Exhibit (C)(8)(G)

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

October 13, 2015

Strictly Private and Confidential

Preview of the Analysis of the Reorganization of Enersis S.A.

Prepared for the Enersis S.A. Board of Directors

Enersis

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

|

Important information

This document has been prepared by IM Trust Asesorías Financieras [Financial Consultants], S.A. (hereinafter “IM Trust”) at the request of the Board of Directors of Enersis S.A. (“Enersis” or the “Company”) for the exclusive and private use of the Company and its Board of Directors.

The recommendations and conclusions of this document constitute the best view or opinion of IM Trust regarding the reorganization of Enersis at the time of issuance of this document, considering the methodologies used for this purpose and the information that was available. This document’s conclusions may vary if additional or other background information were available. IM Trust shall be under no obligation to report such variations nor when the opinions or information contained in the document are modified.

For the preparation of this document, IM Trust has based itself solely and exclusively on information provided by Enersis and public information, which IM Trust has assumed, without independent verification, to have complete and total integrity and accuracy. In this way, IM Trust assumes no responsibility with regard to the information reviewed nor the conclusions that may arise out of any error, inaccuracy and/or falsity of such information.

Likewise, the conclusions of the document may be based on assumptions that may be subject to significant uncertainties and economic and market contingencies, such as flows, projections, estimates, and interpretations, whose occurrence can be difficult to predict and many of them could even be beyond the reach of Enersis, so there is no certainty at all about the degree of fulfillment of such assumptions. Under no circumstances may the use or incorporation of such flows, projections or estimates be considered as a representation, warranty, or prediction of IM Trust regarding their occurrence, nor of the assumptions that underlie them.

Strictly Private and Confidential 2

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

Contents

1. Introduction 4

2. Business Model Considerations 7

3. Stock Impacts of the Reorganization at Enersis 11 i. Enersis’ Stock Market Situation and Preliminary Assessments 11 ii. Business Models Differentiation and Corporate Structure Simplification 16 iii. Liquidity Considerations 22

4. Cash Flow Impacts of the Reorganization at Enersis 25

5. Conclusions and Next Steps 28

6. Attachments 31

Strictly Private and Confidential 3

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

1 |

|

INTRODUCTION

Strictly Private and Confidential 4

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

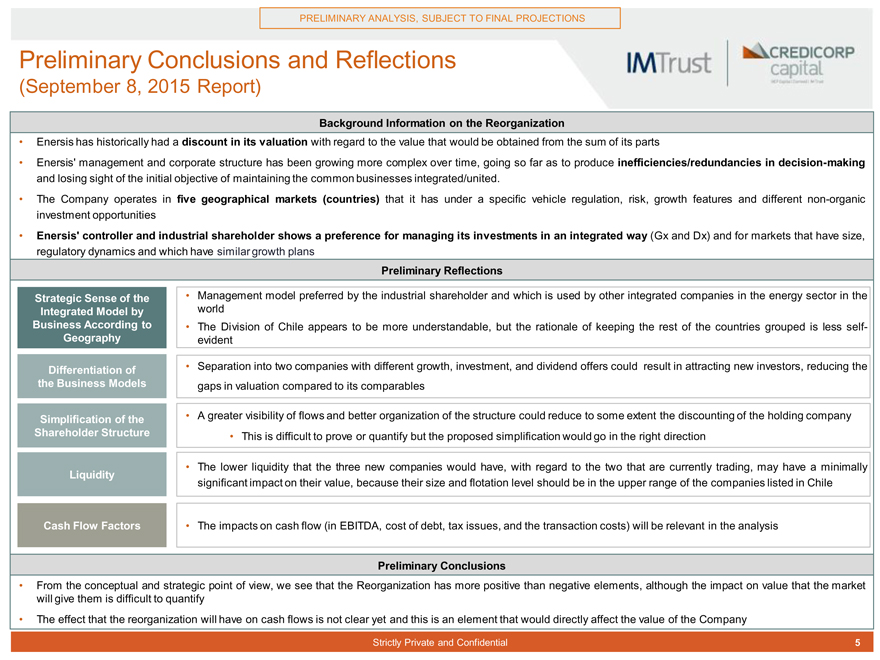

Preliminary Conclusions and Reflections

(September 8, 2015 Report)

Background Information on the Reorganization

Enersis has historically had a discount in its valuation with regard to the value that would be obtained from the sum of its parts

Enersis’ management and corporate structure has been growing more complex over time, going so far as to produce inefficiencies/redundancies in decision-making and losing sight of the initial objective of maintaining the common businesses integrated/united.

The Company operates in five geographical markets (countries) that it has under a specific vehicle regulation, risk, growth features and different non-organic investment opportunities

Enersis’ controller and industrial shareholder shows a preference for managing its investments in an integrated way (Gx and Dx) and for markets that have size, regulatory dynamics and which have similar growth plans

Preliminary Reflections

Management model preferred by the industrial shareholder and which is used by other integrated companies in the energy sector in the

Strategic Sense of the

Integrated Model by world

Business According to The Division of Chile appears to be more understandable, but the rationale of keeping the rest of the countries grouped is less self-

Geography evident

Differentiation of Separation into two companies with different growth, investment, and dividend offers could result in attracting new investors, reducing the the Business Models gaps in valuation compared to its comparables

Simplification of the A greater visibility of flows and better organization of the structure could reduce to some extent the discounting of the holding company Shareholder Structure This is difficult to prove or quantify but the proposed simplification would go in the right direction

The lower liquidity that the three new companies would have, with regard to the two that are currently trading, may have a minimally

Liquidity significant impact on their value, because their size and flotation level should be in the upper range of the companies listed in Chile

Cash Flow Factors The impacts on cash flow (in EBITDA, cost of debt, tax issues, and the transaction costs) will be relevant in the analysis

Preliminary Conclusions

From the conceptual and strategic point of view, we see that the Reorganization has more positive than negative elements, although the impact on value that the market will give them is difficult to quantify

The effect that the reorganization will have on cash flows is not clear yet and this is an element that would directly affect the value of the Company

Strictly Private and Confidential 5

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

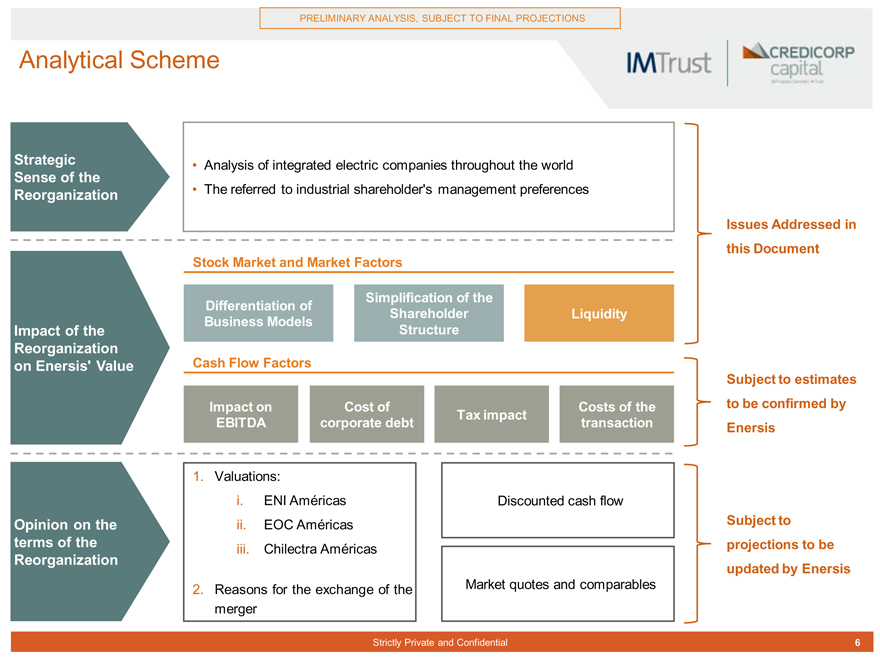

Analytical Scheme

Strategic Analysis of integrated electric companies throughout the world

Sense of the

Reorganization The referred to industrial shareholder’s management preferences

Issues Addressed in Stock Market and Market Factors this Document Simplification of the Differentiation of Shareholder Liquidity Business Models

Impact of the Structure Reorganization on Enersis’ Value Cash Flow Factors

Subject to estimates Impact on Cost of Costs of the to be confirmed by Tax impact EBITDA corporate debt transaction Enersis

1. Valuations: i. ENI Américas Discounted cash flow

Opinion on the ii. EOC Américas Subject to terms of the iii. Chilectra Américas projections to be

Reorganization updated by Enersis

2. Reasons for the exchange of the Market quotes and comparables merger

Strictly Private and Confidential 6

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

BUSINESS MODEL CONSIDERATIONS 2

Strictly Private and Confidential 7

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

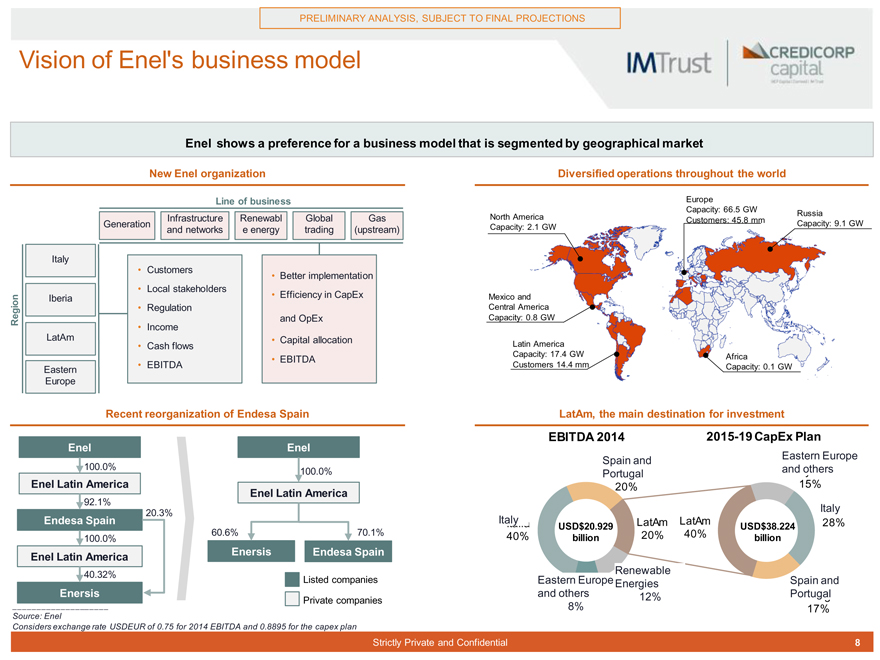

Vision of Enel’s business model

Enel shows a preference for a business model that is segmented by geographical market

New Enel organization Diversified operations throughout the world

Line of business Europe

Capacity: 66.5 GW Russia

Infrastructure Renewabl Global Gas North America Customers: 45.8 mm

Generation Capacity: 2.1 GW Capacity: 9.1 GW and networks e energy trading (upstream)

Italy

Customers

Better implementation

Local stakeholders

Iberia Efficiency in CapEx Mexico and

Regulation Central America

Region Income and OpEx Capacity: 0.8 GW LatAm Capital allocation

Cash flows Latin America

EBITDA Capacity: 17.4 GW Africa

Eastern EBITDA Customers 14.4 mm Capacity: 0.1 GW

Europe

Recent reorganization of Endesa Spain LatAm, the main destination for investment

Enel Enel EBITDA 2014 2015-19 CapEx Plan

100.0% Spain and Eastern Europe 100.0% Portugal and others

Enel Latin America 20% 15% Enel Latin America

92.1%

20.3% Italy Italy lia

Endesa Spain Italia LatAm LatAm 28%

USD$20.929 USD$38.224

60.6% 70.1% 40% 20% 40%

100.0% billion billion

Enel Latin America Enersis Endesa Spain

40.32% Renewable

Listed companies Eastern EuropeEnergies Spain and Enersis and others 12% Portugal

Private companies

8% 17% Source: Enel Considers exchange rate USDEUR of 0.75 for 2014 EBITDA and 0.8895 for the capex plan

Strictly Private and Confidential 8

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

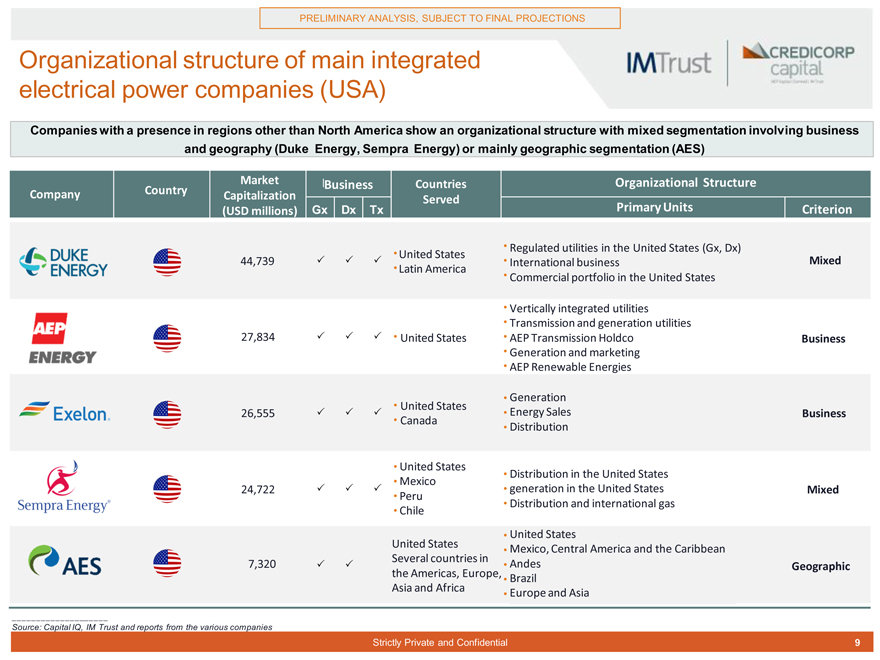

Organizational structure of main integrated electrical power companies (USA)

Companies with a presence in regions other than North America show an organizational structure with mixed segmentation involving business and geography (Duke Energy, Sempra Energy) or mainly geographic segmentation (AES)

Market Business Countries Organizational Structure

Company Country Capitalization

Served

(USD millions) Gx Dx Tx Primary Units Criterion

Regulated utilities in the United States (Gx, Dx) United States

44,739 International business Mixed Latin America

Commercial portfolio in the United States

Vertically integrated utilities

Transmission and generation utilities

27,834 United States AEP Transmission Holdco Business

Generation and marketing

AEP Renewable Energies

Generation

United States

26,555 Energy Sales Business

Canada

Distribution

United States

Distribution in the United States

Mexico

24,722 generation in the United States Mixed

Peru

Distribution and international gas

Chile

United States United States

Mexico, Central America and the Caribbean 7,320 Several countries in Andes

Geographic the Americas, Europe, Brazil

Asia and Africa Europe and Asia

Source: Capital IQ, IM Trust and reports from the various companies

Strictly Private and Confidential 9

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

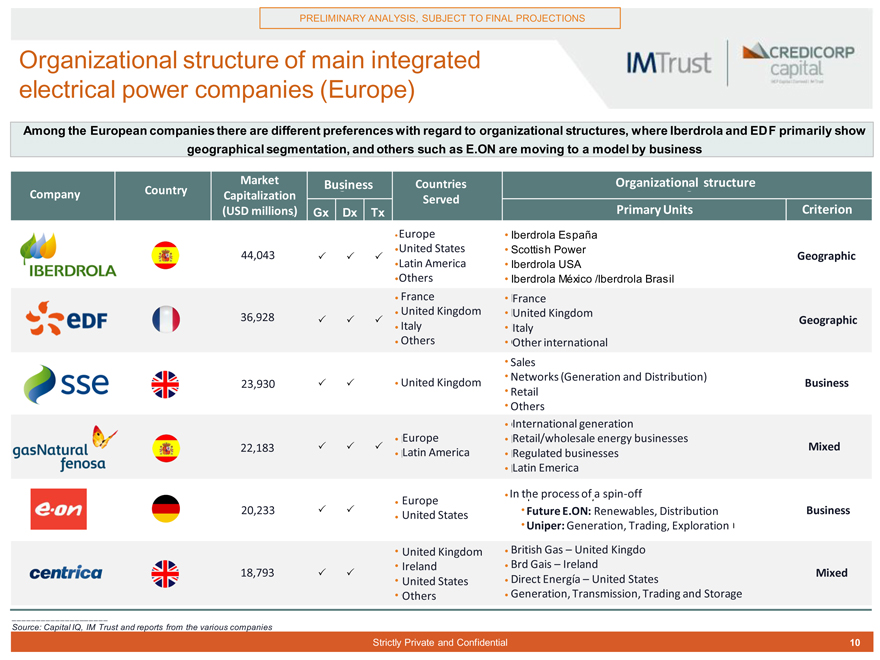

Organizational structure of main integrated electrical power companies (Europe)

Among the European companies there are different preferences with regard to organizational structures, where Iberdrola and EDF primarily show geographical segmentation, and others such as E.ON are moving to a model by business

Market Business Countries Organizational structure

Country Company Capitalization Served

(USD millions) Gx Dx Tx Primary Units Criterion

Europe Iberdrola España United States Scottish Power

44,043 Geographic

Latin America Iberdrola USA

Others Iberdrola México /Iberdrola Brasil

France France

United Kingdom United Kingdom

36,928 Geographic

Italy Italy

Others Other international

Sales

Networks (Generation and Distribution)

23,930 United Kingdom Business

Retail

Others

International generation

Europe Retail/wholesale energy businesses

22,183 Latin America Regulated businesses Mixed

Latin Emerica

In En the proceso process de of spin-off a spin-off

Europe

20,233 United States Future E.ON: Renewables, Distribution Business

Uniper: Generation, Trading, Exploration

United Kingdom British Gas – United Kingdo

Ireland Brd Gais – Ireland

18,793 Direct Energía – United States Mixed

United States

Others Generation, Transmission, Trading and Storage

Source: Capital IQ, IM Trust and reports from the various companies

Strictly Private and Confidential 10

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

STOCK IMPACTS OF THE REORGANIZATION AT

ENERSIS 3 i. Enersis’ Stock Market Situation and Preliminary Assessments

Strictly Private and Confidential 11

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

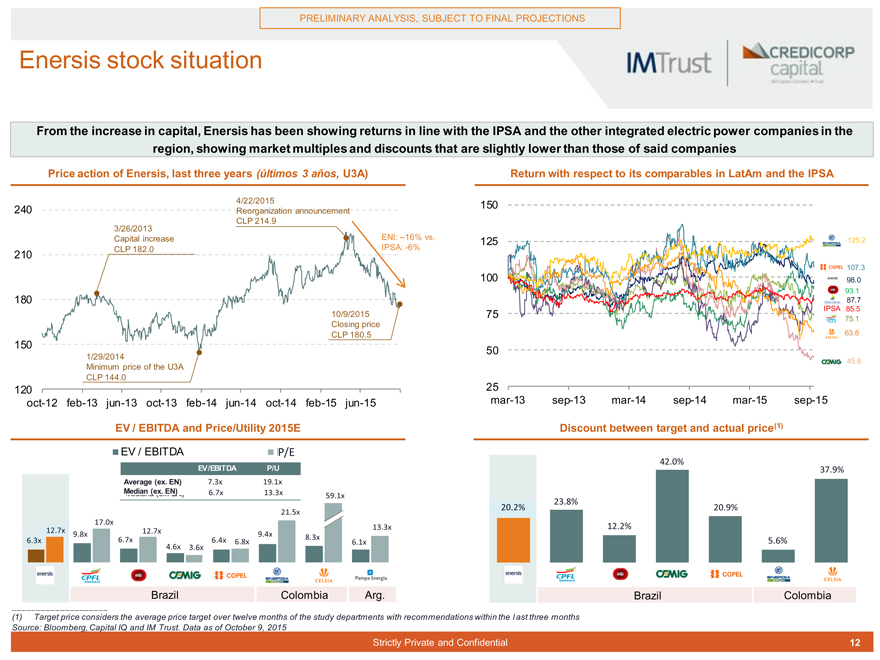

Enersis stock situation

From the increase in capital, Enersis has been showing returns in line with the IPSA and the other integrated electric power companies in the region, showing market multiples and discounts that are slightly lower than those of said companies

Price action of Enersis, last three years (últimos 3 años, U3A) Return with respect to its comparables in LatAm and the IPSA

4/22/2015 150 240 Reorganization announcement CLP 214.9 3/26/2013

Capital increase ENI: –16% vs. 125 1125. ,2 CLP 182.0 IPSA: -6%

210

100 1 107. ,3

98, 98.0 93. 3,1 1

180 85, 87, 87.7

IPSA 85.5

10/9/2015 75

75. |

| 5,1 1 |

Closing price

CLP 180.5 63. 3,8 8

150

50

1/29/2014

45, 45.6

Minimum price of the U3A CLP 144.0

120 25 oct-12 feb-13 jun-13 oct-13 feb-14 jun-14 oct-14 feb-15 jun-15 mar-13 sep-13 mar-14 sep-14 mar-15 sep-15

EV / EBITDA and Price/Utility 2015E Discount between target and actual price(1)

EV / EBITDA P/E 42,0% 42.0%

EV/EBITDA P/U 37. 7,9% 9%

Average (ex. EN) 7. 7,3xx 19,1 19.1x

Median (ex. EN)

6. 6,7xx 13,3 13.3x 59, 59.1x 23. 3,8% 8%

21, 20.2% 20. 0,9% 9%

21.5x 17. 7,0x

12. |

| 2,7x 7x 12, 13. 3,3x 12,2% 12.2% 9.8x 9, x 12.7x 9, 9.4x 6. 6,3xx 6.,7x x 6. 6,4xx 6,8 8.,3xx |

4,6x 6.8x 6,1 6.1x 5,6% 5.6% 4.6x 3. 3,6xx

Brazil Colombia Arg. Brazil Colombia

(1) Target price considers the average price target over twelve months of the study departments with recommendations within the last three months Source: Bloomberg, Capital IQ and IM Trust. Data as of October 9, 2015

Strictly Private and Confidential 12

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

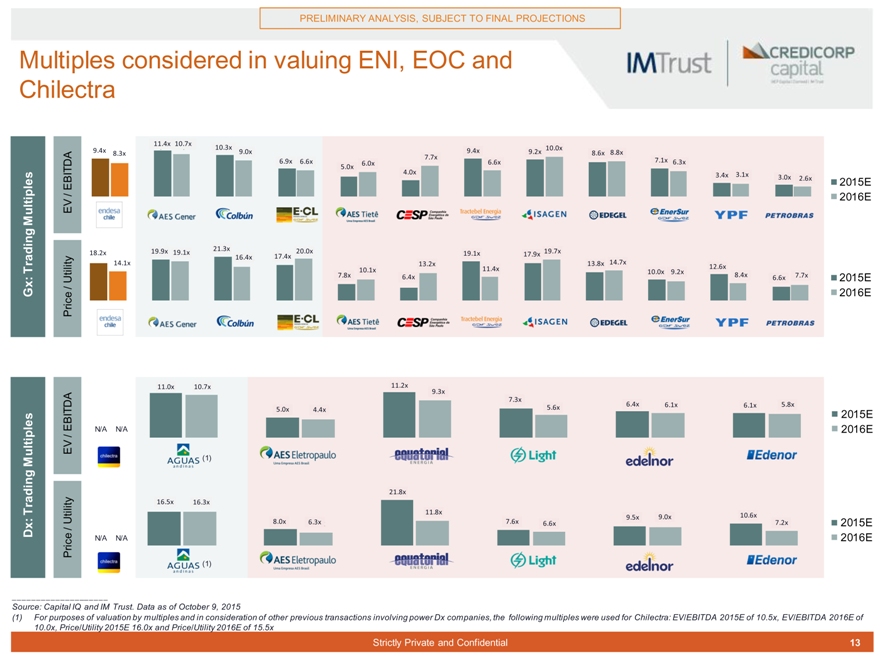

Multiples considered in valuing ENI, EOC and Chilectra

11,4x 11.4x 10. 10,7x 7x 10,

9. 9,4x 10.3x 9, 9.4x 9, 10, 10.0x

8, 8.3x 9. 9,0x 9.2x 8, 8.6x 8, 8.8x

6, 7. 7,7x 7x 7, 7.1x

6.9x 6. 6,6x 6. 6,0x 0x 6. 6,6x 6, 6.3x 5. 5,0x

4. 4,0x 3,4x 3.4x 3.1x

3, 3, 3.0x 2, 2.6x

EBITDA 2015E /

Multiples EV 2016E

19, 21. 21,3x 20, 19,

18.2x 19.9x 19. 19,1x 20.0x 19, 19.1x 19.7x

18, 16. 16,4x 17. 17,4x 17. 17,9x 14,

14, 14.1x 13. 13,2x 13, 13.8x 14.7x 12,6x Trading 10.1x 11, 11.4x 12.6x

10,1x 10, 10.0x 9. 9,2x 2x 8,

Utility 7. 7,8x 8x 6. 6,4x 8.4x 6, 6.6x 7, 7.7x 2015E

/

Gx: Price 2016E

11. |

| 11,0x 10, 10.7x 11,2x 11.2x |

9. 9,3x

7, 7.3x 6,

5. 5,6x 6.4x 6. 6,1x 6, 6.1x 5. 5,8x 8x 5, 5.0x 4.4x

EBITDA 4,4x 2015E

N/A N/A 2016E

/ EV

Multiples (1)

21, 21.8x Trading 16, 16.5x 16,3 16.3x x

11,8 11.8x x 10, 10.6x

8, 9, 9.5x 9. 9,0xx

Utility 8.0x 6. 6,3x x 7. 7,6x 6, 6.6xx 7, 7.2xx 2015E

Dx:/

Price N/A N/A 2016E (1)

Source: Capital IQ and IM Trust. Data as of October 9, 2015

(1) For purposes of valuation by multiples and in consideration of other previous transactions involving power Dx companies, the following multiples were used for Chilectra: EV/EBITDA 2015E of 10.5x, EV/EBITDA 2016E of 10.0x, Price/Utility 2015E 16.0x and Price/Utility 2016E of 15.5x

Strictly Private and Confidential 13

|

Strictly Private and Confidential 13

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

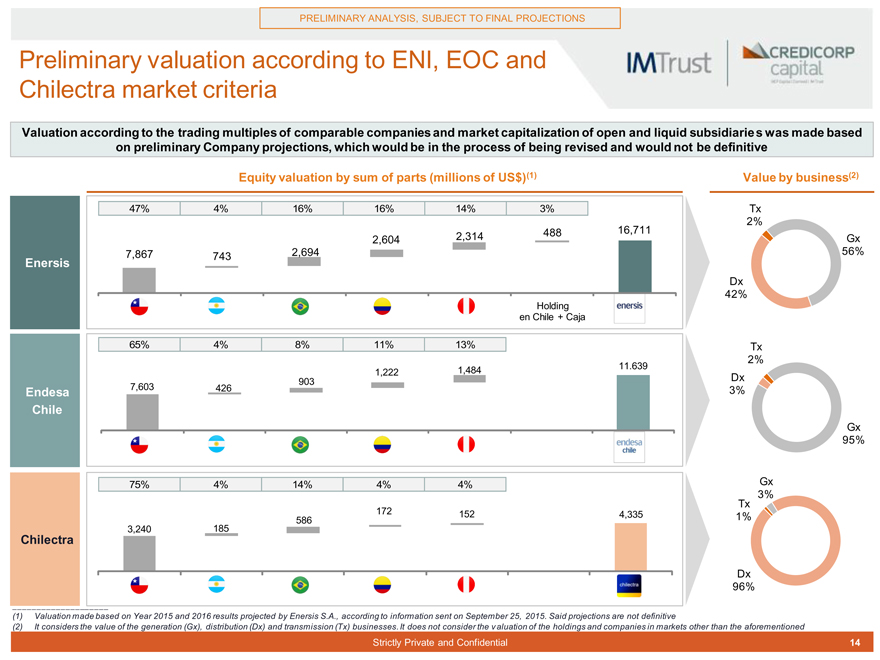

Preliminary valuation according to ENI, EOC and Chilectra market criteria

Valuation according to the trading multiples of comparable companies and market capitalization of open and liquid subsidiaries was made based on preliminary Company projections, which would be in the process of being revised and would not be definitive

Equity valuation by sum of parts (millions of US$)(1) Value by business(2)

47% 4% 16% 16% 14% 3% Tx 2%

488 16,711

2,604 2,314 Gx Enersis 7,867 743 2,694 56% Dx 42%

Holding en Chile + Caja

65% 4% 8% 11% 13% Tx 2%

1,484 11.639

903 1,222 Dx Endesa 7,603 426 3%

Chile

Gx 95%

75% 4% 14% 4% 4% Gx 3% Tx

172 152 4,335 1% 586

Chilectra 3,240 185

Dx 96%

(1) Valuation made based on Year 2015 and 2016 results projected by Enersis S.A., according to information sent on September 25, 2015. Said projections are not definitive

(2) It considers the value of the generation (Gx), distribution (Dx) and transmission (Tx) businesses. It does not consider the valuation of the holdings and companies in markets other than the aforementioned

Strictly Private and Confidential 14

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

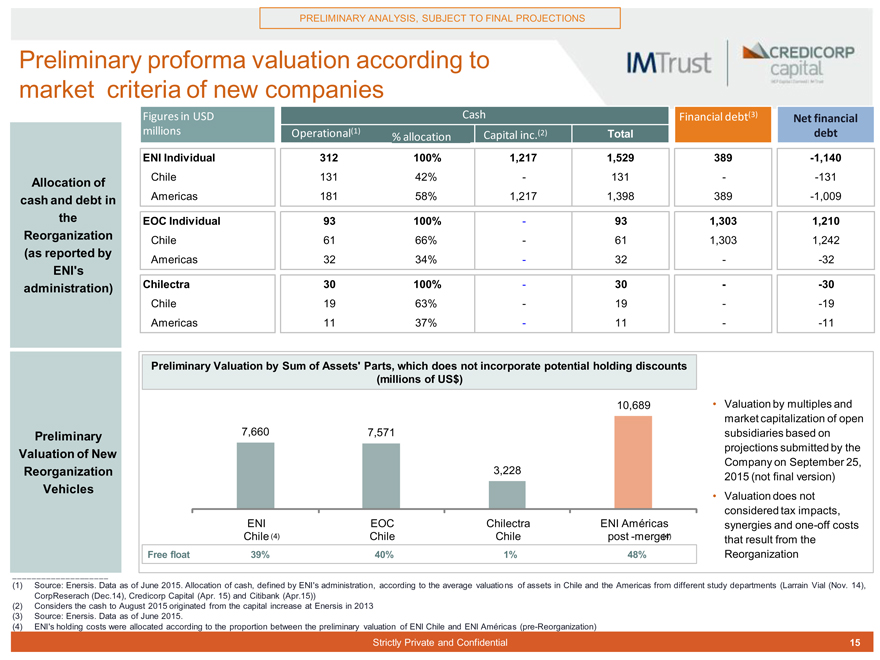

Preliminary proforma valuation according to market criteria of new companies

Figures in USD Cash Financial debt(3) Net financial millions Operational(1) % allocation asignación Capital Aum. capital inc.(2) (2) Total debt

(1) |

|

ENI Individual 312 100% 1,217 1,529 389 -1,140

Allocation of Chile 131 42%—131 —131 cash and debt in Americas 181 58% 1,217 1,398 389 -1,009 the EOC Individual 93 100%—93 1,303 1,210

Reorganization Chile 61 66%—61 1,303 1,242

(as reported by

Americas 32 34%—32 —32

ENI’s administration) Chilectra 30 100%—30 —30

Chile 19 63%—19 —19 Americas 11 37%—11 —11

Preliminary Valuation by Sum of Assets’ Parts, which does not incorporate potential holding discounts (millions of US$)

10,689 Valuation by multiples and market capitalization of open Preliminary 7,660 7,571 subsidiaries based on projections submitted by the

Valuation of New

Company on September 25,

Reorganization 3,228

2015 (not final version)

Vehicles

Valuation does not considered tax impacts, ENI EOC Chilectra ENI Américas synergies and one-off costs Chile (4) Chile Chile post -merger (4) that result from the

Free float 39% 40% 1% 48% Reorganization

(1) Source: Enersis. Data as of June 2015. Allocation of cash, defined by ENI’s administration, according to the average valuations of assets in Chile and the Americas from different study departments (Larrain Vial (Nov. 14), CorpReserach (Dec.14), Credicorp Capital (Apr. 15) and Citibank (Apr.15)) (2) Considers the cash to August 2015 originated from the capital increase at Enersis in 2013 (3) Source: Enersis. Data as of June 2015.

(4) ENI’s holding costs were allocated according to the proportion between the preliminary valuation of ENI Chile and ENI Américas (pre-Reorganization)

Strictly Private and Confidential 15

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

STOCK IMPACTS OF THE REORGANIZATION AT

ENERSIS 3 ii. Business Models Differentiation and Corporate Structure Simplification

Strictly Private and Confidential 16

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

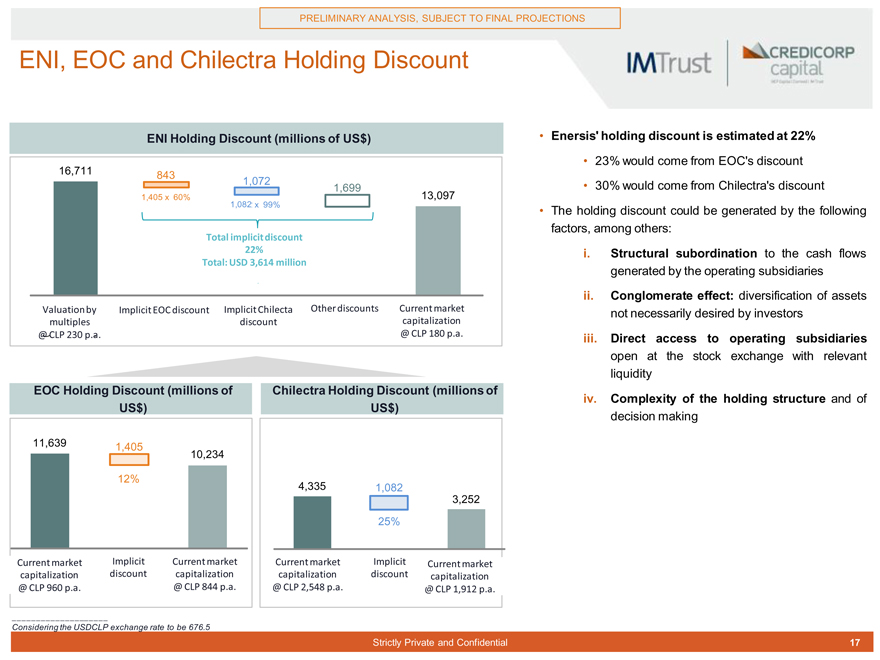

ENI, EOC and Chilectra Holding Discount

ENI Holding Discount (millions of US$) Enersis’ holding discount is estimated at 22%

23% would come from EOC’s discount

16,711

843

1,072 30% would come from Chilectra’s discount

1,699

1,405. x 60% 13,097

1,082 . x 99% The holding discount could be generated by the following factors, among others:

Total implicit discount

22% i. Structural subordination to the cash flows

Total: USD 3,614 million generated by the operating subsidiaries ii. Conglomerate effect: diversification of assets

Valuation by Implicit EOC discount Implicit Chilecta Other discounts Current market not necessarily desired by investors multiples discount capitalization

@ CLP 230 p.a. @ CLP 180 p.a. iii. Direct access to operating subsidiaries open at the stock exchange with relevant liquidity

EOC Holding Discount (millions of Chilectra Holding Discount (millions of iv. Complexity of the holding structure and of US$) US$) decision making

11,639 1,405 10,234 12% 4,335 1,082 3,252 25%

Current market Implicit Current market Current market Implicit Current market capitalization discount capitalization capitalization discount capitalization

@ CLP 960 p.a. @ CLP 844 p.a. @ CLP 2,548 p.a. @ CLP 1,912 p.a.

Considering the USDCLP exchange rate to be 676.5

Strictly Private and Confidential 17

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

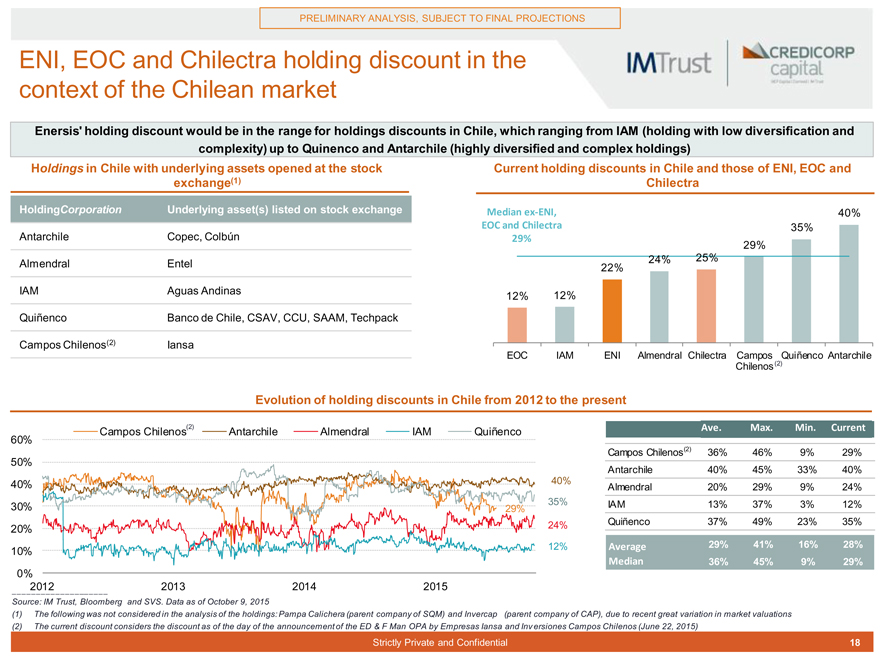

ENI, EOC and Chilectra holding discount in the context of the Chilean market

Enersis’ holding discount would be in the range for holdings discounts in Chile, which ranging from IAM (holding with low diversification and complexity) up to Quinenco and Antarchile (highly diversified and complex holdings) Holdings in Chile with underlying assets opened at the stock Current holding discounts in Chile and those of ENI, EOC and exchange(1) Chilectra

HoldingCorporation Underlying asset(s) listed on stock exchange Median ex-ENI, 40%

EOC and Chilectra 35%

Antarchile Copec, Colbún 29%

29% 24% 25%

Almendral Entel 22% IAM Aguas Andinas 12% 12% Quiñenco Banco de Chile, CSAV, CCU, SAAM, Techpack

Campos Chilenos(2) Iansa

EOC IAM ENI Almendral Chilectra Campos Quiñenco Antarchile Chilenos(2)

Evolution of holding discounts in Chile from 2012 to the present

Campos Chilenos(2) Antarchile Almendral IAM Quiñenco Ave. Max. Min. Current 60%

Campos Chilenos(2) 36% 46% 9% 29%

50%

Antarchile 40% 45% 33% 40%

40% 40%

Almendral 20% 29% 9% 24% 30% 35% IAM 13% 37% 3% 12%

29%

24% Quiñenco 37% 49% 23% 35%

20%

12% Average 29% 41% 16% 28%

10%

Median 36% 45% 9% 29%

0%

2012 2013 2014 2015 Source: IM Trust, Bloomberg and SVS. Data as of October 9, 2015

(1) The following was not considered in the analysis of the holdings: Pampa Calichera (parent company of SQM) and Invercap (parent company of CAP), due to recent great variation in market valuations (2) The current discount considers the discount as of the day of the announcement of the ED & F Man OPA by Empresas Iansa and Inversiones Campos Chilenos (June 22, 2015)

Strictly Private and Confidential 18

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

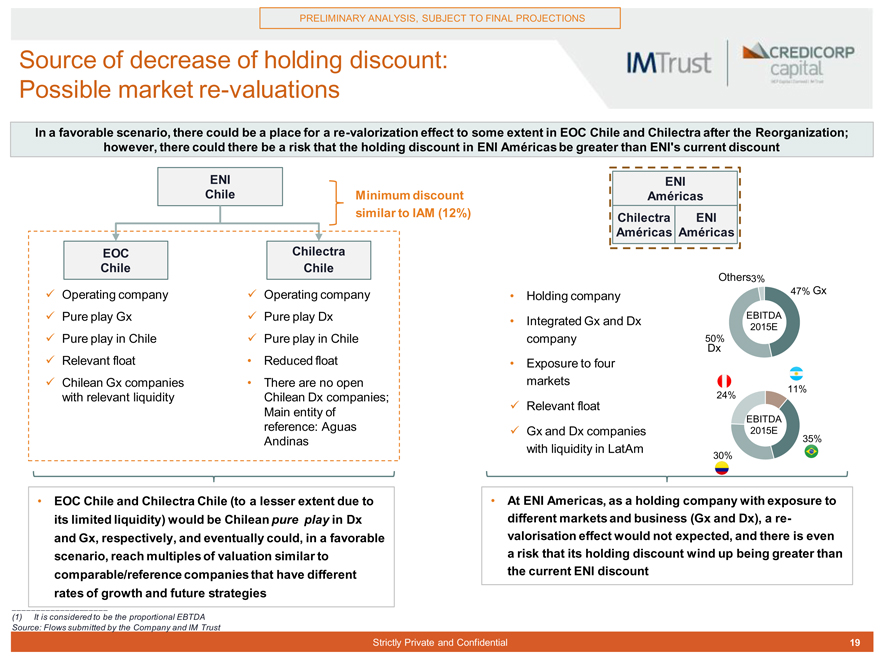

Source of decrease of holding discount: Possible market re-valuations

In a favorable scenario, there could be a place for a re-valorization effect to some extent in EOC Chile and Chilectra after the Reorganization; however, there could there be a risk that the holding discount in ENI Américas be greater than ENI’s current discount

ENI ENI Chile Minimum discount Américas similar to IAM (12%) Chilectra ENI

Américas Américas EOC Chilectra Chile Chile

Others3%

??Operating company ??Operating company Holding company 47% Gx ??Pure play Gx ??Pure play Dx Integrated Gx and Dx EBITDA

2015E

??Pure play in Chile ??Pure play in Chile company 50%

Dx

??Relevant float Reduced float Exposure to four ??Chilean Gx companies There are no open markets

11% with relevant liquidity Chilean Dx companies; 24% Main entity of ??Relevant float

EBITDA reference: Aguas ??Gx and Dx companies 2015E Andinas 35% with liquidity in LatAm

30%

EOC Chile and Chilectra Chile (to a lesser extent due to At ENI Americas, as a holding company with exposure to its limited liquidity) would be Chilean pure play in Dx different markets and business (Gx and Dx), a re-and Gx, respectively, and eventually could, in a favorable valorisation effect would not expected, and there is even scenario, reach multiples of valuation similar to a risk that its holding discount wind up being greater than comparable/reference companies that have different the current ENI discount rates of growth and future strategies

(1) |

| It is considered to be the proportional EBTDA Source: Flows submitted by the Company and IM Trust |

Strictly Private and Confidential 19

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

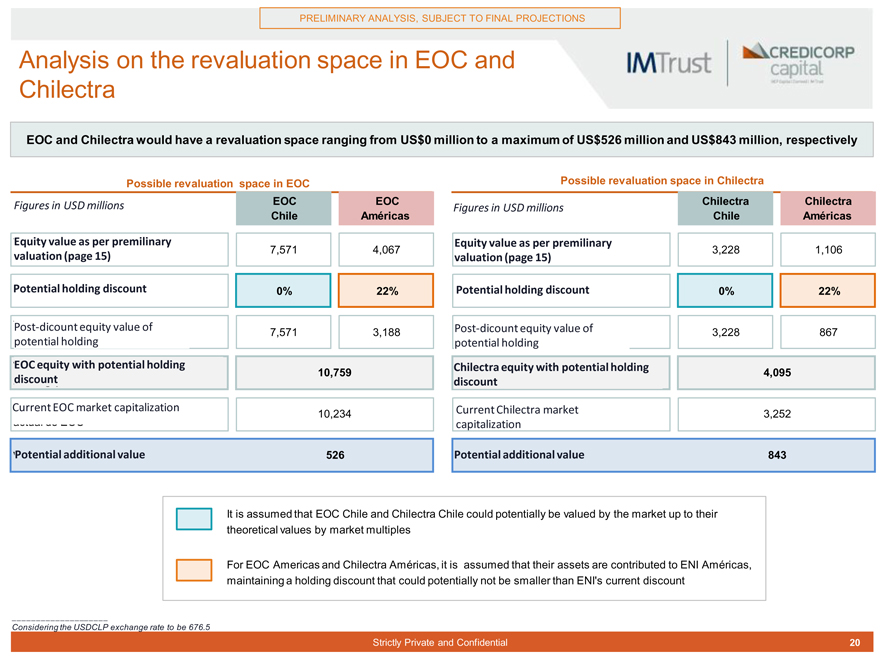

Analysis on the revaluation space in EOC and Chilectra

EOC and Chilectra would have a revaluation space ranging from US$0 million to a maximum of US$526 million and US$843 million, respectively

Possible revaluation space in EOC Possible revaluation space in Chilectra

Figures in USD millions EOC EOC Chilectra Chilectra

Figures in USD millions

Chile Américas Chile Américas

Equity value as per premilinary Equity value as per premilinary

7,571 4,067 3,228 1,106 valuation (page 15) valuation (page 15)

Potential holding discount 0% 22% Potential holding discount 0% 22%

Post-dicount equity value of Post-dicount equity value of

7,571 3,188 3,228 867 potential holding potential holding

EOC equity with potential holding Chilectra equity with potential holding

10,759 4,095 discount discount

Current EOC market capitalization Current Chilectra market

10,234 3,252 capitalization

Potential additional value 526 Potential additional value 843

It is assumed that EOC Chile and Chilectra Chile could potentially be valued by the market up to their theoretical values by market multiples

For EOC Americas and Chilectra Américas, it is assumed that their assets are contributed to ENI Américas, maintaining a holding discount that could potentially not be smaller than ENI’s current discount

Considering the USDCLP exchange rate to be 676.5

Strictly Private and Confidential 20

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

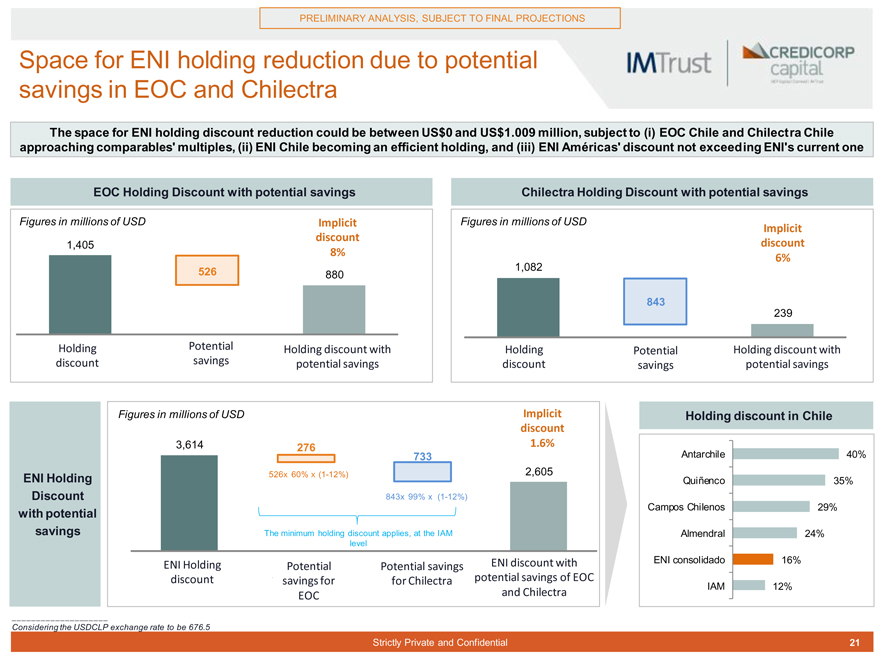

Space for ENI holding reduction due to potential savings in EOC and Chilectra

The space for ENI holding discount reduction could be between US$0 and US$1.009 million, subject to (i) EOC Chile and Chilectra Chile approaching comparables’ multiples, (ii) ENI Chile becoming an efficient holding, and (iii) ENI Américas’ discount not exceeding ENI’s current one

EOC Holding Discount with potential savings Chilectra Holding Discount with potential savings

Figures in millions of USD Implicit Figures in millions of USD

Implicit discount discount

1,405

8% 6%

526 1,082 880

843 239

Holding Potential Holding discount with Holding Potential Holding discount with discount savings potential savings discount savings potential savings

Figures in millions of USD Implicit Holding discount in Chile discount

3,614 276 1.6%

733 Antarchile 40%

526x 60% x (1-12%) 2,605

ENI Holding Quiñenco 35%

Discount 843x 99% x (1-12%) with potential Campos Chilenos 29% savings The minimum holding discount applies, at the IAM Almendral 24% level

ENI Holding ENI discount with ENI consolidado 16% Potential Potential savings discount savings for for Chilectra potential savings of EOC IAM and Chilectra 12% EOC

Considering the USDCLP exchange rate to be 676.5

Strictly Private and Confidential 21

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

STOCK IMPACTS OF THE REORGANIZATION AT

ENERSIS 3 iii. Liquidity Considerations

Strictly Private and Confidential 22

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

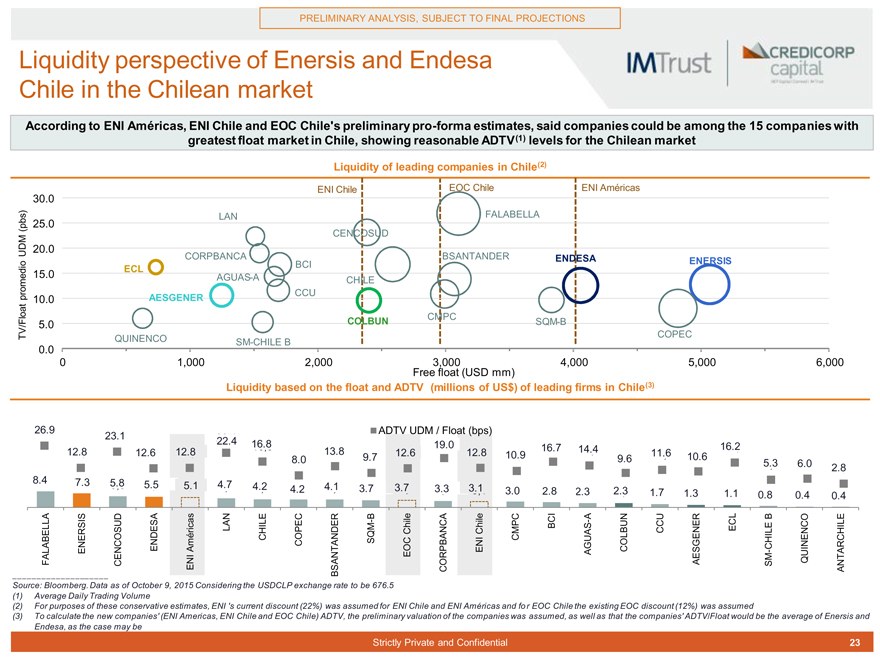

Liquidity perspective of Enersis and Endesa Chile in the Chilean market

According to ENI Américas, ENI Chile and EOC Chile’s preliminary pro-forma estimates, said companies could be among the 15 companies with greatest float market in Chile, showing reasonable ADTV(1) levels for the Chilean market

Liquidity of leading companies in Chile(2)

30.0 ENI Chile EOC Chile ENI Américas LAN FALABELLA

(pbs) 25.0

CENCOSUD

UDM 20.0

CORPBANCA BCI BSANTANDER ENDESA ENERSIS

15.0 ECL

AGUAS-A CHILE promedio AESGENER CCU

10.0

COLBUN CMPC

5.0 SQM-B

TV/Float QUINENCO COPEC SM-CHILE B

0.0

0 1,000 2,000 3,000 4,000 5,000 6,000 Free float (USD mm)

Liquidity based on the float and ADTV (millions of US$) of leading firms in Chile(3)

26, 26.9 ADTV UDM / Float (bps) 23. 23,1 1 22, 22.4

16. |

| 16,8 8 19. 19,0 16. 16,7 7 16.2 16,2 12.8 12,8 12.6 12,6 12.8 12,8 13.8 13, 12. 12,6 6 12.8 12,8 14.4 14,4 11.6 |

8.0 9.,7 7 10.9 10,9 9.6 ,6 11,6 10.6 10,

,0 5.3 ,3 6. 6,0 0

2.8 2,8 8.4 8,4 7.3 ,3 5.8 5.5 4.7

,8 5,5 5.1 ,1 4,7 4.2 4,2 4.2 ,2 4.1 4,1 3.7 3,7 3.7 3,7 3.3 3,3 3.1

3,1 3.0 3,0 2.8 2,8 2. 2,3 3 2.3 2,3 1.7 1,7 1.3 1,3 1.1 ,1 0.8 0,8 0.4 0,4 0.4 0,4

LAN B—Chile Chile BCI A—CCU ECL B ENDESA Américas CHILE COPEC SQM CMPC COLBUN CHILE

FALABELLA ENERSIS CENCOSUD EOC ENI AGUAS AESGENER—SM QUINENCO ENI BSANTANDER CORPBANCA ANTARCHILE

Source: Bloomberg. Data as of October 9, 2015 Considering the USDCLP exchange rate to be 676.5 (1) Average Daily Trading Volume

(2) For purposes of these conservative estimates, ENI ‘s current discount (22%) was assumed for ENI Chile and ENI Américas and for EOC Chile the existing EOC discount (12%) was assumed

(3) To calculate the new companies’ (ENI Americas, ENI Chile and EOC Chile) ADTV, the preliminary valuation of the companies was assumed, as well as that the companies’ ADTV/Float would be the average of Enersis and Endesa, as the case may be

Strictly Private and Confidential 23

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

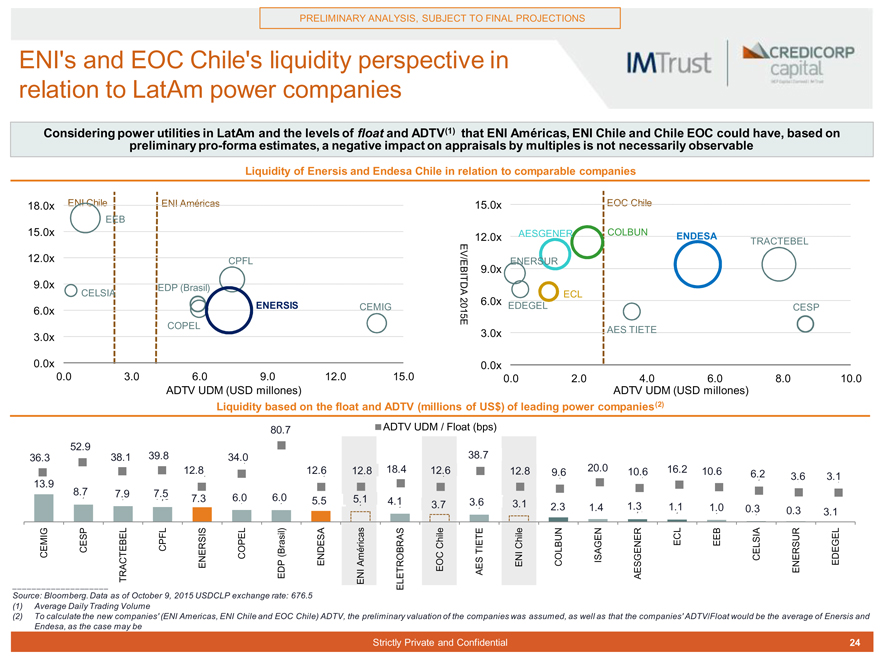

ENI’s and EOC Chile’s liquidity perspective in relation to LatAm power companies

Considering power utilities in LatAm and the levels of float and ADTV(1) that ENI Américas, ENI Chile and Chile EOC could have, based on preliminary pro-forma estimates, a negative impact on appraisals by multiples is not necessarily observable

Liquidity of Enersis and Endesa Chile in relation to comparable companies

18.0x ENI Chile ENI Américas 15.0x EOC Chile EEB

15.0x 12.0x AESGENER COLBUN ENDESA

TRACTEBEL 12.0x CPFL 9.0x ENERSUR

9.0x EDP (Brasil) EV/EBITDA

CELSIA ECL

ENERSIS 6.0x

6.0x CEMIG 2015E EDEGEL CESP COPEL 3.0x AES TIETE

3.0x

0.0x 0.0x

0.0 3.0 6.0 9.0 12.0 15.0 0.0 2.0 4.0 6.0 8.0 10.0 ADTV UDM (USD millones) ADTV UDM (USD millones)

Liquidity based on the float and ADTV (millions of US$) of leading power companies(2)

80. |

| 80,7 ADTV UDM / Float (bps) |

52. |

| 52,9 9 36. 36,3 3 38. 38,1 1 39. 39,8 8 34. 34,0 0 38. 38,7 7 |

12. |

| 12,8 8 12. 12,6 6 12, 12.8 18. 18,4 4 12. 12,6 12. 12,8 9.6 20. 20,0 0 10.6 16. 16,2 2 10. 12,1 6 |

13, 13.9 9,6 10,6 6. 6,2 2 3.,6 6 3. 3,1 1 8.7 8,7 7.9 ,9 7.5 7,5 7,3

7.3 6.0 6,0 6.0 6,0 5.5 5,5 5.1 ,1 4.1 3.6

4,1 3.7 ,7 3,6 3.1 ,1 2.,3 3 1. 1,4 4 1.3 1.1 1.0

1,3 1,1 ,0 0. 0,3 3 0. 0,3 3 3. 0,1 1

CPFL Chile Chile ECL EEB CESP TIETE

CEMIG ENERSIS COPEL(Brasil) ENDESA Américas ENI COLBUN ISAGEN CELSIA EDEGEL TRACTEBEL EDP ENI EOC AES AESGENER ENERSUR

ELETROBRAS Source: Bloomberg. Data as of October 9, 2015 USDCLP exchange rate: 676.5 (1) Average Daily Trading Volume

(2) To calculate the new companies’ (ENI Americas, ENI Chile and EOC Chile) ADTV, the preliminary valuation of the companies was assumed, as well as that the companies’ ADTV/Float would be the average of Enersis and Endesa, as the case may be

Strictly Private and Confidential 24

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

CASH FLOW IMPACTS OF THE REORGANIZATION

AT ENERSIS 4

Strictly Private and Confidential 25

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

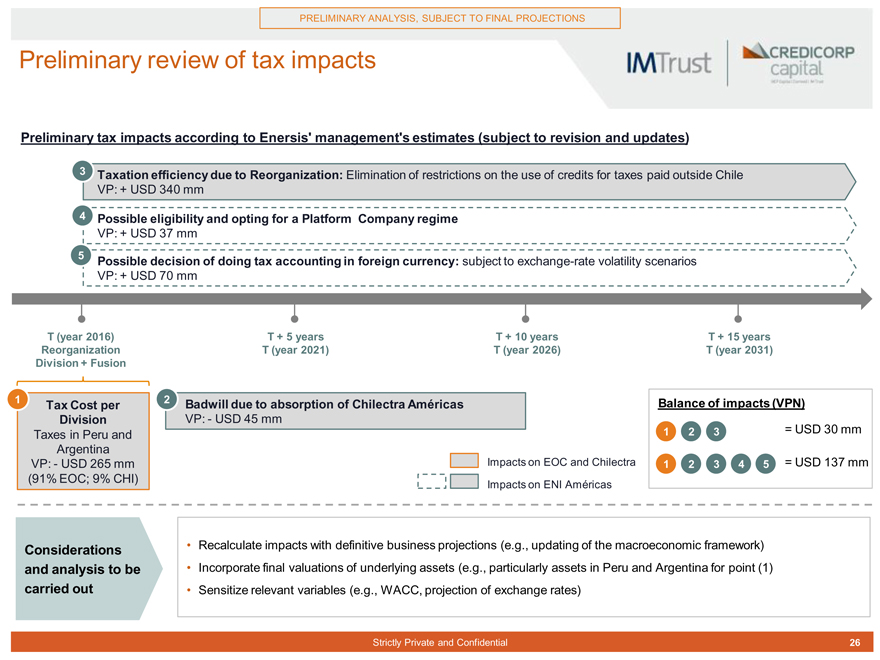

Preliminary review of tax impacts

Preliminary tax impacts according to Enersis’ management’s estimates (subject to revision and updates)

3 Taxation efficiency due to Reorganization: Elimination of restrictions on the use of credits for taxes paid outside Chile VP: + USD 340 mm

4 |

| Possible eligibility and opting for a Platform Company regime |

VP: + USD 37 mm

5 |

| Possible decision of doing tax accounting in foreign currency: subject to exchange-rate volatility scenarios |

VP: + USD 70 mm

T (year 2016) T + 5 years T + 10 years T + 15 years Reorganization T (year 2021) T (year 2026) T (year 2031) Division + Fusion

1 |

| Tax Cost per 2 Badwill due to absorption of Chilectra Américas Balance of impacts (VPN) |

Division VP:—USD 45 mm

Taxes in Peru and 1 2 3 = USD 30 mm Argentina

VP:—USD 265 mm Impacts on EOC and Chilectra 1 2 3 4 5 = USD 137 mm

(91% EOC; 9% CHI)

Impacts on ENI Américas

Considerations Recalculate impacts with definitive business projections (e.g., updating of the macroeconomic framework) and analysis to be Incorporate final valuations of underlying assets (e.g., particularly assets in Peru and Argentina for point (1) carried out Sensitize relevant variables (e.g., WACC, projection of exchange rates)

Strictly Private and Confidential 26

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

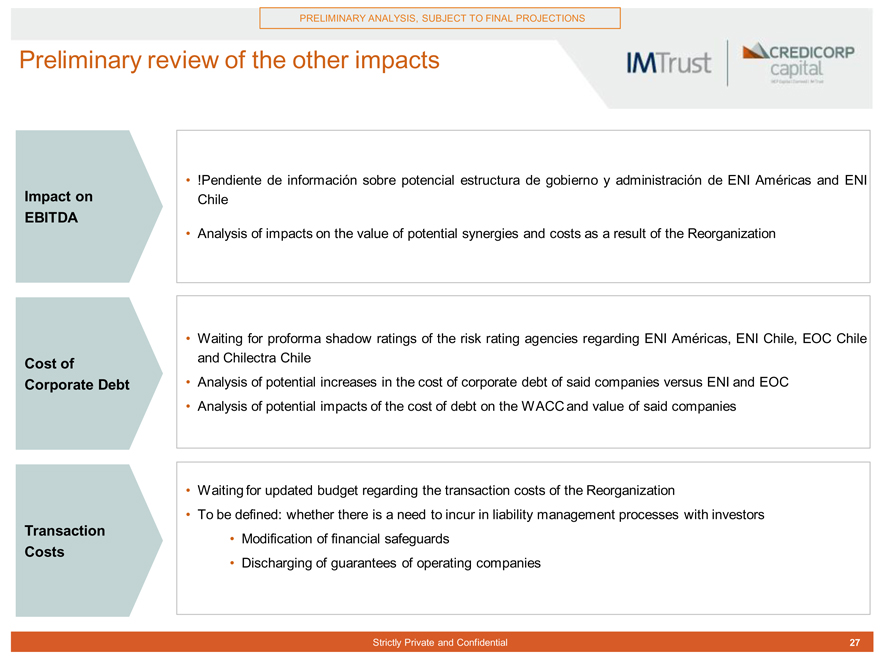

Preliminary review of the other impacts

!Pendiente de información sobre potencial estructura de gobierno y administración de ENI Américas and ENI

Impact on Chile EBITDA

Analysis of impacts on the value of potential synergies and costs as a result of the Reorganization

Waiting for proforma shadow ratings of the risk rating agencies regarding ENI Américas, ENI Chile, EOC Chile Cost of and Chilectra Chile Corporate Debt Analysis of potential increases in the cost of corporate debt of said companies versus ENI and EOC

Analysis of potential impacts of the cost of debt on the WACC and value of said companies

Waiting for updated budget regarding the transaction costs of the Reorganization

To be defined: whether there is a need to incur in liability management processes with investors

Transaction

Modification of financial safeguards

Costs

Discharging of guarantees of operating companies

Strictly Private and Confidential 27

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

CONCLUSIONS AND FURTHER STEPS 5

Strictly Private and Confidential 28

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

Conclusions

It is not yet possible to comment on the desirability of the Reorganization due to the lack of definitive projections and impacts of the transaction on Enersis’ cash flows

We understand that it is natural that the organizational structure model is a control tool of the controlling shareholder and industrialist

We don’t see a predominant organizational model among the main integrated electric power companies (business, geographical, mixed, etc.) Business Model Enel shows a preference for a business model that is organized mainly by geographical market Considerations From the point of view of simplification and discount reduction, the division of Chile is understandable, but the rationale of keeping the rest of the countries grouped is less self-evident

From the standpoint of market similarity and dynamics it could be logical to also separate Brazil or leave Chile, Peru and Colombia together

The idea that the Reorganization could contribute to a reduction in ENI’s holding discount has been raised

According to preliminary estimates, ENI’s holding discount is 22%, which is in line with other Chilean holdings

The main source of reduction of said discount could occur due to a possible revaluation of EOC Chile and Chilectra Chile when a strengthening

Differentiation of takes place of their status as pure-play operating companies in the Chilean Gx and Dx market, respectively

Business Models

& Our preliminary estimate is that said space of savings (expressed as a reduction of the of ENI’s holding discount) could be in the range of US$0-Simplification of the 1.009 million, which mainly depends on the following considerations:

Shareholder

That EOC Chile and Chilectra Chile reach the local comparable’s multiples that have different growth rates and strategies

Structure

That ENI Chile’s holding be very cost-effective and that cash flows from the subsidiaries be fully transferred to shareholders with an explicit dividend policy (such as IAM’s)

That ENI Américas’ discount does not wind up being greater than ENI’s current discount (22%)

While ENI Americas, ENI Chile and EOC Chile would have a stock market capitalization and flotation lower than those of ENI and EOC, as the case may be, its size and level of flotation should be in the upper range of companies listed in Chile with levels of liquidity also in the upper

Liquidity range

Based on quotes from electric power utilities in LatAm, there is no evidence that the possible lower liquidity of the new corporations can necessarily generate a significant impact on their value

The impact on cash flow (in EBITDA, cost of debt, tax issues, and the transaction costs) will be relevant in the analysis of the Reorganization Cash Flow Factors and might affect the exchange rates of the merger and/or potential trade-offs between ENI, EOC and Chilectra

To date, we are waiting for final estimates by ENI, to be reviewed and incorporated into our analysis

Strictly Private and Confidential 29

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

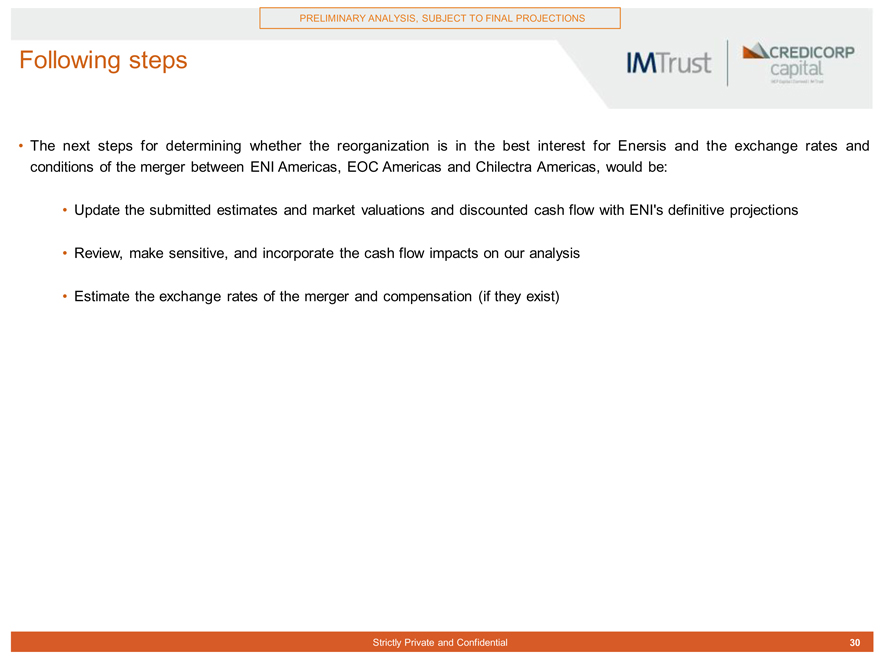

Following steps

The next steps for determining whether the reorganization is in the best interest for Enersis and the exchange rates and conditions of the merger between ENI Americas, EOC Americas and Chilectra Americas, would be:

Update the submitted estimates and market valuations and discounted cash flow with ENI’s definitive projections

Review, make sensitive, and incorporate the cash flow impacts on our analysis

Estimate the exchange rates of the merger and compensation (if they exist)

Strictly Private and Confidential 30

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

ATTACHMENTS 6

Strictly Private and Confidential 31

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

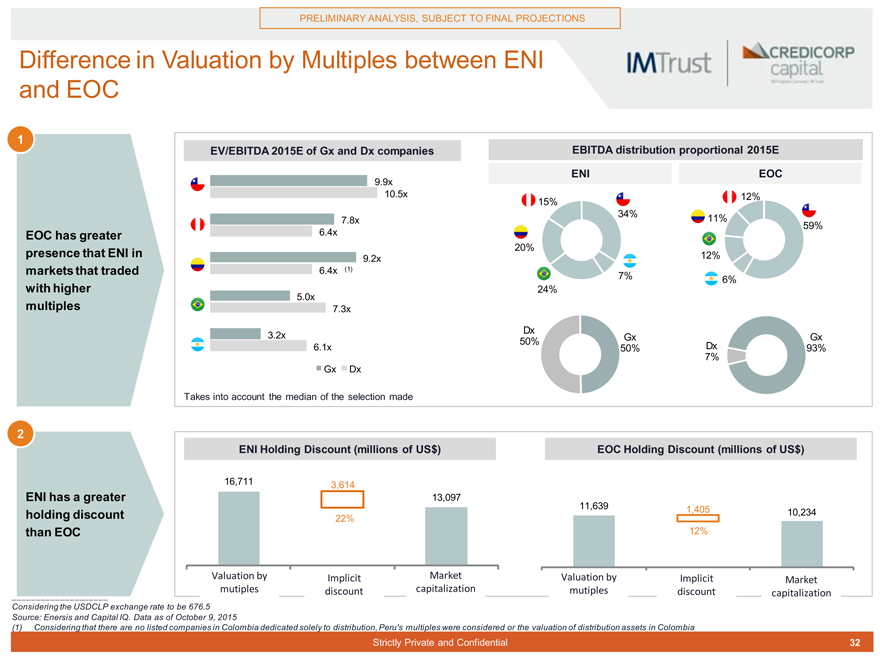

Difference in Valuation by Multiples between ENI and EOC

1 |

|

EV/EBITDA 2015E of Gx and Dx companies EBITDA distribution proportional 2015E ENI EOC

9.9x

10.5x 12% 15% 34% 11%

7.8x

59%

EOC has greater 6.4x presence that ENI in 20%

9.2x 12% markets that traded 6.4x (1)

7% 6% with higher 24%

5.0x multiples 7.3x

3.2x Dx

50% Gx Gx 6.1x 50% Dx 93% 7%

Gx Dx

Takes into account the median of the selection made

2 |

|

ENI Holding Discount (millions of US$) EOC Holding Discount (millions of US$)

16,711 3,614

ENI has a greater 13,097

11,639 1,405 holding discount 10,234

22% than EOC 12%

Valuation by Implicit Market Valuation by Implicit Market mutiples discount capitalization mutiples discount capitalization

Considering the USDCLP exchange rate to be 676.5 Source: Enersis and Capital IQ. Data as of October 9, 2015

(1) Considering that there are no listed companies in Colombia dedicated solely to distribution, Peru’s multiples were considered or the valuation of distribution assets in Colombia

Strictly Private and Confidential 32

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

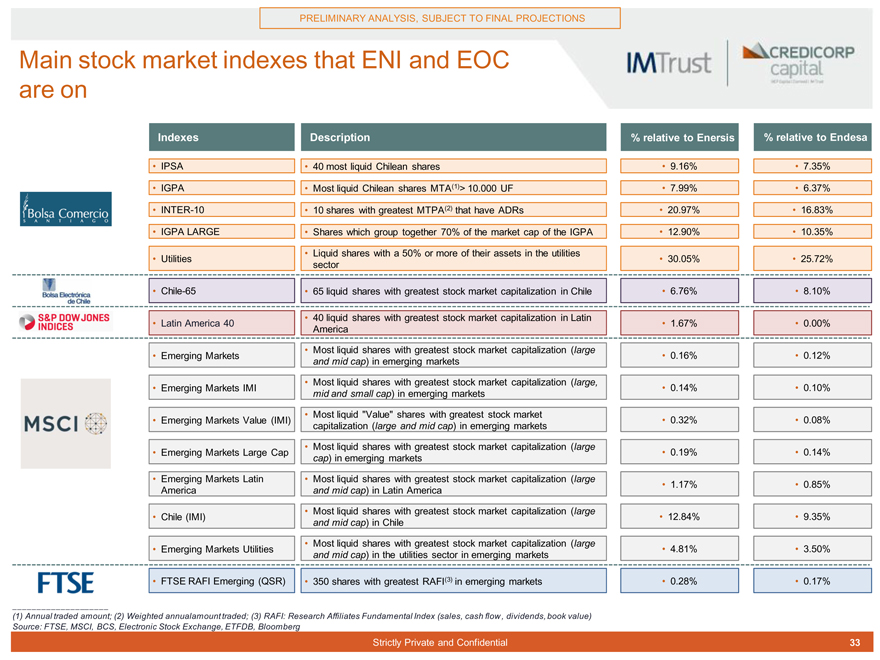

Main stock market indexes that ENI and EOC are on

Indexes Description % relative to Enersis % relative to Endesa

IPSA 40 most liquid Chilean shares 9.16% 7.35%

IGPA Most liquid Chilean shares MTA(1)> 10.000 UF 7.99% 6.37%

INTER-10 10 shares with greatest MTPA(2) that have ADRs 20.97% 16.83%

IGPA LARGE Shares which group together 70% of the market cap of the IGPA 12.90% 10.35%

Liquid shares with a 50% or more of their assets in the utilities

Utilities 30.05% 25.72% sector

Chile-65 65 liquid shares with greatest stock market capitalization in Chile 6.76% 8.10%

40 liquid shares with greatest stock market capitalization in Latin

Latin America 40 1.67% 0.00% America

Most liquid shares with greatest stock market capitalization (large

Emerging Markets 0.16% 0.12% and mid cap) in emerging markets

Most liquid shares with greatest stock market capitalization (large,

Emerging Markets IMI 0.14% 0.10% mid and small cap) in emerging markets

Most liquid “Value” shares with greatest stock market

Emerging Markets Value (IMI) 0.32% 0.08% capitalization (large and mid cap) in emerging markets

Most liquid shares with greatest stock market capitalization (large

Emerging Markets Large Cap 0.19% 0.14% cap) in emerging markets

Emerging Markets Latin Most liquid shares with greatest stock market capitalization (large

1.17% 0.85% America and mid cap) in Latin America

Most liquid shares with greatest stock market capitalization (large

Chile (IMI) 12.84% 9.35% and mid cap) in Chile

Most liquid shares with greatest stock market capitalization (large

Emerging Markets Utilities 4.81% 3.50% and mid cap) in the utilities sector in emerging markets

FTSE RAFI Emerging (QSR) 350 shares with greatest RAFI(3) in emerging markets 0.28% 0.17%

(1) Annual traded amount; (2) Weighted annualamount traded; (3) RAFI: Research Affiliates Fundamental Index (sales, cash flow, dividends, book value) Source: FTSE, MSCI, BCS, Electronic Stock Exchange, ETFDB, Bloomberg

Strictly Private and Confidential 33

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

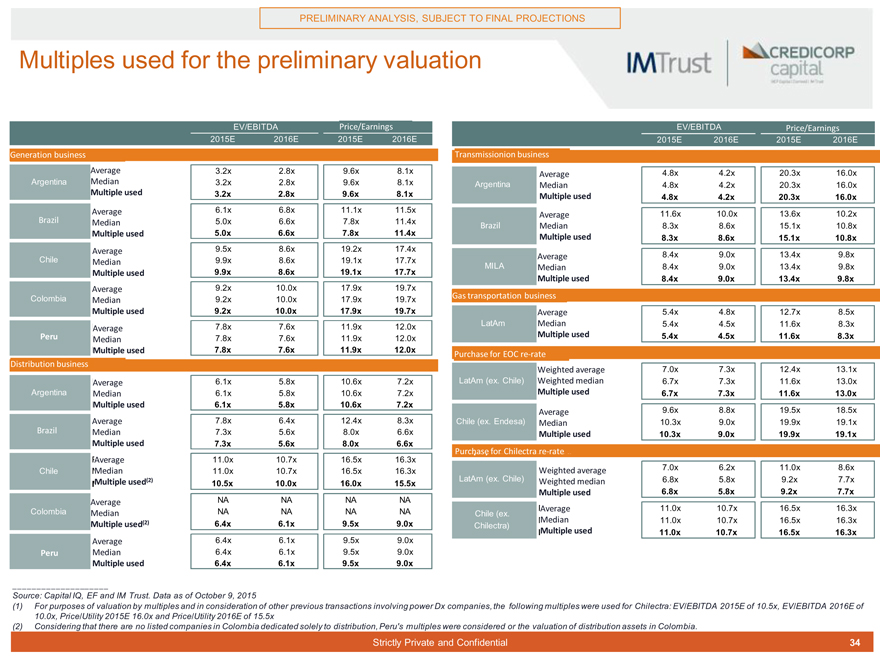

Multiples used for the preliminary valuation

EV/EBITDA Price/Earnings Precio/Utilidad EV/EBITDA Price/Earnings Precio/Utilidad 2015E 2016E 2015E 2016E 2015E 2016E 2015E 2016E

Generation Negoc o de business ge ración Negocio Transmissionion de transmisión business

Average 3.2x 2.8x 9.6x 8.1x Average 4.8x 4.2x 20.3x 16.0x Argentina Median 3.2x 2.8x 9.6x 8.1x Argentina Median 4.8x 4.2x 20.3x 16.0x

Multiple used 3.2x 2.8x 9.6x 8.1x Multiple used

4.8x 4.2x 20.3x 16.0x

Average 6.1x 6.8x 11.1x 11.5x 11.6x 10.0x 13.6x 10.2x

Average

Brazil Median 5.0x 6.6x 7.8x 11.4x

Brazil Median 8.3x 8.6x 15.1x 10.8x

Multiple used 5.0x 6.6x 7.8x 11.4x Multiple used

8.3x 8.6x 15.1x 10.8x

Average 9.5x 8.6x 19.2x 17.4x

Average 8.4x 9.0x 13.4x 9.8x Chile Median 9.9x 8.6x 19.1x 17.7x MILA Median 8.4x 9.0x 13.4x 9.8x

Multiple used 9.9x 8.6x 19.1x 17.7x

Multiple used 8.4x 9.0x 13.4x 9.8x

Average 9.2x 10.0x 17.9x 19.7x

Colombia 9.2x 10.0x 17.9x 19.7x Gas Negocio transportation t ansp rte business de gas

Median

Multiple used 9.2x 10.0x 17.9x 19.7x Average 5.4x 4.8x 12.7x 8.5x

7.8x 7.6x 11.9x 12.0x LatAm Median 5.4x 4.5x 11.6x 8.3x

Average

Peru 7.8x 7.6x 11.9x 12.0x Multiple used 5.4x 4.5x 11.6x 8.3x

Median

Multiple used 7.8x 7.6x 11.9x 12.0x Purchase Comp para for EOC re-rate re-rate EOC

Distribution Negocio de business distribución

Weighted average 7.0x 7.3x 12.4x 13.1x Average 6.1x 5.8x 10.6x 7.2x LatAm (ex. Chile) Weighted median 6.7x 7.3x 11.6x 13.0x Argentina Median 6.1x 5.8x 10.6x 7.2x Multiple used 6.7x 7.3x 11.6x 13.0x

Multiple used 6.1x 5.8x 10.6x 7.2x

Average 9.6x 8.8x 19.5x 18.5x Average 7.8x 6.4x 12.4x 8.3x Chile (ex. Endesa) Median 10.3x 9.0x 19.9x 19.1x

Brazil Median 7.3x 5.6x 8.0x 6.6x Multiple used 10.3x 9.0x 19.9x 19.1x Multiple used 7.3x 5.6x 8.0x 6.6x

Average 11.0x 10.7x 16.5x 16.3x Comps Purchase para for Chilectra re-rate Chilectra re-rate

Chile Median 11.0x 10.7x 16.5x 16.3x Weighted average 7.0x 6.2x 11.0x 8.6x Multiple used(2) LatAm (ex. Chile) Weighted median 6.8x 5.8x 9.2x 7.7x

10.5x 10.0x 16.0x 15.5x Multiple used 6.8x 5.8x 9.2x 7.7x

Average NA NA NA NA Average 11.0x 10.7x 16.5x 16.3x Colombia Median NA NA NA NA Chile (ex.

(2) |

| Median 11.0x 10.7x 16.5x 16.3x |

Multiple used 6.4x 6.1x 9.5x 9.0x Chilectra)

Multiple used 11.0x 10.7x 16.5x 16.3x

Average 6.4x 6.1x 9.5x 9.0x Peru Median 6.4x 6.1x 9.5x 9.0x

Multiple used 6.4x 6.1x 9.5x 9.0x

Source: Capital IQ, EF and IM Trust. Data as of October 9, 2015

(1) For purposes of valuation by multiples and in consideration of other previous transactions involving power Dx companies, the following multiples were used for Chilectra: EV/EBITDA 2015E of 10.5x, EV/EBITDA 2016E of 10.0x, Price/Utility 2015E 16.0x and Price/Utility 2016E of 15.5x (2) Considering that there are no listed companies in Colombia dedicated solely to distribution, Peru’s multiples were considered or the valuation of distribution assets in Colombia.

Strictly Private and Confidential 34

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

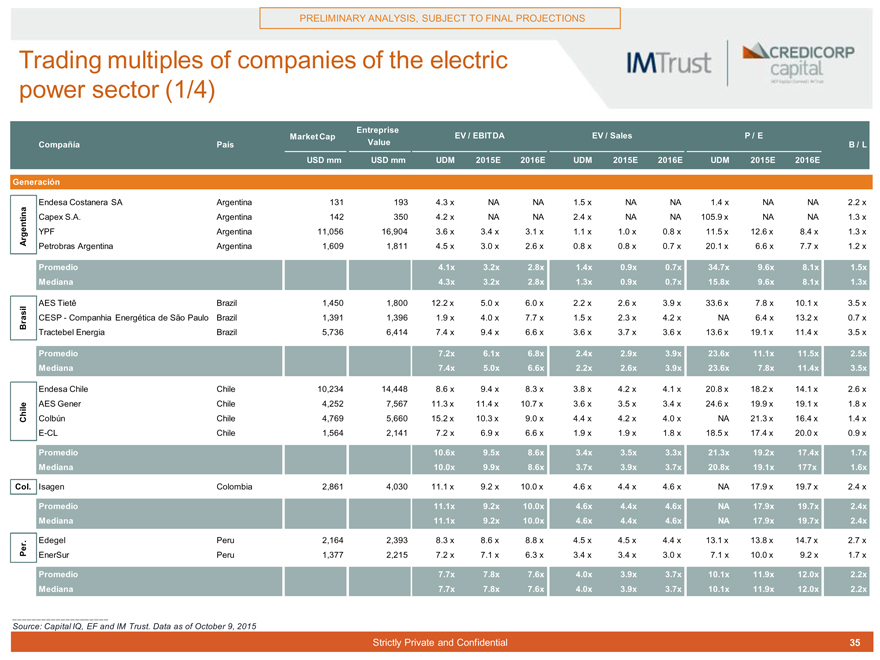

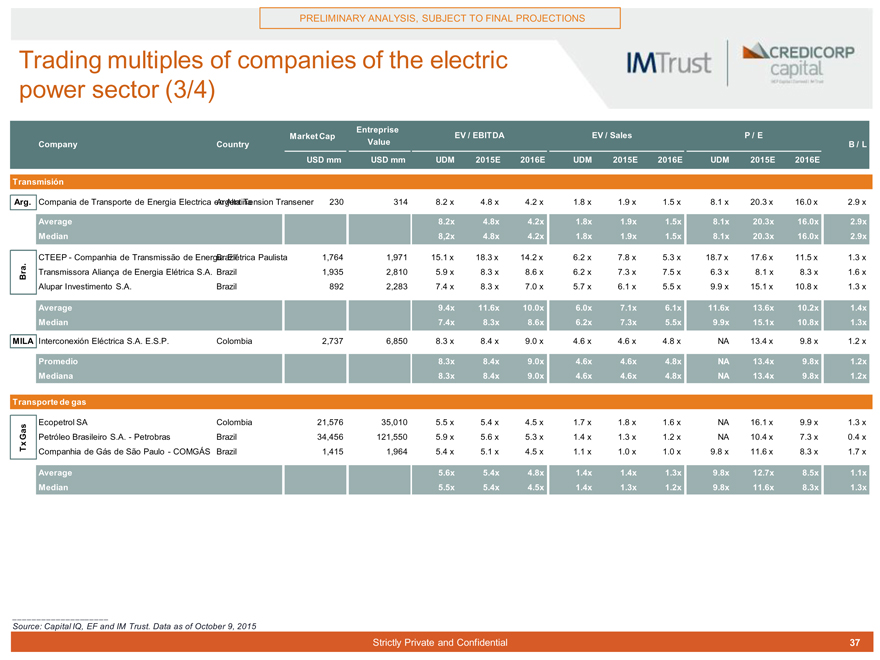

Trading multiples of companies of the electric power sector (1/4)

Entreprise

Market Cap EV / EBITDA EV / Sales P / E

Compañía País Value B / L USD mm USD mm UDM 2015E 2016E UDM 2015E 2016E UDM 2015E 2016E

Generación

Endesa Costanera SA Argentina 131 193 4.3 x NA NA 1.5 x NA NA 1.4 x NA NA 2.2 x Capex S.A. Argentina 142 350 4.2 x NA NA 2.4 x NA NA 105.9 x NA NA 1.3 x Argentina YPF Argentina 11,056 16,904 3.6 x 3.4 x 3.1 x 1.1 x 1.0 x 0.8 x 11.5 x 12.6 x 8.4 x 1.3 x Petrobras Argentina Argentina 1,609 1,811 4.5 x 3.0 x 2.6 x 0.8 x 0.8 x 0.7 x 20.1 x 6.6 x 7.7 x 1.2 x

Promedio 4.1x 3.2x 2.8x 1.4x 0.9x 0.7x 34.7x 9.6x 8.1x 1.5x Mediana 4.3x 3.2x 2.8x 1.3x 0.9x 0.7x 15.8x 9.6x 8.1x 1.3x

AES Tietê Brazil 1,450 1,800 12.2 x 5.0 x 6.0 x 2.2 x 2.6 x 3.9 x 33.6 x 7.8 x 10.1 x 3.5 x Brasil CESP—Companhia Energética de São Paulo Brazil 1,391 1,396 1.9 x 4.0 x 7.7 x 1.5 x 2.3 x 4.2 x NA 6.4 x 13.2 x 0.7 x Tractebel Energia Brazil 5,736 6,414 7.4 x 9.4 x 6.6 x 3.6 x 3.7 x 3.6 x 13.6 x 19.1 x 11.4 x 3.5 x

Promedio 7.2x 6.1x 6.8x 2.4x 2.9x 3.9x 23.6x 11.1x 11.5x 2.5x Mediana 7.4x 5.0x 6.6x 2.2x 2.6x 3.9x 23.6x 7.8x 11.4x 3.5x

Endesa Chile Chile 10,234 14,448 8.6 x 9.4 x 8.3 x 3.8 x 4.2 x 4.1 x 20.8 x 18.2 x 14.1 x 2.6 x AES Gener Chile 4,252 7,567 11.3 x 11.4 x 10.7 x 3.6 x 3.5 x 3.4 x 24.6 x 19.9 x 19.1 x 1.8 x Chile Colbún Chile 4,769 5,660 15.2 x 10.3 x 9.0 x 4.4 x 4.2 x 4.0 x NA 21.3 x 16.4 x 1.4 x E-CL Chile 1,564 2,141 7.2 x 6.9 x 6.6 x 1.9 x 1.9 x 1.8 x 18.5 x 17.4 x 20.0 x 0.9 x

Promedio 10.6x 9.5x 8.6x 3.4x 3.5x 3.3x 21.3x 19.2x 17.4x 1.7x Mediana 10.0x 9.9x 8.6x 3.7x 3.9x 3.7x 20.8x 19.1x 177x 1.6x

Col. Isagen Colombia 2,861 4,030 11.1 x 9.2 x 10.0 x 4.6 x 4.4 x 4.6 x NA 17.9 x 19.7 x 2.4 x

Promedio 11.1x 9.2x 10.0x 4.6x 4.4x 4.6x NA 17.9x 19.7x 2.4x Mediana 11.1x 9.2x 10.0x 4.6x 4.4x 4.6x NA 17.9x 19.7x 2.4x

Per. Edegel Peru 2,164 2,393 8.3 x 8.6 x 8.8 x 4.5 x 4.5 x 4.4 x 13.1 x 13.8 x 14.7 x 2.7 x EnerSur Peru 1,377 2,215 7.2 x 7.1 x 6.3 x 3.4 x 3.4 x 3.0 x 7.1 x 10.0 x 9.2 x 1.7 x

Promedio 7.7x 7.8x 7.6x 4.0x 3.9x 3.7x 10.1x 11.9x 12.0x 2.2x Mediana 7.7x 7.8x 7.6x 4.0x 3.9x 3.7x 10.1x 11.9x 12.0x 2.2x

Source: Capital IQ, EF and IM Trust. Data as of October 9, 2015

Strictly Private and Confidential 35

|

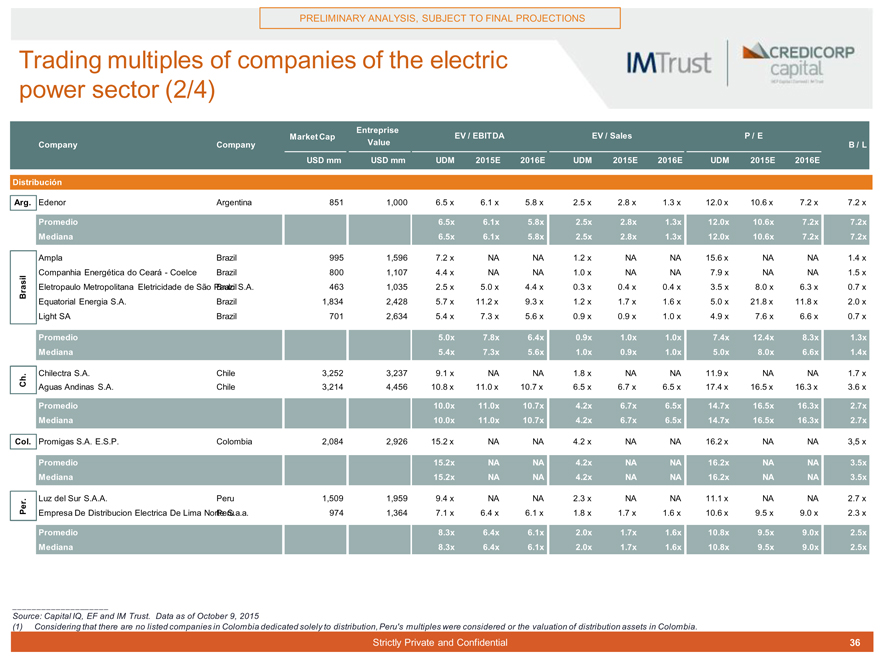

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

Trading multiples of companies of the electric power sector (2/4)

Entreprise

Market Cap EV / EBITDA EV / Sales P / E

Company Company Value B / L USD mm USD mm UDM 2015E 2016E UDM 2015E 2016E UDM 2015E 2016E

Distribución

Arg. Edenor Argentina 851 1,000 6.5 x 6.1 x 5.8 x 2.5 x 2.8 x 1.3 x 12.0 x 10.6 x 7.2 x 7.2 x

Promedio 6.5x 6.1x 5.8x 2.5x 2.8x 1.3x 12.0x 10.6x 7.2x 7.2x Mediana 6.5x 6.1x 5.8x 2.5x 2.8x 1.3x 12.0x 10.6x 7.2x 7.2x

Ampla Brazil 995 1,596 7.2 x NA NA 1.2 x NA NA 15.6 x NA NA 1.4 x Companhia Energética do Ceará—Coelce Brazil 800 1,107 4.4 x NA NA 1.0 x NA NA 7.9 x NA NA 1.5 x Brasil Eletropaulo Metropolitana Eletricidade de São Paulo Brazil S.A. 463 1,035 2.5 x 5.0 x 4.4 x 0.3 x 0.4 x 0.4 x 3.5 x 8.0 x 6.3 x 0.7 x Equatorial Energia S.A. Brazil 1,834 2,428 5.7 x 11.2 x 9.3 x 1.2 x 1.7 x 1.6 x 5.0 x 21.8 x 11.8 x 2.0 x Light SA Brazil 701 2,634 5.4 x 7.3 x 5.6 x 0.9 x 0.9 x 1.0 x 4.9 x 7.6 x 6.6 x 0.7 x

Promedio 5.0x 7.8x 6.4x 0.9x 1.0x 1.0x 7.4x 12.4x 8.3x 1.3x Mediana 5.4x 7.3x 5.6x 1.0x 0.9x 1.0x 5.0x 8.0x 6.6x 1.4x

Ch. Chilectra S.A. Chile 3,252 3,237 9.1 x NA NA 1.8 x NA NA 11.9 x NA NA 1.7 x Aguas Andinas S.A. Chile 3,214 4,456 10.8 x 11.0 x 10.7 x 6.5 x 6.7 x 6.5 x 17.4 x 16.5 x 16.3 x 3.6 x

Promedio 10.0x 11.0x 10.7x 4.2x 6.7x 6.5x 14.7x 16.5x 16.3x 2.7x Mediana 10.0x 11.0x 10.7x 4.2x 6.7x 6.5x 14.7x 16.5x 16.3x 2.7x

Col. Promigas S.A. E.S.P. Colombia 2,084 2,926 15.2 x NA NA 4.2 x NA NA 16.2 x NA NA 3,5 x

Promedio 15.2x NA NA 4.2x NA NA 16.2x NA NA 3.5x Mediana 15.2x NA NA 4.2x NA NA 16.2x NA NA 3.5x

Per. Luz del Sur S.A.A. Peru 1,509 1,959 9.4 x NA NA 2.3 x NA NA 11.1 x NA NA 2.7 x Empresa De Distribucion Electrica De Lima Nort Peru S. a.a. 974 1,364 7.1 x 6.4 x 6.1 x 1.8 x 1.7 x 1.6 x 10.6 x 9.5 x 9.0 x 2.3 x

Promedio 8.3x 6.4x 6.1x 2.0x 1.7x 1.6x 10.8x 9.5x 9.0x 2.5x Mediana 8.3x 6.4x 6.1x 2.0x 1.7x 1.6x 10.8x 9.5x 9.0x 2.5x

Source: Capital IQ, EF and IM Trust. Data as of October 9, 2015

(1) Considering that there are no listed companies in Colombia dedicated solely to distribution, Peru’s multiples were considered or the valuation of distribution assets in Colombia.

Strictly Private and Confidential 36

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

Trading multiples of companies of the electric power sector (3/4)

Entreprise

Market Cap EV / EBITDA EV / Sales P / E

Company Country Value B / L USD mm USD mm UDM 2015E 2016E UDM 2015E 2016E UDM 2015E 2016E

Transmisión

Arg. Compania de Transporte de Energia Electrica en Argentina Al a Tension Transener 230 314 8.2 x 4.8 x 4.2 x 1.8 x 1.9 x 1.5 x 8.1 x 20.3 x 16.0 x 2.9 x

Average 8.2x 4.8x 4.2x 1.8x 1.9x 1.5x 8.1x 20.3x 16.0x 2.9x Median 8,2x 4.8x 4.2x 1.8x 1.9x 1.5x 8.1x 20.3x 16.0x 2.9x

CTEEP—Companhia de Transmissão de Energia Brazil Elétrica Paulista 1,764 1,971 15.1 x 18.3 x 14.2 x 6.2 x 7.8 x 5.3 x 18.7 x 17.6 x 11.5 x 1.3 x Bra. Transmissora Aliança de Energia Elétrica S.A. Brazil 1,935 2,810 5.9 x 8.3 x 8.6 x 6.2 x 7.3 x 7.5 x 6.3 x 8.1 x 8.3 x 1.6 x Alupar Investimento S.A. Brazil 892 2,283 7.4 x 8.3 x 7.0 x 5.7 x 6.1 x 5.5 x 9.9 x 15.1 x 10.8 x 1.3 x

Average 9.4x 11.6x 10.0x 6.0x 7.1x 6.1x 11.6x 13.6x 10.2x 1.4x Median 7.4x 8.3x 8.6x 6.2x 7.3x 5.5x 9.9x 15.1x 10.8x 1.3x

MILA Interconexión Eléctrica S.A. E.S.P. Colombia 2,737 6,850 8.3 x 8.4 x 9.0 x 4.6 x 4.6 x 4.8 x NA 13.4 x 9.8 x 1.2 x

Promedio 8.3x 8.4x 9.0x 4.6x 4.6x 4.8x NA 13.4x 9.8x 1.2x Mediana 8.3x 8.4x 9.0x 4.6x 4.6x 4.8x NA 13.4x 9.8x 1.2x

Transporte de gas

Gas Ecopetrol SA Colombia 21,576 35,010 5.5 x 5.4 x 4.5 x 1.7 x 1.8 x 1.6 x NA 16.1 x 9.9 x 1.3 x Petróleo Brasileiro S.A.—Petrobras Brazil 34,456 121,550 5.9 x 5.6 x 5.3 x 1.4 x 1.3 x 1.2 x NA 10.4 x 7.3 x 0.4 x Tx Companhia de Gás de São Paulo—COMGÁS Brazil 1,415 1,964 5.4 x 5.1 x 4.5 x 1.1 x 1.0 x 1.0 x 9.8 x 11.6 x 8.3 x 1.7 x

Average 5.6x 5.4x 4.8x 1.4x 1.4x 1.3x 9.8x 12.7x 8.5x 1.1x Median 5.5x 5.4x 4.5x 1.4x 1.3x 1.2x 9.8x 11.6x 8.3x 1.3x

Source: Capital IQ, EF and IM Trust. Data as of October 9, 2015

Strictly Private and Confidential 37

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

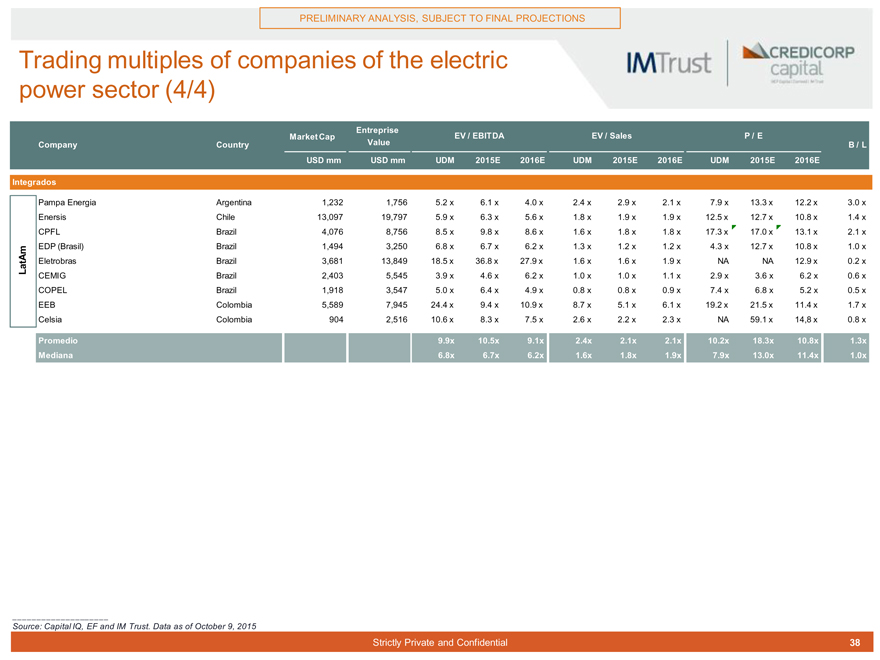

Trading multiples of companies of the electric power sector (4/4)

Entreprise

Market Cap EV / EBITDA EV / Sales P / E

Company Country Value B / L USD mm USD mm UDM 2015E 2016E UDM 2015E 2016E UDM 2015E 2016E

Integrados

Pampa Energia Argentina 1,232 1,756 5.2 x 6.1 x 4.0 x 2.4 x 2.9 x 2.1 x 7.9 x 13.3 x 12.2 x 3.0 x Enersis Chile 13,097 19,797 5.9 x 6.3 x 5.6 x 1.8 x 1.9 x 1.9 x 12.5 x 12.7 x 10.8 x 1.4 x CPFL Brazil 4,076 8,756 8.5 x 9.8 x 8.6 x 1.6 x 1.8 x 1.8 x 17.3 x 17.0 x 13.1 x 2.1 x EDP (Brasil) Brazil 1,494 3,250 6.8 x 6.7 x 6.2 x 1.3 x 1.2 x 1.2 x 4.3 x 12.7 x 10.8 x 1.0 x LatAm Eletrobras Brazil 3,681 13,849 18.5 x 36.8 x 27.9 x 1.6 x 1.6 x 1.9 x NA NA 12.9 x 0.2 x CEMIG Brazil 2,403 5,545 3.9 x 4.6 x 6.2 x 1.0 x 1.0 x 1.1 x 2.9 x 3.6 x 6.2 x 0.6 x COPEL Brazil 1,918 3,547 5.0 x 6.4 x 4.9 x 0.8 x 0.8 x 0.9 x 7.4 x 6.8 x 5.2 x 0.5 x EEB Colombia 5,589 7,945 24.4 x 9.4 x 10.9 x 8.7 x 5.1 x 6.1 x 19.2 x 21.5 x 11.4 x 1.7 x Celsia Colombia 904 2,516 10.6 x 8.3 x 7.5 x 2.6 x 2.2 x 2.3 x NA 59.1 x 14,8 x 0.8 x

Promedio 9.9x 10.5x 9.1x 2.4x 2.1x 2.1x 10.2x 18.3x 10.8x 1.3x Mediana 6.8x 6.7x 6.2x 1.6x 1.8x 1.9x 7.9x 13.0x 11.4x 1.0x

Source: Capital IQ, EF and IM Trust. Data as of October 9, 2015

Strictly Private and Confidential 38

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

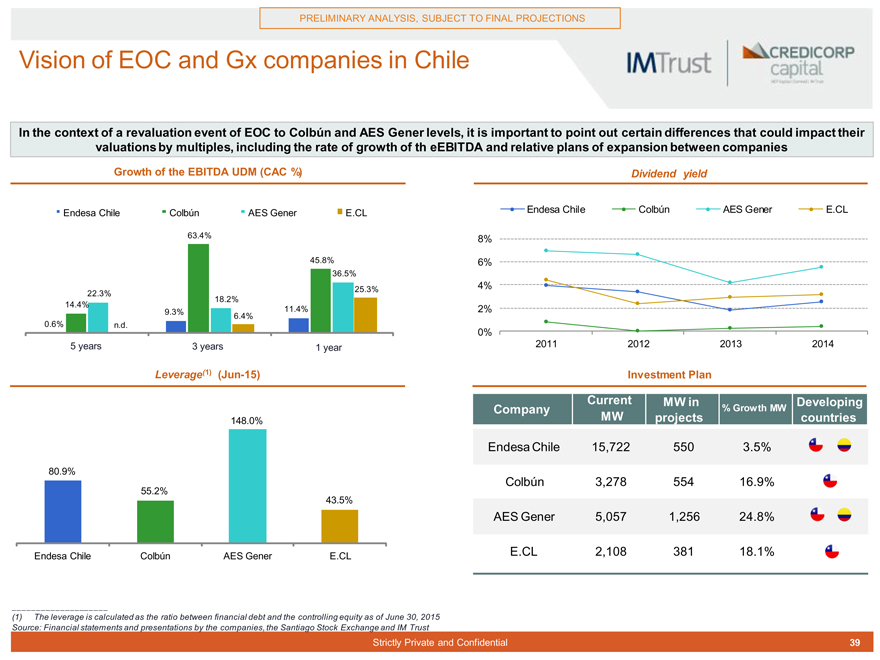

Vision of EOC and Gx companies in Chile

In the context of a revaluation event of EOC to Colbún and AES Gener levels, it is important to point out certain differences that could impact their valuations by multiples, including the rate of growth of th eEBITDA and relative plans of expansion between companies

Growth of the EBITDA UDM (CAC %) Dividend yield

Endesa Chile Colbún AES Gener E.CL Endesa Chile Colbún AES Gener E.CL

63.4% 8% 45.8% 6% 36.5% 25.3% 4% 22.3% 18.2% 14.4% 2% 9.3% 11.4% 0.6% n.d. 6.4%

0%

55 years años 33 years años 11 year año 2011 2012 2013 2014

Leverage(1) (Jun-15) Investment Plan

Current MW in Developing

Company % Growth MW

148.0% MW projects countries

Endesa Chile 15,722 550 3.5%

80.9%

Colbún 3,278 554 16.9%

55.2%

43.5%

AES Gener 5,057 1,256 24.8%

Endesa Chile Colbún AES Gener E.CL E.CL 2,108 381 18.1%

(1) The leverage is calculated as the ratio between financial debt and the controlling equity as of June 30, 2015 Source: Financial statements and presentations by the companies, the Santiago Stock Exchange and IM Trust

Strictly Private and Confidential 39

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

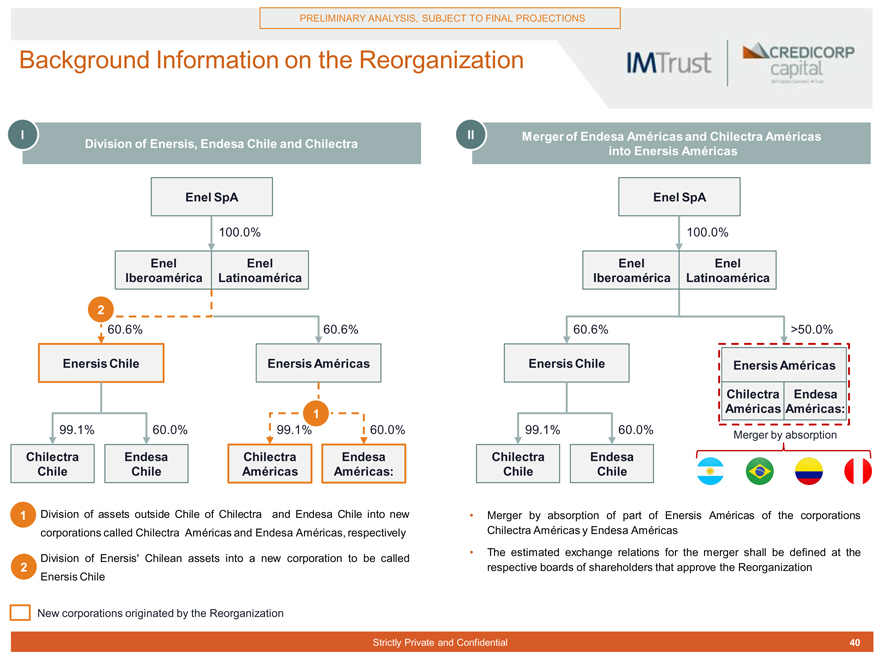

Background Information on the Reorganization

I II Merger of Endesa Américas and Chilectra Américas Division of Enersis, Endesa Chile and Chilectra into Enersis Américas

Enel SpA Enel SpA

100.0% 100.0%

Enel Enel Enel Enel Iberoamérica Latinoamérica Iberoamérica Latinoamérica

2 |

|

60.6% 60.6% 60.6% >50.0%

Enersis Chile Enersis Américas Enersis Chile Enersis Américas Chilectra Endesa

1 |

| Américas Américas: |

99.1% 60.0% 99.1% 60.0% 99.1% 60.0% Merger by absorption

Chilectra Endesa Chilectra Endesa Chilectra Endesa Chile Chile Américas Américas: Chile Chile

1. Division of assets outside Chile of Chilectra and Endesa Chile into new Merger by absorption of part of Enersis Américas of the corporations corporations called Chilectra Américas and Endesa Américas, respectively Chilectra Américas y Endesa Américas

The estimated exchange relations for the merger shall be defined at the

2. Division of Enersis’ Chilean assets into a new corporation to be called

2 |

| respective boards of shareholders that approve the Reorganization Enersis Chile |

New corporations originated by the Reorganization

Strictly Private and Confidential 40

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

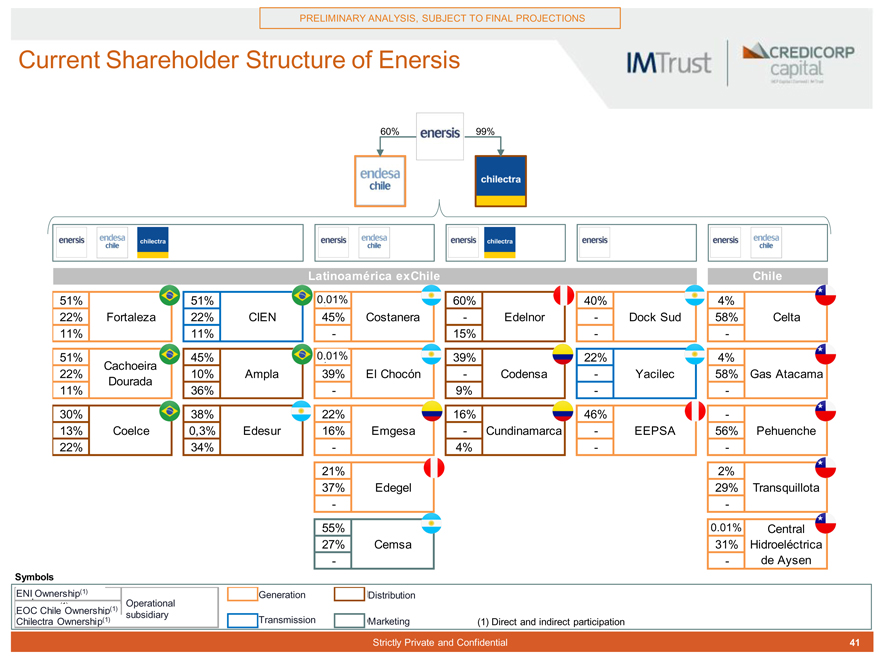

Current Shareholder Structure of Enersis

60% 99%

Latinoamérica exChile Chile

51% 51% 0. 0,01% 60% 40% 4%

22% Fortaleza 22% CIEN 45% Costanera—Edelnor—Dock Sud 58% Celta 11% 11%—15% —51% 45% 0. 0,01% 39% 22% 4% Cachoeira 22% 10% Ampla 39% El Chocón—Codensa—Yacilec 58% Gas Atacama Dourada 11% 36%—9% —30% 38% 22% 16% 46% -13% Coelce 0,3% Edesur 16% Emgesa—Cundinamarca—EEPSA 56% Pehuenche 22% 34%—4% —21% 2% 37% Edegel 29% Transquillota

—

55% 0, 0.01% Central 27% Cemsa 31% Hidroeléctrica

— de Aysen

Symbols

ENI Propiedad Ownership (1) ENI (1) Generation ación Distribution istribuc ón (1) Operational EOC Propiedad Chile Ownership EOC Chile (1) subsidiary

Chilectra Propiedad Ownership (1) Chilectra (1) Transmission ión Comercialización Marketing (1) Direct and indirect participation

Strictly Private and Confidential 41

|

PRELIMINARY ANALYSIS, SUBJECT TO FINAL PROJECTIONS

Santiago Office

Avenida Apoquindo 3721, Piso 9 Las Condes 7550177 Chile

+56 (2) 2450 1600