united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-23611

James Alpha Funds Trust

(Exact name of registrant as specified in charter)

515 Madison Avenue, 24th Floor, New York, NY 10022

(Address of principal executive offices) (Zip code)

Emile R. Molineaux

80 Arkay Drive, Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 888-814-8180

Date of fiscal year end: 8/31

Date of reporting period: 8/31/2023

Item 1. Reports to Stockholders.

| |

| |

| |

| |

| |

|

| |

| JAMES ALPHA FUNDS TRUST d/b/a EASTERLY FUNDS TRUST |

| |

| |

| |

| |

| |

| CLASS A, C, I AND R6 SHARES |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| ANNUAL REPORT |

| AUGUST 31, 2023 |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| THIS REPORT IS AUTHORIZED FOR DISTRIBUTION ONLY TO SHAREHOLDERS AND TO OTHERS WHO HAVE RECEIVED A COPY OF THE PROSPECTUS. |

| |

| |

| |

| |

| |

James Alpha Funds Trust d/b/a Easterly Funds Trust

ANNUAL REPORT TO SHAREHOLDERS

September 15, 2023

Dear Shareholder:

We are pleased to provide you with this annual report on the investment strategies and performance of the funds in the James Alpha Funds Trust d/b/a Easterly Funds Trust (the “Trust”). This report covers the twelve months from September 1, 2022 through August 31, 2023.

We believe that successful investing requires discipline and patience. Try to stay focused on your long-term investment goals. Don’t let short-term stock and bond market fluctuations or investment manias change your long-term investment strategy. In our opinion, the Easterly Funds are managed by some of the world’s leading institutional investment advisory firms. It is our belief that combining the strength of the Trust’s performance with a well-designed asset allocation plan can help you to achieve your long-term investment goals.

ECONOMIC OVERVIEW

As measured by Real Gross Domestic Product (GDP), the value of the production of goods and services in the United States accelerated to an annualized growth rate (AGR) of 2.1% during the second quarter of 2023. The economy added an average of 271,000 nonfarm payroll jobs per month over the last year. This happened while the unemployment rate held a low 3.8% level in August and the inflation decreased to 3.2% from above 9% a year ago. Small businesses and consumer sentiments started to increase during the summer of 2023 indicating less risk of a potential recession. This market has been largely controlled by the Federal Reserve, who have signaled their commitment to tightening financial conditions in order to get inflation under control. This is a material break from a decades long precedent where the Fed has been there to provide support during market turmoil. Time will tell whether the Fed is able to engineer its desired ’soft landing’ or if their actions will induce an economic recession. So far it has been working while FED maintained its policy to fight against inflation. Following the Fed’s July 2023 meeting, Powell stated “We intend to keep policy restrictive until we’re confident inflation is coming down sustainably to our 2% target, and we’re prepared to further tighten if that’s appropriate.”

Interest Rates: Treasury yields bottomed in August 2020 and have increased ever since, although the rise has been volatile. In the twelve months since the end of August 2022, 10-year treasury rate has risen from 3.2% to 4.1%. With the Fed continuing to hike rates and aggressively reducing its balance sheet, we believe the environment is supportive for the current interest rates range, and yields will remain steady over the next 12 months.

FUND SPECIFIC OVERVIEW

Real Estate (JARIX)

Global real estate stocks posted a loss for the period between September 1, 2022 and August 31, 2023, as multiple exogenous factors weighed on the capital markets during the year (e.g., central bank tightening to rein in inflation, the war in Ukraine, China’s transition from COVID lock-downs to re-opening its economy, and the regional bank mini-crisis) and continued to distract investors, causing them to keep their attention focused mostly away from industry and company fundamentals. The FTSE EPRA Nareit Developed Index (the “Index”) had a total return of -4.20%, while the Easterly Global Real Estate Fund (the “Fund”) generated a total net return of -6.78%, underperforming the Index by 258 basis points.

20231026-3194948

A historical review of listed real estate returns during periods of high inflation serves as a reminder that real estate values tend to increase with inflation, as rising inflation is typically consistent with a growing economy – the most important driver of demand for most property types. Additionally, commercial real estate leases often incorporate annual rent escalators, helping to provide additional protection of real estate cash flows during inflationary periods.

Higher energy prices, particularly in Europe, reduced consumer spending and negatively impacted sectors exposed to discretionary spending. Notably, the Fund was positioned defensively in Europe, with a substantial portion of its European holdings invested in German residential companies, whose fundamentals are not only unimpacted by rising energy prices but are in fact bolstered by increased demand for housing, spurred by the tide of migrants fleeing Ukraine. Other European positions were similarly insulated from the economic fallout of the conflict in Ukraine, with Specialty property type positions (e.g., Cell Towers, Student Housing and Medical Office Buildings) representing the bulk of the Fund’s remaining European exposure.

The regional bank mini-crisis, thus far, has revealed the lagged effect of rate hikes to date—and the resulting duration mismatch that created an inherent instability among the deposit base. Uncertainty among lenders over the regulatory response (what adjustments if any will be made to the current $250k per account FDIC insurance limit) will likely have a chilling effect on their willingness to make new loans and/or re-finance existing ones. The flipside is that the resulting tightening of credit will do some of the Fed’s work for it, thus shifting the narrative around future rate hikes from “higher for longer” to “just high for longer.” Thus, the path forward in terms of potential impact on the business of commercial real estate will be determined largely, if not solely by the Fed and the Treasury acting in concert to contain and thus prevent the isolated challenges at a small number of regional banks from evolving into widespread contagion that could present a systemic challenge.

Finally, as it relates to the highly challenging outlook for office buildings, particularly those located in Central Business Districts, the impact of fundamental changes in how companies manage their office space needs in the new world order of hybrid work models, owners of office buildings will experience significant headwinds over the next five plus years as existing leases expire and tenants downsize their space needs. The ensuing erosion of value will in some ways be similar to the secular decline in regional malls resulting from the “Amazon effect,” i.e., the disruptive impact of e-commerce. Just as the commercial real estate industry writ large managed to thrive in the face of substantial value destruction in the regional mall sector (which at one time had a larger market capitalization than the office sector), it is certainly plausible that the coming difficulties in the office sector can be contained without spreading to other sectors or the funding markets for commercial real estate.

Despite the macroeconomic and geopolitical stress that is capturing headlines, our outlook for the global real estate market continues to be constructive. Real estate fundamentals and earnings growth remain healthy in an environment characterized by low supply in many sectors, paired with high construction costs. Our high conviction, benchmark-agnostic investment approach allows us to maintain a laser-focus on identifying and owning only the 50 highest-quality companies in our investable universe. We have high conviction in our fundamental research and confidence in the management teams of the companies we own. While global capital markets continue to experience periods of market fixation on non-fundamental factors, we believe our portfolio is well positioned as investor attention turns back to fundamentals.

Hedged Equity (JDIEX)

The investment environment early in the period was characterized by concerns that the Federal reserve would over tighten policy in its efforts to rein in inflationary forces. The four 50 basis point hikes from June through November put equities on notice and spiked the VIX up into the 30+ range in the 4th

20231026-3194948

quarter. This hurt September equity returns as the enormity of the increases began to be absorbed. However, the markets began to position for a slowing pace of inflation expecting Chair Powell’s hopes for a disinflationary path to translate into equity exuberance. While the rhetoric helped drive improved hopes over the next several months for a pause or pivot in FED hikes, the reality did not quite match the expectation. Despite solid economic data and earnings that (while softer) did meet expectations, the concerns around FED policy kept volatility somewhat elevated into March of 2023 leading to a very volatile period despite positive equity returns. Through that period from 8/31/22 until the close of the 1st qtr. 2023 JDIEX delivered 5.45% returns vs the S&P’s 4.95%. Much of that improved return came from the ability of the strategy to collect income from the options positioning in the fund. The period that followed was markedly different in that the market’s hopes for a more dovish FED and moderating inflation with still solid growth allowed for a goldilocks scenario to gain credibility. During that subsequent 3/31 - 8/31/23 period the VIX dropped from the 20 level to 13 and the S&P gained 10.45% vs JDIEX providing 5.08% gains. While the fund’s performance still lay in the middle of its targeted 40-60% of the S&P the impact of reduced volatility could clearly be seen. Over the 8/31/22 - 8/31/23 period, JDIEX gained 10.80% vs the SPX 15.92%. JDIEX provided a very solid 68% participation rate, which looks particularly attractive considering our ~40% of the market’s volatility level. Given the drop in volatility, the manager’s use of shorter dated options expiries while seeking to maximize income of the overlay resulted in a better than one would expect participation rate.

The transitional period of underlying fundamentals and still very involved FOMC gave a very bi-modal feel to the period. Between dovish and hawkish datapoints and FED meetings that all were in play, trading ranges for both equities and the VIX were quite wide. As the period progressed, however, greater bullishness took hold making it imperative to actively manage the overlay structure to optimize the best levels from which to defend (the put spreads) without giving up excessive upside (the short calls). While market momentum and technical indicators became positive after the first quarter, it is important to note that both global and domestic economic datapoints showed some risk of recession. With very strong consumer and services sector data, however, those calls for recession have been held at bay. Both the labor and inflation data have to date allowed for the safe landing narrative to hold true. Additional impetus was also felt as the summer progressed in the hopes of an AI led tech sector and overall productivity boom. Despite that powerful AI driven hope, as the period ended, there were rumblings that tech and high PE stocks, which have powered the S&P, may be growing vulnerable to price for perfection realities if inflation, earnings, the macro, and geopolitical levers stop pulling in such synchronized fashion. As such, August was a more difficult month for the index and the fund defended appropriately. While the downdraft was relatively small, we point out that many of those priced for perfection factors remain in place and make a strong case for the defensive approach the fund takes. As we have said before, the market correction process is rarely a one-time event or straight-line process. We continue to see volatility levels as too complacent but can never predict when spikes will come. We remain committed as a result, to a systematic approach executed by the managers that reconciles the levels of volatility, equity price levels, and the skew of bullishness and bearishness in the market mathematically to keep the options positions in a net neutral to positive carry.

The fund has not changed its distribution policy since the last report.

The fund accesses exposure to the S&P 500 by entering into a 13-month swap with Goldman Sachs for up to 130% of the return of the index. The second way the fund uses derivatives is through the put spread collar strategy the fund uses. The fund remains long the market to a 30% level (the excess achieved in the swap) and generally targets between 40-60% S&P exposure which can, in market declines, move towards zero exposure if the market approaches our short put within expiry constraints. The derivatives strategy targets a positive carry result which trades off some upside for meaningful downside protection.

Both the investment process and results were consistent in keeping with the stated policy and objectives.

20231026-3194948

COMPARING THE FUND PERFORMANCE TO BENCHMARKS

When reviewing the performance of the funds against their benchmarks, it is important to note that the Trust is designed to help investors to implement an asset allocation strategy to meet their individual needs as well as select individual investments within each asset category among the myriad of choices available. Each Easterly Fund was formed to represent an asset class, and each portfolio’s institutional money manager was selected based on their ability to manage money within that class.

Therefore, the Easterly Funds may be able to help investors to properly implement their asset allocation decisions and keep their investments within the risk parameters that they establish with their investment consultants. Without the intended asset class consistency of the Easterly Funds, even the most carefully crafted allocation strategy could be negated. Furthermore, we believe the benchmarks do not necessarily provide precise standards against which to measure the portfolios, in that the characteristics of the benchmarks can vary widely at different points in time from the Easterly Funds (e.g., characteristics such as: average market capitalizations, price-to-earnings and price-to-book ratios, bond quality ratings and maturities, etc.) . In addition, the benchmarks can potentially have a survivor bias built into them (i.e., the performance of only funds that are still in existence may remain part of the benchmark’s performance while funds that do not exist anymore may be removed from the benchmark’s performance).

ELECTRONIC DELIVERY AVAILABLE

This report can be delivered to you electronically. Electronic delivery can help simplify your record keeping. With electronic delivery, you’ll receive an email with a link to your James Alpha Funds Trust quarterly statement, daily confirmations and/or semi-annual and annual reports each time one is available. You have the ability to choose which items you want delivered electronically. Choose one item or all items. It’s up to you. Please call our Customer Service Department toll-free at (833) 999-2636 for instructions on how to establish electronic delivery.

Investors should consider the investment objectives, risks, charges and expenses of the Easterly Funds carefully. This and other information about the Easterly Funds is contained in your prospectus, which should be read carefully. To obtain an additional copy of the prospectus, please call 888.814.8180. Past performance is not indicative of future results. Investments in stocks, bonds and mutual funds are not guaranteed and the principal value and investment return can fluctuate. Consequently, investors may receive back less than invested.

The S&P 500 is an unmanaged, capitalization-weighted index. It is not possible to invest directly in the S&P 500.

The security holdings discussed may not be representative of the Funds’ current or future investments. Fund holdings are subject to change and should not be considered to be investment advice. Any statements not of a factual nature constitute opinions which are subject to change without notice. Information contained herein was obtained from recognized statistical services and other sources believed to be reliable and we therefore cannot make any representation as to its completeness or accuracy.

Easterly Funds, LLC serves as the Adviser to the Easterly Fund family of mutual funds and related portfolios. Easterly Funds, LLC is registered as investment advisers with the SEC. Effective 10/2/2023, the Easterly mutual funds are distributed by Easterly Securities, LLC. Although Easterly Funds, LLC is a registered investment adviser, registration itself does not imply and should not be interpreted to imply any particular level of skill or training.

20231026-3194948

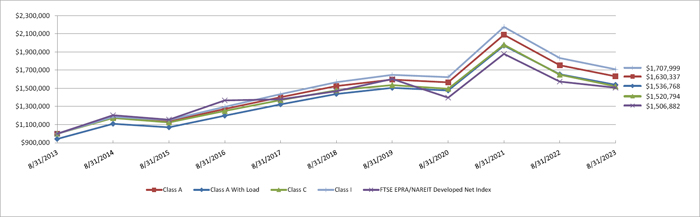

Easterly Global Real Estate Fund

PORTFOLIO REVIEW (Unaudited)

August 31, 2023

The Fund’s performance figures* for the year ended August 31, 2023, as compared to its benchmark:

| | | Annualized | Annualized | Annualized | Annualized | Annualized | Annualized |

| | One Year | Five Year | Ten Year | Since Inception (a) | Since Inception (b) | Since Inception (c) | Since Inception (d) |

| Class A | (7.06)% | 1.35% | 5.01% | 6.92% | n/a | n/a | n/a |

| Class A With Load | (12.41)% | 0.16% | 4.39% | 6.47% | n/a | n/a | n/a |

| Class C | (7.80)% | 0.58% | 4.28% | n/a | 5.90% | n/a | n/a |

| Class I | (6.78)% | 1.73% | 5.50% | n/a | n/a | 5.96% | n/a |

| Class R6 | (6.61)% | 1.93% | n/a | n/a | n/a | n/a | 3.28% |

FTSE EPRA/NAREIT

Developed Net Index (e) | (4.20)% | 0.52% | 4.18% | 5.92% | 5.72% | 4.46% | 1.59% |

Comparison of the Change in Value of a $1,000,000 Investment

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (833) 999-2636. The total operating expense ratio as stated in the fee table to the Fund’s prospectus dated December 31, 2022, is 1.36%, 2.11%, 1.11% and 1.11% for the A, C, I and R6 Classes, respectively.

| (a) | Inception date for Class A is October 26, 2009. |

| (b) | Inception date for Class C is January 5, 2012. |

| (c) | Inception date for Class I is August 1, 2011. |

| (d) | Inception date for Class R6 is August 17, 2017. |

| (e) | The FTSE EPRA/NAREIT Developed Net Index is designed to represent general trends in eligible real estate equities worldwide. Relevant real estate activities are defined as the ownership, disposure and development of income-producing real estate. |

| Top 10 Holdings by Country | | % of Net Assets | |

| United States | | | 45.5 | % |

| Germany | | | 10.2 | % |

| Japan | | | 9.4 | % |

| United Kingdom | | | 8.9 | % |

| Spain | | | 6.9 | % |

| Hong Kong | | | 5.5 | % |

| Cayman Islands | | | 3.5 | % |

| Bermuda | | | 2.4 | % |

| Singapore | | | 2.1 | % |

| Canada | | | 1.5 | % |

| Other/Cash & Equivalents | | | 4.1 | % |

| | | | 100.0 | % |

Please refer to the Schedule of Investments for a more detailed breakdown of the Fund’s assets.

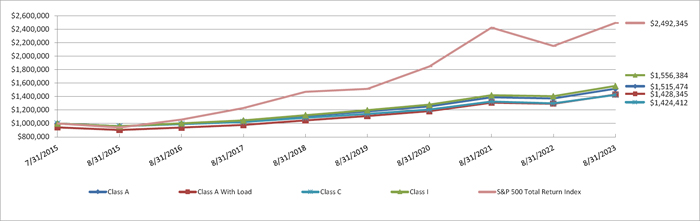

Easterly Hedged Equity Fund

PORTFOLIO REVIEW (Unaudited)

August 31, 2023

The Fund’s performance figures* for the year ended August 31, 2023, as compared to its benchmark:

| | | Annualized | Annualized | Annualized |

| | One Year | Five Year | Since Inception (a) | Since Inception (b) |

| Class A | 10.45% | 6.47% | 5.28% | n/a |

| Class A With Load | 8.28% | 5.21% | 4.51% | n/a |

| Class C | 9.70% | 5.61% | 4.47% | n/a |

| Class I | 10.80% | 6.73% | 5.62% | n/a |

| Class R6 | 11.10% | 7.16% | n/a | 7.42% |

| S&P 500 Total Return Index (c) | 15.94% | 11.12% | 11.96% | 12.75% |

Comparison of the Change in Value of a $1,000,000 Investment

Performance data quoted above is historical. Past performance does not guarantee future results and current performance may be lower or higher than the performance data quoted. The investment return and principal value of an investment will fluctuate, so that shares when redeemed, may be worth more or less than their original cost. For more performance numbers current to the most recent month-end please call (833) 999-2636. The total operating expense ratio as stated in the fee table to the Fund’s prospectus dated December 31, 2022, is 2.10%, 2.85%, 1.85% and 1.85% for the A, C, I and R6 Classes, respectively.

| (a) | Inception date for Class A, C and I is July 31, 2015. |

| (b) | Inception date for Class R6 is August 17, 2017. |

| (c) | The S&P 500 Total Return Index is an unmanaged free-float capitalization-weighted index which measures the performance of 500 large-cap common stocks actively traded in the United States. Index returns assume reinvestment of dividends. Investors may not invest in the Index directly. Unlike the Fund’s returns, the Index does not reflect any fees or expenses. |

| Top 10 Holdings by Security Type | | % of Net Assets | |

| Exchange Traded Funds | | | 91.9 | % |

| Put Options Purchased | | | 0.4 | % |

| Put Options Written | | | (0.1 | )% |

| Call Options Written | | | (1.1 | )% |

| Other/Cash & Equivalents | | | 8.9 | % |

| | | | 100.0 | % |

Please refer to the Schedule of Investments for a more detailed breakdown of the Fund’s assets.

| EASTERLY GLOBAL REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS |

| August 31, 2023 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 97.8% | | | | |

| | | | | Bermuda - 2.4% | | | | |

| | 3,335,447 | | | Hongkong Land Holdings Ltd. | | $ | 11,840,837 | |

| | | | | | | | | |

| | | | | Canada - 1.5% | | | | |

| | 209,885 | | | Canadian Apartment Properties REIT | | | 7,527,675 | |

| | | | | | | | | |

| | | | | Cayman Islands - 3.5% | | | | |

| | 571,760 | | | CK Asset Holdings Ltd. | | | 3,154,844 | |

| | 4,003,464 | | | ESR Group Ltd. | | | 6,007,316 | |

| | 487,957 | | | GDS Holdings Ltd. - ADR(a) | | | 5,835,966 | |

| | 568,505 | | | Wharf Real Estate Investment Company Ltd. | | | 2,369,293 | |

| | | | | | | | 17,367,419 | |

| | | | | France - 1.2% | | | | |

| | 229,632 | | | Klepierre S.A. | | | 6,068,774 | |

| | | | | | | | | |

| | | | | Germany - 10.2% | | | | |

| | 864,650 | | | Deutsche Wohnen S.E. | | | 19,812,462 | |

| | 1,379,456 | | | Instone Real Estate Group A.G. | | | 8,821,112 | |

| | 950,506 | | | TAG Immobilien A.G.(a) | | | 10,780,985 | |

| | 489,472 | | | Vonovia S.E. | | | 11,750,555 | |

| | | | | | | | 51,165,114 | |

| | | | | Guernsey - 0.7% | | | | |

| | 3,376,570 | | | Sirius Real Estate Ltd. | | | 3,721,533 | |

| | | | | | | | | |

| | | | | Hong Kong - 5.5% | | | | |

| | 5,568,225 | | | Link REIT | | | 27,607,498 | |

| | | | | | | | | |

| | | | | Japan - 9.4% | | | | |

| | 18,274 | | | Japan Hotel REIT Investment Corporation | | | 9,263,251 | |

| | 2,323,497 | | | Mitsubishi Estate Company Ltd. | | | 29,601,316 | |

| | 2,368 | | | Mitsui Fudosan Logistics Park, Inc. | | | 8,059,762 | |

| | | | | | | | 46,924,329 | |

| | | | | Singapore - 2.1% | | | | |

| | 4,763,417 | | | Keppel DC REIT | | | 7,749,598 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| EASTERLY GLOBAL REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| August 31, 2023 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 97.8% (Continued) | | | | |

| | | | | Singapore - 2.1% (Continued) | | | | |

| | 2,609,628 | | | Mapletree Pan Asia Commercial Trust | | $ | 2,933,111 | |

| | | | | | | | 10,682,709 | |

| | | | | Spain - 6.9% | | | | |

| | 895,755 | | | Cellnex Telecom S.A. | | | 34,277,568 | |

| | | | | | | | | |

| | | | | United Kingdom - 8.9% | | | | |

| | 15,982,849 | | | Assura PLC | | | 9,278,155 | |

| | 5,586,591 | | | Empiric Student Property PLC | | | 6,167,259 | |

| | 3,250,002 | | | Grainger PLC | | | 9,710,627 | |

| | 411,379 | | | Great Portland Estates PLC | | | 2,186,475 | |

| | 605,512 | | | Segro PLC | | | 5,644,608 | |

| | 954,848 | | | UNITE Group PLC (The) | | | 11,356,119 | |

| | | | | | | | 44,343,243 | |

| | | | | United States - 45.5% | | | | |

| | 969,085 | | | Acadia Realty Trust | | | 14,429,676 | |

| | 140,404 | | | Alexandria Real Estate Equities, Inc. | | | 16,334,601 | |

| | 24,738 | | | Americold Realty Trust, Inc. | | | 832,434 | |

| | 586,479 | | | Broadstone Net Lease, Inc. | | | 9,483,365 | |

| | 76,014 | | | Camden Property Trust | | | 8,180,627 | |

| | 57,423 | | | CBRE Group, Inc., Class A(a) | | | 4,883,826 | |

| | 463,810 | | | CoreCivic, Inc.(a) | | | 4,990,596 | |

| | 1,022,175 | | | DigitalBridge Group, Inc. | | | 17,806,289 | |

| | 368,532 | | | Easterly Government Properties, Inc. | | | 4,927,273 | |

| | 1,069,204 | | | Ellington Financial, Inc. | | | 14,295,257 | |

| | 197,265 | | | Elme Communities | | | 3,033,936 | |

| | 440,546 | | | Equity Commonwealth | | | 8,383,590 | |

| | 859,032 | | | GEO Group, Inc. (The)(a) | | | 6,219,391 | |

| | 842,606 | | | Independence Realty Trust, Inc. | | | 14,181,059 | |

| | 213,704 | | | Kilroy Realty Corporation | | | 7,896,363 | |

| | 173,910 | | | Prologis, Inc. | | | 21,599,622 | |

| | 25,000 | | | Realty Income Corporation | | | 1,401,000 | |

| | 692,494 | | | Retail Opportunity Investments Corporation | | | 9,320,969 | |

| | 36,005 | | | SBA Communications Corporation | | | 8,084,203 | |

| | 191,039 | | | Sun Communities, Inc. | | | 23,386,995 | |

| | | | | | | | | |

See accompanying notes to financial statements.

| EASTERLY GLOBAL REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| August 31, 2023 |

| Shares | | | | | Fair Value | |

| | | | | COMMON STOCKS — 97.8% (Continued) | | | | |

| | | | | United States - 45.5% (Continued) | | | | |

| | 560,566 | | | UDR, Inc. | | $ | 22,366,583 | |

| | 118,949 | | | Ventas, Inc. | | | 5,195,692 | |

| | | | | | | | 227,233,347 | |

| | | | | | | | | |

| | | | | TOTAL COMMON STOCKS (Cost $871,103,510) | | | 488,760,046 | |

| | | | | | | | | |

| | | | | TOTAL INVESTMENTS – 97.8% (Cost $871,103,510) | | $ | 488,760,046 | |

| | | | | OTHER ASSETS IN EXCESS OF LIABILITIES – 2.2% | | | 11,170,583 | |

| | | | | NET ASSETS - 100.0% | | $ | 499,930,629 | |

ADR - American Depositary Receipt

Ltd. - Limited Company

PLC - Public Limited Company

REIT - Real Estate Investment Trust

A.G. - Aktiengesellschaft

S.A. - Société Anonyme

S.E. - Societas Europeae

| (a) | Non-income producing security. |

See accompanying notes to financial statements.

| EASTERLY GLOBAL REAL ESTATE FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| August 31, 2023 |

Forward Currency Contracts

| Units to | | | | | | US Dollar | | | | | Settlement | | Unrealized | |

| Receive/Deliver | | | In Exchange For | | | Value | | | Counterparty | | Date | | Appreciation/(Depreciation) | |

| To Sell: | | | | | | | | | | | | | | | | | |

| $ | (353,008,058 | ) JPY | | $ | (2,416,324 | ) USD | | $ | (2,426,822 | ) | | Brown Brothers Harriman | | 9/1/2023 | | $ | (10,498 | ) |

| | (412,744,750 | ) JPY | | | (2,837,240 | ) USD | | | (2,837,494 | ) | | Brown Brothers Harriman | | 9/5/2023 | | | (254 | ) |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | Total: | | $ | (10,752 | ) |

Currency Abbreviations:

JPY - Japanes Yen

USD - U.S. Dollar

See accompanying notes to financial statements.

| EASTERLY HEDGED EQUITY FUND |

| SCHEDULE OF INVESTMENTS |

| August 31, 2023 |

| Shares | | | | | | | | | | | | | | | Fair Value | |

| | | | | EXCHANGE-TRADED FUNDS — 91.9% | | | | | | |

| | | | | EQUITY - 91.9% | | | | | | | | | | |

| | 242,500 | | | SPDR S&P 500 ETF Trust(a) | | | | $ | 109,209,875 | |

| | | | | TOTAL EXCHANGE-TRADED FUNDS (Cost $91,812,151) | | | | | | |

| | | | | | | | | | | | | | | | | | | | | |

| Contracts(b) | | | | | Counterparty | | Expiration Date | | Exercise Price | | | Notional Value | | | | | |

| | | | | INDEX OPTIONS PURCHASED - 0.4% | | | | | | | | | | | | |

| | | | | PUT OPTIONS PURCHASED - 0.4% | | | | | | | | | | | | |

| | 50 | | | S&P 500 Index | | PER | | 09/01/2023 | | $ | 4,400 | | | $ | 22,538,300 | | | $ | 1,500 | |

| | 100 | | | S&P 500 Index | | PER | | 09/08/2023 | | | 4,375 | | | | 45,076,600 | | | | 19,750 | |

| | 210 | | | S&P 500 Index | | PER | | 09/15/2023 | | | 4,325 | | | | 94,660,860 | | | | 94,500 | |

| | 150 | | | S&P 500 Index | | PER | | 09/29/2023 | | | 4,350 | | | | 67,614,900 | | | | 243,000 | |

| | 55 | | | S&P 500 Index | | PER | | 09/29/2023 | | | 4,415 | | | | 24,792,130 | | | | 139,425 | |

| | | | | TOTAL PUT OPTIONS PURCHASED (Cost - $2,156,717) | | | | | 498,175 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | TOTAL INVESTMENTS – 92.3% (Cost $93,968,868) | | | | | | | $ | 109,708,050 | |

| | | | | PUT OPTIONS WRITTEN - (0.1)% (Proceeds - $561,202) | | | | | (144,250 | ) |

| | | | | CALL OPTIONS WRITTEN - (1.1)% (Proceeds - $691,127) | | | | | (1,341,400 | ) |

| | | | | OTHER ASSETS IN EXCESS OF LIABILITIES – 8.9% | | | | | | 10,614,007 | |

| | | | | NET ASSETS - 100.0% | | | | | | | | $ | 118,836,407 | |

| | | | | | | | | | | | | | | | | | | | | |

| Contracts(b) | | | | | Counterparty | | Expiration Date | | Exercise Price | | | Notional Value | | | | | |

| | | | | WRITTEN INDEX OPTIONS - (0.1)% | | | | | | | | | | | | |

| | | | | PUT OPTIONS WRITTEN - (0.1)% | | | | | | | | | | | | |

| | 50 | | | S&P 500 Index | | PER | | 09/01/2023 | | $ | 4,180 | | | $ | 22,538,300 | | | $ | 750 | |

| | 100 | | | S&P 500 Index | | PER | | 09/08/2023 | | | 4,160 | | | | 45,076,600 | | | | 6,750 | |

| | 210 | | | S&P 500 Index | | PER | | 09/15/2023 | | | 4,100 | | | | 94,660,860 | | | | 30,975 | |

| | 150 | | | S&P 500 Index | | PER | | 09/29/2023 | | | 4,130 | | | | 67,614,900 | | | | 69,750 | |

| | 55 | | | S&P 500 Index | | PER | | 09/29/2023 | | | 4,200 | | | | 24,792,130 | | | | 36,025 | |

| | | | | TOTAL PUT OPTIONS WRITTEN (Proceeds - $561,202) | | | | | | 144,250 | |

| | | | | | | | | | | | | | | | | | | | | |

| | | | | WRITTEN EQUITY OPTIONS - (1.1)% | | | | | | | |

| | | | | CALL OPTIONS WRITTEN- (1.1)% | | | | | | |

| | 500 | | | SPDR S&P 500 ETF Trust | | PER | | 09/01/2023 | | | 441 | | | | 22,517,500 | | | | 491,000 | |

| | 500 | | | SPDR S&P 500 ETF Trust | | PER | | 09/15/2023 | | | 448 | | | | 22,517,500 | | | | 296,000 | |

| | 250 | | | SPDR S&P 500 ETF Trust | | PER | | 09/15/2023 | | | 450 | | | | 11,258,750 | | | | 115,500 | |

| | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to financial statements.

| EASTERLY HEDGED EQUITY FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| August 31, 2023 |

| Contracts(b) | | | | | Counterparty | | Expiration Date | | Exercise Price | | | Notional Value | | | Fair Value | |

| | | | | WRITTEN EQUITY OPTIONS - (1.1)% (Continued) | | | | | | | | | | | | |

| | | | | CALL OPTIONS WRITTEN - (1.1)% (Continued) | | | | | | | | | | | | |

| | 450 | | | SPDR S&P 500 ETF Trust | | PER | | 09/15/2023 | | $ | 455 | | | $ | 20,265,750 | | | $ | 96,750 | |

| | 450 | | | SPDR S&P 500 ETF Trust | | PER | | 09/22/2023 | | | 450 | | | | 20,265,750 | | | | 245,250 | |

| | 300 | | | SPDR S&P 500 ETF Trust | | PER | | 09/29/2023 | | | 456 | | | | 13,510,500 | | | | 96,900 | |

| | | | | TOTAL CALL OPTIONS WRITTEN (Proceeds - $691,127) | | | | | 1,341,400 | |

ETF - Exchange-Traded Fund

SPDR - Standard & Poor’s Depositary Receipt

PER - Pershing

| (a) | A portion of this security is held as collateral for written options. |

| (b) | Each option contract allows the holder of the option to purchase or sell 100 shares of the underlying security. |

See accompanying notes to financial statements.

| EASTERLY HEDGED EQUITY FUND |

| SCHEDULE OF INVESTMENTS (Continued) |

| August 31, 2023 |

TOTAL RETURN SWAP

| | | | | | | | | | | | | | | | | | | | | | Upfront | | | Unrealized | |

| | | Payment | | | | | | | | | | | | Number Of | | Maturity | | Notional | | | Payments/ | | | Appreciation/ | |

| Description | | Frequency | | Long/Short | | Currency | | Index | | Spread | | Counterparty | | Contracts | | Date | | Amount | | | Receipts | | | (Depreciation) | |

| SPDR S&P 500 ETF Trust | | Monthly | | Long | | USD | | Federal Funds Rate | | 0.55% | | Goldman Sachs | | 15,000 | | 10/2/2023 | | $ | 6,004,950 | | | $ | — | | | $ | 552,901 | |

| SPDR S&P 500 ETF Trust | | Monthly | | Long | | USD | | Federal Funds Rate | | 0.55% | | Goldman Sachs | | 10,000 | | 5/20/2024 | | | 4,125,191 | | | | — | | | | 310,116 | |

| SPDR S&P 500 ETF Trust | | Monthly | | Long | | USD | | Federal Funds Rate | | 0.55% | | Goldman Sachs | | 67,500 | | 8/21/2024 | | | 30,522,150 | | | | — | | | | (311,597 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | 551,420 | |

See accompanying notes to financial statements.

| STATEMENTS OF ASSETS AND LIABILITIES |

| August 31, 2023 |

| | | Easterly | | | Easterly | |

| | | Global Real Estate | | | Hedged Equity | |

| | | Fund | | | Fund | |

| | | | | | | |

| Assets: | | | | | | | | |

| Total Investments, at cost | | $ | 871,103,510 | | | $ | 93,968,868 | |

| Total Investments, at value | | | 488,760,046 | | | | 109,708,050 | |

| Cash | | | 3,883,413 | | | | 8,606,365 | |

| Foreign Cash (Cost $164,327, $0) | | | 165,576 | | | | — | |

| Deposit at Broker | | | — | | | | 1,635,216 | |

| Unrealized appreciation on swaps | | | — | | | | 863,017 | |

| Interest and dividends receivable | | | 1,928,902 | | | | — | |

| Receivable for securities sold | | | 8,499,809 | | | | 35,724 | |

| Receivable for fund shares sold | | | 115,406 | | | | 131,228 | |

| Prepaid expenses and other assets | | | 39,754 | | | | 32,703 | |

| Total Assets | | | 503,392,906 | | | | 121,012,303 | |

| | | | | | | | | |

| Liabilities: | | | | | | | | |

| Options Written (premiums received $0, $1,252,329) | | | — | | | | 1,485,650 | |

| Payable for securities purchased | | | 1,402,968 | | | | 138,626 | |

| Payable to manager | | | 359,569 | | | | 83,761 | |

| Payable for distribution (12b-1) fees | | | 77,821 | | | | 1,191 | |

| Payable for fund shares redeemed | | | 1,310,828 | | | | 80,323 | |

| Administration fees payable | | | 63,160 | | | | 23,168 | |

| Trustee fees payable | | | 3,589 | | | | 3,919 | |

| Unrealized depreciation on forward currency contracts | | | 10,752 | | | | — | |

| Unrealized depreciation on swaps | | | — | | | | 311,597 | |

| Accrued expenses and other liabilities | | | 233,590 | | | | 47,661 | |

| Total Liabilities | | | 3,462,277 | | | | 2,175,896 | |

| | | | | | | | | |

| Net Assets | | $ | 499,930,629 | | | $ | 118,836,407 | |

| | | | | | | | | |

| Net Assets: | | | | | | | | |

| Paid in capital | | | 898,366,871 | | | | 110,677,268 | |

| Accumulated earnings (loss) | | | (398,436,242 | ) | | | 8,159,139 | |

| Net Assets | | $ | 499,930,629 | | | $ | 118,836,407 | |

| | | | | | | | | |

| Net Asset Value Per Share | | | | | | | | |

| Class A | | | | | | | | |

| Net Assets | | $ | 56,486,609 | | | $ | 3,347,511 | |

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | | | 4,360,006 | | | | 310,683 | |

| Net asset value, redemption price per share | | $ | 12.96 | | | $ | 10.77 | |

| Offering price per share (maximum sales charge of 5.75% and 5.75%, respectively) | | $ | 13.75 | | | $ | 11.43 | |

| | | | | | | | | |

| Class C | | | | | | | | |

| Net Assets | | $ | 34,242,680 | | | $ | 459,654 | |

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | | | 2,634,144 | | | | 43,721 | |

| Net asset value, offering price per share (a) | | $ | 13.00 | | | $ | 10.51 | |

| | | | | | | | | |

| Class I | | | | | | | | |

| Net Assets | | $ | 376,980,300 | | | $ | 113,263,732 | |

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | | | 27,513,907 | | | | 10,333,699 | |

| Net asset value, redemption price and offering price per share | | $ | 13.70 | | | $ | 10.96 | |

| | | | | | | | | |

| Class R6 | | | | | | | | |

| Net Assets | | $ | 32,221,040 | | | $ | 1,765,510 | |

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] | | | 2,313,680 | | | | 156,335 | |

| Net asset value, redemption price and offering price per share | | $ | 13.93 | | | $ | 11.29 | |

| | | | | | | | | |

| (a) | Redemption price per C share varies based on length of time shares are held. |

See accompanying notes to financial statements.

| STATEMENTS OF OPERATIONS |

| For the Year Ended August 31, 2023 |

| | | Easterly | | | Easterly | |

| | | Global Real Estate | | | Hedged Equity | |

| | | Fund | | | Fund | |

| | | | | | | |

| Investment Income: | | | | | | | | |

| Dividend income | | $ | 17,494,489 | | | $ | 1,345,156 | |

| Interest income | | | 81,167 | | | | 140,281 | |

| Less: Foreign withholding taxes | | | (70,511 | ) | | | — | |

| Total Investment Income | | | 17,505,145 | | | | 1,485,437 | |

| | | | | | | | | |

| Operating Expenses: | | | | | | | | |

| Management fees | | | 5,333,095 | | | | 1,180,990 | |

| Distribution (12b-1) fees | | | | | | | | |

| Class A Shares | | | 169,942 | | | | 6,387 | |

| Class C Shares | | | 409,440 | | | | 3,684 | |

| Shareholder servicing fees | | | 776,078 | | | | 87,765 | |

| Administration fees | | | 401,028 | | | | 113,623 | |

| Registration fees | | | 108,117 | | | | 36,459 | |

| Custodian fees | | | 65,793 | | | | 21,072 | |

| Legal fees | | | 63,985 | | | | 67,559 | |

| Printing and postage expense | | | 63,928 | | | | 9,061 | |

| Audit fees | | | 41,501 | | | | 19,512 | |

| Trustees’ fees | | | 17,480 | | | | 15,241 | |

| Compliance officer fees | | | 8,250 | | | | 6,691 | |

| Interest Expense | | | — | | | | 101,745 | |

| Insurance expense | | | 25,313 | | | | 3,427 | |

| Miscellaneous expenses | | | 15,457 | | | | 6,387 | |

| Total Operating Expenses | | | 7,499,407 | | | | 1,679,603 | |

| Less: Expenses waived and/or reimbursed | | | (664,778 | ) | | | (355,145 | ) |

| Net Operating Expenses | | | 6,834,629 | | | | 1,324,458 | |

| | | | | | | | | |

| Net Investment Income | | | 10,670,516 | | | | 160,979 | |

| | | | | | | | | |

| Realized and Unrealized Gain (Loss) on Investments: | | | | | | | | |

| Net realized gain (loss) from: | | | | | | | | |

| Investments and Foreign currency transactions | | | (20,483,354 | ) | | | 993,984 | |

| Options purchased | | | — | | | | (11,040,817 | ) |

| Options written | | | 1,054,208 | | | | 9,816,199 | |

| Swaps | | | — | | | | (259,679 | ) |

| Net realized loss from: | | | (19,429,146 | ) | | | (490,313 | ) |

| | | | | | | | | |

| Net change in unrealized appreciation (depreciation) on: | | | | | | | | |

| Investments and Foreign currency transactions | | | (47,189,949 | ) | | | 12,868,633 | |

| Options purchased | | | — | | | | (7,460,213 | ) |

| Options written | | | — | | | | 1,548,457 | |

| Swaps | | | — | | | | 3,807,593 | |

| | | | | | | | | |

| Net change in unrealized appreciation (depreciation) | | | (47,189,949 | ) | | | 10,764,470 | |

| | | | | | | | | |

| Net Realized and Unrealized Gain (Loss) on investments | | | (66,619,095 | ) | | | 10,274,157 | |

| | | | | | | | | |

| Net Increase (Decrease) in Net Assets Resulting From Operations | | $ | (55,948,579 | ) | | $ | 10,435,136 | |

See accompanying notes to financial statements.

| STATEMENTS OF CHANGES IN NET ASSETS |

| | | Easterly | | | Easterly | |

| | | Global Real Estate Fund | | | Hedged Equity Fund | |

| | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, 2023 | | | August 31, 2022 | | | August 31, 2023 | | | August 31, 2022 | |

| | | | | | | | | | | | | | | | | |

| Operations: | | | | | | | | | | | | | | | | |

| Net investment income (loss) | | $ | 10,670,516 | | | $ | 8,831,585 | | | $ | 160,979 | | | $ | (30,416 | ) |

| Net realized gain (loss) on investments, options, swaps and foreign currency transactions | | | (19,429,146 | ) | | | 53,090,350 | | | | (490,313 | ) | | | 5,594,111 | |

| Net change in unrealized appreciation (depreciation) on investments, options, swaps and foreign currency transactions | | | (47,189,949 | ) | | | (210,858,339 | ) | | | 10,764,470 | | | | (5,775,863 | ) |

| Net increase (decrease) in net assets resulting from operations | | | (55,948,579 | ) | | | (148,936,404 | ) | | | 10,435,136 | | | | (212,168 | ) |

| | | | | | | | | | | | | | | | | |

| Distributions to Shareholders: | | | | | | | | | | | | | | | | |

| Total Distributions Paid: | | | | | | | | | | | | | | | | |

| Class A | | | (2,994,528 | ) | | | (10,389,606 | ) | | | (52,730 | ) | | | (159,839 | ) |

| Class C | | | (1,532,971 | ) | | | (5,756,611 | ) | | | (9,205 | ) | | | (46,485 | ) |

| Class I | | | (18,980,290 | ) | | | (58,618,796 | ) | | | (1,701,742 | ) | | | (3,349,453 | ) |

| Class R6 | | | (1,722,951 | ) | | | (2,967,024 | ) | | | (233,071 | ) | | | (1,728,423 | ) |

| Total Dividends and Distributions to Shareholders | | | (25,230,740 | ) | | | (77,732,037 | ) | | | (1,996,748 | ) | | | (5,284,200 | ) |

| | | | | | | | | | | | | | | | | |

| Share Transactions of Beneficial Interest: | | | | | | | | | | | | | | | | |

| Beneficial Interest: | | | | | | | | | | | | | | | | |

| Net proceeds from shares sold | | | | | | | | | | | | | | | | |

| Class A | | | 4,782,117 | | | | 16,302,732 | | | | 2,116,408 | | | | 229,649 | |

| Class C | | | 1,088,594 | | | | 4,775,820 | | | | 158,993 | | | | 58,000 | |

| Class I | | | 79,179,790 | | | | 230,263,714 | | | | 70,237,091 | | | | 39,952,049 | |

| Class R6 | | | 11,825,628 | | | | 40,438,846 | | | | 245,626 | | | | 2,178,179 | |

| Reinvestment of dividends and distributions | | | | | | | | | | | | | | | | |

| Class A | | | 2,715,520 | | | | 9,136,407 | | | | 50,354 | | | | 148,171 | |

| Class C | | | 1,412,599 | | | | 4,933,360 | | | | 9,204 | | | | 41,686 | |

| Class I | | | 13,897,461 | | | | 40,226,193 | | | | 1,596,104 | | | | 1,869,684 | |

| Class R6 | | | 1,171,675 | | | | 2,542,936 | | | | 181,506 | | | | 1,035,979 | |

| Cost of shares redeemed | | | | | | | | | | | | | | | | |

| Class A | | | (37,528,473 | ) | | | (17,161,581 | ) | | | (583,456 | ) | | | (560,903 | ) |

| Class C | | | (15,121,168 | ) | | | (16,200,811 | ) | | | (99,271 | ) | | | (424,084 | ) |

| Class I | | | (228,192,330 | ) | | | (208,222,388 | ) | | | (28,314,246 | ) | | | (9,900,348 | ) |

| Class R6 | | | (25,860,842 | ) | | | (13,394,297 | ) | | | (10,375,514 | ) | | | (8,048,979 | ) |

| | | | | | | | | | | | | | | | | |

| Net increase (decrease) in net assets from share transactions of beneficial interest | | | (190,629,429 | ) | | | 93,640,931 | | | | 35,222,799 | | | | 26,579,083 | |

| | | | | | | | | | | | | | | | | |

| Total Increase (Decrease) in Net Assets | | | (271,808,748 | ) | | | (133,027,510 | ) | | | 43,661,187 | | | | 21,082,715 | |

| | | | | | | | | | | | | | | | | |

| Net Assets: | | | | | | | | | | | | | | | | |

| Beginning of year | | | 771,739,377 | | | | 904,766,887 | | | | 75,175,220 | | | | 54,092,505 | |

| End of year | | $ | 499,930,629 | | | $ | 771,739,377 | | | $ | 118,836,407 | | | $ | 75,175,220 | |

| | | | | | | | | | | | | | | | | |

| Share Activity | | | | | | | | | | | | | | | | |

| Shares sold | | | | | | | | | | | | | | | | |

| Class A | | | 365,902 | | | | 937,001 | | | | 208,051 | | | | 21,445 | |

| Class C | | | 81,935 | | | | 273,452 | | | | 15,453 | | | | 5,409 | |

| Class I | | | 5,679,009 | | | | 12,693,288 | | | | 6,768,998 | | | | 3,941,739 | |

| Class R6 | | | 840,457 | | | | 2,232,739 | | | | 23,538 | | | | 201,456 | |

| Shares Reinvested | | | | | | | | | | | | | | | | |

| Class A | | | 214,237 | | | | 516,499 | | | | 5,045 | | | | 14,344 | |

| Class C | | | 110,770 | | | | 276,044 | | | | 940 | | | | 4,083 | |

| Class I | | | 1,038,822 | | | | 2,167,738 | | | | 157,562 | | | | 178,746 | |

| Class R6 | | | 86,167 | | | | 134,943 | | | | 17,419 | | | | 96,640 | |

| Shares Redeemed | | | | | | | | | | | | | | | | |

| Class A | | | (2,924,600 | ) | | | (1,010,377 | ) | | | (56,444 | ) | | | (51,643 | ) |

| Class C | | | (1,137,526 | ) | | | (942,378 | ) | | | (9,940 | ) | | | (40,623 | ) |

| Class I | | | (16,475,176 | ) | | | (11,788,231 | ) | | | (2,711,746 | ) | | | (956,371 | ) |

| Class R6 | | | (1,830,175 | ) | | | (745,543 | ) | | | (969,938 | ) | | | (765,085 | ) |

| Net increase (decrease) in shares of beneficial interest | | | (13,950,178 | ) | | | 4,745,175 | | | | 3,448,938 | | | | 2,650,140 | |

See accompanying notes to financial statements.

| FINANCIAL HIGHLIGHTS (For a share outstanding throughout each year) |

| Easterly Global Real Estate Fund |

| | | CLASS A | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 14.56 | | | $ | 18.94 | | | $ | 15.56 | | | $ | 17.81 | | | $ | 18.73 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (1) | | | 0.20 | | | | 0.14 | | | | 0.11 | | | | 0.19 | | | | 0.09 | |

| Net realized and unrealized gain (loss) | | | (1.25 | ) | | | (2.93 | ) | | | 4.85 | | | | (0.51 | ) | | | 0.65 | |

| Total from investment operations | �� | | (1.05 | ) | | | (2.79 | ) | | | 4.96 | | | | (0.32 | ) | | | 0.74 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.19 | ) | | | (0.41 | ) | | | (0.28 | ) | | | (0.28 | ) | | | (0.64 | ) |

| Distributions from realized gains | | | (0.36 | ) | | | (1.18 | ) | | | (1.30 | ) | | | (1.65 | ) | | | (1.02 | ) |

| Total dividends and distributions | | | (0.55 | ) | | | (1.59 | ) | | | (1.58 | ) | | | (1.93 | ) | | | (1.66 | ) |

| Net Asset Value, End of Year | | $ | 12.96 | | | $ | 14.56 | | | $ | 18.94 | | | $ | 15.56 | | | $ | 17.81 | |

| Total Return* | | | (7.06 | )% | | | (16.03 | )% | | | 33.47 | % | | | (1.93 | )% | | | 4.67 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 56,487 | | | $ | 97,639 | | | $ | 118,587 | | | $ | 88,222 | | | $ | 104,815 | |

| Ratio of gross operating expenses to average net assets | | | 1.42 | % | | | 1.36 | % | | | 1.51 | % | | | 1.60 | % | | | 1.60 | % |

| Ratio of net operating expenses to average net assets | | | 1.42 | % | | | 1.36 | % | | | 1.51 | % | | | 1.60 | % | | | 1.60 | % |

| Ratio of net investment income after expense reimbursement/recoupment to average net assets | | | 1.53 | % | | | 0.80 | % | | | 0.64 | % | | | 1.16 | % | | | 0.52 | % |

| Portfolio Turnover Rate | | | 12 | % | | | 116 | % | | | 160 | % | | | 187 | % | | | 172 | % |

| | | | | | | | | | | | | | | | | | | | | |

| | | CLASS C | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 14.63 | | | $ | 19.06 | | | $ | 15.68 | | | $ | 17.95 | | | $ | 18.89 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) (1) | | | 0.10 | | | | 0.01 | | | | (0.02 | ) | | | 0.07 | | | | (0.04 | ) |

| Net realized and unrealized gain (loss) | | | (1.26 | ) | | | (2.94 | ) | | | 4.89 | | | | (0.51 | ) | | | 0.65 | |

| Total from investment operations | | | (1.16 | ) | | | (2.93 | ) | | | 4.87 | | | | (0.44 | ) | | | 0.61 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.11 | ) | | | (0.32 | ) | | | (0.19 | ) | | | (0.18 | ) | | | (0.53 | ) |

| Distributions from realized gains | | | (0.36 | ) | | | (1.18 | ) | | | (1.30 | ) | | | (1.65 | ) | | | (1.02 | ) |

| Total dividends and distributions | | | (0.47 | ) | | | (1.50 | ) | | | (1.49 | ) | | | (1.83 | ) | | | (1.55 | ) |

| Net Asset Value, End of Year | | $ | 13.00 | | | $ | 14.63 | | | $ | 19.06 | | | $ | 15.68 | | | $ | 17.95 | |

| Total Return* | | | (7.80 | )% | | | (16.64 | )% | | | 32.51 | % | | | (2.62 | )% | | | 3.87 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 34,243 | | | $ | 52,362 | | | $ | 75,701 | | | $ | 65,907 | | | $ | 80,048 | |

| Ratio of gross operating expenses to average net assets | | | 2.17 | % | | | 2.11 | % | | | 2.26 | % | | | 2.35 | % | | | 2.37 | % |

| Ratio of net operating expenses to average net assets | | | 2.17 | % | | | 2.11 | % | | | 2.26 | % | | | 2.35 | % | | | 2.37 | % |

| Ratio of net investment income (loss) after expense reimbursement/recoupment to average net assets | | | 0.79 | % | | | 0.05 | % | | | (0.11 | )% | | | 0.42 | % | | | (0.25 | )% |

| Portfolio Turnover Rate | | | 12 | % | | | 116 | % | | | 160 | % | | | 187 | % | | | 172 | % |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| * | Assumes reinvestment of all dividends and distributions and does not assume the effects of any sales charges. Aggregate (not annualized) total return is shown for any period shorter than one year. Total return does not reflect the deduction of taxes that a shareholder would pay on distributions or on the redemption of shares. |

See accompanying notes to financial statements.

| FINANCIAL HIGHLIGHTS (For a share outstanding throughout each year) |

| Easterly Global Real Estate Fund |

| | | CLASS I | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 15.34 | | | $ | 19.84 | | | $ | 16.19 | | | $ | 18.42 | | | $ | 19.29 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (1) | | | 0.27 | | | | 0.20 | | | | 0.18 | | | | 0.28 | | | | 0.17 | |

| Net realized and unrealized gain (loss) | | | (1.34 | ) | | | (3.07 | ) | | | 5.08 | | | | (0.54 | ) | | | 0.66 | |

| Total from investment operations | | | (1.07 | ) | | | (2.87 | ) | | | 5.26 | | | | (0.26 | ) | | | 0.83 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.21 | ) | | | (0.45 | ) | | | (0.31 | ) | | | (0.32 | ) | | | (0.68 | ) |

| Distributions from realized gains | | | (0.36 | ) | | | (1.18 | ) | | | (1.30 | ) | | | (1.65 | ) | | | (1.02 | ) |

| Total dividends and distributions | | | (0.57 | ) | | | (1.63 | ) | | | (1.61 | ) | | | (1.97 | ) | | | (1.70 | ) |

| Net Asset Value, End of Year | | $ | 13.70 | | | $ | 15.34 | | | $ | 19.84 | | | $ | 16.19 | | | $ | 18.42 | |

| Total Return* | | | (6.78 | )% | | | (15.74 | )% | | | 34.06 | % | | | (1.51 | )% | | | 5.06 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 376,980 | | | $ | 571,664 | | | $ | 678,440 | | | $ | 544,432 | | | $ | 643,866 | |

| Ratio of gross operating expenses to average net assets | | | 1.17 | % | | | 1.11 | % | | | 1.26 | % | | | 1.35 | % | | | 1.33 | % |

| Ratio of net operating expenses to average net assets | | | 1.04 | % | | | 1.04 | % | | | 1.12 | % | | | 1.19 | % | | | 1.19 | % |

| Ratio of net investment income after expense reimbursement/recoupment to average net assets | | | 1.92 | % | | | 1.12 | % | | | 1.02 | % | | | 1.68 | % | | | 0.93 | % |

| Portfolio Turnover Rate | | | 12 | % | | | 116 | % | | | 160 | % | | | 187 | % | | | 172 | % |

| | | | | | | | | | | | | | | | |

| | | CLASS R6 | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 15.56 | | | $ | 20.09 | | | $ | 16.35 | | | $ | 18.55 | | | $ | 19.35 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (1) | | | 0.29 | | | | 0.23 | | | | 0.22 | | | | 0.31 | | | | 0.22 | |

| Net realized and unrealized gain (loss) | | | (1.35 | ) | | | (3.13 | ) | | | 5.13 | | | | (0.54 | ) | | | 0.69 | |

| Total from investment operations | | | (1.06 | ) | | | (2.90 | ) | | | 5.35 | | | | (0.23 | ) | | | 0.91 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | (0.21 | ) | | | (0.45 | ) | | | (0.31 | ) | | | (0.32 | ) | | | (0.69 | ) |

| Distributions from realized gains | | | (0.36 | ) | | | (1.18 | ) | | | (1.30 | ) | | | (1.65 | ) | | | (1.02 | ) |

| Total dividends and distributions | | | (0.57 | ) | | | (1.63 | ) | | | (1.61 | ) | | | (1.97 | ) | | | (1.71 | ) |

| Net Asset Value, End of Year | | $ | 13.93 | | | $ | 15.56 | | | $ | 20.09 | | | $ | 16.35 | | | $ | 18.55 | |

| Total Return* | | | (6.61 | )% | | | (15.69 | )% | | | 34.29 | % | | | (1.32 | )% | | | 5.44 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 32,221 | | | $ | 50,074 | | | $ | 32,039 | | | $ | 31,355 | | | $ | 12,238 | |

| Ratio of gross operating expenses to average net assets | | | 1.17 | % | | | 1.11 | % | | | 1.26 | % | | | 1.36 | % | | | 1.33 | % |

| Ratio of net operating expenses to average net assets | | | 0.94 | % | | | 0.94 | % | | | 0.97 | % | | | 1.00 | % | | | 0.88 | % |

| Ratio of net investment income after expense reimbursement/recoupment to average net assets | | | 2.02 | % | | | 1.30 | % | | | 1.18 | % | | | 1.86 | % | | | 1.20 | % |

| Portfolio Turnover Rate | | | 12 | % | | | 116 | % | | | 160 | % | | | 187 | % | | | 172 | % |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| * | Assumes reinvestment of all dividends and distributions and does not assume the effects of any sales charges. Aggregate (not annualized) total return is shown for any period shorter than one year. Total return does not reflect the deduction of taxes that a shareholder would pay on distributions or on the redemption of shares. |

See accompanying notes to financial statements.

| FINANCIAL HIGHLIGHTS (For a share outstanding throughout each year) |

| Easterly Hedged Equity Fund |

| | | CLASS A | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 9.99 | | | $ | 11.18 | | | $ | 10.83 | | | $ | 10.42 | | | $ | 10.80 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss (1) | | | (0.01 | ) | | | (0.03 | ) | | | (0.08 | ) | | | (0.05 | ) | | | (0.13 | ) |

| Net realized and unrealized gain (loss) | | | 1.03 | | | | (0.06 | ) | | | 1.17 | | | | 0.72 | | | | 0.75 | |

| Total from investment operations | | | 1.02 | | | | (0.09 | ) | | | 1.09 | | | | 0.67 | | | | 0.62 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | — | | | | (1.10 | ) | | | (0.74 | ) | | | — | | | | (0.31 | ) |

| Distributions from realized gains | | | (0.24 | ) | | | — | | | | — | | | | (0.26 | ) | | | (0.69 | ) |

| Total dividends and distributions | | | (0.24 | ) | | | (1.10 | ) | | | (0.74 | ) | | | (0.26 | ) | | | (1.00 | ) |

| Net Asset Value, End of Year | | $ | 10.77 | | | $ | 9.99 | | | $ | 11.18 | | | $ | 10.83 | | | $ | 10.42 | |

| Total Return* | | | 10.45 | % | | | (1.17 | )% | | | 10.67 | % | | | 6.56 | % | | | 6.26 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 3,348 | | | $ | 1,538 | | | $ | 1,899 | | | $ | 1,537 | | | $ | 519 | |

| Ratio of gross operating expenses (including dividend and interest expense) to average net assets (2) | | | 1.95 | % | | | 2.02 | % | | | 2.04 | % | | | 2.07 | % | | | 2.22 | % |

| Ratio of net operating expenses (including dividend and interest expense) to average net assets (3) | | | 1.61 | % | | | 1.54 | % | | | 2.04 | % | | | 2.01 | % | | | 2.20 | % |

| Ratio of net investment loss (including dividend and interest expense) after expense reimbursement/recoupment to average net assets | | | (0.14 | )% | | | (0.33 | )% | | | (0.73 | )% | | | (0.44 | )% | | | (1.28 | )% |

| Portfolio Turnover Rate | | | 12 | % | | | 23 | % | | | 44 | % | | | 173 | % | | | 245 | % |

| | | | | | | | | | | | | | | | |

| | | CLASS C | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 9.82 | | | $ | 10.90 | | | $ | 10.57 | | | $ | 10.28 | | | $ | 10.66 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment loss (1) | | | (0.08 | ) | | | (0.10 | ) | | | (0.14 | ) | | | (0.14 | ) | | | (0.18 | ) |

| Net realized and unrealized gain (loss) | | | 1.01 | | | | (0.08 | ) | | | 1.12 | | | | 0.69 | | | | 0.72 | |

| Total from investment operations | | | 0.93 | | | | (0.18 | ) | | | 0.98 | | | | 0.55 | | | | 0.54 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | — | | | | (0.90 | ) | | | (0.65 | ) | | | — | | | | (0.23 | ) |

| Distributions from realized gains | | | (0.24 | ) | | | — | | | | — | | | | (0.26 | ) | | | (0.69 | ) |

| Total dividends and distributions | | | (0.24 | ) | | | (0.90 | ) | | | (0.65 | ) | | | (0.26 | ) | | | (0.92 | ) |

| Net Asset Value, End of Year | | $ | 10.51 | | | $ | 9.82 | | | $ | 10.90 | | | $ | 10.57 | | | $ | 10.28 | |

| Total Return* | | | 9.70 | % | | | (1.95 | )% | | | 9.77 | % | | | 5.47 | % + | | | 5.51 | % + |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 460 | | | $ | 366 | | | $ | 746 | | | $ | 1,781 | | | $ | 524 | |

| Ratio of gross operating expenses (including dividend and interest expense) to average net assets (4) | | | 2.70 | % | | | 2.77 | % | | | 2.68 | % | | | 2.81 | % | | | 2.96 | % |

| Ratio of net operating expenses (including dividend and interest expense) to average net assets (5) | | | 2.36 | % | | | 2.29 | % | | | 2.68 | % | | | 2.94 | % | | | 2.96 | % |

| Ratio of net investment loss (including dividend and interest expense) after expense reimbursement/recoupment to average net assets | | | (0.81 | )% | | | (1.02 | )% | | | (1.31 | )% | | | (1.36 | )% | | | (1.74 | )% |

| Portfolio Turnover Rate | | | 12 | % | | | 23 | % | | | 44 | % | | | 173 | % | | | 245 | % |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Ratio of gross expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class A: |

| | | | 1.84 | % | | | 1.99 | % | | | 1.99 | % | | | 2.05 | % | | | 2.19 | % |

| (3) | Ratio of net operating expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class A: |

| | | | 1.50 | % | | | 1.51 | % | | | 1.99 | % | | | 1.99 | % | | | 2.17 | % |

| (4) | Ratio of gross expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class C: |

| | | | 2.59 | % | | | 2.74 | % | | | 2.63 | % | | | 2.79 | % | | | 2.93 | % |

| (5) | Ratio of net operating expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class C: |

| | | | 2.25 | % | | | 2.26 | % | | | 2.63 | % | | | 2.92 | % | | | 2.93 | % |

| + | Includes adjustments in accordance with accounting principles generally accepted in the United States and, consequently, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset values and returns for shareholder transactions. |

| * | Assumes reinvestment of all dividends and distributions and does not assume the effects of any sales charges. Aggregate (not annualized) total return is shown for any period shorter than one year. Total return does not reflect the deduction of taxes that a shareholder would pay on distributions or on the redemption of shares. |

See accompanying notes to financial statements.

| FINANCIAL HIGHLIGHTS (For a share outstanding throughout each year) |

| Easterly Hedged Equity Fund |

| | | CLASS I | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 10.13 | | | $ | 11.33 | | | $ | 10.96 | | | $ | 10.53 | | | $ | 10.90 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) (1) | | | 0.01 | | | | (0.01 | ) | | | (0.06 | ) | | | (0.03 | ) | | | (0.10 | ) |

| Net realized and unrealized gain (loss) | | | 1.06 | | | | (0.07 | ) | | | 1.19 | | | | 0.72 | | | | 0.76 | |

| Total from investment operations | | | 1.07 | | | | (0.08 | ) | | | 1.13 | | | | 0.69 | | | | 0.66 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | — | | | | (1.12 | ) | | | (0.76 | ) | | | — | | | | (0.34 | ) |

| Distributions from realized gains | | | (0.24 | ) | | | — | | | | — | | | | (0.26 | ) | | | (0.69 | ) |

| Total dividends and distributions | | | (0.24 | ) | | | (1.12 | ) | | | (0.76 | ) | | | (0.26 | ) | | | (1.03 | ) |

| Net Asset Value, End of Year | | $ | 10.96 | | | $ | 10.13 | | | $ | 11.33 | | | $ | 10.96 | | | $ | 10.53 | |

| Total Return* | | | 10.80 | % | | | (0.98 | )% | | | 10.91 | % | | | 6.69 | % | | | 6.68 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 113,264 | | | $ | 61,982 | | | $ | 33,478 | | | $ | 41,145 | | | $ | 19,673 | |

| Ratio of gross operating expenses (including dividend and interest expense) to average net assets (2) | | | 1.70 | % | | | 1.77 | % | | | 1.84 | % | | | 1.82 | % | | | 1.99 | % |

| Ratio of net operating expenses (including dividend and interest expense) to average net assets (3) | | | 1.36 | % | | | 1.29 | % | | | 1.84 | % | | | 1.81 | % | | | 1.86 | % |

| Ratio of net investment income (loss) (including dividend and interest expense) after expense reimbursement/recoupment to average net assets | | | 0.14 | % | | | (0.13 | )% | | | (0.51 | )% | | | (0.29 | )% | | | (0.93 | )% |

| Portfolio Turnover Rate | | | 12 | % | | | 23 | % | | | 44 | % | | | 173 | % | | | 245 | % |

| | | | | | | | | | | | | | | | |

| | | CLASS R6 | |

| | | | | | | | | | | | | | | | |

| | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | | | Year Ended | |

| | | August 31, | | | August 31, | | | August 31, | | | August 31, | | | August 31, | |

| | | 2023 | | | 2022 | | | 2021 | | | 2020 | | | 2019 | |

| Net Asset Value, Beginning of Year | | $ | 10.40 | | | $ | 11.58 | | | $ | 11.13 | | | $ | 10.64 | | | $ | 10.95 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | | | | | | | | | | | |

| Net investment income (loss) (1) | | | 0.07 | | | | 0.02 | | | | (0.02 | ) | | | 0.02 | | | | — | |

| Net realized and unrealized gain (loss) | | | 1.06 | | | | (0.08 | ) | | | 1.23 | | | | 0.73 | | | | 0.72 | |

| Total from investment operations | | | 1.13 | | | | (0.06 | ) | | | 1.21 | | | | 0.75 | | | | 0.72 | |

| Dividends and Distributions: | | | | | | | | | | | | | | | | | | | | |

| Dividends from net investment income | | | — | | | | (1.12 | ) | | | (0.76 | ) | | | — | | | | (0.34 | ) |

| Distributions from realized gains | | | (0.24 | ) | | | — | | | | — | | | | (0.26 | ) | | | (0.69 | ) |

| Total dividends and distributions | | | (0.24 | ) | | | (1.12 | ) | | | (0.76 | ) | | | (0.26 | ) | | | (1.03 | ) |

| Net Asset Value, End of Year | | $ | 11.29 | | | $ | 10.40 | | | $ | 11.58 | | | $ | 11.13 | | | $ | 10.64 | |

| Total Return* | | | 11.10 | % | | | (0.77 | )% | | | 11.49 | % | | | 7.19 | % | | | 7.23 | % |

| Ratios and Supplemental Data: | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of year (000s) | | $ | 1,766 | | | $ | 11,289 | | | $ | 17,970 | | | $ | 9,702 | | | $ | 13,365 | |

| Ratio of gross operating expenses (including dividend and interest expense) to average net assets (4) | | | 1.70 | % | | | 1.77 | % | | | 1.84 | % | | | 1.81 | % | | | 1.94 | % |

| Ratio of net operating expenses (including dividend and interest expense) to average net assets (5) | | | 1.10 | % | | | 1.03 | % | | | 1.38 | % | | | 1.36 | % | | | 1.33 | % |

| Ratio of net investment income (loss) (including dividend and interest expense) after expense reimbursement/recoupment to average net assets | | | 0.64 | % | | | 0.20 | % | | | (0.20 | )% | | | 0.16 | % | | | (0.03 | )% |

| Portfolio Turnover Rate | | | 12 | % | | | 23 | % | | | 44 | % | | | 173 | % | | | 245 | % |

| | | | | | | | | | | | | | | | | | | | | |

| (1) | Per share amounts calculated using the average shares method, which more appropriately presents the per share data for the period. |

| (2) | Ratio of gross expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class I: |

| | | | 1.59 | % | | | 1.74 | % | | | 1.79 | % | | | 1.79 | % | | | 1.95 | % |

| (3) | Ratio of net operating expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class I: |

| | | | 1.25 | % | | | 1.26 | % | | | 1.79 | % | | | 1.79 | % | | | 1.82 | % |

| (4) | Ratio of gross expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class R6: |

| | | | 1.59 | % | | | 1.74 | % | | | 1.79 | % | | | 1.78 | % | | | 1.90 | % |

| (5) | Ratio of net operating expenses to average net assets (excluding dividend and interest expenses) for the Easterly Hedged Equity Fund - Class R6: |

| | | | 0.99 | % | | | 1.00 | % | | | 1.33 | % | | | 1.34 | % | | | 1.30 | % |

| * | Assumes reinvestment of all dividends and distributions and does not assume the effects of any sales charges. Aggregate (not annualized) total return is shown for any period shorter than one year. Total return does not reflect the deduction of taxes that a shareholder would pay on distributions or on the redemption of shares. |

See accompanying notes to financial statements.

| NOTES TO FINANCIAL STATEMENTS |

| Year Ended August 31, 2023 |

| 1. | ORGANIZATION AND SIGNIFICANT ACCOUNTING POLICIES |

James Alpha Funds Trust (the “Trust”) was organized in 2020, as a Delaware Statutory Trust and is registered under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Trust currently consists of five series. Easterly Funds LLC serves as the Funds’ advisor. These financial statements include the following two series:

| Fund | Sub-Advisor |

| Easterly Global Real Estate Fund | Ranger Global Real Estate Advisors, LLC |

| Easterly Hedged Equity Fund | EAB Investment Group, LLC |

Ultimus Fund Solutions, LLC (the “Administrator”), serves the Trust as administrator, custody administrator, transfer agent and fund accounting agent. Ultimus Fund Distributors, LLC (“NLD” or the “Distributor”) is the Trust’s Distributor.

The Easterly Global Real Estate Fund and the Easterly Hedged Equity Fund are diversified Funds.

| Fund | Primary Objective |

| Easterly Global Real Estate | Total return through a combination of current income and capital appreciation |

| Easterly Hedged Equity | Capital appreciation |

Easterly Hedged Equity is a “fund of funds”, in that the Fund will generally invest in other investment companies. Currently, each Fund offers Class A, Class C, Class I and Class R6 shares. Class A shares of each fund are offered at net asset value plus a maximum sales load of 5.75%. Class C shares are offered subject to a CDSC of 1.00%. Class I and Class R6 shares are offered at net asset value. Each class represents an interest in the same assets of the applicable Fund, and the classes are identical except for differences in their sales charge structures, ongoing service and distribution charges. Class R6 shares are only available to certain qualified investors and the minimum initial investment will vary depending on the type of qualified investor. All classes of shares have equal voting privileges except that each class has exclusive voting rights with respect to its service and/or distribution plans. Fund level income and expenses, and realized and unrealized capital gains and losses are allocated to each class of shares based on their relative net assets within each Fund. Class specific expenses are allocated to that share class.

The following is a summary of significant accounting policies followed by the Funds in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. Each Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update ASU 2013-08.

(a) Valuation of Investments

Investment securities listed on a national securities exchange are valued at the last reported sale price on the valuation date. NASDAQ traded securities are valued at the NASDAQ Official Closing Price (NOCP). If there are no such reported sales, the securities are valued at the mean between current bid and ask. Debt securities (other than short-term obligations) are valued each day by an independent pricing service approved by the Board of Trustees using methods which include current market quotations from a major market maker in the securities and trader-reviewed “matrix” prices. Short-term debt securities having a remaining maturity of sixty days or less may be valued at amortized cost or amortized value, which approximates market value. U.S. Government Money Market values all of its securities on the basis of amortized cost, which approximates market value. Options listed on a securities exchange or board of trade for which market quotations are readily available shall be valued at the last quoted sales price or, in the absence of a sale, at the mean between the last bid and ask price. Options not listed on a securities exchange or board of trade for which over-the-counter market quotations are readily available shall be valued at the mean of the current bid and asked prices. Futures are valued based on their daily settlement value. Swap transactions are valued through an independent pricing service or at fair value based on daily price reporting from the swap counterparty issuing the swap. Total return swaps on securities listed on an exchange shall be valued at the last quoted sales price or, in the absence of a sale, at the mean between the current bid and ask prices. Any securities or other assets for which market quotations are not readily available are valued at their fair value as determined in good faith under procedures established by the Board of Trustees (the “Board”). There is no single standard for determining the fair value of such securities. Rather, in determining the fair value of a security, the board-appointed Valuation Designee shall take into account the relevant factors and surrounding circumstances, a few of which may include: (i) the nature and pricing history (if any) of the security; (ii) whether any dealer quotations for the security are available; and (iii) possible valuation methodologies that could be used to determine the fair value of a security. The Easterly Global Real Estate Fund uses fair value prices as provided by an independent pricing vendor on a daily basis for those securities traded on a foreign exchange. Foreign currency and Forward currency exchange contracts are valued daily at the London close each day. The ability of issuers of debt securities held by the Funds to meet their obligations may be affected by economic or political developments in a specific state, industry or region. Investments in foreign countries may involve certain considerations and risks not typically associated with domestic investments, including, but not limited to, the possibility of future political and economic developments and the level of government supervision and regulation of foreign securities markets.