Exhibit (C)(8)(H)

|

September 8, 2015 Strictly Private and Confidential

Preliminary Discussion on the Reorganization of Enersis S.A.

Prepared for the Directors’ Committee of Enersis S.A.

ENERSIS imtrust credicorpcapital

|

imtrust credicorpcapital

Important Information

This document has been prepared by IM Trust Asesorías Financieras S.A. (hereinafter “IM Trust”) at the request of the Directors’ Committee of Enersis S.A. (“Enersis” or the “Company”) for the private and exclusive use of the Company and its Directors’ Committee.

The recommendations and conclusions in this document constitute the best judgment or opinion of IM Trust with respect to the Reorganization of Enersis (as this term is defined below) at the time this document is issued, considering the methods used to this end and the information that was available. The conclusions of this document could change if other data or additional information becomes available. IM Trust will have no obligation whatsoever to give notice of such changes or of any modifications to the opinions or information contained in this document.

This document has been prepared by IM Trust on the sole and exclusive basis of the information delivered by Enersis and public information, and IM Trust has assumed that this information is fully complete and accurate without conducting any independent verification. As such, IM Trust assumes no liability with regard to the information reviewed or for the conclusions that may derive from any error, inaccuracy, and/or falsehood in such information.

Likewise, the conclusions in this document may be based on assumptions that are subject to significant uncertainties and economic and market contingencies, such as flows, projections, estimates, and assessments, whose occurrence may be difficult to foresee and many of which may even be outside the control of Enersis, to the extent that there exists no certainty as to the actual fulfillment of these assumptions. Under no circumstance may the use or inclusion of such flows, projections, or estimates be considered as a representation, guarantee, or prediction of IM Trust with respect to their occurrence or to their underlying assumptions.

Strictly Private and Confidential 2

|

Contents

imtrust credicorpcapital

1. Background Info and Structure of the Reorganization 4

2. Current Situation of Enersis 9

3. Scope of the Advisory Services 12

4. Reflections and Preliminary Conclusions 16

5. Annexes 18 a) Methods of the Advisory Services 19 b) Market Analysis 22 c) Organization of Enel 30

Strictly Private and Confidential 3

|

BACKGROUND INFO AND STRUCTURE OF THE

REORGANIZATION 1

imtrust credicorpcapital

Strictly Private and Confidential 4

|

Background Info on the Reorganization (1/3)

imtrust credicorpcapital

Enersis S.A. (“Enersis” or the “Company”) has notified the market that it is beginning a corporate reorganization process (the “Reorganization”), with the aim of:

1. Simplifying the corporate structure of the Company and the decision-making process

2. Facilitating understanding on the part of the market, thereby growing the value of all of the companies that comprise the Enersis group

The Reorganization is to include the separation of generation and distribution activities in Chile from the rest of the activities conducted outside Chile by the Enersis group, and is to be carried out in two stages:

Splitting of Empresa Nacional de Electricidad S.A. (“Endesa Chile”) and Chilectra S.A. (“Chilectra”), and Enersis, resulting in:

“Chilectra Américas”, to be assigned the holdings, assets, and liabilities held by Chilectra outside of Chile

Stage 1: • “Endesa Américas”, to be assigned the holdings, assets, and liabilities held by Endesa Chile outside of Chile, and

Splitting of

“Enersis Chile”, to be assigned the holdings, assets, and liabilities of Enersis in Chile, including the holdings in Chilectra and

Enersis,

Endesa Chile, Endesa Chile (after the splitting of those two companies) and Chilectra • The company to be spun off from Enersis (to be called “Enersis Américas”) will maintain the holdings, assets, and liabilities of Enersis outside of Chile, including the holdings in Chilectra Américas and Endesa Américas

Merger of the companies that constitute the holdings of Endesa Chile, Chilectra, and Enersis outside of Chile

Stage 2: • This is to be implemented by way of a merger through absorption into Enersis Américas of the companies Endesa América and

Merger into Enersis

Chilectra Américas

Américas

It is estimated that Stage 2 and the entire Reorganization could be completed during the third quarter of 2016

Enersis Chile and Enersis Américas are to be headquartered in Chile and their stock is to be traded in the same markets as Enersis

Neither of the operations described above would require any additional financial contribution on the part of shareholders

Strictly Private and Confidential 5

|

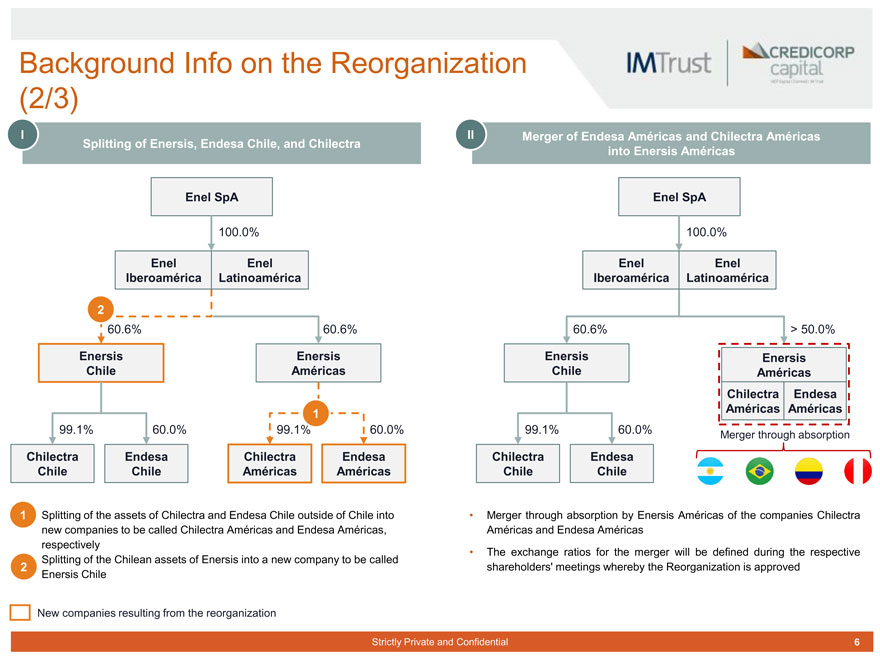

Background Info on the Reorganization (2/3)

imtrust credicorpcapital

I II Merger of Endesa Américas and Chilectra Américas Splitting of Enersis, Endesa Chile, and Chilectra into Enersis Américas

Enel SpA Enel SpA

100.0% 100.0%

Enel Enel Enel Enel Iberoamérica Latinoamérica Iberoamérica Latinoamérica

2

60.6% 60.6% 60.6% > 50.0%

Enersis Enersis Enersis Enersis Chile Américas Chile Américas Chilectra Endesa

1 Américas Américas

99.1% 60.0% 99.1% 60.0% 99.1% 60.0% Merger through absorption

Chilectra Endesa Chilectra Endesa Chilectra Endesa Chile Chile Américas Américas Chile Chile

1 Splitting of the assets of Chilectra and Endesa Chile outside of Chile into • Merger through absorption by Enersis Américas of the companies Chilectra new companies to be called Chilectra Américas and Endesa Américas, Américas and Endesa Américas respectively

The exchange ratios for the merger will be defined during the respective Splitting of the Chilean assets of Enersis into a new company to be called 2 shareholders’ meetings whereby the Reorganization is approved Enersis Chile

New companies resulting from the reorganization

Strictly Private and Confidential 6

|

Background Info on the Reorganization (3/3)

imtrust credicorpcapital

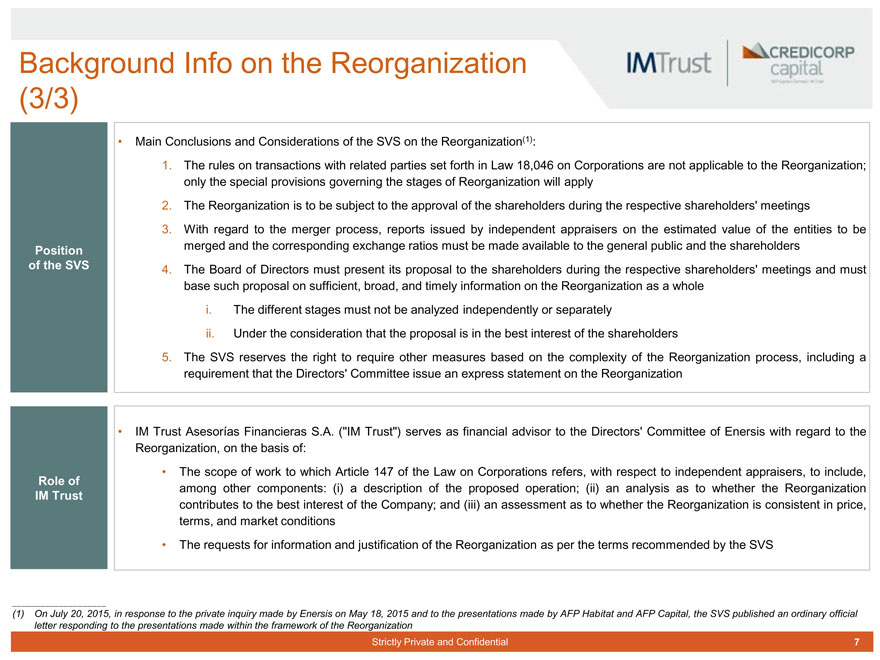

Main Conclusions and Considerations of the SVS on the Reorganization(1):

1. The rules on transactions with related parties set forth in Law 18,046 on Corporations are not applicable to the Reorganization; only the special provisions governing the stages of Reorganization will apply

2. The Reorganization is to be subject to the approval of the shareholders during the respective shareholders’ meetings

3. With regard to the merger process, reports issued by independent appraisers on the estimated value of the entities to be Position merged and the corresponding exchange ratios must be made available to the general public and the shareholders of the SVS 4. The Board of Directors must present its proposal to the shareholders during the respective shareholders’ meetings and must base such proposal on sufficient, broad, and timely information on the Reorganization as a whole i. The different stages must not be analyzed independently or separately ii. Under the consideration that the proposal is in the best interest of the shareholders

5. The SVS reserves the right to require other measures based on the complexity of the Reorganization process, including a requirement that the Directors’ Committee issue an express statement on the Reorganization

IM Trust Asesorías Financieras S.A. (“IM Trust”) serves as financial advisor to the Directors’ Committee of Enersis with regard to the

Reorganization, on the basis of:

The scope of work to which Article 147 of the Law on Corporations refers, with respect to independent appraisers, to include,

Role of among other components: (i) a description of the proposed operation; (ii) an analysis as to whether the Reorganization

IM Trust contributes to the best interest of the Company; and (iii) an assessment as to whether the Reorganization is consistent in price, terms, and market conditions

The requests for information and justification of the Reorganization as per the terms recommended by the SVS

(1) On July 20, 2015, in response to the private inquiry made by Enersis on May 18, 2015 and to the presentations made by AFP Habitat and AFP Capital, the SVS published an ordinary official letter responding to the presentations made within the framework of the Reorganization

Strictly Private and Confidential 7

|

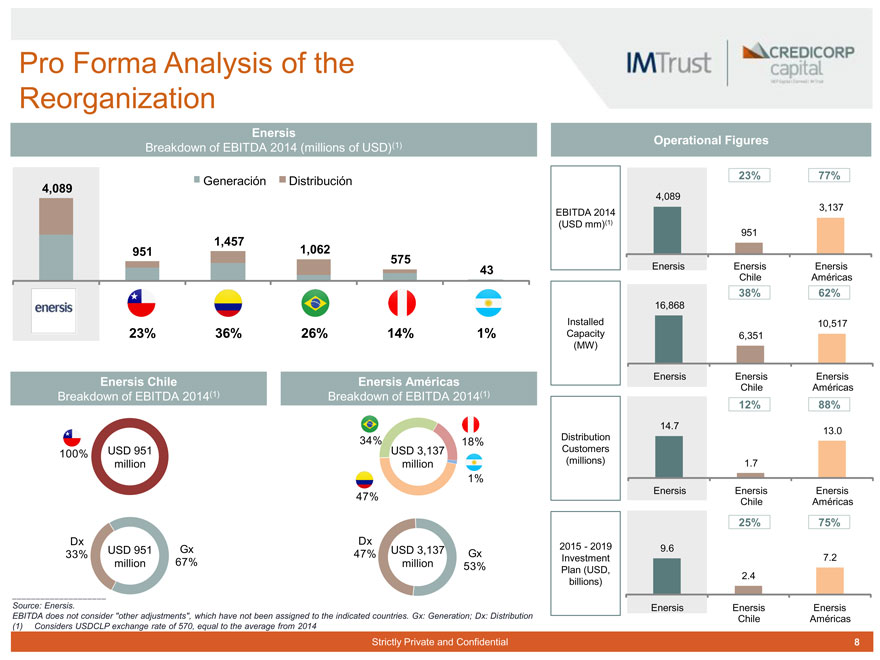

Pro Forma Analysis of the Reorganization

imtrust credicorpcapital

Enersis

Operational Figures

Breakdown of EBITDA 2014 (millions of USD)(1)

Generación Distribución 23% 77%

4,089

4,089

3,137 EBITDA 2014 (USD mm)(1) 951

1,457

951 1,062

575

43 Enersis Enersis Enersis Chile Américas

38% 62%

16,868

Installed 10,517

23% 36% 26% 14% 1% Capacity 6,351

(MW)

Enersis Chile Enersis Américas Enersis Enersis Enersis

Chile Américas

Breakdown of EBITDA 2014(1) Breakdown of EBITDA 2014(1)

12% 88%

14.7

13.0 34% 18% Distribution

USD 951 USD 3,137 Customers 100% million million (millions) 1.7 1%

Enersis Enersis Enersis

47%

Chile Américas

25% 75%

Dx Dx

USD 951 Gx USD 3,137 2015—2019 9.6

33% 47% Gx Investment 7.2 million 67% million 53%

Plan (USD,

2.4 billions)

Source: Enersis. Enersis Enersis Enersis

EBITDA does not consider “other adjustments”, which have not been assigned to the indicated countries. Gx: Generation; Dx: Distribution Chile Américas (1) Considers USDCLP exchange rate of 570, equal to the average from 2014

Strictly Private and Confidential 8

|

CURRENT SITUATION OF ENERSIS 2

imtrust credicorpcapital

Strictly Private and Confidential 9

|

Stock Situation of Enersis

imtrust credicorpcapital

1 |

|

Behavior of the

Price of Enersis

Stock

2 |

|

Market multiples

of companies

from the

electricity sector

in Chile

3 |

|

Market discount

on target price of

Enersis

4 |

|

Liquidity of

Enersis and

Endesa Chile

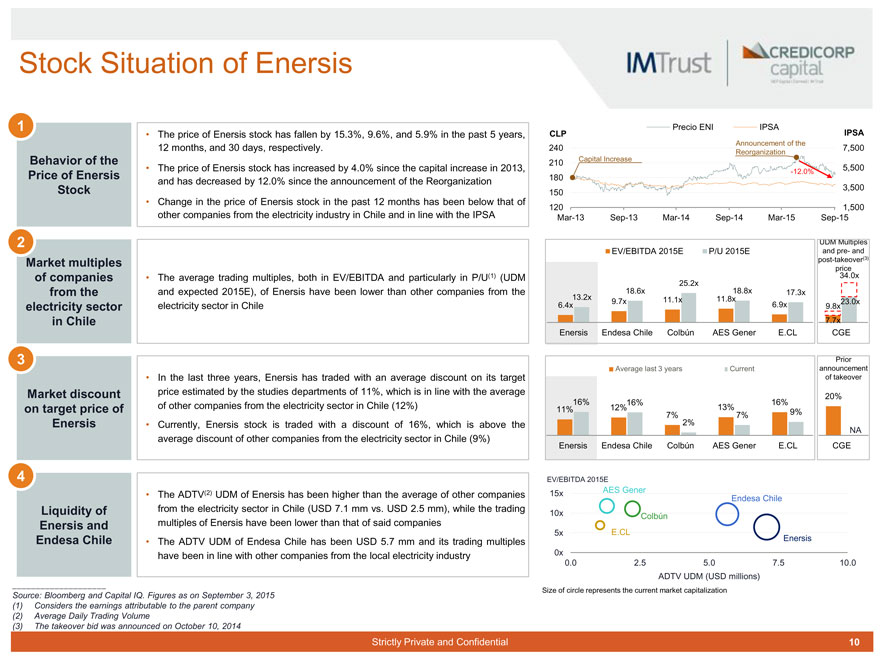

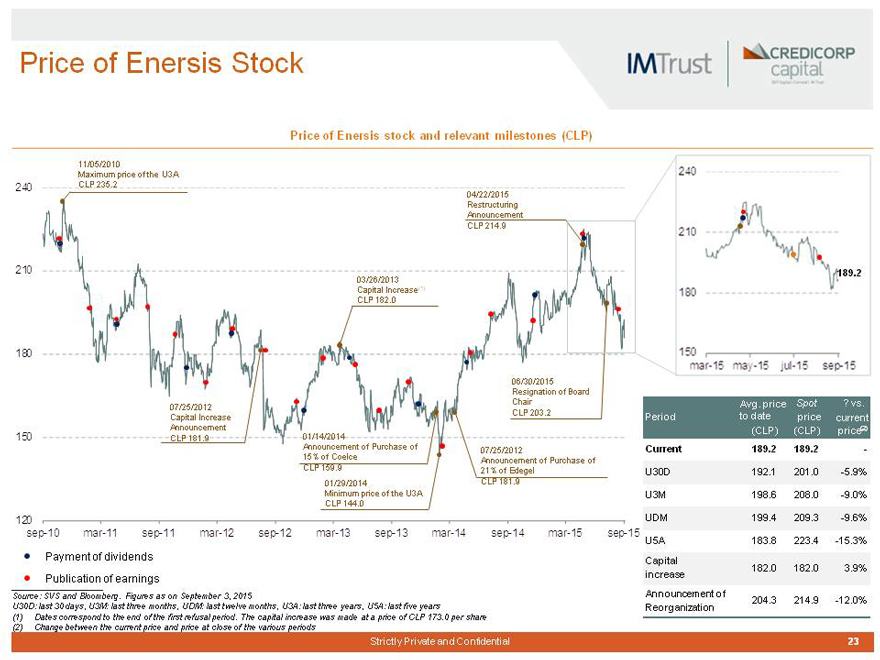

The price of Enersis stock has fallen by 15.3%, 9.6%, and 5.9% in the past 5 years, 12 months, and 30 days, respectively.

The price of Enersis stock has increased by 4.0% since the capital increase in 2013, and has decreased by 12.0% since the announcement of the Reorganization

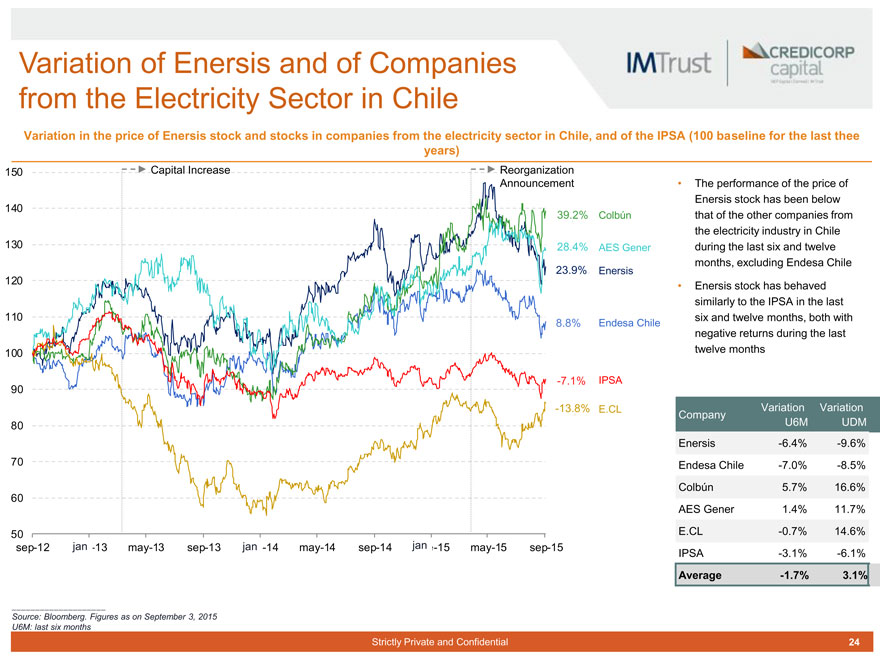

Change in the price of Enersis stock in the past 12 months has been below that of other companies from the electricity industry in Chile and in line with the IPSA

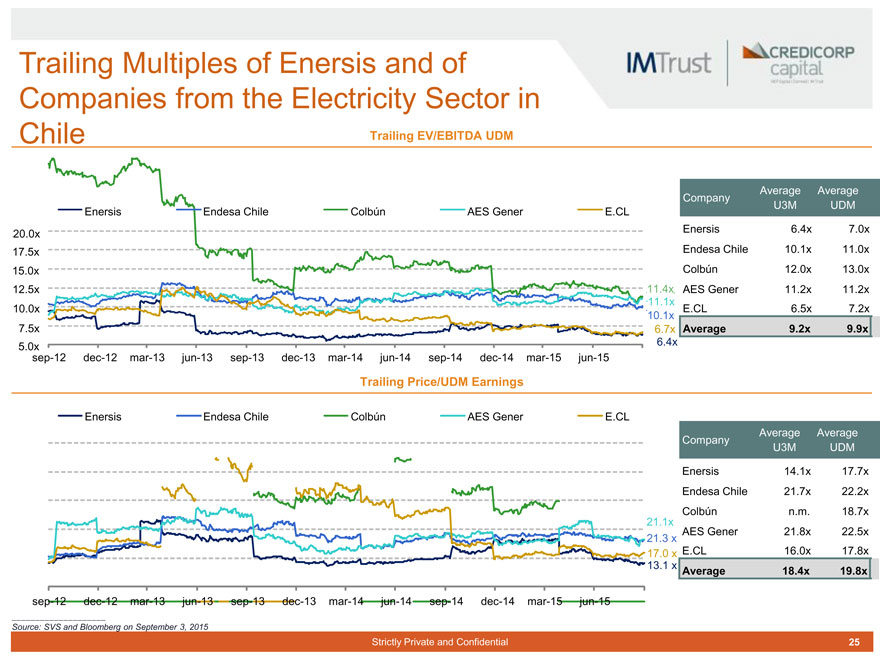

The average trading multiples, both in EV/EBITDA and particularly in P/U(1) (UDM and expected 2015E), of Enersis have been lower than other companies from the electricity sector in Chile

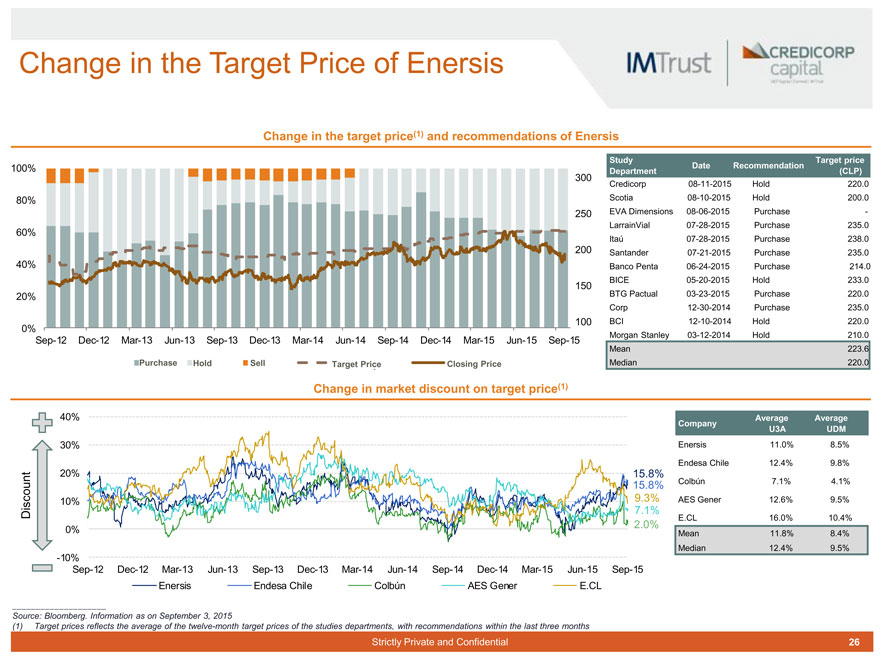

In the last three years, Enersis has traded with an average discount on its target price estimated by the studies departments of 11%, which is in line with the average of other companies from the electricity sector in Chile (12%)

Currently, Enersis stock is traded with a discount of 16%, which is above the average discount of other companies from the electricity sector in Chile (9%)

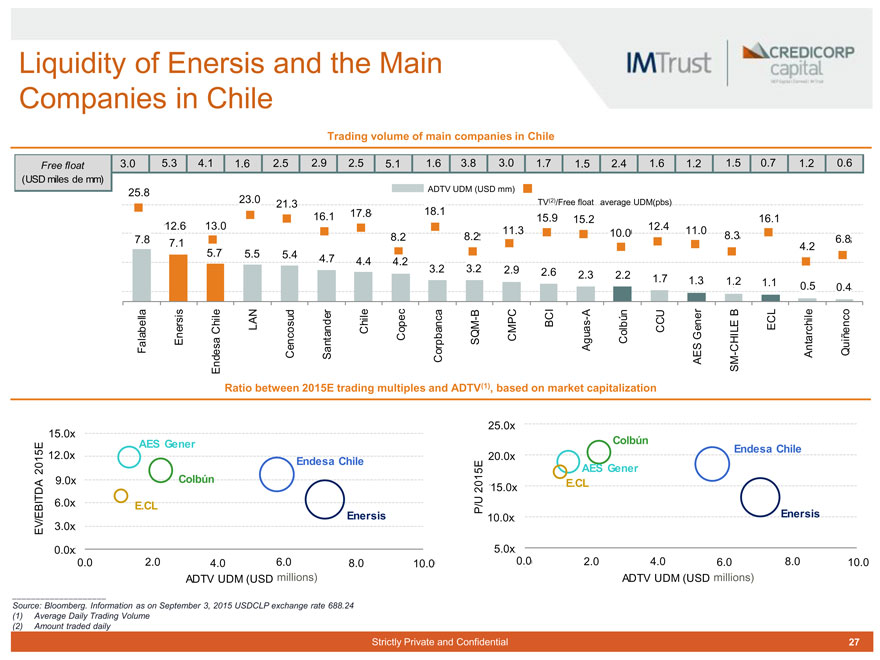

The ADTV(2) UDM of Enersis has been higher than the average of other companies from the electricity sector in Chile (USD 7.1 mm vs. USD 2.5 mm), while the trading multiples of Enersis have been lower than that of said companies

The ADTV UDM of Endesa Chile has been USD 5.7 mm and its trading multiples have been in line with other companies from the local electricity industry

Precio ENI IPSA

CLP IPSA

Announcement of the

240 7,500

Reorganization

210 Capital Increase

-12.0% |

| 5,500 |

180

150 3,500

120 1,500

Mar-13 Sep-13 Mar-14 Sep-14 Mar-15 Sep-15

UDM Multiples

EV/EBITDA 2015E P/U 2015E and pre- and

post-takeover(3)

price

34.0x

25.2x

18.6x |

| 18.8x 17.3x |

13.2x |

| 9.7x 11.1x 11.8x 23.0x |

6.4x |

| 6.9x 9.8x |

7.7x

Enersis Endesa Chile Colbún AES Gener E.CL CGE

Prior

Average last 3 years Current announcement

of takeover

20%

16% 16% 16%

11% 12% 7% 13% 7% 9%

2%

NA

Enersis Endesa Chile Colbún AES Gener E.CL CGE

EV/EBITDA 2015E

15x AES Gener

Endesa Chile

10x Colbún

5x E.CL Enersis

0x

0.0 |

| 2.5 5.0 7.5 10.0 |

ADTV UDM (USD millions)

Size of circle represents the current market capitalization

• |

| Source: Bloomberg and Capital IQ. Figures as on September 3, 2015 (1) Considers the earnings attributable to the parent company (2) Average Daily Trading Volume (3) The takeover bid was announced on October 10, 2014 |

Strictly Private and Confidential 10

|

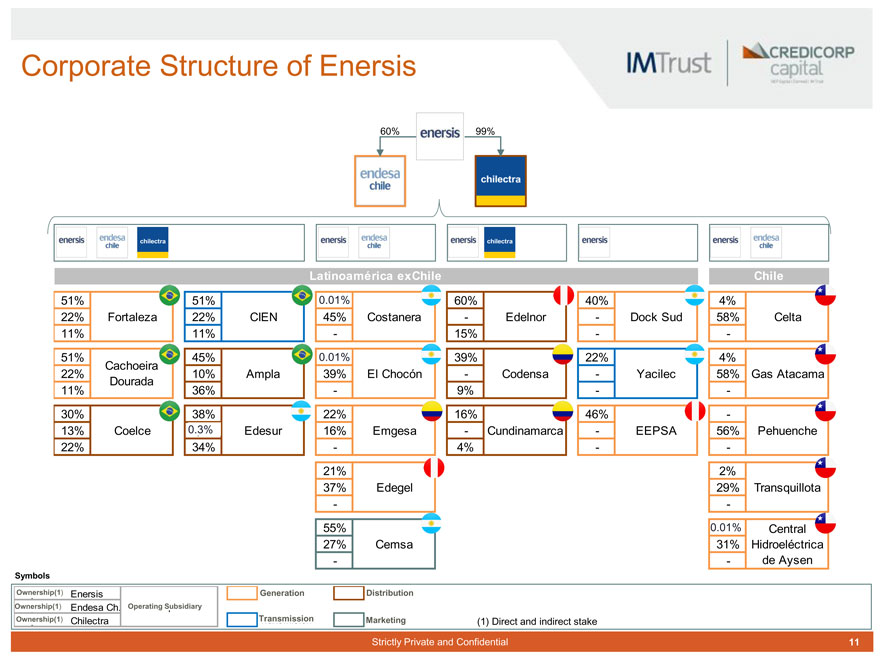

Corporate Structure of Enersis

imtrust credicorpcapital

60% 99%

Latinoamérica exChile Chile

51% 51% 0. ,01% 60% 40% 4%

22% Fortaleza 22% CIEN 45% Costanera—Edelnor—Dock Sud 58% Celta 11% 11%—15% —

51% 45% 0. ,01% 39% 22% 4% Cachoeira

22% 10% Ampla 39% El Chocón—Codensa—Yacilec 58% Gas Atacama Dourada 11% 36%—9% —

30% 38% 22% 16% 46% -

13% Coelce 0. 0, 3% % Edesur 16% Emgesa—Cundinamarca—EEPSA 56% Pehuenche 22% 34%—4% —

21% 2%

37% Edegel 29% Transquillota

—

55% 0.,01% 1 Central 27% Cemsa 31% Hidroeléctrica

— de Aysen

Symbols

Propiedad Ownership(1) (1) Enersis Generation erac ón Distribution tr c ón

Ownership(1) Propiedad(1) Endesa Ch. Operating Filial Operat Subsidiary va

Ownership(1) Propiedad(1) Chilectra Transmission Transmisión Marketing Comercialización (1) Direct and indirect stake

Strictly Private and Confidential 11

|

SCOPE OF THE ADVISORY SERVICES 3

imtrust credicorpcapital

Strictly Private and Confidential 12

|

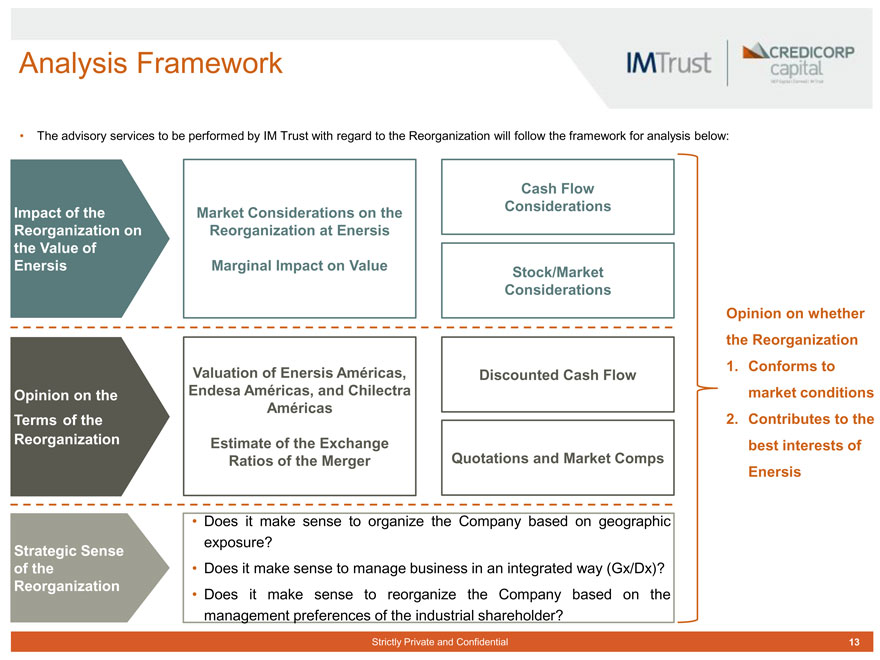

Analysis Framework

imtrust credicorpcapital

The advisory services to be performed by IM Trust with regard to the Reorganization will follow the framework for analysis below:

Impact of the

Reorganization on

the Value of

Enersis

Opinion on the

Terms of the

Reorganization

Strategic Sense

of the

Reorganization

Market Considerations on the Reorganization at Enersis

Marginal Impact on Value

Cash Flow Considerations

Stock/Market Considerations

Valuation of Enersis Américas, Endesa Américas, and Chilectra Américas

Estimate of the Exchange Ratios of the Merger

Discounted Cash Flow

Quotations and Market Comps

• Does it make sense to organize the Company based on geographic exposure?

Does it make sense to manage business in an integrated way (Gx/Dx)?

Does it make sense to reorganize the Company based on the management preferences of the industrial shareholder?

Opinion on whether the Reorganization

1. Conforms to market conditions

2. Contributes to the best interests of Enersis

Strictly Private and Confidential 13

|

Main Value Considerations

imtrust credicorpcapital

Cash Flow Factors

1 1

Impacts on EBITDA

Corporate governance (boards, regulations, etc.)

Structural costs

Operating costs

2

Cost of Corporate Debt

Impact on credit profile of surviving companies

Considerations based on allocation of net debt in process of Splitting

3

Tax Impact

Splitting and merger processes (one off)

Tax efficiency/inefficiency under new structure

4

Costs of the Transaction

Legal

Regulatory

Advisory

Liability managements

Other

Stock and Market Factors

5

Differentiation of business models

“Clientele effect” (interest of new investors):

Geographic/risk focus

Dividends policy/investment plan (income vs growth)

Best market comps by country

6

Simplification of corporate structure

Greater efficiency in decision-making process and approvals

Greater visibility and transparency of financial information

Clarity in investment vehicles

7

Liquidity

Impact on liquidity due to smaller size of surviving companies

Strictly Private and Confidential 14

|

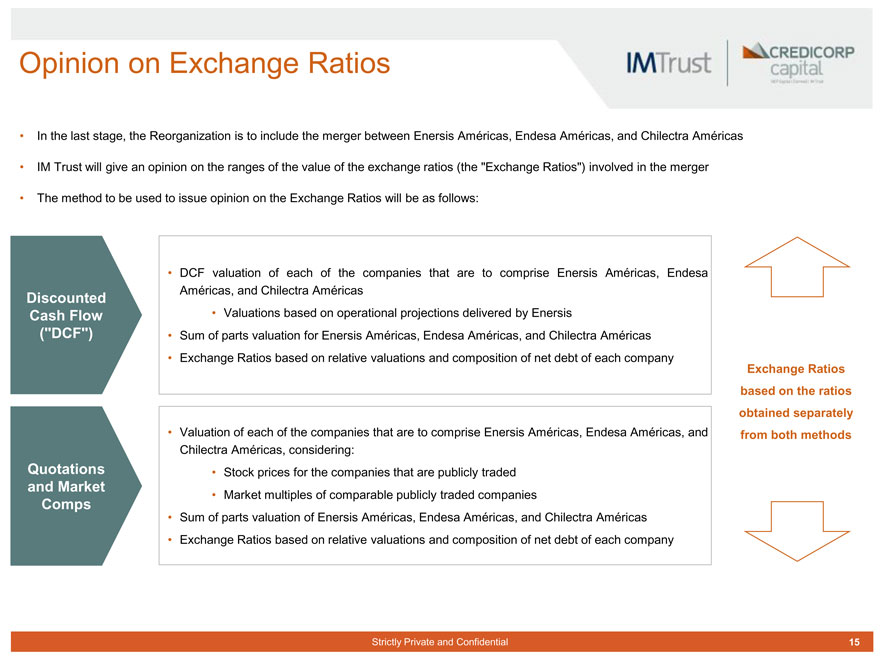

Opinion on Exchange Ratios

imtrust credicorpcapital

In the last stage, the Reorganization is to include the merger between Enersis Américas, Endesa Américas, and Chilectra Américas

IM Trust will give an opinion on the ranges of the value of the exchange ratios (the “Exchange Ratios”) involved in the merger

The method to be used to issue opinion on the Exchange Ratios will be as follows:

DCF valuation of each of the companies that are to comprise Enersis Américas, Endesa

Américas, and Chilectra Américas

Discounted

Cash Flow • Valuations based on operational projections delivered by Enersis

(“DCF”) • Sum of parts valuation for Enersis Américas, Endesa Américas, and Chilectra Américas

Exchange Ratios based on relative valuations and composition of net debt of each company Exchange Ratios based on the ratios obtained separately

Valuation of each of the companies that are to comprise Enersis Américas, Endesa Américas, and from both methods Chilectra Américas, considering: Quotations Stock prices for the companies that are publicly traded

and Market

Market multiples of comparable publicly traded companies

Comps

Sum of parts valuation of Enersis Américas, Endesa Américas, and Chilectra Américas

Exchange Ratios based on relative valuations and composition of net debt of each company

Strictly Private and Confidential 15

|

REFLECTIONS AND PRELIMINARY

CONCLUSIONS 4

imtrust credicorpcapital

Strictly Private and Confidential 16

|

Reflections and Preliminary Conclusions

imtrust credicorpcapital

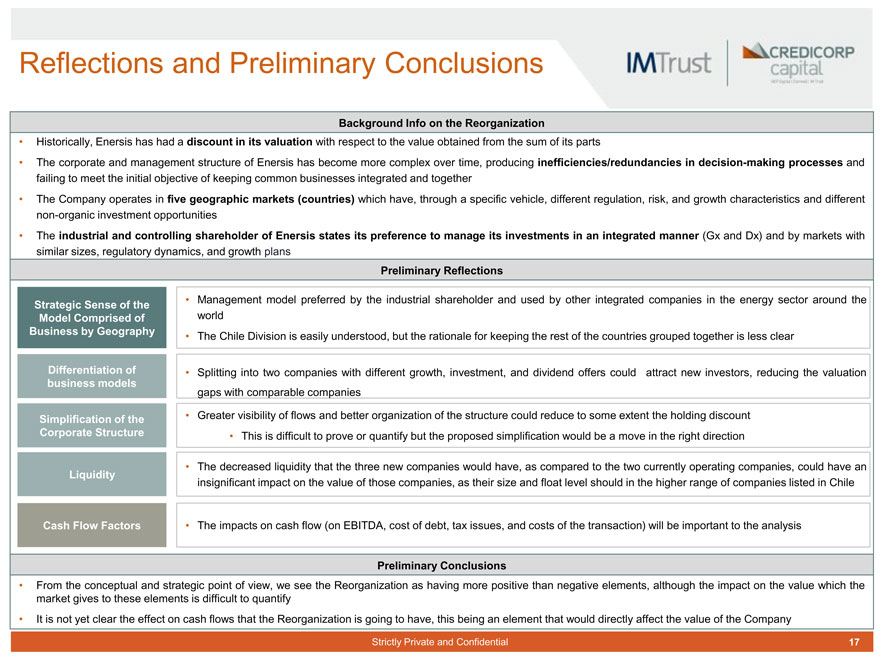

Background Info on the Reorganization

Historically, Enersis has had a discount in its valuation with respect to the value obtained from the sum of its parts

The corporate and management structure of Enersis has become more complex over time, producing inefficiencies/redundancies in decision-making processes and failing to meet the initial objective of keeping common businesses integrated and together

The Company operates in five geographic markets (countries) which have, through a specific vehicle, different regulation, risk, and growth characteristics and different non-organic investment opportunities

The industrial and controlling shareholder of Enersis states its preference to manage its investments in an integrated manner (Gx and Dx) and by markets with similar sizes, regulatory dynamics, and growth plans

Preliminary Reflections

Management model preferred by the industrial shareholder and used by other integrated companies in the energy sector around the

Strategic Sense of the

Model Comprised of world Business by Geography

The Chile Division is easily understood, but the rationale for keeping the rest of the countries grouped together is less clear

Differentiation of • Splitting into two companies with different growth, investment, and dividend offers could attract new investors, reducing the valuation business models gaps with comparable companies Simplification of the • Greater visibility of flows and better organization of the structure could reduce to some extent the holding discount Corporate Structure • This is difficult to prove or quantify but the proposed simplification would be a move in the right direction

The decreased liquidity that the three new companies would have, as compared to the two currently operating companies, could have an

Liquidity insignificant impact on the value of those companies, as their size and float level should in the higher range of companies listed in Chile

Cash Flow Factors • The impacts on cash flow (on EBITDA, cost of debt, tax issues, and costs of the transaction) will be important to the analysis

Preliminary Conclusions

From the conceptual and strategic point of view, we see the Reorganization as having more positive than negative elements, although the impact on the value which the market gives to these elements is difficult to quantify

It is not yet clear the effect on cash flows that the Reorganization is going to have, this being an element that would directly affect the value of the Company

Strictly Private and Confidential 17

|

ANNEXES 5

imtrust credicorpcapital

Strictly Private and Confidential 18

|

METHODS OF THE ADVISORY SERVICES

5a

imtrust credicorpcapital

Strictly Private and Confidential 19

|

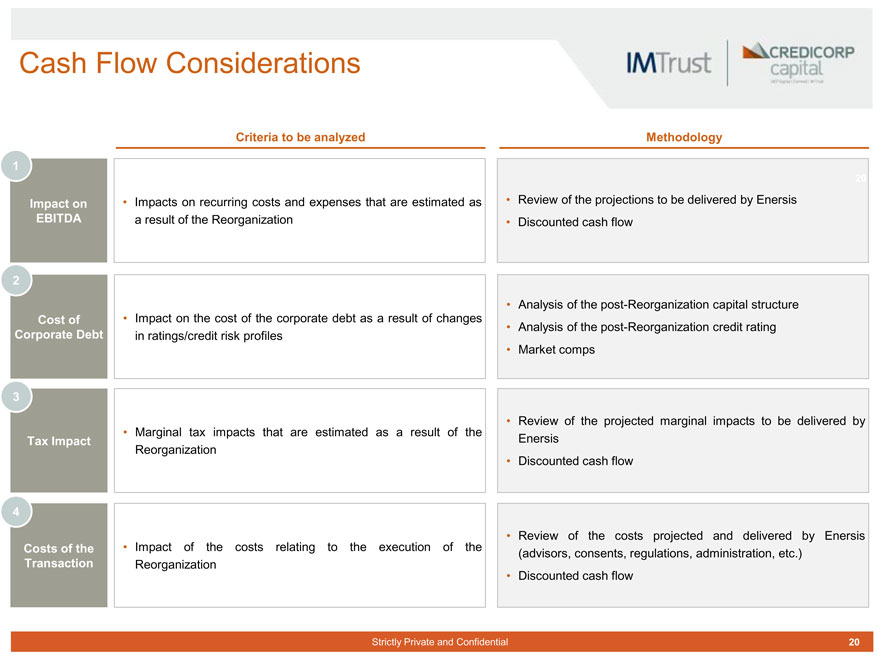

Cash Flow Considerations

imtrust credicorpcapital

Criteria to be analyzed Methodology

1

20

Impact on • Impacts on recurring costs and expenses that are estimated as • Review of the projections to be delivered by Enersis EBITDA a result of the Reorganization • Discounted cash flow

2

Analysis of the post-Reorganization capital structure Cost of Impact on the cost of the corporate debt as a result of changes

Analysis of the post-Reorganization credit rating Corporate Debt in ratings/credit risk profiles

Market comps

3

Review of the projected marginal impacts to be delivered by

Marginal tax impacts that are estimated as a result of the

Tax Impact Enersis

Reorganization • Discounted cash flow

4

Review of the costs projected and delivered by Enersis Costs of the Impact of the costs relating to the execution of the (advisors, consents, regulations, administration, etc.) Transaction Reorganization

Discounted cash flow

Strictly Private and Confidential 20

|

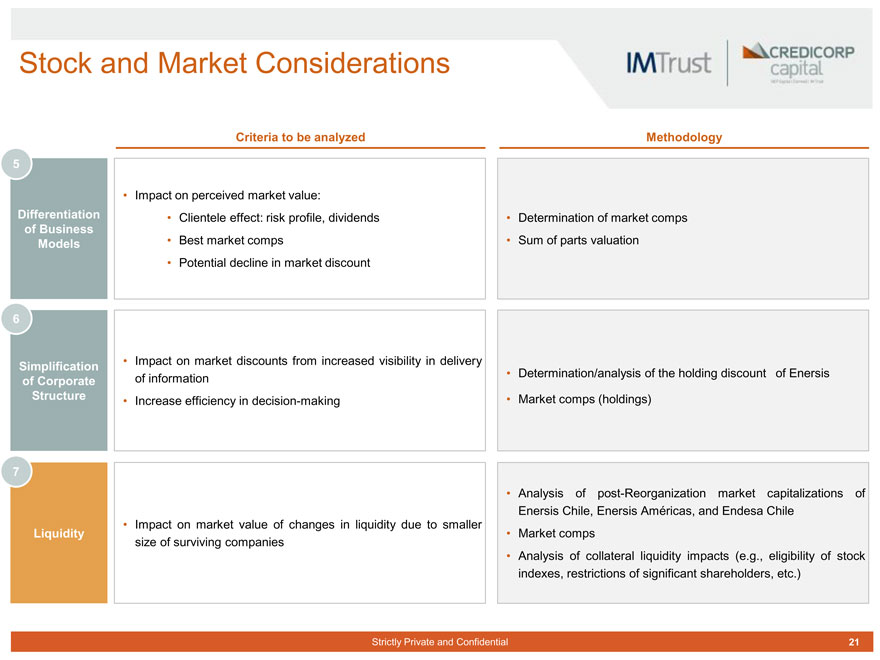

Stock and Market Considerations

imtrust credicorpcapital

Criteria to be analyzed Methodology

5

Impact on perceived market value:

Differentiation • Clientele effect: risk profile, dividends • Determination of market comps of Business • Best market comps • Sum of parts valuation

Models

Potential decline in market discount

6

Impact on market discounts from increased visibility in delivery

Simplification of information • Determination/analysis of the holding discount of Enersis of Corporate Structure • Increase efficiency in decision-making • Market comps (holdings)

7

Analysis of post-Reorganization market capitalizations of Enersis Chile, Enersis Américas, and Endesa Chile

Impact on market value of changes in liquidity due to smaller

Liquidity • Market comps size of surviving companies

Analysis of collateral liquidity impacts (e.g., eligibility of stock indexes, restrictions of significant shareholders, etc.)

Strictly Private and Confidential 21

|

MARKET ANALYSIS

5b

imtrust credicorpcapital

Strictly Private and Confidential 22

|

Price of Enersis Stock

imtrust credicorpcapital

Price of Enersis stock and relevant milestones (CLP)

11/05/2010

Maximum price of the U3A 240 240 CLP 235.2 04/22/2015 Restructuring Announcement CLP 214.9

210

210 189.,2 2

03/26/2013

Capital Increase(1) 180 CLP 182.0

180 150 mar-15 may-15 jul-15 sep-15

06/30/2015

Resignation of Board

Chair Avg. price Spot ? vs.

07/25/2012

CLP 203.2 to date

Capital Increase Period price current Announcement (CLP) (CLP) price(2)

150 CLP 181.9 01/14/2014

Announcement of Purchase of 07/25/2012 Current 189.2 189.2—15% of Coelce Announcement of Purchase of CLP 159.9

21% of Edegel U30D 192.1 201.0 -5.9%

01/29/2014 CLP 181.9

Minimum price of the U3A U3M 198.6 208.0 -9.0% CLP 144.0

120 UDM 199.4 209.3 -9.6% sep-10 mar-11 sep-11 mar-12 sep-12 mar-13 sep-13 mar-14 sep-14 mar-15 sep-15

U5A 183.8 223.4 -15.3%

Payment of dividends

Capital

182.0 182.0 3.9%

Publication of earnings increase

Announcement of Source: SVS and Bloomberg. Figures as on September 3, 2015

204.3 214.9 -12.0%

U30D: last 30 days, U3M: last three months, UDM: last twelve months, U3A: last three years, U5A: last five years Reorganization (1) Dates correspond to the end of the first refusal period. The capital increase was made at a price of CLP 173.0 per share (2) Change between the current price and price at close of the various periods

Strictly Private and Confidential 23

|

Variation of Enersis and of Companies from the Electricity Sector in Chile

imtrust credicorpcapital

Variation in the price of Enersis stock and stocks in companies from the electricity sector in Chile, and of the IPSA (100 baseline for the last thee years)

150 Capital Increase Reorganization

Announcement • The performance of the price of 140 Enersis stock has been below 39. 39,2 2% Colbún that of the other companies from the electricity industry in Chile 130 28.,4% AES Gener during the last six and twelve months, excluding Endesa Chile

23. 23,9 9% Enersis

120

Enersis stock has behaved similarly to the IPSA in the last 110 six and twelve months, both with

8.,8% Endesa Chile negative returns during the last 100 twelve months

90 -7. ,1% IPSA

-13. -13,8% 8% E.CL Variation Variation Company

80 U6M UDM

Enersis -6.4% -9.6%

70 Endesa Chile -7.0% -8.5% Colbún 5.7% 16.6% 60 AES Gener 1.4% 11.7%

50 E.CL -0.7% 14.6% sep-12 jan e e-13 may-13 sep-13 jan e e-14 may-14 sep-14 jan ee-15 may-15 sep-15 IPSA -3.1% -6.1%

Average -1.7% 3.1%

Source: Bloomberg. Figures as on September 3, 2015 U6M: last six months

Strictly Private and Confidential 24

|

Trailing Multiples of Enersis and of Companies from the Electricity Sector in

imtrust credicorpcapital

Enersis Endesa Chile Colbún AES Gener E.CL 20. ,0 0x 17. ,5 5x 15. ,0 0x

12. |

| ,5 5x 11.4x 11,4 x 11,1 11.1x 10. ,0 0x 10,1 x 10.1x |

7. ,5 5x 6,7 6.7x x

6,4 6.4x

5. 5,0x 0x sep-12 dec-12 mar-13 jun-13 sep-13 dec-13 mar-14 jun-14 sep-14 dec-14 mar-15 jun-15

Trailing Price/UDM Earnings

Enersis Endesa Chile Colbún AES Gener E.CL

21.1x 10 21.1x 3 x 17. 6 0 7x x 13. 6. 1 4 x

sep-12 dec-12 mar-13 jun-13 sep-13 dec-13 mar-14 jun-14 sep-14 dec-14 mar-15 jun-15

Source: SVS and Bloomberg on September 3, 2015

Average Average

Company

U3M UDM

Enersis 6.4x 7.0x

Endesa Chile 10.1x 11.0x

Colbún 12.0x 13.0x

AES Gener 11.2x 11.2x

E.CL 6.5x 7.2x

Average 9.2x 9.9x

Average Average

Company

U3M UDM

Enersis 14.1x 17.7x

Endesa Chile 21.7x 22.2x

Colbún n.m. 18.7x

AES Gener 21.8x 22.5x

E.CL 16.0x 17.8x

Average 18.4x 19.8x

Source: SVS and Bloomberg on September 3, 2015

Strictly Private and Confidential 25

|

Change in the Target Price of Enersis

imtrust credicorpcapital

Change in the target price(1) and recommendations of Enersis

Study Target price 100% Date Recommendation Department (CLP)

300

Credicorp 08-11-2015 Hold 220.0 80% Scotia 08-10-2015 Hold 200.0 250 EVA Dimensions 08-06-2015 Purchase—LarrainVial 07-28-2015 Purchase 235.0

60%

Itaú 07-28-2015 Purchase 238.0 200 Santander 07-21-2015 Purchase 235.0 40% Banco Penta 06-24-2015 Purchase 214.0 BICE 05-20-2015 Hold 233.0 150 BTG Pactual 03-23-2015 Purchase 220.0

20%

Corp 12-30-2014 Purchase 235.0 100 BCI 12-10-2014 Hold 220.0

0%

Morgan Stanley 03-12-2014 Hold 210.0

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Mean 223.6

Purchase Compr Purcha r Hold Mantener Sell Vender Target Precio Price objtivo Closing Prec o cierr Price Median 220.0

Change in market discount on target price(1)

40% Average Average Company U3A UDM

30% Enersis 11.0% 8.5% Endesa Chile 12.4% 9.8%

20% 15. ,8% 8%

15. |

| , 8% Colbún 7.1% 4.1% 10% 9. ,3% AES Gener 12.6% 9.5% |

Discount 7. ,1%

E.CL 16.0% 10.4%

2.,0%

0% Mean 11.8% 8.4% Median 12.4% 9.5%

-10%

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Enersis Endesa Chile Colbún AES Gener E.CL

Source: Bloomberg. Information as on September 3, 2015

(1) Target prices reflects the average of the twelve-month target prices of the studies departments, with recommendations within the last three months

Strictly Private and Confidential 26

|

Liquidity of Enersis and the Main Companies in Chile

imtrust credicorpcapital

Trading volume of main companies in Chile

Free float 3. 3,0 0 5. ,3 4.,1 1. 1,6 2.,5 2. ,9 2.,5 5.,1 1. , 6 3.,8 3.,0 1.,7 1. ,5 2.,4 1.,6 1.,2 1. ,5 0. 0,7 1.,2 0.,6 (USD miles de mm) 25. ,8 ADTV UDM (USD mm) 23.,0 21.3 , TV(2)/Free float average UDM(pbs) 17.8 , 18.1 , 16.,1 15. ,9 15.,2 16.,1 12. .,6 13,0 13.0 11,3 12. ,4 11.3 10.,0 11. ,0 7. ,8 8.,2 8.,2 8.,3 6.8 7.1 , , 4. ,2 5.,7 5. ,5 5. ,4 4. ,7 4. ,4 4. ,2 3.2 3.,2 , 2. ,9 2. ,6 2. ,3 2. ,2 1. ,7 1.,3 1. ,2 1.,1 0.5 , 0.4 ,

Strictly Private and Confidential 27

Falabella

Enersis

Endesa Chile

LAN

Cencosud

Santander

Chile

Copec

Corpbanca

SQM-B

CMPC

BCI

Aguas-A

Colbún

CCU

AES Gener

SM-CHILE B

ECL

Antarchile

Quiñenco

Ratio between 2015E trading multiples and ADTV(1), based on market capitalization

15. |

| ,0x |

AES Gener

12. |

| ,0x |

2015E Endesa Chile

9. ,0x Colbún

6.,0x E.CL

Enersis

EV/EBITDA 3.,0x

0.,0x

0. ,0 2. ,0 4. 4,0 0 6. 6,0 0 8.,0 10. ,0

ADTV UDM (USD millions)

25. |

| ,0x |

Colbún

Endesa Chile

20. |

| ,0x |

AES Gener

2015E 15. , 0x x E.CL P/U

10.,0x Enersis

5.,0x

0.,0 2. ,0 4. ,0 6.,0 8. ,0 10. ,0

ADTV UDM (USD millions)

Source: Bloomberg. Information as on September 3, 2015 USDCLP exchange rate 688.24 (1) Average Daily Trading Volume (2) Amount traded daily

Strictly Private and Confidential 27

|

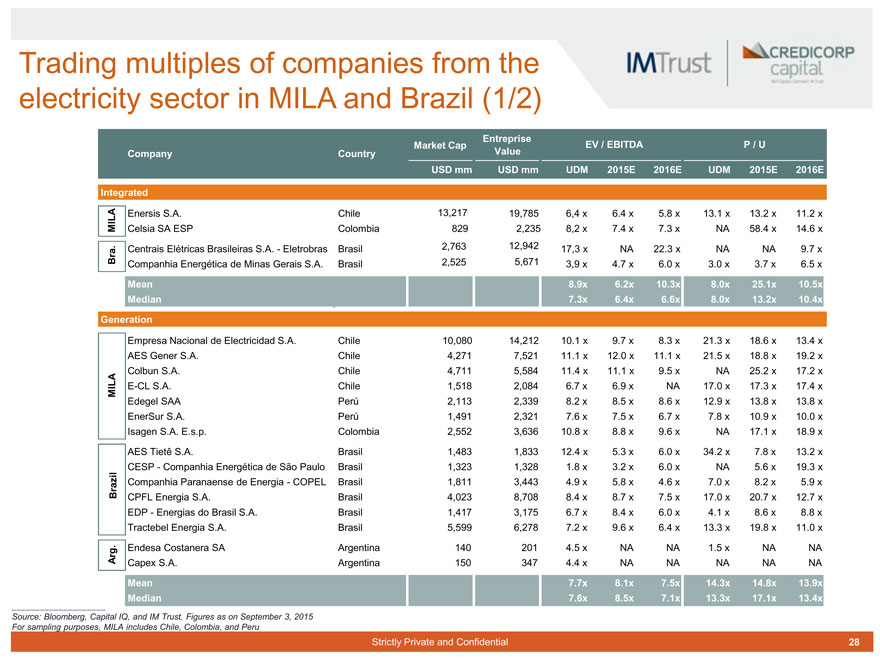

Trading multiples of companies from the electricity sector in MILA and Brazil (1/2)

imtrust credicorpcapital

Entreprise

Entreprise

Market Cap EV / EBITDA P / U

Company Country Value

USD mm USD mm UDM 2015E 2016E UDM 2015E 2016E

Integrated

Enersis S.A. Chile 13,217 19,785 6,4 x 6.4 x 5.8 x 13.1 x 13.2 x 11.2 x

MILA Celsia SA ESP Colombia 829 2,235 8,2 x 7.4 x 7.3 x NA 58.4 x 14.6 x

Centrais Elétricas Brasileiras S.A.—Eletrobras Brasil 2,763 12,942 17,3 x NA 22.3 x NA NA 9.7 x

Bra. Companhia Energética de Minas Gerais S.A. Brasil 2,525 5,671 3,9 x 4.7 x 6.0 x 3.0 x 3.7 x 6.5 x

Mean 8.9x 6.2x 10.3x 8.0x 25.1x 10.5x

Median 7.3x 6.4x 6.6x 8.0x 13.2x 10.4x

Generation

Empresa Nacional de Electricidad S.A. Chile 10,080 14,212 10.1 x 9.7 x 8.3 x 21.3 x 18.6 x 13.4 x

AES Gener S.A. Chile 4,271 7,521 11.1 x 12.0 x 11.1 x 21.5 x 18.8 x 19.2 x

Colbun S.A. Chile 4,711 5,584 11.4 x 11.1 x 9.5 x NA 25.2 x 17.2 x

MILA E-CL S.A. Chile 1,518 2,084 6.7 x 6.9 x NA 17.0 x 17.3 x 17.4 x

Edegel SAA Perú 2,113 2,339 8.2 x 8.5 x 8.6 x 12.9 x 13.8 x 13.8 x

EnerSur S.A. Perú 1,491 2,321 7.6 x 7.5 x 6.7 x 7.8 x 10.9 x 10.0 x

Isagen S.A. E.s.p. Colombia 2,552 3,636 10.8 x 8.8 x 9.6 x NA 17.1 x 18.9 x

AES Tietê S.A. Brasil 1,483 1,833 12.4 x 5.3 x 6.0 x 34.2 x 7.8 x 13.2 x

CESP—Companhia Energética de São Paulo Brasil 1,323 1,328 1.8 x 3.2 x 6.0 x NA 5.6 x 19.3 x

Brazil Companhia Paranaense de Energia—COPEL Brasil 1,811 3,443 4.9 x 5.8 x 4.6 x 7.0 x 8.2 x 5.9 x

CPFL Energia S.A. Brasil 4,023 8,708 8.4 x 8.7 x 7.5 x 17.0 x 20.7 x 12.7 x

EDP—Energias do Brasil S.A. Brasil 1,417 3,175 6.7 x 8.4 x 6.0 x 4.1 x 8.6 x 8.8 x

Tractebel Energia S.A. Brasil 5,599 6,278 7.2 x 9.6 x 6.4 x 13.3 x 19.8 x 11.0 x

Endesa Costanera SA Argentina 140 201 4.5 x NA NA 1.5 x NA NA

Arg. Capex S.A. Argentina 150 347 4.4 x NA NA NA NA NA

Mean 7.7x 8.1x 7.5x 14.3x 14.8x 13.9x

Median 7.6x 8.5x 7.1x 13.3x 17.1x 13.4x

Source: Bloomberg, Capital IQ, and IM Trust. Figures as on September 3, 2015 For sampling purposes, MILA includes Chile, Colombia, and Peru

Strictly Private and Confidential 28

|

Trading multiples of companies from the electricity sector in MILA and Brazil (2/2)

imtrust credicorpcapital

Entreprise

Market Cap EV / EBITDA P / U

Company Country Value

USD mm USD mm UDM 2015E 2016E UDM 2015E 2016E

Distribución

Luz del Sur S.A.A. Perú 1,502 1,947 9.4 x 9.9 x 10.4 x 11.1 x 13.0 x 13.6 x

MILA Empresa De Distribucion Electrica De Lima Norte Perú 964 1,349 7.1 x 6.4 x 6.1 x 10.6 x 9.6 x 9.0 x

Ampla Energia e Serviços S.A. Brasil 954 1,556 7.0 x NA NA 14.9 x NA NA

Companhia Energética do Ceará—Coelce Brasil 770 1,077 4.3 x NA NA 7.6 x NA NA

Brazil Eletropaulo Metropolitana Eletricidade de S. Paulo Brasil 525 1,097 2.7 x 4.2 x 3.6 x 3.9 x 8.5 x 6.3 x

Equatorial Energia S.A. Brasil 1,765 2,360 5.5 x 9.0 x 7.0 x 4.8 x 19.9 x 10.8 x

Light SA Brasil 665 2,600 5.3 x 6.9 x 5.4 x 4.6 x 7.3 x 5.3 x

Pampa Energia SA Argentina 1,254 1,783 5.3 x 5.8 x 3.6 x 7.9 x 17.4 x 15.9 x

Arg. Empresa Distribuidora y Comercializadora Norte Argentina 874 1,025 6.6 x NA NA 12.2 x 11.9 x 6.3 x

Transener Argentina 234 319 8.3 x 4.7 x 4.1 x 8.2 x 18.1 x 16.3 x

Mean 6.2x 6.7x 5.7x 8.6x 13.2x 10.4x

Median 6.1x 6.4x 5.4x 8.0x 12.5x 9.9x

Source: Bloomberg, Capital IQ, and IM Trust. Figures as on September 3, 2015 For sampling purposes, MILA includes Chile, Colombia, and Peru

Strictly Private and Confidential 29

|

ORGANIZATION OF ENEL

5C

imtrust credicorpcapital

Strictly Private and Confidential 30

|

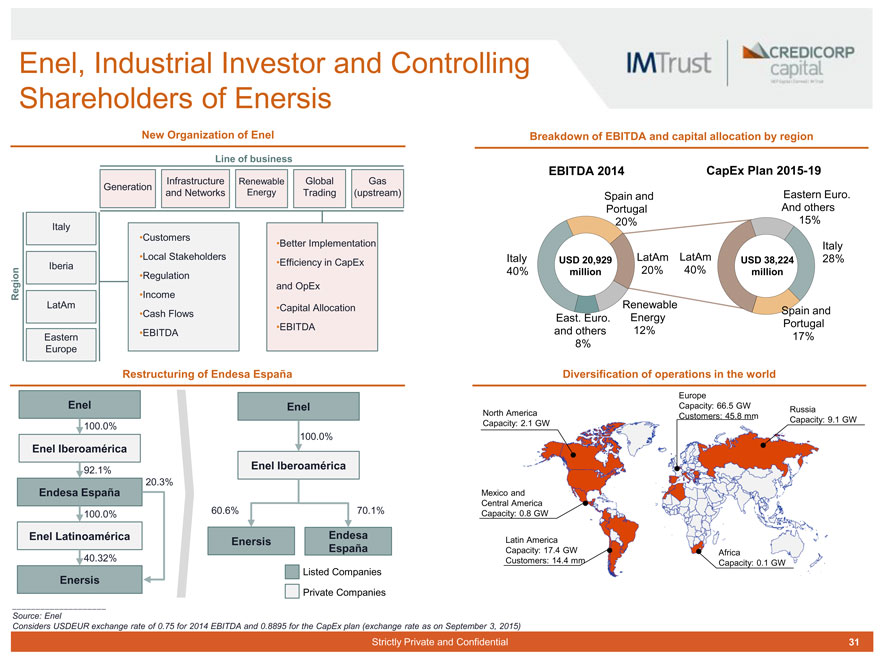

Enel, Industrial Investor and Controlling Shareholders of Enersis

New Organization of Enel

Line of business

Infrastructure Renewable Global Gas Generation and Networks Energy Trading (upstream)

Italy

Customers

Better Implementation Local Stakeholders

Efficiency in CapEx

Iberia

Regulation

Region •Income and OpEx

LatAm •Cash Flows •Capital Allocation

EBITDA EBITDA

Eastern Europe

Breakdown of EBITDA and capital allocation by region

EBITDA 2014 CapEx Plan 2015-19

Spain and Eastern Euro. Portugal And others 20% 15%

Italy Italy USD 20,929 LatAm LatAm USD 38,224 28%

40% million 20% 40% million

Renewable

Spain and East. Euro. Energy Portugal and others 12% 17% 8%

Restructuring of Endesa España

Enel Enel

100.0%

100.0%

Enel Iberoamérica

92.1% Enel Iberoamérica

20.3%

Endesa España

100.0% 60.6% 70.1%

Enel Latinoamérica Endesa Enersis España

40.32%

Listed Companies

Enersis

Private Companies

Diversification of operations in the world

Europe

North America Capacity: 66.5 GW Russia

Capacity: 2.1 GW Customers: 45.8 mm Capacity: 9.1 GW

Mexico and Central America Capacity: 0.8 GW

Latin America

Capacity: 17.4 GW Africa

Customers: 14.4 mm Capacity: 0.1 GW

Source: Enel

Considers USDEUR exchange rate of 0.75 for 2014 EBITDA and 0.8895 for the CapEx plan (exchange rate as on September 3, 2015)

Strictly Private and Confidential 31

Source: Enel

Considers USDEUR exchange rate of 0.75 for 2014 EBITDA and 0.8895 for the CapEx plan (exchange rate as on September 3, 2015)

Strictly Private and Confidential 31

|

Santiago Office

Avenida Apoquindo 3721, Piso 9 Las Condes 7550177 Chile

+56 (2) 2450 1600

imtrust credicorpcapital