UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-01829 |

|

Columbia Acorn Trust |

(Exact name of registrant as specified in charter) |

|

One Financial Center, Boston, Massachusetts | | 02111 |

(Address of principal executive offices) | | (Zip code) |

|

Scott R. Plummer

5228 Ameriprise Financial Center

Minneapolis, MN 55474 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-612-671-1947 | |

|

Date of fiscal year end: | December 31 | |

|

Date of reporting period: | December 31, 2010 | |

| | | | | | | | |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

Q4 2010

Columbia Acorn Family of Funds

Class Z Shares

Managed by Columbia Wanger Asset Management, LLC

Annual Report

December 31, 2010

n ColumbiaSM

Acorn® Fund

n ColumbiaSM

Acorn International®

n ColumbiaSM

Acorn USA®

n ColumbiaSM

Acorn International SelectSM

n ColumbiaSM

Acorn SelectSM

n ColumbiaSM

Thermostat FundSM

Not FDIC insured • No bank guarantee • May lose value

Columbia Acorn Family of Funds

The views expressed in the "Squirrel Chatter II" and "In a Nutshell" commentaries reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective authors disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for a Columbia Acorn Fund are based on numerous factors, may not be relied upon as an indication of trading intent on behalf of any particular Columbia Acorn Fund. References to specific company's securities should not be construed as a recommendation or investment advice and there can be no assurance that as of the date of publication of this report, the securities mentioned in each Fund's portfolio are still held or that the securities sold have not been repurchased.

Letter to Shareholders from the

Columbia Acorn Board of Trustees

40 Years of Vision, Stability and Growth

Fellow Shareholders:

This has been an eventful year for the Columbia Acorn Funds. Early in the year, the Board negotiated new management and administrative agreements with the Funds' adviser, Columbia Wanger Asset Management ("CWAM"), following its acquisition by Ameriprise Financial, Inc. These new agreements were crafted with the objective of preserving CWAM's autonomy and culture and ensuring that the terms of these agreements were in Fund shareholders' best interests. Finally, I am especially pleased to report that the CWAM investment team remains in place following the ownership transition. Together with Ameriprise's expressed commitment to support and maintain the unique culture of CWAM and the Acorn Funds, your trustees are optimistic that the necessary foundation has been laid to perpetuate a vibrant and successful investment organization.

Last year's letter spoke of change and continuity in the governance of your Funds. That process has continued with the retirement of two long-serving trustees, David Kleinman and Jack Wing, and the selection of three new trustees, David Small, John Heaton and David Rudis. Mr. Small is a senior partner at Grosvenor Capital Management, a successful manager of investment partnerships. Mr. Rudis was formerly the president of LaSalle Bank, a major Chicago bank until its sale a few years ago, and Mr. Heaton is a distinguished professor of finance at the University of Chicago. Our new trustees collectively bring extensive business, investment and financial expertise to the job of overseeing your Funds, and we are glad to have them on board. At the same time, we will miss David and Jack, each of whom served shareholders faithfully and well for many years.

The markets continued to recover in 2010, and all the Funds delivered strong absolute returns during the year. While these results are important, your trustees—each a shareholder—focus especially on long-term performance. To this end, we salute present and past members of the investment team at CWAM for the remarkable record that they have created for the Acorn Fund. Since the Fund's inception 40 years ago, the original Class Z shares have enjoyed average annual total returns in excess of the S&P 500, as have the Fund's other classes of shares, which were instituted in 2000. As a result of this performance, the Acorn Fund was ranked the number one U.S.-based mutual fund over its lifetime, ahead of 149 other U.S.-based funds in existence during the period.* This is an extraordinary legacy, which your trustees will work to see perpetuated.

Thank you for your confidence in the Acorn Funds, and best wishes for the new year.

James A. Star

Independent Chairman of the Board of Trustees

Columbia Acorn Trust

* According to Morningstar, Columbia Acorn Fund Class Z ranked #1 of 149 U.S.-based mutual funds in existence since June 10, 1970. These rankings are based on returns for Z Class shares for the period June 10, 1970, the inception date of the Fund, to December 31, 2010. Please refer to Page 1 for complete performance data.

| | | From Inception to

12/31/10 | | 10 years | | 5 years | | 1 year | |

Acorn Fund

compound return | | | 15.01% | | | | 9.40% | | | | 5.91% | | | | 26.00% | | |

Morningstar

ranking | | | 1 of 149 | | | | 10 of 167 | | | | 24 of 169 | | | | 14 of 169 | | |

Source: ©2011 Morningstar, Inc. All rights reserved. Morningstar rankings are based on annualized total returns and do not reflect sales charges. Criteria: Open-ended mutual funds; inception date on or before Columbia Acorn Fund; oldest share class only; USD-based currency.

Columbia Acorn Family of Funds

Table of Contents

| Performance At A Glance | | | 1 | | |

| Description of Indexes | | | 2 | | |

| Squirrel Chatter II: The Keys to Prosperity | | | 3 | | |

| Understanding Your Expenses | | | 6 | | |

| Columbia Acorn Fund | |

| In a Nutshell | | | 8 | | |

| At a Glance | | | 9 | | |

| Major Portfolio Changes | | | 20 | | |

| Statement of Investments | | | 23 | | |

| Columbia Acorn International | |

| In a Nutshell | | | 10 | | |

| At a Glance | | | 11 | | |

| Major Portfolio Changes | | | 37 | | |

| Statement of Investments | | | 39 | | |

| Portfolio Diversification | | | 48 | | |

| Columbia Acorn USA | |

| In a Nutshell | | | 12 | | |

| At a Glance | | | 13 | | |

| Major Portfolio Changes | | | 49 | | |

| Statement of Investments | | | 50 | | |

| Columbia Acorn International Select | |

| In a Nutshell | | | 14 | | |

| At a Glance | | | 15 | | |

| Major Portfolio Changes | | | 58 | | |

| Statement of Investments | | | 59 | | |

| Portfolio Diversification | | | 63 | | |

| Columbia Acorn Select | |

| In a Nutshell | | | 16 | | |

| At a Glance | | | 17 | | |

| Major Portfolio Changes | | | 64 | | |

| Statement of Investments | | | 65 | | |

| Columbia Thermostat Fund | |

| In a Nutshell | | | 18 | | |

| At a Glance | | | 19 | | |

| Statement of Investments | | | 70 | | |

| Columbia Acorn Family of Funds | |

| Statements of Assets and Liabilities | | | 72 | | |

| Statements of Operations | | | 73 | | |

| Statements of Changes in Net Assets | | | 74 | | |

| Financial Highlights | | | 78 | | |

| Notes to Financial Statements | | | 81 | | |

Report of Independent Registered

Public Accounting Firm | | | 91 | | |

| Federal Income Tax Information | | | 92 | | |

Board of Trustees and Management

of Columbia Acorn Funds | | | 93 | | |

| Columbia Acorn Family of Funds Information | | | 96 | | |

2010 Year-End Distributions

The following table details the year-end distributions for the Columbia Acorn Funds. Except for Columbia Thermostat Fund, the record date was December 14, 2010, the ex-dividend date was December 15, 2010, and the payable date was December 16, 2010. For Columbia Thermostat Fund, the record date was December 21, 2010, the ex-dividend date was December 22, 2010, and the payable date was December 23, 2010.

| | | Short-term

Capital

Gains | | Long-term

Capital

Gains | | Ordinary

Income | | Reinvestment

Price | |

| Columbia Acorn Fund | | | None | | | $ | 0.8374 | | | $ | 0.0140 | | | $ | 29.55 | | |

| Columbia Acorn International | | | None | | | | None | | | $ | 0.3276 | | | $ | 39.79 | | |

| Columbia Acorn USA | | | None | | | | None | | | | None | | | | NA | | |

| Columbia Acorn International Select | | | None | | | | None | | | | None | | | | NA | | |

| Columbia Acorn Select | | | None | | | | None | | | | None | | | | NA | | |

| Columbia Thermostat Fund | | | None | | | | None | | | $ | 0.0678 | | | $ | 12.39 | | |

Columbia Acorn Family of Funds

Performance At A Glance Class Z Average Annual Total Returns through 12/31/10

| | | NAV on

12/31/10 | | 4th

quarter* | | 1 year | | 3 years | | 5 years | | 10 years | | Life

of Fund | |

Columbia Acorn Fund

(ACRNX) (6/10/70) | | $ | 30.19 | | | | 14.57 | % | | | 26.00 | % | | | 2.64 | % | | | 5.91 | % | | | 9.40 | % | | | 15.01 | % | |

| Russell 2500 Index | | | | | 14.86 | % | | | 26.71 | % | | | 2.48 | % | | | 4.86 | % | | | 6.98 | % | | | NA | | |

| S&P 500 Index** | | | | | 10.76 | % | | | 15.06 | % | | | -2.86 | % | | | 2.29 | % | | | 1.41 | % | | | 10.65 | % | |

| Lipper Small-Cap Core Funds Index | | | | | 15.40 | % | | | 25.71 | % | | | 2.88 | % | | | 4.76 | % | | | 6.96 | % | | | NA | | |

| Lipper Mid-Cap Growth Funds Index | | | | | 13.93 | % | | | 25.66 | % | | | 0.11 | % | | | 6.22 | % | | | 2.59 | % | | | NA | | |

Columbia Acorn International

(ACINX) (9/23/92) | | $ | 40.92 | | | | 8.57 | % | | | 22.70 | % | | | 0.08 | % | | | 9.60 | % | | | 9.33 | % | | | 12.17 | % | |

S&P Global Ex-U.S. Between

$500M and $5B Index | | | | | 10.58 | % | | | 24.36 | % | | | 0.28 | % | | | 8.19 | % | | | 11.75 | % | | | 9.45 | % | |

| S&P Global Ex-U.S. SmallCap Index | | | | | 10.65 | % | | | 22.96 | % | | | -1.11 | % | | | 7.29 | % | | | 10.69 | % | | | 8.64 | % | |

| MSCI EAFE Index | | | | | 6.61 | % | | | 7.75 | % | | | -7.02 | % | | | 2.46 | % | | | 3.50 | % | | | 6.24 | % | |

Lipper International Small/

Mid Growth Funds Index | | | | | 11.64 | % | | | 23.77 | % | | | -1.96 | % | | | 6.34 | % | | | 7.63 | % | | | NA | | |

Columbia Acorn USA

(AUSAX) (9/4/96) | | $ | 28.56 | | | | 16.43 | % | | | 23.16 | % | | | 1.93 | % | | | 3.48 | % | | | 8.74 | % | | | 10.57 | % | |

| Russell 2000 Index | | | | | 16.25 | % | | | 26.85 | % | | | 2.22 | % | | | 4.47 | % | | | 6.33 | % | | | 7.55 | % | |

| Russell 2500 Index | | | | | 14.86 | % | | | 26.71 | % | | | 2.48 | % | | | 4.86 | % | | | 6.98 | % | | | 9.14 | % | |

| S&P 500 Index** | | | | | 10.76 | % | | | 15.06 | % | | | -2.86 | % | | | 2.29 | % | | | 1.41 | % | | | 6.53 | % | |

| Lipper Small-Cap Growth Funds Index | | | | | 15.57 | % | | | 26.08 | % | | | -0.04 | % | | | 3.92 | % | | | 2.58 | % | | | 5.84 | % | |

Columbia Acorn Int'l Select

(ACFFX) (11/23/98) | | $ | 28.33 | | | | 8.09 | % | | | 21.89 | % | | | -2.45 | % | | | 9.04 | % | | | 6.63 | % | | | 10.33 | % | |

S&P Developed Ex-U.S. Between

$2B and $10B Index | | | | | 9.75 | % | | | 20.16 | % | | | -3.22 | % | | | 4.95 | % | | | 8.22 | % | | | 8.36 | % | |

| MSCI EAFE Index | | | | | 6.61 | % | | | 7.75 | % | | | -7.02 | % | | | 2.46 | % | | | 3.50 | % | | | 3.96 | % | |

Lipper International Small/

Mid Growth Funds Index | | | | | 11.64 | % | | | 23.77 | % | | | -1.96 | % | | | 6.34 | % | | | 7.63 | % | | | 11.35 | % | |

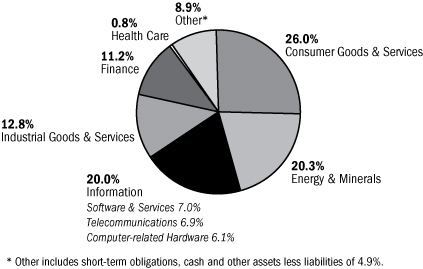

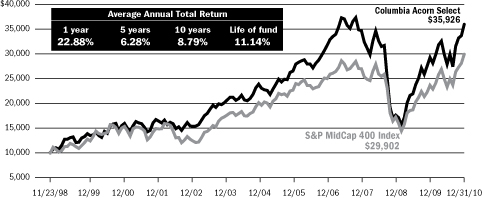

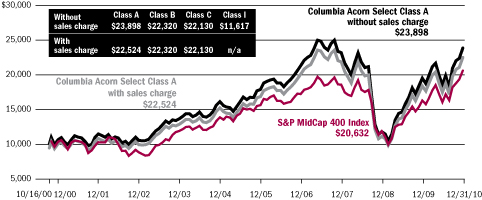

Columbia Acorn Select

(ACTWX) (11/23/98) | | $ | 28.73 | | | | 14.05 | % | | | 22.88 | % | | | 1.24 | % | | | 6.28 | % | | | 8.79 | % | | | 11.14 | % | |

| S&P MidCap 400 Index | | | | | 13.50 | % | | | 26.64 | % | | | 3.52 | % | | | 5.74 | % | | | 7.16 | % | | | 9.47 | % | |

| S&P 500 Index** | | | | | 10.76 | % | | | 15.06 | % | | | -2.86 | % | | | 2.29 | % | | | 1.41 | % | | | 2.44 | % | |

| Lipper Mid-Cap Growth Funds Index | | | | | 13.93 | % | | | 25.66 | % | | | 0.11 | % | | | 6.22 | % | | | 2.59 | % | | | 6.50 | % | |

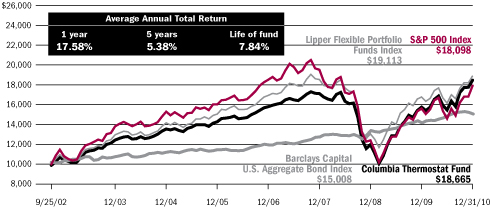

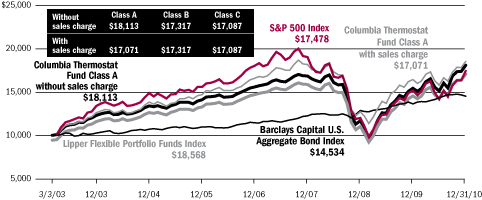

Columbia Thermostat Fund

(COTZX) (9/25/02)† | | | $12.44 | | | | 7.37% | | | | 17.58% | | | | 2.62% | | | | 5.38% | | | | — | | | | 7.84% | | |

| S&P 500 Index | | | | | 10.76 | % | | | 15.06 | % | | | -2.86 | % | | | 2.29 | % | | | — | | | | 7.44 | % | |

Barclays Capital U.S.

Aggregate Bond Index | | | | | -1.30 | % | | | 6.54 | % | | | 5.90 | % | | | 5.80 | % | | | — | | | | 5.03 | % | |

| Lipper Flexible Portfolio Funds Index | | | | | 7.29 | % | | | 12.91 | % | | | 0.68 | % | | | 4.75 | % | | | — | | | | 8.15 | % | |

| 50/50 Blended Benchmark†† | | | | | 4.65 | % | | | 11.29 | % | | | 2.04 | % | | | 4.44 | % | | | — | | | | 6.57 | % | |

*Not annualized.

**Although the Fund typically invests in small- and mid-sized companies, the comparison to the S&P 500 Index is presented to show performance against a widely recognized market index over the life of the Fund.

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for daily and most recent month-end updates.

Net asset value (NAV) returns do not include sales charges or contingent deferred sales charges (CDSC). If they were included, returns would have been lower. Class Z shares are sold only at NAV with no distribution and service (Rule 12b-1) fees. Only eligible investors may purchase Class Z shares of the Funds, directly or by exchange. Please see each Fund's prospectus for eligibility and other details. Class Z shares have limited eligibility and the investment minimum requirement may vary.

Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers or expense reimbursement arrangements, performance results would have been lower.

†A "fund of funds" bears its allocable share of the costs and expenses of the underlying funds in which it invests. Such funds are thus subject to two levels of fees and potentially higher expense ratios than would be associated with an investment in a fund that invests and trades directly in financial instruments under the direction of a single manager.

††The 50/50 Blended Benchmark is a custom supplemental benchmark established by the adviser.

All results shown assume reinvestment of distributions and do not reflect the deduction of taxes that a shareholder would pay on fund distributions or on the redemption of fund shares.

Unlike mutual funds, indexes are not actively managed and do not incur fees or expenses. It is not possible to invest directly in an index. For index definitions, see Page 2.

1

Columbia Acorn Family of Funds

Descriptions of Indexes Included in this Report

• 50/50 Blended Benchmark, established by the Fund's adviser, is an equally weighted custom composite of Columbia Thermostat Fund's primary equity and primary debt benchmarks, the S&P 500 Index and the Barclays Capital U.S. Aggregate Bond Index, respectively. The percentage of the Fund's assets allocated to underlying stock and bond portfolio funds will vary, and accordingly the composition of the Fund's portfolio will not always reflect the composition of the 50/50 Blended Benchmark.

• Barclays Capital U.S. Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs and total return performance of fixed-rate, publicly placed, dollar-denominated and non-convertible investment grade debt issues with at least $250 million par amount outstanding and with at least one year to final maturity.

• Lipper Indexes include the largest funds tracked by Lipper, Inc. in the named category. Lipper Small-Cap Core Funds Index, 30 largest small-cap core funds; Lipper Mid-Cap Growth Funds Index, 30 largest mid-cap growth funds, including Columbia Acorn Fund and Columbia Acorn Select; Lipper International Small/Mid Growth Funds Index, 10 largest non-U.S. small/mid growth funds, including Columbia Acorn International; Lipper Small-Cap Growth Funds Index, 30 largest small-cap growth funds, including Columbia Acorn USA; Lipper International Funds Index, 30 largest non-U.S. funds, excluding non-U.S. small-cap funds; Lipper Flexible Portfolio Funds Index, an equal-weighted index of the 30 largest mutual funds within the Flexible Portfolio fund classification, as defined by Lipper.

• Morgan Stanley Capital International Europe, Australasia, Far East (MSCI EAFE) Index is a capitalization-weighted index that tracks the total return of common stocks in 22 developed-market countries within Europe, Australasia and the Far East. The returns of the MSCI EAFE Index are presented net of taxes.

• Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 8% of the total market capitalization of the Russell 3000 Index.

• Russell 2500 Index measures the performance of the 2,500 smallest companies in the Russell 3000 Index, which represents approximately 17% of the total market capitalization of the Russell 3000 Index.

• Standard & Poor's (S&P) 500 Index tracks the performance of 500 widely held, large-capitalization U.S. stocks.

• Standard & Poor's (S&P) MidCap 400 Index is a market value-weighted index that tracks the performance of 400 mid-cap U.S. companies.

• S&P Developed Ex-U.S. Between $2B and $10B Index is a subset of the broad market selected by the index sponsor representing the mid-cap developed market, excluding the United States.

• S&P Global Ex-U.S. SmallCap Index consists of the bottom 20% of institutionally investable capital of developed and emerging countries, outside the United States. The performance of the S&P Global Ex-U.S. SmallCap Index is provided to show how Columbia Acorn International's performance compares to foreign market performance with a similar geographic distribution and wider market cap range than the Fund's primary benchmark.

• S&P Global Ex-U.S. Between $500M and $5B Index is a subset of the broad market selected by the index sponsor representing the mid- and small-cap developed and emerging markets, excluding the United States.

Unlike mutual funds, indexes are not managed and do not incur fees or expenses. It is not possible to invest directly in an index.

2

Squirrel Chatter II: The Keys to Prosperity

In 1651, Thomas Hobbes described human life as "poor, nasty, brutish and short." Today, 360 years later, humanity has achieved record levels of prosperity, safety and longevity. The United Nations estimates that poverty was reduced more in the last 50 years than the previous 500.1 In the developing world, life expectancy rose from 44 years to 64 years from 1950 to 1999, while in the developed world, life expectancy rose from 66 years to 78 years.2

In 1651, Thomas Hobbes described human life as "poor, nasty, brutish and short." Today, 360 years later, humanity has achieved record levels of prosperity, safety and longevity. The United Nations estimates that poverty was reduced more in the last 50 years than the previous 500.1 In the developing world, life expectancy rose from 44 years to 64 years from 1950 to 1999, while in the developed world, life expectancy rose from 66 years to 78 years.2

Hobbes's perspective was accurate for his time. There was very little growth in worldwide per capita GDP until about 1820; income in Europe had dropped for centuries following the decline and collapse of the Roman Empire.3 England and much of Europe were caught in a Malthusian trap, with population gyrating up and down largely due to plagues, famines and wars. But sometime around 1820, economic growth accelerated, and per capita GDP growth has averaged over 2% yearly since then, compounding into excellent gains in living standards.4 Why?

Four Conditions for Growth

William Bernstein's The Birth of Plenty, How Prosperity in the Modern World was Created is a fascinating history of worldwide economic circumstances. He discusses reasons for the successes and failures of many empires and countries. Bernstein believes that four institutional conditions are necessary for sustained growth: property rights and civil liberties, scientific rationalism, efficient capital markets, and fast and cheap transportation and communications. He notes that these four factors existed temporarily in sixteenth century Holland, then firmly in the English speaking countries, and in the last 50 years, increasingly over much of the world.5

Physical and intellectual property rights plus civil liberties create incentives and intellectual freedom to work hard, innovate and create wealth. In empires, totalitarian states and feudalistic societies, incentives to produce beyond immediate needs are nil, because governments or lords tend to impose confiscatory taxes and arbitrarily seize property. Bernstein believes that Rome fell, in part, due to excessive taxation on farmers. He also thinks that an independent judiciary is necessary to enforce property rights and civil liberties.

Scientific rationalism is needed for technological progress and innovation. Throughout history, various regimes run by church and state ossified due to the rejection of scientific observations in favor of dogma or preconceived beliefs. During medieval times, for example, astronomers who concluded the earth revolved around the sun were tortured. Bernstein cites the trial of Galileo as a turning point toward scientific rationalism. Early inventors then tended to be tinkerers rather than scientists, but science became increasingly important. For example, by the nineteenth century the steel industry had initiated the use of modern science laboratories staffed by full-time researchers.6

Efficient capital markets enable entrepreneurs and enterprises to raise capital at reasonable costs. I remember Jesse Jackson citing a lack of capital as a cause for inner city poverty: "Capitalism without capital is just plain ism."7 Bernstein notes that entrepreneurs once had huge downside risk from failures, namely debtors prisons in recent centuries and enslavement by creditors in ancient times. The creation of limited liability corporations during the nineteenth century in Britain and the United States was a breakthrough in reducing downside risks for capitalists.

Fast and cheap transportation and communication are also needed for prosperity. Bernstein explains that before railroads and the telegraph, transportation and communication were horribly expensive and slow. Rarely could bulk goods be transported over land more than 20 miles a day, and theft was rampant. Local crop failures often caused starvation. Mass markets did not exist. The reach of rail and telegraph grew incredibly rapidly during their first decades, spurring economic growth.

Bernstein provides plenty of case studies of regimes and countries that stagnated or failed due to the lack of one or more conditions, ranging from ancient societies and Japan under the samurai to Communist countries of the twentieth century. He states, "Institutions, not the bounty of nature or freedom from imperialist domination, separate the winners from the losers in the global economy."8

3

Trade Drives Prosperity

Matt Ridley's The Rational Optimist, How Prosperity Evolves adds substantial perspective to Bernstein's work and provides comforting thoughts about the future. Though Ridley does not mention Bernstein by name, it is clear that he agrees with Bernstein's basic contentions. Ridley sees property rights as the primary key to prosperity. He quotes a study by MIT economist Daron Acemoglu, which compared measures of property rights to economic growth across countries and determined that three-quarters of the variation of economic growth is explained by property rights.9 Ridley adds, "In a sample of 127 countries, the sixty-three with higher economic freedom had more than four times the income per capita and twice the growth rate of the countries that did not."10

Ridley's emphasis is on trade, which he believes allows increasing specialization, expertise, productivity and innovation. Humans seem to be hard-wired for trade. Archaeological evidence indicates that some 100,000 years ago humans began to barter.11 People traded things and also absorbed ideas. Human intelligence became collective and cumulative. Ridley states that, more recently, the history of the modern world is a history of ideas meeting, mixing, mating and mutating.12 Innovation results from an exchange of ideas. I think of the iPhone. Steve Jobs utilizes technologies and resources developed over centuries and components originated in many countries to make an incredibly inno vative and useful device.

Ridley notes that societies that halted trade regressed. After ocean levels rose 10,000 years ago and cut off Tasmania from Australia, people there gradually lost the ability to fish and make tools out of bones. European mariners discovered Tasmanians wearing nothing but wallaby pelts and seal-fat grease.13 As another example of a closed-off society, Ridley writes, "China went from a state of economic and technological exuberance in around AD 1000 to one of dense population, agrarian backwardness and desperate poverty in 1950;" per capita income there was about flat in those 950 years.14

Ridley takes a libertarian view, highly skeptical of government. He states, "...governments generally tend to be good things at first and bad things the longer they last. First they improve society's ability to flourish by providing central services and removing impediments to trade and specialization... But...governments gradually employ more and more ambitious elites who... give themselves more and more rules to enforce, until they kill the goose that lays the golden eggs. ... Because it is a monopoly, government brings inefficiency and stagnation to most things it runs..."15

Ridley asserts that African governments have largely caused economic problems in Africa. He writes that famines in Darfur and Zimbabwe were the result of government policies. Setting up a company in Tanzania takes 379 days and $5,500, a huge sum there. Botswana has done substantially better, growing per capita GDP nearly 8% annually since its independence in 1966. That growth exceeded China's, and is largely due to secure property rights, Ridley says. Ridley is optimistic for much of Africa, however. Cell phones are spreading rapidly, providing both communication and micro-finance (two of Bernstein's conditions for prosperity). Ridley cites wonderful examples of products and labor reaching optimal markets and payments being made over cell phones.16

Ridley has comforting thoughts about the future, debunking naysayers. He notes that (oddly enough) over time humans have temporarily exhausted or driven to extinction renewable resources like forests and certain animal species, while non-renewable resources have lasted much longer than many expected. In 1865, an economist said Britain's coal was running out, and as early as 1914 the U.S. Bureau of Mines wrote that American oil reserves would last 10 years.17

Ridley believes supplies of oil, coal and gas "will last decades, perhaps centuries, and people will find alternatives long before they run out."18 He states that prices of conventional fuels need to rise and prices of alternatives need to fall, and both will occur as conventional supplies run down and efficiencies of alternatives rise. Ridley notes that wind, solar and biomass alternatives envelop enormous quantities of land. He denounces organic farming, noting that if farm yields fell back to 1961 levels, 82% of the land area of the earth would be needed for farming, up from 38%. "The Dark Ages were a massive experiment in back-to-the-land hippy lifestyle (without the trust fund)," he says.19

4

Ridley largely dismisses climate change fears. The scenario that calls for significant climate change by the year 2100 is a scenario of dramatic economic growth. He believes the world, and especially developing countries, will be much, much richer and better able to adapt to and mitigate climate change. In the meantime, carbon intensity20 of the worldwide economy is rapidly dropping, as wood, dung and coal become relatively less important and natural gas and nuclear power gain share, in an environment of substantially more efficient lighting, heating, transportation and manufacturing.

While some of Ridley's arguments seem a bit over the top, I think they generally appear coherent and largely believable. As to the climate change issue, I advocate taking reasonable steps to mitigate global warming. Most of my family's road miles are in a hybrid vehicle and both my home and Columbia Wanger Asset Management have adopted compact florescent lighting. Several years ago we calculated that replacing over 100 incandescent bulbs at the office saved enough electricity to power three average-sized homes.

I agree that prosperity is driven by the factors named by Bernstein and Ridley and, though there are imbalances in world economics, I think things will be okay. The Great Recession has ended, growth has resumed and the keys to prosperity remain in place. Many parts of the developing world are booming and we have invested accordingly. About 22% of Columbia Acorn International is invested in the developing world and many Fund investments in non-emerging market companies have some business tied to developing markets. Other Columbia Acorn Funds also own some stocks that benefit directly or indirectly from developing markets.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, LLC

The information and data provided in this analysis are derived from sources that we deem to be reliable and accurate. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. The views/opinions expressed in Squirrel Chatter II are those of the author and not of the Columbia Acorn Trust Board, are subject to change at any time based upon economic, market or other conditions, may differ from views expressed by other Columbia Management associates and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Acorn Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Acorn Fund.

The information included on Pages 3, 4 and 5 of this report is unaudited.

1 Ridley, Matt, The Rational Optimist, How Prosperity Evolves, (New York, New York, HarperCollins 2010), p. 15.

2 Bernstein, William J., The Birth of Plenty, How the Prosperity of the Modern World was Created, (New York, New York, McGraw-Hill 2004), p. 10.

3 Ibid, p. 3.

4 Ibid, p. 12, 23.

5 Ibid, p. 15-17.

6 Ibid, p. 123.

7 Rev. Jesse Jackson quoted in an article that appeared in Ebony magazine, August 1967, titled "Apostles of Economics," p. 84.

8 Bernstein, William J., op. cit, p. 293.

9 Ridley, Matt, op. cit, p. 321.

10 Ibid, p. 117.

11 Ibid, p. 350.

12 Ibid, p. 272.

13 Ibid, p. 78.

14 Ibid, p. 180.

15 Ibid, p. 182.

16 Ibid, p. 320-326.

17 Ibid, p. 237.

18 Ibid, p. 238.

19 Ibid, p. 144, 175.

20 Carbon intensity is defined as the amount of CO2 produced divided by worldwide GDP.

5

Understanding Your Expenses

As a Fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption or exchange fees. There are also ongoing costs, which generally include investment advisory fees and other Fund expenses. The following information is intended to help you understand your ongoing costs of investing in the Columbia Acorn Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing Your Fund's Expenses

To illustrate these ongoing costs, we have provided examples and calculated the expenses paid by investors in the Class Z shares of the Columbia Acorn Funds for the last six months. The information in the following table is based on an initial investment of $1,000, which is invested at the beginning of the reporting period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using each Fund's actual operating expenses and total return for the period. The amount listed in the "Hypothetical" column assumes that the return each year is 5% before expenses and then applies each Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the reporting period. See the "Compare With Other Funds" information for details on using the hypothetical data.

July 1, 2010 – December 31, 2010

| | | Account value at

the beginning of

the period ($) | | Account value at

the end of

the period ($) | | Expenses paid

during the period ($) | | Fund's

annualized

expense

ratio (%)* | |

| | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | | Hypothetical | | Actual | |

| Class Z Shares | |

| Columbia Acorn Fund | | | 1,000.00 | | | | 1,000.00 | | | | 1,301.20 | | | | 1,021.37 | | | | 4.41 | | | | 3.87 | | | | 0.76 | | |

| Columbia Acorn International | | | 1,000.00 | | | | 1,000.00 | | | | 1,284.10 | | | | 1,020.21 | | | | 5.70 | | | | 5.04 | | | | 0.99 | | |

| Columbia Acorn USA | | | 1,000.00 | | | | 1,000.00 | | | | 1,313.70 | | | | 1,020.06 | | | | 5.95 | | | | 5.19 | | | | 1.02 | | |

| Columbia Acorn International Select | | | 1,000.00 | | | | 1,000.00 | | | | 1,265.90 | | | | 1,019.31 | | | | 6.68 | | | | 5.96 | | | | 1.17 | | |

| Columbia Acorn Select | | | 1,000.00 | | | | 1,000.00 | | | | 1,290.10 | | | | 1,020.27 | | | | 5.66 | | | | 4.99 | | | | 0.98 | | |

| Columbia Thermostat Fund** | | | 1,000.00 | | | | 1,000.00 | | | | 1,198.10 | | | | 1,023.95 | | | | 1.39 | | | | 1.28 | | | | 0.25 | | |

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Funds and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning different funds. If these transaction costs were included, your costs would have been higher.

*Expenses paid during the period are equal to each Fund's annualized expense ratio, multiplied by the average account value over the period and then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 365.

**Columbia Thermostat Fund's expenses do not include fees and expenses incurred by the Fund from the underlying portfolio funds in which it invests. Had the investment adviser and/or any of its affiliates not waived fees or reimbursed a portion of expenses, account value at the end of the period would have been reduced.

Compare With Other Funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Funds with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical examples are meant to highlight the continuing costs of investing in a fund and do not reflect any transaction costs, such as sales charges, or redemption or exchange fees.

6

Estimating Your Actual Expenses

To estimate the expenses that you actually paid over the period, first you will need your account balance at the end of the period:

• For shareholders who receive their account statements from Columbia Management Investment Services Corp., your account balance is available online at columbiafunds.com or by calling Shareholder Services at (800) 922-6769.

• For shareholders who receive their account statements from their brokerage firm, contact your brokerage firm to obtain your account balance.

1. Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6.

2. In the section of the table titled "Expenses paid during the period," locate the amount for your Fund. You will find this number is in the column labeled "Actual." Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

7

Columbia Acorn Fund

In a Nutshell

| |  | |

|

| Charles P. McQuaid | | Robert A. Mohn | |

|

| Lead Portfolio Manager | | Co-Portfolio Manager | |

|

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for daily and most recent month-end performance updates.

Fund Positions

in Mentioned Holdings

As a percentage of net assets,

as of 12/31/10

| lululemon athletica | | | 1.5 | % | |

| FMC Technologies | | | 1.5 | % | |

| Ametek | | | 1.5 | % | |

| Donaldson | | | 1.4 | % | |

| Fugro | | | 1.2 | % | |

| Pacific Rubiales Energy | | | 0.9 | % | |

| Abercrombie & Fitch | | | 0.9 | % | |

| Coach | | | 0.6 | % | |

| Silver Wheaton | | | 0.5 | % | |

| Southwestern Energy | | | 0.4 | % | |

| Talbots | | | 0.2 | % | |

Columbia Acorn Fund rose an even 26.00% in 2010, building on its 39.65% gain achieved in 2009. We are happy to say that at year end 2010, the Fund, adjusted for distributions, was within 0.2% of its all-time high, which was achieved in October 2007, prior to the Great Recession. As shown on Page 1, Columbia Acorn Fund's gains for 2010 were a bit below its primary benchmark, the Russell 2500 Index, a bit above peer funds as represented by Lipper, and well above the large-cap S&P 500 Index. During the fourth quarter of 2010, the Fund rose 14.57%, approximately matching its benchmark and again beating the S&P 500.

Active apparel company lululemon athletica was up 125% during the year and 53% in the quarter and was the Fund's top dollar winner in both periods. Handbag designer and retailer Coach also did well, rising 53% for the year and 29% for the quarter. Both companies had excellent product offerings and fine earnings growth.

Other retail stocks held in the Fund had mixed results. Teen apparel retailer Abercrombie & Fitch jumped 68% in the year and 47% in the quarter, as it became more price-competitive and gained market share. Women's specialty apparel retailer Charming Shoppes and branded multi-channel retailer J Crew Group had disappointing results for the year, sinking 45% and 30% respectively, while Talbots, a women's retailer, was the biggest dollar loser in the quarter, dropping 35%. We sold the Fund's positions in Charming Shoppes and J Crew. We weighted consumer stocks correctly, as lululemon's dollar gains were five-times that of the largest consumer stock loser in the Fund and Abercrombie & Fitch's gains were more than twice that of the biggest loser.

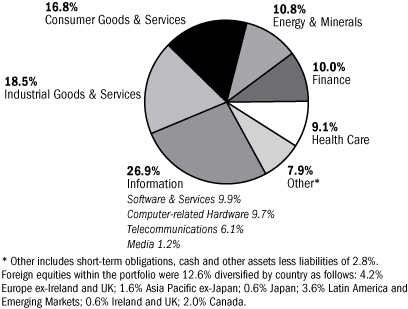

Industrial stocks provided fine upside. Aerospace and industrial instrument maker Ametek measured a 55% gain during the year and 23% in the quarter, ranking in the Fund's top five dollar contributors for both periods. Filter maker Donaldson rose 39% in the year and 24% in the quarter. Both companies reported excellent earnings gains. Industrial stocks made up 18.5% of the Fund at year end.

Oil production and service stocks did very well. Oil and gas wellhead manufacturer FMC Technologies was the Fund's second largest dollar winner during the year, rising 54%, and Colombian oil producer Pacific Rubiales Energy nailed third place, gaining 130%. During the quarter, these stocks were up 30% and 21%, respectively. Holland-based sub-sea oilfield services provider Fugro jumped 48% in the year and 25% in the quarter. Natural gas related stocks, in contrast, fizzled. Oil and gas producer Southwestern Energy was off 22% during the year and was the Fund's largest dollar loser, surrendering less than one-third of FMC's gains. Believing that oil prices are likely to stay high relative to natural gas prices, we shifted some investments accordingly.

The portion of Columbia Acorn Fund's portfolio invested in foreign stocks was up 41.24% in the year and accounted for 12.6% of Fund assets at year end.* In addition to the strong international energy names mentioned above, Canada's Silver Wheaton, a company that invests in mines in exchange for favorable purchases of silver by-product, glistened with a 160% gain in the year and a 46% gain in the quarter.

Small- and mid-cap stocks outperformed larger caps in both 2009 and 2010 and are currently valued somewhat higher than large caps. Takeovers of small- and mid-cap companies are accelerating, and we believe that large companies and private capital groups have buying power and increasing confidence in the economy. Columbia Acorn Fund had 13 stocks subject to new or increased takeover offers during the year, mostly in the fourth quarter. Small- and mid-cap earnings growth was greater than large-cap earnings growth in 2010. We believe that, should takeovers and faster earnings growth continue, small- and mid-cap stocks could continue to outperform large caps.

*These returns are not comparable to mutual fund returns, as they are gross of fees and other expenses and do not portray the cash effects incurred by actual mutual funds. Columbia Acorn Fund's foreign stockholdings were not purchased as a balanced, stand-alone portfolio.

Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

8

Columbia Acorn Fund (ACRNX)

At a Glance

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. Please visit columbiamanagement.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2010

| Inception 6/10/70 | | 1 year | | 5 years | | 10 years | |

| Returns before taxes | | | 26.00 | % | | | 5.91 | % | | | 9.40 | % | |

| Returns after taxes on distributions | | | 25.44 | | | | 5.24 | | | | 8.84 | | |

Returns after taxes on distributions

and sale of fund shares | | | 17.60 | | | | 5.04 | | | | 8.26 | | |

| Russell 2500 Index (pretax)* | | | 26.71 | | | | 4.86 | | | | 6.98 | | |

All results shown assume reinvestment of distributions.

*The Fund's primary benchmark.

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

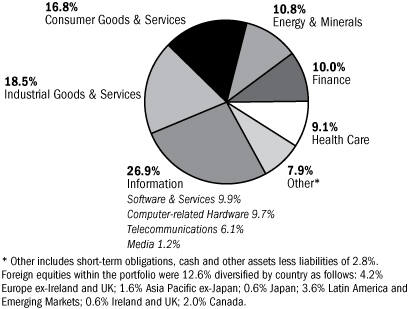

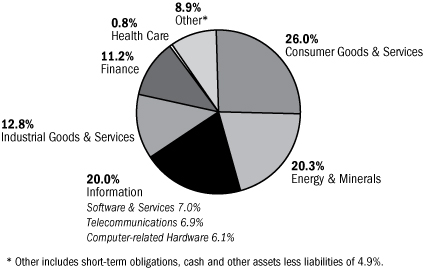

Columbia Acorn Fund Portfolio Diversification

as a percentage of net assets, as of 12/31/10

Columbia Acorn Fund Top 10 Holdings

as a percentage of net assets, as of 12/31/10

| 1. | | Crown Castle International

Communications Towers | | | 1.5

| % | |

| 2. | | lululemon athletica

Premium Active Apparel Retailer | | | 1.5

| % | |

| 3. | | FMC Technologies

Oil & Gas Wellhead Manufacturer | | | 1.5

| % | |

| 4. | | Ametek

Aerospace/Industrial Instruments | | | 1.5

| % | |

| 5. | | Donaldson

Industrial Air Filtration | | | 1.4

| % | |

| 6. | | Mettler Toledo

Laboratory Equipment | | | 1.3

| % | |

| 7. | | Informatica

Enterprise Data Integration Software | | | 1.3

| % | |

| 8. | | Fugro (Netherlands)

Sub-sea Oilfield Services | | | 1.2

| % | |

| 9. | | Amphenol

Electronic Connectors | | | 1.1

| % | |

| 10. | | Expeditors International of Washington

International Freight Forwarder | | | 1.0

| % | |

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

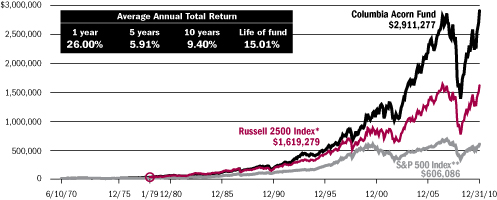

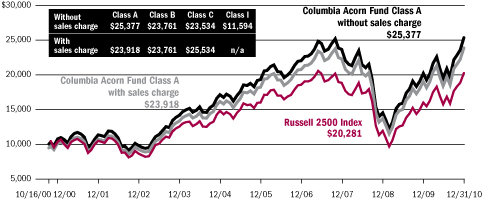

The Growth of a $10,000 Investment in Columbia Acorn Fund (Class Z)

June 10, 1970 through December 31, 2010

This graph compares the results of $10,000 invested in Columbia Acorn Fund at inception on June 10, 1970 to the S&P 500 Index and to an initial $31,777 investment in the Russell 2500 Index on the index's December 31, 1978 inception date. Although the indexes are provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the indexes. The indexes are unmanaged and returns for both the indexes and the Fund include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect taxes that a shareholder would pay on Fund distributions or on a sale of Fund shares.

Total Net Assets of the Fund: $18.1 billion

* A $10,000 investment in Columbia Acorn Fund at inception appreciated to $31,777 on December 31, 1978, the inception date of the Russell 2500 Index. For comparison with the Russell 2500 Index, we assigned the index the same value as the Fund at index inception.

**Although the Fund typically invests in small- and mid-sized companies, the comparison to the S&P 500 Index is presented to show performance against a widely recognized market index over the life of the Fund.

9

Columbia Acorn International

In a Nutshell

| |  | |

|

| P. Zachary Egan | | Louis J. Mendes III | |

|

| Co-Portfolio Manager | | Co-Portfolio Manager | |

|

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for daily and most recent month-end performance updates.

Fund's Positions

in Mentioned Holdings

As a percentage of net assets,

as of 12/31/10

| Zhaojin Mining Industry | | | 1.1 | % | |

| Mr. Price | | | 0.8 | % | |

| Shandong Weigao | | | 0.6 | % | |

| Shriram Transport Finance | | | 0.5 | % | |

| Intralot | | | 0.4 | % | |

| CIR | | | 0.3 | % | |

Columbia Acorn International finished the year up 22.70%, underperforming the 24.36% return of the S&P Global Ex-U.S. Between $500M and $5B Index, the Fund's primary benchmark. The Fund's 2010 fourth quarter return was 8.57%, versus a benchmark return of 10.58%. Smaller international stocks continued to outperform their larger-cap counterparts for the second consecutive year, and for four out of the last five years. The large-cap MSCI EAFE Index returned 7.75% in the year.

Emerging market demand continues to explain much of the ongoing rebound from 2008 in corporate earnings and stock returns around the world. While the U.S. grapples with rising budget deficits and Europeans ponder the possibility of default among one or more euro zone members, formerly troubled economies such as Thailand and Brazil now enjoy strong economic growth and corporate earnings and comparatively good public balance sheets. Indeed, as reported in the Financial Times, the World Bank calculates that domestic demand in developing economies contributed fully 46% of global growth in 2010.*

We believe this represents a significant opportunity for investors, although a highly differentiated one, as valuation and other intervening variables often stand between GDP growth and stock returns. While China, for example, continued to post high growth in 2010, its stock market (as measured by the Hang Seng China Enterprises Index) rose less than 2%. Emerging market stocks represented, in the course of the year, almost one quarter of Columbia Acorn International's assets. However, emerging market demand for goods and services provided by companies domiciled elsewhere remains a core component of the Fund's strategy, so implicit emerging market exposure is higher. With these companies we seek to access growth at either a more reasonable price or with less risk.

Unsurprisingly, emerging market stocks were among the largest contributors to positive returns in 2010. South African apparel, household and sporting goods retailer Mr. Price rose over 100% as improved merchandising and working capital levels bolstered the company's already strong fundamentals. Zhaojin Mining Industry, a Chinese gold miner, posted a similar return on the back of rising gold prices, value-accretive acquisitions, exploration on current properties, and rising production. Also in China, Shandong Weigao, a manufacturer of vertically integrated hospital consumables, rose over 70% on strong demand for medical consumables and improving results from its joint venture with Medtronic. In India, Shriram Transport Finance also increased over 70% on high growth and low defaults in its core used truck finance business.

Disappointments in 2010 included Greek lottery company Intralot, which declined nearly 40% on adverse tax developments in Bulgaria and Greece and start-up costs in the United States and Italy. A weak currency in Bulgaria further impacted earnings. Japanese retailer Point fell 30% on weak same-store sales and heavy upfront investments. We no longer hold this name in the Fund. Italian holding company CIR fell 29% as gas prices squeezed its electricity generation business.

It is notable that the U.S. dollar has fallen over 30% versus the yen, 28% versus the Swiss franc, and over 55% versus gold over the last five years. As managers, we take an agnostic view on currency, notwithstanding volatile movements and long-term uncertainties about the creditworthiness of certain countries. Instead, we consider carefully how currency movements might impact competitiveness and profitability within individual companies. And we seek to hedge out some of the risk relative to our benchmark caused by overweighting or underweighting countries or regions. Particularly in the present context of "quantitative easing" (printing money) and competitive devaluation, however, we take comfort as managers and investors in the Fund, knowing that equities confer claims on real businesses. Among the attractions of an internationally diversified equity portfolio is the possibility it offers of retaining purchasing power through economic cyc les and bouts of monetary experimentation. We believe it may prove to be an important component of a capital preservation strategy.

*Beattie, Alan, "World Bank backs efforts to counter rapid inflows," Financial Times, January 13, 2011, p. 4.

International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investing in emerging markets may involve greater risks than investing in more developed countries. In addition, concentration of investments in a single region may result in greater volatility.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

10

Columbia Acorn International (ACINX)

At a Glance

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. Please visit columbiamanagement.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2010

| Inception 9/23/92 | | 1 year | | 5 years | | 10 years | |

| Returns before taxes | | | 22.70 | % | | | 9.60 | % | | | 9.33 | % | |

| Returns after taxes on distributions | | | 22.40 | | | | 8.84 | | | | 8.81 | | |

Returns after taxes on distributions

and sale of fund shares | | | 15.42 | | | | 8.31 | | | | 8.24 | | |

S&P Global Ex-U.S. Between $500M

and $5B Index (pretax)* | | | 24.36 | | | | 8.19 | | | | 11.75 | | |

All results shown assume reinvestment of distributions.

*The Fund's primary benchmark.

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

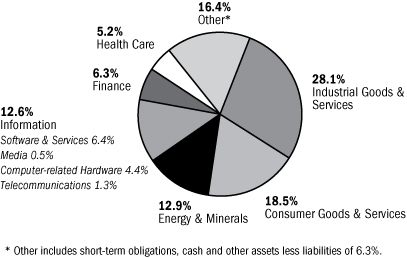

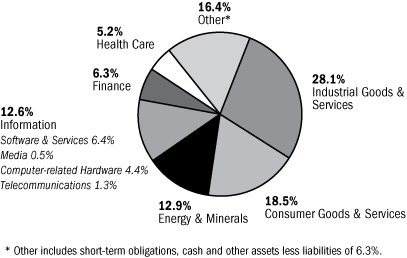

Columbia Acorn International Portfolio Diversification

as a percentage of net assets, as of 12/31/10

Columbia Acorn International Top 10 Holdings

as a percentage of net assets, as of 12/31/10

| 1. | | Naspers (South Africa)

Media in Africa, China, Russia & Other Emerging Markets | | | 1.6

| % | |

| 2. | | Hexagon (Sweden)

Measurement Equipment & Software | | | 1.5

| % | |

| 3. | | Olam International (Singapore)

Agriculture Supply Chain Manager | | | 1.4

| % | |

| 4. | | Localiza Rent A Car (Brazil)

Car Rental | | | 1.2

| % | |

| 5. | | Kansai Paint (Japan)

Paint Producer in Japan, India, China & Southeast Asia | | | 1.2

| % | |

| 6. | | Imtech (Netherlands)

Electromechanical & Information & Communications

Technologies Installation & Maintenance | | | 1.2

| % | |

| 7. | | Zhaojin Mining Industry (China)

Gold Mining & Refining in China | | | 1.1

| % | |

| 8. | | Fugro (Netherlands)

Sub-sea Oilfield Services | | | 1.0

| % | |

| 9. | | NHN (South Korea)

South Korea's Largest Online Search Engine | | | 1.0

| % | |

| 10. | | Advance Residence Investment (Japan)

Residential REIT | | | 1.0

| % | |

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

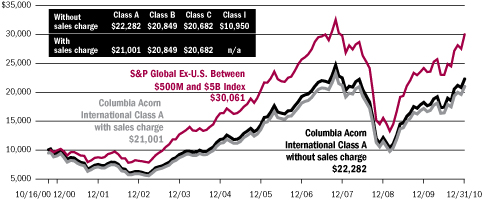

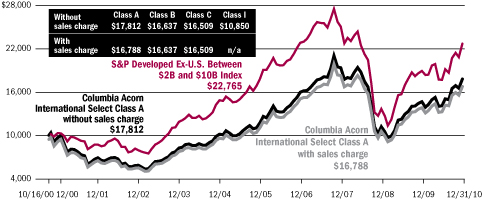

The Growth of a $10,000 Investment in Columbia Acorn International (Class Z)

September 23, 1992 through December 31, 2010

This graph compares the results of $10,000 invested in Columbia Acorn International at inception on September 23, 1992 to the S&P Global Ex-U.S. Between $500M and $5B Index. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index. The index is unmanaged and returns for both the index and Fund include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect taxes that a shareholder would pay on Fund distributions or on a sale of Fund shares.

Total Net Assets of the Fund: $6.1 billion

11

Columbia Acorn USA

In a Nutshell

| | | |

|

| Robert A. Mohn | | | |

|

| Co-Portfolio Manager | | | |

|

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for daily and most recent month-end performance updates.

Fund Positions

in Mentioned Holdings

As a percentage of net assets,

as of 12/31/10

| FMC Technologies | | | 2.6 | % | |

| Informatica | | | 2.6 | % | |

| Ametek | | | 2.2 | % | |

| Nordson | | | 2.0 | % | |

| tw telecom | | | 1.6 | % | |

| lululemon athletica | | | 1.6 | % | |

| Atmel | | | 1.4 | % | |

| Abercrombie & Fitch | | | 1.4 | % | |

| Finisar | | | 1.3 | % | |

| ITT Educational Services | | | 0.6 | % | |

| Global Payments | | | 0.5 | % | |

| Monolithic Power Systems | | | 0.3 | % | |

| Talbots | | | 0.2 | % | |

| Equinix | | | 0.2 | % | |

*The Lehman Brothers bankruptcy was announced on Monday, September 15, 2008. On Friday, September 12, 2008, Columbia Acorn USA's net asset value (NAV) was $24.16. On December 31, 2010, the Fund's NAV was $28.56. In 2008, the Fund's peak NAV was $28.22. As of December 31, 2010, the Fund was just 2.28% below its dividend-adjusted, all-time high, which it reached on June 4, 2007.

Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

Columbia Acorn USA ended the fourth quarter of 2010 up 16.43%, which compares to a 16.25% gain for its primary benchmark, the Russell 2000 Index. Small-cap stocks were very strong in 2010. For the annual period, the Fund was up 23.16% while its benchmark gained 26.85%. The Fund's relative annual return was hurt by poor performance of some of the Fund's positions in women's apparel stocks and small-cap semiconductor names, as well as the Fund's overweight position in the lagging telecom sector.

Several stocks in the retail, technology and industrial sectors were among the Fund's winners for the quarter and the year. lululemon athletica, a retailer of premium activewear, enjoyed blistering sales growth of 56% over the prior year, driving the Fund's investment up 53% in the fourth quarter and more than 125% for the year. Teen apparel retailer Abercrombie & Fitch grew same-store sales by 15% in December, outpacing competitors, most of whom posted negative year-over-year sales for this important retail month. The stock was up 47% in the fourth quarter and had an annual gain of 70% in the Fund.

Technology winners included Atmel, a leader in touchscreen microcontrollers, radio frequency and memory semiconductors. Its business has benefited from surging sales of smart phones and tablet computers. Atmel gained 55% in the fourth quarter and was up 130% for the Fund during the year. Finisar provides optical sub-systems and components for communications networks. The Fund's investment rose 67% in the quarter and 169% for the year as the company benefited from a surge in demand for data transmission and storage. Informatica, a data integration software provider that helps companies manage their disparate data streams, has also enjoyed strong revenue growth and Fund gains in the stock were 15% in the quarter and 70% for the year.

Two niche industrial companies rounded out the list of top contributors. Ametek, a manufacturer of aerospace and industrial instruments, gained 23% in the fourth quarter and was up 55% for the Fund during the year. Nordson, a maker of dispensing systems for adhesives and coatings, was up 25% in the quarter and 52% for the year in Columbia Acorn USA. Both companies have benefited from strong revenue growth and productivity improvements through wise expense control.

Outside these winning sectors, FMC Technologies, the largest position in the Fund at the end of 2010, was the top contributor to performance in the fourth quarter and ranked second for the year. Order flow at this oil and gas wellhead manufacturer climbed dramatically, nearly reaching pre-recession peaks. The stock was up 30% for the quarter and 54% for the year.

Laggards for the quarter included fiber optic telephone and data services provider tw telecom. Its stock fell 8% on underwhelming sales growth. Women's specialty retailer Talbots fell 35% in the quarter on declining sales. Equinix, a provider of offsite data centers for larger companies, suffered from price cutting in its sector and difficulties in integrating a recent acquisition. The stock fell 21% in the fourth quarter.

For the annual period, ITT Educational Services, a provider of post-secondary degree education, suffered as new regulatory requirements dogged the for-profit education sector, leading to declines in new enrollment. The stock was down 33% in the Fund for the year. Credit card processor Global Payments fell 14% during the annual period as a pricing war in its Canadian credit and debit processing business drove down margins. Monolithic Power Systems, a manufacturer of high performance analog and mixed-signal integrated circuits, fell 31% for the year due to pricing pressure and management's reduction of company profit margin targets.

Here are some fun facts for long-term stock investors: at the end of 2010, the S&P 500 large-cap index was higher than it was that fateful day before Lehman Brothers went bankrupt in September 2008, and so was Acorn USA; the Russell 2000 small-cap index was trading higher than at any point during the entire year of 2008, and so was Acorn USA; and the S&P 400 mid-cap index ended 2010 a mere 2% below its all-time high! And so did Acorn USA.* A stock market Rip Van Winkle waking up from his stress-free, two-year nap would find the market just as he left it. Turns out, buy and HOLD actually works quite well.

12

Columbia Acorn USA (AUSAX)

At a Glance

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. Please visit columbiamanagement.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2010

| Inception 9/4/96 | | 1 year | | 5 years | | 10 years | |

| Returns before taxes | | | 23.16 | % | | | 3.48 | % | | | 8.74 | % | |

| Returns after taxes on distributions | | | 23.16 | | | | 3.12 | | | | 8.42 | | |

Returns after taxes on distributions and

sale of fund shares | | | 15.05 | | | | 2.96 | | | | 7.72 | | |

| Russell 2000 Index (pretax)* | | | 26.85 | | | | 4.47 | | | | 6.33 | | |

All results shown assume reinvestment of distributions.

*The Fund's primary benchmark.

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

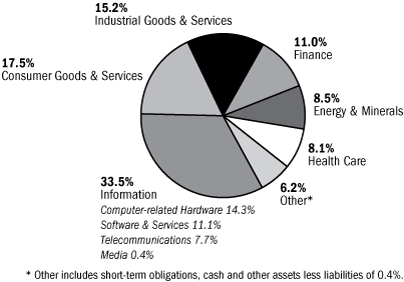

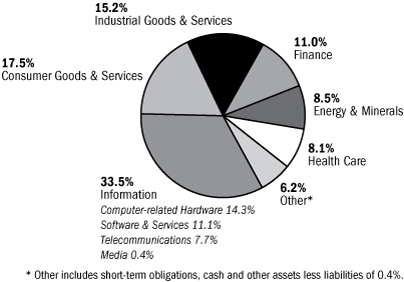

Columbia Acorn USA Portfolio Diversification

as a percentage of net assets, as of 12/31/10

Columbia Acorn USA Top 10 Holdings

as a percentage of net assets, as of 12/31/10

| 1. | | FMC Technologies

Oil & Gas Wellhead Manufacturer | | | 2.6

| % | |

| 2. | | Informatica

Enterprise Data Integration Software | | | 2.6

| % | |

| 3. | | Ametek

Aerospace/Industrial Instruments | | | 2.2

| % | |

| 4. | | Nordson

Dispensing Systems for Adhesives & Coatings | | | 2.0

| % | |

| 5. | | Micros Systems

Information Systems for Hotels, Restaurants & Retailers | | | 1.8

| % | |

| 6. | | Atwood Oceanics

Offshore Drilling Contractor | | | 1.7

| % | |

| 7. | | tw telecom

Fiber Optic Telephone/Data Services | | | 1.6

| % | |

| 8. | | Mettler Toledo

Laboratory Equipment | | | 1.6

| % | |

| 9. | | lululemon athletica

Premium Active Apparel Retailer | | | 1.6

| % | |

| 10. | | Gaylord Entertainment

Convention Hotels | | | 1.6

| % | |

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

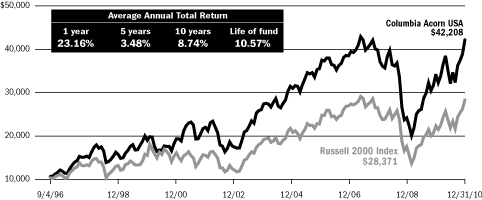

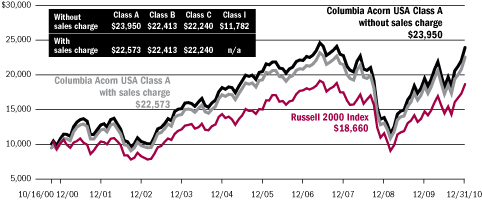

The Growth of a $10,000 Investment in Columbia Acorn USA (Class Z)

September 4, 1996 through December 31, 2010

This graph compares the results of $10,000 invested in Columbia Acorn USA at inception on September 4, 1996 to the Russell 2000 Index. Although the index is provided for use in assessing the Fund's performance, the Fund's holdings may differ significantly from those in the index. The index is unmanaged and returns for both the index and the Fund include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect taxes that a shareholder would pay on Fund distributions or on a sale of Fund shares.

Total Net Assets of the Fund: $1.7 billion

13

Columbia Acorn International Select

In a Nutshell

Christopher J. Olson

Lead Portfolio Manager

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than the performance data shown. Please visit columbiamanagement.com for daily and most recent month-end performance updates.

Fund's Positions

in Mentioned Holdings

As a percentage of net assets,

as of 12/31/10

| Serco | | | 4.1 | % | |

| Hexagon | | | 4.0 | % | |

| Pacific Rubiales Energy | | | 3.9 | % | |

| Naspers | | | 3.5 | % | |

| Fugro | | | 3.2 | % | |

| Pan American Silver | | | 2.6 | % | |

| Zhaojin Mining Industry | | | 2.6 | % | |

| United Drug | | | 2.0 | % | |

| Cobham | | | 1.6 | % | |

| Micro Focus | | | 0.7 | % | |

Columbia Acorn International Select ended the fourth quarter of 2010 up 8.09%, underperforming its primary benchmark, the S&P Developed Ex-U.S. Between $2B and $10B Index, which gained 9.75%. For the annual period, the Fund's 21.89% return topped the benchmark's 20.16% gain in what turned out to be a very strong year for the global equity markets.

Top contributors to Fund performance in the quarter and year included two names in the energy sector. Pacific Rubiales Energy, a Colombian oil exploration and development company, benefited from new oilfield discoveries. The stock was up 20% for the fourth quarter and 129% for the year in the Fund. In the Netherlands, sub-sea oilfield services provider Fugro had a 25% gain in the fourth quarter and ended the year up 48% as customers confirmed their commitment to deep water drilling and higher oil prices led to a recovery in oil industry exploration spending.

Two mining companies were among the top contributors. China's Zhaojin Mining Industry had another strong quarter, gaining 34% and ending the year up 113%. The company continued to benefit from strong production and exploration profiles and rising gold prices. In Canada, Pan American Silver, a silver miner, was up 36% for the quarter and 55% for the year. Silver prices rose 83% over the year and the company continued to move forward on two large exploration projects.

The Fund's investment in Swedish measurement equipment manufacturer Hexagon gained 15% in the quarter and ended the year up 70%. The company has been enjoying strong sales growth both in Europe and emerging markets. Naspers, a media company with assets in South Africa, China and other emerging markets, was up 20% for the quarter and 48% for the year. Results in the company's underlying businesses remained strong, driven by increasing levels of Internet usage throughout its emerging market Internet holdings.

Underperformers in the quarter included UK facilities management company Serco, down 11% on concerns the government austerity program in the United Kingdom would reduce its sales growth. Irish pharmaceutical wholesaler United Drug was off 15% in the quarter on Irish budgetary concerns and worries over the impact cuts could have on the domestic economy. Cobham, a UK manufacturer of aerospace components, was down 10% in the quarter and also ranked among the worst performers for the year, with an annual decline of 17%, as the uncertainty regarding U.S. and UK defense budget cuts delayed sales. Other laggards for the year included MegaStudy, a South Korean provider of online education services that fell 33% after the government moved to subsidize its publicly run competitors. We sold the Fund's position in MegaStudy in the second quarter of 2010. Micro Focus, a UK legacy software provider, had an annual loss of 26% on news of the departure of t he company's CFO and a revenue growth downgrade.

International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. Investing in emerging markets may involve greater risks than investing in more developed countries.

Portfolio holdings are subject to change periodically and may not be representative of current holdings.

14

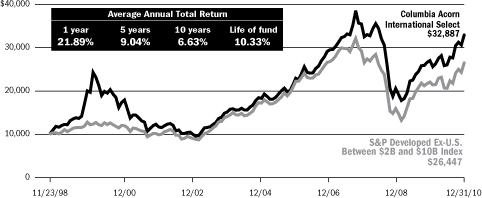

Columbia Acorn International Select (ACFFX)

At a Glance

Performance data shown represents past performance and is not a guarantee of future results. The investment return and principal value of an investment will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data shown. Performance results reflect any fee waivers or reimbursements of Fund expenses by the investment adviser and/or any of its affiliates. Absent these fee waivers and/or expense reimbursement arrangements, performance results would have been lower. Please visit columbiamanagement.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2010

| Inception 11/23/98 | | 1 year | | 5 years | | 10 years | |

| Returns before taxes | | | 21.89 | % | | | 9.04 | % | | | 6.63 | % | |

| Returns after taxes on distributions | | | 21.70 | | | | 8.72 | | | | 6.47 | | |

Returns after taxes on distributions and

sale of fund shares | | | 14.62 | | | | 7.89 | | | | 5.87 | | |

S&P Developed Ex-U.S. Between $2B and $10B

Index (pretax)* | | | 20.16 | | | | 4.95 | | | | 8.22 | | |

All results shown assume reinvestment of distributions.

*The Fund's primary benchmark.

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

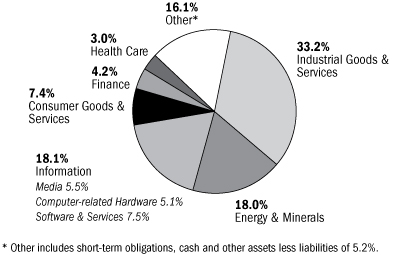

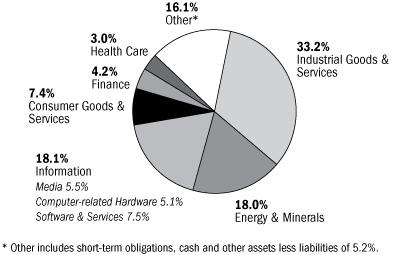

Columbia Acorn International Select Portfolio Diversification

as a percentage of net assets, as of 12/31/10

Columbia Acorn International Select Top 10 Holdings

as a percentage of net assets, as of 12/31/10

| 1. | | Kansai Paint (Japan)

Paint Producer in Japan, India, China & Southeast Asia | | | 4.1

| % | |

| 2. | | Serco (United Kingdom)

Facilities Management | | | 4.1

| % | |

| 3. | | Hexagon (Sweden)

Measurement Equipment & Software | | | 4.0

| % | |

| 4. | | Pacific Rubiales Energy (Colombia)

Oil Production & Exploration in Colombia | | | 3.9

| % | |

| 5. | | NHN (South Korea)

South Korea's Largest Online Search Engine | | | 3.9

| % | |

| 6. | | Ascendas REIT (Singapore)

Singapore Industrial Property Landlord | | | 3.8

| % | |

| 7. | | Jiangsu Expressway (China)

Chinese Toll Road Operator | | | 3.7

| % | |

| 8. | | Naspers (South Africa)

Media in Africa, China, Russia & Other Emerging Markets | | | 3.5

| % | |

| 9. | | Fugro (Netherlands)

Sub-sea Oilfield Services | | | 3.2

| % | |

| 10. | | UGL (Australia)

Engineering & Facilities Management | | | 3.1

| % | |