 2.63 | % | 2.86 | % (4) | ||||||

| Ratio of expenses to average net assets excluding interest and dividend expenses (5) | 2.22 | % | 2.15 | % | 2.21 | % (4) | ||||||

| Ratio of net investment income (loss) to average net assets (5)(6) | (0.49 | )% | 2.23 | % | 0.71 | % (4) | ||||||

| Portfolio turnover rate | 1,409 | % | 1,009 | % | 1,832 | % (3) | ||||||

| * | For the period September 29, 2015 (commencement of operations) through August 31, 2016. |

| ** | Formerly the Investor Class through July 31, 2017. |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Total returns are historical in nature and assume changes in share price, and reinvestment of dividends and capital gains distributions, if any. |

| (3) | Not annualized. |

| (4) | Annualized. |

| (5) | The ratios of expenses to average net assets and net investment income (loss) to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Recognition of net investment income (loss) by the Fund is affected by the timing and declaration of dividends by the underlying investment companies in which the Fund invests. |

| (7) | Amount is less than $0.005. |

See accompanying notes to financial statements.

17

| Anchor Tactical Equity Strategies Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period Presented.

| Institutional Class | ||||||||

| Year | Period | |||||||

| Ended | Ended | |||||||

| August 31, 2018 | August 31, 2017* | |||||||

| Net asset value, beginning of period | $ | 11.05 | $ | 10.00 | ||||

| Activity from investment operations: | ||||||||

| Net investment loss (1) | (0.14 | ) | (0.13 | ) | ||||

| Net realized and unrealized gain on investments | 1.89 | 1.26 | ||||||

| Total from investment operations | 1.75 | 1.13 | ||||||

| Less distributions: | ||||||||

| From net realized gains | (0.67 | ) | (0.09 | ) | ||||

| Total distributions | (0.67 | ) | (0.09 | ) | ||||

| Paid-in capital from redemption fees (1) | 0.00 | (7) | 0.01 | |||||

| Net asset value, end of period | $ | 12.13 | $ | 11.05 | ||||

| Total return (2) | 16.33 | % | 11.48 | % (3) | ||||

| Net assets, end of period (000s) | $ | 160,260 | $ | 60,366 | ||||

| Ratio of expenses to average net assets (5) | 2.19 | % | 2.40 | % (4) | ||||

| Ratio of expenses to average net assets excluding interest and dividend expenses (5) | 2.10 | % | 2.20 | % (4) | ||||

| Ratio of net investment loss to average net assets (5)(6) | (1.25 | )% | (1.24 | )% (4) | ||||

| Portfolio turnover rate | 1,091 | % | 1,576 | % (3) | ||||

| * | For the period September 6, 2016 (commencement of operations) through August 31, 2017. |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Total returns are historical in nature and assume changes in share price, and reinvestment of dividends and capital gains distributions, if any. |

| (3) | Not annualized. |

| (4) | Annualized. |

| (5) | The ratios of expenses to average net assets and net investment loss to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Recognition of net investment loss by the Fund is affected by the timing and declaration of dividends by the underlying investment companies in which the Fund invests. |

| (7) | Amount is less than $0.005. |

See accompanying notes to financial statements.

18

| Anchor Tactical Municipal Strategies Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period Presented.

| Institutional Class | ||||||||

| Year | Period | |||||||

| Ended | Ended | |||||||

| August 31, 2018 | August 31, 2017* | |||||||

| Net asset value, beginning of period | $ | 9.85 | $ | 10.00 | ||||

| Activity from investment operations: | ||||||||

| Net investment income (1) | 0.16 | 0.00 | (7) | |||||

| Net realized and unrealized loss on investments | (0.14 | ) | (0.16 | ) | ||||

| Total from investment operations | 0.02 | (0.16 | ) | |||||

| Less distributions: | ||||||||

| From net investment income | (0.19 | ) | 0.00 | (7) | ||||

| Total distributions | (0.19 | ) | 0.00 | |||||

| Paid-in capital from redemption fees (1) | 0.00 | (7) | 0.01 | |||||

| Net asset value, end of period | $ | 9.68 | $ | 9.85 | ||||

| Total return (2) | 0.25 | % | (1.47 | )% (3) | ||||

| Net assets, end of period (000s) | $ | 21,689 | $ | 71,063 | ||||

| Ratio of expenses to average net assets (5): | ||||||||

| before reimbursement | 2.26 | % | 2.10 | % (4) | ||||

| net of reimbursement | 2.25 | % | 2.10 | % (4) | ||||

| Ratio of net investment income to average net assets (5)(6) | 1.64 | % | 0.02 | % (4) | ||||

| Portfolio turnover rate | 298 | % | 366 | % (3) | ||||

| * | For the period September 6, 2016 (commencement of operations) through August 31, 2017. |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Total returns are historical in nature and assume changes in share price, and reinvestment of dividends and capital gains distributions, if any. |

| (3) | Not annualized. |

| (4) | Annualized. |

| (5) | The ratios of expenses to average net assets and net investment income to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Recognition of net investment income by the Fund is affected by the timing and declaration of dividends by the underlying investment companies in which the Fund invests. |

| (7) | Amount is less than $0.005. |

See accompanying notes to financial statements.

19

| Anchor Tactical Real Estate Fund |

| FINANCIAL HIGHLIGHTS |

Per Share Data and Ratios for a Share of Beneficial Interest Outstanding Throughout Each Period Presented.

| Institutional Class | ||||||||

| Year Ended | Period Ended | |||||||

| August 31, 2018 | August 31, 2017* | |||||||

| Net asset value, beginning of period | $ | 9.76 | $ | 10.00 | ||||

| Activity from investment operations: | ||||||||

| Net investment income (loss) (1) | 0.06 | (0.02 | ) | |||||

| Net realized and unrealized loss on investments | (0.19 | ) | (0.23 | ) (7) | ||||

| Total from investment operations | (0.13 | ) | (0.25 | ) | ||||

| Less distributions: | ||||||||

| From net investment income | (0.10 | ) | — | |||||

| Total distributions | (0.10 | ) | — | |||||

| Paid-in capital from redemption fees (1) | 0.00 | (8) | 0.01 | |||||

| Net asset value, end of period | $ | 9.53 | $ | 9.76 | ||||

| Total return (2) | (1.36 | )% | (2.40 | )% (3) | ||||

| Net assets, end of period (000s) | $ | 31,992 | $ | 99,246 | ||||

| Ratio of expenses to average net assets (5) | 2.38 | % | 2.14 | % (4) | ||||

| Ratio of expenses to average net assets excluding interest and dividend expenses (5) | 2.13 | % | 2.13 | % (4) | ||||

| Ratio of net investment income (loss) to average net assets (5)(6) | 0.67 | % | (0.26 | )% (4) | ||||

| Portfolio turnover rate | 609 | % | 630 | % (3) | ||||

| * | For the period September 6, 2016 (commencement of operations) through August 31, 2017. |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Total returns are historical in nature and assume changes in share price, and reinvestment of dividends and capital gains distributions, if any. |

| (3) | Not annualized. |

| (4) | Annualized. |

| (5) | The ratios of expenses to average net assets and net investment income (loss) to average net assets do not reflect the expenses of the underlying investment companies in which the Fund invests. |

| (6) | Recognition of net investment income (loss) by the Fund is affected by the timing and declaration of dividends by the underlying investment companies in which the Fund invests. |

| (7) | The net realized and unrealized loss on investments per share does not accord with the net of the amounts reported in the statement of operations due to the timing of purchases and redemptions of the Fund shares during the period. |

| (8) | Amount is less than $0.005. |

See accompanying notes to financial statements.

20

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS |

| August 31, 2018 |

| 1. | ORGANIZATION |

The Anchor Tactical Credit Strategies Fund (“Credit Fund”), Anchor Tactical Equity Strategies Fund (“Equity Fund”), Anchor Tactical Municipal Strategies Fund (“Muni Fund”) and Anchor Tactical Real Estate Fund (“Real Estate Fund”) (each a “Fund” or collectively the “Funds”) are diversified series of shares of beneficial interest of Northern Lights Fund Trust IV (the “Trust”), a trust organized under the laws of the State of Delaware on June 2, 2015, and registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Credit Fund, Equity Fund and Muni Fund each have the investment objective to provide total return from income and capital appreciation with a secondary objective of limiting risk during unfavorable market conditions. The Real Estate Fund seeks to achieve above average total returns over a full market cycle with lower correlation and reduced risk when compared to traditional real estate indexes. The Credit Fund commenced operations on September 29, 2015. The Equity Fund, Muni Fund and Real Estate Fund commenced operations on September 6, 2016. Effective October 19, 2018, the Board of Trustees of the Trust (the “Board”) has determined based on the recommendation of Anchor Capital Management Group, Inc. that with respect to the Real Estate Fund, that it is in the best interests of the Real Estate Fund and its shareholders that the Real Estate Fund cease operations. The Board has determined to close the Real Estate Fund and redeem all outstanding shares on November 7, 2018.

Each Fund offers two share classes designated as Investor Class and Institutional Class. The Investor Class of the Credit Fund converted to the Institutional Class of the Credit Fund on August 1, 2017. The Investor Class of the Credit Fund is no longer available for sale and the Investor Class of the Equity Fund, Muni Fund and Real Estate Fund have not commenced operations. Each class represents an interest in the same assets of each Fund and classes are identical except for differences in their ongoing service and distribution charges.

| 2. | SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by each Fund in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. Each Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update ASU 2013-08.

Security Valuation – Securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the exchange on the business day the value is being determined, or in the case of securities listed on NASDAQ at the NASDAQ Official Closing Price (“NOCP”). In the absence of a sale such securities shall be valued at the mean between the current bid and ask prices on the day of valuation. Short-term debt obligations having 60 days or less remaining until maturity, at time of purchase, may be valued at amortized cost.

21

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

Valuation of Underlying Funds – The Funds may invest in portfolios of open-end or closed-end investment companies (the “Underlying Funds”). Investment companies are valued at their respective net asset values as reported by such investment companies. Open-end investment companies value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value to the methods established by the board of directors of the open-end funds. The shares of many closed-end investment companies and exchange traded funds (“ETFs”), after their initial public offering, frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurances that the market discount or market premium on shares of any closed-end investment company or ETF purchased by the Funds will not change.

The Funds may hold securities, such as private investments, interests in commodity pools, other non-traded securities or temporarily illiquid securities, for which market quotations are not readily available or are determined to be unreliable. These securities will be valued using the “fair value” procedures approved by the Trust’s Board of Trustees (the “Board”). The Board has delegated execution of these procedures to a fair value team composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) adviser. The team may also enlist third party consultants such as a valuation specialist at a public accounting firm, valuation consultant, or financial officer of a security issuer on an as-needed basis to assist in determining a security-specific fair value. The Board reviews and ratifies the execution of this process and the resultant fair value prices at least quarterly to assure the process produces reliable results.

Fair Valuation Process. As noted above, the fair value team is composed of one or more representatives from each of the (i) Trust, (ii) administrator, and (iii) adviser. The applicable investments are valued collectively via inputs from each of these groups. For example, fair value determinations are required for the following securities: (i) securities for which market quotations are insufficient or not readily available on a particular business day (including securities for which there is a short and temporary lapse in the provision of a price by the regular pricing source), (ii) securities for which, in the judgment of the adviser, the prices or values available do not represent the fair value of the instrument. Factors which may cause the adviser to make such a judgment include, but are not limited to, the following: only a bid price or an asked price is available; the spread between bid and asked prices is substantial; the frequency of sales; the thinness of the market; the size of reported trades; and actions of the securities markets, such as the suspension or limitation of trading; (iii) securities determined to be illiquid; (iv) securities with respect to which an event that will affect the value thereof has occurred (a “significant event”) since the closing prices were established on the principal exchange on which they are traded, but prior to the Fund’s calculation of its net asset value. Restricted or illiquid securities, such as private investments or non-traded securities are valued via inputs from the adviser based upon the current bid for the security from two or more independent dealers or other parties reasonably familiar with the facts and circumstances of the security (who should take into consideration all relevant factors as may be appropriate under the circumstances). If the adviser is unable to obtain a current bid from such independent dealers or other independent parties, the fair value team shall determine the fair value of such security using the following factors: (i) the type of security; (ii) the cost at date of purchase; (iii) the size and nature of the Fund’s holdings; (iv) the discount from market value of unrestricted securities of the same class at the time of purchase and subsequent thereto; (v) information as to any transactions or offers with respect to the security; (vi) the nature and duration of restrictions on disposition of the security and the existence of any registration rights; (vii) how the yield of the security compares to similar securities of companies of similar or equal creditworthiness; (viii)

22

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

the level of recent trades of similar or comparable securities; (ix) the liquidity characteristics of the security; (x) current market conditions; and (xi) the market value of any securities into which the security is convertible or exchangeable.

The Funds utilize various methods to measure the fair value of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Funds have the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following table summarizes the inputs used as of August 31, 2018 for the Funds’ assets and liabilities measured at fair value:

| Anchor Tactical Credit Strategies Fund | ||||||||||||||||

| Assets * | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Closed-End Fund | $ | 1,846,877 | $ | — | $ | — | $ | 1,846,877 | ||||||||

| Exchange Traded Funds | 37,769,004 | — | — | 37,769,004 | ||||||||||||

| Total | $ | 39,615,881 | $ | — | $ | — | $ | 39,615,881 | ||||||||

23

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

| Anchor Tactical Equity Strategies Fund | ||||||||||||||||

| Assets * | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Exchange Traded Funds | $ | 158,396,001 | $ | — | $ | — | $ | 158,396,001 | ||||||||

| Total | $ | 158,396,001 | $ | — | $ | — | $ | 158,396,001 | ||||||||

| Anchor Tactical Municipal Strategies Fund | ||||||||||||||||

| Assets * | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Closed-End Funds | $ | 10,848,551 | $ | — | $ | — | $ | 10,848,551 | ||||||||

| Mutual Funds | 10,803,455 | — | — | 10,803,455 | ||||||||||||

| Total | $ | 21,652,006 | $ | — | $ | — | $ | 21,652,006 | ||||||||

| Anchor Tactical Real Estate Fund | ||||||||||||||||

| Assets * | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Exchange Traded Funds | $ | 30,027,928 | $ | — | $ | — | $ | 30,027,928 | ||||||||

| Total | $ | 30,027,928 | $ | — | $ | — | $ | 30,027,928 | ||||||||

| Liabilities * | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Exchange Traded Funds | $ | (5,828,250 | ) | $ | — | $ | — | $ | (5,828,250 | ) | ||||||

| Total | $ | (5,828,250 | ) | $ | — | $ | — | $ | (5,828,250 | ) | ||||||

There were no transfers between any level during the year ended August 31, 2018.

It is the Funds’ policy to record transfers into or out of any Level at the end of the reporting period.

The Funds did not hold any Level 2 or Level 3 securities during the period.

| * | Please refer to the Portfolio of Investments for industry classifications. |

Exchange Traded Funds – The Funds may invest in ETFs. ETFs are a type of fund bought and sold on a securities exchange. An ETF trades like common stock and represents a fixed portfolio of securities. The Funds may purchase an ETF to gain exposure to a portion of the U.S. or a foreign market. The risks of owning an ETF generally reflect the risks of owning its underlying securities, although the lack of liquidity on an ETF could result in it being more volatile. Additionally, ETFs have fees and expenses that reduce their value.

Short Sales – A “short sale” is a transaction in which a fund sells a security it does not own but has borrowed in anticipation that the market price of that security will decline. A fund is obligated to replace the security borrowed by purchasing it on the open market at a later date. If the price of the security sold short increases between the time of the short sale and the time a fund replaces the borrowed security, the fund will incur a loss, potentially unlimited in size. Conversely, if the price declines, the fund will realize a gain, limited to the price at which the fund sold the security short.

Security Transactions and Related Income – Security transactions are accounted for on trade date. Interest income is recognized on an accrual basis. Discounts are accreted and premiums are amortized on securities purchased over the lives of the respective securities. Dividend income and expense are recorded on the ex-dividend date. Realized gains or losses from sales of securities are determined by comparing the identified cost of the security lot sold with the net sales proceeds. Withholding taxes on foreign dividends have been provided for in accordance with the Funds’ understanding of the applicable country’s tax rules and rates.

Dividends and Distributions to Shareholders – Dividends from net investment income, if any, are declared and paid quarterly for the Funds. Distributable net realized capital gains, if any, are

24

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

declared and distributed annually. Dividends from net investment income and distributions from net realized gains are determined in accordance with federal income tax regulations, which may differ from GAAP. These “book/tax” differences are considered either temporary (e.g., deferred losses, capital loss carryforwards, etc.) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment; temporary differences do not require reclassification. Any such reclassifications will have no effect on net assets, results of operations, or net asset values per share of the Funds.

Federal Income Tax – It is the Funds’ policy to qualify as regulated investment companies by complying with the provisions of the Internal Revenue Code that are applicable to regulated investment companies and to distribute substantially all of their taxable income and net realized gains to shareholders. Therefore, no Federal income tax provision is required. The Funds recognize the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Funds’ tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years ended August 31, 2016 to August 31, 2017, or expected to be taken in the Funds’ August 31, 2018 year-end tax return. The Funds identify their major tax jurisdictions as U.S. Federal, state of Nebraska, and foreign jurisdictions where the Funds make significant investments; however the Funds are not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

Expenses – Expenses of the Trust that are directly identifiable to a specific Fund are charged to that Fund. Expenses, which are not readily identifiable to a specific Fund, are allocated in such a manner as deemed equitable, taking into consideration the nature and type of expense and the relative sizes of the Funds in the Trust.

Indemnification – The Trust indemnifies its officers and trustees for certain liabilities that may arise from the performance of their duties to the Trust. Additionally, in the normal course of business, the Funds enter into contracts that contain a variety of representations and warranties and which provide general indemnities. The Funds’ maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Funds that have not yet occurred. However, based on experience, the risk of loss due to these warranties and indemnities appears to be remote.

| 3. | CASH – CONCENTRATION IN UNINSURED ACCOUNT |

For cash management purposes the Funds may concentrate cash with the Funds’ custodian. This typically results in cash balances exceeding the Federal Deposit Insurance Corporation (“FDIC”) insurance limits. As of August 31, 2018, the Credit Fund, Equity Fund and Real Estate Fund held $495,450, $2,098,168 and $2,036,911 respectively in cash at MUFG Union Bank, N.A. that exceeded the FDIC insurance limit of $250,000.

| 4. | INVESTMENT TRANSACTIONS |

For the year ended August 31, 2018, cost of purchases and proceeds from sales of portfolio securities, other than short-term investments, amounted to $717,761,556 and $764,475,397, respectively, for the Credit Fund, $807,895,268 and $727,348,307 respectively, for the Equity

25

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

Fund, $138,027,271 and $186,615,848, respectively, for the Muni Fund and $379,880,936 and $442,865,224, respectively, for the Real Estate Fund.

| 5. | INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES |

Anchor Capital Management Group, Inc. serves as the Funds’ investment adviser (the “Adviser”).

Pursuant to an investment advisory agreement with the Trust, on behalf of each Fund, the Adviser, under the supervision of the Board, oversees the daily operations of the Funds and supervises the performance of administrative and professional services provided by others. As compensation for its services and the related expenses borne by the Adviser, each Fund pays the Adviser a management fee, computed and accrued daily and paid monthly, at an annual rate of 1.60% of each Fund’s average daily net assets. For the year ended August 31, 2018, the Funds incurred advisory fees, as follows of $1,107,294 for the Credit Fund, $1,470,406 for the Equity Fund, $814,852 for the Muni Fund and $1,494,231 for the Real Estate Fund.

The Adviser has contractually agreed to reduce its fees and/or absorb expenses of the Credit Fund, the Equity Fund, the Muni Fund and the Real Estate Fund until at least August 31, 2018 to ensure that total annual fund operating expenses after fee waiver and/or reimbursement (exclusive of any front-end or contingent deferred loads, taxes, brokerage fees and commissions, borrowing costs (such as interest and dividend expense on securities sold short), acquired fund fees and expenses, fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses), or extraordinary expenses such as litigation) will not exceed 2.25% of each Fund’s average daily net assets of the Institutional Class Shares. Fees waived or reimbursed by the Adviser may be recouped by the Adviser from the Fund, to the extent that overall expenses fall below the expense limitation, within three years following when such amounts were waived and/or reimbursed if such recoupment can be achieved within the lesser of the foregoing expense limits or the expenses limits in place at the time of the recoupment. During the year ended August 31, 2018, the Adviser waived fees of $6,605 for the Muni Fund, which is subject to recapture by the Adviser before August 31, 2021.

Distributor – The distributor of the Funds is Northern Lights Distributors, LLC (the “Distributor”), The Board has adopted, on behalf of the Funds, the Trust’s Master Distribution and Shareholder Servicing Plan (the “Plan”), as amended, pursuant to Rule 12b-1 under the 1940 Act. Under the Plan, Institutional Class Shares may pay up to 0.25% of their average daily net assets to pay for certain distribution activities and shareholder services. For the year ended August 31, 2018, $173,015, $229,751, $127,321 and $233,474 was incurred under the Plan for the Credit Fund, the Equity Fund, the Muni Fund and the Real Estate Fund, respectively.

The Distributor acts as the Funds’ principal underwriter in a continuous public offering of the Funds’ shares. For the year ended August 31, 2018, the Distributor did not receive any underwriting commissions for sales of the Funds’ shares.

26

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

In addition, certain affiliates of the Distributor provide services to the Funds as follows:

Gemini Fund Services, LLC (“GFS”), an affiliate of the Distributor, provides administration, fund accounting, and transfer agent services to the Trust. Pursuant to separate servicing agreements with GFS, the Funds pay GFS customary fees for providing administration, fund accounting and transfer agency services to the Funds. Certain officers of the Trust are also officers of GFS, and are not paid any fees directly by the Funds for serving in such capacities.

Northern Lights Compliance Services, LLC (“NLCS”) – NLCS, an affiliate of GFS and the Distributor, provides a Chief Compliance Officer to the Trust, as well as related compliance services, pursuant to a consulting agreement between NLCS and the Trust. Under the terms of such agreement, NLCS receives customary fees from the Funds.

Blu Giant, LLC (“Blu Giant”) – Blu Giant, an affiliate of GFS and the Distributor, provides EDGAR conversion and filing services as well as print management services for the Funds on an ad-hoc basis. For the provision of these services, Blu Giant receives customary fees from the Funds for these services.

| 6. | REDEMPTION FEES |

Through July 24, 2017, the Funds assessed a short-term redemption fee of 1.00% of the total redemption amount if a shareholder sells their shares after holding them for less than 60 days. The redemption fee is paid directly to the Funds from which the redemption is made. The Funds received redemption fees for the year ended August 31, 2018 of $2,892, $1,638, $2,849 and $33 for the Credit Fund, Equity Fund, Muni Fund and Real Estate Fund, respectively.

| 7. | AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION – TAX BASIS |

The identified cost of investments in securities owned by the Funds for federal income tax purposes and the respective gross unrealized appreciation and depreciation at August 31, 2018, were as follows:

| Portfolio | Cost for Federal Tax purposes | Unrealized Appreciation | Unrealized Depreciation | Tax Net Unrealized Appreciation (Depreciation) | ||||||||||||

| Anchor Tactical Credit Strategies Fund | $ | 40,595,721 | $ | 252,049 | $ | (1,231,889 | ) | $ | (979,840 | ) | ||||||

| Anchor Tactical Equity Strategies Fund | 153,637,036 | 4,881,865 | (122,900 | ) | 4,758,965 | |||||||||||

| Anchor Tactical Municipal Strategies Fund | 21,688,264 | 59,674 | (95,932 | ) | (36,258 | ) | ||||||||||

| Anchor Tactical Real Estate Fund | 23,677,663 | 576,443 | (54,428 | ) | 522,015 | |||||||||||

27

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

| 8. | DISTRIBUTIONS TO SHAREHOLDERS AND TAX COMPONENTS OF CAPITAL |

The tax character of distributions paid during the periods ended August 31, 2018 and August 31, 2017 was as follows:

| For the period ended August 31, 2018: | ||||||||||||||||||||

| Ordinary | Exempt | Long-Term | Return Of | |||||||||||||||||

| Portfolio | Income | Income | Capital Gains | Capital | Total | |||||||||||||||

| Anchor Tactical Credit Strategies Fund | $ | 1,189,725 | $ | — | $ | 144,140 | $ | — | $ | 1,333,865 | ||||||||||

| Anchor Tactical Equity Strategies Fund | 4,171,001 | — | — | — | 4,171,001 | |||||||||||||||

| Anchor Tactical Municipal Strategies Fund | 48,035 | 854,007 | — | 4,651 | 906,693 | |||||||||||||||

| Anchor Tactical Real Estate Fund | 919,778 | — | — | 148,949 | 1,068,727 | |||||||||||||||

| For the period ended August 31, 2017: | ||||||||||||||||||||

| Ordinary | Exempt | Long-Term | Return Of | |||||||||||||||||

| Portfolio | Income | Income | Capital Gains | Capital | Total | |||||||||||||||

| Anchor Tactical Credit Strategies Fund | $ | 5,312,680 | $ | — | $ | 152,354 | $ | — | $ | 5,465,034 | ||||||||||

| Anchor Tactical Equity Strategies Fund | 494,486 | — | — | — | 494,486 | |||||||||||||||

| Anchor Tactical Municipal Strategies Fund | 6,995 | 13,281 | — | — | 20,276 | |||||||||||||||

| Anchor Tactical Real Estate Fund | — | — | — | — | — | |||||||||||||||

As of August 31, 2018, the components of accumulated earnings/ (deficit) on a tax basis were as follows:

| Undistributed | Undistributed | Undistributed | Post October Loss | Capital Loss | Other | Unrealized | Total | |||||||||||||||||||||||||

| Ordinary | Ordinary | Long-Term | and | Carry | Book/Tax | Appreciation/ | Accumulated | |||||||||||||||||||||||||

| Portfolio | Tax-exempt Income | Income | Capital Gains | Late Year Loss | Forwards | Differences | (Depreciation) | Earnings/(Deficits) | ||||||||||||||||||||||||

| Anchor Tactical Credit Strategies Fund | — | $ | 8,797 | $ | — | $ | (1,492,890 | ) | $ | — | $ | (1,999 | ) | $ | (979,840 | ) | $ | (2,465,932 | ) | |||||||||||||

| Anchor Tactical Equity Strategies Fund | — | 10.832,686 | 513,471 | — | — | (63,776 | ) | 4,758,965 | 16,041,346 | |||||||||||||||||||||||

| Anchor Tactical Municipal Strategies Fund | — | — | — | — | (3,174,566 | ) | — | (36,258 | ) | (3,210,824 | ) | |||||||||||||||||||||

| Anchor Tactical Real Estate Fund | — | — | — | (3,153,009 | ) | (1,803,732 | ) | — | 522,015 | (4,434,726 | ) | |||||||||||||||||||||

The difference between book basis and tax basis undistributed net investment income, accumulated net realized gain(loss), and unrealized appreciation/(depreciation) from investments is primarily attributable to the tax deferral of losses on wash sales and straddles, and the unamortized portion of organizational expenses.

Late year losses incurred after December 31 within the fiscal year are deemed to arise on the first business day of the following fiscal year for tax purposes. The Funds incurred and elected to defer such late year losses as follows:

| Late Year | ||||

| Portfolio | Losses | |||

| Anchor Tactical Credit Strategies Fund | $ | 399,972 | ||

| Anchor Tactical Real Estate Fund | 291,430 | |||

Capital losses incurred after October 31 within the fiscal year are deemed to arise on the first business day of the following fiscal year for tax purposes. The Funds incurred and elected to defer such capital losses as follows:

| Post October | ||||

| Portfolio | Losses | |||

| Anchor Tactical Credit Strategies Fund | $ | 1,092,918 | ||

| Anchor Tactical Real Estate Fund | 2,861,579 | |||

28

| Anchor Funds |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| August 31, 2018 |

At August 31, 2018, the Funds had capital loss carry forwards for federal income tax purposes available to offset future capital gains as follows:

| Non-Expiring | CLCF | |||||||||||||||

| Portfolio | Short-Term | Long-Term | Total | Utilized | ||||||||||||

| Anchor Tactical Municipal Strategies Fund | $ | 3,174,566 | $ | — | $ | 3,174,566 | $ | — | ||||||||

| Anchor Tactical Real Estate Fund | 1,803,732 | — | 1,803,732 | — | ||||||||||||